04 Decarbonising the downstream – opportunity or threat?

Alan Gelder, Wood Mackenzie, surveys the current attempts to decarbonise the refining and petrochemical sectors, alongside considering the challenges operators are facing in these undertakings.

11 A whole systems challenge

James Jenkins, DNV, UK, considers the different strategies used in the decarbonisation of midstream oil and gas and thermal power generation in support of electricity grid resilience.

15 Refinery revolution

Phil Ingram, Johnson Matthey, UK, considers how the energy transition poses both a challenge and an opportunity for refineries, as operators seek to decarbonise processes while maintaining economic viability.

19 A pathway to carbon reduction

Howard Siew, BASF, USA, discusses how co-processing renewable and recyclable feedstocks can help to reduce the carbon footprint in FCC units.

23 Scaling the plastics value chain

Milica Folić, Topsoe, considers how to enable scalable chemical recycling of plastic waste to create drop-in naphtha.

27 What to do with waste

José Miguel González, Tecam, examines the role of chemical recycling in creating a circular economy.

30 Carbon capture sets sail

Sophia Asal, Endress+Hauser, Switzerland, and Anastasija Kuprijanova, Carbon Ridge, USA, outline how carbon capture can be used to decarbonise the hard-to-abate sectors of global trade and infrastructure.

Jeroen Huizinga, John Crane, explores sustainable fuels in the marine transportation industry, charting the development of LNG as a bridge fuel, alongside considering the future role that ammonia, hydrogen, and methanol could play.

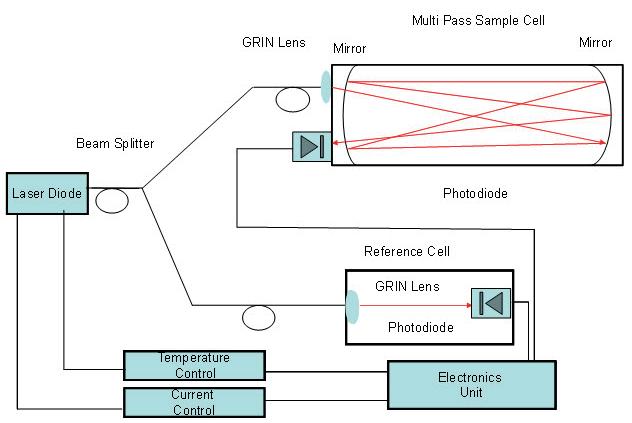

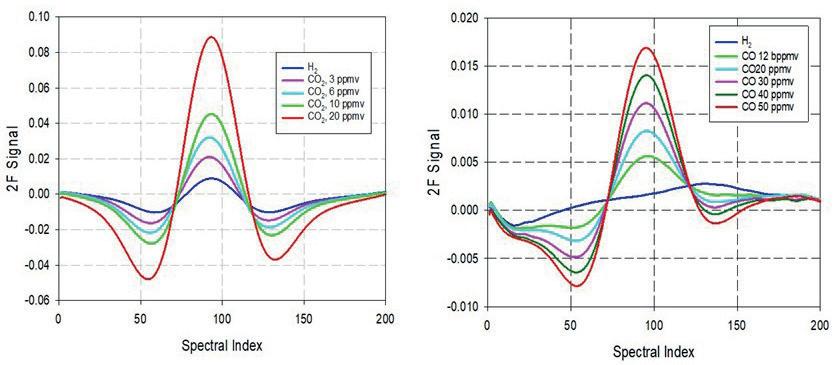

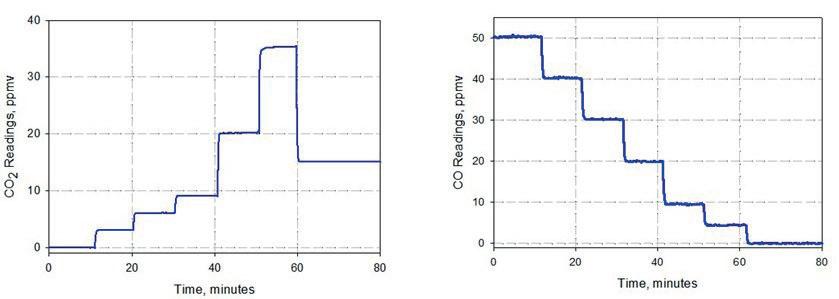

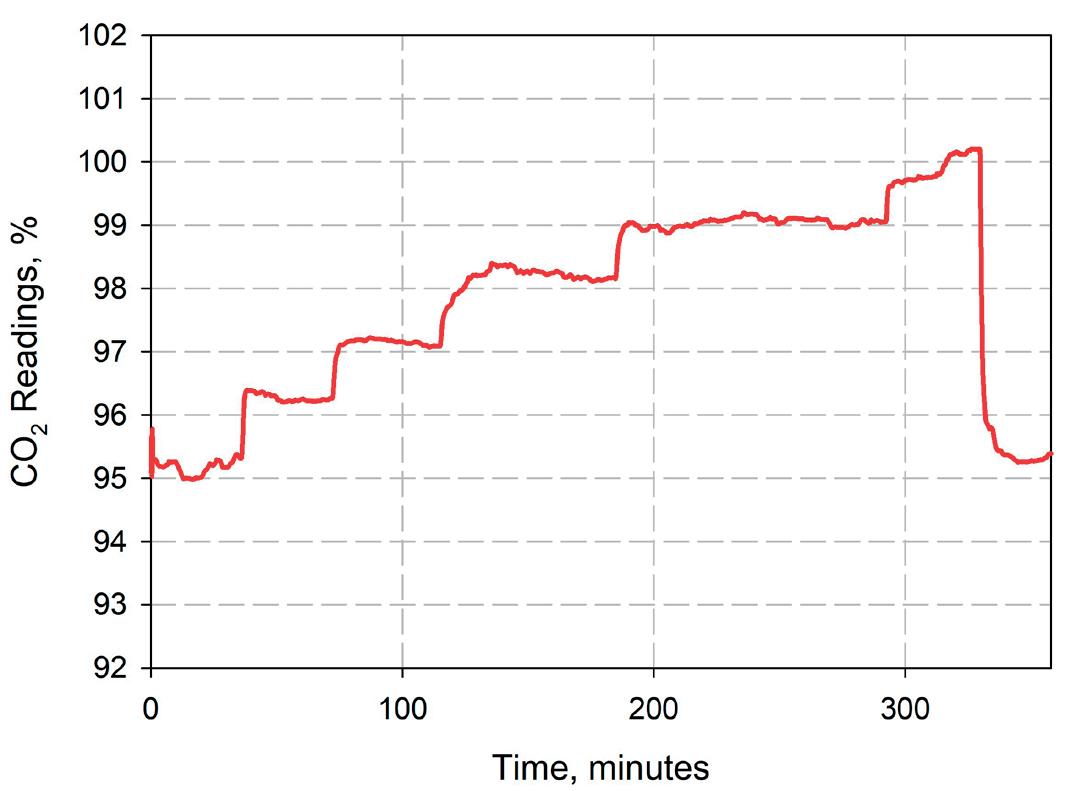

39 Carbon oxidation monitoring in blue hydrogen production

Airat Amerov and Michael Gaura, AMETEK Process Instruments, USA, evaluate the use of tunable diode laser absorption spectroscopy to measure carbon dioxide and monoxide levels in carbon capture and storage.

43 Green hydrogen at scale

Nicolas Carrara, Juan Ruiz, and Carlos Ruiz, KBC (A Yokogawa Company), explore the challenges of industrial scale deployment of green hydrogen and how advanced technologies can help operators to cross the chasm.

49 Keeping it close to home

Andrew Symes, OXCCU, UK, explains why Europe should prioritise producing sustainable aviation fuel locally rather than depending on imported methanol.

51 Sulfur, safety, and sustainability

Juan J. Gonzalez, Merichem Technologies, considers how refineries and petrochemical operations can reduce sulfur emissions for increased safety and sustainability.

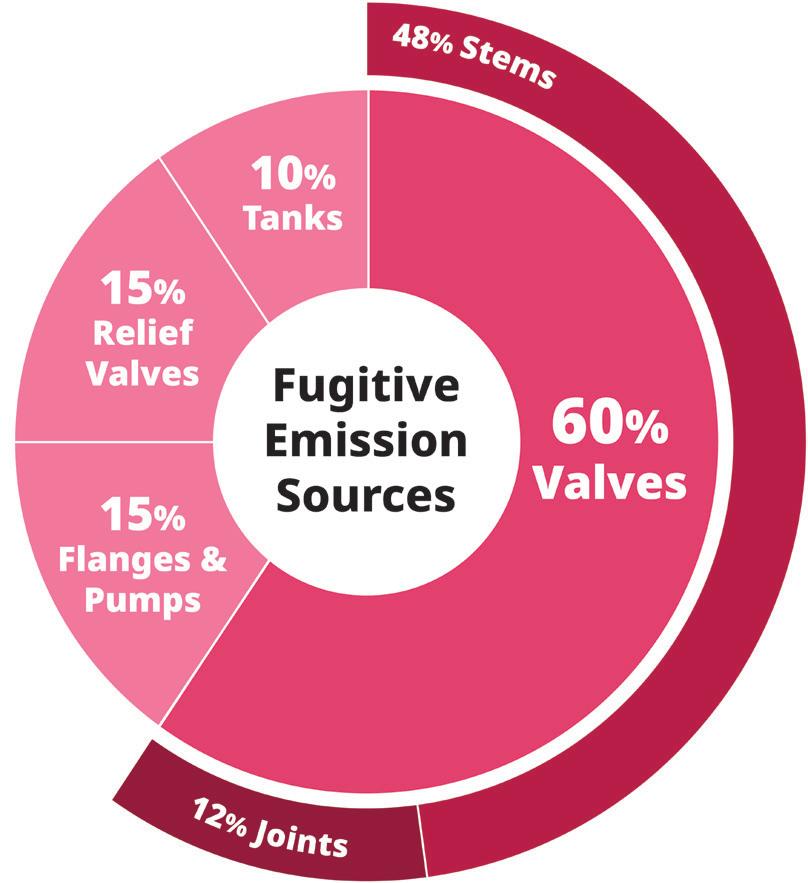

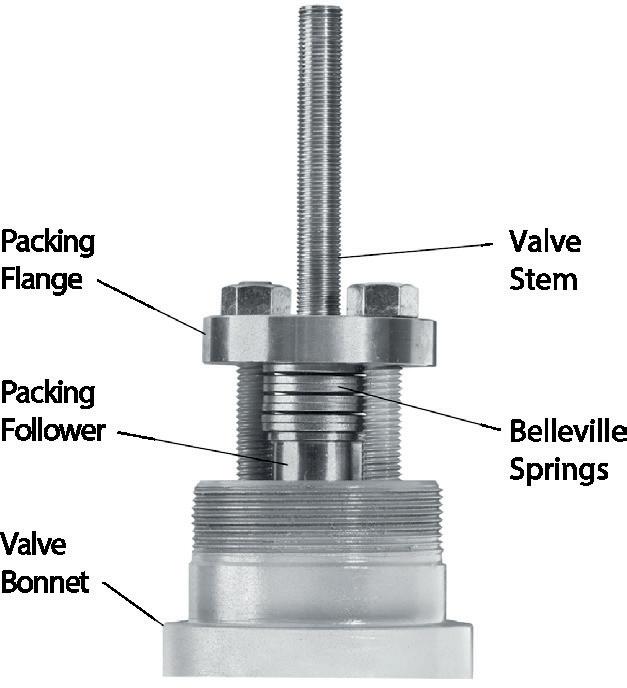

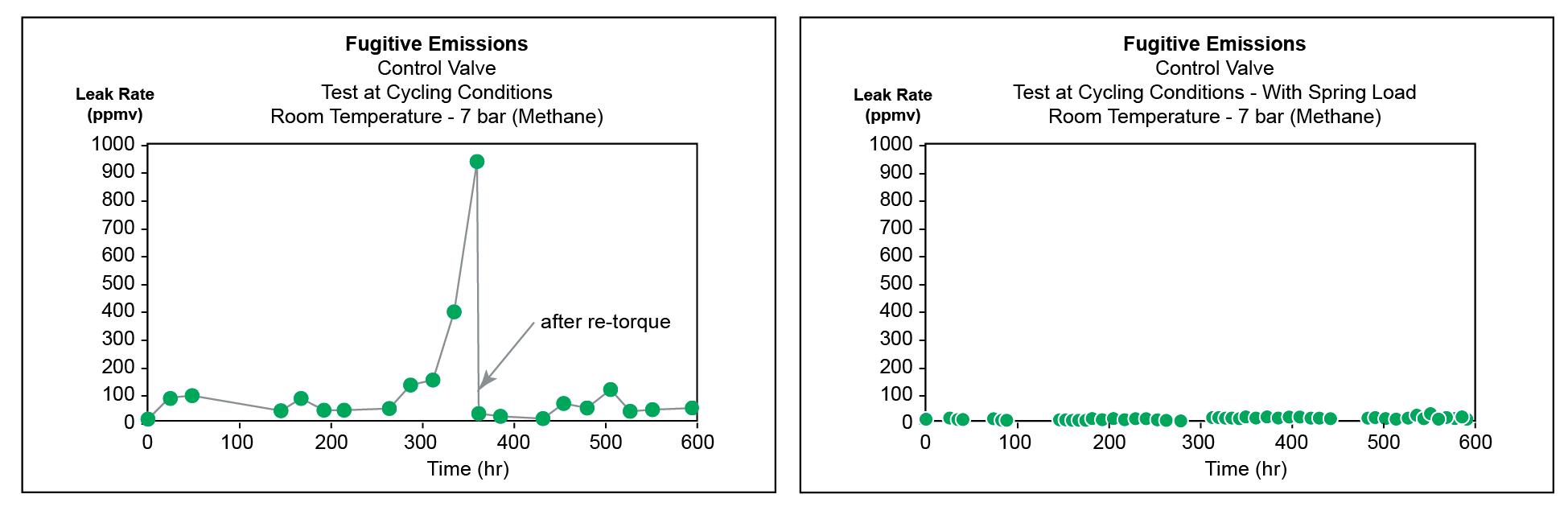

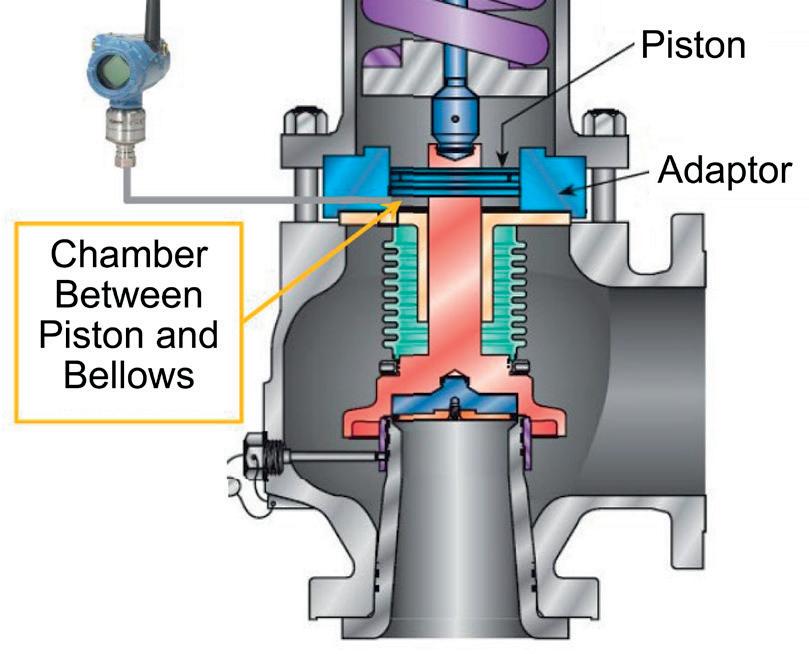

55 Emission reduction solutions

Frank Campagna and Alice Shao, Emerson, USA, discuss how technological improvements in design, valve packing, and relief valves address a host of emission and maintenance problems in downstream oil and gas facilities.

59 Energy efficiency: the ‘first fuel’ of decarbonisation

Dr Ankush Gulati, ABB Motion Services, Singapore, outlines why energy intensive industries should prioritise energy efficiency in order to reach their climate goals.

Carbon Ridge is advancing maritime decarbonisation with its compact, modular onboard carbon capture system – engineered for retrofits or newbuilds. The system delivers high capture efficiency with reduced footprint and low operational costs. Supported by precision instrumentation from Endress+Hauser, the technology enables shipowners to meet emission targets while maintaining fleet value.

ET Black™ Technology

Cut your CO2 emissions by 50% with the future of carbon black production

Compliant and innovative

Meets stringent environmental regulations, keeping your business future-ready

Unparalleled flexibility

Produce all ASTM grades and specialty grades seamlessly in a single plant

Sustainable Uses thermal decomposition of aromatic oils for cleaner production

CONTACT INFO

MANAGING EDITOR James Little james.little@palladianpublications.com

ADMIN MANAGER Laura White laura.white@palladianpublications.com

SUBSCRIPTION RATES

Annual subscription £110 UK including postage /£125 overseas (postage airmail). Two year discounted rate £176 UK including postage/£200 overseas (postage airmail).

SUBSCRIPTION CLAIMS

Claims for non receipt of issues must be made within 3 months of publication of the issue or they will not be honoured without charge.

APPLICABLE ONLY TO USA & CANADA

Hydrocarbon Engineering (ISSN No: 1468-9340, USPS No: 020-998) is published monthly by Palladian Publications Ltd GBR and distributed in the USA by Asendia USA, 701C Ashland Avenue, Folcroft, PA 19032.

Periodicals postage paid at Philadelphia, PA & additional mailing offices.

POSTMASTER: send address changes to HYDROCARBON ENGINEERING, 701C Ashland Ave, Folcroft PA 19032.

15 South Street, Farnham, Surrey

GU9 7QU, UK

Tel: +44 (0) 1252 718 999

COM MENT

CALLUM O'REILLY SENIOR EDITOR

Much has changed in the energy sector since we published the inaugural issue of this EnviroTech supplement last year. Perhaps most notably: the return of President Donald Trump to office, signalling a seismic shift in US energy policy with worldwide implications.

The President has pushed forward with his ‘America first’ energy policy, quickly withdrawing the US from the Paris Agreement (again), reversing clean energy support policies, and promoting the use of fossil fuels to ‘unleash American energy’.

In its latest ‘Energy Transition Outlook’, DNV notes that recent changes in US energy policy – combined with the fact that only six countries have reduced their emissions in line with the Paris Agreement, a decade on from its adoption – have led to broad recognition that the world is unlikely to achieve net zero emissions by 2050. Indeed, DNV’s flagship report now forecasts all the way out to 2060 for the first time, recognising that the transition will by no means be complete a decade earlier. “Faced with these developments, a casual observer might conclude that the energy transition is stalled or in reverse. That is most definitely not the case. The energy transition is rolling on,” reassures Remi Eriksen, DNV’s Group President and CEO, in the foreword to the Outlook.

The report begins with a series of ‘highlights’ for those looking to extract the key findings. Pointedly, highlight number one reads: “Policy reversals in the US will have only a marginal impact on the global energy transition.” DNV estimates that emission decline in North America has slowed down by around 5 years, and projects only a marginally slower energy transition than it forecast last year. However, although current US energy policy may not have a long-term impact on decarbonisation efforts, DNV doesn’t expect to see net zero CO 2 emissions until 2090.

The report reiterates that urgent action is required to limit global warming to well below 2°C.

As we all know, the energy evolution is here, and our sector has a vital role to play. As energy demand continues to grow, fossil fuels will remain a significant part of the energy mix for the foreseeable future. But it is essential that the downstream sector continues to decarbonise its operations and invest in its future.

This issue of EnviroTech is packed with technical articles and case studies exploring how the sector can grasp the opportunities presented by the energy transition and thrive in the new energy reality.

As Alan Gelder, Vice President of Refining, Chemicals and Oil Markets at Wood Mackenzie, explains in his keynote article starting on the next page of this issue, “Industry players must balance immediate operational pressures with long-term positioning for the energy transition.”

Of course, this is an extremely difficult balancing act, but the rewards could be transformative – delivering lasting value for both companies and the planet.

Alan Gelder, Wood Mackenzie, surveys the current attempts to decarbonise the refining and petrochemical sectors, alongside considering the challenges operators are facing in these undertakings.

Fossil fuels remain the backbone of modern life.

But while these low cost, energy dense feedstocks power our economy, a stark paradox emerges. Despite record renewable energy deployment and surging electric vehicle (EV) adoption, global emissions continue rising. In 3Q25, global oil demand is set to breach over 105 million bpd, almost 10 million bpd higher than a decade after the world leaders signed the Paris Agreement. Despite a decade of climate commitments, the energy transition faces mounting headwinds as emissions climb despite unprecedented clean energy investment. The need to decarbonise the oil value chain will remain critical. Decarbonisation requires investment at facilities that must

remain commercially viable for years to come. This presents both opportunities and threats for the downstream sector.

Oil value chain emissions

This emissions challenge becomes clearer when examining where they originate. In 2024, global primary energy demand was 636 exajoules, with over 80% supplied by fossil fuels (Figure 1). Oil’s share has been in slow decline from over 35% in 2000 to just under 30% in 2024. Global CO2 emissions were over 37 billion t in 2024, dominated by the power and industrial sectors. The combined emissions from transportation were just under 22% of the total, mostly from oil. The sheer scale of these emissions and the breadth of

sources across the global economy show the challenge to achieving net zero.

Wind and solar are decarbonising the power sector. Growing electrification is primarily decarbonising the transport sector, with EV penetration moving at pace in China and Europe. EV penetration in the US proceeds at a much slower pace than elsewhere and faces reduced government support. Global oil demand is to continue to grow in the medium-term and remain resilient over the coming decades. Growing adoption of EVs and improving energy efficiency will drive global oil demand into decline. However, the refining sector has a long future ahead of it, supporting sustained petrochemical demand growth either

from integrated refinery and petrochemical sites or by supplying its feedstocks.

Refining is an energy intensive part of the oil value chain, with its emissions often exceeding those from the upstream sector (Figure 2).

Refining process emissions are primarily from combustion (fuel for process heaters and fluid catalytic cracking catalyst regeneration), on purpose hydrogen production, and electricity consumption. Refinery emissions are closely related to asset complexity, given the larger energy requirements from the greater conversion to high value refined products associated with more sophisticated configurations.

Decarbonising the downstream sector is multi-faceted (Figure 3), involving both a reduction of the emissions from refinery operations alongside the carbon intensity of its products, all of which require investment.

Decarbonising operations

There is a clear commercial incentive to lower carbon emissions at sites exposed to emission charges. Good practice is to focus on overall energy efficiency and process optimisation. There are multiple technologies for emissions reductions, pre or post-combustion, but the primary focus is on displacing fossil fuels by low-carbon options, such as low-carbon hydrogen, and capturing emissions using carbon capture and storage (CCS).

CCS is currently capturing over 80 million tpy of carbon dioxide, but the downstream sector accounts for less than 5%. A key challenge to deploying CCS technologies in the downstream sector is that low levels of carbon dioxide in post combustion gases are spread across disparate point sources, resulting in costs that are often higher than the savings from lower emissions. There is significant CCS capacity under active development, but most of the capacity is being developed for the fossil power sector and upstream oil and gas production. CCS deployment will also receive help from recent US legislative developments that has standardised available tax credits. As with any large capital

project, economies of scale prevail for CCS. Refiners located in industrial clusters will have the opportunity to partner with adjacent industries to jointly decarbonise their combined operations.

Low-carbon hydrogen is an interesting example of an opportunity supported by the refining sector in Europe. Like CCS, the economics of emissions reduction are challenging. Displacing hydrogen produced from natural gas with that produced by electrolysis using renewable power typically incurs high power costs. Several green hydrogen projects have targeted the sector, with European refineries already committing more than US$5 billion of capital. This is due to the decarbonisation of refined products adding value to the cost savings benefits.

Decarbonising products

Decarbonising the energy sector is a key European aspiration. This is being achieved by growing biofuel penetration into transport fuels, along with circularity requirements for plastics to reduce demand for virgin material. There are opportunities for liquid biofuels in both the aviation and marine sectors. The current Renewable Energy Directive legislation (RED III) introduces a requirement for renewable fuels of non-biological origin (RFNBO), including multipliers for RFNBOs in the marine and aviation sector to support their commercialisation. Green hydrogen is RFNBO compliant and can be deployed in the refining sector to deliver the 2030 targets.

Decarbonising the maritime sector

The International Maritime Organization (IMO) has introduced a net-zero framework to cover the emissions from virtually all vessels. The greenhouse gas fuel intensity for each vessel is to be reported and improved over time, with a market compliance mechanism introduced to support zero or near zero (ZNZ) fuels.

Marine biofuels are expected to increase steadily over the next decade, also driven by the introduction of the

Source: Wood Mackenzie

Source: Wood Mackenzie

Figure 1. Global primary energy consumption and carbon dioxide emissions (2024).

Reliable Technologies for H2S, Mercaptan & COS Treatment or Removal

Turn yellow into green using our low OPEX, proven sulfur treatment technologies.

Merichem Technologies is a leader in sulfur treatment technologies, providing safe and eco-friendly solutions to remove H2S, mercaptans and COS from both liquid and gas streams. Whether it’s customized or standard, adsorbents or chemical processes, our robust technologies allow you to maximize profitability while meeting your specifications at any scale.

With over 50 years of experience delivering innovative solutions and excellence in service, you can trust we will do the same for you.

Let’s discuss your specific requirements and how we can help.

EU Emissions Trading Scheme (ETS) and Fuel EU Maritime regulations (Figure 4). There are a range of biofuel blends now proven in the marine fuel market, based on fatty acid methyl esters (FAME) or used cooking oil, typically blended in with very-low sulfur fuel oil (VLSFO). Wood Mackenzie expects marine biofuel volumes to increase over the next decade, but long-term growth is restricted by the lack of supply availability and increasing feedstock competition from the aviation sector. Furthermore, liquid biofuels do not achieve the emissions requirements for ZNZ fuels. Over the longer term, e-fuels, such as e-methanol and e-ammonia, will be needed, particularly in Europe. E-diesel could appear as a shipping industry fuel during the 2040s given its drop-in nature.

Europe has also carved out €800 million from its latest Hydrogen Bank auction to support maritime supply projects. However, under the current IMO pricing mechanism, it will take time for hydrogen-based fuels to be competitive with incumbent fuels.

Sustainable aviation fuel (SAF)

International bodies and governments are committed to reducing aviation carbon emissions, with the EU leading the charge. Improvements in aircraft efficiency, infrastructure, and other operational improvements are minor compared with

the opportunity to deploy SAF that is either bio-based or synthetic (e-SAF).

The ReFuelEU Aviation regulatory framework requires SAF to power 6% of the jet pool by 2030, of which an average of 1.2% is to be e-SAF, produced from RFNBO-compliant green hydrogen. By 2050, the SAF blending mandate is 70%, of which half must be e-SAF.

SAF is largely produced from hydroprocessed esters and fatty acids (HEFA) feedstocks, using waste oils and alcohol-to-jet (ATJ) facilities. Biomass to liquids is a potential future route offering a wider feedstock pool but is challenged by high capital costs.

Figure 5 highlights the potential opportunity for significant future growth of SAF supplies. Feedstock, technology, and cost constraints must be overcome if the ambitious long-term net zero targets for aviation are to be met.

Petrochemical circularity

The production of plastics is a major contributor to global carbon emissions, with the long lifetime of plastics presenting a challenge to the broader natural environment. The concept of the circular economy was born out of this dilemma. The circularity of polyolefins requires a vertical sectoral view, as equipment must be dismantled and waste sorted as essential pre-requisites. The promotion of plastics recycling, both mechanical and chemical, requires diversion away from landfills as a start, supported by the development of the sustainable use of materials – rigid materials are far easier to mechanically recycle. Today, 70% of polyolefins are in applications that are hard to recycle. Pyrolysis (chemical recycling) is off to a slow start as an industry. Value chain integration incorporating waste collection and processing will be essential for its success and sustained growth. This will overcome sensitivity to feedstock quality along with a material improvement in selectivity, as the operational yields are currently low. Pyrolysis oils vary in quality and the EU exempting fuels from its mass balance determination of recycled content. In Europe, pyrolysis oils need to be pre-treated to remove contaminants and upgraded to a naphtha boiling range to fully capitalise on EU regulatory support.

Downstream commercial performance will drive choices

Margin pressures across refining and petrochemicals will dictate which facilities can afford decarbonisation investments. The refining system has a diverse asset base of 700 facilities, making any investment case site-specific.

Figure 4. Outlook for marine biofuels by region and e-fuel demand. Source: Wood Mackenzie Product Markets Service.

POWERFUL CHEMISTRY, UNPARALLELED EXPERTISE

KETJEN’S INDUSTRY LEADING CATALYSTS UNLEASH THE POWER OF ADVANCED CHEMISTRY THROUGH:

INVESTMENTS to meet future production supply demands.

INNOVATIONS that expand profitability and efficiency, while lowering costs.

INSIGHTS, based on customer interactions and market factors, allowing for rapid response to industry needs.

Learn more at KETJEN.COM

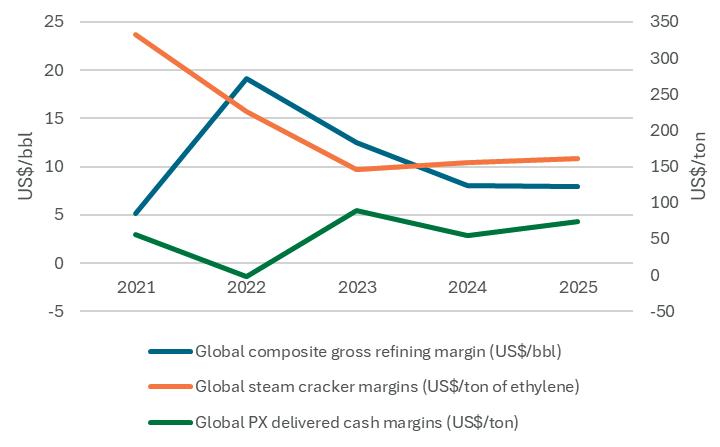

However, the broader market context cannot be ignored, as shown in Figure 6.

Global refining margin performance for 2025 is expected to be broadly flat on 2024, both lower than the highs of 2022. Global ethylene margins are weak, with capacity rationalisation in Europe and other high-cost locations ongoing. The surplus of global steam cracker capacity stems from significant over-build in China. Global paraxylene (PX) margins have been in the doldrums for a while, with signals of recovery in 2025.

The near-term outlook for the sector is still challenged, as global composite refining margins are projected to be at their low point in 2026 before recovering, after which the rising tide of demand lifts global utilisation. For chemicals, particularly the olefins chain, recovery is not projected to happen until the late 2020s, such is the scale of the overbuild in China. The PX recovery is projected to be sooner than olefins, given the shift of olefins to lighter feedstocks. The near-term outlook for the downstream sector is complicated by US trade tariff policy, which could slow economic activity further and lower demand growth for refined products and petrochemicals.

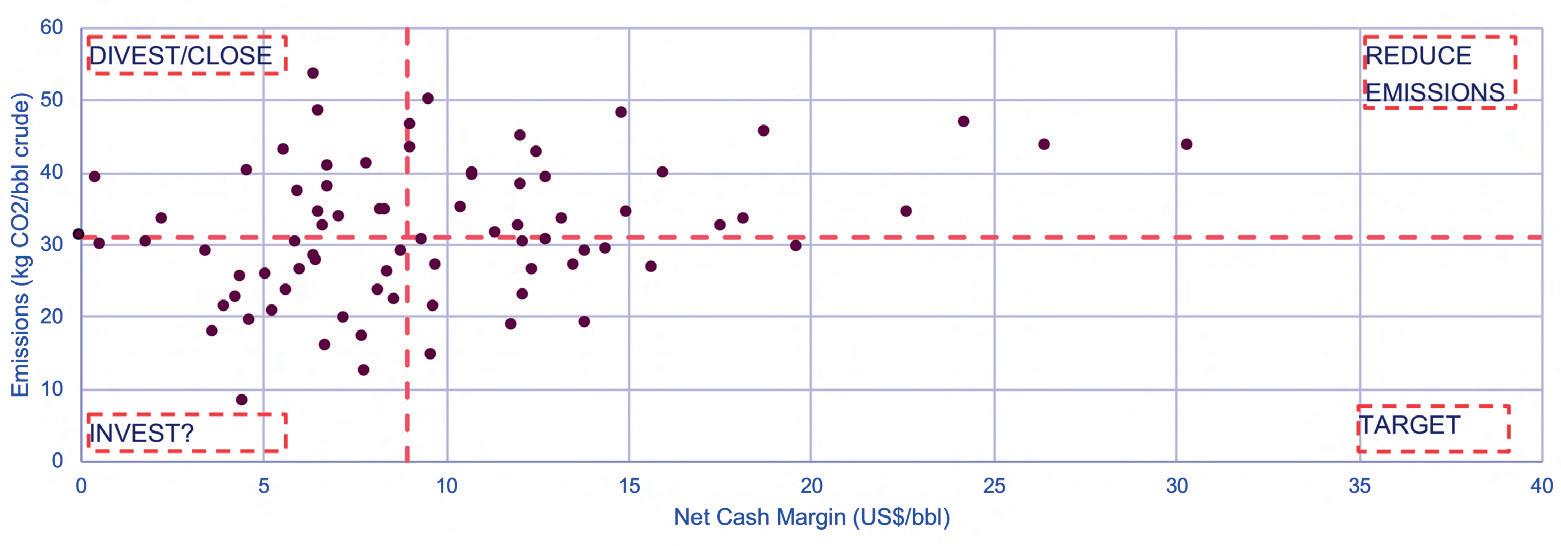

Tight cost management is the order of the day. The market fundamentals of refining and commodity chemicals require sustained focus on reliable operations, value maximisation, and frugal investments. This means that decarbonisation investments will not occur at all sites. Owners of a portfolio of sites need to focus on sites in the ‘target quadrant’ of the matrix of competitive position and emissions (Figure 7). These will be the sites that are well positioned to adapt to decarbonisation, as they deliver higher earnings with low emission intensities.

These sites can benefit from the shift to liquid biofuels and development of RFNBOs, providing they focus on the critical success factors for each specific opportunity, notably securing feedstock supply for liquid biofuels and low-cost renewable power and economies of scale for RFNBOs.

For those sites well positioned for a lower carbon future, in a global environment full of uncertainty, a key challenge will be timing of their transition. Owners need to regularly review market developments and investment metrics to identify when to trigger a material transformation.

Conclusions

Decarbonising the downstream sector is both an opportunity and threat. The threat stems from declining demand for fossil fuels and rising cost of emissions, both driving capacity rationalisation. The opportunity lies in growing demand for liquid renewables, both bio-based and synthetic, along with petrochemical circularity. The transition between the two will not be smooth, requiring each site to focus on their competitive advantage now and in a future lower carbon environment.

Success will depend on timing, feedstock security, and the ability to navigate an increasingly complex regulatory landscape whilst maintaining commercial viability. Industry players must balance immediate operational pressures with long-term positioning for the energy transition. Those who master this balance will emerge as winners in the evolving downstream landscape.

Figure 5. Global SAF demand forecast by fuel type. Source: Wood Mackenzie Liquid Renewable Fuels Service.

Figure 6. Downstream sector commercial performance. Source: Wood Mackenzie offerings on product markets, olefins, and PX.

Figure 7. Europe downstream earnings vs emission matrix (2023). Source: Wood Mackenzie Refinery Evaluation Model.

James Jenkins, DNV, UK, considers the different strategies used in the decarbonisation of midstream oil and gas and thermal power generation in support of electricity grid resilience.

Progress towards net zero is slowing in key geographical regions, increasing pressure on emissions-intensive sectors, particularly fossil fuel thermal power generation and midstream oil and gas. Decarbonising these sectors is critical as they sit at the intersection of two essential, mutually dependent infrastructures: the gas network and the electricity grid. The UK electrical grid relies on natural gas for flexible thermal power and stability, while the gas network

increasingly depends on the grid for its operational control systems.

In the UK, transforming these sectors is essential to meeting legally binding climate targets:

n 2032: 58% reduction in greenhouse gas emissions vs 1990.

n 2037: 68% reduction vs 1990.

n 2050: net zero.

According to DNV’s ‘UK Energy Transition Outlook (ETO) 2025’, emissions could fall to around 145 million t of CO 2 by 2050 – an 82% cut from 1990 levels – yet still miss the net zero goal. The pace must accelerate, and it cannot do so in silos. Decarbonising one backbone of the energy system without the other risks reliability shortfalls, higher costs, and public resistance.

These sectors are both a major industrial emitter and a strategic backbone of the UK’s energy system. Its transformation is a climate imperative and a driver of a more secure, resilient electricity grid. Wide scale electrification and additional grid infrastructure are needed to meet UK decarbonisation targets. The UK’s electrical grid boasts exceptional reliability >99% in 2023/24 – enabled in part by the gas grid, which provides consistent energy to dispatchable power generators, helping to balance fluctuations.

Grid operators are investing in stability solutions like synchronous condensers, batteries, and power electronics. However, these alternatives can be costly or remain at low technological readiness levels. As such, a decarbonised midstream oil and gas sector can play a vital role in ensuring the UK’s expanding electrical grid retains resilience and energy security over both the near and long-term.

This ‘whole systems thinking’ approach is not new –National Energy System Operator (NESO) already models gas-electric interactions in winter planning.

The 2024/25 winter period highlighted the stakes: with peak gas demand for electric generation at 27.9 GW and a couple of days prior a 17 GW increase over a period of 5 hours. Also over the 2024/25 winter period there were 54 days where at least 40% of electricity was generated from gas. Without a gas network ready to deliver, blackouts would have been a real risk.

Whole systems thinking means recognising that one network’s decarbonisation must reinforce – not undermine – the other’s resilience. It also requires considering gas network decommissioning, which will not align neatly with the last customer switching to electricity. Planning is essential to ensure industrial users and thermal power generators are supported throughout the transition.

Decarbonisation levers in a whole system

Three parallel main strategies dominate the decarbonisation toolkit:

n Electrification and fuel switching – removing fossil fuel combustion and replacing it with low-carbon electricity.

n Carbon capture and storage (CCS) – capturing unavoidable CO 2 emissions from industry (e.g. refining, power, cement, and energy from waste).

n Low-carbon hydrogen and derivatives – substituting grey hydrogen in refining, providing hydrogen for high-heat industrial processes, and enabling energy storage with dispatchable power.

Each lever contributes differently to decarbonisation and grid resilience, making integration essential. They are most effective not as isolated measures, but as mutually reinforcing parts of an integrated system.

Electrification

Electrification, particularly replacing fossil fuel combustion with electric heat and power, is one of the most direct ways to cut operational emissions. For example, in refineries, electric boilers, heaters, and motors can displace gas-fired units in process heating, distillation, pumping, and other thermal applications.

The benefits are two-fold:

n Immediate Scope 1 and 2 emissions reductions, especially as the UK grid continues to decarbonise.

n Air quality improvements by eliminating on-site hydrocarbon combustion, reducing NO X and particulate emissions.

From a whole systems perspective, industrial electrification brings both opportunity and challenge. Replacing on-site fossil fuel combustion with cleaner power also increases electricity demand. Meeting that demand reliably requires coordination with the gas network, which can supply dispatchable generation during low renewable output. Thus, electrifying one sector reinforces the need for a clean, flexible gas system to backstop the grid.

Electrification also shifts emissions upstream, making it essential that the additional power demand is met by low-carbon generation and supported by gas system flexibility and storage. Electrifying industry does not mean abandoning the gas network; rather, it means reconfiguring the gas network through repurposing the gas infrastructure with low carbon solutions (e.g. hydrogen, biomethane) to complement a renewables-led grid.

A DNV case study for a European refinery illustrates the impact: replacing two large gas-fired boilers with electric units cut direct CO 2 emissions by over 100 000 tpy but increased site electricity demand by 90 MW – equivalent to around 800 000 MWh yearly, or enough to power approximately 135 000 homes. Such shifts need integrated grid-gas network to ensure stability and resilience.

In the UK, many industrial clusters are in coastal areas with high-voltage connections that may need reinforcement for substantial new loads and renewable supplies. In some regions, grid capacity may already be under pressure from other major projects, including offshore wind landfall points, data centres, and gigafactories. For instance, rapidly growing data centre

demand has prompted recent inquiries for up to 2.5 GW of on-site gas generation due to grid connection delays, underscoring pressure on local capacity.

CCS

CCS is essential for tackling emissions that electrification cannot address – making it indispensable for deep decarbonisation in refining, heavy manufacturing (cement and steel), and energy from waste, where some emissions are inherent to the process. For example, capturing CO 2 from steam methane reformers (SMRs) in hydrogen production or catalyst regeneration units can eliminate large volumes of emissions that switching to electricity alone cannot.

Global CO 2 capture capacity is forecast to reach around 270 million tpy by 2030 and 1300 million tpy by 2050, still far below the net zero requirement. Achieving the needed scale will depend on sustained cost reductions – projected to average about 40% by 2050 –alongside supportive policies and investment frameworks.

In the UK, CCS dovetails with the government’s cluster sequencing programme, advancing industrial carbon capture in North West England, Teesside, Humber, and Scotland – all home to significant downstream oil and gas assets and heavy industry. Linking industrial emissions into these CCS clusters allows captured CO 2 to be transported via shared pipelines to offshore Irish Sea or North Sea storage sites. This ‘cluster’ approach reduces costs and accelerates deployment by aggregating demand for transport and storage infrastructure.

The UK’s CO 2 storage potential is vast – estimated at over 78 Gt in saline aquifers and depleted hydrocarbon fields – enough to support CCS for decades if developed alongside emissions sources.

From a whole system perspective, CCS also bolsters energy security. It enables low-carbon hydrogen and

power generation from domestic natural gas to continue within stringent carbon limits, reducing import reliance during supply disruptions and safeguarding UK energy system resilience.

Low-carbon hydrogen and derivatives

Hydrogen is a crucial energy carrier for a decarbonised system, particularly in hard-to-abate sectors like aviation, shipping, and high-heat industry, as well as an energy storage vector. By 2050 – when much of the world targets net zero – DNV predicts hydrogen and its derivatives will account for over 4% of final energy demand (188 million tpy of H 2). However, to meet the Paris Agreement’s goals, they would need to supply about 15% of global energy demand by 2050.

In the UK, DNV projects hydrogen production will reach 1 million tpy by 2030, with 60% being low-carbon. By 2050, UK production is expected to rise to 5 million tpy, with 23% used for dispatchable low-carbon power and industrial processes.

Low-carbon hydrogen will replace grey hydrogen (hydrogen produced from natural gas through steam methane reforming [SMR], which results in significant CO 2 emissions that are released into the atmosphere) in refining and serve as a dispatchable low-carbon fuel for power. Internationally, projects like the Netherlands’ HyStock and Japan’s Chiyoda SPERA hydrogen chain demonstrate how large scale hydrogen storage can integrate with grid services. The UK could adopt similar models – using curtailed offshore wind to produce hydrogen, storing it in geological structures (e.g. salt caverns), and reconverting it to power when needed.

Hydrogen derivatives (ammonia, e-methanol, and synthetic e-fuels) extend this potential as drop-in fuels or more easily transportable, storable forms of low-carbon energy. Ammonia’s higher energy density and

Figure 1. Illustration of National Gas Network Innovation Competition NIC FutureGrid Phase 1 Project where DNV is the primary partner responsible for design, building and operating the test facility for the research project at Spadeadam, UK.

easier liquefaction make it a candidate for maritime fuel and power station co-firing, although its toxicity does remain a concern for many sectors. E-methanol could find use in shipping and chemicals. However, their deployment depends on overcoming safety and handling challenges.

Closing safety and knowledge gaps

Large scale adoption of hydrogen, CCS, and ammonia demands not only engineering solutions but also robust safety science to manage new hazards. DNV supports the energy transition through research at its Spadeadam facility in the UK and other global testing sites to demonstrate the safe use of low-carbon energy vectors. Some examples of ongoing or future work include the following:

CO2 pipeline transport safety

CCS networks will involve hundreds of km of new and repurposed pipelines. The Skylark Joint Industry Project (JIP), led by DNV with the UK Health and Safety Executive Science Division (HSE SD) and partners, aims to address safety challenges in transporting dense phase CO 2 . It involves large scale rupture, dispersion, and venting scenarios to understand terrain effects, venting operations, emergency planning, and validate consequence models.

CryoCO2 JIP

Two knowledge gaps are identified: the heat transfer and erosion characteristics of impinging CO 2 jets, including protective materials’ performance; and valve and system performance under high-flow, dense-phase CO 2 conditions. The JIP intends to close these gaps through full scale testing to improve understanding and manage risks from high-flow, high-pressure CO 2 releases.

Self-ignition of hydrogen

National Gas FutureGrid – Phase 1 results, including testing at DNV Spadeadam, highlighted that key areas of uncertainty are associated with the generation of damaging overpressures following early ignition from a hydrogen pipeline rupture. These uncertainties can have a strong influence on the calculated risks. Work is ongoing on transient experiments to focus on the probability and timing of self-ignition from a buried hydrogen transmission pipeline rupture.

Hydrogen jet fire erosion

The external flame characteristics of hydrogen and natural gas are not significantly different. Internally, hydrogen jet flame temperatures and convective thermal flux are greater. Hydrogen jet fires may erode reactive passive fire protection (PFP) systems like intumescent coatings more than hydrocarbon jet fires. Gaps relate to properties within large scale hydrogen jet fires, particularly flame temperature and heat flux. Large scale experimental data is needed to confirm equivalence to natural gas jet fires and their relation to propane jet fires used to test PFP systems.

Resolving these technical gaps now ensure safety considerations will not bottleneck the energy vector’s deployment.

Benefits for grid resilience and energy security

Hydrogen-ready gas networks with sufficient storage, like salt caverns, can serve as large scale, distributed storage – converting surplus renewable electricity into hydrogen during excess generation and supplying it back for power during low-renewable periods. This intra-day, week, month, or seasonal balancing role is valuable in the UK, where surplus renewables can be stored for times of low supply and/or high demand.

The benefits of integration are tangible: modelling shows that coordinated gas and electricity system operation can reduce total system costs by billions yearly, avoid unnecessary capacity build-out, and strengthen resilience to extreme events. These synergies exemplify whole systems thinking – the electrical grid and natural gas, CCS, and H 2 networks working in harmony, supporting each other on the energy transition journey.

The road ahead

Momentum is building – electricity supply sector emissions fell 15% in 2024, whilst UK fuel supply sector emissions fell 6% and industry 9% – but the pace must increase to meet net zero milestones. Incremental change is no longer enough: high-emission sectors, like thermal power generation alongside midstream and downstream oil and gas sectors, must scale up hydrogen, CCS, and electrification in a coordinated, safe way.

A whole systems approach is vital to achieving net zero targets without compromising operational continuity or public trust. The downstream oil and gas sector plays a pivotal role in the UK’s energy transition. Decarbonisation efforts, through electrification of industrial processes, CCS, and low-carbon hydrogen, must be integrated with the electricity grid and gas network to ensure reliability and energy security. Industrial clusters in which the downstream sector are located, are central to this transformation, leveraging shared infrastructure and coordinated planning. Research and development with technical advisory and assurance are essential to scaling these solutions, with DNV leading efforts to close knowledge gaps.

DNV’s independent technical advisory and assurance expertise – from hydrogen pipeline testing to CCS dispersion modelling – provides the evidence base for investment, regulation, and safe deployment.

Whole systems thinking, such as planning industrial decarbonisation in lockstep with grid reinforcement and gas network transition, is the route to achieving climate targets without compromising energy security or grid reliability.

For refineries, this is both a challenge and an opportunity. Legacy infrastructure and carbon-intensive processes pose significant hurdles, but the emergence of low-carbon hydrogen, synthetic fuels, and carbon capture technologies provide a clear pathway to a more sustainable future. Governments, investors, and consumers are pushing for change, while policy mechanisms such as carbon pricing and emissions regulations are accelerating the shift. The risk of inaction is growing and refineries that fail to adapt could face increased operating costs, regulatory penalties, and declining competitiveness in a carbon-conscious market.

Advanced technology providers with expertise in catalysis and process technology are delivering innovative solutions to help refineries decarbonise, transition to alternative feedstocks, and produce low-carbon fuels at scale.

The need for energy transition in refining

Refineries play a critical role in the global economy, supplying fuels, chemicals, and materials that power industries and transport networks. However, they are also among the largest industrial sources of GHG emissions. The petrochemical sector alone is the third largest industrial emitter of carbon dioxide (CO 2 ), largely due to its reliance on fossil-based feedstocks such as crude oil, natural gas, and coal. Governments worldwide are introducing stringent emissions regulations, carbon taxes, and incentives to drive the adoption of cleaner technologies. The EU’s Fit for 55 package and China’s 2060 carbon neutrality targets all signal an era of heightened regulatory scrutiny and financial incentives for decarbonisation. Yet beyond regulation, market forces are shifting as

consumers and businesses favour sustainable products. To remain competitive, refineries must take proactive steps, integrating alternative feedstocks such as biomass and captured CO 2 , deploying carbon capture and storage (CCS) technology, and investing in low-carbon hydrogen production.

However, the transition is not without challenges. Unlike the power sector, which can directly adopt renewable energy sources, refineries require solutions that maintain process efficiency, ensure energy security, and allow for gradual infrastructure adaptation. This is where innovation becomes critical.

Innovation in refinery decarbonisation

Proven at scale advanced reforming technologies and future technological innovations are central to the decarbonisation of the refining sector. There are already mature reforming technologies and providers are investing in further improvements and innovations that are delivering solutions to reduce emissions, improve efficiency, and enable the shift to cleaner feedstocks.

Advanced reforming technologies, such as JM’s LCH TM technology, which combines gas-heated reforming and auto-thermal reforming, can achieve up to 99% carbon capture efficiency and offers >15% feedstock efficiency compared to steam methane reforming. 1 This represents a significant advancement over conventional hydrogen production, offering a scalable and cost-effective way to support emission reductions in refining, industry, and hard-to-abate sectors.

Retrofit options are also gaining traction. Catalysts and modular systems that enhance heat transfer or reduce pressure drops are helping refineries to cut emissions without major capital investment. These technologies, such as JM’s CLEANPACE TM technology, allow facilities to modernise incrementally, while maintaining performance and reliability. Beyond hydrogen, the demand for sustainable fuels is also rising. Sustainable aviation fuel (SAF), known in the US as synthetic aviation fuel, is expected to meet 50% of aviation fuel demand by 2050, according to the International Energy Agency (IEA).

Technologies that produce syngas from captured CO 2 and green hydrogen, such as JM’s HyCOgen TM technology, are providing new pathways for low-carbon fuel synthesis. Using processes such as Fischer-Tropsch, this syngas can be converted into synthetic crude oil, and

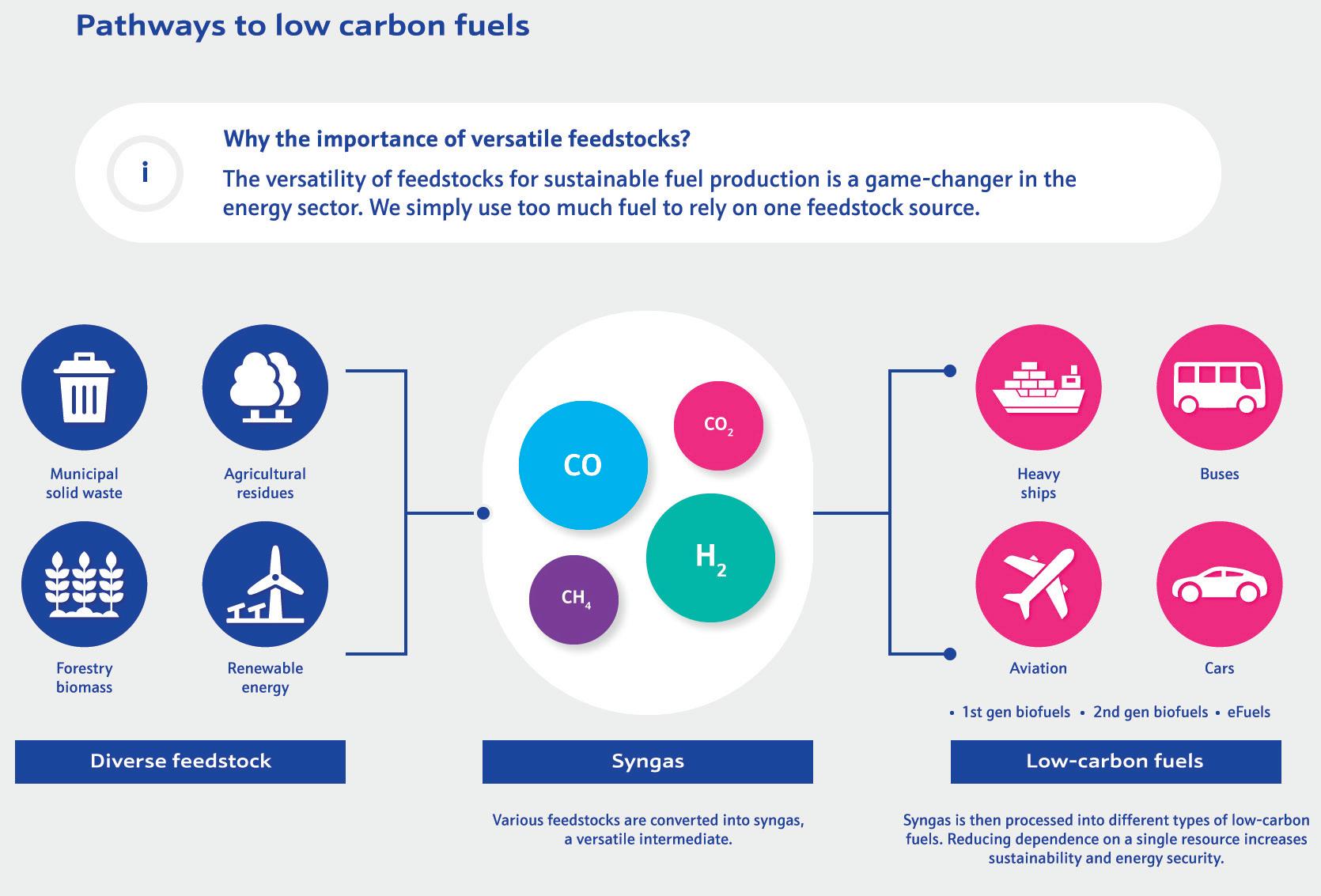

Figure 1. Feedstock versatility is critical to scaling sustainable fuel production.

subsequently into SAF and synthetic diesel: a particularly important step in decarbonising the transport sector.

Similarly, the production of e-methanol from CO 2 and green hydrogen is offering a viable alternative to fossil-based methanol in shipping and chemical applications. As the momentum behind power-to-liquid and e-fuel solutions grows, the availability of commercially deployable systems will be critical to enabling broad adoption.

Real-world applications: decarbonising refineries and beyond

These technologies are already being deployed in large scale decarbonisation projects worldwide. In the UK, the H2Teesside project is set to produce 700 MW of low-carbon hydrogen with 97% CO 2 capture, supporting industrial users in cutting emissions. Led by BP, this project is part of the UK’s broader net zero strategy.

In Spain, Repsol and Aramco are constructing one of the world’s first facilities to produce SAF using electrolytic hydrogen and captured CO 2 . This plant will begin with a production capacity of 2100 tpy of SAF, reducing emissions by 70% compared to conventional jet fuel.

Chile’s Haru Oni facility, developed by HIF Global, with Johnson Matthey and Siemens Energy as technology partners, is another milestone in scaling up e-fuels as an alternative to fossil-based transport fuels. By leveraging captured CO 2 and green hydrogen, the project demonstrates how synthetic fuels can complement the energy transition.

The economics of refinery decarbonisation

One of the biggest challenges facing refineries is ensuring the financial viability of transitioning to low-carbon solutions. While the environmental imperative is clear, business sustainability requires that decarbonisation efforts deliver long-term economic returns.

The initial capital outlay can be substantial, particularly for technologies like hydrogen production,

carbon capture, and synthetic fuel synthesis. However, this investment is increasingly offset by emerging financial incentives. Carbon pricing mechanisms, such as the EU Emissions Trading System, are making it more expensive to emit CO 2 , creating strong economic drivers for change. Meanwhile, governments across the globe are offering tax credits, subsidies, and concessional financing to support industrial decarbonisation.

Adding to these pressures are global policy developments that shape investment strategies. For example, recent US tariffs on Chinese clean energy technologies highlight growing geopolitical concerns over supply chain security and underscore the importance of developing domestic capabilities. These dynamics are reshaping how and where companies invest, particularly in strategic sectors such as hydrogen and synthetic fuels.

Within this context, low-carbon hydrogen emerges not only as a climate solution, but also as a significant economic opportunity. Forecasts suggest the global hydrogen market could reach US$1.4 trillion by 2050 2 , with industrial users driving much of the demand. Refineries that invest early in scalable hydrogen technologies will be well-positioned to meet both policy mandates and market expectations.

The future of refinery decarbonisation

The transformation of refineries is being driven by proven, at scale technologies together with continuous improvement and technological innovation, regulatory policies, and market dynamics. In the coming years, refineries have the option to increasingly integrate low-carbon and clean feedstocks such as biomass and CO 2 , expand their use of power-to-X technologies, and adopt modern catalyst solutions to improve efficiency.

Policymakers will also play a crucial role. Carbon border adjustment mechanisms, tax incentives, and government-backed hydrogen projects will influence the pace of refinery decarbonisation. Companies that act early will gain a competitive advantage, securing market share in the emerging low-carbon economy.

Ultimately, the refining industry is at a pivotal moment. Through advanced process technologies, strategic partnerships, and innovative catalysts, refineries can decarbonise their operations while maintaining economic viability.

Early adopters of low-carbon hydrogen, SAF, and other synthetic fuels will define the future of refining in a decarbonising world.

References

1. Based on a 355MW HHV Hydrogen capacity plant with amine carbon capture technology. SMR data source is IEAGHG Technical Report 2017-02. SMR & Carbon Capture data source is NETL Technical Assessment 2023-12.

2. ‘Green hydrogen: energizing the path to net zero’, Deloitte, (19 June 2023) https://www.deloitte.com/global/en/issues/ climate/green-hydrogen.html

Figure 2. Adapting to low-carbon pathways.

Howard Siew, BASF, USA, discusses how co-processing renewable and recyclable feedstocks can help to reduce the carbon footprint in FCC units.

As the global energy landscape shifts towards sustainability, the refining industry faces increasing regulatory and social pressure to lower its carbon footprint. Refiners become part of the process to balance supply of cost-effective energy, ensuring security of supply and improving the sustainability of its energy products. Fluid catalytic cracking (FCC), a key part of modern refining, is now at the forefront of this change. With rising regulatory demands, regional policy differences, and market incentives, refiners are looking into co-processing renewable and recyclable feedstocks in FCC units to cut greenhouse gas (GHG) emissions and support circular economy goals.

Market trends and regulatory drivers

The effort to reduce carbon footprints is driven by a convergence of global climate agreements, national policies,

and corporate sustainability goals. The Paris Agreements, the EU’s Renewable Directive (RED III)1, US Renewable Fuel Standard (RFS)2, California’s Low Carbon Fuel Standard (LCFS)3, and Canada’s Clean Fuel Regulations4 are among the primary frameworks encouraging refiners to implement low-carbon practices.

In Europe, RED III requires Member States to achieve either a 14.5% reduction in the greenhouse gas intensity of transport fuels or ensure that at least 29% of the energy used in transport comes from renewable sources by 2030.1 In the US, the RFS requires blending renewable fuels, and the LCFS promotes renewable fuel production and carbon intensity reduction, similar to Brazil’s RenovaBio programme, which is accelerating the adoption of renewable feedstocks and circular economy practices.

Together, these regulatory drivers are reshaping the refining industry, creating strong incentives for the integration of renewable and recycled carbon into existing infrastructure. Co-processing in FCC units provides a flexible and cost-effective pathway to meet these evolving requirements while maintaining operational continuity and product quality.

FCC units: role and carbon challenge

The FCC unit is a catalytic process that converts heavy hydrocarbons into lighter, high-value products like gasoline, diesel, and olefins. It typically processes vacuum gas oil (VGO), atmospheric residue, and other heavy fractions. However, FCC units are also major carbon emitters, contributing up to 30% of a refinery’s direct CO2 emissions, according to EPA.5 This is mainly because of carbon rejection, where the process inherently rejects carbon as coke, which is burned to regenerate the catalyst and provide necessary heat to the process, releasing CO2. This makes FCC one of the most carbon-intensive units in a refinery. Traditional fossil-based feeds are high in carbon and lack hydrogen, making it hard to reduce the carbon footprint without changing the feed or the process.

Making FCC more sustainable

Carbon capture at the regenerator stack

Technologies like BASF’s OASE® gas treatment system can capture CO2 from FCC flue gases. These captured emissions can be sequestered underground (CCS), used in chemical production (CCU), or converted into synthetic fuels or building blocks. While promising and proven, these solutions require significant capital investment and infrastructure.

Feedstock changes: co-processing renewables and recyclables

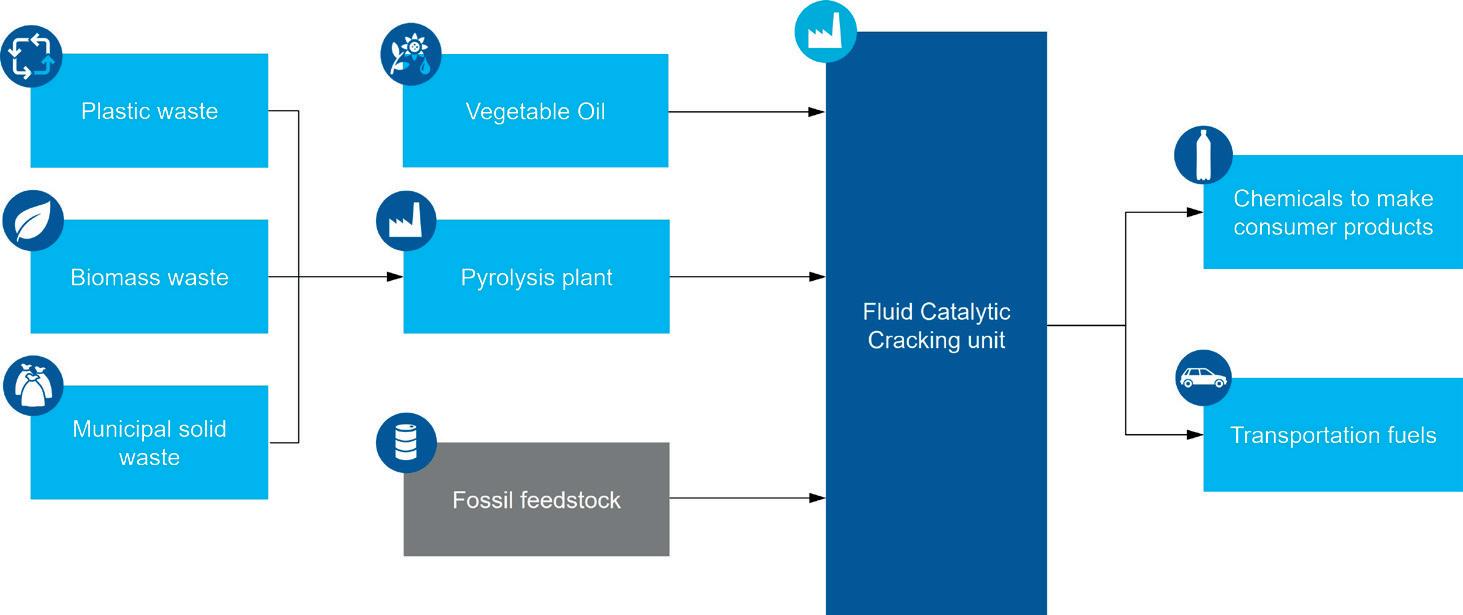

A more immediate and flexible approach to reducing refinery carbon intensity is the co-processing of renewable and recyclable carbon oils (RCOs) in the FCC unit (Figure 1). These RCOs include renewable feedstocks such as vegetable oils, used cooking oil, and animal fats, as well as recyclable streams like pyrolysis oils derived from waste plastics, biomass waste, and municipal solid waste (MSW). This strategy enables refiners to leverage existing FCC infrastructure while integrating circular and renewable carbon into fuel and chemical production.

Understanding renewable and recyclable feedstocks

Renewables

Renewable feedstocks are derived from biological sources and can be broadly categorised into two types:

n Plant and animal-based oils: these include different types of vegetable oil (soybean, rapeseed, corn oils etc.), used cooking oil, and animal fats. They are rich in triglycerides and typically contain moderate levels of oxygen (around 10 wt%) in the form of esters and carboxylic acids. While generally low in aromatics and coke precursors, they may contain alkali and earth alkaline metals such as sodium, potassium, calcium, and magnesium, which can impact catalyst performance and require pretreatment (e.g., degumming or adsorption).

n Biomass pyrolysis oils: produced from lignocellulosic materials such as wood, corn stover, and agricultural residues, these oils have a much wider and higher oxygen content (typically 40 - 45 wt%) and are chemically complex. They contain a wide range of oxygenated compounds including phenols, furans, ketones, and organic acids. These oils also tend to have high water content and may carry metal contaminants like iron, phosphorus, alkali, and earth alkaline metals, making them more challenging to process in FCC units without dilution or pre-treatment, such as mild hydrotreatment.

Recyclables

Recyclable feedstocks are primarily derived from plastic waste and vary in composition depending on the source and sorting process:

n Polyolefin-based plastics: plastics such as polyethylene (PE) and polypropylene (PP) are ideal candidates for pyrolysis due to their high hydrogen-to-carbon (H/C) ratio and low oxygen content. The resulting pyrolysis oils are predominantly aliphatic, with low levels of metals and heteroatoms, making them relatively easy to co-process in FCC units.

n Mixed plastic waste: these streams may include polyvinyl chloride (PVC), polyethylene terephthalate (PET), polystyrene (PS), and other polymers. Pyrolysis of such mixtures can introduce impurities such as chlorine (from PVC), oxygenates (from PET), and aromatics (from PS), which can lead to corrosion, catalyst deactivation, and increased coke formation. Effective sorting, pretreatment, or blending with cleaner feeds is often necessary to manage these risks.

Feedstock chemistry and crackability

The chemical composition of renewable and RCOs significantly influences their behaviour in

Figure 1. Enabling the partial replacement of fossil-based feedstocks with waste or renewable streams to ensure a sustainable future.

FCC units. The referenced study by Dorazio and Fu introduces a more FCC-relevant framework: a cross-plot (Figure 2) of effective hydrogen index (EHI) vs Conradson carbon residue (CCR).6 This approach effectively captures the upgradability of feedstocks in catalytic cracking environments.

The chemical properties of renewable and recyclable feedstocks significantly influence their behaviour in FCC units. Polyolefin-based plastics such as polyethylene and polypropylene exhibit a high EHI ~2.0 and very low CCR, making them ideal for FCC processing with high yields of LPG and naphtha and minimal coke formation. Plant-based oils like soybean or used cooking oil have a moderate EHI ~1.6 and low CCR, but their oxygen content requires deoxygenation during cracking, which produces water and carbon oxides and may necessitate pretreatment to manage metal contaminants. In contrast, biomass pyrolysis oils derived from sources like olive pits or wood have a low EHI ~0.6 (e.g., hydrogen deficiency) and extremely high CCR (up to ~20 wt%), making them the most challenging for the FCC. Their high oxygen and aromatic contents lead to increased coke formation and reduced conversion efficiency, often limiting their use to low co-processing ratios and requiring hydrotreatment or blending with conventional feeds.

These differences in feedstock chemistry directly affect how easily a material can be cracked and upgraded into fuels. Feedstocks with high EHI and low CCR are more compatible with FCC operations, offering higher yields and lower coke. In contrast, low EHI and high CCR feedstocks require careful blending, catalyst tuning, and operational adjustments to avoid performance degradation.

Operational impacts of co-processing

Contaminants

and metals

Renewable and recyclable feedstocks introduce a range of contaminants, as seen in Table 1,8 that can impact FCC catalyst performance and unit reliability. Biomass-derived oils and plant-based feedstocks often contain alkali and earth alkaline metals such as sodium (Na), potassium (K), calcium (Ca), and magnesium (Mg), which can poison active catalyst sites and reduce cracking efficiency. Similarly, plastic-derived pyrolysis oils

may carry chlorides (from PVC), heavy metals, or silicon-based compounds depending on the source and sorting quality. These impurities can lead to increased coke formation, corrosion, and fouling in downstream equipment. BASF addresses these challenges through a combination of adsorbent technologies for contaminant removal and advanced metal passivation strategies to help neutralise the effects of metals and extend catalyst life.7,8

Product yields and selectivity

The chemical nature of each feedstock influences product distribution. Pyrolysis oils from polyolefins (e.g., LDPE) are highly crackable and can yield over 90% conversion into valuable products such as gasoline, LPG, and light cycle oil (LCO) when processed with BASF’s FCC catalysts. Plant oils, while generally compatible with VGO, contain oxygen that must be removed during cracking, often resulting in increased water, CO, and CO2 formation, and potentially higher coke yields. Biomass pyrolysis oils are more complex, with high oxygen and aromatic content, requiring deeper deoxygenation and often resulting in elevated coke and gas production. BASF’s catalyst formulations are

Figure 2. Upgradability of various sustainable feedstocks defined in terms of effective hydrogen index and concarbon.

Table 1. Typical impurities and impact of sustainable feedstocks

Figure 3. BASF catalyst portfolio in FCCU co-processing.

designed to manage these trade-offs, optimising selectivity toward desired products while minimising operational penalties.7,9

Catalyst design and flexibility

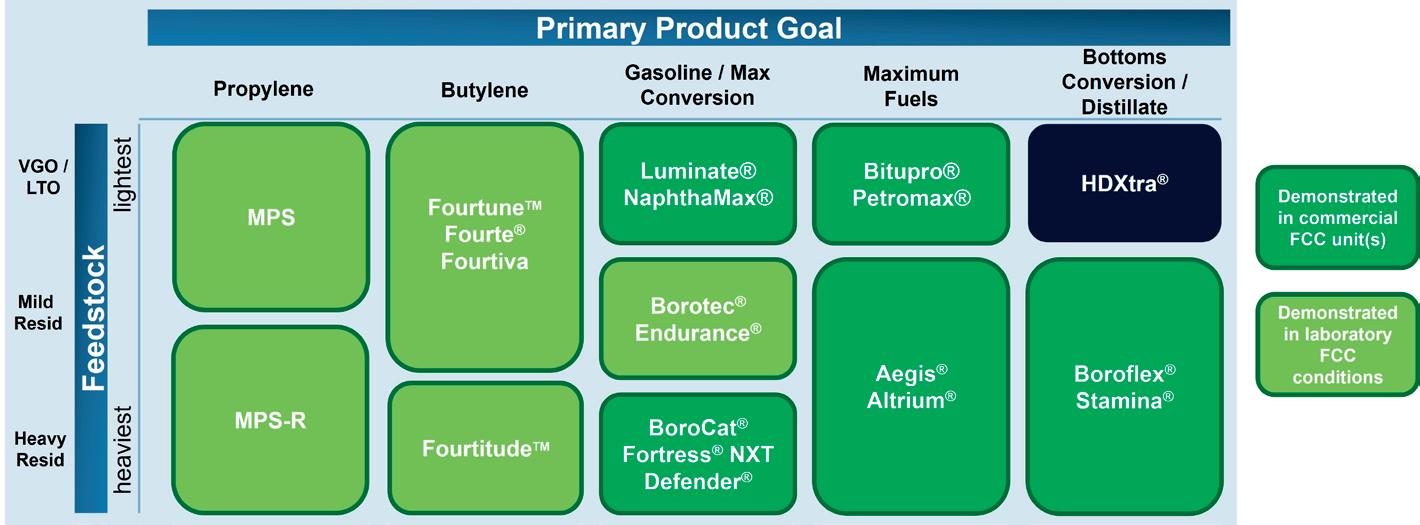

BASF’s FCC catalyst portfolio (Figure 3) is engineered to support the co-processing of a wide range of renewable and waste-based feedstocks. These catalysts are tailored to address specific challenges such as contaminant tolerance, coke suppression, and product selectivity. Whether the goal is to maximise LPG olefins, gasoline, or distillate yields, BASF offers solutions that have been validated in both commercial FCC units and laboratory scale testing. This flexibility enables refiners to adapt to evolving feedstock availability and regulatory pressures while maintaining operational efficiency and product quality.

Pyrolysis oil performance: case studies

Extensive lab-scale testing has demonstrated the strong potential of FCC units to co-process renewable and RCOs with high efficiency. In particular, pyrolysis oils derived from LDPE have shown exceptional crackability, with over 80 - 90% of the feed converted into upgradable products such as gasoline, LPG, and light cycle oil. Further, BASF’s FCC catalyst, specifically designed to maximise LPG olefins, achieved a combined 45.4 wt% yield of propylene and C4 olefins from waxy LDPE pyrolysis oil, demonstrating the ability to tailor product slates through catalyst engineering.7

In co-processing scenarios, studies have shown that blending 10% plastic-derived pyrolysis oil with conventional vacuum gas oil (VGO) had minimal impact on overall product yields and coke selectivity, indicating strong compatibility with existing FCC operations. Even more challenging feedstocks, such as biomass-derived pyrolysis oils from olive pits, were successfully processed when appropriate catalyst designs were used, and feed blending strategies were employed. An example study demonstrates the viability of co-processing biomass pyoil to produce gasoline blend stocks.10

These results underscore the FCC unit’s flexibility and robustness in handling diverse RCOs, provided that catalyst design and process conditions are carefully optimised.

Collaboration with technology licensors

Collaboration with technology licensors plays a critical role in enabling the successful integration of renewable and

waste-based feedstocks into FCC operations. By combining BASF’s catalyst innovation and operational guidance with licensors’ deep expertise in FCC process design, hardware configuration, and operational optimisation, refiners gain access to end-to-end solutions that address the unique challenges of co-processing. Such partnerships accelerate the industry goals of continuously increasing the processability of RCOs, ensuring that FCC units can operate reliably and efficiently while meeting sustainability and regulatory goals.8

Conclusion

FCC is no longer just a tool for maximising transportation fuels – it is becoming a strategic enabler of refinery carbon footprint reduction. By embracing co-processing, renewable feedstocks, and carbon capture when viable, refiners can transform FCC units into engines of sustainability, aligning profitability with planetary responsibility.

Co-processing renewable and RCOs in FCC units offers refiners a practical path to reduce carbon intensity and support circular economy goals. Regulatory frameworks like RED III, LCFS, and RenovaBio accelerate adoption, while BASF’s catalyst technologies enable efficient processing of diverse feedstocks – from polyolefin-derived pyrolysis oils to more challenging biomass oils.

Feedstock chemistry, particularly EHI and CCR, determines FCC compatibility. High-EHI, low-CCR feeds like LDPE pyrolysis oil yield high-value products with minimal coke, while biomass oils require careful blending and pretreatment.

Lab studies confirm that with the right catalyst and process design, FCC units can co-process up to 10% RCOs with minimal impact on yields or coke. Collaborations among refiners, licensors, and catalyst providers can further support industry goals with integrated solutions for reliable and sustainable FCC operations.

References

1. Directive - EU - 2023/2413 - EN - Renewable Energy Directive - EURLex, https://eur-lex.europa.eu/eli/dir/2023/2413/oj/eng

2. US EPA Reformulated Fuel Standards, https://www.epa.gov/ renewable-fuel-standard

3. California Renewable Standard Eligibility Guidebook, Ninth Edition (Revised), https://efiling.energy.ca.gov/getdocument. aspx?tn=217317.

6. DORAZIO, L., and FU, J., ‘Transforming refineries’ opportunities through FCC’, Digital Refining, (2023).

7. MASTRY, M.C., DORAZIO, L., FU, J., GÓMEZ, J.P., SEDANO, S., AIL, S.S., CASTALDI, M.J., and YILMAZ, B., ‘Processing renewable and wastebased feedstocks with fluid catalytic cracking: Impact on catalytic performance and considerations for improved catalyst design’, frontiers, (2023).

8. VINCENT, G., RIVA, S., BARRIOS, F., DUBOIS, F., and GOLCZYNSKI, S. ‘Tackle operational challenges with FCC coprocessing applications’, Hydrocarbon Processing, (2024).

9. VINCENT, G., and KHAZRAIE, T., ‘Chemical recycling of waste plastics: The role of catalysts’, decarbonisation technology, (2024).

10. LUTZ, H., BÜCHELE, M., FLORIAN, K., REICHHOLD, A., VOLLENHOFER, W., and VENDERBOSCH, R., ‘Wood Derived Fast Pyrolysis Bio-liquids as Co-feed in a Fluid Catalytic Cracking Pilot Plant’, ACF, (2022).

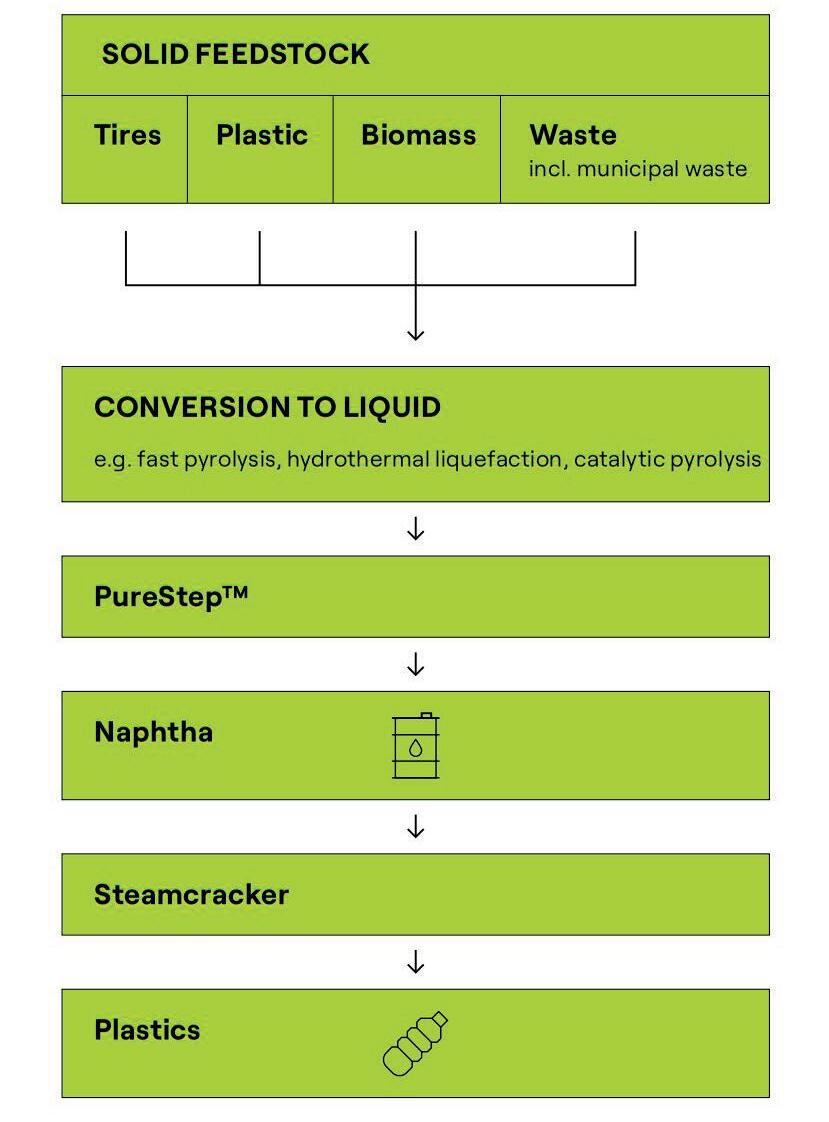

Milica Folić, Topsoe, considers how to enable scalable chemical recycling of plastic waste to create drop-in naphtha.

The shift towards a circular plastic economy has underscored the need for chemical recycling of mixed plastic waste so it can be turned into high-quality, contact-sensitive, and other plastic products. However, the diverse composition of plastic waste and variability of liquefaction methods makes upgrading essential to ensure not only drop-in naphtha quality for steam crackers but to also absorb all the fluctuations in the feedstock quality.

This article will consider these challenges and introduce a technology – developed through over 60 pilot tests on various plastic pyrolysis oils – that delivers on-spec naphtha and heavier steam cracker feedstocks. PureStepTM combines in-depth analysis, decades of hydroprocessing expertise, and tailored solutions for handling specific contaminants like silicon and others. Topsoe’s analytical techniques revealed that major

impurities are not confined to certain boiling fractions, guiding targeted catalyst and process design.

PureStep adapts to different liquefaction technologies and oil qualities, offering the flexibility and robustness needed in chemical recycling. By 2025, the technology had entered commercial operation at two plants. Early insights from these deployments highlight its potential to transform mixed plastic waste into high-value feedstocks, supporting a sounder plastics value chain.

The three Rs

The linear plastic economy, particularly the rise in single-use plastics, has led to rapidly growing plastic waste streams across the globe. The average global recycling rate was just 9.5% in 2020 and according to OECD numbers, global production and use of

plastics will hit 736 million t by 2040, up a massive 70% from 435 million t in 2020.1 The OECD goes on to note that without major change “recycled plastics will continue to make up a mere 6% of all plastics produced in 2040.”

The current landscape and outlook for plastics reveals damaged ecosystems but they also represent a massive missed economic opportunity.

Addressing plastic waste requires a range of solutions that target the problem from multiple angles. These can be broadly grouped into the three Rs: reduce, reuse, and recycle. Reducing involves cutting down on plastic use and minimising how much plastic is used in products from the outset. Reuse focuses on extending the life of products and preventing them from becoming waste prematurely. Recycling, the focus of this article, aims to recover used plastics and convert them into new materials, closing the loop and reducing reliance on virgin plastics.

Mechanical and chemical plastic recycling

Plastic recycling follows two complementary paths: mechanical and chemical. Mechanical recycling works best with clean, sorted, single-polymer waste, such as PET bottles. While this method can produce high-quality products like new bottles and typically has low energy consumption, it has limitations. Each recycling cycle typically lowers material quality, over time leading to downcycling – turning food packaging into lower-value items like textiles or garden furniture.

Chemical recycling, on the other hand, is better suited for mixed and contaminated plastic waste, such as household packaging. It breaks down polymers and removes impurities, producing feedstocks that can be used to make new, virgin-quality plastics – including food – and pharma-grade plastic materials.

Thermochemical liquefaction processes like pyrolysis and hydrothermal liquefaction (HTL) convert solid waste into plastic pyrolysis oil (PPO), a liquid somewhat similar to fossil feedstocks. However, raw PPO contains high levels of contaminants such as metals, halogens, and heteroatoms, which prevent its direct use in steam crackers without extreme dilution and fluid catalytic cracking (FCCs) without dilution.

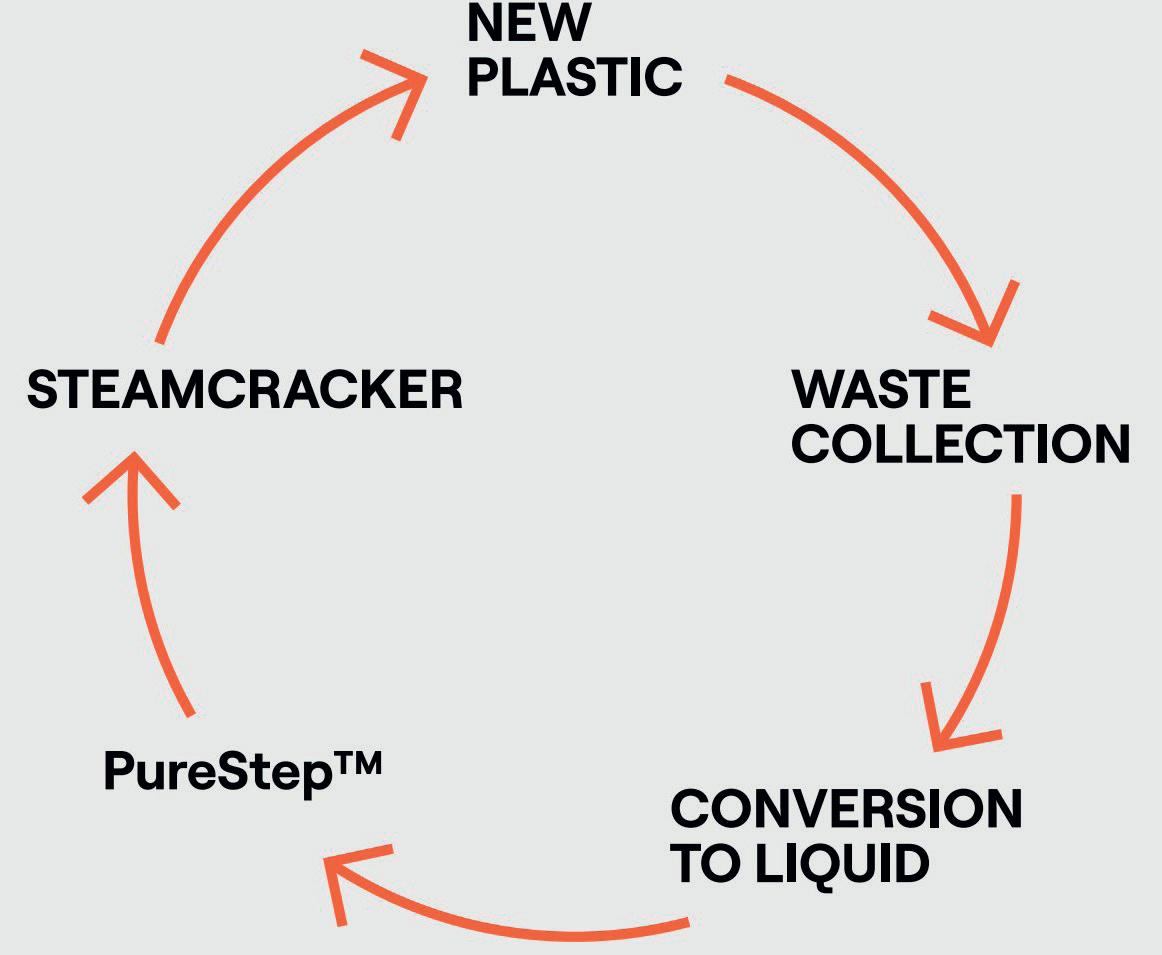

To enable larger scale recycling and reduce reliance on virgin fossil carbon, PPO needs to be upgraded. That is where Topsoe’s PureStep technology comes in. This hydroprocessing solution removes contaminants and adjusts key properties, transforming raw PPO into high-quality feedstock for steam crackers. It closes the quality gap, unlocking higher recycling rates and supporting a circular, recycled-carbon plastics economy.

PPO: a new opportunity

PPOs are emerging as a viable feedstock for the refining and petrochemical industries. Topsoe began working with PPOs in 2014, leveraging decades of hydroprocessing experience to meet growing demand for sustainable feedstock solutions. Upgrading PPOs into drop-in naphtha aligned with the company’s expertise in developing tailored technologies for lower environmental impact.

PPOs share some characteristics with traditional fossil and non-fossil feedstocks, but they also differ in key ways. For instance, they have similar hydrogen content to straight-run diesel but significantly more nitrogen and less sulfur. Compared to tyre-derived oil (TDO), PPOs are less aromatic and contain fewer impurities, resulting in lower hydrogen consumption during processing – both an economic and environmental benefit.

While PPOs are not identical to other feedstocks, their manageable impurity levels make them a strong candidate for hydroprocessing. They offer a promising starting point for customised upgrading solutions that align with circular economy goals and reduce carbon intensity.

Understanding variability

PPOs contain contaminants also found in fossil feedstocks –such as silicon, phosphorus, nitrogen, sulfur, oxygen, and halogens – but in different molecular structures and concentrations. This is due to the very different origin of contaminants, which in plastics is related to their content of

Figure 1. Circular plastic economy with Topsoe’s PureStep technology.

Figure 2. PureStep recycling.

Table 1. Comparison of raw PPO properties with naphtha specification desired for steam crackers: upgrading is needed to close the gap

Property Unit Mixed waste PPO

Final boiling point (FBP)

°C (°F)

400 - 500 (752 - 1022)

Typical naphtha steam cracker feedstock

150 - 250 (302 - 482)

Olefins wt% 40 - 70 <1

Aromatics wt% <20 <10

Sulfur wt ppm <200 <500

Nitrogen wt ppm <2000 <5

Oxygen wt ppm <5000 <25

Halogens wt ppm <700 <3

Total metals wt ppm <200 <1

additives and residues, including stabilisers, flame retardants, adhesives, and post-consumer waste.

Because of this, conventional hydroprocessing must be adapted and optimised. Tailored catalyst development plays a key role, especially for targeting specific contaminants. Some PPOs are also prone to polymerisation and require early stabilisation before hydrotreating (something that can be established via analysis).

To effectively process PPOs, a broad understanding of their variability is essential. This includes sourcing samples from various liquefaction technologies and suppliers and going beyond bulk analysis to identify specific contaminant species.

Successful technology development relies on integrating deep analysis with catalyst design and pilot testing. Building a comprehensive database of results enables faster identification of known patterns and focuses efforts on new challenges –laying a strong foundation for reliable, scalable PPO upgrading solutions.

Targeting naphtha from PPOs

PPOs differ significantly from standard naphtha feedstocks used in steam crackers. A key challenge is that more than 50% of PPO content typically boils above 200°C – well outside the acceptable range for naphtha. For instance, a typical PPO may contain 60% heavy fractions. To meet steam cracker boiling specifications, hydrocracking can be added to Topsoe’s PureStep process to reduce the final boiling point.

Another critical issue is contaminant distribution. A fractionation study on full-range PPOs revealed that contaminants like silicon and chlorine are not isolated in heavy fractions but are spread throughout the boiling range – from light naphtha to vacuum gas oil (VGO).

Some have suggested fractionation alone could remove silicon or chlorine. However, results show that even individual cuts contained 30 - 60% of the total silicon and varying chlorine concentrations, making simple separation ineffective. Combined with the ability to correct the boiling point, the deep contaminant removal allows the whole PPO fraction to be converted into the steam cracker feedstock. These are key elements built into the PureStep approach, enabling the processing of the whole range.

Catalyst development for pyrolysis oils

While fossil-based catalysts can be used for circular feedstocks like PPOs, tailored catalyst development delivers significantly better performance. Contaminants such as silicon and phosphorus originate differently in PPOs than in fossil or bio-derived oils, requiring custom solutions.

Advanced analysis, including SEM imaging, shows that standard fossil catalysts only absorb contaminants near the surface, underutilising the catalyst volume. In contrast, Topsoe’s next-generation guard catalyst, optimised specifically for PPOs, enables full cross-sectional uptake of silicon and phosphorus, significantly increasing capacity.

This tailored catalyst also offers moderate hydrotreating activity – helpful for removing nitrogen and chlorine and reducing coke formation, which can deactivate the catalyst. By combining deep feedstock understanding with targeted formulation, Topsoe maximises catalyst efficiency and reactor utilisation in PPO upgrading.

A flexible solution for upgrading PPOs

Topsoe’s PureStep hydroprocessing technology offers flexible, tailored solutions for upgrading PPOs to steam cracker-ready feedstock. It combines key ‘building blocks’ – optional stabilisation, guard beds with customised catalysts, hydrotreating, and optional hydrocracking – based on feedstock characteristics and product goals.

Typically, at least two blocks are used to address PPO reactivity, contaminants, and boiling point. This enables high recycled content in cracker feed while ensuring smooth operation of existing assets.

PureStep efficiently upgrades the full PPO range, boosting circularity and reducing environmental impact.

Scaling recycling with hydroprocessing

Topsoe has nearly 30 years of experience analysing and upgrading non-fossil feedstocks, from bio-based oils to today’s PPOs. So far, efforts have focused on meeting contaminant limits for cracker feedstocks. Now, the company is expanding this scope through collaboration by studying how hydroprocessed PPOs affect steam cracker performance and yields. This feedback loop is essential for refining both catalyst and process design. PureStep has already been commercialised, with two industrial units in Europe having started up in 2024 and 2025. Operational data from these sites will guide further innovation.

Chemical recycling via pyrolysis is poised to play a key role in the circular economy by supplying recycled feedstocks to existing cracker infrastructure. Hydroprocessing is essential for scaling this value chain – offering compatibility with refinery assets, enabling revamps, and improving economics through higher PPO utilisation.

Challenges remain in scaling pyrolysis and reducing system costs, but momentum is building through industry collaboration and growing investment. As technologies mature and volumes rise, hydroprocessing is set to become a reliable, robust enabler of circular plastic production.

Reference

1. ‘Policy scenarios for eliminating plastic pollution by 2040’, OECD, (2 October 2024).

The concept of chemical recycling

Chemical recycling, also known as advanced recycling, involves transforming plastic waste into monomers, fuels, or other chemical feedstocks. This process helps overcome limitations associated with mechanical recycling, such as contamination issues and the inability to process multi-layered or complex plastics.

There are several chemical recycling techniques. Two of the most common and reliable are:

n Pyrolysis: thermally decomposing plastic waste in the absence of oxygen to produce liquid hydrocarbons, which can be used as fuels or feedstocks for new plastics.

n Gasification: converting waste into syngas, which serves as a building block for fuels, chemicals, and even hydrogen production.

Each of these processes plays a crucial role in addressing the plastic waste crisis while contributing to the circular economy by ensuring materials remain in productive use for as long as possible.

Chemical recycling and the circular economy

The circular economy model aims to eliminate waste by keeping materials in continuous use through recycling, reuse, and remanufacturing. Chemical recycling aligns with this vision by:

n Closing the circle on plastic waste: it allows end-of-life plastics to be reintroduced into the production cycle, reducing dependence on virgin materials.

n Enhancing resource efficiency: by converting waste into valuable chemicals and fuels, chemical recycling maximises resource utilisation.

n Reducing environmental footprint: chemical recycling can help decrease carbon emissions and landfill dependency by diverting non-recyclable plastics from waste streams.

n Fostering industrial symbiosis: chemical recycling facilitates collaboration between industries, where waste from one sector can become a resource for another, thereby optimising material flows and reducing overall environmental impact.

However, the integration of chemical recycling into waste management systems requires innovative technologies, regulatory support, and industry collaboration.

A commitment to sustainable waste treatment

To be at the forefront of sustainable waste treatment, companies should offer customised solutions for industries looking to reduce emissions, optimise waste valorisation, and achieve regulatory compliance. Expertise should span across various industries, including chemical, petrochemical, pharmaceutical, and oil and gas, where waste management is a critical concern.

Approaches to chemical recycling

Companies should employ a mixed strategy to implement chemical recycling within industrial waste treatment systems:

n Customised technology integration: design and install tailored chemical recycling solutions, integrating pyrolysis, gasification, and other techniques into existing waste treatment infrastructure.

n By-product recovery and valorisation: beyond waste elimination, emphasise the recovery of valuable by-products, such as synthetic fuels, hydrogen, and chemical precursors, to enhance economic and environmental benefits.

Figure 2. Chemical recycling fosters industrial symbiosis.

Figure 1. Plastic waste can be transformed into second-generation plastics.

n Regulatory compliance and sustainability optimisation: with global regulatory frameworks tightening around waste management, it is necessary to ensure that solutions align with international environmental standards, including the European Green Deal and UN Sustainable Development Goals (SDGs).

n Collaborative industry partnerships: actively collaborate with waste management operators, project developers, project management companies, and industrial partners to develop scalable chemical recycling projects that drive systemic change towards sustainability.

Case study: chemical recycling solutions in action

A notable project, from Tecam, is a waste-to-fuel chemical recycling plant in the south of Spain where Tecam has just finished the FEL3 engineering phase. Through the implementation of an advanced pyrolysis unit, Tecam enables the conversion of plastic residues into pyrolysis oil, that can be later transformed into biofuel and other chemical by-products. This project not only eliminates plastic waste but also creates new raw materials, aligning completely with circular economy principles and constituting itself as a sustainable and economically viable solution.

The economic and environmental benefits of chemical recycling

Beyond the direct waste treatment advantages, chemical recycling brings significant economic and environmental benefits: