MARKETVIEW | JAPAN OFFICE | Q2 2025

MARKETVIEW | JAPAN OFFICE | Q2 2025

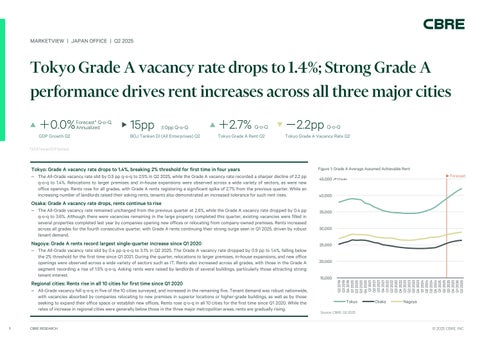

Tokyo Grade A vacancy rate drops to 1.4%; Strong Grade A performance drives rent increases across all three major cities Forecast* Q-o-Q, +0.0% Annualized GDP Growth Q2

15pp

±0pp Q-o-Q

BOJ Tankan DI (All Enterprises) Q2

+2.7% Q-o-Q Tokyo Grade A Rent Q2

-2.2pp Q-o-Q

Tokyo Grade A Vacancy Rate Q2

*JCER Forecast (ESP forecast)

Tokyo: Grade A vacancy rate drops to 1.4%, breaking 2% threshold for first time in four years ‒ The All-Grade vacancy rate slid by 0.5 pp q-o-q to 2.5% in Q2 2025, while the Grade A vacancy rate recorded a sharper decline of 2.2 pp q-o-q to 1.4%. Relocations to larger premises and in-house expansions were observed across a wide variety of sectors, as were new office openings. Rents rose for all grades, with Grade A rents registering a significant spike of 2.7% from the previous quarter. While an increasing number of landlords raised their asking rents, tenants also demonstrated an increased tolerance for such rent rises.

Figure 1: Grade A Average Assumed Achievable Rent

Forecast

45,000 JPY/tsubo 40,000

Osaka: Grade A vacancy rate drops, rents continue to rise

Nagoya: Grade A rents record largest single-quarter increase since Q1 2020 ‒ The All-Grade vacancy rate slid by 0.4 pp q-o-q to 3.1% in Q2 2025. The Grade A vacancy rate dropped by 0.9 pp to 1.4%, falling below the 2% threshold for the first time since Q1 2021. During the quarter, relocations to larger premises, in-house expansions, and new office openings were observed across a wide variety of sectors such as IT. Rents also increased across all grades, with those in the Grade A segment recording a rise of 1.5% q-o-q. Asking rents were raised by landlords of several buildings, particularly those attracting strong tenant interest.

Regional cities: Rents rise in all 10 cities for first time since Q1 2020 ‒ All-Grade vacancy fell q-o-q in five of the 10 cities surveyed, and increased in the remaining five. Tenant demand was robust nationwide, with vacancies absorbed by companies relocating to new premises in superior locations or higher-grade buildings, as well as by those seeking to expand their office space or establish new offices. Rents rose q-o-q in all 10 cities for the first time since Q1 2020. While the rates of increase in regional cities were generally below those in the three major metropolitan areas, rents are gradually rising.

1

CBRE RESEARCH

35,000 30,000 25,000 20,000 15,000

Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q2 2022 Q3 2022 Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Q2 2026

‒ The All-Grade vacancy rate remained unchanged from the previous quarter at 2.6%, while the Grade A vacancy rate dropped by 0.4 pp q-o-q to 3.6%. Although there were vacancies remaining in the large property completed this quarter, existing vacancies were filled in several properties completed last year by companies opening new offices or relocating from company-owned premises. Rents increased across all grades for the fourth consecutive quarter, with Grade A rents continuing their strong surge seen in Q1 2025, driven by robust tenant demand.

Tokyo

Osaka

Nagoya

Source: CBRE, Q2 2025

© 2025 CBRE, INC.