Financials have benefited strongly as economies worldwide continue to move towards a more normalised interest rate environment. Despite this, they continue to offer compelling value at a time when many other sectors are trading on extended valuations.

With a dual focus on dividend and capital growth, the Polar Capital Global Financials Trust is an actively managed, diversified global portfolio that seeks to find the best investment opportunites from across this broad and vital sector.

Wood Group woes reveal the importance of discipline on cash flow and acquisitions

07 Nomination of vaccine sceptic Robert F Kennedy Jnr sends healthcare shares into a spin

08 Shein IPO in sight as Amazon digs in for the long ‘Haul’

09 Chancellor’s drive for ‘mega-funds’ could create ‘mega-challenges’

10 Walt Disney shares soar after CEO Bob Iger’s fourth-quarter breakthrough

10 Troubled semiconductor outfit IQE considers sale of Taiwan subsidiary

12 Can Pets at Home paw its way back to retail like-for-like growth?

13 Dell could be poised for AI-powered server boom

14 UK growth disappoints while Chinese consumer spending perks up

IDEAS

16 Take advantage of International Biotechnology Trust’s big discount

18 Why SDI’s growth star is set to shine again UPDATES

21 Still oodles to like about best-in-class British tech Cerillion

FEATURES

23 The UK takeover market has seen a surge of activity in the last few years

28 COVER STORY

The £1 billion profit club

Discover the titans of UK retail

37 Blockchain is an alternative way to play the crypto rally

43 Is the US stock market just too hot to handle? 40 MONEY MATTERS

My Financial Life – how to think about saving and investing in your 50s

46 DAN COATSWORTH

The benefits of staying invested when the list of worries builds up

50 ASK RACHEL

How is a drawdown pot accounted for when paying care costs?

53 INDEX

Shares, funds, ETFs and investment trusts in this issue

Three important things in this week’s magazine

The giants of UK retail: meet the members of the ‘£1 billion club’

As Christmas approaches, we take a deep dive into the UK’s most successful shopkeepers and discover the secrets to their profitability.

Are US markets still an attractive investment proposition?

After the record-breaking run in US stocks this year, and the fervour which greeted the election result, investors should tread carefully.

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

M&A frenzy as hundreds of UK companies are taken over every quarter

We look at the backdrop to the surge in deals over the last couple of years and explain what to expect if a company you own receives an offer.

Wood Group woes reveal the importance of discipline on cash flow and acquisitions

Three tried and tested market principles were reinforced by the latest update from beleaguered energy services firm Wood Group (WG.).

I have followed this business for nearly two decades and it’s hard to remember a time when it was in a worse state than it is today.

That’s backed up by the share price which traded at all-time lows below 50p in response to the company’s devastating missive on 7 November, down around 60% in the wake of the third-quarter trading statement.

An independent review was announced to decide if any prior-year adjustments are required on contracts in its Projects business. This follows some already hefty write-offs and creates a layer of uncertainty – something markets always hate. That’s principle one ticked off.

Crucially, any references to the previously promised ‘significant’ free cash flow in 2025 were notable by their absence. This was far more important to the market than the retention of underlying EBITDA (earnings before interest, depreciation and amortisation) guidance for 2024.

Earnings metrics can be inflated by clever accounting – it is the hard currency of cash on which companies are rightly judged. If revenue and earnings are not translating into cash flow then it is only fair to surmise all is not well. Principle number two.

The final principle is illustrated by the biggest reason Wood finds itself in this mess. So-called ‘transformational’ acquisitions are more likely to destroy value than create it. The company has been in restructuring mode and has been dealing with legacy issues ever since its 2017 takover of Amec Foster Wheeler as problem contracts put pressure on its balance sheet. This necessitated the 2022 sale of the company’s built environment consulting

business to reduce borrowings.

Chart: Shares magazine • Source: LSEG

The business certainly got bigger, it now employs some 35,000 people across 60 countries, but bigger is not necessarily better and warning signs were there from the start. An initial step change in profit and revenue reversed very rapidly and made the company’s words excitedly selling the deal ring very hollow.

US private equity group Apollo pulling out of a lengthy pursuit of the company in May 2023 having done significant due diligence on the business and Dubai’s Sidara also walking away from a deal in August 2024 told their own story.

The market will casting a beady eye over full-year results due in March and a likely year-end trading update in January for signs of updated cash flow guidance. Chief executive Ken Gilmartin and his management team have very little margin for error.

This week’s issue takes a look at the retail sector ahead of the key Christmas trading period and after a difficult period in the run-up to and in the wake of the Budget. But, as James Crux reminds us, amid the gloom there are still some excellent businesses in this industry which are able to deal with the slings and arrows of uneven consumer demand and increased costs. Three

Nomination of vaccine sceptic Robert F Kennedy Jnr sends healthcare shares into a spin

Kennedy will ‘end the chronic disease epidemic and make America great and healthy again’ says

Donald Trump

The potential appointment of well-known vaccine sceptic Robert F Kennedy Jnr to the Trump cabinet in the role of head of the Department of Health and Human Services sent shivers through pharmaceutical companies on 14 November, with shares falling around 7% on average on both sides of the Atlantic.

Kennedy has previously cast doubts on the Covid-19 vaccine, describing it as ‘the deadliest vaccine ever made’.

Jefferies analyst Michael J Yee commented: ‘While it remains unclear how this would play out, we expect the ‘anti-vax’ sentiment to continue’, impacting Covid-19 vaccine revenue which Yee estimates at between $2 billion and $3 billion annually.

Performance of global healthcare stocks since Kennedy's nomination

Sanofi

GSK

Bristol-Myers Squibb

AstraZeneca

Vertex Pharmaceuticals

Pfizer

Novo Nordisk

Moderna

Bavarian Nordic

Eli Lilly

BioNTech

Chart: Shares magazine • Source: Google Finance

‘In terms of childhood vaccines, RFK has been vocal on their safety and most importantly on the basis that they cause autism.’

‘All of this together could negatively impact vaccine perception in the US and not only lead to lower demand and sales but could potentially cause outbreaks if vaccinations are not consistent over the next four years,’ concluded Yee.

If appointed by Congress, Kennedy would have sway over 10 agencies including the FDA (Food and Drug Administration), which is responsible for drug approvals, and the CDC (Centre for Disease Control and Prevention) which is instrumental in public health matters.

Kennedy has been outspoken about downsizing entire departments inside the FDA. Former biotechnology chief executive and another Trump appointee Vivek Ramaswamy has spoken about the need to reduce barriers to getting new drugs approved.

He believes this stops patients from assessing promising therapies and raises the costs of prescription drugs by impeding competition.

Trump’s nomination of Kennedy is likely to face a difficult Senate confirmation process and even if he is appointed some observers are sceptical any of his ideas will come to pass.

Henrik Juuel, chief executive of rabies and mpox vaccine maker Bavarian Nordic (BAVA:CPH), said recent investor selling in the sector was ‘a significant overreaction’ to Kennedy’s nomination.

‘I don’t think these things will ever happen. I don’t think anyone will allow them to. There must be some smart people advising him,’ added Juuel.

Bavarian Nordic shares fell as much as 17% on 15 November, after the company missed analysts’ profit expectations, before recovering in following the trading session.

Major vaccine makers GSK (GSK), Pfizer (PFE:NYSE), Moderna (MNRA:NASDAQ) and Sanofi (SAN:EPA) have so far remained silent on the issue. [MG]

Shein IPO in sight as Amazon digs in for the long ‘Haul’

Chinese fast fashion giant reportedly eyeing first quarter of 2025 for controversial market debut

Ayear after fast-fashion sensation

Shein was first thought to have filed registration papers for a UK IPO, reports suggest the company is targeting the first quarter of 2025 for a London float that could value the business at £50 billion.

Shein’s position as a fast-growing retailer expanding across multiple geographies and taking market share from established players – it is no coincidence that the downswing in the fortunes of online fashion groups ASOS (ASC) and Boohoo (BOO:AIM) has occurred amid Shein’s meteoric rise - would have made it a no-brainer for fund managers under normal circumstances.

According to The Times, the e-commerce colossus’ founder Chris Xu and executive chair Donald Tang have begun meeting with investors in the UK to test appetites for the issue. They’ll no doubt be fielding questions from portfolio managers about the Singapore-based firm’s business practices, supply chains, corporate governance and alleged intellectual property infringement, after the company’s earlier US listing ambitions faced regulatory push back.

As AJ Bell investment director Russ Mould observes, there is an element of ‘it’s too good to be true’ with Shein: ‘Many people think there is a catch with how it is able to sell goods so cheaply – namely

PDD Holdings - ADR

that it is using a supply chain that relies on workers that are poorly paid and poorly treated,’ says Mould. ‘Shein will need to rigorously prove this is not the case if it is to win over investors for the IPO.’

Decelerating sales growth is another cause for concern at Shein, which has seen intense competition from Chinese online marketplace Temu, a bargain shopping platform owned by PDD Holdings (PDD:NASDAQ) which is growing in popularity in the US.

In a bid to take on Shein and Temu, Amazon (AMZN:NASDAQ) has launched ‘Amazon Haul’, a store available on its mobile app which also offers cheap goods, predominantly shipped from China, at ‘crazy low prices’.

Haul’s broad selection of products are on sale at $20 (£15.80) or less, with most under $10, and its launch could help to keep the growth of Shein and Temu in check. However, this is an uncertain time for Amazon to invest in such a business model, since president-elect Donald Trump has proposed leveraging a 60% tax on goods imported from China. [JC]

DISCLAIMER: Financial services company AJ Bell referenced in this article owns Shares magazine. The author of this article (James Crux) and the editor (Tom Sieber) own shares in AJ Bell.

Chancellor’s drive for ‘mega-funds’ could create ‘mega-challenges’

There are concerns over conflicts of interest and the impact on active managers

At least week’s inaugural Mansion House speech, new chancellor Rachel Reeves announced what she called ‘the biggest set of reforms to the pensions market in decades’ with the plan to merge local government pension schemes (LPGS) into a series of ‘megafunds’ along the lines of Australia’s ‘supers’.

The plan is to pool the assets from 86 LGPS in England and Wales, reportedly managing £500 billion in assets, by 2030, in order to ‘unlock’ up to £80 billion of investment for infrastructure projects.

The chancellor also indicated the government would ‘consult’ on measures such as the minimum size requirement for (DC) defined contribution pension schemes to drive further consolidation into ‘megafunds’.

However, as Nick Reeve, editor of Pensions Expert points out, much of what has been proposed for LGPS has been in the works for some time.

‘Pooling has already been extremely successful in reducing costs – something the government acknowledged in its consultation – and driving investment into local and national infrastructure such as renewable energy sources’, says Reeve.

What the government is doing is speeding up the process, but at the same time it is moving the goalposts – it wants pools to be responsible for all assets as well as providing advice to underlying funds, creating a conflict of interest and countering the progress which has been made in the private sector to separate advice and implementation, adds Reeves.

There are also concerns the needs of savers, whose money is ultimately being put at risk, will be forgotten about, warns AJ Bell’s director of public policy Tom Selby.

‘There’s a reason an occupational scheme has a trustee to look after the interests of members. Part of that is investing their money to maximise returns and get the best retirement outcomes possible.

‘Conflating a government goal of driving investment in the UK and people’s retirement outcomes brings a danger because the risks are all

taken with members’ money.

‘If it goes well, everyone can celebrate, but it’s clearly possible it will go the other way, so there needs to be some caution in this push to use other people’s money to drive economic growth.’

Pooling LGPS schemes could have an unpalatable outcome for the active fund management industry, too, which for decades has run a part of the government’s giant retirement funds.

According to the Investment Association, UK asset managers have around £266 billion in mandates from local authorities, which generated £1.3 billion of management fees and a further £180 million of performance fees in 2022-23.

If management of these funds was moved inhouse, it would be a major headache for the fund management industry on top of competition from passive products.

Disclaimer: Financial services company AJ Bell referenced in the article owns Shares magazine. The author (Ian Conway) and the editor (Tom Sieber) own shares in AJ Bell.

Chancellor Rachel Reeves by HM Treasury. Licensed under CC BY-NC-ND 2.0.

Walt Disney shares soar after CEO Bob Iger’s fourth-quarter breakthrough

Disney becomes the first film studio to cross $4 billion globally in 2024

Media giant Walt Disney (DIS:NYSE) showed investors on 14 November it was capable of a turnaround delivering record fourth-quarter streaming and box office numbers.

Disney Pixar’s Inside Out 2 became the highest-grossing animated movie of all time this summer, surpassing Frozen II at the box office.

The company ended the quarter with more than 120 million DIsney+ Core subscribers, 4.4 million more than the previous quarter, and a total of 174 million Disney+ Core

and Hulu subscriptions all told. Matthew Dolgin, equity analyst at US data firm Morningstar, said: ‘Disney seems to have turned a corner toward robust streaming profitability while maintaining healthy growth.

‘Total direct-to-consumer operating income hit $321 million in the fourth quarter after reaching profitability for the first-time last quarter, with $47 million in operating income.’

Disney is anticipating doubledigit growth in operating income for its entertainment business for fiscal 2025 and double-digit adjusted EPS (earnings per share) growth in fiscal 2026 and fiscal 2027.

Shares are already up 25% year-to-date, which may signal the

Troubled semiconductor outfit IQE considers sale of Taiwan subsidiary

Shares are trading at 15-year lows as firm announces a strategic review

After nearly 25 years of ups and downs on the stock market, compound semiconductor wafer supplier IQE (IQE:AIM) is at a real low point.

The shares are trading at their lowest level in more than 15 years, after the company announced it would look to raise £15 million from its largest shareholder Lombard Odier as it carries out a strategic review from which one

of the options is putting its Taiwan operation up for sale.

The company said revenue for 2024 would be flat at £115 million and that, even on the generous measure of adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) it would make just £5 million –suggesting a loss-making second half after it posted £6.6 million of EBITDA in the first half.

A wafer is a thin slice of semiconductor material used in fabricating integrated circuits. The wafer serves as a base for a microchip, and IQE’s wafers are used in

worst is already over.

With CEO Bob Iger due to leave in 2026 after his contract ends, investors will hope he has done enough pave the way for his successor. [SG]

everything from smartphones to electric vehicles and renewable energy systems.

However, the company’s limited scale and relatively lowly position in the food chain of a cyclical industry have made for uneven sales and it has consistently racked up losses at the pre-tax level in recent years. [TS]

26 Nov: Accsys, AO World, Cranswick, De La Rue, FD Technologies, Halfords, Helical, IG Design, LondonMetric, Sosandar, Supreme, Telecom Plus, Victoria

27 Nov: Iomart, Johnson Matthey, Motorpoint, Pets at Home

28 Nov: Loungers, Pennon, TR Property

TRADING UPDATES

25 Nov: Kingfisher

26 Nov: Hill & Smith, Intertek, Safestore, Seraphim Space Investment Trust

Can Pets at Home paw its way back to

Self-help measures and softer comparatives are tailwinds for the UK pet care leader

Weaker demand for discretionary toys and treats and an ongoing vet industry investigation by the CMA (Competition & Markets Authority), driven by concerns market consolidation has led to pet owners being overcharged for medicines and prescriptions, have kept Pets at Home’s (PETS) shares on a tight leash this past year.

Having previously expressed ‘disappointment’ over the CMA probe, the UK pet care leader failed to mention the investigation in its first quarter trading statement (1 August) and will likely remain tightlipped when it reports first half results on 27 November.

As such, investors’ focus will be on Pets at Home’s like-for-like sales performance, which the FTSE 250 firm expects to improve in future quarters as comparatives ease and it sees the benefits of strong product availability and its new digital platform, as well as any updates on its cost efficiency drive and £25

revenue was up 1.5% to £577 million driven by growing average customer spend and growth in active Pets Club members. Retail like-for-like revenues were down 0.8% due to tough prior year comparatives and a tricky consumer backdrop, but growth improved through the quarter there was relief as Pets at Home reiterated full year 2025 guidance for underlying pre-tax profit of £144 million. [JC]

poop bags and cat litter purveyor

‘resilient’ start to the year to March 2025.

like-for-like growth quarter to 18 consumer

Dell could be poised for AI-powered server boom

Tech infrastructure supplier ships first Nvidia chip backed product

Texas-headquartered Dell Technologies (DELL:NYSE) stock has been making strides since the end of the summer and investors will be anticipating a strong end to 2024 as its AI servers business ramps up activity. Next week’s quarterly earnings are a potential test of this confidence.

Dell is already a key manufacturer in tech infrastructure and that edge is being sharpened by strong demand for next generation of AI-powered servers. Chair and CEO Michael Dell recently tweeted that the world’s first Nvidia (NVDA:NASDAQ) liquidcooled GB200 NVL72 server racks are now shipping. ‘The AI rocket just got a massive boost!’ he wrote.

Projections from Dell call for 48,000 AI servers to ship through 2025 featuring eight Nvidia GPU cores (graphics processing units) reflecting the firm’s expanding role in the AI market.

QUARTERLY RESULTS

25 Nov: Agilent

These shipments are expected to generate approximately $20.6 billion in AI server revenue, representing a 56% upward revision from earlier forecasts. AI servers are projected to account for nearly 20% of Dell’s revenue in fiscal 2026, analysts note, underscoring their significance as a key driver of growth.

Expect Dell to provide more detail next week, but also look out for gross margin hints, which could face pressure if higher manufacturing costs aren’t fully reflected in early pricing. [SF]

26 Nov: Analog Devices, Autodesk, Best Buy, Crowdstrike, Dell, HP, NetApp, JM Smucker, Workday

28 Nov: Kroger

UK growth disappoints while Chinese consumer spending perks up

Meanwhile, King Dollar remains at the top of the pile as rate cut hopes fade

With the ‘sugar rush’ of the US elections fading, attention turned back to the state of the global economy last week with a couple of data points worth mentioning.

UK third-quarter GDP came in short of expectations due to poorer manufacturing output, prompting a good deal of hand-wringing and laments that the nation was ‘stagnating’ due to restrictive interest rates.

For our money, however, the IEA (Institute of

Economic Affairs) had it pretty much right when it observed: ‘The incoming government’s downbeat rhetoric about the "economic inheritance" clearly had a negative effect on business and consumer confidence.’

The other salient data point was Chinese retail sales for October, which surprised to the upside thanks to early promotional activity ahead of Singles Day, leading some commentators to suggest consumer spending was ‘stabilising’.

Chinese industrial production was slightly below forecasts but still grew at a 5%-plus clip, and if anecdotal evidence is to be believed we could see an acceleration into year-end as US companies scramble to buy goods ahead of the introduction of swingeing tariffs.

Meanwhile, expectations for lower US rates have been well and truly rolled back, with one quarter-point cut seen in December and a reduction of just 1% or 100 basis points in 2025 after Fed chair Jerome Powell said last week there was ‘no need to rush rate cuts’ given the US economy is still growing, the job market remains robust and inflation is still above the central bank’s 2% target.

Powell says, it is far too early to tell what impact Trump’s policies will have next year and the Fed’s job is not to predict the future.

This hawkishness means the dollar continues to trade at year-highs against most currencies. [IC]

Jump

European growth

Take advantage of International Biotechnology Trust’s big discount

Ageing populations and accelerating scientific innovation are key tailwinds for the sector

Warren Buffett tells investors to be greedy when others are fearful and take advantage of depressed prices.

That in a nutshell is the investment proposition for International Biotechnology Trust (IBT), which sits on an 11% discount to NAV (net asset value).

The discount is not quite as extreme as it was when we highlighted the trust as a rare buying opportunity in March 2020, at the onset of the pandemic, but it nevertheless represents another great opportunity.

This time around prospective investors will also

Seasoned portfolio managers Ailsa Craig and Marek Poszepcynski delivered another year of outperformance for the 12 months to the end of August, with NAV total return increasing 15.9% International Biotechnology Trust (IBT) 716p

be getting exposure to the biotechnology sector at a time when prices and valuations are depressed.

The NBI (Nasdaq Biotechnology index) languishes 10% below the highs it made in 2021, in stark contrast to the new all-time highs registered by the S&P 500 and Nasdaq Composite indices.

However, there are signs temperament towards the sector is turning more positive as interest rates appear to have peaked.

At the recent annual results (7 November), chair of the trust Kate Cornish-Bowden commented: ‘It is rewarding to report on the green shoots of a recovery in the biotechnology sector following an unprecedented period of share price declines in the sector.

‘Relative valuations are compelling as are the potential rewards for investors in innovative companies.’

IBT has been actively buying its shares and, unusually in the sector, pays a 4% dividend, distributed twice a year from NAV.

In summary, we believe there are many things to like about IBT at the current price. Over time we suspect IBT’s discount to NAV will narrow and the biotechnology sector will recover to new highs, driven by structural tailwinds.

CONSISTENT PERFORMANCE

compared with a 15.3% return for the benchmark.

Over the last three years the trust has produced an annualised return of 3.6% per year, outperforming the NBI’s annualised 0.7% loss.

Demonstrating good risk management and its ‘allweather’ status, the fund has outperformed in both up and down periods for the biotechnology sector.

This reflects the team’s flexible value-driven approach and ability to adapt to evolving market conditions with a focus on capital preservation and selective risk-taking.

DEREGULATION UNDER TRUMP

Given most of the holdings in the portfolio are US companies, it is worth discussing the ramifications of the recent US election.

Craig and Poszepcynski believe Trump is likely to favour market-friendly appointments at regulatory organisations such as the FDA (Food and Drug Administration) and FTC (Federal Trade Commission).

Those comments were made before the recent (14 November) nomination of vaccine sceptic Robert F Kennedy Jnr as head of the Department of Health and Human Services, which sent biotechnology shares lower.

The managers see potential for accelerated

International Biotechnology Trust

Top 10 Holdings

Table: Shares magazine • Source: Schroders, Data at 31 October 2024

deregulation and an increase in mergers and acquisitions in the sector. They highlight the importance of biotech’s role in public health and scientific advancement.

‘Governments rely on biotech innovation to address pressing healthcare challenges, while the industry benefits from supportive regulatory frameworks and funding, and investors who fund biotech’s drug development efforts benefit from the potential for attractive returns on investment.

‘Innovative drugs which play a role in keeping patients out of hospital, are unlikely to be the target of government intervention as it is hospitals which account for the largest share of US healthcare spending,’ explain the managers.

A DIFFERENTIATED INVESTMENT PROCESS

The managers apply a rigorous bottom-up approach to selecting investments with a focus on attractively-valued companies which have developed innovative treatments for unmet medical needs.

The team looks to identify businesses which command powerful competitive positions, have strong balance sheets and experienced management teams.

A differentiating feature of the investment process is that the team mitigate specific risks around drug trials by reducing exposures ahead of key trial data releases.

Another defensive feature of the strategy is that the portfolio is diversified across companies at different stages of commercialisation as well as different therapeutic areas.

The trust also invests in private companies via two venture capital funds managed by sector specialist SV Health. This proportion of the fund represents around 9% of total assets.

Turning to current positioning, the managers see signs that the IPO (initial public offerings) window is gradually opening, which should result in a prolonged period of positive performance.

Around 39% of the portfolio is invested in earlystage biotechnology companies, 42% in mid-stage revenue-generating but unprofitable companies and the rest in later-stage, profitable businesses.

The managers believe increased investment in ‘carefully’ selected smaller companies should prove beneficial for shareholders, despite increased portfolio volatility. [MG]

Why SDI’s growth star is set to shine again

Niche science tools maker has a buy and build model proven over years

SDI (SDI:AIM) 58p Market cap: £60.6 million

The past couple of years have seen many a growth grenade tossed at SDI (SDI:AIM) yet the company has stuck to its largely successful knitting and we expect its fortunes to significantly improve through 2025. A casual glance at the share price chart might put a quick end to investors’ research into this small cap business, but that’s a mistake, in our view.

Consensus analyst estimates for this year (to 30 April 2025) have been sneaking higher in the past few months, a promising sign.

WHAT DOES SDI DO?

SDI is a collection of small niche business involved in the design and manufacture of various scientific, healthcare and manufacturing tools, things like digital imaging, sensing and control equipment used in life sciences, and precision optics used in R&D and astronomy.

It’s a buy and build model which resembles that of health, safety and environmental kit maker Halma (HLMA), a constituent of the FTSE 100, and science tools manufacturing peer Judges Scientific (JDG:AIM). The aim is to buy good value businesses which add consistent cash flow and profits to the

overall company. These subsidiaries are run at arm’s length with growth funding provided when needed, and surplus cash creamed off to reinvest in new acquisitions.

Not only does SDI’s growth stretch back multiple years, but it has also been high-quality compounded growth that largely self-funded. Gross margins typically run at around 60% to 65%, high for a manufacturing business, while returns on investment and operating margins are in the double digits and above industry averages.

The end of the pandemic has tossed many a challenge at SDI as customers de-stocked after a prolonged spell of over-ordering. For example, its Atik cameras business helped carry the company through much of the pandemic, winning booming orders from PCR testing equipment manufacturers at a time when other SDI operating companies were struggling.

Higher borrowing costs haven’t helped either, but both issues now seem set to improve. This leaves substantial upside on the table, partly as SDI continues to find attractively priced acquisition targets to supplement organic growth, and from a change in market mood.

NICHE BUSINESSES

It helps that the company concentrates on industries where regulation is high, competitive moats can be enforced and capital investment is less likely to be impacted by economic downswings. Its recent (30 October 2024) acquisition of InspecVision is a great example, a £6.1 million deal that takes SDI profitably into the industrial metrology market, or precision measurement, an estimated $12 billion industry where British FTSE 250 firm Renishaw (RSW) is a global gorilla.

For the year to 31 December 2023, InspecVision

produced adjusted operating profit of £950,000 on about £3.2 million revenue, numbers that offer plenty of promise that SDI can rebuild operating margins from 11% back toward the mid-teens to 20% of past years.

‘InspecVision is a high-quality, profitable business which fulfils our key investment criteria of trading in a growth sector, with international exposure and a strong management team. The acquisition presents a rare opportunity to buy such a good business poised to capitalise on future growth in the metrology market,’ said SDI chief executive Stephen Brown.

On the downside, SDI recently told the market that it expects a second-half weighted current year, which adds some uncertainty to upcoming interim results, due to report 5 December. It is also very small with limited daily trading volumes, which may not suit every investor.

That said, this is a stock which has previously traded on a 20-plus PE (price to earnings), now below 14 on a rolling 12 months basis. History is on its side, we believe. Over the last 10 years, SDI has grown turnover from £7 million to £65.8 million in the year to 30 April 2024 and adjusted operating profit from around £57,000 to £9.6 million. The share price has increased from around 10p to over 200p at its peak, yet today is available at 58p. [SF]

Still oodles to like about bestin-class British tech Cerillion

Rare opportunity that could double in four or five years, according to broker

Gain to date: 19.8%

Genuine growth stocks may be hard to come by on tne UK market but Cerillion (CER:AIM) is a rare gem which qualifies.

Forecast-beating full year results had analysts gushing, with Canaccord Genuity talking up the stock’s chances of more than doubling. The broker observing ‘more market share gains likely; we see a path to £38 on four to five-year view’.

As we explained in our original Great Idea back in June 2024, Cerillion built its reputation on an integrated enterprise billings and customer relationship management software platform sold to medium-sized telecommunication firms, but has expanded the suite over the years to cover charging, interconnect, mediation, and provisioning solutions.

WHAT HAS HAPPENED SINCE WE SAID BUY?

Full-year results to 30 September 2024, announced on 18 November, impressed again, with record order intake of £38.1 million versus £31.6 million the previous year, a sales of potential new customer sales hitting £262 million (£243 million in 2023), also a record, and sales conversion rates that indicate the level of replenishment activity is strong.

This all stands out, yet importantly, growth is anchored in its ability to secure larger telco clients, which deliver higher long-term income thanks to their activity levels and greater software licence and margin contribution. Two large deals were struck last year worth $11.1 million with a South African operator, and a €12.4 million contract with a European operator, which has now been revealed as Virgin Media.

WHAT SHOULD INVESTORS DO NOW?

Chart: Shares magazine • Source: LSEG

The shares don’t look cheap on a one-year view – Stockopedia data has them on a 12-month rolling PE (price to earnings) multiple of 35 – but high-quality stocks seldom do. With previous talk of upside risk to forecasts having been proved and scope for consensus to creep higher as the new fiscal year progresses, we believe Cerillion is a buy and keep stock for years to come. [SF] Cerillion (CER:AIM) £18.90

mid-teens double-digit organic growth and 40%plus operating margins. Free cash flow last year was £9.7 million, plenty enough to keep the growth compounder machine going.

Cerillion continues to deliver upside to consensus,

The UK takeover market has

seen a surge of activity in the last few years

If it seems as though each week brings news of yet another takeover offer for a UK firm, the actual figures from the ONS (Office for National Statistics) are quite mindboggling.

Aside from the number of listed companies being bought, either by ‘inward’ investors or domestic buyers, hundreds of privately-owned firms are being snapped up every quarter.

If you are in a position where a company you own agrees a takeover bid, however, what is the process and how do you get your money?

In this article, we will walk you through an example of a takeover situation and explain how it

worked, how long the timetable was for the deal to go through and what shareholders received once the deal had completed.

RECENT M&A TRENDS

In terms of background, the provisional number of UK domestic and inward M&A (merger and acquisition) deals involving a change in majority share ownership between April and June of this year was 323, which in itself is staggering, but was actually 70 fewer than the period between January and March.

The value of inward M&A during the second quarter was £5 billion, down £600 million on the

Top 10 takeovers of 2024 by value

Table: Shares magazine • Source: Company accounts, AJ Bell

first quarter, while the value of domestic M&A was £2.6 billion, a drop of £1 billion on the first quarter, possibly due to companies sitting on their hands in the run-up to the general election.

The Bank of England’s summary of business conditions reported a slightly more positive sentiment around investment decisions in the second quarter compared with the first quarter as uncertainty over the economic outlook eased, although it flagged financial constraints including the cost of finance and margin pressures continued to weigh on some companies.

The report also observed: ‘Although expectations have been tempered by geopolitical uncertainties, contacts expect moderate growth in

through 2024. Contacts report that credit supply conditions remain the same. Debt markets are open and private debt funds are active. Lending to the largest borrowers with the lowest credit risk continues to be very competitive. Smaller firms that present greater credit risk report tight access to bank finance, though challenger banks and non-bank lenders are more willing to lend at high interest rates.’

We will have to wait until the start of December to see whether M&A activity picked up in the third quarter, which we sense it did, although with the Budget looming in October we suspect some firms would have kept their powder dry until they heard what the chancellor had to say.

Dan Coatsworth, investment analyst at AJ Bell, comments:

What to bear in mind when you get a bid for your shares.

Anyone who finds one of the companies in their ISA or pension subject to a takeover bid has a few things to consider before accepting the offer.

First, is the bidder offering a fair price? It’s all very well for someone to come along and offer 20% or 30% above the market price, but does that factor in what the company might achieve in the future or is it simply based on what it has achieved in the past year?

Second, how is the bid structured? Companies can pay in cash, shares or a mixture of both. Many investors prefer hard cash in their pocket as inheriting shares means they must weigh up if they want to hold the acquiring company in their portfolio longer-term.

Third, some bidders have their shares quoted on a foreign stock market, so investors in the target company need to work out if they’re happy inheriting such shares. There might be foreign exchange fees to pay and potentially extra tax applicable to dividends on overseaslisted companies.

Fourth, while it is tempting to accept a takeover offer for a nice little bump now, would your portfolio be worse off without that stock? Some companies have proven to be nice little earners for an ISA or pension if held over the long term, so you need to allow for the fact that accepting a bid today means giving up future returns.

MOST DEALS ARE FOR CASH

Most deals tend to be cash offers for companies, which makes the process relatively simple and painless for shareholders in the target once a price has been agreed.

For example, on 20 June, US private equity firm Bridgepoint made a 505p per share or £626 million all-cash offer for Alpha Financial Markets Consulting which the board accepted and recommended to its shareholders.

The Bridgewater offer was by way of what is known as a court-sanctioned ‘scheme of arrangement’ under Part 26 of the 2006 Companies Act rather than under the Takeover Code.

What that means is, subject to a scheme sanction hearing at the High Court, the firms can then deliver a copy of the court order to the Registrar of Companies and the scheme becomes effective.

Once the scheme document was published by Alpha FMC, anyone who was on the share register as of Friday 16 August – the day after the deal was approved by the High Court – was entitled to receive cash for their shares.

Alpha FMC shares were then suspended from the AIM market on Monday 19 August and settlement was either by cheque or a credit to shareholders’ accounts via the CREST system on or before 2 September, so the whole process took just over 10 weeks.

In contrast, under the Takeover Code some deals can drag on a lot longer as the buyer asks for more time to carry out ‘due diligence’, or look at the accounts of the company it is hoping to take over, and even then there is no guarantee there will be a firm offer at the end of it.

Housebuilder Bellway (BWY) made a opportunistic offer for rival Crest Nicholson (CRST) in April, and had to revise up its approach several times, extending the so-called ‘put-up or shut-up’ (PUSU) deadline twice, before eventually announcing in August it wouldn’t actually go ahead with a bid.

OTHER TYPES OF DEALS

There have been several large deals this year where shareholders in the target company have been offered shares as part or all of the consideration, such as Barratt Developments’ takeover of Redrow to form Barratt Redrow (BTRW), Benelux insurer Ageas’ (AGS:EBR) approach to Direct Line (DLG) and International Paper’s (IP:NYSE) offer for DS Smith.

Part- or all-share offers are helpful for the buyer as they reduce the cost of funding – new shares can be issued free – and they can help ‘sell’ the deal to reluctant target shareholders who want to stay in the business under new ownership, with the promise of synergies to come.

Solicitors Slaughter & May, who advise on M&A transactions across the value spectrum and specialise in takeover defence, say they have seen a number of trends develop this year.

First has been the return of higher-value bids, in part due a backlog of deals as interest rates and inflation stabilise; second is corporates looking for ‘strategic’ acquisitions to take them into new markets or build new customer bases; and third is private equity firms using ‘stub equity’ offers, which involve a cash offer with an alternative offer of unlisted securities for eligible shareholders.

WHAT TO EXPECT IF YOU GET A BID

If you own shares through an investment platform and one of your holdings is the subject of a takeover, you should get an email notifying you of a ‘corporate action’.

This means, among other things, that any active orders you might have in the stock, such as a regular investment or dividend reinvestment instruction, may have been canceled.

You should also receive directions to the London Stock Exchange website where you will find details of the proposed offer, and you may also get a separate email from your platform provider answering FAQs (frequently-asked questions) about M&A deals.

If the offer becomes official, you will have the opportunity to sell your shares with no dealing charge at the price offered by the bidder.

Typically, as in the case of Alpha FMC, a courtsanctioned ‘scheme of arrangement’ means the deal has been agreed by the board and recommended to shareholders, so the process should be fairly quick and easy.

You also have the option, particularly if the shares are trading in line or close to the bid price, of selling your shares in the open market ahead of the takeover going through. This reduces the risk of you being exposed to a last minute hitch in the transaction.

Disclaimer: Financial services company AJ Bell referenced in this article owns Shares magazine. The author of this article (Ian Conway) and the editor (Tom Sieber) own shares in AJ Bell.

By Ian Conway Deputy Editor

THE £1 BILLION PROFIT CLUB

DISCOVER THE TITANS OF UK RETAIL

TBy James Crux Funds and Investment Trusts Editor

o date, a small, exclusive club of UK retailers have exceeded £1 billion in annual profits, a high street elite that includes Tesco (TSCO), Marks & Spencer (MKS) and Kingfisher (KGF). Some may view this £1 billion figure as merely symbolic, but breaching this barrier is no mean feat and demonstrates a retailer has a lasting place in consumers’ affections and the scale to win in a competitive marketplace. We address the topic now because, barring any nightmares before or over Christmas, this club will

shortly admit two new members.

Led by Simon Wolfson, fashion giant Next (NXT) recently upgraded its year-to-January 2025 pre-tax profit forecast from £995 million to £1 billion and is in a race to reach the ten figure earnings milestone with JD Sports Fashion (JD.), the trainers seller on track to deliver profits of between £955 million and £1.035 billion for the year to January 2025, so long as shoppers splash out on sneakers and athleisure over the Black Friday (29 November) and Christmas period.

A POISONED CHALICE?

Some British retailers have delivered profits of £1 billion, only for these elevated earnings to plunge afterwards, which might suggest the £1 billion barrier is somewhat of a poisoned chalice. Tesco exceeded the £1 billion level in 2001, then went on an aggressive overseas expansion strategy in Europe, Asia and US which ultimately blew up and was dismantled after the supermarket made a £6 billion loss in 2015 including impairment charges. Thankfully for shareholders, Tesco’s earnings have continued to grow in the intervening years and pre-tax profits closed in on £2.3 billion for the year to February 2024.

Billion pound profit club membership has proved more fleeting for others, such as Marks & Spencer, which has reached the £1 billion barrier on two occasions, in 1998 and 2008, but has struggled to get even close since. As Michael Crawford, manager of the WS Chawton Global Equity Income (BJ1GXX3) fund, recounts: ‘Marks & Spencer was the first to pass the milestone in its fiscal year ended March 1998. However, a combination of changing consumer preferences, increased competition from the likes of Zara and H&M (HM-B:STO) and operational issues, decimated subsequent profits. Even after a muchimproved performance in the last three years, profits are well below the £1 billion threshold over 25 years later.’

B&Q-to-Screwfix owner Kingfisher became the third UK retailer to surpass the £1 billion profit mark when the Covid-era home improvement boom persisted into the year to January 2022, driving pre-tax profits up by a third to a smidge over £1 billion. Unfortunately, earnings have faded since amid waning DIY demand and soft market conditions in France.

Also meriting mention is cut-price clothing seller Primark, a part of groceries, sugar and fashion

MEET THE £1 BILLION PROFIT CLUB'S NEWEST POTENTIAL MEMBERS

conglomerate Associated British Foods (ABF). The discount retailer’s profits soared more than 50% to top £1 billion in the year to 14 September 2024, albeit at the operating rather than the pre-tax level. Nevertheless, Shore Capital’s retail sage Clive Black insists Primark ‘can well and truly sit in the £1 billion club as its EBIT (earnings before interest and tax) sits after rent and depreciation, and Associated British Foods the group has no nonlease debt’.

WELCOME TO THE CLUB

Breaking the £1 billion pound mark will only cement the reputations of JD Sports and Next as two of Britain’s best-run retailers. On 2 October, the former reiterated year-to-January 2025 guidance for adjusted pre-tax profit in the £955 million to £1.035 billion range, having eked out sales-led profit growth in a difficult half to 3 August 2024 in which key supplier Nike (NKE:NYSE) grappled with numerous challenges.

JD Sports Fashion

While the UK business is fairly mature, JD Sports Fashion has significant overseas growth potential, notably in the US, which should propel profits towards the £1.2 billion-to-£1.3 billion range analysts are forecasting for the year to January 2027.

On 30 October, the latter raised its year-toJanuary 2025 profit guidance yet again as colder temperatures boosted third quarter sales at Next, the billion pound profit club member which generates the highest operating margins by some stretch.

Anthony Lynch is co-manager of JPMorgan Claverhouse (JCH), the investment trust with stakes in Next, Tesco and Mark & Spencer. He informs Shares: ‘The main benefit of achieving this level of scale is what it means for distribution efficiency. Over time, we’ve seen many fashion brands and business models come and go in what is ultimately an industry with low barriers to entry but high barriers to success.’

Lynch explains: ‘All the while, Next has been quietly investing in its “Total Platform” offering, which offers logistics and software to third party clothing brands. Due to years of careful investment and scaling, it is now the most profitable route to market for many third-party brands. The result is a healthy ecosystem that serves the needs of consumers, brands, and Next. As the retailer continues to scale beyond the £1 billion profit mark, we anticipate its competitive position only strengthening further.’

Next is the biggest holding in WS Chawton Global Equity Income and Crawford looks forward to the retailer remaining a consistent club member for many years to come. ‘If you ask Lord Wolfson about revenue growth and growth targets you tend to get your head bitten off,’ says Crawford.

‘He equates value creation with managing the business to optimise and sustain high levels of return on capital. He will therefore only pursue projects likely to achieve such returns and will withdraw capital from areas failing to achieve the same. This is evidenced by the fact that in 2017, Next started to reduce capital deployed in its large retail estate across the UK. This was after 20 years of outstanding growth when pre tax EPS delivered compound annual growth of 17% driven by increasing retail selling space.’

Crawford continues: ‘Wolfson realised the future would be dominated by online shopping and started to redeploy capital to take advantage of this structural change. In the period 2017 to 2024 the top line did not grow at all; however, EPS grew a respectable 8% putting the £1 billion profit club membership into range.’

He adds: ‘Wolfson regards 2024 as the start of a new phase in the company’s development and he is as excited over the next five years as he has ever been. He cites three transformative developments. Firstly, retail sales from physical stores only accounts for 30% of sales. Secondly, 42% of online sale come from non-Next branded stock including third party brands such as the

Barbour, Levi’s and River Island and finally, over a quarter of online sales come from overseas. The reduced dependence on the Next brand in the UK mitigates against the risk of loss of relevance. Entering overseas markets as an online disruptor, not requiring risky acquisitions nor expensive investment in assets, reduces the risk of over stretch.’

Eric Burns, deputy manager of the CFP SDL Buffettology Fund (BF0LDZ3), tells Shares that whilst pushing through the £1 billion profit barrier is ‘a fantastic endorsement of everything Simon Wolfson and the team at Next have achieved, it is nothing more than a number to us – and I rather suspect the same for him too. Next is one of those steady long-term compounders having grown pre-tax profit at an annual compound rate of around 5% over the past 20 years.

‘More importantly, though, it has put its free cash flow to good use by managing to invest for future growth whilst at the same time paying a decent dividend and buying back its own shares. This latter point has meant free cash flow per share has compounded at 11% per annum over the same time frame and is the more important metric than the £1 billion profit barrier in our view.’

IT'S BEGINNING TO LOOK A LOT LIKE CHRISTMAS

The so-called ‘Golden Quarter’ is the most hotlycontested period of the year amongst retailers, but Christmas 2024 could be a tricky one with household budgets remaining under pressure. The

doom and gloom around the budget dampened the recovery in UK consumer confidence, though inflation is falling and employment levels are high, so shoppers should have more money in their pockets than this time last year.

For investors, the best strategy is to focus on retailers that are best-placed to bag market share this Christmas, into 2025 and beyond. According to the latest Kantar data, Britain’s two largest supermarkets, Tesco (TSCO) and Sainsbury’s (SBRY), have festive momentum, having outperformed the wider market over the 12 weeks to 3 November 2024.

Christmas shoppers and ravenous office workers grabbing a festive bake and a coffee on the move should boost Greggs (GRG), and we have an inkling cut-price gifts and greetings cards purveyor Card Factory (CARD) and affordable homewares retailer Dunelm (DNLM) should both do well.

MARKS & SPARKS - THE COMEBACK KID?

Shore Capital’s Marks & Spencer forecasts show adjusted pre-tax profits moving back towards the billion pound mark in the years ahead, with £893.9 million and £955.9 million pencilled in for 2026 and 2027 respectively. The billion pound profit club’s founder member has momentum entering the peak period. Alongside forecast-beating first half results (6 November), CEO Stuart Machin insisted his charge has ‘the best Christmas food range I’ve seen in my time at M&S and the most stylish seasonal clothing offer yet’. Marks & Spencer’s dependable food and revitalised clothing and home divisions are both gobbling up market share and Shore Capital believes the high street stalwart is ‘probably in its best condition’ approaching Christmas than it has been ‘for many years’, having upgraded its year to March 2025 profit forecast by 9% to £829.9 million following recent interims.

In its latest update (14 November), discount chain B&M European Value Retail (BME) insisted it is ‘well set up for the Golden Quarter’ and ‘encouraged by recent volume momentum’ entering the peak season, but Christmas could be a moment of truth as the groceries-to-general merchandise seller faces pressure from the supermarkets as well as direct rivals like Home Bargains.

Turning to the new £1 billion club members, only the brave would bet against another solid Christmas from Next. And while the athleisure market remains volatile, JD Sports’ strong brand relationships mean it will have received strong allocations of the most sought-after products in time for Christmas.

It is worth paying up for fashion and homewares giant Next with taxable profits set to surpass the £1 billion mark so long as the winter chills keep the tills ringing this Christmas. The bestin-class operator should deliver good cheer for

shareholders when it kickstarts the retail reporting frenzy on 7 January 2025. CEO Simon Wolfson likes to under-promise and over-deliver, so while growth is guided to slow for the rest of the year, a surprisingly bumper fourth quarter could yet drive further upgrades. Shares sees the cash-generative colossus as a long-term winner UK fashion and homewares winner as competition continues to weaken or exit the market, while overseas expansion and the Total Platform operation provide scope for profitable long-term expansion, along with dividends and buybacks.

PRICE: 77.9P

MARKET CAP: £875.6 MILLION

FORWARD PRICE TO EARNINGS RATIO: 8.5

Following the Covid boom, a technology replacement cycle is upon us with new AIenabled computers exciting customers, which suggests a positive peak trading period is ahead for Currys (CURY). The TVs, laptops and mobile phones seller’s impressive turnaround continues under CEO Alex Baldock and Currys has positive momentum, with UK & Ireland like-for-like sales ticking up 5% in the 17 weeks ended 24 August. Panmure Liberum’s 135p price target implies more than 70% upside from these levels and the broker expects first half results (12 December) to show ‘incremental improvements’

TESCO (TSCO) CURRYS (CURY)

PRICE: 343.6P

MARKET CAP: £23 BILLION

FORWARD PRICE TO EARNINGS RATIO: 12.8

DIVIDEND YIELD: 3.9%

Tesco’s proven strategy of investing in price and analysing data to drive more customers to its stores should help it outgrow the market and boost profits well beyond the near-£2.3 billion delivered last year. Led by CEO Ken Murphy, the supermarket has successfully fought back against German discounters Lidl and Aldi through its effective price-match strategy and according to the latest Kantar data, Tesco’s sales rose by 4.6% in the 12 weeks to 3 November 2024, taking its market share to 27.9%. Half year results (3 October) revealed a near-20% hike in taxable

on last year. With a net cash balance sheet and improved earnings quality, Currys looks well placed as interest rates come down and could deliver upgrades should robust trading continue. For the year to April 2025, Panmure Liberum sees pre-tax profits sparking up from £118 million to £130.2 million ahead of £155.1 million in 2026. Stockopedia data has Currys trading on a dirt cheap forward price to earnings ratio of 8.5 times, so a bumper Christmas could spark a re-rating.

profits to the best part of £1.4 billion. ‘The combination of price, quality and innovation means we are as competitive as we have ever been,’ said Murphy, ‘and we have been the cheapest full-line grocer for nearly two years. As we approach the Christmas season, we are looking forward to sharing the quality of our festive food with customers, and can’t wait for them to taste it.’

Capturing the opportunity in ASEAN markets

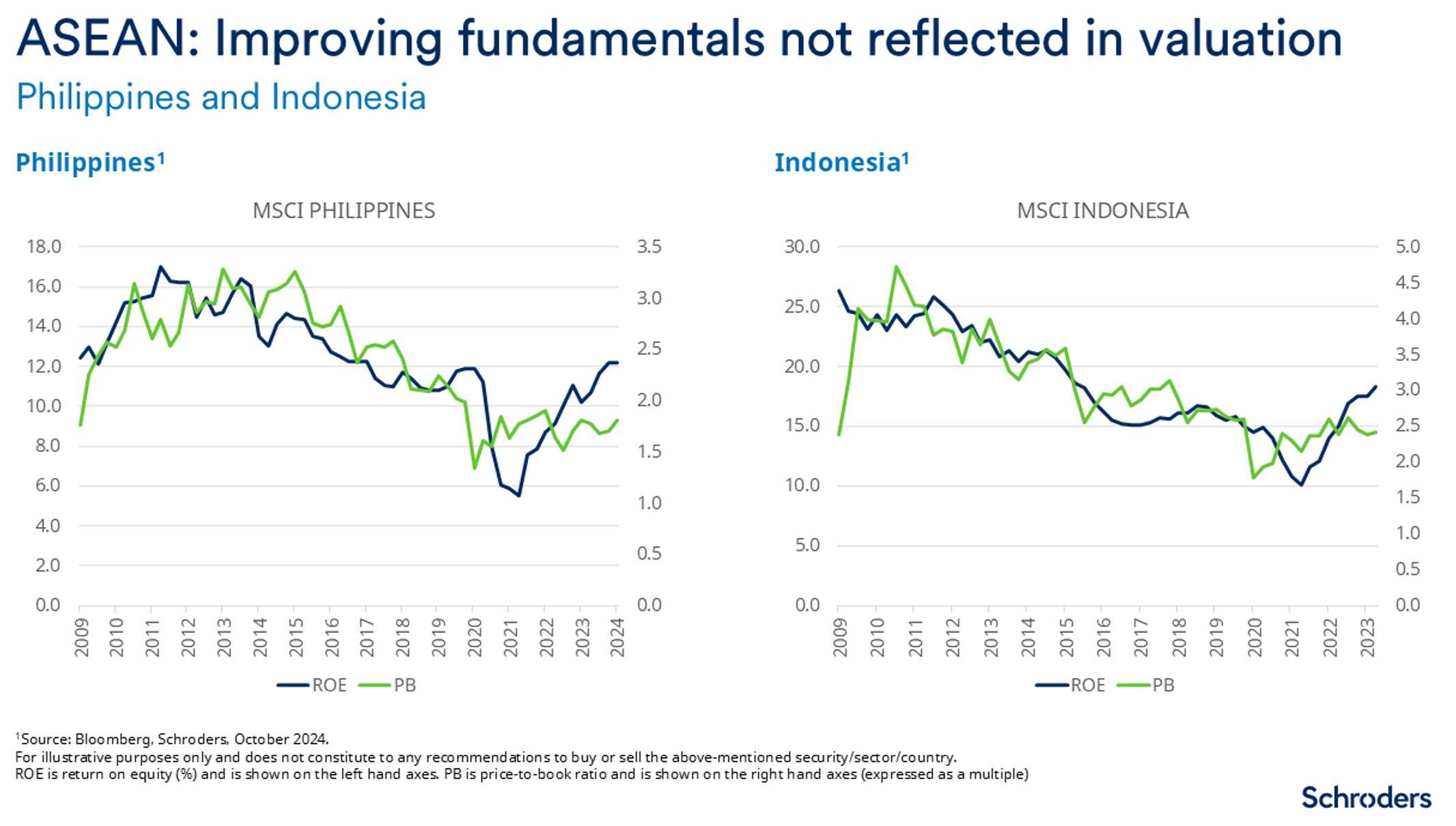

As investors in Asian equities, we are fortunate to operate in a rich and diverse opportunity set. Although the continent is dominated by the economic and geopolitical might of China, there are many other interesting parts of Asia with distinctive characteristics. Indeed, some of these markets may benefit, to an extent, from being somewhat out of the limelight. The ASEAN markets, for example, continue to personify many of the attractive features that investors often associate with the Asian region.

The Association of Southeast Asian Nations (ASEAN) is a regional organisation comprising ten Southeast Asian countries, promoting political and economic cooperation, peace and stability in the region1. The Schroder AsiaPacific Fund portfolio is currently overweight this region, for the reasons we explore below, with particular emphasis on Singapore, Thailand, Vietnam, Indonesia and Philippines.

ATTRACTIVE VALUATIONS

Perhaps as a result of the focus that many investors place towards Asia’s larger economies, we often find interesting valuation anomalies in the overlooked corners of the market. Currently, several of the ASEAN markets fall into this category, with markets like Indonesia and the Philippines looking increasingly attractive in valuation terms. As the charts below clearly illustrates, after a long period of decline, returns on equity have generally been improving in these markets over the last couple of years. This improvement in returns has not yet been reflected in valuations, so this is an area we have been increasing exposure to on a selective basis. The same trend is evident in several other ASEAN markets, which could bode well for future performance.

1 The ASEAN member states are Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam.

SENSITIVITY TO US INTEREST RATES

Meanwhile, there has historically been a relatively close association between the performance of the ASEAN markets and the US interest rate cycle. Higher Federal Reserve rates tend to attract capital back to the US, causing outflows from regions like the ASEAN markets which in turn can cause their currencies to depreciate, unless domestic rates are also raised, potentially impacting economic growth. Meanwhile, many ASEAN nations have US-dollar denominated debt, so higher rates make borrowing more expensive.

On the other hand, when US interest rates are falling, we tend to see better performance from ASEAN markets, as it potentially allows an easing of domestic monetary conditions. Given where we are currently in the US interest rate cycle, we believe the ASEAN markets are relatively well placed and have been keen to capture this opportunity in the Schroder AsiaPacific Fund portfolio.

Indeed, we are already seeing the benefit of this, with better relative performance from the likes of Thailand, Indonesia, Malaysia and the Philippines in recent months. This has coincided with the Federal Reserve’s first interest rate cut since March 2020 and expectations of more to follow.

ECONOMIC GROWTH DRIVERS

With the benefit of lower US interest rates and positive capital inflows, the ASEAN economies look poised to deliver above average economic growth in the years ahead. The region benefits from relatively positive demographics compared to the rest of the region. Indonesia and the Philippines in particular have a young, fast-growing population that is boosting the labour force and driving consumer demand. This demographic advantage is complemented by the benefits that come from being part of the ASEAN community, which advocates more cross-border trade, investment and supply chain connectivity. Together, these factors foster a dynamic environment for sustained growth, attracting investment and creating new economic opportunities.

Within the portfolio, we look to harness this growth through positions like Vietnamese retail business, Mobile World and Philippine property developer, Ayala Land (held as at July 2024)

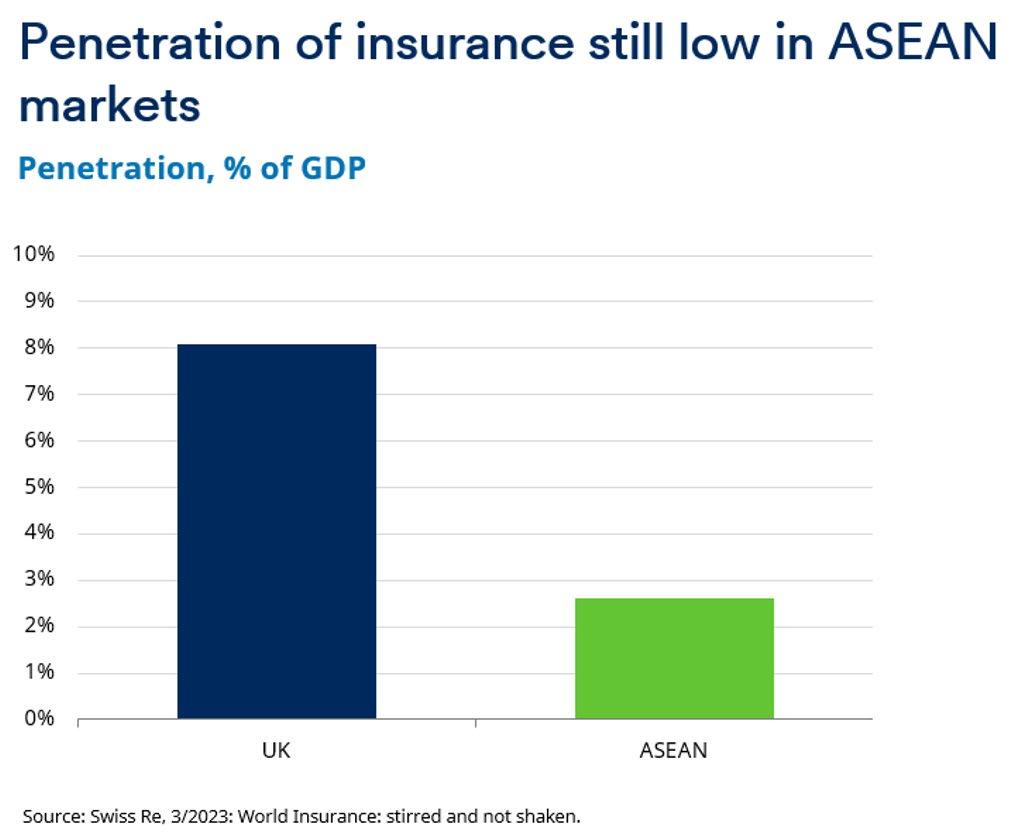

ADVANCING FINANCIAL INCLUSION

Furthermore, the rapid growth potential that we see in ASEAN economies also drives another theme we are looking to capture in the portfolio. Economies at this stage of their development tend to see a longterm trend of rising financial inclusion as economies move towards middle income levels. This means a

greater proportion of the population utilising bank services and accessing other financial products for the first time such as loans and insurance.

Clearly, the best way to access this for the portfolio is through ASEAN financial services businesses, as at July 2024, the trust has positions in Singapore-based DBS, Bank Mandiri in Indonesia and Kasikornbank in Thailand.

NAVIGATING THE FUTURE

For a variety of reasons, including those outlined above, we are optimistic about the outlook for ASEAN markets over the next few years and have positioned the Schroder AsiaPacific Fund to capture this potential through stock specific opportunities. Individually, some of these positions are small in the context of the overall portfolio, but this reflects their relative maturity and a degree of liquidity risk which is always evident in less well-traded markets such as those in the ASEAN region.

Nevertheless, as a collection of high quality, high potential businesses, we are confident our exposure to the ASEAN economies can add value over the long run, particularly in an environment where US interest rates are now falling, and as part of a balanced portfolio strategy that provide attractively diversified exposure to the rest of Asia.

Overall, therefore, the Schroder AsiaPacific Funds overweight position towards ASEAN markets should ultimately spell good news for shareholders.

• China risk: If the fund invests in the China Interbank Bond Market via the Bond Connect or in China “A” shares via the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect or in shares listed on the STAR Board or the ChiNext, this may involve clearing and settlement, regulatory, operational and counterparty risks. If the fund invests in onshore renminbi-denominated securities, currency control decisions made by the Chinese government could affect the value of the fund’s investments and could cause the fund to defer or suspend redemptions of its shares.

• Concentration risk: The Company may be concentrated in a limited number of geographical regions, industry sectors, markets and/or individual positions. This may result in large changes in the value of the company, both up or down.

• Counterparty risk: The Company may have contractual agreements with counterparties. If a counterparty is unable to fulfil their obligations, the sum that they owe to the Company may be lost in part or in whole.

• Currency risk: If the Company’s investments are denominated in currencies different to the currency of the Company’s shares, the Company may lose value as a result of movements in foreign exchange rates, otherwise known as currency rates.

• Derivatives risk: Derivatives, which are financial instruments deriving their value from an underlying asset, may be used to manage the portfolio efficiently. A derivative may not perform as expected, may create losses greater than the cost of the derivative and may result in losses to the fund.

IMPORTANT INFORMATION

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as

• Emerging markets & frontier risk: Emerging markets, and especially frontier markets, generally carry greater political, legal, counterparty, operational and liquidity risk than developed markets.

• Gearing risk: The Company may borrow money to make further investments, this is known as gearing. Gearing will increase returns if the value of the investments purchased increase by more than the cost of borrowing, or reduce returns if they fail to do so. In falling markets, the whole of the value in such investments could be lost, which would result in losses to the Company.

• Liquidity Risk: The price of shares in the Company is determined by market supply and demand, and this may be different to the net asset value of the Company. In difficult market conditions, investors may not be able to find a buyer for their shares or may not get back the amount that they originally invested. Certain investments of the Company, in particular the unquoted investments, may be less liquid and more difficult to value. In difficult market conditions, the Company may not be able to sell an investment for full value or at all and this could affect performance of the Company.

• Market risk: The value of investments can go up and down and an investor may not get back the amount initially invested.

• Operational risk: Operational processes, including those related to the safekeeping of assets, may fail. This may result in losses to the Company.

• Performance risk: Investment objectives express an intended result but there is no guarantee that such a result will be achieved. Depending on market conditions and the macro economic environment, investment objectives may become more difficult to achieve.

amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Blockchain is an alternative way to play the crypto rally

ETFs provide low–cost, diversified exposure to this theme

Whether you love or hate cryptocurrencies, you cannot deny the spectacular performance. Since Donald Trump’s White House race victory (5 November) Bitcoin has surged 35% to an all-time $94,795 high. Since the start of 2024 it has more than doubled. Ethereum and Elon Musk pet crypto Dogecoin, are up 33% and 300% respectively this year.

WHAT IS BLOCKCHAIN?

Blockchain is a type of distributed ledger technology that uses computer code to create, maintain and update information shared by blockchain participants. Each ‘block is a chunk of encrypted data, which is secured, or verified, by cryptography (the Greek word kryptos means hidden).

A block might be one or more crypto transactions, or a loan payment, for instance. When one block of data is verified, it’s then ‘chained’ to the previous block, creating a blockchain.

Blockchain technology is an alternative to records maintained on a central database. With blockchain, risk and management are shared among numerous participants, each of whom has a ‘node’ on the network and works collectively to maintain a permanent list of transactions. All parties on the network have access to a shared, identical, irreversible ledger of transactions.

If you own crypto assets, or are considering doing so, it’s valuable to have at least a basic understanding of blockchain, the technology protocol that powers most cryptocurrencies.

In other words, each node participates in the administration of the blockchain, including the verification of new additions to the blockchain. Each node is able to add new data into the database as long as the addition to the blockchain is agreed by a majority consensus among existing nodes, which enforces the network’s security.

This creates a permanent, transparent record of transactions on the blockchain and prevents users from duplicating transactions.

Blockchain ETFs

Fund size (million) Charges One-year performance Three-year performance

Table: Shares magazine • Source: Just ETF, 18 November 2024

ATTRACTIVE TECHNOLOGY

Blockchain technology excels in moving data securely and transparently. It also offers data safeguards: Records on a blockchain are nearly impossible to alter, making it difficult for a central authority, or bad actor, to falsify or change information. Blockchain technology is also wellsuited to tasks associated with identity verification and data tracking.

Because of these strengths, use of blockchain technology extends beyond the financial sphere. For example, hospitals use blockchain technology to safeguard patient data, global vaccines are tracked and distributed with the help of blockchain technology, and individuals can employ blockchain solutions to verify home or land ownership and create a lifetime portable identity that doesn’t depend on a centralised authority, a government say.

Blockchain has captured the attention of many people who view it as a potentially transformative technology with far wider applications than currently used. That could make it interesting as an investment opportunity, and retail investors have multiple blockchain ETF options to choose from.

ETFS OFFERING BLOCKCHAIN EXPOSURE

The Financial Conduct Authority continues to prevent cryptocurrency ETFs being sold to retail investors in the UK but there are around half a dozen blockchain themed ETFs available. They provide regulated access to a wide range of

stocks exposed to this new technology, including the obvious, like bitcoin investor MicroStrategy (MSTR:NASDAQ), crypto exchange Coinbase Global (COIN:NASDAQ) and crypto mining operation Marathon Digital (MARA:NASDAQ), to the more tangential – such Taiwanese chip manufacturer TSMC (2330:TPE) and Chinese retail platforms Alibaba (BABA:NYSE) and JD.com (9618:HKG). Investors should be aware that charges are higher than for more mainstream products, such as those which track indices like the FTSE 100 and S&P 500. There has been significant variance in terms of performance so it’s worth looking closely at products to get a sense of what’s in them and how they are constructed.

By Steven Frazer News Editor

My Financial Life – how to think about saving and investing in your 50s

You might choose to access your pension or to increase contributions but either way retirement is getting closer

AJBell’s Money Matters campaign aims to help more women feel good investing. As part of the campaign, we’ve been pulling together a series of articles considering the particular issues you might be thinking about as you reach different milestones.

This article looks at some of the specific issues that you might be thinking about in your sixth decade, and this is one that particularly resonates with me because I hit this midlife milestone last year.

It’s the decade when many of us start really thinking about retirement and I have developed a sometimes-unhealthy habit of checking up on my pension pots on a sometimes-weekly basis.

KEEPING ON TOP OF THINGS

I say unhealthy, because it means I am hyper aware of the fluctuations in my investments but at least I know exactly how much I have in my pots and yes I do still have pots plural because

I’m lucky that several of my pensions have some valuable guarantees attached so switching them to a different provider isn’t an option even if consolidating would make it easier to keep track of where I’m at.

For many people consolidating is the answer, especially if you have more than a couple of pensions to keep track of and if you’ve not got your ducks in a row before your 50s there are a couple of really good reasons that now is definitely the time to make the effort.

First, we know there is a gender pensions gap, and chances are you don’t have as much in your retirement fund as you’d like, only a quarter of women we spoke to when we launched our campaign thought their pension was on track to deliver what they will need in retirement.

The cost-of-living crisis has forced many of us to make tough choices but if you are still working make sure you are still paying into a pension because too many women aren’t saving at all.

If you can it’s worth upping your contributions especially if your employer will match that increase – our research found that half of women have never paid more than the minimum requirement into their pension and that’s unlikely to give you the kind of retirement you’re hoping to have.

Even a few extra pounds a month can make a huge difference over potentially 10 or 15 years especially once the magic of compounding is added to the mix.

DECIDING WHETHER TO ACCESS A PENSION

Second, this is the decade when you can choose whether or not to start accessing our defined contribution pots, either by taking a tax-free lump sum or a regular income.

Pension freedoms mean that option is open to you from the age of 55 (57 from 2028) but that decision is always a complicated one and often more so for women who tend to live longer than men.

Because the earlier you dip into your pot the more likely you are to run out and end up relying solely on the state pension for the last years of your retirement. If you are tapping your tax-free cash make sure you are doing it for a reason; for example, some people extended the term of their mortgage when rates jumped up and a lump sum could be an effective way to pay things off earlier, so you don’t have to stretch your pension income to cover housing costs.

Some women find they need to turn to their pension early because they need to quit work or reduce their hours because of caring responsibilities or because of the menopause. Just remember as well as impacting how long your pot might last there will be tax implications to consider as well.

And if you are taking a taxable income from your defined contribution pension you need to be aware of something called ‘the money purchase annual allowance’. Even taking one pound of taxable income flexibly from you pension will reduce the amount you can pay into your pension every year from £60,000 to just £10,000.

AVOIDING LIFESTYLE CREEP

The way we think about midlife has changed considerably over the past decade and whilst we know a huge number of women are economically inactive in their 50s many others are choosing to change careers or rejoin the workforce. This midpoint often brings change and its important not to consider those changes in isolation. If you suddenly find you’ve got a bit of extra

money because you’ve paid off your mortgage or your children have flown the nest, don’t just allow lifestyle creep gobble it up. Think carefully and think proactively about what might come next.

DISCLAIMER: AJ Bell referenced in this article owns Shares magazine. The author (Danni Hewson) and editor (Tom Sieber) own shares in AJ Bell.

MY FINANCIAL LIFE – 50s CHECK LIST

Carry out a mid-life financial MOT – make sure you know what investments you have and how they are performing.

Boost your pension – if you can afford to increase contributions your 50s is a great time to do so.

Consider whether to take a taxfree lump sum – just because you can doesn’t mean you have to.

Think about your housing costs –can you pay off your mortgage or downsize if your family situation has changed.