Canada’s Largest Real Estate Conference and Trade Show

May 14-15, 2025

Toronto Congress Centre

650 Dixon Road

Be inspired by changemakers, innovators, and trailblazers. Take advantage of the expert-led sessions in the PRO Speaker Series and 200+ exhibitors on the trade show floor. Discover the latest trends at Health Quest, Learning and Podcast Hubs, and enjoy 15% off essentials at the REALTOR® Store Pop-Up.

TRREB REALTOR ® QUEST

Where Professionalism Meets Excellence

For more information and to register, visit realtorquest.ca

SUKH SANDHU

VISIONARY, REAL ESTATE DEVELOPER, ENTREPRENEUR & AUTHOR

Sukh Sandhu is a distinguished real estate developer, entrepreneur, and co-author of Winning Strategies For Success, a book featuring insights from industry leaders. Known for his innovative and community-driven approach to real estate, Sukh has transformed countless residential and commercial projects, earning numerous accolades for his excellence, ethics, and creativity.

Coming from a family deeply rooted in agriculture, politics, and business, Sukh developed an entrepreneurial mindset early on, launching a successful car sales enterprise while pursuing a degree in mechanical engineering. His ability to identify untapped opportunities has positioned him as a pioneering figure in the real estate industry. Beyond his business ventures, Sukh is committed to social impact, actively supporting education, healthcare, and welfare initiatives to uplift communities. His dedication to personal growth is evident through his passion for travel, fitness, golf, and other outdoor activities, embodying a well-rounded and dynamic lifestyle.

With his relentless drive for innovation and success, Sukh Sandhu continues to shape the real estate landscape while inspiring others to think creatively and push beyond traditional boundaries. His contributions as a leader, mentor, and now a published author further cement his legacy in the industry and beyond.

PUBLISHERS NOTE

As spring breathes new life into Ontario with its blooming flowers and renewed energy, it’s also a season of growth and opportunity in the real estate market. This issue of the Ontario South Asian Real Estate Magazine is dedicated to delivering insightful, timely, and relevant content that empowers our vibrant South Asian community with the tools and knowledge needed to make informed decisions in real estate, finance, and personal growth. We’re proud to be a trusted resource for homeowners, investors, and professionals navigating the dynamic real estate landscape of Ontario.

We are thrilled to feature Kam Brar, a respected Mortgage Broker with a reputation for exceptional client service and deep industry expertise, as our feature cover story. Kam shares valuable insights on navigating today’s mortgage market, offering practical advice and personal reflections that will inspire both new buyers and seasoned investors alike.

Also in this issue, we shine a spotlight on Pam Pabla—an accomplished Insurance expert and author of the empowering book Unshakable Leadership. Pam’s journey blends professional excellence with a passion for leadership, and her story is a testament to resilience, vision, and community impact. Her contributions remind us of the importance of strength, balance, and integrity in both business and life.

In addition to these compelling profiles, this issue is packed with informative articles focusing on the mortgage industry. From understanding rate trends to exploring strategies for first-time homebuyers, our expert contributors provide clear, actionable content to help our readers make confident financial decisions in a changing market.

We sincerely thank you for your continued support and engagement with our magazine. Your readership inspires us to keep delivering excellence. As we look forward to the upcoming TRREB RealtorQuest event on May 14th and 15th, we encourage you to attend, connect, and take advantage of the incredible networking and learning opportunities it offers.

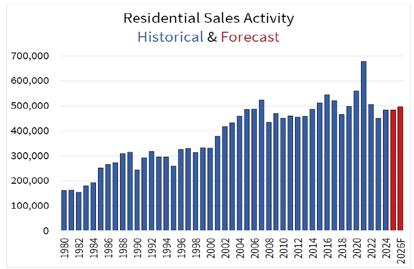

Ottawa, ON April 15, 2025 – The Canadian Real Estate Association (CREA) has updated its 2025 and 2026 forecasts for home sales activity and average home prices via the Multiple Listing Service® (MLS®) Systems of Canadian real estate boards and associations.

CREA released its previous forecast on January 15. While it was too early to incorporate the potential and significant downside risks of a trade war into the forecast at that time, the forecast did state that tariffs targeting the Canadian economy would put what had been expected to be a recovery hear for housing in Canada in jeopardy.

With buyers increasingly fleeing to, or remaining on, the sidelines amid tariff uncertainty, and with the associated economic damage only beginning, sales have continued to fall. Prices in some parts of the country are following suit.

Since CREA briefly paused forecasting at the beginning of the COVID-19 pandemic, this latest CREA forecast constitutes the largest revision in between quarterly forecasts on record going back to the 2008-2009 financial crisis.

Amid ongoing unpredictability and given the fact that it is still far from clear what interest rates will do this year amid a potential stagflation, all forecasts continue to be subject to unprecedented levels of uncertainty.

At this point, some 482,673 residential properties are forecast to trade hands via Canadian MLS® Systems in 2025, representing a 0.02% decline (no change) from 2024. This represents a large downward revision to the 8.6% increase previously forecasted in January.

The national average home price is forecast to decrease a slight 0.3% on an annual basis to $687,898 in 2025, which is about $30,000 lower than forecast back in early January. British Columbia and Ontario are expected to see small declines in average home prices, while in other provinces, expected increases in average home prices have been scaled back to the 3% to 5% range for 2025.

In 2026, national home sales are forecast to improve by 2.9% to 496,487. Sales would fail to crack the half million mark for the fourth straight year. Historically, since 2007, national home sales have surpassed 500,000 units seven times. The national average home price is forecast to edge up by 1.2% from 2025 to $696,074 in 2026.

Each quarter, CREA updates its forecast for home sales activity and average home prices via Multiple Listing Service® (MLS®) Systems of Canadian real estate boards and associations. CREA’s next forecast will be published on Tuesday, July 15, 2025.

RINA GILL FOUNDER

Full-Service Boutique Agency Specializing in Multicultural Marketing

Previous Clientele: Major Banks, Telecoms, Corporates, Small Businesses, Non-Profits & Community Organizations Event Production & Magazine Publications Across Canada Track Record for Securing Corporate Sponsorships & Funding

SIDHU LUXURY PROPERTIES

“Luxury & Off-Market Real Estate Experts”

At Sidhu Luxury Properties, we go beyond the market— specializing in buying, selling, and investing in both commercial and residential real estate, including exclusive offmarket properties. Whether you’re looking for a dream home, a high-return investment, or a prime commercial space, we deliver unmatched expertise and access to the best opportunities.

BUYING?

Gain access to exclusive off-market listings and premium properties before they hit the market. We find the perfect fit for your lifestyle, business, or investment goals.

INVESTING?

We help you maximize returns with exclusive highyield investments, from residential developments to commercial properties, helping you build long-term wealth with insider market insights.

Home Inspections

Commercial Building Inspections

Mold inspections

Air Quality Test, and Mold Remediations

A home inspection is the most important step of Home Buying process. Buying a new home is probably the biggest investment you’ll ever make, and it’s a decision that will affect you for years to come. The process can be extremely stressful and confusing. And of course, there is always considerable risk involved when making such a large purchase decision. A professional inspection will significantly reduce your risk and help make the entire home-buying process easier and less stressful.

We, Technominds Inspection Services Inc. are in the Residential, Commercial, Mold and Environmental inspection business and maintain high professional standards. We all know buying a property, usually is the biggest investment we make. It’s always better to protect this investment by knowing the facts before you own them. We provide educated and valuable information to help our client to make an enlightened decision.

Our reports are detailed, unbiased, and easy to read and understand. We provide you electronic inspection report with pictures and thoroughly explain the report findings at the time of inspection. In addition to reporting any deficiencies or potential failures, our inspections include maintenance tips and other educational information.

KAM BRAR

ON A MISSION TO BUILD DREAMS

Tell us a bit about your background and what led you to become a mortgage broker. What inspired you to pursue this career, and how has your journey shaped your approach to helping clients in the current market?

I was born and raised in Toronto, Ontario, and currently live in Brampton with my husband and our two young children. My parents immigrated from Punjab, India, to Canada in the early 1980s in search of a better future. As the first Canadianborn girl in my family, I dreamed of becoming a businesswoman and one day owning my own company to help others. I pursued a career in law, eventually working with top defence and litigation firms in downtown Toronto at a very young age.

2

I worked on many cases during my legal career before deciding to make a major change.

I was seeking a new challenge and decided to transition into the mortgage industry. While many mortgage brokers come from backgrounds in banking or real estate, I entered this field with determination, a strong client base, and a network of referrals. I worked tirelessly to learn every aspect of the business, and failure was simply not an option. Today, I am proud to be a successful mortgage broker who helps clients navigate financial decisions and achieve their homeownership dreams.

A good mortgage broker stays upto-date with market trends, interest rates, and loan products to provide the best possible advice. I prioritize understanding each client’s unique situation so I can tailor solutions that meet their specific needs.

Can you give us an overview of the Ontario real estate market as we move into Spring 2025? What are some key trends you’re seeing in terms of mortgage rates, home prices, and demand?

Mortgage rates have fluctuated but are generally stabilizing. Central banks have taken a cautious approach, keeping rates moderate to encourage market activity.

Home prices remain high, particularly in urban centers like Toronto and Ottawa. However, the growth has slowed compared to previous years, leading to more balanced conditions

in some areas. There is still strong demand for housing, especially in suburban regions, as remote work continues to shape buyer preferences. Limited inventory contributes to competitive market conditions.

Some key trends include:

n A growing interest in sustainable, energy-efficient homes

n Increased popularity of condos and townhomes as more affordable alternatives

n Rising demand in secondary markets as buyers seek affordability and improved quality of life

Overall, the market remains dynamic, with evolving buyer behavior and economic conditions.

3

What are some of the key challenges first-time homebuyers are facing in Ontario’s current real estate market, and what strategies would you recommend to help them prepare for securing financing?

First-time homebuyers face several obstacles, including these challenges:

n High home prices, especially in major cities

n Difficulty saving for a down payment

n The need for strong credit scores to secure favorable mortgage rates

n Additional expenses such as closing costs and legal fees

Strategies for Credit Repair:

n Review credit reports regularly and dispute any inaccuracies

n Pay down high-interest debts

n Make consistent, on-time payments to build a strong credit history

Down Payment and Savings:

n Create and stick to a monthly budget

n Explore support programs like the FirstTime Home Buyer Incentive

n Use the Tax-Free First Home Savings Account (FHSA) to save with tax advantages

Closing Costs:

n Estimate and include costs like land transfer taxes, legal fees, and home inspections in your budget

n Set aside an emergency fund for unexpected expenses

Pre-Approval and Guidance:

Get pre-approved to understand your purchasing power

Work with a mortgage broker or advisor to receive personalized advice

4

Many first-time buyers are concerned about affordability. How can they best prepare for rising home prices, and are there specific programs or incentives available to help with down payments?

Preparation Strategies:

n Automate savings for your down payment

n Cut non-essential expenses

n Stay informed about market trends and property values

n Consider alternative neighborhoods or housing types

n Explore ways to boost income, such as side jobs or career growth

Programs and Incentives:

n First-Time Home Buyer Incentive: A shared-equity mortgage that helps reduce monthly payments

n Home Buyers’ Plan (HBP): Withdraw up to $35,000 from your RRSPs to buy a home

n Tax-Free First Home Savings Account (FHSA): Save up to $8,000 annually, up to $40,000 total

n Land Transfer Tax Rebates: Available to first-time buyers in Ontario

What are your thoughts on alternative financing options like co-ownership, joint mortgages, or rent-to-own arrangements?

These options can help buyers who are struggling with down payments:

Co-Ownership:

n Shared costs with family or friends

n Requires a clear legal agreement to outline responsibilities and ownership

Joint Mortgages:

n Combines incomes to increase purchasing power

n Important to establish legal and financial agreements

Rent-to-Own:

n Rent payments contribute toward future home purchase

Seek professional advice to understand the legal and financial implications of each option.

In a volatile market, fixed rates offer peace of mind. If you’re comfortable with risk and want potential savings, variable rates can work. Always consult a mortgage advisor. 5 6

n Ensure the contract clearly defines purchase terms and rent contributions

With the current market’s volatility, should homebuyers be considering fixed-rate or variable-rate mortgages more? Can you explain the pros and cons of both?

Fixed-Rate Mortgages:

Pros:

n Predictable monthly payments

n Protection from interest rate increases

Cons:

n Typically, higher initial rates

n Less flexible if rates decrease

Variable-Rate Mortgages:

Pros:

n Lower starting rates

n Potential savings if rates drop

Cons:

n Payments can increase with interest rate changes

n Greater uncertainty and stress

n Ongoing supply challenges 7 8

For clients who are looking to refinance or move into a new home, what advice would you give regarding current mortgage terms?

Refinancing Tips:

n Determine your refinancing goals (lower payments, debt consolidation, etc.)

n Compare offers from different lenders

n Calculate your break-even point to assess if refinancing makes financial sense

Moving Advice:

n Get pre-approved to lock in rates and define your budget

n If your mortgage is portable, consider transferring it to the new property

Protecting Against Rate Hikes:

n Choose a fixed-rate mortgage for stability

n Some lenders offer short-term rate holds

n Look for flexible mortgage terms

n Maintain an emergency fund for financial cushion

What do you predict for Ontario’s real estate market in the next 12 to 24 months? Should buyers and investors be cautious, or is now a good time to act despite some uncertainties?

Market Predictions:

n Moderate home price growth

n Stabilizing interest rates

n Continued demand in suburban and smaller urban areas

Advice for Buyers and Investors:

n Assess financial readiness and long-term goals

n Get pre-approved and act decisively in competitive markets

n For investors, conduct thorough market research and focus on long-term strategies

Opportunities exist for those who are prepared and well-informed.

Do you anticipate more inventory becoming available soon, or will buyers still need to be prepared for bidding wars?

While there may be gradual improvements, inventory shortages are expected to persist:

n New developments are in progress, but completion takes time

n Government initiatives may help, but effects won’t be immediate

Buyers should:

n Be ready for competition in popular areas

n Get pre-approved and consider flexible offer terms

n Expand their search to different neighborhoods or property types

What are your future plans? Where do you see yourself in 5 years?

I look forward to continuing this journey and working with more clients in the years to come. 9 10

In five years, I see myself continuing to grow professionally while expanding my business and knowledge. I’m passionate about promoting financial literacy, especially among Canadian youth. Teaching people how to manage debt, set financial goals, and invest wisely builds resilience and contributes to lifelong well-being.

My goal is to deliver exceptional service, simplify the mortgage process, and help clients find the best financing solutions. A mortgage is a long-term commitment, and I’m here to support my clients every step of the way.

CANADA’S MORTGAGE OUTLOOK: NAVIGATING 2025 AND EARLY 2026

As Canada advances through 2025, the mortgage landscape is experiencing notable transformation. With a combination of decreasing interest rates, impactful policy reforms, and shifting market dynamics, both prospective homeowners and existing borrowers must remain informed to make prudent financial decisions.

INTEREST RATES: A GRADUAL DESCENT

The Bank of Canada has begun a series of interest rate reductions, with the policy rate currently at 2.75% as of March 2025, following a 25 basis point cut. Forecasts suggest continued gradual declines, with the rate potentially reaching 2.25% by the end of the year. For borrowers, this downward trend translates to more favourable mortgage rates. Five-year fixed rates are anticipated to decrease by approximately half a percentage point, likely settling around 4% by late 2025. Variable rates are also projected to fall, with estimates suggesting a drop to near 3.13%.

POLICY REFORMS: ENHANCING ACCESSIBILITY

In December 2024, the federal government enacted substantial mortgage reforms aimed at improving housing affordability. Among the most significant changes are an increased purchase price cap for insured mortgages and extended amortization periods.

The new rules allow homebuyers with less than a 20% down payment to purchase properties valued up to $1,499,999, compared to the previous threshold of $999,999. Additionally, insured mortgages for first-time buyers and newly constructed homes now permit amortization periods of up to 30 years, alleviating monthly payment obligations and broadening accessibility for entry-level buyers.

MARKET DYNAMICS: A REBOUND IN SIGHT

The synergy of declining interest rates and favorable policy reforms is expected to revitalize Canada’s housing market. After a period of subdued activity, market analysts predict a resurgence in home sales throughout late 2025 and into 2026. This recovery is anticipated to be driven by robust population growth and enhanced affordability conditions. However, there are potential headwinds: a considerable number of mortgages initiated during the pandemic’s low-rate environment are set to mature by the end of 2026. As borrowers face higher renewal rates, many could encounter increased financial pressure, which may

influence broader economic activity and consumer confidence.

LOOKING AHEAD: STRATEGIC CONSIDERATIONS

As the mortgage environment continues to evolve, Canadian borrowers are encouraged to approach their financial decisions strategically:

Stay Informed: Keep up with changes in interest rates and regulatory policies to make timely, well-informed decisions.

Evaluate Options: Consider the pros and cons of fixed versus variable mortgage products based on your financial goals and market projections.

Plan for Renewals: Anticipate the impact of renewing mortgages at potentially higher rates and explore strategies to cushion monthly payments.

By remaining vigilant and engaged, Canadians can adeptly navigate the complexities of the mortgage landscape, positioning themselves for long-term financial health and sustainable homeownership.

UPCOMING FEATURE COVER STORY

MANRAJ S. MUKKAR

PARTNER, CASSELS BROCK & BLACKWELL LLP

Manraj (Manny) Mukkar is an experienced lawyer and a partner in the Real Estate & Development Group at Cassels, a leading Canadian national law firm. Manny’s practice focuses on all aspects of commercial real estate law and general corporate matters in which he routinely acts on behalf of developers, vendors, purchasers, lenders, and borrowers on a broad range of complex commercial real estate transactions, with a particular concentration on acquisitions and dispositions of commercial properties, and commercial financing transactions involving all real estate asset classes.

Aside from managing a busy practice, Manny is active in the community contributing his time and experience by serving as a mentor to international students to help nurture their growth and assist with their transition into the Canadian legal market. Manny is also a member of his firm’s Inclusion & Diversity Committee and serves as co-chair of the Asian Affinity Group. He has also held various positions for the Sikh Foundation of Canada, a non-profit organization that seeks to promote Sikh history, arts, and culture.

Drawing from his substantial experience in a wide variety of transactional work, Manny prides himself on delivering professional, practical, and solution-driven advice which enables him to navigate complex legal issues to ensure the most optimal results for his clients.

Unshakable Leadership:

Pam Pabla

on Building Trust, Empowering Others, and Protecting What Matters Most

Can you share a bit about your professional journey and what inspired you to pursue a career in the insurance industry?

My journey in the insurance industry has been both meaningful and deeply rewarding. With over 25 years of experience, I have had the opportunity to serve in various roles—from client service and claims advising to leadership, education, and business ownership. Since opening my agency in 2018, my team and I remain committed to helping individuals, families, and business owners protect what matters most to them.

Witnessing insurance’s real impact during life’s most unexpected moments inspired me to pursue this path. Insurance is not just about policies—it is about people. It promises to provide support, guidance, and peace of mind when it matters most. That purpose continues to guide everything I do.

Over the years, I have remained committed to advancing the profession. I taught Chartered Insurance Professional (CIP) courses with the Insurance Institute of Canada, helping future professionals build the skills and values needed to serve others with care and integrity. I have also been honoured to represent the profession as an Insurance Ambassador.

2 3

Today, as a Chartered Insurance Professional, an Award-Winning Author of Unshakable Leadership, and an entrepreneur leading my insurance agency, I bring together years of experience, deep industry knowledge, and a passion for people. I am proud to serve as a leader and mentor, empowering others through education, delivering meaningful protection, and building a legacy of care, service, and leadership.

“My

agency is built on trust, care, and personalized service. My team is dedicated to guiding clients through every step with clarity and compassion, ensuring that they feel protected, valued, and supported in every decision.”

Health insurance is a key part of protecting your well-being. Please help our readers understand Ontario’s various types of health insurance coverage and how someone might choose the right option for their needs.

Absolutely. In Ontario, while we’re fortunate to have provincial health coverage through OHIP, it doesn’t cover everything. That’s where additional health insurance comes in. Individuals can explore a variety of plans that offer coverage for things like prescription drugs, dental care, vision, paramedical services, and even private or semi-private hospital rooms. There are also options for personal health plans and executive-style coverage tailored to business owners or self-employed individuals.

Choosing the right plan comes down to understanding your lifestyle, current health needs, and gaps in your coverage. I encourage people to ask questions, review their budget, and think long-term. A good insurance advisor will walk you through the options and help you select a plan that gives you flexibility and peace of mind.

Supplemental health insurance can offer extra support beyond what OHIP covers. What are some of its top benefits, and who should seriously consider adding this type of coverage?

Supplemental health insurance is really about protecting your lifestyle and your choices. While OHIP covers many essential services, it doesn’t include everything—especially regarding everyday health needs. That’s where supplemental coverage steps in, offering support for prescription drugs, dental care, vision, mental health services, physiotherapy, chiropractic care, and more.

Think of it as a customized health safety net—giving you the freedom to choose the care you want when you need it without worrying about the financial burden. It benefits self-employed professionals, retirees, young families, and even students starting independently.

Supplemental health insurance is a powerful way to stay ahead of health expenses and protect your savings if you value wellness, independence, and peace of mind. After all, your health is your greatest asset—protecting it means protecting your future.

In today’s world, families are more aware of the financial impact a serious illness can have. How can critical illness insurance provide the support people need during such a life-changing time?

A serious illness can change everything in an instant. That is why critical illness insurance is so important. It provides a tax-free lump sum that helps ease the financial pressure so you can focus on what truly matters — your health and your family.

Whether it covers out-of-pocket medical expenses, helps with everyday bills, or allows you to take time off work to recover, this protection gives you choices. It is not just about money. It is about time, comfort, and peace of mind during some of life’s most difficult moments.

At its heart, critical illness insurance is about being prepared and feeling supported. It allows families to move forward with confidence, knowing they will not have to face a health challenge alone. It is one of the most thoughtful ways to protect the future.

5 6 7

Many people may not fully understand disability insurance. Can you explain the types of coverage available and why it is so essential for anyone who may face a health concern that affects their ability to work?

Disability insurance is one of the most important forms of protection because it helps safeguard your income if an illness or injury prevents you from working. Your income supports everything—your home, family, and future—so protecting it is essential.

There are different types of disability coverage. Some plans offer short-term benefits for temporary situations, while others provide long-term support if you cannot return to work for an extended period. Each type is designed to help cover your daily living expenses so you can focus on recovery without the added stress of financial worries.

I always say that your ability to earn an income is one of your greatest assets. Disability insurance gives you peace of mind, knowing that you have support even if life takes an unexpected turn. It is about planning and staying strong during uncertain times.

The insurance world can sometimes feel overwhelming for people. How do you help your clients feel informed, confident, and supported when making insurance decisions?

My goal is always to make insurance simple, caring, and straightforward. I understand that insurance can initially feel confusing, but with the proper guidance, it becomes a powerful tool to protect what matters most. I take the time to listen and understand my client’s needs and explain coverage in a way that is easy to understand and meaningful to them.

Education is key. I want every person I speak with to walk away feeling confident and empowered about their decisions. I believe in building relationships, not transactions. That means offering honest advice, being available to answer questions, and always keeping their best interest in everything that I do.

When people feel supported, they make strong choices for themselves and their families. That is what real peace of mind looks like, and I strive to deliver it daily.

Many homeowners may not fully understand the purpose of mortgage insurance. Can you explain what it is, how it works, and why homeowners need to consider, especially those buying their first home?

Mortgage insurance protects your loved ones from financial hardship if something unexpected happens to you. It provides a tax-free benefit that the beneficiary can use to help pay down or pay off the remaining mortgage balance in case of a critical illness, disability, or death.

For many families, the home is more than just a property— it is a place of comfort, stability, and security. Mortgage insurance helps ensure that even in the most difficult times, your family is not left with the burden of large monthly payments or even the risk of losing their home.

This coverage is essential for first-time homeowners who are building their financial foundation. It offers peace of mind and a layer of protection that allows you to focus on living life confidently, knowing your home and your family are supported no matter what life brings.

Life insurance is key to protecting your family’s future. Why is it so important to have life insurance, and how can someone choose between term and permanent life coverage?

Life insurance is one of the most powerful ways to protect your loved ones. It provides financial security and peace of mind, ensuring that your family can maintain their lifestyle, cover outstanding debts, and focus on healing—not hardship—in the event of an unexpected loss.

There are two main types of life insurance: term and permanent. Term life insurance protects for a set period, such as 10, 20, or 30 years. It’s often chosen for its affordability and simplicity, making it an excellent option for those with short- to medium-term needs, like paying off a mortgage or securing income replacement during the working years.

On the other hand, permanent life insurance is designed to last a lifetime. It offers long-term protection and can build cash value over time. This makes it an ideal choice for those looking to leave a legacy, fund future expenses like education or estate planning, or ensure lifelong coverage.

Choosing the right solution depends on your goals, stage of life, and family’s needs. My team and I are here to guide clients through every step, helping them make informed, confident decisions that bring lasting protection and peace of mind.

“Life insurance is not just about what happens someday — it is about protecting the life you are building today and every tomorrow that follows.”

Life insurance is one of themostpowerfulwaysto protectyourlovedones.It providesfinancialsecurity andpeaceofmind, ensuringthatyourfamily canmaintaintheirlifestyle, coveroutstandingdebts, andfocusonhealing—not hardship—intheeventof anunexpectedloss

With changes in the housing market, what should homeowners consider when choosing home insurance to make sure they are fully protected from unexpected damage or loss?

Home insurance is more than just a requirement — it is a key part of protecting your home, your belongings, and peace of mind. As the housing market changes and home values shift, homeowners must ensure their coverage keeps pace.

When selecting a home insurance policy, I encourage people to look at more than just the basic coverage. It is about understanding what is included, such as protection against fire, water damage, theft, and personal liability. You also want to ensure the coverage reflects your home’s current rebuilding costs, not just its market value.

Optional coverage, like sewer backup or overland water, can also provide added peace of mind, depending on where you live. Solutions are available for those with high-value belongings or home-based businesses to ensure proper protection.

Home insurance is about feeling secure, knowing that your family, your investment, and future are protected if something unexpected happens. It is a smart step toward financial stability and a strong foundation for life.

A business owner must have the right insurance coverage. Can you explain the different types of business insurance available and why entrepreneurs need to assess their risks and protect their business

with the right coverage?

Business insurance is vital to building and protecting what you have worked so hard to create. Every business is unique, so the coverage should reflect the specific risks involved in your operations.

There are several types of business insurance to consider. Commercial property insurance helps protect your building equipment inventory and contents. Commercial general liability insurance helps cover costs related to third-party injury or property damage. Professional liability, also known as errors and omissions insurance, is important for businesses that provide advice or services. For businesses with vehicles, there is commercial auto insurance. And if you employ staff, you may need coverage that supports your obligations as an employer.

Assessing your risks and having the proper protection in place helps prevent minor setbacks from becoming significant financial challenges. Business insurance provides stability and confidence, allowing entrepreneurs to focus on growth while knowing they are protected from the unexpected.

For

Protecting against potential risks is essential for small service businesses. The right insurance coverage provides financial protection and allows business owners to operate with confidence and peace of mind. 9 10 11

small businesses, especially those in the service industry, what types of insurance are most important to help guard against potential risks, and how can business owners make sure they are getting the best value?

Some of the most essential types of coverage include commercial general liability, which helps cover the legal and/or medical costs if a client or third party is injured or experiences property damage related to your business. Professional liability insurance is also valuable, especially for companies that provide advice consulting or services. Property insurance can help protect your equipment, tools, or office space, whether you own or lease it.

To get the best value, business owners should review their coverage regularly, especially as their operations grow or change. Working with a trusted insurance advisor can help you understand what is necessary and what is optional and how to tailor a plan that fits your needs and your budget.

Smart planning today helps protect your business tomorrow, allowing you to focus on delivering excellent service and building lasting success.

As the author of an upcoming book on leadership, what inspired you to write about this topic, and what do you hope readers will take away from it?

This book reflects my personal and professional journey, which was shaped by leading a team, building a business, and walking through seasons that required strength, faith, and unwavering commitment. Over the years, I have learned that leadership is not about status or position. Rather, it is about how you show up, how you serve, and how you make a difference in the lives of others.

I felt a deep calling to share the principles that have guided me—accountability, responsibility, and faithfulness. These values have helped me grow as a leader and remain grounded in every decision. I hope that by sharing these lessons, others will feel empowered to step confidently and clearly into their leadership journey.

This book is filled with real stories, timeless truths, and practical tools to help readers lead with purpose and impact. It is for anyone who wants to grow and lead with the heart and create a lasting legacy — not just in business, but in life.

If you are ready to rise into the leader you were meant to be, this book will inspire, support and walk with you every step of the way. This is more than just a book; it is an invitation to transform your mindset, strengthen your leadership, and step boldly into your calling.

“Leadership is not about power; it is about purpose. This book invites every reader to lead with courage and integrity and become the difference the world needs today and in the future.”

14

What has been one of the most fulfilling parts of your career so far, both personally and professionally?

One of the most fulfilling parts of my career has been the opportunity to make a real difference in people’s lives. Whether helping a young family protect their future by supporting a business owner with the right coverage or guiding someone through a difficult season, I find purpose in knowing that what we do truly matters.

Professionally, I am proud of building a successful insurance agency that focuses on care education and trust. As a Chartered Insurance Professional and the Award-Winning Author of Unshakable Leadership, I have had the privilege of sharing my knowledge and values with clients and the community. Leading a team that believes in putting people first and watching them grow has been incredibly rewarding.

Personally, the most meaningful moments are the ones where clients become like family, and I get to walk alongside them through life’s journey. I have learned that success is not only measured by numbers but also by the lives you touch, the relationships you build, and the legacy you leave behind.

“True fulfillment comes from knowing that every conversation, every policy, and every decision is impacting lives in a meaningful way. My greatest success is not in what I have achieved — but in the legacy of trust, care, and leadership my team and I continue to build daily.”

What can we expect from your upcoming book, and what is next for you in both your professional journey and personal growth?

This book represents a defining moment in my journey. It captures the essence of growth through resilience and the strength that comes from choosing integrity over comfort.

Readers can expect a deeply meaningful and action-oriented experience that challenges them to reflect, lead, and live with intention. It is not just a book to read but a guide to follow as they build the kind of life and leadership that creates lasting impact.

Professionally, I am focused on deepening the level of care and support that offer through my insurance agency. My vision is to continue building a team and client experience centred on trust, clarity, and service. I am also looking forward to new speaking opportunities, collaborations, and leadership development projects that will expand the reach of this message.

On a personal level, I remain committed to growing in faith, strengthening my family foundation, and living a life that reflects purpose and gratitude. When you lead with your values and walk with vision, every new season becomes an opportunity to rise.

The journey ahead is full of purpose, and I am excited to continue serving, leading, and inspiring — one life, one chapter, and one conversation at a time.

“This new season is filled with purpose, passion, and possibility. My journey forward is a calling to lead with vision, influence with integrity, and build a legacy rooted in faith, excellence, and impactful leadership.”

“This company stands above the rest - quick to respond and shows up on time. I had pot lights put throughout my second floor and was amazed at how efficiently the work was done. Hossein was able to make great suggestions regarding placement that I would have never thought of. I highly recommend Hossein and his crew, and won't hesitate to use them again for future projects.”

“Potlight

BUILDING WEALTH THROUGH REAL ESTATE

Real estate has long been one of the most effective paths to building wealth in Canada. With the right mortgage structure and strategy, individuals can generate long-term equity, establish positive cash flow, and use leverage to expand their property portfolio. Whether you’re a first-time buyer or an aspiring real estate investor, understanding your financing options and how to use them wisely is key to long-term financial growth.

UNDERSTANDING MORTGAGE TYPES IN CANADA

Before diving into advanced strategies, it’s crucial to understand the common mortgage types available:

Fixed-Rate Mortgages

A fixed-rate mortgage locks in your interest rate for a set term (usually 1 to 5 years). This is ideal for buyers who prefer stability in monthly payments and want to avoid surprises during periods of interest rate fluctuation.

Variable-Rate Mortgages

With variable-rate mortgages, your interest rate may fluctuate depending on the prime rate. These usually start lower than fixed rates and can save you money if rates stay low. However, they do involve more risk and require a stronger tolerance for change.

Adjustable-Rate Mortgages (ARMs)

Similar to variable-rate, but with changing monthly payments instead of just adjusting how much goes toward interest vs. principal. ARMs provide flexibility but require a safety buffer in your budget.

Home Equity Line of Credit (HELOC)

Once you have equity in your property, a HELOC allows you to borrow against that equity. This can be a flexible tool for renovations or even purchasing additional property — but it must be managed wisely.

WEALTH-BUILDING STRATEGIES WITH MORTGAGES

Mortgages are not just a debt — they are a tool. When structured strategically, they can accelerate wealth accumulation through equity growth, rental income, and appreciation.

Buy and Hold Strategy

Buy a property in a growth market, rent it out, and hold onto it long-term. Your mortgage is paid down over time by your tenants, while your property (ideally) appreciates in value. This strategy builds equity and passive income.

House Hacking

Live in one unit of a multi-family property while renting out the others. This can cover or significantly reduce your mortgage payments, allowing you to save or invest in additional assets.

Purchase undervalued properties, renovate to increase value, rent them out, refinance to pull out the increased equity, and use that capital to repeat the process. This method relies on forced appreciation and smart use of leverage.

USING LEVERAGE TO SCALE YOUR PORTFOLIO

One of the most powerful tools in real estate is leverage — using borrowed money to increase your potential return on investment. For example:

5%–20% down payments allow you to control

a large asset with a relatively small amount of capital.

Refinancing and pulling equity from one property can fund the down payment on another.

Cash-flowing rental properties help you cover debt service while building equity.

Key Tip: Lenders assess your total debt obligations when approving mortgages, so keeping your debt-to-income ratio healthy is essential when scaling.

ENSURING POSITIVE CASH FLOW

While property value increases build longterm wealth, cash flow keeps your investments sustainable. To ensure positive cash flow:

Choose properties in high-demand rental areas.

Avoid over-leveraging or overpaying on your mortgage.

Budget for property management, taxes, maintenance, and vacancy.

Even modest monthly cash flow can provide a cushion against market shifts or rate increases and add up to significant income over time.

FINAL THOUGHTS

Smart mortgage planning and strategic leverage can empower you to build a real estate portfolio that generates both equity and income. As interest rates begin to stabilize, and more Canadians look toward real estate as a reliable investment vehicle, having a well-informed, long-term strategy is

1994

The App is FREE, check daily for new listings

• Find information, make connections

• Add your own information, do business

• Find a Realtor Member to work with

Four Ways Free for the Public, Buyers and Sellers to Make to make Connections

1. Search Database 1 and 2 for Free, 24/7.

2. Add your Haves and Wants for Free.

3. Search for a Member to post your listing for maximum worldwide exposure.

4. Subscribe to daily email for newest Have & Wants.

Find a Member by language spoken. Call for Assistance.

Search Database 2 for Asian Haves and Wants.

Ask your Realtor to join ICIWorld on your behalf to reach this major world audience.

BILLION

ICIWorld.com was the first real estate service on the Internet (1994) to serve real estate professionals that provides more choice for the public.

of Commercial listings Haves and Wants are exclusive to our networking platform and NOT found elsewhere on the internet.

Search the Wants, Members with buyers ready, willing, able and qualified to buy businesses, commercial and residential properties today!

Real Estate Brokers & Salespeople are the best positioned people in the industry, to network real estate Have and Want information globally, confidentially. They also provide MLS™ services.

Executive Members on ICIWorld.com globally share their exclusive information confidentially and on their websites.

Scan to make an appointment Real Estate Brokers & Salespeople in the USA and Canada provide security for the Public because they are trained in Consumer Protection.