Submarine Telecoms Forum, Inc. https://subtelforum.com/about-us

BOARD OF DIRECTORS: Wayne Nielsen, Margaret Nielsen, Kristian Nielsen, and Kacy Nielsen

Contributions are welcomed and should be forwarded to: pressroom@subtelforum.com.

Submarine Telecoms Cable Industry Report is published annually by Submarine Telecoms Forum, Inc., and is an independent commercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical fiber technologies and techniques. Submarine Telecoms Forum may not be reproduced or transmitted in any form, in whole or in part, without the permission of the publishers.

Liability: While every care is taken in preparation of this publication, the publishers cannot be held responsible for the accuracy of the information herein, or any errors which may occur in advertising or editorial content, or any consequence arising from any errors or omissions, and the editor reserves the right to edit any advertising or editorial material submitted for publication.

New Subscriptions, Enquiries and Changes of Address

19471 Youngs Cliff Road, Suite 100, Sterling, Virginia 20165 United States, or visit https://subtelforum.com.

Your Premier Portal to Locate Companies for Submarine Telecoms Collaboration

Content Highlights:

• All-Encompassing Listings: Dive into a world-class directory of submarine telecom product and service providers.

• Intuitive Search: Effortlessly navigate to the services and solutions tailored to your mission.

• Spotlight on Innovation: Engage with the leaders driving the industry forward through technological advancements.

SET SAIL FOR SUCCESS

BOOKMARK THE SUBTEL FORUM INDUSTRY DIRECTORY TODAY!

Figure

Figure

EXORDIUM

Dear Readers,

Welcome to Issue 14 of SubTel Forum’s Submarine Telecoms Industry Report.

The year 2025 marks the beginning of a new era for the submarine cable industry. The sector has transitioned from an age of unrestrained buildout to one defined by strategic coordination, sustainability, and global accountability. Amid geopolitical friction, evolving regulatory frameworks, and persistent supply chain pressures, the industry continues to demonstrate remarkable adaptability—balancing capacity growth with resilience and stewardship.

As detailed in this year’s report, the submarine telecoms landscape now stands at a point of structural maturity. Over $22 billion in active project capital is currently self-financed, underscoring a confident and independent market. Meanwhile, governments and multilateral institutions are deepening engagement through public-private partnerships and emerging security and sustainability frameworks, including the International Advisory Body on Submarine Cable Resilience. The message is clear: subsea cables are no longer peripheral infrastructure—they are critical assets central to global security, finance, and digital inclusion.

Technological evolution continues apace, though the emphasis has shifted from expansion to optimization. The industry’s focus now rests on operational precision, with innovations such as multi-core and hollow-core fiber, 800G wavelengths, and smart repeaters improving both efficiency and environmental performance. Lit-capacity utilization has reached record levels—averaging 60 percent globally—reflecting a disciplined alignment between deployment and demand.

Equally transformative is the cultural shift toward sustainability and long-term stewardship. Measurable standards such as CUE, PUE, and REF are now embedded in project design, while circular-economy practices are taking hold in system recovery and decommissioning. These advances—alongside a new generation of engineers, analysts, and policymakers—signal a maturing ecosystem that recognizes the enduring balance between growth, resilience, and responsibility.

Each year, our Industry Sentiment Survey provides an invaluable barometer of optimism, investment appetite, and workload trends across every region of the subsea market—data that directly informs the analysis and forecasts presented throughout this report.

The Submarine Telecoms Industry Report remains a cornerstone analytical resource for understanding these dynamics. It complements SubTel Forum’s other products—the Submarine Cable Map (published in January, May, and September), the quarterly Submarine Cable Almanac, the continuously updated Submarine Cables of the World Interactive Map, as well as our upcoming Cableship Codex, launching in December 2025. Together, they form a comprehensive suite of industry intelligence—tracking projects, investment, regulation, and innovation across every region.

This year’s report identifies more than $18.4 billion in new projects under active development, with $9.2 billion already contracted and $4.1 billion expected to reach RFS by the end of 2025. We have drawn on proprietary data from the SubTel Forum Submarine Cable Database and insights from recent SubTel Forum Magazine issues, as well as contributions from leading specialists including:

• Andrés Fígoli

• Kristian Nielsen

We extend special thanks to our 2025 sponsors for their invaluable support in producing this 14th annual edition:

• ACS

• Figoli Consulting

• WFN Strategies

As always, we are honored to feature a Foreword by Doreen Bogdan-Martin, Secretary-General of the International Telecommunication Union, whose leadership continues to advance the global dialogue on connectivity and resilience.

As SubTel Forum enters its 24th year in publication, our mission remains unchanged: to inform, connect, and challenge an industry that is vital to the world’s digital future. The next chapter will be defined not merely by capacity but by coordination—between nations, enterprises, and generations. With more than 175 years of subsea history behind us, the submarine cable community remains a model of innovation, pragmatism, and perseverance.

We thank our readers for your continued engagement with SubTel Forum’s work. As ever, we believe that an informed industry is a productive industry.

Good reading and Slava Ukraini,

Wayne Nielsen Publisher & President, Submarine Telecoms Forum, Inc.

FOREWORD

Thoughts from Doreen Bogdan-Martin, ITU Secretary-General

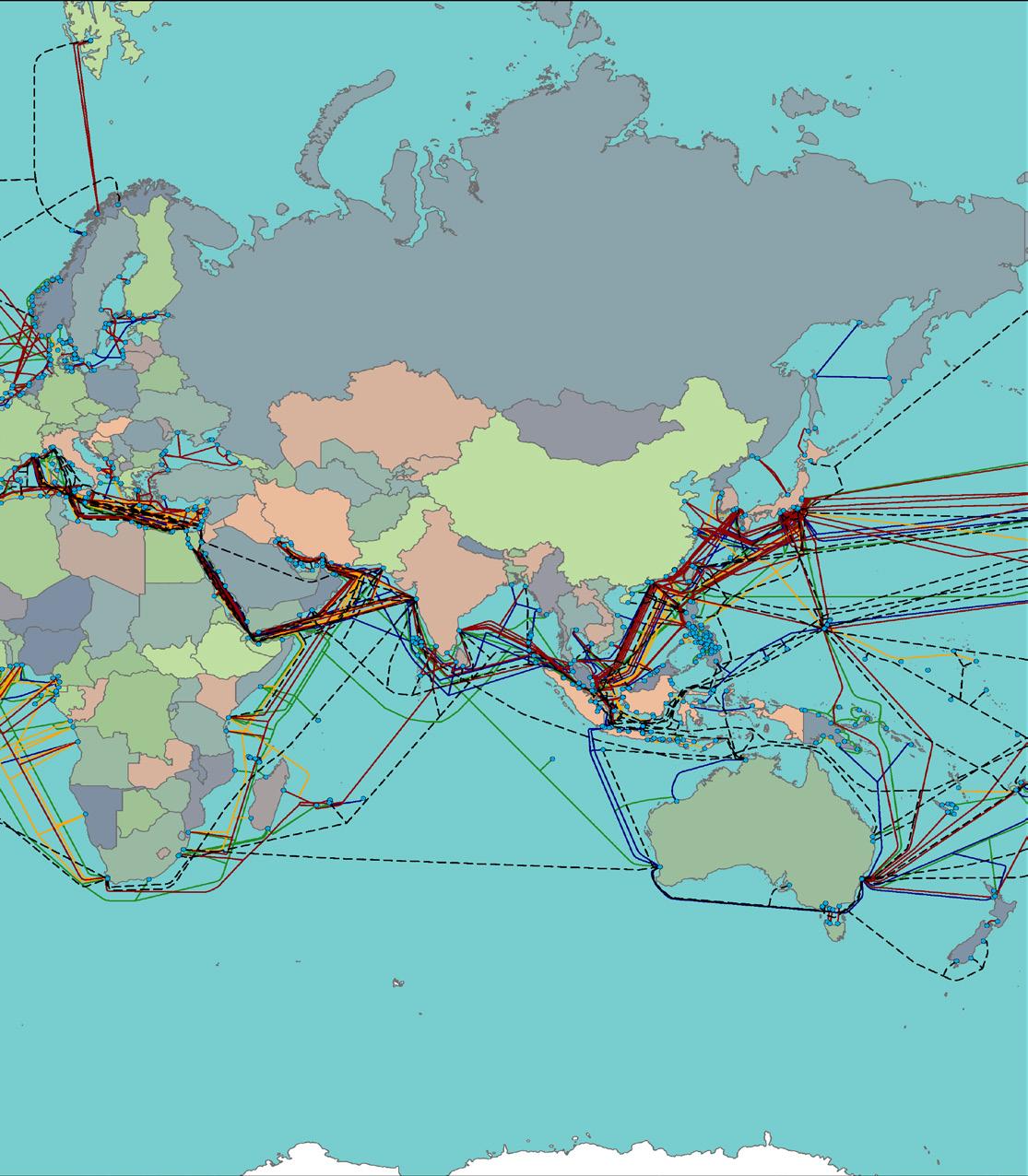

Laid end to end, the submarine cables connecting our world could circle the Earth between 30 and 40 times over.

The immensity of this undersea network reminds me of the vast challenges before us as the United Nations agency for digital technologies.

ITU’s goal is to bring one-third of humanity online, while ensuring that all 5.5 billion people already using the Internet can benefit from meaningful, reliable connectivity.

But when connectivity supplied by cable services is disrupted, entire economies and communities feel the impact.

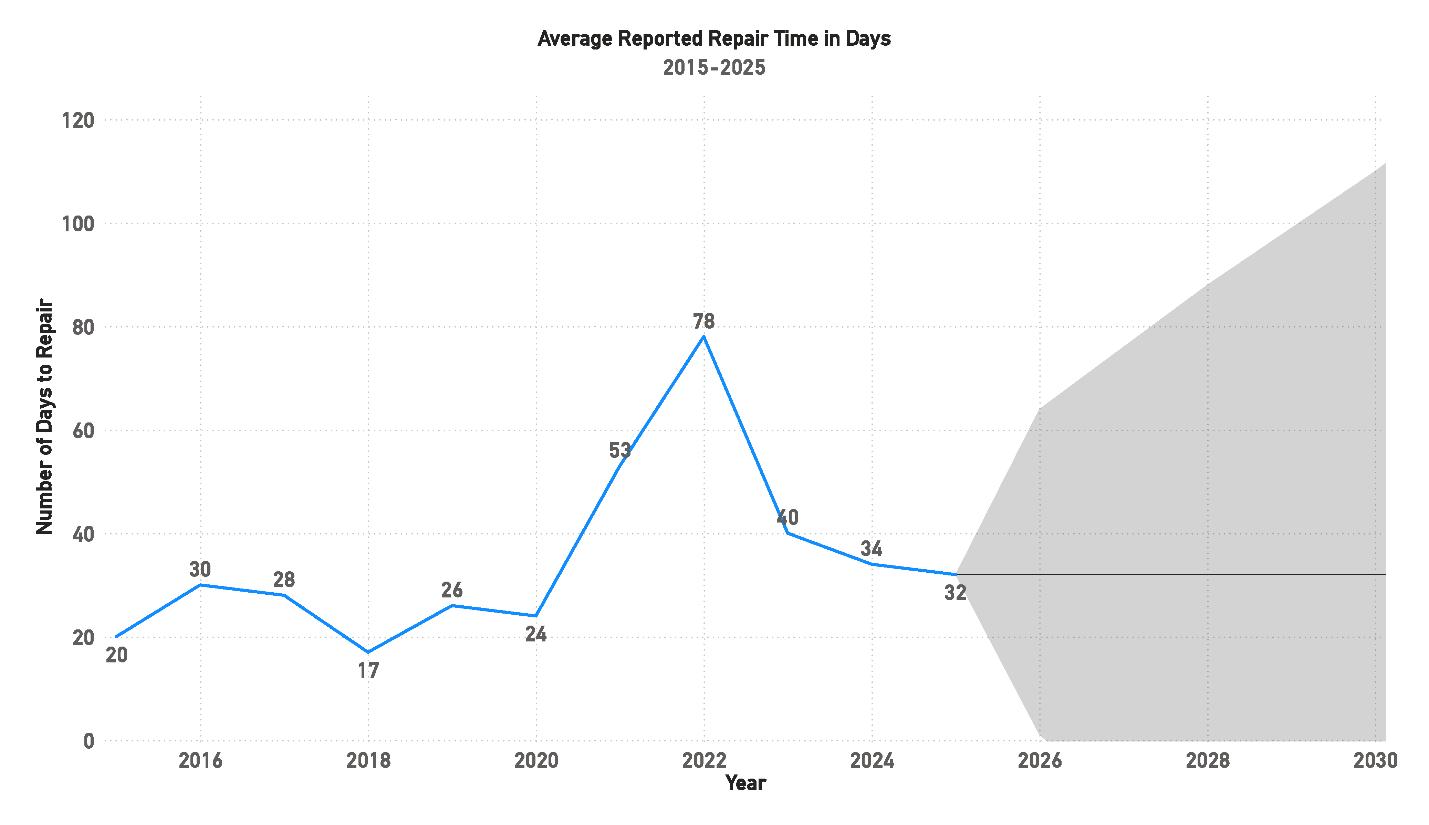

Even though these information superhighways are built to operate for around 25 years, we are seeing over 200 disruptions annually.

Repairs can sometimes face significant delays.

ITU’s goal is to bring one-third of humanity online, while ensuring that all 5.5 billion people already using the internet can benefit from meaningful, reliable connectivity.

Meeting our goal of universal, meaningful connectivity demands more than infrastructure; it calls for shared commitment, fresh ideas, and collaboration on long-term resilience strategies on a global scale.

Developing these strategies is the aim of our International Advisory Body for Submarine Cable Resilience, led by ITU together with the International Cable Protection Committee.

While cable resilience has become a top priority for governments around the world, supporting strategies are at quite different levels of maturity.

The Advisory Body — comprising more than 40 experts and co-chaired by representatives from Nigeria and Portugal — aims to help everyone move forward together.

Its composition reflects ITU’s diverse membership of 194 Member States and over 1,000 companies, academic institutions and standards communities all over the world, and its work is grounded in strong shared incentives to boost cable resilience.

Over the next decade, some estimate that more than two-thirds of new value creation could come from digitally enabled platforms.

Submarine networks are given life by an interplay of technology, business and policy that must be considered holistically — we stand to gain great value from harmonizing our approaches to this fundamentally international matter.

In February, we held our first summit on submarine cable resilience in Abuja, Nigeria.

The summit’s declaration promotes global cooperation on areas including the strengthening of cable resilience through risk mitigation, promoting diverse routes and landings, and facilitating timely deployment and repair.

Alongside rising demand for data, route diversity for resilience has become a key driver for new cable rollouts.

Route diversity also includes an important development dimension, with underserved regions and Small Island Developing States especially vulnerable to cable service disruptions.

Enabling policies and regulations could support faster repairs, as could data-driven approaches to cable monitoring and risk assessment.

The Abuja Declaration also highlights the importance of sustainable approaches, technological innovation, and capacity building, with emphasis on preparing for both present and future connectivity needs.

This momentum continued at the World Summit on the Information Society High-Level event in July, where Advisory Body members gathered with the development community to discuss how to make the invisible backbone of global digital connectivity more resilient.

This year, ITU marks its 160th anniversary.

We are proud to have supported the submarine telecoms industry since its very beginnings, which also date back to the mid-1800s.

ITU standards underpin every technical aspect of this vital infrastructure, from cable design and construction, to deployment, operation, maintenance and repair.

This year, ITU marks its 160th anniversary. We are proud to have supported the submarine telecoms industry since its very beginnings, which also date back to the mid-1800s

Just as standards provide the technical foundations for global business ecosystems, our collective efforts and continued collaboration can help build the consensus essential to cable resilience.

Greater cable resilience will demand synergy in the actions of stakeholders across the public, private, and academic sectors alike.

I am confident readers of this report will rise to the occasion, and wish you every success in your work to ensure that undersea networks connect our world meaningfully and sustainably for generations to come.

Doreen Bogdan-Martin ITU Secretary-General

METHODOLOGY

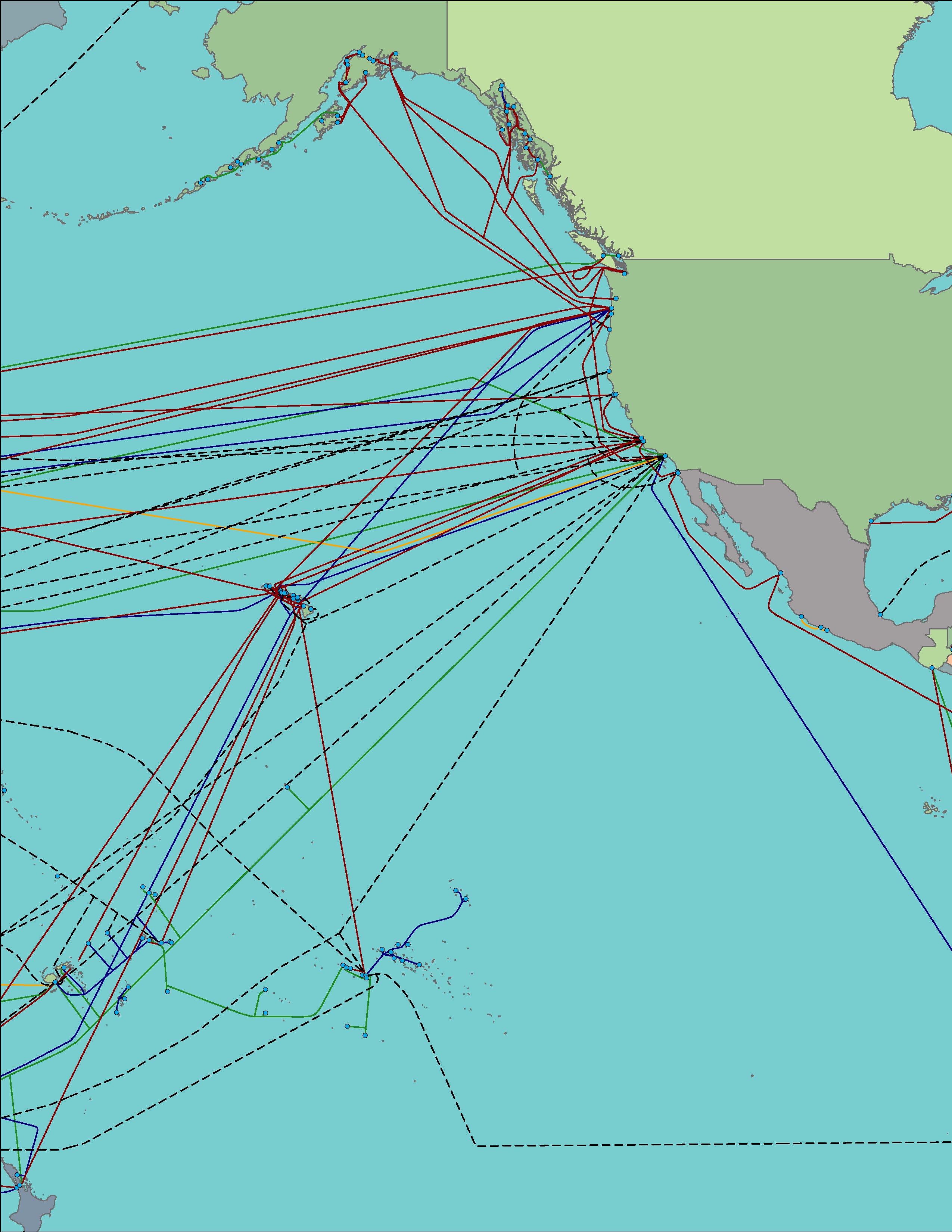

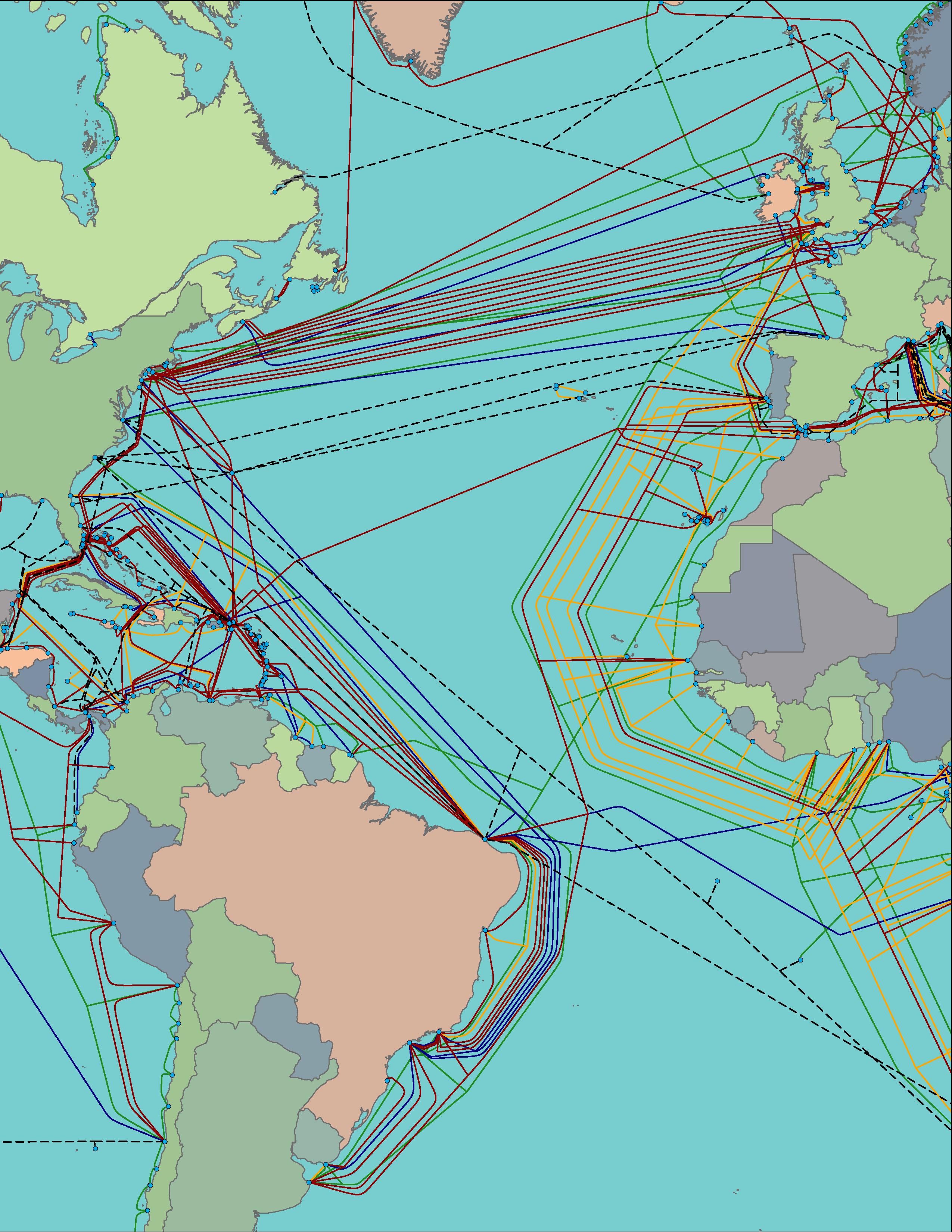

This edition of the Submarine Telecoms Cable Industry Report was developed by the analytical team at Submarine Telecoms Forum, Inc., who also produce ongoing research for SubTel Forum Magazine, the Submarine Cable Almanac, the Submarine Cable Map Series, and the SubTel Industry Newsfeed. The report draws from the Submarine Cable Database, a proprietary data resource continuously maintained since 2013. This database serves as the foundation for all quantitative and visual analyses presented in the report, encompassing more than 500 active and planned domestic and international systems. It enables precise querying by year, region, length, capacity, ownership, installation contractor, project status, data center connectivity, and numerous other parameters

The process of data collection for this report is ongoing throughout the year and involves a diverse network of sources that include public regulatory filings, corporate disclosures, government infrastructure reports, supplier announcements, and industry press releases. In addition to these sources, the SubTel team conducts regular interviews and direct correspondence with cable owners, operators, manufacturers, and installers to verify and enrich available data. Each new data point is ingested through a structured process that includes tagging, classification, and source verification. Where possible, data are cross-referenced against at least two independent sources to ensure reliability. In cases where discrepancies arise, follow-up verification is conducted through direct outreach to industry participants or by consulting archival project documentation.

The Submarine Cable Database operates on a MySQL backend, designed for scalability and efficient data retrieval. Each system record is assigned a unique identifier, allowing for longitudinal tracking of project changes over time. Prior to integration, all data undergo consistency checks to eliminate duplication and ensure proper alignment with historical entries. The team maintains a detailed changelog schema that records each edit, which in turn allows analysts to trace the evolution of individual cable records across multiple reporting cycles/.

Data verification is a key component of this methodology. Automated validation scripts routinely scan the database for internal inconsistencies, such as incorrect length-to-capacity ratios or missing geospatial identifiers. These automated checks are complemented by manual reviews, during which analysts examine geographic accuracy using ArcGIS Pro overlays and other mapping tools. All landing points, regional groupings, and route alignments are visually verified against satellite and published marine route data. Financial fields are audited to ensure that cost estimates are correctly expressed in U.S. dollars and adjusted for inflation where applicable, maintaining uniformity across reporting years.

All visual outputs in this report are generated in ArcGIS Pro and Microsoft Power BI. The former is used to produce maps with consistent geospatial fidelity, following the visual and cartographic standards of the Submarine Cables of the World print map. Power BI is connected directly to the live database, ensuring

that every chart, graph, and data table in the report reflects the most current information available. This real-time integration enables seamless updates to visualizations whenever new data are incorporated into the database.

The analytical framework applied to this report includes descriptive, comparative, and predictive techniques. Descriptive analysis provides an overview of the current cable system landscape, summarizing distributions by geography, technology type, and ownership structure. Comparative analysis explores change over time, examining metrics such as regional growth, deployment trends, and technological advancement. Predictive modeling, executed through Power BI’s Exponential Smoothing (ETS) forecasting function, extends these observations into future projections. This model accounts for seasonality, trend persistence, and random variance within the data to produce forward-looking estimates that balance statistical rigor with practical interpretability.

Forecasting relies on a combination of historical trend modeling and exponential smoothing. The Compound Annual Growth Rate (CAGR) is calculated through two separate approaches: a fixed-period method that measures overall growth over a defined span, and a rolling two-year method that reduces volatility and provides a clearer picture of short-term fluctuations. Where gaps exist in public reporting—particularly following the 2019 adjustments to FCC data disclosure requirements—capacity projections are estimated using averaged historical growth rates from 2015 through 2018 as a baseline. These projections are further refined through model calibration, in which historical deviations are analyzed to fine-tune the forecast parameters.

For unrepeatered cable systems, a maximum modeled length of 500 kilometers is applied except in cases where longer systems are publicly confirmed. Future deployment trends for these systems are extrapolated linearly, based on the ratio of historical installation rates to regional project announcements. System cost estimates are derived from publicly available figures when disclosed; otherwise, a standardized industry average of seventy-five thousand U.S. dollars per kilometer is applied. This figure represents a blended average adjusted for inflation and the typical cost differential between shallow-water and deep-sea deployments.

A rigorous quality assurance process underpins every stage of this methodology. Once the analytical phase concludes, a secondary review is conducted by senior members of the SubTel research team, who re-verify key system data and recalculate sample metrics to confirm the accuracy of both the source database and the analytical outputs. All data visualizations are regenerated directly from live Power BI dashboards, ensuring consistency between graphical elements and the underlying data. This multi-step validation process minimizes the risk of error propagation and reinforces the integrity of both the current dataset and its forward-looking projections.

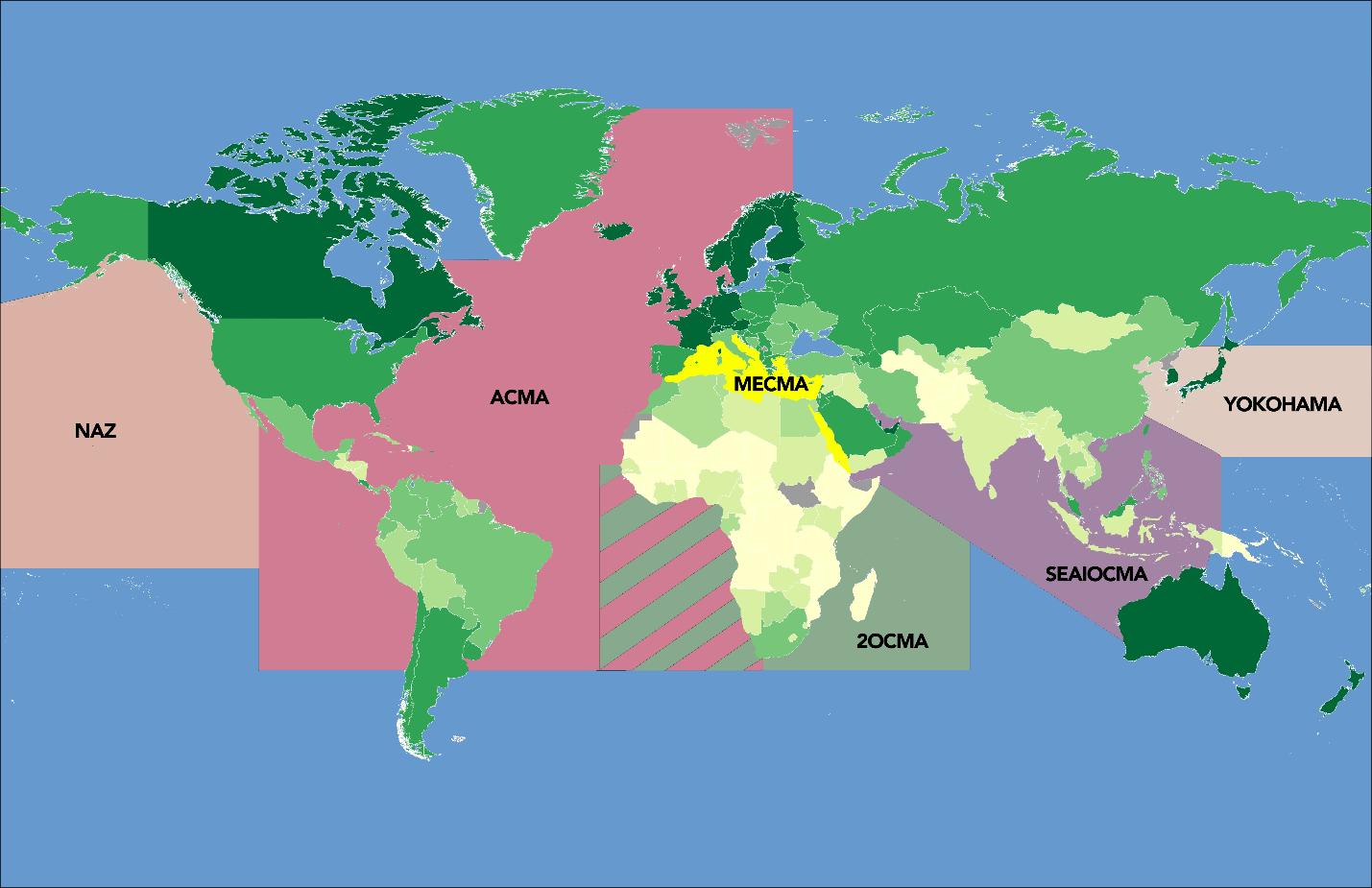

ACRONYMS & DESCRIPTIONS

Acronym

16QAM

2OCMA

4G / 5G

AAE-1

ACMA

ACPL

Definition

16-Level Quadrature Amplitude Modulation – high-order modulation format transmitting 4 bits per symbol for greater spectral efficiency.

2 Oceans Cable Maintenance Agreement – covers southern Atlantic and Indian Oceans; operated from Cape Town.

Fourth / Fifth Generation Mobile Network – wireless technologies that drive higher data demand and subsea backhaul.

Asia–Africa–Europe-1 – subsea cable connecting Asia, the Middle East, and Europe.

Atlantic Cable Maintenance Agreement – covers North Atlantic, SE Pacific, and Northern Europe.

Airtel Cable Partners Ltd. – participant in the SEAIOCMA maintenance framework.

AI Artificial Intelligence – technology enabling machines to perform human-like tasks and driving hyperscale data and bandwidth growth.

AIS

APAC

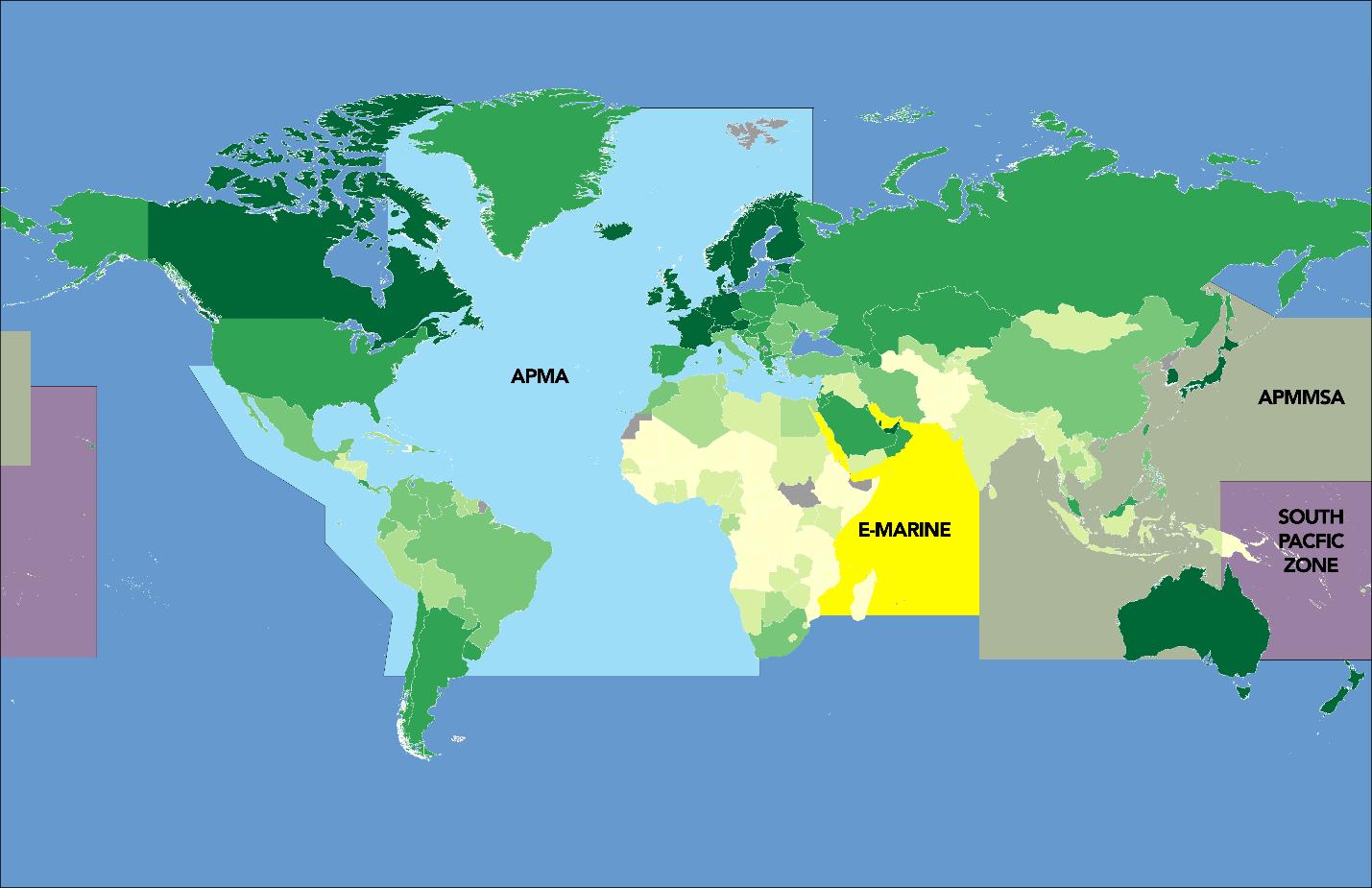

APMA

APMMSA

Automatic Identification System – vessel-tracking technology for monitoring ships near subsea cables.

Asia-Pacific – regional grouping central to hyperscale and subsea growth.

Water Usage Effectiveness – efficiency metric for water consumption in cooling systems.

YoY Year over Year – annualized growth comparison metric. µm Micrometer (Micron) – unit of fiber diameter measurement.

EXECUTIVE SUMMARY

The global submarine cable industry ends 2025 in a phase of structural maturity, characterized by sustained investment, stable financing, and increasing interdependence between infrastructure, regulation, and sustainability. After a decade of exponential buildout, the sector has transitioned from rapid expansion to strategic coordination—balancing growth with resilience, efficiency, and accountability. This year’s report offers a comprehensive analysis of these dynamics, highlighting emerging trends in ownership, financing, technology, and governance across all major regions.

While annual system deployment remains strong, the industry’s defining challenges have shifted. Geopolitical tension, supply chain constraints, and climate considerations now shape investment and project timelines as much as technology does. As subsea infrastructure becomes more deeply embedded in global security and economic systems, 2025 marks the consolidation of a new operational paradigm—one focused on coordination, regulation, and sustainability rather than pure expansion.

Subsea cables have become a focal point of global policy. Building on the momentum of prior security frameworks, 2025 has seen the integration of competition law, national resilience, and sustainability policy into unified governance efforts. The formation of the International Advisory Body on Submarine Cable Resilience underscores growing recognition of cables as critical international infrastructure. Parallel regulatory inquiries, including the UK CMA’s ongoing review of hyperscaler concentration, reflect heightened scrutiny of capacity control and antitrust dynamics in the subsea sector.

Governments are increasingly balancing intervention with collaboration. Public-private partnerships (PPPs) remain a key model for bridging security and innovation, while state-backed repair vessels and infrastructure initiatives hint at an era of deeper government involvement. The geopolitical importance of subsea connectivity is no longer questioned—it is a strategic reality shaping both policy and investment.

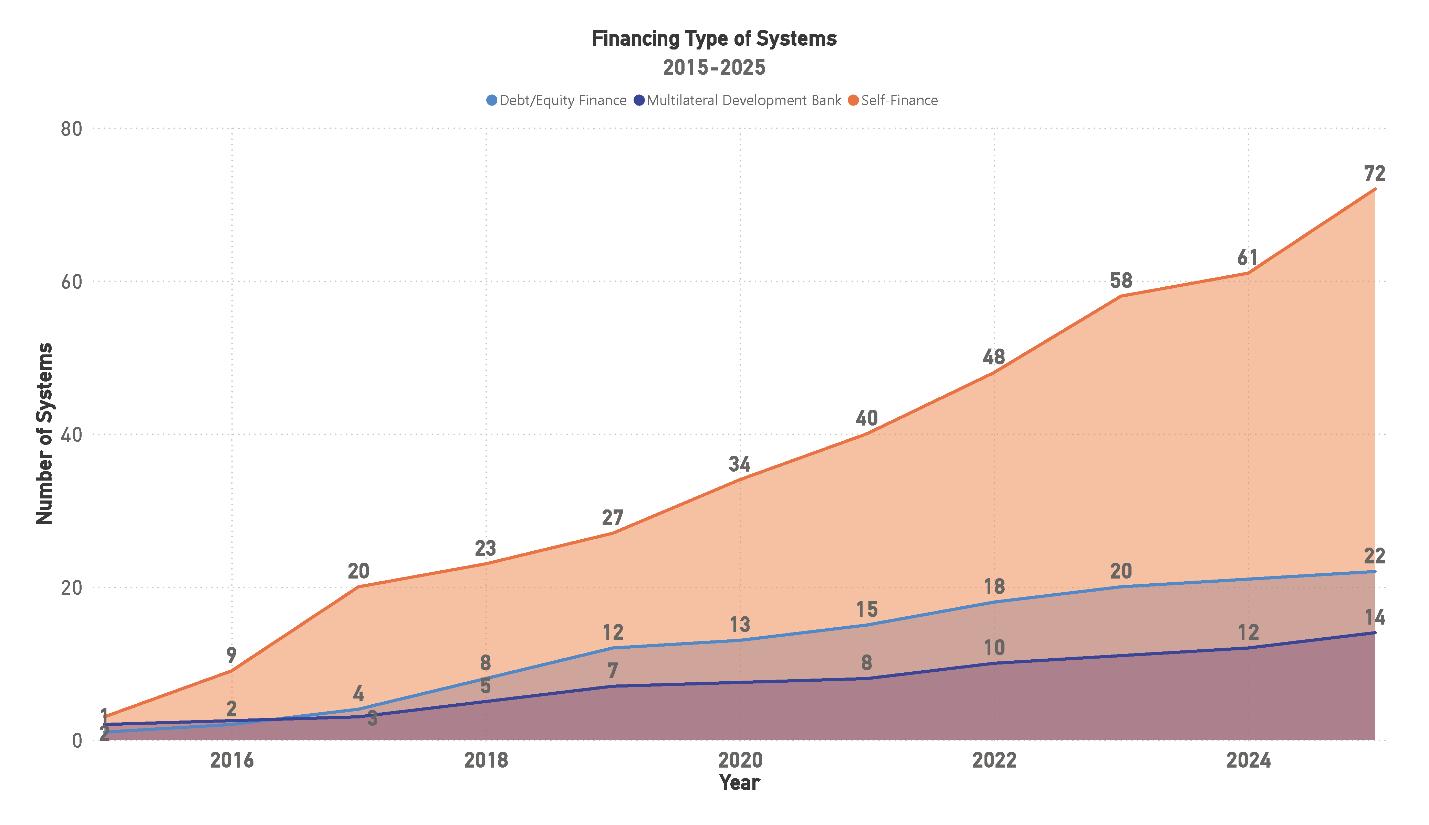

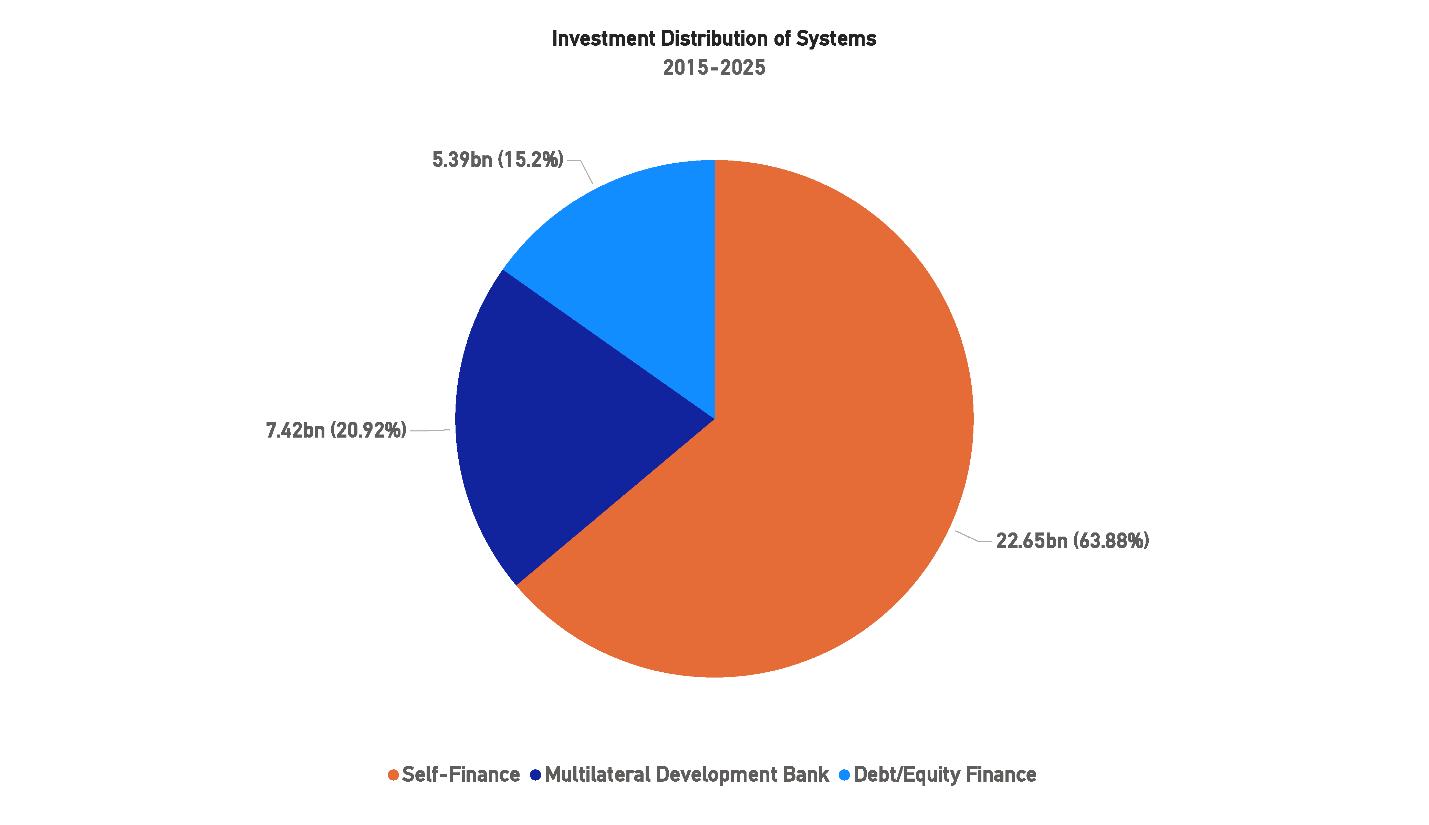

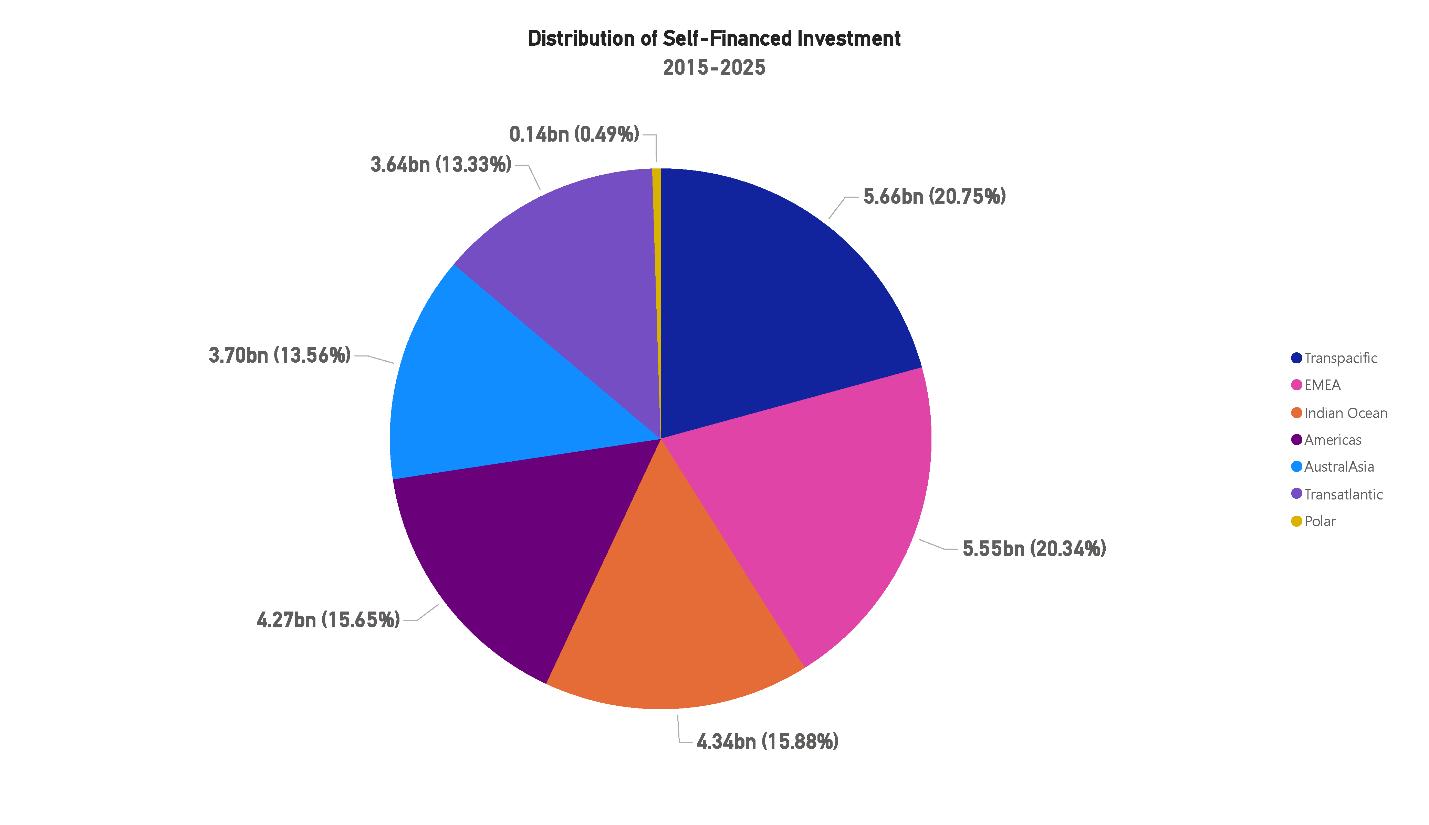

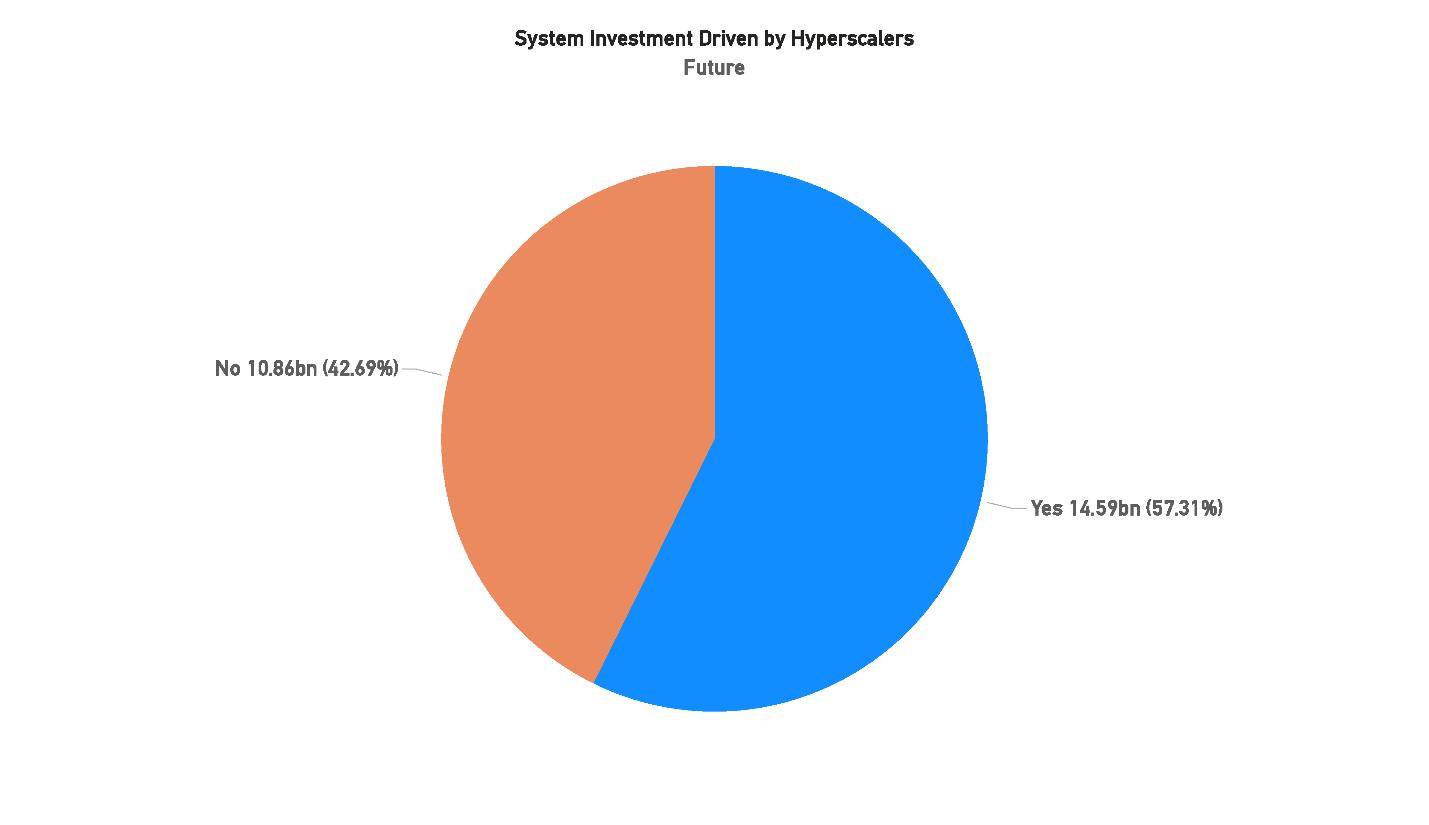

“Self-financing accounts for roughly two-thirds of global project capitalover USD $22 billion.”

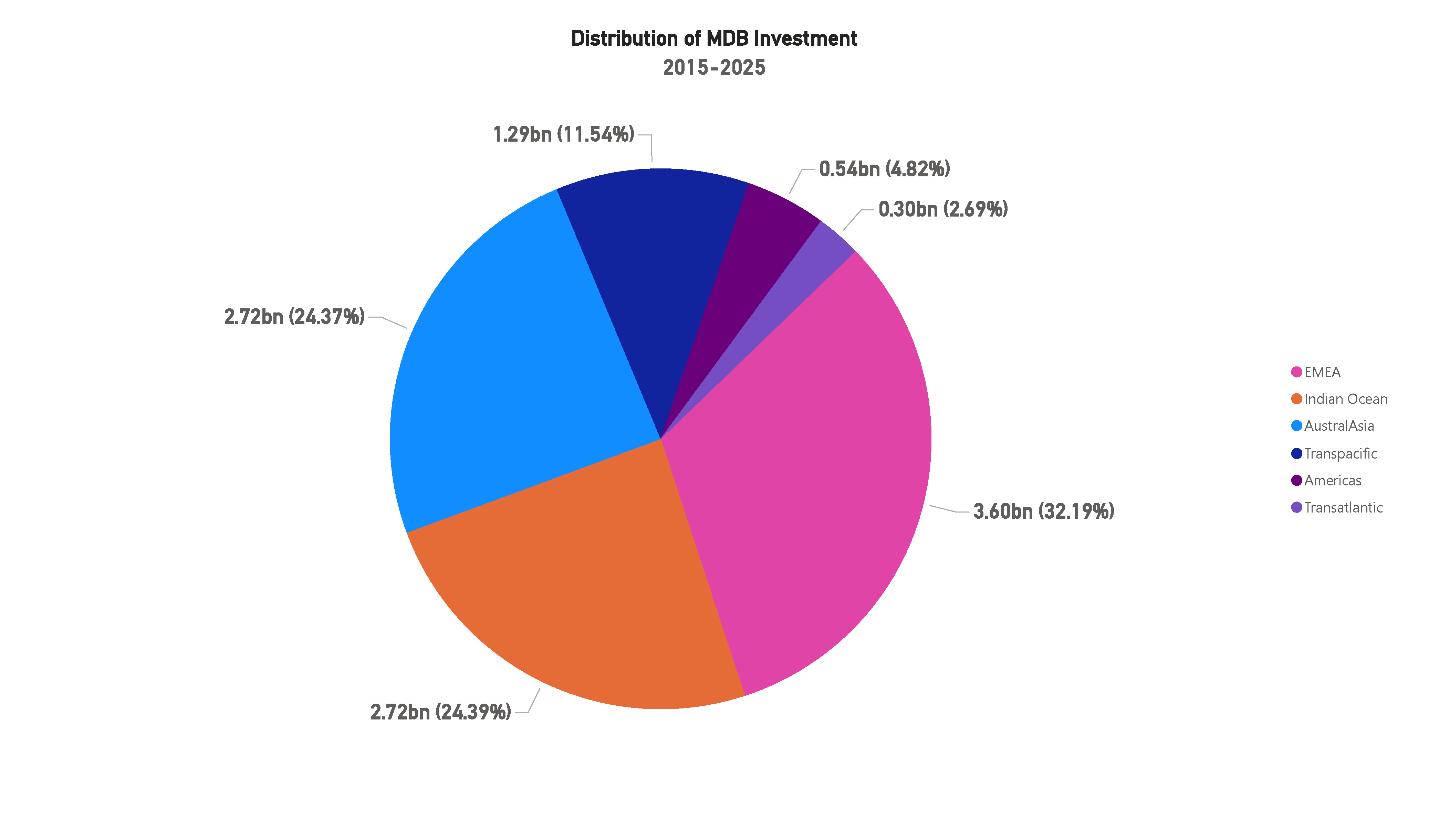

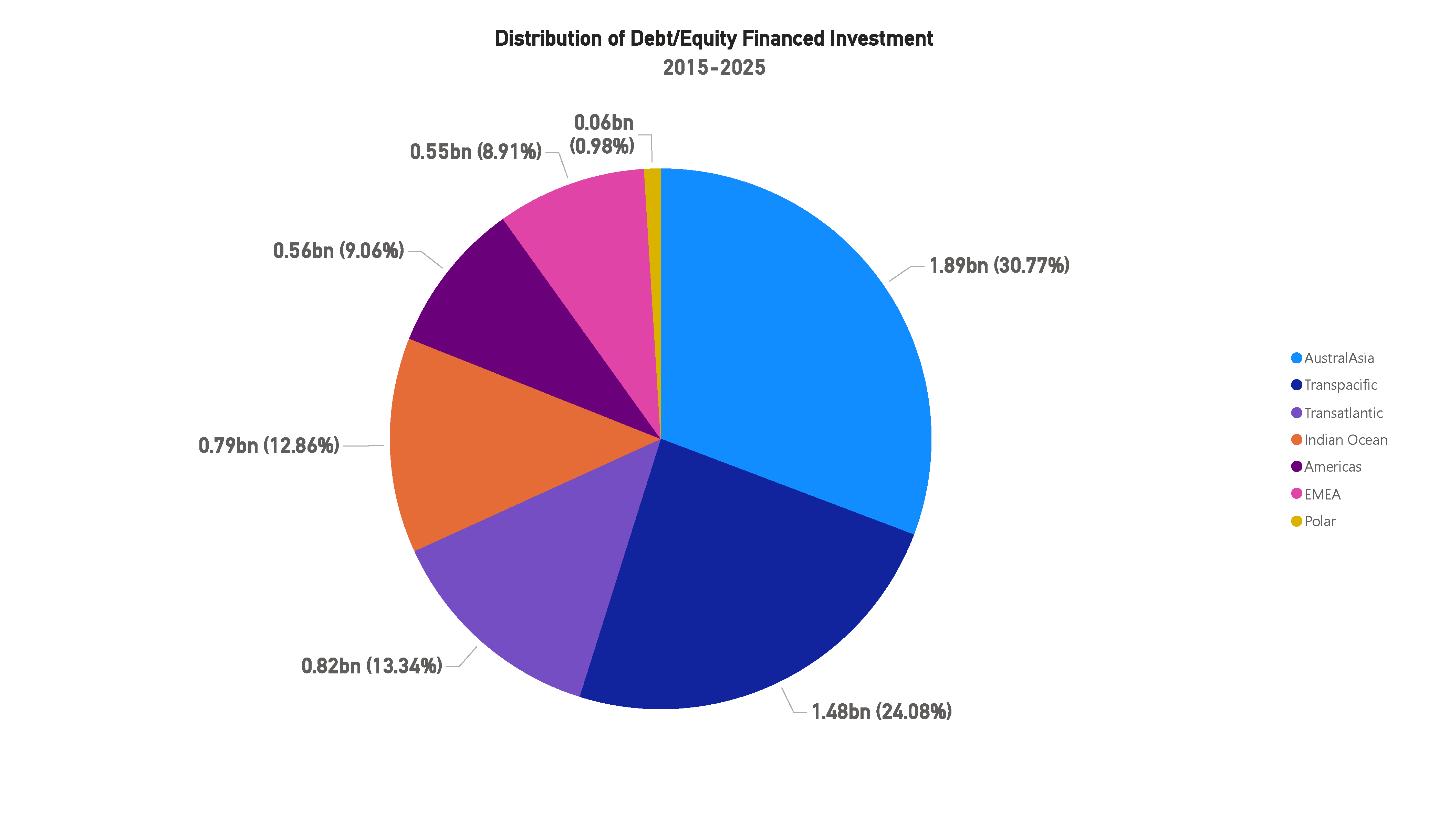

Financing trends reveal a sector that is both independent and adaptive. Self-financing accounts for roughly two-thirds of global project capital—over USD $22 billion—demonstrating the industry’s maturity and confidence. Multilateral Development Bank (MDB) participation remains vital in emerging markets, particularly across Asia-Pacific and the Indian Ocean, where development and security priorities intersect. Debt and equity partnerships are expanding, signaling diversification and risk-sharing as operators pursue long-term stability.

This rebalancing of capital flows illustrates a subtle but important evolution: financial decisions are increasingly driven by geopolitical logic, with investors seeking redundancy, resilience, and regional diversification rather than simply capacity growth.

Technological progress continues to refine, rather than redefine, the industry. The widespread adoption of multi-core and hollow-core fiber, coupled with intelligent network management, is driving efficiency gains across existing infrastructure. Global lit capacity now averages 60% utilization, a historic high that reflects a more disciplined alignment between demand and deployment. Innovations like smart repeaters, 800G wavelengths, and SDM refinements emphasize optimization over expansion—signaling a mature phase of data-driven engineering and operational precision.

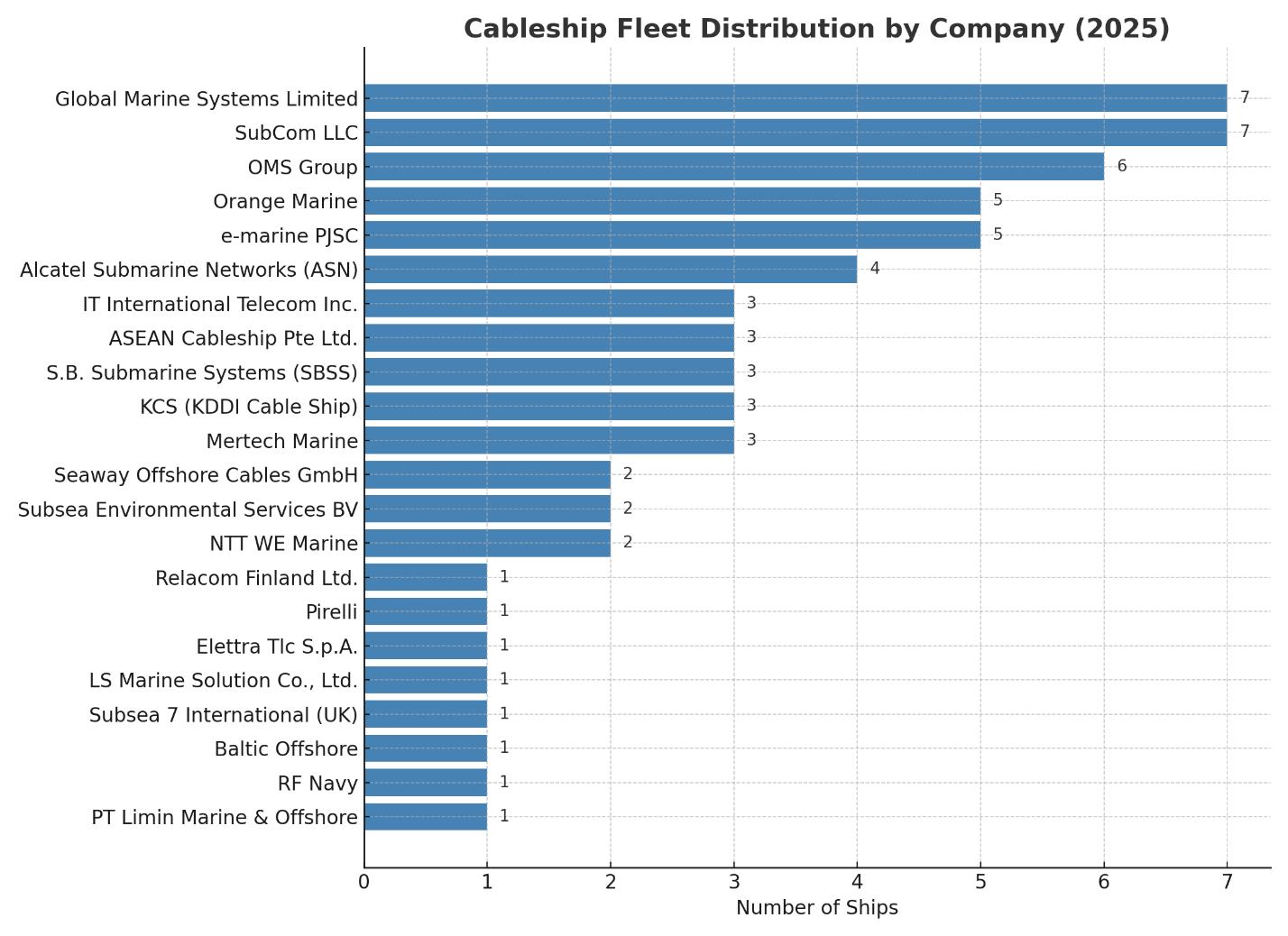

The global cable ship fleet remains a structural bottleneck, holding steady at 63 active vessels. Despite incremental new-

“The global cable ship fleet remains a structural bottleneck, holding steady at 63 active vessels.”

build plans, capacity constraints persist, especially in maintenance coverage across underserved regions such as Africa and the South Pacific. AIS data continues to show vessel concentration near logistical hubs including Singapore, Marseille, and Halifax, underscoring the operational dependence on a limited number of depot clusters. This reality has begun to shape project scheduling, system repair turnaround, and regional resilience planning.

“Perhaps the most transformative development in 2025 is the normalization of sustainability metrics across the industry.”

Perhaps the most transformative development in 2025 is the normalization of sustainability metrics across the industry. Initiatives such as the SubOptic Foundation’s Sustainability Standards and the introduction of PUE, CUE, and REF benchmarks have established measurable baselines for environmental performance. Cable recovery and recycling programs are expanding, while landing stations are increasingly designed to meet verified energy and water efficiency targets. Sustainability is no longer an external expectation—it is now an internal standard embedded in project design, financing, and corporate governance.

A new generation of talent is reshaping the cultural and intellectual fabric of the subsea industry. University programs—such as the University of California, Berkeley’s Sustainable Subsea Networks initiative—are creating formal education pathways that blend engineering, sustainability, and policy. The influx of students and early-career professionals is infusing the sector with fresh perspectives on governance, ethics, and long-term stewardship. This trend signals an enduring shift toward intergenerational continuity and institutional accountability.

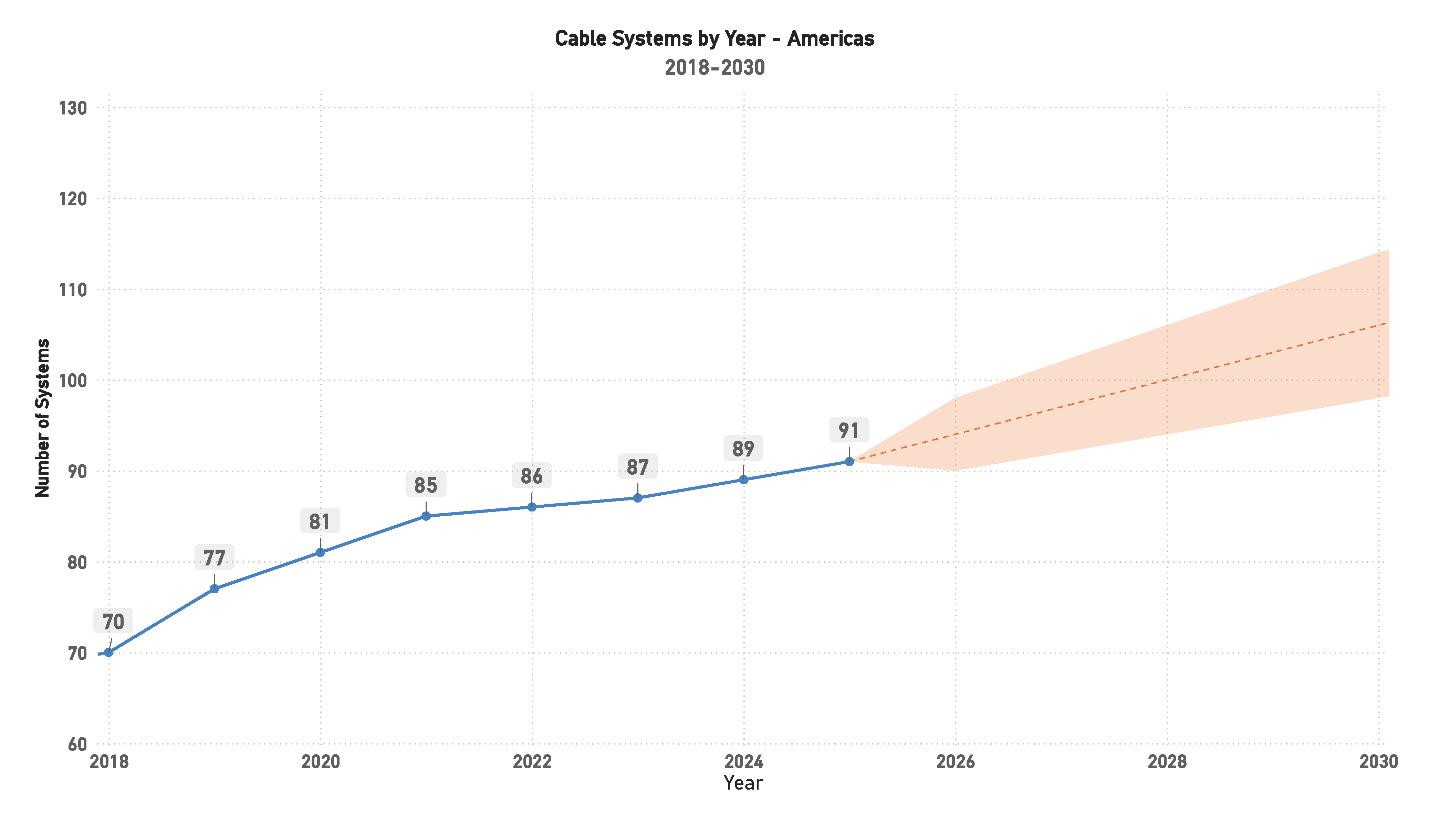

The Americas region continues to show steady growth, driven by hyperscaler investment and system upgrades across North and South America. With 91 active systems, the market remains stable and largely self-financed, reflecting a mature investment environment. Development now centers on modernization and redundancy rather than new routes, though regulatory inconsistency and natural risks still affect project timelines.

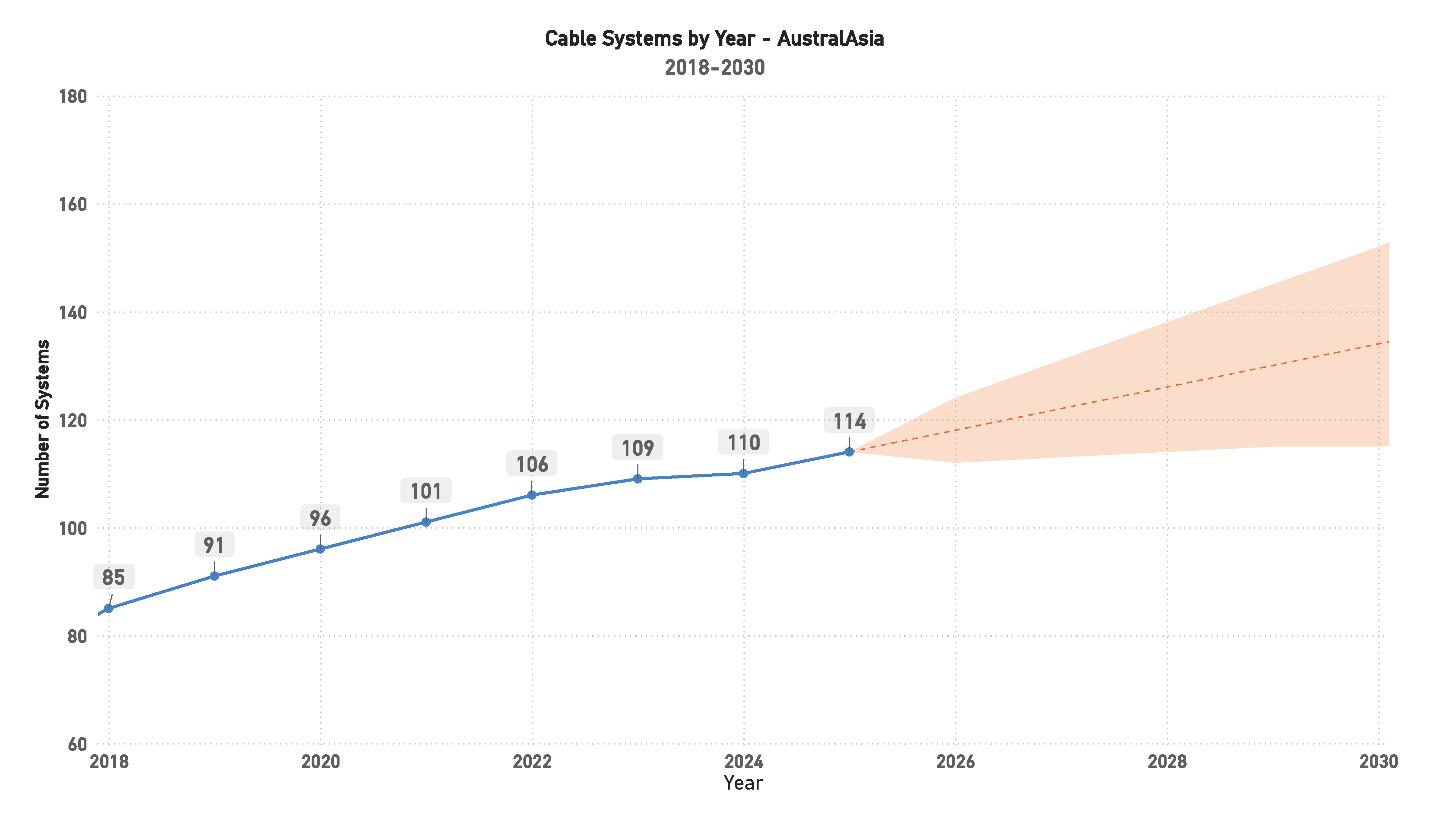

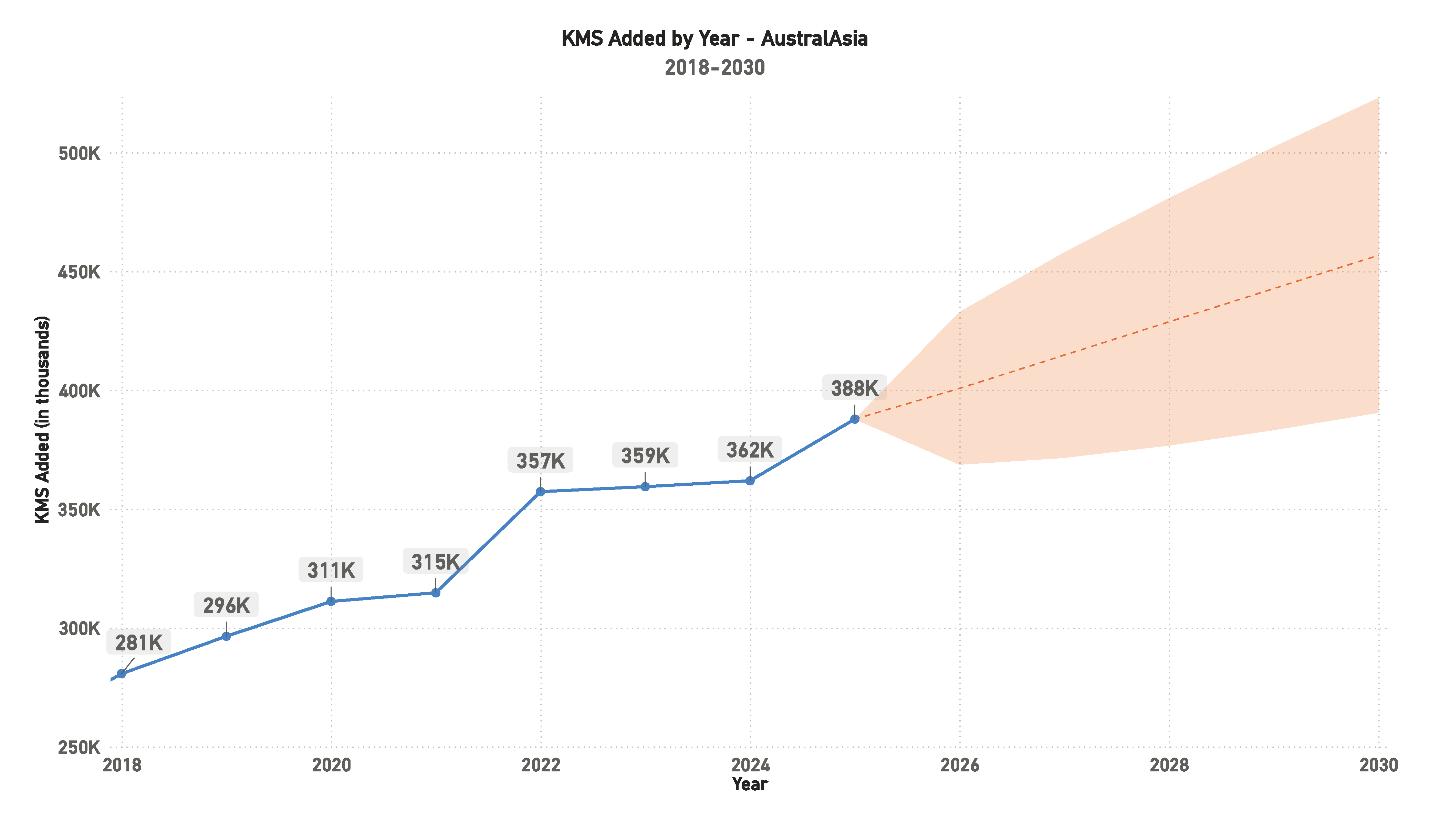

Across the Asia-Pacific and AustralAsia regions, expansion remains strong with 114 systems and 388,000 kilometers of cable in operation. Growth is fueled by large-scale hyperscaler projects and ongoing regional upgrades, supported by rising data center demand. Despite regulatory and environmental challenges in several Southeast Asian markets, the region is projected to surpass 450,000 kilometers by 2030, maintaining its role as a key engine of global capacity growth.

“Across the Asia-Pacific and AustralAsia regions, expansion remains strong with 114 systems and 388,000 kilometers of cable in operation.”

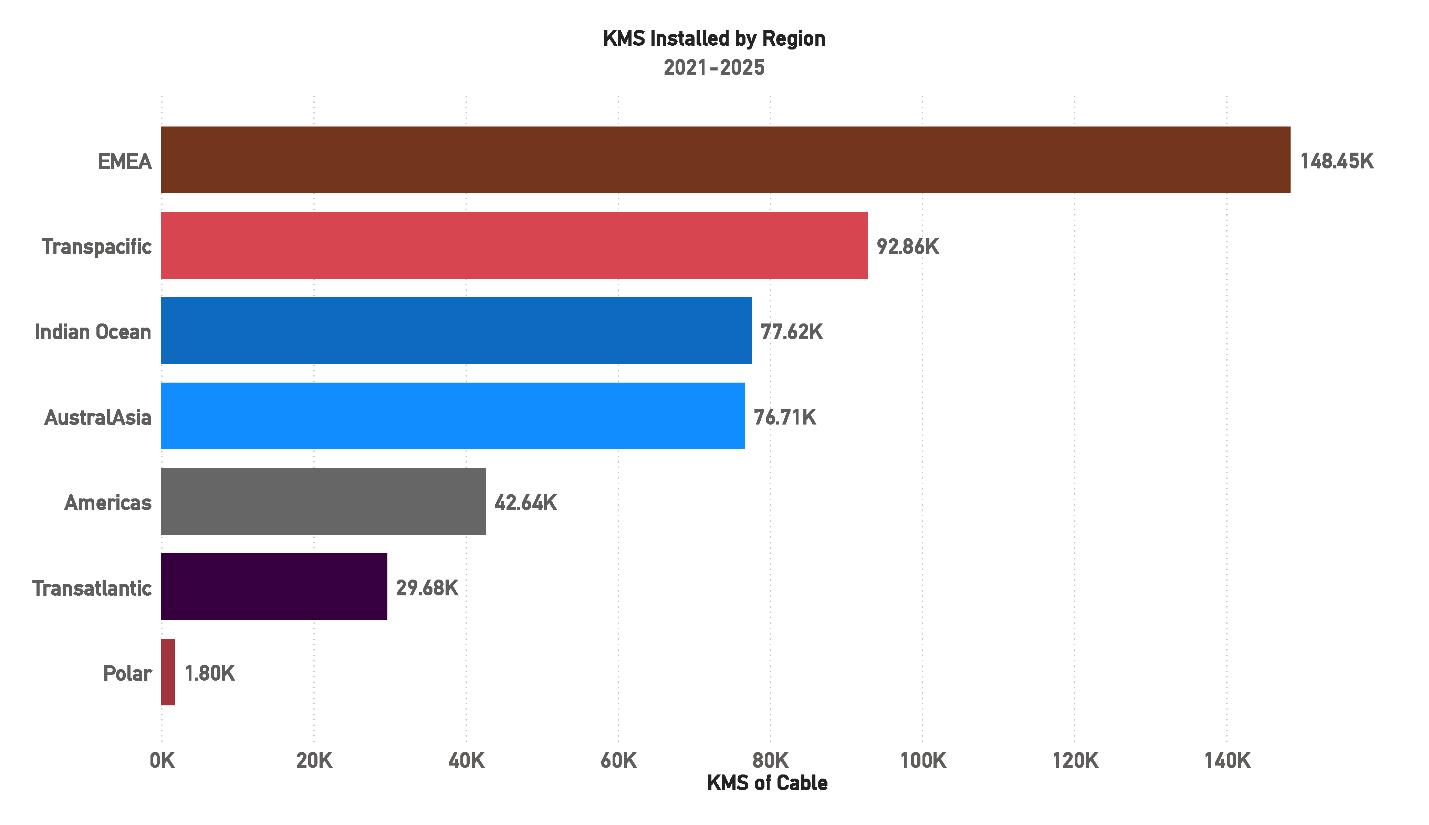

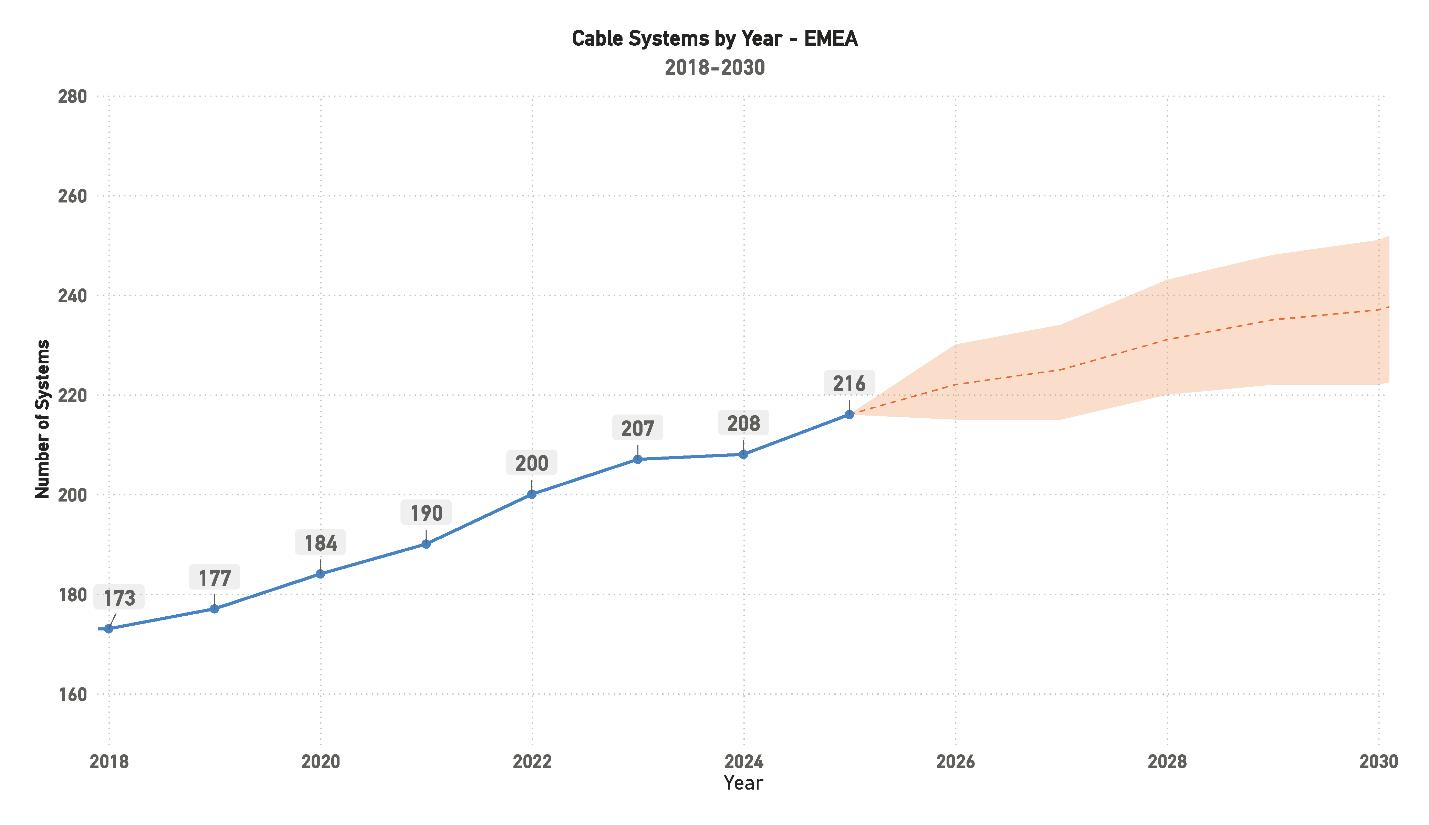

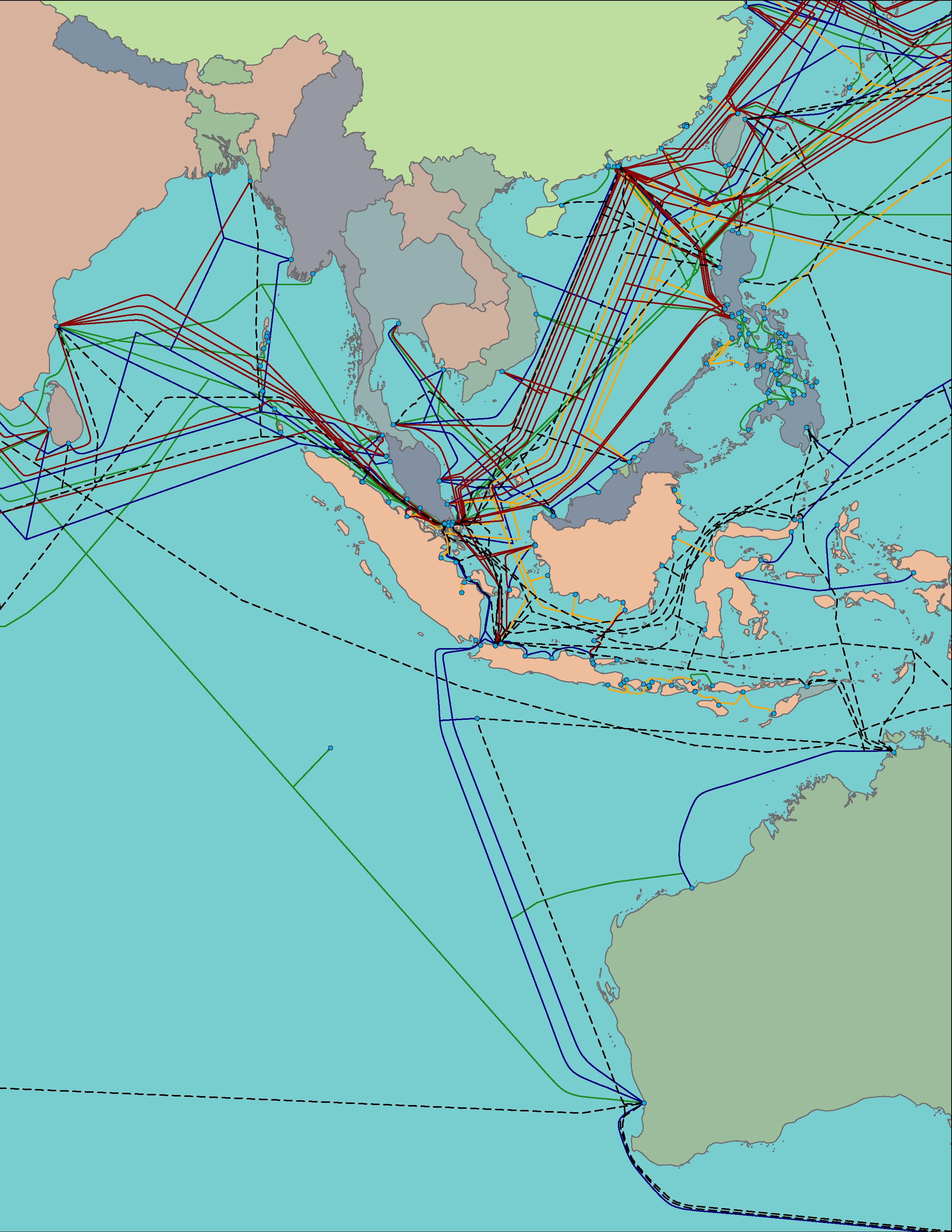

The EMEA region (Europe, Middle East, and Africa) remains the largest and most complex segment of the global subsea market, with 216 systems and 433,000 kilometers of infrastructure. While large-scale expansion continues, particularly in Africa, the region faces regulatory and political challenges, especially around the Red Sea and Suez corridors. Future priorities focus on resilience, route diversity, and network security across the Mediterranean and North Atlantic.

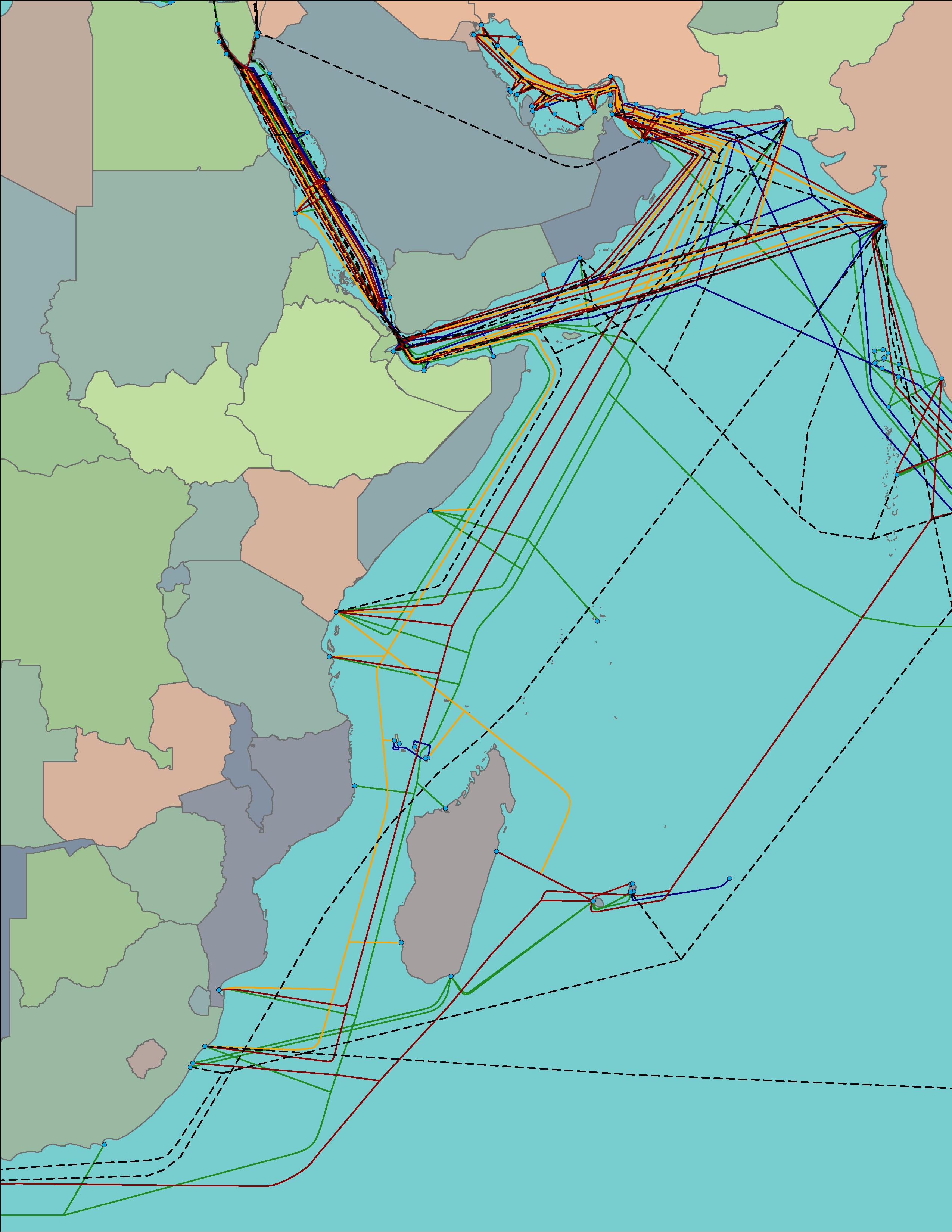

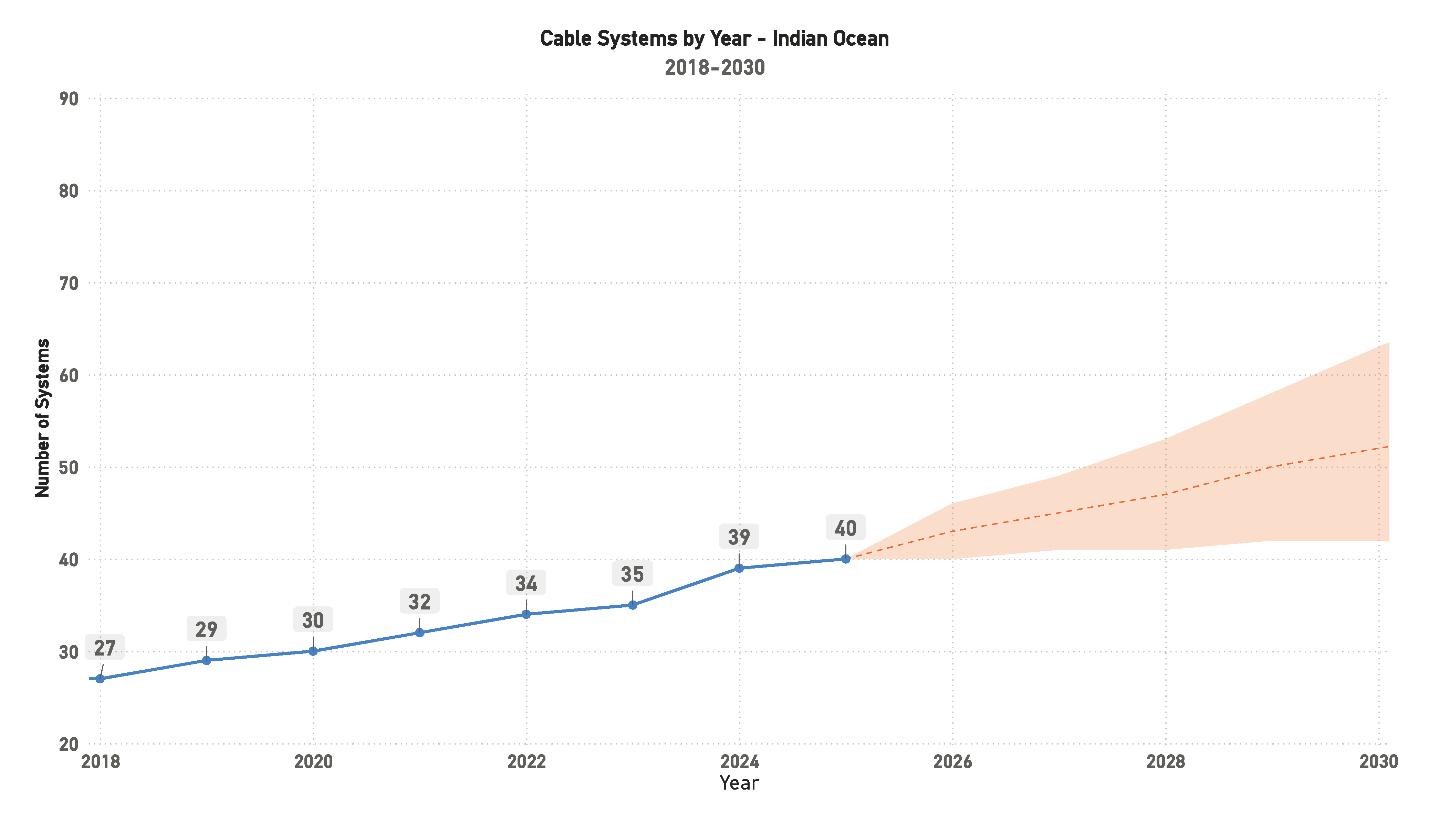

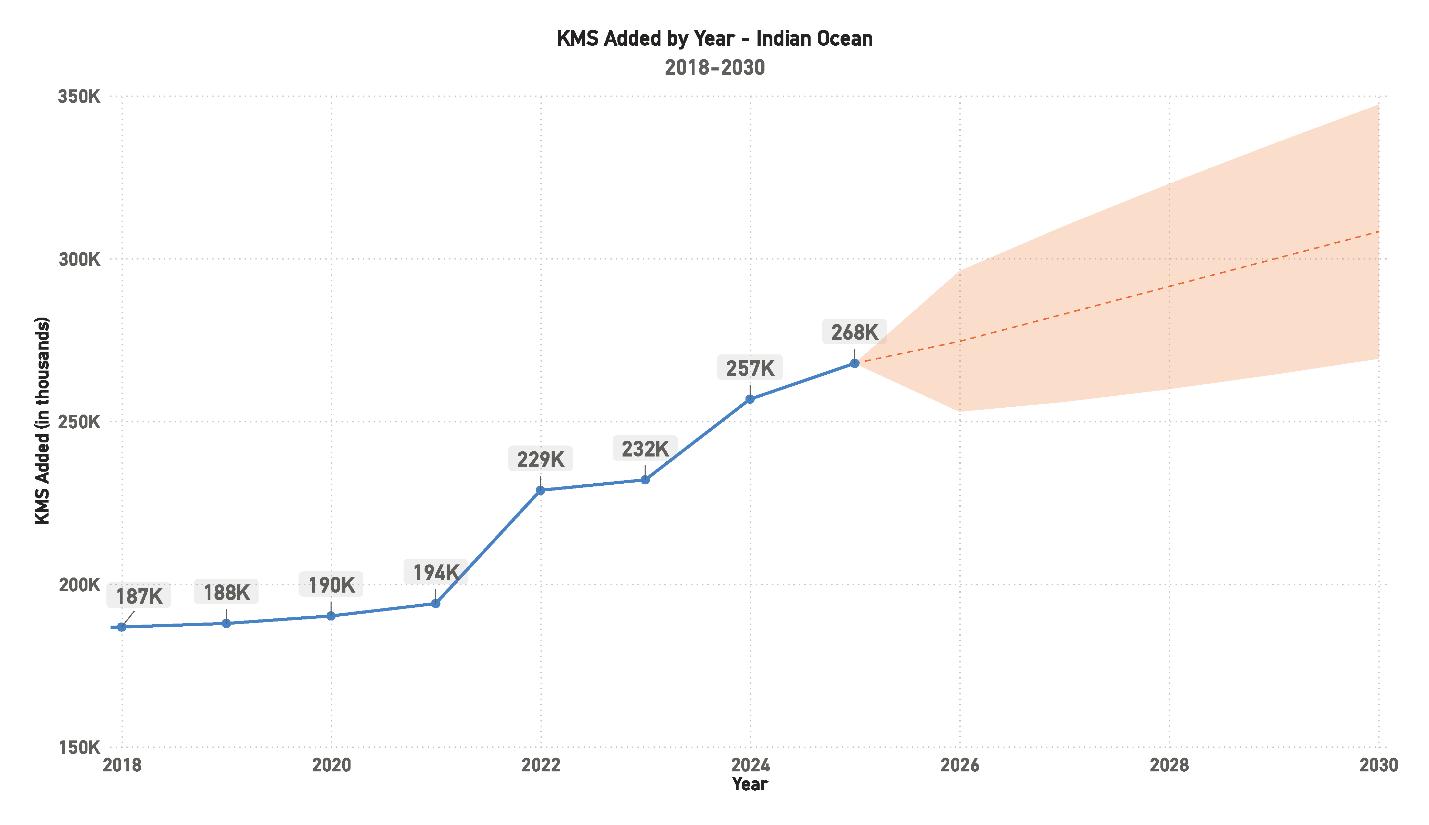

The Indian Ocean region has become an important connectivity bridge between Asia, Africa, and Europe. It now supports 40 systems totaling 268,000 kilometers, projected to exceed 300,000 kilometers by 2030. Growth is steady but uneven, reflecting varied regulatory and economic conditions, while the re-

gion’s strategic role in global redundancy continues to expand.

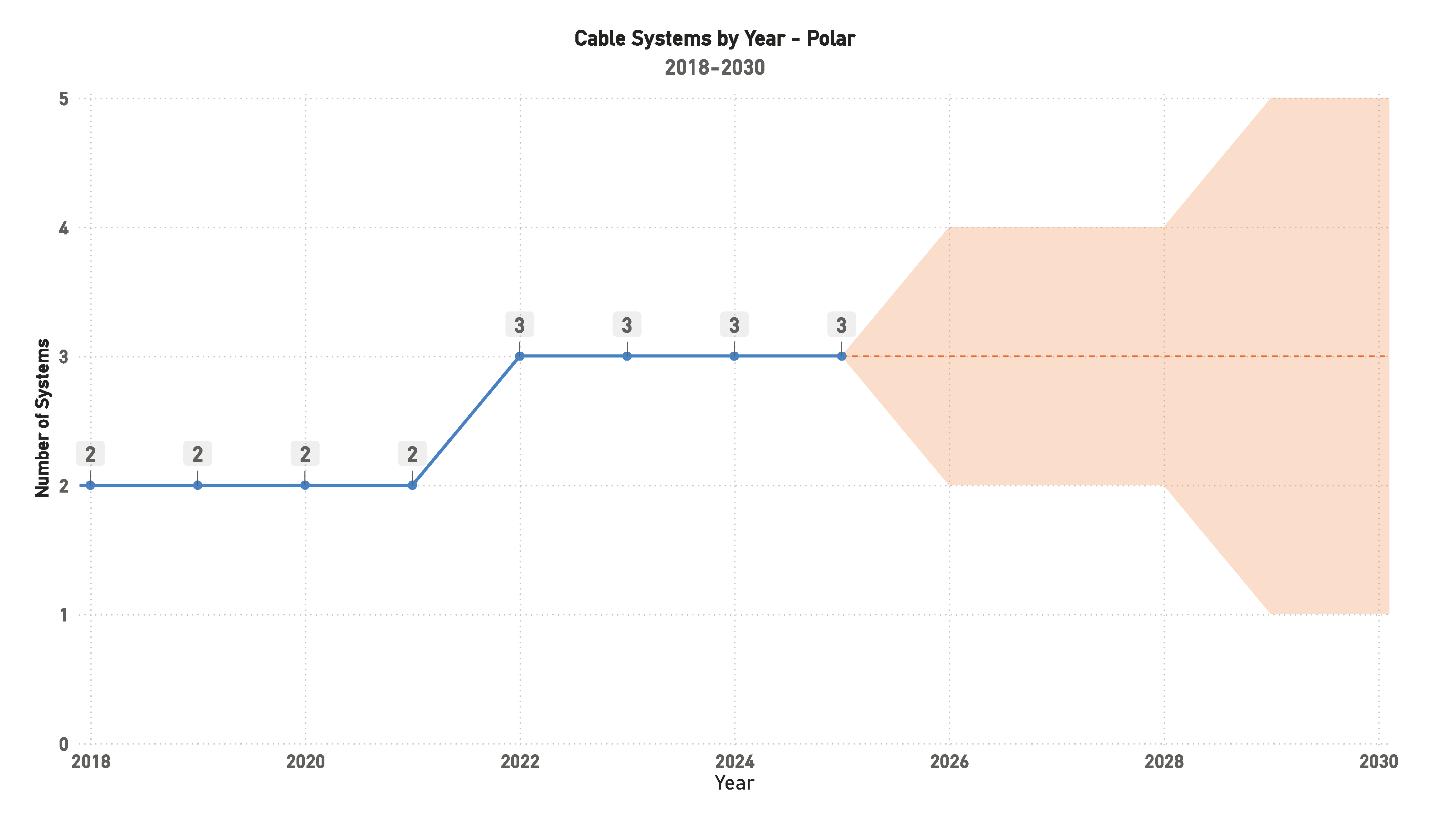

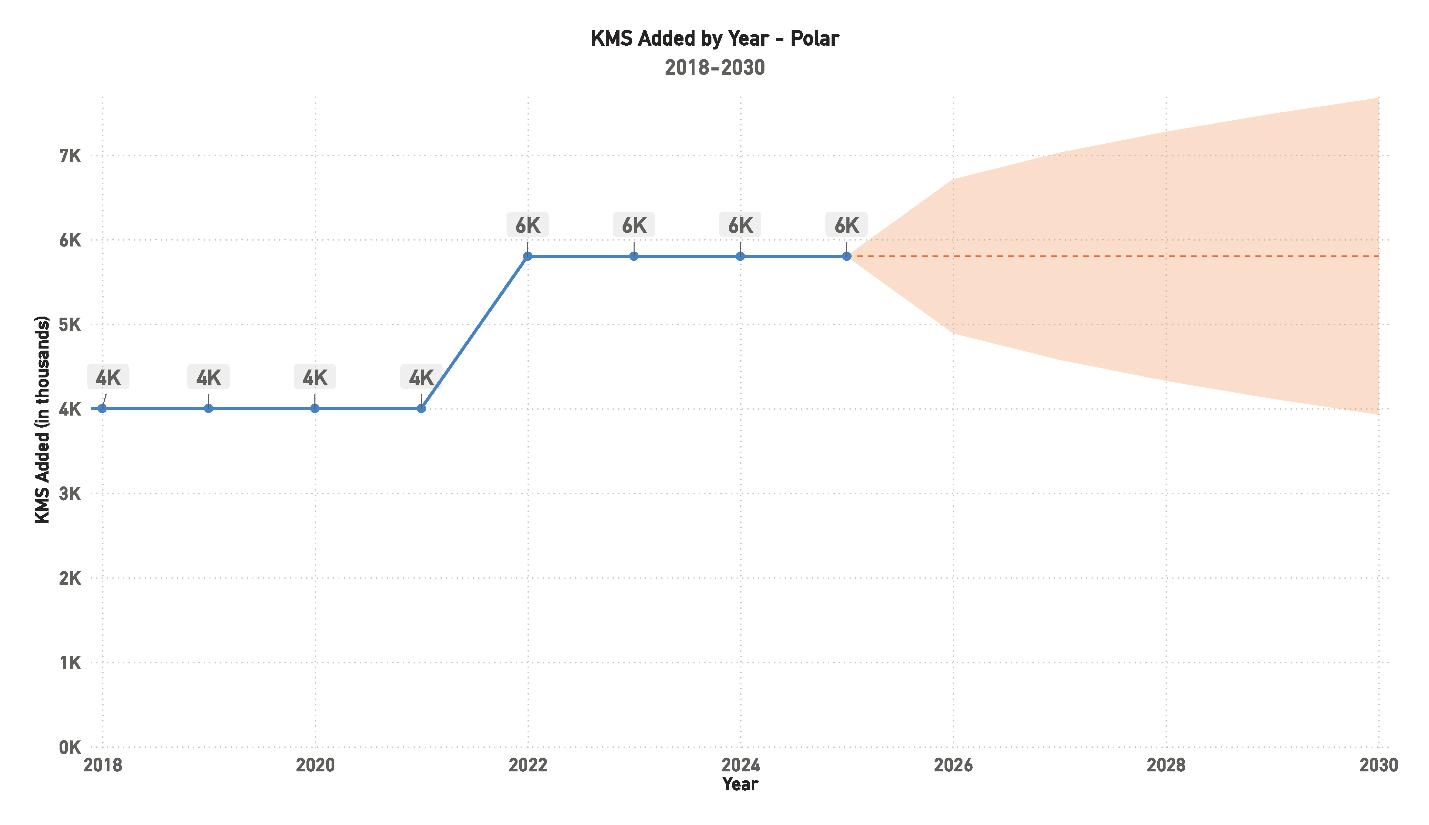

The Polar region remains small but strategically significant, with three operational systems and four in planning. Development is limited by cost, climate, and geopolitical barriers, but long-term prospects include shorter, lower-latency routes between Europe and Asia.

“The Polar region remains small but strategically significant, with three operational systems and four in planning.”

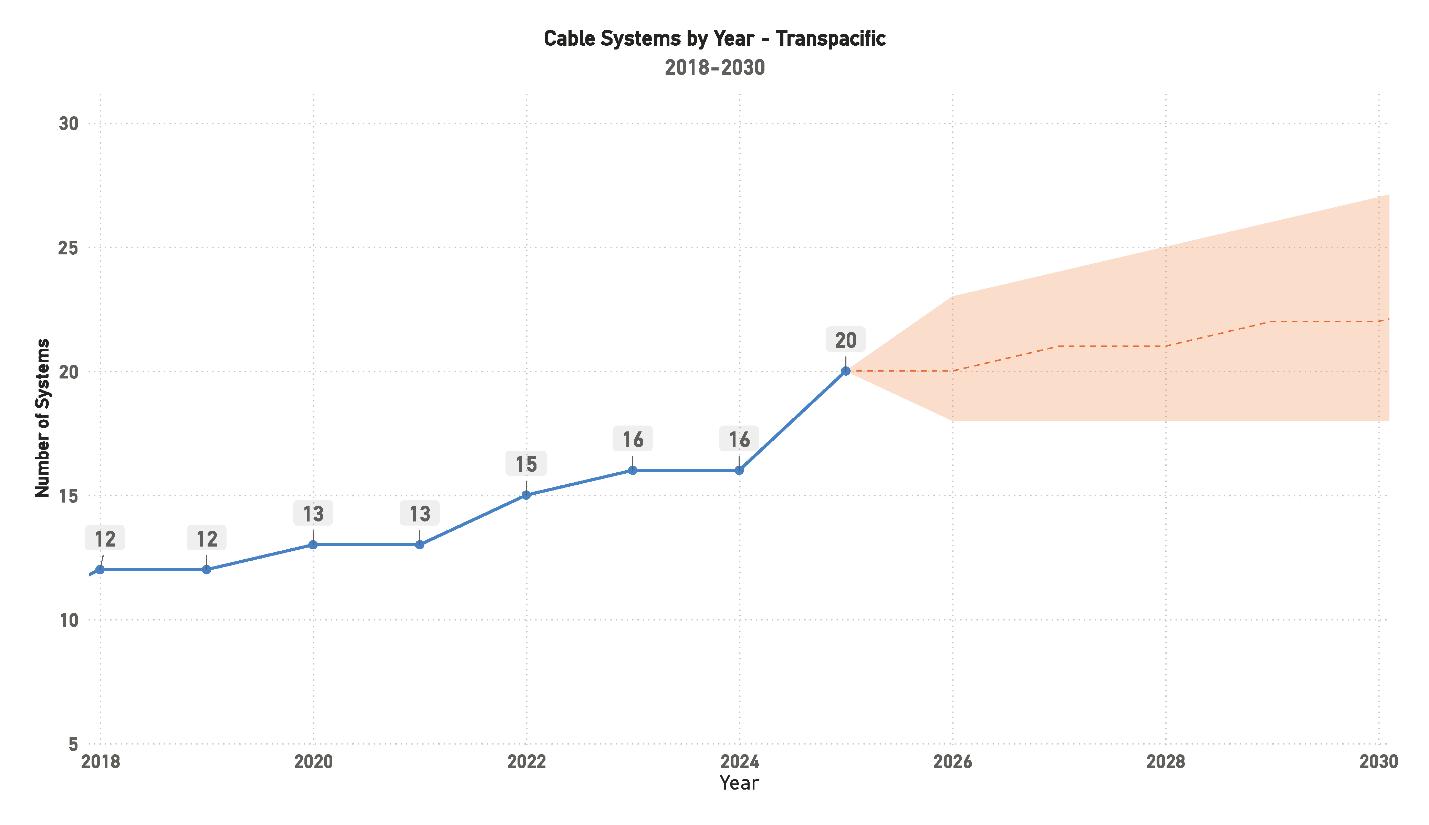

The Transatlantic and Transpacific corridors continue to define the backbone of global data transmission. The Transatlantic route remains the most established and heavily utilized, while the Transpacific corridor— now exceeding 300,000 kilometers of deployed cable—leads in new capacity additions and technology adoption. Both regions are shifting focus from expansion toward optimization, emphasizing efficiency, resilience, and route diversification as global data traffic continues to rise.

The coming years will test the industry’s ability to balance growth, resilience, and environmental responsibility within a fragmented global landscape. Market concentration among hyperscalers will continue to attract regulatory scrutiny, while investment diversification and public-private coordination will shape the next generation of connectivity projects.

Above all, the submarine cable industry stands at the threshold of an integrated era—where governance, technology, and sustainability converge to define its future. The cables that once symbolized raw expansion now represent global coordination: a networked infrastructure not just of fiber and steel, but of policy, accountability, and shared responsibility.

Rewriting how we explore SubTel Forum

Total Unique Authors: 770

Total Tags: 276

TOP 5 TAGS BY ARTICLE COUNT:

Network Operations & Management –943 articles

Technology – 820 articles

Risk & Safety Management – 720 articles

Project Management – 670 articles

Regions & Countries – 508 articles

1. GLOBAL OVERVIEW

1.1. INDUSTRY SENTIMENT

The first dedicated Industry Sentiment Survey was conducted in 2023, providing a foundational snapshot of perspectives within the submarine fiber-optic telecommunications sector. That inaugural effort captured broad industry attitudes around optimism, workload, and market confidence, offering a baseline for measuring growth and change. In 2024, the survey was refined with expanded, standardized questions to improve comparability and analytical depth. This methodological update established a consistent framework, enabling direct year-over-year trend tracking and richer insights into sentiment, investment, and operational dynamics. Now, with aligned datasets from 2024 and 2025, the survey provides a reliable, longitudinal view of how the industry perceives its health, challenges, and direction—an essential tool for understanding how confidence and activity evolve as the market continues to mature.

The 2023 responses reflected a market still emerging from several years of rapid global infrastructure expansion. Overall sentiment was positive, but cautious. Most participants described the industry as optimistic rather than very optimistic, signaling steady confidence tempered by uncertainty around project delivery timelines, regulatory pressures, and cost inflation. Investment expectations were moderate, with respondents citing selective capital deployment and regional disparities in growth potential. Workforce-related feedback emphasized both rising demand for technical expertise and growing concern about talent shortages, particularly in project engineering and marine operations. In retrospect, the 2023 findings captured an industry on the verge of acceleration—poised for the sustained optimism and activity levels that would define 2024 and 2025.

Together, the 2023 baseline and the now-standardized 2024 and 2025 surveys create a comprehensive, comparable dataset. The following analysis examines each question individually, illustrating how industry sentiment has evolved across key themes such as market outlook, investment, project performance, technology readiness, and workforce development. Each chart highlights measurable yearto-year shifts, offering a clear narrative of where the submarine cable industry stands today—and where it is heading.

“The submarine cable industry is best described as ‘coopetition’—a place where competitors and colleagues come together to confront near existential challenges… The unique capacity of this industry to cooperate remains one of its greatest assets.”

Stuart Barnes – Xtera (STF Issue 142)

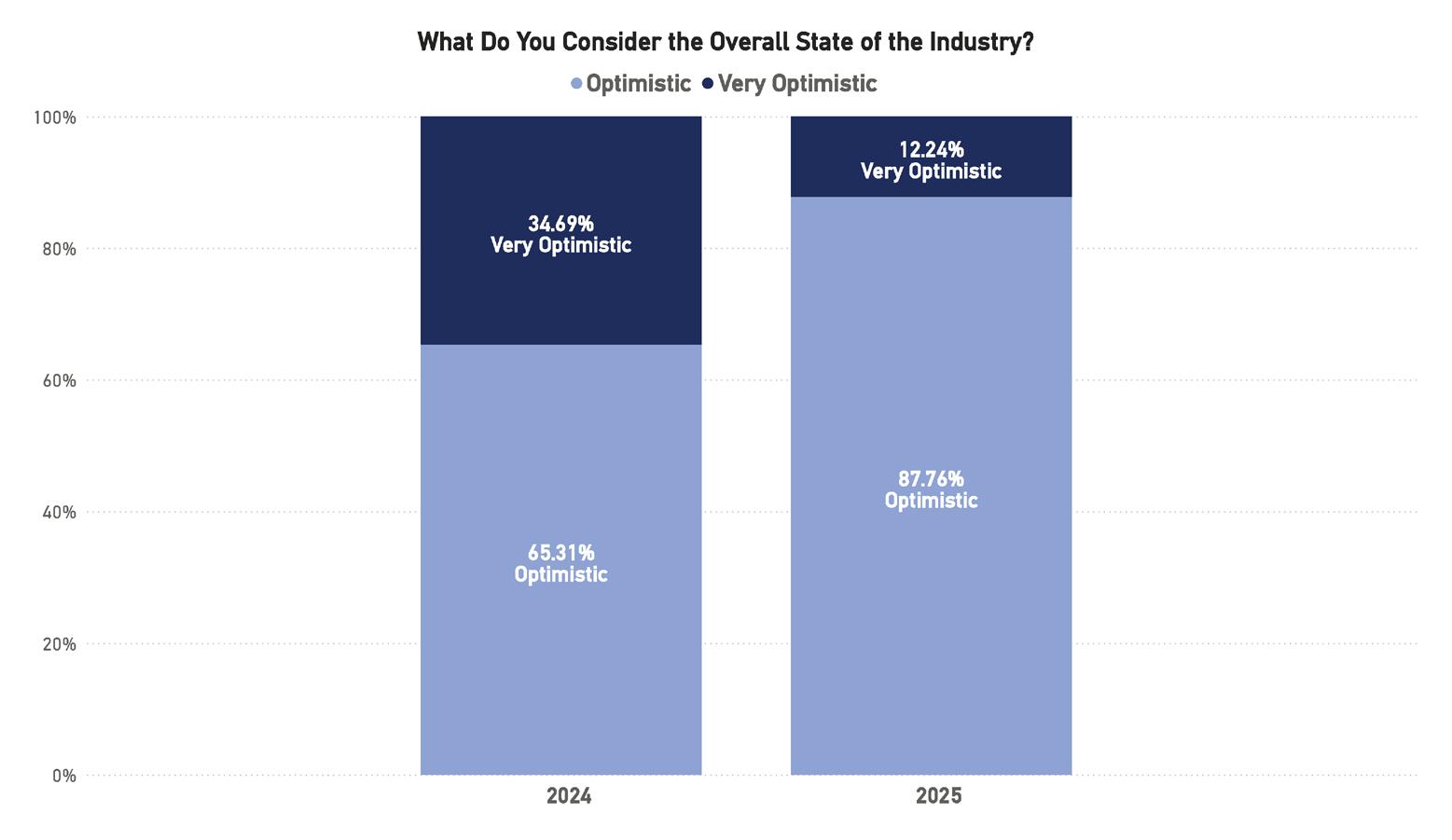

Figure 1: Overall State of the Industry

industry continues to demonstrate exceptionally strong confidence, with 100% of respondents maintaining a positive outlook for 2025. However, the composition of that optimism has shifted. The proportion of those identifying as very optimistic declined from 34.69% in 2024 to 12.24% in 2025, while those describing themselves as optimistic increased to nearly 88%. This adjustment reflects a more balanced confidence—stakeholders remain highly positive about the industry’s direction but are tempering expectations after a sustained period of expansion. Overall, the findings indicate a maturing market: enthusiasm remains high, but with a pragmatic awareness of the logistical, regulatory, and resource challenges that accompany continued growth.

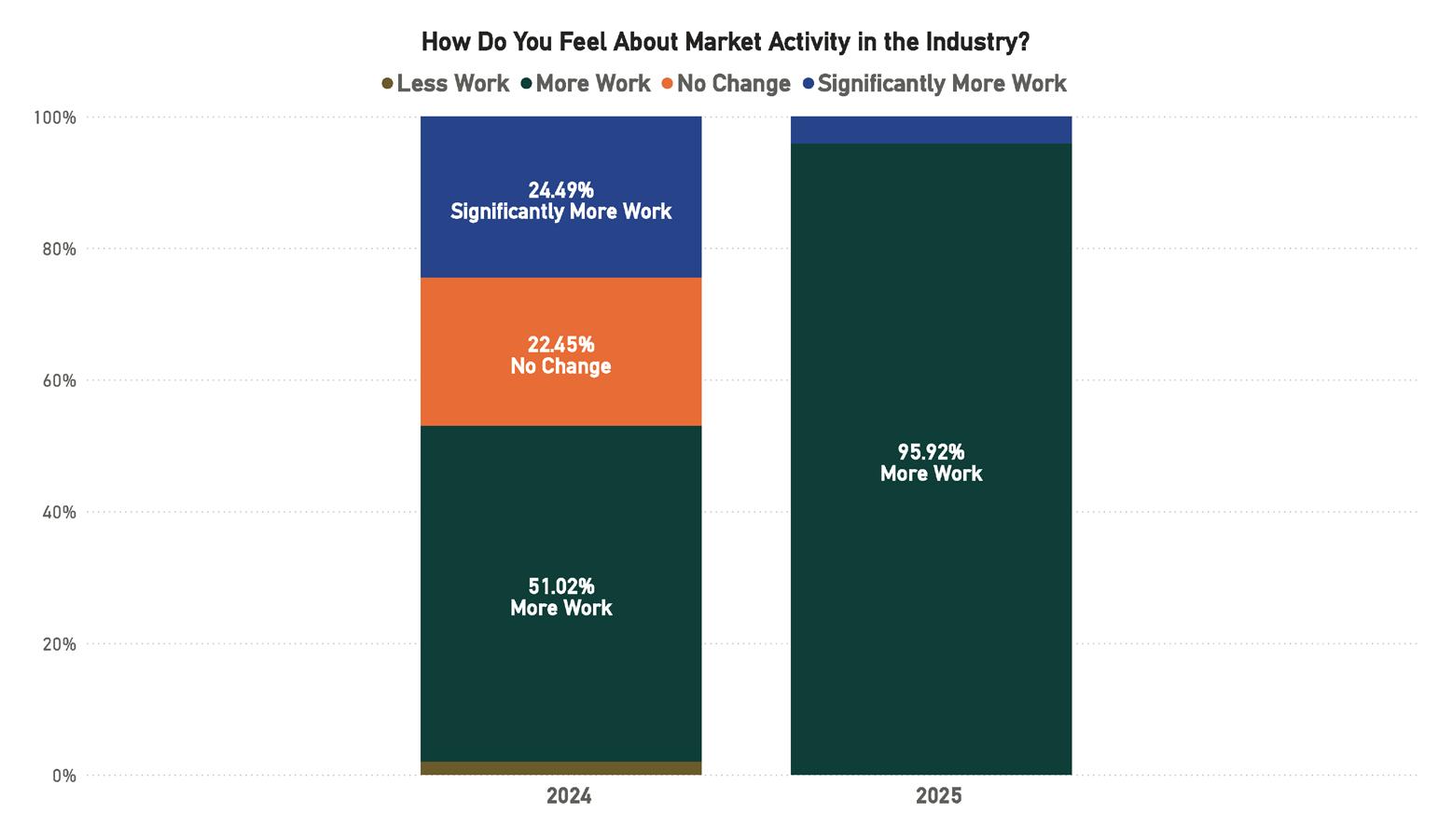

Figure 2: Industry Market Activity

Perceptions of market activity strengthened notably in 2025, marking one of the most pronounced yearover-year improvements in the survey. Nearly 96% of respondents reported experiencing more work than in 2024, compared to just 51% the prior year. Meanwhile, the share reporting no change fell from 22.45% to 0%, and those citing significantly more work consolidated into the broader category of increased activ-

ity. The virtual disappearance of negative or neutral responses underscores a period of unprecedented demand across both mature and emerging cable markets. This expansion reflects the industry’s intensified build cycle, with multiple hyperscale connectivity and intercontinental projects advancing simultaneously. The data suggest that the industry is now operating near full capacity, with sustained workloads expected to carry through 2026.

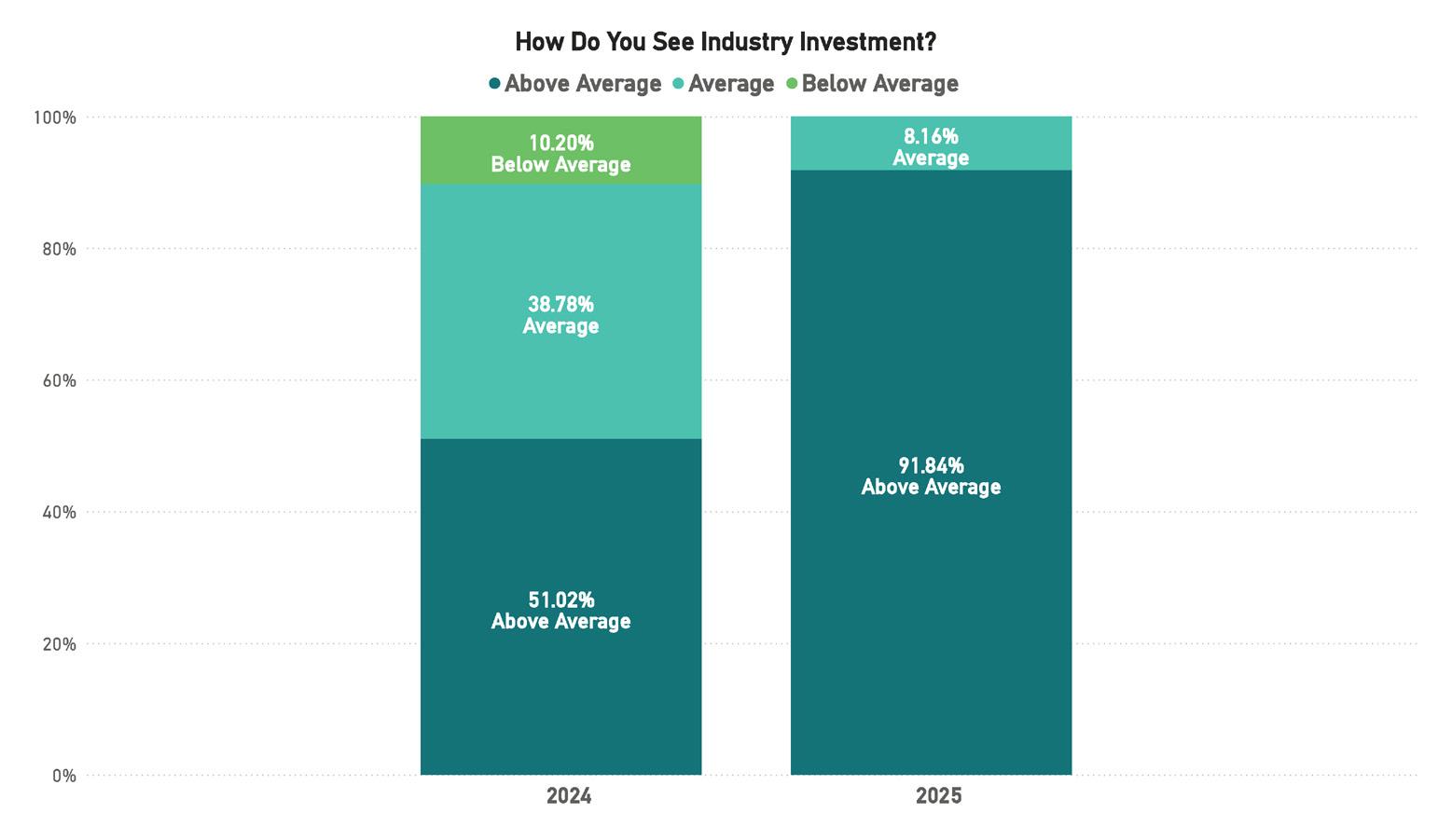

Confidence in investment has surged alongside rising workloads. In 2025, 91.84% of respondents rated industry investment as above average, a dramatic increase from 51.02% in 2024. Meanwhile, the below average category has disappeared, and only a small minority (just over 8%) described investment as average. This sharp upward shift signals robust capital confidence, supported by continued funding for large-scale system builds, technology modernization, and data center integration. The findings reflect a strong correlation between investment sentiment and project activity—capital flows are not only sustaining current growth but actively fueling industry acceleration. While external macroeconomic factors remain a watchpoint, respondents clearly view 2025 as a year of investment strength and long-term strategic commitment.

Figure 3: Industry Investment

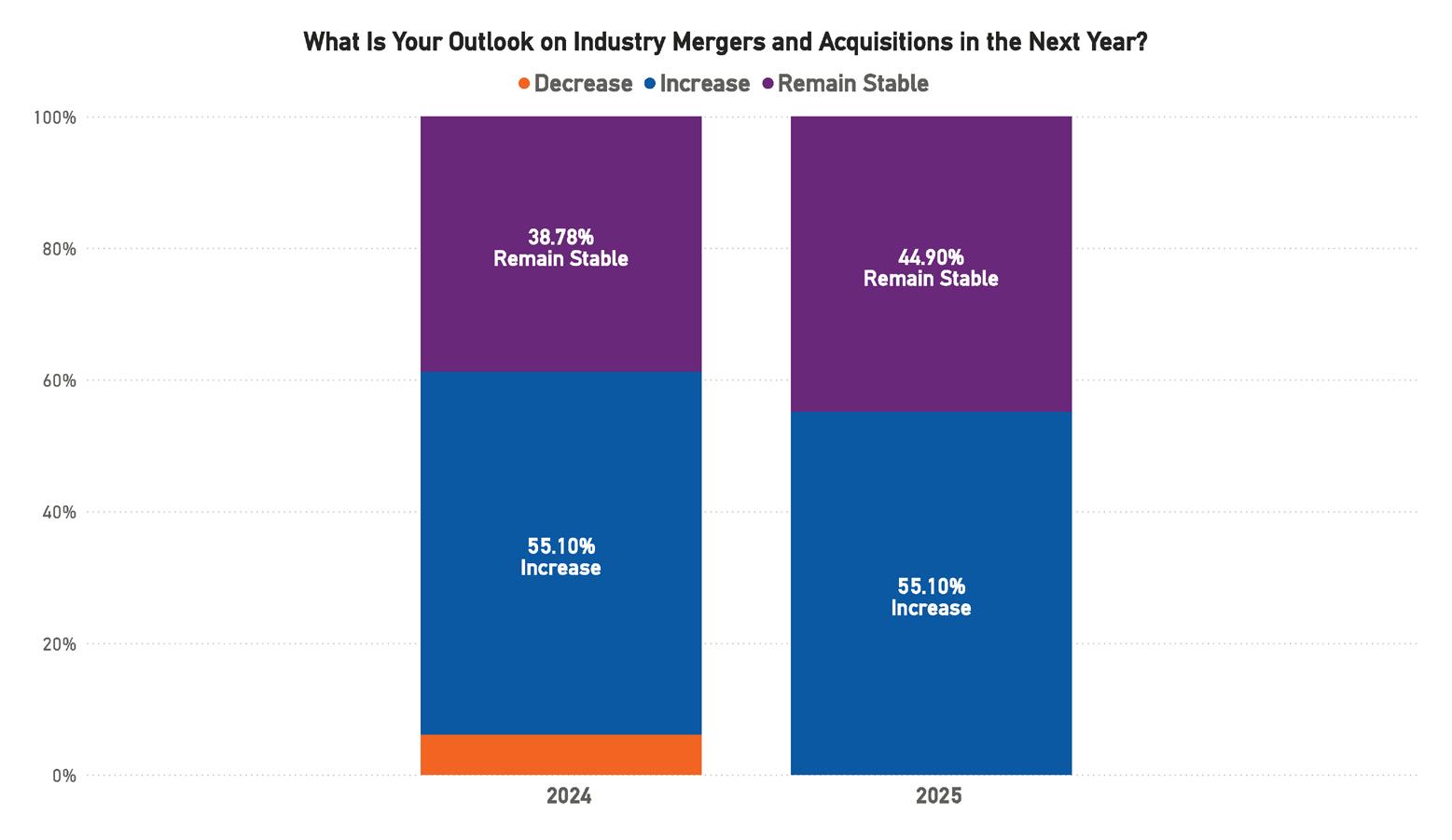

Figure 4: Industry Mergers & Acquisitions

Expectations around mergers and acquisitions remain steady compared to the previous year. In both 2024 and 2025, 55.10% of respondents expect an increase in M&A activity, while the share anticipating stable conditions rose modestly from 38.78% to 44.90%. No respondents forecasted a decrease. The data suggests that consolidation continues to be viewed as a defining feature of the industry, with participants anticipating continued strategic alignments rather than dramatic market shifts. The consistency of these responses underscores the perception that mergers and acquisitions are now a normalized component of the industry’s long-term business cycle, reflecting both investment confidence and the pursuit of scale efficiencies among operators, vendors, and infrastructure investors.

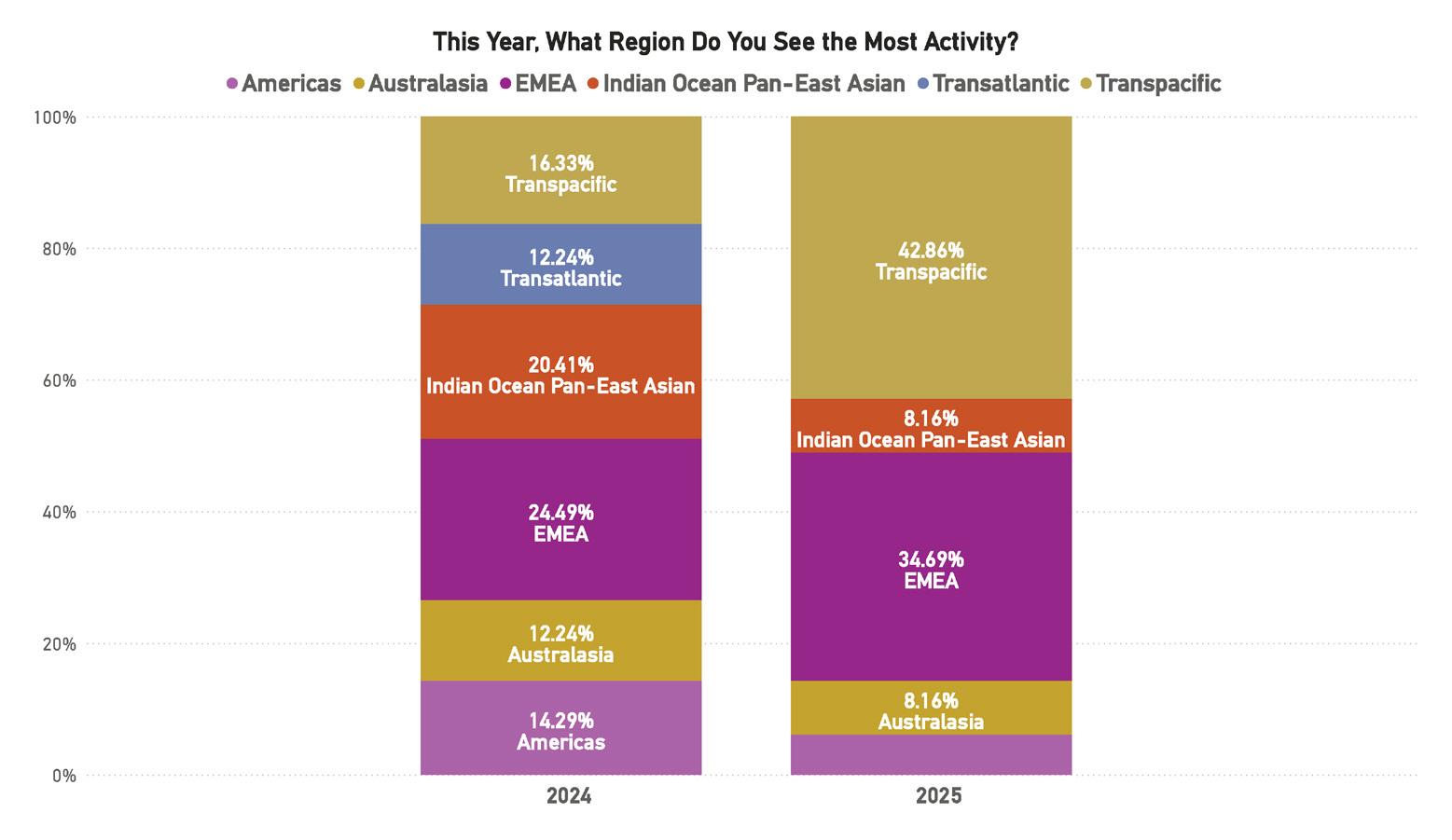

5: Region Activity

Regional market activity has shifted notably in 2025, with a strong concentration of work moving toward the Transpacific region. The Transpacific share of reported activity increased sharply from 16.33% in 2024 to 42.86% in 2025, displacing other regions that had dominated in previous years. EMEA continues to be active at 34.69%, up from 24.49%, while the Indian Ocean Pan–East Asian region saw a marked decline from 20.41% to 8.16%. Australasia and the Americas remained comparatively stable, though both represent smaller overall shares of reported activity. These shifts point to a geographic rebalancing of global infrastructure development, as Transpacific routes attract sustained investment in capacity and resiliency. The change also reflects the increasing prioritization of Asia–U.S. connectivity in global traffic patterns, with EMEA maintaining a strong second position through ongoing regional and intercontinental builds.

Figure

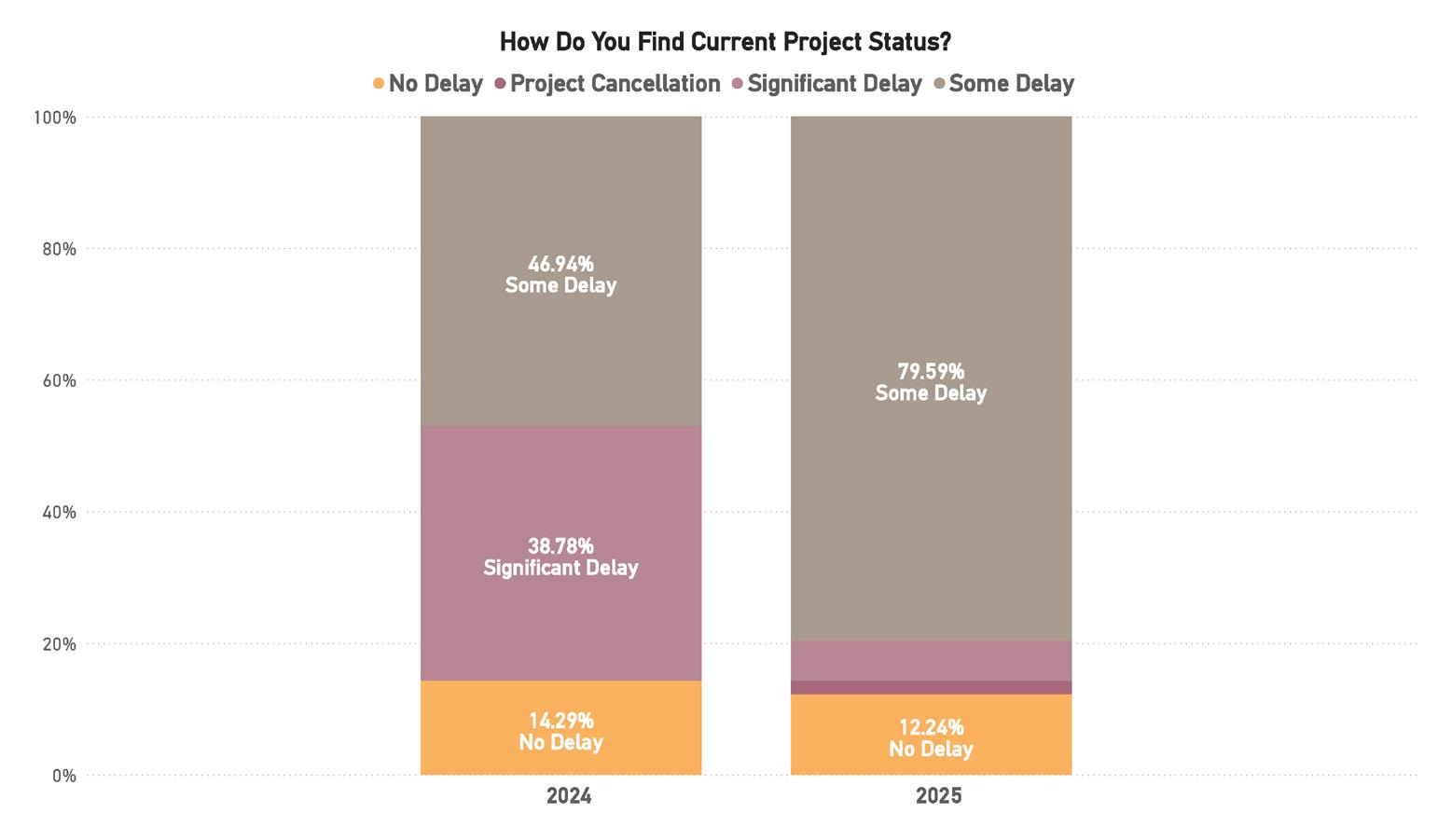

6: Project Status

Project execution challenges have intensified, with a clear increase in reported delays compared to 2024. In the current survey, 79.59% of respondents noted that projects are experiencing some delay, a significant rise from 46.94% the previous year. The share indicating significant delays fell sharply to negligible levels, suggesting that while most projects are behind schedule, fewer are facing critical disruption. The portion reporting no delays declined slightly from 14.29% to 12.24%. This data signals a broad but manageable slowdown, likely tied to ongoing supply chain strain, vessel availability, and regulatory clearance timelines. The industry continues to move forward at high volume, but capacity constraints and logistical bottlenecks remain persistent challenges that are now embedded into standard project planning.

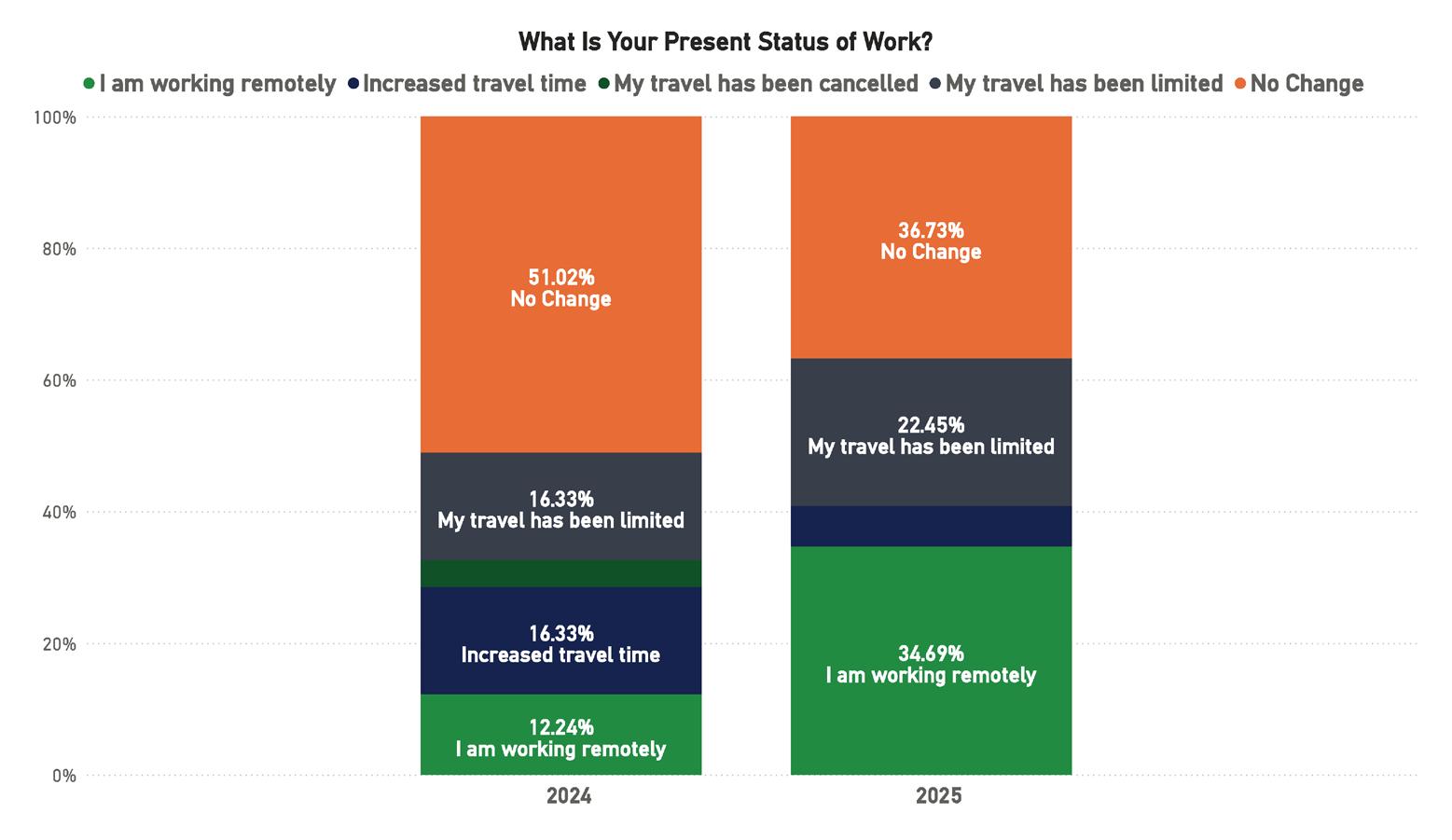

Figure 7: Work Status

Work patterns in the industry continue to evolve, with a clear trend toward greater remote flexibility in 2025. The share of respondents reporting that they are working remotely rose significantly from 12.24% in 2024 to 34.69% in 2025. Meanwhile, those indicating “no change” in their work status fell from 51.02% to 36.73%, showing that the shift in work modes is still ongoing. Reports of limited travel increased modestly, while increased travel time declined slightly, suggesting that logistical constraints continue to affect mobility but are stabilizing overall. The growing share of remote work underscores the lasting impact of hybrid

Figure

and distributed operational models within the submarine cable sector, particularly as organizations adapt to global project footprints and cross-regional collaboration demands.

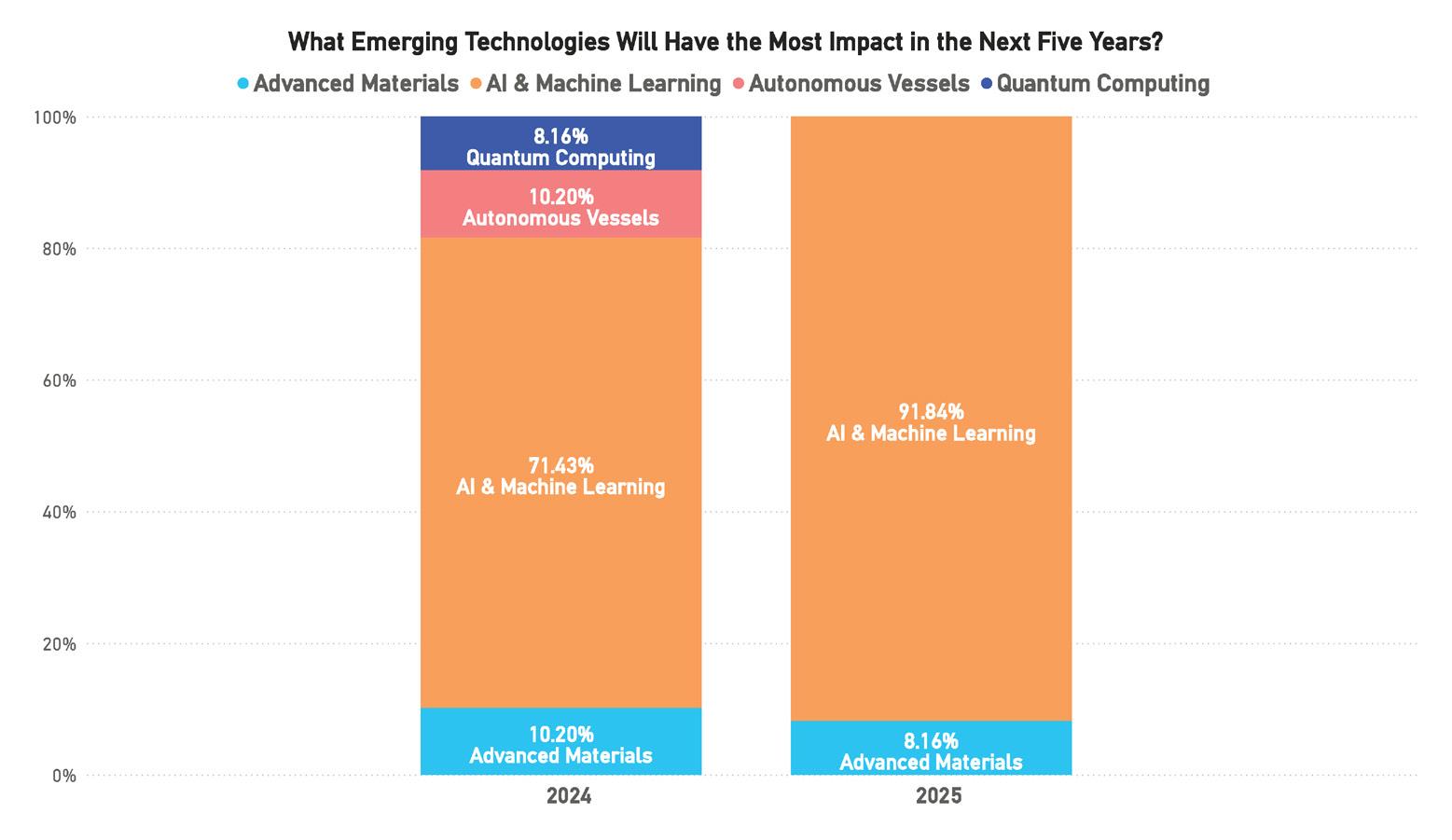

Figure 8: Emerging Technologies

Technological innovation remains a defining force in the industry, with AI and machine learning emerging as the clear frontrunner among transformative technologies. In 2025, 91.84% of respondents identified AI and machine learning as the technology expected to have the greatest impact over the next five years, up sharply from 71.43% in 2024. This steep rise reflects a broadening industry consensus that automation, predictive analytics, and intelligent network management will drive the next wave of efficiency and innovation. Other technologies, such as autonomous vessels, advanced materials, and quantum computing, saw declining mentions year over year, suggesting that while they remain on the radar, they are perceived as secondary to the immediate and tangible applications of AI across network design, maintenance, and data analytics.

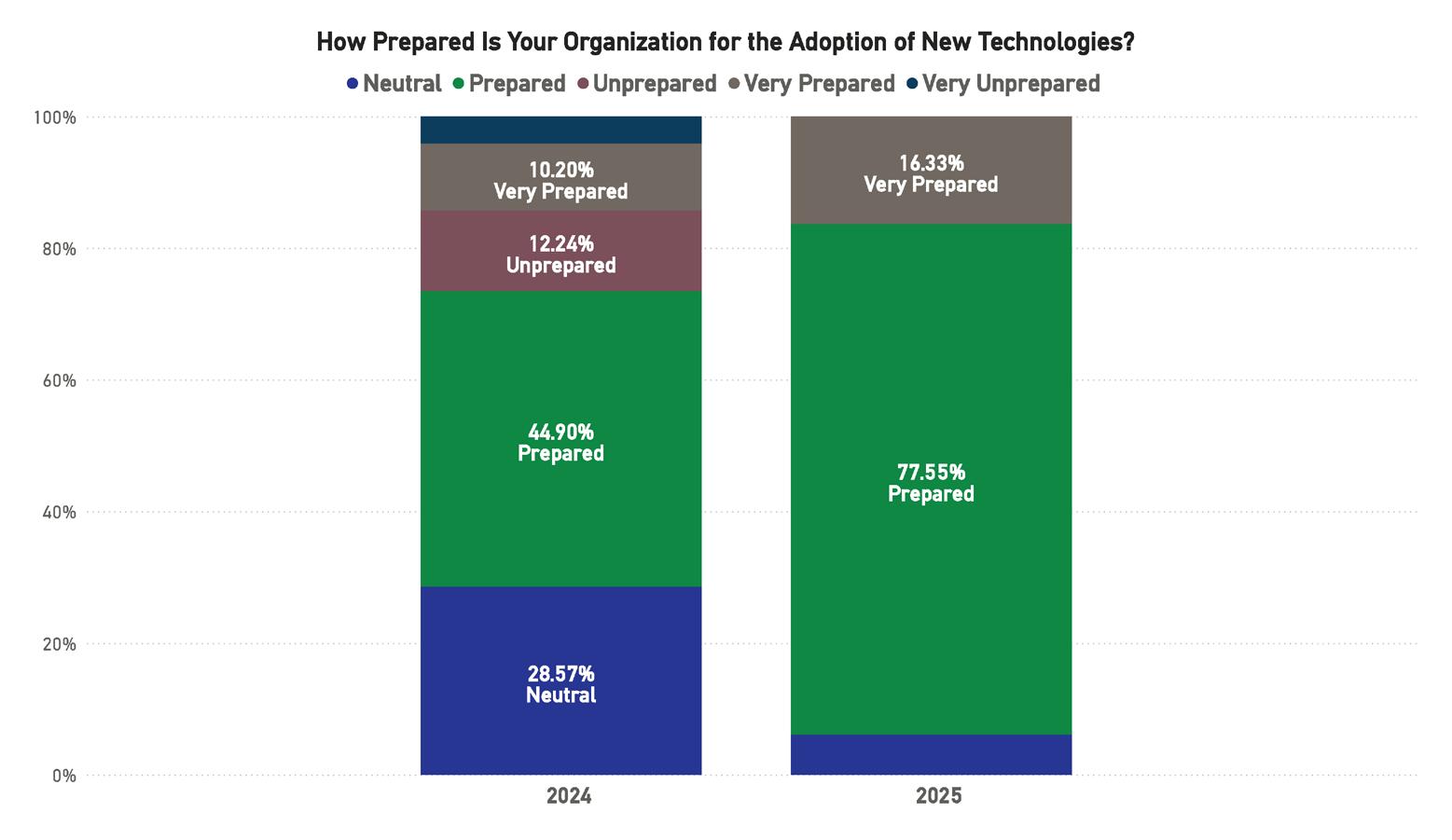

Figure 9: Technology Preparedness

The industry’s readiness for technological change has improved substantially, signaling both strategic alignment and operational progress. In 2025, 77.55% of respondents described their organizations as pre-

pared for the adoption of new technologies, compared to 44.90% in 2024. The “very prepared” category also increased from 10.20% to 16.33%, while the share identifying as unprepared declined to near zero. This strong upward movement indicates a widespread shift from awareness to execution, as companies invest in modernization and skills development. The overall trend reflects a maturing ecosystem where new tools and digital capabilities are no longer aspirational but actively integrated into business models, positioning the industry for faster adaptation in the years ahead.

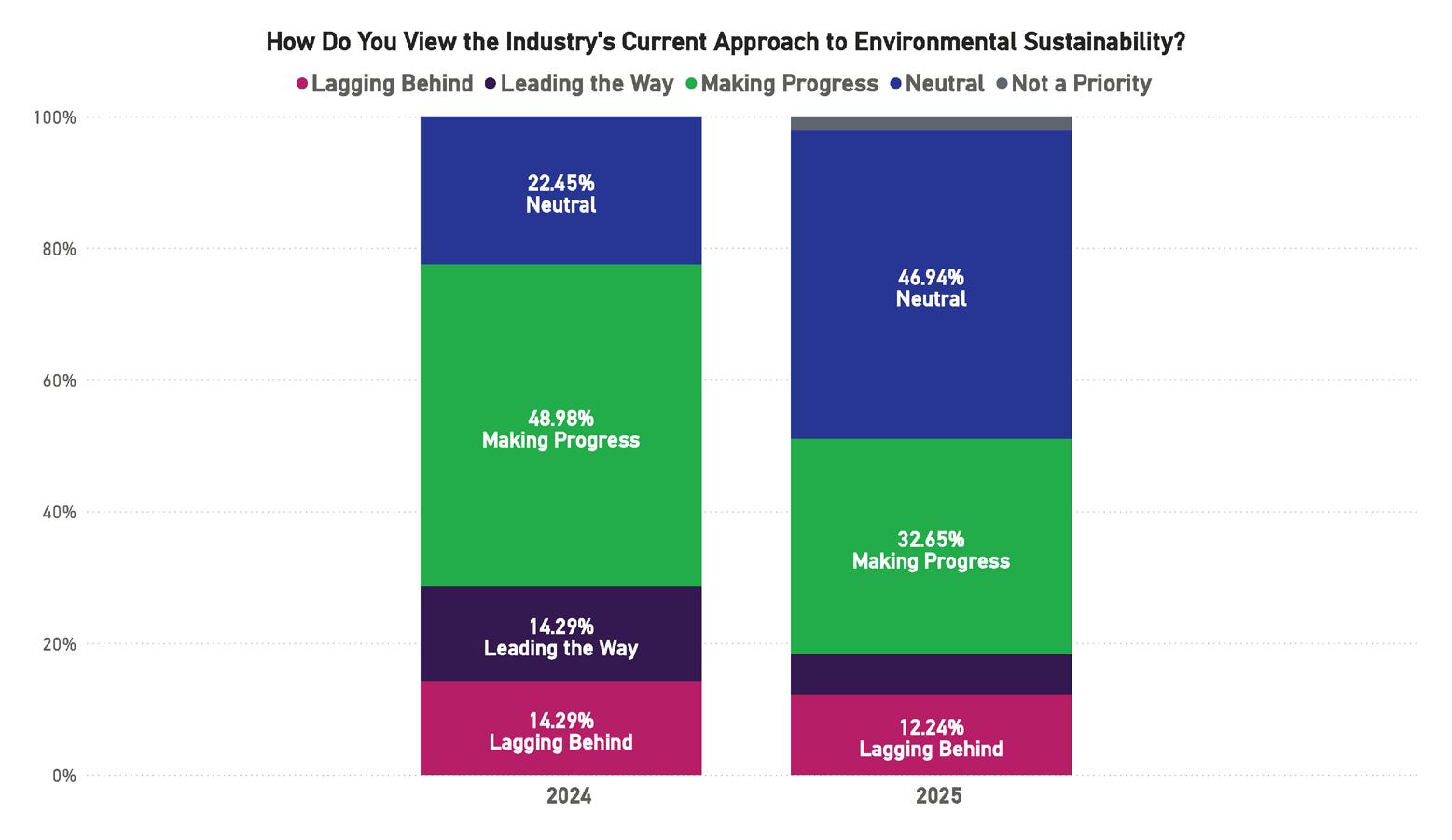

Figure 10: Sustainability Approach

Perceptions of the industry’s environmental progress shifted noticeably in 2025. While nearly half of respondents in 2024 viewed the industry as “making progress,” that share declined to 32.65% this year. Meanwhile, neutrality increased substantially from 22.45% to 46.94%, suggesting that respondents are now less certain about the pace or visibility of sustainability efforts. The shares identifying the industry as “leading the way” or “lagging behind” remained relatively stable, with a slight decline in both categories. These results point to a growing perception plateau—stakeholders acknowledge that environmental initiatives are underway, but many feel progress has slowed or that the industry has yet to demonstrate measurable outcomes. As sustainability expectations continue to rise globally, maintaining momentum and transparency may be key to sustaining confidence in this area.

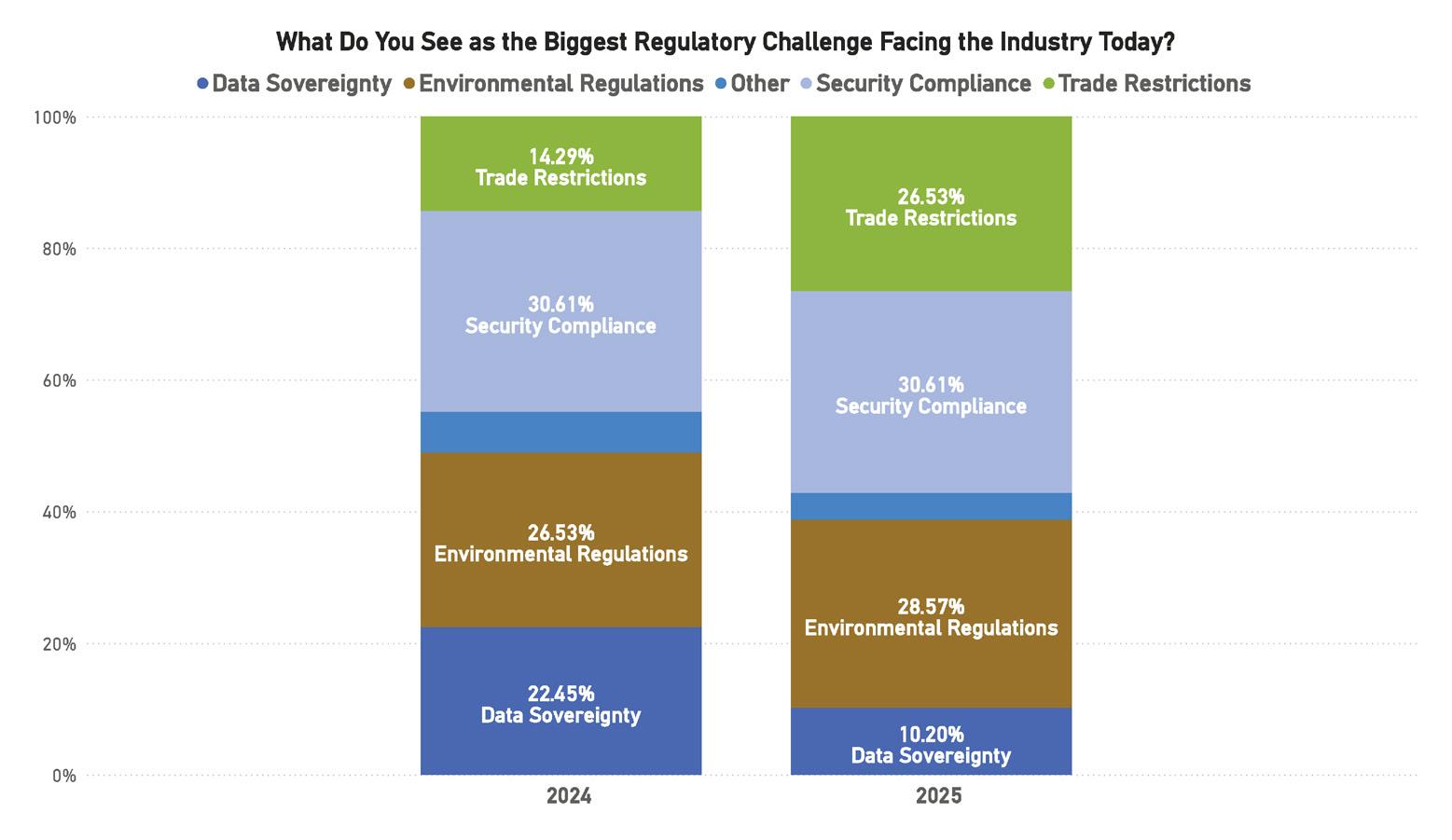

11: Regulatory Challenges

Regulatory complexity remains a defining concern across the industry, though the areas of emphasis continue to shift. In both 2024 and 2025, security compliance held steady as the most frequently cited challenge at 30.61%. However, trade restrictions rose significantly—from 14.29% to 26.53%—reflecting growing geopolitical friction and supply chain considerations. Environmental regulations also edged higher, while data sovereignty concerns declined sharply from 22.45% to 10.20%. This changing mix illustrates a dynamic regulatory landscape increasingly influenced by international trade policy, security governance, and environmental accountability. The decline in data sovereignty as a leading issue may indicate that companies have adapted to data localization requirements, while newer challenges, particularly those linked to cross-border operations and environmental oversight, are now shaping the regulatory conversation.

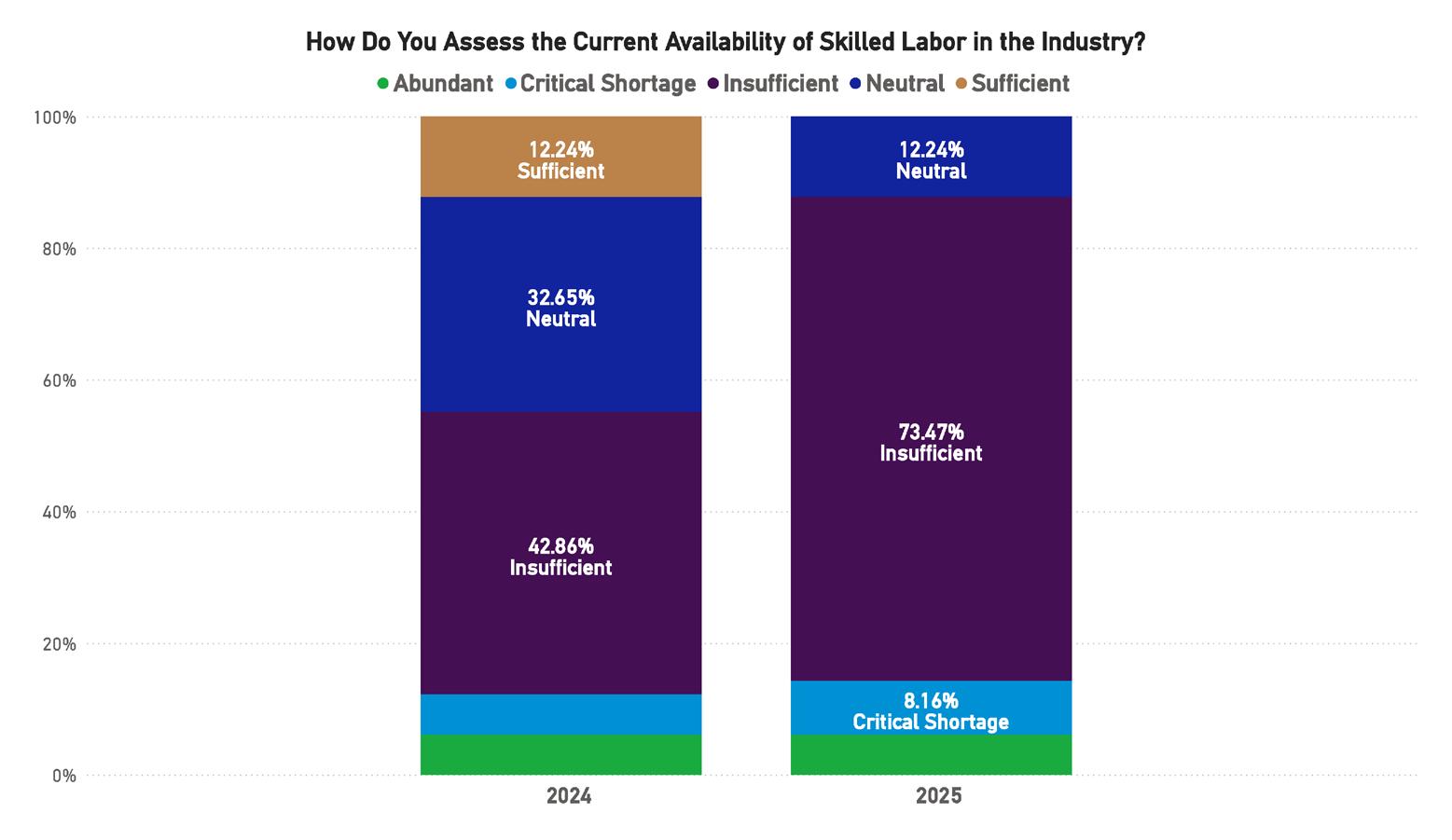

12: Skilled Labor Availability

Concerns over workforce capacity have intensified sharply in 2025. The share of respondents describing skilled labor availability as “insufficient” surged from 42.86% to 73.47%, with an additional 8.16% now identifying a “critical shortage.” The number of respondents rating availability as sufficient or abundant has effectively disappeared, while neutrality dropped from 32.65% to 12.24%. These figures point to an escalating talent gap across the submarine cable ecosystem, driven by sustained project demand, aging

Figure

Figure

technical workforces, and limited new entrant pipelines. The results underscore that skilled labor scarcity is no longer a localized or short-term issue—it has become a defining structural constraint. Industry leaders may need to prioritize workforce development, technical training, and cross-sector partnerships to mitigate long-term operational risks associated with these shortages.

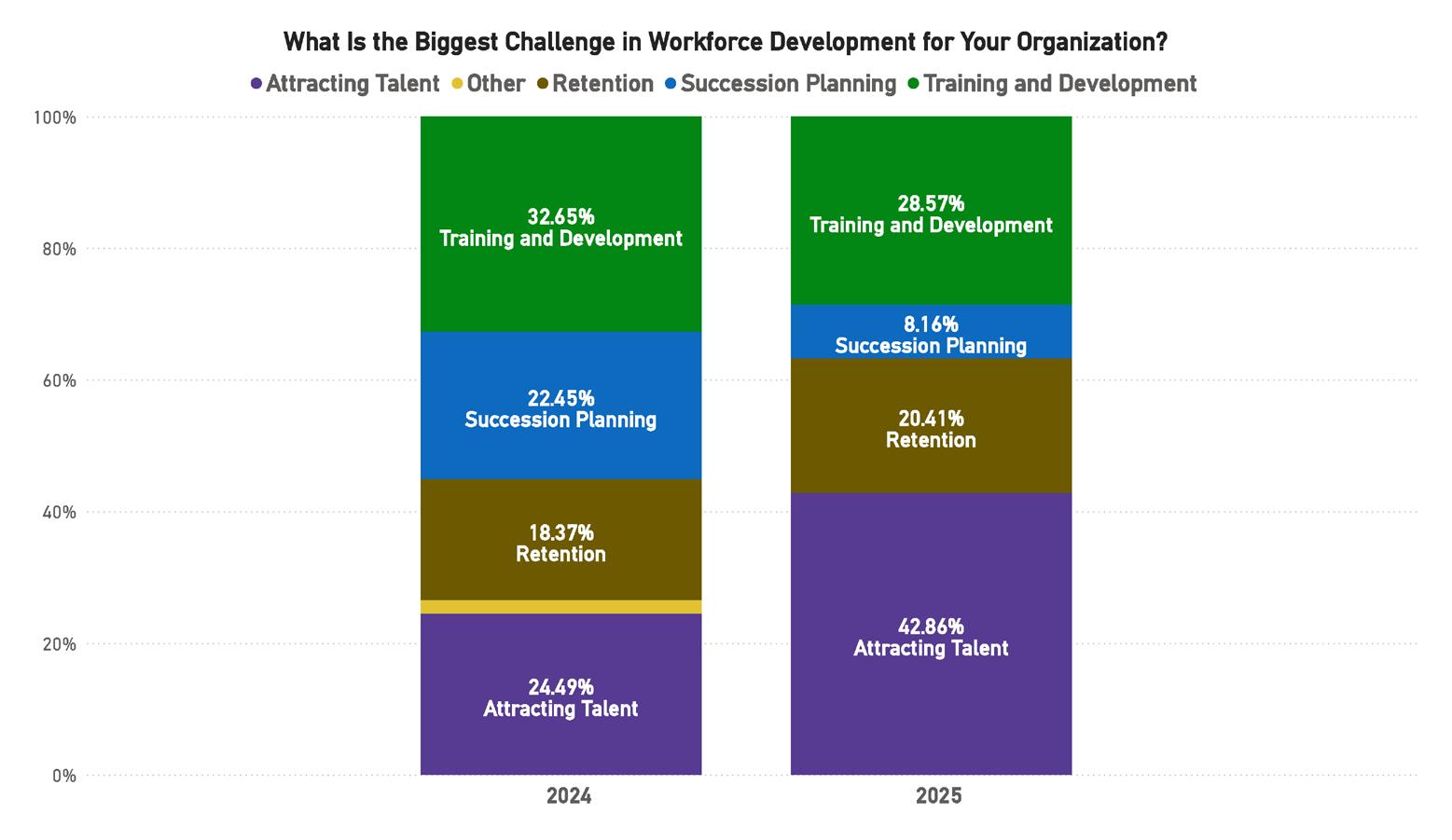

The 2025 results indicate a clear shift in how organizations view workforce development priorities. Attracting new talent has become the dominant concern, rising from 24.49% in 2024 to 42.86% in 2025. Training and development, while still a key focus, fell slightly from 32.65% to 28.57%, suggesting that many organizations now feel internal training is less urgent than replenishing and expanding the talent pipeline. Succession planning declined sharply to 8.16%, and retention increased slightly to 20.41%, pointing to a tightening labor market where recruiting qualified professionals outweighs long-term personnel planning. These findings align closely with the broader skills shortage reported across the industry, highlighting a near-term need for recruitment and outreach strategies that can attract new technical and managerial expertise into the sector.

Figure 13: Workforce Challenges

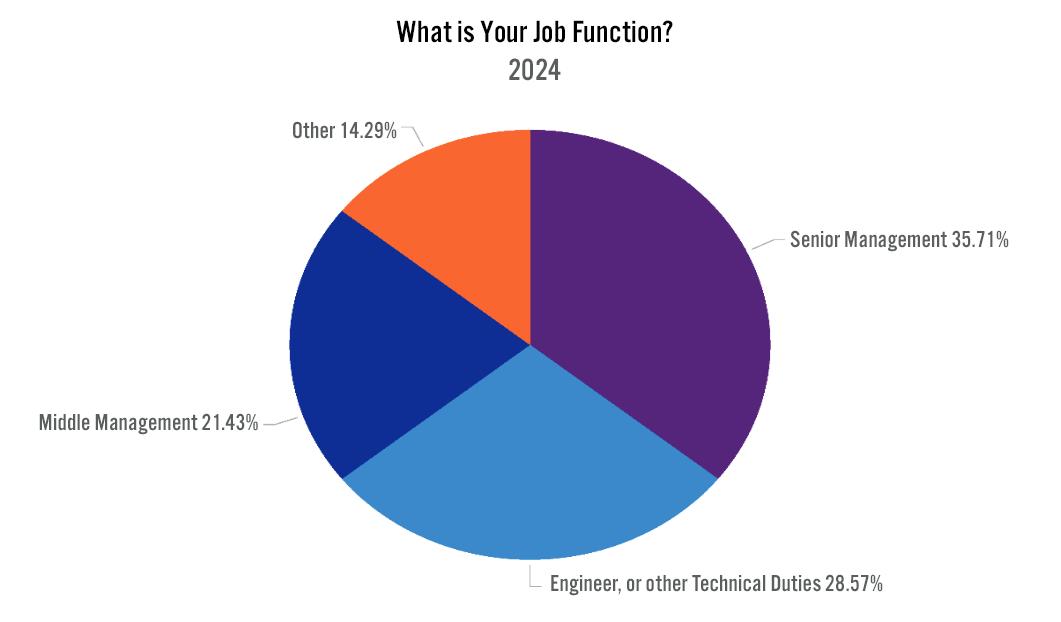

Figure 14: Job Function

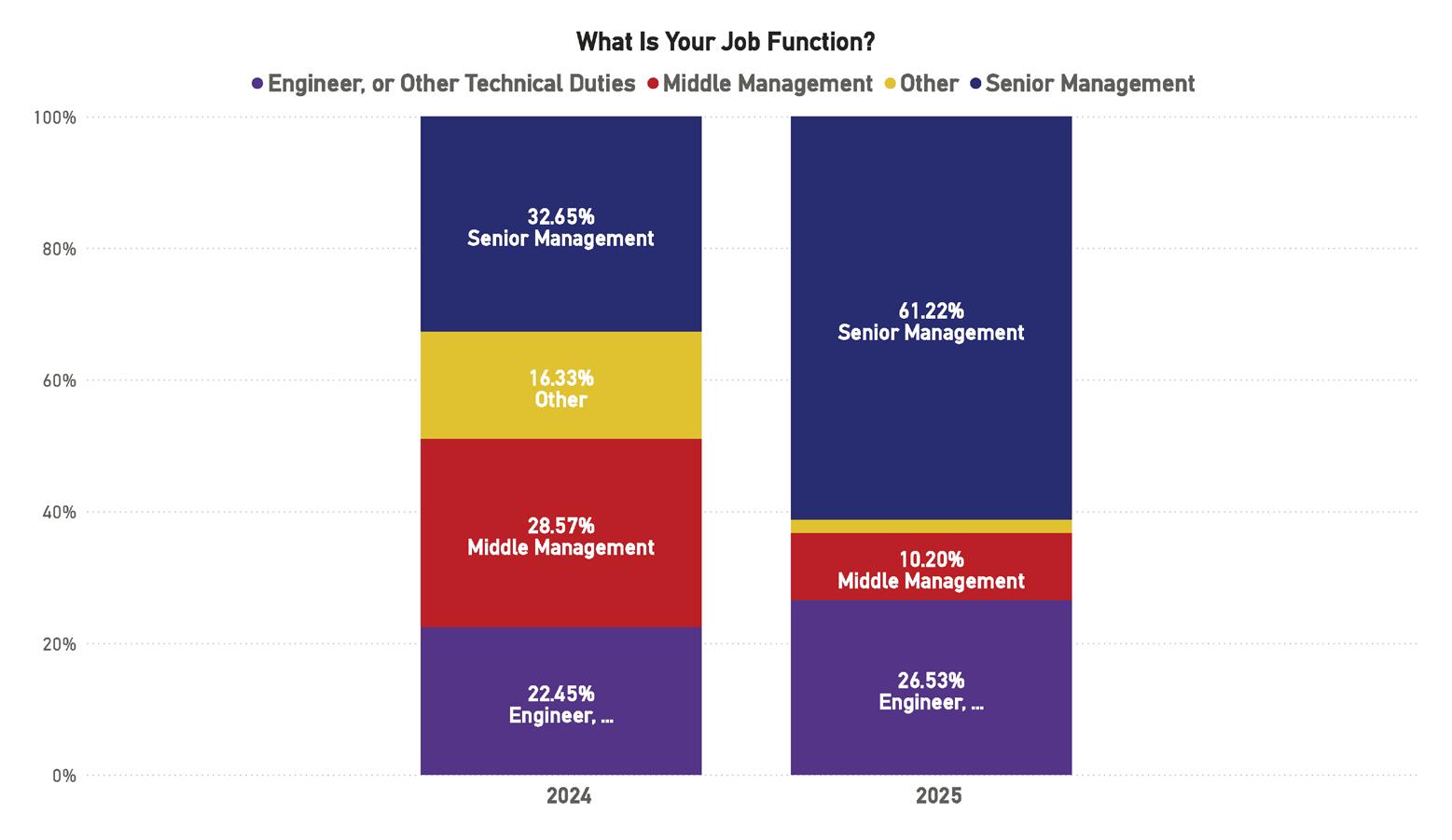

The distribution of job roles among survey respondents has shifted toward senior management positions, which now account for 61.22% of participants compared to 32.65% in 2024. The representation of middle management decreased from 28.57% to 10.20%, while engineers and technical specialists remained relatively stable, rising slightly to 26.53%. The “other” category, which may include consultants or independent contractors, declined notably from 16.33% to negligible levels. This shift suggests that higher-level decision-makers are increasingly represented in the industry’s feedback base, potentially signaling greater executive engagement in strategic discussions around growth, regulation, and technology adoption. The prominence of senior management input also strengthens the survey’s value as a forward-looking indicator of organizational priorities and investment sentiment.

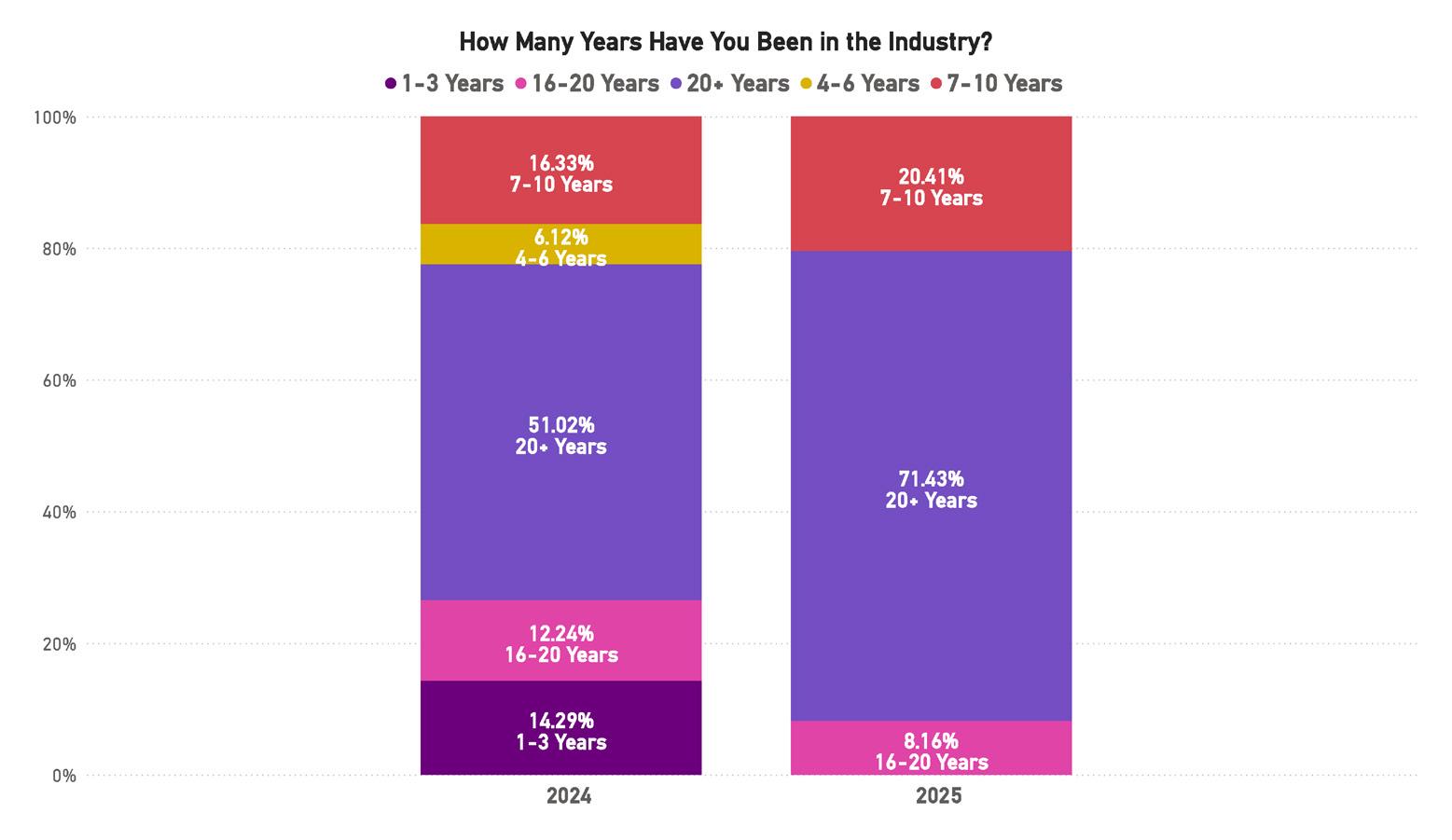

Figure 15: Years in Industry

Experience levels among respondents continue to trend toward the higher end, underscoring the submarine cable sector’s long-established professional base. In 2025, 71.43% of participants reported having over 20 years of experience, up from 51.02% in 2024. This sharp increase reinforces the perception that the industry remains dominated by long-tenured experts, many of whom have witnessed multiple technological and market cycles. Meanwhile, representation from mid-career professionals (7–10 years) grew slightly to 20.41%, while all other experience brackets declined, particularly those with fewer than 10 years in the field. These results highlight both the depth of institutional knowledge within the industry and a looming generational transition challenge, as the gap between veteran professionals and newer entrants widens further. The data suggests that without stronger recruitment and knowledge transfer programs, the industry could face difficulties sustaining expertise over the next decade.

The 2025 survey reflects a notable geographic rebalancing across the industry’s global footprint. Respondents from the Asia-Pacific region rose sharply to 44.90% from 24.49% the prior year, reinforcing the region’s growing importance as both a project hub and investment center. Europe also increased its share to 38.78%, while participation from North America and Africa/Middle East declined, and South America saw minimal representation. The geographic shifts parallel trends observed in project activity, with strong growth in transpacific and EMEA systems reflected in earlier survey questions. This evolving distribution underscores the global nature of the submarine cable industry but also highlights the increasing centrality of Asia and Europe in driving market expansion, capacity upgrades, and infrastructure leadership.

Key Highlights and Conclusions

Across the three-year sentiment timeline, the submarine fiber-optic industry has entered a phase of sustained expansion and operational maturity, marked by high activity, strong investment, and growing structural challenges. The 2025 survey results portray a sector that is confident in its direction and deeply engaged in large-scale delivery but also increasingly constrained by labor shortages, regulatory complexity, and uneven progress in sustainability.

The overall tone of 2025 responses remains strongly optimistic, with nearly nine in ten participants describing the state of the industry as positive and most reporting higher workloads than ever before. This sustained optimism is underpinned by record investment levels, the acceleration of major transpacific and EMEA builds, and the broad integration of AI and digital tools into planning and operations. Industry leaders appear to view this growth period as both a validation of long-term strategy and a call to address emerging bottlenecks in talent and execution capacity.

At the same time, the data reflect a maturing awareness of the challenges that accompany expansion. Skilled labor shortages have reached critical levels, and organizations increasingly identify talent attraction—not training or succession planning—as their foremost workforce challenge. This aligns with demographic trends showing an aging professional base and limited entry of new technical personnel, pointing to an urgent need for education, recruitment, and knowledge transfer initiatives.

Technological preparedness has improved sharply, illustrating that organizations are moving from adaptation to proactive modernization. Yet this progress is tempered by slower movement on environmental sustainability, where confidence appears to have plateaued. Neutrality in this area has grown substantially, suggesting that while sustainability is widely recognized as a strategic imperative, measurable outcomes remain inconsistent.

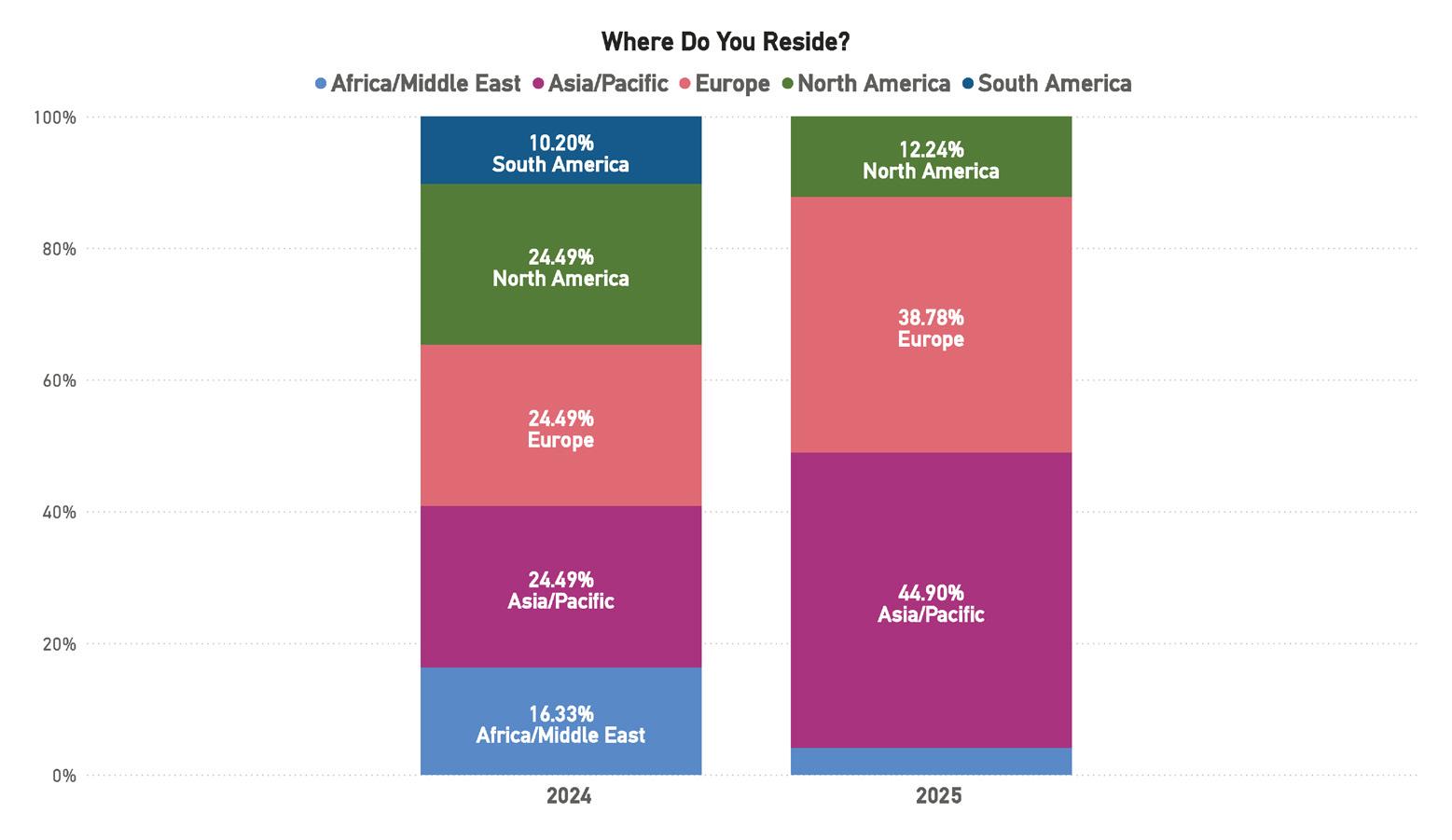

Figure 16: Residency

Geographically, the center of gravity continues to shift eastward. Asia-Pacific and Europe now account for the majority of reported activity and residence among respondents, mirroring global investment flows and the increasing importance of transoceanic capacity routes connecting these regions. This diversification reinforces the truly global character of the industry but also introduces new regional dependencies and policy considerations.

Taken together, the 2025 sentiment data portray an industry operating at peak momentum—expansive, capital-rich, and technologically agile—but navigating constraints that could shape its next phase of evolution. The convergence of optimism, capacity strain, and leadership concentration suggests that the coming years will hinge on strategic investment in people, process, and sustainability to maintain equilibrium between growth and resilience.

Whether you're seeking a reliable landing party or hosted cable landing services, we deliver:

• 24/7 monitoring

• Remote hands support

• Redundant backup power systems

• Secure, scalable infrastructure

Contact us at US1-503-707-5376 to learn more.

1.2. STRATEGIC SHIFTS IN SUBMARINE CABLE POLICY

Insights from Kristian Nielsen

Submarine cables are the unsung infrastructure of the modern world. Carrying an estimated 99% of all intercontinental internet traffic, they are the backbone of financial systems, cloud computing, government communications, and everyday life online.

For much of their history, these systems were treated as neutral infrastructure — engineered, financed, and operated with minimal political involvement. But in the past year, that picture has changed dramatically. Governments now see cables as strategic assets, and in some cases as vulnerabilities.

Policies, regulations, and even naval operations are being reshaped by concerns about espionage, sabotage, vendor trust, and geopolitical rivalry. Major developments since late 2024 have reshaped dynamics in the United States, Europe, Russia, China, Japan, Southeast Asia, and the wider Indo-Pacific.

1.2.1. UNITED STATES: REGULATION, SECURITY, AND VENDOR TRUST

In July 2025, the U.S. Federal Communications Commission (FCC) adopted new rules creating a “presumption of denial” for submarine cable licenses involving equipment or operators linked to “foreign adversaries.” (Latham & Watkins, 2024) The rules also prohibit using technology from companies on the FCC’s “Covered List,” such as Huawei and ZTE (Submarine Networks, 2025).

FCC Commissioner Brendan Carr explained: “We have seen submarine cable infrastructure threatened in recent years by foreign adversaries, like China. We are therefore taking action here to guard our submarine cables against foreign adversary ownership, and access as well as cyber and physical threats.” (IEEE ComSoc Tech Blog)

Congress has also stepped in. In September 2025, the House of Representatives passed the Undersea Cable Control Act, which would restrict exports of sensitive cable technology, direct agencies to identify and secure critical components, and instruct the U.S. to work with allies on global standards (De Bevoise LLP Insights, 2024).

The impact is already visible. Cable projects planning landings in Hong Kong have been cancelled or rerouted (Latham & Watkins, 2024). Consortia are expected to disclose vendor ties, equipment origin, cybersecurity safeguards, and even repair ship availability. The SEA-ME-WE 6 cable is the most high-profile example: although HMN Tech’s bid was cheaper, the contract went to SubCom under U.S. diplomatic pressure, raising costs and delaying delivery (Reuters, 2025). Vendor trust is now an explicit requirement, not a background consideration.

1.2.2. EUROPE: FROM INCIDENTS TO ACTION PLANS

Europe’s awareness of cable vulnerability sharpened in late 2024, when multiple data cables between Sweden, Finland, and the Baltic states were damaged. Some incidents coincided with anchor drags by vessels flagged to China, while another involved simultaneous disruption of cables and a gas pipeline (CSIS, 2025). Although no government has published definitive proof of sabotage, officials increasingly describe such events as hybrid threats.

In February 2025, the European Commission responded with an Action Plan on Cable Security worth nearly €1 billion (Semafor, 2025). Funding is earmarked for enhanced monitoring, spare cable stockpiles, and a fleet of dedicated repair vessels. One EU official described the approach as moving from passive resilience to “active deterrence, detection, and repair.”

NATO has also taken a larger role, deploying naval assets and underwater drones and launching exercises focused on cable protection (IEEE ComSoc Tech Blog). A new Maritime Centre for the Security of Critical Undersea Infrastructure in the UK is coordinating allied responses. Meanwhile, the Critical Entities Resilience Directive requires operators to assess sabotage risks and maintain emergency plans.

Permitting processes for urgent repairs, historically slow, are being streamlined.

Europe is now treating submarine cables with the same seriousness as pipelines and power grids.

“The 2025 ICPC Plenary chose the theme ‘The Big Squeeze: Geopolitics & Spatial Planning’ because geopolitics and spatial planning are putting a squeeze on the planning of new undersea critical infrastructure.”

Ryan Wopschall – ICPC (STF Issue 141)

1.2.3. RUSSIA: ISOLATION AND SOVEREIGN PROJECTS

Since 2022, Russian companies have been largely excluded from international cable consortia (Latham & Watkins, 2024). Western governments view Russian participation as a security risk. At the same time, European navies continue to monitor Russian “research” vessels suspected of mapping or interfering with cables — the so-called “shadow fleet.”

Moscow’s response has been to build sovereign alternatives. The Polar Express cable, a 12,650 km system along Russia’s Arctic coast from Murmansk to Vladivostok, is entirely state funded (Latham & Watkins, 2024). Scheduled for completion by 2026, it will provide Russia with an independent communications corridor between Europe and Asia.

1.2.4. CHINA: EXPANSION MEETS PUSHBACK

China continues to pursue ambitious subsea cable projects under its Digital Silk Road initiative, with systems connecting Asia, Africa, and the Middle East (Subsea Cables Industry News, 2025). Companies such as HMN Technologies remain active, but their participation in global projects is narrowing.

Governments in the U.S., Europe, Japan, and elsewhere cite concerns about supply-chain transparency, foreign state influence, and the risk of espionage or sabotage. As a result, Chinese bids are increasingly excluded even when they are technically strong and economically competitive (Reuters, 2025).

The SEA-ME-WE 6 cable highlights this shift. HMN Tech initially offered the lowest bid, but the contract was reassigned to SubCom after U.S. diplomatic pressure, reflecting the growing role of geopolitics in procurement decisions.

1.2.5. JAPAN: SUBSEA CABLES AS NATIONAL SECURITY

The most significant new development in 2025 came from Japan. In September, Tokyo formally designated subsea cables as a national security priority (Financial Times, 2025).

The government is preparing to subsidize NEC, Japan’s leading subsea cable manufacturer, to acquire a fleet of large cable-laying ships (TS2.Tech, 2025). NEC currently charters vessels — for example, one from a Norwegian company under a four-year lease signed in 2022 — but officials view this as a vulnerability.

One government source told the Financial Times: “The Japanese government thinks this situation is very serious, so we are thinking we need to make some intervention.” Another cited risks of “espionage or cable-cutting sabotage,” and even the possibility that cables could one day serve as submarine detection systems [Source 1 Financial Times].

NEC has already laid more than 400,000 km of cables worldwide. Owning ships would allow NEC to guarantee faster response times for installation and repairs, making it more competitive in major tenders (Tom’s Hardware, 2025). NEC executive Takahisa Ohta acknowledged: “Owning a vessel is a huge fixed cost … but the market is booming now … one option is to acquire our own ship, and it’s something we’re considering.” (RioTimes Online, 2025)

Japan’s move has far-reaching implications. It enhances self-reliance, strengthens competitiveness, aligns with Quad and Indo-Pacific connectivity goals, and may provide a model for other governments to follow.

Southeast Asia is a region where these geopolitical tensions play out daily. Countries such as Vietnam, Indonesia, and the Philippines are building new cables to meet growing demand, but they are also being pulled by competing offers of investment and influence (Reuters, 2025).

Reuters reported in 2025 that U.S. officials have lobbied Vietnam to avoid Chinese suppliers as it plans up to ten new cables by 2030. Chinese companies continue to offer attractive pricing and financing, creating a delicate balance for regional governments.

To manage these pressures, many projects are reconfiguring routes. New trans-Pacific systems are bypassing Hong Kong, while consortia increasingly use mixed suppliers to reduce dependency on any one country (AInvest/Nikkei, 2025). Governments are tightening permits for landings and repairs, requiring local oversight, while some have relaxed cabotage rules to speed emergency work.

1.2.7. INDO-PACIFIC: ALLIANCES AND ALTERNATIVE ROUTES

The Indo-Pacific has emerged as a focal point for cooperative connectivity. The Quad alliance — the U.S., Japan, Australia, and India — has pledged to connect every Pacific Island state by the end of 2025, committing over USD $140 million in combined funding (JFIR, 2025). Japan’s forthcoming fleet would directly support these efforts by providing installation and repair capacity.

Alternative routes are also being developed to enhance resilience and bypass chokepoints. Projects such as Far North Fiber and Polar Connect in the Arctic, along with multi-branch loops across Northeast Asia, North America, and Southeast Asia, are being advanced [Source 12 Rio Times Online]. Japan’s geography makes it both a hub and a vulnerability, with many landing stations concentrated near Tokyo. The government is therefore encouraging diversification of landing sites, while projects such as the Southeast Asia–Japan Cable 2 (SJC2) already provide new routes and over 126 Tbps of capacity (AInvest/Nikkei, 2025).

1.2.8. CONCLUSION

Over the last year, submarine cables have moved from being technical projects managed quietly by private consortia to becoming critical assets at the heart of national and international security.

Key lessons are emerging. Fleet ownership matters, as Japan’s NEC subsidies show (Financial Times, 2025). Vendor trust is central, with U.S. and European policies reshaping procurement (FCC, 2025) (Semafor, 2025). Routing, redundancy, and permitting are now strategic as well as technical. And geopolitical blocs — the U.S., EU, Japan, Australia, and their partners — are increasingly aligning on what constitutes “trusted infrastructure.”

The submarine cable industry stands at a new inflection point. Politics is now as important as bandwidth. For investors, operators, and policymakers alike, understanding these dynamics is no longer optional — it is essential.

1.3. SYSTEM GROWTH

The submarine cable industry continues to demonstrate resilience and steady expansion, with new deployments reflecting the growing demand for global connectivity, low-latency routing, and enhanced resilience across major corridors. While year-to-year fluctuations remain a defining feature of the industry, the longer-term trajectory continues upward, supported by both hyperscaler-backed projects and regional consortia.

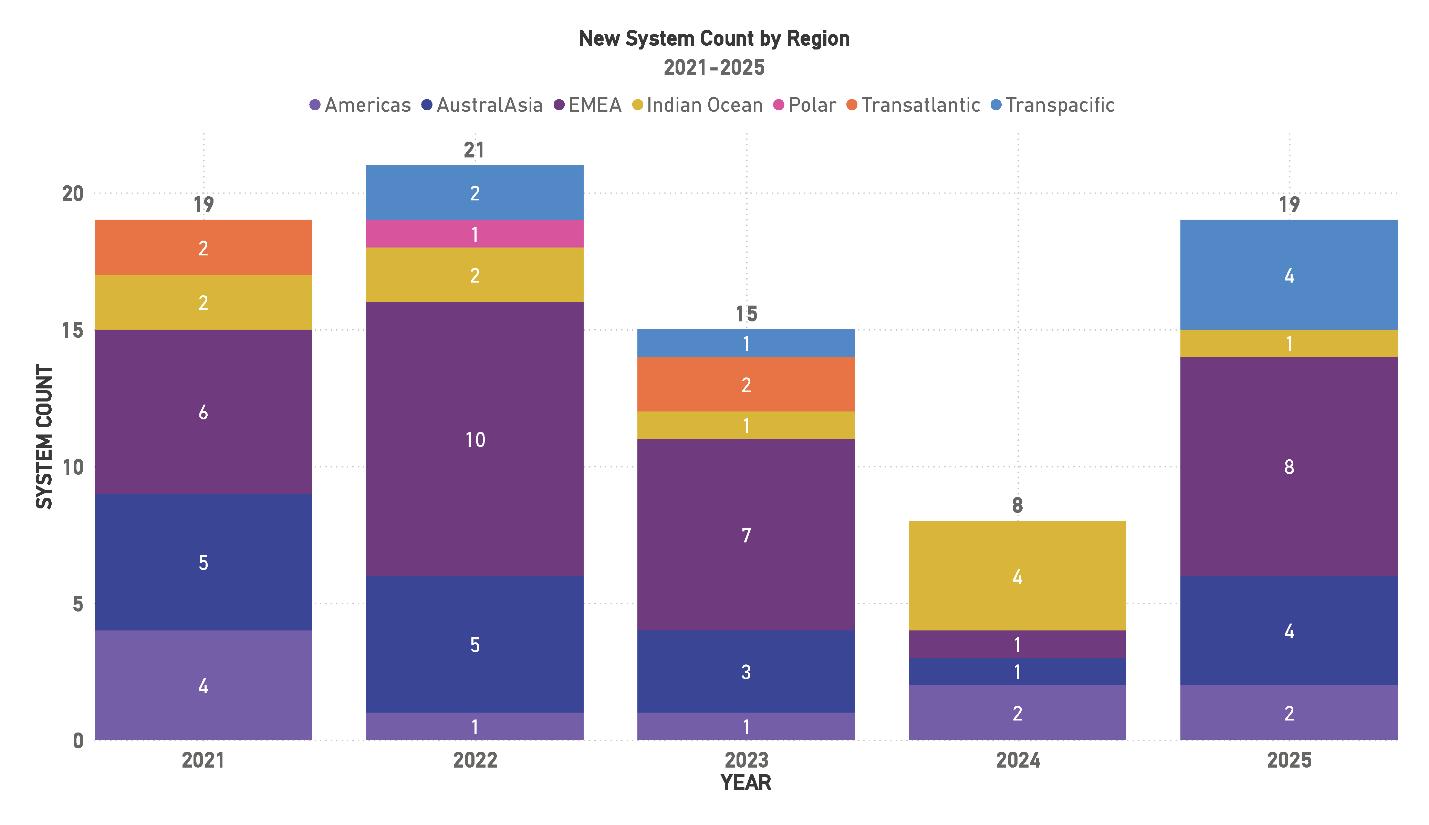

Figure 17: New System Count by Region, 2021-2025

Between 2021 and 2025, new system installations have shown both peaks and troughs as projects move through complex financing, permitting, and construction cycles. The year 2022 marked the high point, with 21 new systems coming online, followed by a decline in 2023 (15 systems) and 2024 (8 systems). Data for 2025, however, shows a rebound to 19 systems, highlighting the cyclical but resilient nature of industry growth. EMEA has consistently led in new system count, underscoring its role as the most active region for cable development, while the Transpacific’s resurgence in 2025 illustrates renewed investment in

transoceanic routes. AustralAsia continues to make steady contributions, while the Indian Ocean and Polar regions remain far less active, reflecting ongoing economic and geographic challenges.

Over the five-year period, EMEA emerges as the dominant contributor to system additions, while Transpacific growth in 2025 signals its return as a priority corridor for global capacity. Compared to last year’s report, which noted a steady decline in new installations after 2020, the updated figures suggest a more uneven but ultimately stronger recovery, with growth concentrated in high-demand long-haul routes.

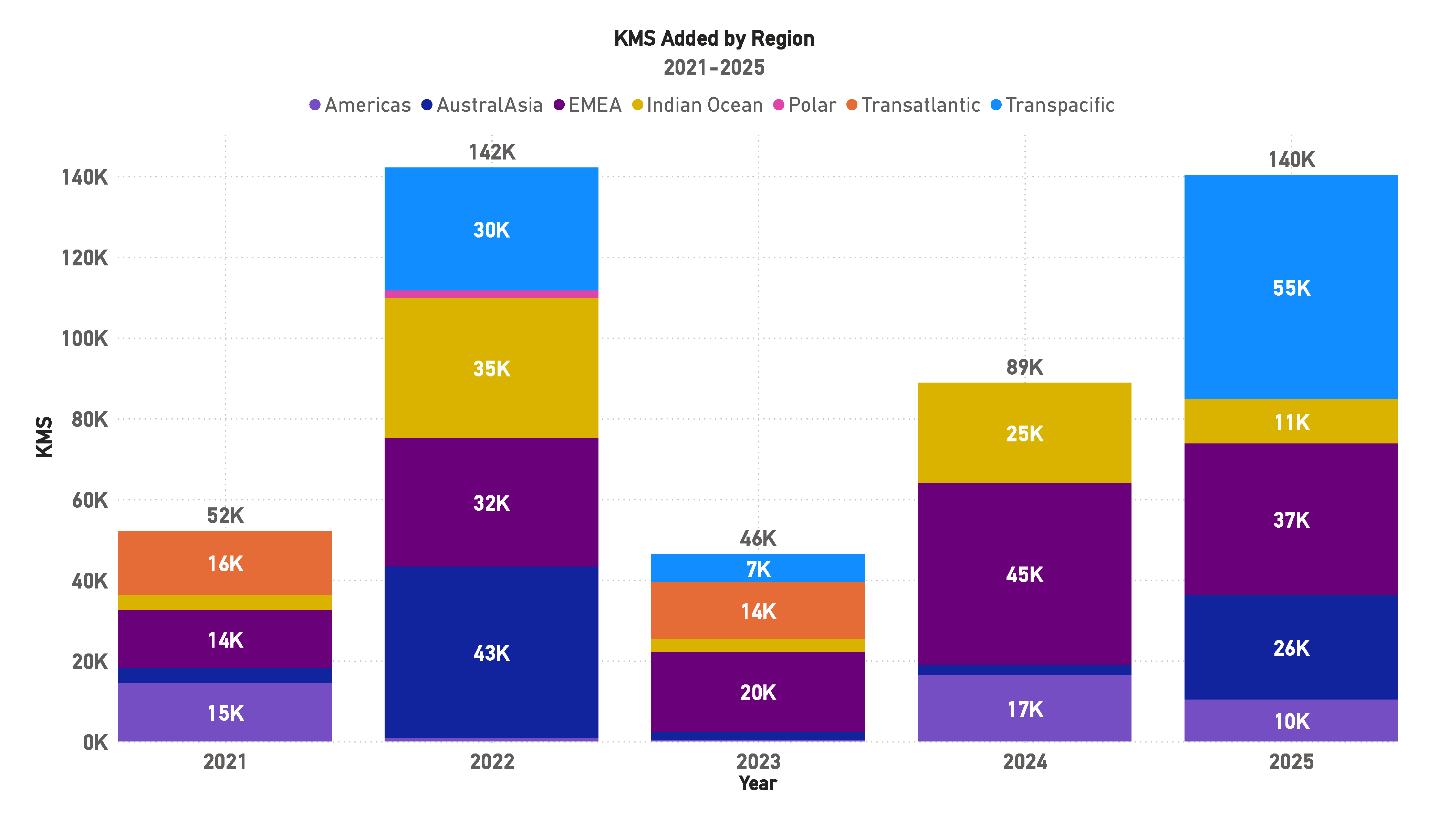

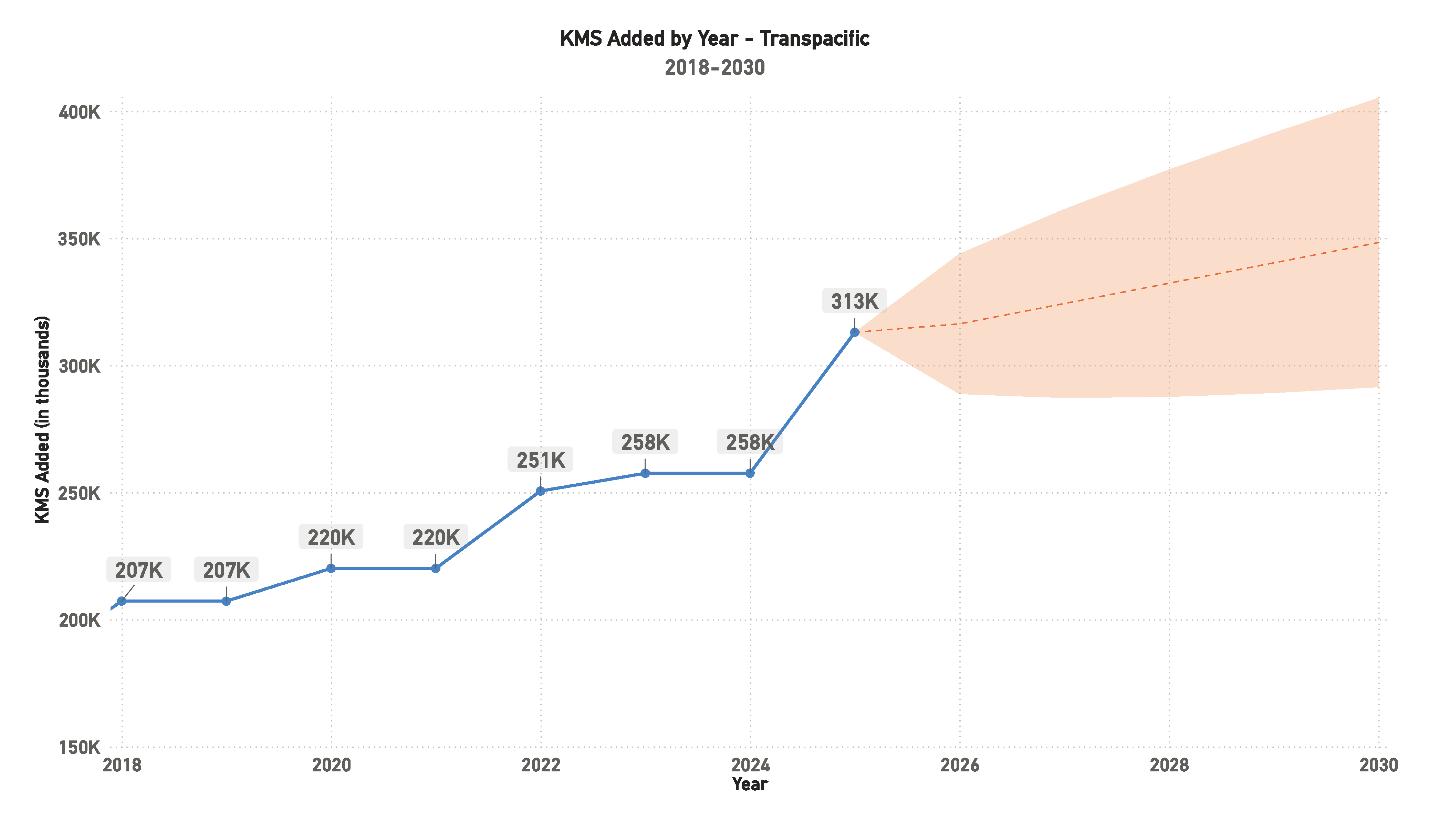

When measured in kilometers of cable installed, the story diverges from system counts, emphasizing the importance of system scale. In 2022, the 21 new systems contributed 142,000 kilometers, making it the standout year of the period. By contrast, 2023 delivered 15 systems but only 46,000 kilometers, reflecting a year dominated by shorter or regional builds. The year 2024, despite having only 8 new systems, recorded 89,000 kilometers, highlighting the scale of large projects in the Indian Ocean and EMEA. Projections for 2025 suggest another strong year, with nearly 140,000 kilometers expected to be added, supported by significant Transpacific and EMEA deployments.

Taken together, these results highlight the disconnect that can occur between system count and total kilometers installed. While smaller regional projects boost the number of systems in a given year, the longest-haul builds, particularly in the Transpacific and EMEA regions, account for the bulk of kilometers added. Compared to last year’s assessment, the growth in kilometers is greater than expected, underscoring the industry’s strategic focus on scaling capacity along its largest and most critical routes.

Figure 18: KMS Added by Region, 2021-2025

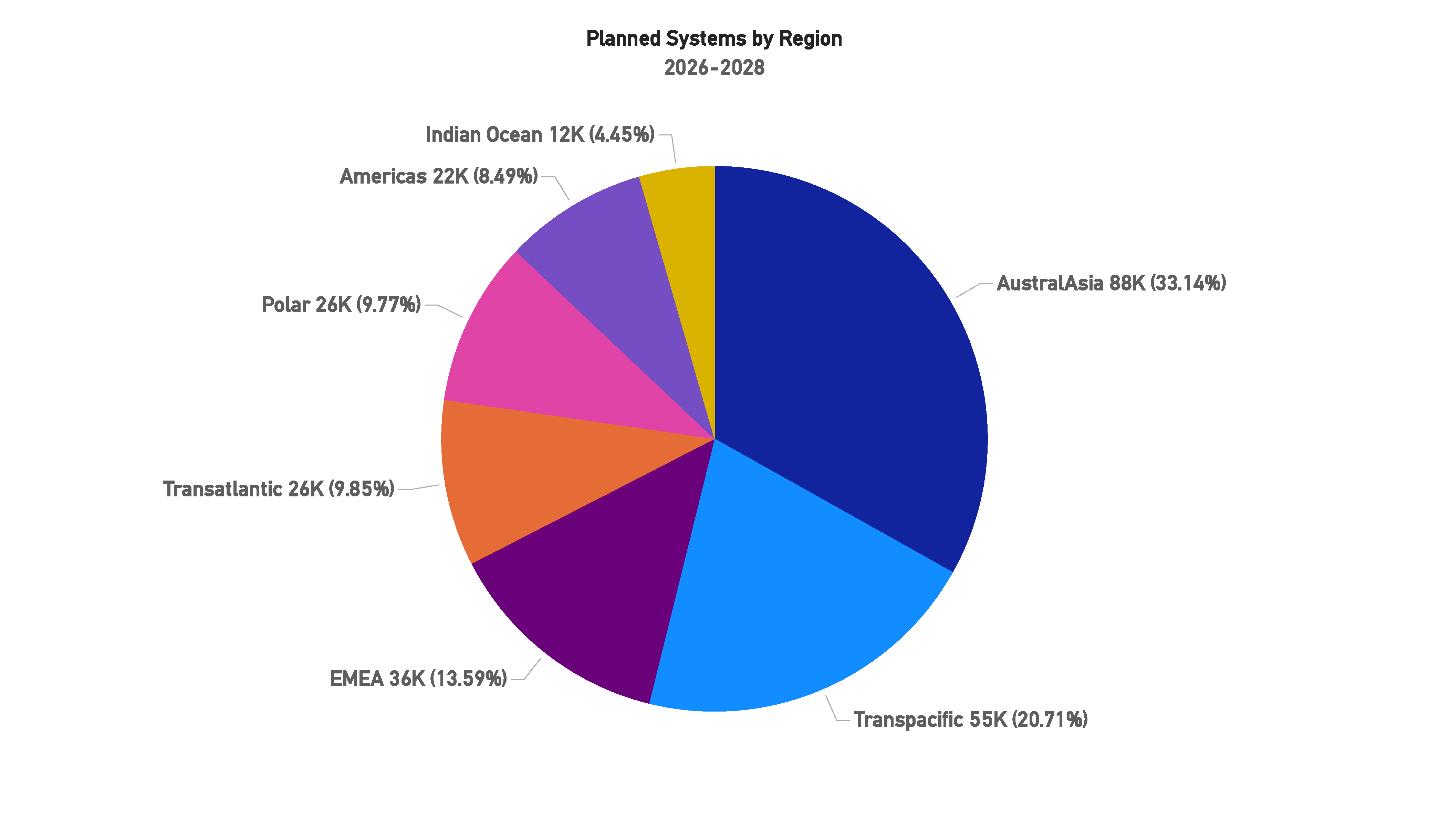

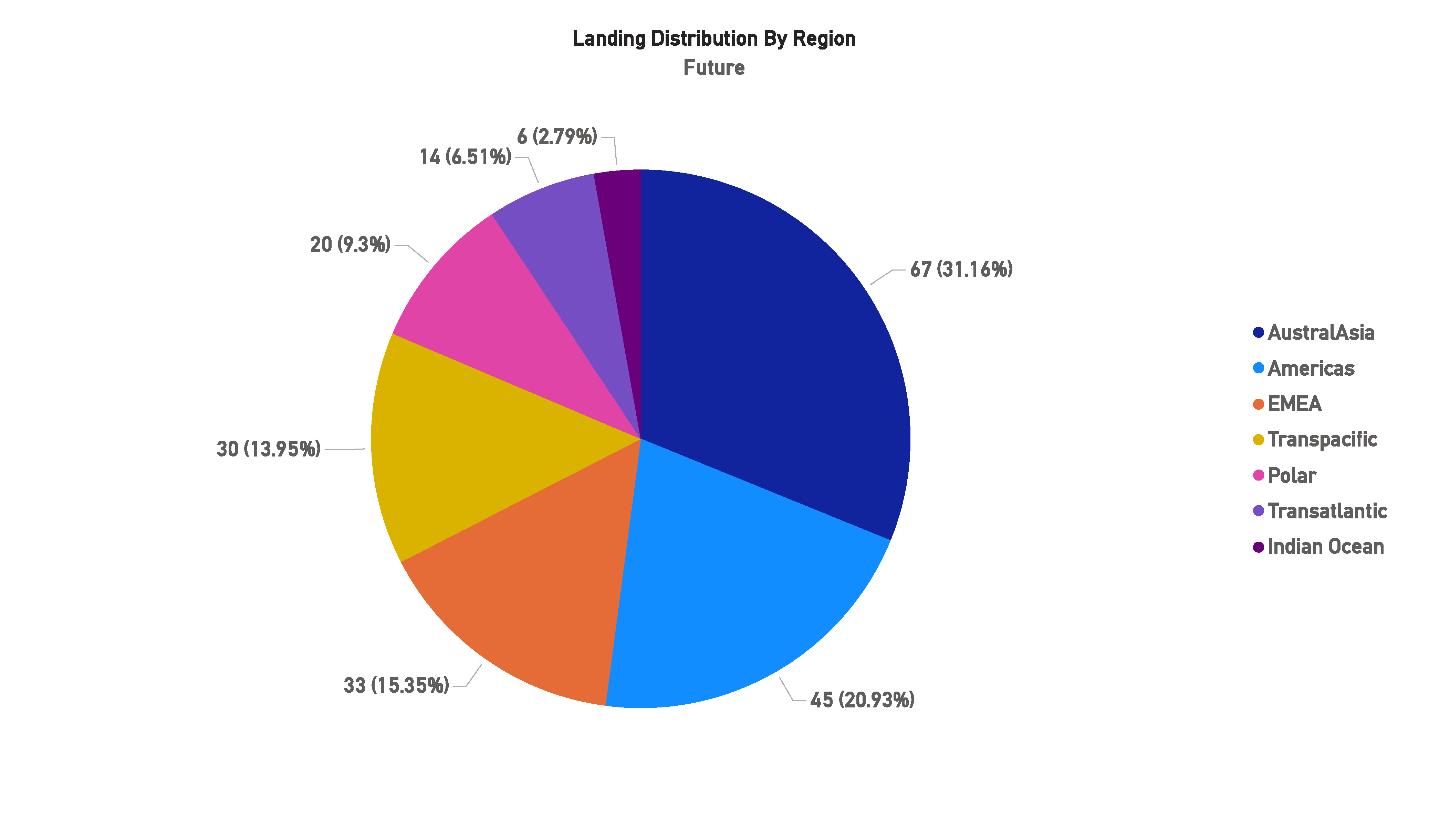

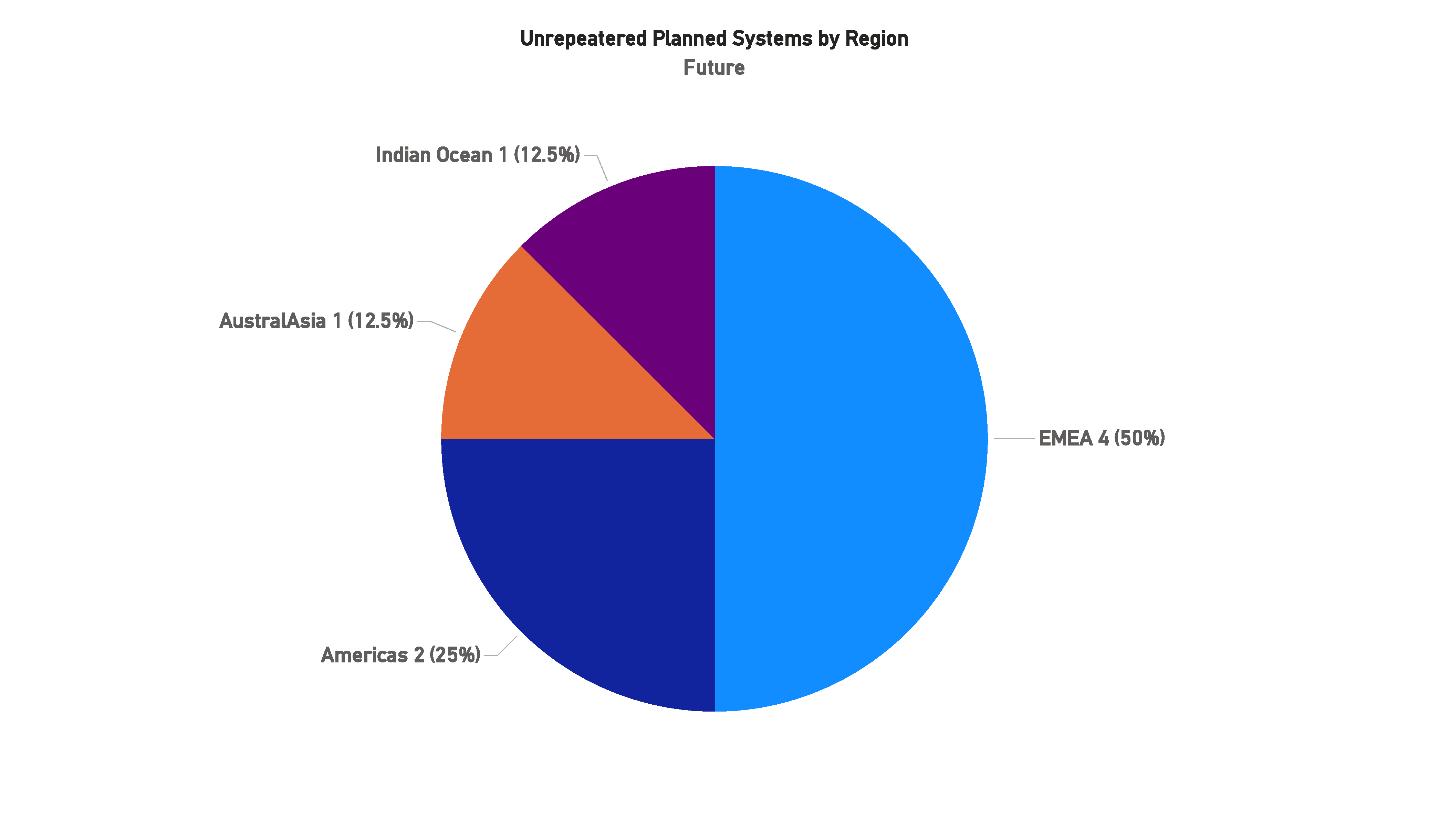

19: Planned Systems by Region, 2026-2028

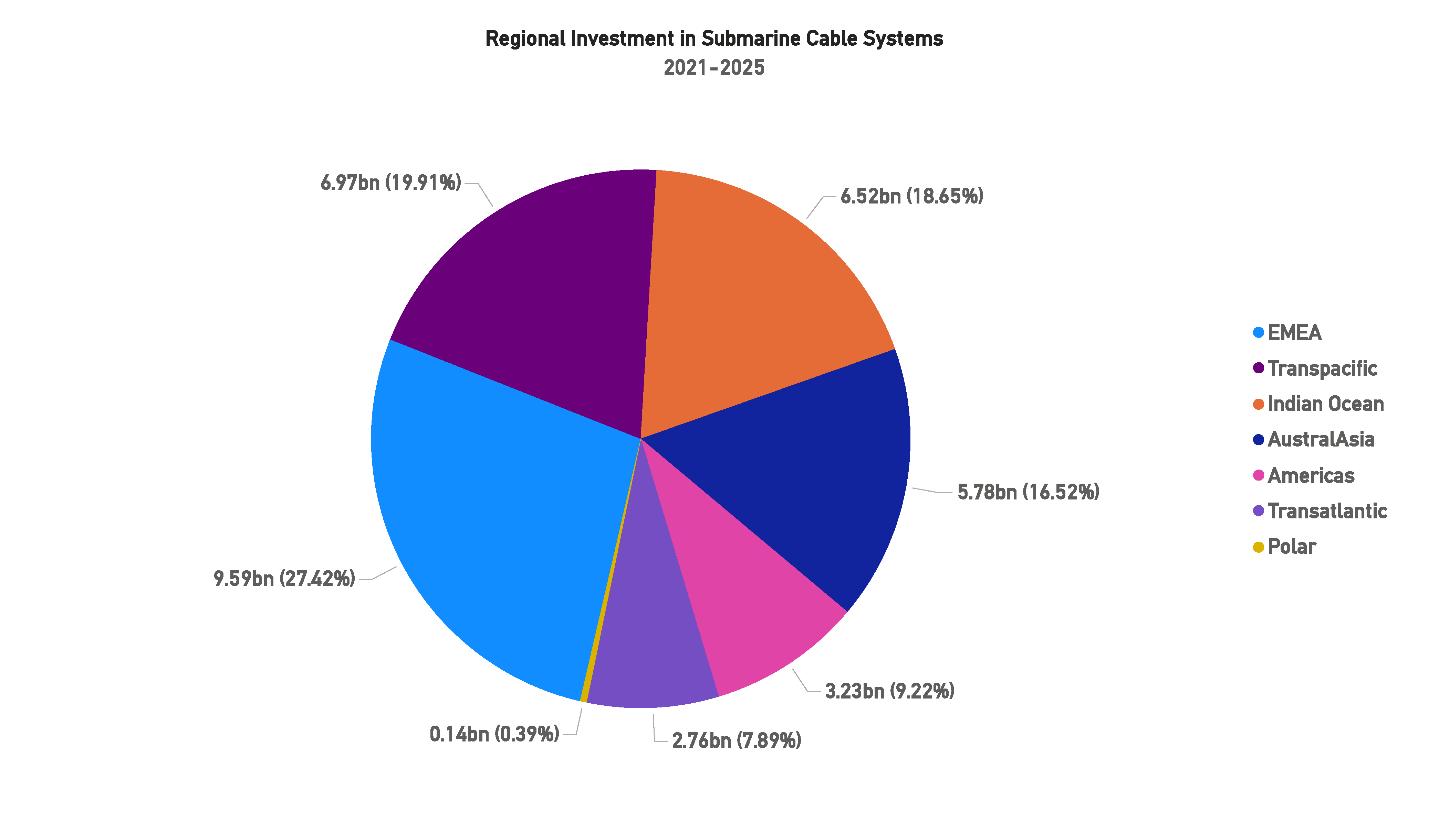

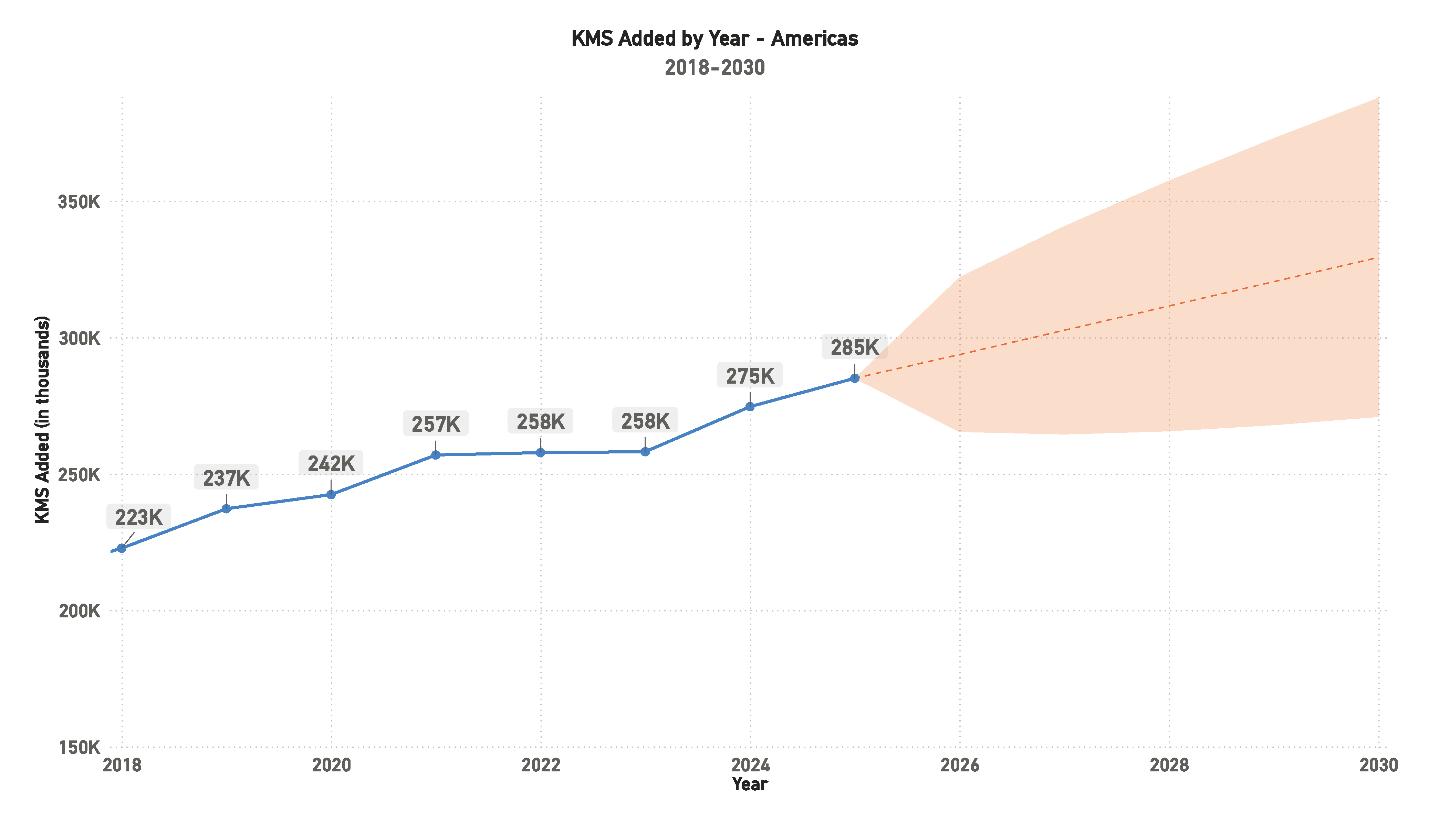

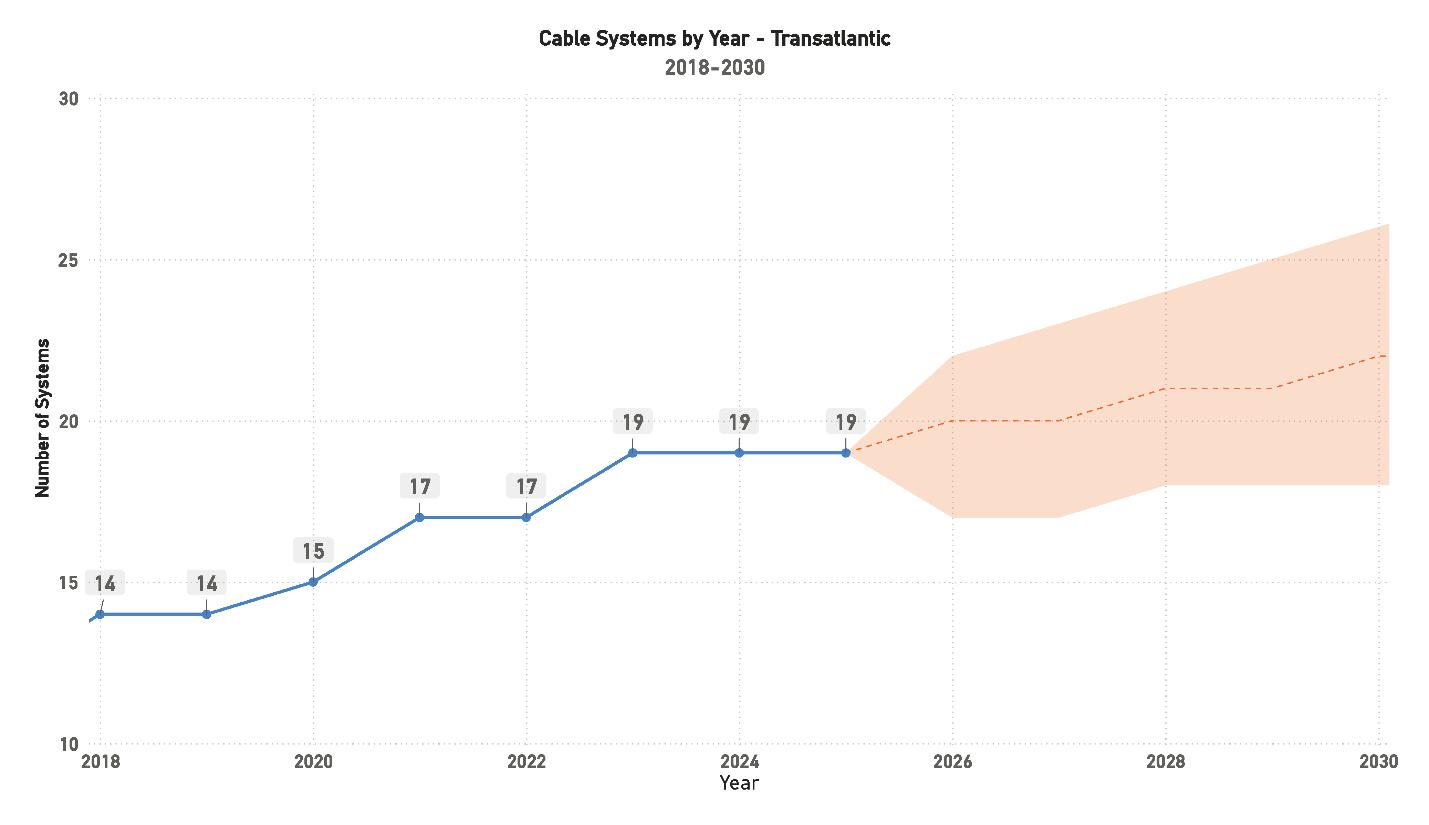

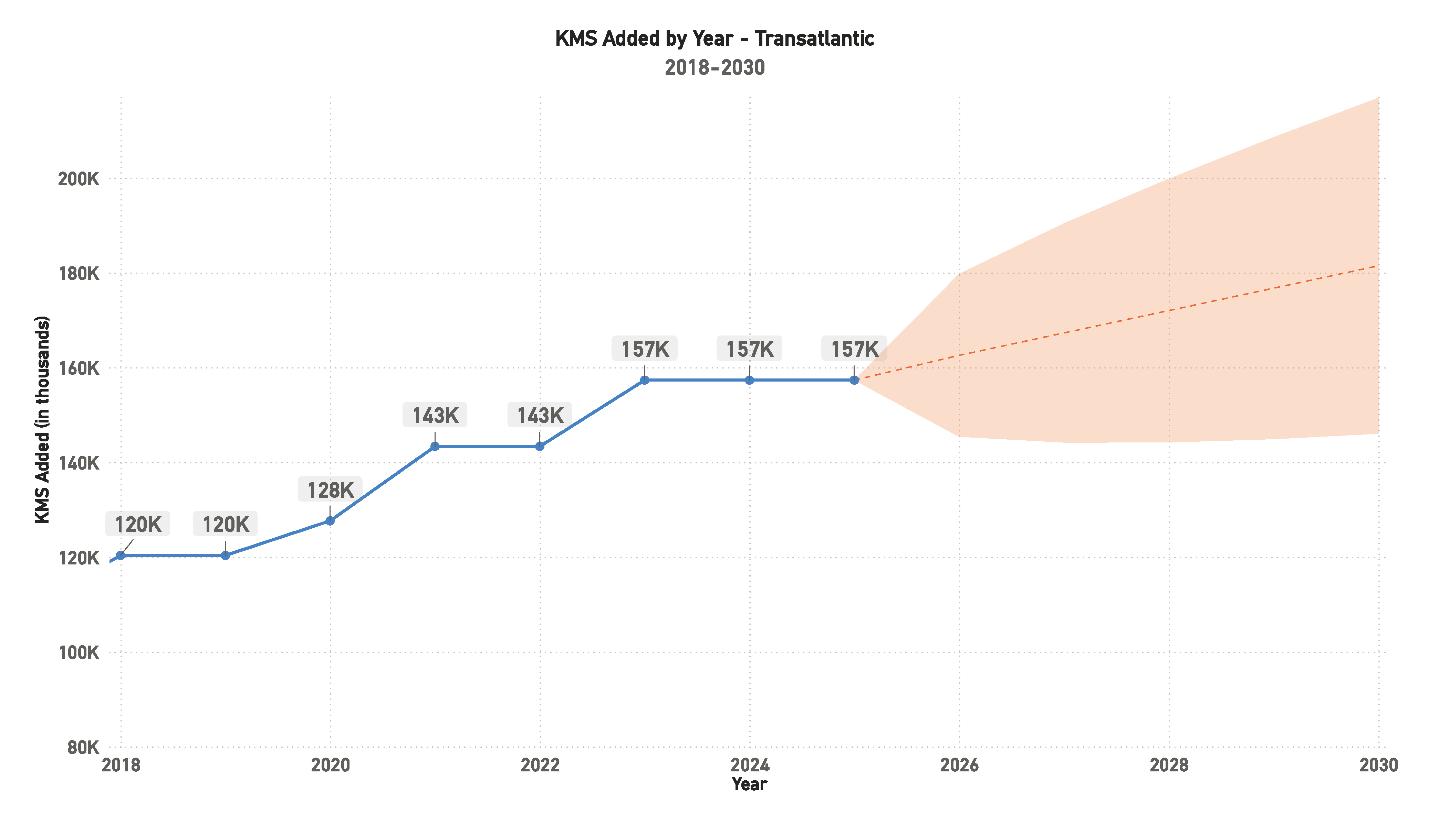

Looking ahead, planned systems between 2026 and 2028 further reinforce these dynamics. AustralAsia leads with 88,000 kilometers of projected builds, accounting for one-third of future deployments, while the Transpacific follows with 55,000 kilometers, or just over 20% of the total. EMEA remains steady, with 36,000 kilometers planned, while the Transatlantic and Polar regions each account for approximately 26,000 kilometers. The Americas and Indian Ocean regions, with 22,000 kilometers and 12,000 kilometers respectively, remain on the lower end of future activity.

These projections suggest that long-haul routes will continue to dominate global growth, with AustralAsia emerging as the most active hub of development. The renewed emphasis on Transpacific builds reflects the need for both replacement of aging systems and diversification of capacity between Asia and the Americas. Compared to last year’s forecast, AustralAsia’s projected share has increased, while EMEA and the Transatlantic remain stable contributors, underscoring the broadening distribution of global infrastructure investment.

“Ten years ago the network carried over 97% of international traffic across one million km of cable with 100–150 Tbps of capacity; by 2025 it spans over 1.5 million km with more than 550 cables and 2 500–3 000 Tbps of capacity—a twenty fold increase in a decade.”

Joel Ogren – Assured Communications (STF Issue 142)

Figure

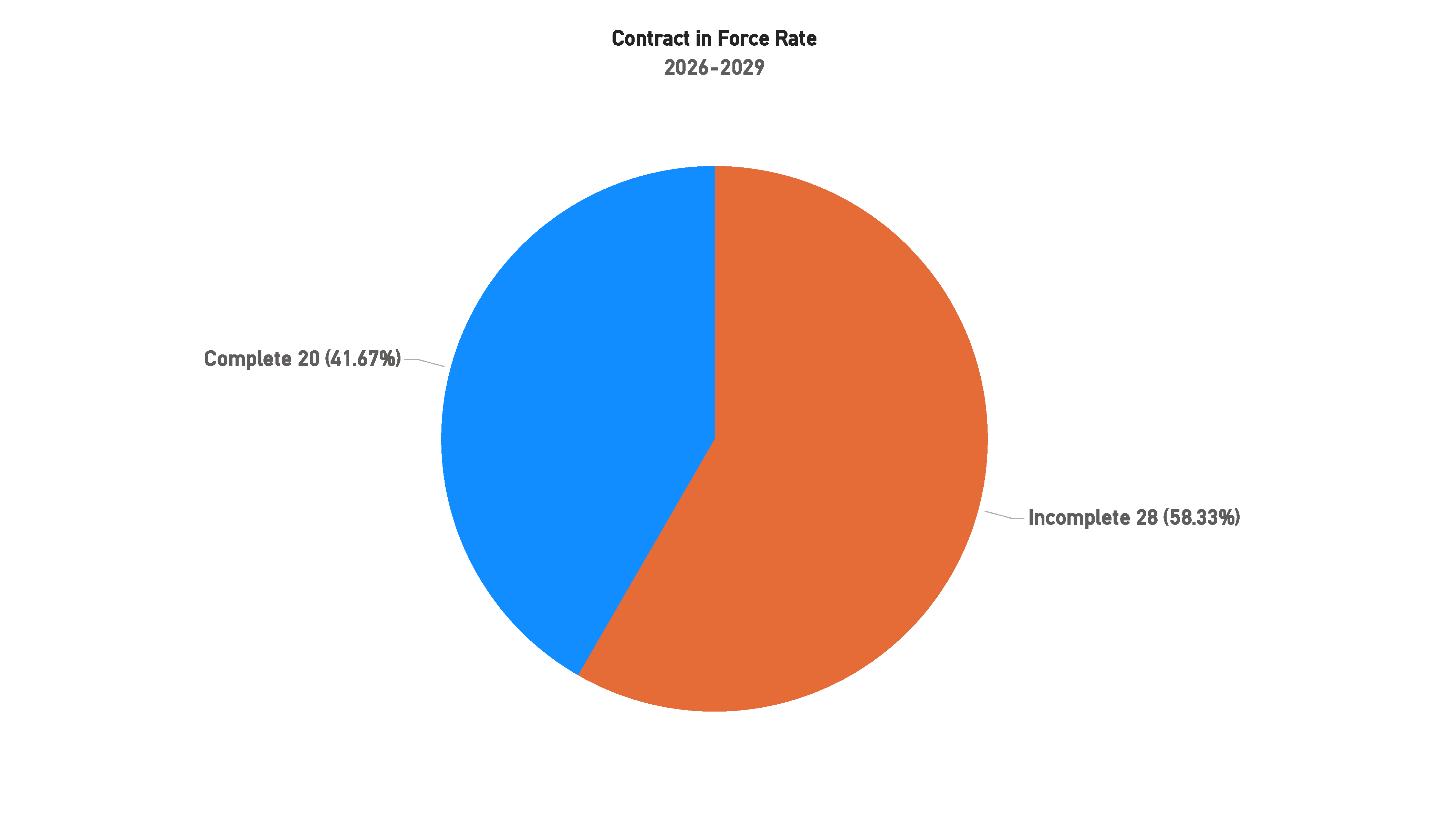

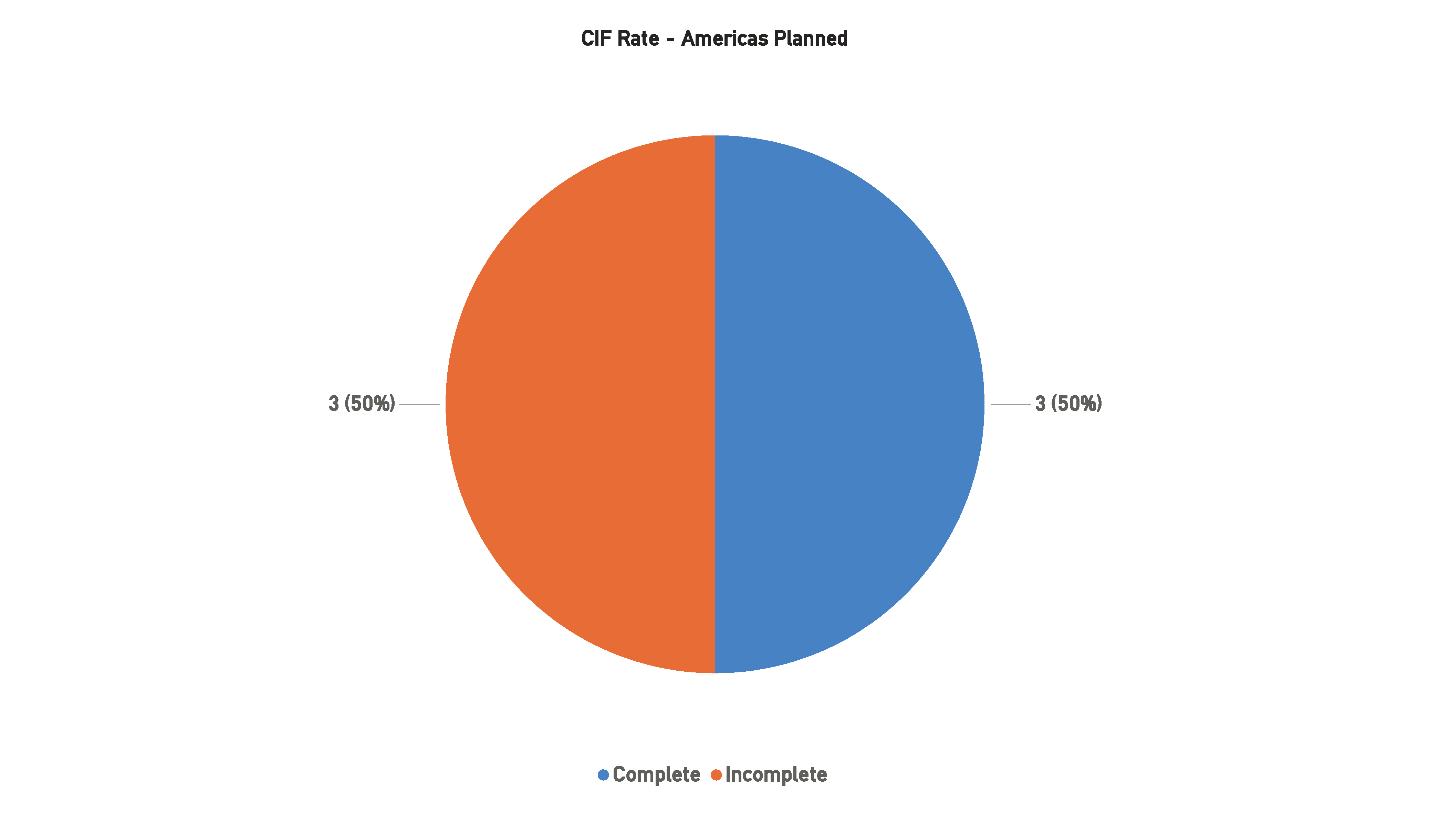

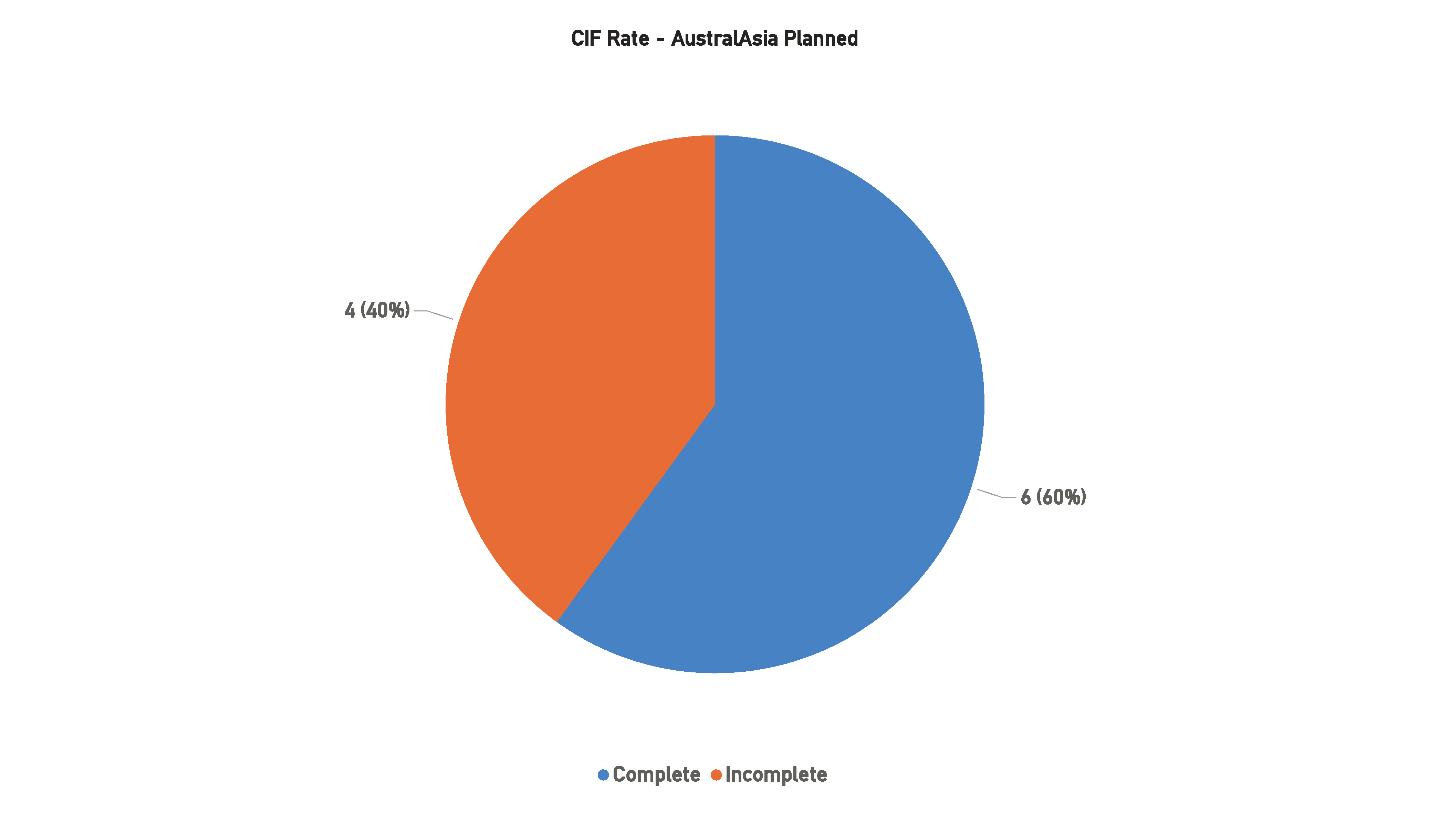

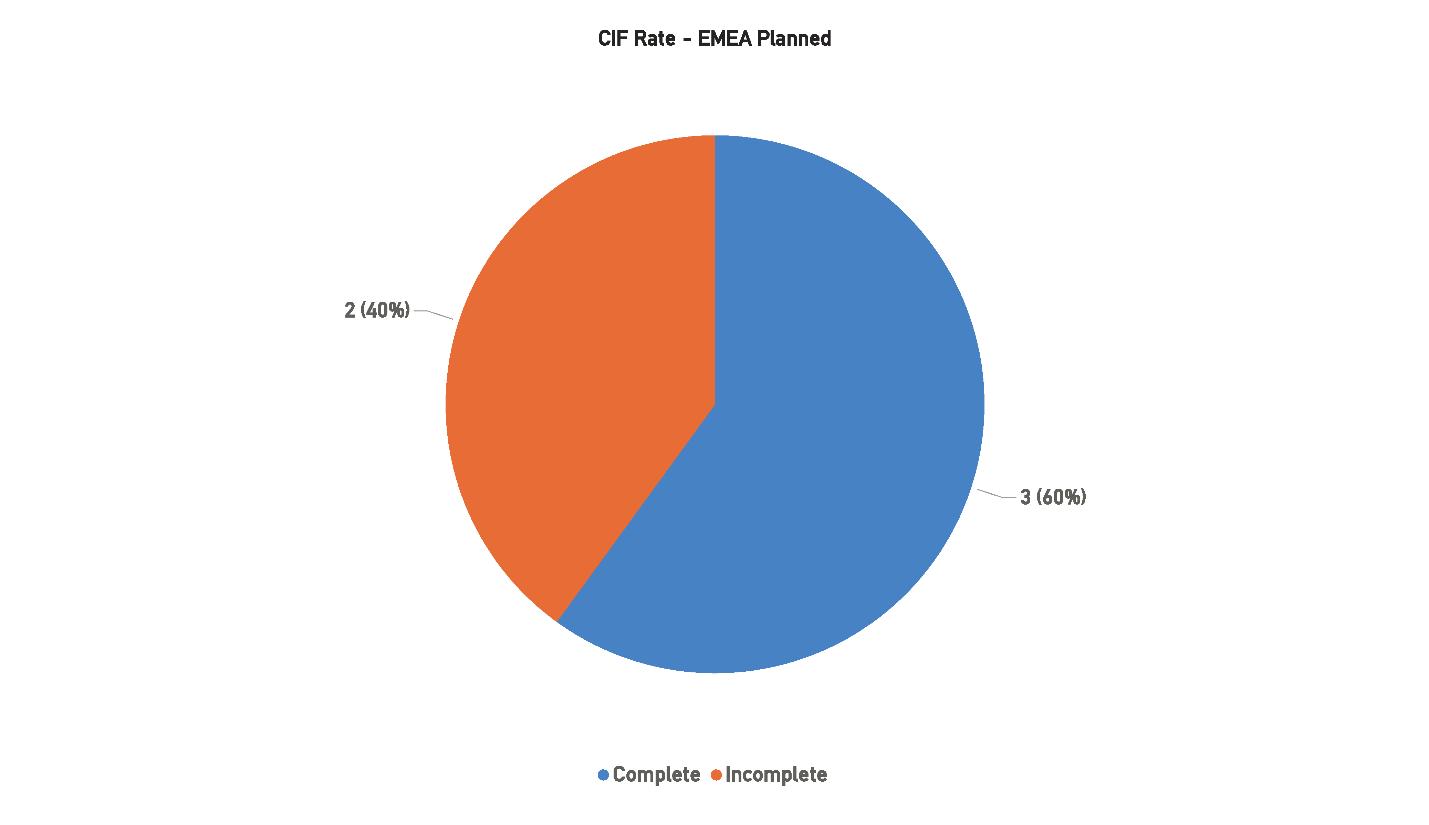

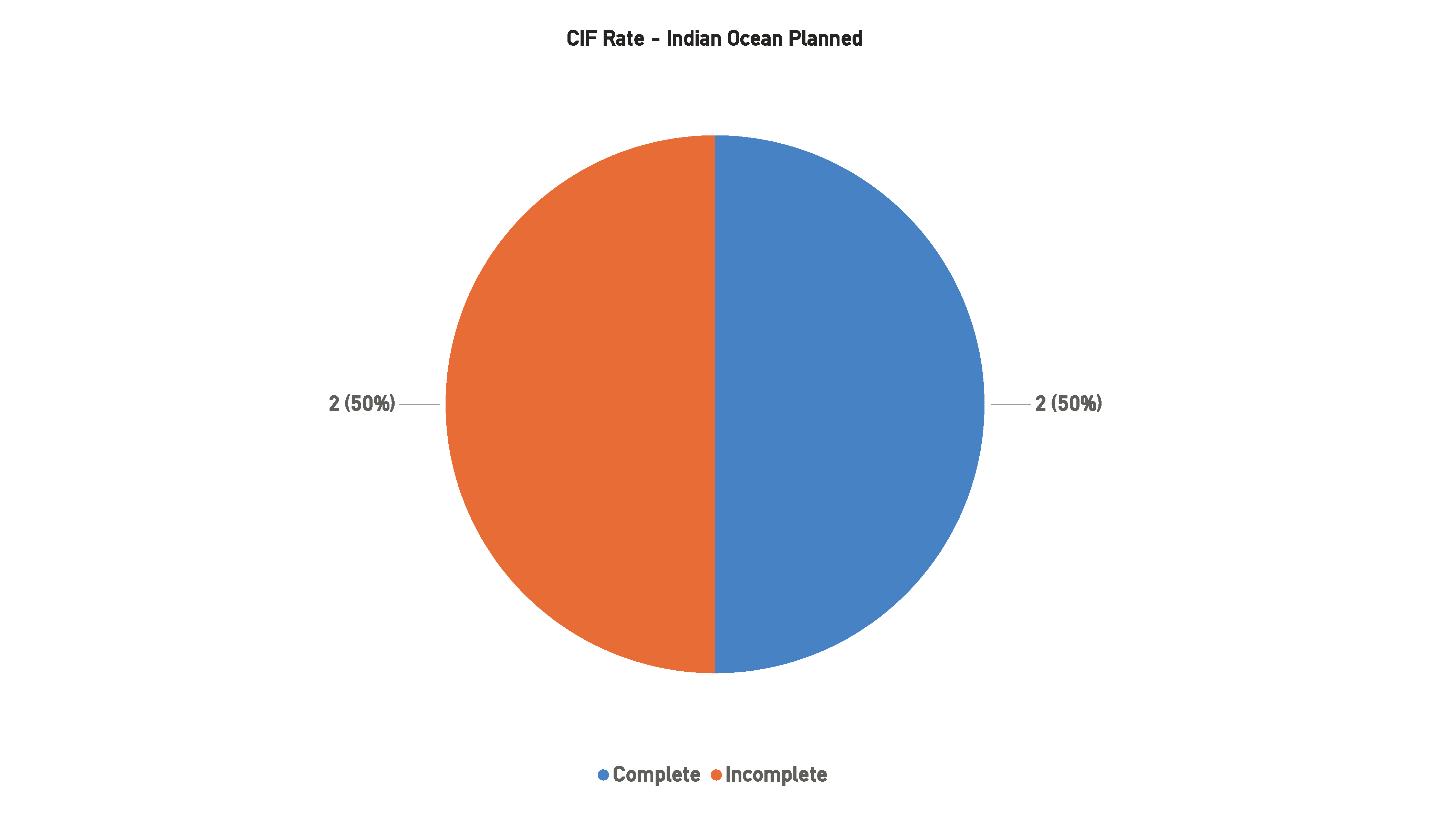

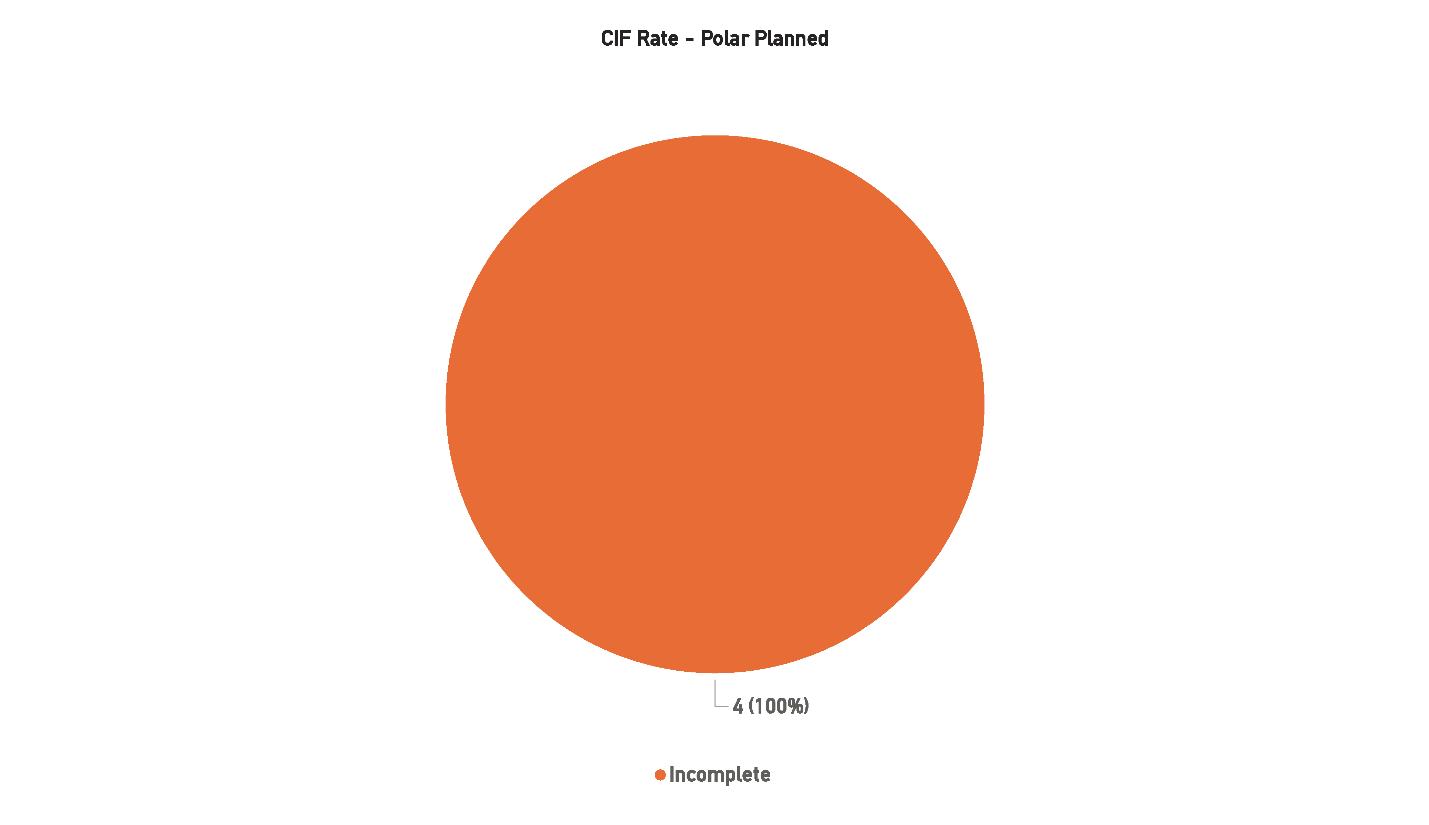

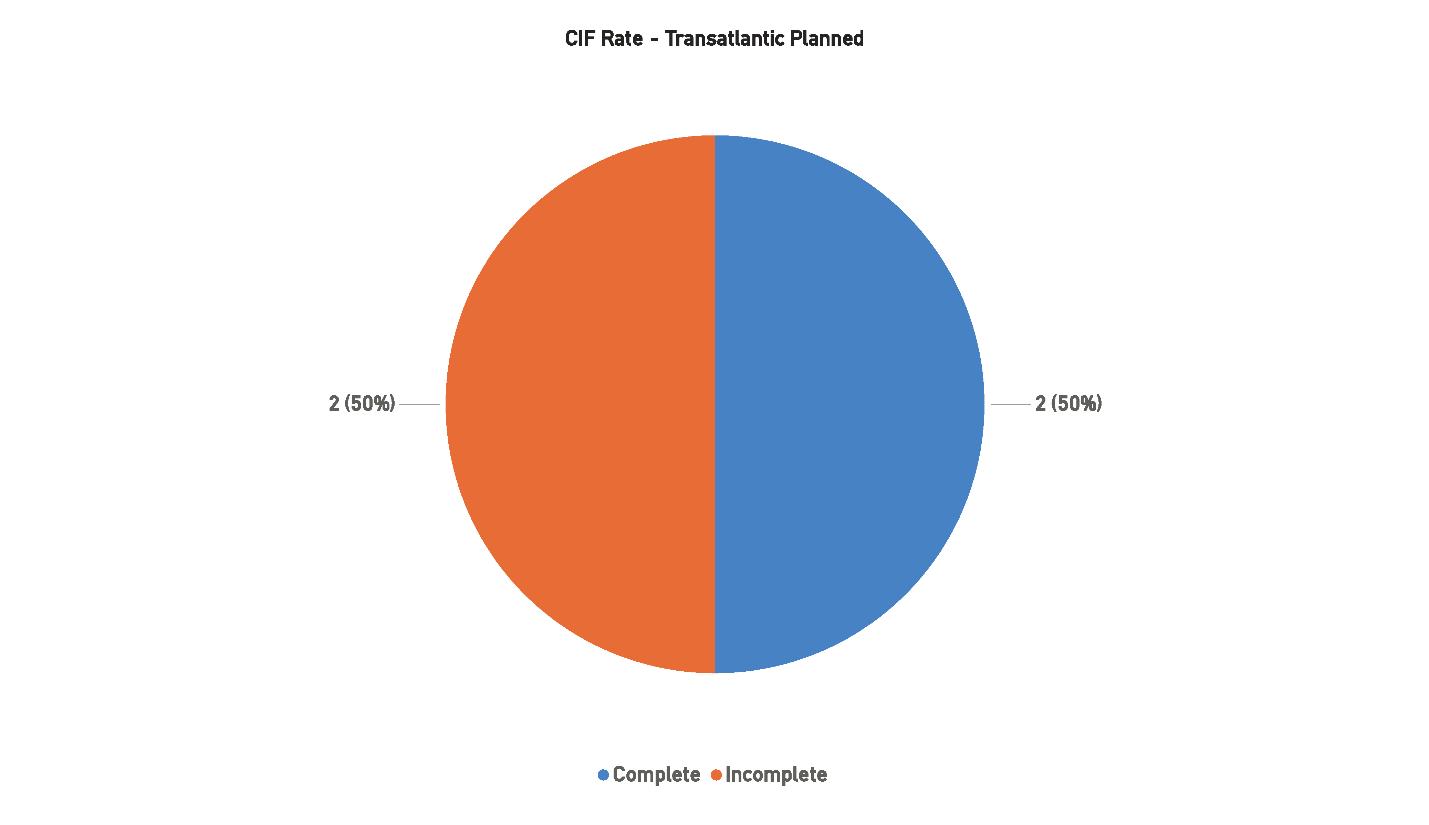

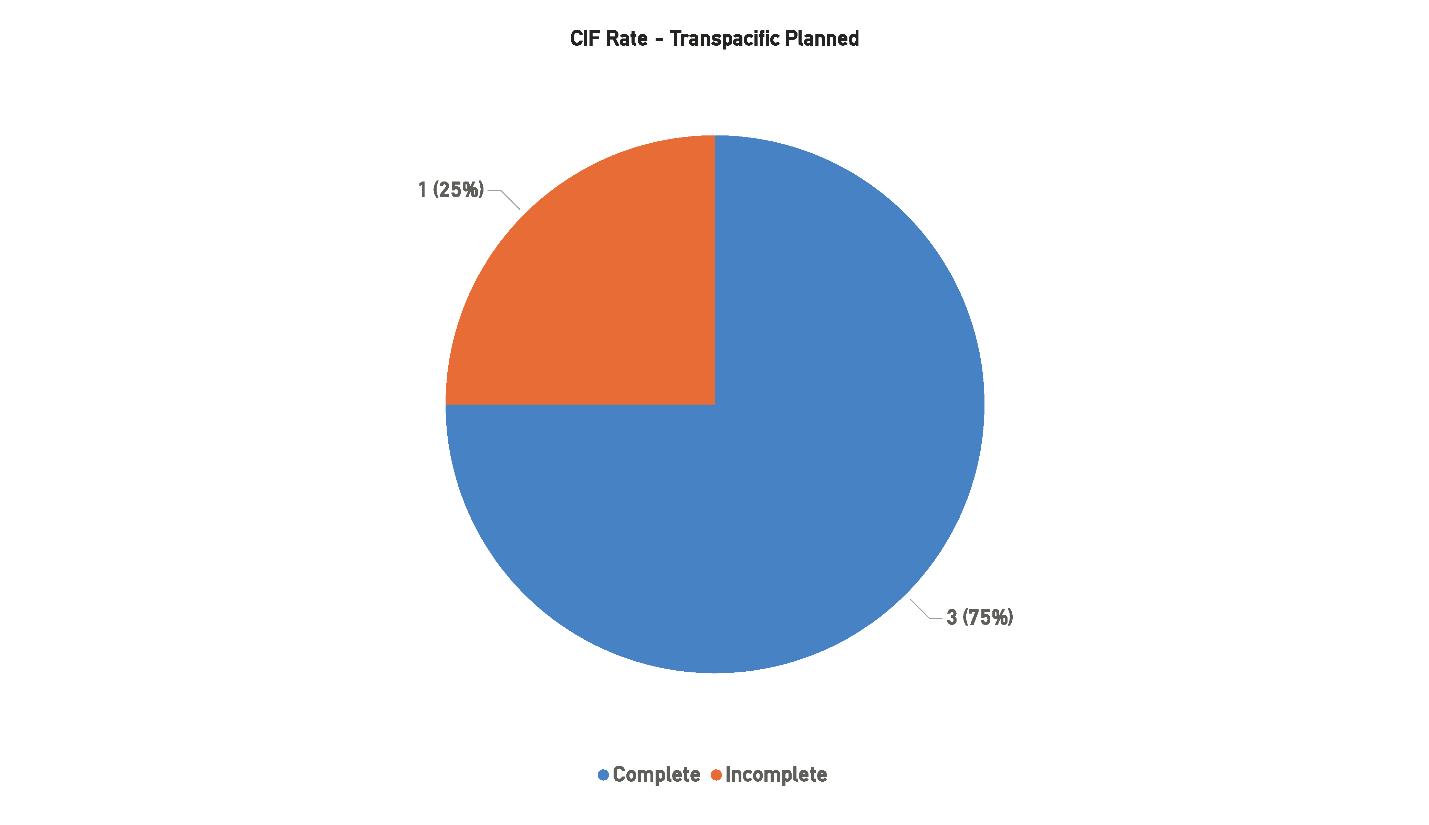

Despite this healthy pipeline, securing financing remains one of the industry’s most pressing challenges. As of the 2026–2029 forecast, 20 of the 48 planned systems have reached Contract in Force (CIF) status, representing 41.67%. While this is an improvement over last year’s report, where just over 20% of systems were CIF, it still leaves the majority of projects awaiting final commitments. The increase suggests progress in overcoming earlier financing hurdles, though challenges persist amid rising costs, regulatory complexities, and continued global economic uncertainty.

The CIF rate remains a key indicator of which systems are most likely to move forward. Projects that achieve CIF status have secured the necessary contractual and financial backing, giving them a far higher likelihood of being realized. Those that remain incomplete face the risk of delay or cancellation, particularly if they lack hyperscaler participation or sufficient consortium support. The current figures suggest that while industry activity remains strong, the timing of deployments will continue to be influenced by financing cycles and broader market conditions.

In summary, the period from 2021 to 2025 highlights the industry’s ability to adapt to fluctuating conditions, while projections through 2029 reaffirm the long-term trajectory of steady growth. EMEA, AustralAsia, and the Transpacific stand out as the primary corridors of expansion, while the CIF rate underscores the challenges that remain in bringing ambitious plans to completion.

Figure 20: Contract In Force Rate, 2026-2029

1.4. OUT OF SERVICE SYSTEMS ANALYSIS

An in-depth examination of the decommissioning of Out-of-Service (OOS) submarine cable systems highlights the growing importance of this often-overlooked stage of the industry’s lifecycle. While many cables continue to operate well past their anticipated End-of-Service (EOS) dates, the process of removing, recycling, or otherwise managing these aging systems has become increasingly relevant as global connectivity infrastructure expands. Companies such as Subsea Environmental Services, Mertech Marine, and Submarine Cable Salvage, Inc. remain at the forefront of recovery and recycling efforts, offering solutions that balance operational, financial, and environmental considerations. Mertech Marine has continued its long-standing focus on the recovery and repurposing of cables, while Subsea Environmental Services and Submarine Cable Salvage, Inc. have emphasized sustainable practices, including materials recycling and environmentally conscious removals.

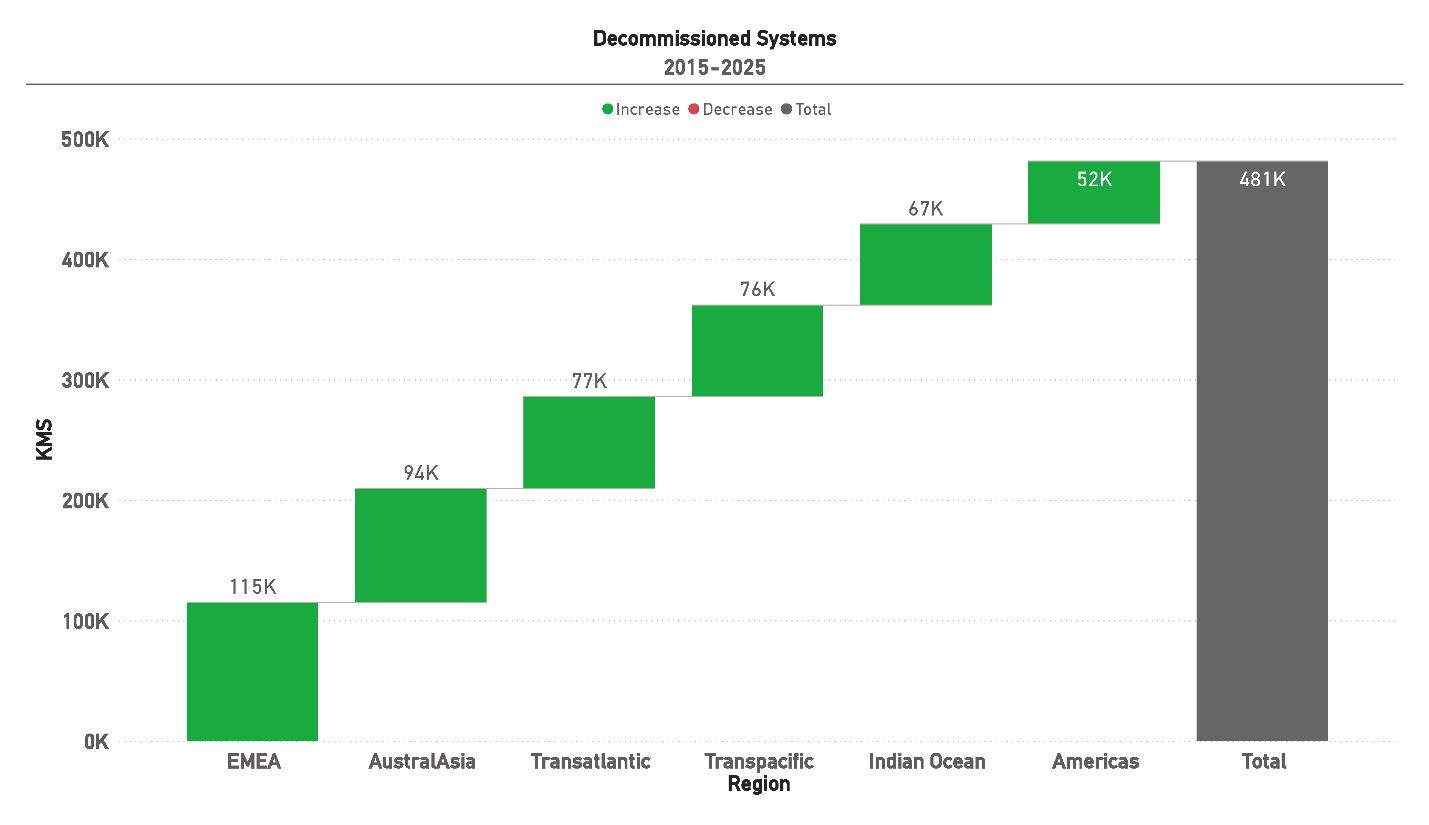

Figure 21: Decommissioned Systems, 2015-2025

Between 2015 and 2025, approximately 481,000 kilometers of submarine cable systems are expected to

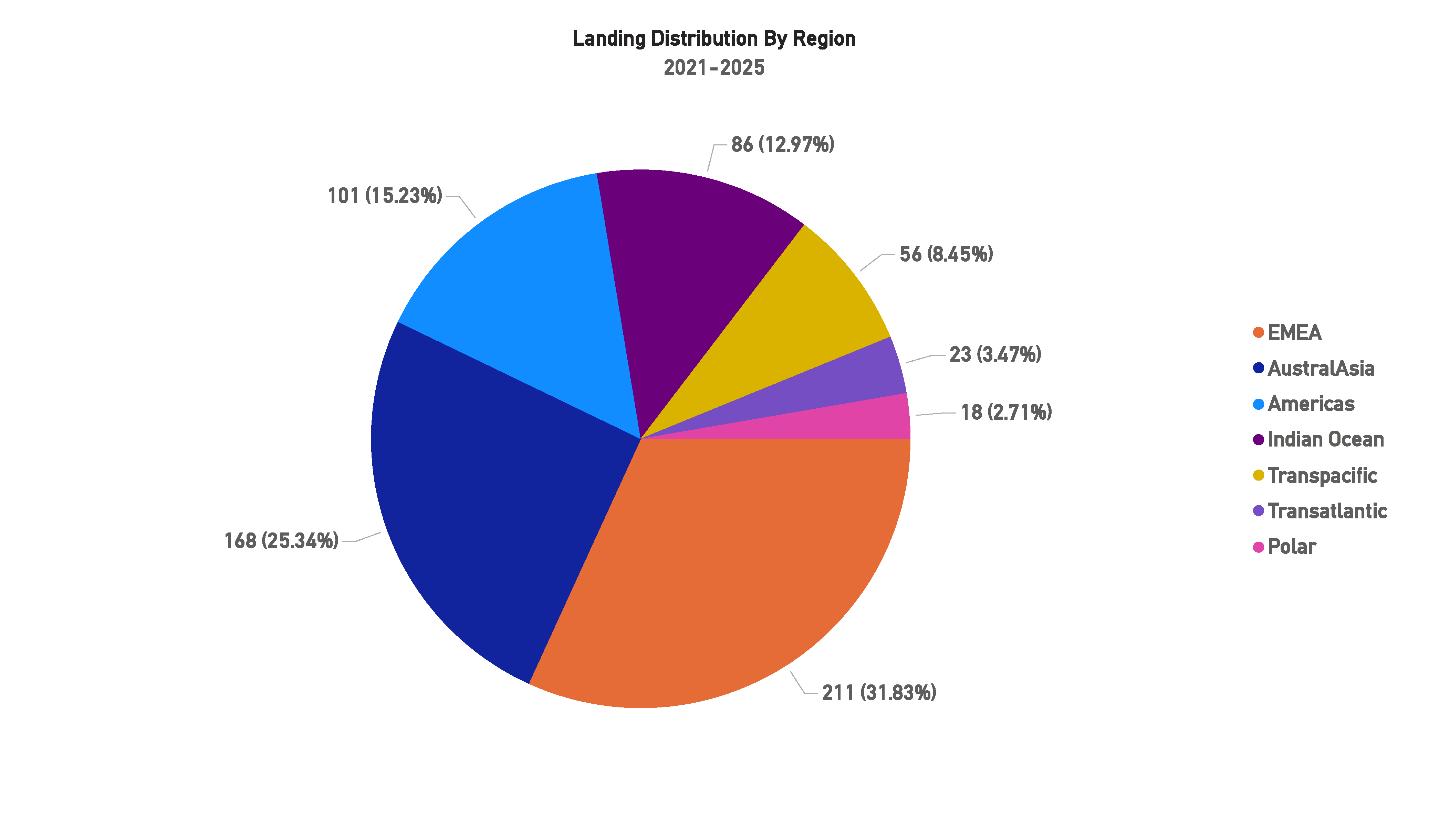

be decommissioned worldwide. The EMEA region accounts for the largest share, with 115,000 kilometers taken out of service, reflecting both its historical role as a hub of subsea connectivity and the aging infrastructure concentrated in the region. AustralAsia follows with 94,000 kilometers, while the Transatlantic and Transpacific regions report 77,000 and 76,000 kilometers, respectively, underscoring the significant turnover in long-haul systems. The Indian Ocean region contributes 67,000 kilometers to global decommissioning totals, and the Americas account for 52,000 kilometers. Together, these figures highlight the ongoing transition as older systems reach the end of their useful life, particularly those built during the rapid build-out of the late 1990s and early 2000s.

Compared to last year’s analysis, which estimated 411,000 kilometers of cables taken out of service from 2014 to 2024, the updated totals reflect both continued retirements and improved tracking of decommissioned systems across multiple regions. EMEA remains the largest contributor, consistent with its status in previous years, while AustralAsia has grown in share as more regional systems age out of service. The Americas and Indian Ocean remain relatively smaller contributors but nonetheless illustrate the steady global spread of decommissioning activity.

Technological advancements have extended the lifespan of many cables beyond their expected EOS, often surpassing the standard 25-year benchmark through upgrades at landing stations and network management improvements. However, aging infrastructure inevitably faces higher risks of equipment failure, service interruptions, and increased maintenance costs, leading operators to transition systems into OOS status. The decision to physically remove these systems remains complex: while environmental regulations in some regions now mandate removal, in others, cables are left on the seafloor due to prohibitive recovery costs and the potential for ecological disturbance.

With an estimated 85 additional systems projected to reach EOS within the next five years, and another 53 by 2032, the issue of decommissioning is expected to intensify. Historical precedent shows that fewer than 60 systems have been fully removed in the past two decades, underscoring the gap between cables aging out of service and those actually reclaimed or recycled. This discrepancy places increasing pressure on both operators and regulators to address the environmental and logistical challenges of managing decommissioned assets.

Specialized companies such as Mertech Marine and Subsea Environmental Services play a vital role in bridging this gap. By focusing on recovery and recycling, these firms ensure that valuable materials can be repurposed while mitigating the environmental impact of aging infrastructure. Their expertise in cable removal and sustainable disposal practices offers a path forward for an industry facing mounting regulatory scrutiny and growing public expectations around environmental responsibility.

In conclusion, the decommissioning of Out-of-Service submarine cable systems remains a multifaceted challenge at the intersection of technical feasibility, financial cost, and environmental stewardship. As hundreds of thousands of kilometers of cable near the end of their operational life, coordinated strategies involving system owners, regulators, and specialized recovery firms will be essential. The coming decade will test the industry’s ability to not only expand global connectivity but also responsibly manage the inevitable retirement of its oldest infrastructure.

“Unrepeated submarine cables form the oldest architecture in subsea communications. They provide regional and inter island links and connect offshore installations; their simplicity and cost effectiveness make them indispensable.”

Tony Frisch (Xtera), Anders Ljung (Hexatronic) & Lynsey Thomas (Lynsey Thomas Consulting) (STF Issue 143)

2. CAPACITY

2.1. GLOBAL CAPACITY

Global capacity growth across major submarine cable routes continues to highlight the shifting dynamics of investment and demand within the industry. Between 2021 and 2025, a clear pattern emerges: while overall demand for international connectivity remains robust, the timing and distribution of new capacity along major arteries such as the Transatlantic, Transpacific, Americas, and AustralAsia routes have varied considerably year by year.

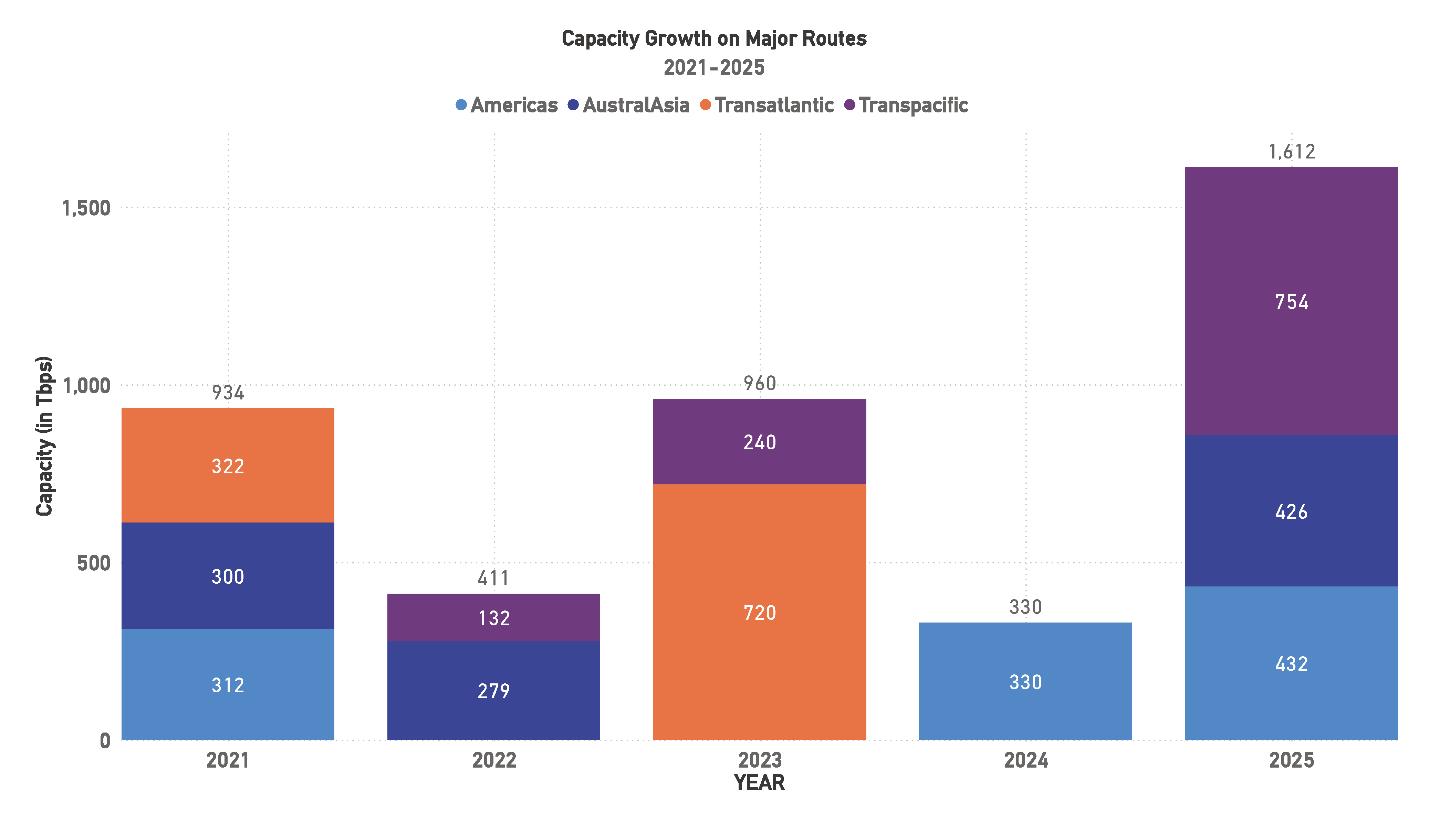

22: Capacity Growth on Major Routes, 2021-2025

In 2021, the industry recorded one of the stronger capacity additions of the period, with 934 Tbps brought online across the major routes. The largest contributions came from the Transatlantic and Americas segments, which together accounted for more than 600 Tbps of new capacity. AustralAsia also played a significant role, adding 300 Tbps during the year. This growth underscored the continued demand across both east–west and north–south routes, particularly for transoceanic systems connecting the U.S. and Europe with Asia and beyond.

Figure

By contrast, 2022 represented a sharp decline in new additions, with only 411 Tbps deployed. This drop was driven largely by a lack of growth across the Americas and Transatlantic routes, with AustralAsia adding just under 280 Tbps and Transpacific contributing a smaller 132 Tbps. The slowdown reflected a gap in the commissioning of large-scale new systems, even as demand fundamentals remained strong.

A recovery took shape in 2023, with 960 Tbps of new capacity added across major routes. The Transatlantic segment dominated with 720 Tbps, underscoring its central role as one of the most competitive and well-developed corridors. The Transpacific route contributed 240 Tbps in the same year, marking an important step forward in expanding links between North America and Asia-Pacific markets. Notably, AustralAsia and the Americas did not register major contributions during this period, highlighting the uneven distribution of capacity growth across routes.

Capacity growth slowed again in 2024, with just 330 Tbps added, all of it on the Americas route. This represented one of the lowest totals in recent years, particularly when compared to the significant volumes added in 2021 and 2023. The limited growth underscores the variability in project completions, as capacity additions remain closely tied to the timing of individual system launches.

In 2025, the industry is preparing for a substantial wave of new capacity across major routes. A total of 1,612 Tbps is projected to be added, the largest annual increase of the five-year period. The Transpacific route is expected to contribute 754 Tbps, representing nearly half of total new growth this year, followed by AustralAsia with 426 Tbps and the Americas with 432 Tbps. Together, these three regions account for more than 95% of projected additions in 2025, reflecting a renewed emphasis on strengthening intercontinental connectivity and expanding east–west traffic corridors.

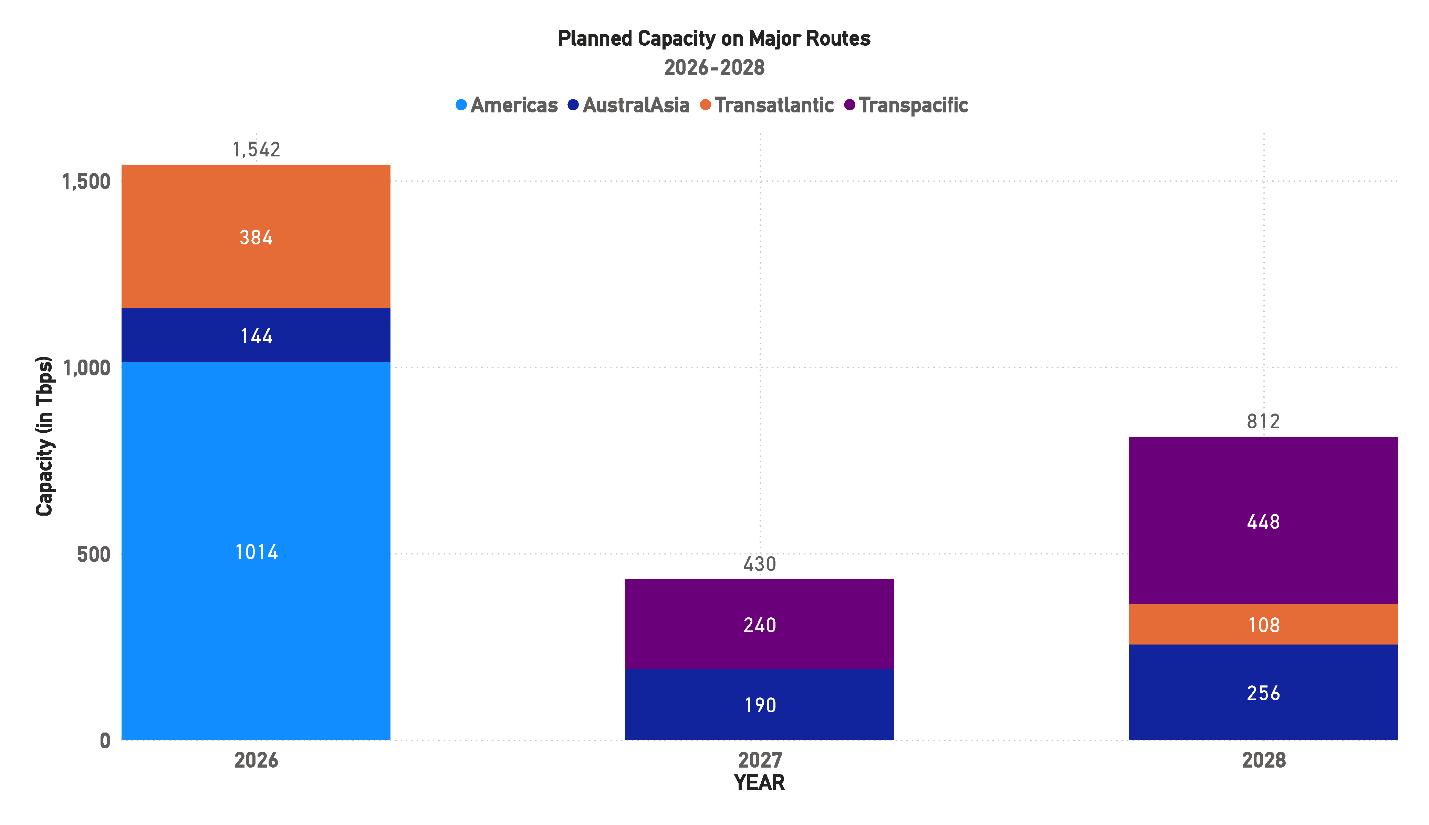

Figure 23: Planned Capacity on Major Routes

Beyond 2025, the outlook indicates continued capacity growth but at a more measured pace. In 2026, an estimated 1,542 Tbps will be added, the majority of which—over 1,000 Tbps—will come from the Americas route. This makes 2026 another high-capacity year, with important implications for data flow between the U.S., Latin America, and other regions. In 2027, capacity additions are projected to decline significantly, with only 430 Tbps planned, largely split between the Transpacific (240 Tbps) and AustralAsia (190 Tbps). By 2028, the pipeline anticipates 812 Tbps of new capacity, with Transpacific once again playing a leading

role at 448 Tbps.

Compared to last year’s projections, the timing of growth has shifted, with some systems now scheduled for later years, particularly in the Transpacific and Transatlantic segments. The concentration of activity in 2025 and 2026 highlights the clustering effect often seen in large-scale submarine cable deployments, where multiple projects reach completion within a short timeframe. At the same time, the forecast suggests slower activity in 2027 before growth resumes in 2028, a reminder of the cyclical nature of the industry.

It is important to note that these figures represent growth across the industry’s major arteries and do not capture all new capacity added globally. They are, however, indicative of where the most competitive and heavily developed routes are headed in terms of near- and medium-term growth. As in previous years, the adoption of advanced transmission technologies—including higher-order modulation, greater fiber pair counts, and spectrum sharing arrangements—will play a critical role in ensuring these new systems meet the escalating demand for global data transmission.

Taken together, the results from 2021 to 2025 and the planned deployments through 2028 underscore the scale and complexity of managing global submarine cable capacity. With demand continuing to rise across all regions, the industry’s ability to deliver large volumes of new capacity on its most important corridors remains central to supporting the world’s digital infrastructure.

“More than 70% of direct traffic between Africa and the United States now runs through the Angola Cables network, providing low latency, high capacity routes.”

Angelo Gama – Angola Cables (STF Issue 142)

2.2. LIT CAPACITY

The global submarine cable landscape continues to expand rapidly, with major routes seeing significant increases in both lit capacity (the in-service bandwidth actively being used) and total design capacity (the theoretical maximum if fully equipped). Year-over-year growth from 2024 to 2025 has been robust across all key routes, driven by hyperscaler investments, data center expansion, and surging demand from 5G and cloud services. However, regional disparities and constraints – from economic and regulatory challenges to geopolitical tensions – are influencing how this capacity is utilized. Below, we provide an updated region-by-region breakdown for the Americas, Intra-Asia, Transatlantic, and Transpacific routes, including 2024 and 2025 figures and projections for 2026, along with analysis of trends, drivers, and emerging technologies.

2.2.1. AMERICAS (NORTH AMERICA–LATIN AMERICA ROUTES)

Capacity Growth: The Americas routes (primarily connecting the U.S. with Latin America and the Caribbean) have sustained strong growth. Total design capacity nearly doubled between 2020 and 2024, rising from about 913 Tbps to 1,524.8 Tbps in 2024, while lit capacity grew from 802 Tbps to 1,102.2 Tbps over the same period. This represents a significant increase, although growth has been uneven year to year. From 2024 to 2025, total capacity continued to climb – bolstered by new systems like Google’s Firmina cable (approximately 12 fiber pairs, ~240 Tbps design) – reaching an estimated ~1,650 Tbps. Lit capacity is likewise up in 2025 to roughly ~1,200 Tbps, reflecting ongoing traffic growth. By 2026, with additional projects coming online (including high-fiber-count cables such as the planned 36-pair AMX-3/Tikal cable at ~360 Tbps (BNAmericas, 2024)), total design capacity is projected to approach ~1,750 Tbps, with lit capacity around ~1,300 Tbps as service uptake gradually fills the available bandwidth.

Table 1: Americas Route Lit Capacity 2024-Present Year

Utilization and Drivers: The Americas region currently utilizes a large share of its capacity – roughly 72% of available capacity was lit in 2024 – but growth in lit bandwidth has been slower and prone to fluctuation. In the years immediately prior, lit capacity saw double-digit growth (29% in 2020) that tapered off to

mid-single digits (around 4% in 2021) before rebounding to about 16% by 2024. This volatility stems from economic and political factors in Latin America. Demand is heavily concentrated in the United States, which continues to drive traffic, whereas many Latin American markets are still ramping up digital adoption. Hyperscalers (like Google, Meta, and Microsoft) have been key investors in new North–South cables connecting the U.S. to Brazil, Chile, Argentina and beyond.

These new private cables (e.g., Google’s Curie and Firmina, Meta’s Juno and others) contribute enormous design capacity, but much of it is dedicated to the hyperscalers’ own cloud and content needs. As a result, unless wider market demand catches up or access to these systems broadens, a significant portion of the theoretical capacity remains unlit. Indeed, the Americas route has struggled with underutilized capacity in certain segments, as cloud and streaming services growth in Latin America, though accelerating, has not yet fully tapped the available bandwidth.

Regional Considerations: Economic challenges and regulatory hurdles in parts of Latin America continue to temper demand growth. Political instability and slower enterprise cloud adoption in some countries mean that the full potential of new cables is not immediately realized. Nevertheless, there are positive signs: telecom and data center investments are increasing in major economies like Brazil, Mexico, and Chile, and 5G rollouts and rising internet use are steadily boosting international bandwidth needs. By 2025, cloud providers and content networks are expanding their presence in Latin America, driving more traffic onto subsea routes.