COMMERCIAL SERVICES PAGE 40:

ASSET/PROPERTY MANAGEMENT FIRMS

BROKERAGE FIRMS

CONSTRUCTION COMPANIES/GENERAL CONTRACTORS

ECONOMIC DEVELOPMENT CORPORATIONS

ENVIRONMENTAL/ENGINEERING FIRMS

COMMERCIAL SERVICES PAGE 40:

ASSET/PROPERTY MANAGEMENT FIRMS

BROKERAGE FIRMS

CONSTRUCTION COMPANIES/GENERAL CONTRACTORS

ECONOMIC DEVELOPMENT CORPORATIONS

ENVIRONMENTAL/ENGINEERING FIRMS

By Dan Rafter, Editor

For decades, the J.L. Hudson Department Store stood as the heart of downtown Detroit—a place where generations of Detroiters gathered to shop and dine. Now, that legacy is being reborn.

Bedrock in October officially unveiled Hudson’s Detroit, marking the completion of a 12-story, 400,000-squarefoot office building at 1240 Woodward Ave. in the city’s downtown.

The milestone is the first major phase of a 1.5-millionsquare-foot mixed-use development that will ultimately reshape Detroit’s central business district. Designed by SHoP Architects, the newly finished office component introduces state-of-the-art workplaces, retail, an event venue and a rooftop lounge slated to open in 2026.

The project’s second phase—a 45-story tower at 1208

Woodward Ave.—is scheduled for completion in 2027 and will feature The Detroit EDITION hotel and The Residences at The Detroit EDITION, adding luxury residential, hospitality and dining to the development’s mix.

A decade in the making

For Bedrock, the vision behind Hudson’s Detroit is about more than real estate. It’s about community.

“Ten years in the making, Hudson’s Detroit is elevating downtown and creating space for the community to come together,” said Dan Gilbert, Founder and Chairman of Bedrock. “Whether you are an office tenant, attending an event or shopping at one of the new retailers, everyone can experience Hudson’s. Through Nick Gilbert Way, we’re delivering a vibrant destination DETROIT (continued on page 20)

TVS project a boon to Iowa community – and proof that the state’s industrial market remains strong

By Dan Rafter, Editor

In a clear signal that the Midwest remains a hotspot for supply chain infrastructure, TVS Supply Chain Solutions in September cut the ribbon on a 225,113-square-foot, build-tosuit logistics facility in Waterloo, Iowa. IOWA

(continued on page 22)

No two problems are alike. Neither are their answers. Each requires a point of view. A new angle. Together, we’ll look for an integrated solution, guided by data and insights. We’ll gain a deep understanding of your business, and consider every part of your commercial real estate strategy, so you can realize anything.

BEST-IN-CLASS DESIGN-BUILD SOLUTIONS LOCALLY & NATIONALLY

ARCO provides turnkey solutions resulting in single-source responsibility, integrated design, and accelerated schedule. Our deep specialization and knowledge of the local Detroit, Michigan, and national markets empower us to anticipate challenges, streamline delivery, and drive consistent success on every project.

A new era for Detroit’s skyline?

That’s the goal of Bedrock’s Hudson’s Detroit: For decades, the J.L. Hudson Department Store stood as the heart of downtown Detroit—a place where generations of Detroiters gathered to shop and dine. Now, that legacy is being reborn.

TVS project a boon to Iowa community – and proof that the state’s industrial market remains strong: In a clear signal that the Midwest remains a hotspot for supply chain infrastructure, TVS Supply Chain Solutions in September cut the ribbon on a 225,113-square-foot, build-tosuit logistics facility in Waterloo, Iowa.

New hotel will be a major milestone in Chicago’s Pullman neighborhood: It’s been more than 40 years since a national brand has opened a new hotel in any of the Chicago communities located south of the city’s Hyde Park neighborhood. That is about to change.

Does September swoon mean future challenges for multifamily sector? The worst monthly rent performance in a September in more than a decade? That’s what Yardi Matrix reported in its most recent multifamily research report.

Thriving in a competitive market for eight decades: It’s what The Missner Group has done: It’s rare that a small business survives for 25 years. But to make it 80 years? That’s the rarest of feats.

Most employees approve of hybrid work: A new study says that employees have for the most part accepted back-to-the-office policies, especially hybrid schedules. That doesn’t mean, though, that all employees are complying.

The Chicago industrial market’s transition continues: The Chicago industrial market is still undergoing a phase of transition and transformation as the record amount of space delivered in recent years is absorbed.

23 million new doctor visits a year: Expect the demand for medical office space across the country to climb as the U.S. population continues to grow older.

Milwaukee’s The Avenue an example of mixed-use ‘lifestyle office markets’ that are outperforming competitors today: Office properties in busy mixed-use districts are outperforming the broader U.S. office market when it comes to leasing activity and vacancy rates.

Sales volume, prices on the rise in single-tenant net-lease retail market: The single-tenant net-lease retail market saw a busy first half of the year, with both sales volume and median sales prices on the rise, according to the latest research from Colliers.

Luxury retailers still seeing significant growth: Luxury retailers were riding high a year ago, having enjoyed several years of growth following the COVID-19 pandemic. Today? New headwinds have hit this slice of the retail sector.

Detroit Suburban State of the Market

St. Louis Commercial Real Estate

The Midwest’s commercial real estate publication, providing useful, unbiased and accurate coverage of the industry and its professionals since 1985.

WWW.REJOURNALS.COM

Publisher | Mark Menzies menzies@rejournals.com 312.933.8559

Editor | Dan Rafter drafter@rejournals.com

ADVERTISING

Vice President of Sales & MW Conference Series Manager | Ernest Abood eabood@rejournals.com

Vice President of Sales | Frank E. Biondo frank.biondo@rejournals.com

Classified Director | Susan Mickey smickey@rejournals.com

Director, National Events & Marketing | Allison Kim Allison.kim@rejournals.com

Midwest Real Estate News brings real estate leaders together to explore the challenges and opportunities unique to their markets.

Editor’s

Multifamily market check-in: Where we stand in H2 2025 36 Unlocking Hidden Value: Transforming Industrial Properties into High-Performing

ADDRESS

7767 Elm Creek Boulevard, Suite 210, Maple Grove, MN 55369

Midwest Real Estate News® (ISSN 0893-2719) is published bimonthly by Real Estate Publishing Corp., Oak Park, Il 60301 (rejournals.com). Current and back issues and additional resources, including subscription request forms and an editorial calendar, are available on the internet at rejournals.com.

W. P. Carey (NYSE: WPC), one of today’s largest net lease REITs, provides long-term sale-leaseback and build-to-suit capital solutions for companies in the U.S. and Europe. With offices in New York, London, Amsterdam and Dallas, the company remains focused on investing primarily in single-tenant, industrial, warehouse and retail properties under long-term net leases with built-in rent escalations.

Why W. P. Carey?

• 50+ years of experience

• Diversified, net lease investor

• All-equity buyer

• Certainty of close

• Cross-border, multi-party capabilities

• Ability to work with all credits (public and private)

By Dan Rafter, Editor

Niche real estate types have long thrived in the broader industrial market, with categories such as cold storage and specialized manufacturing rising and falling in cycles. But in recent years, one of the fastest-growing subsectors has been industrial outdoor storage (IOS), according to CommercialCafe’s September National Industrial Report.

The sector’s growth has been fueled by its low costs and flexibility, offering solutions at a time when supply chain disruptions and shifting trade policy have pressured occupiers to maximize efficiency. As CommercialCafe says in its report, IOS facilities serve a range of uses, from overflow storage and vehicle parking to bulk material yards and infill locations, making them increasingly attractive to tenants and investors.

Supply, however, has not kept pace. Zoning constraints and the frequent redevelopment of IOS sites into higher-value properties have limited availability. That imbalance has driven rents sharply higher, according to CommercialCafe. Newmark reports that IOS rents have surged 123% since 2020, with inland hubs such as Memphis, Atlanta and Phoenix among the hottest markets.

Historically, most IOS properties have been privately held with non-standardized pricing. But institutional players are beginning to take a larger stake. PwC estimated the IOS market at about $200 billion in 2023, with $1.7 billion raised that year alone. Since then, activity has accelerated.

This year, Peakstone Realty Trust acquired a 51-asset IOS portfolio for $490 million, while Barings and Brennan Investment Group launched a joint venture targeting $150 million in IOS investments. Realterm also purchased a 13-property portfolio for $277 million. Analysts expect the asset class to become increasingly institutionalized, with standardized pricing models and growing confidence among lenders.

Still, challenges remain. As CommercialCafe says in its report, local governments and residents often push back against IOS developments, constraining supply even as new demand drivers emerge. Analysts note that future growth could come from the storage needs of technologies such as drone delivery systems and autonomous trucks.

The broader U.S. industrial market remains solid. CommercialCafe reported that in-place rents reached $8.66 per square foot in August, up three cents from July and 6.1% higher yearover-year. Developers are also pressing ahead: 338.3 million square feet of industrial space is under construction nationally, representing a projected inventory increase of 1.6%. By the end of August, 205.4 million square feet

had already been delivered this year.

Manufacturing projects represent 28% of the pipeline, though they have accounted for just 14% of new starts since early 2023, according to CommercialCafe. That’s because manufacturing facilities take longer to complete than logistics projects, keeping them in the pipeline longer. After peaking in 2024, new manufacturing development has slowed considerably. Between 2021 and 2024, about 200 million square feet of space broke ground, but starts so far this year total less than 20 million square feet.

The slowdown is reflected in investment data. The U.S. Census Bureau reported annualized manufacturing construction spending of $223.1 bil-

lion in July 2025, down 7% from the record set in August 2024. Even so, spending remains more than triple its 2020 levels.

Industrial property sales reached $43.2 billion through August, averaging $137 per square foot. Notable deals include LG’s $2 billion buyout of GM’s stake in their Ultium Cells battery plant in Lansing, Michigan. The 2.8-million-square-foot facility is set to produce electric vehicle batteries, though GM has scaled back EV production amid softer demand.

Still, momentum in the EV sector persists. Toyota recently placed a $1.5 billion battery order, and GM continues to back plants in Ohio and Tennessee.

TPG AG Net Lease Real Estate actively seeks investments including net leased properties, sale-leaseback transactions, and forward take-outs of development projects. We are focused on transactions between $25–$500 million across North America and Western Europe. Our approach is flexible and creative across property types and tenants. Recent transactions include:

Million

Single-campus sale-leaseback with an investment grade public technology company

Purchase and leaseback of food grade facilities in connection with multiple corporate aquisitions

$62 Million $231 Million

Take-out financing for corporate headquarters development

Industrial portfolio sale-leaseback with a building products company

GORDON WHITING

Co-Head & Co-Portfolio Manager (212) 883-4157 gwhiting@tpg.com

SAMARTH ARORA

Vice President +44 207 758 5431 sarora@tpg.com

CHRIS CAPOLONGO

Head of Acquisitions (212) 692-2161 ccapolongo@tpg.com

PAUL LEWIS (Europe)

Managing Director +44 207 758 5333 plewis@tpg.com

Sale-leaseback and bolt-on acquisition for large private equity sponsor

$246 Million

Portfolio acquisitions of mission-critical private agricultural equipment dealer

SCOTT SOUSSA

Co-Head & Co-Portfolio Manager (212) 692-7905 ssoussa@tpg.com

CHRISTIAN BLANKE

Director (212) 883-4161 cblanke@tpg.com

NICHOLAS GRACE

Director (646) 634-0286 nmgrace@tpg.com

MICHAEL MINTSKOVSKY Vice President (212) 883-4188 mmintskovsky@tpg.com BENJAMIN L. YETERIAN Vice President (212) 692-7997 byeterian@tpg.com

By Dan Rafter, Editor

It’s been more than 40 years since a national brand has opened a new hotel in any of the Chicago communities located south of the city’s Hyde Park neighborhood.

That is about to change.

That’s because the Pullman Hotel Group is set to bring a nationally branded Hampton by Hilton Hotel to Pullman, a $30 million, 101-room hotel that will serve visitors to Chicago’s Pullman and Roseland communities.

When construction is complete, the Hampton will be the first nationally branded hotel developed in Chicago’s Pullman community.

Construction is expected to begin in early 2026, with the hotel opening in either late 2026 or early 2027. The Chicago Plan Commission earlier this month approved the development.

Antony Beale, alderman for Chicago’s 9th ward, said that the hotel is just the latest step in a years-long economic investment in the Pullman/Roseland areas.

“This builds on everything that we have done over the years,” Beale said. “This will just add to the new jobs and opportunities we are seeing in this community. It will be the perfect addition to the restaurants and industrial buildings that have already opened here, an addition to the thousands of jobs that have already been created here.”

The Pullman area has seen plenty of investment during the last several years. This includes the opening of the Pullman National Park’s Visitor Center and the Pullman State Historic Site.

The historic site includes the neighborhood’s famous clock tower and administration building, while the national park covers the entire Pullman community, celebrating its history as the United States’ first planned industrial community.

The neighborhood has also seen the opening of the 180-acre Pullman Park that is home to two SC Johnson and Gotham Greens industrial facilities, a Whole Foods Midwest Distribution Center and Amazon delivery center. Several new restaurants and retail centers have recently opened in the

neighborhood, too, including the first Chick-fil-A in Chicago’s South Side, Potbelly Sandwich Shop, Culver’s and Lexington Betty Smokehouse.

“People are coming from all over to visit Pullman with the national park and historic site,” Beale said. “It has become a destination, a place for recreation and a place for people to eat and drink in the community. There is shopping here. The only piece we were missing was a place for people to lay their heads. Soon they will be able to stay in the community when they visit.”

Why has it taken so long for Pullman to get a new hotel? The answer is complicated. But Beale said that the Pullman and Roseland area suffered a void for many years with businesses leaving the city’s South Side.

As that changed, and the businesses returned, it boosted foot traffic and spending in the communities. That in turn made the area once again attractive to a national hotel brand.

“Businesses are coming because they see the traffic rising here,” Beale said. “They see the void that needs to be

filled. We have created a positive atmosphere in the area, and we are seeing the results of that.”

The Hampton might not be the only new hotel opening soon in the area, either. Beale said that he and local officials are looking at adding at least one more new hotel to the community after the Hampton opens.

“We did a market analysis. We can support two hotels here, no problem,” Beale said.

The new Hampton will be 62,000 square feet and rise four stories. It is being built at 111th Street and Doty Avenue along Interstate-94 and the Bishop Ford Expressway. Beale said that the hotel is projected to create 25 new jobs once it opens.

The hotel will feature a business center, exercise room, indoor pool and on-site surface parking. The Pullman Hotel Group is using a Chicago Recovery Grant to assist with buying the property on which the hotel will sit from Chicago Neighborhood Initiatives.

By Dan Rafter, Editor

The worst monthly rent performance in a September in more than a decade? That’s what Yardi Matrix reported in its most recent multifamily research report.

According to Yardi Matrix’s September Multifamily National Report, the average advertised apartment rent in the United States fell $6 to $1,750 a month in September. At the same time, yearover-year multifamily rent growth fell 30 basis points to just 0.6%.

That drop of $6 might not seem like much. But the fall in advertised rents represented the worst September showing in more than a decade. The U.S. multifamily market hasn’t seen a decline in average asking rents this large in a September since 2009.

Yardi Matrix said that in markets with too much new multifamily supply, building owners are offering concessions or cutting advertised rents to attract tenants.

That said, U.S. multifamily monthly rents are still close to all-time highs. Because of this, Yardi Matrix said that it is too soon to say that the September decline is part of a trend.

And it’s not just multifamily rents that fell in September. Yardi Matrix reported that single-family build-to-rent advertised rates fell during the month, too. The average build-to-rent advertised monthly rent dropped by $15 in September to $2,194, while the yearover-year growth rate fell 60 basis points to a flat 0.0%.

A key factor for the multifamily market’s rental fall? Yardi Matrix said that more than 525,000 apartment units are in the lease-up phase across the country. That intensifies competition among properties. Markets with the weakest rent growth are often those with the deepest pipeline of units in the lease-up phase.

An example is Dallas, which has 35,000 apartment units in lease-up, representing 3.8% of its multifamily stock. Phoenix has 22,000 units in lease-up, equal to 5.9% of its multifamily stock,

while Austin, Texas, has 18,000 units in lease-up, which is 5.5% of its multifamily stock.

Some Midwest markets are bucking the trend of falling apartment rents, though. Yardi Matrix said that Chicago’s average asking apartment rent rose 3.9% in September on a year-over-year basis while that figure stood at a healthy 3.4% in the Minneapolis-St. Paul market.

Rent growth, though, remained negative in Austin, Texas, where the average advertised monthly rent fell 4% this September when compared to the same month a year ago, and in Dallas, where the advertised rent dropped 1.9% this September compared to the same month in 2024.

The national occupancy rate fell slightly to 94.7% in August, but was unchanged year-over-year, according to Yardi Matrix’s report. The Twin Cities market posted one of the largest increases in occupancy rates with a jump of 0.6% in August.

Short-term rental trends were less positive for some Midwest markets. In

Detroit, the monthly advertised asking rent fell 0.4% from August to September. In Chicago and Columbus, advertised monthly rents fell 0.5% in September when compared to August.

Senior Vice President, Midwest Operations

Year-over-year rent growths were solid in many Midwest markets, though. In the Cleveland-Akron area, monthly advertised rents jumped 3.2% this September when compared to a year earlier. That figure stood at 3.1% for Cincinnati, 2.1% for St. Louis, 2% for Milwaukee and 1% for Louisville.

Jason is a seasoned facility services executive with deep industry expertise in client engagement and operational excellence “We could not be more excited to have Jason on board,” said UG2 COO John Correia “He knows the industry, he knows the region, and he is the ideal leader for this moment, as UG2 expands our footprint and deepens our relationships across the Midwest.”

Based in the company’s new regional office in Minneapolis, Jason will oversee operations within UG2’s Midwest Region He will support business development activities and expand UG2’s impact through vital, lasting customer partnerships

By Dan Rafter, Editor

It’s rare that a small business survives for 25 years. But to make it 80 years? That’s the rarest of feats.

But it’s one that Des Plains, Illinois-based general contractor and real estate developer The Missner Group has accomplished.

The Missner Group is celebrating its 80th anniversary this year. Irving Missner founded the company in 1945. He steered the company until 1975, when his son Judd Missner took over.

Today, Irving Missner’s grandsons, Barry Missner, chief executive officer, and Glen Missner, president, co-lead the company. The two are continuing The Missner Group’s history of success in the Chicago market. Since its founding, the company has taken on more than $3 billion in construction projects and developed more than 20 million square feet of real estate projects in the Chicago market.

We recently spoke with Barry Missner about the company’s success and its bright future. Here is some of what he had to say.

What are some of the reasons for The Missner Group’s success?

Barry Missner: I don’t have a great answer for you. There is not a magic sauce that allows a business to succeed. You always hear that the first generation starts a business, the second generation grows it and the third generation blows it. Thankfully, we’ve avoided doing that.

It’s been a slow climb for us. I can’t identify a turning point or a transformative moment where it became clear that the business was going to succeed. For us, success has been a long hike. Perseverance is the word that I might use. We are always focused on grinding and getting better at the things that we have been doing for a long time.

You could say that we had a big moment in the ‘70s. up until then, we had been a contractor. In the ‘70s, we transitioned into an integrated real estate company. From the ‘70s on, we switched from a builder to a real estate company and developer. We became a bigger, more accomplished and better version of ourself.

My father was the one who initiated that change. That moment of diversifying from construction to construction and real estate expanded our business to more areas. My father thought that we should get involved in the development business. He was able to make this move with the help of some mentors in the business who helped him on the execution side. Now we are a real estate company that develops, manages and leases real estate.

How has The Missner Group grown over the years?

Missner: Right now, we have about 24 employees. We are still a small company. When I started here in 1991, we had a staff of six. It’s been a slow build over the years. Maybe that is the secret of our success: We didn’t get too big, too fast.

What are some of the memorable projects that you and The Missner Group have worked on over the years?

Missner: There are some projects that stand out for me. One is the first development that I oversaw, in Buffalo Grove. It was maybe 13 acres and three buildings, which were all small buildings by today’s standards. But it gave me the

chance to go through the full soupto-nuts entitlement process. That was in 1995, and it was impactful for me. It was the first time I’d overseen a project. I felt like I didn’t know what I was doing. Seeing it come to completion successfully was a great feeling.

There was another project in 2003. We developed a building in Niles. It was a substantial project, costing $25 or $30 million, a big deal for that time. We had to find an institutional equity partner. That was a new kind of capitalization for us. We went beyond our comfort zone with a much bigger construction loan. It was a step up for us. It showed us the size and scope of projects that we could do.

The projects in the city are always impactful, too. They involve a lot of blood, sweat and tears. The challenges of developing on an infill lot are significant. Then you layer on the complexities of working with the city and it makes the challenges even greater. But there is a feeling of satisfaction when you complete projects like that.

What kind of impact on the Chicago market have your projects had?

Missner: We are building warehouses. They provide an economic engine for the city. These projects employ people. We are not building hospitals, of course. There are different types of property that might have a greater impact on the city and its surrounding communities. But if I showed you the sites that we’ve worked on, you’d se that we’ve left them in far better condition than they were when we arrived. There is a great deal of effort involved in cleaning up a site. Development provides jobs, tax revenue and an economic engine for the city.

On our latest project, we spent $6 million remediating environmental contamination. We cleaned up the site and developed a new building. There is no denying that this is a positive for that site.

How has The Missner Group kept a steady stream of new business coming?

Missner: The business is very competitive. You have to work constantly to keep the jobs coming. Our customers often are not repeat customers. If someone has a good experience with us, they might tell a friend that if Missner makes an offer, you should consider working with them. But to succeed, you must continue to create opportunities. We aren’t selling widgets where if the price is right and customers like us, we’ll continue to get business. We must constantly find new customers.

We rely on our reputation. We do what we say we are going to do. I have 30-plus years of relationships with brokers that I rely on to get a seat at the table. We have an established history. We get credibility from clients for going through the process so many times.

What changes have you seen in the local commercial real estate business during your time at The Missner Group?

Missner: The city was much sleepier as a real estate market early in my career. There weren’t a lot of companies developing warehouse projects. Development

“The risk comes from the uncertainty and the upfront costs. The developer takes on the risk in pursuing the development.”

and real estate investment have become more competitive and more complicated, especially development. You must deal with more requirements. It is more costly and time-consuming.

When I worked on that first entitlement deal in Buffalo Grove, we had to get a zoning change, extend a right-of-way and annex property from Lake County. It wasn’t overwhelming. It probably took about three months. It wasn’t free, but it wasn’t a huge cost. That has completely changed. That process might be six to 12 months now. And the cost is much higher.

The risks we take are higher today. When you spend all that money and do all that work, there is still no guarantee that it works out in the end. The timeline is longer and the market changes. The village you are working with might ask for concessions that make the project no longer economically feasible. The big gest changes are the time and risk and money that development requires today versus 25 years ago.

The risk comes from the uncertainty and the upfront costs. It’s not guaranteed that you’ll get the zoning you need, for example. The economic risk falls on the developer. The developer takes on the risk in pursuing the development.

How do you reduce this risk?

Missner: We look at every potential proj ect very closely. You don’t know how the market might look in six months when you finally break ground on a project that you start working on now. If you want to develop something, you have to make the decision now, even though you can’t be certain of what the market will look like in six months. You must do your research and manage the risk as best you can. It is very difficult. Anyone who tells you that they never lose money in this

business is not doing a lot of real estate deals.

How strong is the local industrial market now?

Missner: We develop shallower-bay projects, infill locations that are more immune to the softening we’ve been seeing in industrial leasing activity. Throughout the first half of 2025, there has been slower leasing activity in all phases of the industrial sector, but activity is softer with the bigger buildings.

We have also seen less negative impact on rent growth with infill developments. Even though we had been seeing slower leasing, we were still seeing rent growth in those infill markets.

Leasing activity is starting to pick up. We are optimistic that if leasing continues to pick up, the market will be strong because rents haven’t fallen significantly.

Are there projects that The Missner Group is working on now that you are especially excited about?

Missner: We have broken ground on our industrial project at 4002 S. Princeton in the Stockyards area of Chicago. Construction is about 40% complete. That project required a great deal of predevelopment work, two-plus years of that. We also have some other projects that are earlier in the pipeline. It is too early to discuss those projects, but we are seeing more opportunities in the market today.

The capital is coming back into the market. It is getting better. We think we will be converting more ideas into actual projects.

By Dan Rafter, Editor

Anew study says that employees have for the most part accepted back-to-theoffice policies, especially hybrid schedules. That doesn’t mean, though, that all employees are complying when their companies mandate that they return to the office, whether that mandate is one to two days a week or four to five.

That’s one of the main takeaways from JLL’s Workforce Preference Barometer 2025, a report studying the state of the global workforce.

Another key finding? Most employees told JLL that they are more interested in maintaining a solid work-life balance than they are in a higher salary. This means flexibility: Workers want the flexibility to work remotely when it makes sense and to work non-traditional hours if it results in benefits such as a shorter commute to work.

Others who are caring for children or elderly parents want a schedule that allows them to tackle these caregiving duties even if they arise during normal

working hours, as long as they can complete their duties during non-traditional working hours.

Researchers compiling this year’s JLL’s Workforce Preference Barometer surveyed 8,700 office workers in 31 countries. These respondents worked at companies that each employed more than 1,000 staffers in sectors including finance, technology, manufacturing and public services.

JLL’s survey found that 65% of respondents listed work-life balance as their top priority, ahead of salary. This is evidence of how important it is for companies to provide their workers with a work schedule that does give them the chance to spend time with their families or enjoy downtime away from the office.

“We have been publishing this barometer for several years, and the statistic that stood out to me this time was the importance that employees place on flexibility and work-life balance,” said Peter Miscovich, executive managing director, global future of work director

for JLL. “What we are seeing is that with the accelerated pace of change, accelerated rate of tech adoption, the post-pandemic stressors in the marketplace and uncertainty about the economy, is that people are really looking for greater time flexibility and work-life integration if not full balance.”

Miscovich said that survey respondents said that they want a greater level of autonomy when it comes to their work schedule. They want time to disconnect from their work.

“There is still that always-on workplace mentality that is prevalent today,” Miscovich said. “The high levels of stress and the burnout of multiple cohorts is pervasive. That finding in the barometer supports what we are seeing in the marketplace today. People are feeling stress. We will see if this changes, but it does seem to be part of our new normal.”

Some employers, though, are taking steps to improve the work-life balance of their workers.

Miscovich said that it is important for companies to consider the needs of different workers and to ask them what they need from their work schedules. As Miscovich says, the most successful hybrid work schedules consider input from employees on when they need and don’t need to be in the office.

A manager, for instance, might need to be in the office four days a week while a programmer might only need to be on-site one day a week. Maybe both types of employees need to be in the office when on-site meetings or brainstorming sessions are scheduled.

Other employees might be taking care of both young children and elderly parents. These workers might need to take time off during the day, something that employers can allow if these workers can complete their tasks during non-traditional hours.

Other employees might face long commute times if they must work a traditional 9-to-5 schedule. Companies might allow these workers to come into the office earlier and leave

earlier or get to their desks later in the day and work past 5 p.m.

“Employers should look at the individual cohorts within an organization and ask them what they need in terms of autonomy,” Miscovich said. “If the output is there and the company’s objectives are being met, providing this flexibility can be a win-win for everyone. When companies can execute this, that is where we see the greatest success.”

The study reported that 66% of global office workers say that their company sets clear expectations for the number of days that they are expected to work on-site. The survey found, too, that 72% of respondents viewed these back-tooffice policies positively.

Of those employees with this positive view, 50% said that being in the office at least on a hybrid basis supports better teamwork. A total of 43% of these respondents said that they prefer working in the office to working remotely and 35% said they view hybrid policies as being fairer to all employees.

Miscovich said that those in favor of hybrid policies said that they appreciate the chance to be both visible in an organization and the opportunity to work off-site.

“People are looking for workplace variety and balance,” Miscovich said. “Working seven days a week nonstop is not healthy. If you create the conditions that allow enough flexibility for workers, those are the work arrangements that earn the most positive acceptance.”

As Miscovich says, workers want a positive experience when they go to the office. They want to be able to use a conference room if they need one. They want the technology that makes it easier for them to complete their work. They want the opportunity to grab a quick cup of coffee if they need a break from work.

“They are looking for a higher-quality experience in the office,” Miscovich said. “If companies can provide that, it’s a nice win-win-win opportunity.”

The challenges

But what about those workers who don’t view their companies’ back-tooffice policies favorably? JLL said that 40% of them said that they believe

“Working seven days a week nonstop is not healthy. If you create the conditions that allow enough flexibility for workers, those are the work arrangements that earn the most positive acceptance.”

they will be less productive on the job if they are not able to choose their preferred work setting.

Those employees who don’t have a positive view of their companies’ hybrid policies told JLL that they are less concerned about having to return to the office than they are about a lack of company support that would otherwise make in-office work a comfortable and worthwhile experience.

The JLL survey found that 55% of respondents who had have negative views on hybrid policies are concerned about their quality of life. A total of 42% said they had feelings of being stuck in their job and 41% said that they felt let down by their companies’ return-to-office plans.

Not all workers follow their companies’ hybrid plans, of course. JLL found that compliance ranges from 74% in the United States to 85% in Europe, with compliance rates above 90% in Italy and France.

Consider companies that mandate that employees work one to two days in the office every week. JLL found that 68% of respondents at such companies did work the required one to two days. A total of 19% routinely worked three to four days in the office and 7% regularly worked all five weekdays in the office. However, 5% of respondents continued to work fully remote despite their companies’ back-to-office mandates.

For companies that mandated employees to work three to four days a week in the office, JLL found that 70% of survey respondents did follow that mandate. A total of 12% worked fulltime in the office. But JLL found that 17% routinely worked only one to two days in the office while 1% remained fully remote.

And for respondents whose employers have mandated that they work fulltime in the office? According to the study, 82% of these respondents said that they followed this mandate. A total of 10% of respondents said that they routinely worked three to four days in the office, 5% said that they routinely worked one to two days in the office and 2% said that they remained fully remote.

In its study, JLL said that companies can take steps to increase in-office compliance from workers. Companies should personalize the work experience, recognizing that older employees with more experience might not need to come into the office as frequently as their younger peers. Some employees, depending on the work that they do, can perform more of their tasks remotely.

JLL said that companies should reserve much of employees’ in-office time for

tasks such as meetings, brainstorming sessions and other work that can only be done on-site.

Also important? Taking a more holistic approach to creating an inviting workspace. This means not only providing an office space with amenities such as onsite fitness centers, healthy food options and quiet spaces for creative work, but also providing employees with the option to work non-traditional hours, take time off to care for children or elderly parents or even take a mental break if they face possible burnout.

Employees with a positive view of their work schedules tend to work in environments in which the business’ needs are balanced with employee wellbeing.

A total of 50% of employees who are in favor of their companies’ hybrid policies say that being in the office at least part time supports better teamwork. A total of 71% of survey respondents who viewed their companies’ hybrid policies favorably said that their companies are a great place to work.

Miscovich said that companies that want to persuade their employees to come into the office a greater number of days need to provide an office space that is enticing.

“If employers want to be competitive in attracting great talent, and they want that talent to come into the office three days a week, they need a great workplace environment,” Miscovich said. “Employees are looking for that high-quality building, that high-quality workplace design. They want a building with sustainable practices and energy management. This trend will continue.”

By CommercialCafe

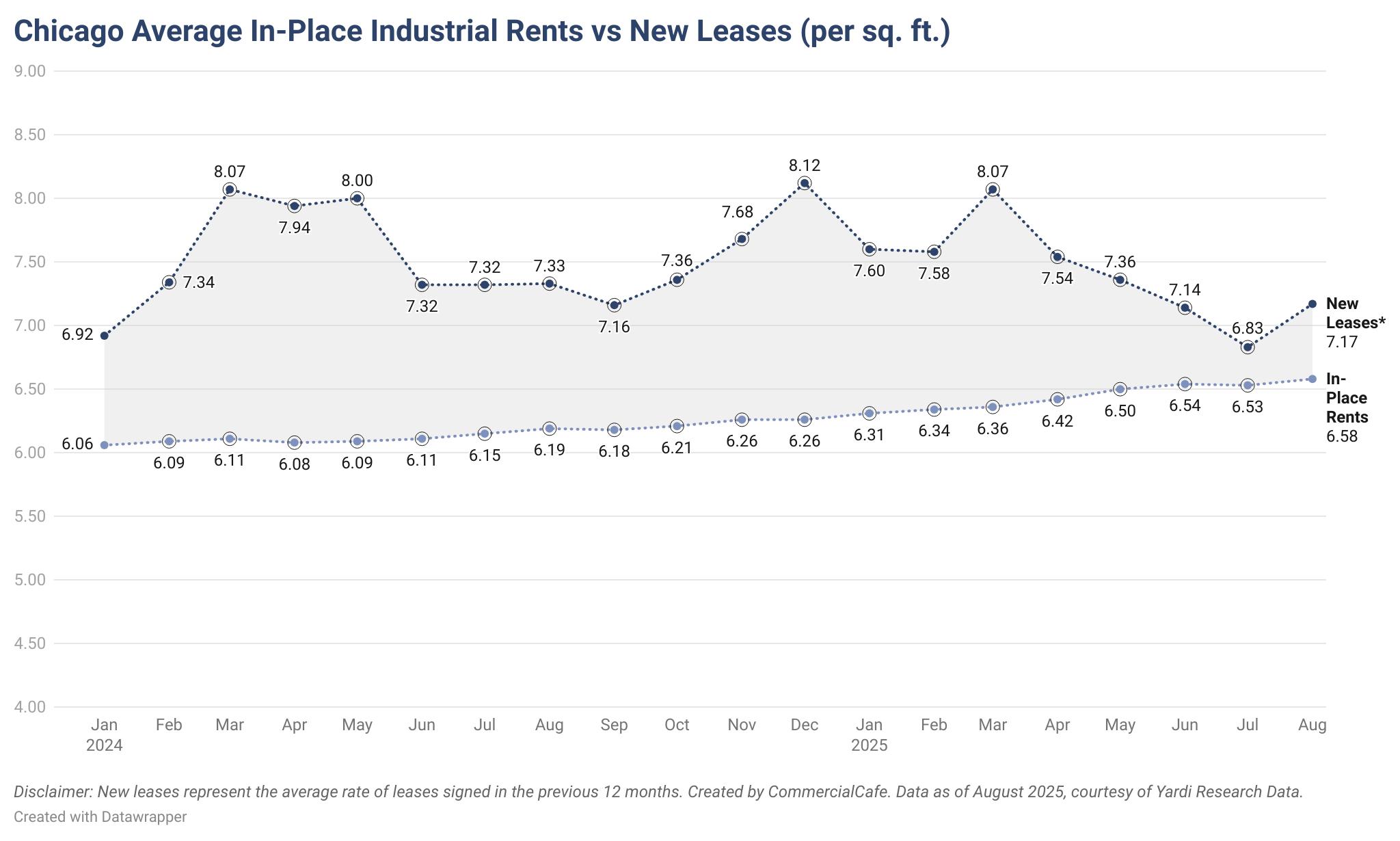

• In-place rents for Chicago industrial space averaged $6.58 per square foot compared to a national average of $8.66 per square foot.

• New lease premiums are flattening out in Chicago, with leases signed in the last 12 months being only 59 cents per square foot more expensive than existing leases.

• Transactions remain healthy but may be reaching a plateau with $1.78b volume so far this year, down 5% compared to 2024.

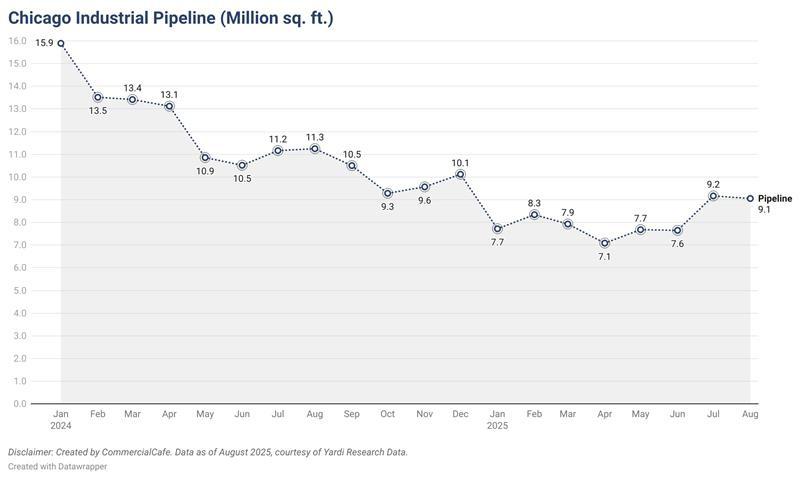

• The market has 9 million square feet of space in the pipeline, reflecting the ongoing cooldown period after a red-hot start to the decade.

The Chicago industrial market is still undergoing a phase of transition and transformation as the record amount of space delivered in recent years is absorbed. While attitudes generally tend toward wait-and-see, rent growth continues at a measured pace even as sales and development hit the brakes.

In-place rents for industrial space in Chicago averaged $6.58 per square foot at the end of August, placing the market among the 10 most affordable nationwide. The current rate is $0.05 above the average rate in July and represents a 7.2% increase compared to August 2024, slightly above the national rent growth of 6.8%.

With just two months in the last year with negative rent growth and measured increases in the remaining months, prices are normalizing in the market following the double-digit spikes of 2022-2023. This is best evidenced by the fact that leases signed in the last 12 months average $7.17 per square foot, only $0.59 more per square foot compared to all in-place leases. Current figures showcase a gradual decrease in new lease premiums from $1.19 per square foot one

year ago and from $1.45 in August 2023, indicating that the market’s rental rate growth is evening out after several years of rapid expansion and tenants may be getting the upper hand in lease negotiations.

Industrial property transactions are mostly keeping pace in Chicago, which in itself is an outlier as sales have been elevated in other major markets so far in 2025. Year-to-date sales through August total $1.78 billion in Chicago for the fifth-highest sales volume na-

tionwide. However, this figure marks a 5% dip from the $1.86 billion recorded at the same time last year. Meanwhile, year-to-date sales in Dallas-Fort Worth are up 34% annually — $3.95b this year compared to $2.95 billion last year — while industrial transactions in New Jersey are 45% more elevated compared to 2024.

Chicago still holds a comfortable lead over other regional entries such as Minneapolis ($907 million), Columbus ($864 million) and Indianapolis ($439 million).

Properties in Chicago traded for an average of $94 per square foot, significantly lower than the national average of $137 per square foot. This affordability is in line with larger regional trends, as the region’s average sale prices for industrial properties ranged between $105 per square foot in Minneapolis and $51.2 per square foot in Cleveland. As such, Chicago remains an attractive option for investors looking for value-add opportunities or those looking to establish themselves in a major industrial hub with accessible price points.

Chicago also maintains the Midwest’s largest development pipeline with just over 9 million square feet currently under construction. This space stands to expand the local inventory by approximately 0.8%, with an additional 1% expansion in the works

from properties currently in the planning stages.

The largest property currently in the pipeline is the 1.3-million-squarefoot facility in DeKalb dubbed “Project Midwest” which will encompass manufacturing as well as warehouse space. Two more properties larger than 1 million square feet are also being built: the Plainfield Logistics Center as well as a warehouse at 21012 W. Mississippi St. in Elwood.

“DarwinPW has been focused on industrial real estate for over 45 years. You could say it’s in our DNA. As times change, we stay ahead of them by developing new tools and skill sets to help the people we serve.”

For over 45 years, Darwin Realty has been a leader in industrial and commercial real estate. The company specializes in brokerage, property management, investment and development services primarily in the Midwest. Darwin’s highly qualified professionals are problem solvers and utilize a breadth of tools and knowledge to serve our clients best.

Chicago’s pipeline is currently the sixth-largest nationwide, ahead of other major markets such as New Jersey (6.08 million square feet) and Los Angeles (4.87 million square feet). At the same time, the current stock under construction is 12% less than the pipeline in August 2024 and much lower than the peak of 33 million square feet in late 2021.

This development downturn is in line with national trends as space

from the construction glut earlier in the decade is still being absorbed, leading to elevated vacancy rates and making new investments less appealing for developers. Markets such as Phoenix and Philadelphia saw their pipelines halve in the last year, with the Texas Triangle being one of the few regions nationally where development is trending up once more.

As Chicago’s industrial market continues to recalibrate with moderate rent growth and selective development, investors may continue to find more appeal in purchasing well-positioned but affordable properties. Chicago’s enduring logistical advantages suggest that the market will be well-positioned once vacancies stabilize and new leases increase in price, leaving the door open for further growth once the readjustment phase is completed.

for people to gather, ideas to spark and memories to be made. This is only the beginning for Hudson’s.”

That public plaza, Nick Gilbert Way, named in honor of Gilbert’s late son, will debut Nov. 6, connecting Woodward Avenue to Farmer Street. The space will feature live music, art installations, retail pop-ups and year-round programming beginning this holiday season.

The plaza’s anchor, Un Deux Trois, a French-inspired coffee truck from Midtown’s Café Sous Terre, will serve pastries and espresso daily.

A modern workplace in the heart of Detroit

The newly completed 12-story office building brings Detroit a next-generation workplace designed for collaboration and flexibility. The space features panoramic skyline views, open layouts and a seven-story atrium filled with natural light and plenty of greenery. Its crowning feature, a skylight inspired by the headlight cover of a 1954 Corvette,

“Whether you are an office tenant, attending an event or shopping at one of the new retailers, everyone can experience Hudson’s. Through Nick Gilbert Way, we’re delivering a vibrant destination for people to gather, ideas to spark and memories to be made. This is only the beginning for Hudson’s.”

is a nod to the city’s deep automotive roots.

Amenities include The Atrium Café, serving healthy meals and drinks; The

Rec Room, designed by Detroit-based Pophouse, which features a lounge, library, pickleball court and kitchenette; and a Sports Suite with a multi-sport simulator. The property also includes a

fitness center, training rooms, underground parking and access to meeting and event space at The Department at Hudson’s, a 56,000-square-foot venue that debuted in spring 2025.

That venue has already hosted major events such as Global Citizen NOW, Crain’s Detroit Business Homecoming and Summit Detroit, drawing thousands of visitors to the city.

GM returns to Woodward

Hudson’s Detroit also represents a symbolic homecoming for one of the city’s most iconic companies.

General Motors will establish its future world headquarters in the Hudson’s Detroit office tower, occupying multiple upper floors and a public showcase space at street level. Its new lobby and showroom, named Entrance One, pays homage to the main employee entrance of the original J.L. Hudson Department Store.

“As the signature tenant at Hudson’s Detroit, General Motors celebrates Detroit’s rich legacy while embracing the city’s bright future,” said David Massaron, GM’s vice president of Infrastructure and Corporate Citizenship.

“Our return to Woodward Avenue in this state-of-the-art building will allow our teams to drive the future of the automotive industry.”

The move will mark GM’s fourth office site in the city, underscoring its long-term commitment to downtown Detroit.

Retail revival on Woodward

Hudson’s Detroit is having a spillover effect, too. Woodward Avenue will reopen between Grand River Avenue

and State Street for the first time in decades, restoring a key stretch of Detroit’s retail corridor.

Several new retailers are already joining the mix. ALO, the wellness apparel brand, opened at Hudson’s in August, while Tecovas, a modern Western outfitter, will open its doors October 10. Additional retailers will

be announced in the coming months, joining established Bedrock tenants such as Apple, Shinola, Lululemon, Nike, Savage X Fenty, H&M, and The Lip Bar.

Honoring the past, building the future

The new development is built on the historic footprint of the J.L. Hudson Department Store. Once the tallest department store in the world, Hudson’s was a symbol of Detroit’s golden era. Bedrock’s reimagined project honors that heritage while redefining the city’s skyline.

When completed in 2027, Hudson’s Detroit will stand as one of the most ambitious urban redevelopments in the Midwest. Along with its 225room EDITION hotel and 97 luxury condominiums, the tower will bring five-star amenities, including a spa, pool and fitness center, to downtown Detroit.

What was once a vacant lot at the city’s core is transforming into a vertical neighborhood—a new anchor for Detroit’s next chapter.

The new facility in Waterloo, about 55 miles from Cedar Rapids, will be TVS’ second logistics facility in Iowa following construction of an earlier facility in Iowa City.

The project was executed in partnership with ElmTree Funds and Ryan Companies US, Inc.

At a Sept. 25 ribbon-cutting, TVS executives, state and city officials, along with the project’s development partners, praised the facility as a strategic stepping stone in expanding the company’s U.S. reach, especially across the manufacturing belt that spans Iowa, Illinois and beyond.

“We’re excited to expand our U.S. operations with this new facility in Iowa,” said Brad Dyer, chief commercial officer for TVS. “Being in Waterloo strengthens our commitment to supporting manufacturing and supply chain needs while positioning ourselves for continued growth in North America.”

With 6,800 square feet of office

space, a driver’s lounge, 30 loading docks and two drive-in doors, the Waterloo site is tailored for heavy logistics and manufacturing flows. The project is a natural fit for Ryan Companies. Ryan is also building a nearly identical 225,000-square-foot facility in Davenport, Iowa, set for completion in October.

“Ryan Companies is proud to partner with TVS and ElmTree to deliver this important project in Waterloo,” said David Wilson, senior vice president of real estate development at Ryan.

“This facility is a prime example of how thoughtful development and collaboration can create lasting value for the community and key industries.”

During the groundbreaking ceremony, James Koman, chief executive officer and founder of ElmTree Funds, praised the investment and the development.

“We are pleased to support TVS’s continued expansion in the U.S. Midwest through this investment, which will help support critical supply chain needs in the region,” Koman said. “ElmTree is honored to partner with TVS and Ryan Companies on this initiative.”

in celebrating the project, framing it as a milestone in Iowa’s evolving identity as a manufacturing and logistics hub.

Why Iowa — and why now?

The Waterloo facility adds heft to TVS’s regional network, filling a gap between its Iowa City operation and anticipated operations in Davenport. For manufacturers serving regional markets across the Midwest, having closer, efficient logistics nodes is increasingly critical in a tight labor and real estate environment.

In Iowa more broadly, industrial real estate remains constrained. Developers say demand for big-box and warehouse space still outpaces supply, even amid rising construction costs and interest rate pressures.

In Cedar Rapids, the industrial market has been remarkably tight. According to GLD Commercial, Cedar Rapids’ industrial inventory clocked in near 14.1 million square feet in 2024, and the vacancy rate — which began 2024 at just 1.25% — rose through the year to end it near 3.97% as older space came

online. For comparison, in the 2023 reporting period, vacancy in Cedar Rapids held at 1.25%.

Cedar Rapids recently attracted a major investment: in February of this year, the city and Alliant Energy announced the development of a $750 million data center by Quality Technology Services, the largest economic development project in the city’s history.

For TVS, the Waterloo facility ushers in immediate scaling capability in the Midwest. For Iowa, it provides jobs, strengthens logistics infrastructure and bolsters the state’s argument as a distribution crossroads.

For the broader industrial market — especially in places like Cedar Rapids — the move serves as another signal of how logistical real estate is under mounting pressure, particularly in infill and second-generation markets where supply is limited and rents are rising.

By Dan Rafter, Editor

Office properties in busy mixed-use districts are outperforming the broader U.S. office market when it comes to leasing activity and vacancy rates. The reason? Shifting demographics and worker preferences, according to a new report from JLL.

In its Lifestyle Office Markets research report released earlier this month, JLL said that these mixed-use districts— often referred to as lifestyle office

markets—combine urban amenities with suburban accessibility and feature high-end property types, transit connections, walkability and roundthe-clock activity.

Although lifestyle office markets currently account for just 4% of U.S. office space, JLL projects they could make up as much as 30% of the nation’s office inventory by 2040 as both tenants and investors increasingly favor live-workplay environments.

“We are witnessing a structural shift in how the market values workplace environments, with massive implications for investors, developers and municipalities alike,” said Jeff Eckert, president of Americas Office Agency Leasing at JLL, in the report. “As workplace strategies evolve, organizations are increasingly willing to pay a premium for location-based amenities that offer their employees authentic, engaging experiences that cannot be replicated through a screen.”

The report found that lifestyle office markets consistently outperform traditional office developments. Properties in these areas command a 32% rent premium over other Class-A office space, lease up twice as quickly and maintain significantly lower vacancy rates—12.5% compared to 22.5% nationally.

Institutional investor interest has also surged. Office acquisitions in lifestyle office markets rose from minimal levels before 2015 to more than 8% of

institutional office investment volume nationwide in 2024, JLL reported.

Popular location-based amenities that make these developments so attractive include proximity to sports and entertainment venues, waterfront settings and access to green space. These features provide measurable rent premiums, according to JLL’s report.

“The pandemic and subsequent push and pull of remote work awakened office tenants to the reality that experience and environment are crucial for attracting and retaining talent,” said Jacob Rowden, senior manager of U.S. office research at JLL. “Companies are flocking to vibrant, mixed-use areas with synergies among diverse property types that create a sense of energy and engagement.”

An example of these developments? One of the more successful is in Milwaukee. The Avenue—a mixed-use redevelopment in the city’s downtown—has achieved nearly 95% office occupancy, JLL says. The development has done this by providing amenities, food and beverage options, and activated public spaces. By offering

“Companies are flocking to vibrant, mixed-use areas with synergies among diverse property types that create a sense of energy and engagement.”

these pluses, The Avenue attracts a significant amount of foot traffic. And employees prefer working in a location close to food, beverage and entertainment options. That makes office space in such districts more attractive to companies hoping to bring their workers back into the office more frequently.

The Battery in Atlanta, a 74-acre development anchored by Truist Park, home

of Major League Baseball’s Atlanta Braves, is another example. Its 630,000 square feet of office space has a direct availability rate of just 0.5%, compared to 25.9% across the metro area. Similar sports-anchored projects, such as The Star in Frisco, Texas, and District Detroit, also report far lower vacancy rates than their surrounding markets.

As demand rises, more professional sports franchises—including the NFL’s

Washington Commanders and Major League Soccer’s Chicago Fire—are moving ahead with mixed-use development plans that integrate office, housing, retail and entertainment.

Other successful lifestyle office markets include suburban hubs like The Domain in Austin, Texas, and Reston Station near Washington, D.C., as well as urban districts such as Hudson Yards in New York and The Wharf in D.C.

Edge-of-downtown submarkets are also benefiting. Since 2019, office occupancy in districts such as Boston’s Seaport, Chicago’s Fulton Market and Miami’s Wynwood has climbed nearly 25%, compared to a 7.5% decline for traditional central business districts.

JLL said the momentum reflects both demographic shifts and evolving workforce dynamics. Post-pandemic challenges, including housing affordability, perceptions of crime, and lagging office attendance downtown, have accelerated demand for office space in areas offering more integrated livework-play ecosystems.

By Dan Rafter, Editor

The single-tenant net-lease retail market saw a busy first half of the year, with both sales volume and median sales prices on the rise, according to the latest research from Colliers.

In its 2025 first-half report, Colliers said that the U.S. single-tenant net-

lease retail sector racked up $5.7 billion in sales volume in the first six months of the year. That is up 9.6% from the second half of 2024.

The median price per square foot of sold properties rose to $309, a jump of 8% from the end of 2024. Colliers said that the net-lease retail sector is seeing a shift toward smaller, more liquid for-

mats, something that reflects changing consumer behavior and a more disciplined approach from investors.

The median cap rate for transactions in the first half of the year dropped to 6.8%, down 10 basis points from the second half of 2024.

Not all net-lease retail sectors are performing as strongly as others. But convenience stores remain an attractive asset type, recording sales volume of $796 million in the first half of 2025, up by nearly 16% from the second half of last year. The median sales price per square foot for convenience store transactions rose to $925.

This doesn’t mean that the convenience store sector doesn’t face challenges. Colliers reported that economic uncertainty and rising prices have forced consumers to cut back on non-essential spending, causing a decline of 4.7% in average visits to U.S. convenience stores in the first half of 2025. Part of this is because U.S. consumers when traveling are opting for shorter, regional “microcations” over long-distance trips, according to Colliers.

Drug stores face challenges, too, with Colliers reporting that the average number of consumer visits to drug stores and pharmacies declined by 3.6% during the first half of 2025. Sales volume in this sector dropped, too, falling to $444 million in the first six months of this year, while the median sales price for drug stores and pharmacies dropped to $257 a square foot.

And what about dollar stores and discount retailers? This sector notched a sales volume of $527 million in the first half of the year and a median sales price of $166 a square foot.

Colliers said that discount and dollar stores saw an increase of 2.9% in foot traffic during the first half of 2025. However, the future is uncertain as these retailers brace for the impact of tariffs as they rely so heavily on low-cost imported goods.

Full-service restaurants racked up $1.07 billion in sales volume during the first half of 2025, with these properties selling for an average of $469 a square foot during this time.

Colliers, though, reported that full-service restaurant visits declined by 1.6% in the first six months of the year. Colliers pointed to economic uncertainty and several years of menu price increases as the reason for this dip.

Colliers reported that quick-service restaurants saw $1.01 billion in sales volume in the first half of 2025, with properties selling for an average of $751 a square foot. However, visits to quick-service restaurants dropped slightly, by 0.6%, in the first half of 2025. Colliers cited a reduction in commuters and fewer long-distance trips leading to a decrease in on-the-go food purchases.

As a national contractor, we know that EVERY

That’s

why we’re committed to investing in local resources and expertise. No matter where we build, our objective remains the same—to deliver residences your tenants are PROUD TO CALL HOME

By Dan Rafter, Editor

Luxury retailers were riding high a year ago, having enjoyed several years of growth following the COVID-19 pandemic. Today? New headwinds have hit this slice of the retail sector, most notably economic uncertainty and concerns over tariffs.

What do these challenges mean?

That’s not yet determined. JLL in its U.S. luxury retail report, released earlier this week, said that while some luxury brands have reported falling revenues, economic concerns have not yet led to a significant decline in luxury store openings.

According to JLL’s report, luxury retailers are opening new locations at

a faster pace than they did in the first half of 2024. In the first six months of this year, newly opened luxury square footage jumped by 65.1% when compared to the same period a year ago.

However, the last quarter of 2024 was even more active. JLL said that luxury openings in the fourth quarter of last year totaled 195,563 square feet, the highest quarterly total that JLL has ever recorded in the luxury retail market.

And so far this year? In the first quarter of 2025, retailers opened 146,888 square feet of new luxury retail space across the United States, JLL said. In the second quarter of this year, they opened 79,625 square feet of new luxury space. That’s a total of 226,513

square feet of new luxury openings in the first half of this year.

Challenges do loom, though. JLL reported that Capri Holdings anticipates an $85 million increase in cost of goods sold for fiscal year 2026 because of tariffs, while Tapestry’s Kate Spade brand is impacted by the 20% Southeast Asian import tariffs, something that is prompting the retailer to reduce its handbag styles by 30%. The company is projecting a total $160 million tariff-related cost for fiscal year 2026.

At the same time, LVMH says that it is increasing local production in the United States by opening a second Louis Vuitton facility in Texas to reduce import costs.

Much of the strength of the luxury retail market today is fueled by the shopping habits of Gen Z and Millennials, according to JLL.

JLL reported that Tapestry’s Coach brand notched a 14% increase in sales during the fiscal fourth quarter of 2025 and a jump of 10% for the full year. Gen Z and Millennials make up 60% to 70% of the brand’s new North American customers, JLL says.

Prada Group’s Miu Miu saw its retail sales surge by 49% in the first half of 2025, with a sizable portion of these sales coming from younger consumers.

The suburban Detroit commercial real estate market remains a resilient one, something that was clear during Michigan REjournal’s Detroit Suburban State of the Market Summit held Oct. 3 at The Community House in Birmingham, Michigan.

A big group of more than 170 local CRE professionals gathered to hear the good news about commercial real estate activity in Detroit’s suburban communities. The consensus? Yes, the suburbs are facing their own challenges. But commercial real estate here is resilient.

As in most markets, the multifamily, industrial and retail sectors are especially strong today in the Detroit suburbs. All three sectors are still seeing solid activity and lower vacancy rates. And while the suburban office market’s vacancy rate is still too high, it’s not quite as alarming as the vacancy rates in Detroit itself.

The event also featured plenty of opportunity for networking, as attendees gathered to discuss the state of their markets, local deal flow and their hopes for the future.

Speaking on the Suburban Market Trends: State of the Market panel were AJ Bower, Vice President – Advisory & Brokerage Services, Friedman Real Estate; Brendan George, Senior Vice President, CBRE; Paul Choukourian, Executive Managing Director, Colliers; Kathleen Garmo, Senior Advisor, Keystone Commercial Real Estate; Scott Jacobson, Chief Executive Officer, S.R. Jacobson Development Corp.; Mason Capitani, Managing Partner, L. Mason Capitani CORFAC International; and Allen Weiss, Senior Vice President, Plante Moran Realpoint, the panel’s moderator.

Participating in the Design, Construction & Property Innovation panel were Nick Weise, Vice President, Principal, Rightsize Facility, the panel’s moderator; Lori James, Senior Principal, Interiors, SmithGroup; Mitch Hudepohl, Director of Business Development, ARCO National Construction; Larry Brinker Jr., Chief Executive Officer, Brinker; and Zack Boisvert, Director of Construction Services, Premier Construction & Design.

The Investment & Financing Opportunities panel closed out the summit. Participating in this panel were Craig Miller, President & Managing Partner, DUFFY+DUFFY COST SEGREGATION; Anne Galbraith Kohn, Senior Vice President, CBRE; Dennis Bernard, President, Bernard Financial Group; Barry Swatsenbarg, Executive VP, Detroit - Investment & Loan Sale, Auction Services, Colliers; Jeffrey Schostak, President, Schostak Brothers & Company Inc.; Robert Pliska, President, SPERRY – Property Investment Counselors; A.J. Weiner, Senior Managing Director, JLL; and Michael Vogt, Member, Dickinson Wright, who served as the panel’s moderator.

The region’s top CRE pros gathered at the Hilton St. Louis Frontenac for the eighth annual St. Louis Commercial Real Estate Summit held Sept. 24.

And what did attendees learn? That the St. Louis-area commercial real estate market, while working through challenges, is a resilient one, one with its best days ahead of it.

Panelists also spoke of the strength of the St. Louis region’s multifamily, industrial and retail sectors, all of which are seeing solid leasing activity even during the country’s economic challenges.

Participating on the Multifamily/Apartment Market Update and Forecast panel were John Morrissey, Jr., Vice President, Broadmoor Group, who served as the panel’s moderator; Dominic Martinez, Managing Director, Northmarq; Bobby Mills, Managing Director, GREA; Tom Kaiman, Founder, Mia Rose Holdings LLC.; Matt Bukhshtaber, Vice Chairman, Investment Properties, CBRE; and Kyle Howerton, Co-Founder and Principal, AHM Group.

Speaking on the St. Louis Market Sector Update panel were Greg Schowe, Division Manager, Asset Preservation, Inc.; Matt Mabie, President, Oakline Construction Group; John Skae, VP, Relationship Manager, Enterprise Bank & Trust; Ben Haas, Investment Leasing Officer, EQT Real Estate; Amanda Enger, Associate, JLL; Adam Glosier, Partner, Scout Realty Group; and Jenn Mesey, CPM, President, Institute of Real Estate Management, St. Louis Chapter, the panel’s moderator.

The event closed with the Transforming Downtown and Suburban Development—Game Changers panel that featured Mike LaMartina, President, Ballpark Village; Greg Gleicher, CEO, Good Developments Group; Otis Williams, Interim President and CEO, St. Louis Development Corporation, the panel’s moderator; and Taylor Reich, Mixed-Use Development and Operations, The Staenberg Group.

The Nashville-area multifamily market remains strong, with tenants still seeking apartment units throughout the region.

That was the big takeaway from the Nashville Multifamily Summit held by Midwest Real Estate News Sept. 4 at the Renaissance Nashville Hotel.

The event featured the biggest names in Nashville’s multifamily sector and plenty of opportunities for area brokers, developers and other CRE professionals to network and mingle.

Panelists said that while demand for Nashville-area multifamily units has slowed slightly, it remains strong while vacancies are still low. Panelists also predicted an even stronger market in the coming months.

This year’s summit kicked off with the Nashville Multifamily Market Outlook panel, which focused on the bright times ahead for this busy city’s apartment market. Speaking on the panel were Monroe Stadler, Director of Acquisitions, Freeman Webb; Matt Evans, Senior Director of Development, Greystar; John Cannon, Executive VP, Commercial Real Estate Manager, Pinnacle Financial Partners; Matthew Robinson, Principal, MRP Realty; Tarek El Gammal, Executive Managing Director, Multifamily Capital Markets, Newmark; and Clayton Williams, Director, Investments, Carter-Haston.

Speaking on the Development, Construction, Design & Property Management Trends panel were Bryan Jacobs, CEO, Bristol Development Group; Jason Breden, VP and Director of Nashville Operations, McShane Construction Company; Kyle Verhasselt, Senior VP of Acquisitions, Origin Investments; Brad Lutz, Managing Principal – Chicago + Practice Leader Multifamily, Baker Barrios; and Keith Randall, Shareholder, Winstead PC.

By Laura Khouri, President and COO of Western National Property Management

As we navigate the second half of 2025, the multifamily sector continues to present opportunities, fueled by persistent demand and a slowdown in new supply.

In 2024, net absorption exceeded 546,000 units, marking the second-highest total in over four decades and underscoring the sector’s longterm resilience. With construction tapering and demand remaining stable, markets across the country are poised to continue experiencing these shifts in varying ways, as outlined in the Marcus & Millichap Investment Forecast.

Institutional investors remain focused on opportunities that deliver both strong returns and lasting value. Many

are concentrating on stable markets and asset types, while closely tracking shifting renter preferences, evolving amenity expectations, and the importance of operational excellence. As the sector progresses through the remainder of 2025, we can identify which opportunities are gaining traction and the key factors shaping their success in the months ahead.

The post-pandemic landscape continues to reshape migration patterns and renter demand, creating clear winners in markets with strong job growth and manageable new supply. In the coming quarters, certain regions are positioned to see stronger occupancy and

rent gains than others, as construction activity slows and renter interest remains resilient.

California, particularly Orange County, has demonstrated notable stability. At the same time, the Sun Belt continues to lead the way, with nearly two-thirds of its metros offering below-median rents and above-average job growth, according to Marcus & Millichap. Larger markets are absorbing new deliveries with relative ease, while smaller cities benefit from a healthy supply-demand balance. Suburban demand is also on the rise as renters prioritize affordability, additional space, and green access while remaining within reach of major metros.

On the asset side, both workforce and affordable housing remain critical in high-cost urban areas where job growth continues to outpace homeownership affordability. Luxury rentals also continue to perform well, especially among younger renters driven by lifestyle and location preferences. With the median age of firsttime homebuyers now at 38, many individuals remain in the rental market and favor high-end living that aligns with amenities and urban identity.

As investors look to deploy their capital, keeping these shifting market dynamics and renter preferences in mind will be essential to identifying the strongest opportunities for growth and long-term stability.

Operational excellence remains a key standard for multifamily assets aiming to attract institutional investment. Properties that meet owners’ specific goals, strong resident retention, and disciplined cost control are capturing the attention of major funds.

As the property management arm of Western National Group—a fully integrated firm spanning acquisition, development, construction, and management—Western National Property Management (WNPM) brings an ownership mindset to every asset it manages. This reflects a broader trend among leading property management firms, where strategic, portfolio-wide oversight is combined with localized management to ensure decisions are thoughtful, proactive, and centered on both client and resident needs.

WNPM uses advanced technologies to streamline after-hours service requests and monitor property and market performance, allowing the firm to stay ahead of operational trends. The firm conducts regular safety and loss prevention walks as well as monthly tailgate meetings to proactively manage risk, especially as insurance costs remain elevated. The firm’s comprehensive approach to operations enables effective stabilization even under challenging conditions. During a recent 90-day takeover of a distressed portfolio, the team applied a structured transition strategy that achieved a 30% occupancy increase within three months while maintaining resident satisfaction from the outset.

Operational centralization further strengthens performance. By streamlining marketing, training, risk management, and CapEx support through in-house departments, the firm enables on-site teams to focus on what matters most: resident satisfaction, leasing velocity, and maintenance responsiveness.

As investors seek resilient assets in a shifting market, partners who exemplify tailored, forward-thinking strategies will be the ones to deliver lasting value.

Lease-Up Success

A critical, often overlooked component of asset success is the strength

of the property management team. The labor market remains tight, with competition for skilled property managers and leasing agents intensifying. Leading firms are investing in robust training programs to ensure staff can navigate lease-up complexities, address resident concerns efficiently, and uphold high service standards.

A leader in the multifamily industry, WNPM launched its Western National University (WNU) in 2010, a comprehensive training platform that aligns employee development with both corporate goals and individual career paths. One standout initiative is the Training Advisory Group (TAG), a peerto-peer mentorship program that pairs each new associate with a seasoned leader from day one, providing immediate, structured support and accelerating on-site readiness.

Additional leadership development programs provide associates with direct insights from decision-makers, helping them better understand the broader multifamily landscape and how to best serve their properties and residents.

For institutional investors, these training initiatives are a strategic advantage when selecting stable assets. Well-trained and engaged teams drive smoother lease-ups, higher resident satisfaction, and lower turnover which are key contributors to operational consistency, risk mitigation, and longterm value creation.

Amenities: What’s Hot in 2025

Amenities remain key drivers of leasing velocity and tenant satisfaction. In today’s market, renters are prioritizing features that enhance convenience, connectivity, and wellness. High-speed

internet, secure package delivery, fitness centers, and flexible communal spaces are in strong demand.

• Co-working spaces and private offices – With hybrid work now permanent, dedicated remote-work areas are a must-have.

• Wellness-focused amenities –Mindfulness rooms, outdoor fitness areas, social spaces, and rooftop terraces are key differentiators.

• Smart home technology – Contactless entry, smart thermostats, and app-based maintenance requests enhance convenience.

• Community-driven experiences – Events such as resident mixers, networking opportunities, and pet-friendly activities foster belonging.

• Activated ground-floor retail –Partnering with nearby restaurant/ cafes, fitness studios, or service providers can create a seamless, vibrant community experience.

Owners and property managers who stay attuned to evolving preferences ensure that amenities are thoughtfully curated to match both the target demographic and local market. Over-investing in costly features that don’t align with resident demand can erode returns. As a result, investors are increasingly drawn to assets with amenities that not only drive leasing velocity but also foster resident loyalty and long-term retention.

Looking Ahead: Positioning for Success

The multifamily sector currently reflects a market in measured transition. Institutional capital remains engaged, but investors are placing greater emphasis on operational performance, stability, and alignment with current renter preferences. Properties that combine experienced management with thoughtfully curated amenities in resilient markets demonstrate the strongest performance and continue to deliver longterm value.