Interested in submitting an article for a future issue? Email: editors@hrra.com

Make Your Commissions Work for You: The Realtor®’s Guide to Mastering Variable Income p 10

REALTORS®

WELCOME

THANK

EDITOR: DR DAWN KENNEDY (dkennedy@hrra com)

SALES: Misty Pritchett (advertising@ hrra com)

HRRA reserves the right to edit or refuse all submissions for publication HRRA reserves the right to receive royalties from some programs and services Views and advertising expressed in this magazine are not necessarily those of, nor endorsed by, HRRA

It's Not Just a House, It's Financial Wellness p 12

Investing in Wellbeing: A Pathway to Savings and Organizational Growth p. 14

What to do, what to do…

JAY MITCHELL: PRESIDENT'S MESSAGE

“All of this is just a lot, and we need help, no matter how smart we think we are.”

Most of us hopefully have some kind of a financial plan…whether it is based in owning property (or properties); investing in the stock market; buying and selling crypto; or storing cash under your mattress. Regardless, a plan is good.

How to make the plan work is another story. I’m reminded of this by financial planners, one of whom called the other day to “touch base” about planning for the future I dread those calls, but I know they are necessary It helps if that person calling is also a friend, so the relationship has real meaning. Hold them close!

Our “financial wellness” is a broad term that covers multiple ideas and scenarios. It always stops me cold when trying to figure out what end is up.

For instance, what about that life insurance policy that will increase in quick premium multiples when reaching a “certain age” (and I’m close!)? Keep it and spend the extra as we go along or gamble and stop paying? Should there be more than one policy? Who’s coming behind you? Spouse, children, other loved ones? It will matter to them if you muster out of this world and leave no provisions for them

What about government retirement funds (Social Security)? Can it be counted on and what are the calculations? Check out www.ssa.gov no matter your age. You can see what the numbers might be. And be prepared to be scared. It’s never enough.

Is there enough in savings for emergencies? Small or large, one will surely pop up, and it’s usually a mystery until it’s right in front of your nose. Being ready to react will be the key to success.

And really, we need someone to help us figure out where our money gets divvied up in the market. Most of us don’t have a clue on what to invest in, so it’s smart to seek professional advice. It’s like hiring a REALTOR® hire a pro!

What about prized belongings? Do they have any value for others? Some really do and it might be time to have them appraised.

All of this is just a lot, and we need help, no matter how smart we think we are. Be sure to use the great resources that are available, including our great HRRA affiliates who are standing by ready to help sort things out on all levels of financial wellness.

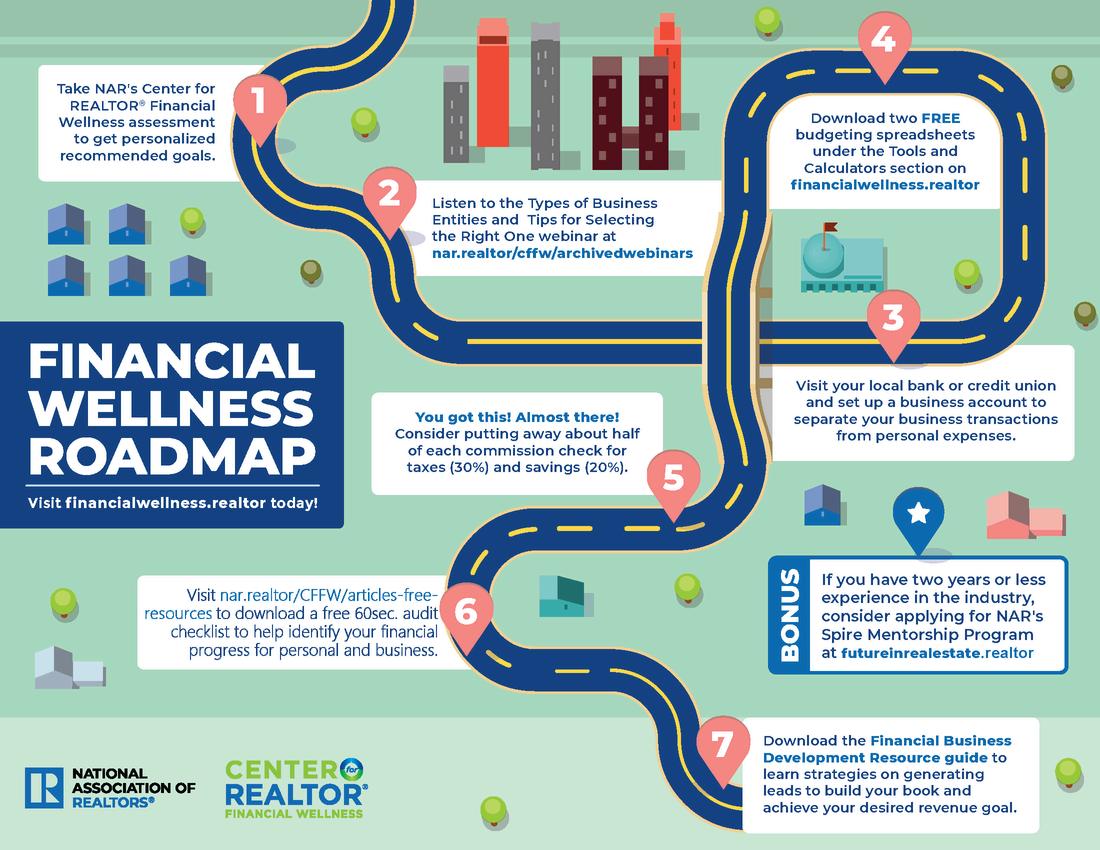

You might start here, with a truly wonderful NAR resource, the Center for REALTOR® Financial Wellness: www.financialwellness.realtor.

Wishing you great financial health that can be a direct result of this outstanding profession we are all in!

Dear HRRA Members,

DR. DAWN KENNEDY: CEO BRIEF

“Every day your REALTOR® Association, on all three levels (federal, state and local), advocates for your financial wellness, ensuring a return on your dues investment.”

I have often promoted the financial wellness center, one of your many National Association of REALTORS® (NAR) member benefits, as a great tool for ensuring your success in the profession However, in this particular brief, I would like to speak to the financial wellness provided to us through the three-way agreement. As a refresher for some, the three-way agreement is the membership structure that requires membership in the local, state, and national associations. One cannot be a member of the Virginia REALTORS® without joining the local board or the National Association of REALTORS®. When you receive your dues invoice, although HRRA does the invoicing and collection, you are paying for membership for all three organizations.

When it comes to financial wellness, NAR’s primary objective is your long-term member success During Covid, NAR pressured our federal government repeatedly to allow REALTORS® to be classified as essential workers, allowing HRRA members to continue practicing, and earning commissions, during the national shut down. One area I believe where NAR doesn’t receive much attention is the constant fight against losing your independent contractor status, most likely because it is such a constant fight, we tend to forget about it.

These cases are not one-and-done because each state has its own labor laws. As late as last year there was a New Jersey case brought forward challenging the classification of REALTORS® as Independent Contractors NAR remains at the

forefront of this issue as reflected in its 2025 legislative priorities:

“Protecting the right to work independently is a core priority for NAR With 88% of REALTORS® operating by choice as self-employed independent contractors, NAR is leading the fight to preserve this flexible business model. Independent contractors do not receive employer-sponsored health insurance, requiring them to seek health care coverage on their own. NAR supports expanding access to affordable, quality health insurance options through Association Health Plans, ensuring REALTORS® and other independent contractors can get the care they need.

Support the Association Health Plans Act (H.R. 2528/S. 1847) to provide REALTORS® with access to quality, affordable health care

Support the Direct Seller and Real Estate Agent Harmonization Act (H R 3495) to ensure real estate agents maintain their independent contractor status under the Fair Labor Standards Act

Support the Main Street Tax Certainty Act (H.R. 703/S .213) to preserve the 20% deduction for pass-through business income”

Every day your REALTOR® Association, on all three levels (federal, state and local), advocates for your financial wellness, ensuring a return on your dues investment.

Hapoy Selling!

Dr Dawn Kennedy

Professional Standards: A Deep Dive

Money Money Money!

When a member joins the association via the application process, that application serves as a contract between the REALTOR® and the REALTOR® Association. The potential member voluntarily agrees to several policies including adhering to the Code of Ethics and participating in the Code of Ethics process. The process itself is a key member benefit in that a panel of one's practicing peers conducts the hearing and issues the verdict, thereby eliminating the need for costly attorneys and court fees. However, members may opt for using an attorney in the process (this is their right), which somewhat defeats the point of selfpolicing and self-adjudicating. In the case interpretation below, we see that attorney fees are strictly the expense of the attorney's client As a reminder, case interpretations are official NAR policy and should be viewed as such

Case #17-6: Request for Arbitration Expenses

REALTOR® A, the listing broker, and REALTOR® B, a cooperating broker, engaged in a heated dispute as to which REALTOR® was the procuring cause of a sale and, therefore, entitled to the commission. Finding that they could not resolve the matter themselves, they agreed to arbitrate in accordance with Article 17 of the Code of Ethics.

REALTOR® A initiated the request for arbitration with a letter to the Board; the letter was received and reviewed by the Grievance Committee which agreed that it was an arbitrable matter The case was sent on to the Professional Standards Committee for a hearing

The President of the Board, consistent with the Board’s Code of Ethics and Arbitration Manual, appointed a five-member Hearing Panel to hear the case. The proper forms agreeing to the arbitration were sent to both REALTORS®, each signed his agreement and returned it to the Professional

Standards Administrator. Prior to the date set for the hearing, REALTOR® A learned that REALTOR® B had practiced law before he entered the real estate business. REALTOR® A then decided that he would be at a disadvantage in presenting his case to the Hearing Panel without an attorney due to the legal background of REALTOR® B. REALTOR® A sent in an amended arbitration request in which he

The case was set and a hearing was held at which REALTOR® A appeared with his attorney and a court reporter. REALTOR® B acted as his own attorney. The Hearing Panel had the Board’s attorney and a Professional Standards Administrator with a tape recorder present After giving both parties the opportunity to present their case, the Hearing Panel adjourned the hearing and went into executive session to reach a decision.

It was the opinion of the Hearing Panel that the arbitration process is provided to all REALTORS® and REALTOR-Associates® by the Board to avoid any unnecessary expenses. The hiring of an attorney was REALTOR® A’s own decision, not required by Article 17 of the Code of Ethics, the Hearing Panel, the Code of Ethics and Arbitration Manual, or the Board of REALTORS®. The Hearing Panel decided the commission dispute based strictly on the merits of the case presented. The Hearing Panel disallowed the request by REALTOR® A that he be awarded attorney’s fees or other administrative expenses

The Big Beautiful Real Estate Win The Big Beautiful Real Estate Win

It is October, the beginning of the fourth quarter, and we are nearer to the end of the year. Whew! That is quite a lot to take in. This is the time of year that many REALTORS® start to assess the past year and often measure success by the number of houses sold or their production.

You might be asking what does this have to do with advocacy? Well, everything. Advocacy begins with protecting the industry and your right to do business It does not end there This year, on July 4, 2025, President Trump signed the Big Beautiful Bill, also known as H R 1 It includes a qualified business income deduction at 20% and includes a $400 minimum deduction for those with at least a thousand dollars. That is a tax savings for you.

1

Another win for your wallet and those of your clients is the preservation of the mortgage interest deduction. The deduction is now permanent. This is a win, especially for first-time home buyers. The affordable housing, and now low-income housing credit , is a huge win, especially since there is a need to build more housing that can help low-income families realize the American dream of home ownership Like the mortgage interest rate deduction, it is now permanent

2

A little-talked-about element is the “Baby Bond.”

3

A child born after the law is enacted gets a $1000 bond. Parents can add up to $5000 each year. By the time the child reaches adulthood, they could have up to 166,000 dollars to use as a down payment for a home! That is crazy cool. This is not down payment assistance, but an incentive for generational saving and wealth. Additionally, those who don’t get an inheritance or cannot rely on family wealth now have a way to save and get into the home of their dreams.

Board (VREB) from charging a fee to a licensee for transferring within a primary place of business, i.e., from branch to branch. That will keep some money in your pocket while you build your business. 4

Your Government Affairs Committee continues to monitor any bills and laws that affect your money. We will act to safeguard your wallet as you continue to grow your business, succeed in your business, and help your clients realize their dreams

RPAC (REALTORS® Political Action Committee) plays a critical role in our efforts to get laws passed and in our efforts to elect candidates who understand the importance of protecting private property rights. That is where you come in. Your RPAC (REALTORS® Political Action Committee) contributions make the fight possible. Please consider joining the fight for you and our precious clients.

At the state level, the General Assembly has passed a law prohibiting the Virginia

As a CERTIFIED FINANCIAL PLANNER™, I’ve seen top-producing REALTORS® earning six figures or more still living paycheck to paycheck. Not because they can’t sell, but because they haven’t structured their cash flow properly. The good news? It’s not about making more; it’s about managing better. With the right systems, your life can feel like a steady W-2 paycheck with even more income and freedom.

Too many agents leave real estate not because they lack talent, but because poor money management sinks them. Taxes sneak up, savings never happen, and credit cards become the safety net. Over time, the stress pushes them back to a traditional job. But with a few smart steps, you can flip the script and build a career that lasts.

Step 1: Automate Everything

Start by creating three key accounts:

Business operating account – commissions land here first.

Business tax account – automatically move a set percentage of every commission into this account. Work with your tax professional to calculate the right percentage (20–25% is a safe starting point).

Personal account – this is your monthly paycheck. All personal expenses get paid from here.

Keep business and personal expenses completely separate!! Mixing the two is one of the fastest ways to lose control of your money.

Pro tip: You can even set up your tax account to pay the IRS directly each quarter for estimated taxes. This eliminates the dreaded April surprise that knocks so many REALTORS® out of the business.

Automation removes temptation Every commission automatically flows into the right buckets, so you never wonder where the money went.

Step 2: The REALTOR® Version of the 50-30-20 Reverse Cash Flow Rule

Here’s where many agents get tripped up: you think your gross commission is your income. A $10,000 closing hits, and before long, all $10,000 is gone.

But in reality, you’re a business owner. That means the first thing you do is set aside for taxes. Next, set aside what you need for your business to keep running What’s left is your true net pay From there, use this framework:

20% = Net Worth Building (automated into savings, investments, or debt payoff).

50% = Needs (housing, insurance, utilities).

30% = Wants (lifestyle and fun).

The key? Set aside the 20% for net worth building first. If you want to flourish, you can’t let lifestyle spending eat up everything. Business will always fluctuate, so build your life around your net, not your gross.

Step 3: Build Your Emergency Fund and Buffer

The fastest way to make variable income feel consistent is by building cushions.

Business buffer: Keep enough in your business account to cover a few months of recurring business expenses This allows you to pay yourself a consistent paycheck even when closings slow down

Personal emergency fund: Keep 3–6 months of living expenses in a separate account. This is your true safety net, protecting your household from unexpected downturns.

Every REALTOR® knows there’s a “real estate winter.” It may not be this season, but it will eventually come. Be prepared for when commissions slow down so you can weather the slow months without stress.

If you’re starting from scratch, don’t get overwhelmed. Aim for one month in each account,

then build from there. Even a small buffer gives you breathing room and keeps you from relying on credit cards.

Closing Thought

You didn’t become a REALTOR® to stress over every commission check You chose this career for freedom and the chance to build a life on your terms. But that freedom only comes when your money is structured to support you, not suffocate you.

By automating your accounts, paying yourself first with the 50-30-20 Reverse Cash Flow Rule, keeping business and personal separate, and building the right buffers, you can turn unpredictable commissions into consistent confidence.

Because here’s the truth: those who master variable cash flow are the ones who last. The rest eventually go back to chasing a W-2

It's Not Just a House— It's Not Just a House—

It's Financial Wellness It's Financial Wellness

It's Not Just a House— It's Financial Wellness

When buyers think about purchasing a home, they’re often focused on two things: the house itself and the monthly payment. But as REALTORS®, you know the conversation has to go deeper. Today’s clients aren’t just buying a property; they’re making one of the biggest financial wellness decisions of their lives. The way you guide them can determine whether homeownership becomes a source of stability and wealth, or stress and regret.

Let’s be honest: buyers are glued to headlines about rates They walk into showings asking, “What’s the rate today?” as if that’s the only factor that matters. But financial wellness is about fit, not just numbers. The lowest rate isn’t always the best deal if it comes with higher points and costs upfront sometimes the “cheaper” rate actually costs buyers more out of pocket. A fixed-rate mortgage can bring peace of mind, while an adjustable-rate mortgage might be the right move for someone planning to sell or relocate in a few years. By helping clients think beyond “lowest rate” and instead ask questions like “How long will I stay in this home?” or “What happens if rates shift?” you position yourself as more than their REALTOR®; you’re the trusted advisor who helps them make decisions that hold up for the long run

We’ve all seen it: a client gets pre-approved for a higher amount than they expected and suddenly they’re off to the races, stretching every dollar to hit the max. But being approved for $450,000 doesn’t mean they should buy at $450,000. Coaching clients to “buy smart” instead of “buy to the ceiling” is one of the biggest gifts you can give them. A home should feel like freedom, not a financial chokehold. Remind buyers that staying under budget now means more breathing room later, and you’ll be the REALTOR® they thank when they’re living comfortably instead of being “house-poor.”

Marty Guy Fink

Branch Manager, Homespire Mortgage

Your role doesn’t stop at the closing table. In fact, the little nuggets you share after closing can make you unforgettable. One of the simplest financial wellness tips is the bi-weekly payment strategy. By splitting their monthly mortgage into two payments every two weeks, homeowners end up making one extra full payment a year. Over time, this can shave years off the loan and save them thousands in interest. Imagine your clients telling their friends, “Our REALTOR® gave us a tip that’s going to save us ten years of payments ” That’s the kind of lasting impact that keeps your name at the top of their referral list

Financial wellness isn t just about making the mortgage work; it’s about how the home can support overall financial health. For clients struggling with high-interest credit card debt, a cash-out refinance or home equity line of credit can sometimes be a lifeline Rolling multiple payments into a single, lower-interest option can change their financial outlook dramatically While these strategies aren’t right for everyone, when you know they exist, you can guide clients toward conversations that help them see real estate as a solution, not just a purchase.

At its core, financial wellness is about giving clients the confidence to see homeownership as more than a transaction it’s a path to stability, equity, and long-term success. When REALTORS® lead the way in these conversations, you don’t just sell homes; you change lives.

Investing in Wellbeing: A Investing in Wellbeing: A Pathway to Savings and Pathway to Savings and Organizational Growth Organizational Growth Investing in Wellbeing: A Pathway to Savings and Organizational Growth

In a climate where individuals, businesses, and organizations are striving to maximize resources, the question of how to save money without compromising performance is more important than ever. One of the most effective answers lies not in budget cuts or new technologies, but in the intentional prioritization of wellbeing. By aligning Employee Assistance Programs (EAPs) with mental health best practices and incorporating executive coaching, organizations can strengthen their workforce and see significant financial benefits.

The Cost of Ignoring Wellbeing

Unchecked stress, burnout, and absenteeism take a substantial toll on both individuals and organizations National data estimates that workplace stress costs U S employers hundreds of billions of dollars annually in lost productivity, medical expenses, and turnover. For employees, unaddressed mental health challenges can lead to personal financial strain due to higher healthcare costs and reduced capacity to work effectively.

Studies suggest that replacing an employee may cost anywhere from half to double their annual salary. Beyond the financial costs, high turnover disrupts organizational stability and diminishes morale. Addressing wellbeing upfront helps prevent these expenses before they accumulate.

Dr. Natalie Halloran

& CEO,

Strengthening Employee Assistance Programs

Many organizations already have Employee Assistance Programs in place, but the effectiveness of these programs depends on how well they align with current mental health best practices. Programs designed decades ago often fail to meet the needs of today’s workforce. A modern EAP should emphasize:

Accessibility: Easy, confidential entry points to support, whether through phone, online platforms, or on-site resources.

Preventive Care: Proactive services such as wellness workshops, counseling for stress management, and mental health check-ins before issues escalate

Cultural Integration: Wellbeing initiatives must be visible in workplace culture When leadership actively communicates the value of mental health and normalizes its use, employees are far more likely to engage with support services.

Organizations that modernize their EAPs typically report reductions in absenteeism, lower healthcare claims, and improved staff retention all of which translate directly into savings.

The Role of Executive Coaching

While EAPs address mental health directly, executive coaching plays a critical role in fostering growth and resilience among leaders and teams Coaching provides leaders with tools to better manage challenges, communicate effectively, and motivate others The benefits extend beyond individual development; stronger leadership often results in healthier organizational cultures, reduced conflict, and greater alignment with goals.

Founder

TillHall Enterprise, LLC

Research consistently shows that companies investing in executive coaching experience high returns, with some studies indicating a multiple of the original investment. Coaching helps leaders make strategic decisions that reduce inefficiencies, enhance collaboration, and ultimately save money by improving overall performance.

Creating a Synergistic Approach

The most impactful organizations combine strong mental health practices with leadership development. When EAPs offer mental health resources and coaching equips leaders to foster supportive environments, the result is a culture where individuals feel valued and capable. This synergy reduces the costly cycle of burnout, turnover, and disengagement while paving the way for innovation and long-term growth.

For individuals, this means access to healthier work environments where personal wellbeing and professional goals are supported in tandem. For organizations, it means maximizing the potential of their workforce while minimizing avoidable costs

H A P P E N I N G S O O N A T H R R A H A P P E N I N G S O O N A T H R R A

SPOTLIGHT

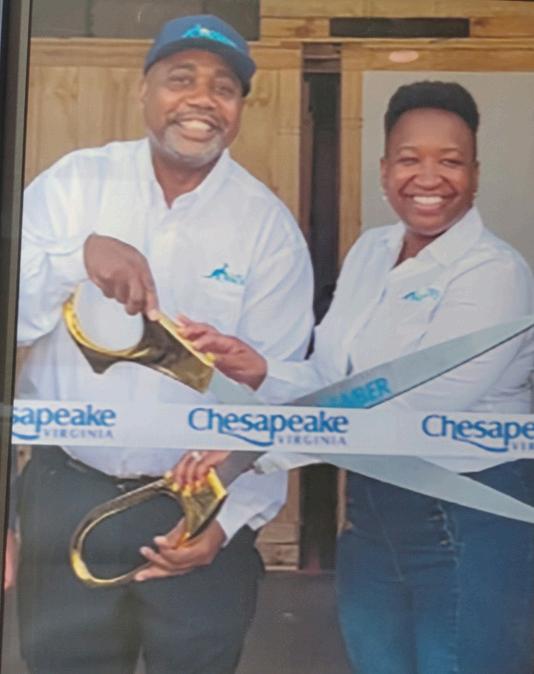

Name: Blue Kangaroo Packoutz

Territory: From the Outer Banks, all of Hampton Roads, Williamsburg, Richmond, as far west as Windsor, Smithfield & Carrollton Year Established: 2024 HRRA Affiliate Member Since: 2025

Contents Restoration, i e restoration of documents, electronics, art, textiles, books, antiques, furniture, upholstery, carpets, rugs, structural cleaning, and more

Why we got into this business: When Ebony & I started Blue Kangaroo Packoutz, it wasn't just about starting a business; it was about answering a calling Years ago, we experienced firsthand what a disaster feels like what it feels like to lose the things that make a house a home That's why we created something that doesn't just restore belongings, but peace of mind. We are the team that shows up and helps people take their first step back to normal. This isn't just work for us. It's personal.

Why we joined HRRA: To tell REALTORS® & PMs about the benefits of Packoutz Too often when homes, offices, or apartments are damaged, people feel they must discard their possessions, not knowing that unless it is unsalvageable, we can restore it! We can be the difference between discarding a treasured item or holding on to what you treasure.

Why we love doing what we do: We love seeing the look on a child's face when they get back a doll or teddy bear or being able to give someone back a one-and-only photo of someone they dearly loved.

Our favorite satisfied customer story: It's got to be Nick Mold had covered nearly all his clothes and bedding When we brought everything back restored, he gave us 5 stars and recommends us often.

Favorite HRRA event: Haven't been to one yet. I injured my back and was unable to join the Affiliate Kickball team, but you just wait till next year!!

Most memorable HRRA moment: That would have to be the moment I first walked into the business office I met Linda, Gene, Sofia and Jackie, and they greeted me like family as soon as I came in My questions were answered, advice was offered, and I walked away assured that joining HRRA was a very smart move.

How Healthy Are How Healthy Are

Your Finances? Your Finances? How Healthy Are Your Finances?

When we think about wellness, we often picture physical or mental health. But have you ever stopped to ask yourself about your financial health?

According to the Financial Health Network, financial health is not only about income or budgeting. It’s also about how your finances support your overall well-being Financial health means that your daily financial system allows you to spend, save, borrow, and plan in ways that help you feel in control today and prepared for tomorrow

It’s a holistic view one that recognizes financial decisions are deeply personal and often emotional. Money touches nearly every part of our lives: where we live, what we eat, how we care for ourselves and others. That’s why improving financial wellness starts with honest self-reflection, not spreadsheets.

Financial well-being isn’t one-size-fits-all, but there are four key areas that serve as a foundation. Each comes with a simple reflective question and an action step you can take with no financial expertise needed

1. Spend: Are you spending less than you earn?

Reflect: When you review your recent spending, do your choices support your personal goals and priorities or are they driven by stress, impulse, or habit? Many people don’t realize how unconscious their spending has become. It’s easy to swipe, tap, or click without connecting it to your bigger goals.

Try this: Give yourself the gift of awareness. Track your spending for one week without judgment and then look for patterns. One small change like packing lunch or canceling a forgotten subscription can free up resources to put toward goals that truly matter to you

2. Save: Are you setting money aside regularly for now and later?

Reflect: Could you handle a $500 emergency without relying on credit or dipping into other savings? Life is full of unexpected expenses a flat tire, a medical co-pay, a last-minute trip. Having a financial cushion helps transform emergencies into inconveniences

Try this: Start by building a $500 “just in case fund ” Automate a small weekly transfer even $10 counts. Once it’s set up, treat your savings like a non-negotiable bill and start gradually increasing your transfers over time, building both your savings and your confidence.

3. Borrow: Are you managing debt wisely?

Reflect: Does your current debt feel manageable, or is it a source of anxiety? Debt itself isn’t inherently bad it can be a tool. But unmanaged debt can quietly chip away at peace of mind and limit your choices.

Try this: Write it all down: balances, minimums, interest rates. Getting a clear picture can be empowering. Choose one small debt to pay off first that “quick win” can help you feel more in control and less overwhelmed

4. Plan: Do you feel confident about your financial future?

Reflect: Do you have clear goals and a roadmap or does thinking about your financial future feel overwhelming? It’s common to avoid planning because the future feels uncertain. But clarity can ease anxiety

Try this: Choose one meaningful goal, whether it’s saving for a major purchase, building your retirement fund, or starting a side business. Write it down, set a target amount, and break it into manageable monthly chunks. Remember, progress beats perfection. Planning doesn’t need to be perfect to be powerful.

Financial health isn’t about being perfect with money. It’s about feeling in control and prepared for what life brings. Reflecting honestly on where you are today is the first step toward where you want to be.

So, ask yourself: What would financial well-being look like for me? Then take one small action. Your future self will thank you.

Congratulations, #842105141! You’ve won this month’s giveaway. Email editors@hrra.com to claim your prize.

How to Forecast Cash Flow & Protect Your Personal Credit

Reprinted with permission from the National Association of REALTORS®

Real estate professionals have a lot to juggle, and properly managing cash flow and credit keeps everything moving forward. One of the best ways to protect your personal and business finances is to use a

planning Determine what you need to take home each month What are you spending on health insurance? How much do you need to save or invest for retirement, and what are your other essential living expenses? Don’t forget to factor in income and selfemployment taxes

In any cash flow forecast as a self-employed professional, that final number is the baseline figure to aim for Next, factor in any business operating expenses

Typical operating expenses for a real estate professional include marketing costs, membership fees, advertising, printing, technology, and, in many cases, the upkeep of an office You may also have staff, or plan on hiring in the future All those costs should go into projected cash flow forecasts

Now that you have a clear idea of what you expect to spend each month or over the course of the year, you can project the number of transactions you need to close based on the level of compensation you’re seeking for your services

Be sure to factor in potential earnings from rental commissions, and any other income streams, such as property investing and flipping

Know When You Are Expecting to Make BIG Purchases

On top of everyday expenses and operating costs, many agents also invest in property.

In some cases, that means buying, renovating, and selling or renting out properties. Whether you’re doing this individually, with a partner, family members, or friends, or in an investment syndicate, investing in properties can be lucrative and an excellent way to leverage your real estate and local knowledge.

Generally speaking, the more you improve or expand a property, and the higher-spec the finish, especially in an up-and-coming neighborhood, the bigger the profit you’ll make.

But this, of course, comes at a cost. If you are flipping real estate, then project those big purchases into your cash flow and be clear how you will finance them. And factor in a contingency budget based on potential cost overruns (estimating at least 10% of the total, to be on the safe side). There’s nothing worse than starting to invest in upgrading a house only to run out of money mid-project, as it can be very hard to offload a halffinished redevelopment, and you could easily lose money in the process.

Avoid Mixing Personal & Business Finances

When your personal and business finances are mixed, you risk damaging your credit file, especially if you are investing in developing properties or making big purchases.

This happened to Ana Sandoval, a broker and owner of Realty Way, in Miami, Fla.. Sandoval is also a real estate investor, and as she was only a couple of years into her real estate brokerage and investing career, it was a significant worry.

Her main focus is flipping properties and investing in real estate alongside her family, friends, and a group

of investors she has worked with for years. It’s handson work, and money is needed at various points during the development process.

It’s been an exciting journey for Sandoval, and once every new property is ready, it’s either sold or put on the market to rent. Unfortunately, for a time, she was using personal accounts, loans, and credit lines to fund some of this work, and that was knocking her personal credit score and ability to apply for loans at lower interest rates.

Fortunately, members of the National Association of REALTORS® can access finance offers from NAR REALTOR Benefits® partners.

Give Yourself Peace of Mind

Sandoval tried applying for a business credit card with Capital One, but they said her brokerage was too new. At that moment, she thought her only option was to wait at least three years and try again.

As an NAR member with automatic access to NAR REALTOR Benefits®, Sandoval was encouraged to apply for the NAR World Elite Business Mastercard, which is managed by Affiniti Finance.

The application process was quick and easy, and her time as a broker didn’t impact Sandoval’s ability to be approved. Having an NAR World Elite Business Mastercard means that her personal and professional finances are now separate, and it makes managing cash flow a lot easier.

Plus, the unlimited 2.1% cashback on all purchases, and 5% on any brokerage marketing expenses, is like getting free money. It’s a win-win for Sandoval and the other investors she works with in her growing real estate portfolio.

Access NAR REALTOR Benefits®: With the NAR World Elite

Business Mastercard

NAR members have exclusive access to apply for the NAR World Elite Business Mastercard, which offers up to 2.1% unlimited cash back on all purchases, 5% cash back on marketing expenses, and the opportunity to get a $500 sign-on bonus to help offset NAR membership dues.

The $500 bonus is available to cardholders who make $30,000 of eligible purchases within the first three months of being approved for their account

Cash back rewards work like this: You will earn a total reward of 5% cash back on the first $5,000 of eligible purchases made at marketing or marketing software product merchants then 1% if you do not have autopay set-up, 2 1% if you have weekly autopay setup, or 1 9% if you have semi-monthly autopay set-up

You will earn 1% unlimited cash back rewards on all of your eligible purchases; if you have set up weekly autopay, you will instead earn 2.1% unlimited cash back rewards on all of your eligible purchases. With semi-monthly autopay, you will earn 1.9% unlimited cash back rewards on all of your eligible purchases.

Please review the cardholder agreement for full details about the terms and conditions of the rewards and benefits.

About the NAR World Elite Business Mastercard

Affiniti Finance Inc. is the program manager of the NAR World Elite Business Mastercard and is responsible for its operations, including but not limited to card issuance, rewards, management, and customer service.

Cardholders are encouraged to review the comprehensive terms and conditions provided by Affiniti Finance Inc., which can be accessed at affiniti.finance/legal. Affiniti Finance Inc. is not an FDIC-insured institution. NAR World Elite Business Mastercard is issued by Patriot Bank, N.A., Member FDIC, pursuant to a license by Mastercard International Incorporated.

Log into the MyHRRA Membership Portal to sign up!

Contract Pitfalls

November 6, December 2

8:30 AM - 12:30 PM, $35

Real Estate Pitfalls

November 6, December 2

1:00 PM - 5:00 PM, $35

8 Hour Required Topics

October 16, November 13, December 11

8:30 AM - 5:00 PM, $65

Broker Real Estate Law

October 20-27

M-F, 9:00 AM–1:00 PM, $300

Broker Real Estate Management 8 HR CE

October 28 8:30 AM–5:30 PM, $60

Broker Real Estate Finance

November 17

9:00 AM–1:00 PM, $370

Brokerage

December 15 9:00 AM–1:00 PM, $370

Designations, Certifications, and Workshops

Buyers by Generation Designation Course

October 14, 9:00 AM - 5:00 PM, $99

Abla Barakat - Epique Realty

Welcome, New Members!

Akiyah Lindsey - Redfin Corporation

Amanda Broadus - Garrett Realty Partners

Aquaetta Wilder - Keller Williams Coastal Virgin

Benjamin Doyle - BHHS RW Towne Crossways Blvd

Brian Shea - LPT Realty, LLC

Brittney Jones - The Bryant Group

Candace Cosby - Keller Williams Coastal Virginia

Christopher Lares - MR Rivera Realty Group

Deisy Lawrence - Harrell Homes Real Estate

Demetrice Thomas - Verian Realty LLC

Devin Lundy - eXp Realty LLC-VB

Emmilee Osbourne - RE/MAX Alliance

Eric Wood - Keller Williams Coastal Virginia

Erica High - Century 21 Nachman Realty

FelinetTorres-Bonano - ERA Real Estate Professionals

Jamecia Hawkins - Summit Realty Group LLC

James Blackwell - Keller Williams Coastal Virginia

Jennifer Franklin - Century 21 Nachman Realty

Joshua Worthley - eXp Realty LLC-VB

Katherine Holloway - Own Real Estate LLC

Kelly Wadlinger - RE/MAX Prime

Kelvin Demps Sr. - eXp Realty LLC-VB

Kim Kirane - RE/MAX Ultra

Kim Lokeman - Real Broker, LLC

Lakisha Brown - Redfin Corporation

Londyn Patterson - LPT Realty, LLC

Melissa Vadnais - Century 21 Gold Market Realty

Myra Davis - Harrell Homes Real Estate

Natasha Randolph - eXp Realty LLC

Peter Schonk - Swell Real Estate Co.

Randall Sim - Mossy Oak Properties Land & Farms

Rowan Whitenack - LPT Realty, LLC

Ryan Ceballo - Coastal Life Realty

Shannan Crayton - Epique Realty

Shannon Kellam Neas - eXp Realty LLC-VB

Shawnda Joynes - Redfin Corporation

Sofiane Nianduillet - eXp Realty LLC-VB

Soraya Bakhshayesh Eghbali - Harrell Homes Real Estate

Stacy Mitchell - RE/MAX Alliance

Stefanie Mendez - Atlantic Sotheby's International