The markets of Bangladesh, Pakistan and Sri Lanka unlocked

Fraud facts

Just how big a problem is fraud –and where is it happening? 19

MENA CONTENT

Understanding the content that is driving MENA mVAS today

How Ooredoo and Evina beat DCB fraud in MENA

Unlocking MENA: a $360bn mVAS opportunity awaits

Mobile’s contribution to the wider MENA economy is set to reach $360 billion by 2030, up from $310 billion in 2023 and will employ some 700,000-plus people as technology continues to reshape the region. And telemedia is getting a big slice of the action.

As World Telemedia Dubai kicks off on 11 May, figures from the GSMA show just how buoyant the MENA market is – and how its growth prospects continue to be enormous in the market. There are already more than 427 million mobile users across MENA, 327 million of

them using mobile internet and therefore ripe for using telemedia mVAS services. Some 81% of them use a smartphone.

For MNOs this translates into revenues of some $66 billion in 2023, predicted to grow to more than $88 billion in 2030.

value added services

FInd out what content drives which leading African markets

Discover how cybercrime is impacting African consumers

The content that has ignited the imagination of Indian consumers

WHERE NEXT FOR DCB?

Carrier billing drives mVAS, but alt.payments are growing fast

Discover the latest techniques for driving traffic worldwide 24 AI SHIFTS MARKETING AI underpins marketing, but it is having surprising effects 25 NEXT GEN MESSAGING RCS needs to be pushed, but has it already lost to OTT?

Meet Shweta Mahajan from Digital Technology

Africa has the potential to be one of the world’s leading mVAS markets – so long as network investment keeps pace with consumer desire to engage with the digital economy.

The African market for mobile value-added services (mVAS) in 2025 is experiencing substantial growth, driven by increasing smartphone adoption, expanding mobile internet access and the proliferation of mobile financial

THE BIG GUY Paul Skeldon paul@telemedia-news.com

ART DIRECTOR Victoria Wren victoria@wr3n.com

CONTRIBUTORS & CONSULTANTS Nick Lane Jarvis Todd Tim Green

SALES & MARKETING info@Telemedia-news.com

PRODUCTION DIRECTOR Annika Micheli annika@Telemedia-news.com

PUBLISHER Jarvis Todd jarvis@Telemedia-news.com TO SUBSCRIBE www.TelemediaOnline.co.uk

WHAT WE’VE BEEN LISTENING TO In the garden, The Band Feel Giving Me That Look In Your Eyes, The Fans WHAT WE HAVE BEEN READING The decline and fall of the human empire, Henry Gee WHAT WE HAVE BEEN AMUSED BY Last one laughing UK SUMMER 2025 WILL BRING…

World Telemedia Dubai: where to see the next gen of mVAS

As World Telemedia Dubai (11-13 May) attests, the mVAS sector across MENA, Africa, India and South Asia is booming. And this issue of telemedia magazine is dedicated to looking at these markets in detail to assess not only where they might be heading, but also where they are at right now. What is interesting about all these ‘evolving and emerging’ regions is that, at a time when the US is playing brinkmanship with a trade war, these are all very much self-contained markets. They have all developed their own localised content and services, they are all finding their way with not only carrier billing but also pioneering the use of wallets and alternative payments and are creating vibrant ecosystems that many markets in the West could well learn a thing or two from (see page 20).

In MENA, for example, the roll out of 4G and 5G networks in many regions – particularly the Gulf Cooperation Council (GCC) countries of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates – has thrust the relatively youthful market into the full-on digital economy. Gaming, streaming, sports, esports and lifestyle all vie for eyeballs, creating a lucrative ecosystem of MNOs,

content providers, billers and marketers all working in a surprising harmony (see page 6). Across Africa, similar things are happening, albeit more piecemeal in such a vast continent. Again, networks and youth are driving the market, but so too is the rapid uptake of mobile money services such as M-Pesa, which has seen all online services, not just commerce, start to thrive (see page 10).

India, meanwhile, has quietly become a regional, if not global, powerhouse in mobile entertainment. Its booming market is again youthdriven, but it is fair to say that the reach of mVAS here is also huge (see page 14). India’s neighbours – Bangladesh, Pakistan and Sri Lanka – meanwhile lag behind, but have huge potential (see page 19).

So, as the US wavers in its position as a global leader, these regional markets are more than able to be themselves and offer huge opportunities that the telemedia industry is ready, willing and able to fill

telemediaonline.co.uk @telemediaTweets

Paul Skeldon. editor

Unlocking MENA: a $360bn mVAS opportunity awaits

DRIVERS OF SUCCESS

Among the most important success factors in this rise and rise of MENA mVAS lies in networks. In 2023 60% of MENA consumers were connected to 4G. By 2030 it is predicted that 50% will be connected to 5G.

Rollout of 5G is, compared to some developed countries, extremely rapid. This is already seeing consumers getting a taste for high-quality streaming and gaming, as well as AR and VR services.

This has all been delivered to consumers at a relatively low cost. The cost of mobile data as a percentage of GDP has halved over recent years, making connectivity more accessible. Growth in locally relevant content such as media, entertainment social media platforms and e-government services has also boosted user engagement (see page 6).

The investment by network operators in the region is significant. While the market is buoyant, it has many political, social and economic challenges (see below), yet MNOs have continued to pour money into the region. This has prompted local governments to work harder on

Regions to be cheerful

Certain countries within MENA stand out for their success in mVAS adoption and others, while successful are still hard to do business in. Some of the standout markets in the region include:

• GCC Countries – The Gulf Cooperation Council (GCC) comprises six Middle Eastern countries: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. High smartphone penetration (88% in 2023) and advanced network infrastructure, including widespread 5G deployment, make GCC states particularly strong markets. The UAE and Saudi Arabia lead in digital transformation initiatives and partnerships between operators and tech firms like Microsoft for cloud-based services.

• North Africa – Countries like Egypt benefit from growing affordability of mobile devices and data plans. Subscriber penetration reached 84% in North Africa by 2023. Increased availability of locally relevant content such as e-government services has also driven adoption.

• Iran – Economic instability, poor payments infrastructure and economic instability caused by sanctions against its government all hamper the Iranian market. However, despite these challenges, Iran has seen significant growth due to expanded mobile broadband networks and increasing demand for mobile entertainment services.

• Algeria and Libya – These countries have poor infrastructure, a huge connectivity gap between urban and rural areas and economic instability. However, while not there yet, these countries are likely to be part of the next wave of MENA growth as their economies come under control and network infrastructure investment arrives.

regulation and compliance and creating favourable business conditions for operators, service providers and the rest of the telemedia value chain to help encourage and continue this investment.

On the content front (see page 6), the MENA mVAS market has also been helped along by Middle Eastern government support of sports. Bring the World Cup to Qatar along with creating a star-studded pro-soccer leagues such as the Saudi Pro League have inculcated and developed a deep appetite for sports content in the region. This along with gaming and localised streaming and social content is also driving the market forward.

CHALLENGES

However, there are challenges. Large swathes of the population, especially outside of the major urban areas, remain unconnected, with no assess to network and so are left in the usage gap. Closing this gap through network investment – with handset sales to then follow – would not only expand the market, but hugely improve the lives of people. It would give them access to healthcare, finance, education and entertainment.

The region also has its fair share of economic instability, seeing hyperinflation and conflicts in certain countries disrupt mobile ecosystems and limit consumer spending power.

On a deeper level there are also issues with regulation and compliance in many markets. In some countries intense regulatory environments are creating barriers for operators and service providers. Ensuring compliance with local laws while expanding services is challenging.

In other markets regulation is light and, while this sees businesses proliferate, fraud, scams and cybercrime also flourish, denting consumer confidence and limiting spend.

There are also growing privacy concerns and data security regulations further complicate the adoption of advanced services like AI-driven mVAS.

That said, the market in MENA is flourishing and, as World Telemedia Dubai shows, there is abundant opportunity in the MENA region and beyond into Africa, India and South Asia as a result.

To learn more about the MENA market, go to: www.dubai.wtevent.com

billing & payments

Unlocking MENA: How Ooredoo tackles DCB fraud

With DCB-powered mVAS gaining ground in MENA, so too are the fraudsters. Here Paul Skeldon takes a look at how MNO Ooredoo worked with Evina to tackle the problem

Ooredoo – which is Arabic for ‘I want’ – is one of the leading telecoms companies in MENA, delivering mobile, fixed, broadband internet and corporate managed services to consumers and businesses across markets in the Middle East, North Africa and Southeast Asia.

The growing use of DCB across these regions has seen Ooredoo not only thrive, but explode, being used for payments among under and unbanked customers across apps, games, entertainment services, as well as subscriptions on platforms such as Google Play Store and Huawei AppGallery. It also supports payments on for streaming services, cloud gaming such as Blacknut and mobile financial services and even ecommerce.

However, where DCB has been such a rampant success, so the fraudsters have followed. As mobile payments have grown rapidly across MENA, fraudsters are becoming more sophisticated, using automated attacks to target users. AI – while a great tool for creating content and services – is becoming a weapon and operators like Ooredoo need to be on the front foot to tackle the problem.

To do this, Ooredoo has partnered with Evina, a global leader in mobile payment security, to integrate AI-powered fraud prevention technology into its DCB processes, strengthening the security of carrier billing and ensuring safer and more reliable digital transactions. It also is an object lesson in DCB fraud prevention that all MNOs everywhere can learn from.

Through the partnership, digital service merchants using Ooredoo’s carrier billing will have access to Evina’s advanced fraud detection and prevention system, allowing them to proactively detect and block fraudulent transactions in real time. This ensures a more secure digital experience for customers, protecting them from unauthorised charges.

Rene Werner, Group Chief Strategy Officer, Ooredoo, explains: “Security and trust are the foundations of customer satisfaction in general and of any successful digital payments ecosystem in particular.

“At Ooredoo, we are committed to lead in customer experience across our markets. By partnering with Evina, we are reinforcing our defences against evolving threats and ensuring that our customers can transact with confidence. This initiative prevents fraud and enables a seamless, secure, and scalable digital payments experience that fuels growth for businesses and empowers millions of users across our markets.”

NEW SECURITY STANDARDS

Through this initiative, Ooredoo is setting new security standards for mobile payments across its operating companies, reinforcing trust in Carrier Billing and supporting the sustainable growth of digital merchants and services.

David Lotfi, CEO of Evina, adds: “Fraud is the biggest challenge in the mobile payment industry, and Ooredoo has taken decisive action to further protect its customers and build a trusted digital ecosystem across the MEA region and Asia. With its unwavering commitment to security and innovation, Ooredoo is setting new standards for a safer digital economy. We are extremely proud to support this vision and to kick off this partnership with them.”

By investing in advanced fraud prevention, Ooredoo continues to upgrade the digital experience for its customers, making mobile payments safer and more accessible while reinforcing its position as a leading digital enabler in the region.

This strategic partnership was officially finalised during MWC 2025 in Barcelona, reinforcing Ooredoo’s commitment to driving innovation and security in digital transactions. Learn more from Evina at World Telemedia Dubai on 11-13 May 2025.

For more detail and to meet Evina, go to: www.dubai.wtevent.com

value added services

Unlocking

services and payments. Games alone generate nearly $2 billion in revenues in Africa in 2024 and, if you consider the wider mVAS market that encompasses this and all other fun and useful mobile services, the total is in the many millions.

While it is easy to think of Africa as a single emerging market, it is in fact made up of 47 separate countries, all with varying needs and demands and each at its own stage in exploiting mVAS. So, what is driving these huge potential markets, where are the hotspots and how can telemedia tap in?

MARKET SIZE AND REVENUE

The African mVAS market is projected to generate billions of dollars in revenue by 2025, with the lion’s share of contributions coming from mobile financial services, entertainment and various flavours of ecommerce. But it is building on a sector that is already quite strong in many parts of the market.

In Southern Africa alone, communication services generated $17 billion in 2024, with annual growth projected at 2.3% through 2028. Ethiopia’s mVAS market is expected to grow from $1.43 billion in 2022 to $7.48 billion by 2031, reflecting a CAGR of 20.14%. Nigeria’s telecom market was valued at $9.1 billion in 2022 and continues to grow at a CAGR of 4.6%.

On the other hand, markets such as Zimbabwe, which is experiencing high-inflation and limited economic momentum are struggling to grow their wider economies, which in turn hampers network and smartphone penetration, and so mVAS growth is also restricted and is likely to remain so for some time to come.

USER BASE GROWTH

However, Africa is a thriving market. Smartphone adoption surged by 24% in early 2024, with countries like Nigeria (42% increase in smartphone shipments), South Africa (19%) and Egypt (39%) leading this growth.

Mobile financial services are a key driver of mVAS adoption. For instance, MTN’s MoMo app connects more than 200 million wallets across 24 African countries, with transaction values jumping from $76 billion in 2018 to $204 billion in 2022.

Mobile money services form the bedrock of this growth. Airtel Africa, for example, reports a 29.6% increase in mobile money revenues year-on-year by March 2023. By now, while numbers are hard to come by, this is likely much higher.

And then there is M-PESA. M-PESA is Africa’s most successful mobile payment service, having debuted in Kenya in 2007 and grown to become a key driver of financial inclusion with millions of customers in seven countries.In 2024, M-PESA contributed 42.9% of parent company Safaricom’s service revenue, totalling $600 million, a 16.6% increase over the previous six months.

This service, perhaps more than any other, is what has made mVAS in Africa possible: allowing millions of unbanked consumers to sample the digital economy and they have really taken to it.

CHALLENGES ABOUND

However, there are challenges to growth across the continent. Countries like Ethiopia and conflict zones such as Sudan face slower growth due to limited infrastructure and economic instability that go with emerging markets. Regulation – too much and too little – can also be a barrier to growth.

For instance, while Ethiopia’s mVAS market is growing rapidly due to urbanisation and improved telecom infrastructure, rural areas remain underpenetrated due to limited network coverage. In fact, limited access to smartphones and high-speed internet restricts mVAS adoption in rural areas across the continent. It might all be good in the city, but the countryside is being left behind.

For true growth, this iniquity must be addressed firstly at a network level before telemedia players can unleash their content and services on the masses.

There is also the risk of fraud (see page 13). All VAS markets have their share of cyber crime, but emerging ones often see a disproportionate level of fraud that can often see these nascent markets grind to a half.

Overcoming this and the networks ubiquity issues will allow services to flourish.

To learn more about the African market, go to: www.dubai.wtevent.com

Unlocking Africa: the content that drives the market

The opportunity for mVAS across Africa is huge, but what content and services is driving that market – and what impact could US tariffs have on this? Paul Skeldon takes a look

Africa is a diverse continent, made up of many countries – each with their own unique interests and mores. Mobile entertainment services in Africa are thriving due to increasing smartphone penetration, affordable data plans and a youthful population.

The development of mobile payment services such as M-PESA have brought millions of unbanked consumers into the market for all things digital and that has seen an explosion in use. So, what are they using?

STREAMING SERVICES

Music and video streaming services are the most popular mVAS across Africa, as might be expected. South Africa’s Showmax – a subscription-based video-ondemand service offering TV shows, movies and original productions – is popular in South Africa and expanding across the continent.

As of 2023, it had 2.1 million subscribers, more than Netflix. Nigeria’s IROKOtv, meanwhile has become the “Netflix of Africa,” specialising in Nollywood films and African TV series, with more than 5000 movies on its platform. And Boomplay – a pan-African music streaming service pre-installed on Transsion phones – now has more than 75 million users as of 2023 and remains a top app in Nigeria, Ghana, and Kenya.

These big names show that video and TV content streaming are big business and telemedia companies looking to get in on the action need to look at how they too can create and sell long and short form video.

On the music side, South Africa’s TRACE Play focuses on Afro-urban music, concerts and TV shows celebrating African culture.

What these all have in common is that they thrive on local content for local people. Typically, success in

streaming lies in localising the content to each country’s market. There are 47 countries in Africa and they are all culturally different. These local players show just how important getting that right is – both in terms of content and price point.

MOBILE GAMING

Games are big digital business the world over and African markets are no exception. Again, though, keeping it local is key. Nigeria generated around $300 million in 2024 from mobile gaming, while South Africa contributed around $278 million driven largely by esports platforms such as Mettlestate.

Esports are particularly popular across Africa, with a relatively youthful population drawn to sports in general, but more affordable and more youth-orientate esports in particular.

What is interesting is that there is increasingly a crop of mVAS players such as YangoPlay, which are combining music, movies and games into a single offering and are already widely used across Nigeria, Kenya and South Africa. India’s Hungama is doing something similar (see page 14).

THINK LOCAL

The key with unlocking African mVAS services lies in thinking local, says Jacqui Jones, MD of Worldplay. Each market is different and wants its own content and services. Successful models can be transferred to other markets, but as the success of local services over global offerings such as Netflix shows, it is understanding what works in each market that is key to unlocking Africa. To learn more about the African content market, go to: www.dubai.wtevent.com

Unlocking India: the massive mVAS market that is going places

While MENA and Africa garner all the attention as growth markets, India, with its vast, young middle class population is a hotbed for mVAS services. Paul Skeldon takes a look

With a population of 1.4 billion people, nearly 500 million of whom are considered middle class, India is a massive and growing mVAS market that for many players. Yet goes somewhat under the radar. But take a look at the numbers and you can see what a huge opportunity this market presents to telemedia companies.

The mVAS market in India is experiencing rapid growth due to increasing smartphone penetration – 162

According to Manpreet Singh Ahuja, chief digital officer and TMT Leader at PwC India: “India’s entertainment and media sector is on the cusp of a major transformation. According to our [data], key growth drivers such as digital advertising, OTT platforms, online gaming and GenAI are shaping the future of the industry. Businesses that adapt and innovate in these areas are poised to seize unparalleled opportunities in this dynamic landscape.”

million as of 2022 – expanding 4G and 5G networks and rising demand for mobile data services. As a guide to how popular mVAS is, just look at data use in the country: average monthly data usage per user is forecast to increase from 16.4GB in 2023 to 37.4GB by 2028, reflecting the growing reliance on mobile internet for entertainment, communication and ecommerce.

According to 2023 data from PwC India, despite economic headwinds and geopolitical uncertainties, entertainment and media revenues saw massive growth of 5.5% and are set to grow by similar rates between now and 2023. And this has a big impact on mVAS.

WHAT DRIVES MVAS IN INDIA

The real drivers for this mVAS growth lie in affordable handsets from brands such as Xiaomi and Realme making smartphones accessible to lower-income groups. Improved networks are also seeing AR and VR services, games and more all explode across the market.

The government too has played a strong role. Programmes like Digital India promote digital inclusion through affordable internet access and e-governance services, have all made India’s MVAS market one of the largest and fastest-growing in the Asia-Pacific (APAC) region.

With all that in mind, it is no surprise that the Indian mobile entertainment market is set to reach some $44.2

Unlocking South Asia: looking to the future

While India is a booming market for mVAS, its neighbours in Pakistan, Bangladesh and Sri Lanka are definitely ones to watch for the next round of growth, says Paul Skeldon

India gets all the attention, but the mVAS markets of Pakistan, Bangladesh and Sri Lanka are already showing promising signs of growth and this region is set to be an interesting area for mVAS investment in the years ahead.

Sandwiched between the mega markets of India and South East Asia – the latter the largest single mVAS market in the world, accounting for more than 34.8% of the market share in 2024, South Asia may look like a minnow that is easy to overlook. But delving into the numbers reveals an intriguing market.

Growing mobile penetration and the roll out of 4G and 5G networks has already started to drive users to the digital economy and, with more localised content arriving, the market is already catching fire.

PAKISTAN

The Pakistani market has some 194 million mobile users, with smartphone penetration growing steadily amongst them. Mobile financial services are also increasingly popular as the largely unbanked population look to use their cash in the digital world. This, along with government initiatives such as Digital Pakistan, has seen uptake of mVAS explode.

Local apps like Tamasha, Bajao and Harpal Geo stand out due to their focus on Pakistani-specific content, including cricket matches, local dramas, and music. These apps cater to cultural preferences and offer affordable subscription models, which resonate well with the local audience.

BANGLADESH

Bangladesh has some 182 million mobile users and is at a similar stage in its digital journey to Pakistan. Here, however, there is more of a mix of international content and home grown – perhaps an indication of how the market in Bangladesh is at a more nascent stage.

With 46.5 million users aged 18 and above in early 2025, TikTok dominates the entertainment space, reaching nearly 60% of the local internet user base. Facebook Lite and Messenger are widely used for communication and entertainment.

Local apps like Chorki and Toffee are highly popular due to their focus on Bangladeshi culture, language, and preferences. These apps provide localized content such as Bangla movies, dramas, and Bangla-dubbed foreign shows. Their affordability and accessibility across devices further enhance their appeal.

SRI LANKA

Sri Lanka, by contrast, is a much smaller market, but one that is much further along its mobile journey and so has a much more engaged audience. High literacy rates see e-learning and educational apps being among the most popular, while international entertainment apps such as Netflix and Spotify have a strong market.

But there are local services emerging. Dialog ViU is Sri Lanka’s largest entertainment ecosystem, offering over 108 local and international live TV channels, 1,000+ local movies and dramas, sports events, and international partner content such as iFlix, Zee5, Hungama Play, and ALT Balaji. It also provides exclusive Sinhala and Tamil content like school cricket matches and national rugby tournaments. Other services such as Airtel Movie Box and SLT OTT Entertainment are also popular.

The key in all these emergent South Asian markets is that local content is a winner and there is still a large untapped market to be had.

To learn more about the South Asian markets, go to: www.dubai.wtevent.com

Sandwiched between the mega markets of India and South East Asia – the latter the largest single mVAS market in the world, accounting for more than 34.8% of the market share in 2024, South Asia may look like a minnow that is easy to overlook. “

billing & payments

Where next for DCB?

Carrier billing is going great guns across developed and emerging markets, but a raft of wallets and other alt.payments are snapping at its heels. What now, asks Paul Skeldon?

Carrier billing is surging in popularity the world over. Already it is forecast by Juniper Research that more than a fifth or all mobile phone subscribers worldwide – that’s around 1.5 billion people – will be using carrier billing (DCB) to buy either digital content, physical goods, or digital tickets, in 2025. Meanwhile, Facts & Factors suggests that where the global carrier billing market was worth around $30 billion in 2021, steady growth of around 8% year on year is going to be maintained and the sector is likely to be worth in excess of $48 billion by 2028.

Interestingly, the largest growth in DCB use is set to be seen in the US, however it is the rest of the world where it is really coming into its own. According to the Facts & Factors’ research, the rapid growth in cloud computing is what is pushing carrier billing. Cloud

computing has detonated an explosion in digital content and services and people the world over are wanting to get a piece of the action. However, adoption of credit cards in these markets is poor and so DCB has been a handy alternative.

This is why Juniper predicts that so many people will be using DCB this year – that an MNOs increasingly now seeing it as a small but necessary new revenue stream as their core earners – voice, messaging and data – become ever more commoditised.

MANY ALTERNATIVES

However, there are many impediments to how far carrier billing can go and, as research shows, many of these developing markets – especially the ones that are relatively new to the digital world, such as Vietnam and the Philippines, for example – are adopting wallets and other alternative payments instead (see panel). This is becoming a universal issue. Digital wallets are garnering significant interest from users because they offer more than just the ability to pay for things. They may well be comparable to carrier billing terms of one-click payment, but they can often support multiple payment mechanisms – cards, bank transfers and, potentially, carrier billing too – all with the enhanced security of tokenisation, encryption and biometric authentication.

But it is their versatility that really appeals to users. Digital wallets provide additional services like budgeting tools, loyalty programmes and cashback offers, which enhance user engagement beyond simple payments. With this in mind, it is easy to see how, in 2023, digital wallets accounted for 44.5% of ecommerce transactions and 33.1% of POS transactions globally and, by 2026, more than 60% of the global population is expected to use digital wallets.

THE MENA CONUNDRUM

While wallets and alternative payments are garnering users across different markets, their uptake in MENA is slow. Here DCB dominates and looks set to for some time to come. Wallets account for around 20% of spend across MENA – 18% in Saudi Arabia – and young people are erring towards them as they are more of a mobile-first payment tool, but there is still a propensity to use DCB in the region.

Much of this is driven by a reliance of cash, which is much easier to buy pay-as-you-go mobile airtime, which can then be used to purchase goods through DCB. There are also significant infrastructure gaps that make mobile broadband-based services unreliable. Interoperability issues across networks is also a problem. However, even in MENA, there is a slow move towards using more than just DCB for mVAS payments.

ORCHESTRATION

The rise of wallets is being seen in all markets and is part of a trend towards consumers using a wide variety of payment tools to do the things that they want to do. This can be a challenge for merchants as, where once you could build a business around using DCB to sell content to mobile users, now you have to manage a raft of payment tools alongside DCB – and manage a process where users graduate from maybe starting their relationship with a merchant through DCB to one where they use a wallet, card or instant payments

This sees many players having to look at how to orchestrate these payments, something that payment provider Celeris has been quick to capitalise on. It orchestrates payment tools for merchants by acting as a central platform that connects and manages various payment gateways, processors, and other financial service providers. This allows merchants to access multiple payment options and tools through a single interface, streamlining their payment processes and improving efficiency.

By centralising payment management, Celeris simplifies the entire payment process for merchants, reducing the need for multiple integrations and interfaces. This orchestration allows merchants to optimize their payment processing, leading to higher approval rates, reduced fraud, and lower costs.

Wallets of the world

Developing markets are increasingly adopting digital wallets over traditional carrier billing for payments due to their convenience, accessibility, and integration with other financial services. Some notable trends include:

• India and China: Countries like India and China lead in digital wallet adoption. India’s UPIbased wallets, such as Paytm, PhonePe and China’s Alipay and WeChat Pay have transformed payment ecosystems, handling billions in transactions daily.

• Africa: Mobile money services like M-Pesa are driving financial inclusion by connecting unbanked populations to financial services. Wallets are expanding into microlending and insurance through partnerships.

• Latin America: Wallets such as PicPay in Brazil are integrating features like customizable insurance and e-commerce services, helping underserved populations access financial tools.

• Southeast Asia: Wallets like GCash in the Philippines offer integrated banking services, including savings accounts and investments, making them a one-stop solution for users. These wallets are preferred over carrier billing due to their ability to provide broader finan

cial services, enhanced security, and seamless integration into super-app ecosystems.

Such orchestration platforms are also flexible and scalable – who knows what the next tranche of payments technology will bring – and help manage and mitigate fraud. They also bring an enhanced user experience to merchant sites.

To learn more about billing and payment, go to: www.dubai.wtevent.com

150+ business ready “virtual” exhibitors

Search by – services, markets, business EVENT DISCOUNTS Inc’ 8.1LIVE, WT25 (Dubai and Marbella)

user

acquisition

Shifting sands How the traffic gen landscape has changed

The telemedia sector has undergone a significant transformation in user acquisition from heavy reliant on affiliate marketing to a focus on social media and Google. Paul Skeldon finds out why

In the early days of telemedia, affiliate marketing was a dominant force in driving traffic and user acquisition. This model cantered around partnerships between the mVAS provider or content owner (the merchant) and third-party entities (the affiliates). Affiliates, which could range from individual website owners and bloggers to larger media companies, would promote the mobile services or content through various online channels.

Merchants provide affiliates with unique links or tracking codes embedded in banners, text links, or other promotional materials and the affiliates are incentivised to drive traffic through commission-based models – typically getting paid on Cost Per Acquisition (CPA), Revenue Share or Cost Per Click (CPC).

Affiliates used a range of methods to attract users, such as display advertising, seach engine marketing,

The future of traffic generation

Imagine a future where an mVAS provider uses AI to analyse a user’s social media activity and search history to deliver highly targeted video ads on TikTok featuring content they are likely to enjoy, with a seamless path to subscription. They might also partner with a niche gaming influencer on Twitch to promote their mobile games to a highly engaged audience. This future of traffic generation for mVAS and mobile entertainment is likely to be characterised by several key trends:

1. Increased Focus on Personalization: Leveraging data and AI to deliver more personalized content and advertising experiences that resonate with individual users.

2. Integration of Multiple Channels: A holistic approach that combines the strengths of social media, search engines, content marketing, and potentially a revitalized form of affiliate marketing (with greater emphasis on quality and transparency).

3. The Rise of Video and Interactive Content: Video content, particularly short-form video on platforms like TikTok and Instagram Reels, will continue to be a powerful driver of engagement and traffic. Interactive content formats like quizzes and polls can also enhance user engagement.

4. The Metaverse and Emerging Platforms: Exploring new traffic generation opportunities within emerging digital environments like the metaverse.

5. Emphasis on User Privacy and Data Ethics: Navigating the evolving landscape of user privacy regulations and building trust through transparent data practices.

6. AI-Powered Optimization: Utilizing artificial intelligence to automate and optimize traffic generation campaigns across various platforms.

7. Influencer Marketing Evolution: A shift towards more authentic and niche influencer partnerships with a focus on genuine engagement.

email shots, content marketing around blogs and other content and SMS marketing. For example, a mobile games provider working with a gaming blog (the affiliate). The blog would feature reviews and articles about the games, embedding affiliate links. When a reader clicks on these links and installs the game, the blog earns a commission.

THE RISE OF SOCIAL MEDIA AND VIRAL TRAFFIC

While affiliate marketing still works well, the advent and rapid growth of social media platforms like Facebook, Instagram, X (formerly Twitter) and TikTok have fundamentally altered the traffic generation landscape for mVAS and mobile entertainment. These platforms offer direct access to vast and highly segmented user bases, enabling more targeted and engaging marketing efforts. Social media channels generate traffic in a wide range of ways. Typically it is through organic content, where entertainment content, behind the scenes insights, information posts and user generated content are all used to organically attract users to the mVAS offering. But there are other ways to leverage social. Paid social media advertising uses the platforms’ advertising features to reach specific demographics, interests and behaviours. This includes integrating visually appealing ads into users’ feeds, display ads and images, immersive full-screen ads and influencer marketing. Creating and nurturing online communities around the mVAS or entertainment content through Facebook groups, Discord servers can also help, with these communities driving organic traffic through engagement and word-of-mouth. And let’s not overlook direct links and calls to action. For example, a mobile video streaming service might share short, captivating clips of their shows on TikTok, with a link in the bio or within paid ads directing users to subscribe. They might also partner with popular lifestyle influencers to promote their content to a wider audience.

GOOGLE’S DOMINANCE

Despite the strong role played by social media – not to mention how affiliate marketing is still a viable way to drive traffic – Google remains an indispensable traffic source for mVAS and mobile entertainment providers, offering a powerful combination of search-driven intent and broad reach through its advertising network.

Google generates traffic in multiple ways, most notably through SEO, where the mVAS site or services is optimised through keywords. page layout and text use. Off-page optimisation, building authority through backlinks, is also key.

However, running paid ad campaigns on Google’s search results and display network is probably the most commonly used telemedia tactic for Google traffic generation. This allows for keyword ad targeting, audience targeting based on behaviour data and re-marketing, where ads are shown to users who have previously interacted with the mVAS provider in some way.

For example, a mobile music streaming app might optimize its website for keywords like “best music streaming apps” to attract organic traffic. Simultaneously, they could run Google Ads campaigns targeting users searching for specific music genres or artists, driving them directly to the app’s download page.

TRAFFIC GENERATION CHALLENGES

While each method offers significant benefits, they also come with their own set of challenges for mVAS and

nels and touchpoint can be challenging. Meanwhile, traffic volumes can be heavily reliant on the efforts of individual affiliates and some affiliate practices, particularly in sensitive areas like mVAS subscriptions, have faced regulatory scrutiny.

Social media isn’t immune to challenges. Social media platform algorithms frequently change, impacting organic reach and requiring constant adaptation of strategies. Competition for ad space on popular platforms can drive up advertising costs. Accurately measuring the return on investment for organic social media efforts can be difficult.

Standing out in crowded social feeds requires consistently creating high-quality and engaging content, while keeping users engaged and converting them into paying customers requires ongoing community management and content updates.

So what about Google? Ranking high in organic search results for competitive keywords can be a long and challenging process and Google’s search algorithms are constantly updated, requiring ongoing monitoring and adaptation of SEO strategies. Highly competitive keywords can have very high cost-per-click rates too and, as any user

marketing & promotion

How AI is reshaping marketing

User acquisition is shifting to a highly targeted, data-driven, social media world and AI is going to be crucial to that. Paul Skeldon takes a look at what this looks like across the wider advertising and marketing world

It is no surprise that digital channels have become the dominant place for advertising and marketing of services, content and ecommerce, however without AI and automation it is hard to stand out from the crowd.

So finds the annual marketing survey of 700 marketing professionals from onmichannel ad company Mediaocean, which reveals how marketers are navigating rapid technological advancements and shifting consumer behaviours.

The report highlights the rise of generative AI (GenAI) as the top consumer trend, but for marketers themselves it is driving an increased investment in automation and the continued prioritisation of digital channels like social media, digital display/video and Connected TV (CTV).

As we enter 2025, the advertising ecosystem continues to evolve rapidly. The interplay between technology, data, and creativity drives new opportunities for marketers to engage meaningfully with consumers. Mediaocean’s insights offer a clear roadmap for navigating these complexities. Brian Wieser, CEO and Principal, Madison and Wall “

THE IMPACT ON ADVERTISING

The study, perhaps unsurprisingly, finds that social media, digital display/video and Connected TV (CTV) are the fastest-growing channels, with 68%, 67% and 55% of marketers planning to increase spending in these areas, respectively.

However, while GenAI has emerged as the leading consumer trend, surpassing CTV, 63% of marketers identify it as critical to their business. Key advancements in AI are reshaping workflows and enabling more sophisticated advertising strategies. This is what is likely to be key for helping advertisers stand out in the increasingly competitive digital marketing arena.

AI is also having to work in close conjunction with automation to not only deliver the right ads at the right time to the right users, but also to make the process as efficient as possible. According to Mediaocean, automation has become the fastest-growing investment area, with a 17% increase in adoption since mid-2024, as marketers seek to improve their workflow across media formats.

Additionally, advertisers are adopting multiple approaches to identity resolution to improve campaign measurement and attribution. Almost half cite this as a top concern for 2025 and, despite slight improvements, 86% of advertisers report a lack of synchronization between creative and media processes, highlighting significant opportunities for growth.

MARKETING EVOLVES

“The report underscores the profound shifts already underway and intensifying across the advertising industry,” says Aaron Goldman, CMO of Mediaocean. “From the rise of AI and automation to the need for more comprehensive measurement frameworks, the insights in this report provide actionable guidance for brands and agencies looking to thrive and compete in a dynamic marketplace.”

“Generative AI is no longer a futuristic concept—it’s a cornerstone of today’s advertising strategies,” says Deborah Wahl, Forbes CMO Hall of Fame member and former global CMO of General Motors. “The moment we’re in reminds me of the electric vehicle transformation in the auto industry. To capitalise on the opportunity, nay – imperative, marketers had to reimagine their business strategies and marketing programs. The same goes for AI and the brands that embrace it now will see outsized returns.”

messaging & engagement

Mixed messages What is happening with RCS?

Interesting times lie ahead for the messaging sector, with the very tech underpinning it changing – from SMS to RCS and OTT – while even those that carry it, the MNOs, potentially facing disruption from new entrants from outer space – well, low Earth orbit. Paul Skeldon reports

As UK operators VMO2 and Three UK start to offer RCS for business messaging, research reveals that globally growth of RCS deployment and indeed its uptake has proved slow. The power of OTT continues to undermine RCS use by businesses, while pricing, lack of communication and integration between MNOs and the risk of fraud are all hurdles to its uptake. Find out what operators need to do – before satellite messaging services come and do it for them.

So, what does this mean for telemedia? Messaging is a key plank in how telemedia can drive traffic. While back in the day PSMS was used as a billing tool (it still is, but the role of messaging has changed), today messaging services are more about marketing and driving traffic, as well as being part of a business-to-consumer customer service and engagement offering. While SMS can and does do all this, the pandemic showed both businesses and consumers that they could do and get so much more with messaging.

OTT services such as WhatsApp – and more deeply exemplified by WeChat in China – readily filled the gap left when consumers could no longer interact face-toface with businesses when Covid struck. These services rapidly adapted and evolved to show just what could be done with rich messaging and created not only the rich business messaging (RBM) market, but also pushed messaging into being an ad medium and traffic generator – it even brought together the worlds of messaging, marketing and payments as the beginnings of transactional rich media messaging have started to emerge.

While Google has plugged away for more than a decade to get its RCS modality accepted as the de facto SMS 2.0 rich messaging platform, it wasn’t until Apple finally embraced it in its iOS18 update at the end of 2024 that RCS looked like it might actually go somewhere.

MNOS DRAGGING FEET

Only it isn’t. Not so far at least. Operators it seems didn’t stand poised to explode RCS offerings on to the market as soon as Apple gave its approval.

Instead, they have largely failed to move forward with working together on interoperability to make sure everyone can send and receive RCS across all the various OSs available. They have also been inconsistent in pricing it and, while it is something of an unknown, there is little they have said about prevent fraud through RCS –which let’s face it is bound to happen as soon as enough people use it; scammers love a new channel.

All this reluctance could be down to RCS being unproven – largely because it is as, with only half of users able to use it until November 2024, no one has, err, used it. But operators need it. With SMS revenues shrinking and with OTT services currently the best game in town for businesses looking for rich business messaging, RCS is the only messaging offering that MNOs will soon be able to leverage.

While seeing UK operators come together to start the roll out is encouraging, globally this is more anomalous. There needs to be much deeper engagement with RCS by both consumers and operators, the latter being the only way that the former will ever see RCS. I myself have yet to receive on. No one I know outside of work even knows what it is.

IS AI THE AI-NSWER?

With AI creating a whole new level of chatbots – not least ones that text like real people – there is more to gain here than just adding a new way to text. Businesses can offer rich messaging, some of it even transactional, but creating engaging, realistic and personal conversations with it (using AI chatbots) is next level – and something that operators have the chance to get into on the ground floor.

Telefonica Labs seems to working towards this with its AI Chatbot tech, but so too are many other tech companies. As the adult industry has shown, there is already a massive market for AI generated personalised text chat; if you can create that as a customer service model with rich, interactive formats then everything from customer service to advertising changes radically.

Couple all this with the fact that satellite messaging – through constellations such as Starlink – are starting to become a reality (especially in developing and un/ under-connected regions) and the messaging market looks very exciting to consumers and tech bros, but really rather bleak for slow to move operators.

cesses, strategies, and tooling, to make ourselves more efficient and to be able to use at scale. Even if fraud teams have irrefutable proof that AI tools are used against their fraud department, this can be a simple, obvious application.

For example, a criminal might use ChatGPT to write a refund abuse claim or a phishing email. But is that groundbreaking or impossible to prevent? I don’t think so,” he says.

AI-powered fraud prevention tools are the most effective line of defence, with machine learning and behavioural analysis emerging as critical weapons in merchants’ anti-fraud arsenals.

Almost three-quarters (71%) of the companies spoken to are using machine learning (ML), large language models (LLMs) or any other AI technology to detect and/or prevent fraud.

Merchants believe AI-enabled fraud will have the most significant impact on online payment fraud (53%), fraudulent chargebacks (46%), and account takeover (ATO) attacks (42%).

With AI-powered fraud techniques evolving rapidly, businesses must take proactive measures to protect themselves. The Ravelin report underscores the need for a multi-layered approach that combines AI-driven fraud prevention tools with human expertise.

WHAT IS BEING DONE?

So, what is the industry doing about it? Across retail in general, most businesses are using the tools available to try and fight fraud. Interestingly, 66.2% of them are looking at machine learning to fight AI fraud, while as many as 46% are also using AI to combat AI fraud.

The biggest impediment however is cost. Nearly 40% of merchants say that finding the budget to do this is the biggest obstacle to tackling all fraud, let alone the deluge of it driven by AI.

In the telemedia sector there has been a lot of work done to counter DCB fraud and other payment fraud thanks to companies such as Evina, Tetra Mobile Solutions and Empello and with compliance increasingly becoming something that players across the market have embraced – as discussed by Kevin Dawson from MCP Insight at Telemedia8.1 LIVE in Barcelona.

Yet there is still much more to be done. While the telemedia industry is strong on fraud prevention, the fraudsters are getting ever more sophisticated and, armed wit state of the art AI, they are only going to do more damage.

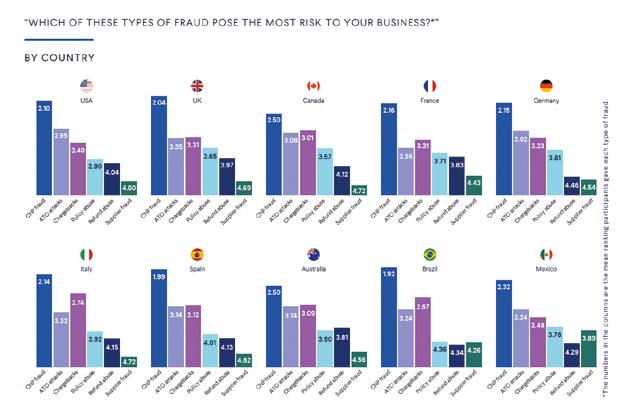

Which countries see the most online fraud?

The United States ranks as the country most affected by online fraud, while with $1.8 billion in total value, France experiences one of the highest financial losses due to fraud. Ireland records the highest online fraud share, with 85% of the cases occurring digitally.

So finds a new study by ZeroBounce, which analysed fraud rates, total fraud value, and online fraud share to determine which countries are most affected by online fraud. The research examined key fraud metrics, including cross-border fraud, domestic fraud, and the number of transactions per card.

The findings highlight the nations that are most vulnerable to digital financial crimes and provide insight into how fraud risks vary across different economies.

viewpoint

Shweta Mahajan head of product and business development, Digital Technology

Digital Technology sits at the forefront of premium digital content and seamless monetization solutions. Here, Shweta Mahajan, head of product and business development, Digital Technology takes a look at the five key areas that will shape our business and the industry as a whole

Cloud gaming and 5G expansion

Cloud gaming platforms like StreamPlay are revolutionizing the gaming industry by eliminating hardware constraints. With the continued expansion of 5G, real-time gameplay will become even more seamless, enhancing accessibility and user engagement worldwide. StreamPlay, our cloud gaming platform, allows users to access high-quality games instantly without the need for expensive consoles or high-end PCs, democratizing gaming access across various devices.

Gamification in learning and wellness

The integration of gamification into education and fitness is transforming engagement levels. Interactive e-learning tools and wellness platforms such as Games2Learn and Learn2BFit are making education more immersive and fitness routines more enjoyable, driving sustained user interest. Games2Learn blends entertainment with learning through interactive and engaging games, while Learn2BFit motivates users with gamified fitness challenges, AI-driven workout plans, and progress tracking, making health and wellness more accessible and fun.

Evolution of Direct Carrier Billing (DCB)

As a leader in Direct Carrier Billing, we are constantly improving accessibility for premium services like Watcho, Docubay, StreamPlay, and many more in discussion. By streamlining transactions, DCB ensures frictionless payments, enabling millions of users to access premium content effortlessly. Watcho, a dynamic content streaming platform, offers exclusive web series, short films, and entertainment, while Docubay provides a curated selection of high-quality documentaries catering to knowledge seekers worldwide.

AI-Driven Personalization

Artificial intelligence plays a pivotal role in enhancing digital experiences. AI-powered recommendations are optimizing content discovery, ensuring users receive tailored gaming, fitness, and educational content that maximizes engagement and satisfaction. Whether it’s personalized learning paths in Games2Learn, customized fitness programs in Learn2BFit, or AI-curated gaming suggestions in StreamPlay, our platforms are leveraging AI to deliver enhanced user experiences.

Culturally relevant and faith-based content

The demand for culturally tailored content, particularly faith-based platforms, is growing significantly. We are developing services that cater to spiritual, educational, and lifestyle needs, with a strong focus on the MENA region’s evolving content consumption trends. Platforms like KidsFlix Club, our dedicated children’s content service, provide safe, engaging, and educational entertainment tailored to young audiences, while faith-based content services cater to users seeking spiritual enrichment and culturally relevant programming.

Top tech tip for tomorrow: think beyond the screen –the future is seamless & integrated

The future of digital experiences is centered around frictionless, personalized and immersive interactions. Whether through:AI-driven personalization for tailored content and services, nstant access to cloud-based platforms, removing hardware constraints, or embedded payments via Direct Carrier Billing (DCB) enabling smooth transactions, success lies in eliminating barriers between users and content.

At Digital Technology, our commitment is to pioneering digital solutions in education, gaming, entertainment, and wellness - creating engaging, empowering, and meaningful experiences for users worldwide.

We are actively working on bringing advanced technology closer to users with innovative solutions like the “AI-Powered Image Enhancement & Resizing Tool”, which utilizes AI to enhance image quality while allowing precise resizing without compromising clarity. This makes it an invaluable tool for content creators, designers, and businesses seeking high-resolution visuals. Additionally, our “AI-Based Voice & Video Call Cloning for Call Centers” introduces an advanced system that replicates voice and video interactions, enabling seamless call handling and automation. This technology enhances efficiency, ensures consistent customer interactions, and optimizes operational costs, making it a game-changer for call center operations.

Looking ahead, we are also exploring Cloud Gaming Innovations to offer seamless, high-performance gaming experiences without the need for expensive hardware, as well as Smart Wallet Charging Solutions that provide users with effortless and secure ways to top up their digital wallets through multiple payment integrations.