Protect assets with superior service and specialty chemical expertise

Henrik W. Rasmussen

Managing Director & SVP, The Americas

Topsoe

→

31 Pioneering the future of aviation

08 2025: The demand dilemma

Alan Gelder, Ann-Louise Hittle, Brittany Martin, Cristina De Santos Torres, Kelly Cui and Shruthi Vangipuram, Wood Mackenzie, provide an in-depth review of downstream markets in 2024 and look ahead to what 2025 may hold for the extended oil value chain and the key trends that are projected.

14 The wave of innovation

Jason Chadee, Avathon, USA, discusses how AI is revolutionising the downstream oil and gas industry by driving innovation and boosting safety and efficiency.

19 Beyond a hammer: technology in the oil and gas industry

Joseph McMullen, AVEVA, USA, explores the rise of Artificial Intelligence (AI) and Machine Learning (ML) in the downstream oil and gas industry, and examines how companies are embracing the digital transformation to revolutionise operations.

23 A downstream digital transformation

Ken Evans, DTN, USA, highlights current trends in digital transformation in the downstream oil and gas sector, as well as future potential.

27 Where clean fuels begin

Matthew Clingerman and Allen Ting, Sulzer, USA, explore how innovative pretreatment technologies are driving the future of biofuel refineries.

Paul Ticehurst, Johnson Matthey, UK, discusses the importance of scaling SAF production as a crucial step in decarbonising the aviation sector, highlighting advancements in technology, feedstock diversity, and regulatory support needed to achieve global decarbonisation targets.

35 Next-generation SAF

Richard Marsh, LanzaJet, and Leigh Hudson, International Airlines Group (IAG), introduce next-generation SAF technology that is helping airlines to meet their decarbonisation targets.

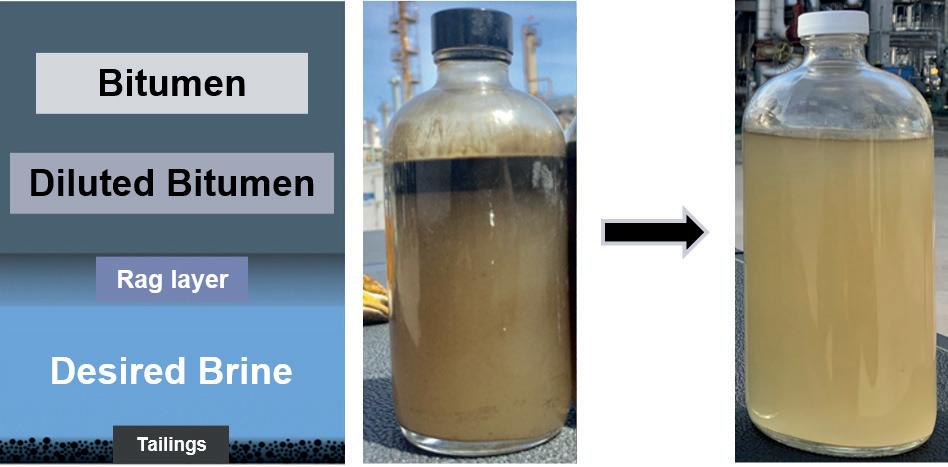

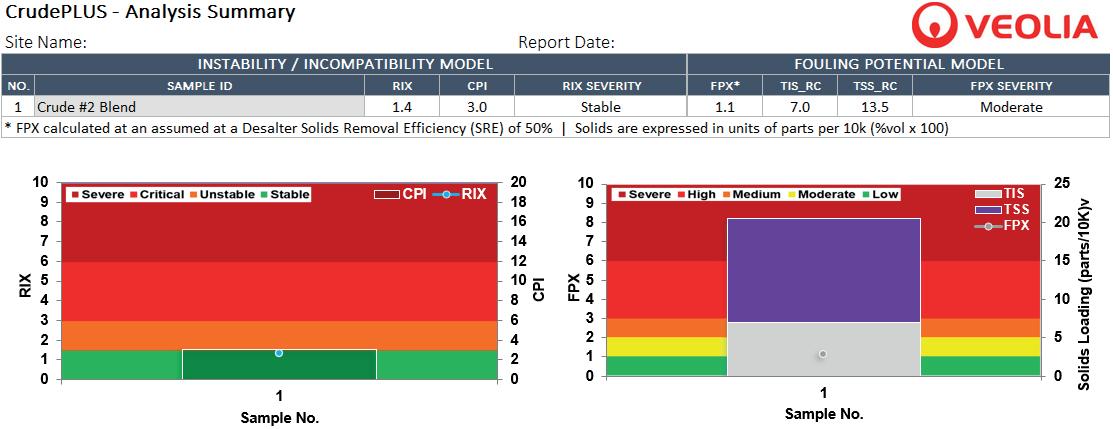

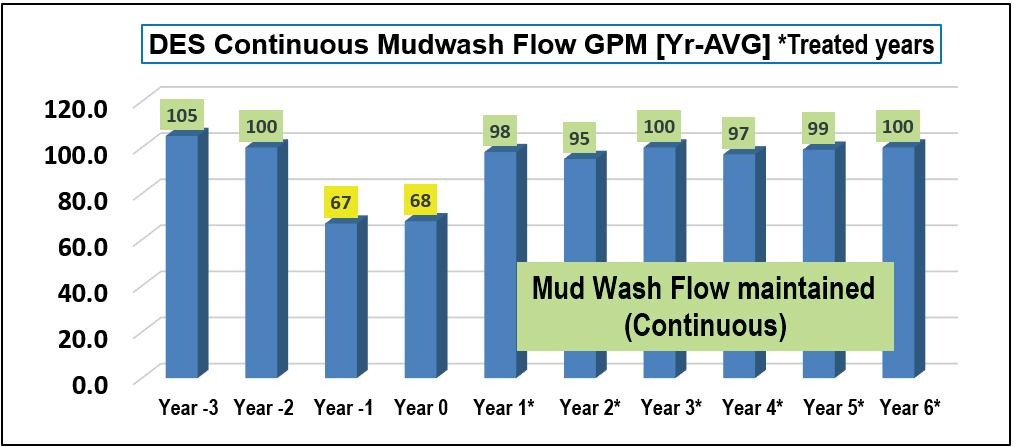

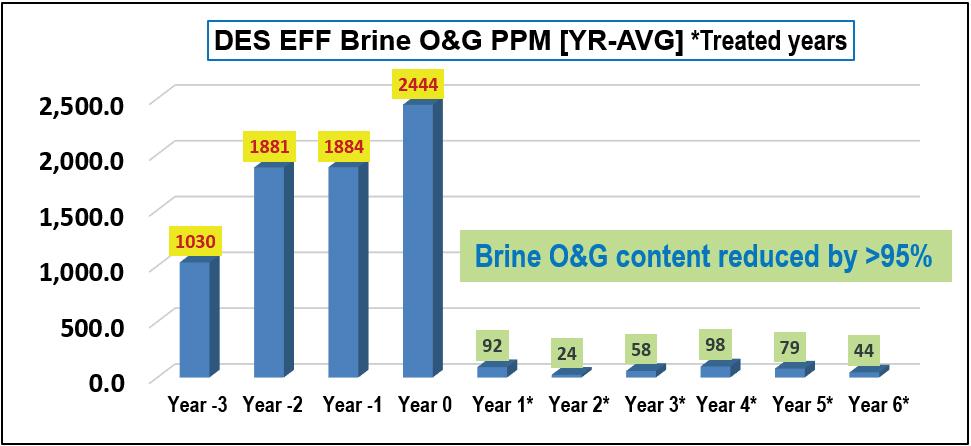

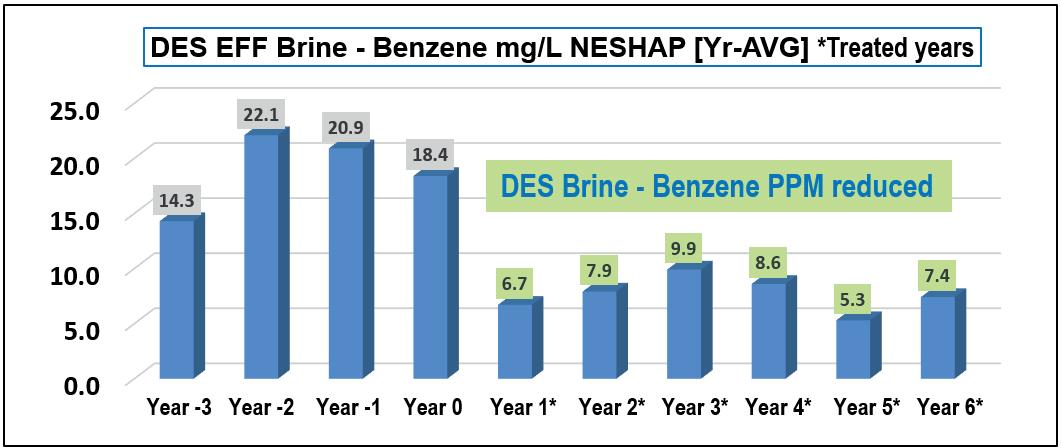

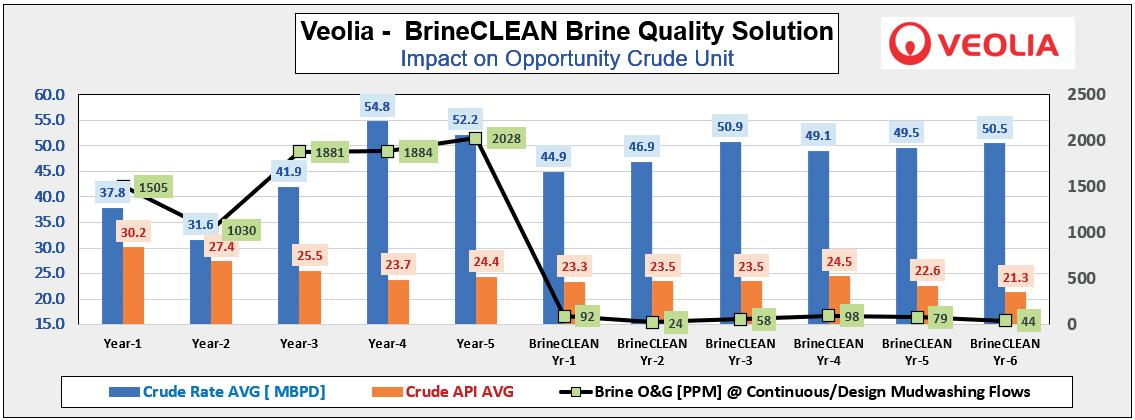

39 Unlocking crude blending opportunities

Sylvain Fontaine, Veolia Water Technologies and Solutions, USA, explores how a desalter brine quality programme can help to enable crude blending opportunities.

45 Centralised water treatment for industrial clusters

Colin Robinson, Evides Industriewater, UK, outlines how centralised industrial water infrastructure is supplying demineralised and process water to chemical companies in the Port of Rotterdam and aiding the transition to low carbon technologies and net zero.

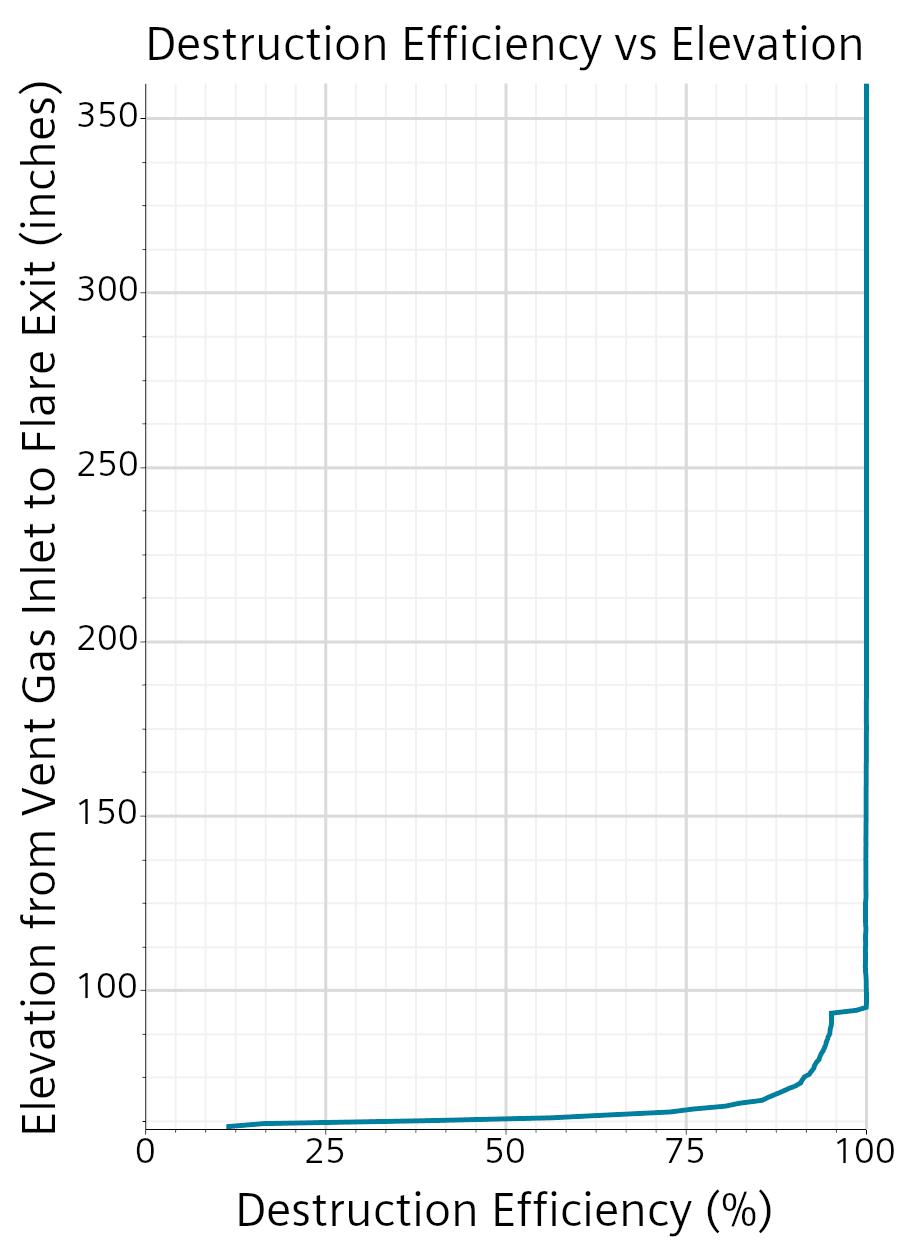

49 Flare play

Matthew Martin and Dharmik Rathod, ClearSign Technologies, explain how new combustor technologies can help strike a fair balance between meeting stringent emissions regulations and maintaining profitable operations when flaring low pressure permeate gas.

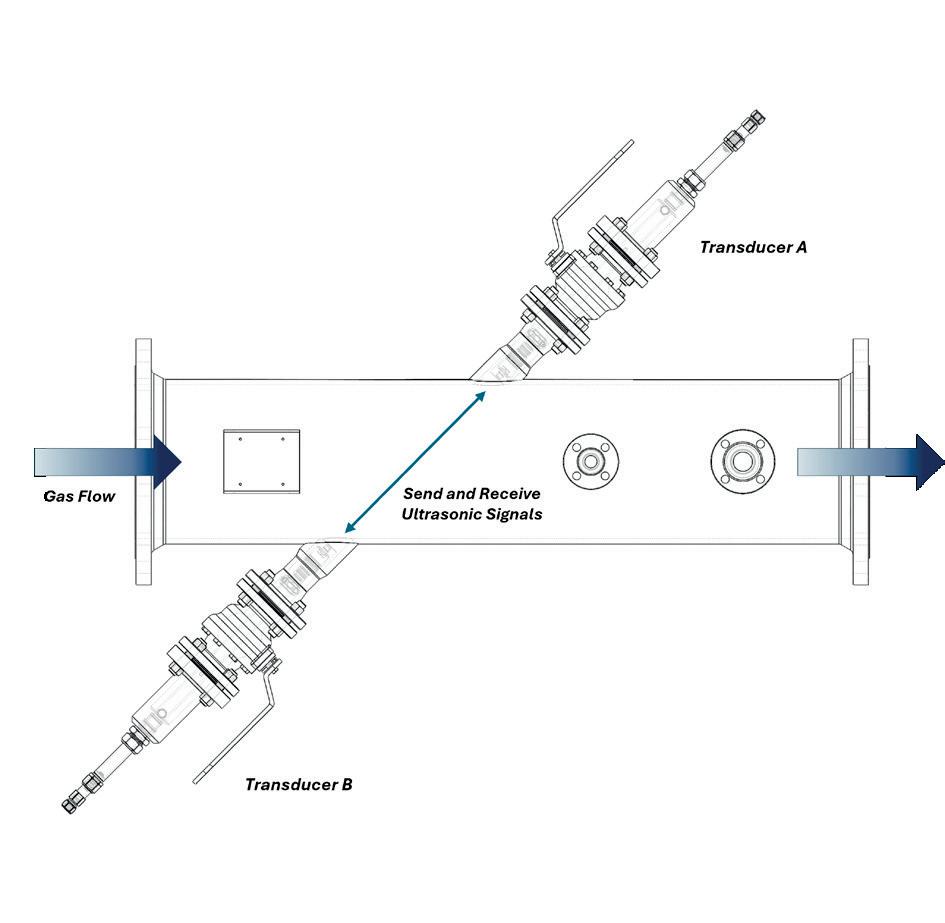

53 Meeting demands and moving forward

Dr Neil Bird, Fluenta, UK, explains how advanced digital technologies can provide an algorithmic solution to ultrasonic flare meter specification and be game-changing for predictive flare gas measurement.

57 Catalyst review

Hydrocarbon Engineering presents a selection of the most advanced catalyst services and technologies that are available to the downstream sector today.

Halliburton Multi-Chem provides industrial water and process treatment solutions to refineries and petrochemical plants. Through onsite technical service and engineering support, the company helps customers with business goals, including improving reliability, increasing throughput, and enhancing the efficiency and flexibility of operating units. Halliburton Multi-Chem’s aim is to protect assets and maximise value.

CONTACT INFO COM MENT

MANAGING EDITOR James Little james.little@palladianpublications.com

ADMIN MANAGER Laura White laura.white@palladianpublications.com

CONTRIBUTING EDITORS Nancy Yamaguchi Gordon Cope

SUBSCRIPTION RATES

Annual subscription £110 UK including postage /£125 overseas (postage airmail). Two year discounted rate £176 UK including postage/£200 overseas (postage airmail).

SUBSCRIPTION CLAIMS

Claims for non receipt of issues must be made within 3 months of publication of the issue or they will not be honoured without charge. APPLICABLE ONLY TO USA & CANADA

Hydrocarbon Engineering (ISSN No: 1468-9340, USPS No: 020-998) is published monthly by Palladian Publications Ltd GBR and distributed in the USA by Asendia USA, 701C Ashland Avenue, Folcroft, PA 19032. Periodicals postage paid at Philadelphia, PA & additional mailing offices. POSTMASTER: send address changes to HYDROCARBON ENGINEERING, 701C Ashland Ave, Folcroft PA 19032.

15 South Street, Farnham, Surrey

GU9 7QU, UK

Tel: +44 (0) 1252 718 999

CALLUM O'REILLY

SENIOR EDITOR

Thirty years ago, the BBC broadcast an edition of its ‘Tomorrow’s World’ programme that predicted what life would be like in 2025.

For the uninitiated, Tomorrow’s World was a British television series that ran for 38 years between 1965 and 2003, exploring contemporary developments in science and technology. The programme introduced its audience to a selection of new technology that would become commonplace, from home computers and mobile phones to compact disc players and robotic vacuum cleaners. And in 1995, the programme focused in on the impossibly futuristic-sounding year that we have just entered into. So, how did the team of experts and leading scientists – including Professor Stephen Hawking – think we would be living our lives today?

Well, aside from a few dud predictions (e.g. the introduction of a gigantic foam gel to slow down space junk), the team at Tomorrow’s World successfully foresaw a number of advancements, including the prevalence of smart speakers, VR headsets and automated banking. On other occasions, the predictions were pretty close, although a little too advanced (even for 2025). For example, in the healthcare sector, Tomorrow’s World predicted that patients would be operated on by robots that are remotely controlled by leading surgeons in far-off locations. While this hasn’t quite materialised, it is certainly true that robotic surgery is helping to improve treatment for patients. The Tomorrow’s World team also offered a vision for self-driving cars that could become a reality in the future, although it did inaccurately predict that society would have given up on the prospect of electric vehicles by 2025.

Of course, the internet was starting to gather momentum back in 1995, and the Tomorrow’s World team anticipated both the huge advantages and significant risks that it presented. They predicted that “business barons” and banks would take control of the internet and establish a restricted-access ‘supernet’, which would lead to hacks, viruses and even violent riots. And while the internet has remained mostly open and cyberspace riots have not materialised, hackers (including nation state hackers) are a real problem in 2025, and cybersecurity is extremely important.

Although it is fair to say that Tomorrow’s World was hit and miss with its predictions for life in 2025, the number of technological advancements that we have seen in the last 30 years is startling. And the intrigue, excitement and concern surrounding the prospect of the internet back in 1995 can be mirrored by the rise of AI today – a topic that we cover in detail in this issue of Hydrocarbon Engineering . As we look to the next 30 years, the words of Stephen Hawking to Tomorrow’s World back in the 90s are just as relevant in today’s world: “Some of these changes are very exciting, and some are alarming. The one thing that we can be sure of is that it will be very different, and probably not what we expect.”

1. FRASER, G., ‘30 years ago Tomorrow’s World predicted 2025 – how did it do?’, BBC, (1 January 2025).

CUSTOM CATALYST SOLUTIONS THAT DRIVE PERFORMANCE

Industry Leading Expertise

The best solutions for the most complex challenges.

Advanced Chemistry

Our catalysts are the industry's gold standard, increasing performance and cost effectiveness, while supporting your energy transition journey.

Partner of Choice for Industry Leaders

Our experts serve as an extension of your team, providing solutions and answers when you need them.

WORLD NEWS

Saudi Arabia | Ebara Elliott Energy awarded AMIRAL petrochemical complex contracts

Ebara Elliott Energy will supply advanced equipment for SATORP’s strategic expansion (AMIRAL) petrochemical complex in Jubail, Saudi Arabia. The contracts for the project were awarded by Hyundai Engineering Co. and Maire Tecnimont.

The AMIRAL project will feature the construction and integration of a 1 650 000 tpy mixed-feed cracker and

associated petrochemical units, integrated into the existing SATORP refinery. This project underscores SATORP’s commitment to achieving carbon neutrality by 2050.

As part of the project, Ebara Elliott Energy will deliver 22 units spanning three of its product lines, including compressors, pumps, and turbines.

Middle East | Wood wins decarbonisation project contract

Wood has secured a contract worth around US$17 million from a leading petrochemical company in the Middle East to improve efficiency and reduce emissions on a process manufacturing plant.

Under this 18-month contract, Wood is providing consultancy and engineering services, process technology and specialist equipment to enhance operations by adding a new heat recovery unit

to an existing process plant. Wood’s solution is estimated to drive a reduction of around 110 000 tpy of CO2 emissions.

As part of the scope, Wood delivered a series of innovative feasibility studies and an early engineering package, designing a complex system to effectively collect the high-temperature flue gas and deliver it to a waste heat recovery transfer system to generate medium-pressure steam.

USA | Cheniere achieves first LNG at the Corpus Christi Stage 3 Project

LNG has been produced for the first time from the first train (Train 1) of Cheniere Energy Inc.’s Corpus Christi Stage 3 Liquefaction Project (CCL Stage 3).

The commissioning process continues, and Cheniere expects substantial completion of Train 1 to be achieved at the end of 1Q25. Upon substantial completion, Bechtel Energy Inc. will transfer care, custody and control of the completed train to Cheniere.

CCL Stage 3 consists of seven midscale trains, with an expected total production capacity of over 10 million tpy of LNG. As of 30 November 2024, overall project completion for CCL Stage 3 was 75.9%. Upon substantial completion of all seven trains of CCL Stage 3, the expected total production capacity of the Corpus Christi liquefaction facility will be over 25 million tpy of LNG.

Italy | Saipem and AVEVA sign MoU to develop AI solutions

Saipem and AVEVA have signed a Memorandum of Understanding (MoU) to co-develop enhanced solutions based on artificial intelligence (AI) and machine learning (ML) to support the engineering design and construction of energy and infrastructure facilities.

The collaboration will focus on three areas of interest: optimisation of both 3D modelling and project planning, streamlining of material procurement and project supply chain.

By implementing AI-driven solutions, Saipem aims to enhance the efficiency and effectiveness of

projects throughout the entire lifecycle, from estimation to plant design and construction.

AVEVA will support Saipem in creating software that leverage generative and predictive design to develop multiple simulation scenarios to optimise plant design in 1D, 2D and 3D.

The goal is to reduce the time required to complete project tasks, foster better communication among stakeholders, improve consistency, and allow people to concentrate on value-added and strategic activities.

Paolo Albini, Chief Supply Chain, Digital and IT Officer at Saipem,

commented: “Saipem’s goal is to define a new way of delivering projects by leveraging on our deep experience and the potential offered by AI applications to develop optimised, fast and innovative engineering solutions that enable our clients to reduce the time-to-market and support them in the path towards net zero.”

Caspar Herzberg, CEO, AVEVA, added: “The new solutions will enhance the performance, efficiency and delivery of world-class engineering projects, ensuring that the carbon footprint is minimised at each step.”

WORLD NEWS

DIARY DATES

24 - 27 February 2025

Laurance Reid Gas Conditioning Conference Norman, Oklahoma, USA pacs.ou.edu/lrgcc

2 - 4 March 2025

AFPM Annual Meeting San Antonio, Texas, USA www.afpm.org/events/AnnualMeeting2025

11 - 12 March 2025

StocExpo Rotterdam, the Netherlands www.stocexpo.com

23 - 25 March 2025

AFPM International Petrochemical Conference San Antonio, Texas, USA www.afpm.org/events/IPC25

6 - 10 April 2025

AMPP Annual Conference + Expo Nashville, Tennessee, USA ace.ampp.org

8 - 10 April 2025

Sulphur World Symposium Florence, Italy www.sulphurinstitute.org/symposium-2025

19 - 23 May 2025

World Gas Conference Beijing, China www.wgc2025.com

20 - 22 May 2025

ESF North America Houston, Texas, USA www.europetro.com/esfnorthamerica

4 - 5 June 2025

Valve World Americas Expo & Conference Houston, Texas, USA www.valveworldexpoamericas.com

10 - 12 June 2025

Global Energy Show Canada Calgary, Alberta, Canada www.globalenergyshow.com

25 - 26 June 2025

Downstream USA Houston, Texas, USA events.reutersevents.com/petchem/downstream-usa

USA | Chevron upgrades Pasadena refinery

Chevron U.S.A. Inc. (CUSA), a wholly owned subsidiary of Chevron Corp., has completed a retrofit of its refinery in Pasadena, Texas, US, which is expected to increase product flexibility and expand the processing capacity of lighter crudes by nearly 15% to 125 000 bpd.

Chevron acquired the Pasadena Refinery in 2019 with the strategic intent to expand its Gulf Coast refining system. This project is expected to allow the company to process more equity crude from the Permian Basin, supply more products to customers in

the US Gulf Coast, and realise synergies with the company’s Pascagoula refinery.

The Light Tight Oil (LTO) Project aims to enhance facility reliability and safety and will ultimately result in an increase in the supply of refined products domestically. The refinery will also begin producing jet fuel and exporting gas oil.

The phased start-up of the asset is expected to last through 1Q25 as project team members work to confirm all plants are operating as planned and products are developed to specification.

USA | EIA expects higher natural gas prices

The US Energy Information Administration (EIA) expects the average price of natural gas for the remainder of the winter heating season to be about 40% higher than the November 2024 spot price, despite expectations that US natural gas inventories will remain higher than average throughout the winter.

Although the price increase is notable, recent US natural gas prices have been at near or record lows, and the increase will keep prices in line with previous end-of-winter prices.

The US started the winter season with 6% more natural gas in storage than average, and the EIA’s December ‘Short-Term Energy Outlook’ (STEO) forecast that natural gas inventories will remain 2% above the five-year average at the end of winter.

In a statement, the EIA said that it expects US benchmark Henry Hub natural gas spot price to increase from just above US$2/million Btu in November to an average of approximately US$3/million Btu for the rest of the winter heating season.

Australia | Final Pluto Train 2 modules arrive

The Scarborough Energy Project has passed a significant milestone with the final Pluto Train 2 modules arriving at the Pluto LNG facility in Karratha, Western Australia.

The successful completion of the Pluto Train 2 module programme advances the Scarborough Energy Project towards the targeted delivery of first LNG in 2026.

Since February 2024, a total of 51 modules have been shipped to Karratha from the module yard in Batam, Indonesia, where they were built.

Expanding the Pluto LNG facility to include a second LNG processing train

provides an efficient way to process gas from the offshore Scarborough field.

Once operational, Pluto Train 2 will have capacity to process approximately 5 million tpy of LNG.

The expanded Pluto facility includes new domestic gas infrastructure and will have the capacity to supply up to 225 TJ/d to the Western Australian market.

Woodside selected Bechtel to execute the engineering, procurement and construction of Pluto Train 2, with construction activities at the Karratha site commencing in August 2022.

Revamp to thrive in the new reality

Ever-changing market conditions, global economic challenges, and the shared journey of the energy transition all mean it is crucial to evaluate easy-to-implement and costeffective improvement opportunities. At Shell Catalysts & Technologies, our solutions open new possibilities for smarter investments while preserving cash through revamping, reconfiguring, or optimising your existing assets. Our experts co-create tailored solutions while keeping your margins in mind – ensuring the investments you make right now can help you maintain your competitive advantage into the future.

Learn more at catalysts.shell.com/revamps.

Alan Gelder, Ann-Louise Hittle, Brittany Martin, Cristina De Santos Torres, Kelly Cui and Shruthi Vangipuram, Wood Mackenzie, provide an in-depth review of downstream markets in 2024 and look ahead to what 2025 may hold for the extended oil value chain and the key trends that are projected.

2024 was the year of the election, with over half of the world’s population involved in the democratic process. In many countries, the incumbents remained in power, but with reduced mandates. Populism prevailed in some form. The run-up to the US election was particularly long, with the victory by former President Trump and the clean sweep by the Republican party offering the potential of 2025 being very different from 2024.

There were many events in 2024 that impacted global energy markets, with the Houthi rebels attacking maritime traffic around the Red Sea, disrupting shipping, and an escalation of the Israel/Hamas conflict that remains today. The conflict in the Middle East widened as Israel confronted Hezbollah in Lebanon and exchanged missile attacks with Iran. The Russia/Ukraine conflict ground on, with no significant breakthrough by either side.

2024 in review Oil market

Global oil demand was projected to reach a new high in 2024, but the oil market has been plagued by concerns that demand is weaker than projected and a focus on potential over-supply, as OPEC+ withheld significant supplies throughout the year. Plans for OPEC+ to increase supply through easing of voluntary cuts have been delayed, as oil prices weakened during the year, particularly in 2H24. Oil prices, however, surged upwards during periods of high geopolitical tension, such as when Israel was threatening to attack Iran’s energy infrastructure. Oil prices fell quickly when tensions eased, due to the ample spare capacity.

In 2024, oil demand growth surpassed the increase in supply with only a small gain in non-OPEC production for the year. This will change in 2025 when non-OPEC growth is equal to the projected increase in demand, another factor weighing on oil prices late in 2024.

The concerns about demand centre on the forecasts for 2024 oil demand growth published by OPEC and the International Energy Agency (IEA) which were unusually divergent, adding to the sense of confusion. Both organisations (and Wood Mackenzie) revised their demand growth projections downwards as the year progressed. US inflation remained high, slowing the pace at which the US Federal Reserve could cut interest rates, delaying the shift to

increased industrial production. China’s economy started 2024 reasonably strongly, but weakened as the year progressed, with a weak housing market depressing a key sector in the Chinese economy. Europe has continued to struggle with high energy costs, weak competitiveness and low investment levels. Despite these woes, oil prices have not collapsed and only flirted at levels below US$70/bbl briefly.

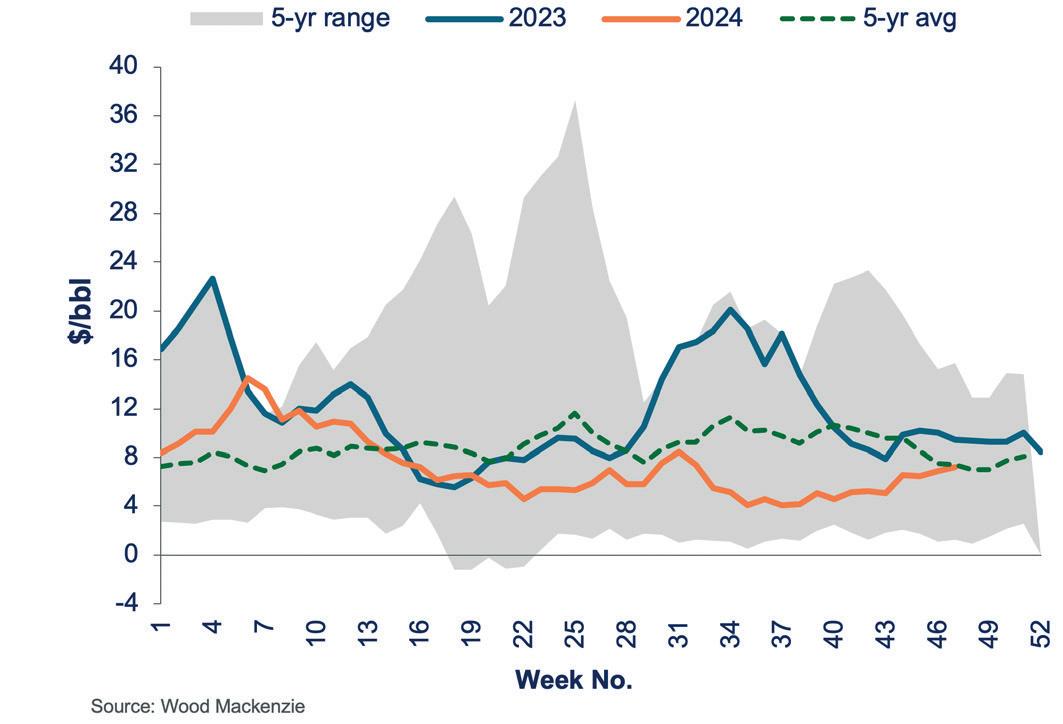

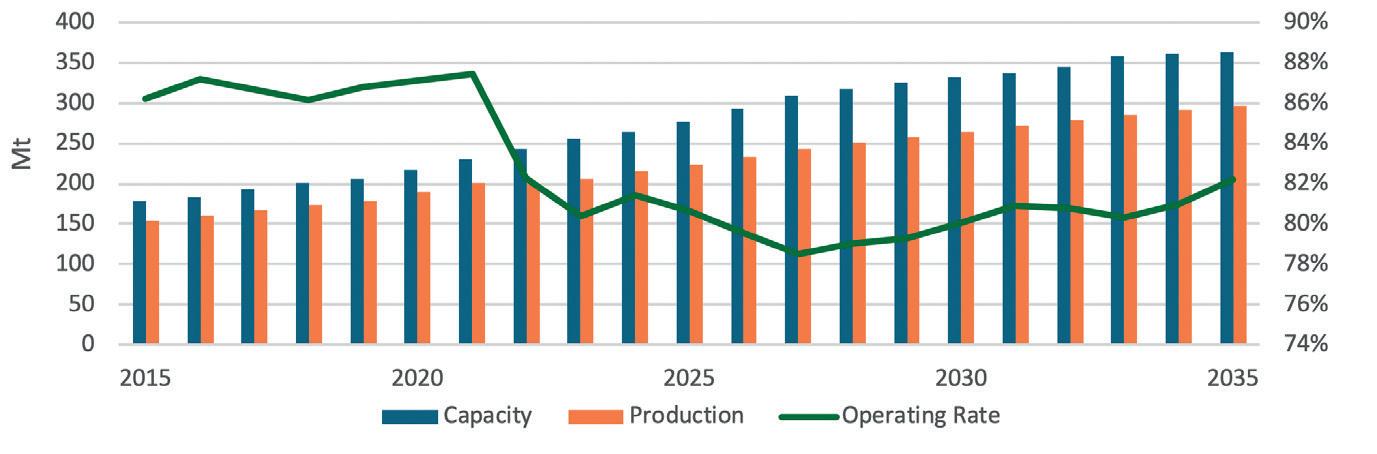

Refining

Refining margins were back to five-year average levels at the end of 2023. Global composite margin has now reset to (or is just below) the five-year average, as shown in Figure 1.

For Europe, the regional reference margin is at pre-pandemic levels. This is despite the disruptions of the Russia/Ukraine conflict and the Red Sea, both of which make global inter-regional trade less efficient and more costly, which would support refining margins.

Refining margins have returned to traditional norms, with competitively weak sites in both Europe and Asia suffering economic run cuts due to the low margin environment.

These lower refining margins reflect several factors, with the key drivers being refinery capacity additions outpacing demand growth and several VLCCs being cleaned and used to transport diesel/gas oil from the Middle East to Europe, mitigating the impact of higher freight costs from vessels diverting around southern Africa. Refineries are complex to commission, with facilities such as Dangote in Nigeria being successfully commissioned during the year, consequently lowering the imports of gasoline to West Africa.

Olefins

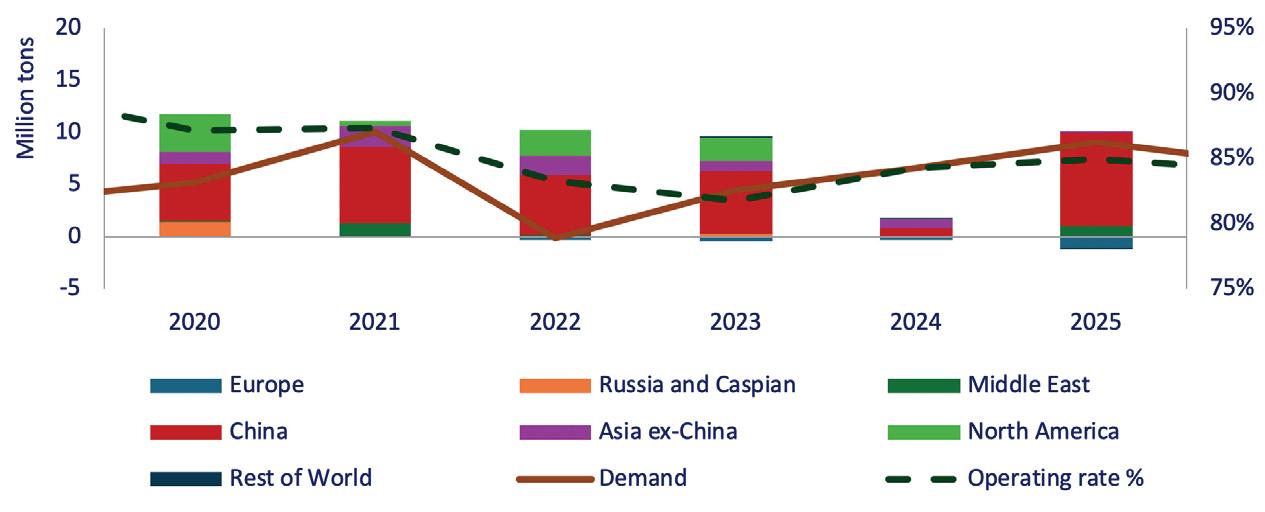

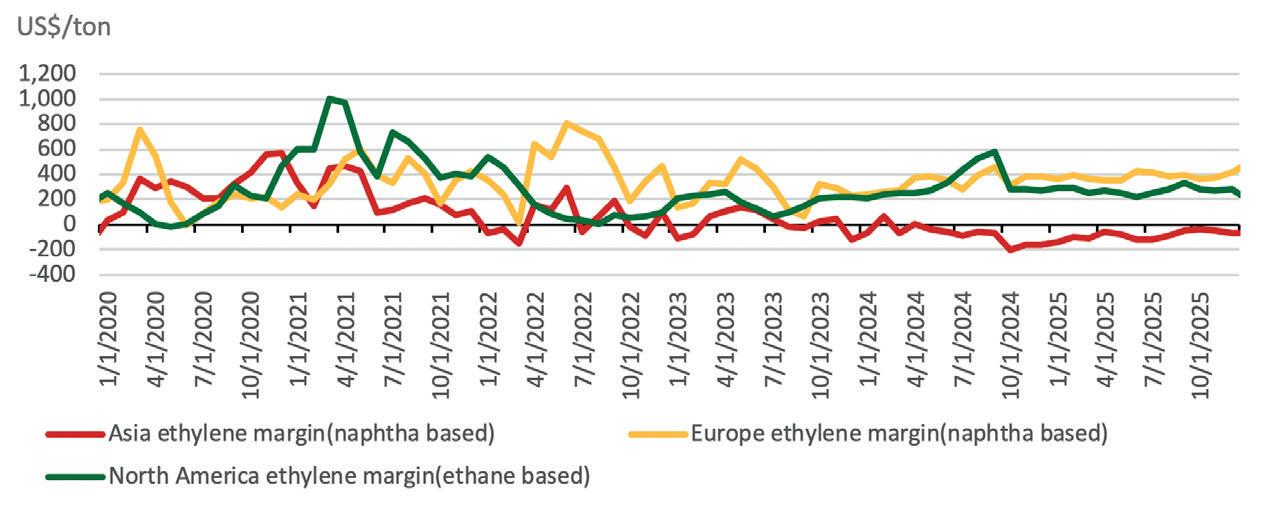

The global olefins market continued its expansion in 2024, but the year marked a low point for ethylene capacity investments due to project delays, as shown in Figure 2. Only 1.3 million tpy of capacity was added in Asia, well below the 2020 - 2025 average of 8.7 million tpy. In contrast, propylene capacity growth continued, primarily driven by PDH unit additions in China. PDH investments were expected to peak in 2024, reflecting poor margins observed in recent years. Rationalisation efforts progressed in Europe and Asia, driven by overcapacity and sluggish demand growth. While European crackers maintained positive margins on average in 2024, two significant closures were announced: ExxonMobil’s facility in Notre-Dame-de-Gravenchon, France, and Sabic’s Geleen unit in the Netherlands. More closures are anticipated, given Europe’s high production cost and weak industrial activity. In China, Sinopec and PetroChina outlined plans to phase out smaller, uncompetitive crackers between 2025 - 2026. Asia’s ethylene margins were negative due to overcapacity and weak economic growth. Conversely, US ethane crackers thrived, supported by low ethane prices averaging US$144/t in 2024, US$38/t lower than in 2023, as shown in Figure 3. This price advantage has spurred interest in additional ethane cracker projects and increasing ethane feedstock use in Asia.

Polyolefins

In 2024, the polyethylene market faced rapid capacity expansion, shipping volatility, geopolitical tensions, rising trade barriers, and weak margins. Several facilities in Europe and Asia permanently closed due to declining demand for virgin polyethylene, stricter regulations, and unfavourable margins. Operating rates, especially in Asia, were pressured by fluctuating upstream prices and margin constraints. However, major capacity

Figure 1. Weekly five-year range global composite gross refining margin (US$/bbl).

Figure 2. Global ethylene annual capacity change vs demand change.

Figure 3. Regional ethylene margins.

For nearly a century, Grace catalysts have kept fuel and petrochemical feedstocks flowing from the industry’s largest refineries to the trucks, trains, planes, and ships that keep our world running.

We are leveraging our long history of innovation in fluid catalytic cracking to develop products that enable lower carbon fuels and help meet the challenges of the energy transition.

expansions, such as Sinopec’s 1.2 million tpy polyethylene plant in China, and Reliance’s 1.5 million tpy polyethylene unit in India, helped alleviate local supply shortages.

Global polyethylene consumption reached 121 million tpy in 2024, driven by strong demand in packaging, automotive, and construction sectors. Meanwhile, rising production costs were offset by increased investment in advanced recycling technologies, which, alongside expanded capacity, stabilised the market.

Aromatics

Since 2022, aromatics pricing has been impacted by above-average octane values. The first half of 2024 continued to see aromatics pricing supported by the elevated alternative value in the gasoline pool. However, as forecasted, this pressure significantly reduced at the end of the 2024 driving season.

Freight disruptions have not been enough to avoid a persistent import substitution of aromatics derivatives in Europe and the Americas. China’s capacity additions pressured margins globally. Even if there were new PX builds in China in 2024, assets entering the market in 2023 ratcheted up operating rates, pushing out more PX imports. China has also structurally transitioned into an exporter of the largest benzene derivative, styrene. Aggressive pricing strategies have enabled Chinese producers of derivatives, such as PTA, to pressure on their counterparts around the world. Europe has been the most impacted region, where rationalisation has been unavoidable.

Key things to watch in 2025

Oil market

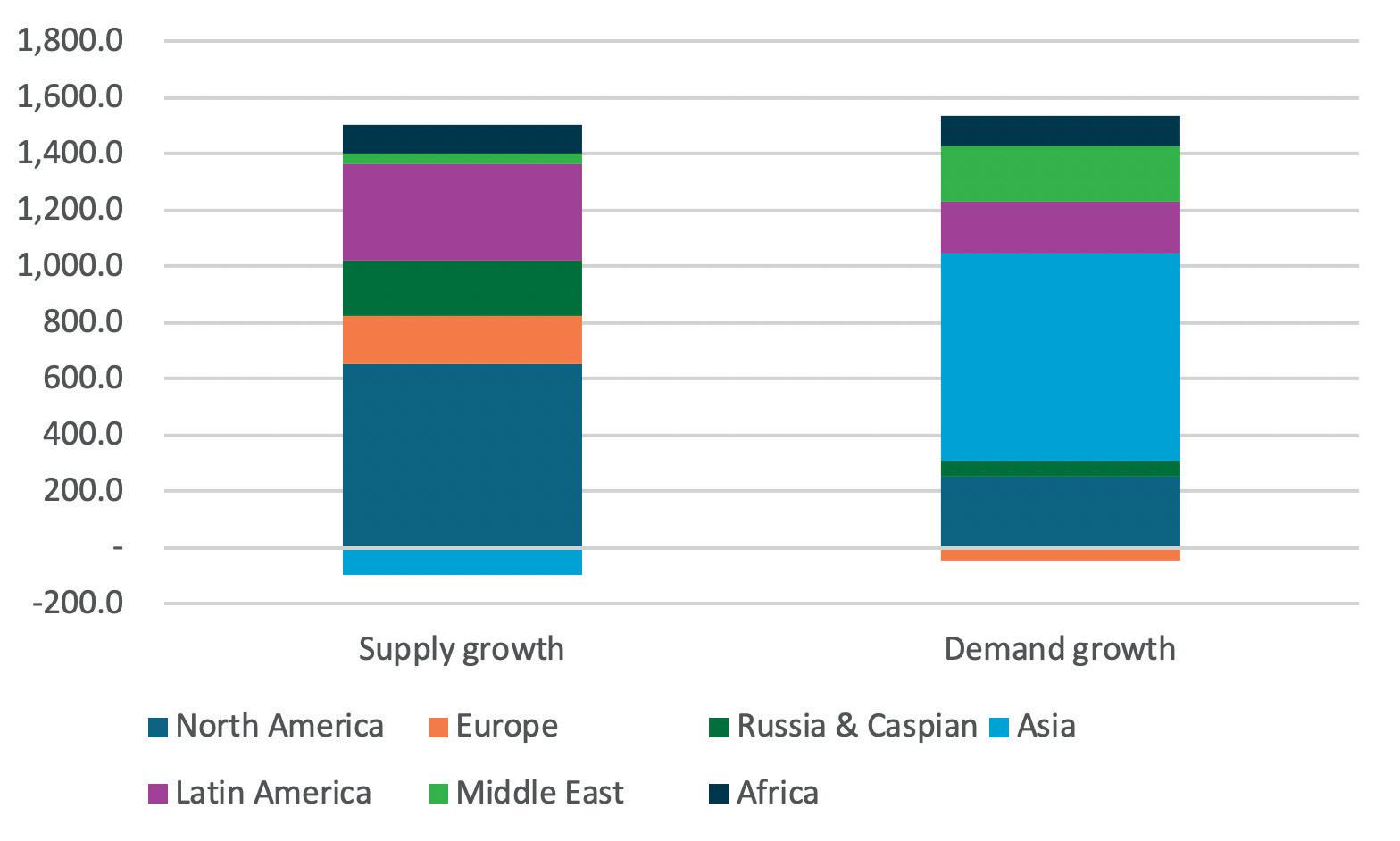

Wood Mackenzie projects 2024 to be the low point of global GDP growth, with 2025 being stronger than 2024, the economy rebalancing to growth in both services and industrial production. Global oil demand growth is projected to increase to 1.5 million bpd for 2025, with oil demand growth across all regions except Europe. However, the challenge for OPEC+ remains – as shown in Figure 4, global demand growth only just outpaces non-OPEC supply growth, providing limited opportunity for OPEC+ to reduce its cuts without significantly weakening the oil price.

Wood Mackenzie’s current Brent oil price projection for 2025 is in the mid-to high US$70s range. Besides the typical risks to the oil price around global GDP growth, geopolitical events and conflict, the recent re-election of President Trump could present a material downside risk to the oil price. The imposition of tariffs on all US imports would dent global economic growth, add inflationary pressure to the US consumer and slow oil demand growth, which could depress oil prices by around US$5 - 7/bbl in 2025, with further declines likely thereafter.

Refining

The crude distillation unit (CDU) capacity investment wave witnessed in 2024 will ease after 1Q25, with crude distillation capacity expected to be effectively flat after 1Q25 as announced closures (PetroIneos at Grangemouth, UK, and LyondellBasell in Houston, Texas, US) and re-configurations (such as Shell at Rhineland, Germany) take place. Global refinery utilisation will remain broadly flat, as refinery projects commissioned in 2024 reach full commercial operations.

Refining margins are projected to remain at current levels through 2025. Oil demand growth can be met by the additional capacity that has become operational during 2024. The slow return of OPEC+ volumes should enable VLCCs to remain in distillate service for some time, keeping downward pressure on freight rates and limiting the upside to refining margins.

The potential imposition of US import tariffs provides an upside to US refining margins, given the support that this will provide to US ex-refinery gate prices on gasoline, which is still imported in significant volumes into the US Atlantic Coast. Higher US crude runs is a downward risk to refiners elsewhere, which when combined with weaker global oil demand growth could lower global composite gross refining margins for 2025 from approximately US$5/bbl to US$2.5/bbl.

Figure 4. 2025 global oil demand and non-OPEC supply growth (‘000 bpd).

Figure 5. Global polyolefins overview.

Olefins

In 2025, global ethylene capacity is poised to resume its growth, with 8.8 million tpy of new capacity coming online, the majority of which will be contributed by China. However, China’s investment in PDH facilities is expected to slow, which could help ease the oversupply in the propylene market, although it is unlikely to resolve the issue in the short-term.

Olefin margins are expected to remain under pressure in 2025. While stronger GDP growth is forecast for 2025, it will be challenging for demand growth to absorb the far greater increase in supply. The market is not expected to recover until after 2027, when capacity additions begin to taper off.

Table 1. Anti-dumping cases (November 2024)

Region/country Start Result

EU November 2023

EU publishes its provisional ADD rates ranging from 6.6 to 24.2% on PET resin from China. From April 2024, these rates were confirmed and made definitive for the next five years.

Argentina October 2013 On 1 June 2023, Argentina announced to suspend the anti-dumping investigation against PET resin originating from China, South Korea and India.

Japan September 2016

South Korea October 2024

Mexico January 2024

US October 2015

The result was announced on 4 February 2023, continuing the anti-dumping duty of 39.8 - 53% to 2 February 2028.

On 17 October 2024, the Trade Committee of the Korean Ministry of Trade, Industry and Energy (MOTIE) recommended to the minister of strategy and finance to impose antidumping duties of 7 - 7.98% on PET resin from China for the next five-year period.

On 9 August 2024, Mexico made a preliminary anti-dumping ruling on PET resin originating from China, with the ratio of 34 - 63%.

Mexico initiates the anti-dumping investigation into Chinese PET resin in January 2024. The relevant HS codes are 3907.60.99 and 3907.61.01, both of which were previously considered in the decree that increased roughly 400 import duties (for PET from 9 - 25%) on 15 August 2023. A second decree, dated 22 April 2024, increasing the import tariff from 25% to 35%, which gets added to the compensatory quotes established by the preliminary ADD ruling.

Implemented an anti-dumping duty of 104.98 - 126.43% and an anti-subsidy duty of 7.53 - 47.56%. In 2022, both anti-dumping and anti-subsidy duties were reviewed, and a decision was made to continue implementing these duties.

Indonesia February 2021 On 3 February 2021, the Indonesian authorities imposed a definitive anti-dumping duty on PET imports from China, with the rate of duty ranging from 2.6 to 10.6%.

Malaysia July 2024

Adding to the challenges, the potential imposition of a hefty import tariff (up to 60%) on Chinese goods by the Trump administration could significantly disrupt China’s plastic exports. Such a measure would further strain demand growth, exacerbating pressure on the already oversupplied market.

Polyolefins

On 10 July 2024, Malaysia announced the initiation of an anti-dumping investigation into PET resin originating from or imported from China and Indonesia. The involved HS code was 3907.61.00. The preliminary ruling of this case is expected to be made within 120 days from the date of filing.

Brazil September 2024 On 18 September 2024, Brazil’s government increased import taxes on 29 chemical products. Import duties for PET raised from 12 - 20%

to decrease starting in 2025, as the growth in supply gradually surpasses the growth in consumption.

In 2025, the global polyolefins market will face a complex mix of opportunities and challenges. Capacity expansions, particularly in Asia and the Middle East, will continue to meet demand across industries, namely those associated with industrialisation. As shown in Figure 5, global utilisation is on a downward trend. However, geopolitical tensions, particularly in major production regions, could lead to supply disruptions, creating continued price volatility. Meanwhile, sustainability efforts will intensify, with companies investing in recycling technologies and circular economy initiatives. These factors, coupled with rising production costs, will drive a market that is both volatile and growth-oriented, with innovation and strategic capacity expansions helping to stabilise supply.

Aromatics

Octane levels are expected to remain close to levels seen in 2H24. With the gasoline market lengthening in the Atlantic basin, polyester production will become the main factor dictating PX margins. Benzene-naphtha spreads are projected

China’s capacities will continue to add pressure to global markets despite export-oriented Chinese players facing tougher conditions in 2025. Overcapacity in China and highly integrated chemical production will be key to its industry competitiveness in 2025. Trump’s return to the White House and the increasing number of Anti-Dumping Duties applied to Chinese-origin products (e.g. PET, as shown in Table 1) will be key to changes to global trade.

Operating rates are expected to continue recovering across the polyester value chain while global styrene operating rates will start bottoming in 2025, but rationalisation risk remains, especially in certain parts of Europe chains.

Conclusion

All parts of the extended oil value chain (from oil markets to aromatics and polyolefins) enter 2025 with ample spare capacity, making demand growth critical to the commercial performance of the individual sectors. Geopolitics and trade tariffs are critical uncertainties to be closely monitored, as these could play a key role in defining the winners and losers.

Unlock exclusive insights with our series of Spotlight interviews with industry experts and contributing authors to Hydrocarbon Engineering magazine.

Brad Cook, Vice President of Sales and Marketing at Sabin Metal Corp., outlines best practice control points for refiners looking to maximise the value and lifecycle of their precious metal catalysts.

Chelsea Hogard, Engineering Team Leader for Watlow’s Industry 4.0 Development Team, discusses the importance of Data Insights in mitigating the risks associated with process heating.

Virginie Bellière-Baca, Global Head of Technology and Innovation at Sulzer Chemtech, considers the importance of customer partnerships, innovation, and the endless evolution of technology.

James Esteban, UNICAT Catalyst Technologies, explores how scientific modelling allows tailored optimisation of filtration grading and loading profiles to deliver improvements in catalyst bed life.

Wolf Spaether, Head of Marketing and Product Management for Ethylene, Clariant Catalysts, talks refinery off-gas (ROG) purification and the role it plays in a more sustainable future.

Dominic Sarachine, Product Manager at FS-Elliott, talks about the development and design of an API 672-compliant centrifugal compressor for one of the world’s largest single-site ethylene facilities.

Luis Hoffmann and Emmanuelle Chauveau, Sulzer Chemtech, consider how polymer recycling presents both a critical challenge and an opportunity to incorporate sustainability in industrial practices worldwide.

for New Energy at Atlas Copco Gas and Process, discusses his recent white paper: ‘The heat pump way to more sustainable energy’.

Dr. Cecilia Mondelli, Global Head of CCUS at Sulzer Chemtech, and Stephen Shields, Head of Advanced Chemical Recycling at Sulzer Chemtech consider how to capitalise on decarbonisation opportunities.

Jason

Chadee, Avathon, USA, discusses how AI is revolutionising the downstream oil and gas industry by driving innovation and boosting safety and efficiency.

Artificial intelligence (AI) is fundamentally transforming the downstream oil and gas industry, bringing with it a wave of innovation and efficiency that is reshaping the entire sector. The complexity of refinery activities is apparent in its roadmap for end-product delivery, which includes energy efficiency and process improvements, environmental performance, inspection and containment boundary integrity, and fuel delivery. Potential issues exist across all those strategic activities.

Integrating automation technologies, including AI-driven solutions, Internet of Things (IoT) devices, and advanced control systems, enhances efficiency, safety, and cost-effectiveness, as well as contributing to the long-term sustainability of downstream operations. In particular, the industry relies heavily on automation technologies to overcome its unique challenges, such as optimising operations and safety, and ensuring a reliable supply of energy in the face of pressures to operate in environmentally responsible ways.

It is a complex and demanding industry that heavily relies on efficient maintenance practices to ensure smooth operations and maximise profitability. Ageing infrastructure poses a significant challenge to refineries. The average age of US refineries is 80 years old, and many are centenarians.1 Refiners in the US alone are estimated to lose around US$6.6 billion/yr due to unplanned downtimes. Maintenance teams are tasked with balancing the need for reliability while managing the increasing risks associated with ageing equipment. Safety is also a concern for refineries. They are considered some of the most dangerous workplaces in the world and, as such, are subject to stringent regulations and standards of safety imposed by local, state, and national regulatory bodies. Ensuring compliance often involves inspections, audits, and preventive maintenance activities, which add additional layers of complexity to maintenance operations and demands high levels of attention to detail, data, and documentation.

The cost of downtime and unsafe practices

Unplanned downtime is one of the most significant sources of lost revenue and a major driver of extra costs in any manufacturing environment, which can be extremely costly to refineries and petrochemical plants. According to the Aberdeen Group, equipment failures cause 42% of unplanned downtime with a price tag of US$10 000/h - 250 000/h, or US$50 billion annually. Outdated maintenance methods leave refining operations vulnerable to unexpected failures and unnecessary downtime.

The cost of catastrophe is even higher. The potential for fires, explosions, leaks, and injuries is significant, underscoring the necessity for stringent safety measures and regulations.

In 2009, an explosion at a refinery in Marcus Hook, Pennsylvania, US, underscored the importance of safety for refineries. It killed five workers and injured 15 others. The cause was a buildup of flammable vapours in a tank farm that caught fire when a spark from a worker’s torch ignited. In addition to the cost of damage repair, there was a multi-million-dollar settlement for the victims and their families, and injured workers received workers’ compensation benefits. In 2021, another US refinery agreed to pay US$19.69 million to resolve federal

and state claims for natural resource damages caused by significant oil discharge into a river, because the river waters and the estuarine environment was subsequently contaminated with petrochemical waste.

Reuters reported in 2020 that US refineries and petrochemical plants were cutting back on insurance because accidents and other disastrous situations were driving up the cost of coverage.1 The decline in coverage for physical damage and business interruption leaves refineries exposed to the costs of repairs and downtime. Inadequate insurance coverage also leaves them open to potential dissolution.

Automation and big data

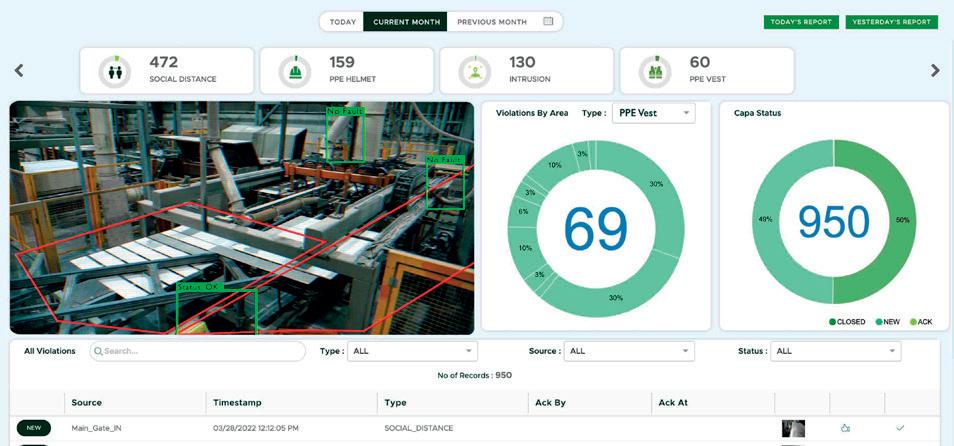

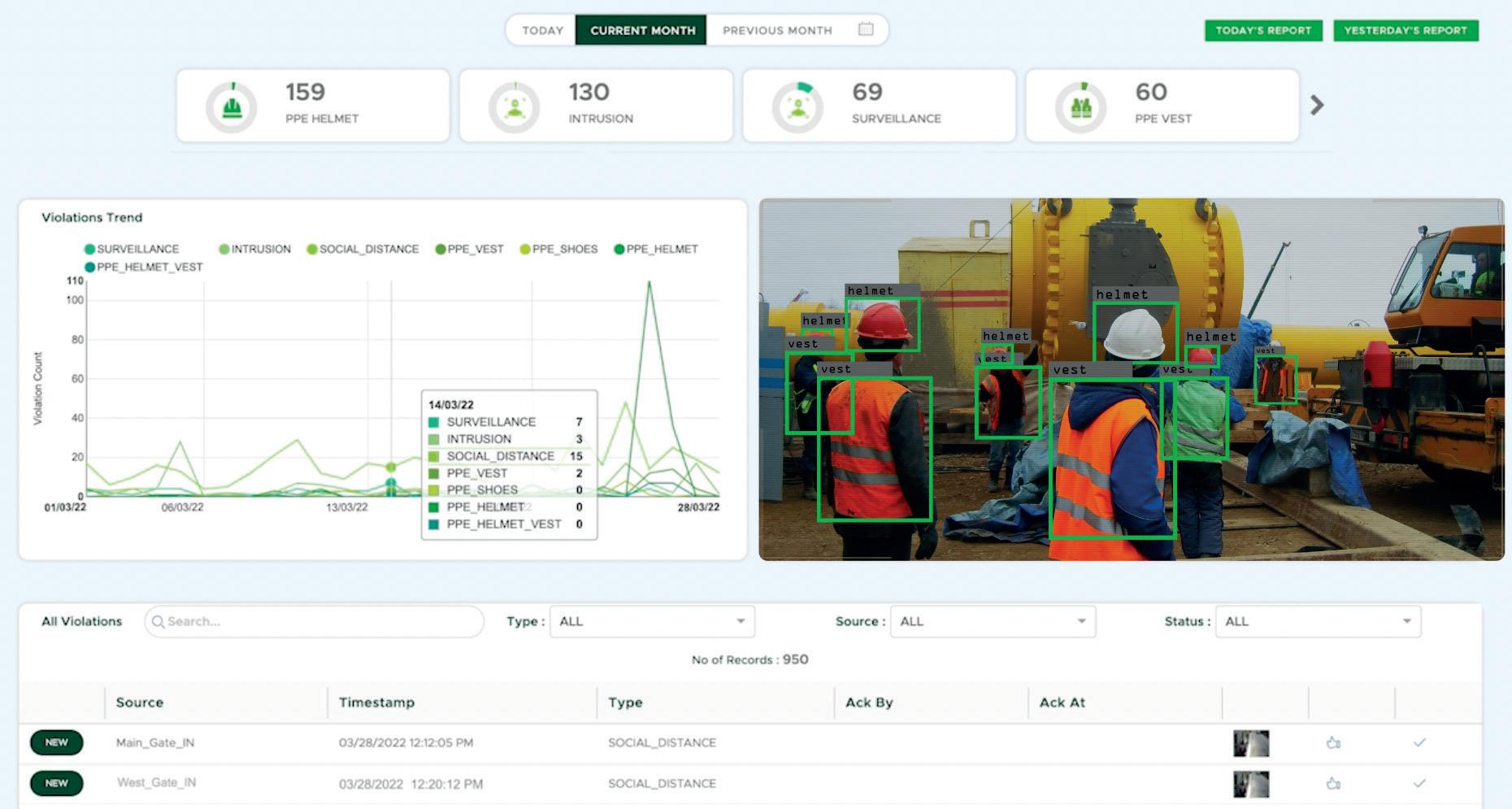

To mitigate downtime and safety issues, refineries turned to technology. In doing so, the amount of data generated by refinery activities has increased proportionally to the technologies it employs to manage them. Process automation technologies, which include DCS, HMI, SCADA, and data historians, have been used for decades for automated data collection, process simulation, and scheduling. They were followed by automated visual control systems that use cameras, sensors, and computer algorithms to remotely monitor, control, and collect data from equipment such as temperature, pressure, and speed data. The advent of IoT and Industrial Internet of Things (IIoT) further revolutionised operations for refiners by transferring data to be accessed by pertinent personnel. Visualising all the data in one place meant operators could theoretically draw conclusions to enhance productivity and improve safety standards.

The issue then became having too much data. The volume and frequency of the data generated made its utility questionable or unmanageable for human operators to act upon.

AI to the rescue

AI has the unique ability to ingest huge amounts of data from multiple sources, analyse the data sets for key trends and connections, and make appropriate recommendations. AI can also significantly reduce false alarms and alarm volume so that operators can focus on what is truly actionable.

AI enables predictive to prescriptive workflows, automated data integration, automated model-building, planning and visualisation toolkits, generative AI workflow solutions, and more. It ‘learns’ from diverse structured and unstructured data types to unlock actionable insights, reduce costs, and optimise processes.

A specific AI technology, Industrial AI, custom-built for refineries, can increase operators’ ability to identify production-impacting events by up to 90%. AI can shorten data-to-insight lead time, so no data science expertise is required. Users can learn to operate intuitive dashboards and reports in a day or less. There are no black-box results, which means AI technology reports when and why an anomaly will happen. The behaviours that caused the anomalies are analysed and trended over time to show progression relative to historical performance and related sensor or process data. It mitigates alert fatigue by auto-calibrating tunable thresholds with real-time SME feedback to automatically categorise, benchmark, and compare alerts, reducing false positives.

Refiners see ROI in days rather than months. If there is no failure data, Industrial AI learns ‘normal’ behaviour vs transitory states from historical operational data to rapidly and accurately identify performance anomalies and detect unknowns. Driven by user knowledge and alert scoring, Industrial AI adjusts to the ‘new normal’ of operational states as assets age and maintenance practices change.

The benefits of AI for refineries

There is a unique combination of factors that makes AI the most impactful technology for enhancing the overall efficiency, safety, and cost-effectiveness of operations. The direct and indirect economic benefits of implementing AI-driven models for refineries are real.

Figure 1. Smart refineries can self-optimise by allowing AI to control the parameters of physical assets.

Figure 2. AI delivers the full-feature performance optimisation solution that refinery operators need to ensure continuously profitable operations.

Figure 3. Visual AI solutions boost safety in refining operations.

WABT Gain (°C)

Feed Sulfur: 1000 ppmwt (10-15% Improvement in Catalyst Cycle Length)

n Optimised production: AI creates situations where equipment failures can be predicted, thereby minimising downtime and enhancing efficiency. The result is heightened production and cost reduction.

n Improved supply chain management: automation technologies give operators real-time visibility into inventory and forecast demand, optimising logistics, which translates to decreased inventory costs and improved profitability.

n Reduced maintenance costs: with automation and AI-driven models, refinery operators can preemptively predict equipment failures, enabling proactive, preventative maintenance. This approach reduces downtime, increases productivity, and lowers maintenance costs.

n Improved asset management: automation offers real-time insights into asset performance, predicts equipment failures, and optimises maintenance schedules.

n Increased operational efficiency: when complex processes are optimised, inefficiencies are pinpointed, volatility and distribution are responded to effectively, efficiency is heightened, costs reduced, and profitability improved.

The equally important indirect benefits

n Improved safety: reducing human intervention in high-risk situations results in fewer accidents, improved worker morale, and cost savings.

n Reporting and compliance: AI can monitor regulatory updates and build a regulatory intelligence knowledgebase to help maintain consistent reporting and compliance.

n Reduced environmental impact: optimising processes reduces emissions and improves operational efficiency, which helps operators lower their environmental impact, meet sustainability goals, and minimise compliance costs.

Conclusion

Refineries have embraced digital transformation to deliver a complex array of products efficiently and cost-effectively, ensuring regulatory compliance, maintaining worker safety, and achieving sustainability goals. An integrated approach to operations optimisation is required – one that evaluates hundreds or even thousands of data points in real-time from interconnected assets, processes, and systems.

AI delivers the full-feature performance optimisation solution that refinery operators need to ensure continuously profitable operations. It enables them to refine and deliver products to market while ensuring worker safety and achieving sustainability goals.

Industrial AI delivers world-class operational results by performing real-time equipment, worker performance, and status analysis based on sensor data, enabling alerts on impending equipment failures and operational abnormalities.

Figure 5. AI can identify and send warnings about potentially dangerous assets, project facilities located in remote and harsh environments, and ensure workplace safety.

Figure 4. AI evaluates thousands of data points in real time from interconnected assets, processes and systems.

Joseph McMullen, AVEVA, USA, explores the rise of Artificial Intelligence (AI) and Machine Learning (ML) in the downstream oil and gas industry, and examines how companies are embracing the digital transformation to revolutionise operations.

The pressures of environmental sustainability and economic profitability has the oil and gas industry split between powerful forces. These forces demand continuous digital transformation to meet their demands. While digital transformation offers massive potential to solve challenges, it is essential to remember that businesses are ultimately driven by profitability, regardless of industry. While sustainability is a critical concern for most stakeholders, it must be balanced with financial feasibility. However, profitability and sustainability are not mutually exclusive; in fact, they often overlap. Increased efficiency, reduced costs, and reduced emissions can all contribute to both financial health and environmental responsibility.

Abraham Maslow’s quote, “If the only tool you have is a hammer, you tend to see every problem as a nail,” rings true in the context of today’s rapidly evolving technological landscape. Innovative technologies offer a powerful toolkit to navigate this complex landscape. If you choose a pragmatic application of the right technology, you can in fact have your cake and eat it too!

There is one technology that has taken not only the oil and gas industry, but the entire world by storm and is worth

discussing: Artificial intelligence (AI). AI is a broad concept that describes how machines can mimic human intelligence. While ChatGPT, Gemini, and MidJourney have captured headlines by allowing people to generate content and pictures, AI has industrial applications that are changing the industrial landscape, driving significant improvements in efficiency, cost-effectiveness, and sustainability.

Machine Learning (ML), a subset of AI that uses mathematical models of data to teach computers how to learn without direct instruction, allows machines to improve and learn from experience. AI, including ML, has many real-world industrial applications.

According to recent data1, the adoption of AI in downstream oil and gas is expected to grow rapidly:

n The global market for AI applications in oil and gas value chains is projected to reach nearly US$3 billion in 2024 and US$5.2 billion by 2029.

n 47% of oil and gas industry professionals surveyed expect their organisations to use AI in operations in 2024.

This trend is likely to accelerate as the technology matures and its benefits become more apparent.

However, here is an overview of some use cases for AI and ML in downstream oil and gas:

n Data analysis: AI and big data technologies convert raw operational data into actionable intelligence, enhancing strategic planning and decision-making.

n Real-time monitoring: AI-powered systems monitor operations, collecting data from energy meters and equipment sensors. This helps boost throughput, minimise energy consumption, and identify potential safety hazards.

n Predictive analytics: AI algorithms can analyse vast amounts of data from sensors and equipment to predict failures and schedule maintenance proactively, reducing downtime and costs. This also provides the ability to schedule repairs and replacements more efficiently.

n Maintenance scheduling: AI creates efficient maintenance schedules by analysing data on equipment usage, production needs, and required costs, optimising performance and extending infrastructure life across the supply chain.

n Process optimisation: process models optimise operations by analysing real-time data to adjust process parameters, improving yields and energy efficiency. These models continuously learn and adapt based on new data, ensuring continuous optimal performance.

n Quality control: ML algorithms analyse produced fuels and petrochemicals against key quality standards (ISO, API, ASTM) directly from production lines. This allows for rapid prediction and correction of quality deviations, minimising waste and ensuring production reliability.

n HSE hazard prevention: AI systems help prevent health, safety, and environmental (HSE) hazards by monitoring for risks such as explosions, fires, leakages, and chemical exposure.

n Emissions detection and monitoring: advanced imaging technology combined with AI is used to detect and remediate of fugitive emissions, supporting environmental sustainability efforts.

n Supply chain optimisation: AI systems will help with planning and scheduling to help adapt to ever-changing conditions.

AI is no longer just theoretical concepts or futuristic ideas. It is driving real, tangible benefits for companies across the globe. The following real-world examples showcase how industry leaders such as Suncor, Saudi Aramco, bp, and Cosmo Oil are actively using AI, ML, and advanced data analytics to solve complex challenges. These companies are not only transforming their internal processes, but are also paving the way for a more efficient, sustainable future. The following case studies explore how they have turned data into actionable insights, reshaping their industries in the process.

Suncor’s use of a data historian and advanced predictive analytics

Suncor2 leverages a historian system across all facilities, providing comprehensive visibility into operations – from controls and engineering to economic and business layers,

all the way up to management. This system allows for real-time monitoring of operational health. However, Suncor is doing more than simply analysing sensor data; the company utilises predictive analytics to identify normal operating patterns. When deviations from these patterns occur, the system can automatically detect potential failures months or even years before they happen.

This predictive capability not only highlights at-risk assets but also diagnoses potential root causes, reducing the need for daily manual inspections. Instead, the system focuses attention on assets exhibiting subtle variations in performance, which may signal the onset of issues. This approach significantly reduces maintenance efforts while supporting an enterprise-wide asset health programme. It also gives facilities ample time to plan maintenance proactively, mitigating risks of unexpected failures, which can increase emissions or other undesirable operational modes.

Beyond asset health, Suncor also utilises simulation models that integrate real-time data. These models enable the company to compare actual performance with design benchmarks and predict operational adjustments based on demand. The insights gained from process performance data further enhance asset health predictions, extending the reach of AI and ML beyond sensor and vibration data. This includes advanced calculations based on first-principle models, applied to variables that cannot be directly measured. Suncor has scaled this approach to monitor hundreds to thousands of assets, ultimately driving reductions in greenhouse gas emissions and energy consumption.

Saudi Aramco’s Unified Operations Center

Saudi Aramco’s Unified Operations Center3 offers a high-level view of the enterprise’s asset health and performance through a panoramic visualisation system. This software acts as a central hub, consolidating data from various sources like sensors, engineering documents, and financial systems. It presents this information in a single, user-friendly interface, allowing operators to visualise asset health, monitor supply chains, and leverage AI and predictive analytics for proactive decision-making.

By providing a holistic view of operations, the Unified Operations Center empowers Saudi Aramco to optimise performance and make data-driven choices that enhance efficiency and profitability. This integrated approach allows the company to monitor supply chain operations and proactively manage asset health using predictive analytics, AI, and ML, alongside online simulations. By optimising both asset health monitoring and process performance in real-time, Saudi Aramco can strategically plan maintenance and optimise their overall operations.

Cosmo Oil’s real-time process optimisation

Cosmo Oil4exemplifies real-time process optimisation by leveraging cloud-based simulation models to optimise its supply chain and operations. Its system uses automated,

Link up with a supplier who can provide alternatives that the others can’t.

Spherical Catalyst Carriers

EXCELLENT SIZE CONTROL WITH UNPRECEDENTED FORMULATION FLEXIBLITY

With Saint-Gobain NorPro, you can count on a secure supply of Accu® spheres catalyst carriers, custom-made to your requirements.

We offer new materials as carriers that were not previously available:

• Narrow size distribution

• Excellent control to average particle size

• Control of porosity

• Alumina, silica, titania, zirconia, zeolite, and mixed oxides

For inquiries or product samples: www.norpro.saint-gobain/accuspheres

real-time simulations based on live plant data to monitor and improve operational performance. For example, Cosmo Oil uses online models to update distillation column calculations in its crude unit. By continuously adjusting for changes in feed and equipment health, these models provide highly accurate predictions of equipment performance and process output.

This level of precision allows Cosmo Oil to optimise key processes, such as pump-around and product draws, to meet specifications while enhancing preheat integration. This reduces fuel usage and energy consumption, ultimately leading to higher yields. The entire process is autonomous, with self-tuning models that adjust throughout the day, ensuring minimal maintenance while improving sustainability, energy efficiency, and profitability.

The best of both worlds: bp

bp is using cloud-based planning models to balance profitability and sustainability. On the one hand, bp significantly improved its downstream5 business efficiency and decision-making process by implementing a unified supply chain solution in the cloud, reducing crude purchase decision time from two days to less than two hours. On the other hand, bp uses the same tool to optimise CO2 emissions6 across its operations. With cloud access to advanced planning tools, including Linear Programming (LP) models, bp can rapidly run complex simulations. This allows bp to make fast decisions that impact the bottom line while being as environmentally friendly as possible.

Conclusion

The journey towards a sustainable and profitable oil and gas industry is complex, but it is achievable. AI and ML can offer a powerful toolkit to achieve this balance. By harnessing these technologies, companies can optimise operations, reduce waste, and minimise environmental impact, all while maintaining financial viability. As AI continues to evolve, the industry can expect even more groundbreaking applications that will reshape the downstream oil and gas sector for a more sustainable and profitable future.

Technology offers a powerful compass, guiding us towards a future where economic growth and environmental responsibility coexist. As we navigate this path, it is essential to remember Maslow’s quote so that we do not view a single technology as a silver bullet. By embracing innovation and harnessing the full potential of new innovative technology, we can create a legacy that benefits both generations to come.

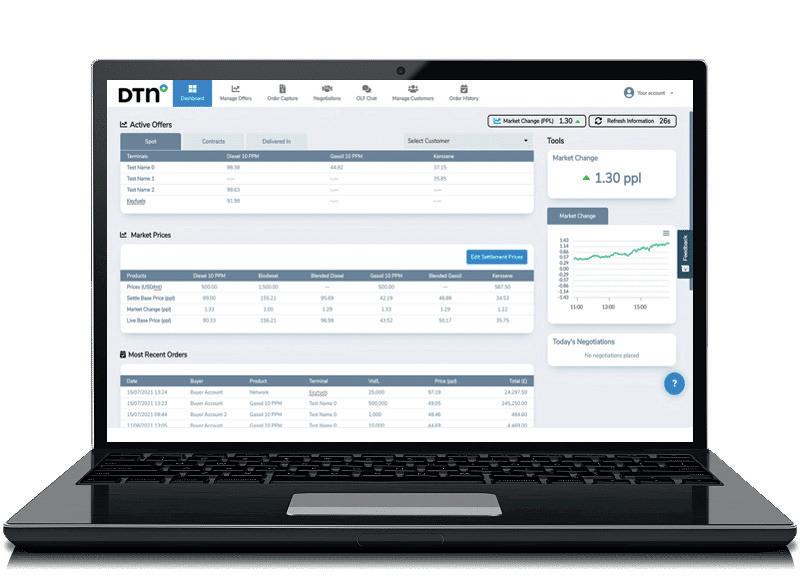

Ken Evans, DTN, USA, highlights current trends in digital transformation in the downstream oil and gas sector, as well as future potential.

The downstream oil and gas sector is undergoing a significant digital transformation that has accelerated over the past few years. This shift has been driven by extraordinary events including a global pandemic, labour shortages, geopolitical unrest, and the evolving energy transition. Furthermore, this industry remains essential to human progress and prosperity and is therefore always seeking ways to remain sustainable. Against this backdrop, energy companies are increasingly harnessing the power of fourth industrial revolution technologies to increase efficiency, reduce costs, optimise margins, and maintain razor-thin profits.

Advanced analytics and AI

One of the technologies that has seen widespread adoption in the sector is artificial intelligence (AI). Advanced analytics and AI have broad applications across the energy supply chain. Companies in the downstream sector are using AI to optimise margins and inventory allocations, as well as to improve operational efficiencies and customer experience.

For example, AI-powered analytics can help suppliers and wholesalers predict future demand more accurately by analysing historical data, market trends, weather patterns, and global events. This allows fuel sellers to maintain optimal inventory levels, minimising both overstocking and stock-outs. Additionally, AI is being used to personalise customer experiences and optimise pricing strategies, enhancing overall customer satisfaction and loyalty.

Digital twin technology

Pioneered by NASA in the 1960s to create simulations for spacecraft and astronauts, digital twin technology has gained traction in the downstream sector. According to a Markets and Markets report, the adoption rate of this technology is expected to grow significantly. 1

A digital twin is a virtual replica of physical assets, processes, or systems. In the downstream sector, digital twin technology uses real-time data from sensors and Internet of Things (IoT) devices to simulate and monitor operations. This enables companies to analyse supply chain performance, predict equipment failures, and optimise maintenance and inventory placements.

For example, Chevron reports implementing digital twin technology across its downstream operations, creating virtual replicas of its refineries and other assets. 2 This has allowed the company to simulate different operational scenarios and optimise processes, resulting in improved operational efficiency, reduced downtime, and enhanced safety performance.

These iterations yield benefits for Chevron, the shareholders, and the consumer by eliminating price and production variability and maximising the efficiency of limited assets.

Cloud computing and edge computing

Cloud computing is used for centralised data storage and advanced analytics. Refineries can use cloud-based platforms to collect and analyse vast amounts of operational data, enabling real-time optimisation of production and distribution processes across their entire supply network.

analytical look at demand activity.

Edge computing, on the other hand, processes data locally at the equipment level. For instance, sensors on refinery equipment can detect anomalies and make immediate decisions, like adjusting flow rates or shutting down operations, without needing to send data to the cloud. This reduces latency and ensures quicker response times in critical operations, especially in remote areas such as oil terminals and distribution centres.

Robotic process automation

Robotic process automation (RPA) is increasingly adopted in the downstream oil and gas industry to automate repetitive, rule-based tasks. This technology helps companies streamline their operations, reduce human error, and free up employees to focus on higher-value activities. For example, workflows that digitally monitor electronic bills of lading (eBOLs) can save an energy supplier as much as US$25 000 per missing BOL in one month.

RPA is also enhancing communication between systems, reducing manual interventions during the loading and unloading of products. This allows operators to focus on more strategic tasks while maintaining throughput and improving turnaround times and operational efficiency.

Figure 1. Integrated advanced analytics enable a digital marketplace where buyers and suppliers can negotiate and buy fuel and manage volume, while automating resource-heavy back-office functions.

Figure 2. Monitoring the delicate balance between supply and demand is one of the most important fundamental factors in today’s petroleum markets. AI-driven data with granular insights allows meaningful location-specific operating statistics as inputs into a multi-dimensional infrastructure model, providing an unparalleled,

Sulzer MellapakEvo™ Packed for Evolution!

The new Sulzer MellapakEvo™ structured packing, in combination with advanced MellaTech™ column internals, delivers unparalleled performance improvement for your columns. Verified at an independent testing facility, this latest mass transfer technology is proven to enhance column performance in both capacity and efficiency.

MellapakEvo has optimized packing geometry as well as an increased effective interfacial area for enhanced liquid spreading and liquid surface renewal. This boosts the vapor-liquid interactions for a superior mass transfer and excellent hydraulic performance.

This innovative design delivers up to 40% better efficiency compared to MellapakPlus 252.Y at a similar capacity. It also offers up to 20% greater capacity than MellapakPlus 452.Y at a similar efficiency, minimizing energy consumption for operators.

Contact Sulzer for a full technical analysis tailored to your needs: chemtech@sulzer.com

Blockchain technology

Blockchain’s decentralised ledger system ensures that all transactions are recorded transparently and cannot be altered, making it ideal for tracking the complex supply chains in the energy sector.

VAKT, a consortium of major oil companies and banks, is one of several blockchain initiatives targeting the oil and gas sector. The company’s blockchain-based platform for post-trade processing aims to eliminate paper-based processes and reduce inefficiencies in trading operations. It reports that initial results show a reduction in reconciliation and dispute resolution times by up to 40%, leading to significant cost savings for participating companies. 3

Integration and single platform

As the industry continues to evolve, further integration of these technologies is expected, leading to more intelligent, automated, and interconnected downstream operations. This will require normalising data, consolidating disparate systems, and integrating data silos for end-to-end visibility and collaboration. A one-platform solution with intuitive visualisation will enable companies to leverage the technology to its fullest potential.

This centralisation improves data accuracy, enabling real-time insights for optimising production, inventory, and distribution. It also simplifies compliance and reporting by ensuring all operations are visible on one platform. Moreover, integrating different systems reduces redundancy, cuts costs, and improves collaboration between departments, leading to increased efficiency and profitability across the value chain.

Advanced cybersecurity measures

With increased digitalisation, the importance of robust cybersecurity measures will grow. These include enhanced AI-driven threat detection systems that can identify and respond to anomalies in real time. Zero trust architecture will be widely implemented, ensuring strict access controls and verifying every user and device. Operational technology (OT) networks will be segmented from IT networks to prevent cross-network attacks. Blockchain will be utilised for secure data transactions, and there will be an increased focus on employee cybersecurity training and cloud security to prevent breaches and minimise risks across the supply chain.

The next big step: enabling the ecosystem economy

The next big step for technology-enabled transformation will be consolidating many of these advancements to enable the ecosystem economy. This represents a transformative shift in how businesses operate, breaking down traditional sector silos and fostering interconnected networks that drive innovation and value creation. The downstream oil and gas marketing and retail segment, which has long

operated as a robust ecosystem, will benefit the consumer through enhanced efficiency and service delivery from a new digital platform.

New ecosystem

Key technologies essential for developing new ecosystem business network platforms include the following:

n Cloud computing: this provides scalable and flexible infrastructure, enabling seamless resource management and integration, leveraging a shared ontology of reference data for all physical assets –the digital twins of various products, terminals, pipelines, transport assets, etc. – needed to eliminate unnecessary data conversions, normalisations, and reconciliations.

n Big data analytics: this facilitates the processing and analysis of vast amounts of data, generating actionable insights and driving informed decision-making.

n AI and machine learning (ML): this automates processes, enhances user experiences, and predicts trends, ensuring the platform remains adaptive and efficient.

By leveraging these technologies, businesses can create robust ecosystem platforms that not only meet current market demands, but also anticipate and adapt to future trends, ensuring sustained growth and innovation.

Future technology requires a strong foundation today

Downstream oil and gas companies that embrace these digital technologies and successfully implement them across their operations will be well-positioned to thrive in an increasingly connected and complex business environment. The convergence of AI, IoT, digital twins, and other technologies will create new opportunities for optimisation and innovation.

However, it is important to note that successful digital transformation requires more than just technology adoption. It requires quality data sources, data integrity, a strategic approach to data management and cybersecurity.

It also involves cultural change and workforce upskilling. According to 2021 research performed by Forrester Consulting on behalf of DTN, 70% of the respondents reported “lack of the right skills” as their biggest challenge to digitalisation. 4 Addressing these challenges and opportunities will be crucial for realising the full potential of digital technologies.

References

1. ‘Digital Twin Market Size, Share & Industry Trends Growth Analysis’, Markets and Markets, (July 2023).

2. ‘The good twin: how digital doppelgängers are driving progress’, Chevron, (7 February 2023).

3. ‘How post-trade digitalisation is modernising commodity trading’, (9 November 2021).

4. Digital Modernization Fuels Downstream Oil And Gas, DTN, (January 2022).

Matthew Clingerman and Allen Ting, Sulzer, USA, explore how innovative pretreatment technologies are driving the future of biofuel refineries.

Clean fuels from renewable sources are critical for meeting the emission targets of the future. Renewable diesel, also known as hydrotreated vegetable oil (HVO), has become a leading alternative for road transportation fuels as companies invest in a more environmentally conscious energy supply. Similarly, the predominant pathway today for production of sustainable aviation fuel (SAF) is via hydrotreated esters

and fatty acids (HEFA). HVO and HEFA are both produced by converting fats, oils, and greases (FOG) into finished fuels using long-proven hydroprocessing technologies. Upstream of the hydrotreater is pretreatment, which is the first step in the process to remove impurities from the feedstocks. Conventional pretreatment processes currently employed to make HEFA have been used in other applications, such as in edible oil refining and

biodiesel production. However, the stringent requirements for producing HEFA have led to new advances in pretreatment technologies that increase flexibility and improve operational efficiency.

Pretreatment overview

The catalogue of potential feedstocks for producing HEFA seems endless, but they all share similar characteristics. Primarily sourced from plant oils or animal fats, these fatty acids and triglycerides also contain several impurities that can negatively impact the conversion process.

Contaminants such as chlorides, phosphorus, and metals contribute to premature deactivation of the hydrotreating catalyst, as well as to corrosion and potential process instability. Waste oils and lower-quality feedstocks, such as used cooking oil (UCO) and low-grade tallow, are gaining popularity. Impurity levels in these feedstocks are often much higher, which further increases process complexity and the risk of complications. Therefore, the pretreatment unit is a critical first step in the fuels production process.

Until now, physical refining has been the technology of choice. It was originally developed for oleochemical and edible oil markets, but extended later to include biodiesel, renewable diesel, and SAF. The multi-step process can vary depending on the concentration and type of impurities to be removed. Physical refining units generally include acid or enzymatic degumming, adsorption, and mechanical separation. Additional steps such as water washing, crystallisation and filtration, and steam stripping may be required to treat and remove other contaminants such as chlorides, polyethylene, and complex structures found in various biomass-based feeds. Multiple stages of these individual processes may be required if impurity levels are high. Although capable of removing impurities, more severe treatment to reach ultra-low levels of key contaminants is not possible without significant additional investment.

Newer pretreatment technologies have been developed as alternatives to physical refining. One such process is thermal cracking. Similar to visbreaking units found in refineries, the fats and oils are converted simply by using heat to break the chemical bonds and reduce the molecular weight. The resulting product is composed of distillate range hydrocarbons that are a mixture of paraffins, olefins, and aromatics, along with some unconverted oils and fatty

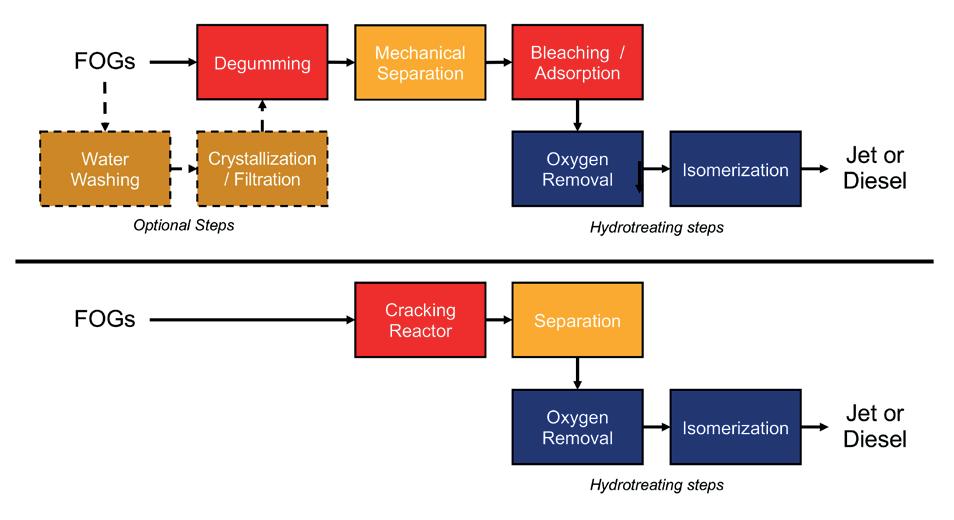

acids. Additionally, the typical targets of FOG pretreatment – metals, phosphorus, and chlorides – are reduced to levels below which the performance of the hydrotreater unit will not be impacted. The process does not require mechanical separation, but instead uses typical process equipment already found in refineries. Nor does it use catalyst or chemicals to carry out conversion and purification of the product. A comparison of thermal cracking vs traditional physical refining is shown in Figure 1.

In addition to breaking down the fats and oils into shorter-chain molecules, a product stream of light hydrocarbons, mainly of light gases ranging from C1 to C4, is produced in the thermal cracking process. Because hydrogen is not added to the unit, oxygen is removed via decarboxylation, and therefore the off-gases also contain some biogenic CO2. Approximately half of the oxygen present in the raw feed will be taken out with the off-gas. The remainder will be removed by hydroprocessing in the downstream unit. Some aqueous waste, which contains the rejected contaminants, is also generated in small quantities that can be treated and recycled.

Thermal cracking improves efficiency and flexibility

Pretreatment is often designed together with the hydrotreating unit to ensure interoperability and maximise efficiency. Typical grassroots HVO and HEFA units consist of two stages: deoxygenation followed by isomerisation (shown in Figure 1). These processes consume a high amount of hydrogen, which is typically around 2500 standard ft3/bbl (410 Nm3/m3). Using the pretreat unit to achieve partial conversion introduces several optimisations that are not possible with physical refining. The cracked feedstock, which is now partially distillate with some of the oxygen removed, requires less hydrogen in the downstream hydrotreater. As a result, the first stage of the hydrotreater will now be smaller and hydrogen consumption will be reduced by up to 60%.

Further economic efficiencies can be gained by operators focused on production of HVO. As outlined above, thermally-cracked triglycerides are now a mixture of distillate range hydrocarbons with a portion of unconverted/under-converted feedstock. The pretreated product needs only minimal further processing with hydrogen to remove the remaining oxygen and adjust the properties to meet the accepted specifications for HVO. At maximum pretreat conversion, it is possible that for what once required two stages of reaction – deoxygenation and isomerisation – only a single reactor might be necessary. In this scenario, the CAPEX savings can be as much as 50%. Base metal catalyst may also be used for isomerisation, which reduces cost as well.

Adjusting operating conditions of the pretreatment unit, namely the internal recycle flowrate, will also have an influence on the final product from the hydrotreater. With a once-through design, the thermal cracking followed by hydrotreating can produce a diesel product with 28°F (-2°C) cloud point with approximately 1230 standard ft3/bbl (200 Nm3/m3) hydrogen consumption. By recycling the unconverted oils from the cracking reactor,

Figure 1. Comparison of SAF and HVO production steps using physical refining (top) or thermal cracking (bottom) pretreatment processes.

the cloud point and hydrogen consumption are reduced to -2°F (-19°C) and 960 standard ft3/bbl (159 Nm3/m3) respectively.

Commercially proven performance

A variety of feeds, including distillers corn oil, soybean oil, used cooking oil, and waste chicken fats have been studied in both a pilot plant and in a commercial unit that began operations in 2023. Table 1 shows the results obtained in the commercial pretreat unit for key impurities compared to the specifications required for the downstream hydrotreater.

As shown in the table, similar product qualities were obtained despite varying impurity concentrations in the feedstock. This suggests that the range of usable

feedstocks may be widened, including those of lower quality, by using a more severe form of pretreatment. It may also allow for upgrade and monetisation of materials that would otherwise have been discarded. The gums and resins formed in physical refining contain not only the heteroatoms that make up the impurities, but also valuable carbon that can be converted to fuels. Cracking these materials can increase the yield of saleable product.

Thermal cracking of the renewable feedstock would also overcome the barriers limiting co-processing of renewable feedstocks with petroleum-derived diesel and jet. Higher reaction exotherms and the oxygen content of biomass-based feedstocks limits co-processing to approximatly 10 - 15% of the total feed rate. With the pretreated product now partially comprised of distillate-range hydrocarbons, the maximum allowable percentage of renewable feedstock can be much higher. Olefin saturation, oxygen removal and some isomerisation would still be required, but to a significantly lesser degree and without major investments in additional equipment or reaction stages.

Lower carbon intensity

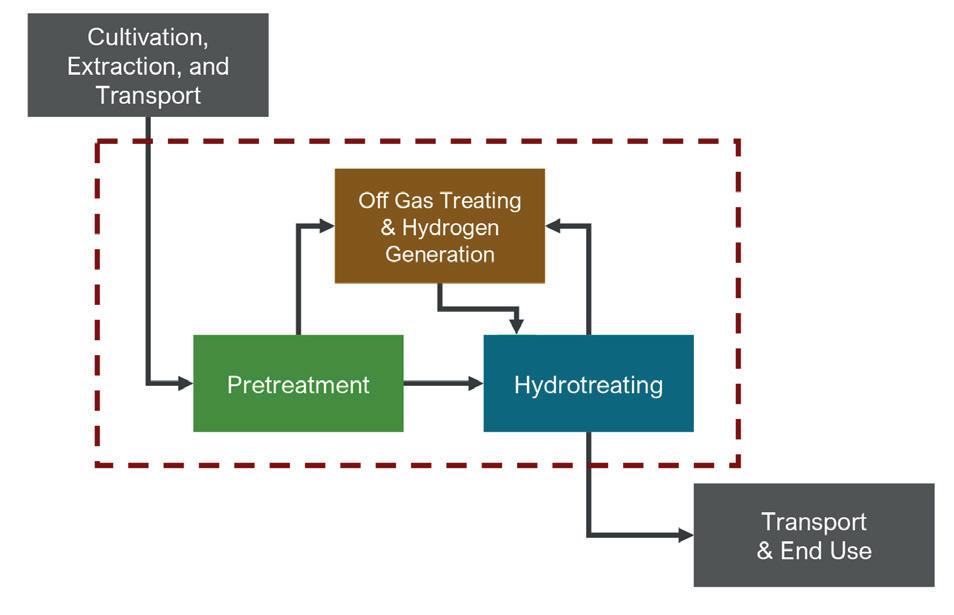

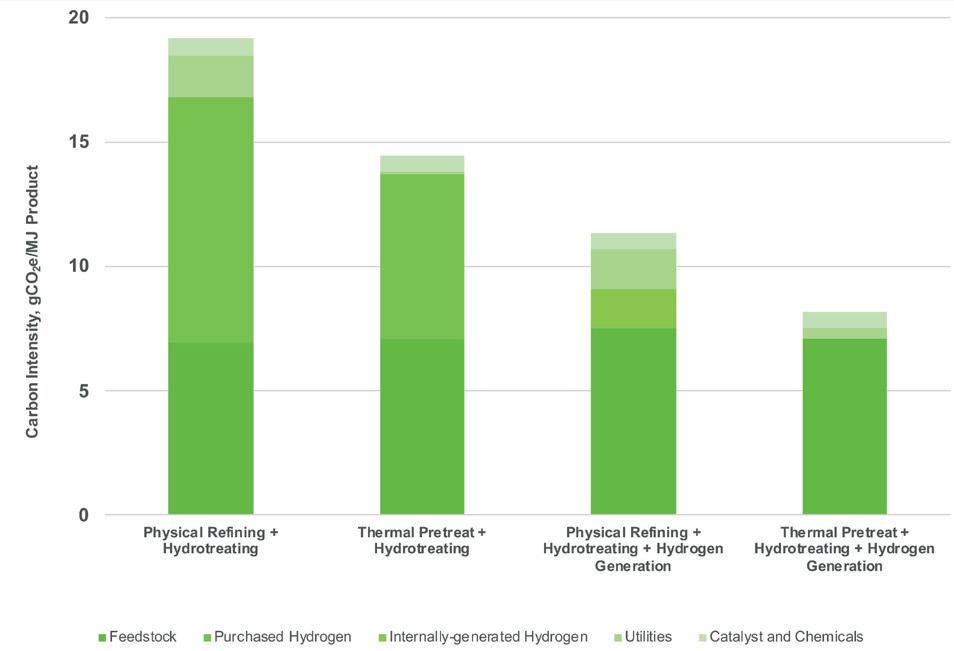

The adoption of renewable feedstocks to produce fuels has been a major driver towards a more sustainable transportation industry. Essential to that is the selection of pretreatment, hydrotreating, and hydrogen generation technologies to be used in the biofuels refinery, as they will have a direct impact on the facility’s economics and carbon footprint. Producers and sellers are incentivised or mandated, depending on jurisdiction, to produce a fuel that adheres to ever decreasing carbon intensity (CI) targets. Improving CI for only the biorefinery portion of the well-to-wheel CI, which is highlighted in Figure 2, can be more economically advantageous due to either the collection of incentives or reduced cost of carbon.

Considering the aforementioned optimisations, thermal cracking pretreatment has a lower carbon footprint relative to the conventional pretreatment process. This comparison is shown in Figure 3. Even though CO2 is generated, the CI is reduced by one-third due to the lower hydrogen consumption. Using produced naphtha and off-gas further reduces CI by eliminating the need for imported natural gas to generate hydrogen. Externally generated hydrogen, at higher quantities, is still required when physical refining is used. Altogether, the CI from the combined processes is almost 30% lower, which for a 10 000 bpd HVO complex, means a reduction in CO2 emissions of up to 30 000 tpy. Additionally, the final CI is up to 90% lower than conventional, petroleum-derived fuels.

Key takeaways