The improving capital markets and operating environment are helping to draw owners of high-quality, well-performing seniors housing properties to the M&A market. If cap rates start to compress, then we may start seeing record-breaking per-unit prices soon.

See article at right

Skilled Nursing Values

Times are pretty good for skilled nursing facilities, as many states have offered more generous Medicaid rates. That is helping to raise prices for SNFs, but the long-term fundamentals of the business may be the main driving factor for buyers.

Given all of the optimism surrounding the operating environment in seniors housing, from national occupancy gains to historic resident rate increases to better expense controls, we would expect prices to be rising for assets of all types and qualities, on an apples-to-apples basis. An analysis of LevinPro LTC’s proprietary deal database shows that, indeed, prices have risen on average for seniors housing properties in the most recent four-quarter period. And it may be the start of a rise that will begin setting records soon.

That previous pricing record was set in 2019, when the average price for seniors housing properties, comprising both independent living and assisted living/memory care properties, hit $244,200 per unit. The market readjusted to a post-COVID world of lower census and higher risk, but it was the sudden and steep rise of interest rates that depressed pricing the

continued on page 22

Skilled Nursing Values on the Rise

A Favorable Reimbursement Environment Is Helping

Will there ever be a better reimbursement environment for skilled nursing facilities? Well, it is tough to beat the golden age of the sector in the 1990s when facilities were reimbursed by Medicare and Medicaid largely based on their reported costs, subject to some caps and efficiency parameters. Other costs like therapy, staffing and administrative overhead were also reimbursed, and there were few incentives to economize, or to get creative at all. Many states also used a cost-based reimbursement system for Medicaid.

It was a predictable and lucrative system, and facilities often exceeded 15% and 20% operating margins. Medicare SNF days were also growing substantially at the time as post-acute care utilization expanded. That’s when we saw many publicly traded providers like Genesis HealthCare, Sun Healthcare, Integrated Health Services and Mariner Health Group

continued on page 2

continued from page 1

enter the market, attracted to the revenue reliability of the sector.

That golden era came to a crashing halt when the Prospective Payment System was implemented in 1998 to address the rising cost of skilled nursing care to the federal government. PPS took a wrecking ball to the way business was done at nearly all facilities across the country, and margins quickly plummeted when high-cost therapy and ancillary billings were capped. The SNF sector went from more than a dozen publicly traded companies in the 1990s to just a handful by the mid-2000s.

Nursing facilities eventually adjusted to the PPS system and margins recovered, but the disruption certainly adversely affected the relationship between the sector and the government. Friction also rose from the fact that Medicaid reimbursement rates consistently did not meet

Inside the World of Senior Care Mergers, Acquisitions and Finance Since 1948

This publication is not a complete analysis of every material fact regarding any company, industry or security. Opinions expressed are subject to change without notice. Statements of fact have been obtained from sources considered reliable but no representation is made as to their completeness or accuracy.

POSTMASTER: Please send address changes to The SeniorCare Investor, P.O. Box 1117, New Canaan, CT 06840.

costs in many states. The implementation of the PatientDriven Payment Model in 2019 was a much better roll-out than PPS, helped by increased communication between CMS and the sector, and facilities were getting better reimbursed for the increased levels of care provided to an increasingly medically complex patient population.

However, ironically, it was the COVID-19 pandemic and ensuing difficulties that may have strengthened the relationship with the government to its best state since the 1990s. The skilled nursing sector was brought to its knees in the early days of the pandemic, with numerous deaths, plummeting census and endless media scrutiny.

To rescue the industry, support poured in from the government in the form of CARES Act grants, Medicare advance payments, temporary COVID Medicaid rate bumps and various regulatory flexibilities. That was once again reinforced with the rising staffing challenges and costs, as well as the effects of inflation, when CMS responded with more substantial rate increases and many states implemented noticeably higher Medicaid rate increases and supplemental payments.

Even the One Big Beautiful Bill Act has carve outs in place with respect to any changes to provider taxes and senior care, as well as a 10-year delay of the federal staffing mandate for nursing homes. Another win for SNFs.

The new administration is also in the process of removing the threat of a minimum staffing mandate, recently announcing that CMS has drafted an interim final rule that would repeal the minimum staffing standards for SNFs. We’ll see what the final version will look like, but it’s another good sign for the industry and suggests that the value of the skilled nursing sector, from its pivotal place in the post-acute care spectrum to its lower cost care setting status, is finally being recognized.

Buoyed by these positive developments, we attended the Zimmet Healthcare and Reimbursement conference in Connecticut last month (a fantastic conference for anyone looking to understand the complexities of the SNF reimbursement landscape, future hurdles, and how their facilities can best perform in the current environment),

and spirits were high. It was a stark contrast to the 2023 conference when Marc Zimmet was sounding the alarm over the rise of Medicare Advantage. Rather, a theme of the 2025 conference seemed to be, “make hay while the sun is shining, things are pretty good in the SNF sector right now,” to paraphrase.

That generalization on our part does not account for the various states that have not implemented as-generous hikes to their Medicaid rates and other forms of payments to SNFs. Not every state can be West Viriginia. And states like North Carolina and Idaho, plus others, may pass Medicaid rate cuts soon as a reaction to budget shortfalls. Federal policy and reimbursement rates make an impact on SNFs’ bottom lines, certainly.

But each state, with its own Medicaid rate, CON requirements and bed supplies, regulatory environments, labor supplies, union preponderance and other financial incentives make up 50 distinct markets for SNFs. Some are great, some are OK, and some make it excruciatingly difficult to run a profitable facility.

But all have buyers that see opportunity, and usually sellers that want to get out quickly, or are being forced out. Despite the disparate state-by-state markets for SNFs, many buyers are looking to the long-term fundamentals of the sector. Simply put, there is a limited supply of beds (a diminishing supply in some states) and an impending surge in demand from older adults. For those planning on staying in the industry for the long-term, the value of those beds will keep rising. That was the response we got from a couple of buyers when we questioned some very high prices paid for facilities. Additional revenue from related ancillary businesses also helps support higher prices.

The high yields offered by skilled nursing investments continue to draw buyers into the space, and as interest rates on permanent debt slowly decrease, that risk cushion should continue to expand. That is, if cap rates remain in their historical range of 12.0% to 13.0%. Right now, the average is 12.10% for the four quarters ended June 2025, down from an average of 12.2% in 2024 and 12.9% in 2023. But, during the buying frenzy of 2021 and 2022 when interest rates were historically low and

government relief payments were flowing, cap rates did decline to the 11% range.

We would still like to see the risk cushion remain for a sector that remains so dependent on the whims of the federal and state governments, even if we are in good times right now and even as interest rates fall. Facilities will be increasingly dependent on a smaller share of Medicare patients to earn their profits, especially if Medicaid rate increases continue to fail to keep up with expenses. If prices also rise, then the debt service will also rise, putting pressure on ownership to increase revenues. That pressure is compounded for any operators with escalating lease payments.

Prices are, in fact, rising due to the ameliorating capital markets, the Medicaid rate increases passed in a number of states and higher overall levels of revenue from care and ancillaries. But the average only eked up 2% from $83,800 per bed in calendar-year 2024 to $85,100 per bed in the four quarters ended June 2025.

Despite the overall positive reimbursement environment that SNFs are currently enjoying, there are still winners and losers in the environment that rewards a facility’s ability to capture more share from a dwindling Medicare share of the population, as well as attract the best case mix. And those “losers” (we don’t like that term, either) are sometimes looking for the nearest exit in the form of a sale. The low end of the market thus weighs down the average price per bed, and we still see a significant share of sales involving struggling facilities in the near future. Vacant facilities are not included in our pricing averages.

But most skilled nursing owners and dealmakers would usually care more about the average pricing in their particular states or markets, since market dynamics that impact a facility’s performance and value are so state and market specific. That is why LevinPro LTC provides five-year average prices, cap rates and Gross Income Multipliers (GIMs) for the top-20 states.

It also helps explain why the average price per bed for sales in Illinois, a notoriously difficult state for operators, pales in comparison to the average price per bed for the

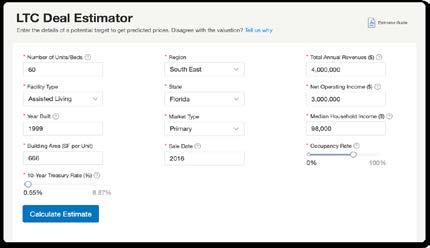

more attractive state of Maryland, $52,800 compared with $184,800. A more exhaustive study of stateby-state trends will be presented in the next Senior Care Acquisition Report. But, of course, state-by-state comparisons are also evident when using LevinPro LTC’s new deal valuation tool, which takes into account most of the transactions in our historical proprietary database.

Will we see a new record set for the sector, in terms of per-bed pricing? Probably not in 2025, but it is possible we could see the average pop above $100,000 per bed by year’s end, especially with several high-priced deals we know have closed or are set to close in the coming months.

The lower end of the market will always be there, but with more buyers looking toward the long-term fundamentals and seeing increased revenues to support higher prices, we could be writing about new records next year. Unless the rug is pulled out from under operators’ feet in a new, creative way.

SKILLED NURSING ACQUISITIONS

The long-term fundamentals of the skilled nursing industry are appealing to investors, with the value of beds expected to keep rising as demand increases and supply remains limited. After attending The Zimmet Healthcare and the Reimbursement conference, it was clear that many owners recognize this, and the overall reimbursement environment is almost as good as it can be, right now. Of course, not all states make it easy to operate profitably, but more states have boosted their Medicaid rates and become much more attractive to investors.

West Virginia has been one of the states that has usually attracted a lot of attention. It is a highly desirable state in which to operate SNFs, with good reimbursement rates and limited competition. The small pool of facilities in the state means that they rarely come up for sale, but the governor, Patrick Morrisey, just announced that West Virginia has agreed to sell four state-owned skilled nursing facilities totaling 511 licensed beds that

BOUTIQUE BY DESIGN

Built organically since 1997 and focused from the outset

were losing around $6 million a year, according to the governor’s office.

The prospective buyer is Marx Development Group, a New York-based real estate developer and manager that is focused on several real estate sectors, including hospitality, residential, commercial and healthcare facilities. The deal appears to be a coup for both the state and for MDG, which has also agreed to build between three and five new facilities to replace the aging facilities while sourcing labor and materials within the state.

The acquired facilities will also receive renovations and expansions, with the quality of care hopefully improving for patients, too. Plus, the state is relieved of covering the operating losses at these facilities while receiving some sale proceeds at the same time. The governor stated that the facilities were purchased for $60 million, or $117,400 per bed, but given that per-bed prices for West Virginia have been as high as $315,000 per bed (for profitable operations) and that low bed supply is met with high investor demand in the state, we suspect that

the total consideration may have been much higher than $60 million.

We knew the deal was in the works for at least a year, since the state announced in July 2024 that it had engaged Laca Wong-Hammond of Lument Securities to assist the Department of Health Facilities in “facilitating a sustainable long-term care strategy, leveraging private capital to revitalize the state’s nursing facilities.” That plan included the sale and license transfer of the four facilities, which were Jackie Withrow Hospital in Beckley, John Manchin Sr. Health Care Center in Fairmont, Hopemont Hospital in Terra Alta, and Lakin Hospital in West Columbia. The deal would also ensure uninterrupted care throughout the transition and “channel millions of dollars into facility modernization, upgrades and expansions.”

The transaction process was kicked off by an extensive marketing campaign from Lument to engage qualified investor groups with operational expertise, and it continued through a change in governorship, although not a change in party control. We believe the bidding

environment was very strong and active, with the governor saying that over 140 parties contacted the state with interest, 62 NDAs were signed and over eight letters of intent were received before Marx Development Group was ultimately selected. The governor stated that the firm “brings to the table a remarkable breadth of resources and extensive experience in renovating and improving healthcare facilities that are in need of thoughtful investment.”

Indeed, Marx is a vertically integrated developer (capable of building the new facilities) and operator. According to MDG’s website, it is affiliated with the skilled nursing operator Majestic Care, which operates over 40 facilities in Ohio, Indiana and Michigan. The state’s announcement referenced MDG owning and operating 55 senior care properties with over 5,000 licensed beds in Indiana, Michigan, New York, Ohio and Kentucky. The deal is set to close either at the end of September or the end of October.

Invesque (OTCMKTS: MHIVF) sold its two remaining skilled nursing facilities in Illinois. They were previously leased via a long-term, triple-net structure that included a tenant purchase option. Proceeds from the transaction allowed the company to fully repay the KeyBank credit facility. With this payoff, Invesque now has two unencumbered assets that were previously secured by the credit facility, providing additional financial flexibility.

While Invesque is exiting the skilled nursing sphere, The Ensign Group (NASDAQ: ENSG) is ever-expanding in it. The company announced three transactions, growing in Wisconsin, Iowa and California. First, through two separate transactions on the same day, Ensign acquired the real estate and operations of Pine Crest Health and Memory Care, a 120-bed skilled nursing facility in Merrill, Wisconsin (with 70% occupancy and a 19.5% quality mix), and Crystal Heights Care Center, a 72-bed skilled nursing facility in Oskaloosa, Iowa. Subsidiaries of Standard Bearer Healthcare REIT, Ensign’s captive real estate company, acquired the real estate for both facilities, which are operated by Ensign-affiliated tenants.

The Giannini Group at Marcus & Millichap handled the

Merrill sale, which saw a price of $9.5 million, or $79,200 per bed. Ryan Saul and Nick Cacciabando of Senior Living Investment Brokerage represented the seller in the Crystal Heights transaction.

On the same day, Ensign acquired the operations of five senior care facilities in California. The acquisitions are subject to new triple net lease arrangements with affiliates of CareTrust REIT (NYSE: CTRE) and International Equity Partners. Courtyard Health Care Center is a 112-bed skilled nursing facility in Davis, and Pacific Gardens Nursing and Rehabilitation Center is a 171-bed SNF in Fresno.

Sitting on the same campus in Modesto, Vintage Faire Residential comprises 31 assisted living units and Vintage Faire Nursing & Rehabilitation Center features 99 skilled nursing beds. Arbor Place and Arbor Rehabilitation & Nursing Center, also sitting on the same campus but in Lodi, feature 48 assisted living units and 149 skilled nursing beds, respectively. Lastly, Turlock Residential and Turlock Nursing and Rehabilitation Center offer 30 assisted living units and 144 skilled nursing beds, respectively, on the same campus in Turlock.

The management assumption also included three additional skilled nursing facilities in California: Shoreline Care Center (193 beds in Oxnard), Buena Vista Care Center (150 beds in Santa Barbara), and Huntington Park Nursing Center (99 beds in Huntington Park). They are being operated under management agreements pending certain state regulatory reviews. In total, Ensign-affiliates added over 1,200 operational beds/units to Ensign’s portfolio through the acquisition of the operations of these eight senior care facilities.

Ensign’s portfolio now comprises 361 healthcare operations, which includes 47 senior living operations, across 17 states. Ensign subsidiaries, including Standard Bearer, own 148 real estate assets.

In another transaction with a REIT as the buyer, Strawberry Fields REIT (NYSEAMERICAN: STRW) acquired a senior care facility with 108 skilled nursing beds and 16 assisted living beds for $5.3 million, or $42,700 per bed, in Poplar

Bluff, Missouri. Ryan Saul, Jeff Binder and Lucas Doll of Senior Living Investment Brokerage arranged the sale, representing a regional owner/operator that was exiting the state of Missouri to focus on communities closer to its corporate headquarters.

Cedargate Healthcare features a 108-bed skilled nursing portion built in 1973 and a 16-unit assisted living community added in 1996. Renovations were also completed in 2021, and the campus benefitted significantly from the new Medicaid reimbursement methodology implemented in 2022, including a $37 per-patient-day increase on January 1, 2025. It still has a long way to go census-wise, with occupancy sitting at 43%. But the campus still generated positive cash flow of $560,000 (EBITDAR) on $5.74 million of revenues.

The deal resulted in a 10.6% cap rate, which seems appropriate given the unit mix. The facility was added to an existing master lease with an affiliate of Reliant Care Group. The acquisition will increase the REIT’s annual rents by $530,000 and is subject to 3% annual increases.

Toby Siefert of SLIB also handled the sale of a skilled nursing/memory care facility in Northborough, Massachusetts, on behalf of a private owner looking to retire from the industry. Finding the right buyer was important to the seller, so Siefert sourced Alliance Health and Human Services, a not-for-profit owner/ operator of several skilled nursing and rehab facilities in Massachusetts, to take over the campus. Built in 1999, the campus includes 45 skilled nursing beds and 12 memory care units (22 MC beds). It was operating profitably. The buyer assumed the existing HUD debt balance through a quick TPA process. According to Community Advocate, the purchase price was $5.95 million, or $88,800 per bed.

Blueprint was engaged by a regional owner/operator, subject to approval by the U.S. Bankruptcy Court for the Eastern District of New York, to conduct a comprehensive marketing process for the sale of Liberty Health and Wellness in Liberty, Missouri. Formerly a 143-bed, highlyprofitable and well-occupied skilled nursing facility, the asset encountered regulatory and survey challenges

that led to its decertification from CMS and the Missouri Department of Health and Service Services. Shortly after the marketing campaign launched in March, the facility closed.

Blueprint repositioned the 75-unit facility offering to appeal to skilled nursing, behavioral health and other alternative-use acquirers. There was strong market interest with multiple competitive offers from both skilled nursing and behavioral health providers. The highest and best offer was from Capital Foresight Limited Partnership at over $40,000 per bed, certainly a strong price for a vacant facility. Michael Segal, Amy Sitzman, Giancarlo Riso and Daniel Waldhorn handled the transaction.

Next for Blueprint, Connor Doherty and Ryan Kelly facilitated the sale of a skilled nursing facility in Ohio on behalf of a group of investors from around the area looking to exit the business. The asset featured a phased physical plant with modernized components and was operating at strong occupancy levels at the time of marketing. The facility benefited from stable operations, a solid patient mix, and established referral relationships.

Blueprint targeted buyers aligned with the facility’s operational consistency and long-term positioning in the market. There was interest from multiple regional and national operators seeking to expand their footprint and add scale within the state, resulting in three competitive offers. The transaction closely smoothly, with the ultimate buyer, a regional operator looking to grow their presence in the area, acquiring the facility for $11.5 million, or $119,800 per bed.

Evans Senior Investments represented a regional, Florida-based owner/operator in the sale of two non-core assets, Pinecrest Rehabilitation Center and Tamarac Rehabilitation and Healthcare Center. That seller was NuVision Management , which commented on the eventual purchase price exceeding its expectations, especially for non-performing assets.

Built in 1967 and 1979, the two skilled nursing facilities are less than 30 miles from each other in Miami, Florida, and encompass 220 total beds. At the time of securing

the buyer, both facilities were losing money, and ESI highlighted the upcoming Medicaid rate increases. No other details were disclosed, but we would guess the per-bed price surpassed $150,000.

Andrew Montgomery and Jeremy Warren of Montgomery Intermediary Group also handled a transaction with a struggling SNF, this time in a smaller central Missouri market. Built in 1967, the facility features more than 90 beds and was between 35% and 40% occupied at the time of sale. The seller was a local Missouri owner, and the buyer was a repeat MIG client. The turnaround asset is in a rural area, and while the purchase price was not disclosed, it was said to be in line with similar deals that MIG has closed in comparable Missouri markets. In addition to this transaction, MIG closed a couple of other deals in the Midwest.

Jeffrey Vegh and Joe Schiff of Forest Healthcare Properties closed three skilled nursing transactions. The first deal involved the sale of two skilled nursing facilities that sit near each other just outside Philadelphia, Pennsylvania. The cash-flowing assets total 242 beds. The seller was a New Jersey-based operator, and the buyer entered the state through the acquisition.

Forest handled two additional closings, both in Kentucky. In Louisville, a SNF with more than 120 beds and an occupancy rate above 85% changed hands. The buyer was a large regional operator looking to expand its existing footprint in the state. The final transaction involved two SNFs in rural Kentucky, near the Tennessee border about 20 minutes apart. The seller was a mom & pop, and the buyer was a prominent Kentucky operator adding to its in-state portfolio.

SENIORS HOUSING ACQUISITIONS

A couple of major operator announcements made news after Labor Day, most notably AlerisLife’s decision to wind down its business and transition all of its operations to other operators. The company had struggled for years as a publicly traded company (previously known as Five Star Senior Living) with chronic operational and governance issues, posting repeated net losses, negative

EBITDA, low operating margins, and underperforming owned communities. Despite some gains and cost savings after Alvarez & Marsal’s operational review in 2022, the company failed to generate meaningful profits, and leadership changes did not reverse declining performance. Shareholder value suffered for some time, with the company finally being acquired in 2023 by ABP Acquisition LLC, a firm majority-owned by Adam Portnoy, the CEO of RMR Group (NASDAQ: RMR), which runs Diversified Healthcare Trust (NASDAQ: DHC).

Now, AlerisLife is transitioning its management of 116 Diversified Healthcare Trust-owned seniors housing communities to seven different operators, while also selling its 17 owned communities. The deal would help fully wind down AlerisLife’s business and operations by the first half of 2026.

AlerisLife engaged a third-party investment banking firm to help with the process of selling its owned communities and management agreements. A marketing process commenced in April 2025, and after outreach to more than 300 potential counterparties and a competitive bidding process, AlerisLife and DHC selected seven operators to purchase the management agreements for the 116 DHC communities. The transition of these management agreements will occur in tranches beginning in September and is expected to be completed by year end, subject to customary closing conditions and lender and regulatory approvals where required.

In connection with AlerisLife’s asset sales and after repayment of debt and payment of estimated wind-down costs, DHC expects to receive estimated net proceeds of between $25 million to $40 million for its 34% interest in the company. DHC plans to use these net proceeds to reduce leverage and for other general business purposes, including reinvestment in its SHOP segment.

The closing of these transactions is expected to strengthen DHC’s balance sheet and improve SHOP community performance with the transfer of management agreements to a diversified pool of more capable operators, unlocking operational efficiencies, driving cost savings, and positioning DHC’s SHOP segment

Chart a course for service.

The Senior Housing and Healthcare Lending team at Synovus offers tailored expertise in welcoming every generational wave, whether they arrive in calm or choppy economic waters.

Contact Jennifer Lawley at (205) 868-4759 or JenniferLawley@synovus.com synovus.com/seniorhousing

for accelerated revenue and NOI growth. Performancebased terms and operator investments will further align interests and drive improved results.

Also, right before we went to print, LCS and Vi announced a strategic merger, adding Vi’s 10 communities and 4,000 residents to the LCS portfolio of more than 130 communities. Depending on regulatory approvals, the merger is expected to close in mid-2026, with both companies continuing to operate independently until that point. Vi is the rebranded Classic Residence by Hyatt portfolio, which was founded by Penny Pritzker in the 1980s. Meanwhile, LCS was founded in 1971 by Fred Weitz.

LevinPro LTC’s proprietary database shows that prices have risen on average for seniors housing assets over the trailing four quarters. It could mark the beginning of an upswing that may soon set new records (read more on the seniors housing environment in the lead on page 1).

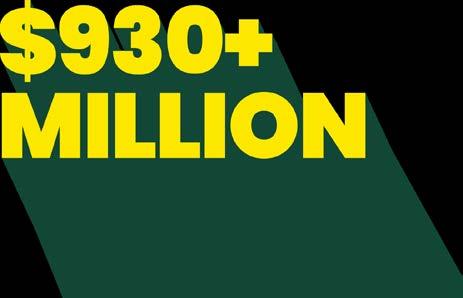

If August is any indicator, average prices will start rising fast, as we recorded the four highest (reported) per-unit prices for the year, so far. One of those deals was a big one, when Harrison Street Asset Management sold five Class-A seniors housing communities throughout central Long Island and New York. The deal was valued at more than $600 million, and it was handled by Newmark.

The portfolio comprises five assets, developed in partnership with B2K Development between 2016 and 2022. The Long Island Business News identified the five properties as part of the “Bristal” brand of assisted living communities, including Bristal Assisted Living in Mount Sinai, Bristal in West Babylon, Bristal in Holtsville, Bristal in Bethpage and Bristal in Jericho, all totaling more than 850 units.

That would put the price above $700,000 per unit. We also understand from those familiar with the portfolio that the operating performance was exceptionally strong, especially considering the majority-assisted living unit mix, although there were independent living and memory care units, as well. According to multiple sources, the buyer appears to be Ventas (NYSE: VTR), and B2K will

continue to manage the portfolio.

In a separate transaction involving another five-asset seniors housing portfolio with a strong price-per-unit, JLL Capital Markets represented a joint venture between Iron Point and Avanti Senior Living that was divesting five Class-A, high-performing communities in Texas and Louisiana with upside potential. Built between 2015 and 2019, the communities comprise approximately 90 units each, with a total of 67 independent living, 201 assisted living and 179 memory care units in the Houston and Dallas, Texas, markets and the Lafayette and New Orleans, Louisiana, markets. The portfolio, which is entirely private pay, was and will continue to be operated by Avanti.

The purchase price was $147.7 million, or $330,000 per unit. The buyer, Ventas, expects Year 1 metrics to include a cash NOI yield of 7%, occupancy of 91%, an NOI margin of 32%, and a RevPOR of roughly $6,700 a month.

There were a few other portfolio transactions that closed this month. Municipal Capital Appreciation Partners (MCAP) acquired nine seniors housing communities totaling more than 780 beds. The portfolio is mostly in Virginia, with locations in Connecticut, Maryland, Michigan and Pennsylvania.

This was part of Invesque’s sale of its 20-property Commonwealth Senior Living portfolio, approved earlier this summer. MCAP emerged to repurchase the properties after selling them to Invesque in 2019 for $340.4 million. Commonwealth Senior Living will continue to operate the portfolio. To fund the acquisition and renovation of the nine properties, BMO’s Healthcare Real Estate Finance group closed a $117.325 million facility for affiliates of MCAP.

Senior Living Investment Brokerage handled the sale of a portfolio of three well-performing seniors housing communities in Montana and Oregon to Integrated Senior Foundation. The properties are in Sweet Home and Cottage Grove, Oregon, and Great Falls, Montana. Jason Punzel, Vincent Viverito, Brad Goodsell, Jake Anderson, and Taylor Graham represented the regional

operator seller, which developed and recently remodeled the communities. The seller will use the proceeds to expand its portfolio.

Built in 1996 and renovated in 2020, Magnolia Gardens is in Cottage Grove, Oregon, with 101 independent living, assisted living and memory care units on a 5.02-acre plot. The community was 96% occupied at the time of sale. Built in 1997 and renovated in 2023, Wiley Creek is in Sweet Home, Oregon, on 6.87 acres with 108 independent living, assisted living and memory care units. It is 96% occupied. Built in 2001 and renovated in 2022, The Lodge is in Great Falls, Montana, with 78 assisted living units on 5.06 acres and was 92% occupied. The three assets collectively comprise 155,058 square feet. They are stabilized with strong cash flow and operating margins.

The three communities sold for a combined $77.8 million, or $271,100 per unit. Occupancy was strong, averaging 95%, and we believe the operating margin was close to 35%. That healthy performance, combined with the

communities’ age, could put the cap rate close to 8%, based on our estimate. The buyer funded the transaction using tax-exempt bonds, and the seller plans to use the proceeds to expand its portfolio.

JLL Securities and JLL Capital Markets arranged $79.32 million in tax-exempt, floating-rate bank financing for the acquisition. JLL secured a low spread bridge loan, financing the acquisition at 103% loan to cost. Greg Fawcett served as placement agent, and the JLL Capital Markets Seniors Housing team was led by Alanna Ellis, Alex Sheaffer and Erik Cassella.

JLL Capital Markets was involved in a separate transaction, this time facilitating the sale of Loma Clara, an 89-licensed-bed, Class-A seniors housing community in Morgan Hill, California. JLL’s Seniors Housing Capital Markets team marketed the property on behalf of the seller, Steadfast Senior Living, and procured the buyer, LTC Properties (NYSE: LTC). The REIT acquired the community within its SHOP segment with an estimated year-one yield of 7%, and will retain Discovery

Management (an affiliate of Discovery Senior Living) as the operator, establishing a new relationship.

Completed in 2018, Loma Clara is a two-story building offering 42 assisted living units and 25 memory care units with 41 MC beds. The property is 92% occupied and is a full private-pay community, with units averaging 529 square feet. It is positioned on a 1.73-acre site, adjacent to an active adult community and numerous medical facilities, including a major Hospital.

LTC Properties’ second quarter press release noted the community was making $2.71 million of EBITDAR, and was acquired for $35.2 million, or $525,400 per unit, at an 8% cap rate. Another one of the highest per-unit prices we have seen so far in 2025. JLL’s Seniors Housing Capital Markets team representing the seller was led by Senior Managing Director Aaron Rosenzweig and Senior Director Dan Baker.

Senior Living Investment Brokerage continued its active month, closing numerous deals across the skilled nursing and seniors housing spectrum. Dave Balow facilitated the sale of an assisted living program community in the Albany, New York MSA, on behalf of a private owner. Built in 1985, Danforth Adult Care Center is in Hoosick Falls and features 57 units with 80 beds, including 42 licensed as ALP. The community sits on 2.49 acres with 29,112 square feet and maintains a roughly equal payor mix of private-pay and Medicaid residents. It generated $303,800 in EBITDAR on $3.17 million of revenues, with 83.8% occupancy.

The offering was marketed in the summer of 2024, attracting several competitive offers. The buyer, a New Jersey-based ALP owner/operator with a growing portfolio across upstate and downstate New York and a strong presence in the Albany MSA, paid $7 million, or $87,500 per unit. The property was HUD-eligible and presented advantages for the new owner, including potential augmentation of ALP bed count every two years under the state’s application process. The buyer financed the acquisition with a bridge loan, intending to eventually transition it into HUD financing.

Next for SLIB, Matthew Alley announced another Lone Star State deal, selling a 20-unit memory care community in Sugar Land, Texas. Built in 1998, Barton House Memory Care was the only seniors housing asset of a notfor-profit organization, which decided to divest. It was 80% occupied but losing around $30,000 a year on $1.26 million of revenues. A local family-owned company will look to take advantage of its market presence to bolster census and improve the operating margin. They paid $1.6 million, or $80,000 per unit.

Bradley Clousing, Daniel Geraghty and Ryan Saul were engaged by a Southeast owner/operator in its divestment of two seniors housing communities that sit a few blocks apart in Wilton Manors, Florida. The buildings total 159 independent living and assisted living units, and were cash flow negative when the seller acquired them in late-2022.

Post-acquisition, the owner/operator completed extensive renovations, and then the operator, Golden Bell Senior Living, was brought on to rebuild census and significantly improve operating performance at both communities. The buyer, a South Florida-based private fund, will keep Golden Bell on as the operator. Seems like a good choice. There was a confidential and competitive market for the offering, with no additional details disclosed.

Clousing and Geraghty, along with Balow, additionally sold a 104-unit assisted living/memory care community in Florence, Kentucky. Built in 2007 on nearly 12 acres, Fields of Florence is well maintained and competes well in the local market. The private equity seller had purchased the asset in March 2024 (see the deal here on LevinPro LTC) when it was 60% occupied, but its operator turned around the operations quickly, with occupancy reaching 85%. So, the PE firm approached SLIB to conduct a tight marketing process, finding another private equity group with a strong Southeast-based operating partner to take over.

Also in Kentucky, DMK Development Group divested a seniors housing portfolio in the Louisville and Lexington MSAs. The four communities were purposefully developed within a 50-mile radius to enhance operational

efficiencies. They are in Bardstown, Danville, Winchester and Shelbyville, totaling 316 assisted living and memory care units with 56 AL and 23 MC units in each community. The communities were opened between late 2020 and early 2022, and each was highly occupied at the time of the sale and maintained occupancy at 90+%.

Trilogy Health Services, a long-time operating partner of DMK’s, managed the portfolio throughout lease-up and stabilization. DMK developed the portfolio with the help of several banking partners, including Stock Yards Bank & Trust, Republic Bank, Independence Bank and Old National Bank. American Healthcare REIT (NYSE: AHR) acquired the portfolio for $65.3 million, or $206,600 per unit, in July. The REIT will keep Trilogy on as operator.

DMK Development Group completed another divestment in July, selling a 167-unit seniors housing community in Venice, Florida. The buyer was New York-based real estate investment manager Town Lane. The company assumed a $25.71 million mortgage on the property in the offmarket transaction. Atlas Senior Living will continue to

operate the community.

Developed by DMK in 2023, The Goldton at Venice was highly occupied at the time of sale. The community offers a full continuum of care, including 114 independent living, 38 assisted living and 15 memory care units. There are a wide range of amenities such as a fitness center, heated saltwater swimming pool, movie theatre, wellness spa and salon, sports bar, pickleball court, putting green and multiple dining venues.

Town Lane is prioritizing recently built, full-continuum assets in growing markets. Earlier in the summer, Town Lane acquired two other Class-A, full continuum seniors housing communities in Florida, Discovery Village Naples in Naples and Discovery Village Sarasota Bay in Brandenton, with this being its third seniors housing acquisition in the region.

Additionally for DMK in July, despite the difficult market conditions surrounding new construction, the company completed the development of a project in West Bend,

Wisconsin, that was 65% pre-leased. The 114-unit community, managed by Charter Senior Living, consists of 50 independent living, 44 assisted living and 20 memory care units.

The company also opened a 79-unit community in Murray, Kentucky, in the same month. The community is also managed by Charter and comprises 56 assisted living and 23 memory care units with strong pre-leasing success.

Back in June, DMK broke ground on a 191,000-squarefoot project in Sheboygan, Wisconsin, that will feature 183 units including 114 IL, 48 AL and 21 MC units.

Construction is scheduled to be completed in Spring of 2027. The company also has a community under construction in Winder, Georgia. Similar to the West Bend prototype, the community will comprise 110,000 square feet and will offer 50 IL, 44 AL and 20 MC units. Construction is scheduled for completion in summer of 2026. Both communities will be managed by Charter Senior Living. DMK Development Group’s pipeline consists of four to five projects slated to start in the next six to nine months.

Continuing with transactions involving Class-A seniors housing communities, Principal Asset Management (Principal Financial Group’s investment management division) and IRA Capital announced the acquisition of American Groves, a Class-A seniors housing community in Gilbert, Arizona, for $44.5 million, or $500,000 per unit. The sale was facilitated by JLL Capital Markets on behalf of the seller, American Care Concepts and Reichmann International Realty Advisors , which developed the community in 2021.

American Groves is a two-story, 89-unit community, offering independent and assisted living services. Each unit has the ability to transition between independent and assisted living in response to changing resident needs, enabling the community to adapt to future demographic and operational trends. It comprises 107,138 square feet and sits on 5.58 acres.

JLL arranged the sale of a Class-A community in Foster

City, California. Built in 2016 by Atria Senior Living as part of a mixed-use master-plan town center development, Atria at Foster Square comprises 155 assisted living and memory care units.

Artemis Real Estate Partners purchased the community in partnership with Atria, and Atria will continue to operate the community under its Atria Signature Collection brand. Aaron Rosenzweig and Dan Baker of JLL’s Seniors Housing Capital Markets team handled the transaction. No additional details were disclosed.

Benchmark Senior Living added another Connecticut community to its portfolio, acquiring the Class-A Church Hill Village in Newtown through a joint venture with National Development, a Massachusetts-based real estate investor. Built in 2019 by a partnership between Senior Lifestyle Corporation and Teton Capital Co., the 71-unit assisted living/memory care community is laid out in four connected residential neighborhoods.

It is Benchmark’s 21st community in Connecticut, and the ninth in the affluent Fairfield County. The company has also made recent investments with National Development in New Jersey and New York. Webster Bank provided acquisition financing for the deal, but no terms were disclosed. Newmark handled the transaction.

Following its involvement in the sale of Church Hill Village, plus Harrison Street’s sale of its Long Island portfolio to Ventas, Newmark handled another transaction featuring a high-end asset. Developed by Bayshore Retirement Living in 2019, The Bayshore on Hilton Head Island comprises 126 independent living and assisted living units in Hilton Head Island, South Carolina. It also expanded in 2023 with 26 additional IL villas.

Occupancy has consistently been strong, and we imagine the operating margin was quite healthy, too. LCS was the in-place operator. The ultimate buyer was not disclosed, but Newmark helped to arrange acquisition financing for them, as well as handling the sale.

Blueprint facilitated the sale of a Class-A, cash-flowing seniors housing community in Glendale, Arizona. Built

in 2015, the 85-unit assisted living and memory care community reflects institutional-quality construction and design, and has benefited from consistently strong occupancy. There was a competitive bidding environment, with nine offers secured. The seller was an institutional joint venture.

The asset was ultimately acquired by a well-established regional owner/operator with a portfolio of nearby, directly competing properties. Their local presence and market familiarity are expected to unlock synergies and performance upside. Amy Sitzman and Giancarlo Riso handled the transaction.

Blueprint was separately engaged in the sale of a 110unit seniors housing community in Perrysburg, Ohio. It operated as an independent living community, but was positioned for conversion to assisted living, with a focus on serving waiver-eligible residents. Ben Firestone, Connor Doherty and Ryan Kelly handled the transaction. A buyer with a track record in executing value-add conversions and an existing Ohio footprint was ultimately selected.

Doherty and Kelly were next engaged to market a 100unit vacant assisted living community located 10 miles south of Cleveland, Ohio, that had been taken offline following operational challenges. The community was profitable during prior operations. Blueprint generated four competitive offers from sophisticated owner/ operators with proven capabilities in executing value-add strategies. The selected buyer, known for opportunistic acquisitions, intends to reopen the community and fill it through the state’s Medicaid waiver program.

In a different transaction involving a vacant seniors housing community, Senior Living Investment Brokerage facilitated the sale of Mount Hood Senior Living. Built in 1962 and renovated in 2022, the vacant community features 44 assisted living and memory care units with 50 beds in Sandy, Oregon. It is situated on a 2.35-acre campus with 26,000 square feet.

This was the seller’s only seniors community, and they are exiting the industry. The buyer is a local operator and will reopen the community. They paid $6.3 million,

or $143,200 per unit, for the asset. Jason Punzel, Brad Goodsell, Vince Viverito, Jake Anderson and Taylor Graham handled the transaction.

Andrew Montgomery and Jeremy Warren of Montgomery Intermediary Group also handled the sale of a vacant community. It comprises 20 assisted living units in Eastern Tennessee and was built in the 1990s. The buyer paid $92,500 per unit and plans to convert it from assisted living into supportive housing for youth aging out of foster care. The buyer is looking to acquire additional assets across Memphis, Chattanooga and Central Tennessee that can be repurposed for similar uses.

Berkadia announced a few closings in the Midwest. First, Dave Fasano, Ross Sanders, Cody Tremper and Mike Garbers were engaged by Ryan Companies US in its divestment of a Class-A seniors housing community in Cedar Rapids, Iowa.

Built in 2017 by Ryan Companies, Grand Living at Indian Creek comprises 165 independent living, assisted living and memory care units. The property is situated near Mercy Medical Center and UnityPoint Health-St. Luke’s Hospital, two of the region’s leading healthcare providers. The in-place operator, Grand Living, will continue to manage the community. The buyer and financials were not disclosed.

Fasano, Sanders, Tremper and Garbers also facilitated the sale of Welstone at Mission Crossing, a 101-unit independent living community in Mission, Kansas, that was opened in 2016. The community was purchased by an affiliate of Livingston Street Capital, LLC , a Pennsylvania-based private equity firm with a national portfolio of active adult, independent living, and multifamily properties. Discovery Senior Living will stay on as the property’s operator.

In a full circle transaction, Blake Bozett and Spud Batt of The Zett Group sold a large seniors housing community in Eugene, Oregon, to a Salem, Oregon-based group in partnership with a new operator through a pre-established JV structure. Bozett represented his grandparents, Ron and Joyce Knutson, a pioneering couple who first got

involved in the seniors housing space in the 1970s in the Pacific Northwest. The Eugene property was one of two communities left in the family’s hands, with the other in Spokane, Washington.

Built in 1979 by the Knutsons, Churchill Estates features 241 units of independent living, assisted living and memory care, one of the largest communities in the state of Oregon. Ronald Roderick, from another pioneering seniors housing family in the Pacific Northwest (he was the father of Greg Roderick, the founder of Frontier Senior Living), was an original partner in the community. It was an operational juggernaut for many years. But the pandemic, combined with the community’s distance from the family’s base in Spokane, took a toll on operations, and the community was not stabilized.

So, the Knutsons decided to sell, enlisting the help of their grandson, Blake Bozett. Unfortunately, after the deal went under contract, Ron, lovingly known as “Poppie,” passed away at the age of 90 and after 71 years of marriage. “Poppie” was a force of nature, a skydiver at 85, an avid golfer, a man of deep faith and a relentless giver, and his legacy is being honored through the newly established 501 (c)(3) called “Poppie’s Legacy Foundation.”

Despite the personal loss, the deal successfully closed a few months later, with the property commanding a purchase price of $18.5 million, or $76,800 per unit. In addition, the family was able to stay in the deal with a piece of senior secured seller financing that would provide consistent trust payments. It solved for the family estate motivations and mitigated any tax liability. The capital stack also included equity and mezzanine financing.

Bozett’s career in seniors housing brokerage also began when a broker had initially reached out to the Knutsons to prospect the family portfolio, prompting a conversation with Bozett, who was in banking at the time, and leading to Bozett’s first seniors housing brokerage job thereafter. Talk about full circle. The Zett Group has an active pipeline, which currently represents over $100 million in active engagements.

A couple additional seniors housing transactions closed

this month. A high-quality independent living community sold in northern Michigan, thanks to Justin Knapp and Jim Knapp of The Knapp-Stahler Group at Marcus & Millichap. Whispering Pines was purpose-built in Lake City with 48 units. It boasted strong in-place occupancy and faced little local competition. Across the 19 acres, there are also wooded walking trails, a large pond and a central clubhouse. The community offered an opportunity for a new owner to serve a broader population through the Michigan Choice Waiver program, which the undisclosed buyer will do.

Three active adult sales closed in August, too. Newmark arranged the sale and financing for an active adult community in Huntington Beach, California. The seller, Bascom Group, was represented by Newmark Vice Chairman Dean Zander, who worked on the deal with Voit Real Estate Services’ Joe Leon and Nick Ingle. Huntington Breeze is a 114-unit, 103,000-square-foot community that was built in 1987 and renovated in 2017.

Newmark Executive Managing Directors Vincent Punzi and Lowell Takahashi facilitated acquisition financing on behalf of the buyer, WSW Property Ventures, a new venture headed by Steve Wasserman, Pamela Scott and George Wu. WSW plans to unlock additional value through strategic initiatives, including the potential development of accessory dwelling units, capturing below-market rents and implementing a renovation program. The purchase price was $35 million, or $307,000 per unit.

The CBRE Capital Markets Houston Multifamily Group and CBRE National Senior Housing also handled the sale of an active adult community in Houston, Texas. Built in two phases in 2006 and 2012, Elate Royal Oaks, previously known as Camden Royal Oaks, consists of 340 units (236 were built in Phase 1, and 104 were built in Phase II). Clint Duncan, Matt Phillips, Jock Naponic, Nolan Mainguy and Philip Kerr of the Multifamily Group, as well as Aron Will and John Sweeny on the seniors housing side, represented the seller.

CBRE National Senior Housing also acted as the advisor in securing acquisition financing on behalf of the buyer through its Debt & Structured Finance team. Aron Will

and Michael Cregan originated the five-year, fixed rate loan on behalf of the joint venture between GEM Realty Capital and Middle Street Partners. Post-closing, the community will be operated by Greystar under a thirdparty management contract.

GEM Realty Capital acquired a separate active adult community in June for $32.925 million, or $204,500 per unit, with Inspired Real Estate Partners. Built in 2020, Lakeview at Germantown, previously known as Avenida Watermarq, is a 161-unit, Class-A community in Germantown, Tennessee, that was 87% occupied at the time of sale. The joint venture brought on Gallery Residential to manage the community. Newmark handled that transaction.

Lastly, Stellar Senior Living announced the close of its first joint venture with $20 million in capital commitments. Stellar’s partner is a large private equity firm, and the joint venture will provide funding to acquire 10 to 15 seniors housing communities over its term.

The first acquisition under this new venture is The Grand at Broomfield Assisted Living & Memory Care, previously known as The Gallery at Broomfield, in Broomfield, Colorado. The Class-A community was built in 2023 and features 115 assisted living and memory care units.

Stellar has managed this community for the past couple of years, and is now also a minority owner. The community leased to 100% occupancy in the first seven months and has not dropped since then. Perhaps it is time for a rate increase. The acquisition marks the first of many more to come from the new capital raise.

AGENCY LOANS

Since launching in February, Ikaria Capital Group, whose team brings more than 100 years of collective experience in financing, structuring, underwriting, servicing, and asset-managing bridge and FHA/HUD loans, has already completed its first HUD transaction. The $16.5 million closing was executed on behalf of a private investment firm.

The borrower, an existing client, had previously acquired a skilled nursing facility in California in 2023. The HUD takeout enabled the borrower to execute its long-term financing plan. Ross Holland originated the loan.

A few separate agency loans were highlighted this month. Helios Healthcare Advisors arranged acquisition financing for a 124-bed skilled nursing facility with a strong quality mix in Pasadena, Texas, on behalf of a regional healthcare operator that had been leasing the property from a third-party landlord. The financing package was $12.9 million, or $104,000 per bed.

Leveraging the facility’s strong occupancy and financial strength, Helios structured a direct HUD acquisition loan through a national HUD lender. The capital structure also included a seller note, allowing the borrower to close the transaction with minimal cash investment.

Pillar Stone Healthcare Company, based in Houston, Texas, acquired Baywood Crossing Rehabilitation & Healthcare Center for $12.5 million, or $100,800 per bed. The HUD loan financed $9.9 million of the purchase price, with a $3 million seller note covering the remainder.

In another transaction, CBRE National Senior Housing originated construction debt from HUD for a seniors housing development in Rancho Cucamonga, California. The project, Rancho Cucamonga Memory Care, is being built by a joint venture between Flatiron Development Group, Spring Capital Group and Anthem Memory Care. Upon completion, it will feature 64 units (72 beds) in a single-story, H-shaped building design. Resident units will make up the north and south wings, while the central portion will house the main entrance, commercial kitchen, laundry facilities, administrative offices, and communal living and dining spaces.

CBRE National Senior Housing’s Debt & Structured Finance Team, led by Aron Will, Joshua Hausfeld and John Turner, originated the $17.26 million loan through CBRE’s direct FHA Lending Platform. The financing, structured under HUD’s Section 232 Mortgage Insurance Program, provides construction funding that converts to a 40-year, non-recourse, fully amortizing permanent loan upon

completion. The community is also pursuing National Green Building Standard Bronze Certification, which would qualify it for reduced Green Mortgage Insurance Premium of 25 basis points.

In May 2025, Berkadia closed a $7.6 million 232/223f HUD loan to refinance Whitewood Gardens, a 39-unit assisted living community built in 2013 in Portland, Oregon. The fully amortizing, 35-year term represents 78% LTV and allowed the sponsor to avoid a loan maturity. Ed Williams and Rob Affleck handled the transaction. Early in the process, they pinpointed HUD’s project eligibility requirements, and, during underwriting, addressed the need for additional bathrooms to meet with compliance. Leveraging relationships with HUD engineering and repairs experts, the team guided the construction process, securing approvals on last-minute requests. The loan covered the initially anticipated bank debt, but also addressed additional debt identified post-submission, thanks to improved operations during underwriting.

KeyBank Community Development Lending and Investment provided a $13 million construction loan to finance the construction of Hawthorne Heights, an 86unit affordable seniors housing project in Gainesville, Florida. KeyBank Commercial Mortgage Group (CMG) also arranged a $6.53 million Freddie Mac permanent loan for the project.

Hawthorne Heights will serve seniors aged 62 and up with five apartment homes specifically set aside for individuals with special needs. The five-story building will be constructed on a 2.9-acre site. The development will set aside three apartments for households earning 22% of the area median income, nine apartments for households earning 40% or below the AMI and 74 apartments for households earning 60% or below the AMI.

The sponsor, National CORE, is an experienced notfor-profit developer with ownership of more than 105 properties serving more than 30,000 residents across California, Florida and Texas. The project secured additional funding from Red Stone, providing Low Income Housing Tax Credit (LIHTC) equity and bonds from Florida

Housing Finance Corporation. The property qualifies for real estate tax abatement, which provides tax exemption for not-for-profit-owned properties that commit to using it for providing affordable housing for at least 99 years.

The CT Group will manage the property, utilizing its more than thirty years of experience in affordable and lowincome housing management. The CT Group currently manages 926 units across 12 properties in Florida, including Hampton Court, a 42-unit Section 8 property in Gainesville.

Completion of Hawthorne Heights is anticipated by November 2026. The lease-up period is expected to commence in August 2026, with stabilization projected for July 2027. Matthew Haas and Cathy Danigelis of KeyBank CDLI structured the financing. Hector Zuniga Jr. and Rod Reynolds of KeyBank CMG arranged the permanent loan.

CONVENTIONAL LOANS

WesBanco Bank launched its dedicated healthcare vertical, under the leadership of Suzanne Myers as EVPCommercial Healthcare Director, and is already off to the races with a handful of closed senior care transactions. The bank’s strategic initiative will provide financing across the continuum of care, including seniors housing, skilled nursing, CCRCs, hospitals and specialty care.

So far this year, the bank has closed over $200 million in loans for acquisitions, recapitalizations, working capital and bridge-to-HUD loans for clients across the Midwest and Mid-Atlantic. Plus, there is a pipeline of closings that exceeds $500 million for 2025. It is great to see that kind of liquidity injected into the industry.

Some of the highlights include a $67 million loan for a northeastern Ohio operator to refinance and cash out of four skilled nursing facilities with 340 total beds in the state. The borrower will use the cash out to construct new buildings and is on the path to a HUD refinance.

On the construction financing front, WesBanco provided a $19 million loan for a new 90-bed skilled nursing facility

in the Midwest. In Nebraska, WesBanco also closed a $10 million bridge-to-HUD loan and revolver to refinance a 50bed skilled nursing facility. This was a recapitalization for a property that was financed with HUD several years ago, and the loan will also serve as a bridge-to-HUD.

Lastly, WesBanco closed a $35 million bridge line for an East Coast operator to acquire skilled nursing facilities. We know there is a lot in the pipeline, so stay tuned for future WesBanco closings.

BWE closed a $330 million financing on behalf of Spectrum Retirement Communities. The transaction refinances an eight-property Class-A seniors housing portfolio developed by the sponsor. They are in major metropolitan areas in four states across the Midwest and Southwest. Ryan Stoll and Taylor Mokris of BWE’s National Seniors Housing and Care team arranged the financing.

The transaction attracted strong interest and competition from an array of lenders, including agencies, life insurance companies, banks and private credit firms. Ultimately, a global private credit investor provided the non-recourse financing, which includes full-term interest-only, a highly competitive interest rate, and favorable structural terms.

A former office-to-senior-care conversion project in New Jersey received a recapitalization and revolver, courtesy of Metropolitan Bank and G Capital. Grant Goodman of G Capital arranged the loan on behalf of an experienced developer/investor with a 30+ year track record and a diversified investment portfolio. The borrower has deep expertise in the hospital sector, but this was its first senior care deal.

It had partnered with a veteran SNF operator to convert the asset into a modern senior care facility inspired by the Green House model, investing significant equity in the project. Featuring both skilled nursing and assisted living services, it re-opened in March 2020. That was unfortunate timing, as the facility faced immediate headwinds dealing with the pandemic, and ownership had to invest more equity in the extended lease-up period. But it has since surpassed 90% occupancy and achieved

a five-star rating.

So, the time came for a recapitalization, and Goodman approached a mix of banks, debt funds and HUD finance companies to provide an array of options. Robert Albano of Metropolitan Bank ultimately led the way in providing $29.5 million in total financing, including a $500,000 ABL revolver. The loan has a three-year term and 12 months of interest only, with a fixed rate featuring a seven handle. There is also exit flexibility to go to HUD in the next year. The borrower is now planning several more similar redevelopment senior care projects.

Helios Healthcare Advisors arranged an $11.63 million refinance for a 191-unit/231-bed portfolio of assisted living and memory care communities in Arkansas on behalf of a regional owner/operator. Spread across four locations in the Ouachita Mountain region of Arkansas and primarily serving a Medicaid population, the portfolio is a sub-set of the borrower’s larger operation. It experienced challenges associated with rising costs and little to no reimbursement rate relief from the Living Choice Medicaid waiver program.

The ask did not pencil out at the time it initially went to market and there was pressure from the borrower’s lender, which had inherited the credit through a recent acquisition. Ultimately, Helios identified a lender that was able to get comfortable with the nuances of the transaction.

Anticipating changes to the reimbursement environment, the borrower engaged Helios, which arranged a refinance with a bridge-to-HUD lender that recognized how the reimbursement shift would affect revenue. The loan was structured as an interest-only, 24-month bridge loan, priced at SOFR + 350. In addition to retiring all the existing matured debt, the financing reset the capital structure for the borrower and its principals.

Berkadia announced the closing of a few financings. First was the refinancing of Monark Grove Madison, a Class-A, 132-unit, independent living and memory care community developed and owned by Michigan-based KIRCO. Steven Muth, Austin Sacco, Garrett Sacco and

Alec Rosenfeld of Berkadia Seniors Housing & Healthcare secured a loan through a national bank. The deal closed on July 15 after a competitive process.

Alabama-based Atlas Senior Living manages Monark Grove in Madison, Alabama. It was built in 2022 and features 105 independent living and 27 memory care units with amenities.

Next for Berkadia, Steven Muth, Austin Sacco and Garrett Sacco utilized Berkadia’s bridge lending program to secure $10 million in bridge financing for a Pacific Northwest repeat sponsor. The loan proceeds were used to retire existing debt on a 60-unit memory care community in Sequim, Washington, while also returning equity to the sponsor. At underwriting, the community was 87% occupied with a LTV of 57.5%. The 24-month, interest-only bridge loan was structured to meet HUD’s debt seasoning requirements, with Berkadia anticipating permanent HUD financing for the facility in early 2027.

Lastly, Steven Muth, Austin Sacco, Garrett Sacco, Jared Flamm and Thomas Croft secured $10 million in bridge financing for a Pacific Northwest client through Berkadia’s Proprietary Bridge Lending program. The refinancing supports a 60-unit memory care community in Washington, which operates at strong occupancy. The 24-month, interest-only bridge loan positions the property for anticipated permanent HUD financing.

MidCap Financial closed an $18.7 million first mortgage loan. The four-year, floating-rate loan refinanced the existing indebtedness on a seniors housing community in a coastal Southeastern market. The sponsor is an experienced Southeastern-based real estate investment firm. The community is newer and comprises more than 100 independent living, assisted living and memory care units. It is in the process of stabilizing.

Greystone provided a $64.96 million bridge loan for a senior care portfolio in Pennsylvania comprising three assets with 506 beds. The financing was originated by Christopher Clare, David Young, Ryan Harkins, Ben Rubin, Parker Nielsen and Liam Gallagher.

LevinPro

Deals, News & Analytics

Long-term care and health care investment intelligence. Gain an informational edge with focused news briefs, expert analysis, and in-depth deals intelligence spanning long-term care and health care industries.

The non-recourse interest-only bridge loan carries a 24-month term, two six-month extension options and a floating rate. It allows the borrower to improve operations while working with Greystone to secure HUD-insured permanent financing. The portfolio includes a combined total of 408 skilled nursing, 76 assisted living, 12 memory care and 10 independent living beds.

ACQUISITION LOANS

Ziegler announced its role as the capital structure advisor and hedge advisor in the placement of a $52.5 million acquisition loan on behalf of a regional owner/operator. The acquisition financing was used to acquire five enhanced independent living communities in Michigan. The portfolio surrounds the Detroit, Michigan MSA, and has a total of 631 units with 695 beds.

Christopher Utz advised and negotiated the transaction for the borrower and placed the loan with Oxford Finance. Ziegler’s Structured Products practice placed an interest rate cap through a competitive bid process, ultimately executing the cap with Goldman Sachs.

A few additional acquisition loans closed throughout August. Alec Blanc of Monarch Advisors closed a new loan for the acquisition of a 42-unit assisted living community in Gaylord, Michigan. Built in two phases in 2019 and 2020, the community was a strong performer, with full occupancy and a healthy margin. The borrower, QualisTerra Senior Ventures, a private seniors housing investment group, engaged Monarch to source senior debt for the transaction. Monarch was successful at securing a three-year non-recourse acquisition term loan commitment from a debt fund lender. The leverage fell between 70% and 75%.

BWE arranged acquisition financing for a seniors housing community in Carlsbad, California. Ryan Stoll and Taylor Mokris led the financing effort on behalf of Harrison Street. Following a competitive marketing process, the sponsor obtained a 10-year, fixed-rate loan with a full term of interest-only payments from a national life insurance company.

Oakmont Santianna comprises 153 independent

living, assisted living and memory care units. Originally developed and leased-up by Oakmont Management Group, the property opened in 2022 and will continue to be operated by Oakmont post-acquisition. Since stabilizing, the community has demonstrated strong performance, currently operating at 95%+ occupancy. Oakmont manages more than 90 communities nationwide and currently operates 23 properties in partnership with Harrison Street.

MONTICELLOAM announced the initial funding of $152 million in total bridge and working capital financing for the acquisition of nine skilled nursing facilities with nearly 1,100 beds across North Carolina. The debt carries a 36-month initial term with two extension options. The sponsor, a returning healthcare client with operating experience in the Southeast, will utilize a $10 million working capital line of credit to manage the daily operational needs of the facilities.

Seniors Housing Values

...cont. from page 1

most. Across all property types and qualities, the prices that investors and lenders were willing to pay and finance plummeted, which also removed many high-quality and well-performing properties from the M&A market. Any owners that could avoid selling for a substandard price did so, leaving the most motivated (and in some cases desperate) sellers to accept whatever bids they received. Most of the buyers also paid in cash, unable to obtain debt at suitable terms or cost. That combination caused the average price per unit, unsurprisingly, to drop to $156,300 in 2023 and even further to an average of $140,200 in the four quarters ended June 2024, the lowest level since 2010.

Thankfully, we had reached the bottom, as the first interest rate cuts were approved by the Fed in September 2024 and the ensuing two meetings. Even earlier than that, the belief that rates had stopped rising encouraged more lenders and sellers to return to the market, helping to push the average price paid for seniors housing communities to $167,300 in calendar-year 2024. Further improvements in the capital markets, from liquidity to

More, but still not many, owners of the highest quality communities finally pulled the trigger on a sale after delays caused by pricing dissatisfaction or by a desire to push through yet another year of high resident rate increases. All of these factors caused the average price per unit to soar 25% from calendar-year 2024 to $209,400 in the four quarters ended June 2025.

Since the turn of the century, assisted living communities have accounted for the majority of sales and of dollar volume in the overall seniors housing market, and so far 2025 is no exception, with assisted living representing close to four of every five seniors housing properties sold. The AL sector thus helped drive the increase in average prices for seniors housing, contributing a 15% rise in the average price per unit compared with 2024, from $160,900 per unit in 2024 to $184,800 in the four quarters ended June 2025.

The independent living market saw a larger increase on a percentage basis, rising 28% from $183,000 per unit in 2024 to $234,100 per unit in the four quarters ended June 2025, which is close to its pre-pandemic highs but still about $25,000 per unit below the record achieved in 2022 of $259,400 per unit.

Meanwhile, the current average price per unit for assisted living stands well below the pre-pandemic averages, which can largely be explained by the relative lack of high-quality property sales. To be fair, the higher end market has rebounded since the worst of the capital markets chaos, but not to the degree or proportion of the pre-pandemic and pre-inflation M&A markets. Poor performing, low quality and “value-add” property sales still make up the majority of deals, and whatever operating improvements that are being celebrated have not flowed through to all properties, particularly on a margin or cash flow basis.

We have heard about the high end of the market returning for a year now, but it has been a slow and steady return, and probably slower than many have expected. The number of sales that we have tracked with a per-unit price above $400,000 has doubled in 2025 so far compared with all of 2024 (albeit from a relatively low level), still a testament to both the increased quality of properties brought to market and the pricing increases for most property types.

In addition, a few August deals drew attention with some of the highest prices we have recorded all year, most notably Harrison Street’s sale of five assisted living communities in New York to a publicly traded REIT (which we believe to be Ventas, NYSE: VTR) for more than $600 million, or over $700,000 per unit. They were developed by Harrison Street Asset Management and B2K Development between 2016 and 2022. The communities have delivered strong operating performance.

We understand from those familiar with the portfolio that the performance was exceptionally strong at the time of sale, especially considering the majority-assisted living unit mix, although there were independent living and memory care units, as well. Newmark handled the deal.

A couple other deals handled by JLL Capital Markets in August topped $500,000 per unit. First was LTC Properties (NYSE: LTC) acquiring a 67-unit community in Morgan Hill, California, for $35.2 million, or $525,000 per unit, with an estimated year-one yield of 7%. Aaron Rosenzweig and Dan Baker of JLL represented the seller, Steadfast Companies, in the deal.

JLL also sold an 89-unit seniors housing community in Gilbert, Arizona, to IRA Capital and Principal Financial Group for $44.5 million, or $500,000 per unit. The seller was American Care Concepts and Reichmann International Realty Advisors , which developed the community in 2021.

These were all Q3 deals, and all August announcements, representing the three highest per-unit prices for the year, based on disclosed figures. We also believe more high-quality, high-priced deals will be announced around more favorable terms and leverage, increased buyer competition among most property types and supported higher prices. At the same time, continued operational and financial improvements (mostly for the newer, higher quality properties) warranted higher prices.

the time of the NIC Fall Conference in Austin and in the ensuing weeks. So, is the tide turning? Is the scarcity of new development, with more capital being redirected to M&A as a result, leading more investors to acquire newer, high-end and cash-flowing properties above replacement cost?

We are not quite there with prices exceeding replacement cost, which is what many developers are needing for their projects to pencil. Aron Will of CBRE agreed on our latest webinar covering LevinPro LTC’s valuation statistics (you can watch the recording of that here), saying that, “we just have not cycled through enough of that high-quality product,” that would trade at prices high enough to entice developers back into building.

“If you can make good returns doing acquisitions, a lot of investors have rationalized that as opposed to putting out common LP equity for development.” However, a “herd mentality” will likely develop with respect to a resurgence in new construction, but that will not happen for another eighteen to twenty-four months. Our gut says it could be sooner, but another further delay in new development will help to boost M&A prices for existing communities, accelerated by a group of new entrants coming into seniors housing from the multifamily, private equity and alternative investments worlds.

A combination of slightly compressed cap rates and significantly higher levels of NOI at certain high-quality communities will start setting records on a per-unit basis very soon, perhaps exceeding $1 million per unit. A figure like that would make an impression on developers and other owners of high-end properties that are sitting on the M&A sidelines. And a virtuous cycle of higher and higher quality properties, and more competition for them, could see cap rates decline further as a result.

However, given the strains the industry has gone through in just the last five years with the pandemic and the capital markets disarray, let alone the period of overdevelopment in the late-2010s that saw occupancy and margins decline across the sectors, we are not advocating for a rapid and irrational decline in cap rates. From the standpoint of risk, that would not be good for the industry,

which saw a lot of owners lose the arbitrage bet when they bought seniors housing or active adult communities for sub-6% and sub-5% cap rates, or even lower for some active adult deals. There are still real operating risks when it comes to seniors housing, even for the higher end product. Staffing challenges could rear their ugly head yet again, or any high-profile negative media attacks.

Another risk for the sector in general is the aging physical plants of thousands of AL communities across the country, approaching 50% of the total product. That could impact the attractiveness of the current inventory to the future baby boomer customers and the trend towards home health.

Inflation and the rises to both capital costs and resident rates as a result has made the affordability factor for middle- and lower-market seniors a serious issue, putting major downward pressure on assisted living’s penetration rate. There are also shortening lengths of stay for an older and frailer move-in population, permanently higher labor needs and costs, plus any major, future disruptive event yet to be considered (like a pandemic).