A slowdown in new construction and investment sales? Sure. But Detroit’s industrial sector remains a resilient one

By Dan Rafter, Editor

As in most major cities across the United States, Detroit is in the middle of a slight industrial sector slowdown. New construction starts are down in Detroit’s industrial market. Leasing activity has slowed.

Despite this, the brokers and developers working in this market say that Detroit’s industrial sector remains a resilient one, a sector that offers plenty of opportunities for investors and tenants.

These CRE professionals say, too, that better days are ahead for this sector. They expect new construction, leasing activity and investment sales to each increase in the coming months as developers and investors work through the challenges of an uncertain economy.

John Boyd, executive vice president and principal with Southfield, Michigan-based Signature Associates, said that the biggest challenge with investment sales in the Detroit market is the disconnect between the prices that sellers want for their industrial assets and the prices that investors are willing to spend.

This doesn’t mean that industrial sales aren’t happening in and around Detroit. Boyd said that deals are still happening, just not as many as during the industrial sector’s boom years in 2021 and 2022. Some of the industrial deals happening in the Detroit market are confidential, Boyd said, while others involve national REITs that are buying properties along the I-275 corridor. Local investors are also occasionally closing sale-leaseback deals.

“There are opportunities in the market,” Boyd said.

Boyd said that rising construction costs have played a role in limiting investment sales. These higher costs have slowed new construction starts. There aren’t as many properties, then, for investors to buy. The demand among buyers for existing properties, especially those under 40,000 square feet, remains strong, Boyd said. But because of the lack of new supply, the cost of these smaller properties continues to rise, making it more difficult for many investors to afford such purchases.

Boyd said that properties of 10,000 to 20,000 square

DETROIT (continued on page 16)

Prepping for the World Cup: Despite slowdowns, tenants, investors still eyeing Kansas City market

By Dan Rafter, Editor

It’s true that investment sales and new commercial construction activity have slowed in the Kansas City market. But it’s not correct to say that the Kansas City commercial real estate market is in a slump.

It’s more like a correction, a return to normalcy.

And the CRE professionals working in this market say that demand remains high for most of Kansas City’s commercial sectors. They are

DETROIT

The Flint Commerce Center in Flint, Michigan. (Photo courtesy of Detroit Regional Partnership.)

Welcome back everyone; to a workspace not as we know it. Let our deep relationships and intelligence at scale inform new work models that work just for you. By re-engineering the way teams interact with adaptive, agile design, we provide unique thinking on a work future that works for everyone. Evolve everything. Realize anything.

A slowdown in new construction and investment sales? Sure. But Detroit’s industrial sector remains a resilient one: As in most major cities across the United States, Detroit is in the middle of a slight industrial sector slowdown. New construction starts are down in Detroit’s industrial market. Leasing activity has slowed.

Prepping for the World Cup: Despite slowdowns, tenants, investors still eyeing Kansas City market: It’s true that investment sales and new commercial construction activity have slowed in the Kansas City market. But it’s not correct to say that the Kansas City commercial real estate market is in a slump.

Cleveland CRE overview: Industrial and retail remain top performers: Cleveland has long been known for its industrial sector. And that sector remains resilient here, still attracting plenty of demand from tenants.

Demand for multifamily remains strong in Cleveland market: The multifamily sector remains resilient across the Midwest. It’s no different in the Cleveland market, where tenants continue to hunt for new apartment units in both the suburbs and downtown Cleveland.

Mid-year Chicago office reports show higher vacancies, but larger leases: Rising vacancies but larger leases closed. That’s the mixed bag of office news from the latest research from Bradford Allen.

U.S. multifamily market continues strong recovery: The U.S. multifamily market continued its strong recovery in the second quarter, as robust absorption reduced the national vacancy rate, according to CBRE’s latest research.

42 Signs of Chicago’s office revival

43 The balancing act: Technology company workplaces evolve to balance innovation with optimization during transformation to AI

44 Maximizing value in industrial real estate: Execution, agility and crossfunctional strategy

45 5 strategies for safeguarding your Midwest business’ liability

47 The 1031 exchange “Napkin Test”: A simple rule of thumb for a complex tax code

The Midwest’s commercial real estate publication, providing useful, unbiased and accurate coverage of the industry and its professionals since 1985.

WWW.REJOURNALS.COM

Publisher | Mark Menzies menzies@rejournals.com 312.933.8559

Editor | Dan Rafter drafter@rejournals.com

ADVERTISING

Vice President of Sales & MW Conference Series Manager | Ernest Abood eabood@rejournals.com

Vice President of Sales | Frank E. Biondo frank.biondo@rejournals.com

Classified Director | Susan Mickey smickey@rejournals.com

Director, National Events & Marketing | Allison Kim Allison.kim@rejournals.com

Midwest Real Estate News brings real estate leaders together to explore the challenges and opportunities unique to their markets.

ADDRESS

7767 Elm Creek Boulevard, Suite 210, Maple Grove, MN 55369

Midwest Real Estate News® (ISSN 0893-2719) is published bimonthly by Real Estate Publishing Corp., Oak Park, Il 60301 (rejournals.com). Current and back issues and additional resources, including subscription request forms and an editorial calendar, are available on the internet at rejournals.com.

40 Multifamily in neutral: A

Some more good multifamily news: More than 816,000 U.S. apartment units leased during the last six quarters

By Dan Rafter, Editor

The multifamily sector remains one of the strongest commercial real estate asset classes, even as economic uncertainty continues to hit the United States. And the latest research shows that tenants are still scooping up apartment space at a healthy clip.

This shouldn’t be a surprise. Mortgage interest rates remain high today. The median price of an existing home across the United States continues to rise, too. The National Association of REALTORS® reported that in June, the median sales price of existing U.S. homes rose to $435,300. That’s the highest this figure has ever been.

These numbers are pricing many potential homebuyers out of the market. These people have to live somewhere, and many of them are choosing to rent apartments.

The demand from renters for multifamily units remains strong across the United States, according to the latest research from Lee & Associates.

In its second quarter 2025 multifamily report, Lee & Associates said that net multifamily absorption during the quarter in the United States totaled 136,007 units. That big number isn’t unusual: Lee & Associates said that during the last six quarters, renters have leased 816,814 multifamily units across the country.

This strong leasing activity has brought vacancy rates down. The report says that the U.S. multifamily vacancy rate fell 10 basis points to 8.1% as of the end of the second quarter. This is largely due to the rising demand for Class-A apartment units, a segment of the multifamily market in which demand still exceeds supply.

This isn’t surprising, either. Many of the market’s renters-by-choice are looking for apartment buildings that come with amenities, everything from rooftop pools to decked-out onsite fitness centers. Lobby storage units for Amazon deliveries matter, too. And most important? Connectivity. Renters want high-speed Internet access as many of them continue to work from home, at least on a part-time basis.

According to Lee & Associates’ report, U.S. rental demand stood at 267,273 units in the second quarter. This follows the leasing of 548,911 rental units in 2024, the second-highest amount on record. This can be partly attributed to the members of Gen Z who are entering the prime apartment rental age. At the same time, a growing number of Baby Boomers are reaching an age in which renting is becoming a good option, especially as their children move out.

Expect vacancy rates to remain low in the multifamily sector. Lee & Associates reported that new construction activity in this sector has tapered off.

Lee & Associates reported that net apartment deliveries have declined for three consecutive quarters, falling nearly 30% to less than 130,000 units in the first quarter of this year. And forecasts show that fewer than 80,000 multifamily units are scheduled for delivery in the fourth quarter of this year.

What does this mean? Only that demand for existing apartment space will continue to rise and that the multifamily sector will remain a strong one.

Image by Pexels from Pixabay.

As a national contractor, we know that

EVERY PROJECT IS UNIQUE

That’s why we’re committed to investing in local resources and expertise. No matter where we build, our objective remains the same—to deliver residences your tenants are PROUD TO CALL HOME.

Cleveland CRE overview: Industrial and retail remain top performers

By Dan Rafter, Editor

Cleveland has long been known for its industrial sector. And that sector remains resilient here, still attracting plenty of demand from tenants.

But the retail sector has been a pleasant surprise, too, according to Kevin Malinowski, executive managing director for Cleveland and Akron with Colliers. This sector also features low vacancies, with plenty of retailers eyeing Cleveland’s neighborhoods for new locations.

We spoke with Malinowski about the state of Cleveland’s commercial real estate sector. Here is some of what he had to say.

What asset classes are the strongest in the Cleveland market today?

“ Our busiest asset classes are industrial and retail. Those are the two if we are looking at the height of our market that are seeing the most activity.”

Kevin Malinowski: Our busiest asset classes are industrial and retail. Those are the two if we are looking at the height of our market that are seeing the most activity. They are at the good equilibrium part of the market between expansion and hyper-supply. These two sectors have stayed in that sweet spot for several years.

Our vacancy in the industrial sector in Northeast Ohio is especially low. Because of that we are seeing some new industrial construction. That new construction usually comes with a tenant in tow as opposed to a speculative build.

Why are these two sectors performing so well right now?

Malinowski: The thing that I would say about Cleveland and many of our peers in the Midwest is that we are at that point in the market curve between expansion and hyper-supply. A lot of

Image by James Smith from Pixabay.

the United States sits in hyper-supply. They are seeing their vacancies growing in these sectors. The Midwest has been holding strong with lower vacancies. The Midwest cities are right at that sweet spot from an industrial standpoint.

Historically in Cleveland we have not had a lot of speculative building in our industrial market. If you need space, our developers will build it.

When you have a vacancy rate near 3.1%, that’s a pretty tough industrial market when you’re looking for space. That lower rate is allowing us to see more conversions of existing buildings and new construction on the industrial side.

How about on the retail side? That’s performing well, too, right?

Malinowski: We see a lot of the same

struggling across the country. How is it performing in Cleveland?

Malinowski: The office sector’s vacancy rates have been steady for several years now. Its overall vacancy rate is about 15%. That’s not as good as industrial or retail, but our office sector is in a much better place than it is in other markets. More markets have higher rates. They have lost rent.

Cleveland is one of the cities leading the United States in office-to-multifamily conversions. It’s a wonderful thing. It takes the denominator of the equation and reduces it. Without the conversions, we’d probably be in the same trough of the market curve with everyone else.

Can you talk about those conversions and their impact on the Cleveland-area office sector?

Malinowski: Our B- and C-class office buildings are the ones being converted. The nice thing about that is you gain new residential units in downtown Cleveland. And these buildings don’t look generic. Some of the new apartments have a generic feel. They don’t have a lot of character. That’s not the case with these office-to-multifamily conversions. Some of the older buildings have construction that you can’t replicate. It would be too expensive. Conversions are a win-win. You retain the character and you build a stronger residential presence downtown.

We have well over 21,000 residents in downtown Cleveland now. It’s like Baskin-Robbins with 31 flavors. Not everyone likes vanilla. Renters can choose the style of apartment, building and location that suits their personalities. That is a win-win.

things with retail as we see with industrial. The retail sector is right in that part of the market curve between expansion and hyper-supply, too. We are not getting ahead of ourselves with too much new construction. If you look at our vacancy rate with retail, it’s about 7.9%. That’s pretty low, too.

What about the Cleveland-area office sector? I know that office is

The city of Cleveland is focused on getting 30,000 residents living downtown. They feel that they can do this. The goal is to get 30,000 by 2030. There is alignment between our county and city leaders. They have a unified vision of where downtown Cleveland should go. That plays a huge role in making things happen. For developers, nothing is harder than when you have a vision but you must convince 10 different parties with 10 different visions of your vision. It’s a lot easier for developers when there is that unified vision.

Image by Reinlin from Pixabay.

Speaking of multifamily, how is that sector performing in the Cleveland area?

Malinowski: Market forces still make multifamily a compelling story. The construction that is going on in downtown Cleveland is primarily conversions to multifamily. It’s a healthy evolution of the market. People like living in multifamily buildings. They want to be connected to their communities. Then there are the mortgage interest rates and housing prices that make it difficult for many people to buy a single-family home. These factors are encouraging the growth of multifamily.

This is a good thing for downtown Cleveland. You need residents to make a vibrant downtown. If you go back to the early 2000s, there were pockets of residential downtown. Now you have full neighborhoods that are blooming. Cleveland is seeing residential growth not just in downtown but in the nearer surrounding areas, too, places like Ohio City and Tremont. We can now support activity in downtown after 5 p.m. Once you get that tipping point, an additional accelerant kicks in. One feeds on another.

Are there any new developments taking place in the Cleveland market that you’d want to mention?

Malinowski: What’s exciting is that all our major employers in Northeast Ohio are growing. We track the S&P 500 and our 20 largest employers. They have been exceeding the Fortune 500 average. That’s a strong value for Northeast Ohio.

I’m also excited about the projects and growth we see with NASA at the Glenn Research Center by Cleveland Hopkins International Airport. Then there is Blue Abyss, which purchased land in Brook Park. Blue Abyss picked Cleveland to build the deepest deep-water testing facility in the United States. These are both exciting for Cleveland. We have one of just 10 NASA centers nationally. That gives us a competitive edge. To have one out of 10 is a good thing.

The Cleveland Clinic is in full construction mode of its neurological institute, too. We have some exciting projects that are continuing to add fuel to the growth of Northeastern Ohio.

James Smith from Pixabay.

Demand for multifamily remains strong in Cleveland market

By Dan Rafter, Editor

The multifamily sector remains resilient across the Midwest. It’s no different in the Cleveland market, where tenants continue to hunt for new apartment units in both the suburbs and downtown Cleveland.

We spoke with Nick Soeder, president and principal broker of Cleveland’s Adams Lynch, about the enduring strength of the region’s multifamily sector. Here is some of what he had to say.

How strong is the demand from rent-

ers for multifamily units in the Cleveland market?

Nick Soeder: We are seeing strong demand from renters still. Our vacancy rates might be a little above the national average. But this is because of so many apartment units coming online, especially in downtown Cleveland and in neighborhoods such as University Circle and Ohio City. All these new units have caused our multifamily vacancy rate to spike a bit over 8%.

Even with that higher vacancy rate, we are seeing increased monthly mul-

tifamily rents. Cleveland is one of the strongest markets for rent growth in the Midwest.

Are you seeing greater demand from renters in different parts of the market?

Soeder: The vacancy rate is lower in the suburbs, around 5%, give or take. The downtown apartment buildings and CBD apartments are higher-rent properties with more bells and whistles. In the suburbs, you can find space at a lower rent. You might also get more size. And you don’t have to add

the cost of parking downtown, which can add another $100 or $200 a month to your cost. In the suburbs, you can just pull into a lot and walk up to your unit. That might account a bit for why we are seeing lower vacancies in the suburbs.

Are you still seeing a steady addition of new apartment units in the market?

Soeder: In 2025 there are more new apartment units coming online than in 2024. The number of new units scheduled for 2026 is a little lower. After

Image by Michal Jarmoluk from Pixabay.

that, we’ll see where it goes. There are still a lot of new units planned, with many developers targeting the suburban areas such as Lakewood and Middleburg Heights. There are several multifamily projects planned for Cleveland Heights, too. We are seeing a lot of planned activity for the suburban markets.

That’s not surprising. The City of Cleveland has had a population loss during the last 10 years. But when you look at greater Cleveland, areas like Lorain County and Medina County, you see population growth. You might start to see more development in those areas because of this. There is also more land available in those areas. It can often be easier to start a new development

Photo by DJ Johnson on Unsplash

“The downtown population has certainly increased over the last few years from where it was 10 years ago. We will see what happens. It’d be good to see better occupancy in buildings in the CBD and downtown.

But it is a tremendous difference from where it was a decade ago. Now you see people out walking their dogs and going grocery shopping.”

from the ground up than it is to convert an old office building and build in the city limits.

Overall, we are in a good place when it comes to multifamily demand. Developers are still interested in this sector.

I’ve read that Cleveland is leading the Midwest when it comes to the number of conversions from office and other outdated properties to multifamily. What impact is that having on the market?

Soeder: We have seen quite a few conversions to multifamily. We lost a lot of office workers over the years. What do you do with these large high-rise properties in the CBD? With the workfrom-home folks and companies not needing as much office space, office conversions have become more popular. We have seen several downtown.

It can be challenging, though. I’m not a developer. But it’s certainly not as easy as having a piece of land and building from the ground up. It must be a developer that is really interested in building downtown or in the CBD to take on a project like that. It is not an easy process. Some of the downtown conversions have worked out well. But there are hurdles to overcome. Those

buildings do have more character, though. There are pros and cons.

Are more people interested in living in downtown Cleveland?

Soeder: The downtown population has certainly increased over the last few years from where it was 10 years ago. We will see what happens. It’d be good to see better occupancy in buildings in the CBD and downtown. But it is a tremendous difference from where it was a decade ago. Now you see people out walking their dogs and going grocery shopping. There is activity even when there is not a game or concert. The demand for downtown multifamily is there.

Is demand strong enough to support the number of new multifamily units coming to the Cleveland market?

Soeder: It seems to be. People smarter than me are building these. They wouldn’t do it if they didn’t see the possibility. They wouldn’t be putting shovels in the ground if they didn’t think these developments would be successful.

feet are selling for up to $100 or $120 a square foot.

“That is up significantly from the pre-pandemic days,” Boyd said. “It’s the basic economics of supply and demand. There is more demand than supply.”

Tariffs, and the uncertainty surrounding them, is also slowing industrial leasing activity in the Detroit market, a market that still relies heavily on the automotive industry. Boyd says that the suppliers working in the auto industry are hesitant to lease large swaths of space until they see the impact from tariffs.

Automakers also face challenges from a presidential administration that doesn’t seem as enamored with electric vehicles as past administrations.

“We are waiting to see the impact of

EV policy decisions,” Boyd said. “This is causing significant heartburn with suppliers who geared up to meet the volumes of EV production anticipated by GM and Ford, volumes that did not happen. That is continuing to have an impact on Tier 2 and Tier 3 suppliers.”

Again, though, these challenges haven’t shut down all industrial activity in the Detroit market. Fisher Dynamics plans to build a 300,000-square-foot factory at the Former Eastland Center mall site in Harper Woods.

And in another big deal, Magna completed construction on a 285,000-square-foot EV seating plant in Auburn Hills, while Piston Automotive is building a 715,012-square-foot logistics center in Auburn Hills to supply GM’s EV Orion assembly plant.

On the positive side, the demand for data centers has continued to grow in the Detroit-area market, Boyd said. The state of Michigan still has a limited number of data centers. That is start-

ing to change as the country’s appetite for these centers only grows.

Boyd said that he expects to see several announcements for new data centers throughout the state in the next six to 12 months.

“Overall, there is still good demand and absorption across the market,” Boyd said. “The market is normalizing slightly, but the demand for industrial space is still solid.”

What has to happen, though, to see an increase in new industrial construction in the Detroit market? Boyd said that vacancy rates need to fall again first.

This might happen sooner rather than later. Boyd said that he is working with several large users who are looking for 300,000 to 500,000 square feet. That type of property is limited today, and the rents on existing industrial properties of this size are increasing. This might eventually lead to a jump in new construction.

The Detroit market also faces a lack of quality land parcels suitable for industrial construction.

“There are build-to-suits going on,” Boyd said. “There will be infill projects. But I think the scarcity of good land parcels is contributing to the higher costs of existing industrial properties.”

An industrial construction slowdown

Kyle Morton, vice president of development in the Detroit office of Ashley Capital, said that Detroit experienced a massive spec industrial construction wave that hit and delivered in 2023.

During this year, the market saw more than 5 million square feet of spec industrial construction come online. Morton said that is two to three times the amount of new spec industrial space that the Detroit market typically sees.

Because of this boom, it’s not surprising that spec industrial construction

DETROIT (continued from page 1)

Ashley Capital’s Crossroads Distribution Center North in Van Buren Township, Michigan. (Photo courtesy of Ashley Capital.)

DETROIT

has mostly come to a halt here since, Morton said. He said that Ashley Capital started developing two spec projects in 2023, one in Flint and another in Van Buren Township. He said that these were the only two spec industrial buildings that started construction in 2023. And in 2024? Morton said that he can’t think of a single spec industrial project that began construction.

“We had such an oversupply of spec industrial, it had to slow down,” Morton said. “But the market today is looking more optimistic.”

Morton said that Ashley Capital has started earth work on four sites in the local market. The company isn’t committed yet to building, but it is getting the sites ready for future work.

“We are hoping that in the next few months, we’ll see a little uptick in industrial leasing activity here,” Morton said. “We are already seeing little signs of optimism.”

Both of Ashley Capital’s 2023 spec buildings are fully leased.

Morton, too, said that the effect of tariffs and a slowdown in EV production are both holding up new construction in the Detroit industrial market. As Morton says, a good portion of the industrial construction and leasing activity in 2021 and 2022 was fueled by automotive plant expansions as automakers geared up to increase EV production.

“But that has all gotten kicked to the road,” he said.

Consider the Orion Assembly plant in Orion Township, Michigan. General Motors originally planned to use the plant for EV production. GM has since abandoned those plans and will instead build the Cadillac Escalade, Chevrolet Silverado and GMC Sierra light-duty pickups at this plant beginning in early 2027.

“If we get a little more auto contracts signed, you’d see a big uptick in industrial activity in this market,” Morton said. “The uncertainty that comes with tariffs is causing a lot of delays. There is interest from numerous companies for industrial space here. But many of them are not doing anything yet until they can see what happens with tar-

We Provide:

• Asbestos / Lead /Mold Consulting

• Building & Infrastruc ture E valuations

• Construction Materials Testing

• Environmental Services

• Geotechnical Ser vices

• Indoor Air Qualit y Consulting

Morton said that the major automakers all poured massive amounts of money into EV production. But now that EV tax credits are going away, and demand for EVs seems to be waning, the automakers are being forced to change their business plans.

“Everything keeps changing,” Morton said. “Clearly, GM biting the bullet and switching EV back to gas vehicle production shows you where EV demand is now. There is an acknowledgement of the lack of demand for EV.”

While Detroit’s industrial market serves a variety of end users, historically, as the auto industry goes, so does Detroit. That is still the case, Morton said.

“When the auto industry starts seeking more space again, the market here will switch pretty quickly,” he said.

A key tool for users seeking industrial space in Detroit market

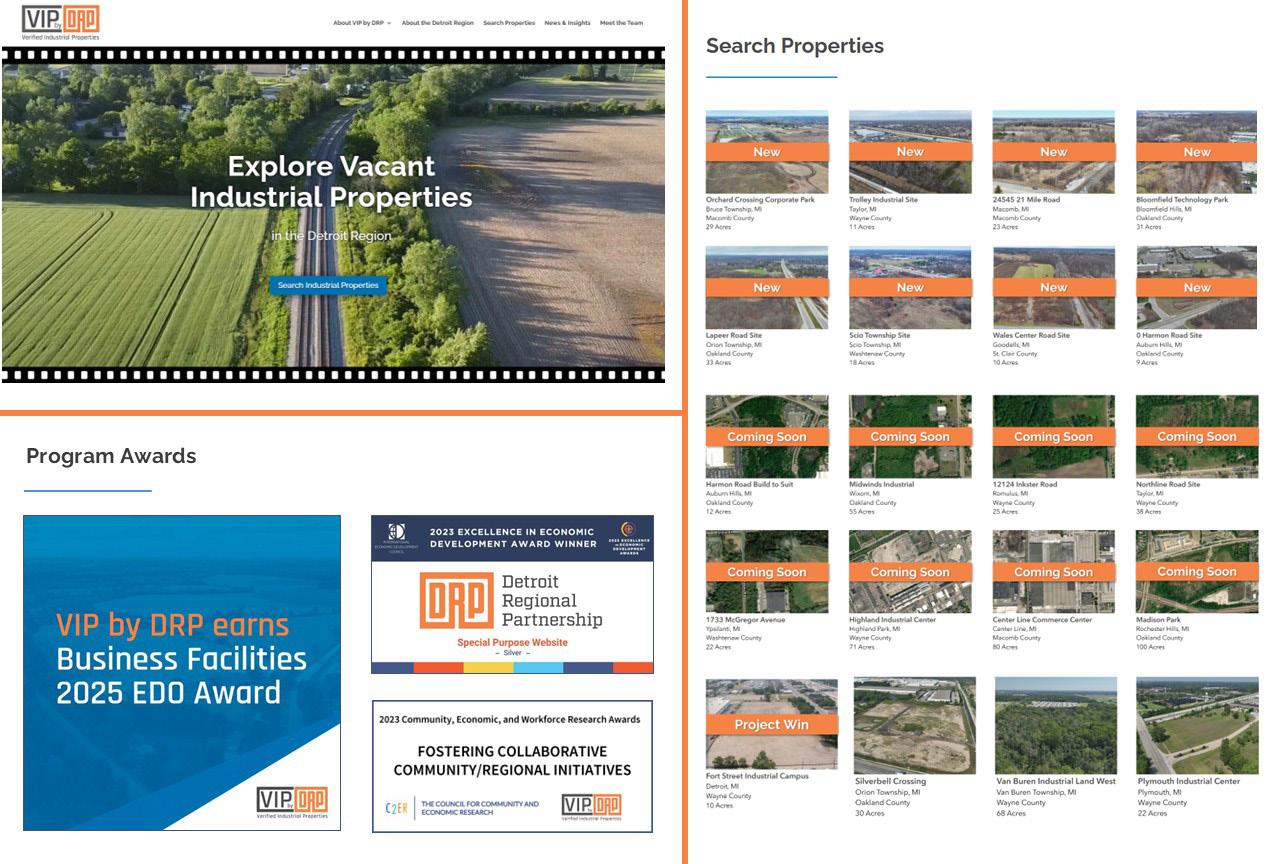

Developers looking for sites in the

region on which they can build new industrial developments can turn to the Verified Industrial Properties Program (VIP) offered by The Detroit Regional Partnership.

The goal of this program is to boost the site-readiness of brownfields throughout Southeast Michigan. The program, which launched in October of 2022, offers incentives to encourage partners to submit available properties to an online portal run by the Detroit Regional Partnership. Developers can then search the portal to find developable sites that fit their needs.

That portal, verifiedindustrialproperties.com, is a key to the program: It highlights former brownfield sites that have been vetted for environmental, zoning and other development-readiness factors. Third-party engineers verify the condition of vacant industrial parcels of 10 acres or more by evaluating how easy or difficult it would be to connect to utilities, whether wetlands mark the site, if there are easements for developers to deal with and other key factors.

“The VIP program was an answer for site consultants who wanted to have the facts on sites throughout the region verified,” said Shannon Selby, vice president of real estate for the Detroit Regional Partnership’s Verified Industrial Properties program. “This program saves developers time and money when they are looking at possible sites.”

Visitors reviewing sites on the VIP by DRP homepage can pull up assessment reports on available land sites in Southeast Michigan. Site reports include drone videos, mapping and sometimes a letter of support.

John Boyd (Photo courtesy of Signature Associates.)

Kyle Morton (Photo courtesy of Ashley Capital.)

Shannon Selby (Photo courtesy of Detroit Regional Partnership.)

READY FOR YOUR CLOSEUP?

VIP BY DRP PUTS SOUTHEAST MICHIGAN INDUSTRIAL PROPERTIES IN THE SPOTLIGHT

We’ll cover the cost of due diligence data verified by thirdparty experts. Not only does that make your site more marketable, we’ll actively promote it in-state, out-of-state and out-of-country. We know that more looks mean more opportunities for more prospects.

To learn more about the Detroit region’s premiere site-readiness program, scan here:

DETROIT

Selby says that the site reports can save developers six to 10 months of work that they would otherwise have to perform on their own.

“The response to this program has been overwhelming,” Selby said. “The site owners and brokers are very involved in the VIP program. The development community supports it. No one has done this before, pulled this information together. It’s a tool to get developers to say ‘yes’ to working in our region.”

Today, developers and owners can review about 50 land sites on the VRP by DRP website.

Justin Robinson, senior vice president of business development with the Detroit Regional Partnership, said that he and his fellow staffers are constantly analyzing new sites to add to the VIP program.

Robinson said that partnership staffers each quarter analyze new RFPs, studying what developers are looking for regarding site sizes, urban or suburban locations or greenfields vs. brownfields.

“We use that information when we decide which sites to invite into the program,” Robinson said. “We closely monitor that live demand.”

Robinson said that partnership staffers also work with site selectors to determine the information they need, the studies they need done, before they can bring a land site to a potential partner and end user.

“The demands from end users are constantly changing,” Robinson said. “We are constantly adjusting to these changing demands. We are always looking for the latest

The online home of the Detroit Regional Partnership’s Verified Industrial Properties program. (Image courtesy of Detroit Regional Partnership.)

information to continue to build this program.”

The VIP program is especially important today. People from outside the region think that Detroit has plenty of industrial land. However, Detroit’s industrial market currently has a low overall vacancy rate. That can make finding industrial space a bit like finding a needle in a haystack, Robinson said.

“We know that we need to help companies identify land on which they want to build new buildings,” Robinson said.

Selby said that the goal is to add 10 sites to the VIP online home every quarter and to hit 120 total sites by the first quarter of 2027.

“We have a very organized and strategic program to help us reach these goals,” Selby said. “We have boots on the ground testing land sites.”

End users can search sites by greenfield or brownfield, by acreage and by county, Selby said. The VIP program lists industrial sites that are 10 acres and up.

“It’s about bringing better and more jobs to Michiganders,” Selby said. “We expect this toolkit to be something that can be used across the state. We are pretty excited about that.”

“This is the core of the program,” Selby said. “We want to provide an answer to every end user searching for a site in our region.”

Robinson said that he expects demand for industrial space, both existing buildings and sites on which to develop, to continue to rise in the Detroit market and throughout Southeast Michigan.

“Detroit is almost the only underserved major, medium-sized regional market when it comes to industrial space,”

he said. “In a lot of markets, there had been some overdevelopment of spec industrial space. Here, developers were more conservative. There is still demand in the market.”

The Detroit Regional Partnership is working steadily to improve the existing VIP program, too. Selby pointed to the industrial site readiness playbook that the partnership plans to unveil soon.

As Selby says, some communities are fearful of allowing industrial develop-

ment. The partnership’s site readiness guide will help educate communities on what it means to have an industrial project in their cities or towns. It will showcase the economic benefits that such projects can bring.

“It’s about bringing better and more jobs to Michiganders,” Selby said. “We expect this toolkit to be something that can be used across the state. We are pretty excited about that. Industrial developments bring great opportunities to communities in the form of better fire, police and economic stability.”

these sectors.

“We have seen the opening of a number of new restaurants, coffee shops and salon concepts,” Buland said. “For a while, post-COVID, those had been softer markets. To see those rebounding strong for us has been nice.”

a boost so that it doesn’t have much vacancy at all,” Buland said.

The last piece of the puzzle for Kansas City’s CRE market? Buland says it’s the office sector. As in most Midwest markets, the office sector is struggling in Kansas City with high vacancy rates.

Exact Architects’ ABC at Main redevelopment will feature 50 residential lofts, a speakeasy and a coffee shop. (Photo courtesy of Exact Architects.)

Providing another boon to Kansasing of CPKC Stadium, home of the KC Current professional women’s soccerdium in the world purpose-built for a -

tivity in its surrounding neighborhood, Buland said. This includes both retail development and new multifamily

portant. Like many Midwest cities, Kansas City is working to attract more full-time residents to its downtown areas. The addition of amenities like the soccer stadium and new apartment

“As jobs are coming back downtown, the people are coming back to the center of the city, too,” Buland said.

ployees get hired downtown. They are coming with strong offer letters from-

ments. You walk around downtown, and everyone is out there walking their dogs. That’s a positive sign.”

Steady construction now. More activity in the future?

Sam Stahnke, vice president of the Kansas City office of ARCO National Construction, said that most of the commercial construction taking place in the Kansas City market today is of the build-to-suit variety, with end users already in tow.

The market is also seeing some new construction from owner-users who are seeking to expand or modernize their commercial properties, Stahnke said.

“That has been the biggest shift,” Stahnke said. “Kansas City was a spec distribution market. Now we are seeing more end-user-driven building.”

Stahnke says that 2025 so far has been a steady year for ARCO. It hasn’t been a boom year, like during the pandemic. But the slight slowdown in activity has given ARCO team members the chance to earn additional certifications, learn

new skills and become better for the future, Stahnke said.

Part of what has made 2025 more of a challenge has been the threat of tariffs, Stahnke said. The fear that tariffs will cause construction costs to rise even higher has slowed new construction activity.

On the positive side, Stahnke said, ARCO is seeing an uptick in projects that had been delayed ramping up again. Other projects are slated to start construction in early 2026 and are now going through the planning phase, he said.

“The hope is that these projects start to come out of the ground in 2026,” Stahnke said.

Much of the work that ARCO is seeing is in the manufacturing space. Demand for distribution and warehouse space remains steady, too, Stahnke said.

“More groups nationally are starting to see that if you look at UPS’ delivery map, you can get to something like 80% of the U.S. population in a 48hour drive or less from Kansas City,”

Exact Architects’ Aiden Hotel, which will bring 80 new hotel rooms to the Kansas City market. (Photo courtesy of Exact Architects.)

KANSAS CITY

Stahnke said. “For the Amazons of the world, it’s a positive to be in the center of the nation.”

Multifamily construction demand remains strong, too, Stahnke said, with many developers looking to start construction on new apartment developments later this year or in the spring of 2026.

tenant-improvement jobs for companies such as ARCO.

Of course, not all the submarkets in the Kansas City region are seeing as much construction activity as others. Stahnke pointed to the Northland submarket, north of the Missouri River, as being a particularly strong one for distribution projects. Southern Johnson

“More groups nationally are starting to see that if you look at UPS’ delivery map, you can get to something like 80% of the U.S. population in a 48-hour drive or less from Kansas City.”

Caleb Buland (Photo courtesy of Exact Architects.)

Sam Stahnke (Photo courtesy of ARCO.)

KANSAS CITY

“We are adding new multifamily developments. We are adding entertainment and youth sports facilities. We are creating this mecca with great businesses and a top quality of life. It’s a combination that encourages top talent to move here. It’s all about that talent attraction.”

off of Interstate-70, too. Many of the industrial properties here total 250,000 square feet or less.

Another busy real estate type for the Kansas City market? Entertainment and sports venues. Stahnke said that youth sports are popular in the market. It’s why in the last three years construction crews have built two baseball and softball complexes here and renovated a third.

ARCO is also building Live Nation Entertainment’s Riverside Amphitheater in Kansas City, a venue slated to open for the 2026 concert season. When finished, it will seat 20,000 people.

“We’ve seen an influx of new businesses and people into the Kansas City market,” Stahnke said. “Now city officials and developers are working to boost the quality of life here. We

are adding new multifamily developments. We are adding entertainment and youth sports facilities. We are creating this mecca with great businesses and a top quality of life. It’s a combination that encourages top talent to move here. It’s all about that talent attraction.”

Stahnke said that this improved qualify of life is encouraging more people to move to Kansas City. But the re -

gion is attractive to newcomers, too, because of its low cost of living.

“A lot of call centers or central offices for larger companies are moving to Kansas City,” Stahnke said. “These end users don’t need to be in San Francisco or Los Angeles or Chicago where it is more expensive for their employees to live.”

Mid-year Chicago office reports: Vacancies tick up but large leases signed, more properties sold for conversion

By Bradford Allen

Rising vacancies but larger leases closed. That’s the mixed bag of office news from the latest research from Bradford Allen.

According to Bradford Allen’s Q2/25 Office Market Report: Downtown Chicago and Mid-Year 2025 Office Market Report: Suburban Chicago, the Chicago CBD office vacancy rate rose to 24.7%, up from 23.4% in the first quarter. Bradford Allen found, too, that average gross asking rates declined to $41.54 from $42.56 in the same period.

Meanwhile, the suburban vacancy rate reached 25.1%, up from 24.6% at the end of 2024, and gross asking rents declined to $24 per square foot.

Still, companies continued to sign large leases and investors acquired

more distressed and obsolete properties, whether to recapitalize or convert to new uses. Move-in-ready office suites, which comprise builtout and speculative spaces, remained popular, accounting for almost onethird of downtown leases and more than a third of suburban leases. Those between 3,000 and 12,000 square feet are leasing the fastest, according to Bradford Allen.

“Behind the numbers is a market that’s continuing to find balance but healthier than some might realize based on recent headlines,” said Neil Bouhan, senior managing director, research and communications, at Bradford Allen. “As conversions take obsolete product off the market and distressed properties find new owners and tenants, vacancy will decline further and better reflect current market conditions.”

Downtown Chicago

Tenants signed approximately 1.9 million square feet of leases in downtown Chicago in the second quarter, with about half of that in the West Loop. Golub Capital’s 205,450-square-foot lease at 225 W. Randolph St. was the quarter’s largest. Throughout downtown, direct net absorption was negative 1.5 million square feet for the quarter, making second-quarter 2025 among the weakest periods for overall demand since first-quarter 2024.

Investment sales totaled $118.3 million in the second quarter, down from $156.7 million in the first quarter, a 24.5% decrease. Kohan Retail Investment Group’s purchase of 311 S. Wacker Drive for $45 million was the quarter’s largest investment deal. The purchase price equated to $34 per square foot, down significantly

from the $230 per square foot paid in 2014 but a low enough basis for the new owners, who are considering converting some of the office space into a hotel, to pursue a strategic repositioning.

Other conversion deals are expected to add a combined total of 734 residential units to the market, including:

• The Primera Group secured $67 million in TIF funding to convert 105 W. Adams St. into 400 residential units.

• WindWave Real Estate and Path Construction bought a portion of 111 W. Illinois St. for $17 million for conversion into 153 residential units.

• Concord Capital bought 223 W. Erie St. for $6.85 million and plans to convert it into 66 residential units.

Photo courtesy of Bradford Allen.

Additional conversion projects announced were 1500 N. Halsted St. near Goose Island (31 units) and 309 W. Washington St. (84 units).

Suburban Chicago

The vacancy rate in the suburbs was 25.1% for the first half of 2025, up from 24.6% at year-end 2024. Gross asking rents declined to $24 per square foot.

Suburban office leasing activity was 2.9 million square feet at mid-year, ahead of the pace for 2024, which saw a total of 5.7 million square feet. Net absorption was negative 5,639 square feet, an improvement over the net negative 770,000 square feet of absorption in the first half of last year.

Investment sales totaled $121 million through June, well below the pace for last year, when $368 million in sales were recorded at year-end.

Market conditions continue to present opportunities for patient capital looking to acquire quality assets in prime suburban locations, according to Bradford Allen. For example, GTZ Properties acquired the 327,000-square-foot Oak Brook Office

“Tenants signed approximately 1.9 million

205,450-square-foot lease at 225 W. Randolph St. was the quarter’s largest.”

Center for just under $9 million, a significant discount from the 2013 purchase price of $33 million. GTZ plans to maintain 100,000 square feet of upgraded office space while exploring retail and entertainment conversions

for the remainder of the property, located about 3 miles from the Oakbrook Center mall.

Fortune Brands Innovations leased two of three buildings at 1 Horizon Way in

Deerfield, the former Horizon Therapeutics campus. The deal was backed by Illinois EDGE tax credits in exchange for creating 400 new jobs by late 2027.

It’s not always about the physical skyline, but about improving communities. Clients who want a construction company with a different vantage point turn to McCownGordon. Through transparency, collaboration and a genuine good time, we are tranforming spaces that improve lives and connect communities. McCownGordon is proud to be Kansas City’s community builder.

U.S. multifamily market continues strong recovery

By CBRE

The U.S. multifamily market continued its strong recovery in the second quarter, as robust absorption reduced the national vacancy rate, according to CBRE’s latest research.

Positive net absorption, which measures the change in the number of occupied units, totaled 188,200 units in Q2 2025, the strongest second-quarter performance on record. This marks the fifth consecutive quarter in which demand surpassed construction completions. As a result, the overall multifamily vacancy rate fell by 70 basis points to 4.1%, well below its long-term average of 5.0%.

After a record 450,000 new units in 2024, only 83,000 units were delivered in Q2 2025, with a more pronounced slowdown expected in coming quarters.

“Multifamily fundamentals strengthened dramatically in the second quarter, as robust renter demand continues to outpace new deliveries.

“Multifamily fundamentals strengthened dramatically in the second quarter, as robust renter demand continues to outpace new deliveries.”

We expect the gains to continue this year and accelerate in 2026,” said Kelli Carhart, Head of Multifamily Capital Markets for CBRE.

Average monthly rent increased 1.2% year-over-year in Q2 2025 to $2,228, the first time in two years that rent

growth exceeded 1%. Rent growth is likely to further improve amid slowing construction completions and healthy absorption.

Multifamily investment volume rose 7.1% year-over-year in Q2 2025 to $32.9 billion. The multifamily sector

accounted for the largest share of total commercial real estate investment volume in Q2 2025 (34%).

Other Q2 2025 Multifamily Sector Highlights:

• The Midwest (3.7%), Northeast (3.1%) and Pacific (1%) regions experienced solid year-over-year rent growth.

• All 69 markets tracked by CBRE recorded positive net absorption in Q2 2025, with New York (19,300 units), Chicago (9,300) and Dallas (8,700) leading the way.

• Sixty-eight markets saw net absorption exceed new supply in Q2 2025, up from 52 markets in Q1 2025 and 65 in Q4 2024.

• Vacancy rates declined in 68 markets quarter-over-quarter in Q2 2025, up from 52 markets in Q1 2025.

Image by Michal Jarmoluk from Pixabay.

Big crowd hits downtown Chicago for wisdom, networking and knowledge during 11th annual National Net Lease Summit

A big crowd packed the halls of the University Club of Chicago in downtown Chicago July 24 for the 11th annual National Net Lease Summit held by Midwest Real Estate News. And why not? The biggest names in the net lease industry were on hand to share their thoughts on the reliable but continually evolving commercial sector.

And what did attendees hear? The net lease sector faces challenges, as do all commercial real estate sectors. But net lease remains one of the most resilient sectors. Investors still view commercial real estate, and net lease real estate, as a safe place to park and grow their dollars. That doesn’t change even if the U.S. economy is going through challenging times.

Panelists spoke, too, about the strength of specific net lease asset types, properties such as dollar stores, auto care and quick-service dining facilities. These assets continue to draw customers and investors.

What will the future hold for net lease? Panelists said that they see even brighter days ahead for this sector as some of the uncertainties facing the economy -- such as the threat of tariffs -- are resolved.

Randy Blankstein, president of Wilmette, Illinois-based The Boulder Group, and a participant in the summit, said that the industrial and quick-service-restaurant sectors of the net lease market are seeing the most demand from tenants today.

He also said that sale-leaseback activity accelerated in the first half of the year as companies seek to bolster their balance sheets even as interest rates remain high and economic uncertainty continues to hit the United States.

And what about the thoughts of net lease professionals? Are they optimistic about the state of the net lease sector?

Blankstein said that he is cautiously positive about the future.

“The net lease market continues to show signs of stabilization after three years

of cap rate increases, with the second quarter marking a notable change in pricing momentum,” Blankstein said. “While transaction volume remains below historical peaks, particularly in the 1031 exchange space, the narrowing bid-ask spreads and continued institutional participation suggest improved market liquidity.”

Blankstein said that investors are closely watching Federal Reserve policy signals and broader capital market conditions as they evaluate acquisition opportunities. He said that with cap rate movements moderating and supply-demand dynamics showing greater balance, net lease activity should gain momentum through the rest of 2025.

Another highlight of the day? The networking opportunities. With hundreds of commercial real estate professionals in attendance, guests to the summit had plenty of chances to meet with their peers to discuss the state of the market, swap notes on intriguing properties and maybe plant the seeds of future deals.

Kicking off the event was the National Net Lease Market Overview panel, which focused on the challenges of navigating today’s volatile market. Participating in this panel were Zachary Pasanen, Managing Director, Investments, W. P. Carey;

Randy Blankstein, President, The Boulder Group, who also served as the panel’s moderator; Joel Tomlinson, Managing Director, Ares Management; Barclay Jones, Managing Director, The Carlyle Group; Gordon Whiting, Managing Director, Founder and Co-Head Net Lease Real Estate strategy, TPG Angelo Gordon; Richard Hurd, Founder and President, Hurd Real Estate; and Nicoletti DePaul, Chief Operating Officer, SURMOUNT.

The Industrial Net Lease – Leading the Marketplace panel focused on the performance of the still-resilient industrial sector. Speakers were Sean Hostert, Author, Net Lease Observer, the panel’s moderator; Angie Wethington, Senior Director, Scannell Properties; Jeff Lizzo, Managing Director, STREAM Capital Partners; and Briggs Goldberg, Managing Director, Newmark.

The event’s third panel, 1031 Exchange Trends – Navigating a Changing Landscape, focused on the challenges facing 1031 exchanges and the potential rewards in this sector. Participating in this panel were Todd Phillips, CEO, Legacy Property Trust, moderator; Matthew Douglas, Senior Director, Accruit; Greg Schowe, Division Manager, Asset Preservation, Inc.; Chris Newton, Executive Vice President, Chicago Deferred Exchange Company; Spencer Lund, Chief Investment Officer, NAI Legacy; James Lockhart, Tax Partner, Real Estate, Aprio Advisory Group, LLC; and Paul Abdow, CIMA, Managing Director, Net Lease Capital.

Speaking on the Sale-Leaseback Market Update – Gaining Momentum panel were Steven Chod, Managing Director, Kroll Real Estate Advisory Group; James Hanson, Principal, Capital Markets Group, Avison Young; Karly Iacono, Senior Vice President, National Net Lease, CBRE Investment Properties; David Piasecki, Managing Member, Blue Vista Capital Management LLC; JC Asensio, Executive Managing Director, Newmark; Elizabeth J. Randall, CCIM, President, Randall Commercial Group, LLC (Moderator); and Dennis Cisterna III, Managing Partner and Chief Investment Officer, Sentinel Net Lease.

Looking into their crystal balls for the Net Lease Market Conditions and Forecast 2025 – Waiting for a Rebound panel were Evan Beeson, Senior Investment Advisor, Sands Investment Group; Anthony Walters,/ Senior Director, JLL Capital Markets; Neil Abraham, President, Realty Income International; Christian Tremblay, Vice President, Northmarq; Maury Vanden Eykel, Executive Vice President, CBRE (Moderator); and Daniel M. Taub, Senior Vice President, National Director, Retail, Marcus & Millichap.

The Capital Markets Overview – State of Refinancing panel closed out the day. Speaking on this panel were Caity McLaughlin, Principal, Credit Tenant Lease Financing, PGIM Private Capital (Moderator); Bob Farina, Senior Vice President, Commercial Real Estate Division, Old National Bank; Chris Miller, Managing Director, Triple Net Lending; and Sean Keane, Senior Vice President, NNN Finance Director, First Savings Bank.

Celebrating the resiliency of Columbus’ CRE market at Columbus Commercial Real Estate Summit

The Columbus, Ohio, commercial real estate market remains a resilient one, according to the speakers at Midwest Real Estate News’ 11th annual Columbus Commercial Real Estate Summit.

During the summit, held by Midwest Real Estate News July 31 at The Plaza hotel Columbus at Capitol Square, a crowd of local CRE professionals gathered to network and listen to the market analysis provided by the biggest names in the local commercial market.

These professionals pointed to the strength of the multifamily and industrial sectors -- even though both, of course, face their own challenges -- as highlights of the Columbus CRE market. They also said that retail has proven more resilient than many expected.

The office sector here continues to face challenges, as it does across the country. But speakers said that there are signs of hope in this sector, too, especially in Class-A office properties that boast top-end amenities.

The summit also focused on some of the bigger commercial developments taking place in or being planned for the Columbus region.

The summit kicked off with the Apartment Market Update & Forecast: Opportunities & Challenges panel, which looked at the enduring strength of the Columbus multifamily sector. Speaking on this panel were Paul Kiebler, CEO and Founder, Pepper Pike Capital Partners; Don Brunner, President and CEO, BRG Apartments (Moderator); Tessa Greb, Regional Vice President, Towne Properties; Rowland S. (Tre’) Giller III, CEO, DRK & Company; Jason Krug, Senior Managing Director, Berkadia; and Patrick Kempton, Regional Production Manager, KeyBank Real Estate Capital.

Speaking on the Columbus Market Sector Update: Industrial, Office, Retail, Finance, Investment panel were Christopher Potts, Brokerage Senior Vice President and Principal, Colliers – Columbus; Brian Marsh, Executive Managing Director, Columbus, JLL; Shawn Dorsey, SVP, CRE Relationship Manager, Northwest Bank; Craig Miller, President and Managing Partner, DUFFY+DUFFY COST SEGREGATION; Brent Myers, VP, Development, CASTO; and Matthew E. Drane, Chief Revenue Officer and Senior Managing Director, Verti Commercial Real Estate (Moderator).

The summit ended with the Transforming Downtown and Suburban Development—Game Changers panel featuring Jeremiah Gracia, CEcD, Director of Economic Development, City of Dublin; Quinten L. Harris, Deputy Director of Jobs and Economic Development, City of Columbus (Moderator); Franz Geiger, Managing Director, N.P. Limited Partnership, POLARIS Centers of Commerce; and Skip Weiler, President, The Robert Weiler Company.

Cleveland Commercial Real Estate Summit highlights the victories among the challenges in this key Midwest market

Panelists spoke about the strength of the industrial and multifamily sectors and the resilience of the retail and healthcare sectors. And while speakers agreed that the office sector -- as it is across the country -- continues to struggle, they did find some bright spots, especially with high-end, amenity-rich Class-A properties.

The biggest challenge that Cleveland faces? Population loss. The city’s population continues to shrink, an issue that municipal officials are working now to resolve.

Brokers, developers, commercial finance professionals, municipal executives and real estate lawyers shared plenty of good news during the 11th annual Cleveland Commercial Real Estate Summit held June 26 at Windows on the River in Cleveland.

Chris Ronayne, Cuyahoga County Executive, gave the keynote speech of the event. He focused on the many positive news stories taking place now in Cleveland, highlighting new developments, multifamily projects and businesses.

Speaking on the Multifamily/Apartment Market Update and Forecast panel were Ryan Bartizal, Senior Managing Partner , The Max Collaborative; Samantha Belin, VP Residential, GCI Residential, LLC.; Rob Garrison, SVP Senior Mortgage Banker, KeyBank Real Estate Capital; Nick Soeder, President/Principal BrokerMultifamily Investments, Adams Lynch Associates; Rob Starrett, Managing Director, Berkadia; and Aaron Pechota, Executive Vice President, The NRP Group.

Speaking during the Cleveland Market Sector Update panel were Tim Breckner, Senior Vice President, Colliers; Steve Ross, First Vice President, Advisory & Transaction Services, CBRE; Matt Wilson, Associate Broker, Anchor Retail; Paul DiGiacobbe, Business Development, ARCO National Construction – Cleveland; Matt Grashoff, Partner, Hahn Loeser Parks; and Craig Miller, President and Managing Partner, DUFFY+DUFFY COST SEGREGATION.

The summit concluded with the Transforming Downtown and Suburban Development -- Game Changers panel that featured Spencer Pisczak, President, Premier Development Partners, LLC.; Kevin Malinowski, Executive Managing Director, Colliers; Scott Skinner, President and Executive Director, North Coast Waterfront Development Corporation; Christine Nelson, Vice President, Project Management and Site Strategies, Team Northeast Ohio; Tom McNair, Director of the Department of Economic Development, City of Cleveland; and Ian Jones, Partner, AVID Architects.

A packed house gathers to celebrate a resilient sector at Detroit Industrial Real Estate Summit

The Detroit industrial market continues to thrive, despite economic uncertainty. That’s the takeaway from the Detroit Industrial Real Estate Summit held by Michigan Real Estate Journal Aug. 21 at The Community House in Birmingham, Michigan.

A crowd of more than 200 attendees packed the house to hear from the biggest names in Detroit’s industrial sector. Panelists spoke about the Detroit Regional Partnership’s VIP by DRP program, which helps end users find available sites for industrial development; the many benefits of doing business in the Detroit area; the newest industrial developments powering the market; and the resiliency of industrial real estate today.

The event also provided networking opportunities for all attendees. With so many industrial specialists at The Community House, attendees had the chance to discuss upcoming projects, the latest deals and the future of this sector with each other.

The summit opened with the Detroit Industrial Real Estate Market Outlook 2025 panel, with speakers focusing on the bright future of the area’s industrial sector. Participating in this panel were John Boyd, Executive Vice President, Principal, Signature Associates; Jared Friedman, Co-CEO, Friedman Real Estate; Jason Capitani, Managing Partner, L. Mason Capitani CORFAC International; Randall Allman, Senior Vice President, Principal, Director of Industrial and Logistics Specialist, Lee & Associates; moderator Elizabeth Rogers, Partner, Taft; and Ryan Brittain, Vice President, Detroit, Colliers.

The Development & Design: Building Tomorrow’s Facilities panel featured Trae Allman, Principal & Co-Founder, Innovo Development Group; Emily D’Agostini Kunath, Principal, D’Agostini Companies; Curtis Hoffman, Operations Manager, ARCO National Construction; Shannon Selby, Vice President, Real Estate, Detroit Regional Partnership; Marc Werner, Regional Vice President, NorthPoint Development; and moderator Chris Martella, Member, Dawda.

Speakers on the Capital Markets & Investment Strategies included Jeffrey Schostak, President, Schostak Brothers & Company Inc.; Steven Chaben, Senior Vice President, Regional Manager, Marcus & Millichap; Luke Timmis, Principal, Investment Division, Signature Associates; Dave Dismondy, Managing Director, District Capital; Anne Galbraith Kohn, Senior Vice President, CBRE; and moderator Mark J. Bennett, Managing Member, MJBennett.

This year’s summit concluded with the Economic Development & Regional Incentives panel featuring Robert McCraight, Mayor, City of Romulus; Paul O’Connell, VP Real Estate Development, Michigan Economic Development Corporation; moderator Kurt Brauer, Partner, Warner Norcross + Judd; Jazmine Danci, Economic Development Administrator, Downriver Community Conference; and Phil Santer, Senior Vice President & Chief of Staff, Ann Arbor SPARK.

Multifamily in neutral: A mid-year reassessment

By Bryan Lamb, Executive Vice President – Multifamily Sector Leader, Ryan Companies

The multifamily real estate sector sends mixed signals as we cross the halfway mark of 2025. Activity has slowed but not stopped, and market conditions are neither recessionary nor red-hot. It’s a year of recalibration, not retreat.

For developers, investors, and capital partners, this is a moment to reassess and not react impulsively but plan strategically for what comes next. While economic uncertainty and capital constraints persist, the long-term outlook for multifamily remains sound. The fundamentals haven’t changed, but the playbook has.

Capital Markets: Still the Primary Headwind

The capital markets environment continues to weigh down multifamily deal flow. Elevated interest rates remain the most significant drag on investment and development activity. As of Q1 2025, the average interest rate for permanent multifamily loans hovers around 6.1%, according to Newmark, up from sub-4% just three years ago.

The result is persistent negative leverage, where borrowing costs exceed unlevered yields. This dynamic has discouraged transactions and kept both buyers and sellers sidelined. Buyers aren’t willing to pay premium prices in today’s financing climate, and sellers are reluctant to realize losses after years of cap rate expansion.

A related ripple effect is limited liquidity. Many LPs are still waiting for

capital to be returned from previous investments before committing to new ones. The development spread, the yield differential between new builds

and stabilized asset cap rates, looks relatively more attractive, especially compared to value-add acquisitions, but few are willing to act until the capital bottleneck clears.

Demand Remains Strong, But Supply Can’t Catch Up

Here lies the paradox: demand is not the problem. Demographic and economic conditions continue to support strong demand. Homeownership remains out of reach for many Americans, with mortgage rates above 6.5% and home prices near record highs. Meanwhile, new household formation has increased in many markets, especially among millennials and Gen Z renters.

According to Newmark data, national

Bryan Lamb (Photo courtesy of Ryan Companies.)

Image by Tori Cheatham from Pixabay

occupancy rates remain stable at around 94.5%, and effective rents increased slightly in Q1 2025, especially in suburban and Sunbelt markets.

What’s missing is new supply. According to FRED, construction starts remain well below pre-slowdown levels, down more than 30% compared to Q1 2023. While there was an 8% uptick from Q1 2024, it’s more of a modest rebound than a proper recovery. Many projects expected to break ground in early 2025 are still sitting on the sidelines. Permits may be in hand, and designs may be complete, but those developments have been shelved or delayed indefinitely without viable capital structures and unnecessary uncertainty on labor and tariff policy, which can dramatically impact construction costs. Roughly speaking, labor and materials each represent about 50% of direct construction costs. With both sides of that equation being challenged, construction cost relief would defy basic economic theory. The result? We’re simply not adding enough new inventory to meet long-term housing demand.

Strategic Shifts: Developers Adapt to Meet the Market

The smartest players aren’t standing still. They’re retooling strategies to match the moment.

One major shift is product type. Developers are moving away from urban high-rise luxury towers in favor of suburban, low-to-mid-density woodframe products. These communities are less expensive to build, faster to deliver, and more aligned with where today’s renters want to live.

There’s also a growing emphasis on attainability, targeting renters earning 80–120% of the area median income (AMI). It’s not “affordable housing” in the regulatory sense, but it is affordable by design: modest unit sizes, practical finishes, and reasonable common-area amenities. States like Florida are leaning into this model with programs like the “Live Local Act,” which offers tax incentives for mixed-income projects built “by right” in commercial zones.

Developers, especially those with integrated architecture and construction teams like ours at Ryan, can use typology and unit prototyping to streamline design, lower costs, and increase construction cost predictability.

“When the market turns, and it will, those with thoughtful discipline and pre-positioned projects will lead the next growth cycle.”

Regional Priorities: Where Development Is Still Happening

While many projects are paused, development hasn’t disappeared entirely and remains attractive where fundamentals are strong and capital confidence is higher.

For example:

• Dallas and Tampa continue to attract development interest due to population and job growth, business-friendly climates, and deeper institutional buyer pools.

• San Diego and Seattle remain appealing as high-barrier markets with long-term rent growth potential, even if entry is more difficult.

• Key indicators guiding development decisions include job growth, employment diversity, housing supply pipelines, and infrastructure investment.

The Rest of 2025: What Could Shift the Market

While the current slowdown feels prolonged, most industry leaders see this as a cyclical pause, not a structural decline.

Multifamily’s underlying strengths: short lease durations, dynamic rent pricing, and essential housing utility, make it historically resilient during recessionary times. The market recovered faster than any other asset class post-2008 and during the COVID bounce-back.

What will it take to reignite activity?

• Rate cuts from the Federal Reserve, projected to begin in late 2025, could tip the balance back toward neutral or even positive leverage.

• Geopolitical stability, including easing tensions in the Middle East and more clarity on tariff policies, would also improve market confidence.

• Stabilized inflation and better construction cost predictability could restore underwriting confidence. Thoughtful labor and immigration policy could go a long way on this front. Until then, most developers plan for 2026 as the more likely window for new starts.

Final Thought: Quietly Building for What’s Next

Multifamily may be in neutral, but developers with a long-term vision are not standing still. They’re using this time to assemble land, refine products, optimize cost structures, and deepen relationships with capital.

When the market turns, and it will, those with thoughtful discipline and pre-positioned projects will lead the next growth cycle.

Bryan Lamb is executive vice president – multifamily sector leader with Minneapolis-based Ryan Companies.

Shaping the Future of Commercial Real Estate

Newmark Zimmer is a leading commercial real estate advisor and service provider to institutional investors, global corporations, and other owners and occupiers.

nmrkzimmer.com

Back on track: Signs of Chicago’s office revival

By Nicole McAleese, Leasing Associate, Urban Innovations

Like any other Monday, I started my day traveling on the Metra from the northwest suburbs—a commute that, for the past four years, often felt like stepping onto a ghost train. Entire cars to myself, eerily quiet rides and a trickle of passengers even during peak hours at Ogilvie Transportation Center.

But this past Monday was different. With the summer heat finally here, the train was bustling. For the first time in years, I struggled to find a seat—and not just once. All week long, trains were packed, standing-room-only in both directions.

Nearly five years since COVID cast its long shadow over Chicago’s commercial real estate market, we’re finally seeing a surge in professionals returning to the office—and it’s backed up by data.

According to Kastle Systems, office occupancy in the top 10 U.S. metros, including Chicago, has risen to around 54.2% of pre-pandemic levels, with a 6.5 percentage point jump in just one month.

On peak days (generally Tuesdays), Chicago’s office occupancy has reached approximately 74%, with

recent reports from Kastle Systems stating occupancy ranging from 74% up to 94% in Chicago’s Class A+ buildings.

Still, Chicago lags behind other major U.S. cities—office visits here remain about 40–45% below the pre-pandemic benchmark.

But the direction is clear—and that optimism is reflected in how spaces are being used and leased. According to Crain’s/Chicago Fed report, Chicago’s office vacancy has continued climbing, reaching a 30-year high of roughly 15% by late 2024. With dig-

ital access data showing office visits steading at 50-55% range.

And industry sentiment remains strong—Avison Young named Chicago a top market to watch in 2025 as leasing and foot traffic begin to accelerate.

With a busy and bright first half of 2025 behind us, it’s thrilling to see River North regaining the hustle and bustle we remember from pre-COVID days. Auctions are turning, transit is packed, and desks are getting filled once again.

Image by Jürgen Polle from Pixabay.

The balancing act: Technology company workplaces evolve to balance innovation with optimization during transformation to AI

By JLL

Technology companies are strategically optimizing their real estate portfolios to free up capital for artificial intelligence investments while simultaneously enhancing workplace effectiveness, according to JLL.

JLL’s 2025 Technology Spaces Report explores how technology organizations are using data-driven strategies to balance cost optimization with innovation demands across office and specialized research spaces.

“The race to lead in artificial intelligence is driving technology companies to innovate faster and to increase investment by driving revenue growth and cutting costs,” said Rob Kolar, Global Division President, Technology, JLL Work Dynamics. “Technology companies are taking a more strategic approach to their real estate, focusing on both optimization and innovation to support rapid AI growth while maximizing the effectiveness of their office environments.”

While many technology companies maintain hybrid work policies, they are increasingly focused on boosting office attendance and effectiveness.

Insights from JLL’s 2025 Global Occupancy Planning Benchmark Report reveals that 56% of technology organizations reduced space in the last year to increase utilization, with 73% having added collaboration space to support hybrid work programs. However, enforcement of in-office policies remains inconsistent, with 24% not enforcing requirements and 45% relying on individual managers to implement attendance on their teams.

Lab and R&D spaces, representing approximately 10% of technology companies’ real estate portfolios, are becoming increasingly important for AI innovation. Despite this growing significance, these specialized spaces lag behind in utilization tracking and data-driven design, with 47% of

companies that have lab spaces not currently tracking their utilization.

“To maximize space effectiveness, technology companies need a smart, goal-driven data strategy,” noted Kari Beets, Senior Manager, Technology Research, JLL. “Quality data is para mount in making impactful decisions, but it’s essential to streamline what metrics are collected and presented in light of overall strategy to trim costs and lead to more optimized space.”

Looking ahead, JLL forecasts four key ways technology workspaces will transform in the next 3-5 years:

1. The learning workplace: Agentic AI will create workplaces that adapt au tomatically to improve efficiency and human experience

2. Innovation-driven investment: In creased spending on AI compute, lab spaces and R&D facilities to support innovation

3. Collaboration over cubicles: Greater emphasis on human collaboration and AI-supported work environments

4. Energy-conscious design: Technol ogy companies will increasingly focus on clean power and energy efficiency to support AI computing demands

The technology workplace of the fu ture will be a learning workspace that

is innovation-driven, collaborative –between humans and with machines

indicates that 82% of technology real estate leaders believe AI can help solve major CRE challenges.

“To prepare for the future, corporate real estate teams must establish a clear vision that’s aligned with business goals and flexible enough to respond to rapid change,” added Nick LiVigne, Managing Director, Consulting Lead, Technology, JLL. “This means building strong data capabilities to be more predictive, applying AI to the right business problems, and having a test and learn approach to how the teams operate.”

IImage by Shadab Mohammad from Pixabay.

Maximizing value in industrial real estate: Execution, agility and cross-functional strategy

By Kevin Bufalino, Clear Height Properties

In today’s industrial real estate market, delivering strong, risk-adjusted returns isn’t just about buying right or riding cap rates, it’s about execution, operational discipline, and a cross-functional approach that drives value throughout the life of an asset.

Balance and Diversification Absorb Volatility

Smart portfolio construction demands more than just a focus on location. While real estate fundamentals will always value geography, truly resilient portfolios are built with broader strategic intent. Factors like asset mix, tenant profile, and market exposure play a critical role in weathering economic cycles.

Portfolios that thoughtfully combine single- and multi-tenant assets across both infill and geographically diverse markets tend to outperform through periods of leasing volatility and shifting interest rate environments. This diversification not only enhances stability but also position owners to capitalize on emerging market dynamics.

Clear Height Properties recently put this strategy into action through the acquisition of a five-building, 231,000-square-foot industrial portfolio in the Cincinnati metro area. This expansion reflects a broader investment thesis: targeting stable, under-recognized submarkets where tenant demand is steady and acquisition pricing remains disciplined. The Cincinnati acquisition not only broadened geographic exposure but also aligned with Clear Height’s longterm goals for leasing velocity and portfolio balance.

In short, smart portfolio construction isn’t about chasing the obvious, it’s about building for resilience and opportunity in any market condition.

Acquiring an asset is only the beginning. Real value is created when operators engage proactively with tenants, identify opportunities for improvement, and structure deals to serve both short-term needs and long-term performance.

Through Q2 2025, Clear Height executed 80 lease transactions totaling 426,000 square feet. Many of these transactions involved proactive tenant discussions with creative structuring or in-house construction support. These were not passive renewals. In fact, they were the result of deliberate, integrated execution between asset managers, property managers, and leasing partners.

Integrated Teams Drive Strategic Results

Siloed decision-making often leads to inefficient capital deployment and missed opportunities. When leasing, asset management, and property operations operate in isolation, critical insights fall through the cracks and strategic momentum stalls.

Organizations that embrace cross-functional integration are

better equipped to capitalize on opportunities in real time with precision. When teams are aligned, decisions move faster, and execution improves. Then value is unlocked more efficiently through proactive lease structuring, targeted capital investments, or operational agility.

In today’s environment, speed and alignment are not just operational strengths, they’re strategic imperatives.