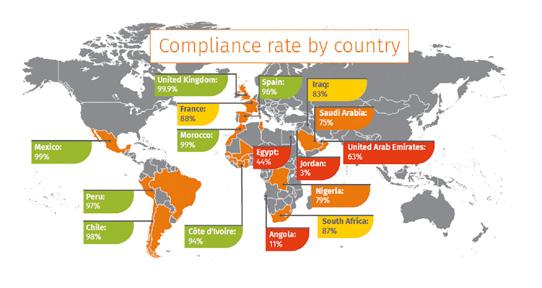

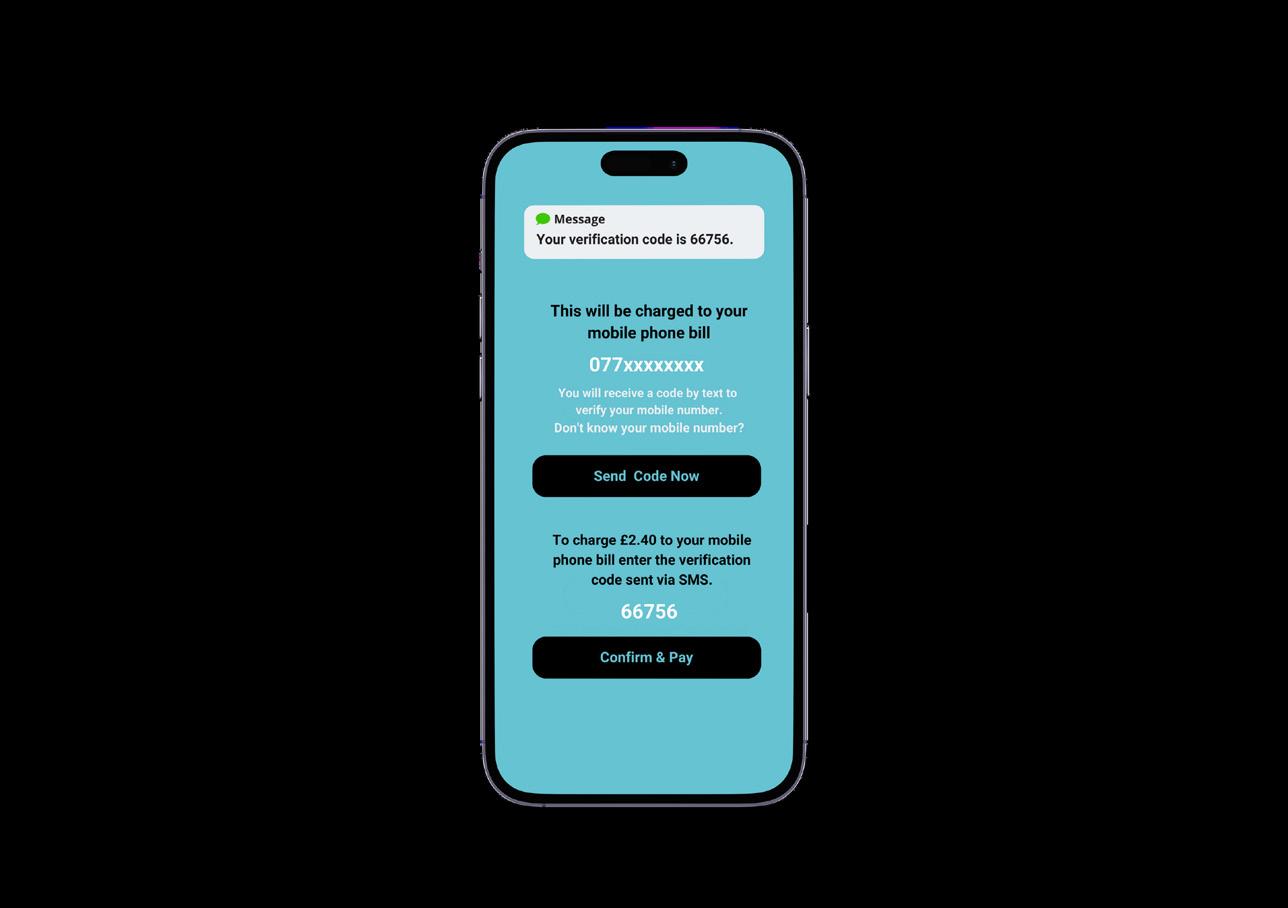

Compliance across carrier billing-based ads fell from 93% in 2022 to 88% in 2023, with analysis of some 5 million digital journeys and 500,000 VAS tests worldwide finding around 65,000 issues.

According to Empello’s Annual Review 2023, the primary reason for the decrease in compliance has been a raft of changes to banner requirements in the Middle East and LATAM, which have resulted in significant fluctuations in the compliance rates in some countries or carriers. The removal of moderation from X –formerly Twitter – has also had an impact. At one extreme over the course of this year, Empello has seen an example of one carrier’s compliance falling from 83% compliance to 8% purely due to changes in banner guidelines.

PERFORMANCE ASSESSED

As has become usual, performance varied from market to market and region to region, with LATAM being the most compliant region and the Middle East being least compliant, lagging far behind the other regions.

The level of compliance in Europe has fallen in 2023 and that is mainly driven by the results in France and Spain which drove half of all issues we found in Europe.

Drilling down to specific countries, Em

TELECOMS & NETWORK OPERATORS

Mobile network operators (MNOs) are no longer just connectivity providers – they are set to become media companies. Sitting on a treasure trove of data – user behaviour, location and preferences – they are stand at the doors to a goldmine: commerce media, and $820bn opportunity if analysts are to be believed.

One of the biggest content channels is education

Making SMS secure is key to its enterprise future, says

The latest MEF consumer research reveals just how messaging use changes

Making SMS quantum computer hacking proof is more important than you think

Robocalls are becoming the latest security risk – here’s how to beat them

State of the industry

pello’s data shows a dramatic improvement in South Africa this year, rising from 63% to 87% compliance. Conversely there has been a fall in France from 98% compliant to 88%.

Fresh markets researched, including Angola and Jordan, showed what Empello says are “extraordinarily high levels of non-compliance”.

In Nigeria, however, compliance was found to sit at a rate of 79%, high for a market with no formal compliance programme, says Empello’s report, adding: “Key to achieving and maintaining high compliance rates is participation by all parties in any compliance programme, but specifically active engagement by the carriers involved”.

COMPLIANCE ISSUES

With that in mind, the study shows that the main sources of non-compliance was content locking and misleading flows, which accounted for 56% of all issues found globally. This is exactly the same as in 2022. Content Locking remains the highest category in 2023 and continues the resurgence seen from the last quarter of 2021 and throughout 2022.

“It goes to prove that when it comes to advertising fraud, the old tricks are still working on consumers and fraudsters continue to deploy them in various guises,” says the report.

Brand passing, however, has declined further in 2023, with 2415 instances found compared with 3451 in 2022 and 8672 in 2021. However, this year Empello has introduced a sub-category called Impersonation of a Public Figure, in order to better capture misuse of personal identities, particularly in the Middle East compared to misuse of brand identities. This added an additional 473 instances.

Auto subscriptions have decreased from 941 in 2022 to 582 in 2023, but Saudi Arabia leads the pack with 219 auto-subscriptions showing the presence of widespread and systemic payment fraud. Attempted auto subscriptions have also declined by around 30% from 940 to 668.

Take down times in the Google Playstore have reached a record high, with take down

and predominantly found in the Middle East.

Web advertising still accounts for 90% of campaigns Empello discovered in-market. The compliance of Facebook advertising is particularly problematic with 98% non-compliance on this channel (up from 84% in 2022), with Instagram and Tik Tok following a similar pattern at 96% each (up from 43% and 53% in 2022).

of rogue apps happening in as little as 24 hours.

“However,” says the report, “it does beg the question of why these apps make it through to the Playstore in the 1st place when it’s so easy to take them down? Surely it would be better to prevent them going live at all than suffer the damage they can cause in even 24 hours live on the Playstore?”

SERVICE TYPES IN 2023

There has been little change in the types of services advertised and their relative compliance rates. Games services remain the most advertised services in 2023, followed by Video Streaming and Mixed Content. More specialised services remain in the minority, but typically have much higher compliance rates.

The most common form of payment flow found by Empello is a header enrichment two click flow, although this is heavily influenced by the LATAM markets. MSISDN PIN flow is the second most common flow

introduction of a new compliance category of Misleading Placement of a Google Banner. This has been separated from the general Misleading Flow category as the merchant may have little or no control over how and where Google places its banners.

LOOKING ON THE BRIGHT SIDE

This year’s new entrant is X, previously known as Twitter, which due to a lack of content moderation and controls over publishers has shown a 100% rise in discoveries from 4712 to 9921 in 2023, with a non-compliance rate of 96% also.

“This means that, if merchants are advertising on social media, 96 times out of 100 it will be non-compliant.,” says Empello’s report. “Of course, that is not to say that direct buy media from Social Media channels is all bad, but affiliate networks typically use social media channels for misleading and content locking campaigns. The social media companies do have a responsibility to ensure that there are proper policies in place to prevent these practices.”

The company also identified new threats to the compliance of web advertising in 2023, including so-called Banner Farm websites on Google Display, as well the increase in Shell Apps via the Google Play Store. These continue in 2023, leading to the

Overall, it is disappointing to see the average level of compliance fall in the global market in 2023. However, there are a number of markets and carriers that continue to maintain consistently high standards, such as Vodafone UK, and many that have improved from 2022, such as the South African market. Other markets such as Qatar and Oman have suffered from changes to banner guidelines dramatically impacting their compliance rates.

Stand out countries that are still ripe for compliance improvement are Saudi Arabia, the UAE and Egypt – just as they were in 2022.

“Maintaining compliance is very much like weeding a garden,” says Empello. “It has to be done diligently and regularly because if you let weeds get a hold whilst you are not looking, a garden can be quickly overrun which then requires a major clean-up effort. As ever, our global mission is to create compliant and fraud free environments where VAS services can thrive in the long term, so if you have some weeding to be done, or you want your VAS garden to be weed free from the get-go, then please get in touch.”

Download the full report at https://www.empello.com/ empello-releases-its-annualreview-for-2023/

Commerce media and MNOs

Commerce media leverages user data to deliver targeted advertising within the purchase funnel, significantly influencing consumer decisions. This presents a phenomenal opportunity for MNOs to transform themselves from connectivity providers to key players in the advertising ecosystem.

THE POWER OF FIRSTPARTY DATA

MNOs possess a unique advantage in the digital world, they ‘own’ a wealth of first-party data on their subscribers. This data is unmatched by other players in the advertising landscape and includes demographic data such as age, gender, location, income bracket; device usage patterns such as how long they dwell and where; and how much data they use, their location and the kind of content they like.

This rich tapestry of data allows MNOs to create highly targeted consumer segments with incredible accuracy. Imagine targeting a fitness app campaign – with MNO data, you can show ads to

users with high evening activity levels and frequent downloads of health apps, significantly improving campaign effectiveness.

And it is a massive potential market. The global commerce media market is projected to reach a staggering $820bn by 2030, according to a report by McKinsey. This explosive growth highlights the immense potential for MNOs to carve out a significant share in this lucrative space.

BEYOND TARGETING

However, MNOs can go beyond basic targeting by leveraging realtime contextual data. Imagine a user searching for a new pair of running shoes online. Through their network activity, the MNO can identify this user and serve them a targeted ad for a sports apparel store in their vicinity. This contextual relevance delivers a seamless user experience and significantly increases the likelihood of conversion.

MNOs can also offer advertisers a variety of engaging formats to reach their target audience within the mobile ecosystem.

Paving the way: who has taken a lead in MNO commerce media?

So, who is doing this today and how is it going? Several MNOs are already taking bold steps to integrate commerce media into their offerings:

• Verizon Media: Verizon, a leading American MNO, launched its own advertising platform, Verizon Media. This platform leverages its vast user data to offer targeted advertising solutions for brands, demonstrating their commitment to the commerce media space. In 2022, Verizon Media reported advertising and subscription revenues exceeding $2bn, highlighting the potential financial gains from this venture.

• Singtel’s Amobee: Singtel, a major Singaporean telecommunications company, acquired Amobee, a global ad tech company. This acquisition demonstrates Singtel’s strategic move to establish itself as a player in the commerce media arena, leveraging Amobee’s expertise in ad targeting and campaign management.

• Telefonica’s AdTech unit: Telefonica, a Spanish MNO, established a dedicated AdTech unit to develop and sell targeted advertising solutions to brands. This dedicated unit signifies Telefonica’s commitment to building expertise in commerce media and carving out a niche in this growing market.

SMS is a key one. Targeted promotional offers and discount codes delivered directly to users’ phones. A 2023 study by SMS Marketing Trends found that SMS marketing boasts a staggering 98% open rate, making it a highly effective format.

Serving targeted ads within popular mobile apps based on user data and app usage patterns opens another window of opportunity for many MNOs. The global in-app advertising market was valued at $188.3bn billion in 2023, according to Statista, highlighting the potential reach and revenue opportunities.

Rich media ads are also becoming a reality, not least as RCS gets rolled out. Interactive video ads or location-based banners with click-to-call functionalities for immediate conversions. Rich media ads can increase brand recall and engagement compared to traditional static banners.

Native advertising also plays a role. Seamlessly integrating branded content within mobile apps or websites, creating a less intrusive advertising experience. Native advertising can generate higher click-through rates compared to traditional banner ads.

A MULTIFACETED OPPORTUNITY FOR MNOS

Embracing commerce media offers a multi-pronged benefit for MNOs potentially brings operators a raft of opportunities. Creating a new revenue stream through targeted advertising partnerships with brands seeking a highly engaged customer base, being the main one.

But there are many others. Enhanced customer value can also be added. Providing a more personalised and enriching mobile experience for subscribers with relevant advertising, potentially leading to increased satisfaction and loyalty.

Analysing user behaviour within the commerce media platform can provide MNOs with valuable insights to optimise their

network offerings, personalise future campaigns and develop new value-added services. There are also improved customer retention possibilities. By delivering relevant and engaging advertising experiences, MNOs can potentially increase customer satisfaction and loyalty, reducing churn.

NAVIGATING THE LANDSCAPE

While the opportunity is undeniable, there are challenges MNOs need to consider. As with any consumer-facing service that leverages first-party data, data privacy is a paramount concern. MNOs need to ensure transparency and user consent regarding data collection and usage for advertising purposes. Building trust with their subscribers is crucial for the long-term success of commerce media initiatives.

To cope with this – as well as with creating a media business – MNOs may need to invest in building expertise in ad targeting, campaign management and data analytics and management to effectively compete in the commerce media space. This might involve hiring specialists or partnering with established adtech companies.

Competition is also a growing concern. Established advertising platforms like Google and Facebook are formidable competitors with extensive infrastructure and established relationships with advertisers. MNOs need to offer unique value propositions and data insights to attract advertisers in this crowded space.

Data privacy regulations are constantly evolving. MNOs need to stay compliant with all current and future legislation. This requires ongoing monitoring of changing regulations and adapting their data collection and usage practices accordingly.

COLLABORATIVE FUTURE

The future of commerce media within the mobile ecosystem is

collaborative. MNOs can unlock their full potential by partnering with key players:

• Ad tech companies: MNOs can leverage the expertise of ad tech companies in ad targeting, campaign management, and data analytics to build robust commerce media platforms and compete effectively with established players.

• Brands: MNOs offer brands access to highly targeted user segments and unique advertising formats that traditional advertising platforms might not provide. Building strong relationships with brands will be crucial for MNOs to attract advertising dollars.

• App developers: Integrating commerce media functionalities within popular mobile apps can create a seamless user experience. MNOs can partner with app developers to create targeted advertising opportunities within their apps, generating a revenue stream for both parties.

By working together, MNOs,

ad-tech companies, brands, and app developers can create a winwin situation for all stakeholders.

Advertisers gain access to valuable first-party data for targeted campaigns, MNOs create new revenue streams, and users receive a more personalized mobile experience.

The mobile commerce media market represents a golden op-

The superbundling add on

Bango has spent more than a year pushing the idea that telcos can generate increased revenues if they allow users to aggregate streaming services and then pay via the telco for them.

This idea of super bundling isn’t new, but the latest push towards sportsVOD is timely. This summer sees the European football championships take place in Germany across June and July, followed swiftly by the Olympics in Paris in July and August. These are crammed in around the host of other on-going sporting events taking place worldwide this summer and cements just how important sports are commercially to anyone in the content business.

Sports fans are the biggest adopters of streaming package, with the average US sports fan having seven and spending some $1440 a year. However, many of them – 73% according to Bango – want more but can’t afford it and are also put off by the complexity and scale of just how many sports services there are out there.

portunity for MNOs. MNOs possess a unique advantage through their vast first-party data and the ability to leverage real-time contextual insights. By overcoming challenges like data privacy concerns and building expertise in the advertising space, MNOs can unlock substantial revenue streams and enhance the value proposition for their subscribers.

Given this fragmentation, 87% of those paying for SportsVOD subscriptions are calling for a single ‘content hub’ to centralise all of their sports subscriptions (and more) into one place. Without this sort of all-in-one solution, 55% of sports streamers admit to using pirate streaming services to access all of their favourite content in one place.

The piracy aside – which indicated a market in crisis, rather than unwilling consumers – this shows, believes Bango, that sports fans are more than ready for super bundling. Further, they say that they want their MNO to provide it.

Running the numbers, Bango believes that telco customers would pay around 38% more on their monthly phone bill for this – a substantial increase in revenues.

What is intriguing is that there still seems to be some degree of reticence among MNOs to do this. They need to create new revenue streams to counter commoditisation of messaging and voice, an aggregating content and billing for it – potentially with

Collaborative partnerships with ad-tech companies, brands, and app developers will be key to success in this rapidly evolving landscape.

As commerce media continues to grow, MNOs who embrace this opportunity are poised to become significant players in the mobile advertising ecosystem of the future.

DCB – is one option for them.

There are challenges with super bundling for telcos. Securing rights to bundle popular content from different providers can be expensive. Telcos need to negotiate favourable deals while offering a diverse and attractive range of content. Telcos would also be entering a crowded market already occupied by established streaming giants. They would need to differentiate their offerings by providing unique value propositions or competitive pricing. Likewise, negotiating revenue sharing agreements with content providers can be complex. Telcos need to ensure they get a fair share of the profits while keeping their bundles affordable for customers.

Then there are the tech integration and data issues – telcos need to invest in robust infrastructure to ensure a smooth user experience and super bundles often include unlimited or generous data allowances to accommodate streaming – both of which are costly.

• Search & connect with 1,600+ qualified users

• Search & connect with 120+ virtual exhibitors

• Go “premium” & generate sales leads

• View 140+ on-demand presentations

• Post requirements & offers in the Chatroom

Content: time to mix it up and start again?

A

look at

the most popular streaming services in the UK in 2023 reveals an interesting development in what consumers want. Paul Skeldon takes a look at how the content market needs to be about more than just, well, content – and how that is driving mVAS explosive growth

Content is indeed king, but as consumers demand more and more of it, content alone is no longer enough. In fact, the content needed to drive VAS and carrier billing is increasingly relying on a complex mix of lengths, formats and channels to create a value proposition that consumers are prepared to pay for.

Take a look at the digital streaming market if you want proof. A study by Digital Climax out in May has shown that Amazon was the most popular streaming site in the UK in 2023. Netflix was third. No surprises there – but the report does contain something quite telling. Fourth and fifth in the rankings were The Daily Express, a newspaper, and Radio Times, a TV listings magazine.

So, the top five most popular streaming sites in the UK in 2023 contains two ‘old media’ players and a retailer and shows that, increasingly, the content market isn’t just about the kinds of content that streams. In fact, it isn’t just about TV and movie content in the streaming world, it is about way more. And that is symptomatic of the broader

content market.

Looked at the other way round, what the report tells us, I believe, is that consumers are looking for a multimedia experience. While that may all sound a bit ‘90s (and it does, I was there), it marks an evolution in the content market, certainly in the UK, away from just dedicated TV-like streaming content to something richer and more holistic.

While Netflix is a pure streamer – as is number two in the UK, Sky – Amazon isn’t and nor are The Express and Radio Times. All have other strings to their bows.

Amazon originally used the lure of free delivery through Amazon Prime to tempt users into its streaming business. Today it uses each to temp users to pay a yearly subscription, guaranteeing a massive and steady income from millions of users. The fact that you only get some content for free is testament to how powerful the lure of Amazon is.

Netflix, conversely, has been a focussed subscriptions-based content streaming service and, while it still attracts the users in large numbers, it is having to consider selling advertising and

creating a premium level of service to help balance the books.

Much of this has been because it has spent a large sum creating excellent content. Amazon, which has done the same, augments that cost with subscriptions and pay-per-view. Amazon too has a very strong retail media ad business, which generated $47bn in 2023 – and it uses its streaming platform as part of that offering to brands. This also helps it pay for content.

But look at what is happening at the other two in the UK top five streamers. The Daily Express and Radio Times, however, come at this from a very different place. Both are old school media companies – inky publishers, at least originally – and rely on display advertising, banners, sponsored copy, subscriptions to news services and sales of physical publications to bank roll what it does. Its streaming content sits around this and is used to pull people into the site to watch, thus putting them in front of all those adverts and sponsor opportunities.

And this old-fashioned way of doing things seems to be work-

ing. The Daily Express had around 103.8 million visits throughout 2023. It had the most hits in January 2023, with 11.1 million visits, and receives an average of 8.6 million web visits per month. The digital platform of the Daily Express and Sunday Express, has online access to global news stories and additional entertainment like puzzles and games. Similarly, Radio Times ranked fifth with approximately 73.4 million visits in 2023. Known for its television and radio programme schedules, the website had the most visits in January 2023, with 6.9 million total visits, and receives an average of 6.1 million visits per month. Radio Times also provides film, TV, and entertainment news and interviews with many of the biggest stars.

So, what does this mean for the content market? As Julia Dimambro, CEO of Seriously Fresh Media attests, the content market is shifting and creating the right content to satisfy what is becoming an increasingly diverse consumer demand is now a big challenge for telemedia companies. There is so much demand, but while many are pursuing just TV and movie quality long-form content, or pushing deeper into shorts, perhaps what is really needed is a more mixed bag of

mVAS set to hit $3.5bn by 2030

As platforms and channels explode – and marketing across those channel also booms – mVAS services are set to also see explosive growth.

In fact, the global mVAS market is estimated to be worth US$880.4m in 2024 and is likely to grow at a 14.9% CAGR through 2034. The market is expected to surpass a valuation of US$3.5bn by 2034.

According to data from FactMR, reduced prices of smartphones due to intense competition among manufacturers have raised the adoption of mobile phones in emerging countries filled with lower-income populations are driving the growth of mVAS globally. Technological advancements including virtual reality (VR), augmented reality (AR) and high-definition video streaming are also critical for growing the market.

Enhanced connectivity, says the report, enables businesses to develop and offer better and more interactive mVAS offerings that elevate user experiences, which in turn is also driving up use.

The increasing use of mVAS by enterprises to streamline communication with clients and customers is also propelling market growth. Furthermore, mobile apps and services facilitate project management, boost employee collaboration and enable data analysis.

East Asia is projected to account for a share of 36.5% in 2024. By 2034, the region

media types, as well as content formats?

With the increasing use of AI, there are increasing ways to create a cornucopia of content, but as Dimambro points out, you still need the human touch. And I think this means looking not just at creating video content, but looking at the whole range of things people consume. Pictures, text, memes and GIFs to create services that encourage visitors and engagement.

This has the added advantage of being able to also leverage messaging tech – especially RCS and WhatsApp – to drive traffic, and for carrier billing to micro bill for additional content and access.

Underpining all this, however, is advertising. As we have seen

is anticipated to acquire a market share of 38.4%. The regional market value is expected to reach US$1.35bn by 2034. North America’s market is estimated to attain a value of US$1.02bn by 2034. The region is projected to be led by the United States.

Underexploited countries such as South Korea and Mexico are also forecast to show a high adoption rate for mobile value added services. Leading players can focus on their expansion efforts in these economies.

Leading market players are emphasising the development of compact and costeffective mobile value added services to gain more customers. Furthermore, active players in the mobile value added service market are attempting to attract additional customers.

In addition, leading players in the market are focusing on inorganic growth strategies like strategic mergers and acquisitions, and collaborations with technology partners to enhance their offerings and reach.

In 2023, Google unveiled a new range of AI-powered features in its translation application at its Paris virtual event. These new features consist of more contextual translation options with examples and descriptions, an augmented-reality translation feature via Google Lens, and a redesigned app for Apple’s iOS operating system.

Deutsche Telekom, Ericsson and Samsung, in June 2021 successfully executed a

(see page 1), commerce media – where any consumer facing entity with first-party consumer data is poised to capitalise on selling brand ads, especially as cookies are no more – is a growth market for many and will soon be a key marketing channel for telemedia and VAS companies.

However, for all these streamers – and by that I also include all those content players that make up the telemedia market – advertising based around this content as well as to advertise the content itself is set to explode.

With publishers now coming round to multiple content formats, delivered across multiple platforms, the opportunity to create marketing networks has never been bigger or more ripe.

5G end-to-end (E2E) network slicing pilot. This trial was conducted on Samsung S21 commercial equipment, which is combined with Virtual Reality headset at Bonn lab of Deutsche Telekom.

The network provider’s market share is poised to ascend, projected to increase from 62.9% in 2024 to 63.3% by 2034, with an impressive Compound Annual Growth Rate (CAGR) of 14.9%. The segment is forecasted to achieve a substantial market valuation of US$2.2bn by 2034.

This growth is fuelled by the escalating adoption of mVAS by network providers, leveraging it to fortify customer relationships, reduce acquisition costs and mitigate customer churn rates, contributing significantly to the segment’s expansion.

Simultaneously, the enterprise segment is expected to experience robust growth with a CAGR of 14.6% through 2034. The surge is driven by a growing number of enterprises integrating mVAS to enhance operational efficiency and customer engagement. Utilising mVAS, enterprises seek to improve communication, receive real-time updates, personalised offers, and transaction notifications.

Moreover, these services play a pivotal role in optimizing internal functions, project management,sfostering employee collaboration, and facilitating data analysis, says the study.

Your AI toolbox for subscriber acquisition and retention in 2024

Julia Dimambro, CEO, Seriously Fresh Media offers a look at the tools you need to create content that is great for subscriber acquisition and retention using AI – and how there is still very much a need for the human touch

After the positive response to my interview with Paul Skeldon at Telemedia 8.1 in February 2024 about AI advancements in content creation, we figured it was time for an update. And let me tell you, in just three months, the progress in generative AI is mind-blowing.

As a quick example of how quickly things are progressing,

check out this QR code for a YouTube short featuring Will Smith, created using AI just a year ago. It’s insane how far we’ve come in 12 months.

And it’s not just content creation. For those of us in the Telemedia industry, the way we acquire, engage with, and keep customers will evolve dramatically this year.

So, let’s take a look at some of the main tools that can help with all of this in 2024. And given we are knee deep into AI research and applications here at SFM, if we can help save you guys time and money, it means you’ll have more for Seriously Fresh content!

1 AI-Powered Audience Insights – Platforms like Google Analytics and Facebook Audience Insights use AI to give you deep insights into your audience’s demographics and behaviours. This helps you tailor your marketing strategies for maximum impact.

2 Predictive Content Performance Analytics – Adobe Analytics or IBM Watson Customer Experience use AI algorithms to predict how your marketing campaigns will perform, so you can optimize your strategies accordingly.

3 Automated Personalization Platforms – HubSpot and Marketo are godsends for marketers. They offer AI-driven automation and personalisation across multiple channels, making sure your audience gets the right message at the right time.

4 AI-Powered Content Recommendation Engines – Amazon Personalise and Netflix’s recommendation algorithms analyse user behaviour to serve up personalized content recommendations, keeping your audience engaged and coming back for more.

5 AI-Enhanced CRM Solutions – Check out CRM platforms such as Salesforce Einstein and Zoho CRM Plus for AIenhanced customer relationship management. They use AI algorithms to automate

marketing and communication processes, segment customers, and deliver targeted messages and offers.

THE CAVEAT

However, there’s a caveat: while AI is revolutionising the Telemedia industry, it hasn’t yet been able to truly recreate premium video content that captures the essence of what it means to be human. It struggles to evoke what moves and inspires us, what resonates with our specific interests, tastes, and beliefs, and it doesn’t quite mimic our speech either; you can still tell when it’s AI.

That’s where Seriously Fresh comes in. With more than 20 years of experience in premium video licensing, we understand the Telemedia industry and its unique challenges for launching video services. Whether you need AI-powered solutions or

emotive productions that speak to your audience, we’ve got you covered.

That’s why at Seriously Fresh, we’re proud to be HUMANS, CREATING CONTENT FOR HUMANS.

In conclusion, as I was pon-

dering what to write, I couldn’t resist using AI to possibly prove a point. Can you guess which part I used the help of an AI tool? Drop me a message with your guess, or reach out if you want to chat more about premium video content. Seriously

Fresh has something for all budgets, audiences and objectives.

Julia Dimambro is CEO, Seriously Fresh Media julia@seriouslyfreshmedia.com

That’s edutainment

Paul Skeldon takes a look at how edutainment has become the latest content craze, blending learning with fun and games, and just how that engagement can be monetised

The traditional model of education, with rows of students passively absorbing information from textbooks and lectures, is facing a revolution. Enter edutainment, the dynamic merging of education and entertainment that prioritses engagement and interactivity. This trend is fuelled by a growing understanding of how people learn best: through active participation, exploration, and a touch of fun.

This shift is driven by several factors. Mobile apps have become ubiquitous and the educational app market is booming. Platforms such as Duolingo (language learning) and Khan Academy (math and science) offer bite-sized learning modules, gamified elements like points and badges, and personalised learning paths that cater to individual needs.

Educational app developer Duolingo, for example, boasts over 500 million users world-

wide, demonstrating the massive potential of this approach.

GOT GAME?

Traditional learning can be dry and monotonous. Gamified learning injects a dose of fun by incorporating game mechanics like points, leaderboards, and challenges into the learning process. Educational games like Minecraft Education Edition allow students to collaborate and problem-solve in immersive virtual worlds, while platforms like Quizizz transform quizzes into engaging competitions.

Minecraft Education Edition, a version of the popular sandbox game specifically designed for education, is used by over 100 million students globally, highlighting the power of gamification in learning. ([invalid URL removed])

Virtual Reality (VR) is also creating a new level of immersive learning. VR technology offers

the potential for truly immersive learning experiences. Imagine exploring the ancient pyramids of Egypt or dissecting a virtual frog in a biology class – VR makes these experiences possible and can significantly increase engagement and knowledge retention.

Companies like Talespin offer VR field trips that transport students to historical locations or natural wonders, making learning geography and history more exciting and interactive.

THE BENEFITS OF EDUTAINMENT

Edutainment makes learning more enjoyable, which leads to increased engagement and motivation. Interactive elements like games and simulations keep students actively involved, fostering a sense of accomplishment and a desire to learn more.

Active learning experiences offered by edutainment have

DCB: fuelling frictionless learning in edutainment

Direct carrier billing (DCB) can play a transformative role in the edutainment landscape, acting as a bridge between learners and valuable educational resources. Here’s how:

DCB allows users to pay for edutainment apps and subscriptions directly through their mobile phone bill. This eliminates the need for credit cards or complicated payment gateways, simplifying the process for users, especially those in regions with limited access to traditional payment methods.

The ease and convenience of DCB can encourage impulse learning experiences. A student intrigued by a specific app or game tied to a subject can readily access it without needing parental credit card information, potentially sparking a lifelong passion for learning.

While DCB facilitates payments, most carriers offer spending caps and usage alerts. Parents can leverage these features to control their children’s access to paid edutainment content while still

allowing them to explore learning opportunities safely.

DCB expands the potential customer base for edutainment platforms, reaching individuals who might not have access to credit cards or prefer alternative payment methods. This provides developers with a wider revenue stream, allowing them to invest in even richer and more engaging learning experiences.

DCB often transcends geographical limitations. Developers can offer their edutainment tools globally, knowing that local carrier networks will handle payments, increasing the reach and impact of their learning content.

In conclusion, DCB acts as a vital facilitator in the edutainment industry, removing payment barriers, promoting impulse learning, and driving revenue for developers. As edutainment continues to grow, DCB will be a key player in making engaging and effective learning experiences accessible to a wider audience.

been shown to improve knowledge retention compared to traditional methods. Immersive experiences like VR simulations can create lasting memories and a deeper understanding of complex concepts.

Many edutainment platforms offer personalized learning paths that cater to individual needs and learning styles. This allows students to learn at their own pace and focus on areas where they need the most help. For example, language learning apps like Duolingo adapt the difficulty level of lessons based on the user’s performance.

Meanwhile, edutainment resources are often readily available on mobile devices and computers, making learning accessible anytime and anywhere. This flexibility allows students to learn on their own schedule and revisit concepts as needed.

CHALLENGES ABOUND

But there are challenges. While technology can be a powerful learning tool, excessive screen time can have negative consequences for children’s development. It’s crucial to find a balance between edutainment and other activities that encourage physical activity and social interaction.

Access to technology and reliable internet connections can vary significantly – and cost can be an issue. Inequitable access can exacerbate educational disparities if certain groups lack the resources to take advantage of edutainment tools.

Gamified elements and the interactive nature of edutainment can also sometimes become distractions, diverting attention away from the core learning objectives. It’s important to ensure that the games and activities are welldesigned and aligned with the educational goals.

And, with the rapid growth of the edutainment market, ensuring the quality and accuracy of educational content is essential. Parents and educators need to carefully

evaluate apps and programs before introducing them to children.

THE BUSINESS OF EDUTAINMENT

Despite these challenges and its relative new-ness, the edutainment market booming and is now a multi-billion dollar industry, with significant growth potential.

Many edutainment apps are freemium, offering a basic level of content for free, with premium features and in-app purchases available for a subscription fee. This allows users to try before they buy and generates revenue for app developers.

Some platforms like Rosetta Stone offer subscription-based access to their entire library of language learning tools and resources. This provides a predictable revenue stream for companies and ensures users have access to all available content. Educational institutions like

schools and libraries can purchase licenses for educational software and apps, allowing them to provide these resources to students. This model allows companies to reach a wider audience and cater to the specific needs of educational institutions.

Some edutainment apps utilize

Edutainment

The rise of Artificial Intelligence (AI) will lead to AI-powered tutors and personalised learning platforms will further customise the learning experience, catering to individual needs and learning styles.

At the same time, AR technology will allow learners to interact

offers a compelling alternative to traditional learning methods – with engagement

in-app advertising to generate revenue. This model can be effective for free apps, but it’s important to ensure that ads don’t interfere with the learning experience.

LEARNING THE FUTURE

Edutainment is poised to become an even more dominant force in the education landscape. As technology continues to evolve, we can expect to see:

with educational content in the real world, further bridging the gap between theory and application. Imagine history students being able to view historical figures and events through an AR app while visiting a museum.

Alongside core academic subjects, edutainment platforms will increasingly focus on developing essential soft skills like critical thinking, collaboration, and

problem-solving.

Effective edutainment tools will incorporate ongoing assessment and feedback mechanisms to track progress and identify areas where learners need additional support.

Edutainment offers a compelling alternative to traditional learning methods. By fostering engagement, interactivity, and accessibility, edutainment has the potential to revolutionise the educational experience for learners of all ages. However, careful consideration needs to be given to potential drawbacks like screen time limitations and ensuring equitable access. As the edutainment market continues to evolve, collaboration between educators, app developers, and technology companies will be crucial to harness the power of this approach to create engaging and effective learning experiences for future generations.

& ENGAGEMENT

Why is integrating security in SMS trading essential?

A messaging platform should stand as a bastion of security, with an all-encompassing suite of security operations crucial for the preservation and protection of valuable data. Here Horisen explains what that means in practice

The security of information takes precedence in the digital sphere nowadays, especially within professional messaging businesses where seamless communication is imperative. Therefore, security must be your top priority when considering a platform for your messaging business. A messaging platform should stand as a bastion of security, with an all-encompassing suite of security operations crucial for the preservation and protection of valuable data.

Security should not be an afterthought; it should be the foundation upon which the entire system is built. With a commitment to meeting the highest security standards, the platform should be designed, monitored, and maintained according to the strictest security protocols. It should ensure a fortified environment to safeguard sensitive information, complying with GDPR regulations and hosting data in a secure cloud environment.

A FORTIFIED FORTRESS

A secure platform should boast servers collocated in bankcertified data centres, employing state-of-the-art layered security measures. These measures should include a fully redundant virtualization infrastructure and zero single-point-of-failure network setup nested behind a high-security firewall setup. It should be protected by redundant Distributed Denial of

Service (DDoS) protec tion at the internet service provider (ISP) level, ensuring that only cleansed IP traffic enters the system.

STRICT ACCESS CONTROL

Access to the platform should be accurately controlled, with connec tions restricted solely to trusted IP addresses. For enhanced security, VPN connectivity should be available upon request, while secure IPSec and TLS connec tions should be encouraged as best practices for customers. This fortification ensures that only authorized and secure channels are permitted, minimizing the risk of unauthorized access and potential breaches.

prompt response and resolution to any potential issues. In the event of an incident, everyone involved should be promptly notified within 24 hours, with detailed information regarding the incident provided. Emphasis should be placed on transparency and accountability, with a dedicated team readily available to respond and address incidents at any time, ensuring proactive measures are taken to minimize disruptions and maintain the reliability and security of the platform.

CERTIFICATION, STANDARDISATION AND COMPLIANCE

FIRM RELIABILITY AND AVAILABILITY

A secure platform should be distinguished by its high availability and exceptional robustness. With a system boasting 99.999% availability and a no-downtime policy even during maintenance, it should ensure uninterrupted service. The auto-rebinding process should kick in if a connection falters, guaranteeing continuous service without interruptions.

The platform should not only fortify its defences, but also actively monitor and repair any potential system issues. The 24/7 availability of a professional support team should ensure that any concerns or challenges are swiftly addressed. Equipped with a dedicated team of developers well-versed in industry standards, the platform should undertake hands-on maintenance, problem detection, and swift resolution, ensuring the system remains resilient and secure at all times.

INCIDENT MANAGEMENT

To emphasize the commitment to providing customers with a secure platform for their messaging needs, Incident Management within the platform ensures

To achieve a high level of security, the platform should utilize a framework of controls based on ISO, NIST, OWASP, and CIS requirements. In addition to ISO 27001:2022 certification and GDPR compliance, system hardening measures should be applied based on CIS controls on all cloud and system components. To apply security best practices in secure software development and testing, vulnerability scans should be performed daily, and 3rd party penetration tests yearly to ensure staying up to date with the newest OWASP TOP 10 and NIST guidelines.

EMBRACING A SECURE FUTURE

The significance of security operations within an SMS platform cannot be overstated. A secure platform is essential for safeguarding sensitive information and ensuring the integrity of communication. HORISEN SMS Platform is a security-rich SMS trading solution that safeguards and elevates SMS trading businesses to new heights of secure communication.

www.horisen.com/contact/

THE

paul@telemedia-news.com

ART DIRECTOR Victoria Wren

FROM THE EDITOR

2024: an esoterically interesting year so far for telemedia

PRODUCTION

PUBLISHER

2023 was an exciting year for telemedia: RCS adopted by Apple, carrier billing exploding across all sorts of service, content and AI joining forces to great some really interesting services. The market has become buoyant and, largely, quite compliant (see page 1). 2024 – thus far, and we are now half way through it believe it or not – has been much more sedate. However, there are some really strange and esoteric things happening that may yet reshape the industry in some quite profound ways. The concept of commerce media has been with us for a while – it is really just digital advertising reach out across more sites – but 2024 is seeing it start to become a real force to be reckoned with (see page

1). As cookies become effectively outlawed, brands needing to market to consumers have to turn to those with first party data and that suddenly puts any organisation, such as MNOs front and centre when it comes to being able to carry adverts. This is nothing new, but done right could be a massive new revenue stream for carriers. Commerce media is already becoming a multi-billion dollar industry in the US for retailers. MNOs – with their location data and device information – are well placed to really seize this opportunity.

It is also an excellent new performance marketing channel for VAS, offering them an excellent way to engage with consumers. It could also lead to a bonanza in carrier billing off the back of

these services going live. The downside is that marketing and advertising are under attack. Invalid traffic created by AI and bots is really starting to hammer advertising (see page 18), while AI tools (see page 10) – useful as they are in content and service creation –are now being regulated (see pages 22 and 24). So, 2024 may look quiet, but actually there is a lot going down – and expect more in the second half.

telemediaonline.co.uk

@telemediaTweets

Paul Skeldon. editor

Getting the message How consumers are changing how they use messaging

Messaging have slowly morphed into a powerful business comms channel – but what do consumers think about it and how are they using it? We take a look at the latest MEF survey data from around the world

Business messaging has steadily evolved from a series of individual channels siloed into specific use cases to a more interwoven solution where organisations increasingly look to offer communications platform as a service (CPaaS).

At the same time, however, the P2P behaviour of consumers, and different demographic preferences for how organisations actually contact them, has also evolved – largely driven by the growing availability and capabilities of richer channels.

To find out just how digital transformation is modifying the messaging and channel behaviour, experiences and expectations of consumers, Mobile Ecosystem Forum (MEF) has surveyed 9,750 smartphone users across 15 countries.

What it has found makes interesting reading. A total of 91% of smartphone users across the 15 countries surveyed by MEF this year now receive com-

mercial messaging. However, this number is unchanged from last year indicating that we may have reached saturation point in users, and specifically as far as Text messaging (SMS) is concerned.

CHANGING OF THE GUARD

Year-on-year, this survey has shown that users appreciate a rich mix of communication solutions – but with email always a hot favourite for A2P. This year, however, we have seen significant decrease in the number of people who prefer to receive commercial messages via email while there has been a significant increase in the number of people who would prefer WhatsApp.

The older the demographic, the more likely it is to receive either email, SMS or phone calls – while Instagram is primarily youth-focused with most messaging going to the 25-34 age group and decreasing steadily in

the older demographics. Spam continues to be an issue regardless of the market with 47% of all respondents receiving unsolicited messages. However, this number is down slightly from 49% in 2023 and eight of the 13 countries survey by MEF last year saw a decrease in unsolicited messages.

FRAUD STILL AN ISSUE

Although instances of data harm are generally lower than last year they are still reported most on the most-used A2P channels, and WhatsApp managed to buck the trend with a 4-point rise in reported attacks perhaps due to the fact that more people are now using the OTT channel. We are seeing an increase in positive action being taken by those affected by data harm, with examples of users engaging credit monitoring or identity theft companies, closing accounts and cancelling credit cards all on the rise.

Gavin Patterson, Director of

Data, MEF, comments: “2024 marked another important milestone in the development of our coverage with the addition of two new markets – Egypt and Indonesia – to our overall survey population. In total, MEF now surveys respondents in 15 countries across the world representing almost 56% of the world’s total population.

“Mobile messaging gives enterprises the most direct and personal communication channel imaginable, so our experiences, our preferences and our behaviour are important and valuable tools to help ensure that the business messaging market can continue to grow – and grow in the right direction. Mobile messaging gives enterprises the most direct and personal communication channel imaginable, so our experiences, our preferences and our behaviour are important and valuable tools to help ensure that the business messaging market can continue to grow – and grow in the right direction. I hope you enjoy having a look through these, and all our other, consumer survey results.”

A quantum of SMS solace

Quantum computing offers much to the world, but it may be the hackers that get the first use out of it… and messaging could be their target. Paul Skeldon takes a look at how secure messaging apps might be to quantum hackers – and finds them wanting

Quantum computing – using the wave-particle duality of subatomic particles to act as super diodes – may sound like science fiction, but it is already finding practical uses in the digital world – and not just with the good guys.

Quantum computing has significantly elevated the threat of hacking, highlighting the critical importance of implementing quantum-level security measures in application algorithms.

To assess the risk, Surfshark – a cybersecurity company focused on developing humanised privacy and security solutions such as VPNs – has assessed 12 widely used messaging apps to determine their quantum security status, identifying those capable of withstanding quantum hacking attempts. This assessment is based on known quantum threats and the emergence of new threats remains a possibility. Consequently, apps deemed quantum-secure today may need to adjust their defences in the

future. Nonetheless, those currently recognised as quantum-secure are demonstrating proactive measures, while those relying on traditional encryption or lacking encryption altogether are falling behind.

According to the research, only two messaging applications are currently prepared for the quantum computing era: Signal and iMessage. Signal’s recently announced Post-Quantum Extended Diffie-Hellman (PQXDH) encryption protocol may not be as advanced as Apple’s PQ3², but it is nonetheless equipped to defend against the present quantum computing threats.

Half of the most popular analysed applications provide End-to-End (E2E) encryption by default, which protects against conventional threats. However, classical cryptography is not secure against quantum computing threats.

Notably, even though Skype encrypts messages, when a Skype call is made to a mobile or

landline phone, the segment of the call transmitted via the Public Switched Telephone Network (PSTN) is not encrypted by Skype.

Are big tech companies lagging behind? Facebook only introduced default encryption of messages a few months ago –seemingly a delayed reaction, especially since Apple has recently introduced its quantum-secure messaging encryption protocols. Another major player, Google, has had encrypted messages in its pre-installed Android messenger (Google Messages) by default for about half a year, slightly earlier than Facebook Messenger. Nevertheless, both of these tech giants’ messaging applications significantly trail behind Apple in terms of security.

Some messaging applications are not only vulnerable to quantum threats but also fail to provide default protection against current dangers. Telegram, WeChat, and QQ do not have encryption enabled as the standard setting. Snapchat encrypts images but not text messages.

The absence of E2E encryption leaves a conversation vulnerable to interception by hackers,

governments, or private entities. And the results of such interception can be dire — even a seemingly innocent joke shared in a private conversation can result in arrest.

Messaging apps developed in authoritarian countries often lack straightforward default encryption. WeChat and QQ (both lacking encryption) originate from China, while Telegram (also without default encryption) was founded by brothers with Russian origins and is headquartered in the United Arab Emirates. The same brothers also founded the widely-used platform VK, which was later acquired by the Russian state.

At least one in six people worldwide could be subject to surveillance through unencrypted messaging. WeChat boasts over 1.3 billion users, with around half a billion residing outside China. Telegram recently reached 900 million users. To be on the safe side, Surfshark has assumed that all Telegram users use WeChat as well, which most likely is not true and would mean that even more people are vulnerable to unencrypted message peaking.

Invalid traffic: How AI bots are eating advertising

Digital transformation and AI have worked wonders in the ad market, but they have also seen a massive rise in invalid traffic – traffic from bots that skews ad stats and costs advertisers and publishers dear. Paul Skeldon reports

More than a fifth of internet traffic is invalid. Or to put it another way, one out of five website visits is not a real person, but an automated program –a bot – with no intention or capability to convert into a paying customer.

When you look at in-ad traffic in programmatic campaigns this figure sometimes hits 90%. That is a lot of non-paying traffic.

So finds a study by Fraud0, which analysed data from its largest 100+ customers and analysed a total of more than 2.9 billion sessions in 2023.

It is important to note that Fraud0 excluded crawlers, such as the Google Search Engine Crawler, from the invalid traffic data in order to obtain more

meaningful results. And the results are shocking – but why is this happening and what can be done about it?

THANKS DIGITAL TRANSFORMATION

Taking a step back, digital transformation has revolutionised the business world, enabling companies to leverage AI for growth and efficiency. However, it also creates new challenges and risks, especially in the realm of digital advertising. One of the most pervasive and persistent threats is this invalid traffic, which refers to any clicks or impressions that are not generated by genuine human users.

The cost is huge. Services and

ads are made and sold based on traffic and, if you can’t trust what or where that is coming from – nor, indeed, if it is actually real – then the business of digital marketing looks shaky. With more companies poised to make a commerce media play (see page 1), anything that undermines digital marketing could be extremely costly.

So, where are the problems and what can be done to fix them?

CHANNELS AND INDUSTRIES

According to the research, invalid traffic is a major threat across all digital marketing channels – no channel is exempt. Its uncontrolled presence means wasted ad budgets and has negative consequences such as ineffective campaigns, skewed analysis, and misleading attribution.

The biggest proportion of invalid traffic is seen, perhaps unsurprisingly, on Google Shopping, which hi 67% in 2023. TikTok’s rapid growth has also seen it rocket up the charts for invalid traffic, hitting nearly 40%. Interestingly, The Trade Desk – a commerce media platform – is the second biggest, coming in not far behind Google Shopping on 55%. LinkedIn Ads is also seeing some issues, with nearly half its traffic being invalid.

The issue of invalid traffic and bots naturally affects every industry. But there are some significant differences in terms of the extent. The sector most impacted by invalid traffic is gambling, which sees nearly 40% of

its traffic being invalid. Typically this is being seen in fake account creation to take advantage of promotions, credential stuffing and account take over – where criminals use bots to break into customer accounts by automating login attempts using compromised or predictable passwords. There is also growth in polluted analytics that distort customer numbers and ad stacking, where multiple ads are piled up in one place so a click on the top, genuine, ad registers impressions on all the others. This is costing the advertisers as they pay for clicks they don’t receive.

Ecommerce and retail see almost a third of its traffic being invalid. Here scalping and scraping – where bots reserve limited availability or desirable goods to drive up prices and bots that harvest data respectively – are the biggest headaches. Inventory hoarding and wasted ad spend are also a big deal.

But it is domain spoofing that has the biggest impact. Domain spoofing is a widespread technique used by fraudsters to siphon off ad budgets. Inferior websites are created that pretend to be well-known websites. They are often an exact copy of these websites or are simply created by AI.

The approach sounds simple and effective – and it is. Advertisers pay for this supposed premium traffic, but never see a conversion or the hoped-for branding effects.

Telecoms and tech/SaaS sector players are each seeing around a fifth of their traffic (21% and 19%

respectively) being invalid. Media and marketing hits 18%.

WHERE AND WHEN

Interestingly, the majority of invalid traffic originates from Germany. However, this does not necessarily mean that the persons are also physically located in Germany. Cybercriminals often use data centres or proxy servers to organise bot attacks, so the analysis of web traffic in different countries is likely to reflect proxy locations rather than the actual locations of the attackers.

According to Fraud0, the result is not surprising, as the majority of companies in this evaluation come from Germany. Attackers also benefit from lower latency when they choose proxies that are closer to their targets – a key advantage when conducting high-volume attacks.

Similarly, when it comes to the distribution of operating systems,

cybercriminals follow the market. Both Windows and Android are market leaders (>70% in desktop and mobile) and are therefore more often abused for invalid traffic in order to get buried in the crowd and not attract attention in the corresponding analyses and security systems.

Android accounts for 48.88% of invalid traffic, while Windows has 12.26%. MacOS is under 10%, while iOS doesn’t quite make it to 2%.

THE FUTURE – AND THE SOLUTION

Advances in AI, exemplified by the likes of Bard or ChatGPT, will lead to an increase in fake internet activity, as the barriers to creating bots are lowered and the sophistication and capabilities of malicious bots are improved. Using modern AI, it is now trivial to spin up hundreds of thousands of fake bot accounts

with human-like behaviour for less than a penny per account. We are coming to the end of this version of the internet and it will be replaced by something entirely different.

This evolving landscape turns cybersecurity into a constant game of adaptation, where defence mechanisms are continually challenged by advancing opponents. The availability of advanced, free AI models potentially offers those with malicious intentions a tactical advantage.

In today’s world, organisations must employ proactive strategies, monitor inbound activity and automatically intercept and identify spoofed traffic before it enters their systems. Bot management is challenging, but by implementing effective bot detection and mitigation strategies, you can protect your website from threats.

Fighting bots is all about identi-

fying visiting bots and minimising their negative impact on your company, your users,and your customers. Bot detection and mitigation solutions are tailored to enable uninterrupted website access for humans and legitimate bots and act as barriers to prevent unauthorized access by malicious bots.

With bot activity on the rise, it is important to detect and deal with traffic generated by bots. Nowadays, software continuously monitors bot activity within your online platforms, meaning it automatically fights threats in real-time as soon as they appear or try to gain access.

Download the full report https://www.fraud0.com/ wp-content/uploads/2024/02/ Unmasking-the-ShadowsInvalid-Traffic-2024-Report.pdf

CYBERSECURITY & FRAUD

The silent siege Robocalling fraud and how the fight back begins

Blame AI, but while it brings many wonderful things, it also brings a surge in fraud. The latest, Paul Skeldon discovers, is robocalling fraud – however, the fightback has begun

Robocalling fraud is on the rise – and AI is to blame. Robocalling involves the use of automated dialling systems to place pre-recorded messages with the intent to deceive or trick the recipient. These calls often impersonate legitimate businesses like banks, credit card companies, or government agencies. The scammers attempt to steal personal information, financial details, or trick victims into sending money.

The sheer volume of robocalls is staggering. According to Juniper Research, a leading technology research firm, an estimated 179 billion robocalls were made globally in 2023, with a projected increase to 200 billion by 2027. This translates to bil-

lions of unwanted calls, causing frustration, disruption, and significant financial losses for individuals and businesses alike.

Some of the common tactics used by robocallers, include:

• Caller ID Spoofing: Robocallers often use technology to manipulate the Caller ID on your phone, making it appear as if the call is coming from a legitimate source, like a local phone number or a well-known company. This increases the likelihood that the recipient will answer the call.

• Phishing Scams: Robocallers may try to trick you into revealing personal information, such as your Social Security number,

bank account details, or passwords. This information can then be used for identity theft or fraudulent transactions.

• Preying on Fear and Urgency: Robocallers may use scare tactics, claiming your Social Security number has been compromised or that you owe money to the IRS. The sense of urgency created by these tactics can lead victims to make rushed decisions and disclose sensitive information. The financial impact of robocalling fraud is substantial. Juniper Research estimates that global losses from robocalling fraud will reach $48bn by 2027. These losses are borne by individuals who fall victim to scams, as well as businesses who experience reputational damage and a decrease in customer trust.

COMBATING THE THREAT: ENTER SHAKEN/STIR

The rise of robocalling fraud has necessitated the development of new solutions. Here’s where SHAKEN/STIR comes in. SHAKEN/STIR, also known as Secure Telephone Identity Revisited and Signaturebased Handling of Asserted Information Using Tokens, is a suite of protocols and procedures designed to combat caller ID spoofing.

SHAKEN/STIR consists of two key elements. SHAKEN (Secure Telephone Identity Revisited), is a protocol estab-

lishes a framework for issuing digital certificates to phone numbers. These certificates verify the legitimacy of the caller’s identity and ensure that the caller ID displayed on the receiving phone is accurate.

STIR (Signature-based Handling of Asserted Information Using Tokens), meanwhile, is a protocol defining the process of using digital signatures to authenticate the caller ID information.

The originating phone service provider signs a digital token with the caller’s information, and this token is then transmitted to the receiving phone service provider. The receiving provider can then verify the signature and determine if the caller ID is legitimate.

Here’s a simplified explanation of how SHAKEN/STIR works to prevent caller ID spoofing:

• Digital certificate issuance: phone service providers issue digital certificates to their customers, verifying their phone numbers.

• Call initiation: when a call is placed, the originating phone service provider signs a digital token with the caller’s information using the issued certificate.

• Call transmission: the signed token is transmitted along with the call to the receiving phone service provider.

• Signature verification: the receiving phone service provider verifies the signature on the token using the public key associated with the originating phone service provider’s certificate.

• Caller ID authentication: if the signature is valid, the call is authenti-

cated, and the correct caller ID information is displayed on the receiving phone.

• Potential warning: if the signature verification fails or no token is present, the receiving phone service provider can choose to block the call or display a warning message to the recipient about a potential scam call.

While still under development and implementation, SHAKEN/ STIR holds immense promise in combating robocalling fraud. But it can make a difference. For starters it can reduce spoofing and scam calls by verifying caller ID information, SHAKEN/STIR makes it significantly harder for robocallers to spoof legitimate numbers, reducing the number of scam calls reaching consumers. This can lead to a decrease in financial losses from robocalling fraud.

declines, consumers will regain trust in answering their phones. This can lead to a more positive mobile communication experience.

SHAKEN/STIR can provide valuable information to law enforcement agencies investigating robocalling scams. The digital certificates and tokens associated with calls can help identify the origin of robocalls and track down those responsible.

While SHAKEN/STIR represents a significant step forward, there are still a number of challenges to consider. For SHAKEN/STIR to be truly effective, widespread adoption by phone service providers across the globe is necessary. This requires ongoing collaboration and international agreements to ensure compatibility between different networks.

lance and innovation are required to stay ahead of evolving spoofing tactics.

For SHAKEN/STIR to reach its full potential, consumers need to be aware of its existence and understand how it works. Public education campaigns are crucial to ensure people are informed and can take advantage of the protections it offers.

A COLLABORATIVE EFFORT

The fight against robocalling fraud requires a multi-pronged approach. SHAKEN/STIR is a powerful tool, but it’s one piece of the puzzle. Developing and implementing new technologies to identify and block robocalls is essential. This includes advancements in call filtering systems and artificial intelligence-powered solutions.

track down the perpetrators of robocalling scams and hold them accountable.

Ongoing public education campaigns are critical to empower consumers to identify and avoid robocall scams. Educating people about the tactics used by robocallers and the functionalities of SHAKEN/STIR will increase their vigilance and decrease the success rate of these scams.

As the number of spoofed calls

Scammers may develop new techniques to bypass SHAKEN/ STIR protocols. Continued vigi-

Stronger international cooperation between law enforcement agencies is necessary to

Can branded voice calling end the siege?

In today’s world, the constant barrage of unknown phone numbers can be frustrating and suspicious. However, a new technology is emerging that aims to transform the way businesses connect with their customers – branded voice calling.

This innovative solution not only streamlines communication but also offers a powerful weapon against caller ID spoofing and fraud.

Branded voice calling allows businesses to display their brand name, logo and even a call reason alongside the caller ID information when they make calls to customers. This eliminates the uncertainty of unknown numbers and fosters trust by clearly identifying the legitimate source of the call.

Imagine receiving a call with your bank’s logo and a message like “Important account update” instead of just an unfamiliar number. Branded voice calling offers a more transparent and secure communication experience.

Fraudsters often rely on caller ID spoofing to impersonate legitimate businesses like banks, credit card companies, or government agencies. This tactic deceives victims into answering the call and potentially

revealing personal information or falling for scams. Branded voice calling acts as a powerful deterrent against these tactics in several ways:

By displaying the brand name and logo, branded voice calling makes it immediately clear to the recipient who is calling. Since the caller ID information is verified by the phone service provider, spoofing a brand’s identity becomes significantly more difficult. This makes it harder for fraudsters to trick consumers into answering their calls.

Branded voice calling reinforces a company’s commitment to secure communication and protects its brand image from being misused by scammers.

Several innovative service providers have emerged to offer branded voice calling solutions to businesses. Hiya Connect is a platform that allows businesses to display their brand information when making outbound calls, boosting call answer rates and building trust with customers.

Twilio, meanwhile, uses its cloud communications platform to provide branded voice calling functionalities as part of its suite of communication solutions for businesses.

Robocalling fraud remains a significant threat, but with the combined efforts of phone service providers, technology developers, law enforcement, and consumers, we can turn the tide. SHAKEN/STIR offers a powerful tool in this fight, but its success depends on widespread adoption, continued innovation, and public awareness. By working together, we can create a safer and more secure mobile communication experience for everyone.

Leading brands across various industries are recognizing the benefits of branded voice calling. Banks and credit unions use branded voice calling to improve customer confidence when receiving important account information updates or fraud alerts. Hospitals and clinics, too, use branded voice calling to remind patients about appointments, reducing missed appointments and improving communication.

Brands use branded voice calling to connect with customers regarding order confirmations, special offers, or loyalty programme updates.

So, what does branded voice calling offer these businesses? For starters, customers are more likely to answer calls when they recognise the brand calling them, leading to better communication and improved customer satisfaction. Branded voice calling also projects a professional and trustworthy image, fostering stronger customer relationships.

Some branded voice calling platforms offer analytics that provide businesses with insights into call performance and customer engagement.

US, UK and EU all make moves to regulate AI What does it mean for telemedia?

The UK and US have signed a memorandum of understanding to look at the regulation of AI, hot on the heels of the EU’s AI Act being ratified in March as the world starts to take seriously the regulation of this new technology. But what are the ramifications for the telemedia industry, asks Paul Skeldon ?

The UK and US have signed a memorandum of understanding to look at the regulation of AI, hot on the heels of the EU’s AI Act being ratified in March (see panel). The governments of the world are finally waking up to the need to, if not control, then try and tame rampant AI development and turn it into a force for good. We also want to avoid the cliched Terminator-style ‘AI destroys the world’ as a possible outcome too.

But what is it likely to mean for the telemedia sector, which has become so inherently reliant on AI?

Well, the main use of AI in parsing vast data sets to better target consumers is unlikely to be readily impacted by these attempts at corralling the wild west of AI. The thrust of both the US-UK and EU rulings is to outlaw things like biometric targeting and profiling, as well as the European catch-all of

EU becomes first to regulate AI

The EU has become the first government to implement a law regulating AI. t aims to protect fundamental rights, democracy, the rule of law and environmental sustainability from high-risk AI, while boosting innovation and establishing Europe as a leader in the field. The regulation establishes obligations for AI based on its potential risks and level of impact.

BANNED APPLICATIONS

The new rules ban certain AI applications that threaten citizens’ rights, including biometric categorisation systems based on sensitive characteristics and untargeted scraping of facial images from the internet or CCTV footage to create facial recognition databases.

Emotion recognition in the workplace and schools, social scoring, predictive policing (when it is based solely on profiling a person or assessing their characteristics), and AI that manipulates human behaviour or exploits people’s vulnerabilities will also be forbidden.

Measures to support innovation and SMEs

Regulatory sandboxes and real-world testing will have to be established at the national level, and made accessible to SMEs and start-ups, to develop and train innovative AI before its place-

“other high-risk AI systems”, which include – today, at least… who knows what the future may hold in high-risk AI? – critical infrastructure, education and vocational training, employment, essential private and public services, to name but a few. The laws are also heavily targeting emotion recognition and profiling, particularly on and around social media and even more particularly of the young. All these have no direct impact

ment on the market.

During the plenary debate prior to passing the Act into law, the Internal Market Committee corapporteur Brando Benifei (S&D, Italy) said: “We finally have the world’s first binding law on artificial intelligence, to reduce risks, create opportunities, combat discrimination, and bring transparency. Thanks to Parliament, unacceptable AI practices will be banned in Europe and the rights of workers and citizens will be protected. The AI Office will now be set up to support companies to start complying with the rules before they enter into force. We ensured that human beings and European values are at the very centre of AI’s development”.