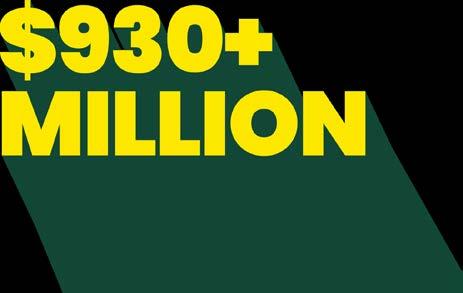

The M&A market is heating up and set to break records in 2025. Deal activity accelerated throughout the summer, and the third quarter ended with more than 200 deals. Q4 could top that.

See article at right

Thoughts on NIC

Everyone was cheerful in Austin at the NIC Fall Conference, buoyed by improving operations, falling capital costs and plenty of deals hitting the market. The “good deals” are still out there but may run out soon in some pockets. And what are the new entrants attracted to?

The NIC Fall conference in early September was filled with optimism from brokers, investors, operators and lenders (see “Thoughts on Fall NIC” to read about our takeaways). Last Fall NIC also carried a positive tone that had not been seen in some time, but that was largely fueled by the Federal Reserve’s 50-basis point rate cut just beforehand, the first since March 2020, more than four years earlier. However, the soaring optimism present at the Fall 2025 conference has been underpinned by three already active M&A quarters, with a gangbusters fourth quarter expected, plus an improved operating environment, according to market participants. Investors and operators are in growth mode and lenders are now well-positioned with the appetite to provide capital to both existing and new relationships.

In the first few months of 2025, we were skeptical about whether this

continued on page 25

Thoughts on Fall NIC

The Mood Was Overwhelmingly Positive in Austin

We have never been to such a universally positive industry event as the 2025 NIC Fall Conference in Austin, Texas. We were also hard-pressed to find any disagreement with that. It was well attended, with nearly 3,200 people there according to NIC, which is a post-pandemic record. Many new faces populated the crowds, coming from investment firms, lifecos and banks eager to learn more about the space. It helped that the 10-Year Treasury rate plunged to nearly 4.00% as the conference kicked off, and that the Federal Reserve’s meeting to cut rates was looming (and ultimately delivered on a 25-basis point cut).

There was also a sea of green lanyards of capital providers eagerly searching for new deals. More sidelined lenders and their seniors housing originations teams have gotten word to put out capital. Stresses on the balance sheet from other industries continue to abate. More operators

continued on page 2

continued from page 1

and communities are on surer financial footing and point to demographic and development tailwinds to support future strong performance and to mitigate risk. There is also a sense that the “good deals” will run out soon from a spread, leverage and valuation perspective, and that lenders do not want to miss the party. More on that later.

Banks Are Back. Much of the buzz centered around the banks. We consistently heard that they were “back.” Distress from other commercial real estate sectors was ebbing from many banks’ balance sheets, freeing up space for new originations. The expected (and eventual) 25-basis point cut in interest rates from the Fed may have convinced more credit committees to get off the fence, particularly for seniors housing deals with the industry seeing operational improvements nearly across the board.

Not all banks are frantically putting money out, but some are already oversubscribed, and they are getting much more competitive on terms. We even heard that some spreads fell below 200 basis points. Of course, if you ask most of these banks, they will say that they are looking to lend on newer properties with best-in-class sponsors. For those Class-A, stabilized transactions, competition is intense, and we expect spreads to further shrink as a result.

But another feature of the healthier capital markets is the variety of capital sources. Lifecos are returning to the space with large allocations for loans, including some new entrants that were learning about the sector at NIC. And to fill the gap on higher-leverage, interest-only and more flexible transactions, the debt funds are still there to provide liquidity.

Inside the World of Senior Care Mergers, Acquisitions and Finance Since 1948

This publication is not a complete analysis of every material fact regarding any company, industry or security. Opinions expressed are subject to change without notice. Statements of fact have been obtained from sources considered reliable but no representation is made as to their completeness or accuracy.

POSTMASTER: Please send address changes to The SeniorCare Investor, P.O. Box 1117, New Canaan, CT 06840.

However, in the lending world, HUD seems to be making the biggest waves, or rather, Frank Cassidy keeps making news. Welcome news. The newly appointed Principal Deputy Assistant Secretary at HUD and the FHA spoke at NIC, giving an update on the changes made to the program under the new administration, most notably the Express Lane, which is off to a successful start. He hinted that the changes are not over. HUD recently removed the MIP for all multifamily properties, leaving those in health care to wonder if that is coming down the line.

Importantly, Cassidy said this at NIC: “The days of closed doors at HUD are over.” That is the advantage of having an “insider” in this role at HUD. He knows the impacts of regulatory changes (positive and negative), the queue length (hence the Express Lane) and also messaging to the market. HUD has a mandate to provide needed, lowcost, fixed-rate liquidity to the market, and we hear that the staff is taking that mandate and running with it with a fervor. With the fiscal year just ending, we will see what the final 232 program firm commitments will total, but we know it is a record, by far.

After all, HUD financing when done with the right guardrails is a win-win for the government and for borrowers, but also for the trickle-down effects. More investors will be willing to acquire facilities and invest in the necessary capital

improvements to keep them competitive if they know that HUD financing is their end goal. More bridge lenders will be willing to lend on acquisitions or refinances as well, increasing competition for the product and reducing costs for borrowers. Lower costs could and should ultimately trickle down to the resident, as well. Take advantage of the open door while we have it.

Cap Rates on the Move. One thing that was confirmed at the conference was the recent movement in cap rates for Class-A communities. By “confirmed,” we mean we collected more anecdotal evidence. Our mid-year update to The Senior Care Acquisition Report, which is available to read here, showed a decline in average cap rates for assisted living properties from 8.6% in calendar-year 2024 to 8.3% in the four quarters ended June 2025. The average for Class-A properties mirrored that decline, going from 7.6% to 7.3% in the same period. Those are 30-basis point declines, tempered by the fact that the second half of 2024 is still included in the most recent average.

But in the summer months, we heard that cap rates for the best properties were compressing at an even faster rate, attributable to a minor fall in treasury rates and a meaningful increase in buyer demand. As mentioned previously, this part of the market is also flush with liquidity from the banks. The consensus, and based on some of the transactions we have recorded, was that cap rates may have correspondingly posted another 30-basis point drop from June until NIC. We know of some deals that have recently closed with cap rates lower than previously seen in the last few years.

BBG just released a Fall update to their Seniors Housing Investor Survey, six months after releasing its Spring 2025 survey, and the changing responses on cap rates were particularly illuminating. All levels of care saw a decline in average cap rates over the past six months, according to the respondents. Focusing on just assisted living, independent living and memory care, the average cap rate fell by 91 basis points, 90 basis points and 45 basis points, respectively, from the Spring to the Fall survey. That is just six months’ difference. Looking at how the 10-Year Treasury rate changed between the two

survey periods, it fell by approximately 40 to 50 basis points, albeit very unevenly. So, the survey suggests that cap rates have shifted far more dramatically than interest rates, moved by improved operations (thus less risk) and increased buyer demand forcing up prices, combining to compress cap rates.

BBG broke out its survey responses by Class and Market Type, and the declines in cap rates were consistent across the board. Class-A assisted living communities in primary markets saw the average cap rate decline from 7.14% in the Spring to 6.26% in the Fall, an 88-basis point decline in just six months, according to the sentiments of respondents. Class-B AL communities in primary markets saw a 92-bps decline to an average of 7.11% in the same period. The cap rate spread between A and B assisted living communities also shrunk in both primary and secondary markets, but only slightly by four basis points from the Spring to the Fall.

Memory care properties saw a less dramatic decline in average cap rates, or so said the respondents, falling 45 basis points to an average of 8.00% for Class-A communities in primary markets and also by 45 basis points for Class-A communities in secondary markets, to 8.54%. There were similar declines for Class-B memory care communities, dropping to 8.8% in primary markets and to 9.45% in secondary markets.

Independent living is typically at a lower cap rate level, so we would have expected to see a smaller absolute decline in average cap rates, but we were surprised to see an 87-bps decline for Class-A communities in primary markets to just 5.59% in the Fall survey compared with Spring. Class-A IL communities in secondary markets, meanwhile, registered an 88-bps drop to 6.19% in the Fall. Class-B communities in the two market types fell to 6.24% and 6.88%, respectively, or 90+bps decreases from Spring to Fall.

Even though they are investor sentiment data, and not actual transactions, these average cap rates are starting to get back to where cap rates were before inflation caused capital costs to soar. Even active adult saw its average cap rate for Class-A assets in primary markets fall

below 5%, plummeting from 5.59% in the Spring survey to 4.71% in the Fall, inching closer to the 10-Year Treasury rate. Sentiment alone could entice some property owners that acquired their assets when cap rates were low to come back into the market, if they need to sell, that is. And if they increased cash flow in the meantime, even at a higher cap rate, they could still achieve a return on the community. Also, if the flight to quality among both buyers and lenders leads to more active bidding environments for the best-in-class properties, the cap rates should compress further, especially if interest rates continue their slow descent. But we are still looking for more transaction comp data to back up the lower-cap rate environment we appear to be entering.

We will also wait to see if our cap rate data bears that out in our 31st Edition of The Senior Care Acquisition Report in March 2026, which breaks out pricing and cap rate averages for the A, B and C markets.

REIT Activity. A few people commented on Ventas’s (NYSE: VTR) recent acquisition surge, and how it seemed

like the REIT was trying to catch up to its Big 2 counterpart in taking advantage of the opportunities in the M&A space. It bought two five-property seniors housing portfolios over the summer, one for $600 million and the other for $148 million, plus a smattering of singleasset deals and likely others where they were not publicly named as the buyer, yet.

Ventas reported in its second quarter earnings report that it had spent $1.2 billion on closed seniors housing investments to that point, not including the two fiveproperty deals which would have brought the year-to-date total to roughly $2.0 billion. By comparison, Welltower (NYSE: WELL) had closed $3.6 billion in seniors housing and skilled nursing acquisitions in the first half of the year, including $1.19 billion in SNF investments. The two big Ventas deals were high-quality transactions, too, with the $600 million deal involving five Harrison Streetowned communities on Long Island that sold for over $700,000 per unit.

Welltower has an advantage over Ventas from a cost

of capital perspective, with its share price continuing to soar, more than tripling since October 2022. But some of that increase in share price has to do with the positive reaction to Welltower’s aggressive buying spree in the post-pandemic years, when many buyers exited the market and property values hit bottom. It has been snapping up “good deals” for years now, and well before the good deals will start to disappear. The REIT and its operating partners have also done supremely well in pushing occupancy and margins. It is even developing at a faster clip than most. But Ventas’s shares are trading near record highs, giving it a cost of capital boost over its competitors, and the REIT may continue to exercise that advantage more for Class-A, performing properties, while the pricing still makes sense.

Other REITs like LTC Properties (NYSE: LTC), Sabra Health Care REIT (NASDAQ: SBRA) and National Health Investors (NYSE: NHI) have also been active as acquirers. NHI estimated its current investment pipeline at $330 million, or nearly double the size of its pipeline at the same time in 2024. LTC Properties is making good progress

on its projected $460 million pipeline for 2025, having just closed a $195 million acquisition for five seniors housing properties in Wisconsin last month. And Sabra announced $122 million of total investments closed as of its second quarter earnings report, plus an additional $220 million of investments that it had been awarded at the time.

When Will the Good Deals End? One question we did ask many attendees was how long they thought the “good deals” would last, meaning when property prices would surpass “replacement cost” or the combined cost to develop and fill a community. Even Class-A communities, which have seen the most buyer demand and movement in pricing, are still trading below the cost to develop them.

It would dissuade many builders from developing if they cannot hope to sell their communities for a profit down the road. And if capital costs stay elevated in the next several years, at least relative to the days of ZIRP, and construction costs are still somewhat affected by tariffs, then the prohibitive cost to develop may be dragged out

even longer for most projects. That makes the current sales of Class-A, well-performing properties at or below replacement cost even better for the buyers, if they theoretically have a longer runway of being the newest thing in town, charging the highest rents in their markets and facing less competition for staff and residents.

Some developers may need some comps with pricing above replacement cost before they build a new community, to give some assurance that the property could sell for a higher basis once it is filled. But there may be some of those comps soon, including deals valued at over $1 million per unit. One may have already closed around the time of NIC. Psychologically, that could encourage some developers to put shovels in the ground.

So, the good deals may come to an end for the brandnew, Class-A buildings relatively soon, considering the flood of interest from buyers and lenders flowing in their direction, and as cap rates continue to compress to pre-capital markets crisis levels. But what about the B and C markets? It is certainly tougher to measure the

U.S. Department of Housing and Urban Development Office of Housing Seller

Healthcare Loan Sale 2026-1 (“HLS 2026-1”)

Bid Submission Date: October 22, 2025

8 Section 232 healthcare loans backed by 8 properties. Eight (8) first-lien loans with a total unpaid principal loan balance of approximately $58 million

Secretary-Held commercial loans secured by first liens

Falcon Capital Advisors, Transaction Specialist supported by Mission Capital Advisors For further information: www.falconassetsales.com; 1-844-709-0763; HUDsales@falconassetsales.com Interested participants must execute a Qualification Statement and Confidentiality Agreement. This is a sale of due and payable notes.

This announcement is not an offer to sell or a solicitation of an offer to buy mortgage loans. Information concerning the mortgage loans will be furnished only to, and bids will be accepted only from, bidders who certify that they have such knowledge and experience in financial and business matters as to be capable of evaluating the merits and risks and who certify that they have the resources to bear the risk of a purchase of the mortgage loans.

replacement cost of these lower-quality communities, because what would you spend to replace an older, less competitive building with another similar one? Also, how much would you have to spend on renovations to make an older community compete with the newer ones, and just how effective could it be in the end? Many of these older communities may have different operating futures, as well, switching to a Medicaid waiver model, another care type or an alternative use.

Nevertheless, the lack of new construction combined with improving demographics should push pricing for the lower-quality communities. Operations will continue to improve, generally speaking, and buyer demand could increase if the “good deals” start running out at the high end of the market. Not all buyers of Class-A buildings would suddenly switch to acquiring non-core assets, but if development is not an option and the thesis to invest in seniors housing is still there, then these lower-quality communities would be their only option.

One could argue that lower- and middle-market communities could offer more stability from an occupancy perspective, if they are seen as more affordable options. But occupancy is expected to rise across all property types in the coming years, and the lower-quality communities will not be able to pass through rising expenses to its residents as easily as Class-A communities can.

So investors in lower-quality communities will almost surely have to sacrifice a higher return. But you can either lower your cap rate when acquiring a Class-A community and diminish your return on your exit cap rate, or go the lower-quality route and hope to see a bigger bump in your basis. Both come with risks, of course, but should light a fire under anyone thinking about investing in M&A. Do it now while the good deals are out there.

Too Much Focus on the High End. We of course have to end on a negative tone and talk about our disappointments from the conference. First, nearly all of the positivity on the operating environment, the capital markets, the M&A market and just about everything centered on the high-end of the market. “Banks are back,” but really only for the best-in-class sponsors

and for new communities. Margins and cash flow are reaching pre-pandemic levels, but only for the high-end communities that can charge eye-popping rents. There were presentations on innovative ways to enhance the lifestyles and well-being of seniors, or of your staff. Great, but how can lower- and middle-market communities afford this programming, amenities or benefits?

And perhaps most importantly, the seniors housing industry is entering its golden age but is at serious risk of becoming an industry bifurcated between a luxury product that only the wealthy can afford and a subsidized, regulated product that provides more bare-bones housing and care to the rest of seniors who need it. That leaves a huge opportunity for disruption from home health to active adult or some hybrid of the two to fill the gap and offer a more appealing and affordable solution.

We understand that most of the conversation and attention is going towards the shinier, more profitable, higher-yielding product. But B and C communities represent the majority of properties in the seniors

housing industry, and the optimism and opportunities stemming from demographics will not all trickle down to them.

We were also disappointed by the conversation surrounding new development, particularly building for the middle market. Again, we do not fault anyone for being constrained by the simple math of the cost to build and the rents needed to cover those costs. If anything, the industry may need some irrational capital, or “dumb money,” to come in and build, leaning on the demographics thesis to bring them ultimate success. Or as one broker better put it, we need long-term capital to invest in development.

But the public talk on development seemed to be a little pie-in-the-sky, given the real cost constraints on building today. Maybe those sessions will make more sense in the Spring. In all of our private conversations, there was much more realism on that fact and also the resignation that the main solution for the middle market will be a government solution. And that could scare away capital.

SKILLED NURSING ACQUISITIONS

The skilled nursing M&A market continues to see steady deal flow, with pricing remaining highly dependent on asset quality and a state’s reimbursement environment. Investor sentiment has soared in those states with reimbursement tailwinds and higher Medicaid funding.

One of those states is Kentucky, where the legislature approved a favorable rebasing change in July 2024 that led to a significant increase in Medicaid funding, along with increased interest in owning and operating facilities in the Commonwealth. We imagine that facilities are realizing an immediate boost to their value as a result of the changes to the reimbursement environment, and Blueprint is likely securing great prices for its Kentucky clients. The firm has announced four closings totaling more than $200 million in September alone in the Commonwealth, probably helped by the fact that its own Kyle “Bluegrass” Hallion is from and lives in Louisville.

The latest deal was one of the largest portfolio sales in Kentucky, featuring seven facilities (including two in Louisville) and 818 total licensed beds. Blueprint represented the seller, North Carolina-based Principle LTC, a private owner/operator that wanted to capitalize on the rebasing change and increased investor demand. The portfolio generated a very competitive bidding environment, procuring 12 qualified offers from a mix of in-state and out-of-state investors and operators. After multiple rounds of comprehensive bidding, the seller ultimately selected a New Jersey-based owner/operator, with meaningful existing scale, that was eager to enter the Kentucky market. Michael Segal, Steve Thomes, Kory Buzin, Kyle “Bluegrass” Hallion and Daniel Waldhorn handled the transaction.

Blueprint also recently closed the sale of Wellington Parc Nursing and Rehabilitation, an 80-bed skilled nursing facility in Owensboro, Kentucky. The seller was a long-tenured ownership group, but after a 40-year history of operating in Kentucky, it exited with the deal. Majestic Care, affiliated with Marx Development Group, was the buyer, emerging from seven qualified LOIs and a competitive final round of bidding. Segal, Hallion and

Waldhorn handled the deal.

Another state, Iowa, also recently pushed through increases to its Medicaid rates, and Nick Cacciabando and Ryan Saul of Senior Living Investment Brokerage found a publicly traded buyer for a 72-bed facility there. The SLIB pair helped an industry veteran sell his last solely-owned senior care facility with the deal. The facility in question was Crystal Heights Care Center in Oskaloosa, about one hour southeast of Des Moines. Set on a 12acre campus, the facility was built in phases from 1975 to 1995 to 2017. The last addition consisted of a stateof-the-art rehabilitation wing with 14 private suites and a therapy gym at a cost of approximately $2.5 million. The wing stabilized within just a few months of opening.

Total occupancy was around 87.5%, and the facility earned around $135,000 of EBITDAR on $5.62 million of revenues. Plus, it has historically earned a four- or five-star rating from CMS. A marketing process in early 2023 did not yield a satisfactory price for the seller. However, the improved Medicaid rate boosted revenues significantly. So, another process was launched.

The Ensign Group (NASDAQ: ENSG) set its eyes on the property as a strategic acquisition to bolster its presence in Iowa. It paid $4.2 million, or $58,300 per bed, or more than double the highest bid from 2023. There was a delay in the real estate closing in order to obtain a clear title, but the seller agreed to let Ensign take over operations on August 1, before closing the real estate sale with Ensign’s affiliate Standard Bearer Healthcare REIT on September 17.

Next, Cacciabando and Jeff Binder returned to a familiar place, in Junction City, Kansas, to sell a senior care community. This property was Cacciabando’s first ever sale back in 2007, which he closed with Binder. The pair, plus Vince Viverito, are now representing that 2007 buyer in the community’s sale, as the regional owner/operator is choosing to focus on its remaining core assets.

Built in phases in the 1970s and 1980s, Valley View Senior Life features 28 independent living units, 13 assisted living units and 61 skilled nursing beds on

16.5 acres. It was 65% occupied and operated at an 8% margin on $8.4 million of revenues, so things could be improved. A California-based operator was looking to expand its footprint outside of California, Colorado and Montana, and made its first Midwest purchase, acquiring Valley View for $8.75 million, or $85,800 per unit, at a 7.7% cap rate.

Cacciabando and Binder also sold a skilled nursing facility in Kirkwood, Missouri, a suburb of St. Louis. Sitting on a 3.8-acre campus, the facility has been built over the years, with the original colonial-style part of the building constructed in 1927. It has also received renovations as recently as 2010. Known as Manor Grove, the facility has 117 beds, with 90 private and 13 semi-private units.

Owned by a local not-for-profit Board of Directors, the facility was struggling operationally, with a more than $1.3 million loss on $10.77 million of revenues and 72% occupancy. The seller was looking for a buyer to not only turn around the operations but to continue its legacy. A Missouri-exclusive owner/operator was ultimately chosen amid a handful of competitive offers, for a price

of $5 million, or $42,750 per bed.

A senior care campus in Pine Island, Minnesota, with some operational issues in the past found a new owner thanks to Saul, Jake Anderson and Dan Geraghty. The campus includes Pine Haven with 70 skilled nursing beds and Evergreen featuring 24 assisted living units. Pine Haven was built in stages over the years, starting in the mid-1960s, while the AL portion was added in 1995.

In 2022, the Minnesota Department of Health stepped in after the nursing facility failed to pay its employees wages, healthcare insurance and other vendor fees. The receivership began in June 2022, and the MDH kept the campus operating until a sale process was initiated. The seller of Pine Haven was the USDA, and the seller of Evergreen was the City of Pine Island. SLIB eventually sold both properties to a regional operator with other communities in the state.

Anderson was then joined by Jason Punzel, Brad Goodsell, Vince Viverito and Taylor Graham to sell a 59-unit assisted living/memory care community, also in Minnesota. Trails of Orono was built in 2012 in Wayzata and was occupied in the high-80s. It was being sold by an institutional developer located in the Twin Cities. The buyer is a regional owner/operator looking to grow in the state. The purchase price was not disclosed.

Marx Development Group and its affiliate Majestic Care’s acquisition of four skilled nursing facilities in West Virginia is set to close at the end of October, and the deal is still attracting a lot of attention in the state. That is because the seller is the State of West Virginia, and headlines are usually made when a for-profit buyer is taking over any state-owned or not-for-profit facility.

The scrutiny is often unfair, given the single-factor analysis most journalists perform on or parrot the results of private equity’s ownership of skilled nursing facilities. They almost always mislead the public on the impact of these acquisitions on the operations and financial health of the facilities, and on quality of care. Plus, do you ever see the positives of these acquisitions spelled out in the press, from planned investments in the building’s

physical plant to simply keeping the facility open, and thus most of the jobs it creates? No, and there is always more to the story.

We asked Majestic Care, which is taking over the operations of these four facilities, to fill in some details about the takeover. We know that the deal includes the sale and license transfer of the four facilities, which included Jackie Withrow Hospital in Beckley, John Manchin Sr. Health Care Center in Fairmont, Hopemont Hospital in Terra Alta, and Lakin Hospital in West Columbia. In total, there are 511 licensed beds. The state had been covering the operating losses at these facilities for years, totaling more than $6 million annually, and their aging physical plants were in need of some serious capex.

So, as part of the deal, Majestic/Marx is “launching a multi-year capital program to modernize the infrastructure, clinical equipment and resident amenities,” to the tune of millions of dollars. It is also being done in partnership and collaboration with the state. “No closures are planned, the residents stay where they are, and staff remain in

place.” All current employees are also being offered continued employment with no cuts to pay. New benefits will include retirement, health insurance, and paid time off, along with supports like tuition reimbursement, sign-on bonuses, a care team member relief fund for emergencies, and leadership development programs. That is one of the benefits to private ownership, “allowing [Marx] to move faster on investment in staff and facilities, with the goal of raising quality.”

Marx confirmed that its “committed investment reaches nine figures.” And in response to a FOIA request submitted by Erin Beck, a reporter from Mountain State Spotlight, on September 30 the state released the executed Asset Purchase Agreement for the portfolio. It confirmed the $60 million payment (in cash) that the governor of West Virginia had announced earlier this summer but also revealed a minimum of $80 million in “ancillary consideration” to be allocated by Marx post-closing. That brings the total consideration to $140 million, or $274,000 per bed.

The $80 million in ancillary consideration will cover net operating losses from continued operation of the facilities by Marx, inclusive of the costs of maintenance and repair of the facilities. But the majority of allocation will go towards the development of between three and five new skilled nursing facilities, with the $80 million figure only being a “minimum” spend.

The purchase agreement lays out a schedule of escrow deposit requirements on certain milestones, going in $5 million increments upon real property acquisition of at least three new development sites within 180 days after the October 31 closing date, to application for government approvals on the new facilities and construction financing closed within 240 days after closing, to building permits applied within 300 days. Construction must begin within 420 days of closing, after which substantial completion of each facility must be done within 450 days of securing the building permits, and finally, Marx must apply for final Certificate of Occupancy on each new facility on or before 480 days after receiving the building permits. The last step would result in just $3 million deposited in escrow.

If Marx elects not to develop and otherwise occupy at least three new facilities within 780 days after the closing date or to acquire the new development sites within one year of the closing date, then it must pay the state a one-time payment of $45 million. If Marx satisfies the deadlines, it would not have to pay that amount provided that a minimum of $50 million has been spent by Marx on the development of the new facilities. But the agreement clarifies that if Marx has not expended the whole $80 million even after satisfying the development requirements, it must pay the state the difference as additional cash consideration.

The agreement also stipulates that Marx must, “to the maximum extent practicable,” procure all of its labor, materials, equipment and supplies needed to build the new facilities from local, in-state sources, “even if slightly higher costs are incurred.” The quality and suitability of the products and services should still be comparable to non-local options, and the project schedules cannot be materially adversely impacted. That must have made Marx’s bid that much more appealing compared with

others that were submitted.

Speaking of the bidding process, we knew the deal was in the works for at least a year, since the state announced in July 2024 that it had engaged Lument Securities to assist the Department of Health Facilities in “facilitating a sustainable long-term care strategy, leveraging private capital to revitalize the state’s nursing facilities.” The transaction process was kicked off by an extensive marketing campaign from Lument to engage qualified investor groups with operational expertise, and it continued through a change in governorship, although not a change in party control.

We believe the bidding environment was very strong and active, with the governor saying that over 140 parties contacted the state with interest, 62 NDAs were signed and over eight letters of intent were received before Marx Development Group was ultimately selected. The governor stated that the firm “brings to the table a remarkable breadth of resources and extensive experience in renovating and improving healthcare facilities that are in need of thoughtful investment.”

Indeed, Marx is a vertically integrated developer (capable of building the new facilities) and operator. According to MDG’s website, its affiliate Majestic Care operates over 40 facilities in Ohio, Indiana and Michigan. The state’s announcement referenced MDG owning and operating 55 senior care properties with over 5,000 licensed beds in Indiana, Michigan, New York, Ohio and Kentucky.

The deal appears to be a coup for both the state and for MDG, which has also agreed to build between three and five new facilities to replace the aging facilities while sourcing labor and materials within the state. And a statement to us from the governor’s office says, “we prioritized future investment, employee retention, quality of care, and continued access for residents and communities.”

Blueprint handled several skilled nursing portfolio sales in September. First, during the NIC Fall conference in Austin, the firm announced that Amy Sitzman and Giancarlo Riso facilitated the sale of five skilled nursing

facilities located throughout the Texas Hill Country and Houston. All five facilities are within four hours of each other, offering scale and operational efficiencies.

The portfolio features 469 beds and has a diverse payor mix with a strong track record of financial performance. The facilities were generating over $2.2 million of inplace cash flow, with portfolio-wide occupancy at 71% and trending upward at the time of marketing, so there is room for an incoming investor to reduce expenses and increase value. Blueprint procured multiple competitive offers, ultimately advising the seller to move forward with a well-established SNF owner/operator that was looking to expand its footprint within Texas.

A second portfolio sold with the help of Sitzman and Riso, as well as Kyle Hallion. It featured four senior care assets in the Dallas-Fort Worth MSA with 585 skilled nursing beds and 401 seniors housing units across a mix of CCRC, assisted living, and skilled nursing campuses. The seller was a national owner/operator looking to divest these assets that no longer fit their long-term strategy.

At the time of marketing, the assets faced a variety of operational headwinds: elevated expenses, significant deferred capex, and below-market seniors housing rates. Blueprint secured seven offers spanning single-asset to full-portfolio buyers. The selected buyer, an experienced turnaround investor with roots in the municipal bond market, partnered with a local Dallas-based operator familiar with the properties. They intend to deploy significant capital improvements at the flagship 372bed CCRC, execute a turnaround plan for the 191-bed assisted living/skilled nursing campus and repurpose the two remaining campuses to alternative uses.

Sitzman and Riso handled another five-property portfolio, also in Texas. They advised a client on the sale and HUD 232 process for skilled nursing facilities in central and west Texas. The facilities totaled 424 beds and featured positive cash flow. They had attractive, fixed-rate HUD debt of 2.8% and long remaining terms with maturity dates starting in 2035 through 2044, presenting an incoming investor with significant cash-on-cash returns, especially if they invested in a targeted capex program

FINANCING THE FUTURE OF CARE. ONE RELATIONSHIP AT A TIME.

MERIDIAN’S SENIOR HOUSING AND HEALTHCARE FINANCE PRACTICE IS BUILT ON DEEP EXPERIENCE—AND A LONG-TERM COMMITMENT TO THE SECTOR. GUIDED BY SEASONED LEADERSHIP AND A FOCUS ON MARKET INSIGHT AND CLIENT OUTCOMES, OUR HEALTHCARE PLATFORM CONTINUES TO BE A KEY DRIVER OF THE FIRM’S GROWTH.

AMY HELLER Senior Managing Director

AVI BEGUN Managing Director

to raise the facilities’ competitive profiles. Further upside potential existed by improving the CMS star rating at each facility, and establishing additional referral relationships with nearby acute care hospitals.

Blueprint procured multiple competitive offers ultimately advising the seller to move forward with a growing skilled nursing operator that was looking to expand its footprint within Texas and grow its relationship with one of their existing capital partners. Blueprint also leaned on its experience with the HUD 232 TPA process to shepherd the various stakeholders towards closing.

Next, Sitzman and Riso were joined by Connor Doherty, Ryan Kelly and Will Roberts to market Project Golden Gopher, which features two properties with 230 skilled nursing beds in Hopkins and Rochester, Minnesota. The assets were owned by a publicly traded REIT and marketed on a distressed basis. Though the facilities were challenged, they presented clear upside through census growth and operational enhancements. The properties are near acute care hospitals, enabling an incoming

operator to establish strong referral relationships.

Following a targeted marketing process, Blueprint generated significant investor interest and ultimately selected a well-capitalized regional owner/operator with an established Minnesota footprint. The buyer intends to leverage its existing infrastructure, clinical resources and local market expertise to drive census growth and return the portfolio to stabilized performance.

In one final skilled nursing closing announced by Blueprint this month, the firm facilitated the sale of Welbrook Senior Living Farmington, a 50-bed Medicare-only transitional rehab skilled nursing facility in Farmington, New Mexico. Jacob Gehl and Dillon Rudy represented the buyer, a highnet-worth private investor/operator, which took over the facility from a private equity seller.

The facility, built in 2018, was a turnaround opportunity, operating at below market occupancy and experiencing an EBITDAR loss on approximately $5 million in revenue at the time of marketing. The buyer was looking to

expand their presence in New Mexico and saw significant potential in repositioning the asset, which it intends to do by expanding the facility’s existing licensure capacity and enhancing operational efficiency.

Mark Myers has had an active year since leaving Walker & Dunlop in January 2025 to go to SVN Senior Living Advisors (SVN SLA) before exiting that shop in May to co-create a seniors housing brokerage platform with Kiser Group. But a few deals that he worked on with his previous teams have also recently closed. The largest was the sale of Sarah Neuman, a 301-bed skilled nursing facility in Mamaroneck, New York, that was owned by The New Jewish Home (NJH). Despite negative EBITDA, the high-end, well-located facility sold for $76 million, or $252,500 per bed.

The private buyer has significant SNF holdings across the country and showed considerable patience as it took over three years for the state to issue the Change of Ownership (CHOW). New York has become stringent on the CHOW from not-for-profit to for-profit entities. Myers closed this

sale in conjunction with Walker & Dunlop and his former partners, Josh Jandris and Brett Gardner, who are now at Cushman & Wakefield.

The W&D team closed another sale for NJH in April, selling the 295-unit senior apartment community known as Kittay House. The sales price was $40.5 million, or $137,300 per unit. The property was part of New York’s Mitchell-Lama program that provides affordable rental and cooperative housing to moderate- and middleincome families.

The property operated at a small profit so there was no cap rate. This deal also took years to conclude, for the same reasons related to New York’s tight scrutiny over not-for-profit properties being sold to for profits. The buyer owns a 744-bed SNF on the same campus, which Myers and Jandris sold in 2016, and plans to incorporate Kittay as a feeder to his long-term care operation.

In June in conjunction with his former teammates at SVN SLA, Myers closed on the sale of the 112-bed AU Wellcare

SNF in Breese, Illinois, for $5 million, or $44,600 per bed. The facility had significant EBITDA resulting from a good quality mix, including a daily average of 18 Medicare residents. The seller also owns a nephrology company that provides dialysis in nursing homes and sold a handful of hotels that he owned with partners, rolling the sales proceeds into the acquisition of several nursing homes and seniors housing communities in southern Illinois.

Operating nursing homes is a lot different than operating other commercial real estate, including hotels, and the seller found himself in some financial difficulties with the closing of his SNF in Maryville, Illinois, which he purchased just a year ago. He is also trying to open a vacant CCRC that was purchased in nearby Highland, Illinois. However, the buyer owns and operates a significant number of skilled nursing facilities in the region.

Also in conjunction with his former team at SVN SLA, Mark Myers closed the sale of Forest Ridge, an 80-bed skilled nursing facility in Woodland Park, Colorado. Built in 2016, the facility features all private suites and is located near medical facilities, including Pikes Peak Regional Hospital. It was nearly fully occupied and operated at a strong 16.5% margin. SVN SLA represented the private seller and found the buyer, Cottonwood Healthcare, which owns and operates more than 30 skilled nursing facilities in the West. Forest Glen will be a flagship facility for Cottonwood, which has other transactions under way and is set for further growth. It paid $13 million, or $162,500 per bed, at a 12.1% cap rate.

SVN Senior Living Advisors’ Josh Salzman led the way on the sale of a lender-owned skilled nursing facility in San Antonio, Texas. The large facility had more than 230 licensed beds and was non-stabilized at the time of sale. The national bridge lender had owned and controlled the facility after completing a foreclosure action. It retained SVN to conduct a confidential marketing process and target buyers with a high degree of closing certainty. A national owner/operator looking to increase its portfolio in Texas emerged as the buyer.

Shifting from Texas to Mississippi, 3G Healthcare Real Estate, which mainly focuses on skilled nursing

transactions and has a side focus of debt and equity placement, facilitated the sale of a skilled nursing facility in the Magnolia State on behalf of a small, local skilled nursing owner. Built in the 1970s, the asset faced occupancy and operational challenges, including staffing shortages, the need for resident mix improvements, and significant bad debt, compounded by reduced state Medicaid rates.

During the marketing process, the turnaround potential and long-term opportunities were emphasized, resulting in six competitive offers. Ultimately, an owner/operator with a local presence paid $116,000 per operational bed for the facility, with plans to invest capital, enhance the facility’s standing within the community, improve the quality mix, and leverage its scale and regional teams to turnaround performance. Stan Klos III worked closely with the city to overcome a couple of hurdles, and he successfully got the transaction across the finish line.

Evans Senior Investments facilitated the sale of Mahoning Valley Nursing & Rehab Center, a 142-bed skilled nursing facility in Lehighton, Pennsylvania. The seller, an independent owner, faced increasing financial and operational pressures in today’s skilled nursing environment. The selected buyer was a regional operator with a growing presence in the state and will rebrand the facility as Mahoning Post Acute Nursing and Rehab.

According to Time News, Lakewood, New Jersey-based Outcome Healthcare was the buyer, and the seller was a mom & pop, Mike and Devon Mickey. The pair purchased the SNF in 1999 from Norman Berger, who had owned it since the late-1970s.

Also in Pennsylvania, Senwell Senior Investment Advisors facilitated the successful sale of a 100-bed skilled nursing facility. Built in 1987, the facility was developed by an Ohio-based operator as part of a broader growth initiative. Its occupancy rate was consistently strong, often exceeding 95%. It was the seller’s only out-of-state asset, leading to the decision to divest and refocus operations within Ohio.

The sale process attracted five strong offers. Senwell

and the seller ultimately moved forward with a buyer that demonstrated the clearest ability to execute a smooth operational transition and align with the long-term needs of the community. The buyer will look to enhance its broader care delivery model with additional ancillary services. Ben Bohland and Collin Hempfling facilitated the transaction.

Lastly, a large not-for-profit owner of skilled nursing facilities in Texas added another facility to its portfolio in the Lone Star State. Set in the town of Georgetown just north of Austin, The Wesleyan was founded in 1962 in collaboration with The Methodist Church, but the current 40-acre campus was built in 2008 and expanded its offerings to include a 142-bed skilled nursing facility, 240 units of independent living, 24 IL cottages and 84 units of assisted living and memory care. The SNF portion was bringing in positive cash flow but operated below industry margins. It also operated below its licensed capacity.

So, the owners decided to sell the standalone skilled nursing facility to Wellsential Health, which owns more

than 60 facilities in Texas. Regency Integrated Health Services operates all of Wellsential’s locations. Dominic Porretta of Cain Brothers advised The Wesleyan on the strategic divestiture, generating significant interest among Texas-based owners and operators. Based on other transactions that have recently closed in the state, we believe pricing may have exceeded $100,000 per operational bed. In conjunction with the transaction, Cain Brothers also assisted The Wesleyan on the remediation of its tax-exempt bonds associated with the sale.

SENIORS HOUSING ACQUISITIONS

After attending NIC last month, where the rooms and halls were full of optimism from brokers, lenders, operators and investors, it became clear that we will certainly break the annual record for publicly announced transactions for the second year in a row. So far this year, LevinPro LTC has recorded more than 560 publicly announced deals, with the past three quarters annualizing to roughly 750 transactions for 2025. For comparison, the industry announced 716 deals in 2024, surpassing the previous

record of 561 set in 2022. We’re also hearing of a very active fourth quarter, and even if some of these closings slip into early next year, 2025’s total will almost certainly be a record.

The assets trading this year look a bit different from those that changed hands last year. While many older buildings and distressed communities continue to sell, there has been a noticeable uptick in Class-A seniors housing communities and stabilized properties among the closings. New players are also entering the market, focusing on the Class-A market, with a few publicly announced transactions marking buyers’ first seniors housing acquisitions. Even more new entrants are expected. And of course existing industry participants remain active, especially the publicly traded REITs.

LTC Properties (NYSE: LTC) made a dent in its 2025 acquisition pipeline with a two-asset Kentucky deal and then a five-property Wisconsin portfolio acquisition. The two Kentucky properties were added to its SHOP portfolio through an off-market transaction. Both assets opened in the first half of 2023 with 158 total assisted living/memory care units. More than 50% of those units were pre-leased, and they achieved full stabilization in an average of 20 months. Since then, they consistently performed well and were stabilized at the time of closing. It is expected that the communities will deliver a year-one yield of approximately 7%. One of the buildings appears to be Charter Senior Living of Hopkinsville, which has 56 assisted living and 23 memory care units.

The seller, DMK Development Group, developed the assets and brought on Charter Senior Living to handle the operations. DMK and Charter have collaborated on 10 ground-up development projects since 2017, with several currently under construction and more in the pipeline. DMK’s investors included Charter, Planters Bank, Central Bank & Trust Co., Poppy Bank and PACE Loan Group

The REIT bought both communities for $40 million, or $253,000 per unit, and will keep Charter on as operator. This marks a new partnership between the two companies, though LTC has previously worked with Keven Bennema, Charter’s CEO and Co-Founder.

Just days later, the REIT announced a larger SHOP acquisition involving five seniors housing properties in Wisconsin. The Class-A portfolio features a total of 520 units of independent living, assisted living and memory care. It was stabilized, with an average property age of six years and an expected year-one yield of approximately 7%. Lifespark, a new LTC operating partner, has managed the communities since 2021 and will continue to do so.

LTC Properties paid $195 million, or $375,000 per unit, financed through a line of credit, proceeds from previously disclosed property sales and loan payoffs from the second half of 2025, and proceeds from sales of common stock under the company’s ATM program. The deal has brought LTC to 80% of its projected $460 million acquisition pipeline for 2025. Of those acquisitions, $270 million has been added to its SHOP portfolio, and LTC expects to close an additional $90 million in SHOP acquisitions by the end of the year.

We suspect a Senior Living Investment Brokerage sale of a Class-A seniors housing community in Wisconsin may have been related to the LTC portfolio. Jason Punzel, Jake Anderson and Ryan Saul worked on the deal. Built in the last couple of years, the high-quality asset featured approximately 125 units of independent living, assisted living and memory care. Occupancy was strong above 90%, and financial performance was solid. Its newer vintage attracted significant interest from national, regional and institutional investors, and SLIB procured multiple offers for the seller. A public REIT was disclosed as the selected buyer and will keep the current management company as the operator.

LTC Properties was not the only publicly traded company active on the acquisition front this month. Austin Diamond and Nick Stahler of The Knapp-Stahler Group at Marcus & Millichap announced their role representing the seller of a seniors housing community in Mansfield, Texas (Dallas-Fort Worth area). Sonida Senior Living (NYSE: SNDA) bought the asset, which comprises 82 assisted living and 36 memory care units. The operator paid $15.55 million, or $159,200 per unit, which was funded with cash on hand and proceeds from its senior secured revolving credit facility. The Knapp-Stahler Group

navigated a challenging renegotiation at the expiration of due diligence, ensuring a favorable outcome and smooth closing for all parties.

That is an attractive price, from Sonida’s perspective, for a 2016-vintage, recently renovated, Class-A property, which Sonida described as having the “highest quality physical plant in this market” for the operator. Plus, The Jasper of Mansfield is strategically situated near existing Sonida assets, shares a driveway with senior-centric healthcare providers and referral sources (including a kidney dialysis center, renal care, orthopedic specialists and GI specialists), and sits immediately across the street from a 294-bed hospital.

However, it was not stabilized at the time of sale. This was the only seniors housing asset of the seller, a regional hotel developer that originally built the community. Nevertheless, the property attracted significant investor interest before Sonida emerged as the eventual buyer. Sonida plans to invest additional capital to complete an aesthetic refresh to common areas and amenity spaces

over the coming year. And it expects a double-digit cap rate upon stabilization. This purchase brings the company’s Dallas-Fort Worth portfolio to nine assets and 21 total in the state.

Welltower (NYSE: WELL) acquired a 118-unit assisted living/memory care community in Marana, Arizona, northeast of Tucson. The Watermark at Continental Ranch was developed in 2019 by Kayne Anderson Real Estate and Watermark Senior Living. Watermark bought the land in 2017 for $1.34 million, and Kayne Anderson bought the community in 2019 upon receipt of the certificate of occupancy and licensure, according to the deal in LevinPro LTC. BMO Harris Bank financed that purchase with a $21 million credit facility. There are studio, one- and two-bedroom layouts, plus specialized memory care wings. Welltower has rebranded the community Cogir at Continental Ranch.

Another Class-A community with assisted living and memory care services traded hands this month. The well performing property is outside of Allentown,

Pennsylvania, and traded to a joint venture between Legend Senior Living and a new capital partner. Alex Florea and Kevin Lukehart of Blueprint handled the transaction. Legend has been operating The Vero at Bethlehem, which opened in July 2023 and stabilized within 18 months. At the time of marketing, the 124-unit asset achieved industry-leading occupancy and margins, which we would guess were in the high-90s and high-30s range, respectively.

The builder of the project, KBE Building Corporation, listed Columbia Pacific Advisors as the developer. Given the community’s outstanding performance and trajectory, ownership decided to monetize the asset and lock in returns through a targeted recapitalization process in recognition of Legend’s efforts and success so far. This strategy led to competitive offers from all groups approached and allowed Legend to maintain operations and co-invest alongside a new partner. The deal closed at the agreed-upon pricing.

Two assisted living/memory care communities set in between Orlando and Gainesville, Florida, found a new in-state owner. Located about 10 miles apart in Ocala and Belleview, the communities total 83 units and were previously owned by a partnership between a Floridabased capital partner and a regional operator. Both assets are cash-flowing but have upside potential for a new owner. There is also a third asset currently awaiting a HUD assumption that will transition once the approval is complete. Its new owner will be a Florida-based owner/ operator, which is acquiring the whole portfolio. Brad Clousing and Dan Geraghty of Senior Living Investment Brokerage handled the transaction.

Clousing and Geraghty were joined by Jeff Binder to help a seniors housing portfolio in Michigan trade hands. Set in secondary markets, the portfolio consists of four late1990s vintage properties that are well maintained and well regarded in their respective communities. They also experienced continued occupancy growth throughout 2025 but still represented an opportunity for a new regional owner/operator to hit the ground running in boosting performance through a hands-on management approach and leveraging existing referral networks. A

national owner/operator deemed the portfolio no longer fit with its long-term operational objectives and slated it for divestment. SLIB presented more than five bids from a mix of local, regional and family office groups before a regional owner was selected.

Two faith-based, not-for-profit CCRCs in central Pennsylvania were acquired by a private East Coastbased investor. Located an hour’s drive from each other, Church of God Home has 50 independent living units and 109 skilled nursing beds in Carlisle, while Towne Centre in Myerstown has 152 skilled nursing beds, plus some “borrowed” IL units from the Carlisle location that gives it a CCRC designation. They were built in 1948 and 1972, respectively, and operated at a profit. But this was not a “cap rate deal,” as the Towne Centre location struggled more with occupancy, and the price was not disclosed.

The selling organization is based in south central Pennsylvania and appears to be StoneRidge Retirement Living, which was looking to focus on its flagship CCRC and other opportunities. Meanwhile, the East Coastbased buyer has an existing presence throughout eastern Pennsylvania. Toby Siefert and Nick Cacciabando of SLIB handled the transaction.

In a separate transaction involving a not-for-profit, a high-end seniors housing community that caters to the Japanese-American population in the San Francisco, California, area completed a delicate operational transfer, with the help of Ziegler. Kokoro Assisted Living is located in the heart of San Francisco’s historic Japantown and is known for providing culturally sensitive care and an environment that blends Japanese and American heritage through meaningful activities, celebrations and cuisine. The main structure was originally a synagogue and has since been converted to seniors housing, expanding in the early 2000s.

It had decent occupancy, but operations were never optimized, operating just above breakeven. Sequoia Living, another not-for-profit organization, managed the community. In early 2025, Kokoro’s Board of Directors engaged Ziegler to lead a strategic process to identify a new management partner aligned with the community’s

THE WHITE GLOVE APPROACH TO SENIOR LIVING FINANCE

billion in FHA/HUD loans

Jason Dopoulos | Managing Principal jdopoulos@ikariacg.com

Ken Gould | Managing Principal kgould@ikariacg.com

very specific mission and cultural values. So, Ziegler focused on management companies with proven experience in delivering specialized cultural care.

That search and evaluation process led to a partnership with Northstar Senior Living, a seniors housing operator with communities across the country. Northstar also operates another Asian American-focused community in Los Angeles, known as Sakura Gardens, which added to its appeal. Humair Sabir led the transaction.

Blueprint facilitated the sale of a Class-A seniors housing community in Jasper, Georgia. Built in 2022, The Lodge at Stephens Lake includes 83 units of independent living cottages, assisted living and memory care. It is adjacent to a large active adult development and benefits from significant planned residential and commercial growth. At the time of launch, the community was approaching 95% occupancy and generating annualized revenue of $4.7 million with EBITDAR margins of 30%+.

Engaged by the original developer, Blueprint launched

a 30-day marketing campaign that generated multiple initial round offers from both public and private investors. Following a competitive final round process, a public REIT emerged as the winning bidder, which partnered with a Georgia-based operator already active in the Jasper market. The offering included expansion land, and the REIT intends to begin construction shortly after closing.

The manager will be Phoenix Senior Living , which operates a well-performing community not far from The Lodge at Stephens Lake. This brings its portfolio to 46 managed seniors housing communities across the Southeast. Amy Sitzman, Giancarlo Riso and Kyle Hallion handled the transaction, which closed at the LOI pricing.

A vacant assisted living community in Birmingham, Alabama, found a new owner thanks to Sitzman and Riso. Originally built in 1999, the community faced significant physical plant needs and operational challenges that rendered it unviable, without substantial capital investment. So, ownership decided to shutter it and divest. Blueprint utilized both its proprietary platform and

the Ten-X online auction platform to generate multiple competitive bids from regional and national operators. The successful bidder, Pines Senior Living, plans to reopen and reposition the community.

Sitzman and Riso were then joined by Connor Doherty and Ryan Kelly to get another seniors housing deal across the finish line. Built in 2013 as part of an expansion to an adjacent CCRC, the building has 67 assisted living and memory care units in Odessa, Texas. It had gone through multiple operator changes over the years. Blueprint procured multiple competitive offers, advising the seller to move forward with a value-add regional owner/ operator with an existing presence in the Dallas-Fort Worth market that was looking to expand within the state.

Doherty and Kelly were engaged to market a 225-unit CCRC in St. Louis, Missouri, that was experiencing operational challenges. The seller, a large owner/ operator, was looking to address immediate performance issues and position the asset for long-term stability and value. So, the deal was marketed either as an outright sale or a lease with a purchase option. Following a competitive process, the selected transaction structure was a lease with a purchase option. The incoming operator, a regional owner/operator, brings local market knowledge with an established footprint in Missouri as well as Illinois.

The duo then teamed up with Jacob Gehl and Dillon Rudy to handle the sale of an 80-unit assisted living and memory care community in the Syracuse, New York MSA. At the time of marketing, it was generating strong cash flow and had recently benefited from significant renovations, positioning it as stabilized.

A diverse buyer pool was targeted, including local, regional and national groups. The process generated three competitive offers, ultimately resulting in the selection of a regional owner with an existing footprint. The buyer will retain the incumbent operator.

A private equity firm based in La Jolla, California, purchased its fourth seniors housing property, with Scott Frazier and Brooks Blackmon of Blueprint facilitating the transaction. Bakerson Companies bought Truewood by Merrill, Clovis, a 115-unit assisted living/memory

care community in Clovis, an affluent suburb of Fresno, California. The property was an older vintage but showed well. Bakerson will bring in a new operating partner, Calson Management, to operate it going forward under a new name: Saddle Ridge Senior Living, which honors the city’s celebrated Clovis Rodeo and its deep-rooted western heritage. The firm paid all cash for the property, at an attractive per-unit value.

In a story announcing its previous acquisition in Rock Hill, South Carolina, in March 2024, we described Bakerson as “playing offense right now” in the seniors housing M&A market. Helped by its ability to pay all cash, the firm is backed by Latin American family office capital. It was launched in 2021 by Pablo Linero, who brings investment experience from Brookfield Properties, HP Investors and Frontera Real Estate Investments. Other investments include Blossom Vale Senior Living in Orangevale, California, and another property in McAllen, Texas, both as a co-GP investor. All fit the investment criteria for Bakerson, which is searching for larger, B-quality seniors housing properties (usually above 150 units) that have existing cash flow with some upside.

Turning from California to Florida, Berkadia handled the sale of Summer Vista, a seniors housing community in Pensacola. Ross Sanders, Dave Fasano, Cody Tremper and Mike Garbers closed the transaction. Built in 2016, the 89-unit AL/MC community has always been a strong performer. In fact, after opening in February 2016, it had reached stabilization after just five months.

According to LevinPro LTC’s M&A database, a 2017 sale of Summer Vista to CNL Healthcare Properties had occupancy at 95% (it sold for $21.4 million, or $240,400 per unit at the time). Then in February 2020, Summer Vista and a 92-unit AL/MC community in Tampa sold to Waypoint Residential for a combined $48.85 million, or $270,000 per unit. Occupancy was nearly full at Summer Vista at the time, while performance at the Tampa location lagged, so we imagine the per-unit allocation was higher for the Pensacola property.

Today, we understand that occupancy is still in the 90s, and according to those familiar with the listing, the operating margin was consistently in the high-30s. That

is very strong considering there are no independent living units. SRI Management has operated the building since opening, and will continue to do so. The buyer was not disclosed but was described as a leading owner of seniors housing. The purchase price was also not disclosed, but we imagine it was high for a Florida panhandle deal.

In another transaction, not far from the NIC venue in Austin, Berkadia closed the sale of Village on the Park Onion Creek, a 124-unit independent and assisted living community located in an Austin suburb. Cody Tremper, Mike Garbers, Ross Sanders and Dave Fasano closed the deal on behalf of Bridgewood Property Company, a Houston-based developer, owner and operator, and the original developer of the community. Bridgewood’s wholly owned management company, The Aspenwood Company, will continue managing the property for its new owner, a publicly traded REIT. We hope a bottle of champagne was popped at NIC.

Opened in 2016, Village on the Park Onion Creek is located in South Austin and boasts consistently strong

3rd Quarter Investor Call

October 23, 2025

Sponsored by

About the Webinar

The SeniorCare Investor is convening a panel to discuss the latest seniors housing and care M&A data, relevant case studies on recent transactions and answer all audience questions. It’s an industry event that you don’t want to miss.

www.levinassociates.com/2510webinar

occupancy. In addition to its 102 independent and assisted living units, the property also features 22 indemand independent living cottages.

Continuum Advisors announced the sale of Laurel Circle, a luxury 270-unit CCRC on 25 acres in Bridgewater Township, New Jersey. Built in 1996, Laurel Circle offers a full continuum of care with 183 independent living apartments, 19 independent living villas, 30 assisted living units, 10 memory care units and 28 skilled nursing units, plus an additional five acres of undeveloped land for future expansion.

A joint venture that included LCS retained Continuum to represent them in the sales transaction. David Kliewer and Jay Jordan led the transaction, which generated strong buyer interest and culminated in the sale to an affiliate of Maxwell Group, Senior Living Communities Kliewer and Jordan had previously arranged the sale of Laurel Circle (formerly Arbor Glen) in 2018, when it was acquired out of a defaulted bond sale process. It had previously been owned and operated by the not-for-

PANELISTS:

Swett, Managing Editor, The SeniorCare Investor (moderator)

Lindenauer, President, FHA, NewPoint

Sarah Anderson, Senior Managing Director, Newmark

profit Friends Retirement Concepts, Inc. The LevinPro LTC database shows the 2018 purchase price was $39.7 million, or $132,800 per unit. Apparently, the community is performing well now, and the seller had invested more than $15 million in capital improvements, including villa and apartment renovations, a substantially rehabbed community center, and extensive health center modernizations. The community also executed a strategic shift to Type C (Fee-for-Service) entrance fee contracts.

A standalone independent living community in Great Falls, Montana, just sold for one of the highest per-unit prices in the state. Developed in 1995, The Iris Senior Living was the highest-quality IL building in the area and was consistently fully occupied. It features 60 units and operates at a nearly 40% margin. Even though it is an older building, it is in good condition and commanded a $253,000 per unit price (or $15.2 million in total), at an 8.8% cap rate. The cap rate makes sense given the market and vintage of the asset, and the price is the highest on a per-unit basis in the LevinPro LTC deal database in the state of Montana.

Blake Bozett and Spud Batt of The Zett Group represented the seller, Compass Senior Living, which bought the former Brookdale Senior Living (NYSE: BKD) asset about five years ago. Bozett and Batt also sourced the buyer, a Minnesota-based operator. There were several bids.

David Young of Greystone arranged attractive acquisition financing from a local credit union for the deal. The loan comes with a 6.4% fixed rate for five years, a 10-year term and no prepayment penalty, at 80% loan-to-cost. Because of the smaller loan size, Young targeted local banks and credit unions that could stretch high in the capital stack at great pricing, and he secured two competitive terms. Young works on Chris Clare’s team at Greystone, which includes Ben Rubin, Ryan Harkins, Parker Nielsen and Liam Gallagher. As a team, they have closed over $600 million year-to-date within seniors housing and skilled nursing, and they are currently engaged on over $750 million of transactions.

Madison Meiser and Bill Meiser of Meiser Commercial Real Estate completed two separate seniors housing

transactions in Michigan. All parties involved had experience in the senior care sector, making the transactions smooth, aside from routine negotiations. The first transaction to close was in Plymouth.

Built in 1980, the assisted living community featured 50 units and was licensed for 75 beds. The buyer, an owner/operator, has opportunities to reduce expenses and enhance the property’s value. At the time of sale, occupancy was 84%, and the community was operating at a loss. For the trailing 12 months ending February 2025, the property generated $2.36 million in revenues. A hurdle presented itself late in the transaction, but the Meisers successfully navigated it and closed the deal. The buyer paid $3.3 million, or $66,000 per unit, in cash to acquire the asset.

A couple of weeks later, the firm closed another deal involving an assisted living community, this time in Clinton Township and on behalf of a different seller. Built in 1988 and renovated in 2024, the building features 18 units and is licensed for 20 beds. It was 40% occupied, and losing money. The buyer was a skilled nursing owner/operator that paid $1.5 million, or $83,300 per unit, in an allcash transaction. The seller, an owner/operator, agreed to a substantial holdback. This is not the buyer’s first seniors housing asset, and they are looking to continue expanding their seniors footprint.

On the other end of the spectrum, an AL/MC community reporting strong occupancy traded in Twin Falls, Idaho, with the help of Chad Mundy and Nick Stahler of The Knapp-Stahler Group at Marcus & Millichap. The campus opened in 1989 with an eight-unit building, and added two 15-unit buildings in 2009 and 2015, respectively. Some units were added to each building in 2023 and 2024, and now, the campus totals 43 private beds. Occupancy was between 95% and 100%, and the campus generated well over $900,000 of NOI on more than $2.5 million of revenues.

A new investor group entering the sector emerged as the buyer, paying an undisclosed sum for the community. At the release of contingencies, Mundy and Stahler confronted multiple obstacles that threatened the

transaction, but resolved the issues to close at the originally contracted purchase price.

Foundry Commercial and funds managed by affiliates of Fortress Investment Group acquired the RoseWood Village Assisted Living and Memory Care communities in Charlottesville, Virginia. The two communities, RoseWood Village at Greenbrier and RoseWood Village at Hollymead, will be operated by Foundry Commercial’s management company, Allegro Living, under its Spring Arbor brand. With these additions, Allegro Living’s footprint now comprises 54 communities across 14 states.

The Greenbrier community was built in 2001 and expanded in 2018, while the Hollymead community was constructed in 2008. Together they feature 104 assisted living and 62 memory care units. Allegro Living plans on making interior improvements for both properties in the near future, with committed funding from Foundry and Fortress. The seller was represented by JLL

Also built in 2001, Evans Senior Investments facilitated the sale of Heirloom Inn, a 67-unit assisted living community in Price, Utah. The seller, which developed the community over 20 years ago, was independent owner/operator Shauna O’Brien. At the time of sale, the property was performing well, albeit with opportunities for expense management and revenue growth. There was strong interest from buyers due to the limited supply of assisted living communities in the surrounding market, with a regional operator that offers scale being a good fit for the asset. The transaction was completed ahead of schedule, within four months.

Phorcys Capital Partners acquired Village Veranda at Lady Lake, a 125-unit assisted living/memory care community in Lady Lake, Florida, adjacent to The Villages. Opened in 2019, the community was developed by Gordon Cos., Village Veranda Lady Lake LLC and SRI Management, which has operated the community since the start. SRI will stay on as operator. The property was acquired through a receivership sale, with Phorcys as the stalking horse.

The deal marks Phorcys’s fifth seniors housing

investment. The company is an alternative asset manager focused on investing in distressed assets and municipal bonds with strategic investments across senior living, multifamily, student housing and hospitality. Stride Bank provided acquisition financing for the deal.

Lastly, we learned that Eureka Capital Partners is working on AlerisLife’s exit from its 17 owned properties and management transition of 116 Diversified Healthcare Trust -owned (NASDAQ: DHC) properties. A marketing process commenced in April 2025, and after a competitive bidding process, AlerisLife and DHC selected seven operators to purchase the management agreements of the 116 DHC communities, and the transition has already started in tranches and should be completed by year-end. The whole business is expected to be wound down by the first half of 2026.

Q3 Surpasses 200 Deals...cont.

from page

1

year’s activity could surpass 2024’s annual record of 716 publicly announced transactions, which eclipsed the previous record of 561 in 2022. It seemed particularly challenging, as the new Trump Administration added some uncertainty surrounding tariffs and their effect on interest rates. Also, 2024’s elevated total was partly driven by larger portfolio divestments being broken into one-off sales to maximize the value of both performing and non-performing assets, while larger portfolio divestments were expected in 2025.

However, the third quarter finished strong, with 202 deals, bringing the senior care M&A market to 567 publicly announced transactions in the first three quarters of this year, which annualizes to roughly 750 deals for 2025. By comparison, Q2 and Q1 reached 181 and 179 deals, respectively, and Q3:24 saw 181 deals publicly announced. Combining 2025’s activity thus far with the expectation of a highly active fourth quarter, which has already proven to be off to an active start with a slew of closings announced in just the first few days, it seems safe to say the industry is on track to set a new annual record of publicly announced transactions for the second year in a row.

The fourth quarter was the most active quarter of 2024. That end-of-year increased transaction volume followed the Federal Reserve’s interest rate cut, which brought back investor confidence and a general feeling that interest rates would indeed start declining. There could be a similar trend in Q4:25 with the Fed resuming its interest rate cutting. But also, the seniors housing operating market is in a much stronger position than a year ago, which is helping to drive transaction activity and value.

September alone recorded 71 publicly announced transactions, and only two other months have surpassed 70 deals, both in 2024. Plus, it’s a preliminary figure that is sure to rise. Over the trailing 24-month period, the M&A market averaged 60 publicly announced transactions per month, up from an average of 44 per month in the previous 24-month period. And while some months will naturally fall below this level as outliers, the general trend has pointed upward.

Census is on the rise, translating into stronger revenues and usually higher cash flow, which in turn supports rising valuations. As investors are willing to pay more for that cash flow, prices are being pushed upward, drawing even more participants into the industry if potentially sellers believe they can exit at more attractive pricing.