Creative Director / Designer Ashlee Nobel Lee Lee Arts + Design

Contributing Writers

Latrecia Carroll, Brad Chambless, Mike East, Susannah Marshall, Roger Morris Jr, Rob Nichols, Bob Sprague, Brett Taylor, Deborah Temple

The Arkansas Banker (ISSN 004-1726) is published quarterly by the Arkansas Bankers Association, 1220 West Third Street, Little Rock, AR 72201. Phone: 501.376.3741.

Periodical postage paid at Little Rock, AR. Postmaster: Send address changes to Arkansas Bankers Association, 1220 West Third Street, Little Rock, AR 72201. Subscription to The Arkansas Banker magazine is included in the membership fees to the Arkansas Bankers Association. Cover price is $5.95 each. Annual subscription rates are $40.00 for members and $60.00 for non-members.

Federal tax law prohibits the deduction of lobbying expenses for federal incomes tax purposes. Organizations like ABA, which assess member dues, are required by law to notify their members of the portion of their dues attributable to lobbing/and therefore non-deductible on your federal tax return. For the year 2023, it is estimated that 9.32% of your dues will be attributable to lobbing as defined by the IRS. Contributions to ABA are not charitable contributions, however, they may be deductible as a legitimate business expense.

Chairman’s Column Washington Update Commissioner's Column Emerging Leaders The Road Less Traveled

Brad Chambless is a leader with passion for his bank and the ABA.

Durbin 2.0

Bankers express concerns.

2024-25 Leadership

Our new Executive Committee and Board of Directors.

Women’s Business Fund

Empowering women entrepreneurs.

Non-Compete Final Rule

The FTC makes a bold move.

When is a Card a Card?

Debit vs. credit vs. HELOC Access Annual Convention Recap

A look at our successful annual bankers meeting.

NEWS & MOVES

PRESIDENT’S MESSAGE

Lorrie

Trogden

| President & CEO | Arkansas Bankers

Association

We want you! – to get involved with YOUR association! There are so many ways to be active with the ABA and we would love to have you join us! Listed below are many ways for you to “get in the game.”

COMMITTEES:

• Education Committee – This committee partners with our Professional Development department to suggest hot topics for continuing education. Our world-class education department wants to optimize our offerings for the most up-to-date training to meet our members’ needs.

• Emerging Leaders Committee – Open to everyone, this committee coordinates with the Emerging Leaders Council to create and promote networking events, further financial literacy, and advance banking as a career.

• Government Relations Advisory Council – This committee reads bills as needed and meets every week during the state legislative session. Committee members also contact legislators and testify at legislative committee meetings.

• Member Engagement and Marketing Committee – This committee ensures that our members understand all of the many benefits ABA offers its members and ensures our programs and services are reaching their target audiences.

Please contact any of us at the ABA or ABA leadership to join a committee!

PROFESSIONAL DEVELOPMENT:

We offer a plethora of educational options for every employee in your bank with our Annual Convention, conferences, schools, and seminars! Both in-person and virtual. We can also bring development directly to you by arranging for a speaker to come to the bank for your own personalized in-house training. We are so very grateful when you choose to invest your education dollars with us. This allows us to then invest them back in you with our programs and services.

GOVERNMENT RELATIONS:

Speaking in one voice matters, and this is our number one member benefit! ABA tirelessly advocates for our industry every day at the state and federal level. The easiest micro-volunteer opportunity for you is utilizing the Advocacy Alert links found weekly in the Tuesday eNews, as well as occasional special alerts about pending legislation or rule making. You’ve heard me say it before, but CLICK THE LINK and let your Legislators, Congressmen and Regulators know how what they are proposing affects our industry and your customers! Those links are pre-populated with talking points that you can edit to customize for your bank and your community. Once you’ve clicked the link, send it to other bank employees as well as customers. Customers are often directly impacted by many of these proposals, and they should also weigh

“You must get involved to have an impact, no one is impressed with the won-lost record of the referee.”

in; we may be their only avenue to participate in the legislative process.

ABA BANKPAC:

Yet another path to speak with one voice. Our PAC gives to friends of banking, no matter what side of the aisle they are on. We NEED those who understand our industry and understand banking issues to be at the table when important decisions are being made. If we are not at the table, we will absolutely be on the menu. Your contributions to our PACs make a huge difference in getting candidates elected that will support banking. I encourage you to strive for the 100% club, but any amount makes a difference. (Yes, I am personally a 100% club member!) A heartfelt thank you for those that have contributed, you will see our current 2024 PAC members further back in the magazine. You can contribute online on our website or by mailing a check to the association. Please also consider holding a 13th Board meeting which provides a great opportunity for your board members to learn about what government relations items are pertinent to the bank.

These are just a few ways to get involved with the ABA, and I hope you will consider one or several of them! Your time and talent keep our association vibrant and relevant, and we welcome any new ideas you may have. I, as well as ABA leadership, are only a phone call or email away. I’m traveling the state and would love to hear your ideas in person with a bank visit. Please let me know when I can come and spend time with you at your bank. Happy summer, and I hope to see you soon!

Lorrie Trogden, President & CEO

ABA OFFICERS

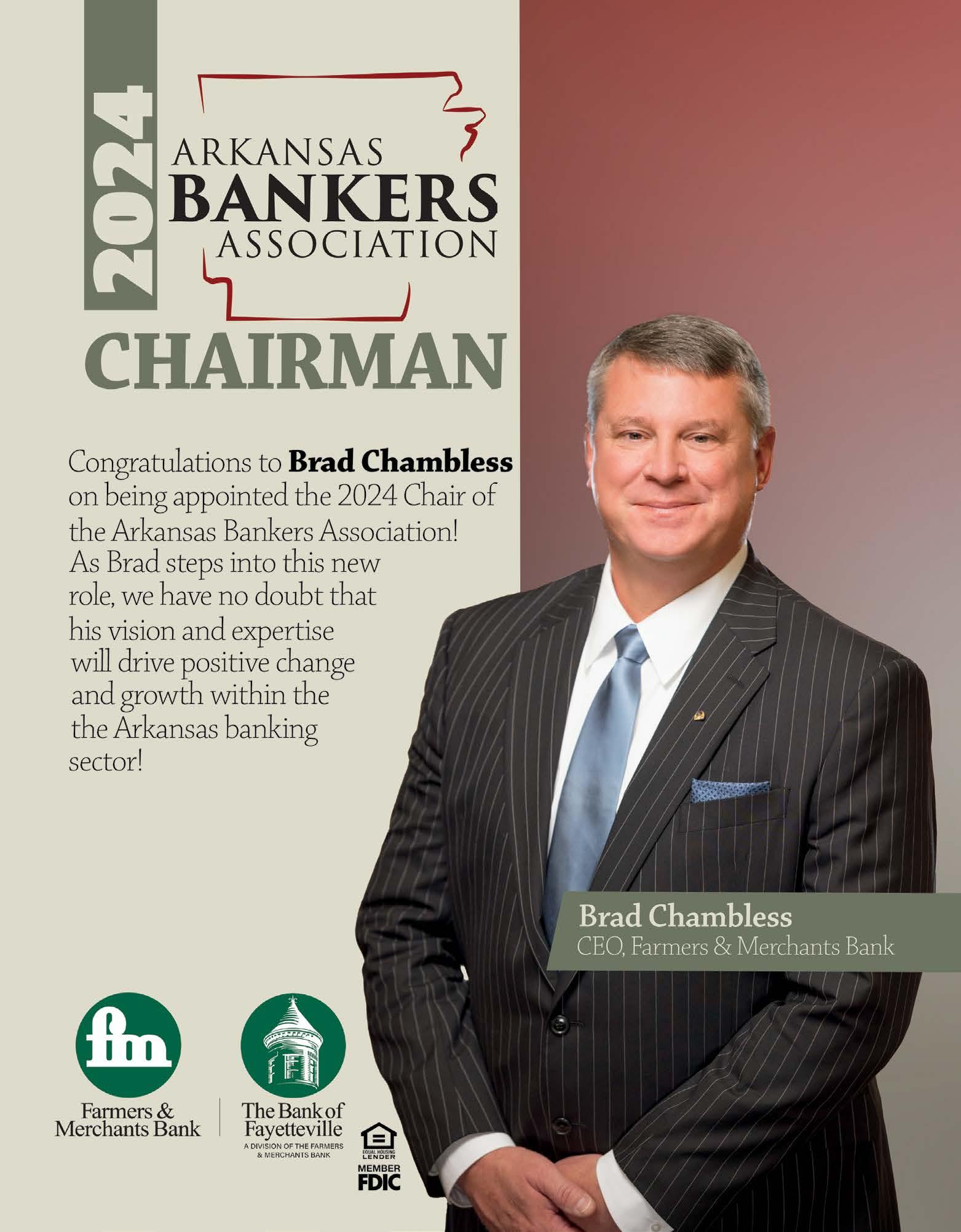

Brad Chambless, Chairman Farmers and Merchants Bank, Stuttgart

Chris Gosnell, Chairman-Elect Farmers Bank & Trust Company, Magnolia

Jason Tennant, Vice Chairman CS Bank, Eureka Springs

Scott Saffold, Treasurer Union Bank & Trust Co., Monticello

Jim Taylor, Past Chairman First Security Bancorp, Rogers

Lorrie Trogden, President & CEO Arkansas Bankers Association, Little Rock

BOARD OF DIRECTORS

Johnny Adams, Conway

Ben Buergler, Bentonville

Latrecia Carroll, Little Rock

Asa Cottrell, Little Rock

Joe Dunn, Little Rock

Robin Hackett, Greenbrier

Heather Jones, Little Rock

Jeff Lynch, Little Rock

Katherine Mitchell, White Hall

John Olaimey, Little Rock

Calvin Puryear, Dumas

Randy Rawls, Warren

Lori Ross, Arkadelphia

Loren Shackelford, Fayetteville

Rob S. Tiffee, Little Rock

Ron Witherspoon, Little Rock

Durbin 2.0

Letters to the Editor | Published in Arkansas Business on April 22, 2024

BANK AND CREDIT CARD NETWORK

PERSPECTIVES NEEDED ON ‘SWIPE FEES’

Iread Monday’s story “Swiped Out: Card Fees Cost Arkansas Businesses $600M in 2022” and kept waiting to see some perspective from the payments industry. To my surprise, the Arkansas banks that I represent and the card networks that foot the bill for the nation’s modern payments system were nowhere to be found in the story.

The good news is that Arkansans are smart enough to recognize that the infrastructure the business owner mentioned in the story used to process a record number of credit card transactions in 2023 did not materialize out of thin air. The financial services industry spends billions every year investing in the technology that makes those payments so convenient, efficient and safe for merchants and their customers.

The National Retail Federation, National Federation of Independent Business and their friends in Congress want merchants and retailers to enjoy the many benefits of that modern payments system without paying anything for it. In Arkansas, we call that freeloading.

Even worse, if the retailers preferred legislation ever cleared Congress, consumers would lose their popular credit card reward programs that have helped so many Arkansas families navigate this period of high prices. History (and Federal Reserve data) also tells us that any potential “savings” would simply pad the profits of those same retailers and never make it back into consumers’ pockets.

Next time, I would appreciate a little more balance from Arkansas Business and a few more facts, especially when there is so much on the line for Arkansans.

Lorrie Trogden President and CEO, Arkansas Bankers Association, Little Rock

To the Editor: The April 8 edition of Arkansas Business had the usual informative articles and focused on the banking industry with the 2023 year-end “report cards” for banks that had become available from the FDIC.

It was surprising to see in that same edition, an article about “swipe fees” that focused entirely on the retailers who pay those fees, without indicating any benefits to the millions of consumers who appreciate and enjoy the convenience of the use of credit cards or to the hundreds of card issuers who deal with fraud and the collection of the balances owed on the cards.

Let’s remember, credit cards came into being to meet the needs of consumers who wanted to “charge” purchases without setting up accounts at every retail store where they shopped. The merchants were glad to accept the credit cards because they were helping their customers by allowing them to purchase goods on credit, and the merchants were getting almost 98% (100% minus the swipe fee of 2.26%) of the sale in cash that day! The merchants had zero risk in the transaction and simply priced their goods for sale at a price that included their cost to accept the credit cards swipe fees and cover their other overhead (rent, labor, utilities, etc.).

Because the use of credit cards has increased significantly in the past several years, the amount of total dollars being spent on swipe fees has increased in proportion, but the amount of the merchant swipe fee rate has remained virtually the same as in the past at about 2.26%.

The article cites data from the Federal Reserve which indicates that retailers’ swipe fees increased from $160.7 billion in 2022 to $172.1 in 2023. Using the average of 2.26% for swipe fees, that means that retailers’ credit card sales increased from $7,111 trillion in 2022 to $7,615 trillion in 2023. That’s a 7.1% increase in credit card sales in one year! Merchants should be ecstatic that their credit card sales have increased that much in one year with those same merchants taking zero risk in collections or fraud involving those sales.

Because of an exponential increase in credit card fraud in the past several years and the popularity of “rewards” programs that consumers expect and demand, the credit card issuers are the ones that are under “financial pressure” of the swipe fees…not the retailers (as stated in the article). Do appropriate research and you will see that the consumers will be the losers if the retailers’ Credit Card Competition Act passes in Congress. That proposed Act is merely a wolf in sheep’s clothing!

Larry T. Wilson Chairman and CEO, First Arkansas Bank & Trust, Jacksonville

The Evolution of Consumer Payments

by Brad Chambless

Since the beginning of time, people have used some form of payment to purchase goods and services. From the creation of the Mesopotamian Shekel around 2,150 BC, society has always endeavored to design payment methods with fair and equitable values. That is the foundation of a free market economy.

The evolution of digital payment by debit and credit cards is no exception. For many years, customer traffic within physical bank branches has declined as technology has provided consumers with improved access to their finances. In essence, digital payment has significantly reduced the amount of cash used by the average Arkansan.

While the fundamental currency remains the same, the form of the payment has evolved due to consumer demand. This was readily evident during the pandemic, as evidenced by data from the Federal Reserve.

The ability to provide consumers with the digital payment options of debit cards, credit cards, or both, was developed through investments made by the financial services sector. When a debit or credit card is used by a consumer, there is a small transaction cost referred to as “interchange” which is the processing expense between the retail and customer banks. This interchange serves to assist in the development of the digital payment system, manage the technology, and support further evolution to mitigate customer fraud.

One of the more well-known evolutions in the fraud prevention and security realm was the creation of the digital EMV chip card, which significantly reduced consumer fraud. Continued investment in innovation is necessary for consumer protection from criminal activity.

Recently, there has been legislation proposed to reduce the interchange on digital payments under the guise that it is either

unnecessary or unfair to retail businesses. This is simply not true nor accurate. As mentioned above, the expense for the development, operation, maintenance, and innovation was borne by the financial sector, not the retailers.

Second, the interchange on most digital payment systems has not materially changed since it was declared reasonable in 2011 upon the passage of the Dodd-Frank Act. The higher volume reported by the Federal Reserve is due to increased consumer card use and considerably higher merchant sales, not an increase in the interchange rate.

Third, Federal Reserve research indicates there is no evidence that any interchange reduction will reduce the price of goods nor benefit the consumer. In fact, many retailers pass the interchange on to the consumer at the point of sale.

Finally, retailers and small businesses actually benefit from the digital payment methods of debit and credit cards. There are significant advantages to be gained in receiving immediate payment with no fraud risk, not having to handle physical cash, no worry about checks clearing nor being returned, speeding up the transaction, and enhancing the customer experience.

Not unlike our Founders who minted the first United States coin, our society will continue to develop and adapt payment systems into the future. However, it is important to fully understand the importance of innovation and the expense associated therewith.

Fraud takes many forms and whether it is a forged check, counterfeit bill, or fraudulent credit card transaction, the impact to the consumer is the same. Arkansans have readily adopted digital payments. Interchange should not be about profitability, but providing consumers the best digital payment system and fraud protection they deserve.

“RESEARCH INDICATES THERE IS NO EVIDENCE THAT ANY INTERCHANGE REDUCTION WILL REDUCE THE PRICE OF GOODS NOR BENEFIT THE CONSUMER.”

Under Siege

Irecently had the opportunity to have lunch with an amazing Arkansas banker, and during our conversation, we discussed all the challenges we face on a daily basis. While our dialogue included the standard operational issues of staffing, liquidity and loan demand, it quickly turned to the massive regulatory burden banks are facing today. At the conclusion of our meal, I made the comment that I felt like our industry is under siege.

challenging the bureau’s expansion of rules affecting our industry.

Banking has always been one of the most highly regulated industries in the United States — and for good reason. Arguably, banks are the most important component of our country’s stream of commerce. As the primary source of credit and custodian of deposits for Americans, banks are the conduit that makes our economy possible. As a result, our government has a vested interest in ensuring that banks operate in a safe and sound manner to promote a strong economy. What’s more, the banking model has always been based on free market negotiation promoting innovation, financial inclusion, and multiple products and services from which our customers may choose.

Honestly, I can accept a regulatory framework that serves a purpose and is reasonably related to sound banking and the protection of our customers. As a symbiotic relationship, our industry cannot thrive without both. But we are experiencing regulation and legislation that materially affects the core banking business model from an income and expense perspective. Well-run banks should never have regulations imposed upon them for failures and misfortunes they had nothing to do with.

As bankers, we are focused on providing safe products and services to our customers while protecting them from bad actors using scams and fraud. Essentially, our focus on safety and soundness promotes

the well-being of the industry and our customers alike. Additional regulations should always be considered using sound reasoning and data to protect the stability of our financial system. During a speech earlier this year, Federal Reserve Governor Michelle Bowman outlined the importance of having regulators “appropriately calibrate and prioritize supervisory and regulatory actions.”

The expense and operational challenges presented by so many new regulations is overwhelming to the banking business model, to say the least. Bowman recognized this as well and said, “The lessons learned from the supervisory failures during the bank stress last Spring clearly illustrate that bank examiners and bank management should be focused on core issues, like credit risk, interest rate risk, and liquidity risk.” Simply stated, more regulations are unnecessary.

The banking industry was materially impacted by the recent U.S. Supreme Court decision that found the Consumer Financial Protection Bureau was legally funded under the appropriations clause. Albeit a setback, the Supreme Court’s decision was limited to the CFPB’s funding, and the bureau will still have to operate within the confines of its regulatory authority. Based on the aggressive demeanor of the CFPB’s supervision and enforcement actions, we should expect to see continued litigation

Webster defines “siege” as “a persistent or serious attack.” When you consider all the recent regulatory actions affecting the banking industry, I think the term “siege” is fairly descriptive. Whether the regulation is related to overdrafts or insufficient charges on deposit accounts, transaction fees on debit and credit cards, or late fees, they all directly reduce a bank’s revenue. More importantly, they have been imposed without consideration of the impact on our customers, not because of any failure requiring additional regulation. Market competition and technology have allowed banks to develop products and services to serve the needs of our customers. But technology and innovation are expensive, and the continued pressure on bank revenue will most certainly have a chilling effect on innovation.

As bankers, we are the subject matter experts and must take an active role in protecting our industry. Our regulators and legislators might have forgotten this after the Payroll Protection Program, but banking is an essential service to all Americans. That said, the most important time that we can unify and make an impact is now — while we are under siege.

At the Arkansas Bankers Association, we will continue to advocate on every member bank’s behalf. We are already working to analyze several pieces of state legislation that we expect to be filed in the 2025 General Session. I encourage you to make your voices heard, and I personally invite you to reach out and join our advocacy efforts to protect our industry. Together we can make a difference and provide a positive impact for our customers today and for future generations.

Brad Chambless | Chairman | Arkansas Bankers Association

Calendar of Events

JULY - SEPTEMBER 2024

July

01

MONDAY 1:30 P.M. – 3 P.M.

LOAN STRUCTURING BASICS

As commercial and middle market lenders know, loan structure has an important influence on the repayment of loans. In this webinar, we’ll discuss the different types of loans - seasonal, term, bridge, and permanent capital, and how to properly structure a loan. We’ll also provide strategies for explaining loan structuring decisions to your customers.

INSTRUCTOR: Tom Carlin

LOCATION: Virtual

02

TUESDAY 10 A.M. –11:30 A.M. REPORTING CRITICAL INFORMATION SECURITY AREAS UPSTREAM

One of the most critical aspects of any Information Security Program is communication and sharing information. This is especially true with executives and Boards of Director, who need education and information on all aspects of information security so they can ask better questions and make appropriate decisions. If the top level of the institution better understands the risks and the impact potential, it will help build a stronger information security culture throughout the institution.

INSTRUCTOR: Lynda Hartup

LOCATION: Virtual

02

TUESDAY 1:30 P.M. – 3:30 P.M.

DISASTER PROOFING EXCEL SPREADSHEETS

Learn to configure AutoRecover settings and enable automatic backups, set up worksheet and workbook protection to prevent unauthorized changes, and how to repair damaged workbooks. Every technique will be demonstrated twice: first, on a PowerPoint slide with numbered steps, and second, in the subscriptionbased Excel for Microsoft 365. We’ll cover differences in Excel 2021, 2019 or 2016.

INSTRUCTOR: David Ringstrom

LOCATION: Virtual

09

TUESDAY 10 A.M. – 12 P.M. DO’S AND DON’TS OF SIGNATURE CARD CONTRACTS

In this webinar, we'll discuss fundamental rules that will keep account representatives and officers from creating liability and future losses on the deposit side of the institution. We'll cover when you should retype the signature card and when it can go with small changes. We'll identify typos, whiteout, initialing and other significant issues. Common errors on ownership types and how that can create big problems on deceased accounts will also be covered. Plus, account stylings and taxpayer identification numbers - at $50 per error, how many can you afford?

INSTRUCTOR: Deborah Crawford

LOCATION: Virtual

10

WEDNESDAY 9 A.M. –THURSDAY 4 P.M.

COMPLIANCE CONFERENCE

11

This conference has been specifically developed for experienced compliance professionals who require the most up-to-date information affecting regulatory compliance taught by industry experts. Attendees should have a working knowledge of compliance and applicable regulations. Delve into Lending Compliance, Deposit Compliance, and BSA. Updates on TRID, CIP, CRA, and Fair Lending will keep participants informed about the latest compliance requirements. Gain valuable insights into Reg CC, Advertising and UDAP, SARs and more.

We'll also kick things off with the latest from Washington, D.C.

LOCATION: Little Rock, AR

16

TUESDAY 10 A.M. – 12 P.M.

NEW BSA OFFICER TRAINING

We have designed the perfect program for new BSA officers and will help you set up a framework to begin your new job and organize the sections of the BSA exam manual and law so that you will know how to begin. You will go from panic to calm, as this program will break down the components of the regulation, the exam manual and the functions so that you can begin to look at each piece one at a time.

INSTRUCTOR: Deborah Crawford

LOCATION: Virtual

FOR MORE INFORMATION ABOUT ABA TRAINING & EVENTS, AND TO REGISTER, LOG ON TO WWW.ARKBANKERS.ORG

During this program, we will look at three groups of accounts - consumer, business and specialty accounts. You won't want to miss this chance to learn how to expand or begin an online account opening program.

INSTRUCTOR: Deborah Crawford

LOCATION: Virtual

Aug

23 23 27 26 27

07 09

WEDNESDAY 5 P.M. –FRIDAY 12 P.M. BANK MANAGEMENT SEMINAR

Join the Arkansas Bankers Association for a laid-back, family friendly event: the 81st Bank Management Seminar! We encourage you to bring members of your family, and your bank family, to this annual retreat both for some R&R, and to gain insight into their increasingly important role within the financial organization.

LOCATION: The Ledger, Bentonville, AR

MONDAY 8 A.M. –FRIDAY 5 P.M.

GSB FINANCIAL MANAGERS SCHOOL

This prestigious school goes beyond the basics to present best practices and provide community financial institution financial managers the tools to build a solid foundation in asset/ liability management. Learn the unique concepts and terminology of bank finance and asset/liability management along with the practical implementation tools to profitably manage a financial institution’s balance sheet, develop effective strategies, and communicate strategies to the board and senior management.

LOCATION: University of Wisconsin

THURSDAY 9 A.M. –FRIDAY 4 P.M.

2024 IRA SCHOOL

IRA providers nationwide are fighting uphill battles as they strive to comply with numerous recent changes to the laws governing IRAs. As the IRS continues to issue guidance concerning the implementation of these changes, it is imperative that IRA providers stay abreast of these developments. By keeping abreast of these changes, IRA providers will be well positioned to better understand and implement the ongoing changes that are being made to the provider’s systems, forms, and procedures and be able to identify when additional steps may be warranted to help ensure ongoing compliance.

INSTRUCTOR: Jonathan Yahn LOCATION: Arkansas Bankers

AT A GLANCE

Live events are subject to a virtual learning environment. For more information, contact the ABA at (501) 376-3741 or Kami Coleman at kami.coleman@arkbankers.org.

The ‘Other’ CRA: A LESSER-KNOWN TOOL IN THE POLICY TOOLBOX

Rob Nichols | President and CEO | American Bankers Association

The banking agencies are tasked with writing implementing regulations for the laws enacted by Congress, but they do not have free reign. In creating these rules, regulators must act within the boundaries of their statutory authority or run the risk of legal challenge—and ABA has not been afraid to hold them accountable in court when they get it wrong. But Congress can also hold agencies accountable when there are policy disagreements by simply overriding final rules.

In ABA’s view, regulators have exceeded their authority in several recent regulatory actions, including the 1071 final rule, the credit card late fee final rule, the new Community Reinvestment Act final rule, and the expansion of UDAAP authority via an update to an examination manual.

When I addressed bankers at the 2024 ABA Washington Summit earlier this year, I assured them that ABA would use every tool in our toolbox to push back against the “regulatory tsunami” that regulators have unleashed upon the banking industry. Litigation is obviously a tool that we’ve been forced to use now several times—as evidenced by our four current legal challenges against bank regulators—but it isn’t the only option.

Among the other tools available is a lesser-known mechanism called the Congressional Review Act—which we sometimes refer to as “the other CRA.”

The Congressional Review Act was enacted in 1996 to provide Congress with an avenue for overturning certain federal regulatory actions, but inexperience with the new law and divided government meant it was only used once in its first 21 years. During the Trump administration, however, when Congress and the White House were controlled by the same party, the CRA was used successfully 16 times. Highlights included ABA-backed resolutions to overturn

“The Congressional Review Act is so powerful because resolutions can move to the Senate floor quickly through an expedited “fast track” procedure and ... a simple majority vote to pass ...”

the CFPB’s rule effectively banning the use of mandatory arbitration for financial products—a rule that ABA strongly opposed— and a resolution to nullify the bureau’s 2013 indirect auto lending guidance, after the Government Accountability Office issued a formal decision in 2017 that the guidance constituted a rule.

Congress passed CRA resolutions three more times during the Biden administration, and lawmakers continue to introduce them. Recently, ABA supported a CRA challenge to the CFPB’s 1071 final rule. That CRA challenge was passed by a bipartisan majority in both the House and Senate—and though President Biden ultimately vetoed the measure, it sent a strong and clear signal that Congress disagreed with the bureau’s rule.

In addition, a resolution of disproval under the CRA was also passed in May to invalidate the Securities and Exchange Commission’s Staff Accounting Bulletin 121, which changed the way that banks and other publicly traded entities are expected to account for digital assets held in custody. ABA is also supporting a CRA challenge to the CFPB’s recently finalized credit card late fee rule. The House Financial Services Committee favorably reported that resolution of disapproval in April.

The Congressional Review Act is so powerful because resolutions can move to the Senate floor quickly through an expedited “fast track” procedure and that, once on the floor, a resolution requires only a simple majority vote to pass—not 60 votes, like most legislation. This fast-track process stipulates a specific timeframe during which rules issued in this Congress can be invalidated by the next Congress: the rule must be issued during a window of 60 session or legislative days prior to Congress’ adjournment at the end of the year in order for the next Congress to have an opportunity to invalidate the rule. We are now nearing the window where any final rules that are issued by the agencies could be challenged under the CRA in the next Congress—yet another reason why electoral outcomes matter.

However the elections shake out in November, ABA’s focus will remain unchanged: supporting a policy environment that supports America’s banks in their mission to supply credit to their customers, clients and communities. And we’ll continue to use every tool in the toolbox to ensure that our broad and diverse banking sector can continue to thrive.

Email Rob at nichols@aba.com.

KEEPING AN EYE on Asset Quality

Susannah Marshall | Commissioner | Arkansas State Bank Department

Bankers and regulators alike have spent a significant amount of time recently commenting and discussing the fact that Asset Quality has generally been stellar for several years now and continues to perform at a high level. I am seeing and hearing a few signals that indicate an ever so slight change in some loan performance metrics across the state as well as regionally and nationally. As we all continue to monitor this area of bank operations, I think now is an important time for us to focus on another component of the Asset Quality conversation – the Allowance for Credit Losses (ACL).

I was recently in a discussion with a few federal regulators and the conversation turned to the topic of Asset Quality and the ACL. One question was posed as to where does our industry stand in the adoption of the Current Expected Credit Losses (CECL) methodology? Have banks appropriately adopted CECL and what is the examination process telling us about the banks’ analysis, documentation and implementation of CECL? I can answer that question quite easily as it pertains to Arkansas state banks. Overall, at this stage, we are not seeing any issues regarding the adoption of CECL by our state banks; however, we continue to acknowledge that it is a process and with each examination, additional information will be obtained, and further reviews will be conducted to more fully ascertain how banks have transitioned to the new methodology.

This accounting change comes at a very interesting time in the cycle of the banking industry. The consumer impact due to the unprecedented rise in interest rates between 2022 and 2023, remains to be seen; however, we are beginning to hear and see incremental changes in performance metrics within banks’ loan portfolios. Additionally, the regulators are increasingly concerned about recent changes in third-party evaluations and appraisals. State Bank Department examiners are beginning to report that in some cases, updated appraisals are reflecting notable declines in values on certain property types in certain markets; however, this remains limited and not a systemic issue at this time. Although we are not seeing this as often in local markets, it is telling that an early indicator of economic stress is beginning to emerge. Now, is the time to truly strengthen your risk management and risk mitigant processes (stress testing) around credit, especially if your institution holds loan concentrations and more specifically concentrations in commercial real estate. The enhanced focus on credit risk should

also cover other types of credit portfolios, in particular, the C&I lending sector and the strength of credit card portfolios in relation to the larger pressures on the economy and households.

Further, an additional focus is on the recent comments we are receiving about banks reporting negative provisions or a decrease in provision expense. This topic presents challenges as it is difficult to reconcile all current factors: strong asset quality, new accounting guidelines, interest rate pressure and valuation decay. I will share that regulators often respond with skepticism when we learn of institutions planning or executing negative provisions. We truly understand that the analysis to support a proper reserve or ACL is challenging, even in the best of circumstances or more definitive economic conditions, but in the current environment, additional pressure exists when making the determination how to analyze, estimate and budget provision expense in relation to the qualitative factors. However, from a regulator’s opinion, now is the time to ensure the ACL is funded appropriately, the analysis is well documented and supported and above all, the bank is prepared for the uncertain, but likely, downturn in asset quality that may occur in the near future.

“ ... updated appraisals are reflecting notable declines in values on certain property types in certain markets; however, this remains limited and not a systemic issue at this time. Although we are not seeing this as often in local markets, it is telling that an early indicator of economic stress is beginning to emerge.”

THE FACES OF ARKANSAS BANKING

with Matthew Gill

SVP Retail Operations - Security Officer Legacy National Bank, Springdale

WHAT ARE YOU MOST PROUD OF REGARDING YOUR LEADERSHIP AT LEGACY NATIONAL BANK?

There is nothing better than to see someone on my team take that next step in their career. I view the teller line as the farm system with major league baseball. We start from the basics and get them prepared for their career. I have seen people on my team move to assistant managers, credit analysts, and loan assistants. It is tough dealing with the turnover, but if my team isn’t being promoted then we are not doing our jobs.

OVER THE COURSE OF YOUR CAREER, WHAT IS THE BIGGEST SHIFT YOU HAVE SEEN IN BANKING?

I think Covid has had the biggest impact on banking since I started in 1994. It forced everyone to embrace technology that their banks offered since most banks had their lobbies closed for an extended period of time. We always had customers that used technology, but we also had those that would come into the branch for face-to-face interaction. Once people were used to the technology, they continued to use it after the pandemic. Our lobby traffic has seen a decrease while our online and mobile activity has steadily increased.

WHAT IS THE DIFFERENCE BETWEEN A BOSS AND A LEADER?

To me, a boss is someone who has knowledge of a job. A leader is someone who has the same knowledge but also has a vested interest in their team. They want to see the people on their team grow and further their career. They are willing to roll up their sleeves and get in the trenches and help their employees when needed. Also, I think a leader is accessible to their team. Let them know you are available and will make time for them.

WHAT ADVICE DO YOU HAVE FOR YOUNG BANKERS STARTING THEIR CAREERS?

Get involved and meet other bankers. Networking is so important in today’s banking environment. The way fraud is evolving, it is vital for me to have contacts at other banks. Getting involved with the Emerging Leaders was a great way for me to make connections with bankers from all across the state.

“Get involved and meet other bankers. Networking is so important in today’s banking environment.”

MY SECRET WEAPON IS: My quick wit and sense of humor.

I ALWAYS START MY DAY WITH: Wordle

HOW WOULD YOU SPEND ONE MILLION DOLLARS? Quickly

WHAT CAN YOU SIMPLY NOT RESIST? One donut

WHERE WOULD YOU TRAVEL? Fiji

TALKING OR TEXTING? Texting

FAVORITE PAIR OF SHOES? Flip flops

IF YOU WERE AN ACTION FIGURE, WHAT ACCESSORIES WOULD YOU BE SOLD WITH? Ice chest and golf clubs

WHAT TIME DO YOU GET UP IN THE MORNING? 6:05

WHAT ARE THREE THINGS STILL LEFT ON YOUR BUCKET LIST?

Seeing a concert at Red Rocks and Ryman Auditorium, and an African safari.

THE IMPORTANCE of Mentorship

Latrecia Carroll | President | Emerging Leaders Section

Mentorship is a cornerstone of professional development, providing individuals with invaluable guidance, support, and insights to navigate their career paths. The importance of having a mentor cannot be overstated, as they offer a unique perspective gained from their own experiences, successes, and failures.

Mentors serve as trusted advisors who can help mentees identify their strengths, weaknesses, and areas for improvement. By sharing their own career journeys, mentors provide valuable lessons and insights that can help mentees make informed decisions and avoid common pitfalls. Additionally, mentors can offer constructive feedback and guidance on specific skills or competencies, helping mentees develop professionally and excel in their chosen field.

One of the key benefits of mentorship is the opportunity for mentees to expand their professional network and gain access to new opportunities. Mentors often have extensive networks within their industry or field of expertise. They can leverage to connect mentees with potential employers, collaborators, or mentors. By fostering relationships with their mentor's contacts, mentees can gain valuable insights, learn about emerging trends, and explore new career paths.

Mentors serve as role models and sources of inspiration for mentees, demonstrating what is possible through hard work, determination, and perseverance. By observing their mentor's successes and learning from their challenges, mentees can gain confidence in their own abilities and aspirations. Mentors can also help mentees set realistic goals and develop actionable plans to achieve them, providing encouragement and support along the way.

Approaching a potential mentor requires careful consideration and preparation. Start by identifying individuals who have achieved success in your field or possess the skills and expertise you admire. Consider past connections, bosses, or professionals in your network. Research their background, accomplishments, and professional interests to ensure they align with your own career goals and aspirations. Once you have identified a potential mentor, reach out to them personally with a clear and concise message expressing your admiration for their work and explaining why you believe they would be a great mentor for you. If you do not know them personally, consider sending them a message or email through professional networking platforms to introduce yourself.

When reaching out to a potential mentor, it is important to be respectful of their time and expertise. Be specific about what you hope to gain from the mentorship and how you believe they can help you achieve your goals. Offer to meet for coffee or a virtual chat to discuss your career aspirations and explore the possibility of working together.

Be prepared to discuss your strengths, weaknesses, and areas for growth, and demonstrate your willingness to learn and grow under their guidance.

Once you have established a mentor-mentee relationship, it is important to nurture and maintain it over time. Schedule regular check-ins or meetings to discuss your progress, seek advice on specific challenges, and celebrate your successes. Be open to feedback and constructive criticism, and show gratitude for your mentor's time and insights. Remember that mentorship is a two-way street. Be proactive in seeking out opportunities to learn from your mentor and contribute to their professional growth as well.

Fostering a trusting relationship with your mentor will provide a sense of safety to explore new challenges. Your mentor will gradually introduce tasks slightly outside your comfort zone, providing guidance and reassurance along the way. Mentors are happy to celebrate your progress and emphasize the value of growth and learning from setbacks. Mentors reinforce the idea that discomfort often leads to personal and professional development.

Whether in professional career paths or personal pursuits, mentorship is an invaluable resource for development. As we continue to recognize the importance of mentorship in shaping emerging leaders and innovators, let us embrace the opportunity to be mentors and mentees. These connections will fuel growth and success for generations to come.

“When reaching out to a potential mentor, it is important to be respectful of their time and expertise. Be specific about what you hope to gain from the mentorship ... ”

ELS EXECUTIVE COMMITTEE

LATRECIA CARROLL PRESIDENT

STONE BANK

Little Rock

Group 1

AMBER MURPHY SECRETARY/ TREASURER

FIRST FINANCIAL BANK

El Dorado

Group 3

ELS COUNCIL MEMBERS

IAN BRYAN VICE PRESIDENT

SIMMONS BANK

Russellville

Group 2

BRITT BURRIS

CONNECT BANK

Star City

Group 3

CHANCE ROBBINS

CS BANK

Eureka Springs

Group 2

JAKE EARNEY

CHAMBERS BANK

Fayetteville

Group 2

GABE ROBERTS

FIRST COMMUNITY BANK

Jonesboro

Group 1

BRITTANY HELMS

SIMMONS BANK

Little Rock

Group 1

RHETT SHEPARD

CENTENNIAL BANK

Little Rock

Group 1

BRANDON KNOWLTON

SOUTHERN BANCORP

Arkadelphia

Group 3

SARAH LYNCH

GENERATIONS BANK

Fayetteville

Group 2

LAUREN STATON

RELYANCE BANK

White Hall

Group 3

EMERGING LEADERS

minutes with...

VE

FIVE Tanya Mims

Fayetteville Community President |

Q. OVER THE COURSE OF YOUR CAREER, WHAT IS THE BIGGEST SHIFT YOU’VE SEEN IN BANKING?

A. The tightening of lending policies after the Great Recession of 2007-2009 is the one that impacted me the most. The Dodd-Frank Act of 2010, creation of the CFPB and TRID dramatically changed how we operated to prove our compliance with all the new regulations and reforms created during that timeframe.

Q. WHAT’S THE DIFFERENCE BETWEEN A BOSS AND A LEADER?

A. A boss seems to emphasize directing, controlling, micromanaging and results. Too much focus here can lead to solutions focused too much on profit at the expense of the people they manage or the customer. However, leaders encourage, inspire and support their teammates to reach their full potential. They are typically less focused on the path to success and how the person gets there and more focused on collaboration and long-term solutions.

Q. WHAT ADVICE DO YOU HAVE FOR YOUNG BANKERS STARTING THEIR CAREERS?

A. You aren’t expected to know it all. Ask more questions and be more curious. Be extremely transparent when you make a mistake. Mistakes are excellent opportunities to develop a plan to prevent them in the future. Don’t resist menial tasks. Excel at each level and you will get trusted with more! Study the lives of those you want to emulate. Ask what they did to get where they are.

Q. WHERE DO YOU FIND YOUR SUPPORT/INSPIRATION? A. Wise friends and the Bible.

Q. HOW WOULD YOU SPEND ONE MILLION DOLLARS?

A. Most likely on income -producing real estate.

Q. WHERE WOULD YOU LIKE TO TRAVEL?

A. The Amalfi Coast, Lake Como & Portofino in Italy, Banff in Canada, Greece and Jerusalem.

Q. WHAT IS YOUR FAVORITE PAIR OF SHOES?

A. An adorable pair of fuzzy slippers from my BFF.

Q. WHAT IS THE BEST GIFT YOU EVER RECEIVED?

A. A 10-person Mariachi band that sang seven songs to me on a beach in Mexico. It was beautiful and magical!

“ You aren’t expected to know it all. Ask more questions and be more curious. Be extremely transparent when you make a mistake.”

2024-25 ABA

EXECUTIVE

CHAIRMAN BRAD CHAMBLESS STUTTGART | GROUP 3

Brad Chambless is Chief Executive Officer of The Farmers & Merchants Bank and The Bank of Fayetteville, as well as the President of The Farmers and Merchants Bankshares.

Chambless joined Farmers & Merchants Bank in 2006 where his roles there included Executive Vice President and member of the Board of Directors. He is a graduate of Dumas High School and received his undergraduate degree from the University of Arkansas at Monticello. He went on to earn a law degree from the University of Arkansas at Fayetteville, practicing law in Arkansas for 10 years before entering the banking industry.

Chambless is active throughout the regional community as a board of director of Acres of Help, Inc., the Arkansas County Imagination Library, the Stuttgart Rotary Club and the Arkansas Bar Association. Chambless also formerly served as a foundation board member for the Phillips County Community College of the University of Arkansas, the Arkansas Bankers Association agricultural sub-committee and director and vice chairman of Arkansas Capital Corporation.

CHAIRMAN-ELECT CHRIS GOSNELL MAGNOLIA | GROUP 3

Chris Gosnell joined Farmers Bank & Trust in 2010 and was elected President and CEO on January 16, 2017. Chris brought with him 6 years of banking experience from Northwest Arkansas when he joined the Bank and previously served as President and Chief Banking Officer for Farmers Bank & Trust.

Gosnell received his Bachelor of Arts in Administrative Management from the University of Arkansas in 2023, as well as his Master of Science in Operations Management in 2005. He graduated from the Graduate School of Banking in Colorado and serves on the Arkansas Bankers Association Board of Directors. In addition, Gosnell was named in Arkansas Business’s 40 Under 40 list for 2015.

Involved in numerous community activities and organizations which include: Leadership Fayetteville Graduate, 2009, Ducks Unlimited Local Board Member, Fayetteville Chapter, 2007 to 2010, Leadership Saline County Class XI, 2011, Arkansas Business 40 under 40, Arkansas Bankers Association Director, Texas Bankers Association Government Relations Committee, Southwest Arkansas Water District Director, Rotary Club of Magnolia, AR, Finance Committee - First United Methodist Church, Magnolia, AR, Southwest Arkansas Water District in Texarkana; Board Member, FBI 2018 Citizens Academy, Arkansas Game & Fish Foundation; Board Member and Arkansas State Police Foundation; Board Member.

VICE CHAIRMAN JASON TENNANT EUREKA SPRINGS | GROUP 2

Jason Tennant is President/Chief Lending Officer of CS Bank in Eureka Springs (2012-present).

Born in Fayetteville in April 1962, and raised in Lincoln, Arkansas, Mr. Tennant's journey in the banking industry has been marked by dedication and achievement. He graduated in 1980 before earning a Bachelor of Science in Business Administration from Arkansas Tech University in 1985. He further his education by graduating from the National Commercial Lending School at the University of Oklahoma and the Southwestern School of Banking at SMU in Dallas. Mr. Tennant has also completed multiple courses from esteemed institutions such as Sheshunoff, the Arkansas Bankers Association, and the American Bankers Association.

Mr. Tennant has served at various financial institutions across the state. He began his career at Union National Bank of Arkansas in Little Rock from 1985 to 1990. Subsequently, he joined the Arvest Bank Group, where he served in Fayetteville, Prairie Grove, Pea Ridge, and Berryville from 1990 to 2001. He continued his career in banking as a member of the First National Bank of North Arkansas (now Bank of 1889) in Berryville from 2001 to 2012. Since 2012 he has served at CS Bank.

TREASURER SCOTT SAFFOLD

MONTICELLO | GROUP 3

Scott serves as the EVP/Chief Lending Officer at Union Bank & Trust Company, Monticello. He has served as a member of the executive management team for nineteen years. He is a Certified Public Accountant, graduate of the Southwestern Graduate School of Banking at SMU, ABA Commercial Lending School, and numerous other banking courses.

A graduate of the University of Arkansas at Monticello, BS Accounting, a graduate of Leadership Arkansas Class V. As a Monticello native, Scott is actively involved in the local community, and currently serves on the following: Vice Chairman of the University of Arkansas Foundation Fund Board as a member of the Executive and Audit Committee, Vice Chairman of the UAM Board of Visitors, and UAM Foundation Fund Board, and past board member of numerous local organizations.

PAST CHAIRMAN JIM TAYLOR ROGERS | GROUP 2

Jim Taylor is Senior Vice President at First Security Bancorp in Rogers. Prior to transitioning to the holding company, Taylor was the Regional President of First Security Bank with management oversight of all operations in Northwest Arkansas, including retail and commercial banking activities at 16 full-service banking centers. He started with First Security Bank in April 1998 opening a Loan Production Office in Fayetteville and oversaw First Security’s expansion into Northwest Arkansas. Taylor attended Arkansas Tech University, where he earned his BS in Agricultural Business.

Taylor is a member of the Government Relations Advisory Committee for Arkansas Bankers Association, Advisory Board for Arkansas Tech University School of Business, Law Enforcement Assistance Program, and serves as the General Volunteer Chairman for the LPGA NWA Championship.

2024-25 ABA

BOARD OF

JOHNNY ADAMS

President / Conway Market

FIRST SECURITY BANK

Conway | Group 2

BEN BUERGLER

Senior Vice President

FIRST NATIONAL BANK OF NWA

Bentonville | Group 2

LATRECIA CARROLL

SVP/Operations Manager

STONE BANK

Little Rock | Group 1

ASA COTTRELL

SVP/Sales Manager

ARVEST BANK

Little Rock | Group 1

JOE DUNN

Chief Lending Officer

STONE BANK

Little Rock | Group 1

ROBIN HACKETT

Chief Mortgage &

Chief Operation Officer

FIRST SERVICE BANK

Greenbrier | Group 2

HEATHER JONES

President, Arkansas

BANK OF AMERICA

Little Rock | Group 1

JEFF LYNCH

President & CEO

EAGLE BANK & TRUST COMPANY

Little Rock | Group 1

DIRECTORS

KATHERINE MITCHELL

SVP – Bank Services

RELYANCE BANK

White Hall | Group 3

JOHN OLAIMEY

President & CEO

SOUTHERN BANCORP BANK

Little Rock | Group 1

CALVIN PURYEAR

SVP/COO

MERCHANTS & FARMERS BANK

Dumas | Group 3

RANDY RAWLS

Vice President

UNION BANK & TRUST COMPANY

Warren | Group 3

LORI ROSS

City President

CITIZENS BANK

Arkadelphia | Group 3

LOREN SHACKELFORD

President, Chief Lending Officer, N. Arkansas

CHAMBERS BANK

Fayetteville | Group 2

ROB S. TIFFEE

Senior Vice President

REGIONS BANK

Little Rock | Group 1

RON WITHERSPOON

President & CEO, Central Arkansas

ARVEST BANK

Little Rock | Group 1

THE Making

by Roby Brock

FROM AGRICULTURE TO LAW TO BANKING, ABA CHAIRMAN BRAD CHAMBLESS MAY BE ONE OF THE MOST VERSATILE BANKERS IN ARKANSAS.

Growing up in Dumas, Arkansas, the last thing Brad Chambless thought he would be doing for a living was in banking.

His parents moved to the southeast Arkansas town in 1970 from Louisiana when Brad was very young. His father was a hometown pharmacist and his mother was a school teacher. Brad grew up in the ‘70’s like most Arkansas kids did – outside all the time playing with neighborhood friends, riding bikes, and generally unwatched because Dumas was a safe small town.

“Dumas was a thriving agriculture community. It had about 6,000-7,000 citizens,” Chambless said. “We were outside the entire time growing up, and one of the great memories is riding your bicycle because you could ride it for miles and miles and no one ever asked questions. Today, that would probably be frowned upon, but it was just a great, great environment to raise a family, and I always look back at that and have a very deep affection for Dumas in that area of the state.”

After graduating from Dumas High School, Chambless enrolled at nearby University of Arkansas at Monticello. He didn’t have much scholarship money to attend, so his goal was to get a degree in three years and finish debt-free. Majoring in agricultural business and economics, he worked for a local farmer through college and had instant employment upon graduation in the agriculture sector.

Community

2024 PAST CHAIRMAN’S DINNER

FROM AGRICULTURE TO LAW TO BANKING

“There are several seed companies in that part of the state, and I already had an offer to go get your degree, come back and you can take over for us. That was the plan and that's exactly what happened. I came back home in 1990 and started work operating that seed company and realized very quickly I didn't want to work 16 and 18 hours a day when trucks are coming in and out,” Chambless said.

Soon after working full-time for the seed company, he took the LSAT pre-law school exam and took off to Fayetteville to get his law degree.

“I graduated from there in 1996 - which seems like a million years ago now - took the bar and passed. During that interim period when I'd taken the bar and got my score for licensure, I worked for a local attorney. Kenny Johnson gave me my first job and I began immediately in litigation. That was the path. He was a great litigator. I started trying cases with him, as I was not a transactional type lawyer. I always wanted to be in court and practice,” he said.

Chambless and his wife, Ja, located in DeWitt to practice law and raise a family.

He represented some area banks, but Farmers and Merchants Bank headquartered in Stuttgart wasn’t one of them. Still, they came calling on Chambless. Being as well-connected in southeast Arkansas as he was, the bank wanted him to be a market president and commercial lender. Chambless couldn’t see the path of exiting his law practice and going to work for the bank, so he turned them down.

Also capitalizing on his agricultural background, Chambless represented a variety of farm-related cases, including a seed company that proved to be a landmark case.

“In 2005, I tried at that time the largest seed intellectual property case in the nation in federal court. I'd also just had my first child and was living the dream. Practicing law is one thing, but when you layer in your first child, it kind of changes your perspective,” he recalled.

The new dad had been in court for more than a half-month on the trial and had not seen his newborn son during most of that time.

“When I came home from that long jury trial and had not seen my son in two-and-a-half weeks, the bank showed up at the door and they were like, ‘We want to talk to you again.’ And I'm like, ‘I'm not as hardheaded as I used to be.’ We started a conversation. I took that leap of faith and they've been better to me than I could have ever asked for my family. It also gave me structure and the ability to go home on my terms and know where I was supposed to be for my family. That's how I pivoted and came into banking,” he said.

FAMILY FIRST

Putting family first was the motivation that shifted Chambless’ career path into banking. He beams with pride when the conversation turns to his wife, Ja. She is the director of the Pattillo Center-School in DeWitt, now the family’s hometown.

The school was established to meet the needs of children with developmental disabilities and their families in the Arkansas County region. The center focuses on intervention and offers speech therapy, occupational therapy, and physical therapy.

“She services the entire county of Arkansas County and services about 105 children every day. Most of those families don't have the means to get them there and they certainly couldn't get them to metropolitan area like in Easter Seals here that they would love to get to. It is just not economically possible and it's her passion and her calling.”

The Pattillo Center is named after Don Pattillo's family, a previous president and CEO of Farmers and Merchants Bank. Chambless described him as “a great banker, a great mentor.” Pattillo had been in business a long time and had a similar background to Chambless having also been an attorney.

Chambless’ two sons are 19-year old Reece, a student at the University of Central

MAJORING IN AGRICULTURAL BUSINESS AND ECONOMICS, HE WORKED FOR A LOCAL FARMER THROUGH COLLEGE AND HAD INSTANT EMPLOYMENT UPON GRADUATION IN THE AGRICULTURE SECTOR.

PHOTO: Left to Right: Eddie Holt, Don Pattillo, Jim Cargill, Randy Scott, Rob Robinson, I. Joe Miles, Jon Harrell, Larry Kircher, Cathy Owen, Jim Taylor, Larry Wilson, John Womack, Sean Williams, Reynie Rutledge, Charles Blanchard, Robert Taylor

“WHEN I CAME HOME ... AND HAD NOT SEEN MY SON IN TWO-AND-A-HALF WEEKS, THE BANK SHOWED UP AT THE DOOR ... WE STARTED A CONVERSATION. I TOOK THAT LEAP OF FAITH AND THEY’VE BEEN BETTER TO ME THAN I COULD HAVE EVER ASKED FOR MY FAMILY.”

Arkansas, and 15-year old Jackson, a 10th grader at DeWitt High School (Go Dragons!). He’s been known to coach a team or two for the boys, who have been active in baseball, basketball and golf.

CLIMBING THE BANKING LADDER

Farmers and Merchants Bank is headquartered in Stuttgart, Arkansas and has branches in Des Arc, DeWitt, Hazen, Morrilton, and Perryville. It was founded in 1945 and has made two major acquisitions in the last decade. In 2015, Farmers and Merchants acquired The Bank of Fayetteville to broaden its footprint into bustling Northwest Arkansas. In 2019, the bank’s holding company purchased Integrity Bank of Mountain Home, which also had branches in Bentonville, Gassville, Lakeview, Pocahontas and Jonesboro. Chambless was named President and CEO in 2021.

When Chambless started his banking career, Pattillo was the president. His advice to Chambless?

“You're going to make mistakes. Just make sure they're little ones,” Chambless laughs.

Gary Hudson succeeded Pattillo, and Chambless also considers him a great mentor and role model.

“I was very fortunate beginning with Mr. Pattillo and then further with Gary Hudson. They encouraged me and asked me to engage and be a part of the legislative side of the Banker's Association,” he said, noting that his legal background positioned him to be knowledgeable and tactical on dealing with state and federal legislation and its potential impact on banking.

Brad Chambless ABA Chairman

“I BEGAN TRAVELING SOME WITH THE STATE ASSOCIATION TO WASHINGTON D.C. LEARNING THE REGULATORY SIDE OF BANKING AND THEN DEALING WITH OUR DELEGATION ON AN IN-PERSON BASIS THERE.”

“I began traveling some with the state association to Washington D.C. learning the regulatory side of banking and then dealing with our delegation on an in-person basis there. That moved from one trip a year to two trips a year, and I continued to grow with the association. I was then asked to come onto the board and worked up through the leadership program,” he added.

As he has moved into the ABA Chairman's role, Chambless' experience as government relations chair for the association, which puts him square in the middle of a plethora of state and federal legal issues. At the state level, Arkansas lawmakers have pushed for protections for elder abuse and have chosen to regulate state investments regarding Environmental, Social and Governance (ESG) decisions.

“When the legislature goes into the session, which will happen in six months, we'll be super busy and start tracking all of the state bills along with everything that's federal,” he said.

THE CHAIRMAN’S BIGGEST ISSUES

Elder abuse is a major concern for Chambless. He has seen it happen to unsuspected elderly customers with his bank and he knows it’s a widespread issue. The warning signs can range from nervous customers with strangers, online scams to simply noticing checks out of sequential order.

“I deal with elder exploitation almost daily. This week alone, I've had two cases that I've had to deal with,” he said.

He sees three overarching themes in most cases where elderly customers are exploited. Older Arkansans are more trustworthy than younger generations and that can often lead to them helping someone in need without being careful. Social media and technology have developed new methods for predators to prey on the elderly. And, the COVID-19 pandemic created a new wave of scams that targeted older bank customers who were isolated and lonely.

“It's hard to believe it's possible, but it's heartbreaking,” Chambless said.

In the month of June, the Arkansas Bankers Association made a big push to its member banks to provide materials to raise awareness of elder financial exploitation.

“The other thing that I really have a passion for are veterans and service members. We are really trying to make a big push to make products available, especially in some of our more rural markets, some of the markets that I operate in. We're creating products and services just to give a reward and service for those who've already served and allow us to do what we do,” he said. “Out of utter respect, there are a lot of service members who need

some help and some support, whether they're active or inactive as veterans.”

Other regulatory issues that will be on Chambless’ radar during his term as ABA Chairman include:

• Section 1071 of the Dodd-Frank Act, where small business owners will have onerous data reporting requirements put on them;

• The Corporate Transparency Act that will require business owners to submit additional data to a government type repository or database; and

• The Durbin amendment, which would reduce credit card transaction fees and shift fraud costs onto issuers and consumers.

As chairman of the Arkansas Bankers Association, Chambless expresses a lot of pride in the organization and the difference it is making for the industry and the communities they serve.

“For me, it's about small town banking, rural Arkansas. There are more banks in rural Arkansas than there are in our urban areas just because we can't afford to have banking deserts. Community banks have always carried that burden of making sure that all of our communities have consumer and business products that are fair and equitable to keep that community thriving and growing,” he said. “I think it was never more true than when the government asked us to engage in PPP, the Payroll Protection Program. The government could not have pulled that off without Arkansas banks.”

“FOR ME, IT’S ABOUT SMALL TOWN BANKING, RURAL ARKANSAS. COMMUNITY BANKS HAVE ALWAYS CARRIED THAT BURDEN OF MAKING SURE THAT ALL OF OUR COMMUNITIES HAVE

CONSUMER AND BUSINESS PRODUCTS ... TO KEEP THAT COMMUNITY THRIVING AND GROWING.”

“My goal is to always say 'thank you' to the member banks we have around the state for what they do and make sure that it's a source of pride. It should be. Every banker in Arkansas should have that pride when they wake up. A community bank is only known as a community bank by its customers, but if you do it correctly, that community should see you every day taking care of that community and all of the people that have needs in it,” Chambless said. “It's just super important that we keep our community banks very strong.”

YOUR COMPANY UNCOVERS Financial Fraud.

NOW WHAT?

by Mike East, CFE SafeHaven Security Group

Imagine you are the CEO of a company, and there is a knock at your office door. You tell them to come in, and your CFO and HR Director quickly enter your office and close the door behind them. The CFO tells you that Mary, an Accounts Payable Supervisor who has been with the company for over 15 years, is in the main conference room crying.

You know Mary, she is the employee that everyone likes and trusts. In fact, Mary is so well respected that you let her plan the annual Christmas Party, and she handles purchasing gift cards to give out to the employees. Mary also helps get ready for the annual audit when the outside accounting firm shows up, and pays the monthly credit card statements for you, the CFO, and the 6 salespersons that work for the company.

The CFO states that it appears Mary has misappropriated approximately $15,000 from the company.

Now, you feel like you got hit by a semi-truck that just kept going. Not Mary. She wouldn’t steal from the company, nor from me. We are not just co-workers; we are a family here. You then ask the CFO a thousand questions.

How did this happen?

Who discovered it?

Why would Mary steal from the company?

Is there anyone else involved?

How long has this been going on?

How come our outside Auditors didn’t find anything in the annual audit?

The CFO’s answer to all these questions is the same, “I don’t know…”

Then you start to realize that your shock has turned into anger. You order the CFO and HR Director to fire Mary at once and have her escorted off the property. After that’s done, you want to speak to the head of the accounting firm that conducted your yearly audits and find out why this wasn’t detected sooner. Then you want to talk to your lawyer to discuss your legal options regarding suing Mary and the accounting firm. Somebody is going to pay for this, and you want to lash out at everyone. You have been deeply hurt by Mary, but most of all, you feel a deep sense of both personal and professional betrayal.

These events that I just described were taken from an actual case that my agents and I worked on several years ago from the Financial Crimes Unit of the North Carolina State Bureau of Investigation. For those of you who like to skip to the last chapter of a book, I’ll be glad to summarize

SHE STOLE APPROXIMATELY $1,000,000 IN EACH OF THESE YEARS, FOR A TOTAL LOSS OF $5,000,000.

NO ONE WAS GOING BEHIND HER. SO, THE NEXT QUESTION IS, WHY WASN’T THIS PICKED UP IN THE YEARLY AUDITS CONDUCTED BY THE OUTSIDE ACCOUNTING FIRM.

it for you. Mary had an on-line gambling addiction, which grew into trips to the casinos in Las Vegas a couple of times a year. Mary was using 3 of the company credit cards that were assigned to the 6 salespersons. At some point, 3 of the salespersons left the company to pursue other jobs. Since she was the Accounts Payable Supervisor, no one was going behind her looking at monthly credit card bills for 3 employees that were no longer there. The 3 former employees’ credit cards also showed expensive dinners, vacation trips, rental cars, airfare, hotels, name brand purses, and various other items that could be easily explained if she was ever questioned about them. As for the gift cards for the employees at the Christmas party, Mary did purchase about $2,000 in gift cards for the party each year that were given out to the employees. However, she also purchased an additional $8,000 in gift cards for herself that she used throughout the year for meals, electronics, or just general shopping. We found stacks of gift cards, wrapped in rubber bands in her kitchen drawers when we executed a search warrant at her residence.

We went back and traced every transaction that Mary did for the past 5 years while she worked at the company. She stole approximately $1,000,000 in each of these years, for a total loss of $5,000,000. I asked the CEO and CFO of the company how they did not miss $1,000,000 in revenue each year. The CEO said, “Mike, our company brings in a half billion dollars in revenue each year. If you had five hundred, $1 dollar bills on a table, regardless of if they were stacked up or scattered around, would you be able to easily see that one of them was missing?” He made an excellent point. This is one of the most profound statements I have ever heard, and I have shared it with clients who are in a similar situation. The more successful your business becomes, the more important it is to stay on top of your finances.

So how did $15,000 grow into $5,000,000? The obvious answer is no one was going behind her. So, the next question is, why wasn’t this picked up in the yearly audits conducted by the outside accounting firm. That’s because audits are designed to look at a company with a high-level view, to determine if the company is making more money than it is spending. Most audits do random sampling of invoices, credit cards, and expenses. Mary was smart enough to use the salespersons’ credit cards that were still working at the company, and of course, all those expenses and payments were properly documented for the auditors. Mary has become comfortable and adept at covering her tracks after all these years.

As the officer of a company, regardless of if it is privately held, publicly traded, a non-profit, or a governmental entity, what happens next if you unfortunately find yourself in a similar situation? There are many questions to consider, but at the end of the day as the CEO, you are worried about the financial health of your company, the potential reputational damage this incident will cause, and can your company survive?

I encourage you to find an expert to guide you through this extremely critical point in your company’s history and to help evaluate and navigate this terrain. You can use a financial investigator…

TECHNIQUES FOR FRAUD

Detection & Prevention

by Bob Sprague Forvis Mazars

The story of Mary is an all-too-common narrative that organizations across the globe face every day. A long-term employee everyone trusted had been given a key role in an accounting function where opportunities existed. When facing financial pressure, the employee resorted to occupational fraud to escape her financial situation. Management is left searching for answers on how they fell victim to the fraud and wondering how they could have prevented it.

The Association of Certified Fraud Examiners (ACFE) estimates that organizations, just like Mary’s company, lose approximately 5% of revenue to fraud annually. In its most recent biannual study on occupational fraud, the ACFE examined 1,921 cases of occupational fraud across 138 countries and territories, which led to total losses of $3.1 billion to the organizations included in the survey.1 Among the fraud schemes that led to these losses, the most common types fell into the category of asset misappropriation—theft of a company’s assets by its employees—like the fraud that Mary perpetrated.

As the underlying facts of these types of fraud develop, management, like the CEO of Mary’s organization, asks the types of questions posed here. How could this have happened? Where were the auditors? Auditors are specifically hired to prevent issues like this, aren’t they? These last two questions expose a common expectation gap that many have about the role of an external audit and the responsibilities of the external auditor.

The roles and responsibilities of the external auditor are defined in AU Section 110, Responsibilities and Functions of the Independent Auditor. Auditors have “a responsibility to plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether caused by error or fraud.”2 Reasonable assurance is not the absolute assurance that some expect from an auditor creating this gap between expectations of management and other stakeholders as it relates to auditors identifying fraud

during their work. As much as organizations and other stakeholders may want to rely on external auditors to identify fraud, the reality is that organizations need to put in place multiple controls and processes to help fight fraud. An external audit is just one of many anti-fraud controls that can help with the battle.

THREE RECOMMENDATIONS FOR COMBATING FRAUD – BE PROACTIVE

Confidential Reporting Tool

If an external audit is not the silver bullet for detecting fraud, how else can organizations better combat the issue of occupational fraud? One of the areas the ACFE examines in its biannual study is how frauds are initially detected. Each year the ACFE study is published, the most common detection method by far is via a tip. In the 2024 study, 43% of all frauds studied were detected by a tip from an employee, customer, vendor, or other

IN THE 2024 STUDY, 43% OF ALL FRAUDS STUDIED WERE DETECTED BY A TIP FROM AN EMPLOYEE, CUSTOMER, VENDOR, OR OTHER TIPSTER.

tipster.3 No other method was even close, with internal audit following at 14%, and management review at 13%.4 Surprisingly, only 3% of the cases studied were initially detected by the organization’s external auditors.5 This statistic provides a compelling argument for companies to bring about a confidential reporting mechanism that can be used by employees and others, including external third parties, to confidentially come forward with a tip if they witness a fraud. Would-be tipsters are more likely to come forward if they can do so confidentially, as many may fear retribution if their identity is known. Further, tipsters are better equipped to help fight fraud if there is a formal mechanism they can use to report. The ACFE found that organizations with hotlines are almost twice as likely to uncover fraud via a tip than organizations that do not have a hotline.6 A proactive tool such as a hotline may not prevent fraud from occurring, but it will help organizations identify an issue earlier to mitigate possible losses.

Surprise Internal Audits

It is difficult to dissuade a fraudster if they believe nobody is looking. External audits may fail to detect a fraud if fraudsters

are able to know where the auditors are looking, or the fraudulent transactions are not selected in a random audit sample. A more effective approach is to go looking for fraud. A broad fraud detection program should include a risk assessment to help identify the areas most susceptible to fraud risk. Once those areas are identified, surprise internal audits can be a highly effective tool for detecting and deterring fraud. A well designed internal audit process that focuses on fraud risk areas can allow organizations to complete a more in-depth audit, specifically searching for indicators of fraud. Fraudsters will be less likely to commit fraud if they fear detection, but, at a minimum, when fraudsters know the organization is monitoring activities, they may be deterred.

Proactive Data Monitoring

Every day, organizations generate vast amounts of data that can be analyzed for potential indicators of fraud. In an increasingly more complex and digital world, the amount of data available for analysis continues to explode. However, with complexity comes opportunity for fraudsters. Organizations should use the available data at their fingertips to help with fighting fraud. There are numerous data analytic tools on the market that organizations can purchase that are specifically designed to search for potential fraud indicators. Alternatively, many organizations develop their own tools to assist with this effort. Regardless of whether organizations choose to purchase or develop their own fraud-fighting tools, cost should not be a deterrent. Organizations are prone to waiting until they have had an issue because they do not want to spend the money to be proactive. They wait until they have lost $5,000,000 to Mary.

If you have questions or need assistance, please reach out to a professional at Forvis Mazars today.

This article is for general information purposes only and is not to be considered as legal advice. This information was written by qualified, experienced professionals at Forvis Mazars, but applying this information to your particular situation requires careful consideration of your specific facts and circumstances. Consult a professional at Forvis Mazars or legal counsel before acting on any matter covered in this update.

EMPOWERING WOMEN ENTREPRENEURS

ARKANSAS WOMEN’S BUSINESS FUND

by Deborah Temple Financing Strategies

Small businesses are the backbone of our communities, driving economic growth, generating employment opportunities, and fostering innovation. Women entrepreneurs are at the core of this dynamic ecosystem, and their contributions are vital to community prosperity. However, despite their indispensable role, women-owned businesses often encounter obstacles when accessing the capital necessary for success.

As advocates for financial inclusion and economic empowerment, banks play a crucial role in dismantling these barriers and supporting the aspirations of women entrepreneurs. Enter the Arkansas Women’s Business Fund (AWBF), a new initiative to help transform the lending landscape of women-owned businesses in our state.

BUILDING ON BANK ON ARKANSAS+ PROGRESS: THE PIVOTAL ROLE OF COMMUNITY BANKS