To deliver a strong, rising and reliable income from equities, we believe it’s important to target exceptional companies.

That’s why our investment process is built to interrogate every potential company’s management, finances, and business model. Only when we find those that meet our definition of ‘quality’ companies, do we invest.

So we can aim to build a portfolio with potential to deliver a high and growing income.

Murray Income Trust – made with quality, built for income.

Please remember, the value of shares and the income from them can go down as well as up and you may get back less than the amount invested.

Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

05

The shifting ISA landscape and the case for investing

07 Tech stocks slump as US recession fears extend the recent sell-off

09 UK M&A gets off to a slow start but investment trusts are in demand

1 1 Schroders looks to turn the corner with new strategy 1 1 Rentokil’s latest results fail to reassure the doubters

13 Can Next pull another rabbit out of the hat?

14 All eyes on economic bellwether FedEx’s third-quarter earnings next week

1 6 Growth and income-hungry investors should take a bite out of Bakkavor

1 9 JPMorgan European Growth & Income is the perfect way to invest in outperforming European shares UPDATES

22 Games Workshop marches on after full-year upgrade FEATURES

24 COVER STORY STEP INTO AN ISA How to make the most of the tax efficient wrapper

32 Markets have hit a rough patch but investors can take some comfort in corporate earnings

42 Is it wrong to chase performance as an investor?

36 FUNDS

How one fund manager looks to find the next generation of US market stars

45 DAN COATSWORTH

Six of the Magnificent Seven are nursing share price losses this year

49 ASK RACHEL

How can I check my entitlement to a full state pension?

52 INDEX Shares, funds, ETFs and investment trusts in this issue

Three important things in this week’s magazine

As debate about the future of ISAs hits the newspapers, Shares walks you through the choices

ISAs are one of the most successful government savings initiatives in history, yet many people have yet to unlock the benefits of tax-free investments.

Does the sudden sell-off in US markets mean we should start worrying about the economy and company earnings?

Despite the recent increase in market volatility, analysts aren’t changing their forecasts and are still expecting profits to rise by double digits this year.

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Why Games Workshop is still one of our preferred stocks

Even though it is now part of the prestigious FTSE 100, the table-top games maker has proved once again it can grow faster than analysts expect as it raises guidance.

Analyst weighs in on ‘buy the dip’ debate as Nvidia sinks to lowest valuation since 2019

Domino’s Pizza serves up strong year of profit growth Clarkson shares plunge 17% on tariff concerns and slow start to 2025 Energy companies

The shifting ISA landscape and the case for investing

Simplifying the tax wrapper makes more sense than cutting the cash allowance

This week we extol the virtues of ISAs.

For the last quarter of a century or so, these products have allowed savers and investors to shield their cash from HMRC and avoid having to fill out complicated paperwork at the end of the tax year.

As of the end of the 2022/23 tax year, Britons had squirreled away more than £725 billion in these vehicles making them among the most successful UK government innovations on record.

In some ways ISAs, and particularly the core stock and shares and cash iterations, have faced less tinkering than other areas like pensions, with the £20,000 annual allowance unchanged since April 2017.

While this limit hasn’t been increased in line with inflation, it still feels pretty generous given most of us would struggle to put away more than this sum in a single year, particularly if we’re already making contributions to our pension.

Nonetheless, there are probably unnecessary levels of complexity in the broader ISA set-up as it stands today. Addressing these seems more urgent than cutting the cash ISA limit, as the Government is rumoured to be considering, partly as a way of encouraging more people to invest their money.

AJ Bell has put forward some pretty sensible ideas on how the ISA universe could be simplified and made more user-friendly in a policy paper issued last summer. It has already played a part in seeing off the idea of a British ISA, but merging the cash and stocks and shares, Junior and Innovative Finance ISAs into a single product, as the investment platform has suggested, might be a better way to encourage more people to put funds to work in the market without reducing the generosity of the cash limit.

AJ Bell's proposed simplified ISA structure

AJ Bell's proposed simplified ISA structure

AJ Bell's proposed simplified ISA structure

Annual ISA allowance

Annual ISA allowance

Annual ISA allowance

Under 18 18 or over

Under 18 18 or over

£9,000, rising with CPI each year

Under 18 18 or over

£9,000, rising with CPI each year

£9,000, rising with CPI each year

Eligibility UK resident

Eligibility UK resident

Eligibility UK resident

£25,000 or in-force ISA allowance at introduction if higher, rising with CPI each tax year

£25,000 or in-force ISA allowance at introduction if higher, rising with CPI each tax year

£25,000 or in-force ISA allowance at introduction if higher, rising with CPI each tax year

Person with parental responsibility will be responsible for ISA for under-16s

Person with parental responsibility will be responsible for ISA for under-16s

Perimitted investments As for current stocks and shares ISA

Person with parental responsibility will be responsible for ISA for under-16s

Perimitted investments As for current stocks and shares ISA

Perimitted investments

As for current stocks and shares ISA

Tax treatments No capital gains tax on realised gains or income tax on interest or dividends

Tax treatments No capital gains tax on realised gains or income tax on interest or dividends

Tax treatments

No capital gains tax on realised gains or income tax on interest or dividends

Withdrawals Allowed from age 18 onwards, with no withdrawal penalty

Withdrawals Allowed from age 18 onwards, with no withdrawal penalty

Transfers Full and partial transfers allowed

Withdrawals Allowed from age 18 onwards, with no withdrawal penalty

Transfers Full and partial transfers allowed

Transfers Full and partial transfers allowed

Table: Shares magazine • Source: AJ Bell

Table: Shares magazine • Source: AJ Bell

Table: Shares magazine • Source: AJ Bell

This wouldn’t mean existing providers of cash ISAs would suddenly have to start offering the ability to buy equities, merely that it would be up to said provider which options they provided within the universe of eligible investments. As AJ Bell points out, we don’t distinguish between cash and stocks and shares pensions, for example.

Also, not overtly penalising people for making withdrawals from a Lifetime ISA which are not for retirement, due to a terminal illness or to buy a first home seems a reasonable reform.

It’s fine for the state to claw back the free cash it has doled out, but that would be achieved by applying a 20% exit charge (as it did during Covid) rather than the current 25% which leaves someone with less money than they started with.

As of the end of the 2022/23 tax year, Britons had squirreled away more than £725 billion in these vehicles”

In our main article in this issue, we discuss how to start or restart your ISA investment journey step by step. Read on to discover more and get the latest on the sell-off in the US market.

DISCLAIMER: AJ Bell, referenced in this article, owns Shares magazine. The author (Tom Sieber) and editor (Ian Conway) of this article own shares in AJ Bell.

STICK

• Guinness Global Investors was established over 20 years ago

• We focus on identifying sustainable profitability which is under-priced by the market

• Our experienced team of senior employees and fund managers have worked together for many years

• The Fund seeks capital growth and income from companies in Asia Pacific

• We target the growing number and breadth of high-quality companies in Asia’s growing consumer economy

Visit guinnessgi.com/wsaei or call 020 7042 6555.

• We invest in companies with consistent returns and the potential for sustainable dividend growth

Scan the QR code to find out the length of the largest tree frog in the world.

POSITIVELY DIFFERENT

GLOBAL INVESTORS

Risk: Past performance is not a guide to future performance. The value of this investment and any income arising from it can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested. Guinness Global Investors is a trading name of Guinness Asset Management Ltd., which is authorised and regulated by the Financial Conduct Authority. Calls will be recorded.

About Us

About the Fund

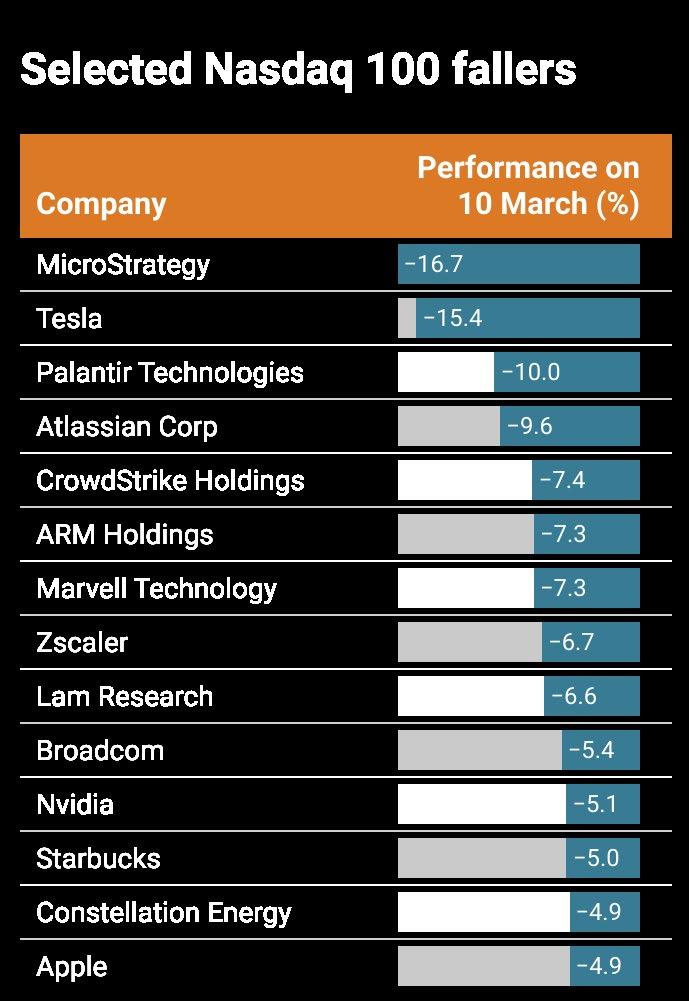

Tech stocks slump as US recession fears extend the recent sell-off

Recession noises seem to be getting louder which partly explains why 10year treasury yields have dropped by more than half a percentage point since president Donald Trump was inaugurated in the middle of January.

Trump has further stoked concerns as he failed to dispel recession fears, saying the economy was entering a ‘period of transition’. The Trump

administration is warning of short-term pain on the path to a ‘Golden Age’ while treasury secretary Scott Bessent has said the economy needs to ‘detox’.

In response US stocks fell hard on 10 March driven by a 4% drop in the technology-heavy Nasdaq 100, its worst one-day fall since 2022. The index has now entered correction territory, falling more than 10% from the peak.

The benchmark S&P 500 index has given back all the gains it made since the election and sits more than 8% below its recent peak. Meanwhile the so-called Magnificent Seven stocks have entered bear-market territory after losing 20% of their value since the end of 2024.

Electric vehicle maker Telsa (TSLA:NASDAQ) has slumped by around 40% and AI darling Nvidia (NVDA:NASDAQ) has lost a fifth of its value from the recent peak.

Airline stocks were weaker after Delta Airlines (DAL:NYSE) slashed its quarterly revenue and profit outlooks citing weaker domestic demand.

CEO Ed Bastian told CNBC that the outlook has been impacted by the recent reduction in consumer and corporate confidence, caused by macro uncertainty.

Delta shares fell 11% in aftermarket trading,

Policy implementation and front-loaded policy uncertainty push recession risks higher”

MICHALE GAPEN, Morgan Stanley

dragging down American Airlines (AAL:NASDAQ) by 6% and United Airlines (UAL:NASDAQ) by 9%.

The so-called fear index, VIX, has spiked to 22 reflecting expectations for increased daily volatility. Digital currencies have taken a bath with bitcoin losing more than 3%, taking losses to a 26% since January.

The bearish reaction spilled over into Asian markets with the Asia-Pacific excluding Japan index slumping more nearly 2% before recovering slightly in early trading, as a modicum of calm returned.

Safe haven assets such as the Japanese yen and Swiss franc were in demand with the yen touching a five-month high against the US dollar.

Uncertainty has been stirred by Trump’s tariff polices which seem to be dampening sentiment and causing businesses to postpone investment decisions.

Economist Michale Gapen at Morgan Stanley believes the economy will avoid a recession while acknowledging ‘policy implementation and front-loaded policy uncertainty push recession risks higher’.

Goldman Sachs reduced its 2025 GDP forecast to 1.7% from 2.2% on 7 March as it sees larger tariffs impacting disposable income and consumer spending while increasing uncertainty for businesses.

The investment bank increased its probability of recession to 20% from 15%, a relatively small amount because ‘the White House has the option to pull back if the downside risks begin to look more serious.’

Meanwhile, the US Federal Reserve looks set to keep its powder dry with the latest reading of the labour market showing resilience and inflation remaining above target.

Market implied interest rates suggest one

The White House has the option to pull back if the downside risks begin to look more serious”

interest rate cut in June and two further cuts by the end of the year.

Bank of America’s Shruti Mishra is in the camp that argues the Fed will not cut rates further with inflation above target. The question is, will falling stock prices force the central bank’s hand?

There is a record amount of household wealth tied up in equities according to data from the Federal Reserve, which means a large fall in prices could impact consumer spending. [MG]

UK M&A gets off to a slow start but investment trusts are in demand

Arevised approach for FTSE 250 healthcare facilities owner Assura (AGR) by US buyout fund KKR (KKR:NYSE) and Stonepeak Partners brings UK M&A deal values so far this year to around £3.6 billion by our calculation.

That is only around 25% of the value of deals announced in the first quarter of last year, although in fairness we haven’t included Sidara’s reported interest in energy services firm Wood Group (WG.) as no financial details have been released yet.

Higher-for-longer interest rates may be deterring some trade buyers, but the amount of ‘dry powder’ in the private equity industry is still colossal and UK companies are still relatively cheap so the odds must favour a pick-up in deal activity this year.

On a positive note, the average premium so far this year is 50%, slightly higher than the 47% average last year, but the biggest deal to date in 2025 – the proposed takeover of Assura – is worth less than one third of last year’s biggest deal, the acquisition of DS Smith by International Paper (IP:NYSE).

In the investment trust world, aside from Assura and high-yielding BBGI Global Infrastructure, which is the subject of a £1.06 billion bid from Canadian pension investor BCI, most of the corporate activity has been in the form of mergers rather than acquisitions.

The combination late last year of two of the largest trusts, Alliance Trust and Witan, to form £4.8 billion market-cap behemoth Alliance Witan (ALW), sent an unmistakable message that bigger is better when it comes to courting investors.

That message was reinforced last month when JPMorgan Global Growth & Income (JGGI) – which has already absorbed Scottish Investment Trust, JPMorgan Elect and JPMorgan Multi-Asset Growth in the last few years – revealed it was in talks to take over rival Henderson International Income Trust (HINT) to create a vehicle with £3.4 billion of assets.

Yet, as KKR and BCI have shown, trusts are just like any other company, and if the price is right

Biggest M&A deals of 2024-2025

there is a take-private deal to be done. It’s worth noting KKR’s offer is equal to Assura’s September 2024 EPRA NAV (net asset value) while BCI’s offer for BGGI Infrastructure (BGGI) is at a small premium to its last NAV – that seems like a clear sign to potential bidders as to what level to pitch an approach at if they want a positive reception. [IC]

Schroders looks to turn the corner with new strategy

In late February, when we ran our screen of the UK’s biggest five-year laggards, investment management firm Schroders (SDR) was one of the worst FTSE 100 performers with its shares languishing 33% below their pre-pandemic level.

Last week, the firm surprised the market not only by beating forecasts with its 2024 result but by unveiling a threeyear strategic plan to return to profitable growth.

‘We are unashamed advocates of the power of active management to address our clients’ complex needs,’ said chief executive Richard Oldfield, adding:

Rentokil’s

‘Schroders is an exceptional company. We have all we need to ensure this business thrives.’

The market responded positively, sending the stock price up nearly 13%, taking year-to-date gains to more than 25% and making Schroders one of the best big-cap performers as analysts upgraded their forecasts.

‘Profits ahead of estimates for 2024 is a good starting point for a Strategy Update which does all that could be hoped for,’ said Panmure Liberum’s Rae Maile, hailing its growth aspirations, a commitment to ‘long overdue’

Chart: Shares magazine • Source: LSEG cost cutting and a return to ‘proper’ reporting.

‘Schroders had been in need of an investment case: the potential for 10%-plus compound annual growth in operating profit backed by continued financial strength gives it one,’ concluded Maile. [IC]

results fail to reassure the doubters

A few weeks ago we flagged the need for pest control and hygiene group Rentokil (RTO) to come up with a positive spin on its 2024 results or the outlook for 2025, but in the event there was little in this month’s announcement to inspire confidence and the shares headed south once more, losing over 10% and taking them back the lows of last October.

Revenue and earnings were broadly in line with (lowered) estimates as a positive performance in international markets was dragged down by weakness in North America,

but operating profits slipped and free cash flow was notably lower due to working capital outflows.

The outlook brought little comfort either, with investors sensing weakness in North American sales and lead generation, and the decision to withdraw the previous £200 million cost saving target from the Terminix deal went down particularly poorly no matter how management tried to spin it.

The firm says it is ‘comfortable’ with market expectations for the current year and it is plodding on with bolt-on

Chart: Shares magazine • Source: LSEG

acquisitions as per usual, but as we have flagged several times in the past, the gulf in performance between Rentokil and US peer Rollins (ROL:NYSE) suggests investors in the UK firm are being short-changed. [IC]

In Asia money talks. But it needs an interpreter.

Living and working in Asia, our investment team navigate Asia’s fast-growing markets as locals.

With a history stretching back decades, we look for the best opportunities to invest your money in quality smaller companies with the potential to grow.

20 March: Central Asia Metals, Energean, Eurocell, Foresight Solar Fund, Hostelworld, Robinson, Schroders Capital Global Innovation Trust FIRST-HALF RESULTS

The retail bellwether has played down expectations ahead of full-year results

Business and consumer confidence has been rocked by Rachel Reeves’ Budget decisions, yet shares in Next (NXT) remain firmly in positive territory year-to-date with the stock trading close to all-time highs.

To retain interest in the story the fashion-to-homewares giant will need to deliver some positive surprises with its full year results, penciled in for 27 March.

Investors will be hoping for signs of improvement in Next’s UK brick and mortar sales, which slipped into negative territory in the nine weeks to 28 December 2024, and counting on continued momentum in overseas online sales, a key growth area for the FTSE 100 retailer these days.

As ever, chief executive Simon Wolfson’s pronouncements on the consumer, the shifting retail landscape and Next’s plans for returning surplus cash will be pored over by investors, who will also be eager for an update on the profit performance of Next’s Total Platform.

On 7 January, the group raised its year-to-January 2025 profit guidance by £5 million to £1.01 billion following better-than-expected festive trading, implying 10% year-on-year growth and admitting the high street stalwart to retail’s billion-poundprofit club.

Over the nine weeks to 28 December 2024, online sales growth accelerated but at the

expense of growth at retail stores. Guidance for the year to January 2026 came in below market expectations, with the company warning it expects UK growth to slow as employer tax increases and their potential impact on prices and employment begin to filter through into the economy.

For the current year, Next forecast full-price sales would rise by 3.5% to £5.22 billion and guided for a 3.6% increase in profit before tax to £1.046 billion with operating cost increases expected to overshadow cost savings. However, the firm is adept at winning market share, and retail supremo Wolfson is renowned for his conservative guidance, preferring to set expectations low and under-promise then over-deliver on the day. [JC]

What the market expects from Next

What the market expects from Next

Logistics giant FedEx (FDX:NYSE) is due to report earnings for the third quarter to the end of February on 20 March after the closing bell, and given its status as a bellwether of US and global economic activity investors will be looking for clues as to the strength of consumer and corporate demand.

Analysts at US investment bank

JP Morgan expect the ‘persistent uncertainty’ from tariffs will likely push FedEx’s EPS (earnings per share) guidance for the year to May 2025 to the low end of its forecast $19 to $20 range.

However, in contrast, Deutsche Bank analysts are upbeat about the firm's prospects, describing its DRIVE initiative which is aimed at making more than $4 billion in structural cost savings as a ‘game changer.’

‘Management have identified an opportunity to improve earnings by over 100%,’ say the Deutsche Bank team, adding that the company has previously proven its ability to boost operating profits in a declining revenue environment.

FedEx disappointed investors with its second-quarter earnings update in December, reporting revenue of $22 billion compared to $22.2 billion in the same quarter a year earlier

and the $22.09 billion Wall Street consensus.

The company also created uncertainty over the full-year outcome saying it was unable to forecast fiscal 2025 MTM (mark-tomarket) retirement plan accounting adjustments.

This time round, as well as scrutinising the results, investors will be keen to find out how the separation of the freight business is progressing after the company revealed its plans in December and whether there are any share buybacks planned for the 2026 financial year.

FedEx bought back $2 billion of shares in the first nine months of this financial year and is aiming to purchase a further $500 million of common stock by the end of the current quarter making a total of $2.5 billion. [SG]

Growth and incomehungry investors should take a bite out of Bakkavor

Margins are improving and financial risk is reducing at this private label food processor

Bakkavor (BAKK) 150.5p

Market cap: £872 million

Investors fretting over geopolitical uncertainties, downbeat economic outlooks on both sides of the Atlantic and frothy valuations across the pond should consider tucking into an attractively valued, cash generative and dividend paying UK stock with defensive qualities.

One name that fits the bill is Bakkavor (BAKK), the chilled prepared food manufacturer with positive trading momentum, which is not only rebuilding its margins, but also reducing leverage. Shares believes this combination of improving returns and falling debt levels could drive a further re-rating of Bakkavor, even after a strong run over the past year or more.

The £872 million cap is also well-positioned should consumers cut back on dining out and spend more on food products that can be eaten

at home and could treat investors to additional forecast upgrades, potentially as early as May’s first quarter update. Despite rising employment costs, this private label pizza-to-hummus maker remains confident of achieving a 6% operating margin by 2027, which suggests outer year forecasts could prove overly conservative.

ABOUT BAKKAVOR

Bakkavor, which joined the stock market at 180p in November 2017, is the leading provider in a large and growing UK fresh prepared food market being driven by structural trends towards convenience, while its presence in the US and China positions the group well in these high-growth markets.

Guided by CEO Mike Edwards, the FTSE 250 firm supplies UK and US grocers including Tesco (TSCO), Sainsbury’s (SBRY), Waitrose, ASDA, Morrisons and Marks & Spencer (MKS) as well as international

food brands in China with everything from meals, salads and sandwiches to desserts, pizzas and bread, soups, sauces and more.

Focusing on retailers’ own label brands, the company’s competitive strengths include its sheer scale and close partnerships with customers, not to mention strong capabilities in salads, ready meals, pizza and desserts and the high service levels which are helping it to win new business.

TASTY MOMENTUM

Bakkavor is enjoying positive trading momentum with shoppers making more frequent trips to the supermarket, which has supported growing demand for the company’s fresh, convenient and high-quality meal solutions.

Impressive results (4 March) for the year ended 28 December 2024 showed adjusted operating profits fattening up more than 20% to £113.6 million, helped by positive volume growth and efficiency gains across all markets, and Bakkavor’s adjusted operating margin moved up from 4.3% to a better-than-expected 5%.

In the UK, the company generated 5.2% likefor-like growth which came from a welcome combination of both volume and price. The US business returned to growth in the second half, and the US margin should recover further, while losses in China were significantly pared, with 13.8% like-for-like growth in mainland China driven by retail and new food service customers.

Crucially, the FTSE 250 firm’s net debt fell by £36 million to a year-end £194 million, paring Bakkavor’s net debt to EBITDA ratio from 1.5 times to 1.1 times, at the lower end of the target range, despite capital expenditure and a

Profitable

growth on the menu

generous 10% increase in the dividend to 8p. By reducing its debt load, Bakkavor’s finance costs are coming down, cash is being freed up which can be reinvested back into the business or deployed for earnings-enhancing acquisitions, while financial risk for investors is lessening.

For the current financial year, Peel Hunt forecasts adjusted pre-tax profits of £90 million rising to £93 million and £97 million in 2026 and 2027 respectively. Based on the broker’s 11.3p earnings forecast and an expected 8.5p dividend this year, Bakkavor trades on a palatable prospective price to earnings ratio of 13.3 times which implies scope for further multiple expansion, and the stock offers income seekers a juicy 5.6% yield.

Risks to consider with Bakkavor include any additional rises in labour-related cost inflation, or a sustained rise in raw material input costs, which could interrupt progress in delivering against margin targets. [JC]

JPMorgan European Growth & Income is the perfect way to invest in outperforming European shares

The trust offers investors exposure to a collection of robust businesses along with attractive income

JPMorgan European Growth & Income (JEGI) 110.9p

Market cap:

£466.3 million

European equities have outperformed their US counterparts by the widest margin since 2000 so far this year according to Morgan Stanley.

All of the major European indices have rallied this year. The German DAX index has risen nearly 17%. France’s CAC 40 has gained 11.5% and the UK’s leading blue-chip index the FTSE 100 has gained 4%.

In contrast, the S&P 500 has fallen over 4% year-to-date and the tech-heavy Nasdaq fell nearly 10% due to US recession fears and Trump tariff uncertainty.

Global bank HSBC (HSBA) has recently downgraded US equities (10 March) citing tariff uncertainty while turning bullish on European stocks following Germany loosening its fiscal rules.

Peter Oppenheimer, chief global strategist at Goldman Sachs research says: ‘The potential for greater fiscal spending following the German election, and a pick-up in European governments’ push to deregulate and stimulate growth means that, after all things may not be quite as bad as markets have been pricing.’

A great way to play Europe’s recent momentum is JPMorgan European Growth & Income (JEGI) which has returned 12% on an annualised basis over the last three years according to the trust’s latest factsheet.

The trust has an impressive investment team

Regions (%)

Figures shown may not add up to 100 due to rounding

Table: Shares magazine • Source: JPMorgan European Growth & Income as of 31 January 2025

behind it comprising of Alexander Fitzalen Howard, Zenah Shuhaiber and Timothy Lewis who have a combined 65 years of investment experience. Tim Lewis, co-manager of the trust tells Shares: ‘European equities are an attractive investment

right now after a forgotten decade. Energy price hikes, the war in Ukraine had put off investors [before]. However, with the likelihood of a ceasefire in Ukraine and Europe now beating expectations [investors] are now talking about Europe once again.’

WHAT’S IN THE PORTFOLIO?

The investment team take a bottom-up approach to stock picking focusing on businesses which are better quality than the market is giving them credit for, following a similar approach to its popular stablemate JPMorgan Global Growth & Income (JGGI). They tend to ignore the noise from popular and recently volatile technology sector and will look to outperform in different market environments. There is a focus on the operational momentum of the business, i.e. are things improving at a macro and a micro level?

The trust’s top 10 holdings are mainly from defensive sectors such as healthcare, food, beverages and tobacco. The portfolio includes some pharmaceutical heavyweights like Danish pharmaceutical Novo Nordisk (NOVO-B:CPH), Swiss pharmaceutical Novartis (NOVN:SWX) and Swiss multi-national healthcare company Roche

JPMorgan European Growth and Income trust – top 10 holdings

JPMorgan European Growth & Income

Holdings (ROG:SWX).

The trust also holds Nestle (NESN:SWX) and energy giant TotalEnergies (TTE:NYSE)

Co-manager Lewis says: ‘We see our [portfolio] as balanced in different market environments. We are neutral to the technology sector; we see opportunities in the banking sector post GFC (global financial crisis), and we are keen to champion consistent alpha for investors. We know investors want income and we offer an attractive yield of circa 4% to 4.1%.’

The trust which pays four dividends per financial year in July, October, January, and March has an ongoing charge of 0.66% per year and is trading at a rough discount of 8%.

HOW HAS THE TRUST PERFORMED?

The trust’s longer-term track record is good, returning 12.7% over five years and 9.6% over 10 years on annualised basis, outperforming its benchmark the MSCI Europe excluding UK.

Lewis mentions stocks the investment team are ‘particularly excited about’ which include Prysmian (PRY:BIT), an energy and industrial cables company which connects offshore wind farms to the electrical grid.

‘We’re also positive about the outlook for Publicis (PUB:EPA), the global media and advertising business, which is seeing strong topline growth despite industry dynamics, as their data-first strategy has allowed them to win market share, growing almost twice as fast as peers since 2000,’ Lewis adds. (SG)

Chart: Shares magazine • Source: LSEG

Games Workshop marches on after full-year upgrade

Jefferies estimates a 10-part Warhammer series could net Games Workshop $10 million of royalty income

Games

Workshop (GAW) £144.80

Gain to date: 21%

At the end of October 2024, we identified the potential for shares in fantasy games and miniatures maker Games Workshop (GAW) to break new ground, driven by the next growth phase of its business, after the post-pandemic pause.

We were encouraged by analyst upgrades to 2026 earnings estimates which we believed could mark the start of a new upward revisions cycle for the company.

WHAT HAS HAPPENED SINCE?

Games Workshop released an unscheduled trading update on 22 November where it raised sales and profit guidance for the half year. The Warhammer franchise owner subsequently beat those expectations when reporting first-half results on 14 January.

CEO Kevin Rowntree described the results as ‘our best first half-year performance’.

The shares were promoted to the blue-chip FTSE 100 benchmark in December and management confirmed that creative guidelines have been agreed with Amazon (AMZN:NASDAQ) to create a Warhammer 40K film and TV series.

The agreement gives Amazon exclusive rights with an option to license equivalent rights in the broader Warhammer universe after any initial productions have been released.

Games Workshop reminded investors that production processes in respect of films and television series may take several years, and it

Games Workshop (p) Apr 2024 Jul Oct Jan 2025

made no change to its forecast for the full year to 1 June 2025.

That is, until 5 March when the firm issued another short, unscheduled trading update saying full year profit will be ahead of expectations. This was prompted by ‘strong’ trading across both the core business and licensing.

Jefferies noted that while this is clearly positive it should not be too surprising given the success of video game Warhammer 40K: Space Marine 2, one of two new games released by Games Workshop’s license partners in the first half.

WHAT SHOULD INVESTORS DO NOW?

The business looks to be in fine fettle, and arguably has only just scratched the surface of the global expansion opportunity. We remain happy to keep backing the shares.

Historically, Games Workshop has released a quarterly trading update in the middle of March, but whether we will get one given the unscheduled update on the 5 March is unclear. [MG]

Chart: Shares magazine • Source: LSEG

WATCH RECENT PRESENTATIONS

CleanTech Lithium (CTL)

Gordon Stein, CFO

CleanTech Lithium is an exploration and development company advancing lithium projects in Chile. The group holds mining exploration and mining exploitation licenses over the Projects which are prospective for lithium resources based on the lithium-enriched brine in the surface and sub-surface of the basins.

Majedie Investments (MAJE)

Dan Higgins, CIO of Marylebone Partners

Majedie Investments seeks to deliver long-term capital growth at an attractive rate above inflation, while preserving shareholders’ capital. The portfolio is managed by Marylebone Partners LLP. The approach is focused on the three main investment strategies: hard-to-access special investments, allocations to specialist external funds, and direct investments in public equities.

Shires Income (SHRS)

Iain Pyle, Lead Manager

The company’s investment objective is to provide shareholders with a high level of income, together with the potential for growth of both income and capital from a diversified portfolio substantially invested in UK equities but also in preference shares, convertibles and other fixed income securities.

Speculation about the fate of the cash ISA allowance has revived the debate about the merits of using a stocks and shares ISA to put your money to work in the financial markets.

Regardless of whether the Government follows through on a reported plan to limit contributions to a cash ISA to £4,000, there is a strong argument for considering turning to the markets through a stocks and shares ISA as long as you have five years or more to leave your cash to grow.

A stocks and shares ISA is the perfect place to grow the value of your investments given any returns are kept safely away from the clutches of HMRC.

Over 20

years

UK stocks have delivered 3.1% a year adjusted for inflation compared with -1.8% for cash

The Barclays Equity Gilt Study is the main reference point for returns from the UK market. The latest edition, out in April 2024, revealed that over the preceding 20 years, the real, or inflation-adjusted, return from cash was -1.8% compared with 3.1% from equities. Demonstrating that investing your money has historically been much more likely to protect you from the impact of rising prices than cash in the bank.

In this article we will take you step by step through the process, from choosing the right ISA type for you, the mechanics of setting up an account and examining how to populate it with a diversified portfolio of investments, before touching on how you should think about managing your holdings going forward.

While aimed at those who are at the outset of their investing journey, the insights which follow could still be useful to existing ISA investors who want to bring some order to an investment pot that might have got into a bit of a jumble, for example, or someone whose participation in the markets has stalled for whatever reason but who now wants get back in the investing habit.

STEP 1: CHOOSING THE RIGHT TYPE OF ISA

Introduced in 1999, the tax-efficient ISA wrapper has several guises and different types of ISA will suit different types of savers and investors.

The most compelling feature of an ISA is tax efficiency says Wesley Harrison, head of financial planning at Benchmark Capital, a subsidiary of Schroders.

‘You can benefit from tax-free growth on income and no capital gains, that is the biggest selling point for us [and that’s what we tell our clients],’ says Harrison.

This point on income is worth remembering outside of an ISA if you receive more than £500 in dividend income from shares you would pay tax on it, within the tax wrapper you don’t.

There are five different categories of ISA:

1. JUNIOR ISA

2. CASH ISA

3. STOCKS AND SHARES ISA

4. LIFETIME ISA

5. INNOVATIVE FINANCE ISA

ISAs are portable, so it is possible to take your ISA with you to a different platform or provider and to combine multiple existing ISAs (as long as they aren’t different types) into a single account. You can only pay into one Lifetime ISA in each tax year and a child can only have one Junior ISA of each type(cash and stocks and shares). The overall annual ISA limit for an adult is £20,000.

KEY FEATURES OF THE DIFFERENT ACCOUNTS

A Junior ISA, Lifetime ISA or stocks and shares ISA will enable you to invest in UK and overseas stocks, funds, investment trusts and exchangetraded funds.

Each ISA has different features. The Lifetime ISA, for example, can help get on the housing ladder or fund your retirement.

You can invest up to £4,000 every tax year until you’re 50. The Lifetime ISA limit of £4,000 counts towards your annual ISA limit.

You need to be 18-39 to open an account and make your first payment before you’re 40.

The government will add 25% bonus to your savings up to a maximum of £1,000 per year. You can withdraw money from your Lifetime ISA if you’re buying your first home, aged 60 or over or terminally ill, with less than 12 months to live. In any other circumstances you would face onerous withdrawal charges.

A Junior ISA can help you save for your child’s future until they turn 18. You can invest up to £9,000 each tax year for your child. They can access the cash when they turn 18 – not before.

Parents and guardians can open a Junior ISA, but anyone can pay into them. [SG]

TOP TIPS FOR ISA INVESTORS

USE IT OR LOSE IT

Benchmark Capital’s Harrison says one of the biggest mistakes people make is not using their tax-free ISA allowance and leaving it too late (like towards the end of the tax year) before they save and invest.

He says: ‘If you do this, you have potentially missed out on a full year of compounded returns.’

KEEP TRACK OF YOUR ISAS

Some of Harrison’s clients have lost track of the number of ISA accounts they have opened during the tax year, and they end up contributing to too many and going over the limit. So don’t forget how many ISAs you have and keep track of your ISA investments.

MANAGE YOUR ISAS

If you are going to be using ISAs for investment, don’t think in the short-term, but have a long-term view, says Harrison.

Some clients incorporate their ISAs as part of their retirement planning and generate an income from their ISA products.

Make sure you are properly diversified, monitoring and rebalancing your ISA or ISAs.

STEP 2: OPENING AND FUNDING AN ACCOUNT

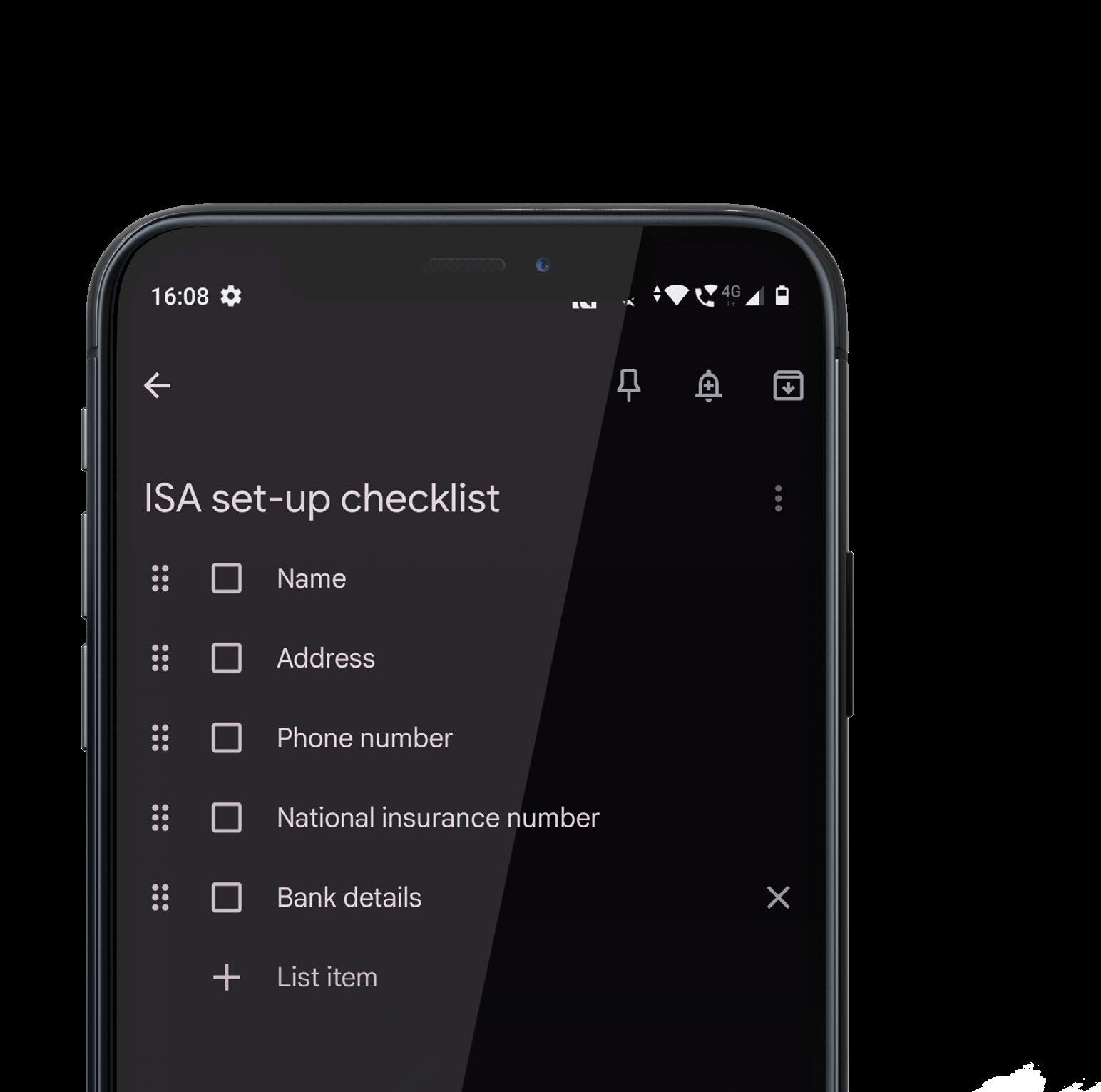

So, you have established your financial goals, have some money to put to work in the markets and familiarised yourself with the ISA rules. You are all out of excuses and it is time to take the leap and open your stocks and shares ISA. The good news is the process is painless. Filling in the application with your ISA provider should take 10 minutes or so.

In order to open your account, you’ll need your name, address and mobile phone number, as well as your date of birth and national insurance number. You’ll also need to punch in your debit card details if you are making a lump sum

including bonds, shares, funds, investment trusts, and ETFs.

You can use your ISA allowance by funding one lump sum, or in smaller amounts. The minimum lump sum investment for an ISA is £500, and you can top it up again later. But remember to stay within the annual ISA allowance, which for the 2024/25 tax year is £20,000. The regular investment service from Shares parent AJ Bell lets you invest as little as £25 a month.

With AJ Bell’s stocks and shares ISA, you can instantly pay money into your account by logging in and selecting the ‘Single payment’ option. Another way to fund your account is by making regular payments by direct debit from your nominated bank account. To set this up, log in and select ‘Regular payments’.

One of the advantages of saving regularly into your ISA, rather than periodically investing big one-off lump sums, is this can help insulate you from stock market fluctuations through a phenomenon known as ‘pound-cost averaging’. By buying shares or fund units with a regular payment, you buy more shares or units in months when their prices are lower than when their prices are higher. As prices move up and down, your investment return is ‘smoothed out’.

With the AJ Bell platform, buying selling investments really couldn’t be simpler. Just log in to your account and from the ‘My account’ menu, click on ‘Buy and sell’, which takes you to the screen where you can choose which investments you want to trade. For shares and other listed entities like ETFs and trusts, you can only place a direct deal during market hours. In the UK these are 8am to 4.30pm. For funds, you can buy or sell outside market hours, although your deal won’t be executed until the next valuation point, which is usually the next business day. [JC]

STEP 3: CHOOSING YOUR INVESTMENTS

Investing can appear daunting, but like any longterm endeavour, breaking the task down into baby steps makes the whole process easier to undertake.

A stocks and shares ISA is a tax efficient way to invest in the stock market and other asset classes like bonds, property, infrastructure, renewables and commodities.

But just because all these choices exist does not mean they are appropriate for everyone.

Think of it like a restaurant menu. Instead of looking at the names of the meals, we can break the menu down by the essential ‘macro nutrients’ of proteins, fats and carbohydrates.

Achieving a good balance between these essential nutrients is important for general physical health.

Investing is all about managing risk, and each asset class has a different risk profile and return expectation. Just like a pursuing an individually balanced diet, investors should aim to achieve a balance of investment risks which reflect their personal circumstances and investment goals.

Essentially there are three broad buckets of risk. Equities are the riskiest asset class, government bonds (a type of government IOU) are lower risk than stocks and cash is the lowest risk asset.

What do we mean by risk? Well, think about risk as the ‘lumpiness’ of returns. In any single year stocks can go up or down in value a lot more than bonds while cash always delivers a steady positive, but relatively low rate of return.

That deals with risk but what about returns? Well, over the long run stocks have provided investors with the highest investment returns, while bonds and cash have delivered the

lowest returns.

While it is important to understand that stocks can fall in value from time to time, the longer they are held, the more likely they are to provide a positive return. This is due to growth in corporate profits which has averaged between 6% and 7% a year.

The annual Barclay’s Equity Gilt study demonstrates that over the last 100 years, there has never been a decade which resulted in negative returns from owning UK stocks. This does not mean it can never happen, but the chances are slim.

PASSIVE OR ACTIVE?

Now we have a better idea of the risks and returns from investing across different assets, the next question is to decide whether to self-manage your investments or outsource it to a financial advisor.

It is worth pointing out that even if you decide to manage your own investment portfolio, it may still be worthwhile speaking with a professional financial advisor.

Assuming you take full control, the next step is to decide whether you want to track broad indices like the S&P 500, FTSE All-Share or MSCI World index, or to actively manage your portfolio.

Higher returns can be made through active management, but even professional fund managers find it hard to consistently beat the indices over the long run.

Picking successful fund managers can be just as difficult to get right as picking the right stocks. There are no right or wrong approaches, it just comes down to personal preference and temperament.

Investing through active or passive funds provides instant diversification which is a big advantage for investors starting out.

Active funds are more expensive than passive funds, and minimising costs is an important consideration in investing. The upside is that successful funds can deliver superior returns to the benchmark over time, but remember, they may also lag.

Some investors may decide to build their own portfolios by choosing which stocks to hold. It saves paying fund fees, but it also requires a certain amount of capital to achieve diversification and investment knowledge.

A minimum of 25 to 30 stocks is required to achieve a reasonable level of diversification. Therefore, it can make sense for investors starting

out to use ETFs to achieve core diversification, then consider adding individual stocks to the portfolio later, if desired.

This is a called a passive core, active satellite approach to managing investments and was used by an investment firm I worked for many years ago to good effect.

HOW MUCH TO PUT INTO EACH RISK BUCKET?

Individual risk appetite should drive asset allocation and in general, younger investors with a longer investment horizon, and investors with a higher risk appetite can afford to allocate a higher proportion to stocks.

To some extent this decision can be outsourced to a one-stop shop which takes care of asset allocation by adopting a multi-asset strategy. For example, the Alliance Witan trust (ALW) is designed to be a core investment with a focus on long-term capital growth and a rising dividend.

Another option in this category is F&C Investment trust (FCIT) which also invests in private equities. Remember, asset allocation is decided by the manager, which means, it may not be suitable for everyone.

Another way to achieve diversification at a competitive cost is to consider starter or readymade portfolios, which are available on most investment platforms.

The platforms typically ask you to select an investment goal, such as growth or income, and your level of risk, which might be conservative,

balanced or adventurous.

You’re then directed to a ready-made portfolio that contains a mixture of actively managed funds or ETFs designed to meet the required risk level. Although from this starting point you would then be expected to manage the investments yourself.

STARTER ISA PORTFOLIO WITH ETFs

Exchange traded funds are primarily passive vehicles which track an index, although increasingly actively managed ETFs are becoming available.

Passive ETFs track major indices like the S&P 500 index and benefit from low costs and good liquidity. They trade like individual stocks, unlike funds which trade once a day or weekly.

Let’s look at two different types of investors, Jane and Sharon, to discover how their portfolios might differ due to their risk appetite.

Jane is in her mid-20s, lives with her parents and works at a software company. Jane considers herself risk tolerant and comfortable dealing with the ups and downs of the stock market and because she has modest outgoings she can put significant sums to work as she looks to build up money to buy her first home.

Sharon is in her late 30s and married with two teenage children. She is working part time and has a more cautious approach to investment risk and has a more modest amount of available cash to invest. [MG]

STEP 4: MAINTAINING YOUR PORTFOLIO

Now you’ve got your ISA up and running you’ll want to keep on top of it to make sure it continues to meet your needs. This may sound like one big headache, but you can keep things relatively stress-free by following a few simple steps.

1

First, work out where you are in relation to your investment goals. If you’re investing for the long term, more than 10 years say, you may be able to tolerate more risk and benefit from higher potential returns. If you’re investing over a shorter period, a greater focus on preserving your capital and minimising risk may be more appropriate.

2

Second, consider contributing regularly to your ISA from your normal income, which can be easily done by setting up a monthly direct debit from your bank. This means you’ll be constantly building your tax efficient savings without having to remember to do it. As your funds build up, you can invest larger chunks of savings in fewer trades, keeping your costs to a minimum.

3

Whichever ISA you choose, maintaining diversification in your portfolio is an important part of sensible financial planning. Diversification means spreading your investments across different types of assets (stocks, funds, bonds, gold etc) and sectors (US, UK, tech, property, income etc) to reduce the impact of market volatility. By rebalancing your portfolio, say annually, you can make sure your holdings remain appropriate for your circumstances.

Say for example you have a portfolio comprised of 60% stocks, 40% bonds (whether directly or through funds), and the stocks do well while the

return from the bonds goes down.

In this case, the value of the various holdings in your portfolio will change and may now look more like 70% shares, 30% bonds.

The concept of portfolio rebalancing is that you then take your profit on the shares that have done well and buy bonds that haven’t done as well for the time being, until the stocks part of your portfolio makes up 60% again.

This helps to keep a more consistent level of risk exposure and also encourages the discipline of selling assets that have appreciated and buying those that may have become relatively undervalued.

4

Remember time in the markets beats timing the markets. It’s notoriously tricky to accurately time the markets and buy at exactly the right time, and even the professionals struggle to do it consistently.

What history shows is that time is your friend when it comes to investing, and the longer you leave your money invested, the better chance you have of getting superior returns. It is also the case that missing just a handful of the best days for the market can seriously undermine your long-term returns, and often the best days follow market corrections.

5

Finally, five, and perhaps most crucial, it’s OK to mostly do nothing. Markets have shown time and again that they can bounce back from the greatest of blows far quicker than you might think. The UK’s FTSE 100 Index took less than two years to recover all its Covid pandemic losses, while the US S&P 500 Index took barely six months.

Investors are frequently tempted to do something in response to bad news, be it a poor set of company results, ugly economic figures, geopolitical volatility, or simply a year of poor returns. It is often exactly the wrong thing to do, which is why you should avoid checking up on your portfolio too often. If your personal circumstances have altered, or the original investment case of a holding has changed, by all means act, but otherwise, trust yourself, relax, and let time in the markets demonstrate its true wealth-generating power. [SF]

AJ Bell referenced in this article owns Shares magazine. The editor (Tom Sieber) and authors of this article (James Crux, Sabuhi Gard, Martin Gamble, Steven Frazer) own shares in AJ Bell.

What Is the Best Second Term “Trump Trade”?

EJF Capital (EJF) believes that Trump’s tariff policy will not uniformly affect financial institutions and that small and community banks, in particular, will largely operate in the protective cove of the domestic economy. In its almost twenty-year history, EJF has never felt more confident about the direction of travel for small U.S. banks given the deregulatory and interest rate environments, predictably low corporate tax rates and fiscal stimulus policies that the second Trump administration will bring. EJF strongly believes as small bank loan growth and M&A heats up, there will be no better “Trump Trade” than owning small bank debt.

TRUMP ADMINISTRATION 2.0

In EJF’s opinion, one can anticipate at least six policy directional moves in Trump’s second term. The first is the continuation of low corporate taxes. The margin of Trump’s victory almost ensures a permanent continuation of Trump’s domestic corporate tax rate of 21% as enacted during his first term. Second, we can anticipate a repeat of Trump’s first term push for deregulation. In his first term, Trump required that for every new regulation proposed two must be revoked. In his

campaign, Trump vowed to increase that ratio to 10:1. President Trump will not need Congress to significantly impact, and reduce to a meaningful degree, the regulatory apparatus of the federal administrative state. Third, and related, we can anticipate a wave of M&A. Approval for M&A in industries under direct federal administrative oversight, like banks, do not need Congressional input. Two of the last four years have seen the fewest bank M&A deals since the 1990s and we are already seeing the anticipated rebound in deal activity after the election as small and regional bank share prices – the currency for M&A transactions –have risen throughout 2024. Fourth, we can expect newfound support for regulating and supporting cryptocurrencies, which EJF believes will most significantly result in the additional commercial embrace of blockchain technology and the use of stablecoins. Finally, we can anticipate more restrictive immigration policies. Some, or all, of these five policy directions have the potential to spur growth and fan inflationary pressures in the economy. This viewpoint has been expressed in the market in the form of increased yields in the 10-year U.S. Treasury bond as well as a steepening yield curve.

EJF’s Expertise Investing in Bank Issued Debt

EJF and its affiliates manage a securitisation platform dedicated to financials with $4.2 billion1 securitised since November 2015.

EJF is one of the leading investors in U.S. community and regional banks across all levels of the capital structure

Extensive industry knowledge and capital markets experience allows EJF to identify and monetise market dislocations and catalyst driven opportinities

EJF was an early adopter in the community bank sub-debt space, inititialising its first purchase in mid-2013. Since 2013, EJF has made total bank sub-debt purchases of approximately $1.3 billion1

1As of 30 September 2024

EJF believes that one subset of companies in America that will benefit from Trump’s five likely policy shifts and a steepening yield curve is smaller banks, i.e. those with less than $100 billion in assets. A steepening yield curve is very positive for bank fundamentals due to a combination of lower deposit costs, as well as fixed asset repricing given the medium duration of most small and mid-size loan portfolios. Valuations of bank equities are highly correlated with margin improvement. While higher interest rates may increase the probability of credit deterioration, we believe that the combination of fiscal stimulus, healthy economic growth and fewer regulatory hurdles should more than offset this risk. It is also worth looking back to Trump’s first term to see how small banks performed. Between 2016 and 2020, small banks grew at 10.6% annualized versus large banks at 2.5%. Today, small banks are growing at 3.3% versus large banks at 0.7% annualized. Therefore, we believe that the potential for a tripling of small bank loan growth may lead to much higher earnings expectations for the

THE TRUMP TARIFFS – EJF TAKEAWAYS EJF’s view is that Trump’s tariffs will have a disparate impact in the financial sector, with a more negative impact on money center, large banks. Although small banks will not be immune to the tariff policies of Trump, particularly as they relate to loans made to American companies with ties to Canada and Mexico, small banks are substantially more domestically focused. U.S. banks under $100 billion of assets have less than 0.5% of loans outside of the U.S. and source less than 0.2% of deposits from outside of the country. By contrast, the largest banks, over $700 billion of assets, are much more exposed to international loans and deposits, with over 17.5% of loans and over 12.5% of deposits originating outside of the U.S.1 01

sector, a catalyst for higher bank share prices and strengthening bank issued credit.

This advertisement is being provided to you in the form of general market commentary by EJF Capital and is not a solicitation or offer of EJF’s advisory services. Additionally, the information contained herein shall not constitute a solicitation or an offer to buy or sell any security or service, or an endorsement of any particular investment strategy. Nothing in this material constitutes investment, legal, or other advice nor is it to be relied upon in making investment decisions. Offering of EJF funds is made by prospectus only. Certain information contained herein has been provided by outside parties or vendors. Although the information herein contained is, or is based on, sources believed by EJF to be reliable, no guarantee is made as to its accuracy or completeness. Accordingly, EJF has relied upon and assumed, without independent verification, the accuracy and completeness of all information available to it. EJF expressly disclaims any liability whatsoever for any loss arising from or in reliance upon the whole or any part of the content therein.

Neal Wilson, Co-Chief Executive Officer

Markets have hit a rough patch but investors can take some comfort in corporate earnings

US earnings - Q4 beats vs recent history

as stocks re-price to take account of all the geopolitical upheaval since the start of the new Trump administration.

FUNDAMENTALS REMAIN SOLID FOR NOW

The good news is that as far as fundamentals go, with around 95% of S&P 500 companies having filed, as-reported fourth-quarter earnings in the US were ahead of expectations across every industry and at least on a par with the third quarter in terms of beats to misses.

In other words, companies in general are in good health and growth isn’t restricted to a few pockets of the economy.

Indeed, in the sectors with the largest number of constituents – financials, industrials and information technology – a higher proportion of stocks beat expectations than across the market in general (roughly 80% against 74%).

For the year to December 2024 ‘earnings per share’ for the S&P 500 were $211, in line with forecasts dating back to last June and representing an increase of just under 10% on the previous year.

For 2025, analysts are forecasting index earnings of $250 or an increase of around 18.5%, although estimates will probably come down as the year

progresses, as they do every year, so we would pencil in 10% to 15% growth to leave scope for a small downward revision.

FURTHER GROWTH EXPECTED IN 2026

For the first time we also have estimates for 2026, where analysts are expecting growth of 15% to $287 although again we would expect that consensus to fade over time.

If we assume earnings are in the region of $240 this year and say $275 next year, based on a

Average contribution to S&P 500 earnings in 2024 and 2025

current reading of 5,789 points it puts the index on a multiple of 24 times falling to 21 times.

The bulk of this year’s operating earnings (around 67%) are expected to come from technology, financial, health care and communication services stocks, the same four sectors which generated most (around 64%) of last year’s earnings.

However, it is worth noting financials and communications services are seen contributing less than they did last year while health care and technology are seen providing a significant lift.

Energy stocks are also seen contributing slightly less than last year (4.9% against 5.7%), while consumer stocks – both staple and discretionary –are expected to be challenged by tariffs and rising prices and are expected to contribute just 14.1% of overall earnings against 15.9% last year.

By Ian Conway Deputy Editor

Fidelity European Trust PLC

Chosen by AJ Bell for its Select List

Fidelity European Trust PLC aims to be the cornerstone long-term investment of choice for those seeking European exposure across market cycles.

Aiming to capture the diversity of Europe across a range of countries and sectors, this Trust looks beyond the noise of market sentiment and concentrates on the real-life progress of European businesses. It researches and selects stocks that can grow their dividends consistently, irrespective of the economic environment.

Holding a steady course throughout market cycles

It is an uncertain time for the world and Europe is no exception. It is however vitally important for investors not to be blown off course. Good companies are still good companies and finding them remains the ‘secret sauce’ of any effective investment strategy.

We will remain focused on the companies in which we have invested and, in particular, on their ability to continue to grow their dividends. As always, we will ask ourselves if that rate of dividend growth is already discounted in the share price.

Performance over five years

We continue to seek new opportunities to add to the portfolio at the right price and remain confident in those names we currently hold. This approach has historically served the portfolio well - including through the recent volatility of the last few months - and we see no reason to change course.

Past performance is not a reliable indicator of future returns.

The value of investments and the income from them can go down as well as up, so you may get back less than you invest. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. This trust can use financial derivative instruments for investment purposes, which may expose them to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The shares in the investment trust are listed on the London Stock Exchange and their price is affected by supply and demand. The investment trust can gain additional exposure to the market, known as gearing, potentially increasing volatility. This information is not a personal recommendation for any particular investment. If you are unsure about the suitability of an investment you should speak to an authorised financial adviser.

The latest annual reports, key information documents (KID) and factsheets can be obtained from our website at www.fidelity.co.uk/its or by calling 0800 41 41 10. The full prospectus may also be obtained from Fidelity. The Alternative Investment Fund Manager (AIFM) of Fidelity Investment Trusts is FIL

(UK) Limited. Issued by FIL Investment Services (UK) Ltd, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and

UKM0225/399910/SSO/0525

How one fund manager looks to find the next generation of US market stars

VT Tyndall North American invests beyond the big familiar names across the Atlantic

US

-focused exchange-traded funds (ETFs) and passive strategies have grown in popularity over the past decade, but this trend has created concentration risk since so many investors are now crowded in US stocks and the mega-cap tech names in particular.

For investors seeking differentiated exposure to the world’s largest, most liquid stock market, then a vehicle that does not mimic any index and offers a play on some of the most exciting and innovative growth companies across the pond merits consideration.

One collective that has caught Shares’ eye is VT Tyndall North American Fund (BYPZY05). First the negatives. The fund is still very small, with just £18.9 million in assets at last count, and ranks fourth quartile over five years with its 63.83% cumulative total return lagging the IA North America Sector’s 97.61% haul. And yet, the portfolio’s more recent performance is encouraging, with VT Tyndall North American ranked first quartile over six months with a 13.55% gain, comfortably ahead of the sector’s 8.35% return.

FLYWHEEL SPINNING FASTER

A unique growth story held in the fund is the innovative SharkNinja (SN:NYSE) the cleaning and cooking appliance maker behind the Shark and Ninja brands whose innovation flywheel is spinning faster.

A 2023 IPO, SharkNinja has established a track record of beating Wall Street estimates and is ‘constantly finding products which are either out of patent or need to be improved. It is quite a differentiated story that most other

TIME TO GET ACTIVE

This high-conviction, long-only portfolio is managed by a true active manager in Felix Wintle, who dares to differ from the index and starts with a top-down analytical process to determine where we are in the cycle. More specifically, Wintle applies a ‘split approach’ to his portfolio: core stock selection based on finding long-term thematic winners and tactical selection driven by the outlook for growth and inflation. An admirer of the late great American broker and investor William O’Neil –author of How To Make Money In Stocks and one of the first investors to incorporate computers into his research, Wintle thinks about the US differently from rival long-only peers.

Not content to follow the herd, Wintle runs a multi-cap portfolio in the belief there is ‘so much more to play for in the US in terms of trying to get those names right and increasing the probability of owning stock picks that are going to work. I do the fundamental work, but also marry that with a macro appreciation and a technical view’, he

long-only managers would not have heard of’, says Wintle. Sharing his bullishness on the name is Jefferies, which believes SharkNinja is well positioned to grow market share across categories and geographies thanks to its ‘best-in-class brands and management team. Its global TAM (total addressable market) is large while penetration remains low, and the company’s proven international expansion playbooks keeps gaining speed’, argues the broker.

informs Shares.

Wintle puts in the hours poring over charts and identifying trends because it is so important to be ‘in synch’ with the market, to find stocks the market already wants to own that are in relative uptrends. ‘If we like the stock fundamentals, the macro backdrop is supportive of taking equity risk and we are buying something that the market already wants to own, that massively increases the probability of that fundamental stock pick being right,’ he explains.

Valuation forms part of his toolkit, but Wintle argues valuations can be inaccurate and subjective. ‘I’d much rather find a stock which is going through a growth phase that is already performing and pay a bit more for it, because that works much better than saying “I can’t possibly own it because it trades on 20 times earnings”.’

Fund info

Fund info

*Measures the difference between fund portfolio and the benchmark

Table: Shares magazine • Source: Tyndall Investment Management, as at 28 February 2025

*Measures the difference between fund portfolio and the benchmark Table: Shares magazine • Source: Tyndall Investment Management, as at 28 February 2025

SHUNTING HIGH & LOW

As at 28 February, VT Tyndall North American owned 31 names with top 10 holdings spanning giants such as Amazon (AMZN:NASDAQ), Costco (COST:NASDAQ) and Goldman Sachs (GS:NYSE), as well as payments company Fiserv (FI:NYSE) and Axon Enterprise (AXON:NASDAQ). The manager is excited about the potential of the latter, which sells tasers, body cameras and software systems to local law enforcement agencies and has morphed into ‘a real practical AI story. The bodycam videos the arrest and there is an AI capability that writes the report for the police officer afterwards. From an investment point of view that’s super interesting because Axon is going

IPOS AND SPIN-OFFS

In contrast to many other managers, who look for a long-term track record on the public markets before they invest, Wintle is a fan of IPOs (initial public offerings) and spin-offs. This aligns with his focus on new leaders and newness. ‘When you look at where the big winners in stock market returns come from, a lot of them are new companies, IPOs, companies with new products, because typically they are the beginning of their growth trajectory and if those products take hold, they can be absolute monsters. I have an issue with this idea that the best companies are the ones that have been around for 140 years.’

Also known as de-mergers, he says ‘spinoffs are almost always a really good source of alpha and new ideas, because most of these businesses get lost in the conglomerates. When you break them up, you get proper management in, proper funding, a proper vision and away you go.’

from a hardware margin profile, the tasers and bodycams, to a software margin profile, which is about 20 percentage points of uplift,’ he enthuses. Illustrating the diversification within the fund, holdings outside the top 10 span the likes of fantasy sports betting firm DraftKings (DKNG:NASDAQ) to trading platform Robinhood (HOOD:NASDAQ), the latter giving investors some

NO ROOM FOR NVIDIA?

One notable absentee from the portfolio is chips champ Nvidia (NVDA:NASDAQ). ‘The reason we don’t own Nvidia right now is everything is a cycle, including the best ideas you’ve ever had in the world,’ explains Wintle. ‘There’s a rate of change deceleration in Nvidia’s revenue growth and the market doesn’t like that. For all its genius, Nvidia is still a cyclical stock. The time to own it was 18 months to two years ago when it was hockeysticking up, but now it is beginning to crest.’

Funds: VT Tyndall North American

exposure to crypto.

Wintle tells Shares he is loathe to own any ‘filler stocks’ and while the fund does own some mega caps, his unwavering focus is on finding the next big growth story. ‘Generally, I generate alpha by finding the new leaders. Companies with strong fundamentals, continued growth potential, and sector outperformance. And typically, the new leadership stocks in the market tend to be small and mid caps. If you are going to generate alpha, you’ve got to be active, because only 4% of stocks in the US actually account for alpha.’

AVOIDING THE ‘ROUND TRIP’

VT Tyndall North American’s core names tend to be in sectors where there’s pricing power and innovation such as consumer discretionary, healthcare, technology and industrials, and he is seeing lots of innovation in the consumer discretionary sector right now.

Fast-food restaurant chain Brinker, the Chili’s owner which flies under the radar as better known companies like McDonalds (MCD:NYSE), Starbucks (SBUX:NASDAQ) and Chipotle (CMG:NYSE), is growing earnings at a rapid clip, taking share from competitors and has ‘stolen a march on the value proposition in America. We sold it because we wanted to take some profits, but I’d be happy to buy back in again if the opportunity arises. If something has done really well, I don’t want to “round-trip”” it. One of the mistakes that fund managers make is falling in love with stocks, but we are quite aggressive in terms of selling on the up.’

A consumer stock Wintle recently sold is the once high-flying fitness and energy drinks company Celsius (CELH:NASDAQ) Monster Beverage (MNST:NASDAQ) was one of the most successful stocks in the S&P 500 ever, so when these growth names really get it right, it can be absolutely transformational,’ he explains. ‘Admittedly Celsius was a one product story, but it was a really successful investment for us, but I did round-trip this one and its painful.’ Celsius’ recent $1.8 billion acquisition of rival energy drink brand Alani Nu makes Wintle think he was right to exit the position. ‘If you’ve got the hottest product in energy drinks, you don’t need to go an buy another product,’ he cautions.

That said, he recently sold two restaurant stocks which had been big contributors to performance, namely Cava (CAVA:NYSE) and Brinker (EAT:NYSE), feeling the time was right to bank some profits. Mediterranean-inspired fast-casual restaurant Cava, which joined the stock market in 2023, was sold ahead of a fourth quarter earnings miss (25 February) and that turned out to be a good decision. ‘Cava is going through a nice growth trajectory, but we feel Wall Street has got way ahead of itself in terms of expectations,’ observes Wintle.

A new consumer name Wintle has added to the portfolio is Planet Fitness (PLNT:NYSE), the largest budget gyms owner in the US whose new CEO has wasted no time in turning around the fundamentals of the business. ‘A new pricing cycle around their black card membership and an expansion plan make for a compelling growth story,’ Wintle insists. Jefferies shares his enthusiasm for the name, having made Planet Fitness, which it describes as ‘The Walmart of Gyms’ with a new ‘laser-focused’ CEO, its top pick for 2025 with a $150 price target versus the current $96.9 market price.

By James Crux Funds and Investment Trusts Editor

Add A New Element to Your Portfolio

Is it wrong to chase performance as an investor?

Examining whether a momentum strategy work when it comes to the markets

One of the basic tenets of investment is not to buy something an asset just because its price has gone up. And yet in the last decade, performance chasing has been a much better strategy than buying investments which have seen their prices fall sharply, a blind bargain-hunting approach which appeals to many people but comes with its own health warnings.

AJ Bell has put five common investing strategies to the test to see how they stacked up against each other (see table below). Perhaps not surprisingly in such momentum-driven markets, performance chasing came out top, with bargain-hunting bringing up the rear.

MODELLING THE STRATEGIES

We modelled these strategies using fund sectors, and the analysis is meant to be instructive rather than exhaustive. For performance chasers, we assumed that at the beginning of each year, they

How different strategies compare

bought a fund in the best performing sector of the previous 12 months. Our bargain hunters bought a fund from the worst performing sector of the previous 12 months.

Herd investors bought a fund from the most popular sector, and contrarian investors bought a fund from the least popular sector. Our egg spreaders diversified across five equity fund sectors, putting 20% in each of US, UK, Europe, Japan and Emerging Markets funds, and rebalancing each year to achieve an equal weight in each.

Performance chasing returned 23.5% in 2024 and 154.7% over ten years. In other words, £10,000 invested in this strategy a decade ago would now be worth £25,468. Throughout 2024, this meant being invested in the Technology and Telecoms sector, which was the best performing sector in 2023, returning 38.9% in that year. Despite its success over the last 10 years, performance chasing comes with large risk warnings attached. An area which has performed well in one year has probably

become a crowded trade and vulnerable to both overvaluation and profit-taking.

A HIGH-OCTANE RIDE