N E E D S F U N D I N G AN INITIATIVE OF VISION 2030 REHOBOTH BEACH COUNTRY CLUB JUNE 2024

EXECUTIVE COMMITTEE

SHARON COVINGTON

President

JOHN CARUSO

Vice President, Governance Chair

ED BROWN

Secretary, Golf Chair

JOHN MCCOOEY Treasurer, Finance Chair

GERRY DESMOND

Executive At Large, Racquets Chair

BOARD OF DIRECTORS

ANDREW METZ

Legal Affairs & Insurance Chair

DANIEL COAR

Long Range Planning Chair

DANIEL LUCKENBAUGH Membership Chair

JAMES A. HORTY, III House Chair

JOE KIRCHNER Buildings Chair

KAREN SCHNEIDERMAN

Hospitality & Centennial Chair

MIKE MCGUINESS

Greens Chair

WILLIAM BOOTH

Pool & Fitness Chair

CARPIU “C” CHERECHES

GM/COO - Ex Officio

IN THIS ISSUE

THE NEED FOR CAPITAL DUES

THE WHY

Current Financial Structure

How Have We Funded Repair and Replacement?

Important Definitions

THE HOW

How Did We Determine the Need for Capital Dues?

View Some of RBCC’s Assets

Why Do We Need Capital Dues?

THE WHAT

What is the Request?

How will it be Structured?

How Does This Impact Me? How will it be Managed?

WHAT’S NEXT

Member Q&A Meetings

Dedicated Coffee with C The Vote

A LETTER FROM THE PRESIDENT &

Dear RBCC Members,

June 8, 2024

We hope by now you have had the opportunity to thoroughly review the Vision 2030 document shared in March, along with our weekly Eagle Tracks, monthly Eagle Point newsletter, and Board Briefs. In Vision 2030, the RBCC Board and Leadership team presented a plan for carrying us into our next 100 years. This document was developed from listening to you, the membership, in the two surveys conducted last year as well as ongoing discussions. From your feedback and our analysis, the Board has developed a RBCC Strategic Plan with related initiatives to provide a framework for how to sustain and grow this beautiful Club in the future. Throughout this process, we have maintained a listening ear, understanding heart, and thoughtful mind to ensure the transparency and clarity needed to make these important decisions.

If you have read our monthly letters, you know we have been talking about the need for Capital Dues to cover the growing obligatory costs necessary to maintain the campus and facilities. During these months, the Board, Talon Tribe members and Club Committees have spent well over a thousand hours going through a thorough analysis of the Club’s capital assets and the repair and replacement needs. In addition, we’ve spoken to scores of you--in committee meetings, in focus groups, at Coffees with C, and casual conversations--to learn and to listen to your thoughts about RBCC and the need for Capital Dues. A consistent theme we heard was how much the Members love the experience at RBCC and how much they want to support a plan for the future that is fiscally responsible, transparent, fair, and accountable.

We have developed this communication to explain the WHY, the HOW and the WHAT of Capital Dues. It is important that you know and comprehend the deep dive we’ve taken to understand the need, before coming to the Board’s unanimous decision to recommend to membership a vote to institute Capital Dues As one of our Core Values states, our stewardship requires “…a well-being of RBCC today and for the future.” Let’s think of the es as our gift for the Centennial and beyond!

u “C” Chereches ral Manager/COO

JOHN MCCOOEY

Treasurer, Finance Chair, Ad-Hoc Chair

JOHN CARUSO

Vice President, Governance Chair

SHARON COVINGTON President

DAN COAR

Long Range Planning Chair

NANCY FREEBERY

Member, Communications Advisor

ANDREW METZ

Legal Affairs & Insurance Chair

JIM ZAMBITO

Finance Committee Member

CARPIU “C” CHERECHES

General Manager, COO

BETHANY ACKERMAN

Membership & Communications Director

THE WHY

WHAT IS RBCC’S CURRENT FINANCIAL STRUCTURE?

RBCC’s current financial structure can be summed up as follows: Annual dues and monthly member charges fund operating expenses.

The Renovation Assessment fee funds the approved 2019-2020 Club Improvement Plan (CIP).

This might be confusing to some Members who recall this assessment was originally named “Capital Dues.” This charge was renamed to Renovation Assessment because assessments have an expiration date and dues are ongoing The $9 9M CIP loan with Fulton Bank was signed in November, 2019 with principal payments beginning in 2020 The loan has a 20-year term and matures in November 2040.

RBCC does not collect Capital Dues for repair and replacement of capital assets. Initiation fees are the current primary source of funding.

SO, HOW HAVE WE FUNDED REPAIR AND REPLACEMENT OF CAPITAL ASSETS IN THE PAST?

New member initiation fees

Bank loans – for example: the irrigation system replacement in 2019. By necessity, over the past 10-year period, initiation fees have also been used to partially fund debt interest payments, prepayment of debt principal (irrigation system replacement loan) as well as fund repair and replacement of capital assets. In some years, initiation fees were utilized to offset operational deficits at the end of the fiscal year. The balance remains in cash reserves.

Click here for a more detailed explanation on where initiation fees have been spent over the last 10 years.

THE RESULT?

With no consistent, reliable revenue source for capital funds, this has often led to many important replacements or refurbishments being de-prioritized or deferred.

OPERATIONAL DUES: Fund day-to-day operations. The goal is to break even in operations, matching revenue to expenses.

From the April Member Focus Groups on the topic of capital dues, it became crystal clear that the Club should have provided the membership with a thorough explanation about why operational dues have increased 10% three years in a row.

The following provides a simplified explanation. To further understand the increase, please click here for a detailed explanation.

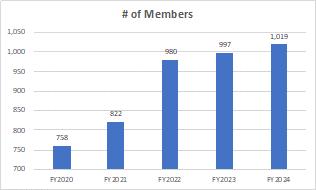

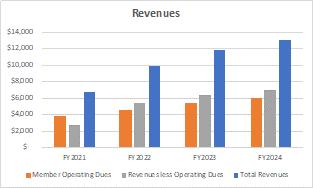

RBCC had an unanticipated growth that started with 758 memberships in FY2020 and expanded to 1,019 memberships in FY2024 equating to roughly 375 new memberships. This impacted the financial structure with a 25 percent compound growth in total revenues and total expenses, five times more than what was expected year after year, following COVID-19 and the Club Improvement Plan (CIP) Total expenses were severely impacted by inflation, the upward pressure of labor costs, increased member usage of the pre-existing and new amenities (additional outdoor dining, pickleball, fitness classes, etc.), and the desire to deliver the expected exceptional level of service for the RBCC member experience.

RBCC CAPITAL DUES: Would be completely separate from operational dues Capital dues are a special class of dues determined and collected specifically to fund obligatory capital repair and replacement of the club’s physical assets as they age.

Examples of obligatory projects:

Bulkhead Repairs

HVAC

Parking Lot

Equipment Replacement

ASPIRATIONAL PROJECTS : Projects the Club completes to evolve and grow. They are not funded by capital dues but instead are funded by initiation fees and/or assessments.

Examples of aspirational projects:

Golf Course Redesign Master Plan

Outdoor Dining Patio and Bar

Fitness Center Renovation

Halfway House Expansion

LEARN More

Click here to see a summary of the in-depth study.

THE HOW WHAT DID THE AD-HOC COMMITTEE AND BOARD DO TO DETERMINE THE NEED FOR CAPITAL DUES?

The recently released Vision 2030 plan, based on two Member surveys and RBCC’s Strategic Plan, solidified the necessity to focus on an ongoing source of funding for the repair and replacement of capital assets.

In 2023, to better understand the need and help plan for the replacement of the Club’s assets, an outside consulting firm, Club Benchmarking, was contracted to conduct an in-depth study. This study has been thoroughly examined and fine-tuned many times over by the RBCC operational management team and the Board.

From this very thorough examination, it has been determined that replacement or refurbishment costs for RBCC’s existing fixed assets are projected to be at least $18 million over the next 10 years.

WHAT ARE RBCC’S EXISTING FIXED ASSETS?

“TODAY 80% OF CLUBS HAVE COME TO UNDERSTAND THE UNSUSTAINABILITY OF OLD MODELS AND CURRENTLY HAVE MONTHLY CAPITAL DUES TO MANAGE THE COMPLEXITY OF AGING FACILITIES.”

Club Benchmarking

SO WHY DOES RBCC NEED CAPITAL DUES?

Short and simple – to establish a consistent, reliable funding stream to maintain the campus and facilities.

We expect future initiation fees will decrease to approximately $1M per year based on a full membership and low Member turnover. If we continue to rely solely on initiation fees to fund the repair and replacement of capital assets, the amount would be insufficient to fund the expected average of $1.8M per year of obligatory capital required. The result? Only projects absolutely necessary to the safety and functioning of the Club will be executed Then capital projects will be scheduled according to which ones are likely to fail suddenly; with the least urgent capital projects, and any aspirational projects, being put on hold.

THE WHAT

WHAT DO WE NEED?

As stated in the preceding section, the study conducted by Club Benchmarking in 2023 documented the Club would need $18M over the next 10 years to repair and replace the Club’s capital assets.

WHAT IS THE REQUEST OF THE BOARD?

The Board recognizes that asking to fully fund and collect $1.8M per year over the next 10 years is a big request. We believe that reducing that to approximately 75 percent of that amount, or $1.3M per year, positions us well to fund most of our needs and have cash reserves (accumulated from Initiation Fees) as a back-up if needed, thus avoiding loans and assessments.

HOW WILL CAPITAL DUES BE STRUCTURED?

As the country club industry is learning, the ideal primary source for asset repair and replacement is steady, predictable funding from membership capital dues. The most common industry practice is to fairly tier those dues based on membership categories The Board agreed that tiering by membership category is both fair and consistent with industry practice Arriving at the dues per individual required one more consideration

What is the appropriate split between the Club’s membership categories: Regular, Social, Clubhouse? The Board exercised due diligence on this matter by: Benchmarking with similar private clubs, Evaluating several possible Capital Dues scenarios against financial ratios provided by Club Benchmarking Best Practices, It was then decided that the Board choose one capital dues amount per membership category. The tiering between membership categories is 100% for Regular, 80% for Social and 20% for Clubhouse. The table below shows the percentage of capital dues by membership category.

WHAT ASSETS WILL BE INVOLVED IN REPAIR AND REPLACEMENT?

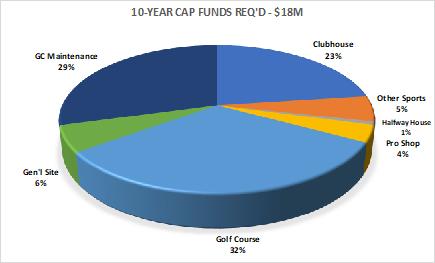

All assets have been evaluated by Club Benchmarking, and a 10year plan outlining anticipated repair and replacement estimated dates and cost for each asset has been developed. This plan has been fine-tuned by the Leadership team and will serve as the Club’s road map. Each year there will be a list of expected repair and replacement projects generated from the 10-year plan. The 10-Year Required Capital Funds pie chart to the left showcases the overview of distribution by department from FY25 to FY34. This list will then be vetted by the Leadership team and Board-assigned committees.

The planned list is understandably fluid. When appropriate some projects may be deferred, and in the case of emergencies, others added. The final plan each year will be presented to, reviewed and approved by the Board. CLICK HERE TO REVIEW THE FIRST YEAR OF ASSET REPAIR AND REPLACEMENT.

HOW MUCH WILL EACH MEMBER BE CHARGED PER MONTH?

Based on the annual amount of $1.3M and the tiering structure as described on page 8, the amount per membership is shown below.

Capital Dues will be ongoing unlike an assessment. Absent any significant change in the Club’s finances, the intent of this Board is to freeze this annual amount for the next 5 years and then have the amount be re-evaluated by the future Board.

HOW WILL CAPITAL DUES BE MANAGED?

The Leadership team, along with Board-assigned committees, will review obligatory capital funds required by project, by department, and by cost with the Finance Committee. The list will be presented to the Board for approval and communicated to the Members as part of the annual budget process. Leadership will track and report on the actual spend versus budget monthly to the Finance Committee.

HOW WILL OBLIGATORY PROJECTS BE MANAGED?

Recognizing the absolute necessity to successfully manage the projects, the Leadership team will collaborate with outside construction management professionals for guidance to review the year’s projected projects as approved by the Board. Following the approval of the budget, the Leadership team will formulate a plan breaking it down month by month and following procedural steps to implement.

WHAT’S NEXT MEETING Register

Click here to Register for a Member Q&A Meeting and submit a question to be answered at the Meeting. Click here to listen in on

Submitted questions during registration will be acknowledged at all Member Q&A Meetings.

Now that you’re an informed Member who has an understanding of how the Board came to a decision, you may be asking yourself... what’s next regarding this topic?

MEMBER Q&A MEETINGS

Just as we recognized the need for Member focus groups before making the decision about capital dues and developing this kickoff communication, we recognize the need for Member meetings to further open up the communication and answer important questions to ensure the membership is fully informed before the vote on capital dues.

MEETING DATES:

June 22 | 3pm - 4pm

June 28 | 4pm - 5pm

July 19 | 5:30pm - 6:30pm

Meetings will be held on the second floor of the Clubhouse in the Bayview Room. Zoom access will be available for those who can’t make it in person. To register for a Member Meeting, use the ForeTees app, Club Website or call the Club at 302-227-3811. YOU CAN ALSO CLICK HERE TO REGISTER!

COFFEE WITH C

C is back to the first Saturday of every month on July 6 at 8am. He will host Coffee with C in the Eagles Nest Bar. This session will not be strictly dedicated to Capital Dues, but all questions are welcome.

NOTICE OF REQUEST FOR A SHAREHOLDERS VOTE

ASK A Question

Can’t attend a Member

Q&A Meeting, but have a question?

Click here to submit a Question for someone to contact you personally. Or

SCAN THE QR CODE

The Board requests the Shareholding Membership of Rehoboth Beach Country Club review the Capital Needs Funding Initiative and vote by Monday, July 22 at 11am to implement Capital Dues.

Three ways for Shareholding Members to vote will be available which include the following with more details below:

Mailing in a ballot

Digital voting via emailed ballot

In person at the Club on Monday, July 22

YOUR VOTE AND VOICE MATTER.

MAILED VOTING

Mailed proxies will be sent to each Shareholding Member on Friday, June 21 and must be received by Parkowski, Guerke & Swayze, P.A. 909 Silver Lake Blvd, Dover, DE 19904 by Friday, July 19 at 4:00pm.

DIGITAL VOTING

Emailed proxies will be sent to each Shareholding Member of Rehoboth Beach Country Club on Friday, June 21, 2024. You must submit your digital proxy on or before 4:00pm on Friday, July 19, 2024. For questions regarding digital proxies, email the Club at office@rehobothbeachcc.com.

By email to mteichman@pgslegal.com. For your proxy to be counted, a signed and checked copy of this proxy must be attached to your e-mail as a .PDF file. Please make sure that the subject line of the e-mail reads “RBCC Proxy.”

IN-PERSON VOTING

In-person voting will be available in the Clubhouse Lobby on Monday, July 22, 2024, from 8:00am to 11:00am. You may deliver your completed ballot in a sealed envelope to the General Manager no later than Monday, July 22 at 11am.

N E E D S F U N D I N G AN INITIATIVE OF VISION 2030

A MORE DETAILED EXPLANATION ON WHY HAVE OPERATING DUES INCREASED 10 PERCENT THREE YEARS IN A ROW

2024

MEMBERSHIP

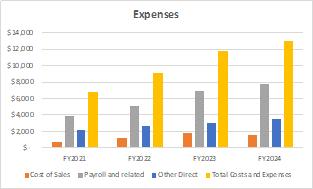

After two years of partial shutdowns and interruptions in service in FY2020 and FY2021, RBCC had record growth in membership, well beyond what was foreseen and planned. From FY2021 until the end of FY2024, total revenues rose from $6.6M to $13M and total expenses rose from $6.8M to $13M, increases amounting to 97% and 90% respectively, or compounded growth per year of 25% and 24% respectively. And the growth in expenses, which we limit to ensure a breakeven operating result, was severely impacted by both overall inflation as a result of COVID programs and the continuing upward pressure on wages and benefits.

During that same three-year period, Membership Dues, in dollars, grew a total of $2.2M with Member usage of club amenities and outside use of club facilities, accounting for the balance or $4.2M. As Member usage increased so did expenses to provide the expected service for the pre-existing amenities as well as the new and expanded amenities that resulted from the Clubhouse Improvement Project and other improvements, e.g. outdoor dining, pickleball courts, fitness classes, etc.

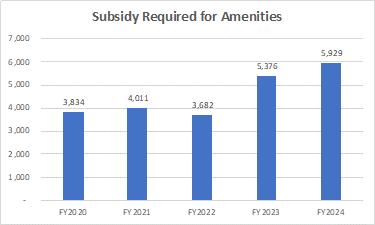

Therein lies the issue. Club amenities are funded by the revenues they generate, e.g. F&B chits, golf fees, guest fees, etc., and portions of the annual Member dues. Call that last piece a “subsidy”. All Club amenities, by design, require a “subsidy” from operational dues. So why doesn’t the increased Member usage cover more of the costs rather than operational dues? The answer is in the math. One dollar of operational dues produces a full dollar of available subsidy funding

One dollar of Member usage produces less than fifty cents. Member usage has to cover its own costs first, whether that’s the cost of goods for F&B, labor costs for fitness, racquets and golf instructors, etc. And some club costs are 100% paid by Member operational dues, e.g. G&A, which includes not only staff salaries but mundane things like insurance, real estate taxes, energy, etc.

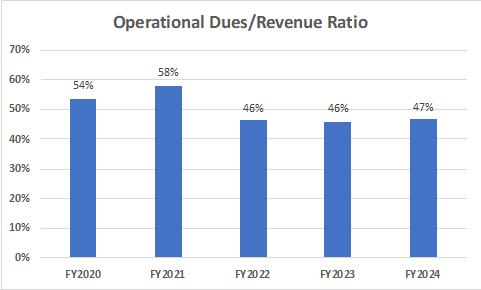

MAINTAINING A BALANCE

Ideally, clubs try to maintain a balance of 50-52% operational dues to total revenues with the most successful clubs targeting 55%. That provides a good mix of dollars available for amenity “subsidies”. RBCC’s ratio rose to 58% in FY2021 (due to low Member usage but steady operational dues in the shutdowns) but then fell to 46% in FY2022 with the rapid growth before recovering a bit to 47% in FY2024. The reason that fell was due to rapid rise in Member usage versus operational dues Member operational dues were increased 3% in FY2022, followed by 10% per year in FY2023 and FY2024

The bottom line is that Member operational dues are required to partially fund all amenities and totally fund some club services The huge increase in membership in a short period time drove the balance of operational dues to total revenue out of kilter.

A MORE DETAILED EXPLANATION ON WHERE INTIATION FEES HAVE BEEN SPENT OVER THE PAST 10 YEARS

A QUICK EXPLANATION

By necessity, over the past 10-year period, initiation fees have been used to partially fund debt interest payments, prepayment of debt principal (Irrigation Loan) and capex projects. The balance remains in cash reserves.

A MORE IN-DEPTH EXPLANATION

From an accounting standpoint, initiation fees are shown on the cash flow statement as part of the cash flows from operating activities, along with the Renovation and Golf Assessment fees, the surplus/deficit from operations and the change in net working capital for operations (inventory, accounts receivable and accounts payable). The Renovation Assessment fee is accounted for separately in that its use is restricted by the Board to pay for the CIP project including the CIP Loan principal & interest and the $2.1M “borrowed” from cash reserves. All other funds in cash flows from operating activities go into an accounting bucket to pay for debt interest (other than the CIP Loan), capex, repayment of debt principal and the annual change in net working capital The surplus that remains is accumulated in cash savings and investment accounts and a Board-designated cash reserve for future Club improvements That designated fund is currently at $3 8M The Board has the authority to change the designation of funds at its discretion as was done in FY2023 and FY2024 to pay down the high interest rate Irrigation Loan

INITIATION FEES PAST FIVE YEARS

Looking at the shorter more recent past 5 years, $7.7M of initiation fees were collected as part of the overall $12M of cash flow from operating activities. After paying for capex projects, bank interest, and repayment of the Irrigation Loan, the remaining funds increased the Board’s designated cash reserve by $2.7M.

Important Note: Future initiation fees are expected to decrease to roughly $1M per year which is insufficient to fund the expected average of $1 8M per year of obligatory capital required

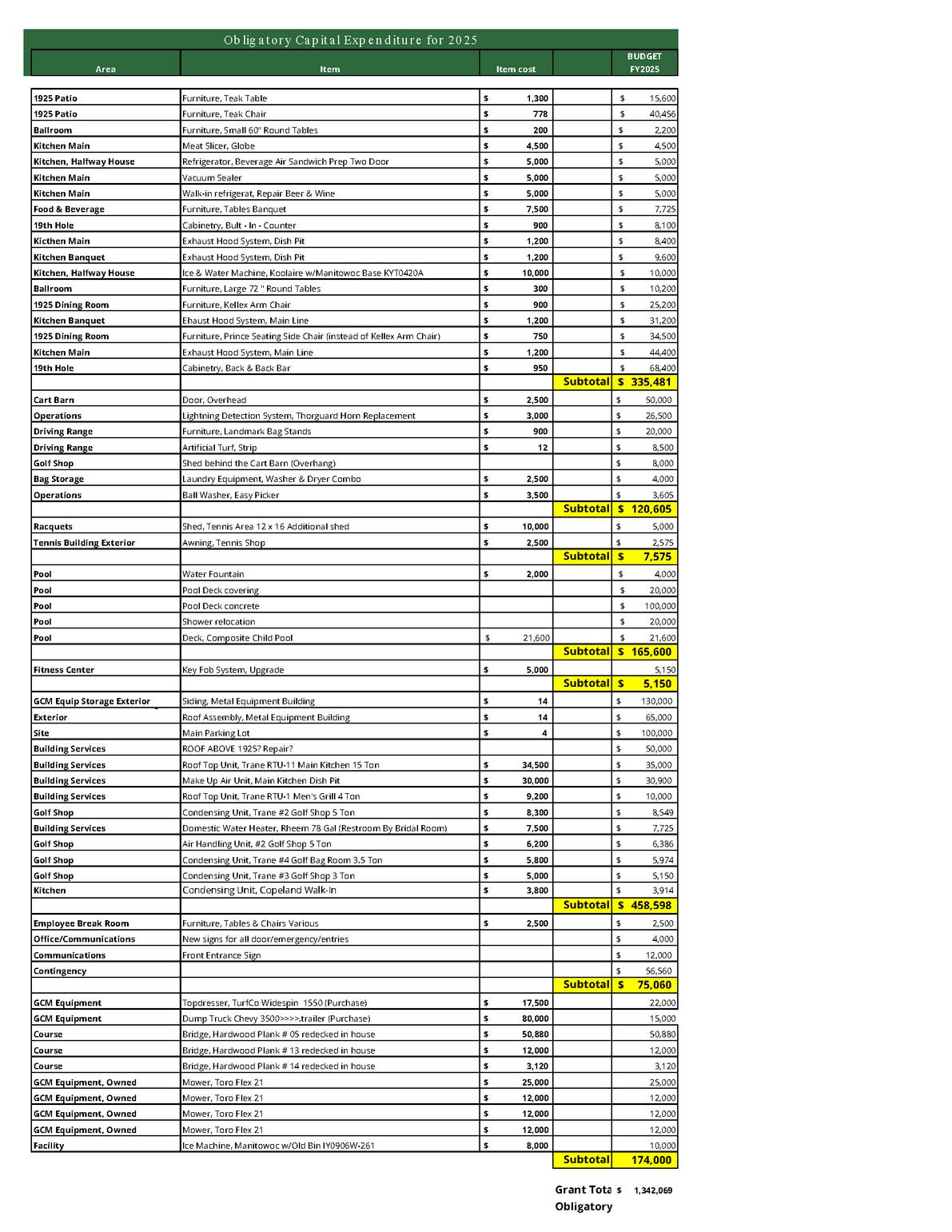

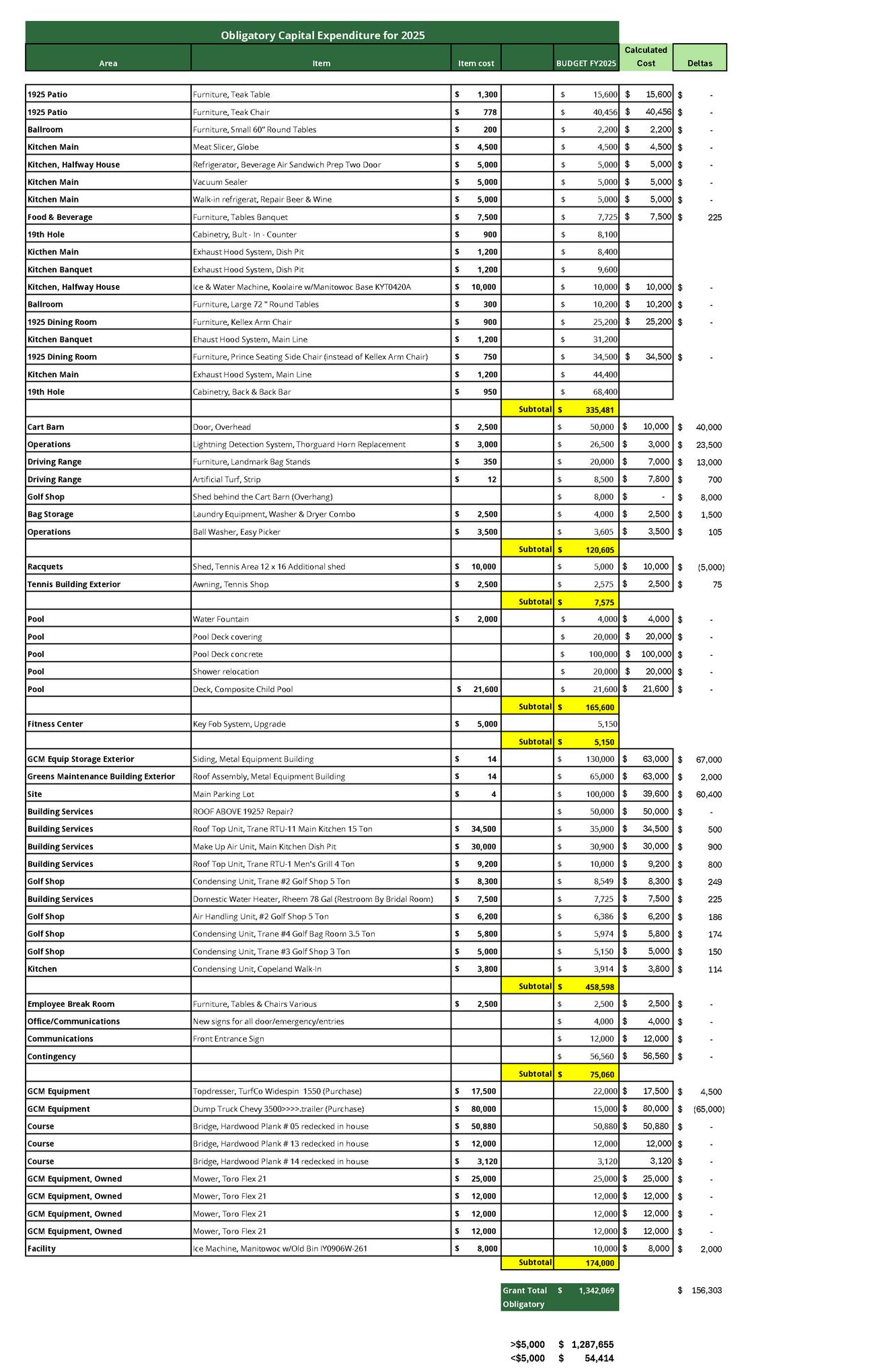

WHAT ASSETS WILL BE INVOLVED IN REPAIR AND REPLACEMENT IN FY2025

The below table shows the Board-approved list of items up for repair and replacement in fiscal year 2025. This list is not yet prioritized by the Leadership team and Board-assigned committees. The list is subject to change.