Danieli Intelligent Plant Control Desk utilises mixed reality technologies while emphasizing inter-operability and human factors. It offers a direct view of processes, equipment and information to operators and managers.

Tony Crinion tonycrinion@quartzltd.com / Tel: +44 (0) 1737 855164

Steel Times International is published eight times a year and is available on subscription. Annual subscription: UK £226.00 Other countries: £299.00

2 years subscription: UK £407.00 Other countries: £536.00

3 years subscription: UK £453.00 Other countries: £625.00 Single copy (inc postage): £50.00 Email: steel@quartzltd.com

Digital subscription: (8 times a year) - 1 year: £215.00 - 2 years: £344.00 3 years: £442.00. Singe issue: £34.00

Published by: Quartz Business Media Ltd, Quartz House, 20 Clarendon Road, Redhill, Surrey, RH1 1QX, England. Tel: +44 (0)1737 855000 Fax: +44 (0)1737 855034 www.steeltimesint.com

Steel Times International (USPS No: 020-958) is published monthly except Feb, May, July, Dec by Quartz Business Media Ltd and distributed in the US by DSW, 75 Aberdeen Road, Emigsville, PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER send address changes to Steel Times International c/o PO Box 437, Emigsville, PA 17318-0437.

Printed in England by: Stephens and George Ltd • Goat Mill Road • Dowlais • Merthyr Tydfi • CF48 3TD. Tel: +44 (0)1685 352063 Web: www.stephensandgeorge.co.uk

Sandvik Coromant on high-speed rail infrastructure. 9 USA update

The tariff storm rages in the US. 11

Latin America update

Scraping export restrictions. 13

India update

Protection from cheap imports.

Carbon capture

Carbon capture: utile or futile?

Automotive

Myra Pinkham on the US automotive industry and President Trump.

Automation Automation and efficiency.

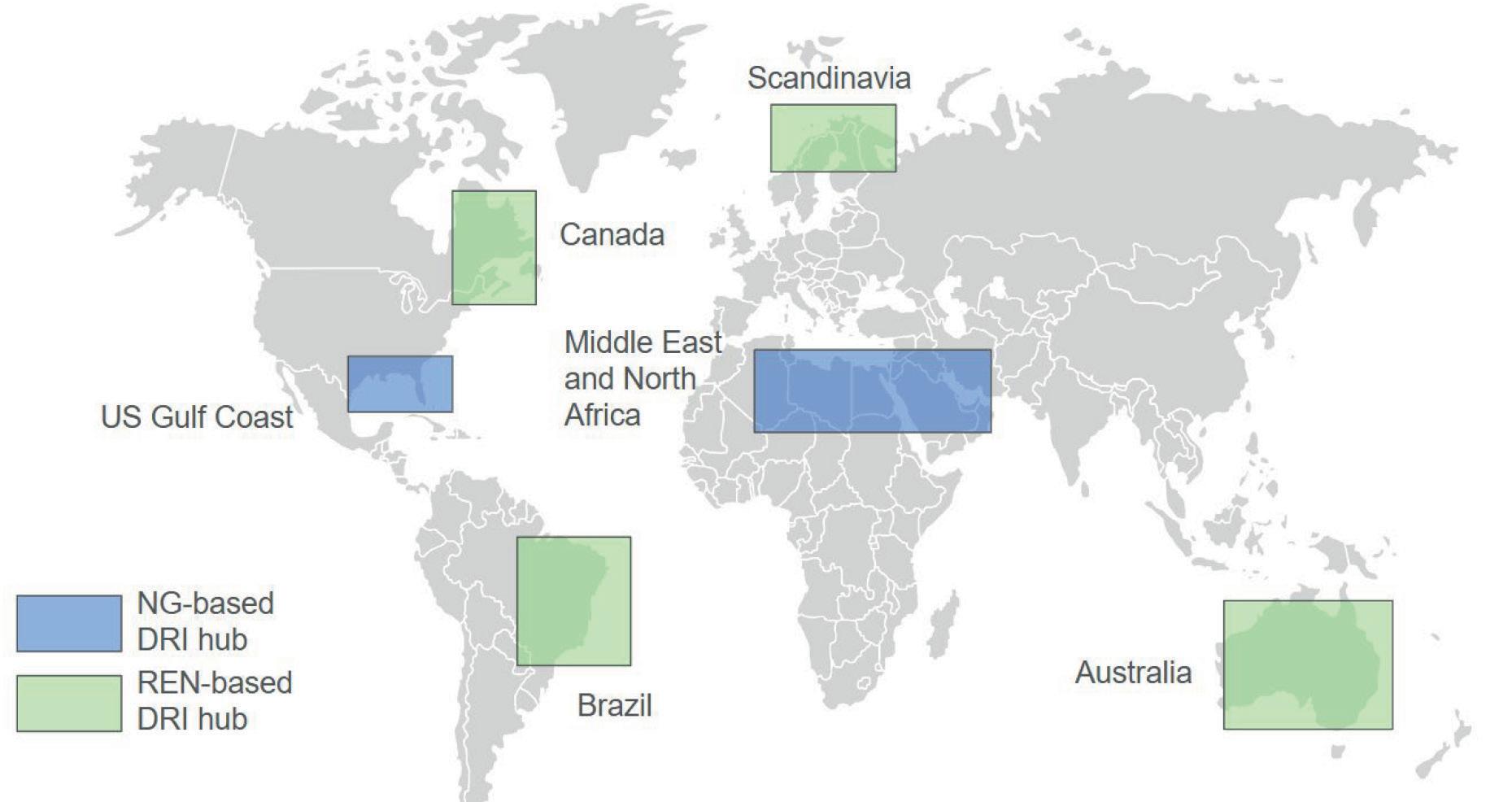

Direct reduced iron

DRI Hubs for the energy transition.

Molten Oxide Electrolysis.

Nickel production – urgent ethical issues.

Filtration Filtration and decarbonization. 41

Decarbonization

Forging the future. 44

Climate policy EU CBAM – the implications.

48

Perspectives: Marr Consulting “We can add significant value.” 51 History

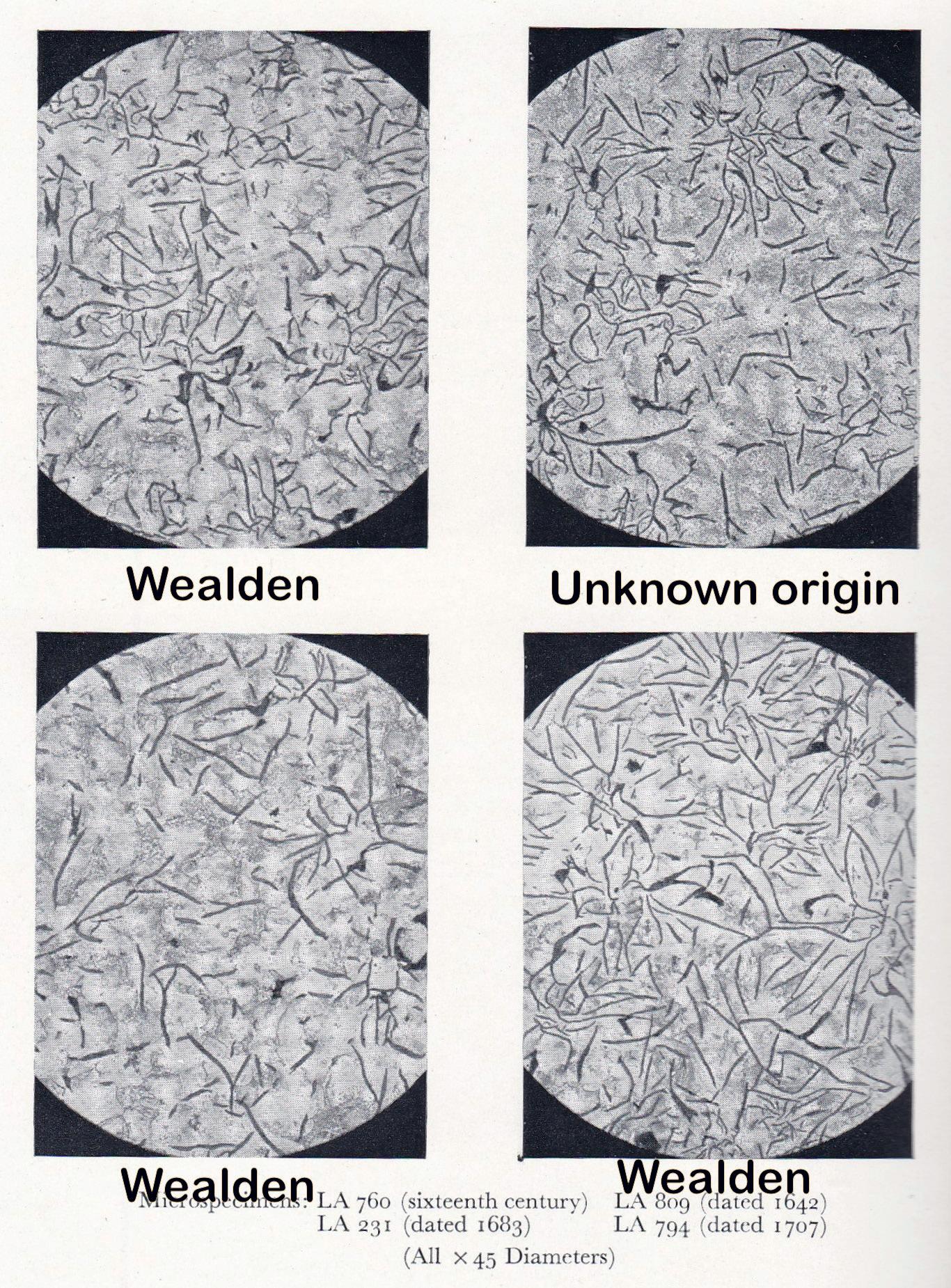

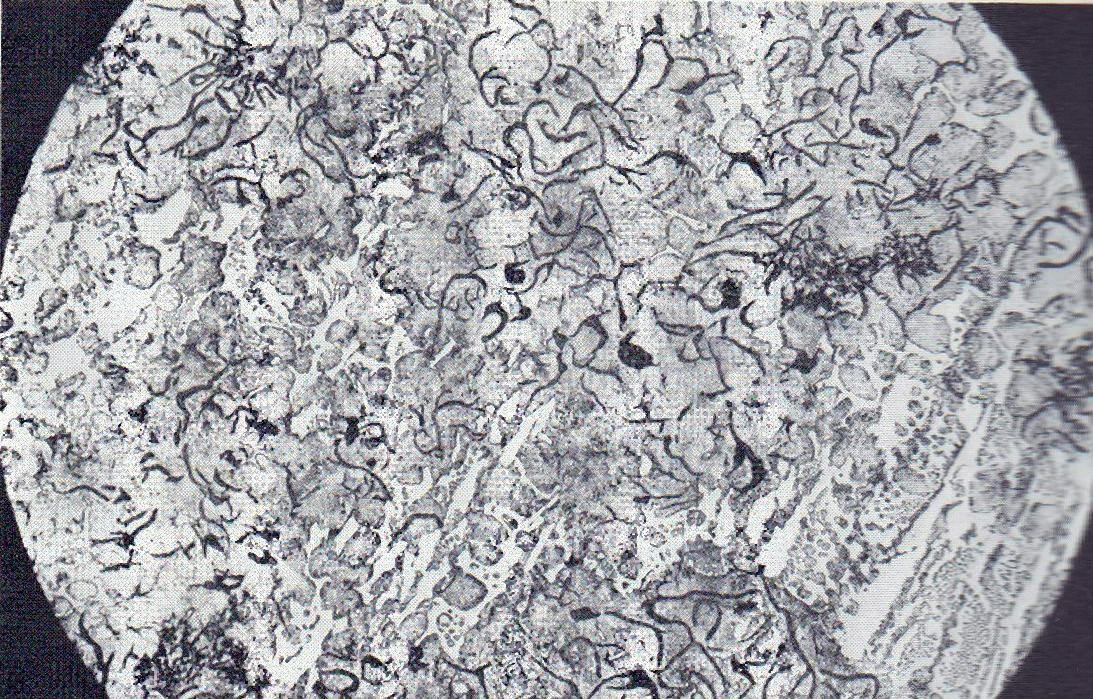

Analysing cast iron firebacks.

Photo courtesy Andrea Fragiacomo (Danieli Automation).

Solid support for President Trump’s tariffs at AISTech 2025

Matthew Moggridge Editor

matthewmoggridge@quartzltd.com

On 3 May I flew direct to Nashville in Tennessee, USA, for what would have been my 12th AISTech convention (had the pandemic not messed up the numbers). As it stands, I’ve attended 10 live events and, as readers know, I love it! This year, like every year, the event was on the money, bringing together the great and the good from the North American steel industry and beyond. In fact, the event is now so popular that it has outgrown previous host venues.

As always, there was plenty to discuss. The key issue was trade, and with President Donald Trump’s second term barely exceeding 100 days, the North American steel industry is 100% on-side with tariffs.

The Town Hall Forum ran with the title of Shake, Battle and Roll and as delegates took their seats in the Karl F Dean Grand Ballroom, battle commenced. Or rather, it didn’t, as everybody appeared to be in agreement, which was good news for the North American steel industry, but not so good for steel industries elsewhere in the world; except, of course, the United Kingdom, which – while I was in Nashville – had its slate wiped clean.

Nicholas R

Kohlhas, senior vice president

of operations and steelmaking at Cleveland Cliffs, said 25% was not enough, telling the audience: “We look at tariffs as a good thing.” He supported across-the-board tariffs with no exemptions and spoke of how there were some products that needed help due to low demand and low pricing. Imports, he argued, played a big role in plant closures.

Dan M Killeen, vice president, Gary Works, for US Steel, agreed, claiming he had been a huge supporter of Section 232. “The Government has made a stand to protect what we value,” he added, stating that tariffs will provide a lot of sustainability moving forward.

While there are counter arguments regarding tariffs, one has to respect the American stance. As Dan J Keown, vice president of Steel Dynamics put it, ‘tariffs are a net benefit to the US steel industry’, arguing that 25% was a good starting point and calling for a targeted approach for the biggest offenders. Perhaps the last word should go to Trevor Saunders of DJJ (part of Nucor) who said a healthy and vibrant steel industry was the end goal as, indeed, was competing on a level playing field. “The health of the industry matters.”

Process

improvement is like climbing. With a strong partner, you

can overcome any

obstacle.

Just as athletes rely on their teammates, we know that partnering with our customers brings the same level of support and dependability in the area of manufacturing productivity. Together, we can overcome challenges and achieve a shared goal, optimizing processes with regards to economic efficiency, safety, and environmental protection. Let’s improve together.

Do you want to learn more? www.endress.com

• A report by Steel Orbis claims that Pittini, a long steel producer from Italy, is to invest in a new rebar rolling mill at the company’s Verona facility. The plan is to be operational by the end of 2025. The plant will produce rebar for the construction industry and will be jampacked with hi-tech systems focused on energy efficiency, process optimization and environmental sustainability. Pittini plans to consolidate it’s competitiveness in the Italian and central European markets.

Source: Steel Orbis, 12 May 2025.

• Submarines are flavour of the month in Singapore at present, as witnessed by the country’s Ministry of Defence ordering two more subs from the German company ThyssenKrupp Marine Systems.

• Following the UK Government’s decision to take Chinese-owned British Steel under its wing in an eleventh hour move to save the steel business from collapse, attention is now focused on Mingyang, China’s biggest offshore wind company, the preferred choice for an offshore wind farm being developed by Green Volt, which is building the first commercial scale floating offshore wind farm in Europe. Green Volt is owned by a Scottish company, Flotation Energy and a Norwegian business, Vårgrønn.

Source: The Guardian, 12 May 2025.

The country had already ordered four subs, two of which have already been delivered and commissioned last September (2024). The latest two subs will be delivered around 2034, it is claimed. Why the interest in submarines? It’s all to do with ‘security’ concerns after Russia’s illegal invasion of Ukraine.

Source: The Defense Post, 13 May 2025.

• Jorge Gerdau Johannpeter, owner and chairman of Brazilian steel giant Gerdau, has blasted US President Donald Trump’s tariffs for dismantling ‘decades of global economic agreements built on international co-operation’, according to a report by Valor International. He accepts, however, that Trump’s actions might be part of ‘a broader negotiating strategy’.

Source: Valor International, 12 May 2025.

• Directors of South Korean steel giant POSCO subsidiary Posco Future M – a manufacturer of battery materials – have approved a rights offering to raise 1.1 trillion won (£771 million) to expand production in

• India’s Supreme Court has ordered the liquidation of 3Mt/yr Bhushan Power and Steel (BPSL) and has rejected an acquisition bid from Indian steelmaker JSW Steel. According to a report by MSN, JSW’s failure to implement a resolution plan over a two-year period was cited by the court. While it is possible for JSW to appeal the decision, a ‘review petition’ is restricted to correcting errors or presenting new evidence. A rehearing is not permitted. The National Company Law Tribunal has adjourned a petition by Janjay Singhal of BPSL for one month.

Source: MSN, 13 May 2025.

• Good news for convenience store owners located close to the construction site of Nucor Steel’s planned West Virginia mill. Elise Crank, store manager of Jerry’s Run Food Mart at the southern end of the Nucor site is reporting booming business and claims that Nucor is keeping her ‘very busy’. Construction workers at the Nucor site can indulge themselves with prepared meals to enjoy at the store or as a takeaway offering. At the northern end of the site, Williams Apple Grove Market, which had a soft opening recently, is expecting similar results.

Source: Mountain Media News, 12 May 2025.

preparation for the growth of electric vehicle sales in the country. The plan is to enhance and expand production in Korea and North America.

Source: The Korea Herald, 13 May 2025.

• Following approval by the Reserve Bank of India, Tata Steel plans to invest $2.5 million in T Steel Holdings, its Singapore-based business. According to a report by Times of India the reason behind the investment is two-fold: one, to bolster its European operations and two, to repay debt. T Steel Holdings is 100% owned by Tata Steel. As is now well known and reported, Tata Steel’s UK and Netherlands businesses are under transformation due to regulatory changes that are ‘driving decarbonization in Europe’.

Source: Times of India, 13 May 2025.

• Governments in Westminster and Cardiff Bay should have been better prepared when Tata Steel UK announced its plan to switch from blast furnaces to one huge electric arc furnace. According to the UK’s Climate Control Committee, Government ministers “should

• News about US tariffs impositions is fast-changing, but Reuters has reported that India is considering import duties (tariffs) on products made in the USA to counter the USA’s steel and aluminium tariffs. No mention of specific products was made.

Source: Reuters, 13 May 2025.

have been better at planning ahead and making sure other green jobs were available locally”, according to a BBC News report. The CCC said that ‘a more proactive and decisive transition plan should have been developed.”

Source: BBC News, 14 May 2025.

• In mining news, Rio Tinto is expecting it’s first shipment of iron ore from Guinea’s Simandou project in November, according to the mining giant’s managing director for Simandou, Gerard Rheinberger. The Simandou project is a Chinese venture in the main with companies like Baosteel controlling 75% of production. The other 25% is in the hands of Rio Tinto, the largest iron ore miner in the world.

Source: Mining Weekly, 13th May 2025.

• A cyber security incident has forced North American steel giant Nucor Corporation to halt certain production at various locations, according

• At the recent China International Metal & Metallurgy Exhibition in Guangzhou, China, Russian steelmaker Magnitogorsk Iron & Steel Works (MMK) was present and looking to drum up business in the Asian market. MMK focused on the sale of hot-rolled coils which, claims a report by Metal Info, are in high demand.

Source: Metal Info, 13 May 2025.

to a report by Reuters. The company has now begun a process of restart operations as an investigation into the attack continues apace. The Reuters report claims that ‘potentially affected systems’ have been taken offline and that Nucor has implemented ‘other containment, remediation or recovery measures’.

Source: Reuters, 14 May 2025.

• International plant builder and technology provider Primetals Technologies is working with a Chinese steelmaker on upgrading the company’s 1-strand thick-slab continuous caster. The upgrade is to expand the caster’s thickness range to 360mm and thus enable heavy gauge plate production for highend applications such as wind turbines, according to a report by Yieh Corp.

The two companies have a long-established association with one another, it is reported.

Source: Yieh Corp, 15 May 2025.

Dedicated solutions to improve your productivity

TotalEnergies Lubrifiants provides a comprehensive range of innovative steel rolling oils, casting fluids and maintenance lubricants. With TotalEnergies Lubrifiants you can:

• Improve product quality and safety standards

• Reduce overall operating costs (TCO) and CO2 footprint (TCO2)

• Significantly increase your productivity

• Decrease in maintenance failures

Tracks to the future

The world’s railway network spans over 1.3 million routekilometres. Urban and highspeed rail infrastructures have scaled up rapidly over the past decade, laying the foundation for convenient, low-emissions transport. As one of the most efficient modes of transport for freight and passengers, continued investment in rail forms a high priority for a more sustainable and resilient future. But how can this look from an engineering level? Here, Harish Maniyoor* analyses the opportunities.

ACCORDING to the International Energy Agency, rail is among the most energy-efficient modes of transport — representing just 2% of total transport energy demand, while accounting for 8% of world passenger and 7% of global freight transport. It’s easy to see why world leaders are taking rail investment seriously.

Railway advancements

In Europe, significant investments are being made to double high-speed rail traffic and increase rail freight volumes by 50% by 2030, as part of the European Union’s sustainable mobility strategy. Elsewhere, the Biden Administration announced nearly $30 billion in investments for rail projects, demonstrating a commitment to enhancing rail infrastructure and service.

Perhaps most significant of all, the railway sector in India has undergone many developments in recent years, driven by government initiatives like dedicated freight corridors (DFCs), high-speed rail projects and the modernisation of railway

infrastructure.

But, to continue driving progress, rail infrastructure will need to undergo substantial upgrades and expansions to meet rising demand, ensure safety and accommodate technological advancements. This includes modernising aging rail networks, increasing capacity through electrification, implementing advanced signalling systems and integrating digital technologies for more efficient operations.

Meeting tough demands

The production of railway components such as axles, wheels, railway tracks, suspension tubes and other structural parts requires high-quality machining tools, capable of delivering exceptional accuracy, durability and efficiency. These components must withstand heavy loads, intense wear and harsh environmental conditions, making precision machining critical to ensuring the reliability and safety of rail systems. High-quality machining tools must offer tight tolerances, con-

sistent performance and the ability to work with a wide range of materials.

Take rail wheels, for instance, which are subject to extreme stresses and wear from continuous contact with rails, often under heavy loads and at high speeds. Several machining challenges present themselves here. First is the need to maintain very tight tolerances, with even a slight deviation from the specified dimensions possibly leading to issues like uneven wear, vibrations or noise during train operation, compromising both passenger comfort and safety.

Another major challenge is working with materials that can withstand the intense mechanical stresses and harsh environmental conditions trains are exposed to. Train wheels are typically made from high-strength steel or steel alloys with excellent fatigue resistance and wear properties. However, these materials are often difficult to machine due to their hardness and toughness. As a result, thermal management during machining is also a key consideration. Machining high-

strength steel generates significant heat, which can cause thermal deformation in the workpiece, affecting dimensional accuracy.

It’s important to recognise that components for different rail types will present their own sets of requirements. Freight trains for instance are heavy, hence the wear on the wheels is high and brake marks from cargo cars often appear on the outer diameter of the wheels. Metro wheels, in contrast, are far smaller and may feature rubber layers between the outer diameter of the wheel and hub to minimise noise. On the other hand, those operating on high-speed rail networks have high demands on exact wheel dimensions, as it is directly related to the comfort of the passenger. To ensure that the wheels are balanced, the tolerances on the outer diameters are high and wheels are frequently re-tuned.

On track with precision machining

There are several machining strategies that, when paired with robust machine tools, can support the production of resilient rail components. Heavy turning is an excellent strategy for machining rail components due to its ability to

handle the large components and high-strength materials involved, as well as its efficiency and precision when working with complex shapes and heavy-duty parts.

Buying tips

When performing heavy turning for rail components, tool life can be significantly improved by focusing on a few key factors. First, choose a cutting tool with a strong, wear-resistant grade that suits the material’s hardness, ensuring stability throughout the cut. Minimise cutting forces by using the right feed rate and depth-of-cut to balance tool pressure, and always ensure proper coolant application to control heat and prevent thermal deformation. Finally, ensure that tool setup and machine stability are optimised to handle high forces and maintain accuracy in turning.

External turning

Sandvik Coromant recommends the T-Max® P product range for external turning, offering enhanced cutting stability, improved chip control and extended tool life to enable precise and efficient machining of tough rail components

such as wheels and axles. Optimised for external turning, from roughing to finishing, T-Max® P handles medium-to-large components in steel, stainless steel, cast iron, heat-resistant alloys and hardened steel. Available with high precision over-and-under coolant and Coromant Capto® quick tool change interface, high stability and minimised tool inventory can be easily achieved in rail machining.

The most suitable turning grades

Additionally, Sandvik Coromant offers recommendations on the most suitable turning grades for your rail application, ensuring a complete machining solution tailored to the specific requirements of the workpiece.

The future of rail infrastructure hinges on precision machining and innovative technologies to meet increasing demands for safety and efficiency. By focusing on effective machining strategies and tailored recommendations, we can ensure that the rail industry not only meets today’s challenges but also paves the way for a sustainable and efficient transportation network for the future. �

With over 50 years in the Steel Industry, we have a wide variety of solutions to keep your mill rolling.

Traversing Restbars

allow for quick and accurate pass changes

· Honours existing mill attachment points and guide base, no machining on your stands required

· Made from stainless steel and speci cally tailored to your mill ensuring perfect t, operation and longevity

Our roller entry guides keep your product on the pass

· Single point, centralized adjustment during operation

· 2, 3 and 4 roller con gurations

· Rigid, stainless steel construction

· Broad size range

Maximize your mill speed while meeting your quenching requirements on all bar sizes. Not just controlled cooling, but correct cooling

· Fewer surface defects and better scale control

· Available in Box, Trough and Restbar-mounted con gurations

The domestic steel industry welcomes President Trump’s “bold new measures” to protect the US steel sector. By Manik Mehta*

The tariff storm rages in the US

THE tariff storm, with tariffs on many products imported into the US, has shaken steel-consuming industries which complain about the rising production costs because of the import tariffs, pointing out that US consumers will bear the brunt of rising costs as they are passed on to them.

Inflation is a sensitive issue in a nation which, some pundits say, is headed towards a recession and high unemployment, thus defeating the purpose of tariffs as an employment-generating tool.

The US announced a sweeping 25% tariff on steel and aluminium imports from all countries. This is the first time that the administration announced sector-based tariffs in President Donald Trump’s second term.

Reaction from the affected trading nations was swift, with the European Union, for example, announcing retaliatory tariffs against the move, targeting US exports worth some $28 billion. China also announced substantial tariffs on US products.

The Japanese chief cabinet secretary Yoshimasa Hayashi called the US tariffs “regrettable”, adding that high-quality steel and aluminium products imported by the US are “irreplaceable and essential” for strengthening the US manufacturing sector’s competitiveness, and did not threaten US national security.

But US Commerce Secretary Howard Lutnick rejected this argument on Fox TV, alleging that “Japan dumps steel.

China dumps steel. That means … they overproduce and sell it dirt cheap to try to drive our guys out of business”.

In 2018, during his first term, President Trump had announced 25% tariffs on steel against China and other countries, citing national security concerns. But the EU and Japan were allowed duty-free quotas for steel imports during Joe Biden’s presidency, with Japan’s annual quota fixed at 1.25Mt effective April 2022. Steel exported in excess of the quota would face tariffs.

While Japan and the US have now agreed to hold further discussions in Washington, Japan’s minister for economic revitalization, Ryosei Akazawa, ‘strongly’ urged the US to reconsider the tariffs on automobiles, steel, aluminium and other products.

Cleveland-Cliffs lays off over 1,200 workers

While the tariffs’ purported aim is to preserve American jobs, it is ironic that some US steel companies are laying off workers. Cleveland-Cliffs said it will lay off workers in Michigan and Minnesota. The company’s operations at its Dearborn, Michigan, plant have been affected by falling automotive demand affecting 600 jobs, according to a company statement. It will also idle work at two iron-ore mines in Minnesota, affecting 630 jobs. ClevelandCliffs said that these actions would allow it to operate more efficiently and in a “more cost-competitive way for the current market environment”, hoping that once

*US correspondent, New York.

President Trump’s policies take full effect and automotive production is re-shored, the company would be able to resume steel production at Dearborn.

Cleveland-Cliffs’ chairman/president/CEO Lourenco Goncalves had maintained during an earnings call on 25 February that tariffs would “penalize the foreign competitors who have been playing by a different set of rules, while strengthening the domestic producers who actually invest in American workers, American manufacturing and American supply chains”.

Nucor also voiced support for the Trump tariffs, though it has some operations in Mexico, a joint venture with Japan’s JFE Steel; the joint venture produces hot-dip galvanized sheet steel for automotive concerns. But Nucor’s performance has fallen short of expectations, considering that its steel mills are predicted to again fall in its Q1 2025 earnings as it did in Q4 2024.

Steel industry applauds Trump Trump claimed that he had saved the US steel industry during his first presidency by using tariffs against China’s ‘massive’ dumping. Indeed, the Section 232 tariffs imposed during his first term were softened by allowing exclusions and exemptions for certain nations if they met some conditions. This time round, such exclusions and exemptions have now been ruled out. Trump claimed recently that his aim was to fortify and invigorate the steel industry.

The steel industry and trade associations welcomed Trump’s tariff announcement. Indeed, in a 2 April statement the Steel Manufacturers Association (SMA) president Philip Bell hailed Trump as a “champion of the domestic steel industry”.

“President Trump is a champion of the domestic steel industry, and his America First Trade Policy is designed to fight the unfair trade that has harmed American workers and weakened manufacturing in the United States,” he said. “On a level playing field, American workers can outcompete anyone,” Bell noted, adding that Trump’s “America First Trade Policy had already started to create American jobs and bolster the domestic steel industry”.

Kevin Dempsey, the president/CEO of the American Iron and Steel Institute (AISI), echoed similar sentiments, saying that the AISI thanked President Trump “for standing up for American workers by restoring fairness in international trade and addressing non-reciprocal trade relationships”.

“American steel producers are all too familiar with the detrimental effects of unfair foreign trade practices on domestic

industries and their workers,” he said.

CFIUS to re-examine US Steel-Nippon merger

After emphasizing last year that he would not like US Steel, a steel industry icon, to be acquired by a foreign corporation, President Trump recently directed the Committee on Foreign Investment in the US (CFIUS) to reexamine the national security aspects of the proposed merger.

A re-examination would ‘help the President determine whether further action would be appropriate’, the administration said.

The CFIUS, during its first review, was unable to make any recommendation to former President Joe Biden who, ultimately, blocked the deal; thereupon, US Steel and Nippon Steel decided to sue the administration on the decision.

US Steel welcomed President Trump’s action, saying that the move by the two merging partners had validated the ‘bold decision’ by the company’s board to challenge President Biden’s ‘unlawful order’.

However, many observers were surprised

by President Trump’s comment that US Steel should remain an American company, after directing the CFIUS to re-examine. “We don’t want to see it go to Japan,” he said.

Nevertheless, some steel industry experts believe the administration would, ultimately, approve the deal though it could stipulate some conditions to be met by Nippon and US Steel.

The two partners argued that the proposed merger could raise the efficiency and competitive vitality of a major player in the strategically important American steel industry, thus also contributing to the overall competitiveness of the American steel industry.

US Steel shareholders had formally approved Nippon’s bid to acquire it for $ 14.9 billion in April 2024.

According to some US studies, including an Atlantic Council analysis, the deal would benefit both the merger partners as well as the US economy, besides enabling Nippon to compete against Chinese firms that dominate global steel markets.

It remains to be seen how this merger saga will further evolve. �

UNLOCK

Scraping export restrictions

Germano Mendes de Paula* looks at the lifting of a 16-year ban on the export of metallic scrap from Argentina following scrap export restrictions since January 2009.

JAVIER Milei is seen as having been elected President because of his promises to deregulate many aspects of life and commerce in Argentina. In January 2025, the government lifted a 16-year ban on the export of metallic scrap. Argentina had put restrictions on scrap exports starting on 8 January 2009, which included materials classified under HS codes 7204.10.00, 7204.21.00, 7204.29.00, 7204.30.00, 7204.41.00, 7204.49.00, 7204.50.00, 7404.00.00, and 7602.00.00.

Initially, the export prohibition on metallic scrap was set to last for 180 days. However, it was renewed multiple times in July 2009, December 2009, June 2010, August 2012, March 2014, June 2015, June 2016, October 2017, October 2018, September 2019, December 2020, December 2021, and February 2023. As a result, the ban was extended 13 times (STI, Nov-Dec 2023, p. 16). This illustrates the persistent nature of restrictions on ferrous scrap exports.

The announcement to end the embargo came from Federico Sturzenegger, Argentina’s Minister of Deregulation and State Transformation, via the Ministry’s website and the Minister’s X account (formerly known as Twitter). The two decrees, 1040/20 and 70/23, were not renewed. The government stated that this decision aims to facilitate the import and export of metallic scrap, thereby reducing production costs for small to medium-sized enterprises (SMEs).

Minister Sturzenegger pointed out that the previous ban was detrimental for several reasons. First, it depressed the local price of scrap, discouraging recycling efforts.

More importantly, the embargo hindered a multitude of recycling businesses across various sectors of the economy. Through his X account, the minister underscored: “President Javier Milei has consistently stated that the power of the State should not be used to arbitrarily redistribute income among market players,” and that “the elimination of such measures is the triumph of freedom over lobbying.”

The removal of the embargo had adverse effects on the interests of Argentinian steelmakers. This development is particularly concerning, as during the first year of Milei’s administration, the country saw a decline in production, including: a 15.4% decrease in pig iron production, a 25.9% drop in DRI, a 21.8% reduction in crude steel, a 32.9% decline in hot-rolled longs (including seamless tubes), a 22.9% decrease in hot-rolled flats, and a 23.5% diminution in cold-rolled flats (STI Digital, Feb 2025, p. 22).

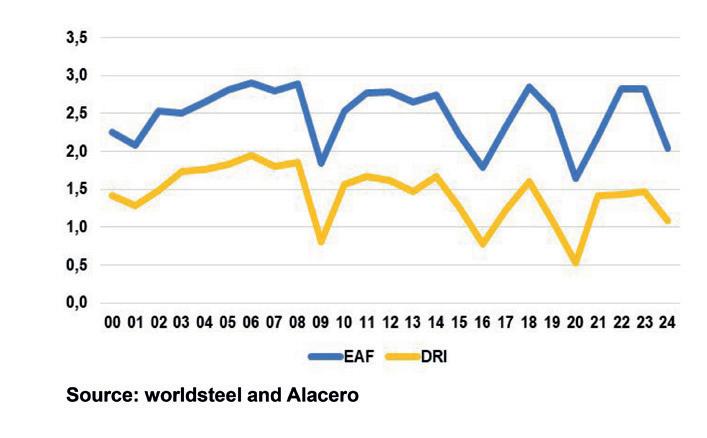

DRI ouput and crude steel production via EAFs

Before analysing the international trade of ferrous scrap, it is important to discuss Argentina’s DRI output and crude steel production via EAFs. Argentina was among the pioneers of adopting direct reduction technology, with TenarisSiderca, a seamless tube manufacturer based in Campana, Buenos Aires Province, commissioning a Midrex module in 1976. This facility currently has a capacity of 960kt/yr and produced 870kt of DRI in 2023, according to the latest available data. Similarly, ArcelorMittal Acindar Villa Constitución,

a long steel producer based in Villa Constitución, Santa Fe Province, began operations with a Midrex module in 1978. This facility now has a nominal capacity of 600kt/yr and produced 558kt of DRI in 2023.

It is noteworthy that Argentina is believed to have very low natural gas prices. As reported by GlobalPetrolPrices, in June 2024, the price of natural gas was $0.017/ kWh for businesses in Argentina, compared to a global average price of $0.065/kWh in the same month.

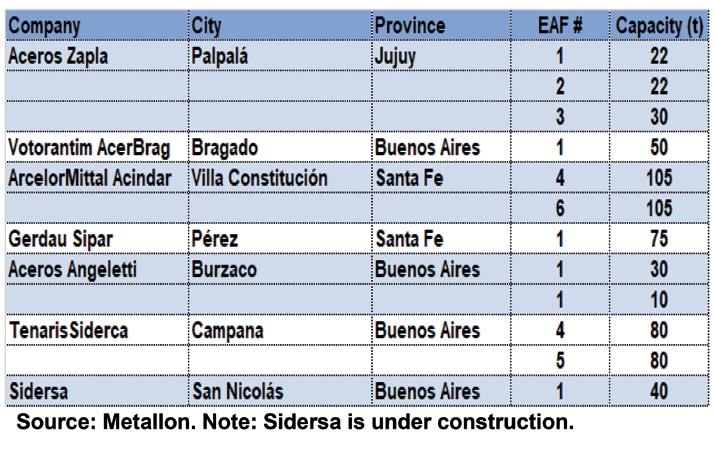

Sidersa’s 360kt/yr steel mill

Fig 1 summarizes the characteristics of the EAFs currently installed and under construction in the Argentinian steel industry. In June 2024, the domestic steel distributor and service centre Sidersa announced plans to establish a steel mill in San Nicolás, Buenos Aires Province, where Ternium Argentina (former Siderar) operates the country’s only coke-integrated mill. The proposed new steel mill will have a capacity of 360kt/yr, focusing on rebar production, and is projected to require an investment of $300 million. The InterAmerican Development Bank is in the process of structuring a sustainability-linked loan, guaranteed for the long-term, for up to $100 million. It is estimated that 30% of output will be exported.

Fig 1 illustrates the trends in crude steel production from EAFs between 2000 and 2024, indicating that it fluctuated around a plateau of roughly 2.5Mt/yr. The lowest production level was 1.6Mt in 2020, impacted by COVID-19, while the

* Professor in Economics, Federal University of Uberlândia, Brazil. E-mail: germano@ufu.br

highest was 2.9Mt in 2006, during the commodities boom. Notably, in 2017, Gerdau commissioned a greenfield steel shop in Pérez, Santa Fe Province, with a capacity of 650kt/yr at a cost of $232 million. Despite this new EAF, the country was unable to surpass the production peak recorded in 2006.

Additionally, Fig 1 indicates that DRI production between 2000 and 2024 averaged around 1.4Mt/yr, exhibiting a similar timing pattern with minimum and maximum values of 525kt in 2020 and 1.9Mt in 2026, respectively. On average, DRI output was equivalent to 58% of total steel production through EAFs, along the period 2000-2024.

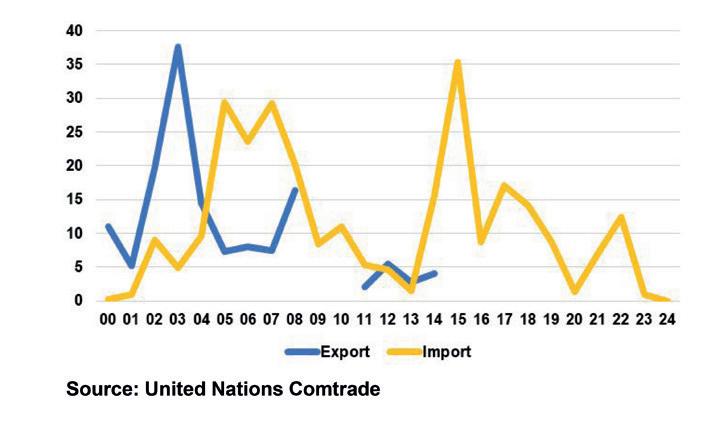

Ferrous scrap trade

Fig 2 focuses on Argentina’s international trade in ferrous scrap, utilising data from United Nations Comtrade. From 2000 to 2008, the year prior to the imposition of the export embargo, Argentina maintained a balanced trade flow, exporting and importing an average of 14 kt/yr. However, following the embargo, exports occurred in only five years, averaging just 3 kt/yr, while imports decreased to 9kt/yr.

The highest level of ferrous scrap exports was reached in 2003, with an export volume of 38kt. Conversely, the peak of import volume was recorded in 2015 at 35kt. It is noteworthy that even prior to the export ban, the volume of international

trade was relatively modest. Following the embargo, as mentioned previously, annual imports declined too. In this context, Argentina managed to navigate the restricted scrap reservoir, which is common in emerging countries, by adopting DRI technology early on.

President Milei’s choice not to renew the ferrous scrap embargo was part of broader efforts toward trade liberalisation. Nevertheless, this decision contradicts the prevailing trend observed in the global steel industry, where an increasing number of countries have been imposing restrictions on scrap exports due to limited scrap reservoirs and rising demand for decarbonisation efforts. �

1500C for

> MAX efficient – maximum service life with optimum cost-effectiveness

> MAX flexible – easy handling and installation, blankets are highly flexible and provide high mechanical strength

> MAX compatible – fits with the entire ALTRA® product range – non-classified according to CLP

Fig 1. Argentina’s DRI and EAF steel production, 20202025 (Mt).

Fig 2. Argentina’s ferrous scrap exports and imports, 2000-2024 (kt).

Table 1. EAFs in Argentina.

Protection from cheap imports

The recommendation by the Directorate General of Trade Remedies (DGTR), the Indian agency responsible for investigating fair overseas trade practices, to levy a 12% safeguard duty for 200 days on cheap steel imports has brought much-needed relief to domestic primary steel producers, says Dilip Kumar Jha*

FOLLOWING the DGTR’s recommendation, India’s Finance Ministry must notify the same or modified guidelines to ensure the implementation of the safeguard levy. The categories covered under the proposed duty include hot-rolled, cold-rolled, and coated steel products.

Until then, finished steel imports will continue at an accelerated pace, especially from China and Vietnam, as these countries face a challenging global business environment amid US President Donald Trump’s persistent threats to impose secondary import tariffs, either directly or indirectly. Surplus-producing countries, such as China and Vietnam, are finding it increasingly difficult to access the US market. The safeguard duty has been proposed for 5.34Mt of flat steel imports, representing 62% of the total import volume in the financial year (FY) 2023-24, thereby limiting the scope for a significant reduction in import volumes.

As European markets continue to struggle with economic growth, the only viable market left for these steel-surplus countries is India, which has achieved the fastest economic growth even in a challenging environment. Notably, the Reserve Bank of India (RBI) projects India’s GDP growth at 6.5% for FY 2024-25 (April-March), potentially the fastest among major economies, although lower than the 9.2% recorded in the previous year.

Rationale behind the duty

India, the world’s second-largest steel producer, recorded its highest finished steel imports in recent years at 8.32Mt during

Source: Joint Plant Committee

FY 2023-24, compared with 6.02Mt the previous year and 4.67Mt in FY 2021-22. The over 38% increase in imports from the previous year and an almost 100% surge from FY 2021-22 were driven by the economic slowdown in Europe and trade disruptions in the Red Sea caused by continuous Houthi attacks on merchant ships in the Suez Canal.

As a result of these disruptions, exporters from China, South Korea, and Japan redirected their shipments to India, offering steel at prices substantially lower than the prevailing domestic market rates. Local steel producers experienced reduced orders from downstream industries, despite robust demand, as their products with similar specifications were 7–8% more expensive than imported alternatives.

The DGTR has determined that critical circumstances exist where any delay in applying provisional safeguard measures would cause irreparable damage, necessitating immediate action. The imposition of a safeguard duty on steel imports has been a long-standing demand of the industry. While the government sympathizes with the concerns of the

*India correspondent.

domestic steel sector, it seeks to balance the interests of local producers with those of downstream and end-users, ensuring the availability of affordable steel.

India’s leading brokerage firm, Kotak Institutional Equities, noted that domestic steel prices are already at a 7–8% premium to import parity, leaving little room for further price hikes if a safeguard duty is implemented. “While margins for these companies have bottomed out in the December quarter, potential supply reforms in China pose an upside risk,” it added.

A breather

If implemented, the 12% safeguard duty on imports of alloy and non-alloy steel flat products for a period of 200 days will provide significant support to domestic steel prices. The levy is expected to create room for an increase in domestic steel prices by up to 13% (comprising the safeguard duty of 12% and a 10% cess on the safeguard duty), amounting to approximately INR 6,000 (~US$71) per metric tonne of hotrolled coil (HRC) based on prevailing prices in February 2025, while keeping prices competitive.

India’s steel scenario

“The move is likely to provide some relief to the subdued profitability of domestic steel players, who have been facing headwinds due to increasing import volumes of low-cost products since October–December 2023. The surge in imports resulted in a decline in EBITDA margins to around 10% in April–December 2025, compared to approximately 12% in FY 2022-23 and FY 2023-24. The anticipated increase in steel realisations will improve the spreads of domestic steel producers, as raw material prices are unlikely to rise in the same proportion. Furthermore, debt levels are expected to reduce from FY 2024-25, as major industry players completed significant capital expenditures to capitalise on the demand prospects for FY 2025-26,” said Rohit Sadaka, director and head of materials and diversified industrials at India Ratings, a leading credit rating agency.

Impact

Imports originating from developing countries, except China and Vietnam, shall be exempt from the levy of safeguard duty

as they account for less than 3% individually and less than 9% cumulatively of the total imports of non-alloy and alloy steel flat products. These imports are not considered a threat. The safeguard duty has been imposed on 5.34Mt of flat steel imports in FY 2023-24, representing 62% of the total flat steel import volume and 58% of the total import volume into India in 2024. This may limit the scope for a significant reduction in import volumes.

The safeguard duty on steel imports will primarily benefit flat products, including hot-rolled flat products, cold-rolled flat products, and coated steel coils, sheets, and plates. These include hot-rolled (HR) coils, sheets, and plates, HR plate mill plates, cold-rolled (CR) coils and sheets, metalliccoated steel (zinc, aluminium-zinc, or zincaluminium-magnesium), and colour-coated steel. However, higher-priced value-added and specialized steel products, such as cold-rolled grain-oriented electrical steel, cold-rolled non-oriented electrical steel coils and sheets, coated electro-galvanized steel, tinplate, stainless steel, and various other coated or clad steels, are exempt from the duty.

Imports of hot-rolled coils, sheets and plates, HR plate mill plates, cold-rolled coils and sheets, metallic-coated steel, and colour-coated steel will also be exempt if their cost, insurance, and freight (CIF) import prices meet the specified thresholds. Currently, the CIF prices of these products are approximately 25% lower than the threshold prices. This will help protect end-user industries from significant cost increases, thereby limiting the overall impact of the duty.

Outlook

India’s move is expected to support the profitability of the domestic steel sector by enabling higher realisations, particularly for large integrated flat steel producers, thereby providing sufficient headroom to absorb external challenges. However, given the sustained global oversupply scenario, the measure may not significantly curb import volumes if exporters choose to lower their base prices to remain competitive in the Indian market until the global demandsupply balance improves. �

Exclusive Sale at Hyundai Steel Dangjin, South Korea

Hot Compact Strip Mill

Hyundai Steel Dangjin Facility (widely known as “Thin Plate Mill”) is a premier steel production plant featuring a Compact Strip Process (CSP) as the main production line, complemented by a 150 -ton Heat-size.

Carbon capture: utile or futile?

Is carbon

capture

an ‘essential tool’ in the fight against climate change, or a distraction from the reality of its true potential?

By

Stefan Erdmann*

LAST year was the planet’s warmest year on record. Global average temperatures reached 1.46°C above pre-industrial levels. Scientists warn that if greenhouse gas emissions continue at current levels, we could see temperature increases of up to 5°C in the coming decades.

Steel production accounts for 10% of global greenhouse gas emissions. On average, for every ton produced, 1.89 tons of CO2 are released. In 2023, the steel industry reached a market value of $928 billion, producing nearly 2 billion tons of steel. By 2050, we need to cut emissions by 90% compared to 2022 levels to meet global decarbonization targets.

Innovation, then, is imperative – but where should the focus be? One of the critical debates today is the role of carbon capture and storage. Is it an essential tool in the fight against industrial carbon emissions? Or could it be a distraction that diverts attention from deeper systemic change?

Reduction versus removal: getting the balance right At Outokumpu, despite the high alloying

content of our stainless steel, we have managed to lower our emissions to 1.52 tons of CO2 per ton of crude steel (2023). This progress highlights the importance of tackling carbon reduction at every stage of production.

Direct emissions are primarily from fossil fuels used in ferrochrome production. Switching to bio-based alternatives or moving towards a carbon-free reduction process could dramatically cut emissions. Buying in carbon-free electricity sources – wind, solar, nuclear and hydro – can address indirect emissions. That shift is speeding up thanks to regulatory pressures like the European Union’s Emissions Trading System.

But what of value chain emissions? Low-carbon raw materials might not yet be

:*Chief technology officer, Outokumpu

viable at scale – but we can’t afford to wait for the perfect solution. So that’s an area where carbon capture can come into play.

In my view, we should always prioritize carbon reduction where it’s feasible and economically viable. Carbon capture can play a part only where deep reductions are currently unachievable. Economic realities, advances in technology and industrial collaborations will ultimately dictate the optimal balance between the two.

Repurposing captured carbon presents a strategic opportunity

Critics argue that carbon capture risks becoming a costly excuse for maintaining business-as-usual operations, rather than driving necessary systemic change. Others see it as a vital technology that complements other decarbonization efforts.

For instance, in sustainable fuels and green chemicals manufacturing, captured CO2 and CO can serve as essential feedstocks – helping other industries to decarbonize in the process.

At Outokumpu, we are actively exploring carbon capture for both utilization and storage as part of our broader

decarbonization roadmap. As we increase our use of biocoke, these carbon gases will transition from gray to green – creating new industrial opportunities while reducing emissions.

So why isn’t carbon capture scaling up faster?

It’s a sizeable upfront investment to build the infrastructure for storing or utilizing captured carbon. Businesses will hesitate to make large-scale commitments without strong economic incentives, and dedicated infrastructure for CO2 transportation and storage is not yet widely available in many key steel-producing regions.

Captured carbon must also have viable market applications, for which we need more cross-industry collaboration. Industrial symbiosis, where companies share resources and infrastructure, is still in its infancy.

Expanding global carbon pricing mechanisms and trade policies to encourage decarbonization could also make capture and storage more viable, while regulatory support and green procurement policies – along with private investment –

can drive stable demand for low-emission steel.

We need a co-ordinated policy framework for carbon capture

We can make carbon capture a meaningful part of the decarbonization toolkit. To do that, we need:

• regulatory frameworks to encourage industries to share CO2 resources and infrastructure, creating viable carbon markets

• government investment in zeroemission energy, prioritizing grid

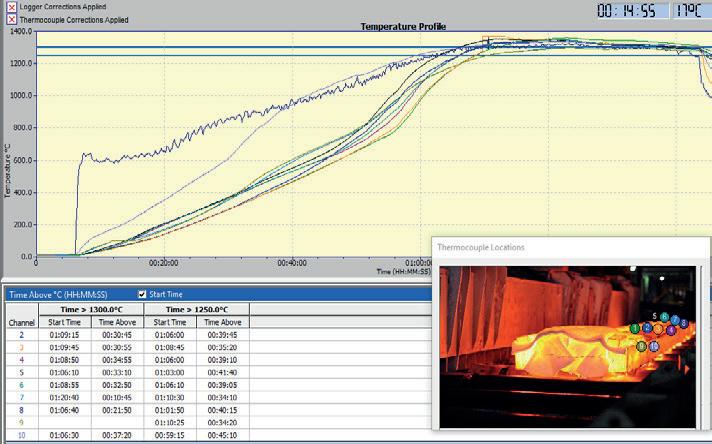

Temperature profiling for Steel Reheat Applications

decarbonization and energy storage solutions

• expanded emissions trading systems and harmonized carbon border adjustment mechanisms to drive investment in lowcarbon steel production

• regulatory alignment with clear, long-term incentives for decarbonization technology investments, rather than shortterm subsidies.

Let’s embrace carbon capture as a tool, not a support

At Outokumpu, we are driving the next generation of low-emission stainless steel by investing in both direct reductions and smart carbon capture applications. As the transition speeds up, steelmakers cannot wait for regulations to force change – we must create scalable, economically viable solutions now.

The green transition is not just a necessity – it is an opportunity. But to seize it, industry players must act decisively and collaboratively. The time for debate is over; the time for large-scale implementation is now. �

Tariffs are causing problems for everybody, but the North American automotive industry finds itself in a state of flux as it tries to second guess what’s going to happen next in terms of tariffs and retaliatory tariffs. Auto production is expected to slip and it will never go back to pre-pandemic levels, says Myra Pinkham*

In a state of flux

MUCH like many other steel consuming end-use markets, the North American automotive market – which had been relatively flattish for much of the past year or so – is currently somewhat in a state of flux given a lack of clarity about what impact tariffs, tariff retaliations and other changes under Trump 2.0 will have.

This has been increasingly challenging given the ever-changing news about the auto, reciprocal and retaliatory tariffs. That was well illustrated by the 9 April announcement by the Trump administration that certain reciprocal tariffs (not including those upon imports from China) that were to be implemented that day will now be delayed another 90 days. However, at least for the time being, it appears that the recent automotive, steel and aluminium and Chinese, Canadian and Mexican tariffs remain in effect.

At the time of going to press, US reciprocal tariffs upon Chinese imports and retaliatory tariffs upon US imports by China were being raised measurably, sometimes on a daily basis. However, it appears as if the US tariffs upon Canadian and Mexican autos and auto parts and the 25% Canadian retaliatory tariff upon those imported from the US only include those that aren’t compliant with terms of the United States-Mexico-Canada Agreement (USMCA), which is very significant given that, several industry observers have noted that at times auto parts and components are transported between the three countries

six times or more.

Meanwhile another question being asked is what this means for the companies that supply the steel used by automotive and auto parts manufacturers.

“Actually, NA auto sales and production have been on a wild ride for a while,” Mike Wall, executive director of automotive analysis for S&P Global Mobility, said. That started in 2020 at the beginning of the Covid pandemic when North American light vehicle output fell to about 13 million units, Wall noted, but was followed by the resultant supply chain issues and a rebuilding, then a drawdown, of inventories.

He pointed out that even with consumer demand generally holding up, NA light vehicle production over the past several years never got back up to the 16.3 million unit level it had achieved pre-Covid. In fact, after its production peaked in 2023 at 15.7 million vehicles, it inched back down to 15.4 million units last year – largely because the automakers built up their inventories too well.

*North America correspondent

The NA automotive industry is now at an interesting crossroads, Jonathan Smoke, Cox Automotive’s chief economist, declared during the company’s recent forecast webcast. He noted that while at the end of last year Cox believed that the auto market would perform to the upside this year, it has since downwardly revised its forecast, largely because of concerns that both recently implemented tariffs and the expected additional tariffs (and retaliation to them) will likely be highly disruptive to NA vehicle production and could lead to a full-scale global trade war and a much weaker economy.

Smoke said that not only have the Trump administration’s policy changes been far more aggressive than expected, but that he doesn’t believe that they are a negotiation gambit, but rather an attempt to restructure the US auto market in a way to favour domestic production.

Other analysts have expressed a similar point of view. Bill Rinna, director of Americas vehicle forecasts for GlobalData, said that, while prior to the Trump

administration’s tariff announcements NA auto production was expected to remain largely flattish this year, there is now considerable downside risk with the output potentially falling to 14.5 million light vehicles in 2025 and to 14.3 million light vehicles next year.

John Anton, director of S&P Global Market Intelligence’s pricing and purchasing service, said perhaps the biggest problem has been the Trump administration’s tendency to constantly change its policies, particularly those related to import tariffs, including that on auto and auto parts, on steel and aluminium or on other products.

It has, however, been going beyond that, noted Philip Gibbs, a senior equity analyst, explaining that while there was initially a lot of optimism about the pro-business nature of the new Trump administration, now

changing market dynamics and regulatory policies.

“The automakers want the certainty that they get from long-term consistent policies to enable them to make the necessary investment and business decisions, Mark Schirmer, Cox Automotive’s director of industry insights, declared. “However, the uncertainty surrounding such factors as tariffs, interest rates, fuel economy and emissions standards and electric vehicle (EV) incentives has made it hard for the auto OEMs to make such plans.”

In fact, while it varies by company, there have been reports that the 25% auto tariffs are having at least a temporary negative impact upon the domestic Big Three automakers. Most notably Stellantis announced that it was temporarily laying off a total of 900 workers at five of its US

many see its actions as being more proconfusion and pro-inflation.

He said that is the case for the tariffs that the administration has imposed upon autos and are expected to be imposed upon automotive components in early May (although, based upon recent history that it isn’t absolutely certain when they will go into effect if they do at all), as they could impact automotive production cost and, if so, that cost increase would flow down to the consumer. “That will definitely be a watch point.”

It is widely believed that government policies as a whole have been and will continue to have an impact upon the auto market and that automakers will be adjusting their product offerings and production strategies in response to these

facilities as well as pausing production at two assembly plants in Canada and Mexico.

Ultimately it is expected that the tariffs will result in more reshoring, but industry observers note that it will take time for the automakers to reconfigure their operations and supply chains.

While recently a lot of attention has clearly been paid to the impact that tariffs will have upon the US auto market, some of Trump’s other policies, as well as other market dynamics, have been and could continue to impact the auto market in a number of ways, including its vehicle and materials mix, and, therefore, have an impact upon demand for steel (and other metals) for automotive applications and, therefore, investments in auto and steel plants.

Even under past administrations –including Biden’s – internal combustion engine (ICE) vehicles have remained the vehicle of choice in the US. However, largely due to incentives, such as those that were in the Inflation Reduction Act (IRA), and the general push towards sustainability and lower carbon emissions, demand for electric vehicles – both battery electric vehicles (BEVs) and hybrids – have been picking up, albeit much slower than was anticipated about five years ago.

S&P Global’s Wall noted BEVs in particular remain very much a work in progress with their consumer demand being clearly not as strong as US automakers had hoped. In 2024 they only had about a 10% share of domestic sales and that share is only expected to grow to about 10% this year given the still strong consumer interest in certain higher fuel efficiency ICE vehicle models.

But he said that there has been growing interest in hybrid vehicles – both traditional full hybrids and plug-in hybrids. KeyBanc’s Gibbs called hybrids an intriguing consumer option given that they are not as dependent upon charging infrastructure and could be a more affordable option. Other market observers agree, calling them a great bridge between ICE vehicles and BEVs.

Bill Rinna, director of Americas vehicle forecasts for GlobalData, believes that BEVs could potentially see some downward pressure from the Trump administration, especially if it eliminates some of the incentives which currently make BEVs somewhat more affordable. He noted that this comes while BEV demand continues to be hampered by the range anxiety of consumers given the weight of their battery packs and with charging infrastructure availability paling.

Amid these dynamics some domestic BEV programmes have been pushed back, delayed or cancelled by both legacy and start-up BEV automakers. For example, Leonard Ling, automotive knowledge manager at Ducker Carlisle, noted that Ford’s new West Tennessee plant has been delayed from 2025 to 2027, Toyota delayed the start of EV production at its new North Carolina plant until the first half of 2026 after delaying EV drive unit production at its Toledo (OH) Propulsion Systems plant until Q4 2024. General Motors delayed the start of production at its Indiana battery plant until 2027 and temporarily halted production of its BrightDrop electric delivery

van in Ontario.

On the other hand, in late March Hyundai formally announced plans to invest $21 billion in the US, including a 2.7Mt/ yr electric arc furnace (EAF) steel mill in Louisiana (its first in the US) that, once online in 2029, will provide steel for the EVs it plans to produce in Georgia and Alabama.

Philip Bell, president of the Steel Manufacturers Association (SMA) said he viewed this announcement as being positive for the US steel industry seeing it as an indication that the tariffs are incentivizing steel industry investment and production in the US and that mills can make a variety of auto grade steels using EAFs.

But given that consumers are voting with their dollars (especially in these uncertain economic times), and with BEVs continuing to be more expensive than other types of cars, S&P Global’s Wall said they are particularly showing interest in higher fuel efficiency ICE and hybrid vehicle models. GlobalData’s Rinna agreed, noting that while down from 95% in 2019, ICE vehicles still have a 75% share of US light vehicle sales and that the hybrid share has increased to 12% from 3% over that timeframe.

Even with these dynamics, as well as expectations that the Trump administration could eventually seek to ease US emissions and fuel efficiency regulations, Abey Abraham, Ducker Carlisle’s managing principal, said that automakers will continue to take a mixed mosaic material approach to further lightweight their vehicles, declaring that there isn’t one silver bullet strategy to do that.

Abraham said that automotive engineers are increasingly using different materials for different applications. “They are not taking square pegs and trying to fit them into round holes,” he explained. “Automakers need to be very precise about how they control the weight of their vehicles and how they balance that with their costs, while also making vehicles that consumers want to drive,” which, he said, isn’t an easy task.

Ryan McKinley, a senior CRU steel analyst,

said that for a while – especially after Ford introduced its aluminium-bodied F150 pickup truck in 2016 and when demand expectations for BEVs (which use about 30% more aluminium than ICE vehicles) were higher – that aluminium would be overtaking steel in many vehicles.

But while aluminium is expected to make further inroads, it is generally believed that the rate of the transition will not be nearly as pronounced going forward, especially given the cost differential between steel and aluminium.

Less pressure to use aluminium?

Also, under the Trump administration’s policies, automakers could feel less pressure to lower the steel content for North American-produced vehicles, which, McKinley said, averages about one ton per vehicle (but about 0.8 ton for BEVs). He noted, however, that steel volumes could also be affected by moves to replace some of the vehicles’ mild steel with advanced high strength steels (AHSS), which is lighter in weight.

While AHSS is more expensive than some of the mild steel it is replacing, it is less expensive than aluminium.

This comes as NA steelmakers are making moves to either maintain or increase their automotive exposure.

KeyBanc’s Gibbs pointed out that given their incumbency, the few remaining domestic integrated steelmakers –Cleveland-Cliffs and US Steel – continue to have a stronghold upon the auto sector and are desperately trying to hold onto that, given that it is pretty much their last market niche, with the potential exception of white goods.

Cleveland-Cliffs, however, announced in late March that it was idling some of the operations at its Dearborn, MI, plant due to softer than desired automotive demand. However, the company expressed confidence that production would be resumed should the policies of the Trump administration result in the reshoring of auto production as expected.

But at the same time EAF steelmakers are

making some inroads supported by all of the new EAF steelmaking capacity that has either recently come online, is expected to come online soon or has been announced.

S&P Global’s Anton pointed out that in addition to Hyundai’s planned Louisiana steel mill, there are a number of other EAF capacity increases or planned increases to produce steel for auto applications.

While it has come online slower than initially anticipated, Steel Dynamics has recently announced that its Sinton, TX, greenfield sheet mill is now at over 80% of its production capacity. Anton said that similarly, Nucor has completed the expansion of its Gallatin mill in Ghent, KY. The company’s greenfield Apple Grove, West Virginia, flat roll mill is expected to come online either next year or early in 2027. Anton said there was some additional capacity coming online to produce rod and bar for automotive applications.

One looming question, however, remains whether US EAF steelmakers will also be able to make exposed auto sheet.

While SMA’s Bell says that EAF steelmakers can make any type of steel required for automotive applications, Anton pointed out that despite trying to break into that market for the past 15-20 years, to date they have only made very meager inroads with the auto OEMs being reluctant to buy steel for those applications from them and he said he isn’t sure if and when that will change.

“In the near term, the US auto market is in a bit of a holding pattern with all of the uncertainty – including the impact of the tariffs and other governmental policies having a negative impact upon consumer sentiment,” Gibbs said.

Wall agreed, stating that S&P Global believes that while NA auto production will slip slightly this year, it will still remain well above pandemic lows, albeit not quite back to its pre-Covid levels. “Also, as long as the market doesn’t blow up because of the tariffs I am hopeful that light vehicle production will improve year-on-year in 2026.” �

DYSENCASTER®

HYDROGEN-READY AND ELECTRIC TUNNEL FURNACES

Performances, operational reliability and quick startups are the result of 30 years of continuous R&D activities, carried out at the Danieli research center and onsite together with partnering customers.

QSP-DUE can make use of more than 20 Danieli patents covering technological layouts, production equipment and Danieli Automation solutions, such as power, instrumentation and intelligent digital controls.

— The most efficient, digitally controlled electric steelmaking with no impact on the power grid.

— 6 m/min casting speed, allowing up to 4.5-Mtpy productivity on a single strand, with dynamic adjustment of slab thickness and width at any speed. In-mould fluidodynamic control with MultiMode Electromagnetic Mould Brake (MM-EMB) for no quality limitation.

— Hydro-MAB burners ready for 100% hydrogen operations and electric tunnel furnaces for carbon-free slab reheating.

— Split mill layout, intensive cooling and dynamic transfer bar reheating for true thermomechanical rolling and endless operation of ultra-thin gauges.

— Danieli Automation robotics and artificial intelligence for zero-men on the floor.

— Least power-consuming process with the lowest carbon footprint.

— The most competitive plant in terms of CapEx and OpEx.

— The highest production flexibility due to three rolling modes available in a single line.

QSP-DUE® ENDLESS CASTING-ROLLING PLANTS

UNIQUE PATENTED DANIELI TECHNOLOGIES

THE TRUE AND ONLY ONES

PERFORMING WORLDWIDE

SGJT and Yukun are enjoing their QSP-DUE plants operating in coil-to-coil, semi-endless and endless mode, based on HRC market requests. The Nucor Steel QSP-DUE plant is under construction.

15 QSP PLANTS

DANIELI THE COMPETITIVE GREEN STEEL

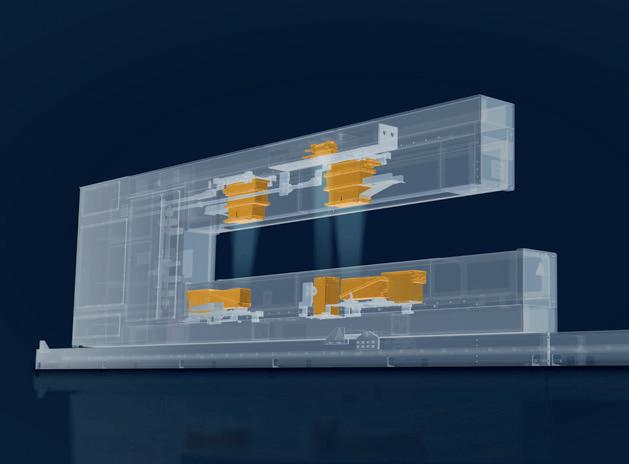

How automation orchestrates efficiency

IN the world of metal processing, the journey from raw material to a highquality finished product is an intricate series of steps. While the metallurgical processes themselves – annealing, pickling, galvanizing – take centre stage, the unseen maestro behind peak performance is often the control and automation system.

The quality of processed metal is determined by the quality of the technology used in its processing. Surface characteristics, flatness, and strip tensions must be perfectly monitored and controlled to produce a flawless product. Ensuring each element of the processing line is synchronized and operating harmoniously is the exact job that the control system is there to do. It dictates the precise speed and tension of the metal strip as it travels through numerous stages, from unwinding to coiling. This seemingly simple task becomes critical when dealing with materials of varying thicknesses, widths, and material grades.

The power of precise control

Control and automation systems act as the central nervous system of processing lines, silently ensuring efficient and consistent operation. At the heart of

these systems lie sophisticated control algorithms that constantly monitor and adjust strip speed and tension throughout the line. These algorithms consider multiple factors, including material properties, line configuration, and real-time feedback from sensors positioned along the line.

By maintaining continuous monitoring and precise adjustments, ABB’s control systems, including ABB Ability™ System 800xA distributed control system (DCS) with the Roll@xA and the ABB Ability™ Manufacturing Operations Management for metals software solutions, as well as digital twin solutions, contribute to reduced product defects, improved productivity, and material savings. Consistent tension throughout the line minimizes the risk of breaks, tears, or uneven coiling. Optimized speed settings ensure the line operates at its peak capacity without compromising quality. These improvements translate to significant cost reductions for metals manufacturers.

One prime example of this efficiency in action is the recent implementation of ABB’s advanced processing line solutions based on the aforementioned DCS, for Jindal Stainless Ltd. at its Kalinganagar facility. This complex project, commissioned

in 2023, underscores how automation can transform a metal processing line, driving productivity while maintaining superior quality.

Jindal Stainless Ltd case study: Orchestrating success through automation

In 2021, Jindal Stainless Ltd, an Indian stainless-steel producer, embarked on an ambitious project to install a Direct Reduction Annealing and Pickling (DRAP) line at its facility in Kalinganagar, Odisha. The DRAP line was designed to enhance the company’s production capabilities by enabling the processing of both hot- and cold-rolled stainless steel coils – earning it the moniker ‘Combo Line.’

The project was a collaboration between Jindal Stainless Ltd. and ABB, with ABB providing the advanced control and automation systems required to manage this complex processing line. ABB’s comprehensive solution included the Ability™ System 800xA automation platform, incorporating the high-end AC 800PEC controller for process control and the AC 800HI controller for safety functions. In addition, ABB implemented low- and medium-voltage line drives, auxiliary drives, and advanced mathematical set-up models

In metals processing, the smallest variations can significantly impact quality, explain Andreas Vollmer* and Deng Bo**

Beyond control:

for inline tandem mills, ensuring precise synchronization and optimal operation. The project team worked diligently from 2021 to 2023, utilizing digital twin technology for in-house testing, which enabled seamless system implementation.

Challenges and solutions

One of the primary challenges faced in this project was the need to commission a highly complex processing line equipped with advanced technology, including a 3-stand S6-high inline tandem cold mill, degreasing section, furnace section, scale breaker, shot blaster, pickling section and 2-high skin pass mill. This required precise synchronization of multiple sophisticated components, such as the automatic roll change device, the auto sequences for entry and exit sections, and micro-tracking for section setpoint handling, all while maintaining high-speed operation and quality output.

Based on ABB’s extensive experience with similar projects, including their previous work with Jindal Stainless Ltd. on the hotand cold rolled annealing and pickling lines in 2010-11, ABB delivered a control system that included features such as accurate load share control of driven rolls, tension control across the line, and advanced thickness control solutions. These features ensured

that the processing line could operate smoothly, even under the demanding conditions of producing both hot- and cold-rolled coils.

Technical innovations

The DRAP line was outfitted with several technical innovations that [ABB claims] set it apart from other solutions available on the market. Key among these was the rollable weld system, which allowed for seamless transition through the inline 3-stand tandem cold mill and the inline skin pass mill. The system featured an auto-sequence for the tandem cold mill roll change device and a 4-roll carousel stand that enabled roll changes without reducing line speed. These advancements were made possible by ABB’s advanced Direct Torque Control (DTC) technology for AC drives and a wide range of metals standard for processing line control.

These innovations improved the efficiency and reliability of the processing line and enhanced the final product’s quality. Within six months of the commissioning process, Jindal Stainless Ltd started producing 2BD surface quality stainless steel ideal for use cases such as pipes and tubing, a new product developed specifically for the DRAP line.

advanced diagnostics and data insights ABB’s control and automation systems extend beyond maintaining optimal speed and tension. They provide a wealth of data and insights that empower operators to proactively manage the processing line. The system continuously monitors equipment health and performance, identifying potential issues before they can lead to downtime. This proactive approach allows for implementing preventive maintenance strategies, maximizing equipment lifespan and minimizing unexpected disruptions. By analyzing historical data and realtime performance metrics, the system can identify trends and patterns. This information can be used to further optimize control settings, identify areas for improvement, and even predict potential issues before they occur. In the case of Jindal Stainless Ltd., these capabilities translated to significant reductions in downtime and maintenance costs, ensuring the processing line operated at peak efficiency.

Collaborative approach and seamless integration

One of the strengths of ABB’s control and automation solutions lies in their ability to integrate seamlessly with existing equipment, regardless of brand. This allows metal manufacturers to leverage advanced automation without the need for a complete line overhaul. ABB’s systems harmonize the various elements of a processing line – from older equipment to newer technology – into an efficient, well-co-ordinated production line. This collaborative approach ensures that companies can maximize the value of their existing assets while improving overall performance.

For Jindal Stainless Ltd, this meant integrating the new DRAP line with existing infrastructure at its Kalinganagar facility, creating a cohesive system that operated efficiently and effectively. The result was a processing line that not only met but exceeded the customer’s expectations, driving productivity and product quality to new heights.

The future of metal processing: evolving for efficiency

The world of processing lines is constantly evolving, with new materials and processes emerging all the time. ABB remains at the

AUTOMATION 24

forefront of this evolution, continuously developing and refining its control and automation solutions.

High quality results

The intricate world of metal processing demands consistent, high-quality results. By leveraging advancements in areas like artificial intelligence and machine learning, ABB is exploring ways to further optimize control strategies, predict potential issues with even greater accuracy, and unlock new levels of efficiency. Through sophisticated algorithms, advanced diagnostics, and seamless integration capabilities, ABB empowers companies like Jindal Stainless Ltd to achieve optimal speed, tension, and overall line performance. These technologies are poised to revolutionize the way metal processing lines operate, driving even greater productivity and quality in the years to come.

The big picture

While ABB’s advanced automation and control systems are transforming the way metals are processed, the broader

implications extend beyond the steel mill. For customers buying metals or consumers purchasing the end product, these operational gains mean better quality and reliability in everyday items. Whether it’s the steel in home appliances, automotive parts, or industrial equipment, improved consistency and durability are guaranteed. By enhancing efficiency and minimizing defects, ABB’s technology not only lowers costs for manufacturers but also ensures that consumers benefit from longer-lasting, higher-quality products.

Additionally, the automation-driven improvements in energy efficiency and sustainability contribute to reducing

the environmental impact of metal production. For consumers who are increasingly conscious of the carbon footprint of the products they buy, this represents a significant step forward. Metal manufacturers adopting these systems can boost their competitiveness and help shape a more sustainable future for the global supply chain, where innovation leads to responsible production and consumption practices.

To summarize, companies that embrace these technologies today position themselves to meet the challenges of tomorrow, producing higher-quality products more efficiently and sustainably. �

DRI hubs for the energy transition

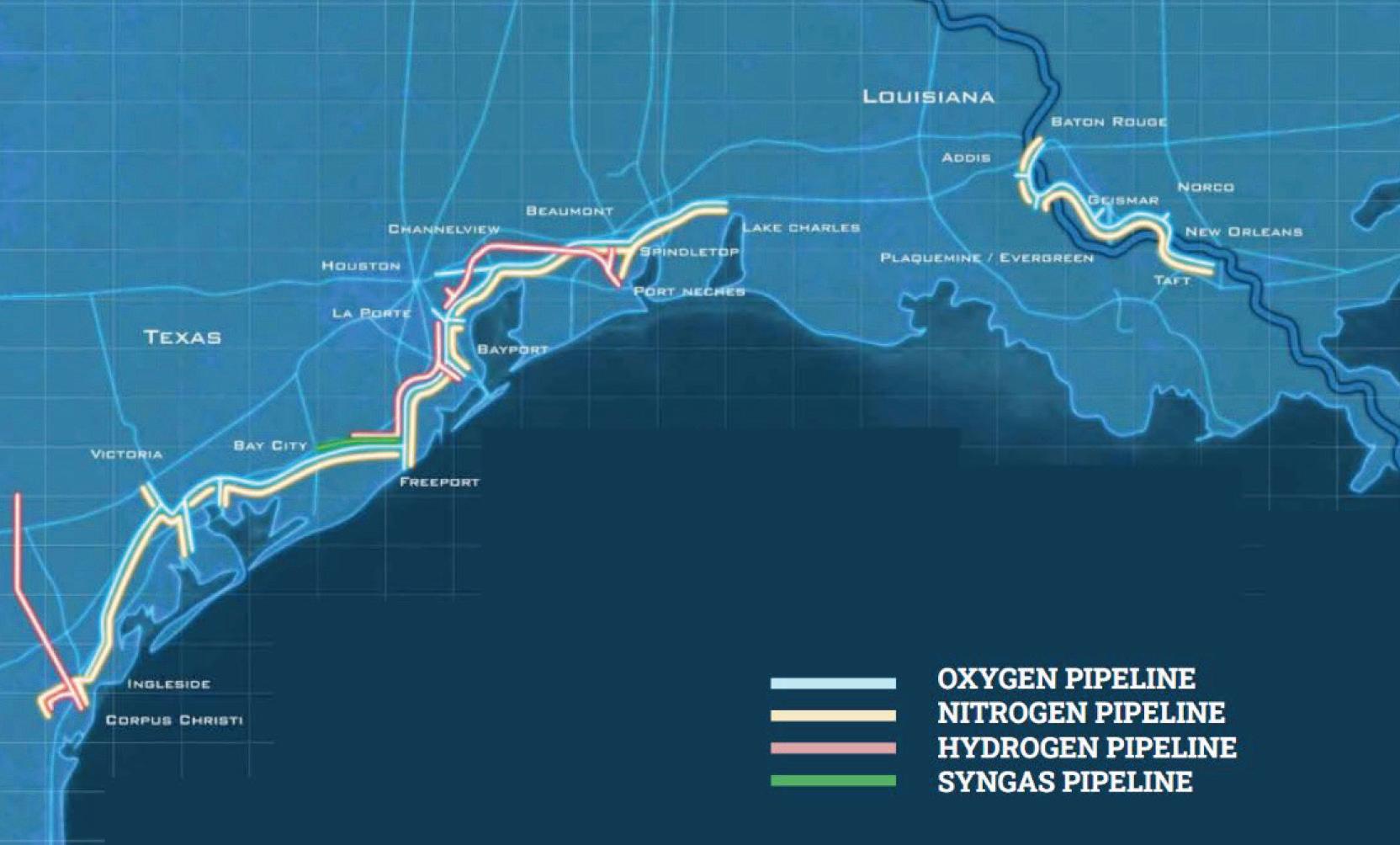

In the frame of energy transition, direct reduced iron (DRI) is a strongly developing technology, with projects based on natural gas (as a classical reducing gas) or hydrogen (in new approaches). This article recalls the merits of using DRI for CO2 emissions reduction, the advantages of potential ‘DRI hubs’ located in suitable regions, such as the US Gulf Coast, and the benefits of having industrial gases networks to provide flexibility for operations. By

Vivienne Balicki, Philippe Blostein, Errico De Francesco, Mike Grant, Geneviève Samson*

THE energy transition is a challenge for society as a whole, including industry. The steel industry in particular, which accounts for 7% of global CO2 emissions, is strongly committed to meeting the challenge of decarbonization.

Since there is no ‘silver bullet’, many different solutions are being explored, and these are regionally dependent. Solutions that apply in the US and in the Middle-East may be very different from solutions that apply in Europe. The two main categories of solutions include, on the one hand, Carbon Capture Utilization and Storage (CCUS), with a wide range of technologies such as cryogenic capture, absorption and adsorption membranes; and, on the other hand, replacement of carbon with another

reducing agent, such as hydrogen.

Blast furnaces are a huge generator of steelmaking emissions, but their potential for decarbonization of the sort required is limited. The most effective steelmaking route for reducing CO2 emissions is the conversion from blast furnaces/basic oxygen furnaces (BOF) to scrap-based electric arc furnaces (EAF), especially where renewable electricity can be found. However, when scrap alone cannot be used, because of its unavailability or because of the quality required, then DRI is the next best alternative.

DRI: a key to decarbonization

DRI is used with gas or coal as a reducing agent. Coal-based DRI is a high CO2

*Air Liquide

emitter. Gas-based DRI can be produced with natural gas (NG), with hydrogen (H2), or by a combination of both. If hydrogen is used, it must be produced through a low-carbon route to achieve overall CO2 emissions reduction objectives. Typically it can be ‘green’ hydrogen, obtained by water electrolysis thanks to renewable electricity, or ‘blue’ hydrogen, obtained through the classical Steam Methane Reformer (SMR) technology but with a CCUS scheme. ‘Pink’ hydrogen, generated from nuclear power plants, can also be a low CO2 emission production route.

Global DRI production has been steadily increasing over years. Production has been multiplied by 20 since 1980 and by three since 2000, and it is set to develop even

further in the years ahead. DRI use enables the decarbonization of steel production. Natural gas-based DRI achieves a substantial 60% reduction in CO2 emissions compared to the conventional BF/BOF route. Hydrogen-based DRI can achieve CO2 emissions reductions higher than 90%. This explains why there have recently been many DRI projects inaugurated or announced around the world, such as the Midrex unit for Tosyali in Algeria (2024), or the Tenova unit for Baosteel in China (2024). Compared with hydrogen-based DRI, the

quality of the DRI produced is generally believed to provide an advantage when DRI is produced in a natural gas based DRI with CCS treatment of its off-gas, since the higher carbon content of the DRI will be a significant energy bonus for downstream EAF operations. With oxygen injection into the bath, carbon will react exothermically to produce carbon monoxide.