VEHICLES WHOSE DIVIDEND PAYOUTS HAVE BEATEN RISING PRICES

Visit the Shares website for the latest company presentations, market commentary, fund manager interviews and explore our extensive video archive.

Manx Financial Group (MFX)

Douglas Grant, Group CEO

A diversified financial services listed entity offering a customer-focused range of deposit, lending, insurance, and wealth management products. The Group includes an established independent bank with both a UK and Isle of Man deposit taking licence, as well as market leading lenders in their field.

Rome Resources (RMR)

Paul Barrett, CEO

A critical minerals exploration company active in the DRC. Its main project is Bisie North, a tin and copper deposit some 8km from the world’s highestgrade tin mine. The Company has been drilling since Admission to AIM in 2024 and is approaching the end of its programme which will lead to the posting of a maiden resource estimate.

Strategic Equity Capital (SEC)

Ken Wotton, Fund Manager

A specialist alternative equity trust. Actively managed by Ken Wotton and the Gresham House UK equity team, it maintains a highly concentrated portfolio of 15-25 high-quality, dynamic, UK smaller companies, each operating in a niche market offering structural growth opportunities

Inflation-busting trusts

One way to offset higher inflation is to look for investment trusts whose dividend growth has outstripped rising prices in recent years.

Finsbury Growth & Income versus Temple Bar

How Temple Bar became the best five-year UK Equity Income performer, and why Nick Train is more excited than ever about Finsbury Growth & Income’s prospects despite its recent struggles.

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Find out which UK companies short sellers are

While controversial, shorting can improve market efficiency by providing

and exposing overvalued companies.

Just Group becomes the latest company to agree to a takeover

The M&A boom in the UK market has shown no signs of abating as deals continue to progress. This raises three big questions: who is doing the buying, is the trend sustainable and what does it mean for investors?

Right at the end of July, life insurer and retirement solutions provider Just Group (JUST) became the latest name to succumb – agreeing to a £2.4 billion takeover by Canadian investment group Brookfield.

According to data from broker Peel Hunt the second quarter saw 19 bid situations, taking the total for the first half as a whole to 31. Bid premiums have been pretty healthy at 39%. This is, as Peel Hunt observes, above historic norms and potentially reflects the attractive relative valuations to be found among UK stocks.

As we have observed before, those healthy premiums may be well received by investors in the short term but do little for the long-term health of the UK market and can mean shareholders miss out on even greater potential returns down the line. The same data from Peel Hunt shows just one new IPO with a valuation of more than £100 million in the first half of the year.

Peel Hunt analyst Charles Hall comments: ‘There have been bids for £16 billion of market cap in the FTSE 250 and £4 billion in the FTSE Small Cap and AIM. The scale of departures from the FTSE SmallCap and AIM, should concern anyone who cares about the health of the equity capital markets.

‘The impact on the FTSE SmallCap is much greater than suggested by the data, as a number of constituents will be promoted to the FTSE 250 to replace the companies being acquired.’

As Hall notes, many of the bids have come from individual companies, rather than private equity.

His counterpart at Berenberg Jonathan Stubbs also notes that a lot of the takeover action is being driven from across the Atlantic. ‘M&A activity in the UK is being increasingly driven by US actors, on both a volume and total activity basis. While UK actors slow

down, due to high costs of funding, macro & political risks, and sluggish earnings, US actors have stepped up over the last four to five years.‘

Stubbs adds: ‘A wide range of factors drive M&A activity however, it is likely that given cheap-relative global valuations, and decent fundamentals UK M&A activity, particularly further down the cap scale, will continue.’

Elsewhere in this week’s issue you can read about the investment trusts which have delivered inflation-busting increases in their dividend as inflationary pressures begin to dial up again. There’s also a look from James Crux at the trusts which top and tail the leaderboard of performance in the Association of Investment Companies UK Equity Income sector with contributions from their respective fund managers and some excellent insights on short selling from Martin Gamble.

President Trump’s latest tariff salvo and July’s non-farm payrolls report conspired to send investors running for the hills on 1 August as volatility spiked, stocks tanked, and two-year treasury yields plummeted by more than a quarter of a percentage point.

Further jangling investors’ nerves, Trump said he would fire Erika McEntarfer, commissioner of the BLS, (Bureau of Labor Statistics) after the agency sharply revised down May and June’s jobs reports by a combined 258,000, the most since the pandemic.

Claiming political interference Trump said on social media: ‘I have directed my Team to fire this Biden Political Appointee, IMMEDIATELY. Important numbers like this must be fair and accurate, they can’t be manipulated for political purposes.’

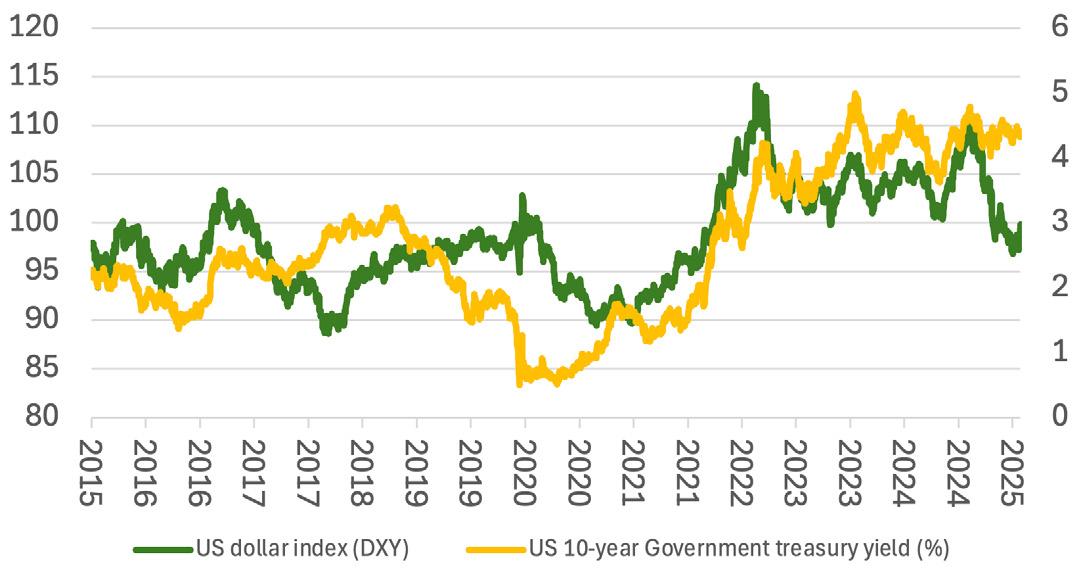

The US dollar index, representing the greenback’s value against a basket of currencies fell 1.4%, potentially reflecting some erosion of confidence in the credibility of US institutions.

The BLS reported that the US economy added just 73,000 jobs in July, undershooting the 104,000-consensus estimate, while the unemployment rate ticked up to 4.2%, in line with forecasts.

Futures markets priced in a greater chance of a September rate cut with odds rising to 60%, compared with 40% before the jobs report.

The 31 July FOMC (Federal Open Markets Committee) meeting saw two members dissent on the Fed’s decision to leave interest rates unchanged, the most governor dissents since 1993.

In another unexpected development, on 1 August Fed governor Adriana Kugler announced she will be stepping down on 8 August, opening the door for Trump to appoint his candidate for the next chair.

On the eve of the 1 August tariff deadline Trump announced new reciprocal tariffs on countries which have yet to negotiate an agreement, which are expected to come into force on 7 August.

For those nations that have a framework deal in place such as the EU and Japan, a floor rate of 15% appears to be the norm, applying to over 40 countries.

Notable exceptions above 15% include Brazil which faces a tariff of 50%, Switzerland at 39%, India at 25%, and Vietnam and Tiawan at 20% apiece. Mexico has agreed a 90-day continuation of existing 25% tariffs.

Canadian goods outside the US-Canada-Mexico free-trade agreement will now face a 35% tariff, up from 25% previously. The US and China are still negotiating with the current 30% levy running out on 12 August. [MG]

Standout

Premium drinks leader Diageo (DGE) served up weak results for the year to June 2025 with operating profits down 27.8% to $4.3 billion (£3.2 billion) due to challenging spirits market conditions, unfavourable currency swings and an earnings hangover from restructuring costs.

The FTSE 100 distiller failed to name a new CEO following the recent departure (16 July) of Debra Crew, forecast flat sales for the new financial year and increased its estimate of the impact of US tariffs from $150 million to $200 million.

So why did the Johnnie Walker-to-Smirnoff purveyor’s shares rally on these numbers?

Well, the profits decline proved better-thanfeared and investors welcomed evidence of ongoing sales improvement, with organic growth delivered in four out of Diageo’s five big markets.

In addition, the Ketel One-to-Captain Morgan maker upped its cost-savings target by $125 million.

Organic sales increased 1.7% in full year 2025, beating the 1.4% analysts were looking for and driven by pricing and volume growth, while Diageo’s free cash flow increased by $0.1 billion to $2.7 billion.

By region, the beverage alcohol behemoth delivered organic growth across North America, Europe, Latin America and Caribbean, and Africa, but Asia Pacific continued to drag on performance with sales down 3.2%.

Turning to individual brands, Don Julio delivered double-digit growth in all regions, while Guinness delivered double-digit growth, iconic whisky brand Johnnie Walker continued to win market share, and Diageo’s non-alcoholic portfolio generated palatepleasing organic sales growth of over 40%.

Led by interim CEO Nik Jhangiani, Diageo increased its cost-savings programme target increased from roughly $500 million to about $625 million over the next three years.

For the new financial year, Diageo expects flat organic sales growth with a more pronounced second-half weighting, while organic operating profit growth to be mid-single-digit ‘including the

Source: LSEG

impact of tariffs as at this time’.

‘While we are encouraged by areas of progress and the standout performance from Don Julio, Guinness and Crown Royal Blackberry, there is clearly much more to do across our broader portfolio and brands,’ conceded Jhangiani.

‘We recognise the need to drive meaningful growth opportunities in an evolving TBA (total beverage alcohol) landscape, and we are sharpening our strategy to accelerate growth.’

AJ Bell investment director Russ Mould says: ‘Guinness remains very successful, and significantly the alcohol-free Guinness Zero has been an important component of that. This may quieten previous suggestions this part of the business might be sold so the company can focus exclusively on spirits.

‘Sales of some brands may be on the agenda for any incoming new boss given a need to get the balance sheet in better shape - although the company will not want to lose any of its crown jewels.’ [JC]

DISCLAIMER: AJ Bell owns Shares magazine. The author (James Crux) and editor (Tom Sieber) of this article own shares in AJ Bell.

Design software firm, once eyed by Adobe, soars 250% on opening day

Wall Street IPO (initial public offering) fever blazed new heights as design software company Figma (FIG:NYSE) hit public markets at a sprint, its shares soaring 250% on opening day (31 July).

The IPO was priced at $33 per share but the stock quickly raced as high as $125, giving the company a $60 billion market cap, outstripping the valuations of other venture capital-backed tech IPOs like CoreWeave (CRWV:NASDAQ) and Circle Internet (CRCL:NYSE) this year.

The excitement is not without foundation. In its filings to go public, Figma disclosed a client base that includes 78% of the Forbes 2000, a list of 2,000 of the biggest publicly

traded companies in the world. Figma’s revenue grew 48% last year.

Figma’s IPO lit up the New York Stock Exchange in both optics and economics. Less than three years ago, Adobe (ABDE:NASDAQ) agreed a $20 billion deal to buy the company, only for the deal to get pulled in 2023 after monopolies regulators raised concerns.

The New York listing also created a lot of money for early VC backers and its bankers. Greylock Partners, Kleiner Perkins, Index Ventures and Sequoia all saw substantial fund returns,

Full year revenue and profit seen materially below consensus

Shares in Scottish free-to-air broadcaster STV (STVG) took a turn for the worse, plummeting 33% in a week to multi-year lows after the firm lowered its outlook on 28 July.

The company warned full-year revenue and adjusted operating

profit would be ‘materially below consensus’ due to continued deterioration in the commissioning and advertising markets.

Group revenue for the full year is now seen in a range of £165 million to £180 million, at an adjusted operating margin of 7%, with £10 million of the group revenue range driven by updated STV Studios guidance.

The firm also forecast third-quarter TAR (total advertising revenue) would be down 8% with July down 20% while August and September taken together would be broadly flat.

However, it wasn’t all doom and gloom for the Scottish free-to-air broadcaster, according to analysts at Shore Capital, who said the firm is

Source: LSEG

some exceeding 17-times, according to reports.

But not everyone was cheering. Investor Bill Gurley, a partner at VC firm Benchmark, argued that the bankers drastically underpriced the deal, enabling insiders to reap disproportionate gains while retail investors bought in after the jump. Time will tell if Figma can successfully grow into its rapidly expanded valuation. [SF]

Source: LSEG

making strategic progress towards its 2030 targets, including the creation of a single audience division and a radio offering.

There are also forthcoming releases of Amadeus for Sky and the third series of Blue Lights for BBC One from the group’s production arm. [SG]

14 August: Rank Group

11 August: Diversified Energy Company, Marshalls

12 August: Derwent London, Entain, Genuit Group, PageGroup, Spirax Sarco, Xaar

13 August: Balfour Beatty, Beazley, Evoke, Hill and Smith, Persimmon

14 August: Antofagasta, Savills

Update will be the last under the leadership of current CEO Leo Quinn

International infrastructure group Balfour Beatty (BBY) is riding high on positive momentum in its key markets, with its shares trading at all-time highs.

Which makes next week’s interim results (1 August) all the more important for investors, and for analysts who have consistently underestimated the firm’s intrinsic growth and ability to continue winning new contracts.

12 August: Bellway

In its AGM (annual general meeting) statement in May, the firm revealed its UK rail business had won £450 million of new work under the latest government spending plan; its US construction business had been awarded a $385 million deal to build a hotel complex and convention centre in Miami Beach; and its US civils business had been awarded an $889 million contract by the Texas Department of Transport to widen a section of Interstate 30.

At the end of June, the company went one better with news it had won an £833 million ($1.1 billion) contract from European energy group Technip to act as the construction partner for the Net Zero Teesside Power project, the world’s first gas-fired power station with CCS (carbon capture and storage).

The full value of the Teesside contract went into Balfour’s order book before the half-year stage, which should be reflected in the interim results.

This will be the last set of results presided over by chief executive Leo Quinn after more than a decade in the role, during which time the business has been transformed into a profitable global business with strong free cash flow generation and an impressive record of shareholder returns.

Philip Hoare, a 30-year veteran of engineering and project management firm AtkinsRealis, and currently that firm’s chief operating officer, is set to take over the reins in September, and investors will be looking to him to drive the business forward. [IC]

Analyst see tailwinds across AI infrastructure, enterprise and sovereign spending

If it talks like tech, and walks like tech, it probably interacts with Cisco Systems (CSCO:NASDAQ), and it is this bellwether status that will have investors clued into upcoming fiscal fourth-quarter earnings.

The $270 billion California-based company is set to release results on 13 August 2025 amid a quietly growing wall of optimism. Deutsche Bank has recently been noting ‘improved visibility towards durable mid-single digit growth in upcoming years’, pointing to tailwinds across AI infrastructure, enterprise deployments, and sovereign spending.

Cisco develops, manufactures, and sells networking hardware, software, telecommunications equipment, and other high-technology services and products, helping to underpin global technology infrastructure.

Drawing close attention to projections of a strengthening earnings outlook over the coming months, Deutsche Bank is now forecasting a high single-digit (7% to 8%) EPS CAGR (earnings per share compound annual growth rate), underpinned by an increasingly attractive revenue mix.

According to Deutsche Bank, around 56% of Cisco’s annual revenue now comes from subscription software and services, good for visibility and cash flows. The shift is expected to support stable margins and allow for continued reinvestment.

According to Koyfin consensus

UPDATES OVER THE NEXT 7 DAYS

QUARTERLY RESULTS

12 August: Cardinal Health

13 August: Cisco Systems

14 August: Applied Materials, Deere & Company, Ross Stores, Tapestry

data, the market anticipates Cisco reporting $0.98 EPS on $14.63 billion revenue, implying roughly 13% and 7% yearon-year growth respectively. Cisco’s has surpassed Wall Street estimates the last eleven quarters. Full year 2025 revenue and EPS are forecast at $56.62 and $3.79, with fiscal 2026 growth seen in the mid-single digits. [SF]

This tried-and-tested Asia trust can continue to outperform for another 30 years

Market cap: £343 million

Investors seeking exposure to smaller Asian companies operating in the world’s fastestgrowing economies and with the potential to become much bigger businesses should buy The Scottish Oriental Smaller Companies Trust (SST).

This total return trust trades at an attractive 11.9% discount to NAV (net asset value) and its stock is now more affordable and liquid following a February’s 5-for-1 share split.

Managed by Singapore-based Sree Agarwal, Scottish Oriental celebrated its 30th anniversary this year, making it one of the longest-running trusts investing in small caps in both developed and emerging Asian markets.

Since its 1995 launch, the fund has delivered a cumulative NAV total return of 2,227.3%, trouncing the 475.7% generated by the MSCI AC Asia ex Japan Small Cap Index, or an annualised total return of 11% against 5% for the benchmark.

Shares believes Scottish Oriental can continue to deliver benchmark-beating performance over the long haul by backing some of Asia’s highest-quality, sustainably growing smaller corporate fry, and all for a reasonable ongoing charge of 0.95%.

This five-star Morningstar-rated trust achieves longterm capital growth by investing in high-quality Asian small caps, defined as having market tags south of US$5 billion at the time of investment.

Singapore-based lead manager Agarwal wears out the shoe leather looking for opportunities in

The Scottish Oriental Smaller Companies Trust

Source: LSEG

China and India, as well as across countries including Indonesia, Malaysia, Pakistan, Philippines, Singapore, Sri Lanka, Taiwan, Thailand and Vietnam, not to mention Australasia and Japan.

Agarwal and his team begin their process by excluding companies which are not run well enough for the trust to invest in.

As minority shareholders, they have to feel aligned with the owners and managers in any company the trust invests in, therefore they rigorously research how various stakeholders including communities, the taxman, employees and so on have been treated by management over time.

‘Only when we conclude a business is investible do we think about the quality of the franchise, the growth, the valuation and so on,’ Agarwal tells Shares

Agarwal’s bottom-up stock picking approach is founded on fundamental research, an on-the-ground presence, strong relationships with management and avoiding the latest investment fads.

‘We like to invest with management teams who are ambitious but at the same time conservative,

particularly about their balance sheets. We avoid leveraged companies and stay away from what is currently the flavour of the season,’ he explains.

Scottish Oriental is also ‘completely benchmark agnostic,’ according to Agarwal. To illustrate the point, he cites Korea, which represents 15% of the benchmark but is not currently represented in the portfolio, an absence which has hurt the trust’s relative performance of late.

‘Historically, from a governance quality perspective, we haven’t been able to find good quality companies in Korea, although that may be changing,’ he teases.

The trust’s focus is on delivering a strong total return to shareholders by investing in smaller companies with potential to become bigger companies in the future.

It is also worth noting the vast majority of Scottish Oriental’s holdings are domestically-focused businesses which tend to be minimally impacted by global trade issues.

‘We are happy to own businesses with lower dividend yields,’ stresses Agarwal, ‘but we want companies which have consistent dividends and whose businesses are predictable and consistent,’ qualities he normally finds in consumer companies.

One example is top 10 holding Uni-President China (0220:HKG), the drinks-to-instant-noodlemaker trading on 15 times earnings with a 5%plus dividend yield which is expanding its Chinese distribution, launching new, higher-margin products and reducing spending on promotions, meaning its profitability should continue to improve.

Among the portfolio’s strongest performers over the past year has been Netease Cloud Music (9899:HKG), China’s answer to music streaming star turn Spotify (SPOT:NYSE).

Another top 10 holding is Philippine Seven (PSVNF:OTCMKTS), the exclusive franchise operator of 7-Eleven convenience stores in the Asian nation with 4,200 sites and counting.

Scottish Oriental recently added a new holding in India in the form of family-owned business KEI Industries (KEI:NSE).

The firm is one of the largest wire and cable manufacturers in India and is benefiting from the country’s shift from thermal electricity to renewable generation.

‘KEI has built a strong track record in India over the last 20 years, is one of the market leaders in India and it also has a net cash balance sheet,’ notes the manager. [JC]

The company is software-driven and has long been an AI user

Market cap: €30.7 billion

Continuing our search for high-quality, undervalued European growth companies, we believe Netherlandsbased provider of business information, software and digital services Wolters Kluwer (WKL:AMS) looks an attractive bet.

As computing power and AI (artificial intelligence) applications grow, companies are realising data is no longer just a by-product of their day-to-day business but a valuable asset which can be used for decision-making and gaining a competitive advantage.

As the volume of data grows, new technologies are enabling companies to find new ways of extracting value, and Wolters Kluwer is a gold mine of high-quality data across the health, tax and accounting, financial and corporate compliance, legal and regulatory and ESG sectors.

Almost all its services are provided digitally, with software accounting for 45% of 2024 revenue, 92% of which was recurring, while digital information services accounted for 40% of revenue, with the balance made up by services (10%) and print (5%).

Over a quarter (27%) of last year’s revenue came from the health industry, where the company provides clinical decision support, drug information, patient engagement tools, medical research and nursing education to healthcare professionals, hospitals and medical institutions.

Source: LSEG

As analysts at Panmure Liberum point out, as Wolters has transformed from delivering services via print to digital over the past decade its operating margin has risen sharply to 27% which is better than many tech and media businesses and well ahead of the broader market.

‘These margins stick to the bottom line, with the company reporting above-market tech and media profit margins over the last decade,’ point out the analysts.

Another plus point for Wolters is that EPS (earnings per share) volatility is a lot lower than the media sector, with its business model largely unaffected by the technology and business cycle, add the analysts.

The firm has also been using AI tools in its software solutions for more than 15 years and is now moving into ‘agentic’ AI in an agreement with Microsoft (MSFT:NASDAQ)

A similar amount (26%) of revenue came from tax and accounting software which enables firms to increase productivity and deal with changing regulations.

The firm’s strong cash generation means it has been able to ramp up investment to improve margins and drive organic growth.

We believe Wolters offers tech-like upside, with a high degree of recurring revenue and earnings – as shown by its forecast-beating first-half results and upgraded full-year guidance – but at a big discount. The shares trade on 23 times 2026 forecast earnings compared with 27 times for UK-listed peer RELX (RELX). [IC]

Strong cash generation allowed the company to announce a £6 million share buyback in the first half

53.4p

Gain to date: 66.9%

It has been 15-months since we first flagged AIM-listed games distributer Gaming Realms (GMR:AIM) as an underappreciated growth story. Pleasingly the market appears to be catching up with the story, with the shares gaining around two-thirds in just over a year.

WHAT HAS HAPPENED SINCE WE SAID TO BUY?

In a pre-close trading update the board said it anticipates reporting 18% year-on-year revenue growth and a 30% increase in adjusted EBITDA (earnings before interest, tax, depreciation, and amortisation) to £7.5 million for the six months to June.

This reflects continued growth in the group’s licensing business and ongoing international expansion.

The company successfully launched six new Slingo (mash-up of slots and bingo) games and added 19 new distribution partners. The group said its strong pipeline of content and operator integrations continued to support its scalable, high margin business model.

With first-half trading in line with expectations, the board believes the company can continue along this trajectory for the remainder of the

Source: LSEG

financial year to 31 December.

As a reminder, the engine of the group’s growth is its ability to launch new Slingo games, increase the penetration of games across existing operators and territories and sign-up new operators.

As the company scales, the large fixed costs of the business mean profit and cash flow margins grow faster than revenues, leading to increasing shareholder value.

SHOULD INVESTORS DO NOW?

The seasoned management team continues to execute on a clear growth strategy. The business appears well on track to generate circa £30 million of free cash flow between 2023 to 2026, suggesting scope for enhanced shareholder returns.

Investors should stick with this niche growth story for the long run. [MG]

By Steven Frazer News Editor

UKinflation is creeping back up again. As measured by the consumer price index, or CPI, the rise in the cost of living was 3.6% in June 2025, up from 3.4% in May, and rising at its fastest rate since January 2024. Prices are almost 28% higher than they were five years ago, according to ONS (Office of National Statistics) data.

Over the past five years, CPI growth has averaged about 4% per year, based on our own simple calculations.

This may not seem like a big deal when compared to double-digit hikes of recent years. Between September 2022 and March 2023, the UK experienced seven months of double-digit inflation, peaking at 11.1% in October 2022, sparking a nationwide costof-living crisis for millions as the economy

Table: Shares magazine • Source: AIC, QuotedData

reopened after the pandemic shutdown. Even so, 3.6% is still way above the Bank of England’s 2% target and towards the top end of ranges Brits have become used to over the past 30odd years.

This creates a unique set of challenges for investors. Rising inflation means most things cost more, and the knock-on effect of that is your savings and investments won’t buy as much in the

future unless the returns you get from them keeps pace with, or outstrips, higher inflation.

That could be the interest rate on your savings, or capital performance and dividend increases from investment trusts in your portfolio.

In short, investors have to net a total return (capital gains plus any income) of at least 3.6% to avoid the real value of their portfolio from eroding.

For those investors reliant on income from their

portfolio, faster inflation growth can put a big dent in your real wealth, income and buying power in the future.

One way to offset higher inflation is to look for investment trusts where dividend growth has outstripped inflation in recent years.

The table shows investment companies with an income objective which have grown their dividends faster than the CPI over the past five years.

An additional check is to look for trusts offering forward income yields above the five-year inflation average.

The caveat with forward yields is they are based on forecasts, and expectations do get missed sometimes, although trusts have the unique ability to maintain income levels in lean years by raising their capital reserves, a route many took to great effect during the worst-hit Covid years.

Shares has picked through the data and come up with three trust options we believe offer investors potential inflation-busting income returns in the years ahead.

If all goes to plan, these trusts should provide the reliability investors seek regardless of short-term spells of increased inflation to deliver real-terms income growth.

JPMORGAN CLAVERHOUSE

TRUST (JCH) 787p

Market cap: £435 million

Discount to NAV: -5.8%

Investors looking to inflation-proof portfolios should look no further than JPMorgan Claverhouse (JCH), the UK Equity Income stalwart trading at a near-6% discount to NAV (net asset value) and offering a plump 4.5% dividend yield.

The £435 million-cap trust boasts a 52-year track

record of uninterrupted dividend growth and has upped the shareholder reward by an annualised 5.9% over the past decade.

While the bulk of the portfolio is in the FTSE 100, through the likes of Shell (SHEL), HSBC (HSBA), AstraZeneca (AZN) and Unilever (ULVR), this quality-infused fund’s managers have increased the focus on sustainable dividend growers across the market cap spectrum which should underpin steadily rising payouts over time.

JPMorgan Claverhouse backs high-quality, resilient companies which can invest capital at high returns to drive strong and sustainable earnings growth.

Relatively new portfolio additions include consulting and administration play XPS Pensions (XPS) and promotional merchandise supplier 4imprint (FOUR), while a holding in FTSE 250 construction group Morgan Sindall (MGNS) has helped recent returns.

The trust’s board seeks to increase the total dividend each year at or close to the rate of inflation. For calendar year 2024, dividends totalled 35.4p, up 2.6% year-on-year, slightly higher than prevailing inflation and supported by the trust’s revenue reserves. [JC]

Market cap: £370 million

Discount to NAV: -19.6%

REITs, or real estate investment trusts, have long been popular with investors seeking a regular source of income as they distribute most of their earnings in dividends and payouts are usually quarterly, which helps with financial planning.

Diversified commercial real estate trust

Custodian Property Income REIT (CREI) has a strong focus on income, as its name suggests, and invests in smaller lot-sized properties leased to high-quality institutional and household-name tenants.

For the year to the end of March 2025, rents grew 2.3% on a like-for-like basis, but those which came up for review were renewed with a 29% uplift, which demonstrates the potential for further increases in income and dividends.

In addition, the manager has sold non-core assets at a substantial premium to their net asset value highlighting the potential for re-rating of its portfolio.

One thing to be aware of is the feast and famine nature of dividend growth, where asset realisations, or lack of them, can lead to bumper income growth some years, and limited increases in others. [IC]

Market cap: £433 million

Discount to NAV: -21%

The NextEnergy Solar Fund (NESF) is the flagship product of NextEnergy Capital, one of the world’s

largest specialist solar investors, managing $3.9 billion worldwide.

The FTSE 250 constituent was listed on the London stock exchange in 2014 making it one of the oldest listed renewable companies in the UK.

The fund provides an attractive dividend yield for income seekers (currently 11%) and offers a natural hedge against inflation with roughly half its revenues backed by inflation-linked government subsidies.

NextEnergy has demonstrated a strong track record of dividend growth annualising at 4.2% per year over the last five and 4.8% per year over the last decade.

Sustainability of the dividend is important for income investors, and it is therefore comforting that NextEnergy has met its target dividend for 11 straight years.

On 16 June it declared a target dividend for the year to the end of March 2026 of 8.43p per share, up 1% and forecast to be covered within a range of 1.1 times to 1.3-times by earnings per share.

The business is highly diversified with 101 operating assets which generated 830GWh (gigawatt hours) of total electricity generation in the year to March 2025, enough to power around 265,000 homes.

The company is currently advancing a pipeline of UK solar, international solar, battery storage and co-investment opportunities to complement the portfolio and further diversify. [MG]

Disclaimer: The editor (Ian Conway) owns shares in NextEnergy Solar Fund.

How Temple Bar became the best five-year UK Equity Income performer, and why Nick Train is more excited than ever about Finsbury Growth & Income’s prospects

Close scrutiny of the AIC’s (Association of Investment Companies) UK Equity

Income sector shows two trusts with strong retail followings occupying top and bottom spots in the five-year share price total return performance table, namely Temple Bar (TMPL) and Finsbury Growth & Income (FGT).

In what represents a reversal of fortunes for two popular portfolios, the value-oriented former has returned almost 180% at the time of writing whereas the latter, managed by Nick Train with a quality-growth philosophy and ‘buy-and-hold’ approach, has delivered a comparatively dull 25%.

In NAV (net asset value) total return terms, Temple Bar is up 145.9% and 110% over five and 10 years respectively, ahead of the sector’s 78.9% and 101.2%, whereas Finsbury Growth & Income has lagged the sector over five years with a 35% return, though it is ahead of the sector over 10 years with a 113.2% haul.

HEADWINDS & TAILWINDS

Sector bedfellows they may be, but each trust pursues a distinct style in its quest to deliver their

shareholders market-beating total returns (capital growth plus dividends).

Veteran money manager Train has steered Finsbury Growth & Income for a quarter of a century with a successful strategy of long-term investment in high-quality companies with durable and cash generative franchises.

More recent periods have been frustrating for shareholders in the charismatic stockpicker’s low

Source: LSEG

turnover portfolio, which aims to beat the FTSE All Share’s total return, with a high interest rate environment and rotation into value and cyclical UK stocks generating headwinds to his approach, and leaving the shares languishing on a near-8% NAV discount.

As such, there is pressure on Train to turn Finsbury Growth & Income’s performance round, and the board has proactively penciled in a continuation vote for early 2026.

Meanwhile, Redwheel’s Ian Lance and Nick Purves have done a terrific job in reviving Temple

Bar’s fortunes since being appointed to run the fund in late 2020, and the shares trade on a modest 0.6% NAV premium as a result.

Value specialist Temple Bar aims to provide growth in income and capital to achieve a longterm total return greater than its FTSE All-Share benchmark, and the investment focus is primarily on UK shares, mainly selected from the FTSE 350.

Temple Bar has delivered outperformance by sticking to the managers’ philosophy rooted in value investing. Lance and Purves scour the UK market for unloved companies with a credible path

Source: The AIC/Morningstar, data correct as of 24 July 2025

Temple Bar

Source: Company factsheets

to recovery, rather than buying beaten-up stocks in structural decline or lacking turnaround potential.

To avoid ‘value traps’, they aim to identify good quality companies which are undervalued and place great emphasis on strong cash flows and robust balance sheets. This gives them confidence a company can survive through a prolonged spell of lower profitability, either due to company specific issues or an economic downturn.

Finsbury Growth & Income is the more concentrated of the two by some stretch. As of 30 June, its top 10 holdings accounted for the thick end of 90% of the portfolio, compared with a top 10 representing 43.7% of the total at Temple Bar.

Train’s trust had 21 high-conviction holdings, an active share of 84.9% and an ongoing charge ratio of 0.6%, whereas quarterly dividend-payer Temple Bar was more diversified across 36 holdings, and ongoing charges were similar at 0.61%.

Both portfolios have allocations to the Consumer and Financial sectors, although Temple Bar has

Source: The AIC, data correct as of 24 July 2025

benefited from exposure to more ‘old economy’ value sectors, such as Energy and Materials, whereas Finsbury Growth & Income has greater exposure to Consumer Staples, Industrials and Technology.

Temple Bar has also adopted a new dividend policy which reflects the increasingly important role of share buybacks in returns. Future dividends will be enhanced to reflect a portion of the buybacks of those companies held by the trust.

THE MANAGERS HAVE THEIR SAY

Ian Lance tells Shares: ‘In the nearly five years since we took over the management of Temple Bar the shares have produced a total return of 187% versus 83% for the UK market (Source: Bloomberg, 30 October 2020 to 22 July 2025). Four stocks – NatWest (NWG), Marks and Spencer (MKS), Centrica (CNA) and Standard Chartered (STAN) – are responsible for half of that outperformance with positive contributions also coming from BP (BP.), Shell (SHEL) and Barclays (BARC).’

Stock Sector Weight

Source: The AIC, data correct as of 24 July 2025

Lance says the common theme among all these stocks is the incredibly low starting valuation which existed in the summer of 2020 when he and Purves were transitioning the portfolio.

‘It is easy to forget that we were in the middle of the first lockdown, and such was the level of fear among investors some shares were driven to irrationally low levels,’ recalls Lance.

‘This was best exemplified by the fact NatWest traded at the same price in 2020 that it reached in 2008 when the UK government had to bail it out even though it was a substantially stronger and higher-quality business. The share price has increased by 400% from that 2020 low to today.’

He continues: ‘Fears the economy would never recover meant the oil price briefly went negative which drove down the share prices of energy stocks to levels which implied profits would never recover. The moral of the story is that sticking with a disciplined valuation-driven investment process can produce the greatest reward during a period when fear and uncertainty lead to completely irrational valuations and throw up the greatest opportunities.’

Nick Train tells Shares: I have been responsible for Finsbury Growth & Income Trust’s investment affairs for 25 years and I am still proud of the longterm track record.

‘However, the last few years have disappointed. In truth, the last five years were always going to be an uphill struggle for an investment approach which tends to avoid Energy, Banks and Defence, which have all performed well. That only tells part of the story though. In hindsight, the portfolio has had insufficient exposure to companies whose services are becoming more relevant as we get deeper into the 21st century. Specifically, not

Source: Company factsheets

enough in “Digital Winners”: Data, Software and Technology Platform companies. It has been our work over the last three years to rectify that, and today our exposure to Digital Winners stands at over 60%.’

Train continues: ‘Now, perhaps more than ever, I am excited about the prospects for Finsbury Growth & Income’s portfolio, comprised of companies with multi-decade growth opportunities at more than reasonable valuations in my view.’

Train, who has raised his personal stake in the trust this year, is not surprised that claim is sometimes met with scepticism, ‘particularly when I tell you these companies with multi-decade growth opportunities are all UK-listed. There is an erroneous assumption the UK stock market is bereft of growth companies, particularly digital

growth companies. Not so. The UK stock market houses several substantive, world-class digital businesses and Finsbury Growth & Income’s portfolio is built around them. We expect the growth rates of of the trust’s major holdings to accelerate in coming years, as technology helps them create new services for customers and new wealth for shareholders. The best investments are often a surprise, and we believe investors will be surprised at the growth opportunities to be found in the UK, and the market and Finsbury Growth & Income will perform better as that realisation sinks in.’

While Finsbury Growth & Income lagged the index over the second quarter of this year, there were standout performers including property portal Rightmove and a trio of British brands or franchises, luxury fashion house Burberry (BRBY), premium mixer drinks firm Fevertree (FEVR:AIM) and football giant Manchester United (MANU:NYSE), a trio with global recognition and globally-derived revenues.

Train recently initiated a new holding in another company which controls formidable data sets, namely automotive online marketplace Autotrader (AUTO). ‘Frankly we should have been invested in this company years ago, because we have long

understood the attractions of companies with dominant positions in classified advertising and it is truly impressive that Autotrader attracts an audience 10 times the size of its nearest rivals,’ explains Train in Finsbury Growth & Income’s latest factsheet.

‘However, better late than never, and some investor quibbles with the current state of the used-car market and the cadence of Autotrader’s introduction of its latest suite of car-retailer services have arguably crimped the rating of the shares and presented an opportunity to initiate, which we have taken.’

As for Temple Bar, it outperformed the FTSE All-Share Index in June, with Capita (CPI) rising strongly after the outsourcer reiterated fullyear guidance and two new holdings made positive contributions, namely Hana Financial (086790:KRX) and Woori Financial (316140:KRX). Purves and Lance view these two Korean lenders as ‘well-run, shareholder-focused and well-capitalised banks which are attractively valued’ and point out both have benefited from government initiatives designed to improve corporate valuations.

But it wasn’t all plain sailing for Temple Bar, which saw a disappointing showing from advertising giant WPP (WPP) following a report Meta (META:NASDAQ) was planning to enable brands to fully create and target ads using AI by the end of next year, heightening concerns the technology will take business from WPP.

GSK (GSK) fell on concerns following a headline the US Secretary of Health was weighing a review of vaccines containing aluminium, an ingredient in some of its vaccines, while Pearson (PSON) weakened after competitor IDP Education (IEL:ASX) warned the international student market continues to be hit by global policy uncertainty.

‘UK equities continue to be valued at a significant discount to global equities generally,’ observe the Redwheel duo in the latest Temple Bar factsheet. ‘Accordingly, we believe notwithstanding the shorter-term uncertainties, UK equities are priced to offer relatively attractive returns into the future.’

By James Crux Funds and Investment Trusts Editor

Shorting can improve market efficiency by providing liquidity and exposing overvalued companies

The FTSE 100 has climbed almost 20% in a straight-line since the dark days of ‘Liberation Day’ in early April to make new all-time highs of 9,175. The relentless rally has also seen more shares notch up highs in the wake of positive sentiment.

This type of market backdrop is often a fertile hunting ground for short sellers, that is, institutions looking to make money from a subsequent fall in share prices.

This article looks at recent activity of short sellers to identify which stocks and sectors institutional investors have targeted, and where those bets have increased the most since early April.

Professional investors have the option to make money from falling share prices in addition to rising ones. These investors follow so-called long/short strategies.

They do this by borrowing stock from a prime broker which they then sell with the intention of making a profit when the shares fall in value. This is risky business compared to buying shares because it exposes the seller to potentially unlimited losses should the shares go up instead of down.

There is also a cost of borrowing stock which needs to be factored in, as well as the prospect of margin calls, where the seller must post collateral to cover short-term losses.

For these reasons short selling is not suitable for most retail investors. However, investors can benefit from the activity by buying long/short hedge funds. Generally, investors need to qualify as sophisticated depending on the fund structure.

One example is Argonaut Absolute Return Fund (B79NKW0), managed by Barry Norris who has notched up 10.6% and 10.3% annualised returns over the

last three and five years.

Norris seeks to generate superior risk-adjusted returns by investing in a concentrated, deeply researched portfolio of equities. The fund typically owns between 30 and 50 long positions and 20 to 50 short positions.

Investors can also access a selection of traditional funds which run short books as part of their wider mandate.

The Financial Times recently reported that long/ short funds saw their first inflows from investors in over a decade following strong returns in the first half of 2025 raking in $10 billion of fresh money.

There is a misconception short sellers are ‘evil’ and spread lies to pull down a share price, so they financially benefit”

There is a misconception short sellers are ‘evil’ and spread lies to pull down a share price, so they financially benefit. While there are examples of short sellers who do operate in such a way they are largely the exception rather than the rule. Many short sellers do in-depth research into a company, and they take a short position if they think the valuation looks excessive and could revert to the mean, they spot something worrying in the accounts, or they think the business is challenged and could struggle, among other factors.

UK REIT (real estate investment trust) Primary Health Properties (PHP) has seen one of the biggest increases in shorting activity in recent months.

The investment trust has been battling US private equity group KKR (KKR:NYSE) to buy

BlackRock Throgmorton (THRG) aims to provide investors with capital growth and an attractive total return by investing primarily in UK small- and midcap companies.

Unusually for the sector, Throgmorton’s portfolio may include an allocation to short as well as long positions. Manager Dan Whitestone recently celebrated 10 years at the trust, as well as his ninth year of outperformance.

Over the 12-months to November 2024, THRG reported an NAV (net asset value) total return of 16.3%, besting its benchmark by 2.2%.

medical centre property owner Assura (AGR)

The target’s board recommended PHP’s cash and shares bid in June, but the subsequent decline in PHP’s shares is telling.

PHP has offered 0.3865 new shares and 12.5p per share in cash, together with a 0.84p special dividend. Shares in PHP are currently trading at 95.40p, meaning the equity component of the offer is worth 36.87p.

Add in the other bits and that values Assura at 50.21p per share. KKR’s best and final offer is 50.42p in cash, meaning Assura shareholders would be better off with the private equity group. Acceptance levels for the PHP bid have been minimal to date.

Short sellers will have been watching this situation closely as Assura’s board seem to be happy to back whoever offers the most money. If PHP loses the bid, its share price could potentially fall back further and that would net the short sellers a profit. After all, Assura would have a new owner with deep pockets to accelerate growth and that could make life harder for PHP to compete.

Food-to-go brand Greggs (GRG) has also been popular with short sellers, fueled by the firm’s dismal operating performance which it blamed on

Analysts at research firm

QuotedData wrote: ‘These results not only highlight Dan’s skill in stock selection, having adapted the portfolio to accommodate for changing market dynamics, but also the significant valuation opportunity presented by the UK market.’

Chris Tennant co-manager of Fidelity Emerging Markets (FEML) says: ‘Taking out short positions allows us to profit not only from the winning businesses in each industry, but also from the losers. We make use of both pair trades, where short positions are paired against long positions, and idiosyncratic shorts.

‘We have a pair trade in the Asian auto battery market, with several short positions in indebted battery makers that are losing market share to Chinese peers such as CATL, in which we have a long position.

‘We hold several idiosyncratic shorts in the paints sector too. In one particular Asian market the paints industry used to be an oligopoly, but a few years ago a new entrant launched a paints brand with a significant capital injection into the market. This has resulted in huge oversupply just as volume growth was slowing rapidly.‘

Source: AJ Bell. FCA, Castellain Capital, data at 29 July

Source: AJ Bell. FCA, Castellain Capital, data at 29 July

the weather.

Those excuses seem to be wearing thin following a first-half report (29 July) where the baker confirmed fullyear 2025 earnings would drop below last year’s levels as the value sausage roll-to-sandwich retailer continues

to grapple with tougher trading conditions.

There is increasing debate around whether Greggs has bitten off more than it can chew and reached ‘peak sausage roll’.

Management is adamant that it can open 140 to 150 net new shops this year and continues to see an opportunity for ‘significantly more than 3,000 shops’ over the longer term.

The weather has also been a theme for the UK’s largest tenpin bowling firm Hollywood Bowl (BOWL) after management Cited a prolonged period of ‘unprecedented’ dry and warm weather in the Spring as impacting short-term trading.

Yet more sunny weather through June appears to have attracted the interest of short sellers, with the amount of shares on loan increasing from 0.6% to 1.7% at the end of July.

President Trump’s 1 August deadline for the imposition of ‘reciprocal tariffs’ on trading partners is now behind us.

The White House can point to several trade deals, notably with the UK, Japan and EU, while negotiations continue with China ahead of a deadline of 12 August.

In the four cases mentioned, America will apply tariffs on imports at a lower rate than that threatened on ‘Liberation Day’ on 2 April, and that is helping stock and bond markets and the dollar rally from the spring lows in the view Trump will not follow through on the full tariff programme and spark a global tit-for-tat trade war which no-one is likely to win.

The imposition of much higher levies on Brazil, Canada and Taiwan, to name but three, and threats of higher duties in pharmaceuticals on the 1 August deadline day is prompting something of a rethink, however, as

this brings the worst-case scenario of 2 April back into view.

As discussed in this column before investors now have to decide whether:

Trump will back down, once a deal of some kind is reached, and tariffs will be reduced from the 2 April proposals to levels which do far less damage to global trade flows.

This is a storm which will pass once Trump’s second term ends in November 2028 (even if tariffs have been an issue since his initial salvo in spring 2018).

Trump’s tendency to rule by Executive Order and bully the US Federal Reserve, in uncanny echoes of emerging markets such as Turkey, means US assets can no longer be afforded their current premium valuations, on the premise the era of American exceptionalism is over.

emerging markets (EMs) are traditionally a beneficiary of a weaker dollar”

Spring’s rally leaned on the first view – any recurrence of fears about the third option could lead to another shift in market mood.

Investors can perhaps track sentiment in three ways. The dollar, as discussed in July, where weakness would point to increased aversion to US assets, strength to renewed comfort with them.

US 10-year treasury yields, where Trump’s tax cut-and-spend plans raise fresh worries about the galloping US deficit, even if tariff income is a potential source of incremental income. Rising yields would speak of concern, especially if they keep going up as the Federal Reserve cuts interest rates, while falling ones would point to an improvement in sentiment.

Trends in overseas equities, as also discussed in

Source: LSEG Refinitiv

Source: LSEG Refinitiv data

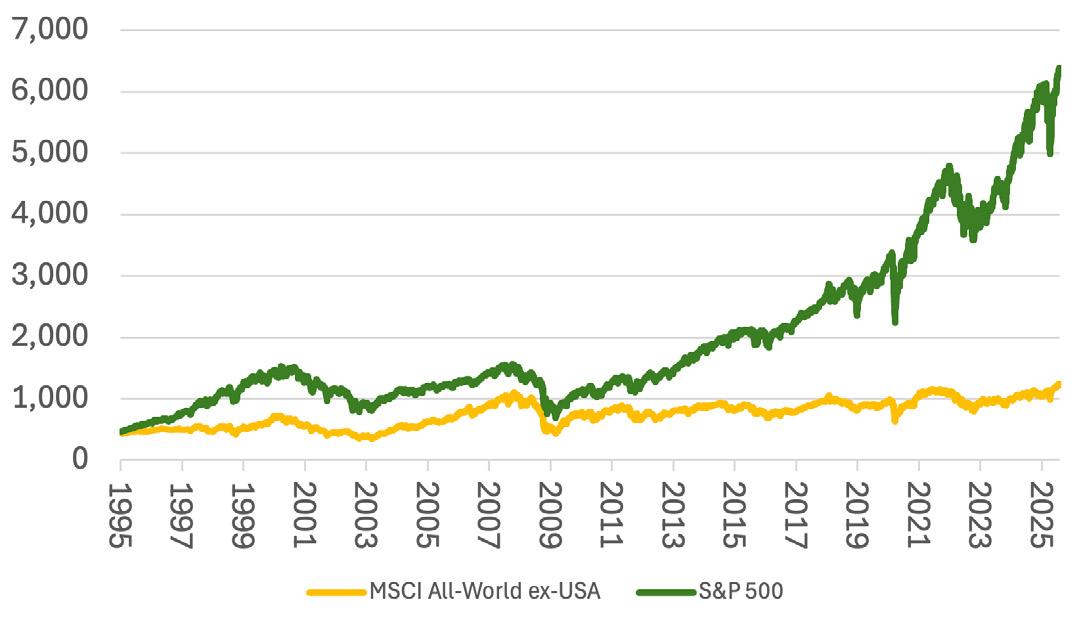

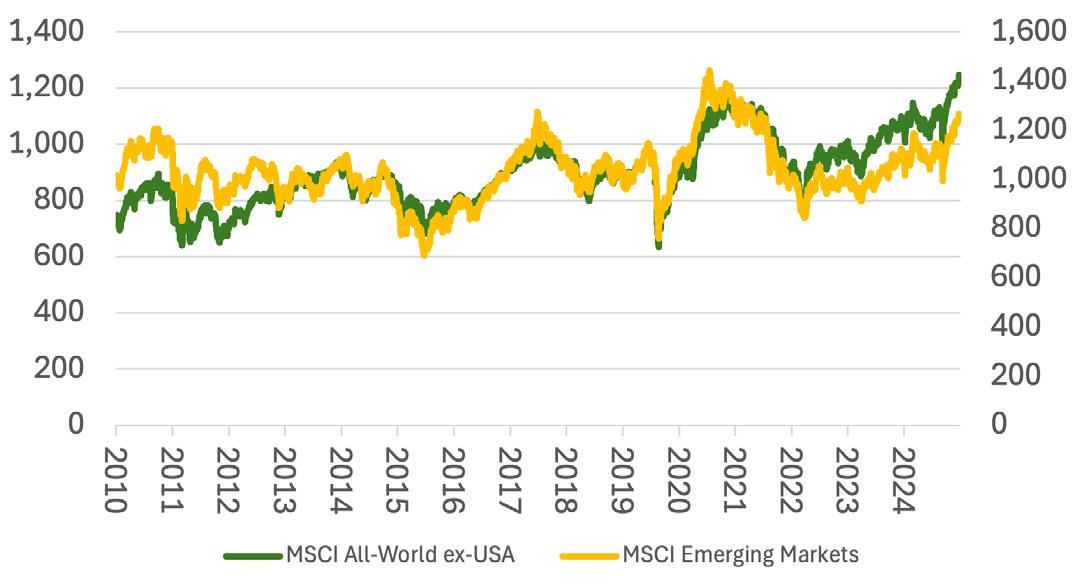

July. US equities have left the rest of the world way behind since the end of the Great Financial Crisis in 2009. However, emerging markets (EMs) are traditionally a beneficiary of a weaker dollar. EMs also learned their lesson from their own debt crisis of the late 1990s and, as a rule, carry healthier sovereign balance sheets than the US (and many other Western nations).

This third trend need not be confined to EMs, either, if investors do decide to diversify away from the dollar and US assets more widely. The MSCI Emerging Markets index is making a run at its prior all-time high of 2021 and the MSCI World ex-US benchmark just might be looking to break out and reach new peaks all of its own. If both indices continue to run, then there really may be something afoot.

Gains for those indices would not mean the US is about to collapse, just that it may be ready to underperform after a lengthy period of dominance. For the record, a classic emerging market like Turkey trades on around 11 times forward earnings for 2025, way less than the 25 times multiple applied to the S&P 500 right now, according to Standard & Poor’s research.

Granted, this is an intentionally provocative comparison, and it can be rebutted quickly on the grounds that the biggest constituents of Istanbul’s BIST-100 are arms manufacturer Aselsan (ASELS:IST), Türkiye Garanti bank (GARAN:IST), holding company Koc (KCHOL:IST), construction

firm ENKA Insaat (ENKAI:IST) and airline Türk Hava Yollari (THYAO:IST). They are all fine companies, but the highest market capitalisation among them is $21 billion and none of them can necessarily be seen as secular growth plays, especially ones with a strong whiff of artificial intelligence, for all the Turkish economy’s considerable long-term potential and the country’s strategic and geopolitical importance.

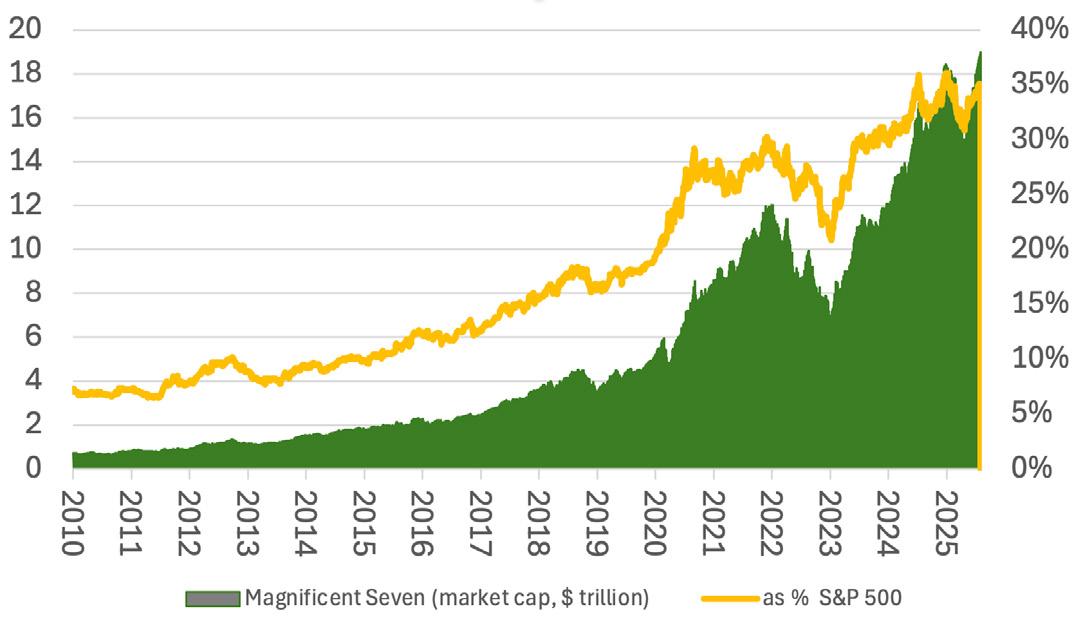

This is in marked contrast to the US equity market where NVIDIA (NVDA:NDQ), Microsoft (MSFT:NDQ), Apple (AAPL:NDQ), Amazon.com (AMZN:NDQ), Alphabet (GOOG:NDQ) and Meta Platforms (META:NDQ) are the six biggest stocks by market capitalisation. The other member of the Magnificent Seven, Tesla (TSLA:NDQ), ranks ninth. Between them they represent 35% of the S&P 500’s $54 trillion stock market valuation, a smidge below the 36% peak reached in late 2024. Again, any move away from them and rotation toward more cyclical names, for whatever reason, could

signal, and play a role in, market sentiment toward US assets more widely, even if that seems hard to believe right now given the unabashed enthusiasm for AI-related narratives.

featuring AJ Bell Editor-in-Chie and Shares’ contributor Dan Coatsworth

LATEST EPISODE

US trade deal with Japan as earnings season kicks off, pensions and IHT plans confirmed, and 24-hour trading on the LSE

Prices rises have been slower than normal in recent years

The past few years have not been a great time to be a homeowner. For those who needed to remortgage, rates soared, while at the same time property prices began to stagnate, leaving homeowners in a sticky situation, paying more for a home where the value was staying the same.

In previous decades, even when you consider the 2008 financial crisis, purchasing a home was a key way many people saved for their futures, and for the most part it worked well.

According to a report from Rathbones, between 1980 and 2016, the value of the average property rose 6.7% per year. That far outpaced inflation, which made owning a home a comfortable investment and helped people take care of their future. (Even if you should not be treating the home you live in as an investment in the traditional sense.) But since 2016, this rate has slowed to 3.7%, meaning the price of a home has barely kept pace with inflation.

Why have price increases slowed recently? It’s not as simple as a single factor but part of it is due to the low interest-rate environment seen post-2016 and into the pandemic and what followed it.

In order to stimulate business growth, the Bank of England set interest rates at extremely low

levels which translated into low mortgage rates.

Because people were able to get cheap mortgages during this period, they could afford to buy more expensive houses. At the same time, new regulations like buy-to-let mortgages came into effect making the purchase of additional properties possible. The net effect was house prices spiked because there was suddenly a flurry of people who were willing and able to buy.

Inflation soared during the pandemic as demand for everything outstripped supply. The government tried to quash rising prices by raising interest rates, but they stayed higher than expected for longer than expected which made mortgage rates cripplingly high.

Without the help of low mortgage rates, house prices quickly became beyond the reach of many prospective buyers.

At that point, the market was faced with a conundrum – house prices had risen to a level where fewer people could afford them, and without multiple buyers competing for the same property price rises slowed sharply, resulting in today’s sluggish environment.

Slowly, demand for mortgages has begun to tick up again. The Bank of England reported 64,167 mortgages were approved in June 2025, 1,500

Source: Nationwide

more than analysts had been forecasting.

There has been a loosening of some of the regulation around mortgages, which allows lenders more flexibility in who they allow to borrow. This could create an easier route for those looking to hop onto the housing ladder

Despite this increase in mortgage demand, however, the average asking price has actually decreased slightly according to research from housing portal Rightmove (RMV).

According to the firm’s July property market survey, the average cost of a home coming to market has decreased by 1.2% in the past month, to £373,709.

For those looking to use their home as an investment, the future may seem a little less rosy. Many of the initiatives being put in place at this point are aimed at making housing more affordable, and efforts to increase the volume of new builds will mean there is more supply coming onto the market.

So, while home values may come back to a range where people can start purchasing again, this may not mean prices jump again, even though demand has been restored.

In recent years, with house prices rising at nearly the same level as inflation, home ownership hasn’t

been that fruitful as an investment.

In contrast, a portfolio comprised of 25% UK equities and 75% global equities has outpaced inflation by an average of 3.4 percentage points each year according to research by Rathbones.

Property investments do come with some unique benefits, however. First, you are able to invest a large amount of money up front, and although you may be paying interest on this money (unless you are a cash buyer), if the property market does well you have a significant stake in it. By contrast, money in a portfolio is usually added bit by bit over many years.

Owning a home can also can remove the expense of rent from your budget. While this will be replaced by a mortgage, at least that works towards ownership and there is potential for your ‘equity’ to grow as an investment.

For now, though, it seems any investment growth might be quite slow. While there’s no way to be sure how markets will move in the future, for the time being the trend of rising house prices has clearly eased.

Hannah Williford AJ Bell Content Writer

There are arguments for making sure you avail yourself of it before the age of 75

My question is about taking 25% tax free cash if you have a number of pension pots and if there are any time constraints.

In my case, I took early retirement after April 2006 and 25% of my defined benefit pension fund, over £100,000 tax free. I have a SIPP with value of £160,000 and I need to decide if I can or able to take 25% tax free before I am 75 in March 2026.

David Rachel Vahey, AJ Bell Head of Public Policy, says:

The pensions tax system has undergone significant change in the last two decades.

First, on 6 April 2006, the tax regimes for occupational pensions and personal pensions were merged creating one set of pension rules.

This was called ‘A-day’, and led to the creation of the lifetime allowance which is a limit on the taxefficient amount you can take out of a pension.

When it was first introduced, it was set at £1.5 million, but after several changes it now stands at £1,073,100.

The annual allowance was also created under this new regime. This is the tax-efficient limit for the contributions someone can pay into a pension, including their own contributions, their employer’s and tax relief.

This was initially set at £215,000, and again after several changes it is now set at £60,000.

Two other (lower) annual allowances have also been introduced, one for very high earners and one for those who ‘flexibly’ access their pension, including taking drawdown.

The second regime change happened last year, when the lifetime allowance was abolished in April 2024 and replaced with two main new limits.

The lump sum allowance (LSA) measures the taxfree lump sums someone can take in their lifetime and is usually set at £268,275.

The lump sum and death benefit allowance (LSDBA) measures the tax-free lump sums someone takes over their lifetime as well as the ones their beneficiaries receive on their death, and is usually set at £1,073,100.

Changing the rules for pensions often results in complications, especially for those who access their pensions under different regimes as you have done.

The new rules calculate how much LSA you have left, taking into account what you previously took

Ask Rachel: Your retirement questions answered from your defined benefit scheme.

You need to have enough remaining LSA to make sure you can take the whole £40,000 (25% of £160,000) tax free from your SIPP, otherwise the excess will be taxed as income.

As you took your tax-free lump sum from your defined benefit pension after 6 April 2006, your remaining LSA is worked out by taking 25% of the lifetime allowance you had used at 5 April 2024 and deducting this from the lump sum allowance.

So, for example, if you had used up 30% of your lifetime allowance by 5 April 2024, then the LSA you have left will be: £268,275 – (25% of 30% of £1,073,100) = £268,275 - £80,482.50 = £187,792.50

You should have enough lump sum allowance to take your whole tax-free lump sum from your SIPP, but you may want to get in touch with a financial adviser who can let you know exactly what your position is.

It’s also worth noting that had you taken your tax-free cash before April 2006 (and not taken any other benefits since then) you would need

to work out your remaining LSA using a different calculation.

There is no time limit on when you have to take your tax-free lump sum, so you can take it after you reach age 75 if you want.

However, a word of caution – if you die after the age of 75 then your beneficiaries may have to pay income tax on the amount they inherit, regardless of whether you had a tax-free amount remaining.

For that reason, it may make sense to take your tax-free amount before you reach age 75 or the taxfree element of it could be lost.

This may be even more relevant if you think inheritance tax (IHT) will apply to your unused pension on death after April 2027.

In that case your beneficiaries may have to pay IHT at 40% and then income tax on some of the unused amount they inherit.

This could mean a combined effective tax rate of 52% if they are a basic rate taxpayer, 64% if they are a higher rate taxpayer or 67% if they are an additional rate taxpayer.

EDITOR: Tom Sieber @SharesMagTom

DEPUTY EDITOR: Ian Conway @SharesMagIan

NEWS EDITOR: Steven Frazer @SharesMagSteve

FUNDS AND INVESTMENT

TRUSTS EDITOR: James Crux @SharesMagJames

EDUCATION EDITOR: Martin Gamble @Chilligg

INVESTMENT WRITER: Sabuhi Gard @sharesmagsabuhi

CONTRIBUTORS:

Dan Coatsworth

Danni Hewson

Laith Khalaf

Russ Mould

Laura Suter

Rachel Vahey

Hannah Williford

Shares magazine is published weekly every Thursday (50 times per year) by AJ Bell Media Limited, 49 Southwark Bridge Road, London, SE1 9HH. Company Registration No: 3733852.

All Shares material is copyright. Reproduction in whole or part is not permitted without written permission from the editor.

Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments published in Shares must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. Shares, its staff and AJ Bell Media Limited do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

Members of staff of Shares may hold shares in companies mentioned in the magazine. This could create a conflict of interests. Where such a conflict exists it will be disclosed. Shares adheres to a strict code of conduct for reporters, as set out below.

1. In keeping with the existing practice, reporters who intend to write about any securities, derivatives or positions with spread betting organisations that they have an interest in should first clear their writing with the editor. If the editor agrees that the

reporter can write about the interest, it should be disclosed to readers at the end of the story. Holdings by third parties including families, trusts, selfselect pension funds, self select ISAs and PEPs and nominee accounts are included in such interests.

2. Reporters will inform the editor on any occasion that they transact shares, derivatives or spread betting positions. This will overcome situations when the interests they are considering might conflict with reports by other writers in the magazine. This notification should be confirmed by e-mail.

3. Reporters are required to hold a full personal interest register. The whereabouts of this register should be revealed to the editor.

4. A reporter should not have made a transaction of shares, derivatives or spread betting positions for 30 days before the publication of an article that mentions such interest. Reporters who have an interest in a company they have written about should not transact the shares within 30 days after the on-sale date of the magazine.