Celebrating over 50 years of the Society of Technical Analysts GOLDSTRIKING The Society of Technical Analysts The Best of the STA Journal

First Published in 2022 by Society of Technical Analysts Paperback Edition

All articles were previously published in the STA Journal Design by Andrew Convery Printed in the UK

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage retrieval system, without permission in writing from the publisher

Copyright © The Society of Technical Analysts ISBN 978-1-3999-3292-9

To all past, present and future members of the Society of Technical Analysts.

The UK’s professional body for Technical Analysts. Founded in 1968. The oldest of its kind in the world.

tel: +44 (0) 20 7125 0038 info@ www.technicalanalysts.comtechnicalanalysts.com

4

The Society of Technical Analysts Dean VernhamHouseDeanAndoverSP110JZ

Dow Theory, Wyckoff and Volume 34 to 59 CHAPTER TWO 34 5 Elliott Wave Fibonacciand 134 to 161 CHAPTER SEVEN 134 PsychologyMarketsand 186 to 201 CHAPTER NINE 186 Theory of Technical Analysis 08 to 33 CHAPTER ONE 8 Moving Averages and Trends 98 to 117 CHAPTER FIVE 98 Pattern Recognition and Pattern Analysis 80 to 97 CHAPTER FOUR 80 Gann Analysis, Cycles and Forecasting 162 to 185 CHAPTER EIGHT 162 SystematicTrading 202 to 217 CHAPTER TEN 202 IndicatorsMomentumand 118 to 133 CHAPTER SIX 118 Charting Types, Point & Figure & Candlesticks 60 to 79 CHAPTER THREE 60 Please note: The job titles and affiliations of the authors featured at the end of the articles were applicable at the time of original publication and as such may not be relevant today. Disclaimer: The Society is not responsible for any material published in this book and publication of any material or expression of opinions does not necessarily imply that the Society agrees with them. The Society is not authorised to conduct investment business and does not provide investment advice or recommendations. Articles are published without responsibility on the part of the Society, the editor or authors for loss occasioned by any person acting or refraining from action as a result of any view expressed therein.

One line of analysis has been the role of crowd behaviour in the regular patterns and trends that dominate financial markets and economic indices. A great deal of research now confirms that crowd behaviour intensifies during the evolution of a trend. Initially, so-called ‘diversity generators’ spot practical investment opportunities but, as the trend progresses, an increasing number of ‘conformity enforcement’ techniques keeps the herd either bullish or bearish. Such techniques include propaganda through the mainstream media, physical proximity, and the choice of associates. The trend, in itself, is a reflection of competition between the bulls and the bears; but, eventually, the winning group will become overstretched. Once this happens, it takes very little to create a reversal.

This means that it is entirely possible to offer more than just a subjective opinion on where a price or an index might be heading. An analyst who concentrates on the long-term has the power to decide whether or not a market is (1) in a trend; (2) undergoing a correction within that trend; and/or (3) undertaking a full trend reversal. Meanwhile, an analyst who focuses on the short-term (and who may not wish to include long-term trend considerations in his or her deliberations) will have a high degree of confidence about the likely outcome from a buy or sell signal.

Reversals can, of course, be just corrections within an ongoing trend, or an actual reversal in the trend. I suspect that the latter involves either a reversal in whatever it is that constitutes fundamentals or in some form of an offset to those fundamentals. This is where the idea of boundaries is important. Many years ago, a number of technical analysts found that the Golden Ratio (38.2:61.8) played an important role in defining these boundaries. Specifically, markets tended to retain 61.8% of their previous impulse waves, and so could retrace 38.2% of any prior advance without triggering a full reversal. This idea can be used to distinguish between a correction and a new trend.

The term ‘Technical Analysis’ means different things to different people: partly, it depends on whether the objective of the analysis is short-term trading or longer-term investment; but partly, too, it depends on training and experience. There is, nevertheless, a basic understanding about the body of knowledge that is known as technical analysis. This is that financial markets (and, indeed, economic indices) are not just random fluctuations within an uncertain environment. They are non-random and coherent phenomena that have the potential to generate observable entry and exit signals. There is, in other words, a functional order behind the apparent chaos.

Foreword

It seems extraordinary that as little as 50 years ago technical analysis was generally regarded as being a fringe pursuit. It might have been accepted that people would look at a price-time chart of a particular market before making a trading or investment decision, but such a chart was to be regarded as being just a picture of history. It was possible to see where a financial price stood in relation to that history, but there was very little appreciation of the fact that price behaviour might actually be telling you something about the future. It has taken the dedication of a relatively small group of people (some of whom are included in this book) to generate the background research that now informs the discipline.

It doesn’t take a genius to recognise that the interaction of internal forces (i.e., forces that are specific to a particular index or market), and external forces (such as those that involve politics), can result in a very complex environment. One approach has been subjectively to simplify the complexity and to use models that are considered appropriate. Another approach, however, is to adopt the idea that a market or index already has all the relevant information contained within itself. This is the realm of technical analysis. It automatically simplifies a very complex environment. The task of the analyst is then to tease out the pertinent information from a specific chart, and use that information to draw conclusions about future probabilities.

By Tony Plummer, FSTA

The research on these phenomena has been profound, and David Watts has undertaken the difficult task of collating that research, as published in the official journal of the Society of Technical Analysts - the Market Technician The result is ten chapters, each of which deals with one of the main subject areas:

As if this were not enough, the situation is complicated by the processes of evolution. First, a system of financial behaviour or economic activity has to recognise that something in its environment has changed. Second, the old system (including its beliefs and infrastructure) has to be downgraded in some way. Third, a new system (in terms of ideas and physical infrastructure)

02 Dow Theory, Wyckoff and Volume 03 Charting Types, Point & Figure & Candlesticks 04 Pattern recognition and Pattern Analysis 05 Moving Averages and Trends 06 Indicators and Momentum 07 Elliott Wave and Fibonacci 08 Gann Analysis, Cycles and Forecasting 09 Psychology and Markets 10 Systematic Trading 6

has to be put in place. And fourth, this new system has to persist until the whole process starts again. All of this takes time - hence the development and persistence of trends. Moreover, evolutionary forces introduce a natural element of expansion and contractionhence the presence of cyclical behaviour.

It is not possible to mention all the contributions that have been made over the years. Names such as Charles Dow, Ralph Elliott, and William Gann are now recognised with an immediacy that was not possible half a century ago. The point, however, is that progress has usually been based on the idea that what matters is trading and investment profitability, not the nicety of the theory. This is why a specific technical analysis tool can ‘work’, even though there is - at the time - no obvious reason for it. It is one of the great truths of technical analysis that it has accessed aspects of reality that have not been considered relevant by conventional thinkers. It has, in this sense, been in the vanguard of change.

01

Technical analysis has accordingly pursued a variety of concepts: the idea that simple line charts might be complemented by phenomena such as bar charts, candle charts, and point and figure charts; the notion that various indicators (investor and marketgenerated) can be used to confirm a market’s progress; and the idea that collective human behaviour is influenced by its own past history, by internal cycles and rhythms, and by external influences such as the planets and natural geophysical forces. Above all there is the idea that specific patterns repeat themselves, often regularly and always frequently. So, when they emerge, these patterns can be used to anticipate future behaviour. Many ideas that might originally have been considered somewhat obscure have now been sufficiently progressed to become taken for granted.

This means that the book can be seen, not just as a history of progress within the Society of Technical Analysts, but also as an upto-date reference work. Readers can therefore either read the whole book sequentially, or delve into specific chapters as they need. Theory of Technical Analysis

The first issue of the Society’s Journal, Market Technician, was published in 1988. It was designed to provide a forum for technical analysts to put forward new ideas and exchange views on market trends and developments. I edited the Journal for 25 years and during that period of time witnessed a revolution in computer technology as well as a radical transformation in the financial

Introduction to the STA’s book of analysistechnicalarticles

The underpinning concepts of technical analysis are covered in the first chapter, Theory of Technical Analysis. Charts are the starting point of all types of technical analysis and, when the Journal was first published, they were all drawn by hand. The articles included in chapter 3 elaborate on the techniques involved in Point and Figure charts, Candlesticks, Heikin-Ashi and Market Profile. Moving averages and indicators are the basic cornerstones of momentum analysis and these subjects are covered in chapters 5 and 6. Chapter 4 expands on the core concepts of pattern recognition. The articles in chapters 2 , 7 and 8 have been selected because they build on the ideas encapsulated in Dow Theory, Fibonacci numbers, Elliott Wave analysis and Gann Theory.

7

Deborah Owen

It is a measure of the extent to which technical analysis has moved into mainstream financial analysis that the STA’s 50th Anniversary book includes articles from academics and a broad spectrum of market participants ranging from short term day traders to long term portfolio managers.

The role of editing the Journal was a stimulating and, at times, challenging exercise (some of the most successful technical analysts are unfamiliar with the basic rules of grammar!). The past half century has seen colossal changes in the financial markets. Collectively, the articles in this book provide an interesting historical record of developments over this period. Analysing the undercurrent of market sentiment will always be the key to profitable trading and investment and these articles also furnish the reader with a portmanteau of tools that can be used to navigate markets over the next 50 years.

The financial markets are rather like a tug-of-war competition in that, in any market, there will be buyers pulling the price up and sellers pushing it down. At any one point in time these conflicting pressures will be resolved into a single price. Academic studies have shown that prices tend to move in trends more often and for longer than could possibly be explained away by the laws of chance. Technical analysis is the study of past trends and patterns with the objective of predicting future price movements.

landscape. The core elements of technical analysis have stood up well to this changing environment. The collection of articles in this book represent not only the breadth of the subject but also the way that the discipline has evolved to encompass new ideas and technological developments.

The Society of Technical Analysts is marking its 50th anniversary by publishing some of the seminal articles that have appeared in its Journal over the years.

technical analysis was regarded as a fringe form of analysis by academics who espoused the Efficient Market Hypothesis (EMH) as the most convincing explanation of how markets behave. However, the 2007-09 financial crisis completely discredited the EMH as a model for describing market behaviour; markets are not perfectly efficient and decision-making by individuals cannot be assumed to be always rational. In the subsequent re-evaluation of market analysis, the ideas and tools of technical analysis have acquired a much wider following.

Extraordinary Popular Delusions and the Madness of Crowds published by Charles Mackay in 1841 is required reading for anyone who wants to understand the mob-psychology of markets and the articles in Chapter 9 focus on this important aspect of trading. Chapter 10 deals with the concept of systematic trading or money management.

To all past, present and future members of the Society of Technical Analysts.

It has long been axiomatic that markets reflect human behaviour and traders have been searching for a reliable way to accurately and consistently tap into the undercurrent of market sentiment since joint-stock companies were first formed in the 17th century. It is thought that Japanese rice traders in the 18th century used a form of technical analysis, known as candlestick charts, to plot movements in the price. In the 19th century, as a result of their (separate) systematic observation of historical price data, Charles Dow, Ralph Nelson Elliott and W.D. Gann each formulated a set of precepts which have, collectively, become the bedrock of technical

Foranalysis.years,

50th Anniversary Party, June 2018 at the London’s Living Room, City Hall

8 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends Theory of Technical AnalysisArticlesin this chapter CHAPTER ONE Tony Plummer FSTA A theoretical basis for Technical Analysis10 Tony Plummer FSTA Towards a new understanding of Technical Analysis20 Tony Plummer FSTA Order and Chaos in Financial Markets22 Tim Parker MSTA Art or science? Ruminations on the meaning of Technical Analysis28

We can then do no better than to start with the article “A theoretical basis of Technical Analysis by Tony Plummer ” in which Tony considers a number of theoretical approaches. This will then begin to lay a foundation of understanding, in this statistics, Chaos Theory and then crowd or market behaviour all feature. Finally Tony then finishes with the mainstream price patterns and waves, which are part of the standard curriculum of Technical Analysis. The variety of behaviours inherent in a market are readily apparent to the student, in the way price actions react at key levels, these key levels being areas of support and resistance or accumulation and distribution. This demonstrates that the market observes a “market memory” that a Technician observes and then maps in his/her analysis.

CHAPTER BSCByINTRODUCTIONONEDavidWattsEngMSTA,MICE

Introduction

9 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

Then it’s worth noting market behaviours are quantified into categories like price ranges, breakout, pullbacks, short covering, Fibonacci retracements and even Elliott Waves to name more than a few, all which are apparent in a price chart. The way the crowd reacts is in fact the basis of the second article in this chapter “Towards a new understanding of Technical Analysis” also by Tony Plummer. Being able to read and understand the crowd behaviour apparent in price action as it develops, is a primary skill of a Technician. Then finally in this trilogy is the article “Order and chaos in financial markets” in which Tony develops a theoretical framework theory using Chaos Theory. I found this chapter aligns with my own understanding of price shocks, from a mathematical approach. In 1982, Benoit Mandelbrot published his classic book “The Fractal Geometry of Nature” which supports the findings of technical analysis, in his seminal study of cotton prices at various time frames. This resulted in many new indicators to classify such chaotic fractal behaviour.

The Society has now been in existence for over 50 years with the journal being published for the last 34 years, such that over that time articles on every conceivable approach to Technical Analysis have been published. So before proceeding to look at the first chapter, what question should we first seek to answer? The perhaps “What is the basis for Technical Analysis? That is almost the title of the first article.

1990’s simple computer models of the market were developed and then found to be wanting, just because there was no awareness of the dependencies that really needed to be included in a successful model. So, in conclusion, if you only take away from this chapter to think about the “Context” your market operates in, Tim would have done his job. It’s the professional technician that is able to consider the inter-market relationships and external influences and modifies his conclusions based upon that all important “Context”.

The final article for this chapter “Art or science, Ruminations on the meaning of Technical Analysis” by Tim Parker approaches the subject quite differently and from another perspective. What I particularly like about Tim’s article is his focus on “Context” or what I would describe as the wider market environment. So how a market behaves often depend upon this “Context” and many have thought they had a strict rule set leading to a pot of gold, only to find out that suddenly the market behaviour changed, just due to the market environment changing. Indeed, in the new age of computers in the

Article originally featured in Market Technician 52 (October 2005)

10 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends

What follows is part of my attempt to meet UKSIP’s challenge. However, there are two important qualifications. First, it only covers the phenomenon of price patterns, it does not cover the extraordinary influence of the Golden Ratio. Second, the analysis is offered only as a small part of an evolving process rather than as an unassailable body of theory.

In any market, prices fluctuate up and down. The implicit assumption of technical analysis is that these fluctuations are not random. The explicit claim of technical analysis, therefore, is that non-random fluctuations create patterns that repeat themselves. It is the repetition of patterns that allows us to forecast - or, better, to anticipate - price movements. So there are a number of questions that need to be answered:

(3) If patterned price movements are present, how quickly can we decide which pattern is evolving?

Figure 1 plots each day’s percentage change (i.e., at time t) in the Dow against the previous day’s percentage change (i.e., at time

has a consistency to it. This encourages certain general market phenomena, and certain specific price patterns, to reproduce themselves through time. Accordingly it is considered appropriate to formulate hypotheses about market behaviour on the basis of historical data and to use these hypotheses to anticipate the future. This process reproduces any other form of scientific enquiry. The problem, however, is that the assumptions about human behaviour used by technical analysts are profoundly different from the assumptions used by economic theorists. Technical analysts assume (usually implicitly) that the market behaves as a coherent whole. Economic analysts assume (very explicitly) that total market behaviour is no more than the arithmetic sum of random decisions by Thisindividuals.difference

Technical analysis and economic theory

Second, there is the question of the degree to which astrology and technical analysis can actually be categorised together. Many technical analysts would argue that, even if astrology is a valid approach to markets, technical analysis is still a distinct and separate discipline because it uses different analytical tools. And this, in a way, points to the real challenge implicit in the forum’s title: is technical analysis just as a set of tools that sometimes work but sometimes don’t? Or does technical analysis actually have a genuine theoretical underpinning that justifies the use of certain analytical tools?

Tony Plummer FSTA

(2) If price movements are non-random, what patterns can we expect to emerge?

A theoretical basis for Technical Analysis

The most fundamental definition of technical analysis is that it is the study of past movements in asset prices in order to forecast future price movements in those prices. However, since past price movements are the outcome of various forms of investor activity, most analysts would also understand that the study of past price movements also includes - where possible - the study of various indicators relating to the supply of, and demand for, the assets in question. This allows us to include not only information - such as volumes, open interest, and put/call ratios - that can be derived directly from the various bourses, but also information - such as opinion surveys and cash holdings in funds - that can be gleaned from external sources. I generally use this broader definition, but want to make clear that excluding by definition does not mean excluding despite value. After all, if a specific indicator helps to make money, why exclude it?

The basic idea underlying technical analysis is that human nature

So much has been written on the subject of the randomness or otherwise of price movements in financial markets that it seems dangerous even to attempt to address the issue. However, using a methodology suggested by the work of Baumol and Benhabib (1989), it is possible to look at the subject pragmatically, without going into a detailed discussion of statistical theory.

in assumptions could not be better designed to foster mutual hostility between the disciplines. Technical analysts are accused of relying on some form of ‘hocus pocus’; economists are berated for ‘living in ivory towers’. The result is that technical analysts tend to ignore the influence of fundamental analysis on trends and that economists tend to ignore the power of technical analysis to forecast turning points. The truth is that both disciplines could usefully learn from one another. However, there is a need first to establish a common ground for understanding the phenomenon of financial markets.

I was recently asked to defend technical analysis to a UKSIP audience in a forum entitled “Technical Analysis: Astrology or Informed Analysis?” This was a challenge on a number of levels. First, it is not my view that the use of planetary alignments or planetary cycles to strengthen entry and exit rules implies ‘uninformed analysis’. On the contrary: there are many important books that suggest that life on earth is directly influenced by cosmic forces (Gaugelin, 1969; Lieber, 1979; Eysenck, 1982). In fact, since the giant planets (Jupiter, Saturn, Uranus and Neptune) usually pull the centre of mass in our solar system outside of the physical body of the sun (Landscheidt, 1989), it would be amazing if the influences were not actually quite significant. Furthermore, many successful traders - including W.D. Gann - have explicitly used astrology to finesse their timing.

Introduction

Random or non-random behaviour

The foundations of technical analysis

(1) Are price movements random or non-random?

Data source: Yahoo.com

Figure 2: Dow in expanded phase space

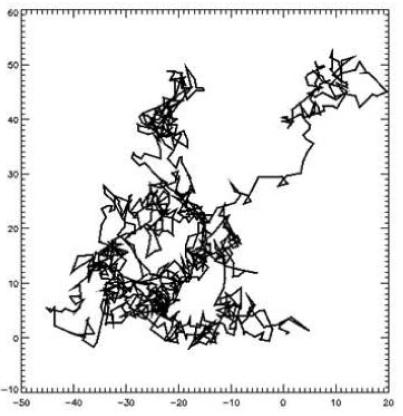

t-1), for every trading day since 2nd January 1990. In other words, movements in the Dow are plotted in what is called “t/t-1 phase space”. The result is exactly the sort of pattern that can be expected if daily movements were indeed random - that is, they are scattered widely throughout the phase space. Nevertheless, what is also relevant is that the movements are actually contained in a very limited area of that phase space. So, although the price movements appear random, they are in some sense contained. This becomes even more apparent if the scales on the chart are (say) quadrupled. See Figure 2 . It is clear that price changes tend not to move out beyond a very specific twodimensional region. Should they do so, they tend to get pulled back in again towards the centre of that region.

1 day percentage changes

DJ Industrial Average: Jan 1990 to Date (Daily close, t/t-1)

The operation of some sort of gravitational pull is particularly noticeable if the chart is extended backwards in time to (say) January 1946. By definition, the data set is a long one, not only covering an important period of economic and social evolution, but also including the 1987 equity crash. See Figure 3. Importantly, the basic region of attraction for the market remains unchanged, and the experience of 18th-20th October 1987 stands out as an idiosyncrasy. It is arguable that, in one sense, the 1987 crash was a truly random event.

Figure 1: Dow in t/t-1 phase space

11 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

1 day percentage changes

DJ Industrial Average: Jan 1990 to Date (Daily close, t/t-1)

The point here is that the idea of randomness obviously has something to do with perspective: the longer the time perspective being taken (or, if you like, the broader the context), the less likely it is that fluctuations will seem random. Anyone who has traded in financial markets for any length of time will know when a price movement is ‘unusual’, based on his or her experience.

-8 -6 -4 -2 0 2 4 6 8-8-6-4-202468t

Data source: Yahoo.com

Figure 4: 5 day changes in the Dow

Data source: Yahoo.com

Data source: Yahoo.com

DJ Industrial Average: Jan 1946 to Date (Daily close, t/t-1)

12 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends

DJ Industrial Average: Jan 1946 to Date (Daily close, t/t-1)

We can take this argument a stage further and look at the price changes over periods that are longer than one day. Figure 4 shows an example of the 5-day percentage changes in the Dow, in t/t-1 phase space. Here, the 5-day percentage change for a particular day is compared with the 5-day percentage change the previous day. What is clear is that the formerly circular ‘bubble’ containing price movements begins to spread out along an upward-sloping diagonal line. And this becomes even clearer for longer time periods. Figure 5 shows 20-day percentage changes in the Dow, in t/t-1 phase space. Oscillations in the Dow seem to be drawn towards the upward-sloping diagonal, where the rate of change at time t is equal to the rate of change at time t-1. Moreover, even though there are obviously unusual events, such as the 1987 equity crash, the oscillations are essentially bounded on the upside and downside. In the language of ‘Chaos Theory’, a strange attractor seems to be at work.

-32 -28 -24 -20 -16 -12 -8 -4 0 4 8 12 16 20 24 28 32 -32-28-24-20-16-12-8-4048121620242832 t-1 t 19/2018/19Oct87-32Oct87 -28 -24 -20 -16 -12 -8 -4 0 4 8 12 16 20 24 28 32-32-28-24-20-16-12-8-4048122032 t-1 t

1 day percentage changes

5 day percentage changes

Strange attractors

It seems that, over longer time periods, changes in the Dow tend towards a stable path of change; but the changes are also persistently induced to accelerate and decelerate along this path. We can hypothesise that something encourages investors to chase the market up until some form of upper boundary is reached, and to chase the market down until some form of lower boundary is reached. This, in itself, is highly suggestive of a deep running ordered process at work. A related question is whether the acceleration/deceleration itself has a cyclical element of some sort. If it did, this would strengthen the case for non-random market behaviour.

Figure 3: Extended Dow data in t/t-1 phase space

Groups and crowds

however, is that once individuals start to be influenced by each other’s behaviour, then their expression of individuality is much reduced. Ultimately, deviation from some measure of average behaviour becomes minimal. This presents a problem for theoreticians because, although basic probability theory breaks down, it is highly likely that a large number of people doing the same thing will produce a forecast-able outcome.

inner need to merge into greater wholes takes on a different imperative when competition or conflict is involved. The associated threat to each individual’s psychological security is reduced when others are involved in meeting that threat (Trotter, 1947). Quite obviously, the greater the threat, the more urgent it is that each individual’s resources are directed towards meeting the purposes of the whole. A competitive environment therefore demands conformity from individuals (Bloom, 2000). Non-conformity is punished by exclusion from the group: individuals are left to meet the threat alone.

This, in a way, was one of the central findings of the late 19th century French sociologist, Gustave le Bon, whose now-famous book, The Crowd, analysed the French Revolution (le Bon, 1895). Le Bon observed that, when people came together in a common cause, the result was something different to just the sum of the parts. People behaved differently to the way that they would as individuals: they would focus on, and follow, the dictates of a recognised leader; they would act to protect their beliefs; and they would quickly see ‘non-believers’ as enemies. In short, the act of people coming together under a unifying belief system would foster conflict.

13 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

Consequently, the ability of individuals to make rational choices, evoke moral judgement and engage in active reality testing is suppressed. This, of course, would help to explain why outsiders have such difficulty in understanding and interpreting group behaviour. Importantly, though, it might also help to explain why stock markets bubble and crash, and why economies boom and slump. Somehow, emotionally laden beliefs are increasingly distributed throughout a market place and throughout an economy.

Data source: Yahoo.com

Figure 5: 20 day changes in the Dow

However,word.the

The truth behind le Bon’s assertions is only too clear in the bloodied history of the twentieth century. There is, however, an important aspect of his analysis that is easily overlooked. This is that le Bon saw crowds, or groups, as psychological phenomena whereby people behave in a unified way once they adopt a shared set of beliefs. This is because belief systems - however unlikely and unreasonable they may seem - mobilise powerful inner emotions. Hence, crowds are held together, and energised by, emotions rather than by cold logic. Moreover - and this is important - the self-awareness of participating individuals is reduced (Neumann, 1990). The psyche is “invaded”by the values of the collective.

-40 -36 -32 -28 -24 -20 -16 -12 -8 -4 0 4 8 12 16 20 24 28 32 36 400-4-36-32-28-24-20-16-12-8-40481216202428323640 t-1 t 18/19Oct87

The suggestion here is that warfare and violence may actually be a specific outcome of the more general tendency towards co-operation amongst human beings. Indeed, this suggestion becomes seriously compelling once account is taken of contemporary ideas relating systems theory, group psychology, and natural evolution. Nature organises itself hierarchically into ever-greater wholes: lower-order parts contribute to higher-order wholes, and the wholes organise the parts. As a result, each whole is qualitatively different to the mere summation of the parts. In human beings, this organisational force finds expression in the need to merge psychologically into a group. At one level this can be explained as the need to reduce the sense of personal isolation. At another level it can be explained as the need to have a sense of purpose. Either way, the outcome is ‘natural’ in the genuine sense of that

Before we look more closely at the possibility of cyclical influences, we need to consider the basis for an ordered process in human behaviour. According to economic theorists, individuals make their decisions independently of one another. Group behaviour is then considered to be forecast-able because, according to probability theory, a large number of uncertainties somewhat spookily create a certainty. As James Surowiecki has recently demonstrated in The Wisdom of Crowds (Surowiecki, 2005), this is not only absolutely correct, but can yield answers and decisions that are amazingly

Theaccurate.problem,

DJ Industrial Average: Jan 1946 to Date (Daily close, t/t-1)

20 day percentage changes

The point is that, once account is taken of the inner dimension of human existence, the need to do things together becomes a viable explanation for a part of human behaviour. Evolution can then be seen in terms not just of random mutation and survival of the fittest individuals but also in terms of the perpetuation of the

Co-operation

Importantly, the idea that group beliefs can induce conformity has found a great deal of support from independent researchers. In the 1950s, Stanley Milgram was able to show that more than 60 per cent of ordinary people could be induced to deliver massive electric shocks to apparent patients just by being told by an authority figure in a white coat that it was alright to do so. Fortunately, the ‘patients’ were actors and no electric shock was actually involved. In the late 1970s, Ed Diener at the University of Illinois published evidence that, in a group setting, people strongly identified with other group members, had little sense of personal identity and tended to act without prior thought. Other evidence - notably from Bristol University in the UK and from Harvard in the US - showed that people’s perception of non-group members and, indeed, of reality itself, could all too easily be influenced by pressure from other group members. In the psychological arena, therefore, a group can be less than the sum of its parts.

Non-rational behaviour

In recent years, the central ideas of self-organisation, group conformity enforcement, and non-rational collective behaviour have been used by a number of important developmental theoreticians to explore the processes of history. Foremost amongst these have been Arthur Koestler (1978), Erich Jantsh (1980), Fritjof Capra (1982), Ken Wilber (1983), and Howard Bloom (1997 and 2000).

The problem, however, is that a clearly defined body of theory that covers this spectrum of economic and financial behaviour is not currently available within the academic community. This suggests that some form of paradigm shift is almost certainly looming as a result of the aftermath of the financial bubble of the late 1990s. After all, how long can academics continue to ignore the tendency of markets to diverge from, and oscillate around, fundamental values? However, it also implies that we need to look for guidance outside of the current ‘rational expectations’ paradigm that embraces economics.

Financial markets

One way forward is to look for patterns that regularly emerge in financial markets. There are three reasons for this. First, largerscale movements in financial markets basically reflect the evolving mood that embraces all economic and social behaviour within a community. Second, financial markets provide a continuous flow of uncontaminated data. Market price action therefore provides a marvellous testing ground for hypotheses about human behaviour. Third, recurring price patterns would (if found) imply recurring behaviour. In other words, the patterns could be interpreted.

Financial markets are characterized by inter-group conflict: it is a contest between the bulls and the bears. Seen in this light, financial markets are not just processes that encourage prices to converge on fundamental induced values. They are reflections of a collective movement between the opposite polarities of optimism and pessimism. Hence, prices are likely to overshoot fundamental values in both directions. One implication is that market participants actually pay less attention to ‘fundamental’ values

A valid point of access for an analysis of market price patterns is to look at investor behaviour during periods of emotional extremes. Traditional economic theory regards such extremes as aberrations. However, insofar as such extremes are actually part of a spectrum of behaviour, they are likely to reveal the basic energies that drive all behaviour. Extremes of behaviour are often noteworthy for their clarity of purpose. Shown in the Figure 6 are the loci of US price action in the Dow Jones Industrial Average from January 1921 to July 1934 and in the NASDAQ from September 1995 to September 2002. The time periods involved are different: the former covers a period of seven years, the latter covers a period of three years. However, when the time elapse relating to the Dow is placed on the lower horizontal axis and the time elapse relating to the NASDAQ is placed on the upper horizontal axis, something very interesting emerges: the patterns of the acceleration into the peak and the subsequent collapse are very similar.

What theory and research are both pointing to is the very real possibility that economic and financial activities are, at heart, less rational than many might want to believe. This does not mean that such activity is always irrational just that it is essentially activated by deeply held psychological needs. These needs are orientated towards obtaining security and meaning, and are universal. Hence, non-random behaviour in economic and financial markets may be the outcome of genuine group influences rather than just the outcome of statistical interactions. This, in turn, would mean that excesses (which are, in any case more easily observed after the event than before it) could well be part of a forecast-able spectrum of behaviour instead of the unforecastable outcome of ‘keeping up with the Joneses’ or of ‘animal spirits’.

Homogeneity

What Professor Sornette is, in fact, describing is a specific - and particularly dramatic - example of a more general mechanism. This is the mechanism that induces conformity from market participants and thereby produces oscillations in financial markets.

This, indeed, is the route that technical analysts have chosen to take. The result is a large body of industry literature confirming

This similarity has been recognized by Didier Sornette, who is Professor of Geophysics at UCLA. Sornette has shown how non-linear mathematics can track and predict a stock market ‘bubble and crash’ (Sornette, 2003). There are two distinct conclusions. The first is that the price acceleration into the final peak is curvilinear, and that the time-elapse of oscillations around that accelerating trend gets progressively shorter. The second is that this specific phenomenon only works because of the impact of “cooperative self-organization”. In other words, non-linear mathematics can predict the timing of the peak (because the oscillations become so fast that they effectively converge on zero), but such non-linear mathematics only work because stock markets are ‘natural’ systems.

Conformity enforcement in financial markets

Bubbles and crashes

Conformity enforcement

14 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends

These conclusions are a dramatic confirmation of the impact of group behaviour in financial markets; and it is almost no accident that they have been generated outside of the discipline of economic theory. Nevertheless, they need to be placed in a wider context of investment behaviour. Professor Sornette notes that, as a stock market bubble accelerates into a peak, investors take more and more notice of what others are doing. Hence, behaviour becomes increasingly homogeneous and local information has long-distance effects. Ultimately, of course, the market becomes satiated, or ‘overbought’, and extremely vulnerable to small perturbations. So only a small amount of profit taking can initiate a full-blown ‘crash’.

most adaptive groups in the face of external threats. Nature is, ultimately, a collaborative enterprise.

that (a) markets oscillate in reasonably regular cycles, that (b) markets spend time in base, top or holding patterns before entering a significant trend, and that (c) these price patterns tend to incorporate certain predictive price configurations, such as ‘head and shoulder tops’. The overriding impression is that market behaviour is not random.

15 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

In modern financial markets, the pressure to conform has become institutionalised. Market professionals are consistently monitored against peer group performances: indices are constructed to show the sector allocations of other funds, and deviations from that ‘norm’ are monitored for success or failure. For the individual fund manager it is a risk to take a marginally different view, let alone an alternative view. So, when a market either begins to run ahead of perceived valuations, or even begins to ‘bubble’, there is huge pressure to join in. Not to do so is a direct risk to personal wealth and personal income.

The basic mechanism

The Wall Street Crash & the NASDAQ Collapse (Weekly closes)

Figure 6: The Wall Street Crash and the NASDAQ Collapse

For whatever reason, the end result is that the psychological environment of the market becomes dominated by a limited set of uncritically held beliefs, known as memes. In a bullish market the meme is that prices are going up; in a bearish market, the meme is that prices are going down. A meme is the glue that holds otherwise disparate individuals together in groups and crowds.

At some early stage, however, such technical buying dries up, and the market begins to retrace back towards the lows. This is a ‘re-test’ of the lows and occurs while those who missed the initial rally will be considering whether or not they now need to react. Investors will take into account the fact that prices have rallied but they will also necessarily re-assess fundamentals. Some may even decide that the market had originally over-discounted fundamentals or that the fundamentals might be shifting. This triggers another bout of buying, which eventually takes the market out of whatever holding pattern it has been in. In other words, a trend starts to materialize. As time progresses, either new information becomes available that confirms that fundamentals are improving and/or the rally in the market enters a feedback relationship with fundamentals such that the latter improve anyway.

Figure 7: The basic mechanism

Data DatastreamEconomagicsources:&

Figure 7 shows some of the basic principles involved. It

Ultimately, however, it is this threat to personal status that provides the main pressure to conform. Individuals participate in markets for reasons of wealth, power and prestige - in other words, to enhance control over future resources. To be out of the market when it is going up, or in the market when it is going down, threatens this control and generates fear. Collective behaviour, of course, reduces fear. So, for the majority, it is easier to trade on the evidence of actual price movements, than it is to invest on the basis of theoretical valuations (which may, in any case, be wrong).

than is usually thought. Partly, this is due to the fact that such values are very difficult to calculate in advance. Partly, though, it is due to the competitive process. So much attention is ultimately given to ensuring that one particular view is right (e.g., prices are going up) that participants lose sight of fundamentals. Energy is spent in generating propaganda to colleagues, clients, other members of the profession and the media. The sub-conscious intention is always to ensure that financial resources continue to underwrite one’s own view. What is missed, however, is that this is also exactly what others are doing. Conformity enforcement is a very subtle process - which is why it is usually deemed not to exist. Nevertheless, it is conformity enforcement that lies at the root of all price trends.

demonstrates the most likely pattern that will be traced out by a broad financial market price index during the course of a complete bull-bear cycle. No account is taken at this stage of the timescale involved. Starting at the lower left-hand side of the chart, a market will be very oversold, probably after some form of crisis. There will then be a bear squeeze of some sort as short positions are covered. This need not entail a significant proportion of investors suddenly becoming bullish - it just needs some investors to close bear positions. This will cause the market to jump sharply. The rise may continue for a little while because investors do not all respond simultaneously. Crucially, they will respond, not so much to ‘fundamental’ considerations, as much as to the fact that prices are rising. In other words, price movements - particularly sharp movements - are a critical item of information.

16 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends

There are a number of very important points that emerge from this simple model of market behaviour. First, a reversal materialises once a market has gone too far. The market is, in some sense, satiated. Second, the reversal is an information shock to the market. It reveals that the market may be out of line with fundamentals and that the market can no longer attract sufficient investor energy to continue the old trend. There is thus an ‘energy gap’. Third, the subsequent re-test of the low occurs while investors absorb the implications of what has just happened. Investors ‘learn’ that something has changed. Fourth, the market ‘signals’ a trend move by breaking out of the holding pattern. Since investors have, in effect, learnt that fundamentals have changed, all subsequent information will be seen in the context of that learning. Data that confirm the trend will increasingly be acted upon; data that contradict the trend will increasingly be ignored. Fifth, market participants will increasingly focus their attention on price action rather than fundamentals. Finally, the market will run ahead of fundamentals and will become overbought, or satiated. This presents the conditions that will trigger a reversal. The whole process then begins in reverse.

The process of learning

Price cycles

In the context of financial market cycles (and, indeed, of economic cycles), it is necessary to understand that downswings are as important as upswings. Nature cannot evolve without periods of rest, because it needs to replenish its energy. Hence, any period of activity will be followed by a period of rest. So, despite the best attempts of governments, bull markets will always be followed by bear markets, and economic expansions will always be followed by recessions. What then determines the extent of a downswing? One answer, of course, is the amplitude of the upswing: the bigger the upswing, the bigger (potentially) the correction. However, it also depends on the time span of the cycle: the longer the cycle, the longer (potentially) the correction. Technical analysis has the capability of determining the difference between big moves and small ones by putting all moves into the context of history and accepting that this history has a valid and vital role to play. Hence, for example, if there is strong evidence that the Dow Jones Industrial Average has, for a very long time, oscillated with a rhythmic periodicity of about 11 years (which it has), then there is every reason to suppose that the oscillation will continue. This will give a strong indication of when an important reversal can be

Markets are exactly the same. At a top or bottom, markets will go through a process of learning that fundamentals have changed. They respond to new information, hesitate while that information is absorbed, and then automatically apply the resulting learning during the thrust of a trend.

The role of prices

Central to technical analysis procedures is the phenomenon of price cycles. It was earlier noted that financial market oscillations might be driven by a natural learning mechanism and that inflexion points might be triggered by an energy gap that arose out of investor satiation. The important point here is that an energy gap reverses the polarity of the market from bullish to bearish, or from bearish to bullish. There are, however, two important questions: First, does this mean that bear markets are inevitable? Second, what determines the difference between a big bear market, such as those that emerge in the form of a ‘crash’, and minor setbacks?

other tasks. However, energy has to be diverted away from other processes in order to facilitate this adjustment, and the ability of a person to do a conscious task actually deteriorates temporarily. After the adjustment, people can apply their learnt techniques to the new task and not even think about it very much.

Normally this ‘slowdown’ is missed because it is only temporary. Nevertheless, it is a real phenomenon, which reflects something important. At some stage during the learning process, information is transferred from short-term memory in the forebrain to longterm memory deeper within the brain. Learning thereby moves from the conscious into the sub-conscious (Hebb, 1949). This is both automatic and necessary, and frees up consciousness for

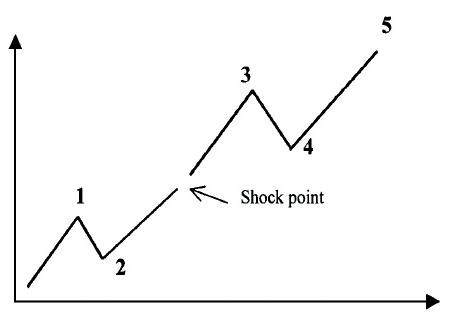

We thus have a three-phase mechanism that accounts for all the basic behaviour within a financial market trend, whether up or down. We also have a specific mechanism that accounts for market reversals. Consequently,we can hypothesize the existence of a six-wave pattern in a full market cycle - three waves up and three waves down. This is an important conclusion. However, there are other important inferences that need to be drawn. The first, which has already been mentioned, is the important role of prices. Individuals can process complex information, but a group can only react to simple information. The most important piece of information to a financial market group is the actual behaviour of prices. The response of the group will be greater, the faster and more pronounced is the change in prices. In a sense, therefore, prices will fulfil the leadership role in a psychological group. The group will accordingly react to this leadership and it will chase trends. The process is dramatically enhanced when high profile individuals confirm their own personal commitment to the trend.

This, of course, stands economic theory on its head. In economics a price is determined by the behaviour of buyers and sellers. This is true, but is only part of the process. When prices generate information, prices also determine behaviour. So a feedback effect is involved. As the biologist and philosopher Gregory Bateson has argued, feedback is one of the characteristics of any living system (Bateson, 1979).

Markets as collective learning processes

Financial markets (and, with them, whole economies) can be viewed as natural self-organizing systems that learn from their interaction with their environment. They are a particular form of what Howard Bloom of New York University calls “collective learning machines” (Bloom, 2000). As such, they organize their lower-order parts in a coherent fashion, oscillate rhythmically, and express themselves in terms of a limited matrix of patterns. This is essentially why the discipline of technical analysis has the power regularly to generate effective buy and sell signals. Analysts will look at indicators of investor energy in order to estimate the intensity of the market’s hold over investors. They know that the stronger the market’s grip, the nearer the market is to a turning point. Analysts will also look at the periodicity of historical oscillations in order to forecast the timing of likely turning points in the future. If a cycle has made itself felt in the past, it is likely to continue into the future. And, finally, analysts will look at the current evolution of price patterns, in the knowledge that certain patterns reproduce themselves. Once the market’s position in the context of a specific pattern is known, it is possible to estimate what might happen in the future. Quite obviously, the most powerful signals are going to be generated when each of the three lines of analysis coincide.

This brings us to the second inference from the market model. In any system that is oscillating in a feedback relationship with its environment, any new information from that environment has to be assimilated and absorbed. A process of learning is therefore involved. So it hardly seems accidental that the mechanism just described mirrors the process of learning that can be found in the human brain. In the early 1960s, Henry Mills found that, although people would initially be very quick at picking up the mechanics of a new task, they would inevitably go through a stage where their ability to apply their new learnings would slow (Mills, 1967). Only after this slowdown could activity speed up again.

This is a significant claim. It means that technical analysis - when properly approached and applied - is an extremely powerful method of interacting with financial markets. This, indeed, is what some of the leading proponents of technical analysis in the last one hundred years have argued. One of these analysts, whose research spanned the traumatic years of the first half of the twentieth century, was Ralph Nelson Elliott (Elliott, 1938). Elliott’s work is usually ignored by economists for the very reasons it is so powerful - namely, it assumes non-random, patterned, group behaviour. However, Elliott made two significant observations.

An important inference is that cycles can be defined by their patterning as well by the precision of their periodicity (Plummer, 2003). This means that the observed variability in cycle periodicities does not invalidate the forecasting potential of cycle analysis because the evolution of a current cycle can be tracked in real time against the pattern of a previous cycle. An example of this is shown in Figure 8, which compares the pattern of fluctuations in the Dow Jones Industrial Average between September 1990 and September 2001 with the pattern of fluctuations between September 1957 and May 1970. Both periods represent one beat of the 11-year cycle in the Dow, and both periods embraced rapid change in the US economy: 1990-01 covered the revolution in information technology, and 1957-70 covered the social revolution of the ‘Swinging Sixties’. In a sense, therefore, the two periods are directly comparable. When the price patterns of the two periods are overlaid on one another, by the simple expedient of plotting each beat of the cycle on a separate time axis, a remarkable similarity emerges. This is not unusual. Once the coincidence of patterns is found, it becomes a simple matter of tracking a new cycle beat against an earlier comparable one and tracking that cycle beat into its final low. Any variations in the periodicity will not matter.

This, in a sense, is where technical analysis brings such great strength to market analysis. It focuses directly on the patterns of market behaviour - both in terms of price movement and investor activity - because its working assumption is that such patterns are both non random and meaningful.

US Dow Jones Industrial Average (Monthly closes, 1 year % Datachange)Source: Bloomberg

Bearing this in mind, it is now appropriate to look at some of the findings of technical analysts regarding specific price patterns.

expected and what order of magnitude that reversal might take. The primary presumption of cycle analysis, therefore, is that this time it will definitely not be different.

Price patterns within cycles

The small and simple shift in emphasis - from the individual to the group - creates a massive shift in our understanding of economic and financial motivation. Economic theory cannot properly explain why a large number of people, who are assumed to be making rational decisions independently of one another, end up (for example) buying red cars or trying to move house, all at the same time.“Mood” may be regarded as being part of the answer; but, then, by what mechanism can a change in mood be made to swarm through a population of separate and rational individuals? Economic theory also cannot properly explain why particular patterns emerge in financial markets. If individuals really do make decisions independently of one another, then prices should just jump about in a random fashion. There is no mechanism for explaining why markets should generate the specific behavioural patterns that have so far been analysed. Nor is there any mechanism for explaining why specific patterns recur.

Derivative price patterns

Figure 8: Patterns in the Dow

If a single beat of a cycle (of whatever length) contains a simple sixwave (three-up / three-down) pattern, then it should be possible to isolate that pattern from whatever trend is driving the market. Or, to put the same thing another way, since a cycle beat consists of six basic waves, these waves can only present themselves in a small number of ways when they are subjected to a trend. Moreover, each trend will itself be part of the six-wave structure of a higherlevel cycle beat. If these conclusions are correct, then not only are price patterns non-random and meaningful, but also they are limited in number.

The fallacy of the rational individual

17 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

This is a very important insight and justifies a lot of the work that technical analysts conduct in relation to market satiation. There are two critical phases after a trend has developed. The first is when it is ‘overbought’ or ‘oversold’. This is the potential point of inflexion in a cycle, and may be captured by indices such as overstretched momentum or by indicators representing panic buying or panic

At first sight, Elliott’s five-three pattern appears to contradict the hypothesis of a three-three archetype. However, the two are entirely consistent, once (a) the role of trends is included and once (b) some allowance is made for the possibility that Elliott himself may not have had all the answers. Shown in Figure 12 is the formation generated when a rising trend is applied to an otherwise balanced three-three cycle. The cycle itself is notated as 1-2-3 up and A-B-C down. Once a trend is applied, however, wave B (which is theoretically a ‘re-test’ wave) actually makes a new high. In other words, the basic three-three profile incorporates a five-wave movement.

Other patterns

Five-three patterns and investor behaviour

Three-wave corrections

critical phase, however, is when a ‘fifth wave’ extends the market into a new high or new low. There are two possibilities. First, the fifth wave is not, by its very nature, truly impulsive. In this case, it may not be ‘confirmed’ by indicators of investor enthusiasm for the trend. Momentum may be weaker, volumes may be lower, and open interest in the relevant futures markets may be falling. Second, the fifth wave may be dynamic enough to create an investor panic. In this case, investment positions are finally driven to satiation. It is quite obvious that new highs or lows that are either not confirmed or generate excesses (or both) could be followed by a sharp reversal.

First, all impulsive movements, whether up or down, consist of five waves (three in the direction of the trend, interspersed with two corrections). Second, all corrections consist of three waves (two in the direction of the corrective trend and one contra-trend move).

18 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends

This particular model does not, of course, automatically generate a three wave correction. There was, however, something missing from Elliott’s original exposition. Elliott was intrigued by the patterning of markets and did not look too closely into their causes. However, the foregoing exposition places great store on the impact on investors of sharp price movements. Such movements are information ‘shocks’. The impact of energy gaps has already been discussed. These are contra-trend shocks. There is, however, another class of information shocks. These are protrend shocks, caused by a higher-level trend, where prices either move into, or extend the length of, an impulse wave. The presence of a pro-trend shock is recognizable by sharp price movements, increases in trading volumes, price gaps between one day’s close and the next day’s open, and rising open interest.

All shocks have to be absorbed by the market and therefore generate a price retracement of some sort. The contra-trend shock produces a re-test of the high or low, the pro-trend shock generates some form of subsequent holding pattern. Figure 13 shows the influence of a pro-trend shock. A break out from the base pattern indicates to investors that a trend is now developing. This is an item of information to which they respond, and buying volumes increase. Eventually, however, satiation sets in and the market hesitates (and, in effect, waits for ‘fundamentals’ to catch up). The market then moves ahead again, reaches its climax and turns down into a relatively deep correction.

Figure 13: Pro-trend information shock

This analysis is very brief and does not do justice to the forces involved. Nevertheless, it already confirms two other aspects of technical analysis. First, it confirms the influence of the famous ‘head and shoulder’ pattern that so often defines a reversal either out of a market high or away from a market low. Figure 14 shows the head and shoulders top formation that was implicit in Figure 13. The top of wave 3 becomes the left shoulder, the peak of wave 5 is the head, and the end of wave B is the right shoulder. A line linking

Note that some capitulation is likely to occur at the end of the third wave. It can also occur at the end of the fifth wave. On rare occasions, it may happen at the end of the first wave. Capitulation is therefore likely to occur between one and three times in a specific trend.

Theselling.second

The combination of simple distortions to lower- level cycles and the more dramatic effect of information shocks produced by highlevel cycles yield the basic five-three pattern observed by Elliott. Underlying this pattern, however, is the operation of a three-three cycle.

Figure 12: The effects of a trend

19 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

Second, the analysis substantiates the presence of genuine trends in markets. This, alone, is a hugely important conclusion. Markets enter a trend when investors have learnt that circumstances have changed: they are only applying ‘learnt’ behaviour. Trends basically continue until markets have run too far ahead of fundamentals.

Bateson, G (1979) Mind and Nature: An Essential Unity. Wildwood House, London. Baumol, W and Benhabib, J (1989) “Chaos: Significance, Mechanism, and Economic Applications” in Journal of Economic Perspectives. Bloom, H (1997) The Lucifer Principle. Grove Press, New York.

the lows of waves 4 and A become the neckline and a sell signal is generated when prices fall through that neckline.

The reason why the pattern works so effectively is that in moving into a trend, the market has probably responded to a higher level information shock. This means that the qualitative structure of the market has shifted - it has incorporated new information and has evolved. Therefore, when a correction occurs at the end of the trend generated by the information, that correction necessarily comes from a ‘higher’ level. It necessarily is longer in price and time than those that preceded it. This, indeed, is what Elliott found.

The discipline of technical analysis has been developed only gradually, over a very long period of time. Its main driving force has been one of profitability rather than theoretical nicety, and this has often militated against effective communication with practitioners in other areas of research, such as economics. Despite its apparent lack of theoretical rigour, technical analysts have observed, catalogued and used a huge volume of very effective tools and predictive techniques. There are, for example, no known price patterns that lie outside of Elliott’s classifications.

Bibliography

The role of technical analysis

Once these tools and techniques are seen in the context of selforganizing groups, which learn (both from their environment and from their own behaviour) then much of it begins to make sense. Markets evolve in a non-random fashion, according to patterned cycles. Different styles of investor behaviour can be identified at each stage of these patterns, and can therefore provide a strong clue as to where a market is in any particular cycle. More to the point, technical analysis has the power - sometimes predictively, but always quickly - to signal serious price reversals. We have shifted from forecasting based on the arcane workings of statistics to forecasting based on the extraordinary forces of Nature.

Bloom, H (2000) Global Brain: The Evolution of the Mass Mind From the Big Bang to the 21st Century. John Wiley, New York Capra, F (1982) The Turning Point. Wildwood House, London. Elliott, R N (1938) The Wave Principle. Elliott, New York. Reprinted in Prechter R. (ed.) (1980) The Major Works of R N Elliott. New Classics Library, New York. Eysenck, H and Nias, D (1982) Astrology: Science or Superstition? Temple Smith, London. Gaugelin, M (1969) The Cosmic Clocks. Paladin, London Hebb, D (1949) The Organization of Behaviour. John Wiley, New York. Jantsh, E (1980) The Self-Organizing Universe. Pergamon, Oxford. Koestler, A (1978) Janus: A Summing Up. Hutchinson, London. Le Bon, G (1895) Psychologie des Foules. Felix Alcan, Paris. Reprinted (1922) as The Crowd. Macmillan, New York. Lieber, A (1979) The Lunar Effect. Corgi, London. Mills, H R (1967) Teaching and Training. Macmillan, London. Neumann, E (1990) Depth Psychology and a New Ethic. Shambhala, New York. Plummer, T (2003) Forecasting Financial Markets. Kogan Page, London. Sornette, D (2003) Why Stock Markets Crash. Princeton University Press, Princeton. Trotter, W (1947) The Instincts of the Herd in Peace and War. Ernest Benn, London Wilber, K (1983) Up From Eden. Routledge & Kegan Paul. London.

Figure 14: The head and shoulders formation

of a new trend, most players are still locked into the emotions and thought processes of the old trend. However, there will always be a large minority who have been successful in recognising the turn. These people will be in a position to look at the fundamentals rationally and will therefore be the stimulus for the new trend. As this new trend develops, more and more people will join it on the basis of changing fundamentals. However, towards the end of that trend, the vast majority will tend to look only at the most recent trend in prices and forget the fundamentals. The process involves a subtle shift from rational to non-rational behaviour. More precisely, since behaviour is always a mix of rational and non-rational, it shifts from a mix of high rational/ low non-rational to a mix of low rational/high non-rational.

Part of the logic involved can be demonstrated with the use of a very simple diagram. It is a limit cycle. Limit cycles are now regarded as being an accurate description of most of Nature’s dynamic processes. In the case of financial markets, one of the relevant limit cycles relates price changes to the level of investor sentiment. Price changes and sentiment move together during the main part of a trend, with no clear cut direction of causation. Volume and open interest rise during this stage. At turning points, however, the relationship breaks down. The limit cycle is biased to the right. Changing prices cannot stimulate further investor involvement because the market is overbought or oversold. This is the first reason why analysts have been able to use the concept of

The equity crash of 1987 has, however, presented the theorists with a problem. First, it was found that “Random Walk” did not operate during the Crash. Second, the theorists could not make the Crash fit into the rigorous theoretical framework of modem economics. The “solution” has (so far) been to assume that everybody responds rationally to irrelevant information (which creates a “bubble”) only to adjust their expectations very quickly when the information is found to be wrong (which creates a crash). Nobody seems to have asked why it is that large numbers of rational people do not recognise that the information is incorrect in the first place?

20 Theory of Technical Analysis Dow Theory, Wyckoff and Volume Charting Types, P&F, Candlesticks Pattern Recognition and Pattern Analysis Moving Averages and Trends

The concept of a “duality” of characteristics has a great deal of validity for Technical Analysis because it can be used to explain the presence of an underlying order in financial markets. Such order has been known to exist ever since stock prices were first plotted on graph paper. However, the reasons for it has essentially eluded all except analysts such as William D. Gann.

Crowds develop in financial markets because participants end up having common beliefs about the future trend in prices.

Movements in prices determine who is right and who is wrong. Emotions are closely involved with the result. The winners will feel pleasure and the losers will feel displeasure, especially fear. Furthermore, these emotions will be intensified by communicating with like-minded individuals. Ultimately, of course, being part of the “wrong” crowd contains no benefits whatsoever. Fear therefore triggers evasive action. Who has not experienced sweaty palms during their trading activities and done precisely the wrong thing as a Atresult?thebeginning

One of the most important ideas to have been developed in the natural sciences in recent years, is that order develops out of chaos. This idea is partly based on the simple - yet profoundnotion that every part of the natural world contains both an element of randomness and an element of predictability. One of the easiest ways of describing the phenomenon is in terms of probability theory: it is not possible to forecast individual events with a great degree of confidence, but it is possible to forecast group events with only a small margin of error.

Most people would intuitively accept this argument. However, the important implication is that the processes involved are not random. Crowds can be analysed just like any other “natural” system. They therefore respond to new information in an elementary way, and they oscillate rhythmically. It is these two simple points which fully justify the assertions of generations of technical analysts that not only do specific price patterns recur, but that it is possible to forecast both the extent and the duration of a potential price movement respond to new information in ,an elementary way, and they oscillate rhythmically. It is these two simple points which fully justify the assertions of, generations, of technical analysts that not only do specific price patterns recur, but that it is possible to forecast both the extent and the duration of a potential price movement.

The source of the current myopia is to be found in the methodology and assumptions of economic theory. The analytical procedures of theorists such as Rene Descartes and Adam Smith have concentrated on the “parts” of a system rather than on the system itself. It has also encouraged an unyielding belief in’ the dominance of rational behaviour in human affairs. Economies are therefore seen as nothing more than the simple summation of all activities, and events such as panics and crashes are regarded as exceptions, rather than as a special case, of a general rule.

The truth of the matter is that the basic assumption of rational behaviour used by modem economic theory is only applicable as a special case. If every part of nature has both an identity of its own and identity derived from its participation in greater wholes, then it follows that every person can be seen both as a unique individual and as a member of large socio-economic groups. Gustave Le Bon was one of the first analysts to recognise that people in a group, or “crowd”, behave non-rationally (and sometimes irrationally). He argued that crowds are psychological phenomena, where common beliefs encourage people to behave alike. It is not necessary for people to be standing shoulder to shoulder. Nations, for example, are “crowds” because the members share the same belief system.

However,“non-confirmation”.behaviour does not stay on the limit cycle all the time.

Article originally featured in Market Technician 4 (February 1989)

Towards a new understanding of Technical Analysis

Tony Plummer FSTA

The re-test may involve a new high in a bull market, or a new low in a bear, but it is not usually accompanied by a noticeable improvement in the sentiment and breadth indicators. This, of course, is the second type of, “non-confirmation”. Such a re-test is invariably followed by a move into a new trend. This is specifically why Elliott discovered that all bear markets are three-waves. The implication of the model, however, is that bull markets are also three-waves. This appears to contradict Elliott’s assertion that all bull markets are five-waves affairs. In fact, five-waves develop when the limit cycle of next higher degree forces a re-test to extend into new territory. Five up-waves are therefore a sign of basic strength. Indeed, it is entirely logical that, during the growth phase of the capitalist system, equity bull markets will always tend to be five-wave affairs. Such a conclusion will not, however, hold true when the economy begins to transfer its belief system into another structure.

As profit-taking develops, prices change direction and a shock is delivered to the limit cycle system. There is a “once-off” change in prices and sentiment inwards from the limit cycle - this is what happened during the 1987 equity “crash”. Next, because of the self-organising processes involved, the path of adjustment involves a spiral back to the limit cycle. This spiral involves a re-test of the earlier turning point. This is what is currently happening in the equity markets.

21 Indicators Momentumand Elliott Wave and Fibonacci Gann Analysis, Cycles and Forecasting Psychology and Markets Systematic Trading

Tony Plummer was formerly a Director of Hambros Bank Ltd. and responsible for their trading positions in the London Gilt-Edged market.

There are many other important implications of this simple model. It can be used to explain all the price patterns which are recognised by Technical Analysis. It enables an analyst to measure prospective price movements with a degree of accuracy which is simply astounding. Furthermore, it confirms the presence of rhythmic oscillations thereby enabling the analyst to forecast the duration of price movements. These features are explored at

length in my new book “Forecasting Financial Markets: The Truth Behind Technical Analysis” which is to be published by Kogan Page this Spring.

whose task it is to test for the nature of reality will formulate their experiments within the context of the common consensus.1 This limitation on the flow of genuinely new ideas means that existing theories are not easily replaced: they tend to evolve without any radical change to the underlying structure. 2 A revolutionary “paradigm” shift usually only materialises either, when a persistent and increasing number of observations no longer accord with consensus beliefs, 3 or when there is a major social crisis. 4

7 Modem economic theory is based on two hypotheses: rationallyformed expectations (after J. F. Muth) and the existance of a natural rate of unemployment (after M. Friedman). James Tobin has called it “Monetarism II”. See J. Tobin, Stabilisation policy ten years after, in “Brookings Papers on Economic Activity”, No. 1, 1980.

The argument of this essay is that our inability to solve the apparently intractable problems of the current era - unemployment, inflation, global pollution, and environmental destruction - is largely the consequence of a significant divergence between economic theory and the underlying economic “reality”. This divergence has essentially occurred for two reasons. First, the analytical procedures which are used to establish the nature of reality in the economic sphere are actually biased against being able to do so. Second, and as a result, there is a genuine misrepresentation of - if not an actual misunderstanding about - the nature of economic

Tony Plummer Article originally featured in Market Technician 9 (October 1990)