Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Keeping Small Business Insurance Customers

Are property/casualty insurers facing a potential retention problem with small business customers?

According to the J.D. Power 2025 U.S. Small Commercial Insurance Study, just 55% of customers say they “definitely will” renew with their current insurer, down six percentage points from a year ago.

The downturn in customer loyalty comes as premiums have been rising, and that could explain why some customers indicate they may jump ship.

But it’s not all about premiums, the survey found. A good percentage (16%) of customers point to a positive service experience as a reason for sticking with their current insurer—and that’s a stronger influence than price, coverage options, or reputation.

“Interestingly, the drop in retention is not solely attributable to higher premiums,” said Stephen Crewdson, managing director of global insurance intelligence at J.D. Power. “In fact, insurers that communicate well and provide a higher level of service can make huge inroads toward keeping customers.”

According to Crewdson, satisfaction is at an identical level among customers who understand why their premium is increasing as it is among those whose premiums are not increasing at all, which he believes “puts a huge onus on insurers to bolster their outreach around rate increases.”

The J.D. Power survey measures overall customer satisfaction among small commercial insurance customers with 50 or fewer employees. It rates insurers on trust, price for coverage, product/coverage offerings, ease of doing business, people, problem resolution, and digital channels.

‘The downturn in customer loyalty comes as premiums have been rising, and that could explain why some customers indicate they may jump ship.’

Following are some key findings of the 2025 study.

Retention declines across the board: After several years of improvement and stability, intended retention has dropped significantly among customers across virtually all demographic groups. The largest dip is among Millennials (-12 percentage points).

Service sets tone for retention: Competitive pricing is a key reason customers select and stay with an insurer—but service is just as important. Overall, 16% of customers say good service experience is the most common driver of retention, beating out price, coverage options, and reputation.

Communication about rate increases is vital to satisfaction: Overall satisfaction, which is 722 (on a 1,000-point scale) among customers who say they completely understand why their premiums increased, is identical to that among customers who have no increase at all.

But independent agents know that retention is not just about the carrier or even the pricing. Happy customers begin with good customer service from agency staff.

Andrea Wells V.P. of Content

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Chief Financial Officer Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus

Andrew Simpson | asimpson@wellsmedia.com

National Editor Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Assistant Editors

Jahna Jacobson | jjacobson@insurancejournal.com

Kimberly Tallon | ktallon@carriermanagement.com

Columnists & Contributors

Contributors: Christopher Boggs, Sarah Morris, Ed Reis, Charles Symington Jr., Daniel Wiessner

Columnists: Mary Newgard, Catherine Oak, Bill Schoeffler

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT) Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator George Jack | gjack@ijacademy.com

THINK AGAIN. Now known as HudsonPro®, our full-service professional lines underwriting and claims handling facility is stronger than ever. Our existing suite of products has been expanded to cover more exposures, from small to large and from conventional to cutting-edge. We proudly serve private companies, non-profits, financial institutions, public companies, groups and individuals, and our seasoned team will craft personalized solutions that fit your needs. When there’s no room for error, THINK HudsonPro.

News & Markets

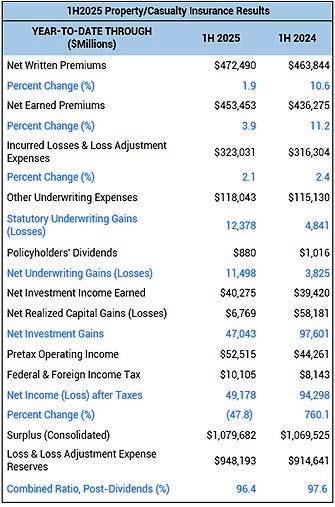

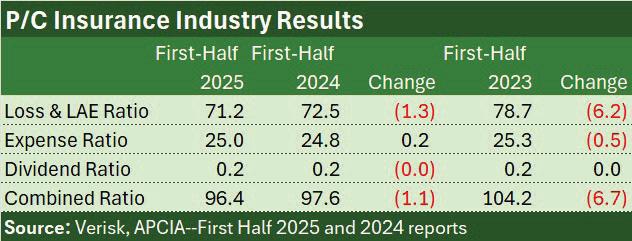

US P/C Insurance Industry First-Half Underwriting Profit Triples

The U.S. property/casualty insurance industry recorded a net underwriting gain of $11.5 billion and net income of $49.1 billion for the first half of 2025, according to a new report.

“The lack of any significant natural catastrophes in the second quarter helped offset the record-breaking catastrophe losses related to the California wildfires and severe convective storms impacting Texas and Georgia earlier in the year,” said Robert Gordon, senior vice president, policy, research and international at the American Property Casualty Insurance Association, in a statement released by APCIA and Verisk.

The underwriting profit figure is three-times the $3.8 billion that APCIA and Verisk reported for first-half 2024.

Net income, however, came in at nearly half of last year’s six-month net income total of $94.3 billion, with a precipitous drop in realized investment gains explaining much of the drop. Last year’s net income figure was inflated by over $50 billion in capital gains realized by one insurer. Excluding that impact, firsthalf net income of $49.1 million is more in line with an adjusted net income figure of roughly $45 billion for first-half 2024.

Based on information from annual statements submitted to insurance regulators by insurers representing roughly 97% of private U.S. property/casualty market insurers, Verisk and APCIA reported that net written premiums grew just under 2% to $472.5 billion.

The 1.9% increase is compared to 10.6%

increase in net written premiums recorded for first-half 2024 over the prior-year six-month period.

First-half 2025 losses and loss adjustment expenses rose at about the same pace, up 2.1% over first-half 2024, but earned premiums rose 3.9%, fueling more than a 1.3-point drop in the industry loss and LAE ratio.

With the expense ratio inching up slightly, the combined ratio for the first half of this year is estimated to be 96.4 compared to 97.6 for last year’s first half, and 104.2 for first-half 2023.

The combined ratio “edged down slightly from this time last year, reflecting underwriting discipline, but escalating catastrophe losses—most notably January’s unprecedented California wildfires—underscore the volatility ahead,” said Saurabh Khemka, co-president of underwriting solutions at Verisk.

“While some lines are showing signs of improvement, the broader industry continues to walk a fine line,” Khemka said.

The Verisk/ APCIA report noted

that private U.S. property/casualty insurers during the first half of this year experienced losses in line with the escalated levels seen in recent years.

“First-quarter losses, driven largely by the Palisades and Eaton wildfires, outpaced historical averages but did not carry over at the same magnitude in the second quarter,” said APCIA and Verisk in the report.

During the first half, surplus levels remained historically high at about $1.08 trillion, up slightly from $1.07 trillion at mid-year 2024.

Choose Wisely

Don’t Leave Your Choice of a Network to Luck

Choosing an insurance network is a big decision. Pick the right one, and you can earn higher commissions – plus gain the support, carrier access and commissions you need to grow your independent insurance agency. Pick the wrong one, and you might not get the local support you need, be forced to pay monthly fees all while losing ownership of your book or control of your business.

The amount of energy a simple AI prompt, such as “Tell me the capital of France,” uses versus the energy used for the same question typed into Google without its AI Overview feature. A complex prompt, such as “Tell me the number of gummy bears that could fit in the Pacific Ocean,” uses 210 times more energy than the AI-free Google search.

$25,000

The amount of money the state of Minnesota is seeking for each instance in which a Minnesota child has accessed TikTok. Minnesota is seeking a declaration that TikTok’s practices are deceptive, unfair, or unconscionable under state law, and seeks a permanent injunction against those practices.

200

The number of horses still in carriage service in Central Park, New York City. There are currently 68 licensed carriage owners with 170 drivers, according to the Transport Workers Union. The Central Park Conservancy argued in an August letter to the City Council that horse carriages have an outsized impact on public safety and road infrastructure in the increasingly crowded park. Other major cities have eliminated or are phasing out similar services.

840,000

The number of homes built in floodplains between 2001 and 2019, according to a 2024 University of Miami study. Construction continues in part because the federally subsidized National Flood Insurance Program will repeatedly pay to rebuild, no matter how high the risk.

Declarations

Sowing Uncertainty

“Farming in the U.S. will change. The fields will all be green. The question is: What grows? And for what purpose? And at what price? It takes time for those chess pieces to move around the board, and we’re kind of in that period today.”

— Gerrit Marx at the annual Farm Progress Show in Illinois. Marx, chief executive officer of CNH Industrial NV, noted that growers are trying to figure out how to adapt to shifting conditions as tariff tensions are making the North American farm market the most uncertain in the world, even as conditions in Europe and Asia start to improve.

Safety Efforts Derailed

“We had an opportunity as a group to make things better and make things safer, and we didn’t do it. Think about how much better and how much safer it could be if we could add all of those 120,000 employees into the mix and all of those operations of hundreds and hundreds of trains a day all across the country.”

— Jim Mathews, president and CEO of the advocacy organization Rail Passengers Association, commenting after none of the nation’s largest freight railroads joined a voluntary federal close call program designed to prevent accidents. Amtrak and smaller freight and passenger railroads do participate, reducing accidents by approximately 20%.

Water Flowing Underground

“If you build a smaller tunnel, OK, it’ll be cheaper, but it can carry less water, so what have you saved? Have you reduced the flooding upstream by an inch? And are you going to spend multimillions of dollars to do that? Well, maybe that’s not worth it.”

— Larry Dunbar, a veteran water resources engineer who has advised Houston, Texasarea governmental agencies on drainage issues, commenting on an initiative to hire Elon Musk’s Boring Co. to build two 12-foot tunnels at a cost of $760 million. Initial proposals for the flood mitigation project suggested 30- to 40-foot diameter tunnels.

Sand, Surf, and Stability

“It’s like a toothpick in wet sand or even a beach umbrella. The deeper you put it, the more likely it is to stand up straight and resist leaning over. But if you only put it down a few inches, it doesn’t take much wind for that umbrella to start leaning. And it starts to tip over.”

— David Hallac, superintendent of the Cape Hatteras National Seashore, commenting on beach homes collapsing along North Carolina’s Outer Banks. Some areas lose up to 15 feet of beachfront a year, and two homes recently fell during Hurricane Erin. At least 11 other houses have toppled into the surf over the past five years.

Turbine Turmoil

“A ‘stop-work order’ is the fancy bureaucratic term, but it means one thing: throwing skilled American workers off the job after they’ve spent a decade training, building, and delivering.”

— Sean McGarvey, president of North America’s Building Trades Unions (NABTU), reacting to the Trump administration’s order to halt work on a nearly completed wind farm off the coast of Rhode Island. NABTU said the order affected the jobs of 1,000 members. ISO New England, which operates the grid for 15 million people in six states, said the company has included the project in its analysis of near-term and future grid reliability.

Feel the Heat

“It’s very easy to underestimate how dangerous heat is. People are usually used to thinking of heat as something that makes them uncomfortable, and that they can tough it out. This type of heat will kill.”

— Abby Wines, Death Valley National Park’s acting deputy superintendent commenting on park visitors seeking out the extreme heat. Death Valley holds the record for the hottest temperature ever officially recorded—134 F (56.67 C) in July 1913—although some experts say the record was 130 F (54.4 C) in July 2021. In the U.S., heat kills more people than all other weather events combined, according to the National Oceanic and Atmospheric Administration.

Data-driven insights. Better agency outcomes.

Business intelligence results in informed decisions. That’s why SIAA provides its independent agency members access to industry leading information systems. Having actionable data means more sales and revenue, operational efficiencies, and meaningful processes. It’s another way we provide our member agencies with the tools they need to enhance their success.

Wherever you are on your journey as an independent insurance agent, or your journey to become one, you owe it to yourself to check out the benefits of becoming a SIAA member. There’s a reason over 5,000 independent agents are availing themselves of the tools, knowledge, and support provided by The Agent Alliance.

Learn how joining our community can make the difference in your long-term success.

siaa.com info@siaa.com

News & Markets

Cyber Outlook Report Finds Gaps, Outlines Holistic Approach to Protections

By Jahna Jacobson

As the cyber market matures, it’s increasingly evident that fighting off cyberattacks is going to be an ongoing team effort. Brokers, carriers, cybersecurity organizations, and insureds all play a role, from security to training to assessing adequate coverage.

According to the latest Cyber Insurance Outlook report from Arctic Wolf, the risk of cyberattack has become part of daily operational concern for many organizations. Yet growing awareness of how organizations can protect themselves from attacks and loss still poses a challenge to the insurance industry.

Seventy percent of insurance professionals responding to this most recent survey (77% of brokers and 63% of carriers) expect the number of new cyber claims to increase, mainly because of steadily growing threat activity.

The Cyber Coverage Gap

One figure the Arctic Wolf report highlights is the discrepancy between cyber coverage figures provided by brokers and those supplied by businesses. While brokers estimate 47% of organizations have the coverage they need, 65% of responding organizations claim they are covered in the event of a cyberattack.

The report hypothesizes that businesses are unaware of the extent of their coverage or what specifically is needed. This 20% gap could represent an opportunity for brokers to reassess clients’ needs and make recommendations for additional protection and mitigation.

Insurers may also initially reject clients for cyber coverage because they have inadequate security controls in place (26%), lack financial stability (21%), or can’t supply the insurer with enough information (21%). While brokers are most likely to reject a client because of financial instability (23%), carriers are more likely to ding potential insureds for missing security protocols (32%).

Cautious Cyber Claimants

In the past year, 12% of clients with cyber insurance made claims, with ransomware accounting for 18% of those claims. Other common claims included data breaches, theft of funds, and phishing incidents, including business email compromise.

However, clients who make claims may find that their rate increases because of a claim (66%) or that they face increased scrutiny during the renewal process (56%). Seven percent reported that they were asked to implement additional controls as a condition of renewal, which could include additional training, upgraded security, or other measures.

Insureds may also have claims rejected because they fall outside the terms of their policy (25% of rejections), their coverage was less than the total claim (19%), the incident fell below the client’s self-insured retention (18%), the incident failed to disclose risk on the client’s application (17%), or the incident was deemed gross negligence.

Fear of higher rates and cancellation drives some insureds to ignore issues that don’t seem to pose a significant financial, security, or “worst case scenario” threat, the report said.

And prices are increasing, with 53% of insurers saying they have seen an overall increase in cyber insurance rates in the

Proactive Protections

North America is considered the global leader in the cyber insurance market. Insurance brokers in North America are more likely to offer both cyber risk control tools and services (73%) compared to the global market (68%). North American brokers are also more likely to have a designated cyber practice (49%) than global counterparts (43%).

However, only 45% of organizations in the North American region have the necessary cyber coverage compared to higher rates in some European countries. Regulatory requirements in places like the U.K. and Ireland incentivize organizations to mitigate cyber risk, with cyber insurance serving as a part of those strategies.

Globally, cyber insurers are proactive with their clients to mitigate damage and loss, with 71% of insurance brokers partnering with cybersecurity providers to better serve clients, while 94% offer ongoing assistance or support to clients.

The majority (69%) also offer in-house cyber risk control tools and services, with 45% charging separately for these services. Another 25% of insurers refer clients to certain cyber risk vendors, with about half of those (12%) negotiating prearranged discounts or terms with the vendors.

last 12 months.

Business Moves

National

Sompo Holdings, Aspen Insurance Holdings

Sompo Holdings, a wholly owned subsidiary of Sompo International Holdings, has an agreement in place to acquire Aspen Insurance Holdings for about $3.5 billion to further its geographical reach outside of its home territory.

With Aspen, Sompo gets a specialty and reinsurance franchise with over $4.6 billion in annual gross written premiums in lines of business such as cyber, credit and political risk, inland marine, U.K. property and construction, and U.S. management liability.

Sompo also gains Aspen’s experience in global casualty, property, property catastrophe, and specialty reinsurance lines. Aspen Lloyd’s syndicate provides access to complex risks and reinsurance licensing across markets untapped by Sompo in the Americas, the U.K., Europe, and the Asia Pacific.

The deal is expected to close during the first half of 2026. The companies’ boards have each unanimously approved the transaction.

Midwest

WalkerHughes Insurance, S&R Insurance

WalkerHughes Insurance acquired S&R Insurance, a retail insurance brokerage headquartered in St. Robert, Missouri. This marks WalkerHughes’ first presence in south-central Missouri. S&R Insurance brings a portfolio of personal and commer-

cial lines, built on decades of relationships and services tailored to local needs. With offices in St. Robert and Houston, Missouri, the agency offers reach into the heart of south-central Missouri.

South Central

AvonRisk, AS&G Claims Administration, Care Logic Inc.

AvonRisk, a national provider of risk management, claims administration, and managed care services, acquired AS&G Claims Administration Inc. and Care Logic Inc., a Houston, Texas-based third-party administrator specializing in workers’ compensation, auto liability, general liability, and medical bill review services. AS&G will continue to operate under its current name, with its existing leadership team remaining in place.

The acquisition gives AvonRisk access to new markets across Texas, Louisiana, Mississippi, and Alabama, deepening its expertise in public entity workers’ compensation and general liability.

Southeast Vision Insurance Exchange Moves Into Florida

Regulators have tentatively approved another new property insurer for the Florida market: Vision Insurance Exchange, led by former Florida Peninsula Insurance CEO Roger Desjadon. Vision is based in Cape Coral, Florida.

If a license is granted, Vision would be at least the 14th property/casualty firm to set

up shop in Florida since state lawmakers approved landmark changes that have reduced what many in the industry had called excessive and frivolous claims litigation.

Vision plans to participate in takeouts of policies held by the state-created Citizens Property Insurance Corp. However, the firm is not on the OIR list of companies approved for takeouts in 2025.

Mark Berset, who was at one time the CEO of Comegys Insurance, is chairman of the Vision exchange oversight committee. Ronald Scalzo Jr., previously with Flagler Insurance Agency, is chief operating officer. Frank Lattanzio is the chief financial officer.

Marsh McLennan Agency, Robins Insurance

Marsh McLennan Agency (MMA), a business of Marsh headquartered in White Plains, New York, acquired Robins Insurance, a Nashville, Tennessee-based independent insurance agency. Terms of the acquisition were not disclosed.

Founded in 1976, Robins primarily provides business insurance and personal lines expertise to clients in the region, with niche expertise in real estate, construction, hospitality, community associations, and manufacturing. All Robins employees, including CEO Van Robins, will work out of their existing Nashville office.

West

Wealthspire Advisors, Marin Financial Advisors

Wealthspire Advisors LLC, an NFP company, has entered into an agreement to acquire Marin Financial Advisors in Larkspur, California. NFP is an Aon company.

Marin Financial Advisors has provided individuals and families with financial services since 1987. The firm is led by Principal Colin Drake, who will continue serving clients alongside Christine Cione, client service director.

Wealthspire Advisors is an independent registered investment advisor with a reported $31 billion in assets under management and 25 U.S. offices.

News & Markets

DOJ Drops Defense of Ban on Employee ‘Non-compete’ Agreements

By Daniel Wiessner

President Donald Trump’s administration has abandoned the U.S. government’s legal defense of a rule adopted under former President Joe Biden that had banned agreements commonly signed by workers not to join rivals of their employers or launch competing businesses.

The U.S. Justice Department filed motions in federal appeals courts in New Orleans and Atlanta to dismiss separate appeals of rulings by two judges that struck down the 2024 U.S. Federal Trade Commission rule concerning “non-compete” agreements. Republicans and business groups have criticized the rule.

The move was expected after FTC Chairman Andrew Ferguson, who was appointed to the post by Trump and had previously criticized the rule, said in February the agency was reviewing it. The appeals involve legal challenges to the rule by a marketing firm and a real estate devel-

oper, as well as the U.S. Chamber of Commerce and other business groups.

Dropping the appeals means the courts will not have a chance to address the novel question of whether the commission, which enforces federal antitrust laws, can adopt sweeping regulations such as its nationwide ban on “non-compete” agreements.

More than 20% of U.S. workers have signed non-compete agreements, according to the FTC. The agency, in adopting the rule, had said the agreements limit worker mobility and suppress wages and competition for labor.

Ferguson and other Republicans on the commission have said the FTC has limited rulemaking powers and cannot adopt blanket bans on what it views as anticompetitive conduct.

selves were not.

During Trump’s first term as president, his administration had argued in court that while specific provisions of non-competes can be unlawful, the agreements them-

The FTC on September 4 announced its first legal action of Trump’s second term related to non-compete agreements, a settlement barring the largest U.S. pet cremation business from enforcing these agreements with 1,800 workers. The agency in that case said the company’s broad agreements, signed even by low-level employees, unlawfully suppressed competitors’ entry into the pet cremation market.

Copyright 2025 Reuters.

US Commercial Lines Prices Increase 3.8%, Falling From Up 6% in Previous Quarters

U.S. commercial insurance rates increased 3.8% in the second quarter of 2025, according to the latest WTW Commercial Lines Insurance Pricing Survey (CLIPS).

WTW said the price increase has been very close to 6% over the past six quarters. Carriers reported an aggregate price increase of 5.3% during the first three months of 2025—down from increases of 5.6% and 6.1% for the fourth and third quarters of 2024, respectively.

“Amidst the ongoing general upward trend, our latest data from the second quarter of 2025 shows a moderation in commercial insurance pricing,” said Yi Jing, senior director of insurance consulting and technology (ICT), WTW. “While some lines con-

tinued to see increases, others remained stable or slightly declined, reflecting a period of more measured rate growth across the market.”

Commercial property saw prices decrease during Q2 2025. Data for most lines continues to indicate moderate to significant price increases in the second quarter of 2025, with the exception of workers’ compensation, directors’ and officers’ liability, commercial property, and cyber.

The largest price increases continued to come from excess/ umbrella liability, with double-digit price increases also seen in commercial auto, reported WTW.

The survey compared prices charged on policies written during the second quarter of 2025, with the prices charged for the same coverage during Q2 2024. Forty-two participating insurers participated in the survey, representing about 20% of the U.S. commercial insurance market.

National

CFC, a specialist insurance provider headquartered in London, appointed Kyle Laudadio as healthcare practice leader in the U.S.

Kyle Laudadio

Laudadio has over 15 years of industry experience and joins CFC from the Great American Insurance Group, where he was divisional vice president. Before that, he worked as an underwriter at Beazley USA.

named James C. Riviezzo head of North American distribution and strategy. Riviezzo has over 25 years of industry experience, joining Resilience from At-Bay, where he was head of national broker relations.

Before At-Bay, Riviezzo held leadership roles at Briza, American International Group (AIG), Safety National Casualty Corporation, and Marsh, USA.

East

Rosenberg & Parker (R&P), headquartered in Wayne, Pennsylvania, named three new owner/partners.

Lawley Medicare Solutions team in Rochester, New York.

Ames & Gough, headquartered in Washington, D.C., appointed equity partners Allison Barefoot and Marguerite Parent as senior vice presidents.

Liberty Global Transaction Solutions (GTS), part of Liberty Mutual Insurance, headquartered in Sydney, Australia, promoted Jason Remsen to head of East, Americas.

Remsen, based in New York City, previously served as a corporate associate at Pepper Hamilton LLP and practiced at Arnold & Porter Kaye Scholer LLP and McDermott Will & Emery LLP.

Amwins, headquartered in Charlotte, North Carolina, appointed Bob Black as national property practice leader within its brokerage division. Black has over 20 years of experience with Amwins as a member of the Georgia leadership team.

Adam Terry assumes the role of national real estate practice leader (property).

Resilience, headquartered in New York City,

New partner President Jack Rosenberg joined R&P as a producer in 2018 after beginning his career at Susquehanna International Group.

James DiSciullo, director of advisory and productions and energy practice leader, joined R&P as a producer in 2019 from Exelon.

Financial Sponsors Practice Leader Harry G. Rosenberg joined R&P as a producer in 2021 following five years at The Blackstone Group on the capital markets team for the private equity and energy groups.

Lawley, headquartered in Buffalo, New York, named Anto Almasian as a surety executive in the Buffalo office. He has expertise in managing a diverse portfolio of clients and an understanding of risk evaluation, operational strategy, and client management.

Andrew Edbauer, employee benefits consultant, also joins the Buffalo office.

Kevin Campbell, insurance advisor, joins the team in Darien, Connecticut.

Evonne Pomerantz, Medicare and individual health insurance consultant, joins the

Barefoot, based in Washington, D.C., has nearly 25 years of insurance brokerage experience, joining Ames & Gough in 2013. Previously, she was a commercial lines account executive and team leader with USI Insurance Services.

Based in the Boston, Massachusetts, office, Parent has 25 years of experience in insurance brokerage and risk management consulting. She joined Ames & Gough in 2006, after having served with William Gallagher Associates in Boston, where she was creator and manager of the emerging client group.

Insurance Services of New England (ISNE), headquartered in Wellesley, Massachusetts, named Mike Chamberlain as manager of membership and sales.

With close to two decades of experience working with independent agents, Chamberlain has held positions at The Hanover and The Concord Group Insurance.

Chamberlain assumes the role following the retirement of Ed Ruhl, who served for over 40 years in the insurance industry.

Kingstone Companies Inc., headquartered in Kingston, New York, appointed Randy L. Patten as chief financial officer (CFO). Patten joins Kingstone Companies, Inc. from NEXT Insurance Inc., most recently serving as vice president, chief accounting officer and treasurer. He also held the position of CFO for the company’s U.S. insurance carrier subsidiary.

Plymouth Rock Assurance Corporation, headquartered in Boston, Massachusetts, hired Brooke Bass as chief operating officer (COO) and Dale Brooks as chief claims officer (CCO). Bass has over 20 years of experience, most recently serving as senior vice president of auto physical damage claims for U.S. retail markets at Liberty Mutual.

Brooks has over 30 years of experience, previously serving in executive roles at Progressive Insurance, including leadership for claims operations in New York and Florida.

Midwest

DOXA, headquartered in Fort Wayne, Indiana, hired Sean Curry as executive vice president of its brokerage vertical. Curry has nearly 20 years of insurance experience in the brokerage market, previously serving as executive/head of brokerage and flood programs for Kraft

Jason Remsen

James C. Riviezzo

Marguerite Parent

Allison Barefoot

Randy L. Patten

Sean Curry

AAA – The Auto Club Group (ACG), headquartered in Dearborn, Michigan, added three senior leaders.

Vincent Fusco joined ACG as executive vice president, chief distribution officer.

Brian Savage joined ACG as senior vice president, chief financial officer (CFO). Savage leads ACG’s treasury, accounting, investments, real estate, and financial planning teams. Savage has over 25 years of industry experience, previously serving as CFO of personal lines at Kemper and product vice president at Allstate.

hired Pete Sayer as a senior vice president in its national property practice.

Based in South Florida, Sayer has over two decades of industry experience, most recently serving as an executive vice president at RT Specialty.

Brown & Riding also named Lauren Root as vice president of its national property practice. Based in the firm’s Houston, Texas, office, Root most recently served as Houston branch manager at Southwest Risk, L.P.

Southeast

in Miami, Florida, Luis has over 30 years of insurance experience, specializing in surety and construction. He previously served as head of bonding for Puerto Rico and the Caribbean, and most recently, as an advisor at the Baldwin Group.

The Liberty Company also named Michael Spirakis as national sales training and development leader. With more than 25 years of experience in the insurance industry, Spirakis most recently served as president of Producer Activity LLC.

for the West region. Yim is the Northern California executive director for the Asian American Insurance Network (AAIN).

Georgina Flores joined ACG as senior vice president, chief marketing officer. She will oversee all aspects of ACG’s marketing, branding, customer engagement, and growth strategies. Flores previously served as chief marketing officer at Encore, vice president of marketing at Aetna, and vice president of consumer marketing at Allstate.

South Central

Brown & Riding, headquartered in Dallas, Texas,

The Liberty Company Insurance Brokers, headquartered in Gainesville, Florida, named Guillermo “Guillo” Luis as vice president, producer. Based Lake Insurance Agency.

Amwins, headquartered in Charlotte, North Carolina, hired Ben Tasse to the newly created role of head of distribution and growth for Amwins’ Underwriting division.

Tasse has nearly two decades of experience, joining Amwins from Sompo North America, where he most recently served as SVP of wholesale business development. He has also served in leadership and underwriting roles at Axis Insurance.

Steven Money joined Alliant Insurance Services, headquartered in Irvine, California, as an assistant vice president within its employee benefits group. With over 20 years of industry experience, Money, based in Atlanta, Georgia, most recently served as a senior account executive at Marsh McLennan Agency.

Scott McCleary joined Alliant Insurance Services as senior vice president within its employee benefits group, based in Charlotte, North Carolina. Before joining Alliant, McCleary served as senior vice president at NFP and previously served as vice president, national accounts at HFCB.

West

Aon, with U.S. headquarters in Chicago, Illinois, named Shelley Yim as Northern California market leader. Yim has over 15 years of experience at Aon, currently serving as chief client officer

Crest Insurance Group, headquartered in Phoenix, Arizona, hired Easton Gibbs as a commercial lines broker. Gibbs previously played professional football with the Seattle Seahawks and the Pittsburgh Steelers. He most recently served as a screening solutions specialist at Exact Sciences.

Crest also named Matt Muehlebach as general counsel. Based in Crest’s Tucson, Arizona, headquarters, Muehlebach most recently served as general counsel and senior vice president of 5Lights LLC and Genius Avenue. Muehlebach has 17 years of experience, with 13 years as a partner at Hecker and Muehlebach, PLLC. He also served as a college basketball analyst for Fox Sports, FS1, ESPN and Pac-12 Networks.

Jennifer Gibbs joined Crest in its San Diego, California, headquarters as relationship development manager for Crest’s personal lines division. Gibbs has over 20 years of leadership experience. Before joining Crest, she held senior roles with 3 Peaks Energy, Hellenic Petroleum, and Kiva Energy.

Vincent Fusco

Brian Savage

Georgina Flores

Pete Sayer

Lauren Root

Ben Tasse

Guillermo Luis

Michael Spirakis

Easton Gibbs

Matt Muehlebach

Jennifer Gibbs

Special Report: Agency Partnerships

By Andrea Wells

Organic growth is a key barometer of an organization’s success in any industry. And it’s critical when it comes to an independent agency’s profitability in a changing market cycle like today.

While no one is predicting a return to “soft market” pricing in 2026, there are noticeable

trends pointing to a changing market, including increased appetite from carriers in many sectors of the insurance business and a declining trend in rate increases across most lines of coverage. Average premium renewal rate changes for all major commercial lines of business except workers’ compensation are up year over year, according to Ivans’ Q2 2025 Index. However,

compared to Q1 2025, Q2 2025 revealed a decrease in average premium renewal rate changes except in general liability.

Most carriers are back to making money, said Keith Captain, president of FirstChoice, a MarshBerry Company. “They’re back to making an underwriting profit, and so you’re starting to hear talk now about the need to deploy capital, meaning they

need to invest in growth,” he said. “You’re actually starting to see certain lines of business where there’s been some rate decreases or carriers are opening up a new company line in order to be able to grow.” Still, that trend depends heavily on the individual carrier’s own appetite and the geography of the risk, he added.

No one is seeing any insurcontinued on page 22

Special Report: Agency Partnerships

Insurance Journal's Top 20 Agency Partnerships

This list includes agency partnerships such as networks, aggregators, clusters, and franchise organizations, all of which play an important role in the independent agency system today.

3

Special Report: Agency Partnerships

continued from page 20

ance carrier return to “full growth mode,” he said. But instead, insurers are drilling down into specific areas where they want to grow—and grow profitably, Captain said. That might mean targeting specific counties in one state rather than opening up to the entire state. What they really learned over the past few years on the road back to profitability is they need to be really focused on exactly where they want to grow, he said.

There have been lessons learned during this market cycle for both the carriers and their agents, Matt Masiello, CEO of SIAA, said. “This was a really difficult market cycle. I think it was more dramatic than any of us thought it was going to be, and it’s been longer and more dramatic in pricing changes,” Masiello said. “And it’s not over yet.”

problems. “What can we do to help agents and carriers solve problems for customers?” Masiello asked.

One future problem in a changing market is growing in a market where pricing might start trending down. That’s why growth-minded agencies, and their agency network partners, will need to re-focus their efforts on growing organically in 2026, Captain predicts.

“That’s the biggest thing people are talking about right now—growth,” Captain said. Not just any growth but organic growth, he added. “I think a lot of agents—not all, but a lot of agents— got comfortable growing through rate increases [throughout the hard market cycle],” he said. “Those agencies had a very retention mindset.”

in 2026, and he sees agency networks as the ideal way for retail agencies to boost organic growth trends next year.

Now is the time to grow, he said. “Competition’s coming back into the market, and that’s good for everybody,” he said. “Independent agents benefit from carrier competition in the marketplace, and we as a network get the benefit of that as well,” he added.

Caldwell sees additional interest from carriers looking to networks for distribution and organic growth through that distribution. He also sees new agencies looking to networks to help them grow.

“So, the more we show we can be an organic growth engine for our carrier partners, the more opportunities we [agency networks] will have next year.”

Despite the challenges, the property/casualty market is in a healthier place, he added. “I think that agencies are better and stronger for having come through a hard market like this,” Masiello said. It’s been good because those dramatic rate adjustments improved the health of insurance carriers today. “We need our carriers to be strong, healthy, and profitable so they have the ability to support our customers and our agencies.”

One of the things this hard market cycle has created is the opportunity for agency networks, like SIAA, to solve

But next year agencies should be focused on changing that retention mindset to an organic growth mindset. “They need to be thinking about, ‘How do I go actually get new storefronts, get new policies?’ Because what we’ve seen over the past few years is a lot of flattening of organic growth,” Captain said. “That’s going to be a really big conversation piece because carriers are asking for it now.”

Now Is the Time

At SmartChoice, new agent recruitment is at an alltime high, Caldwell said. “We’ve added 1,450 new agents over the last year and just had our largest month on record—162 agents in August alone,” he said. “I would say in the last three months of this year, we will appoint more agents than we did in the last two years combined.”

Agency networks are now a proven and profitable distribution model for the independent agency channel, according to Caldwell and others. “We’re a known entity. I’m not explaining what a network is anymore, whereas eight years ago, we all were explaining to an Allstate and Nationwide agency why they should come over to the independent side. We’re not doing that today,” he said. “People have figured out this is the winning side, at least for now,” he added.

“There is such a tremendous opportunity for us and our competitors to take market share, and we have got to take advantage of that,” Caldwell said. “For 2026, the opportunity to grow has never been better. It’s never been better.”

Growth Strategies

Andrew Caldwell, president of Smart Choice, agrees that organic growth will be a focus

Conversations with carrier partners have changed in the last three months as well, he said. Those preferred carriers that for the last two or three years have been very conservative on appointments and capacity are changing the conversation, Caldwell said. “From our meetings with carriers, there’s a ton more saying, now it’s time to grow,” he added.

Like their independent agency members, the largest agency networks and franchise groups listed on Insurance Journal’s Top 20 Agency Partnerships ranking (see page 21) experienced significant growth during the hard market cycle. In aggregate, the total property/casualty revenue of Insurance’s Top 20 Agency Partnerships list grew by $2,681,164,782 in total P/C revenue from the 2024 ranking to the 2025 ranking. Growth strategies in the agency partnerships world are

continued on page 24

Andrew Caldwell

Keith Captain

Matt Masiello

FirstChoice, a MarshBerry Company, caters to insurance agency owners who want to create a path forward through strategic planning, technology enablement, market tools, and education & resources to build their business. Recognized as the #1 top agency partner by Insurance Journal, FirstChoice is available nationwide.

Special Report: Agency Partnerships

continued from page 22

as diverse as the organizations themselves. Some grew by adding hundreds of new member agencies; others grew through mergers and acquisitions; and some grew by both membership numbers and M&A activity.

Renaissance has been active in the acquisition of smaller agency networks in several states in recent years.

Robert A. Bondi, CEO of Renaissance, told Insurance Journal that he sees the strategy as a win for both Renaissance and smaller networks that once acquired have been able to benefit from the scale of a larger group. Like other smaller insurance organizations in the U.S., smaller agency networks are beginning to struggle in today’s competitive environment, he said.

as fragmented as the independent agencies were,” he said. “A little bit of combination is going to make us all stronger, better, and maybe more effective,” he said.

“It’s a very exciting time to be a part of a network, particularly as we all, myself included, are trying to create a more professional, more valuable enterprise that supports agencies and helps them connect better with carriers.”

He believes the evolution of agency networks and how they serve the independent agency channel is only beginning. “We’re still in the beginning of the game on how to actually help independent agencies thrive, and that’s what we’re excited about,” he said.

Previously, most ISU agency members had to be at $1.5 million or more in total revenue. “We had some agencies under that threshold, but it was not easy to do,” he said. McCarthy said the lower threshold for revenue will allow more members to join.

Currently, ISU Steadfast has agency members in 40 states with about 24% of the business written in California. McCarthy said the new ISU Steadfast model will allow for members to access

some products and services on an à la carte basis. “You don’t have to buy the full services at ISU Steadfast. You can come in and say, ‘I just want this,’ for example,” he said.

“We think that the joining of their members with our framework really creates a winwin situation for the members, and for these smaller network owners, who are struggling a bit to try to get carriers to work with them in a constructive way,” he said. Access to certain insurance carriers, products, and services can be more challenging for a smaller organization, he said.

Bondi expects the M&A activity in the agency network world to continue both for Renaissance and other networks. “I don’t think we’re going to end up with only a handful of agency networks, but I do think that the networks in general were just

Other networks like ISU Steadfast and Indium have been on the other side of the M&A game—both were acquired by larger entities but not larger networks.

In October 2023, Steadfast Group, the largest general insurance broker network and underwriting agency group in Australasia, acquired California’s ISU Group to expand the organization into the U.S. Now called ISU Steadfast, the 40-plus-year-old agency network is making a few changes to grow the network and to help additional independent agency members, said Dan McCarthy, CEO of ISU Steadfast.

One big change is that the agency network will be opening membership to smaller agencies with revenues as low as $250,000, McCarthy said.

its current 30 specialist MGA and wholesale solutions to ISU Steadfast and the broader U.S. market. Additionally, with the financial backing of Steadfast Group, McCarthy said there could be perpetuation opportunities for some member agencies as well, either through a fractional purchase or 100% purchase when it makes sense. “They have the capital to do it, and they want to help the agency perpetuate independently,” he said.

McCarthy also said as its new owner continues to make moves into the U.S. market, ISU Steadfast members will see added products and services to help independent agents remain independent. For example, one recent acquisition will help move the Australia-based company’s proprietary programs into the U.S. market.

In early September, Steadfast Group announced its acquisition of a majority stake in U.S.-based specialty managing general agency and wholesale brokerage Novum Underwriting Partners LLC, including the organization’s technology platform, Novum Online. Novum will serve as Steadfast’s program development and management platform in the United States.

McCarthy said the move will help Steadfast bring some of

Columbus, Ohio-based Indium has also grown substantially, partly by being acquired. At the end of 2023, Assurex Global entered the agency network world with their partner firms by acquiring Indium. Katherine Ternes, president of Indium, said the acquisition has led to numerous Assurex Global agencies joining the network. “That was a big part of our increase from 2022 to 2023, the first few [agencies] started participating in 2023, and more have joined since,” she said.

Outlook Bright

Despite changing market trends, the outlook for independent agencies and their network partners is good, Masiello said. “Industry-wise, it’s really a great time to be an independent agency, great time to open new agencies or to run established agencies,” he said. “I think coming out of what we’ve been through over the last 24 to 36 months, the industry should be healthy. And I think that’s good for all of us. It’s an exciting time.”

Dan McCarthy

Bob Bondi

10:46

ISU Steadfast Members

Sam (the new member)

Thanks for welcoming me to the network! Excited to be part of ISU Steadfast.

Carrie (Hanson & Ryan)

Welcome! ISU Steadfast is a game changer! Our profit shares jumped significantly.

Mark - Olson Duncan

You’ve joined the best in the country! We gained access to markets in all 50 states Best decision we ever made.

Jeff - Smith Davis

Ryan - ARMAC

It’s not just business here. It’s a community that genuinely cares about your success. 20 years in, and still thriving. Market access + profit sharing = growth.

Spotlight: Contractors

How Contractor Networks Help to Reduce Repair Costs, Improve Timeliness

The commercial property insurance market is navigating a constantly evolving landscape in 2025, in which rising costs, labor shortages, and the ever-present threat of business interruption are reshaping how claims are managed.

In response, many insurers and risk managers are moving away from ad hoc contractor relationships and toward managed repair models that emphasize trusted networks, transparent pricing, and proactive project oversight.

Commercial claims are an intricate puzzle, and the pressures of today’s market only magnify their complexity.

According to Verisk, U.S. commercial reconstruction costs climbed 5.7% year over year through Q2 2025, driven by material spikes—with concrete alone rising 9.3%—and compounded by persistent labor shortages, with nearly 900,000 skilled trade jobs still unfilled. Turner Construction’s cost index shows a similar 3.8% increase in non-residential building expenses, underscoring how inflationary pressures continue to ripple through the sector.

Against this backdrop, insurers and policyholders alike

face a critical question: How can they adapt now to avoid being overwhelmed by the compounding costs and delays that threaten every claim?

Commercial property claims present a vastly different set of challenges than residential ones. While homeowners insurance claims often involve standardized materials and straightforward repairs, commercial losses need to consider specialized systems, strict regulatory requirements, and the very real risk of business interruption. A hospital may need temporary power solutions and phased repairs to keep critical areas operational; a restaurant may require specialized equipment replacement; a hotel faces immense financial strain if rooms are unavailable for extended periods; a manufacturing

facility may be unable to fulfill contracts until production lines are restored.

And this doesn’t even include how large-scale events continue to test the resilience of claims operations and cost models. For an idea, Lloyd’s estimates it incurred $2.3 billion in losses from the January 2025 wildfires in Los Angeles alone, highlighting how quickly risks can escalate.

These challenges are compounded by the fact that commercial facilities typically already have pre-existing ties with local contractors, often built through routine maintenance or renovations. These relationships can become liabilities in both the renovations and claims process as local contractors may lack the labor capacity, supply chain access, or restoration expertise

to handle large-scale damage. This can result in delays, higher costs, and substandard workmanship that requires rework and extends the claims process.

However, commercial property owners, insurers, and claims professionals do have routes to faster repairs and expedited claims processes.

Step one is to have a broader, and thoroughly vetted, contractor network. This allows all parties involved to leverage a wide pool of pre-qualified contractors, ensuring capacity is available when it’s needed most. This broader pool would also allow relevant parties to identify contractors that are the best fit for the job, rather than defaulting to whoever is closest.

Step two is approaching the job with a smarter pricing

continued on page 27

By Ed Reis and

Sarah Morris

Part of SPG Since 2017. Now One Brand .

WHOLESALE

SAME PEOPLE. SAME SERVICE. A STRONGER, MORE CONNECTED PLATFORM.

Monarch E&S has been part of Specialty Program Group since 2017. We are now joining SPG’s new Wholesale division.

You can continue to count on the same cherished relationships, trusted expertise, and strong carrier connections you’ve always relied on, now enhanced by the broader capabilities of the unified SPG Wholesale platform.

Explore SPG’s Wholesale Division

News & Markets

California Labor Commissioner Cites L.A. Restaurant $680K

The California Labor Commissioner’s Office cited J BBQ, a Koreatown restaurant, more than $680,000 for wage theft violations.

A total of 48 workers were impacted by the violations, which included unpaid wages, denied breaks, and inaccurate wage statements, according to the LCO.

The L CO reportedly found that J BBQ, a restaurant operated by Midri Inc. and its owner, Byung Kwan Lee, frequently failed to pay employees all wages owed, denied their legally required meal and rest breaks, and provided incomplete or inaccurate wage statements.

Some workers were reportedly denied rest periods and were required to remain on the premises even during lunch breaks to help customers. Additionally, staff reportedly worked split shifts without receiving premium pay as required by law.

This investigation was launched by a referral from the Koreatown Immigrant Workers Alliance, a community organization that advocates for restaurant and retail employees.

The total amount cited by the LCO is $680,238, of which $538,638 is payable to the workers. The LCO is a division of the Department of Industrial Relations.

3 Hyundai and 2 GM Products on Mercury’s Most Affordable New EVs to Insure List

California-based Mercury Insurance compiled a list of the most affordable electric vehicles to insure. The list includes 2025 and 2026 model-year vehicles. Factors examined for the list include claims on similar vehicles, costs to repair and vehicle safety records. Mercury examined EVs available at car dealerships today.

This is the 10th year that Mercury has published this list.

The top 10 EVs that are the most affordable to insure, beginning with the most affordable make, are:

• Chevrolet Blazer EV

• Chevrolet Equinox EV

• Nissan Leaf

• Kia Niro EV

• Ford F-150 Lightning

• Hyundai Kona EV

• MINI Cooper SE

• Hyundai IONIQ EV (all models)

• Fiat 500e

• Subaru Solterra/Toyota BZ4X

Mercury put together a list of the most affordable trucks and SUVs to insure earlier in August. Hyundai and GM were also well represented on that list. Two Chevrolets and a Hyundai topped the list of the most affordable new trucks and SUVs to insure for 2025.

SAIF in Oregon Declares $50 Million Dividend

SAIF’s board of directors has declared a $50 million dividend for more than 50,000 workers’ compensation policyholders.

In October, 50,757 policyholders are set to receive the dividend, which will be calculated based on the premium for policies that ended in 2024.

current economic uncertainty and the rising trends in medical costs. However, despite the challenges, SAIF’s strong

This is the 16th consecutive dividend given to SAIF policyholders.

According to Chip Terhune, president and CEO of SAIF, the organization considered the

fiscal position, effective claims handling and proactive safety programs made this year’s dividend possible.

SAIF is Oregon’s notfor-profit workers’ comp insurance company.

California Labor Commissioner Cites LA Developers $2.3M

The California Labor Commissioner’s Office issued citations totaling more than $2.3 million to multiple developers and operators of construction projects at sites in Los Angeles.

The citations stem from an investigation showing there was wage theft and other labor law violations impacting 124 construction workers.

Investigators found workers were being denied overtime pay despite regularly working more than eight hours a day or 40 hours per week. Many were also paid below the Los Angeles minimum wage and were never provided with required sick leave or accurate itemized wage statements, according to the LCO.

Workers frequently received

multiple pay stubs from different corporate entities, despite reporting to the same supervisors, and working on overlapping projects, in a scheme the LCO says was an attempt to evade paying legally mandated overtime and minimum wage.

The investigation also revealed additional violations, including failure to provide workers with paid sick leave and supplemental paid sick leave during the pandemic.

The citations total $2.3 million, including more than $2.1 million in unpaid wages and damages, along with more than $165,000 in accrued interest. The exact amount owed to each worker varies, but the total averages $18,900 per person.

News & Markets

Oregon Workers’ Comp Pure Premium Rate Dropping

Oregon employers on average would pay 87 cents per $100 of payroll for workers’ compensation costs in 2026, down from 91 cents this year, under a new proposal.

The Oregon Department of Consumer

and Business Services called for the decline in costs, which would mark 13 years of average decreases in the pure premium rate.

The DCBS credits the cost decrease to the success of Oregon’s workers’ comp

system, as well as positive, long-term trends. Fewer claims are entering the system over time, along with claims being generally less severe, according to the National Council on Compensation Insurance.

The pure premium rate would drop by an average 3.3% under the proposal. The pure premium per $100 of payroll will have declined by 46.5%, according to the DCBS.

The reduction in costs is due to fewer claims entering the system over time, along with claims being generally less severe, according to NCCI.

Employers’ total cost for workers’ comp insurance includes the pure premium and insurer profit and expenses, plus the premium assessment. Employers also pay at least half of the Workers’ Benefit Fund assessment, which is a cents-per-hourworked rate.

The decrease in the pure premium of 3.3% percent is an average, so individual employers may see larger or smaller decrease, no change or an increase.

The premium assessment, a percentage of the workers’ comp premium employers pay, is added to the premium. It would remain at 9.8% in 2026, the same as 2025, under the DCBS proposal.

The decrease in the pure premium will be effective Jan. 1, 2026, but employers will see the changes when they renew their policies in 2026.

continued from page 26

model. Traditional unit pricing often fails to scale for large commercial losses, leading to significant overpayment. Meanwhile, time-and-material models offer a more accurate reflection of actual labor and material costs while simultaneously capturing economies of scale. For example, Verisk data shows that smarter review models can reduce inflated bills by 20% to 27% on commercial claims, an amount of savings that can make a measurable difference across a portfolio of losses.

Next comes proactive project management and pre-loss agreements. It’s pertinent to remember that managing a commercial repair effectively requires both strong project

oversight during the claim and smart planning before a loss ever occurs. Having established pre-loss agreements lays down clear expectations from the very beginning for pricing, emergency protocols, and response times so when a catastrophe happens, everyone is aligned and mobilization is immediate.

Then once the work begins, proactive project management ensures contractors are held accountable to those agreements. Dedicated repair specialists or virtual project managers can then monitor timelines, coordinate resources strategically, and keep all stakeholders informed as the projects progress.

In tandem with each other, these ideas and practices will

provide both insurers and policyholders with a clearer path forward. As U.S. commercial insurance rates increased 2.8% in the second quarter, according to Novatae Risk Group’s quarterly Market Barometer, organizations can take control of outcomes by adopting solutions that emphasize consistency, transparency, and speed, rather than being overwhelmed by the mounting costs and delays that too often define commercial property claims.

The reality is that the challenges of rising costs, labor shortages, and business interruption aren’t going anywhere any time soon. However, that doesn’t mean these trends have to dictate the trajectory of every claims process. For those

who embrace structured repair models and invest in proactive planning as the commercial property insurance space continues to evolve, they will be the ones better positioned to contain expenses, reduce downtime, and deliver better results for clients.

The message is simple: Prepare now. Build the right relationships, put the right oversight in place, and invest where you can make the loss response as seamless as possible and everybody wins.

Reis is president of managed repair networks at Sedgwick.

Morris is an estimate review consultant at Sedgwick.

ACCELERATE GROWTH WITH STAFF BOOM'S TAILORED OUTSOURCING SOLUTIONS

Embark on a journey of operational optimization and growth with STAFF BOOM, where our tailored outsourcing solutions empower businesses to thrive in today's competitive landscape.

Welcome to Insurance Journal’s 2025 Professional Liability Directory. We’ve compiled this directory of professional liability providers to assist independent agents and brokers in their search for markets. In today’s highly litigious world, professional liability coverages have become critical insurance for many businesses. This directory has been designed to serve as a quick reference guide that allows users to locate carriers, wholesale brokers and managing general agencies offering professional liability coverage. The information published in this directory was submitted directly by the providers and includes their contact information, Web site and states where coverage is available. For a complete listing of markets offered by providers named in this directory, visit: www.insurancejournal. com/directories and type in “professional liability” under the Excess & Surplus, “find a market” option. To submit a listing for future directories, e-mail Kristine Honey at: khoney@insurancejournal.com. We hope you find IJ’s Professional Liability Directory to be a useful tool. To comment on this directory, or any other IJ resource, please e-mail: editorial@insurancejournal.com.

Indemnity

Johnson

Landy Insurance Agency

Inc.

M.J. Hall & Company Insurance Brokers

Markel

MAXIMUM

McGowan, Donnelly & Oberheu, LLC (MDO)

Monarch E&S Insurance

Commonwealth Underwriters, a Division

of Specialty Program Group, LLC

Cooper & McCloskey, Inc.

Costanza Insurance Agency, Inc.

DC MD NC PA SC VA WV

Most States

All States (for Security Industry)

Coterie 38 States

CRC Insurance Services

CRES A Gallagher Company

Donald Gaddis Co., Inc. Insurance Svcs

DUAL North America

All States

All States

All States

All States

Eaton Professional Insurance Services CA

Elite Underwriters CA FL CT NY

EMaxx Assurance Group of Companies, Inc.

All States

Executive Insurance Professionals, PLLC CA NM OK TX

First Choice Insurance Intermediaries, Inc. Most States

Gorst & Compass Insurance

Hudson Insurance Group / Hudson Pro

CA

All States

Insurance Agents & Brokers Service Group, Inc. DE MD PA (for Ins. Agents & Brokers only)

Irwin Siegel Agency

ISC - Integrated Specialty Coverages

J.E. Brown & Associates

All States

All States

All States

James Klein Insurance Service, Inc. Most States

Jamison Risk Services

Johnson & Johnson

All States except AK NV

All States

Kevin Dahlke Insurance Brokerage, Inc. Most States

Keystroke Underwriters

Kinsale Insurance Company

Landy Insurance Agency

All States except HI

All States + DC, Puerto Rico, Virgin Islands

All States except AK

M.J. Hall & Company Insurance Brokers AK AZ CA HI NV OR WA

Markel

Maverick Commercial Insurance Services

All States

All States

National Association of Professional Agents (NAPA) All States

Negley Associates

All States

NeitClem Wholesale Insurance Brokerage, Inc. AZ CA NV

New England Excess Exchange CT DC DE MA MD ME NC NH NJ NY OH PA RI VA VT

NEXT Insurance

All States

Norman-Spencer International, Inc. All States

Novatae Risk Group

OREP Insurance Services, LLC

Philadelphia Insurance Companies

PL Risk Advisors, Inc.

Prime Insurance Company

Professional Governmental Underwriters

Professional Insurance Concepts

Professional Liability Ins. Svcs - Underwriting Facilities

All States

All States

All States except LA

All States

All States

All States

All States

All States (250+ Misc Classes: Vinyard/Farm)

ProLawyer from C&R Insurance Services LLC DC DE MD NJ NY PA VA

Quadrant Insurance Managers

R.E. Chaix & Assoc. CA

States

Roush Insurance Services, Inc. IA IL IN MN ND OH SD WI

RPS Technology & Cyber All States

RT Specialty All States

Sabal Insurance Group, Inc. All States

Select Risk Services, Inc. AR AZ CA CO LA MS NM PA TX

Smart Choice Express Markets All States except AK & HI

SPG ExecuPro All States

STRAVA Specialty All States

Sun Coast General Insurance Agency AZ CA CO NV OR UT

SWBC TX

Synergy Professional Associates, Inc. All States

Target Professional Programs All States

The Hanover Insurance Group Most States

Tokio Marine HCC Professional Lines Group All States

Tokio Marine/HCC All States

U.S. E&O Brokers, a Division of Innovation

Growth Partners Specialty, LLC All States

United Educators All States

USG Insurance Services, Inc. All States

Veracity Insurance Solutions, LLC All States

Victor Insurance Managers LLC All States

Wholesure All States

Woodlands Insurance Services, LLC Most States

Access

Access One80

Alliant Insurance Services

Allsouth Professional Liability

AMIS/Alliance Marketing & Insurance Services

Amwins - 150+ Offices Nationwide

ARC West Coast Excess & Surplus Brokerage, LLC

a CRC Group Company

Artex Risk Solutions, Inc.

Ascendant Insurance Solutions

Ashley General Agency

Aura Risk Management & Insurance Services

Axis Insurance Services, LLC

Bailey Special Risks, Inc.

Baker Insurance and Bonds, LLC

Berkley Select | a Berkley Company

Braishfield Associates, Inc.

Brooks Insurance Agency

Brown & Riding

CAMICO Mutual Insurance Company

CID Insurance Programs, Inc.

Ck Specialty Insurance Associates

Cochrane and Company

Commercial Sector Insurance Brokers, LLC

Commonwealth Underwriters, a Division of Specialty Program Group, LLC

Cooper & McCloskey, Inc.

Costanza Insurance Agency, Inc.

CRC Insurance Services

CRES A Gallagher Company

Donald Gaddis Co., Inc. Insurance Svcs

Eaton Professional Insurance Services

Elite Specialty & Wholesale Insurance Services

Executive Insurance Professionals, PLLC

Gateway Specialty Insurance

Gorst & Compass Insurance

Great American Ins. Group - Executive Liab. Division

States (for Security Industry)

Indemnity Excess & Surplus Agency, Inc. Western States

Insurance Agents & Brokers Service Group, Inc.

IPA Risk Management, LLC

Irwin Siegel Agency

ISC - Integrated Specialty Coverages

J.E. Brown & Associates

James River Insurance Company

Jamison Risk Services

Jencap - Locations Nationwide

Jimcor Agencies

Johnson & Johnson

Joseph Krar & Associates, Inc.

States

States

States

States

States

States except AK NV

States

Brokers only)

States except AK HI IA NE SD WY

States

MA ME NH RI VT

Kevin Dahlke Insurance Brokerage, Inc. Most States

Kinsale Insurance Company All States + DC, Puerto Rico, Virgin Islands

M.J. Hall & Company Insurance Brokers AK AZ CA HI NV OR WA

Markel All States

Maverick Commercial Insurance Services All States

MAXIMUM All States

Monarch E&S Insurance Services Nationwide

Negley Associates

States

NeitClem Wholesale Insurance Brokerage, Inc. AZ CA NV

New Age Underwriters Agency, Inc.

New England Excess Exchange

Norman-Spencer Agency, Inc.

Novatae Risk Group

States

RT Specialty

Sabal Insurance Group, Inc.

Shelly, Middlebrooks & O’Leary, Inc.

Southern Insurance Underwriters, Inc.

Ascendant

Axis

Balance Partners

Berkley Select | a Berkley Company

Brooks Insurance Agency

Cooper & McCloskey, Inc.

Gaddis

Fiduciary

Brooks Insurance Agency

Cooper & McCloskey, Inc.

CRES A Gallagher Company

Donald Gaddis Co., Inc. Insurance Svcs

Elite Specialty & Wholesale Insurance Services

First Choice Insurance Intermediaries, Inc.

Hudson Insurance Group / Hudson Pro

IPA Risk Management, LLC

Johnson & Johnson

Kevin Dahlke Insurance Brokerage, Inc.

Kinsale Insurance Company

Markel

McGowan, Donnelly & Oberheu, LLC (MDO)

National Association of Professional Agents (NAPA)

States + DC, Puerto Rico, Virgin Islands

States

States

NeitClem Wholesale Insurance Brokerage, Inc. AZ CA NV

Norman-Spencer Agency, Inc.

Novatae Risk Group

ProSurance Group, a Div of One80 Intermediaries

R.E. Chaix & Assoc.

U.S. E&O Brokers, a Division of Innovation

States

Amwins

Brooks

Chubb

CID

Ck Specialty Insurance Associates

Commercial Sector Insurance Brokers, LLC

Commonwealth Underwriters, a Division

Specialty Program Group, LLC

Cooper & McCloskey, Inc.

Coterie

Donald Gaddis Co., Inc. Insurance Svcs

States

States

States Elite Underwriters

Gorst & Compass Insurance

Indemnity Excess & Surplus Agency, Inc.

Insurance Agents & Brokers Service Group, Inc.

FL CT NY

States

Sun

Synergy Professional Associates, Inc.

Target Professional Programs

Tokio Marine HCC Professional Lines Group

U.S. Brokers Network, a Division of Innovation

Growth Partners Specialty, LLC

U.S. E&O Brokers, a Division of Innovation

Growth Partners Specialty, LLC

Vanguard Specialty, LLC

Veracity Insurance Solutions, LLC

XPT Specialty

States except Alaska

360

Amwins - 150+ Offices Nationwide

Aon Affinity

ARC West Coast Excess & Surplus Brokerage, LLC

a CRC Group Company

Aura Risk Management & Insurance Services

Berkley Select | a Berkley Company

Brooks Insurance Agency

CID Insurance Programs, Inc.

Cooper & McCloskey, Inc.

CRC Insurance Services

Donald Gaddis Co., Inc. Insurance Svcs

DOXA Insurance Holdings

Gorst & Compass Insurance

Grayhawk General Agency, Inc.

IPA Risk Management, LLC

James River Insurance Company

Jamison Risk Services

Jimcor Agencies

Johnson & Johnson

Kinsale Insurance Company

Landy Insurance Agency

Lawyer’s Protector Plan

M.J. Hall & Company Insurance Brokers

States

States

States except AK

States except AK

States

States + DC, Puerto Rico, Virgin Islands

States except AK

States except AK HI LA OR WV WY

States

MD PA IPA Risk Management, LLC

ISC - Integrated Specialty Coverages

States

J.E. Brown & Associates All States

James River Insurance Company

States

Jamison Risk Services All States except AK NV

Jencap - Locations Nationwide

Johnson & Johnson

Markel

MAXIMUM

States

States

Keystroke Underwriters All States except HI

Kinsale Insurance Company

MAXIMUM

McGowan, Donnelly & Oberheu, LLC (MDO)

National Association of Professional Agents (NAPA)

NeitClem Wholesale Insurance Brokerage, Inc.

New Age Underwriters Agency, Inc.

New

Norman-Spencer Agency, Inc.

Novatae Risk Group

Number One

ProSurance Group, a Div of One80 Intermediaries

ProWriters

Quadrant Insurance Managers

States

States

McGowan, Donnelly & Oberheu, LLC (MDO) All States

Monarch E&S Insurance Services Nationwide

National Association of Professional Agents (NAPA) All States

NeitClem Wholesale Insurance Brokerage, Inc. AZ CA NV

NEXT Insurance

Number One Insurance Agency

States + DC, Puerto Rico, Virgin Islands

States

States

States

States

States

States

States

States

States Professional Liability Brokers & Consultants, Inc.

ProLawyer from C&R

Amwins

Gorst

IPA Risk

Irwin Siegel Agency

James

James

Jencap - Locations

Johnson

Kinsale

Magnolia LTC - (Skilled Nursing, Assisted

Maverick

Negley

PL

Professional

Professional

Promont Insurance Advisors

Psych

RPS

USASIA

Insurance Brokerage, Inc.

New Age Underwriters Agency, Inc.

New England Excess Exchange

Norman-Spencer Agency, Inc.

Norman-Spencer International,

Allsouth Professional Liability

Amwins - 150+ Offices

Aon Affinity

ARC West Coast Excess & Surplus Brokerage, LLC

a CRC Group Company

ARMR.Network - Better Insurance

Cooper

Costanza

Coterie

CRES

R.E.

Roush

AMIS/Alliance Marketing & Insurance Services

Aon Affinity

ARC West Coast Excess & Surplus Brokerage, LLC

a CRC Group Company

States Ascendant Insurance Solutions

Bailey Special Risks, Inc.

Baker Insurance and Bonds, LLC

Berkley Select | a Berkley Company

Brooks Insurance Agency

Cochrane and Company

Commonwealth Underwriters, a Division of Specialty Program Group, LLC

Cooper & McCloskey, Inc.

Donald Gaddis Co., Inc. Insurance Svcs

All States except AK & HI

All States except NY

All States

All States except HI

All States

States

Eaton Professional Insurance Services CA

EMaxx Assurance Group of Companies, Inc.

States

Encore Fiduciary All States (includes Labor PL Insurance)

Executive Insurance Professionals, PLLC

NM OK TX

Gateway Specialty Insurance All States

Great American Ins. Group - Executive Liab. Division

Hudson Insurance Group / Hudson Pro

Indemnity Excess & Surplus Agency, Inc.