Only three months ago, in May, the Reserve Bank said there would be no cut until August nextyear.So,inthespaceofthreemonthstheyhavechangedtheirpredictionbyafullyear. This is a sad indictment of the deterioration in the performance of the Reserve Bank with regard to forecasting inflation. But it is consistent with the errors they made in 2022. It backs up the view economists have been expressing this past year that after loosening too much duringandafterthepandemictheyhadtightenedtoomuch.

So, in that regard the markets are right to factor in some sizeable cuts over the coming 12 months because if the Reserve Bank can change this much in three months they are likely topoweraheadoncetheyfeelthecredibilitylossissmoothedoverbyratecuthappiness. The central bank is picking that come this time next year the cash rate will be near 4.1% and nottheirpreviouspickof5.5%.

This is a timely boost, as we've already seen encouraging activity across our network, with new listings and increased buyer interest. The rate cut sets the stage perfectly for what promisestobeabusySpringseason.

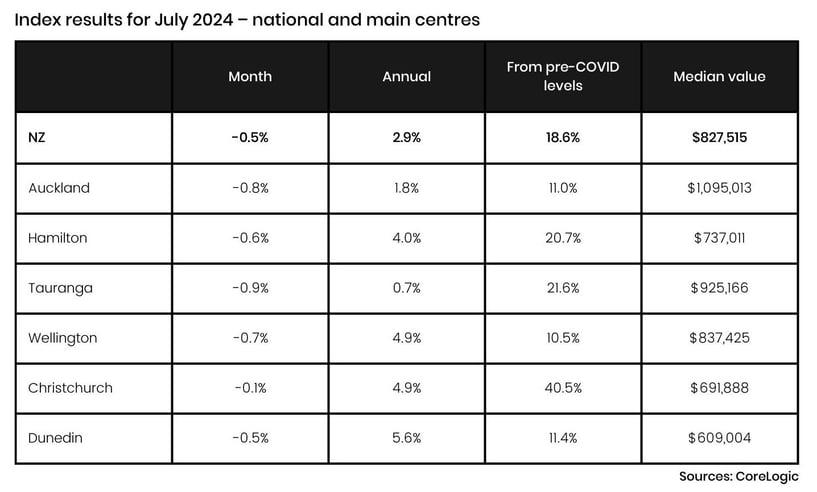

Nationwide, the numbers are holding strong. The median property value has increased by 0.5 percent month-on-month to $827,515. Even more encouraging, values are up 2.9 percent year-on-year and 18.6 percent above pre-COVID levels, demonstrating the ongoing strengthandgrowthofpropertyinvestments.

With the Reserve Bank's decision in place until its next review in October, banks are already beginning to offer relief to borrowers, especially those about to start or refix their mortgages. We can expect more competitive offers from banks over the coming months, withpotentialforfurtherratecutsaseconomicconditionsevolve.

Buyers will feel more confident to return to the market. Property enquiries will pick up, FOMO will recover more than it has, and vendors will feel more emboldened to hold out for the price they dream they can get rather than the one which will allow them to move on with theirlivesstraightaway.

Asalwayswehopeyouenjoythispublication.

Kindregards

Brent

Brent Worthington Principal and Licensee Agent

LJ Hooker Town & Country & Property

1/233 Great South road, Drury

0292 965 362

Management

Shifting Market Dynamics

11 August 2024

Aswintersetsin, the New Zealandpropertymarketcontinuesto navigate througha periodoftransition, characterisedbyfluctuatingvalues, increasedlistings, andvaried regional performances.

Nationaloverview

The latestCoreLogic Home Value Indexreportfor July2024showedacontinuedsoftening inpropertyvaluesacrossNew Zealand, withanational decline of0.5percentforthe month.Thismarksthe fifthconsecutive month of fallingvalues, resultingina2.5percent dropfromthe recentpeakinFebruary

CoreLogic putsthe medianproperty value at$827,515, downapproximately$21,200from February'sfigure of$848,713.Despite thisdecline,valuesare still around19percenthigher thanpre-COVID levelsdespite downabout16 percentfromthe peakobservedinJanuary 2022.

Similar situationswere seeninthe othercentres, withnew listingsup55percentin Wellingtonandthe capital’smedianvalue was$837,425inJuly.

Althoughproperty valuesare downmonth-on-monthandfromrecentpeaksinFebruary, annual pricesare still up, withsignificantgrowthisstill achievedinourcitiessince preCOVID.

“While the month-on-monthpropertymarketin ourcitiesisperforming weakerthan many regional areas, property ownersare still seeingconfidence ingoingtomarket.There are still gainstobe hadinpropertyownership,”Dunoonsaid.

“Asofteninginthe medianproperty value inAucklandisonlyexpectedaswe stillaninflux ofnew townhouse developments.These are oftencheaper thantraditional home and sections, whichwill contribute tothe softeningin the Aucklandmarketas buyershave more choice.”

Regional resilience

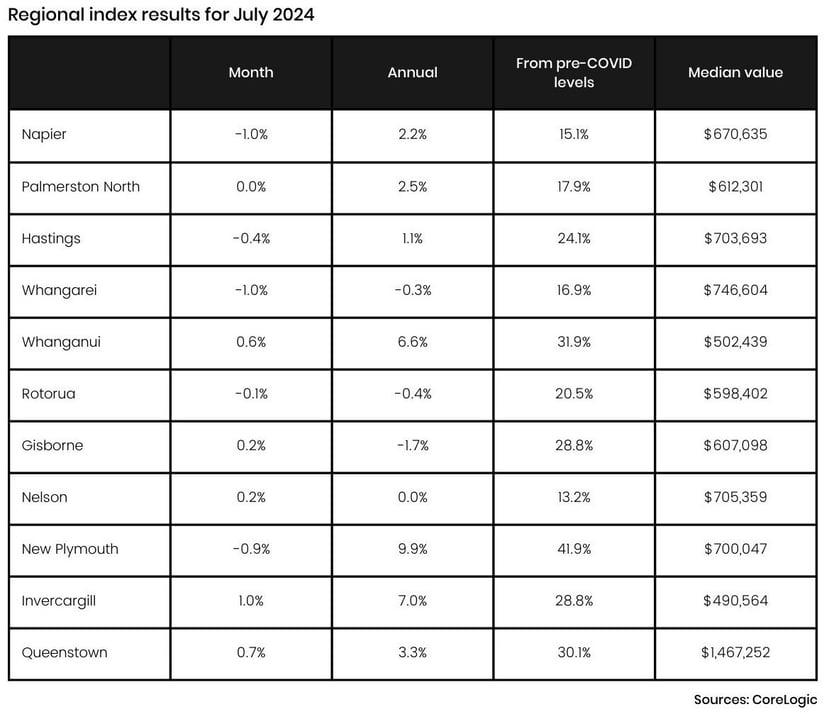

The regions continue to show resilience, however the trend that the regions are holding stronger than the cities is no longer the case as there is a slightly more mixed results in July.

Data from realestate.co.nz shows new listings increased in all regions, except for Taranaki, which was down 4.8 percent. The area with the most new listings was Central North Island, up92.8percent.

Asbanksstarttoease the pressure onmortgage holders, withreductions tofixedterm interestrates, conditions willcontinue toimprove for borrowersandhomeownerswhoare soondue torefinance.

Springisshapinguptobe abusyseason, ifthistrendof new listingscomingtomarket continues.There will beample choice for buyerslookingfor achange or toenter the propertymarket.Sellershave takentime tounderstandthe current marketconditions andhave preparedthemselvestonavigate thismarket.

"The propertymarket'scurrentstate presentsbothchallengesandopportunities.Sellers needtostayinformedandflexible, while buyerscantake advantage ofthe increased choicesandstable prices.The keyistonavigate these conditionswithawell-informed strategy."

Town&Country

Please don't hesitate to contact our team who can ably assist you with any property management matters you may have or if you have any questions about anything in the newsletter or property management in general.

WearandTearvsAccidentalDamage Explained August Newsletter

It is every landlord’s nightmare to receive a bad final inspection report once tenants have moved out of their rental property. The problem often stems from the loose definition of what exactly is classified as ‘fair wear and tear’ and what is defined as ‘accidental damage’.

In NewZealand,tenants are not responsible for paying for what isdeemed to be ‘fair wear and tear’ to a property. Onlywhen the tenant has been irresponsible andaccidentally or intentionally caused damage to a premises is he or she liable to pay for repairs. Let’s take a closer look at how each term is defined and what it means for landlords and tenants.

What is Wear and Tear?

Wear and tear meansthe normal deterioration of a property from ordinary,everyday use. Exposure to the elements, time, as well asday to day living can cause fair wear and tear. Examples include minor scuffs on wooden floors, fadedor chipped paint, loose handles, frayed curtains andtraffic marks on carpets.

What is accidental damage?

This refers to damage that occurs suddenly due to an unexpected and non-deliberate external action. Typically unintentional one-off incidents, it causes, harms, either the property or its contents. Examples include broken windows, carpet stains, torn window screens or burn marks on countertops. Tenants are likely liable for such damage.

What is malicious damage?

This refers to a wrongful act motivated by malice, vindictiveness or spite to damage the property. This includes smashed windows, holes punched in the wall and doors that have been kicked in and often spread throughout the premises.

Knowing the difference between fair wear and tear and accidental damage can eliminate a lot of grief in situations where a lease is about to expire or damage needs to be urgently fixed. Once both tenants and landlords work out what constitutes damage or simple wear and tear, the next step is to determine what their specific home insurance policy will cover and what it will not.

It can come as a bit of a shock when your landlord decides to sell your much-loved 'home'. Naturally, this situation can raise several questions: Do you need to search for a new rental? Are you obligated to keep the property in pristine condition for open homes? What happens when the property is sold?

Your landlord is legally permitted to sell their property at any time; however, they are still governed by several provisions designed to protect tenants. Let's take a look at what happens when a tenanted rental property is sold in New Zealand.

Can your landlord sell your rental property?

In New Zealand, landlords are allowed to sell their property at any time. The good news is that if you have a current fixed-term tenancy agreement, you cannot be asked to leave before the tenancy expires. When the property is sold, it is sold with you, the tenant, in place. You will be notified that the property ownership has changed.

There are many benefits for an owner to sell a tenanted property, particularly as it provides consistent income right up until the property is sold.

Do I have to agree to viewings and open homes?

In New Zealand, while landlords have the right to access their premises to show prospective buyers, they must provide written notice at least 48 hours before each viewing. You are obliged to make all reasonable efforts to agree on a suitable time and day for the showing. If you agree, make sure you get it in writing, signed by both yourself and the landlord or agent.

If an agreement isn’t reached, the landlord is limited to showing the property a maximum of twice per week, with at least 48 hours’ notice each time. Notice can be delivered by email (if you agree to this communication method), mail, or handed to you between 8 am and 7 pm. You are obliged to keep the premises in a "reasonable state of cleanliness".

If the landlord has given you notice within the correct timeframe, they have the right to show people through the premises, whether or not you agree or are present. However, you

do have the right to be at the premises during inspections or have someone else there on your behalf.

It’s a good idea to discuss suitable viewing times with your property owner or property manager and adhere to that routine each week. This way, everyone knows what to expect and when.

Are there any benefits to tenants allowing open homes?

While the sale of a rental property can be disruptive, there can also be benefits. While it is not required, some landlords offer incentives to keep the property inspection-ready, such as:

• Reducing the weekly rent in return for presenting the property nicely for viewings.

• Offering a week’s free rent to help with relocation costs.

• Providing a small fee for tidying and preparing the property for a viewing.

• Hiring a cleaner before the inspection.

• Giving a small thank you gift, such as a box of chocolates or movie tickets, after an open home.

• Offering to provide a reference for future rental applications.

What are the rules around open homes?

Open homes can only take place between 8 am and 7 pm and cannot occur on Sundays or public holidays unless you agree. People cannot stay for an extended period. Notice must be given to you in writing, and the required notice periods differ depending on your tenancy agreement.

Remember, if you refuse access to the property when the landlord is legally allowed, you may be in breach of your tenancy agreement.

What are my rights regarding the advertising and promotion of the property?

Photography: The property can be photographed from the outside without your consent; however, they need your consent to take photos inside the property, including photos of your belongings. The landlord should try to discuss and agree on what will be photographed and how the photos will be used. If you're worried about theft, lock away any valuables that could be easily picked up during an inspection.

Signage: The tenant must give consent for a ‘For Sale’ signboard to be placed on the property outside.

On-site Auctions: If the property is being sold via auction, it cannot be held on-site unless you, the tenant, give consent.

WhatcanIdoifIwanttoterminatemytenancyagreement?

Ifyou have aperiodic agreement, you canserve ano-reasonnotice, whichistypically28 days’ writtennotice, unlessthe landlordagreestoashorter time.

Ifyou are onafixed-termagreementbutwanttomove outbecause the propertyisbeing sold, you maybe able to endthe tenancyagreementearlybymutual consentwiththe landlord.Ensure thisisconfirmedinwritingandsignedbythe landlordoragent.

Some landlordsare happytoendthe tenancyearlytofixanythingbefore theygoto market, allowingaccessforopeninspections.Discussthisoptionwithyour landlordor agentifitsuitsyour needs.

WhathappensIfthelandlordwantsthetenanttoleave?

Alandlordcannotterminate afixed-termagreementdue tothe sale ofthe property.They canhowever endthe tenancy onor after the expiryofthe fixed-termtenancywithatleast 90days’ writtennotice.The landlordalsoneedstostate the buyerhasspecifiedvacant possessionasarequirementinthe unconditional sale ofthe property.

Ifyou have aperiodic tenancyagreement, theycanissue anotice ofterminationgiving the tenant90days’ writtennotice, butonlyiftheyhave exchangedacontractofsale with abuyer, andthe contractspecifiesthatthe propertyissoldasvacantpossession.

Whathappenstoyourtenancyafterthesale?

Ifyou oryourlandlord haven’tterminatedthe agreement, your tenancy agreement remainsinplace and mustbe terminatedcorrectly.Ifyou have afixed-termtenancy agreement, you cannotbe askedtoleave before the endofthe fixedterm.Ifthe property issoldbefore the end of your agreement, the new owner takesoverthe rightsand responsibilitiesofyourpreviouslandlord, meaningyourexistingtermsandconditionsstill apply–includinghow muchrentyou pay, how andwhenyou payit, andthe expirydate of the fixedterm.

Whathappenstomybond?

Whenthe propertyissold, boththe new owner andpreviousowner must notify Tenancy Servicesthatthe propertyhaschangedhands.Your bondwill remainwithTenancy Servicesuntil the endof your tenancywhenthe new landlordcan make aclaimagainstit orhave itpaidouttoyou.

Green shoots appear in New Zealand’s property market.

The Real Estate Institute of New Zealand (REINZ) released its July 2024 data today. The data shows signs of positivity with increases in sales numbers and listing volumes.

REINZ Chief Executive Jen Baird said July brought a new wave of buyer activity not typically seen in late winter. While listings continue to increase, the rise in sales volumes has seen the total number of properties for sale in New Zealand fall compared to last month. However, median prices have decreased by 2.2% nationally compared to a year ago, indicating that houses sold at a lower price in July.

The total number of properties sold in New Zealand increased by 14.5% year-on-year, from 5,070 to 5,806, and by 19.7% compared to June 2024, from 4,851 to 5,806. Thirteen regions saw an increase in sales for July 2024. The most significant increases were in Gisborne (+53.6%), Otago (+45.7%), Marlborough (+42.9%) and Southland (+38.8%). Compared to June 2024, only one region saw a decrease in sales volume, Nelson (-21.2%).

“ Although we have not yet reached the spring

season, we are observing early signs of growth in the market not typically associated with this time of year. This can be seen through the seasonally adjusted data, which indicates an increase of 5.4% in national sales compared to last year, which reflects a market performing above anticipated levels, says Baird.

Fourteen of the fifteen regions have seen a rise in new listings year-on-year, with Wellington (+55.0%), Gisborne (+50.0%) and Southland (+36.9%) leading the way. The only region to see a decrease in new listings year-on-year was Taranaki (-4.8%).

Seven of the sixteen regions had a median price increase year-on-year. West Coast and Tasman stood out, with West Coast’s median price increasing by 21.2% year-on-year ($330,000 to $400,000), and Tasman saw a 10.6% increase ($710,000 to $785,000). Seven regions saw an increase month-on-month (Waikato +3.4% to $725,000, Bay of Plenty +2.0% to $800,000, Tasman +8.7% to $785,000, Nelson +1.4%to $657,000, West Coast +25.0% to $400,000, Otago +6.4% to $665,000 and Southland +9.9% to $482,500).

The national median price decreased by 2.2% year-on-year, from $770,000 to $753,000, and decreased by the same amount month-on-month. For NZ, excluding Auckland, the median price decreased 1.5% year-on-year from $680,000 to $670,000. Month-on-month, the median price also decreased by 1.5%.

“There has been downward pressure on prices in most parts of the country this year and sales volumes have been lower than average as the cost of living, concerns around job security and interest rates challenge many people in New Zealand. However, it seems this sentiment is beginning to change.

Jen

Baird CEO, REINZ

The slight decline in interest rates in July, and a belief that there are more to come, appears to have encouraged buyer activity, as reflected in the increase in sales,” comments Baird.

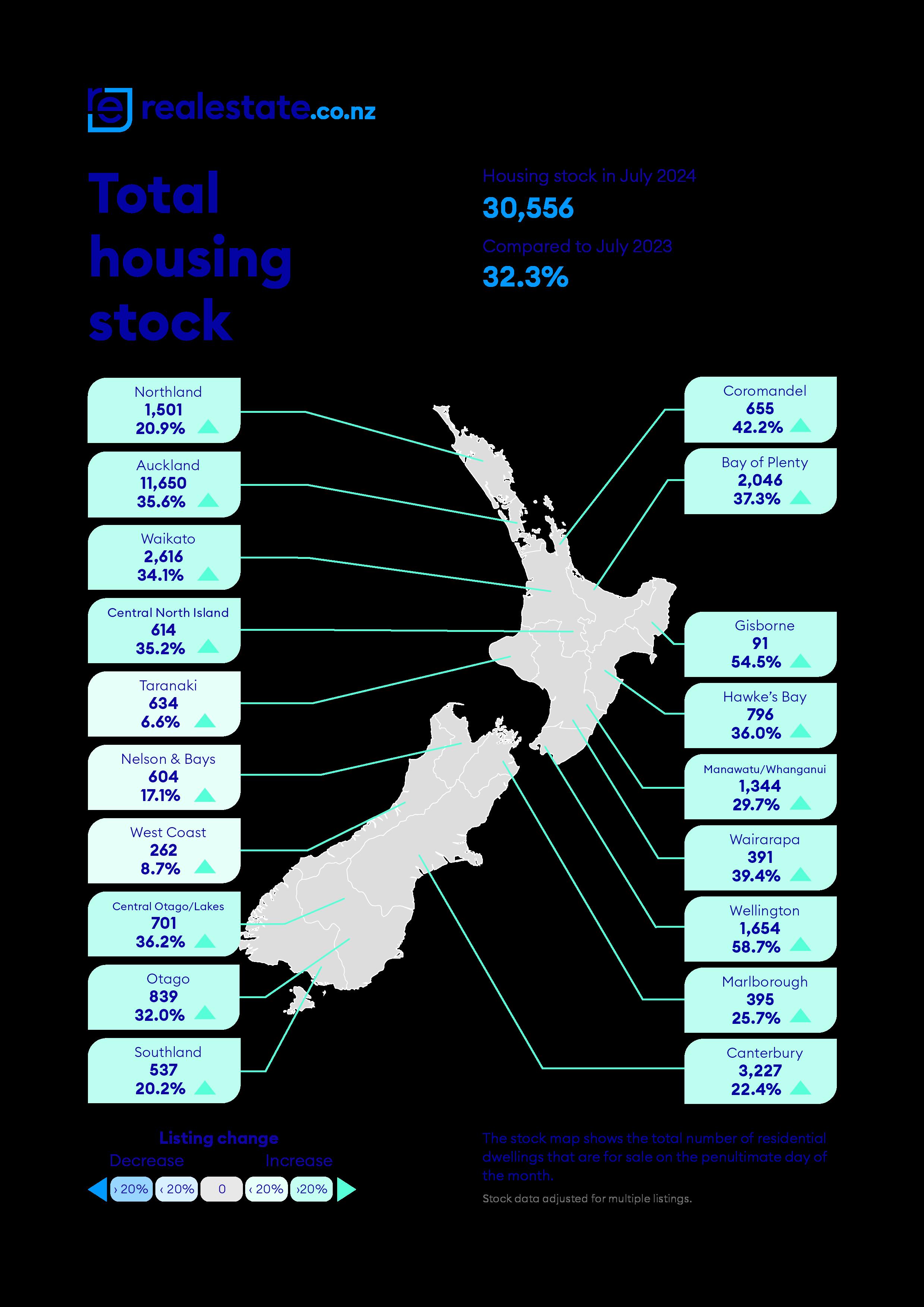

The national inventory level increased by 32.3% (+7,466) in July, from 23,090 to 30,556 year-on-year and decreased by 3.7% from 31,745 month-on-month. For New Zealand ex Auckland, inventory levels increased 30.4% (+4,409) year-on-year from 14,497 to 18,906 and decreased 3.5% (-677) compared to June 2024.

There were 647 auctions nationally in July 2024 (11.1% of all sales), compared to 529 (10.4% of all sales) in July 2023. The Auckland region saw 332 properties sell by auction in July 2024 (18.4% of all sales), compared to 326 properties sold by auction or 19.1% of all sales in July 2023.

“The recent 25 basis point reduction in the OCR, and the strong signals of more reductions to come, will bring relief to households and will provide some confidence to buyers to act soon,” adds Baird.

Nationally, median Days to Sell increased by one day, from 48 to 49 days, compared to a year ago. For New Zealand, excluding Auckland, median Days to Sell had no change yearon-year (49 days). Eight regions had fewer Days to Sell in July 2024 than in July 2023. Manawatu/Whanganui had the highest median Days to Sell at 63 days, a one-day increase compared to a year ago.

The HPI for New Zealand stood at 3,563 in July 2024, a 0.2% increase from July 2023 and down by 0.3% compared to June 2024. The average annual growth in the New Zealand HPI over the past five years has been 5.2% per annum, and it is currently 16.7% below the market peak reached in 2021. Otago is the topranked HPI year-on-year movement this month, reaching a new peak at 4,187.

“In July, we saw an increase in sales across the country compared to last year and June 2024. As more listings hit the well-supplied market, buyers are slower to make decisions, extending the average Days to Sell. Despite ongoing economic challenges, early signs suggest potential improvement, indicating favourable conditions in the residential property landscape might be on the horizon.” adds Baird.

The Real Estate Institute of New Zealand (REINZ) has the latest and most accurate real estate data in New Zealand.

For more information and data on national and regional activity visit the REINZ’s website

Media contact:

Laura Wilmot

Head of Communications and Engagement, REINZ Mobile: 021 953 308 communications@reinz.co.nz

Market Snapshot – July 2024

q National$753,000-2.2%

Days to sell nationally

ANNUAL MEDIAN PRICE CHANGES

JULY 2024

Manawatu-Whanganui

Gisborne

Written by: Liz Studholme

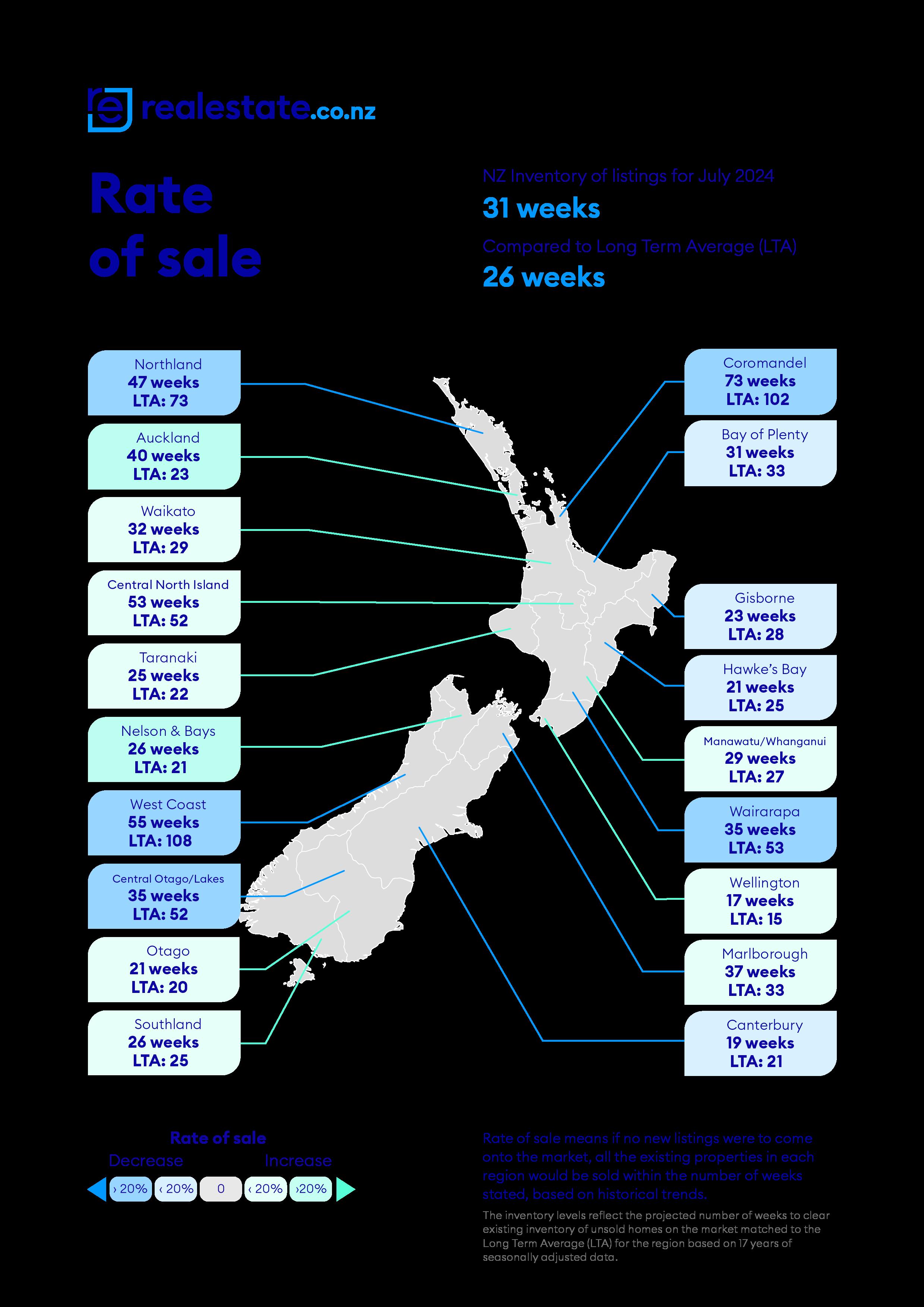

With an increase in the total number of houses for sale and slower-than-average sales, buyers have plenty of choices this winter.

Mortgage interest rate cuts, decreasing inflation, and speculation about the Official Cash Rate dropping sooner than initially signalled may be bringing midwinter economic optimism. However, the latest data from realestate.co.nz suggests we are yet to see the property market warm up, with plenty of choice and slow sales hallmarking the 2024 winter season.

• Plenty of choice for buyers with total stock up and new listings unseasonably high

• Slower than average rate of sale in 10 of 19 regions

• Average asking price fluctuations across the motu

Total stock increased during July by 32.3% year-on-year to 30,556 properties for sale. New listings were also unseasonably high, up 31.3% year-on-year, breaking a seven-year trend of low listing levels in July Adding to the property market’s winter chill, 10 of our 19 regions experienced a slower-than-average rate of sale last month.

Sarah Wood, CEO of realestate.co.nz, notes that supply was unusually high for July, with almost 7,500 more total homes for sale than this time last year:

“17 of our 19 regions saw double-digit growth to total stock levels compared to July 2023, with just Taranaki and West Coast slightly behind at 6.6% and 8.7%, respectively ”

“Buyers have ample choice and time to decide, but this will be a competitive market for many sellers. They should research local market trends and be prepared to negotiate to meet the market ”

Average asking prices experienced regional fluctuations in July, marking a change from the relative stability seen in most regions over the last 18 months.

“It is too early to determine if these changes signal a market shift. Consumer confidence and interest rate adjustments will likely be key drivers of future market trends,” says Wood.

Display price remains the most popular method of sale across our listings, followed by negotiation. “This again indicates that people are taking their time to transact, reflecting the slower pace of the market,” Wood adds.

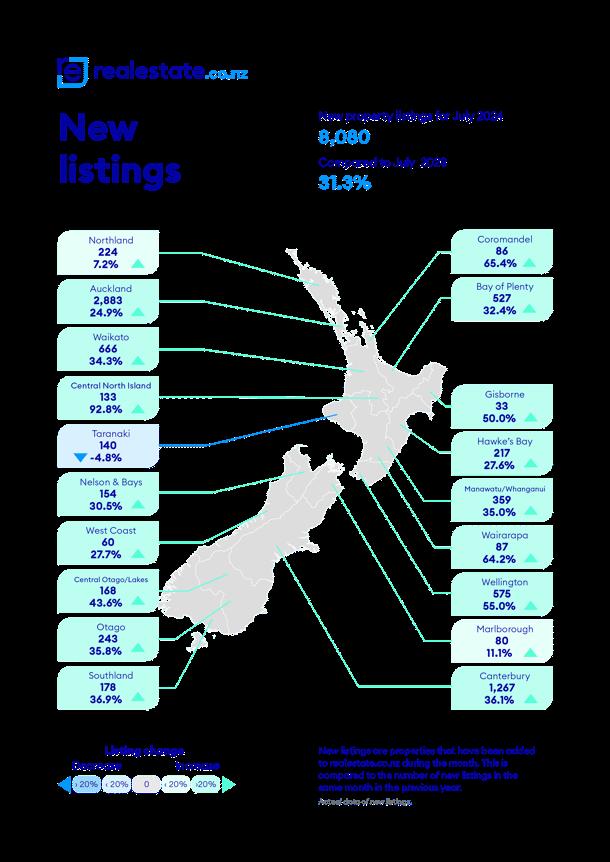

Vendors busier than usual this winter - new listings up 31.3% year-on-year

Breaking a seven-year trend of low listings during July, new listings were up 31.3% nationally last month. This growth was reflected in all regions except Taranaki, where new listings dropped by 4.8% compared to July 2023. However, Taranaki’s smaller market size means this was a drop of just seven listings.

The biggest increase was in Central North Island, where new listings nearly doubled, increasing by 92.8% from 69 in July 2023 to 133 in July 2024.

“In this economic climate, some property owners will be forced to sell. Particularly if they bought at the peak of the market when interest rates were low,” explains Wood.

She notes that several economic factors, including recent policy shake-ups, have influenced the market:

“We’ve seen a spate of changes, such as the shortening of the bright-line test from 10 years to two years, effective 1 July. This change allows investors to sell sooner without incurring capital gains tax.”

“While it is too early to attribute the rise in listings to this change, we understand that many investors were geared up to list their properties on or after 1 July.”

Slower than average rate of sale in 10 of 19 regions

Vendors might have been busy listing their properties and tidying up for weekend open homes, but buyers took their time last month. 10 of our 19 regions saw a slower-than-usual rate of sale in July, signalling that the market is moving more slowly in these regions.

Rate of sale measures how long it would take, theoretically, to sell the current stock at current average rates of sale if no new properties were to be listed for sale. For example, in Auckland, realestate.co.nz calculations show that it would currently take 40 weeks for all stock to be sold, compared to the long-term average of 23 weeks. Auckland saw the biggest slowdown of all regions during July.

Our analysis draws on 17 years of comprehensive property data to ensure accurate insights.

“The high stock levels we have seen throughout 2024, combined with slower sales, could provide opportunities for buyers. However, this depends on individual circumstances. High interest rates and new debt-to-income ratios (DTIs) could impact their ability to purchase.”

“For sellers, understanding current market conditions is crucial. Staying informed, getting advice from your local agent and being flexible can make a significant difference in navigating this slower market,” emphasises Wood.

Average asking price fluctuations across the motu

In July, average asking prices varied across the country. Canterbury, Central Otago/Lakes District, Coromandel, Gisborne, Marlborough, and Otago saw average asking prices grow month-on-month and year-on-year. In contrast, Central North Island, Hawkes Bay, Nelson, Northland, Waikato, and West Coast saw average asking prices decrease month- on-month and year-on-year.

Gisborne’s average asking price reached $710,960 in July, marking the first time it has been above $700,000 since March 2023. Northland, on the other hand, saw its average asking price decrease to $773,623 in July. This is the first time Northland’s average asking price has been below $800,000 since October 2021.

Wood notes these fluctuations are notable as they differ from the more moderate rises and falls of around 5% that have typified the last 18 months:

“It remains to be seen if this signals the end of the 18- month average asking price stability, but vendor expectations may be shifting in some regions.”

The national average asking price in July was down 2.3% year-on-year and 1.4% month-on-month to $848,548. For the last 18 months, the national average asking price has been relatively flat, fluctuating between about $860,000 and $890,000.

Written by Liz Studholme

01 Aug 2024

OneRoof House Price Report - August 2024

Queenstown house prices reach record high as rest of NZ suffers second slump.

Houses in New Zealand’s most expensive region are the most expensive they’ve ever been, new OneRoof figures show.

The average property value in Queenstown-Lakes hit a new peak of just over $2 million at the end of July, but the house price story outside the wealthy enclave wasn’t so encouraging for homeowners.

New Zealand’s average property value dropped 1.5% to $962,000 in the three months to the end of July, as economic uncertainty and high interest rates continued to take their toll on the housing market.

The rate of house price decline accelerated across much of the country, with Auckland and Wellington feeling the worst of the new slump.

Auckland house prices tumbled 2.4% over the quarter and 0.2% year-on-year. At $1.287m, the city’s average property value is only $8000 above its post-slump trough point at the end of June 2023.

Wellington’s average property value is 2.4% higher than a year ago, but its quarterly fall of 2.5% was the country’s steepest.

House prices dropped in another eight regions, reflecting low confidence in the market, although recent positive headlines around interest rates and inflation may put the brakes on further falls.

Several factors have contributed to the recent decline in property values. Interest rates of 7%-plus, higher living costs and rising unemployment have sapped buyer enthusiasm, while the withdrawal of First Home Buyer has put some first-time buyers on the back foot.

There’s still a glut of stock on the market, which has suppressed price growth and led to, in some cases, heavy discounting by stressed vendors.

“Amoresustainedmarketrecoverywilldependonlowermortgagecosts.Thefirst roundofinterestratecuts is likelytoreignitebuyerinterest,althoughthismaybe modestatfirst.”

Tony Alexander: House prices will be rising before the end of the year

The Reserve Bank's rate cut gamble - why the sudden change of heart?

Since July’s drop in annual inflation to 3.3%, expectations have been high that the Reserve Bank will cut the Official Cash Rate this year. Photo / Alex Burton

ANALYSIS: The Reserve Bank has just validated market expectations of an easing of monetary policy with a 0.25 point cut in the cash rate to 5.25% (although I had thought they would hold out to October). The RBNZ predicts the rate will fall below 4.5% in the middle of 2025, then 3% come the end of 2026. On that basis householders can reasonably expect the likes of the one-year fixed mortgage rate will fall to around 5% and perhaps slightly under come the end of 2026.

Only three months ago the RBNZ said it wouldn’t cut the OCR rate until August 2025 and warned that it might in fact need to take the rate higher. ANZ economists even predicted early this year that the rate would rise to 6%. Why such a huge change in a very short time?

First, as I’ve noted here for at least the past year, just as the RBNZ over-loosened monetary policy during and immediately after the pandemic, it has now over-

This tellsussomethingimportant.TheRBNZdecidedtotakeagamble.Itis hoping thatthenewweakness intheeconomy,whichitfailedtoacknowledgeinMay (hintyouguys–readmymonthlysurveyresults),willcrunchpricingplansquite quickly.

Thatmaywellhappen.ButtheRBNZnotedmanytimesinits commentarythis time aroundthatbusinesspricingplans willbeverycloselymonitoredandneedto changefurther.IcanalreadytellfrommylatestmonthlyBusiness Surveyrunwith MintDesignthattheproportionofbusinessessayingtheywon’tnowraisetheir prices has risento26%from18%lastmonthandayearagoanet22%sayingthey wouldraisetheirprices.

Independent economist Tony Alexander: "Only three months ago the RBNZ said it wouldn’t cut the OCR rate until August 2025 and warned that it might in fact need to take the rate higher." Photo / Fiona Goodall

Things are headed in the right direction and borrowers can look forward to lower mortgage interest rates. But before we get to sub-5% fixed rates more people will lose their jobs, more businesses will go under, and there will be a lot more restructuring across most sectors in the economy.

How quickly will the housing market respond to this new-found optimism about interest rates? I can already tell from my surveys of real estate agents and mortgage brokers that buyers are coming back – including some tentative investors. Sentiment is likely to improve further.

But listings are ahead over 33% from a year ago, job security is poor and set to remain that way, net migration flows are falling away very quickly, the rental market has recently shown new weakness, plenty of potential home-buying young Kiwis are leaving the country, and businesses are likely to keep their investment levels low until well into 2025.

Before the end of this year house prices are likely to be rising again. But it pays to remember that while interest rate levels are extremely important when it comes to housing market strength, so too are employment and access to credit. These areas will still take some time to improve.

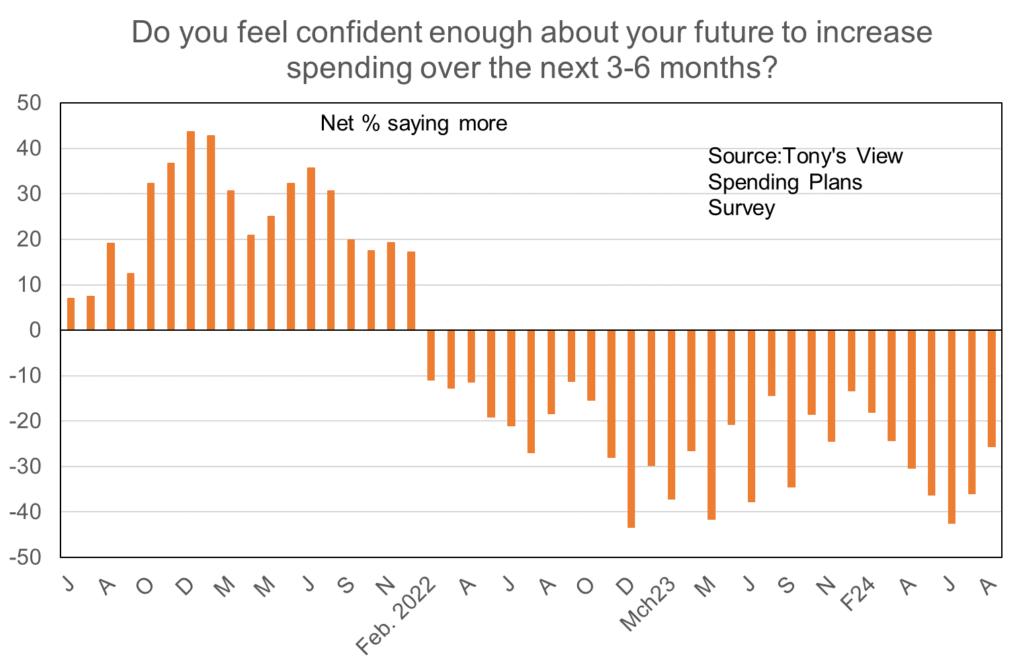

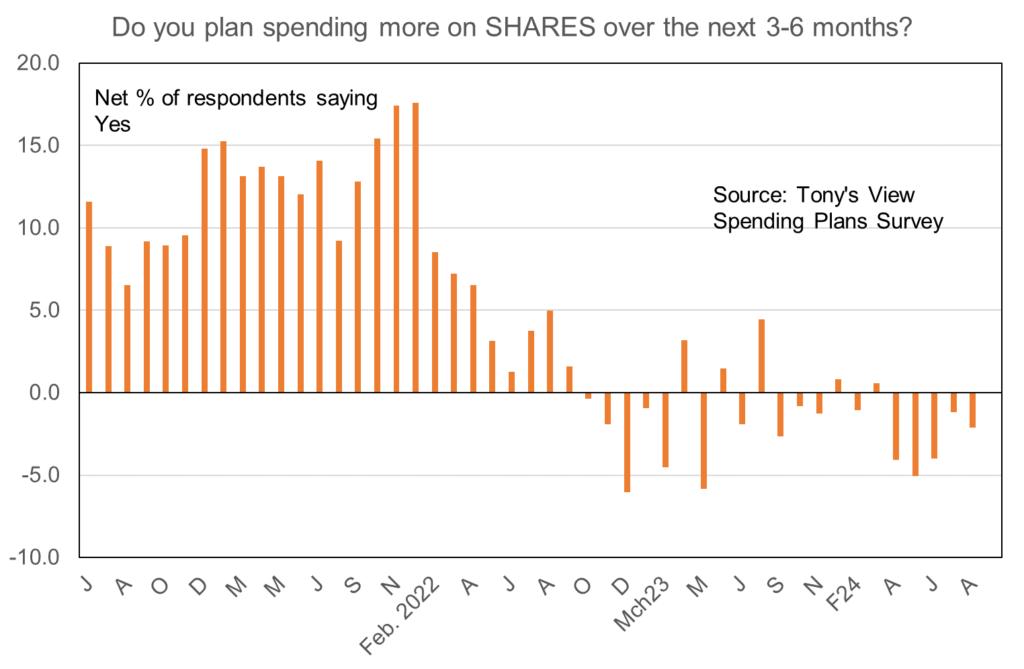

This week I conducted my monthly Spending Plans Survey of Tony’s View readers and although pessimism dominates the degree of woe is easing.

In June a net 42% of people said that they plan spending less on stuff in the next 3-6 months. This improved to a net 36% in July and now in August a net 26% have said they plan cutting back.

This is a reading still well away from the average of -6% seen since I started the survey in June 2020 and only takes things back to where they were in March.

For retailers the main implication is that for the remainder of this year conditions will be tight. We should expect discounted goods and closures of stores to continue. But at least we can talk about light starting to appear at the end of the tunnel next year.

Not that there is any strong reason for believing 2025 will be a firm year for the NZ economy unless consumers and businesses react to falling interest rates by choosing to aggressively boost debt levels. That seems like a bold call to make considering that the unemployment rate will rise through perhaps all of next year, and that people have been burnt recently by debt pressures.

The extent of the interest rate decline-induced recovery in NZ’s pace of economic growth will be constrained by factors including the following.

1. The absence of a large fall in the NZ dollar,

2. The absence of a firm acceleration in the pace of global growth. Worries are deepening about growth in the United States and China in the coming year.

3. The risk of 10% across the board tariffs being introduced in the United States next year and general pullback globally from multilateralism and open borders. This has historically been one of the many key risks facing New Zealand.

4. Rapidly falling net migration inflows and probably a still rising net loss of Kiwis offshore through 2025. It is hard to imagine that the picture young people gain of long-term prospects for living in New Zealand will be enhanced by the deepening media focus on what is wrong across many aspects of central and local government and society overall.

5. The cyclical decline in house construction is likely to continue through 2025.

6. The “weeding out” in all sectors of businesses unable to handle the absence of special pandemic assistance measures and presence of above average interest rates is likely to continue apace through the first half of next year.

7.

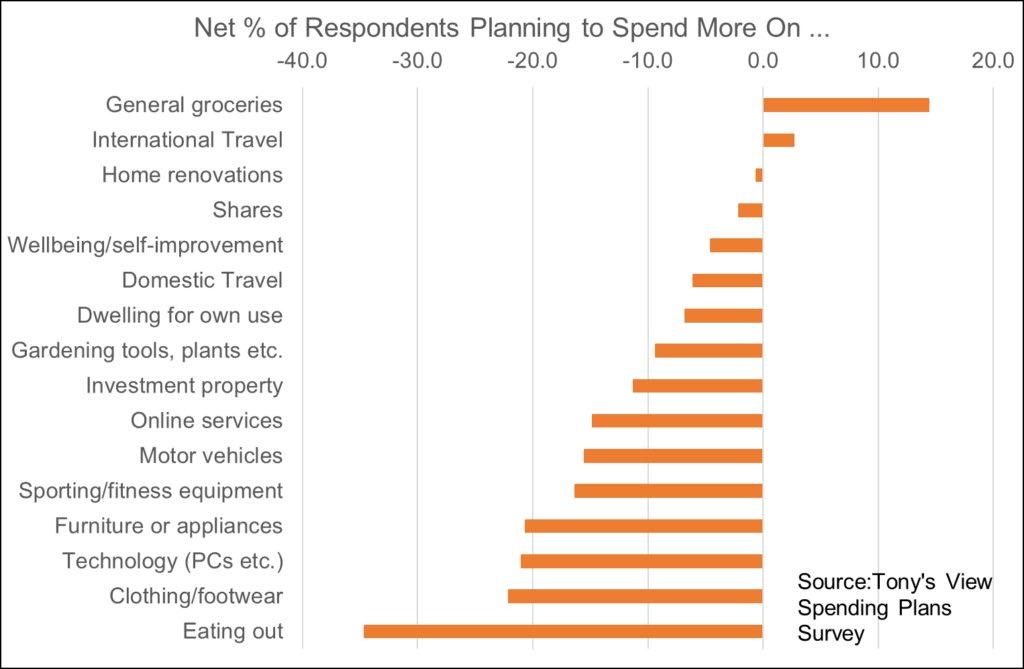

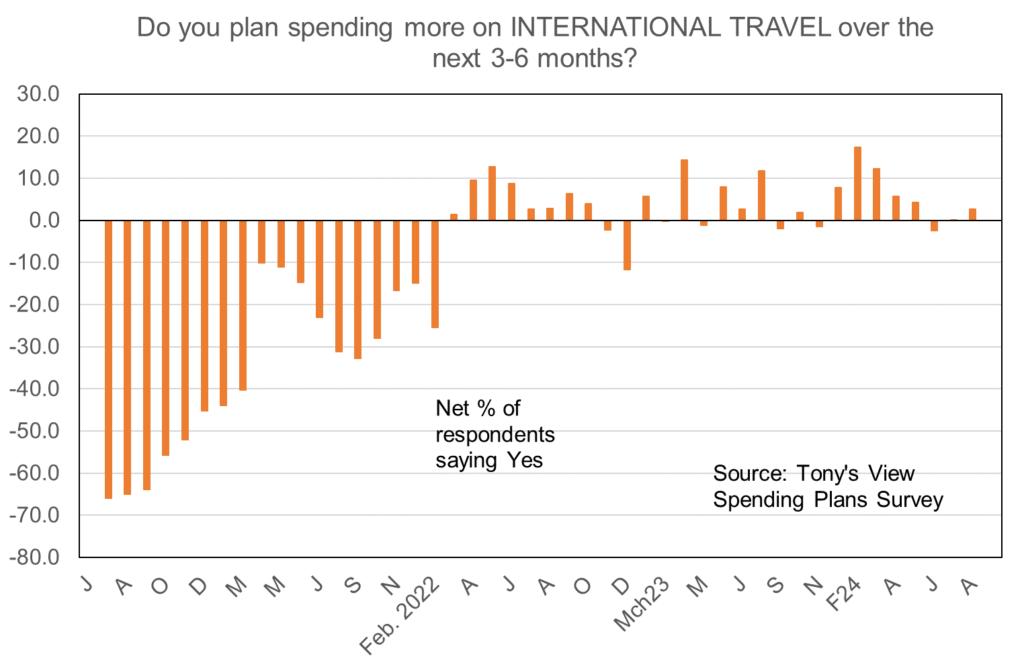

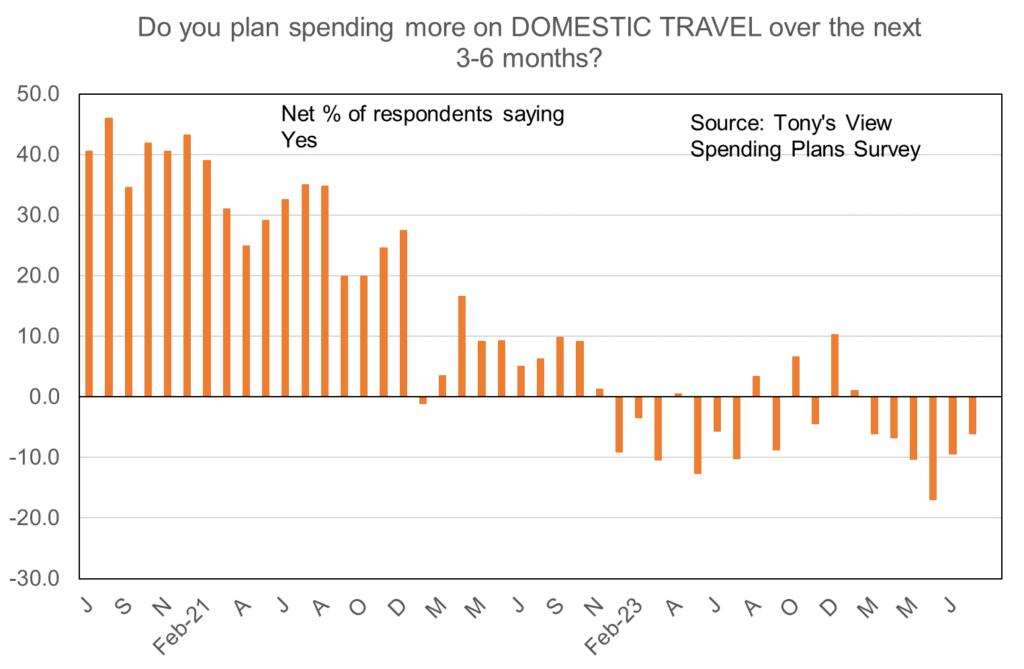

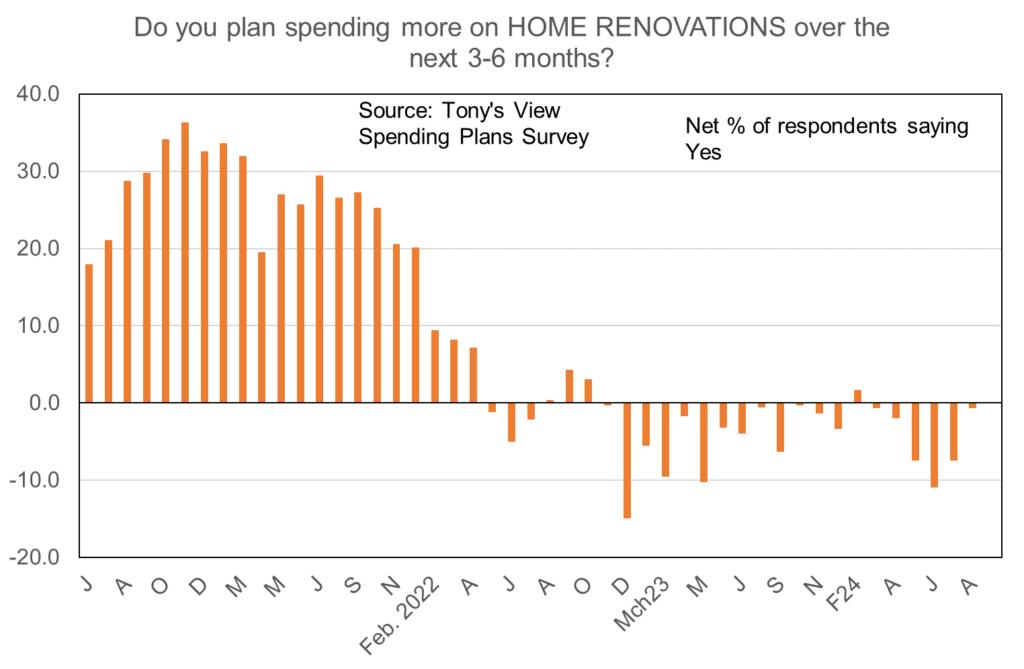

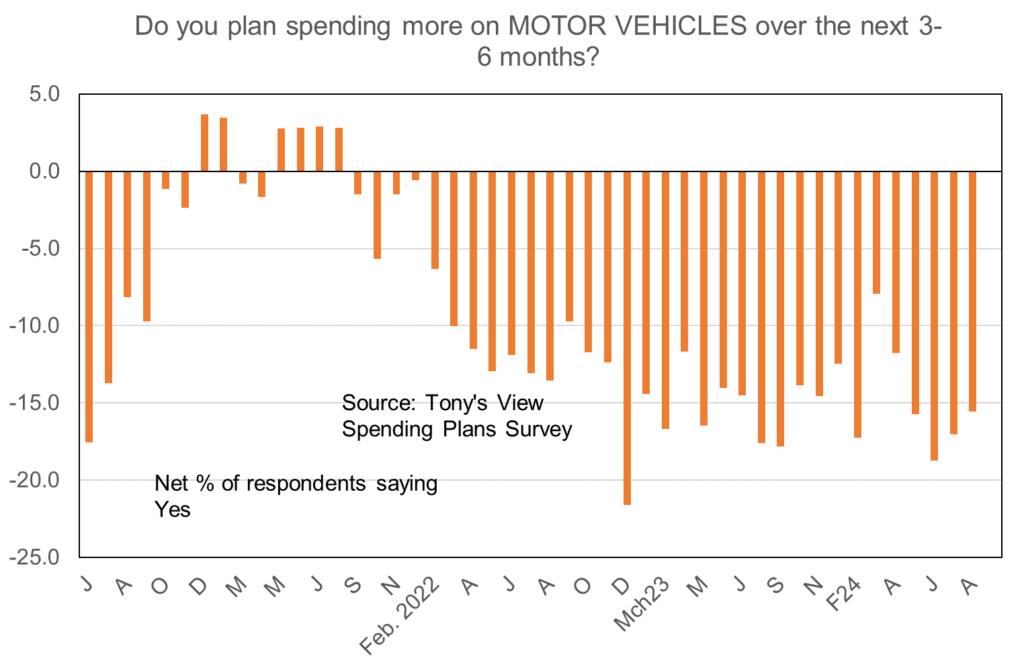

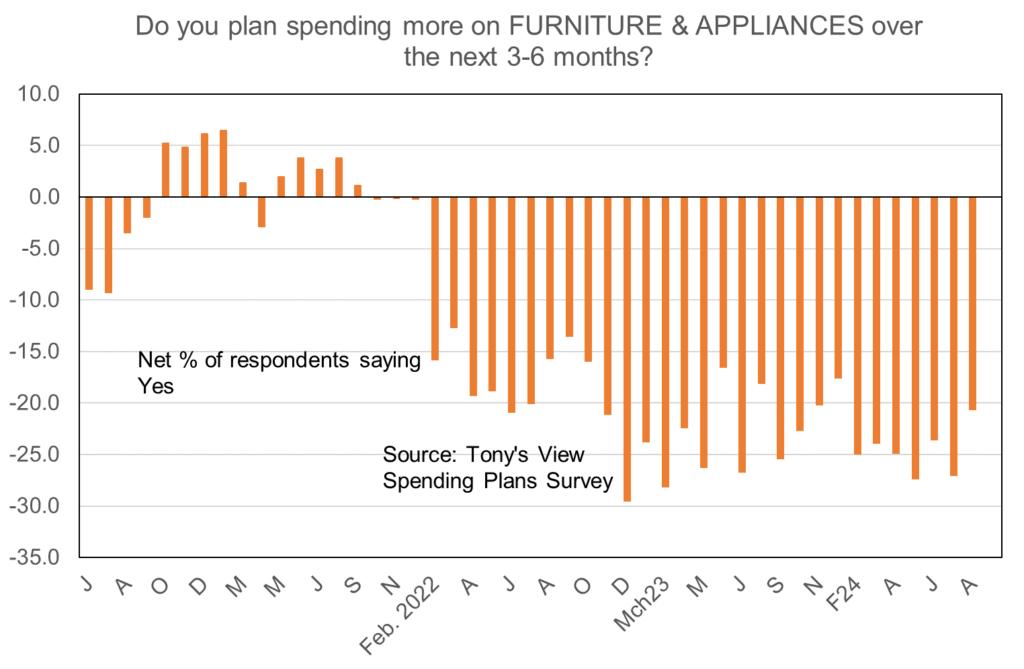

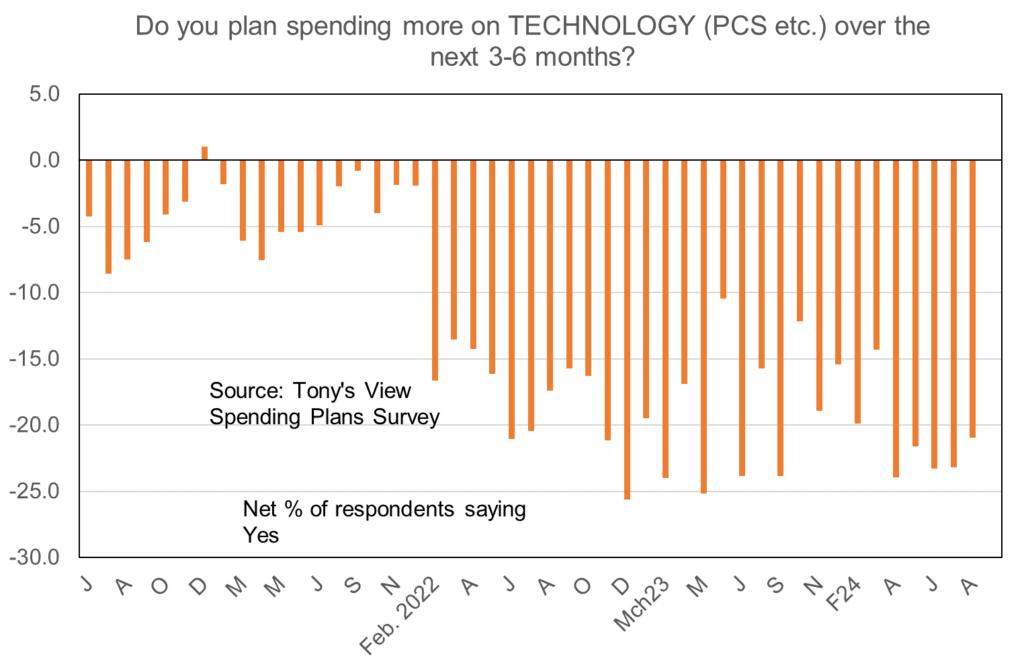

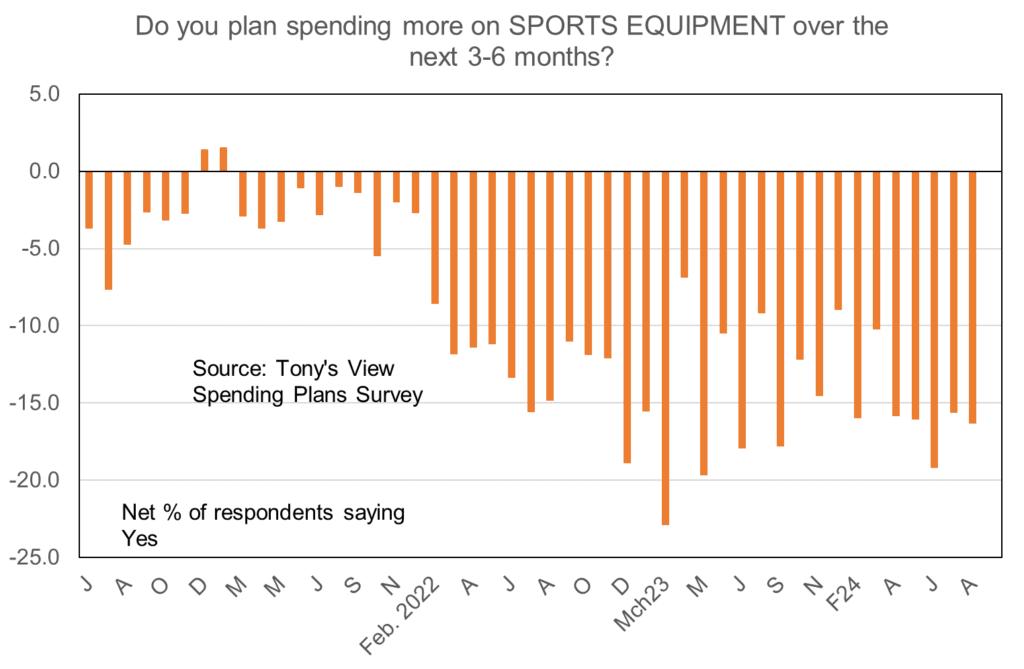

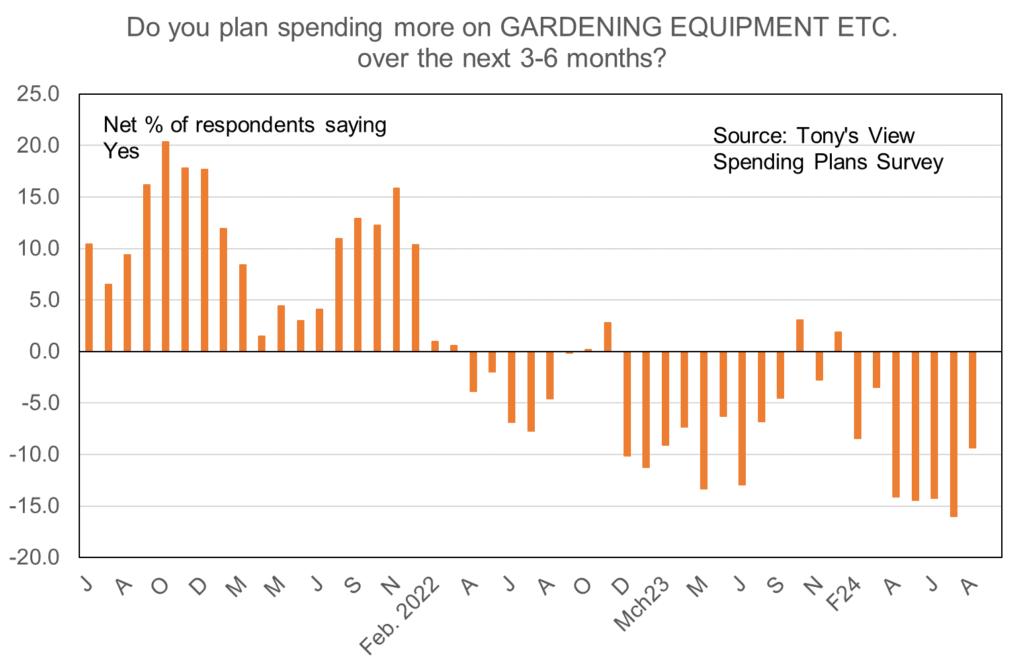

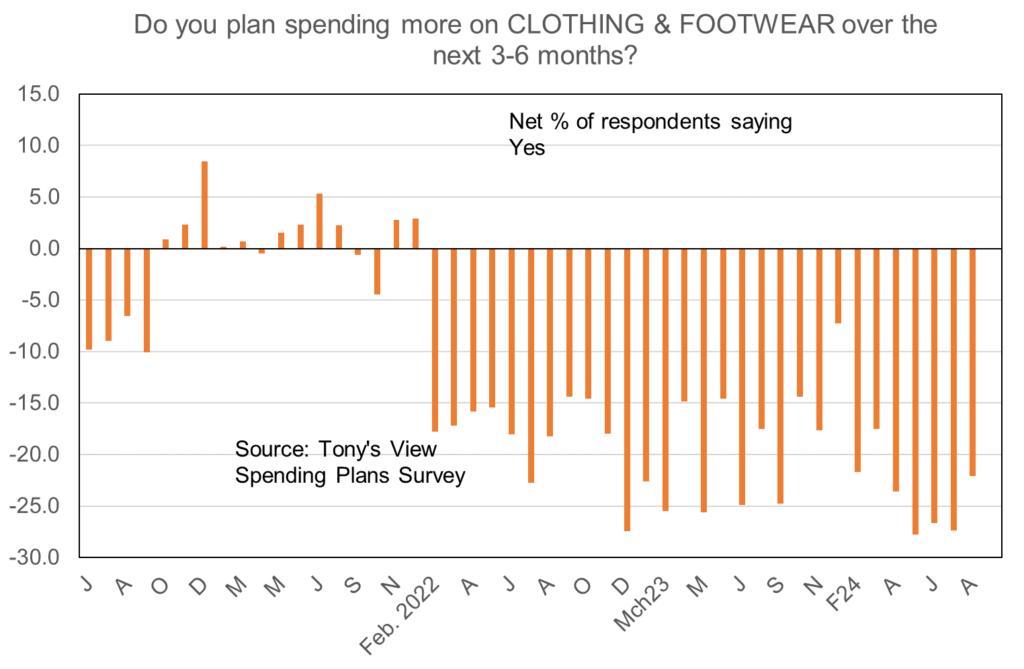

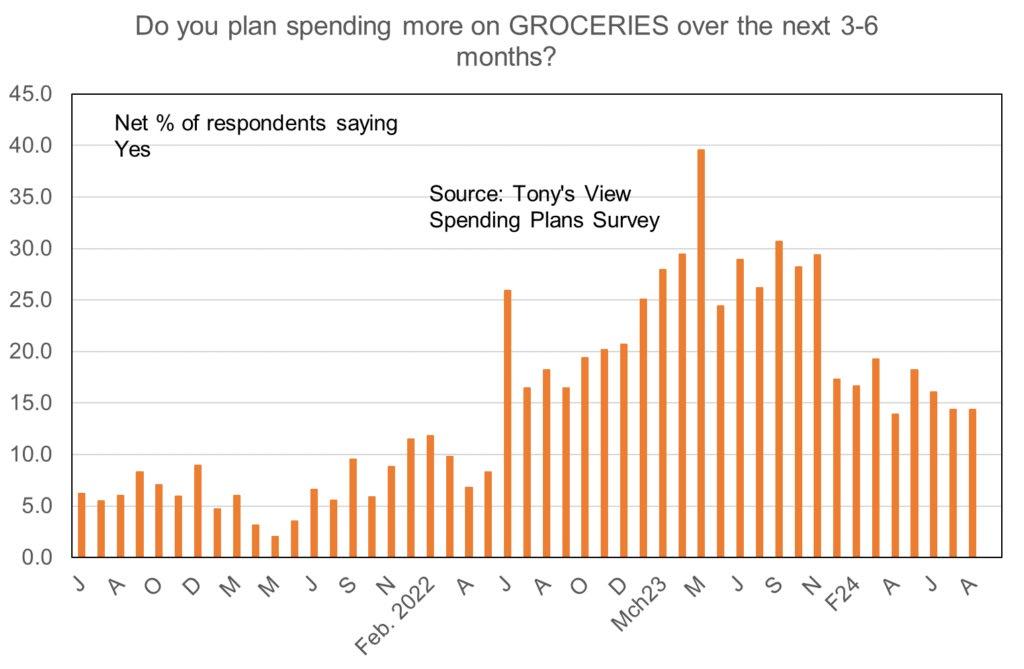

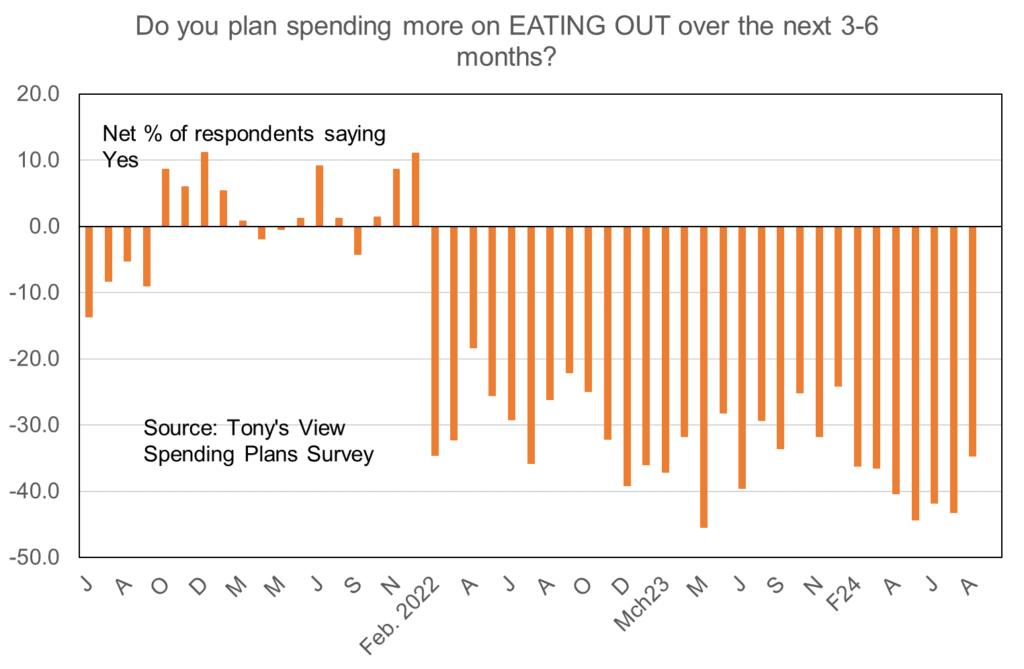

Looking at the detailed results from my Spending Plans Survey we see that cutbacks are planned over the next 3-6 months in all areas except groceries and international travel.

Offshore travel plans continue to hold up and this likely reflects the combined effects of an aging of the population, post-pandemic travel catch-up perhaps still lingering, young people planning to get out of NZ, and the way these days overseas travel is viewed as a normal annual part of life – not a luxury item or one-off retirement event.

Plans for domestic travel remain negative, but an easing of the negativity is underway.

Things remain negative for those in the home renovations sector.

Spending plans on durable goods remain strongly negative. Hence the deep 30% discounting you can find at furniture stores. Even one generally over-priced chain which rarely discounts and instead has focussed on interest rate deals is now cutting prices.

For garden centres the outlook remains poor and as noted previously, this is more than just a seasonal effect.

Based on the weak outlook for clothing and footwear we are likely to see winter sales start very early this year.

Plans for spending on groceries remain firmly positive and above levels before the price jumps of 2022.

Each week we learn of more eateries closing and this is likely to continue for all the rest of this year.

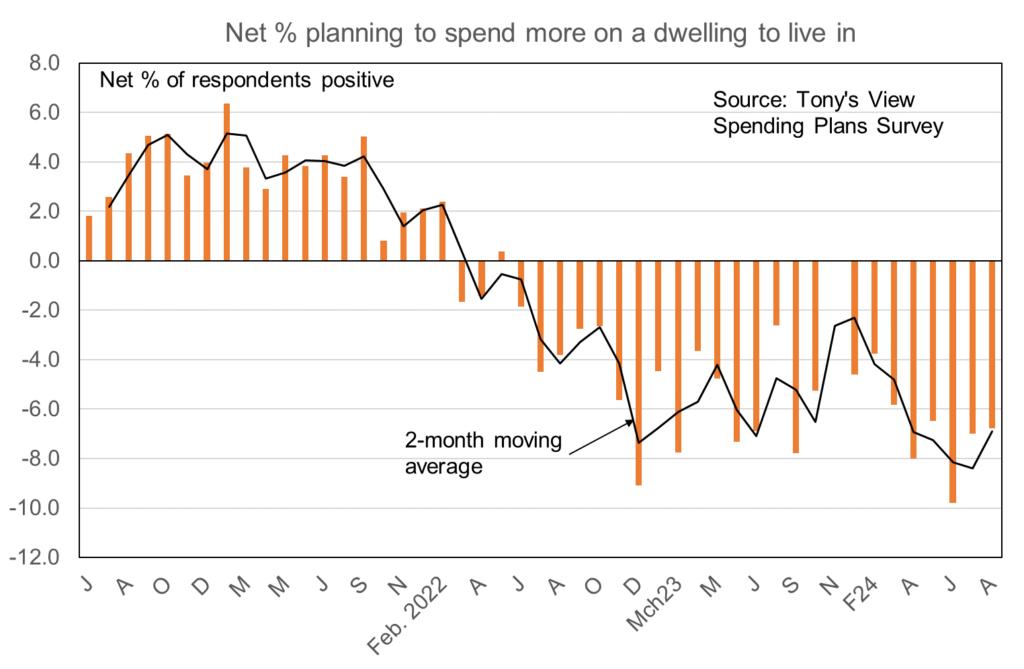

With regard to people’s plans for buying a home to live in things are off their lows but still at very depressed levels.

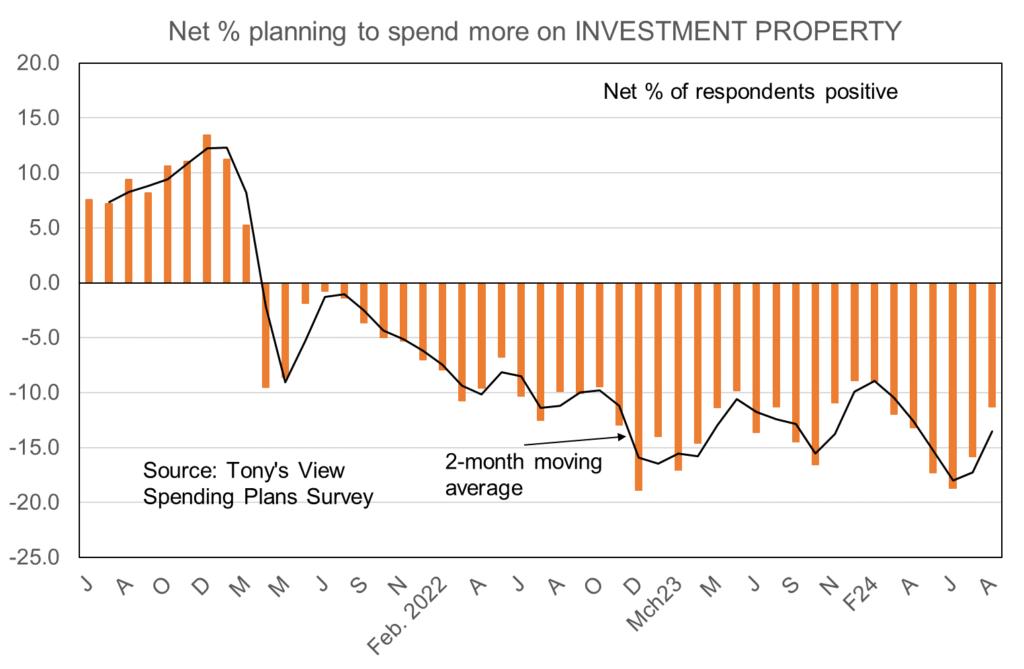

The same comment applies to plans for purchasing an investment property.

Finally, plans for buying shares continue to lie in negative territory.

The rally in wholesale interest rates in New Zealand which has been underway since the second week of July continued this week. Falls were largely driven by a bout of weaker than expected data in the United States, most notably on the labour market.

Measures of employment and unemployment in the US tend to feature larger in inflation forecasts and monetary policy change predictions in the US than in New Zealand. US job numbers only rose by 114,000 in July whereas a gain of near 175,000 had been expected, and the unemployment rate rose from 4.1% to 4.3%.

The data have assumed importance in the US largely because of an underlying fear that the Federal Reserve may have kept interest rates too high for too long and will cause greater than necessary damage to the economy to suppress inflation.

This is the view I have had on NZ monetary policy for some time and discussion of this risk is likely to rise here fairly shortly It will manifest itself in more forecasters bringing forward their predictions for when rates fall, but mainly a focus on the extent of rate cuts here being quite quick and large.

My view for some time has been that come the middle of 2025 the official cash rate will be 1% lower than its current 4.5%. I stick with that and install a risk that the rate won’t be 4.5% but could be 4%.

Local markets have reacted to the weak US data and extra rally in US rates by taking NZ wholesale fixed borrowing costs lower again. Helping things also recently has been a shift in expectations for Australian monetary policy away from one more rise from 4.35% to one cut before Christmas.

Also, the Bank of England recently cut its cash rate 0.25% to 5.0%.

Today, after rallying hard early in the week then backing off as US equity prices recovered and yesterday’s NZ jobs data were stronger than expected, the one year swap rate facing banks stood near 4.68% from 4.77% last week and 5.38% six weeks ago

The three year swap rate is unchanged from last week at 3.91% but down from 4.64% six weeks back.

The margins for bank lending on fixed rate lending have blown out and there is scope for some sizeable mortgage rate reductions. But banks will wait to see what the Reserve Bank does and says in this coming Wednesday’s Monetary Policy Statement.

They are certain to take a less hawkish tone than in recent months but a cut in the official cash rate from 5.5% is unlikely in light of the still too high level of business pricing intentions, wages growth, and even jobs growth.

If I were a borrower, what would I do?

If I were borrowing at the moment, I would look to take advantage of the expected declines in rates from current levels by fixing for just six months.

Nothing I write here or anywhere else in this publication is intended to be personal advice. You should discuss your financing options with a professional.

OCRcutto5.25%,firstcutinyears.

ByKelvinDavidson - 14August2024

ChiefPropertyEconomistKelvinDavidsonunpacks the Augustcashrate decisionand whatitmeansforthehousingmarket

Today’s decision by the Reserve Bank of New Zealand (RBNZ) to cut the official cash rate (OCR) by 0.25% to 5.25% probably wasn’t an earth-shattering surprise, although we had been in the ‘hold’ camp, feeling that the RBNZ wouldn’t want to push through that first cut until inflation was officially back within the 1-3% target band. In the event, however, they deemed the economy to be weak enough and inflation ‘close enough’ (to target) to cut now.

Given this was a full Monetary Policy Statement, we also got the RBNZ’s detailed forecasts for a wide range of economic variables – which now all look weaker than before. Indeed, the RBNZ expects the recession to last a bit longer yet, employment to fall, and the unemployment rate to peak at just short of 5.5% in the middle of next year (compared to previous forecast of around 5%). House prices aren’t really expected to show much growth for another year or so, albeit any further near-term falls could also be small.

Meanwhile, inflation is expected to be back within target in Q3 (2.3%), and stay there over the medium term. The biggest change, therefore, came to the projection for the OCR itself, which is now set to fall by perhaps 1.25% over the next year or so. On the previous projection, the rate wasn’t even envisaged to start falling at all until perhaps mid-2025.

So what about the property market? In reality, not a lot has probably changed as a result of today’s decision and revised economic forecasts. Most people had already been anticipating an easing in monetary policy at some stage soon, and this has

now just been confirmed. Indeed, banks have already been lowering mortgage rates for some fixed terms, and this process looks set to continue – which will be a huge relief for many households.

On the flipside, job security has dropped, and although the unemployment rate isn’t expected to spike higher, the generally softer labour market environment is still likely to be a restraining influence on house sales and prices. Debt to income ratio caps will have a similar effect as mortgage rates drop over the medium term.

Overall, the next phase of monetary policy easing is here, and mortgage rates will drop over the medium term. But the RBNZ was keen to point out that it all still hinges on inflation ‘playing nicely’ (especially non-tradable/domestic price pressures), so that’s obviously a key factor to keep watching closely.

Steve commenced Real Estate in 2001 and since then has continually been in the upper echelon of Real Estate performers. There are many reasons why peopleapproachStevetoworkforthem.

Not only his experience (and in the Real Estate world we now live in, this is a significant benefit to the client), but more-so his integrity. The fact that Steve's business is built around repeat clients (as well as a significant referral network) is testimony to the fact that Steve really understands and appreciates what Real Estateisallabout.

That is, building relationships with integrity, expertise and of course hard work to achievepremiumresults.Thisnodoubtcreatesclientsforlife.

Steve's commitment is also demonstrated by his wife Suzie, who has been along side him for some 43 years. A great sporting family, with four children and now dotinggrandparents.

Being life-long South Auckland residents, Steve enjoys contributing to the local community and sporting associations, further endorsing his strong belief in the familiesandcommunity.

Steve and the team will work hard obtaining the very best result for you too with 100%confidence.

Town&Country

VENITAATTRILL

VenitaAttrill

Sales& Marketing Consutant

0212867792

venita.attrill@ljhooker.co.nz

MeetVenita-YourTrustedRealEstateExpertSince1996!

With an impressive career spanning over three decades, Venita began her journey in Real Estate sales in 1996 with the esteemed LJ Hooker/Harveys Group. Throughout her tenure, Venita has been recognized with numerous national awards, a testament to her unwavering dedication to her clients. In fact, approximately 90% ofVenita's sales are derived from her past clients and client referrals, showcasing the exceptional level of trust and satisfactionsheconsistentlydelivers.

Selecting the right agent is crucial, and there is no better way to make that decision than by evaluating their success and the manner in which they achieve it. Venita's vast clientele, who repeatedly seek her services, skill, and advice, stand as a truetestamenttoherabilitytoexceedexpectations.

While Venita boasts extensive experience and a track record of success, she remains driven and committed to going above and beyond to achieve a premium outcome for every client. Her dedication to continuous improvement ensures that she remains at the forefront of the industry, offering you unparalleledserviceandexpertise.

When you choose Venita as your agent, you can rest assured that you have a trustedpartner by your side, who will tirelessly work to secure the best possible results for you. With Venita, your real estate journey is in safe hands, backed by a legacy ofexcellenceandarelentlesspursuitofsuccess.

Contact Venita today and experience firsthand the difference a seasoned anddeterminedprofessionalcanmakeinyourrealestateendeavours.

Realising he wasn't fixated in winning the game of life based on what college andconventionalwisdomtaughthim,KJfocusedlessonthesecurityaspectof jobs and focused more on helping people in their success on selling to earn his way.

Not only was he scoped out by the high ends of a Real estate Agent in New Zealand to start out by a mere first sentence upon meeting, he's also been buildinghisempireunderthementorshipofthetop10ofNewZealand!

After achieving levels of income, impact and personal freedom he could've only dreamt of as a child, KJ, on top of all his multi 6-8 figure clients, has dedicated his ambitions towards helping people achieve the best prices they canintheirowncircumstancesprovided!

Willyoubenext?

ANU JAY

AnuJay Sales & Marketing Consultant

022 357 7754

anu.jay@ljhooker.co.nz

Introducing Anu Jay, a seasonsed and accomplished sales profession with an impressive track record in the retail sales / financial sales & services industry. With extensive expertise in Sales, Customer Service, Banking, Credit analysis & Business Development, Anu Jay has consistently demonstrated a keen understanding of the industry's nuances and a passion fordrivingsuccess.

Equipped with a Master of Business Administration (MBA) degree in Business Administration and Management from the prestigious London Metropolitan University, Anu Jay possesses a sold foundation of knowledge and strategicacumen,makinghimavaluableassettoanyteamororganisation.

Currently, Anu Jay has ventured into the dynamic world of Real Estate as a Sales & Marketing Consultant. Leveraging his robust experience and innovative approach, he excels in finding tailored solutions for clients, ensuring their needs are met andexceeded.

If you are seeking a seasoned professional with a proven track record in the financial and real estate sectors, look no further. Contact Anu Jay today and discover how his expertise can elevate your business or real estate endeavourstonewheights.

LINAROBAN

LinaRoban LicenseeSalesperson

02102288521

lina.roban@ljhooker.co.nz

Prior to entering the world of real estate, driven by her love of meeting and helping people, Lina had an impressive 20 year career in sales and marketing roles in the telecommunications and corporate marketing industries where her expertise in communication and negotiation always resulted in the delivery of superior customer service to her clients.

Originally from Fiji, Lina epitomises energy, passion integrity and hard work in everything she turns her hand to.

When not delivering superior service to her clients, Lina loves spending time with her family and is a passionate cyclist, owning both road and mountain bikes. With her three children all having "flown the coop", Lina and her husband also have plenty of time to enjoy their love of travel and some of their more memorable adventures include extensive journeys throughout South East Asia, the USA and the South Pacific.

Town&Country

Mark Eklund

Mark Eklund Sales & Marketing Consultant

021244 6692

mark.eklund@ljhooker.co.nz

As an award-winning sales agent with substantial experience across multiple facets of Real Estate, Mark is passionate about the industry. It is his active listening skills and attention to detail that set him apart from others in the field. He is a consummate professional leaving no stone unturned to achieve the objectivesofallpartiesinvolvedincompletingsuccessfultransactions.

Being involved in sales across every real estate demographic, Mark is at ease speaking with anybody and everybody and generates high levels of motivation and satisfaction from the many contacts, friendships, and relationships he has forgedovertheyears.

Mark has strong negotiation skills, skills that he developed whilst serving New Zealand as a detective in the police which have helped him achieve great results for his buyers and sellers throughout his realestatecareer.

Mark is a goal setter but the goal that resonates most with him is to build lasting relationships He believes this is achieved through trust, honesty and communication, and it should be no surprise that a large part of his work is generatedthroughrepeatandreferralbusiness.Whennottalking property, talk to Mark about sport, music, food, wine, travel and of course his adult children of whomheisextremelyproud.

Town&Country

BRENTWORTHINGTON

BrentWorthington

LicensedAgent&Principal

0292965362

Brent.worthington@ljhooker.co.nz

There’s not much Brent doesn’t know when it comes to selling real estate. This town and country agent has had a successful career in the property market and is now the proud owner of his own business. Definitely a quality over quantity man, when you bring Brent on board, you’ll find that accumulating listings is far less important to him than making each one as good as it can get. He prides himself on telling it like it isknowing you’ll be able to make better decisions with a person and information you can trust.

Complementing Brent’s practical and credible approach is a background full to the brim of industry knowledge and business expertise from 30 years working within the construction industry. His capabilities have been well proven as a highly successful business owner.

A family man, with a proven track record of success, Brent has earned an excellent reputation and the trust of his local community and business colleagues.

He places huge emphasis on customer satisfaction, attention to detail and conducting his business with a genuine duty of care. Brent has gained many awards as a business leader during his 12-year tenure in Real Estate.

His entrepreneurial style ensures he reaches out and connects people with like minds. He imparts his wisdom in a warm and friendly manner and helps people to make wise and right decisions before investing in the property market, Auckland wide.

If you are considering a lifestyle change, investing for your future or simply wanting to know the worth of your property in this fluctuating market, feel welcome to call or email Brent to receive the latest updates on the trends and statistics in your area.

DEBBIEHARRISON

Debbie Harrison PropertyManager

021302864

debbie.harrison@ljhooker.co.nz

With a passion and a commitment to providing exceptional service, Debbie has a fantastic attitude of getting things done and ensuring that the clients are happy and well cared for. She takes great pride in her work and goes above andbeyondtoensurethesatisfactionofbothpropertyownersandtenants.

Debbie’s attention to detail and organizational abilities are exceptional, enabling her to efficiently handle all aspects of property management, from tenancy agreements, rent collection to property inspections and maintenance coordination.

Debbie understands that property management requires a compassionate and empathetic approach, and she always strives to create a positive and harmonious living environment for tenants while protecting the interests of propertyowners.

Whether you are a property owner seeking professional management services or a tenant searching for a well-maintained rental property, Debbie is committed to delivering exceptional results and ensuring a smooth and rewardingexperienceforallpartiesinvolved.

With her excellent communication skills, strong work ethic and dedication to excellence,DebbieHarrisonisatrueassettoLJJHooker/RentExchange.

JohnnyBright

AUCTIONEER

Johnny is proud to be a part of the team at Apollo Auctions NZ. Entering real estate in 2014, he has developed and honed his craft of auctioneering and negotiating skills to a level that now sees him as an industry leader. Johnny has worked and collaborated with some of the most notable agents, business owners and auctioneers across New Zealand.

With the fusion of his knowledge and skill together with his personable approach, Johnny creates the ultimate auction experience . He implements drive and dedication to each and every property that he calls - regardless of value, location or personal circumstances. Johnny’s performance style and welcoming nature allows him to capture the audience and motivate buyers. He will guide you through the process and create a solid platform to achieve the best possible outcome for your auction.

Johnny also has a passion for acting. With a Bachelor of Performing and Screen Arts, he has appeared in several TV commercials and films, his most widely recognized being ‘Falling Inn Love’, an American Netflix production which was filmed in New Zealand. He has also worked with the Auckland Theatre Company on a number of occasions.

He currently resides in Beachlands with his wife and two young children.

It’s rare in life that we get something for nothing with no strings attached, especially if it genuinely adds value. Nevertheless, that’s precisely I will give you. Expert home loan advice which has reliably proven to offer significant long-term financial advantage. I keep strict tabs on the country’s largest network of banks plus numerous smaller and second-tier lenders, so you don’t have to. What’s more, this comes at no cost to you because your chosen bank pays for the privilege. You have nothing to lose, yet have a higher chance of securing better terms. Rest assured - if there’s a superior deal out there for you, I’ll find it.

In the typically stoical world of finance, I offer a point of difference. Not only will you receive excellent independent and impartial advice, but you’ll have fun doing it. Even after 15 years in the mortgage arena, my enthusiasm for objectives and commitment to clients shines through at every turn. Endorsement comes from countless glowing testimonials and in my own words: “I’m at my happiest helping people navigate through difficult situations, giving hope and concrete opportunity where they previously had none.”

Prior experience as sales manager in the fields of telecommunications and pharmaceuticals, then later, a small business owner and private property investor, provided me with considerable business acumen across many industries. My customer-focused approach and personable demeanor also reflect a lifetime of experience in client relations. I credit travel to distant locations for creating an enduring interest in different cultures and honing my ability to relate well to the needs of the broader population. In particular, I soundly empathise with people relocating from other countries to make New Zealand their home.

To continue giving my professional best, I maintain balance by travelling and participating in seasonal sports such as paddle boarding and skiing. I enjoy indulging in my creative side; with landscaping, painting watercolours or improving my guitar playing prowess. Additionally, I actively support my community through Christians Against Poverty (CAPNZ), but above all, my wife and our five shared children always take centre stage.

There's little that I haven't seen in my time in the industry, priding myself on an ability to deal with the trickiest of scenarios, never turning anyone away. My philosophy of treating people how I'd like to be treated results in a 360-degree perspective which sets myself apart.

Get in touch if you need any expert guidance. Regards