ABCC Arab-British Business Economic Bulletin Dec 25

After 1.13M+ views of our Egypt issue, we’re turning the spotlight on...

TALK ABOUT

JANUARY 2026 EDITION

INSIDE THE EDITION:

• UAE and UK Drive the Global Clean Energy Transition

• How Dubai and Abu Dhabi Are Redefining Global Finance with British Investors

• British Buyers and Emirati Developers Transforming Real Estate Between Dubai and London

• How UAE–UK Tech Partnerships Are Powering the Future

• Beyond the Horizon: UAE–UK Tourism Soars as Travel and Trade Flourish

WHY GET INVOLVED NOW?

Organisations have the opportunity to secure premium positions for advertising, feature articles, and case studies –ensuring maximum visibility when the edition launches in October.

DELIVERED BY

50TH ANNIVERSARY GALA DINNER

“Fifty years of building friendship through trade”

The Arab British Chamber of Commerce (ABCC) is honoured to mark its 50th Anniversary, five decades at the heart of fostering trade, investment, and collaboration between the United Kingdom and the Arab world.

We extend a cordial invitation to you to join us for this landmark occasion as we celebrate our golden anniversary.

This exclusive Golden Anniversary Gala Dinner will be hosted at the prestigious The Biltmore Mayfair, where we will be bringing together distinguished guests and longstanding friends from across our communities.

This elegant evening will unite leaders from business and government, senior diplomats and executives, high-net-worth individuals, innovators, consultants, media professionals, and public figures who have contributed to the Chamber’s achievements over the past five decades.

The evening will feature a very special Guest of Honour, whose leadership and impact have shaped international collaboration in remarkable ways. More details will be announced soon, stay tuned for details of an inspiring address you won’t want to miss.

We look forward to honouring the past, celebrating the present, and looking ahead to the future with our valued members and strategic partners.

Join us for this celebration of the work of our Chamber and of its mission of building friendship through trade.

We will be honoured by your presence. Dress Code | Dark Lounge Suit-Cocktail Dress Enquiries rana@abcc.org.uk

To Register, visit https://abcc.glueup.com/event/50th-anniversary-gala-dinner-158586/#tickets

Landing in the UAE: A Practical Roadmap for SMEs

The ABCC hosted an exclusive business roundtable with Umm Al Quwain Free Trade Zone Authority.

The Arab British Chamber of Commerce (ABCC) was delighted to host the Umm Al Quwain Free Trade Zone Authority (UAQ FTZ) for an exclusive business roundtable at our offices in London on Monday 10 November 2025.

The event titled Landing in the UAE – A Practical Roadmap for SMEs, was opened by Ms Rita Massoud, Interim Secretary General & CEO of the ABCC, who welcomed Mr Kevin Fernandes, Head of Value Added Services – UAQ Plus. She warmly thanked the UAQ FTZ for partnering with the ABCC on the event.

During the meeting, attendees, who were drawn from among the ABCC membership and beyond, were able to participate in an engaging discussion, followed by a Q&A and networking session. The main focus of the event was on opportunities for growth and partnership across the Arab region using the UAQ Free Trade Zone as the base. Mr Fernandes shared his valuable insights into the latest opportunities and looked at how UK-based enterprises can expand into the UAE and wider GCC region through the UAQ Free Trade Zone. He encouraged UK firms to join the more than 12,000 global companies which had

already chosen to do business in the free zone.

Mr Fernandes explained that Umm Al Quwain was conveniently located in the northern region of the UAE providing seamless connectivity to major emirates and transport hubs; as such, it was only 30 minutes from Dubai International Airport and just 20 minutes from Sharjah International Airport. In terms of sea transport, UAQ FTZ was only an hour away from the global Jebel Ali Port complex.

He went on to outline the main attractions of UAQ FTZ such as the range of business incentives that were available, the ease of the company setup process and the flexible packages that were tailormade to meet the needs of smaller and larger businesses.

Twenty-five year leases on plots of land suited for industrial units, offices, warehouses and showrooms were available, with prospects for expansion. There were flexible options for business licenses, Mr Fernandes explained, meaning that the requirements of most companies could easily be accommodated.

The free zone played host to successful companies operating in a huge number of sectors such as industrial, media, education, commercial trading, services, e-commerce and retail, among others.

Finally, Mr Fernandes said the current drive to attract UK firms to the UAQ FTZ aligned with the campaign, “Make it in the Emirates” which offered an open invitation to UK industrialists, investors, innovators and entrepreneurs to do business in the UAE.

Ms Massoud thanked Kevin Fernandes for his detailed presentation before she opened up the discussion for questions.

His remarks had awakened considerable interest among the UK executives present who raised various questions on aspects of the ease of doing business and the growth of opportunities in the UAE.

Drawing attention to the ABCC’s 50th anniversary year, Ms Massoud stressed that the ABCC remains committed to supporting collaboration and investment between the UK and the Arab world and to bringing the latest opportunities to the attention of its members.

ABCC Interim Secretary General & CEO, Ms Rita Massoud introduces Mr Kevin Fernandes, Head of Value Added Services – UAQ Plus, UAQ FTZ

Mr Kevin Fernandes, UAQ Plus.

Red Sea Luxury Locations Celebrated in Glitzy Exclusive Reception

The Arab British Chamber of Commerce, in partnership with The Red Sea and Marriott’s Luxury Red Sea properties — The St. Regis Red Sea Resort, Nujuma, a Ritz-Carlton Reserve, and The Red Sea EDITION — proudly hosted a glitzy exclusive networking reception at the Bvlgari Hotel, London, on the evening of 6 November.

The invitation-only event brought together diplomats, business leaders, investors and tourism industry experts to celebrate Saudi Arabia’s remarkable progress in the leisure, tourism, and hospitality sectors under its Vision 2030.

Mr Ahmad Darwish, Officer at Red Sea Global, set the tone for the evening by highlighting the importance of environmental sustainability and the empowerment of human capital as central pillars of the Red Sea’s transformative projects.

Following this, Ms Rita Massoud, MBA, FCIPD, Interim Secretary General & CEO of the ABCC, warmly welcomed all the distinguished guests, emphasizing the value of partnership and Arab-British collaboration in advancing shared goals. Mr Tony Coveney, Area General Manager, Marriott Red Sea Region, together with Ms Lana Ghawi Zananiri, Cluster Director of Business Development, Marriott Luxury Group, shared their inspiring perspectives on the Red Sea’s growing prominence as a global luxury destination which was helping to redefine the hospitality industry in Saudi Arabia.

Guests enjoyed a vibrant atmosphere and viewed an engaging video presentation showcasing the Red Sea’s breath-taking beauty, illustrating the location’s exceptional attractions. The evening represented a true celebration of innovation, sustainability, and partnership.

Ms Massoud remarked that the ABCC looked forward to strengthening UK–Saudi collaboration as the chamber marked its 50th anniversary and stressed its ongoing commitment to sustainable growth and excellence.

Ms Rita Massoud, ABCC Interim Secretary General & CEO.

Mr Ahmad Darwish, Officer at Red Sea Global (speaking) with Mr Tony Coveney, Area General Manager, Marriott Red Sea Region, together with Ms Lana Ghawi Zananiri, Cluster Director of Business Development, Marriott Luxury Group.

Empowering Women Entrepreneurs: A Greek Arab Exchange

ABCC Interim Secretary General & CEO, Ms Rita Massoud was delighted to join a panel discussion on 18 November 2025 with BHCC President Ms Anna Kalliani which sought to boost business connections between Greek, British, and Arab businesswomen.

The event formed part of a threeday visit to London by Greek women entrepreneurs from the BHCC organised by the Greek Embassy in London.

Speaking in the panel discussion, Ms Massoud stated that the Arab economies were currently undergoing major transformations enabling women to play their part in the development and growth of their economies.

“As women assume more high-level executive positions in business and across public life, there are greater opportunities for women-led companies

and global collaboration among women entrepreneurs.

“Events such as this one today provide a valuable platform for women to share their experiences and find common ground through networking,” she said, “the collaboration between women entrepreneurs remains an untapped resource”.

“I hope that this meeting is just the beginning of a dialogue that will open up new opportunities for productive engagement and cooperation between women in our different areas and regions” she stated.

Finally, Ms Massoud affirmed that the ABCC viewed collaboration between women entrepreneurs as a vital aspect of its mission of building closer business links.

The Business Mission of Greek Women Entrepreneurs was the first of its kind from Greece to the UK and coincided with International Women’s Entrepreneurship Day on 19 November.

The Greek Embassy expressed its gratitude to the ABCC alongside all panellists, speakers, and everyone who contributed to making the visit a great success.

ABCC Interim Secretary General & CEO, Ms Rita Massoud speaking with BHCC President Ms Anna Kalliani.

H E Yannis Tsaousis, Ambassador of Greece to the UK in discussion with Ms Massoud.

ABCC New Members

The ABCC welcomes our new members and looks forward to working with them in the coming year.

Globetrotters GB Ltd

Spire Insights

Formationlive LTD trading as Formation Global

Relm Interiors Ltd

BrandFull Ltd

Critical Metals Plc

Arab Entrepreneurs Board

Arab National Bank

ProLuxe Travel

Troika International Ltd

Shield Fire Safety & Security Ltd - GOLD

Alinea London Ltd

Al-Bilad Consulting & Solutions Company

OHeeBA

Aston Hub Ltd

ZKR Holdings Limited

Essex Industries Ltd

Algerian Chamber of Commerce & Industry (CACI)PLATINUM

Forsters LLP

Gulf Glass Factory LLC

London emerges as a global hub for the US$2.4tn Halal economy with new strategic partnerships and a media network launch at the first-ever London Halal Forum

• H.E. Mr Yousef H Khalawi, Secretary General of the Islamic Chamber of Commerce and Development (ICCD), addressing the delegates at the London Halal Forum 2025 opening ceremony

• Two-day Forum brings together exhibiting businesses, investors, and media at Excel London

• Major strategic partnerships announced between ICCD–Kenya and Halal Product Development Company–DinarStandard

• Palestinian Breakfast celebrates culture and commerce with remarks from the Palestinian Ambassador to the UK

• The Forum announces the soon-to be-launched Menara Global, a new communications network for 57 OIC member states

The inaugural London Halal Forum 2025, held on Thursday, 20th and Friday, 21st November 2025, concluded at Excel London after two days of trade discussions, investment meetings and cultural programming, marking a significant new platform for the global Halal economy in the UK. The event drew businesses, investors, and media representatives, with more than 1,500 in-person and virtual visitors, exhibitors from over ten countries, and official delegations including the Heads of Chambers of Commerce or their representatives from over 20 nations.

The programme featured 35 international speakers and was supported by over 20 regional and global sponsors and partners, positioning London as a growing gateway to a sector now valued at US$2.4 trillion, according to DinarStandard’s State of the Global Islamic Economy 2024/25.

Delegates from across Europe, the Middle East, Africa and Asia explored emerging trade routes, certification standards and investment opportunities in food, finance, travel, pharmaceuticals, technology and advisory services. The Forum also saw the announcement of two key crossborder partnerships: a new collaboration

between the Islamic Chamber of Commerce and Development (ICCD) and ICCD–Kenya, and a strategic agreement between the Halal Product Development Company (HPDC) and DinarStandard aimed at strengthening data-driven market access and innovation across the Halal economy. In total, the Forum facilitated five new strategic partnerships and unveiled more than five new initiatives designed to strengthen certification systems, investment flows and digital trust across Halal markets.

On day two, a “Taste of Palestine” breakfast took place in collaboration with Yaffa Palestinian Products. It marked the first time H.E. Dr Husam Zomlot had addressed a UK business audience since becoming Ambassador of the State of Palestine. The menu, sourced exclusively from Palestinian producers, was presented as both a cultural showcase and an economic statement about provenance and economic opportunity.

Addressing delegates, H.E. Dr Zomlot reflected on the significance of the occasion:

“This is the first time I have addressed a business community as the Ambassador of Palestine, and it could not have been a more meaningful setting. To see Palestinian products presented with such dignity and sourced exclusively from Palestinian businesses is a reminder that our economic story is one of resilience, talent and opportunity. The global Halal community has an important role to play in amplifying that story.”

Speaking during the session, H.E. Mr Yousef H Khalawi, Secretary General of the Islamic Chamber of Commerce and Development (ICCD), said:

“We believe that the heart of the Halal economy is how you do business. It is not just about the product or service itself, but the ethics of how you have produced that product. Ethical practice, cultural understanding and narrative power are central to shaping the future of the Halal economy.”

On the second day, delegates attended the Halal Echo Afternoon Tea, a roundtable bringing together journalists, PR practitioners, content creators and media professionals from across the UK and the wider OIC diaspora. The session introduced Menara Global, a new communications network dedicated to elevating the voice, capability and economic influence of the 57 OIC member states ahead of its full 2026 launch.

The day also included two Masterclass sessions exploring innovation in Halal, investment strategy, technology-led trust and the future of global Halal integrity.

H.E. Mr Yousef H Khalawi, Secretary General of the Islamic Chamber of Commerce and Development (ICCD), addressing the delegates at the London Halal Forum 2025 opening ceremony

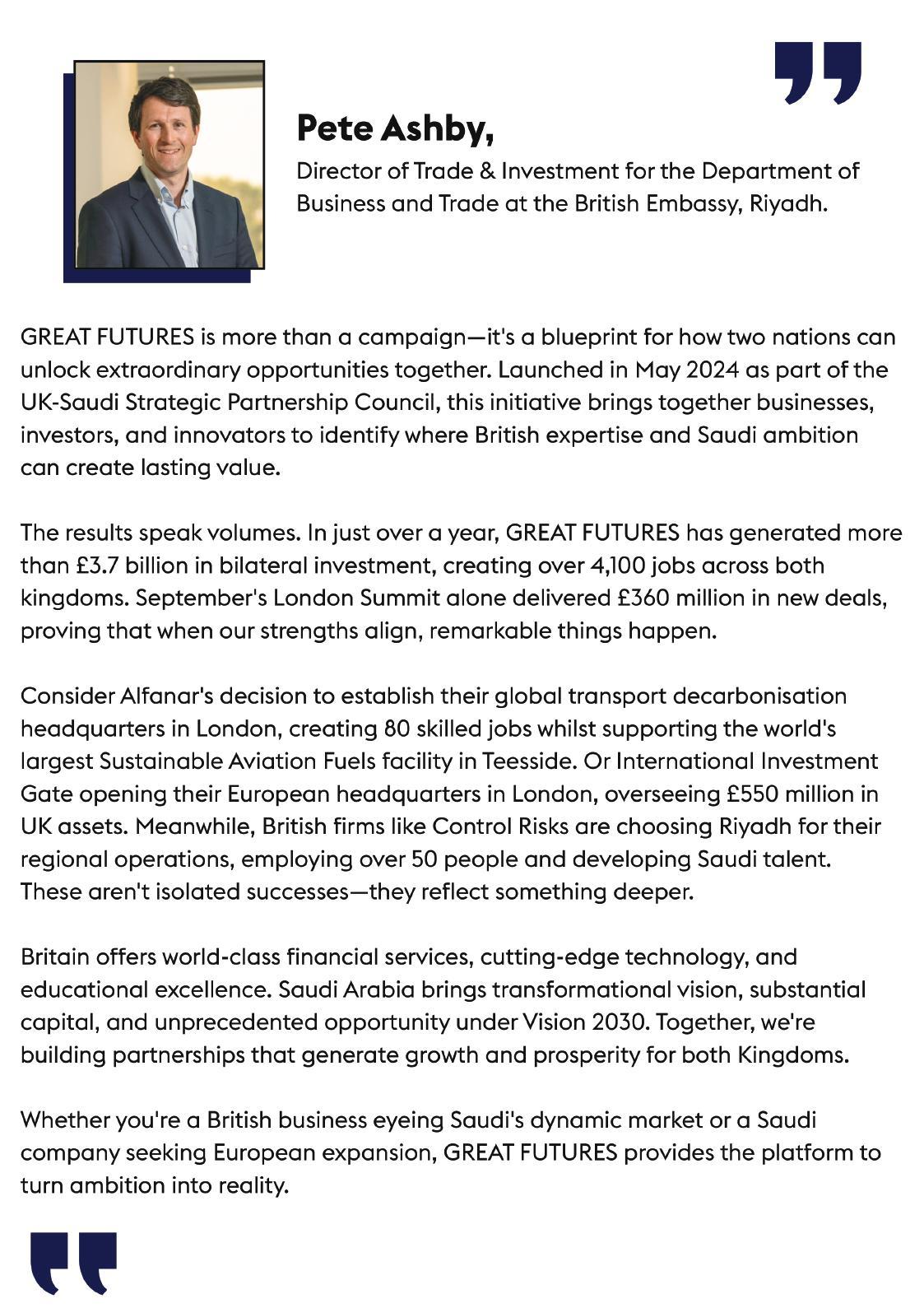

£ 3 . 7 b n £ 3 . 7 b n worth of deals and 4 1 0 0 4 1 0 0 over jobs created between the UK and Saudi Arabia over the last year.

£ 3 . 7 b n £ 3 . 7 b n worth of deals and 4 1 0 0 4 1 0 0 over jobs created between the UK and Saudi Arabia over the last year.

Kuwait Country Profile

KUWAIT

Country Name: State of Kuwait

Capital: Kuwait City

Total area: 17,818 sq km

Border countries: Iraq and Saudi Arabia

Coastline: 499 km

Population: 5.02 million

Population is mostly concentrated in and around Kuwait City and on Bubiyan Island. It is an entirely urban population.

Natural resources: oil, fish, shrimp and natural gas, minerals and others such as gypsum, salt, sulfer, cement and clay; growing agricultural sector and renewables.

Exports: crude and refined petroleum, hydrocarbons, natural gas and acyclic alcohols

Imports: cars, gold, jewellery, garments and packaged medicines.

Kuwait, officially named the State of Kuwait, is situated in the northern edge of Eastern Arabia at the tip of the Persian Gulf, bordering Iraq to the north and Saudi Arabia to the south. The country possesses a coastline of approximately 500 km.

The population of Kuwait reached 5,026,078 by mid-2025, according to UN data. Over 90 percent of the population resides in urban areas in and around Kuwait City, the country’s capital and largest city. In response to the fact that Kuwait possesses limited natural freshwater

resources, the country has developed some of world’s largest and most sophisticated desalination facilities to provide nearly all of its national water needs. The country is divided into 6 governorates.

Kuwait is a small, high-income, oilbased economy with a significant renewable energy. It a regional finance and investment leader and maintains the oldest sovereign wealth fund in the MENA. As it works to diversify its economy, Kuwait has an emerging space and tourism industries.

Kuwait’s main industries are oil, petrochemicals, cement, shipbuilding and repair, water desalination, food processing and construction materials.

According to the IMF, Kuwait’s real GDP was projected to expand by 2.6% after a 2.8% contraction in 2024, as OPEC+ production cuts eased and non-oil activity continues to recover, supported by consumer demand, lower interest rates, and renewed government project execution. The country’s inflation was projected to remain at 2.6% in 2025, largely driven by declining imported food prices and easing demand pressures. Non-oil GDP is forecast to grow also by 2.6%, with support from credit growth, a rebound in domestic demand, and largescale development projects.

Kuwait’s strategic development plan is Vision 2035, launched in 2017, outlines the steps to transform the country into a globally competitive economy by 2035. There are several aspects towards transforming Kuwait into a regional, financial, commercial, cultural and institutional centre. Successful implementation of the national development plan will ensure that Kuwait secures for itself a prosperous and sustainable future.

One key measure consists of establishing a special international economic zone with its own laws

and regulations designed to attract investment. Its independent institutional structure is conducive to attracting global investments with high added value and encouraging innovation while ensuring transparency in the management of financial resources.

Kuwait is being transformed into an attractive environment for investment led by the private sector through an easy-to-do business environment, fair competition and streamlined government procedures with a trend towards innovation and advanced technology across various fields.

Kuwait Vision 2035

Kuwait Vision 2035 is seeking to transform Kuwait into a global financial and trade hub, with the private sector taking a lead in the economy, the foundations will be underpinned by strong governance, clear values and advanced infrastructure for achieving a balanced and competitive growth.

Kuwait is targeting value-added FDI in order to achieve its key objectives and contribute towards its strategic development goals, economic diversification and the promotion of the leading role of the private sector in the economy.

The country’s priorities consist of transforming and adopting new technology and know-how, creating worthwhile jobs for Kuwaiti nationals, providing quality training and education for its people, men and women, as well as supporting local suppliers and producers to strengthen local content in products and projects.

Kuwait is witnessing a growth in its nonoil sector which is a positive development in terms of strengthening its economic diversification and sustainability. The National Bank of Kuwait (NBK) has reported that the non-oil sector is forecast to see an acceleration in growth to 3.2% in 2026 from 2.2% in 2025. Some of this is attributed to a pick-up in oil refining output, which has underperformed so far in 2025, the NBK said, but it is also due to cyclical forces such as lower interest rates, improved business optimism, solid order books and a potential new capex cycle. Some of this is already visible in the performance of various gauges of non-oil activity such as the PMI, credit growth and real estate activity, the bank observes.

The NBK concludes that the adoption of reforms will further stimulate growth and ensure sustainable development for Kuwait. In the longer term, the bank argues, unlocking faster rates of non-oil economic growth will require a range of structural reforms (such as to the business climate, labour market and public sector efficiency) and higher rates of investment – both areas where Kuwait has lagged its Gulf peers. The government formed in May 2024 has been more active on laws and economic reforms (especially fiscal policy) than its predecessors, though presentation of

its multi-year work agenda had been delayed in April 2025, during major global market volatility in the wake of the introduction of US tariffs.

Key Infrastructure Projects

Building major infrastructure is an important ambition mapped out in Vision 2035 and consists of several notable mega projects.

Tallest Tower and Silk City

The Burj Mubarak Al Kabir is a planned skyscraper set to be 1001 metres tall (3,284 feet) making it the world’s tallest tower. The project is to be at the centre of a new city, Madinat Al-Hareer (also known as Silk City) and is expected to take 25 years to complete. Reports suggest that the Silk City project will reportedly cover 250 square kilometres and consist of four distinct quarters, accommodating around 700,000 people and creating 430,000 jobs.

Bubiyan Island

This is the largest island in the Kuwait coastal island chain and has an area of 863 km2.

The Mubarak Al Kabeer Port under construction on the island spans a vast 1,161-hectare expanse and will consist of 24 berths with an impressive capacity of 8.1 million containers.

Based on a feasibility study the projected cost for the port infrastructure has been estimated at $3.2 billion (KD990 million), to be completed through nine distinct executive contracts. Once operational, the Mubarak Al Kabeer Port will help position Kuwait as a key commercial hub and transit point for regional trade and transshipment.

Terminal 2

Kuwait International Airport T2, designed by Foster and Partners, represents a vital component of Vision 2035, aimed at modernising the country’s transportation infrastructure.

South Al-Mutlaa City

This is the largest urban development plan in Kuwait’s history and aims to house around 400,000 people on completion.

South Sabah Al Ahmad Urban Development

The South Sabah Al Ahmad Masterplan is a comprehensive urban development project situated to the south of Kuwait City. The initiative envisions the creation of a modern and sustainable urban community that addresses the evolving needs of Kuwaiti citizens while promoting economic growth and environmental sustainability.

Sovereign Wealth Fund

The Kuwait Investment Authority, the country’s sovereign wealth fund and the oldest such fund in the Middle East, witnessed a significant increase in its assets in 2024 nearing the $1 trillion mark. According to data from the Sovereign Wealth Fund Institute published in July 2024, the fund’s assets rose by approximately $56.55 billion since March 2024, and by about $177 billion over the year. Assets stood at around $980 billion, up from $923.45 billion in March 2024. This marked a substantial increase from July 2023, when the assets were valued at $803 billion.

Kuwait’s fund maintained its position as the fifth largest sovereign wealth fund globally putting it ahead of the Saudi Public Investment Fund which was in sixth place, the Qatar Investment Authority in eighth, and the UAE’s Mubadala Fund in twelfth place.

Telecoms

Kuwait’s telecom infrastructure is well developed, with a focus on mobile infrastructure and services; the telecom sector is important to the country’s economy, and becoming more important as the economy moves away from dependence on oil and gas to one which is increasingly knowledge-based and focused on ICT sector. Investment has been made in 5G networks, which support and promote the growth of data traffic, which is a catalyst for revenue generation.

Kuwait’s mobile sector shows considerable progress but fixed broadband low; the government has stepped up efforts to build up fixed broadband networks, and ultimately this sector offers a potential future growth opportunity. The improvements to fixed broadband infrastructure are helping to develop sectors such as e-commerce, along with smart infrastructure and tech start-ups.

Looking ahead, Kuwait offers great potential for growth in key sectors #especially utilities, housing, transport, tourism and entertainment.

Digital Future

Digital transformation, alongside Kuwaitization, and a focus on environmental, social, and governance (ESG) issues are now seen as central to building a sustainable and inclusive economy. Kuwait is driving forward with efforts to establish a smart, data-driven government and secure, sustainable digital ecosystem that supports innovation and enhances the quality of life and services.

A recent national agreement with Google Cloud was hailed as marking a strategic milestone in building the country’s national digital infrastructure and a qualitative leap in the management and operation of government services. Speaking at a Kuwait Cloud Day event, Kuwait’s Minister for Communications, Omar Al-Omar highlighted that the partnership supported Kuwait’s transition towards a digital economy driven by innovation and artificial intelligence, enabling the development of future government applications and services that leverage advanced data analysis and smart decision-making.

In all sectors, the Kuwaiti private sector and the country’s public institutions are moving towards integrating advanced technologies amid efforts to improve efficiency, raise productivity and service delivery.

Department Services

With over 50 years of delivering accurate and professional Arabic English translations, the Arab-British Chamber of Commerce ensures your business, legal and personal documents are handled with expertise.

FISCAL POLICY, SOVEREIGN WEALTH, AND ECONOMIC RESILIENCE: KUWAIT’S NEXT BIG TEST

A formidable buffer, a narrowing margin

Kuwait’s public finances are anchored by one of the world’s most consequential sovereign investors, the Kuwait Investment Authority (KIA). Through the Future Generations Fund (FGF) and the General Reserve Fund (GRF), KIA underwrites macro-stability, intergenerational equity and, when needed, short-term liquidity. Independent trackers estimate KIA’s assets at roughly the trillion-dollar mark, placing it among the top tier of global sovereign wealth funds. That cushion is real.

Yet the budget math is getting tougher as oil revenues swing with OPEC+ production and prices, and as current spending— especially the wage bill and subsidies— absorbs a growing share of outlays. The policy question for the coming five years is whether Kuwait can convert that sovereign strength into a durable fiscal framework that smooths cycles, protects savings and accelerates diversification.

The budget cycle: from windfalls to widening gaps

The fiscal story of the past two years is a familiar hydrocarbon cycle. Lower oil prices and production curtailed revenues, tipping the budget back into deficit after a brief surplus. The IMF’s 2024 Article IV notes a swing from an 11.7% of GDP surplus in FY2022/23 to a 3.1% deficit in FY2023/24, with the gap expected to widen further in FY2024/25 as oil receipts ease. The composition of spending matters as much as the headline balance. Current expenditures rose sharply, with the public sector wage bill alone accounting for around 5.7% of GDP and subsidies for about 3.4%. Those rigid items leave limited room for capex precisely when Kuwait needs to invest in power capacity, digital infrastructure and industrial diversification. The finance ministry’s FY2024/25 draft also projected

a sizeable nominal deficit, underscoring the need to pair growth initiatives with a credible consolidation path.

The role—and limits—of the sovereign wealth engine

Kuwait’s two-pool structure serves distinct purposes. The GRF is the government’s treasury account for day-to-day financing and shock absorption; the FGF is the long-term savings vehicle, fed historically by mandatory transfers from oil income. During stress episodes, authorities have drawn on the GRF and, when parliamentary debt laws stalled, the financing constraint tightened. That experience sharpened the debate over whether and how to tap the FGF or use it as collateral for market borrowing. The macro case for preserving the FGF is strong: it stabilises expectations, supports Kuwait’s credit profile and compounds returns for future generations. The practical solution is to rebuild the GRF’s liquidity buffer when oil prices are favourable and to maintain regular market access via a medium-term debt management strategy—rather than episodic reliance on ad hoc transfers. With global rates still elevated, predictability in issuance, maturities and investor communications will keep borrowing costs contained without undermining KIA’s longterm mandate.

Reform signals: taxes, tariffs and the investment climate

Kuwait has moved on several fronts that can improve fiscal resilience without sacrificing competitiveness. Most notably, it implemented the OECD Pillar Two 15% domestic minimum top-up tax (DMTT) for large multinational groups from financial years beginning 1 January 2025. In practice, Pillar Two broadens the non-oil revenue base while aligning Kuwait with peers in the region. On the spending side, the government has begun repricing selected public service fees and is reviewing subsidy frameworks to better target support and curb waste. Both trends point in the right direction, but their credibility will depend on transparent implementation and consistent exemptions policy.

On the growth side of the ledger, Kuwait’s investment framework remains a potential differentiator. Under the 2013 Foreign Direct Investment Law, KDIPA can approve up to 100% foreign ownership in qualifying sectors and offer incentives, which helps attract know-how and diversify away from public-sector-led employment. Reducing administrative friction around licensing, land allocation and utilities connection would amplify the impact of these investor-friendly rules and support the private sector’s share of GDP.

Wages, subsidies and the politics of adjustment

The structural challenge is clear: a large share of nationals work in the public sector, and compensation plus generalized subsidies consume a significant portion of the budget. The IMF’s recent assessments quantify this weight and recommend a calibrated mix of civil service reform, targeted social protection, and a multi-year mediumterm fiscal framework. International experience shows that redesigning subsidies—especially for fuel, electricity and water—can be pro-poor and progrowth if it is staged, well-communicated and paired with direct cash transfers to vulnerable households. On employment, right-sizing the public wage bill cannot mean abrupt retrenchment. Rather, Kuwait can phase in hiring controls, link pay progression to performance, and build stronger pipelines from education to private-sector roles, particularly in logistics, finance, healthcare, and cleanenergy services identified under Vision 2035.

KIA’s capital as a catalyst—not a crutch The temptation in any downturn is to let the sovereign wealth fund do the heavy lifting. Used judiciously, KIA can catalyse transformation without diluting savings. Three avenues stand out. First, co-investment: expand the project pipeline of bankable PPPs in power, water, digital and logistics, with KIA anchoring alongside private sponsors to crowd in capital while preserving market discipline. Second, strategic funds: create thematic vehicles—SME growth, venture and climate infrastructure— where KIA’s participation de-risks early stages and accelerates scale. Third, governance spillovers: continue to embed global best practice—IFRS-aligned reporting, transparent mandates, and risk budgeting—so that KIA’s standards permeate state-owned enterprises and the broader investment ecosystem. The aim is to use sovereign balance sheet strength to unlock productivity, not to monetise assets to plug recurrent gaps.

External anchors: ratings, rules and trade

Fiscal frameworks are more credible when they are externally anchored. Kuwait’s rating history shows how liquidity frictions—not solvency—can trigger downgrades when domestic borrowing laws stall. Formalising a debt ceiling, setting a non-oil primary balance target, and publishing a rolling five-year fiscal plan would reassure markets and help ratings recover as reforms take hold.

On the regulatory side, alignment with global tax rules via Pillar Two reduces profit-shifting risks and signals that Kuwait is serious about modernising its revenue regime. The proposed UK-GCC free trade agreement, if concluded, could further lock in rules on services, digital trade and investment protection—useful for Kuwait’s aspiration to be a regional financial and logistics hub. For British corporates, clearer fiscal rules, predictable tariffs and KDIPA pathways will make Kuwait a more bankable play in the Gulf.

Case study lens: when policy clarity moves capital

Recent episodes illustrate the cost of ambiguity and the payoff from clarity. When draft debt laws languished in earlier years, the state leaned heavily on the GRF, tightening domestic liquidity and unsettling investors. Conversely, where Kuwait has spelled out frameworks—such as the DMTT start-date and scope— advisers, lenders and multinational groups have quickly recalibrated structures, and investment committees have treated Kuwait in line with regional peers. The same dynamic can apply to subsidy reform and PPPs: publish timetables, consult widely, and execute to plan. Predictability lowers risk premia and widens the pool of sponsors willing to bid.

A pragmatic fiscal roadmap

A credible path forward rests on five mutually reinforcing steps. First, adopt a medium-term fiscal framework anchored on a non-oil primary balance, with rolling caps on current spending growth and legally protected transfers to the FGF. Second, rebuild GRF liquidity buffers in up-cycles and restore regular market issuance to smooth cash flows. Third, stage subsidy reform with compensatory cash transfers, and channel the savings into targeted capex with high multipliers. Fourth, professionalise workforce policy in the public sector while removing bottlenecks for private employers— labour mobility, commercial courts, contract enforcement. Fifth, leverage KIA as a catalytic, not compensatory, investor in PPPs and productivity-enhancing sectors. None of this requires abandoning Kuwait’s social contract; it requires updating it for a more volatile oil world.

Outlook: resilience by design

Kuwait has the means to engineer resilience by design. It begins with acknowledging that oil windfalls will not always bail out the budget and that the sovereign fund’s primary mission is to protect the future, not finance the

present. By pairing tax and tariff reforms with spending discipline and progrowth investment, Kuwait can shrink the amplitude of its cycles, safeguard intergenerational wealth and create a private sector that absorbs talent outside government payrolls. KIA’s scale is an advantage few countries enjoy. Used wisely, it can be the flywheel that accelerates diversification and raises productivity—exactly the conditions under which fiscal sustainability becomes more than a slogan and economic resilience more than a hope.

References

IMF – Kuwait: 2024 Article IV Consultation – Press Release; Staff Report (wage bill and subsidies shares; fiscal balance): https://www.imf.org/en/Publications/CR/Issues/2024/12/07/ Kuwait-2024-Article-IV-Consultation-Press-Release-StaffReport-and-Statement-by-the-559194

IMF – Staff Concluding Statement of the 2024 Article IV Mission to Kuwait (fiscal swing; composition of spending): https://www.imf.org/en/News/Articles/2024/10/10/mcs101024-kuwait-staff-concluding-statement-of-the-2024-aivmission

Reuters – Kuwait 2024–25 draft budget sees $19.15 bln deficit –finance ministry (headline deficit and revenues): https://www.reuters.com/world/middle-east/kuwait2024-25-draft-budget-sees-1915-bln-deficit-financeministry-2024-01-30/

Reuters – Kuwait finance minister sees boost in projects, diversification under parliament suspension (oil share of revenues; FY2024/25 deficit outcome; reform context): https://www.reuters.com/world/middle-east/kuwaitfinance-minister-sees-boost-projects-diversification-underparliament-2025-09-03/

Global SWF – KIA (Kuwait) – Fund Profile (AUM scale; GRF/FGF structure overview): https://globalswf.com/fund/KIA

Global SWF – Ranking – SWFs and PPFs (comparative scale, methodology): https://globalswf.com/ranking

Reuters – Kuwait asks parliament to approve debt law to help cover deficit (use of GRF; liquidity constraints context): https://www.reuters.com/article/business/kuwait-asksparliament-to-approve-debt-law-to-help-cover-deficitlawmaker-idUSKCN24D0L9/

Moody’s via Reuters – Moody’s downgrades Kuwait on liquidity squeeze, weak governance (ratings sensitivity to liquidity and governance): https://www.reuters.com/article/world/middle-east/moodysdowngrades-kuwait-on-liquidity-squeeze-weak-governanceidUSKCN26E0ZV/

Kuwait Direct Investment Promotion Authority – Law No. 116 of 2013 (FDI Law) (KDIPA framework; up to 100% foreign ownership): https://kdipa.gov.kw/wp-content/uploads/2021/08/ law1162013.pdf

U.S. Department of State – 2025 Investment Climate Statement: Kuwait (KDIPA practice; foreign ownership context): https://www.state.gov/reports/2025-investment-climatestatements/kuwait

Reuters – Kuwait to impose 15% minimum top-up tax on multinational enterprises (Pillar Two implementation timing): https://www.reuters.com/world/middle-east/kuwaitimpose-15-minimum-top-up-tax-multinationalenterprises-2024-12-30/

KPMG – Kuwait: Legislation implementing Pillar Two global minimum tax rules (Decree Law No. 157/2024 summary): https://kpmg.com/us/en/taxnewsflash/news/2025/01/tnfkuwait-legislation-implementing-pillar-two-global-minimumtax-rules.html

PwC – Kuwait implements Pillar Two from 1 January 2025 (scope and mechanics of DMTT): https://www.pwc.com/m1/en/services/tax/me-tax-legalnews/2025/kuwait-implements-pillar-two.html

Economic Diversification and Kuwait Vision 2035

An Oil-Dependent Economy at a Crossroads

Kuwait, long one of the world’s wealthiest oil exporters, is facing a familiar Gulf challenge: how to wean its economy off oil dependency. With petroleum still providing nearly 90% of government revenue, Kuwait’s fortunes rise and fall with global oil prices.

This heavy reliance has sustained a generous welfare state but left the nation vulnerable to market swings. Now, under the banner of New Kuwait Vision 2035, the country is striving to chart a new course – one that transforms Kuwait into a regional financial and trade hub and builds a diversified, sustainable economy for the post-oil era.

For decades, oil has dominated Kuwait’s economy, accounting for roughly half of GDP and the vast majority of export earnings and state income. This has funded high living standards but also stalled incentives for reform. Unlike some of its Gulf neighbours

that accelerated diversification in the early 2000s, Kuwait was slower out of the gate. Political gridlock between the elected parliament and the government often hindered major economic changes, and a sprawling public sector soaked up much of the labour force. The result is an economy where most Kuwaiti citizens hold government jobs, while the private sector relies heavily on expatriate workers. Such a model is widely seen as unsustainable in the long term. By the mid-2010s, recognition grew that Kuwait needed to future-proof its economy – not only by diversifying sources of revenue but also by empowering the private sector and reducing the state’s role in business.

Kuwait Vision 2035: A Blueprint for Diversification

Launched in 2017, Kuwait Vision 2035 (branded as “New Kuwait”) is the government’s ambitious roadmap to transform the country over the coming decade. At its core is the goal of reducing Kuwait’s over-reliance on hydrocarbons. The Vision aims to reposition Kuwait as a leading financial and commercial centre in the region, leveraging its strategic location and wealth to attract investment. Key pillars of the plan focus on developing worldclass infrastructure, fostering new industries, and improving government efficiency.

Economy & Development

CONTINUED FROM PAGE 23...

By 2035, Kuwait intends to have a robust non-oil economy driven by sectors such as finance, logistics, tourism, healthcare, and education.

In practical terms, this means investing oil revenues today into building the backbone of a diversified economy tomorrow – from new ports and highways to hospitals, universities, and digital infrastructure. The government has identified hundreds of projects and initiatives under Vision 2035. For example, the flagship Madinat al-Hareer (“Silk City”) is envisioned as a new metropolis in the north, complete with an iconic 1,001-metre skyscraper and a special economic zone to attract global businesses and tourists. Another major initiative, the South Saad Al Abdullah New City, is planned as a “smart city” for 400,000 residents, integrating advanced technologies and AI to create a model sustainable urban community. Significant undertakings like the recently completed Sheikh Jaber Al-Ahmad Causeway – one of the world’s longest sea bridges –and the ongoing expansion of Kuwait International Airport are set to improve connectivity and logistics capacity. These projects signal Kuwait’s determination to lay the groundwork for a future less dependent on oil.

Investing Beyond Oil: New Sectors and Infrastructure

One of the central strategies of Kuwait’s diversification drive is to grow its nonoil sectors through targeted investment and modernization. Financial services are a top priority: Kuwait is bolstering its banking and finance industry to become a regional financial centre, capitalizing on regulatory reforms and the deep capital reserves of its sovereign wealth fund. Likewise, logistics and trade are getting a boost – the country is expanding port facilities and free trade zones to establish itself as a commercial transit hub between Asia and the Middle East. In tourism and entertainment, traditionally underdeveloped in Kuwait, authorities are launching initiatives to promote cultural tourism, leisure projects, and events that can draw visitors and create jobs. The government’s tourism strategy ties into Vision 2035’s goal of turning Kuwait into not just a financial and business centre but also a cultural hub in the Gulf.

Healthcare and education are also in the spotlight. Billions of dollars are being channeled into new hospitals, research centres, schools and training programmes. These investments not only improve quality of life for citizens but also seed new industries – such as medical services and

education technology – while developing the human capital needed for a competitive economy. Notably, Kuwait is embracing technology and innovation across all these sectors. The Vision 2035 blueprint aligns closely with the digital transformation sweeping the globe. Post-pandemic, Kuwait accelerated efforts to digitise government services and encourage tech startups. From fintech solutions in banking to smart grids in energy and e-learning platforms in education, emerging technologies are seen as key enablers of growth. Ambitious targets have been set as well, such as generating 15% of Kuwait’s energy from renewable sources by 2035 – a move that could spur a homegrown clean-energy industry while freeing up more oil for export. All these efforts reflect a broader shift: Kuwait is attempting to reimagine itself from an oil exporter into a knowledgedriven, service-oriented economy.

Reforms to Attract Investment and Expertise

Economic diversification on this scale requires enormous capital and expertise, and Kuwait is keenly aware it must compete for foreign investment. To that end, the government has undertaken a series of reforms to improve the business climate and open up the economy. The Kuwait Direct Investment Promotion Authority (KDIPA) was established to facilitate foreign projects, and laws have been passed allowing up to 100% foreign ownership in many sectors. Generous incentives – from tax holidays of up to ten years to eased licensing and visa regulations – are on offer for international companies willing to invest in Kuwait’s non-oil industries. These pro-investment policies have begun to pay off: in recent years Kuwait attracted over $3 billion of foreign direct investment into sectors like information technology, healthcare, renewable energy and logistics. The country’s efforts to cut red tape haven’t gone unnoticed; the World Bank at one point ranked Kuwait among the top ten global improvers in ease of doing business, reflecting strides in simplifying permits, streamlining customs, and strengthening legal protections for investors.

International partnerships are also a cornerstone of Vision 2035. Public-private partnerships (PPPs) are being used to fund and operate big infrastructure projects, inviting private capital and know-how into traditionally state-run domains. Kuwait has tapped foreign expertise through joint ventures in everything from port management to healthcare facilities. Longstanding allies such as the United Kingdom have played an active role, with British engineering firms involved in the new airport terminal construction and British technology consultants advising on

telecommunications upgrades. In fact, Kuwait and the UK have deepened their commercial ties via initiatives like the Kuwait-British Business Centre and a Joint Steering Group that align British investors with Kuwait’s development opportunities. Such collaborations not only bring in investment but also help transfer skills and global best practices into the local economy. Furthermore, Kuwait is aligning its policies with international standards – for example, adopting the OECD’s global minimum corporate tax in 2025 to enhance fiscal transparency and investor confidence. As Kuwait looks outward for partners, the ongoing negotiations for a UK-GCC free trade agreement hold promise to further streamline trade and knowledge exchange in areas like digital security and professional mobility. All told, these steps aim to signal that Kuwait is “open for business” like never before – an essential message if it is to become the diversified trade hub it envisions.

Challenges on the Road to “New Kuwait”

Despite the bold vision and considerable wealth at its disposal, Kuwait faces significant obstacles in turning its plans into reality. Bureaucracy remains a chief concern: a slow-moving, complex administrative process has delayed many projects and frustrated investors. Recent reports revealed that only a small fraction of the development budget was actually executed in the first half of the current fiscal year – barely 10% of allocated funds – with just 5 out of 130 planned projects completed in that period. This shortfall highlights implementation bottlenecks that could undermine the Vision 2035 timeline. Administrative inefficiency, overlapping

mandates, and frequent political tussles have all contributed to these delays. Indeed, political instability has been another stumbling block. Over the past two decades, repeated showdowns between Kuwait’s parliament and cabinet led to ministerial reshuffles, dissolutions of parliament, and policy paralysis, which in turn stalled the reform momentum and slowed infrastructure progress. In a dramatic move aimed at breaking the deadlock, Kuwait’s Emir in 2023 temporarily suspended the National Assembly, allowing the government to push ahead with economic measures and projects without legislative gridlock. While this step was controversial, officials argue it has injected muchneeded agility into decision-making and helped accelerate some long-pending development plans.

Another structural challenge is the dominant role of the public sector. Kuwait’s generous public employment and subsidy policies, while popular, have long discouraged entrepreneurship and private initiative. Convincing more Kuwaitis to seek careers in the private sector – and equipping them with the skills to thrive there – is a social shift that will take time. Likewise, regulatory reforms must overcome resistance from entrenched interests that benefited from the status quo. Diversification also doesn’t happen overnight; new industries need talent, infrastructure, and patience to grow. Kuwait must nurture an ecosystem for business and innovation, which includes strengthening legal frameworks, improving governance, and expanding access to financing to support startups and SMEs. The government’s recent moves to impose fiscal discipline (such as reviewing

subsidies and considering new taxes) show it is aware of the need for long-term sustainability, but such measures can face public pushback. In short, Kuwait’s journey to a diversified economy is a race against time – to implement reforms faster than external pressures (like another oil price slump or regional competition) can derail its progress.

Conclusion: Towards a Resilient Kuwaiti Economy

With 2035 on the horizon, Kuwait stands at a pivotal juncture. The Vision 2035 agenda lays out a compelling picture of what the future could hold: gleaming cities powered by innovation, a thriving private sector creating jobs for a young population, and an economy buffered from oil shocks by multiple streams of income. If successful, Kuwait would not only safeguard its own prosperity but also emerge as a dynamic hub in the Gulf, connecting markets and cultures. Achieving this vision will require unwavering commitment – steady investments, policy continuity, and a willingness to break from old ways of doing business. The progress so far has been mixed: foundational projects are underway and reforms have been enacted, yet execution has lagged and key diversification metrics still have far to go. Nevertheless, Kuwait’s advantages are substantial. It boasts one of the world’s largest sovereign wealth funds to finance its dreams, a strategic geographic location, and a well-educated, ambitious citizenry eager for opportunity. These strengths, coupled with lessons learned from peers and support from partners like the UK, give Kuwait the tools to overcome its challenges.

Economy & Development

In the coming years, the real test will be translating plans into tangible outcomes – new industries contributing a larger share of GDP, private enterprises flourishing, and a governance model that supports rapid economic adaptation. The road may be long and occasionally bumpy, but the destination of a diversified, resilient economy is one that Kuwait cannot afford to miss. Vision 2035 has set the course; now Kuwait must navigate it with determination, innovation and inclusive growth at the forefront. The result, if realised, will be a “New Kuwait” that honours its heritage as an oil leader while securing a sustainable future beyond oil.

Delta International (DITRC) – A Complete Guide on What is Kuwait Vision 2035: https://www.ditrc.com/a-complete-guide-on-what-is-kuwaitvision-2035/

Reuters – Kuwait finance minister sees boost in projects, diversification under parliament suspension (3 Sept 2025): https://www.reuters.com/world/middle-east/kuwaitfinance-minister-sees-boost-projects-diversification-underparliament-2025-09-03/

Emirates NBD Research – Kuwait Outlook 2024: https://www.emiratesnbdresearch.com/en/articles/kuwaitoutlook-2024

BusinessCloud – UK tech firms must forge stronger links with Kuwait (17 June 2025): https://businesscloud.co.uk/news/uk-tech-firms-must-forgestronger-links-with-kuwait/

First Forum / The Business Year 2020 – Raed J. Bukhamseen, A shared vision of progress: https://firstforum.org/wp-content/uploads/2021/05/ Report_15782.pdf

The Sycamore Institute – Building Tomorrow: Kuwait’s Path to 2035 (31 March 2023): https://www.sycamoreinstitute.org/post/building-tomorrowkuwait-s-path-to-2035

Economy & Labour Market

LABOUR MARKET AND HUMAN CAPITAL DEVELOPMENT IN KUWAIT: Turning Kuwaitisation into Competitiveness

A workforce built on expatriate labour—and a policy pivot

Kuwait’s labour market has long been defined by a structural split: expatriates make up the overwhelming majority of the workforce, while most Kuwaiti nationals work in the public sector. Recent official and media estimates place expatriates at roughly 70% of the total population and an even higher share of the active workforce, while more than four out of five Kuwaiti citizens hold government jobs. That equilibrium delivered decades of administrative stability but left the private sector reliant on foreign labour and national employment disproportionately concentrated in ministries and state entities. As diversification gathers pace under Vision 2035, Kuwait is accelerating “Kuwaitisation” policies to raise national participation in private firms—shifting the policy focus from headcount targets to skills, productivity and retention.

Kuwaitisation 2.0: from quotas to outcomes

The authorities have strengthened enforcement mechanisms that tie hiring permissions, tender eligibility and

licence renewals to compliance with national employment rules. Procurement documents now frequently require bidders to present a current certificate confirming they meet national manpower ratios, and the Public Authority of Manpower has rolled out new decrees tightening private-sector workforce governance, including working-hours recording and stricter rules on job title and qualification changes. In parallel, measures have emerged to prioritise Kuwaitis in freelance categories and to raise the cost of hiring expatriates into roles that can be filled locally. The policy intent is clear: maintain an open economy while steadily lifting the share of nationals in value-adding private roles.

The approach is beginning to bite, but the friction points are predictable. Private employers report skills mismatches at entry level, salary expectations that are hard to reconcile with productivity in competitive sectors, and difficulties in retaining Kuwaiti graduates once publicsector opportunities arise. A narrow focus on quota compliance risks amplifying

those frictions; a broader focus on capability building, career pathways and mobility between sectors will reduce them. The most successful localisation programmes globally do three things well: they articulate demand from priority industries, align education and training to that demand, and reward firms for measurable outcomes such as sustained employment and progression, not just initial hires.

Youth employment, skills, and the productivity gap

Youth unemployment in Kuwait has hovered in the lower double digits in some recent estimates, a figure that masks the underlying problem: many young Kuwaitis are neither in roles that use their qualifications nor on clear progression ladders in the private sector. If diversification is to stick, a larger cohort of nationals must build careers in logistics, advanced business services, healthcare, tourism and cleanenergy supply chains—the very sectors that Vision 2035 elevates. That requires targeted interventions at three stages.

The first is better signalling. Employers need to be explicit about the skills they value—data analytics for finance and logistics, clinical support tech in healthcare, cybersecurity and cloud operations in digital—and to publish competency frameworks that schools and training providers can teach to. The second is work-integrated learning. Kuwaiti undergraduates and vocational learners should rotate through structured placements with clear learning outcomes, assessed jointly by institutions and employers. The third is early-career support. Wage top-ups, portable training credits and performance-linked bonuses can narrow the initial wage gap between public and private offers while rewarding productivity growth.

Education reform and the innovation ecosystem

Education reform has been a pillar of Kuwait’s development plans for more than a decade, with successive national development plans promoting better outcomes across schools and higher education. The direction of travel is right: elevate STEM attainment, strengthen English proficiency for international business, and embed digital skills across curricula. Around this, a practical innovation ecosystem is taking shape. The Kuwait Foundation for the Advancement of Sciences is scaling corporate innovation programmes with international partners, and leading banks and companies have put cohorts through multi-month challenges focused on building new products, processes and services. For entrepreneurs, the National Fund for SMEs remains the primary policy vehicle; as it continues to streamline processes and strengthen risk management, it can become a more effective springboard for high-potential founders in fintech, healthtech and logistics tech.

A critical next step is joining these dots. The most efficient way to translate education spending into growth is to align it with sector roadmaps. If logistics and financial services are priority engines, then customs digitisation, supply-chain data platforms and regtech become natural focal points for capstone projects, accelerators and corporate innovation briefs. When students solve real problems for prospective employers, placement and retention follow.

A UK lens: qualifications, mobility and partnerships

For British and European stakeholders, Kuwait’s human-capital push intersects with practical collaboration opportunities. UK institutions are

already active in skills and employability programmes in Kuwait, and corporate innovation initiatives have linked Kuwaiti firms with UK and European universities and business schools. As the UK–GCC free trade agreement advances, predictable provisions on services, business mobility and recognition of professional qualifications could make it easier to deploy trainers, assessors and specialist staff into Kuwaiti projects and to run transnational education and apprenticeship pathways. That matters for Kuwaitisation because it expands high-quality training capacity and speeds up the diffusion of international standards in engineering, health, finance and digital.

At the same time, UK regulatory shifts influence Kuwaiti employers that serve UK-linked value chains. Enhanced sustainability and governance disclosure norms mean Kuwaiti firms will need more professionals versed in climate reporting, data assurance and ethical AI—disciplines where UK training providers and consultancies are strong. Strategic partnerships that blend Kuwaiti policy priorities with British training and credentialing know-how can upgrade skills at scale while anchoring Kuwaiti talent in growing private-sector clusters.

Entrepreneurship and SME dynamism Beyond salaried employment, a diversified Kuwait needs more founders building productivity-enhancing products for the local market and the wider Gulf. Policy has moved in that direction: easier licensing for Kuwaiti freelancers, stronger IPP and PPP pipelines that throw off supplier opportunities, and a deeper financial sector that can support venture formation. The test now is to remove practical bottlenecks that stall earlystage companies—slow procurement onboarding, limited access to government sandboxes, and inconsistent data access for building digital services. If the National Fund’s programmes are paired with corporate innovation briefs and public buyers willing to run small, outcomes-based pilots, new entrants will have reasons to hire, train and retain Kuwaiti graduates.

A pragmatic agenda: capability first, compliance second Kuwait can keep its economy open and competitive while elevating national participation if it prioritises capability. The policy menu is clear. Publish occupational standards for priority sectors and align funding to providers who deliver against them. Scale paid, credit-bearing placements and apprenticeships with

guaranteed interviews for those who complete. Reward firms for 12- and 24-month retention rather than firstday hires. Use e-governance to speed licence, visa and qualification recognition decisions so that firms can staff projects on time. And most importantly, celebrate employers and institutions that turn Kuwaitisation into productivity—because that is where the flywheel of sustained private-sector careers really begins.

The transition will take persistence. But the foundations are there: a young population, substantial fiscal capacity to invest in people, and a private sector that is ready to grow as infrastructure, finance and clean-energy projects come to market. If Kuwait aligns incentives around skills and outcomes, it can convert Kuwaitisation from a compliance obligation into a competitive advantage—feeding diversified growth well beyond 2035.

U.S. Department of State – 2025 Investment Climate Statement: Kuwait (public-sector share of citizen employment; FDI and SME context): https://www.state.gov/reports/2025-investment-climatestatements/kuwait

Public Authority of Manpower – Kuwait Labour Law (Law No. 6 of 2010) (institutional basis): https://www.manpower.gov.kw/docs/LaborLaw/E_LaborLaw. pdf

Kuwait Times – Experts: private sector Kuwaitisation hits skill, retention snags (quotas and enforcement trends): https://kuwaittimes.com/article/32444/kuwait/expertsprivate-sector-kuwaitization-hits-skill-retention-snags/

PHDCCI Tender Notice – National Manpower Percentage Compliance certificate requirement (evidence from procurement documentation): https://www.phdcci.in/wp-content/uploads/2025/08/ Tenders-Issue-1752.pdf

HFW briefing – PAM Ministerial Decree No. 15 of 2025 on recording working hours (recent regulatory tightening): https://www.hfw.com/insights/kuwaits-manpower-authoritytightens-regulation-on-recording-working-hours-for-theprivate-sector/

Future Gate – Ministerial Circular No. 1 of 2025 on job titles/ qualifications (labour governance update): https://fgbs.futuregategroup.com/kuwait-news/kuwaitenforces-stricter-rules-on-job-and-qualification-changes/ World Bank – Human Capital Country Brief: Kuwait (education and human-capital indicators): https://thedocs.worldbank.org/en/ doc/64e578cbeaa522631f08f0cafba8960e-0140062023/ related/HCI-AM23-KWT.pdf

British Council Kuwait – Skills for Employability (UK partnerships for skills and entrepreneurship): https://www.britishcouncil.com.kw/en/programmes/ education/skills-for-employability

Times of India – Kuwait restricts 120 freelance job categories to citizens (recent Kuwaitisation measure): https://timesofindia.indiatimes.com/world/middleeast/freelancing-now-only-for-kuwaitis-kuwait-bansexpats-and-gcc-nationals-from-120-freelance-jobs/ articleshow/124024513.cms

British Council – Partnerships in Kuwait (framework for TNE and institutional collaboration): https://www.britishcouncil.com.kw/en/partnerships

Enhancing UK and Kuwait Relations

Relations between the UK and the State of Kuwait are deep, multi-dimensional and historic. In fact, official diplomatic ties between the two countries date back 126 years, but the friendship stretches over 250 years, beginning with trade links that were established in 1775.

Formal mechanisms are in place to advance bilateral relations.

During a Strategic Dialogue held in Kuwait City in July 2025, the two countries renewed their commitment to strengthening bilateral cooperation across various fields.

Then UK Foreign Secretary David Lammy MP met with his counterpart, Kuwait Foreign Minister Abdullah AlYahya, where they explored ways to enhance multilateral cooperation and expand joint initiatives in response to global challenges.

The Kuwait Foreign Minister stressed key milestones in their bilateral relationship, noting cooperation in areas such as

investment, education, healthcare, security, defence and cultural exchange.

Joint Steering Group

The ministerial forum between the UK and Kuwait is the Joint Steering Group (JSG) which advances bilateral relations and addresses shared regional priorities.

The UK hosted the 22nd UK-Kuwait JSG on 23 October in London, where action was agreed to increase cooperation on trade, investment, defence, and regional security. Ministers discussed the breadth of the partnership, including respective industrial strategies, joint military training and deepening development partnerships in third countries. The meeting was also an opportunity to discuss regional priorities.

The JSG was co-chaired by Hamish Falconer MP, Under-Secretary of State for the Middle East, North Africa, Afghanistan and Pakistan at the Foreign, Commonwealth and Development Office, and H.E. Sheikh Jarrah Jaber Al-Ahmad Al-Sabah, Deputy Foreign Minister, Kuwait.

During this latest meeting of the JSG, Ministers oversaw the signing of two Memoranda of Understanding: one on healthcare cooperation and another on hydrographic surveying. These agreements strengthen collaboration in health systems and training and enhance maritime security.

People to People Links

Links between British and Kuwaiti citizens are a vital component of building closer relations at the national level. These contacts are growing and facilitated by enhanced travel processes. Since the UK introduced the Electronic Travel Authorisation (ETA) system for GCC nationals in 2024, Kuwaiti visitors to the UK increased from 120,000 to over 180,000 annually making Kuwaiti tourists the second highest number of visitors to the UK from the Gulf region.

Trade & Investment

His Excellency Mr Bader A. Almunayek, Kuwait’s Ambassador to the UK, has told the Diplomat magazine that enhancing Kuwait’s investment footprint in Britain was a top priority. “The world’s first-ever sovereign wealth fund was established by Kuwait here in London in 1953,” he noted. “Our Kuwait Investment Office (KIO) in London remains our sole international investment arm, covering both Europe and global operations from the UK.”

The Ambassador said that he wanted to strengthen the KIO’s activities in the UK. “Deepening our investment presence here supports the UK economy, and in turn, strengthens our own economic resilience. It’s a winwin,” he said.

“There’s strong potential to expand our trade volume, which currently stands at £6 billion. I’d like to see that figure double during my tenure, and that means identifying key sectors for bilateral cooperation,” he said. “More British companies in Kuwait, more Kuwaiti companies in the UK—that’s the goal,” Kuwait’s UK ambassador told the Diplomat.

Bilateral Trade

According to data released on 31 October 2025 by the UK Department from Business & Trade, the total trade in goods and services (exports plus imports) between the UK and Kuwait was £6.5 billion in the four quarters to the end of Q2 2025, representing an increase of 7.8% or £471 million in current prices from the four quarters to the end of Q2 2024.

In the four quarters to the end of Q2 2025, total UK exports to Kuwait amounted to £2.3 billion, an increase of 13.7% or £280 million in current prices, compared to the same period in 2024.

Of all UK exports to Kuwait in this end Q2 2025 period, £654 million (28.2%) were goods and £1.7 billion (71.8%) were services. UK exports of goods to Kuwait increased by 3.0% or £19 million in current prices, compared to the end Q2 2024 while UK exports of services to Kuwait increased by

18.6% or £261 million in current prices, compared to 2024.

In the four quarters to the end of Q2 2025, total UK imports from Kuwait were £4.2 billion, making an increase of 4.8% or £191 million in current prices, compared to the four quarters to the end of Q2 2024.

Of all UK imports from Kuwait, £4.0 billion (95.3%) were goods and £195 million

(4.7%) were services. In the same period, UK imports of goods from Kuwait increased by 2.7% or £105 million in current prices, compared to 2024 while UK imports of services from Kuwait increased by 78.9%or £86 million in current prices, compared to 2024.

This means the UK reported a total trade deficit of £1.9 billion with Kuwait, compared to a trade deficit of £1.9 billion in 2024. In the four quarters to the end of Q2 2025, the UK had a trade in goods deficit of £3.3 billion with Kuwait, compared to a trade in goods deficit of £3.2 billion in 2024.

Meanwhile, the UK reported a trade in services surplus of £1.5 billion with Kuwait, compared to a trade in services surplus of £1.3 billion in 2024.

These latest figures were published in a DBT factsheet on UK-Kuwait trade which can be accessed on the department’s website.

Energy Transition and Sustainable Development in Kuwait:

FROM AMBITION TO EXECUTION

Why Kuwait’s Energy Transition Matters Now Kuwait sits at a pivotal moment. It is among the world’s highest per-capita emitters, a function of oil-fired power, energy-intensive desalination, and extreme summer cooling demand. That profile carries mounting competitive and policy risks as global markets, financiers and regulators tighten climate expectations.

Vision 2035 sets a clear direction: diversify the energy mix, raise efficiency across power and industry, and develop a pipeline of cleanenergy projects that can stand alongside the country’s oil leadership. The strategic question is not whether to move, but how quickly Kuwait can convert plans into bankable, grid-connected assets and verifiable emissions cuts.

The Target: 15% Renewables by 2030—And the Scale Behind It Kuwait’s official target is to lift renewables to 15% of power generation by 2030. In a system still dominated by fossil fuels, that is a material shift requiring multi-gigawatt solar buildout, grid reinforcement, and storage to manage evening peaks. Flagship developments at Shagaya—most notably the revived Al-Dibdibah

programme—are designed to anchor this ramp-up. Authorities prequalified bidders for a 1.1 GW solar IPP in 2025, while a parallel 500 MW zone proceeds through procurement. These utilityscale parks, if delivered on time, begin to close the gap between ambition and installed capacity.

Kuwait has also signalled a longer runway for clean molecules. In 2024,

Energy & Infrastructure

Kuwait Oil Company commissioned a national roadmap targeting 17 GW of renewables and 25 GW of green hydrogen capacity by 2050. That masterplan positions hydrogen for industrial decarbonisation at refineries and petrochemicals first, with potential export volumes later as costs fall and offtake frameworks mature. For investors, the takeaway is twofold: the 2030 power target can be met only with accelerated project execution; the 2050 hydrogen horizon creates optionality for heavy-industry decarbonisation and new value chains.

Implementation Headwinds: From Procurement to Permitting

Delivering large projects at pace has been Kuwait’s chronic challenge. The cancellation of the original 1.5 GW Al-Dibdibah scheme in 2020 became a cautionary tale about bureaucratic friction and shifting priorities. The relaunch and rebundling of Shagaya

Phase III in 2025 is therefore a credibility test for the state’s energy transition programme. Grid preparedness is equally important. Rapid solar additions will require modernised transmission and distribution, better demand-side management, and grid-scale storage to smooth variability. Kuwait’s utilities and private developers will need bankable offtake terms, timely land allocation, and streamlined permitting to keep schedules intact and finance costs in check.

The power balance is a near-term constraint. Kuwait has been augmenting domestic generation with imported gas to secure summer reliability. A long-term LNG supply agreement with Qatar supports continuity, but it also underlines why efficiency and renewables are not optional: every avoided megawatt of peak demand saves fuel, emissions and cash.

The Efficiency Opportunity: The Fastest, Cheapest “Fuel” Energy efficiency is Kuwait’s most immediate lever. Historical programmes envisaged tightening building codes, retrofitting public assets, and improving power plant performance. Today, that agenda can be updated with digital tools and performance-based contracts that pay for savings delivered. Cooling is the prize. High-SEER HVAC, district cooling expansion, thermal storage and smart controls can shave peaks that drive costly generation and curtailment. Industrial efficiency—waste-heat recovery at refineries, electrification of low-temperature processes, variablespeed drives and advanced analytics— offers additional quick wins with robust paybacks even at conservative carbon prices. The economic logic is straightforward: deferring a gigawatt of peaking capacity through efficiency measures is cheaper and faster than building it. >>>

Energy & Infrastructure

Emerging Technologies: Hydrogen, Storage and Smart Systems

Green hydrogen is gathering momentum in Kuwait’s planning, but the commercial pathway is phased. Early deployments will likely centre on refinery hydrotreating and desulphurisation, displacing grey hydrogen and cutting scope 1 and 2 emissions in the downstream sector. As solar costs continue to fall and electrolyser efficiency improves, Kuwait can scale to export-grade volumes, provided it can secure competitive power, water supplies and offtake contracts aligned with international certification standards.

Battery storage will be pivotal to integrate Kuwait’s planned solar fleet and to shift midday generation toward evening peaks. Utility-scale batteries at Shagaya would reduce curtailment and improve capacity credits for solar assets, strengthening project economics. On the system side, smarter grids—advanced metering, dynamic tariffs, automated demand response—will help reshape

consumption patterns, particularly in commercial buildings and public infrastructure. Over time, electrification of transport, paired with managed charging and vehicle-to-grid pilots, can turn a challenge into a flexibility asset.

Competitive Context: Keeping Pace with the Gulf

Kuwait’s peers have set a fast tempo. Saudi Arabia and the UAE have commissioned multi-gigawatt renewables, paired with tenders that deliver record-low tariffs. Kuwait’s auction design will need to be equally predictable and scalable, with transparent timelines, robust risk allocation, and currency-hedging solutions where relevant.

The recent revival of large tenders is a positive signal, but delivery discipline—financial close, construction milestones, and grid readiness—will ultimately determine credibility with sponsors, lenders and EPCs.

Why UK Policy and Capital Matter to Kuwait’s Transition

For British and European counterparties, Kuwait’s transition intersects with an evolving regulatory

landscape. The UK will introduce a Carbon Border Adjustment Mechanism (CBAM) from 1 January 2027, initially covering emissions-intensive goods such as iron and steel, cement, fertilisers, aluminium and hydrogen. UK-listed and UK-regulated corporates are also moving toward IFRS S1/ S2-aligned climate disclosures that sharpen scrutiny of supply-chain emissions and transition plans. In practice, that means Kuwaiti exporters and joint ventures serving UK markets will face rising expectations for embodied-carbon data and decarbonisation pathways.

On the opportunity side, UK Export Finance has prioritised clean energy and can de-risk cross-border projects through guarantees and direct lending, catalysing private capital into Kuwaiti IPPs and industrial decarbonisation. UK engineering, legal and advisory firms are already active across GCC energy and infrastructure; Kuwait’s project pipeline provides a natural extension for that ecosystem, from bankability studies to owner’s engineering and dispute-avoidance during execution.

Financeability: Turning Plans into Bankable Pipelines

Project finance will flow where structures are predictable. Kuwait’s 30-year PPA model, if consistently applied with clear indexation and curtailment protections, can unlock competitive bids and compressed weighted-average costs of capital. Investors will watch three factors closely. First, sovereign delivery risk, evidenced by timely approvals and adherence to procurement calendars. Second, grid integration, including codified interconnection timelines and compensation rules. Third, ESG reporting that aligns with international frameworks, enabling investors to classify assets as “green” and access lower-cost capital pools. Establishing a centralised, publicly updated dashboard of project status would further improve transparency and confidence.

A Realistic Path Forward

Kuwait’s energy transition is not starting from zero. The renewed Shagaya programme, a hydrogen masterplan focused on industrial decarbonisation, and an explicit 2030 renewables target provide a coherent

spine. The execution agenda is clear: accelerate utility-scale solar with storage; institutionalise efficiency in buildings and industry; modernise the grid for flexibility; and de-risk the first wave of hydrogen projects tied to refinery demand. With disciplined procurement and credible timelines, Kuwait can meet its 2030 target and position itself for a deeper 2040–2050 transformation that preserves competitiveness in a carbonconstrained world.