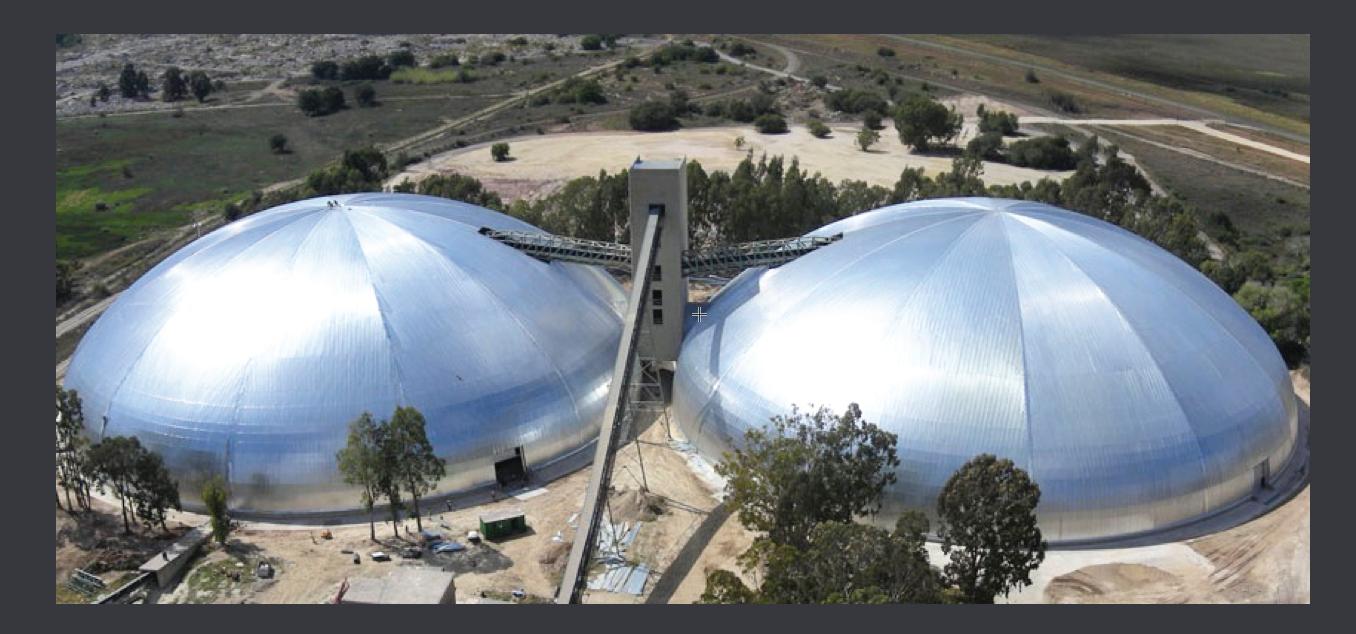

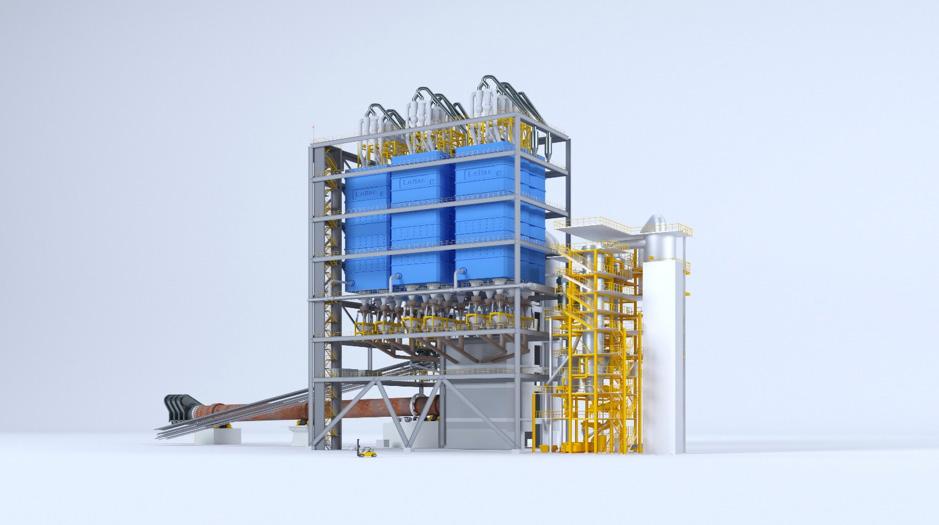

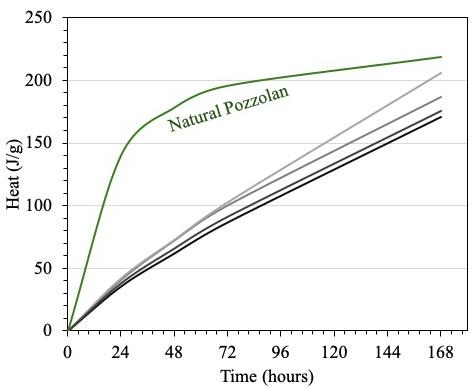

Buzzi Unicem’s Festus Plant with Loadout Powered by PSCL

Post-combustion technology that virtually eliminates CO2 emissions from cement manufacture.

• Captured CO2 is liquefied, purified and available for utilization in the cement manufacturing process, transportation, 3rd party sale or sequestration

• Removes 95 to 99% of carbon dioxide emissions

• Easy retrofit

• Suitable for existing and new plants

• Modular solution scales up to all plant capacities

• Less pre-treatment than alternative technologies

• Amine free

• Handles harmful contaminants, including NOx, SOx and mercury, more robustly than alternative technologies

Technology from:

03 Comment

05 News

REGIONAL REPORT

10 The Sub-Saharan Situation

David Bizley, Senior Editor of World Cement, provides a brief overview of the economic situation in Sub-Saharan Africa’s three largest economies: Nigeria, Ethiopia, and South Africa.

GRINDING & MILLING

14 The Role Of Retrofitting

Michael Lindbichler, CEMTEC, considers the benefits of retrofitting and how it can help cement plants be more sustainable.

PYROPROCESS OPTIMISATION

20 Blazing A Trail

Dr. Robert Pachler, Unitherm Cemcon, provides insight into the factors impacting burner design in the modern cement industry.

28 A Moment For Ammonia

M. Akritopoulos and T. Abbas, Cinar, and Syed Suhail Akhtar, Holcim, explore the advantages of burning green ammonia over hydrogen in a cement kiln.

35 Say ‘Bye’ To Carbon Dioxide

Joel Maia, FCT Combustion, explores the different pathways available for producers to reduce CO2 emissions from cement and clinker production.

CARBON CAPTURE

40 Hurdles To CCUS Adoption

Simon Thomsen, Leilac, explores the reasons for the cement industry’s hesitation to adopt CCUS technology, and explains how these challenges can be overcome.

45 Turning Emissions Into Solutions

Martin Keighley, CarbonFree, answers some of World Cement’s questions regarding carbon capture technology and its potential for application in the cement industry.

GREEN CEMENTS

50 A New ‘It Cement’

Hamed Maraghechi, CalPortland, discusses the development of ternary blended cements in California and considers their contribution to decarbonisation efforts.

56 Going Green

Grant Quasha, Eco Material Technologies, explores the benefits of a green alternative to Portland cement.

MATERIALS HANDLING & LOGISTICS

63 The Mobile App Advantage

Reiner Bachthaler, Axians Industrial Applications, explains how mobile applications can be highly beneficial in bulk goods industries.

69 Conveying Clinker GAMBAROTTA GSCHWENDT reviews different types of conveyors used to transport clinker for the cement production process.

AIR CANNONS & SILO CLEAN-OUT

73 Blasting Assumptions

Dracyon considers the common weaknesses of air cannons, and explains how they can be overcome.

GEARS, DRIVES & MOTORS

77 Driving Sustainability with VFDs

Invertek Drives explains how variable frequency drives can help the cement industry to become more energy efficient.

The Buzzi Unicem Festus Plant in Missouri benefits from comprehensive cement loading and quality solutions courtesy of PSCL. Through recent upgrades, PSCL’s Loading Management and Self-Service Loading solution now efficiently oversees all truck loading operations. Furthermore, PSCL handles all rail loading tasks. The plant uses the Raw Mix Control System by PSCL, guaranteeing top-notch product quality.

HEKO offers the whole range of chains, rollers, sprockets and scrapers for reclaimers. HEKO products are proven in thousands of bucket elevators and conveyors, worldwide.

Our components for the cement industry: central chains, link chains, reclaimer chains, sprockets, bucket elevators and clinker conveyors.

rod.hardy@palladianpublications.com

Sales Manager: Ian Lewis ian.lewis@palladianpublications.com

Sales Executive: Sophie Birss sophie.birss@palladianpublications.com

Head of Events: Louise Cameron louise.cameron@palladianpublications.com

Digital Events Coordinator: Merili Jurivete merili.jurivete@palladianpublications.com

Digital Administrator: Nicole Harman-Smith nicole.harman-smith@palladianpublications.com

Administration Manager: Laura White laura.white@palladianpublications.com

Reprints reprints@worldcement.com

Annual subscription (published monthly): £160 UK including postage/£175 (€245) overseas (postage airmail)/US$280 USA/Canada (postage airmail). Two year subscription (published monthly): £256 UK including postage/£280 (€392) overseas (postage airmail)/US$448 USA/Canada (postage airmail). Claims for non receipt of issues must be made within 4 months of publication of the issue or they will not be honoured without charge.

Applicable only to USA and Canada: WORLD CEMENT (ISSN No: 0263-6050, USPS No: 020-996) is published monthly by Palladian Publications, GBR and is distributed in the USA by Asendia USA, 17B S Middlesex Ave, Monroe NJ 08831.

Periodicals postage paid at Philadelphia, PA and additional mailing offices. POSTMASTER: send address changes to World Cement, 701C Ashland Ave, Folcroft PA 19032

Copyright © Palladian Publications Ltd 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the copyright owner. All views expressed in this journal are those of the respective contributors and are not necessarily the opinions of the publisher, neither do the publishers endorse any of the claims made in the articles or the advertisements. Uncaptioned images courtesy of Adobe Stock. Printed in the UK.

Palladian Publications Ltd 15 South Street, Farnham, Surrey GU9 7QU, UK

Tel +44 (0)1252 718999

Email: mail@worldcement.com Website: www.worldcement.com

DAVID BIZLEY, SENIOR EDITOR

ast month you may recall that I talked about how 2024 was the year of elections, with more than half the world due to visit the polling booth at some point this year. However, another thing that 2024 is likely to be remembered for is being the year that the use of ‘AI’ across business and industry really took off.

You might be wondering about the inverted commas around AI in the previous sentence. Well, allow me to derail the flow of this Comment briefly and explain that that’s because what we’ve come to know as AI isn’t really AI in the true meaning of the name. It’s certainly artificial , but there’s no actual intelligencethere. Tools like ChatGPT, whilst impressive and undeniably useful, remain incapable of actual comprehension, thought, or invention. They’re pattern finding algorithms feeding off data from the internet and reacting to user input, unlike the ‘true’ AI behind fictional entities like C3P0, HAL 9000, or even Skynet, which have their own sense of self.

OK, enough pedantry for now; back to the point – whilst what we know today as AI might not be about to start spouting ‘Cogito, ergo sum’ or develop a sense of existential dread (probably for the best, honestly), it still has huge potential for use across industry, being able to analyse thousands of data points at speeds far beyond human ability. And as much as we might laugh at ChatGPT’s gaffes or habit of ‘hallucinating’ answers, the big players across industry, including cement, are making serious investments into the technology.

Holcim, for example, has announced plans to scale up its use of AI across more than 100 of its plants around the world over the next four years. With AI already deployed at 45 plants to predict and prevent failures before they occur, the company plans to deepen and broaden this application to boost operational resilience. This will involve the further rolling out of a predictive maintenance solution from AI platform software provider C3 AI, as well as piloting generative AI to enhance its capabilities.

Holcim’s CEO, Miljan Gutovic, stated: “AI is a transformative technology that will revolutionise our industry. Already widely embedded across Holcim, AI catalyses operational efficiency and enhances customer service. We will ultimately scale up our use of AI to hundreds of sites worldwide.”

Cemex has also announced its use of a generative AI system to “transform how the salesforce interacts with clients by providing real-time support for a superior customer experience.” The development process involved training a Microsoft AI on Cemex’s product information and expertise in construction regulations. Cemex CEO, Fernando A. González, was equally enthusiastic about the role of AI: “Digital transformation is a top priority at Cemex, as we are continually looking for new digital solutions to innovate and drive more efficient, sustainable, and safer construction projects for our customers.”

Now, if you’d like to hear more about how AI and other cutting-edge technologies are shaping the cement industry, then you’ll be pleased to know that WorldCement’sflagship virtual conference, Optimisation, is coming back for a fifth iteration on 22 October! Featuring Keynote Presentation from Molins’ Chief Technology Officer, Javier Sueiras, this is a fantastic opportunity to learn about the future of cement production. Register today, free of charge: www.worldcement.com/events/optimisation-2024

Convey units

Truck loading

GCCA

UNIDO supports its 172 Member States with economic and industrial development, in line with the UN’s Sustainable Development Goals (SDGs). With its long-standing experience in renewable energy projects and the application of clean energy technologies in industry, UNIDO collaborates with a wide range of partners globally supporting industries on their pathway to net-zero emissions.

The GCCA is the cement and concrete industry’s main membership body, representing 80% of cement production outside of China, as well as a number of leading Chinese manufacturers.

The two organisations have agreed a Memorandum of Understanding (MoU), which will see them working together on key sustainability and decarbonisation issues.

Speaking at the signing ceremony in Austria, Gerd Müller, Director General of UNIDO, said: “Cement and concrete are a vital part of resilient infrastructure development. Decarbonising the cement and concrete sectors worldwide is essential to reducing CO2 emissions and tackling climate change. The GCCA and its members are leading the way on doing so for this important global industry. Our UNIDO Member States face a number of technical, market-related and policy hurdles that make decarbonisation commitments even more challenging. That is why I am very glad to sign this Memorandum of Understanding with the GCCA and start a new phase of closer cooperation that will help our Member States overcome those challenges.”

Thomas Guillot, GCCA CEO, said:

“Through our Net Zero Roadmap and the accelerator programme we have put in place, we are already working with policymakers, governments and industry to overcome procurement and resourcing challenges across the global south. Having this ground-breaking agreement with UNIDO is a natural progression which we hope will fast-track progress in a meaningful way.”

The partnership agreement includes pledges to: f Provide recommendations for decision-makers to create the right market environments for the development of low and near-zero emissions cement and concrete.

f Develop innovative technological solutions to help meet net-zero commitments.

f Organise joint international industry and government events.

f Jointly author and publish documents, recommendations and research tools.

f Identify promising companies and innovative solutions and showcase these at relevant events and in publications.

Vattenfall and Cemvision cooperate to supply near-zero emission cement

Vattenfall and Cemvision have entered an agreement (LOI) for the development and future supply of near-zero emission cement.

The new cement has the potential to reduce carbon dioxide emissions by 95% compared to traditional cement.

It has several potential applications, such as foundations for wind power turbines, power distribution and prefabricated concrete elements. Both Vattenfall and its subcontractors could become important new customers for this new product.

Cemvision develops cement made from recycled residual materials from industries including mining and steel industries manufacturing in a process where Cemvision’s kilns are fuelled by fossil-free energy. Compared to traditional cement production, which emits large amounts of carbon dioxide due to the use of virgin limestone and fossil fuels, Cemvision can reduce the carbon footprint by up to 95%.

“We are delighted to deepen our partnership with Vattenfall and to welcome them to our growing customer base. Already today in our demo production, we are reducing carbon emissions by 80%, and as we optimise processes and supply chain, we will reduce by up to 95% by 2030. Near-zero emission cement is the most efficient way to achieve significant climate benefits without increasing the overall cost of a construction project. It does not have to be difficult to change, but it is important to start in time and help accelerating the transition”, says Oscar Hållén, CEO of Cemvision.

“Vattenfall is very positive about participating in the development of a market for near-zero emission cement by creating demand as a customer. We can also contribute with product verification at our concrete laboratory. The global impact of cement

production makes it necessary to find a way forward with as low carbon emissions as possible, the climate and the future of construction demand it. This is an innovative solution with great potential”, says Annika Ramsköld, Head of Sustainability, Vattenfall.

Cartagena, Colombia www.ficem.org

SOLIDS Dortmund 2024

09 – 10 October, 2024 Dortmund, Germany www.solids-dortmund.de

Virtual Conference: 22 October www.worldcement.com/events/ optimisation-2024

17th TÜRKÇIMENTO Technical Seminar & Exhibition

02 – 05 November, 2024 Antalya, Türkiye teknikseminer.com.tr

AFCM Technical Symposium & Exhibition Malaysia 2024 04 – 07 November, 2024 Kuala Lumpur, Malaysia 26afcm-tse.com

VDZ CONGRESS

06 – 08 November, 2024 Düsseldorf, Germany www.vdz-online.de

AUCBM AICCE27 26 – 28 November, 2024 Tunis, Tunisia www.aucbm.net

09 – 12 March, 2025 Athens, Greece worldcement.com/envirotech2025

As a member and founder of the First Movers Coalition (FMC), Vattenfall has pledged that at least 10% of its cement or concrete purchases will be as close to zero emissions as possible by 2030. The FMC’s overall goal is to take climate action by creating a market for emerging technologies that are crucial to reaching near-zero emissions by 2050.

Heidelberg Materials converts cement plant to a slag grinding facility in Indiana

Heidelberg Materials has announced the successful conversion of its cement plant in Speed, Indiana, USA, to a slag grinding facility to better support the increased demand for sustainable products in the fast-growing Midwest market.

Following last year’s opening of its new state-of-the-art cement plant in Mitchell, Indiana, Heidelberg Materials ceased Portland cement production at its manufacturing site in Speed, Indiana, and invested in modifying the facility to produce slag cement from domestically sourced slag granules. Replacing a portion of conventional Portland cement with slag cement in a concrete mix significantly lowers its environmental impact. The Speed site, which has an annual grinding capacity of more than 400 000 t, also serves as a distribution hub for cement produced at the Mitchell plant as well as a broad range of specialty cementitious products.

The adjustments made at the Speed plant reflect Heidelberg Materials’ strong commitment to achieving net-zero emissions in North America. Recently, the company has been selected for funding of up to US$500 million by the US Department of Energy to advance industrial-scale carbon capture, transport, and storage at its Mitchell cement plant. At the Edmonton cement plant in Alberta, Canada, Heidelberg Materials is currently developing the world’s first full-scale carbon capture, utilisation, and storage solution in the cement industry.

Advancing urbanisation is driving infrastructure demands for residential and industrial space, also spurring increased demand for cement. For cement producers, flexibility and, above all, proximity to the market and speed in logistics are the keys to success and profitability.

In response, HAVER & BOECKER developed the OCTAPLANT®, a new packing concept. The OCTAPLANT, a comparatively compact system for packing and loading cement in bags, consists of a modular design incorporating high quality technology and prefabricated components to allow for quick installation and adaptability.

Significant time saving is the main advantage that OCTAPLANT offers in comparison to conventional systems. With all components on the shelf and many of the assembly tasks completed before the

system ships, the construction phase of the plant is significantly reduced. Less construction needed on site translates to fewer potential errors and reduced labour demands for installation. It also comes into play at the very start of the planning phase. Engineering that is completely planned and finalised down to the last detail accelerates project implementation and ensures the best possible planning security with regard to expected costs, yields, equipping buildings and technology. Moreover, standard delivery of all the tools required for assembly avoids expensive delays that could occur due to missing or incompatible devices and systems. The simple, modular design decreases the need for crane lifts to erect the plant by 80% over the installation of conventional systems. A plug-and-play design, allows for individual elements to simply connect and be operational quickly reducing overall installation time and facilitating quick relocation of the plant based on business potential or demand. The installation time from planning to the start of production is reduced by three and a half months compared to conventional systems, allowing for lower finance costs and a rapid return on investment.

An OCTAPLANT building consists of three segments. The heart is the eponymous octagonal ‘OctaTower’ that houses the HAVER & BOECKER ROTO-PACKER® RVTs packing system, including a foreign body screen, pre-hopper and spillage return system.

These elements are shipped in a simplified and cost-optimised manner in seven standard sea containers, from which the adjacent container building is erected after unloading. It provides space for the bag discharge line, the fully automatic

RADIMAT® bag applicator, the system control and the compressor unit. The final section is a lightweight hall where the filled cement bags are loaded onto trucks. The HB 10 system for rear loading and the HB 17 system for loading open trucks are available here. Moreover, a photovoltaic system can be installed on the roof and thus generate sustainable electricity for the plant.

The OCTAPLANT’s efficient design is adapted to the extreme site conditions of the target markets. The containers are reinforced and reliably withstand wind speeds of up to 200 km/h and earthquake loads. The light-colored façade is designed to reflect solar radiation. In addition, the air flow from the packing machine’s dust extraction system not only creates a low-dust environment, but also provides measurable temperature regulation. The OctaTower and container building can also be sufficiently insulated for colder climates.

Thanks to its mobility and space-saving design, the OCTAPLANT saves on resources and materials. Existing system components and high-quality technical equipment can be easily reused at another location.

Space-optimised transport and a high degree of prefabrication also contribute to a reduced ecological footprint. Finally, the integration of QUAT2RO® products and the PROcheck life cycle approach minimise greenhouse gas emissions, energy consumption and the use of materials during plant operation.

In order to control, monitor and optimise all processes, all the workflows are networked using QUAT2RO System Intelligence. With the PROcheck life cycle approach, HAVER & BOECKER enables comprehensive support: from selecting the right equipment with the right empty bags to offering spare parts and comprehensive services.

When developing the space-optimised and relocatable system, the focus was on ease of operation and maintenance. The OCTAPLANT offers maximum efficiency not only in terms of planning and building design, but customers can also count on maximum output and high quality from the packing machines when it comes to technical equipment and efficient operation.

The engineering for the OCTAPLANT concept was completed by HAVER & BOECKER so that project planning and production could take place immediately. Significant time saving is the main advantage that

David Bizley, Senior Editor of World Cement, provides a brief overview of the economic situation in Sub-Saharan Africa’s three largest economies: Nigeria, Ethiopia, and South Africa.

Sub-Saharan Africa is a vast region, comprising the majority of the continent’s 50+ nations and their 1.2 billion citizens, and is spread across 43.3 million km2 (or 15% of the Earth’s land surface). As such, a full review of the region falls well beyond the scope of this article, which will instead limit itself to a brief discussion of the three major economies: Nigeria, Ethiopia, and South Africa.

Nigeria’s economy has undergone a turbulent period as of late – and that might be putting it mildly, with the BBC referring to the disruption earlier this year as the “worst economic crisis in a generation, leading to widespread hardship and anger.” The economic malaise has even seen the country fall to fourth place, down from first in the IMF’s ranking of the largest economies in Africa.

Like many nations around the world, Nigeria has struggled with inflation over recent years, but the problem had become particularly acute by the beginning of 2024. To list just a few figures: annual inflation rose to 30%, food prices have risen by 35%, and the monthly minimum wage of 30 000 naira has not risen since 2019 and is now worth just US$19. So, what has caused this crisis? In addition to the same external factors being felt by much of the rest of the world, the war in Ukraine for example, Nigeria’s President Tinubu has inherited something of a tricky situation from his predecessor. Former President, Muhammadu Buhari, had taken out loans worth US$19 billion from Nigeria’s central bank to cover government spending – the bank duly obliged and printed the money, thus further exacerbating inflation.

Tinubu’s own policies, however, must take some of the blame for the situation as his attempts to reshape the Nigerian economy for the better have had some unintended consequences. One of his first acts upon being sworn in was to end a long-standing fuel subsidy, which had kept prices low for many citizens. Whilst the subsidy was hugely expensive, and it was (quite reasonably) argued that the money would be better spent on healthcare and education, the sudden rise in fuel prices sent shockwaves down the supply chain with increased transportation costs for goods ultimately being passed on to the end consumer.

Tinubu also brought an end to the policy of pegging the naira to the US dollar. Again, this seemed like a reasonable move because maintaining the dollar peg had been exorbitantly expensive for the central bank. However, once the peg was removed, the value of the naira tumbled by more than two-thirds, briefly reaching all-time lows back in February. In May of 2023, 10 000 naira was worth US$22 – at the time of writing, it is only worth US$6.49.

It’s not all gloom, however. The IMF, which is broadly in favour of Tinubu’s economic reforms and sees the current disruption as a short-term pain needed for long-term gain, expects GDP growth of 3.2% for 2024, and welcomes recent improvements in revenue collection and oil production, a targeted safety net programme of cash transfers to vulnerable households, and a tightening of monetary policy.

In terms of cement demand, IA Cement predicts a ‘relatively normal’ recovery of 3 – 4% in 2024. A possible price war between competing producers, which had been ramping up in 2023 and could have boosted demand this year, appears to have been ruled out by the falling value of the naira. Indeed, prices have actually soared, with the average price for a bag of cement rising from ~4000 naira to a peak of 11 000 – 15 000 naira in May, before falling back to lower, but still high, prices around 7000 – 8000 naira at the time of writing.

Investments are also still being made in the cement sector. In May of this year, Finnish manufacturing group, Wärstilä, signed a 10 year operations & maintenance (O&M) agreement for a captive power plant providing the energy to a new cement plant in Kogi State, owned by Mangal Industries.

The power plant is critical to the facility’s cement production since the site is remotely located with only limited access to the electricity grid. It operates with five Wärtsilä 34DF dual-fuel engines delivering an output of 50 MW. The O&M agreement is designed to ensure that the facility can reliably maintain its cement production target of 3 million tpy.

Ethopia, after Nigeria, is the African continent’s second-most populous nation with a population of 126.5 million. Despite having one of the fastest

growing economies in the region (recording GDP growth of 7.2% in 22/23), it also remains one of the poorest, with per capita gross income of just US$1020.

The World Bank reports that the country’s “consistently high economic growth over the last decade resulted in positive trends in poverty reduction in both urban and rural areas. The share of the population living below the national poverty line decreased from 30% in 2011 to 24% in 2016 and human development indicators improved as well.” The country aims to reach lower middle-income status by 2025.

To maintain this growth, the government has implemented a 10-year development plan, which aims to further work from previous similar plans and promote the shift towards greater involvement of the private sector in the economy.

Recent years have been marred by high levels of insecurity, primarily as a result of the so-called Tigray war, which formally ended in November 2022. Each side (the Ethiopian military and the Tigrayan regional forces) has accused the other of crimes against humanity, including arbitrary detentions and even massacres – a UN report in late 2023 found that there was strong evidence that, even despite the truce, war crimes and crimes against humanity continued to be carried out. The Economist Intelligence Unit reports that while the peace remains fragile, with active insurgencies in the Amhara and Oromia regions, the relative improvement in the security situation will drive a gradual increase in GDP growth.

In terms of cement, at the time of writing, the country is on the verge of welcoming a brand new cement plant in the Amhara region, some 130 km north of Addis Ababa. At a cost of US$2.2 billion, the Lemi National Cement Factory is expected to make significant inroads into addressing building materials shortages in the country by almost doubling national production with its output of 4.5 million tpy. Lemi National Cement PLC currently is a member of the joint venture formed between East African Holding and West International Holding (WIH), a Chinese industrial enterprise.

In other local cement news, the Ethiopian Cement Association has been working with local producers to gradually move away from imported coal supplies, which cost businesses US$300 million a year. Despite having 600 million t of domestic coal reserves, local supply has been oversaturated with low-quality coal from small-scale producers. The few industrial-scale producers have failed to reach demand, ever since exploration was opened up in the 1940s.

Low quality coal has been recognised as a key factor behind the country’s lacklustre cement production and the move towards domestic supplies would be gradual and contingent on the improvement of the quality and availability. Adugna Bekele, president of the Ethiopian Cement Association, noted that “quality would be the deciding factor” in bringing the cement producers on board and emphasised the

importance of adopting coal-washing technologies and establishing industrial-scale processing systems.

News regarding South Africa’s economy has been, to quote the FinancialTimes, “unceasingly negative for years, with power outages, chronic unemployment, state corruption, crime, pitiful economic growth and a downward-trending rand as a constant background.” The World Bank broadly agrees and begins its overview of the country by highlighting that the country’s growth has been hampered for years by electricity supply shortages, with rolling scheduled power cuts (known as ‘load shedding’) starting as far back as 2007, and only intensifying since 2022. The total accumulated duration of the outages (each of which lasts 2 – 4 hours), amounted to a staggering 289 days in 2023, increasing from 157 days in 2022 and 48 days in 2021.

The country has made considerable advances in improving the lives of its citizens since the switch to democracy in the mid-1990s, but progress has stagnated for the last decade. According to the World Bank, the percentage of the population living below the upper-middle-income poverty line between 2005 and 2010 fell from 68% to 56%, but the trend has since reversed with the figure rising to 57% in 2015 and could even be as high as 62.7% for 2023.

Some good news may lie ahead, however. The regular power outages, which have served as a considerable obstacle to business could be due to diminish and ultimately stop within the next couple of years. In 2022, President Cyril Ramaphosa removed limits on how much private generators could produce, which should see some 10 GW of cheap, renewable energy enter the market. The beleaguered state transport & logistics enterprise, Eskom, which oversees rail and ports, is under new management and engaging with private businesses to boost productivity after a year when domestic supply chain issues caused coal exports (as just one example) to fall to 50 million t, their lowest level since 1993. So, whilst challenges remain, the tide may be about to turn for the better.

There is also some positive news from the South African cement sector as the country’s largest producer, PPC, was able to pay its first dividend to investors in nine years. Whilst most of the 20.6% revenue growth came from the company’s Zimbabwe operations, revenues from the South African and Botswanan operations still grew by 5.2%. The company is currently going through the process of divesting its ‘rest of Africa’ assets, having just sold its 51% stake in the Rwandan CIMERWA for US$42.5 million. On the back of the positive results, CEO Matias Cardarelli has struck a note of cautious optimism by stating that the company’s “sustained underperformance and decreasing profitability over a number of years [had] revealed internal gaps that are also clear opportunities.”

N+P’s Subcoal ® portfolio is specifically designed to increase alternative fuel substitution rates up to 100%. This can be done using existing (coal) feed and burner systems. Our alternative fuels are manufactured to high demanding specifications so that it is easy to handle, transport and process, whether co-fired with coal or as a 100% fuel substitute.

All you need to know about reducing CO 2 emissions with alternative fuels: www.npgroup.com

Michael Lindbichler, CEMTEC, considers the benefits of retrofitting and how it can help cement plants be more sustainable.

In the cement industry, the focus on decarbonisation is paramount, but it is not the only concern driving daily operations. Closely related to decarbonisation is the concept of sustainability, particularly through retrofitting. Many cement plants worldwide have been operational for decades. As requirements for product fineness and quality evolve – driven by the increasing substitution of clinker – older systems often reach or exceed their operational limits, necessitating optimisation or upgrades. Additionally, wear material fatigue and the end of the useful lifetime of individual machines or entire plants demand predictive and preventive actions to maintain competitiveness and ensure a secure supply chain.

Addressing these requirements can involve significant investments in new processing lines

or, alternatively, the replacement of single items or assembly groups of affected equipment. From a sustainability perspective, the logical solution in many cases is to retrofit plants to state-of-the-art technology, thereby optimising capital expenses (CAPEX), reducing operational costs (OPEX), and achieving the lowest total cost of ownership (TCO). Retrofitting can extend the operational life of existing plants, improve energy efficiency, and reduce emissions, aligning with global environmental goals. This approach not only supports the environment but also ensures that cement plants remain competitive and economically viable in an increasingly challenging market.

Retrofitting involves adapting existing equipment or plants to meet current requirements. This can range from upgrading small components to replacing complete assembly groups and, in some cases, may involve exchanging all plant equipment constrained only by existing foundations or building dimensions. These extensive projects often necessitate customised solutions derived through reverse engineering. Reverse engineering in combination with retrofitting not only replaces insufficient or broken items but also allows for the incorporation of improvements in rigidity, performance, and safety. Safety has become increasingly crucial in every plant, often serving as the impetus for retrofit projects. Enhanced safety

features can reduce the risk of accidents and ensure compliance with the latest regulatory standards, which are constantly evolving to address new challenges and risks.

A significant challenge in executing retrofit projects is the frequent lack of information, such as incomplete documentation or missing drawings. This can stem from various reasons, including never having received proper documentation, loss of documents, or invalidation due to numerous on-site modifications. However, the engineering phase of retrofitting offers the opportunity to include internals, wear and spare parts, simplifying future maintenance. The ability to reverse-engineer components and systems plays a critical role in overcoming these challenges, enabling the creation of accurate and reliable designs based on existing conditions.

In the past, collecting missing information and dimensions was laborious and time-consuming. Today, technologies like 3D laser scanning facilitate this process. Scans can be easily converted into 3D model files compatible with most CAD systems, providing a solid foundation for new engineering. Scanning entire buildings, including installed equipment, steel structures, and foundations, can be accomplished in just a few days, depending on the required accuracy. This innovation significantly reduces the time and cost associated with the initial assessment and planning stages of retrofit projects. The accuracy of 3D scanning ensures that retrofits are precisely tailored to existing structures, minimising the risk of errors and costly modifications during implementation. Moreover, 3D scanning can be used for regular monitoring and maintenance checks, helping to identify wear and tear before they become critical issues.

Older machines often lack sufficient condition monitoring or interlocking systems that help extend the lifespan of critical parts such as drives, bearings, and other sensitive components. The cost of investing in such monitoring systems is relatively low when considering the reduced maintenance and Retrofit benefits.

repair costs. Incorporating systems like vibration or temperature monitoring in retrofit projects

ensuring that every minute is effectively utilised to enhance plant performance.

Proper lubrication is essential to minimize wear and lengthen equipment life in high-temperature, high-load applications

Easy Bar® with Almasol® is a patented blend of wear-reducing and extreme pressure lubricants suspended in a solid binder that melts after application. It prevents steel-on-steel contact, without risk of flameups, and takes less time to apply than traditional lubricants.

For more about LE’s high-performance lubricants, contact us or visit our website today.

In addition, the integration of renewable energy sources, such as solar or wind power, into the plant’s energy mix can further reduce carbon footprints and operational costs.

The advantages of retrofitting are not limited to cement plants but extend to other mineral processing plants and mining companies. Effective project planning often requires multiple discussions between customers and potential suppliers to fully understand the requirements. The goal is to collaboratively find and offer the best solutions in terms of functionality, quality, and budget. Success begins with professional consulting requiring years of experience and expertise in various disciplines such as mechanical engineering, electrical and automation engineering, and plant and process engineering. Considering the entire grinding plant with all its interrelations is crucial. Detailed analysis of the interrelations between different plant components can lead to more comprehensive and effective retrofit solutions. This holistic approach ensures that all aspects of the plant are optimised, resulting in more cohesive and efficient operations.

Flexibility is essential for suppliers as most projects demand customised solutions rather than standard equipment deliveries. This flexibility extends from organisational style and decision-making processes to the ability to bypass internal procedures throughout the supply chain, from engineering to commissioning and beyond. Tailored solutions can address specific operational challenges and align with the unique goals of each plant, ensuring maximum benefit from retrofit projects. Suppliers must be agile and responsive, able to adapt to changing project requirements and deliver solutions that meet the precise needs of their clients.

Given the rarity of new plant projects or new grinding terminals for cement in Europe and the USA, the retrofit market offers significant opportunities for companies like CEMTEC. Decades of experience in selling ball mills, dryers, cooling drums, and other process-relevant equipment form the basis for executing tailored retrofit projects. CEMTEC also develops digital products that can be implemented, automated, and visualised to optimise and enhance the efficiency of the cement manufacturing process. Continuous condition monitoring and analysis of collected data enable better predictive and preventive maintenance measures, helping to avoid unplanned plant stops and production interruptions which are critical

during high sales periods when produced cement is often dispatched immediately without storage. CEMTEC refers to this type of operation as ‘Smart Grinding’. This approach, combined with the installed base of each original equipment manufacturer (OEM), boosts the aftersales and spare parts business, strengthening customer loyalty and relationships. The integration of digital technologies in retrofitting projects can lead to smarter and more responsive plant operations, enhancing overall productivity and sustainability. Digital twins, for example, can simulate plant operations and predict outcomes, allowing for optimisation before physical changes are implemented.

In conclusion, the concept of sustainability through retrofitting presents a viable and often preferred path for cement plants facing evolving product requirements and ageing equipment. By leveraging advanced technologies, comprehensive planning, and flexible, customised solutions, the cement industry can achieve significant improvements in efficiency, cost savings, and overall sustainability. The retrofit market, particularly in regions with limited new plant projects, provides substantial opportunities for companies to enhance their offerings and support the industry’s transition towards more sustainable operations. The ongoing innovation in retrofitting techniques and technologies promises a future where cement plants can continually improve and adapt, meeting both economic and environmental goals. The role of retrofitting will only grow in importance as industries worldwide strive to reduce their carbon footprints and enhance their sustainability credentials.

Furthermore, the integration of circular economy principles into retrofitting projects can maximise resource efficiency and minimise waste. By reusing and recycling materials and components, cement plants can reduce their environmental impact and create more sustainable production cycles. Collaboration with other industries to repurpose by-products and waste materials can also contribute to this effort, creating a more interconnected and sustainable industrial ecosystem.

Over the last 20 years, Michael Lindbichler has worked on the supplier side for cement and mineral processing plants in various disciplines like machine and plant engineering, occupied the position of mechanical supervisor, and has worked in the sales department at different management levels. Michael is now trying to implement his experience in the most challenging but always interesting field of customised retrofit solutions at CEMTEC.

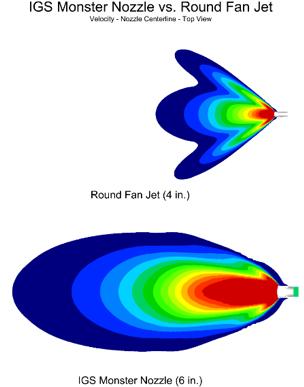

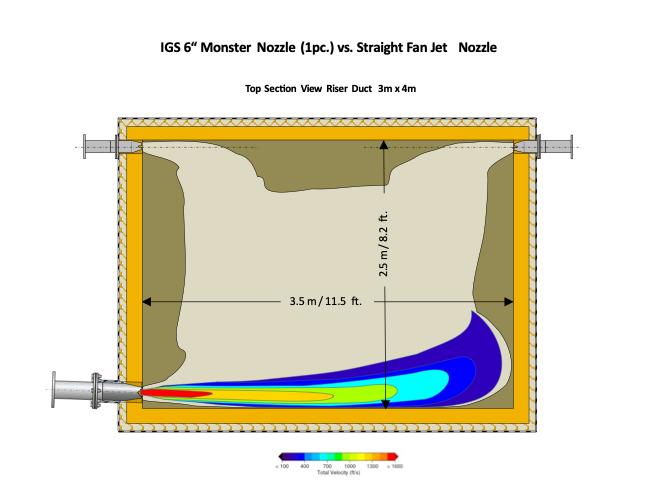

PSCL powers cement loadouts across North America.*

No estimations. No guesswork. Up-to-date accounting. Streamlined user interfaces.

Why aren’t your cement alleys using our Cement Distribution Management Suite yet?

Dr. Robert Pachler, Unitherm Cemcon, provides insight into the factors impacting burner design in the modern cement industry.

As the cement industry undergoes an evolution on its journey to a decarbonised future, a whole range of processes and technologies will need to adapt to the new challenges. This article seeks to provide insight into some of the major considerations facing cement plant operators when it comes to selecting the right burner design for their process.

To mitigate the variability in consistency and quality of alternative fuels (AF) for reliable burner operation, several strategies and considerations must be employed.

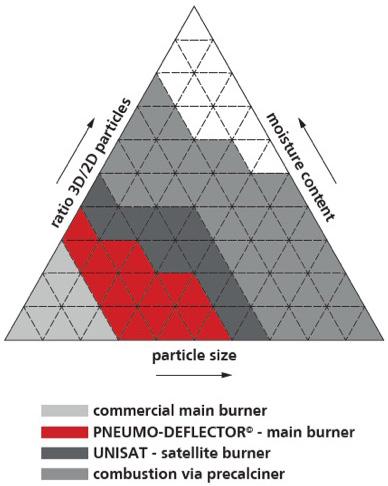

Rigorous quality control measures should be implemented throughout the supply chain to ensure consistency in the AF composition and properties. There are a range of parameters to take into account in order to enable a successful implementation of AF – they include, but are not limited to, the following:

f Particle size distribution.

f Ratio of 3-dimensional to 2-dimensional particles.

f Moisture content.

Standards and procedures for AF collection, handling and storage should be developed and adhered to, in order to ensure consistent quality across different suppliers and batches.

AF from different suppliers or batches should be blended to provide greater consistency and stabilise combustion characteristics and heating values while improving reliability. Foster partnerships with reliable suppliers who demonstrate consistent quality and are committed to addressing any issues that may arise.

Invest in burners equipped with adaptive technology that can adjust combustion parameters based on fuel properties in real-time, thus optimising performance and reliability. Unitherm offers a wide range of products to fire AF with up to 100% thermal

substitution rate (TSR) such as the Pneumo-Deflector or the UNISAT satellite burner. These dynamic burners are equipped with M.A.S. Technology, which provides a reliable and reproducible adjustment option with the highest momentum efficiency over the entire range. This gives operators the opportunity to optimise heat release and emissions according to fluctuating fuel quality.

Provide training for operators and maintenance personnel on the specific requirements and challenges associated with AF, empowering them to identify and address issues effectively.

By implementing these strategies, it is possible to effectively mitigate the challenges presented by the varying consistency and quality of AF, ensuring reliable burner operation while maximising efficiency and sustainability.

Satellite burners can play a significant role in modern cement production, primarily in enhancing the use of biogenic secondary fuel and therefore reducing environmental impact. Especially above a certain TSR (70 – 100%), the satellite burner is the tool for success. The following factors explain why this is the case:

f Temperature control: Together with a flexible main burner, satellite burners can be strategically placed within the kiln to provide localised heat input, allowing for more precise temperature control and uniform heat distribution even with very high substitution rates. This helps optimise the cement clinker formation process, leading to a more stable product quality.

f Fuel flexibility: Satellite burners offer flexibility in fuel selection, enabling cement plants to utilise a variety of AF, including biomass, waste-derived fuels, and other low-carbon alternatives. This diversification reduces reliance on fossil fuels, mitigates environmental impact, and enhances sustainability.

f Emissions reduction: By facilitating more efficient combustion and enabling the use of cleaner fuels, satellite burners contribute to lower emissions of greenhouse gases and pollutants, helping cement plants meet stringent environmental regulations and sustainability targets.

f Cost savings: By improving the TSR of secondary fuels, thereby reducing fossil fuel consumption, and minimising CO2 emissions, satellite burners contribute to cost savings for cement manufacturers in the mid and long term. Additionally, their modular design allows for easier installation, maintenance, and scalability, enhancing overall operational efficiency and profitability.

Overall, satellite burners offer numerous benefits for modern cement production, including enhanced

Finding spare parts like never before.

See what I see

fuel flexibility, emissions reduction, and operational flexibility. Their integration into cement kiln systems can help drive sustainable development and improve competitiveness in the global cement industry.

When looking at ways to decarbonise the cement industry, a diverse range of approaches has to be considered. Green hydrogen is one such approach, as the lack of any carbon involved in hydrogen combustion is well known. Using hydrogen, however,

is not without its technical challenges, particularly when used on a large scale. Focus must be placed on understanding and adapting to hydrogen’s thermodynamic characteristics (Table 1).

Control of flame propagation when using hydrogen is especially important as it has a flame speed eight times greater than methane and a very low density that results in a high nozzle outlet velocity of up to 1300 m/s (depending on pressure difference). This needs to be intelligently controlled in order to avoid double flame formation in combination with other fuels. Unitherm’s dynamic burners with their M.A.S. technology, are well suited to these conditions.

Several additional burner design considerations must be made to ensure safe and efficient combustion when working with hydrogen:

Hydrogen combustion produces high-temperature flames and can lead to increased corrosion rates and embrittlement of materials. Burner components must be made from materials compatible with hydrogen combustion, such as stainless steel or nickel alloys, to ensure durability and longevity.

Flame stability and propagation

Hydrogen has a wide flammability range and burns at a high flame speed. Burner design should prioritise stable flame characteristics to prevent flashback and ensure reliable, efficient and safe combustion over varying operating conditions such as start-up or full operation.

Heat management

To counteract the fast flame propagation which can impact temperature distribution along the kiln, the burner design, ideal with dynamic adjustment possibilities, should incorporate features to manage heat transfer, to obtain a similar heat distribution as with ordinary fuel mixes and maintain equipment integrity. By addressing these burner design considerations, cement plants can effectively leverage green hydrogen as a clean and sustainable fuel source while ensuring safe and efficient combustion processes.

Burner design plays a crucial role in minimising the production of harmful emissions, like NOx, in cement production. This section highlights some ways in which burner design can achieve the goal of reduced emissions:

f Efficient combustion: Proper burner design can optimise combustion efficiency by ensuring that the fuel is thoroughly mixed with the combustion air, resulting in complete combustion of the fuel. This can minimise the production of harmful emissions such as carbon monoxide (CO) and unburned hydrocarbons (UHC). Unitherm Cemcon’s burner designs are

engineered to provide efficient combustion, resulting in reduced emissions.

f Low-NOx technology: NOx emissions in combustion processes are mainly produced through temperature-driven reaction kinetics.

Unitherm Cemcon’s burner designs incorporate low-NOx technology, such as staged combustion, flue gas recirculation (FGR), which can significantly reduce the formation of NOx emissions at the main burner.

f Precise control: Burner design can also enable precise control of combustion parameters, such as temperature, excess air, flame shape and fuel-to-air ratio. This allows for optimal combustion conditions, minimising the formation of emissions.

Unitherm Cemcon’s burner solutions such as the M.A.S. technology incorporate advanced control systems that allow for precise and automated control of combustion parameters, resulting in reduced emissions.

f AF: Cement producers are increasingly using AF, such as biomass, waste-derived fuels, and other low-carbon fuels, to reduce their carbon footprint. Burner design can accommodate the use of AF by providing appropriate fuel injection systems like the Pneumo-Deflector© (Figure 4) when using AF through the main burner only or the UNISAT satellite burner when maximising the TSR between 70 – 100%, that ensure efficient combustion and minimise emissions. The sometimes-high moisture content in AF ‘cools’ the combustion process and thus leads to lower NOx emissions.

In summary, burner design plays a critical role in minimising emissions in cement production.

Unitherm Cemcon’s burner solutions are designed to optimise combustion efficiency, incorporate low-NOx technology, enable precise control, and accommodate AF, all of which contribute to emissions reduction objectives for cement producers.

To reduce maintenance costs and maximise the lifetime of kiln burner, the following steps can be taken:

Regular inspection and maintenance of the burner are essential to identify and address any potential issues before they become major problems. This includes cleaning, checking for wear and tear, and replacing worn-out components as needed. Unitherm Cemcon provides recommended maintenance procedures and schedules for its kiln burners, which should be followed diligently to ensure optimal performance and longevity.

Ensuring that the fuel and air quality meet the specifications recommended by the burner manufacturer is critical for efficient burner

performance and longevity. Poor fuel quality or contaminated combustion air can lead to increased wear and tear on the burner components, reduced combustion efficiency, and higher emissions, which can result in increased maintenance costs and decreased burner lifetime.

Following the recommended operating procedures and guidelines provided for the kiln burners is crucial to ensure optimal performance and extend burner lifetime. This includes proper start-up and shutdown procedures, correct fuel and air settings, and operating within the recommended temperature and pressure ranges.

Proper training of operating and maintenance personnel on the correct operation, maintenance, and troubleshooting procedures for Unitherm Cemcon’s kiln burners is crucial to minimise maintenance costs and maximise burner lifetime. Unitherm Cemcon provides training and technical support to their customers, which should be utilised to ensure that the burner is operated and maintained correctly.

Using genuine spare parts from Unitherm Cemcon for any repairs or replacements is important to ensure that the burner components are of the highest quality and designed specifically for the burner. Genuine spare parts are likely to have better durability and compatibility with the burner, reducing the risk of premature failures and minimising maintenance costs in the long run.

Automation and burner management systems significantly enhance burner operation through precise control, real-time monitoring, and safety features.

These systems enable optimal combustion efficiency, fuel savings, and product quality by controlling parameters like fuel flow rates and air-to-fuel ratios with precision. Real-time monitoring detects deviations from set parameters, allowing prompt corrective actions to maintain

optimal operation. Safety interlocks prevent unsafe conditions like flame failure or overpressure, reducing risks of accidents and environmental hazards.

Remote monitoring and control enable oversight and adjustment of burner performance from a centralised control room or mobile devices, improving efficiency and safety. Data logging and analysis provide insights for performance optimisation, predictive maintenance, and compliance reporting.

Integration with process control systems ensures coordination and optimisation of burner operation with other processes, enhancing energy efficiency and product quality. Energy management features optimise burner operation schedules, load distribution, and fuel switching strategies based on energy pricing and demand, minimising costs and environmental impact.

In summary, automation and burner management systems offer precise control, real-time monitoring, safety features, remote access, data analysis, integration, and energy management capabilities. These contribute to improved efficiency, reliability, safety, and sustainability in industrial burner applications.

Across the cement industry, there is a strong focus on reducing carbon emissions and improving energy efficiency in the cement industry, and this has led to the development of innovative burner designs (e.g. M.A.S. technology, UNISAT) that are able to efficiently combust an extraordinary amount of solid AF and emit fewer greenhouse pollutants.

This path will continue to be followed in the future, but at the same time the variety of fuel specifications is becoming ever wider, as certain fractions will no longer find their way into the combustion process in the pursuit of a functioning circular economy.

Additionally, the trend towards the use of gaseous AF, such as biofuels and green hydrogen, is likely to impact burner design.

These fuels have different combustion characteristics and require specialised burners to achieve optimal performance either under ambient or oxyfuel conditions.

Another trend that is likely to influence burner design is the increasing use of digital technologies, such as artificial intelligence and IoT, in industrial processes.

Burner manufacturers are likely to incorporate these technologies into their products to optimise performance, reduce downtime, and improve safety.

M. Akritopoulos and T. Abbas, Cinar, and Syed Suhail Akhtar, Holcim, explore the advantages of burning green ammonia over hydrogen in a cement kiln.

At cement plants, ammonia (NH3) is considered a pollutant in the flue gases or a reactant to reduce NOx. Its concentration in the atmosphere is monitored, a few parts per million (ppm) being of concern if it escapes without neutralising NOx to N2. A century ago, ammonia was needed to boost the yield of crops so it was produced commercially by combining H2 with N2 to produce NH3-based fertilisers. Used as a fuel, ammonia burns at a moderate rate leaving the combustion products of atmospheric N2 and water vapours.

But one may ask why not burn hydrogen without having to produce ammonia? The rationale behind this approach is the much lower transportation costs and existing infrastructure and transport facilities of ammonia, which do not exist for hydrogen, particularly if it is transported from off-site as a fuel to a plant. Therefore, production of green ammonia, using hydrogen derived from water electrolysis

powered by renewable energy resources cuts down the transportation costs. However, the production of green ammonia will cost up to four times as much to make as conventional ammonia, requiring further developments and ways to reduce green ammonia costs which in turn depend on its utilisation as a fuel other than as a fertiliser.

Ammonia has a higher energy density than hydrogen as a liquid with three hydrogen atoms rather than two. The energy density of liquefied hydrogen is 8491 kJ/l compared to ammonia’s 11 308 kJ/l.1 On a weight basis, ammonia contains 17.65% of hydrogen. As there are three hydrogen atoms attached to a single nitrogen atom, ammonia can contain about 48% more hydrogen by volume than even liquefied hydrogen. From a mass energy density basis, the hydrogen calorific value is 120 MJ/kg, compared to 18.6 MJ/kg for ammonia, which is similar to the calorific value of most green (biomass) solid fuels.1 This makes green ammonia an attractive renewable energy carrier as it has a higher energy density for lower transportation costs. Liquid hydrogen has to be stored at cryogenic conditions of –253˚C, whereas ammonia can be stored in much less energy-intensive vessels maintained at –33˚C. In addition, ammonia, though hazardous to handle, is much less flammable than hydrogen. Hydrogen production and transportation are limited especially when compared to a century-long use of ammonia in agriculture – a vast ammonia infrastructure already exists. Worldwide, some 180 million tpy of ammonia is produced, and 120 ports are equipped with ammonia terminals.

The production of green hydrogen through renewable sources, i.e., solar or wind, is an expensive option but may be justifiable under off-peak power conditions as well as considering CO2 mitigation costs. An alternative approach to the expensive storage and transport issues related with hydrogen, is to combine hydrogen into a compound that preserves the energy value but is easier to transport as a liquid, i.e., methanol (CH3OH) or ammonia. From a CO2 emission reduction perspective, ammonia is the obvious choice, having no carbon molecule.

Under good mixing conditions with oxygen, the only products of the complete oxidation of ammonia are water and nitrogen gas. At standard conditions (298 K, 1 atm), the enthalpy of combustion is 317 kJ/mol or 18.64 MJ/kg as compared with 240 kJ/mol or 120 MJ/kg for hydrogen.

Ammonia is regularly used in cement plants to reduce NOx (SNCR/SCR); however, it has not been used as a fuel. If fired in a kiln, a 100% ammonia flame would have a lower flame speed and a narrower flammability range compared to conventional fuels. It can also be co-fired either with H2 or other biomass-based fuels to reduce combustion generated CO2 emissions. However, it must be questioned whether it is a feasible choice. Ammonia as a fuel has never been fired in a cement kiln so its flame characteristics and

NOx formation potential are unknown, prior to full-scale plant trials. Thus, the use of ammonia as a fuel has been simulated in a cement kiln to evaluate its combustion characteristics as a co-firing fuel, in particular on NOx emissions.

To reduce CO2 emissions, cement plants are replacing carbon rich fuels, i.e., petcoke with

lower C/H ratio fuels as well as modifying the clinker factor to meet with the interim CO2 reduction targets set for 2030. The biomass and biological content in solid and liquid recovered fuels will become less available over the passage of time as other industries have also started competing for these fuels. As a result, the price of these ‘greener’ fuels is expected to rise and may eventually become restrictive and selective, thereby, making it unattractive for co-firing in large proportions. When this happens, green H2 and NH3 firing may be considered as a means to reduce CO2 emissions prior to tackling process generated CO2 emissions, i.e., oxy-combustion and/or CCUS.

A hydrogen flame would be shorter and hotter due to its higher adiabatic flame temperature, hence co-firing with a lower calorific value (CV) NH3, with some modifications in the kiln burner, would overcome biomass-based fuel shortage scenarios as a quick switch-over fuel. A disadvantage would be that, due to air-fuel mixing conditions, NOx formation through NH3 burning would increase. It is significant to highlight this increase, as well as the ways to minimise it – although kiln generated higher NOx emissions can be reduced later in the calciner through fuel reburning and/or using small amounts of NH3 (under selective non-catalytic reduction – SNCR or SCR). Under NH3 and H2 co-firing conditions, CO and NOx formation and destruction reactions rates and regions are expected to be different to those

analysed in one of the first full-scale modelling exercises of a cement kiln.

The limited data for air/ammonia/methane flames, under internal combustion engine or gas turbine combustor conditions for both premixed and non-premixed, shows the significant effect of fuel equivalence ratio on NOx formation. The reported trends show an increase in NOx emissions with a corresponding increase in NH3 content followed by a decrease in the equivalence ratio increases. These conditions are significantly different to those of a kiln flame. In the study presented, NH3 co-firing with H2 and biomass in a kiln burner was simulated and compared with H2 co-firing with biomass. The results are compared regarding the combustion, mineral compositions and NOx emissions.

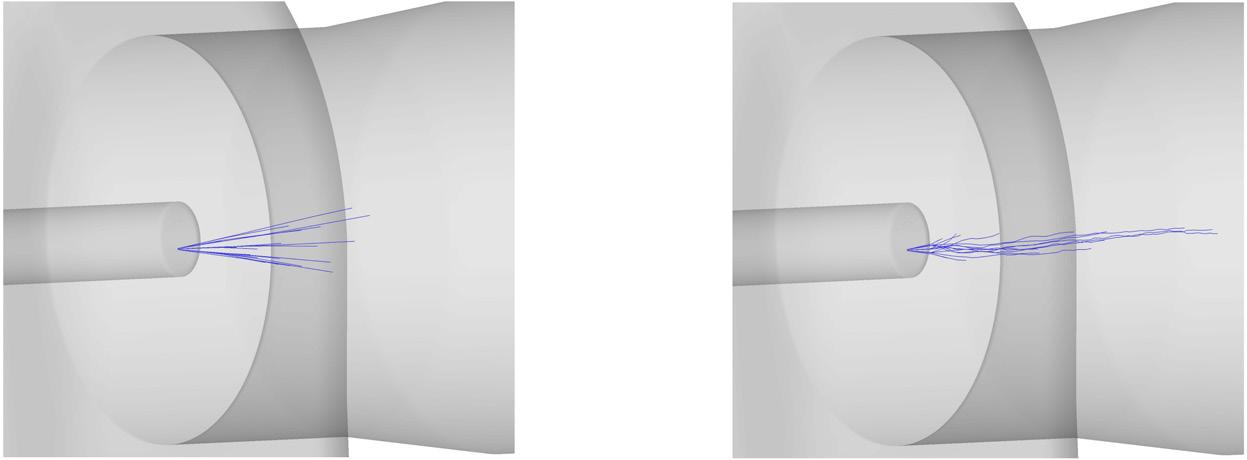

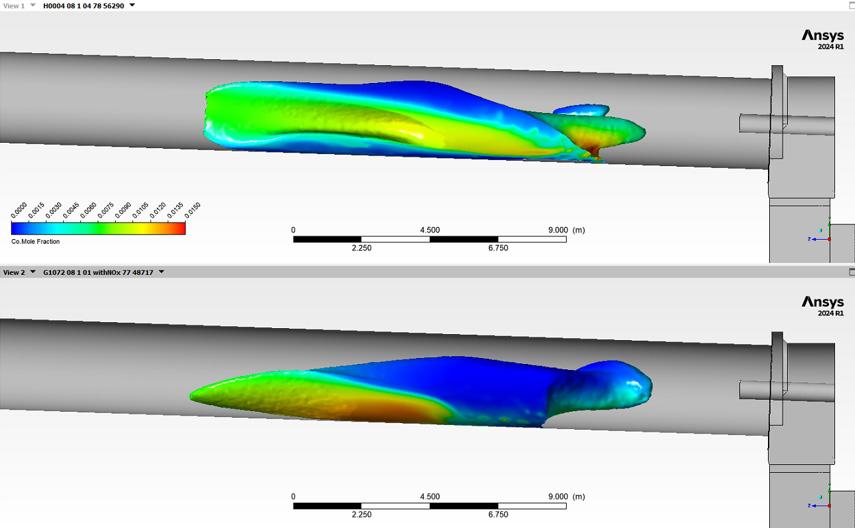

As part of follow-up research and prior to demonstration at full-scale, a sensitivity analysis was carried out for ammonia combustion in a kiln using mathematical modelling, to better understand its combustion and emission behaviour prior to performing expensive plant trials. As part of a recent research campaign, two new simulations are discussed here and compared with the previous H2 and biomass co-firing results which were validated against the plant trial data. Results of ammonia co-firing with hydrogen (Case 1) are compared with the initial simulation of H2 co-firing with biomass – the Base Case (Figure 1). In the Base Case, the biomass (liquid and solid biomass streams) was co-fired with H2 (25% by thermal input) and NH3 was co-fired with H2 with same thermal input ratio.

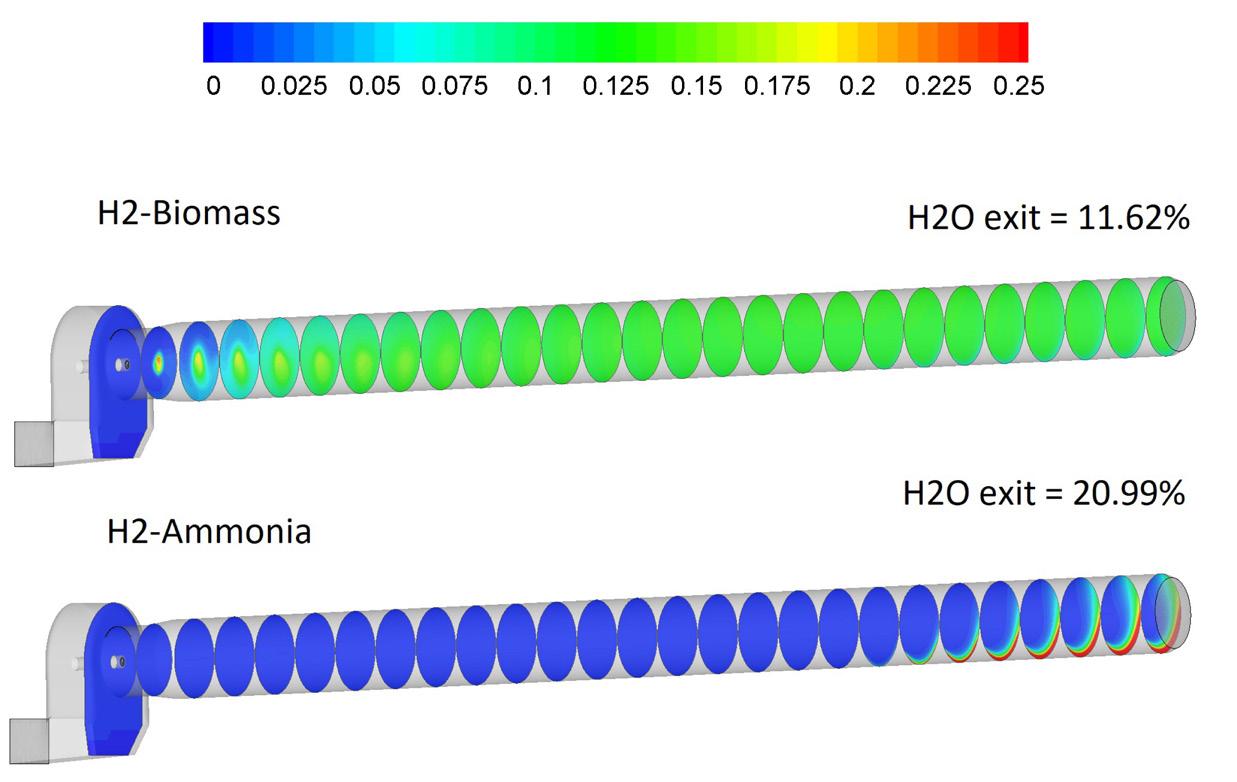

Figure 2 shows an absence of CO2 formation near the kiln front end, as hydrogen (25% by thermal input) co-fired with ammonia (75%) combusts without forming CO2. There was, however, some CO2 formation near the kiln feed-end – this was emitted as a result of calcination reactions of remaining uncalcined hot-meal particles, slowly calcining and releasing CO2. In comparison, three times the amount of CO2 was formed when H2 (25%) was co-fired with biomass corresponding to the carbon content of the biomass.

A higher proportion of water vapour formation was also observed (Figure 3) for the hydrogen/ammonia case, reflecting the absence of CO2 formation, as the combustion products were primarily N2 and H2O, seeing as the fired fuels were carbon-free.

Since stoichiometric combustion of 1 kg NH3 requires around 6.14 kg air and produces 1.59 kg H2O and 7.2 kg N2.

Co-firing ammonia with hydrogen also dampened higher gas temperature peaks (Figure 4) due to the higher adiabatic flame temperature of hydrogen as both gaseous fuels, in this case, burnt in close proximity. In the ammonia/hydrogen firing scenario, ammonia off-set the intensity of the hydrogen flame due to its higher substitution ratio and lower calorific values, i.e., less than 1/6 to that of hydrogen. The temperatures obtained in the ammonia/hydrogen flame were lower and the flame was less sharp and longer (hot region remains further) than the Base Case of hydrogen/biomass co-firing. Ammonia burnt fully while biomass fuel fractions burnt slowly and only up to 97% – for several kiln burner diameters distance. This led to an increased temperature at the kiln back end.

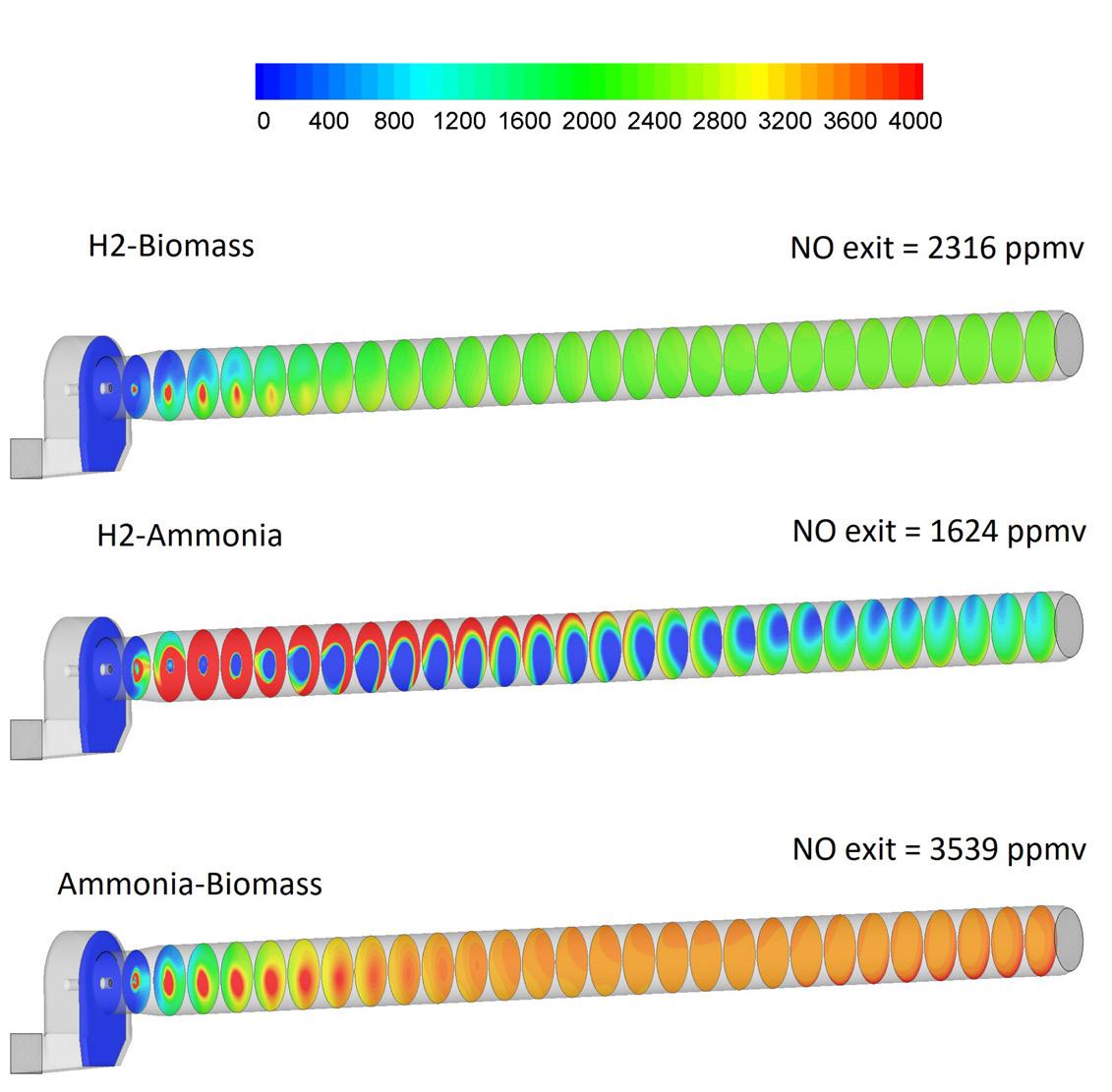

It was expected that the presence of ammonia would lead to a significantly higher NOx formation. Conversely, kiln feed-end NOx emissions dropped in the ammonia-hydrogen co-firing case (Figure 5). This was due to the suppression of peak gas temperatures, leading to lower formation of NOx through the thermal-NOx pathway. In addition, hydrogen, due to its higher reactivity, consumed most of the burner primary air, leaving little oxygen to oxide ammonia, which under starved air conditions was reduced to N2. Hence, reduction of NOx formed both thermal and fuel formation pathways.

In the second scenario, when ammonia was co-fired with biomass, NOx concentrations increased significantly due to the earlier ignition of ammonia in the presence of oxygen in the burner primary air stream. The biomass fuel was a mix of meat and bone meal (MBM -19.4 MJ/kg) and glycerin (CV-15 MJ/kg). For fair comparison, it is important to note that the fuel bond nitrogen content of MBM was five times higher than that of coal – since part of the biomass was burnt in oxygen-rich conditions of the flame in regions where secondary air diffused into the flame. In the ammonia/biomass co-firing case (Case 2), NOx contribution from thermal NOx reduced due to overall lower peak flame temperatures. The increase seen in the formation of NOx was therefore entirely down to the fuel NOx formation, as ammonia oxidised to NO upon predominantly reacting with the oxygen from the burner primary air (available in the absence of H2 combustion). Higher nitrogen content MBM particles released higher fuel bond nitrogen.

The results of the hot gases in the heating up of the bed material did show very similar trends for the three cases. In the case of ammonia/hydrogen, one small difference was that it resulted in a longer flame and lower peak temperatures.

However, heated gases remained at higher levels of temperature for a longer distance, while the bed material also heated up at a faster rate, the full calcination and formation of products occurring faster.

The rationale behind considering ammonia as a fuel is the extremely high cost of hydrogen procurement. Until these costs are justifiable, ammonia may be considered as a co-firing fuel either with hydrogen or biomass-based fuels. For example, in the plant trials, the cost of CO2 avoided (CaCO2) was €1559/t of CO2, which was estimated for a 40% hydrogen thermal substitution rate in the main burner, compared to 100% coal firing conditions. Hydrogen was responsible for about 87% of the fuel mix cost at the burner tip.2 It is difficult to quantify the cost savings of firing ammonia as there are multiple factors, i.e., the costs of long-distance transport, the technology used in the production of hydrogen and or ammonia, the green energy utilisation etc. The cost differential will become larger as the scale of projects increases, and as technologies are developed to reduce transport costs. However, in the absence of hydrogen transport infrastructure (and the prospects of energy savings to reconvert NH3 to H2 at the point of utilisation), it is not only energy efficient to burn ammonia directly, but co-firing it with hydrogen will also suppress peak flame temperatures due to its lower energy density.

Considering combustion and emissions, the presented results demonstrate the small-scale ammonia experimental findings, where 30% reductions in the NOx emissions are observed when ammonia as a fuel was fired in natural gas fired gas turbines.1 The mathematical model used in the predictions, has been validated earlier against the kiln trials for a number of hydrogen co-firing ratios with the biomass and coal as well as alternative fuel flames. Presented results demonstrate the effect of ammonia co-firing scenarios on emerging thermo-fluid dynamic conditions and how to tailor ammonia substitution ratio and its firing strategies to minimise its higher NOx formation potential.

1. JULIE et al, ‘The Potential Role of Ammonia as Marine Fuel – Based on Energy Systems Modelling and Multi-Criteria Decision Analysis’, Hansson, Sustainability (April 2020).

2. ‘State of the art fuel mix for UK cement production to test the path for ‘Net Zero’: a technical, environmental and safety demonstration’, chrome-extension:// efaidnbmnnnibpcajpcglclefindmkaj/https://assets.publishing. service.gov.uk/media/637e4d85d3bf7f154955962d/phase_3_ state_of_the_art_fuel_mix_for_UK_cement_production_to_ test_the_path_for_net_zero.pdf

Joel Maia, FCT Combustion, explores the different pathways available for producers to reduce CO2 emissions from cement and clinker production.

According to the Global Cement and Concrete Association (GCCA), the construction sector produces around 2.5 billion tpy of CO2, with the potential to increase to 3.8 billion tpy by 2050 without CO2 mitigation efforts, due to the rising demand for concrete. Approximately 60% of these emissions stem from limestone decarbonisation, with the remaining 40% from the combustion of fuels used in clinker lines. Additionally, electricity consumption contributes indirectly to CO2 emissions, when not produced renewably.

The construction sector’s value chain, encompassing Cembureau’s 5Cs (Clinker, Cement, Concrete, Construction, and Carbonation), holds significant potential to reduce CO2 emissions, striving toward carbon neutrality. Achieving this goal requires a

collective effort from all stakeholders, with clinker and cement production at its core.

The industry has already been moving toward decarbonisation for several years, employing various technologies. However, with numerous options available, plant environmental teams often feel overwhelmed, lacking clear information on the most cost-effective methods to reduce CO2 emissions for their specific circumstances. This article focuses on decarbonising clinker and cement production, exploring different possibilities and proposing scenarios tailored to each plant’s stage on the decarbonisation path.

CO2 emissions in clinker and cement production can be divided into two primary sources: emissions from raw material decarbonisation and emissions from combustion. Several strategies exist to mitigate both, discussed in this article. To facilitate comparison, a hypothetical ‘standard kiln’ with a 4000 tpd capacity, 800 kcal/kg thermal consumption, and a 40 – 60% energy split between the kiln and calciner respectively will be used, operating for 8000 hours per year.

Improving plant efficiency has a very broad meaning and influences all other methods presented as well. CO2 emissions are directly related to the amount of energy (thermal or electric), needed to produce 1 kg of material. Reducing the energy required to produce 1 kg of material lowers the fuel consumption and the volume of gases generated, thereby reducing both the thermal and electrical energy needed.

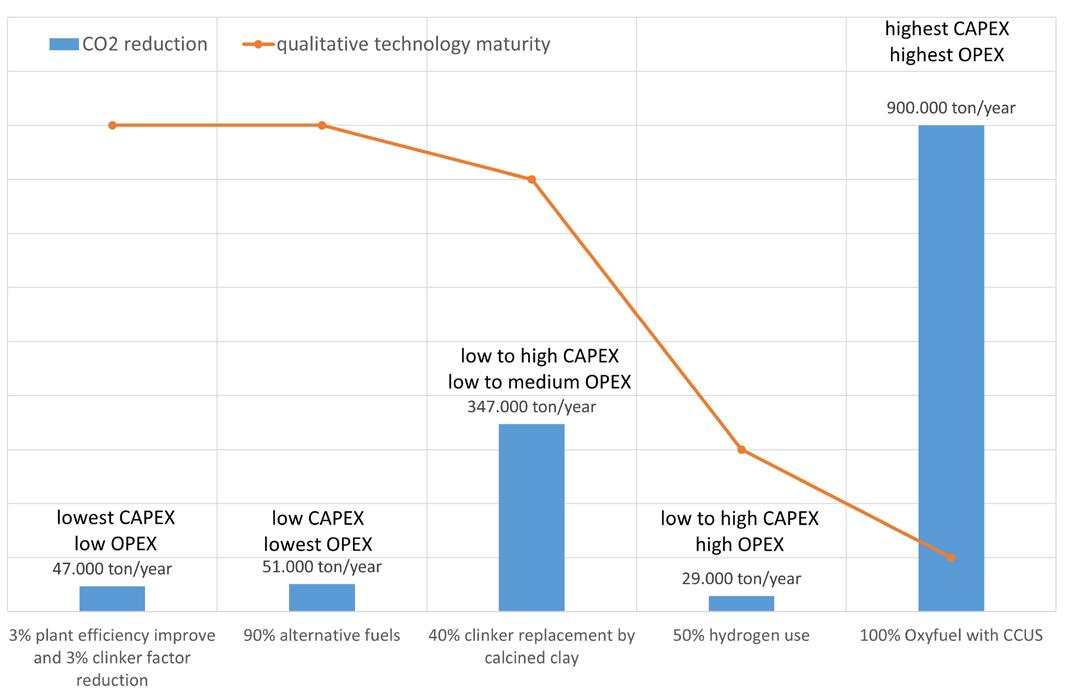

For instance, in the above-mentioned standard kiln, a 3% efficiency improvement would reduce CO2 emissions by approximately 14 000 tpy. It might not seem much but it is worth considering that a 3% improvement in the plant efficiency can be achieved by simple actions and low investment, through, for example, better process control, reducing false air in the system, optimising raw meal composition to allow for easier cooking, upgrading to a combustion system that allows the operation with lower oxygen content in the kiln while keeping the combustion under control.

Similarly, enhancing the clinker quality can lead to significant CO2 reductions. A better-quality clinker means that

less needs to be used to achieve the same cement strength. A 3% reduction in the clinker factor in FCT’s standard plant scenario would decrease CO2 emissions by around 34 000 tpy. Combining this with a 3% efficiency improvement results in a total reduction of approximately 47 000 tpy.

Methods to improve clinker quality include better process control, raw meal composition optimisation and homogeneity, and investing in advanced combustion systems such as the Turbu-Flex™ from FCT.

These options are often overlooked powerful alternatives, at relatively low costs, which allow plants to contribute to their initial share of CO2 emissions reduction.

Use of alternative fuels

It might sound counterintuitive that the use of alternative fuels (AF) would reduce CO2 emissions, as their combustion also releases CO2 While this is true, AF usage prevents additional fossil fuel consumption and the associated emissions. AF, often

instead of using a brand-new font of carbon taken from fossil fuels.

The use of AF is a mature technology, with plants in Europe being able to achieve up to 90% substitution rates by solid AF, and up to 100% when considering a mix of solid and liquid AF.

The cost of converting a plant to high substitution rates varies based on factors such as plant design,

existing equipment residence times, the quality of AF that can be sourced/prepared, and the technology of the combustion equipment, among others.

For this article’s standard kiln, a 10% increase in the thermal substitution rate replacing coal with RDF could reduce CO2 emissions by around 6000 tpy. Achieving a 90% substitution rate would reduce emissions by approximately 51 000 tpy.

Investments in CFD studies for the calciner and advanced combustion systems like the Turbu-Flex™ kiln burner from FCT are relatively low investments that can facilitate this transition.

Materials that possess binding characteristics when mixed with water or other materials, known as supplementary cementitious materials (SCMs), have been used for several decades as a clinker replacement. Fly ash from power plants running on coal, slags from steel production and natural pozzolanic material are common examples of SCMs. However, their availability is decreasing, prompting the search for alternatives, with calcined clay being

a prominent option which has been used in cement for over 40 years in some countries like Brazil, for instance.

The clay used for the calcination is an aluminosilicate mineral within certain ratios of alumina and silica, containing hydroxyl in its structure. Once the clay is submitted to thermal treatment at the right temperatures, the hydroxyl is released from the clay structure. When the clay is mixed with cement, the calcium oxide from the clinker reacts with the clay, strengthening it. The right temperature for clay treatment is very particular for each clay, but in all cases, it is below the clinkerisation temperatures. Therefore, two benefits in terms of CO2 reduction can be achieved when replacing clinker with clay: the CO2 emissions from combustion are reduced (there are further benefits if AF are used), and there are virtually no CO2 emissions from the material (except for some organic and limestone traces).

Once more, the investment costs of this option are within a very wide range. On one side, existing clinker kilns can be adapted for clay calcination with minor adjustments, offering a cost-effective solution, although not the most efficient, even with a pendular operation between clinker and clay. On the other side of the scale, new plants using rotary kilns or flash calciner technologies can be built for optimal efficiency, with an array of different configurations. FCT offers the expertise of its engineers with more than 40 years’ experience in clay calcination, and technologies like the RotaCalx™ (rotary kiln) and FlashCalx™ (flash calciner) for clay production including colour control techniques.

Combustion represented by an isotherm surface coloured by CO molar fraction, on top: oxyfuel combustion, at the bottom: conventional combustion with air. Source: FCT

Comparison between different technologies for CO2 emissions reduction. Source: FCT.

For this article’s standard kiln, replacing 40% of clinker with calcined clay could reduce CO2 emissions by around 347 000 tpy.

Considering that hydrogen gas is a fuel that has no carbon, it should be considered ideal to reduce CO2 emissions. So far, the use of hydrogen in cement production has been limited to very small amounts, in the range of single digits of percentage, from 0.2 – 3%. The limitation is more in the production rather than in the combustion, especially when considering an environmentally friendly production of hydrogen.

Nowadays, the vast majority (above 99%) of hydrogen produced, comes from the reforming of natural gas which releases a substantial amount of CO2 into the atmosphere. If this is the case, burning natural gas directly in the kiln has a lower environmental impact. Moreover, hydrogen is still expensive compared to other fuels and is

not widely available to the industry, hence it is not a feasible option at the moment for cement production. If environmentally friendly hydrogen (for example, when produced via electrolysis of water using solar or wind power) became available at affordable prices in the future, there would be some challenges using hydrogen in cement production at a large scale. This would include reduced flame emissivity, increased NOx emissions and distribution infrastructure. However, these hurdles are significant only when achieving a substitution rate with hydrogen above 50%. There are important investments in order to make hydrogen production more affordable, in larger quantities and clean. FCT wrote a comprehensive article in WorldCementin November 2022 discussing the aspects around hydrogen usage in clinker kilns.