The property market is showing signs of stabilisation, with early indicators pointing towards a potential rebound in 2025.

With mortgages easing a further cut to the OCR and property sales volumes rising, we're starting to see renewed confidence from both buyers and sellers.

While some areas are still seeing price adjustments, overall, the data points to a market that is stablising and setting the stage for future growth.

Stability Leading to Renewed Growth

The latest Core Logic Home Value Index shows that property values in New Zealand declined by just -0.1 percent in January, marking the fifth consecutive month of limited movement. Since August, the total decline has been modest -0.4 percent, compared to the more significant -4.1 percent drop recorded in the first half of 2024.

CoreLogic NZ's Chief Property Economist Kelvin Davison notes that the downturn appears to have run its course.

"Since the mini downturn' seen through the middle part of last year petered out in August national property values have been in a holding pattern - not moving clearly in either direction" he said.

"But with mortgage rates having dropped significantly from their peaks, property sales volumes have continued to rise in recent months and may well start to redcue the available stock of listings on the market in the near term."

The recent stability suggests we could be at the bottom of the cycle, which presents an opportunity for buyers to secure property before prices start to rise again".

One of the most telling signs of improving market conditions is the growing level of mortgage activity. The RBNZ's latest 'lending by purpose' data reveals that mortgage commitments totalled $2.062 billion in January. Roughly a quarter of that was a result of borrowers changing loan providers, which is the highest level of loan provider switching since records began in 2017.

"When people feel confident enough to refinance or take on new loans, it's often a sign of improving sentiment in the market'.

As always we hope you enjoy this publication.

Kind regards

Brent

Brent Worthington Principal and Licensee Agent

0292 965 362

LJ Hooker Town & Country

Rent Exchange Property Management

1/233 Great South road, Drury

Beyond the Address: How Location Impacts Your Home and Lifestyle

Whether you want to be in the heart of the city, close to the coast, or tucked away down a quiet country road, location is always a jewel when finding a home. Although location remains a cornerstone of real estate, but it has evolved.

While it used to primarily focus on being in a popular school zone or having easy access to essential services, today’s buyers are looking for more. It’s no longer just about the suburb, street, or position. House hunters now seek properties that align with their interests, values, and overall well-being, all while staying within their budget.

Why is location so important?

Unlike a dated kitchen or bad wallpaper, one thing buyers can’t change about a property is its address, making location a key factor in any purchase decision.

While affordability determines where people can buy, good neighbourhoods generally have low crime rates and convenient access to shopping, schools, transport links, and medical facilities. For some, being close to beaches or vibrant inner suburbs may be the dream, while others prefer the tranquility of smaller towns.

It’s important to remember that everyone’s priorities differ. Young families often prioritise proximity to schools, parks, and reliable transport links to employment hubs. In contrast, older downsizers and retirees may value being near healthcare services, restaurants, and entertainment options. Investors, on the other hand, may target properties in areas popular with students or professionals.

What are buyers looking for in a location?

High-demand suburbs stand out due to their unique appeal. For example, excellent schools, local cafes, a strong sense of community, coastal charm with easy city access, space and stunning surroundings.

While most homebuyers hope for future value growth, practical needs can sometimes outweigh potential capital gains. A residence on a busy street may not seem ideal at first glance, but for those prioritising access to public transport or living within a sought-after school zone, it might be the perfect fit.

What is a premium location in real estate?

Water views are always highly sought after, homes near golf courses or green spaces are appealing to many buyers, wide street frontage, elevated positions, and proximity to amenities can add significant value.

Housing affordability has also increased demand for properties with potential for future additions, such as a granny flat. Having the flexibility to expand a property’s functionality can make a location even more attractive to buyers.

How do you know if an area is right for you when purchasing a home?

When searching for a new home, it’s crucial to find a property that suits your needs, but equally important is choosing a neighbourhood that feels like home.

Start by visiting the area in person. Explore the local shops, stroll through nearby parklands, and visit community spaces. Enjoy a coffee at a local café and take note of the area’s vibe. These experiences can help you assess if it’s the right fit for your lifestyle.

Another key step is speaking with a local LJ Hooker agent. They can provide insights into the area, including recent sales trends, demographic information, school catchments, transport options, and accessibility Importantly, they can guide you through the buying process, helping you find a property that aligns with your goals and budget

Agents can also help you consider alternative suburbs you might not have initially thought of For example, if your dream area is out of reach financially, they might recommend nearby suburbs with similar features that are more affordable. Often, it’s about making strategic compromises and planning your journey to your ideal location.

What can be done to increase the appeal of a location?

Certain property features can enhance the appeal of a home regardless of its location. In New Zealand, popular features for buyers include outdoor entertaining areas, modern kitchens, and energy-efficient systems. Simple updates like landscaping, repainting, or adding a new letterbox can boost a property’s street appeal

If your property is near a busy road, consider adding hedges or fencing to create a private backyard sanctuary For homes in urban areas, features like off-street parking or a garage can also make a big difference.

Sometimes, small changes can have a big impact. Adding greenery, enhancing outdoor spaces, or making minor interior upgrades can transform a property and make it more desirable to potential buyers.

Location will always be a defining factor in real estate. Whether you’re buying your first home, upgrading, or investing, understanding what makes a location desirable is key. By combining thoughtful research, local knowledge, and strategic planning, you can find a property that meets your needs and provides a great place to call home.

Please don't hesitate to contact our team who can ably assist you withany property management matters you may have or if you have any questionsabout anything in the newsletter or property management in general.

Is It Time to Switch Your Property Manager?

• The key to a successful rental property portfolio lies in having the right team to manage it. Whether you own one rental or several, ensuring your investment is managed effectively is essential for maximising returns and minimising stress.

The property market can be competitive, and tenants expect well-maintained homes and responsive management. That’s why choosing a property manager with the right mix of skills tenant relations, rent collection, overseeing repairs, and problem-solving—is critical.

But what happens when you suspect your property manager isn’t up to scratch? Should you stick with the agency you know, or is it time for a change? Let’s explore some of the most common reasons Kiwis consider switching property managers.

Poor communication

One of the most frustrating experiences as a landlord is being ignored by the person you’ve entrusted to look after your investment.

Effective communication is at the heart of good property management.

“If your current agency is unresponsive or fails to provide timely updates, it can ultimately lead to the mismanagement of your property.”

Good communication doesn’t just benefit you as the landlord; it’s also essential for maintaining positive relationships with tenants. A happy tenant is more likely to renew their agreement, reducing vacancy rates and turnover costs.

As a rule, property managers should respond to emails and calls within 24 hours, with even quicker action in emergencies. If you’re constantly chasing updates or left wondering about the status of your property, it might be time to look elsewhere.

Ineffective rent collection

Your rental property is an investment, and timely rent collection is vital to its financial success. If your current property manager struggles to handle late payments or fails to keep your rent in line with market rates, your returns may suffer.

A skilled property manager will ensure your rental agreement includes clear terms for payment methods, overdue fees, and even eviction procedures, should they be necessary

They’ll also monitor local market trends to keep your rental pricing competitive while helping you reduce tenant turnover.

It’s especially important for property managers to stay on top of legal compliance, including Healthy Homes Standards and Residential Tenancies Act requirements.

Poor property maintenance

Every property requires regular maintenance, and your rental is no exception. If issues like leaky taps, broken appliances, or pest problems aren’t addressed promptly, they can escalate into larger, more expensive repairs.

Landlords are legally required to keep properties in a safe and habitable condition. A good property manager will conduct thorough inspections—up to four times a year with appropriate notice—to ensure tenants are meeting their tenancy terms and to identify any maintenance needs early

Effective property managers should also have a trusted network of local tradespeople to handle repairs efficiently From plumbers to electricians, they’ll manage quotes, supervise work, and ensure everything meets quality standards.

High vacancy rates

A vacant property means lost income, and in today’s rental market, it may point to problems like poor marketing, high rent, or lacklustre tenant placement efforts.

A skilled property manager knows how to attract quality tenants through strategic marketing, professional photography, and well-crafted property listings. They also screen applicants thoroughly, checking references, rental history, and income to ensure a good match.

In New Zealand, where pet-friendly rentals are in high demand, your property manager may even suggest simple updates or policy changes—such as allowing pets or modernising fixtures—to make your property more appealing to tenants.

Lack of transparency

A transparent property manager will provide clear financial reporting and ensure you’re kept informed about your property. You should receive a monthly statement detailing income and expenses, making it easier to stay organised for tax purposes.

If your property manager is disorganised or fails to provide detailed reports, it could cost you financially—both in terms of missed tax deductions and poor decision-making.

Transparency also extends to fees. Make sure your property manager discloses all costs upfront and is clear about their processes.

When

it’s time to make a change

Managing a rental property is about more than collecting rent and organising repairs A good property manager can be a valuable adviser, helping you maximise returns and grow your portfolio.

If you’re dissatisfied with your current property manager, switching to a new agency could be the best decision for your investment. Landlords typically need to provide 30 to 90 days’ notice to change property managers, depending on their agreement. Your new property manager will usually handle the handover process, making the transition seamless.

Take the next step

If you’re considering a change, LJ Hooker’s Rent Exchange property management team is here to help. With a focus on professional service, effective communication, and local market expertise, we’re committed to making your investment as stress-free as possible. Request a free property appraisal today to understand your investment’s potential and how LJ Hooker can help you achieve your financial goals.

Debbie Harrison

Debbie Harrison

Property Manager

021 302 864

debbie.harrison@ljhooker.co.nz

AboutMe

With a passion and a commitment to providing exceptional service, Debbie has a fantastic attitude of getting things done and ensuring that the clients are happy and well cared for. She takes great pride in her work and goes above and beyond to ensure the satisfaction of both property owners and tenants.

Debbie’s attention to detail and organizational abilities are exceptional, enabling her to efficiently handle all aspects of property management, from tenancy agreements, rent collection to property inspections and maintenance coordination.

Debbie understands that property management requires a compassionate and empathetic approach, and she always strives to create a positive and harmonious living environment for tenants while protecting the interests of property owners.

Whether you are a property owner seeking professional management services or a tenant searching for a well-maintained rental property, Debbie is committed to delivering exceptional results and ensuring a smooth and rewarding experience for all parties involved.

With her excellent communication skills, strong work ethic and dedication to excellence, Debbie Harrison is a true asset to LJ Hooker, Drury

Reports, Surveys& Commentaries

Town&Country

A steady market with growing confidence

Published 19 February 2025

The latest figures from the Real Estate Institute of New Zealand (REINZ) for January 2025 showed some positive signs across the New Zealand property market, tempered with the usual slowness of the holiday period.

REINZ Chief Executive Jen Baird stated, “While the numbers predictably show January being a slower month due to the holidays, sales and listings were higher compared to January 2024, and open home volumes were strong across the country with a positive sentiment shown from buyers ”

As expected during the summer holiday period, sales were up 17.5% (from 3,212 to 3,774) compared to January 2024, and were down month-on-month by 37.6% (from 6,048 to 3,774) across New Zealand compared to December 2024. For New Zealand, excluding Auckland, sales saw a 23.4% year-on-year rise, from 2,318 to 2,861. Notable growth in sales was observed in Marlborough (+62.5%) and West Coast (+47.4%) year-on-year while all regions saw a decrease in sales month-on-month.

“When we adjust the sales figures for seasonality, we see that the year-on-year difference is higher than expected, reflecting a shift in buyer sentiment over the past year, from caution to more confidence,” Baird says.

The median price for New Zealand decreased slightly, down 1.7% from $763,000 to $750,000 year-on-year. Excluding Auckland, the median price increased 0.9% year-on-year, rising from $685,000 to $691,500.

Only eight out of sixteen regions reported an increase in median prices compared to January 2024. Gisborne had the highest increases up 28.2% from $515,000 to $660,000, followed by Nelson with a 25.4% increase from $670,000 to $840,000 – a record for this region.

"January is traditionally a slower month as New Zealand enjoys its holidays. Year-on-year January shows prices holding steady. Buyers are still enjoying the choices on offer thanks to rising listing numbers and significant levels of property for sale. First-home buyers and owner-occupiers are still the largest groups at open homes, with salespeople reporting investor interest in pockets of the country. Holiday spots like Taupo and Nelson are also seeing interest from visitors from other parts of the country,” added Baird.

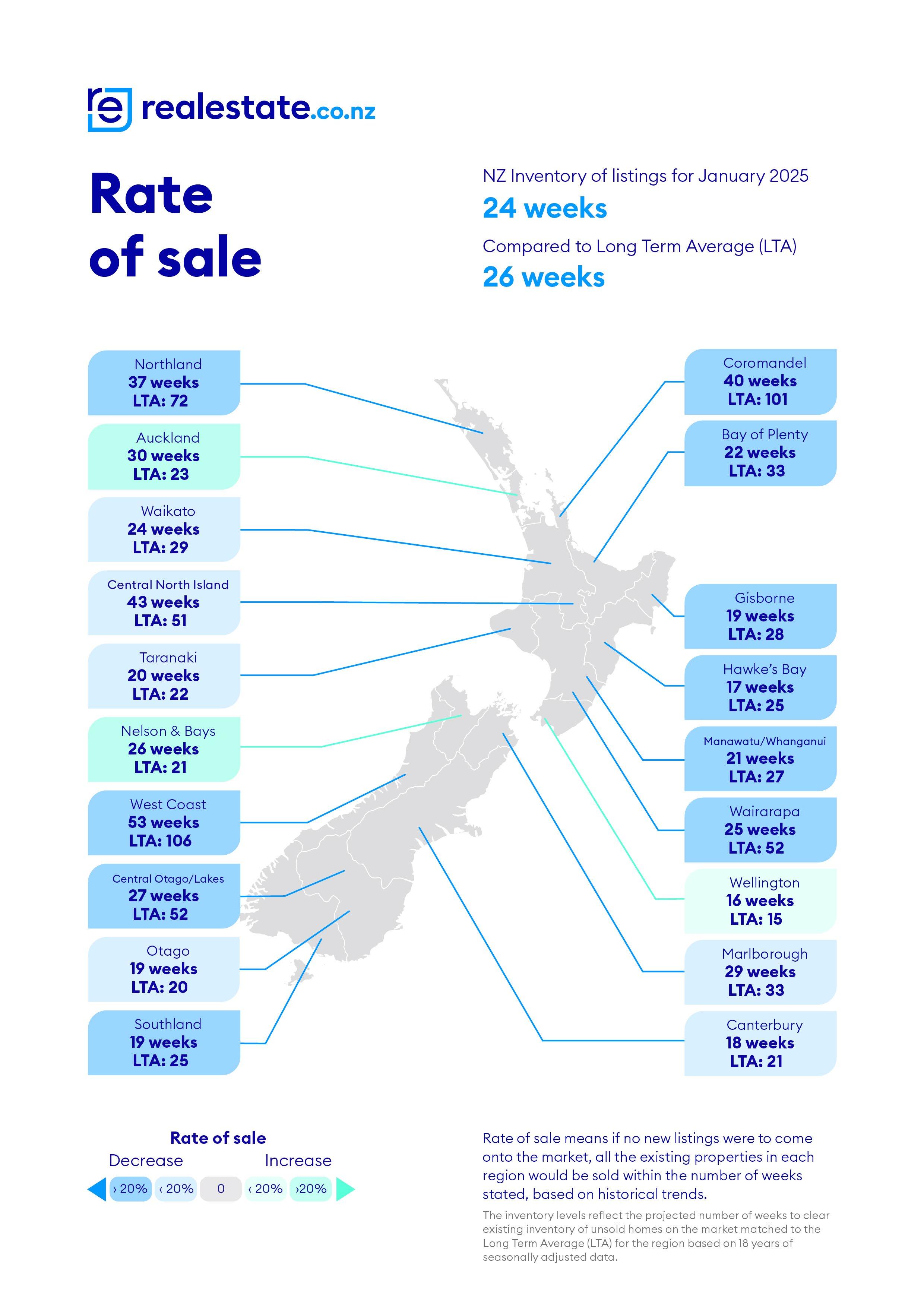

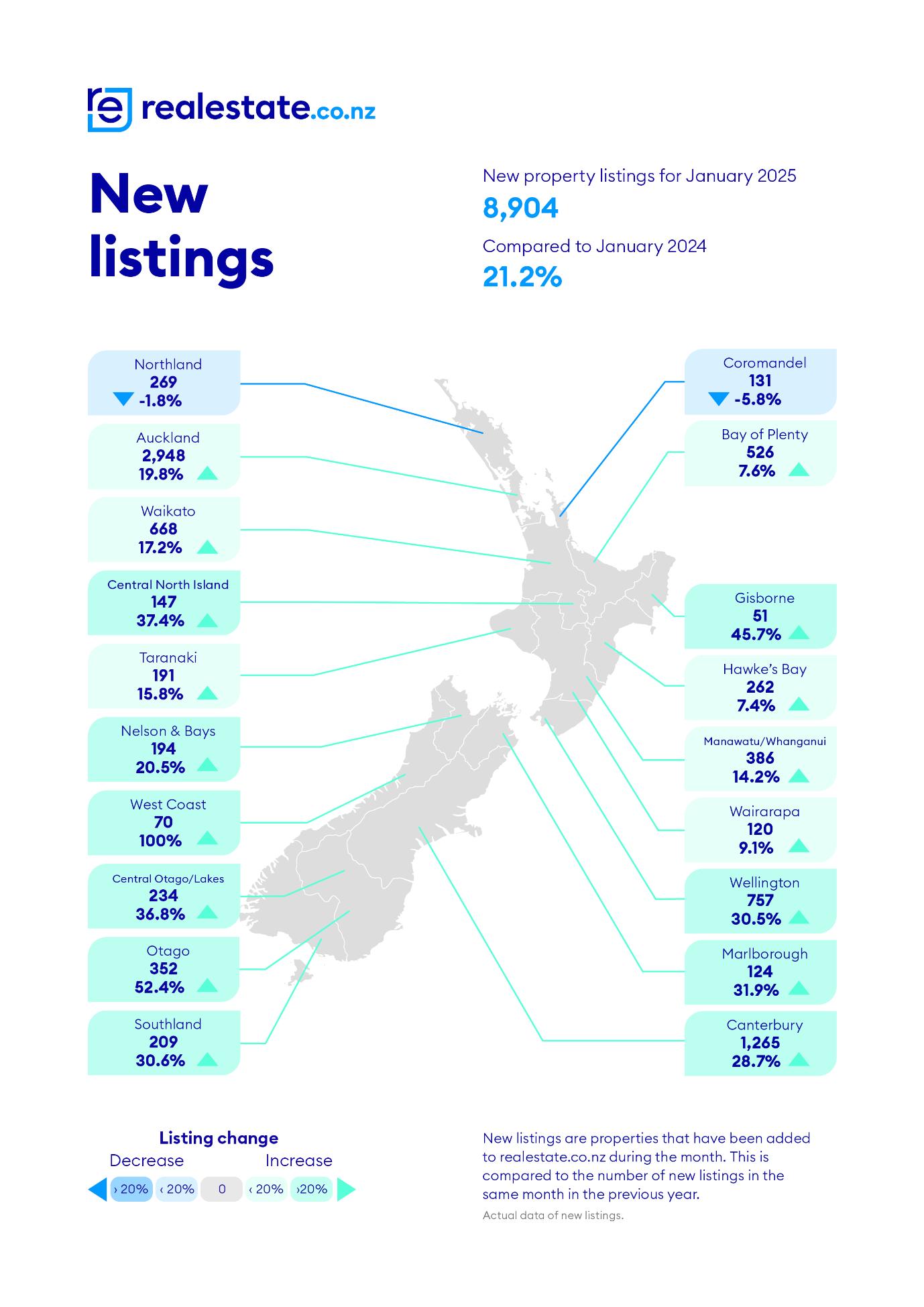

Overall, listings nationally increased year-on-year by 21.2% from 7,347 to 8,904, the highest level of listings for January since 2015. Excluding Auckland, listings rose by 21.9% compared to January 2024, from 4,886 to 5,956. Northland was the only region that didn’t report an increase in listings compared to last year; the most significant gains were reported in the West Coast (+100%), Otago (+52.4%), and Gisborne (+45.7%).

Nationalinventory levels increased by 18.9% year-on-year and also increased by 10.0% compared to December

"All regions are seeing an increase in stock numbers with Gisborne, Marlborough and Otago leading the way,” adds Baird.

“With vendors being realistic in their price expectations and meeting the market, there is a positive sentiment out there amongst agents. Steady and improving is the feedback, with the next few months looking busier with a strong pipeline of property coming to market.”

In January, there were 263 auctions nationally (7.0% of all sales), an increase from the previous year but a sharp decrease from December, as usually happens due to the January holidays. The national median days to sell rose by 3 days, to 54 days, compared to the previous year; excluding Auckland, it increased by five, to 54 days.

The House Price Index (HPI) for New Zealand is currently at 3,606, indicating a decrease of 1.4% year-on-year and 0.2% compared to December 2024. Over the past five years, the average annual growth rate of New Zealand's HPI has been approximately 4.3%. However, it is currently 15.7% lower than its peak in 2021.

The Real Estate Institute of New Zealand (REINZ) has the latest and most accurate real estate data in New Zealand.

ANNUAL MEDIAN PRICE CHANGES

JANUARY 2025

Manawatu-Whanganui

Gisborne

Market Snapshot – January 2025

Days to sell nationally

19 February 2025

Click here to view this report

Published 19 February 2025

February 2025

Coined ‘the perfect market’ in November, the rare stability of high stock levels and stable prices has carried over to 2025. But with confidence on the rise and interest rates declining, the question everyone’s asking is, when will the market change?

Key Takeaways

• New Listings back at levels not seen during January since 2015

• National stock levels up 18.9% year-on-year, close to 2015 levels

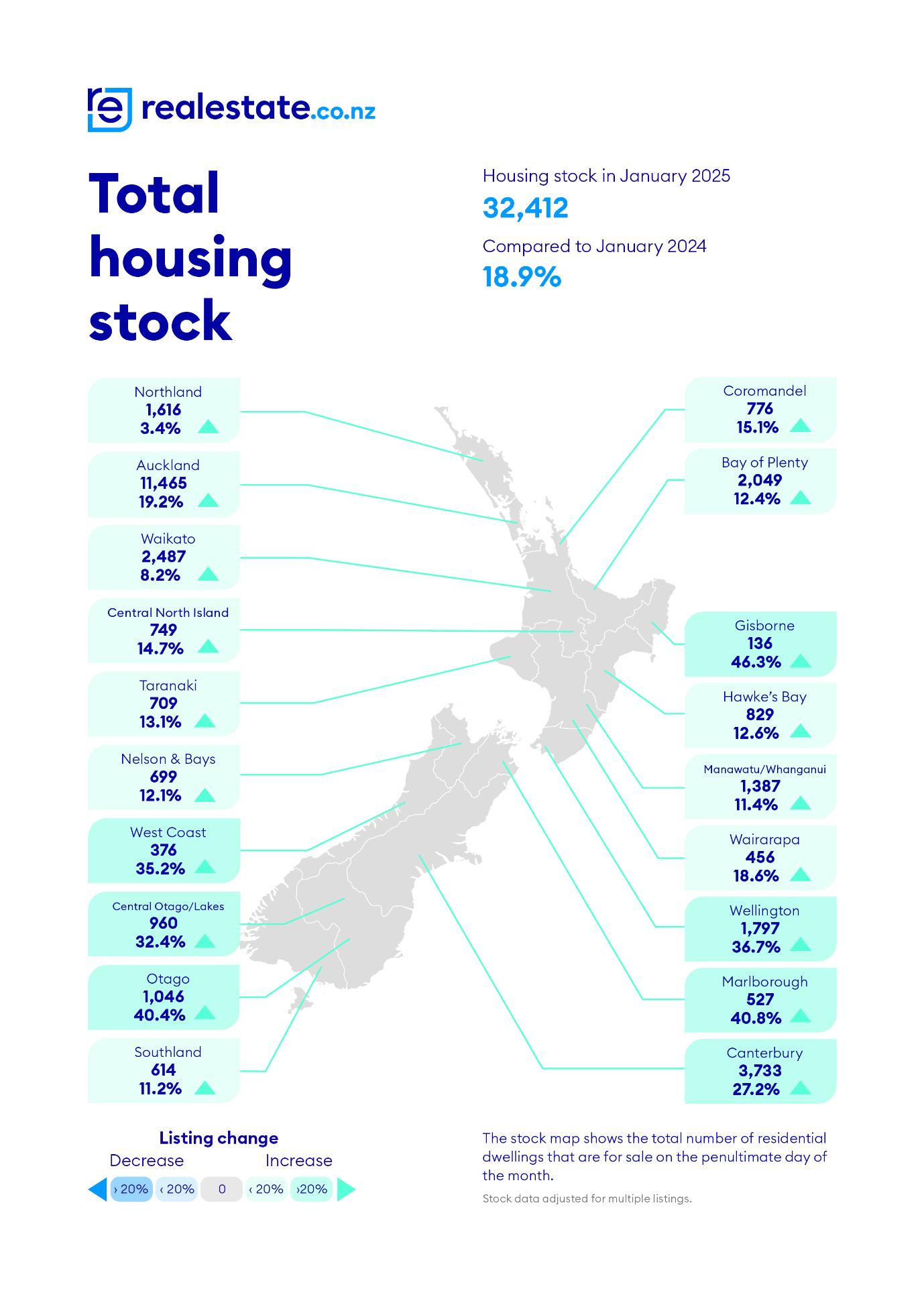

• Auckland stock levels reach 13-year January high

Key Figures

• New listings up 21.2% year-on-year, 8,904 new listings nationally

• National average asking price hits $868,969, down 1.3% year-on-year and up 2.9% compared to December 2024.

• Total stock reached 32,412, an 18.4% increase on last January.

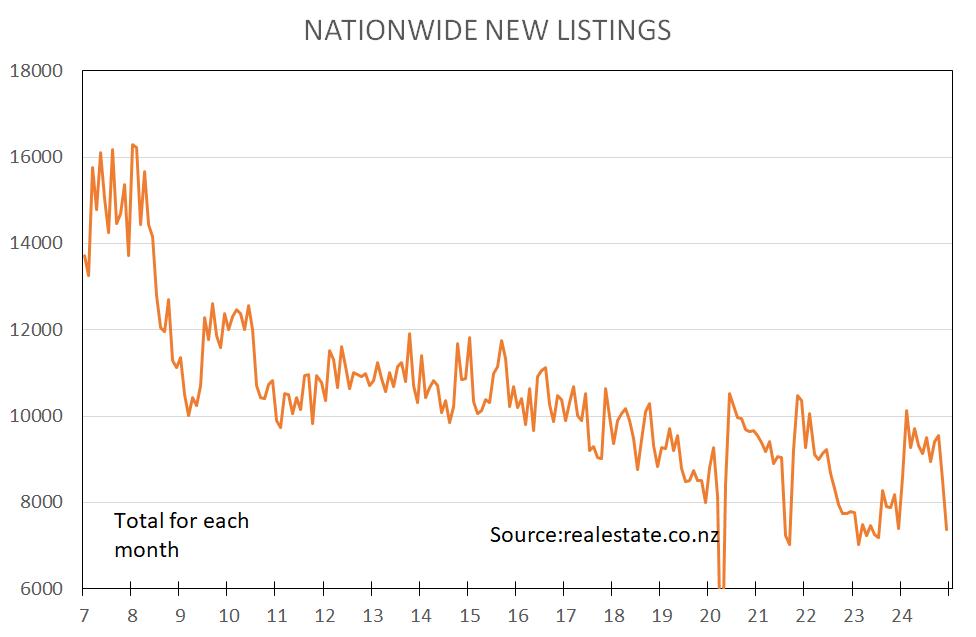

Our latest data shows that after a record low of new listings for any December, sellers jumped into the market in January, with new listings reaching levels not seen during January since 2015. Stock levels were also high last month—closer to levels last seen in January 2015—while average asking prices remained relatively stable year-onyear.

Sarah Wood, CEO of realestate.co.nz, said the market continues to offer strong opportunities for those wanting to buy and sell:

“Lots of choice, combined with relative price stability, offers certainty for both buyers and sellers. And as interest rates decline, the market may become more appealing for those on the sidelines.”

“When things will change is anyone’s guess. And right now, we still have high stock levels to cycle through, so it is unlikely that we will see a frantic rebound. But the market is cyclical, and eventually, we will see a shift ”

New listings return to levels not seen during January since 2015

Nearly 9,000 new listings came onto the market during January, a significant increase from December's record-low new listing figures. Up 21.2% year-on-year, the data suggests sellers dove headfirst into 2025.

Wood said that although it is typical to see more properties come to market in January, this year's numbers are particularly noteworthy:

“The country seems to take a collective holiday during January, and over the past few years, sellers have appeared to do the same. This is the first time new listings have been around 9,000 in the month of January since 2015.”

Year-on-year, the largest increases in new listings were in West Coast (up 100.0% to 70 listings), Otago (up 52.4% to 352 new listings), and Gisborne (up 45.7% to 51 new listings).

Auckland hits 13-year stock high

Stock levels remained high during January, up 18.9% nationally year-on-year to 32,412 properties. All 19 regions saw stock levels increase compared to January 2024. Most notably, 11,465 properties were available for sale in Auckland last month—the highest January level since 2012.

"We haven't seen this level of housing stock in Auckland for more than a decade," said Wood. "There could be a window of opportunity for those looking for property in the region."

Average asking prices hold steady as 2025 begins

The national average asking price has hovered between $840,000 and $890,000 for two years, offering the stability buyers crave and the predictability sellers need. The start of 2025 saw this trend continue, with January’s national average asking price at $868,969, down a modest 1.3% year-on-year. The biggest increase was in West Coast, up 6.3% year-on-year to $505,151, while Coromandel saw the biggest decline, down 20.3% year-on-year to $1,004,312.

Four regions – Auckland, Hawke's Bay, Nelson & Bays, and Southland – saw prices grow both month-on-month and year-on-year, while Coromandel, Waikato, Wairarapa, and Wellington recorded declines over the same periods.

“With interest rates easing and plenty of properties to choose from, the strong start to 2025 creates prime opportunity for those ready to make their move,” concluded Wood.

Written by Hannah Franklin

Finance& Lending

What the OCR cut means for the housing market and home loan costs The housing market is improving but Kiwis still feel wary about the state of the economy.

Tony Alexander 19 Feb 2025

First-home buyers have been strong in the market compared to other buyer groups. Will the cut to the OCR encourage more action? Photo / Fiona Goodall

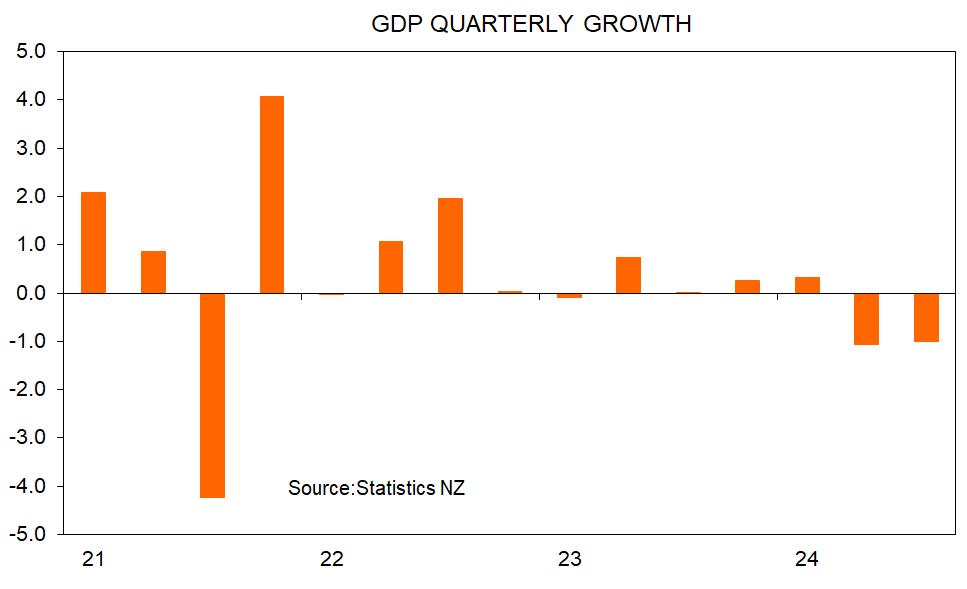

ANALYSIS: The state of New Zealand’s housing market is mildly improving – and the Reserve Bank’s decision today to drop the Official Cash Rate 50 basis points to 3.75% could bring further solace to the sector.

The market turnaround is best seen in the annual number of residential property sales in New Zealand, rising from a low of 59,000 in mid-2023 to close to 71,000 now. Prices have yet to show much improvement overall, with an average gain of about 2.5% since the middle of 2023.

The data tell us that first-home buyers are active in the market, but owner-occupiers are still hesitant. Concerns about employment are likely to be an element in play along with general low confidence in the outlook for the economy.

My monthly Spending Plans Survey, for example, shows a net 10% of people plan to cut their spending in the next three to six months compared with a few months ago when a net 10% of people were planning to spend more.

A more realistic assessment of the economy’s likely performance has occurred, though business surveys still show businesspeople are highly optimistic about what lies ahead. Their reality check may just be starting.

While the absence of owner-occupiers from the market is probably temporary, there is a chance that the so-far low presence of investors could be a characteristic of this cycle. My most recent survey of real estate agents undertaken with support from NZHL showed that a net 48% of agents were seeing more first-home buyers in the market. But only a net 12% were seeing more investors.

The interesting thing is that while the reading for first-home buyers is down only slightly from December, the reading for investors is a sharp fall from net 36% positivity before Christmas.

Why are investors hesitant to buy? One reason is that few will feel the need to beat price rises. Prices are only just edging upward at a very slow pace. Investors will feel that time is on their side, but they will also feel that holding an investment property while waiting for the tax-free capital gain will cost a lot more than it had done in the past.

Councils (which have the power of monopolies) have sharply increased their prices (rates), insurance premiums have soared, and look set for a further boost following the California fires, and maintenance costs are escalating. These cost rises are occurring at the same time that rents in many locations are falling, and landlords are finding it very difficult to secure a good tenant.

Independent economist Tony Alexander: "The data tell us that first-home buyers are active in the market, but owner- occupiers are still hesitant." Photo / Fiona Goodall

Feedback from real estate agents indicates that one or two investors are starting to bump up against the new debt-to-income rules, which limit total investor debt to seven times the property valuation. The numbers are so far quite small given the lack of house price gains. But there will be restraint on the ability of investors to buy to an increasing degree as this upward leg of the housing cycle progresses through 2025.

One important consideration is of course the cost of borrowing money to finance one’s investment. The Reserve Bank has cut the OCR from 4.25% to 3.75% and brought forward by one year to the end of 2025 its prediction of reaching the end- point for cuts this cycle.

The recent revisions to economic growth data in New Zealand have encouraged the Reserve Bank to accept that there is more spare capacity and therefore less inflationary pressure in the economy than it had previously thought.

Will the earlier achievement of the cyclical low for interest rates spur much extra investment? At the margin, some investors will look to purchase earlier than they had been planning. But the numbers may not be large, and it still seems reasonable to expect only mild growth in average property prices this year and next.

- Tony Alexander is an independent economics commentator. Additional commentary from him can be found at www.tonyalexander.nz

Input to your Strategy for Adapting to Challenges

Feel free to pass on to friends and clients wanting independent economic commentary

ISSN: 2703-2825

Sign up for free at www.tonyalexander.nz

Beware interest rates optimism

Welcome to 2025 everyone and another year of trying to interpret what is happening in our economy and attempting to pick where some key things may be headed. Late last year we saw three important pieces of information appear on the same day. One favours a lower interest rates outlook (sortof),theother twohigher.Thatleaves me still warning borrowers not to get optimistic about big rate falls this year, and still expecting a 0.5% cut at 2025’s first cash rate review on February 19. 0.25% is also quite possible but 0.75% highly unlikely.

On December 19 the September quarter Gross Domestic Product data for NZ were released. Our economy shrank 1% whereas the Reserve Bank had been expecting a 0.2% decline and private sectorexpectationswerefora0.4%fall.TheJune quarter fall previously reported as 0.2% was revised to 1.1%.

These are very weak numbers and excluding the pandemic onset period represent the weakest six months period for our economy since 1991. On the face of it you would think extra easing of monetary policy is justified.

16 January 2025

However, each year at this time Statistics NZ revise their data and the revisions this year actually show our economy currently to be 0.6% larger than the Reserve Bank had estimated. How can that be when the last two quarters were so weak? Earlier periods got revised upward and in fact the data now show we were never in recession in 2021, 2022, or 2023.

This actually slots in well with the point I’d been noting through 2024 that it takes 18-24 months for a tightening of monetary policy to have its biggest impact and that the tightening only really started in November 2022 with the 0.75% cash rate rise and warning of recession.

A second caveat is that more up to date data show the economy to be improving so there is no need for extra policy easing to turn things around.

Third, if data can be revised heavily up they can also be revised heavily down further along the track – probably in December this year. Given the poor quality of economic data in New Zealand it is no wonder our central bank and Treasury struggle to get both their forecasts and their policy actions optimally placed.

All up, the data were weaker than expected for sure. But the numbers are out of date, subject to big revisions, and superseded by more recent data showing improvement is underway.

The second thing of note which happened on December 19 our time and 18 US time is that the Federal Reserve cut the US cash rate target by 0.25%.

That was expected. What was not expected was that they changed their prediction for 2025 from four cuts to only two and indicated the economy was in better shape that previously allowed for.

The importance for us here is that scope for falls in fixed borrowing costs in New Zealand for periods of three years and longer looks now to be very limited.

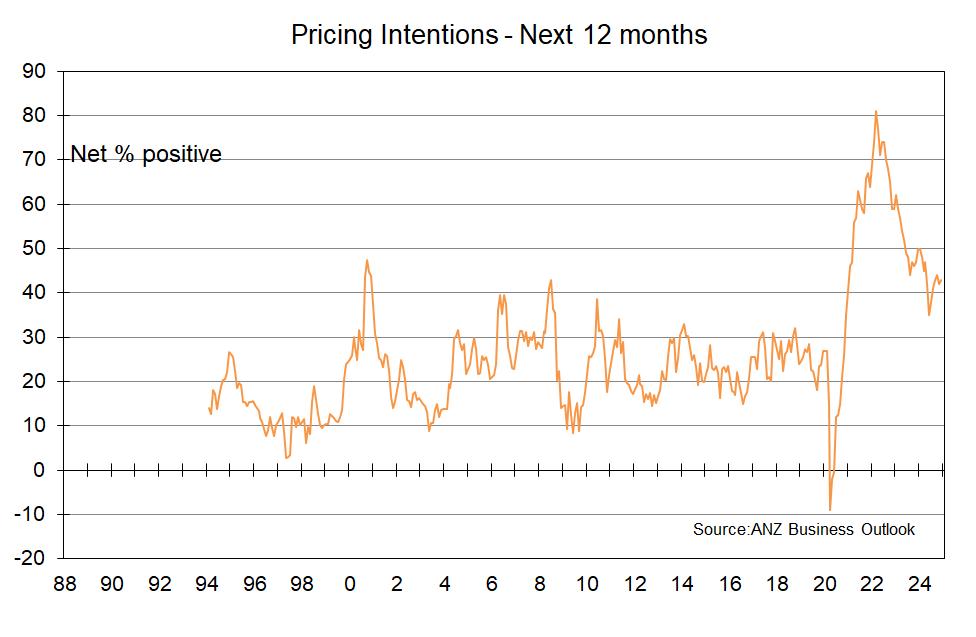

The third thing to happen on December 19 was ANZ releasing their Business Outlook Survey. Throughout 2024 I wrote a lot about this survey and the way it showed business pricing plans not to be falling to levels consistent with near 2% inflation in New Zealand.

In particular I have focussed on the measure showing the net proportion of businesses planning to raise their selling prices a year down the track. This peaked at 81% early in 2022, started 2024 at 50%, fell to 35% in June then rose from there.

In December the reading was 43% from 42% in November.

Businessesarestronglysayingthatwhenthetime is right they will raise their prices.

Of note also from the survey was a rise in year ahead average inflation expectations to 2.63% from 2.53% in November. Also, the netproportion of businesses saying that they expect their costs to go up in the next three months rose to a strong 70% in December from 63% in November.

These measures are moving in the wrong direction.

Looking ahead to 2025, the year is likely to see some mediocre growth in the economy on the

back of lower interest rates, higher dairy sector incomes, higher infrastructure spending, improving standalone house construction (but falling multi-unit building), positive net migration flows, some recovery in household spending and business investment, some recent weakness in the NZ dollar, (haven’t written that for a long time) and ending before the year’s end of the lagged response of employment levels to shrinkage in economic output recorded last year.

The key word to note in the above sentence/paragraph is “mediocre”. New Zealand isnolongeronastronggrowth path,and wehave proven that just because one deregulates one’s economy as happened from 1984-92 does not mean sustained strong outcomes ensue. We are increasinglyreliantonmigrantstoboosteconomic outputbutwithoutevidenceofapercapitaincome growth improvement.

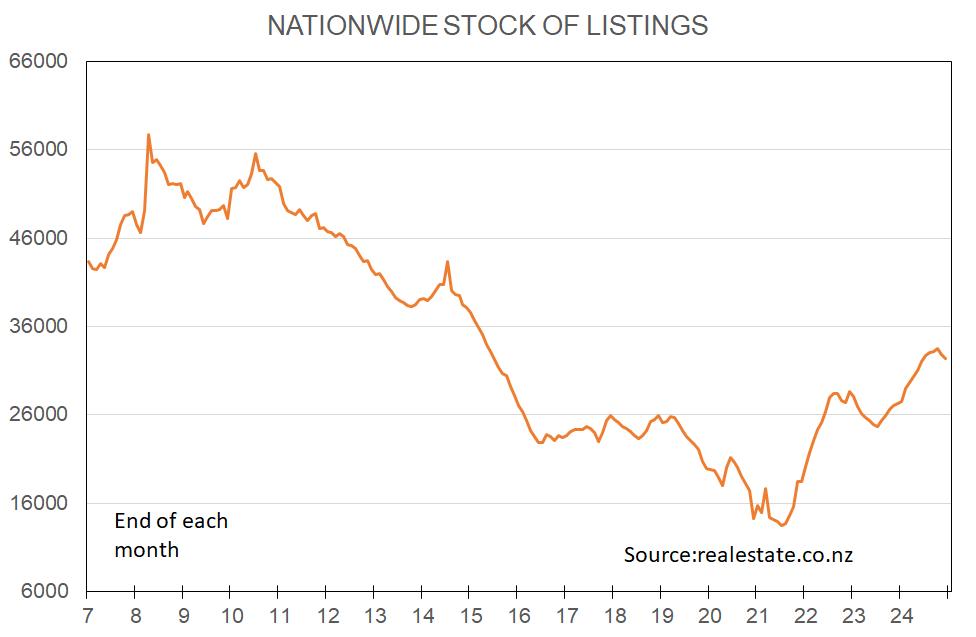

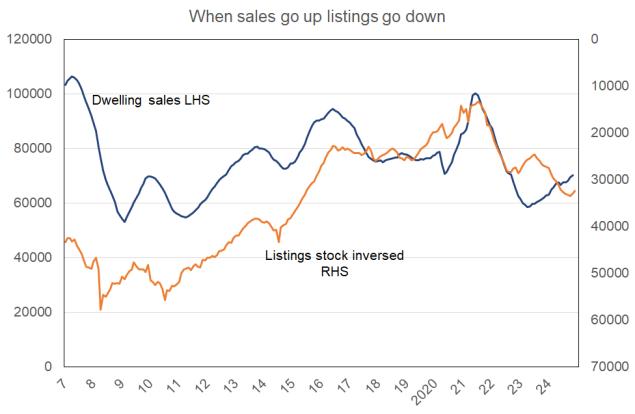

Property listings easing slightly

Data from realestate.co.nz tell us that during the month of December the number of properties freshly listed for sale fell in seasonally adjusted terms by 13% after falling 11% in November. These are quite firm declines over a two month period and what I will be looking for from here is evidence in my monthly surveys that the strong rise in vendor numbers following growth in buyer numbers may be petering out.

With regard to the actual stock of listings at the end of December the total of 32,300 was down slightly from 32,900 at the end of November (data seasonally adjusted) and the peak of 33,500 at the end of October.

Is this the start of a downward trend? In the past when sales have improved listing stocks have tended to fall and maybe that process is now commencing.

Business sentiment improves

We already know from the ANZ Business Outlook Survey undertaken each month plus my own Business Survey with Mint Design that sentiment in the business sector has been improving in recent times since the interest rate direction shifted.

So there is not really any surprise in the NZIER’s Quarterly Survey of Business Opinion showing that a net 9% of businesses expect the economy to improve compared with a net 4% in the September quarter expecting a deterioration. In the June quarter a net 40% expected things to get worse in the next six months.

This improvement in sentiment has been accompanied by small improvements in hiring and investing intentions though the latter two remain slightly negative.

The QSBO is most useful for the insight we can gain into inflationary pressures down the trackor at least in the next three months. Back in the September quarter survey a net 41% of the non-farm businesses surveyed said they expect their costs to rise. That has now eased to 35% which is still above the 29% three decade average.

The net proportion of firms planning to raise their prices has lifted to 15% from 7% where the average is 21%. These developments are okay but not supportive of any acceleration in the pace of monetary policy easing.

In fact, the capacity utilisation rate has climbed to 91.3% (roughly speaking) from 89.1% in the September quarter. But with 67% of businesses saying lack of customers is the main restraint on their output compared with 64% last quarter and an average of 59%, some justification for further slight easing of monetary policy remains.

If I were a borrower, what would I do?

Not be optimistic that interest rates will fall much this year.

People are highly confident that the economy will be stronger this year than last year and 2026 will be even better. As a rule inflationary pressures are stronger the faster the rate of growth in one’s economy unless that growth is driven by a surge in productivity – which hasn’t happened in New Zealand for a long time and doesn’t look likely in the near future.

This means that the natural tendency of inflation will be to start cyclically rising at some point in the next two years and as I noted from probably late in the September quarter last year that is where my focus now is – not the short-term inflation outlook.

This matters because monetary policy aims at influencing inflation 18-24 months down the track and by then from now the unemployment rate looks like it will comfortably be falling again, and businesses will before the end of this year likely have regained pricing power.

This is an especially important consideration because pricing plans have held at well above average levels over the past year even as the economy shrank by 1.1% in the September quarter and 1.0% in the December quarter.

Over the past few months confidence about the speed and extent of monetary policy easings in the United States and Australia has declined. Most notably just this past week the expectations for the US have changed in light of a far stronger pace of jobs growth in December than had been expected. Employment rose 256,000 versus an expected 155,000 and average rise of just above 180,000 a month throughout 2024.

The US economy is in reasonable health and the labour market remains relatively strong with the unemployment rate at just 4.1%. Throw in the risk of higher consumer prices because of likely tariff increases by the incoming President and markets now generally only see scope for two more cuts in the Fed. Funds rate this year. One or two forecasters are picking no further cuts at all.

The changes in policy expectations in the two economies of greatest relevance to ourselves have helped cause increases in NZ medium to long-term bank borrowing costs. Another factor bringing caution here is the declining NZ dollar.

Measured by the Trade Weighted Index average gauge of our currency’s level the NZD currently sits about 5% down from where it was six months ago and 6% down from a year ago. It is 3% below the level assumed by the Reserve Bank in November which implies slightly more imported inflation than they would have expected – but not all that much.

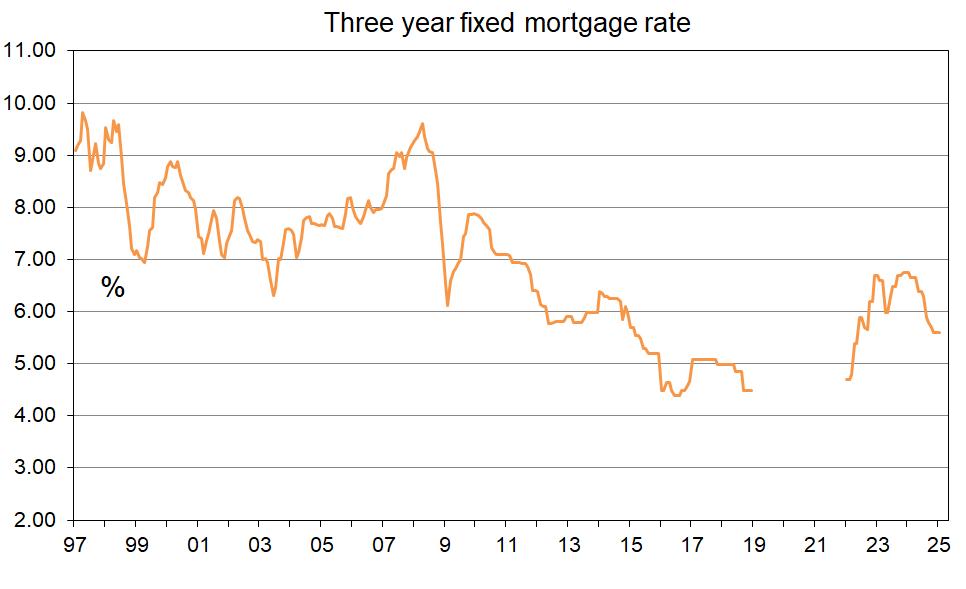

So, given my caution how long will I keep saying I’d just fix six months and when would I likely flick to fixing at least some (half+) of my debt at a fixed rate for at least five years? That is impossible to say but my gut tells me I’ll make the switch before the middle of this year.

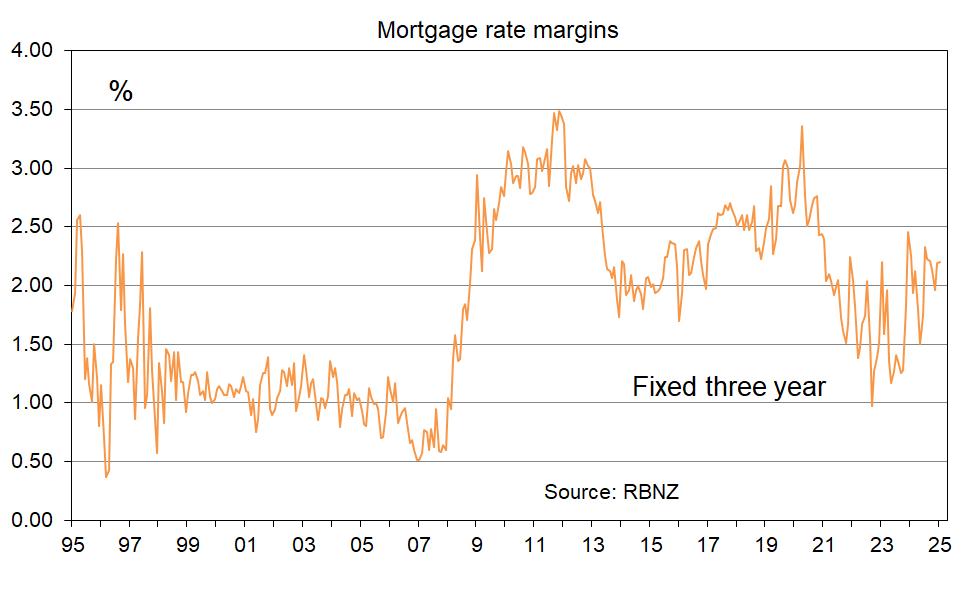

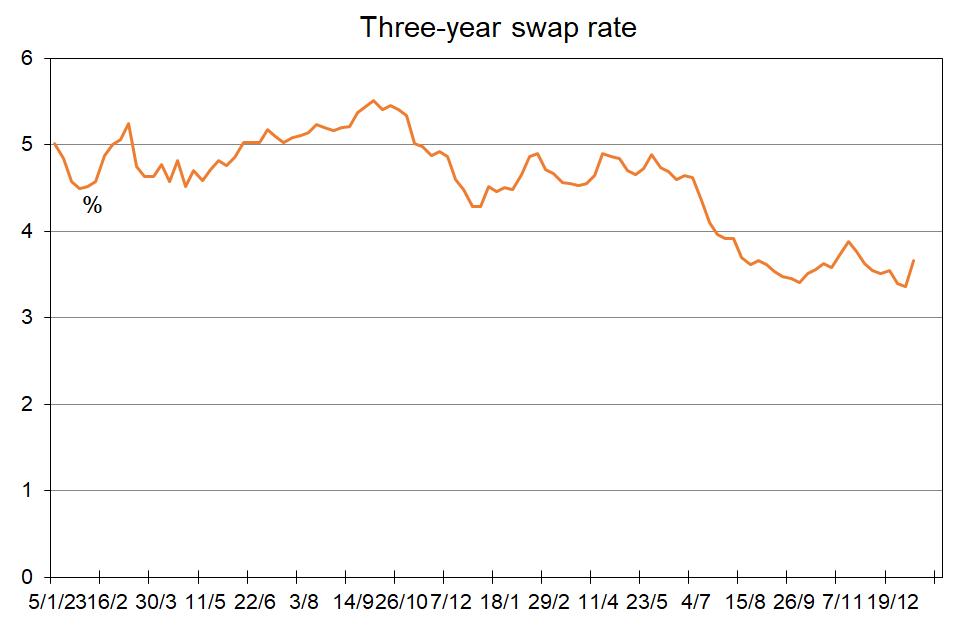

At the moment I could fix for three years at around 5.6%. I feel that with the margin for this rate looking a bit high I’d like to wait for a rise in bank competition to drive a round of cuts before fixing at about three years, or maybe two though that rate currently is only 0.1% less thanfixing for three years.

The main thing which borrowers contemplating a decision like this need to take on board is this. Scope for mortgage rates for terms of two years and beyond to fall much from current levels is quite limited.

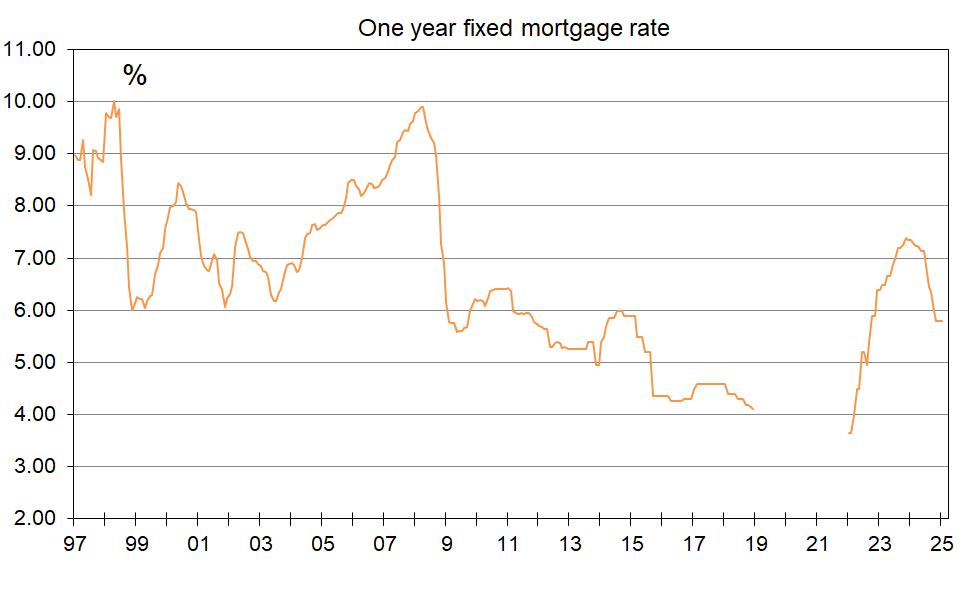

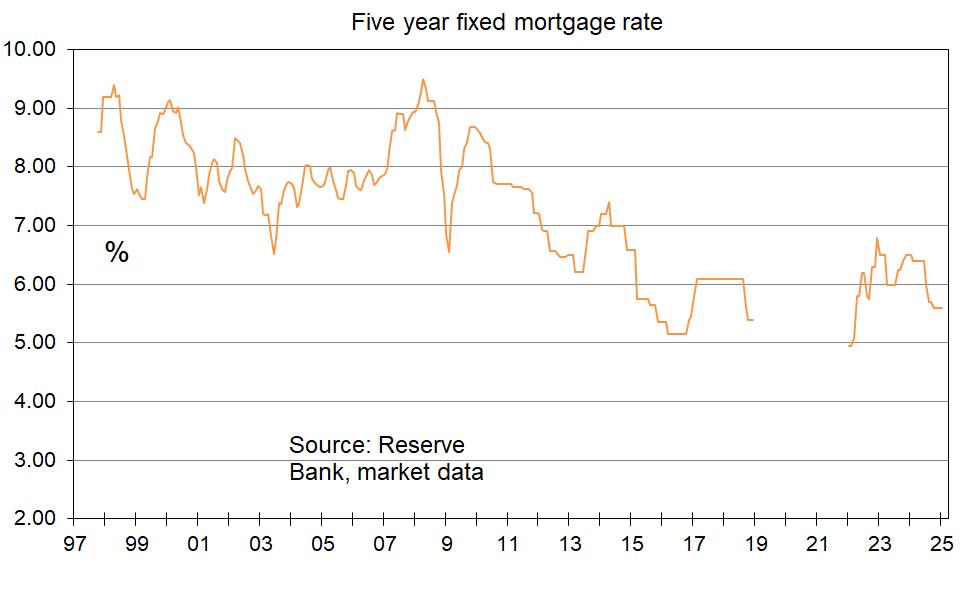

The cost to NZ banks of borrowing money at a fixed rate for one year in the wholesale markets currentlysitsnear 3.55%from3.57%threeweeks ago. The three year cost is near 3.66% from 3.55% and the five year rate near 3.84% from 3.66%.

These three graphs show levels of the one,three, and five year fixed mortgage rates over the past few years excluding the 2019-21 period when rates were absurdly low because of worriesabout deflation and then the effects of the pandemic.

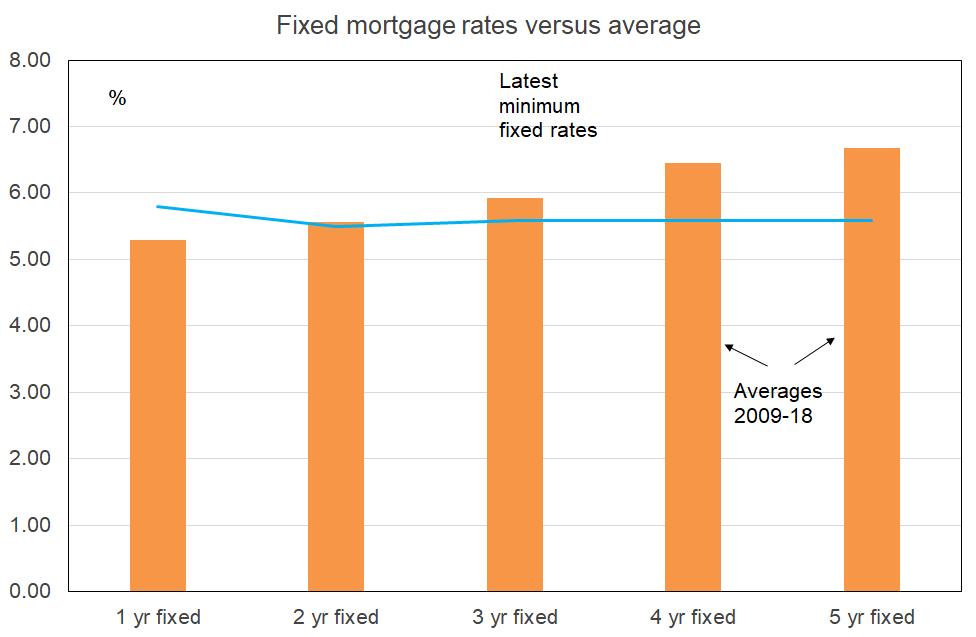

This graphshowshowcurrentratescompare with averages from 2009-19.

To see the interest rates currently charged by major lenders go to www.mortgages.co.nz

Nothing I write here or anywhere else in this publication is intended to be personal advice. You should discuss your financing options with a professional.

These three points, along with professionalism and knowledge in the real estate field, Johnny feels are very important keys to maintaining a happy and trouble-free median between vendors and purchasers.

Many years ago, Johnny was made redundant from his last employment due to a drop-off in the industry so he decided to put his house on the market and relocate his family. After experiencing some of the small things that annoyed him during the marketing of his home, as well as a lack of communication from the agents who were in control of his biggest asset, he decided that if he could work on the things that frustrate vendors when marketing their homes, then he believed he could have a successful career in real estate. So, Johnny decided to take his home off the market, completed his Real Estate papers, sold his own home and relocated to Wattle Downs, where he and his wife still reside today.

Johnny achieved national millionaire sales club status in his first year, which in itself proved he has great product knowledge but also the ability to achieve results. Johnny has now been in real estate for 30 years and has personally been involved in buying, selling, and building property and believes there is nothing like first-hand knowledge of the rewards property can bring.

What he enjoys best about South Auckland is the wide variety of properties from small investments to family homes and larger lifestyle properties. He also loves the many diversities in cultures, nationalities, and the customs that make South Auckland a great place to live.

Johnny and his wife of 40 years have two sons and five grandchildren raised in Wattle Downs, so if you're looking for a salesperson with experience, proven results, and great knowledge of the Wattle Downs and South Auckland market, then give Johnny a call — obligation-free!

Interest rates are coming down and buyer inquiry is way up. It's a great time to move!

Whenyouknow,youknow.

JohnnyBright

AUCTIONEER

Johnny is proud to be a part of the team at Apollo Auctions NZ. Entering real estate in 2014, he has developed and honed his craft of auctioneering and negotiating skills to a level that now sees him as an industry leader. Johnny has worked and collaborated with some of the most notable agents, business owners and auctioneers across New Zealand.

With the fusion of his knowledge and skill together with his personable approach, Johnny creates the ultimate auction experience . He implements drive and dedication to each and every property that he calls - regardless of value, location or personal circumstances. Johnny’s performance style and welcoming nature allows him to capture the audience and motivate buyers. He will guide you through the process and create a solid platform to achieve the best possible outcome for your auction.

Johnny also has a passion for acting. With a Bachelor of Performing and Screen Arts, he has appeared in several TV commercials and films, his most widely recognized being ‘Falling Inn Love’, an American Netflix production which was filmed in New Zealand. He has also worked with the Auckland Theatre Company on a number of occasions.

He currently resides in Beachlands with his wife and two young children.

It’s rare in life that we get something for nothing with no strings attached, especially if it genuinely adds value. Nevertheless, that’s precisely I will give you. Expert home loan advice which has reliably proven to offer significant long-term financial advantage. I keep strict tabs on the country’s largest network of banks plus numerous smaller and second-tier lenders, so you don’t have to. What’s more, this comes at no cost to you because your chosen bank pays for the privilege. You have nothing to lose, yet have a higher chance of securing better terms. Rest assured - if there’s a superior deal out there for you, I’ll find it.

In the typically stoical world of finance, I offer a point of difference. Not only will you receive excellent independent and impartial advice, but you’ll have fun doing it. Even after 15 years in the mortgage arena, my enthusiasm for objectives and commitment to clients shines through at every turn. Endorsement comes from countless glowing testimonials and in my own words: “I’m at my happiest helping people navigate through difficult situations, giving hope and concrete opportunity where they previously had none.”

Prior experience as sales manager in the fields of telecommunications and pharmaceuticals, then later, a small business owner and private property investor, provided me with considerable business acumen across many industries. My customer-focused approach and personable demeanor also reflect a lifetime of experience in client relations. I credit travel to distant locations for creating an enduring interest in different cultures and honing my ability to relate well to the needs of the broader population. In particular, I soundly empathise with people relocating from other countries to make New Zealand their home.

To continue giving my professional best, I maintain balance by travelling and participating in seasonal sports such as paddle boarding and skiing. I enjoy indulging in my creative side; with landscaping, painting watercolours or improving my guitar playing prowess. Additionally, I actively support my community through Christians Against Poverty (CAPNZ), but above all, my wife and our five shared children always take centre stage.

There's little that I haven't seen in my time in the industry, priding myself on an ability to deal with the trickiest of scenarios, never turning anyone away. My philosophy of treating people how I'd like to be treated results in a 360-degree perspective which sets myself apart.

Get in touch if you need any expert guidance. Regards