At Rent Exchange, we provide comprehensive property management services tailored to your needs. Beyond our full-service professional management, we offer a variety of additional services to ensure all your property requirements are met:

Flexible Pay-As-You-Go Options

Inspections Only

Commercial Leasing / Management

Air BnB Casual / Short Stay Letting

Consider Rent Exchange as your on-demand property management consultants Here to help you manage all aspects of your portfolio!

For rental properties, photoelectric smoke alarms are preferred, either hardwired to the mains power or equippedwithalong-lifebattery,andinstalledwithin3 metresofeverybedroomdoor,ineverysleepingroom, andoneachlevelofamulti-storeyhome.

It is essential to ensure investment properties comply with New Zealand’ s regulations, not just for legal reasons but for tenant wellbeing

If it has been a while since you had new tenants, consider a fresh coat of paint to the main areas, steam cleaning the carpet or updating kitchen appliances A neutral décor is likely to be more appealing to more people

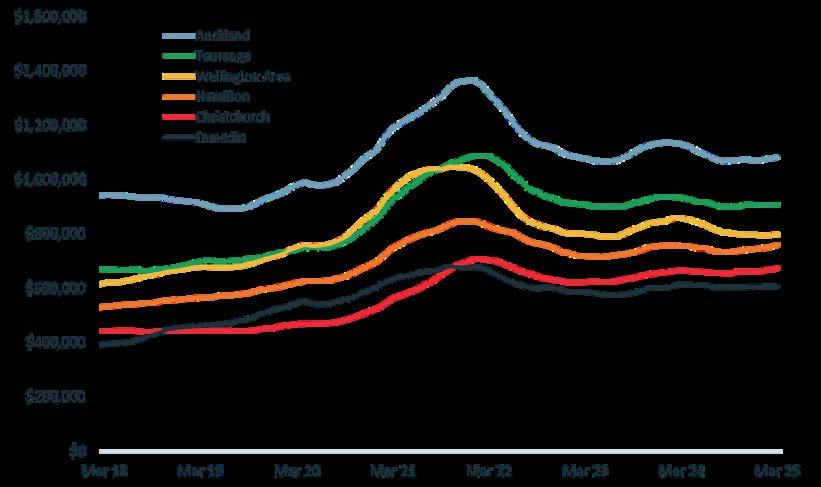

The Real Estate Institute of New Zealand (REINZ) has released March figures, revealing promising trends in the national property market Continuing the momentum from last month, year-on-year sales are rising across the country.

Published 17 March 2025

“As we transition into the cooler months, the market remains vibrant rather than stagnant. There have been reports of increased attendance at open homes and auctions. Even in cases where properties don’t sell at auction, there’ s plenty of post-auction interest, indicating a resilient and engaged buyer community,” says Acting Chief Executive Rowan Dixon.

TheWestCoastregionexperiencedthehighestincrease,risingby11.5%from$370,000to$412,500.Two regionshadnochangefromMarch2024:Canterburyat$695,000andTaranakiat$600,000.Nelson’ s medianpricesignificantlydeclinedyear-on-yearfrom$722,000to$640,000(11.4%).

“Marchsawayear-on-yearincreaseinsales,butmedianpricescontinuetolagbehind NewZealand’ s propertymarketremainsthesame:highlistingsresultindecreasedbuyerurgency.Ifabuyermissesoutona property,theycaneasilyfindasimilaroneforsale,”saysDixon

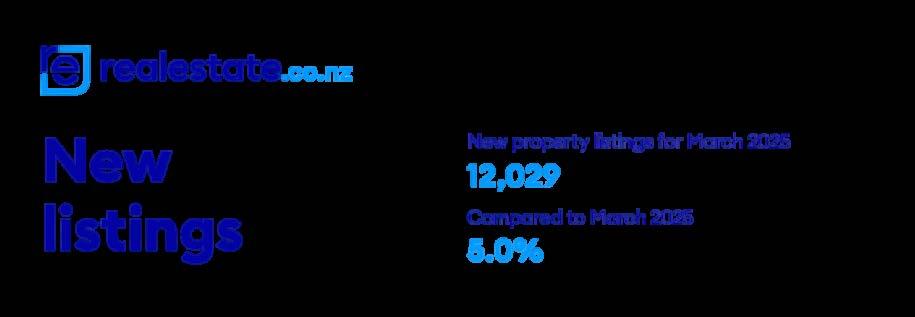

MorepropertieshitthemarketthaninMarch2024,with anincreaseof5.0%nationally,from11,455to 12,029listings ExcludingAuckland,listingsincreasedbyonly2.6%,from7,326to7,513,comparedtolast year Nationalinventorylevelsincreasedby10.9%year-on-yearto36,870and3.2%comparedtothe previousmonth.

The Real Estate Institute of New Zealand (REINZ) has the latest and most accurate real estate data in New Zealand, for more information and data on national and regional activity visit the REINZ’ s website

31 March 2025

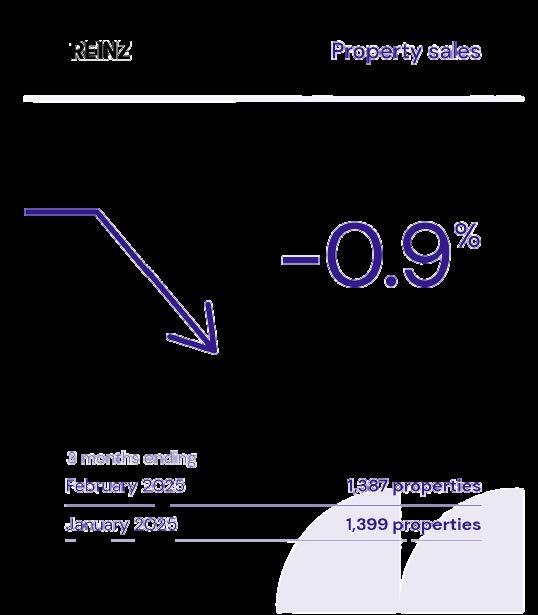

Lifestyle Data: For the three months ended February 2025

Continued Strength in the Lifestyle

Property Market

Data released today by the Real Estate Institute of New Zealand (REINZ) reveals intriguing dynamics in the lifestyle property market. For the three months ended February 2025, there were 12 fewer lifestyle property sales compared to the three months ending in the previous month, marking a slight decline of 0.9%.

In total, 1,387 lifestyle properties changed hands during this period, which is an impressive 18.3% increase from 1,172 sales in February 2024 and a slight dip from January 2025's 1,399 sales. In the year to February 2025, lifestyle property sales increased to 6,181, a rise of 682 properties (12.4%) compared to the previous year. The total value of these sales reached a striking $6.96 billion.

The median price for lifestyle properties sold in the three months ending February 2025 stood at $957,500, reflecting a $24,500 rise (+2.6%) from the same period in 2024. Notably, the median price for Bare Land lifestyle properties sold during this period was $425,000, down $15,000 (-3.4%) compared to the previous year. The median price for Farmlet Lifestyle properties appreciated significantly to $1,100,000, marking a $40,000 increase (+3.8%).

The REINZ rural spokesman commented that despite a slight dip in sales this month, the overall trend in lifestyle property transactions over the past year indicates a robust market, with sales soaring by over 12% and a remarkable total value of nearly $7 billion.

Nine regions experienced an uptick in sales compared to February 2024, with Auckland (+53 sales) and Waikato (+50 sales) leading the way. On the other hand, Nelson/Marlborough (-11 sales) and Gisborne/Hawke’s Bay (-2 sales) saw the most substantial declines in sales over the same period. When comparing to January 2025, five regions reported increased sales.

Interestingly, eight regions saw an increase in median prices for lifestyle blocks in the year to February 2025, particularly the West Coast (+57.3%). However, the largest drops were noted in Southland (-19.2%) an Nelson/Marlborough/Tasman (-13%).

The time it takes to sell lifestyle properties increased by six days, averaging 79 days to sell this February compared to the same time last year. Southland reported the quickest sales at just 56 days, while Northland had the longest wait at 103 days.

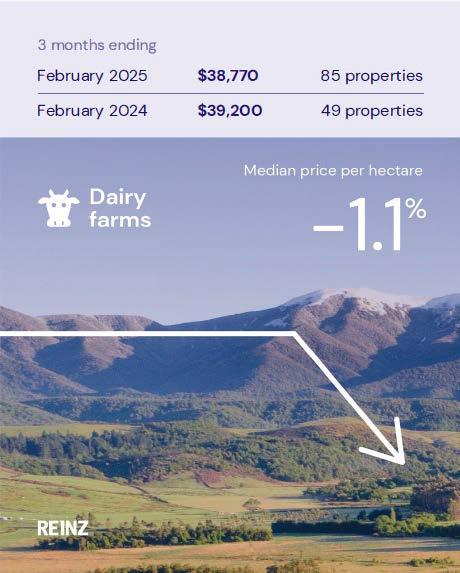

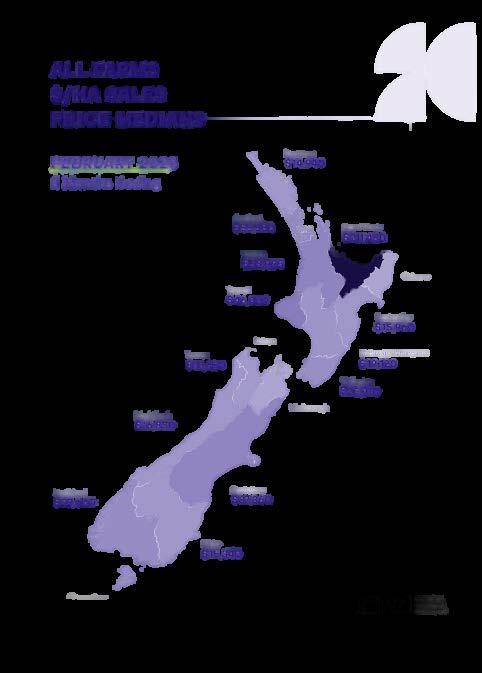

The latest data from the Real Estate Institute of New Zealand (REINZ) reveals an exciting surge in farm sales, with a notable increase of 69 transactions, which is a 32.1% rise for the three months ending in February 2025 compared to the same period in 2024. This means 284 farms changed hands in February 2025, showcasing a dynamic agricultural market. While this is a decrease from the 313 farm sales recorded in the previous three months ending January 2025 (-9.3%), the year-on-year growth from February 2024, which saw only 215 sales, highlights a significant upward trend in the sector

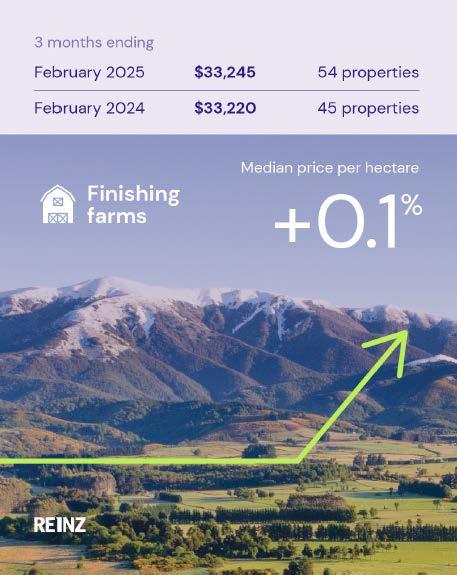

1,084 farms were sold in the year to February 2025, 149 more than were sold in the year to February 2024, with 39.9% more Dairy farms, 37.8% more Dairy Support, 0.4% more Grazing farms, 7.9% fewer Finishing farms and 35.7% more Arable farms sold over the same period. The REINZ rural spokesperson commented on the regional dynamics, stating that the strong increase in farm sales over the past year reflects renewed confidence in the rural property market The rise in sales activity suggests that buyers are taking advantage of market conditions, whether for expansion, investment, or diversification

The median price per hectare for all farms sold in the three months to February 2025 was $28,115 compared to $27,620 recorded for the three months ended February 2024 (+1.8%). The median price per hectare decreased by 3.5% compared to January 2025. The REINZ All Farm Price Index increased 0.2% in the three months to February 2025 compared to the three months to January 2025, and 5.2% compared to the three months ending February 2024. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors

Nine regions recorded an increase in farm sales for the three months ending February 2025 compared to the three months ending February 2024, with the most notable being Southland (+31 sales) and Taranaki (+13 sales). Wellington (-2 sales) and Northland and Waikato (-1 sale) recorded decreases in sales

Despite growing economic optimism, new data from realestate.co.nz shows the property market remains in recovery mode In March, new listings were up nationally, month-on-month and year-on-year, and total stock was up in all but one region, a sign that seller confidence is back Buyer activity remains cautious, but it’ s worth noting that sales volumes were up in February, the Real Estate Institute of New Zealand (REINZ) data showing 6,287 properties sold nationally — a 3.4% increase compared to the same month last year.

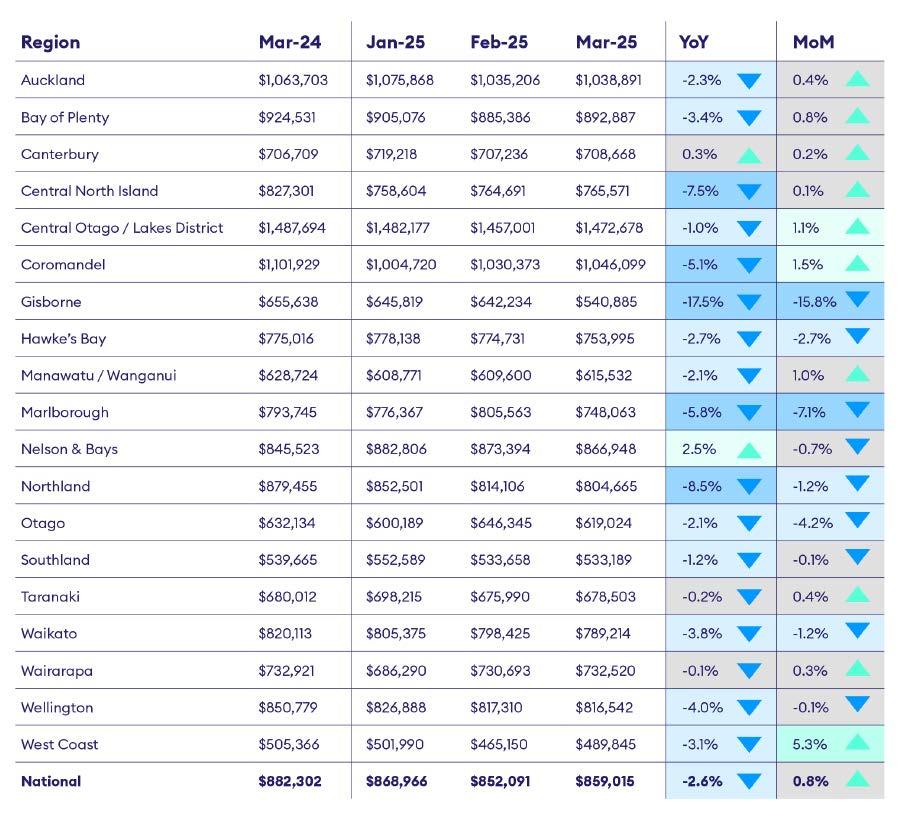

Average asking prices were down year-on-year across most regions in March, declines generally modest, pointing to a relatively stable market. Nationally, the average asking price dipped 2.6% compared to March 2024, with Nelson the only region to record year-on-year growth Properties soldslightly faster during March, with properties spending less time listed on realestate co nz than in February. However, there’ s no sign of a sharp upswing yet Vanessa Williams, spokesperson for realestate.co.nz, says: “This isn’t a runaway market. But there are signs of quiet momentum as 2025 progresses

Twoyearsofsteadypricesshowbuyersstillholdingback

The national average asking price remained relatively stable in March, edging up just 0.8% month-on-month but still down 2.6% compared to March last year. “Williams says it’ s remarkable how consistent prices have been over the past couple of years: ”

“The national average asking price has remained below $900,000 for over two years – last exceeding that mark in December 2022 at a seasonally adjusted $916,487. At the peak of the market, in January 2022, it reached $983,415.”

Year-on-year, only one region, Nelson & Bays, saw average asking price growth during March (up 2.5% to $866,948). Month-on-month, three regions recorded increases: Coromandel (up 1.5% to $1,046,099), Central Otago/Lakes District (up 1.1% to $1,472,678), and the West Coast (up 5.3% to $489,845).

However, the broader trend remained one of caution in March, with six regions (Gisborne, Hawke’ s Bay, Marlborough, Northland, Otago, and Waikato) experiencing both month-onmonth and year-on-year declines

“Despite signs of growing economic confidence, it’ s yet to translate into upward price pressure, and with the stock levels the way they are, we don’t anticipate this changing in the short term,” said Williams.

Stockremainsatdecade-highlevels

With 36,870 properties on the market in March 2025, buyers were spoiled for choice National stock levels were up 10.9% compared to March 2024, signalling growing seller confidence. Every region recorded a year-on-year increase in stock, except Northland, where levels were flat, dipping just 0.4%.

Williams said the lift in stock reflects a shift in the market.

“Two years ago, many sellers hit pause — high interest rates and election uncertainty made people cautious about listing That’ s clearly changed There were 7,586 more properties for sale last month than in the same month in 2023, showing how far we ’ ve come.”

She adds that the data suggests properties sold more quickly last month. “In February, a significant proportion of listings had been on site for 60 to 90 days. In March, a larger share was listed for a shorter period — between 30 and 60 days.”

“Seeing more listings spend less time on site points to properties selling slightly faster This trend is also mirrored in the REINZ sales data from February,” explained Williams.

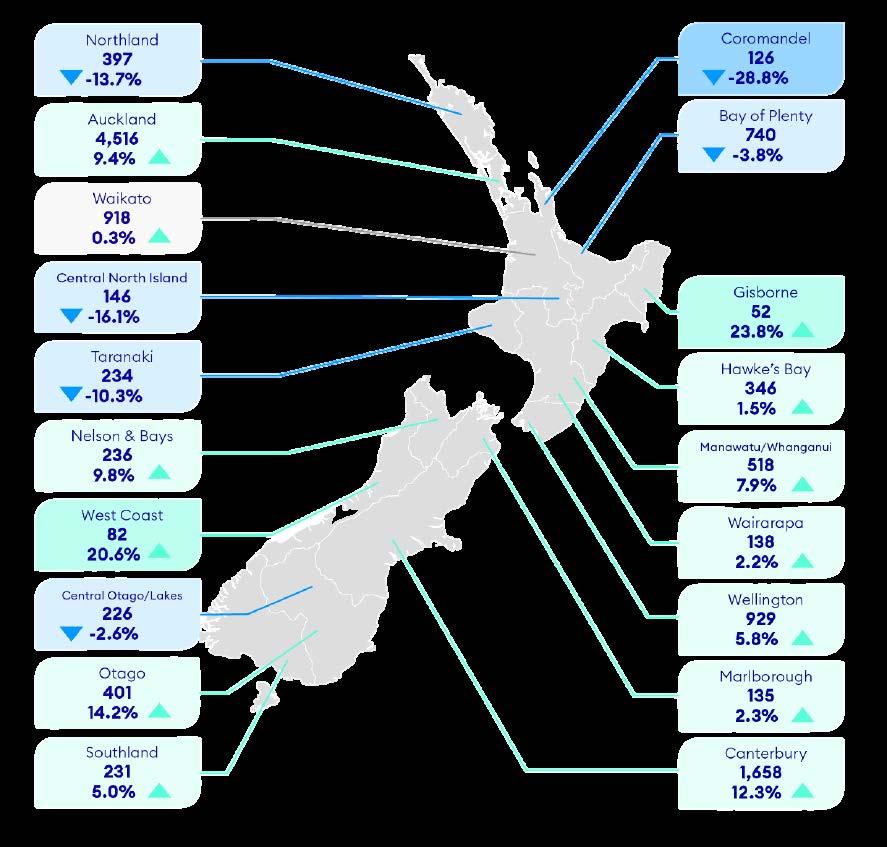

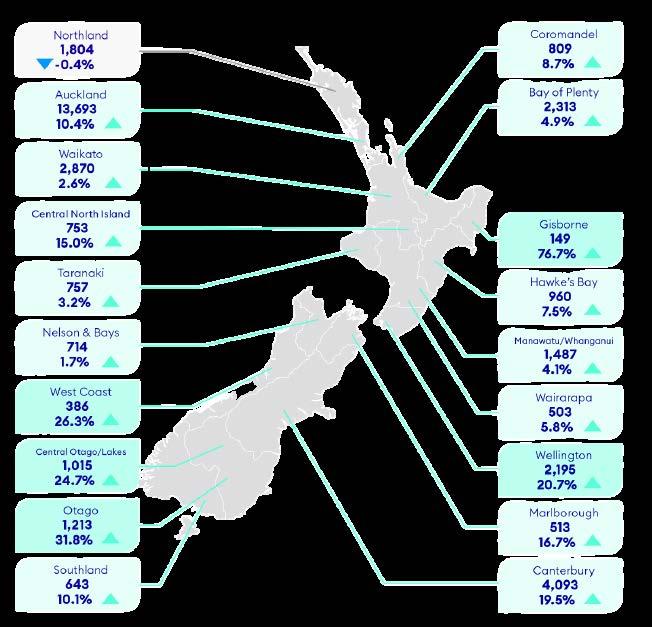

13of19regionsseeyear-on-yearliftinnewlistings

Vendors were busy in March. Nationally, new listings rose 5.0% year-on-year, reaching 12,029 –another signal of growing seller confidence. 13 of our 19 regions recorded year-on-year increases, with Gisborne seeing the largest percentage jump, up 23.8% compared to March 2024. It’ s the second consecutive month the region has led the country in year-on-year growth. At the other end of the spectrum, Coromandel saw the biggest decline, with new listings down 28.8% year-on-year. Williams said this highlights the localised nature of New Zealand’ s property market:

“It’ s a reminder that there’ s no one-size-fits-all in real estate – each region moves to its own rhythm. Getting local advice is invaluable.”

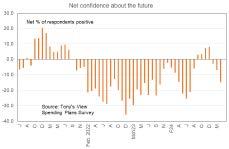

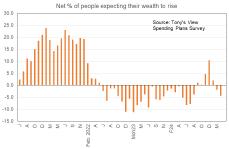

The latest reading is -15% from -7% last month and a peak of +8% in December. A net 4% of people now worry about where their wealth is headed from a net 10% feeling positive about such prospects in December. Note, all results came in after President Trump’ s tariff announcement but before the rout in stock markets around the world.

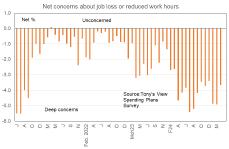

I have highlighted these two factors behind the deterioration in sentiment at the start of this article rather than at the end because of this factor There is no fresh deterioration in feelings about the labour market underway. The measure I create to measure this is minimally changed at a net -4% in April from -5% in March and -3% in December It is the general environment in which people, their businesses, and the economy will be operating that has become of concern, not a round of layoffs

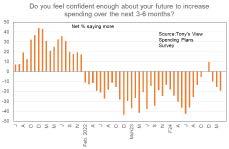

A net 19% of people plan spending less on furniture and appliances

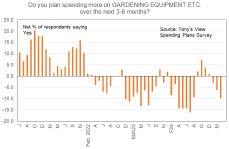

The surge in plans for spending on garden equipment and presumably plants proved shortlived and a net 10% of respondents plan cutting spending on their gardens

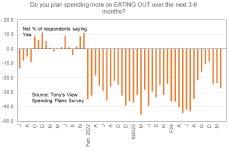

Plans for spending on eating out have turned around quite a bit since December and the surge in prices of food and drinks consumed in cafes and restaurants may be a prime cause – it certainly is for me

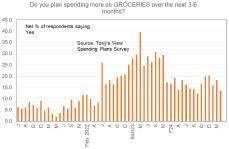

The outlook for supermarkets remains positive with a net 13% of us planning to spend more That will be a function of expecting prices to rise largely but maybe a bit of extra spending to eat at home rather than at cafes and restaurants

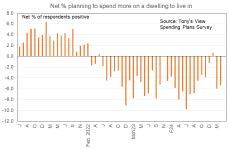

Housingoutlooksubdued

The two residential real estate measures I gather from this survey remain at weak levels A net 5.4% of people plan cutting spending on a house to live in Don’t get hung up on what the number actually means but focus instead on the trend and whether things are getting better or worse There has been a strong deterioration over the past two months On this basis one could not say the housing cycle is yet kicking nicely upward

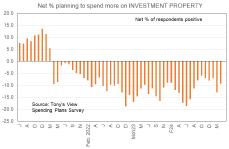

For investors a net 9.3% of people from 13% in March say they plan cutting spending The level of this measure remains poor and there is no improving trend underway. Some of the gains from July to October have been given back

Overall, my Spending Plans Survey tells us that the outlook for our economy is subdued – as warned about in August Consumer spending accounts for over 65% of total spending in a modern economy and if householders keep their wallets tight then the pace of growth in one ’ s economy will be quite constrained unless there is a surge in exports That is hard to see happening given the deteriorating international trade environment

ImpactonNZofthetariffwar

I have held off recently writing anything about the US-initiated global trade war because of the sheer lack of knowledge about what the US would do and how other countries would respond And how the US then responds And how other countries in turn respond. And so on.

But here are some general thoughts which I give for the record only but frankly consider to be a general waffle leading to no real conclusions beyond a recommendation to be cautious as high uncertainty is going to be with us for some time.

Slightly slower NZ growth

Slightly higher NZ inflation

Slightly higher NZ interest rates, or lower Uncertainty is very high and that will retard business investment and consumer spending

Let’ s start with something positive We are currently receiving good prices for the key goods we ship overseas with the ANZ Commodity Price Index in NZ dollar terms ahead about 23% on a year ago The index level is shown as the orange line in the following graph The surge is good for our economy though it places upward pressure on domestic food prices

This means that as world growth slows to something less than it would otherwise have been we will be negatively affected but not to a large degree We might expect slightly slower growth in inbound visitor numbers because of weakness in other countries But the bigger issue there is getting our far flung country back on their list of travel destinations rather than the small changes in world growth prospects

We can expect to see higher inflation in New Zealand than would otherwise be the case. This won ’t be because we will place new tariffs on imported goods from the US because we will not. Instead, the goods which we import from overseas will be more expensive in many cases.

Goods we bring in from the United States will cost more to produce there than before as some of their components will have been imported into the US, incorporated in the final product, then shipped out to us and the rest of the world One clear impact of US tariffs will be reduced competitiveness of US goods in other markets Their exports will suffer

Similarly, goods which we import from other countries will in some cases contain US parts or parts from local factories which use US inputs Higher input costs for them will mean higher imported goods prices here This is important because falling prices for our imports have been a substantial driver of our lower inflation rate

President Trump’ s hope is that businesses will shift production back to the US They will only do that if they expect the tariffs to remain But if they anticipate the eventual return of a Democrat President to lead to them being unwound then the investment will not be undertaken

In this way tariffs negatively impact global productivity which is a similar thing to saying they raise inflation and make people poorer than would otherwise be the case.

One final thought. Most of what we send offshore comes from the primary sector, is minimally processed, and buyers are used to high price fluctuations. They will interpret the coming 10% price hikes in the US as just another fluctuation and the impact on volume demand will be constrained The same will not be the case for our manufactured exports and those are the ones most at risk – not beef and wine

Iwereaborrower,what wouldIdo?

Uncertainty has sharply increased Accepting that situation is vital because it leads to some clear conclusions. First, medium to long-term fixed mortgage rates become more valuable as they removeonepotentially very volatileelement in one ’ s cash flows and leave space and energy for managing other impacts of the changing environment.

Second, well it may be too late for you to do anything about this one Mr Trump is a known quantity. He is a source of instability and represents extreme risk. Equities are financial assets which are highly sensitive to changes in riskassessment Itissurprisingthatglobalshare marketsfailedtotakethisintoaccountwhenhe waselected

TheDowJonesIndustrialsIndex stoodat 41,800 the day before the US Presidential election last year Itthenrosetoapeakof 45,000 onemonth later and was still at 44,600 in the third week of February. The fall now will be a shock to many people Butadjustmenttoheightenedriskfroma known source of instability was going to happen atsomestage

When will the uncertainty end? Not before his second term expires, I suspect Does that mean equities keep weakening? No It just means the discounttoreflectheightenedriskwillbewithus forthenextthreeandahalfyearsatleast

The main influence on wholesale interest rates thisweekwasthedeclineinUSratesasmarkets morestronglyfactoredintheriskofarecessionin the US economy. But there was also some mild downside pressure from the NZIER’ s Quarterly Survey of Business Opinion which was released onTuesday. Allresultswerecollectedbeforethe April 2 announcementofUStariffssothereisno point in undertaking any deep analysis of the results However, onethingthey doclearly show istheextrememarginpressurewhichbusinesses areunder.

On average since 1992 a net 21% of businesses have said they plan raising their selling prices in the coming three months In the December quarter the outcome of the NZIER survey was a below average net 15% planning to raise their prices.

That provided easy justification for loosening monetarypolicy.

Thisquarteronly anet 2% saidthey planraising theirprices Atfacevaluethissuggestsahighrisk ofinflationfallingtosettlebelow 2% andtheneed for a quick cut in the cash rate to below 3%. Borrowersmightrejoice

However, there are cost pressures to consider –pressureswhichwilloneday manifestthemselves as higher prices On average a net 29% of businessessaytheyexpecttheircoststoriseinthe nextthreemonths. IntheDecemberquarterthis proportionwas 35%. Nowitishigherat 42%. We would not expect to see this happening if underlying inflationary pressures in New Zealand wereeasing

Thisgraphshowsthequarterlydifferencebetween the pricing and cost expectation measures. The graph starts in 1995, but the latest result is the worstonrecordgoingbackto1970.

This series strongly tells us cash flows will be bad for many non-rural businesses this year More liquidations are coming It also tells us inflation risks lie on the upside further out where monetary policy is aiming (18-24 months from now).

And so, with all this uncertainty swirling around and with contradictory inflation portents contained in the NZIER’ s survey (capacity measures are low), the Reserve Bank have had to make a monetary policy decision. When times are this uncertain it is not a good idea to make big changes. So, it is unsurprising that the Reserve Bank stuck with their previously indicated track and cut the official cash rate by0.25%.

The only real “news” in their release was a focus on their ability to cut the OCR should the deteriorating international economic environment warrant it They did not discuss raising the cash rate should the environment spring the other way.

As it is, overnight the US President announced a 90 day pause on the over-10% tariffs apart from China which has placed an 84% tariff on US goods and the US has responded with a 125% tariff in total.

The deterioration in the US-China relationship is cause for concern and leaves a mild downside bias to all our interest rate forecasts for now Having said all of that (and in 24 hours who knows what extra can be added to the mix), we find that wholesale interest rates in NZ initially rallied during the week then sold off this morning

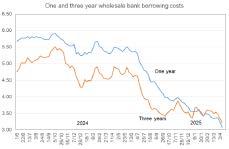

The one year swap rate at which banks borrow to lend at a one year fixed rate to you and I has fallen to near 3.07% from 3.24% last week and 3.5% just before banks reduced their one year mortgage rates to 5.25% from 5.49%. The three year swap rate has fallen to near 3.22% from 3.34% last week and 3.5% just before mortgage rates went from 5.59% to 5.29%.

It looks like scope exists for a cut in the one and maybe two year swap rates Beyond that will depend upon whether banks feel they might gain some competitive market share by discounting their three year rate

If I were borrowing at the moment, I would probablyfixtwoyearsat4.99%butmightwaita bit in case the 4.99% three year rate were to returnagain.

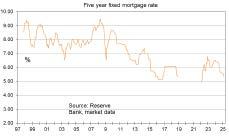

These three graphs show mortgage rates since 1997 excluding the period of deflation worries (2019) and the pandemic

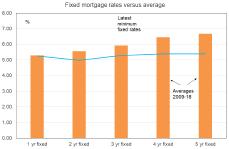

This graph shows how current rates compare with averages from 2009-19

To see the interest rates currently charged by major lenders go to www.mortgages.co.nz Nothing I write here or anywhere else in this publication is intended to be personal advice. You should discuss your financing options with a professional

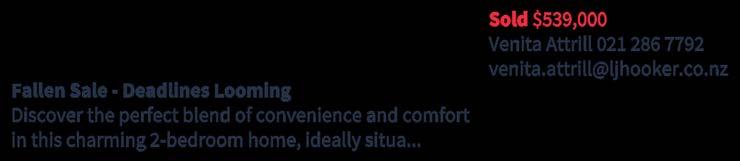

Properties

Newto Market

RelocatingVendorsSellingFamilyHome

3 1 3

Well-presented 220m² solid 1960's home

Downstairs teenage retreat, home office or man-cave

New roof installed in 2022

Single internal garage plus external double garage

Zoned for Opaheke School & Rosehill College

TO

BEAUCTIONED

On Site 21 Clark Road, Pahurehure

Sunday 27th April 2025 at 2.30pm (unless sold prior)

VIEW

As advertised or By Appointment

AGENCY

LJ Hooker Town & Country 09 294 7500

sqm (mol)

2C Waiari Road, Conifer Grove

Price Drop; Urgency Needed

Conifer Grove at entry level price. You've got to see this! A beautiful 1920's bungal..

Winner Harcourts New Zealand Auctioneer of the Year: 2010, 2014 & 2017

Winner of the Australasian Competition: 2011 & 2015

Finalist Australasian Competition: 2010

Runner-up REINZ National Auction Competition: 2020

Local Updates

APRIL2025

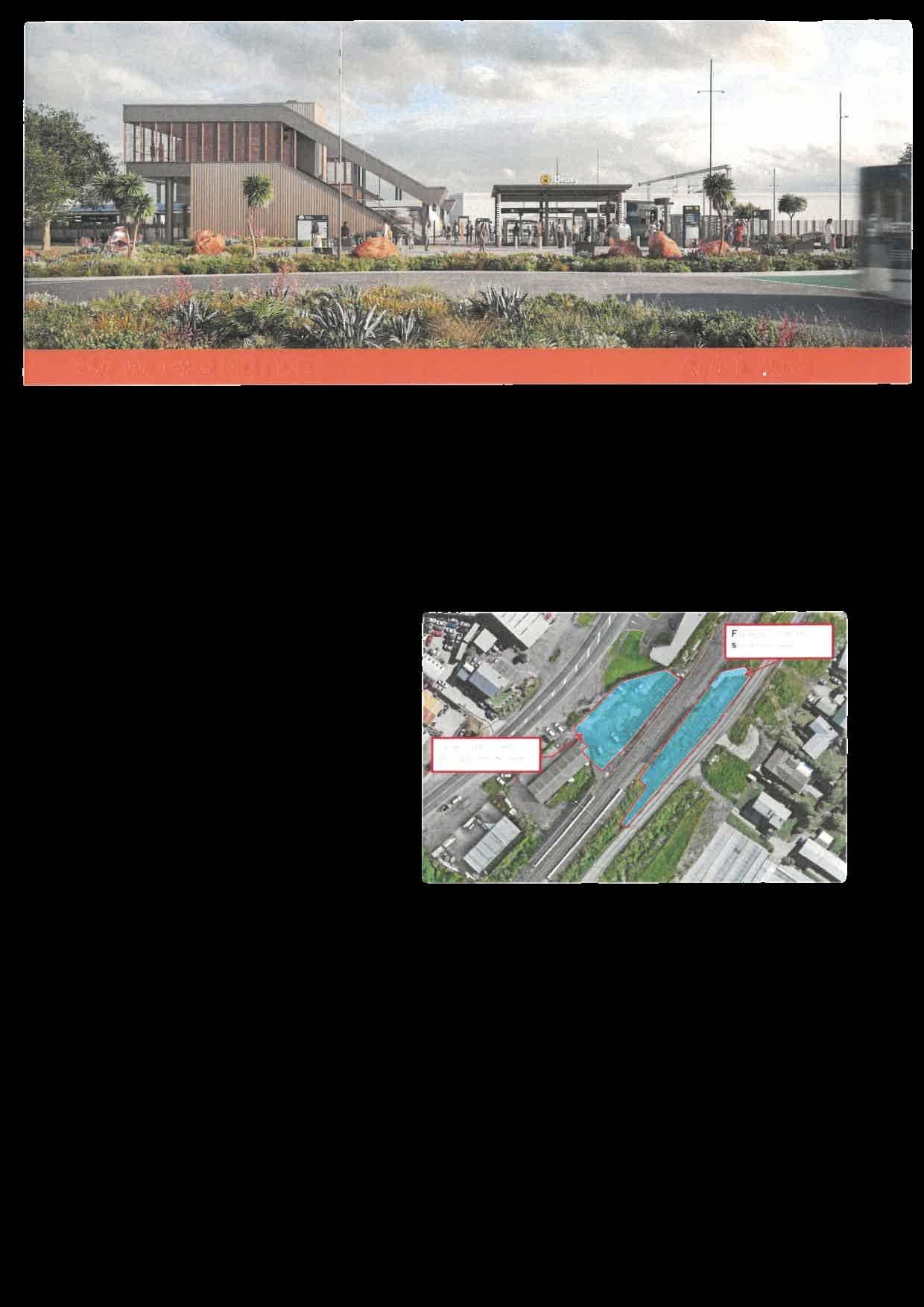

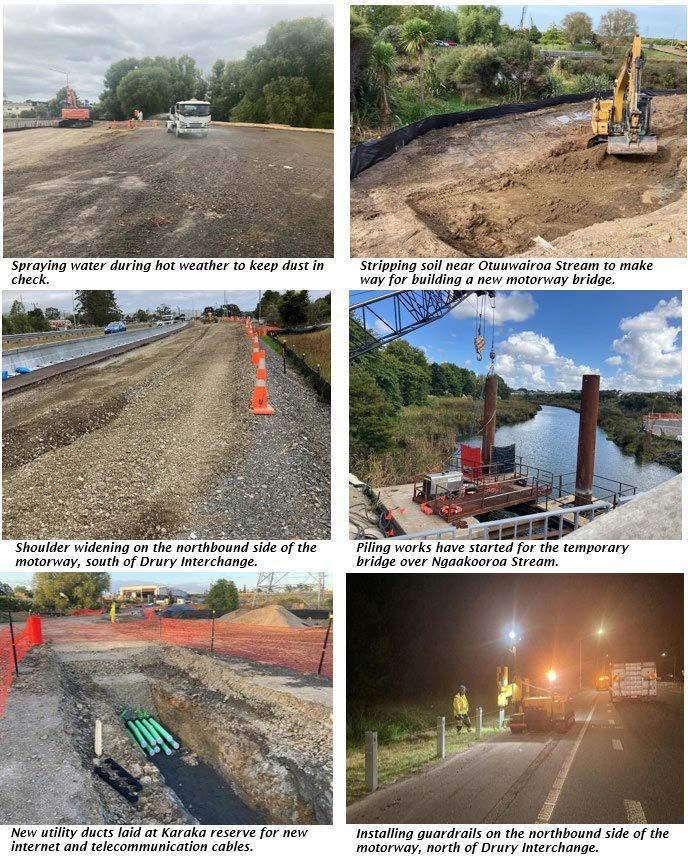

Construction update | He pānui

Daylight saving time may be ending this weekend but the Papakura to Drury project's momentum continues to accelerate.

The project team made great progress over the last month, which was notable due to the establishment of several new work sites.

A critical priority when setting up new sites, and before any earthworks get underway, is the implementation of robust erosion and sediment control (ESC) measures to protect the environment. See the next story for more details.

Currently, we are working across multiple fronts along the length of the project. On Bremner Road, construction of the temporary steel truss bridge is ongoing and underground service investigations continue, including on Creek Steet. At Slippery Creek / Otuuwairoa Stream, earthworks have started ahead of construction beginning on new higher motorway bridges across the stream and raising the motorway higher.

At Flanagan Road, our team is halfway through building an impressive retaining wall that has been under construction for the past several months. Read more on this below.

On the Southern Motorway itself, shoulder widening works have been progressing at pace in preparation for shifting northbound traffic lanes over to the west this Sunday night (weather permitting). Please drive safely as you navigate and become accustomed to the new layout of motorway lanes in the coming weeks.

Combined with the mid-February shift of southbound traffic lanes over to the east, the two traffic shifts put together will enable the team to begin working within the central median of the motorway in the coming month.

A combination of bunds and silt fences used for erosion and sediment control at a Victoria Street site.

Protecting the environment | Tiakitanga o te taiao

Erosion and sediment controls (ESC) are a critical environmental management practice used during construction activities to ensure the land (whenua) and waterways (awa) are protected. If proper care is not taken, soils and material may be lost from the land and end up in waterways – causing contamination, silting and negative impacts on wildlife and their habitats. ESC measures are typically installed when a worksite is first set up and, in many cases, these remain in place until construction works are completed. Later, long-term ESC measures are installed immediately before project completion, to ensure sustained environmental protection.

A range of different ESC measures can be used, with each tailored to the specific conditions of each site and the project’s requirements. ESC measures include silt fences; sediment traps; geotextiles; runoff diversion channels and bunds (earth embankments); and planting selected types of vegetation. Within this project, silt fences are the most frequently used ESC measure, providing an effective barrier against the spread and loss of sediment from the site. Other ESC measures, such as bunds and sediment traps, are installed at individual sites as required by individual site conditions and the potential environmental risks. After the completion of construction works in a particular area, fibre mats are laid to stabilise the soil surface, which supports the establishment of long-term sediment control through planting vegetation. This process ensures ongoing environmental protection even after the project team departs the site.

The fibre mats used exclusively on the Papakura to Drury project are 100% biodegradable coconut husk fibre (coir) mats, which contain a fully biodegradable jute mesh – meaning no plastic components and minimising the project's environmental impact. These coir mats promote natural vegetation growth, further enhancing long-term erosion controls and ecological restoration.

Backfilling in progress at the retaining wall near Flanagan Road.

Retaining wall | Taiapa pupuri whenua

A significant part of the Papakura to Drury project involves the construction of several large retaining walls.

One of these is located near Flanagan Road, which we began construction on last November. This retaining wall (shown above) is being built because both Flanagan Road and the Waikato water pipeline must be realigned eastward closer to Hingaia Stream – necessary as the motorway and Drury Interchange will be shifting eastwards too. When completed around May this year, this retaining wall will have used about 10,000 cubic metres of backfill material, 1,150 tonnes of concrete and 118 steel beams.

These steel beams vary from 12.5 metres to 14 metres in length. Other large retaining walls for the project yet to begin are walls alongside State Highway 1, State Highway 22, Bremner Road, and the North Island Main Trunk railway line.

We will tell you more about these other walls when construction begins for each.

Latest photos from site | Ngā pikitia

We are removing vegetation, investigating underground services, carrying out earthworks, paving and piling across the project extent – all activities require environmental controls.

Looking ahead | E haere ake nei

During the coming months, our project works include:

Completing a large retaining wall at Flanagan Road

Continuing with underground service investigations around Drury Interchange including on the motorway, Great South Road, SH22, Bremner Road, Victoria Street and Mercer Street

Working to realign the Victoria Street intersection with SH22 before installing traffic lights

Building a temporary steel truss bridge over Ngaakooroa Stream for Bremner Road traffic

Demolishing and rebuilding the existing Bremner Road bridge over the Ngaakooroa Stream

Continuing earthworks either side of Slippery Creek / Otuuwairoa Stream in preparation for bridge building works

Starting construction works in the central median of the motorway between the BP motorway service centre and Drury Interchange.

Contact us | Whakapā mai

For further information regarding the project, please contact our team: