• Automate Interactions & Notifications to Streamline Hand-offs Between Parties

Us: sales@trellisplatform.com Or Visit: www.trellisplatform.com

THE WORLD IS CHANGING...

HEDGE FUND DUE DILIGENCE & RISK MANAGEMENT NEED TO CHANGE TOO

DAVID X MARTIN & ENRICO DALLAVECCHIA

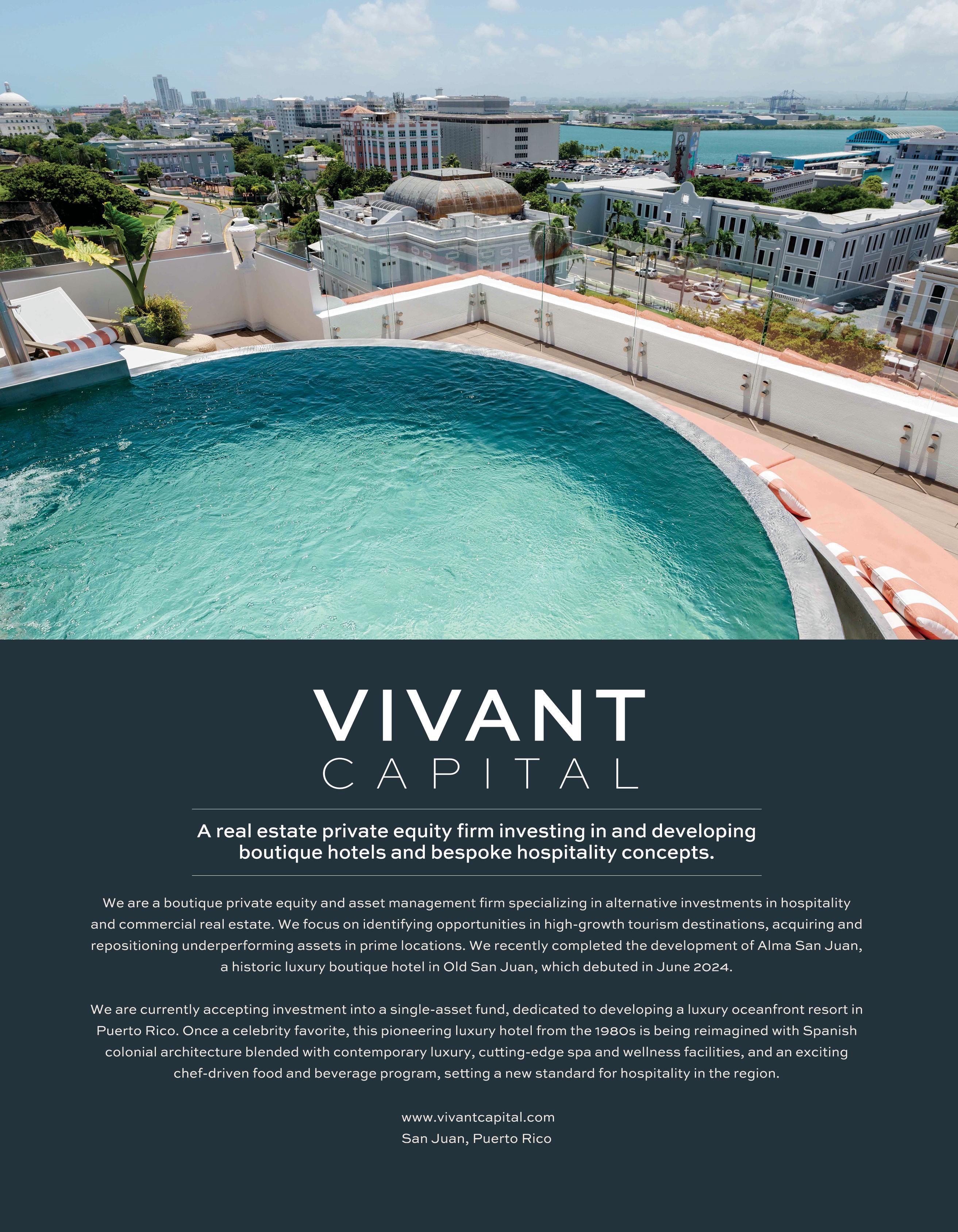

Arctium Capital Management

Management guru W. Edwards Deming famously said: “It is not necessary to change. Survival is not mandatory.”

We all know what he meant. Given the ever-increasing velocity and intensity of change in the past few decades, it’s even truer now than in Deming’s day. Adapt or die.

The Past Versus The Present

Today’s environment of global tariff wars, nearshoring, technological decoupling, and the growing complexity of U.S. geopolitical priorities require a profound reassessment of how hedge fund investors conduct due diligence and how fund managers practice risk management. Investors and managers alike are operating in a regime defined by faster news cycles, greater tail risks, and a collapse of the assumptions that have governed global markets for decades. In short, the

frameworks we have traditionally used to monitor and mitigate risk must now be reinvented for today’s more fragmented, volatile, and dangerous world.

Traditional hedge fund due diligence frameworks were designed to test governance, consistency, operational stability, and alignment. They worked well in a world where volatility was episodic, institutions were predictable, and market regimes were long-lasting. But that world is gone.

But today’s world is totally different: The pace at which narratives shift, capital moves, and confidence erodes has accelerated. Evaluating a fund manager’s strategy, pedigree, and service providers is still important, but it is no longer enough. Investors now need to assess adaptability — that is, how well a manager navigates an environment where macro and geopolitical shocks are not outliers, but structural features of the market.

Behavioral Interviewing

Historical track records during more stable times matter less than the ability to respond well to curve balls that come out of the blue. Investors should ask managers specific questions about past dislocations: “What did you do during the COVID shock? How did you respond to the inflationary regime shift? Tell me about how you managed through geopolitical disruptions, like Brexit or Russia’s invasion of Ukraine. Did you maintain discipline or shift risk aggressively – and why? How did you communicate with investors during these situations – and did investors respond well to your communication? What has been your biggest mistake as a fund manager … and how did you rebound from that mistake?” The best predictor of future behavior is

past behavior, so you want to use behavioral interviewing – asking specific, behavioral questions about their ability to think on their feet, prevent blind spots, and respond in a crisis. Examples of past behavior are far more revealing than a Sharpe ratio or volatility statistic. Beyond individual manager assessments, investors should also reconsider how they evaluate a fund’s contribution to the overall portfolio. It’s time to replace the traditional question, “Does this fund fit into our asset allocation framework,” with a more dynamic inquiry: “Will this fund continue to be additive under correlation breakdowns and volatility spikes?” It may seem counterintuitive, but a fund that complements the portfolio in calm markets may turn out to exacerbate losses in stressed conditions if it is exposed to hidden

betas or crowded trades. Evaluating resilience across regimes is therefore essential – and more relevant than evaluating fit within a static allocation model.

Strategy Shift, Fund Resilience, and Managerial Alignment

Another critical dimension is the detection and response to strategy drift. In calm markets, investment theses remain intact and risk frameworks evolve gradually. In today’s volatile markets, even well-defined strategies may drift — either due to market pressure, investor demands, or subconscious behavioral bias. Therefore, continuous monitoring is just as important as the initial investment decision. Investors need to establish feedback mechanisms to track whether managers are adhering to their mandate, changing their exposure profile, or deviating from their stated risk appetite. Timely detection of such changes can prevent significant losses. Service providers – often an afterthought — take on greater importance as the velocity of change increases. Prime brokers, fund administrators, legal advisors, and custodians must be resilient in their own right. Weaknesses in these relationships may not be visible in bull markets but they are vulnerable fault lines when stressed. Investors should evaluate whether these providers are robust, responsive, and appropriately scaled to the fund’s strategy and assets under management.

Equally vital is the evaluation of the fund’s operational and financial resilience. In a period where funding conditions tighten rapidly, and redemption cycles accelerate, managers with limited operational runway or excessive reliance on “hot money” are particularly vulnerable. A strong fund must not only perform but survive. This includes having lock-up provisions that are appropriate for the liquidity of the strategy, a diversified investor base, and a funding structure that does not rely on leverage to meet redemptions or cover margin calls. In addition, let’s not overlook the importance of managerial alignment. Investors have always asked whether fund managers have “skin in the game.” But in today’s climate, the quality of that alignment matters more than its mere presence. Investors want to know: “Are key principals significantly invested? Are incen-

tives designed for short-term performance fees or longterm capital preservation? Does the firm demonstrate a commitment to continuity and succession planning?” These factors become critical when markets turn and the path forward is unclear.

Fast Forward

Risk management, for both allocators and hedge fund managers, must now morph from a retrospective function to a forward-looking discipline that supports active decision-making. The speed at which information flows and markets reprice demands a new level of responsiveness. In past regimes, drawdowns unfolded over weeks or months. Today, they can materialize in hours. Such acceleration demands tighter trigger frameworks, revised stop-loss protocols, and scenario analyses that reflect not only market volatility, but political instability, policy shifts, and regional conflicts.

One of the major weaknesses in today’s investment ecosystem is the underuse of scenario planning. Many investors and managers continue to build stress tests around historical market events – while tail risks today are less about the recurrence of past shocks and more about the emergence of entirely new disruptions. The task is no longer to predict specific events but to understand how a strategy or portfolio behaves when fundamental assumptions break. This includes scenarios like the failure of a major global counterparty, the fragmentation of capital markets, the imposition of capital controls, or systemic technology failures.

The one thing we know for sure is: The future looks nothing like the past. We must ask ourselves: “What is unthinkable today, that if it happened, would completely transform our business?” Futurist Joel Barker, author of The Business of Paradigms, says that “when a paradigm shift occurs, everyone goes back to zero. Your past success counts for nothing.” Overnight, your highly successful firm can find itself back at Square One, along with everyone else, scrambling to operate within a new, unfamiliar paradigm. In other words, we all need to get proficient at thinking about the unthinkable. Planning for the unthinkable means going beyond the numbers. It involves tabletop exercises, discussions around investment governance, and coordination across functions. The goal is not to eliminate uncertainty

– an impossible task – but to build a decision-making framework that performs under pressure. The best institutions create a pre-defined set of responses that can be executed quickly during a crisis. This includes capital reallocation plans, hedging overlays, and communication protocols. In a crisis, there is rarely time to design new solutions. The ability to act must be embedded in advance. In other words, you need a Plan A, Plan B, Plan C, Plan D, and perhaps a few additional contingency plans.

Reporting frameworks must also evolve. Too many investors rely on risk reports that are backward-looking, overly quantitative, and disconnected from decision-making. These reports often emphasize variance and benchmark-relative returns rather than actual investment insight. What we need is a more holistic view of risk — one that incorporates liquidity, behavioral exposure, operational fragility, and geopolitical sensitivity. Reports should highlight not just what happened, but what is likely to happen and where the vulnerabilities lie.

Learning From Others

Lessons from other domains – particularly enterprise and cyber risk management – are instructive. In cybersecurity, the focus has shifted from how an attack happens to the consequences of the disruption. Similarly, investors should focus on the impact of market shocks, not just their causes. Whether the disruption stems from inflation, geopolitics, or regulation, the key question is: “How does it affect capital flows, portfolio construction, and operational continuity?”

Cyber risk management provides a valuable model for navigating today’s investment landscape. Because cyber threats can emerge and escalate in real time, the field has developed a culture of rapid response, constant monitoring, and contingency planning. This mindset — shaped by the need to act at “warp speed” — offers a useful analogy for investment professionals that are now facing, more than ever, a fast-moving geopolitical and macroeconomic environment.

One lesson we can learn from cyber risk professionals is the focus on identifying the “crown jewels” — assets or functions whose failure would be catastrophic. In hedge funds, this might include proprietary research

models, key staff, execution infrastructure, or critical service provider relationships. These elements must not only be identified, monitored, and stress-tested regularly but also explicitly incorporated into the design and execution of stress testing exercises and crisis simulations. Too often, tabletop exercises are conducted without the direct participation of the individuals or teams responsible for these vital functions — which limits their realism and effectiveness. Ensuring that these stakeholders are actively engaged in scenario planning, decision-tree analysis, and post-mortem reviews helps uncover operational dependencies and coordination failures before a real crisis hits. Their participation strengthens institutional memory, improves cross-functional communication, and ensures that contingency plans are not just theoretical documents but practical tools ready to be deployed under pressure.

Today’s leading funds are already adapting. They are embedding risk teams within the investment process – not as gatekeepers, but as partners. They are using open-source data to detect behavioral changes in markets, applying machine learning to flag anomalies in trading patterns, and building institutional memory around past crises to shorten reaction time. These managers understand that risk is not a static concept but a behavioral process that evolves – often very quickly –along with the market.

Investor Relations

Communication with investors has also changed. Top-performing funds are increasing the frequency of updates, not only to report performance but to contextualize it. During volatile periods, weekly or even daily insights can preserve investor confidence and avoid redemption spirals. More transparency around positioning, risk exposures, and scenario thinking reassures sophisticated clients that the fund is in control, even if the market is not.

Smart allocators, too, are revisiting their approach. Family offices and endowments are re-evaluating how they define risk appetite. Rather than applying a uniform framework across asset classes, they are tailoring their approach to reflect the unique risk-return dynamics of alternatives. This includes defining not just how much volatility they can tolerate, but what kinds

of losses are unacceptable and what types of risks are dealbreakers – risks they’re unwilling to assume under any conditions.

Conclusion

Decision-making in uncertainty remains one of the most difficult challenges in investing. But with the right structure it can become more manageable. Investors who define their values, constraints, and priorities ahead of time can move more decisively when the facts change. Those who wait until uncertainty resolves will likely find that the best opportunities have already passed them by.

This is not a time to retreat into safe havens or to freeze decision-making – nor is it a time to chase alpha blindly. It is a time to elevate process over prediction. Building a resilient investment process means developing the tools, people, and culture to respond ef-

fectively to rapid – sometimes unimaginable – change. It means that due diligence is not a checklist, it’s an ongoing conversation. And it means that risk management is not a shield, it’s a steering wheel.

50+ years ago, futurist Alvin Toffler wrote that both the rate of change and intensity of change were accelerating exponentially over time. Toffler predicted that we’ll ultimately arrive at the point where the speed and intensity of change become overwhelming, even paralyzing, and we will find ourselves living in a state of shock – Future Shock. That day is fast approaching. What can we do to prepare and/or prevent it?

These are parlous times, in which capital preservation and opportunity capture depend on institutional agility. Success will go to those who can identify real-time threats, adapt to new realities, and act swiftly without compromising discipline. That is not just good risk management – it’s survival.

David X Martin CEO and CIO Arctium Capital Management

Enrico Dallavecchia President and CCO

Arctium Capital Management

Arctium Capital Management is an Outsourced CIO service provider specializing in hedge funds and alternative investments, with a core focus on uncorrelated alpha—a strategy designed to deliver returns independent of market swings. Our flagship Arctium Uncorrelated Alpha Fund seeks capital appreciation, particularly during market downturns, by generating returns with minimal correlation to equity and fixed income markets. Led by two former Chief Risk Officers of major financial institutions, our team brings deep expertise in markets and risk management. Arctium partners with endowments, family offices, pension funds, and insurance companies, offering customized OCIO solutions, hedge fund due diligence, and institutional-grade risk management.

THE OPPORTUNITY TO INVEST IN FILM FINANCING THROUGH SECURED DEBT

E.J. KAVOUNAS

Copilot Entertainment

In recent years, the way films and television projects are financed has evolved considerably, with major studios like Netflix, Warner Bros., and Amazon often funding projects directly from their own balance sheets. These vertically integrated giants produce, distribute, and exhibit their content across global streaming platforms, allowing them to absorb the financial risk and retain the lion’s share of profits. However, a significant number of films and television series, including those that eventually appear on streaming platforms or in theaters worldwide, are not studio-backed but instead financed independently. These independently produced projects offer an underexplored investment opportunity, especially in the realm of secured private debt.

Understanding Independent Film Financing

Independent film and television projects are typically financed through a mosaic of funding sources. These include equity investments from high-net-worth individuals, family offices, and private equity firms, combined with soft money such as government grants, tax credits, and rebates. In many cases, producers must also secure loans from private lenders to cover budget gaps. Equity investment is often seen as the riskiest component of the financing stack. These investors are last in line to recoup their investment and only see returns if the film performs well at the box office or garners significant licensing deals. To help mitigate this risk, some

investors rely on federal tax incentives such as IRS Section 181, which allows for an immediate deduction of qualified production expenses. Internationally, similar risk-reduction mechanisms exist, including production grants in Canada, the UK, Germany, and Australia, all of which aim to stimulate local film production by returning a percentage of the budget to qualifying projects.

Yet, beyond equity lies a more stable and potentially lucrative corner of the film financing landscape: secured debt. This form of investment is far less dependent on a project’s commercial success and more reliant on pre-arranged financial structures, making it attractive for investors seeking lower-risk exposure to the entertainment industry.

What Is Secured Debt in Film Finance?

Secured debt in film financing involves lending money to a film or television project with the backing of tangible or contractual assets. These assets may include:

1. Tax Credits and Rebates: Many U.S. states and foreign governments offer refundable cash rebates or transferable tax credits for qualified production expenses. For example, Georgia, New Mexico, and Louisiana in the U.S., and countries like Canada and the UK, provide significant credits that can total 20% to 40% of a production’s local spend. These credits are typically assigned to a lender as collateral and repaid when the credit is monetized (either through a sale or refund from the state).

2. Pre-Sale Contracts: Independent producers often secure distribution deals in advance of production. These contracts guarantee payment from international or domestic distributors upon delivery of the completed film. A lender may advance funds against these contracts, with the sales revenue acting as repayment.

3. Gap Financing: In certain cases, lenders will finance the “gap” between what a producer has already raised and the total production budget. This is generally based on projections of future revenue from unsold distribution territories or rights. While riskier than tax-credit or pre-sale backed

loans, these still involve a degree of structure and collateral.

How the Process Works

A typical secured lending process begins with the production company providing a comprehensive financial plan to the lender. This plan includes:

• A detailed production budget and schedule

• Copies of confirmed pre-sale agreements

• Letters of intent for tax credit eligibility following a pre-production audit, often from a local accounting firm, that provides an Opinion Letter based on spend and legislation.

• Completion bond (an insurance policy that ensures the film will be finished on time and on budget)

• Cash flow schedule detailing when expenses will be incurred and when revenues are expected

Once the lender verifies the collateral, it structures a loan that may cover 30% to 70% of the production budget, depending on the strength of the security. The loan is usually repaid within 12 to 24 months, with interest rates ranging from 8% to 15% annually, depending on risk profile and collateral quality.

Why Investors Should Consider Secured Debt

Investing in secured debt for film and television projects offers several distinct advantages:

1. Reduced Risk: Unlike equity, which depends entirely on the project’s success, debt investments are backed by assets with known or contractual values.

2. Attractive Yields: Interest rates can be significantly higher than traditional corporate bonds or treasury notes.

3. Shorter Duration: Loans are often repaid quickly, sometimes within a year, allowing for higher liquidity and faster reinvestment opportunities.

4. Portfolio Diversification: Entertainment lending is uncorrelated to stock and bond markets, offering an alternative asset class that behaves differently during economic cycles.

5. Cultural Impact: Investors can contribute to the creation of artistic works and cultural products, sometimes receiving credits, invitations to premieres, or other non-financial perks.

Understanding the Risks

Of course, no investment is without risk. For secured debt investors, the primary concerns include:

• Production Delays or Failures: If the project is not completed, the tax credits or pre-sale contracts may not be triggered.

• Regulatory Changes: Tax incentive programs are subject to political and budgetary shifts, which could impact availability or timing.

• Counterparty Risk: The solvency of distributors and tax credit buyers must be vetted, as delayed or defaulted payments could impact returns.

• Completion Risk: While completion bonds help mitigate this, some projects still run over budget or behind schedule.

These risks are typically addressed through rigorous due diligence, third-party oversight (such as completion bond companies and audit firms), and well-structured legal agreements.

Emerging Trends

The popularity of private debt in entertainment has increased in recent years. While boutique finance firms have helped expand access to this market, it is worth noting that some traditional commercial banks also provide film financing, particularly for the most secure collateral such as tax credits. However, these institutions often struggle to offer the level of leverage or production-specific flexibility that many independent producers require. As a result, more agile private lenders continue to play a vital role in bridging financing gaps. One example is Level Field Media whose principals have financed over 850 film and TV productions. This boutique lender assists producers using structuring, to increase collateral by mixing multiple jurisdiction’s tax incentives. Acting as a consultant, providing finance strategy, boutique lenders help producers reduce their reliance on equity while maximizing returns to investors and minimizing their risk.

Conclusion

While equity investment in film can yield outsized returns, it comes with considerable risk tied to box office performance and commercial viability. For investors looking for a more predictable and secured pathway into

the world of entertainment finance, private debt backed by tax credits and pre-sale agreements offers a compelling alternative. These investments combine the allure of Hollywood with structured asset-backed returns, creating opportunities not just for financiers but for storytellers and audiences alike. As demand for content grows globally, so too does the opportunity for savvy investors to participate in its creation—with less drama and more security.

E.J. Kavounas is an executive with over two decades of experience in media finance and investment banking. He produced the feature Hero Mode, starring Mira Sorvino and Sean Astin. Prior to this, he worked for 15 years in investment banking, including at Credit Suisse in Los Angeles, where he was a Managing Director. He has closed over $10 Billion worth of transactions, including financing the feature films Empire State (Dwayne Johnson) and Escape Plan (Sylvester Stallone and Arnold Schwarzenegger).

He holds an MBA from The Wharton School of the University of Pennsylvania and a BA from Middlebury College. In addition to his professional achievements, he is an advisor to Caltech Connection which supports community college undergrads through mentorship opportunities with Caltech grad students.

E.J. Kavounas Founder Copilot Entertainment

INSIGHTS FROM KEVIN SHEA

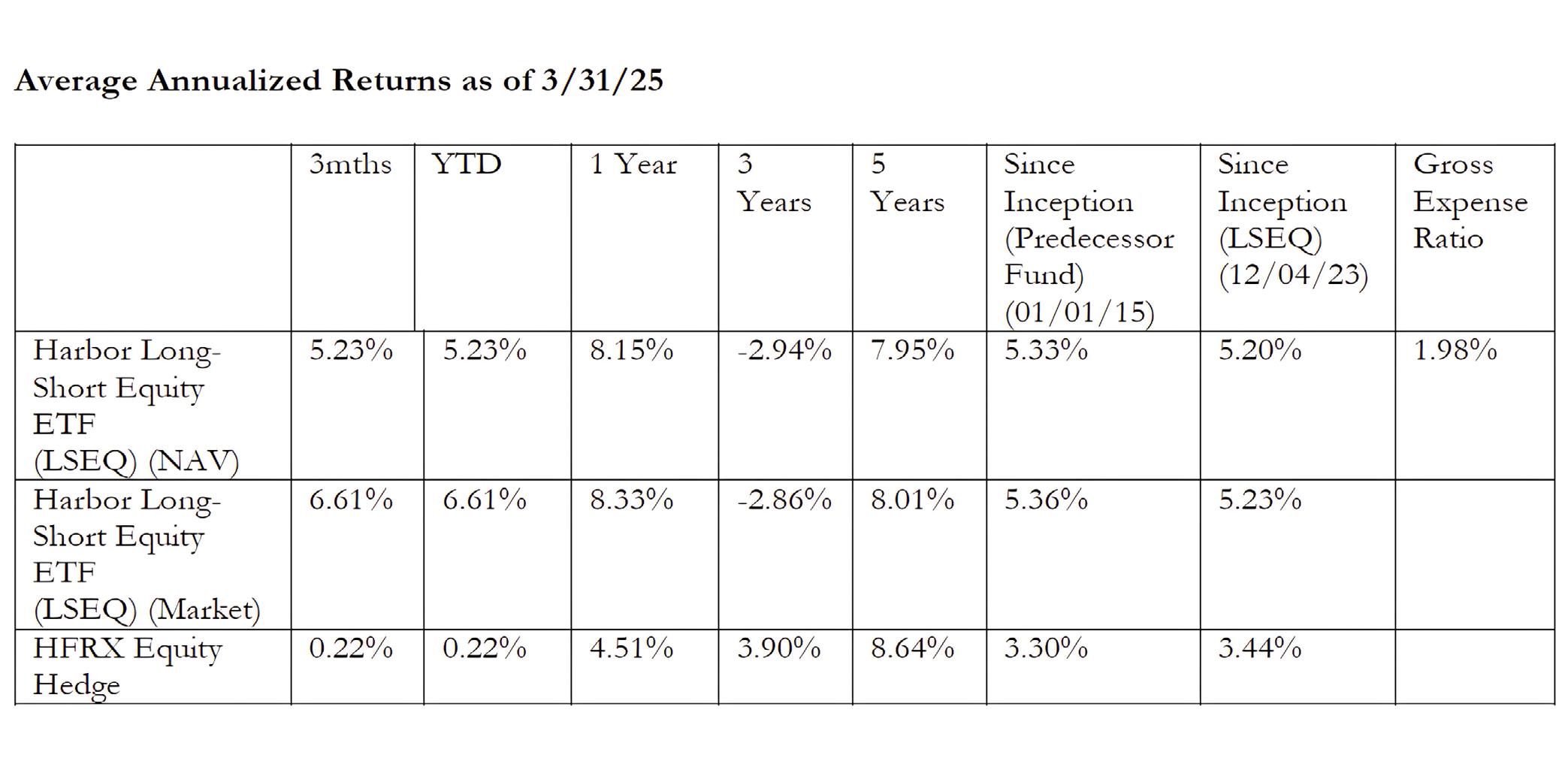

Uncorrelated spoke with Kevin Shea at Disciplined Alpha about the Harbor LongShort Equity ETF and his updated views on the overall U.S. equity market. The discussion is summarized below.

Uncorrelated: Can you provide a summary of the ETF and the compelling features it offers?

Kevin Shea: The ETF invests in Large Cap and Mid Cap U.S. stocks. It has four distinct features that include a Regime Model that determines gross and net exposure and Growth versus Value style tilts, distinct Industry Group based stock selection models, a separate Short Model, and an Alpha Opportunity Model that

determines which parts of the market have the most opportunity to generate alpha.

Uncorrelated: Can you describe how you developed these four features? Perhaps connect them to your broader career and the roles you had over time. For structure, please organize them chronologically. Which feature did you develop first?

KS: While we are probably best known for our Regime Model, the first feature I developed was the distinct Industry Group based stock selection models. My first career was in Biotech. In the early 1990s, I worked at a biotech company in Boston doing HIV research. It was intense work, as there were no drugs on the market for

EDITOR’S NOTE: THIS ARTICLE HAS BEEN UPDATED AS OF APRIL 2025 AND ORGINALLY APPEARED IN OUR JANUARY 2025 ISSUE.

HIV. If somebody got infected, their life expectancy was only 24 months. I worked with a team to develop an antibody. This research turned into a Master’s Thesis, an article, a patent, and ultimately a drug in clinical trials.

Due to the progress on the scientific front, we needed a business development person. I started working in this role part time while pursuing and earning an MBA, with a concentration in Finance and a minor in International Studies.

After graduating in 1995, I entered the Management Development Program at John Hancock that involved rotations in several parts of the firm. The first rotation was in the Health Insurance division. This made me reflect on the fact that Biotech and Health Insurance are both Industry Groups within the same Health Care Sector, but they are fundamentally different from each other. Biotech companies make significant investments in research and development (R&D), to develop distinct products protected by patents, over a decade plus product development cycle, and with heavy national regulatory hurdles to overcome prior to marketing. Health Insurance companies typically make relatively little investments in R&D over a much shorter product development time are more focused on operational product efficiency, and also look for the general account to seek to increase in value over time in order to pay out future claims.

Due to the inherent fundamental differences in the business models of the companies in these Industry Groups, it seemed natural from a stock selection perspective to build Industry Group dependent models.

I subsequently rotated to three different groups in the mutual fund division of John Hancock. I attended meetings with company managements and sellside fundamental analysts across all Industry Groups. The insights gained from these and subsequent meetings, which now number over 1,000, has allowed me to gain insight into the drivers of stock performance within a given Industry Group. I have taken these insights and rigorously backtested them to build Industry Group dependent stock selection models.

This is a very differentiated feature of the strategy. The investment management industry has evolved over the years, but we believe it is still tilted toward fundamental analysis for stock selection. While fun-

damental managers and analysts know a lot about the companies they cover, they generally have not backtested their conclusions about the specific drivers of performance. Quantitative managers and analysts, on the other hand, frequently run backtests, yet in our experience very few ever talk to company managements to understand the business models of the companies they are trying to model. Very few managers and analysts try to both understand the compelling fundamental drivers of performance within a given Industry Group, as well as backtest those ideas before incorporating them into an investment strategy. We think it is important to do both.

Uncorrelated: Interesting. Which were the next of the four features that you developed?

KS: I developed the separate Short Model followed by the Alpha Opportunity Model. I joined Invesco to build a Mid Cap product in 1999. Shortly after I arrived, the market started to decline significantly. While the overall U.S. equity and the Nasdaq declined, I noticed that the stocks that declined the most were not necessarily the worst ranked stocks in our existing Long Model. This led us to explore the idea of building a separate Short Model. We weren’t directly shorting stocks at the time, so we called this a Bomb Avoidance model. It was exciting to find predictors of underperformance, which we combined into an overall Model. It was somewhat frustrating; however, to not just avoid the stocks likely to underperform, but to potentially be able to actively take advantage of this insight by selling them short.

A couple of years later I had the opportunity to build a Market Neutral product at a predecessor firm to Disciplined Alpha, D.A. Capital Management. As there are fewer tools to work with in Market Neutral than a variable exposure product, it is important to focus on those parts of the market where you are rewarded for being correct. This work led to our Alpha Opportunity Model.

Uncorrelated: So that leaves the Regime Model. Can you expand on that? This sounds particularly interesting.

KS: I agree. In business school, it is common for finance professors to review the Fama French model in which the expected “total” return of a stock is driven by the

exposure to the market, size, and value. The market “relative” return of a stock is thus driven by a stock’s exposure to size and value. Finance professors tend to then typically review a lot of data and conclude that over the long run, if one buys small cap value stocks, they may potentially outperform the market. While this is conceptually correct, the long run for an academic might be ten years.

After surveying numerous allocators, I found that historically the most popular time-period that they use to evaluate performance is the most recent three years, followed by the most recent five years.

In the late 1990s, Growth stocks outperformed Value stocks. The internet Bubble finally blew up from 2000 to 2002, during which period Value stocks outperformed Growth stocks. This was followed by a sig-

nificant “Junk Rally” in the second and third quarter of 2003, when low-priced, low-quality stocks performed well.

At a high level, there was a shift from Risk On in the late 1990s, to Risk Off from 2000 to 2002, to an extreme level of Risk On in primarily two quarters in 2003. Put another way, first Growth stocks outperformed, then Value stocks outperformed, then Growth stocks outperformed again.

In my experience, many Growth and Value managers tend to be very passionate about their investing styles. Growth managers look for the latest new technology. Lately this has often had to do with AI. Growth managers also likely then pay a high multiple of future earnings or cashflow to buy these stocks. Value managers historically admit that they seek to provide a steady

allocation in a broader portfolio, likely not investing in companies that may cure cancer or reinvent the internet. They continue to state that they invest in “boring” companies, but these companies have had real earnings, and today, they buy these companies at attractive valuations. They often point out that Value strategies have the potential to hold up in times of market turmoil.

A Regime approach to investing historically does not categorically embrace Growth or Value as an inherently better method of investing. Instead, it relies on a model that indicates one of these styles is likely to outperform over the medium term. In our case we use a combination of Macro data and Relative Valuation to determine which of these styles is likely to outperform.

Very few managers take a Regime approach to investing. Based on manager databases and conversations with sellside strategists that publish on Regime models, we believe there might be about 20 managers in the industry that have a formal Regime approach to investing.

Uncorrelated: This does indeed seem like a very differentiated feature. Can you discuss why a Regime approach to investing may be particularly important at this point in time?

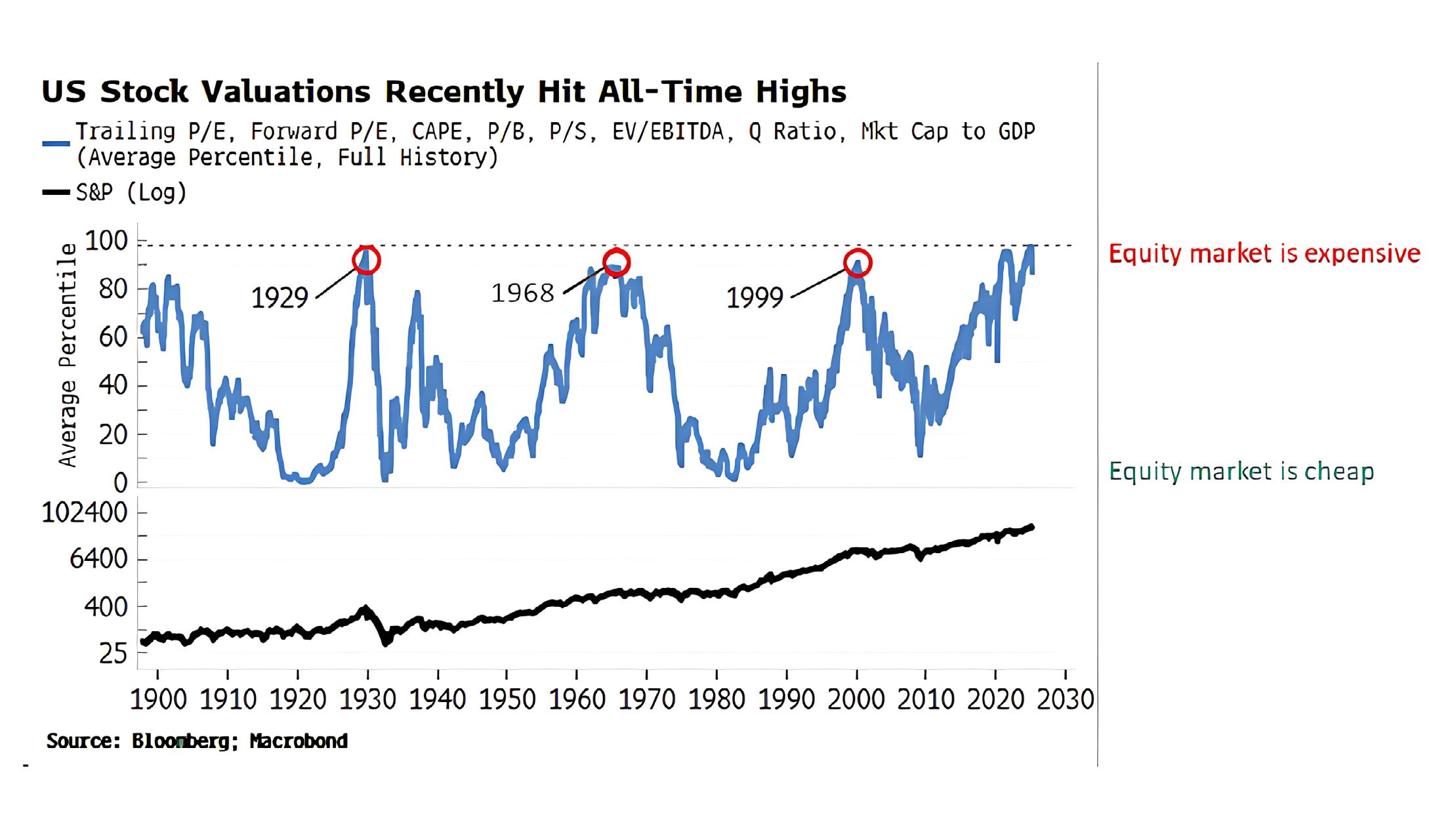

KS: It is the very same reason why I believe your Uncorrelated Conference is timely. I have brought with me a chart showing the relative valuation of the U.S. equity market for the last 130 years. Initially the valuation represented the PE ratio developed by Robert Shiller, known as the Cyclically Adjusted Price to Earnings Ratio, or CAPE. Over time, as additional information became available, other valuation metrics were included. These individual valuation metrics were combined on an equal-weighted basis to establish a composite valuation metric for the U.S. equity market.

The y-axis is on a scale from 0% to 100%. This represents the percentile ranking since inception of the chart for the composite valuation metric up until that point in time. When the line reaches 100%, this indicates that the U.S. equity market has never been as expensive as it had been, up until that point in time.

The U.S. equity market peaked in 1929, as referenced in the first red circle in the chart, just before the market crashed leading to the Depression in the 1930s.

The U.S. equity market finally recovered 25 years later in 1954.

The U.S. equity market then continued to rise until 1968. At that point, as referenced in the second red circle in the chart, the U.S. equity market reached a valuation similar to the level in 1929. The U.S. equity market endured multiple bear market declines during the 1970s, before finally recovering 14 years later in 1982.

The U.S. equity market, once again, then continued to rise until 2000. Just before the peak of the market, as referenced in the third red circle in the chart, the U.S. equity market, once again, reached a valuation similar to the level in 1929. The U.S. equity market, once again, endured two bear market declines consisting of the bursting of the Dot-com Bubble and the Global Financial Crisis, before finally recovering 13 years later in 2013.

Today, the U.S. equity market is, again, at a valuation similar to the level in 1929. When the multiple of the U.S. equity market expands, this corresponds with multi-year periods during which the U.S. equity market generates above-average returns. When the multiple of the U.S. equity market contracts, this corresponds with multi-year periods during which the U.S. equity market generates 0% annualized returns.

I believe the U.S. equity market is due for a multiyear period during which the multiple of the U.S. equity market contracts, and the U.S. equity market generates 0% annualized returns.

Many products that are marketed as solutions to diversify a Long portfolio have correlations with the S&P 500 Index of approximately .85 to .90, and, in my experience, are unlikely to deliver returns that keep up with inflation during a multi-year period when the S&P 500 Index may generate 0% annualized returns. Some Long Short equity strategies have much lower correlations with the S&P 500 Index, and may be better positioned for such a time period. In our case, this is due to the Regime Model. While the S&P 500 Index generated 0% annualized returns from 2000 to 2013, there were several year time periods when Growth stocks outperformed, then Value stocks outperformed, etc. Having the ability to shift between tilting to Growth stocks and Value stocks has the potential ability to generate absolute returns during such a time period.

Reproduced with permission from Simon White, Macro Strategist at Bloomberg Source: Robert Shiller at Yale University; Bloomberg Fundamental data; March 13, 2025; Factors are equally weighted and introduced as they became available, with CAPE being the first factor. An expanding window technique was used to calculate average percentiles; Estimates for S&P were used prior to 1957

Uncorrelated: I understand you have partnered with Harbor Capital, in the launch of an ETF version of your strategy. Can you tell us more about this?

KS: We are very excited about this partnership. Harbor Capital has $58.79 billion in assets under management as of March 31, 2025. In the last few years, the mutual fund industry has shown signs of maturing while the ETF industry has expanded dramatically. As of December 2024, and according to available information on the ETF market, in 2023, the overall ETF market grew 15%, while the Active ETF market grew approximately 46%. The figures for 2024 are ahead of the 2023 pace. The overall ETF market now exceeds $10 trillion in as-

sets. In the last three years, Harbor Capital has focused on bringing compelling ETF products to the marketplace. They now offer about 20 ETF products across a variety of asset classes. They also have a salesforce with coverage throughout the country.

The Disciplined Alpha Onshore Fund LP, which launched almost ten years ago, was reorganized into the Harbor Long-Short Equity ETF in December 2023. We agreed and after a lot of work by both parties, this was one of the first hedge fund to ETF conversions in the industry.

Uncorrelated: Sounds like an exciting partnership. Thank you for your time.

Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which returns would have been lower. Investment returns and principal value will fluctuate and when redeemed may be worth more or less than their original cost. Returns for periods less than one year are not annualized. Current performance may be higher or lower and is available through the most recent month end at harborcapital.com or by calling 800- 422-1050.

ETF performance prior to 12/4/23 is attributable Disciplined Alpha Onshore Fund LP (the “Predecessor Fund”). The historical NAV of the predecessor are used for both NAV and Market Offer Price performance from inception to ETF listing date. Performance periods since LSEQ listing date may contain NAV and MOP data of both the newly formed ETF and the predecessor fund performance. Please refer to the Fund prospectus for further details.

Shares are bought and sold at market price not net asset value (NAV). Market price returns are based upon the closing composite market price and do not represent the returns you would receive if you traded shares at other times.

Important Information

For Institutional Use Only. Not for Distribution to the Public.

The HFRX Equity Hedge Index measures the performance of the hedge fund market. Equity hedge strategies maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment processes can be employed to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation ranges of typical portfolios.

All investments involve risk including the possible loss of principal.

Unlike mutual funds, ETFs may trade at a premium or discount to their net asset value. The ETF is new and has limited operating history to judge.

The views expressed herein are those of Kevin Shea, Disciplined Alpha at the time the comments were made. These views are subject to change at any time based upon market or other conditions, and the author/s disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results.

There is no guarantee that the investment objective of the Fund will be achieved. Stock markets are volatile and equity values can decline significantly in response to adverse issuer, political, regulatory, market and economic

conditions. Short selling securities could potentially have unlimited loss due to the price of securities sold short increasing beyond the cost of replacement and the limitless increase on the value of a security. The Fund utilizes a quantitative model and there are limitations in every quantitative model. There can be no assurances that the strategies pursued or the techniques implemented in the quantitative model will be profitable, and various market conditions may be materially less favorable to certain strategies than others. The Harbor Long-Short Equity ETF (the “Fund”) acquired the assets and assumed the then existing known liabilities of the Disciplined Alpha Onshore Fund LP (the “Predecessor Fund”), a Delaware limited partnership, on 12/4/23, and the Fund is the performance successor of the reorganization. This means that the Predecessor Fund’s performance and financial history will be used by the Fund going forward from the date of reorganization. Performance information prior to 12/4/23 reflects all fees and expenses, including a performance fee, incurred by the Predecessor Fund. Disciplined Alpha LLC (“Disciplined Alpha”) served as the general partner and investment manager to the Predecessor Fund, which commenced operations on 1/1/15 and, since that time, implemented its investment strategy indirectly through its investment in a master fund, which had the same general partner, investment manager, investment policies, objectives, guidelines and restrictions as the Predecessor Fund. Regardless of whether the predecessor fund operate as a stand-alone fund or invested indirectly through a master fund, Disciplined Alpha managed the Predecessor Fund assets using investment policies, objectives, guidelines and restrictions that were in all material respects equivalent to those of the Fund. However, the Predecessor Fund was not a registered fund and so it was not subject to the same investment and tax restrictions as the Fund. If it had been, the Predecessor Fund’s performance may have been lower.

Diversification does not assure a profit or protect against loss in a declining market.

ETFs are subject to capital gains tax and taxation of dividend income. However, ETFs are structured in such a manner that taxes are generally minimized for the holder of the ETF. An ETF manager accommodates investment inflows and outflows by creating or redeeming “creation units,” which are baskets of assets. As a result, the investor usually is not exposed to capital gains on any individual security in the underlying portfolio. However, capital gains tax may be incurred by the investor after the ETF is sold.

Indices listed are unmanaged and do not reflect fees and expenses and are not available for direct investment.

The Standard & Poor’s 500 Index is an unmanaged index generally representative of the U.S stock market.

The Russell 1000 Growth Index is an unmanaged index generally representative of the U.S. market for larger capitalization growth stocks.

The Russell 1000 Value Index is an unmanaged index generally representative of the U.S. market for larger capi- talization value stocks.

Investors should carefully consider the investment objectives, risks, charges and expenses of a Harbor fund before investing. To obtain a summary prospectus or prospectus for this and other information, visit harborcapital.com or call 800-422-1050. Read it carefully before investing.

Foreside Fund Services, LLC is the Distributor of the Harbor Long-Short Equity ETF. 4425052

Mr. Shea is CEO of Disciplined Alpha LLC. and has 25 years of investment experience. Previously he was the Director of Quantitative Research at Cadence Capital, responsible for implementing a regime-based approach across multiple products representing $5 bb. Mr. Shea has also held the positions of Portfolio Manager at Batterymarch where he managed $600 mm, and CIO and Founder of DA Capital where he grew the firm from $10 mm to $450 mm over four years. He has also been a Portfolio Manager at Invesco, responsible for $100 mm, and a Quantitative Analyst at John Hancock Funds. Mr. Shea holds a B.A. in Liberal Studies from the University of Notre Dame, an A.L.M. in Biology from Harvard University, and an M.B.A. in Finance and International Studies from Boston College. Mr. Shea co-teaches a Proseminar in Finance at MIT’s Sloan School of Management. He is a member of the CFA Institute, and the Institute for Quantitative Finance, also known as the Q Group. He is also a member of the Financial Accounting Standard Board’s (FASB’s) Investor Advisor Committee (IAC). Mr. Shea has been quoted in numerous publications including aiCIO, Emerging Manager Monthly, Hedge Fund Alert, HFM Week, Institutional Investor, and WatersTechnology. He has spoken at numerous conferences in the U.S. and internationally sponsored by Allianz, Argyle Executive Forum, Battle of the Quants, Capital IQ, FactSet, HFM Week, International Quality & Productivity Center, Northfield and Sentiment Analysis Symposium.

Kevin W. Shea, CFA Chief Executive Officer Portfolio Manager Disciplined Alpha LLC

WHY COMMERCIAL REAL ESTATE MAY BE THE MOST COMPELLING ALTERNATIVE ASSET CLASS RIGHT NOW

Over the past two years, commercial real estate (CRE) has been at the center of turbulence in the alternative investment world. The combination of soaring interest rates, remote work disruption, and credit contraction hit the sector hard. Office assets lost their luster, cap rates ballooned, and transaction volume stalled. For many investors, CRE became synonymous with risk.

But markets are cyclical, and distress often sets the stage for opportunity. As of 2025, a growing cohort of sophisticated investors is rethinking CRE not as the problem child of alternatives, but as the most actionable opportunity in the space.

Why? Because while much of the alternative asset universe is only now starting to face real cracks, CRE has already repriced—and that makes it uniquely positioned for smart capital to step in.

A Fast and Furious Reset

The distress in commercial real estate wasn’t slow or subtle. It was fast, broad, and very public. Follow-

ing the pandemic-induced demand shifts and a historic surge in interest rates, CRE went through a structural repricing.

Lenders reined in leverage. Refinancing dried up. Office towers emptied out. Even multifamily and industrial—darlings of the pre-2022 cycle—faced valuation cuts as cap rates widened. Suddenly, asset owners were underwater on 2021-vintage deals and equity was wiped out in recap after recap.

But here’s the silver lining: this pain has already worked its way through a large portion of the system. CRE has already experienced a real market-clearing moment. Prices have corrected. Risk has been repriced. Opportunistic capital is returning to the table.

Compare that to other corners of the alternative landscape—where many assets are still marked to outdated valuations, and distress remains unrealized.

Delayed Distress in Other Alternatives

The private credit boom of the past few years may

be heading toward its first major test. Loans originated in 2021 and early 2022 were priced during a low-rate, high-growth environment. Today, many of those borrowers are struggling with debt service, and restructuring activity is picking up.

Venture capital faces a similar reckoning. As of 2025, many portfolios are sitting on markdowns, with flat or no exits. Yet fund-level NAVs often lag the reality on the ground. The illusion of stability masks what will likely be a challenging capital raising cycle for many emerging managers.

Even private equity is feeling the squeeze. Dry powder remains high, but deal activity has slowed, and exits are harder to come by. Multiple compression is real, and GPs are grappling with how to return capital on overvalued legacy assets.

Meanwhile, core infrastructure and real assets— long considered safe havens—are seeing pressure due to rising capital costs, permitting delays, and increased political risk. Once stable yield plays are now experiencing volatility.

In short, distress is a lagging condition in many

alt strategies, but in CRE, it’s already been priced in.

Real Estate’s Unique Characteristics

Unlike many alternatives, real estate has the benefit of being both a cash-flowing asset and a hard asset. That means it has multiple levers to drive value:

• Rental income

• Operational improvements

• Leverage and recapitalization

• Tax efficiency and depreciation

As valuations have reset and interest rates begin to stabilize, real estate investors are seeing cleaner entry points, more conservative underwriting, and genuine upside.

In particular, value-add and opportunistic strategies are gaining traction. Managers are targeting distressed assets, bridge lending opportunities, preferred equity positions, and even direct ownership in mismanaged or over-levered deals. The market is becoming more two-sided again, with willing sellers and data-driven buyers.

Where the Opportunities Are

Not all CRE sectors are created equal. Office remains challenged in many urban cores, but even within that asset class, there are bright spots: life sciences conversions, boutique urban repositioning, and Class A+ assets in high-barrier markets.

Multifamily is seeing renewed interest as rents stabilize and new supply slows. Industrial continues to benefit from supply chain reconfiguration and nearshoring. And hospitality, once thought to be the riskiest play, has roared back with travel and experiential spending returning in force.

Investors are also gravitating toward special situations: distressed debt, note purchases, loan-to-own strategies, and real estate-backed private credit. These strategies provide equity-like upside with credit-like protections.

Geographically, capital is flowing toward the Sun Belt, secondary metros, and regions with demographic tailwinds. Puerto Rico and the U.S. Virgin Islands have even drawn attention from real asset investors looking for tax advantages and yield.

A More Favorable Capital Stack

Another reason CRE is gaining momentum is that the capital stack has become more favorable for new entrants. Debt is more expensive, yes, but it’s also more rational. Banks and private lenders alike have pulled back, opening space for new credit players to step in with well-structured terms.

Preferred equity, mezzanine debt, and bridge loans are all seeing increased demand. For investors who know how to underwrite risk and structure protection, these instruments offer asymmetric return profiles.

Meanwhile, institutional capital—which once crowded into core real estate in gateway markets—is rethinking its approach. Many are shifting to private REITs, club deals, or manager-led co-investments that offer more control and flexibility.

LP Sentiment Is Turning

Perhaps most important, LPs are looking for

places to put capital to work. With other alternative strategies entering periods of uncertainty, real estate— particularly at the value-add and distressed end of the spectrum—is starting to look like a contrarian but logical allocation.

Several large pensions, endowments, and sovereign wealth funds have announced renewed interest in CRE, especially in segments that are demonstrably dislocated. Family offices are also re-engaging, attracted by the combination of income, appreciation potential, and tangible asset backing.

There is also a growing movement to pair CRE with impact or ESG mandates, particularly in affordable housing, adaptive reuse, and energy-efficient retrofits.

Risks Still Exist—But They’re Transparent

Of course, commercial real estate still carries risk. Some office markets may never fully recover. Construction costs remain high. And liquidity is still constrained compared to other asset classes.

But in CRE, these risks are known, priced, and often visible in a way that private equity mark-to-model or early-stage venture capital risk is not. That’s what makes CRE so attractive in this phase of the cycle: you can see the cracks, but you can also underwrite through them.

Conclusion: The Contrarian Opportunity

The best opportunities in alternatives often come from sectors others have written off. In 2020, that was credit. In 2021, it was growth equity. In 2025, it may be commercial real estate.

While other strategies brace for valuation resets and LP skepticism, CRE has already gone through the fire. What’s emerging now is a more disciplined, more transparent, and more actionable investment environment—one where smart capital can find attractive risk-adjusted returns.

For allocators and fund managers willing to lean into dislocation, CRE might not just be a comeback story.

It might be the most compelling alternative bet of

the next cycle.

Bonus: What to Watch in CRE for 2025–2026

• Refinancing Wall: Billions in maturing debt will either force recapitalizations, create buying opportunities for both properties and distressed paper

• Sun Belt vs. Gateway Repricing: Diverging performance will shape capital flows.

• Return of the Local Developer: Smaller operators with strong local knowledge are regaining an edge.

• Private Credit Synergy: CRE-focused credit strategies are offering hybrid returns with downside protection.

• New Structures: Look out for interval funds, NAV-based lines, and more co-investment structures appealing to institutional LPs.

CRE is a complex asset class, but for investors willing to do the work, the reward may be found in this moment of recalibration. Distress creates entry points—and right now, CRE is the rare alternative asset where the worst might already be behind us.

Nathan Whigham Founder and President EN Capital

EN Capital is a leading capital advisory firm specializing in debt and equity placement and capital stack structuring across multiple industries. The firm actively works on deals across the US, Caribbean and LATAM. EN Capital is led by Nathan Whigham who has been structuring and placing capital since 2006.

AUTOMATING FINANCIAL SERVICES WITH AI AGENTS

TOM BLAIR

iClerk

Accelerating Financial Processes

In the 19th century, William Jevons discovered something peculiar. He noticed that as steam engines became more efficient, coal consumption didn’t drop; people began to use more coal. This counterintuitive insight became known as Jevons’Paradox, and for economists and historians, it has become an academic trope. Put in the context of intelligent AI Agents, Jevon’s Paradox means that as tasks become drastically more efficient, organizations find more use cases to automate, unlocking new productivity and demand levels. When a task becomes cheaper, faster, and easier, we don’t stop doing it; we find a hundred new ways to do more. Agents make the work accessible to more people, who find new ways to use it.

The most profound aspect of these agent technologies is their ease of adoption; the ease of implementation is fast, often within 100 development hours for a custom agent. Agents can process transactional data and language data from virtually any system, in any format, and with minimal integration cost. Training staff is as each as a having a conversation with a colleague as these agentic systems leverage natural language interfaces, interactive charts, and automated reporting, and all in real-time. The overall effect is that on a global basis, agentic systems are transitioning from the 30 million programmers that are required today to unlock information value, beyond the 750 million spreadsheet users, to allowing billions of new people, and their ideas, to be unlocked.

In today’s technology environments, the task of moving data between SaaS-based business intelligence

(BI), customer relationship management (CRM), and spreadsheets requires predefined steps and a lot of smart labor. These systems are brittle and unable to adapt to the nuances and the one-off requests that occur in business. By contrast, AI Agents maintain context over time and across different data sources. Armed with persistent memory, Agents can recall context from prior interactions to inform future actions, using advanced reasoning to solve problems and handle exceptions rather than just following rigid rules. Crucially, they semantically integrate with existing software and data sources, indexing any databases, documents, voice, or video, but without the maintenance nightmare of human-maintained web scrapers, programmed spreadsheets, macros, CRM, or BI tools; the difference between a program that automates a calculation and an AI agent that can dynamically and accurately generate

an entire financial report.

Agent Autonomy: Role-based Agents

Agents operate just as human employees operate, according to pre-determined roles and in alignment with contractual obligations, corporate policies, or compliance rules. AI agents can process private information, anonymizing information without sharing it with the LLM providers, while simultaneously providing unfettered data access through interactive, language- based interfaces. Agents can reason through tasks like humans and provide accurate, secure, and repeatable information with traceable provenance.

AI Agents don’t just follow instructions, they learn, adapt, and connect across systems, and through this lens, we have observed three general classes of AI

Agents, each with a distinct role in how work gets done:

Knowledge Agents. Agents that aggregate a specific corpus of knowledge and serve as on- demand experts, curating and delivering information through interactive, graphs, charts, reports, or prompts. These agents can be deployed to access corporate information, databases of large documents, or dense financial contracts, and extract the required information and insights for customers or employees. A Knowledge Agent can make private, confidential information accessible, secure, and interactive.

Workflow Agents automate entire financial processes from start to finish with human checkpoints for quality and control. Agents can log into systems, perform multi-step workflows, and coordinate activities with one-click provenance, allowing professional staff to focus on what is strategic rather than having to manage the minutiae. Agents automate manual data and financial statement gathering, perform interactive scenario modeling and statutory reporting, and generate accurate, traceable KPIs.

Integration Agents serve as the connective tissue of a firm, linking disparate SaaS and manual systems and data into cohesive workflows. Many firms suffer from having numerous specialized tools that don’t communicate, and Integration Agents solve that by orchestrating any tasks on any data that require the integration of isolated systems. To monitor a finance database for reconciliation or to cross-check each against compliance rules, Integration Agents ensure quality, repeatable data collection, transformation, and transmission of critical business processes.

From Spreadsheets to Automation

Many firms outsource their back-office systems to offshore processing or rely on professional services-driven tools like SaaS, spreadsheets, email, and manual processes as the backbone of operations. These tools and the manual processes that drive them are error-prone, complex, and repetitive; no one likes this type of work. Today’s professionals spend dozens of hours monthly on routine administrative work instead of being able to focus on strategic initiatives.

Firms have long relied on stopgap measures like programmed macros or robotic process automation (RPA) tools to mitigate these issues. These handcranked tools cannot adapt to the change of daily business or the ambiguity and nuance of natural language requests. Last generation systems are adept at copying numbers from one system to another, but these systems do not understand context or meaning. A static, deterministic process will fail if a data format changes or an email template differ, a different paradigm from the cognitive reasoning abilities of AI Agents that can adapt, provide maintenance-free resilience, and the analytic flexibility necessary to support modern business processes.

Transforming Professional Services

Consider fund administration and accounting, a domain governed by statutory deadlines, islands of data, compliance policy, and lots of professional services. For example, calculating a fund’s Net Asset Value (NAV) at period-end requires gathering information from custodians, pricing various assets, reconciling transactions, and double-checking everything for compliance with valuation policies. Today, this is a painstaking process involving multiple analysts and layers of manual review and compliance steps. AI agents are streamlining these steps with Fund Administration Agents that can automatically extract data from statements and feeds, validate it against expected patterns, and perform reconciliation, all designed with quality control checkpoints that meet corporate policy requirements. AI-powered tools can ingest and cross- verify financial information from multiple sources, significantly reducing manual errors and speeding up NAV calculations and investor reporting. The finance team can generate accurate NAV reports in minutes and with traceable audit exception handling and provable results. While Agents handle the toil of reconciliation, humans can focus on the strategic aspects of the business.

Precision calculations with traceable citations, and explainable reasoning logic across chains of actions, are the key to Agents that process legal and finance documents, perform compliance actions, and ensuring regulatory compliance actions. Agents can deconstruct

complex contracts, generate searchable tags, and semantically understand the “meaning” of different passages, providing analysis in context to corporate policy objectives and allowing for easy comprehension through interactive, natural language interfaces. AI agents are tackling the mundane, repetitive, critical workflows, allowing firms to retain, not replace professionals, and perform more strategic and less tactical work.

The American Institute of CPAs reported that 75% of today’s public accounting CPAs will retire within the next 15 years. A limited supply of qualified professionals is compounded by increased compliance, reporting complexity, and costs to create an environment that mandates vast automation. AI agents can perform many of the tasks CPA’s, analysts, and other professional staff perform today, from collecting and cleaning data for analysis, to automating logic and inference and complex scenario modeling, allowing expensive staff to concentrate on higher-level strategy and client engagement.

As AI agents replace the tactical work that takes place in the back offices of finance, compliance, and advisory firms, the economics of professional services are being rewritten. What once relied on deep benches of junior staff and expensive, error-prone processes is now shifting to intelligent automation that is faster, cheaper, and auditable by design. The firms that adapt will not only survive the looming talent shortage and increasing industry complexity, but be able to leverage the increased capacity and more efficiency staff while gaining competitive edge. The transformation is not about replacing professionals, but arming them with intelligent collaborators.

Strategic Benefits: Efficiency, Speed, and Accuracy

The strategic advantages of deploying AI Agents in professional services revolve around the operational efficiency gains, the speed of business execution, improved accuracy, labor and inference cost control, and the ease of adoption resulting from using these technologies.

When an autonomous agent can handle a task end-to-end, a firm can reallocate human effort to more strategic work. With AI Agents, a task that might cost thousands of dollars in staff time per quarter can be rep-

licated for a fraction of that cost of the SaaS subscriptions and professional services labor expenses currently employed. This isn’t about replacing professionals, but about a process optimization of current business practices, to benefit the staff and helping them amplify their productivity.

With efficiency gains comes improvement in speed of business execution. Agents can operate in real time or on pre-set schedules and are able to provide alerts and reminders for your custom business processes. Whether for regulatory filings, LP reporting, K1 generation, or Agents that help you perform financial and technical due diligence, AI Agents can dramatically accelerate cycle times, providing real-time, interactive interfaces that allow you easy, logical access to all your data, all the time.

Humans make errors and so do language models. The difference is that AI Agents can be designed so they don’t make errors and provide improved accuracy. By automating the tedious data transfers, calculations, and document cross-checks, AI agents help mitigate mistakes by using both deterministic and non-deterministic models, meaning the AI Agents can process both numerical and language data with auditable accuracy and source data traceability. A well- designed agent will perform a task the same way every time, or flag an exception if something doesn’t match expected parameters. This consistency is invaluable in compliance and accounting workflows, where an oversight can result in regulatory fines or financial losses.

There are two important factors in determining the cost to deploy an Agent, labor expenses and the cost of inference. In the United States, a professional makes an average of ~$100k annually, nearly $200k with full expense load. An Agent designed to perform 40% of the same tasks as an experienced analyst performs, can be performed with an AI Agent for under $1k per month, a fraction of the current cost to perform the task.

AI Agents not only perform work for less, but they also help businesses control the cost variability and exposure of changing technology. Deep reasoning models offered by LLM vendors allow AI Agents to think through problems the way a human, reasons through a problem. For enterprise firms, the fact these models can generate an unpredictable number of tokens, the unit

of cost accounting in language models, results in an exposure to runaway inference costs. It is akin to roaming Europe with your phone and receiving a large phone bill upon your return. This is particularly important in fund administration, where profit margins can be thin, and shaving off a substantial portion of manual effort to minimize labor cost and while controlling inference costs, translates directly into savings.

AI Agents reason across your private data the same way a professional would, looking for patterns in data, early warnings of issues, or opportunities, allowing professionals to make smarter decisions, faster. Agents don’t just cut costs, they are tools of re-engineering, allowing firms to rethink how they surface patterns and insights from the deluge of information. Agents automate 90% of the work for about 10% of the current cost, providing speed, greater accuracy, and accessibility beyond what is currently available. However, the most compelling AI Agent feature is fast deployment, the ability to rapidly develop custom workflows and deploy to staff, usually within one calendar quarter.

Broader Implications

The advent of AI Agents in financial services brings transformative implications not just for efficiency and profit, but also for people and society. Foremost is the elevation of human roles.

As machines assume the mundane and repetitive work, professionals can shift toward more analytical, strategic, and interpersonal responsibilities. This won’t happen comprehensively, but gradually, one agent at a time. This is one of the factors driving AI Agent adoption; each Agent automates a single workflow, which is one logical unit of work, and the entire firm doesn’t need to “adopt AI”, just to automate one workflow at a time. Over time, through use, and acclimation to the technology, firms often find more and more workflows to automate. This is the way Jevons’ Paradox will play out: tasks will become more efficient, organizations will find more use cases, which will unlock new productivity demand levels. Rinse and repeat.

These changes will herald a new age of advisory work where instead of junior analysts burning the midnight oil updating spreadsheets, poring through large documents, or grinding through bank statement rec-

onciliations, they can focus on interpreting results and learning to think like investors or strategists earlier in their careers. GPs, investors, partners, and accountants will have more bandwidth to be proactive advisors, spoong issues before they become problems rather than spending all their time reacting to problems. In essence, work becomes more about thinking and communicating and less about processing, and with a positive social impact. Jobs become more satisfying and creative, human talent is better utilized, and firm retention increases. We have seen these Agents change people’s lives for the better. As Agent adoption permeates the financial industry, firms must apply the same standards, roles, and constraints as any new team member, requiring upfront guidance, monitoring, and clear ethical direction.

As AI Agents make financial processes cheaper, faster, and more accurate, demand for automated workflows will continue to surge, unlocking entirely new use cases across professional services and reshaping how firms manage labor, compliance, and data, at scale. In a world of rising complexity and shrinking margins, AI agents aren’t replacing professionals, they’re elevating them. Firms that leverage these amazing technologies will succeed beyond competitors that do not, resulting in a reimagining of how work gets done.

To learn more about iClerk AI Agents, contact Tom Blair - tom@iclerk.ai

Tom Blair CEO iClerk

AI

iClerk AI is an enterprise platform that deploys accurate, repeatable, and traceable AI Agents to automate complex, labor-intensive, yet critical financial and accounting

IS YOUR FIRM AT RISK? INSURANCE ESSENTIALS FOR

ALTERNATIVE ASSET MANAGERS

MATHEW KRYDER Petschauer Insurance

Managers who treat insurance as a commodity may be jeopardizing their company’s future. Purchasing decisions driven by price with little regard to the insurance contract lend themselves to significant coverage gaps, unnecessarily exposing the firm and its investors to an irrevocable financial loss. Alternative asset managers are especially vulnerable to such gaps due to the unique financial exposures they face. “Off the shelf” insurance policies often fail to adequately cover their operations and the managers who purchase them may be taking on more risk than they realize.

Insurance policies are highly differentiated contracts and insurance carriers specializing in financial services risks have created programs tailored to meet the unique needs of the asset management industry. Managers interested in proper risk transfer should partner with an experienced insurance broker with access to these programs to secure the coverage they need to protect themselves and their stakeholders.

This article takes a closer look at some of the unique financial exposures and rising trends faced by the asset management industry. We also detail the essential insurance coverages needed for an effective risk transfer program while highlighting the coverage gaps to be avoided.

Fund Management & Investment Advisor Exposures

In today’s volatile marketplace and rising government regulation, alternative asset managers face a variety of adverse exposures. Interactions with regulators, shareholders, investors, vendors, creditors and employees can lead to costly litigation. These risks threaten the bottom line and the reputation of your fund and its managing partners. For example, a fund assumes vicarious liability for the actions of its outside service providers. If an error is made in misstating performance or in the financials, the fund will bear the responsibility. Even well-managed operations can be sued for misman-

agement, misrepresentations, employment practices violations, breach of duty, and failure to provide adequate disclosure of the investment risks involved.

Management Liability Insurance

The primary purpose of the Management Liability policy is to pay for defense costs. If a lawsuit is brought against the management entity, the fund’s assets are used to indemnify the fund manager. Management Liability insurance would prevent a fund from needing to liquidate positions or use cash to pay for defense costs. The insurance limit should correlate to the assets under management (AUM), however, this limit typically covers a minimal portion of AUM. It is important to remember that Management Liability is designed to pay defense costs for a mistake, not indemnify the loss of tens of millions of dollars of trading losses. The policy would be prohibitively expensive if it covered the fund’s assets. Management Liability provides an extra degree of security and comfort to your current investors and serves as an excellent selling point to your potential investors.

Examples of Management Liability Gaps

Many fund managers attempt to cover these risks with a traditional Directors and Officers Liability (D&O) policy. D&O alone, however, does not provide adequate protection for a fund. Because a fund manager also serves as an investment advisor to its investors, it may be impossible to determine whether a claim results from professional advice, which is not covered by a traditional D&O Policy. D&O and Professional (a.k.a. ‘Errors and Omissions’) Liability are written together in a Management Liability policy to protect against these risks.

Another common gap is that specific operations may be overlooked when writing the Management Liability policy. For example, if the funds themselves are not listed as the Named Insured on the policy, then the funds are exposed if a lawsuit is brought against the manager and the funds.

Another example of an overlooked operation is the management of ERISA plans. If the firm manages funds for employer sponsored plans such as pensions and 401(k) plans, then they have a fiduciary exposure and Fiduciary Liability coverage should be included.

Fiduciary Liability provides protection for breaches of fiduciary duty by administrators of Employee Benefit Plans. These policies usually include coverage for Errors & Omissions. Unlike the ERISA or fidelity bond, Fiduciary Liability coverage provides liability protection for the fiduciary.

Fund managers serving on outside boards can also expose the fund to decisions made or advice given by these managers. An “Outside Directorship Liability” Endorsement should be added to provide additional protection in connection with outside boards on which they serve. This coverage is especially critical for private capital managers who sit on the boards of their portfolio firms.

Employee Related Exposures

Hiring the right talent is critical to the success of any firm. However, managers need to be aware of the additional risks associated with managing employees, including employee theft and lawsuits stemming from the administration of employee benefits. Managers are especially vulnerable to employee discrimination and harassment suits which can quickly spiral into significant losses for employers. According to the Equal Employment Opportunity Commission (EEOC), the average cost of settling out of court for employment related cases was $75,000 and jury awards averaged $217,000 in 2020. More than half of EEOC claims filed in 2020 involved claims of retaliation.

Employment Practices Liability Insurance

If you have employees, your firm should secure Employment Practices Liability coverage which provides for the legal costs to defend claims involving sexual harassment, wrongful termination, and discrimination including legal liability for such acts. It also covers discrimination suits brought by candidates you chose not to hire. This coverage is also known by various titles: Employment Related Practices Liability, Management Risk Protection, Employers E&O, and Americans with Disabilities Act Insurance which are all basically the same coverage.

Crime Insurance and Financial Institution Bond

A Crime policy and a Financial Institution Bond cover losses stemming from theft of money and securi-

ties, including theft of your firm’s assets by an employee. Managers will want to make sure investors’ assets are covered under this policy as well.

Employee Benefits Liability insurance

Are you providing employee benefits to attract and retain talent? Then you’ll need an Employee Benefits Liability policy which provides protection against claims made by employees caused by a negligent act, error, or omission in the administration of an Employee Benefit Plan. Incidents such as providing incorrect advice concerning an employee’s health insurance plan or failure to enroll employees under a benefit program are covered.

ERISA Bond

An ERISA (Employee Retirement Income Secu-

rity Act) Bond is a fidelity bond that protects against dishonest and/or fraudulent acts of employees or trustees that could arise in the course of maintaining an Employee Retirement Plan. The ERISA Act requires employers to maintain a bond in the amount of at least 10% of the retirement plan assets.

Cyber Risks