Steve Brawner, Latrecia Carroll, Brad Chambless, Jake Fair, Susannah Marshall, Rob Nichols, John T. Olaimey, Tim Schenk, and Barry Thompson

The Arkansas Banker (ISSN 004-1726) is published quarterly by the Arkansas Bankers Association, 1220 West Third Street, Little Rock, AR 72201. Phone: 501.376.3741. Periodical postage paid at Little Rock, AR. Postmaster: Send address changes to Arkansas Bankers Association, 1220 West Third Street, Little Rock, AR 72201. Subscription to The Arkansas Banker magazine is included in the membership fees to the Arkansas Bankers Association. Cover price is $5.95 each. Annual subscription rates are $40.00 for members and $60.00 for non-members.

Federal tax law prohibits the deduction of lobbying expenses for federal incomes tax purposes. Organizations like ABA, which assess member dues, are required by law to notify their members of the portion of their dues attributable to lobbing/and therefore non-deductible on your federal tax return. For the year 2023, it is estimated that 9.32% of your dues will be attributable to lobbing as defined by the IRS. Contributions to ABA are not charitable contributions, however, they may be deductible as a legitimate business expense.

Chairman’s Column Washington Update Commissioner's Column Emerging Leaders

The CFPB is eyeing changes.

Serving Veterans

Banks in Arkansas and across the nation are finding new ways to serve veterans.

Compliance

The FDIC offers guidance on ITMs. CDFI Banks

Leveraging nonprofits to meet customer needs.

Non-Competes

Litigation continues on a complicated issue.

St. Louis Fed President Alberto Musalem visits Little Rock.

Attacking the ITMs

A new security threat is emerging.

Bank Management Seminar

A recap of the annual event in Bentonville.

44 NEWS & MOVES

PRESIDENT’S MESSAGE

Lorrie Trogden | President & CEO | Arkansas Bankers Association

has seen a record number of credit unions purchasing banks.

Per S&P Global, credit unions had acquired $7.2 billion of bank assets. Credit unions are utilizing their tax-free status and exploiting government loopholes to outbid other interested parties. Each time a credit union buys a bank, those tax dollars are gone; eroding state and federal tax bases and weakening remaining community banks who are the backbones of the communities they service.

However, this issue goes beyond just tax dollars. According to the National Credit Union Administration, as of the first quarter of 2024, credit unions are holding $160 billion in commercial loans, which is more than double what they held in 2019. According to a study published in the Journal of Financial Stability, buying banks strengthens credit unions’ abilities to grow commercial lending, however, it may also weaken the system as a whole by weakening credit unions’ net worth. Commercial loans are typically riskier than real estate or credit card loans. The study indicates “business loans could be indicators correlated with more likely subsequent decreases in net worth through the larger increases in loan loss provisions related to underperforming and non-preforming loans, and through the reduction of interest income associated to non-preforming loans...business loans have an effect on future delinquency rates between two and three times higher than that of the other loans of the credit union.” Standards continue to relax and fields of membership continue to grow, which will continue to exacerbate this issue as credit unions persist in increasing commercial lending.

Another very large concern is that credit unions are not required to adhere to the Community Reinvestment Act (CRA), which requires lending and investing in low- to moderate-income neighborhoods and communities of underserved individuals.

The recent Navy Federal Credit Union scandal drives this point home. It reportedly approved 75% of white borrowers while rejecting more than half of black applicants and turning down Latino applicants at a rate approaching 50%. Navy Federal CU should absolutely be called before Congress to explain why our service men and women, including veterans, were harmed by these lending practices. Had it been subject to the Community Reinvestment Act, which it and other credit unions oppose, this may have never happened.

In my home state of Arkansas, there are still many small rural towns that have bank branches but no credit union presence, directly speaking to banks’ commitment to serve all local communities and not just the most profitable areas of the state. Because of instances like this and other problems, some states are enacting state CRA laws for state-chartered credit unions.

According to polling conducted by Morning Consult, 68% of adults said credit union customers should have the same CRA protections that banks provide, while 54% said Congress should investigate whether the credit union tax exemption is still warranted.

Lastly, credit unions are hurting their own members by denying them dividends. Instead of returning profits to members, which is one of the “benefits” of being a credit union member, they

are spending those profits on lavish buildings, executive compensation and marketing.

Northwest Federal Credit Union recently used tax-payer subsidized profits to ink a deal to secure the naming rights to the Washington Commanders stadium. It will pay $7.5 million a year for the naming rights to an NFL stadium, raising the question again of how a tax-exempt entity that is supposed to be serving low and modest means customers can afford such a whopping price tag. (Northwest CU was founded in 1947 to serve CIA employees)

Unlike other non-profit organizations, such as mine, some credit unions are also paying their board members and taking them on extravagant trips and retreats. These practices are again being subsidized by tax-paying citizens.

Unlike other non-profits, credit unions do not have to answer for these sorts of practices or prove to the IRS that they are staying on mission because they are exempt from filing a form 990. My small association with a budget of $1.6 million has to file a form 990 with the IRS that is over 40 pages long, but the $8 billion-dollar Northwest Federal CU submits nothing.

For these and a myriad of other reasons, credit unions should not be able to manipulate their tax-free status to buy banks. This harming of the financial system, their members, and the communities they live in can all be avoided. If credit unions are going to operate like banks in their product offerings, such as high-dollar commercial real estate loans, and acquisition strategies, they should be taxed and regulated like banks.

Lorrie Trogden, President & CEO

CONGRATULATIONS Graduates!

The Arkansas Bankers Association proudly congratulates Zane Ludwick and Brad Martin on their graduation from the esteemed GRADUATE SCHOOL OF BANKING AT COLORADO.

ZANE LUDWICK

ARVEST BANK Fayetteville

BRAD MARTIN

CITIZENS BANK & TRUST Van Buren

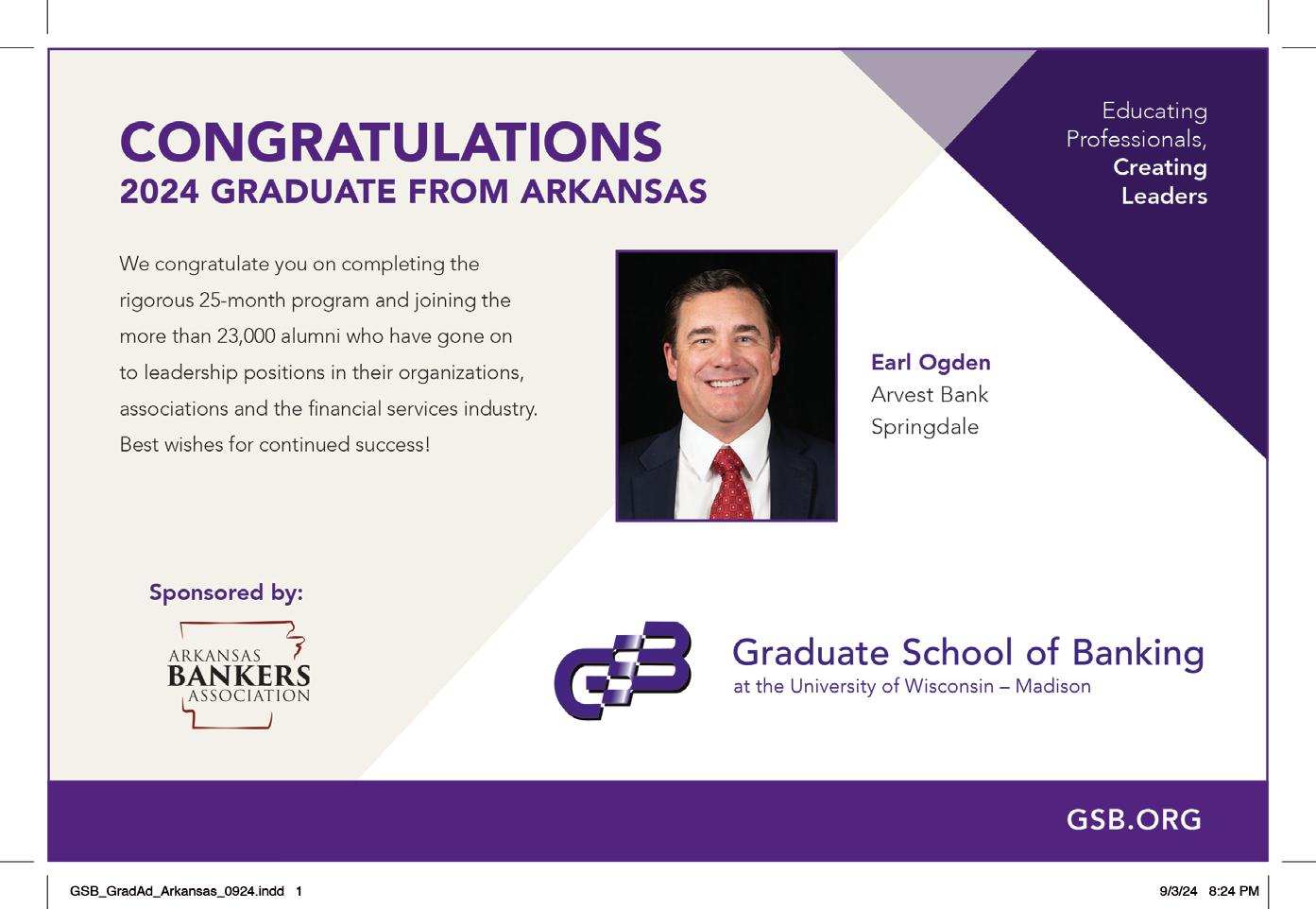

The Arkansas Bankers Association proudly congratulates Levon Ogden on his graduation from the esteemed GRADUATE SCHOOL OF BANKING AT THE UNIVERSITY OF WISCONSIN-MADISON.

LEVON OGDEN

ARVEST BANK Springdale

CONGRATULATIONS TO THE GSB SCHOLARSHIP WINNER

LYNDSAY CARTER

Chief of Staff

FARMERS & MERCHANTS BANK / THE BANK OF FAYETTEVILLE Stuttgart

2024 SCHOLARSHIP to the Graduate School of Banking at the University of Wisconsin-Madison

ABA OFFICERS

Brad Chambless, Chairman Farmers and Merchants Bank, Stuttgart

Chris Gosnell, Chairman-Elect Farmers Bank & Trust Company, Magnolia

Jason Tennant, Vice Chairman CS Bank, Eureka Springs

Scott Saffold, Treasurer Union Bank & Trust Co., Monticello

Jim Taylor, Past Chairman First Security Bancorp, Rogers

Lorrie Trogden, President & CEO

Arkansas Bankers Association, Little Rock

BOARD OF DIRECTORS

Johnny Adams, Conway

Ben Buergler, Bentonville

Latrecia Carroll, Little Rock

Asa Cottrell, Little Rock

Joe Dunn, Little Rock

Robin Hackett, Greenbrier

Heather Jones, Little Rock

Jeff Lynch, Little Rock

Katherine Mitchell, White Hall

John Olaimey, Little Rock

Calvin Puryear, Dumas

Randy Rawls, Warren

Lori Ross, Arkadelphia

Loren Shackelford, Fayetteville

Rob S. Tiffee, Little Rock

Ron Witherspoon, Little Rock

The Good, The Bad, and The Ugly

Brad Chambless | Chairman | Arkansas Bankers Association

Recently, I was addressing a group of new employees during an orientation meeting and drew looks of amazement when I said the smartphone had not been developed when I began my banking career. My point was simply that such a common piece of technology has only been in the market for about 20 years, yet it is so much more powerful than its predecessor, the telephone.

The same advances in technology apply to the world of banking and finance. Many of us have experienced the shift from the green ledger paper and calculators of yesteryear to integrated computers and software that process our work at the click of a button. Massive investments in technology have fueled the velocity of research and development at an amazing pace.

All of this new technology has brought incredible benefits and efficiencies to our industry, but it has also created a plethora of issues that cause concern. While I lack the space to discuss all these issues in depth, I do want to address some of them and how the Arkansas Bankers Association is working to provide solutions for members.

THE GOOD

Some of the great things that technological advancements have brought us include robotic process automation, Integrated Teller Machines, electronic signature capability, remote work and virtual meeting capabilities. In fact, just since the pandemic, virtual meetings have become common. I am confident that there are far more solutions being developed that will enhance customer experience, increase efficiency in product delivery, and help monitor and reduce the risk to the bank.

THE BAD

Arguably, the most prolific technology threat to banks lies in cybersecurity risk. In fact, cybersecurity risk has remained at the top of the Conference of State Bank Supervisors (CSBS) Community Bank Sentiment Survey for the past two quarters. While this threat is not limited only to banks and financial institutions, I would argue

that it is much more impactful to our industry. Banking is and always has been founded on the premise that our customers place their trust in us to keep their assets safe. As an existential threat to our industry, it is imperative that we all vigorously defend to protect our customers’ trust.

Further, while check theft, washing and altering have always plagued banks, now the ability to apply for accounts and wire money online has elevated the threat of fraud. When coupled with ATM thefts using malware and physical removal of the machines, banks are facing more risk daily. Navigating the balance between convenient products and services and the economic and reputational risk to our institutions has never been more difficult.

Two of the newest technological threats that we must deal with quickly are quantum computing and artificial intelligence (AI). As mentioned above, both technologies are rapidly developing and will affect our industry. As bankers, most of us are not equipped nor adequately staffed to have in-house technologists develop adequate mitigation tools. As a result, it is imperative that we become more proactive in our efforts to prepare for these new threats.

THE UGLY

The truth is that technology is expensive. With respect to the economic impact to our institutions, our daily technology costs have increased substantially. This led me to ask, “Are we getting the necessary solutions that we need from these companies?” After considerable discussion, I was simply not convinced. Essentially, the vast majority of our technology platforms are standard or “canned” products developed by a software engineer. Every community bank is somewhat unique, and a one-size-fits-all approach is not logical. Even assuming that we can have a custom solution created, it would involve additional expense, as you know.

The ever-changing landscape of technology and software that affects banks will continue to evolve, and we must be prepared for the rapid changes ahead. I want you to know that the Arkansas Bankers Association is committed to all member banks, and our team is working tirelessly to protect and support our industry.

REGULATIONS & LEGISLATION

We just returned from Washington, D.C., where we discussed technology and fraud with our regulators. Specifically, we addressed the disconnect between our technology vendors and some of the new banking regulations. Section 1071 of the Dodd Frank Act was again at the forefront of this discussion. But the difficulty in using technology to identify represented debit items for purposes of UDAP was a great example of our regulators assuming that our core operating systems can readily be compliant with just the flip of a switch. We all know that is simply not the case. Advocacy is the only way to ensure that our regulators understand the true impact of theory versus practice.

Likewise, the ABA team has begun strategizing to effectuate beneficial legislation in anticipation of the 2025 Arkansas legislative session. In particular, we will be seeking to strengthen criminal penalties for a variety of acts involving banks that we think are currently far too lenient and fall short of being an effective deterrent to bad actors. Alternatively, we will be prepared to defend proposed legislation that is not in the best interest of our member banks and industry. With three full months until the session begins, we are already monitoring more than a dozen potential pieces of state legislation. This looks to be a very busy year at the state level, and I want to assure you the ABA team will represent all member banks each day of the session.

Finally, one of the association’s core values is our commitment to innovation and to be visionaries of positive change. With respect to technology development and innovation, I am very excited about our collaboration with The Venture Center of Little Rock. This is an opportunity for Arkansas banks to communicate our challenges directly with technology companies so they know what solutions we’re seeking. This partnership is expected to provide member banks effective, efficient and economical solutions using technology, and I encourage each of you to reach out to myself or ABA President and CEO Lorrie Trogden to become involved with the Arkansas Banking Solutions Accelerator. As always, I encourage each of you to make your voices heard for our industry — both now and for the future.

Calendar of Events

- DECEMBER 2024

Oct

06 07

SUNDAY 8 A.M. –MONDAY 5 P.M.

ABA BANK MARKETING CONFERENCE

Explore the ever-changing terrain of bank marketing in Chicago, IL, and experience resultsoriented educational sessions you won’t soon forget. Meet like-minded leaders from across the country, have some fun, get the deep dish on hot marketing trends – and leave with rare souvenirs: actionable takeaways and inspiration to power your performance.

LOCATION: Chicago, IL

07 11

MONDAY 8 A.M. –FRIDAY 5 P.M.

GSB BANK TECHNOLOGY SECURITY SCHOOL

This state-of-the-art program will broaden your understanding of the business of banking including key drivers of bank profitability, along with an in depth, interactive and hands-on study of the latest IT security techniques and strategies. The school uses a mix of lecture, small group discussions and interactive computer labs. The hands-on, computer-based simulation labs will allow you to explore penetration and vulnerability testing, security attacks, early detection of data breaches and more.

LOCATION: Fluno Center, University of Wisconsin, Madison, Wisconsin

08

TUESDAY 9 A.M. – 4 P.M. NEW

ACCOUNT DOCUMENTATION & COMPLIANCE

This full-day program is one of the country’s most comprehensive seminars on opening deposit accounts. The session answers many of the complicated questions customers and employees ask. The 200+ page detailed manual, included in the registration and customized to your state law, has become an invaluable resource for banks across the state.

INSTRUCTOR: Matt Dickinson

LOCATION: Arkansas Bankers Association, Little Rock

17

THURSDAY 9 A.M. – 4:30 P.M.

APPRAISAL & EVALUATION COMPLIANCE

This seminar lays the foundation for risk management and is important to anyone involved in the appraisal and/or evaluation function at a bank, whether they are actively ordering/managing/ reviewing appraisals, performing/ ordering evaluations or involved in real estate lending risk management. This session will update you on current regulations and Agency Guidance including your state laws on evaluations and AMCs. It will focus on the major topics of today including Reconsideration of Value and Bias in the Appraisal Process in addition to discussing hot topics with examiners.

INSTRUCTOR: Cheryl Bonnaffons Bella LOCATION: Arkansas Bankers Association, Little Rock

22

TUESDAY 9 A.M. – 3 P.M.

2024 FDIC BANKER OUTREACH

The Arkansas Bankers Association has partnered with the FDIC to bring you these important sessions that will be tailored to directors, risk management, and consumer compliance staff to bring participants up to date on current economic trends and regulatory issues. Resource materials will be provided for future reference.

LOCATION: ABA, Little Rock

23

WEDNESDAY 9 A.M. – 4 P.M.

LENDING CASH FLOW & FINANCIAL STATEMENT ANALYSIS

During this course we’ll discuss some of the key elements in the underwriting process for Commercial Lending. Through analyzing the customer’s data we can learn to assess their capacity to repay the loan.

INSTRUCTOR: Adam Trower

LOCATION: ABA, Little Rock

24

THURSDAY 9 A.M. – 4 P.M.

INTRODUCTION TO BANK MANAGEMENT

This course will give attendees a broad knowledge of the components involved in managing a bank. It will cover Liquidity, Capital Planning, Asset Liability, Sales, Loans, and Deposits from a high level. This session is ideal for new and potential bank management, lenders, personal bankers, and operations personnel.

This conference offers a unique educational experience focused on banking industry trends, leadership development skills, and peer networking opportunities. The Emerging Leaders Section works to engage, connect, and empower banking professionals from around Arkansas to shape and lead the future of the financial industry. Get access to top industry thought leaders and grow your network. Share ideas with your peers and get strategies for solving your challenges.

LOCATION: Clinton Presidential Center, 1200 President Clinton Avenue Little Rock, AR

TUESDAY 9 A.M. – 4 P.M. ABA

SECURITY CONFERENCE

Bank security officers are challenged each day to be aware of the perils affecting their banks, while also modifying the policies, procedures, and practices to prevent losses. As we confront increasing threats worldwide, it has become more essential than ever for you and your security team to ensure your bank’s security program can address today’s wide range of physical and virtual threats. This conference will provide you with an opportunity to learn from industry experts, network with colleagues, and visit with exhibitors to see and experience the latest in products and services.

LOCATION: TBA

20

WEDNESDAY 9 A.M. – 4 P.M. ABA TECHNOLOGY

CONFERENCE

MONDAY 9 A.M. –FRIDAY 4 P.M.

COMMERCIAL LENDING SCHOOL

This school is an intensive, one-week school that exposes students to the major issues commercial lenders face. Eleven different instructional modules throughout the week along with group case study work will address multiple topics and are taught and led by top-notch banking veterans who will give you plenty of opportunity to ask questions and share concerns.

INSTRUCTOR: Mike Rushing & Ron Wasson

LOCATION: ABA, Little Rock

Stay on top of technology trends and sustain your bank’s technology strategy! Technology and innovation have been transforming financial services since long before artificial intelligence and iPhones, and your role as an IT professional is ever-changing, especially in today’s environment. This event is designed to provide support as you keep on top of technology trends, navigate the business of banking, and build your bank’s technology strategy—all to improve access and better serve your customers. This conference will provide you with an opportunity to learn from industry experts, network with IT colleagues, and visit with exhibitors to see and experience the latest in products and services.

LOCATION: TBA

AT A GLANCE

Live events are subject to a virtual learning environment. For more information, contact the ABA at (501) 376-3741 or Kami Coleman at kami.coleman@arkbankers.org.

DEFEND THE DUAL BANKING SYSTEM

Rob Nichols | President and CEO | American Bankers Association

Since the time of President Lincoln, American consumers have benefited from a dual banking system, made up of both state-chartered institutions and federally chartered national banks.

This system—which can trace its roots back to the U.S. Constitution—allows consumers to have more choices. It offers them a robust marketplace of banks of different sizes and business models to meet their needs. And it enables the nation’s more than 750 national banks to operate safely, soundly and efficiently across multiple jurisdictions under the supervision of the OCC, while at the same time allowing state banks to serve their communities with local supervision.

But this system, which has served our country well for more than 150 years, is now coming under threat, as lawmakers in both red states and blue states have begun to pass laws that will interfere with national bank operations, violate federal preemption and tread squarely on the OCC’s turf.

Just look at the situation currently unfolding in Illinois, with the Interchange Fee Prohibition Act that was signed into law this summer as part of the state’s budget legislation. This misguided law bans banks, credit unions, payments networks and other entities from charging or receiving interchange fees in Illinois on taxes and tips charged as part of a credit or debit card transaction.

This law—which will create unprecedented chaos and confusion for consumers and businesses if allowed to take effect—violates

multiple federal statutes, including the National Bank Act and the Federal Credit Union Act, and cannot be enforced against national banks, federal savings institutions or state-chartered banks, as well as federally and state-chartered credit unions. It also runs afoul of the Electronic Fund Transfer Act, which directly addresses the permissible amount of interchange fees for debit card transactions and does not carve out taxes and gratuities.

This law, a gift to corporate mega-retailers as part of a last-minute budget deal, is the first of its kind to pass in the nation. We can’t let it stand and run the risk other states follow, which is why ABA is fighting back.

Together with the Illinois Bankers Association, America’s Credit Unions and the Illinois Credit Union League, we filed a lawsuit challenging the law, and we are

“Banks are being asked by states to pick a side in service of performative politics rather than deliberative policy.”

seeking a preliminary injunction pausing implementation until the court can rule on the merits of our case. With top outside lawyers assisting us, we have confidence we will prevail in this case, sending a strong message to other states looking to follow Illinois’ lead.

We’ve seen a different kind of challenge to the dual banking system in other states. Florida and Tennessee have put in place their own safety and soundness tests, encroaching on the OCC’s federal overnight of national banks.

Like ABA, the OCC has taken notice.

“Just look

at the situation currently unfolding

in

Illinois

...

This misguided law bans banks, credit unions, payments networks and other entities from charging or receiving interchange fees in Illinois on taxes and tips charged as part of a credit or debit card transaction.”

We’ve been encouraged by comments from Acting Comptroller Michael Hsu noting that his agency will continue to defend the dual banking system. The acting comptroller pointed out in recent remarks that “increasingly, banks are being asked by states to pick a side in service of performative politics rather than deliberative policy.” This simply shouldn’t be the case, and we will continue to urge the OCC to exercise its authority when states cross the line.

Our dual banking system has served Americans well for decades. ABA will continue to push back against efforts to undermine that system, and we’ll keep pressure on regulators to do the same.

Email Rob at nichols@aba.com.

MAINTAINING VIGILANCE IS KEY to Cyber Security Threats

Susannah Marshall | Commissioner | Arkansas State Bank Department

Cyber security risk and the overall threat landscape continue to evolve, becoming more sophisticated with each passing day. This statement has been true for quite some time, and it is clear that cyber risk will be a significant topic for our industry for the foreseeable future. In fact, cyber risk continually ranks as one of, if not the top, risk reported by bankers in most industry surveys. Not surprising, it also ranks very high from a regulatory standpoint as well as a significant concern of the general public.

One of the primary reasons cyber risk is so impactful is because it permeates every aspect of our professional and personal lives, but of grave concern is how it impacts us in the financial services sector. Banks are trusted by their customers to protect their money, privacy and financial data. That trust is supported by a regulatory environment that requires banks to implement strong oversight and controls and operate within the bounds of laws and regulations that are in place to protect the consumer and help to ensure a safe and sound banking system.

Our society is very much “connected”, and we are becoming increasingly more dependent and reliant on technology to perform many functions in our lives, including our banking activities. Banks are heavily focused on adopting technology to improve efficiencies in operations, enhance customer experiences and meet their requests and provide innovative products and services to remain competitive. The adoption and utilization of technology provides many benefits to businesses and individuals such as easier and more timely access to banking services, personalized financial recommendations through data-driven insights, convenience, enhanced security, and faster payment processing. As a result, both banks and their customers benefit from more seamless, user-friendly experiences that are accessible anytime and anywhere.

These all represent positive advances in our industry. However, the downside of cyber risk is considerable. A cyber attack can pose significant financial, reputational and operational risk. The increased speed that enables us to more efficiently conduct our banking business also comes with risk that cyber threats are spreading just as rapidly which can impact a bank or a customer without proper cyber security controls. The vast amount of financial data within a bank that is exposed to potential cyber breaches or attacks is staggering.

The frequency of cyber attacks has reached alarming levels in recent years leading me to worry if we might become somewhat “de-sensitized” to the impacts of cyber breach notifications in the future? While customers may grow weary of these incidents, banks cannot afford the luxury of becoming complacent. Banks must remain hyper-vigilant and consistently focused on addressing cyber risk at all times and continually enhancing and elevating their cyber security posture and implementing risk mitigation tools as promptly as possible. I also

“ Banks must remain hyper-vigilant and consistently focused on addressing cyber risk at all times and continually enhancing and elevating their cyber security posture and implementing risk mitigation tools as promptly as possible.”

want to remind all banks that a proper cyber security culture is most impactful when the institution approaches it in a holistic manner. Strong cyber security programs penetrate every segment of a financial institution, from the front-line customer service staff up to the board of directors.

Overall, I am very proud of the results I’ve seen from our Information Systems examinations of your institutions and how banks are actively managing their cyber risk management processes. I want to take this opportunity to remind all institutions of the notification requirements to report computer-security incidents requirements to your federal regulatory authority and our specific requirement to also notify the Bank Department of a cyber breach. In most of the instances where we have been notified, the bank has responded swiftly and effectively, implementing their incident response plans to remediate the situation in a timely manner. We are pleased with the overall responsiveness by our Arkansas banks as it relates to cyber related events and preparedness.

With the recent announcement by the FFIEC to sunset the Cybersecurity Assessment Tool (CAT) by August 2025, community banks should begin evaluating and preparing to adopt a suitable cybersecurity framework to effectively continue to demonstrate their cyber security preparedness.

I recognize that our industry faces a multitude of operational challenges every day, and the growing risks that exist within our society’s increasing reliance and dependence on technology will continue to place significant pressure on each institution. While I am encouraged by our current position, I am fully aware that cyber security risk will remain a top priority for the industry, and maintaining constant vigilance is essential.

THE FACES OF ARKANSAS BANKING

with David Tolentino

Branch Manager

First State Bank, Ola

YOUR BANK IS A FAMILY-OWNED BANK, HOW IMPORTANT ARE FAMILY-RUN BUSINESSES TO THE SUCCESS OF OUR STATE?

Very important! As a family-owned business, it is easier to take care of our customers directly. We are able to make every encounter personable while enhancing our ability to better serve the community. All decisions are made locally.

WHAT IS THE BEST PART OF BEING A HOMETOWN BANKER?

The relationships that I am able to build and cultivate with the community. I am able to assist different generations with their banking needs. There is no better feeling than being able to help families accomplish their dreams.

WHAT ADVICE DO YOU HAVE FOR YOUNG BANKERS STARTING THEIR CAREERS?

To always be Teachable and Engaging.

WHAT DO YOU LISTEN TO ON YOUR MORNING COMMUTE?

The Dave Ramsey show. My favorite quote from him is “Quit Spending like you are in Congress.”

I ALWAYS START MY DAY WITH… Prayer because when we put God in the center of our lives everything falls into place.

WHAT GAME DO YOU ALWAYS WIN AT...AND WHAT GAME DO YOU ALWAYS LOSE AT?

I always win at Mexican Train Dominoes and Bible Quiz games, but always lose at Jenga.

“ALWAYS BE TEACHABLE AND ENGAGING.”

“I

am able to assist different generations with their banking needs. There is no better feeling than being able to help families accomplish their dreams.”

TEAMWORK AND WORKPLACE Collaboration

Latrecia Carroll | President | Emerging Leaders Section

Teamwork is one of the cornerstones of success in any organization, group, or project. It extends far beyond just working together; it’s the art of blending diverse talents, experiences, and perspectives to reach a shared goal.

Teamwork happens when individuals come together, contributing their unique strengths to a collective task. It’s not just about working on the same project but understanding that each member has a role that complements the others. Whether in a large group or a small partnership, teamwork involves clear communication, mutual respect, trust and accountability and a shared vision of success. It’s a fluid dynamic that relies on collaboration, where everyone’s contribution— big or small—counts towards the final outcome.

The power of teamwork lies in its ability to amplify the strengths of each member while compensating for individual weaknesses. Teamwork has so many benefits including Increased Creativity and Innovation, Enhanced Efficiency, Shared Responsibility and Support and Motivation.

Diverse perspectives fuel creativity. Different minds approaching the same problem can lead to unexpected, innovative solutions. Dividing tasks among team members allows for specialization, enabling people to focus on what they do best, making the process more efficient. Working together spreads the load, so no one person carries the entire burden. It builds resilience as teams can handle challenges better than individuals can. A dedicated team provides support when challenges arise and offers encouragement, which can increase motivation and job satisfaction.

As an introvert, it is natural to prefer working in solitary environments, and that is completely valid. However, being an introvert does not mean you can’t thrive in a team setting. It’s about finding your role within that team. There are ways in which introverts can adapt.

Choose Roles that Suit Your Strengths. As an introvert, you may excel in tasks requiring deep thinking, planning, and analysis. These are vital contributions to any team.

Leverage Your Listening Skills. Introverts often listen more than they speak, which can make you the most attentive person in the room. Use this to your advantage in understanding team dynamics and identifying areas of improvement.

Set Boundaries. Find ways to carve out moments of solitude to recharge while still being engaged in the team.

Fostering teamwork starts with creating a culture of inclusivity and open communication. You can encourage teamwork, even if you do not naturally gravitate towards collaborative settings.

Lead by Example. Demonstrate that teamwork does not mean constantly being in meetings. Show that working together can happen through clear communication and trust.

Create Opportunities for Collaboration. Organize structured times for team members to work together, but balance that with periods for independent work. This way, both extroverts and introverts can thrive.

Encourage Team Building. Invest time in helping team members get to know each other on a personal level. Building trust strengthens the bonds that make teamwork more natural and enjoyable.

Celebrate Collaborative Success. Acknowledge and reward when teams work well together. Highlight the strengths of individuals in the team so everyone feels valued for their contribution.

While introverts may prefer solitary work, they also have a vital role in team settings. By understanding the dynamics of teamwork, embracing your strengths, and encouraging an environment of respect and collaboration, you can help foster successful teamwork, even if it is outside your comfort zone.

“Teamwork has so many benefits including Increased Creativity and Innovation, Enhanced Efficiency, Shared Responsibility and Support and Motivation.”

ELS EXECUTIVE COMMITTEE

LATRECIA CARROLL PRESIDENT

STONE BANK

Little Rock

Group 1

AMBER MURPHY

SECRETARY/ TREASURER

FIRST FINANCIAL BANK

El Dorado

Group 3

ELS COUNCIL MEMBERS

IAN BRYAN VICE PRESIDENT

SIMMONS BANK

Russellville

Group 2

BRITT BURRIS

CONNECT BANK

Star City

Group 3

CHANCE ROBBINS

CS BANK

Eureka Springs

Group 2

JAKE EARNEY

CHAMBERS BANK

Fayetteville

Group 2

GABE ROBERTS

FIRST COMMUNITY BANK

Jonesboro

Group 1

BRITTANY HELMS

SIMMONS BANK

Little Rock

Group 1

LAUREN STATON

RELYANCE BANK

White Hall

Group 3

BRANDON KNOWLTON

SOUTHERN BANCORP

Arkadelphia

Group 3

SARAH TEFTELLER

GENERATIONS BANK

Fayetteville

Group 2

EMERGING LEADERS

Guidance on ITMs: THE FDIC’S USE ONLY AS DIRECTED

On August 9, 2024, the FDIC released a Financial Institution Letter (“FIL”) offering limited guidance on the use of interactive teller machines or ITMs. Specifically, the FDIC addressed the question of whether an ITM would be considered a remote service unit (“RSU”), which a bank may establish without approval, or a branch, which requires approval under Section 18(d) of the FDI Act.

The guidance states that an ITM would require approval as a branch unless:

• The ITM is an automated, unstaffed banking facility owned or operated by, or operated exclusively for, the bank, which is equipped to enable existing customers to initiate an interactive session with remotely located bank personnel; and

• To the extent that bank personnel have the ability to remotely assist the customer with the operation of the ITM to perform core banking functions, customers must also be able to perform such transactions without the involvement of bank personnel and must have the sole discretion to initiate and terminate interactive sessions with bank personnel

It seems, essentially, that an ITM will require a branch application unless it functions primarily as an ATM, with any interactive assistance from bank personnel being 1) unnecessary for core banking functions, 2) provided by remotely-located bank employees, and 3) initiated and terminated by the customer.

The guidance further states “This FIL relates exclusively to the applicability of section 18(d)’s branch establishment requirements to state nonmember banks.” This is an important part of the guidance, because it places substantial limits on how it can be used and clarifies that ITMs and branches are not fully interchangeable for all purposes. It also leaves several questions unanswered, so banks should be careful not to read too much into this FIL.

First, of course, this guidance can only be used by state nonmember banks. Because this is not interagency guidance, banks regulated by agencies other than the FDIC should probably consult their regulators directly.

“Although an ITM may be a ‘branch’ for purposes of whether an application is required, it may not be considered a branch for other purposes, such as the Community Reinvestment Act.”

Additionally, the FDIC does not discuss how the rules about branch closings would apply to ITMs, which leaves open questions like:

• Would closing an ITM be considered a branch closure?

• What would be the appropriate process if a bank wants to place a brickand-mortar branch at a location that currently has an ITM, or within 1,000 feet of an ITM? Would the brick-andmortar branch require an application for a new branch?

• What would be the process for a bank that wants to close a brick-andmortar branch and replace it with an ITM? Would this be considered a branch closure?

Similarly, for signage purposes, it’s probably clear that FDIC signage will be required if the ITM is taking insured deposits. It seems like an ITM would likely be in the category of “ATMs and like devices” that are considered “digital deposit taking channels” requiring the new digital sign, but clarifying guidance would be useful in this area as well.

Finally, although an ITM may be a ‘branch’ for purposes of whether an application is required, it may not be considered a branch for other purposes, such as the Community Reinvestment Act (“CRA”). Because branch locations are the basis for determining a bank’s CRA assessment areas, treating ITMs as branches for CRA purposes could have significant consequences for banks. The CRA defines a branch as “a staffed banking facility approved as a branch.” The FDIC guidance indicates that ITMs may need to be “approved as a branch,” but it is unclear whether ITMs would be considered “staffed” because of the interactive features available. Until we have further guidance on this question, it may be worthwhile for banks to include a review of potential CRA consequences when determining whether and where to place ITMs.

Because the guidance is explicitly limited only to whether a branch application is required to establish a new ITM, banks should avoid extrapolating too much from this guidance, continue to be cautious about using ITMs and, when in doubt, contact regulators for additional guidance. As always, Compliance Alliance will continue to monitor developments in this area, and provide updates as they come available. If you have any further questions, do not hesitate to let us know.

“Because the guidance is explicitly limited only to whether a branch application is required to establish a new ITM, banks should avoid extrapolating too much from this guidance, continue to be cautious.”

SERVING

VETERANS

FREEDOM ACCOUNTS FOR THOSE WHO’VE KEPT US FREE

by Steve Brawner

THERE’S A REASON FARMERS AND MERCHANTS BANK IS LOOKING FOR WAYS TO SERVE ACTIVE DUTY MILITARY PERSONNEL AND VETERANS.

“Freedom isn’t free,” said Brad Chambless, the bank’s president and CEO and the chairman of the Arkansas Bankers Association. “We want to make sure that all of our service members, active and veteran’s status, know how much we appreciate what they’ve done for our country and our ability to do what we do with our families.”

Association of Military Banks of America (AMBA)

was formed in 1959 to help banks that serve military bases and communities.

BRAD CHAMBLESS

PRESIDENT / CEO

FARMERS AND MERCHANTS BANK

CHAIRMAN

ARKANSAS BANKERS ASSOCIATION

The Freedom Checking Account is the first of what he hopes will be a suite of products and services. There are also ongoing efforts to provide general financial counseling as well as help in restoring credit.

Chambless’ bank, which has 25 branches, has partnered with the Association of Military Banks of America’s (AMBA) Veterans Benefits Banking Program (VBBP) to create a Freedom Checking Account limited to active-duty service members and veterans.

AMBA was formed in 1959 to help banks that serve military bases and communities. It and the Department of Veterans Affairs created the VBBP in 2019 to provide a marketplace of banks and credit unions serving veterans, beneficiaries, survivors and caregivers. VA monetary benefits can be directly deposited into accounts offered by participating banks and credit unions. The accounts offer debit cards so veterans can use them at ATMs or at points of sale around the world.

Last year, the American Bankers Association announced that the ABA Foundation had signed a formal agreement with the AMBA. It will serve as AMBA’s fiscal sponsor for managing the donations that fund the VBBP. The foundation also will encourage banks to participate in the program and provide access for unbanked veterans. Banks must provide free checking accounts to any veteran using direct deposit for their VA benefits and must commit to help veterans overcome obstacles to opening an account.

Farmers and Merchants Bank’s Freedom Checking Account bears interest on a monthly basis with a current annual rate of 1.78%. The bank provides free paper statements to those who want them and will refund up to $20 a month in ATM fees. Customers receive a patriotic-themed debit card. Account owners also qualify for a onetime rate bump of 75 basis points above the stated rate on any of the bank’s CD products.

Chambless said the account is the first of what he hopes will be a suite of products and services. There are also ongoing efforts to provide general financial counseling as well as help in restoring credit. The bank is trying to implement the Federal Home Loan Bank of Dallas’ Housing Assistance for Veterans (HAVEN) program. It provides grants for home modifications such as wheelchair ramps, new construction and down payment assistance. The program serves veterans, service members with a service-related disability, and families who lost a loved one between Aug. 2, 1990, and now.

Farmers and Merchants Bank is reaching out to service members to inform them about its offerings. On Nov. 5, it will launch the Freedom Checking Account at an open house for invited active and veteran service member guests in Arkansas and Prairie Counties. A speaker from Fields of Honor will do a presentation. That organization provides scholarships to families of fallen or disabled military personnel and first responders. Chambless also will be talking to veterans at the local Veterans of Foreign Wars headquarters.

Both AMBA and AFFN have programs providing $1,500 grants to military banks if the banks will match them and donate the money to worthy organizations on military installations.

Larry Wilson, chairman and CEO of Jacksonville-based First Arkansas Bank and Trust, knows from long experience that military personnel face challenges. His bank, formed in 1948, opened a branch location on the Little Rock Air Force Base in 1956, one year after the base opened.

Wilson said military spouses often must work to make ends meet. Living far away from one’s roots can create additional financial challenges. Service members often have to move, which creates expenses.

“The government pays for most of it, but still there are incidentals and a lot of expenses that the government doesn’t cover,” Wilson said.

Now with a main bank location and 20 branches, First Arkansas Bank and Trust offers veterans-specific bank accounts through AMBA’s Veterans Benefit Banking Program. Its charter, in order to have a branch on the base, requires it to offer financial counseling. Bank employees attend monthly meetings at the base to educate airmen about budgeting and saving.

Like many Arkansas banks, First Arkansas Bank and Trust also hires veterans and military spouses. The American Bankers Association has partnered with the U.S. Chamber of Commerce Foundation’s Hiring Our Heroes program to provide banking jobs to veterans, service members transitioning into civilian life, and military spouses.

Wilson serves as a board member for AMBA and also for the Armed Forces Financial Network, an electronic transfer network that provides active-duty military veterans access to ATM services and point of sale terminals located on or near overseas U.S. bases.

Both AMBA and AFFN have programs providing $1,500 grants to military banks if the banks will match them and donate the money to worthy organizations on military installations. Wilson estimated that First Arkansas Bank and Trust has donated $50,000 over 20 years. One recipient, Operation Warm Heart, helps airmen and families with emergency situations such as funerals.

Chambless wants the Arkansas Bankers Association to help the state’s banks serve veterans and current personnel. Retired Air Force Maj. Gen. Steve Lepper, president and chief executive officer of the Association of Military Banks of America, spoke at the most recent ABA Bank Management Seminar in Bentonville to give bankers a wider vision of what they can offer.

Chambless said several bankers since that presentation have asked for more information.

“We may be competitors as banks, but I’m more than willing to share my data with another bank if they’re going to reach out and try to lift a program that supports, helps and pays respect and tribute to our veterans,” he said.

LARRY WILSON

CHAIRMAN / CEO

First Arkansas Bank and Trust offers veterans-specific bank accounts ... and bank employees attend monthly meetings at the base to educate airmen about budgeting and saving.

CREDIT REWARDS CARD UNDER FIRE!

by Tim Schenk KBA General Counsel

Seven in ten people say they have a rewards, points, or cashback credit card. Folks across America use these rewards for travel, discounts at retail stores, or just to bank a few extra dollars at the end of the year. Needless to say, these unique perks are wildly popular. So why have these benefits recently come under fire from the CFPB? As usual, Rohit Chopra leads the charge of regulatory overreach under the false pretense of consumer protection.

On May 9th, the Consumer Financial Protection Bureau issued a report highlighting consumer frustration with credit card rewards programs. In its press release, the CFPB said, “Consumers tell the CFPB that rewards are often devalued or denied even after program terms are met. Credit card companies focus marketing efforts on rewards, like cash back and travel, instead of low interest rates and fees. Consumers who carry revolving balances often pay far more interest and fees than they get back on rewards. Credit card companies often use rewards programs as a ‘bait and switch’ by burying terms in vague language or fine print and changing the value of rewards after people sign up and earn them. New problems have been created by the growth of co-brand credit cards and rewards programs where consumers can transfer miles or points to merchants.”

90% OF AMERICANS MAKE PAYMENTS WITH A CREDIT OR DEBIT CARD

75% OF THOSE OPTING TO USE A REWARD CARD WITH NEARLY

“If you tell people those things are worthless, it seems easier to take them away.”

CFPB Director Rohit Chopra said, “Credit card companies promise upfront benefits for signing up and using their rewards card, but often bury complex terms in the fine print for using the rewards. The CFPB will be looking for ways to protect people’s points, stop bait-and-switch scams, and promote a fair and competitive market for credit card rewards.”

The CFPB comes to wholesale conclusions that: “Credit card issuers impose vague or hidden conditions that keep consumers from receiving rewards; Companies devalue rewards; Consumers encounter redemption issues with earned benefits; and Companies revoke previously earned rewards. If true, these conclusions are concerning and worthy of a Congressional hearing.”

So, who are these consumers being misled and having their reward points stolen? On the first page of the CFPB’s Credit Card Rewards

Issue Spotlight, the basis for the conclusions above states, “We analyzed several hundred consumer complaints relating to the administration of credit card rewards programs and identified four recurring themes that resulted in consumers not receiving the rewards.” Several hundred? Will the CFPB determine the validity of credit card rewards programs based on several hundred complaints?! I’m sure those several hundred consumers adequately represent the roughly one hundred and ninety-one million Americans with credit cards. I’m sure they represent these one hundred and ninety-one million Americans with credit cards so well that we should forego all statistical analyses such as standard deviation or a survey not based solely on complaints. I hope you can feel the sarcasm here dripping off the page.

The day before the CFPB released its “Spotlight,” the Electronic Payments Coalition (EPC) released its study, which showed that

“credit card rewards are a lifeline for working-class Americans.” Now wait. How can that be true? The CFPB just said that credit card rewards are a problem. The EPC study was conducted in the first quarter of 2024 and “represents more than half of the credit card market measured by purchase volume.” Half of the credit card market? There is no way that can be more statistically accurate than a few hundred complaints. Again, excuse my sarcasm, but this is ridiculous.

Unsurprisingly, the EPC study reached drastically different conclusions than the CFPB “Spotlight.” The EPC study found that:

• REWARDS ARE FOR EVERYONE. Since 2020, rewards card ownership has grown the fastest among the low-to-moderate (LMI) income segment. Currently, more than two-thirds of LMI cardholders own a rewards card. This result illustrates that reward cards are popular among low-income households, and reward programs do not exclusively serve upper-income customers.

• REWARDS SUPPLEMENT CONSUMER INCOME. All cardholders receive a boost to income from their rewards. Many cardholders save up rewards over months to supplement holiday and back-to-school shopping. Total rewards savings in 2023 accounted for 23% to 32% of planned holiday purchasing.

• THERE IS NO CROSS-SUBSIDY OR SO-CALLED “REVERSE ROBIN HOOD.” Rewards redemption rates are similar across income groups, suggesting that each income group is taking advantage of their rewards at the same level.

• REWARDS ARE ESSENTIAL TO LOWER-INCOME CONSUMERS. LMI accounts are most likely to redeem cash rewards, implying that this income segment uses rewards for everyday spending needs.

In short, the EPC study found that credit card rewards are valuable to customers of all demographics. This makes sense when ninety percent (90%) of Americans make payments with a credit or debit card, with nearly seventy-five percent (75%) of those opting to use a reward card.

Director Chopra expressed deep concern during his testimony in his joint hearing with the Department of Transportation that consumers were storing points that could become unusable. EPC explained that “reward cardholders often carry a balance of unredeemed rewards. This represents an important safety net for these cardholders.”

So, who is right? I tend to believe a study with a larger group of consumers whose sole identification was not a complaint. But there is a larger question: Why is this happening now?

In my personal opinion, federal agencies want to create the impression that points are worthless. If something is worthless, it is easier to take it away. As regulations such as Reg II and the Durbin Amendment loom, pressure on the card market will increase, and points, miles, and benefits will suffer. If you tell people those things are worthless, it seems easier to take them away.

Regardless of my thoughts, the reality is that if you value your points, miles and card services, let your elected officials know it before those benefits, and this argument, becomes a thing of the past.

A NONPROFIT

ALONGSIDE A CDFI MAXIMUM IMPACT FOR LEVERAGING

by John T. Olaimey President & CEO, Southern Bancorp Bank

Not long ago, a small business customer in West Memphis walked inside one of our Southern Bancorp Bank branches looking for help. Struggling through a post-pandemic economy and a slow season of the year left him short on cash and with a subpar credit history. To stay afloat, he borrowed from an online “merchant advance” company – lenders that, in many cases, function essentially as modern-day payday lenders for businesses.

Fortunately for this auto shop owner, our bank lending team has an in-house collaborator that specializes in helping people access flexible capital when a traditional bank loan may not be in the cards – Southern Bancorp Community Partners (SBCP), our nonprofit CDFI loan fund and financial development organization. SBCP’s lending team put together a responsive and responsible debt consolidation loan that was within reach of this business owner’s financial position, which allowed him to get out from under this predatory debt and put his business back on the right track.

There are countless examples like this throughout Southern Bancorp’s nearly 40-year history, from first-time homeowners to second-chance savers and small business startups to family farms. As a CDFI bank, we can support many of these customers entirely on the bank side of our operations; but plenty can still benefit from the additional support of our nonprofit CDFI, SBCP, to find their path to opportunity.

WE HAVE GROWN TO $2.6 BILLION IN ASSETS AND ORIGINATE MORE THAN 8,000 LOANS ANNUALLY, 96 PERCENT OF WHICH ARE IN CDFI TARGET MARKETS. OUR NONPROFIT HAS REACHED MORE THAN $44 MILLION IN ASSET SIZE , ORIGINATED MORE THAN 100 LOANS IN 2023, AND LED THE PREPARATION OF 4,403 FREE TAX RETURNS.

We believe the collaboration between Southern Bancorp Bank and SBCP offers a unique model for community development, blending financial services with mission-driven programs that address the broader challenges faced by our communities. This synergy allows us to make a more profound and lasting impact – one that benefits both our customers and the communities in which we operate.

One of the primary advantages of this partnership is our ability to address a wide range of community needs that extend beyond traditional banking. While Southern Bancorp Bank focuses on providing accessible financial services to underserved communities – such as affordable home loans, small business loans, checking and savings accounts, and community development – SBCP complements these efforts by providing the flexible lending of a nonprofit alongside educational programs, financial counseling, credit building, and specialized services for low-to-moderate income (LMI) families.

For example, SBCP’s financial counseling and literacy workshops equip individuals with the knowledge and skills they need to manage their finances effectively. Whether it’s our HUD-certified homebuyer counseling or credit counseling, these programs are especially critical in underserved areas, where financial education is often limited. By providing these services, SBCP helps individuals and families build a strong financial foundation, making them more likely to benefit from the slate of traditional banking services we offer.

Such benefits include building generational wealth through affordable homeownership, which frequently transpires through collaboration. Programs and services provided by SBCP, such as forgivable and repayable down payment assistance, matched savings Individual Development Accounts (IDAs), and HUD-certified homebuyer counseling,

pair hand-in-hand with our bank’s mortgage division to help folks along every step of their homeownership journey – from eliminating the barriers to entry many families face all the way to signing the mortgage documents at the finish line.

Moreover, the nonprofit status of SBCP allows it to access grant funding and philanthropic support that would otherwise be unavailable to a for-profit financial institution, even, in some cases, a CDFI. These additional resources enable SBCP to expand its programs and our overall reach to more people throughout our communities, thereby amplifying the impact of our community development efforts. The down payment assistance and IDA programs, as well as our Minority Business Empowerment Program, are made possible with the support of these grants and investments into our nonprofit.

In the banking world, many of us are sensitive to the distrust that some communities have toward banks. When the FDIC studied households that were un- or under-banked throughout the United States a few years ago, “Don’t trust banks” was the second most common reason for not having a bank account, behind only, “Don’t have enough money to meet minimum balance requirements.” There’s not one silver bullet to solve this systemic problem overnight, but from our vantage point, one of our operating arms being a nonprofit does help break down some of these perceptions.

Be it a financial workshop at a local church, free tax assistance for customers and non-customers alike, one-on-one counseling, or otherwise, our SBCP programs are often a positive first impression leading to a warm handoff to our bank side, or a lasting impression that builds a bridge over previous presumptions about banks in general. Put simply, it helps us foster more long-term relationships in the places we serve with people who view us as more than just a bank, but a true partner in their financial journey.

Our unique structure is also one of the main components to the growth we have achieved over the past decade, as well as the lofty goals we have set course toward over the next. On the bank side, we have grown to $2.6 billion in assets and originate more than 8,000 loans annually, 96 percent of which are in CDFI target markets. Our nonprofit has reached more than $44 million in asset size, originated more than 100 loans in 2023, and led the preparation of 4,403 free tax returns throughout our markets, the most we’ve ever done. Not bad for a scrappy CDFI serving primarily underserved communities.

The collaborative partnership with which we, and other banks like us, operate should serve as a successful example of how financial institutions can go beyond traditional banking to make a real difference in their communities – for the whole of their communities. By combining the strengths and mission-driven nature of a CDFI bank with the agility and flexibility of a nonprofit, we are able to better meet people where they are and address the complex and interconnected challenges that our communities face.

As we look to the future, this model of collaboration offers a path forward for other banks and financial institutions that are as committed to community development as we are at Southern Bancorp. In doing so, we can build stronger, more vibrant communities that benefit everyone.

ABOUT THE AUTHOR

John T. Olaimey, President and Chief Executive Officer of Southern Bancorp Bank, has over 20 years of experience in banking, finance, corporate law and executive management.

TO COMPETE OR NOT TO COMPETE THAT IS THE QUESTION

by Jake Fair Wright Lindsey Jennings

There has been a great deal of press and some understandable confusion about the developments surrounding non-compete agreements. So, let’s explore how this all started.

Earlier this year, the Federal Trade Commission (FTC) published a rule that would eliminate non-compete agreements. The result of the proposed rule meant that employers would no longer be able to enter into non-compete agreements with most workers and many existing non-compete agreements were invalidated (with the exception of existing non-competes for “senior management” as defined by the FTC, among other exceptions).

A number of legal challenges ensued. Specifically, the first lawsuit was filed by a tax-service firm in the Northern District of Texas, mere hours after the vote approving the rule for publication. The U.S. Chamber of Commerce and several other business organizations also filed a lawsuit in the Eastern District of Texas seeking, among other things, a declaratory judgment finding the rule to be unlawful and an order prohibiting the FTC from enforcing the rule. This second case was stayed while the first one proceeded.

Before we review the FTC rule and the recent decision by Judge Ada Brown of the U.S. District Court for the Northern District of Texas, it is important to understand the differences between

a non-compete agreement, a non-solicitation agreement, and a non-disclosure agreement.

WHAT IS A NON-COMPETE AGREEMENT?

A non-compete agreement is used to prevent a bank employee from leaving the bank for a competitor or engaging in activities that would compete with the employee’s former bank. These agreements typically prevent the employee from competing with the former bank for a specified period of time and within a certain geographic area after the employee leaves.

Courts have generally held that non-compete agreements are enforceable so long as the clause contains reasonable limitations as to the geographical area, type of subsequent employment, and the time period in which the employee may not compete.

WHAT IS A NON-SOLICITATION AGREEMENT?

A non-solicitation agreement is less constraining than a non-compete agreement, and serves to protect an employer’s existing

“The first lawsuit was filed by a tax-service firm in the Northern District of Texas, mere hours after the vote approving the rule for publication.”

customer relationships and employees. The non-solicitation agreement is a contractual obligation by a bank employee that prevents the individual from soliciting the bank’s customers, prospects, clients, or employees to conduct business with the employee or competitor. This agreement takes effect when the individual’s employment with the bank ends, and is usually for a limited duration.

WHAT IS A NON-DISCLOSURE AGREEMENT?

A non-disclosure agreement prevents bank employees from disclosing any confidential information received during their employment with the bank. This type of agreement is primarily used to prevent banks’ proprietary information from getting into the hands of competitors who often seek to gain an advantage. Additionally, non-disclosure agreements can be used outside of the employment context when interacting with third parties and seeking to protect confidential and proprietary information.

DOES THE FTC RULE APPLY TO BANKS?

Now, back to the FTC rule. The FTC describes the rule as a comprehensive rule; however, it also acknowledges that the rule does not apply to regulated financial institutions. That is because the non-compete ban applies only to entities covered by the FTC Act and banks and credit unions are excluded from FTC jurisdiction. Notably, non-solicitation agreements are also still permitted and likely not impacted by the rule.

In some other contexts, however, federal regulators are

authorized to enforce certain FTC actions against banks. In the rule, the FTC acknowledges that whether the federal bank regulators apply the rule to entities under their own jurisdiction is a question for those agencies.

It is important to note that the FTC declined to exclude bank holding companies, subsidiaries, and other affiliates of excluded financial institutions from the rule if those entities otherwise fall within the FTC’s jurisdiction. What does this mean? While banks are currently excluded from the rule, their parent companies and affiliates are subject to the non-compete ban and the FTC’s enforcement. This is an important consideration for banks – especially those with shared or dual employees involving holding companies or affiliates.

WHAT HAPPENED WITH THE TEXAS CASE?

Judge Brown initially enjoined the implementation and enforcement of the rule as to only the named plaintiffs. However, on August 20, Judge Brown entered her final ruling finding that the FTC exceeded its statutory authority and that the rule was arbitrary and capricious. Judge Brown noted the FTC’s lack of evidence as to why it chose to impose such a sweeping prohibition—one that prohibits essentially all non-competes—instead of targeting specific and harmful non-competes.

What’s next? At the moment, Judge Brown’s ruling will prevent the rule from going into effect in September as originally scheduled. It is expected that the FTC will appeal the ruling to the Fifth Circuit. There is also ongoing litigation in other federal courts. Stay tuned!

ST. LOUIS FED PRESIDENT DISCUSSES ECONOMY IN LITTLE ROCK

by Roby Brock

photos courtesy St. Louis Federal Reserve Bank

In July, St. Louis Fed President Alberto Musalem shared his views on various aspects of the U.S. economy and monetary policy during a fireside chat at the Little Rock Regional Chamber’s Power Up Little Rock event. Jay Chesshir, CEO of the Little Rock Chamber of Commerce, interviewed Musalem. The following is a partial transcript, slightly edited for grammatical consistency.

JAY CHESSHIR: One of the things that we really appreciate from you is the fact that you’re here and you want to engage with businesses in Little Rock, in central Arkansas, in Arkansas, obviously across the district. Can you give us just your thoughts as to how you envision that relationship to grow?

ALBERTO MUSALEM: I derive tremendous value from engagement. When we go to the FOMC [Federal Open Market Committee] meetings to talk about interest rates, all the presidents spend a fair

amount of time sharing at the table with each other, what we are seeing in our different districts, what we’re seeing in labor markets, what we’re seeing in inflation, what we’re seeing in wages, and a whole host of impressions. It’s really valuable data.

So just zooming out, Congress created a Federal Reserve which has the board of governors in Washington, which oversee 12 reserve banks, which are 12 reserve bank districts that span the country. The intent there was for monetary policy to reflect economic conditions in all 12 districts. So we only have one monetary policy. We can’t make monetary policy for different districts or states. It’s one monetary policy, but it’s informed by what happens in different districts and we at the Fed are accountable to the public through Congress to be transparent about what we’re doing, how we’re doing it, and why we’re doing it.

And I view the relationship with my district, which is the Eighth District, Little Rock is a part of that, as a two-way street where I come and I benefit and my team also benefits from having conversations

“I’m hearing that the turnover rate of employees has declined and .... that wage growth is returning to normal levels, pre-pandemic normal levels, which are all very encouraging things from an inflation and labor market perspective.”

with business leaders, community leaders about what’s happening on the ground, but also to explain what we’re thinking, why we’re doing what we’re doing and how we’re doing it.

CHESSHIR: As you’ve started your tenure here, and when you talk to businesses as you’re going through this learning period about this district, are you hearing any common themes or concerns from businesses that are starting to create a common thread?

MUSALEM: I’ve been to two FOMC meetings and one thing that of course I can’t say what happens in the meetings, but I think I can share this across the 12 districts, you do hear a lot of common themes. Surprisingly, you would expect to hear very different stories depending on which part of the country. But there are very some common themes. Some themes that I’ve learned about in my district are as follows.

Companies are still facing cost pressures in their inputs and also labor insurance costs are a big part of it, particularly for smaller businesses. That’s very clear. I’m also hearing that labor conditions are improving. Companies seem to be having a less difficult time in filling vacancies than they had six months, 12 months, 24 months ago when the labor market was extremely out of balance.

I’m hearing that the turnover rate of employees has declined and that’s consistent with the hard macro data that we look at. I’m hearing that wage growth is returning to normal levels, pre-pandemic normal levels, which are all very encouraging things from an inflation and labor market perspective. We, of course, are hearing that interest rates at the level that they are at is straining some balance sheets. They’re straining low- and moderate-income household balance sheets, they are straining small business balance sheets. Home builders clearly are being affected by high interest rates and they’re clearly having

a restraining impact on housing and real estate markets. These are common themes.

CHESSHIR: From our perspective in talking with not only our existing companies, but those companies that are looking at this area, this region, from the standpoint of location, it seems like people are trying to find that equilibrium as to what will this look like going forward? Recognizing something else is going to change… We’ve seen some encouraging data that what you’re doing continues to work. Based upon that, what’s your outlook for the rest of this year?

MUSALEM: I’ll talk about activity first and then inflation second. So on activity, I see the economy as continuing to grow consistent with its long-term growth rate. I see an economy this year that probably will grow between one point and a half and two percent. I don’t want to pin it to the 10th decimal point, but it’s around there. I don’t think anybody has that kind of level of precision. I don’t think the probability of a recession is very high right now. I see a labor market that is still strong. I see employment levels as high. I see monetary policy as restrictive, but not overly restrictive. I see financial conditions which are tight for some parts of the economy, but I see broader financial conditions that are either neutral or maybe even accommodative for other parts of the economy.

If you look at firms that have access to capital markets, capital markets are very buoyant right now. Firms are taking advantage of a low cost of equity or debt financing to issue meaningful amounts of debt and equity at a pace higher than the last two years. I see credit as generally available for households, businesses, and municipalities. I think putting all those things together, I don’t see a recession as highly likely. There’s a rule of thumb out there, at least when I was in the markets, it was a rule of thumb that just counting years not based

PHOTO: Jay Chesshir (left), CEO of the Little Rock Chamber of Commerce, interviews St. Louis Fed President Alberto Musalem.

on anything else, just one on average, every one in five years you get a recession, right? So what we call the unconditional probability of recession, meaning if nothing else happens, it’s like one in five, right? Twenty percent. I kind of believe that’s an appropriate number right now, a twenty percent chance of recession, eighty percent chance of no recession. I don’t see anything that would suggest it is higher probably than that in terms of inflation.

With inflation, the data has been very encouraging. The way I like to think about inflation is I try not to focus on the last data point. It’s just one data point. I try to think of what is the overall environment and what does that tell me about what inflation is likely to be twelve months from now, eighteen months from now, what we call the forecast horizon. I try to be as forward looking as I can now. Of course, the last data point does give you a lot of information about that potential path and the data has been encouraging, although I would say from my perspective, I’ll speak for myself of course, I’m not sure I would call the first four months of the year a bump in the road or an anomaly. I think we had a good six months at the latter half of last year. We had an unfavorable four months in the beginning of this year. We had two months of favorable inflation data. I think when you add it all together, we have continued progress to where we want to be, but I think it’ll be prudent to look forward to the next twelve months and think of what that environment is going to look like and what inflation may look like going forward.

CHESSHIR: There are those out there that talk about the two percent inflation target and its potential needing to be increased to three or four percent. What are your thoughts on that?

MUSALEM: I think right now we are trying to bring inflation back to two percent. I think it would be a bad idea to change the inflation target... The job is not done, but it was successful. A reason for that was because inflation expectations remain anchored, right? We never lost the general public, never lost confidence that inflation would be brought back down to target. I believe that if we begin to change the

“Every time there’s innovation like this, there’ll be a change in the match between skills of people and jobs available for people. I’m confident that over time people will re-skill and I’m confident that over time it’s going to not negatively impact employment.”

inflation target from two to three, then the next question is going to be, ‘well, why not four? Why not three and a half?’ And then it would muddy the waters in terms of the formation of inflation expectations for the general public, and people would start having difficulty entering into long-term investment project decisions or buying homes because they wouldn’t be sure what the target actually is. So I think it would be counterproductive at this stage.

CHESSHIR: I can only imagine from an economist perspective how the world has changed not only in trying to manage an economy in an effective way, but also the different tools that are used in that work. Generative AI [artificial intelligence] is something on everyone’s mind today. It’s impacting all of our lives. How do you see that impact, especially from the labor market perspective? Do you see that as a way to overcome the lack of population growth as it has slowed or do you see it as creating problems in the labor market from the standpoint of people’s jobs being lost?

MUSALEM: Let me focus on the labor market. Part of the question, I view generally AI as just another wave of innovation. In humankind’s history travel through time, there’ve been a lot of innovations that we now benefit from the wheel and then other innovations. And every time there’s been an innovation like that, I don’t see it as being negative for employment. So if the question was ‘will this negatively affect the level of employment in the economy,’ I don’t think that’s the case. I think there will be, every time there’s innovation like this, there’ll be a change in the match between skills of people and jobs available for people. I’m confident that over time people will re-skill and I’m confident that over time it’s going to not negatively impact employment.

I think AI holds tremendous promise. Like many of you, I’ve been trying to inform myself as much as I can about this development and my understanding is the combination of AI, which is the thinking - the information processing part with the robotics part - with the biotechnology part, combining all those things together holds good promise for us in terms of productivity.

PHOTO: Scott Ford (left), Westrock Coffee CEO, and St. Louis Fed President Alberto Musalem.

ATTACKING THE INTERACTIVE TELLER MACHINE

A NEW SECURITY CONCERN EMERGING IN THE PACIFIC NORTHWEST

by Barry Thompson Thompson Consulting Group

Financial institutions utilizing Interactive Teller Machines (ITMs) or Virtual Teller Machines (VTM) in thePacific Northwest are facing a pressing security challenge that demands immediate attention. Criminals have devised a simple yet effective method of robbing individuals by exploiting vulnerabilities in these systems. By merely approaching the machine and initiating a call, they are able to coerce staff into dispensing funds.