As we approach the mid-point of the year, market conditions across food categories remain mixed. Some sectors are showing early signs of recovery, with positive signs to match the uplift in consumer mood during grilling and outdoor dining season. Others have not emerged from a rather more gloomy climate, and continue to feel the strain of reduced supply, rising input costs, and ongoing global disruption.

In dairy and eggs, we’re beginning to see stabilisation, with improved weather and eased biosecurity controls supporting better supply dynamics. Coffee prices have softened slightly on the back of stronger crop forecasts, and the Irish fresh produce season is progressing well, offering a welcome boost in local availability.

However, much of the protein category remains under pressure. Poultry and turkey markets are grappling with the continued impact of Avian Influenza, lamb throughput is significantly behind last year’s levels, and pork and seafood face rising demand amid limited international supply. Meanwhile, cooked meats are seeing broad-based inflation driven by raw material and operational cost increases.

This report provides a full overview of these developments and more, helping you stay informed and plan with confidence. Our team remains on hand to support you with tailored advice, product alternatives, and long-term sourcing solutions.

Warm regards, Sysco Ireland

Centre of Plate | Produce | Bakery & Dessert Catering Supplies & Beverage 04

The global food market can be unpredictable, but your supply doesn’t have to be. Our specialist team is here to help you stay stocked with quality options that fit your budget. Whether it’s discovering new products, exploring different price tiers, or finding the best value, we’ve got solutions for you. Talk to your ASM to arrange a meeting.

Centre of Plate

MICHAEL JOYCE

Mick has been in the industry for over 30 years. He is a qualified master butcher and provides his customers with expert information to add value to their business.

Centre of Plate

NEIL BRISLANE

Neil has been part of the Sysco team for over 20 years, with the last decade dedicated to Centre of Plate. His deep knowledge helps customers make informed decisions, adding real value to their business.

Centre of Plate

PHILL WARING

Phill joined the business in 2023 after 18 years working as a Chef. His roles were primarily in Fine Dining establishments throughout Northern Ireland, but he also spent time in Australia.

Produce

NOEL RYAN

Noel joined Sysco in 2022, however with 35 years in the produce business he brings a wealth of experience to his role. Noel’s belief in Sysco’s customer centric values plays an important role in how he does his job.

Produce

ALASDAIR MacINNES

Alasdair joined the business over 20 years ago, following 25 years as a chef working in busy restaurants. He began his career with Sysco in purchasing before moving to a produce specialist role.

Produce

RUTH POLLOCK

Ruth joined Sysco in 2024 and has over 20 years’ experience within fresh produce. Ruth enjoys working in partnership with her customers to come up with the best solution for their business.

Centre of Plate

KELAN McMICHAEL

Kelan has worked in the industry as a chef for over 25 years, in some of the finest kitchens in the UK and Ireland. He was honoured to be part of a team that cooked in the Hague, representing Ireland and Irish produce.

Produce

SIMON DOHERTY

Simon has over 35 years’ experience in the industry and is an expert in the industry and the produce category. Simon is always willing to go above and beyond to ensure the highest quality service.

PROTEIN

BEEF

The beef trade remains strong, underpinned by tight supply and firm export demand. Manufacturing categories such as mince, burgers, and diced beef are seeing brisk movement, while tighter kill numbers and rising live exports continue to add upward pressure on prices. Retail sales have proven more resilient than expected, even amid inflation, as roast products show typical seasonal decline.

KEY POINTS

Pricing Trends

Cattle price inflation stands at 38% year-to-date, significantly outpacing customer inflation at 24%. While some price softening was seen earlier this year, prices have returned to an upward trend over the past two weeks and are expected to hold firm as supply tightens.

Retail Demand

Despite early fears of a 10% decline, retail volumes are down just 3.3%, with price increases successfully passed through by all six major Irish retailers. The decline is largely attributed to lower demand for roast-type products typically associated with winter.

Export Activity

Live exports are up 25% year-on-year overall. Weanling, store, and finished cattle exports are up 46% year-on-year, contributing to tightening domestic supply and rising cattle prices.

Production Outlook

Kill numbers have fallen 24% since March’s peak. Bord Bia now forecasts a 7-8% decline in 2025 slaughter volumes compared to 2024, tightening supply further into the second half of the year.

European Trends

Beef prices are also rising in Germany and Central Europe, where shortfalls in manufacturing meat are emerging ahead of the BBQ season.

PORK

The European pork market is experiencing firming demand, supported by seasonal trends, improved foodservice activity, and growing international interest. While prices are expected to peak during Q3, the overall outlook for the sector remains positive, particularly in out-of-home and retail segments.

Source: Pigment Dashboard

KEY POINTS

Rising Domestic Demand

Mild weather in May and June has boosted interest in pork across both retail and foodservice. The grilling season has further supported increased consumption, with demand from industrial users rising in anticipation of stronger enduser activity into the second half of Q2.

Food-to-Go & Out-of-Home Growth

As more consumers return to the office and dining habits normalise, demand for on-the-go pork products (e.g. sandwiches, baguettes) is growing. Pork continues to be well-positioned in this space due to its affordability, versatility, and convenience, with food-to-go formats gaining traction as cost-effective dining options.

International Market Outlook

Geopolitical tensions, particularly between China and the USA, are shifting global trade dynamics. Chinese importers are seeking alternative sourcing routes, which could benefit EU and South American pork exporters, driving further international demand.

Pricing Trends

Prices are expected to peak in Q3 in line with seasonal demand and may soften slightly in Q4, depending on disease developments or shifts in protein market dynamics. Broader inflationary pressures may return towards late 2025 into early 2026, particularly if other protein costs increase.

Irish Average Grade E Pig Prices per 100kgs

LAMB

The Irish lamb sector continues to face a significant supply shortfall, driven by reduced ewe numbers, higher mortality rates, and increased live exports. Strong and sustained demand, both domestically and across export markets, is maintaining upward pressure on prices, particularly for manufacturing and middle cuts.

KEY POINTS

Supply Shortages

• National throughput levels for new season lambs are down by approximately 150,000 head year-on-year, with forecasts indicating a further 250,000 head shortfall up to the end of May 2025.

• The Irish sheep census (Dec 2023) reported a 7% reduction in ewe numbers, contributing to lower lamb availability.

• Higher mortality rates and increased live exports, influenced by Blue Tongue-related movement shifts, are further tightening supply.

Strong Demand Across All Segments

• Demand for lamb has remained robust through 2024, with no signs of easing into 2025.

• Manufacturing lamb has seen a marked uptick in demand over the past 6-8 weeks, compounded by reduced supply and tight global availability.

• Southern Hemisphere supply to Europe remains limited, intensifying pressure on middles and manufacturing cuts.

Carcase Trade & Processing Impact

The strength of the carcase trade has led many processors to avoid deboning, further limiting the volume of product available for manufacturing and added-value markets.

Pricing Trends

• Middle cuts continue to command high prices due to persistent short supply.

• Shoulder prices remain strong, driven by both retail demand and limited manufacturing stock.

• Leg prices are now increasing as Christmas procurement begins in earnest.

Source: Bord Bia

CHICKEN

Inflationary pressure and deepening supply shortages remain the dominant themes of the European and wider poultry markets. Prices have surged by over 20% since mid-February 2025, driven by Avian Influenza (AI) outbreaks, significant culls of breeding stock, and restricted imports. With no market recovery anticipated until early 2026, producers and processors are navigating an increasingly constrained landscape.

KEY POINTS

Severe Hatchery Shortages

Prices for hatching eggs have doubled in just two months, driven by a global shortage following extensive AI-related culls. Grandparent, parent, and hatchery flocks have been hit hard, significantly reducing supply capacity across global markets.

The island of Ireland implemented a housing order in February 2025 and more than 112,000 birds have been culled in Northern Ireland. Irish farmers and processing partners are increasingly reliant on imports of hatching eggs from the European market to offset local shortages.

Supply Challenges

• Avian Influenza outbreaks continue to rise across Europe. New containment measures came into effect in Poland from the week commencing 21st April, which included the expansion of restriction zones, 60-day quarantine periods, longer intervals between flock cycles, and reduced maximum stocking densities.

• Newcastle Disease outbreaks also persist, further straining supply chains.

• Since June through the end of 2025, the EU will dramatically reduce poultry import quotas from Ukraine, intensifying supply pressure within the region.

• Brazil has reported its first Avian Influenza outbreak, prompting a 60-day export ban from major importers including the EU, China, and South Korea, tightening global availability further.

• Shortages and inflation across other protein categories are driving increased demand for poultry, reinforcing upward price trends.

• The BBQ season commenced in May, historically the peak demand period for poultry, placing additional strain on already limited supply.

EUROPEAN TURKEY

The European turkey market is under renewed pressure as Avian Influenza (AI) continues to spread aggressively across the continent. Outbreaks have more than doubled year-on-year, with severe losses across key producing countries. As a result, availability of both fresh and frozen turkey is constrained, and costs have returned to peak levels last seen during the 2024 Christmas period.

In the 2024/25 reporting year (1 July 2024 – 30 June 2025), there have been 653 confirmed outbreaks of Avian Influenza across Europe, affecting a total of 37.4 million animals. This marks a sharp increase from the same period last year, which saw 320 outbreaks and 11.6 million animals impacted.

With AI outbreaks still active and affecting major producers, the European turkey market is expected to remain tight in supply and elevated in cost through the summer and into Q3 2025.

Approximately 3.3 million turkeys have been affected by AI outbreaks in the current season. The most significant losses have occurred in:

• Poland: 1.85 million turkeys (+247,038 vs. previous year)

• Italy: 581,753 turkeys (no change vs. previous year)

• England: 425,715 turkeys (+50,809)

• Hungary: 253,767 turkeys (+58,914)

• Germany: 184,750 turkeys (+5,435)

COOKED MEATS

COOKED MEATS

Ongoing protein shortages, rising raw material costs, and operational inflation continue to drive up pricing across the cooked meats and value-added poultry categories. The sector is under pressure from surging beef and poultry costs, packaging and energy inflation, and sustained wage increases.

KEY POINTS

Chicken (Fresh/Frozen, Sliced & Whole)

Prices have increased by over 20% since February 2025, mirroring the inflation in the fresh poultry market.

Sliced Turkey

European turkey pricing remains at the high levels seen during the 2024 Christmas peak, representing a 40% increase from Q3 2024.

Sliced Beef

Beef prices have surged by approximately 40% from January to June 2025, placing significant cost pressure on cooked beef products.

Cooked Pork Products

Pork is also facing steady inflation, with Irish prices rising by approximately 6% and EU pork increasing by 9% over the same period.

Operational Cost Pressures

In addition to raw material inflation, processors are contending with higher packaging and energy costs. Labour-related costs are also rising, with minimum wage increases of nearly 20% since 2023 further compounding margin pressures.

Value-Added Chicken Products

The breaded fillet and goujon ranges are expected to see further price increases of approximately 8% in H2 2025. This follows cumulative inflation of around 16% across value-added chicken lines since January 2025, driven by broader protein market volatility and input cost escalation.

Outlook

The cooked meats and value-added poultry categories will continue to reflect upstream cost inflation through the second half of 2025. With no signs of immediate relief on raw materials or operational inputs, pricing is expected to remain elevated.

SEAFOOD

SEAFOOD

The seafood sector continues to experience volatility across key species due to biological constraints, quota reductions, and global demand pressures. While some species show signs of stabilisation, others remain under significant supply stress with elevated prices expected through the remainder of the year.

SALMON

Atlantic farmed salmon production is forecast to grow by 2.5% in 2025, subject to biological conditions. Prices remain relatively high, but increased harvest availability from July is expected to ease pressure. A seasonal price increase is likely again from late November into December.

COD

Supply of Atlantic cod has been cut by 30% this year, pushing prices to record highs, approximately 80% above January 2024 levels. Pacific cod prices have stabilised due to steady demand, but long-term availability remains dependent on upcoming 2026 quotas, with low volumes expected until at least 2028.

HAKE

Fresh hake supply has been inconsistent, mainly landed by Spanish vessels off the south coast of Ireland. Prices are currently stable but expected to rise later in the year. Frozen hake supply has declined due to reduced quotas and poor fishing conditions, contributing to price inflation across markets.

HADDOCK

Prices remain high due to lower quotas and increased demand, with no significant change expected in 2025. Current elevated pricing levels are likely to persist.

BASS & BREAM

A challenging year ahead for both species. Global supply remains tight, with notable price increases expected across June and July. High seawater temperatures at the end of 2024 led to elevated mortality rates, further straining 2025 availability.

PRAWNS

Prices are trending 7.5% higher year-onyear, largely due to low productivity. Some improvement in supply is anticipated during the summer months, which could bring modest price relief.

SQUID

Global squid prices are at multi-year highs, driven by reduced catches in key regions like Peru and the Indian Ocean. Raw material availability remains limited, and processors face ongoing supply challenges. Elevated pricing is expected to persist through the rest of 2025.

DAIRY

DAIRY

As we move into the summer months, the dairy and egg sectors are beginning to stabilise following a period of sustained pressure. Improved spring weather has supported milk production across parts of Europe, while the easing of biosecurity restrictions in Ireland is helping egg supplies rally. Though pricing remains elevated in certain categories, particularly for butter, early signs point to a more balanced outlook. That said, market conditions remain sensitive, and ongoing vigilance will be essential through the second half of the year.

EGGS

After a challenging period marked by Avian Influenza (AI) outbreaks and strict biosecurity measures, the Irish egg market is beginning to stabilise. Recent regulatory changes and improved disease control have supported a modest recovery in supply.

KEY POINTS

Avian Influenza Impact

Bird flu has continued to pose a significant threat to poultry populations across multiple regions in recent years, often transmitted via wild birds. The virus, which crosses borders easily, has led to widespread mortality and disruption, particularly in egg production.

Biosecurity Restrictions Lifted

In response to the elevated risk of AI, special biosecurity regulations for poultry were introduced in December 2024. These included a housing order for poultry flocks and captive birds. The housing order was revoked earlier this month. Remaining biosecurity measures will be lifted from the end of May 2025.

Recovery in Supply

With restrictions easing and no major new outbreaks reported locally, egg supply in Ireland has begun to improve. While full recovery may take time, early indicators suggest stabilisation is underway.

BUTTER

The EU butter market continues to experience elevated pricing, driven by robust demand and limited availability. Despite a modest increase in supply as more processors re-enter the market, overall volumes remain tight, sustaining upward pressure on prices.

Expana Benchmark for European Butter

OIL

Spain’s olive oil sector is showing signs of bouncing back, following two years of drought-induced disruption and record-high pricing. Improved weather conditions and rainfall have led to expectations of a strong current harvest and positive outlook for the season ahead. However, global dynamics across the broader edible oils market continue to keep pricing elevated.

KEY POINTS

Global Demand vs. Production

While global demand for edible oils and fats has grown approximately 4% over the past two years, this season’s consumption growth is expected to slow to around 1%. Nonetheless, global consumption is still projected to exceed production, maintaining upward pressure on prices.

ONGOING SUPPLY CONSTRAINTS

Rapeseed & Sunflower Oil: Past harvest shortfalls and strong demand continue to support elevated pricing.

Palm Oil: Production has lagged expectations in recent weeks, tightening supply and firming global prices.

Market Volatility: Ongoing tariff discussions and trade uncertainties could further influence pricing and availability across all major oil categories.

BEVERAGE & IMPULSE

COFFEE

Coffee markets have seen some price softening in recent weeks, largely driven by improved weather conditions in key producing regions. Forecasts for upcoming harvests in Brazil and Vietnam suggest stable to average production levels, contributing to a more balanced near-term outlook.

Monthly Price Movements: ICE London Robusta Futures (Nearby)

KEY POINTS

Improved weather conditions across Brazil have eased concerns over the upcoming crop. Seasonal rains in Vietnam are tracking close to average levels. While some regions are experiencing minor dry spells, conditions overall remain favourable for crop development. Vietnam’s next coffee harvest, scheduled for later this year, is progressing well under current conditions.

APPLE JUICE

The price outlook remains uncertain as market players assess the potential impact of future US-China tariffs on the apple concentrate market. According to market sources, there are limited supplies. The industry is now looking ahead to the spring and the prospects for the next crop. Apple Juice EU - €/mt 3,000 2,500 2,000 1,500 1,000

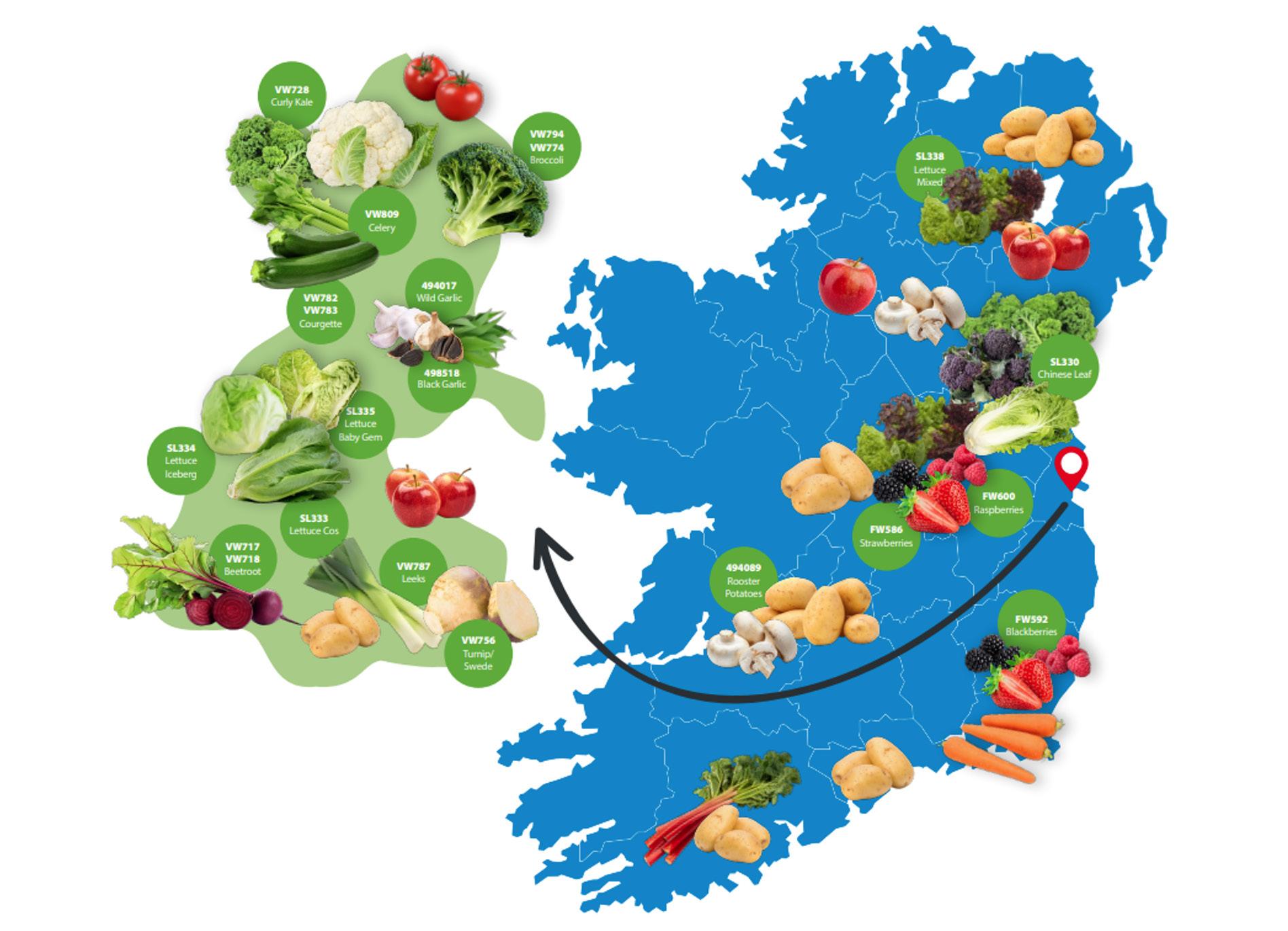

FRESH PRODUCE

At Sysco, we continue to prioritise our partnerships with local growers as we transition into peak Irish season across a broad range of produce.

IRELAND: IN SEASON NOW

Irish-grown strawberries, raspberries, lettuce varieties (including Iceberg, Butterhead, Lollo, and Oak Leaf), broccoli, curly kale, and baby vegetables are now available and in good supply.

COMING INTO SEASON

Mid-July to early August

Irish celery, carrots, courgettes, and blackberries are expected to come into full season, supporting local sourcing through summer.

MELONS

Sourcing has transitioned from Spain’s Almeria region to Murcia, where growing conditions are more challenging. Crop quality is being closely monitored.

ONIONS

Dutch onions are currently in full season. Spanish new season onions are re-entering the market, with pricing expected to improve as availability increases.

POTATOES

This year’s plantings are complete and notably more timely than last season. Despite dry conditions, crops are developing well.

New Season Queens are becoming available now.

New Season Roosters expected from late July to early August.

BAKERY

WHEAT

The global wheat market is facing a mixed outlook, with early signs of weather-related stress emerging in some key growing regions. Despite this, expectations for a strong carry-over in Europe and positive crop reports from the U.S. and Russia are contributing to a more balanced view. Pricing remains under pressure, but confidence among growers is low as current levels risk unprofitable returns.

KEY POINTS

Carry-Over & EU Export Position

Europe is heading into the next season with aboveaverage carry-over stocks. Limited export demand and favourable financial incentives are encouraging both growers and commercial stores to hold onto grain, particularly as UK pricing remains uncompetitive globally.

Emerging Weather Concerns

Dry conditions are intensifying across the UK, France, Germany, Poland, and the Baltics, with little rain forecast. Russia is also facing dryness, while Ukraine continues to benefit from rain. Longer-term dryness in Australia and China is raising additional concern for winter wheat crops.

U.S. Crop Outlook

In contrast, U.S. wheat crops are performing well, with 61% rated Good/Excellent, up 2% week-on-week. Corn planting is progressing rapidly, 40% ahead of the five-year average, reinforcing confidence in North American grain supply.

Monthly Price Movements

Global Production & Pricing

Russia, the world’s largest wheat exporter, is forecasting a 2025 crop of 83.8 million tonnes, with an exportable surplus of 41.3 million tonnes. Despite strong fundamentals in some regions, macroeconomic factors such as U.S. tariffs, a strong dollar, and softening oil prices are influencing contract lows in many markets.

Grower Sentiment

While the pricing outlook may favour buyers, confidence remains low among growers globally, many of whom are unwilling to sell at current price levels due to concerns over negative returns.

KEY POINTS

Reduced EU & UK Beet Acreage

The latest planting data indicates a 9% year-on-year decrease in EU sugar beet acreage, slightly higher than previous expectations. UK and EU combined acreage is down an estimated 5-7%, suggesting reduced domestic output for the 2025/26 marketing year.

Progress in Sowing

Despite acreage reductions, sowing progress has been strong, with favourable weather conditions supporting timely planting across Europe. The first yield assessments will become available in the coming months once sugar beet weight results are reported.

Raw and White Sugar Futures Prices

SUGAR

The global sugar market remains finely balanced as macroeconomic concerns and shifting weather patterns create mixed signals. While production forecasts in the EU and UK point to reduced acreage, favourable weather in Brazil is supporting global output. Overall, the market remains cautious, with early estimates suggesting a modest decline in total production for the year ahead.

Brazilian Production Gains

Milling activity in Brazil accelerated in late March, alleviating early-season concerns. April brought ample rainfall, further supporting cane development and reinforcing expectations for a strong 2025 harvest.

COCOA

Cocoa markets remain under upward pressure following extreme weather conditions in West Africa and regulatory changes in Europe.

KEY POINTS

Extreme Weather in Côte d’Ivoire

April 2025 marked one of the driest on record in Côte d’Ivoire, the world’s largest cocoa producer. Prolonged dryness has sparked concerns over the remaining mid-crop and raised alarms about the potential impact on the upcoming main crop.

Supply Risk & Market Tension

While Q1 grindings are no longer the market focus, the weather-driven uncertainty has taken centre stage. Participants are closely monitoring whether early-season surpluses may be eroded if current conditions persist.

EUDR Compliance Pressure

Prices are also being supported by new traceability and documentation requirements under the EU Deforestation Regulation (EUDR). Compliance challenges are adding cost and complexity to the supply chain, especially for exporters into the EU market.

Port Arrivals

Despite the weather challenges, port arrivals in Côte d’Ivoire are up 11.2% year-on-year, a rare bearish indicator in what has otherwise been a bullish market environment.