Making moves with modular regasification terminals

10 LNG in Latin America: A tale of two markets

Kilian de Cintré, Partner, Chris Taufatofua, Partner, Chris Strong, Partner, and Ruairi McGill, Associate, Vinson & Elkins, assess the current state of the LNG market in Latin America and the Caribbean.

14 Energy on the Elbe

The Hanseatic Energy Hub, Germany’s latest LNG terminal, is a testament to the country’s growing LNG infrastructure. However, as Germany’s energy market evolves, so too must its capability to import a fuel in an entirely new manner. Thies Holm, Managing Director, GAC Germany, looks at the role the terminal will play in the energy transition.

19 Nickel, powered by LNG

Karthik Sathyamoorthy, CEO, AG&P LNG, and DeLaine Mayer, Director of External Affairs, Nebula Energy/AG&P LNG, detail how LNG can be used to help decarbonise nickel’s value chain.

21 Monetising Congolese gas

Frederik Van Nuffel and Maria Carolina Chang, EXMAR, Belgium, provide an overview of the implementation of the floating LNG terminal offshore Pointe Noire, Republic of the Congo.

Danielle Murphy-Cannella, Head of Sustainability, and Kristoffer Evju, Vice President Commercial, ECOnnect Energy, explore some of the challenges and possibilities within the current state of the global LNG market, and technological solutions that can contribute towards cleaner and sustained energy security.

29 Compressor Q&A

LNG Industry asked Burckhardt Compression to discuss some key factors regarding compressors for use in the LNG industry.

33

The next generation of cryogenic insulation

Harry Walkoff, President, H.R. Walkoff LLC, Technical Insulation Consultant, explains Alkegen’s evolution of aerogel blankets and the development of a new product for LNG applications.

38

Lessons from LNG for shipping's multi-fuel future

Jesper Sørensen, Global Head of Alternative Fuels & Carbon Markets, KPI OceanConnect, considers the lessons LNG can teach us as a viable decarbonisation pathway for marine energy.

41 Navigating sustainability, efficiency, and risk

Dr Valentina Dedi, Lead Economic Advisor at KBR, highlights the role of maritime logistics in the oil and gas industry.

45

One step further

Bill Howe, Chief Executive, and Geoff Skinner, Technical Director, Gasconsult Ltd, and David Champion, LNG Technology Manager, McDermott, outline how liquefaction technology can be developed to support decarbonisation initiatives, both now and

MAN Energy Solutions enables its customers to achieve sustainable value creation in the transition towards a carbon-neutral future.

Addressing tomorrow’s challenges within the marine, energy, and industrial sectors, the company improves efficiency and performance at a systemic level.

Leading the way in advanced engineering for more than 250 years, MAN Energy Solutions offers a range of advanced technologies for decarbonisation that includes highly efficient compression solutions together with longstanding experience in high-pressure CO2 compression and plant designs.

Find out more: www.man-es.com/our-focus

THEODORE REED-MARTIN EDITORIAL ASSISTANT

COMMENT

June and July brought the return of one of Europe’s most popular sporting events across the continent. The 2024 UEFA European Football Championship is here, and Germany, the host nation, are off to a blistering start. They opened the tournament with a 5 – 1 victory against Scotland, followed by a 2 – 0 victory over Hungary. Their momentum teetered at the end of the group stages with a 1 – 1 draw against Switzerland, though they succeeded in qualifying through to the round of 16. This slow pace was replicated in their recent 2 – 0 victory over Denmark, which was largely down to a stroke of VAR-induced luck. Certainly, the Danes left scratching their heads feeling rather harddone-by after a goal was scrubbed due to a toe offside, and a penalty was awarded for an accidental handball. Regardless, Germany are through to the quarter-finals and remain one of the favourites to win the tournament.

Though football is not the only area in which Germany is making strides, with the nation also doing well in its LNG sector.

Just one example is how SEFE has recently completed its first import of LNG into Germany using its booked slot in Wilhelmshaven LNG terminal. The regasified LNG will be managed by SEFE and its sales arm, WINGAS, as part of SEFE’s European gas portfolio.1 Similarly, ECOnnect Energy has signed a contract with FSRU Wilhelmshaven GmbH, a joint venture between Tree Energy Solution (TES) and ENGIE, for the installation of the Jettyless ready IQuay solution for LNG import to Wilhelmshaven, bolstering the nation’s energy security. All of this news comes as a result Wilhelmshaven being on the list of the priority projects supported by Germany’s LNG Acceleration Law, passed in May 2022, in order to strength the country’s energy security by 2025. The terminal is strategically positioned to import a significant amount of Germany’s natural gas demand and will play an important role in future decarbonisation efforts commencing

Managing Editor

James Little james.little@palladianpublications.com

Senior Editor Elizabeth Corner elizabeth.corner@palladianpublications.com

Sales Director Rod Hardy rod.hardy@palladianpublications.com

in 2025.2

In other news, Germany’s first land-based terminal for liquefied gases is set to commence operation in 2027, making a significant contribution to the security of affordable energy supply in Europe. At peak times, over 1100 people will work on the construction site to connect the two largest LNG tanks in Europe, each with a capacity of 240 000 m3 and ammonia-ready, to the grid in three years. This project kicked off with a joint ground breaking ceremony attended by around 200 partners and backers. Besides the German energy suppliers EnBW and SEFE, which have booked substantial capacities at the terminal, the Czech energy company, ĈEZ, has also secured long-term import rights. This terminal will not only support Germany’s energy infrastructure, but also help bolster the energy needs of the Czech Republic.3

After six years of planning and permitting, the Hanseatic Energy Hub (HEH) project in Stade is now entering the construction phase. This project is Germany’s latest LNG terminal and exemplifies the country’s growing LNG infrastructure. Detailed in an article on this issue by GAC Germany, titled ‘Energy on the Elbe’ (p.14), which explains how Germany is leveraging LNG imports amidst a broader European surge driven by geopolitical factors and the push for renewable energy. The future shines bright for the LNG industry as a whole, with Germany playing a pivotal role in its development.4

Additionally, this issue features a range of articles covering FSRUs to tank maintenance, providing up-to-date insights on the global LNG landscape. Exciting times lie ahead, particularly in Germany, whose LNG industry grows as the nation strives to win the championships.

References

References available upon request.

Sales Manager Will Powell will.powell@palladianpublications.com

Production Designer Amy Babington amy.babington@palladianpublications.com

Head of Events

Louise Cameron louise.cameron@palladianpublications.com

Digital Events Coordinator Merili Jurivete merili.jurivete@palladianpublications.com

Digital Content Assistant Kristian Ilasko kristian.ilasko@palladianpublications.com

Specially designed LNG valve lines can minimize product loss due to conductive heat transfer by using the superior insulating properties of vacuum jacket technology.

• Designed for LNG

• Available in both jacketed and non-jacketed models

• Industry standard for LNG applications.

CryoMac® 4 LNG Fueling Nozzle Maximum safety for LNG fuel technology

SAFE

“Safety Stop” for added safety and operator protection.

Ball cage interface with receptacle adapter ring guides and locks the nozzle in place for optimum engagement and user interface to increase environmental seal life. DURABILITY þ

Patented nozzle safety feature is recognized in the market as a major failsafe advantage for the operator.

For more information on our LNG offerings, scan the QR Code above

Canada Cedar LNG announces positive FID

The Haisla Nation and Pembina Pipeline Corp., partners in Cedar LNG Partners LP, have announced a positive final investment decision (FID) on the Cedar LNG project, a floating LNG (FLNG) facility with a nameplate capacity of 3.3 million tpy, located in the traditional territory of the Haisla Nation, on Canada’s West Coast.

The project is expected to be funded with asset-level debt financing for approximately 60% of the project cost. Cedar LNG has secured a construction term loan with a syndicate of banks.

The remaining approximately 40% of the costs of the project are expected to be financed through equity contributions from both partners. The Haisla Nation have obtained committed capital through the First Nations Finance Authority to fund their 20% equity contribution to the project. Pembina continues to anticipate its equity contribution will be funded from cash flow from operating activities. Pembina expects no material change to its 2024 Cedar LNG equity contributions disclosed previously, with no incremental post-FID contributions in 2024 anticipated.

Prior to FID, Pembina was required to provide financial assurances to advance project-related upstream infrastructure projects. Following the positive FID, the required financial assurances will be transferred to Cedar LNG. Cedar LNG has secured a letter of credit facility for the ongoing funding of the required financial assurances.

Canada

LNGNEWS

Nigeria

TotalEnergies launches Ubeta gas development to supply Nigeria LNG liquefaction plant

TotalEnergies, operator of OML 58 onshore license in Nigeria with a 40% interest, together with the Nigerian National Petroleum Corp. Ltd (NNPCL, 60%), have taken the final investment decision (FID) for the development of the Ubeta gas field.

Located about 80 km northwest of Port Harcourt in Rivers state, the OML 58 license contains two fields currently in production, the Obagi oil field and the Ibewa gas and condensate field. OML58 gas production is processed in the Obite treatment centre and supplied to both the Nigerian domestic gas market and to Nigeria LNG (NLNG) plant.

Also located in OML58, the Ubeta gas condensate field will be developed with a new six-well cluster connected to the existing Obite facilities through a 11 km buried pipeline. Production start-up is expected in 2027, with a plateau of 300 million ft3/d (about 70 000 boe/d including condensates). Gas from Ubeta will be supplied to NLNG, a liquefaction plant located in Bonny Island with an ongoing capacity expansion from 22 – 30 million tpy, in which TotalEnergies holds a 15% interest.

Ubeta is a low-emission and low-cost development, leveraging on OML58 existing gas processing facilities. The carbon intensity of the project will be further reduced through a 5 MW solar plant currently under construction at the Obite site and the electrification of the drilling rig.

Galileo Technologies announces project with Saint John LNG

Galileo Technologies has announced a significant project with Saint John LNG, a fully-owned subsidiary of Repsol. This project aims to address the challenge of boil-off gas (BOG), a part of normal operations in the LNG industry. Traditionally, BOG is compressed and sent back to the pipeline. Through the installation of Galileo Technologies' reliquefaction solution, Saint John LNG will be able to recover and store this resource to serve the market, especially during times of high demand.

The agreement encompasses the design, fabrication, and installation of eight BOG compressors, 15 CryoboxTM units,

and associated utility packages, which will be provided from Galileo’s manufacturing centre in Middlesex, New Jersey, and marks an important milestone in the company's commitment to innovation and sustainability.

The impact of this project is substantial, with the potential to reliquefy approximately 10 million ft3/d of natural gas, equivalent to 120 000 gal. of LNG. By implementing advanced compression and reliquefaction technologies, the new technology will enhance operational efficiency and improve service to local customers.

LNGNEWS USA

the Netherlands EverLoNG's second demonstration campaign underway

The SSCV Sleipnir from Heerema Marine Contractors has set sail with the EverLoNG ship-based carbon capture (SBCC) prototype on board. The unit was developed in the Netherlands by Carbotreat and VDL Carbon Capture.

The objective of the campaign is to test all aspects of the SBCC on the LNG-fuelled vessel. This will be done over an operating period of around 500 hours and includes storing carbon dioxide (CO2) on board as a liquid in a specially designed container. The container will then be offloaded, and the CO2 transported to an industrial site for utilisation, or stored permanently in the geological subsurface.

Canada Woodfibre LNG receives BCEAO order to move floatel to site

Woodfibre LNG has received a Compliance Order from the BC Environmental Assessment Office, requiring Woodfibre LNG to deploy the floatel to site and to use the vessel for non-local workforce accommodation in accordance with the amended Environmental Assessment Certificate.

Woodfibre LNG views compliance with all regulatory conditions as a top priority. The company will prepare to proceed with moving the floatel to the project site to ensure compliance with the Order and our regulatory conditions, and to use the floatel for workforce housing as had been intended.

In response to feedback received through a widespread community engagement process which began in 2019, Woodfibre LNG received approval of an amendment to its Environmental Assessment Certificate in November 2023, authorising use of a temporary floating worker accommodation, or ‘floatel’, to accommodate up to 650 members of the project workforce outside the community of Squamish.

The floatel represents an investment of CAN$100 million that will support a di-verse workforce, provide fully contained, on-board dining, recreation, and medical services and ensure that the community will not be strained by a large influx of workers.

The floatel is currently anchored near Nanaimo, ready to move to Howe Sound to accommodate non-local construction workers as it was designed to do.

Argent LNG, a leader in innovative energy solutions, has announced its strategic decision to select Chart Industries' mid scale modular liquefaction solution for its upcoming 20 million tpy LNG facility in Port Fourchon, Louisiana, the US. This move represents a significant departure from conventional large scale LNG facilities, challenging the industry's traditional operational paradigm.

Chart Industries' IPSMR® (Integrated Pre-Cooled Single Mixed Refrigerant) process technology lies at the heart of this disruptive approach. IPSMR sets a new standard for efficiency and performance in liquefaction, surpassing conventional technologies and enabling Argent LNG to tailor its liquefaction systems precisely to site-specific conditions. This capability optimises the matching of gas turbine power with single cold box capacity, ensuring maximum operational efficiency and cost-effectiveness.

Chart has begun engineering work related to the project and anticipates booking an IPSMR technology and equipment order in 2025.

THE LNG ROUNDUP

X Shell signs agreement to acquire Pavilion Energy X D.TEK and Venture Global sign HoA for Ukraine and Eastern Europe X Technip Energies, JGC, and NMDC Energy awarded contract for ADNOC's Ruwais LNG project

BRIGHTER FUTURE COOLER BY DESIGN ®

Chart’s LNG power generation solutions provide natural gas to hundreds of thousands of homes. This is one way Chart facilitates LNG as a safe, clean-burning fuel for energy, transportation and industry.

Global Hydrogen Conference 2024 Online www.accelevents.com/e/ghc2024

19 – 23 May 2025

29th World Gas Conference (WGC2025)

Beijing, China

www.wgc2025.com/eng/home

GTT receives order for tank design of 10 LNG carriers

GTT has received an order from its partner Hudong-Zhonghua Shipbuilding (Group) Co. Ltd for the tank design of 10 new very large LNG carriers. Each will offer five tanks with a total capacity of 271 000 m3. The tanks will be fitted with the NO96 Super+ membrane containment system developed by GTT.

Delivery is scheduled between 1Q30 – 4Q31.

USA

Aramco and Sempra announce HOA for Port Arthur LNG Phase 2

Aramco, one of the world’s leading integrated energy and chemicals companies, and Sempra, one of North America’s leading energy infrastructure companies, have announced that their respective subsidiaries have executed a non-binding heads of agreement (HoA) for a 20-year sale and purchase agreement (SPA) for LNG offtake of 5 million tpy from the Port Arthur LNG Phase 2 expansion project. The HoA further contemplates Aramco’s 25% participation in the project-level equity of Phase 2.

The parties expect to execute a binding LNG SPA and definitive equity agreements with terms substantially equivalent to those in the HoA, with the SPA and equity agreements subject to a number of conditions.

Port Arthur LNG is a natural gas liquefaction and export terminal in Southeast Texas with direct access to the Gulf of Mexico. The Port Arthur LNG Phase 1 project is currently under construction and consists of trains 1 and 2, as well as two LNG storage tanks and associated facilities. The Port Arthur LNG Phase 2 project is a competitively positioned expansion of the site to include the addition of up to two trains capable of producing up to 13 million tpy.

Australia

Baker Hughes awarded multi-year services frame agreement by Woodside Energy

Baker Hughes, an energy technology company, has entered into a new 10-year services frame agreement with Woodside Energy to support its LNG operations in Australia..

Under the multi-year services frame agreement, Baker Hughes will provide spare parts and field service resources for onsite turbomachinery equipment maintenance and upgrades, equipment refurbishment and advanced digital asset performance services.

This latest agreement builds on the strategic partnership between Baker Hughes and Woodside Energy in the LNG sector that first started in 1989 and has since included collaboration on multiple projects. In 2021, Baker Hughes was awarded the supply of high-efficiency gas turbine and compressor technology for Woodside Energy’s Pluto LNG train 2 project in Western Australia, which serves Woodside Energy’s Scarborough offshore gas project and provides LNG exports to countries across Asia. Most recently, in 2022, the two companies signed a memorandum of understanding to collaborate on possible decarbonising solutions leveraging Baker Hughes’ broad portfolio of carbon management and climate technology solutions.

LNG IN LATIN AMERICA:

Despite gas deposits totalling at least 7.3% of global reserves and gas usage accounting for only 6.3% of global consumption, pointing to future export opportunities, Latin America and the Caribbean remain a net gas importer, with only Trinidad and Tobago and Peru regularly exporting LNG in meaningful quantities. Declining production from mature fields, inhospitable terrain, and a lack of regional

gas interconnection remain barriers to gas self-sufficiency and estimates suggest that, without additional development, gas imports will potentially soar to 12 billion ft3/d from current levels of 5.2 billion ft3/d by 2035.

The governments of Latin American and Caribbean gas producers have had to strike a fine balance between supporting domestic industry and regional gas demand

A TALE OF TWO MARKETS

Kilian de Cintré, Partner, Chris Taufatofua, Partner, Chris Strong, Partner, and Ruairi McGill, Associate, Vinson & Elkins, assess the current state of the LNG market in Latin America and the Caribbean.

(particularly in relation to using gas to provide back-up generation power or to decarbonise oil or coal fired industry) and meeting their net-zero commitments, with the ability to export LNG to more lucrative international markets.1 Coupled with this, historical regional gas producers are experiencing declines in production and higher extraction costs from more mature fields. Bolivia, for example, whilst still a key

regional exporter, has seen natural gas production fall from a peak of 2.1 billion ft3/d in 2014 to 1.3 billion ft3/d in 2023, as their reserves become more difficult and expensive to extract at commercially viable levels, leading to failures to fulfil volume requirements under export contracts. This repositioning of countries as exporters is resulting in the redirection of gas flows in existing infrastructure as the

market reacts with energy companies from Brazil, Argentina, and Bolivia, for example, in discussions to reverse the flow of the pipeline between the three countries (currently flowing from Bolivia to Argentina) to allow Argentinian gas to be exported to Brazil via Bolivia.

Despite this, new discoveries, the changing global political and economic landscape, and policy shifts by the LNG market’s key players are presenting opportunities for Latin America and the Caribbean market to assert itself as both gas self-sufficient, and potentially a key exporting region.

Fuelling growth: The role of LNG imports in Latin America and the Caribbean

With more regasification capacity than any other country in the region, Brazil remains one of the largest LNG importers in the region and is the sixth largest importer of US LNG globally. Whilst traditionally Brazil has been reliant on hydropower, changing weather patterns – both in terms of rainfall quantity and the timing of wet seasons since 2021 – have caused a rebalancing of the sources of its power production, increasing its reliance on gas-generated power to replace shortfalls in its hydropower production. Whilst gas as a percentage of its energy mix has varied year on year, this peak reversed a decline in import levels since the previous high in 2014. Brazil expects to launch a power auction in 2024, with expectations that ‘base’ electricity supply will continue to transition from hydropower to thermal gas plants, adding certainty to import volumes as gas moves from a replacement source to a core constituent of its energy mix, fuelling import requirements. The transition from hydropower to gas, however, is not unique to Brazil, and depleted hydropower reservoir levels elsewhere in the region have caused a surge in LNG import volumes. The significant distances from import terminals and the challenging topography of Brazil mean that transportation of pipeline gas remains prohibitively expensive, meaning LNG is one of the only ways to safely deliver affordable gas to regional industrial and power sectors. With declining domestic gas production, and a forecast decline in imports from neighbouring Bolivia, Brazil has taken advantage of the recent liberalisation of domestic gas regulations to lead the region in new LNG import projects, with recent developments in Barcarena and Santa Caterina commencing operations earlier this year. However, key challenges for Brazilian LNG import terminals remain: a lack of pipeline interconnection and liquidity in local gas markets act as an impediment to the development of local LNG projects. Historic issues have also included underutilisation, with the average Brazilian LNG import terminal operating at under 40% in 2020. There is growing sentiment within the market that this is likely to change in light of the next power auction, and with new facilities being set-up as multi-user import facilities, as opposed to standalone single-user LNG-to-power terminals –creating greater liquidity in the market and driving competition in pricing and product offerings from the facilities.

Turning the tide: Latin America’s

rising LNG production and export potential

The US’ decision to pause the issuance of LNG export permits to non-FTA countries has caused uncertainty around the

future maintenance and expansion of international US LNG supply and has presented opportunities for other regions to step into the supply gap, either domestically or to ramp up export-focused production. With uncertainty around the length of the US’ permit pause, it remains to be seen whether a potentially short-term issue will have an impact on the final investment decisions for new LNG projects in Latin America and the Caribbean.

Spurred by a potential shortfall in international LNG exports and domestic demand, Argentina is developing the world’s second largest shale gas reserves at Vaca Muerta, and is poised to become a key gas producer and exporter. Within the region, both Argentina’s existing and planned gas pipeline transportation networks will allow it to export gas locally to key gas importers such as Chile and Brazil (reversing historic gas flows). The development of the field presents an opportunity for Argentina to meet pre-existing local demand and potentially replace Bolivia as the main regional exporter. Given the size of the discovery, Argentina has ambitions to become a key international player in LNG exports. The memorandum of understanding signed between YPF and Petronas in 2022 to develop a floating LNG processing plant in Argentina by 2027, with the aim to export up to 2 million tpy and a potential second phase increasing export capacity to 9 million tpy, demonstrates the potential routes to market that exist. Whilst historically Argentina has been viewed as a challenging investment destination, as policy and currency instability, inflation, and other factors have led to issues such as cost overruns and currency repatriation concerns, there are indications the country is ripe with opportunity for experienced players, and investors’ appetite for LNG projects in the region is returning.

Increased integration of Mexican infrastructure with the US gas grid is allowing Mexico to offer innovative solutions to long standing logistical issues with Pacific-coast US-LNG exports. With up to eight LNG export projects at various stages of planning and development and four more in advanced stages of development, Mexico is likely to become a key export hub for Texan basin gas through liquefaction and export facilities developed on its Pacific coast. Projects are aiming to profit from price differentials and the construction of new US-Mexico gas pipelines. Whilst the regional benefit may initially be limited to tax receipts, the development of a Pacific LNG maritime trade in Latin America will boost export opportunities in the region.

Recent major discoveries offshore of Suriname and Guyana have the potential to further transform the LNG landscape. While total gas discoveries are as-yet undisclosed, the limited local gas demand in both Suriname and Guyana makes both countries ideal candidates for major LNG production projects. Both Suriname and Guyana are investigating options to commercialise these gas reserves, with Suriname progressing with the development of a 4-million tpy LNG project, which is due to complete in 2025. More will need to be done to incentivise international investment and long-term offtake, given the risk the recent territorial dispute between Guyana and Venezuela presents and the potential for significant changes in Guyana’s investment environment as it grapples with double-digit percent economic growth and with LNG comprising such a large percentage of its GDP and tax receipts. Investors are cognisant that a change in LNG pricing and any state budget over-extension could present significant issues.

Bridging the gap: LNG investment challenges in Latin America

Political risk is still a fundamental challenge to attracting investment into Latin America and the Caribbean, with the role of the public sector, inflation, currency instability, opaque public procurement and permit approval processes, debt defaults, and even international sanctions, meaning that investors are especially sensitive to making investment decisions in large capital intensive projects. 2 With key international economies, including the UK, the US, South Korea, India, and Australia going to elections in 2024, changes in the foreign policies of key LNG importers and exporters are likely, which may present opportunities for countries in Latin America and the Caribbean. Despite the dangers, international investors are well versed in deploying risk mitigation techniques such as US$-denominated construction and sales agreements, offshore bank accounts for sales proceeds and innovative payment and financing techniques, such as prepayments and inventory monetisation, but further macroeconomic certainty will serve as a catalyst for projects.

Recent changes in government, for instance in Mexico and Argentina, have focussed political attention on the role of the state-owned petrochemicals companies in the gas network, particularly in the development of the gas transportation infrastructure and LNG export projects where there is traditionally limited private sector appetite, leading to the potential for both countries to become regional exporters in the future. Conversely, the Colombian government’s policy to restrict new exploration has acted

as a break on investment into new gas assets. Whilst historically a lack of any united regional gas policy has caused a fragmentation of the regional gas market, leading to different regional gas markets, including within individual countries, there has been increasing governmental focus on policy harmonisation, particularly within the Southern cone, leading to increasing interconnection within the region, though it remains to be seen as to how fundamentally this will impact local gas markets.

The success of Latin American and Caribbean LNG projects will likely turn on overcoming the barriers to investment and navigating the various challenges of the region and the LNG market of a transaction. With many LNG projects successfully operating in the region, well-advised developers have substantial opportunity to take advantage of the region’s LNG market to support the growth of the LNG industry in Latin America and the Caribbean and fuel the development and decarbonisation of the region.

Notes

1. Whilst significant fuel and electricity subsidies exist within the Latin American and Caribbean market and an increase in the size of exports at market-driven prices will increase revenues and tax receipts for the exporting countries, there are tensions within domestic markets, such as Peru, at the amounts currently earmarked for sale outside of the country.

2. Investors and developers are likely to be encouraged by the numerous examples of LNG projects being successfully completed across the region, from Brazil and Chile to Peru and Trinidad and Tobago.

Elbe Elbe on the Energy Energy on the

The Hanseatic Energy Hub, Germany’s latest LNG terminal, is a testament to the country’s growing LNG infrastructure. However, as Germany’s energy market evolves, so too must its capability to import a fuel in an entirely new manner.

Thies Holm, Managing Director, GAC Germany, looks at the role the terminal will play in the energy transition.

European demand for LNG is at its highest level in years. According to a report by the European Union Agency for the Cooperation of Energy Regulators, the EU imported 134 billion m 3 of LNG in 2023, representing 42% of the region’s total gas imports and making the EU the top global LNG import market. 1

Demand for recent LNG consumption is being driven by several factors, including the ongoing geopolitical situations, Europe’s accelerated transition to renewable energy and a particular long and cold winter season. Countries across the region have been ramping up their LNG terminal infrastructure over the past two years to

bolster their capacity, cater to growing regional demand and alleviate some of Europe’s LNG capacity pressures.

In Belgium, for example, the expanded Zeebrugge LNG import terminal came into operation at the start of the year, with a storage capacity of 566 000 m 3 and a regasification capacity of about 6.6 million tpy. 2 Meanwhile, in Italy, more than €1 billion (US$1.06 billion) is being invested in a new FSRU with an annual capacity of 5 billion m 3 to complement an existing LNG terminal. 3

LNG leader

But it is Germany that is leading the pack with a steep rise in the number and capacity of its onshore LNG terminals. According to data from Statista, Germany has more planned and operational LNG terminals than any other country in Europe, with a total of 15 import terminals either planned, under construction or fully operational. 4

The Hanseatic Energy Hub at the Port of Stade just outside of Hamburg – ‘the heart of the German shipping industry’ – on the River Elbe, is one of the country’s newest facilities to support its ambitious drive to boost energy security and transition to more sustainable fuel options. Due to formally begin operations in 2027 following a total investment of more than €1.6 billion (US$1.7 billion), Germany’s first land-based LNG terminal will have a total capacity of 13.3 billion m 3 and is forecast to meet more than 15% of Germany’s existing demand for LNG, whilst also managing other low-carbon energy sources, such as ammonia and hydrogen, and also being entirely emission free.

The pieces are already being put in place to ensure the Hub will be firing on all cylinders by 2027. In December 2023, GAC Germany provided ship agency and logistics support to LNG carriers to ensure their efficient unloading and turnaround at ports elsewhere in the country, drawing on the Group’s experience serving the gas sector in Germany and across Europe, as well as its dynamic footprint at some the LNG sector’s leading markets.

Until the terminal is operational, however, the Port of Stade is also a crucial location for Germany’s regasification capabilities. In March 2024, to shore up its LNG import capabilities, the port became home to the FSRU Energos Force, the first unit in Stade and the fourth overall in Germany. Similar vessels are operating at the Brunsbüttel and Wilhelmshaven terminals, with another due to come online later this year. Those four FSRUs are only expected to be temporary until all of Germany’s planned terminals are fully operational.

The total regasification capacity of Germany’s terminals, once all of the planned facilities are operational, will rise to 54 billion m 3 by the time the Hanseatic Energy Hub is operational in 2027 compared to 13.5 billion m 3 in 2023. The construction of new LNG terminals in northern Germany on such a large scale, together with increasing gas imports from Norway, the Netherlands, and Belgium, will result in a fundamental shift in the way Germany’s gas supply functions.

Stade is making its mark as one of the leading hubs for LNG imports, not just in Germany but in Europe.

Rapid development

For a long time, there had been no viable reason for Germany to directly import LNG via commercial vessels due to the effectiveness of gas pipelines from neighbouring countries. While other countries in Europe, including Spain, France, and Italy, had more LNG facilities and terminals, Germany’s infrastructure was relatively immature. Up until the end of 2022, gas was only imported to Germany via pipelines. 5

Figure 1. Arctic Princess LNG tanker.

Figure 2. Boarding officer looking at Arctic Princess LNG tanker.

The Turbomachinery & Pump Symposia is recognized worldwide as the industry’s must-attend event. Connect with more than 4,900 delegates, meet with leading suppliers, observe product demos, and get answers to your technical questions. We look forward to seeing you in Houston!

4,945 ATTENDEES

323 EXHIBITING COMPANIES

53 COUNTRIES

TPS.TAMU.EDU #TPS2024

HOSTED BY

That has all changed, and the drive to develop sufficient, effective, and sustainable long-term infrastructure for LNG carriers and FSRUs to provide a home-grown LNG capability has been swift.

Germany has raced ahead to build up its own LNG import infrastructure in record time, with Chancellor Olaf Scholz saying he wants to use this “new Germany-speed” for the expansion of renewable energy capabilities, adding that geopolitical tensions have further accelerated Germany’s desire to transition to more sustainable fuel choices. 6 The country has a goal of being greenhouse gas neutral by 2045, with a following aim of being greenhouse gas negative by 2050.

This is especially apparent at the Port of Stade, which was better known for supporting dry bulk, barge and general cargo vessels due to its non-tidal access for ocean-going vessels.

In December 2023, the port officially opened its new landing pier for FSRUs less than a year after construction began. 7 At a cost of €300 million (US$321 million), it is also the largest waterside construction project in German port history.

The accelerated timeframe and levels of investment of this infrastructure project is a clear example of the country’s bold vision to ensure LNG is a cornerstone of its future energy capacity, with Stade and the Hanseatic Energy Hub a jewel in Germany’s crown.

Growing the LNG-fuelled fleet

While the infrastructure to support Germany’s LNG capacity for domestic purposes is developing at a rapid pace, the shipping industry itself could also benefit from Germany’s growing energy capabilities, particularly amid concerns of long-term overcapacity challenges.

There is not a week that goes by without news of another newbuilding hitting the water that runs exclusively on LNG. According to data supplied by the International Maritime Organization (IMO), more than 1000 vessels running on LNG as its primary fuel are now in operation – more than hydrogen, ammonia, LPG, and methanol combined – with another 2000 expected to come into service by 2028. 8

One of the critical challenges behind the uptake of LNG-powered vessels is the need for bunkering terminals and distribution networks that can safely support such vessels. Yet, in a ‘chicken and egg’ scenario, there are concerns that the investment needed for these types of facilities will not be available until there is sufficient demand.

This is why facilities like the Hanseatic Energy Hub and its supporting network and partners could prove to be so effective in the long term to support the shipping industry’s race to decarbonise by 2050.

Europe is expected to have developed a total LNG terminal capacity of 400 billion m 3 by 2030, based on current infrastructure plans. 9 However, forecast regional demand is expected to reach just 190 billion m 3 by the same period, leading to a serious concern of overcapacity of LNG.

This abundance of a more sustainable source of fuel for commercial vessels stored at leading European ports and terminals such as Stade could prove a bellwether for

all manner of vessel types turning to LNG as a primary fuel source.

Decarbonisation drive

The Hanseatic Energy Hub will play a key role in helping Germany meet its decarbonisation goals. As part of the terminal’s development, the facility has begun sounding out the market to determine whether its longer-term plans should be based largely on ammonia to be reconverted into clean hydrogen.

It is crucial that Germany’s LNG terminals can be retrofitted to support a decarbonised energy system, either through importing other green fuel options such as ammonia or green hydrogen, or improving Germany’s regasification capabilities. No matter the choice, flexibility in services and offerings across Germany’s energy terminals will be vital if they are to remain competitive in the long term.

This is another reason why the Port of Stade turned to long-term partners to provide long-term support for the Hanseatic Energy Hub. If Germany’s nascent homegrown energy capabilities are to remain successful and support domestic energy supplies, they need to be flexible in the long term to adapt to market trends and fuel developments. Germany rapid development of its LNG terminal infrastructure, including the Hanseatic Energy Hub, will alleviate short-term concerns. However, with their long-term viability being thrown into question, they must also play a leading role in Europe’s decarbonisation efforts.

References

1. ‘Analysis of the European LNG market developments’, European Union Agency for the Cooperation of Energy Regulators, (19 April 2024), www.acer.europa.eu/monitoring/ MMR/LNG_market_developments_2024

2. ‘Zeebrugge LNG expansion work progresses’, LNG Prime, (5 April 2023), https://lngprime.com/europe/zeebrugge-lngexpansion-work-progresses/78139/

3. ‘Italy’s Snam to invest €1bn in new offshore LNG terminal’, Offshore Technology, (15 November 2023), www.offshoretechnology.com/news/snam-lng-terminal-investment/

4. ‘Number of operational and planned LNG terminals in Europe as of January 2024, by country’, Statista, (26 March 2024), www.statista.com/statistics/326008/lngimport-terminals-by-country-europe/

5. ‘Versorgungssicherheit bei Erdgas: MonitoringBericht nach § 51 EnWG’, Bundesministerium für Wirtschaft und Energie, (February 2019), www. bmwk.de/Redaktion/DE/Publikationen/Energie/ monitoringbericht-versorgungssicherheit-2017.pdf?__ blob=publicationFile&v=24

6. ‘German government plans extensive LNG infrastructure build-up to ensure security of European supply’, Clean Energy Wire, (3 March 2023), www.cleanenergywire. org/news/german-government-plans-extensive-lnginfrastructure-build-ensure-security-european-supply

7. ‘New Stade LNG jetty opens doors for independent energy supply in Germany’, Offshore Energy, (19 December 2023), www.offshore-energy.biz/new-stade-lng-jetty-opens-doorsfor-independent-energy-supply-in-germany/

8. ‘Uptake of Alternative Fuels’, The Future Fuels and Technology Project, https://futurefuels.imo.org/home/ latest-information/fuel-uptake/

9. ‘Over half of Europe’s LNG infrastructure assets could be left unused by 2030’, Institute for Energy Economics and Financial Analysis, (21 March 2023), https://ieefa.org/articles/ over-half-europes-lng-infrastructure-assets-could-be-leftunused-2030

Karthik Sathyamoorthy, CEO, AG&P LNG, and DeLaine Mayer, Director of External Affairs, Nebula Energy/AG&P LNG, detail how LNG can be used to help decarbonise nickel’s value chain.

The urgent need to reduce carbon dioxide emissions to mitigate the worst effects of climate change demands transformation of key industries, particularly a rapid shift towards electric vehicles (EVs) to reduce dependence on carbon-intense fossil fuels. This pivot towards a lower-carbon economy hinges on electrification and the adoption of low-carbon energy sources.

The transportation sector has witnessed a notable shift in the adoption of EVs, with the US, Europe, and China leading global sales. Decisions by major automakers to wholly adopt low-carbon product lines underscore this shift: Jaguar recently announced an end to the production of internal combustion engines by year-end1 and Mitsubishi Motors has pledged to produce only EVs and hybrids by 2035.2 As EV sales surge, global battery demand escalates, amplifying scrutiny on battery supply chains, with particular attention on critical materials like nickel, where Indonesia plays a pivotal role.

Nickel, a crucial component in lithium-ion batteries, enhances battery lifespan and charge efficiency, making it indispensable for green technologies.3 Indonesia has ascended as the world’s leading nickel producer, with its global extraction share skyrocketing from 5% in 2015 to 50% in 2023.4 President Joko Widodo’s 2020 ban on nickel ore exports, aimed at promoting onshore processing, catalysed a surge in processing plants and investments from automakers into Indonesia.5 Despite challenges, including EU opposition to the ban at the World Trade Organization and ecological concerns, Indonesia’s burgeoning nickel industry, driven by demand for EVs and renewable energy technologies, positions its supply chain dominance as a linchpin in the nation’s economic development. However, optimising EVs’ environmental benefits necessitates reducing the carbon intensity across the EV value chain.

Reducing nickel’s carbon intensity

The expansion of Indonesia’s nickel industry has strained the country’s ambitious target of reaching net-zero emissions by 2060. Indonesia, one of the largest coal producers in the world and a major coal consumer, aims to add 35 GW to the national grid to power the economy, including the metals industry. Indonesia’s industrial parks on the islands of Sulawesi and Halmahera are nickel and aluminium processing hubs. Reliant on coal, they consume 15% of the country’s coal-fired generation.6

To transition away from coal, state electricity company PT PLN has begun a gasification programme to develop LNG midstream infrastructure in the Sulawesi-Maluku region.7 In March 2024, AG&P LNG, a terminals and downstream infrastructure firm majority-owned by US-based developer and investor Nebula Energy, announced the award of a 20-year contract for LNG infrastructure from PLN EPI. This is a familiar blueprint for AG&P LNG: now with 11 LNG import terminals at different stages of commercial development in high-growth markets across Southeast Asia and India, the firm is well-suited to support Indonesia’s transition from coal to natural gas. Globally, AG&P builds downstream LNG distribution and logistics focused platforms, from import regasification terminals connecting LNG/gas to a wide range of LNG distribution infrastructure.

In Indonesia, AG&P LNG, together with consortium partners Suasa Benua Sukses (SBS) and KPMOG (collectively known as the consortium), secured a tender for the co-development, ownership, and operation of LNG import terminal infrastructure and downstream logistics across seven locations in the Sulawesi-Maluku cluster. The import facilities have a combined regasification capacity of 2.3 million tpy across its seven sites. Among these are Indonesia’s nickel smelting facilities.

Developing LNG infrastructure

The consortium’s involvement in developing LNG infrastructure in Indonesia brings several key benefits: it facilitates the transition from coal to natural gas, significantly reducing greenhouse gas emissions and other pollutants, supporting Indonesia’s ambitious 2060 net-zero emissions target. Additionally, the consortium’s expertise and investment ensure the reliability and efficiency of LNG supply chains, fostering economic stability and energy security. By establishing robust LNG infrastructure, the consortium also paves the way for further industrial growth and modernisation in the Sulawesi-Maluku region, enhancing the competitiveness of Indonesia’s

nickel industry on the global stage. This strategic move not only aligns with global sustainability goals but also bolsters Indonesia’s position as a leading player in the EV battery supply chain, advancing the broader objective of a low-carbon global economy.

Furthermore, the modernisation of the Sulawesi-Maluku region through the establishment of advanced LNG infrastructure represents a significant leap forward for local industry. The adoption of LNG technology will introduce state-of-the-art processes and systems for resource-efficient manufacturing and lower-carbon energy consumption, fostering innovation and efficiency within the nickel and aluminium processing sectors. This modernisation effort is likely to attract further foreign investment, boosting local economies and creating job opportunities. Enhanced infrastructure and technological capabilities will also enable the region to meet stringent international environmental standards, rendering Indonesian nickel more appealing to sustainability-focused global markets.

Conclusion

The transition to LNG not only enhances the environmental credentials of the region’s industries but also augments their global competitiveness. By reducing reliance on coal and lowering emissions, Indonesian nickel products will meet the growing demand for environmentally responsible materials, particularly from automakers and technology companies striving to minimise their carbon footprints. This positioning establishes Indonesia as a preferred supplier in the global EV battery and green technology supply chain. As international markets place higher premiums on sustainability, the modernisation driven by this consortium ensures that Indonesia can maintain and expand its dominance in the global nickel industry, securing long-term economic benefits and leadership in the transition to a low-carbon economy.

References

1. FITZGERALD, J., ‘Jaguar Ending Production of Gas Cars Entirely before New EVs Arrive’, Card and Driver, (4 March 2024), www.caranddriver.com/news/a60075224/ jaguar-gas-cars-production-ending

2. ‘Mitsubishi Motors to sell only EVs, hybrids by mid-2030s’, Reuters, (14 March 2023), www.reuters.com/business/autostransportation/mitsubishi-motors-electrify-100-its-fleet-by2035-yomiuri-2023-03-10

3. ‘The role of nickel in EV battery manufacturing’, Innovation News Network, (27 October 2023), www.innovationnewsnetwork.com/the-role-of-nickel-in-evbattery-manufacturing/38877

4. MICHEL, T., ‘The Prospects of Indonesia’s Nickel Boom Amidst a Systemic Challenge from Coal’, French Institute of International Relations, (May 2024), www.ifri.org/en/publications/notes-de-lifri/prospectsindonesias-nickel-boom-amidst-systemic-challenge-coal

5. DAGA, A., ‘Indonesia’s nickel policy looks fragile’, Reuters, (26 January 2024), www.reuters.com/breakingviews/ indonesias-nickel-policy-looks-fragile-2024-01-26

6. JONG, H., N., ‘Indonesia’s coal burning hits record high –and ‘green’ nickel is largely why’, Mongaby, (3 July 2023), https://news.mongabay.com/2023/07/indonesias-coalburning-hits-record-high-and-green-nickel-is-largely-why

7. DA COSTA, G., ‘PLN Energi Primer Indonesia prepares gasification of Sulawesi-Maluku cluster plants’, Indonesia Business Post, (1 April 2024), https://indonesiabusinesspost. com/risks-opportunities/pln-energi-primer-indonesiaprepares-gasification-of-sulawesi-maluku-cluster-plants/

Figure 1. AG&P LNG awarded 20-year contract by PLN EPI, Indonesia for co-development, ownership, and operations of LNG import terminals in Sulawesi-Maluku Power Cluster.

Frederik Van Nuffel and Maria Carolina Chang, EXMAR, Belgium, provides an overview of the implementation of the floating LNG terminal offshore Pointe Noire, Republic of the Congo.

In 2022, EXMAR, a Belgium-based provider of innovative shipping and floating gas infrastructure solutions, was approached by Eni to monetise gas reserves of the Marine XII field in Congo.

The exploitation of the Marine XII oil and gas field in Congo faced limitations due to excessive natural gas production alongside the oil. While the oil was valuable, the natural gas was less so, primarily because the country’s consumption levels were too low to deal with all the associated gas. Consequently, the strategy of Eni to liquefy this associated gas enabled not only the sale of LNG, but also an increase in oil production output.

To implement an LNG export solution in a short timeline, a combined system was developed with two existing units. The TANGO floating LNG (FLNG), a liquefaction barge with liquefaction capacity of approximately 1 billion m3/y of gas

originally designed for benign conditions with limited storage capacity, and the EXCALIBUR, an LNG carrier to serve as permanent storage unit (FSU) for the terminal.

In early 2022, the EXMAR teams were tasked to find a solution to moor TANGO FLNG offshore Congo and position FSU EXCALIBUR alongside the FLNG, based on the environmental conditions of the area and considering the short timeframe to implement the new design.

EXMAR, with its expertise across the whole LNG value chain, including FLNG, and serving as the EPC contractor for this project for the implementation of the FLNG and FSU EXCALIBUR, designed the mooring system and performed the refurbishments on both vessels at Dry Docks World yard in Dubai.

Eni’s Congo LNG project leveraged the Marine XII block’s gas resources and existing production infrastructure,

adopting a phased approach to achieve the goal of zero routine gas flaring. This strategy allowed for increased oil production in the Marine XII block, with previously flared gas now being monetised through TANGO FLNG’s LNG production,

thereby minimising flaring to the lowest possible levels. All this was targeted to be completed in less than a year till first gas, underwriting.

A fully-integrated project

The development of the Congo LNG project was a good example of how an opportunity can become reality in a short timeframe when several companies work together to one common goal. Various divisions within the EXMAR Group worked jointly with the Eni teams to come up with an innovative solution creating value using existing assets.

To moor an FLNG barge close to an FSU in offshore conditions with a substantial swell, a new mooring system was invented. The ‘split mooring’ system is a combination of a reinforced side-by-side mooring with a conventional spread mooring system. The design from Exmar Offshore Company in Houston is made to keep both floating units close enough together to easily facilitate LNG and crew transfer while keeping a safe distance between both units in a 100-year storm design condition. In spring 2022, the concept was proven to Eni via wave basin tests. Since split mooring is a completely new concept, it means that the EXMAR teams had to prove via a technology qualification assessment (TQA) by the classification society Bureau Veritas that it would work.

In parallel with the further maturing of the split mooring, several other upgrades were engineered.

Since no helicopter platform was available, boat landing towers were added to both TANGO FLNG and the FSU EXCALIBUR to cater for personnel transfer. In this way, classical surfer boats (which were already available in Congo) could be used for the personnel transfer.

A normal LNG ship-to-ship (STS) system to transfer LNG from TANGO FLNG to FSU EXCALIBUR could not be used because of the motions of both units, and because the distance between both units is too large. A new liquid transfer system (LTS) was designed to overcome these operational challenges. On both FSU EXCALIBUR and TANGO FLNG, a tower was built to increase the height of the LNG manifold well above the mooring lines in between both units. On top of the towers, LNG swivel arms of a dedicated design were installed to always ensure that the LNG transfer hoses are free of stress and torsion. The entire system uses one 10 in. hose for LNG transfer from the FLNG to the FSU and a second 10 in. hose for vapour return from the FSU back to the FLNG. All excess boil-off gas generated by the FSU can be reliquefied on the FLNG increasing the efficiency of the terminal and avoiding unnecessary venting or flaring of natural gas.

The feed gas inlet manifold also required a full revision. In the original design, feed gas was brought to the FLNG through shore high-pressure gas hoses from an onshore manifold. As the FLNG is now 3 km offshore, a new design was necessary. Together with Eni, the feed gas supply was changed to a high-pressure riser connection. On the upstream side, a riser tower was put on the seabed by Eni where the rigid subsea feed gas piping was connected to a flexible riser. On the downstream side, a riser balcony structure was added to TANGO FLNG to support the riser loads. The flexible riser itself was then installed as an aerial hose, partially submerged in the water.

The EXCALIBUR is a vessel built in 2001 with a membrane system and without a reinforced cargo containment system.

Figure 1. Congo LNG export terminal.

Figure 2. Split mooring configuration.

Figure 3. FSU boat landing tower.

Join the discussion under the motto “Setting a green course”

SMM, the leading international maritime trade fair, is inviting you to navigate tomorrow and engage with experts pioneering the path to greener shipping at gmec, the global maritime environmental congress.

Cutting-edge sessions will focus on the latest in maritime sustainability, encompassing immediate solutions for decarbonisation and exploring alternative fuels such as methanol, LNG, ammonia, hydrogen, and wind. There will also be a debate on nuclear power and the circular economy in ship recycling. Choose your topics, gain fresh insights and make valuable contacts. Participation is free of charge – all you need is your SMM exhibition ticket. Step Forward for Sustainability.

smm-hamburg.com /gmec the leading international maritime trade fair

get your ticket now

smm-hamburg.com/ticket in cooperation with

smm-hamburg.com/news

youtube.com/SMMfair linkedin.com/company/ smmfair

facebook.com/SMMfair

For a terminal which needs to be online all the time, it is important that partial filling of the cargo tanks is possible. Thanks to the relative directional wave climate offshore Congo, it has been proven together with GTT, the cargo containment designer, that most of the time, no filling restrictions apply to FSU EXCALIBUR. Close monitoring is done on the terminal to verify the cargo tanks loading condition

against the predicted sea states. Whenever there would be a risk of sloshing, mitigating measures have been put in place to avoid such risk.

The offshore sea conditions also had an impact on the process plant of TANGO FLNG. Originally, the process plant was designed with very limited motion and acceleration criteria since it was meant to operate at shore moored conditions. Detailed studies have been conducted with the topside process licensor, Black & Veatch, to ensure that the process was validated for the new offshore conditions and mitigating measures were put in place where required.

Further implementation

For the implementation, an integrated project team of both EXMAR and Eni personnel was set up to lead all efforts in the right direction. The team consisted of 180 people at peak from all parts of EXMAR Group, closely co-operating with all the contractors involved. Detailed design and engineering were ongoing while, in parallel, a team in Dubai was busy overseeing the first steel cutting and welding of all new structures. Despite the extremely challenging timeline, the project was implemented on time in about one year after Eni’s final investment decision.

Together with Eni, EXMAR Infrastructure, EXMAR Offshore Company, EXMAR Shipmanagement, EXMAR Technical, DV Offshore, and BEXCO all worked side-by-side to bring the project to life, with 3 million working hours put into the conversion of both vessels without lost time injury.

Future operations and maintenance (O&M) would be managed as a single terminal, rather than two separate assets, with a fully-integrated terminal organisation by EXMAR Shipmanagement, developed to enhance efficiency and collaboration.

The project development strength lies in the synergy of diverse teams, with an EXMAR operations team engaged from the outset. Some of its current crew members have been involved since the initial phase of development and construction, throughout the previous commissioning and operations, and they continue to be an integral part of the vessel’s core crew. Their intimate knowledge of the assets is unparalleled and fundamental for the execution of the conversion scope and preparations for the operations in Congo.

Mobilisation, installation, and start-up

In October 2023, in the presence of the Ministry of Hydrocarbons of the Republic of Congo, senior representatives from Eni, EXMAR, and Dry Docks World Dubai celebrated the sail away of the TANGO FLNG and FSU EXCALIBUR vessels from Dubai to Congo. The FLNG was dry towed to Luanda, Angola. From there, the FLNG was wet towed to Pointe Noire. FSU EXCALIBUR sailed straight to Congo where she was moored at the port of Pointe Noire.

The offshore installation activities by Eni started immediately thereafter. By the end of December 2023, Eni announced the introduction of gas into the TANGO FLNG facility moored in Congolese waters, only 12 months after the final investment decision, a key milestone for the project. Following completion of the commissioning phase, TANGO FLNG produced its first LNG cargo in February 2024, placing the Republic of the Congo on the list of LNG-producing countries.

Figure 4. TANGO FLNG and FSU connected with gangway.

Figure 5. LNG transfer system.

Making moves with modular regasification terminals

Danielle Murphy-Cannella, Head of Sustainability, and Kristoffer Evju, Vice President Commercial, ECOnnect Energy, explore some of the challenges and possibilities within the current state of the global LNG market, and technological solutions that can contribute towards cleaner and sustained energy security.

The global market for LNG is in a state of flux due to various geopolitical and market factors, diverging from market trends in the last decade. The recent supply disruptions due to war and regional conflicts such as in Ukraine and the Gaza region have underscored the

importance of resilient value chains and flexible responses to secure supply.

Access to import terminals and liquid gas markets is becoming increasingly vital, aligning with the key objectives of regional energy strategies, notably prominent in the EU.

Figure 2. Rendering of the gas balcony mounted directly onto an FSRU with minimal disturbance to the seabed.

Figure 1. The jettyless ECOnnect IQuay C class for transfer of LNG, ammonia, CCS, and other cryogenic fluids.

These strategies aim to enhance resilience to disruptions and ensure a stable supply of LNG as a cleaner alternative to other fossil fuels. The growing significance of LNG in the energy mix of countries worldwide further emphasises the need for adaptable and robust LNG value chains to meet the evolving demands of the market. This article explores the evolving landscape of the LNG market and the strategies needed to ensure a secure regasification capacity in the context of increasing global demand and supply disruptions.

LNG demand

Globally, natural gas accounts for approximately 24%, or roughly 3.94 trillion m3 of total energy consumption. Consumption varies from region to region due to varying levels of infrastructure and market demand. For example, North America and Europe have mature LNG networks and natural gas accounts for approximately 25% of total energy consumption.

The European gas demand is currently estimated to be around 400 billion m3, which is assumed to stay relatively stable over the coming years. Seasonal dips in demand over the summer is currently being offset by the mandate to refill the storages for energy security in the coming winter. According to the European Commission, the overall gas import capacity from LNG regasification and natural gas pipelines in Europe is covering 40% (157 billion m3) of its current demand for gas. This creates a gap between capacity and demand which will be crucial to diminish in the following years by either increasing import capacity or reducing demand. For the latter, the EU has agreed to reduce its consumption by 15% compared to the past five years average.

To enhance energy security on the continent, the European Commission created the policy initiative of Projects of Common Interest (PCI) for key cross border infrastructure projects that link the energy systems of EU countries. Based on the list of EU’s PCIs, the LNG strategy includes a list of key infrastructure projects which are essential to ensure that all EU countries can benefit from a stable supply of LNG.

LNG demand in Asia has historically been strong, making the region a key market since the beginning of the LNG industry. The three founding markets of Japan, South Korea, and Taiwan have been joined by China and India, forming the ‘Big 5’ that attract considerable attention. Emerging Asian markets show great potential for LNG demand, with countries like Malaysia, Indonesia, Thailand, Pakistan, Bangladesh, Vietnam, and the Philippines having the ability to satisfy a significant portion of their energy demands via LNG. Asia continues to demonstrate rapid growth in energy demand, driving LNG to become the preferred fuel source.

LNG supply

While gas imports and LNG imports from Norway have increased significantly, only 10% of the total European gas needs are today met with domestic production, which has been decreasing over the recent years due to production limits in the Groningen Field in the Netherlands and decline in the mature fields in the North Sea.

The US exported 91.2 million t of LNG in 2023, a record for the country, according to data compiled by Bloomberg.1 Qatar, the top LNG supplier in 2022, saw its volumes shrink for the first time since at least 2016, with a 1.9% decline dropping the nation into third spot for shipments of the super-chilled fuel. Australia ranked second, with exports that were little changed from 2022. The US’s position as the largest LNG exporter is expected to continue in the coming years, with 17 more LNG plants on track to be built in the US by 2028.

Export increase from the US is a result of the global demand and the current sizeable difference in prices between the US and the European trading hubs – making the EU a lucrative market. Higher gas prices thus give the producers incentives to increase their spot volumes to cover the excess demand in the market. Furthermore, the global liquefaction capacity is set to increase in the coming years in response to these market dynamics.

Asia’s demand for LNG has been increasing due to expanding populations, rising standards of living, and urbanisation. Countries such as Japan, Korea, China, India, Indonesia, the Philippines, Thailand, Vietnam, and Bangladesh have been driving the demand for LNG. Asia, particularly Southeast Asia, has become the main export destination for growing US LNG exports. The region’s imports of LNG have been robust, with record supply keeping spot prices muted. Despite representing a relatively small volume of the world’s LNG trades, South American LNG imports have been increasing. Several countries including Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, and Venezuela have been involved in LNG trade and have been exploring the potential for LNG utilisation.

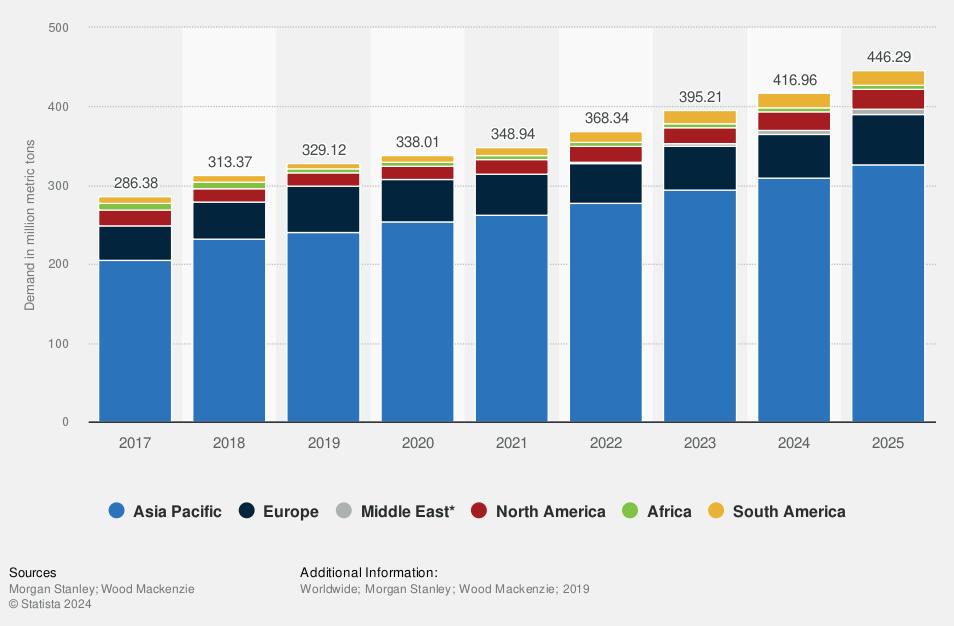

Figure 3. Projected LNG demand worldwide from 2017 – 2025, by region (million t).

The growing significance of LNG in the energy mix of countries worldwide further emphasises the need for adaptable and robust LNG value chains to meet the evolving demands of the market.

Current infrastructure challenges

Europe is still struggling to make use of the increased LNG production due to a lack of sufficient infrastructure. The ability for a country to import LNG is largely dependent the capacity for LNG regasification, storage, and cross-country pipeline networks.

The EU region has expanded its LNG import capacity by 34%, or 6.8 billion ft3/d, by 2024 compared with 2021, with several countries developing new FSRU terminals and expanding existing ones.2

In South America and Asia, demand for LNG has been growing, but the infrastructure has not kept pace with the demand, leading to supply shortages and higher prices.

In the process of operating LNG terminals, the main challenge is the length of time it takes to build the infrastructure and acquire other critical components, such as permits, financing, and construction. An onshore plant’s environmental impact, including both terrestrial and marine ecosystem impacts, should also be considered.

FSRUs have been a major contributor towards fast-tracking LNG import, storage, and regasification capacity in the near-term. They serve as a time saving, cost-efficient, and flexible alternative to building onshore

regasification plants, which may take up to five years to reach operational status.

The fleet of FSRUs in the market as of the end of 2021 was 48 vessels, with demand skyrocketing after the outbreak of conflicts. The result is a worldwide shortage of FSRUs and high chartering rates. The construction of new vessels takes approximately 3 – 4 years and the conversion of FSUs of LNG carriers into FSRUs may serve as a viable alternative, with a lead-time of around two years. With shipyards having backlogs for conversion all the way to 2027, the combined supply of new FSRUs will likely remain constant over the next few years.

There are infrastructure gaps in the current global LNG market that cannot accommodate the urgent demand for LNG import and regasification. There is therefore a need in the market for new technology to provide a cheaper, more flexible and environmentally friendly solution with less lead time than the current alternatives.

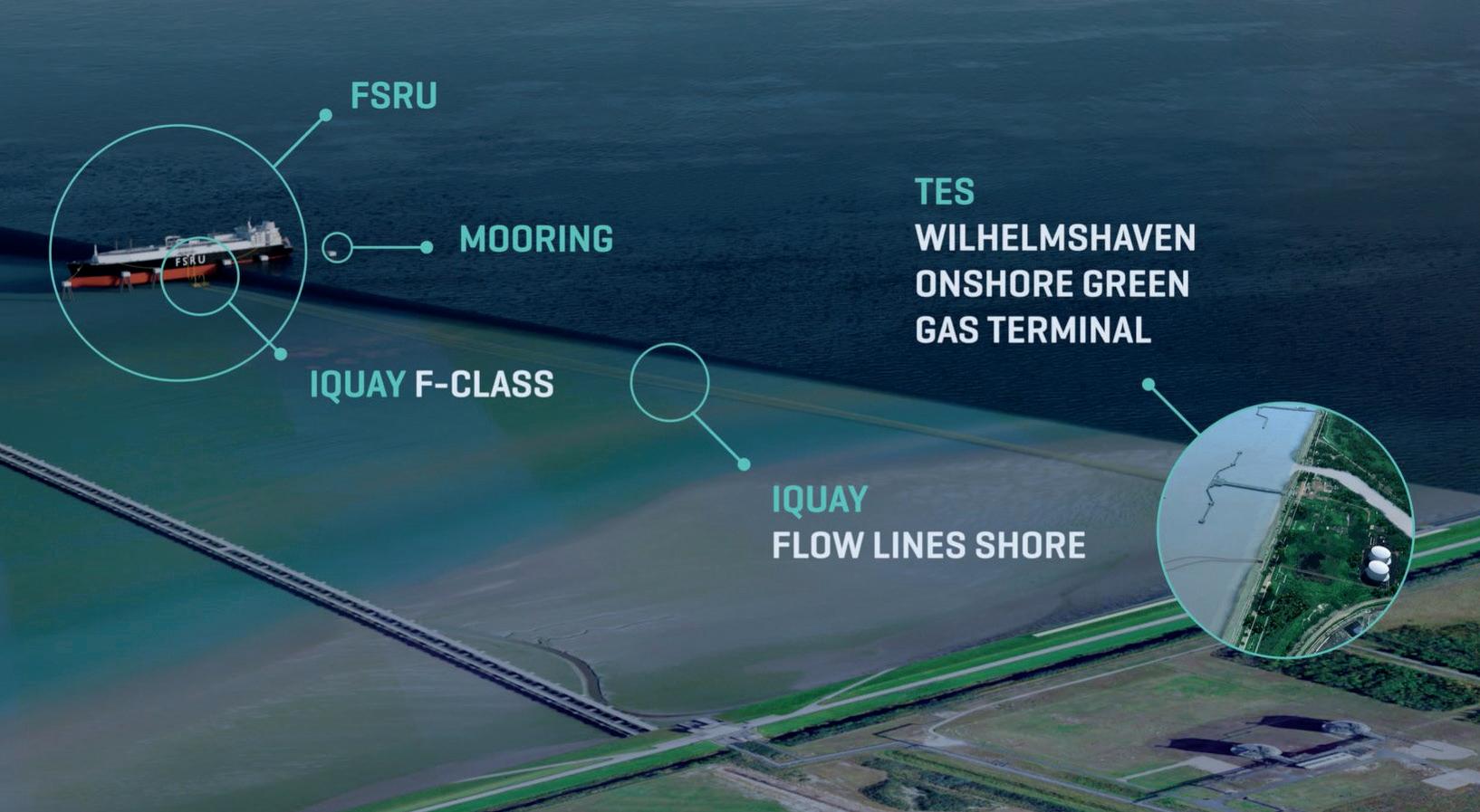

Fast-tracking LNG import in Wilhelmshaven, Germany

Seeking greater flexibility to suit vessel and storage facility availability, LNG and gas operators have chosen jettyless and low-impact import solutions to accelerate energy security options. One example of this is in Wilhelmshaven Port; needing to fast-track Germany’s fifth FSRU project, a jettyless LNG terminal design was selected to accelerate gas import accommodating 8.5% of Germany’s energy demand.

Everyone wants to get what they paid for.

LNG Industry is independently verified by ABC, because we want our advertisers to know they’re getting the exposure they’ve been promised. ABC. See it. Believe it. Trust it.

ECOnnect Energy designed, constructed, and installed a jettyless infrastructure solution linking the offshore gas storage to the onshore terminal in Wilhelmshaven, with a gas balcony and a low-impact subsea pipeline. The jettyless delivery includes an emergency release system, flexible risers, a pipeline end manifold, and thermoplastic composite pipes. The gas balcony is minimally intrusive on the FSRU as the pre-fabricated foundations were welded during dry dock, allowing for quick installation and integration without requiring hot work.

The project will commence operations in Autumn 2024 and initially import as much as 16 – 20 billion m3, while also accommodating 1.6 million m3 for direct connection to the Open Grid Europe (OGE) gas grid. The Wilhelmshaven project, operated by Tree Energy Solutions (TES), E.ON, and ENGIE, will also be at the centre of a future hydrogen hub beginning in 2025.

The gas balcony design from ECOnnect Energy has also been used for upstream applications in the Gulf of Mexico for NASDAQ-listed New Fortress Energy’s Fast LNG projects, and the flexibility of the design has since been applied to fasttracking FSRU projects to bolster Europe’s energy security. Natural gas import into existing and new ports will require new import solutions that can be implemented quickly and can

accommodate current LNG demand, while also allowing for future ‘clean and renewable hydrogen-ready’ import.3

From an environmental perspective the jettyless, gas balcony solution reduces: embodied emissions (carbon dioxide) from construction, resource use, biodiversity loss, and physical impact. The system specification requires minimal, if any, environmental assessment and permitting from relevant authorities and does not require any civil works nor the impact from fixed-marine infrastructure. The system is fully removable with little disturbance to the seabed, offers a greener solution with a low visual impact, and is fully re-usable and certified for carbon dioxide and/or hydrogen carrier liquids for future import.

Floating LNG terminals and the way forward

For fast and cost-effective regasification needs, a solution based on the existing field-proven jettyless infrastructure consisting of a modular, floating regasification, and transfer system for gas transfer from an FSU to an onshore natural gas receipt facility or pipeline effectively replaces the need for both a fixed marine structure and also FSRUs/onshore regasification plants.

The full terminal solution, consisting of a floating terminal, an FSU, a comprehensive mooring solution, LNG transfer system, and gas transportation lines to shore, can be equipped with modular regasification skid types, power generation equipment, and appurtenant regasification and gas transfer components required to best fit project specific and local regulations and requirements. The terminal can also be equipped with carbon capture facilities for the capture, liquefaction, and storage of carbon dioxide emissions from nearby industrial areas or to capture vessel emissions, creating a green, closed-loop emission terminal.

The modular design of the floating terminal enable construction at any yard, with universal installation on any transporting vessel effectively removing the constraints of open FSRU yard slots or negotiating onshore real estate for land-based regasification configurations.

Modular, plug-and-play infrastructure could enable rapid LNG import into strategic global ports, while also providing the flexibility to be adapted for future renewable energy import. The regasification solution makes LNG accessible to new locations without requiring new regasification infrastructure, with shorter lead time than other floating or onshore regasification options.

References

1. ‘US Becomes Top LNG Exporter After Overtaking Australia and Qatar’, Bloomberg Markets, (January 2024), www.bloomberg.com/news/articles/2024-01-02/ us-becomes-world-s-top-lng-supplier-after-exportseclipse-australia-and-qatar

2. ‘Today in Energy: Europe’s LNG import capacity set to expand one-third by end of 2024’, U.S. Energy Information Administration (November 2022), www. eia.gov/todayinenergy/detail.php?id=54780

3. ‘Joint Statement between the European Commission and the United States on European Energy Security’, European Commission, (25 March 2022), https:// ec.europa.eu/commission/presscorner/detail/en/ statement_22_2041

Bibliography

Sources available upon request.

Figure 4. FSRUs are in high demand to accommodate LNG import into Europe resulting in a worldwide shortage of units and high chartering rates.

Figure 5. ECOnnect is delivering the IQuay F-class Solution to Wilhelmshaven, an infrastructure solution linking the offshore gas storage to the onshore terminal, with a gas balcony and subsea pipelines.

LNG Industry asked Burckhardt Compression to discuss some key factors regarding compressors for use in the LNG industry.

Thomas Hess, Product Manager LNG Marine/PCI, Burckhardt Compression

Thomas Hess is a German citizen and graduated in Mechanical Engineering in 2002. He joined Burckhardt Compression directly after graduating, working in R&D and the engineering division. Further experience was gained in project management before taking up a new position as Head of Contracting in China, where he lived for six years. On returning to the head office in 2012, he took over responsibility for project execution in the marine business, leading to his current position in product management. He has more than 20 years’ experience with compression machinery and their auxiliary systems for land and marine based hydrocarbon transport and storage installations.

Q1. How can the right compressor improve cost-efficiency, and overall efficiency of the LNG process?

Thomas Hess, Burckhardt Compression

Selecting the right compressor can significantly impact product and process costs. Whereas shaft power efficiency is obvious and easy to compare, there are other – rather hidden and equipment-specific – features and requirements which can play a major role.

Decision makers should therefore pay good attention on the required all-over utility consumption of the equipment. Some compressors can operate under cryogenic conditions, some require pre-warming of the gas consuming extra energy and coolant. Compressors operating with lubricated compression stages will require constant supply of special oils and, at the same time, special filtration equipment might be required for oil removal depending on the process needs.

Gas tight compressors can operate with almost zero leakages (down to few ppm) and none of the valuable product handled is lost. This feature, however, is not available for all types of compressors which are offered to the market, and continuous purging with nitrogen and

ventilation of the compressor crankgear or gearbox to the vent respiratory flare might be required.

Total cost of ownership can therefore vary widely with the chosen type of compressor for an application. Over time, if the decision was wisely made under consideration of previously listed aspects, cost and overall efficiency can be positively impacted.

Q2. What factors are considered when deciding on a compressor for a project?

Thomas Hess, Burckhardt Compression

It definitely takes much more information as offered within the equipment data sheet.

Deciding factors might be entirely different when specifying and evaluating compressors for cases where existing and aged machines need to be replaced; an existing facility is enlarged and requires additional capacity or a new plant is built. In the latter case, decision makers are more open in equipment evaluation, as there are no or less stringent constraints in available space or utilities defined by the existing infrastructure, limiting the product selection.

In any case, the compressor application and the role of the compressor in the specific process should always be carefully reviewed on criticality of the machine respiration, the impact of a potential machine failure, and related downtime. Decision makers need to define if the process requires redundancy or if there are back-up systems available. A clear picture should be available on the expected annual operating hours of the equipment as products available on the market will vary in maintenance requirements and offered mean time between overhaul.