Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started. Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

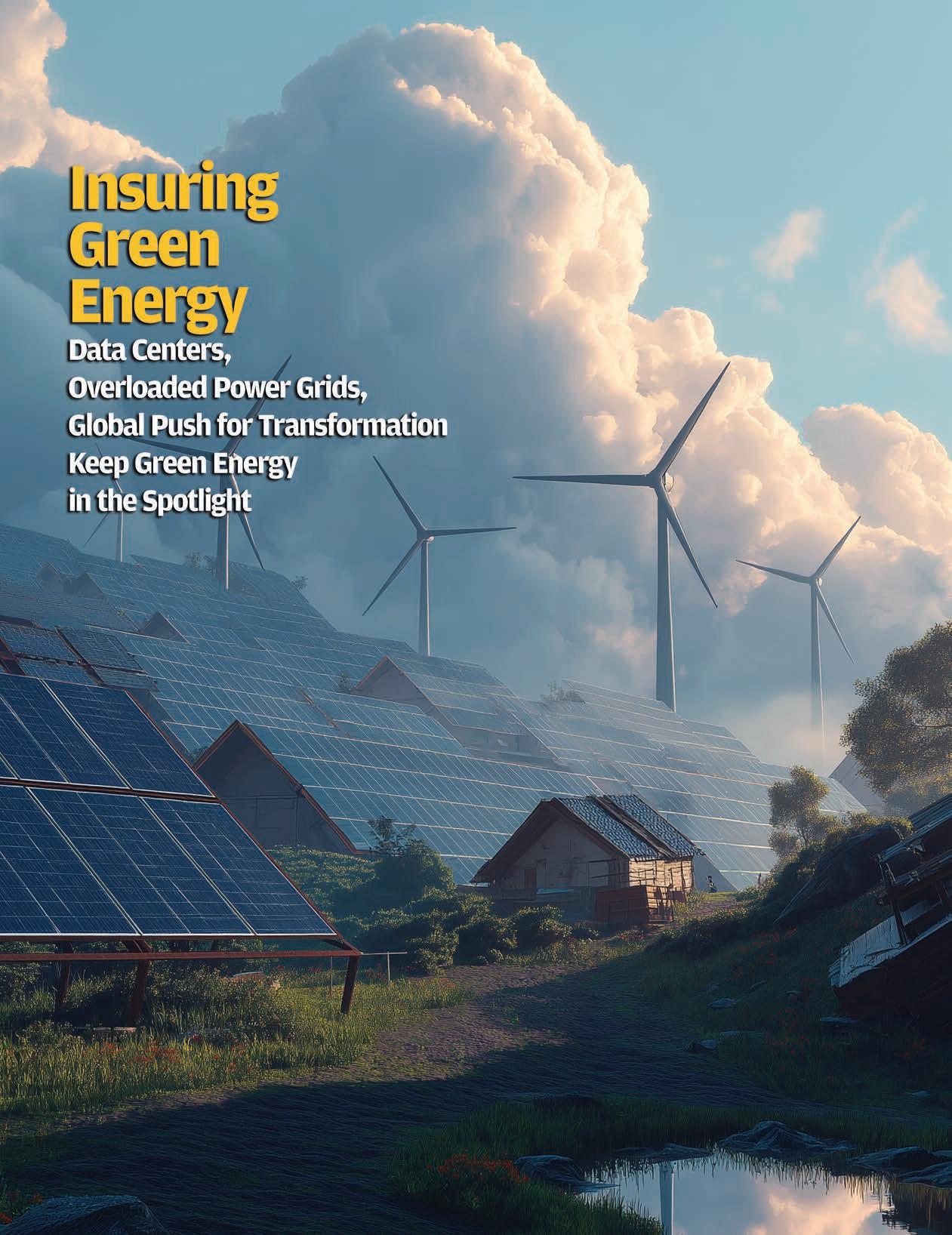

Powering the Future

Grid stability and system strength have become major issues around the world. At press time, New York is in the midst of rolling blackouts. Blistering heat is straining power grids across the eastern half of the U.S., leading to a blackout in part of New York City’s borough of Queens as the local utility issued a warning to conserve electricity.

The scenario is not new. My home state of Texas sees alerts every summer for residents to turn down the A/C on extremely hot summer days due to high power demands. And with the growing energy demand due to more and more technology needs, such as AI data centers, the U.S. and the world need to think about a mix of energy supply that works together to keep the lights, and A/C, on.

This special issue of Insurance Journal highlights the growing renewable energy industry and speaks with insurance specialists dedicated to this increasingly important sector of the economy. Because without power there might not be an economy—at least not one that operates on technology.

Renewable energy is growing in the United States and worldwide. In the U.S., wind and solar energy generated more electricity in 2024 than coal for the first time ever. But growth extends far beyond wind and solar. There’s growing interest in nuclear energy, hydropower, and geothermal power. And then there’s the expanding industry of power storage to relieve pressure on U.S. power grids during heavy energy months.

“We need power for everything, for our daily lives, down to different industries—from manufacturing to technology. We need reliable power,” Priscilla Pazmino-Vitela, head of natural resources – Americas for Allianz Commercial, told Insurance Journal in this special report (see page 28). The energy industry will continue to see growth from a variety of energy providers, including renewables “because we need to have reliable energy just to meet the demand that we’re seeing in innovation technology, or data centers,” she said.

While U.S. renewable energy maybe hit a road bump in investment due to a possible repeal of federal tax credits in some areas, global investment isn’t slowing down overall. Investment in clean technologies—renewables, nuclear, grids, storage, low-emissions fuels, efficiency, and electrification—is on course to hit a record $2.2 trillion this year.

And that’s good news for insurance specialists in this space.

‘We need power for everything, for our daily lives, down to different industries—from manufacturing to technology. We need reliable power.’

“There absolutely is an opportunity to drive this green transition and help this green transition along the way,” Fraser McLachlan, CEO of GCube and recently appointed chairman of the newly formed Tokio Marine GX (TMGX), says. “And make some premium out of it, as well.”

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant

Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content

Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus

Andrew Simpson | asimpson@wellsmedia.com

National Editor

Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor

William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor

Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Assistant Editors

Jahna Jacobson | jjacobson@insurancejournal.com

Kimberly Tallon | ktallon@carriermanagement.com

Columnists & Contributors

Contributors: Marc Adee, Mark Berven, Mike Erlandson

Columnists: Chris Burand, Erin Dwyer, Mary Newgard

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales

Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT) Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator George Jack | gjack@ijacademy.com

Artificial intelligence is positioned to transform healthcare, even if AI’s most alluring and headline-grabbing promises— like predictive diagnostics that anticipate illness before symptoms appear—remain projections for the future. While much of the spotlight is on what is to come, a quiet AI transformation is underway.

A survey conducted by the Medical Group Management Association in the summer of 2024 found that 42% of medical group leaders reported using some form of ambient listening AI.1 These systems, sometimes called “AI scribes,” aim to capture interactions between physicians and patients through discrete microphones installed in examination rooms. The AI then generates suggested notes and billing codes for physicians to review and enter into the medical record.

With the promise of increased efficiency in the documentation process, it is easy to see why physicians are drawn to this technology. A 2024 American Medical Informatics Association (AMIA) survey revealed that nearly 75% of healthcare professionals believe the time and effort required for documentation impedes patient care.2 In another study, over 77% of respondents indicated they often work later than desired or take work home due to excessive documentation tasks.3 Less time spent documenting allows physicians to spend more time with patients and potentially helps combat physician burnout.

The benefits of this technology are obvious and potentially transformational for physicians, but AI also brings new risks to consider. Not the least of which is patient consent. Recent evidence suggests that most patients are skeptical about the utilization of AI in healthcare. In a 2022 survey by the Pew Research Center, 60% of respondents reported they would feel uncomfortable if their provider relied on AI for their medical care.4 To help alleviate such concerns, physicians should have patients execute a detailed consent form that explains how the ambient listening system works, what is preserved, and the system’s deletion policy.

Physicians should also obtain and document a patient’s verbal consent at every visit before triggering the listening system. This ensures the patient remains comfortable having their protected health information shared with the system. Additionally, this verification is a legal necessity in states that require consent from all participants to a recorded conversation.

Discoverability is another issue physicians should be mindful of when utilizing this technology. By now, it is well known that most, if not all, malpractice litigation includes a discovery request for all relevant digital communications and metadata stored in the electronic medical record. Such data has provided fertile ground for plaintiffs’ attorneys seeking to weave a narrative in favor of their client, and ambient listening AI could be even more problematic.

While physicians are typically only privy to the AI-generated notes, ambient listening systems may also capture and store a raw audio recording of the entire patient encounter. Whether this data is retained depends on the design and configuration of the specific system. As such, physicians and practices must work with vendors to determine whether their chosen system stores complete audio recordings. If a system retains a complete audio recording of the patient-physician interaction, it will undoubtedly be discoverable in litigation.

In a worst-case scenario, there could be an inconsistency between the note in the EMR and the audio recording. Even a seemingly minor inconsistency could undermine the accuracy and reliability of the entire medical record. It may also be used to suggest that the physician failed to review the AI-generated notes adequately. Negative optics of this nature can derail otherwise defensible cases.

Against this backdrop, there is scant justification for retaining these audio logs once the AI-assisted note has been accurately added to the electronic medical record. To address this, practices should implement clearly articulated retention policies for all data captured by the AI system that is not added to the medical record. Beyond preventing the creation of unnecessarily discoverable data, a well-defined retention protocol that is consistently adhered to should ward off allegations of spoliation. Collaboration with vendors will be needed to ensure the chosen retention protocol is in place.

AI is already reshaping how healthcare operates, and these are just a few risk issues that need to be considered. As this technology evolves, its integration into everyday medical practice will only deepen. Amid these rapid advancements, physicians must remain vigilant to emerging risks, even as they navigate the often-dazzling promise of innovation.

Risk Recommendations

Physicians utilizing ambient listening AI systems should consider the following risk management steps to reduce legal risks:

2. Implement policies for retention and destruction of audio data.

3. Train providers on what is being captured and how to communicate accordingly.

4. Engage legal counsel in evaluating how these systems intersect with controlling discovery rules.

Bradley E. Byrne Jr., Esq., Southeast Regional Risk Manager

News & Markets

Insurance Industry Rejects Proposed Moratorium on State Artificial Intelligence Regulation

By Chad Hemenway

Aproposed decade-long moratorium on state regulation of artificial intelligence has gained the attention of many, including those within the insurance industry.

The 10-year prohibition of AI regulation is contained within the sweeping tax bill, “One Big Beautiful Bill,” and would preempt laws and regulations already in place in dozens of states.

The National Association of Professional Insurance Agents (PIA) on June 16 sent a letter “expressing significant concern” to Senate leadership, who submitted a reconciliation budget bill that has already passed through the House of Representatives.

“PIA strongly urges the Senate to eliminate the reconciliation language enforcing a 10-year moratorium on state AI legislation and regulation, or explicitly exempt the insurance industry’s state

regulation of AI because the industry is already appropriately regulated by the state,” said the letter, signed by Mike Skiados, CEO of PIA.

PIA referenced a model already adopted by the National Association of Insurance Commissioners (NAIC) that requires insurers to implement AI governance programs in accordance with all existing state and federal laws. Nearly 30 states have adopted the NAIC’s model on the use of AI by insurers.

Earlier in June, NAIC sent a letter to federal lawmakers following the passage of the bill in the House. The commissioners said state regulation has been effective in evolving market conditions.

“This system has not only protected consumers and fostered innovation but has also allowed for the flexibility and experimentation that is essential in a rapidly changing world,” said NAIC leadership in the letter. “By allowing states to develop and implement appropriately tai-

lored regulatory frameworks, the system ensures that oversight is both robust and adaptable.”

“State insurance regulators understand that AI is a transformative technology that can be leveraged to benefit insurance policyholders by, among other things, creating new product offerings, improving the efficiency of the insurance business, and transforming the consumer experience.”

The language—more specifically the definition of AI within the bill—is also of concern. NAIC called it “overly broad” and questioned whether it not only applies to machine learning but “existing analytical tools and software that insurers rely on every day, including calculations, simulations, and stochastic forecasts…and a multitude of insurtech provided analytical systems for rate setting, underwriting, and claims processing.”

To that end, the American InsurTech Council (AITC) said it “strongly opposes” the AI state regulation moratorium, which it said would “create a dangerous vacuum in oversight during a period of rapid technological change.”

“Such a ban would undermine the foundational principles of insurance regulation in the United States and jeopardize consumer protections at a time when AI is rapidly transforming the way insurance is developed, priced, marketed, underwritten, and delivered,” said the AITC in a statement.

In May, state attorneys general in 40 states urged Congress to get rid of the moratorium proposal within the bill.

On June 16, the National Council of Insurance Legislators (NCOIL) in a statement said a ban on state regulation would “disrupt the overall markets that we oversee” and “wrongly curtail” state legislators’ ability to make policy.

The group said constituents have “been steadfast in asking for protections against the current unknowns surrounding AI, and they cannot wait 10 years for a statebased policy response.”

THE POWER OF PARTNERSHIP

For this independent insurance agent and Taekwondo World Champion, partnering with Smart Choice has led to breakthrough business results. Clients notice when an insurance broker has their back. The Smart Choice partnership has helped the agency keep its retention rates up, even as policyholders increasingly compare rates. With access to a broader range of property/casualty, life/disability and annuity carriers, for both commercial and personal clients, the Short Associates team can offer clients more choices and win more business.

Breaking through barriers to success

“Clients have called to ask why their costs are going up and if there are options. Without my partnership with Smart Choice, I would have lost a lot of business because my phone has rung way more than it ever has in the last two years.”

Short Associate’s Darrell Swanson and Smart Choice-Midwest Regional Director Luke Royal

News & Markets

Agents Must Take the Lead on Personal Cyber Coverage, Report Says

By Jahna Jacobson

While major corporate cyber hacking makes the news nearly every day, what about hackers in homes?

As personal lives and residences become more intertwined with the internet, consumers are at greater risk of personal cybercrime. As risk grows, so does the need to protect consumers—although they may not know it.

Exposure to Personal Cyber Crime

Three out of four consumers have had their personal information lost or stolen, and 28% have had a social media account hacked, according to the new report, “Addressing the Personal Cyber Protection Gap,” from the Insurance Information Institute (Triple-I) and Hartford Steam Boiler (HSB), a Munich Re company.

The average payout for a home cyber claim is over $10,000, the new report found.

While consumer concerns used to be limited to financial accounts and identity theft, there are now opportunities to hack wherever there is an internet-connected device, including doorbells, thermostats, and security cameras. If a device is connected to the web, it can be infected with malware and collect information to be used by bad actors.

The risks have become a hot topic, particularly since the rise of “deepfake” technology and generative artificial intelligence (GenAI).

“As digital lifestyles evolve and become more interconnected, so do the risks,” said Neil Rekhi, product manager, personal cyber insurance, HSB, in the report. “The pace of personal cyber threats is increasing at an accelerating rate, and personal cyber insurance is one way to protect against these increasing risks.”

The Cyber Coverage Gap

Cyber insurance is one of the fastestgrowing property/casualty segments. The proliferation and potential severity of

personal cyber threats has forced insurers to clarify policy coverage and exclusions, improve risk managers’ understanding of product value, and better manage costs and rate stability. While 84% of the agents and brokers surveyed said they understand the value of personal cyber insurance, only 43% believe their clients share the same understanding.

The majority of agents (77%) say they have presented personal lines cyber insurance to clients at least once in the last month, but 56% of agents report that clients don’t understand or see the value of cyber insurance. Most agents (71%) said the price and breadth of coverage were clients’ most important criteria for purchasing personal cyber insurance.

While most agents understand the value of personal cyber coverage, only 73% said they are comfortable explaining it to clients and only 68% are comfortable selling the coverage.

“The disconnect between agent/broker and consumer perceptions of personal cyber risk—and the role of insurance in

addressing it—is a call to action from insurance professionals,” said Triple-I Chief Insurance Officer Dale Porfilio in the report.

The new report suggests that it will be up to agents and brokers to break new ground and get comfortable confronting consumers about potential risks and available protections.

“Agents need to be prepared to respond to—or, better yet, anticipate—customers’ questions and concerns about exclusions, deductibles, or other policy characteristics that might erode the perceived value of the product,” the report posits. “Agents should be able to explain in detail the breadth of a policy’s coverage, as well as any deductibles or exclusions that might apply.”

“In other words, better educated agents can help consumers be more aware of cyber scams and the importance of personal cyber insurance in protecting their assets. This will help them be less likely to become victims and ensure that they’re protected if they do.”

‘While consumer concerns used to be limited to financial accounts and identity theft, there are now opportunities to hack wherever there is an internet-connected device, including doorbells, thermostats, and security cameras.’

News & Markets

AM Best: US P/C Industry Records $1.1B Underwriting Loss for Q1

Growth in net earned premiums during the first three months of 2025 was offset by losses and expenses, resulting in a $1.1 billion net underwriting loss for the U.S. P/C industry. According to industry rating agency AM Best, the January wildfires in California were to blame for the increase in losses

for personal and commercial insurance lines in the first quarter.

Fitch Ratings said insured losses during the first quarter were an estimated $50 billion, with $38 billion from the California wildfires. The total is $19 billion more than Q1 2024.

Losses incurred during Q1 were about $147.1 billion, up

about 17% from the same period a year ago. Losses and loss adjustment expenses (LAE) were up 15.8% to about $167.5 billion, which significantly offset a 7.8% increase in net premiums earned to $226.3 billion, said AM Best in a first look at industry financial results.

Q1 net investment income of

$20.5 billion was up just 2.4% from Q1 2024.

Net income dropped more than 50% to about $19.8 billion during Q1 2025.

The industry’s combined ratio worsened to 99.4 from 94.4 during Q1 2024. Excluding $9.6 billion of favorable reserve development during Q1, the combined ratio was 103.6, said AM Best.

Fitch said the industry reported net income of $20.1 billion and a combined ratio of 98.8 for Q1 2025.

AM Best said its first-quarter analysis was based on company reports received by May 29. These insurers represent about 96% of both the industry’s total net premiums written and industry surplus, which increased 6.9% to about $1.1 billion.

US Homeowners Insurance Rates Rose 40.4% in Six Years: Report

U.S. homeowners insurance rates rose 40.4% over the past six years, with the biggest increases hitting in the last two years, a new report shows.

LendingTree’s 2025 State of Home Insurance Report shows rates from 2019 through 2021 remained stable, with increases of 2% in 2019, 2.1% in 2020, and 3% in 2021. Then rates started rising in 2022 with increases of 5.4%, 11% in 2023, and 11.4% in 2024.

The average annual cost of home insurance across the U.S. is now $2,801. The most expensive states for homeowners insurance are Oklahoma ($6,133), Nebraska ($5,912), and Kansas ($5,412), according to the report.

Hawaii has the lowest average rate at $632, followed by California ($1,260) and Vermont ($1,339), the report shows.

The states with the largest rate increases between 2019 and 2024 were: Colorado (76.6%), Nebraska (72.3%), and Utah (70.6%).

Colorado’s increase was partly due to an uptick in billion-dollar natural disaster events. There were 24 between 2019 and 2024. Nebraska experienced 25 natural catastrophes, and Utah has seen growing losses from disasters in wildfire-prone areas, the report shows.

Other key findings

in the report:

• Montana and Nebraska saw the largest jumps in home insurance rates in 2024, both at 22.1%. Minnesota and Washington each saw an increase of 19.5%.

• The smallest rate increases in 2024 included Florida (1.7%), Texas (3.4%), and New York (3.8%).

• States with the smallest

cumulative increases from 2019 to 2024 were Vermont (12.2%), Alaska (12.9%), and Maine (17.9%).

LendingTree’s analysis is based on home insurance data from Quadrant Information Services, sourced from insurer filings, and RateWatch from S&P Global. The analysis used standard coverage amounts and deductibles unless otherwise noted.

The following coverages and deductibles were used:

• $400,000 dwelling coverage

• $40,000 other structures

• $200,000 personal property

• $80,000 loss of use coverage

• $100,000 liability

• $5,000 medical payments

• $1,000 deductible

US Commercial Lines Prices Up 5.3%, Continue Downward Trend: WTW CLIPS

U.S. commercial insurance rates went up again in first-quarter 2025, according to the latest findings from WTW’s Commercial Lines Insurance Pricing Survey (CLIPS).

Carriers reported an aggregate price increase of 5.3% during the first three months of 2025—down from increases of 5.6% and 6.1% for the fourth and third quarters of 2024.

The aggregate price increase for the first quarter of 2024 was 6.3%.

“Overall, the continued reduction in rate increases is a very positive sign for buyers,” said Yi Jing, senior director of insurance consulting and technology at WTW.

However, Jing added, “consistent double-digit rate jumps for areas like commercial auto signify continued pricing difficult in the market. The only other coverage area maintaining double-digit rate increases is excess/umbrella liability.”

In Q4 2024, excess and umbrella liability recorded its highest price increase in the past three years, and commercial auto recorded its highest

For Q1 2025, commercial auto had the largest downward movement from the prior quarter among all surveyed lines.

Commercial property continued a strong downward

pricing trend, with just a small increase during Q1 2025, after large price increases were seen in 2023.

Forty-one participating insurers representing approximately 20% of the U.S. commercial insurance market

(excluding state workers compensation funds) contributed data to the survey.

WTW’s CLIPS data is based on new and renewal business figures obtained directly from carriers underwriting the business.

40.4%

The amount U.S. homeowners insurance rates rose over the past six years, with the biggest increases hitting in the last two years. LendingTree’s 2025 State of Home Insurance Report shows rates from 2019 through 2021 remained stable, with increases of 2% in 2019, 2.1% in 2020, and 3% in 2021. Then rates started rising in 2022, with increases of 5.4%, 11% in 2023, and 11.4% in 2024.

$5,000

A tax break proposed by Missouri lawmakers to offset the cost of property insurance deductibles. In the wake of a May 16 tornado, lawmakers approved $100 million of open-ended aid for St. Louis and $25 million for emergency housing assistance in any areas covered under requests for presidential disaster declarations. State budget director Dan Haug said the deductible provision could eventually cost up to $600 million.

$10,000

The amount awarded to a New Orleans, Louisiana, family by jury in federal court after a city police officer shot and killed their Catahoula Leopard puppy. The court found the officer had violated the puppy owners’ constitutional rights but was shielded from punishment under qualified immunity because of his government role. The jury awarded $10,000 in damages for emotional distress to the puppy’s owners, to be paid by the city. An additional $400 was awarded for the rescue dog’s market value.

Declarations

FEMA Farewell?

“This just means you should not expect to see FEMA on the ground unless it’s 9/11, Katrina, Superstorm Sandy.”

— Carrie Speranza, who used to advise the agency and is now president of the U.S. Council of the International Association of Emergency Managers, commenting on “Abolishing FEMA,” the memo addressed from then-acting FEMA head Cameron Hamilton to his bosses at the Department of Homeland Security. The memo outlines a number of functions that “should be drastically reformed, transferred to another agency, or abolished in their entirety,” possibly as soon as late 2025. Potential changes included eliminating long-term housing assistance for disaster survivors, halting enrollments in the National Flood Insurance Program, and providing smaller amounts of aid for fewer incidents.

Better Battery Boom

“Batteries are very good at handling these types of events. Things have gotten a lot better than a couple years ago.”

— Andrew Gilligan, director of commercial strategy at Fluence Energy Inc., a battery developer with three storage sites in Texas. When temperatures recently climbed to seasonal levels not seen in over a century, power demand surged. Meanwhile, scores of natural gas-powered generators were offline, getting tuned up for summer. Battery banks kicked in to cover 8% of demand, keeping power flowing. In the 12 months through April, energy storage in the U.S. rose from roughly 18 gigawatts to 25 gigawatts, a 41% increase, according to a Bloomberg Green analysis of federal data.

Record Fire Risk

“Don’t say this is going to be the worst fire season. You say that every year.”

— Nevada Gov. Joe Lombardo, jokingly, to State Forester and Fire Warden Kacey KC at a June wildfire briefing in Carson City, Nevada. KC’s cautious forecast for the coming fire season didn’t quite comply with the governor’s request. The state is “abnormally dry for this time of year,” she told him, primarily because of minimal snow at lower elevations during the winter followed by a warm spring that rapidly melted the snowpack at higher elevations. The annual briefing brought together a conglomeration of agencies and groups, including the U.S. Forest Service, Bureau of Land Management, Nevada National Guard, and city, county, and tribal representatives.

The Right to Invest

“We are very happy with the resolution and Bally’s decision not to use race in this investment. This case should serve as a warning to other companies that hope to dole out investment opportunities based on race. It is illegal, and we’ll fight it wherever we can.”

— Attorney Dan Lennington, who represented Richard Fisher, Phillip Aronoff, and the American Alliance for Equal Rights (AAER) in a discrimination case against gaming company Bally. Bally initially offered a 25% stake in a Chicago development to only women and minority investors to win the casino license from the Illinois city in 2022. The suit claimed the men's civil rights had been violated because they were white men.

Reining in Rates

“With factors such as distracted driving, excessive speeding, and increased automobile repair costs putting upward pressure on insurance rates, I am happy that we were able to hold the average increase to 5%.”

— North Carolina Insurance Commissioner Mike Causey commenting on the state’s automobile insurance rates, which are poised to increase statewide by a 5% average this fall. The settlement is lower than the average 22.6% rate increase for private passenger vehicles that had been initially requested in February by the North Carolina Rate Bureau, which represents insurance companies. The agreement also includes an average statewide 16.3% decrease on motorcycle liability insurance rates. The rate changes will take effect on new and renewed policies starting Oct. 1.

Lower Coverage Costs for Cabbies

“For years, New York City’s for-hire drivers have been crushed by an unjust, outdated insurance mandate that inflated costs, limited their options, and unleashed widespread fraud. In the middle of an affordability crisis, drivers were stuck paying the price for a broken system. But today, the Council came through.”

— New York City Council Member Carmen De La Rosa on the June 11 vote to lower for-hire vehicles’ per-person personal injury protection (PIP) coverage from a minimum limit of $200,000 to $100,000 and prohibiting the Taxi and Limousine Commission from requiring those licensed in the city to have PIP liability coverage over 200% of what's required for drivers elsewhere in the state.

Business Moves

National

Brown & Brown, Accession Risk Management

Brown & Brown Inc. has entered into an agreement to buy Accession Risk Management, the parent company of the specialty brokerage firm Risk Strategies and wholesaler One80 Intermediaries, for about $9.8 billion.

Daytona Beach, Florida-based Brown & Brown will purchase RSC Topco Inc., the holding company for Boston-based Accession—one of the largest privately held brokerages in the U.S.

After the close of the transaction, expected in the third quarter, the Risk Strategies team will become part of Brown & Brown’s retail segment. Accession CEO John Mina will join the retail senior leadership team.

Accession, founded in 1997, has over 5,300 employees in the U.S. and Canada and reported revenue of approximately $1.7 billion in 2024.

Brown & Brown, the seventh largest global broker with nearly $4.3 billion in revenue, according to AM Best’s 2024 ranking, enters the recent M&A action from the world’s top brokers.

Midwest

Risk Strategies, Schroeder Insurance

Risk Strategies acquired Schroeder Insurance, a Missouri-based firm with a specialty focus in the commercial lines and private client sectors. Terms of the deal were not disclosed.

Led by brothers Paul and Ted Schroeder, who each have over 30 years of industry experience, Schroeder Insurance’s business is closely split between commercial and private clients. The agency has specialty experience in hospitality, the public sector, and emergency response organizations, among others.

Schroeder Insurance traces its beginnings back to 1953 and founding partners A.C. Schroeder and Charles H. Schroeder. Its two offices in Union and Washington are located just west of St. Louis, Missouri.

In Missouri alone, Risk Strategies has recently acquired Thomas McGee Group, Stephens & Associates, and Beattie & Associates, all based in St. Louis and Kansas City.

Taylor Oswald Moves Headquarters to Cleveland, Ohio

Taylor Oswald, a provider of group benefits and property and casualty insurance, announced it is relocating its corporate headquarters in Cleveland.

With the move, Taylor Oswald joins its partner, Oswald Companies, at Oswald Tower on the East Bank of the Flats. Taylor Oswald said the move triples its office footprint and deepens its commitment to Cleveland.

Taylor Oswald President and CEO Eddie Taylor said the move allows the company to tap into the local talent pool and maintain strong ties with the community.

Taylor Oswald is an insurance advisor in the areas of property and casualty, employee benefits, retirement plan services, personal and family risk management,

life insurance and wealth preservation. In 2025, it also expanded to provide workers’ compensation third-party administration.

Ryan Specialty, JM Wilson

Ryan Specialty signed a definitive agreement to acquire the business of JM Wilson Corporation. JM Wilson is based in Michigan and its operations will become part of RT Binding Authority, the binding authority specialty of Ryan Specialty.

Founded in 1920, JM Wilson has six offices throughout the United States. The business has a broad range of offerings, including products ranging from personal lines to surety, and is well known for its expertise in transportation. JM Wilson generated approximately $19 million of operating revenue for the 12 months ended January 31.

Terms of the deal were not disclosed. The transaction is expected to close in the third quarter of 2025. Philo Smith served as exclusive financial advisor to JM Wilson.

South Central

Artemis Insurance, Tyner Jeter Insurance

Artemis Insurance, the parent brand of Texan Insurance, Ozark Insurance, and Marek Insurance, announced the acquisition of Baton Rouge-based Tyner Jeter Insurance.

Formerly part of McInnis Tyner Agency since 1972, the team launched Tyner Jeter Insurance in August 2012.

Earlier this year Artemis expanded into Louisiana by partnering with Ozark Insurance. Kyle Watson, managing partner for Ozark Insurance, will expand his role to oversee both Louisiana-based agencies.

Southeast

Unison Risk Advisors, Hatcher Insurance

The Orlando, Florida-based boutique agency and brokerage Hatcher Insurance is now part of Unison Risk Advisors.

Hatcher, founded almost 80 years ago, offers property and liability insurance, surety bonding, employee benefits, and personal insurance services. Billy Palmer, Bryan Robertson, and Cory Broadaway acquired the brokerage in 2020. They will

continue with the firm under Unison, the companies said.

The addition of Hatcher complements Unison’s 2023 partnership with Miamibased NSI Insurance Group.

Unison Risk Advisors was formed in 2020 with the merger of Cleveland-based Oswald Companies and RCM&D of Baltimore. It is headquartered in Cleveland and has over 1,200 employees across 25 offices. Robert Klonk is chairman and chief executive officer.

Patriot Growth Services, Brennan & Co.

Brennan & Co. insurance agency, based in Savannah, Georgia, is now part of Patriot Growth Services, a brokerage and insurance services firm that has grown rapidly since its founding in 2019. Patriot Growth has its headquarters in Pennsylvania and operates 170 offices nationwide.

Brennan began business in 2005, specializing in commercial marine insurance, including coverage for terminals, stevedores, shipyards, and towing, dredging and marine construction firms. The firm also offers property-casualty coverage and employee benefits services. It is led by principals Edward Brennan, Austin Denney, and Owen Brennan.

King Risk Partners, Nobles Insurance Agency

King Risk Partners has acquired Nobles Insurance Agency in North Carolina.

Nobles, with offices in Raleigh, Clayton, and other cities, has been in business for almost 60 years, binding life, homeowners, auto, and commercial insurance plans. Terry Nobles Jr. is owner of the agency. King Risk, based in Gainesville, Florida, has operated since 1974 and has expanded steadily in recent years through acquisitions across the eastern United States.

CRC Group Rebrands BenefitMall

Three years after it purchased BenefitMall, Alabama-based CRC Group is rebranding its employee benefits division as CRC Benefits.

The change marks a significant step in aligning the division with CRC Group's broader go-to-market strategy and will include a new logo. CRC Benefits will offer

a comprehensive wholesale employee benefits platform and will continue to work with agencies nationwide.

CRC Group, headquartered in Birmingham, Alabama, is an independent insurance wholesaler founded in the 1980s.

The group is part of Truist Insurance Holdings. CRC acquired Dallas-based BenefitMall, a wholesale benefits general agency, in September 2022.

West

Hub International Ltd., Wycoff Insurance Agency Inc.

Hub International Ltd., headquartered in Chicago, Illinois, acquired the assets of Wycoff Insurance Agency Inc. in Mount Vernon, Washington. Wycoff Insurance will be referred to as Wycoff Insurance Agency, a Hub International company. Chris Eisses, president; Donnie Keltz, vice president, secretary and treasurer; and the Wycoff Insurance team will join Hub Northwest.

Wycoff Insurance is a locally owned insurance agency providing commercial and personal insurance.

Monarch E&S Insurance Services, Market Finders Inc.

Monarch E&S Insurance Services acquired Market Finders Inc. (MFI) in Albuquerque, New Mexico. Monarch E&S Insurance Services is a division of Specialty Program Group LLC.

MFI is a managing general agent and wholesale broker founded in 1971. MFI specializes in both personal and commercial lines, including transportation risks, led by President Steve Shaffer.

Arthur J. Gallagher & Co., Wilkins & Associates Insurance Services

Arthur J. Gallagher & Co., headquartered in Rolling Meadows, Illinois, acquired Reno, Nevada-based Wilkins & Associates Insurance Services Inc.

Steve Wilkins, Jared Wilkins, and their team will operate under the direction of Scott Firestone, head of Gallagher’s Southwest region retail property/casualty brokerage operations.

Wilkins & Associates, founded by Tom and Melanie Wilkins, is a retail insurance broker serving commercial and personal lines clients in Reno and western Nevada.

InterWest Insurance Services, headquartered in Sacramento, California, has acquired Armstrong & Associates Insurance Services in the state of California.

Martin Armstrong will remain in a leadership role, with all employees coming over to InterWest.

Founded in 2004, Armstrong specializes in agribusiness and serves clients throughout California and beyond.

Inszone Insurance Services, Denver West Insurance Brokers

Inszone Insurance Services acquired Denver West Insurance Brokers in Golden, Colorado. Denver West Insurance Brokers will retain the same office and team members.

Founded in 2003 by Tina Kiel, Denver West Insurance Brokers is a provider of commercial, personal and benefits insurance services.

Inzone Insurance Services, Evers Insurance LLC

Inszone Insurance Services, headquartered in Sacramento, California, acquired Evers Insurance LLC in Cave Creek, Arizona.

Evers Insurance specializes in commercial insurance, particularly in the garage and auto dealer industries. It was founded in 2011 by Britt Evers. Jake Evers also contributed to the firm's growth as a generalist in commercial lines.

Alliant Insurance Services, Johnson Benefit Planning

Alliant Insurance Services acquired Johnson Benefit Planning in Oregon. The Johnson Benefit Planning team will join Alliant.

Johnson Benefit Planning is an employee benefits consulting firm with offices in Bend and West Linn, Oregon. Alliant is headquartered in Irvine, California.

National Starwind Specialty Insurance Services named Graham Jenks the president of JH Blades Group, which encompasses JH Blades Energy, JH Blades Marine, Southern Marine, and Energy Technical Underwriters. JH Blades is a specialty platform of Starwind Specialty Insurance Services, a CRC Group company headquartered in New York City. Jenks has served as president of Southern Marine for eight years. He previously served at the company as a vice president and marine underwriter. Before joining the company in 2012, Jenks was a marine cargo broker at Price Forbes and Partners.

Richard Martin, long-time leader of JH Blades, has retired following a career spanning many years of service.

Michael Gonzales joined Alliant Insurance Services, headquartered in Irvine, California, as first vice president with the value-based healthcare and risk management solutions team within its employee benefits group. Based in North Carolina, Gonzales will work closely with clients across the healthcare spectrum. Gonzales has over 20 years of experience in business development, sales operations, and go-to-market strategy, as well as 15 years of experience focused on partnering with hospitals, health systems, physician provider groups, and Managed Service Organizations (MSOs). Before joining Alliant, Gonzales most recently served

as vice president of sales at MedEvolve.

Former Willis Group

Holdings CEO Joe Plumeri was named to the new role of chairman at Insurance Advisory Partners (IAP). He will start the role on September 1. Plumeri served as chairman and CEO of Willis Group, beginning in 2000, after previously serving as CEO of Citibank, North America. He then joined KKR & Co., a former investor in Willis Group, as a senior adviser.

York, has elected Kelly Gonyo as chair of the board for the 2025–2026 term. Gonyo is the founder and president of Blue Line Insurance Agency, headquartered in Lake Placid, New York. Gonyo has served on the Big “I” New York Board of Directors since 2020, previously holding the roles of vice chair and secretary/treasurer.

Ryan Specialty, headquartered in Chicago, Illinois, has appointed Brad Storey as president of Irwin Siegel Agency (ISA), a social service industryfocused managing general underwriter that is part of the Ryan Specialty Underwriting Managers division of Ryan Specialty. ISA is headquartered in Rock Hill, New York.

Mosaic Insurance, headquartered in Hamilton, Bermuda, promoted Yosha DeLong to the new role of global engagement officer and hired cyber and technology liability executive Brian Bonkoski to lead the company’s cyber business.

Based in Chicago, Illinois, DeLong has built Mosaic’s cyber business since the company’s launch in 2021, spanning a global footprint that includes the U.S., Canada, Bermuda, the U.K., Germany, and the United Arab Emirates.

Bonkoski, based in Philadelphia, Pennsylvania, is the global head of cyber at Mosaic. He has 20 years of experience in underwriting and distribution leadership, with previous executive roles at Chubb and AIG. Most recently, he served as senior vice president and head of field operations at Chubb.

East

Big “I” New York, a trade association for independent insurance agents in New

Also elected to the executive committee was David Borg, who will serve a one-year term as vice chair and secretary/ treasurer. Borg is a past president of Big “I” Suffolk and a former Chair of the Big “I” NY NextGen Committee.

Gonyo and Borg join David Bodenstein (immediate past chair) and Ron Brunell (national director).

Big I New York members also elected regional directors: Lisa Hussainov of Walsh Duffield Companies Inc. in Buffalo, New York, to a two-year term representing the West Central region; Eric Diamond of Marshall & Sterling in Chappaqua to a two-year term representing the East North region; Eileen Frank of J.P. West Inc. in New York, to a two-year representing the Metro Suburban region; and Robert Bleistein of Eastern Classic Coverage Insurance Agency on Long Island, to a two-year term representing the Metro Suburban region.

Big “I” NY’s regional directors are Mike Zwas, Deena McCullough, Emmanuel Osuyah, Rob Bowen Jr., and Doug Benz, and at-large directors are Frank Marullo and Sydney Roe.

Storey has been with the Irwin Siegel business for over 17 years and is currently executive vice president of the managing general underwriter.

With this appointment, Howard Siegel becomes executive chairman of ISA.

Davis & Towle Insurance Group, headquartered in Concord, New Hampshire, named former New Hampshire Insurance Commissioner Christopher (Chris) Nicolopoulos as the agency’s new CEO.

Jeffrey Towle, previously the agency’s president, has been appointed chairman of the board, while his son, Ryan Towle, who was previously vice president, has assumed the role of president.

Nicolopoulos previously served as president and CEO of the New Hampshire Association of Insurance

Graham Jenks

Yosha DeLong

Kelly Gonyo

Brad Storey

Howard Siegel

Chris Nicolopoulos

Agents and New Hampshire’s insurance commissioner. Most recently, he held a regional government affairs position at the National Association of Mutual Insurance Companies.

Sandra Margeson has assumed the role of chief financial officer and treasurer.

Lori Tobin is now vice president, personal lines/branch management.

Brian Parsons has been promoted to vice president, sales.

Midwest

– affiliates. He joined Brotherhood Mutual in 2000 as an assistant underwriter and most recently served as assistant vice president, sales and special markets, since 2015. He has also held the positions of property claims adjuster, senior marketing specialist, and manager of the special markets division.

Urbana, Ohio, named four new equity partners. All are based in the Springfield office.

Ben Galbreath has nearly two decades of experience in personal, commercial, life, and supplemental benefits insurance.

Jason Heims has been with Wallace & Turner since 2007, specializing in both personal and commercial lines and overseeing claims management.

Mary Jo Leventhal serves as director of operations and business development.

Frankenmuth Insurance, headquartered in Frankenmuth, Michigan, appointed Kelly Ott as chief legal officer and corporate secretary. Ott is the company’s top legal advisor, overseeing corporate legal matters, governance, and regulatory compliance across all Frankenmuth Insurance companies and subsidiaries.

Ott has over 30 years of experience in private practice and in-house legal leadership. She previously served as legislative and regulatory counsel and managing attorney for claims litigation at State Farm, as vice president and assistant general counsel at Horace Mann, and most recently as vice president and counsel at The Hanover Group.

Brotherhood Mutual Insurance Company, headquartered in Fort Wayne, Indiana, made three executive team changes.

Gabe Brown was named vice president, sales and operations – Brotherhood Works

Drew Smith is now vice president of marketing. He joins Brotherhood Mutual after over 27 years with American Specialty Insurance & Risk Services, Inc., where he served as vice president, client services, and chief marketing officer and was president of the company for over nine years. He most recently served as a senior advisor.

O’Day has over 20 years of public service experience in Oregon, previously serving as the deputy director of the Oregon Department of Veterans’ Affairs, executive director of the Mid-Willamette Valley Council of Governments, general counsel for the League of Oregon Cities, deputy city attorney and deputy city manager for Salem, deputy legal counsel to the Office of the Governor, and law clerk to the chief justice of the Oregon Supreme Court.

Myles Trempe is a second-generation Wallace & Turner employee, handling both personal and commercial lines coverage.

Southeast

TK Keen, deputy insurance commissioner and administrator of DCBS’ Division of Financial Regulation, will serve as acting insurance commissioner. Keen has led several National Association of Insurance Commissioners’ working groups. Before joining the division, he practiced law as a sole practitioner in Washington, with a focus on employment law cases.

Mitzi Thomas has had a 30-year career with Brotherhood Mutual, where she has served as vice president of marketing for the past 12 years.

With plans to retire at the end of 2025, Thomas has stepped into the role of vice president and marketing advisor. She previously served as marketing communications manager, assistant vice president of corporate communications.

Wallace & Turner Inc., located in Springfield and

Lake Mary, Florida-based Trident Reciprocal Exchange, launched in 2024, named Ryan Hodges as CEO. Hodges has 25 years in the property and casualty insurance business and was previously vice president of commercial insurance for Bankers Insurance Group. Hodges also worked as a commercial underwriting manager for Citizens Property Insurance Corp.

West

Oregon Gov. Tina Kotek named Sean O’Day as acting director of the Oregon Department of Consumer and Business Services (DCBS). O’Day is currently the deputy director for DCBS.

He replaces Andrew R. Stolfi, who the Oregon State Senate recently confirmed to be the director of the Oregon Employment Department. Stolfi presently serves as both the DCBS director and the Oregon insurance commissioner.

Coalition, headquartered in San Francisco, California, hired Ilsa Derfus as its director of capacity. Derfus is responsible for managing relationships with carrier partners and will serve as the primary point of contact for all capacity-related matters.

Derfus joins Coalition from McGill & Partners, where she was a partner and previously worked with Coalition and other clients in a reinsurance brokerage capacity. In the decade before McGill, Derfus served as an associate director at Aon Benfield and a pro-rata technician at Guy Carpenter.

Kelly Ott

Isla Derfus

Mitzi Thomas

Drew Smith

Gabe Brown

News & Markets

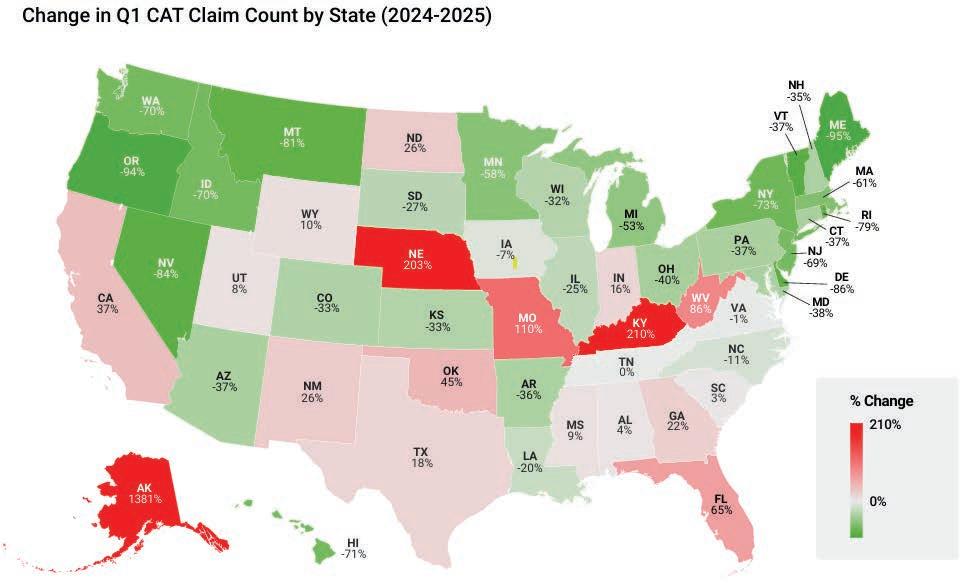

Verisk: Q1 Claims Volume Hits 5-Year Low but Severity Up on Wildfire Losses

By Ezra Amacher

The first three months of 2025 brought devastating wildfires to California, significant wind and hail events to Texas, and substantial increases in tornado activity to “Tornado Alley,” but claim volume decreased to a five-year low, according to a quarterly property report from Verisk.

The findings in Verisk’s “Quarterly Property Report January–March 2025” show that claims severity rose due to the California wildfires while property claims continued a downward trend that began in 2023.

Claims costs skyrocketed in the first three months, with the national average replacement cost value (RCV) increasing 46% compared to the same period a year ago. The increase in RCV was primarily driven by the Palisades and Eaton fires, which generated approximately 48,000 claims totaling roughly $10 billion, Verisk found.

California experienced a 1,805% increase in RCV from Q1 2024 to 2025, the report found. The average claims estimate from the wildfires was $337,000.

This extreme increase in RCV was counterbalanced in the first quarter by the fact that 33 states experienced a decrease in severity from the same quarter in 2024, the report said. Maine, Delaware, Montana, and Oregon saw an average 80-95% decrease in severity.

Total claim volume for the quarter was down about 7%. The decrease came primarily from non-catastrophe claims, while catastrophe claims stayed steady, Verisk found.

Texas led the country in claim volume with 161,000 claims. California had the next highest with 96,600, followed by Florida (48,500), Missouri (48,200), North Carolina (36,000), and Pennsylvania (35,700).

Texas accounted for 95% of all Q1 catastrophe (CAT) events, driven by wind and hail events. Several other states

saw significant increases in CAT claims, the study found, ranging from 45% in Oklahoma to over 200% in Kentucky and Nebraska. Most of these CAT claim increases were from wind and hail claims tied to tornadoes, the study said.

Many states, including those in the Pacific Northwest, saw a drop-off in CAT claims. Washington had a 99% decrease in freeze claims, Oregon had a 98% decrease in ice and snow claims, and Maine had a 98% decrease in wind claims from 2024 to 2025, the report found.

Verisk found that billable labor costs slowed in the first quarter. Labor costs increased 1.06% across the United States compared to 1.42% in the previous quarter.

The report cautioned that U.S. immigration and tariff policies could also have a potential impact on construction and material costs. The construction industry relies heavily on imported materials (28% of lumber, 24% of concrete, 36% of gypsum) and immigrant workers (26% of the workforce), the report said.

News & Markets

Insurance Sector Should Be on the Lookout for ‘Scattered Spider’ Hackers

By Chad Hemenway

Watch out, insurance industry. A well-known cybercrime group appears to have shifted focus to insurers.

Apparently, recent cybersecurity incidents at Erie Insurance, Philadelphia Insurance Cos., and Aflac are indicative of a trend. The largely decentralized hacking group known as Scattered Spider have switched focus from retailers to insurance companies, according to Google Threat Intelligence Group.

“Actors that bear the hallmarks of Scattered Spider are now targeting the insurance industry,” John Hultquist, chief analyst at Google’s Mandiant, posted to X. “They have a habit of working their way through a sector. Insurance companies should be on the lookout for social engineering schemes targeting their call centers.”

Scattered Spider, partnering with ran-

somware-as-a-service group DragonForce, had in recent months been concentrating on the retail sector in the U.S. and U.K., causing havoc to Whole Foods supplier United Natural Foods, Marks & Spencer, Co-op, Adidas, The North Face, Cartier, and Victoria’s Secret, among others.

Since Hultquist’s first post on the cybercrime group’s change in industry focus, the U.S. has bombed Iran—raising some concern that retaliation could include cyberattacks. Even with the increased cyber threat from Iran, Hultquist said the “threat I lose sleep over is Scattered Spider.”

“They are already taking food off shelves and freezing businesses. The Iranian hackers may not even have Internet access, but these kids are in play right now,” he posted.

Keith Wojcieszek, global head of threat intelligence at Kroll, told Insurance Journal he recently received some infor-

mation that one insurer was the victim of phishing, which gained access to the company’s information technology. The hackers then use the information they can see to research the company’s hierarchy and fuel social engineering efforts.

Like the retail sector, insurers have a huge amount of valuable personally identifiable information and financial data to store, use, and sell. Also, insurers have information on insureds, which may be used to identify the next targets, according to Wojcieszek.

“These attacks may be about money, but there could also be a two-prong approach,” he said, explaining that insurers now gather a lot of information on companies in order to insure them. “The network security of each company—[insurers] are so detailed on the cybersecurity each company has. What a wealth of knowledge to have to know how to attack the next company or industry, or develop tools to go in and attack.”

Spotlight: Claims

Wildfire Experience Inspires New Contents Claims Insurtech

By Allen Laman

When Michael Balarezo emerged from the basement office of his Boulder, Colorado, home in December 2021, smoke plumes from the nearby Marshall Fire were visible from his driveway. Balarezo, his wife, and daughter swiftly stowed emergency clothing, sensitive documents, and toys into duffel bags and loaded them in the back of their car.

“And we say bye to our home,” Balarezo said, “because we think it’s going to go in flames.”

Eighty-mile-per-hour wind gusts whipped debris through the air. The smoke thickened and limited visibility to distances shorter than half a

When the flames subsided, the house was one of the lucky survivors in the Balarezos’ neighborhood. But soot and ash flooded into the home through doors believed to be opened by emergency personnel. The entire main level and upstairs bedroom needed to be gutted.

Two years after leaving, Balarezo and his family moved back in. It took a lot of time to work with all the parties needed to get everything fixed,

he said. A former insurance claims adjuster himself, the process gave Balarezo a new perspective on how much policyholders go through when disaster strikes.

He described the experience as chaotic. Family arguments erupt over how much time repairs are taking, he said.

Stress arises when policyholders wonder why the resolution is dragging on and why they haven’t heard from their insurance company. Living in a townhome, Balarezo spoke of issues that can surface when alignment is needed with neighbors on contractors and services.

“It’s almost like working a full-time job on top of the

full-time job that you have,” he said of the repair process.

The idea for Adjusto, his new contents claims platform, didn’t hit Balarezo until the very end of this claim. He and his wife told their daughter that they could finally return home. After hearing the news, she began sobbing as all the emotions of the previous two years were released. She was happy it was over and ready to move on.

“That moment, it hit me really hard, personally,” Balarezo said. “She shouldn’t have to suffer through all of this. And it made me realize that she witnessed mom and dad arguing and fighting over the claim. She witnessed

football field.

News & Markets

Wildfire Season Preview: Rest of 2025

Is High-Risk, May Follow LA Wildfires Paradigm

Following the “paradigm-shifting” Los Angeles wildfires in January, the 2024-2025 wildfire season will be remembered as a turning point for the insurance industry, and a warning that “wildfire is no longer a seasonal or rural phenomenon,” a new outlook asserts.

The rest of 2025 poses severe wildfire risk in numerous states thanks to developing drought conditions, including high risk in wildfire-prone California, according to a report from ZestyAI.

The L.A. wildfires killed 29 people, and damaged or destroyed thousands of properties. The fallout of the fires included large losses for major California insurers, including State Farm. The carrier is asking the California Department of Insurance to approve a large rate increase. According to the California Department of Insurance, 37,749 claims have been filed related to the fires and $12.1 billion has been paid out.

However, the wildfire perils weren’t only in California.

“From New Mexico, where one of the state’s most destructive wildfires validated early high-risk forecasts, to blazes in the Midwest and Southeast, the 2024

season revealed wildfire’s expanding geographic footprint, relentless pace, and increasingly unpredictable behavior,” the report stated. “For insurance carriers, it exposed the limits of legacy models still tied to historical fire perimeters or broad geographic zones, and accelerated adoption of next-generation tools that assess parcel-level vulnerability—including structural features, defensible space, and vegetation overhang.”

The rest of the year is shaping up to be more volatile following a moderate 2024 wildfire season. Severe drought conditions are expected to return and spread across the country, with intensified dryness in the Southwest and deep into the Northern Rockies and the Plains, according to the report.

“Heavy rains in California, Oregon, and Washington during the past two years have driven significant vegetation growth. If heat and dryness persist into late summer as forecasted, these areas could once again become highly combustible,” the report states. “This familiar pattern, where wet years boost fuel loads that turn dangerous when conditions shift, remains a long-term

driver of wildfire risk in these historically vulnerable states.”

The report notes that states like Arizona, New Mexico, Nevada, Utah, and Colorado remain in multi-year droughts, while Montana, Wyoming, North Dakota, and South Dakota are emerging as new high-risk zones due to a dry, snow-starved winter and unusually warm spring. Drought signals are also coming out of Texas and Florida, according to the report.

The report also touches on how new state rules and laws are reshaping how insurers are assessing and communicating risk:

In late 2024, the California Department of Insurance finalized its Sustainable Insurance Strategy, a reform to stabilize the state’s insurance market. Central to the strategy is the approval of forward-looking catastrophe models in rate filings—allowing insurers to price wildfire risk based on future exposure rather than past losses.

In 2025, Colorado enacted House Bill 25-1182, establishing a new benchmark for transparency in wildfire risk modeling. The law applies to all admitted carriers and the FAIR Plan. It requires insurers to disclose how wildfire models impact rates, recognize both property- and community-level mitigation efforts, notify policyholders annually of their risk scores and discounts and provide an appeals process for disputed scores.

In 2024, Washington adopted new regulations aimed at improving transparency around insurance premium increases. Insurers are required to notify policyholders that they may request a written explanation for any increase in their homeowners or auto insurance premiums. Upon request, carriers must provide a rationale within 20 days.

In April, Oregon passed Senate Bill 83, repealing the state’s mandatory wildfire hazard map following sustained public opposition. The original map had classified properties into risk zones that triggered defensible space requirements and stricter building codes—measures that some property owners argued were based on incomplete or inaccurate data and had unintended consequences on insurance availability and property values.

mom and dad talking with the insurance company or with the adjusters, trying to figure out how we can move forward and being aggravated.”

All the stress impacted her. And Balarezo didn’t think that was fair.

“That moment is when I thought, ‘I feel like I can do something about this,’” Balarezo said. “Someone should do something about this.”

FairMatch platform provides fast, accurate, and automated personal property valuation for carriers, MGAs, TPAs, and adjusting firms at scale and provides “new ways for adjusters to collaborate with policyholders to resolve claims quickly while building trust.”

He felt the time was right to combine his policyholder experience, adjuster know-how, and decade of software engineering expertise. Adjusto was formed in April 2024 and was publicly announced in March 2025.

After months of beta testing, Adjusto launched FairMatch, an AI-powered platform.

Rather than rushing to replace items through vendor catalogs or shopping links, Adjusto’s FairMatch gives adjusters the tools to determine what people are truly owed and deliver it with clarity and care, according to the Adjusto release on June 18.

Balarezo said Adjusto’s new

FairMatch accepts handwritten, spreadsheet-based, or in-platform item lists and automates line-by-line matching to likekind-and-quality (LKQ) items that adjusters and policyholder can agree on. Adjusto says the platform also automates depreciation and valuation logic, as well as settlement prep and flag reviews—automating 85% of the heavy lifting for adjusters and giving them the space to provide a personalized and empathetic claims experience.

Professional Background

Balarezo became an all-lines claims adjuster after college. His future father-in-law worked as head of an auto salvage team, and he tipped Balarezo off to an opening at Oklahoma Farm Bureau Insurance.

Balarezo enjoyed the investigative nature of the job. He liked digging into claims during his three years in the role.

“Also, I enjoyed the fact that I got to help people as part of my day-to-day [duties],” he said.

Balarezo ultimately pursued his dream of becoming a software engineer and moved to Silicon Valley to build automation solutions for companies including Google, Amazon, and Disney. Still, he carried the lessons he learned in insurance with him.

‘I think there’s too many tools in the market that just complete tasks but don’t actually resolve the issues of claims.’

Balarezo recalled working extensively to defend auto insurance policyholders in third-party arbitration during his time as a claims adjuster. He’d review police reports, have deep conversations with affected parties, and give the process his all until the very end.

Seeing things through is

also a core tenet of software engineering.

“Because [in] software engineering, you fail a lot, very quickly,” Balarezo explained.

“And you kind of need this resilience to just keep on going. And it ended up proving to be a skill that I learned in adjusting that I was able to put into practice as a software engineer professionally.”

Balarezo launched Adjusto and returned to insurance 12 years after leaving Oklahoma Farm Bureau. To his surprise, not much had changed. He spoke with many adjusters and other industry folks to understand the problems they faced, and he learned that some of the processes he was familiar with were exactly the same.

Adjusto

Before forming Adjusto, Balarezo set out to identify real problems that claims professionals face. He took paid time off from his job to attend insurance industry events to understand pain points and make connections.

Meanwhile, he also reopened his old phonebook and began reconnecting with contacts from his adjusting days and continued on page 26

Adjusto Co-Founders Michael Balarezo, James Terry, and Reid Greer

Spotlight: Claims

interviewed neighbors who had struggled to settle claims. Balarezo and his team found that a lack of transparency is eroding policyholder trust.

They noted the frustration that policyholders feel about delays and the expectations they have of how claims should be settled. And the Adjusto team recognized the need for improved data accuracy and valuation in the claims process.

The new FairMatch platform is designed to be used by anyone who services contents claims. That includes carriers, MGAs, TPAs, independent adjusters, and other contents specialists. Balarezo said the company brings a science-based approach to its solution, which is deeply rooted in data science, machine learning, and statistics.

“We like to focus on building solutions that actually are meant to solve the actual problems,” Balarezo said. “I think there’s too many tools in the market that just complete tasks but don’t actually resolve the issues of claims.”

‘We automate what doesn’t require human attention, and we create transparency across the board so that everyone from policyholders to carriers can move forward with clarity and confidence.’

They certainly don’t help adjusters build trust with

policyholders, he said, and the quality of the data and responses back to policyholders need a “tremendous amount of improvement.”

He said that overall, the claims process and experience are broken. The Adjusto team believes the contents claims arena is simultaneously one of the most under-innovated and high-friction areas in insurance.

“We surface critical information faster to the adjuster,” Balarezo said. “We automate what doesn’t require human attention, and we create transparency across the board so that everyone from policyholders to carriers can move forward with clarity and confidence.”

Adjusto aims to turn moments of potential friction into trust-building opportuni-

ties for adjusters, which ultimately turns into decreasing churn and increasing loyalty. The platform is designed to be intuitive, friendly, and fast, Balarezo said, freeing up space for adjusters to focus on empathizing with policyholders and rebuilding that trust.

“I think that’s the big thing that tooling is missing today,” Balarezo added. “Adjusters largely can’t really trust the output that comes out of it. I’ve had conversations where adjusters literally have to go back and then redo their work because the automation that’s built into it just isn’t accurate. It’s not intelligent.”

Go Deeper

Claims of any size and scale can benefit from FairMatch, Balarezo said.

He explained that the Adjusto team thinks of itself as a thought leader, partner, and trusted advisor to the company’s clients. They deeply understand enterprise structure and process, he said, and they also understand the needs of smaller companies.

“What that means is for us, we very intentionally built our software in a way to fit directly into an existing tech stack with minimal friction,” Balarezo explained, pointing to Adjusto’s seamless integration and rapid onboarding.

He later added that Adjusto is “here to be a partner and help modernize. We’re ready to roll up our sleeves and help lay the groundwork for the future.”

This article was originally published in Carrier Management but has been updated to reflect the new launch of Adjusto’s FairMatch platform. continued from page 25

My New Markets

Entertainment

Market Detail: Greenwood’s Entertainment commercial insurance program offers tailored coverage with a minimum premium starting at $1,500, catering to a diverse range of businesses and venues, including auditoriums, theaters, axe throwing venues, bowling alleys, campgrounds, RV parks, convention and performing arts centers, country clubs, tennis clubs, golf clubs, escape rooms, equestrian centers, family entertainment and amusement centers, firearm stores, go-karting facilities, batting cages, mini golf courses, gyms, fitness centers, hunt clubs, museums, paintball and laser tag facilities, race tracks, ATV parks, rage rooms, resorts, shooting ranges, special events, tourist attractions, zoos, and aquariums.

Each class benefits from specialized coverage to address the unique risks associated with entertainment and leisure activities.

Submission Requirements: ACORD

Commercial Insurance application and General Liability application, including comprehensive descriptions of operations/ exposures, signed and dated by the insured upon binding. Supplemental application, as required, signed and dated by the insured at the time of binding. Five-year loss runs for currently valued company, including descriptions for losses exceeding $10,000. Information from website.

Available Limits: Not disclosed.

Carrier: Kinsale; non-admitted; rated A by AM Best.

States: Arizona, California, Idaho, Illinois, Iowa, Kansas, Michigan, Missouri, Nevada, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, and Wisconsin.

Contact: Catherine Mcmackin, Catherine@ gwgeneral.com, 626-817-9100 x 515.

Tech E&O

Market Detail: Built for modern specialty. Anzen simplifies executive and specialty risk—fast. Anzen combines deep underwriting expertise, AI-powered tools, and access to 70+ markets to help brokers quote, compare, and close with speed and precision. The company has led retail distribution, built tech companies, and

shaped executive risk programs across every stage of growth. Anzen brings it all together, so clients don’t have to choose between scale, service, or speed. Backed by top investors in both tech and insurance and trusted by 40+ founders and executives nationwide.

Available Limits: Not disclosed.

Carrier: Not disclosed.

States: All 50 states and the District of Columbia.

Market Detail: Thimble makes it easy to cover a wide range of food, beverage, and restaurant businesses—especially those seeking fast, flexible, and affordable coverage. Whether a client runs a food truck or a neighborhood café, Thimble can help! What Thimble covers (eligible for GL, BOP, and WC—depending on business class and state availability): bakery cafés, cookie stores, donut shops, and bagel shops; cafés, diners, and bistros; buffets and cafeterias; caterers and catering services; coffee shops, smoothie bars, and juice bars; delis and sandwich shops; fast food restaurants and limited-service eateries; family-style and full-service restaurants; ice cream, frozen yogurt, or custard shops; food trucks, lunch wagons, and mobile food vendors—food stands, kiosks, and concessionaires; pretzel stands and snack carts; pizza parlors and pizzerias (excluding hired/non-owned auto liability); food service contractors (cafeteria, institutional, or industrial) and restaurants with alcohol sales under 50% of total receipts.

Coming soon: coffee roasting and tea blending; cheese making and dairy substitute manufacturing; baked goods manufacturing (commercial or smallbatch); confectionery and candy production; nut and snack food processing; spice, sauce, and condiment manufacturing; ice cream and frozen dessert production; juice, soda, and bottled water production (non-alcoholic); and specialty food stores (cheese, chocolate, spices, etc.)

Instant quotes and flexible policy terms. Coverage by the hour, day, month, or year. COIs delivered in minutes.

Available Limits: Not disclosed.

Carrier: Admitted.

States: All 50 states and the District of Columbia.

Contact: Laura Thornton, laura.thornton@ thimble.com, 862-591-3111.

Professional Employment Organizations

Market Detail: An MGA specializing in PEO placements — partner with MartinoWest Business & Insurance Solutions and open the door to specialty markets competitors can’t reach. Offering an established override contingency for qualified retail brokers and a generous commission split structure. Get appointed today.

Available Limits: $5M maximum premium; $10K minimum premium.

Carrier: Not disclosed.

States: All 50 states and the District of Columbia.

Market Detail: Applied Specialty Underwriters® offers Primary and Excess Liability for electric power and distribution, solar and wind turbine erection, roads and bridges, tunnels, rail, telecom and broadband, airports, pipelines, coastal and inland ports, locks, levees and dams, water treatment plants, waterline projects, and government infrastructure.

Available Limits: Not disclosed.

Carrier: Admitted and non-admitted.

States: All 50 states and the District of Columbia.

Renewable energy is growing in the U.S. In fact, wind and solar energy generated more electricity in the U.S. than coal for the first time ever in 2024.

Growth extends far beyond wind and solar, renewable energy insurance experts told Insurance Journal for this special report. There’s growing interest in nuclear energy, hydropower, and geothermal power. And then there’s the expanding industry of power storage to relieve pressure on U.S. power grids during heavy energy months.

One thing is clear: the need for power is growing, and so is the industry that works to protect renewable energy assets.

Fraser McLachlan, CEO of GCube and recently appointed chairman of the newly formed Tokio Marine GX (TMGX), expects significant investment in green energy as the transition to be green takes place across many classes of business and countries worldwide. The investment into green energy is expected to be about $15 trillion in the next 10 years, he said.

“There absolutely is an opportunity to drive this green transition and help this green transition along the way and make some premium out of it, as well,” he said. Launched in May, TMGX, an abbreviation of green transformation, is Tokio Marine Group’s response to the increasing demand for insurance that is critical to transitioning

to a more decarbonized, sustainable society.

The primary driver of “green transformation” is renewable energy. Renewables are growing worldwide, and in the U.S., renewable energy outpaced other energy generation sources in 2024, collectively accounting for about 90% of the United States’ new installed capacity, according to the World Resources Institute.

“With the new projects online, renewables (including wind, solar, geothermal, and hydropower) and battery storage now make up 30% of the country’s large-scale power generating capacity,” wrote WRI’s energy specialists Lori Bird, Andrew Light, and Ian Goldsmith in a February 21, 2025, article. “In 2024, all carbon free electricity sources, including nuclear, supplied nearly 44% of electricity, while renewables, including smallscale solar, supplied nearly 25%.”

There are challenges as well as opportunities when it comes to insuring the fast-changing renewable energy world.

One challenge is keeping up with emerging technologies as the renewable energy sector continues to divest in various

segments, McLachlan said. That’s where green energy insurance specialists can help, he said. “Things like hydrogen, small-medium nuclear reactors, new types of solar, new types of electric vehicles—there’s a whole bunch of stuff that is going on that is really not being catered to at the moment by the more traditional insurance providers.”

Solar Differences