AEQUITAS

Insightful commentary on market issues

The case for and against US stocks and shares We examine the reasons to be cheerful and fearful on the American market

A

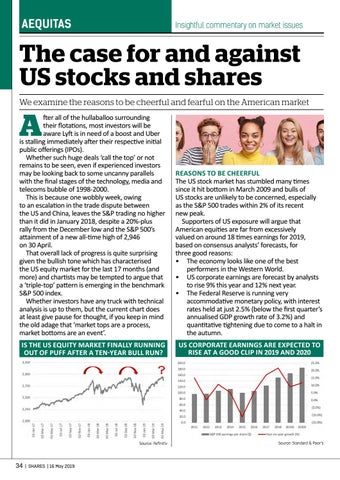

fter all of the hullaballoo surrounding their flotations, most investors will be aware Lyft is in need of a boost and Uber is stalling immediately after their respective initial public offerings (IPOs). Whether such huge deals ‘call the top’ or not remains to be seen, even if experienced investors may be looking back to some uncanny parallels with the final stages of the technology, media and telecoms bubble of 1998-2000. This is because one wobbly week, owing to an escalation in the trade dispute between the US and China, leaves the S&P trading no higher than it did in January 2018, despite a 20%-plus rally from the December low and the S&P 500’s attainment of a new all-time high of 2,946 on 30 April. That overall lack of progress is quite surprising given the bullish tone which has characterised the US equity market for the last 17 months (and more) and chartists may be tempted to argue that a ‘triple-top’ pattern is emerging in the benchmark S&P 500 index. Whether investors have any truck with technical analysis is up to them, but the current chart does at least give pause for thought, if you keep in mind the old adage that ‘market tops are a process, market bottoms are an event’.

REASONS TO BE CHEERFUL The US stock market has stumbled many times since it hit bottom in March 2009 and bulls of US stocks are unlikely to be concerned, especially as the S&P 500 trades within 2% of its recent new peak. Supporters of US exposure will argue that American equities are far from excessively valued on around 18 times earnings for 2019, based on consensus analysts’ forecasts, for three good reasons: • The economy looks like one of the best performers in the Western World. • US corporate earnings are forecast by analysts to rise 9% this year and 12% next year. • The Federal Reserve is running very accommodative monetary policy, with interest rates held at just 2.5% (below the first quarter’s annualised GDP growth rate of 3.2%) and quantitative tightening due to come to a halt in the autumn.

IS THE US EQUITY MARKET FINALLY RUNNING OUT OF PUFF AFTER A TEN-YEAR BULL RUN?

US CORPORATE EARNINGS ARE EXPECTED TO RISE AT A GOOD CLIP IN 2019 AND 2020

Source: Refinitiv

34

| SHARES | 16 May 2019

Source: Standard & Poor’s