Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Closer Look: US Excess & Surplus Lines Growth Slowed Again in 2024; Berkshire, AIG Top Premium Rankings

Is It Covered: When Insurance Isn’t the Optimal Risk Management Approach

Minding Your Business: Valuation & Terms of Small Books of Business

Turning Non-Standard Risks into New Revenue: How Agents Can Capitalize on the Specialty Market

Workers' Comp: Validating Mental Health Claims in Today’s Workforce

Closing Quote: Behind the Surge: What Cyber Claims Say About the Future of Risk

Texas Flood

As of press time, Texas and the world are watching yet another unprecedented natural catastrophe unfold. More than 250 lives could be lost in this one event and billions of dollars in property have been destroyed.

This storm is tragic on many levels, but it also hits close to home as I’ve lived and spent most of my life in and around the beautiful Texas Hill Country. It’s a region of Texas that is unlike any other, which is why so many Texans return year after year to enjoy its beauty.

Natural beauty, and water, like in Texas Hill Country, is why everyone wants to visit and live in areas with extreme catastrophic risk. Whether it’s the breathtaking landscapes of California, the pristine beaches in Florida, or the eastern shoreline—people live, work, and play in dangerous places. That isn’t going to change. Destruction occurs, and people rebuild in the same dangerous areas—and the risk goes on.

The National Flood Insurance Program says that over the past 20 years, 99% of counties in the U.S. have experienced a flood event, and yet some estimate that less than 7% of property owners nationwide purchase flood insurance coverage.

In Kerr County, Texas, where the most devastating flooding occurred, that figure is less than 2%.

We know there is no coverage for flooding in standard homeowners policies, renters policies, or in most commercial property insurance policies. And we know the risk of flooding is everywhere. Yet so few purchase the right coverage to protect their most precious assets. And those purchasing habits likely will not change either.

‘Insurance

coverage is one way to protect property and life. Another way is to simply manage the risk through better mitigation efforts.’

Insurance coverage is one way to protect property and life. Another way is to simply manage the risk through better mitigation efforts. That might mean building stronger, improving building codes, offering risk management tools to insureds that reduce risk. I think of water sensors, fire sensors for electrical risk—heck, even complimentary “weather radios” for high-risk flooding zones. Perhaps more can be done to offer policy premium credits when people and businesses make investments to reduce risk on their own.

The Triple-I states that “risk” is just another word for “peril,” which refers to something that can go wrong. Today, there’s no greater peril than natural catastrophe risk.

So, what more can be done to prepare for the next big catastrophe? Is the insurance industry doing enough to help insureds manage their risk for these CATs? After all, it’s not just about buying coverage—it’s about managing the risk before the catastrophe strikes. How can this industry be part of the solution?

| jcarlson@insurancejournal.com

ADMINISTRATION / CIRCULATION

Chief Financial Officer Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant

Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus Andrew Simpson | asimpson@wellsmedia.com

National Editor Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor

William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Contributors: Trent Cooksley, Susanne Sclafane, Karen Thomas, David Wilson

Columnists: Catherine Oak, Bill Wilson

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT) Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Administrator

Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer

Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director

Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator

George Jack | gjack@ijacademy.com

More than London access A London advantage.

You already know Amwins for our specialty brokerage expertise and skilled underwriting. Now it’s time to put our London broker to work for you.

Amwins Global Risks has spent 50+ years placing complex risks across the globe, with over $4 billion placed into the London market annually and highly specialized teams across Property, Financial & Professional Lines, Cargo/Marine, Energy, Casualty and US Transportation.

So when the placement gets tough—or just deserves better—work with the independent London broker that’s already on your side.

Wherever risk takes you, Amwins Global Risks is in your corner - in almost every corner of the world.

News & Markets

Marsh Suit Against Alliant Alleges Poaching of Commercial Surety Team, Accounts

By Andrew G. Simpson

Insurance broker Marsh USA is suing rival Alliant Insurance Services, this time for allegedly poaching key commercial surety employees and clients.

New York-based Marsh is accusing Californiabased Alliant of inducing key commercial surety employees to breach their non-solicitation and confidentiality agreements and of wrongfully interfering in Marsh’s business relationships.

Marsh and Alliant are two of the biggest insurance agencies in the country.

Marsh alleges Alliant wanted a commercial surety practice and targeted Glenn Pelletiere, Marsh’s commercial surety leader for the Northeast. Pelletiere had spent nearly a decade at Marsh, building a commercial surety book of business, anchored by four marquee clients.

On January 24, 2025, when Pelletiere resigned to join Alliant, Marsh said he promised to refrain from taking any clients or employees. However, according to the complaint, three key surety team employees—Colin Horgan, Madison Diaz,

and Nicholas Manning—resigned minutes later. Marsh says “each one played a critical role” in keeping Marsh’s surety clients close and each was bound by one-year post-employment restrictions prohibiting solicitation or servicing of Marsh clients and solicitation of Marsh employees. According to the complaint, after the employees resigned, the client solicitation of Marsh clients began, and in March, one of the largest commercial surety clients in Pelletiere’s book of business moved to Alliant.

Marsh calls this case “yet another chapter in Alliant’s execution of its corporate strategy of theft. Alliant does not build—it raids. And once again, it has raided a Marsh McLennan entity for a high-performing team, led by a key producer managing a substantial book of business, in deliberate violation of binding contractual restrictions and settled law.”

Marsh is suing to enforce its former employees’ restrictive covenants, protect its confidential and trade secret information, enjoin the employees and Alliant from taking more accounts, and halt what

it says is “Alliant’s campaign of unfair competition.” In addition to injunctive relief against the employees and Alliant, Marsh seeks to recover its business losses, legal costs, and damages including punitive damages.

“This raid is no outlier,” Marsh says in its new complaint, claiming that as many as 70 cases with similar claims have been filed against Alliant.

This is also not the first feud between the two. Marsh McLennan Agency (MMA) sued Alliant for similar claims in December 2024. In January, a judge blocked Alliant from soliciting MMA clients, and in May, MMA won a permanent injunction prohibiting Alliant from soliciting certain “restricted” Marsh clients and from using confidential information. The injunction applies to Alliant and Johnny Osborne, a former producer in MMA’s Huntsville, Alabama office, and two members of his team—all three of whom simultaneously resigned in December 2024 to join Alliant.

In that case, the judge concluded that MMA “clearly is entitled” to a prohibitory injunction against Osborne and Alliant to prevent further losses of client relationships and customer goodwill and further use or disclosure of protected confidential information.

Erie Insurance Restores All Operations After Month Outage; Says No

Data Breached

Erie Insurance reports that it has restored full business operations that have been affected by a monthlong network outage.

The company said there is “no evidence” of a breach of any sensitive personal information, financial records, or legally protected data by the threat actor during this incident.

“Key services and systems have been safely and securely restored and our local agents, claims teams, and customer care teams have returned to regular ways

of serving customers,” the company announced on July 7.

The insurer previously said the outage it initiated on June 7 helped contain a threat. The insurer also earlier said “there is no evidence of ransomware and no indication of ongoing threat actor activity.”

Erie’s announcement that it has restored all operations came five days after Philadelphia Insurance reported that all of its systems were back up and running after its network outage. “We

have resumed regular operations, though we continue to address minor technical issues as they arise,” the company stated in a July 2 update on its handling of its network outage that began June 9.

While neither insurer has spoken of the source of its cybersecurity incident, Google Threat Intelligence Group has said the hacking group known as Scattered Spider appears to have switched focus from retailers to insurance companies and is likely behind the Erie and Philadelphia events.

News & Markets

Tax Increase on Litigation Funders Does Not Make Final Budget Bill

By Chad Hemenway

When Trump’s huge tax bill was signed into law July 4, missing were changes to the taxes third-party litigation funders pay.

Once included within the One Big Beautiful Bill (OBBB) was language to tax earnings by litigation funders at a rate of nearly 41%. Critics have said the litigation funding industry was not taxed enough or, in some cases, not at all—especially foreign investors.

The insurance industry has routinely blamed third-party litigation funding (TPLF)— investments in lawsuits in exchange for a percentage of a settlement or judgment—for the rapid increase in litigation costs. According to a new consumer guide on legal system abuse from the Insurance Information Institute (Triple-I) and Munich Re US, legal system abuse costs each American family about $6,664 more for goods and services, and costs small businesses $160 billion in tort costs.

The insurance industry has

lobbied to rein in the practice, looking to potential tax reform as an opportunity.

In a statement sent to Insurance Journal, Jimi Grande, senior vice president of federal and political affairs for the National Association of Mutual Insurance Companies (NAMIC), said the provisions once in the bill would have been a “win for Congress, the Trump Administration, and American consumers and businesses.”

Instead, shortly before the House vote, the Senate parliamentarian ruled the proposed tax increases for profits connected to TPLF violated certain budget rules. The language was removed from the mammoth bill.

“Due to some misinformation, partisanship, and efforts of those who profit off the U.S. court system, the Senate parliamentarian decided to rule against the closing of the tax loophole, which led to its removal from the OBBB,” Grande said. “Keeping this foreign funder loophole open means additional billions will fuel legal system abuse, and these foreign entities will

continue paying nothing in U.S. taxes. American citizens will keep footing the bill as trial lawyers and litigation funders are incentivized to keep doing business as usual, contributing to a more litigious society and out-of-control tort costs impacting nearly the entire economy.”

Meanwhile, the International Legal Finance Association (ILFA) called the decision to omit the tax on TPLF a “clear victory for Americans.” The ILFA said litigation funding

is “a vital mechanism that enables individuals and small businesses to seek justice against well-funded defendants.”

“Rather than curbing ‘predatory’ behavior, this bill would shift power away from consumers and small businesses and into the hands of the very industries—Big Tech, Big Pharma, and Big Insurance—that most often seek to avoid liability for their misconduct,” said the global TPLF trade association.

Big ‘I’ Celebrates Continued Tax Deduction for Many Independent Agents

The Independent Insurance Agents & Brokers of America

(Big “I”) on July 4 celebrated the passage of the “One Big Beautiful Bill.”

“The Big ‘I’ would like to thank the U.S. Congress and President Trump for their work to bring more certainty and growth to the economy by passing tax reform,” said Charles Symington, Big “I”

president & CEO, in a statement.

“Passage of this reconciliation bill delivers on the promise to protect and make permanent much of the 2017 Tax Cuts and Jobs Act (TCJA) that so many of our members have come to rely on,” he said.

The tax cuts signed into law during President Trump’s first term were set to expire at the end of this year. The

TCJA included the Section 199A tax deduction on qualified business income for pass-through entities (sole proprietorships, partnerships, limited liability companies, and S-corporations).

The Big “I” said 86% of independent agencies are structured as pass-through entities.

“We would like to thank the president and congressional

leaders for making the 20% small business deduction for pass-through entities permanent,” Symington continued.

“That certainty, along with the existing low corporate rate, will allow our members to continue investing in jobs across Main Street America and better serve their customers and communities,” Symington added.

31%

The number of executives who cite cyber risk as their greatest threat, up from 22% in 2024, according to Beazley’s report, Spotlight on Tech Transformation & Cyber Risk 2025. The report shows U.S.-based executives feel more prepared to counter cyber threats, with the perception of cyber resilience rising to 81% from 73% a year ago, potentially indicating a false sense of security.

16.5%

The decrease in the number of lightning-related claims in 2024. Insurers in the U.S. paid out about $1.04 billion in claims in 2024 compared to $1.24 billion in 2023, according to the Insurance Information Institute (Triple-I). More than half of the claims were filed in the top 10 states—with Florida, Texas and California the top 3—but the total number of lightning-caused claims fell 21.5% to 55,537 in 2024, the lowest number of claims since before 2017.

414

The number of outstanding traffic citations one Maryland resident incurred, including 360 for excessive speeding. Ashley Yvette Kibler is being hauled into court by District of Columbia Attorney General Brian L. Schwalb, who is seeking to collect the $168,168 in unpaid fines and penalties she owes the District. Schwalb also announced lawsuits against three other drivers. Altogether, the four have amassed more than 1,000 traffic infractions totaling over $340,000 in unpaid fines, penalties and fees, according to Schwalb.

$100,000

The amount of insurance liability for-hire drivers must now carry in New York City, reduced from $200,000. New York City Mayor Eric Adams has signed legislation that reduces the amount of personal injury protection (PIP), or no-fault, insurance coverage that the city’s 74,000 Uber, Lyft, yellow taxi, and livery drivers have to buy from the current $200,000 to $100,000 per person.

For Most Everything

Declarations

NOAA Loses Data Source

“NOAA’s data sources are fully capable of providing a complete suite of cutting-edge data and models that ensure the gold-standard weather forecasting the American people deserve.”

— Kim Doster, National Oceanic and Atmospheric Administration (NOAA) communications director, commenting on how NOAA and the U.S. Navy and will no longer accept and distribute readings from the long-running Defense Meteorological Satellite Program. The military satellite data is just one piece of a “robust suite of hurricane forecasting and modeling tools,” Doster said. Storm models still include data from other satellite systems and from NOAA’s hurricane hunter aircraft, among other sources.

Blocking FAIR Unfair

“We support the Department of Insurance’s effort to dismiss Consumer Watchdog’s reckless lawsuit—a necessary step to prevent further destabilization of California’s already fragile insurance market. Blocking FAIR Plan cost recovery would jeopardize the last-resort coverage option for homeowners and push the market closer to collapse. It is critical that recovery costs be spread equitably across a broader pool of policyholders to stabilize the system and protect access to coverage for all Californians.”

— American Property Casualty Insurance Association (APCIA) statement on a lawsuit from Consumer Watchdog that challenges the way the FAIR Plan recovers costs.

More Options for Florida

“More companies entering the Florida market is a surefire sign that the legislative reforms to address legal system abuse are working. As competition in the marketplace increases, rates are stabilizing and even decreasing for consumers. Florida is doing something right and other states are taking notice.”

— Adam Shores, senior vice president of state government relations at the American Property Casualty Insurance Association, commenting on the number of property insurers venturing into the catastrophe-prone state’s insurance market. Two more property insurers have put their toes in the Florida market this summer, making 14 new carriers in the state since 2023.

Reasonable Effort

“I have no legal obligation to do so.”

— Bicyclist Brendan Linton, when asked in court why he didn’t pull his bike off the road to allow traffic to pass. Linton fought a $25 ticket for violating the provision on slow speed impeding of traffic all the way to the Pennsylvania Supreme Court, arguing that the slow-speed laws did not apply to bicyclists, or were at the very least ambiguous. The court’s decision: While Pennsylvania cyclists must make “reasonable efforts” to not impede traffic, the law does not mandate that they always and immediately pull off the road to let faster traffic pass. The law does require slow-going motor vehicles to pull off the road. Linton was clocked going 19 mph in a 55 mph zone.

Natural Gas Deemed Green

“I don’t think it’s anything crippling to wind or solar, but you got to realize the wind don’t blow all the time and the sun don’t shine every day.”

— Said Louisiana Republican Rep. Jacob Landry, the author of a new state law redefining natural gas as green energy. Louisiana’s law orders state agencies and utilities regulators to “prioritize” natural gas, along with nuclear power, on the grounds that it will improve the affordability and reliability of the state’s electricity. Landry runs an oil and gas industry consulting firm. The legislation “is saying we need to prioritize what keeps the grid energized,” he added.

Fraud Hurts Healthcare

“The submission of false claims undermines the integrity of our federal healthcare system.”

— Said Linda T. Hanley, Special Agent in Charge with the United States Department of Health and Human Services Office of Inspector General, after Illinois chiropractor Carrie Musselman was guilty of one count of healthcare fraud and five counts of wire fraud. Musselman was sentenced to 20 months in prison and ordered to repay more than $2.3 million following convictions on multiple charges related to a scheme to defraud Medicare and 12 other insurance companies.

News & Markets

Q2

Composite Personal

According to the MarketScout Market Barometer, the composite rate for U.S. personal lines increased in the second quarter by 4.6% compared to 4.9% during the first quarter.

Dallas-based MarketScout, a division of Novatae Risk Group, said high-net-worth homes valued over $1 million saw the largest hikes of 6.7% during the second quarter.

“We have just now entered hurricane season, so for those owning homes in coastal areas, expect homeowners’ rates to go up, not down,” said Richard Kerr, CEO of Novatae Risk Group, in a statement. “Agents should advise their clients in coastal areas to renew their insurance between January

Lines Rates Up 4.6%; Commercial Up 2.8%

and March, as rates are often much more favorable during those months.”

Personal auto insurance rates increased 5.7% on average in Q2, added MarketScout.

Switching to commercial lines, the composite rate increased 2.8% in Q2, remaining fairly steady from the average increase of 3% during Q1 2025.

than previous quarters.

Like Q1, commercial auto rates went up 6.7% to lead all coverage classes during Q2. Umbrella and excess liability came in at up 5%, an improvement over average increases of 6 7% in Q1. General liability saw rates go up an average 3.7% in Q2 compared to up 2.3% in Q1.

Commercial property was up 3.6% in Q2—the same result as Q1. Kerr said the distribution and underwriting company is “seeing steady improvement in property insurance rates, which is encouraging for insurance buyers.”

Other Findings

In earlier reports, commercial lines premiums also trended up during the first quarter of 2025 but at a slower pace

In early June, The Council of Insurance Agents & Brokers (CIAB) quarterly survey found that commercial property/ casualty premiums across all account sizes rose by 4.2% in Q1 2025, down 22% from the last three months of 2024. The CIAB noted at the time that the trend marked a “clear” signal of soft market conditions.

In mid-June, WTW’s Commercial Lines Insurance Pricing Survey (CLIPS) showed that U.S. commercial insurance rates went up by 5.2% in Q1 2025, down from increases of 5.6% and 6.1% for the fourth and third quarters of 2024.

coastal communities.

News & Markets

Reputation Risk Can Overshadow Ransom in Cyberattacks, Aon Says

By Jahna Jacobson

The cost of a cyberattack extends far beyond any immediate mitigation expenses or ransoms paid.

Reputational costs and dipping stock values can be a significant portion of losses, according to the new Aon Global 2025 Cyber Risk Report. Reputation risk events can cause shareholder value to fall by an average of 27%, according to Aon—and reputation risks are nontransferable.

The Growing Cyberattack Severity

In 2024, the frequency of reported cyber incidents was up 22% on the previous year. The 776 reported cyber incidents or litigation represented the most claims, an increase of 31% year over year, ranging from ransomware and business interruption to class action litigation and regulatory investigations. In the U.S., for example, Aon cyber and errors and omissions (E&O) claims data revealed 1,228 reported incidents across broking clients in 2024, reflecting an increase of 22% year over year.

While ransomware claims frequency

increased, the average ransom payment amount for Aon broking clients declined by 77%. Midsized organizations filed more cyber claims than any other group—over half of all incidents.

Reputation Risk Factors

Damage to brand or reputation is a top risk facing organizations globally today, according to Aon’s latest Global Risk Management Survey (GRMS), and has been since 2007.

Specific cyberattack techniques are more likely to become reputation risk events than others, the Aon report stated. Malware/ransomware attacks make up a disproportionate number of the identified reputation risk events, accounting for approximately 60% of reputation risk cyber events but only 45% of all cyber events.

Malware attacks are the most common (57% of all) and have a high propensity to have a reputational impact (20% likelihood) but have a limited impact on shareholder value (-28% on average). A system exploits attack, in comparison, has just an 8% chance of reputational impact.

For cyber events, there is also a likely large-scale media pickup when there are opportunities for consumer impact or outrage or issues that could be deemed to be in the public interest.

The Aon report analyzed 1,414 cyber events reported in the media up to the end of 2024, of which more than 95% were malicious. The analysis showed that 56 developed into reputation risk events, causing shareholder value to fall by 27%.

However, reputation risk is one of a growing number of risks that are either uninsurable or only partially insurable. Prevention and management are critical to avert reputation risk and its associated costs.

‘[R]eputation risk is one of a growing number of risks that are either uninsurable or only partially insurable. Prevention and management are critical to avert reputation risk

and its associated costs.’

Mitigating Cyber Losses

Prioritization of controls and red flags continued to change in 2024, with privacy-oriented, third-party, and supply chain controls emerging as new areas of interest for insurance. According to the report, Aon clients who invested in security controls reported a 9% improvement in critical—or ‘red flag’—controls, which can impact insurability. Organizations across sectors continued to invest in and improve their critical controls over the course of 2024. Insurance carriers are also becoming more sophisticated in their risk underwriting and are more focused on the overall cyber maturity profile and an organization’s narrative around specific controls. This new climate was driven in part by intense global cyber insurance market competition and is expected to continue into 2025.

Spotlight: Reinsurance

Reinsurance Renewal Prices Moderate as Capacity Exceeds Cedent Demand: Brokers

By L.S. Howard

Strong returns in the reinsurance sector are attracting capital and leading to favorable pricing outcomes for buyers—but underwriting discipline continues, according to renewal reports from three reinsurance brokers.

Despite heavy natural catastrophe losses in the first quarter, reinsurance capacity has exceeded demand.

“[T]raditional reinsurers targeted growth and deployed more capacity at the midyear renewals, which is accelerating the trend toward buyer-friendly conditions and leading to greater flexibility in terms and conditions as well as options to purchase expanded coverage,” said Aon in its report titled “Reinsurance Market Dynamics—Midyear 2025 Renewal.”

Reinsurers’ balance sheets continue to be strong, which is driving an appetite for growth—despite insured losses through the first half that are nearing $70 billion, said Guy Carpenter in its report titled “Strong returns in reinsurance

sector attracts capital, leading to favorable client outcomes.”

For the first quarter alone, global insured losses from natural catastrophes were estimated at around $60 billion—the second highest Q1 loss on record—which was driven by the $40 billion California wildfire loss, Aon said. “The first half of 2025 is likely to become the second costliest on record due to additional catastrophe activity in the second quarter, including two large severe weather outbreaks in the U.S. on May 14-17 and May 18-20.”

Nevertheless, the mid-year renewals saw overall pricing continue to moderate. Aon noted “significant variation in renewal outcomes” as reinsurers differentiated cedents by loss experience and performance.

“Clients were largely able to secure risk-adjusted rate reductions for property treaties and were well-placed to hold pricing broadly flat in casualty lines—in part, as underlying pricing increases continue to flow through to reinsurers,” agreed Gallagher Re in its report titled “1st View:

Challenging the Status Quo.”

“After several highly profitable years, reinsurers are increasingly looking to deploy their significant capital, but they are disciplined in approach. In some businesses and geographies, we are still seeing reinsurers willing to sacrifice share to protect profitability—particularly larger, less growth-oriented players,” said Gallagher Re.

Increasing Client Demand

Reinsurers easily absorbed the 5% to 7% increase in client continued on page 16

Spotlight: Reinsurance

continued from page 15

demand for property catastrophe limit, Guy Carpenter said, noting that reinsurer capacity exceeded demand by more than 20%, driving risk-adjusted rate decreases of 5% to 15% for non-loss impacted programs, and risk-adjusted rate increases of 10% to 20% for loss-impacted programs.

“Reinsurance capacity was more than sufficient to absorb a near 10% increase in global demand for property catastrophe limit,” Aon affirmed.

Rising demand for reinsurance protection was largely driven by insurers in the U.S. and the significant “depopulation” of Citizens—Florida’s windstorm insurer of last resort, Aon said, explaining that the depopulation program transferred more than 428,000 Citizens policies to the private insurance market in 2024, generating additional limit demand from insurers.

“Other factors included inflation, model changes, and revised views of natural catastrophe exposure, with recent wildfires in the U.S. and floods in Brazil prompting insurers to evaluate loss potential and protection needs,” Aon added.

“The number of start-up reinsurers remains small, although new players in the property catastrophe space are gaining traction and adding to competitive pressures. Competition was greatest in middle layers of catastrophe programs, in particular alternative capital created competitive tension,” Aon continued.

Casualty Renewals

Aon said casualty insurers entered the mid-year renewals in a relatively strong position “as robust underlying rating and underwriting actions taken in recent years helped ensure ongoing reinsurer support.”

“Reinsurers continue to support the casualty market, but remain watchful of negative trends in the market, including adverse reserve development, the frequency of nuclear verdicts and impact of litigation financing, as well as emerging areas of liability,” Aon added.

Gallagher Re pointed to the $8.1 billion of adverse prior-year development reported by U.S. property/casualty carriers in 2024, related to the trailing 10 accident years, which was up from $3.8 billion in 2023.

“Offsetting these concerns, however, are relatively high interest rates, the robust underlying rate environment, and the underwriting actions taken by insurers in recent years,” Aon said.

Indeed, Gallagher Re discussed the proactive steps that many cedents are taking with their underwriting strategies and claims management practices to mitigate the impact of loss trends and improve their profits. Such remedial actions on the part of ceding companies ultimately have benefited their renewal outcomes, Gallagher indicated in its report.

“The current trading environment is one of the most favorable for reinsurers in many years, evidenced by the additional capital being attracted to the sector,” said Dean Klisura, president and CEO, Guy Carpenter, in the broker’s renewal report.

“We see this as a tremendous opportunity to re-balance the market dynamics in our clients’ favor. More capacity will continue to moderate pricing, give clients more diversification of reinsurance partners, and provide better solutions to protect earnings,” Klisura added.

“Reinsurers showed greater confidence in those cedents who articulated the actions they have taken to improve performance, and how their actions tangibly improve future performance,” Gallagher Re said.

On the other hand, a clear market divide was demonstrated for cedents that were unable to provide reinsurers with evidence on how they were tackling performance issues, Gallagher continued. Those insurers saw less favorable outcomes.

Guy Carpenter confirmed that the casualty reinsurance renewals remained disciplined but there were two factors that drove more stable outcomes.

“First, reinsurers and clients evaluated trading relationships across property, casualty, and specialty programs. Reinsurers looked to find balanced support across all programs for a given client,” Guy Carpenter said. “Second, carrier underwriting actions have improved casualty economics for reinsurers, particularly proportional programs where insurers share ground-up premium and loss.”

“Reinsurers continue to be attracted to international placements with limited severity loss and good geographic diversification,” Aon added. “However, accounts with U.S. exposures that experienced further deterioration in U.S. loss severity saw a significant reduction in reinsurer appetite and increased pricing.”

Strong Reinsurer Performance

The 2025 renewals—in April and mid-year—have been greatly affected by reinsurers’ strong profits and capital positions.

“Reinsurers came into the renewal in good financial shape. They reported strong results for 2024, with ROEs well above the cost of capital,” said Gallagher Re. “Q1 results were weaker due to the impact of January’s unprecedented wildfires in Los Angeles, California, but barring further exception cat events, reinsurers remain on track for another good year overall.”

That sentiment was reiterated by Guy Carpenter, which said that strong reinsurer performance is expected to continue this year, despite heavy natural catastrophe claims in the first quarter. “Reinsurer returns on equity were 16% in 2024 and are projected to be 15% in 2025,” Guy Carpenter added.

Aon said most major reinsurers remain on course to deliver good results in 2025. “Notably, the four composite European reinsurers have maintained their (increased) full-year earnings guidance, despite the impact of the California wildfires.”

Record Reinsurance Capital Levels

Reinsurance capital closed 2024 at an all-time high of $607 billion—a trend Guy Carpenter expects to continue with growth of 5% to 7% by year-end 2025.

On the other hand, Aon said global reinsurer capital reached a new high of $715 billion in 2024 and expanded by a further $5 billion to $720 billion during the first quarter of 2025, despite the California wildfire claims. (The $720 billion figure includes $115 billion of alternative capital, according to Mike Van Slooten, head of Market Analysis at Aon, in an emailed explanation.)

Gallagher estimated dedicated reinsurance capital was US$769 billion at year-end 2024 (which includes alternative capital such as insurance linked securities) and is set to increase by another 6% this year, assuming average results for the remainder of the year.

‘Reinsurers continue to support the casualty market, but remain watchful of negative trends in the market, including adverse reserve development, the frequency of nuclear verdicts and impact of litigation financing, as well as emerging areas of liability.’

The main driver of the growth in reinsurance capital continues to be the retained earnings of established reinsurers, said Aon and Gallagher Re.

“Strong capital positions are continuing to translate into healthy risk appetites, particularly in property and most specialty classes, and these dynamics are expected to persist into future renewals,” Aon added.

Insurance Linked Securities

Capital supply has been supported by inflows into the insurance linked securities market, said Gallagher Re, pointing to the growth in non-life ILS assets-under-management of $4 billion during the first quarter, which backed $15.2 billion in catastrophe bond issuance through June 13, an increase of 36%, year-on-year.

Guy Carpenter agreed that client property catastrophe needs are being

met by a strong cat bond market. “During the first half of 2025, approximately $17 billion of limit was placed through 56 property catastrophe bonds and one health catastrophe bond,” Guy Carpenter said, adding that GC Securities has placed 23 catastrophe bonds in 2025—the highest number of any broker year to date.

Aon noted total capacity from ILS has now exceeded $115 billion as of the end of Q1 2025, with growth overwhelmingly driven by the increasing size of the 144A cat bond market. However, interest from institutional investors in sidecar opportunities continues to grow, especially for casualty risk,” Aon added.

Just

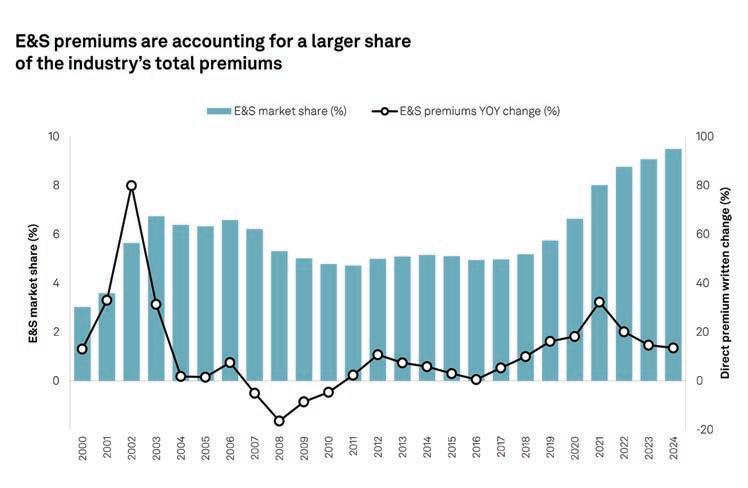

Closer Look: Excess & Surplus Lines

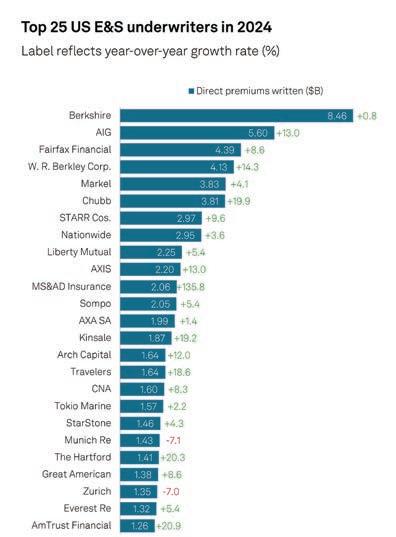

US Excess & Surplus Lines Growth Slowed Again in 2024; Berkshire, AIG Top Premium Rankings

By Susanne Sclafane

Arecent analysis by S&P Global Market Intelligence reveals that the pace of growth in the U.S. excess and surplus lines market slowed to 13.4% in 2024, down from 14.5% a year earlier.

While growth stayed up in double digits in both years, the jumps paled in comparison to a 32.3% rate of growth recorded in 2021, according to the S&P GMI “2025 U.S. Excess & Surplus Market Report” published in June.

“The E&S market continues to grow at a faster pace than the U.S. P/C industry as a whole, even as its pace of expansion slowed in 2024,” said Tim Zawacki, principal insurance analyst, S&P Global Market Intelligence. Earlier this year, S&P GMI reported that overall P/C premiums— across standard and E&S business—grew by 8% in 2024.

Focusing on E&S premiums, Zawacki noted that national growth in the E&S residential and commercial property lines moderated in 2024, increasing by 15.4%, compared to the over 20% year-over-year growth rates observed in each of the prior

five years. “Weakness in commercial property rates in catastrophe-exposed geographies could lead to a continued slowing in the E&S market’s expansion in 2025,” Zawacki said.

In spite of the diminishing E&S growth last year, 2024 was still the sixth straight year of double-digit growth overall (across all lines), S&P GMI said in its “2025 U.S. Excess & Surplus Market report,” which also shows changes in E&S market share and growth rates for each of the last 20 years, lists the top 25 E&S writers in 2024, and delivers information on leaders and 2024 E&S market share by line and state.

commercial auto ($5.7 billion, or 5.8%).

E&S premiums represented 9.5% of the U.S. total direct premiums written in 2024.

What’s Driving the Slowdown?

For full-year 2024, the U.S. E&S direct premiums written reached nearly $100 billion—coming in at $98.2 billion across all lines, up from $86.6 billion in 2023 and $75.5 billion in 2022. As in prior years, the bulk of E&S premiums in 2024 were written within various liability coverages ($51.3 billion, or 52.2%), several property lines of business ($31.7 billion, or 32.3%), and

Source: S&P Global Market Intelligence “2025 U.S. Excess & Surplus Market Report”

The line-of-business reports included in S&P GMI’s analysis reveal that the 15.4% jump in E&S premiums for commercial property and homeowners lines in 2024 marked the slowest pace of growth since 2018 (9.3%). In 2023, the E&S property growth rate had surged to 40.6%. In contrast, E&S liability premium growth, after slowing to 4.3% in 2023, returned to double-digit growth in 2024. The overall 2024 E&S liability growth rate was 12.4% across four lines (other liability-claims made, other liability-occurrence, medical professional, and product liability).

Analyzing top players in the various lines, S&P GMI found that Berkshire Hathaway Group, the second biggest E&S property writer (behind STARR Cos.)—and the largest writer across all E&S lines—actually shrunk its E&S property premiums 1.5% to $4.0 billion in 2024 across four property lines (fire, allied, commercial multi-peril/non-liability, and homeowners). Contributing to the decline, Berkshire’s E&S allied lines premiums fell by 17.1% to $1.5 billion, according to S&P GMI’s calculations. In contrast, in 2023, Berkshire’s E&S premiums for allied lines soared by 66.4%.

Across all writers, homeowners, the smallest of the E&S property lines, saw outsized growth of 45.2% in 2024, rising to $3.2 billion from $2.2 billion in 2023. This jump was fueled by an 86% increase in California’s domestic E&S homeowners premiums, which climbed to $962.1 million.

Across all E&S property lines, geographies with significant exposures to hurricanes and wildfires reported the largest annual E&S growth rates last year, S&P

thing they liked better on the commercial lines side,” Adee said.

“But that market moved hard and fast—and in a strange way,” he suggested, later encouraging investors and analysts at the conference to weigh what risk models are showing against how the market is moving. “The different versions of the models keep creeping up the return periods.” While modeled expected losses are trending in the upward direction, commercial property rates are going down.

“I would suggest that doesn’t make a lot of sense other than just there’s a lot of capital chasing, and not as much business as [carriers] might want,” he said. “It’s just an interesting moment on the commercial property side—[and it’s] a little bit of a head-scratcher why people find that as attractive as they do at the moment.”

C&F, he said, “dialed back a lot on property just within the last quarter,” adding that E&S companies can “turn on a dime.”

officer of American Financial Group, reported that AFG writes a broad range of property in different parts of its specialty businesses.

“I think overall after quite a few years of increases that our property books are pretty adequate. We’re still getting price increases that exceed loss ratio trends on a good number of those businesses. [But] there are some businesses, on the E&S side, where prices are more flat,” he said.

“As much as anything, we’re trying to get the proper insurance-to-value where we can. That really adds to the profitability of property lines.”

Lindner continued: “We’re not a homeowners writer, and traditionally we’ve had lower relative catastrophe volatility on the hurricane and earthquake side than our peers.”

“I’m a Christian, and if you think God can do whatever he wants wherever he wants with whatever frequency, we think

Source: S&P Global Market Intelligence “2025 U.S. Excess & Surplus Market Report” continued on page 20

GMI reported. Geographically, the S&P GMI analysis tracks the growth in each state’s share of E&S premiums relative to the total property market since 2019, finding changes of more than 10 percentage points in Hawaii, South Carolina, and California.

Views of the 2025 E&S Property Market

Separately, at the S&P Global Ratings 41st Annual Insurance Conference in early June, specialty insurers writing commercial property on E&S paper discussed 2025 changes in the market and their appetites for E&S commercial property risks.

Marc Adee, chair and chief executive officer of Crum & Forster Holdings Corp., highlighted recent market movement toward shared and layered business, which he said generally has broader terms and tends to be cheaper. The push to write this business occurred even after the January 2025 fires in California had “put a fair dent” in a lot of carriers’ results—when “a subdued approach to the market” would have been anticipated.

“The speed with which that market moved down might indicate that maybe some of the people that were moving the capacity from homeowners found some-

Carl Lindner III, co-chief executive

Closer Look: Excess & Surplus Lines

continued from page 19

it’s hard to really adequately price coastal property and things like earthquake,” he said, reporting that AFG’s 1-in-500-year exposure in hurricane and earthquake is roughly 2% of equity. … We’re not as regulated, and I think we can pick and choose how we want to write property.”

While AFG will write coastal and earthquake, the choice to write that property business might be made when it’s part of a larger book of business, he indicated.

Back to the 2024 Leaderboards

Both AFG’s P/C insurance subsidiary, Great American Insurance Group, and Fairfax Financial Group, which includes C&F, were among the top writers of E&S business across all lines in 2024, according to S&P GMI, although neither showed up among the top 10 for any of the property lines analyzed. Both groups grew overall direct E&S written premiums by about 9% last year. Great American ranked No. 22 in overall E&S premiums with about $1.4 billion reported for the year. Fairfax, which includes Allied World and Odyssey Re’s Hudson in addition to the C&F companies, ranked third with $4.4 billion.

Ranking above Fairfax are Berkshire and AIG, with $8.5 billion and $5.6 billion in 2024 direct E&S premiums, respectively. (Editor’s Note: S&P GMI’s U.S. E&S ranking does not include Lloyd’s.)

Among growing E&S writers, Berkshire recorded the lowest overall growth rate at 0.8% last year, while two top 25 E&S insur-

ers—Munich Re and Zurich—each reported E&S premium drops. The declines pushed each down six spots in the rankings, with Munich falling to 20th and Zurich to 23rd.

‘Weakness in commercial property rates in catastrophe-exposed geographies could lead to a continued slowing in the E&S market’s expansion in 2025.’

— Tim Zawacki, S&P GMI

Retaining its second-place spot on the overall ranking (and a lead rank in product liability), AIG saw its 2024 E&S premium leap nearly 13% in 2024, following a 9% jump in 2023.

In terms of overall E&S growth, the biggest sprinters in 2024 were The Hartford

and Chubb, each growing around 20%, followed by Kinsale, Travelers, and W.R. Berkley.

W.R. Berkley, with $3.8 billion of its $4.2 billion 2024 E&S direct written premiums coming from the four liability lines analyzed by S&P GMI, became the largest E&S liability writer, surpassing Berkshire, the report notes.

Combining growth rates from the latest S&P GMI analysis of E&S leaders with those in a report published last year at the same time (based on 2023 writings), Carrier Management finds that the groups with the biggest overall growth rates across the two-year period were Starstone, Travelers, Kinsale, Starr Cos., and AXIS.

S&P GMI’s Methodology

The S&P GMI E&S report is derived from data running the S&P Global Market Intelligence E&S market share templates, P&C–Market Share (All exhibits) and P&C–Market Share (E&S Lines), the report notes in an introduction explaining the methodology.

Template results are based on U.S.domiciled entities that submit regulatory statements to the National Association of Insurance Commissioners and excludes so-called alien surplus lines insurers that are domiciled outside the U.S. but write domestic business, including certain Lloyd’s of London syndicates.

According to S&P GMI, the data is derived from Schedule T of annual and quarterly statutory statements for individual entities to identify those companies that list their status as “not licensed,” “eligible surplus lines,” or “domestic surplus lines insurer.” The data was compiled on April 17, 2025.

This article was originally published in Carrier Management, Insurance Journal’s sister publication.

Sclafane is Executive Editor of Carrier Management, a publication of Wells Media Group serving property/casualty insurance carrier executives.

Crum & Forster’s Marc Adee and American Financial Group’s Carl Lindner III speaking at the S&P Global Ratings conference in early June 2025.

Business Moves

National

ReSource Pro, Propellint

ReSource Pro, headquartered in New York City, acquired Propellint, a technology services firm specializing in implementation and support for insurance platforms including Insurity among others.

The acquisition expands ReSource Pro’s ability to assist with complex data migrations and core system implementations, complementing its existing strengths in workflow optimization and transformation services. Propellint’s clients can expect continued service, now backed by ReSource Pro’s expanded resources.

East

World Insurance Associates LLC, Healey & Associates

Global insurance broker World Insurance Associates LLC acquired the business of Healey & Associates of Portland, Maine.

Healey has been offering employee benefits to clients throughout New England since 1982, with a special focus on serving nonprofits. Healey is World Insurance’s first employee benefits agency in Maine.

World Insurance, headquartered in Iselin, N.J., serves its clients from more than 300 offices in the U.S. and the U.K. Terms of the deal were not disclosed.

COVU Inc., Ford Insurance Agency

San Francisco, California-based COVU Inc. acquired Ford Insurance Agency, a 100-plus year-old, family-owned business based in Eliot, Maine. Operated by the

Lonsinger family, Ford Insurance Agency provides commercial and personal lines coverage. The price was not disclosed. The transaction includes a three-year non-compete.

Midwest

First Financial, Westfield Bancorp

First Financial entered into a definitive agreement to acquire Westfield Bancorp, in a cash and stock transaction, from Ohio Farmers Insurance Company. Ohio Farmers is the parent company of the global property and casualty insurance group conducting business as Westfield.

The acquisition adds all of Westfield Bank’s retail banking locations and its commercial, insurance agency and private banking services. First Financial’s larger balance sheet will provide expanded credit capacity for Westfield Bank.

Under the terms of the agreement, First Financial will purchase 100% of the stock of Westfield Bancorp from its sole shareholder, Ohio Farmers. The transaction is valued at $325 million, which will be paid 80% in cash and 20% in stock of First Financial. The transaction is expected to close in the fourth quarter of 2025, subject to regulatory approvals and satisfaction of customary closing conditions. No First Financial shareholder approval is required. Approval of Westfield Bancorp’s sole shareholder, Ohio Farmers, has been received.

Bishop Street Underwriters, Aerospace Insurance Managers

Bishop Street Underwriters acquired

Ohio-based Aerospace Insurance Managers, a general aviation insurance services provider, from Hallmark Financial. This acquisition marks Bishop Street’s entry into the aviation insurance market. Financial terms of the deal were not disclosed.

AIM provides general aviation coverage for aircraft hull, aircraft and airport liability, with a focus on small aircraft flown for pleasure or business, as well as hangar owners, FBO operators, private and municipal airports, and flight school and charter operators. Operating across 47 states, AIM’s 16-person team will be led by Sean Kelley, vice president – chief underwriting officer, and Randy Kasen, vice president – business development and operations.

South Central

Inszone Insurance Services, Osterts and Associates LLC

Inszone Insurance Services acquired Osterts and Associates LLC, an insurance agency based in Plano, Texas.

Osterts and Associates, owned by Jerry and Kim Ostert, was founded in 1992 by Kim’s father, George Wynn, as the George Wynn Agency. Osterts and Associates specializes in all lines of personal insurance—including auto, umbrella, RV, boat—as well as life, financial services and business and commercial insurance.

Southeast

World Insurance Associates

World Insurance Associates acquired the business of five entities with locations across Louisiana on March 1.

The agencies are Insurance Unlimited of Louisiana LLC, Erwin Insurance Agency Inc., Burke & Burke Insurance Marketing Inc., Courtney Insurance Services Inc., and U.S. Principal Insurance.

Terms of the transaction were not disclosed.

The entities provide comprehensive property and casualty and employee benefit insurance products to businesses across numerous industries, as well as to individuals.

People

National

Jeff Miller rejoined Lockton, headquartered in Kansas City, Missouri, as national practice leader for the stop loss and pharmacy practices. Miller has over three decades of industry leadership. Previously, Miller served as president of Point6 Healthcare and office president at Ryan Specialty Benefits. Additionally, Miller has held leadership roles at Aetna and PacifiCare of Texas and previously worked at Prudential and BlueCross BlueShield in Oklahoma. During his previous tenure at Lockton, Miller served as executive vice president and practice leader.

Marty Andrejko rejoined Zurich North America, headquartered in Schaumberg, Illinois, as head of construction professional liability. Andrejko most recently served as managing director of construction professional liability at Aon. Andrejko, based in Philadelphia, has over 35 years of industry experience, including leadership roles at Convex, Berkshire Hathaway Specialty Insurance and AXA XL, as well as a nearly eight-year tenure at Zurich.

corporate and middle-market marine risks across the Northeast U.S.

Verisk’s Property Claims Services (PCS), headquartered in Jersey City, New Jersey, named Harry White head of commercial strategy. With over 14 years at Verisk and deep expertise in the risk transfer market, Harry brings a global perspective and a proven track record of client engagement and highly technical market insights.

Ted Gregory, who has been with PCS since 2013, will see his current leadership responsibilities expanded as the new head of research and operations.

new leadership within its U.S. wholesale and specialty division. The company is simplifying its structure from six U.S. wholesale and two U.S. retail regions to four integrated U.S. regions. As part of the new structure, the following appointments have been made to lead the four U.S. regions: West, Central, Northeast and Southeast.

ident, will lead the Southeast region. She has been with Markel for seven years and served as regional president for Markel’s former Mid-Atlantic region.

Three additional appointments were:

Brian Gray, regional president, will lead the West region with expanded oversight. Gray has been with Markel for 22 years and served as regional president for the West region for eight years.

Matt Huels has been appointed chief growth officer, U.S. wholesale and specialty. Huels has been with Markel for 10 years, most recently serving as regional president, West retail region.

Tom Losquadro

Canopius Group, headquartered in Chicago, Illinois, appointed Tom Losquadro as vice president of underwriting for national hull and liability U.S. Losquadro previously held senior roles at both AIG and Marsh McLennan. He joins Canopius from AIG, where he led the hull and liabilities underwriting team, focusing on large

Alliant Insurance Services, based in Irvine, California, named Lisa Paul leader of its new nationwide vertical specialty platform dedicated to serving clients in the transportation sector. With three decades of transportation insurance and risk management experience, Paul most recently served as an executive vice president at HUB International.

Mimi Fiske, regional president, will lead the Central region. She has been with Markel for 11 years and served as regional president for Markel’s former Midwest region.

Jim Hinchley has been appointed president, workers’ compensation and small commercial package. Hinchley joined Markel in 2024 as chief retail officer.

Markel Insurance, the insurance operations within Markel Group Inc., headquartered in Richmond, Virginia, appointed

Sal Pollaro has been appointed regional president for the expanded Northeast region with scope for wholesale and retail. He has been with Markel for 16 years, most recently serving as executive underwriting officer, professional liability.

Hollis Zyglocke, regional pres-

Scott Whitehead has been appointed executive underwriting officer, casualty. Whitehead has been with Markel for 26 years, serving in various underwriting leadership roles, most recently as senior managing director, Markel Insurtech.

East

Plymouth Rock Home Assurance Corporation, headquartered in Boston, Massachusetts, appointed Colleen Finn as chief marketing officer. Finn has over a decade of experience in property and casualty insurance and is

Harry White

Ted Gregory

Lisa Paul

Matt Huels

Brian Gray

Mimi Fiske

Sal Pollaro

Hollis Zyglocke

Jim Hinchley

Scott Whitehead

responsible for developing and executing growth strategies. Finn previously served as managing director of product management at Plymouth Rock Home Assurance Corporation. Before joining Plymouth Rock, Finn spent nine years at Liberty Mutual.

advisor to the GRS North America leadership team.

Willis, a WTW business, headquartered in New York City, appointed Linda Fisher as the sub-vertical leader for law firms within the Financial Services and Professional Services (FIPS) industry vertical division within North America. Fisher, based in Chicago, Illinois, previously served as a managing director in the national law firm vertical at Marsh McLennan Agency. She was also a leader in Gallagher’s law firm group and the law firm practice leader at Old Republic Professional.

Liberty Mutual Insurance, headquartered in Boston, Massachusetts, named Neal Bhatnagar president, major accounts, of Global Risk Solutions (GRS) North America. Bhatnagar joined GRS in 2021 in his current role, executive vice president, major accounts casualty. He succeeds Mike Fallon, who retires in January 2026 and remains as a senior

Tokio Marine HCC (TMHCC), based in Houston, Texas, appointed Elizabeth Geary to the newly created role of president and CEO of North America P&C. Geary will be based in New York City. Geary has over two decades of underwriting and senior leadership experience, joining from Liberty Mutual, where she was president of insurance solutions. Geary began her career at TransRe, gaining underwriting experience in U.S. property and healthcare, progressing to global head of cyber, and ultimately serving in a dual role as chief underwriting officer, North America, and president, global portfolio management.

Midwest

Frankenmuth Insurance, headquartered in Frankenmuth, Michigan, promoted Scott Merrihew to chief underwriting officer. In this expanded role, he oversees commercial lines and personal lines underwriting and continues to serve on the executive committee for Frankenmuth Mutual Holding Company and all subsidiary companies. Merrihew joined Frankenmuth Insurance 30 years ago and was promoted to chief commercial lines officer in 2024 after serving as head of commercial lines operations.

Circadian Risk, headquartered in Ann Arbor, Michigan, named Frank Schools as chief financial officer (CFO). Schools

previously worked with Circadian Risk principals while serving as the CFO of Universal Services of America (now Allied Universal). Schools’ 46-year career includes positions with Partners Group and Warburg Pincus, Ares Management, Blackstone and Onex. He has also held senior finance roles at 99 Cents Only and Pacific Sunwear.

group. Based in San Francisco, California, Jauregui has nearly two decades of experience and previously served as vice president of sales at EPIC Insurance Brokers and Consultants and in health and benefit sales at Mercer.

Caroline Buse joined Alliant as vice president within its employee benefits group. Based in South Carolina, Buse previously served as vice president at Gallagher.

Finys, an insurance software solutions provider headquartered in Troy, Michigan, appointed Tim Norman as chief growth officer and Rishi Khetrapal as director of finance.

Norman has over 20 years of experience in insurance technology and most recently served as vice president, enterprise sales at e123. Previous roles include vice president of sales at Applied Systems.

Khetrapal has over a decade of experience most recently serving in strategic finance and accounting at TruckSmarter. He previously served as investment director at Prudential Private Capital.

West

Faby Jauregui joined Alliant Insurance Services, headquartered in Irvine, California, as vice president within its employee benefits

Mercury Insurance, headquartered in Los Angeles, California, appointed Steve Bennett as its senior director of climate and catastrophe science. Bennett joins Mercury with over three decades of leadership in studying extreme weather, climate risk and effective risk management. He also serves on the adjunct faculty at the University of North Carolina at Chapel Hill.

Previously, he was co-founder and chief scientist at Demex.

The Liberty Company Insurance Brokers, headquartered in Gainesville, Florida, hired Connor Dann as vice president, producer. Dann is based in Liberty’s Woodland Hills, California, office.

Dann began his career at Assured Partners and most recently served as a sales executive. In his new role, Dann focuses on expanding Liberty’s presence in the construction and real estate sectors.

Frank Schools

Colleen Finn

Linda Fisher

Neal Bhatnagar

Scott Merrihew

Tim Norman

Rishi Khetrapal

Steve Bennett

Connor Dann

Idea Exchange: Is It Covered?

Logic & Language and Forms & Facts When Insurance Isn’t the Optimal Risk Management Approach

On March 14, 2024, I made a blog post titled “Do You Have The Right Kind of Insurance?” The article was initiated by an email I received through my website from a professional photographer who claimed that one of his photographs was posted on my website without his permission. I was told that, to stop the legal process that had already begun for copyright infringement, I should deposit bitcoin or ethereum funds in a crypto wallet address.

By Bill Wilson

titled “Insurance Is NOT a Commodity... Real Life Example #2,146: Acquired Autos.”

So, as before, I initiated my own investigation and found that PicRights had initiated such actions against a lot of people, based on information I found in a Google search. One individual claimed he refused to pay and was hit with a lawsuit that cost him $7,000 in attorney fees to settle. The information I found led me to believe this might be a legitimate claim.

PicRights is a Canadian-based firm that provides licensing compliance services to intellectual property owners. AFP is a French International news agency with locations around the world. So, the orga-

nizations involved in this matter appeared to be legitimate. The email was also very detailed and included attachments and links for resolving the claim. In addition, several days later I received a hard copy of the email in the form of a letter that was dated May 21, 2025. So, along with other information I had gathered, I concluded that this was not a scam but rather a real claim for copyright infringement because I had not licensed the image from AFP.

Over the years, I have published literally thousands of articles, seminar manuals, and six books. I have never deliberately and knowingly included any copyrighted material without express permission.

The email smelled intensely of being a scam, so I started to investigate the claim. First, I determined that the photographer was indeed a real person and, according to one news account, he had actually (and successfully) sued someone for copyright infringement. So, I contacted the photographer and forwarded the email to him.

Literally within minutes, he responded with, “Sorry…we are both victims of ‘phishing.’ Anything that requests payment via bitcoins is going to be a scam.”

In my blog post, I said, “I have photos on my website, but they are either license-free images provided through the WordPress platform or, in a few instances, photos for which I received express permission to reproduce.” What I learned recently is that using “license-free” or “royalty-free” images is not a guarantee of immunity from a copyright infringement claim.

On May 23 of this year, I received an email from someone at PicRights International Inc. alleging that I had posted an image owned by Agence France-Presse (AFP). They asked for proof that I had licensed a photo of five penguins that was copyrighted by AFP. If I could not produce such proof, they demanded that I remove the image immediately from my website AND pay, via credit card or PayPal, $534 for the past use of the image on a blog post

Sometimes, others have allowed me to use their material gratis with an attribution, such as some photos in my book “20/20 Vision: Why Insurance Doesn’t Cover the COVID 19 Pandemic.” In other instances, I’ve actually paid to reproduce images.

For example, in my book “Presentation Skills for the ‘Unprofessional’ Speaker,” I included several cartoons for which I paid a fee to reproduce.

In a string of correspondence with the representative from PicRights, I explained that any unlicensed use of the AFP photo was unintentional on my part. I knew that was immaterial from a legal standpoint, but I was looking for a little sympathy. And, not only was my misuse innocent, but I also had reason to believe it was permissible.

WordPress’s website touts the benefit of royalty-free images from Unsplash, Pixaby, Pexel, and other sources that change

over time. What I discovered that meant was that I don’t have to pay WordPress, Unsplash, Pixabay, etc., for such images but that doesn’t mean I don’t have to pay someone else if a copyrighted image is posted on one of the sources. This isn’t clear in the terms and conditions on both the WordPress or Unsplash websites.

I contacted both WordPress and Unsplash multiple times and never got a response from either of them. In addition, the name of the person who submitted the photo to Unsplash was shown on their website and I tracked her down. According to the short bio on Unsplash, she is a professional wildlife photographer that has traveled the world. She told me via email that this was HER photo, but when I told her that PicRights disputed that, she never responded to subsequent emails.

I made a final appeal to PicRights, again explaining that I myself had been the past

victim of people deliberately taking presentations I had made and delivering them as their own and others incorporating significant passages from a book of mine without attribution. However, in this case, once again, I felt like I was an innocent victim and that the entity that should be pursued is Unsplash and/or WordPress, who provided the platform that enabled the distribution of intellectual property without a valid license.

Unfortunately, my appeal fell on deaf ears, but PicRights was agreeable, under the circumstances, to reducing the $534 claim by 30%. Long story short, I settled the claim and moved on even though I felt like the victim of shake-down.

So, what does this have to do with insurance and risk management? First of all, you can insure the copyright infringement peril. However, such policies may have a deductible and, otherwise, is it worth it to file a $300-plus claim?

Second, there are other risk management approaches that can be used. In my case, looking to the future, I chose “Avoidance.” I spent a long day deleting every image on my website that I had downloaded through the WordPress platform. I also practice loss prevention by being more diligent to ensure I don’t even innocently incorporate the intellectual property of others in anything I produce.

Do you or your employer have a website that uses “royalty-free” images? If so, be aware that there are organizations using image search apps and even more sophisticated bots to patrol the internet.

Have you had an experience similar to mine? If so, feel free to share your story in the Comments section or send an email.

Finally, I’d be interested in what you think about this practice of going after the “little guy.” Recently, I spoke at a conference on ethics, and one of the issues I discussed was that an act can be legal but unethical or arguably ethical but illegal. In my case, this was legal, but was it ethical or moral?

Wilson, CPCU, ARM, AIM, AAM, is the founder and CEO of InsuranceCommentary.com and the author of six books. He can be reached at Bill@InsuranceCommentary.com.

Idea Exchange: Minding Your Business

Valuation & Terms of Small Books of Business

We get many calls about valuing small books of busi ness and if it is worth it to do a valuation. The seller may know what he/she wants, and the buyer may not want to spend a lot of money and needs some good advice. Usually on a small deal, like under $150,000, a fair market valuation does not make sense. Instead, we usually do an Opinion of Value if a book of business is under $500,000 in commissions or less.

By Catherine Oak

$200,000 book—that's 43.8% profit.

Valuing the Book

Deal Example Math

Let’s say you are looking at a $200,000 book to buy, mainly personal and commercial lines accounts.

You are looking at expenses to put in a CSR for like $36,000 plus benefits of 15% (or $5,400), and then your time at renewal and maybe a call or two. Then let’s pay the owner or a producer 20% ($40,000) plus 15% benefits ($6,000) and then throw in another $25,000 in miscellaneous expenses, like phone, accounting, rent, automation, etc. This totals $112,400. So, now we have $87,600 in profit on a

If you use a 6-times multiple of 43.8% profit, that is 2.6-times commissions, or in dollars a $200,000 book is then $525,600. If you give them 30% down, that is $157,680. Then you still owe $367,920. You turn that amount that you still owe, which is 70% of the money, into a percentage for the next three years. That 70% divided by three years is 23.3%. And with an earn-out you don’t pay interest. That way you can tell them no matter what comes in, you will give them 23.3% of the money. So, then you are paying on retention and are protected, as if only $175,000 comes in.

Ask us to send you the spreadsheet of a pro forma for this little book, and then to be astute you value it based on the bottom line. Then use perhaps a 6-times pro forma pretax multiple times profit, not the top line.

Two-times commission is usually a minimum for any size book today.

Typical Terms

In general, typical terms with an independent agency (not regional or national broker) are usually 20% to 50% down and

the balance on an earn-out, which means paying a percentage of what you still owe for each year based on what renews. The first year is paid by the down payment, so the buyer doesn’t start paying until the beginning of the second year and then can pay monthly, quarterly, or annually. With an older seller, the buyer usually has three years or less to pay this off.

The multiple varies between usually 5.0 for a riskier book with a higher profit to 7.0 multiple of cash flow or profit. On this book example, a 6-times profit is used because the profit was high at 43.8%. The profit range is usually 15% to 30% today.

Letter of Intent

A letter of intent (LOI) that each party signs before a purchase agreement is drafted by an attorney is helpful. An LOI may help the attorney to assist the seller or buyer with the Purchase Agreement. (Note: I can send a sample LOI that will not suffice as a legal agreement but can save a lot of the attorney’s time and is in layman’s language.)

Contingent Buy-Sell with Retiring Principals

A contingent buy-sell agreement can be put in place to set up a deal with producers that are not ready to let go yet but want back-up. This puts the price in writing in case something happens to the seller so that valuation is not done after a death or disability and protects the seller from a fire sale. The buyer is screened well, and both parties agree they are a good “fit” and want this to be done in the future. (Note: I can send a sample agreement to amend and use, but it should be reviewed by an attorney.)

Oak is the founder of consulting firm Oak & Associates, based in Northern California and Central Oregon. Oak & Associates specializes in financial and management consulting for independent insurance agencies, including valuations, mergers acquisitions, sales and marketing planning as well as perpetuation planning. Phone: 707-935-6565. Email: catoak@ gmail.com.

News & Markets

WCIRB: 2024 Losses, Expenses in California Workers’

Comp 108% of Earned Premium

Total losses and expenses in

California’s workers’ compensation system incurred in 2024 were $16.7 billion, or 108% percent of earned

premium, a report shows.

The Workers’ Compensation Insurance Rating Bureau of California released the 2024 California Workers’ Compensation

Losses and Expenses report, an overview of statewide insurer losses and expenses for the 2024 calendar year.

In calendar year 2024, earned premium totaled $15.5 billion, down from $15.8 billion of premium earned in 2023. Total insurer paid losses in 2024 were $9.5 billion, or 61% percent of calendar year earned premium, according to the WCIRB.

Based on insurer statutory annual statement information, the bureau estimates policyholder dividends incurred in 2024 to be 0.7% of 2024 earned premium, resulting in an underwriting loss of $1.3 billion, or 8.4% of premium.

The report shows that $5.2 billion, or 54% of total loss payments, were for medical benefits last year. Additionally, $4.4 billion, or 46% of total loss payments, was for indemnity benefits (including vocational rehabilitation benefits).

Washington Board to Eye Insurer AI Use

Washington Insurance Commissioner Patty Kuderer convened her first Artificial Intelligence Advisory Board meeting in Seattle to look at the insurance industry’s use of AI and to get recommendations on policy development, oversight and consumer education.

The board reviewed its charter and expectations, discussed AI in insurance, identified priorities and working groups and planned next steps during its inaugural meeting.

The board follows an Office of the Insurance Commissioner bulletin sent last year to insurers doing business in the state reminding them that decisions or actions impacting consumers that are made or supported by AI or other advanced analytical and computer technologies must follow insurance laws and regulations. The bulletin was based on a model advisory adopted by the National Association of Insurance Commissioners.

Idea Exchange: Specialty Markets

Turning Non-Standard Risks into New Revenue: How Agents Can Capitalize on the Specialty Market

Independent agents could be turning away nearly half of their prospective clients

The years of independent agents chasing “standard and preferred” home and auto risks are quickly coming to an end.

By David Wilson

As the risk landscape evolves, the traditional “ideal” customer profile— stable income, home ownership, clean driving record—is no longer the reliable foundation for agency growth it once was.

Economic pressures, climate-related exposures, and demographic shifts are forcing many clients out of standard underwriting guidelines and into non-standard, niche, or E&S (excess and surplus lines) territory.

For every six standard risks that walk into an agency, there are likely four more that don’t fit the mold. These non-standard risks, once dismissed as too niche or time-consuming, are now essential for agency revenue growth, client retention, and diversification.

By approaching this segment with the right strategy and tools, agents can stay competitive and serve a broader range of clients. Here are five ways to turn those out-of-the-box risks into revenue.

Redefine Non-Standard Risks

Non-standard home and auto risks aren’t inherently bad; they just fall outside typical carrier appetites. For example, standard carriers might be hesitant to insure a home on the coast with storm exposure, or a property with prior water or fire loss.

Similarly, they may shy away from auto clients with a foreign driver’s license or an imperfect driving record. While these prospective clients may not qualify for preferred coverage, there are many non-standard solutions that can meet their needs.