Business intelligence results in informed decisions. That’s why SIAA provides its independent agency members access to industry leading information systems. Having actionable data means more sales and revenue, operational efficiencies, and meaningful processes. It’s another way we provide our member agencies with the tools they need to enhance their success.

Wherever you are on your journey as an independent insurance agent, or your journey to become one, you owe it to yourself to check out the benefits of becoming a SIAA member. There’s a reason over 5,000 independent agents are availing themselves of the tools, knowledge, and support provided by The Agent Alliance.

Learn how joining our community can make the difference in your long-term success.

siaa.com info@siaa.com

Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Top 100 Agencies

This year marks the 21st annual publication of Insurance Journal’s Top 100 Independent Agencies special report. Nearly all of the firms in the Top 100 saw notable increases in total property/casualty revenue year-over-year. From 2023 to 2024 the Total P/C Revenue combined of all 100 firms grew by more than $3.1 billion. (See the full report on page 28.)

This year’s Top 100 welcomes a handful of firms not listed on last year’s report, as well. Newcomers and one returning firm this year include the following: Keystone Agency Partners LLC; OneDigital; Superior Insurance Partners; Vantage Insurance Partners; The Mahoney Group; Reliance Partners; OVD Insurance; C3 Risk & Insurance; Snellings Walters Insurance Agency.

While the list added new agencies, there were again agencies that fell off the ranking due to acquisitions, including: NFP (now part of Aon); Woodruff Sawyer (now part of Arthur J. Gallagher); The Horton Group (now part of Marsh); and Wallace Welch & Willingham (now part of IMA).

And what about the Future Top 100? While the following agencies didn’t make the cut in 2025, their total property/casualty revenue for 2024 came very close.

Special mention goes out to the following agencies:

• Beehive Insurance Agency Inc.

• Morris & Garritano

• Ori-Gen Agency Insurance Services Inc.

• Biltmore Insurance Services

• Windermere Insurance Group LLC.

Insurance Journal’s Top 100 report would not be possible without the willing participation of all the agencies, brokerages, and agency groups that have shared their information over the years.

Insurance Journal’s Top 100 report would not be possible without the willing participation of all the agencies, brokerages, and agency groups that have

shared their information over

the years.

All information in this report is gathered from voluntary online submissions and best estimates based on other public information sources.

We thank the many agencies that have contributed and invite others that have never submitted information for the report to consider it next year. Be proud of what you have accomplished.

For questions, comments, or criticisms, write to us at Insurance Journal. And congratulations to this year’s top agencies!

| jcarlson@insurancejournal.com

ADMINISTRATION / CIRCULATION

Chief Financial Officer Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant

Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content

Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus

Andrew Simpson | asimpson@wellsmedia.com

National Editor Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor

William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Online Training Coordinator George Jack | gjack@ijacademy.com

Every day, we create unique risk solutions for unique businesses.

When it comes to insurance for midsize and large businesses, we get it. We do it for all kinds of industries, tailoring our policy solutions from traditional to specialized coverage. With our experience in underwriting, innovative service, and claims, we are your one-stop shop.

Connect with your underwriter at The Hartford.

News & Markets

Independent Agencies’ Market Share Shows Small Decline; Strong Hold on Commercial Lines with Opportunity to Grow in Personal Lines

By Andrea Wells

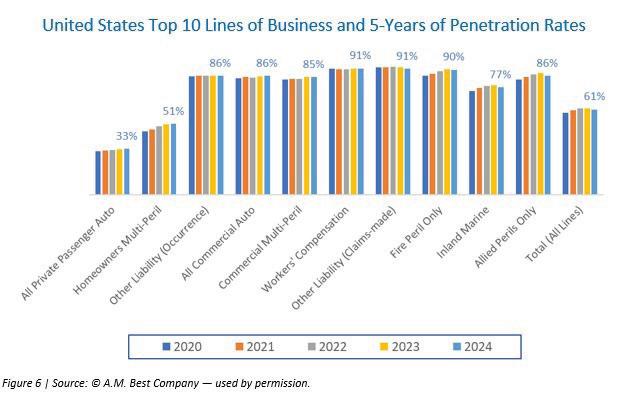

The independent agency channel placed 61.5% of all property/casualty insurance written in the U.S. in 2024, a slight decline from 2023 where independent agents placed 62.2% of P/C lines nationwide.

That’s according to the 2025 Market Share Report published by the Big “I” trade association for independent agents. IAs hold a steady five-year average of P/C coverages written at 61.3% despite the challenges of the hard market, the report noted.

The annual Market Share Report compiles and analyzes P/C premium data from AM Best and provides insights for agencies and carriers on current market share by distribution types.

Overall, the independent agency channel held steady in both commercial and personal lines business written in 2024. Independent agencies wrote 87.2% of commercial lines written premiums, consistent with 87.3% in 2023. But in personal lines, opportunities for independent agency channel growth remain.

According to the study, independent agents wrote 39% of personal lines written

premiums in 2024, compared to 38.7% in 2023. The good news: independent agents have continued to retain gains in personal lines market share from 2020 where IAs only held about 35.7% of the market.

The state with the highest independent agent penetration rate was Massachusetts (78.8%), and the state with the lowest rate was Alaska (51.4%), the study revealed.

By line of business, the top penetration rates were: International (100.0%), Multi-Peril Crop (96.9%), and Private Crop (96.4%). The lowest penetration rates were: Financial Guaranty (4%), Mortgage Guaranty (14%), and All Private Passenger Auto (32%), with Farmowners Multi-Peril (40%) and Warranty (40%) following.

The hard market led to additional premium growth as direct written premiums for total P/C business reached $1.05 trillion in 2024, up from $952 billion in 2023.

The Big “I” said that despite loss factors continuing to impact the P/C market— including $113 billion in insured natural catastrophe losses in the U.S., according to Aon—direct written premium increases of 9.6% in 2024 resulted in combined ratios of 92% for 2024, down from 96% in 2023 and 98% in 2022.

The highest average loss ratios occurred in Federal Flood at 278.8%, Private Crop at 93.0%, and Multi-Peril Crop at 85.9%.

“The hard market conditions of the last few years have presented independent agencies across the country with significant challenges, but the results of the 2025 Market Share Report demonstrate agencies’ ability to adapt to serve their communities,” said Charles Symington, Big “I” president & CEO, in a statement.

“In a complicated and fast-evolving market, the personalization, choices, and education that independent agents provide are crucial, proving once again their role as key partners in the insurance distribution channel.”

Other Findings

• Surplus Lines. In the United States in 2024, the percentage of premiums going to Surplus Lines Domestic insurers was 9.7%, up from 9.4% in 2023, and 7.0% in 2020. The five-year average is 8.7%, the report said. Nationwide, the top three lines of business with premiums going to Surplus Lines insurers were: Other Liability (Occurrence), Other Liability (Claimsmade), and Fire Peril Only.

• Flood. Private flood continued to grow with a 50.6% utilization rate, up from 46% in 2023 and 44.9% over the past five years.

• Commissions. The average U.S. commission rate in 2024 was 11.5% for all P/C lines of business combined. The highest average commission rate was 13.6% (Massachusetts), and the lowest was 10.1% (Delaware). The highest average commission rate by line of business was Surety at 27%, followed by Burglary & Theft at 20% and Private Crop at 19%. The lines with the lowest average commission rates were All Private Passenger Auto, Excess Workers’ Comp, and Multi-Peril Crop—all at 8%.

The Market Share Report is free for Big “I” members and states associations. To order or purchase a copy of the complete 2025 Market Share Report, visit the Big “I” Market Share Report webpage.

Artificial intelligence is positioned to transform healthcare, even if AI’s most alluring and headline-grabbing promises— like predictive diagnostics that anticipate illness before symptoms appear—remain projections for the future. While much of the spotlight is on what is to come, a quiet AI transformation is underway.

A survey conducted by the Medical Group Management Association in the summer of 2024 found that 42% of medical group leaders reported using some form of ambient listening AI.1 These systems, sometimes called “AI scribes,” aim to capture interactions between physicians and patients through discrete microphones installed in examination rooms. The AI then generates suggested notes and billing codes for physicians to review and enter into the medical record.

With the promise of increased efficiency in the documentation process, it is easy to see why physicians are drawn to this technology. A 2024 American Medical Informatics Association (AMIA) survey revealed that nearly 75% of healthcare professionals believe the time and effort required for documentation impedes patient care.2 In another study, over 77% of respondents indicated they often work later than desired or take work home due to excessive documentation tasks.3 Less time spent documenting allows physicians to spend more time with patients and potentially helps combat physician burnout.

The benefits of this technology are obvious and potentially transformational for physicians, but AI also brings new risks to consider. Not the least of which is patient consent. Recent evidence suggests that most patients are skeptical about the utilization of AI in healthcare. In a 2022 survey by the Pew Research Center, 60% of respondents reported they would feel uncomfortable if their provider relied on AI for their medical care.4 To help alleviate such concerns, physicians should have patients execute a detailed consent form that explains how the ambient listening system works, what is preserved, and the system’s deletion policy.

Physicians should also obtain and document a patient’s verbal consent at every visit before triggering the listening system. This ensures the patient remains comfortable having their protected health information shared with the system. Additionally, this verification is a legal necessity in states that require consent from all participants to a recorded conversation.

Discoverability is another issue physicians should be mindful of when utilizing this technology. By now, it is well known that most, if not all, malpractice litigation includes a discovery request for all relevant digital communications and metadata stored in the electronic medical record. Such data has provided fertile ground for plaintiffs’ attorneys seeking to weave a narrative in favor of their client, and ambient listening AI could be even more problematic.

While physicians are typically only privy to the AI-generated notes, ambient listening systems may also capture and store a raw audio recording of the entire patient encounter. Whether this data is retained depends on the design and configuration of the specific system. As such, physicians and practices must work with vendors to determine whether their chosen system stores complete audio recordings. If a system retains a complete audio recording of the patient-physician interaction, it will undoubtedly be discoverable in litigation.

In a worst-case scenario, there could be an inconsistency between the note in the EMR and the audio recording. Even a seemingly minor inconsistency could undermine the accuracy and reliability of the entire medical record. It may also be used to suggest that the physician failed to review the AI-generated notes adequately. Negative optics of this nature can derail otherwise defensible cases.

Against this backdrop, there is scant justification for retaining these audio logs once the AI-assisted note has been accurately added to the electronic medical record. To address this, practices should implement clearly articulated retention policies for all data captured by the AI system that is not added to the medical record. Beyond preventing the creation of unnecessarily discoverable data, a well-defined retention protocol that is consistently adhered to should ward off allegations of spoliation. Collaboration with vendors will be needed to ensure the chosen retention protocol is in place.

AI is already reshaping how healthcare operates, and these are just a few risk issues that need to be considered. As this technology evolves, its integration into everyday medical practice will only deepen. Amid these rapid advancements, physicians must remain vigilant to emerging risks, even as they navigate the often-dazzling promise of innovation.

Risk Recommendations

Physicians utilizing ambient listening AI systems should consider the following risk management steps to reduce legal risks:

2. Implement policies for retention and destruction of audio data.

3. Train providers on what is being captured and how to communicate accordingly.

4. Engage legal counsel in evaluating how these systems intersect with controlling discovery rules.

Bradley E. Byrne Jr., Esq., Southeast Regional Risk Manager

$400

27%

How much it costs to subscribe to hurricane reports from Global Weather Oscillations, led by former National Weather Service and U.S. Air Force meteorologist David Dilley. Dilley’s model predicts where hurricanes will make landfall, within about 100 miles. He’s calling for one hurricane to hit Florida this season but said he can’t reveal exactly which area. “It wouldn’t be fair to customers who have purchased subscriptions” to say publicly where the storms will hit, he told Insurance Journal recently. 82

The average rate hike Illinois State Farm homeowner policyholders may see this year. State Farm is raising the state’s homeowners’ rates by an average of 27% and requiring customers to carry a minimum 1% wind/hail deductible in their home insurance policy. The rate increases went into effect July 15 for new business and start August 15 for renewals.

$58.8 Billion

The amount workplace accidents cost U.S. employers each year, according to Liberty Mutual’s latest Workplace Safety Index. The top 10 causes of injuries account for 86% of those costs, or $50.87 billion. Overexertion involving outside sources remains the top cause, accounting for $13.7 billion in costs. This has held true for 25 years. Falls on the same level is second with $10.5 billion in costs.

The temperature The Los Angeles County Board of Supervisors is considering as a cooling requirement for rental units. The board recently held an initial hearing on an ordinance to require rental units to maintain indoor temperatures at or below 82 degrees Fahrenheit to protect tenants from heat-related health risks. The ordinance doesn’t require air conditioners; it also allows methods like cool roofs, insulation and shade.

Declarations

Gun End-Run

“The intent of Congress when it closes a door is not for States to thus jimmy a window.”

— Circuit Judge Dennis Jacobs, responding with reservations while concurring with a federal appeals court to uphold a New York state law holding gun manufacturers potentially liable when their weapons are used in deadly shootings. The law requires the gun industry to create reasonable controls to prevent unlawful possession, use, marketing or sale of their products in New York. It allows them to be sued for unlawful acts that create or contribute to threats to public health or safety.

Warning from New Florida CFO

“I want the insurance companies to listen … if an insurance company does not do what they say they’re going to do and are contractually obligated to do, I am going to call you out.”

— Blaise Ingoglia, a millionaire home builder and recent state legislator, who was recently appointed head of the Florida Department of Financial Services by Gov. Ron DeSantis. The quote first appeared on the Orlando Sentinel news site. “I am going to be a proactive fiscal watchdog for Florida,” Ingoglia said, the Associated Press reported. “I’ve had a history of calling out wasteful spending, whether it’s Democrats or Republicans.”

Construction Fraud Crackdown

“Construction projects are a major investment, and consumers deserve to be treated honestly and fairly when hiring a business to perform work on their homes. Contractors cannot take thousands of dollars in deposits and then disappear. Where possible, given the constraints we have under the Consumer Protection Act, my office will hold bad actors who exploit Michigan residents accountable.”

— Michigan Attorney General Dana Nessel, discussing a lawsuit against Hummingbird Construction Co., LLC and its owner, Matthew Ashline, for allegedly scamming multiple customers by accepting deposits for construction projects never started and then failing to return the funds.

Autopilot On Trial

“It engenders a lot more inappropriate confidence in the car, because autopilot is such a good technology in aviation. Somehow, we feel like that is going to translate to a really effective tech in the car.”

— Mary “Missy” Cummings, an engineering professor at George Mason University, and expert witness on safety in Tesla Inc.’s face off with the California Department of Motor Vehicles over claims the company exaggerated the capabilities of its Autopilot and Full Self-Driving technology. Cummings, who was a U.S. Navy fighter pilot, told jurors those kinds of statements can encourage driver “complacency.”

Coastal Crisis

“It is going to result in one of the largest setbacks for our coast and the protection of our communities in decades. I don’t know what chiropractor or palm reader they got advice from on this, but—baffling that someone thought this was a good idea.”

— Former Louisiana Rep. Garret Graves, a Republican who once led Louisiana’s coastal restoration agency, commenting on the state’s cancelation of $3 billion in repairs to its disappearing Gulf coastline, funded by the 2010 Deepwater Horizon oil spill settlement. The move scrapped what conservationists called an urgent response to climate change, but Gov. Jeff Landry viewed as a threat to the state’s way of life.

No-Drone Zones

“We have both good and bad actors in the air, and right now we can’t identify which is which. These are not hypothetical threats. They’re happening now in active emergency zones and putting lives at risk.”

— Tom Walker, CEO of DroneUp, supporting local agency rights in drone safety. DroneUp works with governments on UAV-related training and operational support, policy development, mission coordination and integrated airspace management. State governors and industry experts are asking Congress to give state and local officials more leeway to control drones. Those rights are now solely for the Departments of Homeland Security, Justice, Defense and Energy.

Business Moves

National

Keystone

Agency Partners, Warburg Pincus

Private equity firm Warburg Pincus will acquire a majority stake in insurance broker and agency network Keystone Agency Partners (Keystone).

Keystone was formed in 2020, in partnership with Keystone Insurers Group Inc. and Bain Capital LP.

Bain Capital will retain minority ownership in Keystone through a new investment from Bain Capital Insurance.

Keystone is a national retail broker and agency network, comprised of 28 platform partners and more than 350 independent network partners that together write more than $8 billion in annual premiums.

The transaction is expected to close in Q3 2025 and is subject to regulatory approvals. Financial details of the transaction were not disclosed.

White

Mountains Insurance Group, Distinguished Programs

White Mountains Insurance Group has a deal in place to acquire about 50% of Distinguished Programs for $230 million.

With the buy of the outstanding equity shares, White Mountains will own 51% of Distinguished, an independent program manager and managing general agency for specialty insurance. The Bermudabased holding company owned 1% of Distinguished outstanding equity interests before this transaction.

Founded in 1995, New York-based Distinguished will continue to be led by

CEO Bill Malloy, President Jason Rotman, and CEO Steve Sitterly.

Aquiline Capital Partners, the current controlling equityholder of Distinguished, will continue to hold a significant minority interest.

The transaction is expected to close in the third quarter of 2025, subject to regulatory approvals.

East

World Insurance Associates LLC, Healey & Associates

World Insurance Associates LLC acquired the business of Healey & Associates of Portland, Maine.

Healey has offered employee benefits throughout New England since 1982, with a focus on the non-profit sector.

World Insurance Associates is a financial services organization headquartered in Iselin, New Jersey, with more than 300 offices across the U.S. and the U.K.

Terms of the transaction were not disclosed.

Smith Brothers Insurance LLC, Charter Oak Agency

Glastonbury, Connecticut-based Smith Brothers Insurance LLC acquired Charter Oak Agency. Charter Oak Agency, an independent insurance agency with offices in Westport and Derby, Connecticut, will retain these locations.

Marissa Barbera, president and owner of Charter Oak Insurance Agency, and her team will join Smith Brothers Insurance. Smith Brothers Insurance is an

independently operated insurance broker with more than 250 professionals, licensed in every state with offices throughout Connecticut, Massachusetts, New Jersey, and New York.

Midwest

WalkerHughes, Apogee Insurance Solutions LLC

Apogee Insurance Solutions LLC, a St. Peters, Missouri-based insurance agency, joined WalkerHughes Insurance, a privately held, founder-led retail insurance brokerage headquartered in Indianapolis, Indiana.

This marks WalkerHughes’ second acquisition in Missouri and a continued step forward in its regional expansion strategy.

Apogee, which specializes in personal lines and commercial insurance, serves the St. Louis metro area. Agency owner Kyle Heywood is exiting the business. Longtime team members Jessica Grotewiel and Amanda Knott will be integrated into the WalkerHughes Missouri operations.

Inszone Insurance Services, Snell-Nelson Insurance Agency Inc.

Inszone Insurance Services acquired Snell-Nelson Insurance Agency Inc, an agency based in Ashland, Kansas, with additional operations throughout Kansas and Oklahoma. Snell-Nelson has 40 years of history and experience in the region.

Lemonade Expands Auto to Indiana

Lemonade expanded its Lemonade Car insurance product statewide in Indiana. With this addition, Lemonade Car is now available in states representing approximately 42% of the U.S. car insurance market.

Lemonade Car’s sequential in-force premium growth outpaced the rest of Lemonade’s book for Q1 2025.

Reliance Global Group Sells Fortman Insurance Services

Reliance Global Group announced it has completed an asset sale of Ottawa, Ohiobased Fortman Insurance Services, wholly owned subsidiary, for $5 million.

Reliance didn't disclose the buyer of Fortman.

Reliance sold Fortman at a value above the initial purchase price Reliance purchased the agency for in 2019.

Southeast

NFP, Levine Group LLC

Global insurance and benefits broker NFP acquired Levine Group LLC, a financial services firm based in Brentwood, Tennessee.

Levine Group has served Nashville and the surrounding area since 1963. The firm offers investment management, retirement plan consulting, employee benefits, and insurance.

NFP, an Aon company, has more than 8,000 employees in the U.S., Puerto Rico, Canada, the U.K., and Ireland. Michael Levine, who leads Levine Group, will join NFP, working with Mike Schneider, president of NFP’s central and West regions. Trevor Coe and Zach Levine will also join NFP.

All of TailoredRisk’s employees will join Afore, and TailoredRisk will eventually operate under the Afore name.

Afore also appointed TailoredRisk’s principal, John Paolini, to the role of executive vice president of its national personal lines division. Paolini will fill the vacancy created by Andrew Muller’s recent elevation to executive vice president of strategy and partnerships.

Afore has acquired more than 50 agencies and has more than 20 offices nationwide.

Hancock Claims Consultants, Knight’s Solutions

Hancock Claims Consultants, a 22-yearold claims adjusting firm with offices in Georgia and Kentucky, acquired Knight’s Solutions, an inspection firm that works claims in the Midwest and Southeast.

Neither company is a public adjuster firm, but they work for property insurers, providing inspections and claims adjusting.

Terms of the deal were not disclosed.

Knight’s, with offices in Mobile, Alabama, and Bardstown, Kentucky, also offers ladder assist services, providing roof inspections on steep or tall buildings for insurance adjusters. Ryan Knight is the owner.

Hancock also has offices in Bardstown and Alpharetta, Georgia, and works for insurers across the country.

The firms plan to complete operational integration over the next 90 days. Ryan Knight will report to Ray Tant, Hancock’s senior vice president of inspections and estimating.

Florida-based Legacy Insurance Solutions joined Patriot Growth Insurance Services, a national insurance brokerage and partnership platform headquartered in Fort Washington, Pennsylvania.

Founded in 2011, Legacy is a familyfounded insurance agency with offices in Tallahassee and Palm Beach Gardens, Florida.

Patriot Growth was founded in 2019. Terms of the deal were not disclosed.

King Risk Partners, Cummings Insurance Agency

King Risk Partners, a national insurance brokerage with home offices in Gainesville, Florida, has acquired Cummings Insurance Agency in Aiken, South Carolina.

Ted Cummings is principal of the agency, founded in 2014 and specializing in agricultural and equestrian clients.

The agency is not affiliated with other Cummings insurance agencies in Alabama, Florida, and Pennsylvania.

Marsh McLennan Agency, Excel Insurance

Marsh McLennan Agency, part of the global Marsh insurance brokerage and services companies, acquired Excel Insurance, in Medley, Florida.

Excel was founded in 2020 and provides property/casualty solutions, including

auto, watercraft, commercial coverage, homeowners, and workers’ compensation insurance, for small businesses and residents in south Florida.

All Excel employees, including President Jacob Pared, will now join MMA in its existing Doral office.

West

Trucordia, Vegas Valley Benefit Plans

Trucordia acquired the business of Vegas Valley Benefit Plans, a provider of employee benefits and insurance services based in Las Vegas, Nevada.

Trucordia is the group name for an insurance brokerage headquartered in Lindon, Utah, offering commercial and personal lines, life and health, and employee benefits insurance services.

Trucordia, Fuhriman Insurance

Trucordia also acquired the Fuhriman Insurance business.

Based in Boise, Idaho, Fuhriman Insurance offers insurance solutions for auto, home, commercial, life, umbrella, renters, workers’ compensation, toys, and pest control.

International

CRC Group,

Atrium Underwriting Group Ltd.

CRC Group, the Charlotte, North Carolina-based wholesale specialty insurance distributor, has entered a definitive agreement to acquire Lloyd's managing agency Atrium Underwriting Group Ltd. from investment funds managed by Stone Point Capital and other investors.

Atrium will retain its brand name and independence under the leadership of its current management team within the CRC Group, making its first investment outside of North America. A trium manages Syndicate 609 and writes specialty insurance and reinsurance across property, casualty, and specialty business groups.

Financial details of the transaction were not disclosed. It is expected to close in the third quarter, subject to customary closing conditions and regulatory approvals.

National Chubb, headquartered in Warren, New Jersey, appointed Scott Williams as private equity industry practice leader.

Williams has over 15 years of insurance industry experience, joining Chubb in 2009 as division counsel for the private/ not-for-profit practice. He succeeds Seth Gillston, who was recently appointed head of global casualty for major accounts in North America.

pany’s Eastern zone. Before joining Liberty, Weiss held underwriting and insurance specialist roles, most recently at XL Catlin.

Adam Denninger chief operating officer. Denninger will lead Hiscox USA’s operations across strategy, transformation, data, and delivery. With over 25 years of experience, Denninger most recently served as Capgemini’s global industry leader for insurance.

East

Trucordia, headquartered in Lindon, Utah, appointed Rajeev Khanna as chief information officer. Khanna has over three decades of experience, most recently serving as global chief technology officer for Aon plc. Prior to Aon, Khanna was vice president of global infrastructure services at Expecia and senior director of global infrastructure services at Asurion.

Liberty Global Transaction Solutions (GTS), part of Liberty Mutual Insurance, headquartered in London, promoted Hilary Weiss to head of Americas.

Weiss joined Liberty Mutual in 2018 as associate vice president, Americas

M&A, before moving to Liberty GTS in 2021 as head of the com-

Aspen Insurance Holdings Limited, headquartered in Hamilton, Bermuda, appointed Mariza Costa to the newly created role of head of investor relations. Costa has over 20 years’ experience and most recently served as vice president, rating agency relations and corporate finance, at Everest Group. She previously held roles at AM Best Company’s ratings division as associate director, reinsurance and large commercial and Allianz Global Corporate & Specialty as broker compensation manager.

Arch Insurance North America, headquartered in Jersey City, New Jersey, appointed Jeff Kaufmann to the newly created role of executive vice president, head of marine. The unit includes both ocean marine and inland marine products. Kaufmann, who is based in New York, joins Arch from MSIG USA, where he was EVP and head of marine.

Hiscox, headquartered in Atlanta, Georgia, appointed

Northeast region distribution leader. Petrone has over 30 years of industry experience, most recently serving as major accounts New York zone leader at Chubb. He also spent over a decade at Marsh as a managing director and senior client executive.

MAPFRE USA, headquartered in Boston, Massachusetts, appointed Mark Pasko as executive vice president, general counsel and secretary. Pasko most recently served as chief legal officer of QBE North America, where he managed the legal and regulatory affairs for QBE’s North American and Bermuda operations.

Roosevelt Road Specialty, headquartered in New York City, appointed Brendan Cook as chief underwriting officer of property. Cook has over 20 years of experience, joining Roosevelt Road Specialty from RB Jones, Inc., where he served as vice president and managing director. Cook previously held senior roles at QBE North America and Crum & Forster.

MSIG USA, headquartered in New York City, appointed David Petrone as

The MEMIC Group, headquartered in Portland, Maine, promoted Karl Lagasse to vice president of business technology and hired Jason Ennis as director of architecture and innovation.

Lagasse joined MEMIC in 2021 and has 20 years of insurance technology experience. Ennis has 29 years of experience in IT, previously serving as enterprise architecture manager at MMG Insurance, technical architect at Unum and enterprise services manager at Wolters Kluwer.

Midwest

Rockford Mutual Insurance Company (RMIC), headquartered in Rockford, Illinois, promoted Ann Kriens to the position of claims vice president.

Kriens joined RMIC in 2014 with 20 years of claims experience at Economy/ MetLife, serving as an adjuster, support supervisor, property subrogation manager and home operations manager. She most recently served as RMIC’s assistant vice president of claims. Kriens’ promotion follows the

Scott Williams

Rajeev Khanna

Hilary Weiss

Mariza Costa

Brendan Cook

David Petrone

Karl Lagasse

Ann Kriens

Jeff Kaufmann

Adam Denninger

Mark Pasko

retirement of Patrick Kennedy, former vice president of claims and internal counsel.

Tokio Marine HCC, based in Houston, Texas, announced a key leadership transition at its travel-focused subsidiary, WorldTrips, a provider of travel insurance located in Carmel, Indiana. Mark Carney will transition from his role as CEO of WorldTrips to become its chairman.

Philip Hsia has been appointed CEO of WorldTrips. Hsia has led Tokio Marine HCC’s Global Travel Group, including oversight responsibility of WorldTrips, since 2018.

Burns & Wilcox, headquartered in Farmington Hills, Michigan, promoted Bill Gatewood to executive vice president, personal insurance.

Burns & Wilcox is a member of H.W. Kaufman Group, a privately held global insurance organization. Gatewood’s insurance career spans 30 years, with over 14 years of service at Burns & Wilcox and over 10 with H.W. Kaufman Group.

South Central

Hull & Company-Texas, headquartered in Dallas, Texas, promoted Brandt Wilkins to underwriter/broker. Wilkins has been with Hull Texas for three years, managing a book with emphasis in the south-central region of the U.S. He previously served as a commercial lines account manager at Frost and an associate broker at Amwins Group.

Hull & Company-Texas also

hired Angelika Gambino, who joins the agency as a commercial lines underwriter/ broker. Gambino has over 15 years of experience, with specializations in commercial property and casualty, serving as an underwriter at Burns & Wilcox and a commercial producer at TWFG.

Southeast

The Liberty Company Insurance Brokers, headquartered in Gainesville, Florida, hired Will Bradshaw as a producer based in the firm’s The Browning Agency office in Ponte Vedra, Florida. Bradshaw previously served as a manager for Southern Table Hospitality. Bradshaw focuses on delivering insurance solutions to clients with complex needs.

West

Acrisure Re, headquartered in Grand Rapids, Michigan, named Danny Souza, senior vice president, as leader of Acrisure Re’s new West Coast office in San Francisco, California.

Souza joined Acrisure Re in 2016 and maintains his leadership responsibilities in New York, ensuring collaboration and continuity across both offices.

Alliant Insurance Services, headquartered in Irvine, California, hired Jordan Leclair as vice president. The Phoenix, Arizona-based benefits consultant previously

served as vice president, employee benefits, at USI, where he served a broad portfolio of clients.

The National Association of Insurance Commissioners (NAIC) elected Washington State Insurance Commissioner Patty Kuderer to serve as secretary/treasurer for the Western Zone committee and in an official role on the NAIC’s executive committee.

LP Insurance Services

LLC, headquartered in Reno, Nevada, named Founder and CEO Nick Rossi as executive chairman. Rossi founded the company in 2010.

Brian Cushard, president since 2022, was appointed president and CEO. Cushard joined LP Insurance Services in 2020 as vice president of strategic growth. He previously served as a senior vice president at both Woodruff Sawyer and Beecher Carlson.

The Workers’ Compensation Insurance Rating Bureau of California (WCIRB) appointed Eric Sanders as senior vice president and chief customer operations officer. Sanders has over 25 years of industry experience, including over a decade at QBE, where he served as chief claims and risk solutions officer. He held claims and loss control leadership roles at Fireman’s Fund.

Victor Insurance appointed Mark Damico as president and chief operating officer (COO) of Torrent Technologies, Victor’s U.S. flood insurance technology and services business based in Kalispell, Montana.

Based in Brookfield, Wisconsin, Damico has over 30 years of industry experience, joining Torrent as COO in 2018. Damico succeeds Kevin Tobin, who is retiring after over 35 years of service.

Cheryl Blake joined Alliant Insurance Services, headquartered in Irvine, California, as senior vice president within its employee benefits group. Based in Georgia, Blake has served in multiple leadership roles, most recently as principal with OneDigital.

Ned Gaines was appointed acting commissioner at the Nevada Division of Insurance. Gaines has over 25 years of experience and recently joined the Nevada Division of Insurance as the chief deputy commissioner. He previously served 12 years with the Washington Office of Insurance Commissioner, most recently as the deputy commissioner of rates, forms and provider networks.

Alliant Insurance Services, headquartered in Irvine, California, hired Karston King as vice president. Based in Utah, King previously served as an insurance broker with GBS Benefits Inc., working in the oil and gas, technology and manufacturing sectors.

Danny Souza

Jordan Leclair

Nick Rossi

Patrick Kennedy

Brian Cushard

Mark Damico

News & Markets

US Tariffs Projected to Slow Global Economy and Insurance Premium Growth: Swiss Re

By L.S. Howard

Global growth is slowing as U.S. tariff policy reduces trade and heightens geopolitical uncertainty, which ultimately will lead to decelerating growth in insurance premiums, according to Swiss Re.

Global GDP growth (adjusted for inflation) is expected to slow to 2.3% in 2025 and 2.4% in 2026, down from 2.8% in 2024, Swiss Re Institute said in its report titled “World insurance in 2025: a riskier, more fragmented world order.”

The global insurance industry (life and non-life) is expected to follow the trend with total premiums slowing to 2% this year from 5.2% in 2024, and picking up marginally to 2.3% in 2026, Swiss Re said.

“U.S. tariffs create new risks for insurers, with negative impacts expected through inflation, trade, supply chain, and economic growth outcomes,” the report said.

Property/Casualty Sector

“The primary non-life insurance sector is seeing decelerating premium growth as insurance pricing softens and policy uncertainty cuts economic momentum,” said Swiss Re, forecasting 2.6% growth in real terms in 2025 (versus 4.7% in 2024) and 2.3% in 2026.

Real premium growth in advanced markets reached 4.5% in 2024—higher than the 3.8% reported in 2023 as well as the previous 10-year average of 3.5%, the report said, noting that the decadehigh growth in 2024 was driven by rate hardening, with insurers increasing prices to cover rising claims severity.

Global life premium growth will also slow down—forecast by Swiss Re to drop to 1% this year in real terms, after a strong 6.1% gain in 2024.

Localized Pricing Strength

While the U.S. tariffs will affect the insurance industry differently across geographies, they likely will increase U.S. loss trends the most, Swiss Re said, noting that U.S. motor and construction claims are due to see the greatest and most direct impact, but the effects should be manageable.

There will be some localized pricing strength in lines such as U.S. casualty due to higher loss cost trends, but this is unlikely “to offset the overall growth downtrend,” Swiss Re said.

Outside the U.S., Swiss Re predicted that tariffs are more likely to be disinflationary, thereby reducing pressure on claims. “Premium growth will likely be lower in the environment of economic slowdown, more so in trade-exposed areas such as

marine and trade credit insurance, and in sectors like construction.”

Some Opportunities

On a more positive note, Swiss Re said the tariff crisis may provide some underwriting growth opportunities. “A heightened awareness of risk typically benefits insurers, provided the economic shock is not severe. This is particularly the case for lines of business offering protection against economic and financial disruption, such as credit and surety insurance.”

In addition, marine insurance outside the U.S. could benefit from realignment of supply chains “if other economic blocs increase trade among themselves.”

Investment Results to Drive Profits

Swiss Re said investment results will be a key driver of P/C sector profitability in the next three years. “We see global P/C underwriting results broadly stable at around 1.5% to 2% of net premiums earned, and we estimate industry return on equity (ROE) at 9.7% from 2025 onward.”

“While insurers’ profitability outlook is still benefiting from rising investment income, we expect tariffs to slow global GDP growth, and consequently weigh on insurance demand. In the long term,

U.S. tariff policy is another move toward more market fragmentation, which would reduce the affordability and availability of insurance, and so diminish global risk resilience,” said Jérôme Haegeli, Swiss Re’s group chief economist, in a statement accompanying the report.

Stagflationary Shock

The report warned that tariff rates—the highest since the Great Depression—will create a stagflationary shock for the U.S. economy. (Stagflation refers to an economy simultaneously hit by slow or no growth, high unemployment, and rising prices/inflation.)

“The volatile nature of U.S. policy changes under the current administration has ushered in a paradigm shift of diminished confidence in the U.S. government, eroding its status as a ‘safe haven’ for global capital,” said the reinsurer in a press release accompanying the report. “Consequently, Swiss Re Institute has lowered growth expectations for most major economies in 2025.”

Fragmentation a Danger

The word “fragmentation” or “fragmented” is used 43 times in the report because the fragmentation of geopolitics, economies, and markets could have serious long-term risk and cost impacts for insurers and society.

“Trade barriers and supply chain disruptions or reshoring may push up inflation for prolonged periods, feeding into higher claims costs. Restrictions on free capital flows for re/insurers can lead to inefficient capital allocation, higher capital costs, and higher insurance prices, possibly curtailing insurability of peak risks,” the report added.

Swiss Re cited the example of the “exceptional” 2005 U.S. hurricane season, when 12% of U.S. insurers received reinsurance payments equal to 100% of their equity, and 23% received payments exceeding one-third of equity.

(In 2005, Hurricane Katrina hit the Gulf Coast of the U.S., causing catastrophic damage in Louisiana and Mississippi, which Swiss Re described as a “watershed event” for the insurance industry in a report published on June 23, 2025. With

an insured price tag of $105 billion at 2024 prices, Katrina is the most expensive natural catastrophe for the global insurance industry on record, Swiss Re confirmed.)

Swiss Re warned (in its world insurance report, published on July 9) that fragmentation could reduce the insurability of such peak risks and would likely lead to limited underwriting capacity, which in

turn would raise insurance prices.

“Political fragmentation reduces international cooperation on mitigating critical global risks such as climate change, pandemics, and cyber risks, increasing global exposures. Society ultimately bears the cost of fragmentation as firms and individuals have less insurance coverage, keeping protection gaps wide.”

News & Markets

Travelers Q2 Net Income Soars on Less Losses, Favorable Reserves

By Chad Hemenway

The Travelers Cos. increased second-quarter net income $975 million for a total of about $1.5 billion, and reversed an underwriting loss posted last year for the same period.

Travelers’ secondquarter underwriting profit was about $1 billion compared to a loss of $65 million for Q2 2024, as catastrophe losses net of reinsurance during the timeframe were lower—$927 million this year versus about $1.5 billion a year ago. The insurer said the losses were primarily from wind and hail storms in multiple states.

million compared to $230 million for Q2 2024.

The Q2 combined ratio for the New York-based insurer was 90.3, almost a 10-point improvement over last year.

Overall net premiums written (NPW) grew 4% to about $11.5 billion during Q2, and in a statement CEO Alan Schnitzer credited contributions from all three insurance segments—business, personal, and bond & specialty.

year ago, and the combined ratio came in at 88.4 versus 108.5 for Q2 2024. U.S. homeowners insurance NPW increased 7% to about $2.5 billion.

NPW in the business segment increased 5% to $5.8 billion as renewal premiums were up 8.6% for middle-market business and 10.7% for small commercial. The Q2 combined ratio in the business segment was 88.3 compared to 89.2 last year during the same time.

Additionally, Travelers booked favorable prior-year reserve development of $315

However, the most dramatic results were seen in personal lines, where Travelers reversed a Q2 2024 underwriting loss of $373 million to a gain of $480 million for the same quarter this year. Income for the segment was $534 million compared to a loss of $153 million a

The second quarter turned around results from the first three months of 2025. Looking at year-to-date results, net income is up 15% to about $1.9 billion. The company recorded net income of $395 million for Q1, down 65%, with an underwriting loss of $305 million. Travelers paid out about $2.3 billion in Q1 catastrophe losses, mostly on the California wildfires.

Renewal Rates in Q2 Tell of ‘Slowly Softening’ Commercial Lines Market, Says Ivans

Premium renewal rates increased year-over-year for all major commercial lines, except workers’ compensation, according to second-quarter 2025 results of the Ivans Index.

The Chicago-based technology provider for insurance carriers, agents, and managing general agents said the average premium renewal rate for all major commercial lines except workers’ compensation increased in Q2 2025 but was overall lower compared to the averages from Q1 2025.

“Similar to last quarter, premium renewal rates decreased for nearly all major commercial lines during Q2, continuing the trend of a slowly softening market after several hard market years,” said Kathy Hrach, senior vice

president of product management, Ivans.

The Ivans Index found renewal rate increases were lower compared to Q1 2025 in commercial auto, commercial property, businessowners policy (BOP), and umbrella. The rate change for workers comp was down again in Q2, but fell even

more (-1.75% versus -1.5% in Q1 2025).

General liability was the only line of business tracked where the increase in Q2 was higher than that of Q1 (about 4.7% compared to nearly 4%).

Premium renewal rates in Q2 increased about 8.4% in commercial auto—down from increases of about 9.2% in Q1. Commercial property rates were up nearly 8% in Q2, which was down from renewal rates that were up about 8.6% in Q1. Premiums renewals were 10.85% in Q2 2024.

BOP renewal rates were up about 7.9% in Q2 compared to up about 8.6% in Q1. Umbrella rates changes increased about 9.1% in Q2, slightly lower than when renewals were up about 9.3% in Q1.

Workplace Injuries Costs Near $60B Per Year; Overexertion, Falls Top Causes: Liberty Mutual

Liberty Mutual’s latest Workplace Safety Index has found that workplace accidents cost U.S. employers about $58.8 billion annually.

The top 10 causes of injuries account for 86% of those costs, or $50.87 billion.

The index marks its 25th year identifying the top 10 causes of the most serious workplace injuries—those causing an employee to miss more than five days of work—and ranking them by their medical and lost-wage payments.

Even as the rate of serious workplace accidents fell by about 40% over the 25 years represented by the Index, the total cost of workers compensation benefits increased by 30%, according to data from the Bureau of Labor Statistics and National Academy of Social Insurance.

Source: Liberty Mutual Workplace Safety Index

Workplace Safety Index.

“Struck by object or equipment” and “falls to a lower level” also continue to be major injury drivers, together accounting for nearly $11.6 billion in costs.

Overexertion involving outside sources remains the top cause, accounting for $13.7 billion in costs, largely due to manual material handling. This has held true for 25 years.

Falls on the same level is the second leading cause, with $10.5 billion in costs, emphasizing the need for slip, trip, and fall prevention strategies, according to the

Injuries due to other exertions and bodily reactions, roadway incidents, and caught-in or compressed by equipment also feature prominently in the top 10, underlining the diverse risks present in today’s workplaces.

While still making the top 10, costs associated with repetitive motion injuries from micro tasks has dipped by 44%. The

report outlines safety efforts that are helping to reduce these types of injuries. Workers being struck against object or equipment rounded out the top 10 causes of workplace injuries, totaling $1.7 billion in costs.

The report found that more than half (56%) of workplace injuries involving the back, shoulder, knee, or multiple body parts drive nearly $32.6 billion in costs.

Seven of this year’s top 10 injury causes appeared in all 25 indices. Each index is based on data three years prior. As such, the 2025 index reflects 2022 data.

My New Markets

Armored Car Services

Market Detail: For more than 25 years, The Mechanic Group has specialized in delivering custom-built private security insurance programs to armed and unarmed security guard, private investigation, intelligence, electronic security, alarm installation and monitoring and security consulting firms. Today, they are one of the leading insurance providers to all of these communities, working as an MGA for agents and brokers seeking a market for these insureds. Coverages include: E&O, commercial excess, CGL, workers’ comp, fidelity bonds, D&O, umbrella, liability, contractors license bonds, EPLI.

Available Limits: Not disclosed.

Carrier: Admitted and Non-admitted. States: All 50 states and the District of Columbia.

Contact: Marc Katz, mkatz@mechanicgroup.com, 800-214-0207

Mobile Homes, Motorcycles

Market Detail: Aegis Security Insurance Company has been providing insurance protection since 1977. Licensed in all 50 states and the District of Columbia, they insure a variety of products including manufactured homes, select dwellings, motorcycles, travel trailers and more. Sign on to www.aegisfirst.com and quote, bind and access policy information online. Contact achase@neee.com to receive a username and password.

Available Limits: Not disclosed.

Carrier: AEGIS, Rated A by AM Best States: Motorcycle: Prod. Code 18 –Connecticut, Pennsylvania and Rhode Island. Manufactured Home: Prod. Code 21 – Connecticut, Massachusetts, Maine, New Hampshire, New York, Pennsylvania, Rhode Island and Vermont.

Market Detail: High mods, bad claims history, lapse or even start-ups. Specializing in workers’ compensation and offering competitive options for high-hazard industries.

Program highlights: A-rated carrier, 95%

approval rate for standard market declinations, tailored workers’ compensation programs, proactive claims management, competitive rates, above average commissions, pay-as-you-go billing, coverage across multiple states, no need for annual audits and access to discounted workers’ compensation premiums.

Available Limits: $12,000 minimum premium; $2.5 million maximum premium. Carrier: Lions, Sunz, Prescient National, Chubb, AIG and State National; Admitted; Rated A by AM Best. States: All 50 states and the District of Columbia except Alaska and Hawaii. Contact: Evan Swan, proposals@cprbrokers.com, 714-928-3858

Fire & Rescue Insurance Program

Market Detail: Amynta EOB’s Fire & Rescue Insurance Program has been custom-designed for Departments throughout the U.S. that serve a population of 25,000 or less. We have a comprehensive program including both P&C and Accident & Sickness.

Eligibility: Volunteer departments (up to 20% career will be considered); services population less than 25,000; preferred serviced population less than 5,000; wellness/safety culture; prefer volunteer organizations with no emergency medical services or ambulance exposure; second tier preferred provides only basic life support; written bylaws reviewed by outside counsel; prefer no converted vehicles; training for bariatric patient handling

Available Limits: Not disclosed. Carrier: Not disclosed.

States: All 50 states and the District of Columbia.

Contact: Mark Harrington, mark.har-

rington@amyntagroup.com, 607-749-9080

Public Auto Liability Coverage

Market Detail: For many organizations, the most serious bodily injury or property damage losses are the result of automobile accidents. Shelly, Middlebrooks & O’Leary provides commercial auto liability and physical damage coverage for all classes of airport transportation. Contact their office to discuss shuttle bus, van or limo transportation accounts.

Coverages: Auto liability limits up to $5 million; commercial auto liability; physical damage; general liability; excess auto and general liability.

Risk appetite: SMO is well-positioned to provide insurance solutions for a wide range of public auto businesses, including airport shuttles, courtesy auto, entertainer/ athlete bus, limousines, non-emergency medical transport, taxicabs and wilderness expedition buses. Has pen.

Available Limits: Auto liability limits up to $5 million.

Carrier: Not disclosed.

States: Florida, Georgia, North Carolina, South Carolina and Texas.

News & Markets Attempts to Reform Litigation Funding Disclosure Continue on the Hill

By Chad Hemenway

Changes to the taxes paid by litigation investors did not make it into the final version of the expansive One Big Beautiful Bill, but the issue of third-party litigating funding continues to have the attention of at least some lawmakers in Washington.

Rep. Darell Issa, R-Calif., chairman of the House Subcommittee on Courts, Intellectual Property, Artificial Intelligence, and the Internet, held a hearing July 22 titled “Foreign Abuse of U.S. Courts.” He said the Chinese Communist Party is “waging what they call legal warfare, using the U.S. courts.”

Issa in February introduced the Litigation Transparency Act of 2025 (HR 1109) that would require disclosure of third-party litigation funding (TPLF) in federal civil cases.

“This is using our patent system, our trademark system, and our courts to their advantage,” he said. “Legislation and rule changes by the administration need to happen, and happen now.”

The American Property Casualty Insurance Association (APCIA), which has made TPLF reform a top priority, submitted a statement to the subcommittee.

“TPLF poses a major risk to America’s civil justice system and its economic and national security,” said Sam Whitfield, APCIA’s senior vice president of federal government relations. “This rapidly growing practice inflates the cost of litigation, particularly the growth of non-economic damages. These increased litigation costs impact the cost of living for consumers and businesses, including insurance costs.”

According to a new consumer guide on legal system abuse from the Insurance Information Institute (Triple-I) and Munich Re US, legal system abuse costs each American family about $6,664 more for goods and services, and costs small businesses $160 billion in tort costs.

“TPLF allows hedge funds and other financiers, including sovereign wealth funds and foreign interests, to secretly

invest in and potentially control lawsuits within the U.S. in exchange for a profit by claiming a healthy percentage of any settlement or award,” according to Whitfield, who added support for Issa’s bill as well as another, Protecting Our Courts from Foreign Manipulation Act of 2025 (HR

2675), introduced in April by Rep. Ben Cline, R-Va.

Cline’s bill would require disclosure of TPLF by foreign persons and prohibit foreign governments and sovereign wealth funds from investing in federal court litigation, APCIA said.

We speak human, not fine print.

We believe insurance should sound like a conversation, not a contract. So, we skip the jargon and meet you where you are—with tools, insights, and people who know your customers’ industries inside and out, from manufacturers and contractors to breweries and wineries.

That’s how partnerships work. And that’s how we work. Because at EMC, we’re all about Keeping insurance human®

Let’s get to know each other at emcinsurance.com

Special Report: Top 100 Agencies

About This Report:

Welcome to the 21st annual Insurance Journal Top 100 Independent P/C Agencies report.

The Top 100 list is ranked by total property/casualty agency revenue for 2024 and comprises only those agencies whose business is primarily retail, and not exclusively wholesale.

Also included is a list of the nation’s Top 20 Bank Holding Companies and Top 20 Banks in Insurance, courtesy of Michael White’s Bank Insurance Fee Income Report - 2025 Edition. (See page 31.)

Insurance Journal wishes to thank all of the agencies and brokerages that were willing to share their information and cooperated in the process for the Top 100 report. The result is a glimpse at some of the nation’s most successful independent insurance agencies and brokerages.

All information in this report has been gathered from voluntary online submissions from agencies and brokerages and best estimates based on other public information sources. There may be agencies eligible for listing but for which no information was received or located.

We encourage all qualifying agencies to submit data for future reports. The more

submissions Insurance Journal receives, the more accurate and comprehensive this listing can be. Also, submitted data was not independently verified.

For more information about this report, contact Andrea Wells at: awells@ insurancejournal.com.

Is your agency on this list?

Tell everyone! For reprints, badges, plaques, and more, call (800) 897-9965 x125 or email us at: reprints@insurancejournal.com.

Insurance Journal’s 2025 Top 100 Property/Casualty Agencies

Insurance Journal’s 2025 Top 100 Property/Casualty Agencies

Top 20 Banks in Insurance Brokerage Fee Income

®Insurance Journal

Closer Look: Higher Ed Sports

As Schools Prepare to Pay Athletes, What Role Will Insurance Play?

By Allen Laman

As colleges and universities prepare to legally pay athletes for the first time in National Collegiate Athletic Association history, collegiate sports programs are exploring insurance policies designed to mitigate the risks that come with dishing out tens of millions of dollars annually to players.

A recently approved antitrust settlement deal between the NCAA and five major collegiate sports conferences will allow schools to directly compensate students for the first time in 119 years of organized competition. Total pay will be capped at about $20 million per school.

“The reason why insurance is now being introduced more consistently is that there are now real dollars at risk,” said Tyrre Burks, founder and CEO of Players Health, a sports-centric managing general agency.

“And we’re not talking a small amount of dollars, either. We’re talking billions

of dollars that are now going to athletes. Universities, for the first time, are now sharing athletic department revenues back to the athletes.”

Burks said Players Health gives clients greater visibility of their risks while supplying them with tools and resources to mitigate them. One of those resources is insurance; the Minneapolis-based company writes general liability, equipment and property, D&O, and more lines of coverage for youth, amateur, and collegiate sports organizations.

Following decades of a strict no-pay policy enforced by the NCAA, athletes were cleared to begin profiting off their name, image, and likeness (NIL) in 2021. They have since been legally allowed to receive money from third parties like donor collectives and brand sponsorship deals—but they haven’t been cleared to receive funds directly from their schools.

That has now changed with approval of the landmark "House vs. NCAA"

settlement on June 6.

Leading up to the approval, Players Health developed and began selling policies aimed at addressing the risks schools will face under the new payment system. Because while the NCAA has long pulled from a pool of carriers to provide participant accident policies for collegiate athletes, that health insurance only covers medical costs to athletes.

The critical injury insurance policy offered by Players Health is designed to insure payment from a school or collective to a student athlete should that athlete suffer an injury that forces them to miss at least 40% of a sports season. The product is parametric; pre-determined injuries are covered, and if the insured athlete suffers one of them and meets the 40% threshold, the policy triggers.

“It’s a very flexible product for these universities,” Burks said. “They can protect their downside, and we’ll insure up to a million dollars with that product.”

Players Health calculates an injury probability for every athlete to determine policy premiums. Burks said his company has aggregated one of the largest injury databases in amateur sports and uses that data to create the predictive model.

The MGA also offers a contract protection product that insures against player transferring. When the NCAA’s transfer portal system launched in 2018, it made it easier than ever for athletes to switch schools. In the current sports calendar, Burks said that front-loading cash to players who want upfront payments has its pitfalls.

An athlete could sign a deal with a school when the first open transfer portal period begins in December, Burks said, and then transfer away in the spring—when the second portal period begins—without ever playing a game for the school that paid them.

“You could insure the transfer risk that you have for that athlete,” Burks said,

explaining that Players Health has created a model that predicts the likelihood an athlete will transfer and bakes that into the premium. This policy is designed to help keep predatory language out of contracts, Burks said, while also preventing litigation and making schools whole.

‘The reason why insurance is now being introduced more consistently is that there are now real dollars at risk.’

In addition to critical injury and contract protection, Players Health offers schools a fair market value bonus product that Burks said allows schools to punch above their weight when it comes to attracting and retaining athletes.

Colleges and universities aren’t allowed to award performance bonuses directly to players, but Burks explained that through

these policies, payment triggers to a school if an athlete hits on-the-field milestones that increase their value, like being named to an all-conference team or winning the Heisman trophy.

“Ultimately, the athlete now has these triggers that they can shoot for,” Burks said. “They know their value is worth more, and … they’ve got an extra half a million dollars that they can go and achieve if they hit these milestones. Now, they’re worth more in the market.”

Schools from the Big 12, SEC, and Big East conferences have purchased policies outlined in this piece from Players Health. Burks said the MGA’s focus is to democratize data and use insights to drive changes in behavior and decision-making.

“We’re not trying to just push papers and just send over a policy,” he added. “We want the client to understand why they’re buying it, and we want them to be just as educated about why they’re buying it and the product as we are.”

Spotlight: Recreation & Leisure

From Golf Greens to Sausage Fests: The Wild World of Prize Insurance

By Ezra Amacher

Mark Gilmartin grew up around golf, playing in national tournaments from a young age and competing in college. When his amateur golf career didn’t translate into a spot on the professional tour, he turned his love of golf into a professional occupation: insuring hole-in-one contests.

Gilmartin and a former college teammate formed Hole In One International in 1991, a business that provides insurance for organizations sponsoring golf tournaments.

Hole-in-one shots and other sports-related contests are a common occurrence today, but when Gilmartin was getting the operation off the ground in the early 90s, few people believed it would catch on.

“We tried to raise some money; we put a business plan together,” said Gilmartin. “Everybody kind of laughed at us, saying that’s crazy.”

When another of Gilmartin’s ex-college teammates, Kirk Triplett, won $30,000 in a professional tournament, Triplett invested about $12,000 into the company to get it off the ground.

Before long, Hole In One International grew into one of the biggest programs of its kind. As demand grew for in-game contests like half-court basketball shots, Gilmartin’s business evolved into other sports.

In the early 2000s, Gilmartin founded Odds On Promotions. Odds On insures any skills-based contest from field goal kicks to fishing tournaments. The company also covers sweepstakes, like a win-a-car game that an auto dealership puts on.

Gilmartin added to his portfolio by purchasing a third brand, Hole in One USA, after the COVID-19 pandemic.

Gilmartin’s business is firmly at the center of the expanding and ever-changing world of prize indemnification insurance.

“The idea of prize indemnification, the idea of offering the chance to win a new car or a million dollars to do something has grown exponentially since it was

just hole-in-one insurance in 1990,” said Gilmartin.

Not Your Standard Risk

There are three main types of risks in prize indemnity insurance.

The first is math-based risk, which is equivalent to flipping a coin and having a 50/50 chance of winning. “Pick an envelope off a wall out of a hundred envelopes,” said Gilmartin. “One is a winner; 99 aren’t.”

The second is skill-based risk, which includes the hole-in-one challenge, halfcourt shot, and field goal kick.

The third is odds-based risk, like whether a running back will score two touchdowns in an NFL game.

Gilmartin’s businesses cover all three types with a focus on writing skill-based risk. With more than three decades of experience, he and his team have formulated their own numbers on what the odds are of someone winning a contest.

“Somebody can make the half-court shot and it can cost us $5,000 or it could cost us a million dollars. It’s still one guy, one shot,” said Gilmartin. “That’s insurance in general, right? You take a large universe of all the risk and you boil it into one, and then it averages out in the end and hopefully you’ve built in some profit.”

Contests are

priced differently based on how a client selects the contestant. If a client selects someone five minutes before they’re going to attempt a shot, that’s random selection. The person walked into the area with no notice they would be attempting a halfcourt shot for several thousand dollars.

“They might have high heels on, might be a grandma. They could be anybody,” said Gilmartin.

A different type of pricing is designed for clients who might hold a drawing in advance of a contest. Only the people that think they might win or want to do it are going to sign up.

“My grandma’s not going to sign up. Only the basketball jocks and those kinds

of people are going to sign up, and then they get drawn and obviously they’ve got to be given notice that they’re going to do it,” said Gilmartin.

It’s not just hole-in-ones and half-court shots that the Reno, Nevada-based companies insure. Over the years, clients have come in the door with off-the-cuff skill-based contests. It’s up to the staff to do their own research on the probability of a contestant winning.

Once, a sausage festival in the Midwest wanted to run a sausage-throwing contest in which a sausage was thrown through a car window from a certain distance to win a car. Gilmartin and some coworkers determined the risk themselves, using a sausage-sized object and throwing it from the same distance through the same size opening. Nobody at the sausage festival

won the contest.

“Those are the types of things that we have to [consider to] determine our own underwriting and our own probability,” said Gilmartin.

Close-Call Claims

For a hole-in-one contest, there is an independent observer—somebody who isn’t playing in the event and is there, designated in a certain location, to watch the contestants and make sure the ball went in the hole. For a basketball half-court shot, there must be video of the person taking the shot, where they release it, and whether it went in.

The majority of videos that come in are from clients themselves, as is part of the policy. One of the requirements of the client is that they need to clearly video the

contest from certain places so the claims team can see everything they need to see.

“The bigger the prize is, the better the chance it’s being recorded on video,” Gilmartin said. “There’s always video out there to assist us in the claims process.”

Gilmartin said there’s always a physical presence at the contest to make sure a contest is conducted properly and to determine whether or not there was a legitimate winner. In some cases, they’ll send an adjuster to be there physically, while other times they’ll rely on the client to provide an independent observer.

Claims adjusters will peel over footage to see, for example, whether a contestant’s foot was right on the half-court line, in which case a claim could be deemed illegitimate if the policy states the contestant must be behind the line. Similarly, a claim could come down to whether a field goal was kicked in time or whether the clock had just expired.

The growth of smartphones and social media has made the claims process both easier and harder for the claims staff. The claims team has more videos it can potentially use to corroborate whether a contestant’s attempt was successful.

“I’ve got 10,000 witnesses taking a video of what actually happened, because all we’re after is the truth,” said Gilmartin. “Once we find the truth, we determine whether or not the claim is legitimate.”

The claims process is not all that different than NFL officials using instant replay technology to review a crucial call on the field. Like professional sports, when a decision doesn’t go the home team’s way, fans will complain about it online.

“That has happened a number of times over the years when the truth is black and white and they still think that the truth doesn’t matter, that you should pay anyway,” said Gilmartin. “That’s when social media can turn on us.”

While technology and on-site observers provide more tools than ever to determine a contest’s true outcome, the court of public opinion can still present a significant challenge for insurers in the prize indemnification space.

It’s all part of the game.

Spotlight: Real Estate

When Business as Usual Isn’t Enough: Rethinking Assault & Battery Liability in Commercial Real Estate

In urban centers across the U.S., property owners and managers are welcoming a return to pre-2020 levels of foot traffic in retail corridors, mixed-use developments, and multifamily buildings. While this rebound signals a healthy recovery for local economies, it also revives a longstanding and often underestimated exposure: assault and battery (A&B) liability.

increasingly large sums in A&B cases, driven by public sentiment that favors plaintiffs and the rise of third-party litigation funding. In this environment, implementing reasonable security measures may not be enough for landlords to avoid liability.

By Corey Alison

Many property owners assume that their general liability policies will protect them if violence occurs on their premises. Unfortunately, this assumption can leave them dangerously exposed.

As insurance professionals, it’s our job to illuminate these gaps and help clients navigate the evolving landscape of premises liability, especially as social inflation, litigation funding, and public expectations reshape the risk environment.

Rising Foot Traffic, Rising Exposure

A&B claims are not new, but they are becoming more visible, more costly, and more complex to manage. As cities and commercial areas see renewed activity, landlords face evolving legal and social expectations around security and tenant safety.

Several converging factors, from shifting security practices to rising jury awards, are making this risk more pressing and harder to ignore.

• Social inflation and nuclear verdicts. Juries are awarding

• Changing tenant dynamics. The COVID pandemic disrupted tenant relationships. Many property owners were restricted from evicting problematic tenants, creating backlogs and introducing behavioral risks that persist even as legal restrictions have eased.

• Shifts in security practices. In an effort to manage costs and adapt to changing technologies, many owners have reduced on-site security staff in favor of surveillance systems. While cameras offer valuable evidence and enhance security monitoring, they do not actively prevent incidents as they occur.

• Increased foot traffic in entertainment zones. Properties located near nightlife venues, college campuses, or in busy downtown districts are more susceptible to incidents simply due to higher volumes of visitors and heightened activity at night.

The Coverage Misunderstanding

A significant driver of underinsurance in A&B is misunderstanding what many general liability policies actually cover.

In the current market, a large

number of commercial general liability (CGL) policies contain explicit exclusions for A&B, and in many cases, for firearms-related incidents, as well. Even if a policy does not mention firearms separately, the broader A&B exclusion often applies to losses involving weapons. Property owners may mistakenly believe that absence of a specific firearms exclusion implies coverage. However, if an assault or battery incident involves a firearm, it is likely to be excluded under the standard A&B language. This nuance is easily overlooked, yet critical, especially as gun-related incidents continue to draw public attention and legal scrutiny. Additionally, A&B exclusions or sublimits may also apply to related risks such as abuse or molestation. This is particularly relevant for properties that include amenities like gyms, pools, or childcare facilities.

Layering Coverage (It’s Not Just About Limits)

When brokers and risk advisors discuss A&B exposure with clients, the conversation often focuses on limits—how high and how broad.

However, this focus on dollar amounts can obscure crucial details about how coverage functions in a claim scenario, what is included or excluded, and how different policy structures impact a client’s true protection.

Effective coverage goes far beyond policy form names and requires a nuanced understanding of form language and practical risk realities.

It’s crucial to clarify:

• Defense costs. Are defense costs included within policy limits or outside of them?

Defense inside the limits can erode available indemnity dollars rapidly, especially in drawn-out cases.

• Sublimits. A few specialized programs offer sublimits for A&B coverage on a monoline basis. The size of the sublimits can be as low as 50/100 but can also be as high as $1 million. In addition, defense is normally inside limits and excess markets typically will not sit over these programs.

• Exclusion carve-outs. Brokers should examine whether abuse and molestation or firearms exclusions are nested within broader A&B exclusions and how these interact with sublimits.

In many cases, a creative solution for A&B coverage is necessary to comply with lenders.

While the market for this coverage is limited with few carriers offering tailored solutions, brokers should still explore these options. Even if a policy includes restrictive

terms such as defense costs inside limits or partial exclusions, providing your client with additional avenues for protection is beneficial.

Practical Steps for Property Owners

Beyond insurance placements, property owners have a proactive role to play in mitigating A&B risk.