• Automate Interactions & Notifications to Streamline Hand-offs Between Parties

To lead what’s next, you need to think differently now.

Investment professionals leading today’s markets aren’t just knowledgeable—they bring clarity, judgment, and a deep understanding of where capital is moving next.

The CAIA Charter gives you all three.

If you want to stay relevant, build influence, and earn the confidence to navigate what’s coming next, CAIA is where you start.

Learn more at caia.org.

Next isn’t coming. It’s here.

The Power of Integrating Technology and Investment Operations

FROM FRINGE TO FINANCIAL FRONTIER:

HOW CRYPTO IS REWRITING THE RULES OF INSTITUTIONAL INVESTING

BY GAUTAM GANESHAN KPMG in the Cayman Islands

Once relegated to the fringes of the financial world, digital assets are now part of everyday conversation. Cryptocurrencies, NFTs, and the entire blockchain ecosystem are no longer restricted to the sphere of emerging technology and frontier investors. As the industry continues to mature, established and institutional market participants are realizing the potential that digital assets have to offer. Institutions stand to benefit from the tokenization of real-world assets, digital asset ETFs, and innovative institutional grade products.

Tokenization of Real-World Assets

The tokenization of real-world assets has received a significant amount of attention as the market continues to mature. Tokenization is the process where an asset’s interest is valued and divided into digital units where ownership is recorded on a blockchain. This asset could be a building, a bond, or even an investment fund. This process provides transparency and tamper-proof record-keeping, attracting the attention of large finan-

cial institutions. This includes the likes of BlackRock, JP Morgan, Citibank, Goldman Sachs, KKR, and Hamilton Lane, all of whom have already begun to offer some form of tokenized products to their clients or have begun to integrate the use of tokenized products into their service offerings.

So, what are the benefits of tokenized real-world assets? Enhanced liquidity, accessibility, transparency, and streamlining costs are just a few that deserve mention.

• Traditionally, illiquid assets (e.g., real estate, investment fund interests) become more accessible through fractional ownership, allowing a greater number of individuals to access investment opportunities. Sponsors can also choose to lower the investment threshold. As an example, Hamilton Lane reduced the investment minimum to US$10,000 from US$2M on their tokenized private fund offering. This lower threshold ultimately democratizes access to investment products and increases accessibility.

• The blockchain technology, on which the tokenized products are offered, provides an immutable and transparent record of ownership and transaction history, enhancing trust and security.

• Tokenized products have smart contracts built into them, which can automate several of the functions associated with these products, including redemptions, recording of ownership transfers and distributions, which significantly reduces costs and streamlines operations such as reducing settlement periods.

As tokenized funds continue to gain popularity, they will unlock a new era of democratized and transparent investing.

Exchanged Traded Funds (“ETFs”) and Digital Asset Treasury Companies (“DATs”)

In January 2024, after ten years of rejecting Bitcoin ETF applications, the SEC approved the first spot Bitcoin ETFs and since then have approved Ethereum ETFs in May 2024. Since then, amongst other regulatory changes, in September 2025, the SEC ap-

proved generic listing standards for commodity-based exchange traded products, which would include digital assets. This is expected to increase the number of ETFs approved focusing on other digital assets (e.g. Solana, XRP, Cardano and Hedera). Additionally, it is widely anticipated the SEC will also approve ETFs to stake their assets promoting further mainstream acceptance of digital assets.

There have been further developments in 2025 which have been brought as competition to the ETFs – namely Digital Asset Treasuries (“DATs”). DATs are companies which hold a digital asset as a means of treasury and aims to increase shareholder value by increasing the amount of tokens per share. This is achieved through various means including financial engineering, yield generation, running an operating business or through acquisition.

The approval of the spot Bitcoin and Ethereum ETFs in the United States changed the game. It allowed institutions such as pension plans, endowments, and other institutional investors, to gain exposure to Bitcoin and Ethereum. This is achieved without the technical complexities of a self-custody wallet or dealing with less familiar counterparties. DATs take the opportunity for these institutional investors further by providing an opportunity for investors to accrete more digital assets per share relative to an ETF. This is because a DAT has the ability to engage in alternative capital raising options (through issuing convertible bonds and preferred shares) or yield generating activities (such as staking or decentralized finance) whereas an ETF is more restricted.

However, there are certain disadvantages with owning the ETF or DAT. Most notably, the investor does not own the actual digital asset itself, and is instead relying on the sponsor to carry out the strategy and mitigate the risks of directly owning the digital assets. Additionally, there are fees associated with the ETFs and DAT operating costs which are not present when you hold the asset directly.

The approval of the spot Bitcoin and Ethereum ETFs along with the introduction of DATs in the United States represents a significant milestone, bridging the gap between traditional finance and the digital frontier.

Institutional Grade Products and Services

Digital assets did not evolve from Wall Street institutions as traditional assets did in the past. As a result, the infrastructure that institutions were accustomed to (e.g. custody, derivatives and risk management tools) was not in place until recent years.

From a custody perspective, Coinbase has been offering custody as a service since 2012 and is seen as the leading institutional custody offering in the market. There have been other large, financial market institutions who have also begun offering digital asset custody solutions, such as Fidelity Digital Assets in 2019, BNY Mellon in 2022, State Street Custody in 2023 and Deutsche Bank in 2023.

In 2017, CME introduced the Bitcoin futures contact, and since then has launched additional derivative products over Bitcoin and Ether. These futures products have allowed institutions to hedge their positions or gain exposure to the underlying asset. Additionally, CBOE in January 2024 launched spot and leveraged derivatives trading for Bitcoin and Ether futures. Further, there are other native digital asset exchanges which offer opportunities for institutions to enter into derivatives. One example is Deribit, who offers options on digital assets, and several exchanges including Binance and OKx who offer futures on digital assets.

Finally, staking represents a significant market opportunity for institutions to capture yield, and a return on their investments which may be held passively, such as fixed term deposits. There are several well-known market participants who are offering staking as a service, including custodians (e.g. Coinbase) and specific staking service providers (e.g. Figment).

The Future of Institutional Crypto

The institutional digital asset infrastructure ecosystem is rapidly maturing, presenting exciting possibilities for market participants to invest in a similar manner to how they have been investing in the traditional investment market.

However, there remain several challenges facing institutional participants, including identifying experi-

enced and knowledgeable service providers. In our experience, there have been numerous instances where an initial service provider was identified but did not have the requisite knowledge of digital assets. This resulted in a change in service providers, increased efforts, and costs to rectify the issues.

In my opinion, digital assets represent a foundational shift in financial markets. They have the ability to meaningfully change how the world operates, and present a vast spectrum of possibilities for institutions, unlocking potential avenues for significant growth. Those that adopt a proactive approach in investing the time and resources will be well-positioned to seize the opportunities offered by the digital asset market. This includes the tokenization of real-world assets, digital asset ETFs, and pioneering institutional grade solutions.

Gautam Ganeshan President

CFA Society Cayman Islands

Partner

KPMG in the Cayman Islands

KPMG in the Cayman Islands is one of the leading professional services firms, with over 400 employees from more than 40 countries and 30 Partners delivering audit, tax and advisory services to clients worldwide. We provide industry insights to help organizations negotiate risks and perform in the dynamic and challenging environments in which they do business. Our high performing people are our greatest asset. We use our expertise and insight to cut through complexity and deliver informed perspectives and clear solutions that our clients and stakeholders value.

RULES OF THE GAME:

TACTICAL ASSET ALLOCATION VS. COMPETITION FOR CAPITAL

BY AARON FILBECK, CAIA, CFA, CFP®, CIPM, FDP CAIA Association

Since late 2022, we’ve been actively exploring the evolution of portfolio construction through the lens of the Total Portfolio Approach (TPA)—a shift in mindset that challenges traditional asset allocation frameworks. Through two in-depth reports, Innovation Unleashed: The Rise of Total Portfolio Approach (March 2024)1 and From Vision to Execution: How Investors Are Operationalizing the Total Portfolio Approach (October 2025)2, and the launch of our dedicated TPA Hub3, we’ve examined how leading institutional investors are rethinking governance, decision-making, and performance measurement. In this article, we build on that body of work by contrasting TPA’s “competition for capital” mindset with the more

familiar structure of tactical asset allocation (TAA)— not to say one is better, but to show how each is a different game entirely.

As we’ve been discussing the rise of the Total Portfolio Approach, and the dimensions that are associated with it, one of the most common statements I’ve heard is some variation of the following:

“I like this concept of competition for capital, but it really just sounds like tactical asset allocation with a new name attached it.”

Chess vs. Monopoly

When it comes to portfolio design, the game you choose to play determines the rules, the scoreboard,

and even the types of moves on the board that are possible.

In many ways, tactical asset allocation is a lot like playing chess: the board is fixed, the rules are strict, and the path to success (checkmate) is defined by executing within that structure. Competition for capital, on the other hand, looks more like Monopoly. The objective is clear (accumulate the most wealth), but there’s no predetermined path for how to get there. Success comes from making directional bets on properties, trading op-

portunistically, and deciding when to take on concentrated risk by building houses or hotels.

Monopoly can feel uncomfortable because the structure is looser and outcomes depend on both foresight and flexibility, but that very openness creates the possibility of winning by a large margin. Both games are fun, and certain types of people may gravitate towards one over the other. The same thing can be said for designing and governing a long-term pool of capital.

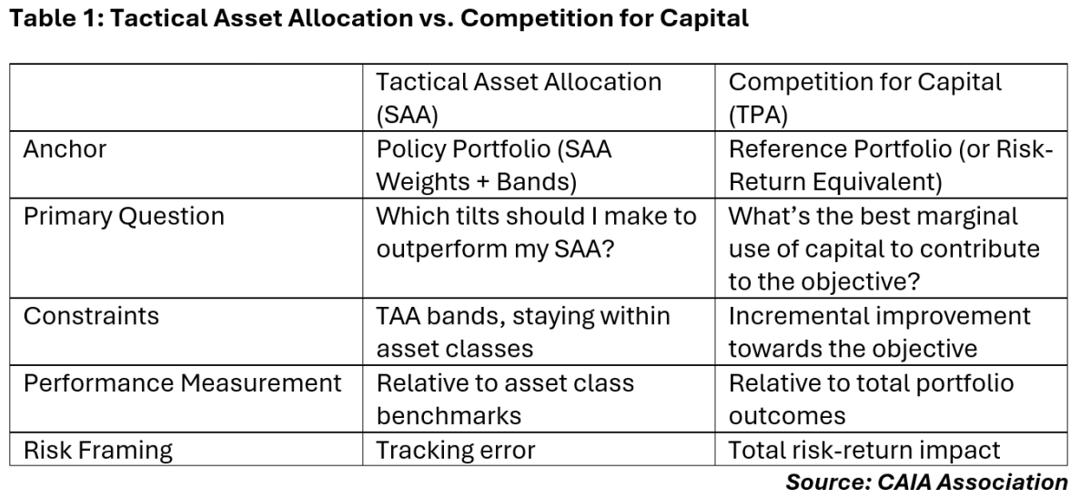

TAA vs. Competition for Capital

In a governance structure that elects for SAA, the rules are set forth by building a prescriptive policy portfolio that the investment team is responsible for managing around. The scoreboard is measured against that policy portfolio, and the moves available are modest, deliberate deviations to capture short- to medium-term opportunities. You may sacrifice a few pawns to distract your opponent as you plan your next move. With this framing, TAA is framed as an “alpha decision,” designed to add value while staying close to the policy guardrails. It’s quantifiable and comfortable, but doesn’t allow for much creativity.

In a governance structure that elects for TPA and, by extension, a competition for capital mindset, the rules are set forth by a very different prescription: maximize value without losing your money along the way.

The scoreboard is measured against an appropriate risk and return target, often in the form of a reference portfolio. The moves available to the team are wide open, so long as they advance that objective. Instead of managing relative to asset class benchmarks, you’re asking: “What’s the best use of the next marginal dollar?” Every potential investment, from a public equity to a private infrastructure project, competes directly for a spot in the portfolio. In this framing, competition for capital is a “beta decision,” designed to improve long-term outcomes by working across the whole opportunity set. While this opens the door to true cross-asset decision-making, it is challenging to implement if the guardrails are not established and ownership of decisions is unclear. It requires the governing body and the investment office to have clear accountabilities between who is responsible for setting the objective and who is responsible for managing the portfolio. Those who have embraced TPA tend to have clearer delineation than those who embrace SAA, which can often have CIOs implicitly being held accountable for policy portfolios set by their boards.

Shifting from TAA to C4C

Moving from TAA to competition for capital changes governance, performance measurement, and the scope of opportunities. TAA is benchmark-driven, while competition for capital is outcome-driven. TAA’s risk lens is tracking error, while TPA looks at the total portfolio’s risk-return efficiency. And while TAA tends to source ideas on an existing relative basis, competition for capital encourages a global, unconstrained search for opportunities. This can be summarized in Table 1.

Putting It All Together: Play the Game You’re Good At

While seemingly similar at face value, tactical asset allocation and competition for capital are different games entirely: one is chess, which rewards discipline within structure; the other is monopoly, which rewards creativity within less restrictive rules. The choice depends on how the organization is governed, and specifically how decision-making rights are allocated between the board and the investment office. Without clarity on who sets the objectives and who plays the moves, either

game quickly devolves into confusion and frustration. With clarity, both can be effective, but the nature of the experience and the outcomes will differ significantly. These are different games, and people can excel at either one of them. But isn’t Monopoly a lot more fun?

About the Contributor

Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP is Managing Director, Content & Community Strategy at CAIA Association. His industry experience lies in private wealth management, where he was responsible for asset allocation, portfolio construction, and manager research efforts for high-net-worth individuals. He earned a BS with distinction in finance and a master of finance from Pennsylvania State University.

Managing Director, Content & Community Strategy CAIA Association

CAIA Association is a global network of forward-thinking investment professionals, redefining the future of capital allocation in a world where traditional and alternative converge. United by a commitment to improving investment outcomes, we lead with authority, educate to inspire, and connect people who turn insight into action. To learn more about the CAIA Association and how to become part of the most energized professional network shaping the future of investing, please visit us at https://caia.org/.

THE POWER OF PRIVATE EQUITY:

CATALYSING ECONOMIC GROWTH IN UNDERSERVED NATIONS

BY CANDICE CZEREMUSZKIN

Moore

Global

&

Moore

in the Cayman Islands

In the modern era of global investment, private equity (PE) is increasingly recognised not only as a vehicle for financial returns but also as a catalyst for structural economic transformation. Long established as a force within developed markets, the sector’s potential to drive inclusive, sustainable growth in underserved nations — particularly across Africa, South America and parts of Asia — is now coming into sharper focus.

Private Equity as a Long-Term Partner in Development

Private equity does far more than inject capital. It brings a blend of strategic insight, operational rigour and long-term thinking that can fundamentally

alter a company’s trajectory. In developing economies, where businesses often face limited access to finance, infrastructure and management expertise, this partnership model can be the difference between stagnation and scale.

Unlike public market investors, PE firms typically hold assets for five to ten years, giving them both the incentive and the capacity to nurture growth. That patience aligns well with the realities of building sustainable businesses in emerging markets, where success often depends on navigating regulatory uncertainty, addressing skills gaps and developing local supply chains. Moore’s global private equity team, led by Candice Czeremuszkin, has observed that investors increasingly recognise the dual opportunity these regions represent — the potential for attractive returns, paired with tangible social and economic impact.

Infrastructure remains the backbone of any developing economy, and yet many countries face chronic underinvestment. From roads and ports to renewable energy grids, the opportunities for private capital are vast. In Sub-Saharan Africa, for example, less than half the population has access to electricity. PE-backed firms are increasingly stepping into the gap — financing solar microgrids, clean power storage, and next-generation logistics platforms that enable regional trade. Such investments are not merely philanthropic. Reliable power and efficient transport systems reduce business costs, increase productivity, and open up entirely new markets. In Moore’s experience, infrastructure-focused funds that combine financial discipline with strong local partnerships are often the ones achieving both scale and resilience.

Agriculture and AgriTech

Agriculture continues to underpin livelihoods across much of the developing world, yet inefficiencies persist across production and distribution. Private equity is now fuelling innovation through AgriTech — from precision farming tools to digital supply chains that connect farmers directly with international buyers.

In Latin America, PE capital has supported technology-led cooperatives that help smallholders secure better pricing and access to sustainable certification schemes. These models do more than raise yields; they embed transparency and traceability into food systems, aligning local growth with global ESG standards.

Czeremuszkin notes that agricultural technology is one of the fastest-growing areas of private investment within Moore’s client base.

Perhaps no sector demonstrates the democratising power of private equity more vividly than financial technology. With billions of people globally still unbanked, mobile payments and micro-lending platforms are rewriting the rules of access to finance.

Across Africa and South Asia, PE-backed FinTech start-ups are enabling customers to build credit histories, access insurance, and make digital payments securely for the first time. This is not just a social good; it is the foundation for new consumer markets and thriv-

ing small businesses.

The next generation of FinTech success stories may emerge not from Silicon Valley, but from Lagos, Nairobi or Dhaka — cities where innovation meets pressing local need. Moore’s sector specialists have seen strong deal flow in these regions, driven by investors seeking diversification and by governments creating innovation-friendly regulatory frameworks.

The global convergence of trends

The growing momentum behind private equity in underserved nations is not accidental. Several macroeconomic and structural trends are converging to make these markets increasingly attractive.

Demographics and urbanisation

Africa’s population is expected to reach 2.5 billion by 2050, with a rapidly expanding middle class and urban workforce. This demographic surge translates into escalating demand for housing, education, healthcare and digital services — all sectors where private equity can provide the scale and sophistication to meet emerging needs.

Digitisation and leapfrogging

Developing countries often bypass the legacy systems that constrain mature economies. Mobile networks and cloud-based infrastructure allow them to ‘leapfrog’ traditional stages of development. For PE investors, this opens a frontier for technology-driven growth, particularly in consumer services, logistics and e-commerce.

Moore has seen first-hand how digital adoption drives value creation. In one recent engagement, the firm supported a fund expanding a cloud-based healthcare platform into secondary cities in Southeast Asia. The project delivered not only strong returns but also measurable community outcomes — a case study in the intersection of profit and purpose.

ESG integration and impact investing

Environmental, Social and Governance (ESG) factors have moved from the margins to the mainstream of private capital. Increasingly, investors demand proof that returns are being generated responsibly. In frontier

markets, this alignment of profit with purpose has become a key differentiator.

Impact-focused funds are deploying blended finance — combining private, public and philanthropic capital — to achieve outcomes that would be impossible through commercial funding alone. For PE firms, integrating ESG principles from the outset is no longer optional; it’s essential for long-term credibility and access to global capital pools.

Moore’s global network has noted a rise in investor mandates explicitly linking carried interest to sustainability outcomes, reflecting the industry’s shift towards measurable impact.

Navigating the risks

Despite its promise, investing in emerging markets presents real challenges. Political instability, foreign exchange volatility and governance issues can all threaten returns. Yet, as experienced firms know, these risks can be managed with the right structures and local insight.

Successful investors are increasingly embedding themselves in the regions where they operate. They build relationships with local entrepreneurs, regulators and community stakeholders — a strategy that provides invaluable context and early warning against potential pitfalls.

Currency risk, too, can be mitigated through careful hedging and by structuring revenues in stable foreign currencies where possible. Likewise, partnerships with multilateral institutions and development finance bodies can provide political risk insurance and enhance credibility with local governments.

Czeremuszkin observes that the most effective funds are those that treat local partnerships as strategic, not transactional.

“Weoftenseethedifferenceinportfolioperformancebetweenfirmsthat truly understand the operating environmentandthosethattrytoimposea Westernmodelwholesale.Theformer tend to outperform, both financially andsocially.”

The role of policy and regulation

Government support remains a crucial enabler of private investment. Predictable legal frameworks, transparent procurement processes, and efficient capital markets are all essential for sustained investor confidence.

Some countries are taking significant steps in this direction. Kenya’s public–private partnership framework, for example, has unlocked billions in infrastructure investment, while Brazil’s updated insolvency laws have improved exit visibility for investors. These reforms matter — they turn theoretical opportunity into investable reality.

Moore’s advisory teams often work alongside regulators and policymakers to translate complex international standards into locally practical solutions. That collaborative model strengthens ecosystems from within, ensuring that capital inflows are matched by institutional resilience.

Looking ahead: Private Equity as a catalyst for inclusive growth

To unlock the full potential of private equity in underserved nations, the ecosystem must evolve on several fronts. Limited Partners (LPs) need to broaden their mandates to include emerging markets as a core allocation rather than a peripheral ‘impact’ category. Local fund managers require greater access to global networks, training, and governance support. And regulators must strike the balance between investor protection and development facilitation.

The next decade will likely see deeper integration between global and regional funds, more blended finance models, and greater use of data analytics to measure non-financial outcomes. If harnessed effectively, private equity could become one of the defining forces of sustainable development in the 21st century.

As Moore’s global team continues to advise investors across multiple jurisdictions, a consistent theme emerges: the future of private equity will be built as much in Nairobi, São Paulo and Jakarta as in London or New York. Those willing to engage early — with patience, cultural awareness and genuine partnership — will help shape not only the growth trajectories of their portfolios, but of entire economies.

From capital to catalyst

Private equity’s greatest strength lies in its capacity to convert capital into capability. By investing in sectors that underpin everyday life — power, food, finance, education and health — the industry can help redefine the economic narrative of developing nations. The success stories of tomorrow will not be confined to the boardrooms of established financial centres, but will emerge from local founders and communities who partner with investors to build resilient, scalable businesses.

In this sense, private equity is far more than a source of funding. In underserved nations, it represents the convergence of ambition, innovation and impact — a catalyst for change that is as transformative for investors as it is for the societies they invest in.

Global Private Equity

Lead (Moore Global) and Managing Partner (Moore in the Cayman Islands)

Moore Global is a leading accounting, advisory and consulting network with over 500 offices across more than 100 countries. The network supports clients in navigating complex financial and operational challenges, with specialist expertise spanning audit, tax, corporate finance, and private equity advisory. Through its collaborative approach and deep sector knowledge, Moore helps businesses and investors unlock growth opportunities across both established and emerging markets.

Candice Czeremuszkin

BRIDGING THE LIQUIDITY GAP:

A Scalable Investment Strategy in Commercial Real Estate Credit Enhancement

BY CONRAD WICKER

Amplifi CRE

Real estate is a capital-intensive business and relies heavily on debt. Debt providers, both recourse and non-recourse, generally have minimum net worth and liquidity requirements for their borrowers (among other credit requirements). Conversely, there are many experienced, qualified real estate professionals who understand how to prudently develop and operate commercial real estate assets, and have investors who will back their projects, but do not present an adequate balance sheet to qualify for loans. The infrastructure to help borrowers bridge the gap to qualify for the financial covenants of their loans remains under-developed.

Novel Delivery, not Concept

Amplifi was formed by a team of former commer-

cial real estate bankers to provide a programmatic, institutional solution to this common problem, one that we were seeing frequently in our corporate roles. commercial real estate borrowers were often falling short of lender net worth and liquidity requirements, and, as a result, failing to qualify for loans. Amplifi bridges the gap by co-guarantying non-recourse loans alongside experienced borrowers in exchange for fees and/or profit participation in the underlying properties.

The concept of third-party credit enhancement/ support is not a novel one, but the need is being fulfilled mostly by ultra-high-net-worth individuals on a oneoff basis. Those ultra-high-net-worth individuals may demand unpredictable economics and are not programmatic providers. Accordingly, Amplifi’s competition is fragmented, non-institutional, and unpredictable. Am-

plifi’s competitors do not have access to the deal flow that Amplifi sees, given its team’s strong track record and relationships in commercial real estate credit spanning nearly all asset types and geographies. Amplifi’s competitors also often lack the institutional credit and risk management approach that Amplifi employs in every transaction.

Large Market Opportunity

Over $2.8 trillion in commercial real estate loans will mature over the next three years. Many of these loans were originated at lower rates, higher valuations, and looser terms. In the current environment, refinancing requires fresh capital, stronger guarantees, and creative solutions.

An estimated $147 billion market for third-party

guarantees exists, yet today this market is fragmented, opaque, and ad hoc. Borrowers often scramble to find high-net-worth individuals willing to co-sign, with unpredictable terms and limited scalability. Amplifi only needs to capture a small portion of this market share to deliver compelling returns to its investors.

A Niche Asset Class: Managed Credit Exposure with Real Estate Alpha

Our investment vehicles are structured as 10-year funds with a 7-year investment period and quarterly distributions. The capital raised is not deployed into real estate deals at the outset, but instead held in liquid, investment-grade securities—primarily short-duration

Treasuries. These liquid investments serve as the financial backing for co-guarantee commitments from which the Amplifi generates revenue for its investors. Returns are driven by a combination of:

• Origination fees for underwriting and issuance of guarantees

• Annual maintenance fees based on the size and duration of the guarantee

• Profit participation in select deals where the platform takes a small equity or promote interest as part of the compensation package

• Yield from low-risk fixed income holdings

Target returns may include average annual yields in the low-to-mid 20% range with a 3.0x+ multiple on invested capital. Importantly, this is achieved without directly deploying capital into real estate or relying on property appreciation. Capital stays within the four walls of the vehicle unless a loss is incurred or could be incurred—an unlikely outcome given sound risk management controls.

This structure allows for a new type of return profile: one that mirrors the upside of equity, with far more insulation from the downside.

Institutional Risk Management, Purpose Built for CRE Guarantees

Every aspect of the underwriting process is designed to mitigate the potential for liability. Risk is evaluated across four distinct vectors:

Project Fundamentals

The first and most important filter is the quality of the real estate project itself. Focus remains exclusively on deals with sound fundamentals, clear exit strategies, and institutional-grade underwriting. Full third-party diligence is conducted, including appraisals, property condition and environmental reports, rent and sale comps, and local market intelligence. Site visits and broker interviews help assess the nuances of each market.

Sponsor Evaluation

Borrower integrity, reputation, and track record are

critical. This includes background checks, litigation reviews, credit evaluations, and reference calls. Red flags such as failed projects, adverse litigation, or poor reputation are disqualifiers. Indemnification provisions ensure the borrower stands behind any losses incurred due to their conduct.

Lender and Loan Terms

Only established institutional lenders with a history of reasonable enforcement and transparent practices are considered. Loan terms are scrutinized for leverage, rate structure, maturity, and covenant risk. Aggressive structures or risky sponsor-lender dynamics are avoided.

Guarantee Structure

Non-recourse carve-out language is negotiated with experienced counsel to ensure clarity and limit liability. Each provision is modeled for potential impact, and structures are built with rights to intervene in the event of borrower default. Involvement includes direct notice rights, step-in authority, and the ability to force a sale or restructure to protect exposure.

Downside Protection: Layered and Modeled

Unlike equity or even traditional debt, exposure is not binary. For a credit enhancement vehicle to incur a loss, several unlikely events must occur simultaneously:

1. The project must experience significant value loss (equity fully wiped out).

2. The loan must be underwater (debt is impaired).

3. A carve-out violation must occur.

4. That violation must directly cause a loss.

5. The borrower must fail to honor its indemnity.

6. Amplifi must be unable to step in and cure or restructure the default.

This highly layered model makes loss events both rare and containable. That said, we plan for the worst in our vehicles. We maintain reserves and underwrite a loss provision in our anticipated return analysis.

Even if a loss were to occur, capital remains liquid and exposure is capped to the impairment, not the full loan amount or property value.

Why Capital Allocators Are Taking Notice

For institutional investors, family offices, and sophisticated portfolio managers, this strategy offers a compelling value proposition: differentiated commercial real estate exposure with reduced risk, lower correlation to traditional CRE investments, and high cash-on-cash returns. Effectively earning equity like returns while taking very limited credit risk - lower than traditional private credit.

Unlike equity or debt investments that rely on market timing, cap rate compression, or borrower execution, returns are derived primarily from contractual fee streams and credit enhancement economics. This creates a unique risk-adjusted return profile that complements a broader real estate allocation. It also introduces real estate credit exposure without direct lending or investing risk.

Moreover, because capital is held in liquid securities and only deployed upon specific guarantee triggers, such vehicles maintain a strong liquidity position while still benefiting from the economics of real estate transactions. This makes the strategy especially attractive for allocators seeking capital-efficient alternatives that perform across market cycles.

In an environment where volatility and repricing are disrupting traditional CRE equity and debt strategies, credit enhancement offers a forward-looking, resilient way to stay invested in the space.

Benefit for All Parties Involved

A prudently executed credit enhancement model succeeds because all parties win:

• Good borrowers secure the loans they need, without diluting ownership or over-raising equity.

• Prudent lenders gain added protection and confidence in their underwriting.

• Savvy investors gain access to an innovative yield strategy with controlled downside

Built by Practitioners

This strategy was conceived by lenders who have been borrowers. We understand the nuances of both

sides of the table. We have experience underwriting billions in real estate loans, managing structured credit portfolios, and developing real estate across multiple cycles. This 360 degree perspective informs every element of the approach—from legal architecture to investor reporting.

Conclusion: A New Pillar of Capital Formation

The credit enhancement model is a large market opportunity in an otherwise fragmented marketplace; it is a new pillar of capital formation for commercial real estate. In a time of tightening credit and rising barriers to financing, it offers a bridge—backed by institutional risk management, powered by market demand, and designed to deliver superior returns.

For investors seeking differentiated exposure to commercial real estate with a highly risk-managed, programmatic strategy, this model offers a timely and scalable solution. The capital markets are changing, and those who adapt with innovative solutions will define the next era of real estate investing.

Conrad Wicker Managing Principal Amplifi CRE

Amplifi is a middle-market commercial real estate finance and investment company and fund manager. Through niche credit enhancement solutions and strategic co-GP equity investments, we partner with owners and lenders to fill critical needs in the capital stack.

TOKENIZATION CONSIDERATIONS

BY DOUGLAS SPENCER Monetaforge

Tokenization of real-world assets is rapidly gaining traction across numerous industries, with the financial sector leading the way. At its core, tokenization involves linking a crypto token to a tangible asset or entitlement, establishing a legal connection that can facilitate ownership, transfer, and investment. As this innovative approach evolves, several critical considerations must be

addressed to ensure successful and compliant tokenization.

Purpose

The first step is clearly defining the purpose of the tokenization. This involves identifying the specific asset or entitlements the token represents, its expected lifespan, target investors, target jurisdictions, and applicable

regulations.

For example, tokens might represent: a 5-year bond with quarterly interest payments, rental income sharing from a property, capital raise linked to future profits, fractional ownership of artwork, private or mutual funds, stocks, options, royalties, employee payroll, or participation in illiquid asset portfolios.

Understanding whether the token will be marketed to investors residing in jurisdictions with regulations, such as the United States, Australia or Canada is crucial, as each jurisdiction has unique securities regulations and varying seasoning (holding) periods.

Since tokenization is still emerging, investor education and communications plans as to the purpose and value are vital to build awareness, trust and understanding of the token project within the target market.

Technological

Blockchain is an internet technology that manages a “ledger” keeping track of all token transactions with a distributed and immutable database ensuring accurate accounting. The secure, efficient, scalable, transparent, immutable nature of blockchain technology is what makes tokenization work.

Selecting the appropriate blockchain network infrastructure is fundamental. Key considerations include choosing the blockchain network suitable for the token target market, designing smart contracts, and adhering to standards like ERC-20 and ERC-3643.

Ethereum-based blockchains are popular choices due to their mature ecosystem, ability to run smart contracts, and compatibility with Layer 2 scaling solutions such as Arbitrum and Optimism, as well as sidechains like Polygon. Compatibility with the Ethereum Virtual Machine (EVM) allows seamless deployment of tokens and applications across various blockchain networks, including Polygon, BNB Chain, Avalanche, Fantom, Celo, Base, Arbritrum and Cronos.

ERC-20 is a technical standard for enabling tokens on an Ethereum blockchain. ERC-20 is a set of rules that ensures tokens are interchangeable and compatible with smart contracts, wallets, and exchanges within the Ethereum ecosystem. This standard defines a common interface for tokens, which includes functions for transferring tokens, checking balances, and manag-

ing approvals.

ERC-3643 standard provides permissioning capabilities, enabling on-chain identity management and claims or rules that can restrict token access based on investor qualifications—such as being an accredited investor or jurisdiction. ERC-3643 is also useful to better enable self-custody of tokens while still ensuring enforcement of regulatory or other token specific rules.

Transaction fees (gas fees) vary across networks; for instance, Polygon offers notably lower costs compared to other networks, which can be advantageous for high-volume token related activities during the lifespan of the token.

Marketplace

Enabling a marketplace and how the tokens will be marketed, sold, and managed within regulatory frameworks is important. If issuing security tokens restricted to certain investors (e.g., SEC Reg D or Reg S offerings), compliance with marketing restrictions, having a workflow process for the investor purchase subscription agreements, and investor accreditation is essential.

After the Primary Offering and seasoning (holding) periods end, resale or secondary market trading will need to be supported. For tokens with expected high trading volumes, listing on exchanges may be appropriate. Conversely, tokens with limited holders or low trading activity require a strategy for resale and peer to peer transfer mechanisms.

Many tokenization providers are also crypto exchanges that enable via their platform the onboarding of investors, initial investment, secondary trading, promotion of the tokens to their investor base, and management of the transfer restrictions. This model works well, but usually requires all investors to register, invest, trade and maintain their token holdings exclusively on the provider exchange platform. There may be limitations of what jurisdictions investors can be accepted from. Investors must also trust the exchange to hold their tokens.

Providers using permissioning standards like ERC-3643, enable a marketplace to promote the tokens to a global investor community, manage the investor onboarding with KYC and accredited investor verifications, enable the initial investment subscription

agreement signing process, and provide access to an existing pool of registered investors that are pre-qualified and familiar with investing in tokens. This permissioning model also allows investors to hold their token in self-custody wallets and opens the secondary market trading to a wider range of exchanges and other token trading bulletin board posting systems.

Legal

Legal preparations are vital and include drafting core documents such as the Token Statement of Entitlements (also referred to as a Master Token Agreement), technical token White Paper, Private Placement Memorandum for the token Offering, Subscription Agreements, and marketing materials. Ensuring these documents align with jurisdictional regulations helps mitigate legal risks and provides clarity to investors. Depending on the type of tokenized project and jurisdictions the token investment is offered in, there may be a range of legal and regulatory compliance considerations to be aware of.

Operational

Operational planning must account for ongoing management of the token’s lifecycle and ongoing related activities. This includes handling distributions (payouts, dividends, royalties), maintaining accurate records of token holders, and implementing secure wallet verification processes.

Tokens may have a fixed term—such as a 5-year bond—or be perpetual. In either case, provisions for termination (burning tokens), re-issuance, or cross-chain deployment should be considered. Additionally, mechanisms for stakeholder voting on token-related decisions can enhance governance and transparency.

Considerations for what happens if a token holder loses access to their wallet can include having the ability to confirm a token holder identity and legitimate situation, then enabling an authorized recovery or forced transfer of their tokens to a new wallet.

Administration

Finally, effective administrative controls are essential for maintaining token integrity and investor trust. This encompasses functions like minting, burning, re-

covery, forced transfers, lock-ups, and enforcing regulatory restrictions.

Investor administration involves onboarding, Know Your Customer (KYC) and Anti-Money Laundering (AML) screenings, wallet forensics, and ongoing compliance management—especially when tokens are restricted to accredited investors. Implementing robust systems ensures regulatory adherence and smooth operation throughout the token’s lifecycle.

Provider

By carefully addressing these considerations, you can select a suitable tokenization provider (Virtual Asset Service Provider - VASP) capable of executing your tokenization project in compliance with regulations and ensuring all the key aspects are taken care of, paving the way for successful asset tokenization.

Douglas Spencer Founder

Monetaforge is a Virtual Asset Service Provider registered with and regulated by the Cayman Islands Monetary Authority, offering compliant tokenization services in accordance with the US SEC and other jurisdictional regulations.

Monetaforge

THE CAYMAN ISLANDS PRIVATE FUNDS SURGE:

UNDERSTANDING THE DRIVERS

BEHIND SUSTAINED GROWTH

BY SAMANTHA WIDMER Cayman Finance

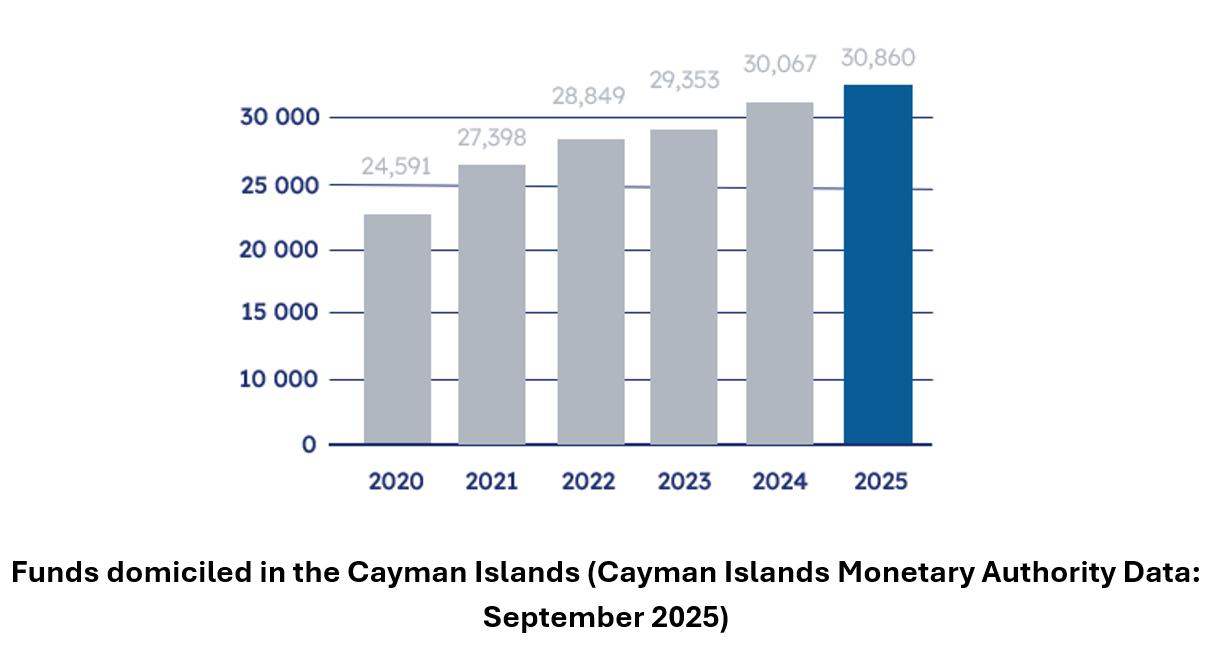

The Cayman Islands has experienced a remarkable transformation in its private funds sector over the past five years. Since the introduction of the Private Funds Act in 2020, private fund registrations have surged from 12,700 to more than 17,700, representing just under a 40% increase. As of September 2025, the Cayman Islands hosts almost 31,000 registered funds in total with over $8.5 trillion in assets under management, cementing its position as the world’s premier offshore funds domicile.

This growth warrants closer attention. What factors are driving fund managers to choose Cayman for their private fund structures? And why has the jurisdiction maintained its dominance over the past five years?

The foundation: Tax neutrality and legal certainty

At the heart of Cayman’s appeal lies its tax-neutral

framework, a concept frequently misunderstood, but fundamental to cross-border investment. Tax neutrality simply means the jurisdiction does not impose an additional layer of taxation on top of what investors already owe in their home countries.

International investors remain fully liable to pay taxes on distributions and capital gains in their home jurisdictions. The Cayman Islands automatically reports fund investments to investors’ respective tax authorities worldwide in accordance with the OECD Common Reporting Standard and the US Foreign Account Tax Compliance Act. In 2022, Cayman exchanged information on 550,000 accounts from 19,000 financial institutions, demonstrating its active commitment to transparency. Meanwhile, portfolio investments remain subject to tax in the countries where those investments are made.

Cayman’s commitment to transparency and financial crime prevention further strengthens its position as

a trusted jurisdiction. The Cayman Islands holds leadership roles in the OECD’s global forum on transparency and exchange of information for tax purposes and was one of 65 countries to receive the highest rating in the OECD’s peer reviews. In recognition of its robust frameworks, the jurisdiction was appointed as one of the first two guest members under the Financial Action Task Force’s Regional Bodies’ Guest Initiative to participate in FATF meetings and working groups during 2024/25. The Cayman Islands has also established the Office for Strategic Action on Illicit Finance (OSAIF), a centralised authority that coordinates the jurisdiction’s anti-money laundering and counter-terrorist financing efforts in alignment with international standards.

For fund managers, Cayman’s tax neutrality supports efficient access to global capital markets. It allows international investors to participate in global funds without incurring unintended tax liabilities or complexities that dual locations may bring. Cayman provides managers, particularly those based in the US, with a simple, well-tested vehicle for pooling international capital. This clarity and efficiency have made Cayman the preferred choice for fund managers seeking to attract a diversified investor base.

Cayman’s legal system, based on English common law, reinforces investor confidence through its strong precedents, modern legislation, and respected judiciary. The courts operate efficiently with an investor- and creditor-friendly approach and appeals ultimately go to

the Privy Council in London. Many lawyers who specialise in Cayman funds come from top international firms, and the Grand Court’s Financial Services Division specialises in complex financial and commercial cases. Together, tax neutrality and legal certainty underpin Cayman’s global reputation.

According to the US Securities and Exchange Commission’s private funds statistics, the Cayman Islands accounts for around 32% of the net assets of US private funds, far ahead of other competing jurisdictions. For qualifying hedge funds specifically, more than half (54%) of all net assets reported to the SEC are managed by Cayman-domiciled funds. These figures underscore Cayman’s entrenched position as the preferred offshore jurisdiction for US fund managers seeking to attract international capital.

The Private Funds Act: Regulatory evolution supporting growth

Cayman’s success is also the product of thoughtful regulatory evolution. The introduction of the Private Funds Act in 2020, followed by subsequent enhancements, created a comprehensive system of oversight for private funds. The legislation established mandatory registration with the Cayman Islands Monetary Authority (CIMA), required annual audits, and formalised independent oversight functions for valuation, cash

monitoring, and safekeeping of assets.

These measures codified practices that many sophisticated managers were already following and aligned Cayman with global regulatory standards. Rather than discouraging growth, they have strengthened investor confidence by ensuring a consistent and transparent framework. Institutional investors, including pension funds, sovereign wealth funds, and insurance companies, increasingly view Cayman’s regulatory system as a mark of credibility.

Cayman’s approach remains pragmatic and commercially balanced. Its regulatory framework protects investors and upholds international standards while allowing sufficient flexibility for fund managers to operate efficiently. This balance of strong governance and practical implementation has made Cayman the jurisdiction of choice for managers seeking both stability and speed to market.

Private credit: the primary growth engine

Private credit has emerged as a dominant force driving private fund formations in Cayman. This growth reflects fundamental shifts in the global financial system following the 2008 financial crisis. Stricter banking reg-

ulations have limited banks’ capacity and willingness to lend, particularly to middle-market companies. Private credit funds have stepped into this financing gap, offering customised loan structures with faster execution than traditional syndicated loans or public markets.

Cayman has been a central platform for this growth. Its fund structures accommodate both openand closed-ended formats, enabling managers to tailor liquidity and governance provisions to specific investment strategies. The jurisdiction’s familiarity with global investors, efficient registration processes, and trusted reputation all contribute to its continued dominance in this space.

Although market momentum may moderate as interest rate cycles evolve, the fundamental drivers of private credit remain intact. Demand for private financing continues to expand, and Cayman’s adaptable framework ensures it remains the domicile of choice for managers pursuing these opportunities.

Private equity’s continued evolution

Private equity continues to be a cornerstone of the Cayman funds sector. While fundraising conditions have become more challenging, the jurisdiction’s flex-

ibility in accommodating complex fund structures has proven particularly valuable as private equity managers adapt to changing market conditions.

The emergence of continuation funds and secondary market strategies exemplifies this innovation. These vehicles allow managers to extend the life of legacy assets, provide liquidity to existing investors, and inject fresh capital, often requiring specialised “hybrid” liquidity and financing structures that differ from traditional master-feeder setups. Cayman’s flexible legal framework and experienced service provider ecosystem make it particularly well-suited to support these evolving structures.

Cayman’s legislation also allows fund documentation to align closely with onshore requirements, ensuring consistency for global investors. This ability to replicate or integrate with onshore fund terms gives managers and investors confidence that Cayman structures will operate seamlessly alongside their domestic arrangements.

Supported by an extensive network of experienced legal, administrative, and audit professionals, the jurisdiction provides the expertise needed to design and operate increasingly sophisticated private equity platforms. As Cayman hosts more funds than any other offshore jurisdiction, it is also home to some of the most experienced funds professionals in the world. The sophistication of Cayman’s financial services industry attracts experts with a depth of knowledge continues to attract managers who value both innovation and reliability in their fund domicile.

Hedge Funds: A Resurgence Built on Liquidity

After several years of subdued inflows, hedge funds are once again experiencing a resurgence. As of mid2025, the Cayman Islands hosts more than 75% of the world’s offshore hedge funds and nearly half of the industry’s estimated $1.1 trillion in assets under management.

Performance has driven this resurgence. According to Citco, hedge funds delivered their highest annual returns since 2020, achieving a weighted average return

of 15.7% in 2024, with around 80% of funds posting positive returns in recent months. In a financial environment where many private market strategies tie up capital for extended periods, hedge funds offer flexibility that appeals to a wide range of institutional investors. Cayman’s efficient structures, clear governance framework, and regulatory certainty enable these funds to launch and operate quickly, often within weeks.

The jurisdiction’s reputation for reliability and consistency continues to attract managers seeking to combine agility with transparency. Hedge funds established in Cayman benefit from both the jurisdiction’s operational efficiency and the credibility associated with its mature financial infrastructure.

Family Offices: Sophisticated Capital Seeking Institutional Infrastructure

The increasing sophistication of family offices represents another key growth driver for Cayman’s private funds sector. The number of single-family offices worldwide has risen sharply, and their collective assets under management is now around $5 trillion. These entities are increasingly allocating capital to private markets, seeking access to high-quality investments in private equity, private credit, and infrastructure.

Cayman’s reputation, legal certainty, and efficient fund structures make it a natural home for this growing segment. Family offices require the same level of professionalism and governance as institutional investors, and Cayman provides that through its network of experienced service providers. The jurisdiction’s expertise in establishing “access funds” has also enabled high-networth investors to participate in institutional-grade opportunities by pooling capital efficiently.

Regulatory attitudes toward access funds have also shifted favourably. While previous SEC administrations sought to limit retail exposure to alternatives, the current administration has encouraged greater access, citing the significant wealth generated in the sector. Cayman’s efficient and well-understood structures are positioned to facilitate continued inflows from family offices and private wealth managers worldwide.

Time-to-market: Speed as a competitive advantage

In an industry where timing can determine success or failure, Cayman’s ability to launch funds rapidly represents a significant advantage. With CIMA’s online REEFS portal, many funds can be registered and launched within weeks, provided service providers are aligned, and documentation is in order.

This speed stems from several factors: streamlined regulatory processes, experienced service providers who understand CIMA’s requirements, standardised documentation approaches, and regulatory pragmatism that balances investor protection with commercial efficiency. For fund managers under pressure to deploy capital or capture market opportunities, these advantages are often decisive in domicile selection.

Looking ahead: Sustainable growth

The factors driving private fund growth in Cayman appear durable rather than cyclical. Private funds are growing at approximately 5% annually, with continued diversification into private capital, ESG strategies, and virtual assets expected. The jurisdiction is well-positioned to benefit from several emerging trends.

First, increased fund flows from emerging and growth markets including Brazil, the UAE, India, China, and Japan are creating new sources of capital seeking stable, internationally recognised structures. Japanese institutional investors alone have over $645 billion invested overseas, with approximately 80% flowing into Cayman-domiciled funds.

Second, the growing interest in virtual asset strategies and fund tokenisation positions Cayman to capture innovative fund structures. The jurisdiction is already home to approximately 63% of crypto and digital-asset hedge funds according to research published by the Alternative Investment Management Association (AIMA) and PwC, and a bespoke regulatory framework for tokenised funds is under development.

Third, the retailisation of alternative investments promises to expand the addressable market significantly. As alternatives reach broader markets beyond tradition-

al institutional investors, Cayman’s efficient structures and experienced service providers position the jurisdiction to capture a substantial share of this growth.

Conclusion: A foundation built on fundamentals

The substantial increase in private funds registered in the Cayman Islands reflects more than favourable regulation or tax treatment. It stems from a comprehensive value proposition encompassing legal certainty under English common law, regulatory credibility backed by international standards, operational efficiency enabled by experienced service providers, structural flexibility accommodating diverse strategies and investor bases, and tax neutrality that enables global capital flows.

As fund managers navigate an increasingly complex global landscape characterised by geopolitical uncertainty, regulatory harmonisation pressures, and rapid technological change, Cayman’s ability to balance innovation with compliance, flexibility with governance, and commercial pragmatism with international standards positions the jurisdiction to maintain its leadership in the private funds sector for years to come.

Samantha Widmer Associate Director of Funds & Capital Markets Cayman Finance

Cayman Finance is a public-private partnership and the leading industry association representing the Cayman Islands’ financial services sector. Its mission is to protect, promote, develop, and grow the jurisdiction’s financial services industry through strategic engagement with domestic and international stakeholders.

TOKENIZING REINSURANCE AS AN RWA - THE NEXT GENERATION OF UNCORRELATED RETURNS

BY JAY MADHU Oxbridge / SurancePlus

A New Frontier in Real-World Assets (RWAs)

Reinsurance has always been one of finance’s most stable yet least understood asset classes - grounded in real-world economics and historically reserved for major institutions writing contracts worth tens of millions. It’s the original “uncorrelated” asset - delivering steady

returns even when equity and bond markets swing wildly.

Now, through blockchain and tokenization, reinsurance is entering the spotlight as a Real-World Asset (RWA) - a tangible, cash-generating investment category that’s rapidly becoming one of the biggest narratives in digital finance.

By bringing reinsurance on-chain, platforms like

SurancePlus, a subsidiary of Oxbridge (NASDAQ: OXBR), are connecting traditional insurance economics to modern blockchain infrastructure. It’s the convergence of two worlds: the stability of a proven institutional market and the transparency and accessibility of Web3.

The result is a true RWA play with uncorrelated, institutional-grade returns - built not on speculation, but on real premiums, real contracts, and real-world value.

Why Reinsurance Has Been the Quiet Performer

Reinsurance is insurance for insurers. It protects carriers after major natural catastrophes like hurricanes or earthquakes - events that have no correlation to the stock market. That’s what makes it such an attractive RWA: it’s backed by real economic activity rather than synthetic leverage.

For decades, institutional investors have relied on reinsurance for diversification and yield. But access required scale - minimum commitments of $10 million or more - and was limited to reinsurers, hedge funds, and a handful of specialized ILS managers.

Tokenization changes that. With blockchain-based structures, accredited investors can now participate in fractionalized reinsurance contracts starting at much lower entry points. It’s a new level of access to an asset class that has historically been reserved for the few.

From Traditional Reinsurance to the Blockchain Era

Reinsurance has always been a global businessanchored in disciplined underwriting, strong capital standards, and decades of actuarial experience. Whether domiciled in the Cayman Islands, Bermuda, London, or Singapore, licensed reinsurers follow strict regulatory frameworks designed to ensure transparency, solvency, and reliability.

Today, digital platforms are extending those same principles into tokenized investment structures. Through tokenization, each digital reinsurance token represents a fractionalized interest in a real-world reinsurance contract. Built on blockchain rails, these tokens

provide verifiable transparency, automated settlements, and efficient distribution - all within regulated, auditable frameworks that align with international standards. This evolution blends the trust and oversight of traditional finance with the efficiency and accessibility of blockchain - turning reinsurance into one of the most credible and scalable Real-World Asset (RWA) models now emerging.

Transparency, Trust, and Fractionalization

Blockchain is beginning to make its way into the operational layers of insurance and reinsurance - enhancing how policies, underwriting data, customer service, and even claims are recorded and verified. While still early in its adoption, these integrations are steadily improving the flow of information and trust across the value chain.

Where the technology is also proving transformative is on the investment side - and this is where the real opportunity lies for investors. By fractionalizing reinsurance exposure through tokenization, blockchain makes it possible to participate with smaller commitments while still accessing institutional-grade returns. This is where the big payoff happens: blockchain doesn’t just modernize reinsurance - it opens the door to a previously unreachable, high-yield asset class.

How the Returns Work

Reinsurance returns are generated from premiums collected by insurance companies, offset by any losses from catastrophic events. Because these cash flows are tied to real-world risk rather than market sentiment, they tend to remain stable and uncorrelated with equities, bonds, or crypto.

Traditionally, such returns have only been available to large reinsurers and institutional investors able to deploy tens of millions per contract. Reinsurance contracts can yield strong annualized returns - sometimes as high as 60% - depending on market conditions and loss experience. Today, through tokenization and blockchain-based access, that same class of returns can be reached by a much broader pool of accredited investors, bringing an institutional-grade, uncorrelated asset class into the modern digital economy.

Governance and Oversight

Governance remains a critical part of the reinsurance ecosystem. Licensed reinsurers operate under strict regulatory supervision - for example, in the Cayman Islands, reinsurance entities are overseen by the Cayman Islands Monetary Authority (CIMA) - ensuring capital adequacy, solvency, and adherence to international standards.

In parallel, robust Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures remain paramount. Blockchain technology is helping streamline these processes - what once took days can now, in most cases, be completed in close to three minutes. This advancement not only enhances compliance but also makes investor onboarding far more efficient, lowering the friction traditionally associated with regulated investment participation.

When a reinsurance platform is also part of a publicly listed group, it adds yet another layer of oversight - not only through independent audits, but also through securities-law compliance and continuous disclosure obligations. Together, these safeguards provide the transparency and accountability that give investors confidence as the reinsurance industry evolves into the Real-World Asset (RWA) era.

The Broader RWA Landscape

Real-World Assets (RWAs) have become one of the most discussed themes in crypto and institutional finance alike. From real estate to private credit, the tokenization of tangible, cash-flow-generating assets is reshaping how capital moves.

Reinsurance sits at the very heart of this movement. It’s one of the few asset classes that’s both verifiable and uncorrelated - a perfect fit for institutional investors seeking diversification in a tokenized format. As on-chain infrastructure matures, RWA-backed reinsurance products are likely to attract increasing attention from fund managers and treasury allocators alike.

Looking Ahead: A New Era for Reinsurance and Digital Assets

Over the next decade, reinsurance is poised to be-

come a cornerstone of the Real-World Asset (RWA) ecosystem. As transparency, liquidity, and regulatory clarity improve, tokenized reinsurance could redefine how institutional capital interacts with global insurance markets.

For investors, it represents a rare combination of yield, stability, and innovation. For the reinsurance industry, it’s a chance to expand capacity and resilience through a broader capital base.

This is more than a technical shift - it’s a generational change in how risk and capital meet. And it’s happening now, on-chain.

Jay

Madhu Chairman & CEO, Oxbridge / SurancePlus

Oxbridge (NASDAQ: OXBR) is a Cayman Islands–based reinsurer specializing in property catastrophe risks. Its subsidiary, SurancePlus, is pioneering tokenized reinsurance investments that open access to accredited investors globally. The companies currently issue their reinsurance security tokens on the Avalanche blockchain.

THE RISE OF HEDGE FUND SMASHOW TO CAPITALIZE ON INVESTOR DEMAND

BY SS&C

Hedge fund separately managed accounts (SMAs) have grown increasingly popular with investors in the past few years. As a result, many hedge fund managers are joining SMA platforms and adding SMAs to their offerings. In the process, they are running into significant operational complexities that make managing SMAs at scale very different from running a conventional hedge fund. This paper explains the benefits of SMAs as well as the challenges they pose, and what managers need to take advantage of this growing trend.

By all accounts, hedge fund separately managed accounts (SMAs) appear to be having their moment. The Alternative Investment Management Association calls it a “renaissance,” observing that SMAs have “evolved from a niche allocation vehicle to a method of preference for deploying capital by institutional investors.” At a recent AIMA forum, JP Morgan predicted that 58% of new fund launches in the year ahead will be SMAs, while Goldman Sachs projects the SMA space to grow by $400 billion by 2027.1

The appeal of SMAs is understandable. In contrast to a conventional commingled hedge fund structure, a hedge fund SMA gives a single investor exposure to a hedge fund manager’s strategies—and the potential for exceptional returns—combined with direct ownership and control of the assets in the fund. SMAs allow for customization to investor mandates—for example, ESG-based selections or exclusions, risk parameters, tax strategies, limits on leverage or derivatives, or other criteria. Moreover, investors can negotiate customized fee structures, which typically do not include a performance component. And, with no lock-up periods or redemption windows, SMAs afford investors greater flexibility in liquidity.

In a recent BNP Paribas survey of institutional allocators, 26% of respondents said they use SMAs among their hedge fund allocations, while 15% said they expect to increase their allocations to SMAs.2 Hedge fund managers are moving quickly to respond to this growing investor demand, particularly as fundraising for pooled vehicles becomes increasingly competitive

and challenging. From a manager’s perspective, set-up is less complicated, since an SMA does not require a legal-entity wrapper. Hedge fund SMA platforms have proliferated in recent years to more efficiently connect investors and managers in a streamlined manner.

SMA platforms also perform many investor onboarding and servicing functions, freeing the manager to focus on strategy and work with the client on investment decisions.

OPERATIONAL COMPLEXITY

For all the optimism and energy around this segment, however, running SMAs carries significant operational complexity, especially for firms looking to offer this capability to multiple investors at scale.

Institutional investors have high standards of governance and oversight. SMA managers must be able to demonstrate operational integrity that can withstand rigorous due diligence, with institutional-grade controls, strong cybersecurity and measures to mitigate counterparty risk.

THE ROLE OF A FUND ADMINISTRATOR

A third-party fund administrator can play a critical role in enabling managers to scale SMA operations efficiently, and should be able to relieve much of the complexity associated with servicing multiple accounts. As with the prime broker, the selection of an administrator for an SMA is up to the investor. In practice, however, investors are likely to rely on their managers’ experience and recommendations. The SMA is more of a collaborative relationship between the investor and manager than a typical pooled fund, grounded in a high degree of trust and confidence.

An SMA is not too dissimilar from a regular hedge fund from an administrative servicing standpoint. However, there are some nuances to take into consideration. SMAs require an infrastructure that can handle accounting and reporting for several individualized accounts. Among the biggest challenges:

• Transparency and reporting: Greater visibility into fund holdings and trades is a key reason inves-

tors will choose an SMA over a commingled fund. Where a manager of a conventional fund can simply issue monthly statements, SMA investors will expect more frequent and detailed reporting—daily, in some cases—on performance, attribution, risk and other bespoke requirements. This will require aggregating data from multiple sources and delivery of custom reports for every investor via client portals or dashboards.

• Prime broker: SMA investors can choose their own prime brokers, which means the manager is likely to have several prime broker relationships instead of just the one or two associated with conventional hedge funds. This puts the onus on the manager to reconcile across multiple prime brokers and counterparties.

• Post-trade allocations: Managers must ensure that trades are allocated fairly across all accounts. This requires having systems that can track the entire trade lifecycle and automate allocations while ensuring compliance with each account’s investment guide-

lines.

• Compliance: Managers must be able to meet regulatory reporting and investor disclosure requirements across multiple SMAs.

The key considerations in selecting an administrator include:

• Technology infrastructure: The administrator must have a highly scalable infrastructure to handle multiple individual SMA books—the key difference between SMA and pooled fund accounting. The accounting system should offer look-through capabilities that enable visibility into portfolio data and activity. Connectivity with prime brokers and all the major SMA platforms is also critical. And because SMA managers are in possession of highly sensitive client data, the provider needs to have strong cybersecurity controls.

• Reconciliation: The administrator can take a major back-office burden off the manager by performing trade, position and cash reconciliations with every SMA’s prime broker.

• Custom reporting: The provider should be able to deliver comprehensive, customized performance, attribution and risk reporting for each individual account, ideally via secure client portals. SMAs don’t normally have a daily NAV calculation like a pooled fund, but the administrator should be able to provide portfolio valuations for each account. The provider should also have the capability to handle customized fee schedules and calculations.

• Compliance monitoring: The administrator should be able to perform automated, rules-based checking against investor mandates, including any restrictions, sector weightings, ESG or other criteria spelled out in the investment agreement.

Hedge fund SMAs are clearly gaining traction. Their influence in the alternative space is only likely to grow, as allocators increasingly signal their preference for individualized investment solutions. Expertise in SMAs provides hedge fund managers with an opportunity to diversify their offerings, deepen relationships and capture more allocations.

What’s needed to succeed is a true data and opera-

tions partner that can alleviate much of the administrative complexity that comes with managing and servicing multiple SMAs.

With the right combination of technology, scale, service capabilities and expertise, managers can better position themselves to take full advantage of this growing trend.

1“The SMA Renaissance,” Alternative Investment Management Association, February 5, 2025 https://www.aima.org/article/the-sma-renaissance.html 2“Coming Up Trumps: Allocators add to hedge funds as alpha rises,” BNP Paribas, February 10, 2025 https://globalmarkets.cib.bnpparibas/coming-up-trumps-allocators-add-to-hedge-funds-as-alpha-rises/

SS&C is a leading innovator in technology-powered solutions and operational services for the global investment management industry, with particular expertise in the full range of alternative investments, including hedge funds and SMAs, private equity, private credit, funds of funds, real estate, real assets and direct investments. We are also the industry’s largest global fund administrator as measured by assets under administration.

SS&C develops, owns and operates the technology that powers our fund administration services. We continually reinvest a significant percentage of our annual revenue into technology research and new solution development. SS&C serves a worldwide clientele with a network spanning the major financial centers of North America, Europe, Asia and Australia.

Learn more at ssctech.com

WHY CAYMAN IS EMERGING AS THE TECH JURISDICTION OF CHOICE

BY TECHCAYMAN

The world’s technology leaders are racing into uncharted territory. McKinsey’s 2025 Technology Trends Outlook projects that Alphabet, Amazon, Meta, and Microsoft will each spend $70–$100+ billion on AI-related capex in 2025—from data centers to custom silicon. Marquee listings are returning to public markets, exemplified by Figma’s NYSE debut in July 2025. Together, these shifts signal surging institutional appetite and a new era of technology innovation. At the same time, family offices are deploying capital directly into startups and digital infrastructure, expanding the pool of long-horizon capital.

But while the opportunities are extraordinary, the obstacles are real. Regulations diverge market by market. Immigration backlogs choke the flow of skilled talent. Infrastructure readiness varies widely, and the winning jurisdictions are those that combine regulatory clarity with durable professional and physical infrastructure. For founders and investors alike, the question is no lon-

ger what to build, but where to build it.

One jurisdiction is proving itself uniquely capable of bridging finance and technology: the Cayman Islands.

From funds to founders

Cayman’s story begins with finance. For decades, it has been the jurisdiction of choice for the world’s leading investment funds. Today, Cayman is home to more than 30,000 regulated funds, supported by a deep ecosystem of international law firms, administrators, auditors, and banks, according to Cayman Finance.