• REINZ Press Release – Activity Heats Up While Prices Remain Cool (Jen Baird, CEO) o Market Snap Shot o Annual Median Price Changes

• REINZ Property Report 17 December 24 (November Data) withlink

• REINZ House Price Index Report (HPI) 17 December 24 (November Data) withlink

Hi

Property Market Confidence Grows with Further OCR Cut

17December2024

The Reserve Bank’s latest Official Cash Rate (OCR) by a further 50 basis points to 4.25% sends a strong signal to the property market. With this being the last OCR announcement until mid-February 2025, we expect many borrowers on floating rates to take this opportunity to secure fixed-term rates, especially as some banks have already moved early to adjust their offerings.

For new borrowers, the competitive environment among lenders is likely to intensify, creating more favourable conditions for those entering the market. Any relief to borrowers is welcomed and reinforces the broader sentiment that 2024 has been a year of transition.

Looking ahead to 2025, we anticipate greater stability and renewed optimism in the real estate market. Regional areas have shown early signs of recovery and now we’re seeing similar momentum in major centres like Auckland, Wellington, and Christchurch as buyer activity picks up.

First home buyers have been particularly active, with recent CoreLogic data showing they now account for 27 percent of the market. This highlights growing confidence that the market has turned a corner. As affordability improves, we expect this trend to strengthen further.

For those sitting on the fence OCR’s latest decision should provide confidence to re-engage in property— whether it’s relocating, up-sizing or investing.

On a larger scale, we’ve also noticed an increase in interest from high-net-worth expats returning to New Zealand. Many are drawn back by a combination of factors, including high property taxes overseas and potential global shifts, such as recent election outcomes.

This optimism is mirrored in ASB’s latest Housing Confidence Survey, which revealed a marked increase in people believing it’s a good time to buy and expecting house prices to rise in 2025. The survey also showed 57 percent of respondents anticipate further interest rate declines, the highest rate of such expectations since the survey began in 1996.

From a historical perspective, the OCR remains low compared to past peaks. During the 2008 Global Financial Crisis, the OCR reached 8.25 percent and stayed there for 13 months before declining rapidly to 2.5 percent within 10 months. Property market recoveries also tend to take longer than downturns. CoreLogic data shows that after the GFC, property values dropped by 10 percent in a year but required three years to recover, during which sustainable growth was observed.

At present, CoreLogic data highlights that property values are approximately 18 percent below the postCOVID peak of November 2021 but remain 16 percent higher than pre-COVID levels from March 2020. While the market has faced challenges, there are clear signs we’ve reached the bottom, and some areas are already in recovery.

As always we hope you enjoy this publication.

Kind regards

Brent

Brent Worthington Principal and Licensee Agent

0292 965 362

LJ Hooker Town & Country Rent Exchange Property Management

1/233 Great South road, Drury

All You Need to Know to Prepare for a Summer Sale

Summer is the season when everything shines its brightest – the sun is out, the temperatures are up, and your garden is in full bloom. These natural advantages make summer an ideal time to sell your home. Properties often look their best in the warmer months, and buyers are more inclined to visit open homes when the weather is on their side.

While it may be tempting to slip on your jandals and head to the beach, if you’re planning to list your property this summer, take a moment to ensure it’s perfectly presented for potential buyers.

Here’s how to make the most of the season

Style for the season

Summer is all about life, light, and warmth – and your home’s interior should reflect these vibes to make a lasting impression on buyers. Start by swapping out heavy curtains, rugs, or dark-coloured cushions for lighter fabrics and brighter hues. Think breezy linen curtains, coastal tones like soft blues or whites, and cushions with summery patterns. These small changes can create a fresh, airy feel that aligns with the warmth and vibrancy of the season.

Don’t underestimate the power of scent to evoke positive emotions. Introduce fresh flowers like lilies, peonies, or gardenias, or use fragrant diffusers with summery scents like citrus or lavender. These aromas can fill your home with a sense of life and vitality, helping buyers form an emotional connection with the space.

Make sure your interiors are uncluttered and full of natural light. Clean your windows, pull back curtains, and remove any furniture that blocks sunlight to create a bright and inviting atmosphere.

Create irresistible outdoor living spaces

Outdoor spaces become an extension of your living area in summer, and buyers will be looking for areas where they can soak up the sun or entertain friends and family. Set the scene by arranging outdoor furniture that invites buyers to imagine themselves relaxing or hosting gatherings. A simple setup of a dining table with chairs, some cosy outdoor cushions, or a lounge set can transform a plain patio into an attractive entertaining area.

Introduce colour and life to your garden with vibrant plants, potted flowers, or hanging baskets. Plants like lavender, marigold, or bougainvillea add a pop of colour and can provide a delightful aroma. Consider creating zones for different activities, such as a BBQ area or a shaded spot with comfortable seating.

Make sure the outdoor areas are well-maintained. Keep lawns neatly mowed, pull out weeds, and tidy up garden beds to create a polished look. Don’t overlook the exterior of your home either – give the walls a wash to remove dust and grime, and consider a fresh coat of paint for areas that look weathered. Crystal-clear windows will also allow buyers to admire the natural light inside while showing off the surrounding views.

Tackle those repairs

A stunning exterior or light-filled interior will only go so far if buyers notice lingering maintenance issues. Whether it’s a squeaky door, peeling wallpaper, or a dripping tap, small problems can suggest to buyers that the home hasn’t been properly cared for. Summer is the perfect time to address these issues and present your home as move-in ready.

Start with the basics – repair any cracked tiles, touch up peeling paint, and fix leaky pipes or taps. If there are areas that have been bothering you for months, it’s likely buyers will notice them too. These small updates can prevent buyers from negotiating down the price over minor concerns. Don’t forget the home’s exterior –check fences for damage, clean out gutters, and make sure pathways are in good condition.

Buyers may also look for larger red flags, like signs of moisture damage or outdated electrical work. Consider hiring a professional to inspect areas you may not have noticed, ensuring you’re presenting the best version of your home.

Keep it cool

One of the best ways to win over buyers during the summer heat is by showing them that your home can be a comfortable retreat. If you have air conditioning, ensure it’s running during open homes to create a cool, refreshing environment. Set the temperature to a comfortable level that shows the system is effective without being overly cold.

If your home doesn’t have air conditioning, don’t worry – you can still create a pleasant atmosphere. Open windows to let in a natural breeze and use fans strategically to circulate air. Highlight any features that help keep the house cool, such as ceiling fans, tinted windows, or shaded outdoor areas. If possible, schedule open homes during cooler parts of the day to keep the environment comfortable for visitors.

By providing a cool escape from the summer heat, you’ll leave buyers feeling positive and at ease as they view your property, helping them focus on its best features.

Why summer is the perfect time to sell

Selling your home in summer isn’t just about good weather – it’s about showcasing your property at its absolute best. From sun-drenched interiors to vibrant gardens and relaxing outdoor spaces, summer allows your home to shine in ways that aren’t possible during other seasons.

With a little effort to style and maintain your property for the season, you’ll maximise your chances of attracting serious buyers and achieving a successful sale. So, while the beach will still be there tomorrow, today is your chance to create a home that buyers will fall in love with.

Tapping into the mindset of renters is an important way for savvy investors to maximise returns. Affordability, location and length of lease will always be important, but other features can make a property more popular. Having a chat with your property manager is a good place to start, as they will be able to provide insight as to what is in demand in your suburb. Investing in some simple changes, such as built-in wardrobes or new kitchen appliances, could attract a longer-term tenant who will look after the property like it was their own.

Pet friendly

About64%ofNewZealandhouseholds own a pet, so it makes sense for landlords to be accepting of a tenant’s furry family members. Researchdataalso found oneof the most frequentlysearched keyword for rental properties is ‘pet friendly’.Only minor modifications may be needed, such aslaying hard-wearing floors or fencing the yard.

Air-conditioning and heating

While there is no obligation for landlordsto install air conditioning, there is a growingmarket expectation.

Bathrooms and ensuites

A master bedroom with an ensuite is also high on a tenant’s wish list, particularly for couples or housemates sharing a property. Not having a freestanding bathtub will also reduce the pool of potential renters, particularly families with young children.

Outdoor entertaining

As tenants are usually responsible for keeping the garden tidy, there is a preference for easy-to-care yards. Pools can be apopular inclusion in familyfriendlyareas, and while tenants are responsible for theupkeep, many are happy to make this trade-off.

Home office

A built-in desk, a spare room, or a nook suitable for working from home can make a property stand out in the market.

Updated kitchens

If your budget doesn’t stretch for a full makeover, consider simple updates such as new appliances, countertops or splashback tiles. Properties without a dishwasher may take longer to find a tenant.

Parking

Renters want a designated car space or a secure lockup garage with remote access. Extra storage space for bikes, tools, or seasonal items are highly desirable.

Get a free property management appraisal and learn how our expert strategies can simplify your portfolio management for greater efficiency and profit.

HealthyHabitsforInvestorsin2025

Setting up sustainable habits can set you on a path to becoming a smarter and more successful property investor. Being better organised, increasing your market knowledge and staying on top of new legislation are just some of the steps you can take to improve your overall strategy. Importantly, you need to define your investment goals and surround yourself with the right team to help you get there.

1. Stay Informed

Property managers are invaluable for looking after your investment, but visiting it in person offers a first-hand perspective and better insight. If it has been a while since you last visited, then schedule a personal inspection. It is also a great way to see any changes or trends happening in the local area. Listen to the advice of your property manager and tackle small problems quickly before they turn into something more costly. The last thing you want is for a dripping tap to turn into water damage or a broken pipe.

2. Build a solid budget

Make sure your cash flow can handle unexpected expenses such as vacancy or maintenance. Setting aside a little extra every week could come in handy in an emergency. Ideally, you should have a three-month buffer in a separate bank account.

3. Research the Market

Regularly check rental listings in your area and compare them with your own investment. Your property manager will be able to provide insight on any improvements that could help attract and retain quality tenants. If it is time to update the kitchen or bathroom - set a budget and work towards it rather than over-stretching your finances. Keep in mind that any renovations should be aimed at a wide pool of tenants rather than reflecting your style.

4. Be tax ready

Don’t wait until the last minute to get everything ready for your tax time. Keep accurate records of all income and expenses related to your investment property, including rent received, maintenance costs, loan interest, property management fees and council rates. Familiarise yourself with expenses that you can claim, such as property management fees and depreciation.

5. Keep looking forward

Investing in property is a long-term investment – but it doesn’t mean that you can set and forget. Do you want higher rental yields, long-term growth, or to add another property to your portfolio? Communicate your goals with your property manager, local real estate agent and accountant.

Please don't hesitate tocontact ourteam who canably assist you withanyproperty management mattersyou may have or ifyou have any questionsabout anything in thenewsletter or propertymanagementin general.

Brent from LJ Hooker Drury is outstanding. His meticulous attention to detail and proactive follow-up are truly unmatched. I cannot recommend LJ Hooker highly enough. The team at LJ Hooker is exceptional.

We have two properties on Great South Road, and Brent serves as our property manager. Initially, I thought managing the rentals myself would save money, but I quickly realized how much easier and stress-free it is to have Brent and his team handle everything.

Not only has LJ Hooker removed the hassle from my plate, but they have also maximized the returns on our rental properties. Their expertise, thorough approach, and industry knowledge ensure no detail is overlooked.

If you're considering professional property management, I strongly encourage you to trust Brent and the LJ Hooker team with your investments. Anthony, Commercial Landlord.

Anthony, Commercial Landlord

Brent Worthington Principal and Licensee Agent 0292 965 362

LJ Hooker Town & Country Rent Exchange Property Management 1/233 Great South road, Drury

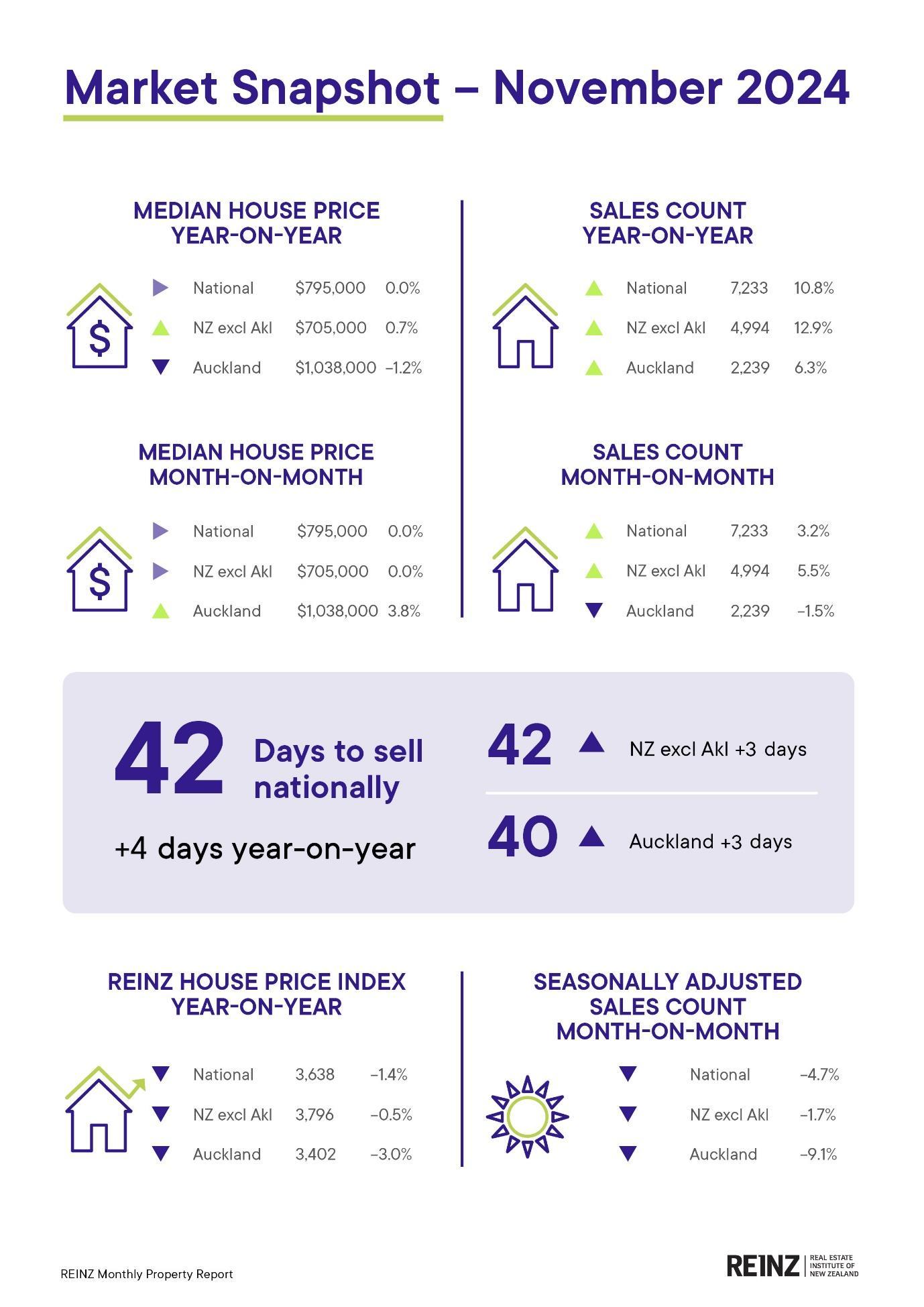

REINZ November Data: Activity Heats Up While Prices Remain Cool

Published 17 December 2024

As we approach summer, market activity is on the rise. In November, the New Zealand property market experienced a wave of confidence, as evidenced by the latest figures from the Real Estate Institute of New Zealand (REINZ).

Buyers are showing increased interest, spurred by the recent reduction in the Official Cash Rate (OCR), prompting more transactions nationwide. At the same time, fewer sellers are bringing their property to market, which is reflected in the nationwide decline in property listings.

REINZ Chief Executive Jen Baird says, “There’s been a shift in market sentiment nationwide in November. After a challenging year, recent data indicates promising signs of increased activity, which we hope will continue into 2025. This is a good time to make transactions, as prices remain stable, and interest rates decrease.”

Nationwide, sales rose by 10.8% compared to November 2023. In New Zealand, excluding Auckland, sales increased by 12.9% year-on-year, with notable gains in Gisborne (+55.6%), Hawke's Bay (+34.4%), and Wellington (+32.3%).

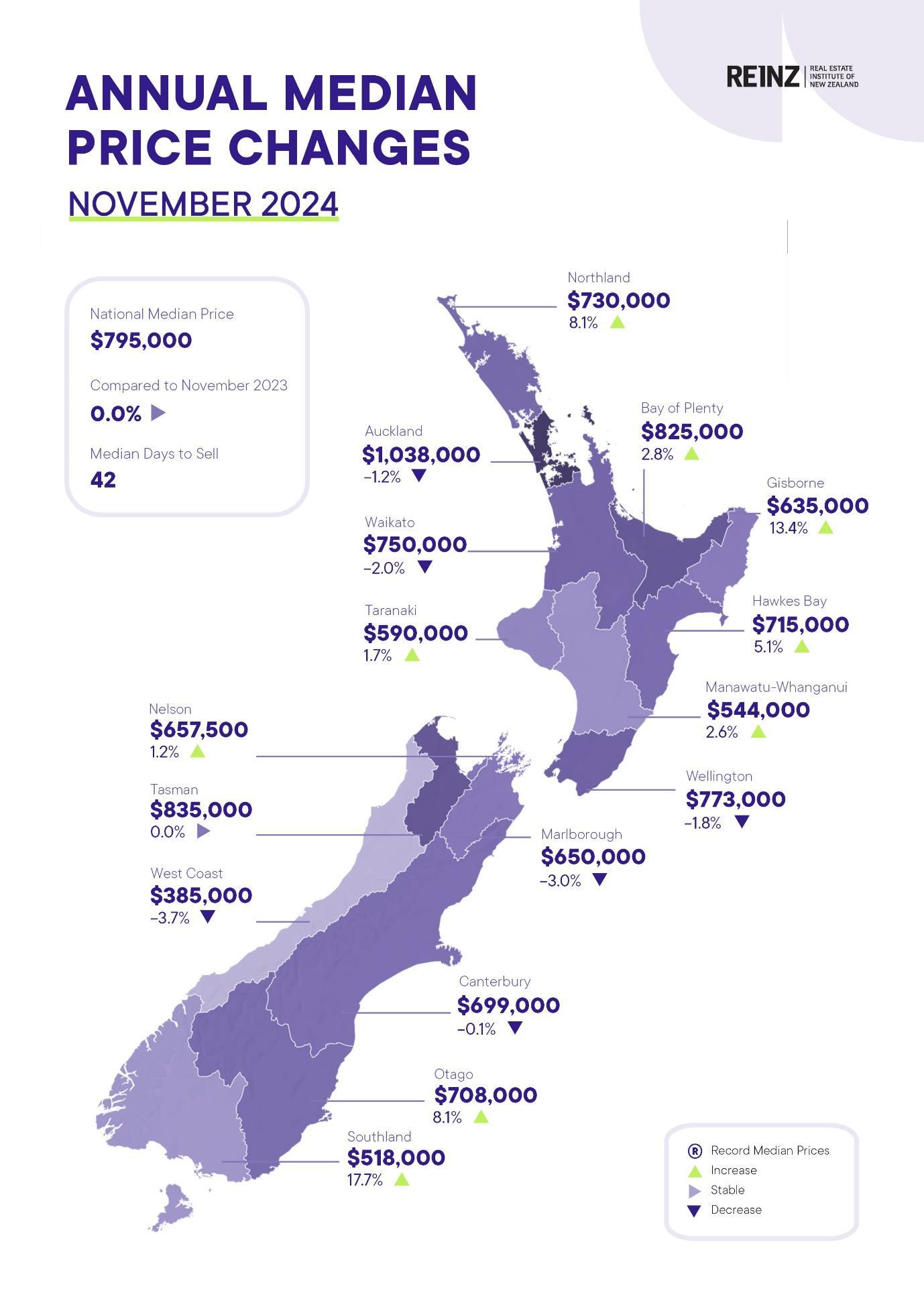

Median prices in New Zealand remained unchanged year-on-year and month-on-month, holding steady at $795,000. Excluding Auckland, the median price saw a slight year-on-year increase of $5,000, rising from $700,000 to $705,000 while remaining stable month-on-month.

Nine out of sixteen areas reported an increase in median prices over the past year, with Southland leading the way with a 17.7% from $440,000 to $518,000, a record high for the region and the first time it has recorded a median price over $500K. Gisborne followed with a 13.4% rise year-on-year to $635,000.

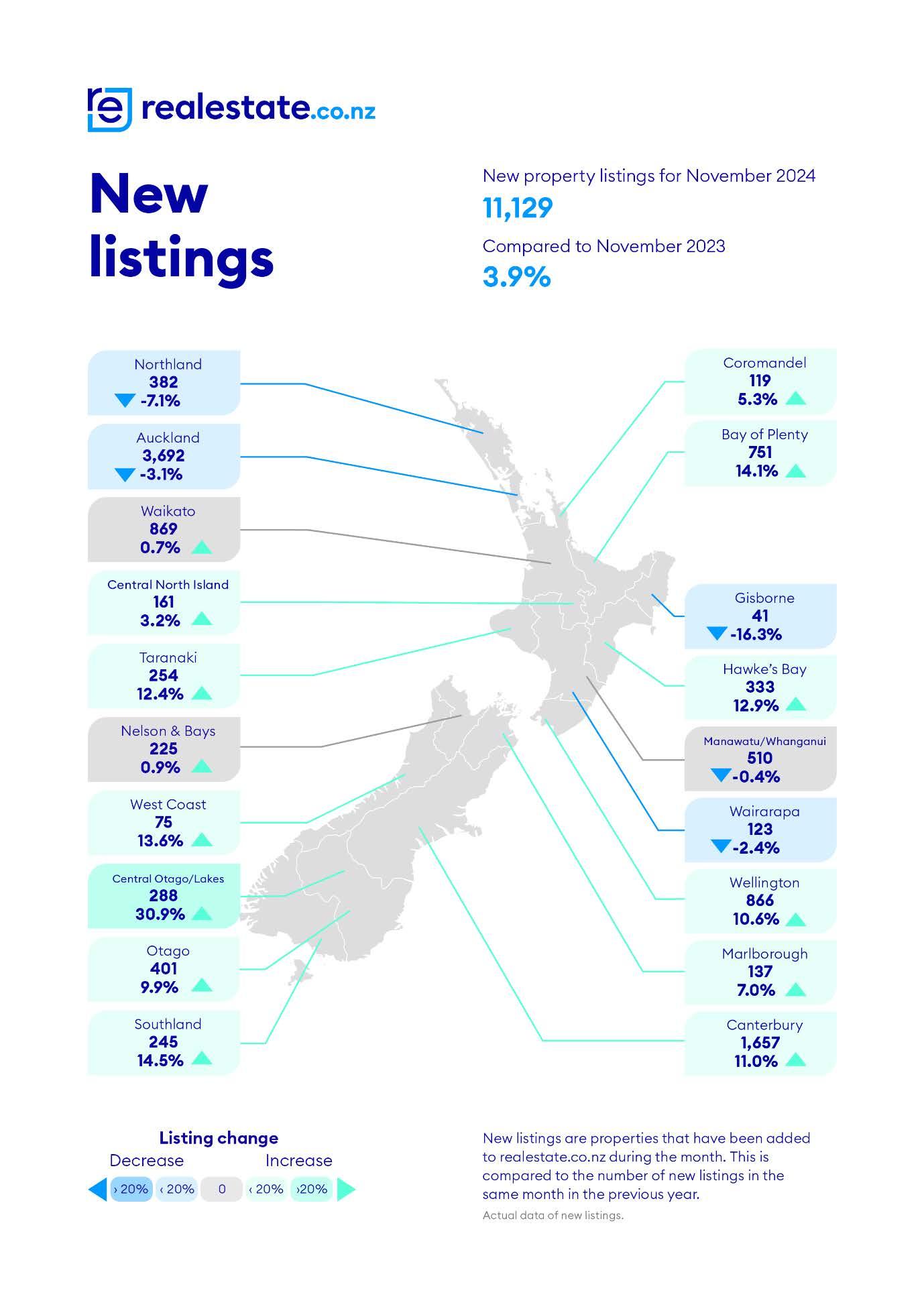

“November saw more life in the property market. Buyers are benefiting from steady prices and increasing options, while sellers in many areas are seeing stronger interest,” adds Baird. Overall, listings nationally increased year-on-year by 3.9% from 10,712 to 11,129, and New Zealand (excluding Auckland) increased by 7.8% from 6,901 to 7,437 compared to November 2023. Eleven out of fifteen regions reported increases in listings compared to last year. The regions with the most significant increases were Southland (+14.5%), the Bay of Plenty (+14.1%), and the West Coast (+13.6%).

For the first time this year, the number of listings in the market decreased compared to the previous month, with a nationwide decline of 3.8% compared to October 2024. Additionally, listings across New Zealand, excluding Auckland, decreased by 0.4% month-on-month.

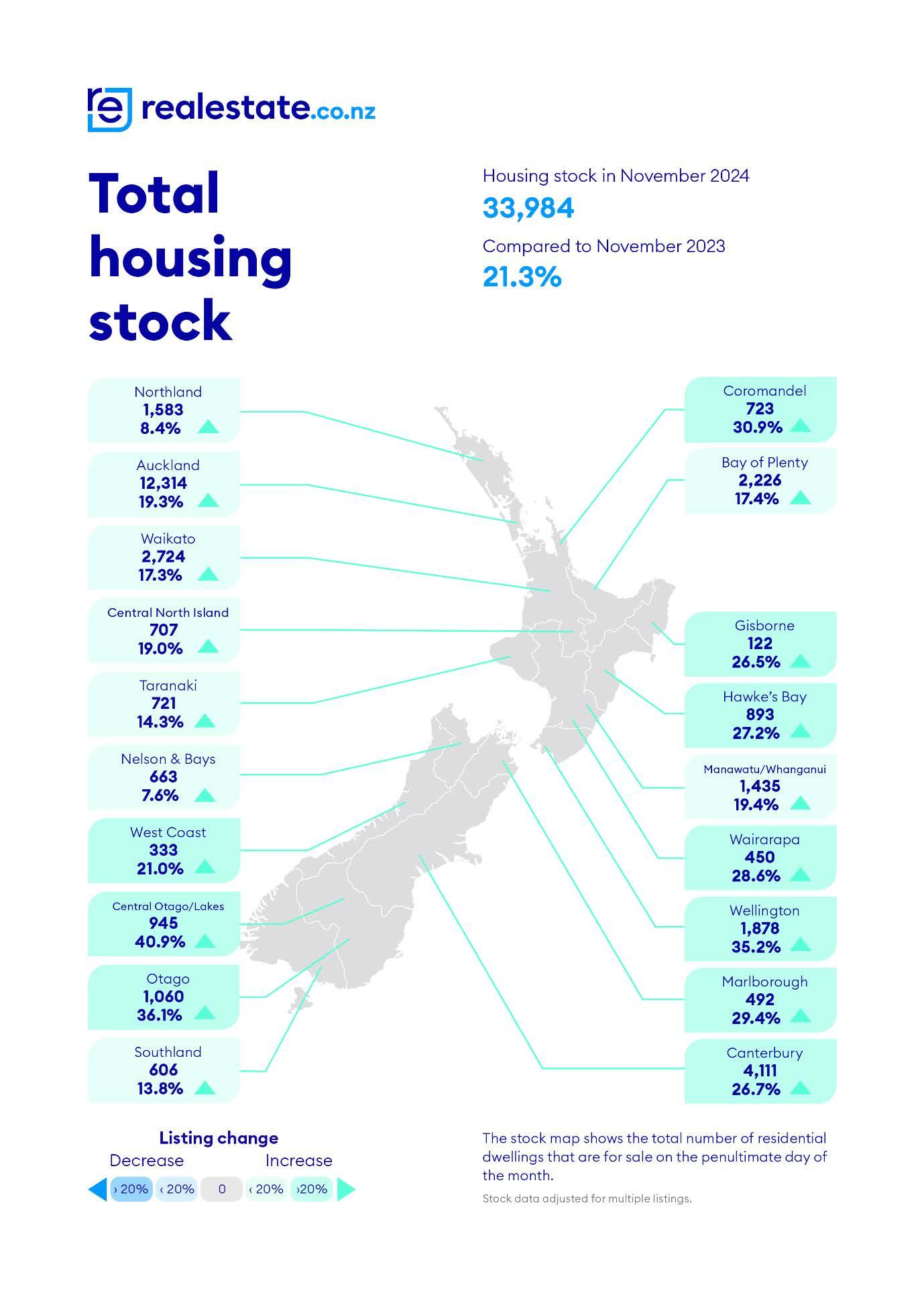

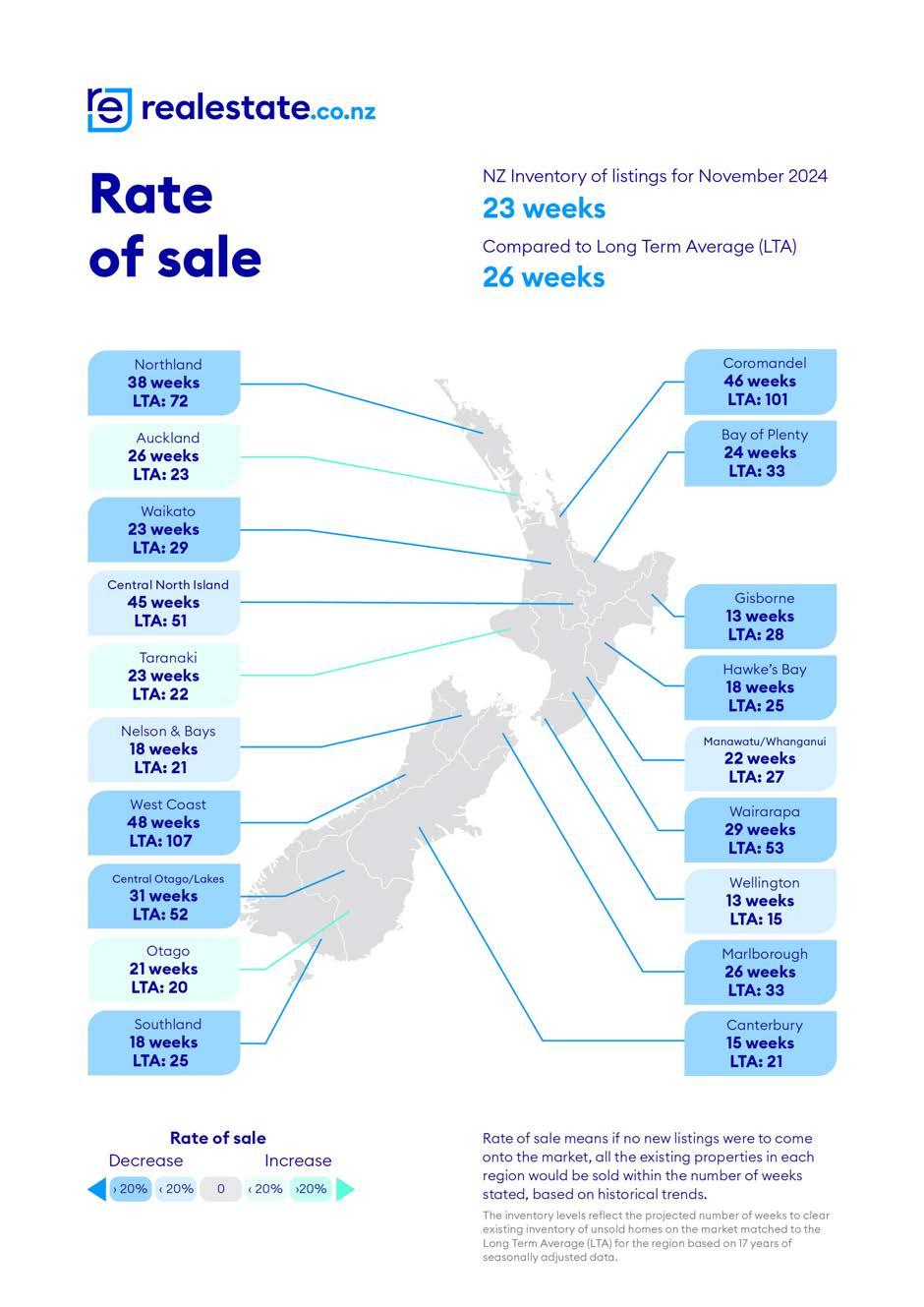

Inventory levels are rising, with a national increase of 21.3% year-on-year and a 5.1% increase month-on-month, totalling 33,984.

Baird notes, “November marks the first month in a while that we have seen an increase in demand and a slight reduction in new property coming to market. We expect the summer months to bring the usual upswing in sales activity across the market, this year with both buyers and sellers feeling a little more confident.”

In November, there were 1,209 auctions nationally (16.7% of all sales), a decrease from 20.3% in November 2023. The national median days to sell rose by four to 42 days compared to last year; excluding Auckland, it increased by three to 42 days this month.

The House Price Index (HPI) for New Zealand is currently at 3,638, reflecting a year-on-year decrease of 1.4% but a month-on-month increase of 0.6%. Over the past five years, the average annual growth rate of New Zealand's HPI has been approximately 4.6%. However, it is currently 14.9% lower than its peak in 2021. In November 2024, Southland reported the highest HPI movement, reaching an index level of 4,652, which marks a new high for the region.

The Real Estate Institute of New Zealand (REINZ) has the latest and most accurate real estate data in New Zealand.

We declared the November property market the 'perfect market' for buyers and sellers - the data shows stable prices and plenty of options for buyers, while REINZ data shows sales activity is also gaining momentum.

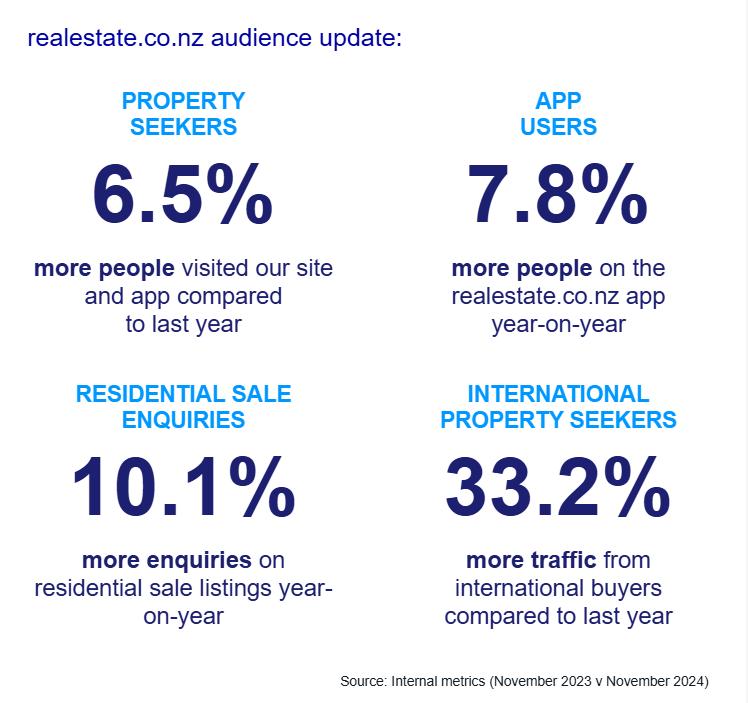

The number of property browsers on our site was up by 6.5% compared to November last year, and people searching on the app was up by 7.8%.

Enquiries on residential properties for sale were also up by 10.1% year-on-year. It seems international buyers have a renewed interest in New Zealand, unsurprisingly, with property seekers based overseas up by a whopping 33.2% year-on-year.

November 2024 - Stable prices, strong stock levels, falling interest rates, and rising buyer activity create the ideal ‘Goldilocks’ market for buyers and sellers.

• Two years on, property prices remain the same, offering the stability buyers crave and the predictability sellers need.

• Highest November stock levels in eight years give buyers more choice, while property sales pick up pace for sellers.

• The OCR drops, for the third consecutive time, to 4.25%, making borrowing more affordable.

• New listings growth slows to single digits, reflecting a stabilising market. Kiwis have long wished for a property market that offers stability and opportunity, and it seems that moment has finally arrived.

The latest data from realestate.co.nz paints a picture of balance: property prices have remained steady for nearly two years, hovering between $850,000 and $890,000, while healthy stock levels up 21.3% year-on-year are giving buyers substantial choice.

Sales activity is also gaining momentum, with the Real Estate Institute of New Zealand (REINZ) reporting over 6,500 properties sold in October the highest monthly total since March 2022.

Vanessa Williams, spokesperson for realestate.co.nz, describes it as “the perfect market.”

“After 18 years of tracking the property market,” she says, “this is one of those rare moments where certainty and opportunity align, creating a true ‘Goldilocks market’ that benefits buyers and sellers.”

Falling interest rates and the absence of election-year uncertainty when many Kiwis traditionally delay property decisions further reinforce market stability. “This isn’t a frantic rebound,” Williams explains. “It’s a steady uptick that provides confidence for both buyers and sellers ideal circumstances for making one of the biggest purchases of your life.”

She adds that debt-to-income (DTI) ratios are also helping to maintain this equilibrium, ensuring buyers make measured decisions while keeping investor activity in check.

Two years on, property prices remain the same, offering the stability buyers crave and the predictability sellers need.

The national average asking price held steady in November, marking 23 months of prices hovering between $850,000 and $890,000. Year-on-year, the national average asking price dipped by 2.8%, while month-on-month, it declined by 1.1%.

“We’re seeing more market activity but not significant price fluctuations. In fact, at $846,150 in November, the national average asking price is at the bottom of the range we’ve observed for nearly two years,” says Williams.

Only two regions have seen month-on-month and year-on-year growth in average asking prices: Central Otago/Lakes District (up 4.8% month-on-month and 2.5% yearon-year) and Wairarapa (up 9.2% month-on-month and 1.4% year-on-year).

At the other end of the spectrum, Bay of Plenty, Central North Island, Marlborough, Otago, Taranaki, Wellington, and the West Coast saw average asking prices decline year-on-year and month-on-month.

Highest November stock levels in eight years give buyers more choice while property sales pick up pace for sellers.

November stock levels reached their highest point since April 2015, with just under 34,000 properties available nationwide. Up 21.3% year-on-year, property seekers have significantly more options than this time last year.

All regions experienced stock growth both month-on-month and year-on-year, except Gisborne and Coromandel, which saw month-on-month declines of 9.5% and 4.2%, respectively.

Williams notes that despite ample choice for buyers, sellers also stand to gain. The proportion of listings on-site for less than 30 days before being sold or withdrawn rose by 1.4%, and those on-site for 30 to 60 days increased by 3.1%. Meanwhile, listings on-site for more than 60 days declined across the board.

“There’s plenty of choice, but properties are starting to move—it’s a win/win,” says Williams.

She adds that properties listed with a displayed price remained the most popular selling method, accounting for 29.4% of listings in November. “This gives buyers a clearer indication of the price expectation and likely results in a more informed and prepared buyer.”

New listings growth slows to single digits, reflecting a stabilising market.

National new listings in November saw their first single-digit year-on-year growth of 3.9%—a notable shift after months of double-digit increases throughout 2024.

This steady rise marks a return to more typical market patterns after a volatile 2023.

“Sellers seemed to hit pause last year, with high interest rates and uncertainty leading up to the election deterring many Kiwis from listing their homes. Following this, we saw a ‘post-election sugar rush’ in November 2023 as new listings peaked before dropping significantly in December,” says Williams.

This year, however, the market is showing signs of balance. New listings dipped 3.8% month-on-month in November. The last time new listings dipped between October and November was 2018. However, this dip aligns with typical seasonal patterns observed over the past 18 years.

“This steadying of new listings provides buyers with predictability while giving sellers confidence in a consistent market,” says Williams.

My house price hunch: Why 2025 could be the ‘year of conflicting forces’

The five things you need to know about the housing market this week.

Lower interest rates will likely support house price growth next year, but other economic factors could pull the market in the opposite direction. Photo / Fiona Goodall

1. Another variable year in suburbia

Our annual deep-dive into suburb-level data showed a continuation of the patchiness in the property market that’s now been in play ever since the downturn started in early 2022. For example, seven suburbs recorded double-digit gains in median values in 2024 including Blaketown and Cobden, in Grey District; Kaikoura, in Canterbury; Fernhill, in Queenstown; and Otautau, in Southland. But areas such as Mataura, in Gore, and Pipitea, in Wellington, both declined by around 10%. To be fair, you also tend to see quite a bit of variability across suburbs even in an overall market that’s booming. But the variability seen in 2024 certainly fits with the continued challenges that the property market has faced, including the weakening labour market.

2. 2025 could be the ‘year of conflicting forces’

It’s also that time again when thoughts start turning to what might lie ahead next year, and my hunch is that we’ll largely see a continuation of a market being pushed in opposite directions by a range of different forces. On the one hand, the falls in mortgage rates will tend to support house sales activity and property values, especially as existing borrowers increasingly roll off their current payments and onto the new lower rates. However, (un-)affordability is still a significant challenge, listings remain abundant, and jobs are still being lost. Debt-to-income ratio restrictions aren’t binding right now, but they are also likely to become a greater consideration in 2025. I anticipate house prices will rise in 2025, but perhaps by only 5-7% That’s great for those who own property, but it’s still only a modest rise compared to the early stages of past upturns.

CoreLogic chief economist Kelvin Davidson:

"I anticipate house prices will rise in 2025, but perhaps by only 5-7%."

The theme of trade-offs or conflicting forces may be relevant for other aspects of the property market too. For investors, for example, lower mortgage rates will make the cashflow for a typical rental purchase look more appealing. But DTIs may make it a little more difficult to get finance in the first place. Meanwhile, people choosing a mortgage rate must decide between fixing short or returning to longer terms again.

3. The economy remains lacklustre

Another reason to take a relatively cautious view about the housing market’s performance in 2025 is that the economy remains subdued, and may not kick into gear again for a while yet. The latest soggy results came from November’s electronic card spending (core retail activity up by only 0.1% from October) and the BNZ-BusinessNZ manufacturing indicator, which was in shrinking territory for the 21st month in a row.

4. Rental market still looks subdued

This week, Stats NZ will publish its rental price data for November, and there’s every chance we’ll see another subdued result. After all, net migration continues to drop –which is slowing overall property demand growth – and the stock of available rental listings has also risen; up by 17% year-on-year, and essentially the highest level for this time of year since 2020.

5. Another recession?

Finally, we’ll sign off 2024 (in terms of headline economic data) with the Q3 GDP figures from Stats NZ on Thursday The expectation is that GDP will have fallen by perhaps 0.3-0.4%, which means another technical recession, after the drop in Q2. But as always, remember these figures for July-September are already a bit old (we’re in December), and the timelier measures suggest that Q4 probably hasn’t been as bad, albeit not great either.

-Kelvin Davidson is chief economist at property insights firm CoreLogic

Input to your Strategy for Adapting to Challenges

Feel free to pass on to friends and clients wanting independent economic commentary

ISSN: 2703-2825

Sign up for free at www.tonyalexander.nz

Consumers to spend more

My central themes are that an economic upturn is getting started but it will be muted and won’t prevent some more businessesclosingdown over the first part of 2025 as cash flows will still be too poor to get them through to the stronger customer flow environment. Also, interest rates will ease but the bulk of declines in rates for two years and beyond have already happened and the extent of growth stimulus will be less than many people are expecting.

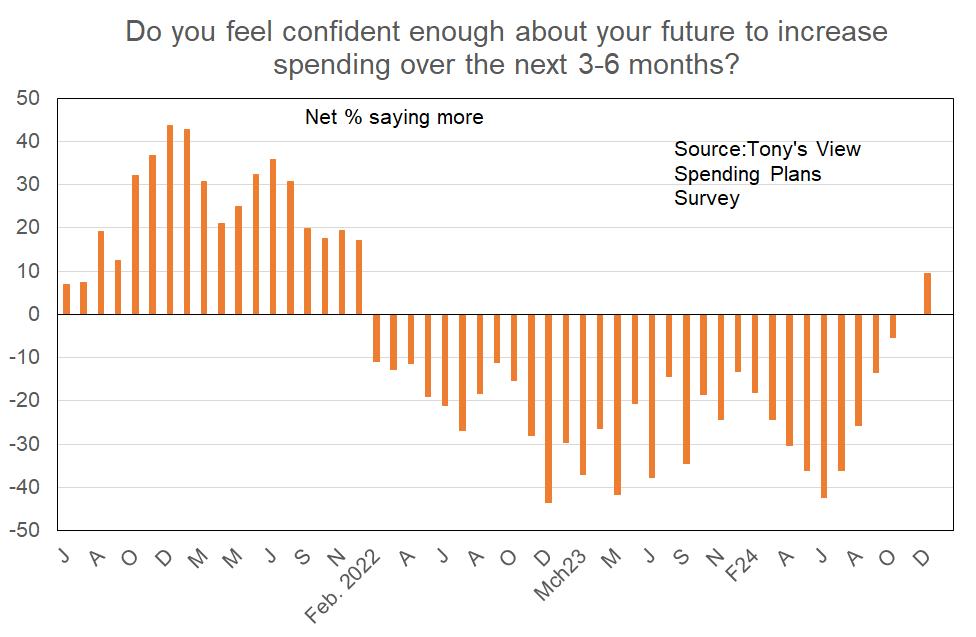

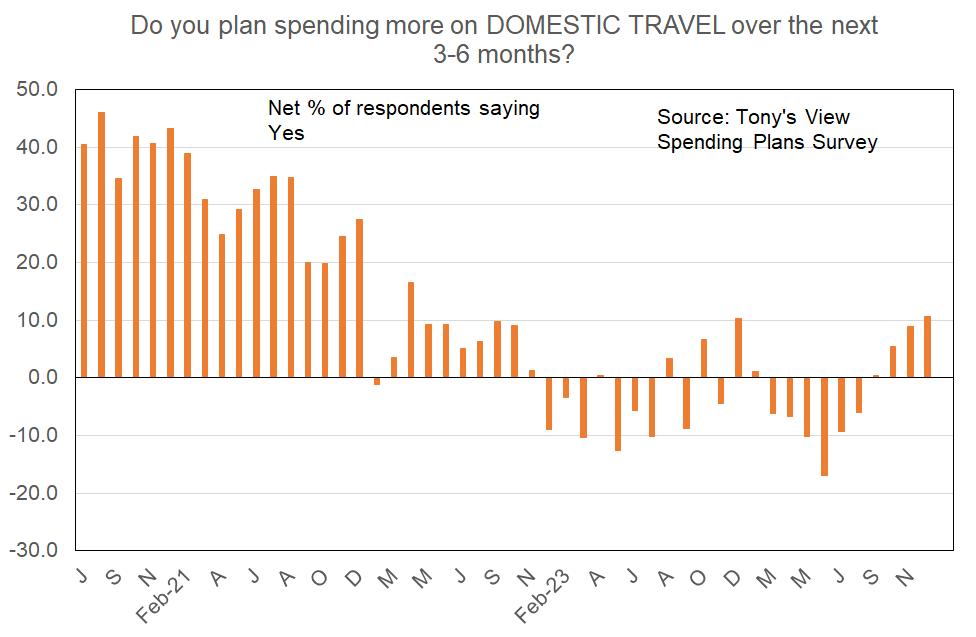

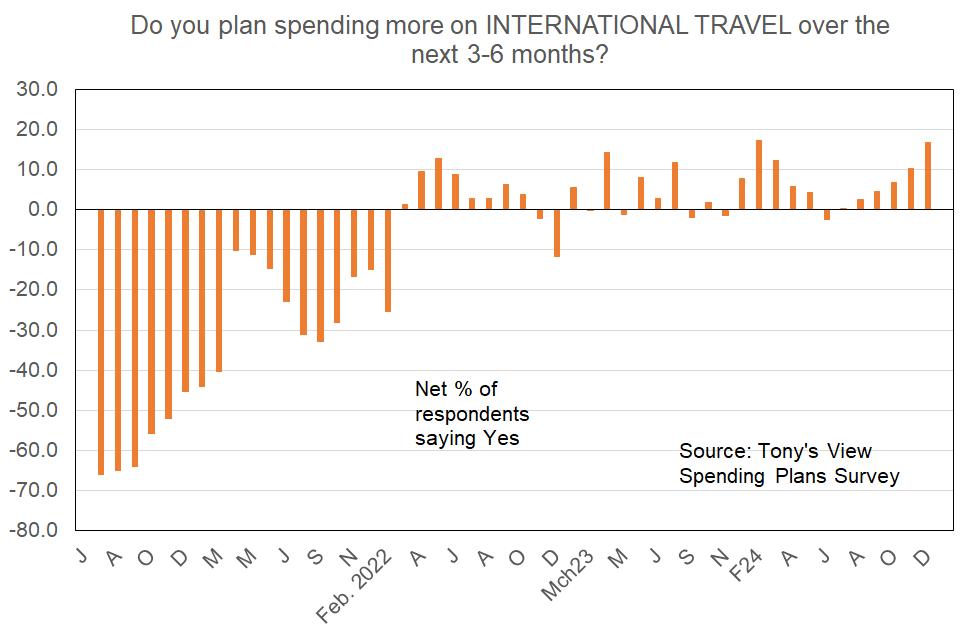

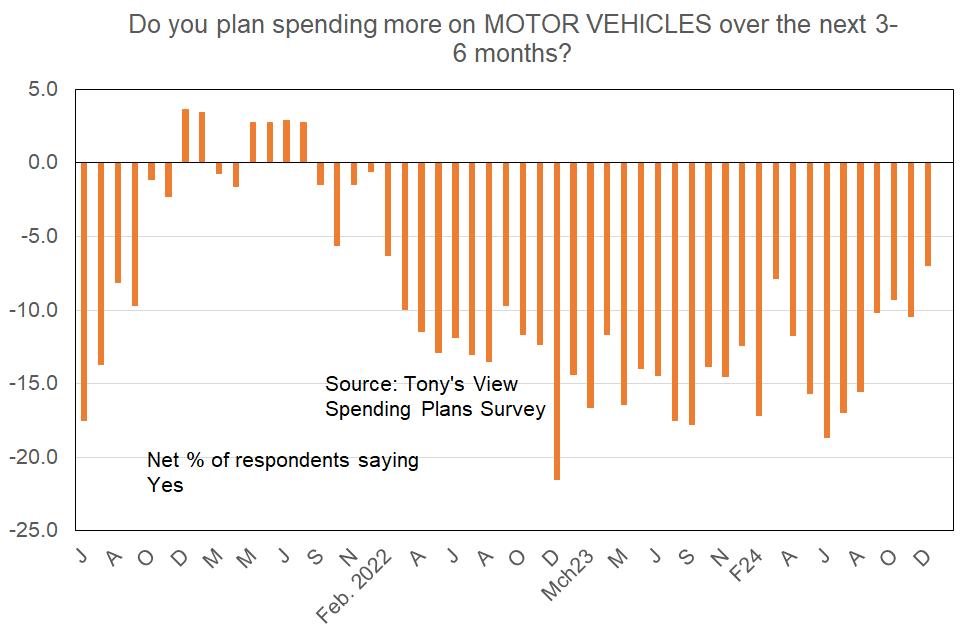

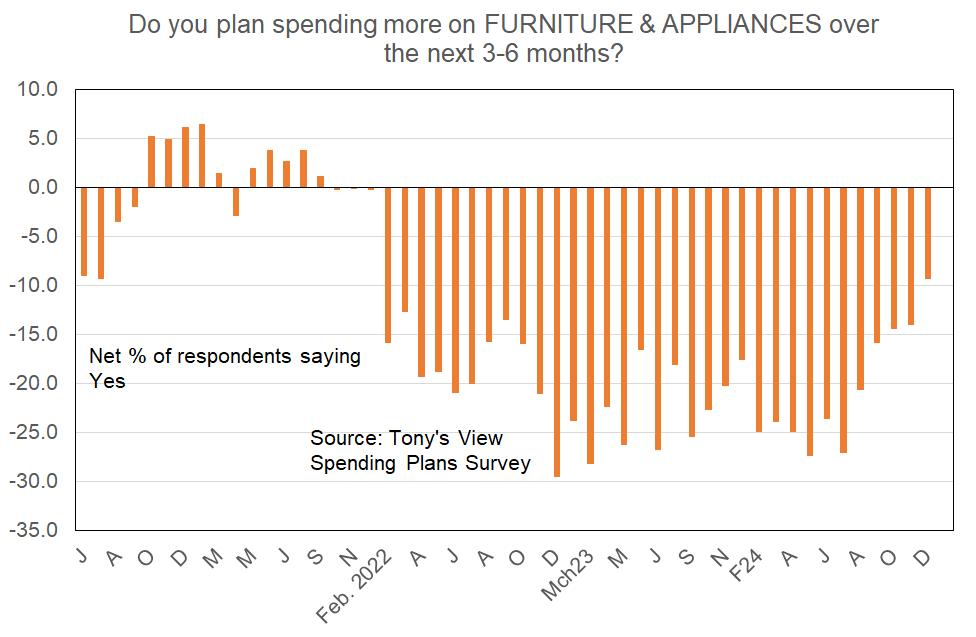

In a modern economy like ours some 65% or so of spending is undertaken by households and that is why it is useful to pay attention to leading indicators of what you and I as consumers look likely to do with our money. This week I have in hand the results from my final Spending Plans Survey for 2024 and they show that these plans for spending over the next 3-6 months are the strongest in exactly three years.

A net 10% of the 558 respondents have reported that they intend raising their spending levels on stuff generally.

12 December 2024

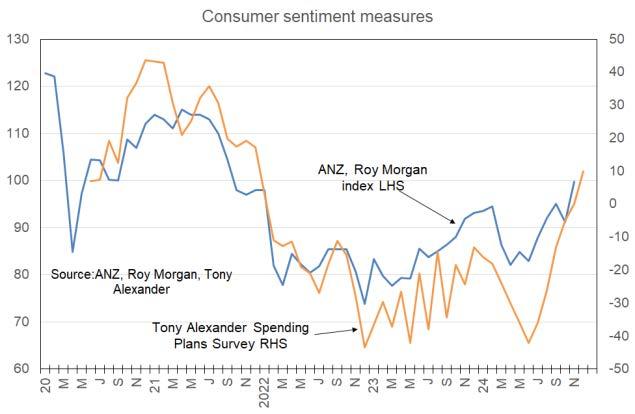

This survey tends to lead or coincide with the long-running ANZ Roy Morgan Consumer Confidence gauge. That means we can reasonably expect some more strength to show through there fairly soon and that this will add to the cautionary feeling in financial markets regarding the extent to which the Reserve Bank will feel extra stimulus (less restraint actually) needs to be applied to the economyonce the cash rate reaches 3.5%.

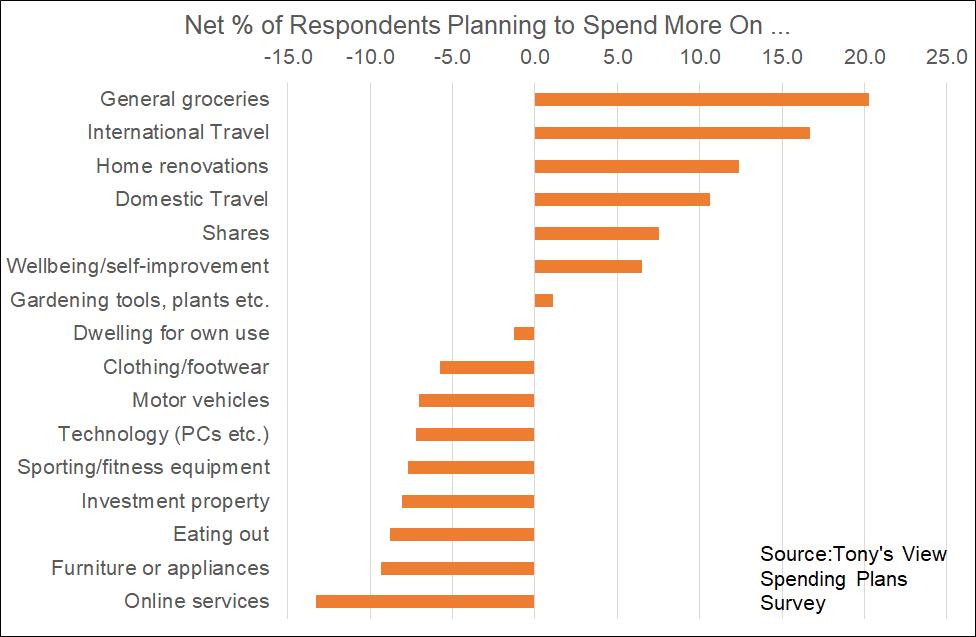

People are planning to boost their spending in seven of the offered categories with greatest strength in groceries where the factor in play is probably still the impact of well remembered price rises. International travel is back in favour and the lift in plans for home renovations is confirmed.

Here are graphs for some of the categories listed above.

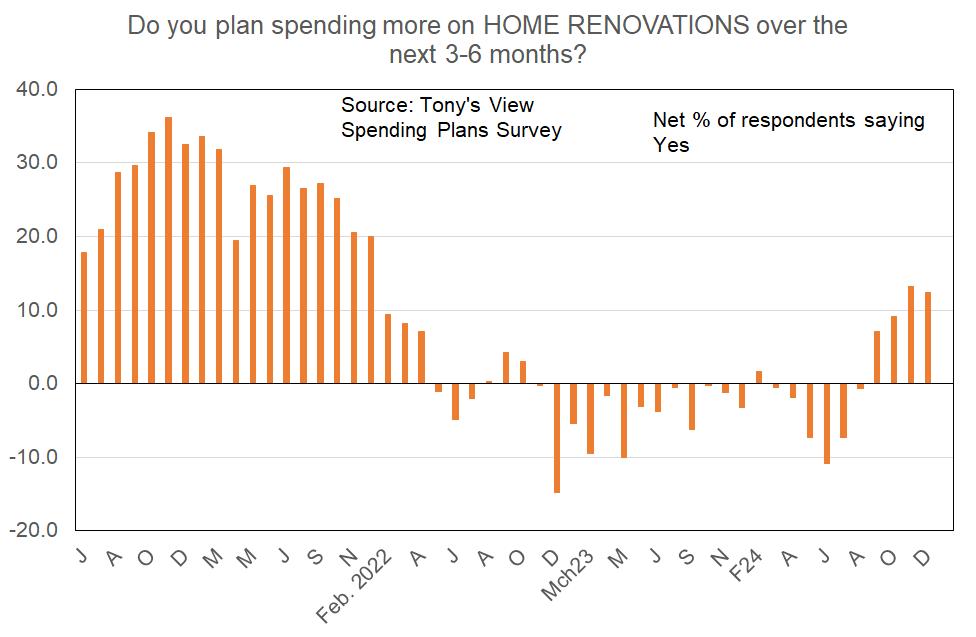

As mentioned above and noted also recently in a newspaper article, those involved in the home renovations sector are experiencing a solid upturn.

Domestic travel plans are firming while those for offshore travel are as strong as they have ever been in the past for the period covered by this survey since mid-2020.

It is interesting that the solidity and implication of seriousness about the spending improvement

signalled by the lift in renovations plans is not yet being seen in a net positive result for motor vehicle purchasing. The sector is one in a state of flux with reduced interest in fully electric vehicles, increased interest in hybrids, and perhaps awareness of a wave of the former coming out of China.

Plans for spending on furniture and appliances arealsostill firmly net negative.Thissuggests that some tentativeness about spending plans by Kiwi households remains amidst cost of living pressures and rising unemployment.

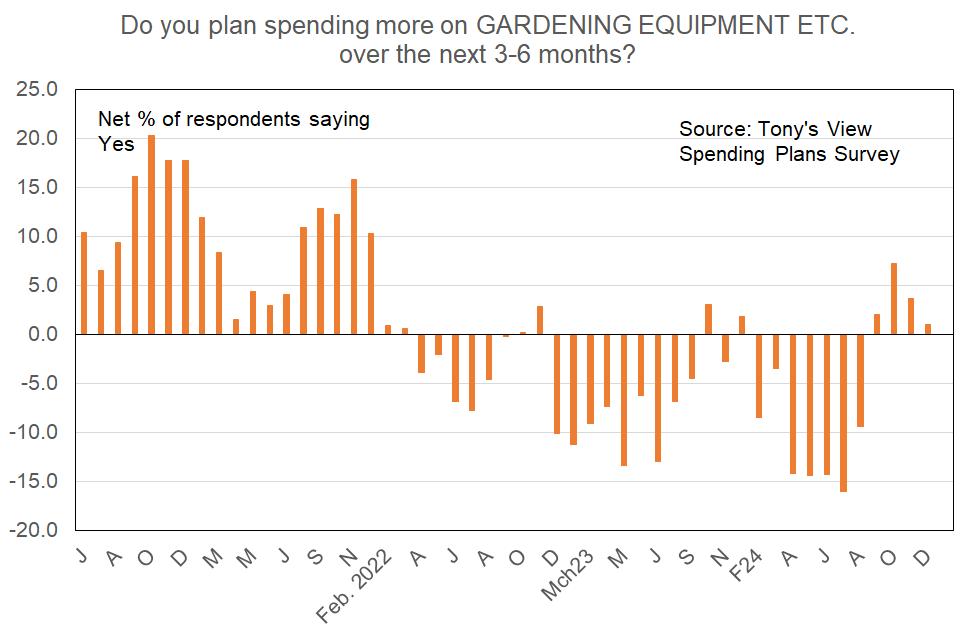

The gardening upturn has remained muted.

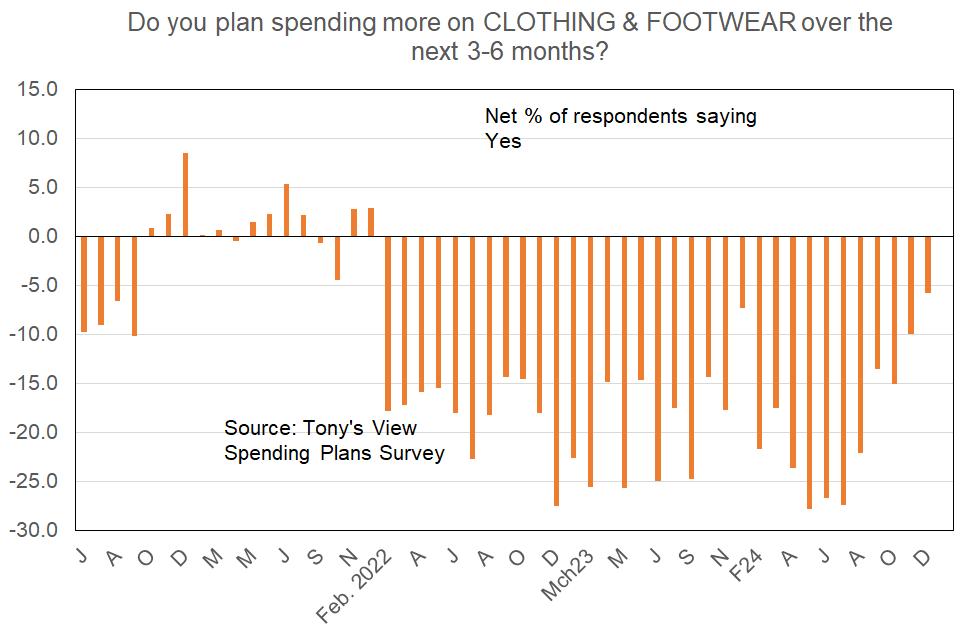

Prospects for clothing and footwear retailers are better but still poor overall.

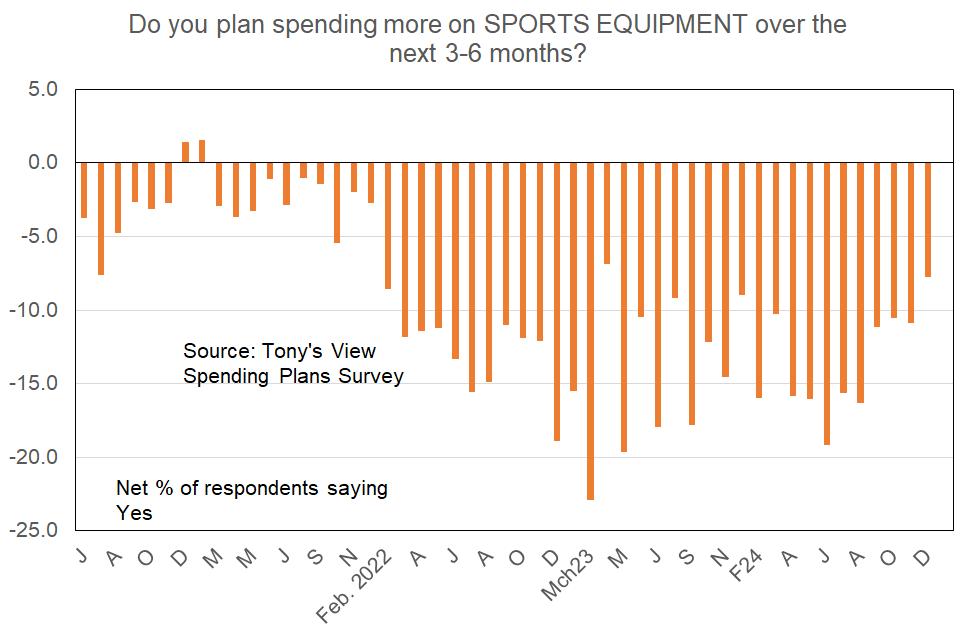

Same for sports equipment.

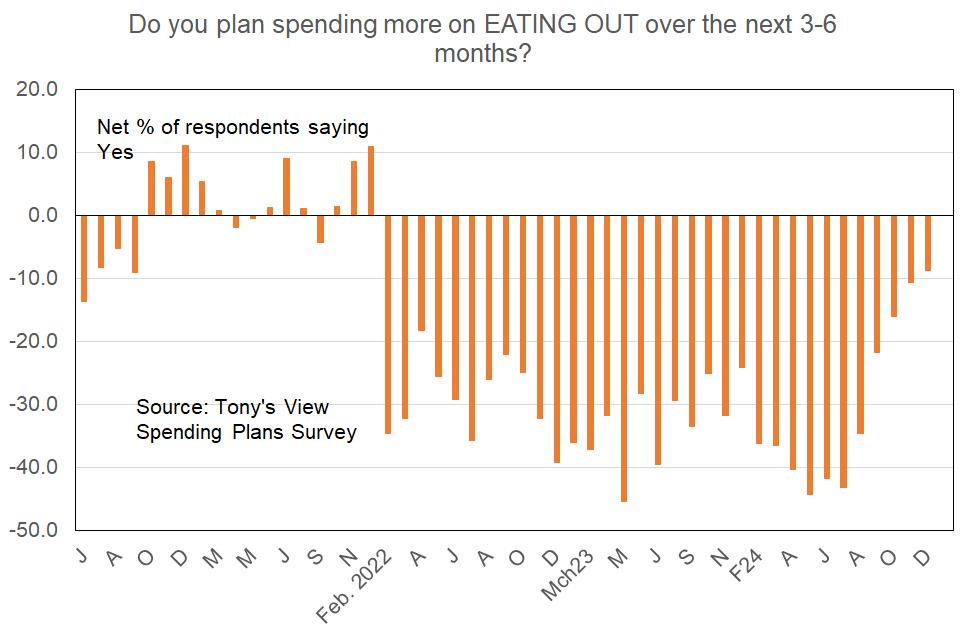

For the areaofspending which had the worst level of spending plans in the past things are close to being net positive – but not yet. What my survey hasn’t been able to capture is the lift in eating out which involves takeaways as opposed to going to a restaurant or café.

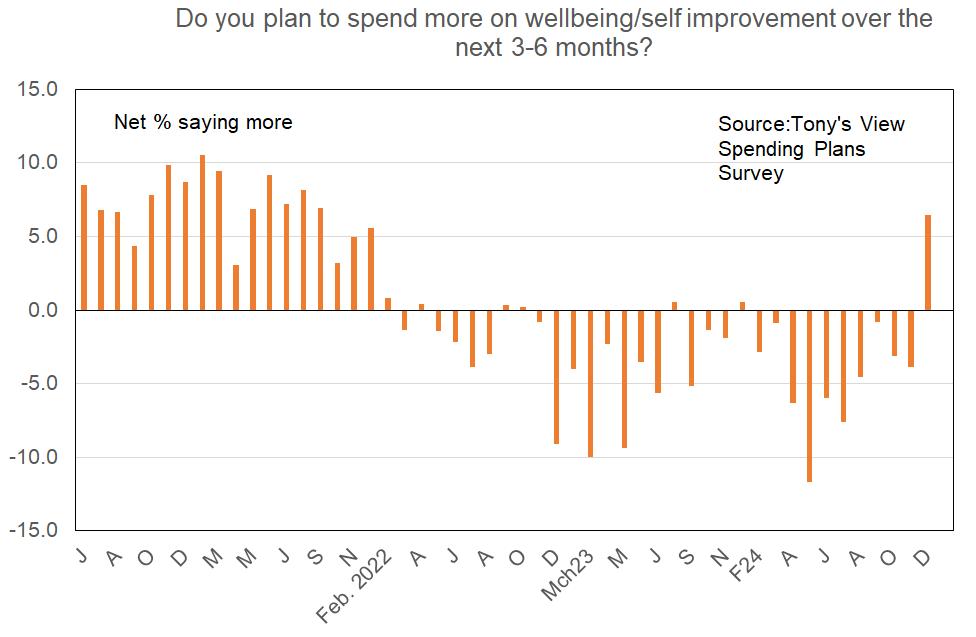

I’m not sure what to make of the firm jump in people’s plans for spending on their wellbeing. But it seems reasonable to assume that the outlook is getting better for those providing such services.

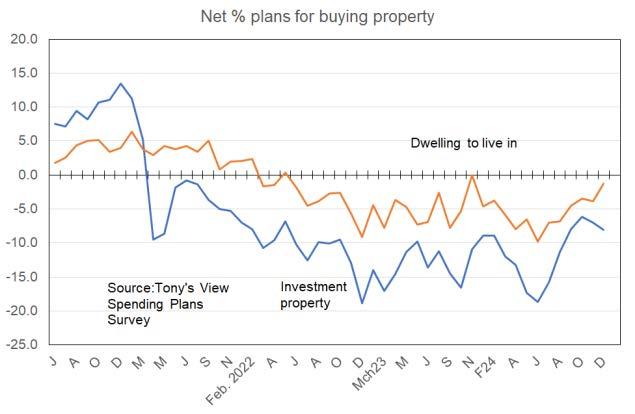

Backing up the data from my other surveys showing an improving trend in residential real estate but no frenzy, only a net 1.3% of people now plan cutting spending on a place to live in This is the least negative such result since May 2022.

Net plans for purchasing an investment property (the blue line above) however are not showing a continuation of the improving trend which emerged mid-year.

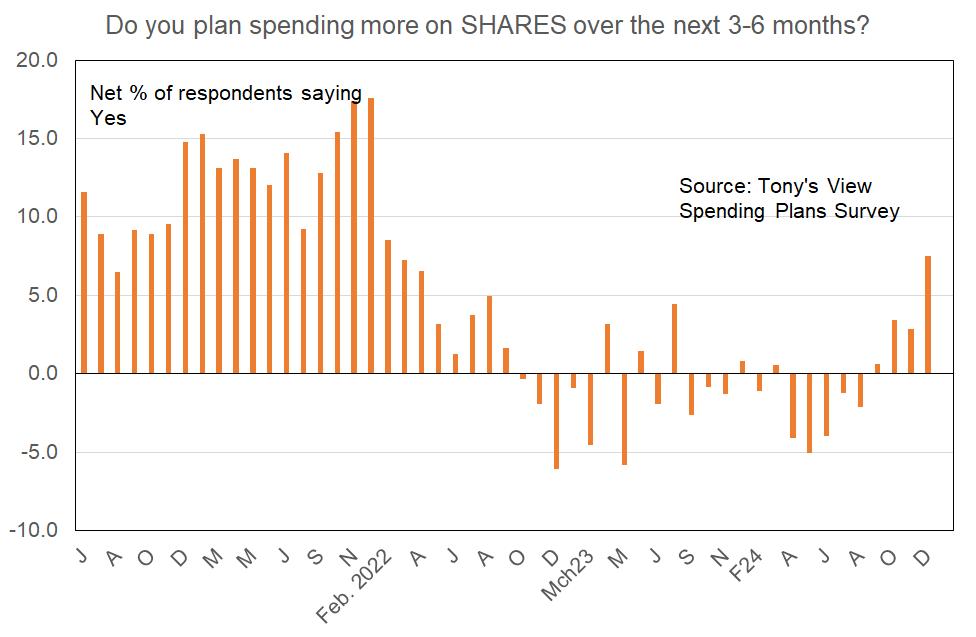

Finally, when it comes to shares people are getting a tad excited.

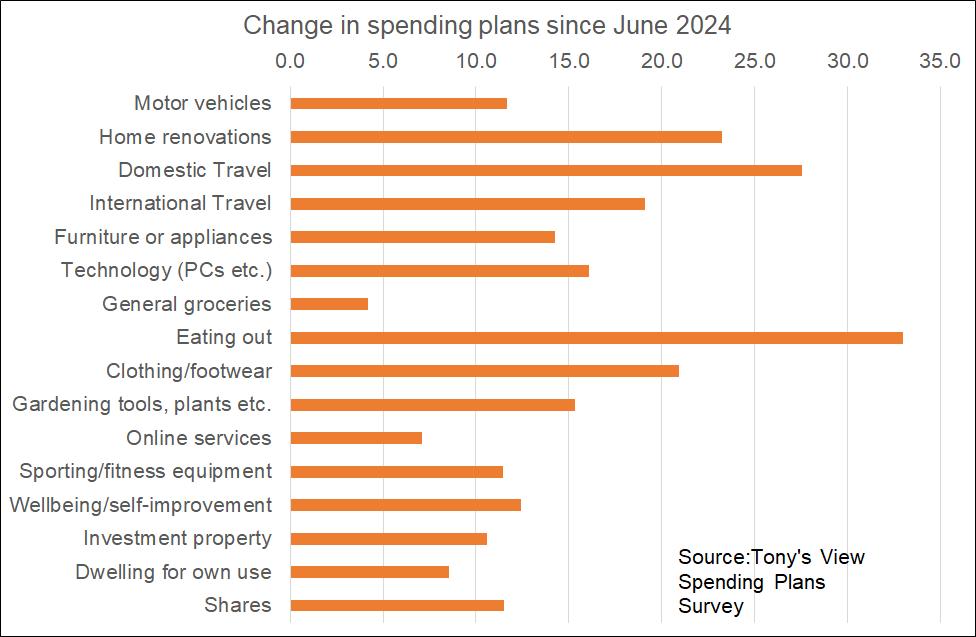

Next week I will take a look at the developments in factors which people cite as driving their decisions to spend more or spend less. But to finish with here is a graph showing the extent of improvement for each category I track since the depths of despair in June this year.

• Some things which people might normally be thinking about buying in the coming year as conditions improve, they have in fact already bought during the pandemic binge.

• Business failures in the extended “weeding out” period alongside right-sizing by many others will see employment confidence sit on the low side for employees all through 2025.

• At some stage general discussion about interest rates will shift from great optimism associated with them falling to “is that it?”

• Discussions of capital gains taxes, wealth taxes, new levies, fiscal deficits and the old saw of superannuation unaffordability etc. will make people wary of spending at the margin and encourage emigration.

• Councils are promising much higher rates, costs related to climate change are growing, and electricity companies are promising more price rises. Anticipation of ongoing cost of living pressure will in particular restrain the willingness to spend of older people.

• House price gains this cycle are likely to be restrained. That means a smaller than usual positive wealth effect on consumer spending for the next three years.

If you are a retailer or a supplier of goods and services to retailers you can justifiably expect better conditions over 2025-26. However, the strength of rebound in consumer spending is unlikely to be so large that the other sectorspecific challenges you face (new competitors, ways of shopping etc.) will be smoothed over. Your need to adapt will remain strong.

This all largely sounds positive. But is consumer spending going to truly surge? Probably not.

If I were a borrower, what would I do?

My answer = start thinking about this little sentence. “Is that it?”

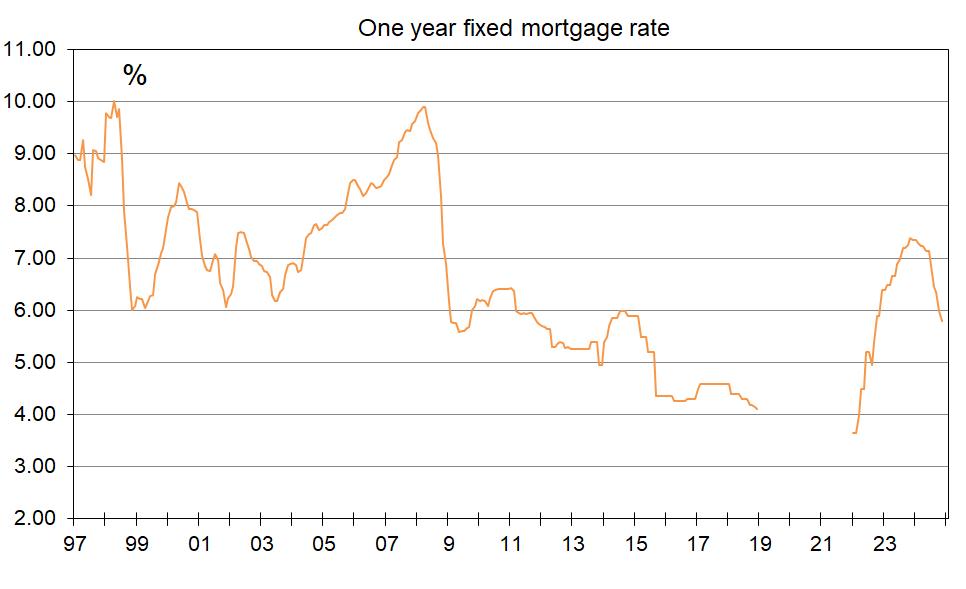

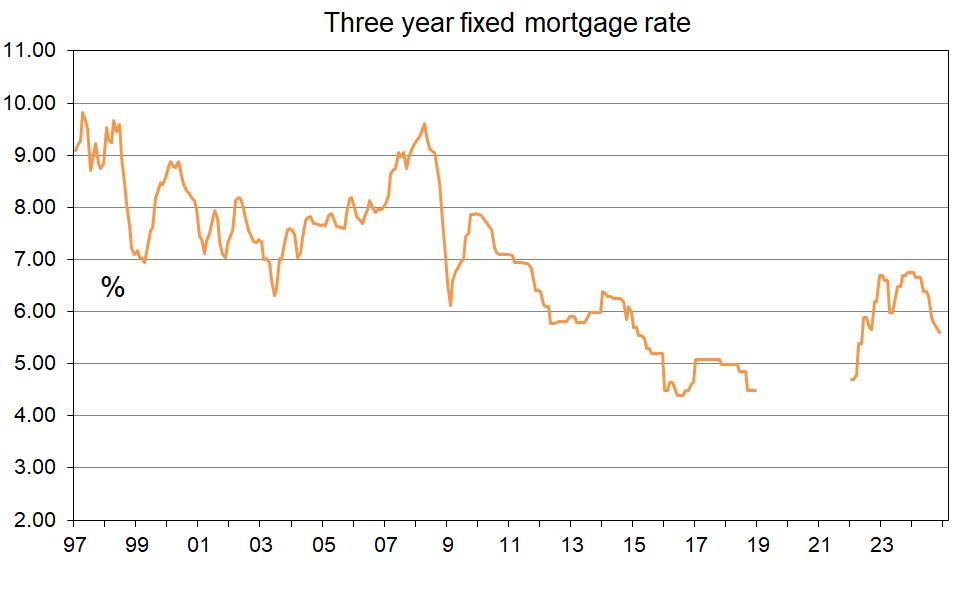

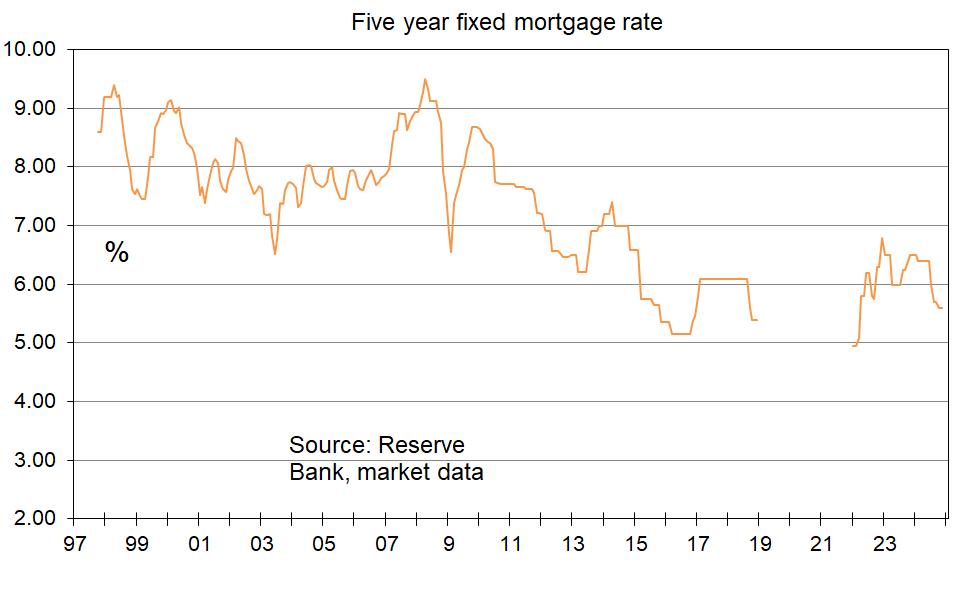

I see quitea highriskthatpeopleexpectmortgage rates to fall a lot further from current levels than they have so far. With the official cash rate so far downby 1.25% and likely to fall another 0.75% we have seen one year fixed mortgage rates decline about 1.5%, three year rates about 1.4%, and five year rates about 1.0%.

From current levels Isee scopefor maybe another 0.5% coming off the one year rate and less than that for rates two years and longer. That means the one-year rate may optimistically bottom out just above 5% from near 5.8% commonly at the moment. The three year rate may fall from near 5.6% towards 5.2%, the five year rate from near 5.6% also to just over 5.2%.

Butasnoted, this looks like theoptimisticscenario from a borrower’s point of view. In fact, it pays to note that over 2017-18 when the official cash rate averaged 1.75% the one year rate averaged 4.4%, the three year rate 4.9%, and the five year mortgage rate 6%.

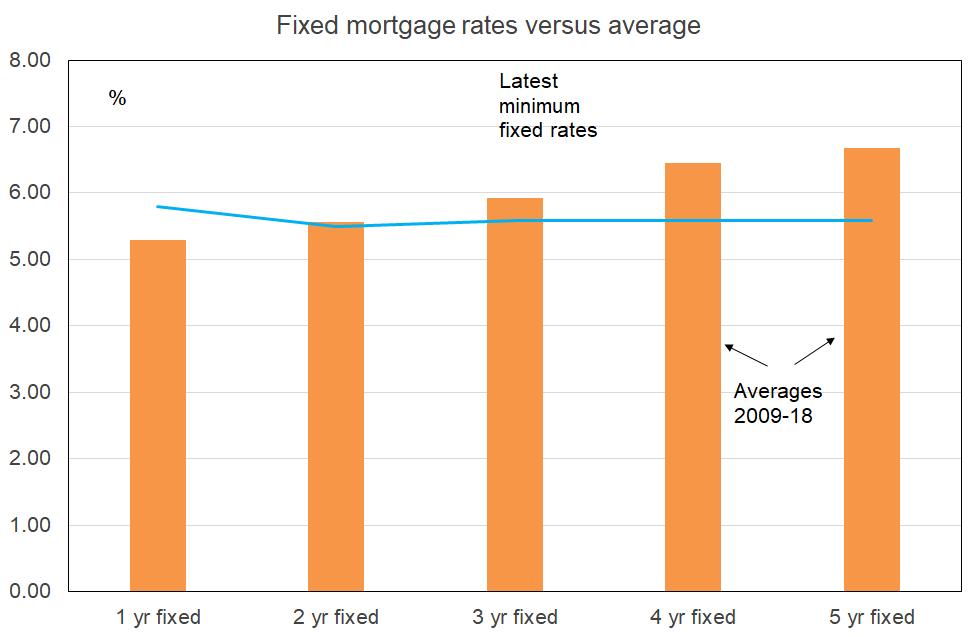

Note the graph I include in TV each week below showing how the current fixed rates represented by the blue line compare with averages for each over the post-GFC period before the worries about deflation and pandemic. We are already below average for terms of three years and beyond. Here it is for the scrollingly challenged.

The question of course is to what extent will the Reserve Bank feel that monetary policy needs to be quite accommodative (very low rates) in order to ensure inflation does not look like settling towards the low end of the 1% - 3% target range. My view is that they won’t feel much need to pump the accelerator at all. Taking the foot off the brake will probably be enough this time around.

As noted, there are boosts to inflation to come from increases in council rates, electricity, climate change-related things, and the environment of rising house prices (calm, not frenzied). Rising dairy prices (great for the NZ economy) will mean higher prices for cheese etc.

Add in the structural decline in New Zealand’s underlying rate of productivity growth. Then consider the factor I have been harping on about for the second half of the year here. Business margins are crunched, and survey results suggest that once customer demand improves, they are going to recoup crunched margins by raising prices.

Note that I am not taking a position on global inflation. I do not know how things are going to change there. A higher global inflation scenario on the basis of the return of tariffs and decline in multilateralism seems a reasonable assumption. But a lower environment seems reasonable if one focuses on deflation in China and their diversion of exports from the US to other markets such as our tiny one.

What all of this adds up to is something quite simple from a borrower’s point of view. Run your numbers assuming an interest rate of 5.25% for the next three years. As for when the time will be optimal to switch from fixing six months to three-plus years – I don’t really have a view and can only see myself jumping up and down again to suggest fixing long if one lender decides to radically discount a long rate sometime next year.

Given the lack of competition between banks for mortgage business at the moment amply revealed in my monthly survey of mortgage brokers that does not look like a high probability scenario at this point.

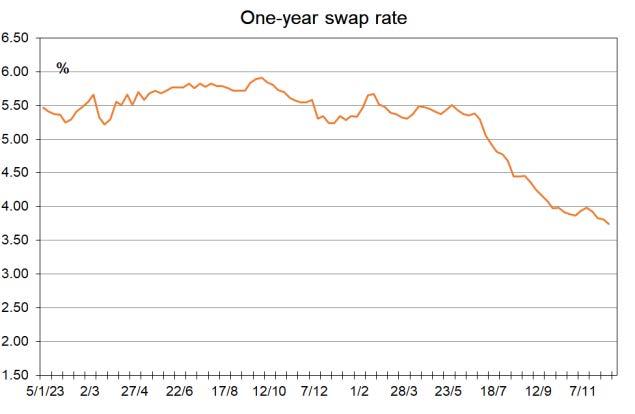

This week the wholesale fixed borrowing costs which banks pay in order to offset fixed mortgage rate lending have edged only marginally lower. At 3.74% the one year wholesale fixed rate is down from 3.81% last week, 3.98% four weeks ago, and 5.24% at the start of the year.

These three graphs show levels of the one, three, and five year fixed mortgage rates over the past few years excluding the 2019-21 period when rates were absurdly low because of worries about deflation and then the effects of the pandemic.

This graph shows how current rates compare with averages from 2009-19.

I reckon scope exists for the 3-5 year fixed rates to be cut further once banks start more assertively competing for business. For the moment I don’t think they are really feeling it. So, I’d still probably fix for a short-term (six months though some feel 12-18 is good), with a view to fixing 3-5 years probably sometime next year. When is anyone’s guess in this very uncertain environment.

To see the interest rates currently charged by major lenders go to www.mortgages.co.nz

Nothing I write here or anywhere else in this publication is intended to be personal advice. You should discuss your financing options with a professional.

Town

2CWaiariRoad, CONIFERGROVE

CharacterandComfortinConifer Grove

Charming 1920s bungalow: This delightful home blends character with modern conveniences, featuring three spacious bedrooms, a modern kitchen, and a cozy sunroom. Spacious living areas: Open-plan living with high ceilings creates a warm, inviting space for family gatherings, while the man cave/rumpus room at the rear adds versatility for hobbies or entertainment.

Secure and private section: Fully fenced freehold property ideal for families and pets, offering privacy and peace of mind.

Prime location in Conifer Grove: Situated near a cul-de-sac and greenbelt, with excellent school zoning, shops, schools, parks, and public transport within walking distance. Convenience and charm: A perfect combination of accessibility to daily needs and a welcoming community spirit – call today to arrange a viewing!

Sold Mark Eklund0212446692 mark.eklund@ljhooker.co.nz

Sold VenitaAttrill0212867792 venita.attrill@ljhooker.co.nz

Sold View ByAppointment Paula Cox021396977 paula.cox@ljhooker.co.nz

Sold Steve Reilly021930352 steve.reilly@ljhooker.co.nz

Sold KJ Klavenes0275566194 knut.klavenes@ljhooker.co.nz

Local Updates

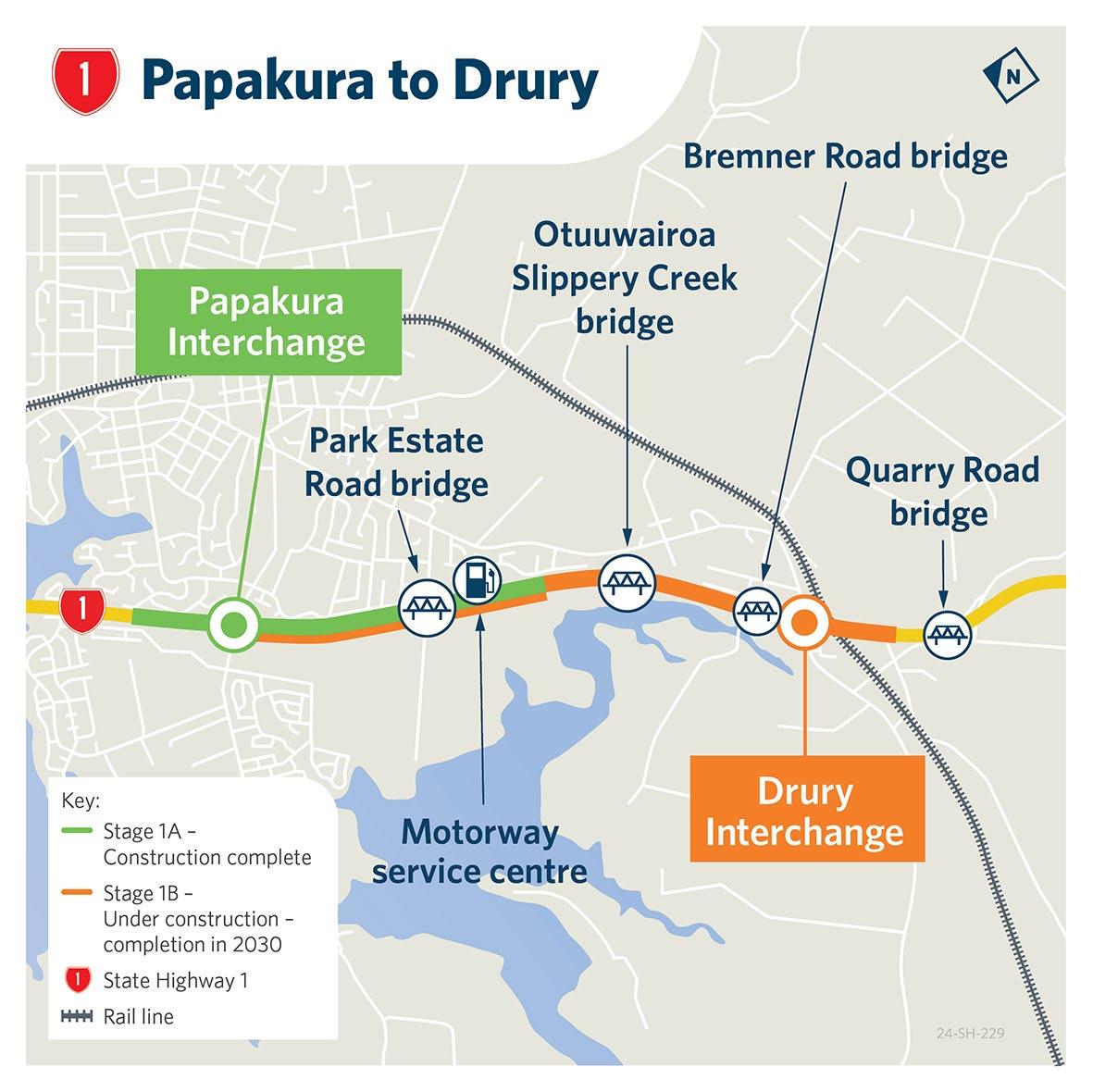

SH1 Papakura to Drury

Construction update

6 December 2024

Construction update | He pānui

Kia ora

We are now well into summer with long days and warmer weather - with the wet weather hopefully behind us! Over the last month the team has completed the final layer of asphalt on both sides of the motorway – the final 'icing on the cake'. Earlier this week we also completed laying final asphalt on Beach Road, which marks the end of the asphalting programme for Stage 1A of the project.

With asphalting now done, a second 'long-life' coat of line markings will be applied on both sides of the motorway and on Beach Road in the New Year – we need to

wait for a bit until the asphalt is sufficiently cured to ensure the long-life markings stay put.

While some early works have been underway since September, this month construction officially started on the next stage (Stage 1B) of the project.

Stage 1B is a much larger and more complex construction project than Stage 1A, meaning the construction timeframe will be significantly longer. The estimated completion date for Stage 1B is August 2030. Read on for more information.

Work will also begin early in 2025 on installing traffic lights at the intersection of SH22 and Great South Road. Signalising this intersection is required for traffic mitigation as part of Stage 1B of the project and will improve safety over the current intersection layout.

An aerial view of Drury Interchange looking northwards – the interchange will be raised and shifted across to the east where three new bridges have already been built over the railway.

Stage 1B

Key features of Stage 1B of the Papakura to Drury project include:

• Continuing the new third motorway lane in both directions from the BP service centre down to Drury Interchange, including safety and lighting upgrades

• Relocating Drury Interchange across to the east and raising it up higher –due to the safety clearance needed above the newly-electrified North Island Main Trunk (NIMT) railway, and to improve over-dimensional vehicle access along Great South Road under the motorway. Three bridges have already been built across the NIMT railway, purposefully in advance of KiwiRail’s electrification to Pukekohe project

• Replacing the SH1 motorway bridge across Great South Road; the Bremner Road bridges over SH1 and Ngaakooroa Stream (beside Auranga); and the two SH1 bridges over Otuuwairoa Stream / Slippery Creek

• Realigning the Victoria Street intersection on SH22 to line up opposite Mercer Street, and signalising the intersection (installing traffic lights)

• Realigning the southern end of Flanagan Road (as the motorway will move over to where the end of Flanagan Road currently lies)

• Building a shared walking and cycling path on the western (northbound) side of SH1 between Papakura and Drury Interchanges, with connections at Park Estate and Bremner Roads, and upgrading walking and cycling facilities on Great South Road through Drury Interchange

• Significant upgrades of utility services including improvements to stormwater management and realignment of the existing Waikato water supply pipeline beside Flanagan Road.

For more information on Stage 1B and the project overall, visit the project website at www.nzta.govt.nz/p2b

We will continue to keep the community updated on the progress of our construction works via these e-newsletters, the project website and regular community information days. We are also happy to meet with and give presentations to business and community groups on request.

There was a great turn out at the recent Drury / South Auckland community information day.

Community information day | Te rā hapori

The Papakura to Drury project team recently attended the Drury / South Auckland community information day held on Saturday 30 November at the Drury School Hall. It was our busiest event yet with over 270 people attending!

From the conversations held on Saturday, some of the common queries raised about our project were:

• When is the next stage starting and how long will it take?

Stage 1B of the project officially began earlier this week and the estimated completion date is August 2030. This length of time is necessary due to the complexities of the project and the need to keep both SH1 and SH22 operating during construction.

• What is happening with the two bridges on Bremner Road and what happens to Auranga access when the bridge over the motorway is demolished?

The Bremner Road bridges over SH1 and Ngaakooroa Stream must be replaced with higher bridges as part of Stage 1B. During construction, there will always be at least two ways available to get in and out of Auranga. When the bridge over SH1 is demolished and rebuilt over ~2 years, Auranga residents and visitors can use either the Victoria Street / SH22 / Mercer Street intersection (which in 2025 will have traffic lights installed) or the existing Jesmond Road / SH22 intersection.

• Why wasn't the cycleway built as part of Stage 1A, at least between Papakura Interchange and Park Estate Road bridge?

Extra land outside the previous motorway boundaries was needed to build the shared walking and cycling path and this land needed to be purchased from adjacent landowners first – which can take time. The shared path was always intended to be built as part of Stage 1B between Papakura and Drury Interchanges, extending the existing Southern Path between Takanini and Papakura Interchanges.

• Is the SH22 / Great South Road intersection going to get traffic lights?

Yes, this intersection will be signalised soon as a required mitigation during coming phases of Stage 1B, when the Drury northbound off-ramp will need to be closed for an extended period of time, and the Drury southbound onramp for shorter periods. These ramps closures will mean more vehicles using Great South Road as the detour from Ramarama back to Drury Interchange. As the existing SH22 / Great South Road intersection has congestion and safety concerns, we are required to install traffic lights here first before any of the planned ramp closures.

The next community information day will be held on Saturday 22 February 2025. If you have any questions in the meantime about the Papakura to Drury project, feel free to contact us by replying to this newsletter or using our other contacts as listed in the "Contact Us" section below.

The old Police weigh station building being loaded on a transporter to be taken off-site.

New traffic lights | Ngā rama hou

On SH22 just west of Drury Interchange, the southern end of Victoria Street (beside the Drury sports complex) will be realigned directly opposite Mercer Street and upgraded with traffic lights. To allow for this intersection realignment, the old weigh station building opposite Mercer Street was removed last week so construction can begin. Our team has installed temporary fencing around the old weigh bridge site and put measures in place (such as silt fences) to protect the environment during our upcoming works.

This intersection will be signalised for the safety of motorists turning right into or out of Victoria and Mercer Streets. The traffic lights must be installed before the future demolition of the Bremner Road bridge across the motorway to provide a safe alternative access for the Auranga community.

Further to the west, we are also installing traffic lights at the SH22 / Great South Road intersection – which is a requirement ahead of the future motorway ramp closures mentioned earlier.

Looking ahead | E haere ake nei

During the coming months, our project works include:

• Building a large retaining wall needed for the realignment of Flanagan Road (on the southeastern side of Drury Interchange)

• Underground service investigations around Drury Interchange - including on the motorway, Great South Road, SH22, Bremner Road, Victoria Street and Mercer Street

• Working to realign the Victoria Street intersection with SH22 before installing traffic lights

• Starting works at the SH22 / Great South Road intersection to install traffic lights

• Building a temporary bridge on the south side of the existing Bremner Road bridge over the Ngaakooroa Stream for traffic to use while we rebuild the existing bridge over this stream.

P: 0800 796 796 - for construction-related queries

P: 0800 741 722 - for general project queries

E: p2b@nzta.govt.nz

W: www.nzta.govt.nz/p2b

VenitaAttrill

Sales&MarketingConsultant

M: 0212867792

E: venita.attrill@ljhooker.co.nz

KJ Klavenes

Sales&MarketingConsultant

M: 0275566194

E: knut.klavenes@ljhooker.co.nz

Christine Forster Administrator

E:: christine.forster@ljhooker.co.nz

Paula Cox

Sales&MarketingConsultant

M:: 021396977

E: paula.cox@ljhooker.co.nz

Anu Jay

Sales&MarketingConsultant

M :0223577554

E: anu.jay@ljhooker.co.nz

ShashikaFernando Administrator

M: 0273022588

E:: shashika.fernando@ljhooker.co.nz

Steve Reilly

Sales&MarketingConsultant

M: 021930352

E: steve.reilly@ljhooker.co.nz

Mark Eklund

Sales&MarketingConsultant

M: 0212446692

E: mark.eklund@ljhooker.co.nz

JohnnyCleven

Sales&MarketingConsultant

M: 0274816422

E: johnny.cleven@ljhooker.co.nz

DebbieHarrison

PropertyManager

M: 021303864

E: debbie.harrison@ljhooker.co.nz

Atesh Narayan

Sales&MarketingConsultant

M: 0212721912

E: atesh.narayan@ljhooker.co.nz

BrentWorthington

Principal/Licensee Agent

M:0292965 362

E: brent.worthington@ljhooker.co.nz

Mark Eklund

MarkEklund Sales & Marketing Consultant

021 244 6692

mark.eklund@ljhooker.co.nz

As an award-winning sales agent with substantial experience across multiple facets of Real Estate, Mark is passionate about the industry. It is his active listening skills and attention to detail that set him apart from others in the field. He is a consummate professional leaving no stone unturned to achieve the objectives of all parties involved in completing successful transactions.

Being involved in sales across every real estate demographic, Mark is at ease speaking with anybody and everybody and generates high levels of motivation and satisfaction from the many contacts, friendships, and relationships he has forged over the years.

Mark has strong negotiation skills, skills that he developed whilst serving New Zealand as a detective in the police which have helped him achieve great results for his buyers and sellers throughout his real estate career.

Mark is a goal setter but the goal that resonates most with him is to build lasting relationships He believes this is achieved through trust, honesty and communication, and it should be no surprise that a large part of his work is generated through repeat and referral business.When not talking property, talk to Mark about sport, music, food, wine, travel and of course his adult children of whom he is extremely proud.

JohnnyBright

AUCTIONEER

Johnny is proud to be a part of the team at Apollo Auctions NZ. Entering real estate in 2014, he has developed and honed his craft of auctioneering and negotiating skills to a level that now sees him as an industry leader. Johnny has worked and collaborated with some of the most notable agents, business owners and auctioneers across New Zealand.

With the fusion of his knowledge and skill together with his personable approach, Johnny creates the ultimate auction experience . He implements drive and dedication to each and every property that he calls - regardless of value, location or personal circumstances. Johnny’s performance style and welcoming nature allows him to capture the audience and motivate buyers. He will guide you through the process and create a solid platform to achieve the best possible outcome for your auction.

Johnny also has a passion for acting. With a Bachelor of Performing and Screen Arts, he has appeared in several TV commercials and films, his most widely recognized being ‘Falling Inn Love’, an American Netflix production which was filmed in New Zealand. He has also worked with the Auckland Theatre Company on a number of occasions.

He currently resides in Beachlands with his wife and two young children.

It’s rare in life that we get something for nothing with no strings attached, especially if it genuinely adds value. Nevertheless, that’s precisely I will give you. Expert home loan advice which has reliably proven to offer significant long-term financial advantage. I keep strict tabs on the country’s largest network of banks plus numerous smaller and second-tier lenders, so you don’t have to. What’s more, this comes at no cost to you because your chosen bank pays for the privilege. You have nothing to lose, yet have a higher chance of securing better terms. Rest assured - if there’s a superior deal out there for you, I’ll find it.

In the typically stoical world of finance, I offer a point of difference. Not only will you receive excellent independent and impartial advice, but you’ll have fun doing it. Even after 15 years in the mortgage arena, my enthusiasm for objectives and commitment to clients shines through at every turn. Endorsement comes from countless glowing testimonials and in my own words: “I’m at my happiest helping people navigate through difficult situations, giving hope and concrete opportunity where they previously had none.”

Prior experience as sales manager in the fields of telecommunications and pharmaceuticals, then later, a small business owner and private property investor, provided me with considerable business acumen across many industries. My customer-focused approach and personable demeanor also reflect a lifetime of experience in client relations. I credit travel to distant locations for creating an enduring interest in different cultures and honing my ability to relate well to the needs of the broader population. In particular, I soundly empathise with people relocating from other countries to make New Zealand their home.

To continue giving my professional best, I maintain balance by travelling and participating in seasonal sports such as paddle boarding and skiing. I enjoy indulging in my creative side; with landscaping, painting watercolours or improving my guitar playing prowess. Additionally, I actively support my community through Christians Against Poverty (CAPNZ), but above all, my wife and our five shared children always take centre stage.

There's little that I haven't seen in my time in the industry, priding myself on an ability to deal with the trickiest of scenarios, never turning anyone away. My philosophy of treating people how I'd like to be treated results in a 360-degree perspective which sets myself apart.

Get in touch if you need any expert guidance. Regards