“Investment Committee Leadership: Driving Governance and Leadership”

Mr. Akhileh Gupta Chief Investment Officer, Aviva India

“Rise of Passive Investing in India”

Dr. Riya Singla Assistant Professor, IIM Amritsar

“Investment Committee Leadership: Driving Governance and Leadership”

Mr. Akhileh Gupta Chief Investment Officer, Aviva India

“Rise of Passive Investing in India”

Dr. Riya Singla Assistant Professor, IIM Amritsar

1. FOREWORD 02

Dr. Nagarajan Ramamoorthy Director, IIM Amritsar

2. COVER INTERVIEW 03

“Investment Committee Leadership: Driving Governance and Leadership”

Mr. Akhileh Gupta Chief Investment Officer, Aviva India

3. FACULTY ARTICLE 06

“Rise of Passive Investing in India”

Dr. Riya Singla Assistant Professor, IIM Amritsar

We are back with another edition of Vitta Artha. The publication provides in-depth coverage of contemporary financial trends, featuring insightful articles, interviews with industry leaders, and engaging content that enriches readers’ understanding of the financial world. Previous editions have featured prominent figures such as Mr. Amit Jeswani, CIO at Stallion Asset Management, Mr. Sankaran Narayan, CIO at ICICI Prudential AMC, Additionally, Vitta Artha includes thought-provoking book and movie reviews offering a comprehensive platform for both learning and engagement.

Rahul Saha

IIM Ranchi

Shreya

IIM

Sammridhi Jadhav

Hritabhash

IIM

Swagat

IIM

Dear All,

Dr. Nagarajan Ramamoorthy Director

Amritsar

I am delighted to introduce the thirteenth edition of Vitta Artha, the bi-annual magazine published by the Finance and Economics Club (FEC) of IIM Amritsar. FEC works interminably at the college and industry levels to further the students’ interests by exposing them to various aspects of the world of finance and economics—the club endeavours to harness talent and enhance the learning experience of our student community. Vitta Artha – The Finance and Economics magazine of IIM Amritsar is one such effort in the same direction. Varied views in the form of articles given by students from prominent B-schools across India, finance and economics faculties, and the esteemed insights of industry professionals help the students and readers better understand the real-life implications and nuances in the fields of finance and economics.

This edition of Vitta Artha looks at how leadership within investment committees determines direction, risk propensity and handling the tough terrain of investment management. It covers best practices for generating sound and rational decision on investments and shows how the structures of governance affect portfolio stability and future worth. In turn, this feature prepares readers to have profound insight into the phenomena of leadership within the investment committees and its effects on the obtainment of sustainable financial results. In addition, it provides information on contingency planning for future adversities it plays a role of making advance changes on investment and risks it also offers broader views on financial responsibility and management including stable and sustainable portfolio management.

This issue lays out the shift towards passive investments with a detailed report on the Passive Investment space in India. The article discusses such aspects as the rationale for this occurrence, including the efficiency of low-cost index fund tracking, or difficulties that passive actively managed investments face in the present unstable market environment. It emphasises the rising adoption of passive products, such as Index Funds and ETFs and explores the influence of the higher financial literacy level, and internet connectivity.

Alongside this, this edition also features articles across various domains in Finance and Economics from students across various reputed institutions, CFA preparation strategies. Moreover, this issue brings out books and movie recommendations to generate interest and enthusiasm amongst its readers. Like the previous editions, I hope that this issue of Vitta Artha adds value to its readers and thus augments their interest and inquisitiveness in the enriching domain of finance and economics.

Akhilesh Gupta is a veteran investment professional with over 25 years of experience managing multi-asset class portfolios, including equities, fixed income, FX, and alternative assets. Currently the Chief Investment Officer (CIO) at Aviva India. His investment philosophy emphasizes disciplined, rule- based strategies to create value while managing risk effectively.

Akhilesh has navigated major financial crises like the Asian Financial Crisis, Dot-Com Bubble, and Global Financial Crisis. He is known for his sharp analytical skills, connecting the dots to generate alpha while maintaining high governance standards. He has also held senior roles at Reliance Nippon Life Insurance and Dundee Mutual Funds.

A mentor and visiting faculty at top business schools, Akhilesh is passionate about financial literacy, impact investing and philanthropy. Influenced by Warren Buffett’s dispassionate thinking and Wayne W. Dyer’s belief in self, he is respected for his ability to manage risk and communicate complex concepts clearly.

Given your extensive experience, what are the typical responsibilities of an investment committee, and how does it ensure sound decision-making regarding asset allocation and risk management?

The Investment Committee (IC) provides an overarching guidance while adhering to the prescriptive exposure and prudential norms, set by, be it IRDAI / SEBI / PFRDAI for their respective asset managers. Over the years we have witnessed harmonisation of the regulatory norms across the regulators, which is again imperative for the smooth functioning of the financial markets while safeguarding the interest of the investors be it retail or Institutional.

The Chief Investment Officer (CIO) recommends further guardrails to be accepted by the IC to augment reinforcements to deliver the superior risk adjusted performance to both shareholders and investors (policyholders). These additional measures are helpful in upholding the credentials during the uncertain times in the financial markets as well as to mitigate the employees related fiduciary risks.

In terms of asset allocation, the IC is appraised by the CIO about the valuations of the different asset classes. Then IC is recommended to move into asset classes which is cheaper from the asset class which is rich in case of multi asset portfolios and normally a range is approved to work-on to provide flexibility to the Fund Managers.

The IC is also appraised of various risk repots like Value at Risk (VAR), Beta, Sharp Ratios etc. of the portfolios to showcase the source of risks and whether they are within limits. In case, if they are out of the agreed range, then Chief Risk Officer (CRO) provides the explanation and process to bring them back within the tolerance range. The IC usually meets every quarter to review outlook and strategy of fund management and performance as per agreed benchmarks and compliance.

How do you ensure the investment committee aligns portfolio strategies with the organization’s broader financial goals, especially in navigating multi-asset portfolios and managing risk?

The investment Policy (IP) is a document recommend by the CIO to IC, where in, there are

well defined asset allocations are mentioned while adhering to regulatory and internal exposure and prudential norms. These allocations are designed on the basis of risk taking capacity which in turn offered to the investors / shareholders.

For example, in terms of equities, if the firm has a conservative risk appetite, then allocation may be restricted to NIFTY 100 stocks to reflect this thought process.

The risk tolerance for Fixed Income is defined in terms of the portfolio duration as well as allocation between Sovereign Bonds and Corporate Bonds. Normally, there is a range allocated to different asset class in the multi asset portfolio and it can be altered depending upon the valuation outlook and strong arguments to do so.

In your experience, how do investment committees incorporate macroeconomic data into their decision-making process to ensure portfolios remain resilient during periods of economic uncertainty?

IC deliberates on the economic outlook and valuations of different asset classes shared by the CIO and then looks for what has been changed since last time and how portfolios were navigated which is reflected in the performance against the index. Obviously, consistent good out- performance against index and Peers reflects well of the strategy and actions taken to navigate the uncertain and unanticipated events in the financial markets

What are some of the key challenges you face in maintaining effective performance within the investment committee, especially during periods of market volatility? How do you address these challenges?

Yes, there are periods of under- performance for variety of reasons. Possibly, once you have initiated the position and it so happen that it may take longer the anticipated time to perform. Conversely, you have initiated a position, which is failing to perform as per original hypothesis. The idea is to cling to conviction while reduce / exit the mistakes at the earliest. In addition, the rule based process of selection and allocation is the gold standard to deliver the consistent performance over long period of time and this is what should be conveyed to the IC.

What are the emerging trends like Stewardship / ESG etc. in portfolio construction reshape investment committees and how should finance professionals prepare to contribute effectively?

Stewardship Policy, approved by the IC while adhering to regulatory norms, is now a integral part of the investment management. There are five pillars which help guide investment team that how to monitor investments by interacting management of the investee companies as well as collaborating with fellow institutional share-holders while discharging the fiduciary responsibilities towards the investors. There are proxy advisory companies likes, IIAS/ In Govern which assist asset managers while voting for the resolutions proposed by the investee companies. Stewardship Policy as well as voting pattern is available on the website of the asset managers.

The climate risk is clear and present danger and there is where ESG is compelling companies to act in the greater good of environment / social.

You’ve held leadership roles across several financial institutions, including your current role at Aviva India. How has your approach to portfolio management evolved over the years as you’ve taken on larger responsibilities?

The secret sauce of consistent compounding of capital is “Boring” way of increasing your circle of competence by regular updating and upskilling yourself and team. There is a never a dull day in the investing world for passionate investors. Imagine today we are learning about e- commerce which was not there a decade ago and forming an intelligent views on it to invest. One of my favourite saying is if you consider yourself as a successful investor, then you should be wealthy and achieved the financial freedom.

As someone who has worked through multiple market cycles, including the 2008 financial crisis, how do you prepare portfolios to withstand such crises?

This is simple. It is the guardrails in terms of exposure and prudential norms which itself help

whether the storm. Secondly, the selection and allocation in the portfolios should be based on the “Home Work” done on each and every investment so that once you go through the storm, you have the conviction that drawdown will lower than the index and eventually you will gain much more then index once you pass through the tunnel.

Looking back at your career, is there a particular decision or project that you are most proud of? What made it significant, and how did it shape your perspective as a leader in finance?

I fondly remember how I learned the tricks of the trade once I commenced my investment journey with Cargill. It was where I have honed my skills in trading Fixed Income / Equity / FX. It has evolved me as a person how to maintain a balanced personality whether you have made a profit or loss. This has also laid the foundation of learning consistent compounding of capital through equities and achieving financial freedom.

What core financial skills and leadership qualities should MBA finance students develop to succeed in future investment manager?

One has to has passion for investment, being curious and consistent learnability to succeed in managing money. In addition, behavioural skills like how to behave in an uncertain scenario, when markets are testing your nerves in terms of your position is yet to perform etc. will be utmost important to thrive in the market. A dispassionate and disciplined approach is the key to success.

Dr. Riya Singla Assistant Professor Finance, Accounting, and Control

For time immemorial, wealth creation in the financial markets has been synonymous with the ability to buy the right stocks at the right time. The belief is that the investors who can actively engage in the market will only be able to generate abnormal returns. However, in the past few years the markets world over have witnessed the rise of an alternate investing phenomenon

Without engaging actively in the market, passive investment opportunities have taken the financial markets by storm and are now reshaping the dialogue about wealth creation. Passive investment funds, like the Index Fund and Exchange Traded Funds (ETFs), try to replicate the composition of indexes like Nifty 50 and Sensex. Unlike active investment strategies, the aim is not to beat the market by buying and selling the right stocks. The intention here is to mimic the composition of these indexes and track the performance over time. Various developed financial markets have seen a shift of retail investors and institutional investors towards passive investment. On the aligned path, the rapidly growing Indian capital market observes passive investment becoming a formidable force. Indian Investors are looking at a transition from traditional, actively managed mutual funds to a systematic, cost-effective investing medium.

Indian stock market was predominantly an arena for active fund managers. However, as the market becomes unpredictable, the appeal of passive investment grows. According to the study ‘Where money flows’ by Motilal Oswal Asset Management Company, the asset management industry in India has grown 7X in the past decade, with Asset Under Management (AUM) soaring from 8.3 lakhs in December 2013 to 61.2 lakhs in June 2024. Notably, passive equity has attracted the secondhighest net inflows for the mutual fund industry by mid of 2024 and has shown a CAGR of 56% in the past decade. Moreover, of the 106 new fund offers in the Indian market in 2024, about 59% have been passive schemes, clearly highlighting the rise in its popularity.

The rising prominence of passive funds reflects the evolving landscape of the Indian market. In the past few years, actively managed funds in India have been unable to outperform their benchmarks. A 2024 report by SPIVA (S & P Indices versus Active) finds that about 77 %, 82 %, and 100 % of actively managed funds have underperformed their assigned benchmarks over 1-, 3-, and 5-year period respectively. Investors naturally are inclined to question the efficacy of active investment funds as returns hardly justify the cost. Passive funds are inherently less costly due to lesser expenditure on research, fund management, and operational expenses.

The average expense ratio of an actively managed equity fund is 1.5% to 2%, whereas passive funds charge less than 1%. If compounded over the years, the cost difference relative to the return difference can significantly contribute to the corpus of the investors. Moreover, the younger investing population of India, mainly millennials and firsttime investors, find these investment avenues less time-consuming, liquid, and simple to understand. They are able to reap the benefit of market growth by holding the index fund and not worrying about selling or buying stocks each time the market shows volatility. In addition, the Indian investors are gradually becoming more financially literate. Internet penetration into the Indian hinterland has allowed easy access to the financial advice of experts. The surge in information avenues has created awareness among investors about available choices and empowered them to make choices based on their risk appetite and financial goals. Complimenting the other information sources, the continuous efforts by the Securities and Exchange Board of India (SEBI) to protect and educate small investors have allowed them to make decisions independently and not rely on the advice of big fund managers.

The attractiveness of passive funds is not just limited to retail investors, as Indian institutional investors are gradually following the same path. The Association of Mutual Funds in India (AMFI), in its latest report, suggests that approximately 43% of the investment in index funds is contributed by Institutional Investors. In 2023, the Employees’ Provident Fund Organisation (EPFO) invested approximately 22% more in passive funds than the last year. In the past seven years, the investment by EPFO in passive funds has crossed INR 2.5 trillion. The increased institutional investment in passive fund schemes could be driven by the cost advantage, the expectation of consistent returns, and, most importantly, increased transparency, which is crucial for these investors. The endorsement from such a prominent and credible investing institution not only infuses funds for the growth of passive funds but also builds faith amongst retail investors about the reliability of the investing strategy.

The growth of passive investment funds in India has been impressive.

has been impressive. However, the journey ahead has a few challenges. The Indian mutual fund industry is still dominated by active funds. Many investors, particularly older generations, still prefer the potential for outsized returns promised by active management. Furthermore, India’s equity market is still in a growing phase. It can be characterized by its high volatility, thus offering ample opportunities for skilled active managers to outperform during specific periods. However, the consistency of passive investment will still emerge as a less complex and hands-off approach to wealth creation.

As we advance, the passive investment strategy is going to deepen its roots in India. Indian investors are gradually learning from the developed markets about the potential of passive investing. The market participants and regulators continually strive for a more efficient Indian financial market with more transparency, lower costs, and better investor protection. Passive investment funds fulfill all these characteristics; hence, massive growth is yet to be witnessed.

• https://iongroup.com/blog/markets/how-the-rise-inpassive-investing-in-india-drives-sell-side-automation/

• https://economictimes.indiatimes.com/mf/mf-news/ passive-investing-booms-mutual-funds-cross-rs-10lakh-crore-aum/articleshow/112687323.cms?from=mdr

• https://www.business-standard.com/economy/news/ investment-by-epfo-in-etfs-crosses-rs-2-5-trillion-saysgovt-123121101027_1.html

• https://www.motilaloswalgroup.com/Media-Room/ Press-Release/-/indias-passive-mutual-fund-industrysurpassin/AM/20626#:~:text=Mumbai%2021%20 August%202024:%20According,Hybrid%20and%20 4.44%25%20in%20others.

• https://www.cnbctv18.com/personal-finance/passivemutual-funds-vs-active-funds-nfo-new-offer-rise-indiareturns-investment-19471534.htm

• https://www.spglobal.com/spdji/en/documents/spiva/ spiva-infographic.pdf

• https://www.amfiindia.com/research-information/aumdata/age-wise-folio-data

“An investment in knowledge pays the best interest.”

— Benjamin Franklin

Rahul Saha IIM Ranchi

Quick commerce, offering delivery within 30 minutes via online platforms, has transformed retail by providing fast and convenient shopping. This article examines the hyperlocal delivery networks enabling quick commerce, focusing on operational strategies, unit economics, and the role of dark stores. Key companies like Zepto, Blinkit, and Dunzo are analysed for their approaches to profitability and efficiency. The article explores the impact of optimized order value, strategic dark store locations, and data analytics on operational success. The challenges and benefits of last mile delivery and economies of scale are discussed, along with the broader implications for consumers and delivery agents. The conclusion highlights the importance of continuous innovation and strategic adaptation for sustaining growth in the competitive quick commerce market, which shows significant potential for future expansion.

Quick commerce is the delivery of goods purchased within few hours or even under half an hour through online application. This encourages seamless shopping experience as well as faster delivery and frequent orders for the delivery agents. This instant gratification and convenience works with the help of a strong hyperlocal delivery network as dark stores in each neighbour to guarantee delivery under 10-minutes (example: zepto). Dark stores are mini warehouses that work as distribution centres and are located in a non-premium area to avoid higher rent and are exclusively for online shopping. Recent startups that currently hold a major market share are Zepto, Blinkit, Instamart, Dunzo and BigBasket as well as some companies that got shut down due to high competition are Ola Dash, Fraazo and JioMart.

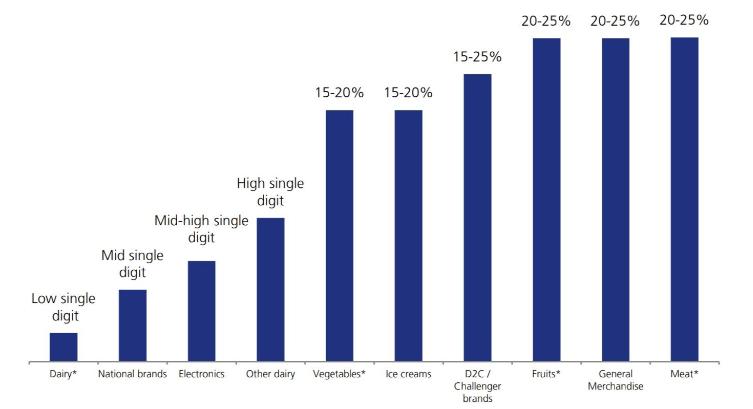

Unit Economics refers to the mechanism behind turning each unit of sale into profit for the sustainability of the company. In reference to quick commerce, we take one delivery as one unit to calculate profit per unit with direct costs and revenue. Companies like Zepto and Blinkit are in the negative profit per unit whereas Dunzo has achieved a positive profit per unit goal. These quick commerce companies earn a significant portion of their income from commissions on the products they sell to the online consumer. The margin percentages differ with every application and every category of product, for instance: Fresh vegetables and fresh fruits have a high margin of around 15-25% whereas dairy products have a lower margin.

Quick commerce got its opportunity to flourish and grow through several lockdowns during the Covid-19 pandemic as no-contact and faster deliveries of groceries were preferable by the consumers for daily consumption. This led to countless startups and companies to fill the gap and innovate their applications in the field quick commerce. Considering strong competitive landscape and complicated market dynamics, only four major players survived while several other initiatives had to fold up.

Dynamics of Hyperlocal Delivery

The main three areas to focus in order to recover costs are:

• Right order value: setting an appropriate order value directly affects the revenue of the company as with the increase in average order value, the level of commissions earned also increases. Example- Zepto and Instamart has Rs. 400 order value and Blinkit has Rs. 553 order value.

• Right population density around dark stores the location of the dark stores plays an important part as it should be located close enough to customers for faster deliveries but should also be far from premium rent area to avoid high rent expenditure.

• Monetization through advertisements: the companies can use data analytics to track the consumption pattern in neighbourhoods to accordingly manage the inventory. They can also micro target relevant audiences for better returns and track the real time visibility of effectiveness of advertisements for brands.

The internal factors also play a crucial role in smooth operations of quick commerce as these provide cross functional synergy which sets the company apart and show real time analysis, like inventory accuracy, operational metrics, availability

•

of delivery resources and wide product portfolio. The growth of quick commerce come with both benefits and challenges for the consumers and staff involved. The benefits can be broadly classified as better services at cheaper and faster rates and the convenience of seamless shopping as well as cognitive ease for the consumer. The challenges may be invisible but quite detrimental in the long term making the consumer impatient and restless as well as encouraging a pampered generation and disloyal customer base. The delivery agent also faces the challenges in the form of penalties to be paid for late deliveries and the issue of rating system as well as increased rate of accident with no insurance cover as they fall under the category of gig economy.

Last mile delivery is the last leg of the final journey of the product to the customer and focuses on correct location of the warehouse network and distribution centres, whoever cracks this equation solves the issue of delivery time and is successful in fulfilling customer satisfaction. The last area of concern remains the long term sustainability of this sector as swiggy and Zomato, being the leading companies in food delivery segment are still a loss making venture, which begs the question how quick commerce can sustain?

The answer lies within the question as quick commerce refers to the deliveries made within a short amount of time which gives every rider/ delivery agent more time to deliver new orders thereby increasing the rider’s efficiency by 3x. Therefore, faster delivery equals to cheaper deliver signifying the economies of scale. The existence of dark stores in every neighbourhood also helps by reduction in fuel cost and increased use of electronic vehicles.

In conclusion I would like to summarise the article by stating that the only way to survive in this hyper competitive, highly unsustainable and profit challenged market is by having a well- researched and product portfolio and constant updates with the help of data analytics to track consumer behaviour. Innovation and diversification will keep the company fresh in consumer’s perspective, for instance, new launch of Zepto Café in Mumbai to deliver fresh coffee in under 10minutes, exclusive launch of PS5 on Blinkit, quick fashion entrance into the market with IPL jerseys and several incentives and partnerships.

The quick commerce market in India is forecasted to generate a revenue of US$3,349.00m in 2024 and the user penetration rate, which currently stands at 1.8% in 2024, is projected to rise to 4.0% by 2029 which shows the untapped potential in this sector and the evolving trends of India’s retail economy.

• https://www.marketbrew.in/weekly-insights/growingquick-commerce-india

• JM Financial- Deep Dive : Quick Commerce (3278 (jmfl.com))

• https://www.linkedin.com/pulse/how-unit-economicswork-quick-commerce-saad- fazil/

• https://www.statista.com/outlook/emo/online-fooddelivery/grocery-delivery/quick- commerce/india

• Forbes India: Why quick commerce is a better business model than e-commerce, with Deepinder Goyal (https:// youtu.be/VyqjbDAYyWY?si=EcxlHPK3zKfTTZnH)

• Forbes India: Will quick commerce ever be profitable, and if so, how? (https://youtu.be/-_bkP6W7MSE?si=_ LnaB1Cf4bW711iH)

• Backstage with Millionaires: Why 10-minute delivery startups are taking over India’s online grocery space (https:// youtu.be/7rARKQD8HNU?si=PHH3TCymC59F56_h)

Shreya IIM Lucknow

What are robo-advisors?

A robo-advisor is a digital platform that provides automated financial planning and investment advice driven by algorithms requiring little or no human supervision. A typical robo-advisor evaluates the candidate’s financial goals, risk tolerance, and time horizon through an online survey. This data is further used to offer tailored investment advice and automatic portfolio management / rebalancing service.

In the recent times, they have gained significant popularity, especially among younger investors who are seeking low-cost and convenient investment solutions.

As of July 2024, Vanguard Digital Advisor is the largest robo-advisor by AUM ($200Bn+) and the market is growing at a CAGR of ~30%.

Portfolio rebalancing

Most of the robo-advisors use modern portfolio theory to build passive, indexed portfolios that are continuously monitored. Optimal asset-class weightings are maintained through rebalancing

• Rebalancing - Involves allocation of a target weight and a corresponding tolerance range to every asset class. Robo-advisors continuously monitor and automatically rebalance the portfolio by adjusting the weights of risky and risk-free assets.

• Tax-loss harvesting strategy - Involves sale of securities at a loss in an attempt to save on capital gains tax. It is usually done towards the end of the tax year and involves simultaneous investment in a similar security to maintain the portfolio allocation and benefit from an upturn in the markets

Revenue generation They earn revenue by charging a fee based on AuM, through payment for order flow – i.e. amount generated from directing trade orders to market makers, and promoting financial products / services via partnership with other firms.

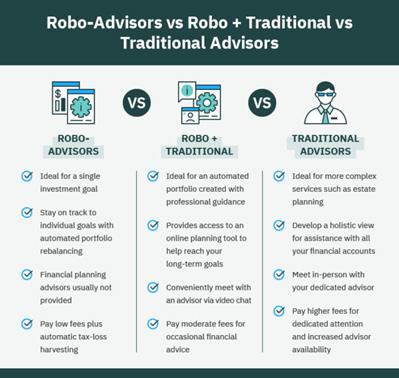

Benefits of robo-advisors vs. traditional financial advisors

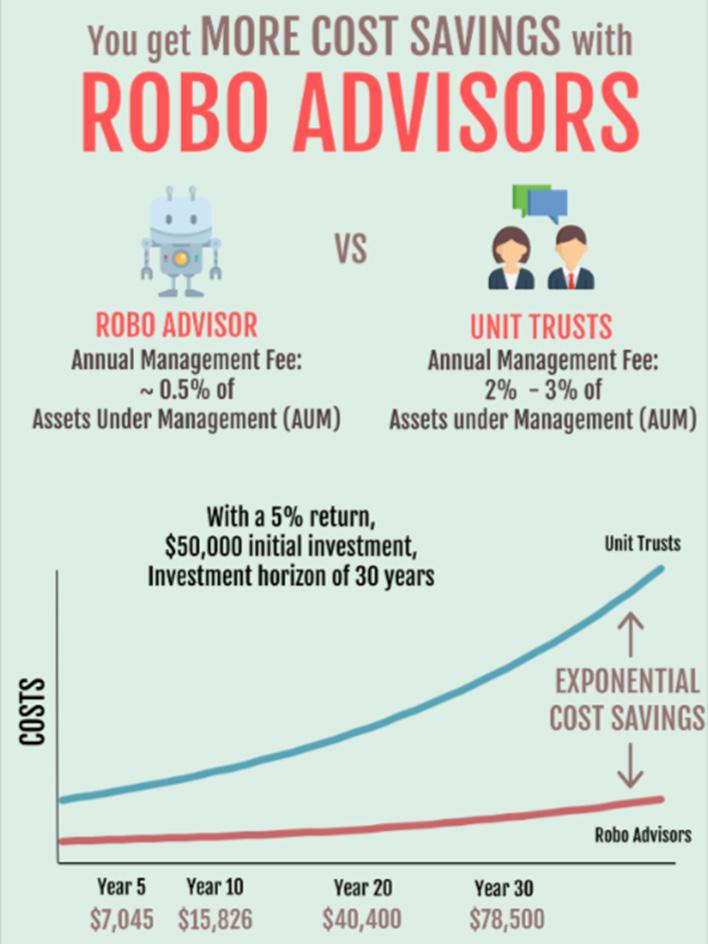

• Lower fees - Traditional financial advisors usually charge around 1% of AUM while roboadvisors typically charge below 0.4%, making investing more inclusive.

• Accessibility - With just a few clicks, one can open an account and there’s no requirement of multiple in-person meetings or lengthy paperwork. Robo-advisors offer a convenient and streamlined investment experience with a very low minimum investment policy.

• Tailored advice - AI can offer tailored investment advice based on a candidate’s financial goals, risk tolerance, and time horizon.

• Efficient portfolio management - Routine tasks like diversification and rebalancing is executed efficiently by the algorithms. In terms of data analysis, AI can analyse vast amounts of historical market data and trends to identify ideal assets for making real-time portfolio adjustments.

• No emotional bias - usage of AI/ML algorithms ensures rational decision making

• Limited flexibility & personalization - While roboadvisors find ready takers among the young generation, it is less accepted among HNIs having a large portfolio or entities looking to invest a significant portion of their savings. They typically require more sophisticated strategies like selling call options on current portfolio or buying specific stocks. Such investors are more likely to look for human validation, especially when the markets become volatile.

• Unexpected crises - Roboadvisors are ill-equipped to deal with extraordinary situations. For example, robo-advisors won’t know if you are between jobs or have an unexpected expense - automatic withdrawals can drain your funds quickly.

• Cybersecurity concerns – Ensuring robust security measures is crucial to protect the customer data from any potential cyber attacks and virus expense - automatic withdrawals can drain your funds quickly.

Source: Tokenist

Looking ahead, the future of investment lies in a hybrid model that combines the efficiency and precision of AI with the oversight and experience of humans.

• Cierra Murry, Suzanne Kvilhaug (2024, February) What Is a Robo-Advisor?

- Retrieved from: https://www. investopedia.com/terms/r/roboadvisorroboadviser.asp

• The Muse Editors (2024, April) What is a Robo-Advisor and is the Right Choice for You? - Retrieved from: https:// www.themuse.com/advice/what-is-arobo-advisor

• Bluestock (2023, December) RoboAdvisors: AI in Personal Finance and Investment - Retrieved from: https:// medium.com/@bluestock.in/roboadvisors-ai-in-personal-finance-andinvestment-d05b0d3acd83

Samriddhi Jadhav IPS Academy, IBMR

The world is facing some of the unprecedented environmental challenges: climate change, depletion of resources, and waste accumulation. The linear economic model, which emphasizes consumption and disposal, is unsustainable in the long run. On the other hand, circular economy has been a model of minimizing waste and maximizing resource efficiency which has gained big tides as part of the sustainable development strategy. This is because AI is emerging as a powerful catalyst for innovation and optimizing circular economy activities. By harnessing the capabilities of AI, businesses and organizations can revolutionize resource management, waste reduction, and product design, paving the way for a more sustainable future.

AI Applications in the Circular Economy

1. Waste Management and Recycling: Rebalancing

• Waste Sorting and Classification: AI-based computer vision algorithms will ensure complete identification and separation of waste materials, thus affording better efficiency in recycling and reducing contamination.

• Predictive Maintenance: AI can predict equipment failures in recycling facilities, minimizing downtime and reducing costs.

• Optimized Collection Routes: AI can optimize waste collection routes, reducing transportation emissions and improving efficiency.

According to market.us, The Global AI in Waste Management Market size is expected to be worth around USD 18.2 Billion by 2033, from USD 1.6 Billion in 2023, growing at a CAGR of 27.5% during the forecast period from 2024 to 2033.

• Sustainable Design: Products are designed with AI such that they may be durable, repairable, or recyclable for an extended time frame, thus reducing the amount of waste.

• Material Optimization: AI would be able to find the most sustainable material for a product and optimize its usage to minimize all the environmental impacts.

• Predictive Analytics: AI can predict product demand and optimize production schedules, reducing waste and excess inventory.

Fashion Industry: The fashion industry is one such sector where AI is bringing a tremendous change to the concept of a circular economy. AI-powered systems study consumer behavior and preferences, where companies can reduce overstocking and avoid making too much. The approach reduces waste but also increases the usage of environmentally-friendly resources. This AI technique is also applied in the creation of digital dressing rooms, reducing returns that often result in waste. AI also permits the design of products that are intended to be recyclable and easily broken down for recycling purposes.

• Traceability: AI can track the entire lifecycle of products, ensuring transparency and accountability in supply chains.

• Demand Forecasting: AI can predict the demands for products with good accuracy, reducing over-production and wastage of products.

• Reverse Logistics: Reverse logistics process can be optimized using AI, hence collection of used products, their reuse, or recycle becomes easy.

• Energy Efficiency: AI can optimize energy consumption in manufacturing processes and buildings, reducing greenhouse gas emissions.

• Water Conservation: AI can monitor water usage and identify opportunities for conservation, reducing water scarcity.

• Material Recovery: AI can identify valuable materials in waste streams and optimize their recovery, reducing the need for virgin resources.

Agriculture: In agriculture, the role of AI in the circular economy can be easily seen through optimization in the use of resources. AI-powered precision agriculture avails an automated system that uses minimal quantities of water, fertilizers, and pesticides. Thus, such systems help the environment and create less waste. AI instruments can also predict crop yields, which enables the farmer to plan and subsequently reduce food wastage.

• Enhanced Resource Efficiency: AI may lead to better resource optimization, reducing wastage and mitigating environmental impacts.

• Improved Sustainability: AI can contribute to a more sustainable future by promoting circular economic principles and reducing greenhouse gas emissions.

• Economic Growth: AI will be unlocking new economic opportunities for business and stimulating economic growth through innovative solutions for circular economy.

• Social Benefits: AI can improve quality of life by reducing pollution and creating jobs in the circular economy sector.

• Waste Management: Companies like Recycleye use AI-powered computer vision to ultimately streamline waste sorting, making it more efficient and reducing contamination.

• Product Design: Adidas has implemented AI to design shoes with a longer lifespan, incorporating sustainable materials and optimizing product design for durability.

• Supply Chain Optimization: Walmart had been using AI to reduce transportation costs and also increase sustainability within their supply chain.

Although AI may be seen as having great promise for pushing the circular economy forward, it has still to deal with some challenges, not least the question of data privacy and more ethical aspects. There are also needs for skills and a well-skilled workforce also on one other hand. But overcoming these challenges is what will open new possibilities in innovation and sustainable development.

AI can certainly make a very significant impact on the transition toward a circular economy. We could minimize resource use and unnecessary waste through AI-powered solutions and create sustainable life for the generations to come. As we progress with the boundaries of AI within the circular economy, there is a need to face challenges and opportunities to build a more resilient and equitable world.

• https://www.unido.org/sites/default/files/2017-07/ Circular_Economy_UNIDO_0.pdf

• https://www.linkedin.com/pulse/what-ai-impact-wastemanagement-hamed-aghayan/

• https://www.africanmediamalta.com/post/how-artificialintelligence-ai-is-revolutionising-the-circular-economy

• https://www.sustamize.com/blog/6-ways-ai-canhelp-reduce-carbon-emissions#:~:text=By%20 leveraging%20AI%2C%20companies%20now,of%20 improvement%2C%20and%20reduce%20their

• https://www.linkedin.com/pulse/ai-waste-managementmarket-reach-usd-182-billion-2033-markets-us-w0yyc/

Hritabhash Ghosh IIM Amritsar

Black Swan event, a concept popularised by Nassim Nicholas Tayeb, in his eponymous book “The Black Swan: The Impact of the Highly Improbable.”, represent extreme unpredictable developments that have severe and far-reaching consequences. [1][2] These extreme events like the COVID 19 Pandemic, override traditional financial models and risk management methodologies. Their rarity makes them very difficult to predict however they can have massive long-time impact. In this paper we try to explore these enigmatic events through a mathematical lens and try to find novel ways to understand these events.

Black Swan events have two defining characteristics, 1. Rarity: These events are outliers and lie beyond the traditional limits of our sample space of events. [3]

2. Severe Impact: They have immense impact, that have the potential to reshape industries. [1][3]

Examples like the 2008 Financial Crisis or the COVID 19 Pandemic represent black swan events that can disrupt financial markets, and cause systemic risk to the overall financial stability of the world. Classical financial models, designed to assess risk using Normal Distributions dismiss these rare events as outliers, underestimating their likelihood.

These risk models are due to their fundamental structure assign negligible probabilities to these extreme events thereby struggling with Black Swan Events. To address these limitations, we will look at the work of Chichilnisky [4], who has proposed an axiomatic approach to addressing these events,

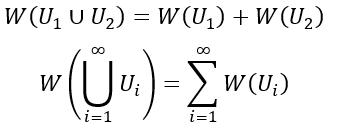

1. Classical Models assume that the likelihood of 2 disjoint events is the summation of their individual likelihoods [5][6] i.e. for events U1 and U2:

2. New Axiomatic Approach, proposed by Chichinlisky blends the ideas of countably additive and finitely additive measures. This method allows us to assign more weightage to rare events which is of critical importance in predicting and managing risks posed by Black Swan events [4]. This idea reflects the heavy tails observed in real world data, which represent the high likelihood of extreme events relative to standard models. Mathematically this creates a convex combination of the two measures:

Some ways to mitigate the adverse developments due Black Swan Events include,

1. Diversification: Expanding the investments across different geographies and asset classes.

2. Stress Testing: Scenario Analysis and Stress Tests can help prepare for extreme situations that traditional models overlook.

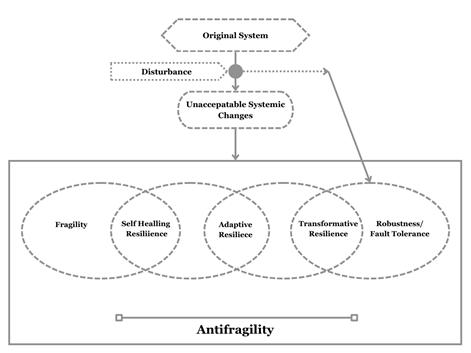

3. Antifragility: Drawing directly from Taleb’s concept, financial systems must be designed in such a way that they benefit from volatility instead of collapsing under stress [2]. Antifragile tend to get stronger when faced with disorder making them well suited to face black swan events.

Likelihood of Black Swan events become increasingly higher as financial markets become integrated and complex, underscoring the urgent need for designing financial models that integrate extreme outliers in their foundations so that we can remain prepared for the next unexpected shock.

Referrences:

1. Nafday, A.M., 2009. Strategies for managing the consequences of black swan events. Leadership and Management in Engineering, 9(4), pp.191197.

2. Taleb, N.N., 2007. “, The black swan: the impact of the highly improbable, Random House, New York, USA.

3. Mueller, J. and Stewart, M.G., 2016. The curse of the Black Swan. Journal of Risk Research, 19(10), pp.1319-1330.

4. Chichilnisky, Graciela. “The foundations of statistics with black swans.” Mathematical Social Sciences 59.2 (2010): 184-192.

5. DeGroot, M.H., 2005. Optimal statistical decisions. John Wiley & Sons.

6. Arrow, K.J., 1974. Essays in the theory of risk-bearing (Vol. 121). Amsterdam: NorthHolland.

7. Bangui, H. and Buhnova, B., 2022. Blockchain Patterns in Critical Infrastructures: Limitations and Recommendations. ICSOFT, pp.457-468.

““When you develop your opinions on the basis of weak evidence, you will have difficulty interpreting subsequent information that contradicts these opinions, even if this new information is obviously more accurate.”” — Nassim Nicholas Taleb, The Black Swan: The Impact of the Highly Improbable

Swagat Gongle IIM Amritsar

In the complex world of economic governance, countries must balance their financial needs while ensuring long-term economic stability. Two critical concepts in this context are sovereign default— when a nation fails to meet its debt obligations— and tax smoothing, a fiscal strategy that aims to minimize the disruptive effects of fluctuating tax rates. While developed countries have effectively integrated tax smoothing into their financial systems, many emerging economies, including India, have faced challenges in achieving this balance. India’s fiscal journey provides valuable lessons on the importance of responsible fiscal management and the role that tax smoothing plays in preventing sovereign debt crises.

Sovereign Default and the Indian Experience

Sovereign default occurs when a government cannot repay its debts, which can severely affect its economy and credibility. Historically, India has come dangerously close to a sovereign default during periods of economic turmoil, the most notable example being the 1991 Balance of Payments Crisis.

In the late 1980s and early 1990s, India’s foreign exchange reserves fell to dangerously low levels, unable to cover even two weeks’ worth of imports. The government was forced to take drastic

steps, including pledging its gold reserves to the International Monetary Fund (IMF) and enacting structural reforms to liberalize the economy. The crisis exposed India’s vulnerability to external shocks and highlighted the risks of poor fiscal management, particularly during high spending. While India did not formally default, it teetered on the edge, as a stark reminder of the dangers of fiscal indiscipline.

The 1991 crisis underscored the importance of fiscal reforms, paving the way for policy changes that aimed to stabilize the economy, promote growth, and reduce fiscal deficits. One key takeaway from the crisis was the need to adopt tax smoothing practices to prevent such close calls in the future.4

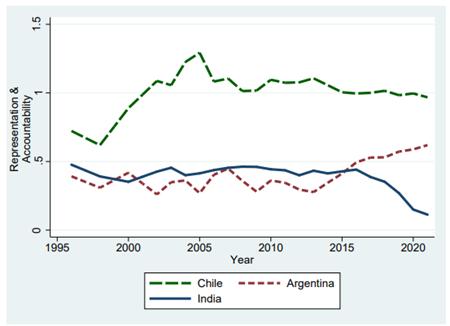

Representation and Accountability over time

Understanding Tax Smoothing

Tax smoothing is an economic theory introduced by economist Robert Barro. It suggests that governments should strive to keep tax rates relatively stable over time rather than allowing them to fluctuate drastically in response to temporary shocks. By doing so, governments can avoid economic inefficiencies and reduce the burden on businesses and consumers. During recessions, instead of raising taxes sharply to meet increased spending needs, governments can

borrow, and in boom times, they can repay the debt, thus maintaining a consistent tax rate. The goal is to avoid tax spikes that could stifle growth or reduce consumer spending.

Since the 1991 crisis, India has taken significant steps to stabilize its fiscal policy and smooth out tax rates, mainly through institutional reforms and more prudent borrowing practices. A notable example is the Fiscal Responsibility and Budget Management (FRBM) Act of 2003, which was introduced to ensure fiscal discipline by controlling deficits and reducing debt levels. The FRBM Act set targets for fiscal deficit reduction and limited the government’s borrowing. By mandating that borrowing should only be used in exceptional circumstances, the FRBM Act promoted the idea of spreading fiscal responsibility over time rather than allowing large tax fluctuations or uncontrolled lending in response to short-term needs. However, India’s adherence to tax smoothing has been tested during periods of economic crisis. For example, during the 2008 Global Financial Crisis, the Indian government temporarily suspended the FRBM Act to allow for more lavish public spending to stimulate the economy. Rather than raising taxes significantly to meet increased spending needs, India opted to borrow in the short term, reflecting a tax smoothing approach. This allowed the government to stimulate the economy without placing a heavy tax burden on businesses or individuals during a recession.

A more recent test of India’s fiscal management came during the COVID-19 pandemic when the government faced unprecedented pressure to increase spending while revenues plummeted. In response, the government temporarily widened the budgetary deficit, borrowing more to fund stimulus measures and relief programs. This decision to rely on lending rather than sudden tax hikes was in line with the principles of tax smoothing, as it spread the cost of recovery over time, avoiding the risk of stifling an already fragile economy.

Another important step in India’s tax reform journey was the introduction of the Goods and Services Tax (GST) in 2017. The GST replaced a complicated web of state and national taxes with a unified tax structure, helping to create a more predictable and stable revenue stream for the government. Although not explicitly designed as a tax smoothing measure, the GST has contributed to more excellent fiscal stability by providing a steady and broad-based source of revenue. This, in turn, reduces the need for erratic changes in tax rates during economic downturns or booms.

Additionally, reforms such as the Direct Benefit Transfer (DBT) scheme, which replaced inefficient subsidy programs, helped India better manage its fiscal burden. By reducing the government’s expenditure on subsidies and targeting benefits directly to the needy, the DBT scheme freed up resources that could be used to smooth out fiscal policies without resorting to significant tax increases.

India’s fiscal journey demonstrates the importance of institutional reforms in promoting tax smoothing and preventing sovereign debt crises. By adopting prudent borrowing practices and reforms like the FRBM Act and GST, India has made strides toward stabilizing its fiscal policy and avoiding drastic changes in tax rates. However, challenges remain. India’s fiscal deficit has widened in recent years, and its ability to manage its debt sustainably will depend on its commitment to responsible fiscal management.

• The 1991 crisis, the FRBM Act, and the introduction of GST all offer valuable lessons for emerging economies grappling with fiscal volatility. The key to avoiding sovereign default and promoting longterm economic growth lies in balancing the need for government spending with the need to maintain stable tax policies. While borrowing can provide a short-term solution to fiscal shocks, maintaining fiscal discipline and avoiding over-reliance on debt is crucial for long-term stability.

In conclusion, India’s efforts toward tax smoothing and fiscal discipline have helped the country avoid the worst consequences of budgetary crises. However, as the global economic landscape evolves, India must continue refining its fiscal policies, ensuring it can weather future financial storms while maintaining steady and predictable tax rates.

References

• https://www.data.gov.in/resource/year-wise-detailsloans-borrowed-government-india-and-alongrepayment-and-interest

• https://testbook.com/ias-preparation/balance-paymentcrisis-1991#:~:text=A%20bop%20crisis%20in%20 1991,and%20services%20to%20other%20countries

• https://testbook.com/ias-preparation/fiscalresponsibility-budget-management#:~:text=The%20 Fiscal%20Responsibility%20and%20Budget,and%20 transparency%20in%20the%20budgetary

• https://tradingeconomics.com/india/governmentdebt-to-gdp#:~:text=India%20recorded%20a%20 Government%20Debt,percent%20of%20GDP%20 in%201980

• https://www.nber.org/system/files/working_papers/ w31943/w31943.pdf

“Thoughtful disagreement is not a battle; its goal is not to convince the other party that he or she is wrong and you are right, but to find out what is true and what to do about it.”

― Ray Dalio, Principles: Life and Work

“Innovation is not just about having a good idea. It’s about executing on that idea and creating value for customers and society.” – Ajay Banga, former CEO of Mastercard.

The Fintech sector has grown through full transformation in the past years. Its transformation is inspired by innovations regarding digital payments, alternative lending, insurtech, wealth management, and enabling technologies. The global fintech market size, based on 2024, is USD 111.14 billion and is estimated to reach USD 421.48 billion in 2029 with a CAGR of 30.55%.

India is emerging as a significant hub for the fintech ecosystem, especially in digital payments, which grew exponentially. This report does in-depth sectoral analysis of the global fintech landscape, market size, growth factors, and trends, focusing specially on India.

Fintech is the marriage of finance with technology to provide digital solutions for all financial services, ranging from payment, lending, insurance, wealth management, and banking. The main growth is due to financial inclusion, digital adoption, and changing expectations among consumers, especially worldwide.

Digital Payments: The largest subsector, represented by platforms like UPI (Unified Payments Interface), which has been one of the biggest contributors to the digitization of the Indian economy.

Alternative Lending: This includes peer-to-peer lending as well as digital lending products that allow the consumer loan.

Insurtech: It enables modes of management of insurance policy and its claim through digital. Wealth Tech: This is technology-based solutions for wealth management. The same includes roboadvisory platforms.

Enabling Tech: Provides the underlying infrastructure through blockchain, cybersecurity, and cloud computing.

Market Size and Growth

Global Fintech Growth

Fintech Market, Global Global revenue, 2023 to 2028: The fintech market is forecast to grow the revenue from US$79.38 billion in 2023 to US$141.18 billion in 2028 due to increased investments in digital financial infrastructure and changed consumer preference.

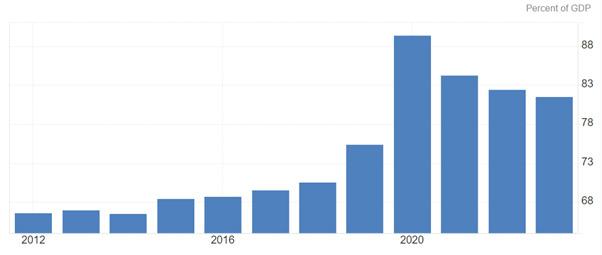

Indian Digital Payment Growth

In India, as of 2017 to 2024, there has been outstanding growth in digital payments, and the growth in the value of transactions was largely driven by UPI:

The growth score for digital payments in India has also increased sharply, and it has moved from 0.08 in the year 2017 to 0.97 in the year 2023.

Global Fintech Landscape

The number of fintechs worldwide has been increasing steadily with the following figures for regions like America, EMEA (Europe, Middle East, Africa), and Asia-Pacific:

Sectoral Analysis: The Fintech Boom in India

Favorable regulations, an opulent young population, and widespread internet penetration have propelled the fintech industry in India to become one of the most innovative in the world. The fintech market size in the country is anticipated to reach USD 1.3 trillion by 2030 while it expands across Lendingtech, Payments, and Insurtech segments.

Key Fintech Startup Hubs

During 2014 to Q3 2022, cities like Bengaluru and Pune became the hub for fintech with an impressive CAGR growth rates:

Market Segmentation and Competitive

Landscape

Digital Payments

Major Players: Paytm (40%), G-Pay (30%), PhonePe (15%).

Growth Drivers: UPI, QR-based transactions, and wallet adoption.

Challenges: Regulatory hindrances and rising competition due to new entrants in the business.

Wealth Tech

Leaders: Groww at 25.09%, Zerodha at 17.07%, Angel One at 15.25%.

Growth Catalysts: Expanded scope of investment opportunities and robo-advisory platforms. Alternative Lending and Insurtech, Lending tech and insurtech have gained stable adoption especially by MSMEs and the unbanked segment.

Growth Drivers

Internet Penetration: With India having more than 700 million internet users, the fintech can look forward to increasing online population

Demand for Digital Financial Services: Consumers increasingly demanding a digital channel for payments, lending, and insurance, offering flexibility at lower costs.

Regulatory Support: A initiatives like Jan Dhan Yojana, Digital India, and policies for financial inclusion have been a supportive government role in the growth of fintech.

Emerging Technologies: Innovation in AI, blockchain, and machine learning introduces new opportunities for fintech development

Challenges

Regulatory Uncertainty: Although the government policies are friendly, difficulty arises in applying rules in areas such as data security and privacy for emerging fintech players.

Capital Raising: For most fintech companies, the level of difficulties in capital raising is particularly high when they are at the early stages of growth.

Security Risks: Fintech companies face high risks of data breaches and cyber attacks because they handle super sensitive customer data.

Industry Trends

Artificial Intelligence Focus: Fintech-related services such as robo advisors and automated services often feature AI.

Increased M&A Activity: Consolidation in the fintech space has become the new trend, as large financial institutions buy the innovative startups. ESG Initiatives: Fintechs are now increasingly adopting environmental, social, and governance initiatives.

Real Economy Partnering: The fintech and traditional financial institution collaboration is changing the landscape of the industry.

Targeting SMEs: Fintechs are targeting the small and medium enterprises, which were previously under-served, with solutions tailored to their requirements.

Conclusion and Future Outlook

This would generally promise a period of stable growth for the Indian fintech sector, weighed in by factors such as increased digital adoption, regulatory support, and emerging technologies. Market maturation will require competition where fintech companies must bolster customer retention, regulatory compliance, and enhance user experience.

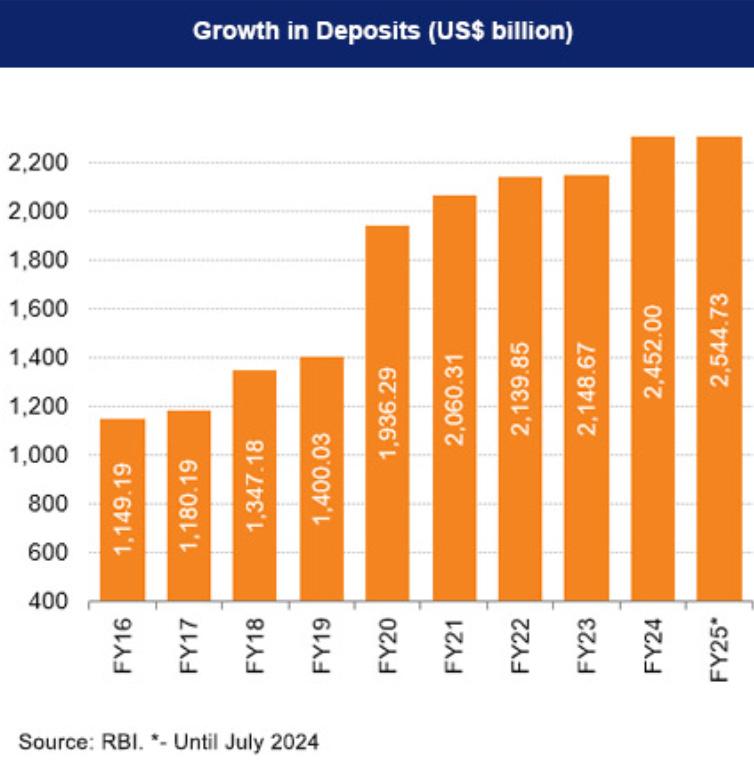

The Indian banking sector, a heterogeneous amalgam of public, private, and foreign institutions, operates under stringent Reserve Bank of India regulations. Despite structural challenges like burgeoning NPAs, the industry’s pivot towards digitalization and inclusive financial paradigms underscores its transformative role.

Policy updates

• Investment Portfolio Classification: Updated guidelines now align investment categorization with international standards, requiring banks to use principle-based approach and transparent reporting.

• Interest Rate Risk in Banking Book: New guidelines direct banks to measure, monitor, and disclose risks arising from interest rate changes.

Highlights

• The sector achieved record profits in FY24, with combined net profits of public and private banks exceeding ₹3 trillions.

• The Union Budget 2024–25 introduced a forthcoming strategy document, emphasizing reforms for public sector banks and addressing digital lending growth.

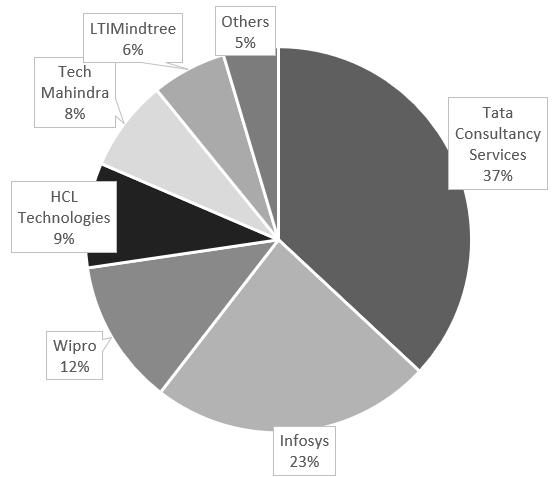

India’s IT sector, a cornerstone of global outsourcing, embodies unparalleled growth, driven by advanced digitalization, robust R&D, and a skilled workforce. Amidst complex regulatory landscapes, the industry pioneers in AI, cloud computing, and cybersecurity.

Policy updates

• The government initiated the NQM, targeting the advancement of quantum computing and quantum technology to bolster high-end computational research across industries.

• The Ministry of Electronics and Information Technology (MeitY) has increased funding for AI development, especially in healthcare and e-governance, to integrate AI with public services.

Highlights

• IT spending projected to reach nearly $139 billion, the IT sector is growing at over 13%, driven by cloud adoption, software investment, and devices. Software spending alone is expected to increase by 18.6% due to growth initiatives from CIOs across India, prioritizing customer experience and operational efficiency.

• India’s data center industry, currently 13th globally, is expected to increase by $8 billion by 2026.

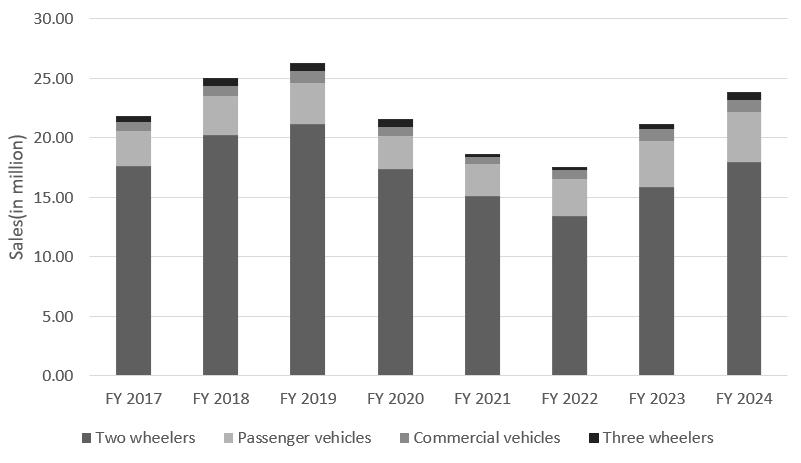

India’s automobile industry, a crucial pillar of its manufacturing ecosystem, melds robust domestic demand with burgeoning exports. Dominated by two- and four-wheeler production, it embraces electric mobility amid complex regulatory landscapes. With stringent emission norms and advances in automation, the sector is aligning with global standards, fostering sustainable growth and innovation.

Policy updates

• The government approved a PLI of ₹26,058 crore to enhance the indigenous production of electric vehicles (EVs) and hydrogen-cell technologies, aiming to reduce reliance on imports.

• The budget proposed a reduction in basic customs duty rates from 21% to 13%, which could enhance the affordability of vehicles, although customs duty on fully imported luxury cars was increased from 60% to 70%.

Highlights

• Hyundai Motor India launched one of the largest IPOs in India’s recent history, gathering substantial investment and marking a significant entry on the stock market.

• Tata Technologies partnered with BMW to launch a joint venture focused on automotive software development, aiming to drive technological innovation in the sector.

India’s FMCG sector, a resilient cornerstone of consumer-driven demand, combines vast rural outreach with digital integration to cater to evolving preferences. Faced with volatile input costs, the industry pivots on innovative distribution channels and sustainable packaging, enabling robust growth while navigating regulatory pressures and intensifying competition in both urban and rural markets.

Policy updates

• Liberalized foreign direct investment (FDI) norms in retail have encouraged international investment, fostering competition and expanding market opportunities.

• GST benefits, especially on FMCG products, have streamlined tax structures, improving supply chain efficiencies and overall competitiveness across the sector.

Highlights

• The FMCG sector saw a record $938 million in M&A activity in the first half of 2024. Significant deals included Tata Consumer Products’ acquisition of Capital Foods (brands include Ching’s Secret) and a stake in Organic India, underscoring an industry-wide trend of consolidation.

• According to CRISIL Ratings, the sector is expected to see 7-9% revenue growth in FY25, driven by increased volumes and steady demand in both rural and urban markets, as well as by expanding categories like health and wellness products.

India’s energy sector, balancing robust demand growth with transition imperatives, has undergone sweeping changes. With an emphasis on renewables, policy incentives drive investment in solar, wind, and green hydrogen. However, complex challenges persist in grid modernization and resource allocation as the industry shifts toward sustainable, self-reliant, low-emission energy production.

• The Indian government allocated ₹19,700 crore to support the production of 5 million metric tons of green hydrogen annually by 2030, aiming to reduce carbon emissions and energy dependence.

• With a central fund of ₹20,700 crore, the government is expanding interstate transmission lines to connect 13 GW of renewable energy from Ladakh to urban centers.

Highlights

• India is expected to add over 20 GW of renewable energy capacity in 2024, driven by hybrid and stand-alone storage tenders to improve grid stability. New regulatory frameworks also encourage corporate demand for sustainable energy, aligning with climate goals set during G20 and COP28.

• India’s focus on green hydrogen continues, backed by schemes like the Green Credit Program (GCP) and the Carbon Credit Trading Scheme (CCTS).

India’s iron and steel industry, a vital sector underpinning industrial growth, grapples with balancing robust domestic demand and global competition. Amid stringent decarbonization targets, the industry integrates advanced manufacturing technologies, like electric arc furnaces, and renewable energy sources. With substantial government support, India aims to maintain its competitive edge in sustainable, highquality steel production.

Policy updates

• The Ministry of Steel allocated approximately INR 14.66 billion (USD 177 million) to advance the use of green hydrogen in steel production, as part of a larger effort to reduce the industry’s carbon footprint by supporting green hydrogen pilot projects. This includes new tenders aimed at producing 450,000 tonnes of green hydrogen annually.

• Under the Union Budget 2023-24, the government allocated Rs. 70.15 crore (US$ 8.6 million) to the Ministry of Steel.

• The Ministry of Steel initiated 13 task forces focused on sustainable practices, aiming to define a clear pathway for “green steel” production without fossil fuels, addressing global competitiveness and aligning with India’s net-zero goals.

Highlights

• ISA Steel Conclave 2023 held in November 2023, this industry event focused on “Steel Shaping the Sustainable Future,” urging companies to double production to meet India’s target of 300 million tonnes annually by 2030.

• In February 2024, The JSW Group is set to build a steel plant in Jagatsinghpur, Odisha, with an investment of US$ 7.8 billion (Rs. 65,000 crore). The plant will have a production capacity of 13.2 million tons of steel per year and is expected to create 30,000 jobs.

• In April-June 2024, crude steel production in India stood at 36.6 MT.

I have been interested in equities, investing and trading since the last year of my engineering. I opted to do the CFA Course to have a better understanding and more extensive knowledge of the financial markets. After enrolling at IIM Amritsar, I got to learn about the CFA exam. I started preparation in April, I chose May as the best month for scheduling my exam. Here is how I prepared for my CFA Level 1 Exam.

The first is Schweser’s notes. They were really useful since they were much more concise and straightforward than CFA textbooks. IFT’s YouTube channel is another great resource for video lectures. Although it covers limited topics, it is a great place to start. A lot of the topics in the CFA curriculum are already covered in your first-year of MBA. Topics covered in Business Statistics, Financial Accounting, Managerial and Macroeconomics, Foundation of Finance, and Corporate Finance cover a lot of the CFA curriculum. In the CFA Level 1 exam, the biggest challenge I faced was Ethics and Standards. It is a highly subjective topic and often requires rigorous practice. Practicing ethics questions from the “Learning Eco System” would be the best way to tackle this subject.

The second category includes all of the multiplechoice practice questions included in CFA textbooks. The majority of these questions are extremely close to those on the actual exam. I went through all of the questions, so when I took the actual exam, everything felt quite familiar to me. The CFA L1 exam pattern is not a speed-based test like the CAT.

It tests your understanding, and sometimes spending time on questions is more beneficial than directly jumping on to answers to save time. Also, CFA L1 tests more concept-based questions than real-world calculations, so don’t squander the last few days of your study time on lengthy calculationintensive problems. The third point to mention is the mock tests supplied by CFA to candidates. A week before my actual CFA exam, I took the simulated examinations to gauge my readiness. Mock examinations, in my opinion, are more complicated than genuine exams. I also practiced all the practice tests from Schweser’s notes. Practicing and analyzing the test is more time-consuming and exhausting, but it will prepare you for D Day as there would be only one optional break between the exams. Getting used to exam patterns is essential cause the second session can be challenging. Examine the curriculum and depth of each subject, and carefully plan out your study schedule. It is preferable to get a financial calculator at the start of the preparation process to become acquainted with it. Learn as many functions as you can because just a handful of them are effective in solving complex Fixed Income Security questions.

My summer internship was initially in offline mode, but after a couple of weeks, it converted into an online mode, allowing me to devote significant time to preparing for the next 40-50 days. A head start in the beginning has significantly helped in my preparation. I have dedicated a whole day to the preparation in the last month before the exam. Schweser’s Secret Sauce is beneficial in the last of preparation because it almost summarises every topic of the curriculum.

It would be ok to leave one or two tough topics with lower weightage rather than wasting time on them and failing to revise commonly questioned topics during the final days of preparation. This phase is critical since most subjects must be reviewed, which considerably improves exam performance. During the critical phase, I devoted most of my time to revising important concepts and giving the mock test. Mistakes in the mock test and learning from those mistakes have significantly helped me in improving my exam performance.

Finally, I’d like to highlight that you shouldn’t be concerned about CFA examinations; most ideas are already taught in the MBA curriculum; you simply need to brush up on certain of them depending on the test format and your current level of preparation.

Directed by: Ben Younger

Distributed by: New Line Cinema

Release Date: 18th February, 2000

Duration: 120 mins

Country: USA

Language: English

Seth Davis is a 20-year-old college dropout who operates a soft core porn web site and an underground casino from his apartment, against his father’s wishes who is a federal judge. Famished for his dad’s approval and the legal method of making a lot of money, Seth gains employment with J.T Marlin, a petty bullish brokerage firm. Visions of a better life, more money, and the good life, Seth joins the firm and is guided into selling low millions and more often, and risky stocks to middle-class investors who are just as often disregarded or forgotten by the firm. Thus, Seth introduction to J.T. Marlin is energizing and threatening all at the same time. The brokers themselves are well dressed young men with a professional and ambitious air about them: wearing sharp suits and driving flashy cars. “... the firm’s culture of hyper-aggression in the pursuit of profit...” The aggressive nature and goal of the firm becomes apparent to Seth in the very first scenes as he learns that the only mission of the company in question is the amassing of cash, with the means used to do it being inconsequential at best. The style of work used by the firm is doubtful and almost close to a violation of the law. Brokers are trained to sell stock out in high-volume cold calling techniques in which they are able to persuade people to invest in low-quality or overvalued equities. Everything about the business’ operation seems to focus on the ‘boiler room’ style of brokering where the brokers are peddling the deals and schemes with the sole purpose of making money, not thinking about the impact to their clients. This world is a very cold and unkind place where any dog is not just allowed to eat a bucket but anything that he/ she can seize.

As he grows through the ranks at J.T. Marlin, Seth begins to realize the nature of the moral turpitude that defines the firm. It’s a pure pyramid, an

organization that has evolved from fraudulent activities, conning investors into buying stocks in companies that in reality are worth pennies or don’t even exist, artificially inflating the prices of the stocks they need for a quick exit once they’ve made their money. Seth struggles with his conscience at work and the desire gains legitimacy for the company he builds.

Boiler Room is a movie about the kinds of decisions which separate one person from another. It offers a social critique related to the greed and materialism in the society to get to the top of the social life. The characters in the film have what many would consider American dreams, their desire for wealth becomes a darkness they willingly carry out on others.

The film presents the themes such as success and materialism, thus making the audiences and viewers think about the fact that sometimes the people can easily cross the line in the aspiration to succeed at work. Starting out as an innocent and easily influenced clerk and turning into a broker with a troubled conscience, Seth’s story underscores the truth about the lack of ethical standards in business. Boiler Room also points to a number of social aspects related to financial voracity. The appropriation of reality that the film shows in J.T. Marlin imitates real-life cases of misconducts, ranging from the Enron scandal, to the financial crisis of 2008, where financial companies’ gross mistreatment of the public caused great losses and suffering.

Since the release of Boiler Room, this theme has only remained more pertinent as scandals and the standards of Wall Street hold the limelight. The plot of the film has to do with the moral lesson that greed is bad and that the power of ethical recourse should be embraced in financial operations.

It is valuable for finance lovers and gives a number of perspectives on the rather unsafe sphere and the moral issues of those people who work in it. It’s a film that tells that everything that brings money is good but the good thing is actually doing the right thing.

In the book The Warren Buffett Portfolio, Robert G. Hagstrom explains the investment philosophy that made the great Warren Buffett. A contrast to most investors who hold equity positions in tens of thousands of equities, Buffett concentrates his capital on a few businesses through the policy of concentration investing. With some outstanding and well-known companies, he easily generates astronomical returns on investment; in fact, his portfolio averages around 10 to 15 stocks.

Buffett likes to invest in just a few high-class companies he can hold for an indeterminate time. He views stocks as equities in businesses and prefers holding periods that are virtually “forever.” This long-term view enables the benefits of compounding, where those earnings are reinvested to generate even higher returns over time. Buffett dislikes churning, so the cost of purchase and sale and taxes become insignificant as investments rise unabated. He will tend to wait for opportunities when the markets fall and buy more shares of the great companies at bargain prices in terms of long-term potential and not at short-term market fluctuations.

He is an advocate of the concept of the value investing principles which he learned from his mentor, Benjamin Graham. That is, buying stocks for less than their intrinsic value-the true value of an entity based on its earnings growth and cash flow. The gap between intrinsic value and market price is the margin of safety, a kind of umbrella that covers one above potential losses. Unlike Graham’s “cigar-butt investing” in undervalued stocks, Buffett invests in companies with growth strength potential, and instead of buying “a cheap stock”, he looks for “a wonderful business at a fair price”.

Economic Moats: Competitive Advantage

Buffett looks for businesses with moats or economic barriers, which make it really hard for anyone else to compete with a company in its industry, allowing them to have a profit-making business. Moats are brand loyalty, such as Coca-Cola, cost advantages, such as Amazon because of scale, network effects, such as the Apple ecosystem, or regulatory protections, such as utilities. The moat serves to protect the business; it is not easy for competition to erode the market standing and profitability of a business. Good moats, according to Buffett, make a business go to long-term returns.

The bottom line for Hagstrom is that emotional control allows Buffett to succeed. According to Buffett, “be fearful when others are greedy and greedy when others are fearful.” Therefore he boasts calm when the markets are correcting and buys at stocks which are undervalued. He was not making mistakes of usually entertaining investors in charged time because he was fixated on the real sense of what his businesses are.

Conclusion

The Warren Buffett Portfolio” outlines the investment philosophy of focus investing, longterm holding, value, and emotional discipline by Warren Buffett. Not one to follow the whim of hot investment fads, Buffett instead invests in businesses with a durable competitive advantage where compounding of wealth occurs over time. Hagstrom’s book is a guide for interested investors looking to put into practice the proven formula Buffett expounds on, reminding them of success arising from owning high-quality businesses and letting them grow over the long haul.

Since its inception in 2017, FEC has been one of the most enthusiastic student interest groups of IIM Amritsar. The club organises numerous interactive events throughout the year to provide students with an enriching learning experience in finance. It supports students in their journey at IIM Amritsar, helping them harness their potential and enthusiasm and guiding them at every turn. From providing advice about additional certifications and online courses, like Bloomberg Market Certification, to helping them with subject choices and interview experiences, FEC facilitates outside- classroom training to upskill them, leading to brighter career opportunities.

The club has kept up its tradition over the months that have passed, working very hard to provide students with the best possible education and experience.

• Golden Investment Fund (GIF): It is a student-managed investment fund composed of experts in F&O and intraday trading. GIF team releases monthly fact sheets of its portfolio under management. Along with an overhaul of their reports, the GIF team also contributes to the IIM Amritsar’s culture by conducting knowledge sessions and investment lectures to engage peers and motivate students to invest in capital markets and develop financial understanding among students.

• Pariprekshya: Pariprekshya is IIMAmritsar’s Annual Finance and Marketing Conclave, where eminent industry experts share their views and experience on the bigstage before IIM Amritsar faculty and students. Being

conducted since 2017, the FEC has been pivotal in conceptualising the event and helping students get relevant industry insights and familiarise themselves with industry trends.

• Starry Nights: FEC is known for its trademark “Starry Nights” sessions, where members share their knowledge and experience in an informal setting. In Starry Nights, an informal discussion occurs on topics in which every attending student can share their point of view, contributing to a healthy conversation on important issues. Various Starry Nights sessions have been conducted since July 2021 on topics ranging from venture capital to the future of Hedge Funds in India.

• Fin-League: FEC’s Fin-League quizzes put the students’ business acumen to the test and help them keep their minds sharp and ready while fostering a competitive environment. Winners of Fin-League quizzes were awarded prizes and certificates. The competition is organised in a league format with three progressively challenging rounds. The examinations encompass various topics from Finance and Economics, providing a unique and enjoyable way to comprehend the relevant concepts and principles.

• Guest Talks: FEC regularly organises industry guest lectures and workshops to give students more practical exposure. In the past, FEC has hosted CFOs and senior management from prominent companies belonging to the financial sector.

• AArunya: FEC organised three events as a part of Aarunya 8.0 – IIM Amritsar’s Annual Management, Cultural, and Sports Fest. The events for AArunya 8.0 were– InSight Out (600+ registrations), Impetus – A Case Competition (600+ registrations), and EcoBatean Economics Debate.