Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Di erence. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Opening Note

Critical Thinking

The recent news that Acrisure would be laying off about 400 employees in early 2026 in its accounting workforce due to advances in technology and artificial intelligence rattled a few nerves. It’s not surprising that advances in AI tools might reduce the need of some employees in the industry. AI has been cited as the reason for other significant layoffs this year, so why not insurance.

In September, Accenture announced a “restructuring plan” that includes exits for workers that aren’t able to reskill on AI.

Salesforce eliminated 4,000 customer support roles citing AI can do 50% of the work now.

But while AI is “killing jobs,” there is some evidence that when AI is focused on specific tasks within a job role, employment in that role can actually grow. That’s because with those specific tasks automated by AI, employees can then focus on activities where AI is less capable, such as critical thinking or idea generation.

That’s according to a recently released study by the National Bureau of Economic Research, “Artificial Intelligence and the Labor Market.” According to a recent article by Seb Murray, for MIT Management Sloan School’s Ideas Made to Matter, the study found that when AI can perform most of the tasks that make up a particular job, the share of people in that role within a company falls by about 14%. However, if AI is only concentrated in just a few tasks within a role—leaving other job responsibilities up to the worker—employment in that role can grow due to significant productivity boosts.

“Firms that adopt AI don’t necessarily need to shed workers; they can grow and make more stuff and use workers more efficiently than other firms,” said Lawrence Schmidt, MIT Sloan associate professor, co-author of the study, in the article.

‘Firms that adopt AI don’t necessarily need to shed workers; they can grow and make more stuff and use workers more efficiently than other

firms.’

The study, was co-authored by Schmidt, Menaka Hampole of the Yale School of Management, and Dimitris Papanikolaou and Bryan Seegmiller of Northwestern University’s Kellogg School of Management.

“Employees may feel anxious about their roles as organizations adopt AI technologies,” wrote the authors of a recent study, “The future of AI in the insurance industry,” by McKinsey & Company. “However, history has shown that technology typically creates new needs and opportunities, leading to the emergence of different roles and responsibilities.” The authors advised employees that going forward it’s important to seek out the right skills and develop a clear understanding of AI’s enabling role in helping with their jobs.

How do you feel about the future of work in insurance with AI rushing through the door?

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Chief Financial Officer Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus Andrew Simpson | asimpson@wellsmedia.com

National Editor Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Assistant Editors

Jahna Jacobson | jjacobson@insurancejournal.com

Kimberly Tallon | ktallon@carriermanagement.com

Columnists & Contributors

Contributors: Grahame Cohen, Todd Henderson, Zach Lerner, Aviad Pinkovezky, Carmen Sharp Columnists: Chris Burand

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT)

Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Administrator

Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design

Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator

George Jack | gjack@ijacademy.com

Andrea Wells V.P. of Content

Making a predict-and-prevent mindset shift in personal lines

“At

its core, insurance is a human business. It’s built on reassurance, not transactions.”

By Casey Kempton, President, Nationwide® Personal Lines

Economic pressures, rising repair costs and volatile weather are testing the limits of the traditional “repair-and-replace” model in personal lines insurance. Claims are rising faster than premiums can keep pace, driving higher rates, frustrating customers and eroding trust.

At the same time, consumers are delaying maintenance and assume that insurance will cover whatever they have lost, widening the gap between customer expectations and what insurance can realistically — and sustainably — deliver.

That’s why Nationwide is leading the shift to a predict-andprevent mindset. Consumers, agents and insurers gain more control by anticipating and remediating risks before they become costly claims. This approach is not abstract. It’s the path to long-term sustainability for our industry and a new way of thinking for our personal lines customers, especially those who prioritize protection.

How we got here

In many ways, our industry shaped how consumers think about insurance. We haven’t always explained the connection between economic and weather changes and rising property insurance costs, leaving many customers uncertain and confused.

Price-driven advertising and online shopping trained consumers to “switch and save” or bundle for discounts. This reinforced the idea that price, not value or level of protection, should be the deciding factor in coverage. Over time, this mindset eroded the perceived value of insurance and weakened relationships among insurers, agents and consumers.

The path forward

To shift the consumer to a predict-and-prevent frame of mind, we will give customers more control and confidence in protecting what matters most to them. Insurance must deliver day-to-day assurance through better experiences, clear communication, stronger agent and community engagement, and smarter technology. This approach accelerates the mindset shift and helps customers feel more in control.

What it takes:

• Demonstrate and communicate value: Show customers how personal lines insurance and industry professionals help protect what matters most before loss occurs.

• Build resilient customers and communities: Unite across the insurance industry to advocate for smarter community planning, stronger building standards, distracted driving laws and prevention-focused engagement.

• Embrace innovation: Adopt smart technology and usagebased insurance programs that give consumers more control, personalization and peace of mind.

This shift does more than ease anxiety; it also rebuilds trust. Customers demand safety, confidence and control, and they reward insurers and agents who deliver it.

Tools to help customers predict and prevent

Nationwide puts this mindset into practice with our smart protection suite — innovative programs and smart technology that help customers reduce risks at home and on the road:

• Ting, a plug-in smart sensor that helps protect families and homes from electrical fire hazards. Ting has already prevented thousands of potential fires.

• LeakBot, a device that attaches to a home’s main water pipe to detect hidden leaks before they cause major water damage.

• SmartRide®, which uses real-time driving feedback to encourage safer driving and reward good habits.

• Focused Driving Rewards®, a newer initiative open to all drivers, not just Nationwide customers. It’s designed to reduce phone-related distractions and reward safe driving with e-gift cards from popular retailers.

A call to action: Let’s shift mindsets together

A predict-and-prevent mindset will define the new standard of personal lines insurance. Our industry is at a turning point. Rising costs, unpredictable weather and shaken consumer confidence expose the limits of today’s unsustainable, reactive model. The cycle ends now.

Let’s chart a path grounded in foresight and resilience. A predict-and-prevent approach shifts customer focus from payouts to protection, from a passive financial burden to an active tool for prevention, security and a sense of control.

Like every pivotal moment in history, progress depends on all of us. We’re not only protecting what matters today; we’re pioneering what protection means for tomorrow. By embracing a predict-and-prevent mindset, we can lead boldly, protect our customers and communities, and set a new standard for our industry’s future.

“The time to act is now.”

News & Markets

An Unsustainable Trend – Declining P/C Rates and Rising Cost of Risk: Marsh’s John Doyle

By L.S. Howard

Property/casualty prices are declining, while the cost of risk continues to rise—a trend that is unsustainable over time, according to John Doyle, president and chief executive officer of Marsh McLennan (MMC).

Nevertheless, without significant changes in large loss activity as well as in the broader macro-economic environment, “we anticipate insurance and reinsurance market conditions seen so far this year will likely continue in 2026,” Doyle said during an analysts’ call to discuss MMC’s third-quarter earnings.

“We continue to see a competitive market characterized by slower growth from an uneven economy, stronger carrier ROEs, and continued decreases in overall rates, particularly in property reinsurance and property [catastrophe] reinsurance,” he said.

Indeed, Doyle noted that global property rates decreased by 8% during the third quarter, compared with a 7% decline in Q2 2025.

Further detailing the “unsustainable” mismatch between softening prices and the rising cost of risk, Doyle pointed to the “big pressure points” of a global economy that may be slowing, declining interest rates, growing exposure to extreme weather, the rapidly rising cost of liability

Rates in Review

Gin some markets—including in the U.S.—and increasing health care costs.

Cost-Saving Program

Launched

It is perhaps with an eye on these pressure points that Doyle announced a new program called “Thrive,” which will include “automation efforts and workforce actions” to optimize the company’s scale and specialization.

Over the next three years, he said, Thrive is expected to “generate approximately $400 million in savings with a portion being reinvested to drive additional growth. We will incur around $500 million in charges to achieve these savings.”

MMC announced last month that it was rebranding as Marsh while forming a new unit called Business and Client Services (BCS), which Doyle explained are core parts of the Thrive program. Thrive aims “to deliver greater value to clients, accelerate growth and improve efficiency,” Doyle said.

lobal commercial insurance rates during the third quarter decreased 4%— driven by property—which follows a 4% decline in Q2 2025, said John Doyle, president and CEO of Marsh McLennan, quoting Marsh’s Global Insurance Market Index, which skews toward large account business.

Overall, rates were down in the U.S. by 1%; Canada by 3%; the UK, EMEA, Latin America, and Asia were all down mid-single digits; and Pacific decreased by double digits, he said during MMC’s Q3 earnings call with equity analysts.

Bucking the trend toward softening rates was global casualty, which increased 3%, while U.S. excess casualty rose 16%, “reflecting continued pressure in the liability environment,” Doyle said.

Workers’ compensation decreased by 5%, global financial and professional liability rates were down 5%, while cyber decreased 6%, he added.

“The efficiencies we gain through the program will support investments in talent and technology. As we increasingly deploy AI, we can deliver even greater value for clients and colleagues. Thrive will also help us continue to expand margins,” he added.

Competitors’ Hiring Practices

Doyle went on to discuss talent in the re/insurance marketplace with a pointed complaint about competitors that poach MMC colleagues.

“A few competitors have engaged in unlawful and unethical hiring practices and encourage talent to violate their covenants as a deliberate strategy to build their businesses. In these cases, I believe it’s important to call out this behavior and to protect our rates,” he said.

The company has responded with lawsuits, including one against rival Willis Towers Watson in May for allegedly stealing clients and another in October against Granite Insurance Agency for poaching former staff.

“This is a people business, and we have an unmatched depth of talent with over 90,000 colleagues, and we love to compete because it makes us better,” he said, adding that colleague mobility is good for the industry “and has served us well because we are an employer of choice with a strong colleague value proposition.”

News & Markets

Workers’ Comp Continues to Lead P/C industry With Strong Profits

Although economic uncertainty could affect insurers in the near to midterm, workers’ compensation continues to be a key driver of the profitability of the entire property/casualty insurance industry even as prices for the line are falling, according to a new AM Best report.

Workers’ comp remained profitable in 2024 with a combined ratio of 88.8—the lowest among the major P/C lines of business—even as net premium written for the industry fell nearly 7% due to rate decreases and pricing cuts, says Best’s aptly titled market report, “Workers’ Compensation Continues With Strong Profits, Despite Pricing Cuts.”

The picture isn’t expected to change. Midyear results indicate 2025 will be another profitable year and another year with a decrease in premium in line with more rate decreases.

Christopher Graham, senior industry analyst, Industry Research and Analytics, AM Best, noted that workers’ comp underwriting profits over the past decade have been largely attributable to favorable prior-year loss development. “While the reserve cushion appears to be shrinking, it is expected to provide benefits to calendar-year profitability in the medium term,” Graham added.

California remains the state with the largest share of national workers’ comp premium, with more than 20% of direct premium written in the country—twice as much as any other state. The top 10 states represent more than 60% of the national premium. According to AM Best, as good as the overall results were in 2024, in six of these top 10 states, results were even better: The statewide combined ratio was better than the national combined ratio.

The report touches on what forces could alter the positive outlook. For one, the segment’s payroll exposure base is susceptible to macroeconomic shocks, the report points out. AM Best sees the possibility of a recession, tariff and immigration policies, and legislative changes as potential headwinds for this line of business.

“A key question for the workers’ compensation line is how much longer will rate and pricing declines continue and cause dissipating profit margins before insurers begin to hold the line on pricing, since, for many companies, workers’ compensation profits help offset more uncertain underwriting results for other lines of coverage,” said David Blades, associate director, Industry Research & Analytics.

‘A key question for the workers’ compensation line is how much longer will rate and pricing declines continue and cause dissipating profit margins before insurers begin to hold the line on pricing ...’

In one executive’s view, the workers’ comp market in California may already be headed in a different direction. John Bennett, chief underwriting officer at BindDesk Insurance Services, recently wrote that while California employers have enjoyed a soft market for the last decade, there are indications of the market hardening. Bennett says workers’ comp rates in California are increasing due to a combination of higher medical costs, more expensive claims, and changes in legal or regulatory requirements. He noted that the California projected accident year

combined ratio for 2024 is 127. Rising costs prompted the Workers’ Compensation Insurance Rating Bureau of California to propose an 11.2% advisory pure premium rate increase for September 1, 2025. California Insurance Commissioner Ricardo Lara approved an average 8.7% increase in advisory pure premium rates.

Opportunity Market

Overall, the commercial insurance industry is entering a period of stability and opportunity made possible by an abundance of capital and the power of artificial intelligence (AI), according to another report from global broker Willis. According to Willis, nearly every commercial line of insurance—except for excess casualty—is in soft market territory. Workers’ comp remains favorable, supported by a $16 billion reserve surplus.

This report finds that insurers, with backing from industry surplus capital exceeding $1 trillion and reinsurance capacity over $725 billion, are pursuing growth across multiple product lines. Capital abundance is only part of the story. Artificial intelligence is “actively reshaping” the industry. “From the boardroom to the underwriting desk, AI-enabled tools are unlocking deeper insights, driving more informed decision making and expanding the very definition of insurability,” the authors contend.

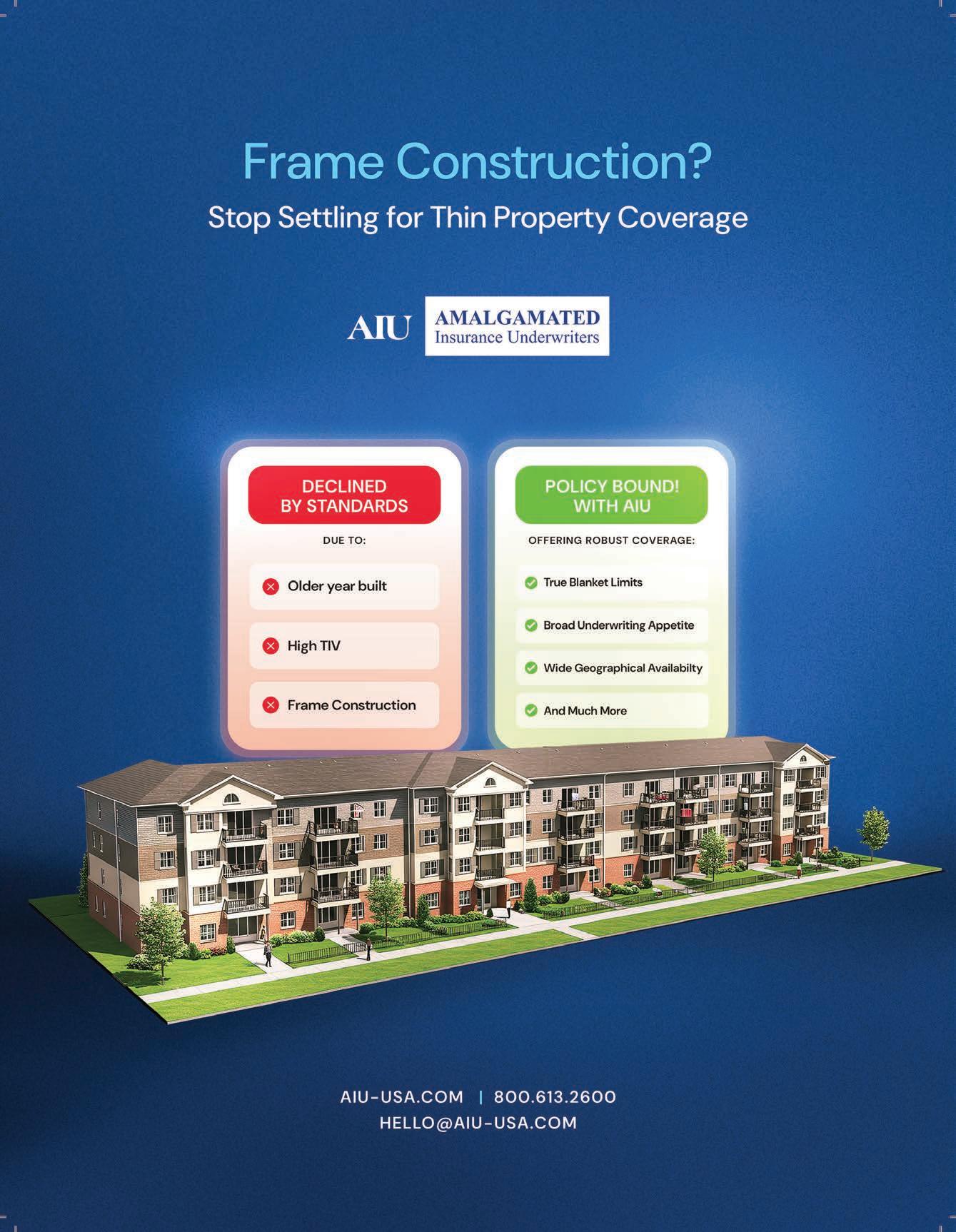

Understanding Hidden Gaps in Commercial Property Coverage Advertisement

The defining feature of today’s commercial property market isn’t simply hardening or softening—it’s volatility. After years of record rate hikes and restricted capacity, the pendulum is rapidly swinging toward lower premiums and broader availability. This instability makes long-term planning difficult for brokers and carriers alike, as today’s push to regain market share can be just as unpredictable as the hard market that came before it. The result is often thinner coverage, and more exclusions.

“I have seen it firsthand,” says Aaron Lowenthal Senior Sales Director at Amalgamated Insurance Underwriters. “Well-managed properties with strong valuations can appear fully protected on paper, only to face limitations that leave them millions short when a loss strikes.”

In today’s environment, the biggest shock isn’t the premium, it’s discovering the coverage doesn’t reach as far as expected when a loss occurs.

These Gaps Are Real

Valuation Gaps:

An apartment operator in Southern California insured a 120,000-square-foot complex at $225 per square foot—$27 million in total insured value. A 125% margin clause limited recovery to $33.75 million, yet rebuilding costs had climbed to $400 per square foot, or $48 million. When a wildfire destroyed the property, the owner faced a $14 million shortfall. What looked like full replacement cost on paper turned into a devastating coverage gap and months of costly litigation against the brokerage.

Nonrenewal Despite Renovations:

A hotel owner in the Midwest invested heavily in renovations for a $12 million property—new plumbing, roofs, and full interior upgrades. Yet when renewal came up, multiple carriers declined due to older exterior entrances, remediated aluminum wiring, and a lack of central fire alarms. Those details outweighed the owner’s improvements in the eyes of many underwriters, leaving the property without coverage despite strong operations and occupancy. It’s the kind of situation that highlights the need for an E&S carrier capable of nuanced underwriting—one that recognizes remediation efforts and responds with robust coverage instead of blanket declinations.

Hidden Exclusions:

The board of a California HOA believed their $48 million policy provided protection against core perils like fire and wind. When a $2 million blaze struck, their claim was denied due to a fine-print exclusion for fire losses tied to outdated breaker panels. Months of back-and-forth ended with no payout, leaving the community uninsured and the broker facing litigation from frustrated board members. Exclusions like these, often buried deep in policy language, can erase coverage for the very risks owners assume are included—turning a standard loss into a financial shock.

Why These Gaps Are Increasing

Margin clauses, rigid eligibility criteria, and hidden exclusions are appearing with greater frequency across property markets. As carriers expand appetite to regain premium, coverage forms often tighten quietly. Policies that appear competitive may hide constraints that erode protection when losses occur. This is why brokers need to look beyond pricing and capacity—and focus on the fine print and intent behind each form.

and sub-limits that reduce coverage on forms appearing to offer full replacement cost. Focusing on how each market handles blanket limits versus capped values is essential to evaluating true exposure and identifying potential shortfalls.

•Exclusions with teeth. Routine exclusions— breaker panels, wiring types, roof age, or year of construction—can wipe out protection for entire risk categories. Anticipating these terms allows brokers to redirect clients toward markets that assess properties holistically instead of through restrictive checklists.

Turning Challenges into Opportunities

In a volatile market, the challenge isn’t understanding insurance fundamentals—it’s execution.

•Remediation as leverage. Many hard-toplace properties are well-run, with responsible ownership and solid fundamentals. When paired with good documentation this can help underwriters see beyond surface risk indicators and unlock coverage options when the standards decline.

•Margin clause awareness. Brokers are increasingly encountering margin clauses

Working with specialty markets like AIU gives brokers and agents more options when standard carriers say no. AIU evaluates each property on its full merits—recognizing remediation efforts, valuing sound management, and avoiding one-size-fits-all criteria. By focusing on underwriting nuance rather than rigid rules, AIU helps brokers turn difficult or previously declined accounts into viable,

$87,000

The amount a North Carolina woman defrauded insurance companies by illegally obtaining and administering weight-loss medication, the state department of insurance alleges. Heather Ann Robinson, 37, of Kenly, was charged with 170 felonies, including insurance fraud, identity theft, and credit card fraud. She also used stolen identity information to siphon some $46,614 from victims’ 401(k) retirement accounts, DOI officials said.

2.88 Million

400

The number of Acrisure employees expected to be impacted by layoffs in early 2026. The company cites advancements in technology and artificial intelligence as the reason behind the move.

The number of Tesla vehicles equipped with a Full Self-Driving system involved in an investigation by the U.S. National Highway Traffic Safety Administration. The investigation was prompted by more than 50 reports of traffic-safety violations and a series of crashes. The auto safety agency said FSD—an assistance system that requires drivers to pay attention and intervene if needed—has “induced vehicle behavior that violated traffic safety laws.”

2.5 Million

The number of cubic yards (1.9 million cubic meters) of sand that’s being dredged and pumped from offshore to replenish Florida’s beaches. Beaches are being widened by as much as 100 feet along a 35-mile stretch of hurricane-depleted shoreline in Pinellas County that includes cities such as Clearwater Beach, Indian Rocks Beach, Belleair Beach, and Redington Beach. Pinellas County is spending more than $125 million in tourism tax revenue to cover the costs.

Declarations

Shock to the System

“Climate-related shocks are likely to be wide-reaching and secular, rather than narrow and cyclical. There’s a long-term trend, certainly on the physical risk side, that could impact bank business models.”

— Kevin Stiroh, who left the Fed earlier this year after it wound down large parts of its work on monitoring how global warming is impacting financial stability, speaking on how banks should expect to see the fallout “materialize” in balance sheets and income statements. Despite those risks, banks and investors have yet to properly map out how climate-related losses will be distributed, Stiroh said. Those at risk include homeowners, banks, insurers, and the holders of securitized financial instruments.

Data Out to Dry

“These new data centers are enormous. I don’t know where you get the water to do that in a state that’s already waterstressed, not only from drought but also rapid population growth in both the population and industry.”

— Robert Mace, executive director of the Meadows Center, speaking on water supply concerns and the plans for more Texas data centers. There are four data centers planned for the state’s Panhandle region, including in Amarillo, Turkey, Pampa, and Claude, and across the state as AI campuses expand in the Permian Basin, and 30 data centers are planned for Sulphur Springs, a small town in East Texas.

Fraud Squad

“The cost of insurance is something all families must be concerned with. Insurance fraud only adds to that cost. In this case, the defendant is someone who worked in the industry. We need to be able to trust the people who are working for insurers to do their jobs fairly and honestly.”

— New Jersey Attorney General Matthew J. Platkin speaking on the case of a former New Jersey insurance adjuster charged with creating and submitting phony claims, approving them himself, and directing nearly $200,000 in payments to bank accounts he controlled. John Philbin, of Clementon, has been charged with insurance fraud and theft by deception.

Human Rules Apply

“If a practice is prohibited for a human to do on behalf of an insurance company, it is prohibited for AI to do. Artificial intelligence is not an end run for insurance companies around a state’s statutes or its regulations.”

— Paul Martin, vice president of state affairs for the National Association of Mutual Insurance Companies, testifying before the Florida House Subcommittee on Insurance and Banking ahead of the 2026 legislative session. Despite the rapid rise of AI in the insurance sector and claims of widespread errors and even discrimination by algorithms, insureds will be protected by existing statutes, insurance advocates told Florida lawmakers.

Small Hail, Bigger Claims?

“This data challenges long-standing opinions by insurance company experts that have denied or minimized damage from small hail. If the science says these storms age shingles years ahead of schedule and set the stage for catastrophic failure in later storms, then dismissing that damage at the claims desk is at odds with the evidence.”

— Attorney Chip Merlin, commenting on a new study by the Insurance Institute for Business and Home Safety that found roof damage from smaller hailstones may be more significant than previously believed. Insurance policies generally consider minor hail damage as normal wear and tear, requiring a singular event causing actual physical damage for a claim.

No Driver, No Ticket

“That’s right … no driver, no hands, no clue.”

— A post written by the San Bruno Police Department in Northern California, when they pulled over a Waymo taxi after it made an illegal U-turn, only to find no driver behind the wheel and, therefore, no one to ticket. Officers were conducting a DUI operation early Saturday morning when a self-driving Waymo made an illegal turn in front of them. Officers contacted Waymo to report what they called a “glitch,” and, in the post, they said they hope reprogramming will deter more illegal moves.

People

National

Joe Gates

Boxx Insurance, headquartered in Miami, Florida, appointed Joe Gates head of distribution, central. Gates has over 20 years of experience in insurance distribution, marketing and underwriting experience from At-Bay, Beazley and AIG. Claims Manager Ray Moylan joined the global claims and hackbusters team. Moylan has almost a decade of cyber, commercial and property claims experience at Marsh and Travelers.

lines insurance, previously serving as a personal lines underwriter/broker at Risk Placement Services Inc. and a commercial lines underwriter at Nationwide.

Luceno joins the team as a personal lines insurance broker, bringing more than six years of experience in personal lines insurance. He most recently served as an assistant vice president at AmWins.

GEICO, headquartered in Chevy Chase, Maryland, named Arianna Orpello as its new chief marketing officer.

Thomas Beale joins Boxx’s technology team as head of engineering and architecture. Beale has experience in security and cyber insurance from Converge Insurance, Guidewire Software and Corax.

XPT Specialty, headquartered in New Haven, Connecticut, added Phil Staver and Zach Luceno to its personal lines division.

Staver joins XPT Specialty as a senior personal lines underwriter/ broker. He has over 18 years in personal

Orpello will join the company on Jan. 5, 2026, from Goldman Sachs, where she most recently served as global chief brand officer. She has over 20 years of experience, including leadership roles at TD Bank, Capital One and ING Direct.

Howden appointed Tom O’Donnell as practice head of logistics, Howden US, which is headquartered in Depew, New York. O’Donnell is based in New York. He has over 25 years of experience, joining Howden from Aon, where he has held leadership roles since 2016, most recently as logistics practice leader – global. Previously, he was a senior director, head of contract risk – Americas at DHL and senior manager, insurance & claims risk manager at Schenker.

CFC, with U.S. headquarters in New York City, created a new U.S.-based cyber development team.

John Keebler joins the busi-

ness as its new national cyber development leader, U.S., based in Chicago, Illinois.

With a career in cyber insurance spanning over 15 years, Keebler joins CFC from Coalition, where he most recently served as national director for business development.

Morgan Justice was hired as cyber development manager for the Western region, U.S. She previously served as West Coast underwriting and business development leader at Coalition. She is based in the San Francisco Bay Area, California.

Brokerage Brown & Brown, based in Daytona Beach, Florida, revamped its retail segment leadership team as part of its ongoing integration efforts following the acquisition of Risk Strategies.

Leaders from Risk Strategies will join the existing retail segment leadership team, taking on expanded responsibilities.

Retail senior leaders include John Mina, John Greenbaum, John Scroope and John Vaglica.

Retail vice presidents include Ed Flanagan, Steve Giannone, Neil Krauter Sr., Robert Rosenzweig and Patrick Roth

CFC’s cyber development manager, based in New York, Annie Lyons, will also report to Keebler.

American International Group (AIG) promoted three AIG employees to lead commercial insurance in North America starting Jan. 1, 2026.

Allison Cooper and Barbara Luck will be co-presidents of AIG’s retail commercial business in North America.

Lou Levinson is now president of wholesale for North America Commercial.

Don Bailey is retiring from his role as CEO of North America commercial insurance at year’s end. He joined AIG from Bristlecone Partners at the start of 2023 as global head of distribution and field operations.

The ACORD board of directors appointed Chris Newman to lead ACORD Solutions Group (ASG) as CEO. Newman most recently served as president international of ACORD. Newman previously led (re) insurance company operations, including setting up operations in North America, Latin America, Asia and the Middle East.

East

World Insurance Associates LLC named John Cicchelli as head of its employee benefits practice.

Cicchelli, who will work out of the Iselin, New Jersey headquarters, has been in the insurance industry for over 30 years.

He most recently worked at Gallagher as their New York/ New Jersey metro growth leader. Before Gallagher, he served at Marsh & McLennan Agency.

continued on page 20

Ray Moylan

Thomas Beale

Arianna Orpello

Phil Staver

Zach Luceno

John Keebler

Morgan Justice

John Cicchelli

Every

day,

we create unique risk solutions for unique businesses.

When it comes to insurance for midsize and large businesses, we get it. We do it for all kinds of industries, tailoring our policy solutions from traditional to specialized coverage. With our experience in underwriting, innovative service, and claims, we are your one-stop shop.

Connect with your underwriter at The Hartford.

continued from page 18

James River Group Holdings Ltd. appointed Georgia Collier and Matt Sinosky to its excess and surplus (E&S) leadership team.

With more than two decades of experience in the E&S market, Collier rejoins James River from the Markel Group, where she served as a managing director and product line leader. She previously spent nearly 20 years at James River and will work from the company’s Richmond, Virginia, office.

Sinosky, based in Pennsylvania, joins from Arch Capital Group Ltd., where he served as vice president of wholesale distribution and led wholesale efforts across six business units. He has spent over 15 years in insurance distribution.

NFP, an Aon company, added two new benefits leaders, Mark Carroll and Bill Schmidt, and their respective books of business. Carroll and Schmidt join as vice president, Benefits, in NFP’s Atlantic region. Based in northern Virginia, Carroll and Schmidt each have three decades of experience and co-founded Small Business Insurance Solutions Inc. (SBIS). In hiring Schmidt, NFP has acquired the business operations of SBIS.

Carroll most recently served as a managing partner of Capital Group Benefits (CGB). As he joins NFP, he is selling his ownership stake in CGB.

Highstreet Insurance Partners, headquartered in Traverse City, Michigan, named Kristen Stokes as its chief broking officer. Stokes is based out of Highstreet’s New York

City office. She has over 20 years of industry experience, most recently serving as a qualified solutions group leader at Marsh McLennan.

Moines, Iowa, appointed Greg Bailey as CEO and Charlie Turri as chief technology officer (CTO).

Protecdiv, headquartered in Philadelphia, Pennsylvania, promoted Cate DelaCruz to executive vice president and head of analytics. DelaCruz joined Protecdiv as senior director of analytics in May 2020. She previously served as a quality assurance engineer/property insurance risk analysis domain expert at Insurity SpatialKey Solutions and as a U.S. property insurance portfolio manager at Argo Group.

Bailey previously founded and served as CEO of Rivet Co. Previously, Bailey founded and served as the CEO of Denim. He co-founded Insure.vc and held senior leadership roles with Athene, Pacific Life and TruStage.

Turri most recently served as CTO of Lenders Cooperative. Previously, he was CTO for Denim and ITPeopleNetwork. He has also held senior IT leadership roles at Athene and AIG. At Recoop, Turri leads efforts into data and AI integration, platform scalability, and automation.

South Central USG Insurance Services Inc. named Jeremy Hernandez as an underwriter in its Houston, Texas, office. Hernandez has over three years of underwriting experience at Bass Underwriters. Before entering the insurance industry, Hernandez worked at COSCO Shipping Lines and HapagLloyd AG.

West

The MEMIC Group, headquartered in Portland, Maine, hired Eric Stager as a safety management consultant on its loss control team, working with policyholders throughout the Northeast. Stager served as chief master sergeant and senior enlisted leader of the 439th Civil Engineer Squadron in the U.S. Air Force, and later as a compliance safety and health officer with the U.S. Department of Labor’s Occupational Safety and Health Administration (OSHA). He also held the role of high voltage electrical supervisor at Hanscom Air Force Base.

Midwest

Recoop Disaster Insurance, headquartered in West Des

Holmes Murphy, headquartered in Waukee, Iowa, hired Jordan Anderson as vice president and employee benefits sales leader in its Sioux Falls, South Dakota, office. He most recently served as vice president of sales and account management at Avera Health Plans, and previously worked at United Healthcare and Aetna.

DOXA, headquartered in Fort Wayne, Indiana, appointed Kevin Wall as president. Wall has over 15 years of experience. Before joining DOXA in 2017, Wall served as director and senior financial analyst at Aon Affinity.

Pinnacol Assurance, headquartered in Denver, Colorado, named Dr. Gabriel Lockhart its senior medical director. Dr. Lockhart previously served as medical director of the ICU and quality improvement chairman at Saint Joseph Hospital. Lockhart is a board-certified pulmonary and critical care physician. He was recently elected president of medical staff at National Jewish Health and is a member of the faculty at the University of Colorado School of Medicine.

The MJ Companies named Melinda Eckard vice president of employee benefits operations and client experience.

Eckard, based in Phoenix, Arizona, has nearly two decades of expertise in insurance, risk management, and employee benefits, having held various roles with Willis Towers Watson. The MJ Companies is headquartered in Indianapolis, Indiana.

Cate DelaCruz

Eric Stager

Kevin Wall

Melinda Eckard

Dr. Gabriel Lockhart

Jordan Anderson

Business Moves

National

Marsh McLennan to Become Marsh

Marsh McLennan will change its brand to “Marsh,” effective January 2026, and has created a new unit, Business and Client Services (BCS).

The company’s four businesses will adopt the Marsh brand beginning in 2027, following a transition period. After that transition period, Marsh and Mercer will each go to market under the new Marsh brand. Guy Carpenter will become “Marsh Re.” Oliver Wyman will go to market as “Oliver Wyman, a Marsh business,” while the operating unit Oliver Wyman Group will become “Marsh Management Consulting.” The company’s stock ticker symbol becomes “MRSH” in January 2026.

BCS brings together the firm’s technology, data, and operations teams under the leadership of Paul Beswick, chief information and operations officer.

Bold Penguin, SquareRisk

Dublin, Ohio-based Bold Penguin, founded in 2016, acquired SquareRisk, a digital, artificial intelligence-enabled wholesale insurance marketplace.

The acquisition positions Bold Penguin, a subsidiary of American Family Insurance, to accelerate its integration speed and expansion into specialty and excess and surplus (E&S) markets while building immediate scale into digital wholesale operations.

SquareRisk, founded in 2022, connects retail brokers to over 45 specialty carriers and MGAs for industries such as

contractors, transportation, hospitality, manufacturing, and more.

Terms of the deal were not disclosed.

East

Lawley, ROC Insurance Services

Buffalo, New York-based independent insurance brokerage Lawley merged with ROC Insurance Services in Rochester.

Founded in 2012, ROC Insurance Services is a Medicare and individual health insurance agency. ROC Insurance Services founders Rick and Lynda Grossmann and 13 employees will join Lawley, which has more than 600 associates nationwide.

This partnership adds Lawley’s 19th location. Lawley has branch offices across New York, New Jersey, Connecticut, and Florida.

Midwest

Arthur J. Gallagher & Co., Strategic Services Group Inc.

Arthur J. Gallagher & Co. acquired Rochester Hills, Michigan-based Strategic Services Group Inc. Terms of the transaction were not disclosed.

Strategic Services Group provides employee benefits consulting services across a range of industries in Michigan and the Midwest. Doug Roehm, Greg Sudderth, and their team will remain in their current location under the direction of Brian Lomas, head of Gallagher’s Great Lakes region employee benefits consulting and brokerage operations.

South Central

Higginbotham,

Stephens Insurance Services

Higginbotham acquired Lubbock, Texas-based Stephens Insurance Services, a benefits specialist. The acquisition pairs on-the-ground relationships with added resources to enhance combined service offerings across West Texas and into eastern New Mexico.

Stephens Insurance Services specializes in group benefits, individual health and life benefits, and Medicare advisory assistance.

Southeast

Engle Martin & Associates, Technical Services

Engle Martin & Associates, based in Atlanta, acquired Integra Technical Services, an international adjusting firm headquartered in London.

Integra manages claims in construction, engineering, energy, manufacturing, and mining, and has adjusters in the U.S. and on four continents.

Integra will continue operating as a standalone business, retaining its brand, leadership team, and service model. The current leadership will maintain oversight of the company’s portfolio. Terms of the deal were not disclosed.

Engle Martin, in business since the late 1990s, has some 800 claims professionals in 75 U.S. locales.

West

The Liberty Company Insurance Brokers, High Ground Insurance Services

The Liberty Company Insurance Brokers acquired High Ground Insurance Services in Torrance, California.

High Ground is a locally owned regional insurance broker and risk management consultant with a national reach. The firm offers specialized services in workers’ compensation claims management, employee benefits plan administration, loss-sensitive insurance program design, and coverage analysis.

The Liberty Company Insurance Brokers is a privately held insurance brokerage.

News & Markets

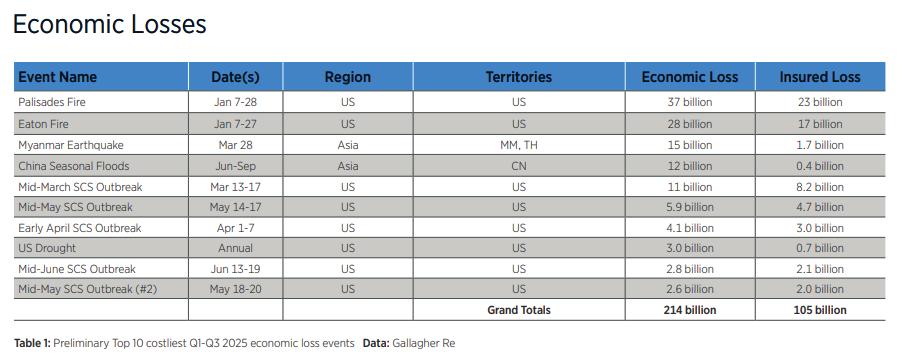

Natural Disaster Claims in 2025 to Again Top $100B Despite ‘Abnormally Low’ Q3 Events

By L.S. Howard

Global insured losses from natural catastrophes during the first nine months of 2025 are estimated to hit $105 billion, bringing the sixth consecutive calendar year with losses topping $100 billion and the eighth year since 2017, according to Gallagher Re.

Ironically, there was an uncharacteristic lack of major natural disasters between July and September, which led to one of the least expensive third quarters for insurers since 2000, said Gallagher Re in a report titled “Natural Catastrophe and Climate Report: Q3 2025.”

“The abnormally low frequency of highcost events has, thus far, left the year well within annual catastrophe budgets for governments and the insurance industry,” the report said, explaining that the below-average claims are largely the result of quieter-than-expected tropical cyclone activity in the Atlantic and Pacific oceans and generally manageable flood and storm events worldwide.

Looking at Q3 on its own, Gallagher Re said it tentatively has produced less than $15 billion in insured claims—the lowest total since 2016 ($18 billion).

The estimated $214 billion in overall economic losses (which include insured losses) from all natural perils during Q1-Q3

was well below the 10-year Q1-Q3 average of $338 billion.

Gallagher Re described 2025 as “topheavy,” with the top five costliest events in January accounting for 53% of all global insured losses. These events were the two major January wildfires in the Los Angeles area and three outbreaks of severe convective storms (SCS) in the U.S.

Entering the fourth quarter, preliminary data indicates this year’s natural cat losses will remain well below recent averages, said the report, explaining that Q4 is typically one of the least expensive on an economic and insured loss basis.

“Late-season tropical cyclone landfalls remain an ongoing risk, as is the constant possibility of a consequential earthquake,” the report said.

Source: Gallagher Re

If the final quarter of 2025 produces manageable losses, “this will likely be a further boost to the re/insurance industry’s financial buffers,” the report added.

Gallagher Re estimates it would now take an event, or series of large events, resulting in an insured loss of at least $115 billion to meaningfully impact the re/insurance industry. “This suggests that even a singular $100 billion event may not strongly change the recent softening shift in property reinsurance renewal pricing.”

Despite the lower insured losses for the first three quarters, Gallagher Re emphasized that with the increasing influence of climate change, the trend of greater losses over time is likely to persist as weather events becomes more extreme “or shift their geographical occurrence patterns.”

Other findings from the report include:

• There have been 16 billion-dollar insured loss events thus far this year—15 in the U.S. and one in Asia Pacific—marking the lowest Q1-Q3 total since 2017 when 16 events occurred.

• The costliest individual non-U.S. event is the March 28 Myanmar earthquake, which also caused major damage in Thailand.

• Other notable events included Cyclone Alfred (March 8-10 in Australia); Windstorm Éowyn (which hit Ireland, the Isle of Man, and the UK on January 24 and Norway on January 24-25); the Taiwan earthquake (January 21); and a series of severe summer hailstorms and flooding in Europe.

• U.S. severe convective storms cost insurers an estimated $46 billion, the third consecutive year in which U.S. SCS claims through September exceeded $40 billion. Insured SCS losses in the U.S. this year already amount to the fourth-costliest year on record, behind 2023 ($62 billion), 2024 ($57 billion), and 2020 ($47 billion).

Rescuers work at the site a high-rise building under construction that collapsed after an earthquake, in Bangkok, Thailand, on March 28, 2025. (AP Photo/Wason Wanichakorn, File)

News & Markets

Can a More Unified Front Be Formed Against Legal System Abuse?

By Chad Hemenway

To tell the public what it spends on insurance—an amount largely affected by what it calls legal system abuse—Uber has started to provide information on customers’ receipts.

“To give you a sense of how bad the problem has gotten in certain places, our worst market—LA County—48% of the average rider fare goes toward insurance,” said Adam Blinick, senior director of public policy and communications for Uber.

“That doesn’t make any sense in the reasonable universe we operate in,” he said during a panel discussion at the American Property Casualty Insurance Association’s annual meeting in Orlando.

The company has started to go on the offensive. Uber has filed Racketeer Influenced and Corrupt Organizations (RICO) lawsuits in New York, Florida, California, and Pennsylvania against lawyers and medical providers it thinks are committing fraud and driving up costs.

“Our desire is not to settle these things out. We want to see them through,” Blinick

said, adding that other corporations have reached out to ask advice on methodologies and building cases. This seems to indicate a willingness or desire to share information. “Let’s build the case to show the kinds of information we could be sharing amongst ourselves to get to the root of fraud and billing malpractice and the like, and make a case for reform.”

Plaintiffs’ lawyers are already highly coordinated, sharing theories, recruiting firms into new mass torts, and investing heavily in political campaigns. In the meantime, third-party litigation funding (TPLF) has become big business.

Gareth Kennedy, principal of insurance and actuarial advisory service for EY, said the firm has found the average cost for a commercial claim has gone up 10% to 11% per year since 2017. In looking at the root cause, TPLF came to the surface.

Though transparency was an issue since TPLF disclosure is only just starting to grab hold in some jurisdictions, EY concluded that over the next five years TPLF will cost the insurance industry up to $50 billion in direct and indirect costs, Kennedy said. “If

you look at that in terms of loss-ratio point drag, you’re talking a 4%-5.2% drag on loss ratios in [2024] premium dollars.”

Panelists urged businesses to respond with smarter political giving, coalition building, and consumer-focused messaging to combat legal system abuse.

Nathan Morris, senior counsel, litigation policy and risk mitigation at Johnson & Johnson, said trial lawyers are singularly focused and mission-driven, while outside interests of businesses are much more than just litigation, so “they don’t always have that kind of freedom of movement politically.”

“Businesses have the ability to do more politically and to be more engaged and more thoughtful,” Morris said. “I don’t think you need to match [trial lawyers] dollar-for-dollar.”

The focus should be on the consumer’s benefit of TPLF. “Is the consumer actually benefitting from that financing? Can we have an honest conversation about that?” he asked. Claims are being filed to “benefit people who are building up an asset class and not people that are seeking justice.”

News & Markets

State Officials Say New Rules, Delays for FEMA Grants Put Disaster Response at Risk

By Gabriela Aoun Angueira

State officials on the front lines of preparing for natural disasters and responding to emergencies say severe cuts to federal security grants, restrictions on money intended for readiness, and funding delays tied to litigation are posing a growing risk to their ability to respond to crises.

It’s all causing confusion, frustration, and concern. The federal government shutdown isn’t helping.

“Every day we remain in this grant purgatory reduces the time available to responsibly and effectively spend these critical funds,” said Kiele Amundson, communications director at the Hawaii Emergency Management Agency.

The uncertainty has led some emergency management agencies to hold off on filling vacant positions and make rushed decisions on training and purchases.

Experts say the developments complicate state-led emergency efforts, undermining the Republican administration’s stated goals of shifting more responsibility to states and local governments for disaster response.

In an emailed statement, the Department of Homeland Security said the new requirements were necessary because of “recent population shifts” and that changes to security grants were made “to be responsive to new and urgent threats facing our nation.”

Updates on Population

Several DHS and FEMA grants help states, tribes, and territories prepare for climate disasters and deter a variety of threats. The money pays for salaries and training, and such things as vehicles, communications equipment, and software.

State emergency managers say that money has become increasingly important because the range of threats they must prepare for is expanding, including pandemics and cyberattacks.

FEMA, a part of DHS, divided a $320 mil-

lion Emergency Management Performance Grant among states on September 29. The next day, it told states the money was on hold until they submitted new population counts. The directive demanded they omit people “removed from the State pursuant to the immigration laws of the United States” and to explain their methodology.

The amount of money distributed to states is based on U.S. census population data. The new requirement forcing states to submit revised counts “is something we have never seen before,” said Trina Sheets, executive director of the National Emergency Management Association, a group representing emergency managers. “It’s certainly not the responsibility of emergency management to certify population.”

With no guidance on how to calculate the numbers, Amundson said staff scrambled to gather data from the 2020 census and other sources, then subtracted the number of “noncitizens” based on estimates from an advocacy group.

They are not sure the methodology will be accepted. But with their FEMA contacts furloughed and the grant portal down during the federal shutdown, they cannot find out. Other states said they were assessing the request or awaiting further guidance.

In its statement, DHS said FEMA needs to be certain of its funding levels before awarding grant money, and that includes updates to a state’s population due to deportations.

Experts said delays caused by the request could most affect local governments and agencies that receive grant money passed down by states because their budgets and staffs are smaller. At the same time, FEMA also reduced the time frame that recipients have to spend the money, from three years to one. That could prevent agencies from taking on longer-term projects.

Bryan Koon, president and CEO of the consulting firm IEM and a former Florida emergency management chief, said state governments and local agencies need time to adjust their budgets.

“An interruption in those services could place American lives in jeopardy,” he said.

Grant Programs Tied Up

In another move that has caused uncertainty, FEMA in September drastically cut some states’ allocations from another source of funding. The $1 billion Homeland Security Grant Program is supposed to be based on assessed risks, and states pass most of the money to police and fire departments.

New York received $100 million less than it expected, a 79% reduction, while Illinois saw a 69% reduction. Both states are politically controlled by Democrats. Meanwhile, some territories received unexpected windfalls, including the U.S. Virgin Islands, which got more than twice its expected allocation.

The National Emergency Management Association said the grants are meant to be distributed based on risk and that it “remains unclear what risk methodology was used” to determine the new funding allocation.

After a group of Democratic states challenged the cuts in court, a federal judge in Rhode Island issued a temporary restraining order on September 30. That forced FEMA to rescind award notifications and refrain from making payments until a further court order.

The freeze “underscores the uncertainty and political volatility surrounding these awards,” said Frank Pace, administrator of

the Hawaii Office of Homeland Security. The state received more money than expected but anticipates the bonus being taken away with the lawsuit.

In Hawaii, where a 2023 wildfire devastated the Maui town of Lahaina and killed more than 100 people, the state, counties, and nonprofits “face the real possibility” of delays in paying contractors, completing projects, and “even staff furloughs or layoffs” if the grant freeze and government shutdown continue, Pace said.

The setbacks prompted Washington state’s Emergency Management Division to pause filling some positions “out of an abundance of caution,” communications director Karina Shagren said.

Disruption

Emergency management experts said the moves have created uncertainty for those in charge of preparedness.

The Trump administration has suspend-

ed a $3.6 billion FEMA disaster resilience program, cut the FEMA workforce, and disrupted routine training.

Other lawsuits also are complicating decision-making.

A Manhattan federal judge in September ordered DHS and FEMA to restore $34 million in transit security grants it had withheld from New York City because of its immigration policies. Another judge in Rhode Island ordered DHS to permanently stop imposing grant conditions tied to immigration enforcement, after ruling in September that the conditions were unlawful—only to have DHS again try to impose them.

Taken together, the turbulence surrounding what was once a reliable partner is prompting some states to prepare for a different relationship with FEMA.

Copyright 2025 Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

Closer Look: Commercial Lines Leaders

Commercial Lines Leaders

Top 50 Commercial Lines Agencies

About the Commercial Lines Leaders: The 2025 Commercial Lines Leaders in this special feature are taken from Insurance Journal’s Top 100 Property/Casualty Independent Agencies as reported in August. This list utilizes only the 2024 commercial lines property/casualty revenue numbers of the independent agencies and brokerages that submitted data to the Top 100 agencies report. For more information on Insurance Journal’s Top 100 Property/Casualty Independent Agencies list, contact awells@insurancejournal.com.

Ranked by Total 2024 Commercial Lines P/C Revenue

1 Alliant Insurance Services/Confie

2 HUB International Ltd.

$2 ,469,998,814 $17,636,809,076 $3, 430,361,887 14 ,141 Irvine, California

$250,000,000 $1,450,000,000 $265 ,000,000 1,200 Ladera Ranch, California

$222,504,788

26

28

33

34

35

36

37

38

39

40

41

42

43

50

1,148 Bangor, Maine

,626,295 595 Cedar Rapids, Iowa

,469,840 397 Bowling Green, Kentucky

,981,223 571 Carmel, Indiana

484 Norfolk, Virginia

573 Buffalo, New York

My New Markets

Sports, Leisure & Entertainment

Market Detail: Renaissance Specialty brings decades of experience insuring everything from major arenas and stadiums to festivals and local fairs. Renaissance strives to modernize and streamline special event insurance—delivering a more efficient, forward-thinking solution for the evolving needs of the entertainment industry.

Coverages include:

Sports, including amateur associations, national governing bodies, sports events, sports venues and complexes and professional teams and leagues.

Entertainment including casino and gaming operations, convention and civic centers, stadiums and arenas, performing arts centers, live music venues and amphitheaters.

Leisure, including amusement parks, water parks, family entertainment centers, gyms and workout facilities, trampoline parks and special events.

Venues, including casino and gaming operations, convention and civic centers, stadiums and arenas, performing arts centers, live music venues and amphitheaters.

Special events, including concerts, festivals, trade shows, fundraisers, parades, auctions, balls and galas, and many more.

Available Limits: Not disclosed.

Carrier: Not disclosed.

States: All 50 states and the District of Columbia.

Market Detail: Fire and water restoration contractors work on locations that have experienced natural or accidental disasters. These disasters may be small, such as a burst pipe, or bigger problems like fires, smoke damage, storm damage, damage from heavy rains, floods, tornadoes, hurricanes, even tsunamis. They can be devastating for the businesses that have to be restored; however, if a restoration contractor exacerbates or creates an adverse environmental condition during restoration activities, their client, and their own business, may never recover.

Available coverages include: contractors’ pollution liability, E&O, site pollution liability, auto, workers comp, and excess. Environmental concerns for fire/water restoration contractors: Examination of the area, cleanup of the area, bringing in heavy equipment if needed, and cleanup/ removal of trash.

Security during examination of the area: because they often don’t know what they may encounter, fire-water restoration contractors have to secure their work areas and make sure that third parties do not enter the work area where they may be exposed to hazardous materials.

Cleanup of areas: fire-water restoration contractors often have to clean possessions on and off-site. Often, these possessions may have been affected by chemicals on-site, or when water intrusion has occurred, mold can appear. Mold may become airborne and affect contractor employees or third parties.

Bringing in heavy equipment when needed: spills may occur from tanks containing fuel for heavy equipment, or exhaust fumes from equipment may be generated. Hazardous and non-hazardous materials may spill during loading/unloading activities.

Transporting waste or materials to or from a job site: Spills may occur while chemicals or equipment are being transported to or from the job site, or during loading/unloading. Spills may occur while waste, debris, etc., are being transported from the job site to a disposal site.

Disposal of waste at non-owned facilities: Restoration debris may be inadvertently mixed with hazardous waste and then disposed of improperly, causing contamination conditions at the landfill or disposal facility. Improper disposal of air conditioning and refrigeration units, which could result in fines, penalties, or claims against restoration entities. Improper disposal of asbestos, lead, and polychlorinated biphenyls (PCBs) containing components, which are regulated and should be handled as hazardous waste.

Insured’s owned premises: Materials that are being cleaned off-site may contain hazardous materials and could spill at the restoration contractor’s premises.

Contamination at owned premises could be caused by cleaning/maintenance chemicals or storage of heavy equipment, mobile equipment, or vehicles. Storage of paints, chemicals, solvents, etc. at owned premises. ASTs used for waste oil, hydraulic fluids, or fuel. USTs used for refueling vehicles or heating oil.

Available Limits: Not disclosed.

Carrier: Not disclosed.

States: All 50 states and the District of Columbia.

Market Detail: Trusted solutions for medical equipment businesses. ProTek, powered by NFP, provides a portfolio of enhanced general and professional liability insurance products to help companies that sell, service and manufacture medical equipment mitigate risks and manage costs. Experienced staff offers expertise and insurance coverages that help protect the medical device sales and service industry.

Available Limits: Not disclosed.

Carrier: Not disclosed.

States: All 50 states and the District of Columbia.

Truckers Seek Detours Around Rising Costs and Litigation

Tort Reform, Safety Tech, Claims Control

Seen as Best Routes

By Andrea Wells

The COVID-era boom in trucking is definitely over.

The trucking sector is experiencing one of its most challenging times, with trucking operators’ profitability dropping across all sectors, total costs continuing to rise, and freight tonnage and rates remaining stagnant or even slightly down.

Costs are up for diesel fuel, tractors and trailers, and insurance. Plus, there are the ongoing concerns over a shortage of drivers and the impact of runaway litigation.

Trucking activity in the United States decreased in September, pushing the level down to the lowest in three months. Specifically, truck freight tonnage declined 0.9% after gaining 0.9% in August and 1.1% in July, according to the American Trucking Association.

“Tonnage levels remain choppy, but they are up 2.1% since hitting a low in January,” said ATA Chief Economist Bob Costello. “Compared to the high three years earlier, however, truck tonnage is still off by 3.9%.”

Since the COVID trucking boom—where trucking company growth surged from the start of the pandemic until the end of 2023—there’s been a significant decline in freight volumes and rates nationwide. According to Denis Brady Jr., transportation broker at Burns & Wilcox, that loss of business has forced a large number of trucking businesses to scale back operations or shut down completely.

Data from the Federal Motor Carrier Safety Administration

(FMCSA) shows that the number of motor carriers declined 10% in 2024. In the first half of the year alone, nearly 10,000 carriers closed their doors. In 2025, more major trucking businesses have filed for bankruptcy as profit margins have been spread thin due to tariffs, heavy debt from overinvestments during the pandemic, and overall higher operating costs including higher insurance costs.

All of this has made trucking a very challenging insurance market. “Over the last decade, the insurance carriers have struggled to be profitable and at the same time the trucking industry is struggling to be profitable as well,” said Mark Gallagher, transportation practice leader at Risk Placement Services (RPS). “That’s a tough spot for truckers right now and for carriers alike.”

Some states are tougher than others when it comes to the insurance market. According to Gallagher, New York, New Jersey, Georgia, Texas, Florida, and California are historically tough states, along with Cook County in Illinois. “Rates are typically higher in those venues,” he said.

Gallagher has seen a lot of trucking firms shutter their doors during the past two years.

“Mergers and acquisitions are a big part of what we’re seeing with larger fleets purchasing some smaller ones,” he said. “We’re also seeing owner/

operators that acquired their own authority over the last few years now shut down their authority and lease their truck, or go back to a larger entity to become a driver—in essence, closing their doors.”

Litigation Against Truckers

Insurance is among the bumps in the road for trucking firms.

Burns & Wilcox’s Brady maintains the driver of skyrocketing liability rates in transportation is clear: litigation. “The personal injury attorneys are winning. They have been for a decade,” he said.

‘The personal injury attorneys are winning. They have been for a decade.’

RPS’s 2025 Transportation Market Outlook found that the cost to insure physical damage has increased by 18% in 2025 over 2024, while umbrella liability increased by 12%.

Settlement creep, a newer phenomenon where insured losses gradually increase over time, has led to auto liability

increases between 7.5% and 20%, the report said.

Litigation costs are higher than ever. According to the American Transportation Research Institute (ATRI), which tracks verdicts and settlements in the trucking industry, the number of cases resulting in verdicts over $1 million increased by 235% when comparing the 2005-2011 period and 2012-2019 period. The ATRI also noted that from 2010-2018, the average verdict over $1 million grew from $5 million in 2010 to $23.5 million by 2018.

While social inflation and nuclear verdicts are driving premium increases throughout the industry, some states are more difficult than others, as Gallagher noted.

In some regions, like New York City’s Bronx Borough, “it’s totally become a free-for-all,” said Greg Kroeger, managing partner at World Insurance Associates LLC.

“There’s certain venues where carriers just don’t want to write because they know that it’s going to be an uphill battle to defend the claim,” he said. “If you’re a carrier, you continued on page 30

Special Report: Trucking

continued from page 29

don’t argue a case in the Bronx. You just don’t.”

According to a recent report by Amwins, “State of the Market Transportation H1 2025,” the states of New York, California, Texas, and Illinois continue to see limited active players, and the casualty marketplace in New Jersey is “essentially non-existent” due to high-frequency claims and the increased limit requirement of $1.5 million.

But it’s not all bad news.

Jennifer Nuest, senior vice president, transportation practice leader at Amwins, sees some good news on the litigation front. She said the market appetite in states like Florida and Georgia is picking up in part due to recent tort reform measures.

Also, the industry sees some good news in the overturning of a $90 million nuclear verdict against trucking firm Werner Enterprises in Texas. While it’s too early to tell if the outcome of this case will help to set a new precedent in Texas, transportation leaders see the ruling and other tort reform

measures as positive.

“I would say these are very positive things for the industry to see some of the litigation reforms starting to get passed in various states, especially tough ones like Florida and Georgia that really need it,” Nuest said. “Unfortunately, the flip side of that is a waitand-see approach for many insurers,” she said.

Nuest doesn’t expect significant market changes until insurers see how these new state efforts play out. Even so, she believes the measures will likely open up the insurance

‘We need a lot more litigation reform to really move the needle on commercial auto...’

market for truckers in small but helpful ways.

“Maybe insurers make small creeps in their appetite,” she said. “For example, a carrier may say, ‘I’ll only write a risk in Florida if less than 40% of their miles are in Florida.’ And then they’ll change it to less than 50% of miles in Florida.”

Another effort that could provide some market relief in difficult states is recently enacted legislation requiring third-party litigation disclosure in several states. But Nuest cautions that any effects of the disclosure laws will not be seen for some time. “It’ll take at least a couple years before we really understand what the impacts are going to be there, but it’s good progress,” she said.

There’s a long road ahead to better times for trucking insurance and the commercial auto market in general, Nuest said.

“We need a lot more litigation reform to really move the needle on commercial auto as social inflation and especially a third-party litigation funding has added a lot of costs to claims,” she said.

Fighting Back

The primary line of defense against rising costs for insurance and against potential litigation is staying focused on safety. This can include encouraging the use of technologies like telematics and dashboard cameras.

“The more insurance carriers continue to lean into technology implementation requirements, such as forward-facing cameras, the better chance the insured will have to fight back against personal injury attorneys,” Brady said.

Telematics, or on-board devices that combine GPS and telecommunications to collect and transmit data on the truck’s location, performance, and driver behavior, have become the standard in safety for trucking companies and a requirement of many insurers for coverage, said Roman

Atkielski, senior vice president, commercial auto and garage division, at Jencap.

“It’s monitoring driver behavior, routes, things like hard brakes and hard turns and speed. These are all just safety issues that motor carriers really need to take seriously,” Atkielski said. “Cameras are also wildly important because they take all the guesswork out of a claim,” he added. “We can actually see the footage as to an incident, so that can tell us who was liable in a claim, and oftentimes it shows that our insureds are not liable.”

Years ago, if a truck rear-ended another vehicle, in most cases the truck driver would be named at-fault, Atkielski said. But what if the other vehicle swerved and cut off the truck in an unsafe manner? “So, cameras can really take all the ambiguity out of what happened in an accident,” he noted.

Claims Management

The industry can also fight rising costs through better management of the overall claims process. Early claim reporting and resolving claims faster dramatically reduces litigation risk and claim severity, Atkielski said.

“What we see is when these claims linger—nobody’s done anything for three months or 60 days or whatever it is—all of a sudden the claimant’s got an attorney involved because nobody’s talking to them,” he said. “But if we can get involved and say, ‘Hey, listen, we’re on this and we’re going to make you whole as quickly as humanly possible,’ if it’s a compensable claim, then the likelihood of them lawyering up is mitigated.”

Adjusters and carriers need to emphasize their time early in the claims process, said Harish Kapur, CEO of Across America Insurance Services, a Riverside, California-based commercial trucking and transportation-focused managing general agency. When claims get litigated, it’s often because the claim process and lifecycle of the claim simply took too long, according to Kapur. “What are you doing in the six months or three months? That’s your crucial time. That’s your money right there.”

This is one reason Kapur brought his firm’s claims process in-house. “We did this six years ago, and I wish we had done it sooner,” he said. “Why did I become a claims guy? I think because I felt like my defense attorneys or our TPA that we hired didn’t do as good of a job as they should have. They didn’t prepare the file as they should have, did not work the file the way they should have.” That led to some claims fights over damages or liability that “we should be accepting,” he said. “But the question really becomes are we fighting for the right reasons.”

Kapur said managing the claims process gives insight into what claims should be fought. “So, this year alone, we’ve taken a total of seven cases to trial. We just finished one yesterday, and we’ve got another one going in trial on Monday,” he said. “On three of them, we had 100% defense verdicts. We paid $0,” he said.

“I feel like insurance companies are not trying enough cases—they’re not trying enough cases, and that is giving a sense to the plaintiff’s side that it’s OK to ask for whatever they want to,” he said.

Handling claims in-house helps identify what claims are worth fighting and helps in preparation to defend those cases, he said. “We prepare the mediation brief, we prepare and go through every medical record, we tie it together, making sure things are lining up. That’s what we do, and we’ve had success on it.”

Kapur said out of the seven cases that have gone to trial, so far there’s only been one loss. “I wouldn’t even call that a loss because we ended up paying a reasonable amount,” he said.

“So, I feel like it’s been a good win because we’re not fighting for the wrong reason.”

Back to the Basics

For agents and brokers approaching the market for their trucking clients, Brady advises to keep it simple. “Go back to basics,” he said. “The three main things a trucking company can do to keep their insurance costs down are to focus on their safety scores, focus on driver hiring and in-house training, and to install dual-facing cameras in all trucks to record accident involvement as a better way to defend their interests against the personal injury attorneys.”

Historically, 70%-80% of accidents are caused by personal autos, yet most of the time the trucker’s insurance carrier ends up paying out due to lack of documentation or because the safety scores of the trucking company make it impossible to defend, he explained.

RPS’s Gallagher recommends that agents always be students of the industry. “Attend as many webinars and educational sessions as you can. We try to provide those on a regular

basis and as much as we can throughout the year for our agents,” he said.

Encourage trucking clients to keep a focus on safety, Jencap’s Atkielski said. “Report claims early, use cameras, telematics, and partner with trucking professionals who understand the market.” Take a look at usage-based insurance options, too. “There are some options out there for usage-based insurance, which will reduce the cost for operators,” he said.

“It’s usually monthly pay so there’s no premium financing.” And do whatever it takes to put the brakes on social inflation. “The industry really needs to find more ways to get in front of that, and a lot of that has to start with claims at the carrier level,” Amwins’ Nuest said. “How are we investing in claims more thoroughly and putting the foot down a little bit more, especially where third-party litigation funding is involved.”

New Cargo Theft Tactics Driving Claims

Cargo theft losses are also driving up costs for truckers. According to data from Verisk CargoNet, cargo theft surged 27% in 2024. The National Insurance Crime Bureau predicts a further 22% increase in 2025, driven by criminal profitability, advanced technology implementation, and geopolitical tensions.