Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Top Business Risks

It’s probably not a surprise that geopolitical volatility has surged into a list of the top 10 business risks worldwide. But cyber risk remains the number one concern globally, followed by business interruption at number two.

That’s according to Aon’s 2025 Global Risk Management Survey, which has tracked the most pressing risks for business decision-makers for nearly 20 years.

Geopolitical volatility rose 12 places since the last Aon survey in 2023, breaking into the top 10 global risks (at number nine) for the first time in the survey’s history—and is forecast to rise to fifth by 2028, said the survey report, which was based on interviews with nearly 3,000 risk managers, C-suite leaders, and executives in 63 countries.

Aon noted that the depth of business concerns about geopolitical volatility depend on the region and differing exposures to geopolitical flashpoints. However, businesses in all regions predicted that this risk would rise in their future list of business concerns.

“Cyber Attack or Data Breach” remains the number one current and future risk, according to survey respondents, as the rapid adoption of digital platforms and AI technologies has expanded the attack surface for threat actors, the Aon report said.

Respondents identified the top 10 global risks in 2025 as:

1. Cyber attack or data breach

2. Business interruption

3. Economic slowdown or slow recovery

4. Regulatory or legislative changes

5. Increasing competition

6 Commodity price risk or scarcity of materials

7 Supply chain or distribution failure

8. Damage to reputation or brand

9 Geopolitical volatility

10. Cash flow or liquidity risk

Aon’s 2025 survey also provided a forward-looking perspective on the risks business leaders expect to be most critical by 2028. Respondents identified the predicted top 10 future risks in 2028 as:

1. Cyber attack or data breach

2. Economic slowdown or slow recovery

3. Increasing competition

4. Commodity price risk or scarcity of materials

5. Geopolitical volatility

6. Regulatory or legislative changes

7. Business interruption

8 Artificial intelligence

9. Climate change

10. Cash flow or liquidity risk

Aon’s 10th Global Risk Management Survey, a biennial web-based research report, was conducted between April and June 2025 in 11 languages. The research gathered responses from 2,941 decision-makers.

Andrea Wells V.P. of Content

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Online Training Coordinator George Jack | gjack@ijacademy.com

PHLYSense is a property monitoring solution that installs in minutes. Organizations get real-time alerts if water is detected or temperatures reach a hazardous level. The program includes sensors and 24/7 monitoring and support, all at no-cost to policyholders with property coverage. Alerts can be sent through SMS text, email, and phone call, and the system can be managed through an innovative mobile app. Avoid costly damages and repairs. Simply set sensor devices in strategic areas of your building and add another layer of property risk mitigation. Enroll at PHLY.com/PHLYSenseInfo or call

News & Markets

Swiss Re Takes a Look at Hidden Behavioral Forces Behind Skyrocketing Jury Awards

By L.S. Howard

The exponential growth of liability claims costs and social inflation in the United States is being driven, in part, by changing juror sentiment and shifts in societal norms, according to analysis from Swiss Re.

“This growing gap between economic fundamentals and actual claims experience has been termed ‘social inflation,’ which is in large part driven by legal system abuse,” the article explained.

In its 2025 Behavioral Social Inflation Study, Swiss Re aimed to assess the behavioral reasons behind legal system abuse, which was based on a nationally representative survey of 1,150 U.S. adults who were presented with a series of randomized legal simulations.

“Crucially, the effect is not confined to Fortune 500 companies. In cases involving severe injury, jurors are nearly as likely to recommend high compensation against small and medium-sized enterprises (SMEs) as they are against large corporations,” the article added.

“We’re seeing growing strain on the civil justice system, with more lawsuits yielding damages that often outpace the actual harm. Jury awards in the tens of millions are becoming more frequent, shaped by emotion, not just evidence,” said Monica Ningen, CEO P&C Reinsurance US, Swiss Re, in a statement accompanying the report.

“Liability claims costs in the United States have entered a self-reinforcing spiral. Traditional economic drivers such as wage inflation, medical-cost trends, and CPI growth no longer explain the pace at which liability claims are escalating,” said an article published by Swiss Re, titled “Verdicts on trial: The behavioral science behind America’s skyrocketing legal payouts.” continued on page 14

“The findings confirm that juror sentiment has shifted decisively toward plaintiffs, and this shift is influencing verdicts in measurable ways,” said the article, which laid out the findings of the study.

“These rising liability costs don’t stay in

Figures 464 Miles

2

Eight months after the Palisades Fire destroyed almost 600 Malibu houses, the city has issued only two rebuilding permits. Delays are attributed to low insurance payouts, slow permit approvals and high costs. Prices for burnt-out lots are dropping as some former residents give up on returning.

The orbital height of a new mapping satellite called NISAR, short for NASA-ISRO Synthetic Aperture Radar. The joint U.S.-India mission, worth $1.3 billion, will survey virtually all the world’s land and ice masses multiple times. By tracking even the slightest shifts in land and ice, the satellite will give forecasters and first responders a leg up in dealing with floods, landslides, volcanic eruptions and other disasters. ISRO is the Indian Space Research Organization.

$1.5 Billion

A federal judge in California preliminarily approved a landmark $1.5 billion settlement of a copyright class action brought by a group of authors against artificial intelligence company Anthropic, according to the authors’ representatives. The proposed deal marks the first settlement in a string of lawsuits against tech companies, including OpenAI, Microsoft and Meta Platforms, over their use of copyrighted material to train generative AI systems.

$877,000

The U.S. Occupational Safety and Health Administration fined a Florida commercial painting contractor $877,000—one of the largest OSHA fines in recent years—six months after a worker fell from a bridge near Savannah, Georgia. Seminole Equipment Co., based in Tarpon Springs, Florida, failed to provide fall protection and life jackets to workers painting the Interstate 95 bridge over the Ogeechee River, OSHA said. Painters were removing scaffolding when Jose Hernandez Garcia fell and drowned in the river.

Declarations

Cannabis Risks

“We’ve had entire crops where, maybe the insured harvests 600 plants, [and] the next day, there’s a box truck that rams through their roll-up door and steals all of the product. They come in, and they’ll take whatever they can get their hands on.”

— When asked about the most significant exposures in the cannabis industry, Beth Ossino, claims manager at Golden Bear Insurance Company, pointed to theft and robbery. During Insurance Journal’s annual Insuring Cannabis Summit, Ossino recalled a couple of instances of devastating losses for insureds, including thieves carrying a safe out of a business and robbers making off with huge amounts of product.

Flat-out Fraud

“It’s just flat-out theft of taxpayer money… At the end of the day, he stole money from the citizens and masked it as legitimate fees.”

— Chris Yates, Texas Department of Insurance (TDI) fraud unit investigator, discussing the case of former insurance agent Carlyle Poindexter, who overcharged almost $300,000 in insurance premiums. Poindexter pleaded guilty to conspiracy to commit wire fraud in August and was sentenced to five years in federal prison and a $50,000 fine. Over six years, Poindexter charged Maverick County Solid Waste Authority $712,350 in premiums but gave Lexon Insurance Company just $329,313. He kept almost $300,000 plus a portion of commissions.

Sinkhole Protection

“I want you all to imagine being a newlywed starting a life with somebody, putting your life savings into a house because you have been told that this is the way that you build generational wealth; this is how you take care of your family moving forward. And then, because of a major rainstorm, your house, and everything in it is gone in an instant.”

— Pennsylvania Rep. Emily Kinkead, D-Bellevue, endorsing House Bill 589, which established an insurance fund for landslides, slope movement, and sinkholes through the state’s Department of Community and Economic Development.

Helene Recovery Continues

“I hope I never see another one in my lifetime, and I’m hoping that if I do, it does hold up. I mean, that’s all we can (do). Mother Nature does whatever she wants to do, and you just have to roll with it.”

— Vickie Revis, whose North Carolina home was swept away by the Swannanoa River in the wake of Hurricane Helene. After a year in a donated camper, she and her husband, Paul, will soon move into a double-wide modular home, also donated by a local Christian charity. It sits atop a 6-foot mound that Paul Revis piled up near the front of the property, farther from the river. At the time of the storm, their home was uninsured. They have since purchased insurance.

Electric Tractors

“If we were to mechanize all the smallholder farmers in the world, there isn’t enough diesel out there to power them. So, we have to find some other source.”

— Ajit Srivastava, an agricultural engineer and Michigan State professor, who is working to improve the viability of large-scale electric tractor adoption. Srivastava wants to help smallholder farmers, who grow about a third of the world’s food. Agriculture is among the largest sources of climate-warming emissions worldwide. Though tractors are a small culprit, experts believe an environmentally friendly machine would still attract buyers interested in sustainability.

Trial by Fire

“What we’ve learned in California and Oregon is it’s the non-economic damages that can really, really get you.”

— Andy DeVries at CreditSights, commenting prior to the announcement that Utility Xcel Energy Inc. has agreed to pay about $640 million to resolve claims that its power lines contributed to the 2021 ignition of the costliest wildfire in Colorado history. The company reached settlements with individual property owners, public entities and insurers ahead of a trial with billions of dollars stake. The company could have faced damages of more than $7 billion, including awards to victims for emotional distress. The company isn’t admitting fault or wrongdoing in connection with the settlements.

News & Markets

continued from page 8

the courtroom. They contribute to higher insurance premiums, reduced coverage availability, and increased costs for everyday goods and services,” she emphasized.

“The growing role of third-party litigation funding adds another layer of pressure, often prolonging cases and inflating awards. Given the magnitude of these costs, businesses must pass these pressures along the value chain, and ultimately, consumers bear the impact,” Ningen said.

The Case for Tort Reform

As a result of these trends, the report said, the case for tort reform is clear.

“Our research shows how public attitudes shaped by a desire to hold companies accountable and a receptiveness to high compensation demands create fertile ground for the plaintiff’s bar, often backed by third-party litigation funders,” the article said.

“Targeted tort reforms have historically helped restore balance to the system,” Swiss Re said, pointing to states like Florida, Georgia, and Louisiana, “where legislatures have introduced reforms to cap damages, limit attorney fees, and create transparency in litigation funding.”

For insurers and reinsurers, the study reinforces the scale and persistence of uncertainty in the U.S. liability market, but the data offer little hope for near-term relief, the article affirmed.

“These rising liability costs don’t stay in the courtroom. They contribute to higher insurance premiums, reduced coverage availability, and increased costs for everyday goods and services,”

“Legal system abuse shows no signs of abating, and pricing uncertainty remains extraordinarily high. Maintaining underwriting discipline through prudent limit structures, appropriate attachment points, and rate increases that reflect the underlying loss cost trend—is essential to sustaining profitability.”

Diving into the hidden behavioral forces behind legal system abuse, the report pointed to three key findings:

• Attitudinal trends: Litigation becomes a social norm. “At the heart of legal system abuse lies a fundamental shift in public

sentiment. Litigation is no longer viewed by the average American as a last resort or an excessive burden on society.” According to Swiss Re’s 2025 behavioral study, just 56% of respondents believe there are too many lawsuits in the U.S., which is a sharp decline from 90% in 2016. “This signals a major shift in perception, with lawsuits increasingly seen as a legitimate tool for exacting justice.”

• Behavioral scenario findings: It’s not the company, it’s the injury. To understand how attitudes toward litigation translate into actual monetary outcomes, survey participants were asked to weigh in on a series of real-world scenarios, which covered slip-and-fall incidents, motor vehicle accidents, and product liability cases. Swiss Re found that a clear pattern emerged: Injury severity, not company size, is the strongest driver of verdict behavior. “Large corporates drew slightly more blame and larger awards, but in most cases the differences were modest and not statistically significant.”

• Who’s on the jury matters more than you think. The survey results reveal a strong political, generational, and economic skew. For example, self-identified Democratic respondents selected award amounts that were 25% to 65% higher than those proposed by Republicans, with Independents tending to fall between the two groups in terms of award size.

Age and income levels were also factors affecting jury awards. “Younger respondents—especially those under 40—expressed significantly more plaintiff-friendly views than older generations,” the study said. At the same time, respondents with lower incomes “favored broader corporate accountability and were more likely to support legal action.” Swiss Re’s analysis determined that this group could “view the legal system as a form of redistributive justice, further reinforcing the trend toward higher awards.”

The article on the social inflation study was authored by Martin Boerlin, head of Casualty Pricing North America and chief underwriting officer P&C Reinsurance, and Surbhi Gupta, senior portfolio analyst and CUO for P&C Reinsurance.

News & Markets

Responsible AI Deployment Linked to Better Business Outcomes: EY

As broader adoption of AI technologies continues to accelerate, companies that implement more advanced Responsible AI (RAI) measures are pulling ahead while others stall.

According to the second Responsible AI Pulse survey from the EY organization, four in five respondents said their company has improved innovation (81%) and efficiency and productivity gains (79%), while about half report boosts in revenue growth (54%), cost savings (48%), and employee satisfaction (56%).

The global survey of large corporations also reveals that nearly all organizations report financial losses and widespread impact from compliance failures, sustainability setbacks, and biased outputs.

According to EY, Responsible AI adoption involves defining and communicating principles before advancing to implementation and governance. The transition from principles to practice happens through 10 RAI measures that embed commitments into operations.

The survey suggests greater adherence to RAI principles is correlated with positive business performance. For instance, those respondents with real-time monitoring are 34% more likely to see improvements in revenue growth and 65% more likely to see improved cost savings.

On average, organizations surveyed have already implemented seven RAI measures, and among those yet to act, the vast majority plan to do so. Across all measures, fewer than 2% of respondents reported having no plans for implementation.

“The widespread and increasing costs of unmanaged AI underscore a critical need for organizations to embed practices deep within their operations to not only reduce risks but also accelerate value creation,” commented Raj Sharma, EY Global Managing Partner, Growth & Innovation.

“This is not simply a compliance exercise; it is a driver of trust, innovation, and market differentiation. Enterprises that view these principles as a core business function are better positioned to achieve faster productivity gains, unlock stronger

revenue growth, and sustain competitive advantage in an AI-driven economy.”

EY’s survey insights were gathered in August and September 2025 from 975 C-suite leaders across 11 roles and 21 countries. All respondents had some level of responsibility for AI within their organization. Respondents represented organizations with over $1 billion in annual revenue across all major sectors and 21 countries in the Americas, Asia-Pacific, Europe, the Middle East, India, and Africa.

Other findings include:

• Inadequate controls for AI risks lead to negative impacts: Almost all (99%) organizations surveyed reported financial losses from AI-related risks, with 64% suffering losses of more than $1 million. On average, the financial loss to companies that have experienced risks is conservatively estimated at $4.4 million. The most common AI risks are non-compliance with AI regulations (57%), negative impacts to sustainability goals (55%), and biased outputs (53%).

• C-suite knowledge gaps in identifying appropriate controls: On average, when asked to identify the appropriate controls against five AI-related risks, only 12% of C-suite respondents answered correctly. Chief risk officers, who are ultimately responsible for AI risks, performed slightly below average (11%). As agentic AI becomes more prevalent in the workplace and employees experiment with citizen development, the risks—and the need for appropriate controls—are only set to grow.

• Citizen developers highlight governance and talent readiness gaps: Organizations face a growing challenge in managing “citizen developers”—employees independently developing or deploying AI agents. Two-thirds of surveyed companies allow this activity in some form, yet only 60% of them provide formal, organization-wide policies and frameworks to ensure these agents are deployed in line with responsible AI principles. Half also report they do not have a high level of visibility in employee use of AI agents. Companies that actively encourage citizen development were more likely to report a need for talent models to evolve in preparation for a hybrid human-AI workforce. These organizations cite the scarcity of future talent as their top concern.

Business Moves

National

White Mountains Insurance, Bamboo

White Mountains Insurance is selling a controlling interest in insurance distribution platform Bamboo to European private equity firm CVC in a deal that values the company at $1.75 billion.

White Mountains bought a majority stake in Bamboo in January 2024 for nearly $300 million.

Bamboo was launched in 2018 by leader John Chu. The company provides residential homeowners’ insurance and related products.

White Mountains is holding company that owns and manages businesses in the insurance and financial services industries.

The company will retain a 15% fully diluted equity stake in Bamboo post-closing, worth $250 million.

The deal is expected to close by the end of the year.

East

ALKEME Insurance, Alliance Brokerage Corp.

California-based ALKEME Insurance acquired Alliance Brokerage Corp., a Melville, New York-based property/casualty agency. The acquisition strengthens ALKEME’s presence on the East Coast, adding insurance and risk management expertise in both real estate and construction insurance.

Alliance Brokerage Corp. serves a range of clients. Alan and Jonathan Zack head the firm.

ALKEME, Gotham Brokerage Co., Gotham Brokerage

California-based ALKEME Insurance acquired Gotham Brokerage Co., a New York City insurance agency founded 60 years ago. Gotham specializes in insurance for condos, co-ops, and apartments with a concentration in the high-value real estate markets of Brooklyn and Manhattan. The acquisition enhances ALKEME’s personal insurance capabilities.

Northern Neck Insurance Co., Frederick Mutual Insurance Co.

Northern Neck Insurance Co. and Frederick Mutual Insurance Co. intend to affiliate, pending regulatory approval, in a move to grow across the Mid-Atlantic region.

The partnership will unite Northern Neck’s personal lines focus with Frederick Mutual’s commercial lines experience. The insurers will continue to operate under their existing brands. Together, the companies will have more than 90 employees and 450 independent agency locations in Virginia, Maryland, Pennsylvania, Delaware, the District of Columbia, and North Carolina.

Frederick Mutual Insurance Co. is jointly owned by Frederick Mutual Group, Inc., a stock corporation with majority ownership, and Mutual Capital Investment Fund (MCIF). Northern Neck has agreed to purchase MCIF’s preferred stock. Upon closing, the preferred stock will convert to common stock. After the transaction closes, management intends to pool results for both companies.

As part of the agreement, Northern Neck will enter into a management agreement with Frederick Mutual, with Peter Cammarata as president and CEO of both organizations and Northern Neck’s board of directors providing unified governance.

The transaction is expected to close before the end of 2025.

Novacore, Minglewood Risk

Novacore, the specialty insurance managing general agent (MGA) formerly the U.S. commercial division of NSM Insurance Group, will acquire Minglewood Risk, an MGA specializing in habitational and real estate coverages.

Founded in Langhorne, Pennsylvania, with core markets in New York, New Jersey, Pennsylvania, Colorado and California, Minglewood Risk specializes in commercial package and excess and umbrella insurance for residential real estate.

Minglewood Risk will become part of Novacore’s real estate segment, with a focus on expanding into the five boroughs of New York City. Novacore partners with more than 20,000 agents nationwide and offers more than 15 specialty programs.

Terms of the deal were not disclosed.

Midwest

The MEMIC Group, The Dakota Group Workers’ compensation specialist The MEMIC Group, led by parent company Maine Employers’ Mutual Insurance Company, entered into an agreement to acquire The Dakota Group, including Risk Administration Services, Inc. and its four affiliated insurance services companies.

The combining of the companies will make The MEMIC Group the third largest multi-state workers’ compensation specialist in the U.S., with estimated combined 2025 writings of more than $600 million and coverage for more than 25,000 employers nationwide.

Both companies are rated A (Excellent) by A.M. Best.

This acquisition includes the purchase of The Dakota Group’s subsidiary-affiliated service companies, including OHARA LLC, TLC Advantage LLC, and Precision Bill

Review LLC. These entities provide both insurance coverage and cost-containment services, such as case management, PPO networks, and medical bill review, to a broad client base across the Midwest.

The transaction also includes Risk Administration Services, Inc. (RAS), which serves as attorney-in-fact to the reciprocal insurer Dakota Truck Underwriters (DTU), as well as a controlling interest in First Dakota Indemnity Company, which is managed by RAS.

With a significant presence in the upper Midwest, The Dakota Group has a growing market share in workers’ compensation that aligns with The MEMIC Group’s growth along the Eastern seaboard.

The Dakota Group is the leading voluntary workers’ compensation writer in South Dakota and a top writer in Minnesota, Iowa, Kansas, and Nebraska.

The transaction is subject to regulatory approval and is expected to be finalized in early January 2026.

World Insurance Associates LLC, ACB Insurance Inc.

World Insurance Associates LLC acquired the business of ACB Insurance Inc. ("ACB") of Indianapolis, Indiana on June 1, 2025. Terms of the transaction were not disclosed.

ACB provides insurance to individuals, families and businesses. The agency is led by Corey Kunkleman, who joined ACB in 2003 as president.

WalkerHughes, Brady Benefits

WalkerHughes Insurance added Brady Benefits, a Fort Wayne-based Employee Benefits brokerage, to its growing Midwest platform.

Brady Benefits, led by Matt Brady, specializes in group health and ancillary benefits. Brady and his team, including Shannon Martin and Angie Lash, will join WalkerHughes,

South Central

Inzone Insurance Services, Arkansas Best Insurance Agency Inc.

Inszone Insurance Services announced its expansion into Arkansas through the

acquisition of Arkansas Best Insurance Agency, Inc., an independent agency based in Hot Springs, Arkansas.

Founded in 1905, Arkansas Best Insurance Agency has served clients across Arkansas and neighboring states for well over a century. Michael Lipton has served as primary owner for 15 years.

Arkansas Best Insurance Agency has operated as a generalist, providing insurance solutions for businesses of all sizes while also maintaining a presence in personal lines.

Amynta Group, Global Surety LLC

Amynta Group has entered into a definitive agreement to acquire Global Surety, LLC, International Sureties Limited and International Sureties SARL (collectively, “International Sureties”), a commercial surety broker based in New Orleans, Louisiana.

The transaction is subject to regulatory approvals and is expected to close during the fourth quarter of 2025. Terms of the transaction were not disclosed.

International Sureties, founded in 1972, is a specialty surety broker, providing a broad range of commercial surety products, including admiralty, court, bankruptcy, logistics and license and permit bonds.

The company provides surety bond services for a wide variety of industries operating from offices in New Orleans, the UK and Belgium.

Clark Fitz-Hugh, president and CEO of International Sureties, will continue to lead the business.

Southeast

King Risk Partners, LH Griffith & Co.

King Risk Partners, headquartered in Gainesville, Florida, acquired LH Griffith & Co., an agency with offices in Walterboro and Goose Creek, in southeast South Carolina.

The Griffith agency was founded 25 years ago. Heath Griffith is principal. The merger will guarantee continuity of service to parts of coastal South Carolina.

King now has offices in 16 cities in North and South Carolina.

Gifford Carr Insurance Group, Omni One Insurance Agency

Gifford Carr Insurance Group, headquartered in Ottowa, Ontario, made its first expansion outside of Canada by acquiring Omni One Insurance Agency, part of the Team Aubuchon group, based in Coral Gables, Florida.

The Florida agency will operate as Omni One Insurance, by Gifford Carr, and the firm's team will remain on board. The agency offers home, auto, commercial and other lines of property-casualty insurance.

Matthew Carr is listed as president of Gifford Carr and as CEO at Omni One.

West

Farmer Woods Group,

iinsure

Farmer Woods Group acquired iinsure, based in Scottsdale, Arizona.

iinsure clients will continue working directly with Jeff Martin, owner of iinsure, while also gaining access to Farmer Woods Group's resources.

iinsure is an independent, multi-line insurance agency specializing in complex commercial and personal profiles.

Farmer Woods Group is a Leavitt Group affiliate based in Phoenix, Arizona. Leavitt Group a privately held insurance brokerage with a network of more than 85 agencies and 250 locations across 28 states.

The McGowan Companies, Limit

The McGowan Companies acquired Limit, a digital wholesale insurance brokerage headquartered in Covina, California, via an asset purchase agreement.

After the transaction is closed, Limit will continue to operate under the “Limit” brand, within The McGowan Companies envelope, led by Shea McNamara, Limit’s facility director. All Limit staff will remain in place.

Limit has two divisions: Limit Wholesale and Limit AI. Limit Wholesale is an Artificial Intelligence-enabled, digital, wholesale insurance brokerage that specializes in cyber liability and technology errors and omissions.

The McGowan Companies is an insurance broker and intermediary located in Fairview Park, Ohio.

Mary Ann Stewart

National Allianz Commercial, with U.S. headquarters in New York City, named Mary Ann Stewart as regional head of liability, North America. Based in Chicago, Stewart is responsible for the strategic direction and management of Allianz Commercial’s North American liability portfolio and talent development across the U.S. and Canada. Stewart joins from Markel, where she most recently served as senior director, global casualty underwriting, within Markel’s casualty business line.

International specialty MGA Rokstone appointed Adrianna Allman and Charles Turgeon as senior underwriters in its North American inland marine division. Joining from AIG and based in Boston and San Francisco, respectively, they have expertise in inland marine trucking, extending Rokstone’s reach across North America.

Jessica Cullen was appointed head of excess casualty and operations. Cullen joined Lockton in 2024 as head of the U.S. casualty practice, London. She has 20 years of industry experience, most recently serving as managing director of the casualty practice at Gallagher. Cullen will report to Rapciewicz.

Hippo, headquartered in San Jose, California, appointed Robin Gordon as chief data officer. Gordon spent the past decade in executive roles as chief data officer and chief technology officer at global companies including Blackstone, KPMG and CoreLogic. She also served as global chief data and analytics officer at MetLife.

Howden US appointed Christine Palomba as deputy head, natural resources, Howden US, headquartered in Columbia, South Carolina. Palomba has 29 years of industry experience, most recently at Aon, as managing director, U.S. power and renewables practice leader. Palomba's appointment follows the announcement of Mike Parrish as CEO, Howden US, to lead Howden's U.S. retail broking business.

eastern region leader for major accounts excess casualty, managing underwriting operations.

East

AXA XL, in Stamford, Connecticut, hired Eric Judd as an executive underwriter on its energy underwriting team in the Americas in New York. With over three decades of experience, Judd previously served in senior underwriting roles at Zurich North America, Liberty International Underwriters and Starr Insurance.

Insurance broker Willis has appointed Steve Blumhagen as a producer in the Upstate New York market. Based in the Buffalo office, Blumhagen has over 10 years of experience in property/casualty insurance. He most recently served as practice leader for property and casualty at USI.

Brokerage Lockton appointed Peter Rapciewicz as U.S. casualty leader. Rapciewicz has over 20 years of insurance industry experience, including over a decade of leadership at Lockton.

Most recently, he served as alternative risk solutions practice leader. Rapciewicz will oversee the strategic direction and growth of Lockton’s casualty offerings across the U.S.

QBE North America, headquartered in New York City, appointed Jayne Cunningham as senior vice president and environmental underwriting leader. Based in North Carolina, Cunningham has over 30 years of insurance experience, including more than 20 years of leadership in the environmental space. Before joining QBE, Cunningham previously held roles at Beazley, XL Capital, Zurich and AIG.

MSIG USA , headquartered in Warren, New Jersey, appointed Martin J. Sullivan as chairman of the board of MSIG Holdings (U.S.A.), Inc. With more than five decades of experience, Sullivan previously served as president and chief executive officer of AIG Inc., deputy chairman of Willis Group Holdings plc, and, most recently, senior advisor at Lightyear Capital LLC.

Insurance agent Jason Bartow was elected president of the Professional Insurance Agents of New York State (PIANY), an association for independent insurance agents. Bartow is commercial lines executive vice president of Eugene A. Bartow Insurance Agency Inc. and Jebb Brokerage Inc.

Chubb, headquartered in New York City, appointed Joe Gaspero as senior vice president, national account segment leader of major accounts excess casualty. Based in Philadelphia, Gaspero has nearly 15 years of insurance industry experience, joining Chubb in 2013. He most recently served as

Bartow is co-chairperson of the PIA Northeast Regional Carrier Program; chairperson of the agency operations, carrier relations and Industry Affairs Committee and treasurer of the Agency Advocacy Coalition, as well as a member of PIANY’s executive/budget & finance and government affairs committees and the Long Island Advisory Committee.

The association also elected new officers to serve

Jessica Cullen

Peter Rapciewicz

Martin Sullivan

Christine Palomba

Joe Gaspero

Jayne Cunningham

Robin Gordon

in 2025-26: President-elect

Michael Loguercio Jr., of Ridge, N.Y., producer for BELFOR Property Restoration; First Vice President Jorge Hernandez of Merrick, N.Y., owner of North Franklin Brokerage Inc.; Vice President Eric Cohen of Fairlawn, N.J., CEO/managing director of Benefit Quest Inc./Eric Cohen Insurance; Treasurer Ed Chadwick of Buffalo, N.Y., who works for Jencap Specialty Insurance Services; Secretary Justin Fries of Roslyn, N.Y., owner of Garber, Atlas, Fries & Associates in Oceanside, N.Y. Richard Andrews is the immediate past president. Andrews is the owner/principal of Andrews Agency in Ithaca.

Midwest

Zach Posey joined World Insurance Associates as the leader of market relationships. Posey, who is based in Chicago, spent the past 15 years at Aon plc, where he most recently served as managing director of Inpoint, the firm’s management consulting and advisory arm. Before that, he spent 10 years in Aon’s National Casualty practice.

Alliant Human Capital, a division of Alliant Insurance Services, appointed Brian Muller as vice president. Muller has over 15 years of experience in corporate and consulting HR. Based in Columbus, Ohio, he joined Alliant in 2025. He began his career in the retail industry and later held consulting roles with several of the nation’s largest insurance brokerage and consulting firms.

South Central

Alliant Insurance Services, headquartered in Irvine,

California, hired Alex Gramling as senior vice president within its employee benefits group. Based in Fayetteville, Arkansas, Gramling serves a national client base. Before joining Alliant, Gramling was senior director, total rewards at Tyson Foods. He previously served as first vice president and lead consultant at Alliant.

Benefits consultant Terry Cox also joined Alliant as senior vice president within its employee benefits group. Based in Austin, Texas, Based in Austin, Texas, Cox serves a national client base. Cox has over three decades of experience in the health and benefits industry. Before joining Alliant, Cox served as a senior principal and sales consultant with Mercer.

IMA Financial Group, headquartered in Denver, Colorado, made two leadership appointments in its Houston, Texas, office. IMA named Joey Dryden as Houston market president. Dryden continues his production responsibilities while partnering with both the property and casualty and employee benefits teams.

IMA also hired its first local employee benefits leader. Will Ogilvie has over 16 years of experience consulting with private and public sector employers, school districts, municipalities, and non-profit organizations. Before joining IMA, Ogilvie served as senior vice president, life and health at Stephens Insurance LLC.

Southeast

ICW Group Insurance Companies, headquartered in San Diego, California, named

Tracey Estes as chief underwriting officer of ICW Specialty, a newly formed business unit that includes VerTerra Insurance, ICW Group’s excess and surplus lines carrier. Estes and her team will be based out of Atlanta, Georgia. Estes has over 20 years of insurance industry experience, most recently serving as head of casualty at MSIG USA. Before that, she was an executive vice president at Arch Insurance and held several leadership roles at AIG.

The CRC Group, based in Charlotte, North Carolina, named Brennan Paris chief revenue officer of CRC Specialty. Paris will also remain president of CRC Select, CRC Specialty’s binding operations, and oversee revenue growth for CRC Specialty’s brokerage, Select, and Insurisk divisions. Paris joined CRC Specialty in 2019. He previously served as the director of business development for Markel.

USG Insurance Services added Shannon Smith as associate producer/broker in its Georgia office. Smith, based in Senoia, Georgia, has seven years of experience in casualty risk placement in the excess and surplus market and is a licensed property and casualty agent in Georgia. Smith previously worked at Amwins, an insurance brokerage.

Alliant Insurance Services, headquartered in Irvine, California, hired Nick Martin as senior vice president within Alliant Specialty to lead the

company’s national alternative risk transfer platform. Martin, based in Atlanta, previously spent over a decade at Lockton Companies, most recently serving as vice president and alternative risk solutions consultant.

West

IMA Financial Group, Inc. named Greg Boothroyd chief people officer. Boothroyd has over 15 years of human resources experience across multiple industries and leadership positions. He most recently served as vice president of HR business solutions and chief of staff to the CEO at Vail Resorts. IMA is headquartered in Denver, Colorado.

bolt expanded Curtis Scott’s role as head of strategy and industry verticals. Scott will lead bolt’s enterprise vertical strategy and North America business planning. Scott has over 15 years of global experience, most recently serving as executive vice president, future mobility and digital economy at Aon. Scott also held roles at Lyft as vice president, GM core services and Lyft Business, and Uber as global head of insurance. bolt is headquartered in San Francisco, California.

Tracey Estes

Nick Martin

Greg Boothroyd

Curtis Scott

Closer Look: Coverage Gaps

Risk Reality vs. Commercial Insurance: Coverage Holes Exposed

By Susanne Sclafane

Two recent reports—one reviewing property and business interruption risks and the other, liability—highlight a growing divide between escalating risk and shrinking insurance coverage. They also suggest decision-makers need more insight into the risks they face.

A written report from FM, titled “Ready for the Storm: Closing the Extreme Weather Resilience Gap,” and a webinar report from Zywave, “A Look Behind the Headlines: Casualty Market Insights,” both offer data points showing that businesses are buying less insurance to cover growing risks, with costs being a major factor. And both suggest that while risk decision-makers are aware of escalating risks, they may be seriously underestimating the degree of risk specific to their businesses or the regions in which they operate.

Jim Blinn, principal account executive for Zywave,

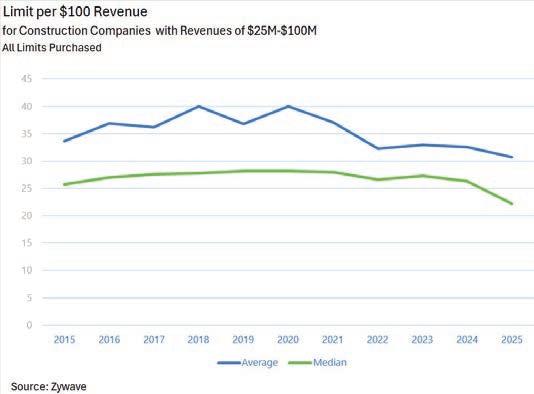

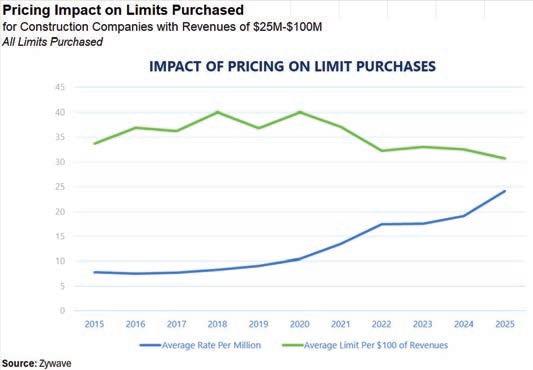

presented a series of graphs displaying escalating excess liability insurance rates per million (per million dollars of program limit), ever-increasing loss severities, and declining limits purchased for casualty insurance in recent years. He called out the limits picture as a “concerning trend.”

“It raises the possibility that organizations are making ill-informed decisions relative to the limits they are purchasing,” Blinn said, before he and co-presenter Senior Account Executive Lauren Boehm highlighted the value to insurance

buyers of reviewing litigation outcomes specific to their business types with Zywave models to better inform their limits purchases.

The mutual insurer, FM, didn’t directly list buying more insurance among recommendations in its property-based report. But like Zywave, FM offered recommendations grounded in the insurer’s expertise—delivering longterm risk and resilience insights—when considering strategies to deal with rapidly evolving extreme weather risk hitting their businesses directly or indirectly impacting them through events at supplier locations.

“Minimizing your insurance coverage to cut costs is a false economy. Instead, taking informed, concrete action to boost resilience—throughout the lifecycle of an asset—can not only minimize the risk but keep insurance markets open and affordable,” according to a concluding page in the FM report summarizing recommendations.

Coverage Gaps Quantified “Insurance is, of course, a

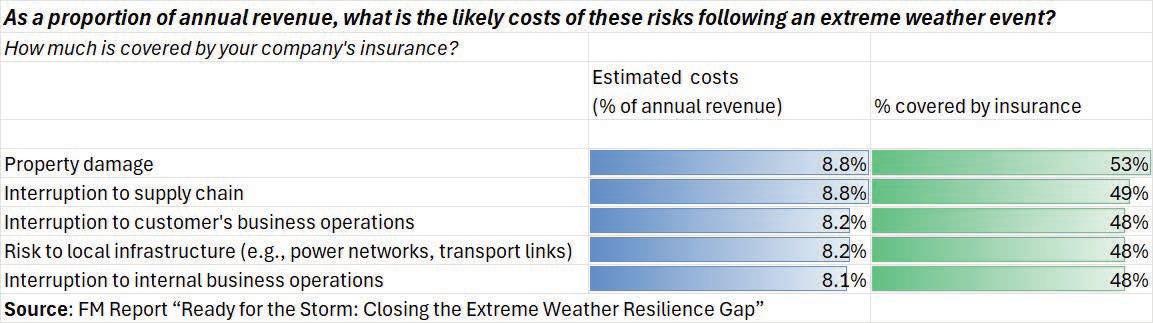

vital tool in mitigating the potential financial impact of extreme weather events.” But respondents to an FM survey reported that “their current insurance policy covers less than half of the potential cost of extreme weather’s various effects,” the FM report says, summarizing one of the key results of a survey of 800 risk decision-makers.

Asked about insurance coverage for 11 specific weather-related risks, these risk decision-makers—half from the C-suite and half from risk management in industrial, manufacturing, and technology businesses around the world with revenue ranging from $250 million to more than $10 billion—indicated that property damage was the only weather-related risk that was more than half covered. And that risk was only 53% covered.

On top of page 21 we show the responses for five of the 11 categories of extreme weather events for which respondents said that likely event loss costs could be 8% or 9% of their annual revenue but that insurance covered 46%-53% of those costs.

Brokers were more pessimistic. FM surveyed 150 insurance brokers who estimated, on average, their clients’ insurance would cover around 40% of the losses experienced due to an extreme weather event.

In an earlier section of the report, broker survey results also suggested that risk decision-makers aren’t fully aware of their risks. Only about two-thirds (67%) of brokers surveyed believe their clients are “mostly” or “fully” aware of how exposed their operations are to extreme weather. That compares to 95% of CEOs and risk managers surveyed.

But in this section of the report, FM pointed to the cost of insurance, rather than

awareness, as the main issue fueling a coverage gap.

Forty-four percent of the buyers surveyed reported that the cost of insurance is too high to secure full coverage— representing the largest share of responses among the risk decision-makers. Similarly, the largest share of brokers surveyed—49%—said cost was the key reason full coverage hasn’t been purchased.

The report noted some opposing factors fueling the problem: a frequency of catastrophic weather events that has forced insurers to increase rates, and rising inflation overall that has put buyers under pressure to focus on short-term cost reduction.

“When insurance rates are going up, risk managers face the question: ‘Why are we spending so much on insurance?’” said Adriano Lanzilotto, VP, client and partner learning at FM.

The report also indicated that one-third of risk decision-makers ranked limited availability of insurance among their top three challenges in mitigating the risks of extreme weather events.

At the Zywave event, Blinn said he didn’t think availability problems explained the declining limits trends for the sizes of companies his firm studied.

“The limits that we’re seeing that organizations of this size are buying [are] not that huge. And so I think there is availability but not necessarily a desire to purchase it at these [levels] of pricing,” he said, referring to an example that he and Boehm repeated throughout the event: construction companies with between $25 million and $100 million in revenue.

Instead of surveying buyers, Blinn used commercial policy data from Zywave’s benchmarking data to compare trends in limits purchased for these construction companies with prices of insurance coverage.

is $1 million, Blinn specifically showed that average casualty umbrella limits per $100 revenue fell about 25% between 2018 and 2025, while the average rate per million dollars of program limit more than doubled. Does this limits reduction make sense when considered against casualty loss trends?

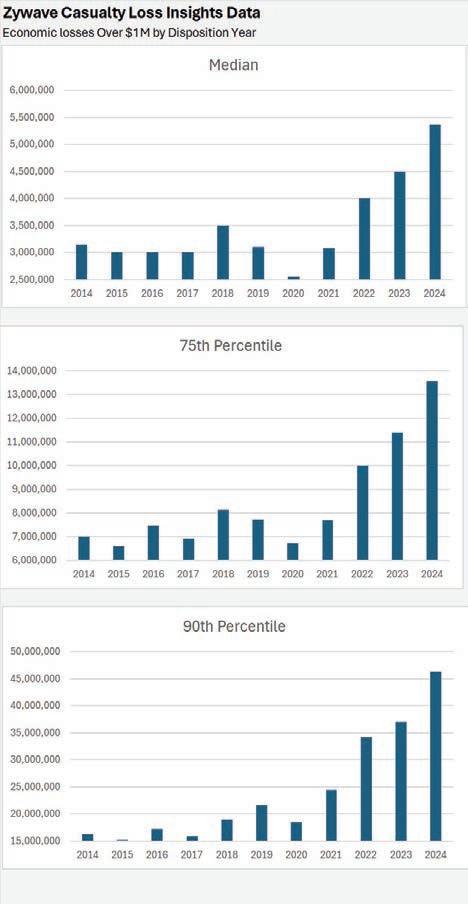

While social inflation and litigation are hot topics, an analysis based on loss data from Zywave’s Excess Casualty Loss Insight Data revealed some eye-opening pops in loss severity.

On page 22, we have captured some of the median, 75th percentile, and 90th percentile loss amounts Blinn displayed for casualty cases in the data base (general liability and auto liability for all types of companies, not just for construction companies, by case disposition year for the last decade).

The graphs reveal that the median casualty loss amount in excess of $1 million jumped more than 70% to over $5 million in the past decade, while the 75th and 90th percentile figures nearly doubled and tripled—to more than $13.5 million and more than $46 million, respectively.

“That hook upward is what insurance companies are dealing with as they think about their pricing,” Blinn said. “This is part of the reason that this median pricing has gone up,” he stated.

Increasing Risk Awareness

Moving from the representations of all the casualty claims to a specific example corresponding more closely

The above graph shows an average limit per $100 of revenue of $30/$100 in 2024, which Carrier Management calculates to be $7.5 million of program limit purchased by the smallest firms in the example—those with $25 million in annual revenues—and $30 million for the $100 million annual-revenue firms. continued on page 22

Noting at one point that the typical retention for the casualty insurance programs

Closer Look: Coverage Gaps

continued from page 21

to the example that Blinn referred to in the limits discussion, Boehm zeroed in on some loss and limits benchmarking data for construction companies. Imagining a construction firm looking to renew its casualty program with $10 million of umbrella limit ($1 million retention) and facing a 20% price hike, she was able to show that that limit was right in the middle of its peers in a benchmarking analysis.

Going further, she showed details of losses experienced by similar firms that would have exceeded lower selected limits.

Blinn later illustrated the variations in average loss amounts in excess of $1

million for different industries, different firm sizes, and different jurisdictions where cases are brought.

Separately, Swiss Re recently reported that injury type mattered more than company type or company size as a determinant of jury verdict amounts in liability cases.

Back in the property world, FM’s report suggests that risk decision-makers need to get a better handle on the weather risks they face, too. “While most businesses are confident they understand the nature of the risk, FM’s research shows they may not have the full picture,” wrote Dr. Louis Gritzo, staff senior vice president, chief science officer, FM, in a foreward to the report.

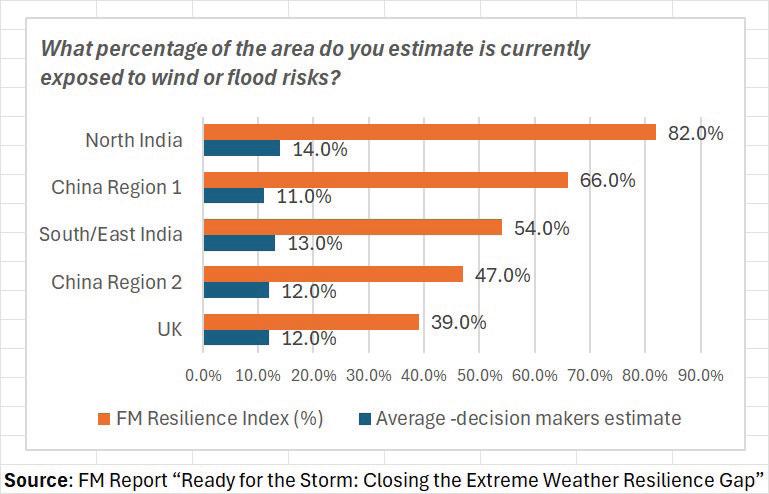

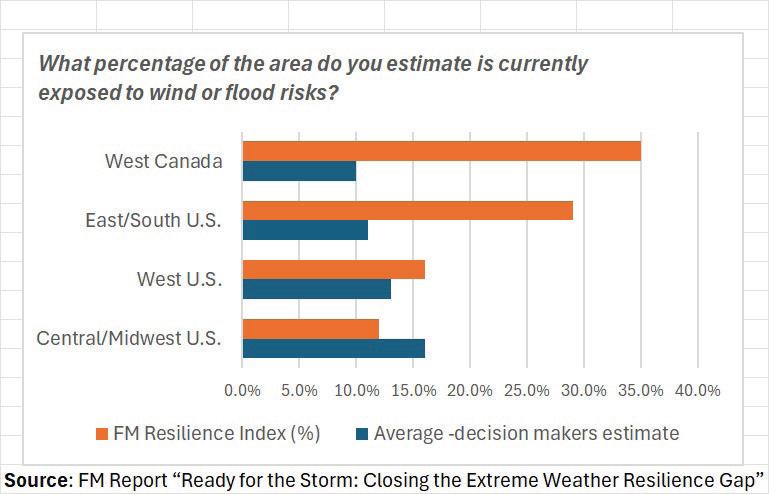

An analysis in the report showed a particular lack of extreme weather risk awareness by location. FM specifically asked risk decision-makers to consider the country or region in which their most critical businesses are based and to estimate how much of the economic activity in that area is exposed to wind or flood. The insurer then compared these estimates with FM’s Resilience Index, a ranking of 130 countries and territories’ resilience to risk, which includes a measure of their wind and flood exposure. The comparison revealed that 74% of risk decision-makers underestimate the exposure when compared to calculations in the FM Resilience Index. Estimates varied

significantly by country and region, but businesses with operations in North India, parts of China, and the UK substantially underestimate the wind and flood exposures of these areas. For example, while the FM Resilience Index indicates that 82% of Northern India is exposed, risk officers estimated a 14% exposure—a gap of 68%.

There were gaps of 20% or more in half of the 17 regions the FM analysis asked about. Risk decision-makers were better able to estimate exposure in North America, actually overestimating their exposure in the Midwest vs. the FM Resilience Index.

“Awareness is all about education, and it is incumbent upon insurers like FM to use all our expertise and insight to provide that to corporates and their brokers,” said Benedict McKenna, division claims manager for the UK and Asia Pacific at FM.

This is why FM invests significantly into exploring the science of changing weather patterns. But tracking the weather alone won’t provide a complete picture of a business’s risk exposure, the report stresses, noting that the impact of extreme weather on a given site is specific to its individual characteristics and that the evolution of business practices and building design is changing the nature and severity of risks.

“You may have two facilities located two miles away, and exposures may be very different,” said Stuart Keller, chief engineer of FM in the report. “That’s why site-level assessment is really critical.”

‘A Better Way’

Beyond the survey results, the FM

report focuses on a message on the benefits of investing in resilience measures— ranging from embedding risk engineering into the design and construction of new sites to conducting regular site inspection of existing sites to extreme weather.

Businesses’ focus on the cost of insurance may explain “why many powerful measures to mitigate extreme weather risk are under-adopted… Ultimately, though,

this short-term view is leaving businesses exposed,” the report says.

“A better way is possible,” the FM report stresses.

“Investing in resilience against extreme weather creates a virtuous circle, in which insurance savings can be reinvested in further risk mitigation measures. While there may be extra upfront costs, a more strategic approach to resilience can make a real difference to the cost—and availability—of insurance.”

FM noted that optimizing insurance spending by investing in resilience “requires a collaborative relationship with insurers.” But using the words of one interviewee for this report, some buyers

view their insurers as risk “police” and try to keep interaction to a minimum.

“It’s difficult for some clients to move from viewing insurance as occupying a risk oversight role to one of mutual loss prevention,” Dr. Gritzo said. “That is our challenge as an industry: to partner with clients and move from transactional oversight to working together to mitigate the risks.”

He suggested that FM’s mutual model is conducive to a more collaborative relationship, noting that FM issued nearly $1.5 billion in membership and resilience credits to our clients in 2024 to improve their resilience.

This story was originally published in Carrier Management.

Sclafane is Executive Editor of Carrier Management, a publication of Wells Media Group serving property/casualty insurance carrier executives.

Closer Look: Commercial Property/Condos

What to Consider When Building Insurance Programs for Aging Properties

In July 2021, after the collapse of the Champlain Towers

By Patrick Wraight

South in Surfside, Florida, the city of Miami ordered structural inspections of all buildings over 40 years old. Since then, two other condominium buildings have been deemed unsafe and evacuated. The residents of Crestview Towers were ordered out of their homes in July 2021, and the city allowed them to return in April 2025. According to a CBS News Miami online article, even though the city is allowing residents to return, some are still concerned about the safety of the building, and during the building’s retrofit, many of their units suffered damage that hasn’t been fully repaired.

This highlights some of the issues that come up with older buildings, and specifically with their insurance programs. I’d like to highlight a few areas, including underwriting and pricing challenges, claims problems, ordinance and law coverage requirements, and some risk management strategies for condo associations to consider.

Underwriting Aging Properties

Sometimes, as underwriters, we receive applications that paint a glowing picture of a risk. It’s the way the agent and applicant want us to see their building. It’s not wrong or false normally. It’s just optimistic.

The problem with older buildings is that applications may be too optimistic about their actual condition. Underwriters must evaluate these buildings as they exist today, not what they were like when they were built.

Consider a high-rise condominium building with a requested replacement cost of $10 million. What does an underwriter want to know about the building? The agent has already sent in the basic information, like year built, construction class, status of the sprinkler system, the type of occupancy, how much of the building has a commercial occupancy, whether or not there are short-term rental

spaces, and the like. That’s a baseline for information that an underwriter may ask for, but other items might cause an underwriter to dig deeper. Depending on what the loss runs look like, or whether or not they have been submitted, the underwriter will ask for more information, such as the last building structural report, data related to the ages of four critical building systems (HVAC, electrical, plumbing, and roof), including when they were inspected, replaced, or upgraded, and pictures. There will always be more pictures requested.

When the underwriter understands the entire picture of the risk, that’s when

decisions are made. In the best situations, the underwriter approves the risk without any coverage restrictions, at a limit of insurance reasonably close to what the insured requested, and at a premium that can be afforded. The problem comes when the underwriter sees things like deferred maintenance, a lack of loss history, or a 40-year-old building where no structural or critical system updates have been made. If the underwriter finds any of those items (along with other potential red flags), conversations will need to be had. The underwriter may offer to write the policy on the condition that certain items be inspected, repaired, or docu-

mented before coverage can be bound. She may also impose certain coverage restrictions, such as adding an Actual Cash Value for roofing material endorsement, providing coverage only for the first $1-$2 million of replacement cost, or declining to offer a quote at all.

Then there’s the issue of price. It will be high.

Losses Will Tell the Tale

Once the policy is written, there is also the potential issue of how it will respond in the event of a claim. Will there be enough coverage? Will the coverage respond in the way that the insured needs it to?

When a building is damaged, and the insured contacts their insurance company, the first thing that a company will do is determine whether or not coverage is in place for the claim. So, they will take the information, confirm that the policy exists, and if it does, then confirm that the building is listed on the policy. There are more details than that, but that’s the essence of it.

Once it’s determined that coverage exists, the work of adjusting the claim begins. Statements are recorded. Pictures are taken. Measurements are done. When all of the adjusting happens, in a perfect world, the adjuster tells the insured how much they estimate the claim to be worth, the insured receives estimates that agree with the adjuster, checks are written, work gets done, and the building is back in shape in relatively short order.

However, when you’re dealing with an older building, it’s not that simple. Consider buildings like Crestview Towers, which broke ground in

1969 and opened for occupancy in 1972. Crestview Towers was built under building codes that were in effect in 1972. The building codes in that area have been updated every two to three years since then, and when building codes are updated, older buildings do not have to comply with the changes until certain renovations happen, or the building is damaged and needs repair.

Even if the building was properly insured on the date when it was completed, over the following 50 years, it becomes more difficult to make sure that the cost to replace it matches the limit on the policy. Some policies include an inflation guard optional coverage. This optional coverage will increase the limit of insurance on covered property (the building) by a set percentage annually. It also increases the limit of insurance daily based on a fraction of the annual

percentage.

If we consider a building that had an initial replacement cost of $1,000,000 and an inflation guard percentage of 5%, we find that the building limit will be $1,050,000 after the first year. If the policy is allowed to renew annually, keeping the inflation guard in place and not adjusting the limit of insurance based on new cost estimates, after 50 years, the limit of insurance would be approximately $11,500,000. This seems like a huge change in limit, and it is, but is it enough?

We understand that this isn’t a reasonable example because insureds do not stay with insurance companies for that long, and insurance companies won’t go that long without running an updated cost estimator on the value of the building. When the insurance company increases the limit of insurance based on their updated cost estimate, the insured begins to

look for coverage elsewhere, and often tries to justify their old limits so that the premium doesn’t go up.

Additionally, the older a building gets, the more out of code it is. This means that even in the event of a partial loss, the local code enforcement officer arrives on site to inspect before issuing building permits for the repairs and finds that the building needs some upgrades. Those upgrades might be related to federal requirements of ADA, or simply updates of critical systems within the building. That’s another issue.

A Primer on Adding on Ordinance or Law Coverage

Even when a building is valued at replacement cost on a commercial property policy, it really isn’t the cost to replace the building. Replacement cost is generally defined as continued on page 26

Closer Look: Commercial Property/Condos

continued from page 25

the cost to replace an item of property with property of like, kind, quality, and utility. So, when an agent tells an insured that they have replacement cost on their building, or the insured reads their policy and sees replacement cost, they can believe that it means that if the building is damaged or destroyed, the insurance company will pay to replace it. And they will, kind of.

When insureds think about replacing a building, they may think about just replacing the building, even if certain things have had to change over the years. Think about the electrical needs for a condo in 1972 compared to today. Back then, there were appliances, lights, televisions, and stereo equipment—and that’s about it. Today, people have computers, tablets, phones, gaming systems, and more that require power.

When the insurance policy mentions replacing the building, it means replacing the building that was there. It does not include replacing the building and upgrading the electrical system or the plumbing system. It does not include making any changes that are required to comply with any kind of federal, state, or local building code or ordinance. It doesn’t care if the city says that you can’t rebuild that building here; you have to move it across the street, or 10 blocks south.

This is where we lean on ordinance or law coverage. On several commercial property policies, including the ISO Condominium Association Coverage Form, this critical coverage is not included. There are carriers that may include

it by default, but making sure that it’s there before a loss is better than assuming it’s there and finding out that it isn’t after a loss. Consider two potential loss situations.

In the first case, there is a fire that damages several units and common areas on three floors. The building is not a total loss, and the building code allows for it to be repaired. The code enforcement officer comes in to inspect and discovers that the last time the electrical system in the entire building was updated was 25 years ago, and the plumbing system in the building is 15 years old. He determines that these need to be updated before he approves the work. The insurance policy will pay for the repairs to the common areas, and the unit owners’ insurance policies will pay for repairs to their units, but without ordinance or law coverage, none of the required updates will be paid for, and those costs will come out of the association’s (and unit owners’) pockets.

‘Even when a building is valued at replacement cost on a commercial property policy, it really isn’t the cost to replace the building.’

In the second case, we have a smaller building that also suffered fire damage. In the investigation, it’s determined that 60% of the building was damaged in the fire, and the city requires that the remaining portion of the building be torn down and rebuilt. The insurance policy will cover the damage that was done by the

fire, but the loss of value of the remaining portion of the building is not covered without ordinance or law coverage.

Ordinance or law coverage provides three separate and related coverages. When the city says that the building cannot be repaired but must be torn down and replaced completely, Coverage A provides that remaining limit of insurance. It’s always the difference between the direct physical loss of the building and the limit of insurance, and it covers that lost value when they say the building needs to be torn down.

Once that undamaged part of the building is knocked down, someone has to come and pick up that rubble, or more directly, remove the debris. The policy provides coverage for the debris from the damaged portion of the building, but we rely on Coverage B to provide coverage for the debris that exists because we had to tear down the rest of the building. This requires a limit of insurance, and finding that limit is complicated, especially when you consider that older buildings might have materials in them that are considered hazardous today.

We also have to deal with the increased cost of construction—and that’s where Coverage C comes in. It provides a limit of insurance so that the building can be upgraded to meet today’s building codes and other requirements.

Here’s another limit that can be hard to come up with because the older the building, the more code upgrades might be needed. This is part of the reason why coverages B and C can share a blanket limit.

That can allow the insured to select a lower limit, but if there’s a total loss, they might find themselves underinsured, which is what we have been trying to avoid.

Managing the Risks

What do we do about it?

Whether you’re a risk manager, board member, or insurance agent, the right answer is not the easy one. It’s important to keep up with maintenance so that deferred maintenance doesn’t turn into a safety issue that needs to be addressed, with a price tag that will be higher than it could have been several years before.

Annual insurance policy reviews are a must. The board may not like it, and it may create uncomfortable conversations, but we can’t manage the risks we don’t know about. We can’t insure against the exposures we haven’t considered. That means reviewing limits of insurance to determine whether they are enough to pay for losses. Even if the odds are that there will never be a total loss, do you want to explain the coinsurance condition after the check comes in with a significant reduction?

Lastly, making sure that the policy covers everything that everyone thinks it does, and when there are exclusions or gaps in coverage, determining if there is a way to provide coverage for those items, what they’ll cost, and whether the insured wants to pay for it, is a good way to make sure that they have their eyes open if a loss happens.

Wraight, CIC, CRM, AU, is director of Insurance Journal’s Academy of Insurance. He can be reached at pwraight@ijacademy.com.

News & Markets

California Department of Insurance Taking Actions Against Tesla Over Claims Handling

The California Department of Insurance launched enforcement actions against Tesla Insurance Services Inc. and Tesla Insurance Company companies for allegedly failing to adequately handle hundreds of California automobile policy claims.

The actions are also aimed at State National Insurance Company. Tesla Insurance Services Inc. is an appointed agent for State National, an admitted insurer in California.

Unless these issues are resolved in favor of policyholders, the companies will be ordered to a hearing before an administrative law judge to determine whether they will be able to continue to transact insurance business in California, as well as face significant monetary penalties.

The actions allege that, despite being repeatedly warned by the California Department of Insurance, the Tesla Companies and State National chose per-

sisted with non-compliant claims-handling practices.

The CDI said it has received consumer complaints related to the handling of auto policy claims beginning in 2022. The department reportedly repeatedly warned the Tesla Companies and State National, and had meetings and correspondence, but the number of consumer complaints and violations continued to mount.

The companies face monetary penalties up to $5,000 for each unlawful, unfair, or deceptive act, or up to $10,000 for each such act determined to be willful.

The department’s accusations, including the following alleged violations:

• Egregious delays in responding to policyholder claims in all steps of the

• Unreasonable denials and delays in fully paying valid claims to consumers

• Failure to conduct thorough, fair, and objective investigations of claims.

• Failure to advise policyholders of their rights to have their claims denials reviewed by the department.

California Police Pulled Over A Waymo for An Illegal U-Turn, But They Couldn’t Cite

By Janie Har

Police in Northern California were understandably perplexed when they pulled over a Waymo taxi after it made an illegal U-turn, only to find no driver behind the wheel and therefore, no one to ticket.

The San Bruno Police Department wrote in a now viral weekend social media posts that officers were conducting a DUI operation on an early October morning when a self-driving Waymo made the illegal turn in front of them.

the car.

Officers contacted Waymo to report what they called a “glitch,” and in the post, they said they hope reprogramming will deter more illegal moves.

The department’s Facebook post has generated more than 500 comments, with many people outraged that police didn’t ticket the company. People also wanted to know how police got the car to pull over.

Officers stopped the vehicle, but declined to write a ticket as their “citation books don’t have a box for ‘robot’.”

“That’s right … no driver, no hands, no clue,” read the post, which was accompanied by photos of an officer peering into

But San Bruno Sgt. Scott Smithmatungol said they can only ticket a human driver or operator for a moving violation, unlike parking tickets that can be left with the vehicle.

A new state law that kicks in next year will allow police to report moving violations to the Department of Motor Vehicles, which is figuring out the specifics, including potential penalties, the Los

Angeles Times reports.

Waymo spokesperson Julia Ilina told the LA Times that the company’s autonomous driving system is closely monitored by regulators. “We are looking into this situation and are committed to improving road safety through our ongoing learnings and experience,” Ilina said.

Waymos currently operate in Phoenix, Los Angeles and San Francisco and in areas south of the city, including the suburb of San Bruno.

“It blew up a lot bigger than we thought,” Smithmatungol said of the viral post to The Associated Press on Tuesday. “We’re not a large agency like San Francisco.”

San Bruno has about 40,000 residents and a sworn police force of 50 officers, he said.

Waymo is owned by Google’s parent company, Alphabet.

Copyright 2025 Associated Press. All rights reserved.

News & Markets

Study Shows California Heat Standard Reduced Work Injuries on Hot Days

California’s worker heat standards led to fewer work-related injuries on hot days, a new study from the Workers Compensation Research Institute found.

The WCRI study, Impact of California’s Heat Standard on Workers’ Compensation Outcomes, measured how California’s heat standard impacted the frequency of injuries in heat-exposed occupations like construction, agriculture and transportation.

The state’s heat standard requires employers to provide water, shade,

rest breaks, acclimatization plans and emergency response protocols during excessive heat.

According to WCRI, heat-related illnesses are 11 to 18 times more frequent on days above 95°F compared with days between 75 and 80°F, yet they represent 20% to 25% of all injuries attributable to heat.

In 2005, after several deaths of agricultural workers due to heat, California implemented emergency outdoor heat regulations. They were expanded to include indoor workplaces in 2024.

The core components of the heat standard include:

• Access to water: Employers must provide at least one quart of cool, free, potable water per worker per hour, located close to where they work.

• Access to shade: Workers must be allowed to rest in shade at any time. If the temperature reaches 80 °F or higher, shade must be made available for all during breaks.

• High-heat procedures (greater than 95 °F): In specified industries, such as agriculture, construction, landscaping, and oil and gas, additional rules apply. Those include buddy systems or monitoring, water reminders, supervisor contact and extra breaks.

• Emergency response and heat-illness prevention plan: Employers must ensure communication with emergency services, first-aid protocols, transport ill workers to cooler locations, and maintain a written Heat Illness Prevention Plan.

• Acclimatization protocols: Workers new to high heat exposures or that are starting shifts during heat waves should be monitored especially for the first 14 days.

• Training: Workers must be trained on types of heat illnesses, symptoms, prevention, hydration, acclimatization, employer obligations and how to report heat illness. Supervisors receive training on how to monitor conditions, weather, employee symptoms and implementing standard procedures.

J&J Must Pay $966M After Jury Finds Company Liable in Talc Cancer Case

By Diana Novak Jones

ALos Angeles jury ordered Johnson & Johnson to pay $966 million to the family of a woman who died from mesothelioma, finding the company liable in the latest lawsuit alleging its baby powder products cause cancer.

The family of Mae Moore, who died in 2021, sued the company the same year, claiming Johnson & Johnson’s talc baby powder products contained asbestos fibers that caused her rare cancer.

The jury ordered the company to pay $16 million in compensatory damages and $950 million in punitive damages, according to court filings.

The verdict could be reduced on appeal as the U.S. Supreme Court has found that punitive damages should generally be no more than nine times compensatory damages.

safe, do not contain asbestos, and do not cause cancer.

Representatives for Johnson & Johnson did not respond to a request for comment. The company has said its products are

J&J stopped selling talc-based baby powder in the U.S. in 2020, switching to a cornstarch product.

(Reporting by Novak Jones; Editing by Chizu Nomiyama, Alexia Garamfalvi and Rod Nickel)

Copyright 2025 Reuters. All rights reserved.

My New Markets

Cannabis Insurance

Professional Lines (E&O, D&O, Cyber and EPLI)

Market Detail: Professional Lines

Coverage Available: Offering a full suite of Professional Liability solutions to protect clients from today’s evolving risks: errors & omissions (E&O), directors & officers (D&O), cyber liability, and employment practices liability (EPLI).

Get in contact to learn more about appetite, limits, and get help placing tough accounts with confidence. Has Pen.

Available Limits: $1,800 minimum premium; $500,000 maximum premium.

Carrier: Admitted. Rated A or better by AM Best.

States: All 50 states and the District of Columbia.

Market Detail: If there’s sawdust, it’s probably us - insurance for wood-based businesses. Pennsylvania Lumbermens Mutual Insurance Company (PLM) is America’s premier commercial property and casualty insurance carrier dedicated to serving the lumber, woodworking, and building materials industries since 1895. Crafting unique, comprehensive coverage, they offer a diverse and tailored range of commercial insurance products for client’s specific business needs. Clients like sawmills and resaw operations; debarker

& veneer mills; plywood manufacturing; concentration yards and wood drying (kilns) wood-mizer/portable sawmills. Write business without contracts. Working with PLM is easy to do when it comes to getting appointed or obtaining a contract. No contracts or appointments required. No premium volume or production requirements. Open brokerageinsureds work with any licensed insurance producer. Protect contingencies - use a unique carrier for unique risks.

Whether it's one account or 100 that fit PLM’s appetite, reach out today for a quote knowing there is a right home for unique insurance programs. Has Pen.

Available Limits: Not disclosed.

Carrier: Admitted. Rated A- (Excellent) by AM Best.

States: All 50 states and the District of Columbia, except Alaska and Hawaii.

Contact: Alex Beyer, abeyer@plmins.com, 800-752-1895

Lawyers Professional Liability

Market Detail: Protexure provides tailored Lawyers Professional Liability Insurance backed by nearly 50 years of experience through ISMIE Mutual Insurance Company—rated A- (Excellent) by A.M. Best. Designed specifically for solo to mid-sized law firms, policies deliver comprehensive protection, exceptional service, and claims expertise in today’s most litigious environments.

Key Policy Features: broad definition of professional services; disciplinary proceedings coverage up to $100,000; 50% deductible reduction for claims resolved entirely through mediation; regulatory coverage up to $25,000; crisis event coverage up to $50,000; no Hammer Clause; unlimited subpoena assistance; loss of earnings coverage: $1,000/day; free ERP for qualifying non-practicing attorneys; personal injury and advertising liability; and prior acts and loyalty deductible credits for eligible firms. Claims expertise that makes a difference with specialized claims professionals offer guidance at every step and legal defense from a vetted panel of experienced liability attorneys. Aggressive defense approach— frivolous claims are not settled to avoid cost. Has Pen.

Available Limits: Disciplinary proceedings coverage up to $100,000; 50% deductible reduction for claims resolved entirely through mediation; regulatory coverage up to $25,000; crisis event coverage up to $50,000; no Hammer Clause; unlimited subpoena assistance; and loss of earnings coverage: $1,000/day.

Carrier: ISMIE Mutual Insurance Company. Admitted. Rating A- (Excellent) by AM Best.

States: Arizona, California, Colorado, Connecticut, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Massachusetts, Michigan, Minnesota, Missouri, Nebraska, Nevada, New Jersey, North Carolina, Ohio, Pennsylvania, South Carolina, Tennessee, Texas, Utah, Virginia, Washington, and Wisconsin.

Market Detail: Trusted solutions for medical equipment businesses. ProTek, powered by NFP, provides a portfolio of enhanced general and professional liability insurance products to help companies that sell, service and manufacture medical equipment mitigate risks and manage costs. Experienced staff offers expertise and insurance coverages that help protect the medical device sales and service industry.

Available Limits: Not disclosed. Carrier: Not disclosed.

States: All 50 states and the District of Columbia.