Last year it was financial institutions catering to the crypto and tech startup communities; this year it is all about commercial real estate exposure

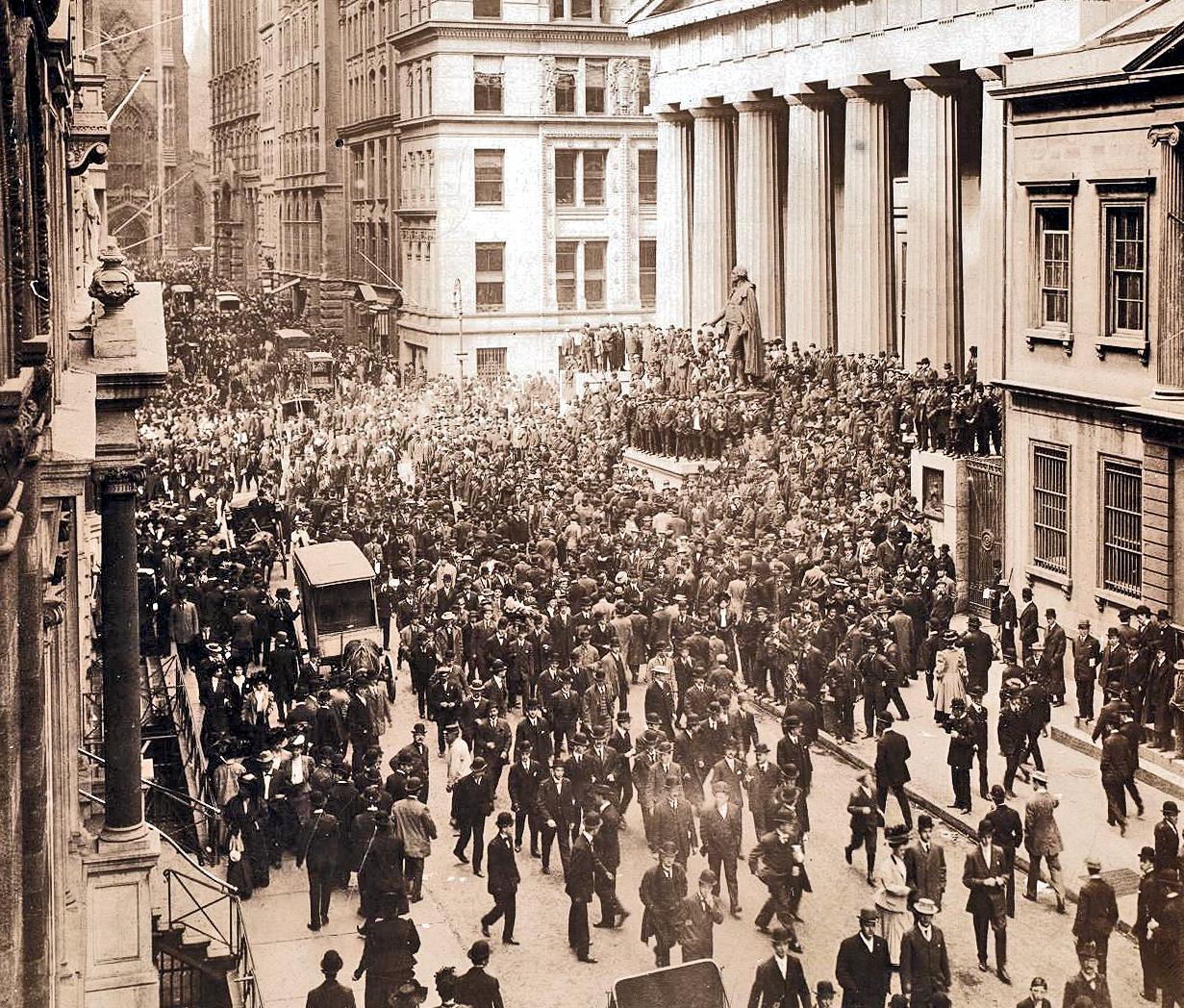

The Panic of 1907

At the turn of the 20th century, a few greedy men unwittingly helped to expose seismic cracks within the US banking system

Before the Fed begins a new easing cycle, investors are scrambling to rebuild their bond portfolios

Volume 12 Issue 01

From the Editor

Looking back at the Greenspan years and the easing cycle of 2001 can offer valuable lessons for today’s investor

The Panic of 1907

At the turn of the 20th century, a few greedy men helped to expose the seismic deficiencies within the US banking system

have

Last year it was financial institutions catering to the crypto and tech startup communities; this year it is all about commercial real estate

Photo

The Penn Wealth Report

need exposure to the

they couldn’t diversify away

26 Why we are not excited about Capital One’s acquisition of Discover Financial

China is wearing out its welcome in Latin America, even among leftist leaders

Whether Boston Beer wants to sell itself is up for debate, but the need for change at the brewer is not

Americans’ savings rate and credit card debt levels are going in two different directions—and both point to trouble ahead

Potential bellwether for the economy: pool sales are sinking

Dear lawless FTC, prepare to go down in flames yet again

Top quotes of the month...

Poe on Perspective Lincoln on Preparation Whitman on Finding Joy

From the Editor/

Remembering the easing cycle of 2001

There are some real similarities between today’s market and the market of a generation ago; wise investors will learn from the past with the realization that circumstances can change on a dime

As we prepare for Jackson Hole and a near-certain cut in interest rates at the September FOMC meeting, we thought it would be fun to enter the Wayback Machine and re-visit the markets of a generation ago.

There are some similarities between the stock market of today and the markets of the late 1990s, though few seem willing to make the connection. Back then, equities—especially tech stocks—were flying high on the back of a so-called “new paradigm.” The Internet, it seemed, had changed everything; even typical economic cycles would be upended by this incredible new phenomenon. Today, AI is the catalyst for calls to throw out the old playbook.

Investors have been clamoring for Fed Chair Jerome Powell to begin an easing cycle, claiming that an effective federal funds rate of 5.33% is harming the economy—especially the housing market. Between the summer of 1999 and the following spring, Fed Chair Alan Greenspan hiked rates six times to dampen what he saw as an overheated stock market and concerns that the strong US economy would spur high inflation. In August 2000 the effective federal funds rate hit 6.65%.

After the dot-com bust, Greenspan was forced to cut rates a whopping eleven times in 2001, with eight of those being 50-basis-point cuts. Of course, the economic shock caused by 9/11 necessitated the Fed’s actions later in the year.

As the catalyst for this latest easing cycle is not an economic crisis but, rather, moderating inflation, we certainly do not see eleven cuts coming down the pike, nor do we expect any to be more than 25-basis-points in size; however, we could envision the effective federal funds rate dropping to the 4% range. That

Penn Wealth Publishing

Subscription Information

https://www.pennwealthreport.com

Penn Wealth Publishing Commerce Plaza, 7th Floor

7300 West 110th Street, Suite 700

Overland Park, KS 66210-2332

would be the best possible outcome, as it would allow for a pickup in the housing market, a more favorable environment for small-cap companies which must refinance their debt, and (still) a decent environment for fixed-income investors.

One ominous similarity between today and a generation ago: Too many Americans neglected the fixed-income portion of their portfolios back then as well, despite solid rates. That cavalier attitude came back to haunt them. Armed with the lessons of the past and before the first cut, it is an ideal time to take a hard look at our portfolio’s diversification, especially the firewall asset classes of cash and fixed income. Your future self will thank you.

Michael S. Hazell Editor-in-Chief

The MonTh in CharTs

Follow our lead...

When the United States government (actually, 536 individuals, counting the president) racks up a $34.8 trillion national debt, costing taxpayers an extra trillion per year in interest payments alone, why would we be surprised that Americans have racked up $1.338 trillion in revolving debt which carries an average interest rate in excess of 22%? The comedy is when Bank of America CEO Brian Moynihan, who makes $28.6 million per year, laments a potential slowdown in consumer spending. Sure he does: credit card debtors are keeping his bank’s net interest income so high.

Charts tell the story. Here are some of our favorites from the past month. For the top business and economic stories of the month, visit Penn After Hours at www.penneconomics.com.

The return of Bitcoin?..

After peaking around $68k per coin in November of 2021, Bitcoin began its great tumble—falling to $15k per coin a year later. Those who hung on were rewarded, however, as this past spring prices rose above $73k— nearly a 400% gain. More recently, it fell back to the $55k range, but now sits near $60k. Head spinning yet? Ours as well. Crypto may be a new asset class, but it is certainly no hedge against a market drop. Investors need to realize this before buying in, or asking their employer to pay them in Bitcoin.

Mortgage rates finally moving...

In 2017, the average monthly mortgage payment for the median-priced new home was $1,250. That figure has now doubled, based on loans originating over the past twelve months and accounting for the rise in home values, mortgage rates, and higher property tax and homeowner’s insurance costs—the four factors making up PITI. Finally, however, it appears that buyers are getting a reprieve as rates have dropped back below the 7% level. What will the terminal point be, based on Fed rate cuts? We could see the average 30-year going as low as 5%.

American Business History

The Panic of 1907

At the turn of the 20th century, a few devious men helped to expose the seismic deficiencies within the US banking system

In the early months of 1907, skies were bright within the United States. The Gilded Age brought forth an unprecedented period of expansion within the country, and the US economy had grown to become the largest in the world, supplanting that of the United Kingdom. As is so often the case, just as a sense of sanguine bullishness begins to set in, a storm begins to coalesce on the horizon.

By the end of the year, a panic would cause the New York Stock Exchange to plunge, a recession would be triggered, imports would decrease by 26%, and reverberations from the event would be felt around the world. The first global economic crisis of the century would also sow the seeds for the Federal Reserve System—a central bank within the United States which would emulate the macroeconomics of Europe.

The backdrop

Frederick “Fritz” Augustus Heinze was an American businessman born in Brooklyn to German immigrant parents. At age 20, he took his degree from the Columbia School of Mines and headed out to Butte, Montana as an engineer for the Boston and Montana Company. When his father died not long after, this hard-drinking, boisterous entrepreneur used his $50,000 inheritance to develop an advanced new smelter in the region. Unsatisfied with leasing mines to secure the ore for his smelter, Heinze stumbled across an area abundant with ore deposits and purchased the surrounding land.

With his gregarious nature and an uncanny political acumen, Heinze took on the two “Copper Kings” in the region and built what would become the United Copper Company, which produced

some 40 million pounds of copper per year. After a tumultuous few years, filled with legal challenges and even hand-to-hand combat within the veins between miners of opposing companies, Heinze agreed to sell his Butte operations to one of the Copper Kings for $12 million. It was off to New York with his United Copper, where he planned on becoming a major financial force within the industry.

As fate would have it, the wealthy would-be potentate struck up a friendship with Charles W. Morse, a speculator and businessman of questionable character who had previously cornered the lucrative ice business in New York, gaining the moniker “Ice King.” (At the time, commercial ice was cut from lakes and rivers, taken to an ice house, and packed with straw and sawdust for insulation; remarkably, these giant ice blocks often had the ability to stay frozen until the following winter!) Morse attempted to use his monopoly to jack up the price of the frozen commodity, but his plan fell apart when it was revealed he had colluded with local politicians in exchange for a kickback.

Banks, trusts, and bucket shops

In the early 20th century, banks within the US operated with far fewer rules than they do today. With the ascendancy of America’s economic might came an increase in the demand for financial services, leading to a proliferation of trust companies to fill the void. Trust companies were subject to even fewer rules than the banks—a fact that would come back to haunt depositors. One such association was the Knickerbocker Trust Company, chartered in 1884 by a friend and classmate of J.P. Morgan. The firm

F. Augustus Heinze (Public Domain)

Charles W. Morse (Public Domain)

served as trustee for individuals, corporations, and estates. By 1907, under the leadership of Charles T. Barney, Knickerbocker had become the third-largest trust company in New York City. That was about to change.

There was another component to the banking/investment environment in the early 20th century: a nexus between the two worlds known as a bucket shop. These seedy establishments were street corner “offices” which allowed for the betting on stock and commodity prices without the transfer or delivery of actual shares or goods ever taking place. These archaic derivative houses would ultimately be outlawed in the US, but they were a fixture within the financial zeitgeist of the early 1900s.

Cornering United Copper

It was Augustus Heinze’s brother, Otto, who originally hatched the scheme to corner the market on United Copper, the firm his brother built in Montana. Believing that his family already controlled a majority of the company, the plan was to aggressively buy more shares in an effort to run the price up, thus squeezing all of the bucket shop short sellers by calling the shares.

Ironically, Knickerbocker’s president had turned down the plan to fund the scheme when the two brothers and Morse presented it to him. Despite the fact that Augustus and Morse both sat on a number of bank and trust boards at the time,

Barney warned that the plan was too risky and too costly for his trust company. Otto didn’t heed that warning when he began accumulating more shares despite the lack of funding, and the refusal would not insulate Barney from the carnage which would ensue.

When Otto put his plan into motion on Monday the 14th of October, he quickly drove shares of United Copper from the $40 range to around $60. To his shock and dismay, when he called the short sellers’ bluff on Tuesday, they had little problem finding enough shares (outside of Heinze family control) to meet his demands. By Wednesday, the stock price had collapsed to $10 per share. Otto’s fledgling empire was reduced to rubble.

While the New York Stock Exchange suspended Otto’s trading privileges, both his brother and co-conspirator Morse began losing their lucrative board seats. Banks holding large amounts of United Copper stock as collateral against outstanding loans began to fail.

Because of his relationship to Morse and Heinze, Barney was forced to resign, but that didn’t stop nervous depositors from yanking their funds out of the trust. Like a wildfire among dry brush, the panic quickly spread to other financial institutions.

The city’s wealthiest and most respected banker, J.P Morgan, decided it was too late to save Knickerbocker Trust, but he was able to staunch the bleeding at healthier institutions by cajoling a group of the

city’s other trust presidents. Not only did the group agree to provide over $8 million in emergency loans to the Trust Company of America, Morgan persuaded John D. Rockefeller—the richest man in the world at the time—to pledge up to half his wealth to preserve the system.

Most importantly, Treasury Secretary George Cortelyou pumped some $25 million of government funds into several New York banks to instill confidence. None of these actions, however, soothed the nerves of investors, who began selling shares on the New York Stock Exchange at breakneck speed. When the dust settled, the Exchange had lost some 50% of its value from the previous year’s peak.

It would take more strong-arm tactics by Morgan (like locking the bankers in his library until enough funds were committed) and an intervention by trust-busting President Theodore Roosevelt to end the crisis, but the damage had been done. The banking system in America would never be the same.

From the gold standard to Jekyll Island

The shock waves at home from the Panic sent ripples across the pond to Europe. European banks had significant investments in America; investments which began to plunge in late 1907. Banks on the continent began to tighten standards, causing a slowdown in economic activity. Additionally, policymakers begin to question the viability—and limitations—of a monetary system built upon a country’s store of gold.

Back at home, the US Congress passed the Aldrich-Vreeland Act which established the National Monetary Commission. This group’s mandate was to identify ways to overhaul the banking industry. One glaring problem became clear: the country needed a central bank to manage the flow of funds.

One of the Act’s namesakes, Senator Nelson Aldrich, called a secret meeting—not publicly acknowledged until the 1930s—at a secluded island off the coast of Georgia in 1910. Six wealthy and powerful men met at the ultra-exclusive Jekyll Island Club to rewrite the country’s entire banking system.

The Aldrich Plan called for a system of 15 regional central banks which would make emergency loans to commercial member banks, and serve as a fiscal agent between the federal government and the banking industry. The Fed was born.

The Panic of 1907 led to a realization that global economies were intertwined as never before. Sadly, that fact would be borne out some twenty-two years later.

Last

Will CRE Foment New Bank Runs?

year it was financial institutions catering to the crypto and tech startup communities; this year it is all about commercial real estate

The law of unintended consequences in economics. Libraries could be filled with examples from throughout history, so why do so many thickheaded politicians and policymakers ignore the evidence. Add another book stack to the library and entitle it 2023 Bank Failures

The most recent iteration of banking instability could be traced directly back to the Global Financial Crisis of 2008/09. That is when the Federal Reserve made the monumental decision to pound interest rates down to zero. Prior to this steep and rapid descent, the lowest rates had ever been was 1% back in 2003 as the Fed tried to contain the recession of 2001.

Ultra-low rates are great for borrowers, but this unnatural condition carries with it a host of problems if allowed to persist. And persist it did—for some seven years before the Fed began raising in December 2015. Just as rates clawed their way back to more normalized levels, along came the nightmare from Wuhan, and back down they went. They would remain there until March 2022 when the Fed began its marathon, eleven-hike tightening cycle.

In addition to forcing fixed-income investors to take on more risk via the equity market in a search for yield, banks also felt backed into a corner as their net interest income—the spread between what they earn on loans and the interest paid to depositors—contracted. When rates hit 4.5% in February 2023, the stage was set for the spring banking debacle.

A niche banking market emerges: providing financial services to the crypto world

Founded in 1988, Silvergate Bank was a rather boring savings and loan association based out of the San Diego region. Around a decade after its founding, it was re-capitalized and reorganized into a bank, but it remained a small, regional institution.

In 2013 the bank’s CEO, Alan Lane, got the crypto bug and began investing his own money in the digital currency. Three years later he started an initiative to attract cryptocurrency clients. The bank’s bespoke suit approach was buried; time to put on the chinos and enter the future of finance.

By 2021, Silvergate had amassed some $16 billion in assets, serving major crypto clients like Coinbase, Crypto.com, Cboe Digital Markets, and perhaps its most favored customer, FTX Trading Ltd. FTX and its related firm, Alameda Research, had nearly two dozen accounts at the bank by early 2022.

Things were swimming along for Silvergate Capital, the holding company for the bank, in early 2022. Bitcoin prices just kept rising, hitting a peak near $70,000 per coin the prior November. But by March, as the Fed began its long tightening cycle, crypto was in trouble. As rates rise, some semblance of sanity returns to investors’ psyche as viable fixed-income options return.

In addition to the rate hikes, the US Congress began turning up the heat on the largely unregulated crypto industry. As quickly as prices had risen in 2021, they plunged back to earth in 2022. By mid-July, bitcoin had fallen below the $20,000 mark.

As could be expected, crypto companies began yanking cash out of their Silvergate accounts as their own investors fled. The bank was able to keep pace with the mounting bank run until a monumental fraud was exposed: FTX, led by crypto wonder-boy Sam Bankman-Fried, turned out to be a house of cards.

Even a well-capitalized bank couldn’t survive the implosion of an industry it had tied its future to, which should be a classic lesson on client diversification. Silvergate collapsed on 08 March 2023.

SVB: bank of choice for tech startups and the venture capitalist community Imagine being a relationship manager in charge of new business development at a relatively small regional bank in Washington State in the mid-1990s. One day you are introduced to a young entrepreneur by the name of Jeff Bezos. This guy has just started an online company he is billing as “Earth’s biggest bookstore.”

Despite the high odds of failure among news businesses, you convince the bank to extend a line of credit to Bezos. Of course, whether expressed implicitly or explicitly, the understanding is that Cadabra, which would soon be renamed Amazon, would reciprocate for the extension of credit by holding its deposits at the bank.

The relationship would end up being a wild success story for both parties: Bezos got the credit his young firm needed to scale, and the bank was building a relationship with the future “richest person on the planet.” Thus was the concept behind Silicon Valley Bank: cater to promising tech startups, earn net interest income along the way, and reap the rewards when their ventures hit it big.

By early 2022 the plan was working beyond the rosiest of expectations. Assets had grown from around $75 billion a few years earlier to over $200 billion by that spring. Of course, in addition to making interest on bank loans, these institutions also make money by investing the assets held on their books. And that is where the trouble began.

A prolonged zero-interest-rate environment presents big problems for lending institutions. Consider the math: loans must be made at very low rates, but the yield on fixed-income assets purchased

will also be low—a double whammy. Executives could increase their risk tolerance for these assets in a chase for yield, but regulatory agencies are supposed to provide guardrails to prevent banks from going too far out on a limb. In the case of SVB, the Federal Reserve was the primary and the FDIC was the secondary federal regulator.

For some inexplicable reason, the bank began buying longer-duration bonds. This is economic suicide when rates are near zero, as values move down when rates finally do move up—and the longer the duration the greater the swing. As the eleven-hike tightening cycle moved along, the current market value of SVB’s longdated Treasuries and mortgage-backed securities (MBS) plunged. It was a sophomoric but tragic mistake, and one which could have so easily been avoided.

As the tech wreck of 2022 gained momentum, investors began pulling out funds, forcing the bank to sell assets at a steep loss. In an effort to be transparent, SVB CEO Greg Becker telegraphed that the bank found itself in a challenging situation. That was all it took for social media to foment a panic and cause a modern-day bank run. It is unclear where the Federal Reserve Bank of San Francisco was while the bank loaded up on these toxic assets. It should also be noted that the bank’s risk management officer left the company in October—but stopped performing her role the prior April!

Another travesty (in our opinion) was the fact that the bank was able to value these assets at par—or the return of principal they would receive if held to maturity. But the long bonds they held couldn’t be sold anywhere near par, meaning the books were a mirage.

On the 9th of March, 2023, SVB shares fell 60% in value. The bank was shut down the following day by California’s financial regulator. Two days later, the contagion had spread to New York-based Signature bank, forcing it to shut its doors. One month, three sizable bank failures. But the carnage was not over.

First Republic: banker to high-net-worth individuals—and student loan debtors Like Silvergate, First Republic Bank was founded in the mid-1980s. The amount of financial engineering that took place over the subsequent forty years is staggering. If it wasn’t making acquisitions, it was busy being acquired—and subsequently sold off—by the likes of Merrill Lynch/Bank of America. Rapid, unfettered growth was its mantra.

First Republic held over $200 billion in assets, then it collapsed

Silivergate’s high risk was due to a lack of diversification among clientele

...First Republic’s loan-to-deposit ratio was a staggering 111% in early 2023. This meant that the bank had loaned out in excess of what it held in deposits.

Also headquartered in San Francisco, the last decade or so of its existence the bank focused its efforts on buying wealth management firms catering to highnet-worth individuals. It also began zeroing in on the student loan debt market—a lucrative business considering the $1 trillion of outstanding student loans.

While student loans cannot be written off in a personal bankruptcy, they are still considered unsecured and uninsured. Additionally, due to the bank’s highnet-worth customer base, there were massive amounts of uninsured deposits on the books—those that exceeded the FDIC’s $250,000 insurable limits.

Furthermore, First Republic’s loan-to-deposit ratio (LDR) was a staggering 111% in early 2023. This meant that the bank had loaned out in excess of what it held in total deposits. Typically, an ideal LDR is somewhere in the neighborhood of 80-90%. Forget for a moment the board’s role in this; where were the regulators? This was a red-flag-waving situation that took years to develop.

Perhaps the bank could have gotten away with their irresponsible behavior had a crisis not hit their figurative doorstep, but what was going on at neighboring Silvergate and SVB was a crisis of epic proportions. In its earnings release for the first quarter, First Republic reported customer withdrawals of over $100 billion, or nearly half of the bank’s deposits. Like SVB, the bank had loaded up on longer-term Treasuries which they were forced to sell at deep discounts to cover client withdrawals. An infusion of emergency capital was needed quickly. Enter Jamie Dimon.

It is amazing how often history repeats, or at least “rhymes.” Recall who led the charge to staunch the bleeding in the Panic of 1907. This time it was his eponymous company, led by Dimon, who cobbled together a group of eleven major banks to pledge $30 billion in assistance to try and keep First Republic afloat. It quickly became obvious that even that large amount would not suffice, forcing the FDIC to seize the bank on 01 May 2023.

Agreeing to pay back the $25 billion or so that JPMorgan did not put forth, Dimon’s company acquired the bank and absorbed what was left of the assets and customer base, ending the First Republic name.

There would be one more domino to fall thanks to the 2023 bank run. PacWest Bancorp, a Beverly Hills-based holding company operating 69 Pacific Western Bank branches, had a similar business model to First Republic, and customers were pulling deposits with equal vigor. With billions of dollars worth of unrealized losses in its bond portfolio, investors were also fleeing: The share price of PACW fell from $51 in early 2022 to $3 in May 2023. In July, Banc of California agreed to buy PacWest with the assistance of two large private equity firms.

2023 offered a sober lesson in the irresponsible management of bank assets by too many executives at publicly traded financial institutions. Individuals who should have known better were making egregiously bad decisions while banking regulators were, to a large degree, AWOL. Regional bank investors got suckered in by fat dividend yields and promises of future growth; they were rewarded with massive losses of principal.

Will commercial real estate be 2024’s banking flashpoint?

The pandemic led to a massive shift in the way Americans think about work. Imagine a decade ago telling office workers they could perform their duties from home, at least several days a week. That was a scenario outside the realm of possibility for virtually all white-collar positions.

The nightmare that occurred in early 2020 allowed for technological advances that would have normally taken a generation to manifest, but were now being developed and adopted within years or even months. Suddenly, Americans were “buying up” in the real estate market and converting that extra space into their home office. But residential gains were commercial real estate’s pains.

Owners and landlords of commercial real estate (CRE) used to hold all the cards. They could get lower interest rate loans from banks to finance the purchase and maintenance of their buildings and then extract (arguably) confiscatory rates from tenants on gross or net leases. They would argue that the overhead on these structures, from utilities to insurance to property taxes, is enormous—a fair point. Post pandemic, however, the dynamic changed immensely.

For the first time ever, companies suddenly had the ability to allow a large percentage of their workforce to telecommute; i.e., work from home. This brought that enormous SG&A expense line on their income statement into focus. If office workers no longer needed to be in their cubicles five days a week, it only made sense to reconsider those massively expensive leases at renewal time. And did they ever.

According to Moody’s Analytics, US office vacancies rose to a fresh record of 20% in the first quarter of 2024 as tenants continue to downsize. This is doubly bad news for the owners of CRE, as they are also facing much stiffer terms as they refinance bank loans coming due. Many, in fact, are simply choosing to walk away from their properties, letting the bank which holds the note deal with the problem.

Recall the challenges faced by the regionals which had too much long-term debt in their portfolio. At least they knew this debt would ultimately mature at face value; but banks holding too much CRE exposure have no such guarantee.

The $20 trillion CRE market in America is, in fact, getting pummeled.

A Blackstone-owned office building in Manhattan, for example, is currently on the market at a 50% discount to its listed value five years ago. This past December, a Class A office building in LA sold for roughly half its purchase price from a decade ago. Buyers simply cannot justify

paying much higher interest rates without the seller taking a large haircut on the asking price. The situation will get better when the Fed lowers interest rates, but the hybrid work model is here to stay.

NYCB: poster boy for outstanding CRE loans

Of course, none of this really matters to banks which do not carry an inordinate amount of CRE paper on their books, percentage wise. For example, a glance at the accompanying graph shows JPMorgan holding a whopping $178 billion worth of CRE loans, but that amounts to a reasonable 12.6% of their total loan portfolio. Some banks went all in on this segment, however.

When Signature Bank failed in March 2023, New York Community Bancorp (NYCB) bought most of its assets. Trouble began appearing this past January when the bank announced Q4 losses that were $2.4 billion worse that previously reported. What really raised red flags during the release were the comments by management: it attributed the losses to “material weaknesses” in its loan review process. Shares plunged from $10 to $5.75 in a matter of days.

We are being told by many in the CRE world that the worst is behind us, but is it? According to a recent Bloomberg report, nearly one-third of the 112 state chartered banks in California have property debt sitting above the 300% threshold. One, River City Bank (RCBC), had commercial real estate loans on its books equal to 660% of its capital going into 2024.

The carnage continued when NYCB slashed its dividend from $0.15 per share to $0.05 per share and the CEO of 27 years abruptly announced he was leaving. Moody’s downgraded the bank’s credit rating to junk status and warned of further downgrades to come.

NYCB had become not only a major lender to office building owners, but also to New York apartment landlords, and some 50% of their properties were rent-controlled buildings. Rents were allowed to increase, but at much lower rates than the expenses associated with operating the properties. Furthermore, pandemic-era laws preventing the eviction of tenants not paying their leases accounted for $1.25 billion worth of uncollected back rent. No rental income, no evictions, rising costs, and higher refinancing rates; it is no wonder so many owners simply walked away from their properties leaving the banks holding the bag.

The Fed’s vice chair for supervision, Michael Barr, called the situation a “slow-moving train wreck.” Rates are elevated, making it harder for the landlords to get new financing; values of office and apartment buildings are dropping; and banks are not only raising their loan standards but being forced to put more in capital reserve for the inevitable wave of sour loans they will be forced to cover. And while inflation is subsiding, the Fed is still expected to cut at a very measured and methodical pace. Hence, the slow-moving train wreck.

Investors are now being inundated with stories of the generational opportunity in regional banks: companies with fat yields, multi-year-low share prices, and “five-star” or “buy” ratings from the analysts. They would be well-advised to dig deeper into these companies’ financials, looking for heavy debt loads and oversized exposure to CRE. Those with skin in the game may be telling us that blue skies are ahead, but we see new storm clouds forming on the horizon.

NYCB’s excessive exposure to CRE (VentureCapitalist)

Intuitive Machines Wins NASA Lunar Rover Contract

The Moon offers great potential for private space companies, and one American firm is beyond the drawing board stage

Just a few short months ago, Houston-based Intuitive MachinesLUNR $3 made history by successfully landing the first private spacecraft on the lunar surface. While the Odysseus craft ultimately ended up on its side, the mission was reminiscent of the 1976 landing of the American craft Viking on the surface of Mars. Shares of publicly traded Intuitive spiked 19% as Odysseus skimmed the lunar landscape.

The stated goal of the company’s Lunar Access Services is to offer a reliable and affordable means for governments and private companies to place objects in cislunar (between the Earth and the Moon) orbit or on the lunar surface. Other divisions of the company include Lunar Data Services, Space Systems & Services, and Orbital Services.

In April, it was the Space Systems division which garnered attention; specifically, the Lunar Mobility unit. As astronauts begin exploring the lunar surface once again, they will need a reliable space buggy to get around. After a NASA competition, three companies were awarded contracts worth up to $4.6 billion to build these vehicles: privately held Lunar Outpost and Venturi Astrolab, and Intuitive Machines.

NASA’s ambitious Artemis program calls for astronauts to return to the lunar surface by 2026 (though persistent problems at major contractor BoeingBA $167 may push that timeline out), with the new fleet of rovers scheduled to arrive ahead of the Artemis V crew, slated to launch by 2030. Not only are the vehicles meant to be driven by astronauts, they will also be autonomous, able to be sent out on solo lunar treks.

Most exciting from Intuitive’s point of view, these will not be simple contracts to purchase the vehicles. Instead, NASA will lease rides on the buggies, allowing for the company to find other paying customers to purchase trips as well. Intuitive teamed up with aerospace giants Boeing and Northrop GrummanNOC $481 on the project, as well as French tire and rubber company MichelinMGDDY $19 and Austrian engineering firm AVL.

What else is Intuitive Machines working on?

In addition to landers and rovers, Intuitive is also heavily involved in space telecom operations. Its Lunar Tracking, Telemetry, and Command Network (LTN) provides continuous line-of-sight communications with the Moon utilizing nine ground stations in seven locations around the world. Developed under contract with York Space Systems, five data relay satellites known collectively as Khon can be placed in a variety of orbits to support continuous communication capabilities for customers.

As lunar posts and establishments begin to take form, next to oxygen, food, and water to sustain life, reliable power supplies will be critical. The US Department of Energy (DoE) recently awarded a contract to a joint venture between Intuitive and X-energy for a design study of a Fission Surface Power (FSP) solution. An FSP system works by splitting uranium atoms inside of a reactor to generate heat, which is then converted to electricity. The initial aim is to provide a working model on the lunar surface by the end of the decade.

From drawing board to fruition

It is one thing to draw up plans, quite another to build working solutions. While most Americans had probably never heard of Intuitive Machines until Odysseus landed on the Moon, this eleven-year-old firm is already delivering on its grand promises. An investment in LUNR would certainly be speculative, but the company is winning contracts and, unlike most other nascent space players, turning a profit.

High-Speed Rail is Finally Taking Shape in America

Construction has begun on Brightline West, a high-speed rail project that will transport travelers from LA to Vegas in just over two hours

Considering the sheer size of America, from sea to shining sea, it is amazing that the sort of high-speed trains which have operated successfully in Europe and Japan for decades are nowhere to be found in this country. Granted, Americans love their automobiles, but congested highways and the less-thanstellar air travel experience have left many yearning for the glory days of train travel—with some added speed, of course.

The only long-distance, intercity rail system in the country, Amtrak, is operated by the government, and its only line that remotely resembles high-speed travel is the Acela, which connects several major Northeastern cities and can travel at speeds up to 150 mph. That government monopoly ended last year, however, as privately owned high-speed rail provider Brightline began running trains between Orlando and Miami—the first private passenger train service in the US in a century.

Due to the heavy infrastructure (bridges, highways, existing tracks, etc.) between the two cities, Brightline’s neon yellow trains have been limited to speeds of 125 mph or less, but the success of the Florida experiment spurred the company on to a much more ambitious project: Brightline West.

Brightline West will soon become America’s first true highspeed rail system. Connecting Southern California to Las Vegas, the line will almost precisely follow the current I-15 route between Rancho Cucamonga and Vegas. This makes for a much “cleaner” journey, allowing the trains to traverse the 218-mile track at speeds of up to 200 mph.

Today, nearly 50 million trips per year are made between LA and Vegas, with over 85% of them taking place on the highway. This has led to congested roadways, pollution, accidents, and frustrated travelers. The average drive time is around four hours; the all-electric Brightline trains will cut that time down to just over half that. The company believes it will serve over eleven million one-way passengers annually when up and running.

Ready to go by the 2028 Summer Olympics

Ground was broken last month on the project, and the firm expects the route to be fully operational in time for the 2028 Summer Olympic Games to be held in Los Angeles. The cost for the line’s development is estimated to be in the $12 billion range, with $3 billion in federal funds already secured. Another quarter of that amount will come from the sale of revenue bonds initiated by the US Department of Transportation, and the remaining funds will come from private investors.

Brightline estimates the line will generate $1 billion worth of tax revenue and have a $10 billion economic impact on the region. From an environmental standpoint, up to 700 million fewer vehicle miles will be driven per year, removing over 400,000 tons of CO2 from the atmosphere.

Needless to say, the most exciting aspect of this project is the the vision of it being replicated between major cities around the United States; perhaps even the manifestation of a high-speed, transcontinental line in the not-too-distant future. We believe the prospects for this industry are bright.

Investing in the future of high-speed rail in America

While Fortress Investment Group, the owner of Brightline, is no longer publicly traded, there will still be plenty of opportunities in this space. For example, Brightline has selected Siemens Mobility, a division of German conglomerate SiemensSIEGY $87, to build a fleet of ten American Pioneer 220 (AP220) trainsets for the project. Founded in 1847, this $150 billion firm operates in the automation, electrification, mobility, and healthcare arenas.

Alstom SAAOMFF $18 is a French firm which has built over 70% of the world’s high-speed trains, while US-based Jacobs SolutionsJ $145 works in transportation infrastructure. Jacobs is a holding in our preferred vehicle for the industry, the Global X US Infrastructure ETFPAVE $37. It may be time to climb aboard.

Artist’s rendering of Brightline’s flagship Las Vegas station; Image courtesy of Brightline

Liquidity Analysis

Your Emergency Reserve Fund

Just as term life insurance is crucial for young households, an Emergency Reserve Fund for life’s unexpected expenses should be in everyone’s vault

Maria was on her way to work, mulling over her family’s strained financial situation, when she noticed her vehicle making an odd clunking sound. She ignored it at first, but then the “check engine” light came on and she noticed a strange burning smell. Her anxiety level skyrocketed; there was barely enough money coming in each month to pay the bills, let alone a surprise vehicle repair charge. She ignored the disturbing sounds and drove on.

A week later, Maria’s car was in the shop after being towed from the highway. Then she got the call she was dreading: the transmission was shot, and it would cost $3,500 to replace. Her mind raced. They didn’t have the cash, but she needed the vehicle to get to work. Credit cards? A loan on her 401(k)? It was a terrible feeling.

Most Americans have been in a similar situation at least once—for many, it is a recurring nightmare. A costly auto repair is bad enough, but what if the emergency was the unexpected loss of a job? If one month’s income is needed to pay that month’s bills, what happens if the income stops? It highlights the need for an emergency reserve of cash for when the inevitable surprises rear their ugly heads, but just because something is needed doesn’t mean it exists.

According to recent data, just over 50% of Americans don’t have any emergency savings at all. Another 25% or so have somewhere between $1,000 and $10,000 set aside, and the remainder have north of $10,000 ready to deploy. Those are scary figures, considering what is considered an appropriate amount.

viewed using the Liquidity Analysis tool within their Personal Financial Website (PFW). Data is culled from the Profile and Budget sections of the website to form the liquidity chart as shown on the following page.

It can be both sobering and discouraging to view these figures in front of us; but knowledge is power, and we should always be cognizant of our financial situation. Once we are, the steady journey toward financial stability can be set in motion.

Where should I maintain my ERF?

Within the Personal Financial Website, the emergency fund includes cash sitting in bank accounts as well as the cash portion of taxable investment accounts. But we highly recommend having a dedicated account earmarked for emergencies. Furthermore, it may even be a good idea to house this account at a separate bank or brokerage, assuming the money can be

How much should I have set aside for emergencies?

The general financial planning rule of thumb is to have three to six months’ worth of fixed and variable expenses set aside in an Emergency Reserve Fund (ERF). In other words, take every bill you must pay each month, include the appropriate percentage of bills due on a recurring basis (like semiannual insurance payments and annual HOA dues), and take that figure times six. You arrive at what should probably be the size of your ERF.

For clients or members of Penn Wealth, this figure—along with any surplus or deficit—is easily

quickly accessed for emergency use either through an ACH transfer or a debit card.

There are a couple of challenges we have with intermingling emergency funds with other cash or assets in a single account. First and foremost, it is too easy to dip into this source of funds for non-emergency purposes. Also, it can become rather confusing to try and separate the precise dollar amount available for emergencies versus the cash needed for the payment of bills. It is much “cleaner” to have a separate account dedicated to this end; a “break glass in case of emergency” fund.

Financial emergencies seem to arise when we can least afford them

One contention we have heard over the years is that this money is just sitting there, not earning anything. Even when rates were flatlined at zero and cash was losing ground to inflation, that was no excuse not to have an Emergency Reserve Fund. With money market yields now hovering around 5%, with no minimum investment requirement and the ability to access the funds on a daily basis, that argument certainly holds no merit.

That said, your bank probably isn’t going to simply offer up these rates and “sweep” your money into them. Even after calling, emailing, or chatting, they probably will either A) require a fat minimum amount for a decent yield, or B) try to offer you something other than daily liquidity, such as a bank CD. Therefore, it makes sense to have a no-fee brokerage account nicknamed “Reserve Fund” for this purpose. Talk to your advisor or the custodian of your funds for more details.

If there is no money left at the end of each month, how can I fund my account? We are often asked, “Should I pay off all of my revolving debt before funding an emergency account?” The answer is a resounding “No!” True, paying monthly interest charges calculated off of a 20.55% rate on the balances carried (the 3-month national average as of this writing) is outrageous, but both sides of the ledger must be dealt with immediately: reducing debt while increasing liquid assets.

One more note on the figurative prison credit card debt puts so many Americans in. We have a client with a perfect 850 credit score (believe it or not, about 1% of consumers have reached that storied height). I asked them to pull up one of their credit card statements and tell me what the current rate would be if they carried a balance on that particular card. They were shocked to see the 16.99% figure sitting on page three. And that is for someone with a perfect credit score!

While it is critical to your fiscal health to get out of the credit card/revolving credit death trap, it is equally important that you fund your emergency account. After all, if you find yourself with no cash when the next emergency arises, odds are great that your credit card will be the poison of choice. So let’s consider a few simple methods to build the former while still reducing the latter.

First and foremost, don’t be afraid to start small. If your financial institution has a program which automatically rounds up purchases to the nearest dollar and transfers the difference to a savings account, take advantage of it. If not, start by taking just 1% of your weekly spend and transfer that amount into your savings account each weekend. By completing this simple task weekly, the amount is small enough that the impact should be completely manageable.

Everyone should be operating with a robust monthly budget rather than simply looking at account balances and taking an occasional glance at the transactions. By having a budget which lists every variable (e.g., electric bill) and fixed (e.g., car payment) expense on its own line, we can begin scouring for sources of cash for our fund.

For example, most of us have numerous subscriptions which are automatically deducted from our accounts each month. While we may not be able to live without those five streaming services we are paying for (after all, each has that one show we just can’t miss), odds are strong that we have a few memberships lurking in the app store which we could cancel without doing harm to our lifestyle. If so, earmark 100% of that money for the savings account each month—the differences will net out within the budget.

Phone bills and insurance premiums are two other common sources of spare change. While we may not be able to get that War of 1812 surtax removed from

our phone bill, there are probably a few superfluous items hiding in those fifteen pages of small type. If push comes to shove, tell your service provider and insurance rep that you are looking at switching to reduce your monthly expenses. In order to prevent you from walking, they will probably offer some sort of discount for being such a “faithful” customer. Once again, take any reductions, dollar for dollar, and move that amount to the savings line on your budget.

While most of us don’t have many windfalls coming our way each year, more than half of all tax filers expect to get a fat refund (a topic for another day). Earmark a healthy chunk—if not all—of that refund for your emergency fund and enjoy the increased sense of well-being.

Many people consider the equity in what may be their largest asset—their home—to be an acceptable source of funds for crisis situations. While better than pulling out a high-rate credit card, it is still not a good solution. Your home is the golden goose which generally rises in value each year without much effort on your part. Try to keep those home equity lines of credit at bay—despite all the enticing offers from your mortgage lender.

The same goes for borrowing against your 401(k) or 403(b). You may be able to pay these loans back with zero interest, but try to leave retirement funds alone. You will thank yourself later in life.

Define what constitutes an emergency

Your Emergency Reserve Fund is a cornerstone to your fiscal health and, quite frankly, to your overall level of happiness. Think back to the level of stress and anxiety the last real financial strain brought about in your life. That incident also provided you with a gauge to define what constitutes a real emergency.

If something seems urgent at the time, like funding an upcoming weekend getaway or buying that set of irons which are 50% off for one week only, take a step back and consider where this “need” ranks in comparison to that angst-filled crisis. If it is not an actual fiscal emergency, don’t touch this fund.

Here’s the bottom line: If you had a new expense come along that you were forced to build into your budget, like an increase in rent or mortgage, you would find a way to pay it. Treat your savings just as seriously: make it a line item and an obligation you must pay each month. Even if your starting point is just 1% of income, you will begin creating a habit you can build upon. And the larger your emergency fund becomes, the greater your peace of mind will be.

Liquidity analysis helps you determine appropriate funding of your ERF

What Should Your Bond Ladder Look Like Right Now?

Why would investors buy longer-duration bonds when their shorter-term cousins have a better yield? It’s all about the trajectory of rates going forward

Investing in bonds used to be a rather simple proposition: These vehicles almost always went up in value when stocks were floundering due to economic conditions. They offered a nice balance, or hedge, to the equity side of a portfolio and provided a steady stream of income in the process. Furthermore, an intelligent investor could deploy a strategy known as laddering to make their fixed-income segment as efficient as possible. No matter one’s risk level, some exposure to bonds was a must.

In normal times, the longer out on the maturity or duration ladder one was willing to go, they higher the reward in terms of yield. This makes perfect sense, as why else would someone lock money up for a longer term if they weren’t paid more to do so?

The left side of the graph below provides a great example of a normal yield curve. Ten years ago, a 2-year Treasury note (fuchsia line) was yielding a paltry 0.31%, or 31 basis points. Investors buying a 5-year note (green line), however, would have received a “whopping” 1.5%. Extending this example out, a 10-year note (blue line) would pay 2.7%; a 20-year bond (orange line), 3.4%; and a 30-year bond, 3.7%.

Historically, the average of this particular spread has been 88 basis points. It must be noted, however, that the spread is not limited to positive values.

A condition known as the inverted yield curve In six instances since 1978, something odd has occurred: the 2-year Treasury has yielded more than the 10-year Treasury. Note the spike in the fuchsia line in 2022; its rise was so rapid that it sped past the 10-year note as represented by the blue line. This condition is known as an inverted yield curve, but what does it tell us?

Historically, an inverted yield curve serves as a harbinger of recession. Recall that rates are typically higher on longer bonds to entice buyers, but the law of supply and demand is very much at work here. If investors believe a recession is coming, they also believe that the Fed will be forced to lower rates to combat the condition. By rushing into longer-term maturities, buyers are trying to lock in higher rates before they fall. But as they do so, rates will naturally fall due to the higher demand—even if the Fed does nothing. In the six cases since 1978, the yield on the 10-year fell below that of the 2-year Treasury.

Economists typically look at the spread between what the 2-year and 10-year US Treasury notes are yielding to gauge the overall health of the economy.

It now appears that the Fed is ready to begin a new easing cycle, with a 25-basispoint cut fully baked in by markets for the September meeting, and a series of cuts at subsequent meetings. But the economy is not floundering, so we expect these cuts to be very orderly.

Rather than play the Fed guessing game, the most risk-averse investors tend to stick with shorter maturities. This has to do with an instrument’s sensitivity to interest rates. The longer the maturity, the more sensitive bond prices are to changes in rates. In other words, as bond rates rise, bond prices fall; and the longer the maturity the more they tend to get hammered. If held to maturity, that isn’t necessarily a problem—holders continue to get the same rate. But steep discounts would await bond sellers if they needed to liquidate before maturity—like the failed banks of 2023 were forced to do.

A normal (left) versus inverted (right) yield curve

A brief look at duration

While it is true that longer bonds are more sensitive to rate changes than short-term vehicles, it is more accurate to say that the longer a bond’s duration, the greater the impact of these changes.

Maturity is just one factor of duration; the credit rating of the bond issuer is another. Consider this scenario: Rates remained low for the better part of a decade, and two companies took advantage of the situation by selling large amounts of bonds to raise capital. One company is a large pharmaceutical firm which has been operating in the black for years, while the other one is a small biotech which has yet to turn a profit. Both issued bonds with two year maturities, with the pharma bond yielding 3% and the biotech having a 5% coupon.

Suddenly, rates begin rising and both companies must issue new bonds because the original ones are maturing. Now, the larger firm must offer a coupon of 5% and the biotech with the lower credit rating must offer 9% to entice buyers to take the additional risk. Despite both sets of bonds having the same maturity, the riskier issuance was more greatly affected by the change in rates; hence, the duration was longer.

Another issue affecting duration has to do with a bond’s call features, or the ability of a company to “call away” the bonds at a point prior to maturity.

Say, for instance, that rates were high when two companies issued bonds with five-year maturities. One company placed a two-year call feature on their bonds, while the other did not. The two years have passed, and the Fed has been on an easing cycle to stimulate a moribund economy. Rates are now half as high as they had been at the time of issuance.

One company can call away the bonds and issue a new series at a much lower rate, while the other must continue paying the coupon until maturity. The duration of the callable bond would be lower than the series which must be held to maturity.

Here’s the point: A lot more than a bond’s maturity date must go into an investor’s decision to purchase. A number of factors must be weighed.

Is there a sweet spot right now between short-term CDs and 30-year bonds?

While borrowers weren’t happy with the Fed’s eleven rate hikes, fixed income investors hailed the period. Finally, the bond market was working once more as these investments provided both a hedge to market downturns and a decent yield. Even money markets looked attractive.

For the better part of a decade, money market rates floated around zero. For those willing to do some shopping, rates around 5.25% could suddenly be had for that extra cash sitting in accounts. That is well above the current yield of the 30-year Treasury bond! Some $6 trillion came flooding into money market funds.

Here’s the problem: when the Fed adjusts the funds rate down, these yields will immediately follow. And holders of one- or two-year CDs will face reinvestment risk—the high odds that an equivalent yield will not be available under the same terms. Back to where we began this story: the bond laddering strategy.

Suppose an investor had $100,000 sitting in cash and wished to put these funds to work in a portfolio of bonds. Instead of trying to read the tea leaves with respect to the Fed and rates—a fool’s errand, this investor puts onefifth of the total amount to work in a 2-year, 4-year, 6-year, 8-year, and 10-year bond, respectively.

While we like individual bonds for clients, not everyone is comfortable searching for the best vehicles. For most investors, the easiest and most efficient way to take advantage of our sweet spot on the fixed-income ladder is through ETFs and open-ended mutual funds. In fact, our Penn Strategic Income Portfolio has several great options.

For example, the PIMCO Investment Grade Corporate Bond ETFCORP $95 has a duration of 6.4 and holds nearly 1,400 corporate bonds. The Hartford Strategic Income FundHSNIX $7 has a duration of 6 and a mix of government and corporate bonds—and a current yield of 6.35%.

Source: Fidelity via MunicipalBonds.com

For simplicity, let’s assume that each bond’s maturity is closely correlated to its duration. Some simple math shows us that we now have a nice little portfolio of five bonds with an average duration of six.

In two years our first bond will mature, assuming no pesky call features were attached. (A brief aside. You should always be aware of a bond’s characteristics, avoiding call features when possible and seeking out a feature known as a death put—meaning a beneficiary would not be punished for selling early if anything happened to the owner.) Instead of reinvesting the proceeds in another 2-year bond, a 10-year bond is purchased (the gold box in the diagram). This step is repeated when each subsequent bond matures.

Before long, we have five, ten-year bonds—getting the maximum possible yield in a normal curve environment—but our duration remains six. Furthermore, should we need cash, $20,000 becomes available every two years.

Granted, this strategy would not have worked well during the zero-rate environment, but that period was an anomaly. The Fed may be on an easing trajectory with respect to rates, but they are not going to zero again. In fact, this peak-rate stretch is an ideal time to put it to work.

The Capital Group US Multi-Sector Income FundCGMS $27 has a great mix of 35% government bonds, 50% corporates, and 15% securitized obligations (think packaged mortgages and other loans), plus a yield of 6%. We also highlighted one of our favorite managed bond funds for the Fund Spotlight column. That article can be found on page 20.

And don’t forget about municipal bonds and bond funds. These vehicles generally come in two varieties, revenue and general obligation, and offer a stream of income free from federal, state, and local taxes. To figure out what a muni’s tax-free rate would equate to were it a taxable bond, visit the BankRate.com TEY calculator here.

Investors should never ignore the “boring” fixed-income segment of their investment mix, as it has saved many a portfolio in turbulent times. Acting as the loan officer to corporate America pays handsomely, and while commentators and Fed watchers are busy wringing their hands over what the central bank may do next, we are celebrating the fact that investors can finally rebuild a viable bond portfolio which A) has a real yield, and B) probably won’t drop double digits in value like it did in that horrendous year of 2022. As the Fed begins its methodical easing cycle, we welcome a return to the “old normal.”

Nordea Bank Abp

Investors need to have exposure to the financials sector, but nobody said they couldn’t diversify away the risks unique to the American corner of the industry

While American investors are weighing the threats versus opportunities in the financials sector right now, one point often escapes them: there are plenty of other figurative fish in the global waters. And just because US banks face a crisis with respect to commercial real estate doesn’t mean that their overseas counterparts face the same level of risk.

Nordea is a dominant player in one of the fastest-growing regions of europe.

One interesting global financial services firm we have had on our radar is Nordea Bank AbpNRDBY $11. Impressively, this $43 billion firm opened its doors over two hundred years ago—in 1820. It has since acquired locations dating back to 1832 in Sweden, 1848 in Norway, and 1862 in Finland. Today, it is the largest bank in the Nordics, carrying $657 billion of total assets on its books at the end of the first quarter.

Having exited Russia in 2022, Nordea is a diversified financial services group serving ten million private, corporate, and institutional customers throughout northern Europe. The bank operates in four Business Areas (BAs), with each contributing to its annual revenue of $13 billion: Personal Banking ($5B), Business Banking ($4B), Large Corporates & Institutions ($2.5B), and Asset & Wealth Management ($1.5B).

A good potential fit for two Penn portfolios

While we consider Nordea a suitable fit for the Penn International Investor, its 8% dividend yield also makes it a good candidate for the cash-generating Penn Strategic Income Portfolio. Its has a healthy payout ratio of 64% (total annual dividends divided by net income), and its dividends are well-covered by earnings. It increased its year-on-year payout rate by 15% in 2024, and we see the rate holding up for the next several years. Operating revenue has been steady to rising over the past decade, as have the company’s net income levels. Of last year’s $13 billion in revenue, $5.3 billion flowed down as net interest income. In the first quarter of 2024, in fact, Nordea recorded an alltime high 1.36 billion euros of quarterly net income—the difference between what the bank pays for deposits and what it earns from lending.

Stronghold in a growing region

While Nordea’s business has been on an upward trajectory thanks to organic growth, acquisitions, and higher interest rates, it has also benefited from strong economic growth in the Nordics. Not only has population growth in the region outpaced the rest of Europe, industries such as software development—and subsequent exports of related products and services—have been growing at an impressive clip. We see this trend continuing, yet few investors have exposure to the zone.

NRDBY

@ $11

While few analysts cover Nordea, we believe the shares of this two-century-old company could rally back to the $15 range (its high price) within the next few years. In the meantime, investors can reap the fat quarterly income stream being generated, and brag about being invested in one of the fastest-growing regions of Europe.

Nordea Copenhagen Metro HQ (Photo courtesy of Nordea)

Symbol: NRDBY

Action Price: $11

Dividend Yield*: 8.7%

*As of date/time written

Nordea Bank Abp opened its doors in Copenhagen in 1820 as a local savings bank. Since then, it has grown to become the leading financial institution in the Nordics, offering a wide range of financial services. While the bank generates most of its income through vanilla lending products such as mortgages, household loans, and corporate loans, it is also a leading equity and debt underwriter in the Nordics. The company operates primarily in the countries of Denmark, Norway, Sweden, and Finland.

Net interest income (NII), revenue from interest-bearing assets, is the life blood of a bank. Since 2020, Nordea’s NII has nearly doubled, growing from just over $4 billion to over $8 billion. The bank’s multiple has continued a slow descent, however, with the current P/E ratio sitting below eight.

Based out of Helsinki, Finland, Nordea is the largest bank in the Nordics

An Unconstrained, AllWeather Bond Portfolio

With bond portfolios finally beginning to shine once again, this well-managed fund has outperformed its peer group

It has been a frustrating decade for investors counting on their portfolios to provide them with a steady stream of income. After eleven rate hikes, however, they are finally done wandering the desert and now have a plethora of higher-yielding choices in front of them. But that green fixed-income meadow ahead holds plenty of noxious strains which could wreak havoc as economic conditions change. Expert guidance is needed.

For clients at Penn Wealth Management, we generally prefer to stick with individual issues; instruments which allow us to highly control the quality and duration of a fixed-income portfolio. But there are some exceptionally skilled money managers out there with proven track records of successfully navigating this complex arena. Two would be Dan Ivascyn and Alfred Murata, portfolio managers of the Pimco Institutional Income FundPIMIX $10 for the past decade.

The stated objective of this fund is to “seek maximum income” with “long-term capital appreciation” listed as a secondary goal. As we write this, the fund carries a TTM yield of 6.2% (spitting out a monthly income stream) and has a positive aggregate return over the past three years. Maintaining a positive return in the midst of nearly a dozen rate hikes is simply remarkable for a bond fund.

To illustrate this point, consider the accompanying graph of PIMIX’s three-year return versus that of the overall bond universe, 7-10-year Treasuries, and the 20-year T-bond. A portfolio of wide-ranging US bonds would have dropped nearly 16% over that time frame, while a basket of 7-10-year Treasuries would be down 21%, and holding nothing but long bonds would have meant a scorching 43% drop in value.

The freedom to pursue opportunities wherever they may be—domestic or abroad

The economic landscape is constantly shifting, causing different bond sectors to move in and out of favor. This fund’s prospectus allows these two adroit managers to go wherever they see the best opportunities.

The fund could go longer out on the duration ladder, for example, if they believe long rates have peaked. Right now, the average duration of the portfolio is 4.22 years while the average effective maturity is 5.5 years. We could see the team increasing duration over the coming months—especially with rate cuts on the short-term horizon.

The current mix of the portfolio is roughly 40% government bonds (both US and foreign), 20% securitized, 30% cash equivalent (which is interesting), and the remaining 10% or so in corporates and derivatives. Per the managers’ most recent monthly commentary, “tactical exposure across the European yield curve and short exposure to Japanese rates both contributed to performance.” Securitized credit detracted from performance.

We have been so impressed with the fund that we made it a core holding within the Penn Strategic Income Portfolio

PIMIX has a minimum initial investment of $1 million, but institutional clients of Penn Wealth are able to access the fund with much smaller amounts. For more information, contact the team at Client. Services@PennWealth.com. Penn Wealth Management is a legally separate entity from the publisher of this report, Penn Wealth Publishing.

PIMIX @ $10

Under The radar

Four investments being ignored—or missed—by the financial press

Celestica Inc

Information Technology

Electronic Equipment & Components

Raiffeisen Bank AG

Financials

International Banks

Asahi Kasei Corp

Basic Materials

Chemicals

Arca Continental SAB

Consumer Defensives

Beverages

Celestica IncCLS $55 is a supply chain solutions company. Its Advanced Technology Solutions segment works with aerospace & defense, industrial, health tech, and capital equipment businesses. The latter is comprised of semiconductor, display, and robotics equipment companies. The firm’s Connectivity & Cloud Solutions segment works with communications and electronics storage businesses. Celestica works with its client firms through every step of the supply chain, from design and manufacturing to full-scale production and after-market services, with the aim of reducing costs, improving speed-tomarket, and driving innovation. We would place a fair value of $70 on the shares.

Raiffeisen Bank International AGRAIFF $18 is the largest bank in Austria in terms of total assets, accounting for a full quarter of the country’s banking sector. Regarding Austria and Central/Western Europe as its home markets, the bank operates in three major geographical regions: Central Europe (Czech Republic, Hungary, Poland), Southeastern Europe (Albnania, Bosnia, Bulgaria, Serbia), and Eastern Europe (Belarus, Ukraine). A mid-cap institution ($6B), Raiffeisen has a multiple of two, positive net income (the bank earned $2.9 billion on $10 billion in revenue last year), and a fat dividend yield of 7.86%. We would place a fair value of $25 on the shares.

Asahi Kasei CorpAHKSY $14 is a Tokyo-based holding company founded precisely 100 years ago. Through its various subsidiaries, the firm is organized into four segments based on product or service: chemical and fibers, homes and construction, electronics, and healthcare. The majority of Asahi’s revenue comes from Japan, making it a pure international play. (It should be noted that we are bullish on Japanese equities for 2024.) This $10 billion Basic Materials company has a clean balance sheet, low beta (0.6717), and 3.5% dividend yield, making it worthy of review for investors searching for solid overseas companies.

It has been quite a while since we talked about a beverage distributorship, and when we did it typically involved booze delivery. Arca ContinentalEMBVF $10 is a Mexico-based bottler and distributor of primarily Coca-Cola products throughout Latin America. Beverage sales account for 90% of the company’s revenue, with snacks accounting for the other 10%. Arca primarily operates within Mexico, Ecuador, Peru, and northern Argentina, though the company’s snack brands include Wise in the US. With a multiple of 5 and a forward dividend yield of 4.6%, this $14 billion mid-cap value firm might be a good fit for international exposure within a portfolio. The company has free cash flow of $1 billion and earned $1 billion from $12.7 billion in revenue over the trailing twelve months. 3 2 1 4

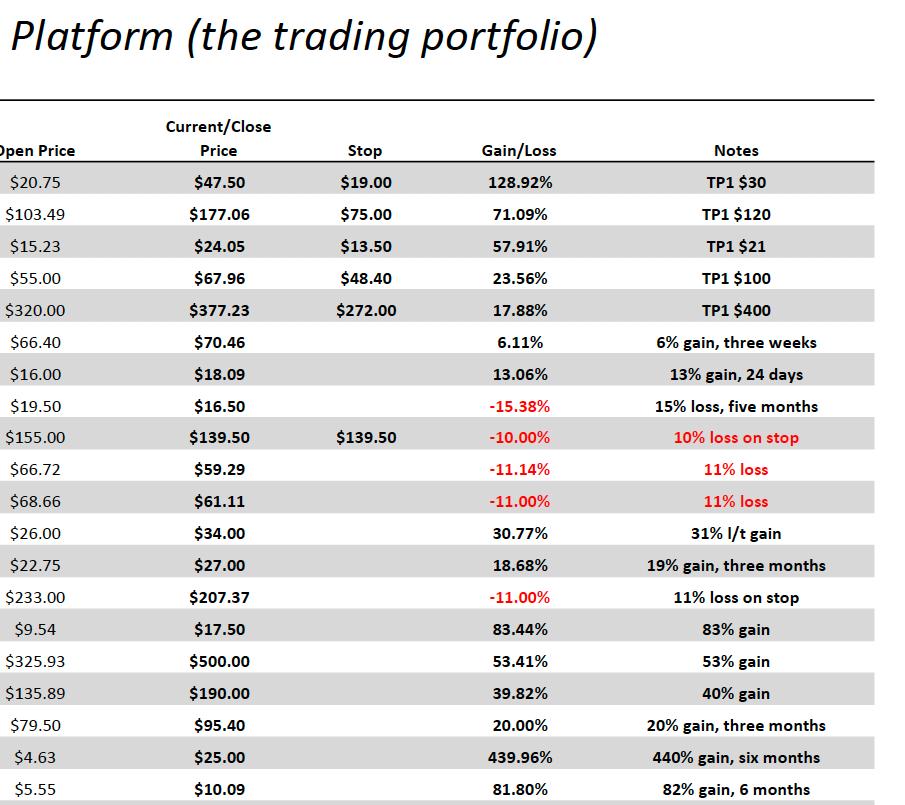

Trading Desk

Actions we have taken at the Penn Trading Desk, plus a look at what other Wall Street analysts have to say...

Penn: Buy Pioneer income Fund

Penn: Add AerosPAce leAder

To remain on top of all trades as they happen, subscribe to our X feed @ PennWealth. All trade details can be found at the Penn Wealth Trading Desk .

While we typically buy individual bond issues for clients, the fixed-income arena boasts some impressive management teams. One such team manages the Pimco Institutional Income FundPIMIX $10, which we have just added to the Strategic Income Portfolio. For a bond fund to have a positive return through nearly a dozen rate hikes is remarkable. The fund accomplished this feat by having the ability to go where the fund managers see the best opportunities. The average duration for the fund is about five years, the average maturity seven years, and the TTM yield is 7.08%.

Penn: Add FinTech To inTrePid

PayPalPYPL $55 could be considered one of the OGs of FinTech. Founded in 1998, the firm operates a digital payments platform on behalf of merchants and consumers worldwide. A darling of the pandemic, investors seemed to lose interest in 2022. Keep in mind that this market leader also owns Venmo and Braintree (among others), has 400 million active users in 200 global markets, and carries a forward multiple of eleven. We added PYPL shares to the Intrepid at $55 with an initial price target of $100 and a stop loss at $48.40.

Penn: Add indusTriAl equiP mAker

Lakeland IndustriesLAKE $15 is a small-cap maker of safety garments and protective gear for a wide range of industries, from fire suppression and chemicals, to munitions and pharmaceutical. The Alabama-based firm has virtually zero debt on its books, has turned a profit each year for over a decade, and carries a low beta (risk measure) of 0.55. We added LAKE to the Intrepid Trading Platform at $15.23 with an initial price target of $21, which equates to a 40% upside. We are placing a stop on the shares at $13.50.

RTX CorpRTX $73 is the product of a merger between Raytheon and United Technologies, two storied defense contractors. Units include Collins Aerospace, Pratt & Whitney, Raytheon Intelligence & Space, and Raytheon Missiles & Defense. The company offers an excellent balance between its civilian and defense lines, and we believe investors are ignoring the firm’s strong growth potential going forward—it is, after all, a “boring” industrial. We re-opened in the Global Leaders Club @ $73.30 per share with $100 initial target price.

Penn: remove TArgeT

When shares of TargetTGT $170 popped 13% midday on strong Q4 earnings, we took the opportunity to close the position from the Penn Global Leaders Club and record our 170% profit in the stock. We are underwhelmed with the retailer’s growth plans, and have a fair market value on the shares below our sale price of $170—just $1 below their 52-week high. We believe the cash could be better deployed elsewhere.

Penn: Add nordic BAnk

Nordea Bank AbpNRDBY $12 has been around some 224 years and is the largest commercial bank in the Nordics. The company has a conservative portfolio, with revenues generally deriving from mortgage, personal, and corporate loans. With a multiple of seven and a dividend yield of 8%, we added Nordea to the Penn International Investor at $12/share.

Penn: Add ulTA BeAuTy

We noticed shares of Ulta BeautyULTA $377 were highly undervalued, and immediately added the name to our Intrepid Trading Platform at $320/share. The very next day, Warren Buffett took a major stake in the beauty retailer and shares skyrocketed. Our initial price target is $400, which would represent a 25% gain.

A Canadian gold miner operating in lower-risk jurisdictions...

Shares of Ulta Beauty were trading too low to pass up. Buffett bought the next day.

When you think of the future of robotics and automation, think Rockwell

Investors are missing the big picture on this “boring” industrial

Open RTX Corp in Global Leaders Fund

Open AEM in Global Leaders Club

Open ULTA in Intrepid Trading Platform

Open Rockwell in New Frontier Fund

New Zealand’s Adventure Paradise

With its rich history and surreal natural beauty, Fiordland National Park is a required stop for visitors to New Zealand

It may be the heart of summer in the United States, but now is a great time to start planning an escape from the coming winter’s frigid grasp. For sports enthusiasts and adventure seekers, New Zealand’s Fiordland National Park should be high on the list of destinations.

Nestled in the South Pacific Ocean in the southwestern section of the Polynesian Islands, New Zealand is almost an afterthought for many, especially when compared to its much larger neighbor to the northwest—Australia. But the country’s immense beauty and ecological diversity—from subtropical forests on the North Island to glaciers, pristine lakes, and snow-covered mountains on the South Island—make it nearly a mandatory item on any traveler’s wish list. A focal point for visitors must be the cherished jewel of Fiordland National Park.

Early history

Storied British explorer Captain James Cook quite literally put Fiordland on the map, as he and his shipmates aboard the HMS Resolution became the first Europeans to visit the area in 1773 following a grueling, 123-day trip around Antactarcia. The region must have seemed like a paradise to the weary sailors, who had set sail to prove or disprove the existence of a great southern landmass known as Terra Australis.

On the site of what would become known as Astronomer’s Point, the most advanced chronometer of the time was deployed to establish the precise global location of New Zealand. Cook also set up a brewery during his five-week stay, making the country’s first beer—it was hoped that this ale would help prevent

top Rainbow over Fiordland middle Milford Sound, Southland (Pexels)

Snow-capped mountains, Southland (Pexels)

scurvy among the crew. Like so much of Fiordland, current-day visitors to Astronomer’s Point, located in the remote region of Dusky Sound, are greeted with virtually the same view Captain Cook enjoyed 250 years ago.

What to do once in Fiordland

Encompassing an area nearly 5,000 square miles in size, Fiordland is one of the largest national parks in the world. And it is hard to fathom a more diverse natural environment; an area which includes rainforests, stunning mountain lakes, spectacular waterfalls, and—of course— glacier-carved fiords. Best of all, travelers never have to leave the park thanks to a multitude of accommodations.

One ideal base camp for visitors is Te Anau, a tranquil lakeside town which serves as the gateway to the park. Despite its laid-back vibe, guests have a number of restaurants at which to dine, a supermarket for groceries, and even the Foridland Cinema to catch a flick. A seventeen-minute drive south down State Highway 95 lies Manapouri, namesake town to New Zealand’s “loveliest lake.” With its 33 islands, there is no shortage of day cruises to traverse its pristine waters.

While there are more accommodations in Te Anau, Manapouri provides a more rustic stay. For $200 per night or less, visitors can select from a wide array of hotels, cabins, or cozy cottages in either town.