Justin Allen, Latrecia Carroll, Paul Gatling, Dr. Kuan Liu, Susannah Marshall, Megan McGovern, Rob Nichols, Timothy Schenk, Mickey Belle Shields-Manley, Jim Taylor, and Dr. Timothy J. Yeager

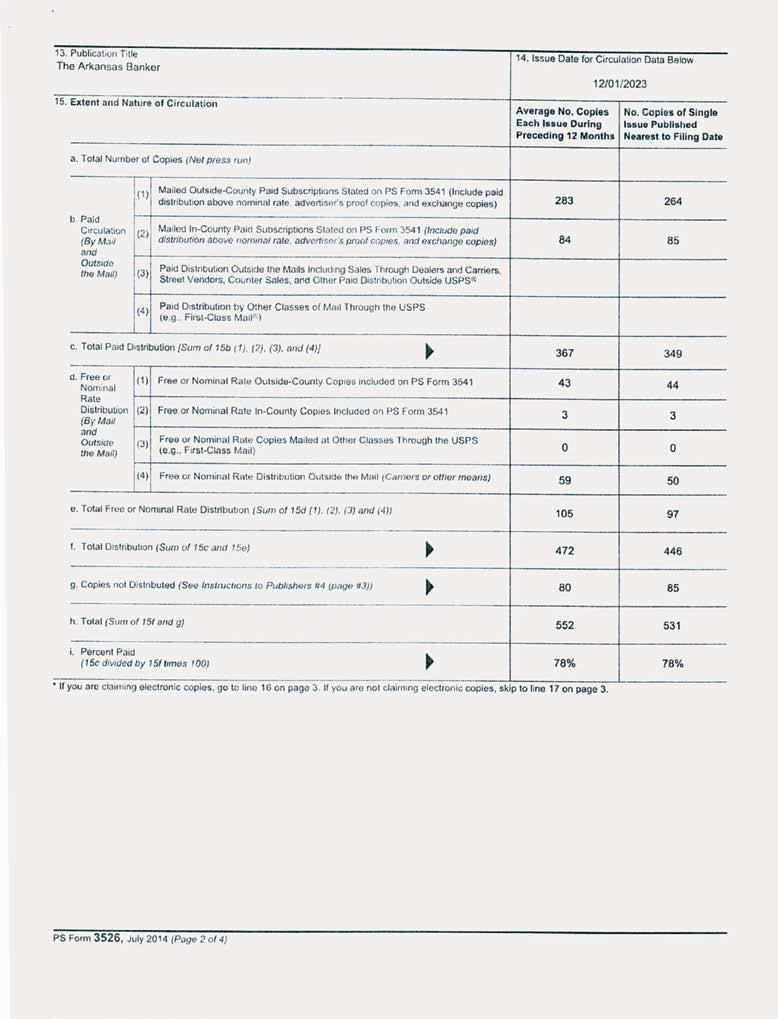

The Arkansas Banker (ISSN 004-1726) is published quarterly by the Arkansas Bankers Association, 1220 West Third Street, Little Rock, AR 72201. Phone: 501.376.3741. Periodical postage paid at Little Rock, AR.

Postmaster: Send address changes to Arkansas Bankers Association, 1220 West Third Street, Little Rock, AR 72201. Subscription to The Arkansas Banker magazine is included in the membership fees to the Arkansas Bankers Association. Cover price is $5.95 each. Annual subscription rates are $40.00 for members and $60.00 for non-members.

Federal tax law prohibits the deduction of lobbying expenses for federal incomes tax purposes. Organizations like ABA, which assess member dues, are required by law to notify their members of the portion of their dues attributable to lobbing/and therefore non-deductible on your federal tax return. For the year 2023, it is estimated that 9.32% of your dues will be attributable to lobbing as defined by the IRS. Contributions to ABA are not charitable contributions, however, they may be deductible as a legitimate business expense.

Insurance Concerns

Rapidly rising insurance premiums are adding stress to businesses, homeowners.

New Rules For Beneficial Ownership

FinCEN issues new guidance.

of

Elections What could be on your ballot in November? Evolution of Passport

A scheme to monitor.

Credit Bureau Triggers

An explanation for those unsolicited calls.

Bank Entry Decline

A Dodd-Frank fallout.

Banking Legal

Updates

Pending litigation could impact the financial system.

Women in Banking

Women bankers convene for annual session.

ABA Goes to D.C. Bankers meet with Cotton, Womack, and Hill.

PRESIDENT’S MESSAGE

Lorrie Trogden | President & CEO | Arkansas Bankers Association

Elections are upon us, the state legislative session starts soon, and regulatory issues abound – what do we do in the face of all that? Advocate, advocate, advocate! We work every day to change “what is” into “what should be.” The “what should be” has a direct impact on our communities and our customers, and we are on the right side of fighting the good fight for them and for our industry.

Let’s start with the state. On April 10th Arkansas will begin its fiscal legislative session. Because it is a fiscal only session, no substantive bills can be voted on without a 2/3rd majority vote of the House and Senate. Does that mean nothing is happening? Short answer, No. We will be monitoring the session for anything that might affect banking or the budget of the State Bank Department. As you know, they are a cash agency funded by your assessments and anything affecting the department typically affects us. In addition, legislators are already contemplating ideas and bills for the 2025 substantive session. It will be here before you know it. I have already been contacted a couple of times about different subject matter being considered.

The southern states around us are also a good precursor to what is likely to head our way in 2025. These are the active issues in other states right now:

• Merchant Category Code (MCC): This did not pass in AR in 2023. As of March 2024, 27 bills are active in addition to 8 that passed.

• ESG: There are 32 active general ESG bills, along with 16 that are fiduciary only, 19 divestment bills, 5 firearm specific bills and 4 fossil fuel specific bills.

• Social Credit Score: There are 17 active credit score bills.

• Payments: There are 7 of these state level interchange bills.

• Crypto and Central Bank Digital Currency: There are 15 active bills in this arena.

As you can see, there is still a hotbed of anti-bank legislation out there and most of it will be heading in our direction. We are being proactive and on the lookout before filing starts for 2025.

Continuing the state-side of things, the ABA was a guest at several legislative committee hearing tables over the last several months. First, Senator Bryan King, Chairman of the Senate Children and Youth committee, asked the State Bank Department and the ABA to testify at a hearing. My focus was on scamming and fraud with examples of what is happening across the industry and its impact on customers. Members were very interested in the educational resources the ABA offers, and a couple of have shared some of our #banksneveraskthat content on their social media. I also accompanied incoming Vice Chairman Jason Tennant to a joint Insurance and Commerce committee meeting, where Jason focused on the effect rising insurance rates and deductibles are having on our customers’ mortgage and escrow accounts. He did a great job, and we are thankful for his participation and his advocacy!

Moving on to federal, we once again descended on the Hill during the Washington Summit in March to visit with our congressional delegation. Advocacy, Advocacy, Advocacy! We focused on several hot topics:

• 1071 – Despite the current injunction (you can read more about that in our legal update article), we advocated for passage of the Small LENDER Act and continued pressure on CFPB oversight. Big thanks to Congressman Hill for his work on LENDER!

• ACRE – We continue to push for the passage of ACRE and are thankful it has the support of our delegation. It is gaining bipartisan support, but once spending bills are passed, I don’t know if anything else will move before elections.

• Credit Unions – The credit unions were on the Hill a week before us and apparently were spreading a false narrative about why they deserve a tax exemption. An Arkansas credit union claimed that CUs are serving rural areas that banks are not. Fact Check: bankers in the room from Eureka Springs quickly pointed out that there were no credit unions in their entire footprint of small towns, and that was also true of other bankers in attendance. Busted!

• Durbin 2.0 – We have been in constant contact with our delegation about this bill since it was introduced and have lobbied hard for our delegation not to join as co-sponsors or allow it to be attached to a must-pass spending bill. The bill is not scheduled for a committee markup, but we cannot take our foot off the gas! Retailers are contacting them regularly and we must do the same!

• Beneficial Ownership Database – As you all know, the rule making and implementation of the database fell flat on its face, causing nothing but customer confusion and blame on banks. A federal judge in Alabama issued an injunction, so there will be more to come here. Our ask was that FinCEN take a step back and delay compliance until there is a chance for further education, implementation processes are worked out, and privacy concerns are addressed.

We will continue our Advocacy, Advocacy, Advocacy efforts to bring home wins for our industry, your customers, and your communities! I also encourage you to participate in campaigns reminding your bankers to vote. Regardless of who they vote for, it is so important to take part in the process. We want people who understand our industry at the table so that we stay off the menu! Thank you for everything that you do, and I look forward to visiting your bank in 2024!

“We have three priorities: Advocacy, Advocacy, Advocacy!”

Lorrie Trogden, President & CEO

ABA OFFICERS

Jim Taylor, Chairman First Security Bancorp, Rogers

Brad Chambless, Chairman-Elect Farmers and Merchants Bank, Stuttgart

Chris Gosnell, Vice Chairman Farmers Bank & Trust Company, Magnolia

Scott Saffold, Treasurer Union Bank & Trust Co., Monticello

Randy Scott, Past Chairman Farmers Bank and Trust, Blytheville

Lorrie Trogden, President & CEO Arkansas Bankers Association, Little Rock

BOARD OF DIRECTORS

Heather Albright, Little Rock

Duncan Bellingrath, Hot Springs

Asa Cottrell, Little Rock

Joe Dunn, Little Rock

Robert Husong, Rogers

Katherine Mitchell, White Hall

Brandi Ray, Malvern

Gabe Roberts, Jonesboro

Lori Ross, Arkadelphia

Joe Ruddell, Rogers

Loren Shackelford, Fayetteville

Jason Tennant, Eureka Springs

Rob S. Tiffee, Little Rock

Scott Walker, El Dorado

Jay Wisener, Little Rock

Corporate Transparency Act Beneficial for Banks

The Corporate Transparency Act (CTA) represents a significant legislative milestone aimed at promoting corporate transparency, combating illicit financial activities, and enhancing accountability in the financial system. This article provides a comprehensive analysis of the

CTA and its implications for banks, exploring key provisions, compliance challenges, and opportunities for fostering a more transparent and secure financial environment.

In an era marked by increasing scrutiny of corporate structures and financial transactions, the Corporate Transparency Act (CTA) stands as a landmark piece of legislation designed to address longstanding concerns regarding the misuse of anonymous shell companies for illicit purposes. Effective in 2024, the CTA represents a bipartisan effort to enhance transparency

and accountability in corporate ownership, with profound implications for banks and financial institutions tasked with ensuring compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations.

The CTA mandates the establishment of a beneficial ownership registry, requiring corporations and limited liability companies (LLCs) to disclose information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN). Beneficial owners are individuals who directly or

indirectly own or control 25% or more of the ownership interests in the entity or exercise substantial control over its operations.

The implementation of the CTA has significant implications for banks, particularly in the realm of customer due diligence (CDD) and AML compliance. Banks are now required to verify the identity of beneficial owners of corporate customers and maintain accurate records of such information. This entails conducting thorough background checks and risk assessments to ensure compliance with regulatory requirements and mitigate the risk of facilitating illicit financial activities. However, banks cannot access the CTA database without the customer’s consent.

While the CTA represents a critical step towards enhancing transparency and

“Effective in 2024, the CTA represents a bipartisan effort to enhance transparency and accountability in corporate ownership, with profound implications for banks and financial institutions tasked with ensuring compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations.”

Jim Taylor | Chairman | Arkansas Bankers Association

“The CTA mandates the establishment of a beneficial ownership registry, requiring corporations and limited liability companies (LLCs) to disclose information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN).”

combating financial crime, its implementation poses several challenges for banks. Identifying and verifying beneficial owners can be a complex and resource-intensive process, particularly for entities with intricate ownership structures or offshore holdings. Banks must also navigate privacy concerns and data protection regulations while adhering to strict AML/CFT requirements, striking a delicate balance between transparency and customer confidentiality.

Despite the challenges posed by the CTA, it also presents opportunities for collaboration and innovation within the banking industry. Banks can leverage technology and data analytics to streamline the customer onboarding process, enhance risk assessment capabilities, and improve compliance efficiency. Collaborative initiatives between banks, regulators, and law enforcement agencies can facilitate information sharing and strengthen the effectiveness of AML/CFT efforts, ultimately promoting a more transparent and secure financial ecosystem.

By promoting greater transparency and accountability in corporate ownership structures, the CTA serves as a critical tool in the fight against money laundering, terrorist financing, and other illicit financial

activities. Banks play a pivotal role in this endeavor, serving as gatekeepers of the financial system and frontline defenders against financial crime. Through robust compliance measures, proactive risk management, and ongoing vigilance, banks can uphold the integrity of the financial system and safeguard against abuses of corporate entities for illicit purposes.

It is a common misconception that banks were the impetus for the creation of the CTA, I can assure you we were not. However, we could be the benefactor of the beneficial ownership registry database. The Corporate Transparency Act represents a significant step towards fostering greater transparency, accountability, and integrity in the financial system. While its implementation poses challenges for banks, it also presents opportunities for collaboration, innovation, and strengthening AML/ CFT efforts. By embracing the principles of transparency and accountability, banks can fulfill their role as responsible stewards of the financial system and contribute to a safer and more secure environment for businesses, consumers, and society as a whole. I encourage you to seek further knowledge of the CTA to ensure proper compliance with the act.

Calendar of Events

- JUNE 2024

April

15 19

MONDAY 8 A.M. – FRIDAY 5 P.M.

GSB HUMAN RESOURCE MANAGEMENT SCHOOL

From recruitment to selection, performance management to career development, the human resource function has a direct impact on a financial institution’s productivity and bottomline results. That’s why GSB offers the Human Resource Management School, a respected one-week school that provides the foundation for new or veteran human resource professionals to tie together important issues in human resource management with an understanding of the business of banking. A scholarship is offered through the ABA -- please contact Kami at kami.coleman@arkbankers.org for an application!

LOCATION: University of Wisconsin – Madison

22

MONDAY 1:30 P.M. – 3 P.M.

CASH FLOW ANALYSIS

In this webinar, you'll learn the fundamentals of constructing and analyzing direct and indirect cash flow statements in order to enhance the quality and effectiveness of the entire credit decision process.

INSTRUCTOR: Tom Carlin

LOCATION: Virtual

22 26

MONDAY 8 A.M. – FRIDAY 5 P.M.

BANK TECHNOLOGY MANAGEMENT SCHOOL

Don’t miss this innovative school that’s designed by, and especially for, IT professionals and information security officers in the financial industry. This state-of-the-art program will broaden your understanding of the business of banking including key drivers of bank profitability, along with an in depth and interactive study of information technology management. The school will share practical insights for disaster response and business continuity, IT exam preparation, technology risk assessment, vendor management, IT strategic planning, project management and more. Designed to help improve your productivity and value at your bank, you’ll also establish a network of professional colleagues with whom to collaborate and exchange ideas for years to come. Apply today to take advantage of this opportunity to learn from experts in the banking industry about today’s key issues in information technology management and how those critical issues relate to the bank’s goals and bottom line.

LOCATION: University of Wisconsin – Madison

23 24

TUESDAY 9 A.M. –WEDNESDAY 4 P.M.

2024 COMPLIANCE SCHOOL

Join us and sharpen your compliance expertise to develop a basic foundation to maintain an effective compliance program! This school is intended for those with less than five years of experience in the compliance field, or for those wanting knowledge in overall compliance rules and requirements. These sessions will provide an overview of concentration in the consumer compliance areas, including deposit/ operations, lending, and overall strategies for an effective Compliance Management System (CMS).

INSTRUCTOR: Shaun Harms

LOCATION: Arkansas Bankers Association, Little Rock

25

THURSDAY 9 A.M. – 4 P.M.

IRAS:

ADVANCED ISSUES

In this session, we’ll get into the nitty gritty of the new distribution regulations, exploring—in depth—how these new rules affect both IRA owners and IRA beneficiaries. After thoroughly dissecting the new rules and their impact on IRA owners and beneficiaries, we’ll discuss concrete steps your financial organization can take to help ensure ongoing compliance, while also providing top-notch customer service.

INSTRUCTOR: Johnathan Yahn

LOCATION: Arkansas Bankers Association, Little Rock

29

MONDAY 10 A.M. – 12 P.M.

THIRD-PARTY MANAGEMENT

ESSENTIALS

Financial institutions have had specific vendor management guidance to follow for decades. Each primary financial institution regulatory body has issued specific requirements for working with third parties. To avoid costly fines, reputation risk, and consumer harm, vendor management must be embedded in all lines of business. Siloed approaches to vendor management are outdated. This program provides a thorough review of the basic requirements and guidance for sustaining a compliant and risk-based program.

INSTRUCTOR: Kimberly Boatwright, CAMS, CRCM

LOCATION: Virtual

TUESDAY 9 A.M. – 4 P.M. 2024 CONSUMER LENDING

SCHOOL

This informative, intensive three-day school is designed to educate and prepare consumer lenders. This educational program provides essential knowledge and skills and establishes a network of lenders for continued support by sharing experiences with fellow lending professionals. Newly appointed loan officers and bankers in the credit administration and loan processing areas will especially benefit.

INSTRUCTOR: David Kemp

LOCATION: Arkansas Bankers Association, Little Rock

May

30 03 30

TUESDAY

This webinar series will encompass opening personal, business, trust, minor, power of attorney, estate accounts, and much more! Although not customized to specific state law, it will answer the more complicated and challenging questions customers and employees ask. Whether you are new to new accounts or have decades of experience, you will gain more confidence and be prepared to handle even the most complicated scenario!

INSTRUCTOR: Matthew Dickson LOCATION: Virtual

FRIDAY 10 A.M. – 12 P.M.

CALL REPORT FOR BEGINNERS5 PART SERIES

This course is designed for bankers new to Call Report preparation, as well as those seeking a refresher course. This webinar series will primarily follow the structure of the Call Report, progressing through the schedules in order. However, to enhance the learning experience and better convey related reporting content, certain schedules will be grouped together within the curriculum. This approach ensures that attendees can grasp both the individual schedules and their interconnections, facilitating a comprehensive understanding of the reporting process.

INSTRUCTOR: Andrea Lambert

LOCATION: Virtual

AT A GLANCE

Live events are subject to a virtual learning environment. For more information, contact the ABA at (501) 376-3741 or Kami Coleman at kami.coleman@arkbankers.org.

Against a Rising Tide of Regulation, BANKS MUST ROW TOGETHER

Rob Nichols | President and CEO | American Bankers Association

Whenever a new election cycle comes along, it’s not uncommon to hear pundits make mention of “red waves” or “blue waves,” denoting potential power swings in Congress. But as bankers contemplate the future of our country and the policy environment that will shape the future of our industry, there’s another wave that we need to talk about: a tsunami of complex regulation that’s hitting the banking sector as we speak.

To be sure, the tide turned quickly: last year’s turbulent spring ignited a rulemaking frenzy at the banking agencies. Suddenly, new proposals sprang up to increase bank capital levels, impose a new long-term debt requirement and make the resolution planning process more complex.

Simultaneously, the CFPB imposed long-awaited small business reporting requirements under Section 1071 of the Dodd-Frank Act—which went far above and beyond what was outlined in the statute. The Federal Reserve issued a proposal to cap interchange fees under Regulation II, and the FDIC is now pursuing significant changes to its corporate governance guidelines.

Against all that, the agencies finalized a long-awaited update to the Community Reinvestment Act framework—a staggeringly complex, 1,500-page final rule that creates significant new requirements that have the potential to fundamentally alter banks’ business strategies.

Meanwhile, in Congress, banks are facing the resurgent threat of the so-called “Credit Card Competition Act,” which would apply Durbin Amendment-like provisions to credit cards—the equivalent of lawmakers taking money from banks and putting it into the cash registers of mega retailers.

“We need to make sure policymakers in Washington ... understand that regulatory burden has a realworld cost, not just for banks, but for consumers, small businesses and the American economy... If you’re reading this, I urge you to help us tell that story.”

Taken together, these policies place a tremendous cost and compliance burden on banks of all sizes—at a time when they are already facing a tough operating environment due to a protracted period of high interest rates and ongoing geopolitical tensions.

These policies will also have devastating effects for consumers. Banking is, after all, a business—and in order for banks to offer the full range of financial products and services to meet the needs of communities, they need to be profitable, and have an operating environment that supports growth.

The current regulatory landscape will do the opposite. Banks that are already considered well-capitalized by regulators’ own admission will be forced to hold even more capital in reserve—which means less capital will be available to lend to the local small business looking to expand, or to the young family looking to buy their first home. Simultaneously, changes to the fee income streams upon which banks have long depended could spell the end of free or low-cost checking products, and popular rewards programs that consumers value.

What’s perhaps most concerning, however, is the fact that regulators don’t seem to understand the full impact of their actions. As we observed with the Reg II rulemaking and the so-called “Basel III endgame”

proposal, regulators are failing to adequately assess the potential costs of the individual regulations on banks and consumers—let alone contemplate what the cumulative impact of all these rules would be.

ABA is sounding the alarm. We need to make sure policymakers in Washington— from members of the administration to lawmakers in Congress to the regulators holding the rule-writing pens—understand that regulatory burden has a real-world cost, not just for banks, but for consumers, small businesses and the American economy.

If you’re reading this, I urge you to help us tell that story. Join our Bank Ambassador program to rekindle relationships with your congressional delegation and help educate policymakers about banking. Stay informed and send a letter about an issue that will affect your bank through ABA’s grassroots platform, SecureAmericanOpportunity.com. Make a plan to come to the nation’s capital in March for the ABA Washington Summit, and tap a colleague or two to come along.

The sobering reality for banks right now is that rougher seas are likely ahead—but our best hope is to row together.

Email Rob at nichols@aba.com.

To learn more about the Bank Ambassador program, email ABA’s Laura Lily at llily@aba.com.

Director Training Part 2 –Education is the Key

Susannah Marshall | Commissioner | Arkansas State Bank Department

In my previous article, I briefly touched on the topic of director training. In the past few months, there have been several issues that have arisen during both routine examinations and outside of the on-site examination process which align with the topic of director training, and I would like to use this issue to expand on the following topics. Although one session of director training, within the first twelve months of Board membership, is all that is required by the Arkansas State Bank Department, I can’t express enough how important it is to evaluate opportunities for further training for Board members, both internal and external members.

The Directorate is tasked with significant responsibility, and they accept enormous responsibility and liability including financial, fiduciary and legal risk in exchange for their service to the institution and our industry. Although, it is important to note that the vast majority of time, Board members execute their duties and serve the institution with normal and routine processes and oversight. However, circumstances and situations do arise where the institution and the Board face considerable challenges. One key to success for both the institution and the Directorate, is the execution of sound principles, knowledge of regulations and implementation of appropriate corrective measures when necessary.

With the sheer volume of both state and federal rules and regulations, as well as the basic tenets of Capital Adequacy, Asset Quality, Earnings Performance, Liquidity and Funds Management and Sensitivity to Market Risk, it can be overwhelming for any director to feel knowledgeable and prepared to appropriately lead and direct the affairs of the institution. But the following major rules and regulations warrant an increased understanding and awareness in order to diminish some of the risk to individual Board members and the bank itself. As I previously stated, our team has engaged in many recent discussions around these supervisory requirements.

Each Board member and each management team should possess a strong understanding of both Regulation O and Regulation W. Specifically, these two regulations point to the limitations and requirements which Board members must adhere to and can present significant risk if the institution is found in violation of either federal regulation. Also, we are seeing an increase in violations or supervisory findings pertaining to the Bank Secrecy Act. The breadth and complexity of the Bank Secrecy Act requires a much deeper understanding hence the annual training requirements for this regulation. The impact of failing to maintain a strong Bank Secrecy Act program can lead to the highest level of regulatory oversight and potential for financial obligations and penalties against the bank. Further, we continue to work with management teams to ensure proper oversight and application of the Legal Lending Limit. Although most banks rarely have issues regarding compliance with the Legal Lending Limit, violations can

create issues both individually and collectively for the Directorate hence requiring a high level of diligence and oversight.

Although a bank’s management team is charged with leading the institution on a daily basis and implementing strong compliance programs for the adoption and adherence for all applicable laws and regulations, it is of utmost importance that Board members maintain an individual understanding and competency for certain regulations. I fully appreciate that this objective can be especially challenging for external directors. As we are starting a new year and Board members are being selected and reappointed, I encourage each bank to consider an assessment of your Board’s training and consider if now is the time to identify ways to enhance or supplement the training and education of your Board. If the assessment proves that the Board has not had an opportunity to be exposed to external training or industry presentations or speakers in the past few years, perhaps consider options to provide or implement even a small session for the Directorate of the bank.

“Each Board member and each management team should possess a strong understanding of both Regulation O and Regulation W.”

Many director education programs exist. Whether it is an offering by one of the many Graduate Banking Schools, or the Arkansas Bankers Association or American Bankers Association, an in-house session or a consultant facilitated program or even the upcoming annual Day with the Commissioner event held in conjunction with the Arkansas Bankers Association Annual Convention, I propose you consider taking advantage of the multitude of resources to provide your Board members with a new opportunity for training and support. I bet they would be interested in furthering their knowledge and awareness and enhancing their ability to better serve the institution, our industry, and their communities!

THE FACES OF ARKANSAS BANKING with Dwayne Dickey

SVP/IT Director

First Community Bank, Batesville, AR

Dwayne Dickey is the senior vice president and information technology director at First Community Bank. This year marks his 35th year in banking. Dickey, who is married to Suzanne, has two children, Kyler and Brendan. Outside of work, he enjoys running and spending time with his family.

In his role, Dickey oversees all information technology operations as well as the management, strategy, and execution of the IT infrastructure for the bank. He also oversees technical projects and directs the effective delivery of networks, development, and disaster recovery systems and processes. Additionally, he organized an IT in Banking group.

WHAT’S THE DIFFERENCE BETWEEN A BOSS AND A LEADER?

A boss is typically focused on getting the job done, often through instruction and oversight. A leader, on the other hand, inspires and guides their team by setting a vision, empowering them, and fostering a sense of ownership and pride in the work. Leaders often prioritize the growth and development of their team members, creating a more engaged and motivated workforce.

WHY IS IT IMPORTANT FOR THE YOUNGER GENERATION OF BANKERS TO GET INVOLVED IN THE GOINGS ON IN OUR INDUSTRY?

It's crucial for the younger generation of bankers to stay involved and informed about the industry for several reasons. Firstly, staying abreast of the latest developments and trends in banking ensures that they remain competitive and relevant in their careers. This includes staying informed about changes in regulations, technology, and cybersecurity.

Secondly, the banking industry is rapidly evolving, especially with the emergence of new technologies like AI. Understanding these technologies and how they can be leveraged in banking operations is essential for future success. Additionally, as cyber threats become

“Leaders

often prioritize the growth and development of their team members, creating a more engaged and motivated workforce.”

more sophisticated, staying informed about cybersecurity is crucial to protect both the bank and its customers.

Finally, getting involved in the industry allows younger bankers to network with professionals, exchange ideas, and gain insights from experienced leaders. This not only helps them stay informed but also provides opportunities for career advancement and personal growth.

WHAT IS THE BEST ADVICE YOU EVER RECEIVED?

One of the best pieces of advice I've received is from Karl Kemp, the former IT Director for First Community Bank. He once said, "Don't procrastinate; the situation almost never improves by waiting." This advice has stuck with me because it reminds me of the importance of taking action and addressing issues promptly. Waiting often only allows problems to worsen, so it's crucial to tackle challenges head-on and not delay in finding solutions.

WHAT SUBJECT COULD YOU GIVE A ONE-HOUR IMPROMPTU LECTURE ON?

I could easily talk for an hour about running! I've been at it since 2006, and as I always say, "The only thing that runners like more than running is talking about running." In my impromptu lecture, I'd cover everything from establishing solid running routines to helping beginners get started on the right foot. I'd dive into the joy and benefits of running, share tips on staying motivated, and discuss the mental and physical aspects of the sport. It's a passion of mine, and I love sharing that enthusiasm with others!

Mastering Hard Conversations

Latrecia Carroll | President | Emerging Leaders Section

Let’s face it, tackling hard conversations is not for the faint of heart. Experts agree that we are wired to avoid confrontation. I will be the first to admit that I often dread confrontation, but it is crucial for success as a leader. Even with a rockstar team, difficult conversations are sometimes necessary. You might hesitate to approach because you’re unsure of the employee’s reaction. While your fear is valid, avoiding them sends a message that current actions are acceptable. These challenging conversations also prevent issues from growing and affecting other team members. There are approaches we can use to make hard conversations a little easier.

If you need to address a challenging issue, check your mental state. Don’t jump headfirst into the height of emotions; it only makes issues worse. Spend time sorting through your feelings, then pushing them aside. Ensure your concerns don’t arise from an exhaustive mental state.

Prepare yourself for the conversation; the more you prepare, the better it should go. Write down your concerns and propose solutions. Vent about the issue to a trusted friend or colleague, sharing the good, bad, and ugly. Take feedback to help prepare your words. Talking through it with others allows you to see an objective perspective, turning it into a compassionate and connecting conversation instead of accusations and defensiveness.

Be open-minded to different points of view during difficult conversations. Try to understand the other person’s perspective by imagining yourself in their shoes. Walk through the experience through their eyes, attempting to understand their emotions, triggers, and desires. This triggers empathy and self-awareness. At the same time, don’t let the issues fester. Take heart and go. It might not be pleasant, but the goal is to deliver in an honest, fair way.

When you decide to carry out the conversation, make room for the person to talk. Always be willing to listen more than you talk. The worst thing you can do is speak over them

and refuse to hear them out. People want to know they’re being heard. You don’t have to agree with them, but at least acknowledge their point of view. There should be a sense of respect in your tone. Be specific with the issue and clarify that it’s not with the person, but a certain behavior.

The conclusion to any hard conversation is follow-up. Set ground rules for moving forward. Make your intentions clear and get acknowledgment from the other person. Offer resources that could help them improve or correct the issue at hand. Always recognize their efforts to make progress. Emphasize your willingness to help them succeed and reach their goals. Failure to follow up could cause the behavior to creep back over time.

Difficult conversations promote positive change and strengthen team culture. Remember, everyone is battling their own problems. People aren’t always aware of the impact their behavior has on the entire team or organization. Take a deep breath, prepare, and approach the conversation with empathy to find a resolution. Always look at the bigger picture.

“Difficult conversations promote positive change and strengthen team culture... Take a deep breath, prepare, and approach the conversation with empathy to find a resolution.”

ELS EXECUTIVE COMMITTEE

LATRECIA CARROLL PRESIDENT

STONE BANK

Little Rock

Group 1

AMBER MURPHY SECRETARY/ TREASURER

FIRST FINANCIAL BANK

El Dorado

Group 3

ELS COUNCIL MEMBERS

IAN BRYAN VICE PRESIDENT

SIMMONS BANK

Russellville

Group 2

BRITT BURRIS

CONNECT BANK

Star City

Group 3

CHANCE ROBBINS

CS BANK

Eureka Springs

Group 2

JAKE EARNEY

CHAMBERS BANK

Fayetteville

Group 2

GABE ROBERTS

FIRST COMMUNITY BANK

Jonesboro

Group 1

BRITTANY HELMS

SIMMONS BANK

Little Rock

Group 1

RHETT SHEPARD

CENTENNIAL BANK

Little Rock

Group 1

BRANDON KNOWLTON

SOUTHERN BANCORP

Arkadelphia

Group 3

SARAH LYNCH

GENERATIONS BANK

Fayetteville

Group 2

LAUREN STATON

RELYANCE BANK

White Hall

Group 3

EMERGING LEADERS

minutes with...

FIVE Brittany Little

Q.

A.

VE

Market President | Today’s Bank, Huntsville, AR

HOW DID YOU GET STARTED IN BANKING?

I have always loved small businesses, how they work, and how your community benefits from them. I knew I wanted to do something with small businesses and fell in love with banking while working at the bank in college. Without your community bank, you have no one supporting your community and small businesses.

Q. WHAT ADVICE DO YOU HAVE FOR YOUNG BANKERS STARTING THEIR CAREERS?

A.

Never be afraid to learn something. Dig in and learn all you can about a topic. I wouldn’t be where I was today if I hadn’t dug in and tried to learn at an early age. When I first started, the bank was going through key management changes, a core conversion, and making some other major software changes, and I was able to be there on the ground floor learning the new products. Because I was able to learn a lot about how they all worked together, it served me in my various roles throughout my career more than I could ever imagine. Whether it be a trick on our banking system, or where to find some information, looking at a new report for trends, or just learning what something means, everyone enjoys knowing more information about what they work with daily. I have been fortunate to have some great teachers during my career and hope to pass on the knowledge. Knowledge is power, and when you are able to do your job better then we can serve our customers better with the more we all know.

Q. WHAT IS THE MOST INTERESTING THING ABOUT WORKING AT A SMALL BANK?

A. I love working at a small community bank. I love that over the years the bank has grown and I have grown with it. Every single day is different and I didn’t get pigeonholed working on the same thing each day. I was able to grow in my knowledge. Every day presents itself with new challenges, and there isn’t a lot of red tape on making change happen when things aren’t working. Don’t be afraid to change or look at how things are being done, and how they can be better. Things are always evolving, and sometimes there could be better ways to do it.

Q. HOW HAS YOUR LIFE EXPERIENCE MADE YOU THE LEADER YOU ARE TODAY?

A.

Parenting children has helped my leadership. We have a set of twin girls, Ava and Emma (age 8), and Barrett (age 3). By having the girls and raising them in the exact same environment, it has helped me realize not everyone learns the same under the same conditions. They are as different as day and night. It also has helped me focus. I know that my time is valuable. I only get so many waking hours with my family and at work. When I get home at night, and we are doing dinner as a family, baths, and homework, I try my best to be focused on them. After we get them to bed, and we get the house reset for another day, then I will focus on my work. My kids know I love my job, but I always want them to know they come first.

“ Never be afraid to learn something. Dig in and learn all you can about a topic.”

Q. WHERE WOULD YOU LIKE TO TRAVEL?

A. Italy is definitely on my bucket list. I hope in the next couple of years, my husband and I can go over there and stay for a couple of weeks wandering the countryside. I really would like to avoid touristy places and spend time on the off-beat path discovering all the gems!

Fall Candidate ELECTIONS SET

But Still Waiting on Issue Campaigns

by Roby Brock

While the presidential election will suck much of the political oxygen out of the room in 2024, Arkansas’ November ballot will be unusually lower profile.

Arkansas won’t have a governor or U.S. Senate race this cycle, but we will have four contested Congressional elections.

In Arkansas’ 1st Congressional District, U.S. Rep. Rick Crawford, R-Jonesboro, will face Democrat Rodney Govens, a 40year year old Operation Iraqi Freedom veteran from Cabot, and Libertarian Steve Parsons in the November general election.

U.S. Rep. French Hill, R-Little Rock, will square off against Democrat Marcus Jones, a retired U.S. Army Lt. Col., in the general election for the 2nd Congressional District job.

In the 3rd Congressional District, U.S. Rep. Steve Womack, faces Democrat Caitlin Draper in the general election. Draper is a licensed clinical social worker (LCSW), small business owner and community advocate. The Libertarian Party nominated Bobby Wilson in the Third District.

U.S. Rep. Bruce Westerman, R-Hot Springs, will have two general election opponents in the 4th Congressional District race. Democrat Risie Howard, a lawyer from Pine Bluff and daughter of former U.S. District Court Judge George Howard Jr., and Independent John White, who ran and lost as a Democrat in the 2022 election, filed Tuesday to enter the race.

There will also be the run-off election for Arkansas Supreme Court’s Chief Justice position between Justice Karen Baker and Justice Rhonda Wood. Whoever loses the race, will still serve on

the state’s high court. Gov. Sarah Sanders will get to appoint a replacement for the vacancy that will be created by the winner.

In November, Arkansas will see a rare off-year special election for Treasurer of State due to the untimely death of former Treasurer Mark Lowery in 2023. The special election this year will be to fill the remaining two years of the four-year term. Republican Secretary of State John Thurston, Democrat John Pagan, and Libertarian Dr. Michael Pakko are all seeking the treasurer’s post.

Of course, local races for legislature, county and municipal seats will also draw attention. For bankers, electing state representatives and senators who understand financial and banking issues will be key.

What may be the most high-profile elections this fall will center around ballot issues, assuming some of the potential amendments and acts qualify and stay on the ballot. There are seven proposals that must gather anywhere from 72,000 (initiated acts) to 93,000 (constitutional amendments) valid voter signatures to qualify. After that, they must be certified by the Secretary of State’s office and survive probable legal challenges. If all of those thresholds are met, then voters will get a chance to cast ballots on them this Fall.

The General Assembly only referred one proposal to voters, and it simply allows lottery scholarship money to be used for vocational and technical school scholarships. It will be known as Issue 1.

The rest must overcome their largest hurdle: your signature. In the coming weeks, you’ll be asked to sign a petition when you come out of the grocery store, attend a Spring festival, or any other gathering such as a reunion, concert, or baseball game.

To help you decide now if you want to have a chance to vote for any of these measures, here is a handy overview of each one of the proposals that has garnered approval by the Attorney General to seek signatures to qualify.

AN ACT TO EXEMPT FEMININE HYGIENE PRODUCTS AND DIAPERS FROM SALES AND USE TAX

This one does what it says. It would eliminate the sales tax on items like tampons as well as diapers. The thought originally was feminine hygiene products are an extra sales tax burden on women, not men. The diaper clause was added to broaden its appeal to help younger families who are in their child-bearing years and could use the tax break.

ABSENTEE VOTING AMENDMENT OF 2024

Supporters of this proposal claim there needs to be more oversight and restrictions for the absentee voter process. It sets a time and procedures for obtaining a ballot; spells out rules for who can qualify to obtain a ballot; and sets forth the process for counting

those ballots as well as stipulates “elections cannot be conducted in this state using an internet, Bluetooth, or wireless connection.”

ARKANSAS MEDICAL MARIJUANA AMENDMENT OF 2024

This measure is supported by the medical marijuana industry, which contends there are improvements that need to be made to the constitutional amendment passed in 2016. It allows for telemedicine assessments; extends registry cards from one year to three years; broadens the requirements for a "qualifying medical condition"; and allows qualifying patients or caregivers at least 21 years old to keep and to plant marijuana plants in limited quantities and sizes at their domicile. The main reason for the last provision, according to supporters, is to help provide medical marijuana to those who must travel a great distance to a retail store.

ARKANSAS EDUCATIONAL RIGHTS AMENDMENT OF 2024

The proposed amendment would require private schools that receive local and state funds to comply with state academic and accreditation standards, including student and school assessments. Failure to do so would result in a loss of state funds. The amendment also says the state will provide universal access to early childhood education from age 3 until a student qualifies for kindergarten; universal access to afterschool and summer programs; services for students with disabilities; and assistance to children within 200% of the federal poverty line to deal with circumstances that contribute to poor learning outcomes.

ARKANSAS GOVERNMENT DISCLOSURE AMENDMENT (AND ACT) OF 2024

This proposal is a double-feature. Sprouted from the controversy of last year’s special session to restrict the state’s Freedom of Information Act (FOIA), the bipartisan group supporting this amendment change want to enshrine FOIA into the constitution. They are also offering a complimentary initiated act with details normally enacted by legislators. The amendment defines "government transparency," and the act goes further in prescribing penalties for bad actors who knowingly violate the FOIA. It also creates a state commission for records requests.

ARKANSAS HISTORIC OR SPECIAL INTEREST VEHICLE ACT OF 2024

Last, but not least, a proposal has qualified to collect signatures to amend the law at which certain vehicles can be registered as historic or special interest. Current law puts that historic registration for vehicles that are 45 years or older, but this initiated act would lower the minimum age requirement of the vehicle to 25 years.

To summarize, these potential changes to the Constitution and state law are citizen-led initiatives. Arkansas is one of only 15 states with this type of referendum process where a group of citizens can propose laws. The Secretary of State will make a determination on the validity of the signatures in late July, so it won’t be until this Summer before the final issues are determined.

There

are seven proposals that must gather anywhere from 72,000 (initiated acts) to 93,000 (constitutional amendments) valid voter signatures to qualify.

According to the state’s top banking official, the uncertain interest rate environment is the most significant conversation topic entering the year.

Marshall said banks with strong mortgage divisions bore the brunt of the interest rate volatility in 2023 and will remain impacted until a downward movement emerges.

“I don’t want to attempt to predict what will happen with interest rates in 2024 or the timeframe of any potential rate decreases,” she said. “Regardless of whether we will see any additional increases or rates remain flat for the foreseeable future, I believe any potential declines could be further out in 2024.”

82 FEDERALLY INSURED LENDERS DOING BUSINESS IN ARKANSAS HAD A CUMULATIVE NET INCOME OF

THE BANKS GREW THEIR COMBINED ASSETS ROBUSTLY TO

THROUGH THE THIRD QUARTER OF 2023, UP 7.3% YEAR-OVER-YEAR. $1.49 BILLION $165.6 BILLION FROM THE PREVIOUS YEAR. UP 4.1%

Marshall and other Arkansas banking leaders offered various thoughts on the industry entering 2024. According to the latest data from the Federal Deposit Insurance Corp. (FDIC), 82 federally insured lenders doing business in Arkansas had a cumulative net income of $1.49 billion through the third quarter of 2023, up 4.1% from the previous year. The banks grew their combined assets robustly to $165.6 billion, up 7.3% year-over-year. Loan growth was even stronger at 13.8%. Construction loans accounted for a third of that growth, reflecting the vibrant economy.

Tim Yeager expects banks to remain strong — Arkansas’ average return on assets (ROA) of 1.23% is well above the benchmark ratio of 1% — but they are unlikely to match their 2023 performance.

“The lagged effect from high interest rates will lead to slower loan growth, an increase in problem loans, and a shortage of core [stable] deposits,” said Yeager, a finance professor who holds the Arkansas Bankers Association Chair in Banking at the University of Arkansas. His responsibilities include teaching, research and outreach to Arkansas bankers. “Loan demand will slow as businesses and consumers adjust to higher interest rates. In addition, borrowers will struggle to repay the higher interest payments on their debts, leading to more problem loans.”

Like many analysts, Yeager said he expects the Federal Reserve to lower interest rates in the coming months, which will somewhat reduce the pressure on loan demand and funding costs. He said Arkansas bankers are most concerned about a longer-term issue: the ability to hire and maintain qualified workers. He noted that many top students in finance want careers in investment banking, primarily because they think they can make more money on Wall Street.

That might be true, but he tries to explain that there are other advantages of working for a bank.

“We need to get the message across that this is a soul-fulfilling career,” Yeager said. “You’re going to do well, but will you be a millionaire or a billionaire? It’s less likely. But you will have a much more balanced, satisfactory life by doing this.”

According to the American Bankers Association, Arkansas banks employ around 16,000 people at over 1,000 offices and branch locations and have around 5 million customers.

‘ARTIFICIAL’

ECONOMY

Simmons First National Corp. (Simmons Bank) of Pine Bluff is one of the state’s largest banks, with $27.5 billion in assets. It’s one of four Arkansas-based lenders with assets greater than $21 billion at the end of last

year’s third quarter. Bank OZK of Little Rock ($32.7 billion), Arvest Bank of Fayetteville ($27.3 billion) and Centennial Bank of Conway ($21.8 billion) were the others.

George Makris Jr. is the bank’s president and CEO. He said that after a decade marked by growth through acquisition, Simmons Bank is focused on organic growth and efficiency in 2024.

“We acquired 13 banks [in five states] in the past 10 years, which has given us access to some of the best markets,” he said. “We are improving our delivery channels and standardizing many internal functions. That combination should produce favorable financial results leading to capital growth and additional capacity to offer to our customers.”

Makris said the uncertainty around interest rates coupled with government spending and its upward pressure on inflation makes for an “artificial” economy, and that environment will trickle down to consumers.

“Banks are in the risk management business and will shift as much of the risk to the borrower as possible under uncertain times, which will restrict credit access,” he said. “That is more severe for the least credit-worthy borrowers. Loan funding costs and the cost of capital are also negative drivers of access to credit. That said, access to credit is still there for solid projects. Speculative projects will sit on the sidelines.”

ARKANSAS BANKERS ARE MOST CONCERNED ABOUT A LONGER-TERM ISSUE: THE ABILITY TO HIRE AND MAINTAIN QUALIFIED WORKERS.

“We need to get the message across that this is a soul-fulfilling career.”

Makris joked that his crystal ball has a crack in it, but he predicted that if inflation remains steady for the first half of the year – the current U.S. inflation rate is 3.4% for the 12-month period leading up to December 2023, according to the Bureau of Labor Statistics – a modest rate reduction could come in late 2024.

“However, this is an election year, and whether we like it or not, politics plays a role in many governmental decisions,” he said.

Makris also offered an opinion on artificial intelligence (AI) in banking.

“Banks are certainly aware of the proliferation of AI discussion,” he said. “That has driven much of the buzz for tech stocks.

However, I believe we need to be very cautious and deliberate in advancing AI. It will be used for nefarious purposes well before we have maturity and risk protocols to mitigate bad actors.

“The other element not discussed much is who is teaching AI to deploy its logic. Banks have been using variations of AI to determine probability, relationships and other integrated data sets.”

Marshall also alluded to the increasing threat landscape regarding cyber risks and their impact on the industry.

“This increasing risk also translates into increased costs and pressure on resources,” she said. “Unfortunately, many comments I

have received lately center around bankers’ concerns about the increases in fraud attacks on their customers and the impact it is having on the industry.”

“The rate environment is posing headwinds for many institutions, but tailwinds for others,” said Susannah Marshall, Arkansas State Bank Department commissioner. “Especially those that have structured their balance sheets to be in an asset sensitive position and to take advantage of repricing assets at higher interest rates.”

Editor’s note: This article appears courtesy of Talk Business & Politics as part of its "State of the State" series.

LAWMAKERS & INDUSTRY OFFICIALS CONCERNED ABOUT

INSURANCE

Affordability Availability &

by Roby Brock

Rapidly rising premiums and reliable carriers to issue insurance are of growing concern to Arkansas lawmakers, bankers, industry officials, business owners and consumers of all walks of life.

At a March legislative hearing at the Arkansas state capitol, legislators quizzed the state’s Insurance Commissioner as well as national and state insurance representatives, and CS Bank President and Chief Lending Officer Jason Tennant.

Describing current insurance conditions as a “hard market,” Arkansas Insurance Commissioner Alan McClain told lawmakers that rising premiums and carrier reliability is a national problem.

“IT REALLY HASN’T AFFECTED THE MARKET TOO BADLY YET BECAUSE IT’S PRETTY NEW, BUT IT’S A HEADWIND THAT I THINK HAS GOT OUR INDUSTRY VERY CONCERNED AND I THINK IT’S SOMETHING THAT’S GOING TO BE IMPACTFUL COMING DOWN THE LINE.”

“As you’re likely aware, property insurance premiums have been increasing significantly and anytime this happens, there’s a burden on almost every Arkansan and we’re sensitive to that at the insurance department,” McClain said. “A review of insurance news would quickly illustrate that Arkansas is not alone as we face these unprecedented conditions in market behavior.”

There are a number of contributing factors to rising insurance premiums. For starters, catastrophic weather conditions have hammered insurance payouts. Compounding the number of claims due to weather-related incidents is the inflationary costs of materials and labor to replace lost property. Construction materials have risen as much as 42% over the past three years, wages have accelerated, and supply chain kinks have slowed repairs to a crawl in some instances.

In short, there have been more losses than calculated, and premiums – which are normally adjusted annually – haven’t been able to keep up. The situation is likely to get worse before it gets better.

In early March, the largest insurance credit rating agency in the world AM Best downgraded their outlooks on personal lines, auto insurance and homeowner insurance to “negative” and noted that “underwriting profitability over the near term appears highly unlikely.”

McClain said that the Arkansas insurance companies he regulates saw average loss ratios in homeowners insurance hit 121% in 2022 and 131% in 2023. As of December 31, 2023, insurers had paid over $489 million from claims just related to the March 31, 2023 tornado events in central and eastern Arkansas. That calamity was followed up with additional severe weather and hailstorms in the spring and summer.

$ $ $

“On the average, our insurance carriers are paying out more than they’re bringing in. So it’s just kind of simple math,” McClain said.

Tennant brought to the attention of lawmakers how the insurance disaster is impacting banks, especially the mortgage business.

Homeowners often have their home insurance collected in escrow and pay through their mortgage payment. That’s a fixed amount, in most instances, but spiraling insurance costs are going to complicate this process.

“We’re seeing the deductibles become a real factor in a lot of the insurance that’s there because they are primarily going to the percentage of the value of those buildings and those properties,” Tennant told lawmakers. “Our concerns are the impact and the suddenness of this impact, especially to the homeowners that are out

AVERAGE LOSS RATIOS IN HOMEOWNERS INSURANCE HIT AND 121% in 2022 131% in 2023

INSURERS HAD PAID OVER $489 MILLION

FROM CLAIMS JUST RELATED TO THE MARCH 31, 2023 TORNADO EVENTS IN CENTRAL AND EASTERN ARKANSAS

IN SHORT, THERE HAVE BEEN MORE LOSSES THAN CALCULATED, AND PREMIUMS –WHICH ARE NORMALLY ADJUSTED ANNUALLY – HAVEN’T BEEN ABLE TO KEEP UP. THE SITUATION IS LIKELY TO GET WORSE BEFORE IT GETS BETTER.

there because so many of these people escrow their taxes and insurance, which as you all know, that ties into your monthly mortgage payment.”

He highlighted another area where the insurance crisis is proving difficult. For agricultural clients, insurance carriers are adapting policies to spread risks and increase premiums in order to strengthen underwriting. But that comes with a consequence.

“We’re a big ag lender. We are big in the poultry business in Northwest Arkansas. The changes to insurance for the farmer has poultry houses where the deductible is now per house instead of just one big blanket policy,” Tennant said. “So if you’re a farmer that’s raising chickens or turkeys and you’ve got six houses and you have damage to five of them, suddenly there’s a $5,000 deductible on each house.”

Tennant warned that while these examples are happening in real-time, he fears the worst is yet to come.

“It really hasn’t affected the market too badly yet because it’s pretty new, but it’s a headwind that I think has got our industry very concerned and I think it’s something that’s going to be impactful coming down the line,” he said.

It’s unclear what can be done at the state level. For now, lawmakers are responding to constituent concerns over the rising premiums and are awaiting more data and national direction.

Commissioner McClain said the National Association of Insurance Commissioners has launched a 90-day data collection effort from more than 300 property insurers across the U.S.

“We’re asking for 70 data points for our insurers to report to us. So ultimately, we hope to answer what’s driving affordability and availability,” McClain said.

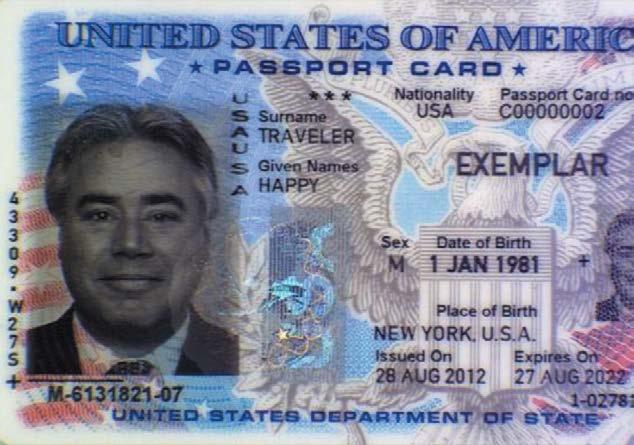

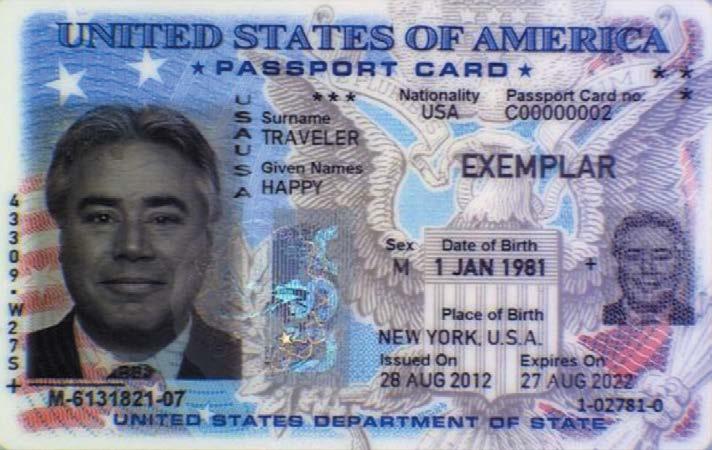

Evolution of the PASSPORT CARD FRAUD SCHEME

The U.S. passport card is a REAL ID compliant identity and travel document issued by the U.S. Department of State. It can be used for purposes of identity, proof of U.S. citizenship, domestic air travel, and land and sea border crossings from Canada, Mexico, the Caribbean, and Bermuda.

U.S. passports are well known, however their cousin, the passport card is not. This makes the card a great document for counterfeiters, since most people have never seen one. This allows organized criminal groups an open door to schemes targeting financial institutions. The following are some of those schemes:

DIRECT WITHDRAWAL AND WIRE TRANSFERS

Early in the evolution, the fraudsters simply used the counterfeit passport cards and other identity documents to impersonate a known bank customer and withdraw cash directly from the victim’s account or conduct a wire transfer to a money-mule’s account. Low success rates and transaction limits reduced profits. Recently, however there has been an uptick in this scheme. Mules will enter a bank, present a passport card and request a copy of their bank account information. After reviewing the account, they will then attempt to withdraw from the same account.

JOINT SAVINGS ACCOUNT (AKA ACCOUNT TAKEOVER)

The same fraudsters began using money-mules to open joint savings accounts with the imposter. Mid-level facilitators began recruiting mules from social media and personal referrals. These recruiters collected approximately 10 percent of the proceeds. The mules only needed to have a legitimate bank account in their true name at the targeted financial institution. The mid-level facilitator would transport the mule and the imposter to the targeted bank and direct the two to open a joint savings account. The mule rarely knew the true name of

the imposter and would be told they weren’t doing anything illegal since they were using their true name. The mule’s connection to the conspiracy was limited to the person who recruited them – they either knew them personally or knew them through social media. Once a mule is attached to a victim’s account, they could not be used again. Mules were well paid if successful and usually collected between $5,000 and $10,000, or 10 to 20 percent for the use of their true identity.

Once the joint account was established a co-conspirator would call the bank impersonating the customer and request to transfer funds to the newly opened joint account. A typical amount is between $20,000 and $35,000; however, losses have reached as high as $99,100 per victim.

As soon as the joint account was funded from the victim’s account, the mules would be directed to log into their accounts, transfer funds from the joint account to their previously established personal account. The mid-level facilitators/recruiter would

AUTHENTIC

U.S. PASSPORT CARD

✓ The photo is crisp, square, and blends into the card.

✓ The microprinting in the background artwork reads “UNITED STATES OF

✓ The optically variable device (OVD) on the lower right of the photo reads “Department of State” and “United States of America” (in a circular formation) with a rectangular shape on the right that reads “USA” vertically.

✓ On the front of the card, the date of birth, serial number, and some letters in “USA” on the right side of photo should feel raised; on the back of the card, the card number should feel raised.

✓ Under UV light, the front of the passport card shows a red eagle surrounded by blue stars and text that reads “FROM SEA TO SHINING SEA”

✓ When dropped on a non nonmetallic surface, striking an edge, it will make a metallic sound.

then drive them to other bank branches and direct the mules to withdraw less than $10,000 cash from the teller windows. This repeats at as many local branches as needed until the funds were depleted or frozen by the bank.

WHERE DOES IT END?

These are just a couple of ways the fraudsters are creating havoc, but some of this can be prevented. If the tellers are aware of some of the security features on the passport cards,

COUNTERFEIT

U.S. PASSPORT CARD

X The photo often has a white blurry border or a dark gray square surrounding the photo.

X Under magnification counterfeit biodata will have distinguishable cyan, magenta, yellow, and black (CMYK) dots instead of pure colors.

X If there is an optically variable device (OVD) it may contain incorrect language or images (e.g. “U.S. Supreme Court” laminate).

X The counterfeit may lack light reflecting, closely set, vertical lines that are placed behind the OVD.

X Under UV light there will be no images or text, or incorrect images and/or text.

X The date of birth, serial number, and other data fields on the card are printed rather than laser etched / raised.

X When dropped on a non non-metallic surface, striking an edge, it will not make a metallic sound.

it can be fairly easy to know if they are handling a real document or a counterfeit card. Here in Arkansas, there are no land borders with foreign countries. Most people do not have a passport card, especially in a state that is not near a border. This is not to say people do not have them, but more are in states bordering Mexico and Canada. The other people who utilize the cards are people who like to go on cruises. With this in mind, that eliminates the frequent use of the document in our region.

Another telltale in the feel of the document, there are raised areas, which resemble the numbers on a credit card, there are colorful holograms, tiny, tiny print, and NO layers. The cards are not laminated so there are no layers. Another tell tale is the sound of the card. When it is dropped on a counter, the card “clinks” with the sound of metal. If you drop a credit card on a counter it doesn’t clink, but the passport card, if genuine, will make the metallic clinking sound. The colors on the card are pure colors, not little dots of ink.

“U.S. passports are well known, however their cousin, the passport card is not. This makes the card a great document for counterfeiters, since most people have never seen one. ”

THE NEW RULES FOR BENEFICIAL OWNERSHIP IN 2024

by Megan McGovern

The Financial Crimes Enforcement Network (FinCEN) continues to issue rules and guidance relating to beneficial ownership following the enactment of the Corporate Transparency Act (CTA) in 2021. Many banks continue to anticipate the release of the third and final rule which will arguably contain the biggest changes for impacted institutions under the CTA. Overall, 2024 may prove to be a pivotal year for potential changes to Customer Due Diligence (CDD) programs and policies.

In the first final rule, FinCEN established the beneficial ownership information (BOI) database per 31 CFR 1010.380. This rule released in September 2022 is often referred to as the “Reporting Rule.” The Reporting Rule compiles information provided by business entities into a main database to assist in anti-money laundering (AML) efforts by financial institutions and government agencies. Starting January 1, 2024, most entities created in or registered to do business in the United States are now required to report BOI to FinCEN. The FinCEN website also allows individuals and reporting companies to request a FinCEN identifier, although FinCEN identifiers are not required to be obtained. Generally, this Reporting Rule did not contain specific changes for financial institutions to make. While some banks may now be choosing to include reference to FinCEN’s website and the BOI filing information requirements or E-Filing system as part of general resources offered to commercial customers, this is not explicitly required under the final Reporting Rule.

The second final rule, known as the “Access Rule” was released in December 2023, with FinCEN setting forth the protocols for disclosure of BOI. The Access Rule dictates which “authorized recipients” have access to the information from the filed BOI reports which are maintained in the nonpublic database, named “Beneficial Ownership Technology System.” Perhaps the most important part of the Access Rule for banks is that financial institutions subject to CDD requirements are deemed “authorized recipients” under these provisions.

Despite the final Access Rule taking effect on February 20, 2024, FinCEN stated that authorized recipients will be given access to the database in different phases over the course of 2024. The first group granted access is limited to certain key authorized

THIS THIRD RULE IS EXPECTED TO REVISE THE EXISTING CDD REGULATIONS AS PART OF A CONFORMING RULE TO ALIGN WITH THE GOALS OF THE CTA.

comply with FinCEN’s existing Customer Due Diligence rule (the “current CDD Rule”) at this time. For now, banks may continue to rely on the current CDD rule, and once access to the new database is granted, authorized banks will have the ability to take this information into consideration, pending the release of the third rule.

Under the Access Rule, authorized banks will need to take certain steps to receive permission to view information in the BOI database and maintain the information received in a confidential manner. In order to receive access to a reporting company’s information in the Beneficial Ownership Technology System, the bank must first receive a reporting company’s consent and “develop and implement administrative, technical, and physical safeguards reasonably designed to protect the information” obtained. FinCEN notes that consent is not required specifically to be in writing but requires consent to be documented, leaving this to the financial institution’s discretion to determine the method of obtaining and documenting each customer’s consent. Further, if a bank is granted access to the BOI system, then the bank’s regulators will also have access to beneficial ownership information when they supervise the financial institutions. It is likely that further guidance will be released in this area once access is granted to financial institutions as authorized recipients and banks begin requesting consent from companies to obtain the BOI information from the database.

Authorized financial institutions continue to await the proposal of the third rule, which will be the final implementing rule of the CTA. This third rule is expected to revise the existing CDD regulations as part of a conforming rule to align with the goals of the CTA. These revisions are projected to ensure the CDD rules follow along with the new BOI database. At this time, it appears unlikely that this third rule containing the CDD changes will be made effective within 2024. As such, aspects of this third rule are expected to carry over into 2025.

FinCEN recently issued Version 1.0 of the “Small Entity Compliance Guide for Beneficial Ownership Information Access and Safeguards Requirements”, which provides useful interpretations for banks to take into consideration relating to the Access Rule. FinCEN notes that this Small Entity Compliance Guide will be updated in the future to include the final requirements from the third rule, referred to in the Guide as the revised CDD Rule. FinCEN plans to further update the Guide to provide direction on how financial institutions can access BOI from FinCEN. FinCEN has been actively providing insights through updated BOI FAQs to address common issues and questions following the implementation of the two final rules. While the FAQs may assist in guiding determinations absent clarity in the rules, the FAQs do not replace or fulfill what may be missing from the regulation itself. FinCEN is expected to continue to release further guidance throughout the year.

=Overall, 2024 has been an active year for the CTA’s two finalized rules, as the BOI database goes live and access is granted in phases to the defined authorized recipients. As banks await the release of the third and final rule containing the conforming changes to the current CDD rules, it remains to be seen how a bank’s current BSA/AML compliance program and practice will be altered by the third rule once finalized.

government agencies, while the second group granted access includes Treasury offices and certain Federal agencies engaged in law enforcement and national security activities. Subsequent stages of the rollout are expected to extend access to additional Federal agencies engaged in law enforcement, national security, and intelligence activities, as well as to State, local, and Tribal law enforcement partners; and finally, to financial institutions that meet the requirements of the final Access Rule.

It is important to distinguish that the Access Rule itself does not create a different regulatory requirement for banks to access BOI from the database. Further, the Access Rule does not require changes to Bank Secrecy Act (BSA)/anti-money laundering (AML) compliance programs designed to

NOTE: On March 1, 2024, shortly after the writing of this article, a Federal judge in Alabama issued a judgment concluding that the Corporate Transparency Act (CTA) exceeded Congress’s authority and enjoined the Department of the Treasury and FinCEN from enforcing the CTA as to the plaintiffs in the case. It’s important to note that as of publication of this article, the lawsuit does not directly affect bank obligations under the current Customer Due Diligence rules and further, an appeal of the decision has since been filed by the government. FinCEN has published the following on its website while the litigation continues:

ABOUT THE AUTHOR

Megan McGovern, JD, serves as Associate General Counsel for Compliance Alliance; bringing over a decade of diverse legal experience to the role. Megan is a graduate of the State University of New York at Albany and Albany Law School.

TRIGGERED!

HOW FEDERAL AGENCIES AND CREDIT BUREAUS ARE WORKING AGAINST YOU

by Timothy Schenk General Counsel, Kentucky Bankers Association

Have you heard customers complain about receiving junk phone calls from other lenders after applying for credit? Based on what we’re hearing from banks, it’s an issue happening across the board. The cause for these unwanted solicitations? Trigger leads.

Trigger leads are leads that come from mortgage trigger products offered by the three major credit bureaus. When a lender requests a credit report, that inquiry automatically “triggers” lenders that a customer is looking for credit. Lenders of all sorts purchase that information and then begin calling your customer, tens, if not hundreds, of times.

The nature of these calls is concerning. One bank president who recently asked what we are doing to combat trigger leads told a shocking, but not unique, story of harassment.

His credit report was pulled on a Tuesday at 9:30 a.m. His first call from a lender came just ten minutes later. By Friday, he had received fifty-one harassing calls.

Lenders refused to stop calling, would not provide their full names, offered unrealistic loan terms (often the source of bait and switch), and knew personal details that he could not trace. It all began when the credit bureau sold his personal information. He asked the same thing that many bankers ask: How is this legal?

Trigger leads are not only legal, but are encouraged by some regulators. The Federal Trade Commission and Consumer Financial Protection Bureau believe these triggers are valuable because they offer more options for customers. While the regulatory compliance side of me wonders how any of this passes the ever-obscure standards of UDAAP, I’ll digress for purposes of this article.

So what is being done? The good news is that we are taking the fight to the credit bureaus.

On the federal level, bipartisan legislation has been introduced – the Homebuyers Protection Act (S.3502/H.R. 7297). These bills would not only enhance consumer protection and strengthen trust in the financial system, but would significantly limit the ability of credit bureaus to share your customers’ information with third parties.

On the state level, several other states that are currently in legislative session are running bills around trigger leads. The ABA is actively watching these bills and is considering running the same type of legislation in the 2025 substantive Arkansas legislative session. This will depend on what happens at the federal level.

While legislative action is in process, you can educate customers to minimize the impact of trigger leads. Optoutprescreen.com will take your customers’ name off of the “trigger lists” from the credit reporting agencies for five (5) years or permanently.

The site will ask your customers for personal information, including their name, address, social security number and address and may take several weeks to process, but it

When a lender requests a credit report, that inquiry automatically “triggers” lenders that a customer is looking for credit. Lenders of all sorts purchase that information and then begin calling your customer, tens, if not hundreds, of times.

“His credit report was pulled on a Tuesday at 9:30 a.m. His first call from a lender came just ten minutes later. By Friday, he had received fifty-one harassing calls.”

has proven to be effective. The customer can even selectively choose which portions of “trigger leads” they would like to screen (calls, but not mail, for example).

OptOutPrescreen.com is the only internet website authorized by Equifax, Experian, Innovis and TransUnion for consumers to opt-out of firm offers of credit or insurance.

Another option is for customers to register their number on DoNotCall.gov. The process takes a minute or two but can prevent unsolicited phone calls. It can take up to thirty-one (31) days to process, but it can prevent many unwanted calls.

The other means of protecting your customers is education. You are likely the first person to discuss trigger leads with your customer. By bringing their attention to the issue, you may prevent them from falling prey to scams and fraud while also protecting your institution from losing that customer.

While we cannot promise an overnight fix to these issues, we are fighting for you on every front to stop trigger leads. In the meantime, please make your customers aware of the options they do have to fight trigger leads to avoid potential harassment, confusion and deception.