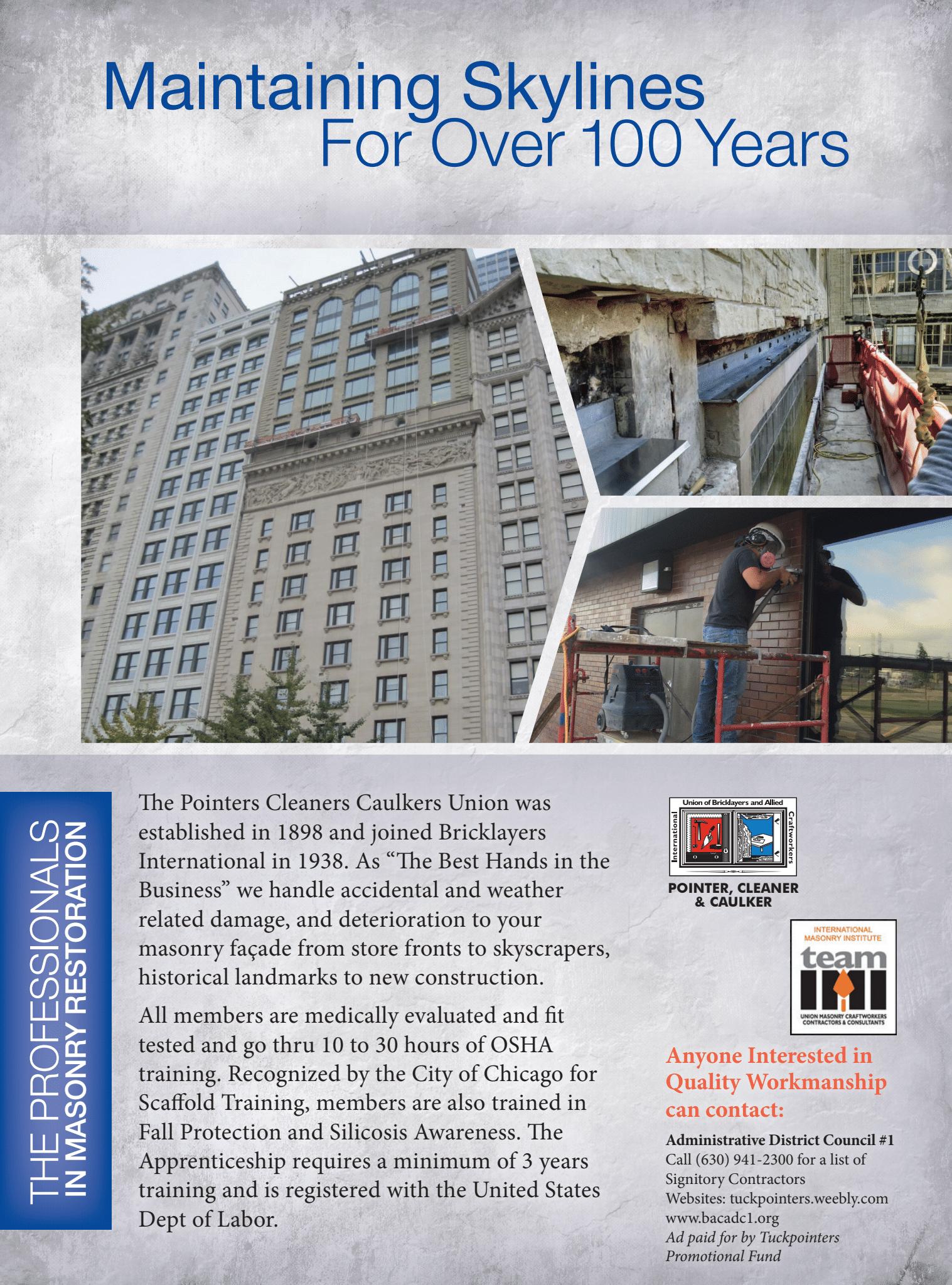

From Scale to Selectivity Why CenterPoint’s 2026 pipeline favors entitled land and infrastructure-led strategy

aleksandarlittlewolf

Everyone is talking about rising industrial demand heading into 2026, but that’s not the story developers are living. Their real bottlenecks sit deeper in the system: power access, build-to-suit complexity, lender scrutiny and capital partners that now expect sustainability baked into every inch of design. For most developers that reality is a drag. For CenterPoint

Properties, it has become a competitive advantage.

Chicago’s industrial market is heading into 2026 with an unusual mix of momentum and restraint.

Leasing activity has rebounded sharply, hitting 35.9 million square feet through Q3 according to Avison Young’s latest market data, and big-box commitments have returned with force. Yet de -

velopment has throttled back. Only 12.9 million square feet are under construction across the metro, down 55 percent from the peak two years ago (AY Q3 report, page 2). This tightening pipeline has reshaped not just what gets built, but who is positioned to build it.

DEVELOPERS (continued on page 12)

for freepik

PUBLISHER

Mark Menzies menzies@rejournals.com 312.933.8559

MANAGING EDITOR Dan Rafter drafter@rejournals.com

VICE PRESIDENT OF SALES & MW CONFERENCE SERIES MANAGER Ernie Abood eabood@rejournals.com

VICE PRESIDENT OF SALES Frank E. Biondo Frank.biondo@rejournals.com

From Scale to Selectivity: Why CenterPoint’s 2026 pipeline favors entitled land and infrastructure-led strategy Everyone is talking about rising industrial demand heading into 2026, but that’s not the story developers are living. Their real bottlenecks sit deeper in the system: power access, build-to-suit complexity, lender scrutiny and capital partners that now expect sustainability baked into every inch of design. For most developers that reality is a drag. For CenterPoint Properties, it has become a competitive advantage.

4

Beyond the Warehouse: IOS emerges as Chicago’s most competitive industrial asset Chicago’s industrial market has spent two years fixated on construction pullbacks, big-box rebounds and the question of how quickly tenants will reengage. But the next cycle may hinge on something far simpler: the land that no one can build again.

6

Pent-Up Potential: Chicago’s industrial market eyes a rebound in 2026 Chicago’s industrial market spent most of 2025 looking more complicated on the ground than it did on paper.

8

Unlocking Hidden Value: Transforming Industrial Properties into High-Performing Assets Industrial real estate is often called the backbone of the economy, but not every building is performing at its full potential. At Clear Height Properties, we focus on finding those “diamonds in the rough” and transforming them into strong, reliable assets.

10

SIOR Panel Sheds Light on Property Tax Reform, Fairness, and Real-World Strategies In Cook County, property taxes can be one of the most unpredictable and most influential variables in the region’s commercial real estate.

14

16

17

The fundamentals remain strong. That’s the message from Marcus & Millichap The fundamentals are strong. That's the takeaway from Marcus & Millichap's latest commercial real estate research brief.

A commercial construction industry in flux? JLL’s Project and Development Services group predicts a construction industry in 2026 defined by policy-driven pressures,

NAI Hiffman: Improving fundamentals buoying Chicago-area industrial sector The Chicago industrial market saw improving fundamentals during the third quarter of 2025, with net absorption of nearly 7.5 million square feet and the sector's vacancy rate falling to 6.1%.

18

COMMERCIAL SERVICES: COMMERCIAL LENDERS/CONSTRUCTION COMPANIES/GENERAL CONTRACTORS/ ECONOMIC DEVELOPMENT CORPORATIONS/RE LAW FIRMS

Beyond the Warehouse: IOS emerges as Chicago’s most competitive industrial asset

By Brandi Smith

Chicago’s industrial market has spent two years fixated on construction pullbacks, big-box rebounds and the question of how quickly tenants will reengage. But the next cycle may hinge on something far simpler: the land that no one can build again. As developers trim pipelines and the mid-range bulk segment hollowed out entirely this year, a different corner of the market has emerged as the most strategic battleground heading into 2026. It’s not Class A warehouses or speculative megasites; it’s the infill industrial outdoor storage yards in the beltline where trucking, intermodal traffic and last-mile networks intersect.

These sites have always been operational necessities. The difference now is that they have become financial ones too. Chicago’s Q3 2025 data makes the point clearly. Construction has fallen 55 percent from its 2023 peak, leaving only 12.9 million square feet underway across a metro with more than 1.2 billion square feet of inventory. Not one square foot is under development in the 500,000 to 749,000 square foot size range — a segment that historically helped balance the region’s supply pipeline. With development hollowed out in that middle band and the remaining large-format construction tilted toward build-to-suit, the pressure on infill land has only intensified.

Nowhere is that pressure clearer than in the IOS segment. These sites were already scarce. Redevelopment, rezoning and infrastructure expansion have pushed them into near-extinction, reshaping the competitive landscape in ways that aren’t reflected in traditional vacancy or absorption data. IOS availability contracts even when the broader market appears stable. It’s a land-use story, not a leasing one.

“My view of Chicago in 2025 is largely shaped by the scarcity of highly functional, strategic real estate in core infill areas,” said Cary Goldman, founder and CEO of Timber Hill Group. “The mainstream focus on massive, speculative bulk warehouses along the outer edges of the market often overlooks the mission-critical segments closer to the urban core.”

That scarcity has only intensified as redevelopment pressure mounts. Data centers, higher-value warehouses and infrastructure projects are absorbing land that once supported IOS functions. Even as overall vacancy holds at 6.2 percent, according to Avison Young’s Q3

"My view of Chicago in 2025 is largely shaped by the scarcity of highly functional, strategic real estate in core infill areas."

2025 report, the supply of IOS-compatible parcels is shrinking in ways vacancy rates cannot show. These sites don’t replenish through new construction cycles. They disappear permanently unless an operator is willing to undertake complex, occasionally contentious entitlement work.

This is exactly why Timber Hill has leaned into assets where zoning, functionality and connectivity overlap. The firm operates four IOS cross-dock terminals in Chicago and recently repositioned one following the expiration of an inherited below-market lease. The property sits six miles from the Loop at I-55 and Cicero, a location that leverages the dense interplay of interstate access and the BNSF and CSX intermodal networks. The site includes a 55-door terminal with an executive office, a free-standing 10,000-square-foot truck repair building and parking for 70 trailers and 59 tractors. Leasing has moved quickly, underscoring an infill theme

that is increasingly dominating tenant behavior.

Goldman pointed to why these “messy” assets matter more in today’s network-driven environment.

“The 'overlooked' properties aren't necessarily obsolete buildings; they are often the highly constrained, legally zoned parcels used for fleet management, last-mile staging, and container storage — the critical 'parking lots' of the supply chain that enable efficient movement of goods,” Goldman said.

Institutions have historically treated IOS as an operational afterthought. As more capital sources tune into the structural scarcity of IOS-compatible land, competition has followed. With few viable options for ground-up IOS development, acquisition and conversion strategies have become the most realistic and efficient plays. Older low-coverage buildings, once discounted, now trade at premiums because their zoning and locations can’t be replicated.

That supply-side pressure is meeting a demand profile that looks nothing like the broader industrial market. Chicago’s logistical advantages are unusually dense. Four interstates intersect here. Six Class I railroads run intermodal operations across the metro. O’Hare ranks among the top cargo airports in the country. According to the AY report’s freight movement data, roughly half of the nation’s intermodal trains pass through Chicago on any given day, and Q3 leasing activity reached 35.9 million square feet — pacing ahead of 2024’s full-year total. Those concentrations of movement are exactly what

turn IOS sites from niche assets into strategic infrastructure.

“Chicago sits at the convergence of four major interstate highways (I-55, I-65, I-80 and I-90), providing direct east–west and north–south connectivity,” Goldman said. “All six U.S. Class I railroads operate intermodal facilities in the metro area, and roughly 50% of all U.S. intermodal trains — about 1,300 trains per day — move through the region. This concentration of rail infrastructure is unmatched elsewhere in the country.”

The region’s freight behavior is stabilizing too. After several years of rate volatility, trucking markets show more balanced routing, better service reliability and fewer extreme swings. That predictability gives operators the confidence to make longer-term location decisions, especially for nodes that support staging, parking and asset maintenance. With data center construction surging and manufacturing activity picking up, flatbed spot rates have shown the first sustained increase in months. Those indicators typically correlate with increased need for IOS capacity.

But the most consequential shift is likely to be psychological rather than statistical. For the first time, IOS is emerging as a primary investment category, not a residual one. The institutionalization of the asset class driven by rising rents, operational needs and persistent land scarcity is pulling new capital into a segment that once required specialist knowledge.

“The next evolution, in my view, is land scarcity,” Goldman said. “Inside the 294/290/55 beltline, the amount of industrial-zoned acreage that can support open storage, equipment yards or fleet operations is shrinking every year.”

That accelerating scarcity will define 2026 more than any movement in headline vacancy or absorption metrics. As developers stay cautious and mid-range bulk construction remains absent, the assets that depend on land rather than walls will set the tone for the region’s industrial performance. IOS may not grab headlines, but its influence runs deeper than most market indicators reveal. In a market built on movement, the most valuable assets may be the ones that never move at all.

Cary Goldman

Pent-Up Potential: Chicago’s industrial market eyes a rebound in 2026

By Brandi Smith

Chicago’s industrial market spent most of 2025 looking more complicated on the ground than it did on paper. Activity appeared constant, yet the correlation to executed deals was weaker than anyone expected. Brokers who anticipated a midyear acceleration instead watched activity cluster without translating into the absorption that typically follows. The headline story wasn’t a lack of interest; it was a backlog of decisions that kept getting pushed just out of reach.

“Liberation Day threw a wrench into demand around most submarkets within Chicago,” said Ben Dickey, Vice President at Stream Realty Partners, whose team saw the mismatch create a sense of suspended animation: a market that looked and felt engaged but kept failing to commit. “There were many cases of buildings that had the perfect unit size for the submarket, or well-priced, functional assets, not seeing any tenant demand for months at a time.”

That pause is now beginning to unwind. By late 2025, brokers were reporting renewed energy across leasing channels. Tours began converting. O’Hare saw a noticeable uptick in deal flow. Users who sat out most of the year began revisiting previously shelved moves, a trend several brokers described as most visible in the airport submarket.

“O’Hare has really flipped from a demand perspective over the past three months compared to the first six in 2025,” Dickey said. “Today, we are seeing renewals and new deals signing with more tours and RFP velocity behind them across all sizes and building class ranges.”

Still, the year’s uneven momentum reset expectations around leverage. Older commodity space lost ground, especially in suburban corridors where second-gen supply grew quickly.

“We are seeing TI allowances and free rent increase and, in some cases, aggressive phase-in rent schedules to maintain a higher base rent that hits developer underwriting,” Dickey said.

Owners waiting for the urgency of the prior cycle found less traction and many faced pressure to adjust underwriting or offer more flexible terms.

“The biggest surprise was how busy the market felt versus how little of that activity translated into true absorption,” said Ken Franzese, Principal at Lee & Associates of Illinois. “Tours,

"Big Box activity, which I would define as

200,000

square feet or larger, seems to be picking up again. A lot of the fortune 500 tenants made big expansion moves pre-pandemic or early on during that fun time, and then the middle market tenant followed ... The rumblings across the market point to a bounce back on big box activity."

RFPs and renewal discussions were strong. However, trade policy, interest rates and inflation stretched decision timelines and kept users cautious.”

That contrast helped define 2025: a market with plenty of activity but inconsistent follow-through. Some brokers argue that oversupply in mid-tier submarkets could keep certain owners concession-heavy into next year. Others point to stronger-than-expected big box activity along I-80, Joliet and Southeast Wisconsin as evidence that demand is already on the move.

“Big Box activity, which I would define as 200,000 square feet or larger, seems to be picking up again,” said Dan Prendergast, Vice President of DarwinPW Realty/CORFAC International. “A lot of the fortune 500 tenants made big expansion moves pre-pandemic or early on during that fun time, and then the middle market tenant followed. But during the last 24 months some owners, or developers that delivered late, were left carrying substantial vacancies. The rumblings across the market point to a bounce back on big box activity.”

The market’s split personality is likely to define early 2026: tight and competitive in infill, improving but selective in bulk corridors and still challenged for older legacy product.

Investors spent 2025 with a similarly cautious hand. Capital focused on predictable asset profiles and passed on anything with unusual characteristics or execution risk. Yet when buyers did act, pricing showed real conviction, especially for infill portfolios. Brokers expect that selectivity to hold, though they anticipate a wider range of buyers

Ben Dickey

Kenneth Franzese

Dan Prendergast

returning as debt stabilizes and underwriting becomes more predictable.

“Buyers stayed very disciplined in 2025,” said Kurt Sarbaugh, Managing Director of JLL Capital Markets. “Opportunities that hit specific buyer profiles were very competitive, while deals that had some uniqueness in the profile had shallower bid pools. Investors were willing to push pricing in certain spots, but the fairway remained narrow.”

That discipline is likely to loosen at the margins next year. Banks are lending again under tighter structures and several capital sources that sat out most of 2025 are showing early movement. Larger portfolio deals are reappearing. There’s growing confidence that Cook County assets, long dismissed by some investors, remain too central to ignore in a region where labor, logistics and rooftops drive every decision.

On the leasing side, tenant outlooks are also shifting. Companies that entered 2025 with caution now cite improving business confidence, a steadier understanding of tariff impacts and a more predictable interest rate environment. For many, 2025 functioned as a recalibration year that

clarified real estate priorities after two volatile cycles.

“Overall tenant activity in 2025 was sluggish,” Prendergast said. “New customer engagement remained flat, and cautious decision-making with increased price sensitivity was a regular theme throughout the year.”

A major wildcard for 2026 is how fast second-generation space is absorbed. That supply kept renewal rates lower in 2025 and pressured asking rents in

certain suburban corridors, particularly for buildings that lacked modern clear heights or trailer capacity. If leasing momentum accelerates as expected, that inventory could tighten faster than the market anticipates, especially with speculative development still muted.

But the most durable momentum remains in the city and its first-ring suburbs. In those locations, multimodal infrastructure, labor access, and proximity to consumers outweigh

temporary uncertainty. Franzese’s broader framing of the year reinforces that divergence.

“Today, the story is less about demand going away and more about the market sorting winners and losers by location and quality,” Franzese said.

“The influx of second-generation space in the 2025 market led to a notable decrease in renewal rates compared to previous years,” said Jackie L. Shropshire, Chicago Industrial Lead at JLL.

The consensus from Chicagoland experts is that 2026 will be defined by a release of pent-up demand rather than a redefinition of market fundamentals. Tenants who hesitated will move. Investors who circled will bid. And landlords who adapted in 2025 will be first to benefit.

The year ahead won’t erase the complexities of the past twelve months, but it will mark a pivot, a shift from waiting to acting, from caution to recalibrated confidence and from surface-level activity to real transactions that reshape the market.

Kurt Sarbaugh

Jackie Shropshire

Unlocking Hidden Value: Transforming Industrial Properties into HighPerforming Assets

By Lauren Posey, Clear Height Properties

Industrial real estate is often called the backbone of the economy, but not every building is performing at its full potential. At Clear Height Properties, we focus on finding those “diamonds in the rough” and transforming them into strong, reliable assets. The opportunity lies in seeing potential where others see problems, breathing new life into overlooked or underutilized properties with the right improvements, smart execution, and a vision for what they can become.

Our approach is simple: stick to real estate fundamentals, make targeted upgrades, and reposition buildings to meet tenant demand. The result is more than strong returns. It is spaces that work better for tenants and add value to communities.

The “Diamond in the Rough” Approach

We look for buildings with good bones: clear height that works for modern users, efficient layouts, solid slabs, and flexible configurations. With these basics in place, we can avoid heavy structural costs and focus our investment on improvements that directly increase value.

Often, the buildings we buy have years of deferred maintenance. Parking lots are worn, landscaping is tired, or systems are past their useful life. Rather than seeing this as a drawback, we see it as an opportunity. By tackling these issues head on, we immediately reposition the property in the market.

Sometimes that means resolving compliance gaps, upgrading fire alarms, making ADA improvements, or rethinking inefficient office space. In many cases, reducing or reconfiguring office areas creates more warehouse space and better suits today’s tenants. Where others see headaches, we see potential.

Modern Systems and Tenant Friendly Features

Bringing properties up to current standards is a big part of what we do. One of the simplest but most impactful changes is upgrading to LED lighting. It reduces energy use, meets new code requirements, and creates brighter, safer work environments. We also integrate sustainable finishes like low flow plumbing, low VOC paints, and ceiling tiles, choices that lower

"Many tenants today need less office and more flexible layouts, so we design spaces that can easily adapt."

operating costs while aligning with ESG goals.

Tenant expectations are also evolving. Features like EV charging stations, once considered extras, are quickly becoming the norm. We install them in strategic locations that support ten-

ants without disrupting traffic flow or parking.

The balance between office and warehouse space is another area where we create value. Many tenants today need less office and more flexible layouts, so we design spaces that can easily

adapt. We have also leaned into adaptive reuse, turning a brewery into pickleball courts and a former distribution center into a baseball training facility. Creative solutions like these meet real market demand, often faster and more cost effectively than new construction.

Execution: Vision into Value

The key to success is execution. Our capital programs are not just about fixing problems; they are about preparing properties for the long term. Roofs, paving, HVAC, and tuckpointing are all handled with trusted vendors who deliver quality and speed, while also helping us secure savings and priority scheduling.

Timing matters too. Immediately upon closing, we start prepping vacant spaces, so they are ready to lease. This includes simple but impactful upgrades like fresh exterior paint or painting interior warehouse walls white, which can dramatically brighten a space and make a big impact on first impressions.

We also think ahead when it comes to functionality: adding drive-in doors, enlarging undersized doors, or upgrading loading docks with seals, levelers, and edge-of-dock equipment are all evaluated during due diligence. Even if these improvements are not immediately necessary, we plan ahead, recognizing that they may be required during our hold period or when a tenant vacates. This forward-thinking approach minimizes downtime and ensures we are ready to move quickly.

Sustainability and Compliance

Sustainability and compliance are not optional anymore, they are expected. At Clear Height, we prioritize upgrades that reduce energy consumption, improve indoor environmental quality, and extend the useful life of assets. Replacing outdated fluorescent or metal halide fixtures with LEDs, using low-VOC paints, and installing water-efficient fixtures are just a few of the ways we integrate sustainability into our repositioning strategy.

Compliance is equally important. We systematically address ADA requirements by modifying layouts, restrooms, ramps, and door hardware. These investments not only protect our tenants and their employees but also minimize landlord liability. By taking a proactive stance on compliance,

605 Bonnie Lane in Elk Grove Village before exterior upgrades.

Repainted façade and cladding with a new concrete apron and freshened curb appeal.

we create safer, more inclusive, and more marketable properties.

From Challenges to Opportunities

The results speak for themselves. One of our acquisitions with significant deferred maintenance is now fully leased after LED upgrades, parking lot resurfacing, and interior reconfigurations. Another vacant distribution building is now thriving as a community sports facility.

In each case, the common thread is Clear Height’s ability to look beyond current conditions and envision what the property could become. By executing quickly, leveraging strong vendor partnerships, and focusing on tenant needs, we consistently deliver outcomes that exceed expectations.

A Holistic Commitment to Value Creation

Individually, roof replacements, ADA upgrades, or LED retrofits may not seem transformative. However, when

combined into a comprehensive strategy, these investments create a strategy that consistently unlocks value. They differentiate Clear Height Properties from owners who simply maintain the status quo.

Our philosophy is that every building has potential if you know where to look and how to unlock it. By focusing on fundamentals, addressing deferred maintenance, implementing modern systems, and reimagining space to meet evolving tenant needs, we trans -

form underperforming assets into high-performing ones.

At Clear Height, we are not just investing in buildings, we are investing in the future of industrial real estate, one “diamond in the rough” at a time.

About

Lauren Posey

Lauren is the architect of operational excellence at Clear Height. She joined the team in 2020 and quickly built the property operations department, creating a vital connection.

Mark

Ryan

Original fluorescent fixtures at 1400 Morse Road in Elk Grove Village.

High-efficiency LED replacement units.

SIOR Panel Sheds Light on Property Tax Reform, Fairness,

and Real-World

Strategies

By Joshua Hearne

If you have ever tried to underwrite a deal or value an investment property in Cook County, you know that property taxes can most unpredictable and one of the most influential variables in the region’s commercial real estate. That uncertainty was the focus of a recent SIOR Chicago Chapter luncheon in Glenview that I moderated with George Cardenas of the Cook County Board of Review and Jay Rock of Rock Fusco & Connelly, LLC.

The discussion covered the complexities of real estate tax assessments and the appeal process, emphasizing the roles of assessors, boards of review, and the importance of providing evidence when contesting property valuations. The panel also explored tax incentives such as the 6b program, including eligibility, renewal, and the political considerations involved in securing and maintaining these incentives. The conversation also compared tax trends and infrastructure challenges across Cook County and neighboring counties, highlighting how new developments and population shifts impact tax rates.

How Assessments Work and Why Appeals Are Important

I opened the discussion with a question that nearly every investor and broker has asked at some point. How can one property can be taxed at $1.50 per square foot, while the property next door is taxed at $4.00 per square foot?

Rock explained that while assessors can’t legally chase sales or automatically increase valuations based on sales price, they do use sales data to guide their models. That, he said, can lead to outliers, especially when new construction or high-priced transactions can distort the data.

“That is why there is an appeal process,” he said. “Just because the assessor says something, that doesn’t mean that it’s the final word.”

Rock went on to explain that every county in Illinois has a Board of Review, where property owners are able to challenge assessments, provide comparable property data and make the argument on the basis of uniformity, which is guaranteed under section nine of the owner constitution.

Cardenas described the Board of Review simply as “the people’s agency,”

"That is why there is an appeal process. Just because the assessor says something, that doesn’t mean that it’s the final word."

noting that that is where due process comes in, is upheld, and where property owners can engage directly with analysts as well as commissioners to make their case.

Unlike the assessor’s office, which typically sets values based on a limited

amount of data or formulas, it allows everyone to be treated fairly and have evidence in hand, he continued.

Importance of Evidence and Transparency

Throughout the discussion, the panelists noted that the key to a successful appeal lies in preparation and evidence, and that owners appealing on an income basis should be ready to submit detailed income and expense statements, rental data, and vacancy information.

“If you’re going to claim your property is over-assessed, you have to back it up with data,” Rock said.

Cardenas agreed, noting that while some owners might be tempted to “play cute” with their numbers, the Board can easily spot inconsistencies. He also encouraged property owners to stay engaged throughout the process and to communicate with your municipal leaders or government contacts if you run into issues. Transparency goes a long way, he added.

The Advantage of Incentive Programs

Much of the conversation focused on Cook County’s Class 6b incentive, an important tool used to attract and retain industrial investment. The 6b provides a 12-year reduced assessment rate of 10% for the first 10 years and a gradual increase in years 11 and 12

Left to Right: Jay Rock, Partner, Rock, Fusco & Connelly: Joshua Hearne, SIOR, Principal, Cawley Chicago Commercial Real Estate; George Cardenas, Commissioner, Cook County Board of Review

for qualifying properties that undergo new construction, substantial rehabilitation, or reactivation of abandoned building after at least 12 months of vacancy.

But municipal support is the real key to success, panelists explained. “If the municipality is in favor of it, the county is usually a rubber stamp,” Rock said. He encouraged investors and owners to begin renewal discussions about 18 to 24 months before expiration as well as to document how the tax savings were used, whether that was through job creation, facility upgrades, or community reinvestment.

Cardenas added that transparency and visibility are powerful allies. If a property owner has created new jobs, improved the property, or invested in the community, they should show it off. “Invite local officials to ribbon cuttings. Share your success stories. It’s good politics and good business.”

Renewals of the 6b classification, however, should never be thought of as automatic. Panelists noted that municipalities are sometimes counting down the days until that 6b expires to see that full tax revenue. The best way to improve your odds for renewal,

"Good communication and good citizenship are just as valuable as good data."

Rock added, is to show tangible and ongoing benefits to the community.

Regional Trends and Rising Rates

Surrounding counties like Will, DuPage, and Lake are also facing their own set of tax challenges. As Rock explained, the rapid pace of industrial and residential development in these areas has created other infrastructure needs such as roads, schools, utilities, and emergency services, which inevitably can drive the need for higher tax rates.

While panelists said their tax rates aren’t catching up to Cook County as of yet, there has been an increase.

Cardenas was quick to point out that relocating purely to avoid high taxes, though, may not be the solution. “There’s no free lunch. If demand rises and values go up, taxes follow. It’s market economics,” he explained.

He also notes that Cook County has many advantages such as connectivity, access, and infrastructure. “I can get anywhere in 30 or 40 minutes,” he explained.

Practical Takeaways

As the panel moved into audience Q&A, the conversation turned more into the practical strategies for owners and investors in managing taxes

and avoiding missteps. The top pieces of advice offered early included:

• Engage early and don’t wait until after a sale to explore appeals or incentives. For 6b applications, initiate conversations well before closing.

• Being accurate and honest. Overstating jobs or investment commitments can backfire, as municipalities often verify compliance and can revoke incentives or impose penalties.

• Keep detailed records like marketing materials, vacancy affidavits, and financial statements. Records can strengthen a case during appeals or renewal applications.

Most counties require appeals to be filed within 30 days of receiving an assessment, so understanding the timeline is key. Board of Review decisions typically follow within 60 days, though appeals to the Property Tax Appeal Board can take up to two years.

And lastly, staying connected and maintaining relationships with municipal and county officials is critical. As Cardenas said, “Good communication and good citizenship are just as valuable as good data.”

CenterPoint spent 2025 doubling down on the fundamentals that many others treated as secondary during the frothier development years. Entitled land, resilient infrastructure and capital discipline shaped its pipeline more than any single macro variable. Rather than chasing the cycle, CenterPoint positioned itself to benefit when the cycle turned. That shift arrived earlier than many expected, and it has reshaped the conversation about what gets built next.

“Timing became everything as speculative development slowed and capital markets tightened,” said Carmine Bottigliero, Vice President of Development at CenterPoint. “Successful projects were those positioned in markets with resilient demand and infrastructure.”

The data supports that recalibration. After years of record deliveries, developers are putting fewer chips on the table. Mid-range bulk construction between 500,000 and 749,000 square feet has disappeared entirely, according to the Avison Young report, while largescale projects that do move ahead are either highly specialized or build-tosuit. The result is a market where users are active but choices are limited. And while brokers have spent much of 2025 talking about decision-making delays, the development community has been adapting to a tighter landscape.

That landscape plays directly to CenterPoint’s strengths. The Intermodal Center at Joliet and Elwood, its flagship, 6,500-acre logistics ecosystem, sits at the confluence of Class I rail, interstate access and labor density. Large format sites with direct intermodal connectivity are scarce and many competitors are grappling with rising utility requirements and entitlement headwinds. The infrastructure advantage that the firm secured years ago is becoming harder for the rest of the market to replicate.

“Land strategy shifted toward securing strategic parcels early, especially those that are entitled and in power-constrained regions, while maintaining flexibility in design,” Bottigliero said.

Developers across the market felt those constraints in 2025. Even though debt availability improved late in the year, lenders were more selective and capital partners demanded tighter alignment on ESG, sustainability credentials and municipal coordination. Those requirements slowed speculative projects, but gave a lift to developers with established entitlements and relationships. The gap between “shovel-ready” and “shovel-possible” has not been this wide in years.

That gap is shaping occupier behavior too. Build-to-suit demand rose across Chicago as tenants sought speed, customization and access to labor, even as they wrestled with rising operating costs. The Avison Young report shows

Centerpoint

"Timing became everything as speculative development slowed and capital markets tightened. Successful projects were those positioned in markets with resilient demand and infrastructure."

big-box leasing over 750,000 square feet is one of the few sectors accelerating and it has done so in a submarket ecosystem where new supply has thinned out.

“Build-to-suit inquiries have surged, signaling occupiers’ desire for speed and customization,” Bottigliero said.

CenterPoint’s upcoming 1.1 million square foot Class A facility at the Intermodal Center fits squarely into this market direction. Scheduled to break ground in spring 2026, the project draws on pre-entitled land, multimodal connectivity and a submarket that continues to outperform on leasing velocity. More importantly, it re-

flects the shift toward sites that can solve infrastructure challenges first, speculative risk second.

Labor dynamics sit just behind those infrastructure challenges and Bottigliero sees them as the quiet variable that will shape next year’s feasibility math. While vacancy remains a healthy 6.2 percent across the metro, several submarkets — particularly those with strong labor footprints — have tightened faster than others. Developers are beginning to triangulate around these locations, weighing workforce reliability as heavily as land cost and utility capacity.

“Persistent talent shortages and rising labor and transportation costs will influence construction timelines and operational strategies,” Bottigliero said.

That pressure adds another layer of discipline to a market already grappling with capital tightening. Rising insurance costs, conservative underwriting and higher operating expenses have forced developers to scrutinize every assumption in their models. CenterPoint’s approach has been to build flexibility into design and delivery, avoiding product types that risk oversupply while focusing on assets with long-term tenant relevance. As more developers chase mid-bay or small-bay opportunities, the firm continues to prioritize infrastructure-heavy big-box

formats where user demand is the most consistent.

Foreign capital has noticed that discipline. International investors have reentered the Midwest with renewed urgency, and Chicago with its multimodal network, deep labor pool, and relative affordability has risen on the list of preferred U.S. industrial markets. Developers that can demonstrate entitlement certainty and infrastructure access have captured the most attention.

“Foreign capital — particularly from Asia — continues to target U.S. industrial assets, with the Midwest, specifically Chicago, emerging as a preferred region,” Bottigliero said.

The story heading into 2026 is not one of runaway development or speculative exuberance. It is a market defined by constraints — of land, of capital, of power, of labor — and by the developers who anticipated those constraints early enough to turn them into opportunities. CenterPoint’s bet on timing and strategic positioning reflects the shift from an era of scale to an era of selectivity. With entitled land, resilient infrastructure and a pipeline aligned with occupier demand, the firm enters the next cycle with a level of clarity many developers are still searching for.

DEVELOPERS (continued from page 1)

Carmine Bottigliero

Intermodal Center

The fundamentals remain strong. That’s the message from Marcus & Millichap

By Dan Rafter

The fundamentals are strong. That's the takeaway from Marcus & Millichap's latest commercial real estate research brief.

In its third-quarter fundamentals report, Marcus & Millichap said that the CRE market's fundamentals are holding firm. That's good news.

But that doesn't mean that commercial real estate professionals won't face challenges throughout the rest of 2025 and in 2026.

In its latest report, Marcus & Millichap analyzed the state of the commercial real estate sector's main asset types. The findings? These sectors might not be booming, but they are, mostly, holding steady even during national economic challenges.

Balance is returning to the multifamily market, according to Marcus & Millichap's report. Demand growth in this sector is moderating, but so is new supply. That could lead to a more stable multifamily market across the

United States, Marcus & Millichap reported.

According to Marcus & Millichap, while the national multifamily vacancy rate is still down 100 basis points on a year-over-year basis, this number did increase to 4.6% in the third quarter of this year.

Certain markets have also seen so much new apartment development that they are now experiencing higher vacancy rates. Marcus & Millichap pointed to markets such as Austin, Dallas-Fort Worth and Nashville. On the other side of the equation, markets with limited development, including Chicago, Cincinnati, Cleveland, Detroit and Minneapolis-St. Paul, have seen rent growth higher than 5%, Marcus & Millichap reported.

In a bit of good news, Marcus & Millichap reported that the U.S. office sector continued to post a positive performance in the third quarter, which might signal a modest recovery in some metropolitan areas.

According to Marcus & Millichap, nearly 38 million square feet of office space was absorbed across the United States in the third quarter. That marks the sixth consecutive quarter of positive net absorption in this sector.

This helped drop the national office vacancy rate down 30 basis points to 16.4% in September, Marcus & Millichap reported.

The office vacancy rate fell a strong 170 basis points in Milwaukee, making this Wisconsin city one of the stronger performers in this sector during the third quarter. Marcus & Millichap reported, too, that Cleveland and Indianapolis ranked among the least-vacant office metropolitan areas in the third quarter.

And in the industrial sector? Marcus & Millichap reported that years of heavy industrial supply continue to influence this sector's performance.

According to Marcus & Millichap, nearly 20 million square feet of industrial space was absorbed from July to

September following a second quarter that saw negative net absorption in this sector. Even with the absorption in the third quarter, though, increased construction activity pushed the vacancy rate in the U.S. industrial sector to a 12-year high of 7.8%.

Construction activity is the reason behind this higher vacancy rate. Marcus & Millichap reported that about 3.5 billion square feet of industrial space has been completed during the past 10 years in the United States. That space is still being absorbed.

The retail sector is holding steady, according to Marcus & Millichap. Net absorption in this sector was positive in the third quarter, but its vacancy rate edged up to a below-average 4.9%.

Retail vacancy rates, though, were below 3.5% in Indianapolis and Minneapolis-St. Paul. Marcus & Millichap reported that well-located retail space, especially space in centers with a higher concentration of necessity retailers, remains in demand by investors.

Photo by Pixabay

A commercial construction industry in flux?

By Dan Rafter

JLL’s Project and Development Services group predicts a construction industry in 2026 defined by policy-driven pressures, local-market nuance and the need for sharper strategic planning. And this evolving construction market will have a significant impact on new development activity in the industrial sector.

That’s the key takeaway from Jll's 2026 U.S. Construction Perspective, a report released this November that highlights how shifting federal and economic policies are reshaping construction opportunities across the country.

“The construction industry is navigating an unprecedented convergence of policy impacts that are fundamentally reshaping market dynamics,” said Louis Molinini, head of project and development Services for the Americas at JLL, in a statement. “While much of 2025 was at a standstill due to uncertainty, we now have directional clarity that enables strategic positioning for

organizations ready to move beyond reactive approaches.”

That uncertainty has slowed new development in all sectors, including industrial. Construction spending dropped 4.7% in 2025, JLL reported, as developers and investors paused projects amid fluctuating costs, regulatory debates and inconsistent demand.

For 2026, JLL expects a modest rebound of just 0.4% growth in new commercial construction activity. This suggests that construction firms will continue to face tight margins and operational pressures, even as activity begins to stabilize.

Much of that strain will come from rising material costs. According to the report, policy instability and a slowdown in overall building activity delayed the full impact of trade and supply-chain pressures. As projects ramp back up in 2026, JLL anticipates that cost increases will accelerate, making early budgeting and procurement strategies even more important.

Workforce challenges are also expected to add stress to construction companies. The industry’s labor shortages, long masked by reduced demand, could increase as construction starts rise. The presidential administration's immigration policies are also reducing the pipeline of labor available to work on new developments, creating staffing bottlenecks that could slow project timelines and push labor costs higher.

“Success in 2026 will require big-picture thinking with granular attention to local market details,” said Jaymie Gelino, chief operating officer and head of work dynamics accounts with JLL’s Project and Development Services group, in a statement.

Gelino said that regional differences in construction activity and demand are widening.

“Even markets facing bigger impacts from ongoing uncertainty remain viable for projects that are matched to local conditions and risks,” she added.

Gateway markets illustrate that tension. Their diverse populations, reliance on immigrant labor and deep global ties make them more vulnerable to policy shifts. But these same attributes also strengthen their longterm prospects.

These major metros boast robust infrastructure, deep talent pools and broad capital access, advantages that can outweigh short-term disruptions. According to JLL, organizations can mitigate risks through early contractor involvement, flexible risk-sharing models and procurement strategies tailored to local conditions.

“Planning for future activity must account for structural workforce constraints now, as market challenges may compound when construction activity accelerates,” said Andrew Volz, research manager with JLL’s Project and Development Services team, in a statement. “The intersection of trade policy, immigration enforcement and local economic conditions requires a wholly integrated approach to accurately assess risks.”

Photo by Pixabay

NAI Hiffman: Improving fundamentals buoying Chicago-area industrial sector

By Dan Rafter

The Chicago industrial market saw improving fundamentals during the third quarter of 2025, with net absorption of nearly 7.5 million square feet and the sector's vacancy rate falling to 6.1%.

That's the positive news from NAI Hiffman's third quarter metropolitan Chicago industrial report.

As NAI Hiffman writes, the demand for industrial space in the Chicago market is down from where it was from 2021 through mid-2023. But the high demand during those years was an anomaly. NAI Hiffman says that demand in this sector is now at a more sustainable level.

Year-to-date absorption in the Chicago-area industrial sector totaled 10.8 million square feet as of the end of the third quarter. That's an improvement

over the 8 million square feet reported during the same period in 2024.

The vacancy rate in the Chicago-area industrial market fell 30 basis points on a quarter-over-quarter basis to

6.1%. NAI Hiffman said that this drop was fueled by several major tenant move-ins, including RJW Logistics' occupancy of 1.1 million square feet at 201 W. Compass Blvd. in Joliet.

The Chicago industrial market recorded 9.7 million square feet of new leasing activity in the third quarter, down from 12.1 million square feet in the previous quarter. Year-to-date total new leasing volume stands at 32.7 million square feet.

NAI Hiffman reported that the I-80/ Joliet Corridor led all submarkets during the third quarter, accounting for 1.6 millions square feet of new leasing activity. The largest industrial lease of the quarter, though, occurred in the South Cook submarket, where Peopleworks committed to 757,504 square feet at 21500 Gateway Drive in Matteson.

Photo credit: gorodenkoff

COMMERCIAL SERVICES

CONSTRUCTION COMPANIES/GENERAL CONTRACTORS

MERIDIAN DESIGN BUILD

9550 W. Higgins Road, Suite 400 Rosemont, IL 60018

P: 847.374.9200 • F: 847.374.9222

Website: meridiandb.com

Key Contact: Paul Chuma, President; Howard Green, Executive Vice President

Services Provided: Meridian Design Build provides construction and design/ build construction services on a national basis with a primary focus on industrial, office, medical office, retail and food and beverage work. Company Description: With a team of in-house professional project managers, Meridian has extensive experience coordinating the design and construction of new buildings, tenant improvements, and additions/renovations from 15,000 square feet to 1,000,000+ square feet. Meridian Design Build has been a Member of the U.S. Green Building Council since 2007.

Notable/Recent Projects: Venture Park 47, Huntley, IL - 729,800 sf speculative industrial facility for Venture One Real Estate. Lion Electric, Joliet, IL - 928,500 sf electric bus / medium duty truck assembly plant for Clarius Partners. Greenwood Truck Terminal, Greenwood, IN - 125 door truck terminal on 43 acres for Scannell Properties.

PRINCIPLE CONSTRUCTION CORP.

9450 West Bryn Mawr Ave., Suite 120 Rosemont, IL 60018

P: 847.615.1515 | F: 847.615.1598

Website: pccdb.com

Key Contacts: Mark L Augustyn, COO, maugustyn@pccdb.com, James A. Brucato, President, jbrucato@pccdb.com

Services Provided: Since 1999, Principle Construction Corp. has been a leading design-build general contractor serving the industrial markets of Chicago Metro, Southern Wisconsin, and Northwest Indiana. We specialize in designing and constructing exacting solutions for our clients, including:

• Built-to-Suit Facilities • Speculative Facilities • Warehouse and Distribution Centers • Logistics and Cross-Dock Facilities • Industrial Outdoor Storage • Industrial and Manufacturing Plant • Tenant Improvements • Expansions and Additions • Food Processing Facilities • Specialty Projects

Recently Completed Projects include:

• 8,205 SF animal shelter for Heartland Animal Shelter, at 586 Palwaukee Dr., in Wheeling, IL.

• 12,560 SF showroom and outdoor pool park for Doheny Enterprises, at 5307 Green Bay Rd., in Kenosha, WI

• Phase 1 renovation project for SMW Autoblok, at 285 Egidi Dr., Wheeling, IL

VICTOR CONSTRUCTION

2000 Center Dr., Suite East C219 Hoffman Estates, IL 60192

Services Provided: Victor Construction Co., Inc. manages projects from ground-up site developments to interior buildouts, specializing in retail, industrial, and commercial markets.

Company Profile: Established in 1954, Victor Construction Co., Inc. is a third generation general contractor that specializes in commercial, industrial, and retail construction. Victor Construction is known as one of the most efficient and dependable general contractors in the Chicago metropolitan area and has earned the reputation due to meticulous project management, cost-effectiveness, budget awareness, and prime first-rate workmanship. Commitment to the clients’ goals is what keeps satisfied customers returning to Victor Construction for all of their construction needs—We Build for Your Success!

Notable/Recent Projects: Owens + Minor Distribution – 600K SqFt distribution facility that involved a full LED lighting upgrade, new HVLS fans, 200K SqFt section that required new cooling for medical distribution, an office renovation of 20K SqFt, and a new exterior employee pavilion.

ECONOMIC DEVELOPMENT CORPORATIONS

VILLAGE OF HOMER GLEN ECONOMIC DEVELOPMENT

14240 W. 151st Street

Homer Glen, IL 60491

P: 708.301.0632

Website: HomerGlenIL.org

Key Contact: Janie Patch, Economic Development Director, jpatch@homerglenil.org

Services: Resource center for brokers, developers, site selectors and businesses providing space and property inventory, trade area demographics, site selection assistance, custom tours, coordination through entitlement process, business opening process guidance and retention services. Demographic Info: Strategic Will County location 25 miles southwest of Chicago with two I-355 interchanges between I-55 and I-80. Average household income of $154,800. Trade area population of 83,000. Prime commercial corridors include Bell Road, 143rd Street and 159th Street (State Route 7). 159th Street is improved with 4 lanes and access to Lake Michigan water and sanitary sewer.

Recent CRE Activity: The Villas of Old Oak (46 ranch duplexes) completing full build out. New food specialty and restaurant openings include South Viet, OneZo Boba Tea, Sultan Sweets and Cervantino’s. Restaurant with drive-thru position available at Homer Glen Bell Plaza with Pet Supplies Plus, Dollar Tree and Taco Bell, SWC 143rd/Bell.

Recent CRE Activity: Double Track Northwest Indiana: $1.6 Billion development reducing train travel to Chicago to 60 minutes; The Franklin at 11th St. Station: $100 Million Development with Residential & Retail Space; “You are Beautiful”/ SoLa: $311 Million Mixed-Use Multi-Family Development with 235 boutique hotel rooms & 174 Luxury Condos; Burn ‘Em Brewing: $3 Million Expansion project with 30 new jobs.

ENVIRONMENTAL/ENGINEERING FIRMS

DEIGAN & ASSOCIATES, PLLC 28835 N. Herky Drive Lake Bluff, IL 60044

P: 847.682.7381

Website: www.deiganassociates.com

Key Contact: Michele Brady, Director Business Development & Real Estate Services, mbrady@deiganassociates.com

Services Provided: The Deigan Group provides client responsive, results oriented environmental consulting and remediation services, with a focus in land-based work, including Brownfield Redevelopment, Power Plant Decommissioning/Redevelopment, Strategic Environmental Planning, Property Assessments and Site Remediation, Compliance/Permitting, Employee Exposure Testing/Safety Monitoring

Asbestos Surveys/Mold/Indoor Air Quality, Waste Minimization/ Recycling/ Sustainability Plans, Successful Grant Writing.

Company Profile: A full-service environmental consulting organization specializing in defining environmental business risk and removing environmental uncertainties for property development sites. Our wide range of experience within the environmental industry helps us provide realistic cost-saving strategies for our clients with the goal of reducing their overall environmental liability and obstacles to redevelopment.

Services Provided: Full line of Commercial, Business and Real Estate loans customized to your individual needs including: commercial and residential construction loans, commercial mortgages, equipment loans and working capital lines of credit.

Company Profile: Marquette Bank started in Chicagoland in 1945 and is still locally-owned/operated. Expect quick decisions, competitive rates, easy application and personal service. Personal/business banking and lending, home mortgages, land trust services, estate planning, insurance services, wealth management and multifamily lending.

REAL ESTATE LAW FIRMS

REINHART BOERNER VAN DEUREN S.C.

1000 N Water Street, Suite 1700 Milwaukee, WI 53202

P: 414.298.1000

Website: reinhartlaw.com

Key Contact: Joseph Shumow, Shareholder, jshumow@reinhartlaw.com

Services Provided: Reinhart is a full-service, business-oriented law firm that delivers innovative, value-added solutions for today’s most important real estate needs, including land use and zoning; tax-incremental financing; tax credits; leasing; construction; and condemnation and eminent domain issues.

Company Profile: With the largest real estate practice in Wisconsin and offices throughout the Midwest and across the country, Reinhart’s attorneys offer clients customized real estate insight rooted in broad knowledge and deep experience to help you capitalize on opportunities no matter where you do business.

SARNOFF

PROPERTY TAX

100 N. LaSalle St., 10th Floor Chicago, IL 60602

P: 312.782.8310

Website: sarnoffpropertytax.com

Key Contact: James Sarnoff, jsarnoff@sarnoffpropertytax.com P: 312.448.5337

Services Provided: Since 1986, Sarnoff Property Tax has been a leading and recognized law firm concentrating solely in the field of property taxation. We help client’s secure favorable taxes in Illinois through property tax appeals, incentives and consulting.

Company Profile: Sarnoff Property Tax’s clients include Owners, Developers, Managers, REIT’s, Fortune 500 Companies, Private Equity Firms, etc., in connection with commercial property, high-rise and low-rise apartment buildings, condominium associations and single-family home portfolios

WORSEK & VIHON, LLP

180 North LaSalle Street, Suite 3010 Chicago, IL 60601

P: 312.917.2307 P: 312.917.2312 | F: 312.596.6412

Website: wvproptax.com

Key Contacts: Francis W. O’Malley, Managing Partner fomalley@wvproptax.com; Jessica L. MacLean, Partner jmaclean@wvproptax.com

Services Provided: Worsek & Vihon, LLP represents tax payers in Illinois by limiting their property tax liabilities through ad valorem appeals. We have over 40 years of experience and can handle basic to the most complex assessment issues while offering the dependable, personalized attention our clients deserve. We have experience representing owners of all property types. In addition to filing thousands of appeals with the Cook County Assessor, we have been involved in numerous proceedings before various Boards of Review, the Illinois Property Tax Appeal Board, and the Circuit Court of Illinois, and have appeared before the Illinois Appellate and Supreme Courts.

Company Profile: Worsek & Vihon LLP, is a team of experienced attorneys singularly focused on real estate tax law. The firm is dedicated to minimizing property tax liabilities through strategic tax portfolio management, wellresearched, creative appeal preparation and aggressive advocacy.