Gold takes out inflationadjusted high as central banks look set to keep buying

06 The IPO market is showing signs of life in both the UK and US 07 Strategic Equity Capital offers investors their money back via tender offer

08 Airtel Africa is one of the big surprise success stories of 2025

08 Hikma Pharmaceuticals shares plumb new 20-month lows

09 Why Kingfisher shares are under the hammer

10 Category killer Costco needs to deliver the goods next week

IDEAS 11 Buy Rightmove for its resilient earnings growth 12 Johnson Service Group looks cheap for the quality of the business

13 How Oracle investors can strike a risk reward balance after 82% share price surge

15 COVER STORY Our Fund Selection The names which take the Shares team’s fancy 26 Are we about to see a resurgence of bad loans as the US economy slows? 28 RUSS MOULD Is it time for some heavy metal?

Three important things in this week’s magazine

OUR FUND SELECTION

The Shares team picks its top five funds

Buying funds and trusts is a great way to tap into the collective expertise of some of the best investment managers in the business and letting them do the work for you. Here the team picks five standout funds to own for the long term.

Bad debts are on the rise again in an echo of the financial crisis

While US bank shares continue to all-time highs, credit quality is quietly deteriorating, according to Fed data, and the recent collapse of an auto loan company has thrown the spotlight back on complicated debt products.

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Is it time to look at commodity stocks?

Away from the excitement surrounding AI, the CRB Commodity index has pushed to new highs and has outperformed global equities over five years. Does that mean investors should now reappraise ‘old economy’ stocks like miners?

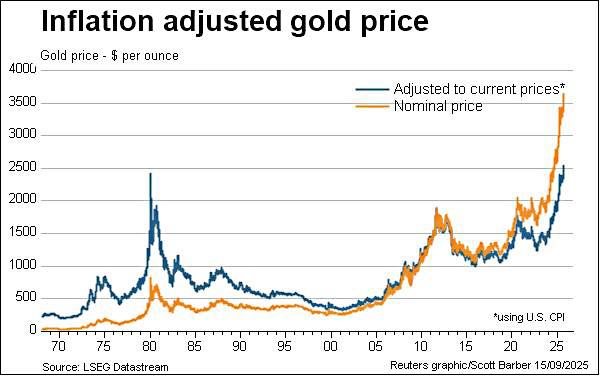

Gold takes out inflationadjusted high as central banks look set to keep buying

Precious metal is already up over 40% this year but some think the momentum can be maintained

It is almost always more instructive to consider inflation when looking at how the value of something has changed over time.

As a fan of classic cinema it can be depressing to look at the highest grossing films of all time and see a list which includes just one film made before this millennium – but adjust this list for inflation and there is a much broader spread across the decades.

The nominal price of lots of goods and commodities will reach record levels with a fair degree of regularity but, by factoring in the impact of price movements, we get a clearer sense of just how much notice we should take of these all-time highs.

In that context, gold achieved a big milestone recently as it took out the previous inflationadjusted high set in 1980. More than 40 years ago rising prices, a collapsing dollar and geopolitical tensions acted as catalysts for a pretty astonishing bull market in the precious metal. Sound familiar?

The latest driver for the gold price, now up roughly 40% in 2025 alone, and which we suggested could reach $4,000 in the not to distant future back in April, appears to be growing fears about stagflation. Inflation in the world’s largest economy remains sticky while economic data-points continue

to point to a slowdown in economic activity.

Longer-term support for gold has come from buying by central banks, which have accounted for 20% of global demand since 2022 compared to an average of around half that between 2011 and 2021 according to Berenberg analyst Jonathan Stubbs. There are reasons to think this trend can continue.

Stubbs adds: ‘According to the World Gold Council 2025 survey, 95% of central bank respondents expect gold-denominated reserves to increase. Central banks highlight crisis performance, inflation hedging, portfolio diversification and geopolitical risk as key drivers.

‘We anticipate demand for gold to remain strong given various risk dynamics, including fiscal dominance/fragility, fiat debasement, financial repression and geopolitical frictions,’ concludes the analyst.

In this, our penultimate issue as a weekly publication, the Shares team highlights the funds they like best from the large universe of options which are available to investors. Next week we will sign off in our current format in a style befitting our name and heritage with a list of our best stock ideas. Look out for that on 25 September.

In the meantime you can read Ian Conway’s thoughts on a trend of mounting bad debts in the US, find out about the latest developments in the investment trust space and some encouraging signs of life in the IPO market on both sides of the Atlantic.

The IPO market is showing signs of life in both the UK and US

The number of businesses joining the stock market on both sides of the Atlantic is ticking up

Despite ongoing geopolitical tensions and economic and market uncertainty there have been several signs of life for the IPO market recently both on these shores and across the Atlantic.

‘London remains the fifth largest exchange globally for equity capital raised with over £7.5 billion raised so far this year,’ says EY-Parthenon UK IPO leader Scott McCubbin.

‘We anticipate renewed momentum in the M&A market in the second half of 2025, which could pave the way for a recovery in IPO activity. For companies considering going public, early preparation, a clear path to profitability, and operational resilience will be key,’ adds McCubbin.

London’s junior market AIM has seen the number of companies listing on this exchange hit a three-year high – rising from nine to 16 in 2024/5, according to data national accountancy group UHY Hacker Young.

The average amount of new money raised per IPO was £9.9 million in 2024/25 – a bounce from the low of £6.8 million recorded in 2022/23.

Colin Wright, chair of UHY Hacker Young, says AIM has emerged from a period of underperformance but if plans to simplify admission and broaden the range of accepted accounting standards go ahead it will enhance its appeal to companies.

Analysts at Peel Hunt are upbeat about future IPO activity in their latest review.

‘Despite a cautious tone from investors postsummer, the backdrop is getting increasingly supportive for UK IPOs. The UK pipeline of potential

London remains the fifth largest exchange globally for equity capital raised with over £7.5 billion raised so far this year”

IPO candidates continues to build, both for later this year and next.’

Examples of prospective UK IPOs include Project Glow Topco Limited (the ultimate holding company of The Beauty Tech Group) which announced its intention to float (8 September) on London’s main market in October this year.

The at-home beauty device company owns brands such as CurrentBody Skin, ZIIP Beauty and Tria Laser.

A report in the Financial Times recently suggested Rolls-Royce (RR.) is looking at funding options for its small nuclear reactor business, with one potential avenue being a standalone stock market listing for the unit.

In the US, the success of the recent Swedish fintech IPO Klarna (KLAR:NYSE) which debuted on the NYSE (New York Stock Exchange) on 10 September raising $1.37 billion might encourage other names to float.

Among those already scheduled to make their NYSE debut this year including online ticket marketplace StubHub. The offering is said to be 20 times oversubscribed, in another vote of confidence for the IPO market.

According to Rainmaker Securities an IPO advisory firm, the 20 largest offerings (out of the 241 US IPOs so far this year) have seen large price spikes on their first day of trading, with an average advance of 36%. [SG]

Strategic Equity Capital offers investors their money back via tender offer

At the same time, Murray Income is weighing up how to improve returns

Long before activists such as Saba Capital appeared on the scene, UK investment trusts were already thinking of ways to improve shareholder returns.

Take Strategic Equity Capital [SEC), which since 2020 has been owned by Gresham House and managed by Ken Wotton and his team.

Back in February 2022, the trust’s board announced a series of proposals designed to improve value creation and strengthen SEC’s investment proposition.

One of the proposals was to scrap the continuation resolutions which would have come up in the 2022, 2023 and 2024 AGMs in favour of a 100% ‘realisation’ event in 2025.

Having considered the options, the board and the management team have opted for a tender offer which allows investors who want to exit the trust the opportunity to do so while keeping it open to those who want to remain.

Shareholders will be asked to vote on a special resolution to allow the trust to buy back shares, after which the assets will be managed as a Continuing Pool and a Tender Pool, with the capital from the Tender Pool being returned over the following months.

Gresham House, which now owns 17% of the shares compared with 5.4% in February 2022, is not selling, arguing in favour of SEC’s track record and the team’s ability to continue generating value for shareholders.

In fairness, since Wotton’s appointment as lead manager in September 2020 the trust’s NAV return per share has been 75% while the share price return has been 102%.

By comparison, the FTSE Small-Cap index

excluding investment trusts has returned 84% and the UK Smaller Companies trust sector has returned 65% over the same period.

Shareholders wanting to take advantage of the tender should note that given the trust invests in smaller companies, which are generally less liquid than larger ones, it may take some time to realise their investments, and tendered shares could be held in escrow for up to 12 months or more.

Another trust deciding on its future is Murray Income (MUT), managed by Charles Luke and the team from Aberdeen Asset Management, which invests in ‘quality companies’.

As part of a review begun in July this year, the board is considering proposals from outside managers as well as Aberdeen on how to deliver improved performance.

Over the year to the end of June, the NAV total return was 2.7% and the share price total return was 4.3% compared with 11.2% for the FTSE All Share total return index, meaning the trust has now lagged the index over one, three, five and 10 years. [IC]

Murray Income Trust

Source: LSEG

Airtel Africa is one of the big surprise success stories of 2025

Rising demand for mobile services, especially mobile money, drives performance

Not many FTSE 100 stocks have more than doubled year-to-date, and back in January few people would have put money on one of them being mobile phone and internet carrier Airtel Africa (AAF)

The firm had a strong year to March 2025, posting a 21% increase in revenue to just under $5 billion on a constant-currency basis, although due to the devaluation of some

African currencies, revenue was more or less flat on a reported basis.

Customer numbers grew 9% to 166 million, with data customers up 14% to 73 million, and usage per customer jumped 30% with the expansion of the Airtel Money network and improved offerings driving a 17% increase in money mobile subscribers.

The current financial year also got off to a good start with revenue for the

Hikma Pharmaceuticals shares plumb new 20-month lows

In June Hikma announced a $1 billion investment in the US to expand its domestic manufacturing of generic medicines

Multinational pharmaceutical company Hikma Pharmaceuticals (HIK) has seen its shares plumb 20-month lows in recent weeks, taking running losses in 2025 to around 21%, compared with a 23% gain in the FTSE index.

The last leg of share price weakness has taken place since 7 August when the generic drug maker released first-half earnings.

Hikma’s core operating profit fell 7% to $373 million due to a strong comparator in 2024 and

a change in product mix, beating the company-complied consensus of $368 million.

However, management lowered full-year core operating margin guidance for its injectables business unit to a range of 32% to 33% from the midthirties’ percentage range communicated at a 24 April trading update.

The company said it expects to return to growth in the second half and reiterated 2025

three months to June up 22%, led by data and voice, while operating profit was up 30% and earnings per share were up 70%.

In May, the firm signed a deal with SpaceX to distribute Starlink internet services in nine African countries, boosting its prospects further, while the IPO of Airtel Money in 2026 could generate further excitement. [IC]

full-year guidance for the group. Hikma generates around 70% of its US sales in the country and has made a $1 billion US investment to further its presence in the country. [MG]

UK UPDATES OVER T HE NEXT 7 DAYS

FULL-YEAR RESULTS

22 Sep: Wilmington

23 Sep: Fonix, Smiths Group

24 Sep: Redcentric, Time Finance

25 Sep: DFS Furniture

FIRST-HALF RESULTS

22 Sep: Elixirr International

23 Sep: Henry Boot, Hvivo, Keystone Law, Kingfisher, Oxford Biomedica, Raspberry Pi, The Mission Group, Yu Group

Consumers remain cautious about starting DIY projects but the retailer is ready to capitalise on a recovery when it comes

B&Q-to-Screwfix owner Kingfisher’s (KGF) shares are down roughly 11.5% over the past month with investors fearing a slowdown in consumer spending in the second half of 2025 which would delay the recovery in ‘bigticket’ spending. Kingfisher’s smaller home improvement rival Wickes (WIX) recently observed (10 September) that UK consumer confidence has ‘remained subdued’ and savings rates remain high with consumers ‘cautious of undertaking major home improvement projects’.

To restore optimism in the story, Kingfisher will need to confirm continued market share gains in all key regions, reiterate full-year 2026 guidance for adjusted pre-tax profits in the £480 million to £540 million range and please investors with its utterances on cost savings and capital returns when it posts first-half results on 23 September.

Mr. Market will be seeking signs of improving trading trends in Poland as well as France, the latter showing signs of stabilisation after a prolonged

What the market expects of Kingfisher

Source: LSEG

downturn in 2023 and 2024. Given the big divergence in performance between Kingfisher’s UK business and its operations in France and Poland, questions may start to surface about whether it might look to focus on these shores and divest other parts of the group.

Berenberg forecasts a ‘solid’ half-year showing from Kingfisher, looking for a 1% year-on-year rise in adjusted pre-tax profits to £338 million on a 0.8% rise in group-wide like-for-like sales. However, the broker expects to hear of a secondquarter like-for-like sales slowdown at B&Q as this summer’s searing UK temperatures ‘may have stifled DIY projects’. [JC]

Source: Berenberg, year-end January

Category killer Costco needs to deliver the goods next week

Shares in US warehouse retailer Costco Wholesale (COST:NASDAQ) have struggled to make headway this year, despite the firm posting high singledigit sales growth throughout the summer months as it picks up cashstrapped customers looking to buy in bulk and save money.

The issue looks to be valuation, with the shares trading on 53 times consensus 2025 earnings and 48 times consensus 2026 earnings.

That compares with an average of 22 times this year for the retail sector and ‘just’ 40 times this year and 29 times next year for AI chip designer Nvidia (NVDA:NASDAQ), the world’s most valuable company by market cap.

Meanwhile, whereas Nvidia is growing its earnings at more than 25% per year, Costco is growing at around 10%, so that 53 times valuation is a major barrier to further progress in many investors’ eyes.

The firm has a chance to change that perception on 25 September when it releases its results for the fourth quarter to the end of August, with analysts expecting quarterly sales of $86.1 billion, up 8% on last year, and EPS (earnings per share) of $5.79, up 12.4% on last year.

For the record, over the three previous quarters Costco has topped profit expectations each time by around 1%, which again given the valuation doesn’t really cut the mustard, so it will need to pull off a decent ‘beat and raise’ this month. Among recent initiatives to drive more spending, the firm introduced extended shopping hours for executive

club members, its highest and most expensive membership level, giving them the opportunity to enjoy an hour-long private shopping experience most mornings before it opens its stores to the general public.

The company had over 37 million executive members at the end of the third quarter, and is famous for selling just about every conceivable type of good including one-ounce gold bars. [IC] US UPDATES OVER THE NEXT 7 DAYS

QUARTERLY RESULTS

23 Sep: AutoZone, Micron

24 Sep: Cintas, Paychex

25 Sep: Accenture, CarMax, Costco

Source: Zacks

Buy Rightmove for its resilient earnings growth

A dominant market position and asset-light model are reflected in enviable margins

Rightmove (RMV)

725.2p

Market Cap: £5.6 billion

Ashare price pullback from peaks at Rightmove (RMV) presents a compelling entry point for investors eager to add a high-quality, asset-light and resilient growth business to portfolios. As an advertising platform, the UK’s biggest property portal is more exposed to estate agent budgets than house prices and transactions, lending Rightmove some protection from the sluggish UK economy.

Nevertheless, interest rate cuts by the Bank of England should help the UK housing market and deliver a tailwind for Rightmove, whose shares trade below a final takeover offer of 780p from Australian property listings company REA Group (REA:ASX), which the company rebuffed a year ago.

Steered by CEO Johan Svanstrom, Rightmove provides advertising for UK estate agents and new home developers and is the market leader in the UK property portal patch. Berenberg observes that the £5.6 billion cap is in ‘a strong defensive position, with challenges from rivals failing to take meaningful market share’.

Eric Burns, fund manager at Sanford DeLand, tells Shares there is ‘a textbook network effect at play’ at Rightmove, whereby ‘the more homes it lists on the site, the more house hunters use it to search for properties, which in turn leads to more listings. It has become so ubiquitous in the property market that estate agents cannot afford to withdraw from it - even in a tough market. As a result, with the exception of the Covid period, it has grown earnings per share every year since its IPO in 2006.’

Rightmove’s results (25 July) for the half to June 2025 came in a smidge ahead of consensus expectations with revenue up 10% year-on-year

to £211.7 million and underlying operating profit increased by 9% to £151.3 million, meaning the asset-light platform company achieved an enviable 71.4% margin.

Crucially, the results revealed little impact on Rightmove from CoStar’s (CSGP:NASDAQ) entry into the market following its 2023 acquisition of OnTheMarket with Rightmove’s key Strategic Growth Areas (SGAs) gaining traction. Rightmove reiterated its full-year 2025 guidance for revenue growth of 8% to 10% and reported sustained traffic growth with a total of 9.1 billion minutes spent on the platform in the half, the second-highest on record.

Rightmove said technology innovation and AI usage had accelerated in the period, and the company has also launched a new product called Ascend to help developers of new builds compete for buyers.

Based on Berenberg’s year-to-December 2025 and 2026 earnings per share estimates of 29.7p and 33.5p respectively, Rightmove trades on a forward price-to-earnings ratio of 24.5 times falling to 21.6 on next year’s numbers. While not optically cheap, this is still a discount to the ratings of European platform peers which seems unwarranted given Rightmove’s improving earnings growth profile, and the company is also returning surplus cash to shareholders through a progressive dividend and earningsenhancing buybacks. [JC]

Johnson Service Group looks cheap for the quality of the business

The firm has set itself an ambitious margin target and is buying back shares

Johnson Service Group (JSG) 152p

Market cap: £600 million

We have talked in recent issues about companies with durable competitive advantages, or ‘moats’ as Warren Buffett calls them.

One such business is textile and workwear rental firm Johnson Service Group (JSG), which thanks to its national presence and high levels of service has built a loyal customer base with a strong retention rate.

Having recently completed its move from AIM to the main market, the company will be on more investors’ radars than previously and could enjoy a whole new level of interest.

The group’s core business is textile rental and cleaning services to the hotel, restaurant and catering trade, collectively known as HORECA, which accounts for around 70% of revenue.

The other 30% comes from renting and cleaning workwear, with both divisions serving thousands of loyal customers.

With the UK hospitality industry still not back to its full potential, revenue growth has mainly come from price increases, backed up by top-notch levels of service, but the HORECA business has also steadily grown its market share and when the upturn comes the firm has the capacity to increase volumes.

Source: LSEG

deliver textiles and clothing to customers.

‘Our continued focus on operational excellence and margin improvement has positioned us well to achieve our target of at least a 14% adjusted operating profit margin in 2026, and we are on track to meet full year adjusted operating profit in line with market expectations,’ said Egan at the half-year stage.

In the meantime, as long-standing chief executive Peter Egan says, it’s a question of constantly improving and finding marginal gains to improve profitability.

That could mean investing in more efficient sorting systems or driers, or recycling heat and water better, or using more modern, greener vehicles to

Achieving a 14% margin target next year will be no mean feat, considering half-way through this year the firm made an 11.1% return, and Egan and finance director Yvonne Monaghan are aware of the challenge, given the burden of increased labour costs and taxes on UK employers since this April. However, energy costs have fallen as a proportion of revenue and prices for electricity, gas and diesel have been fixed for the rest of 2025 and 2026, while lower interest rates over the next 18 months will also help.

In a sign of confidence in its forecasts, the firm announced a new £30 million buyback this month which equates to 5% of its current market cap.

With the shares having gone sideways for the last five years, while operating profits have risen to well above their pre-pandemic peak, the current rating of 11 times current-year 2025 earnings looks undemanding for such a quality business. [IC]

How Oracle investors can strike a risk reward balance after 82% share price surge

Storming earnings see infrastructure IT firm tear up growth assumptions

Gain to date: 82%

Investors won’t often see a company’s market cap jump $250 billion in a single day, and of all the tech companies to reinvent themselves through the power of AI, Oracle (ORCL:NYSE) may be one of the more surprising.

Blowout earnings (9 September) saw shares in the software infrastructure giant surge 36%, its biggest single-day gain in more than 30 years, after its report left analysts ‘in shock’, according to CNBC. It also made co-founder and chair Larry Ellison the world’s richest man, thanks to his 41% stake, overtaking Elon Musk, on paper anyway.

WHAT HAS HAPPENED SINCE WE SAID BUY?

AI has breathed new life into the old dog, something Shares has been discussing for two years or more, leading us to pitch the stock as one of our Great Ideas a year ago.

Oracle tore up growth expectations after announcing hundreds of billions of dollars’ worth of contracted revenue from cloud deals with AI giants, including OpenAI.

WHAT SHOULD INVESTORS DO NOW?

Oracle is banking on this big investment paying off in the years to come and that its quarterly revenue growth has accelerated over the past 12 months from 7% in the first quarter of fiscal 2025 to an expected 13% for the first quarter of fiscal 2026 is encouraging. CEO Safra Catz has forecast 16% revenue growth in fiscal 2026 and analysts see that growth accelerating to 20% in fiscal 2027 and 24% in fiscal 2028. Analyst consensus, according to Koyfin data, anticipates much more. But top line growth is no guarantee of higher profits if costs rise even more, something to watch right across the AI space.

Oracle is expecting to rake in $455 billion over the next few years for contracts booked last quarter, a fourfold increase from the same time last year. That’ll skyrocket its cloud infrastructure revenue from $10 billion last fiscal year to $144 billion by 2030, Oracle projected.

Run your winners is good advice for longterm investors, as countless tech stocks have proven time and again. More cautious investors may decide that a average three year PE (price to earnings) multiple above 36 is a tempting exit point. Top slicing your stake to return your original investment while leaving the ‘profit’ invested is perhaps the sensible risk/reward balance to strike. [SF]

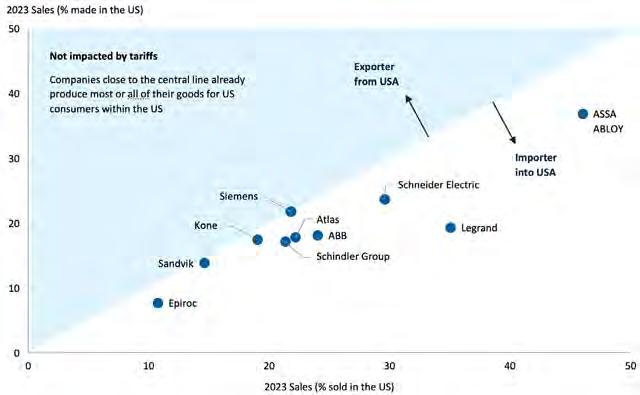

Multinationals go multilocal as globalisation changes course

Capital Group UK – New Perspective Fund

Rising tariffs and simmering trade wars sound like a daunting environment for multinational companies. They would seem to be the most heavily impacted by the current headwinds affecting global trade. However, the reality is, many multinationals are well positioned for it — simply because they’ve navigated choppy trade waters for years.

“Many multinationals are developing a ‘multi-local’ approach to business, moving closer to customers in the countries where they operate,” says Capital Group equity portfolio manager Jody Jonsson. “They are finding ways to adapt and succeed regardless of the environment.”

Examples from this year include German industrials giant Siemens which opened a US$190 million electrical equipment manufacturing plant in Fort

Worth, Texas. US companies known for building their products overseas are taking the same approach. Apple announced it would spend US$500 billion on new US-based manufacturing facilities over the next four years.

That’s one way to get around US tariffs.

MANY MULTINATIONALS HAVE ALREADY SHIFTED SOME PRODUCTION TO THE US

“You would think domesticallyoriented US companies are ideally positioned for today’s trade environment,” Jonsson adds. “And some of them are. But we’ve also seen that globally diversified, multinational companies have the flexibility, resources and management expertise to compete very effectively, even when the ground is shifting beneath their feet.”

Jody Jonsson is a portfolio manager with Capital Group UK –New Perspective Fund

If you act as representative of a client it is your responsibility to ensure that the offering or sale of fund shares complies with relevant

or

or

OUR FUND SELECTION

The names which take the Shares team’s fancy

In our penultimate issue in the current weekly format the Shares team identifies some of the actively-managed funds and trusts they like the best from the thousands on offer to UK investors. We have not used any specific selection criteria to come up with our list, these are just our

writers’ best ideas based on our assessment of the relevant vehicle’s track record, management and investment process. Read on to discover more. And, in next week’s final weekly edition of Shares, we will take our leave by sharing with you our very best stock ideas for the long term.

OUR FAVOURITES

Blue Whale Growth (BD6PG78)

Price – 297p

I first invested in Blue Whale Growth (BD6PG78), a fund which prides itself on doing its own modeling to identify top quality growth companies, in the teeth of the Covid lockdown.

My many conversations with manager Stephen Yiu revealed a laser focus on identifying ‘quality growth’ companies which not only survive but thrive, generating sustainable free cash flow while expanding market share in growing industries.

Delivering superior returns remains Yiu’s first and foremost objective, and this is a fund which has repeatedly done so year after year, not just beating its Investment Association Global benchmark, but frequently smashing it.

Since 2018 (the fund’s first full year of performance data), it has averaged a 14.6% annualised return, or 5.9% delta outperformance versus the benchmark.

With a solid covering of global indices (S&P 500, Nasdaq, for example) in my portfolio, it makes me very comfortable backing a fund that is betting it can find better returns away from most of the ‘Magnificent Seven’, with AI chip firm Nvidia (NVDA:NASDAQ) its only pick from that group.

Blue Whale Growth is not a tech fund – it

has previously deployed capital into oil sands in Canada and railroads in the US – merely one which sees many of the better investment opportunities in and around the tech sphere, a theme which has been in play since the internet emerged more than two decades ago.

Since then, we’ve seen rampant growth in ecommerce, automation, cloud computing and now, AI, setting the scene for that to continue.

So far, infrastructure technology specialists have stolen the AI show, providing crucial chip technology to lay the foundations for what many experts see as a brave new AI world ahead of us.

Blue Whale was ahead of the curve when it first invested in Nvidia nearly five years ago, and the fund continues to see the best opportunities in infrastructure, hence names like Broadcom (AVGO:NASDAQ), TSMC (TSM:NYSE), Lam Research (LRCX:NASDAQ) and Applied Materials (AMAT:NASDAQ) featuring prominently in the portfolio.

This month, the fund celebrated its eighth year since launch, and as mentioned earlier, the track record is better than good, having outstripped its IA Global benchmark every single year bar 2022.

Top 10 holdings (61.8% weighting)

Source: Blue Whale Growth Fund, data correct as of 29 August 2025

Fidelity Special Values (FSV)

Price – 377p

While I am a self-confessed income investor, with the majority of my holdings compounding dividends monthly or quarterly, there is one fund which stands out from the crowd for its ability to generate superior long-term NAV (net asset value) total returns while taking a contrarian approach.

As Sir John Templeton said, it’s impossible to produce a superior performance unless you do something different from the majority, and nowhere is that approach clearer than at investment trust Fidelity Special Values [FSV), which has beaten the market over one year, three years, five years and all the way back to its inception in 1994.

Current managers Alex Wright and Jonathan Winton haven’t achieved this track record just by picking unloved stocks, though – they have a clearly-defined process for selecting ideas, with a focus first and foremost on downside protection, and they stick to that process rigorously.

Blue Whale Growth has done better than twice as well as its benchmark in each year since. Cumulative returns since launch are 195.6% versus 94.3%.

Past conversations with Yiu also reveal that, barring some property investments, his private portfolio is exclusively in the Blue Whale fund, so you could hardly ask for more in terms of aligning his interests with ordinary investors who choose to back the fund.

Annual charges are 1.07%, available for both the accumulation or income-bearing units, while there is an intention to bring charges down as scale increases.

That’s useful to know and I don’t see fees as unreasonable for the performance delivered to date and the potential for more superior returns down the line. [SF]

DISCLAIMER: Steven Frazer has a personal investment in Blue Whale Growth.

Companies are chosen based on fundamental factors rather than top-down ‘macro’ views, with a focus on those undergoing some kind of positive change which the market has yet to appreciate.

With the help of Fidelity’s enormous internal research resources, as well as access to

company management, ideas are whittled down and those which pass muster are added to the portfolio.

In the first stage, the managers take an initial position in the stock with a view to increasing their holding as their conviction increases, and once the operational change takes effect and growth improves, it moves to stage two.

Stage two is where the wider market recognises change is happening and the shares re-rate, at which point the managers let the position run and increase in size.

Stage three is where the recovery is well under way and the share prices closes in on the managers’ upside target, meaning less upside potential and more downside risk, so the position is gradually reduced, and the proceeds are recycled into new stage one ideas.

In areas where stocks have performed well, like banks, the trust has reduced its exposure and recycled gains into consumer-facing businesses like retailers along with building materials companies and builders’ merchants.

Even though the UK stock market has beaten many of its peers year-to-date and the FTSE 100 has hit new highs, Alex Wright is still optimistic

Managers take a contrarian, index-agnostic approach

Weight = weighting of each stock in the FTSE All Share

Source: Fidelity Special Value, data as of 31 July 2025

about the opportunities available.

‘Current market conditions continue to favour our contrarian-value investment style,’ says Wright. ‘The UK offers a rich pool of investment opportunities for diligent investors, combining strong earnings growth, high dividend yields and low valuations.’

He adds: ‘The combination of attractive valuations, particularly in small and mid-cap stocks, improving sentiment, and a broadening rally beyond large caps creates a compelling investment case.’ [IC]

Long-term performance speaks for itself

Source: Fidelity Special Value, data as of 31 July 2025

TM SDL UK Buffettology Fund (BF0LDZ3)

Price – 135p

I believe interest rate cuts on both sides of the Atlantic could offer a big performance boon for the quality-focused TM SDL UK Buffettology Fund (BF0LDZ3), managed by straighttalking Keith Ashworth-Lord, an experienced practitioner of ‘Business Perspective Investing’ as championed by legendary investors Benjamin Graham, Warren Buffett and Charlie Munger.

This £300 million fund focuses on companies whose characteristics include easily understandable business models, fortress balance sheets, relatively predictable earnings and high returns on capital employed.

I like the fact Ashworth-Lord and his comanagers look for firms which are growing organically and run by experienced management teams who act with the ‘owner’s eye’, allocating shareholders’ capital in a rational way and not destroying value through high-risk acquisitions.

The fund avoids overly cyclical sectors such as oil and gas and mining, where earnings depend on commodity prices over which the companies themselves have no control, and also eschews banks on the basis Ashworth-Lord observes their returns are woeful once leverage is stripped out.

Having identified a truly outstanding company with a wide ‘moat’, patient investor AshworthLord and his team wait until the shares can be bought at a price which is substantially less than their true economic worth. As Buffett puts it, ‘Price is what you pay, value is what you get’.

Since its March 2011 launch, TM SDL UK Buffettology is ranked first quartile in the IA UK All Companies sector, although the higher-rate environment and heightened market uncertainty of recent periods has left the fund lagging peers as a fourth quartile performer over one, three and five years.

Nevertheless, I believe this unconstrained, concentrated fund – with just 25 holdings at last count – can bounce back as the market re-rates the array of quality, cash generative compounders that make up the portfolio.

Top 10 holdings as of the end of August 2025

Cumulative performance

Source: Sanford DeLand Asset Management

included fantasy miniatures maker Games Workshop (GAW), business information and data analytics star turn RELX (REL) and another AI and data winner in London Stock Exchange Group (LSEG), not to mention best-in-class retailer Next (NXT), North American pest control powerhouse Rollins (ROL:NYSE) and a stake in Warren Buffett’s Omaha-based investment vehicle Berkshire Hathaway (BRK.B:NYSE).

Outside the top 10, the fund offers investors exposure to Johnnie-Walker, Smirnoff and Guinness maker Diageo (DGE), where AshworthLord believes we may have passed ‘peak pessimism’, as well as promotional products supplier 4imprint (FOUR), a market leader with a ‘cast iron balance sheet’ which Ashworth-Lord believes should emerge from any downturn in an even stronger position versus its weaker competitors. [JC]

Scottish American Investment Trust (SAIN)

Price – 505p

Sticky inflation and stalling economic growth pose a double threat to investors looking for reliable income and growth above the level of inflation.

One fund which is laser-focused on these issues is the Baillie Gifford-managed Scottish

American Investment Company (SAIN), or SAINTS as it is known. The trust has delivered unbroken annual dividend increases for over 50-years, through thick and thin.

Since Baillie Gifford took over the mandate in 2003, the dividend per share has grown at an annualised 5% compared with average CPI of 2%.

The trust aims to be a core investment for private investors seeking income and has an objective to grow the dividend at a faster rate than inflation by increasing capital and growing income.

The fund has a global equity focus but investments are also made in bonds, property and other asset types.

The high-quality investing style of the managers has been out of favour, partly due to high interest rates, while the fund’s performance has not been helped by an underweight towards US stocks.

Consequently, the trust trades at a 10% discount to net asset value, providing long-term investors with an attractive entry point.

We believe that as interest rates fall and growth stalls, quality companies with durable businesses will come back into favour, benefiting the portfolio.

Managers James Dow and Ross Mathison look to populate the portfolio with long-term compounders which have resilient dividends supported by surplus cash flow.

The starting point is always a company’s potential to deliver earnings and cash flow growth above inflation. Importantly, the managers believe share prices and dividends follow the trajectory of company earnings and cash flow over the long run.

The managers split the investment universe into four broad buckets which they describe as compounding machines, exceptional revenue opportunities, management acceleration, and long-cycle returns.

The first two buckets are characterised by companies with enduring competitive positions, strong balance sheets, pricing power, proven management and strong volume growth.

The latter two buckets comprise companies

with margin potential accompanied by a catalyst for change, strategic development, a shift of asset allocation priorities and strong management teams.

Over 90% of the portfolio is invested in the compounders and exceptional revenue opportunities buckets. Top holdings include Microsoft (MSFT:NASDAQ), TSMC (TSM:NYSE), Apple (AAPL:NASDAQ) and Deutsche Borse (DB1:ETR).

The trust has an ongoing charge of 0.58% a year. [MG]

Scottish American Investment top 10 holdings

Company % of portfolio

Source: Baillie Gifford

JP Morgan Global Growth & Income (JGGI)

Price – 563p

If there is one fund which looks extremely well set to deliver long-term growth and income in my opinion, it’s JP Morgan Global Growth & Income (JGGI).

This investment trust has an impressive track record returning 312% and 96.5% over 10 and five years as well as paying a consistent dividend to shareholders, four times a year, at a current yield above 4%.

Structure wise, JP Morgan Global Growth & Income makes full use of being a trust, funding its dividend from a combination of capital reserves and the income generated by its underlying holdings.

This gives it the flexibility to invest in stocks with greater potential for capital appreciation that may not be accessible to conventional equity income strategies, as these companies tend to offer low or no dividend yield.

JP Morgan Global Growth & Income Top 10 Holdings

The trust offers investors a portfolio of 50 to 90 stocks, which it expects to exhibit superior earnings quality and faster earnings growth, it is therefore not surprising that some ‘Magnificent Seven’ stocks make an appearance in its top 10. Microsoft (MSFT:NASDAQ), Nvidia (NVDA:NASDAQ) Amazon (AMZN:NASDAQ), Meta Platforms (META:NASDAQ) and Apple (AAPL:NASDAQ) are all present and correct. Other US stocks in the top 10 include media giant Walt Disney (WALT) and US healthcare giant Johnson & Johnson (JNJ:NYSE).

Having merged with rival Henderson High Income Trust in February this year, it now has total net assets of approximately £3.4 billion (as of 11 September 2025) and it has a track record of being known as a ‘consolidator vehicle’, having merged with the Scottish Investment Trust in 2022, JP Morgan Elect in December 2022 and JP Morgan Multi Asset Growth & Income in March 2024.

It is currently managed by Timothy Woodhouse (who is due to step down on 30 September), James Cook and Helge Skibeli who have created a resilient global ideas portfolio by using proprietary analysis from JP Morgan’s research team to identify companies that will produce the best total returns.

Since Woodhouse was appointed portfolio manager in September 2017, the trust has produced NAV (net asset value) total returns of 160% (12.9% per annum) versus a return of 132% for its benchmark the MSCI AC World (in sterling terms).The ongoing charges are kept to a minimum at 0.43% with no performance fee.

Looking ahead, two key areas where the

trust’s managers continue to see attractive opportunities are high growth stocks, particularly those exposed to semiconductor production, and defensive sectors, where, in their view, valuations have not looked as attractive for more than 15 years.

Consequently, the portfolio is positioned to benefit from several major structural trends, such as the AI (artificial intelligence) revolution, cloud computing and the transition to renewable energy, as well as sectors such as healthcare and assisted living. [SG]

on 25 September

Jamie Hossain Lead Portfolio Manager of International Public Partnerships (‘INPP’)

The RAB model: The key to investing in UK nuclear energy

A new funding model for nuclear has paved the way to the UK’s latest, Gigawatt-scale nuclear power plant. Here’s all you need to know about the project.

Nuclear energy has long been a vital part of the UK’s energy mix, offering reliable, baseload, low-carbon electricity at scale. Yet financing new projects has proved challenging due to high upfront costs, long construction periods, and risks placed heavily on developers.

The Regulated Asset Base (RAB) model is changing that. For the first time, a UK nuclear plant, Sizewell C in Suffolk, will be financed using this approach, unlocking capital for c.3.2GW of new low-carbon capacity, equivalent to 7% of the UK’s electricity needs.

The project is a landmark for UK nuclear, showing how the RAB model can unlock capital to meet the country’s energy needs while protecting both consumers and investors. With the involvement of FTSE250 listed investors like INPP, advised by Amber Infrastructure, it also opens access to opportunities traditionally out of reach for retail investors.

What is the RAB model?

For monopolistic infrastructure assets, regulation ensures consumers are treated fairly while allowing government to attract private capital. The RAB model balances these interests by protecting consumers and creating attractive investment opportunities otherwise not available to investors.

A key feature of the RAB model is that investors begin earning a return from day one of the project, rather than waiting until construction is complete.

Consumers contribute through regulated charges, while investors benefit from predictable, inflationlinked returns.

This structure is designed to:

• Lower overall financing costs: financing is usually one of the biggest expenses in building infrastructure. By offering adequate protections, the RAB model optimises the risk and return profile for investors and lenders - in turn lowering the cost of capital for the project;

• Provide value for money for consumers: optimised financing is anticipated to translate into lower bills over the lifetime of the project; and

• Offer greater delivery certainty: optimal governance structures help projects stay on track.

From a policy perspective, the RAB model helps deliver critical infrastructure without placing the full burden on public funds. By reducing construction and operational risks, it enables long-term private capital to support national priorities such as energy security and net zero.

Proven track record

The RAB model is not new to the UK, and INPP has a long track record investing in such projects. A prime example is Tideway, London’s 25km

Image: Sizewell C, UK. Photo credit: Sizewell C

“super sewer”, financed under the RAB model, where Amber played a central role in structuring the transaction. INPP’s investors have benefitted from predictable cashflows and inflation protection, making Tideway a benchmark for how the model can de-risk large construction projects for both investors and consumers. Tideway has recently celebrated intercepting more than 9 million tonnes of storm sewage that would otherwise have spilled into the River Thames1

Another example is Cadent, the UK’s largest gas distribution network, acquired by INPP when fully operational, which operates under a RAB structure. Demonstrating the model’s flexibility across both operational utilities and well as those requiring construction.

Given Sizewell C is the first nuclear power project to use the RAB financing model, Amber and INPP worked closely with the government and the economic regulator, Ofgem, to tailor the RAB framework specifically for use in the nuclear power sector. The resulting model includes a Government Support Package that strongly insulates investor exposure to overruns and nuclear-specific risks while maintaining strong consumer safeguards. Even in severe downside scenarios, investor exposure is capped through the Government Support Package, which steps in if costs exceed set thresholds. Investors are not required to commit additional capital, and nuclear-specific risks such as decommissioning are ringfenced, making Sizewell C one of the most insulated infrastructure investments in the UK.

By incentivising investors to deliver the construction programme efficiently and prioritise safe, responsible operation of the plant, the overarching objective is to secure safe, low-carbon energy at-scale and value for money for UK energy consumers.

Why nuclear, why now?

To reach net zero and ensure energy security, the UK needs a balanced mix of sources. While

renewables are growing, their intermittency means nuclear is essential for reliable baseload power, helping keep the grid stable and reducing reliance on imported gas. It also delivers wider economic benefits, including thousands of skilled jobs. Nuclear currently provides about 15% of UK electricity2, but most existing plants will retire by 20303, creating urgent need for replacements. Meeting this challenge requires significant private investment, where the RAB model could be key. Sizewell C alone is expected to supply 3.2GW—around 7% of UK demand—for at least 60 years, while boosting jobs and the supply chain.

Why this matters

With inflation and market volatility weighing on portfolios, infrastructure can act as a stabilising anchor, providing long-term, reliable cashflows and exposure to assets that serve real societal needs.

Yet retail investors have had limited access. Listed funds like INPP change that. Since its IPO in 2006, INPP has delivered predictable, inflationlinked returns across transport, energy, and social infrastructure, supporting a progressive dividend policy growing at least 2.5% annually. Early involvement in Tideway and Sizewell C gives it a first-mover advantage as the UK builds critical new infrastructure. For Sizewell C, investors can expect predictable and stable, inflation-linked income as well as the potential for capital growth as construction of the plant progresses underpinned by strong protections against nuclear-specific risks. The project is expected to deliver a low-teen internal rate of return, above INPP’s target return policy, and comes with enhanced protections through the Government Support Package and bespoke licence arrangements that insulate investors from severe construction overruns and nuclear-specific risks.

Backed by government and regulators, the RAB model is reshaping how the UK finances infrastructure - with nuclear now firmly on the agenda - opening up opportunities once out of reach for individual investors.

1 Tideway | HRH The Princess Royal switches on giant water feature as Tideway celebrates Bazalgette Embankment

This information is for general purposes only and does not constitute an offer, invitation, or inducement to buy or subscribe to any securities, nor should it be relied upon as the basis for any contract or investment decision. References to International Public Partnerships Ltd are illustrative only. Past performance is not a reliable indicator of future results. The value of investments can go down as well as up and investors may not get back the amount originally invested. Investors should conduct their own research and seek independent financial advice before making any investment decisions.

Are we about to see a resurgence of bad loans as the US economy slows?

Despite a ‘resilient’ backdrop, banks continue to salt away provisions

Although most US banks reported forecast-busting earnings for last quarter, with many describing the US economy and the consumer as ‘resilient’, we have started to notice a subtle increase in bad loans, which is often the precursor to a more general malaise.

That doesn’t mean the US is necessarily going into a recession, or that the banks will go through a repeat of the Global Financial Crisis, but the obvious slowdown in the US economy since the start of the year does mean we should keep our eyes and ears open for signs of trouble.

Also, it is typically at the end of a bull market that fraud and other misdeeds get exposed, and we may be witnessing the first of a string of defaults with the demise last week of sub-prime vehicle finance provider Tricolor.

AND SO IT BEGINS

Last week, Ohio-based lender Fifth Third Bancorp (FITB:NASDAQ) revealed in a regulatory filing it had discovered ‘alleged external fraudulent activity’ at a commercial borrower associated with their assetbacked finance loan.

The bank said the outstanding balance on the borrowing was $200 million, and estimated it would need to take a non-cash impairment charge in the third quarter of between $170 million and $200

St Louis Fed Consumer Bad Loans

million, without naming the counterparty.

However, it soon emerged the customer was Tricolor, and alongside Fifth Third, Barclays (BARC) and JPMorgan Chase (JPM:NYSE) may also be on the hook, potentially for hundreds of millions of dollars.

According to Bloomberg, Tricolor focuses on lending to ‘borrowers across the US southwest who typically have poor or no credit scores’.

It funds its loans to customers by packaging them into ABS (asset-backed securities) and selling them to bond investors, exactly the kind of practice which subprime mortgage lenders were engaged in

Source: LSEG

St Louis Fed Business Loan Defaults

Source: LSEG

during the mid-2000s and which led to the property market crash.

Barclays and JPMorgan recently led a $217 million sale of Tricolor bonds, and together with Fifth Third have been ‘warehouse lenders’ to the firm meaning they supplied short-term revolving credit facilities.

Since 2022, Tricolor has sold some $2 billion worth of asset-backed loans, many of which remain outstanding and are sitting on investors’ books.

PROVISIONS CREEPING UP

JPMorgan Chase made no mention of Tricolor in its second quarter results, although it did increase its provision for credit losses to $2.8 billion, most of which was for card services, and it increased reserves against bad loans in its wholesale lending business, but it maintained the economy was ‘robust’.

Rival Bank of America (BAC:NYSE) said consumers ‘remained resilient, with healthy spending and asset quality’, and commercial borrowing increased.

The bank also said asset quality remained

strong, with net charge-offs at $1.5 billion for the sixth consecutive quarter, and claimed consumer delinquencies were stabilizing, while card net charge-offs improved year-over-year and commercial nonperforming loans actually declined from the previous quarter.

The interesting thing is, data from the various Federal Reserve banks show a clear upward trend in bad debts across the US banking system.

Household debt in the US reached $18.4 trillion in the second quarter, up $185 billion on the first quarter, mostly due to growth in mortgage borrowing and car loans.

Aggregate delinquency rates ‘remained elevated in the second quarter, with 4.4% of outstanding debt in some kind of delinquency’ according to the New York Fed’s Quarterly Report on Household Debt and Credit.

Also, data from the St Louis Federal Reserve shows household delinquencies and business delinquencies rising towards levels last seen during the pandemic, when many businesses found themselves in trouble and were only saved by the central bank slashing interest rates and the government handing out ‘stimulus cheques’.

Investors might therefore want to do their own due diligence to satisfy themselves we aren’t looking at a rise in bad debts and a subsequent drop in profitability, particularly given how well banks both in the US and the UK have performed in the last couple of years.

By Ian Conway Deputy Editor

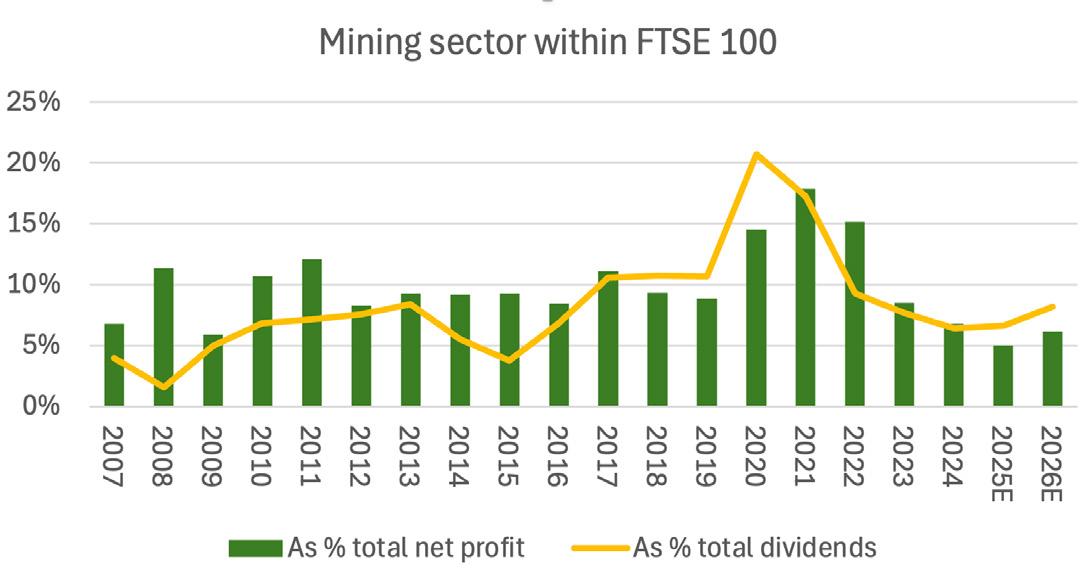

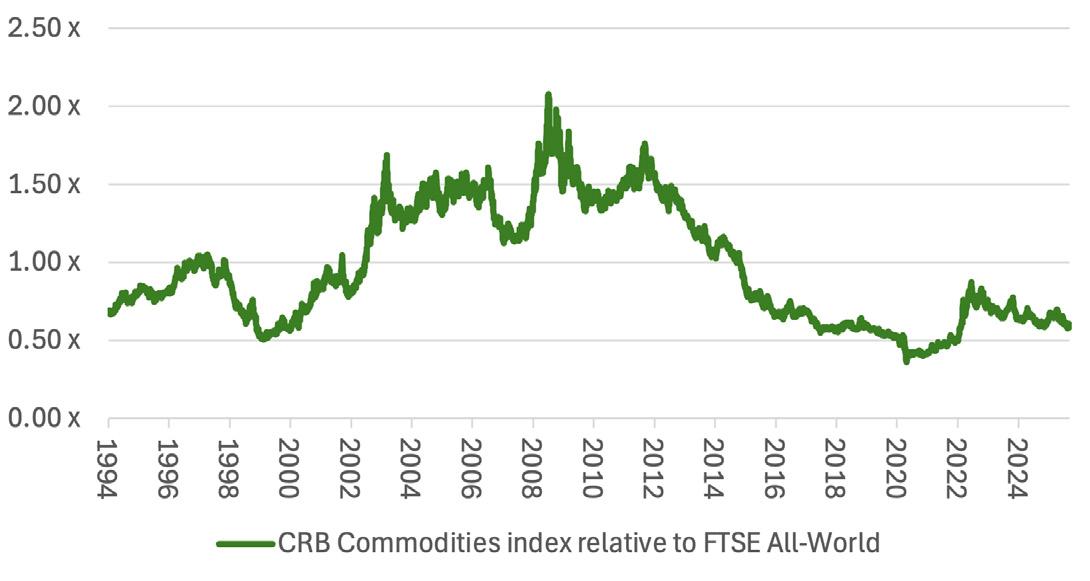

Is it time for some heavy metal?

The putative coming together between Anglo American (AAL) and Canada’s Teck Resources (TECK.B:TSE) is the fifth $1 billion-plus merger and acquisition deal with a major focus on copper mining since 2022. Gold saw a similar rash of activity between producers of the precious metal earlier this decade, and the commodity price has since gone into orbit. It now remains to be seen whether copper miners’ management teams are similarly ahead of the game and providing investors with a hint as to where big commodity and share price moves may be coming next.

ACE OF SPADES

At just under $10,000 a tonne, copper trades within 12% of the all-time high reached in 2021.

The CRB Commodities index overall stands 20% below its 2008 zenith. Energy is the chief culprit here, along with some agricultural crops and nickel,

LSEG Refinitiv data

but gold, coffee and cocoa can all point to new highs in 2005.

Their momentum, along with gains in copper, means the CRB Commodities index is approaching a 17-year higher all the same. A break-out to the upside by the index could be a telling sign. Commodities and ‘real’ assets have historically done well during periods of dollar weakness, or inflation, or both. Most commodities are priced in the US currency, so a falling greenback makes them less expensive to buy for those countries whose own counters are not tied to the buck. Meanwhile, rising prices persuade investors to look for perceived

stores of value and physical assets, and shun paper ones, such as cash and bonds, where purchasing power will be lost if prevailing the rates of interest and coupons languish below the rate of inflation.

HELLRAISER

A drop in the dollar and a resurgence in commodity prices would represent a major change from the 2010s, when the buck was strong and a low-growth, low-inflation, low-interest-rate environment prevailed.

Portfolio options that offered a reliable income (at a yield that exceeded inflation) or provided secular increases in profit and cash flow when growth was scarce shone in such an environment and that included long-duration assets such as government bonds, and ‘growth’ equities such as technology companies, while serial dividend growers and compounders were popular too.

The question now is whether the resurgence of commodities means investors think the times are changing. It is possible that slashing interest rate cuts and more quantitative easing, or QE for short, in response to Covid let the inflation genie out of the bottle after four decades in which central bank policy, Chinese and Eastern European entry to global trade flows and the emasculation of unions kept it stoppered up.

It is also possible that President Trump’s desire to boost US growth by means of lower taxes, a lower dollar, lower energy prices, lower interest rates

Miners’ profit and dividend contribution to FTSE 100 is nearer to historic lows than the highs

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

Source:

and less regulation could stoke rapid growth and further fuel inflation, especially if Germany and China embark upon fiscal stimulus of their own. Inflation, and thus rapid GDP growth, would, after all, help salt down many Western governments’ debt-to-GDP ratios, too, providing they can hold interest rates below the nominal rate at which economic output increases.

Perhaps the CRB Commodity index is telling us that this shift to a higher-inflation, higher-nominalgrowth world, where interest rates are more volatile, is already here. The benchmark has quietly outperformed the FTSE All-World equity index 2020.

Sceptics will point out that commodities’ outperformance peaked in 2022 as Russia invaded Ukraine and prompted a scramble for raw materials such as aluminium, natural gas and oil, for which many had previously relied upon Moscow for supply. Equities have been back in the box seat since then.

IRON HORSE

Analysts still seem unconvinced that a major regime change is upon us. The FTSE 100’s six mining companies are expected to produce just 5% of the index’s aggregate net profits in 2025 and pay out 6.6% of its dividends. The post-2007 averages are 10.2% and 8.3% respectively, while the peak

The

CRB Commodities index has outperformed equities since 2020

Source: LSEG Refinitiv data

profit contribution was 17.8% (in 2021) and highest dividend offering was 20.7% of the total (in 2020). This may catch the eyes of contrarians (or just of those who are weary of the letters ‘AI’). If raw material prices surge, for whatever reason, and miners’ profits and dividends get anywhere near to prior highs, then their current weighting within of the FTSE 100’s total market capitalisation of 7.4% could look low, even if it looks about right today, given their estimated share of the index’s profits and cash payouts to shareholders.

What are the costs and benefits of retiring early?

Find out the impact of drawing on your pension in your 50s compared to waiting until you’re older

Retirement has long been associated with golf courses, cruises, and relaxing on the beach with a drink in your hand. Traditionally, these retirement luxuries have been reserved for the later years in life. But some don’t want to wait until their 60s or even 50s to be tied down by a job and aim to retire at a younger age. This brings some lifestyle perks: you have more time where you are physically capable of travelling and enjoying the hobbies you choose. But if you haven’t prepared properly financially, this can leave you without enough savings later in life, forcing you into a difficult position in the later years of life where you are less equipped to work.

It might seem obvious to say, but another struggle of retiring early is having less time to save. Pensions benefit massively from compound returns, which can mean that the final 10 years in your pension are likely to be when the most significant gains happen, as long as your investments trend upwards. So, can you really afford to retire early, and is it the right choice for you?

HOW DO I LOSE OUT IF I RETIRE EARLY?

You currently don’t gain access to your state

pension until the age of 66 (rising to 67) and can’t access your private pension until you’re 55 (rising to 57). If you’re retiring before state pension age, you won’t get the £11,973 income for those first years. And if you’re younger than private pension access age, you’ll need to fund your lifestyle through other savings.

Retiring too early means you’ll either need to find money to fund the rest of your retirement or significantly change the amount you take from your pension each year.

For example, if you retired at 55 with a £200,000 pension pot, you could withdraw £15,000 each year, but it would run out by 72. That £15,000 also doesn’t increase with inflation, meaning its spending power will decrease over time.

However, retiring five years later would mean that pot lasted until age 83 (even without adding to it during that five-year period) based on 4% investment growth post any charges.

You’ll also need to factor in income tax. While you get 25% of your pension free from income tax, you will have to pay on the rest. The state pension will give a nice boost to your retirement income once it kicks in, but this also counts as part of your income and uses up most of the tax-free allowance.

Personal Finance:

Retiring with at £91,000 pension pot

Taking the same income - £10,000

Varying the income so the pot lasts until age 90

AJ Bell. FE Analytics figures assume 4% investment growth post charges each year and are based on a £91,000 pot at age 55, taking a £10,000 a year income via drawdown.

WHAT ABOUT TAKING LESS INCOME?

What if someone decided to retire at 55 but changed the amount of income they took from their pension? For it to last until they turned 90, they would have to take £7,650 less from their pension each year, compared to retiring at 65 (£17,800 versus £10,150). Even retiring at 60 would mean withdrawing £4,600 less each year.

The average pension pot in the UK is £91,000, according to The Investing and Saving Alliance (TISA). This means it would pay out an income of £8,000 a year if you took it at age 65 and wanted it to last until the age of 90. (Assumes 4% investment growth post charges each year.)

However, to retire 10 years earlier at age 55, you’d have to take over a 40% pension pay cut.

But these often come with a price tag. It doesn’t mean it’s impossible to retire early – it just means that you need to be realistic with how far your pension pot can really get you.

WHEN SHOULD I RETIRE?

There’s no perfect formula for when to retire, because of the unknown factors of how long you’ll need that income, and how your money will grow if it’s left in the market. But keeping estimates conservative can allow for a more relaxing experience and ensure you have enough money left in your pot for care towards the end of life, if needed.

WHAT WILL EARLY RETIREMENT LOOK LIKE?

The Pensions and Lifetime Savings Association estimates that an average UK retiree will need at least £13,400 per year in retirement for a minimum lifestyle, rising to £31,700 per year for a moderate lifestyle as a single person. While the state pension can help retirees reach that income level, those entering retirement early will feel a much larger strain on their pension pot until the state pension kicks in.

For many, the appeal of retiring early is socialising, travelling, or enjoying other hobbies.

To get an idea of how much you will spend each year in retirement, you can take a look at your current spending and eliminate any costs that will go away (such as commuting to work), while anticipating new costs (like a few extra holidays or paying for hobbies, for example).

Retirement can take different forms for different people, and if you don’t feel financially ready to fully retire, you could opt for part-time or consulting work. This can help the income keep flowing while giving you additional free time and flexibility.

Hannah Williford AJ Bell Content Writer

Source:

How will the chancellor’s inheritance tax plans affect my pension wishes?

Can I leave money to non-family members without burdening them?

I am 73 years old and want to understand more how my pensions will be caught by inheritance tax. Is it likely pension pots will count in one’s estate for all ages (not just 75 plus) for inheritance tax? Is it possible for conversion to a bare trust to be offered to customers? I wish to leave to friends’ grandchildren who are many years away from turning 18.

Anonymous

Rachel Vahey, AJ Bell Head of Public Policy, says:

In the Autumn Budget last year, Rachel Reeves announced pensions would be brought into the calculations for inheritance tax (IHT) from April 2027. HMRC published proposals on how this could work in practice, and over the summer it set out revised plans, but there are still several issues with these rules and it’s likely they will change further before being finally introduced.

Under the proposals, any ‘unused pensions’ will be included for inheritance tax, which could be a SIPP pension pot you have not yet accessed, or a drawdown fund from which you may be withdrawing an income.

Any pension funds passed to a spouse or civil partner (to whom you are not married or in a civil partnership) will be exempt from IHT, but if you pass the money to another, say a partner or a child or a friend, then generally it will be ‘caught’ by the new IHT rules (the exception to this is if you have bought a joint annuity or have a scheme pension).

Your age when you die doesn’t matter for working out whether inheritance tax will apply to unused pension funds. Under the proposed rules, even if you died before the minimum age you can access a pension pot – which is 55 today, rising to 57 from 2028 – your pension pot would still be

included when working out how much IHT is due. Your age when you die does matter, however, when working out if any income tax will also apply to any money your beneficiaries take from inherited pensions.

If you die before the age of 75, your beneficiaries won’t have to pay any income tax on any money they take from the pension.

The exception to this rule is if they take a lump sum and the value of all the tax-free lump sums you have taken in your life and your loved ones take on death is more than, usually, £1,073,100.

If it’s more than this amount, which is called the LSDBA (lump sum and death benefit allowance), then the excess will be subject to income tax.

Ask Rachel: Your retirement questions answered

If you are aged 75 or older when you die, then income tax may apply regardless of whether your loved ones take a lump sum or an income.

To answer your question, you cannot ‘convert’ a pension into a bare trust to provide benefits for your friends’ grandchildren, but you can withdraw money from a pension and place it under trust for beneficiaries such as family or friends, although any money you withdraw will be subject to income tax.

When you die, the money in the trust shouldn’t be subject to IHT unless you die within seven years of moving it into the trust.

Alternatively, you can complete a nomination of wishes form to leave your pension money to a trust when you die.

If you die after April 2027, the money will be included when working out if any IHT is due, and if you are 75 or older when you die, there will be a special tax charge of 45% as well.

Another option is to nominate the children to receive the pension funds when you die.

They will be able to keep them within the

Money & Markets podcast

pension wrapper with their parent or legal guardian managing it until they are 18 years old, with the investments continuing to benefit from tax-advantageous growth.

The beneficiaries can then withdraw the money when they want to, and if you are 75 or over when you die, they will pay income tax on any withdrawals, which may be basic rate or within their personal allowance. The pension funds will be included when working out what, if any, IHT is due.

DO YOU HAVE A QUESTION ON RETIREMENT ISSUES?

Send an email to askrachel@ajbell.co.uk with the words ‘Retirement question’ in the subject line. We’ll do our best to respond in a future edition of Shares

Please note, we only provide information and we do not provide financial advice. If you’re unsure please consult a suitably qualified financial adviser. We cannot comment on individual investment portfolios.

WATCH RECENT PRESENTATIONS

Aberdeen Asian Income Fund (AAIF)

Isaac Thong, Portfolio Manager

Aberdeen Asian Income Fund (AAIF) Limited targets the income and growth potential of Asias most compelling and sustainable companies. It does this by using a bottom-up, unconstrained strategy focused on delivering rising income and capital growth by investing in quality Asia-Pacific companies at sensible valuations.

JPMorgan Claverhouse Investment Trust (JCH)

Anthony Lynch, Portfolio Manager

JPMorgan Claverhouse Investment Trust (JCH) has been helping investors tap directly into the long-term growth potential of UK large cap stocks since 1963. The trust focuses on attractively valued, high quality stocks with the ability to generate consistent and growing dividends.

Strategic Equity Capital (SEC)

Ken Wotton, Fund Manager

Strategic Equity Capital (SEC) is a specialist alternative equity trust. Actively managed by Ken Wotton and the Gresham House UK equity team, it maintains a highly concentrated portfolio of 15-25 high-quality, dynamic, UK smaller companies, each operating in a niche market offering structural growth opportunities.

WHO WE ARE

EDITOR: Tom Sieber @SharesMagTom

DEPUTY EDITOR: Ian Conway @SharesMagIan

NEWS EDITOR: Steven Frazer @SharesMagSteve

FUNDS AND INVESTMENT

TRUSTS EDITOR: James Crux @SharesMagJames

EDUCATION EDITOR: Martin Gamble @Chilligg

INVESTMENT WRITER: Sabuhi Gard @sharesmagsabuhi

CONTRIBUTORS:

Dan Coatsworth

Danni Hewson

Laith Khalaf

Russ Mould

Laura Suter

Rachel Vahey

Hannah Williford

Shares magazine is published weekly every Thursday (50 times per year) by AJ Bell Media Limited, 49 Southwark Bridge Road, London, SE1 9HH. Company Registration No: 3733852.

All Shares material is copyright. Reproduction in whole or part is not permitted without written permission from the editor.

Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments published in Shares must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. Shares, its staff and AJ Bell Media Limited do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

Members of staff of Shares may hold shares in companies mentioned in the magazine. This could create a conflict of interests. Where such a conflict exists it will be disclosed. Shares adheres to a strict code of conduct for reporters, as set out below.

1. In keeping with the existing practice, reporters who intend to write about any securities, derivatives or positions with spread betting organisations that they have an interest in should first clear their writing with the editor. If the editor agrees that the

reporter can write about the interest, it should be disclosed to readers at the end of the story. Holdings by third parties including families, trusts, selfselect pension funds, self select ISAs and PEPs and nominee accounts are included in such interests.

2. Reporters will inform the editor on any occasion that they transact shares, derivatives or spread betting positions. This will overcome situations when the interests they are considering might conflict with reports by other writers in the magazine. This notification should be confirmed by e-mail.

3. Reporters are required to hold a full personal interest register. The whereabouts of this register should be revealed to the editor.

4. A reporter should not have made a transaction of shares, derivatives or spread betting positions for 30 days before the publication of an article that mentions such interest. Reporters who have an interest in a company they have written about should not transact the shares within 30 days after the on-sale date of the magazine.