Indian law, amidst a maze of legislation, sets a specific period within which any claimant can approach the court and file a claim. This period, commonly known as the 'Limitation Period', is a crucial concept in the legal landscape, and understanding it is one of the keys to navigating the complexities of legaldisputes.

The Hon'ble Supreme Court of India has observed in a recent judgment that the law of limitation is founded on public policy. This means that it is for the general welfare that a limitation period be prescribed so that every legal remedy has a fixed period of life, and a dispute/litigation is not kept pending indefinitely.

a Maritime Lien, it is advisable to file the suit within one (1) or two (2) years (depending on the type of claim) to take benefit of the provisions giving priority to maritime liens. Section 9 of the Admiralty Act provides for which maritime claims a claimant can exercisemaritimelien.

This article attempts to highlight and simplify the understanding regarding limitation periods in reference to shippingdisputes.

While more than one legislation will be considered to determine the limitation period for shipping disputes, the starting point will be the Limitation Act 1963 (Limitation Act). The Limitation Act, a procedural law, among other things, prescribes the limitation period within which every suit, appeal or application must be instituted before the appropriate court of law. Further, the Limitation Act also prescribes when the limitation period will commence, how the same is to be calculated, the exclusions to be accounted for while calculating the limitation period, the circumstancesinwhichthelimitationclockwillreset,etc.

For almost all suits arising from contracts, the Limitation Act prescribes a limitation period of three (3) years. The said period commences from the occurrence of an event that entitles a claimant to file the suit before the court of law. For example, the non-payment of wages or outstanding sums past the due date is an occurrence that entitles a claimant to file a suit for recovery of outstanding wages/sums. Further, some examples of suits arising from shipping contracts can includesuitsforunpaidseamenwages,suitsforcompensation for lost/damaged cargo, suits for compensation due to nondeliveryordelayindeliveryofcargo,suitsforunpaidfreightor demurrage or detention, suit for damages due to breach of contract, suit for recovery of outstanding amounts, etc. However, Section 29 of the Limitation Act provides that if a special law prescribes a limitation period, the Limitation Act, to the extent the special law does not exclude its application, shall apply as if the limitation period contained in the special lawwasthelimitationperiodprescribedbytheLimitationAct.

This brings us to the special laws that govern Shipping / Maritime disputes in India. These special laws include The Admiralty (Jurisdiction and Settlement of Maritime Claims)Act2017,TheIndianCarriageofGoodsbySea1925,and TheMultimodalTransportationofGoodsAct1993.

While The Admiralty (Jurisdiction and Settlement of Maritime Claims) Act, 2017 (Admiralty Act) does not prescribe a period within which suits invoking the admiralty jurisdictionoughttobefiled,itprovidesthatallmaritimeliens, exceptcrewwagesandcontributions,shallexistonavesselfor one (1) year, irrespective of any change of ownership. Claims towards crew wages and contributions shall continue as a maritime lien for two (2) years. Accordingly, when the Limitation Act and the Admiralty Act are read together, the limitation period for filing any suit invoking the admiralty jurisdiction must be filed within three (3) years from the occurrence of an event that gives rise to a Maritime Claim as defined in Section 4 of the Admiralty Act. However, this is further subject to the provisions of The Indian Carriage of Goods by Sea Act 1925 and The Multimodal Transportation of Goods Act 1993. Additionally, suppose a Maritime Claim is also

The Indian Carriage of Goods bySea1925 (COGSA1925) provides that a carrier and the ship shall be discharged from all liability in respect of loss or damage to cargo unless the suit is brought within one (1) year after the delivery of the cargo or the date when the cargo should have been delivered. It is worth noting here that COGSA 1925 only applies to suits arising from a contract of carriage of cargo from any Indian port to another Indian or Foreign Port. Further,tothebestoftheauthor'sknowledge,whetherCOGSA 1925 will apply to a contract of carriage without a specific statement giving effect to COGSA 1925 in the contract of carriageisacontroversythatremainsatlarge.However,toerr on the side of caution, it is always advisable that any cargorelated claims against the carrier are brought before the expiryofone(1)yearfromthedateofthedeliveryofthecargo.

The Multimodal Transportation of Goods Act 1993 (MMT Act), inter alia, governs the registration of multimodal operators and the multimodal transportation of cargo from IndiatoadestinationoutsideIndia.Multimodaltransportation means transporting cargo using two (2) or more modes. For the provisions of the MMT Act to be applicable, the transport should be undertaken by a registered multimodal operator, the transport should be through two or more modes of transport, and the transport should be from India to a destination outside India. In case the MMT Act applies to a particular transport, then as per the provisions of Section 24 of the MMT Act, the multimodal operator is liable for any claim only up to nine (9) months from a) the date of delivery of the cargoorb)thedatewhenthecargoshouldhavebeendelivered or c) the date on and from which the party entitled to receive delivery of the goods has the right to treat the cargo as lost under sub-section (2) of section 13. Section 13(2) of the MMT Act provides that the cargo may be treated as lost if it is not delivered within ninety (90) consecutive days following the expresslyagreeddeliverydateandifnodeliverydateisagreed uponthenwithinareasonabletime.

In conclusion, although the details of calculating the limitation period can seem confusing, it is generally advisable that, as a thumb rule, for any claims pertaining to ocean transport of cargo (loss, damage, delayed delivery, misdelivery, etc.), the suit is brought before the expiry of one (1) year, and in cases of multimodal transport the suit is broughtbeforetheexpiryofnine(9)months.

For any other claims found in contracts, the suit should be brought before the expiry of three (3) years as prescribed in the Limitation Act. As a parting note, in certain specific scenarios, the Limitation Act permits resetting the limitation clock or excluding time from the limitation period. However, in the author's opinion, not all reset and/or exclusion provisions apply to claims covered by COGSA 1925 and the MMT Act. Hence, claims arising from shipping disputes warrant aspecializedandcasespecificapproach.

For further information or clarifications, the author, a commercial lawyer specializing in Maritime Laws, can be reachedat sukumar@tirthanilegal.com.

The views expressed are only intended for general information purposes and not for solicitation of any work. Undernocircumstancesshouldtheviewsberegardedaslegal advice,andnolegalorbusinessdecisionshouldbemadebased ontheviewsexpressed.

MUMBAI : (022)22661756 / 1422, 22691407

AHMEDABAD : (079) 26569995, E-Mail:dstgujarat@gmail.com

KANDLA : (02836)222665/225790, E-Mail:dstimeskdl@gmail.com

MUMBAI: Adani Group expects its ports business to growatarobustpace,withtheIndianoperationsexpected to double the volume in five years, said a senior company executive. Mr. Karan Adani, Managing Director of Adani Ports and SEZ (APSEZ) was recently quoted as saying that the aim is to transform India's leading port operator into a global ports hub by boosting the share of internationaltraffic.

The ports business currently gets about 5% of its

NEW DELHI: A regulatory framework to push the country's exports through e-commerce medium is expected to be ready by September, a top government officialsaidrecently.

total volume from International Operations, which it is aimingtodoubleby2030,saidAdani.

Theportsbusinesshasbeenseeingexponentialgrowth in the past few years, and Adani expects the trajectory to continue "Currently, the split between our ports and logistics segment is 70:30, and we expect the same to continue because while our logistics segment is growing, soisourportssegment,andthattooatamuchfasterpace," hesaid.

Mr. Koul is set to lead an expanded Board of Directors

Commerce Secretary Sunil Barthwal said that at present India's exports through this medium are only about USD 5 billion as compared to China's USD300billion, annually.

Cont’d. Pg. 23

Cont’d. Pg. 8

NEW DELHI: Je en a an d Co mp an y, a leading freight forwarding company and supply chain solution provider, proudly announces the appointment of Mr Prediman Koul as the new Chief Executive Ofcer.

MUMBAI: The logistics subsector is undergoing numerous changes to address infrastructure and technology challenges. As the lifeline of the MSME sector, the logistics and supply chain industry plays a crucial role in efficiently deliveringtheirproductsandenablingthemtoreachthe marketortheirdestination.MSMEsrelyheavilyontheir third-party logistics providers to operate smoothly, as they often face limitations due to a lack of capital or resources.

The upcoming budget should create an environment where MSMEs can flourish with well-developed logistic infrastructures based on sustainable practices.

We expect the budget to prioritize investments in infrastructure development, digitalization, and skill development, which will further empower MSMEs. Our commitment goes beyond providing logistics; we actively support programs that enhance operational efficiency and competitiveness for MSMEs. Through various initiatives like capacity-building workshops, digital transformation projects, and skill development programs, we strive to growandsustainMSMEs.

WASHINGTON: The International Monetary Fund raised India’s growth forecast for FY25 to 7 percent from 6.8 percent projected in April, according to its World Economic Outlook released on July 16.

“The forecast for growth in India has also been revised upward, to 7 percent, this year, with the change reflecting carryover from upward revisions to growth in 2023 and improvedprospectsforprivateconsumption,particularlyin ruralareas,”thefundnoted.

The Global financial institution expects the economy to grow6.5percentinFY26,unchangedfromApril.

In June, the Reserve Bank of India had revised India’s growthforecastupwardto7.2from7percentearlier.

Thecountryhasgrownover7percentoverthelastthree years. The economy grew 8.2 percent in FY24, with investment and manufacturing supporting growth.

But private consumption spending was lower at 4 percent. Economists indicate a pick up in rural consumption in FY25, but note that a revival would be contingent on good monsoon and lower inflation.

India’sinflationrosebackabove5percentinJuneaftera four month hiatus, as food inflation surged to 9.4 percent from 8.7 percent earlier.

Globalgrowthstable

On the global front, the fund kept its forecast unchanged at 3.2 percent in 2024, predicting a rise to 3.3 percent next year. The multilateral institution projected growth to slowdown for the US and Japan from April estimates, while it predicted a faster pace of rise for China.

The fund noted that risks to growth were balanced, with rising risks to inflation, which are expected to increase prospects for higher-for-even-longer rates.

Cont’d. from Pg. 4

Revenue from the ports segment grew to Rs 20,972 crore in FY24, from Rs 17,304 crore in the previous year On the other hand, revenue from the logistics segment grew toRs2,079crorefromRs1,744croreinthesameperiod

APSEZ is India's largest port developer and operator with 15 ports across the West and East Coast of the country. It also runs a port each in Colombo (Sri Lanka), Haifa(Israel),andDaresSalaam(Tanzania).

Adani attributed growth in the ports business to India's thriving exports and imports demand, and the Country's growing potential globally. He said APSEZ has a target of handling 1 billion tonnes of cargo by 2030. It is projecting "roughly 900 million tonnes of that coming in from existing Indian ports," with remaining 10% focused on

internationalventures,Adanisaid.

Explaining the company's strategy, Adani said APSEZ expects "organic growth" at its existing ports. Capacity expansion is also a potential avenue for future development, as these regions continue to grow and require increasedtradecapabilities.

For inorganic growth, the company will continue to evaluate potential acquisition opportunities. "We see a lot of opportunities coming in from PPP (public-private partnership) projects as the government keeps moving towards mega ports such as Vadhavan port (in Maharashtra), therewillbeopportunitiesforeveryone."

Adani Ports has a multi-pronged approach for international growth including making India a hub for global traderoutes.

ZURICH: Union Commerce and Industry

Minister Shri Piyush Goyal met with Mr. Diego Aponte, Group President at MSC Cargo, a renowned Global Container Shipping & Logistics

Group with a significant presence in India. At Zurich, they discussed potential collaborations with the Indian industry and the growth of Container Shipping &Indian-FlagVessels.

Mr. Koul is set to lead an expanded

Cont’d. from Pg. 4

This decision highlights Jeena's commitment to enhancingitsexecutiveteamwith seasoned professionals, aiming to drive innovation, improve operational efficiency, andexpanditsglobalfootprint.

WitharemarkabletenureatJeenathatbeganin1997, Mr. Koul has risen through the ranks, demonstrating an unwavering dedication to excellence. His appointment as the CEO, reflects his exceptional leadership and strategicvision.

Having joined the company 27 years ago, Mr. Koul has dedicated his career to fostering growth and excellence within the organization. He joined Jeena & Company in the finance division and quickly developed a keen interest in the core business operations. Over the years, Mr. Koul has progressed through various levels. He has served in roles such as Air Freight Manager, Delhi and then advanced to Branch Manager, Delhi, continuously demonstrating his commitment and leadership.

Having ascended to Executive Director & COO in 2022, Mr. Prediman Koul now steps into the CEO role, driving Jeena & Company forward. His commitment to continuous learning is underscored by his participation in leadership programs at the Indian School of Business and IMD Switzerland. Additionally, he serves as the ChairmanoftheACFIDelhiChapter.

Welcoming Mr. Prediman Koul into his new role, the Partners of Jeena & Company collectively congratulated Mr. Koul, saying, “Mr. Koul has been an integral part of Jeena & Company, witnessing and participating through various phases of growth and transformation.Hisextensiveexperience,alongwithhis long-standing association with the company, provides him with an unparalleled understanding of the business and operations. He truly embodies the purpose of the brand. His enduring dedication and steadfast commitment to Jeena & Company highlight the core values we uphold. Recognizing and celebrating those who have invested their lives in the growth and

betterment of the company is fundamental to the strengthofalegacybrandlikeJeena&Company.”

Mr. Prediman Koul will also be taking charge of an expandedBoardofDirectors.OurBoardmembersarea powerhouse of experience and expertise namely, Mr. Hector Patel, CMO and Director, leverages over 30yearsinSalesandMarketingtodriveglobalexpansion and innovative strategies, Mr.HomyarDesai,Director of Sea Freight and Board Member has shaped the Sea Freight division over his 34-year tenure, spearheading IT advancements and major projects, Mr. Malcolm D'Souza, Director of Air Freight and Board Member, brings 15 years of success in pricing, procurement, and business intelligence, and Mrs. Lucky Kulkarni, Director & Group Head of HR and Board Member, with over 25 years in HR, has earned prestigious awards for her strategic initiatives since 2018; The Group CFO and Executive Director, Mr. Gayomard Driver, a Chartered Accountant, ensuresfinancialstabilityandgrowthwhile championingtransformativeindustrychange.

Expressing his enthusiasm for the new role, Mr. Prediman Koul stated, “I am thrilled to begin my journey as CEO of Jeena & Company. I am deeply grateful to our Partners for their trust and to everyone who has supported me over my 27 years here. Congratulations to the newly appointed members of our Management Board. With the support of an exceptional team, I am dedicated to actively listening to your perspectives, understanding your ideas, and embracing the challenges and opportunities you see. Together, we will uphold our commitment to delivering value to our customers, driving sustainable growth, and creating an inclusive workplace where everyone feels valued and empowered. Let's continue to prioritize teamwork, positivity,andagilityasthepillarsofoursuccess.”

Jeena & Company's leadership transformation underscores its intent to harness the expertise and vision of its trusted members to drive the company's goals. By prioritizing workforce development and adapting to the evolving needs of the industry, Jeena & Company iswell-positionedfor enduring success.

GANDHIDHAM: The Kandla Port Steamship Agents Association (KPSAA) expressed its heartfelt gratitude to Shri Sushil Kumar Singh, IRSME, Chairman of Deendayal Port Authority, and Shri Nandeesh Shukla, IRTS, Dy. Chairman for the swift development and implementationofthenewberthingpolicy.

The association commended the leadership and dedication of Shri Sushil Kumar Singh, Shri Nandeesh Shukla and the Heads of Departments for their efforts in creating a policy that significantly benefits the trade and shipping fraternity. The policy's efficiency and speed are a testament to their commitment to improving port

operations and enhancing the overall efficiency and competitivenessofDPA.

The KPSAA delegation, comprising President Mr.BharatGupta,Hon.SecretaryMr.EbezYesudas, Committee Members Mr. Mitesh Dharamshi, Mr. Madhu Menon, Mr. Sabukuttan, and Mr.GiriVisweswaraoIlla, congratulatedandshowered appreciation upon Shri Sushil Kumar Singh and Shri Nandeesh Shukla assured him of their full cooperationandsupport.

The association acknowledged the exceptional work done by Shri Sushil Kumar Singh and his team, recognizing their dedication and swift execution of this crucialpolicy.

RIYADH: Bahri, a global leader in logistics and transportation,hasenteredinto a training agreement with the Saudi Logistics Academy (SLA), a non-profit training facility established to qualify young Saudi talent across several industries including logistics, supply chain, e-commerce, and marketing. The agreement aims to enhance employment opportunities and skill developmentinthemaritimelogisticssector.

Underthetermsofthetwo-yearagreement,SLAwill trainandqualifyanumberofSaudicandidatesinvarious specializations for placement across Bahri’s business units. Through a structured 12-month program, participants will gain hands-on experience and theoretical knowledge tailored to meet Bahri's specific job requirements. This initiative not only fosters career growth for aspiring professionals but also contributes to the sustainability of the logistics sector by nurturing askillednationalworkforcecapableofdrivinginnovation andindustryexcellence.

Hisham AlKhaldi, Chief Support Ofcer at Bahri highlighted the significance of this agreement, stating, "Our agreement with SLA stems from a desire to enrich Bahri with highly-trained young specialists and create greater synergy between national training organization, educational institutions, and the increasingly competitive Saudi job market. By leveraging our combined expertise, we aim to establish a thriving ecosystem for the students, fresh graduates, and early careerists who will become tomorrow’s industry leaders.”

Dr. Abdullah Alabdulkarim, CEO of SLA,

commended the partnership, stating, "With more international talent present within the Kingdom than ever before, providing the Saudi workforce with ample opportunities for upskilling and career development is essential to enhance competitiveness, foster innovation, and drive sustainable economic growth. At SLA, we eagerly anticipate our partnership with Bahri, which will see us train nearly a dozen Saudi talents to assume leading roles within one of the Kingdom’s most vital sectors."

Established in 1978, Bahri has leveraged its established capabilities, locally-sourced talents, andtechnicalexcellenceacrosssixkeybusinessunitsto emerge as a cornerstone in the nation's efforts to transform and propel growth within the maritime logistics sector. With a commitment to bolstering Saudi Arabia’s position as a premier international gateway for logistical services, Bahri is dedicated to strengtheningtheKingdom’spresenceinglobalmarkets.

by Dr. Pramod Sant, A distinguished Industry Expert

Question: WewishtoestablishMISforExportsincluding General Information to Management / Business, Export Compliance, Exports Incentive, Logistics and Timelinesetc.canyougiveusplanforsame.

SOLUTION: In last Daily Shipping Times issue dated 3.7.2024 I gave details of MIS in two main areas of Exports namely 1) General Information on Exports 2) Export Logistics -MIS this was followed by twomoretopics3)ForeignTradePolicy(FTP)-Schemes and Export Obligations 4) Export Incentives and Benefits in DST issue dated 10.7.2024.

Now last part of this solution includes two balance topics

5)ExportTimelinesMIS

6)Accounting,EMA/IDPMSMIS

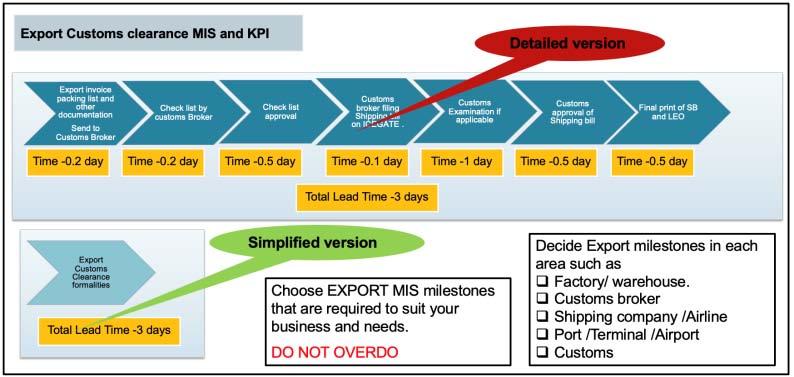

Export Timelines MIS

To measure Export Timelines is complex as export process varies based on the mode of dispatch, Incoterms, and type of export etc While capturing timelines there is need to be familiar with the specific requirements and procedures for each mode, the responsibilities defined by Incoterms, and the documentation neededfordifferenttypes of exports to ensure a smoothandcompliantexportprocess.

monitoringofexporttimelines.

Export timeline MIS need to be prepared in collaboration with stakeholders internal and external.

Most important is do not overdo and increase time pointers which do not add value to businessornotcontrollable.BelowchartExportcustoms clearance MIS /KPI will give idea about simple version and detailed version. Always ensure that data entry is avoided and data flow from Freight forwarder / Customs brokertoyoursystem.

Most important is keep modular structure so that you can add new parameters incorporate changes.

After listing down all steps in export, stakeholder connected with same systems used for same need to be mentioned. Next action is to select steps which are critical, and which needs to be recorded.

For Example –for exporter who is away from port, step of calling empty container and stuffing container and transportation to port may be critical step. Delay in receipt of empty container or delay in transportation to port will result in additional cost and risk of not catching vessel. Further it will result in penalty by customer and loss of reputation. Insuchcasesprecarriagestepsarecritical.

In other example, if exporter is having warehouse at Bhiwandi or Gurgaon and shipment is by airfreight from Mumbai/Delhiprecarriageisrelativelysimple.

Similarly, if export goods need inspection by authorized agency appointed by exporting customer /country or export documents needs to be authenticated by Consulate then it is important to consider such steps in

It is important to know cost of handling export with breakup of Logistics cost, freight, other handling, customs clarence etc. When these costs break up are available, informed decision can be taken while making export offer and selection of INCOTERMS etc.

Cost MIS helps you to take projects to analysis cost and reduce them. Cost compilation needs to be done at shipment level first and then at products, export order level. You can have compilation at business level or country wise and customer wise also. Finally, MIS at company level should have option to drill down at each levelandvariouscombinations.

PS: - Export Management Information Systems (MIS) are multidimensional tools that can be tailored to meet specific needs, strategies, organizational goals, and operational areas. When choosing an Export MIS, it's essential to consider factors such as your business objectives, the scale of operations, the complexity of your export processes, and the regulatory requirements. By aligning the MIS with your strategic goals and operational needs, you can enhance efficiency, ensure compliance,andgainvaluableinsightsfordecision-making,ultimatelydrivingthe success of your export activities.

I.G.M. No. 2382355 Dtd. 12-07-2024

The above vessel has arrived at Mundra on 17/07/2024 as per following details. Item Nos. B/L NOS. 1 EPIRKEMBFL200600

Consignees are requested to obtain the DELIVERY ORDERS on presentation of ORIGINAL BILLS OF LADING duly discharged and on payment of relative charges as applicable within 5 days or else Detention Charges will be applicable.

If there is any delay in CY-CFS / lCD's movement due to port congestion or any other cause beyond the control of the Shipping Line / Agents are not responsible for the same. Also note that the Shipping Line / or their Agents will not be held responsible for auction by Port / Customs / Custodian of uncleared cargo on expiry of stipulated period as laid down in the byelaws.

Consignees are advised that the carriers and/or their Agents are not bound to send individual notifications regarding the arrival of the vessel or the goods.

For vessel ETA / IGM- ITEM/ Exchange Rate / Local charges & Detention Charges please contact our office.

Rajkamal-II, Office No. 103, 1st Floor, Plot No. 342, Ward - 12/B, Gandhidham - 370201. India. In case of any query kindly contact the below E-mail IDS & Phone Numbers : IMPORT related : ravi.vaghela@in.emiratesline.com

Tel. No. : +91-2836-239378 / 239379 - Mob. : +91 89809 97977

EXPORT related : hardik.jadeja@in.emiratesline.com

Tel. No. : +91-2836-239378 / 239379 - Mob. : +91 98980 76324

IGM Tracking : http://www.emiratesline.com : 8090/eadmins/igm_main.jsp.

m.v. “ESL BUSAN” V - 02424 E I.G.M. NO. 2382259 DTD. 11-07-2024

The above vessel has arrived at Mundra on 15-07-2024 as per following details.

7 EPIRCHNNBO256783

8 EPIRCHNNBO256787

9 SZOE24060225

10 EPIRCHNCWA262140

5 EPIRCHNNBO256777

6 EPIRCHNNBO256778 Item Nos. B/L NOS.

11 EPIRCHNGUA201462

EPIRCHNQGA254980 18

EPIRCHNSHA249328 19

EPIRCHNSHA249329 20

21

EPIRCHNNBO256737

EPIRCHNCWA262129

Consignees are requested to obtain the DELIVERY ORDERS on presentation of ORIGINAL BILLS OF LADING duly discharged and on payment of relative charges as applicable within 5 days or else Detention Charges will be applicable.

If there is any delay in CY-CFS / lCD's movement due to port congestion or any other cause beyond the control of the Shipping Line / Agents are not responsible for the same. Also note that the Shipping Line / or their Agents will not be held responsible for auction by Port / Customs / Custodian of uncleared cargo on expiry of stipulated period as laid down in the byelaws.

Consignees are advised that the carriers and/or their Agents are not bound to send individual notifications regarding the arrival of the vessel or the goods.

For vessel ETA / IGM- ITEM/ Exchange Rate / Local charges & Detention Charges please contact our office.

Rajkamal-II, Office No. 103, 1st Floor, Plot No. 342, Ward - 12/B, Gandhidham - 370201. India. In case of any query kindly contact the below E-mail IDS & Phone Numbers : IMPORT related : ravi.vaghela@in.emiratesline.com

Tel. No. : +91-2836-239378 / 239379 - Mob. : +91 89809 97977

EXPORT related : hardik.jadeja@in.emiratesline.com

Tel. No. : +91-2836-239378 / 239379 - Mob. : +91 98980 76324

IGM Tracking : http://www.emiratesline.com : 8090/eadmins/igm_main.jsp.

Also Offers Regular Weekly Services to the Following Destinations:

l l l NHAVA SHEVA : Tel:27471601/05, Fax:27246415

Continuous Carting at Balmer Lawrie CFS, N.Sheva Accepting Cargoes from ICD Delhi, ICD Ahmedabad Accepting Reefer/Chilled Cargoes

Marathon Nextgen, Innova ‘A ’-G01,

E-mail:nxvexp@evergreen-shipping.co.in

CHENNAI : Tel:044-39849999, Fax:044-39849998

COCHIN : Tel:0484-3983999, Fax:0484-3983998

E-mail:cokbiz@evergreen-shipping.co.in

TUTICORIN : Tel:0461-3984999, Fax:0461-3984997/8 E-mail:tutbiz@evergreen-shipping.co.in

E-mail:cenbiz@evergreen-shipping.co.in NEW DELHI : Tel:011-39849999 (Hunting), Fax:011-39849997/98 E-mail:ndimgt@evergreen-shipping.co.in

AHMEDABAD : Tel:079-39849700,Fax:079-39849998 E-mail:zhdbiz@evergreen-shipping.co.in

KOLKATA : Tel:033-39829999, Fax:033-39829998

E-mail:ccubiz@evergreen-shipping.co.in

Cargo Steamer's Agent's ETD

Jetty Name Name

CJ-I SW South Wind Synergy Seaport 21/07

CJ-II Doris Arnav Shpg. 19/07

CJ-III Haj Abdallah T DBC 20/07

CJ-IV Kwai Kwai ACT Infra 22/07

CJ-V Kaley

CJ-VI Wu Yang Glory Dariya Shpg. 23/07

CJ-VII Jin Ning 16 Sea Link 21/07

CJ-VIII VACANT

CJ-IX Billy Jim Interocean 19/07

CJ-X Martin Merchant Shpg. 20/07

CJ-XI TCI Express TCI Seaways 19/07

CJ-XII VACANT

CJ-XIII African Wagtail Cross Trade 22/07

CJ-XIV Jaador Mihir & Co. 24/07

CJ-XV VACANT

CJ-XVAVACANT

CJ-XVI Hampton Ocean Shantilal Shpg. 23/07

TUNA VESSEL'S NAME AGENT'S NAME ETD

Maroulio S Interocean 19/07

Propel Shakti Ambica Log. 19/07

OIL JETTY VESSEL'S NAME AGENT'S NAME ETD

OJ-I Telendos

OJ-II Risha Samudra 19/07

OJ-III Antares J M Baxi 19/07

OJ-IV Southern Robin

OJ-V VACANT

OJ-VI Patriot Malara Shpg. 19/07

CJ-XIII

CJ-II Doris Arnav Shpg.

23/07 Encore Krishna Shpg. China

OJ-VII Silver Valerie Interocean 19/07 Stream Aeriko Dariya Shpg. Paradip

SHIPS SAILED WITH NEXT EXPORT CARGOS DESTN.

Doctor O 14/07 Hodeidah

Fuji Harmony 13/07 Korea

SSF Dream 16/07 Port Khalifa

Ageri 16/07

Hansa Europe 17/07 Jebel Ali

Propel Success 17/07 UAE

Kingfisher 17/07 China

African Bari Bird 18/07 USA

Steamer's Name Agents Arrival on Hai Phoung 87 Chowgule S. 13/07

Aruna Eagle Aditya Marine 13/07

Sweet Lady III BS Shpg. 12/07

Gramba Synergy Seaport 11/07

Della Synergy Seaport 10/07

African Raptor Dariya Shpg. 14/07

Athos Arnav Shpg. 14/07

MO Joud DBC 13/07

SHIPS NOT READY FOR BERTH

CJ-IX Billy Jim Interocean San Lorenzo

Stream Cariboo Synergy Seaport New

22/07 Flag Seaman Taurus USA

Stream Gramba Synergy Seaport

Stream Hai Phoung 87 Chowgule S.

18/07 Ince Ilgaz Arnav Shpg. Ukrain

Stream Jal Kamal Dariya Shpg. Indonesia

CJ-VII Jin Ning 16 Sea Link

Stream Linda Hope Taurus

Tuna Maroulio S Interocean San Lorenzo

CJ-X Martin Merchant Shpg.

INIXY124070137

T. MOP In Bulk INIXY124070103

INIXY124070023

Stream CNC Dream Samudra

19/07 Elandra Maple Interocean

Stream Furano Galaxy GAC Shpg.

26/07 GW Dolphin Interocean Argentina

Stream Hanyu Azalea Seaport

Stream Jag Pavitra J M Baxi

Stream KRA Samudra UAE

18/07 Lavender Ray Samudra China

19/07 Penna J M Baxi

Stream PVT Aurora Kanoo Shpg.

Stream Raon Teresa Samudra Al Jubail

OJ-II Risha Samudra Saudi Arabia

Stream Sanman Sitar Malara Shpg.

18/07 Seapromise Interocean

Stream Silver Gwen Interocean

Stream Solar Roma J M Baxi

Stream Southern Quokka GAC Shpg.

Stream Southern Wolf J M Baxi

Stream Stolt Maple J M Baxi

CDSBO In Bulk

INIXY124070112

IN Bulk INIXY124070095

INIXY124070127

INIXY124070021

In Bulk INIXY124070069

In Bulk INIXY124070111

In Bulk INIXY124070085

INIXY124070105

T. MS BSVI

(C16) 19/07

21/07 20/07-PM GSL Nicoletta 429E X-Press Feeder Sea Consortium Singapore, Dalian, Xingang, Qingdao, Busan, Kwangyang, 22/07 02/08 01/08-PM CCNI Angol 430E 4072683 Maersk Line Maersk India Ningbo, Tanjung, Pelepas, Port Kelang (NWX)

24/07 24/07-AM Inter Sydney 160 4062630 Interworld Efficient Marine China (BMM)

TBA

Asyad Line Seabridge Marine Haiphong, Shekou, Laem Chabang, Port Kelang (FEX1)

TBA Asyad Line Seabridge Marine Haiphong, Shekou, Laem Chabang, (FEX) TO LOAD FOR INDIAN SUB CONTINENT

18/07 18/07-PM Beijing Bridge 2404 4072582 Global Feeder Sima Marine Karachi (CSC)

20/07 19/07-PM Kmarin Azur 427W 4062350 Maersk Line Maersk India Tema, Lome, Abidjan (MW2 MEWA)

18/07 Beijing Bridge (V-2404) 4072582 MBK Logistix Nhava Sheva

18/07 SM Neyyar (V-427) 4062528 MBK Logistics Jebel Ali 19/07 Wan Hai 510 (V-180E) 4072604 Wan Hai Line Nhava Sheva

Maersk Cabo Verde (V-428S) Salalah 13-07-2024 Northern Guard (V-924E) Port Kelang 14-07-2024 Seaspan Jakarta (V-428W) Pipavav 14-07-2024

Evergreen/ONE Evergreen Shpg/ONE Port Kelang, Tanjin Pelepas, Singapore, Xingang, Qingdao, Ningbo 20/07 21/07 21/07-PM TS Hongkong 24002W 2402530 Feedertech/TS Lines Feedertech / TS Line Shanghai (CISC)

20/07 20/07-AM Northern Practise 31E 2402384 FeedertechFeedertech Port Kelang, Singapore, Leam Chabang.(AGI)

22/07 21/07-PM Hyundai Jakarta 130W 2402529 Hyundai Seabridge Maritime Port klang, Singapore, Shekou, Ningbo, Shangai, Kwangyang, Busan (FIM) 23/07 22/07 19/07-PM Xin Chang Shu 87E 2402525 Wan Hai Line Wan Hai Lines Port Kleang (W), Hong Kong, Qingdao, Kwangyang, Pusan, 23/07 24/07 23/07-PM Wan Hai 625 13E 2402639 COSCO/Evergreen COSCO / Evergreen Ningbo, Shekou, Singapore, Shanghai (PMX) 25/07 22/07 22/07-AM Zhong Gu Ji Nan 24004E 2402636 KMTC/COSCO KMTC / COSCO Shpg. Port Kelang, Hongkong, Qingdao. (AIS) 23/07 TS Lines Samsara Shpg

29/07 29/07-PM Zoi 115E 2402545 Interasia/GSL Aissa M./Star Shpg Port Kelang, Singapore, Tanjung Pelepas, Xingang, Qingdao, 30/07 Evergreen/KMTCEvergreen/KMTC (FIVE) TO LOAD FOR INDIAN SUB

Port —/— X-Press Pisces 24005E 2402483 One/X-Press Feeder One India / Sea Consortium Karachi, Colombo. (CWX)

Felixstowe. Dunkirk, Le Havre 19/07 18/07 18/07-AM MSC Fie X IP427B 2402624 CMA CGM CMA CGM Ag.(I) & Other Inland Destination in Europe, Med,Red Sea, Black Sea

20/07 24/07 24/07-AM MSC Thais IS428A 2402635 MSC/SCI MSC Ag / J.M.Baxi Gioia Tauro, Feixstowe, Hamburg, Antwerp & Other Inland Destn.

19/07 18/07-1800 Maersk Sentosa 428W 24229 Maersk Line Maersk India Algeciras

26/07 25/07-1800 W

20/07 20/07-0500 MOL Presence 015E 24243 X-Press Feeders Merchant Shpg. Port Kelang, Singapore, Laem Chabang. 21/07 02/08 02/08-0500 Dimitris Y 0246E ONE ONE (India) (TIP) 03/08 29/07 29/07-2000 Xin Beijing 146E COSCO COSCO Shpg. Singapor, Cai Mep, Hongkong, Shanghai, Ningbo, Shekou, 30/07 Nansha, Port Kelang (CI1)

27/07 27/07-2000 CCNI Angol 430E 24241 Maersk Line Maersk India Singapore, Dalian, Xingang, Qingdao, Busan, Kwangyang, 28/07 02/08 02/08-2000 X-Press Odyssey 24031E 24246 X-Press Feeders Merchant Shpg. Ningbo, Tanjung Pelepas. (NWX) 03/08 Sinokor / Heung A Sinokor India Port kelang, Singapore, Qindao, Xingang, Pusan. In Port —/— Pusan 32E 24236 COSCO / OOCL COSCO Shpg./OOCL(I) Port Kelang, Singapore, Hong Kong, Shanghai, Xiamen, Shekou. 18/07 21/07 21/07-0400 Aka Bhum 022E 24242 Gold Star / RCL Star Shpg/RCL Ag. (CIXA) 22/07 24/07 24/07-0600 OOCL Hamburg 151E 24245

19/07 18/07-2100 One Arcadia 069E 24230 ONE ONE (India) Port Kelang, Singapore, Haiphong, Cai Mep, Pusan, Shahghai, 20/07 22/07 21/07-1900 One Theseus 088E 24241 HMM / YML HMM(I) / YML(I) Ningbo, Shekou (PS3)

19/07 18/07-1800 Maersk Sentosa 428W 24229 Maersk Line Maersk India Salallah, Port Said, Djibouti, Jebel Ali, Port Qasim. (MECL)

30/07 30/07-0300 Seaspan Jakarta 430W 24247 Maersk/GFS Maersk India/GFS Jabel Ali, Dammam (SHAEX)

02/08-0300 SM Neyyar 429W 24248

20/07 20/07-0500 MOL Presence 015E 24243 X-Press Feeders Merchant Shpg. Muhammad Bin Qasim, Karachi, Colombo.

29/07-2000 Xin Beijing 146E COSCO COSCO Shpg. Karachi, Colombo (CI1)

27/07 27/07-2000 CCNI Angol 430E 24241 Maersk Line Maersk India Colombo. (NWX)

In Port —/— Pusan 32E 24236 COSCO/OOCL COSCO Shpg./OOCL(I) Colombo. (CIXA)

21/07 21/07-0400 Aka Bhum 022E 24242

18/07 18/07-1200 SCI Chennai 2407 24238 SCI J M Baxi Mundra, Cochin, Tuticorine. (SMILE)

19/07 18/07-1900 Mogral 0084 CCG Sima Marine Hazira, Mangalore, Cochin, Colombo, Katupalli, Vishakhapatanam, 20/07 Krishnapatanam, Cochin, Mundra. (CCG)

22/07-0600 SSL Bharat 158 24237 SLSSLS Hazira, Cohin, Mangalore, Tuticorin, Mundra. (PIC 1)

20/07 20/07-0500 MOL Presence 015E 24243 X-Press Feeders Merchant Shpg Seattle, Vancouver, Long Beach, Los Angeles, New York, 21/07 02/08 02/08-0500 Dimitris

NO. 2381476 DTD. 03-07-2024

The above vessel has arrived at Mundra on 10-07-2024 as per following details.

EPIRCHNNBO256545 8 EPIRCHNQGA254430

EPIRCHNQGA254468 10 YSNBF24062606

11 PACIND240601

12 YSY2406232A

Consignees are requested to obtain the DELIVERY ORDERS on presentation of ORIGINAL BILLS OF LADING duly discharged and on payment of relative charges as applicable within 5 days or else Detention Charges will be applicable.

If there is any delay in CY-CFS / lCD's movement due to port congestion or any other cause beyond the control of the Shipping Line / Agents are not responsible for the same. Also note that the Shipping Line / or their Agents will not be held responsible for auction by Port / Customs / Custodian of uncleared cargo on expiry of stipulated period as laid down in the byelaws.

Consignees are advised that the carriers and/or their Agents are not bound to send individual notifications regarding the arrival of the vessel or the goods.

For vessel ETA / IGM- ITEM/ Exchange Rate / Local charges & Detention Charges please contact our office.

Rajkamal-II, Office No. 103, 1st Floor, Plot No. 342, Ward - 12/B, Gandhidham - 370201. India. In case of any query kindly contact the below E-mail IDS & Phone Numbers : IMPORT related : ravi.vaghela@in.emiratesline.com

Tel. No. : +91-2836-239378

POST - SHEVA, TALUKA : URAN, DIST : RAIGAD, MAHARASHTRA - 400707.

DIN : 20240678NV000000BA3C

Dated : 24-06-2024

Sub. : Guidelines for verification under CAROTAR 2020, of the Country of Origin Certificates (COO) issued under various Preferential Trade Agreements (commonly also referred to as Free Trade Agreements - FTAs)

Attention is drawn towards Section 28DA of the Customs Act, 1962, read with Rules 4, 5 and 6 of the Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020, notified vide Notification No. 81/2020Customs (N.T.) dated, 21st August, 2020, also known as CAROTAR 2020, and CBIC Circular No. 38/2020- Customs dated 21.08.2020, which empower the proper officer to seek information and supporting documents from the importer claiming preferential rate of duty, if the proper officer has reason to believe that origin criteria prescribed in the respective Rules of Origin have not been met.

2. The officials of Turant Suvidha Kendra (TSK) are responsible for verification of relevant documents uploaded in e-Sanchit module of ICES and defacing of original documents, including the Country of Origin Certificate issued under the Preferential Trade Agreements (hereinafter referred to as FTA-COO). In recent past, following difficulties were being faced by the officials of TSK in verification and defacing of FTA-COO in case of third country invoicing:

(i) The presented FTA-COO does not provide FOB value in the relevant column;

(ii) The third country invoice does not indicate FOB value indicated in the FTA-COO;

(iii) The third country invoice indicates a greater number of items than indicated in the FTA-COO;

(iv) The Bill of Entry presented before Customs on the basis of third country invoice indicates a different CTH as compared to the CTH indicated in the FTA- COO.

3. The procedure for verification of the FTA-COO, as provided in Public Notice No. 33/2024 dated 20.03.2024 has been reviewed in detail, taking into account the pattern of documentation in respect of third country invoicing for imports made with claim of benefit under the Preferential Trade Agreements, trade practices in vogue and in light of the relevant statutory provisions. In supersession of the procedure prescribed vide the said Public Notice, for verification of eligibility of benefit of the relevant FTA on the basis of scrutiny of documents, the following procedure is prescribed:

i. The importer will need to submit the FTA-COO indicating the FOB value in the relevant column of the FTA-COO, along with the third country invoice details. The amount of freight and insurance will also need to be disclosed, either in the third country invoice or by submission of freight certificate and insurance receipt. However, this will not be applicable in case of FTA-COO which does not have FOB value column, e.g. FTA-COO issued under India-Japan CEPA.

ii. If the INCOTERMS of third country invoice is FOB, and the FOB value indicated on the third country invoice is same as that indicated on the FTA-COO, the same prima facie indicates that the FOB value indicated on the FTA-COO includes the value addition (profit and other charges) of the third country supplier. The same is not permitted under the Preferential Trade Agreements. In such cases, the importer shall include an explanation for the identical FOB values mentioned in the two documents, viz. FTA-COO and the third country invoice at the time of submission of self- assessed Bill of Entry.

iii. If the Bill of Lading which indicates “FREIGHT PREPAID”, and which is issued in favour of the Shipper located in the country of origin (exporting country), then the importer will need to submit freight certificate if the freight has been paid by any person other than the Shipper indicated on the Bill of Lading.

iv In the cases wherein the FTA-COO is issued on the basis of third country invoice, i.e. the details of the third country invoice are mentioned in the FTA-COO, then the values mentioned in the said two documents FTA-COO and third country invoice need to be in the same currency. This will help in quick verification of eligibility of benefit of the relevant FTA on the basis of scrutiny of documents.

v. If the third country invoice indicates a greater number of items than indicated in the FTA-COO, then benefit of FTA will be admissible to only the items covered in the FTA-COO and the balance items will be assessed at merit rate.

vi. If the third country invoice indicates a different CTH as compared to the CTH indicated in the FTA-COO, and the product description is the same in both the documents, then the importer will be required to self-declare the preferred CTH in the Bill of Entry. The proper officer will scrutinise the documents and take appropriate decision as part of assessment and as per provisions of the relevant FTA notifications including related nontariff notification. In case the product description in the third country invoice and FTA-COO are different, the eligibility for FTA benefits will be scrutinised as per the provisions of the law

4. The proper officer will give option to the importer for early clearance against bond and Bank Guarantee if the importer needs more time to submit information and supporting documents sought by the proper officer under Rule 5 of CAROTAR, 2020.

5. If verification request under Rule 6 of CAROTAR, 2020 is required to be sent, then the proper officer shall submit specific questionnaire to DIC (Directorate of International Customs), after obtaining necessary details from the importer

6. This Public Notice should be considered as a Standing Order for the concerned Officers and Staff of this Custom House.

7. Any difficulty faced in implementation of this public notice may be brought to the notice of Assistant Commissioner in charge of TSK at email address: tsk-jnch@gov.in.

8. This is issued with approval of the Chief Commissioner of Customs, Zone-II

Sd/Ashwini Kumar Commissioner of Customs, NS-III, JNCH, Mumbai-II

Cont’d. from Pg. 4

He said there is a huge potential to boost these exports. In this regard, a meeting was held in the Ministry with concerned departments such as revenue and industry representatives from areas like logistics and marketplace platforms.

"We are working on setting up e-commerce export hubs in the country. We discussed on its framework. It is in our 100-day agenda," Barthwal told reporters here.

When asked about the timeline for the framework to be ready, he said by September.

There is a potential to take it to USD 50-100 billion in the coming years.

Through these hubs, small producers will be facilitated to sell to aggregatorsandthenthataggregator willfindmarketsandsell.

"It will be a framework for e-commerce export hubs and regulatory ecosystem. These hubs willcomeupnearairports,andports," hesaid.

Export products which hold huge potential include jewellery, apparel, handicrafts and ODOP (one district oneproduct)goods.

He added that the industry is not seeking any financial assistance and just needs a good regulatory ecosystem like taxation and how returnedgoodswillbetreated.

The Commerce Ministry's arm DGFT is working with the RBI and concerned Ministries, including the Finance Ministry, on several steps to promote exports through e-commerce medium as huge export opportunitiesarethereinthesector.

In such hubs, export clearances

can be facilitated. Besides, it can also have warehousing facilities, customs clearance, returns processing, labelling, testing and repackaging.

Federation of Indian Export Organisations Director General Ajay Sahai has earlier stated that it will be a kind of bonded zone which will facilitate exports and imports of e-commerce cargo and to a large extent address the problem of re-imports because in e-commerce, about 25 per cent of goods are re-imported.

Last year, the cross-border e-commercetradewasaboutUSD800 billion and is estimated to reach USD 2trillionby2030.

A report by economic think tank GTRI India's e-commerce exports have the potential to reach USD 350 billion by 2030, but banking issues hinder growth and increase operationalcosts.

India has set a target of USD1trillionofmerchandiseexports by2030andcross-bordere-commerce tradehasbeenidentifiedasoneofthe mediums to meet this aim.

NEW DELHI:

Responding to the Monthly exports figures of June 2024, FIEO President, Mr Ashwani Kumar said that the third consecutive increase in merchandise exports by 2.55 percent to USD 35.2 shows the resilience of the sector. MrKumarsaidthathaditnotbeenfor the logistics disruptions such as lack of container availability, shipping space, irregular shipping schedule and ships skipping Indian ports, the exports would have recorded close to double-digitgrowthinJune2024.

President FIEO added that the continuous hard work put in by the exporting community is paying dividends though there is also slowdownindemandfromseveralkey markets, reflected in sluggish growth projections. Mr Kumar, however, reiterated that he is optimistic of better growth numbers with improved demand coming in from the European Union, UK, West Asia and the US in months to come, which will not only further give a boost to the overall order bookings but also to the labour-intensivesectorsofexports.

FIEO Chief said that key sectors which have shown positive growth

during the month of June 2024, include engineering goods, electronic goods, drugs & pharmaceuticals, organic & inorganic chemicals, plastics & linoleum, cotton yarn/fabs./made-ups, handloom products etc., man-made yarn/fabs./made-ups, handloom products etc., cereal preparations & miscellaneous processed items, iron ore, mica, coal & other ores, minerals including processed minerals, ceramic products and glassware, RMG of all textiles, tea, coffee, rice, tobacco, spices, carpet and fruits & vegetables.

Our exports to eight of all our top ten markets including US, UAE, Netherland, UK, Saudi Arabia, Bangladesh, Germany and Malaysia were positive except with minor declines in China and Singapore, also with many of them recording healthy double-digitgrowth.

Month-on-month merchandise imports during June 2024 was US$ 56.18 billion with growth of 4.9percent,takingthetradedeficitfor the month to US$ 20.98 billion, said Mr Ashwani Kumar. However, a negative trade balance is not always bad, if a country is importing raw materialsorintermediaryproductsto

boost manufacturing and exports, addedFIEOPresident.

Overall exports of (goods and services) increased to US$ 200.33 billion during April-June FY 2024-25 withagrowthof8.6percentcompared to April-June FY 2023-24, whileoverallimportssawanincrease of 8.47 percent to USD 222.89 billion. He also added that though there is an increaseinimportsduringApril-June 2024 mainly due to petroleum products, silver, electronic goods, pulses and vegetable oil but the increase in petroleum products, silver import will lead to increase in exports of petroleum products and gems&jewellerywithatimelag.

FIEO President, Mr Ashwani Kumar further reiterated that the needofthehouristotakestepsonthe liquidity front with deeper interest subvention support and extension of interest equalisation scheme for 5years.Besides,addressingtheMiddle East geopolitical situation, Red Sea challengesbyensuringavailabilityof containers, marine insurance and rationaleincreaseinfreightcharges. The sector also needs easy & low cost of credit, marketing support and conclusion of some of the key FTAs withUK,PeruandOmansoon.

NEW DELHI: India’s total exports are projected to grow by 5.40 per cent in June 2024, with cumulative exports from April to June increasing by 8.60 per cent.

The Ministry of Commerce and IndustrysaidinareleaseonMonday, July 12, that merchandise exports reached USD 35.20 billion in June 2024, compared to USD 34.32 billion in June 2023, marking a growthof2.55percent.

The growth was driven by significant increases in engineering goods, electronic goods, drugs and pharmaceuticals,andcoffeeexports.

During the first quarter of the fiscal year, cumulative merchandise exports amounted to USD 109.96 billion, up from USD 103.89 billion in

thesameperiodlastyear,indicatinga growthrateof5.84percent.

India's total goods exported are expectedtorise2.56percentto$35.20 billioninJune2024,from$34.32billion inJune2023.Thetotalgoodsimported are expected to rise 4.98 per cent to $56.18 billion in June 2024, from$53.51 billioninJune 2023.

The Ministry of Commerce and Industry projects that total services exports will increase by 1.72 per cent to $30.27 billion in June 2024, up from $27.79 billion in June 2023. Additionally, services imports are expected to rise by 10.76 per cent to $17.29 billion in June 2024, compared to $15.61 billion in June 2023, accordingtotherelease.

According to June 2024 data

provided by the Ministry of Commerce and Industry, coffee, tobacco, iron ore, and electronic goods were the few commodities India estimated would significantly increaseitsexports.

Pulses,dyeingmaterials,machine tools, project goods, and silver are estimated to notice a significant increaseinimports.

According to government data, India is increasing its exports to countries like the United Kingdom, Bangladesh,Malaysia,andMexico.In addition to exports, India is also increasing its imports from the United Arab Emirates (UAE), Indonesia, Thailand, Taiwan, and Vietnam.

NEW DELHI: The Commerce Department has decided to take up withtheGSTCouncilandtheFinance Ministry the GST related problems faced by exporters, such as compliance issues, refunds and audits, to ensure speedy redressal of grievances,sourceshavesaid.

Exporters have been complaining about receiving show-cause notices fromGSTauthorities,eithersuomoto or based on audit objection, to pay GST on overseas bank charges, along with interest and penalty, despite the GST council agreeing that the Indian banksshouldpayit.

With the Red Sea crisis slowing down shipments, exporters also want more than the 90-days time allowed rightnowforEGMfilingformerchant exporters when procuring goods for exports at 0.1 per cent concessional GST.

“The Commerce Department has sought inputs from various export bodies on their GST related woes so that these could be collated, analysed

and presented before the GST Council and Finance Ministry for action,”asourcesaid.

Exporters’ body FIEO has also separately submitted to Finance Minister Nirmala Sitharaman the problems faced by the exporting community under the GST regime andsoughtsolutions.

On the notices being received by exporters for non-payment of GST on overseas bank charges, the letter pointed out that the matter was discussedintheGSTCouncilmeeting in June 2022 wherein it was decided that GST on such charges should be paid by the Indian bank as they are availing the services of the overseas bank.

“The recommendation of the Fitment Committee makes it very clear that IGST on such services has to be discharged by the service recipient for which recipient is entitled to ITC (input tax credit) that can be utilised to set off tax liability. ThedomesticbankscouldavailITCof

tax paid by them on reverse charge,” itsaid.

The GST Council agreed with the same and recommended accordingly, the letter added. FIEO asked the FM todirecttheCBICtosuitablyclarifyto the GST authorities so that the show cause notices/demand can be stopped.

Another issue faced by exporters, largely owing to the Red Sea crisis and lack of containers and shipping space, is not being able to meet the 90 days time period given for exports and EGM filling in cases where the merchant exporter procures the goods from a manufacturer at 0.1 percent concessionalGST.

“We request that the 90 days’ time periodmaybeextended,onmerits,by another 60-90 days by the jurisdictional authorities. This will help the exporters who, despite their best efforts, are failing to complete exports within the 90 days time limit,” theletterstated.

MUMBAI: The Directorate General of Shipping, India’s Maritime administration, has mandated the Indian Institute of Management Indore (IIM-Indore) to undertake an in-depth, comprehensive study on the ‘Age Norms and Other Qualitative Parameters’ for ships it introduced in 2023 which drew flak from the industry.

“Followingaseriesofconsultationswithkeyindustry stakeholders, it was decided that an independent, third-party agency should be engaged to undertake an in-depth study to evaluate the concerns and suggestions presented.IIM-Indorehasbeenselectedtocarryoutthis important task,” the DG Shipping said.

IIM-Indorehasbeenmandatedtoconductathorough policy analysis and the submissions made by industry stakeholders, evaluate the impact and implications of theagenormsorder,writeadetailedreportoutliningthe findings of the study, recommend policy measures along

Piyush

with a strategic plan for implementing the recommendations.

The 24 February 2023 order issued by the DG Shipping on ‘Age Norms and Other Qualitative Parameters with Respect to Vessels’ set an age limit of 25 years for oil tankers, bulk carriers, and general cargo vessels – both Indian registered and foreign flagged –calling at the country’s ports to load and unload cargo, triggering concerns among stakeholders. This led the administrationtopartlyamendtheorderon1July2023.

The age norms were designed to encourage a younger fleet to improve safety, meet global rules on ship emissions and protect the marine environment frompollutionduringmishaps.

However, following a pushback from the industry, the D G Shipping has decided to undertake a sweeping review of its order with a holistic approach, encompassingtheentiremaritimesector.

Minister Shri Piyush Goyal paid an official visit to Switzerland at the invitation of his Swiss counterpart Federal Councillor Mr.GuyParmelin.

During this highly successful and productive visit, Shri Goyal’s engagements included bilateral delegation level talks and lunch with Minister Parmelin. The two Ministers had a joint breakfast meeting with captainsofSwissandIndianindustriesonthesameday.

During the bilateral talks with Minister Parmelin, both sides acknowledged that TEPA provides an excellent framework for deepening of trade and investment partnership. A focused approach to creating an enabling environment would expedite realising the goals/targetsetunderTEPA.

The two Ministers had engaging and fruitful

discussions with prominent Swiss and Indian captains of industry over the breakfast meeting on 15 July. Hon’ble CIM encouraged Swiss companies to become a part of India’s growth story and invest in its growing and dynamic market. A 12-member strong Indian business delegationmountedbyCIIalsohadbusinessnetworking opportunitywiththeirSwisscounterparts.

Earlier, Commerce Minister received Chairman/CEOs of select Swiss industry with business and investment interests in India. He also had a productive engagement with members of Indian diaspora. Director General, WTO, Ms. Ngozi OkonjoIweala calledontheMinisteratZurich.

The key objectives of the visit were to discuss next steps for the implementation of the historic India-EFTA Trade and Economic Partnership Agreement (TEPA) which was signed on 10 March, 2024 in New Delhi and to identifywaysandmeansofrealisingtheambitioustarget of US$ 100 billion investment and creation of one million jobs in India by EFTA countries in next 15 years as providedforintheAgreement.

NEW DELHI: India’s Dedicated Freight Corridor, a special-purpose vehicle of the Indian Railways, is likely to be exempted from the purview of an 18 per cent GST, thereby eliminating the need to work out a new revenue modelorchangeinfreightrates.

The tax obligation was reportedly on track access charges – remittances paid for accessing the rail network–whichareafixedcostoftheDedicatedFreight CorridorCorporationofIndiaLtd(DFCCIL).

EstimatedremittancesunderthisheadwasRs.5,000 crore, which could have gone up subsequently as more tracksofthecorridorbecameoperational,sourcessaid.

On Friday (July 12), the indirect taxes board, CBIC, notified the Goods and Services Tax ( GST ) exemption onservicesprovidedbytheIndianRailwaystothepublic and the services provided by Special Purpose Vehicles (SPVs ) to the Railways. The exemption shall come into

forcefromJuly15,2024,onwards.

“Services provided by SPVs to Indian Railways –by allowing Indian Railways to use the infrastructure built and owned by them during the concession period against consideration- and services of maintenance supplied by Indian Railways to SPVs in relation to the said infrastructure built by the SPVs during the concession period against consideration, is said to be exempt from purview of GST, it was decided at a recent councilmeeting,”apartofthenotificationread.

“A simple interpretation of this would mean track accesscharges–whicharereceivedasremittancesfrom the Railways would be exempt from GST. So there need notbearequirementtocategorisesuchachargeundera separate head (for accounting purposes) or hike freight rates for users of the corridor,” a Railway official told requestinganonymity.