Withtherightstrategy,anytimeoftheyearcanbeagoodtimetolistyourhomefor sale Remember,yourlocalLJHookeragentisasuburbexpertwhocanprovide insightsintoyourarea’spropertymarketandensureyouexperiencetheLJHooker differencewhenitcomestoappraisingandsellingyourhome.

Autumnisapopularandaestheticseason,soembraceit.Youcanaddsubtleautumn remindersaroundyourhometomakeitmoreinviting.Ifyourhomehasafireplace,having alowburningfireduringtheopenhomecanhelptocreateaninvitingandcosy atmosphere.Potentialbuyerswillenvisagethemselvesloungingbythefireafteralong day

Accessorieslikepoolfloats,gardenlights,outdoordécorandwateringcanscanclutteryourspaceandrisk damageifleftoutside Thoroughlycleanandstoretheseitemstokeeptheminexcellentconditionfornext year

At Rent Exchange, we provide comprehensive property management services tailored to your needs. Beyond our full-service professional management, we offer a variety of additional services to ensure all your property requirements are met:

Flexible Pay-As-You-Go Options

Inspections Only

Commercial Leasing / Management

Air BnB Casual / Short Stay Letting

Consider Rent Exchange as your on-demand property management consultants

Here to help you manage all aspects of your portfolio!

The latest Real Estate Institute of New Zealand (REINZ) data provides insight into the country ’ s lifestyle property market Sales activity slowed in the three months ending January 2025, with 1,390 lifestyle properties sold 157 fewer than in the three months ending December 2024, representing a 10.1% decline. However, compared to the same period in 2024, sales increased by 17.3%, with 205 more properties changing hands

Over the past year, lifestyle property sales totalled 5,916, an increase of 11 6% compared to the year ending January 2024. The total value of these sales reached $6.65 billion. The median price for all lifestyle properties in the three months to January 2025 was $984,250, reflecting a 4.2% rise from the previous year Bare land lifestyle properties had a median price of $450,000, increasing by 9 1%, while farmlet lifestyle properties reached $1,115,000, up 5 2%

A REINZ Rural spokesperson says that lifestyle properties remain a sought-after market segment despite short-term fluctuations. The annual increase in sales and steady price growth indicated continued buyer confidence and high levels of engagement

Regional trends showed varying levels of activity Ten regions recorded an increase in sales compared to January 2024, with Auckland leading the way with 70 additional sales, followed by Waikato with 61. In contrast, Nelson/Marlborough saw the largest decline, with eight fewer sales in the three months to January 2025 compared to the same period in 2024 Sales rose in three regions compared to the three months ending December 2024

Median prices for lifestyle blocks increased in eight regions between the three months ending January 2024 and the same period in 2025. The West Coast (+28.9%) and Northland (+24.1%) were the most notable increases Meanwhile, Southland recorded the sharpest decline at -19 0%, followed by Nelson/Marlborough/Tasman at -14 2%

The median number of days it took to sell a lifestyle property increased by five days compared to the previous year, reaching 69 days in the three months ending January 2025 Canterbury recorded the shortest selling time, at 56 days, while Northland properties took the longest to sell, averaging 95 days

Demand for lifestyle properties remains strong, even though there were some seasonal slowdowns. Rising prices in many regions suggest that buyers see value, especially in areas with good infrastructure and long-term investment potential, adds REINZ

While sales slowed in late 2024, the overall market remains active Demand continues to be strong in many regions, and price trends suggest ongoing interest in lifestyle properties across New Zealand.

National stock levels climb to over 35,000, the highest since 2015

New listings below expectations for February

Average asking prices cool as sellers flex to meet buyers

KeyFigures:

11,363 new listings - a 3.6% dip compared to February last year

Stock was up by 13 6% year-on-year

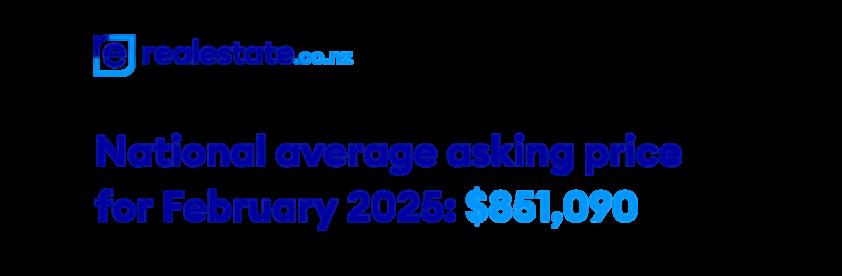

The national average asking price was $851,090 - down by 4.7% year-on-year

Sarah Wood, CEO of realestate co nz says that even though buyers continue to be spoilt for choice, the market remains active

“The market currently looks relatively breezy, especially compared to the frantic pace we saw in 2021

“Buyers have time to breathe and do their due diligence as stable market conditions continue, while properties are still selling through, which is good news for sellers ”

Nationalstockcontinuestoclimb

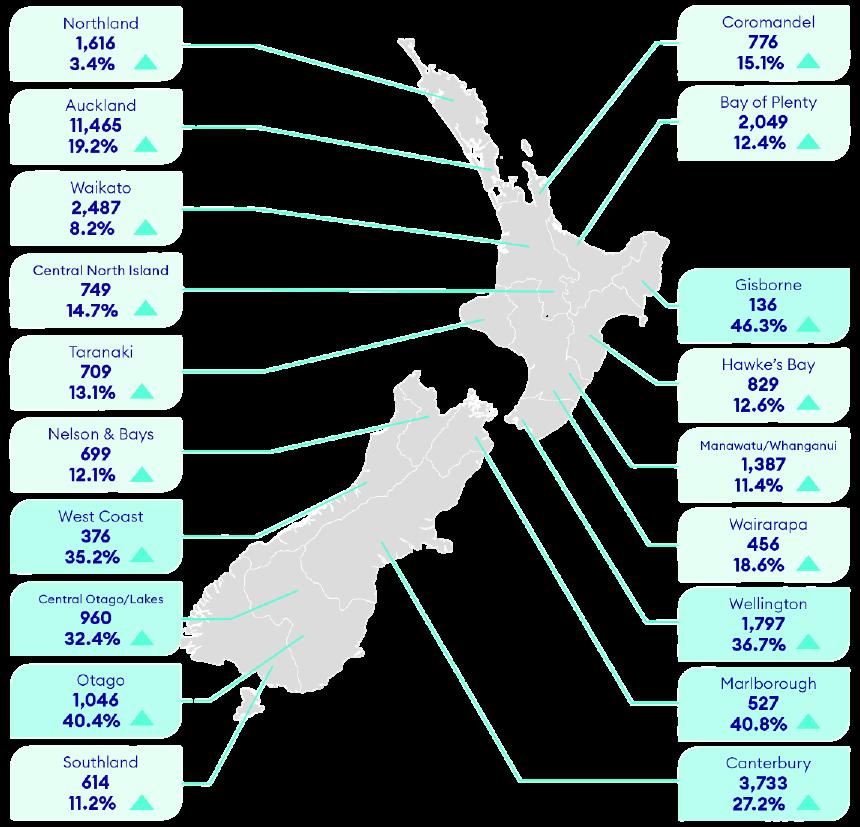

Nationally, stock climbed to 35,712 in February, a 10 2% increase from January The increase was seen across all regions, with 14 of 19 regions recording double-digit increases Gisborne experienced the biggest rise in stock, rising 80.2% month-on-month. Wood explains that high stock and new listings percentages are often seen in less populated regions like Gisborne due to its small listing set.

“Nationally, the continued rise in stock levels brings us back to levels we haven’t seen in ten years, though not the highest ever recorded. ”

Newlistingslift,belowusualexpectations

Over 11,000 new listings came onto the market in February, marking a 27.6% increase from January Wood says that although February is usually a busy month for new listings, this February was lower than expected:

“We’ re used to seeing a rush of new listings as everyone gets back from the beach and into business as usual This year it’ s less dramatic than the 40% uplift we would usually see. ”

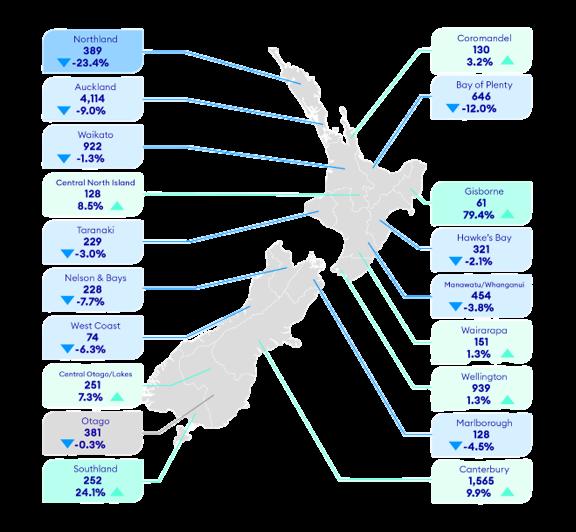

Compared to the same time last year, new listings were down 3 6% nationally A mixed bag of growth and decline was seen across the regions, with Gisborne seeing a 79.4% increase in new listings, and Northland the largest decline, down 23 4%

Pricesdipassellersflextomeetbuyers

The national average asking price dipped to $851,090 in February, down 4.7% year-onyear and down 2.0% month-on-month. Despite the drop, the national average asking price remains between $840,000 and $890,000, as it has for the past two years Wood notes that the slight decline nationally, suggests sellers are becoming more flexible as stock levels remain high:

“With high stock levels, sellers are having to be more willing to negotiate. ”

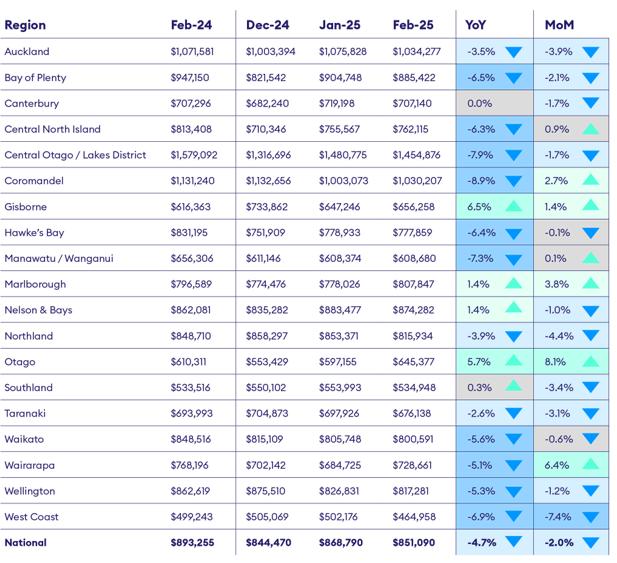

Seven of nineteen regions saw both year-on-year and month-on-month decreases in average asking prices Leading the way was Central Otago/Lakes District (down 7 9%), Wellington (down 5.3%), West Coast (down 6.9%), Bay of Plenty (down 6.5%), Northland (down 3 9%), Auckland (down 3 5%), and Taranaki (down 2 6%)

At the other end of the spectrum, only three regions saw month-on-month and yearon-year growth: Gisborne, Otago, and Marlborough Two regions achieved all-time February average asking price highs: Marlborough ($807,847) and Otago ($645,377)

Marketmoving,slowandsteady

While buyers have more negotiating power due to the number of properties on the market, the market isn’t fully in buyers ’ power nationwide Just two regions, Auckland and Nelson & Bays remain buyers ’ markets, where properties are selling at a slower rate than usual Wood explains that the data shows a more balanced playing field between buyers and sellers:

“Properties are still selling, but at a steady pace This is great news for buyers who have more options and more negotiating power. The good news for sellers is that properties are selling, with the number of properties sold increasing in January by 17 5% year-onyear according to the Real Estate Institute of New Zealand, so working with agents and other experts to make your property attractive is key. ” .

Written by Hannah Franklin

Finance& Lending

InputtoyourStrategyforAdaptingtoChallenges

Feel free to pass on to friends and clients wanting independent economic commentary

ISSN: 2703-2825

Sign up for free at www tonyalexander nz

Businessesplanpricerises

The ANZ Business Outlook survey for February released last week shows things little changed from where they were in January In particular, the measure which I am paying greatest attention to of the net percent of businesses planning to raise their prices in the next 12 months held steady at 46%

I consider that a continuing cause for concern because the average reading for this gauge since inflation settled near 2% in 1992 has been 26% and the measure has risen since reaching 35% in the middle of last year

Business margins are tight, and the result tells me there is a risk that businesses will seek to rebuild those margins via higher prices once the flow of customers is strong enough that they feel they can get away with it.

Add in rising prices for electricity, council rates, climate change, and higher offshore inflation and we get an early cyclical recovery in inflation threatening people’ s happiness about interest rates for the next few years before this year is out This is why I favour aiming for a good rate to fix three years+ rather than just two years which is really not that much insurance at all

Published 6 March 2025

For now, we wait and as yet there is no justification for panic After all, the inflation rate businesses think will prevail in a year ’ s time fell slightly to 2 53% from 2 67%

Of positive import are the upward trends in investment intentions (18%) and employment intentions (17%) A net 34% of construction businesses expect to hire more people in the coming year versus a net 10% of ag businesses planning to hire fewer.

I mention this divergence specifically because of the theme being pushed by some this past week that the recovery in our economy will be driven by the farming sector. No it won ’t.

The Kiwi dollar is only four cents down from a year earlier whereas coming out of the three previous recessions it has fallen 10-15 cents or so and caused the recovery to be export led

There is a drought in place in parts of the North Island important to dairying Costs continue to rise Land continues to switch from sheep and beef to trees

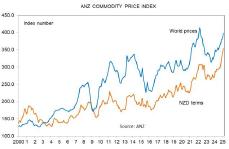

Having said that, courtesy of higher dairy prices, in NZ dollar terms commodity prices for our exports are 23% ahead of a year ago as shown in the orange line’ s strong rise to the right side in the following graph So, there is a positive effect in play, and this is relevant much more to the non-drought non-city regions than the cities

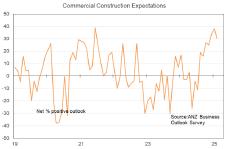

But is the outlook for construction really as bright as the very strong net 34% employment intentions suggest? There is an over-supply of townhouses in our two biggest cities - meaning now is a good time to buy one at a discounted price Townhouse construction will fall through to 2026

For infrastructure there is a lot of talk about more activity But the sector is short of resources and if the poor management of the SH58 upgrade near my place is any indication no-one should anticipate any infrastructure surge in New Zealand

bFor standalone house construction the prospects for growth however look positive as the dynamics are different from townhouses and apartments. For retirement villages however the track is clearly downward over the next 12+ months. For commercial construction of things like offices, warehouses and factors however I do feel the outlook is positive Many businesses need to boost productivity, and better premises can be part of that solution

Real estate agent insights

Each month in my survey of real estate agents sponsored by NZHL I invite respondents to pen a sentence or two regarding what they are seeing at their particular coalface This month these comments stretched to cover nine pages and have already been supplied back to the agents who responded Here are a select few comments for each region to help you better understand what is happening out there These are comments written by the agents, not me Enjoy

Northland

• A noticeable pick up in activity since the start of 2025 in Kerikeri area

In the mid-North, there appears to have been a huge uptick in families wanting to upgrade from their existing home There are also a number of older down-sizers coming through open homes However, I would say 80-90% have a property to sell first

We are in the Far North; our market is moving modestly Buyers are very price conscious and taking their time Vendors are having to come to terms with their property not being worth what they think it is, or 'need' in order to move But we are making sales, people are back in the market with a bit more appetite to make things happen ith regard to the actual stock of listings at the end of December the total of 32,300 was down slightly from 32,900 at the end of November (data seasonally adjusted) and the peak of 33,500 at the end of October

Auckland

Finally some actual light at the end of the tunnel Auction clearance rates up Still too much stock but some good months ahead will hopefully clear some of that out We don't want to jinx things but there is real evidence things are changing now rather than misplaced hope South/East Auckland Mainly new builds Very little interest at present Low numbers to open homes Interest rate drop hasn’t made a huge difference as yet. Tons of completed stock not selling, even after prices have been reduced. Existing stock and do-ups are faring much better but more competition for listings. Development sites are faring badly with little interest unless price is extremely viable as council and Watercare costs have risen sharply.

•Rodney area Never been busier Finding it a little alarming at the number of people asking for appraisals Buyers are coming forward with some ridiculous offers as the result of clearly knowing they have the upper hand right now as we become more swamped with listings Mainly cash buyers, very little financing going on

BayofPlenty

In Papamoa and the Mount, the market has picked up since October 2024. A definite increase in buyer activity and auction clearance rate now close to 30-40%. We are seeing buyers able to access finance more easily I feel it’ s a more balanced market than we have seen in a while

Coastal towns in the Bay Of Plenty- we have plenty of listings, however, it' s hard to make a sale Buyers a giving low offers and aren 't in any hurry to transact

• Properties in sought after locations are selling quickly but sellers need to be right on price to get any action

Waikato

A lot of stock out there, so buyers aren 't in a rush to make an offer as plenty of properties to view Quite a few buyers looking that have property on the market but haven't had any luck in selling theirs

In our beach town we have done more business in the 4th quarter of this financial year than the other 3 quarters combined. Mainly due to the interest rate drops bringing buyers back into the market. Cambridge region, very active market between $7k - $1m. Between $1.2m-$1.4m there is a lot of stock on the market for buyers

Hawke’sBay

Fewer people are in a financial position and/or have the confidence to buy a holiday home in the current market Offers are coming in much lower than vendor' s expectations Vendors tend to be holding out for prices of two to three years ago, despite most still making a significant capital gain at today ' s levels

•Surge in buyers attending open homes over the past couple of weeks, seeing multiple offers on properties now, buyers more eager to act on making offers now rather than just looking market is feeling quite positive here in HB at the moment Survive to 25 was a slogan that sounded good but a bit optimistic Likely end of year before we see rising volumes Around 410 properties available in Napier from high 300s last year, so not a dramatic increase in stock Finance and employment issues more in play

This rate drop has done nothing in Taranaki. Open homes are dead - too many listings no buyers. Have spoken to other agents all saying the same and have noticed homes are on the market for a month or two and then taken off or other agency takes over and still no sale. Vendors quick to blame to salesperson but this market is heading for a crash in prices to have to sel

I’ ve had offers after first open homes on my last five listings -all to First Home Buyers

Great to see some positivity moving forward from these buyers

A solid start to the year with multiple buyers showing interest on all properties Starting to get multiple offers on good properties

Buyers are starting to appear more urgent to transact Some buyers who have missed out on a multi offer or haven't acted quick enough will potentially start to move quicker FOMO may start coming into play within the next six months The lack of construction will also make the existing homes more attractive

Wellington

Wellington Definitely more activity in the market and more people in the auction rooms Some vendors still unrealistic about their sale price"need" as opposed to market value - age old problem that will never disappear!

Kapiti market continues to be well balanced with good amounts of new listings and ample amounts of sellers. First home buyers seem to be well represented with the lower value homes getting good attention. There' s a lot of homes coming to market providing plenty of choice for buyers who remain a bit wary although first home buyers are active It' s a great time to be a buyer in the Porirua City area

Tasman

Steady as it goes. Sale numbers are up with a few multi offers around however buyers are not being silly with their offers They would rather miss out on the property than over pay On the flip side, new listings are way up and out pacing the number of sales

Auctions in Tasman area are having a low success rate with only 22% selling under the hammer No price marketing achieving positive results with multiple offers coming in $1m to $1 5m selling strong in Tasman area, lower priced properties taking a little longer

We have yet to see an increase in overseas interest unless they are Kiwi' s looking to secure a foothold in the country At our end of the market we don't see many first home buyers so really cannot comment on this We hope buyers will start to feel FOMO and put pen to paper and we are seeing more sales but usually with tired sellers lowering their asking price Not always, but it is happening

Marlborough

• Supply still outweighs demand First home buyers are really active, which we hope will stimulate the middle level Very quiet in the million plus market

Residential Buyers for the best suburbs in the$1 2-1 6M are very active and seem to want to purchase quickly Lifestyle buyers are a rare find but when viewing are out for a bargain If the property can ’t be purchased at the right level, they move on quickly! First home and investors under $600k are purchasing and there are plenty of these buyers in the market

• We are seeing a real mix of numbers attending open homes Stock levels are still high so there is plenty of choice for buyers, that said when it is good stock in the lower to mid range, we are seeing buyers act quickly to get offers in and multi offers are starting to come back into the market The higher end of the market is slow

Taranaki

Manawatu-Wanganui

No comments received this month

The market is strong in the under $800,000 bracket and steady above this Vendors are more realistic pricewise, and buyers are getting more motivated (although this is a work in progress, and they need quite a bit of encouragement to make a decision) Very positive about 2025 Lower interest rates and more stock are attracting more buyers

Buyer activity has definitely picked up, but the number of new listings has largely balanced that out In Christchurch In Christchurch, it feels like stock levels are high (almost worryingly high), but there are enough buyers out there to match We are happy

Otagoexcl.QueenstownLakes

Soft start to 2025 after a buoyant end to 2024 for buyer enquiry A bit surprising and hopefully it'll pick up shortly Lots of vendors talking about selling though, which might just add to the ever increasing number of homes on the market

Our area Alexandra Basin is seeing high level of interest from outside the Otago region especially in higher value properties For those inside Otago there is increased interest from Qtown lakes looking to move as well as Cromwell home buyers looking for more affordable options

High levels of housing stock available in Dunedin with over 900 listings The oversupply is providing plenty of choice for buyers, which doesn't encourage prompt action for making an offer

QueenstownLakes

Buyers are still very hesitant to purchase, holding off for further interest rate drops and hoping prices might drop Also worries about economic conditions

Feels like the market is only slowly gearing up for the year after a quiet Christmas period.

Some Vendors hanging out to see what comes of the OIO rules.

Vendor expectation continues to be biggest hurdle in getting an agreement over the line despite good $ gains It’ s not until there is vendor desperation that we are seeing a sale come together

Southland

No comments received this month

Nolistingsboom

Realestate co nz this week released their monthly data on listings received during the month and the stock at the end of the month

The end of February stock of 32,700 dwellings in seasonally adjusted terms was unchanged from the end of January and ahead 13% from a year earlier Stocks have been reasonably steady since about June of last year

The number of fresh property listings received during the month fell 8% after rising 40% in January This series is displaying some unusually high month to month variations so I’ m not focussing at all on the monthly changes but instead the three monthly variations

In that regard over the three months to the end of February fresh listings were down about 3% from the three months to November These is no new listings boom The last true surge was exactly this time a year ago

Nelson Canterbury

IfIwereaborrower,whatwouldIdo?

Not be optimistic that interest rates will fall much this year

There is a lot of uncertainty in global financial markets currently as we watch the on and off again policy changes imposed by the new US President, wonder where Ukraine is headed, and ponder how much the Australian central bank can afford to cut interest rates when their labour market is so strong

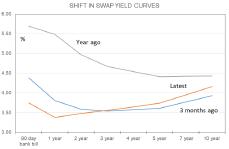

Out of it all the wholesale rates which banks borrow at in order to lend at a fixed rate to you and I have ended this week barely changed from last week

The situation can be best summed up in this following graph It shows the 1-5 year swap rates last year – the grey line – three months ago – the blue line – and now – the orange line Rates are well down from March of 2024 But note how for terms of three years and beyond rates are now above where they were three months ago

New Zealand’ s easing cycle has been well factored into the medium to long-term borrowing costs and they are now creeping up as focus slowly shifts to how the cyclical recovery in economic activity will eventually lead to a cyclical recovery in inflation

The short end of the curve is still falling because of the greater relevance of the current and immediately expected official cash rate The cash rate currently is at 3 75% and is expected to be either 3 0% or 3 25% by perhaps the September quarter at which point the falling phase of the monetary policy cycle will be over Is there any relevance from the surprise resignation of the Reserve Bank Governor Adrian Orr? Some disgruntled people may think so, but it pays to remember a few things

Cash rate changes are decided by a committee these days and not one person taking or not taking advice Also, the Reserve Bank have already reacted to surprising news on weakness in our economy last year by bringing forward their predicted bottoming out of the cash rate to this year from late-2026

Will the outgoing Governor’ s legacy be a good one? No. He oversaw excessively loose monetary policy over 2021 into 2022 and failed to see what virtually every non-Reserve Bank economist in the country could see – an unsustainable and ultimately highly inflationary economic boom.

The Governor and his people then failed to recognise the weakness in our economy last year He often failed to react calmly to criticism (then again, who does?), and appeared to devote too much focus to wellbeing issues rather than good economic analysis and policy implementation

We can anticipate a change in style once a new Governor is appointed, perhaps with someone more aligned with the new government’ s view of the world In that regard the governor perhaps is merely joining a growing list of public servants who have “resigned” from their top of the pile positions in recent times Health, Police, etc

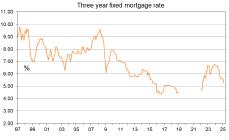

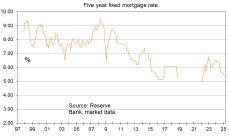

These three graphs show mortgage rates since 1997 excluding the period of deflation worries (2019) and the pandemic

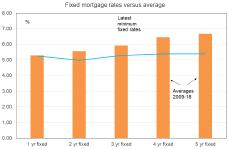

This graph shows how current rates compare with averages from 2009-19

To see the interest rates currently charged by major lenders go to

Nothing I write here or anywhere else in this publication is intended to be personal advice You should discuss your financing options with a professional www.mortgages.co.nz

Thispublicationhasbeenprovidedforgeneralinformationonly Althoughevery efforthasbeenmadetoensurethepublicationisaccuratethecontentsshouldnotberelied uponorusedasbasisforenteringintoany productsdescriptioninthispublication Totheextentthatany informationorrecommendationsinthispublicationconstitute financialadvice, they donottakeintoaccountany person ’sparticularfinancialsituationorgoals Westrongly recommendreadersseekindependentlegal/financialadvice priortoactinginrelationtoany ofthemattersdiscussedinthispublication Nopersoninvolvedinthispublicationacceptsany liability forany lossordamagewhatsoever whichmay directly orindirectly resultfromany advice, opinion, information, representation, oromission, whethernegligentorotherwise, containedinthispublication No materialinthispublicationwasproducedby AI

Properties

HittingTheRealEstateJackpot!

Generous 771m² (mol) fully fenced section

4 bedroom home including consented sleepout with ensuite

Inviting sun-drenched courtyard

Garaging, carport and plentiful off-street parking

Convenient location for schools, shops and transport

PRICE As Advertised

VIEW By Appointment Only

AGENCY

LJ Hooker Town & Country 09 294 7500

Town&Country

Current Listings

2C Waiari Road, Conifer Grove

Price Drop; Urgency Needed

Conifer Grove at entry level price. You've got to

see this! A beautiful 1920's bungal

Lot 13/717-719 Sandringham Road Extension, Sandringham

Must Sell, Call Today To View

Welcome to a unique opportunity to own a stunning home in nearly completed multi-unit development th

48A Sinclair Road, Ararimu

A Luxury haven in a magical setting

Discover the ultimate sanctuary for your family in this expansive, luxury home designed to cater to

For Sale $778,000 View By Appointment

Steve Reilly 021930352 steve.reilly@ljhooker.co.nz

430 Twilight Road, Brookby

Secluded Elegance

Nestled in a sunny spot amongst the trees, is this wonderful private residence. If you are looking f...

For Sale Enquiries over $889,000 View By Appointment

KJ Klavenes 027 5566 194 knut klavenes@ljhooker co nz

An absolutely incredible opportunity for larger families or those looking for the ultimate investmen

For Sale Price By Negotiation View By Appointment Paula Cox 021396 977 paula cox@ljhooker co nz

RecentSales

114 Harbourside Drive, Karaka

RIPE FOR DEVELOPMENT in KARAKA

Located in the "sought after" Karaka Harboursidez Estate, the opportunity to purchase another land ho. ..

80 Sutton Road, Drury

RARE OPPORTUNITY -Zoned Future Urban

80 Sutton Road

*8.4731 ha (more or less)

*8 Bay Milking Shed -130sqm approx

150 Sutton Road, Drury

A rare opportunity-Zoned Future Urban

150 Sutton Road *11.9382ha (more or less)

*2 Bedroom Cottage -124sqm approx

029 296 5362

029 296 5362

029 296 5362

Our People

Sales&MarketingConsultant

M:0212867792

E:venitaattrill@ljhooker.conz

Sales&MarketingConsultant

M:0274816422

E:johnny.cleven@ljhooker.co.nz

Sales&MarketingConsultant

M:0223577554

E:anujay@ljhooker.conz

M:021303864

E:debbieharrison@ljhooker.conz

Sales&MarketingConsultant M:021396977

E:paulacox@ljhooker.conz

Sales&MarketingConsultant M:0212721912

E:atesh.narayan@ljhooker.co.nz

E:christineforster@ljhooker.conz

Sales&MarketingConsultant

M:021930352

E:stevereilly@ljhooker.conz

Sales&MarketingConsultant M:0275566194

E:knut.klavenes@ljhooker.co.nz

Ph:092947500

E:meganvanwinden@ljhooker.conz

KJ Klavenes

Realisinghewasn’tfixatedinwinningthegameoflifebasedon what college and conventional wisdom taught him, KJ focused lessonthesecurityaspectofjobsandfocusedmoreonhelping peopleintheirsuccessonsellingtoearnhisway.

Not only was he scoped out by the high ends of a Real Estate Agent in New Zealand to start out by a mere first sentence upon meeting, he’s also been building his empire under the mentorshipofthetop10ofNewZealand!

After achieving levels of income, impact and personal freedom he could’ve only dreamt of as a child, KJ, on top of all his multi 6-8figureclients,hasdedicatedhisambitionstowardshelping people achieve the best prices they can in their own circumstancesprovided!