Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Opening Note

Six-Month Review

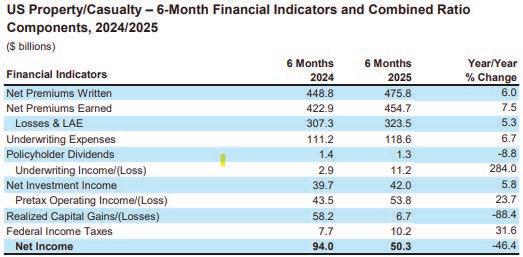

An early look by AM Best at the financial results of the U.S. property/casualty industry revealed insurers recorded an estimated $11.2 billion in net underwriting income in the first half of 2025.

That’s a significant jump from last year when the P/C industry booked $2.9 billion in the first six months, according to a report from the rating agency.

In a separate report, the American Property Casualty Insurance Association and Verisk reported the U.S. property/casualty insurance industry recorded a net underwriting gain of $11.5 billion and net income of $49.1 billion for the first half of 2025. “The lack of any significant natural catastrophes in the second quarter helped offset the record-breaking catastrophe losses related to the California wildfires and severe convective storms impacting Texas and Georgia earlier in the year,” said Robert Gordon, senior vice president, policy, research, and international at the APCIA and Verisk, when discussing the results.

AM Best noted that the P/C industry’s combined ratio improved to 96.4 in first-half 2025 from 97.8 in the same period of 2024.

APCIA/Verisk estimated first-half 2025’s combined ratio to be 96.4 compared to 97.6 for last year’s first half, and 104.2 for first-half 2023.

The combined ratio “edged down slightly from this time last year, reflecting underwriting discipline, but escalating catastrophe losses—most notably January’s unprecedented California wildfires—underscore the volatility ahead,” said Saurabh Khemka, co-president of underwriting solutions at Verisk. “While some lines are showing signs of improvement, the broader industry continues to walk a fine line,” Khemka said.

‘While some lines are showing signs of improvement, the broader industry continues to walk a fine line.’

AM Best reported that catastrophe losses accounted for 10.9 points on the six-month 2025 combined ratio, up from an estimated 8.8 points the previous year.

However, excluding prior-year reserve development of nearly $13 billion, the combined ratio was 99.2, according to AM Best.

Growth of 7.5% in net earned premiums in the six-month period offset increases in incurred losses and loss adjustment expenses (LAE), largely attributable to the January wildfires in California and other underwriting expenses. Plus, an increase in net investment income aided the underwriting gain.

A substantial reduction in net realized capital gains, driven primarily by a $47.5 billion decline at Berkshire Hathaway’s National Indemnity Company, contributed to the industry’s net income being cut nearly in half from the same prior-year period to $50.3 billion.

Based on information from annual statements submitted to insurance regulators by insurers representing roughly 97% of the private U.S. property/casualty market, Verisk and APCIA reported that net written premiums grew just 1.9% to $472.5 billion compared to a 10.6% increase in net written premiums recorded for first-half 2024 over the prior-year six-month period.

Andrea Wells V.P. of Content

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Contributors: Benjamin Burch, Scott Freiday, James Keane, Susanne Sclafane, Lee Shavel

Columnists: Chris Burand, Bill Wilson

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT) Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator George Jack | gjack@ijacademy.com

News & Markets

Industry Reps Back Reauthorization of Federal Terrorism Backstop

By Chad Hemenway

Michelle

Sartain,

president Marsh U.S. and Canada, who has worked at Marsh for more than 28 years, encouraged lawmakers on Capitol Hill last month to reauthorize the Terrorism Risk Insurance Act. More than two decades after Marsh McLennan lost 358 employees in the terrorist attack on the World Trade Center on Sept. 11, 2001, the backstop remains a necessary component to a stable insurance market, she said.

“By all accounts, the program has been a model public-private partnership,” said Sartain. “The backstop remains a critical component to a stable terror insurance market, particularly for nuclear, biological, chemical, and radiological (NBCR) events, and has enabled insurance to be placed and investments to be made.”

The federal backstop for terrorism risk was first initiated late in 2002 to respond to insurers’ forced exclusion of terrorism risks from commercial property/casualty insurance policies following losses from the terrorist attacks. The change put construction projects on hold since financers required the insurance. Meanwhile, a crisis began in workers’ compensation due to the high levels of exposure faced in the line of business since state laws prohibited a terrorism exclusion.

The legislation requires insurers to offer terrorism coverage while the industry has the assurance that if losses from an event reach certain thresholds (the event needs to exceed $5 million in damages to be certified as an act of terrorism and cost insurers $200 million in industry losses to trigger coverage), the government will step in. TRIA has been reauthorized several times, the latest at the end of 2019. It is due to expire again on Dec. 31, 2027.

Sartain offered 17 pages of testimony covering TRIA’s history and features, and outlined how certain industries such as healthcare and higher education rely on

TRIA. On Sept. 17 she told the U.S. House Financial Services Subcommittee on Housing and Insurance that the terrorism backstop allows for insurers and reinsurers to quantify exposures and provide capacity into the market.

Although the expiration is two years away, “insurers and rating agencies closely monitor legislative activity related to [TRIA],” Sartain explained. “Any uncertainty regarding the future of the federal backstop as the deadline approaches will have an impact on the availability and nature of insurance coverage. That, in turn, could send ripple effects through the economy and potentially affect companies’ decision-making processes about hiring and investing.”

If the backstop expires without a replacement, “insurers that are still able to offer terrorism coverage will likely only write coverage for buyers with operations in preferred locations, and could consider increasing prices for other locations,” Sartain wrote. “This would lead to capacity shortfalls for central business districts, at-risk industries, and employers with significant workers’ compensation accumulations, such as office workers, manufacturing facilities, and healthcare and education facilities,” she continued. Elizabeth Heck, former chair of the National Association of Mutual Insurance Companies (NAMIC), also testified before the subcommittee. She said TRIA provides certainty and has allowed insurers

to offer coverage.

“Thankfully, the program has yet to be tested, and as we look back nearly 25 years after the attacks, it is important to recognize how much construction and economic development TRIA has supported, all at no cost to the taxpayers,” she said.

Heck, president and CEO of Greater New York Insurance Company, said she has experience as a “major writer of terror-exposed property in New York City.”

“While insuring against the financial devastation that could accompany a catastrophic terrorist attack might sound like a reasonable protective measure for markets to take on, a large-scale terrorist attack—like an act of war—is not insurable,” Heck submitted to the committee.

About 79% of commercial multiperil policies in the U.S. include some level of terrorism coverage, and insurer appetite for the risk has increased. While NAMIC generally opposes federal backstop programs, Heck said TRIA “represents the rare situation where a clearly defined problem can only be solved by a federal partnership to facilitate insurability in a way that does not harm markets or market participants and ultimately reduces risk against scenarios where other solutions have been exhausted.”

NAMIC proposed a 10-year reauthorization with no significant changes to the program’s structure.

The American Property Casualty Insurance Association (APCIA) did not testify at the hearing but called on Congress to reauthorize TRIA with no change to financial thresholds. In a statement, Sam Whitfield, senior vice president of federal government relations, added: “TRIA is a fiscally sound program that has operated for 23 years with minimal cost to taxpayers. Its continued existence is vital to maintaining confidence in the marketplace and ensuring the availability of terrorism coverage that businesses and communities rely on.”

INSURANCE INDUSTRY CHARITABLE FOUNDATION

Helping communities and enriching lives, together.

Insurance Industry Charitable Foundation (IICF) is a unique nonprofit that unites the collective strengths of the insurance industry to help communities and enrich lives through grants, volunteer service and leadership. IICF has awarded more than $50 million in community grants and contributed $12 million in volunteer service value over the past 30+ years.

Join us for the IICF Month of Giving Register as a team or individual volunteer and find projects near you at: volunteer.iicf.org

Month of Giving October 2025

Since 1998, IICF has hosted the largest ongoing volunteer initiative in the insurance industry. This tradition continues with our month-long celebration of industry volunteerism in October.

IICF also offers year-round volunteering for sustained community involvement and impact. Join with thousands of your insurance industry colleagues as we come together and give back to our neighbors in need.

4.9%

The amount the average annual insurance payment for a mortgaged single-family home in the U.S. rose in the first half of 2025, increasing the average yearly payment to almost $2,370, according to a recent Mortgage Monitor report from Intercontinental Exchange Inc. In Los Angeles, where sprawling wildfires obliterated entire neighborhoods, homeowners’ insurance bills rose by 9% in the first six months of this year, or almost 20% from mid-2024.

The amount James and Levi Garrett of South Dakota have been ordered to pay to resolve violations of the False Claims Act, according to the U.S. Attorney’s Office, District of South Dakota. In 2018, the father and son falsely certified to a crop insurance company that they planted 2,200 total acres of sunflowers, and in 2019, James Garrett falsely certified that he planted 47.5 acres of corn. They allegedly did not plant any sunflowers or corn but wrongfully received a total $1.3 million indemnity from the insurance company.

7

Years Over $4 Million

The length of the double-digit growth streak for the U.S. excess and surplus lines market. Excluding $20.8 billion from the Lloyd’s market, the top 25 groups accounted for less than half (49.7%) of surplus lines premium, down from 51.3% in 2023 and 53.5% in 2022.

174,000

The number of 2021 Tesla TSLA.O Model Y cars being looked at by the U.S. National Highway Traffic Safety Administration (NHTSA) over reports that electronic door handles can become inoperative. NHTSA said it had received reports citing an inability to open doors from the outside.

Declarations

Fighting for TRIA

“The backstop remains a critical component to a stable terror insurance market, particularly for nuclear, biological, chemical, and radiological (NBCR) events, and has enabled insurance to be placed and investments to be made.”

— Michelle Sartain, president, Marsh U.S. and Canada, encouraging federal lawmakers to reauthorize the Terrorism Risk Insurance Act (TRIA). Marsh McLennan lost 358 employees in the terrorist attack on the World Trade Center on Sept. 11, 2001. The program has been a model public-private partnership, said Sartain, who has worked at Marsh for over 28 years. She offered 17 pages of testimony covering TRIA’s history and features—and outlined how industries such as healthcare and higher education rely on TRIA.

Safety Snaps Stalled

“You have to be a little crazy to do this job.”

— Kellen Cloud, longtime employee at Green Mountain Flagging, a company that stations traffic controllers at construction sites across Vermont. Data shows more people are injured or killed in work zones today than a decade ago. A pilot program surveilling work zones using automated cameras was slated to begin July 1, 2025, but the Vermont Agency of Transportation leaders said no law enforcement agency has signed on to help out. While police officers typically park near construction sites with their cruisers’ lights flashing, they’re encouraged to remain at their posts rather than leave to chase down a speeder, several state officials said.

Where’s The Beef?

“This law has nothing to do with protecting public health and safety and everything to do with protecting conventional agriculture from innovative out-of-state competition. That is not a legitimate use of government power.”

— Paul Sherman, a senior attorney at the Institute for Justice, a nonprofit law firm representing UPSIDE Foods and Wildtype, cultivated meat companies that filed a lawsuit against Texas officials over a new law banning the sale of lab-grown meat in Texas for two years. During the Senate committee hearing on the bill, lawmakers expressed concerns that cultured meat will disrupt traditional family farms, as well as concerns over product labelling and safety.

Post-disaster Scholastics

“People think, natural disaster—mental health. They don’t think about the academic component to it. You put that aside when you have a little kiddo crying because they don’t have a house to live in. You’re not going to say, ‘OK, snap out of it. We’ve got math to do.’”

— Carrie Dawes, health and wellness coordinator for Paradise Unified. After the Paradise, California, area was devastated by the 2018 Camp Fire, officials found continuing challenges in getting kids on track academically. After the fire, schools set academics aside and focused on mental health. Today, student testing shows that even once the immediate effects of the fire subsided, scores still lagged.

Vax Attacks

“We don’t need to do any projections. We handle outbreaks all the time. So, there’s nothing special that we would need to do.”

— Florida Surgeon General Joseph Ladapo, when asked about studying the impacts of halting immunization requirements for children, on CNN’s State of the Union. Florida Governor Ron DeSantis is pushing to make his state the first one to dismiss immunization requirements. Florida’s current plan would lift mandates on school vaccines for hepatitis B, chickenpox, Hib influenza, and pneumococcal diseases such as meningitis, according to the state’s health department.

Seeking Federal Flood Funds

“I will continue to urge the Trump administration to approve the remainder of my request, and I will keep fighting to make sure Wisconsin receives every resource that is needed and available.”

— Democratic Wisconsin Gov. Tony Evers, who requested federal flood aid for residents in six counties, but Trump approved it for three. More than 1,500 Wisconsin residential structures were destroyed or damaged in August floods at a cost of more than $33 million, along with more than $43 million in public sector damage. Trump’s latest declarations approved public assistance for local governments and nonprofits in all affected states except Wisconsin, where assistance for individuals was approved.

News & Markets

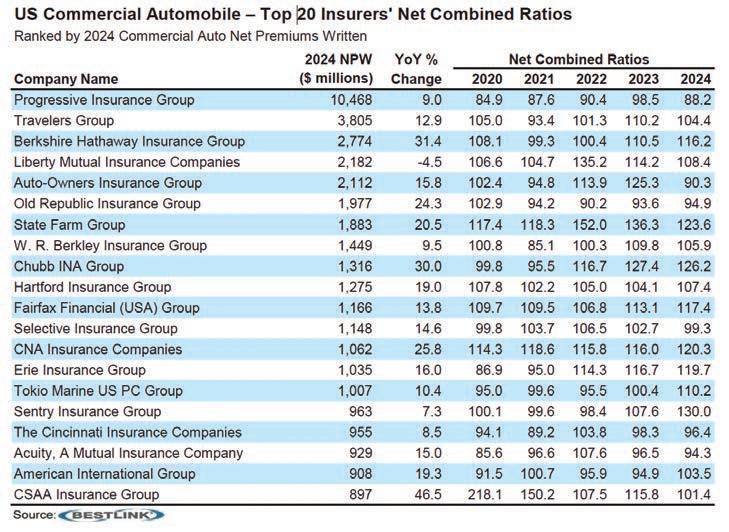

AM Best: Commercial Auto Liability Drags Down Segment, and It Could Get Worse

Commercial auto has been a dark cloud hanging over the U.S. property/casualty industry for more than a dozen years—and things are getting worse.

Commercial auto has posted an underwriting loss for the 14th consecutive year and has accumulated more than $10 billion in net underwriting losses over the last two years, according to insurance industry rating agency AM Best. In addition, rate increases have not kept up with increases in loss costs.

In its new report, “Stuck in Reverse: Commercial Auto Losses Keep Mounting,” AM Best said underwriting losses in 2024 totaled about $4.9 billion. Losses the prior year were about $5.5 billion.

Commercial auto physical damage posted an underwriting profit of about $1.5 billion in 2024 and has been profitable five of the last six years. The problem, said AM Best, is with commercial auto liability— having posted the largest underwriting loss in 2024 of about $6.4 billion.

Commercial physical damage and liability are diverting on paths farther away from each other. While physical damage posted a combined ratio of 88.6 in 2024 and hasn’t eclipsed 100 since 2017, liability posted a 2024 combined ratio of 113, similar to the 113.3 posted the prior year. Liability has posted a combined ratio above 100 in each year since 2014 and has reached 113 five times. Were it not for the adoption of technology to improve

efficiency at some underwriters, expenses may have been worse.

AM Best warned that the divergence could hurt insurers. Liability is a compulsory buy, but physical damage is optional. Insureds may determine PD is not worth the extra cost, and even if they do want the coverage, they may choose higher deductibles to offset the cost.

“This would cut into insurers benefiting from the great profitability of the physical damage coverage, potentially worsening

the overall results for the commercial auto lines,” AM Best said in the report.

Inflation and rising replacement and labor costs have long been headwinds in the space. Now, claims are taking longer to resolve. The longer claims remain open, the higher the exposure to a potential nuclear verdict. This has swung open the door for adverse development, and AM Best estimated commercial auto liability is underreserved by $4 billion to $5 billion—“setting up another year of poor results.”

AM Best’s list of top commercial auto insurers still has Progressive at the top, but Nationwide, a longtime top 10 member, has fallen outside the top 20. Its decline in commercial auto premiums is the result of strategic decisions to concentrate on profit over growth. Fourteen of the top 20 writers posted a combined ratio over 100 in 2024.

Leading the way was Sentry, Chubb, and State Farm with combined ratios of 130, 126.2, and 123.6, respectively. The rating agency said continued losses in commercial auto “may have insurers rethinking” whether the line is worth accepting losses for access to other commercial lines.

News & Markets

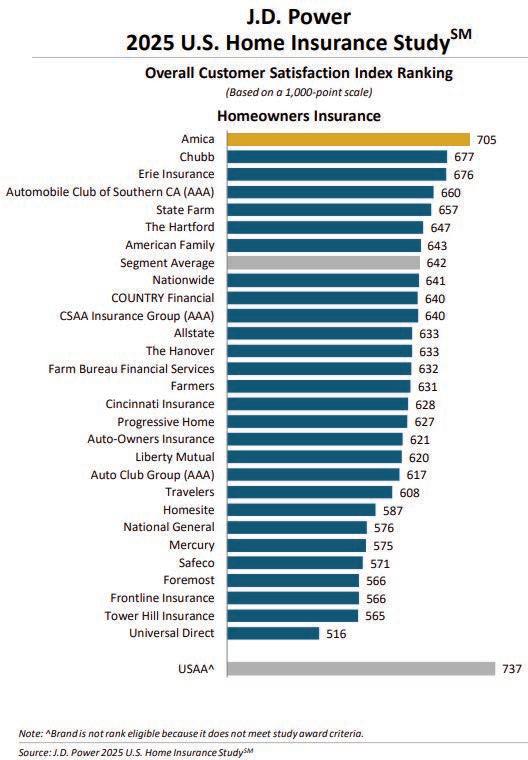

Customers Look to Alternatives as Home Insurance Premiums Rise

Homeowners’ insurance rates are rising at a pace not seen in more than a decade, so more customers are asking why they should stay loyal if they perceive their insurer isn’t reciprocating.

According to a recent survey from J.D. Power, 47% of homeowners have seen at least one rate increase over the previous year. The consumer-data provider found that increases are even more pronounced in what it calls “high-lifetime-value” customers—those with higher annual premiums and a higher proportion of product and services with one insurer. Among these policyholders, 49% have been handed rate increases.

“In a year marked by inflation, severe weather, and tightening reinsurance markets, home insurance premiums have risen sharply in many parts of the country. While

these increases often reflect real cost pressures, they’re also eroding trust and driving customers to shop for alternatives,” said Craig Martin, executive director, global insurance intelligence at J.D. Power.

High-lifetime-value customers may be profitable for insurers, but they are also the most likely to start shopping, according to J.D. Power. Among customers who are unlikely to renew with their insurer, 45% of high-value customers blame price increases, while 30% of low-lifetime-value customers who probably won’t renew cite the repeated price increases.

Rate increases also tend to erode customer-insurer trust and decrease the likelihood customers will say their insurer is easy to work with.

Survey results appear to indicate that communication is key. Policyholders who felt they

understood the reasoning behind rate increases and were presented with options gave much higher overall satisfaction scores—721 on average compared to 537 among customers who do not understand the reasons or were not given options. In fact, the score for customers who received rate increases and options was even 33 points higher than customers who had not seen premium increases at all, J.D. Power said.

Turning to rankings, Amica,

Chubb, and Erie took the top three spots in overall customer satisfaction.

75% of Buyers Are Concerned About Rising Homeowners Insurance Costs: Survey

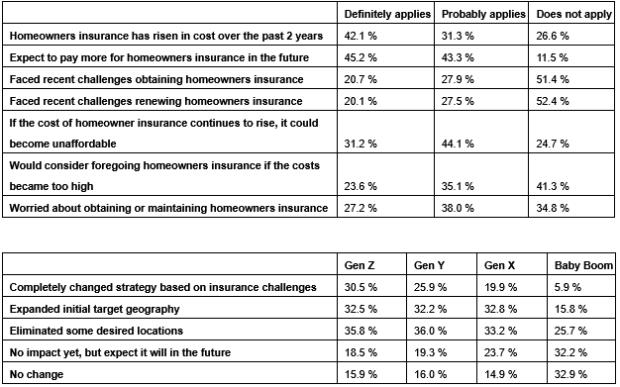

Nearly 75% of recent and prospective buyers believe that homeowners’ insurance could become unaffordable, according to a new survey by Realtor.com.

Eighty-eight percent of those surveyed believe they will pay more for homeowners’ insurance in the future, and 42% have already confirmed they have experienced a rise in home insurance costs.

Even more alarming is that half face or expect to face trouble obtaining and renewing insurance, with

some (58%) indicating they could forgo homeowners’ insurance altogether.

This increases to 76% among Gen Z buyers, even though many of these young buyers are using a mortgage and are required to have homeowners’ insurance.

Of the 1,000 surveyed, 65% are worried about obtaining and maintaining their homeowners’ insurance.

“Homeowners’

insurance offers financial protection for consumers that may help cover damage to

homes and personal property from an extreme weather event or fire, while also providing

Fitch Ratings: U.S. E&S Growth Slows but Remains Strong

Direct written premiums saw double-digit growth for the seventh straight year for U.S. excess and surplus (E&S) insurers, according to Fitch Ratings’ latest annual property/ casualty market review.

Per a Fitch press release, U.S. E&S direct written premiums grew by 11% in 2024—down from 15% the prior year but higher than the 8% increase for U.S. P/C insurers overall.

This represented the 14th consecutive year of E&S premium growth and the seventh straight year of exceeding double-digit growth.

low single-digit growth. Prior to 2023, E&S premium growth was consistently strong across all major product lines for several years, the press release said.

Fitch reported that the current growth spurt, which began in earnest in 2018, places E&S lines at 9% of total

personal property and liability coverage,” said Realtor.com Chief Economist Danielle Hale. “But these benefits come with an upfront cost that has risen as weather events have become more frequent and impactful, and rebuilding costs climb. Homeowners are looking for strategies to lower costs, including adjusting their home searches and potentially shortcharging or forgoing coverage altogether.”

According to the survey’s findings, insurance challenges have forced one-third (33.7%) of home searchers to completely change the geographic area where they are looking for a home, and another 30% have cast a wider net and expanded their initial target geography.

P/C insurance. That is nearly double the segment share it held in 2017 but unchanged from last year, the press release said.

Premium growth was positive across all lines, Fitch

Nearly a quarter of home searchers have completely changed strategies due to insurance challenges.

Additionally, just 30% have looked into the natural disaster risk data for their home or

shared, with other liability-occurrence, allied and fire lines, commercial auto, and medical professional liability reporting double-digit increases. Other liability-claims made and commercial multiperil reported

prospective homes, though 44% plan to do so in the future.

Gen Z home searchers are more likely to have taken action in their search to potentially mitigate homeowners’ insurance challenges compared

E&S underwriting results were reportedly considerably better at an 88 direct combined ratio for 2024, compared to a 95 combined ratio for the total P/C market. While E&S results deteriorated slightly from 86 in 2023, they remain significantly better than the five-year average of 97, Fitch reported.

This marked the third consecutive year that E&S reported better underwriting results than the broader P/C industry.

to other generations, especially Baby Boomers, who said that only 6% had completely changed their home buying strategy and only 15% had expanded their initial search.

Business Moves

National

Lincoln International, MarshBerry

Lincoln International, a global investment banking advisory firm, said it has a definitive agreement to acquire MarshBerry, an advisory firm serving the insurance brokerage, insurance distribution, and wealth management sectors for over 40 years.

MarshBerry operates across six U.S. cities and three international locations in Europe, serving a dedicated client base of private, independent brokers and wealth management firms.

Terms of the deal were not disclosed. The acquisition closing is subject to standard regulatory approvals.

Tropolis Acquires Eight Michigan, Texas and Louisiana Agencies

Tropolis Insurance Services, headquartered in Ann Arbor, Michigan, acquired eight agencies across the United States. Each agency will operate under the Tropolis brand moving forward.

Employees from all eight agencies will participate in the company’s employee purpose plan, an equity incentive program that ensures every team member benefits from Tropolis’ future growth and value creation. Terms of the transactions were not disclosed.

Tropolis acquisitions in Michigan include Warrendale Insurance Agency in Livonia, U.P. Insurance Agency in Iron Mountain, Entrust Insurance and Financial Services in St. Clair Shores, and Canopy Insurance Group in Birmingham.

Texas acquisitions include Infiniti Insurance Services in Spring and King Phillips Insurance in Houston.

Louisiana acquisitions include Beasley Keith Insurance and Safe Harbor Insurance, both in Bossier City.

East

World Insurance Associates, William P. Smart Associates

World Insurance Associates LLC acquired the business of William P. Smart Associates of Fairfield, New Jersey. Terms of the transaction were not disclosed.

William P. Smart’s niche is the entertainment industry. The agency focuses primarily on commercial insurance, with some personal and employee benefits business.

World Insurance, based in Iselin, New Jersey, serves clients from more than 300 offices across the U.S. and U.K.

Duffy Insurance, Satori Insurance

Duffy Insurance Agencies in Lynn, Massachusetts, acquired Sartori Insurance, a family-run agency that has served the Lexington, Massachusetts, community for more than 50 years.

The Sartori team will continue to operate from the agency’s Lexington office, offering personal and commercial lines insurance.

Duffy Insurance was founded in 1996 by the late Paul Duffy and is currently led by his son, Marc Duffy. Sartori is Duffy’s 16th agency acquisition, and it now has Massachusetts offices in Lynn, Gloucester,

Peabody, Lowell, Chelmsford, Georgetown, Marblehead, Salem, Beverly, West Newbury, and now Lexington, as well as in Plaistow, New Hampshire.

Penn-America Underwriters, Sayata

Global Indemnity Group’s subsidiary

Penn-America Underwriters has completed the acquisition of Sayata, an AI-enabled digital distribution marketplace and agency operations platform for commercial insurance with headquarters in Boston, Massachusetts. The company also has operations in Tel Aviv, Israel, and offices in Houston, Texas, and San Francisco, California.

Penn-America Underwriters consists of three agencies: Penn-America Insurance Services; J.H. Ferguson and Associates, which includes the Vacant Express division; and Collectibles Insurance Services. It also now includes three insurance product and service businesses: Sayata, Liberty Insurance Adjustment Agency Inc. and Kaleidoscope Insurance Technologies Inc.

Midwest

World Insurance Associates, Dunaway Insurance Agency, Hoosier Agency

World Insurance Associates acquired the business of Dunaway Insurance Agency of New Palestine, Indiana, and Hoosier Insurance Agency of Bloomfield, Indiana. Terms of the transaction were not disclosed.

Dunaway, founded in 1979, is led by Doug Todd, who works with commercial, agricultural and commercial-affiliated personal lines accounts, and Tina Todd, who manages the personal lines side of the business. Hoosier was founded in 1990 and purchased by Doug Todd in 2005.

Arthur J Gallagher & Co., Bremer Insurance Agencies Inc.

Arthur J. Gallagher & Co. acquired St. Paul, Minnesota-based Bremer Insurance Agencies Inc. Terms of the transaction were not disclosed.

Bremer Insurance Agencies is a subsidiary of Old National Bancorp following the completion of Old National’s acquisition

of Bremer Bank. The agency is a property/ casualty insurance broker serving commercial, agricultural and personal lines clients in Minnesota, North Dakota and Wisconsin. Travis Hoaglund and his team will operate under the direction of Sean Gallagher, head of Gallagher’s Great Lakes region retail property/casualty brokerage operations.

Steadfast Group, Novum Underwriting Partners LLC

Steadfast Group acquired a majority stake in U.S.-based specialty managing general agency and wholesale brokerage, Novum Underwriting Partners LLC.

Founded in 2019 and based in Ohio, Novum is underpinned by a proprietary technology platform, Novum Online, which incorporates a marketplace, submission and underwriting functions that enable quoting, servicing and renewals, as well as policy management for agents and distribution partners.

Novum will serve as Steadfast’s program development and management platform in the United States, offering specialist managing general agency and wholesale solutions to its U.S. agent network, ISU Steadfast, and the broader U.S. market.

The transaction is expected to close during the fourth quarter of 2025.

Gallagher Re, the global reinsurance broker and subsidiary of Arthur J. Gallagher, recently announced an agreement to acquire Steadfast’s reinsurance arm, Steadfast Re Pty Ltd.

Relation Insurance Services,

Joseph M. Wiedemann & Sons Inc.

Relation Insurance Services acquired the assets of Joseph M. Wiedemann & Sons Inc. (JMWS).

Terms of the transaction were not disclosed.

JMWS, a fourth-generation family-owned business based in the Chicago suburb of Arlington Heights, has been serving customers since 1930. They offer a mix of both personal and commercial lines of insurance products and services, focusing on P&C and employee benefits. Their offices will continue to be led by partners John Wiedemann and Ned Cooke.

Southeast

EverPeak Insurance, Method Insurance

Pinnacol Assurance subsidiary EverPeak Insurance has acquired Method Insurance, a workers’ compensation managing general agent based in Nashville, Tennessee. The move will complement EverPeak’s subsidiary Attune, designed to make it easier for brokers to write workers’ comp and commercial insurance.

Method is led by Chairman Richard Rehm and CEO Christopher Rehm, both of whom are physicians.

EverPeak, a workers’ comp specialist with offices in Denver, Colorado, recently announced it had expanded into 11 new states: Alabama, Florida, Illinois, Indiana, Maryland, Michigan, Missouri, Mississippi, Oklahoma, Pennsylvania and Virginia.

SageSure, Olympus, Auros and Interboro Insurance.

In a three-way deal involving carriers, underwriters, holding companies and more, catastrophe-focused managing general underwriter SageSure announced it will acquire the managing general agent for Florida-based Olympus Insurance Co. Olympus CEO Time Stroble and the entire Olympus team are expected to remain in their current positions after the deal is completed. SageSure, with offices in Jersey City, New Jersey, said it now operates in 16 states.

As part of the acquisition move, Valence Insurance Holdings, the parent of Auros and Interboro, will acquire Olympus’ captive reinsurer, Radiant Ltd. SageSure will acquire Gemini Financial Holdings Corp. and its subsidiaries, including Olympus MGA. The same parent company, Slaine Holdings, owns Valence and SageSure.

Terms of the deal were not disclosed.

Brightway Insurance, GlobalGreen Insurance Agency

Jacksonville, Florida-based Brightway Insurance acquired GlobalGreen Insurance Agency, a multi-state network. GlobalGreen is headquartered in Chesterfield, Missouri, and has affiliate operations across the country. Jeffrey Wilson is CEO, and Ray Spears is chairman.

Brightway was founded in 2008 and now has franchise agencies in 45 states. The company promises a distribution platform that helps member agents grow rapidly.

Terms of the deal were not disclosed.

South Central

River Valley Underwriters Inc., Patriot National Underwriters

River Valley Underwriters Inc. will acquire the book of business from Patriot National Underwriters Inc., as well as the current employees. RVU is a family-owned, multi-line MGA based out of Little Rock, Arkansas, specializing in transactional binding authority business as well as wholesale brokerage. RVU will add its carriers and products to the expertise of the current Patriot National staff to continue to deliver the exceptional service that retail agents have come to expect from both parties.

West

Howden, Gravitas Insurance Agency LLC

Howden is acquiring Gravitas Insurance Agency LLC, a Los Angeles-based retail brokerage specializing in contingency insurance for music, sports and live events.

The deal, which is subject to customary closing conditions, follows Howden's other recent sport and entertainment acquisitions, including U.K. performing arts insurance broker Hencilla Canworth, German film and entertainment insurance broker Franz Gossler and Boni Aldaya, an entertainment broking house in Spain.

Gravitas designs and delivers insurance programs for the entertainment sector, representing performing artists and touring acts, live event organizers, talent agencies and record labels. It was founded in 2022 by John Tomlinson as a brokerage exclusively focused on delivering contingency insurance services for the music, sport and live event communities.

Howden is a global insurance intermediary group that operates in 56 countries in Europe, Africa, Asia, the Middle East, Latin America, the U.S., Australia and New Zealand.

National

Chubb Limited, headquartered in Warren, New Jersey, named Steve Haney as president and chief underwriting officer (CUO) of global surety.

Haney previously served as vice president, Chubb Group and division president of North America surety and chief underwriting officer of global surety. He previously served as executive vice president for ACE’s surety business worldwide (now Chubb). He joined the company in 1997 as a surety underwriter.

she most recently served as senior vice president, head of property claims.

Hare succeeds Tim Barziza, who retires in April 2026, after over 30 years in the industry, spending the last 22 years at Chubb.

WTW, headquartered in London, appointed leadership to its North America insurance consulting and technology (ICT) business.

officer. Hallworth, based in New York City, joins AIG from HewlettPackard Inc. He has served as chief data officer at HP Inc. and Capital One and as senior vice president and chief actuary at Travelers.

Patton Kline succeeds Glod as regional aviation and space practice leader, U.S. He has over 21 years of experience in the aviation and space insurance sector.

Teresa Black, executive vice president and chief operating officer of North America surety, was promoted to division president of North America surety. Black has 28 years of insurance industry experience, previously serving as senior vice president of distribution management, vice president and national segment leader for New York and assistant vice president of Chubb’s financial lines business.

Nicolas Carbo, based in Florida, joins as senior director, bringing extensive experience from Corebridge Financial and Oliver Wyman.

Poojan Shah, previously with PwC, was named director and is based in Chicago, Illinois.

Erika Dochney, based in Philadelphia, Pennsylvania, joins as associate director. She was previously with Lincoln Financial Group and Haven Technologies.

HDI Global Insurance Company, headquartered in Chicago, Illinois, appointed Fellipe Aguiar as head of energy and power underwriting in the U.S. for its cross-division energy and power unit.

CNA Financial Corporation, headquartered in Chicago, Illinois, appointed David Haas as president, global specialty, overseeing financial lines, healthcare, affinity and warranty. Haas most recently served as senior vice president, national accounts, casualty.

Michael Nardiello was appointed as the president of global property & casualty. He continues to lead global property and marine and casualty. Nardiello previously served as senior vice president, global property unit business head.

Song Kim was appointed president of global commercial industry segments, including construction, alongside middle market and small business. Kim now leads all global commercial industries.

Ryan Specialty Underwriting Managers (RSUM), the underwriting management division of Ryan Specialty, headquartered in Chicago, Illinois, appointed Alan Ferguson as CEO of US Assure.

Ferguson continues to serve as president of US Assure, a role he assumed in 2019. Ferguson joined Ryan Specialty in 1993 and previously served as chief underwriting officer. He succeeds Ty Petway, who is retiring after over 30 years of service.

FM, headquartered in Johnston, Rhode Island, named Tara Long as senior vice president, chief information officer (CIO).

Chubb also appointed Kim Hare as senior vice president, head of North America property claims. Hare has over 30 years of experience, joining Chubb from Farmers Insurance, where

Aguiar joined the company in August 2024 and has over 26 years of experience in the insurance industry, with a focus on the energy and power sectors across Latin America and the United States.

American International Group Inc., headquartered in New York City, named Scott Hallworth as chief digital

Marsh, headquartered in New York City, appointed Brian Glod, based in New York, as global head of aviation and space and Tony Ambrose, based in London, as global chairman of aviation and space.

Glod joins Marsh’s global specialty executive committee with over 35 years of experience, joining Marsh in 1996. Ambrose joined Marsh in 2020 and has over 30 years of experience working in the global aviation insurance sector.

Long joins FM from MassMutual, most recently serving as chief technology officer and head of enterprise infrastructure services. She previously held roles at Gerber Scientific Inc. and PricewaterhouseCoopers.

Long succeeds Srini Krishnamurthy, who was recently named senior vice president, FM India.

East

The Hanover Insurance

Steve Haney

Teresa Black

Kim Hare

Tim Barziza

Scott Hallworth

Alan Ferguson

Tara Long

Group, Inc., headquartered in Worcester, Massachusetts, appointed Toni E. Mitchell president of its technology and life sciences business.

Mitchell previously served as regional executive for the company’s Pacific Region.

She joined The Hanover in 2010 as regional chief underwriting officer for middle market and previously held leadership roles at One Beacon and Atlantic Mutual.

The MEMIC Group, headquartered in Portland, Maine, promoted Katrice Kelley to director of business analysis, underwriting. Kelley joined MEMIC in 2013. She will continue to lead MEMIC’s underwriting business analysts.

and Allan Egbert to the company’s senior leadership team as chief technology officer and chief platform officer, respectively.

Albert and Egbert, the co-founders of Ask Kodiak, have advised Coterie since early 2025. Ask Kodiak was acquired by Applied Systems in 2021. Albert and Egbert’s also led product strategy at AgencyPort and co-founded Insurtech Boston. Albert will focus on advancing engineering excellence, technical architecture, and Coterie’s innovation roadmap. Egbert leads platform infrastructure, operations, devops, and performance.

Dominic Weber was promoted to senior vice president and chief actuary. With over 42 years of experience, Weber previously served as vice president and chief actuary at Society Insurance.

Doug Duncan was hired in the newly created role of senior vice president and chief information officer. Duncan has over 25 years of technology leadership experience, previously serving as chief information officer at Columbia Insurance Group and senior vice president at Swiss Re.

Southeast

XPT Specialty, headquartered in New Haven, Connecticut, expanded operations into Atlanta, Georgia and North Carolina.

Lindon, Utah, promoted Leslie Greve to senior vice president of marketing. Greve joined Trucordia in 2024 and previously served as vice president of marketing. Before joining Trucordia, she served as CMO at BGZ Brands.

Alliant Human Capital, headquartered in Irvine, California, appointed Mike Chalmers as senior vice president and director of total rewards consulting.

The Mechanic Group, a division of Specialty Program Group LLC, headquartered in Pearl River, New York, appointed Candace Chieppo as practice leader. Chieppo has 27 years of insurance industry experience, joining the firm from Hudson Insurance Group, where she served as assistant director. Previous roles include vice president/senior underwriter at Victor Insurance and roles at Travelers Insurance, Marsh and Lockton.

Midwest

Coterie Insurance, headquartered in Appleton, Wisconsin, named Mike Albert

NI Holdings Inc., headquartered in Fargo, North Dakota, promoted Kevin Elfstrand to senior vice president and chief accounting officer. Elfstrand has over 20 years of P&C experience, including 17 years at Travelers Companies, Inc., most recently as assistant vice president of corporate audit. Brandon Nicol was promoted to senior vice president of reinsurance and chief underwriting officer. He has 19 years of experience, including roles at AmericanAg, XL Catlin, COUNTRY Financial and State Farm.

Chris Oen was promoted to senior vice president and chief claims officer. Oen has over 30 years of experience and will continue to lead the claims department.

Will Pinson, senior underwriter and lead for the North Carolina region, is based in Wilmington, North Carolina. He has over 12 years of experience in specialty and surplus lines underwriting, specializing in placing hard-tobind accounts.

Janet Christenberry, lead underwriter for the Atlanta region, has over 20 years of commercial underwriting experience, previously serving as underwriting supervisor at Jencap and at Genesee General for over 20 years.

Charles Bethishou, commercial lines underwriter for the Atlanta region, has over a decade of experience in underwriting, business development and client retention. Fluent in English, Spanish, and Portuguese, he previously served at Jencap Insurance Services.

West

Trucordia, headquartered in

Chalmers most recently served as senior vice president, compensation and total rewards practice at Lockton and previously served as principal, career practice leader/ Midwest region leader at Buck.

The Liberty Company Insurance Brokers, headquartered in Gainesville, Florida, named Brittany Montoya as vice president and producer at Liberty Naranjo.

Based in Las Vegas, Montoya began her career managing HOAs, ascending from community manager to regional director and vice president. Before joining Liberty, she served as vice president, producer at USI Insurance Services. She previously served as regional vice president at Terra West Management Services.

Toni E. Mitchell

Candance Chieppo

Mike Albert

Allan Egbert

Leslie Greve

Mike Chalmers

Brittany Montoya

Closer Look: Litigation Funding

5-Year Cost of Litigation Funding to Commercial Insurers Could Top $25B

By Susanne Sclafane

“Are you being serious?”

Christopher Swift, chair and chief executive officer of The Hartford, was taken aback by a question from an analyst during the company’s second-quarter earnings call about the impact of litigation finance on the insurer’s results.

“It’s showing up in our loss trend [and] our allocated loss expenses. We’re spending more

time and money on something that turned our judicial system into a gambling system. Are you serious?”

The analyst restated the question, explaining to Swift that he is aware that a variety of issues come together to create social inflation. What he wanted the CEO to pin down was the isolated impact of third-party litigation funding (TPLF), apart from factors such as negative public sentiment and eroding tort reforms. Swift didn’t have figures to share. But two months earlier, an actuary speaking at the Casualty Actuarial Society’s Seminar on Reinsurance, said

the top end of a range of estimates of direct costs that will be paid to funders by casualty insurers is $25 billion over a five-year period (2024-2028).

Mike McComis, a senior manager for EY and a Fellow of the Casualty Actuarial Society, revealed the results of a model developed by his firm last year to measure the impact of litigation funders, using some information from funders’ reports about annual returns and a variety of assumptions to develop the figure. McComis gave an overview of the steps involved in constructing the model and flagged some of the most tenuous assumptions—

including a somewhat shaky guess that insurers will pay about 90% of funders’ returns. He also provided a range of estimates based on 720 scenarios tested with the model, revealing that the five-year cost is most likely to fall between $13 billion and $18 billion (the 25th to 75th percentile), with a mid-range average coming in at around $15.6 billion for the five years from 2024-2028.

(Editor’s Note: McComis revealed that the EY study was performed late last summer, which explains why the estimates begin with the year 2024.)

The figures, he said, repre-

sent direct costs—the portion of TPLF returns that come out of the coffers of P/C insurers. But then there are indirect costs to consider.

“That’s just how much the funders are making. The other element to this is where is that funding going,” he said, suggesting that when funding goes to law firms, they may be able to advertise more, bring in more cases, and fight claims longer. “They have this capital backing, which means they don’t have to settle for cash flow reasons,” he said.

This adds an indirect cost to insurers, McComis said, noting that when cases go on longer, insurers have to pay more legal fees.

“There’s also the potential ability of this to drive up actual results for the plaintiffs, the injured parties themselves,” he said, referring to rising verdict and settlement trends presented by co-panelist Jonathan B. Hayes, managing director and reinsurance actuary at Aon.

the next five years, with the most likely scenario (50th percentile) falling between 4.5 and 5.5 loss ratio points. (McComis estimated the loss ratio boost using 2023 earned premiums for commercial auto liability, other liability occurrence, and medical professional liability.)

“Presumably more of that should be going to the injured parties,” he said.

While McComis and his colleagues didn’t unearth evidence of that as they undertook a massive research project to develop inputs for the model, he did say there is one study that puts total costs, including indirect costs, at roughly double the amount of direct costs. Without identifying the source, McComis noted that if this were true, the high end of the range—now $50 billion—could add 7.8 points to the commercial liability industry loss ratios for each of

Returning to the direct costs modeled by EY, McComis displayed line graphs plotting the most likely (25th and 75th percentile) modeled estimates, as well as the minimum and maximum modeled estimates for each year from 2019 through 2028. The most likely estimates shown on the graphs started at about $1 billion in 2019, growing to $2.5 billion in 2019, and then climbing to around $3.5 billion by 2028. The lines plotting each year’s minimums and maximum estimates showed similar trajectories. Summing up the results in terms of two five-year periods, McComis observed that the model forecasts “basically a doubling effect”—with direct costs of TPLF to the P/C industry increasing by 75%-100% for the early five-year period to the subsequent five-year period.

McComis referred to the conclusion of a separate EY analysis of Schedule P data, which showed no let-up in social inflation post pandemic—with continued commercial auto calendar-year paid claim severity trending at 9.6% on average, and other liability at about 15%. Putting that together with this model’s results, McComis said social inflation trends will persist at a heightened level for longer.

“We haven’t even seen the full impact of this [TPLF] industry because it’s growing, it’s lagged three-and-a-half or four years (the assumed model time frame between TPLF investment and settlement, based on funders’ reports), and they’re making massive returns (around 25%-30%, another model assumption).”

‘We haven’t even seen the full impact of this [third-party litigation funding] industry because it’s growing, it’s lagged three-and-a-half or four years … and they’re making massive returns.’

The model, he said, has “solidified our belief” that TPLF “is going to be one of the key drivers, if not the key driver, of the heightened social inflation-impacted trends going forward, and probably has been in the last several years.”

Building a Model

When actuaries in attendance were polled about the likely cost of TPLF to commercial insurers over the next five years, they mainly guessed $10-$20 billion, not foreseeing the $50 billion potential high-end figure, including indirect costs.

Estimating the cost is not straightforward, McComis noted as he explained his firm’s effort to build a model. It is challenging to identify cases helped by TPLF because there have historically been few requirements to disclose litigation funding (something that is changing now in some states).

That means actuaries can’t tackle the TPLF cost question with a bottom-up approach of extrapolating from historical data. EY chose a top-down approach instead, estimating the portion of returns earned by funders based on returns that some funders have reported in their financial reports, and allocating a share to P/C insurers.

McComis and colleague Abbi Brucea, also a Fellow of the Casualty Actuarial Society, started the modeling with 80-plus hours of research, thoroughly poring over publicly available data and industry reports from firms like Swiss Re and Aon, to derive several key insights:

• Average annual returns from TPLF activities are in the 25%30% range, based on funders’ reports that have posted earnings anywhere from 22% to an outlier of 77% in the past 5-7 years.

• 85%-90% of funded cases succeed, reflecting the selectivity of funders, which some sources said only accepted 5% of commercial cases submitted to them. (The acceptance range extended from 5%-20% based on documents reviewed by EY.)

• Commercial litigation funders’ assets under management (AUM) are growing at a rate of 8.7% per year.

McComis said the last assumption, which came from a past Swiss Re report, would have produced an estimate of $16.5 billion for 2024, noting that this is close to an estimate EY derived by fitting a curve to actual AUM amounts reported in a separate industry report for 2019-2023 ($16.1 billion).

McComis went on to continued on page 22

Closer Look: Litigation Funding

continued from page 21

describe how EY used this information to derive key assumptions for three building blocks of the EY model:

• The amount of capital invested by the TPLF in new cases by calendar year.

• TPLF dollar returns on investment by calendar year.

• The dollar impact to the P/C insurance industry.

For each block, EY selected a range of reasonable assumptions from its research and modeled 720 scenarios, McComis said, before delving into some of the details of modeling building block No. 1: How much money gets invested in new cases each year. Beyond AUM and growth rates, the model needed a range of assumptions about the level of commitment, he said, displaying the assumptions of one scenario that assumed 20% of AUMs were committed to new cases. Likening the concept of commitment to a home equity line of credit, he explained that funders don’t actually earn

anything until the “lifeline of funds,” or amounts they’ve promised to invest in a case, are actually used. According to one of the reports EY read as part of its research, funders deployed 78% of their commitments, on average, when cases were resolved, he said.

Moving from the deployed amounts to the second building block—TPLF earnings on their investments in commercial cases—McComis noted that while EY generally assumed 25%-30% returns per year, the model included scenarios assuming that that will decrease over time. “As this market [becomes] more saturated, maybe [TPLFs] won’t be as successful and so they have more losses,” he said.

The model also required assumptions about the time to resolve cases. “That determines the stopping point of how much interest or return they’ve earned,” he explained, noting that the model assumed three-and-a-half to four years as the midpoint of a fitted distribution.

‘Honestly, there’s not any really good public information out there’ to pinpoint a number… ‘But our belief was that a large proportion of this will be paid by the insurance industry in some fashion,

whether it’s the primary insurers, excess, or reinsurers.’

Finally, the model moved from the sum of the modeled calendar-year projected returns for the TPLF industry to answer the ultimate question for actuaries and insurance executives: How much is the P/C insurance industry going to have to pay for that?

“Some of this is not going to be paid for by the [P/C] industry but [instead] will be absorbed by consumers and corporations,” McComis said, noting the presence of

deductibles or self-insured retentions and increasing commercial insurance costs that may prompt some insureds to increase retentions and reduce towers. EY selected 90% as its best estimate of the portion of TPLF returns that would be paid by insurers, putting a range of scenarios around that in the model.

“Honestly, there’s not any really good public information out there” to pinpoint a number, McComis said. “But our belief was that a large proportion of this will be paid by the insurance industry in some fashion, whether it’s the primary insurers, excess, or reinsurers,” he said. “These are generally cases that are pushing things up into the excess and umbrella layers,” he reasoned.

Takeaways for Actuaries and Executives

“We believe that TPLF is the most significant and measurable driver of social inflation,” said the caption on a slide that graphed the modeled outputs

of minimum, maximum, and most likely direct costs of TPLF to the P/C industry by year.

From an actuarial perspective, for pricing and reserving, “the trends are going to stay high in our opinion,” McComis said, referring to the upward trajectories of the curved line graphs from 2024 through 2028. “So, you shouldn’t be backing off on those,” taking down earlier assumptions. “If you are, we think you’re ignoring the impact of third-party litigation funding continuing to persist in these trends.”

A slide displayed as McComis concluded his presentation included various bullet points referring to the increased duration of litigated claims and incentives for plaintiffs to extract the highest possible values—two considerations that should be included in actuarial analyses going forward.

McComis also offered some advice for claims managers of direct writers.

Start tracking the cases backed by third-party litigation funding, he said, alluding to emerging disclosure requirements. From such data, insurers could potentially build their own models of where TPLF is most likely to be involved.

“Maybe, over time, as you track when you’re fighting those and the outcomes, you can adjust your strategies,” he said, suggesting that the best lawyers and top-performing adjusters might be assigned to cases most likely to be funded by the TPLF firms to get better outcomes.

This story was originally published in Carrier Management, Insurance Journal’s sister publication.

Spotlight: Reinsurance

Exclusive Member of Reinsurance Class of 2025: Duperreault’s Cedar Trace

By L.S. Howard

There are certain traits of hard reinsurance market cycles: prices rise, terms and conditions tighten, and new Bermuda reinsurers are formed to help fill capacity needs—known in the past by the market as the “class of 1992,” “class of 2001,” or the “class of 2005.”

At least that was previously the pattern. During the current hard market, however, there hasn’t been a spate of new entrants—in Bermuda or elsewhere. Only several new reinsurers have been able to find investors with the appetite to provide sufficient financial support that would be needed for underwriting a substantial property/casualty business.

The class of 2025 is mainly limited to Cedar Trace’s Mereo Insurance and Lloyd’s reinsurer OAK Reinsurance.

Mereo Advisors—a Bermuda holding company that was renamed Cedar Trace Ltd.—began reinsurance underwriting as Mereo Insurance in January 2025. The company is led by industry veteran Brian Duperreault, the former executive chairman of American International Group (AIG).

At last month’s reinsurance Rendez-Vous de Septembre, there were rumors (once again) that reinsurance executives were at the meeting seeking investors to help them form three more reinsurers to create a “class of 2026.” But as always, the devil is in the detail as well as the amount of money that

can be raised from investors. (The domiciles of the startups were said to be Bermuda and London.)

Similar rumors about Mereo, OAK Re, and Alpine Re were heard at last year’s RVS—but only Mereo and OAK Re had successful fundraising and were able to launch. Alpine Re wasn’t able to get the funding to launch a $1 billion startup, so it threw in the towel—at least temporarily. (OAK Re’s parent, OAK Global, announced last month it will launch a new syndicate to write retrocession business with an appetite for property and specialty classes in January 2026.)

Some attendees at this year’s RVS meeting questioned the timing of possible 2026 startups, given the softening

pricing seen during this year’s renewals.

But Cedar Trace’s Executive Chairman Duperreault said the timing of the formation of Cedar Trace and Mereo Insurance has worked well because the market continues to be strong across a lot of lines of business. “It’s good to be an underwriter in specialty, casualty, and property right now. So, having this across-the-board strategy is helpful,” he said.

In an interview with Insurance Journal, Duperreault described the reinsurer’s strategy as broad-based and multi-class. “We are writing 25 different classes of insurance business, such as marine, aviation, energy, and property, on a risk-weighted basis,” which creates a portfolio balancing

effect and provides “a pretty steady result.”

“Each one of the 25 is going to go up and down, particularly if they’re in the more volatile portions of the business,” Duperreault continued.

“However, if you put them together with good risks, it balances out, and your loss ratios are actually quite steady over a long period of time,” he said, explaining that there will be a lot of growth in some lines and not much growth in other lines, which balances out to create growth at industry levels.

Cedar Trace’s growth will probably be a little bit above GDP in the early days, but for the long term, Duperreault expects “a steady, profitable business.”

“Over time, if you put a good set of risks together in a balanced portfolio, you’re going to have an average loss ratio and it’s not going to vary very much. It’s like an index fund, an investor index fund.”

Not Reliant on Hard Market

He explained that Cedar Trace’s strategy is not a hard market strategy, so it’s not like the company needs the hard market to continue. “The important thing was would we be able to launch and get a broad-based business in a relatively short period of time, and this market is allowing us to do that.”

He emphasized that it’s impossible to call anything in this world with 100% certainty,

“so having that portfolio balance protects us. And as long as we’re launched—and we are—I’m very comfortable riding out this wave, whichever way it goes.”

Underwriters only have a couple of tools, he said. “One is risk selection, and another is portfolio construction and spread. So, we turn away risks that aren’t priced right, and the pricing takes care of itself.”

The company’s initial plans were to write what Duperreault calls an “aspirational” $520 million during the first year, which he said could be possible if the company writes a full year that includes the January 2026 renewals. “But we’ll see. The important thing is the business is good, sustainable, profitable—and size isn’t as important as that.”

The other positive aspect of the current market for reinsurers is that there is a lot of demand from ceding companies because risk is exploding, he added.

Limited Investor Appetite for Startups

Duperreault attributed the general lack of interest by investors to support reinsurance startups (to create a class of 2023 or 2024) to the sector’s inability to attract long-term capital. (Traditionally, the “class of XXX” terminology has referred to Bermudian reinsurance startups, but it is now being used by many pundits for global formations.)

“Most of the investors don’t want to take long-term balance sheet risks,” he said, noting ILS investments are “hot” because

Brian Duperreault

investors want to know at the end of the year if they had a good year or a bad year.

Indeed, AM Best Ratings has indicated that investors have many additional avenues available to deploy their capital, which didn’t exist in the past.

‘I do think our story itself helped attract our investors in a great way. I think our management expertise helped. Putting those two together, we were able to find enough investors to launch our company. And we’re the only ones.’

The existence of a robust ILS market has “diminished the franchise value of property-catastrophe business to investors,” AM Best said in a July 2024 report titled “The 2023 Reinsurer Class – The Class That Never Was.” (See related article: What Happened to Reinsurance ‘Class of 2023’? Hard Market Defies Age-Old Patterns.)

“Investors today appear much keener to allocate funds to shorter-term ILS instruments

to capitalize on the hardened underwriting conditions, rather than a rated balance sheet,” said the report.

There’s only a very small group of investors who want to take on longer-term risk, Duperreault said, noting that Cedar Trace was able to find a few investors “who understood what we were trying to achieve.” He said that “what we presented was a portfolio approach with the balance that has internal protections.”

Duperreault said that those investors who listened to the pitch understood it and really liked the company’s strategic plan.

He said the company’s portfolio balance was an attractive story to a few wise Cedar Trace investors, which he described as “a nice group who are there for the long haul,” which is a “wonderful thing to have for an investor.”

“They’re not in-and-out types,” Duperreault noted.

At inception, Cedar Trace raised nearly $700 million from several investors and also launched an ILS fund in 2024 with $250-$300 million of capital. Investors include Ares Management Corp. (an alternative asset manager), Susquehanna International Group (a quantitative trading firm), and Andover Cos. (a mutual insurance firm).

“I do think our story itself helped attract our investors in a great way,” he said. “I think our management expertise helped. Putting those two together, we were able to find enough investors to launch our company. And we’re the only ones.”

AM Best has assigned a Financial Strength Rating continued on page 26

Spotlight: Reinsurance

of “A-” (Excellent) and a Long-Term Issuer Credit Rating of “a-” (Excellent) to Mereo Insurance with a stable outlook.

“Initial capitalization in 2024 and retained earnings through the forecast period are expected to support Mereo’s premium growth, which is expected to be rapid in its early years, based on projections,” AM Best said in a Feb. 10, 2025 ratings announcement. “The company’s capital is anticipated to be managed through the use of reinsurance and potentially third-party capital.

Investment risk is projected to be low given its conservative investment portfolio, which will remain matched closely

to the evolution of the liability profile, supporting stability in future balance sheet metrics.”

AM Best went on to say that “Mereo’s senior management team is composed of individuals with extensive experience and strong track records in the industry.”

And, of course, one of those individuals is Duperreault, who previously served as executive chairman for AIG’s Board of Directors and as CEO of AIG from 2017 to 2021. Before joining AIG, he had a 30-year career working in senior executive roles at Hamilton Insurance Group, March & McLennan Companies, and ACE Ltd.

Other veteran executives with Cedar Trace include:

• Lawrence Minicone, chief

executive officer of Cedar Trace. Minicone previously served as the head of Research at Tekmerion Capital Partners, a systematic global macro hedge fund.

• David Croom Johnson, non-executive director, who was formerly CEO of AEGIS London, a successful Lloyd’s managing agency.

• Neil Strong, president of Cedar Trace and CEO of Cedar Trace ILS, who most recently was the CEO of IQUW ILS Ltd.

• Richard Holden, chief underwriting officer of Cedar Trace ILS, who was previously CUO of Fidelis Insurance Bermuda and global CEO of Reinsurance and Capital Management.

• Derek Walsh, chief legal officer and chief operating officer

of Cedar Trace. Previously, Walsh was COO, general counsel, and co-founder of Acacia Holdings, a Bermudabased investment business specializing in insurance-linked securities, focusing on investing collateral for reinsurance contracts.

• Federico Waisman, chief analytics and risk officer of Cedar Trace, who most recently served as head of Underwriting Management at IQUW where he led the portfolio optimization, pricing, exposure management, and underwriting support divisions.

• Jonathan Reiss, interim chief financial officer of all Cedar Trace entities. He also is a managing director at Strategic Risk Solutions (SRS).

ACCELERATE GROWTH WITH STAFF BOOM'S TAILORED OUTSOURCING SOLUTIONS

Embark on a journey of operational optimization and growth with STAFF BOOM, where our tailored outsourcing solutions empower businesses to thrive in today's competitive landscape.

My New Markets

Risk Point Vehicle Inventory Program

Market Detail: Dealer open lot physical damage insurance for car, RV, heavy truck and motorcycle/powersports dealers. Risk Point Mobility Underwriters DOL Program. Features: Program is available for franchised and non-franchised auto dealers, RV dealers, truck dealers and motorcycle/ powersports dealers; Risk Point Alert Weather app sends push notifications to a mobile device when severe weather is within 30 miles, 20 miles, and 5 miles of a target auto dealership; weather loss aggregate deductibles available; economic loss covered to a maximum of $2,500 as a result of collision damage to a new vehicle and $2,500 for additional miles added to the odometer of a new vehicle as a result of a theft loss to a new vehicle; a high sublimit ($200,000 per year) for false pretense (trick, scheme or device) loss; coverage available for stored “off lease” vehicles. An aggregate deductible on collision losses. This is unique in the industry.

Dealer “holdback” covered on total losses to new vehicles – this too is a coverage not often offered by other carriers. The “margin clause” provides coverage equal to 125% of the limit shown in the event that a loss exceeds the limit of insurance shown on the policy. The average monthly value is the limit of insurance shown on the declaration page that will be used as the rating basis. The “margin clause” does not apply to flood or earthquake coverage. Convenient payment plan with 10% down and 11 monthly payments. Monthly Reporter option available. Superior customer service. Claims service is provided by Risk Point and managed from our Dallas, Texas headquarters. Program commission is 12%. Has pen. Available Limits: Not disclosed.

Carrier: Non-admitted.

States: All 50 states and the District of Columbia.

Market Detail: Crypto Shield is the first regulated insurance product for retail crypto investors, covering theft of

crypto while in the custody of qualified exchanges. There have been over 60 exchange hacks, resulting in over $60B in stolen crypto to date. We designed Crypto Shield specifically to protect policyholders from these unfortunate events. Coverages: cyber, directors & officers (D&O), errors & omission (E&O), general liability and wallet risk assessment.

Crypto Shield is backed by an insurance carrier that has earned a Financial Strength Rating of “A-” (Excellent) by AM Best, the largest credit rating agency specializing in assessing the insurance industry.

Breach Insurance is a global insurance underwriter addressing the significant insurance gap in the crypto space by creating regulated insurance solutions for the crypto economy. With a Bermudadomiciled insurance company, U.S.licensed MGA and TPA operations, Breach is able to address the various needs of crypto economy participants.

Why partner with Breach? Licensed & fully regulated, regulated by the Bermuda Monetary Authority as a class IIGB insurer, accepts payment and pays claims denominated in crypto; countrywide licensed as MGA and TPA in the U.S. Has pen.

Available Limits: Not disclosed.

Carrier: Not disclosed. Rated A- (Excellent) by AM Best.

States: All 50 states and the District of Columbia.

Exclusive Workers’ Compensation for Home Health Care

Market Detail: This program was established to reward HHC Agencies that have excellent loss history, with the lowest premiums & upfront dividends & incentives. With an A+ AM Best rating and industry-leading healthcare expertise, our

clients enjoy this well-deserved best-in-industry premium.

Workers’ Compensation Program Highlights: Flexibility to work with you directly or your existing insurance broker; workers’ compensation coverage with bundled risk control, claims, and managed care services; and risk and claims management programs included with all proposals, at no cost.

Risk management solutions meet the specialized needs of healthcare agencies to keep losses at a minimum. Risk control healthcare team – staffed by highly credentialed specialists who can develop customized risk control solutions to address common loss leaders, such as strains, slip/fall, and struck-by injuries. Data analytics – industry-specific performance assessments, peer-to-peer benchmarking, customized reporting, and collaborative analysis reviews. Claims and managed care services – aimed to effectively manage claims, drive positive solutions, and support employees through injury and recovery to achieve a safe return to work. Tailored solutions for workforce challenges – aging workforce, safe return to work, employee health and wellness initiatives. Submission requirements must include the following: Acord form with FEIN #; all available MOD worksheets; 3-5 years of payroll history; 3-5 years of currently valued loss runs; and large loss detail (over $50K).

Available Limits: Not disclosed.

Carrier: Admitted, rated A+ (Excellent) by AM Best.

States: All 50 states and the District of Columbia.

Gold Kulchin Ross Insurance Services, Tarzana, California

Silver Morris & Garritano, San Luis Obispo, California

Bronze Rancho Mesa Insurance Services Inc., San Diego, California

The votes are in for the 2025 Best Independent Insurance Agency to Work For survey by Insurance Journal.

Employees in 2025 highlighted the importance of competitive salaries, employee benefits, training and education, resources, and other employee perks as drivers of satisfaction in the workplace.

But it’s not all about compensation and benefits. Happiness in the workplace has a lot to do with people, relationships, and the agency’s culture. Employees of the winning agencies cite high personal job satisfaction; rate their relationships with their immediate boss or supervisor as positive; and express a high opinion of their agency’s owner or principals and their agency’s reputation in the community. Many employees are grateful

the best agency owners support local charities and the community in which they live. Employees are grateful for the opportunities their agencies provide for them to participate in community service. Employees take pride in working for agencies that are respected and hold strong values and ethics. Employees appreciate the generosity of their agency owners in sharing revenues in the form of bonuses and trips.

The best agencies also provide ways to help their employees grow—by giving them the tools and technology they need, and supporting them with education, training, annual and performance reviews, and, in some cases, mentors. The survey results clearly show employees value this support.

As expected, the winning

agencies score high for overall employee benefits including wellness programs and for working conditions including remote work options, flextime, and other alternative schedules that allow employees to embrace work-life balance.

The best agencies to work for also provide employees with a strong sense of purpose in their profession and deliver a workplace environment where employees feel supported wholeheartedly by management and their peers. Many of the employees say they feel like family in their agencies.

Insurance Journal wishes to thank the thousands of customer service representatives, account managers, producers, managers, and other agency staff who took the time to nominate their independent insurance agency in this year’s survey.

Special Report: Best Agency to Work For

Overall

Robertson Ryan Insurance Milwaukee, Wisconsin

Be a Leader by Listening to Employees and Clients

By Andrea Wells

During the past 60 years, Milwaukee-based Robertson Ryan Insurance has grown from a small, local independent agency into a Top 100 firm employing some 150 agents and 385 associates. But employees say that despite its growth over the years, the agency hasn’t lost its family-style culture in which employees feel valued, heard, and supported.

This year, Robertson Ryan won Insurance Journal’s Overall Best Agency to Work For, an annual awards program where thousands of independent agency employees nominate their organizations, nationwide.

“Robertson Ryan gives you a voice. They listen, encourage, and are there for all of their employees,” said one person when nominating the agency.

Another employee added: “I have worked here for over nine years, and it’s the best place I have ever worked at. Management is very good, you feel heard, and additional education is always available if wanted.”

The recognition as a “Best Place to Work” is not new for RRI. The privately owned agency has been recognized as a top workplace for years, including as Insurance Journal’s Gold Award BATWF winner for the Midwest in 2024.