A SUP PLEMENT TO HYD ROCA RBON ENG INEE RIN G

Euromel® Melamine - the leading and most advanced technology for the production of high-quality melamine used in wood-based products, laminates, moulding compounds and fire-extinguishing foams in the last 40 years.

Delivers high purity, high consistency melamine with total zero pollution (TZP) with extremely lower energy consumption using 30% lesser steam import and 20% lower fuel utilisation than the closest competitor.

Euromel® Melamine Process is now used in 28 plants worldwide, accounting for more than 8 million tonnes of melamine produced cumulatively, making it the most traded and widely used melamine worldwide.

03 Comment

04 Plan to adapt

Alan Gelder, Wood Mackenzie, UK, discusses how refiners can stay ahead on the energy transition pathway.

11 Decarbonisation levers for downstream assets

Jock Hughson, Shell Catalysts & Technologies, Australia, discusses decarbonisation levers that refiners can pull to help them stay aligned with more stringent emissions regulations while staying competitive.

16 Sustaining momentum

Michael Connolly and Man Yiu Tse, ICIS, explore the evolving biofuels market, and examine how economic competition, regulatory dynamics, and shifting corporate strategies shape the industry.

22 Renewables on the rise

Richard Stambaugh, Merichem Technologies, USA, discusses renewable energy integration in refining and petrochemical processes and the rise of renewable diesel as a drop-in replacement for petroleum diesel.

28 Overcoming SAF hurdles

Nabil Ahmed, The Energy Industries Council (EIC), explains why sustainable aviation fuel (SAF) must overcome investment and scalability hurdles in order to prove its promising carbon reduction prospects.

33 Green skies ahead

Giacomo Rispoli and Alessia Borgogna, MAIRE, Italy, discuss the innovations and technologies that are driving

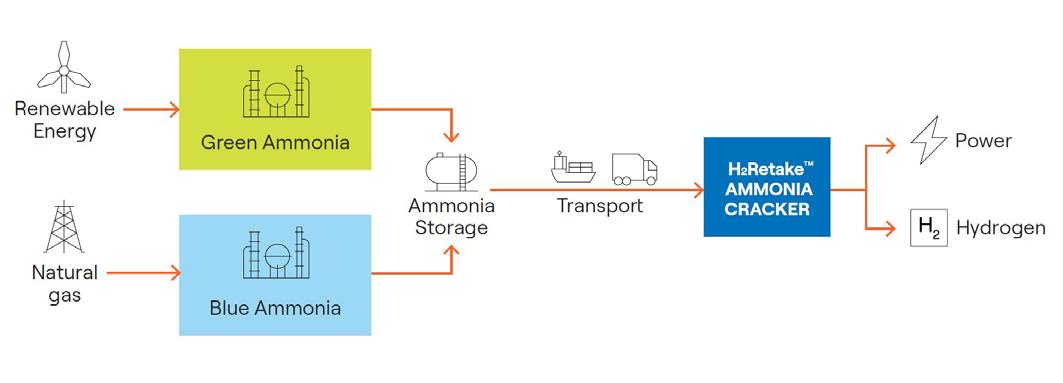

37 A cracking opportunity

Maninder Jit Singh, Topsoe, considers why ammonia cracking will be a key solution for efficient hydrogen transportation.

40 Nature as the blueprint

Thomas Winkler, Sulzer, Switzerland, explores how mimicking the circularity of natural ecosystems can provide an effective roadmap for the development of carbon capture and storage systems.

45 Three steps to CCUS success

Delivering cost-effective carbon capture and storage is critical to meeting climate change objectives. Dr. Marco Ernst, MAN Energy Solutions, explains why the role of scale and the right manufactured solutions cannot be overlooked as key steps to success.

49 Technology for life

Megan Hine, Dräger Safety, UK, outlines the critical importance of accurate carbon dioxide leak detection in onshore carbon capture and storage systems.

53 Empowering a cleaner future

Keith Warren, Servomex, UK, discusses gas analysis strategies for enhancing energy efficiency and reducing emissions.

57 Electrification: a vital step

Volker Metzger, Watlow, Germany, discusses the electrification of process heating in the oil and gas industry to lower carbon emissions.

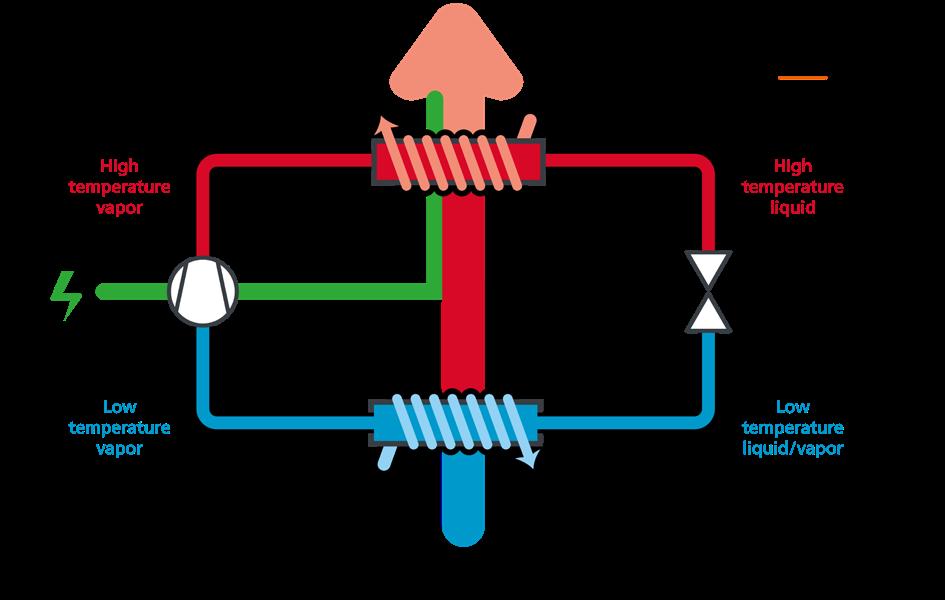

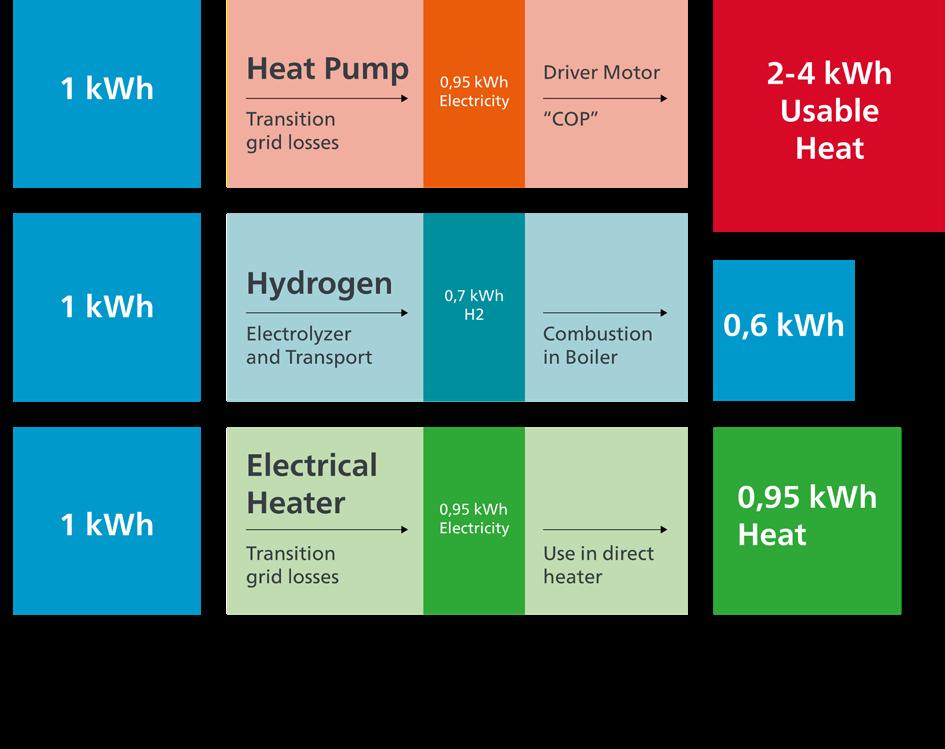

61 Recycle, please!

Rasmus Rubycz, Atlas Copco Gas and Process, considers why the use of industrial heat pumps is a logical solution to help decarbonise the downstream sector.

65 At the heart of the matter

Piotr Kulisz and Andreas Pischke, Valmet Flow Control BL, explore the critical role of flow control technologies in the energy transition.

High-precision measurement devices and solutions enable operators to increase plant safety and availability while ensuring compliance with increasingly stringent environmental guidelines and standards. Endress+Hauser’s analytical reporting software and smart device diagnostics help save time and optimise processes. Partner with Endress+Hauser to make the right process decisions as you move towards a more sustainable future.

For nearly a century, Grace catalysts have kept fuel and petrochemical feedstocks flowing from the industry’s largest refineries to the trucks, trains, planes, and ships that keep our world running.

We are leveraging our long history of innovation in fluid catalytic cracking to develop products that enable lower carbon fuels and help meet the challenges of the energy transition.

MANAGING EDITOR James Little james.little@palladianpublications.com

SENIOR EDITOR Callum O'Reilly callum.oreilly@palladianpublications.com

ASSISTANT EDITOR Poppy Clements poppy.clements@palladianpublications.com

EDITORIAL ASSISTANT Emilie Grant emilie.grant@palladianpublications.com

SALES DIRECTOR Rod Hardy rod.hardy@palladianpublications.com

SALES MANAGER Chris Atkin chris.atkin@palladianpublications.com

SALES EXECUTIVE Ella Hopwood ella.hopwood@palladianpublications.com

PRODUCTION MANAGER Kyla Waller kyla.waller@palladianpublications.com

HEAD OF EVENTS Louise Cameron louise.cameron@palladianpublications.com

DIGITAL EVENTS COORDINATOR Merili Jurivete merili.jurivete@palladianpublications.com

DIGITAL CONTENT COORDINATOR Kristian Ilasko kristian.ilasko@palladianpublications.com

DIGITAL ADMINISTRATOR Nicole Harman-Smith nicole.harman-smith@palladianpublications.com

JUNIOR VIDEO ASSISTANT Amélie Meury-Cashman amelie.meury-cashman@palladianpublications.com

ADMIN MANAGER Laura White laura.white@palladianpublications.com

CONTRIBUTING EDITORS

Nancy Yamaguchi Gordon Cope

SUBSCRIPTION RATES

Annual subscription £110 UK including postage /£125 overseas (postage airmail).

Two year discounted rate £176 UK including postage/£200 overseas (postage airmail).

SUBSCRIPTION CLAIMS

Claims for non receipt of issues must be made within 3 months of publication of the issue or they will not be honoured without charge.

APPLICABLE ONLY TO USA & CANADA

Hydrocarbon Engineering (ISSN No: 1468-9340, USPS No: 020-998) is published monthly by Palladian Publications Ltd GBR and distributed in the USA by Asendia USA, 701C Ashland Avenue, Folcroft, PA 19032.

Periodicals postage paid at Philadelphia, PA & additional mailing offices.

POSTMASTER: send address changes to HYDROCARBON ENGINEERING, 701C Ashland Ave, Folcroft PA 19032.

15 South Street, Farnham, Surrey

GU9 7QU, UK

Tel: +44 (0) 1252 718 999

CALLUM O'REILLY SENIOR EDITOR

Welcome to EnviroTech 2024 , a brand new supplement to Hydrocarbon Engineering that is dedicated to exploring sustainability and decarbonisation initiatives within the downstream sector.

While Hydrocarbon Engineering has long been at the forefront of covering critical developments in this area – and will continue to do so –EnviroTech ’s mission is to place the spotlight firmly on the technologies, whether mature or emerging, that are propelling the energy transition toward a sustainable future.

EnviroTech will serve as an essential resource for professionals navigating the transformative changes, challenges and opportunities that are presented by the energy transition. It will dive deeper into some of the key issues facing our sector, gathering insights from leading industry experts and exploring the innovative technologies, services, and solutions that will not only shape the future of the downstream oil and gas industry, but the planet as a whole.

We have been overwhelmed by the positive response that we have received from the industry since announcing the launch of EnviroTech , and would like to thank all of our contributing authors and advertisers for their support. After a lot of hard work, I am delighted to say that this inaugural issue brings together a diverse range of articles from leading experts covering some of the most pertinent topics at the heart of the energy transition.

We start with a keynote article from Alan Gelder, Vice President of Refining, Chemicals and Oil Markets at Wood Mackenzie, who outlines strategic pathways for refiners to effectively adapt to the evolving energy landscape (p. 4). On p. 11, Jock Hughson, Shell Catalysts & Technologies, considers a number of decarbonisation levers that refiners can pull to help them stay aligned with more stringent emissions regulations. Other articles in this issue explore the rise of biofuels and renewable energy integration in refining and petrochemical processes; innovations in sustainable aviation fuel (SAF) and how to overcome investment and scalability hurdles in order to prove its promising carbon reduction prospects; the use of ammonia cracking as a solution for efficient hydrogen transportation; and roadmaps for the development of carbon capture, utilisation and storage (CCUS) projects. Within these pages you will also find articles exploring energy efficiency and emissions reduction strategies, the electrification of process heating, the use of industrial heat pumps, and the role of flow control technologies in the energy transition, plus much more.

I hope that you enjoy this issue of EnviroTech and find it a valuable tool on your journey to more sustainable operations. We welcome your feedback and editorial suggestions, so please feel free to reach out to us using the contact information on this page.

Alan Gelder, Wood Mackenzie,

discusses how refiners can stay ahead on the energy transition pathway

Global oil demand continues to set records.

3Q23 global oil demand hit 102.8 million bpd, 300 000 bpd higher than 3Q19 and continues to grow. Wood Mackenzie forecasts global oil demand growth of 1.5 million bpd for 2024 and 1.6 million bpd for 2025.

Geopolitical tensions abound – in late summer 2024, Ukraine has occupied Russian territory, peace talks have yet to resolve the Israel/Hamas conflict and a Greek-owned oil tanker was attacked in the Red Sea, continuing the diversion of inter-regional trade around the Cape of Good Hope.

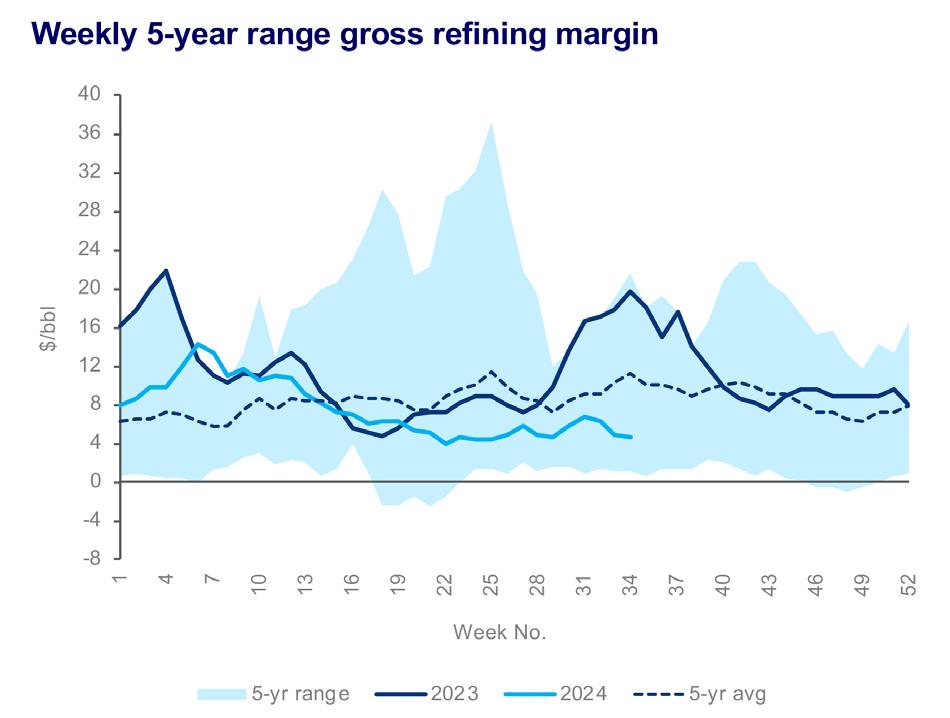

The oil market is languishing in the low US$80/bbl price range for North Sea dated crude, with OPEC+ restricting supply to keep the oil market balanced. Despite these factors, refining gross margins fell below the historical 5-year average during 2Q24 and have stabilised at ‘floor levels’, with low margins

limiting crude runs at weak sites in both Europe and Asia. (Figure 1).

The energy transition decouples the mobility of people and goods from oil demand. It is underway. Electric vehicles represented almost 50% of new vehicle sales in China in June 2024, with Europe at over 20%. Inter-fuel competition is also playing its part, as LNG trucks in China are displacing diesel demand.

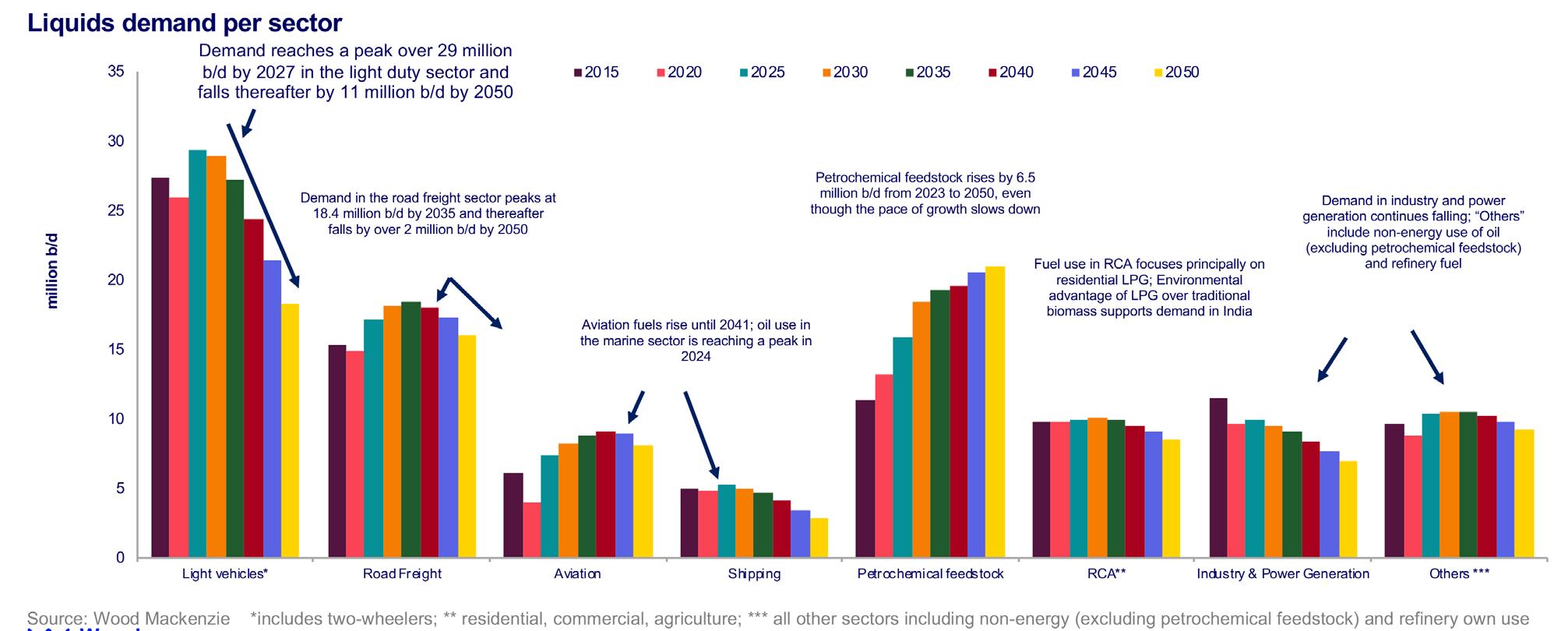

The composition of oil demand continues to evolve. The light duty vehicle sector is leading the energy transition. Heavy duty commercial vehicles, marine and aviation are hard-to-abate sectors due to the challenges of electrification, but they are not immune from fuel efficiency improvements and inter-fuel competition from natural gas or

liquid biofuels. Energy use for oil is projected to peak before the end of this decade.

Petrochemical feedstock demand, however, is forecast to continue to grow through to 2050. As income levels rise in developing countries, the rate of growth of petrochemical demand will slow from ‘GDP plus’ to eventually ‘GDP minus’ growth levels. Recycling and bio-based materials also reduce demand for oil-derived feedstocks, but these factors combine to slow the growth rate of petrochemical feedstock demand. Petrochemical feedstocks delay the onset of ‘peak oil demand’ until the early 2030s, but the sector is not big enough to counter demand declines in gasoline and diesel/gas oil (Figure 2).

From simply a demand perspective, refiners need to shift their focus away from transport fuels, towards petrochemicals. Petrochemicals are also more valuable than transport fuels, showed by the spread between the price of olefins and naphtha/LPG, which are the typical steam cracker feedstocks.

The demand for petrochemicals is far from uniform. Global polyethylene demand is expected to grow by 4.7% from 2023 to 1.2 billion t in 2024. The annual demand growth during 2024 - 2034 will average at 3.3%, higher than the 2.6% GDP growth in the same period. With population growth slowing in the long-term forecast years, polyethylene demand will slow to 1% AAGR during 2034 - 2050, lower than the 2.1% GDP growth.

Global paraxylene (PX) demand will increase to 55 million t in 2024, up from 51 million t in 2023. Robust polyester demand growth will drive PX consumption further, to over 66 million t in 2030 and 81 million t in 2040.

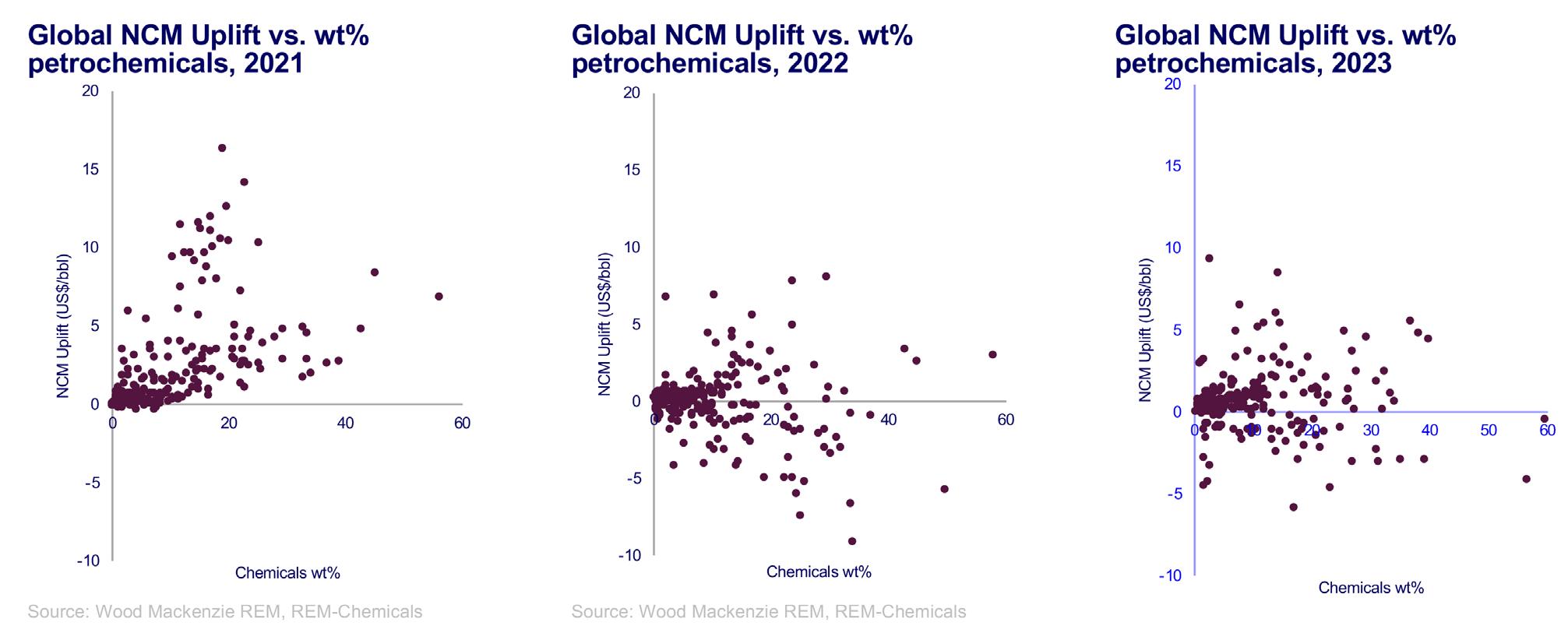

Many refiners are already integrated into petrochemicals, as Wood Mackenzie models over 200 integrated site locations, with several ‘second generation’ sites starting up in China in recent years. The value contribution from petrochemicals is a combination of the overall yield levels, profitability of the specific value chain and the location (as that determines CAPEX and the spread between petrochemical and feedstock pricing). Figure 3 shows the value contribution over the past three years:

n In 2021, petrochemicals added significant value to refining.

n This was not the case in 2022 due to the high value of transport fuels due to the Russia/Ukraine war.

n In 2023, refined product crack spreads declined, but the weak petrochemical margins from capacity over-build weighed on the value contribution.

Petrochemical integration is a ‘mega-trend’ for refiners, as demand for transport fuels declines. However, it is important to note the scale difference between the transport fuel demand and that for petrochemicals. Simply put, not all refiners can viably transition away from fuels to petrochemicals. For refiners to be commercially viable during the energy transition, they need to be strongly competitive, in terms of both earnings and emissions.

ADAM KADHIM Product Line Director, Hydrogen Topsoe

KNOWING YOUR LOW-CARBON POTENTIAL

As decarbonization requirements go up, refining companies are looking for cost-efficient ways to bring their carbon intensity down. One way to go is low-carbon hydrogen. Using low-carbon hydrogen has the potential to support refining businesses and the energy transition by reducing the carbon intensity of fossil transportation fuels. Discover the

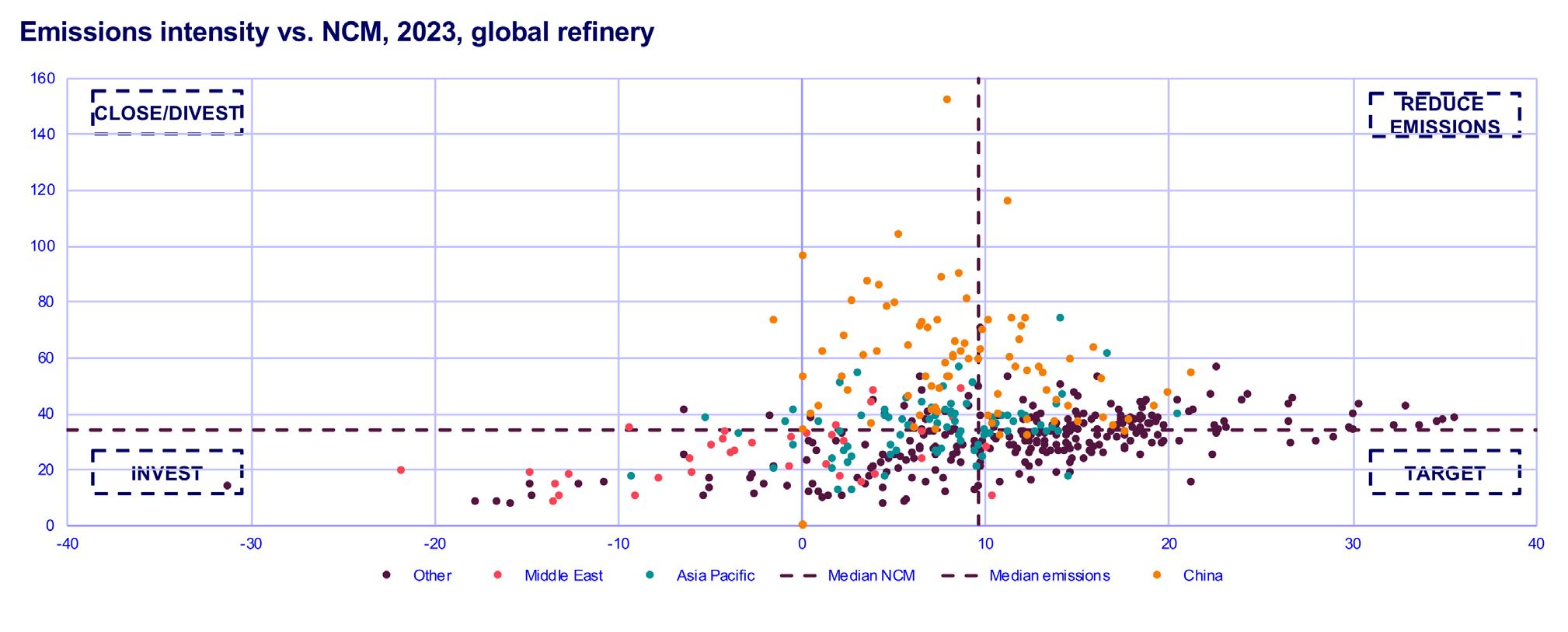

Refiners have traditionally measured their competitiveness in terms of net cash margin (NCM). As margin environment becomes challenging, refiners must continue to focus on improving their margins. However, refiners must now add another dimension to their competitiveness –carbon emissions. Net zero carbon emissions targets may lead to carbon policies which will have a material impact on refiners’ profitability. Using Wood Mackenzie’s PetroPlan simulation for refineries, it is possible to model the Scope 1 and 2 refinery emissions from the process operations used to convert crude oil into refined products.

Figure 4 plots the performance of global refining sites along two dimensions – margin and emissions, separating sites into four categories.

Refiners would want to be in the ‘target’ quadrant, where they achieve above average net cash margin and below average emissions intensity. Refiners with below average margins must first think about improving margin competitiveness, typically through upgrading investments. However, by making these investments, refiners must ensure

they do not move towards high margin and high emission quadrant. Refiners with low margins and high emissions are typically at high risk of closures or divestment.

Decarbonisation will become a necessity rather than a choice. Energy efficiency projects are early responses. For instance, improving furnace efficiency, low temperature waste heat recovery, FCC unit conversion and switching internal combustion fuel from fuel oil or coke to cleaner fuels. However, for a deeper decarbonisation, refiners will have to consider low-carbon technologies such as electric heating, carbon capture, use of renewable power and green hydrogen. There will not be a single solution, instead, a combination of these solutions to solve the complex decarbonisation problem is required. Improvements in technology, collaboration, partnering across multiple industries, and government subsidies will all be crucial to reduce the cost of deployment and accelerate adoption.

Demand for low-carbon liquids is to grow, driven by supportive government and industry policies aimed at

decarbonising the transport sector. Targets are increasing across most major economies, with the more developed regulatory requirements of Europe and North America leading the way, as shown in Figure 5. Three key policies shaping demand are:

n EU’s Fit for 55 package, which sets ambitious emission reduction targets for road, aviation, and marine transport.

n US Renewable Fuel Standard, which needs increasing volumes of renewable transport fuels.

n California’s Low Carbon Fuel Standard, which sets transport carbon intensity reduction targets.

In the rest of the world, policy-driven demand growth is more focused on energy security, reducing reliance on imports, and promoting regional agricultural development.

Robust demand growth is expected this decade for liquid biofuels. Investment in new capacity is required to meet the surging demand over the decade. The current main trend is the addition of hydroprocessing (HEFA) capacity to produce renewable diesel and sustainable aviation fuel (SAF) from oils and fats. HEFA projects account for nearly two-thirds of all announced liquid biofuel investments and over 80% for Europe and North America. This is familiar technology to refiners, producing a drop-in fuel, which can be easily integrated with existing supply chains. Many refiners already co-process small volumes of renewable fuels. However,

the biggest challenge for biofuel expansion is the availability of low-carbon feedstocks that meet stringent regulatory requirements. The ability to use a wider range of feedstock is a focus for bio-distillate projects as producers move away from virgin vegetable oils and

Ketjen’s ReNewFine Catalyst Portfolio for renewable diesel and sustainable aviation fuel is now commercially available.

instead seek alternative sources of waste. Access to secure waste feedstock supply is crucial to being competitive.

Long-term policy goals require the development of advanced renewable fuel technologies. E-fuels are the pinnacle of circularity and are recognised as key to the energy transition for the hard-to-abate maritime and aviation sectors. As e-fuels are reliant on the successful deployment of other technologies that are still nascent and expensive, such as green hydrogen and CO2 capture, Wood Mackenzie does not expect them to become commercially viable until the 2040s. However, there is potential for refiners to use their existing technical, commercial, and marketing capabilities to capitalise on the longer-term e-fuel opportunity. As with liquid biofuels, access to advantaged feedstock will be the main driver of success. Locations with low-cost sources of renewable electricity and CO2 could have that competitive edge.

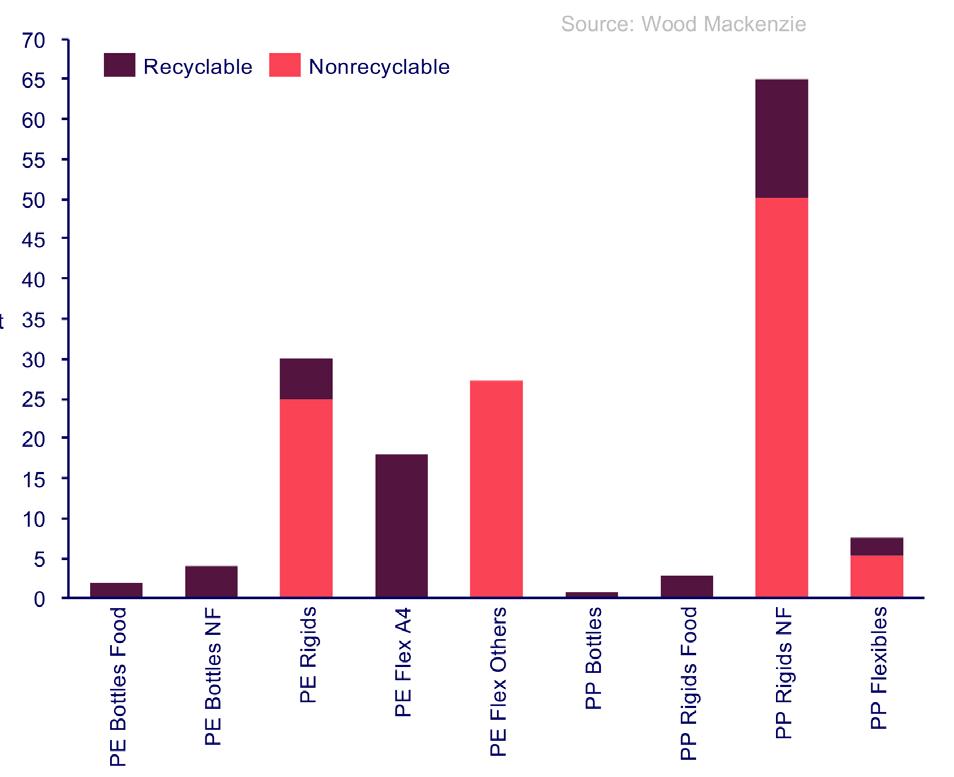

Achieving a net zero world will require keeping the carbon in circulation or utilisation. This will demand that systems and applications are designed with sustainability and circularity in mind. In petrochemicals, being sustainable, however, can sometimes be out of reach, due to the nature of the polymer

or the application. Innovation needs to be geared towards solving this. Where it might not be possible, it is important to keep the end goal in mind, and design recycling systems that can handle applications or materials regardless of how non-recyclable they may be mechanically, after having exhausted all measures possible to keep those materials in circulation.

The issue, in today’s market, is challenging in no other area more than polyolefins, as shown in Figure 6. Whether it is a car bumper or multilayered food packaging, mechanical recycling fails to deliver high-quality recyclates at high yields; this applies to almost 70% of polyolefin applications. Whether it is due to the application itself, or the linear value chain in which it exists, the market needs a solution that can deal with polyolefin waste on a molecular level, and this is where pyrolysis promises to solve the issue on a massive scale.

Pyrolysis is a recycling method that can retrieve concentrated carbon back from plastic waste. In doing so, the thermal breakdown of materials can turn plastic waste into oils, which, once purified and upgraded, can recycled into several applications. It is important to note here that despite the several challenges that lay in front of the pyrolysis industry, the benefits of having a scaled-up pyrolysis industry will be massive. Continuing to innovate to improve the yield and quality of pyrolysis will mean solving an important piece of the circularity puzzle.

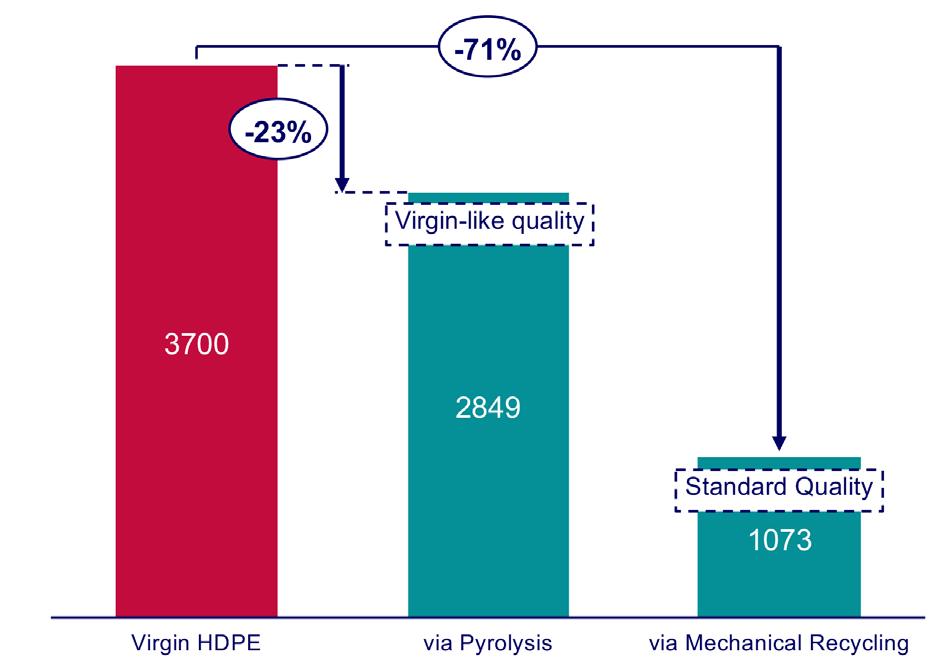

The main goal of pyrolysis is the recycling of polymers, especially mechanically nonrecyclable materials. To put things into context, circular high density polyethylene (HDPE) produces 25% less emissions than fossil virgin, as shown in Figure 7. There is a case for fuels, where pyrolysis oil can produce lower carbon fuels compared to fossil fuels. However, the case needs to be studied from several angles to design a new net zero system, regardless of the technology and application.

Refining margins have largely normalised despite significant geopolitical risk. For the refining industry, continued oil demand growth is supportive to its utilisation, margins and earnings, but an oil demand peak is on the horizon. The long-term viability of a refining asset requires it to be competitive on both earnings and carbon emissions. For many sites, ‘doing nothing’ is an option, but eventually closure will become inevitable for weak sites, particularly those exposed to the cost of carbon emissions. Petrochemicals are the obvious diversification choice for refiners, particularly with petrochemical margins to recover (slowly) from current lows. Integrated refinery/petrochemical sites are highly competitive, but petrochemical markets are, however, relatively small and project timing is often critical for investment success. Liquid biofuels can be attractive for those with secure advantaged feedstock, with the chemical recycling of petrochemical waste providing another opportunity. The ultimate pinnacle of circularity is e-fuels, but it is important to note the rules of competitive advantage remain, as does policy risk. Refiners need to plan to adapt in order to determine which option yields them an advantage to get ahead on the energy transition pathway.

Jock Hughson, Shell Catalysts & Technologies, Australia, discusses decarbonisation levers that refiners can pull to help them stay aligned with more stringent emissions regulations while staying competitive.

Refiners are under increasing pressure to reduce greenhouse gas (GHG) emissions from their operations and from the products they sell. But decarbonising assets is complex and can take many years to plan and implement – and getting it wrong may prove costly. This article will discuss three important decarbonisation levers – decarbonised (blue) hydrogen, carbon capture and storage (CCS) and

renewable fuels – that asset owners can pull to help them stay aligned with more stringent regulations while remaining competitive.

Around the world, oil and gas operations, including downstream refining, account for approximately 15% of global, energy-related carbon emissions, with a further 40% resulting from the use of oil and gas products. However, with atmospheric carbon dioxide (CO 2 ) still

rising and a rapidly shrinking carbon budget to limit global warming to 1.5°C above pre-industrial levels, there is a growing imperative to act – and act quickly.

And next year could prove pivotal for refiners (and hard-to-abate sectors such as steel and cement production) as governments party to the Paris Agreement get ready to announce what are expected to be the boldest updates to nationally determined contributions (NDC) ahead of COP29 in Azerbaijan.

With greater political ambition towards reducing GHG emissions, there is increasing urgency for refiners to develop and implement decarbonisation strategies to reduce direct (Scope 1) and indirect emissions (Scope 2) from onsite operations and those that result from the use of liquid and gas products sold (Scope 3) – which can account for as much as 90% of an asset’s total GHG emissions.

However, decarbonising an asset is complex and can take many years to implement. As the business case for decarbonisation strengthens, how can refiners reduce their carbon emissions while staying competitive?

Hydrogen is a vital fuel and feedstock for many refining applications; however, the majority of hydrogen produced today – natural gas (grey) hydrogen – is carbon-intensive. To decarbonise, industry needs to switch to low-emission sources of hydrogen, ideally renewable (green) hydrogen, produced by electrolysis using renewable power such as wind and solar. However, renewable hydrogen is currently costly to produce.

Alternatively, decarbonised hydrogen, produced from natural gas and using CCS, can offer a cost-effective, interim solution to help meet today’s growing demand while still lowering emissions. Of course, the choice between renewable and

decarbonised hydrogen will depend on the individual circumstances of a refinery.

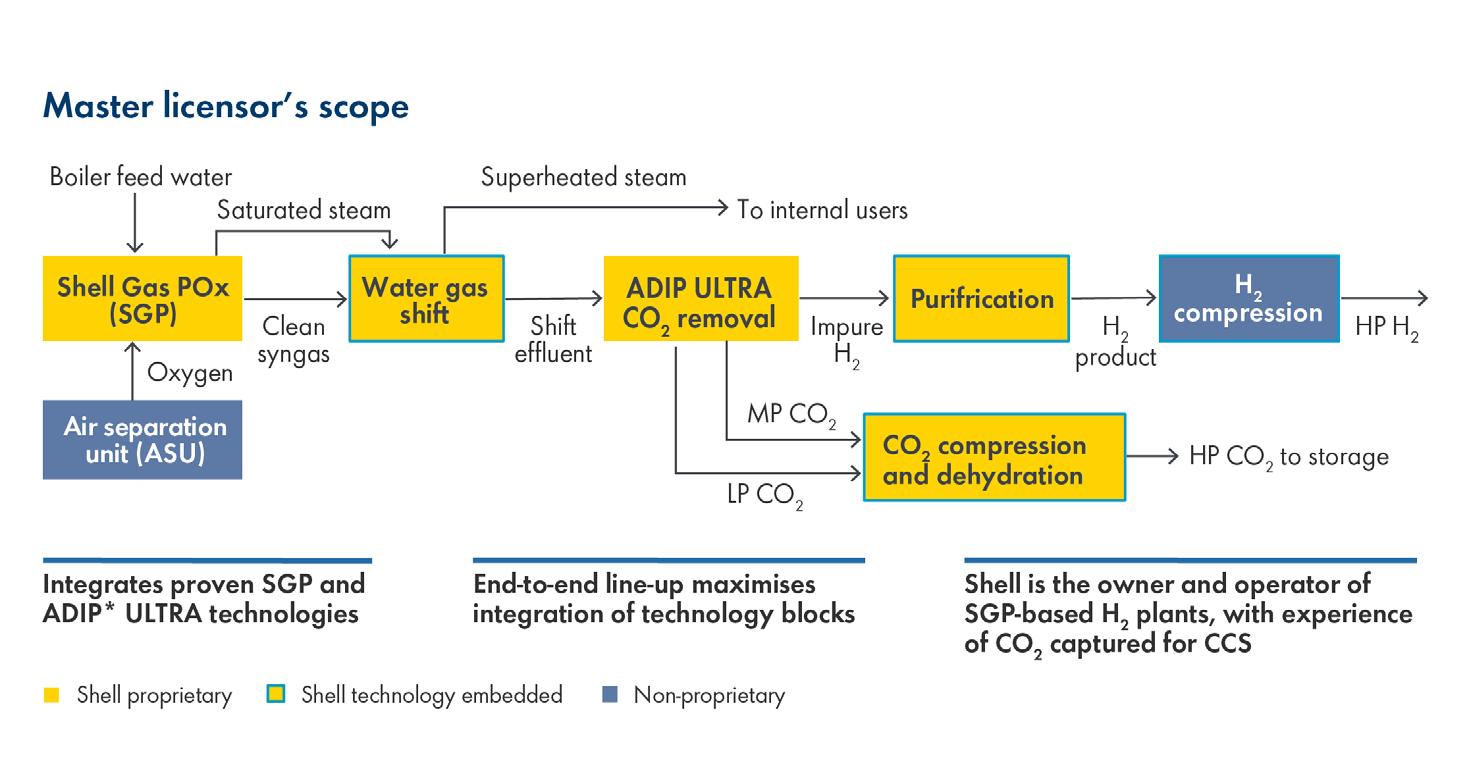

Today, hydrogen project developers have three main decarbonised hydrogen technology options.

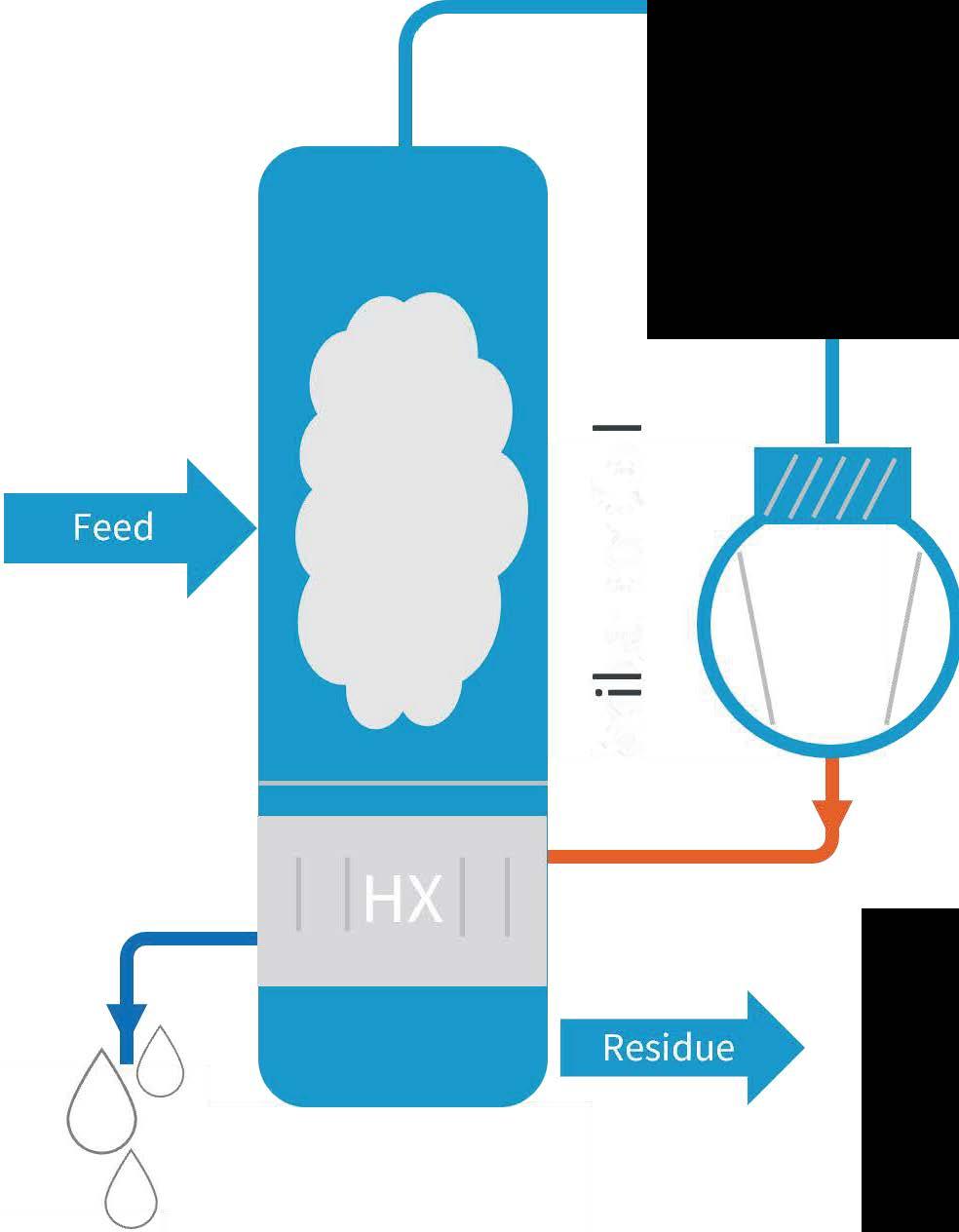

Steam methane reforming (SMR) and autothermal reforming (ATR) are well-established methods. A third option is gas partial oxidisation (POx), which sits at the heart of the Shell Blue Hydrogen Process (SBHP), and leverages Shell gas partial oxidation (SGP) (Figure 1). The SBHP captures CO 2 from high-pressure, precombustion gas streams with higher CO 2 concentrations, thereby making the carbon capture process cost and energy efficient.

According to the International Energy Agency (IEA), any serious ambitions to reduce a facility’s carbon intensity are likely to be spearheaded by CCS. However, capturing CO 2 can be costly, whether from precombustion processes, such as hydrogen production, or from post-combustion flue gases.

Reducing capture costs without compromising performance is crucial to accelerating CCS deployment, which is why Shell Catalysts & Technologies is engaged in continuous research and development to boost performance and efficiency of its amine-based ADIP ULTRA precombustion and CANSOLV * post-combustion capture technologies. Maturing these technologies focuses on:

n Lowering the overall cost of capture.

n Addressing new and evolving performance requirements.

n Improving operability.

Lowering the overall cost of capture means increasing capture efficiency. This can be done by increasing the amount of CO2 captured while decreasing energy consumption. For example, the company’s latest-generation ADIP ULTRA solvent can now capture up to 25% more CO2 from high-pressure, precombustion gas streams – such as those from hydrogen manufacturing units (HMUs) and gasification units – while lowering regeneration energy by up to 25%. This solvent was selected for the Quest CCS project (part of the Scotford upgrader) in Alberta, Canada, where it is capturing approximately 80% of CO2 emissions from the HMU process gas streams.

Similarly, by tailoring the ratio of amine in Shell’s CANSOLV formulations for each asset, the operating range of the solvent can be extended, thus reducing regeneration energy demand by as much as 25%. Moreover,

to keep up with stricter performance demands, CANSOLV can now achieve capture efficiencies of up to 99% – even for streams with relatively low CO2 concentrations. It also exhibits lower volatility and degradation characteristics and meets stringent emissions limits.

CANSOLV has recently been selected for the ADNOC Habshan CCS project, one of the largest post-combustion carbon capture projects in the world, where it will capture and permanently store 1.5 million t of CO2 from the asset’s sulfur recovery unit.

Shell is also increasing the operability of the CANSOLV technology by making it smarter. This means continually generating high-quality data that are monitored and analysed in real time. Examples include analysis of flue gas contaminants (e.g., nitrogen and sulfur oxides, oxygen and iron) and real-time solvent health monitoring for CO2 loading, amine concentration and the presence of degradation products and other contaminants, such as inorganic ions and metals.

High-performing capture technologies are just one part of a larger system that needs to work seamlessly to maximise capture performance and cost efficiencies. But integrating different parts of the systems can be complicated and cost inefficient.

This is why Shell Catalysts & Technologies and Technip Energies (T.EN) established a strategic alliance over a decade ago to offer turnkey carbon capture solutions that can unlock greater performance, as well as offer engineering and logistics benefits.

T.EN offers optimised solutions for CANSOLV units of a wide variety of sizes ranging from 1500 tpy pilot units to 10 000 - 150 000 tpy containerised units that are versatile, redeployable and easily transportable, through to 2 million tpy units for large-scale emitters.

Renewable fuel mandates across Europe and other parts of the world present

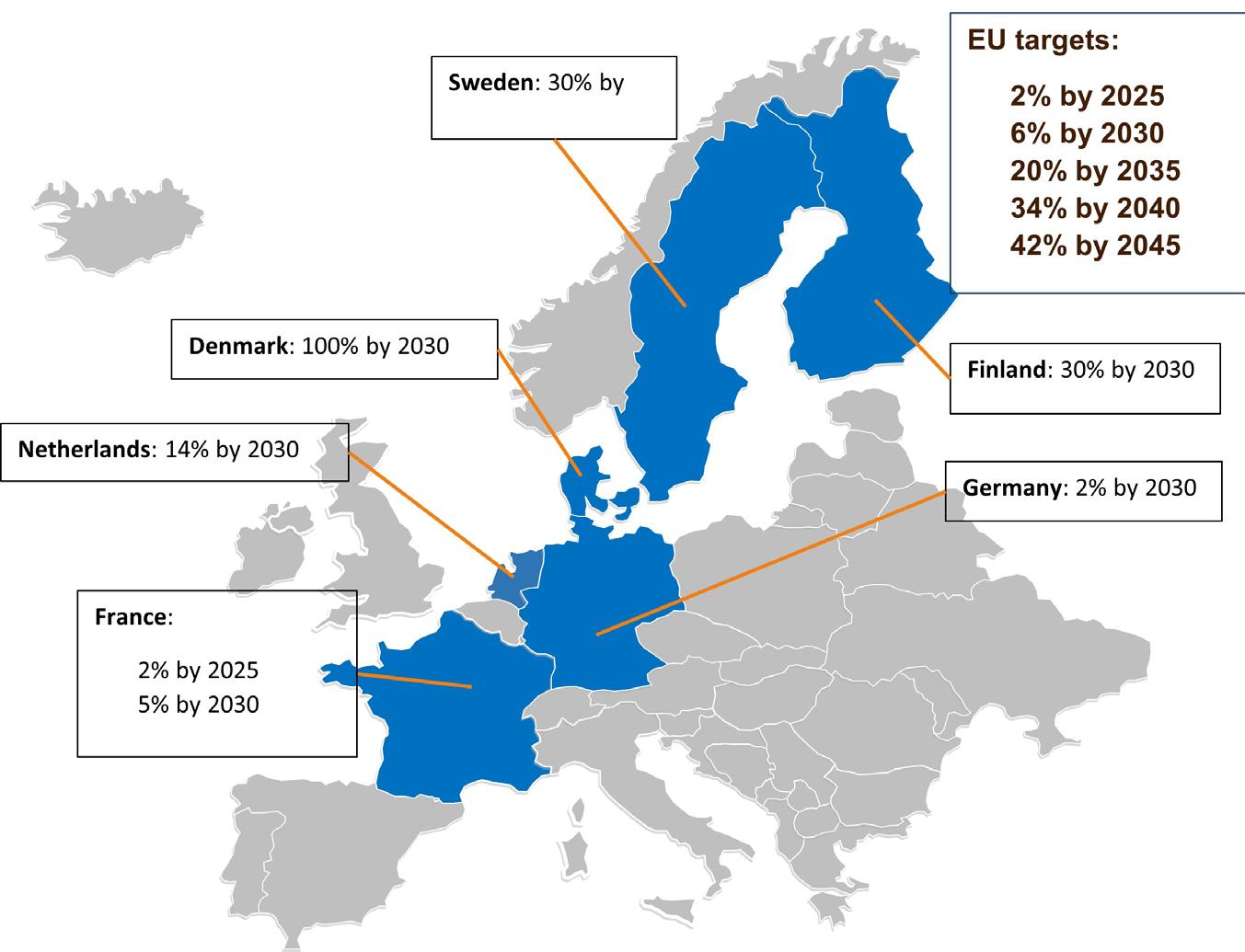

opportunities for fuel producers to support the growing demand for more sustainable fuels, such as bio- and renewable diesel and sustainable aviation fuel (SAF). For example, by 2030 the ReFuelEU initiative obliges a minimum of 6% SAF content in all aviation fuels made available at EU airports, increasing to 20% by 2035 and 70% by 2050. Likewise, the US aims to produce at least 3 billion gal. of SAF annually by 2030.

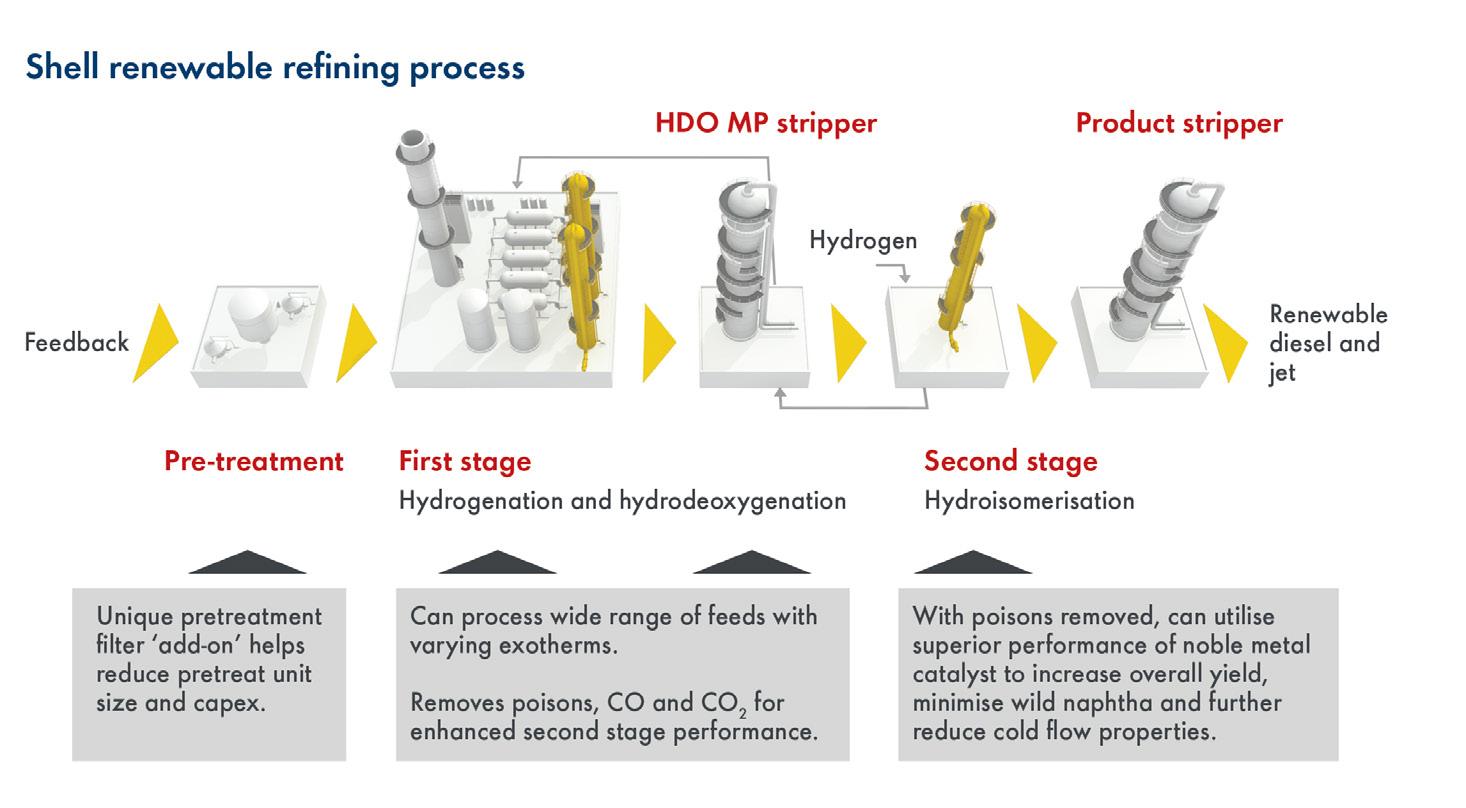

To capture this growing market, an increasing number of refiners are evaluating revamping their assets using the Shell Renewable Refining Process (SRRP) – a two-stage unit that offers higher SAF and renewable diesel yields, and a longer cycle length than a single-stage unit (Figure 2). For operators with a single or two-stage hydroprocessing unit (fossil service) or a single-stage hydrotreated vegetable oil (HVO)/hydrotreated esters

and fatty acids (HEFA) unit, revamping with the SRRP to maximise SAF production could have a significant and positive impact on margins.

Investing in biofeed processing technologies is an important decision; however, understanding the evolving landscape of biofeed availability and regulation is equally important.

For example, the EU’s RED II has introduced a more stringent cap on biofeeds that are easier to use, such as waste cooking oil and certain animal fats, which means that refiners will gradually need to process more challenging feeds like straw, algae and other types of biomass. This limits the amounts of biofuel that can be produced with current HVO units, unless they can be adapted to process more challenging feeds.

Decarbonised hydrogen, carbon capture and biofuels are important decarbonisation levers, but how can they be combined for even greater impact on CO 2 emissions? Knowing where the emissions are coming from and which ones to focus on is key.

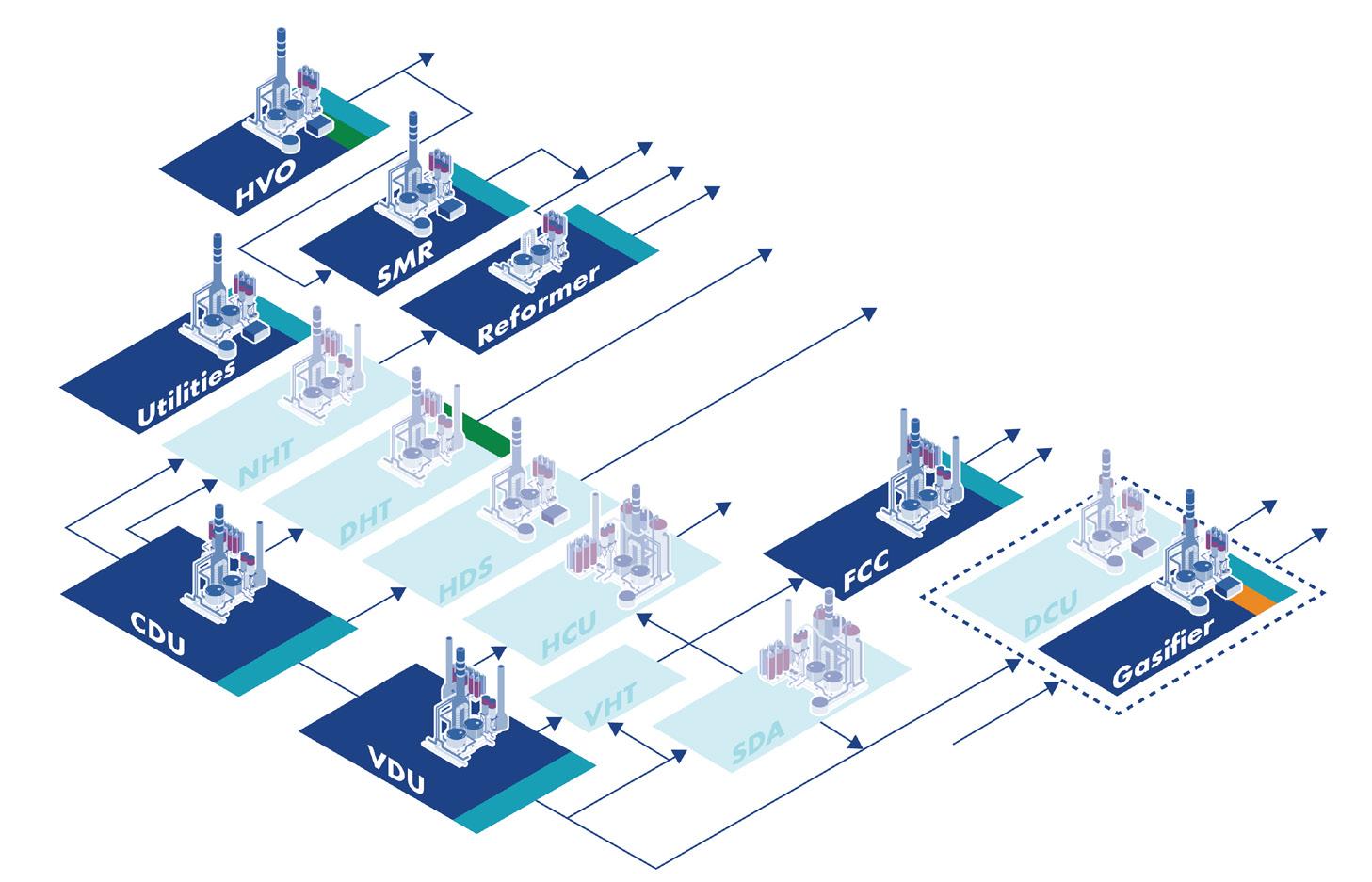

The main CO 2 sources in a typical refinery include the crude distillation and vacuum distillation units, the fluidised catalytic cracker (FCC) and the catalytic reformer, each of which can account for up to 25% of the site’s CO 2 emissions. Additionally, utilities and the HMU contribute about 25 and 5% respectively. When there is a gasification unit in the line-up, this can also be a significant source of CO 2

With different carbon intensities, a range of solutions are needed to avoid and/or capture CO 2 emissions. Figure 3 describes three possible response options. For example, blue stripes indicate where a refiner might use ADIP ULTRA to capture CO 2 from SMR

or gasification units, which produce high-pressure, relatively pure CO 2 steams ideal for carbon capture, or CANSOLV, which might be used to capture CO 2 from various low-pressure flue gases.

Alternatively, a refiner might also upgrade an existing gasifier to generate decarbonised hydrogen using the SBHP (orange stripe) or deploy coprocessing technology in their distillate hydrotreating unit to produce blended biofuels.

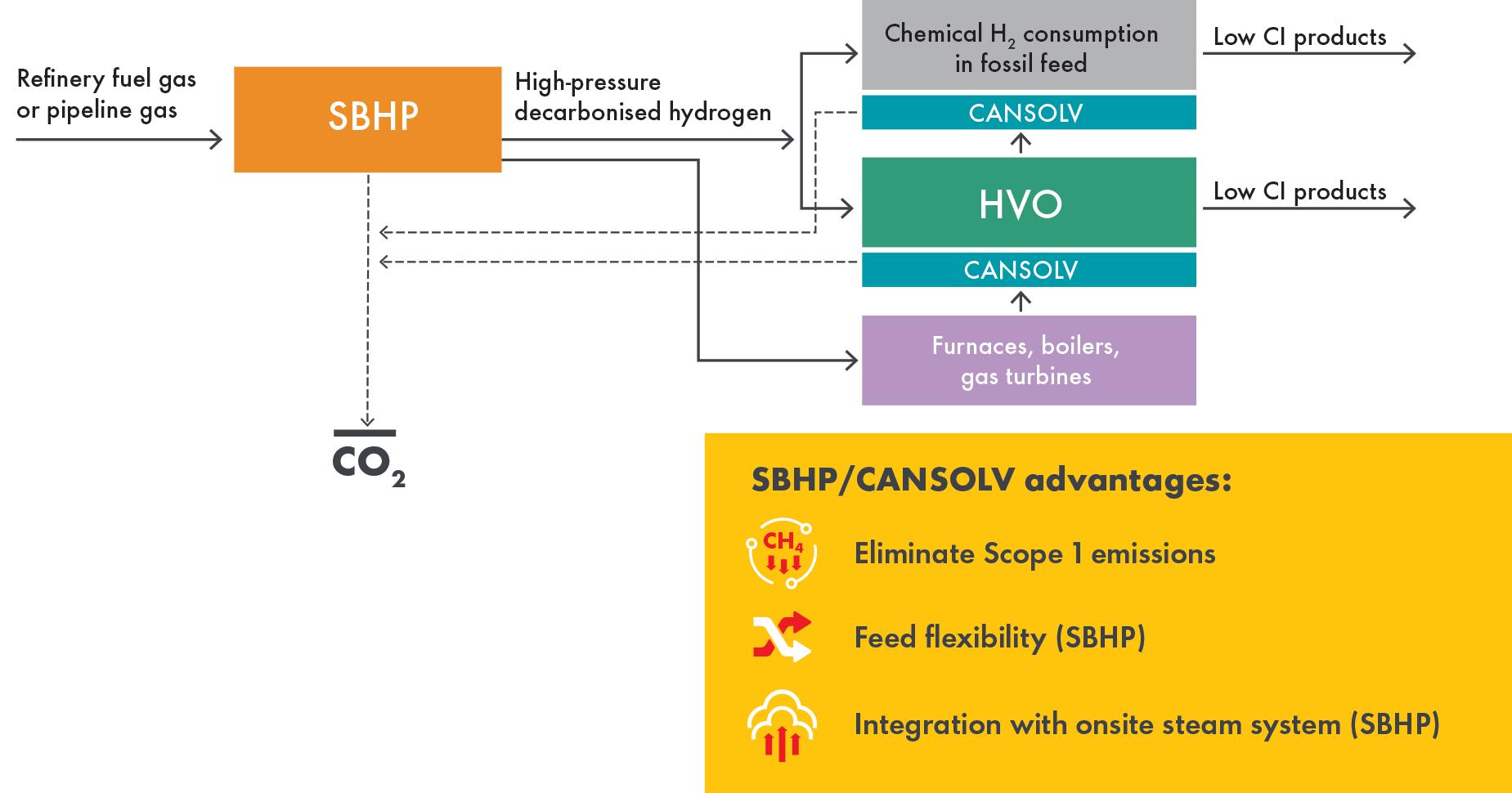

Figure 4 shows an example of how Shell’s hydrogen, carbon capture and biofuels technologies might be integrated to lower the carbon intensity of refinery products. By producing decarbonised hydrogen onsite using the SBHP, refiners can supplement or replace fuel gas (or piped natural gas) in fired equipment. Alternatively, in some cases it may be more economical to capture CO 2 from combustion flue gases using CANSOLV technology or to electrify fired equipment where a sufficient supply of decarbonised electricity exists.

In each case, switching to a decarbonised energy source and/or capturing CO 2 directly from combustion processes can help to significantly reduce operational (Scope 1 and 2) emissions and the carbon intensity of products. Combined with the production of blended biofuels or 100% renewable fuels, a refiner can also take significant steps to reduce emissions from the use of their products (Scope 3).

As countries around the world start drafting their updated NDCs, refiners should assess what bolder climate action and more progressive emissions policies could mean for their operations.

Many refiners are already implementing decarbonisation strategies, but for those yet to start, now is the time to take action to ensure that they are prepared for, and can capture, the market opportunities arising from the shift to low-carbon and more sustainable fuels and operations.

Decarbonised hydrogen using the SBHP and pre- and post-combustion carbon capture using ADIP ULTRA and CANSOLV technologies are proven solutions that can contribute to significant reductions in operational (Scope 1 and 2) emissions. Additionally, revamping HVO and HEFA units using the SRRP can help refiners shift their product slate towards lower-carbon renewable fuels.

Note *ADIP and CANSOLV are Shell trademarks.

The world’s energy system is changing. To solve the challenges, Shell Catalysts & Technologies is developing its Decarbonisation Solutions portfolio to provide integrated value chains of technologies to help industries navigate the energy transition. Our experienced teams of consultants and engineers draw on Shell’s owner–operator–licensor expertise to co-create pathways and technology solutions to address your specific decarbonisation ambitions – creating a cleaner way forward together.

Learn more at shell.com/decarbonisation.

Michael Connolly and Man Yiu Tse, ICIS, explore the evolving biofuels market, and examine how economic competition, regulatory dynamics, and shifting corporate strategies shape the industry.

The global energy transition, spurred by the urgent need to reduce carbon emissions, has placed biofuels at the centre of the decarbonisation agenda. Biofuels have the potential to mitigate climate change by significantly lowering the carbon emissions, particularly in aviation and shipping sectors where there are limited alternatives.

In regions such as the EU, biofuels have been instrumental in reducing carbon emissions, driven by stringent regulatory frameworks and policy support.

However, the landscape for biofuels is far from smooth. The industry faces mounting economic, regulatory, and strategic pressures that threaten to slow its progress despite its critical role in the energy transition.

Biofuels have long been touted as a critical solution for reducing greenhouse gas (GHG) emissions, but they are not immune to the economic pressures that challenge their viability. Rising production costs, volatile feedstock prices,

and market competition from cheap imports create a complex environment for biofuel producers, particularly in Europe.

The closure of Argent Energy, a significant player in the biofuels sector, due to competition from subsidised Chinese and US biodiesel imports and regulatory restrictions on EU feedstock imports, highlights the fragility of the biofuels market.

Neste, the largest biofuels producer by capacity in Europe, recorded its first negative profit in 2Q24, since 4Q14.

Strikingly, Neste reported that the sales margin for its renewable fuels business in 2Q24 fell by more than 50% year on year to US$382/t.

The influx of low-cost biodiesel from China, made possible by low production costs, coupled with state economic support and subsidies, has particularly distorted the market, leaving European producers struggling to compete.

To level the playing field and protect its biofuels industry, the EU imposed provisional anti-dumping duties

of between 12.8 - 36.4% on Chinese biodiesel from 16 August 2024, and will be replaced with definitive measure from February 2025.

Still, competition from imports is just one of many challenges the sector is facing. It is also blighted by the high cost of producing advanced biofuels, such as those derived from waste oils and lignocellulosic materials.

The EU aims to expand the use of advanced biofuels to meet long-term climate goals, in place of first-generation biofuels due to sustainability concerns. This requires a major scale-up of capacities in the region to meet demand. Yet, the high prices of advanced biofuels have been a barrier for producers to secure investments to reach Final Investment Decisions (FIDs). Long-term offtake agreements are key to secure finances. But it is challenging to enter into long-term contracts with potential buyers at high prices.

The lack of demand certainty compounds the challenges in capacity scale-up. The EU has put a limit on the contribution of food- and feed-based biofuels towards the renewable energy target and set a combined secondary target of 5.5% for advanced biofuels and renewable fuels of non-biological origin (RFNBO) in the share of energy supplied to the transport sector in 2030.

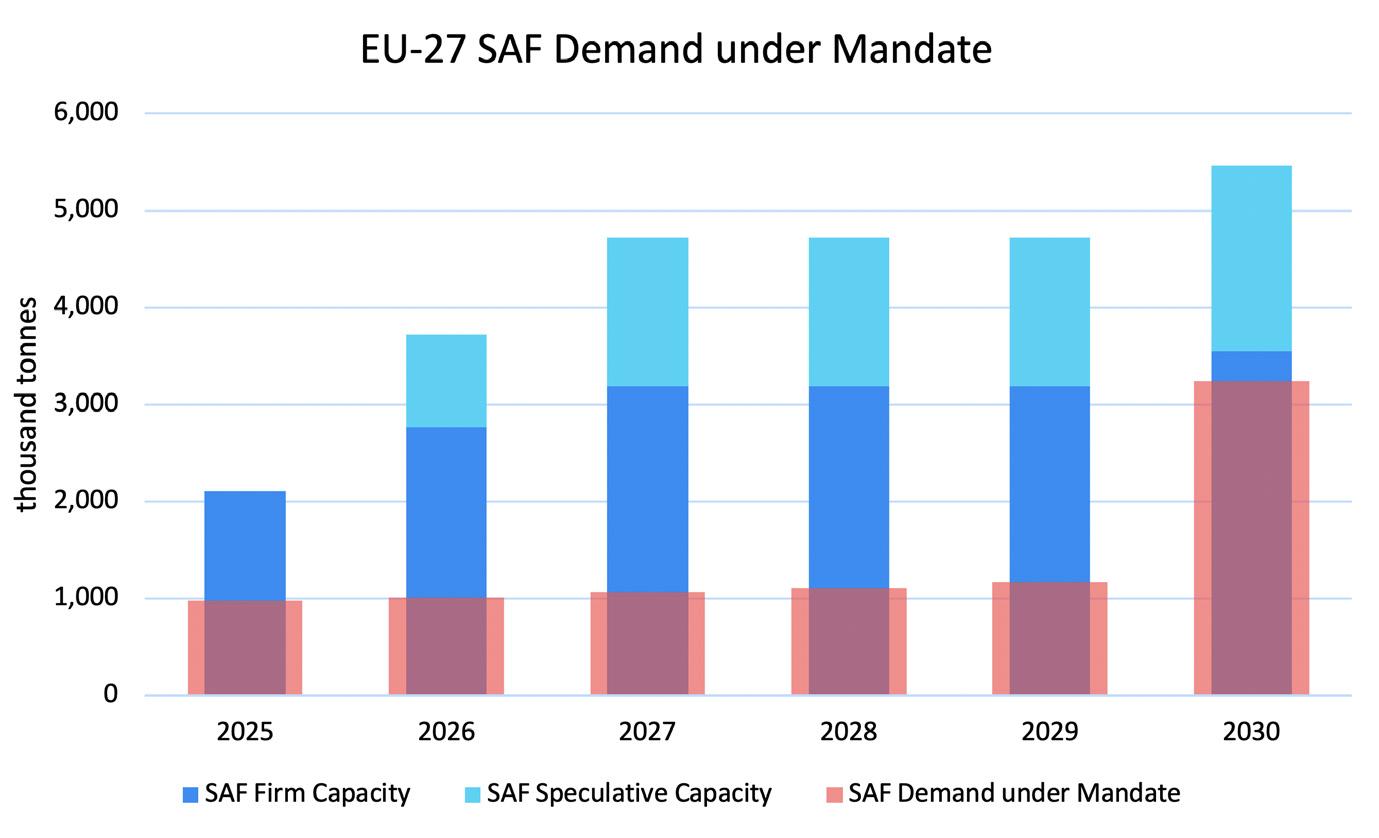

Advanced biofuels will also be needed to meet the ReFuelEU Aviation regulation which mandates a 2% share of sustainable aviation fuels (SAFs) in EU airports from 2025 and 6% from 2030, and progressively reaching 70% share by 2050.

However, mandates are a double-edged sword. While it can drive the market to adopt a certain level of demand, it can also become a limit on demand if there is no complementary policy support.

Take, for example, the ReFuelEU Aviation regulation, the unintended consequence of regulation design is that there will be a step change in SAF demand every five years

when there is an increase in SAF share requirement. This makes it challenging for producers to plan their capacity investments.

Meanwhile, SAF capacity is already more than demand under mandate in the EU. This weak market condition led Shell’s decision to pause the construction of its European biofuels facility in Rotterdam, the Netherlands. BP has also delayed its plans on a bio-refinery in Lingen, Germany, to ‘simplify portfolio and focus on value and returns’, underscoring the pessimism on the returns in the biofuels market.

There are also uncertainties on whether regulations on biofuels may change. Recent policy decisions underscore the tension between short-term economic pressures and long-term climate goals, posing new challenges for biofuel producers.

For example, the government’s decision to reduce the biofuel blending mandate in gasoline and diesel has sparked controversy in Sweden. The move, aimed at lowering consumer fuel costs, is expected to result in higher CO2 emissions, a step backward in the country’s ambitious climate agenda. This decision highlights the difficulty of balancing environmental objectives with economic realities, particularly as energy costs rise and inflationary pressures intensify. While Sweden has been a leader in renewable energy adoption, this policy reversal raises concerns about the stability of the regulatory framework for biofuels in Sweden and across Europe.

Amid these challenges, there are opportunities for biofuels producers to capture in the bio-based chemicals space as the emphasis on a circular economy continues to grow.

Bio-based chemicals, which are derived from renewable biomass, offer a sustainable alternative to traditional petrochemicals. These chemicals are used in a wide range of industries, from plastics and textiles to pharmaceuticals and personal care products. As demand for sustainable materials grows, biofuels producers can extract value from their co-products, bio-naphtha and bio-LPG, enhancing the overall value proposition of biofuels.

This synergy between biofuels and biochemicals drives research into new technologies and processes that can optimise renewable resources. For example, advancements in biorefining technologies enable the efficient conversion of biomass into biofuels and high-value chemicals, creating integrated value chains that maximise the use of feedstocks. This approach not only improves the economic viability of biofuels, but also supports the broader circular economy by reducing waste and promoting the sustainable use of resources.

The future of biofuels will depend on the industry’s ability to overcome the economic, regulatory, and operational challenges it currently faces. Coordinated policy support in every part of the supply chain is essential to sustain momentum. Governments must ensure that biofuel regulations are aligned with long-term climate goals, providing stable and predictable frameworks that encourage investment in sustainable production methods. Policies that level the playing field for domestic producers (like the carbon border adjustment mechanism [CBAM]), protect against unfair competition from subsidised imports, and incentivise the use of advanced feedstocks will be critical.

Innovation will also play a vital role in the future of biofuels. Continued research and development into non-food and feed crop feedstocks, such as agricultural residue and other lignocellulosic materials, as well as advancements in production technologies, will be essential for increasing efficiency and reducing costs. Collaboration between industry, academia, and government will drive these innovations forward.

Finally, increased financial incentives are needed to attract investment in biofuel projects. While biofuels are seen as a key solution to reduce carbon emissions, scaling up production will require significant capital. Governments can support this process through grants, subsidies, and tax incentives that reduce the financial burden on biofuel

producers and share the risk with investors to encourage the development of new projects.

Biofuels remain a pivotal component of the global energy transition, offering a sustainable alternative to traditional hydrocarbons. However, the industry faces significant challenges that must be addressed to unlock its full potential. Economic pressures from subsidised imports, regulatory inconsistencies, and operational hurdles have slowed progress, while strategic shifts by significant energy companies reflect the complexity of the current market environment.

Yet, these challenges also present opportunities for innovation and growth. By investing in advanced feedstocks, improving production technologies, and fostering synergies between biofuels and biochemicals, the industry can create new value streams and contribute more effectively to the global energy transition. To sustain momentum, a coordinated effort is required from policymakers, industry leaders, and investors to support biofuels through clear regulations, financial incentives, and ongoing innovation.

In the end, biofuels have the potential to serve as a bridge between today’s energy system and a future where carbon-neutral technologies dominate. With the proper support and strategic focus, biofuels can continue to play a crucial role in reducing global carbon emissions and driving the shift toward a more sustainable, low-carbon economy.

Superior process and water treatment solutions supported by service excellence

Superior process and water treatment solutions supported by service excellence

Halliburton Multi-Chem collaborates with customers to improve reliability, increase throughput, and enhance operating unit efficiency and flexibility. We offer a broad range of chemistries, equipment, automation, and services to help our customers maximize asset value.

Halliburton Multi-Chem collaborates with customers to improve reliability, increase throughput, and enhance operating unit efficiency and flexibility. We offer a broad range of chemistries, equipment, automation, and services to help our customers maximize asset value.

Our experienced team provides onsite technical services and engineering support. We listen to understand your challenges and respond with solutions.

Our experienced team provides onsite technical services and engineering support. We listen to understand your challenges and respond with solutions.

The world is experiencing the fundamental effects of global warming on the Earth’s climate system. The National Oceanic and Atmospheric Administration (NOAA), a division that provides environmental data, products, and services covering the depths of the ocean to the surface of the sun, reported in January 2024 that the global surface temperature was 2.29°F (1.27°C) above the 20th century average of 54.0°F (12.2°C), making it the warmest January on record. Above average temperatures were recorded across every continent.

A growing coalition of countries, cities, businesses, and other institutions and entities have pledged to combat global warming by getting to net zero emissions. The transition is an immense challenge and the energy sector, which is chronicled as the source of approximately three-quarters of greenhouse gas emissions, holds the key. Energy companies world-wide are sourcing or producing bio-feedstocks and converting or retrofitting operational and idle refineries for processing renewable diesel. It is the number one initiative for lowering the carbon intensity of the transportation industry.

According to the US Energy Information Administration (EIA), US production capacity for renewable diesel could increase significantly throughout 2024.1 Europe accounts for approximately 50% of the total global renewable diesel supply. The EIA also anticipates that, due to increased demand, Europe will transition from an exporter to an importer of renewable diesel over the next five years.

Globally, it is estimated there are currently more than 500 operational biodiesel and renewable diesel refineries across major commercial producing countries, with renewable diesel outpacing the other alternatives in production capability.

In the US market, biofuels consist mostly of ethanol, biodiesel, and renewable diesel. Ethanol accounts for the majority of these biofuels and is used as a blending stock with gasoline. Its production has been steady at approximately 400 million bbl/y since 2021. Biodiesel production likewise has been steady since 2021 but has been declining slightly at approximately 60 million bbl/y. In contrast, since 2021, renewable diesel production has grown considerably – from 15 million bbl/y to over 70 million bbl/y, slightly displacing the demand for biodiesel. The reason for the surge in renewable diesel is easy to explain.

Renewable diesel and biodiesel are both biofuels derived from similar feedstocks like vegetable oils and animal fats, but they differ in their production processes and properties.

Biodiesel is produced chemically through a process called transesterification where fats and oils react with an alcohol (usually methanol) and a catalyst to form fatty acid methyl esters (FAME) and glycerol. As a result, biodiesel contains oxygen in its chemical structure, which can affect its performance and compatibility with engines. Because of its lower energy density, biodiesel is typically blended with petroleum diesel at a ratio of 20% biodiesel to 80% petroleum diesel to minimise its inferior combustion properties.

Renewable diesel, on the other hand, is produced by hydrotreating the same fats and oils used in the production of biodiesel. Hydrotreating involves the introduction of hydrogen into the molecular structure which not only removes organic sulfur but also the oxygen. The result is a

biodiesel fuel that is chemically equivalent to petroleum-based diesel. This hydrogenation process yields a high-quality diesel that can be used as a direct replacement without any blending necessary. This chemical similarity also means that no engine modifications are required. Renewable diesel has the same energy density, providing comparable performance and efficiency.

Because renewable diesel contains no oxygen, the challenges associated with storage, cold temperature operation, and water attraction are eliminated. Its higher cetane number is calculated between 75 and 95, compared to biofuel, which is 50 and 60, which means faster startups in the cold, boosted throttle response, and less noise.

The makeup of the renewable diesel allows the fuel to combust with maximum efficiency while decreasing regenerations in the particulate filters and injector maintenance frequency – and because it does not contain impurities or aromatics, it is odourless.

Both biodiesel and renewable diesel offer environmental benefits by reducing greenhouse gas emissions and reliance on fossil fuels. Renewable diesel’s compatibility with existing infrastructure and engines; however, makes it a much more versatile option.

In the US, federal and state regulations such as the Renewable Fuel Standard (RFS) and California’s Low Carbon Fuel Standard (LCFS) are pivotal in incentivising the production and consumption of renewable fuels, including renewable diesel. Increased blending mandates are making the markets for renewable diesel even stronger, which encourages higher investments in production infrastructure and increases overall production volumes.

In Europe, ‘Fit for 55’ was adopted in 2022. It refers to reducing net greenhouse gas emissions by at least 55% by 2030 and includes two pillars adopted in October 2023. They are the revised Renewable Energy Directive (REDIII) and the ReFuelEU Aviation regulation – with an emphasis on waste-based and low-carbon biofuels in the transportation sector. Canada adopted a country-wide initiative, the Clean Fuel Regulation, which came into effect in 2023. It requires fuel producers and importers to reduce the carbon intensity of transportation fuels to decrease their carbon intensity by approximately 15% (below 2016 levels) by 2030. Asia mandated hikes to more than double regional biofuels demand by 2035.

Before it goes to market, however, renewable diesel must be treated to remove any sulfur and other impurities like nitrogen and olefins. The most common treatments for diesel include hydrotreating, gasification, pyrolysis, or other biochemical and thermochemical technologies. Sulfur may be present in the feedstocks to these processes or be added during a processing

Visual MESA® Greenhouse Gas Emissions Management is a certified Corporate Carbon Footprint software. It continuously monitors emissions and energy consumption across the entire plant operations, giving you accurate, real-time data and alerts for decision making.

Whether you choose cloud-based or on-premise, this solution with automated, auditable reporting enables you to both optimize energy and analyze Scope 1 and 2 emissions to identify and implement operational improvements for energy savings and to meet your emissions reduction targets.

Discover how your industrial plant can save over 25k tonnes of CO2 per year. www.kbc.global/emissions-management

step to facilitate specific reactions. For instance, treatment may include things like the sulfuric acid treatment of feedstocks or the use of sulfur to activate catalyst for a hydrotreating process. Feedstocks such as coal used for gasification could inherently contain sulfur compounds. Regardless, the sulfur either in the feedstock or added to the treatment process must be removed.

Sulfur varieties found in these processes could range from a heavier mercaptan sulfur, which would remain in the diesel, to light mercaptans or H2S, which would be split from the diesel and remain in the lighter hydrocarbon streams. The most effective treatment method is to use a proprietary technology unit specifically designed and fabricated to remove the sulfur species present in the hydrocarbon stream. This will ensure each client’s specifications can be met with a specific solution. Removal of the sulfur species is required to meet emissions requirements in finished products.

There are options when determining what treatment process is most effective and which is required. These are dependent on the hydrocarbon stream being treated, as well as the sulfur impurities present in the feed stream. An example is whether the stream being treated is the diesel stream, or the light end hydrocarbon that was split during the process to make the renewable diesel. This can impact whether the feed stream is a gas or a liquid and what is contained within it. A few options will be discussed below.

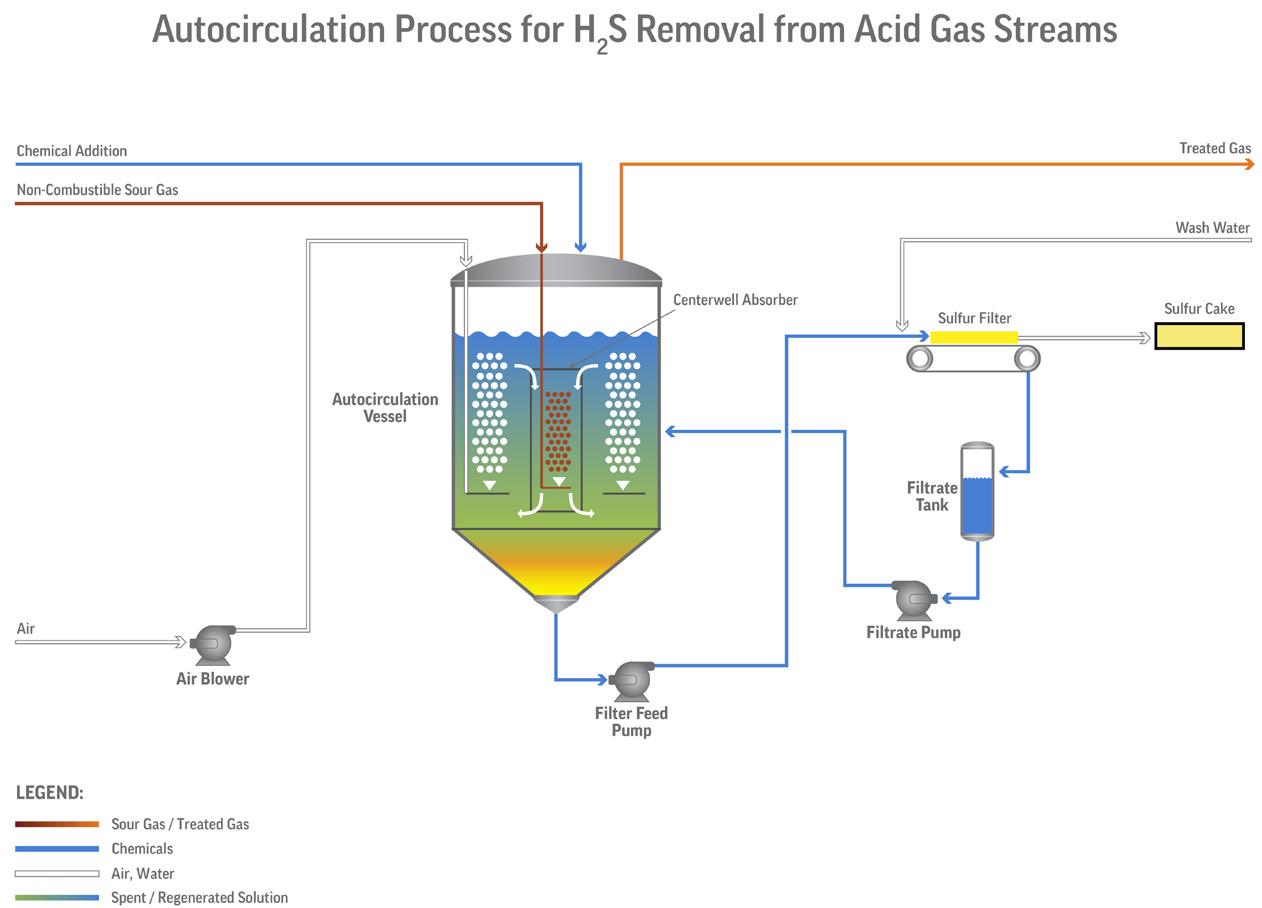

LO-CAT® is a desulfurisation technology for removing 1 to 20 tpd of H2S as sulfur from gas streams. The process chemistry of this technology is embedded in its name –LO-CAT, which stands for Liquid Oxidation CATalyst. The overall system oxidation reaction is as follows:

H2S (gas) + ½ O2 (gas) → H2O + S o

This is a well-known oxidation reaction. This overall reaction is sub-divided into two parts:

(i) Reduction: H2S gas absorption, ionisation and reaction to make solid sulfur in the liquid solution.

(ii) Oxidation: the liquid solution is then oxidised using air and regenerated for re-use.

Therefore, the LO-CAT® process is called a redox (reduction-oxidation) reaction process to reflect these two steps.

LO-CAT does not use any toxic chemicals or produce any hazardous waste byproducts. The environmentally safe catalyst is continuously regenerated in the process.

THIOLEXTM is a technology for removing H2S or mercaptans from gas and liquid streams using an alkaline solution in an acid-base reaction that may also be used depending on the feed and product specifications. THIOLEX units use proprietary, non-dispersive FIBER FILM® Contactors as mass transfer devices, with caustic and/or amine as the treating reagent in gas and liquid hydrocarbon streams. The FIBER FILM Contactor is a vertical vessel packed with proprietary fibre that achieves non-dispersive-phase contact without the problems inherent in conventional dispersive mixing devices, such as aqueous phase carryover, hydrocarbon losses, lack of turndown ability, long settling times, plugging, and flooding. Because the aqueous phase adheres to the fibres rather than being dispersed into the hydrocarbon phase, carryover and uncontrollable emulsions are virtually eliminated.

A further option for H2S removal from gas streams when there is less than 1 tpd of sulfur removal required is to use an adsorbent. SULFURTRAP® EX adsorbent differentiates itself from competing technologies for its ability to easily decrease the H2S content to <1 ppm with continuous low pressure drop (SOR to EOR), loading 2 - 3 times more sulfur than conventional products while keeping the cost of the media low. Low OPEX costs are easily achievable with SULFURTRAP EX due to fewer and easier changeouts. It also provides a safer turnaround experience for operations and maintenance personnel due to the ease of bed changeout, something the competition cannot provide.

These technologies can remove H2S and mercaptans and ensure the renewable diesel product meets its required specifications. The decision between the technologies depends on the inlet contaminant levels and types and the required product specifications.

Companies and government entities are transitioning their fleets to renewable diesel as a low-cost strategy to meet sustainability goals. Renewable diesel allows fleets to substantially reduce carbon emissions and petroleum use, and improve air quality without sacrificing power, performance, or range. Fleet owners and managers can convert their entire diesel-powered fleet to renewable diesel fuel overnight.

The savings may seem minimal at an average of US$0.21 less than diesel. However, the savings are quite substantial. In 2019, there were 3.91 million Class 8 trucks on US roads, which each drove an average of 62 571 miles. If they had all been fuelling and driving with renewable diesel, each truck would have saved an average of US$1317.77/yr. If all Class 8 trucks had used renewable diesel, it would have produced US$5.15 billion in annual savings. Those same trucks fuelled with renewable diesel would have reduced emissions by saving more than 297 million tpy of carbon dioxide (CO2).

With the potential savings and ease of use for renewable diesel, the production and treating requirements to generate it become infinitely doable.

Reliable Technologies for H2S, Mercaptan & COS Treatment or Removal

Turn yellow into green using our low OPEX, proven sulfur treatment technologies.

Merichem Technologies is a leader in sulfur treatment technologies, providing safe and eco-friendly solutions to remove H2S, mercaptans and COS from both liquid and gas streams. Whether it’s customized or standard, adsorbents or chemical processes, our robust technologies allow you to maximize profitability while meeting your specifications at any scale.

With over 50 years of experience delivering innovative solutions and excellence in service, you can trust we will do the same for you.

Let’s discuss your specific requirements and how we can help.

Nabil Ahmed, The Energy Industries Council (EIC), explains why sustainable aviation fuel (SAF) must overcome investment and scalability hurdles in order to prove its promising carbon reduction prospects.

The use of sustainable aviation fuel (SAF) is at the heart of efforts to reduce carbon emissions in aviation. The International Air Transport Association (IATA) has provided a definition that includes fuels made from biomass, and more recently from non-biomass sources through new technologies. SAF can reduce its lifecycle CO2 emissions by up to 80% compared with traditional jet fuel. However, it currently makes up less than 1% of all aviation fuel consumed.

Because it relies on high density energy fuels that can function under extreme circumstances, the aviation sector – which produces between 2 - 3% of global CO2 emissions – faces significant challenges in reducing its carbon footprint. A minimum capital investment of US$10 million is required for each of the 104 SAF projects underway. This level of investment highlights a strong commitment to increasing SAF production, but also demonstrates some major financial and logistical hurdles ahead.

These are produced by varying sources such as agricultural waste, algae, plant-based materials and processing waste converted into ethanol for SAF use. Some advanced methods capture CO2 and combine it with green hydrogen from renewable energy to create ‘e-fuels’. This variety presents many paths for SAF production.

The process begins by selecting the right feedstocks which have to be sustainable, cheap and readily available. These feedstocks are then washed, dried or sometimes grinded. They can be converted into fuels using various techniques such as pyrolysis, gasification or fermentation depending on their types. One advantage is that SAF can be mixed with routine jet fuel and used in existing aircraft engines without any changes, therefore making it easier to incorporate it into the already existing fuel system.

Despite its high cost and difficulty in obtaining enough raw materials for production, SAF has faced a lot of challenges in terms of wider adoption. Currently SAF production costs between two and four times more than traditional aviation fuel, thereby presenting a serious problem to airlines that operate on slender profit margins. Fuel expenses cannot be increased that much.

Furthermore, although potential sources such as agricultural residues and algae exist for scaling up SAF production, these processes are not simple. It will also necessitate substantial investment in infrastructure including new manufacturing plants and improvements to the present fuel distribution network for effective handling of SAF blending, as well as its distribution. Financial incentives or subsidies from governments or companies

have the potential to ensure competitiveness with conventional jet fuel.

The path to the mass use of SAF is difficult, but it can greatly contribute to the sustainability of aviation. Applying new technologies and making substantial investments in them will help introduce a gradual shift towards a cleaner future.

The ‘2024 SAF Insight Report’ by the Energy Industries Council (EIC) highlights both optimism and significant hurdles in today’s SAF environment. While SAF has the potential to reduce carbon emissions from air travel, the current scale remains limited by economic, logistical, and technological obstacles. For SAF development to occur, governments, industries and research institutions should join hands.

North America – with the US in particular taking the lead – has been pioneering various projects involving SAF. The US government is spearheading several initiatives that will improve production of SAFs such as the Sustainable Aviation Fuel Grand Challenge, which has set aims to encourage production of 3 billion gal. annually by

2030 and encourage the use of 100% of aviation fuel from only biofuel sources by 2050.

Key projects in the US, such as Velocys’ Bayou Fuels Biomass to Fuels and GEVO’s Net Zero 1 (NZ1) Project, represent substantial investments in scaling up SAF production. These initiatives leverage advanced technologies to convert biomass and other feedstocks into high-quality aviation fuel, demonstrating SAF’s potential as a mainstream fuel source. The move manifests how the US is leading in shifting towards sustainable aviation.

Europe has also made strides with an impressive portfolio of proposals for SAF, mainly driven by the EU’s ReFuelEU Aviation Initiative. One of its provisions in this project is a gradual increase in blends of SAF. For example, countries like Norway, Sweden and the Netherlands set ambitious national SAF blending targets supported by regulatory frameworks and large investments in infrastructure for SAF production. By 2030 Norway has set goals of 30% blending ratio of sustainable alternatives in the fuels used by airlines while at the same time using its renewable energy resources to produce green hydrogen, as well as other components that make up SAF elements. Similarly, Sweden aims at reducing its emissions from the aviation sector by 30% come 2030 via use of SAF among other sustainable technologies. In addition to these national endeavours, there are EU policies that put forward mandatory requirements for sustainability methods through which a country can involve itself in decarbonising their air travel industry

As an emergent industry, the UK is becoming increasingly important as a critical player in the SAF sector. The Jet Zero initiative of the UK government is aimed at accelerating the development and deployment of SAF with an objective to have 10% SAF blend in aviation fuel by 2030. This is a challenging but achievable target because of the nation’s technological expertise and policy framework.

One vital aspect of this plan is that by 2025, no less than five commercial plants for producing SAFs should be developed. These two projects – including Alfanar’s Lighthouse Green Fuels and Fulcrum BioEnergy’s NorthPoint –demonstrate private sector participation in this crucial area. Concurrently, the Jet Zero strategy emphasises research and development for process optimisation and feedstock expansion. The University of Sheffield has established a SAF Clearing House

in order to show commitment to technological leadership that enhances the research, certification and collaboration which will position the UK as a global hub for SAF innovation.

Among the approved alternative fuels are several types of Fischer-Tropsch synthetic paraffinic kerosene (FT-SPK) and hydroprocessed esters and fatty acids synthetic

increments in blending ratios of SAF, showcasing commitment towards the decarbonisation of aviation. Robust regulatory frameworks ensure that markets are stable for SAF. Governmental clear targets and financial support decrease investment risks, therefore stimulating the participation of the private sector. Policies such as tax credits, subsidies, and blending mandates make it

Explore our library of free-to-access On Demand Webinars, covering a range of topics in the downstream sector covering a range of topics in the downstream sector

Explore our library of free-to-access On Demand Webinars, covering a range of topics in the downstream sector Visit: www.hydrocarbonengineering.com/webinars

Alder Fuels, in concert with Honeywell, to produce carbon-negative SAF at scale. This work aligns with United’s goal of reducing carbon emissions intensity by 50% by 2035, from a 2019 baseline. Other United efforts include collaborations with other SAF producers and investments in pioneering technologies like direct air capture and electric aviation. The following are efforts in a critical direction toward more sustainable practices in aviation, underpinning broader environmental goals for the industry.

In the Asia-Pacific region, countries are starting to recognise the importance of SAF. Japan and Singapore are at the forefront, with Japanese efforts driven primarily by Japan Airlines and All Nippon Airways. Japan Airlines has collaborated with Fulcrum BioEnergy to convert municipal solid waste into SAF. The potential large production capacity of SAF is derived from this partnership, which will contribute to Japan’s aviation emissions reduction process. Singapore Airlines has partnered with Neste for the use of SAF. This agreement with Neste comes amidst the effort by Singapore to gain a place as one of the leading SAF production and deployment hubs in the Asia-Pacific region. Its strategic geographical position – backed up with a robust aviation infrastructure – gives Singapore a good

opportunity to be transformed into a SAF-producing and distribution hub.

The SAF market is also developing in Brazil, which is rich in biomass resources. GOL, a Brazilian airliner, has allied with local and international companies for the development of SAF from sugarcane and other biomass. This would be a significant step towards the reduction of carbon emissions by GOL and put Brazil on the map as a regional leader in SAF production. Brazil’s experience in biofuel production, particularly ethanol from sugarcane, could serve as a good platform in developing SAF. Its agricultural sector is better positioned to supply the required feedstocks, while existing facilities for biofuel production can be adapted to produce SAF. Finally, Brazil’s commitments to the use of renewable energy and sustainable development are consistent with the broader aspirations for SAF.

While the prospects for SAF seem encouraging, it shares similar problems common to most sustainability-linked industries: high production costs and a limited supply of feedstock. Overcoming such challenges will require cooperative efforts from governments and industry stakeholders in the form of supportive policies and investment in research and development. SAF financial incentives in the form of subsidies and tax credits are possible for its production to reduce cost disparities compared with conventional jet fuel. Investment in research and development can provide the needed technological advancement whereby the production cost of these fuels is lowered and efficiency in their production is increased.

Another solution is resilient feedstock supply chains. Combinations of more efficient logistics, better practices in sustainable sourcing, and the creation of regional hubs on feedstock collection and processing can help in setting up a supply of raw materials that are reliable and scalable, which may result in reducing production costs and raising SAF output.

The prospects for SAF look encouraging, with the likelihood of huge reductions in the carbon footprint of the aviation sector. As demand for air travel globally increases, the need to shift to sustainable jet fuel will, therefore, be key in the attainment of climate change goals set and building a sustainable future for the sector.

Another critical component will be technological advancement. Innovations in feedstock processing and fuel conversion technologies can enhance the production efficiency and cost-effectiveness of SAF. In the near-term, developing new feedstocks from algae and waste will make the source of SAF more sustainable.

SAF presents a huge opportunity for reducing the aviation sector’s carbon footprint. Despite the difficulties standing in its way at present, SAF has enormous potential for growth and development. With continuous support from governments and industries, SAF can be a game-changing solution to achieve global climate objectives and ensure a clean future for the world of aviation. As the world moves towards a more sustainable future, the aviation sector has to make SAF an integral part of its decarbonisation strategy.

Giacomo Rispoli and Alessia Borgogna, MAIRE, Italy, discuss the innovations and technologies that are driving sustainable aviation fuel (SAF) production.

The aviation industry stands on the brink of a major transformation as it grapples with the pressing need to reduce its carbon footprint. According to the International Air Transport Association (IATA)1, the best strategy to achieve net zero CO2 emissions from the aviation sector will require a combination of remediation actions: 65% of emissions must be cut by substituting jet-fuel with sustainable aviation fuel (SAF), whereas 35% must come from adopting new technologies (electric and hydrogen), by more efficient infrastructure and operation, by offsets and carbon capture. Therefore, SAF production plays a clear role in achieving net zero emissions.

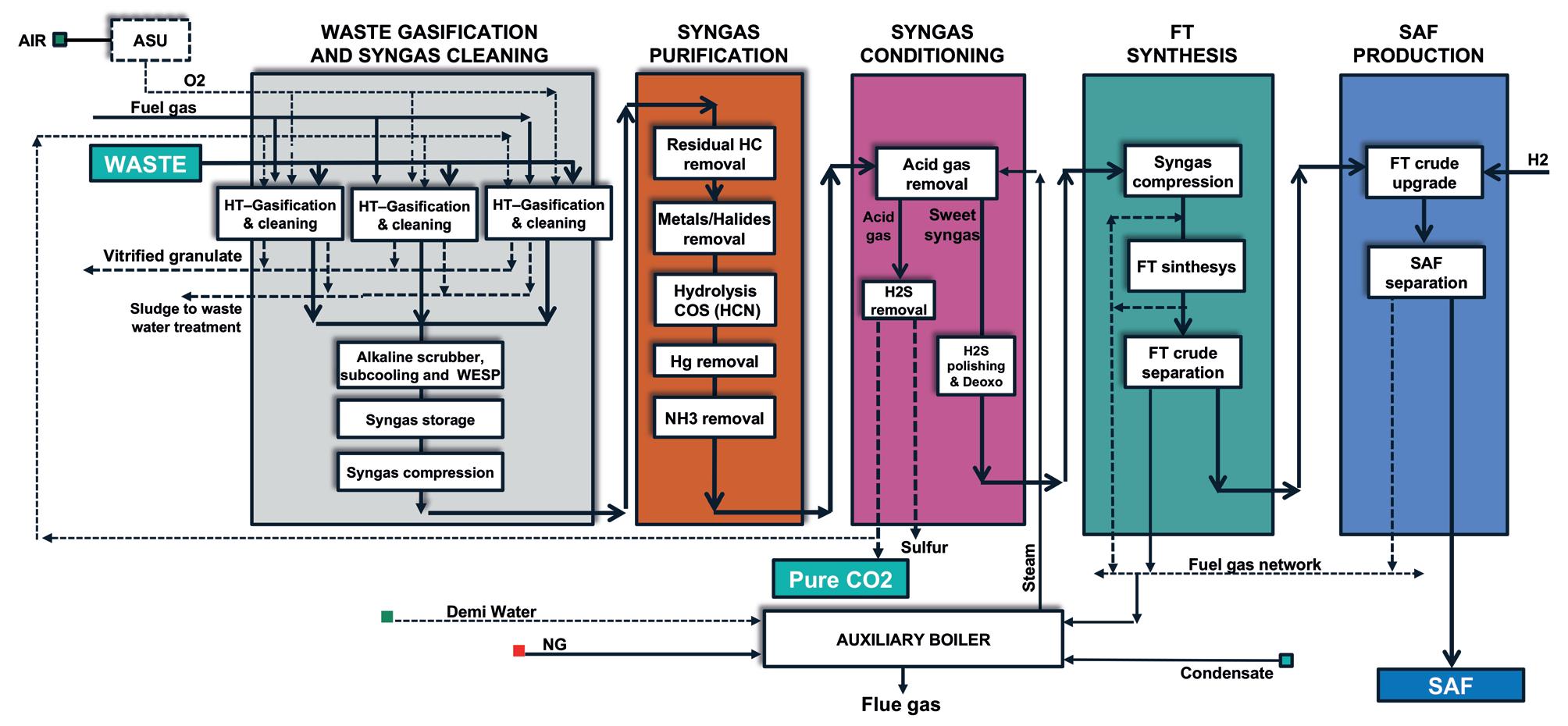

One of the most promising pathways to achieving a sustainable future in aviation is the production of SAF through the gasification of residual feedstocks. This article delves into the potential of this innovative technology exploring its process, economic feasibility, and the challenges it aims to address.

Gasification of residual feedstocks into syngas is a technology poised for industrial use, offering significant potential for fostering sustainability in aviation.

The advantage of gasification technology lies in its ability to utilise a wide variety of waste types, creating a crucial pathway for the circular economy. Wastes that previously had no adequate recovery processes for their chemical elements,

such as carbon and hydrogen, can now be converted into valuable products with high efficiency. Additionally, waste-to-chemical pathways can address issues related to the limited availability of biogenic feedstocks for the hydro-processed esters and fatty acids (HEFA) process2, therefore providing a more robust and sustainable solution for the production of SAF.

Syngas produced by gasification is a versatile mixture of hydrogen, carbon monoxide (CO), and carbon dioxide (CO2), which serves as an intermediate for producing various fuels and chemicals.

Beginning with syngas, multiple technological pathways exist for the production of SAF. These include3:

n The Fischer-Tropsch (FT) process, which converts syngas into liquid hydrocarbons through catalytic reactions.

n The ethanol-to-jet process, which transforms ethanol into jet fuel via dehydration, oligomerisation, and hydro-processing,

n The methanol-based route, which involves either converting methanol to olefins and subsequently to jet fuel, or directly converting methanol to jet fuel using advanced catalysis techniques.

Among the several methods to convert syngas into SAF, the FT conversion stands out as the oldest and

most established. This process involves the chemical reaction of CO and hydrogen, producing light hydrocarbon condensate and waxes, which are subsequently upgraded into jet fuel.

The alcohol-to-jet (AtJ) technology has seen significant advancements in recent years, reaching high levels of technological maturity with the construction of the first industrial plants. This marks a pivotal moment in the journey towards more SAF options, highlighting the increasing viability and potential of such innovative processes.

The methanol-to-jet pathway remains the most underdeveloped pathway. Currently, there are no industrial reference plants available for the technologies that are still being developed, which further underscores the nascent stage of this particular approach. This pathway, however, holds significant promise and continues to be the subject of extensive research and development efforts aimed at enhancing its efficiency and feasibility for large-scale implementation.

One producer and licensor of waste-to-chemical plants is the Italian company NextChem4, part of the MAIRE group, through its subsidiary MyRechemical which develops and licences technological platforms to extract chemical products from non-recyclable and difficult-to-recover waste types, creating entirely new value chains.

MyRechemical has developed a process simulation for the specific design of gasification. The results from advanced and tailored process simulation tools for gasification are then integrated within optimised process schemes for SAF production, both through FT and AtJ, providing insights into the main consumptions and initial equipment capacities required for operation. These results form the foundation for crafting a

robust business case, enabling a rough calculation of investment costs, operative costs, and expected revenues. This financial assessment is crucial for determining the economic viability and sustainability of the proposed scheme.

The simulations reveal that, based on the lower heating value (LHV) of the solid feedstock, approximately 0.15 - 0.18 t of SAF can be produced from 1 t of solid feedstock with an LHV of 16 MJ/kg. This yield can be significantly enhanced by incorporating renewable hydrogen into the process. With the addition of renewable hydrogen, the output increases to 0.34 - 0.37 t of SAF from the same amount of feedstock. This improvement is due to the process’ ability to reuse all the carbon in the residual feedstock, maximising efficiency and sustainability. For both scenarios, the preliminary return on investment is highly promising.

The company’s experience is not only based on simulations, but also on real projects that are underway for the production of SAF. In the case of the FT process, NextChem – in collaboration with Johnson Matthey (JM), selected for the FT technology – has been selected by DG Fuel for the development of the process design package (PDP) for its NX circular gasification technology for a SAF plant in Louisiana, US.5 The project aims to produce up to 450 million litres/yr of SAF from approximately 1 million t of bagasse (extraction residue from the crushing and squeezing of sugar cane). DG Fuel aims to have the plant operational by 2028. Following the PDP, a licence agreement with Nextchem was signed in June 2024.6

Additionally, Nextchem has several ongoing projects through the ethanol-to-jet pathway, particularly in collaboration with Lanzatech and Lanzajet. One example of this is the feasibility study conducted with a company from the UAE for the production of 120 000 tpy of SAF. This is among other projects that have reached a more advanced design phase but are currently not disclosed.7

Decarbonising the aviation sector presents a unique set of challenges due to the high energy density required for long-haul

Process improvement is like sailing. With an experienced partner, you can achieve more.

Optimizing processes and maximizing efficiency is important to remain competitive. We are the partner that helps you master yield, quality, and compliance. With real-time inline insights and close monitoring of crucial parameters, we support manufacturers to optimize processes, reduce waste, and increase yield.

flights and the stringent safety regulations governing fuel performance. Traditional fossil-based jet fuels have been considered as a standard in recent decades, ignoring the substantial environmental impact. The introduction of SAF is a shift towards reducing the carbon footprint of aviation. However, producing SAF at a scale that meets the industry’s demand remains a significant hurdle. Residual feedstocks (such as agricultural waste, forestry residues and municipal solid waste) offer a sustainable and abundant source of raw materials for SAF production. Utilising these feedstocks not only diverts waste from landfills, but also reduces reliance on fossil resources. The gasification of residual feedstocks into syngas is particularly advantageous as it can process diverse feedstocks, converting them into valuable products with high efficiency.

The economic feasibility of the proposed SAF production scheme hinges on several factors, including feedstock availability, process efficiency, and market conditions. Although the initial investment in equipment and infrastructure is substantial, the waste to chemical process is based on a double revenue scheme. In fact, together with SAF (which in order to comply with the ambitious decarbonisation target leads to a substantial increase of price), the business model must also call for generating revenue from the feedstock. Indeed, this revenue comes from disposing and using waste as raw material, by intercepting other common and less environmentally friendly markets for disposing. Meanwhile, this also delivers long-term benefits in terms of reduced carbon emissions and enhanced energy security. Furthermore, integrating renewable hydrogen into the process not only boosts SAF yield but also aligns with broader efforts to transition to a hydrogen economy.

The use of SAF produced from residual feedstocks can significantly reduce the carbon footprint of aviation. Given that the process reuses all the carbon in the feedstock and incorporates renewable hydrogen, the lifecycle emissions of