Global mVAS use explodes past $1bn, driven by better networks, better billing and consumer demand

The global mobile value-added service (mVAS) market is estimated to be worth US$880.4m in 2024 and is likely to grow at a 14.9% CAGR through 2034. The market is expected to surpass a valuation of US$3.5bn by 2034.

According to data from FactMR, technological advancements including virtual reality (VR), augmented reality (AR) and high-definition video streaming are also critical for growing the market, says the study, while enhanced connectivity is enabling businesses – in both mature and emerging markets – to develop and offer better and more interactive mVAS offerings that elevate user experiences, which in turn is also driving use. The increasing use of mVAS by enterprises

to streamline communication with clients and customers is also propelling market growth (see panel on page 3).

The key verticals driving this surge of VAS are what any visitor to World Telemedia or regular reader of this magazine would expect (see chart). Media and entertainment (see page 35) leads the way, but there is growing inter

How cybercrime and fraud is changing

Why edutainment is the content du jour

Julia Dimambro, CEO and founder, Seriously Fresh

spend to hit

in

Carrier billing (DCB) is having a moment: the German market is seeing it rolled out for bus ticketing – in conjunction with RCS – and even the mighty Deutsche Telekom is offering it in its online store as a payment agent for DIMOCO. Globally, too, DCB has exploded – and its rise is set to continue.

Florencia Torres, senior account manager, Mobidea

Opening

THE BIG GUY Paul Skeldon

paul@telemedia-news.com

ART DIRECTOR Victoria Wren

victoria@wr3n.com

CONTRIBUTORS & CONSULTANTS

SALES & MARKETING

info@Telemedia-news.com

PRODUCTION DIRECTOR Annika Micheli

annika@Telemedia-news.com

PUBLISHER

jarvis@Telemedia-news.com

Come together: the continuing mainstream shift of telemedia

World Telemedia Marbella is a great focal point for the industry to take stock of where it has got to in the year just gone and to set itself up for growth and glory in the year to come – and 2024 is no exception.

As this issue of Telemedia magazine attests, much has happened in the past 12 months in the industry – much of what you read in this issue has happened in the past 12 weeks! – and paints an interesting picture of an industry that is bringing together a raft of once disparate business strands into a whole pipeline of innovation.

Take for example what is happening with DCB. The news that Vodafone Germany, DIMOCO Payments and HORISEN (see

Global mVAS

est in education and edutainment services (see page 22).

However, less ‘fun’ services are also becoming money-spinners for VAS players across the globe. Healthcare is increasingly relying on digital channels and this is creating a new market in VAS. Similarly, government and state services are also turning to mVAS platforms to reach the widest possible audience.

THE GLOBAL MARKET

East Asia is projected to account for a share of 36.5% in 2024. By 2034, the region is anticipated to acquire a market share of 38.4%. The regional market value is expected to reach US$1.35bn by 2034. North America’s market is estimated to attain a value of US$1.02bn by 2034. The region is projected to be led by the US. Underexploited countries such as South Korea and Mexico are also forecast to show a high

adoption rate for mobile valueadded services. Leading players can focus on their expansion efforts in these economies.

COMPETITIVE LANDSCAPE

Leading market players are emphasising the development of compact and cost-effective mobile value-added services to gain more customers. Furthermore,

page 1) have teamed up to deliver a mobile bus ticketing service that uses carrier billing via RCS is perhaps the biggest example of this.

But it doesn’t stop there. Also on page 1 we see how mVAS services are exploding globally, driven by tech innovation and a consumer hunger for content and services. Where once it was sport and entertainment only, now we are seeing more around Edutainment (page 22), ecommerce and loyalty programmes (page 25) as well. It is becoming a broad mix.

Marketing these services – generating traffic, as we like to think of it – has also rapidly shifted its focus. Google, unsurprisingly, dominates, but with its RDAs under scrutiny (page 18) many

active players in the mobile value-added service market are attempting to attract additional customers.

In addition to this, leading players in the market are focusing on inorganic growth strategies like strategic mergers and acquisitions, and collaborations with technology partners to enhance their offerings and reach.

FROM THE EDITOR

are looking at alternative channels to get their message out there. Connected TV – Netflix et al – being the prime candidates (page 16).

This surging interest in VAS is also driving increased use of that old stalwart of the telemedia sector IPRS (page 28), which has rehabilitated itself and now, thanks to advances in cyber security across VAS and DCB (page 20), is booming.

But the key is that it is all now working together to create a wonderful world of telemedia that is now established in the mainstream and is set to go from strength to strength – just as World Telemedia Marbella’s stellar growth shows.

telemediaonline.co.uk @telemediaTweets

In 2023, Google unveiled a new range of AI-powered features in its translation application at its Paris virtual event. These new features consist of more contextual translation options with examples and descriptions, an AR translation feature via Google Lens, and a redesigned app for Apple’s iOS operating system.

VALUE ADDED SERVICES

Paul Skeldon. editor

Global mVAS

Deutsche Telekom, Ericsson and Samsung, in June 2021 successfully executed a 5G end-toend (E2E) network slicing pilot. This trial was conducted on Samsung S21 commercial equipment, which is combined with Virtual Reality headset at Bonn lab of Deutsche Telekom.

The network provider’s market share is poised to ascend, projected to increase from 62.9% in 2024 to 63.3% by 2034, with an impressive Compound Annual Growth Rate (CAGR) of 14.9%. The segment is forecasted to achieve a substantial market valuation of US$2.2bn by 2034.

This growth is fuelled by the escalating adoption of mVAS by network providers, leveraging it to fortify customer relationships, reduce acquisition costs and mitigate customer churn rates, contributing significantly to the segment’s expansion.

PLATFORMS TO DOMINATE

The surge in interest in mVAS has seen service offerings morph into companies offering sophisticated VAS platforms that offer more than just a content or service type, but increasingly bring together a range of functions across delivery, content, data management and marketing.

VAS platforms typically operate on a subscription-based model, where customers can subscribe to various services and pay a recurring fee. Key components of a VAS platform include content and service aggregation; billing and payments – especially DCB and alt.payments –content delivery and management, as well as analytics and reporting to help hone and create new VAS offerings.

MVAS IN MENA

mVAS platforms have emerged as a pivotal force in the telemedia and telecoms landscape, particularly in the Middle East and North Africa (MENA) region. These

platforms offer a suite of services that enhance the customer experience, drive revenue, and foster innovation.

As the region continues to experience rapid digital transformation, VAS platforms are playing a crucial role in meeting the evolving needs of consumers and businesses.

Across the MENA region, mVAS platforms deliver a range of advantages for both consumers and business.

For instance, VAS platforms enable telecom operators to provide a more personalised and engaging customer experience. By offering a wide range of services, such as music streaming, gaming, and mobile payments, operators can cater to diverse customer preferences and improve customer loyalty. These platforms also offer a significant opportunity for telecom operators to generate additional revenue streams beyond traditional voice and data services. By partnering with content providers and service providers, operators can offer premium content and services to their customers, generating incremental revenue.

Additionally, VAS platforms can help telecom operators differentiate themselves from competitors and stay ahead of the curve. By investing in innovative VAS offerings, operators can attract new customers, retain existing ones, and position themselves as leaders in the market.

There are several increasingly prominent mVAS platform companies seeking to grow the MENA market, with several big names familiar to anyone who attends World Telemedia.

For example, Golden Goose offers a wide range of services, including mobile gaming, music streaming, and content delivery. MobiMind is another major player in the MENA VAS market, specialising in mobile content and applications. MobiBox, meanwhile, provides VAS solu-

tions to telecom operators and content providers, focusing on mobile gaming and entertainment.

FUTURE TRENDS IN VAS

The VAS market in MENA is a rapidly evolving landscape, part playing catch up with the more developed markets in Europe and parts of Asia and in part driven by the MENA region rapidly finding its own way with creating services and offerings specific to its customer base.

And this evolution is being driven forward, in the short term at least, by a range of technology advances. Key is the rollout of 5G networks and the growth of the Internet of Things (IoT). This is set to create new opportunities for VAS platforms. Services such as connected cars, smart homes and augmented reality will require innovative VAS solutions.

Similarly, AI and machine learning can be used to personalise VAS offerings, improve customer engagement, and detect fraud, while a shift towards more cloud-based VAS platforms – in part propelled by 5G roll out – can offer scalability, flexibility, and cost-effectiveness, making them attractive to telecom operators.

In conclusion, VAS platforms have become an indispensable component of the telemedia and telecoms landscape in the MENA region. By offering a wide range of services, enhancing customer experience, and driving revenue, these platforms are playing a crucial role in the digital transformation of the region.

As the market continues to evolve, VAS platforms will likely play an even more significant role in shaping the future of telecommunications.

Enterprise mVAS on the rise

Mobile Value-Added Services (mVAS) have become an integral part of enterprise strategies, providing innovative solutions to enhance customer engagement, drive revenue, and streamline operations. Typically, this is being seen in:

• Customer engagement: Enterprises are using mVAS to create personalized and interactive customer experiences.For instance, loyalty programs, mobile ticketing, and interactive campaigns can be implemented through mVAS platforms, fostering stronger customer relationships.

• Marketing and promotions: mVAS offers a powerful channel for targeted marketing campaigns. Enterprises can send personalized offers, promotions, and notifications directly to customers’ mobile devices, increasing the effectiveness of their marketing efforts.

• Payment solutions: Mobile payments, such as mobile wallets and QR code scanning, have gained significant traction. Enterprises are integrating these mVAS solutions to provide convenient and secure payment options for their customers.

• Enterprise mobility: mVAS can be used to enable enterprise mobility, allowing employees to access corporate data and applications on their mobile devices. This enhances productivity and flexibility for remote workforces.

• IoT integration: mVAS platforms can be integrated with IoT devices to provide additional services and functionalities. For example, enterprises can offer remote monitoring, asset tracking, and smart home solutions through mVAS. By leveraging mVAS, enterprises can unlock new revenue streams, improve customer satisfaction, and gain a competitive edge in the digital age.

A KARAOKE

VAS in a shifting landscape

Fresh leadership across Europe collides with China’s VAS market opening. Will this spark innovation or a land grab by Chinese giants? Changing regulations, investment tides and data privacy concerns are all up for grabs, so what is the future of Europe’s lucrative value-added services sector, asks Paul Skeldon?

The old Chinese curse warns “may you live in interesting times’ and this Summer’s wave of European governmental changes – particularly in France and the UK – has brought that to the VAS market.

The changes in Europe coincids with a pivotal moment in China, where its VAS sector has recently been liberalised. Brace for impact.

In case you didn’t know, telecom VAS encompasses a wide range of non-core services offered on top of basic connectivity. This includes mobile payments, streaming platforms, cloud storage, gaming and a multitude of other applications. VAS has become a significant revenue driver for telecom operators, offering higher margins compared to traditional voice and data plans.

European governments have historically maintained varying degrees of control over the telecom sector. Some have fostered competition by promoting multiple service providers, while others have allowed dominant national carriers to hold significant sway. This fragmentation has created a complex environment for VAS development.

The new governments across Europe may have different priorities regarding the telecom

industry. Some might favour increased competition and innovation, while others might prioritise infrastructure development or network security. These varying visions will influence regulations that affect VAS providers and their ability to thrive.

THREE EUROPEAN IMPACTS

Typically, there are three key areas of impact. Firstly, governments advocating for a more competitive environment might introduce policies that break dominant player monopolies and encourage new entrants. This could attract foreign investment, especially with China’s recent liberalisation, potentially leading to a surge in innovation and VAS offerings for European users (see below).

Governments across Europe, if not the world, are also prioritising data security and new political will might impose stricter regulations on VAS providers, particularly those handling sensitive user data. Balancing user privacy with innovation will be crucial to ensure a healthy environment for VAS development. Finally, there is infrastructure investment. Governments keen on accelerating digital transformation might prioritise investment in fibre optic networks and 5G infrastructure. This

would not only improve core connectivity but also create a faster and more reliable platform for developing and delivering advanced VAS services.

CHINA’S VAS REFORMS: A DOUBLE-EDGED SWORD?

China’s decision to open its VAS sector to foreign investment presents a double-edged sword for European players.

On the one hand there are a number of interesting opportunities. For example, European VAS providers may forge strategic partnerships with Chinese firms, leveraging China’s vast user base and expertise in certain areas like mobile payments. This could expand their reach and create new revenue streams. Access to Chinese innovations in AI, blockchain and other technologies could also fuel the development of novel and advanced VAS offerings for European markets.

But there are challenges too. Chinese VAS giants, with their vast resources and experience, could pose a significant threat to established European players. This could lead to price wars and consolidation within the European VAS market.

And of course there are the ever-present data security concerns. European governments might be wary of allowing Chi-

nese VAS companies access to sensitive user data, potentially hindering collaborations and market entry for Chinese firms.

NAVIGATING THE NEW LANDSCAPE

Either way, European VAS providers will need to adapt to this evolving environment, maybe not in 2024, but certainly in the years ahead. To do this the telemedia sector needs to up its game. VAS providers need to identify their unique selling points and cater to specific market niches. This could involve specialising in areas like cybersecurity solutions or augmented reality applications. We are already starting to see this happening, but it is going to have to be the norm.

Meanwhile, the VAS sector needs to embrace openness and collaboration. Strategic partnerships with players across Europe and beyond can enable access to new technologies and markets.

And, of course, there needs to be a prioritization of data security and transparency. Building trust with users regarding data handling practices will be paramount in the current climate.

The recent governmental changes in Europe and China’s VAS reforms create a dynamic new environment for the European telecom industry. By navigating the complex interplay of competition, regulation and technological advancement, European VAS providers can seize the opportunities that lie ahead. Their success will depend on their ability to adapt, collaborate and prioritise innovation while ensuring user privacy.

BILLING & PAYMENTS

DCB spend hits $78.5bn

Data from Juniper Research shows that the global DCB market is set to be worth $78.5bn in 2024, rising a staggering 55% to $122bn in just three years’ time – double what it was worth in 2022. This will be driven by the 1.65bn users seen worldwide in 2024 rising to 1.8bn in the same time frame.

WHERE IN THE WORLD

The main driver for this growth continues to come from developing markets across MENA. Currently there are some 742mn DCB users in the region, set to hit 803mn by 2027, according to Statista. Here the explosion in the digital economy and a love of mVAS among a population that has very low bank account and card penetration has seen DCB rise to become a key payment tool.

A similar picture is being seen in the Indian subcontinent, which while not as big a market for DCB as MENA (yet), is set to see the fastest and largest growth in the next three years, logging a projected 37.7% CAGR on spend compared to 37.3% in MENA.

A rise in ecommerce across both India and MENA is also set to drive up DCB – and other alt. payment – spends in the coming years. Global ecommerce transactions could reach $11.4trn by 2029 – up from $7trn in 2024 – driven

by the adoption of ecommerce across emerging markets, finds Juniper Research. In these regions, it will be Alternative Payment Methods (APMs) that enable consumers in non-cardcentric markets to purchase online for the first time – and much of this to start with will be driven by DCB.

However, carrier billing isn’t just a payment tool popular in developing and evolving markets, they are also seeing a surge in use across more developed markets. This has been especially true of Germany. As we shall come to, the German DCB market is one of the most advanced in the world, leveraging new payment models and tying up with other tech such as RCS rich messaging to create some new and very interesting business models.

WHAT IN THE WORLD

Before we get to that, however, it is worth looking at what DCB is being used to buy. It comes as no surprise that digital games are, and will continue to be, the most important segment in the DCB market, with an estimation to reach $40.8bn of spend in 2027.

DCB and RCS join forces in Germany

Vodafone Germany is working with messaging company HORISEN and leading billing company DIMOCO Payments to roll out the firstever public transportation ticketing concept using RCS (Rich Communication Services) and DCB (Direct Carrier Billing) in Germany. Powered by HORISEN’s Business Messenger Platform, the solution allows users to book public transportation tickets and pay directly through their phone bill – all this inside an RCS dialogue.

The process is quite simple: the user just scans the QR code at the bus stop, choose a tariff, selects carrier billing, and enjoys the ride, making public transport more accessible and convenient than ever.

The initiative is part of Vodafone Germany’s UPLIFT project, dedicated to exploring new innovation partnerships. By focusing on future topics like sustainability, data analytics and AI. Vodafone UPLIFT connects innovators with the resources and expertise needed to bring market-ready solutions to life.

Due to the enormous popularity of mobile gaming worldwide and the fact that carrier billing is particularly well suited to facilitate payments in this vertical, digital games will continue to push the rise of DCB.

However, the way in which DCB is finding new outlets in developed markets is also going to be a strong driver of growth. According to Juniper Research’s report, ticketing will be the fastest growing segment from 2024 to 2027. With Mobility as a key driver of this growth, ticketing will be one of the drivers of the evolution of the market.

Currently, the largest market worldwide for ticketing is North America, with tickets for events and travel tickets as a key opportunity for Carrier Billing, together with the digitisation of all tickets. However, Germany is perhaps at the forefront of developments in the this area, with Vodafone Germany teaming up with DIMOCO Payments and messaging company HORISEN to create the world’s first RCS powered bus ticketing system (see panel).

In the same line, physical goods will also be a segment to watch out in the coming years in

the DCB market, as they will account for 21% of the global spend by 2027 ($25.4 billion).

In the physical goods vertical, in regions such as Europe, being compliant with the PSD2 regulation is a must in order to be able to manage these transactions.

Already DIMOCO Payments is providing carrier billing (DCB) services to operator Telekom’s online shop in collaboration with Brodos, strengthening its partnership with Telekom and leveraging the Agent Model that has tempted DCB into being used much more widely.

With the DIMOCO Payments Agent Model, Telekom and Brodos can accept carrier billing payments for physical goods. This next step will allow customers to make friction-free purchases on a wide range of white goods and other products.

The Agent Model is a setup that allows MNOs to facilitate payments on behalf of consumers. It allows for greater flexibility and scalability in carrier billing, catering to a wider range of payment needs in today’s market. Under the Agent Model, DIMOCO payments has the financial license and pays strict adherence to legal frameworks like PSD2 to ensure compliance and security.

Smart payments mean smart business

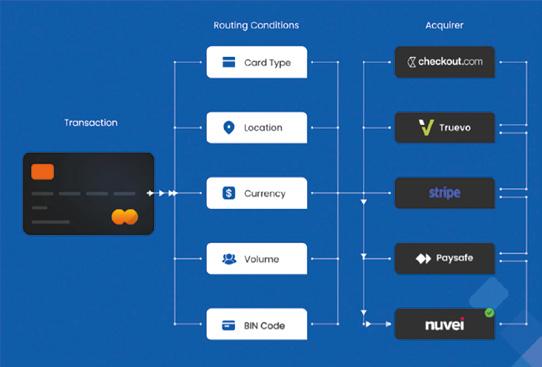

While carrier billing is going from strength to strength, many merchants are looking at adding other forms of payments too – but it can he hard work. Paul Skeldon meets the people lightening that load

Direct carrier billing (DCB) continues to be one of the best ways to monetise telemedia content. Indeed, it has gone from strength to strength in recent years, driven by the growth of the digital economy and the exploding mVAS market (see page 1).

But it comes with challenges. Regulations, transaction caps and an inability to support crossborder payments are all factors that make DCB somewhat selflimiting. It’s a great way to pay, but many merchants – especially those looking to grow revenues, expand in new markets or offer subscriptions services – it needs a little help.

“There are three kinds of merchants out there,” says Nick Dobson, chief revenue officer at Celeris, a company that man-

A case in point

ages and orchestrates payments for merchants and acquirers.

“There are those that are DCB only, but want to expand what they can sell and where; there are those that already augment DCB with credit card, Apple Pay and Google Pay, but want to do more; and there are those that have tried to add these alt. payments, but have struggled to make it work. Our aim is to help these players better manage credit card and alt.payments as an addition to their DCB payments,” he adds.

CHANGING TIMES

The number of consumers using digital services and payments is rapidly increasing, with the latest white paper from Celeris suggesting that where it stood

A well-known mobile games company using DCB for all transactions hit a wall at $100,000, facing issues such as payment delays, high carrier fees and transaction caps, limiting growth.

The company wanted to explore other payment options, but lacked guidance and connections for moving to credit cards and digital wallets and were unsure if the cost and effort would be worth it. So, it decided to test new payment options on a new product it was about to launch.

Celeris played a key role in helping the company transition. Using its extensive network, it introduced the firm to essential industry partners, ensuring smooth onboarding with acquirers. They also connected it with top-notch chargeback and fraud prevention solutions, addressing security concerns. Celeris provided its award-winning Orchestration platform, packed with features to improve transaction success rates and streamline payment processing.

With Celeris’ help, the company expanded its payment options to include credit cards and digital wallets. This boosted its confidence in payment processes, leading to an increased marketing budget. It soon rolled out the new payment options across all its products, seeing a significant revenue increase in just one month.

at 51% of consumers in 2021, it grew in just one year to 62%, as global average. In developed markets it is even higher, with some 90% of US consumers using some form of online payments.

However, at the same time cross border payments are also growing – raking in some $150trn in 2022.

Together, these face many merchants with a dilemma? How to grow their digital sales against a backdrop of DCB that is limited, especially when it comes to looking to sell services and content cross-border.

MANAGING ALT.PAYMENTS

For many merchants, the answer lies in adding other payment channels – typically credit card, Apple Pay and Google Pay. But managing these other payment channels can be hard work.

“Integrating new payment channels means managing relationships with acquirers, currency exchange – for cross border – security and working

within the rules of any given region or jurisdiction,” says Dobson. “Managing flows, chargebacks dn the tech needed is a challenge for many.”

And this is what Celeris aims to offer: a one-stop-shop for merchants looking to add in all these other payment channels – as well as managing subscriptions – as seamlessly as possible.

The company offers intelligent routing and optimisation that increases success rates and reduces costs, enhanced security and fraud prevention using tokenisation and, perhaps more importantly, managing the complexity of subscriptions.

Many merchants using DCB are particularly interested in enhancing their recurring revenue streams with subscription solutions. Celeris offers tailored subscription management tools to effectively meet this need.

“Our recurring payments feature streamlines the process, providing a seamless experience for customers,” explains Dobson. “We also offer zero authorisation solutions, enabling more customers to sign up for free trials without any initial charges. This reduces barriers to entry and increases the likelihood of customers accepting subscriptions, as they don’t need to pay anything upfront.”

Find out more at celerispay.com

Download the latest white paper at celerispay.com

Taking biscuit?the

Google has pulled the plug on blocking cookies, throwing the world of advertising, marketing and media into confusion. So, wonders Paul Skeldon. what happens now?

Google has announced that, after four years, it is abandoning its plan to axe third-party cookies from Chrome, instead offering users the ability to turn cookies off if they want to at the browser level.

The move brings to an end Privacy Sandbox, the project Google set up to end the use of cookies that gather third party user info as people surf the web, a volte face brought about after Google says time spent “considering the impact of the changes on publishers, advertisers and everyone involved in online advertising”.

of this announcement on the broader ecosystem.

vice president of global creative, media and ecosystem at Kantar, told CNBC. “Without third-party cookies, website owners were struggling to figure out how to monetise their audiences and this is one of the reasons there’s been such an increase in gated or paywalled content in recent years.”

Ironically, certain media publishers could even begin to drop content, paywalls, Silvers adds.

commerce media is pointing to it taking a hit from the nondemise of cookies, however some think that it will be boom to brands all round.

However, IAB Europe emphasises the following key considerations that should be addressed in any alternative approach implemented in Chrome: Firstly, user controls in relation to the setting of cookies and processing of personal data for advertising purposes are already the object of industrywide standards that draw on the detailed requirements laid down in the GDPR and ePrivacy Directive. These standards take account of the fact that browser-level user choices cannot enable the establishment of informed and specific consent under GDPR. It is unclear what value the addition of a supplementary choice layer, with the attendant risk of introducing a fragmented user experience, would deliver.

So, what does it mean for the internet and all of us who use it to make a living?

IMPACT ON ADVERTISERS

The bigger implication will be for advertisers. They will continue to be able to gather data on web users and continue to tailor experiences to those users.

Many argue that cookies actually make the web better. While ads can be annoying, the fact that the ads that do pop up are, in theory, of some relevance to each user, does make the web experience more pleasant – at least in the sense that without them it would be horrendous barrage or random ads bombarding users.

IMPACT ON MEDIA

“The number one impact is the internet is going to remain free,” Steve Silvers, executive

This could have an impact on telemedia billing companies and DCB providers, as they have built businesses around micropayments for access to paywall content.

IMPACT ON COMMERCE

The impact of the move on advertising is likely to have a profound impact on commerce, with many merchants able to rely on access to third party data targeted ads and so better click through rates.

However, it may also hit the nascent commerce media market, where merchants and retailers have done much to leverage their first party data to sell advertising space on their websites to brands seeking to target those users. This nascent business could well be dented by the resurrection of cookies as many brands won’t see the need to reinvent the wheel.

The mood music around

Dimitrios Koromilas, Director of Platform Services, EMEA, at Acxiom, says: “Even with Google’s latest decision on cookies, first-party data remains the new currency across the enterprise, not just for the marketing department. Gathering information to create a holistic view of your customer base, which can only be done with first-party data, is pivotal in helping businesses stand out from an increasingly competitive crowd.”

WHAT LIES AHEAD?

The big question is what happens next? Europe’s Internet Advertising Board (IAB) has been quick to point out that, while ending the ending of cookies is probably welcome, the detail lies in what comes after.

Given the lack of detailed information on the user choice functionality that Google proposes to introduce instead of deprecating third-party cookies, it is currently challenging to fully assess the implications

Secondly, it would seem likely that such an approach would entail the same prejudice to publishers as Apple’s ATT, which is currently the object of antitrust scrutiny in several EU jurisdictions. The manner in which controls connected to the availability of third-party cookies will be presented to end-users and articulated with the existing controls already provided for the Privacy Sandbox APIs will be of particular importance to evaluate the impact on competition.

Finally, IAB says it would call on Google to ensure that the development is done in close collaboration with industry standard-setting organisations and takes good account of industry feedback, even as it continues to refine and improve the Sandbox tools. In this connection, it is relevant to acknowledge Google’s record of industry engagement on the Privacy Sandbox up to now, while being clear-eyed about the risks evoked above in relation to the alternative approach announced yesterday.

Jasper Beelen, Managing Director Mobile, Creative

What does your company do?

Creative Clicks is a performancebased marketing company specializing in mobile solutions. We have our own in-house creative studio, where we produce our content, providing our partners with complete 360 solutions.

What sectors does your business operate in?

Here at Creative Clicks, data is the fuel that drives our business. We offer a range of models, including agency, CPA/CPM/ CPI, Cost Plus, and more. For example, we at the Mobile team, that I am heading, are focusing on Mobile Carrier Billing – we enable DCB (or PSMS) as a payment method.

Which countries, or regions do you feel represent the greatest opportunity for your telemedia services in 2024 and why? We have a very strong presence in the MEA, European and APAC regions, where we are enabling millions of users around the world, offering safe and secure payments on their fingertips. In the upcoming period we are also looking to spreading our reach to the LATAM region and smaller emerging markets within the regions we are already present.

Which content and/or applications do you see being the most likely to benefit from telemedia billing technologies? There will be no single word answer to this. We need to keep in mind the needs of the

Clicks

end-users. So, I would say that exclusive, localised, trending content, everything that provides personalised experiences, through regularly updated content, bringing high user engagement and of course user friendly, ad-free platforms with cross-device support included as standard.

Do you think that Direct Carrier Billing can become mainstream and in which markets?

There is a future for Direct Carrier Billing in every market in the world. However, most beneficial markets will be the ones, where the penetration of credit cards and alternative payment methods for micro billings are not so widely spread or accessible to everybody.

How do you balance payment flows, operator relationships and customer satisfaction?

In an ever-evolving digital landscape, where connectivity is key, our Mobile team stands at the forefront of innovation and excellence. We empower Operators, Content Providers and Mobile Users by offering unparalleled access to a world where technical superiority meets human-centric design. Our commitment is to transcend the ordinary, ensuring everyone can engage, grow, and thrive in a seamlessly connected ecosystem.

What are the key drivers and inhibitors for growth?

For sure, I would mention marketing and technical

expertise made to fit the dynamic mobile landscape. High revenue subscription models bringing premium customers. Innovative and responsive team, ensuring rapid market adaptation and long-standing and unique partnerships with top industry players.

Which specific VAS verticals are you expecting to have a great year and why?

Unfortunately, there is no single word answer to this question. Every market, even every user is having different needs. Being flexible and having a rich portfolio of products and verticals, however, is for sure an approach for a great business year.

How might you answer that same question in five years time?

As a company with years of experience we are privileged to be able to regularly invest in new verticals, new products and we have never been relying on a single-vertical approach. Our Content & Partnerships team is constantly on the look for new trends which we can add to our current portfolio.

What’s the most effective business model for an mVAS customer acquisition?

This is a good question! It is important to understand that there is no written manual which has been proven to be most effective. However, the combination of transparent

marketing in combination with anti-fraud solutions, cutting-edge technologies and responsive customer care is something that has been working for Creative Clicks.

In the next 12 months what key technical developments or innovations do you feel will have the most positive impact on mCommerce (VAS / mobile payments / marketing)?

At Creative Clicks, we invest seriously in technologies and our talents. Having that and of course, considering the fast-paced environment of the industry, we take into consideration the needs of our partners and most importantly the needs and demands of our end-users. These have been the success factors in the past 15 years of our history; therefore, we believe these will be turning points for our next 12 months.

Your words of wisdom: On a more personal level, what is the most inspiring piece of advice that has seen you through a life in business to this day and who gave that advice to you?

We try to see the industry from the perspective of our end-users – how do they like to experience payments, how could they utilize the content we are offering. What could we offer to meet their needs. This has brought the personal touch that makes Creative Clicks unique partner.

In 2024, Connected TV (CTV) platforms are poised to revolutionise advertising strategies, with a significant 62% of marketers predicting it will dominate media trends. This shift is already evident in the entertainment sector, where streaming giants like Netflix introduced ad breaks in popular shows such as Bridgerton.

Is it primetime for Connected TV?

Rachel Lyall, Director of Marketing, EMEA and APAC, Mediaocean, takes a look at how connected TV services are forcing a rethink in the performance marketing world, especially now that things are up in the air with cookies

vertising and product perspective and it’s no surprise to see investments surge, with 56% of advertisers looking to increase their CTV spend.

Even as CTV continues to gain momentum, the advertising landscape’s transformation is set to be driven further by technological and regulatory changes. These innovations present both challenges and opportunities for brands aiming to engage with increasingly fragmented audiences.

So, how is CTV reshaping

the future of advertising? Let’s investigate some emerging practices and their potential impact on the industry.

WHERE PERSONALISATION LEADS, AD SPEND WILL FOLLOW

Marketers are beginning to recognise the potential of CTV and streaming from both an ad-

Connected TV: the only channel still growing?

65% of European viewers who have now connected their TV to the internet, directly through Smart TVs, representing an increase of five points YOY, Smart TVs are the only connectivity device type rising across Europe.

So finds AudienceXpress, FreeWheel’s premium video media sales house, in the third iteration of its Streaming Video: CTV Uncovered 2023consumer study, conducted in collaboration with independent research specialist, Happydemics. The research explores viewers’ uptake of CTV and their views on the TV advertising experience, alongside their preferences and perceptions of different channels and platforms. The study was conducted in the UK, Italy, France, Germany, Spain, and the Netherlands – collectively known as the EU6. While broadcast TV content remains a dominant platform, some 51% of EU6 respondents who use CTV and watch free on-demand streaming content shared that they watch these more than live TV. This trend was particularly notable among survey participants aged 15 to 34. Further, almost a half of European respondents

who tune in to free streaming services on their CTV screen (43%) do so every day. Connected TV is now taking centre stage for consumers; allowing them to access a wide array of platforms and services, jumping around from one to another to view their favourite entertainment.

“Evolving viewing habits are continuing to drive the convergence of digital and linear TV, with premium video content from online video aggregators now being watched on the TV screen,” says Stefanie Briec, Director, Head of Demand Sales UK & International for AudienceXpress. “Alongside this, the increase of hybrid streaming services on the market, which include both AVOD (ad-supported video-on-demand) and SVOD in their business models, underscores the reality that high quality, TV-like content retains the power to capture audience attention regardless of channel or platform. Moving forward, marketers require a holistic approach to TV to identify the channels that complement each other and boost the performance of their campaigns.”

Streaming giants like Netflix, Prime Video, and Disney+ are leading the charge by leveraging extensive viewer data and advanced algorithms to segment audiences beyond basic demographics. By analysing viewing history, search behaviour, and time of viewing, these platforms are delivering highly relevant and personalised ads. For example, Netflix gained a deeper understanding of their customers’ needs and preferences through its first-party data, allowing the streaming giant to provide better customer experiences.

The ability to personalise your messages will be key: 71% of consumers expect tailored interactions, and 76% get frustrated when this doesn’t happen. Therefore, ensuring ads do not disrupt the user experience or the flow of the show is paramount for success in the CTV advertising landscape.

PERSONALISATION STARTS WITH THE CREATIVE

In the rapidly evolving world of CTV advertising, the persistent ‘creative media’ gap remains a significant challenge for entertainment marketers. This gap, driven by an overemphasis on media activation at the expense of creative elements, hampers the effectiveness of advertising campaigns. The same research indicates that 86% of respondents lack fully synchronised media and creative processes and technologies.

This disconnects manifests in three primary ways. First, siloed teams and technologies create inefficiencies, leading to higher costs and slower go-to-market times. Secondly, repetitive and irrelevant messaging can desensitise consumers, diminishing their responsiveness. Thirdly,

the absence of creative intelligence prevents marketers from understanding what content truly resonates with audiences.

Addressing these gaps is paramount, particularly in the context of CTV where an innovative approach to media buying holds so much promise.

The temptation to rely on targeting alone to deliver results will only exacerbate the creative-media gap – just as much attention needs to be paid to making sure that the right content is being targeted.

REGULATION AND PUT

CTV CENTRE STAGE

By leveraging advanced ad tech that integrates full marketing workflow, we can craft campaigns that resonate deeply with viewers and drive continued growth in the dynamic advertis

ing is particularly advantageous for entertainment advertisers with access to rich first-party data. Despite Google’s recent announcement that it no longer plans to deprecate third-party cookies and instead demonstrate their commitment to consumer privacy by offering an opt-in action for users (see page 12), advertisers are still encouraged to continue moving forward to shape omnichannel advertising strategies.

Cookies are notoriously unreliable and the growing importance of social media, CTV, and other cookieless channels necessitates the need for advertisers to adapt to a multi-ID, multisignal environment, regardless of Chrome’s changes.

While cookies remain mired in uncertainty, however, the Digital Markets Act (DMA) is certainly

streaming services’ rich firstparty data sets have become invaluable in allowing advertisers to maintain precision targeting without relying on external tracking. Building direct relationships with audiences through owned data ensures continued personalisation and relevance. In tough economic times, performance-driven paid media remains a critical investment for 63% of marketers, while 51% prioritise brand advertising, indicating the necessity of a fullfunnel marketing approach.

Data sharing has long been the backbone of data-driven advertising, but the continuing development of privacy regulations and the restrictions imposed by the DMA means it is imperative to be mindful of consumer choice and consent while adopting technology that isn’t

leverage robust first-party data to connect the dots across channels, ensuring effective audience targeting and outcome measurement. This capability is essential for stronger data consent rules and maintaining impactful, personalised advertising campaigns.

Independent ad tech platforms are not just tools; they are transformative solutions designed to enhance creative relevance and activation across diverse digital marketing channels. These platforms enable a unified, omnichannel workflow supported by a consistent toolkit, which streamlines the creative process and drives growth in the competitive CTV landscape.

Rachel Lyall is Director of Marketing, EMEA and APAC,

MARKETING & ADVERTISING

Double-edged sword

Google’s responsive display ads use AI to take the donkey work out of scaling ads to fit across all sites, platforms and devices – but some are using this power for evil... but a new working group has been set up to set things straight

Google Responsive Display Ads (RDAs) have become a mainstay in the online advertising world. But, while they have been massively successful and offer a powerful tool for marketers, they come with some drawbacks – drawbacks that the telemedia industry is looking to overcome to make RDAs work.

RDAs are a format that allows advertisers to upload various assets like headlines, descriptions and visuals, which Google’s AI then automatically generates different ad combinations based on the available ad space on a website or app. This means a single RDA can trans-

form into a small text ad on one site and a large banner ad with images and video on another.

The allure of RDAs is obvious. This effortless scaling allows the creation of multiple ad variations in one go, making them quick and easy to generate and getting ads out over a multitude of screens and platforms simultaneously. Google’s AI does the heavy lifting.

Because of this, RDAs seamlessly adapt to various ad spaces across the Google Display Network (GDN), which encompasses millions of websites and apps. This expands your reach beyond just search results,

potentially exposing your brand to new customers.

Meanwhile, Google’s AI constantly tests different ad combinations, showing the most effective ones to users. This data-driven approach can lead to better ad performance over time.

However, there is a flipside. While RDAs offer undeniable advantages, there are also potential drawbacks to consider – and it is herein that the telemedia industry is having to act. Since Google’s AI determines the final ad format, you relinquish some control over how your ad appears. This might not

align perfectly with your branding or creative vision.

The responsive nature of RDAs can sometimes lead to misleading banner sizes. An ad designed for a large space might shrink to a thumbnail on a mobile device, potentially losing its visual impact and key messaging. Similarly, while you can set targeting parameters, GDN’s vastness means your ad could appear on unexpected websites, some of which might not align with your brand image.

Research by UK telemedia industry body aimm and market intel company MCP Insight has

found that some ads are also being placed so as to look just like content on websites and so clicks on what look like that websites call to action is in fact diverting to the advertisers –who may not be looking to be one hundred per cent in tune with the website brand.

This has prompted aimm to team up with MCP to create a working group charged with looking at how to make use of RDAs more responsible within the mVAS and DCB sector.

While the working group will tackle these issues of placement, it has also recently announced that it will broaden its scope to to look at another issue plaguing the use of RDAs. Google RDAs use optimised targeting to place ads on highconversion websites and apps. However, some unscrupulous publishers exploit the algorithm by building websites specifi-

cally designed to maximise ad conversions. This results in a poor experience for consumers and advertisers alike.

aimm and MCP Insight believe that by developing and adopting best practice it would reduce the conversion rates of unscrupulous publisher sites, thereby reducing complaints and protecting advertising spend.

In the meantime, there are some key things that mVAS and DCB advertisers can do to maximise the effectiveness of RDAs. These include simple ad best practice, such as providing Google’s AI with a diverse set of compelling headlines, descriptions and visuals. This gives the algorithm more options to create high-performing ad combinations.

Close monitoring is also a must. Don’t

be a passive participant. Regularly analyse ad performance data to see which combinations perform best. You can then adjust your assets or targeting to optimise results.

And be clear with your targeting. While RDAs offer reach, don’t neglect the importance of targeting. Define your ideal audience and set appropriate parameters to minimise the chances of your ad appearing on irrelevant websites.

RDAs offer a powerful tool for advertisers seeking to effortlessly reach a broad audience across the web. However, understanding the limitations and potential pitfalls is crucial. By providing high-quality assets, closely monitoring performance, and maintaining clear targeting, advertisers can leverage the strengths of RDAs while mitigating the downsides.

Vanishing point

Fraud, once the constant companion of digital world, is being tamed. From carrier billing fraud to SMS and voice services, there are signs that all is getting better. But, as Paul Skeldon reports, it has far from gone away

First, the good news. Annual fraud losses from voice and operator messaging channels is likely to decline to around $17bn in 2028, 9% less than 2024’s projected losses. It is also encouraging that carrier billing fraud, while not falling per se, is being wrestled under control. Why, you may ask, has the dark shadow of cyber crime, the once constant companion of the digital world, taken its foot off the gas?

That brings us to the bad news: it hasn’t. However, many of the processes and technologies that have been devised and deployed to make the online and mobile world a safer place, are now bearing fruit.

VOICE AND SMS

The latest report from Kaleido Intelligence, a leading roaming and connectivity market research firm – Mobile Network Fraud & Security: 2024 Outlook – suggests that improved security around 5G, along with the phasing out of old circuit switched networks is seeing fraudsters move away from SMS and voice fraud, instead targeting new channels and digital environments instead.

Kaleido notes that, while voice and SMS fraud will cause fewer material losses over time, the need to maintain backwards compatibility in the networks will keep older vulnerabilities from SS7 and Diameter proto-

cols present long into the 5G era. As a result, Kaleido expects fraud from these channels to plateau rather than disappear altogether, with the rate of decline falling throughout the forecast period.

In the case of SMS, we expect to see declines because of increased adoption of RCS following Apple’s announcement of support for the standard.

However, despite increased encryption, variable implementation will leave messaging open as a potential channel for fraudsters, keeping messaging fraud over $6 million in 2028.

Report author James Moar comments: “The security problems with RCS implementations

How Telecom Egypt drove a 90% reduction in incoming scam calls with voice firewall

Since Telecom Egypt, Egypt’s primary telecom operator, deployed Enea’s voice firewall to protect against scam calls and unwanted robocalls, more than 90% of incoming calls with spoofed caller IDs have disappeared from its network.

When the firewall solution was initially deployed, 8+% of all calls were identified as fraudulent and immediately blocked. This has acted as a deterrent to scammers, who have now ceased targeting the network, resulting in a roughly 90% reduction in spoof calls on the network.

According to a 2023 report from the Global Anti-Scam Alliance (GASA), phone calls are the leading channel for scam attempts worldwide, a sobering fact that underscores the importance of robust telecom security measures. Like many other countries, Egypt suffers from voice call scams where spoofing is used to mislead subscribers about the caller’s identity.

Caller ID spoofing means that the number displayed to a subscriber when receiving a call is not the number from which the call is being

made. Scammers use this method to hide their identities and trick subscribers into believing the call is legitimate. It is often used to impersonate banks or authorities, facilitating the first steps of a financial fraud scheme or personal data theft.

To protect its subscribers, Telecom Egypt has deployed Enea’s voice firewall, a cutting-edge solution that operates on a zero-trust approach. It accurately detects and blocks any spoofed calls coming into the network, ensuring that only genuine calls reach the subscribers and preventing scams at the very first stage before potential victims are reached.

Mohamed Al Fowey, Vice President, Chief Technology Officer at Telecom Egypt says: “Protecting our subscribers is a strategic priority. Improving end-user security to mitigate fraud and abuse in our network adds value to all our users. Enea is instrumental in our work to secure our network against voice call threats such as caller ID spoofing.”

are emblematic of many security issues within the telecoms space; flexibility and variation in standards implementation, while helpful to operators dealing with diverse infrastructure, continues to make high security an option, rather than a necessity.”

TELCO APIS

Similarly, Kaleido notes that while standardised telco APIs will help with service delivery and in some instances provide a new set of anti-fraud tools, they also broaden the attack surface, giving more potential points of ingress and disruption to the telecoms network.

Telcos’ inexperience in dealing with API security is a key reason why more advanced forms of attack will increase to almost $8 billion by 2028.

HOTSPOTS

While voice and SMS fraud have declined, new digital fraud hotspots are likely to emerge in the coming years.

As the number of connected devices increases, the risk of IoT-related fraud will also grow. Attackers may target vulnerable IoT devices to launch attacks on networks and systems.

The increasing reliance on cloud-based services creates new opportunities for fraudsters. Data breaches, phishing attacks, and unauthorized access to cloud-based resources are potential threats.

Fraudsters are becoming increasingly sophisticated in their social engineering tactics. Phishing attacks, smishing (SMS phishing) and vishing (voice phishing) will continue to be a significant challenge.

The growing popularity of cryptocurrencies has led to a surge in cryptocurrency-related scams, such as phishing attacks and Ponzi schemes.

DCB FRAUD

The popularity of Direct carrier billing (DCB) (see page 1 and

8) has been accompanied by a parallel rise in fraudulent activities. Over the past three years, the landscape of DCB fraud has evolved significantly, reflecting the increasing sophistication of cybercriminals and the need for robust countermeasures.

Fraudsters have refined their techniques, leveraging advanced technologies and exploiting vulnerabilities in the DCB ecosystem. This includes the use of malware, phishing attacks, and automated bots to initiate unauthorised transactions.

DCB fraud has also become more widespread and organised, with criminal syndicates engaging in large-scale operations. The financial impact of these fraudulent activities has grown substantially, affecting both consumers and businesses. New trends have emerged, such as the use of deepfakes and social engineering to

deceive consumers. Additionally, the integration of DCB with other payment methods, like mobile wallets and cryptocurrencies, has created new avenues for fraud.

According to fraud prevention companies such as Evina, there are several ways in which the industry, along with specialist companies, can tackle DCB fraud, starting with raising awareness among consumers about the risks of DCB fraud is crucial. Telecom operators and regulatory bodies have intensified their efforts to educate users on how to protect themselves from scams.

Telecom operators and technology providers have implemented advanced security measures to detect and prevent fraudulent transactions. These include fraud analytics, machine learning algorithms, and realtime monitoring systems.

Increasingly, collaboration between telecom operators, technology providers and regulatory bodies has been used to combat DCB fraud effectively (see panel). Sharing information, best practices, and resources can help strengthen defences against emerging threats.

Governments and regulatory authorities have also introduced stricter regulations to address DCB fraud. These regulations aim to protect consumers, hold businesses accountable, and establish clear guidelines for preventing and mitigating fraud.

WHAT LIES AHEAD

Looking ahead to the next two years, several trends are likely to shape the landscape of billing and mVAS fraud. Naturally, Artificial intelligence (AI) will play an increasingly important role in fraud detection – as witness by how the likes of

Evina and MCP Insights are already fighting fraud. These AI-powered systems can analyse vast amounts of data to identify patterns and anomalies that may indicate fraudulent activity.

Biometric authentication methods, such as fingerprint recognition and facial recognition, will become more prevalent in DCB transactions. These technologies can enhance security and reduce the risk of fraud.

Similarly, cloud-based security solutions will gain popularity due to their scalability and flexibility. These solutions can provide realtime threat detection, prevention, and response capabilities. And of course, regulatory frameworks will continue to evolve to address emerging fraud threats. New regulations may be introduced to enhance consumer protection, strengthen data privacy, and impose stricter penalties on fraudulent activities.

Doing it for the kids

Thank goodness – some beneficial screen time for our kids. That’s edutainment and it’s one of the hottest content tickets in telemedia town right now. Here, Julia Dimambro outlines what it is, why its important and how you can get hold of it

With the constant evolution of technology reshaping what we watch and how we watch it, one genre is standing out by delivering real benefits to both service providers and consumers: edutainment.

As the name suggests, edutainment merges education with entertainment, creating a mix of fun and learning that appeals to younger audiences.

For the Telemedia industry — particularly mobile operators and video entertainment platforms – edutainment is more than a lucrative opportunity to tap into a booming market; it offers genuine advantages to consumers by addressing concerns around excessive screen time and mental health, rather than adding to them.

THE RISE OF EDUTAINMENT IN THE MOBILE ERA

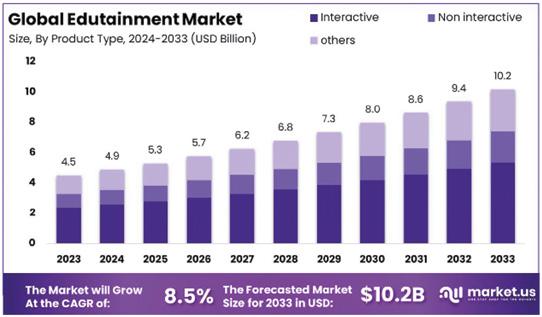

Skyquest Technology predicts the Edutainment market will expand from $5.54 billion in 2022 to $14.5 billion by 2030, with a compound annual growth rate (CAGR) of 16.37% during this period.

According to Market.us, children represent the dominant segment within this, accounting for more than 57.5% of the market share in 2023.

This shift towards edutainment is driven by parents increasingly concerned about the quality of content their children consume and its impact on their mental health and development. The US Center for Disease Control and Prevention (CDC) reports that children ages eight to 10 spend an average of six hours per day in front of

screens, much of it on mobile devices.

Traditional cartoons and animated shows still dominate the market, but studies show the potential downsides. The National Institutes of Health (NIH) found that just 9 minutes of a fast-paced cartoon had immediate negative effects on four-year-olds’ executive function. Non-educational content has also been linked to poorer cognitive development, shorter attention spans, and reduced social skills in children.

Edutainment offers a way to balance children’s need for fun with parents’ desire for content that supports learning and development.

WHY EDUTAINMENT IS A GAME-CHANGER FOR VAS AND VOD

For VAS, VOD and OTT providers, edutainment presents compelling advantages that seamlessly fit with current business and campaign strategies. First, it’s an easier sell to parents. As gatekeepers of their children’s content, parents are more likely to subscribe to services that provide educational value.

This is especially important in today’s market, where ethical concerns and the impact of screen time on children’s mental and physical health are at an all-time high.

Second, offering edutainment can significantly enhance a provider’s brand positioning. By delivering content that contributes positively to a child’s development, providers can differentiate themselves from more generic competitors. This strategy not only attracts subscribers but also builds long-term loyalty, as parents are more inclined to stick with a service they trust to benefit their children.

THE BENEFITS OF EDUTAINMENT FOR KIDS AND PARENTS

Edutainment offers multiple

advantages over traditional cartoons. For kids, it provides an interactive and engaging way to learn new skills—from language and math to socialemotional learning.

Studies have shown that children who engage with educational content tend to perform better academically and demonstrate higher levels of creativity and problem-solving abilities.

For parents, edutainment is appealing because of its ethical and developmental benefits. Unlike traditional entertainment, which can lead to passive consumption and excessive screen time, Edutainment encourages active participation.

This means children are not just passively watching but actively learning, which can mitigate some negative effects of screen time. Additionally, edutainment content is typi-

For leaders in the telemedia industry, integrating premium edutainment is more than a smart business move –it is an opportunity to lead in a rapidly growing segment of the market

cally age-appropriate and free from intrusive ads and harmful material, which addresses parents’ concerns.

POSITIONING YOUR BRAND AS A LEADER IN EDUTAINMENT

For leaders in the Telemedia industry, integrating premium edutainment is more than a smart business move—it’s an opportunity to lead in a rapidly growing market segment. By offering content that aligns with children’s educational

needs and parents’ ethical standards, you can position your platform as a trusted source of high-quality mobile entertainment.

This strategy not only appeals to a broader audience but also enhances your brand’s reputation as a responsible and innovative leader in the industry. As demand foreEdutainment continues to rise, now is the time to invest in this genre and ensure your platform is at the forefront of this transformative trend.

HOW SERIOUSLY FRESH MEDIA CAN HELP

Seriously Fresh Media (SFM) offers a standout catalogue of premium edutainment content, curated for quality, creativity, and global appeal. Predominantly short-form and optimized for mobile viewing it focuses on benefitting young minds in multiple skill sets.

We feature global brands like Smurfs and Masha and the Bear, alongside award-winning series that support child development.

Reach out today at julia@seriouslyfreshmedia.com or meet us at Telemedia in Marbella to see how we can support your Edutainment strategy.

Julia Dimambro, founder and CEO of Seriously Fresh Media

What does your company do?

Seriously Fresh Media (SFM) specialises in secure and easy licensing of premium video content for international, multichannel providers of streamed and VAS entertainment.

SFM doesn’t simply aggregate content and distribute it to clients. Instead, we provide highly specialised access to an international network of renowned producers and studios who create geotargeted, platform-tailored, and language-specific productions. Additionally, we offer bespoke production services for unique content, marketing materials, and branding.

What sectors does your business operate in?

premium content for vas, dcb, vod, ott & streaming platforms

Which countries or regions do you feel represent the greatest opportunity for your telemedia services in 2024 and why? We have clients and partners all over the world because we can deliver locally produced content in various languages. after 25 years in the business, we have seen geographic trends shift and vary depending on local regulations and payment flows at the time. For 2024 specifically, the majority of incoming inquiries are for platforms and services in the Middle East, Latin America, Asia, and Africa.

Which specific VAS verticals are you expecting to have a great year and why?

For 2024, sports content has really stood out. The Eurocup and Paris Olympics appealed to wider audiences, including those who might not typically seek out sports entertainment. This created a significant content trend for 2024. By developing engaging and dynamic propositions around sports and capitalizing on the increased interest that these big international events provide, platforms and services have a unique opportunity to substantially expand their audience reach, diversify their demographics, and enhance their data collection efforts.

How might you answer that same question in five years’ time?

It’s difficult to predict because of the sheer magnitude of Artificial Intelligence’s (AI) impact on content creation and production during this time. The impact will be profound, enabling more personalized and interactive experiences. For instance, a short-form cooking series will be transformed using AI to dynamically tailor the content subscribers see based on their individual preferences, skill level and dietary needs. AI-driven algorithms will analyse viewer data to suggest personalized episodes, making the content more engaging and relevant. It will even create episodes on the fly specific

to the viewers behaviour and preferences within the service.

In production, AI tools will start to streamline all aspects of the production process. From generating scripts, suggesting scene compositions, and even creating realistic visual effects, and all whilst reducing time and costs.

Distribution will also see significant changes. Advanced AI algorithms will predict viewer preferences and optimize content delivery, ensuring that videos reach the right audience at the right time. This will mean that our clients and partners can come to us with very specific requirements and be able to maximise revenue and retention with our content.

Overall, AI will make video entertainment more closely aligned with individual tastes and preferences, transforming the way we consume it.

In the next 12 months what key technical developments or innovations do you feel will have the most positive impact on mCommerce (VAS / mobile payments / marketing)?

As above – AI, AI, AI – I firmly believe we can’t begin to comprehend how our industry will look in an AI future. Even within the next 12 months, I’m sure we’ll see major shifts in how we do business together, how platforms, services, and data collection evolve, and how we create and distribute the content itself.

The most mind-stretching thing I’ve heard about AI is this: Oppenheimer’s IQ was only 2.5 times greater than the least intelligent person on earth, yet look at how he impacted our world. Now, experts predict that AI will be a BILLION times more intelligent than the smartest person alive today. We truly don’t have the brain capacity to comprehend what that could mean.

Your words of wisdom: On a more personal level, what is the most inspiring piece of advice that has seen you through a life in business to this day and who gave that advice to you?

The best bit of advice I ever received was “if you’re presented with two options, always take the option that allows you to do the other one later”.

It has always worked out, and has helped to facilitate a truly amazing life. I took so many chances on opportunities and they resulted in working internationally, living in different countries and cultures and of course, starting businesses and meeting AMAZING people who have stayed in my life for 20, 30, 40 years!

Sup-Uber bundling

Anyone in any doubt that superbundling is just a fanciful idea cooked up by MNOs must think again: Uber has just gone and one it. Here’s why it matters

Uber has joined forces with Bango to expand the reach of its membership programme, Uber One, by bundling the programme into mobile and broadband plans. This strategic move helps Uber to expand its subscriber base by opening-up indirect channels worldwide, to grow its 19 million strong membership base.

Launching in the US, Uber One will be available as an add-on through the Digital Vending Machine(DVM) from Bango.

Uber One offers users exclusive benefits such as discounted rides and deliveries, with monthly memberships available for $9.99 and annual memberships for $96. Uber One also includes part-

nerships with third-party offers, such as discounted memberships to eligible users. Members enjoy perks including a $0 Delivery Fee plus up to 10% off eligible deliveries and orders, as well as 6% Uber Cash on eligible rides.

By joining the Bango DVM, Uber can establish direct relationships with telcos and other reseller partners with ease, enabling Uber One to be included in Super Bundling content hubs and other bundled offers.

The DVM handles all the intricacies involved in resellers creating and managing subscription bundles and targeting offers that include Uber One such as free trials, multi-bundle deals and

discounts.

As subscription costs rise, subscribers seek better deals through new cost-effective methods. Recent research by Bango shows that indirect subscriptions have become a major market in 2024, with combined subscriptions, bundles, and third-party sales driving growth. In the US, one in five subscribers (20%) exclusively sign up through indirect channels.

”Expanding the reach of our Uber One subscription service through indirect channels is an important way for us to increase uptake,” says Danielle Sheridan, Head of Global Membership at Uber. “We look forward to using this partnership to reach new au-

diences and grow our membership base.”

Anil Malhotra, CMO at Bango adds: “Uber extending the reach of its subscription service through telcos is a major validation of the demand for more choice and flexibility in how people access their favourite subscription services. Uber One is already a great example of a multipurpose subscription, providing rides and deliveries, all in one place. It’s exactly that type of all-in-one convenience that today’s subscribers are looking for, and that will be further served through Uber One’s inclusion in the Digital Vending Machine® and future bundles.

“As more users opt for subscription services via indirect channels, the Digital Vending Machine offers a seamless and expedited solution for marketleading products and services such as Uber One.”

Florencia Torres, Senior Account Manager, Mobidea

What does Mobidea do?

Mobidea is a prominent figure in the affiliate marketing industry, specialising in mobile value-added services (mVAS) since 2011. We operate as a leading CPA affiliate network, connecting advertisers and publishers globally. With a robust network of more than 1,500 active advertisers, more than 9,000 offers available across 200+ countries, and a staggering 100,000+ registered affiliates, Mobidea provides a platform where advertisers can reach high-quality users for their mVAS services across Europe, Asia and MENA.

Additionally, our internal media buying team focuses on Google, enhancing our capabilities to deliver targeted and effective advertising solutions. Our core mission is to identify the right channels for our offers and secure high-quality users, ultimately driving success for both our advertisers and affiliates.

Mobidea has a rich history with its board of directors. Can you share their background and how they came to form the company?

Behind Mobidea’s success story are Antoine Moreau and Sebastien Balestas, two visionary leaders who have shaped our journey from the ground up. Antoine’s passion for innovation and sales drove him to pioneer digital solutions for international internet companies. His entrepreneurial journey

began with launching a Latin American company in France, later expanding it across Europe. With a deep understanding of programmatic media buying, Antoine saw the potential in mobile advertising, which led him to pivot Mobidea’s focus in 2011.

Sebastien’s path to Mobidea was equally impactful, with over a decade of experience spanning Avazu in China and AdThink in France. His strategic roles in global business development and customer acquisition solutions underscore his ability to navigate diverse market landscapes and foster meaningful partnerships. Together, Antoine and Sebastien bring a wealth of expertise to Mobidea, blending innovation with a strong commitment to empowering affiliates and advertisers worldwide.

Mobidea recently acquired Traffic.bar and launched subsidiaries like Exclusive by Mobidea. What drove these decisions, and how do they fit into your overall strategy?

Mobidea’s recent strategic moves, such as acquiring Traffic. bar and launching Exclusive by Mobidea, reflect our dedication to enhancing and diversifying our services for clients.

Traffic.bar brings advanced expertise, especially in the dating vertical, enhancing our ability to acquire high-quality traffic efficiently. This acquisition also integrates innovative SmartLink technology, boosting our capac-

ity to deliver effective marketing solutions that drive results for our partners.

Meanwhile, Exclusive by Mobidea focuses on premium, direct CC Submit offers tailored to specific client needs. This subsidiary enriches our service lineup, ensuring we meet diverse market demands effectively. These strategic expansions not only strengthen our market position but also bolster our financial stability, enabling us to navigate industry shifts with agility. At Mobidea, our goal remains clear: to provide exceptional value through diversified offerings that cater to evolving market needs.

You are launching a new Google media buying service. Can you explain what this entails and how it will benefit your clients? Our new Google media buying service is designed to address the evolving regulatory landscape and the need for secure, highquality traffic sources. Over the years, regulations have become stricter to protect businesses from fraud, making Google a safer and more reliable traffic source. By leveraging Google’s robust advertising platform, we can ensure controlled and compliant promotional strategies, reducing risks associated with independent affiliate marketing. This internal media buying initiative positions us as our best affiliate, minimizing dependency on third parties and adding a reliable branch to our value chain. For our clients, this means access to

high-quality, targeted traffic that enhances campaign performance and ROI.

How would you describe the leadership style of Mobidea’s board of directors, and how does it impact company culture and the multicultural team? The leadership at Mobidea is characterised by a strong emphasis on trust and worklife balance. Our board of directors believe in empowering employees rather than micromanaging them, fostering a culture of autonomy and accountability. This approach allows team members to manage their schedules flexibly, as long as they meet their objectives. The supportive environment has led to high employee retention, with many team members having been with the company for over four to five years. This stability enhances job satisfaction, drives productivity, and fosters innovation.

Additionally, Mobidea operates in a global marketplace, and our multicultural team is a significant asset. With team members from various cultural backgrounds and native speakers of over 10 languages, we can effectively bridge cultural gaps and tailor our business approaches to different markets. This diversity enables seamless communication and collaboration with partners worldwide, fostering a deeper understanding of local markets and consumer behaviours.

• Search & connect with 1,600+ qualified users

• Search & connect with 120+ virtual exhibitors

• Go “premium” & generate sales leads

• View 140+ on-demand presentations

• Post requirements & offers in the Chatroom