How digital advertising is changing and AI is becoming

is in the driving seat

More than a fifth or all mobile phone subscribers worldwide – that’s around 1.5 billion people – will be using carrier billing (DCB) to buy either digital content, physical goods, or digital tickets, in 2025

So, why should MNOs be taking a deeper interest in their DCB offerings? According to data, the past decade has seen MNO revenues drop. Minutes and texts have seen a significant decrease in value, with many operators offering unlimited minutes and texts as part of Why 1.5bn people will be using DCB by year end – and here’s why operators need to push it...

However, a study by Juniper Research warns operators that if they wish to capitalise on this sizeable user base, they must maximise attractiveness and value of the carrier billing opportunity to merchants. This they can do by positioning their networks as distribution channels, rather than as mere payment facilitators.

WHY MNOS NEED DCB

MESSAGING & ENGAGEMENT

–

As the world’s MNOs struggle with falling SMS revenues and a drop in voice traffic, they are being forced to reinvent themselves by focussing on other areas. As we have seen (above), DCB is a potentially lucrative source of additional revenues, however what they do with RCS is also going to be crucial. So, what do they need to do?

THE

ART DIRECTOR Victoria Wren victoria@wr3n.com

CONTRIBUTORS & CONSULTANTS

Nick Lane

Sam Barker

Jarvis Todd Tim Green

SALES & MARKETING

info@Telemedia-news.com

PRODUCTION DIRECTOR Annika Micheli

annika@Telemedia-news.com

PUBLISHER Jarvis Todd

jarvis@Telemedia-news.com

TO SUBSCRIBE

FROM THE EDITOR

2025: the year AI totally reshaped how telemedia works

As Telemedia8.1 LIVE in Barcelona – and that other show, what’s it called? Ah yes, Mobile World Congress – hove into view, we find the telemedia industry, much like the rest of the world, undergoing some seismic changes driven by AI.

The impact AI is having and is set to continue to have is transformatory: by this time next year the telemedia industry and the wider world will be very different thanks to the uniquity of agenic AI. Be warned, life is going to change.

But already we are seeing shifts in how the telemedia sector works as a result of basic GenAI. As we see across many of the articles in this issue of the magazine, AI has its virtual hands in pretty much everything the industry does.

AI is being used to enhance customer service with chatbots (see page 20), personalise content (see pages 12 and 22), optimise marketing and advertising (see pages 15 and 17), as well as both perpetrate and combat fraud (see page 26). Its influence runs across all things – and this is just the start.

The changing way that mVAS is marketed is also being impacted by AI and a shift in where consumers are. Affiliate marketing – marketing in general – for mVAS is increasingly using social media (see page 17) is going to be an important topic for the industry, not least as emerging markets are really embracing social for traffic generation and marketing. But there are other issues that are equally as important.

RCS and DCB are both growing in use and are becoming vital to MNOs as revenue generators – not least as their voice and SMS businesses slowly decline. This is particularly important as new payment tools such as instant payments (see page 6) and satellite messaging that by-passes MNO networks (see page 24) also take off, if you pardon the pun. All this sees us head to Barcelona with much to discuss and much to think about. Change is good, but the pace of change we are seeing is rapid so we need to tread carefully.

telemediaonline.co.uk @telemediaTweets

Paul Skeldon. editor

a subscription offering. There has also been a decline in premium SMS (PSMS), to pay for digital content. – and it is not just the volume of PSMS that is declining, but the overall value as well.

Couple this with the price of normal SMS traffic rising in most markets over the past two years – with the average price of an SMS business message rising from $0.019 in 2021 to $0.023 in 2024 – forcing both mobile subscribers and enterprises to look to OTT and network APIs for a cheaper alternative and MNOs have a problem.

This is where carrier billing comes in to play. MNOs benefit from carrier billing in several ways. Firstly, these operators earn a share of the revenue generated from each transaction processed through carrier billing, thus providing them with an additional revenue stream.

Additionally, as subscribers already have a direct billing relationship with their mobile operator, carrier billing can improve customer loyalty by offering a convenient payment options directly linked to the mobile

account. This can help cut churn rates – which itself is a massive cost to MNOs – and lock consumers into buying more through the operator.

But there is more – particularly in emerging markets. Not only can carrier billing provide an alternative payment method for mobile subscribers, but also, it allows the unbanked to play in the digital playground. This opens up the digital market to many more consumers and will generate many more payments, a slice of each going to the operator.

This is particularly prevalent in regions such as Africa and the Middle East and any other emerging markets where mobile phones are more accessible than banking services, points out Juniper’s report. Additionally, whilst there are other markets, including Japan and South Korea in Far East and China that adopt DCB as a mainstream payment type, due to the lack of banked individuals in MENA and subSaharan Africa, this makes this region an ideal location to target for carrier billing.

COMPLICATED MARKET

The carrier billing landscape is

How to grow the DCB market

To ensure the future evolution of the carrier billing market, Juniper Research recommends growing the market through a number of avenues including:

• Carrier billing aggregators and platforms must deepen existing relationships with clients by creating new interactive products and optimising campaigns to increase future tariffs. This will provide high client retention rates to increase market share in core market sectors.

• Adopting a sector-specific focus to target large clients across core markets and geographies.

• Ensuring long-term profitability for stakeholders which will create sustainable growth for carrier billing aggregators and platforms. Improving profitability for companies with limited incremental capital and operational investment will allow carrier billing vendors to develop new customer relationships to create economies of scale.

• Carrier billing vendors can publicly partner with Tier 1 multinational operators and regulators will

a complicated one and includes a range of stakeholders from MNOs, the carrier billing platforms, regulators through to merchants. Throw in aggregators and affiliate marketing of services and it gets even more muddy. And it is constantly changing.

As a result, Juniper believes, as the landscape is constantly evolving due to regulatory changes, technological advancements and evolving consumer expectations, it is essential that all stakeholders in the market collaborate and engage in discussions to maintain the longevity of carrier billing.

As the DCB market continues to grow, it will not only attract a higher number of merchants, but will also be leveraged by a larger number of industries.

To ensure that all stakeholders are able to capitalise on the growth of carrier billing and that the use of carrier billing remains as seamless as possible for consumers, it is vital that all stakeholders participating in the telecom ecosystem collaborate to provide a safe and sustainable environment for consumers. These stakeholders include telecom operators, service providers, payment aggregators, and innovators.

create a trusting relationship when onboarding new clients; providing integration and aggregation for these clients. This will also reduce barriers of entry for other providers looking to form direct network operator connectivity in core markets.

• Widen technological and operational advantage through targeting a limited number of sectors with underlaying niche markets. For example, providing sector-specific intelligent payment routing.

As carrier billing will experience steady growth over the next five years, the points above highlight that there are multiple business models to be explored by carrier billing vendors, for future growth and competitor differentiation. Additionally, several adjacent market trends, including subscriptions and subscription bundling, rich messaging, and the evolution of the payment landscape, will also impact the future growth of carrier billing.

This collaboration will ensure that innovation is achieved securely and can improve the longevity of the market.

As the primary use of carrier billing is for the purchase of digital goods and services, this overall increase in spending benefits both operators and content providers, whilst also providing a convenient payment option.

Specifically, operators stand to benefit from more partnerships and integration to expand the reach of carrier billing. Juniper Research notes that integrating carrier billing as a payment option in popular apps, websites and digital platforms will expose it to a broader audience and increase transactions.

NEXT STEPS FOR MNOS

A key market driver in carrier billing has been the adoption of a new application programming interface (API) called ‘Check Out’ that emerged from the CAMARA project; an open-source framework that standardises APIs for telecoms networks.

Whilst this has been key to increasing subscriber access to carrier billing, the report warns deploying this API alone will not be enough to capitalise on the huge global carrier billing opportunity - with spend forecast to grow from $83 billion in 2025 to over $130 billion by 2029, according to Juniper Research.

The report urges operators to transform their networks into distribution channels; enabling mobile subscribers to purchase digital subscriptions via an operator’s consumer-facing platform. Unlike established bundling, this strategy is underpinned by the integration of content management services; allowing operators to have a direct billing relationship with their subscribers for digital content.

Operators must maximise these platforms through revenue share agreements with digital service providers to capitalise on the large user base.

Instant payment Karma

some sort of bank account to do account to account payments.

The convenience of instant payments, where payments are made from bank account to bank account instantly, have seen them gain traction in both developed and emerging markets as a key way to pay.

Pix, Brazil’s instant payment system, leads with projected growth of 35% per year by 2027. UPI (India), PSE (Colombia), mobile money (Kenya, Nigeria and other African countries), as well as digital wallets (across emerging markets) are all also expected to grow annually by 16% to 20% through 2027.

The projections, from Payments and Commerce Market Intelligence (PCMI), are featured in the new edition of Beyond Borders, EBANX’s annual comprehensive study on the digital market and payment trends in emerging economies and point to just how these payment types are booming. But what does it

mean for carrier billing and for telemedia in general?

“Emerging markets are leading the global shift towards realtime payments, with innovations that match their populations’ demands for speed and convenience,” says João Del Valle, CEO and Co-founder of EBANX.

“This results from an irreversible trend in the payments industry: the development of solutions completely adapted to local consumer behaviour. And our report shows how this is taking place.”

For carrier billing this could be a problem. Currently, DCB leads the way in offering the unbanked – but smartphone-enabled – consumer anywhere in the world the chance to pay and play in the digital world. While Instant Payments offer the same level of convenience and speed, they are typically the preserve of the banked – you have to have

This has seen DCB largely stick to its lane as a payment tool for digital goods and instant payments used for physical ones.

ACROSS THE DIGITAL DIVIDE

But this is changing. Pix exemplifies this transformation pointed out by Del Valle, with a new feature scheduled to be launched by the Central Bank of Brazil in mid-2025. “Pix Automático has the potential to reshape Brazil’s digital market,” he says.

The highly anticipated feature of Pix will enable automated recurring transactions through Brazil’s instant payment system, bringing a whole new customer base to services such as streaming platforms, SaaS, app subscriptions, e-learning, social media, gaming, and more.

Exclusive projections from Beyond Borders indicate that Pix Automático could unlock more than $30 billion in online recurring payments within two

PIX IS USED BY 155 MILLION BRAZILIANS, REACHING 91% OF ADULTS

years, a significant volume for a market dominated by credit cards that currently moves USD 50 billion annually in Brazil. The report also estimates that the new feature will account for 12% of all Pix online transactions by 2027.

“When one payment method gains traction, it creates a ripple effect that elevates the entire ecosystem,” adds Del Valle. “The rise of Pix is not an isolated phenomenon, and we are also witnessing exponential expansion with other types of account-based transactions.”

ROOM FOR TWO?

While this could be bad news for DCB, there is clearly room in the market for both. DCB is well established in many markets and underpins much of the growth in content services in MENA, sub-Saharan Africa and parts of Asia. Its dominance is likely to stick around – especially if operators get behind it with renewed vigour (see page 1).

Instant payments are increasingly going cross-border, which delivers a degree of advantage, what is more likely is that DCB and instant payments will work together. In some cases, DCB providers might integrate instant payment capabilities to offer a more comprehensive payment solution, combining the strengths of both systems.

So, while instant payments will undoubtedly impact the payment landscape, DCB is expected to continue growing, particularly in mobile-centric markets and for digital content purchases.

The key for both payment methods will be to focus on their unique strengths and target markets, allowing them to coexist and serve different consumer needs.

What We Do

We are a digital solutions provider who enables merchants to grow within the credit card or mobile operators Ecosystem in an ever changing connected world.

CREATIVE PUBLISHING

How we do it

Made by Merchants for Merchants. The M4M Concept means we are providing our technology and expertise to digital merchants by creating meaningful and beneficial alliances for long term business growing. MULTICHANNEL MARKETING

Where we do it

Based out of Dubai with point of presence in London Barcelona New York Beirut Karachi

AD Group operates in Europe, MEA, Africa, Southeast Asia, Australia, Latin America and the US.

We are looking for Partners on VAS / DCB ∙ Credit card processing

Build My product time-proof technology

THE PRICE IS RIGHT?

To maximise long-term growth of RCS, the study urges service providers to ensure price parity with SMS and streamline the verification process for businesses, by offering a standard process across network operators and aggregators. In turn, this will enable RCS business messaging users to add custom branding and increase the acceptance of RCS channels amongst mobile subscribers.

With RCS, there is greater potential for conversational use cases to enhance the consumer experience, for example with customer service, or in conversational commerce. The availability of RCS on a wide scale opens up the opportunity for enterprises to use the channel for conversational use cases.

As enterprises adopt RCS business messaging for these use cases, messaging vendors must work with operators to assess consumer engagement with the channel by analysing read receipts and how many messages are typically sent during a conversation. This will allow the development of the session-based monetisation model, which optimises revenue returns for operators for each conversational use case. For example, the cost of a session used for customer care must differ from one used for conversational commerce, and the latter must be charged at a higher rate, since it is more likely to generate a sale for the brand and, therefore, there is greater value associated with that conversation.

Moreover, use cases must be considered down to industry level, as the demand from each industry will differ. For conversational use cases where there is typically a higher number of messages per conversation, these could be charged at a higher rate as the enterprise

is being offered greater value rather than paying per message.

When chatbots are used, sessions can be charged at a premium, since chatbots offer high value to the enterprise by saving time and improving the customer experience, especially as they become more advanced. Their growing popularity will drive the use of RCS for conversations with brands, particularly when a customer has a query they want answering.

The introduction of P2A (person-to-application) RCS messaging will enable customers to reach out to brands easily for customer service, allowing them to direct customers away from voice and email, saving a lot of time. For this to be introduced, a click-to-chat feature must be made possible with RCS as it is with WhatsApp to ensure a seamless experience for the customer and avoid frustration when they are asking something.

However, there are challenges – OTT messaging has already stolen a march on RCS business messaging, being available across devices long before Apple added RCS support late last year; and fraud is a constant issue in the messaging industry.

SEEING OFF OTT AND FIGHTING FRAUD

According to the report, in a number of countries OTT messaging apps have a strong penetration, with a high proportion of the population actively using these apps to send P2P messages. In these countries, messaging vendors must focus on offering RCS as part of an omnichannel approach.

There is also uncertainty surrounding fraud across RCS business messaging, and it is essential to address this. Fraud has had a significant impact on SMS; however, the architecture of the RCS channel is different, and new types of fraud are expected to emerge as a result.

There is no real reason why artificial inflation of traffic (AIT) fraud won’t spill into RCS. Currently, AIT is driven by bots being used to send messages to fake numbers, with enterprises paying for the traffic and not garnering any new users. This could also easily be perpetrated through RCS.

There is also the potential for SIM swap fraud, where fraudsters intercept OTPs. Again, this is happening in SMS and there is no barrier to it working with RCS too.

WHAT DO MNOS NEED TO DO?

When dealing with OTT messaging, operators have a number of options. Firstly, where OTT already has a strong hold, operators must work together to ensure that RCS is widely available. OTT is well established and can add features more quickly and roll out new services with greater agility. In these markets, operators have to look again at pricing to compete, offering a lower price to OTT services for businesses. According to Juniper, this is how MNOs can deliver ROI on RCS business messaging and get RCS reach into these markets.

To deal with RCS fraud quickly, operators must work with vendors which can identify traffic patterns in RCS and compare this to when subscribers are blocking a user or experiencing issues. In turn, measures must be put in place quickly to prevent further cases of the same type of fraud, says the report. It is essential that the RCS messaging ecosystem remains vigilant to emerging types of fraud across RCS and is able to respond quickly. Otherwise, this will have a significant impact on the growth of the channel over the next five years.

• 60+ Leading Exhibitors 12 & 13 May

• 7+ Networking Events 11, 12, 13 May

• Open Bars Hospitality & Live Entertainment

• 5 Star Lunch & Drinks 12 & 13 May

• 8.1 Premium Subscription (worth €300 to 30 June)

• 2 Days Spotlight Session Programme

• 5-star Marriott Resort Palm Jumeirah Hotel Discount (limits apply – book early to avoid disappointment)

Platinum Sponsors

Contact: Jarvis@worldtelemedia.co.uk for sponsorship and exhibition opportunities or to make a speaker application

The amount of customer data captured online nowadays is growing at an exponential rate. Whether it’s opening a bank account, buying a train ticket, or communicating with local government authorities, users are required to share basic personal information, including payment details, email addresses, and home addresses. The more data exchanged online, the greater the risk of data breaches. In 2023 alone, over 2,800 reported data theft incidents compromised more than 8 billion records. Such breaches have a profound impact on consumer trust, which is the cornerstone of customer loyalty.

NIS and DORA Orchestrating safe messaging in the CPaaS era

Messaging has had more than its fair share of security issues and as CPaaS systems leverage more and more data, the need to make messaging safe requires meeting a range of new regulations. HORISEN explains how it works in Europe

According to PCI Pal, 83% of consumers would stop spending with a business for months following a security breach, and 21% might never return. For messaging technology providers like HORISEN, adhering to and even exceeding security standards is essential for maintaining the trust and ensuring the highest level of data protection for our customers’ businesses. Although we, as technology providers, are not directly obligated to comply with these standards, the impact of non-compliance can be significant for our customers. Therefore, as a trusted provider to telecom, governmental, and

banking sectors, HORISEN’s security experts rigorously monitor the latest updates and standards and prioritize aligning with the latest security frameworks such as the NIS 2 Directive for cybersecurity and the Digital Operational Resilience Act (DORA) to protect our clients’ interests and ensure robust, compliant operations.

WHAT IS THE NIS-2 DIRECTIVE?

The Network and Information Security Directive 2 (NIS-2) establishes an EU-wide cybersecurity framework, created in response to escalating threats. Published in December 2022, it

replaces the original NIS Directive, setting higher standards for network and information system security across EU member states. NIS-2 requires essential and significant entities to implement robust measures to manage and mitigate risks, enhancing the resilience of critical sectors and supporting a secure EU digital landscape.

WHAT IS DORA?

The Digital Operational Resilience Act (DORA) is EU legislation focused on strengthening the cybersecurity resilience of financial institutions. It closes regulatory gaps with specific requirements for managing ICT incidents, business continuity, and third-party risk, while mandating threat-led penetration testing. DORA takes a systemic approach to resilience across Europe, prioritizing the financial sector and taking precedence where its requirements overlap with those of NIS-2.

RAISING THE SECURITY AND COMPLIANCE BAR

HORISEN is deeply committed to upholding high security and compliance standards recognizing that robust security is essential to building customer trust. Our foundation in GDPR, ISO/IEC 27001, and ISO/IEC 27002 compliance not only ensures data protection but also enables us to align closely with new regulatory frameworks, such as NIS-2 and DORA, which demand more stringent

cybersecurity measures and operational resilience.

Through an in-depth analysis, HORISEN identified specific areas requiring enhancement to fully comply with these evolving standards. Although ISO 27001 covers nearly all NIS-2 requirements, additional measures were necessary to address areas like crisis management and comprehensive incident reporting, as outlined in NIS-2. To meet these requirements, we have expanded our incident response capabilities to include rapid, structured reporting and a formalised crisis management approach.

For DORA compliance, which emphasises rigorous ICT risk management, incident reporting, and resilience testing, HORISEN is implementing ISO 22301 standards to strengthen our business continuity management, ensuring resilience during disruptions.

Additionally, DORA’s focus on supply chain security led us to adopt ISO 27036, fortifying our vendor risk management process, especially with critical providers like data centres and

ISPs. By managing most key services in-house, we retain greater control over our supply chain and reduce potential security risks.

Furthermore, HORISEN’s proactive security testing practices, including annual third-party penetration tests, align with DORA’s stringent resilience testing requirements, ensuring that our systems remain secure and resistant to emerging threats. Beyond these updates, we also continuously improve employee training programs and have integrated multi-factor authentication (MFA) in line with NIS-2’s cybersecurity expectations. Through these targeted enhancements and rigorous compliance measures, HORISEN upholds a comprehensive approach to data security, meeting today’s regulatory standards and laying a robust foundation for the future.

STANDARDS FOR SAFE AND RELIABLE MESSAGING

In the messaging industry that is growing rapidly, security is not just an obligation - it’s

a competitive advantage. At HORISEN, we take pride in our proactive approach to security, ensuring that we meet and exceed industry standards to protect the data of our customers and their clients.

HORISEN recognises the importance of staying ahead of security standards and regulations. We adhere to these high standards not out of obligation, but because our commitment to our customers’ security and business growth drives us. Our priority is to ensure the most secure and reliable services, reflecting our dedication to their success.

This commitment extends to ensuring that our suppliers, such as data centres, also comply with these high standards. Our cloud services are hosted in Tier IV data centres in Switzerland, demonstrating this commitment through their advanced security concepts that meet the highest requirements.

These partnerships enhance platform reliability, ensuring the utmost integrity and safeguarding clients’ data with unparal-

How AI is reshaping CPaaS in Europe

One of Europe’s leading enablers of B2B digitalisation, Telekom Business Europe –the B2B arm of Deutsche Telekom – is to enhance its telco communications platform to help businesses across Europe establish an omnichannel presence and connect with customers on their preferred channels through a deal with global communications platform Infobip.

Nearly all enterprises are using AIenabled communications platforms to improve their digital competitiveness, and consumers want to reach brands on their favorite channels. Therefore, businesses and brands globally must be able to reach their customers across a range of channels.

Telekom Business Europe’s cloud-based and AI-enabled communication platform, powered by Infobip, enables businesses of all sizes to improve their marketing, sales, and support by unifying their communica-

tion. The centralized communication platform offers an intuitive interface and seamless access, enabling businesses to engage with customers from any location, at any time, through their preferred communication channels, including Rich Business Messaging and Network API use cases.

Telekom Business Europe will gradually launch the solution in different national markets across Europe.

Igor Marušić, CPaaS Lead at Telekom Business Europe, comments: “Our extensive partnership with global CPaaS leader Infobip will help European businesses boost their productivity and set a clear path to future growth. On top of voice and SMS, which remains the most important messaging channel and one that’s still growing, we’re now expanding our portfolio with new channels, including RCS, WhatsApp, Viber, Apple Messages, and

leled diligence while complying with privacy laws. Additionally, we conduct annual penetration tests to ensure that our systems remain resilient against potential threats and vulnerabilities. By adhering to GDPR, ISO/IEC 27001/27002, NIS 2, and DORA, along with hosting our cloud services in most secure environment, we provide a secure foundation for our customers to build their own trusted services.

This comprehensive approach ensures the highest levels of protection and reliability, supporting our customers in delivering secure and trustworthy services to their clients.

For an in-depth look at these standards, HORISEN’s gap analysis and the steps to achieve full alignment with NIS-2 and DORA, check out our paper, Meeting NIS 2 and DORA Requirements in the CPaaS Industry, available on the HORISEN website.

social media. By implementing the communication platform, we’re underpinning our strength in our core channels while also creating new revenue streams and seamlessly adapting to the latest communication trends and customers’ needs for omnipresence.”

Matija Ražem, VP of Business Development at Infobip, adds: “The partnership combines the strengths of both companies to create a powerful and highly versatile communication platform eco-system to help businesses improve customer experience. Moreover, our partnership accelerates digitalization in the European business-to-business market by offering new ideas and tools to the markets. This eco-system is complemented with connected chatbots, contact centres, and marketing campaign services, which are all part of the Infobip platform.”

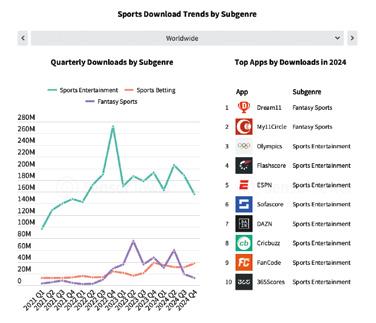

Game on How to score big with subscription sports services in 2025

Sports content is massive worldwide and is set to be a key traffic and billing driver for telemedia VAS across 2025. But how do you mmake the most of it and how do you turn it into a subs service? Julia Dimambro shows you

With a huge selection of major sporting events in 2025, supporter and fan video content around these events is in high demand. Especially on portable devices for that ‘on-the-go’ experience for busy fans who want to keep up to date with the main news and highlights from their favourite tournaments.

As a result, 2025 is also shaping up to be a year of exciting opportunities for the telemedia and VAS sectors. The growing appetite for high-quality, engaging sports content presents a massive opportunity to deliver value to consumers while driving subscription revenue.

But let’s face it, launching a subscription-based service isn’t for the faint-hearted. The high upfront risk, along with marketing and billing expenses, can understandably deprioritise content quality and consumer value. This approach can backfire, increasing the likelihood of products failing to convert or retain subscribers. That’s why strategic insights and trusted partnerships are critical.

WHY SPORTS CONTENT IS A NO-BRAINER ON MOBILE

Sports fans have gone mobile… well, everyone has, but it is particualrly true of sports content consumers. More than 75% of sports fans now prefer streaming highlights, interviews and news on their smartphones. This isn’t a passing tren; global mobile video

traffic is projected to grow by 25% year-over-year, driven largely by the thirst for short-form sports content. The average fan spends about 50 minutes daily watching sports videos, making it one of the most engaging categories in entertainment.

For businesses, the takeaway is clear: if you’re not offering mobile-first, snackable sports content, you’re leaving money on the table. Younger audiences love quick highlights and player soundbites, while seasoned fans appreciate in-depth nálisis and stats. The sweet spot? A mix that keeps subscribers engaged and eager to renew.

TOP SPORTS VIDEO TRENDS FOR 2025

So, what sports content is driving the subscription space?

Tailored content is King: fans crave personalised experiences. AI-driven platforms that curate content based on favourite teams, players, or leagues will win big, fostering loyalty and reducing churn.

Short-form, big impact: quick recaps, bite-sized interviews and highlights are dominating the sports video space. Perfect for mobile consumption, this format boosts engagement and keeps fans coming back for more. Real-time feeds for real-time fans: API integrations are gamechangers, enabling platforms to deliver automated, real-time

updates. This reduces resource costs for providers and meets fan expectations.

Interactive and immersive formats: Augmented reality (AR) and virtual reality (VR) are reshaping fan experiences. Virtual stadium tours and player POV content offer fans a new level of engagement.

MITIGATING RISK WITH MONTHLY LICENSING

Fixed licensing fees can be daunting, especially when factoring in high launch costs, a four-tosix-month break-even point and customer acquisition costs (COA). That’s why monthly licensing is such a smart move: Minimised long-term risk: A structured monthly package allows growth and analysis while keeping launch costs low. This lets you evaluate performance and fine-tune offerings with your supplier for better subscriber retention.

A dynamic fresh service every access: Monthly licensing ensures access to the latest sports news, interviews, and highlights without the need for separate negotiations or added fees.

Scalable solutions: Adjust your package as your audience and needs grow.

At SFM, we’ve spent over two decades helping clients navigate these challenges. By partnering with world-class rights holders and leagues, we provide premium sports content that includes the peace of mind of secure and legal licenses.

PROVEN STRATEGIES FOR SUCCESS

Looking to maximise ROI and grow your audience in 2025? Here are some tried-and-true tips: Focus on regional appeal: Cater to local tastes by including content from local leagues or interviews with regional stars. This not only increases engagement but broadens opportunities to reduce your acquisition costs with more

targeted keywords.

Social media is your friend: Using platforms like TikTok and Instagram has a proven track record of driving new subscribers to your service. SFM’s dynamic sports services include special features specifically for SM.

Tier your pricing: Offer multiple subscription levels to suit different budgets. Freemium models can be great for onboarding new users.

Data is gold: Use analytics to understand what’s working and double down on your most popular content.

FINAL THOUGHTS

2025 promises to be an exciting year for sports video content, particularly on mobile platforms. With the right strategies and the right partner, your subscription service can thrive in this competitive market.

If you’re ready to transform trends into commercial success, let’s chat. At SFM, we’re here to make it happen with Seriously Fresh Media —just like the name says.

WHY CHOOSE SFM?

With more than 20 years in premium video licensing, we’re not just another content provider— we’re your partner in success. Here’s what sets us apart: Unmatched content access: Our long-term partnerships mean you get premium, secure sports content from industry leaders at unbeatable rates.

Tailored solutions: Whether it’s an extensive catalogue or custom API feeds, we’ve got options that fit your needs.

Hassle-free support: From supplier negotiations to seamless delivery, we handle the heavy lifting so you can focus on marketing and acquisition.

At SFM, we’re passionate about helping our clients capitalize on emerging trends. You’ll gain access to top-tier content, proven expertise, and a partnership built on trust.

NEARLY 8 IN 10 SURVEYED USE DIGITAL MEDIA TO CHECK SPORTS NEWS, SCORE AND

UPDATES

Sports video in MENA is the goal

The MENA region is a hot bed for sports content – and creating subscriptionled mVAS services around it are a high priority. While no hard figures exist for the actual value, a look at how the MENA mobile sports market looks shows just what the potential here is:

The overall sports industry in the MENA region is experiencing significant growth. The Middle East sports industry is expected to grow by 8.7% by 2026, which is more than double the rate of the global sports industry’s projected growth of 3.3%.

The MENA region’s SVOD (subscription video on demand) services market generated over $1 billion in revenues in 2023 and is expected to surpass $1.2 billion in 2024. This indicates a growing appetite for video content, which could potentially include sports-related content.

• Information about how to attend a game in-person

• Information about where/when to watch a game on television

• Information about game sports news, scores and updates

• Information about my involvement in fantasy sports leagues

• Information about what my favourite players are doing other than playing

Source: Georgetown University SIM Program

Julia Dimambro is CEO, Seriously Fresh Media www.seriouslyfreshmedia.com julia@seriouslyfreshmedia.com

Online video advertising in MENA is projected to grow by 67% in revenue by 2028, while online video subscription is expected to grow by 19%. This suggests an increasing market for digital content and advertising, which could be relevant if Sport Clips were to expand its digital presence in the region.

The value of sports media rights globally is projected to grow, with in-play clips rights expected to grow by 76% to reach $1.7 billion by 2024, and shortform highlights rights projected to grow by 101% to hit $3.2 billion. This trend could be beneficial if Sport Clips were to leverage sports-related content in its marketing or services.

The MENA region has a young, tech-savvy population with increasing digital penetration. This demographic could be receptive to innovative sports-related services or marketing approaches.

Hashim Abu-Lebdeh, Business Development Manager, 3Anet

What does your company do?

3Anet is a leading mobile billing aggregator, offering Direct Carrier Billing (DCB) connectivity to facilitate seamless transactions between content providers, aggregators and telcos. In addition to DCB, we provide a comprehensive suite of advanced services, including hosting services to ensure reliable and secure platforms, managed services to handle day-to-day operations.

Which countries or regions do you feel represent the greatest opportunity for your telemedia services in 2025 and why? Our services are primarily offered in the MENA region, with Saudi Arabia being the largest market in the region. Iraq still has good potential of growth, while Libya and Algeria are steadily expanding in their adoption of DCB services.

Which content and/or applications do you see being the most likely to benefit from Telemedia billing technologies? AI-powered services and cloud gaming can significantly benefit from telemedia billing by offering seamless payment experiences and broader accessibility. As the entertainment industry continues to grow and target diverse segments, these technologies enable faster transactions, reduce barriers for users and enhance monetisation, particularly in regions with limited access to traditional payment methods.

How do you balance payment flows, operator relationships and customer satisfaction?

We maintain reliable payment systems, build strong partnerships with operators and content providers through transparent communication and implement advanced solutions to ensure secure, reliable payment flows. At the same time, we prioritise simple and userfriendly payment experiences for end users.

What are the key drivers and inhibitors for growth?

Many factors influence growth, but key are technological advancements and stable regulations. Rising customer demand for efficient services, coupled with strategic investments in infrastructure, also play a significant role. However, growth can be hindered by market instability, complex payment flows, economic challenges, and resistance to change from end users.

What major factors do you think will impact the future development of mobile payments and which other payment options represent the biggest opportunity for telemedia?

Technological advancements such as AI and blockchain, increasing demand for contactless and seamless payment experiences, and the growing shift toward digital wallets and mobile apps.

Consumer behaviour and preferences, as well as improved security measures, will also shape the landscape. In terms of other payment options, DCB presents a major opportunity for telemedia, offering a convenient and secure way for consumers to make payments via their mobile carriers, especially in regions with limited access to traditional banking services.

Which specific VAS verticals are you expecting to have a great year and why?

We anticipate significant growth in AI-driven services, cloud gaming and elearning within the VAS landscape. AI-powered solutions are increasingly in demand for their ability to enhance user experiences across industries. Cloud gaming continues to expand as internet speeds improve and the gaming community grows. Elearning, particularly for kids, is expected to thrive due to the rising demand for accessible, interactive, and educational content.

How might you answer that same question in five years?

I expect the VAS landscape to advance significantly, with AI-driven services offering even more personalized and dynamic user experiences. Cloud gaming will likely see widespread adoption as networks evolve, providing smoother and more immersive experiences. Additionally, elearning could evolve into a highly interactive

space with the integration of AR and VR, making educational content more engaging.

Do you see affiliate marketing being a primary, trusted channel for telemedia propositions or do you think alternative routes to market will become more popular – if so, what are they likely to be?

Affiliate marketing is losing popularity due to security concerns, as well as the high potential for fraud and misleading marketing practices. As a result, businesses are shifting toward more secure channels like Google advertising, social media platforms, and app stores. These platforms offer better control, enhanced security, and more reliable ways to engage customers, minimising risks and fostering trust in marketing efforts

What impact is AI going to have on marketing telemedia services in 2025 and beyond – and on your marketing/engagement strategy in particular?

AI will revolutionise telemedia marketing by enabling personalised, data-driven campaigns that enhance customer engagement and satisfaction. It will optimise content delivery, predict behaviour, and automate interactions, allowing for more efficient marketing and stronger customer relationships. This will lead to improved targeting, higher conversion rates, and more effective advertising.

Ad nauseum

How marketing and advertising are changing

Marketing plays a key role in driving users of mVAS, but where best to do that marketing is changing radically. Paul Skeldon takes a look at what that change looks like and where the smart guys are marketing their services

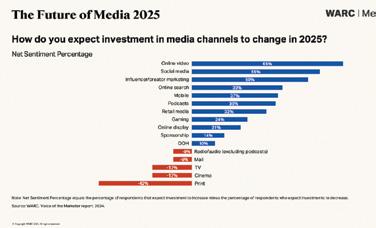

An advertising milestone was reached in 2024: the first year on record that ad spend globally topped $1trn. In 2025 it is expected to grow by 10.7% and hit a whopping $1.08trn. In fact, global ad spend has more than doubled over the last decade, growing nearly three times faster than global economic output since 2014, with more media channels available to marketers than ever before.

Brian Wieser, CEO and Principal of Madison and Wall, an advisory firm focused on the media and technology industries, and oft described as “Madison Avenue’s de facto Chief Economist” says: “As we enter 2025, the advertising ecosystem continues to evolve rapidly. The interplay between technology, data and creativity drives new opportu-

nities for marketers to engage meaningfully with consumers.”

This is backed up by ad industry body WARC’s state of the nation report – The Future of Media 2025 – which stresses that even as the ad market is growing, it is also changing. For instance, Google search is being disrupted by social and retail platforms, as well as the growing influence of artificial intelligence (AI), and finally, the developments within the retail media and commerce sector and how advertisers can adjust to an environment where commerce is increasingly ‘everywhere’.

Paul Stringer, managing editor, research & insights, at WARC, says: “Today, media is so vast, so complex, and so changeable, that it can be difficult for brands to make sense of it all. As we

reach the midpoint of the decade, this is also the most exciting time to be a media planner.

“Digital advertising has matured beyond direct-response to support brand-building and long-term effectiveness, advertisers are focusing more on quality over cost when deciding which media environments to advertise in, and signal fidelity is improving thanks to the growth of AI-powered media solutions and an influx of retail media and commerce media networks.”

So, what should you be looking out for in marketing and how does it impact how you generate traffic?

PLANNING IN AN ERA OF ABUNDANCE

Media diversity brings new opportunities for brands to drive growth over the shortand the long-term using smart combinations of different media channels, finds the study. Planning holistically and

choosing the right combination will be different for every brand and vary by context and objective.

Media quality, reach and price will be critical in helping planners determine the optimum stack for brands.

As spend and sentiment shifts to channels like social, influencers, podcasts and gaming, new tactics for brand building are emerging. Advertisers are adapting campaigns for platforms where attention is more fleeting, and lots of little exposures need to work together to improve brand outcomes.

Across channels like search and social, advertisers will be required to adapt campaigns to fit the preferences of algorithms. This may mean adopting new methods and processes, or putting more trust in AI systems to automate parts of campaign management - even if this means sacrificing autonomy and control.

MARKETING & PROMOTION

NEW CHALLENGES AND OPPORTUNITIES IN SEARCH

This year, more than $220bn will be spent on generic search globally, suggests WARC forecasts, with Google taking more than 80% of the share. However, social media is rivalling Google as the young people’s search platforms of choice for brand discovery.

The future of search appears to be about intent rather than information, supported by sophisticated uses of AI.

Developments in AI are leading traditional search providers and new entrants to compete to ‘identify consumer intent in ever more granular ways’. Access to these insights should help brands build a more sophisticated and nuanced understanding of audience behaviours, leading to more personalised and relevant communications.

AI-driven search requires a

rethinking of search engine optimisation (SEO). In the near future, brands may need to optimise messaging and content to ensure they are visible and represented favourably in AIbased search results.

This approach - which some are calling Large Language Model Optimisation (LLMO) –will require a different set of skills and processes compared to traditional SEO.

The top ad trends for 2025

A recent survey of 700 marketing professionals in late 2024 has highlighted the key trends in marketing and martech that are going to shift the dial in 2025. Published by Mediaocean, the survey offers a compelling view of the marketing world’s immediate trajecetory and backs up just how AI-dependent we are about to become. It finds that the key trends are:

1. Ad spending prioritisation: Social media, digital display/video, and Connected TV (CTV) are the fastest-growing channels, with 68%, 67%, and 55% of marketers planning to increase spending in these areas, respectively.

2. AI is the top trend: Generative AI has emerged as the leading consumer trend, surpassing CTV. 63% of marketers identify it as critical. Key advancements in AI are reshaping workflows and enabling more sophisticated advertising strategies.

3. Automation on the rise: Automation has become the fastest-growing investment area, with a 17% increase in adoption since mid2024, as marketers seek to improve their workflow across media formats.

4. Multi-ID measurement: Advertisers are adopting multiple approaches to identity resolution to improve campaign measurement and at-

Brands may need to adopt more diverse search strategies to account for the growing fragmentation of search experiences across retail and social platforms and variables such as audience, type of search and category.

RETAIL GROWTH FUELS COMMERCE MEDIA EXPANSION

Commerce is increasingly everywhere. Retail media and broader

tribution. Almost half cite this as a top concern for 2025.

5. Creative-media gap: Despite slight improvements, 86% of advertisers report a lack of synchronization between creative and media processes, highlighting significant opportunities for growth.

“This year’s outlook report underscores the profound shifts already underway and intensifying across the advertising industry,” said Aaron Goldman, CMO of Mediaocean. “From the rise of AI and automation to the need for more comprehensive measurement frameworks, the insights in this report provide actionable guidance for brands and agencies looking to thrive and compete in a dynamic marketplace.”

“Generative AI is no longer a futuristic concept—it’s a cornerstone of today’s advertising strategies,” adds Deborah Wahl, Forbes CMO Hall of Fame member and former global CMO of General Motors. “The moment we’re in reminds me of the electric vehicle transformation in the auto industry. To capitalize on the opportunity, nay – imperative, marketers had to reimagine their business strategies and marketing programs. The same goes for AI, and the brands that embrace it now will see outsized returns.”

commerce media is expanding, reaching $154.8bn in advertising spend globally in 2024 with a further 14.8% rise expected in 2025, per WARC Media. New commerce media platforms are launching, and social commerce is continuing to grow rapidly. Commerce media is becoming the infrastructure that underpins the entire digital advertising ecosystem and offers brand building potential. Many retail and commerce media platforms now sell ads that allow advertisers to reach consumers across the purchase journey, from awareness all the way through to conversion.

Advertisers will need to weigh up these opportunities carefully, supported by holistic measurement that allows them to show the impact of commerce on long-term brand and business metrics.

New entrants may struggle to win spend from incumbents. Advertisers already admit to feeling overwhelmed by the number of options available in the commerce space and highlight a lack of standardisation across platforms as their biggest challenge with retailers. In the short-term, this may curtail the growth of new entrants as advertisers prioritise working with just a few large and established networks. Retail spending puts brand budgets at risk. Many advertisers appear to be divesting from traditional advertising channels to spend more on lower-funnel ads on retail media networks. Advertisers should protect traditional advertising budgets to avoid falling into a vicious cycle of weakening their brand, while raising the cost of driving performance on retail media properties

Download the report at https://www.warc.com/content/paywall/article/WarcData/Global_Ad_Spend_Outlook_2024_25/en-GB/156867?

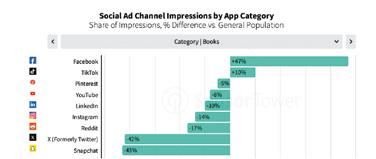

Social climbing

Social media is now at the centre of digital marketing and affiliate marketers are making hay. So, how can mVAS join in and what’s in it for telemedia? Paul Skeldon takes a look

Affiliate marketing has become a dominant force in the digital marketing landscape and has long been a favourite of telemedia as it has become a great traffic driver for mVAS – and mVAS has played an interesting role in the evolution of affiliate marketing. However, the rise of social media has shaken up affiliate marketing in the past five years and increasingly mVAS providers need to be aware of what they can get out of using these platforms and the affliates that leverage them.

Social platforms like Facebook, TikTok,and Snapchat provide access to massive audiences, sophisticated targeting capabilities, and a variety of content formats that can be leveraged to promote products and services. And this has made them very attractive to affiliate marketers.

HOW AFFILIATE MARKETERS USE SOCIAL MEDIA

Affiliate marketers use various strategies to promote products

and services on social media that run the gamut of social marketing.

• Influencer marketing: Partnering with influencers who have a significant following and credibility within a specific niche. Influencers create sponsored content, such as posts, videos, or stories, featuring affiliate links or discount codes.

• Organic content promotion: Creating and sharing valuable content related to the products or services being promoted. This can include product reviews, tutorials, comparisons, or lifestyle content that seamlessly integrates affiliate links.

• Paid advertising: Using social media advertising platforms to target specific demographics, interests, and behaviours. Affiliate marketers can run ads that direct users to landing pages with affiliate links or promote sponsored content.

• Community building: Engaging with followers and building a community around a shared

and automating payouts. Likewise, the service company can also offer content creation and distribution services to affiliate marketers. This can include producing high-quality videos, graphics, and written content optimised for social media platforms.

From a telemedia point of view, mVAS providers can also integrate mobile payment solutions into social media platforms, making it easier for users to purchase products through affiliate links. This can increase conversion rates and drive revenue for affiliate marketers.

interest. This can involve creating groups, hosting contests, or participating in relevant discussions.

• Live shopping: Hosting live streams where products are showcased and affiliate links are shared in real-time. This creates a sense of urgency and encourages immediate purchases.

HOW MVAS CAN LEVERAGE THE RELATIONSHIP

mVAS providers can play a crucial role in facilitating and enhancing the relationship between affiliate marketers and social media platforms. There are a raft of ways in which mVAS providers can leverage and expand the affiliate relationship on social.

For starters, mVAS providers can develop dedicated affiliate marketing platforms that integrate with social media APIs. These platforms can provide tools for tracking affiliate performance, managing campaigns,

From a more ‘soft power’ perspective, mVAS players can leverage their data analytics capabilities to provide insights into audience demographics, interests and behaviours. This information can help affiliate marketers optimize their campaigns and target the right audience. They can also develop loyalty programmes that reward users for engaging with affiliate content and making purchases through social media. This can incentivise users to participate in affiliate marketing campaigns and build brand loyalty.

For both mVAS and advertisers, social media has revolutionised the way affiliate marketers reach and engage with their target audience. By leveraging the power of these platforms, affiliate marketers can promote products and services effectively and drive revenue growth. mVAs providers can play a vital role in supporting this ecosystem by providing the necessary tools, services, and infrastructure to facilitate the relationship between affiliate marketers and social media platforms.

As social media continues to evolve, telemedia must adapt and innovate to stay ahead of the curve and provide cuttingedge solutions for affiliate marketers. And you can learn more at Telemedia Dubai in 11-13 May 2025.

Network or advertiser

Which to choose to market your mVAS

Are you weighing the benefits of joining a CPA network against the potential gains of working directly with advertisers in mVAS? Here, Golden Goose offers a comprehensive comparison of these two approaches, helping you understand the nuances and benefits of each

Leveraging the dynamic market for mobile value added services (mVAS) offers great rewards, but there are several ways to get there. What it comes down to in essence is whether to work with a Cost per Action (CPA) network that sits between an affiliate and advertisers, or whether to work directly with advertisers and cut out the middleman.

While both have pros and cons, choosing what will work best for your business is a tough choice. So how do you choose? Here we take a look at each option, assessing its pros and cons and help guide you to a perfect mVAS decision.

UNDERSTANDING CPA NETWORKS

A Cost Per Action (CPA) network acts as an intermediary between affiliates who want to monetise their traffic and advertisers seeking to promote their products or services. By joining a CPA network, affiliates gain access to a curated list of offers from various

advertisers that are already vetted for quality and profitability. This structure allows affiliates to focus on optimising their traffic strategies without the complexities of direct negotiations with advertisers.

Benefits of CPA networks include:

• Access to a wide variety of offers: CPA networks provide affiliates with a diverse range of advertising offers across different sectors, including mVAS, which are difficult to access independently.

• Pre-negotiated rates and terms: Networks leverage their volume of affiliates to negotiate favourable terms that might be unattainable for an individual affiliate dealing directly with advertisers.

• Reliable tracking and payment systems: CPA networks invest in advanced technology to ensure accurate tracking of actions and timely payments, safeguarding affiliates against discrepancies in reporting and

financial transactions.

• Timely payouts, including daily options: Many CPA networks, including Golden Goose, offer flexible payment terms that can range from weekly to daily payouts, accommodating various forms of payment methods to meet the diverse needs of affiliates globally.

• Support and resources: Networks offer dedicated support teams and resources such as training and market insights, which are invaluable, especially for those new to the mVAS sector or looking to scale their operations.

But there are challenges with using CPA networks. These include:

• Lower margins due to network fees: While CPA networks streamline many aspects of affiliate marketing, they also take a cut of the earnings as compensation for their services, which can mean slightly lower margins for the affiliates.

• Less direct control: Affiliates

working through CPA networks have less control over the campaign specifics like target audience and ad placement because these parameters are often dictated by the network in accordance with advertiser agreements.

WORKING DIRECTLY WITH ADVERTISERS

Working directly with advertisers involves affiliates forging individual partnerships with companies to promote their products or services. This model allows for direct negotiation of terms, rates, and campaign specifics, providing a more hands-on approach to managing mVAS campaigns. It requires a deeper understanding of market trends, audience targeting, and negotiation skills, as affiliates take on the full responsibility of campaign execution and management. There are, as you would expect, a number of advantages to this, including:

• Higher potential revenue per action: Without a middleman, affiliates often receive higher payouts directly from advertisers, as there are no network fees reducing the margins.

• Direct communication and relationship building: Engaging directly with advertisers enables affiliates to build strong, personal relationships, which can lead to better understanding, trust, and potentially more favorable deals and exclusive offers.

• More control over campaigns: Affiliates have complete control over every aspect of their campaigns, from targeting strategies to creative development, allowing for highly customized marketing efforts

that may yield better results.

• Customisation and flexibility: Direct deals often allow for greater flexibility in how campaigns are run, including customizing offers and adapting quickly to changing market conditions or performance feedback.

However, there are some downsides, such as:

• Requires more resources: Managing direct relationships requires more time and effort, including resources for negotiation, contract management, and ongoing communication.

• Higher risk and responsibility: Affiliates are fully responsible for due diligence and compliance, which adds a layer of risk. There’s also the potential for financial instability if an advertiser fails to fulfill payment obligations.

• Limited access to diverse offers: Without the network’s aggregation of multiple offers, affiliates might find it challenging to diversify their portfolio or access a broad range of mVAS opportunities.

• Bureaucratic challenges: Often, direct dealings with big companies involve navigating complex bureaucracies. Affiliates typically rank lower in priority compared to other large corporate partners, making it

challenging to secure attention and resources, and potentially leading to slower decisionmaking and longer wait times for issue resolution.

For affiliates with the capacity to manage direct relationships, this approach can be incredibly rewarding, offering higher margins and more control over their business. However, it demands a significant commitment and a solid understanding of the mVAS market to leverage the opportunities effectively.

COMPARING THE TWO MODELS

When deciding whether to join a CPA network or to work directly with advertisers, affiliates must consider various factors based on their individual capabilities, resources, and business goals. Let’s compare the two models head-on:

Efficiency and ease of use

• CPA networks: These networks offer a plug-and-play approach where affiliates can easily select offers and start campaigns quickly. The support and infrastructure provided by networks like Golden Goose make it particularly efficient for affiliates who want to minimize operational complexities and focus more on scaling their campaigns.

• Direct relationships: Working

directly often involves more setup time and continuous management. The efficiency of this approach depends heavily on the affiliate’s skill in handling negotiations and managing partnerships.

Revenue opportunities

• CPA networks: While the revenue per action might be lower due to network fees, the accessibility of diverse, pre-vetted offers can lead to a more consistent income stream. Networks also often provide optimized campaign strategies that help maximize earnings from available offers.

• Direct relationships: This approach can potentially yield higher payouts per action since there are no intermediary fees. However, achieving this depends on the affiliate’s ability to secure favorable deals and manage campaigns effectively.

Risk management

• CPA networks: Networks generally provide a layer of security for affiliates, handling the due diligence on advertisers and ensuring reliable payment systems. This reduces the risk of non-payment and compliance issues for the affiliate.

• Direct relationships: While offering greater revenue potential, this model carries higher risks, including the burden of vetting advertisers and the

The rise of affiliate marketing in MENA

Affiliate marketing has skyrocketed in the MENA region in recent years as the population has embraced mVAS content and games off the back of exploding mobile phone penetration.

According to Cognitive Market Research figures, MENA accounted for around 2% of global affiliate marketing revenues in 2024, totalling some $4.25bn and is expected to grow at a CAGR of 10% between now and 2031. The biggest growth markets are seen as Egypt, South Africa, Turkey and Nigeria, however a penchant for luxury items is also driving up affiliate marketing in general in the likes of Dubai, Qatar and

Saudi Arabia.

The key things driving these mVAS affiliate programmes in MENA are what drives it everywhere, namely:

• High conversion rates: Digital content like gaming and streaming services appeals strongly to younger demographics.

• Recurring revenue models: Subscription-based services ensure steady income streams for affiliates.

• Localisation: Arabic-language campaigns and culturally relevant offers resonate well with regional audiences.

• Mobile-first approach: With more than 70% of internet users accessing content

possibility of delayed payments or disputes.

Suitability for different types of affiliates

• CPA networks: Ideal for both newcomers and experienced marketers who prefer a streamlined, less hands-on approach to affiliate marketing. Networks provide the tools and support necessary to grow without the need for extensive infrastructure.

• Direct relationships: Best suited for seasoned affiliates who have the capacity to manage complex negotiations and who prefer direct control over their marketing strategies. This model is often more demanding but can be more rewarding for those with the necessary expertise and resources. Each model offers distinct advantages and challenges. CPA networks, like Golden Goose, are generally more user-friendly and less risky, making them a favourable choice for affiliates looking to efficiently scale their operations with reliable support. Direct relationships may appeal to those seeking higher control and potentially greater payouts but require a deeper commitment to managing various aspects of the business.

via mobile devices, mobile-optimised campaigns are essential.

According to Cognitive’s data, virtual products are the fastest-growing category over the forecast period. As more companies offer digital goods and services, the affiliate market is expanding due to the expansion of virtual items. Affiliates are taking advantage of this trend by encouraging viewers to purchase various virtual goods, including software, online courses, and digital downloads. Affiliate marketing for virtual items offers affiliates rich prospects in response to the growing need for digital solutions.

You’ve gotta friend The rise of AI chatbots

AI chatbots are breathing new life into chat services, but it is in combination with CPaaS where they can really create big business. Paul Skeldon explains

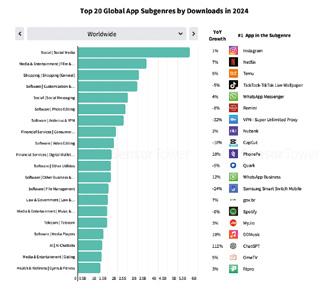

AI chatbots have come a long way in a short time. According to the latest app usage data for 2024, apps mentioning AI were downloaded 17 billion times last year and they have seen 200% year on year growth in terms of spending by consumers and time spent in apps such as Character AI and ChatGPT total nearly 7.7 billion hours.

In fact, thanks to AI, streaming TV and social media, spending on

non-gaming apps outpaced that in gaming apps for the fourth successive year as consumer tastes have shifted to new modes of entertainment (see page 22). This shift to AI chatbots is highly significant. The rise of realistically human chat services powered by AI is not only growing at pace, but is also shifting the dial on the kinds of premium rate services that consumers are spending on.

8 in 10 men believe AI girlfriends could replace humans

The viral prediction of Dr Ian Pearson — a futurologist who claims an 85% accuracy rate for his forecasts — broke the internet last week by claiming that sex with robots will overtake sex with humans by 2050. While that may be some way off in time, if not in actuality, new research suggests a version of this future may be closer than we think: the majority of people are already open to intimacy with AI.

EVA AI (edenai.world), an AI girlfriend platform, decided to explore whether men are ready to embrace the cyber intimacy revolution. A survey of 2,000 men revealed that 8 in 10 believe AI girlfriends could fully replace human companionship, and 81% would even consider marrying one if it were legal.

While sex with robots might not surpass human intimacy until 2050, AI companionship is already accelerating, with 83% of respondents saying they believe they could form a deep emotional bond with an AI girlfriend.

Research shows people are betting on AI to bring back those whose presence they crave, but can no longer reach. 78% of respondents said they’d date an AI clone of their ex, while 80% expressed interest in chatting with an AI clone of

Already there are a number of adult performers on OnlyFans that have opted to use AI-generated virtual versions of themselves to handle text chat with their legion of followers, creating a 24×7 means of staying in touch with many, many people all at once – and generating significant revenues for all involved in making that happen – all the time. They don’t even have to get out of bed (see panel)

a deceased loved one, seeking solace and connection through memories brought to life with technology.

Interestingly, self-reflection also plays a role. Three in four participants said they’d be open to having an AI clone of themselves as a virtual companion and an equal number would create an AI ‘polished’ twin of their current partner.

Cale Jones, head of community growth at EVA AI, on the transformative role AI plays in the societal intimacy shift, says: “AI companionship allows people to be their authentic selves without fear of judgment. It creates a safe space to explore thoughts, emotions, and desires that might feel too vulnerable to share in real life. The benefits extend far beyond the virtual world: one EVA AI user discovered her bisexuality through this platform — something she previously felt too insecure to explore in real life.”

Jones adds: “Our research also found that many people would chat with an AI clone of themselves. It’s an incredible way to gain insights into your own personality, behaviour, and thought processes from a unique perspective. This once-unthinkable future is now closer than ever.”

CPAAS THE REAL WINNER

However, the implications run far deeper than that. As CPaaS service providers look to take things to the next level for businesses looking to make interaction between customers and themselves as rich as possible, the attraction of these personalised AI generated chatbots look like a no-brainer.

Imagine, rather than having a flirty text chat with OnlyFan Amouranth about matters erotic, you are using the tech to offer customers of, say, a bank the ability to talk directly to a friend on customer services who always has the same voice, knows your call history and can talk to you on a much more ‘human’ level. This has, surely, been the thing that has been missing from automated customer service – if not all customer service delivered online or on the phone – and what can make it truly fly?

This shift to AI-powered apps shows that the consumer demand is running in parallel to the technical feasibility of delivering these services. All it takes is for the services to be created and sold. And that is the work of the CPaaS providers.

Several businesses have successfully implemented CPaaS with AI chatbots to enhance their customer service and operational efficiency. Some notable realworld examples include:

• iFood: This South American online food delivery platform integrated a conversational AI chatbot solution on WhatsApp

and their website to improve customer support and automate processes. The chatbot handles 45% of incoming inquiries, resulting in a 70% reduction in delivery costs.

• Aveda: A botanical hair and skincare brand developed an AI chatbot for Facebook Messenger to improve its online booking system. Over a seven-week period, the chatbot achieved impressive results: 378% increase in lifetime users; 6,918 additional bookings; and 33.2% increase in booking conversion rate.

• Subway: The fast-food chain deployed a Google RCS chatbot for business messaging, which delivered exceptional results: 140% and 51% more conversions on two separate offers; and improved customer engagement through rich-media interactive messages.

• Luxury Escapes: This Australian luxury travel agency implemented an AI chatbot that outperformed their website: three times higher conversion rate than the website; generated more than $300,000 in revenue in the first 90 days; and saw an 89% response rate on retargeting efforts.

• Esso: The oil and gas company created an AI-powered chatbot on Facebook Messenger for a hockey-themed community event: 83,000 users engaged with the chatbot; 70,000 users signed up for a contest; and 46,000 posts shared on social media3

• L’Oréal: The beauty company introduced a chatbot platform for recruitment, specifically targeting internship candidates and beauty advisor positions: engaged with 92% of applicants out of the first 10,000 recruitment conversations; and achieved a satisfaction rate close to 100% These examples demonstrate how businesses across various industries are leveraging CPaaS with AI chatbots to automate

processes, improve customer engagement, and drive significant business results.

THE HUMAN TOUCH

The power of AI to drive engagement is perhaps also backed up by how Sensor Tower’s apps data shows (see page 22 for more) that there are signs of digital fatigue among consumers. While on the face of it the data suggests that people want more engaging experiences online, drilling down finds that what they want are experiences that tap into the consumers’ humanity.

While many want apps to help deliver human engagement, the surge seen in food and drink app downloads, for instance, suggests that what consumers want are experience that tap into their needs and wants, their senses and their reward centres.

Again, the examples of OnlyFans performers using AI chatbots to interact ‘as human’ with their fans shows that the need for the human touch and AI are not mutually exclusive. AI can deliver the human experience at scale –something that needs to now be worked into content and services delivered across the telemedia market.

This is the next step in how content and premium services develop. AI can be used for many things, but making things more human is one of the most important. It might also be what stops AI becoming something that controls our lives in an oppressive way and becomes something that works for and with us puny humans and brings richness. With open sourced AI such as China’s recently released DeepSeek making GenAI available to pretty much everyone at a low cost –not to mention the US’s diametrically opposed approach of investing billions of dollars in the same – AI needs to be used for good. It needs to deliver benefits to consumers and improving interaction with business is where that starts.

Learning from OnlyFans: how AI creates a new chat paradigm

One of Twtich and OnlyFans’ biggest adult content creators, Amouranth, is using GenAI to interact via text and chat with her 6.3 million followers as online and messaging come together to create new ways to interact.

Using EVA AI, an artificial intelligence-driven digital interaction platform that enables users to connect with a range of humanlike partners, Amouranth has released a digital duplicate powered by advanced generative AI. The virtual twin is now exclusively available on the EVA AI platform, offering fans an engaging 24/7 digital interaction experience with the online star.

Working closely with Amouranth, EVA AI has meticulously analysed the model’s speech, mannerisms, and experiences. This has enabled the creation of a highly realistic digital model that pushes the boundaries of conversational AI. Utilizing generative AI algorithms trained on Amouranth’s work, EVA AI’s technology authentically responds to messages, allowing fans to foster a sense of personal connection with the hugely popular online star.

Amouranth – real name Kaitlyn Siragusa – ranks as one of the world’s most popular online figures and adult content creators, having amassed more than 6.3 million followers on the Twitch streaming platform and ranking among the top 0.01% of creators on adult content subscription service OnlyFans. With the release of her digital duplicate, she joins a host of famous figures using EVA AI’s proprietary digital twin technology, including adult entertainment sensations Linda Lovelace and Brandi Love.

“Fans of Twitch’s biggest streamers, such as Amouranth, spend hours watching their content, following their lives, and interacting with them through chat during live streams.,” says Caleth Jones, Head of community growth, at EVA AI. “Many form deep connections with their favourite stars and want to keep the conversation going even when the creator goes offline. That’s precisely what EVA AI offers — the ability to chat with your favourite personalities whenever you desire and without having to share the spotlight with countless other fans. Using generative AI to bring themselves to life in the digital world, creators can connect with their fans on a more personal level, while generating an entirely new — and effortless — revenue stream.”