Catch the below pre-Covid level stocks which can rise to the surface

The inherent unpredictability of oil prices and European stocks in demand

07 Trump action on crypto, tariffs and Ukraine shifts markets

08 Tesla looks to AI and robotics to end stock’s three-month slump

10 Rolls-Royce shares hit yet another 52-week high

10 Severfield shares plummet after structural steel group delivers another profit warning 12 Can engineering outfit Spirax revive its fortunes?

13 Adobe may need narrative change to fire stock higher

15 Why trainers titan Nike can be a trendsetter again

18 Time to buy into the real estate recovery with seasoned investor TR Property

21 Share placing at ME International partially removes stock overhang

23 How I think about my investments in the technology space

27 COVER STORY UNDER WATER

Catch the below pre-Covid level stocks which can rise to the surface

38 BP CEO’s hoped-for return to 2010 market value is a big ask

Continuation votes are back on the agenda as investment trusts aim to appease investors

The loophole that gives your child a £36,000 tax-free allowance this year

Berkshire Hathaway readies itself for another home run 52 ASK

Can I still use a cash ISA as a way of saving for retirement?

INDEX Shares, funds, ETFs and investment trusts in this issue

Three important things in this week’s magazine

UNDER WATER

Five years on from the pandemic sell-off there are still plenty of well-known stocks trading at depressed levels

Sifting through the performance tables the Shares team has picked a handful of quality stocks which have been overlooked by the mainstream.

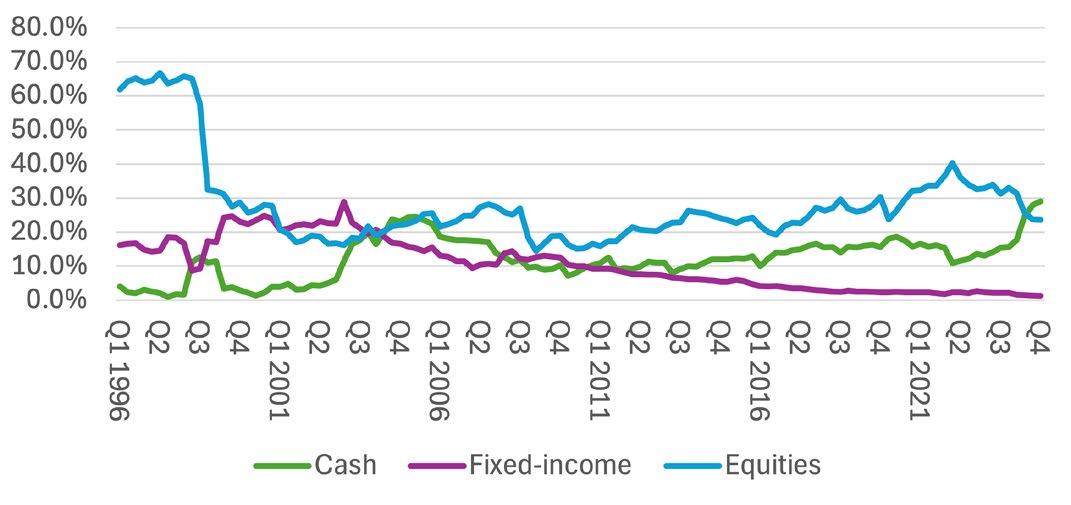

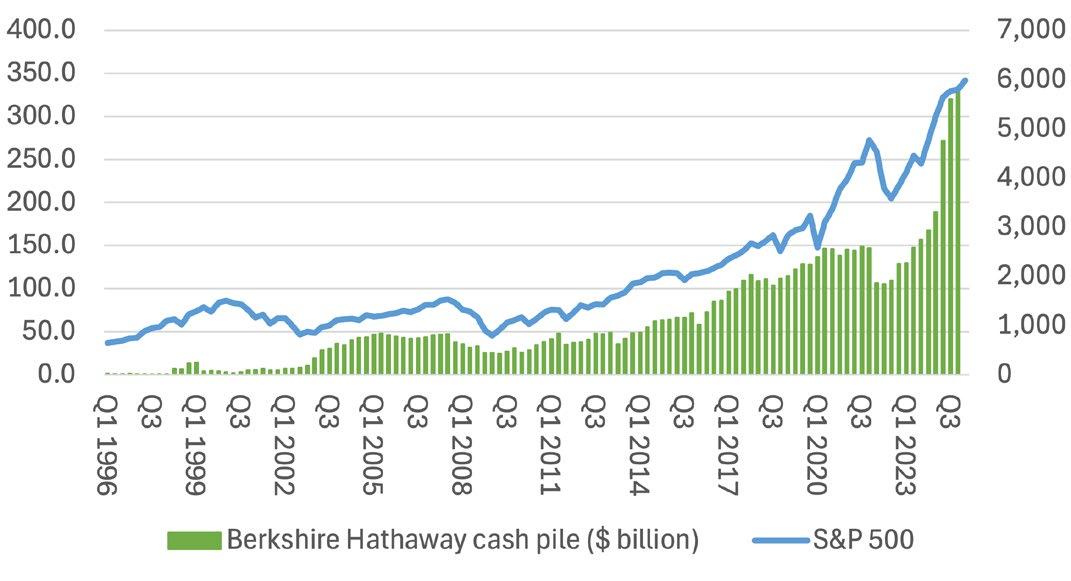

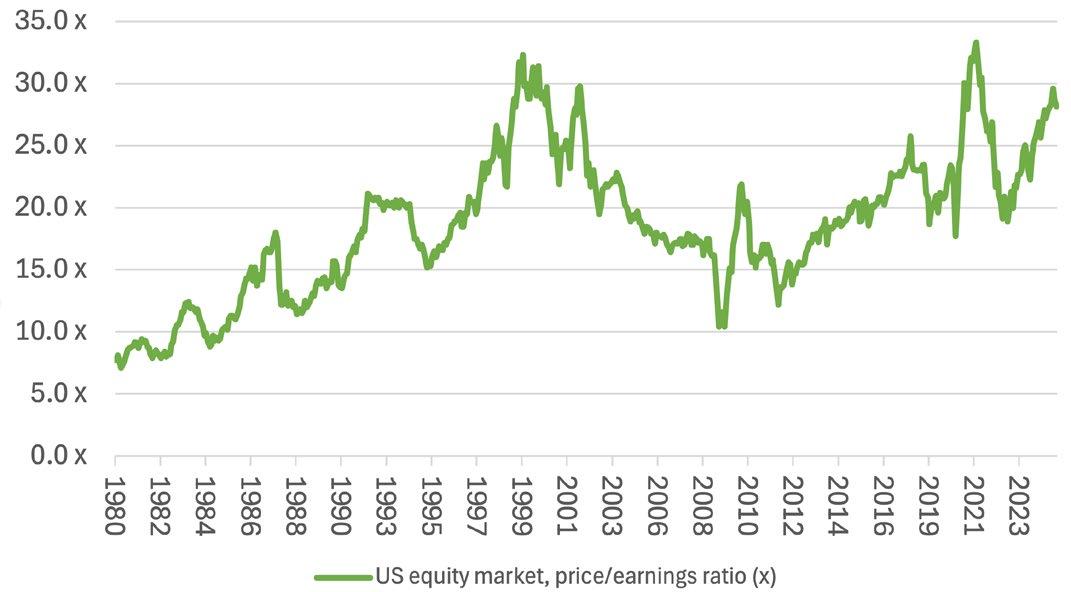

What can Berkshire Hathaway do for an encore if it isn’t buying stocks any more?

Having been a net seller of equities for nine quarters and amassed a record $334 billion of cash, has Warren Buffett finally run out of ideas?

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Tesla investors are pinning their hopes on a pipeline of good news stories after the stock’s collapse this year Falling demand, rising competition and a political backlash have severely dented the electric vehicle maker’s sales so any positive coverage will come as a relief.

Greggs slumps on sales growth slowdown and margin warning

Ashtead shares hit 12-month

sales disappoint

The inherent unpredictability of oil prices and European stocks in demand

The FTSE 100, DAX and CAC-40 have comfortably outstripped US indices

Investors are getting conflicting signals when it comes to the future direction of oil prices, and this week’s fall to three-month lows off the back of crude producers’ cartel OPEC+’s decision to boost output is unlikely to be the end of the story.

The introduction of tariffs on neighbouring countries by the Trump administration could stoke inflation, which would typically be reflected in higher energy prices, but if economic growth is weaker it could lead to reduced hydrocarbon demand.

While developments in Ukraine remain unpredictable, some sort of peace deal might see Russian oil and gas return to global markets, helping tip the supply and demand scales, although escalating Russo-European tensions might well have the reverse effect.

as we largely focused on the larger names, many small-cap oil and gas stocks still bear significant scars from this period despite crude prices actually being higher today than they were in February 2020.

European stocks are enjoying a moment in the sun as US markets teeter. After a long period of underperformance relative to their American counterparts, Germany’s DAX, up 13.7% year-to-date, France’s CAC-40, up 9.7%, and the FTSE 100, up 8.1%, are comfortably outstripping the 0.5% fall in the S&P 500 and 5% slump in the Nasdaq Composite so far in 2025.

As we discuss in our news section, the European defence sector has been particularly in demand in recent weeks.

This inherent volatility and unpredictability is part of the reason we share the market’s scepticism over the turnaround plan unveiled by BP (BP.)

In perhaps the most extreme example of just how far and how fast the oil market can swing, the US crude benchmark WTI actually fell below $0 in April 2020 when the pandemic struck.

This week’s big feature takes the five-year anniversary of the Covid sell-off as an opportunity to highlight the stocks trading materially below their pre-pandemic levels.

Although there wasn’t space to include them,

Yet, as Bank of America points out, European equities ‘have seemingly gone from strength to strength, with the Euro Stoxx 50 making new highs and outperforming the S&P 500 by the most since the quantitative easing era. However, risks this momentum runs out of steam motivates costeffective hedges.

‘The rally was powered by underweight positioning, but that effect may fade. The strength in defence stocks has also supported regional equities, but the subsector isn’t large enough to push broader equities higher, unaided.’

Interest rate cuts from the European Central Bank may be a further catalyst for Europe’s stock markets as weaker inflation leads Morgan Stanley, among other market observers, to predict an additional cut in April.

authorised and regulated by the Financial Conduct Authority. There can be no assurance that the Company’s objectives or performance target will be achieved. Any investment is subject to fees, taxation and charges within the Trust and the investor will receive less than the gross yield. Investors should read and note the risk warnings in the Company’s Key Information Document (KID). Copies of the KID and Report & Accounts are available on Lazard Asset Management’s website or on request. The tax treatment of each client will vary and you should seek professional tax advice. The Trust is listed on the London Stock Exchange and is not authorized or regulated by the Financial Conduct Authority. This information has been issued and approved by Lazard Asset Management Limited and does not in any way constitute investment advice. The company currently conducts its affairs so that the ordinary and subscription shares in issue can be recommended by financial advisers to ordinary retail investors in accordance with the Financial Conduct Authority’s (“FAC’s”) rules in relation to non-mainstream investment products and intends to do so for the foreseeable future.

Trump action on crypto, tariffs and Ukraine shifts markets

European defence stocks surge as leaders talk military expansion

Three recent interventions by the Trump administration are having a major impact on financial markets.

First, plans for a cryptocurrency strategic reserve were announced, helping to light a fire under Bitcoin and other digital assets.

Those gains were soon erased however when, against hopes of a last-minute reprieve, 25% tariffs were introduced on Canada and Mexico along with a 10% levy on Chinese goods.

Canada and China introduced retaliatory measures of their own, raising fears of a prolonged and broad-based global trade war.

Then the White House announced it would suspend military support to Ukraine in the wake of an Oval Office spat between president Donald Trump and vice-president JD Vance and the country’s premier Volodymyr Zelenskyy.

BAE Systems

advisory group deVere, was in no mood to downplay the gravity of the latest news on tariffs.

‘The market implications are vast. The US dollar, often buoyed by trade tensions, is likely to maintain resilience as investors flock to perceived safety. Commodities, already in high demand, could experience further price surges, benefiting energy and industrial sectors.

A day earlier, a gathering of European leaders to discuss support for Ukraine had sparked big gains for the continent’s defence stocks which were extended on the fresh developments.

Until recently, despite his avowed pro-crypto stance, president Donald Trump had simply brought to a close enforcement actions against the industry, but the announcement of a strategic reserve suggests potential for the US government to buy crypto at regular intervals.

A White House cryptocurrency summit on 7 March may reveal more about how the strategic reserve might be established – several relevant proposals are already working their way through federal and state legislatures.

Nigel Green, chief executive of

‘Meanwhile, domestic manufacturing stocks stand to gain as supply chains adjust to new tariff realities. At the same time, businesses reliant on imports face rising costs, forcing either a margin squeeze or price increases for consumers.’

Suggestions European countries will step up their support for Ukraine have seen shares in BAE Systems (BA.), Germany’s Rheinmetall (RHM:ETR) and France’s Thales (HO:EPA) surge, the latter also helped by better-than-expected results on 4 March.

BAE Systems is now up 175% on its level before the invasion of Ukraine in February 2022, although Shore Capital analyst Jamie Murray notes the company is largely reliant on long-term programmes rather than areas like munitions where demand may come through in the near term.

He adds: ‘In addition, BAE is vulnerable to DOGE related cuts given 44% of its revenue comes from the US.’

BAE is vulnerable to DOGE related cuts given 44% of its revenue comes from the US ”

Notably, while European arms makers have been soaring, their US counterparts have seen their share prices come under pressure. [TS]

Tesla looks to AI and robotics to end stock’s three-month slump

Buyer’s strike in Europe as Musk juggles competition and market sentiment

Elon Musk and Tesla (TSLA:NASDAQ) optimists in the analyst community appear to be pinning hopes on AI, robotaxis and robotics to reverse the negative mood surrounding the stock in recent months.

Since peaking at an all-time high close to $480 in mid-December 2024, shares in the electric car firm have lost more than 40% of their value, a plunge that has wiped more than half a trillion dollars off the firm’s market cap.

quarter earnings which missed expectations and left investors in dour mood.

At the start of the week, Tesla investors were handed a welcome lift as the stock was reinstated as a top pick by Morgan Stanley. Analyst Adam Jonas cited advancements in AI and robotics as key drivers for future growth, despite challenges in the core automotive business. Jonas reaffirmed a $430 price target, representing more than 50% upside from recent $285 trading levels.

According to Jonas, a long-time Tesla bull, falling vehicle sales are part of the firm’s transition from a traditional automotive ‘pure play’ to a highly diversified technology provider.

‘While the journey may be volatile and nonlinear, we believe 2025 will be a year where investors will continue to appreciate and value these existing and nascent industries of embodied AI where we believe Tesla has established a material competitive advantage,’ Jonas wrote in a note.

Catalysts for the stock this year could include the scheduled June 2025 robotaxi service launch in Austin, a potential AI day, launches of lower-priced models in the second or third quarter as well as a ‘potential’ third-generation Optimus humanoid robot unveil.

Declining demand, rising costs and Elon Musk’s controversies continue to drag on investor sentiment, with the 45% year-on-year slump in January European vehicle sales a real bombshell.

Worryingly for shareholders, falling demand was not restricted to Europe, with sharp mid-teens January declines in the US and China, its two most crucial markets, even in the face of ticket price cuts designed to attract buyers.

Lower sales have directly impacted Tesla’s revenue and profitability, leading analysts to downgrade their Tesla stock forecasts. This followed lacklustre fourth

Elon Musk has previously said he believes Optimus could be a $10 trillion dollar market opportunity, although sceptics will note Musk has a habit of making bold predictions that fail to materialise.

Tesla bull Cathie Wood, who runs tech-focused Ark Investment Management in the US, also threw her support behind the company and its stock, saying there is a lot of ‘pent-up demand’ for Tesla vehicles. The big valuation unlock, in her view, is Tesla releasing robotaxis across the country, although there remain regulatory hurdles to overcome first. [SF]

Rolls-Royce shares hit yet another 52-week high

Aero-engine maker wows investors with £1 billion share buyback and reinstates dividend

Shares in Rolls-Royce (RR.) surged to a new 52-week high of 792p (3 March) as the aero-engine maker continued to impress investors with its post-pandemic turnaround.

Under the helm of chief executive Tufan Erginbilgic, who was appointed in January 2023, the company has made a steady recovery and recently report stronger-than-forecast full year results.

On 27 February, the Derby-

headquartered company reported a 15.8% jump in revenue to £17.85 billion and a 57% surge in underlying operating profit to £2.5 billion driven by strategic initiatives and cost efficiencies.

In addition, the company announced a £1 billion share buyback and reinstated its dividend – a welcome relief to shareholders after a five-year wait.

With full-year 2025 guidance pointing to underlying operating profit and FCF (free cash flow) in the £2.7 billion to £2.9 billion range two years earlier than planned (2027), what next for the enginemaker?

Rolls-Royce is making solid progress with orders across all

its businesses including for small modular reactors and submarines. While it has exposure to the defence sector, the recovery in air travel and the increase in passenger numbers post-pandemic has meant a strong recovery in trading for the civil aerospace business and by extension for Rolls’ servicing division. [SG]

Severfield shares plummet after structural steel group delivers another profit warning

Shares nearly halve after challenging market conditions in UK and Europe

The outlook looks far from rosy for structural steel group Severfield (SFR) after it delivered another profit warning (3 March) sending its shares down 44% to 26.5p.

In a trading update for the full year ending 29 March, the company said market conditions showed no signs of improvement since it last reported in November and some clients had canceled or delayed projects.

The company is known for working on high-profile London sporting projects such as the expansion of Lord’s cricket ground and the Tottenham Hotspur football stadium.

‘Client decision-making continues to be deferred, and projects are not being awarded or progressing within normal timescales, consistent with the current lower level of business confidence in the UK economy as a whole,’ said the company.

Severfield also canceled the £10 million share buyback programme announced last April as it looks to conserve cash through difficult times.

On the positive side, the structural steel group said it had secured some attractive large projects for full year 2027.

The company added it saw

opportunities in data centres, industrial manufacturing and commercial offices, and that its future and medium-term growth targets remained unchanged. [SG]

Add Definition to Your Portfolio

Defined outcome strategies that increase potential to reduce systematic risk and equity volatility.

12 March: 4imprint, Balfour Beatty, Forterra, Gym Group, Hill & Smith, Hochschild Mining, Legal & General, PensionBee

13 March: Restore

FIRST-HALF RESULTS

11 March: Cranware, Keir Group

13 March: DFS, Seraphim Space Investment Trust, Volution TRADING ANNOUNCEMENTS

13 March: Halma, Trainline

Can engineering outfit Spirax revive its fortunes?

A weaker backdrop and a strategy shift have hit the steam management systems specialist

UK engineering business Spirax (SPX) is expected to deliver mid-single digit organic revenue growth for 2024 when it announces results on 11 March.

As a reminder, the company (once known as Spirax-Sarco Engineering) is a FTSE 100 constituent focused on steam, thermal electric and niche pumping solutions, across a wide range of end-markets.

After a period in the doldrums which has seen the shares drop to £72.05 from the £170.45 peak in late 2021, a recently installed management team will be looking to demonstrate they can turn around the company's fortunes. CEO Nimesh Patel took the helm at the beginning of 2024 and was joined by chief financial officer Louisa Burdett in July of last year.

Spirax has undergone a material shift through acquisitions to position itself for long-term drivers such as the energy transition but this, in turn, has arguably increased the complexity and risk around the business.

Berenberg analyst Andrew Simms comments: 'Spirax had a whirlwind 2024. Rising optimism for a 2024 recovery sent the shares up by 10% in Q1 but the extended Biopharma destocking, slower semiconductor market and cyclical weakness resulted in a 40% peak-to-trough fall.

'With markets that

Spirax Group

deteriorated rather than improved, H1 organic growth in the Steam segment was -1%, while further internal and external headwinds became apparent with declining margins exacerbating a lower-than-expected top line.

'The company’s capital markets day in October 2024 provided some incremental information regarding the scale of the growth opportunity and showcased the new management set-up while highlighting increasing investment requirements. We remain unconvinced that the event achieved what the company envisaged.'

Simms notes an expected fourthquarter weighting to the company's full-year numbers so the upcoming release could be key in showing if Patel and Burdett are making any tangible progress with their recovery strategy. [SG]

What the market expects

What the market expects from Spirax

Adobe may need narrative change to fire stock higher

Creative design software firm’s shares have lost 20% since early December

March will be a busy month for creative software supplier Adobe (ADBE:NASDAQ), with fiscal 2025 Q1 earnings after the market close on 12 March, followed by what could be a crucial investors day less than a week later, on 18 March.

This will be a vital opportunity to give investors a welcome dose of optimism after a testing few months, the stock down 20% since early December 2024.

Adobe’s strategic focus on AI integration across its Creative Cloud, Document Cloud, and Experience Cloud platforms has been a significant driver of growth, with features such as Firefly in Photoshop and Illustrator, enabling users to generate new content, edit images, and create effects with relative ease. Expansion into new markets and strategic acquisitions have further bolstered its growth prospects, yet investors have been getting impatient, with overall growth of 11% last year failing to generate the AI excitement markets were hoping for.

Consensus currently has Adobe growing at around 10% this year and next, so any steer that AI will fire

US UPDATES OVER THE NEXT 7 DAYS

QUARTERLY RESULTS

7 March: Constellation Software, RLX Technology, Algonquin Power

10 March: Asana, BioNTech, NET Power, Paymentus

11 March: Caseys, Dick’s Sporting Goods, Ferguson, United Natural Foods

faster expansion will be needed to take hold of the narrative and set the share price moving higher again.

Adobe has consistently beaten quarterly revenue and earnings expectations, yet the share price reaction has often been muted thanks to cautious commentary. The reaction to these upcoming earnings may depend on management's ability to create some excitement about the story.

The company may also be expected to address the competitive threat posed by Shutterstock (SSTK:NYSE) and Getty Images (GETY:NYSE) after the two rival image providers agreed a $3.7 billion merger at the start of this year. [SF]

12 March: Adobe, Getty Images, UiPath

13 March: Dollar General, Oracle, Ulta Beauty

Why trainers titan Nike can be a trendsetter again

The sportswear leader famed for its iconic swoosh logo is under new management, though this turnaround could prove more marathon than sprint

$79.43

Market cap: $117.5 billion

Patient investors seeking a high-quality, progressive dividend-paying company with one of the globe’s most iconic brands should buy Nike (NKE:NYSE), the lately-unloved sportswear giant trading at a discount to its own history with the shares down 20% over one year and 10% over five.

Despite its recent struggles, Shares believes this is an opportune moment to buy the sneakers-tosoccer ball behemoth.

Nike is in the early stages of a turnaround under new chief executive Elliot Hill, who is laying the foundations for sustainable growth following

strategic missteps under his predecessor, which included reduced product innovation and an overemphasis on direct-to-consumer business Nike Digital which allowed competitors to gain market share.

Hill has come out of retirement with a strategy to return Nike to growth, and the footwear firm is now focused on returning sport to the centre of everything it does.

Turning Nike round could prove more of a marathon than a sprint, however. As such, investors could open a position ahead of third quarter earnings on 20 March, where evidence of an improving North America or Greater China sales performance, or a confident outlook from management, could be the catalyst for the first leg of a rally.

WHAT’S GONE WRONG IN NIKETOWN?

Oregon-based Nike’s recent stumbles reflect mistakes in product and distribution under the previous leadership which led to market share losses and alienated key retail partners at a time when Chinese consumers seemed to lose their appetite for US brands.

Under company veteran Hill, the world’s biggest sportswear firm is refocusing on sport and switching its innovation engine back on in order to regain the customers lost to arch-rival Adidas (ADS:ETR) and upstarts like On Running and Hoka, while Nike’s distribution strategy also needs refining after the shift to selling direct to consumers largely failed to deliver.

Broker Jefferies has been cautious about the

Turnaround will be a marathon not a sprint

Table: Shares magazine • Source: Stockopedia, data as of 3 March 2025

stock due to competition headwinds, but recently upgraded its recommendation from ‘hold’ to ‘buy’, making Nike its new top pick with a $115 price target implying 45% upside from current levels.

The broker pointed out Hill is ‘tackling product and distribution issues head-on, positioning the brand to again outgrow the market and take back lost share. Survey work illustrates Nike’s brand remains very strong, proving that issues were selfinflicted and competitive threats less severe.’

Improving product and adding back distribution will enable Nike to regain share in an athletic footwear and apparel market GlobalData expects to grow at a 3% to 4% compound annual growth rate through to 2028.

THE RIGHT PLAYBOOK

Nike’s results for the second quarter to 30 November 2024 (19 December) proved better than feared, although sales were down 8% year-on-year at $12.4 billion.

Heavy discounting and a lack of product newness drove sales and profit declines, with revenue lower in all four of Nike’s geographic regions including North America and Greater China.

There was also disappointment at the footwear giant’s forecast of a low double-digit revenue fall for the third quarter including Christmas.

Jefferies notes Hill has ‘prioritised restoring wholesale partnerships and driving innovation’ and the new broom is ‘intimately engaged with current and lapsed retail partners. We think Hill has the right playbook; it worked a decade ago, so it’s highly likely to work again.’

The broker’s survey work also shows that more than half of US consumers planning to buy athletic footwear this year will choose Nike shoes, and more than 60% of those aged 18 to 44 will choose Nike.

‘This underscores the brand’s ubiquity and suggests it is still very strong ahead of future innovations with NikeSKIMS and in the running category,’ explained the broker.

For the uninitiated, Nike is partnering with celebrity Kim Kardashian’s SKIMS clothing line to launch a new brand aimed at women, which will focus on apparel, footwear and accessories for the female fitness and activewear sector, with an initial launch this spring through selected US retailers and a global rollout planned for 2026.

Stockopedia shows Nike shares trading on a forward price-to-earnings (PE) ratio of 38 times for the year to May 2025 falling to 32.7 on 2026 estimates.

Not dirt cheap, but investors should expect to stump up for what remains the world’s leading sportswear company, and the rating represents a discount to the 80 times multiple reached at the height of the pandemic.

Investors should also note the stock’s income attraction, with Nike having increased its dividend for 23 years on the spin. [JC]

Time to buy into the real estate recovery with seasoned investor TR Property

There seems no doubt valuations in the European commercial property sector have stopped falling and in some cases have been rising in recent months, but the recovery is uneven with demand for higherquality assets outstripping that for lesserquality ones.

However, allocating part of your portfolio to property by stock picking or even choosing a REIT (real estate investment trust) can be timeconsuming especially if you don’t have the expertise.

Investors looking for broad exposure to high-quality UK and continental European assets to play this recovery should therefore take a look at investment trust TR Property (TRY).

QUALITY ASSETS

Shares magazine•Source: LSEG

quoted shares of property companies, propertyrelated businesses and REITs.

Managed by Thames River Capital, a joint venture with Columbia Threadneedle, the company owns a small amount of UK property directly but the majority of its investments are in

When choosing where to invest, the trust generally prioritises future growth and capital appreciation over yield or discounts to NAV (net asset value), but with many holdings offering a relatively high payouts the shares offer a current yield of around 5.2%, which is fairly attractive.

Interestingly, when we introduced the company to readers a little over a year ago, the UK represented 36% of the portfolio and just two UK stocks made the list of top 10 holdings –today the UK, including directly-owned properties, accounts for just 22% of the portfolio but there are three UK stocks in the top 10 holdings.

The largest weightings, as of January this year, are in industrial property, including Segro (SGRO), German residential, European shopping centres and UK ‘diversified’ companies such as Land Securities (LAND) and LondonMetric (LMP)

For the six months to September, which marked the first half of its financial year, the company

Chart:

Top 10 quoted holdings as of 31

reported an 11.6% increase in earnings per share, from 7.31p to 8.16p, an 8% increase in NAV per share to 378.6p and a 9.4% increase in its share price to 355p.

As a leveraged asset class, the price of debt is a critical driver in the early stages of a valuation recovery, and the decline in interest rates –particularly in continental Europe – not just during the first half to September but just as important in the five months since then, has created a competitive lending environment allowing many companies to refinance at lower interest rates. Therefore, the trust’s focus has shifted from scrutinising firms’ balance sheets to fundamentals, which is the next phase of price recovery, and to portfolio quality as there is a growing mismatch between increasing demand and lack of supply of high-grade property assets. Most of the returns over the six-month period came from European shopping centres and UK diversified REITs.

Klepierre (LI:EPA) in France delivered a 27% return thanks to a stronger earnings outlook and credit upgrades, while Picton Property Income (PCTN) sold its largest office asset for conversion into a residential property, reducing the perceived ‘overhang’ in office space and reducing debt in one go.

Where it has found value the firm has invested in capital raisings, and as merger activity has spread, leading to a smaller number of larger, more liquid companies with better operating efficiencies, it has supported deals such as the takeover of Capital & Regional by New River Retail (NRR).

RECENT PERFORMANCE

After a tough December, European equities shone in January and the ‘value corner’ of real estate stocks even beat the return on the S&P 500 over the month with a 3.9% gain.

The trust’s overweight towards European shopping centres paid off once again as investors sought out high yield and income stability, while French offices surprised to the upside due to the lack of best-in-class space available to rent in Paris (recent estimates put the vacancy rate as low as 4%).

The small share buyback at Picton also helped sentiment towards UK property stocks, even if it was a ‘baby step’ in the scheme of things.

Marcus Phayre-Mudge, lead manager of the trust since 2011, observes: ‘If the board believes in the asset valuation, then nothing is cheaper than their own portfolio at a 30%-plus discount. Buybacks at these discounts are highly accretive. Investors will soon get the message that the non-executives have not abandoned them and are determined to do something about it. It becomes self-reinforcing.’

Phayre-Mudge also sees more M&A to come in the UK: ‘The market wants larger, more liquid names with greater cost efficiencies – just look at the performance of London Metric, an active consolidator. In this environment your share price is a currency and trading at large discounts (to asset value) leaves you in a more vulnerable negotiating position.’

The trust trades at a 9% discount of roughly to NAV, and ongoing charges are 0.82%, in line with the AIC’s Europe peer group, while dividends are paid semi-annually, typically in January and August. [IC]

Share placing at ME International partially removes stock overhang

The company expects to install 1,200 laundry machines in 2025

ME International (MEGP) 197.8p

Gain to date: 23.8%

We highlighted instant-service equipment maker ME International (MEGP) as a compelling investment opportunity a year ago.

The company, formerly known as Photo-Me International, operates a unique business which generates strong cash flow and high returns on capital.

The firm primarily installs and operates photo booths and laundry machines in high footfall locations in return for a commission or fixed fee, underpinned by long-term relationships with site owners which include food retailers and garage forecourts.

WHAT HAPPENED SINCE

WE SAID TO BUY?

The company’s annual results, published on 24 February, showcased another record year of profitability due to the continued rapid expansion of laundry operations and a record pipeline of machine installations with strategic partners.

Revenue from the laundry business increased by 21% to £91 million excluding foreign exchange effects after a record 1,168 machines were installed during the year.

Group revenue and EBITDA (earnings before interest, tax, depreciation, and amortisation) increased by 6.8% and 10% respectively to £307.9 million and £114.2 million.

The group EBITDA margin on sales

increased to 37.1% from 35.8% reflecting the expansion of laundry machines, which achieve a higher margin of 51.4%, and the company hiked the annual dividend by 6.8% to 7.9p per share.

On 27 February, there was a placing of 26.5 million shares (7% of the issued capital) held by private equity investor Montefiore Capital, at a price of 200p per share or a 9% discount to the prior closing price.

The sale took Montefiore’s holding down to 5% and partially removed the overhang, while investment manager Abrdn (ABDN) became a new 5% shareholder.

WHAT SHOULD INVESTORS DO NOW?

We remain happy holders in a growing business which is becoming more profitable due to the superior economics of the laundry business. This should provide strong cash flows to fund growth as well as shareholder returns. (MG)

How I think about my investments in the technology space

Steven Frazer on how he approaches this crucial part of the investment universe

Investing in tech stocks has been making money for ordinary investors for years. Since the internet emerged in the early 1990s, the broadly drawn tech space has consistently delivered market-beating growth in revenues and profits and dominated share price returns. It is no coincidence that aside from Warren Buffett’s Berkshire Hathaway (BRK.B:NYSE), all of

the trillion-dollar companies (currently seven), are universally known as ‘tech’ stocks. But crucially, for me, the tech space looks likely to capture the lion’s share of growth in the years to come – higher revenues, larger profits, bigger cash flows, which should mean superior total returns for investors.

Recent research from Aswath Damodaran, a professor of finance at the Stern School of Business at New York University, supports the idea that tech will remain the preeminent growth sector.

Markets use the term ‘tech’ in a fast and loose

Technology is delivering substantial earnings growth

Nvidia clearly has advantages of rival that can be defended over time, and the growth pathway still looks very healthy and long-term”

fashion, and it captures a wide variety of business models, strategies, risks and rewards. Amazon (AMZN:NASDAQ), Netflix (NFLX:NASDAQ) and Tesla (TSLA:NASDAQ) are all considered tech stocks yet they are completely different businesses with different challenges and opportunities.

THREE KEY MEASURES

Focusing on those differences is, I find, generally more helpful that getting hung up on terminology, with three key measures standing out. First, what advantages does a company have over its competitors, and can they be defended? Second, what growth runway does the company have, and are they capable of exploiting it? Third, how profitably is a company scaling up and does it generate large piles of cash? Other factors need to be considered too, obviously, but these metrics make for a decent starting point.

Let’s look at a topical example; Nvidia (NVDA:NASDAQ). After back-to-back triple-digit returns in 2023 and 2024, the chip designer has faced a choppy 2025, so far, as questions are raised over the firm’s future growth, emerging competition and, possibly, the tightening of Washington’s trading handcuffs with China.

There was also Chinese hedge fund-backed start-

Tech stocks versus S&P 500 Source: S&P

up DeepSeek releasing R1 in January, its open-source reasoning model that reportedly outperformed the best models from US companies, such as OpenAI. R1’s self-reported training cost was less than $6 million, a fraction of the billions that Silicon Valley companies are spending to build their artificial intelligence models, although there remains healthy scepticism among analysts over those cost claims, and the Nvidia chips that power R1.

The stock market’s reaction was swift. In a single day, Nvidia’s stock lost a record-breaking $600 billion in value, a 17% drop. Nvidia, currently the largest producer of advanced semiconductors used for AI development, continues to face questions about DeepSeek’s impact although Nvidia’s comments in response to R1’s launch indicate that it sees DeepSeek’s breakthrough as creating more demand for its graphics processing units.

The immediate concern is that not as many Nvidia chips will be required to develop AI applications. On the other hand, based on timetested economic theory, if programming costs decline, demand for chips could rise. Nvidia was always going to face increased competition, it always has, but backers are betting that management can out-develop opponents to stay at the top.

For now, the fundamentals support that view, as recent forecast-beating Q4 earnings showed, even if the markets reacted badly. Nvidia clearly has advantages of rival that can be defended over time, and the growth pathway still looks very healthy and long-term. Is it doing so profitably and cash generatively?

Returns on capital of 87% and operating margins 62% say yes, with free cash flows accelerating too.

Away from Nvidia, the broader tech space seems

to be in a good place, with the two most crucial sectors on the S&P 500 - Information Technology and Communication Services placed second and fourth in terms of the number of companies to report earnings above estimates during the latest quarterly reporting season (to end December 2024 or January 2025), according to FactSet data at 82% and 8%. Information Technology (83%) saw the largest number of companies to beat the Street on revenues too.

FactSet estimates that total revenue across the S&P 500 is expected to grow at a compound annual growth rate of 8.9% out to 2029, slower than the four sub-sectors identified as tech by the Stern Business School research.

This follows a second consecutive year of stellar technology stock performance, according to US Bank Asset Management. In 2024, the S&P 500 Communications Services and Information Technology index combined gained 37.4%, following 2023’s gain of 57%. By comparison in 2024, the broader S&P 500 Index gained 25%.

Although January’s AI developments added a level of technology sector uncertainty that didn’t exist before, the outlook in general remains favourable, I believe. AI and cloud computing account for a significant portion of today’s corporate spending, as companies seek to enhance productivity and boost their bottom lines.

FactSet estimates that total revenue across the S&P 500 is expected to grow at a compound annual growth rate of 8.9% out to 2029, slower than the four sub-sectors identified as tech by the Stern Business School research”

business-to-business basis, says Eric Freedman, chief investment officer for US Bank Asset Management. ‘That’s what companies are spending their capital on, so that’s where we want to be positioned.’

Sure, in the near-term, investors will home in technology stock valuations. High double-digit PEs (price to earnings) multiples often make investors nervous because a lot of good news is already priced in. But in the long run, I believe that there is scope for the best tech stocks to maintain above average growth rates with solid consensus beating potential to provide upside surprises. It’s why I often look at three-year average PEs and PEGs (price to earnings growth) multiples because I believe they provide a better glance into the future with that extra growth factored in.

The information technology spending we’re seeing is not just from consumers, but on a

Technology companies offer the potential for strong earnings growth that’s not specifically connected to the business cycle, most of the

Tech represents more than 40% of the S&P 500

Chart: Shares magazine • Source: S&P, 28 February 2025

performance US Bank Asset Management sees ahead is driven by secular, rapid business growth, something that tech fund managers have been telling me for a while.

Information Technology stocks currently represent the largest sector of the benchmark S&P 500 Index, comprising more than 30% of the index’s value. When you add in Communications Services stocks, many of which connect with the technology arena, Alphabet (GOOG:NASDAQ) and Meta Platforms (META:NASDAQ), for example, the group represents more than 40% of the S&P 500.

Tech has become so large and influential to almost every aspect of life that investors simply cannot afford to ignore the space”

personally invested in. My conversations with lead managers Mike Seidenberg and Ben Rogoff, respectively, plus many others, help me remain optimistic about the technology stocks space.

While you can significant technology exposure by investing in an S&P 500 tracker, given its heavy weighting in the index, these managers have the ability to go overweight and underweight relative to the index to reflect their levels of confidence in the investment case for individual stocks.

Tech has become so large and influential to almost every aspect of life that investors simply cannot afford to ignore the space. Obviously, you need to be selective, and one way to do that easily to invest in a tech fund run by people with deep experience and expertise, the Allianz Technology Trust (ATT), or Polar Capital Technology Trust (PCT), for example, two investment trusts I am

DISCLAIMER: The author of this article (Steven Frazer) owns shares in Allianz Technology Trust and Polar Capital Technology Trust.

By

Finding Compelling Opportunities in Japan

AVI Japan Opportunity Trust @AVIJapan

Steven Frazer News Editor

UNDER WATER

Catch the below pre-Covid level stocks which can rise to the surface

Just over five years ago the stock market began to react in earnest to news of the Covid pandemic.

The sell-off was short and sharp, with a modest recovery from the lows in the spring followed by sharper gains in November 2020 after AstraZeneca (AZN) made a vaccine breakthrough. However, a large number of UK stocks are still trading below the levels they were at by the close of trading on 21 February 2020, before the selling started in earnest.

In this article we reveal a list of the laggards in

the large- and mid-cap space and analyse the data to look for different trends. We also reveal three names which we think are unfairly languishing below their pre-Covid levels.

We also examine the worst of the worst performers and highlight the names which have performed best over the same five-year timeframe. Read on to discover more.

By The Shares team

LARGE-CAP HOSPITALITY, TRAVEL AND ASSET MANAGEMENT FIRMS STRUGGLE

Large caps have not been spared the worst effects of Covid and the post-pandemic surge in inflation and interest rates which followed.

Hospitality has had to deal with rising wages and an increase in the national living wage and employer national insurance contributions.

These challenges are reflected in Premier Inn owner Whitbread (WTB) shares, which are languishing more than a third below 2020 levels.

Housebuilders have endured the doublewhammy impact of rising cost of mortgages, slowing demand, while increased cost of materials has dented margins.

It is therefore not surprising see housebuilders trading well below 2020 levels with Persimmon (PSN) and Vistry (VTY) two of biggest losers, down 63% and 58% respectively over the last five years.

Property companies have been impacted by higher interest rates which reduce property valuations, while the shift to hybrid working has not been helpful for occupancy levels. This explains why Shaftesbury Capital (SCH) and British Land (BLND) shares sit below 2020 prepandemic levels.

Online food retailer and technology company Ocado (OCDO) briefly became one of the big winners from lockdown, sending the shares from around £10 in February 2020 to a peak of £26 a year later.

We are a long way from those dizzy heights with the shares sitting 72% below the levels where they were in 2020. Embarrassingly the company also got demoted from the FTSE 100 index in the process.

The excitement around the game-changing tie-up with US grocery giant Kroger (KR:NYSE), licensing its whizzy automated warehouse technology seems to have faded.

The cost-of-living crisis has taken its toll on consumer sentiment in recent months, impacting consumer facing firms like JD Sports Fashion (JD.) whose shares are down 54% over the last five years.

Medical products company Smith & Nephew (SN.) has been stymied by the backlog of knee and hip replacement procedures which were postponed during lockdown, leaving its shares trading 46% below 2020 levels.

Travel came to an abrupt halt during the pandemic as countries closed borders to prevent entrance of new strains of Covid.

While the industry has since witnessed a boom from revenge spending, shares in Jet2 (JET2:AIM), British Airways owner International Airlines Group (IAG) and cruise company Carnival (CCL) remain under water over the last five years.

Asset managers have struggled to adapt to a higher interest rate environment which means customers can now earn a decent return on cash deposits for the first time in years. Outflows from equites have put pressure on share prices across the sector. [MG]

Large-cap stocks trading below pre-Covid levels

Data between 21 February 2020 and 21 February 2025

Table: Shares magazine • Source: Sharescope

CONSUMER-FACING MID CAPS UNDER THE COSH

Mid caps whose fortunes are indelibly linked to the struggling consumer, the hardpressed and disrupted hospitality industry and overseas travel have found the road to recovery long, winding and rocky indeed. The likes of global food travel expert SSP (SSPG), travel retailer WH Smith (SMWH) and European airline Wizz Air (WIZZ) all languish significantly below pre-Covid levels, while Magners-toMenabrea maker C&C (CCR) and premium mixer drinks firm Fevertree (FEVR:AIM) remain in the share price doldrums, down 50%-plus on a fiveyear view.

Indebted SSP, which operates restaurants, bars, cafes and other food and drink outlets at airports and railway stations under brands such as Upper Crust, Ritazza and Le Grand Comptoir, has not been helped by geopolitical uncertainty, industrial action and adverse currency swings, while shares in storied WH Smith trade at half the level of five years ago. The retailer is looking to hive off its High Street arm, having successfully repositioned itself as a pure-play travel retailer, at a time when bricks-and-mortar retailing faces online competition, subdued footfall and a sharp rise in labour costs following the recent UK Budget.

Also trading well below pre-pandemic levels are pubs groups JD Wetherspoon (JDW) and Mitchells & Butlers (MAB) as customers

continue to grapple with cost-of-living pressures. Sentiment towards these names has hardly been helped by Rachel Reeves’ Budget, with investors concerned about the bottom-line impact from increased National Insurance costs and another rise in the National Living Wage.

Retail was a tough enough sector to occupy pre-Covid, but subsequent inflation and higher interest rates have crimped consumers’ purchasing power and its constituents are groaning under the strain of rising costs. This largely explains the presence of tech products purveyor Currys (CURY) and UK pet care leader Pets at Home (PETS) on the five year mid cap fallers list, though the former has staged an impressive rally more recently on takeover interest, consistently strong trading and a return to the dividend list, while bid whispers have boosted shares in the latter.

Shares in recruiters Hays (HAS) and PageGroup (PAGE) are 55.1% and 28.8% lower on a five-year view respectively, with candidate and client confidence subdued amid macroeconomic uncertainty in many of their markets. However, the biggest five-year faller is Aston Martin Lagonda (AML), the iconic-yet-indebted car maker whose shares are down almost 90% having hit a series of speed bumps since joining the stock market in 2018. Company-specific challenges, consistent losses, the knock-on effects of weaker consumer demand and more recently, falling business confidence in China, are among the myriad of factors that have dragged on this FTSE 250 loser. [JC]

Mid-cap stocks trading below pre-Covid levels

Data between 21 February 2020 and 21 February 2025

WHO HAS SHONE IN THE FIVE YEARS SINCE COVID HIT?

In some respects it’s harder to pick out trends among those businesses whose shares have performed best in the five years since the Covid correction began.

Some initial Covid winners like online fast fashion firms ASOS (ASC) and Boohoo (BOO:AIM) have endured a big slump since.

Publisher Pearson (PSON) has held on to its gains – up 142% as the group successfully accelerated its digital first strategy and reaped the rewards of offering online learning through various products and its Virtual Schools division – demand for which grew sharply during the pandemic.

In Pearson’s latest full year trading update (on 16 January) the company said Virtual Learning sales had fallen back by 5% in the fourth quarter.

Fellow publishing group Bloomsbury (BMY) benefited from people rediscovering their love of reading during lockdown.

It then struck gold signing new romantasy author Sarah J. Maas and has carved out a meaningful presence in academic publishing, bolstered by its acquisition of assets from US outfit Rowman & Littlefield for £65 million, adding 40,000 academic titles to its library last May.

Cakes, custards, and cooking sauces maker Premier Foods (PFD) has seen its shares rise 427% over a five-year period.

A combination of factors has led to this big move higher – a decade-long balance sheet rehabilitation giving it extra financial firepower and paving the way for further debt reduction and a progressive dividend after a 13-year absence.

Aero-engine maker Rolls Royce (RR.) has proved itself to be the true ‘comeback kid’ after Covid with shares gaining 176% over five years.

Rolls Royce shares recently hit a new record high of 725.4p on the back of excellent full-year results and upgraded targets.

On 27 February, the company reported a significant strengthening of its balance sheet, a £1 billion share buyback and a reinstatement of its dividend – the last time the company paid a dividend was in January 2020.

Further down the list of gainers is uranium mining company Yellow Cake (YCA:AIM) which has benefited from the ‘buzz’ around the future of nuclear power and fantasy miniatures creator Games Workshop (GAW).

The maker of the hit tabletop fantasy game Warhammer entered the FTSE 100 in December 2024, three decades after making its debut on the London stock market. Over the past five years, Games Workshop shares have gained 98.9% giving it a market cap of an impressive £4.76 billion. With a tie-up with tech giant Amazon (AMZN:NASDAQ) expected in the near future – to create films and a TV series based on the Warhammer 40,000 universe – there’s plenty of excitement around this Nottinghambased company. (SG)

Selected winning stocks since Covid

Data between 21 February 2020 and 21 February 2025 Table: Shares magazine • Source: Sharescope

THREE UNDER-WATER STOCKS WHICH CAN RISE TO THE SURFACE

It was almost as if the pandemic did not happen for animal genetics company Genus (GNS) which was riding high after delivering record pre-tax profit of £38.7 million for the half year to 31 December 2020.

Shares magazine • Source: LSEG

Continued royalty growth and high breeding stock sales in China contributed to 11% volume growth in PIC (Pig Improvement Company) while Bovine genetics business ABS (American Breeders Service) delivered 17% revenue growth.

A key driver for the pig business was expansion in China where breeders were restocking pig herds following the spread of Swine Fever in 2019. That progress was

Source: Genus, as at 30 June 2024

Martin Gamble Education Editor

interrupted when China was hit by a slump in pig prices which fell by two thirds between December 2020 and June 2021 due to an oversupply of pork and low consumer demand.

That marked the high for Genus shares, which peaked at £60 in August 2021. Ongoing volatility in the Chinese pig market continued to act as a drag on the overall business, holding back growth in pre-tax profit.

Fast-forward to January 2025 and the business delivered its first positive trading surprise and profit upgrade for three years. First half adjusted pre-tax profit grew 21% to £35.4 million and cash flow from operations surged 284% to £46 million.

PIC China won a further seven new royalty customers taking the number to 20 over the last 18-months. We sense Genus is entering a new earnings growth upcycle after the lull of the last three years.

Shore Capital’s Sean Conroy raised his financial year 2025 pre-tax profit estimate by 5% to £67.3 million after the January trading update.

Commenting on the first half results (27 February) Conroy said: ‘todays results reinforce our view that Genus has come through its recent downgrade cycle and is entering much more cash generative period.’

With the shares languishing 70% blow the peak, and 46% down on prepandemic levels, there is plenty of recovery potential.

Genuit (GEN) 355p Market cap: £885 million

Investors with a few grey hairs may remember a business called Polypipe, which was acquired by IMI (IMI) in the late 1990s before being bought out by management more than once in the 2000s before listing in 2014 and subsequently changing its name to Genuit (GEN)

Ian Conway Deputy Editor

improvement) market exploded, Genuit has faced a more subdued demand environment in the last couple of years and more recently delays to some projects, meaning 2024 earnings will be at the low end of market expectations.

However, the business is geared into a nascent recovery in both residential construction and the RMI market, and any recovery in volumes will lead to a significant improvement in margins thanks to operational gearing.

Added to this, the business is highly cashgenerative, has a strong balance sheet, and leverage is modest at around 1.1 times earnings.

Several listed housebuilders have already noted a sharp pick-up in enquiries this year, and the government’s push to speed up planning is enabling more developments to come on stream.

The business has since been reorganised to focus on residential, commercial and infrastructure markets, and has grown through acquisition to become the UK’s leading producer of sustainable water, climate and ventilation products.

After a surge in orders between 2020 and 2022 as the RMI (repair, maintenance and

Berenberg analyst Robert Chantry says: ‘Genuit has laid out several key medium-term targets: i) organic growth 2-4% ahead of the market, thanks to structural top-line drivers; ii) operating margins greater than 20%; iii) ROCE over 15%; and iv) cash conversion greater than 90%. Genuit is positioning itself as a company with strong structural growth drivers and selfhelp potential, as opposed to a more cyclical story.’

Given these drivers, a rating of 13.8 times 2025 forecast earnings per share does not seem expensive. [IC]

Like all hotel operators Premier Inn-owner Whitbread (WTB) suffered significant disruption during the pandemic.

However, we think it has emerged from Covid in pretty good shape and arguably with an enhanced competitive position as less robust rivals have either fallen by the wayside or been knocked off track.

As Berenberg analyst Jack Cummings observes: ‘Whitbread’s primary market, the UK, has experienced a contraction in supply, particularly as market conditions have accelerated the decline of the independent hotel sector. We expect market conditions to remain tough for independent operators and Whitbread to continue to grow its share of the market.’

The Premier Inn proposition is highly consistent. This isn’t luxury accommodation

Tom Sieber Editor

Changes in the October 2024 UK Budget will lead to increased costs but, on a forecast price to earnings ratio of 12.4 times – significantly below the historical average, this looks more than priced in. [TS] Whitbread (WTB)

Premier Inn open rooms in UK and Germany

but you know exactly what you are getting and its value credentials means it has appeal for commercial and leisure travellers alike.

While net debt remains relatively elevated, the company has the asset backing of its hotel estate and a medium-term ambition to generate £2 billion of cash for dividends, buybacks and investment in the business suggest management is comfortable with the balance sheet position.

Shore Capital analyst Greg Johnson notes the company’s five-year plan could see earnings per share move beyond 300p, from the 226p posted in the year to February 2024 and he highlights the possibility of the company bringing forward capital returns in order to win over the market.

The company’s more nascent business in Germany looks to be approaching a key milestone – anticipated to have reached profitability in the 2024 calendar year. This is another string to Whitbread’s bow for which the market may start giving the company some credit.

Source: Whitbread, data to 31 August 2024

Fidelity European Trust PLC

Chosen by AJ Bell for its Select List

Fidelity European Trust PLC aims to be the cornerstone long-term investment of choice for those seeking European exposure across market cycles.

Aiming to capture the diversity of Europe across a range of countries and sectors, this Trust looks beyond the noise of market sentiment and concentrates on the real-life progress of European businesses. It researches and selects stocks that can grow their dividends consistently, irrespective of the economic environment.

Holding a steady course throughout market cycles

It is an uncertain time for the world and Europe is no exception. It is however vitally important for investors not to be blown off course. Good companies are still good companies and finding them remains the ‘secret sauce’ of any effective investment strategy.

We will remain focused on the companies in which we have invested and, in particular, on their ability to continue to grow their dividends. As always, we will ask ourselves if that rate of dividend growth is already discounted in the share price.

Performance over five years

We continue to seek new opportunities to add to the portfolio at the right price and remain confident in those names we currently hold. This approach has historically served the portfolio well - including through the recent volatility of the last few months - and we see no reason to change course.

Past performance is not a reliable indicator of future returns.

The value of investments and the income from them can go down as well as up, so you may get back less than you invest. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of an investment in overseas markets. This trust can use financial derivative instruments for investment purposes, which may expose them to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The shares in the investment trust are listed on the London Stock Exchange and their price is affected by supply and demand. The investment trust can gain additional exposure to the market, known as gearing, potentially increasing volatility. This information is not a personal recommendation for any particular investment. If you are unsure about the suitability of an investment you should speak to an authorised financial adviser.

The latest annual reports, key information documents (KID) and factsheets can be obtained from our website at www.fidelity.co.uk/its or by calling 0800 41 41 10. The full prospectus may also be obtained from Fidelity. The Alternative Investment Fund Manager (AIFM) of Fidelity Investment Trusts is FIL

(UK) Limited. Issued by FIL Investment Services (UK) Ltd, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and

UKM0225/399910/SSO/0525

BP CEO’s hopedfor return to 2010 market value is a big ask

Big strategic reset greeted with a shrug by a sceptical market

Part of being a successful leader of a public company is managing expectations –setting achievable targets which you can tick off and, by doing so, build credibility with the market.

The under-pressure boss of oil and gas outfit BP (BP.) Murray Auchincloss will have been aware he needed to make a splash during a big strategy event on 26 February but telling the Financial Times he wants to get the market value back to its level before the Gulf of Mexico disaster in 2010 – so around $180 billion – by 2030 makes him a hostage to fortune.

Converted into sterling that is around £140 billion, more than double the current market capitalisation of £69 billion. Let’s be more generous, given the dollar has appreciated significantly against the pound in the interim, and assume he means the £119 billion the company traded at in sterling prior to the disaster.

GETTING BACK TO 2010 LEVELS LOOKS TRICKY

To use Auchincloss’ timeframe, if BP was to achieve this within five years, then by 2030 it would have to enjoy a significant re-rating (assuming no meaningful change in earnings) to 15 times from the current nine times forecast EPS (earnings per share).

This would be significantly richer than the levels its market-preferred US rivals are trading on and would be a pretty lofty multiple for any oil and gas company. After all, these businesses have inherently volatile earnings thanks to the underlying volatility of the price of oil and gas. Something over which they have little or no control.

Or, if it was to stay at the same rating, it would have to increase EPS from the $0.60 forecast by the consensus for 2025 to more than $1.03.

A blend of a more modest re-rating and smaller increase in EPS might just get it there, assuming some impressive execution, but Auchincloss’ big talk means anything less could be dressed up as a disappointment.

CAN BP IMPROVE RETURNS?

The shares actually fell as Auchincloss unveiled his recovery plan which suggests that as a roadmap to achieving the sort of recovery he envisages it fell short.

Most shareholders would probably settle for a simple improvement in the soggy total returns over the last decade, which work out at 4.4% on an annualised basis according to Sharescope. Given you can still get at least 5% from cash in the bank, that provides limited incentive to take on the risks associated with investing in BP.

As expected the strategic reset involved a further dismantling of the energy transition strategy outlined a little more than five years ago by Auchincloss’ predecessor Bernard Looney.

BP will no longer look to shrink its oil and gas production, investments in low-carbon energy will be scaled back and it plans to sell around $20 billion worth of assets by 2027. A strategic review of the Castrol engine oil business and the hunt for a new partner for the Lightsource BP solar power business are top of the agenda. Interestingly, share buybacks were slashed. This may reflect the need to get the balance sheet under control.

Though Berenberg analyst Henry Tarr notes that even if the company manages to reduce borrowings to $14-$15 billion by 2030, as planned, from the current $23 billion its levels of indebtedness would still be higher than its rivals.

The company is also targeting upwards of 20% compound annual growth in adjusted free cash flow out to 2027 and returns on capital employed of more than 16% by 2027.

Reportedly activist investor Elliott, whose presence on the shareholder register emerged earlier this year, is unimpressed with what has been announced – seeing it as lacking in urgency and ambition. It apparently wants BP to trim what it sees as a bloated workforce.

Even with the 5% cuts to employee numbers

already outlined by Auchincloss – its resulting roster of 80,000 staff would be higher than ExxonMobil’s (XOM:NYSE) 62,000 and the US company has a market value which dwarfs BP’s.

FOCUS ON CASH FLOW

For Berenberg’s Tarr the key will be delivering on the cash flow target. He says: ‘Free cash flow growth has three key drivers in our view: lower capex, a recovery in the downstream cash flow contribution, and then operating cost reductions.

‘We have high visibility on the capex, but the downstream recovery and cost reductions are harder to forecast given the partial reliance on a recovery in downstream margins. On a mediumterm view, BP will either need to drive growth in the upstream or pivot towards growth on a pershare basis rather than for absolute cash flow, in our view.’

The consequences if BP can’t win over the sceptics could be pretty seismic. Elliott is already after more dramatic change. Could this even include splitting up the downstream (refining) and upstream (oil and gas production and exploration) assets?

And if BP’s valuation remains depressed it may be vulnerable to a bid. Shell (SHEL) looks the most likely acquirer for cultural, regulatory and political reasons but whether it would be willing to take on what would be an extremely complex integration process while it is trying to get its own house in order is open to question.

By Tom Sieber Editor

Schroder AsiaPacific Fund –embracing a technology opportunity that extends well beyond AI

The diverse growth opportunity obscured by AI hype

The information technology (IT) sector performed strongly in 2024, driven in large part by excitement about recent breakthroughs in generative artificial intelligence (AI). With almost a third of its portfolio exposed to technology, the Schroder AsiaPacific Fund clearly benefited from the sector’s positive performance last year, but portfolio managers Richard Sennitt and Abbas Barkhordar are interested in it for reasons that extend well beyond AI.

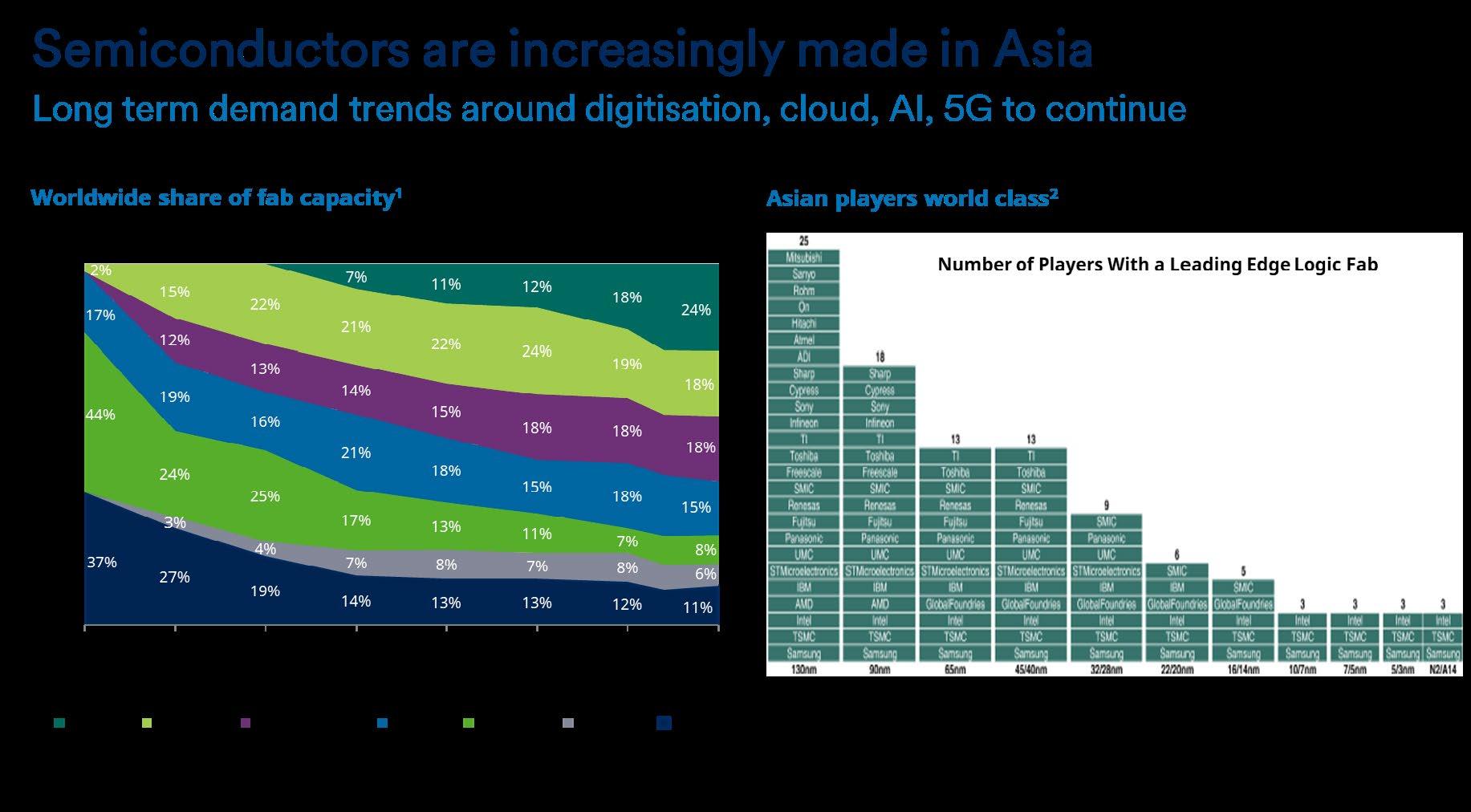

Semiconductor dominance

Over the last thirty years, Asia has become the dominant player in the global semiconductor manufacturing industry. Its powerful position stems from strategic foresight and visionary leadership. Governments in Taiwan and South Korea prioritised semiconductors as a critical industry, investing in research, infrastructure and education to build worldclass capabilities.

TSMC*, established in 1987 with support from Taiwan’s Industrial Technology Research Institute,

became a global leader through innovation and government-backed incentives, such as tax benefits and research grants. In South Korea, Samsung Electronics* grew within the country’s chaebol system, benefiting from favourable policies, including access to low-interest loans and infrastructure investment during the 1980s.

Cost competitiveness initially drew global firms to Asia, sparking a wave of Western outsourcing in the 1990s and 2000s that helped to cement the region’s leadership. Over time, Asia has developed sophisticated ecosystems of technical expertise and supply chain integration, positioning it as the cornerstone of global semiconductor innovation. The continent (including Japan) now controls approximately three-quarters of the global semiconductor market, with particular strength in the most advanced, leading-edge chips, where only three players are active – TSMC, Samsung and Intel. The two dominant Asian semiconductor businesses are significant holdings in the Schroder AsiaPacific Fund portfolio. Of these, TSMC is the largest holding and stands out as the world’s most efficient and innovative chip manufacturer.

AI and beyond – a broadly diverse growth opportunity

As semiconductors have become smaller, faster and more advanced, the role that they play in our everyday lives has grown exponentially. These critical components now power a vast array of devices and technologies, and the opportunity continues to expand. Inevitably, this has been, and remains, a long-term growth opportunity for the likes of TSMC, Samsung and other AsiaPacific Fund holdings such as Taiwan’s MediaTek*

Generative AI, which has captured a great deal of recent media attention, is one prominent example. The immense computational workloads required for machine learning have fuelled significant additional demand for cutting-edge chips. However, Richard and Abbas are equally excited about other transformative trends that are driving the market. For example, cloud computing, the roll-out of 5G mobile networks, digitisation and the ubiquity of the “internet of everything” – the seamless connectivity of devices, systems and processes, spanning everything from smart homes to industrial automation and urban infrastructure – are all creating new and growing demand for advanced semiconductors.

With Asia dominating the production of highperformance chips, companies like TSMC, Samsung and MediaTek are extremely well positioned to capture these structural growth drivers, while solidifying their roles at the forefront of this dynamic industry.

Avoiding the hype

While the potential of AI is undeniable, the hype surrounding it has prompted a degree of caution from Richard and Abbas. The portfolio managers have been keen to limit direct exposure to AI-focused stocks as the euphoria has grown, favouring broader IT themes that offer diversification and resilience, as well as more attractive valuations.

TSMC, for example, manufactures all of nVidia’s cutting-edge AI chips. It has performed exceptionally well as a result, allowing the managers to take profits on several occasions. But there is much more to TSMC than its AI exposure. Richard and Abbas view its valuation as fully justified given its outstanding quality and superb long-term growth prospects. Meanwhile, when compared to similar companies globally, its valuation remains relatively attractive.

Mindful of valuation risks, the portfolio managers are keen to ensure a sensible level of diversification, both in terms of the IT exposure and across the portfolio as a whole. A good example of this diversity is provided by another top ten holding – Indian IT services company Infosys* Although it is based in India, Infosys generates significant revenue from global markets, which provides it with multiple drivers of future growth. Its strong balance sheet, focus on innovation and track record of consistent execution further enhance its appeal as a reliable, long-term growth opportunity.

Also in the portfolio is Delta Electronics*, a Taiwanese company specialising in energy-efficient power and thermal management solutions. Its focus on industrial automation, renewable energy and electric vehicle components adds exposure to long-term structural growth trends that extend far beyond AI.

Navigating risks

Exports are a critical driver of earnings for Asian companies, not just in the IT sector but across many industries. In this context, one of the key questions facing investors is the potential impact of the new US administration’s trade policies, particularly the threat of increased trade restrictions and tariffs.

This is undoubtedly a risk, but Richard and Abbas draw some reassurance from history. Although there are clear differences between President Trump’s first term and now – not least, the starting level of interest rates and the geopolitical backdrop – it is worth remembering that similar policies were introduced last time and, despite that, Asia performed well as a region, albeit after an initial wobble.

Another potential headwind lies in currency markets. Discussions of fiscal loosening under Trump’s second term could lead to a “higher-forlonger” US interest rate outlook and, with it, a stronger dollar. Historically, a stronger dollar has often weighed on Asian market performance. However, it could be argued that much of this risk has already been priced in, given Asia’s underperformance since Trump’s election victory.

While there is always the possibility that policies play out differently or have a greater impact than expected, the managers see attractive opportunities from these levels, supported by the region’s long-term and increasingly diverse growth prospects.

Conclusion

Asia’s multiple growth drivers make it a region ripe with selective opportunities for active stock pickers. The Schroder AsiaPacific Fund reflects this and

benefits from a disciplined and forward-looking investment approach that has delivered strong results over time.

Information technology remains a standout area, offering enticing long-term growth prospects thanks to Asia’s dominance in semiconductors and the structural trends underpinning the sector. Portfolio managers Richard and Abbas are mindful of risks stemming from the market’s exuberance for the AI theme and are keen to ensure that the portfolio’s exposure to technology is diverse and focused on attractively valued, high quality businesses.

Beyond IT, the fund’s exposure to financials and some of Asia’s smaller but faster growing economies, ensures a broad and balanced portfolio that reflects the region’s vast potential. With a carefully constructed portfolio, the Schroder AsiaPacific Fund is well positioned to capture Asia’s long-term growth story and offers investors a compelling way to access this vibrant region.

[*] – Reference to stocks are for illustrative purposes only and are not a recommendation to buy or sell.

We recommend you seek financial advice from an Independent Adviser before making an investment decision. If you don’t already have an Adviser, you can find one at www.unbiased.co.uk or www.vouchedfor.co.uk. Before investing in an Investment Trust, refer to the prospectus, the latest Key Information Document (KID) and Key Features Document (KFD) at www.schroders.co.uk/investor or on request. For help in understanding any terms used, please visit address https://www.schroders.com/en-gb/uk/individual/ glossary/

MARKETING MATERIAL

Please remember that the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. For illustrative purposes only and does not constitute a recommendation to invest in the above-mentioned security / sector / country.

Schroder Unit Trusts Limited is an authorised corporate director, authorised unit trust manager and an ISA plan manager, and is authorised and regulated by the Financial Conduct Authority.

IMPORTANT INFORMATION

For help in understanding any terms used, please visit address www.schroders.com/en/insights/invest-iq/ investiq/education-hub/glossary/

We recommend you seek financial advice from an Independent Adviser before making an investment decision. If you don’t already have an Adviser, you can find one at www.unbiased.co.uk or www.vouchedfor.co.uk

Before investing in an Investment Trust, refer to the prospectus, the latest Key Information Document (KID) and Key Features Document (KFD) at www.schroders.co.uk/investor or on request.

Continuation votes are back on the agenda as investment trusts aim to appease investors

With Saba Capital having turned the spotlight on a handful of underperforming investment trusts, there is now a wave of activity as other trusts look for ways to reduce the persistent discount to NAV (net asset value) which has dogged the asset class.

Some have introduced ‘discount control’ mechanisms, others have launched share buybacks, and some have announced they will hold a ‘continuation vote’, but what exactly does the latter entail?

WHAT IS A CONTINUATION VOTE?

We wrote about continuation votes just over a year ago in late 2023 in the context of music royalty fund Hipgnosis Songs.

In a nutshell, while most listed companies have an indefinite lifespan, investment trusts – which invest in other stocks or asset classes instead of carrying on a business – have to give shareholders the choice of whether or not to continue trading depending on their circumstances.

Many trusts will have a provision in their Articles of Association allowing for a continuation vote to be held every three or five years at the company’s AGM (annual general meeting). However, some trusts also have ‘conditional

Average discount of investment trusts (ex 3i and VCTs) %

triggers’ which require them to hold a continuation vote if, say, their market value falls below a certain level or the discount to NAV (net asset value) is persistently wide.

If shareholders vote against continuation, the assets are sold, the cash proceeds are returned to shareholders and the company is wound up.

WHY ARE VOTES RELEVANT NOW?

According to the AIC (Association of Investment Companies), investment trusts as a group have traded at double-digit discounts since September 2022, or almost the last two and a half years, which is the longest since 1996.

The second-longest period was between August 1998 and October 2000 (27 months), while the

financial crisis saw double-digit discounts persist between September 2008 and September 2010 (25 months).

Excluding the sector’s big beast 3i (III), the current average discount is 14%, which is an improvement on the October 2023 low of 19% but still represents a headwind for investment companies which want to raise funds.

Previous periods of double-digit discounts have ended with those discounts narrowing, contributing to strong returns, as the AIC’s research director Nick Britton points out.

‘Discounts can spell opportunity when it comes to investment trusts. Our research shows that investing at double-digit discounts is generally good for your pocket, and that message has clearly got through to activist investors like Saba.

‘The current period of double-digit discounts has been long, but it can’t last forever. Previous periods like this have ended with some combination of market recovery and corporate activity – and there’s no reason to think this one will be any different.’

WHO IS HAVING A VOTE?

One of the first tests of 2025 comes on 24 March when Herald Investment Trust (HRI) holds a continuation vote at its AGM.

Herald, one of the trusts targeted by US activist hedge fund Saba, received an overwhelming vote in support of its current investment strategy at the requisitioned general meeting on 22 January.

However, as the requisitioned resolutions to