Did eight banks really take the SBP and the government for a ride?

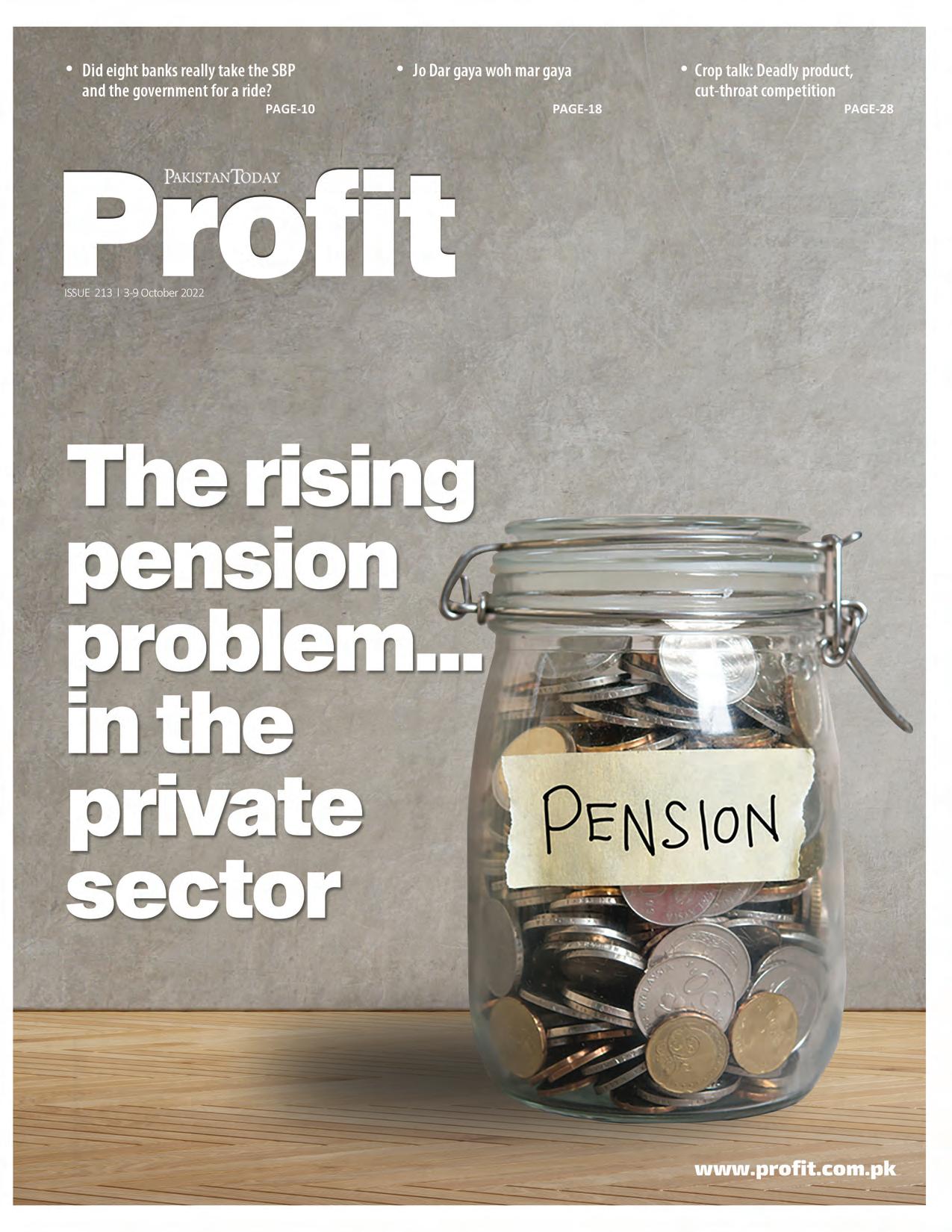

The rising pension problem… in the private sector

Jo Dar

woh

How digitalisation kept aid coming to flood-hit Pakistanis

Will Dar recognise the limits of his

Publishing

Niazi

Babar Nizami

Sabina Qazi

Multimedia: Umar Aziz

Chief

Editor: Yousaf Nizami

Sub-Editors: Mariam Zermina

Talha Farooqi

Basit Munawar

Fawad Shakeel

Ariba Shahid

Aziz Buneri

Shahab Omer

Maliha Abidi

Ghulam Abbass

Ahmad Ahmadani Shehzad Paracha

Daniyal Ahmad

Ahtasam Ahmad

Staff: Maliha Abidi - Regional Heads of Marketing: Mudassir Alam (Khi)

Asad Kamran

Zufiqar Butt (Lhe)

Economic & Financial news by 'Pakistan Today'

profit@pakistantoday.com.pk

Malik Israr (Isb)

10 10

12

16 16

gaya

mar gaya 23

24

power? Khurram Husain 24 24 The economy of eating right Femme Finance 31 Crop talk: Deadly product, cut-throat competition 16 08 12 CON TENTS

Editor:

- Joint

Assistant Editors: Abdullah

I

-

|

Editor

- Video Editors:

I

Reporters:

I Taimoor Hassan l

l

l

l

|

|

|

|

of

|

|

Business,

Contact:

Profit

Did eight banks really take the for a ride? SBP and the government

By Ariba Shahid

By Ariba Shahid

don’t know if the air conditioning was working at the State Bank of Pakistan (SBP) in late September, but the bank treasurers that were filtering in and out of the central bank’s offices during this time all came out sweating.

Eight major banks went through a dimly-lit interrogation at the hands of the SBP after being issued show-cause notices for allegedly manipulating the foreign exchange markets. As the treasury homeboys shuffled into the SBP to offer their explanations to the regulator they were given a dressing down that all but sent them to bed without dessert.

“About eight banks have been summoned so far,” whispers an informed source at the SBP on condition of anonymity. “Treasurers and their teams were getting earfuls from the Supervision Group Directors,” he adds softly. This chewing out allegedly went on for 45 long and very painful minutes. The SBP, it turns out, was being taken for a ride. It is these just these banks, he illustrates holding up eight fingers, that have been called in. “Banks had charged excessive premiums where the spread had be come significantly higher than normal.” Their

names, however, remain a mystery for now.

WeThe first inklings that there was something afoot came when the now erstwhile finance minister, Miftah Ismail, announced that the SBP had issued a show-cause notice to banks over currency-speculation allegations. The SBP was looking to investigate banks that had opened letters of credit (LCs) at higher rates than the spot rate. The banks have auton omy over how and when they issue their LCs, but since the SBP regulates these banks they get to determine the rate of exchange at which these LCs work.

“While banks are not required to run losses, they are regulated by the SBP and have to follow banking regulations. If you’re manipulating the market, action should be taken - even PM Sharif has asked for strong action,” Ismail told Profit. This comes at a time when the rupee has shed nearly 60% of its value in absolute terms in the calendar year to date.

What do the rules say?

Itis a question of dollars. When two trading partners engage in a deal and there is a lack of trust between the two parties, they ask banks to act as the middleman. In short, the bank issues a letter of credit to the person selling their goods, saying that they will bear the risk if the person buying defaults

on the payment. This normally happens in particular on the trade of natural resources such as oil and LNG. Banks make money off of these transactions, but they are also bound by what is known as a spot rate — which is the price quoted for the immediate settlement of a commodity or for the rate of exchange.

To put it even more simply, banks rely on LCs to make money on the foreign exchange market. However, they are restricted by the spot market and exchange rates which are set by the SBP. That is where they have allegedly been trying to run circles around the SBP.

As per chapter 2 of the FE Manual issued by the SBP, banks are barred from charging more than a defined margin set by the SBP. In point number 11 of chapter 2, the SBP states the Authorised Rates of Foreign Exchange. If you explore the manual further or have industry experts comment on it, they will tell you that Section 4(2) of the Act states that unless otherwise directed by the SBP, authorised dealers, authorised money changers and exchange companies are free to determine exchange rates for the conversion of Pakistani currency into any foreign currency or vice versa.

The SBP has granted general permission to authorised dealers which enables them to determine their own rates of exchange, both for ready and forward transactions for the public. This, however, is subject to the condition that the margin between the buying and selling rates should not exceed 50 paisas per US dollar or its equivalent in other currencies.

Now here’s the sticky wicket. Market sources anonymously reveal that the spread between the margin exceeded 50 paisas and had in some cases jumped well above Rs2. In fact, it had even gone up to Rs5. This news has spread both far and wide.

An SBP spokesperson says that the permission granted to authorised dealers to set their own rates of exchange do not apply to inter-bank transactions. “The show cause notice that the SBP has taken is primarily over the previous drastic slump in the PKR. Businesses had also come out complaining against the spread banks charged while retiring LCs. Following this, the SBP went on to investigate. They have sent a show cause notice to eight banks. I do not know the name of those banks nor did I ask,” adds Ismail.

When questioned about the banks’ ac tions, he was non-committal; “It is premature to say that the banks were right or wrong, an investigation is being done by the SBP. Banks are stating their stance.”

On the defensive Banks

were obviously defensive. Sourc es refusing to be named state that the dollar liquidity was extremely low at the time and the reason was that they

Is this a case of collusion, greediness, weak positioning, or all of the above?

10

were buying dollars at expensive rates in the interbank to deal with import transactions. In order to offset their losses, the banks engaged in such acts. A treasurer at a leading bank, also requesting anonymity, added, “At the end of the day, my job is on the line if I don’t make the bank money.”

Another source candidly admitted that banks felt they would be able to get away with it, considering the rarity of the situation and the circumstances they were in. But “Anything that goes against the market trend is investi gated,” said a source in the SBP, so how could they have ever thought they could swing it is the 64-million-dollar question.

To put this in perspective, we will compare the FX earnings banks accumulated in the calendar year 2021 vs just the second quarter of CY2022. In the span of three months, HBL was able to make 95% of the total it made in CY2021. Allied Bank was able to make 180%, meaning it not only made the same amount it did in 2021 but also almost doubled it within the span of a quarter. While not all FX income is made from these premiums, the fact that premiums did shoot up, the rupee shed value, and the banks have increased their FX earnings does raise lots of eyebrows.

An industry expert has an interest ing take on what has happened. “It felt as if the banks had colluded together. In normal circumstances, they compete with each other over providing the best rates possible to clients. However, following instructions to incur losses, it looks like banks went rogue, just in a different way.”

meeting with the treasurers of the eight to 10 leading banks in the coun try. Again, names are shrouded in mystery and people present do not want to say anything on record. But what we do know is that the room was extra chilly that summer afternoon and what transpired is that bank treasuries were called to the SBP because the finance ministry expressed displeasure with the borrowing rates and the current exchange rate. Banks were then cautioned, almost in cold blood, on their FX activities and told to bring the exchange rate down in the interbank even if it meant incurring losses. They were told that it was an issue of national importance and that incurring losses was part of having the privilege of running banking businesses.

A source present at the meeting anon ymously explained that the SBP had asked banks to sell dollars to customers without being allowed to buy them back from the inter bank market. This exposes banks to changes in the FX rate, which could also mean a potential loss of money for them. Moreover, bank treasurers present in the meeting were warned that if banks did not comply, bank presi dents would be called in for a one-on-one meeting for a severe “dressing down” by the SBP.

commercial banks based on the USD deposits put in by customers, said investment banker, Fahd Sheikh.

While it is unknown how much exactly is undertaken through swaps, market sources claim it would be around $4 billion at the moment. For context, the SBP’s forward liabil ities on June 30, 2019 were $8 billion, and $5.8 billion in 2020, added Sheikh.

This implies that the SBP is a net borrower of FX from commercial banks. This also means the SBP should not be calling the kettle names. It is not in as strong a position to dictate terms to commercial banks today as it was during, let’s say, Feb-2020 when it was a borrower of only $2.8 billion from commercial banks. Maybe some retrospection along with a little bit of introspection would be helpful. n

“The profits from these acts are greater than the fines imposed. At the end of the day, banks think about what maximises their earnings,” says a source at the SBP. This could explain why banks would take such a risk.

There is more to it, of course. The first rule of business is to never show all your cards, especially not early in the game. The govern ment and the SBP seemed quick to do so. In December 2021, the term Koonda went viral after Shaukat Tarin threatened banks regarding their bids in the market treasury bills and Pakistan investment bonds auctions. Despite the threat of an action, banks nonchalantly continued as normal, and even pushed yields up.

Expecting banks not to be greedy is naïve. However, expecting them not to be greedy after showing a weak position is like expecting snow in Karachi.

In June 2022, the SBP held a top secret

Now, some months later, and despite the above-men tioned actions, almost the stuff of night mares, hearing the minister complaining about banks seems mind-boggling.

Has the government revealed itself to be in a weak position?

The SBP, on the other hand, has borrowed FX from the interbank market. It has undertaken FX swaps with com mercial banks which means that it is borrowing USD from

Why did the banks think they could do this?

BANKING

12

By Farooq Tirmizi

Ignorea problem in your business long enough, and eventually, the long-term liability becomes a short-term cash outflow. That, it appears, is what is happening to Corporate Pakistan when it comes to retirement liabilities, with the energy, textile, and petrochemical sectors especially vulnerable.

According to an analysis conducted by Elphinstone Pakistan, a securities advisory company that specialises in com pany retirement plans, a majority of companies in the country have retirement expenses and obligations to their employees that have been growing faster than their revenues for much of the past decade, and if left unchecked, will drastically cut into operating profit margins at many companies.

To put it in concrete terms, total retirement liabilities for Pakistani companies have grown from 6.5% of operating profits in 2014 to 9.4% of operating profits by 2020, an alarm ingly fast rise that is likely to have a significant impact on the financial health of most companies.

CORPORATE FINANCE

In this story, we will examine just how bad the problem is, and which companies and sectors have a worse problem than others. We will take a look at how we got to this mess, and the role played by the labour and tax law in Pakistan in creating this problem. Finally, we will examine potential solutions companies might be able to adopt.

(Disclosure: the author of this story is the CEO of Elphinstone, a financial advisory firm that helps set up and administer retirement funds for companies and their employees.)

The scale of the private sector retirement problem

Employeeretirement obligations are a bigger problem than you think. For the 414 publicly listed companies included in Elphinstone’s analysis, the total amount of retirement obligations as of the end of financial year 2021 were Rs 651 billion, or about Rs 937,000 per employee. Even if one excludes some of the government-backed companies – which have excessively onerous pension obligations – the amount of corporate retirement liabilities comes out to Rs 565,000 per employee at the end of 2021.

More importantly from the perspective of companies, this is a problem that is not just big, but growing at a rate faster than most com panies’ ability to pay for it. For the seven years between 2014 and 2021, company spending on retirement obligations towards their employees has grown, on average, 400 basis points faster than revenue growth, for the publicly listed companies included in Elphinstone’s analysis. (One basis point is one-hundredth of one percent.) So, for example, if revenue has been growing at the average company at 10% per year, their retirement spending has been growing at 14% per year.

And in case you are a smart CFO who thinks: “Well, there is a difference between when a liability is incurred and when I actually have to pay it,” the above statistic is not about liabilities. It is about actual cash outflow for a company or the portion of the liability that has actually come due in the relevant year. Liabil ities have been growing slightly faster: about 470 basis points faster than revenue between 2014 and 2021, according to the analysis of publicly listed companies.

Indeed, the relatively narrow gap between the growth rate for liabilities and the growth rate for actual cash paid suggests that many Pakistani companies – particularly those that have been in business for a few decades –have hit a tipping point where their long-serving employees have begun to retire and are now owed those large sums of money that the company has previously been recording as a

liability on its balance sheet.

This problem is particularly acute for some sectors. For refineries, for example, retire ment expenses have been growing at an average of 21% per year faster than revenue growth. For automobile parts manufacturers, it is a nearly 16% per year average over and above revenue growth. For these companies, retirement spending as a percentage of revenues will dou ble in less than five years. For the textile sector, fertilisers, power generation and distribution, and oil and gas companies, retirement expenses will double as a percentage of revenue over the next six to 10 years.

The problem that companies had been kicking down the road, in other words, is here. This is not a problem that will occur in the future. It is a grenade whose pin was taken out a few years ago and which is about to go off on the income statements of most large companies in Pakistan.

This then begs the question: How exactly did we get to this point? Why was this problem allowed to grow for so long? As in most cases, the answer lies in the system enforced on the corporate sector by the government.

Laws governing company retirement plans in Pakistan

Thestory of how and which kinds of retirement benefits are paid to employees in Pakistan starts with the British Raj, though it was a somewhat unintentional beginning.

In 1925, the British Parliament passed a series of laws that would affect governance in British India, and one of the acts in question was the Provident Fund Act of 1925. In its original form, the law was meant to provide retirement security to the employees of the British Indian government and autonomous government agencies controlled by it, such as the railways.

It was an attempt to provide retirement security to Indians in the same way the British government was doing at home with its own citizens, through the Old-Age Pensions Act of 1908. Like most retirement benefits designed at the time, however, its recipients were a limited set of people. In the case of the UK, it was only people who reached the age of 70 (which was a miniscule percentage of the old-age population back then), and in the case of British India, it was restricted to government and quasi-gov ernment employees.

The government Provident Funds established in 1925 were later supplemented with pensions that were completely separate from them and, over time, came to be the dominant form of retirement benefit for government employees. (The problem of ballooning pension

liabilities in the public sector is, by now, a well-documented phenomenon, with Khyber-Pakhtunkhwa Finance Minister Taimoor Khan Jhagra in particular championing reform.)

Soon after the 1925 act, however, the Provident Fund came to be seen as a retirement vehicle that many formal sector employers started using, although from the 1920s through the 1950s, there were not very many employers who were formal sector employers to begin with.

Companies did not offer a Provident Fund out of the goodness of their heart, of course. They offered it owing to a patchwork of legal cases that were brought forth by old, retiring employees that stated that they were owed some form of end-of-service benefit, which courts in British India would recognize – and call Gratuity – in a very haphazard and unpredictable manner. The one bit of predict ability: If a company had a Provident Fund, it was not obliged to pay Gratuity.

After independence in 1947, this largely ad hoc set of arrangements – formalised only for government and public-sector employees –continued, since it affected an almost minis cule proportion of the labour force that was employed by formally incorporated companies that wanted to protect themselves from em ployee lawsuits.

By 1968, however, the formal sector of Pakistan had grown considerably. The Ayub Khan Administration’s famous five-year plans were producing industrial growth and encour aging many previously informal businesses to incorporate and causing the already incorpo rated businesses to expand their labour force rapidly. The question of what was to become of private sector employees in their old age was no longer one that concerned only a small handful of people.

And so, that year the government of Pakistan enacted what became known as the Industrial and Commercial Establishments (Standing Orders) Ordinance, 1968, which laid out many protections for employees, including end-of-service benefits (not just retirement), which included formalising the arrangement that employers previously followed: Gratuity was defined as the default benefit, but was legally substitutable with a Provident Fund. Employers could provide one or the other but were not legally mandated to provide both.

Gratuity was initially defined as roughly half the employee’s last month’s salary multiplied by the whole number of years they had worked at the company. Contrary to common misconceptions, gratuity is owed to any employee who has been at a company for one year or more (in the case where gratuity is the only end-of-service benefit offered). In 1973 the law was amended to make it two-thirds of a month’s salary multiplied by the number of years, and by 1994, it was increased to the

14

employee’s last full month’s salary multiplied by the number of years they had worked at a company.

(Yes, our jiyala readers, both increases in gratuity were enacted into the law during Pakistan Peoples’ Party (PPP)-led governments.)

Provident Funds, the alternative to gratuity, was defined as a separate trust to be managed by a company into which both employees and the employer would put in an equal amount of money each month, and which would be administered and invested separately from the company’s finances.

Through a combination of both legal text in some provinces and precedents established through litigation in others, in general, a company offering a Provident Fund must ensure that the total amount received by an employee (the sum of both employer and employee contributions) is not less than what they would receive through gratuity.

The third option – Voluntary Pension Schemes (VPS) – was introduced in 2005 as a product and in 2008 as a legally acceptable alternative to both of these. But more on that later.

Gratuity vs Provident Funds

Each of the options laid out above have different considerations, and different reason for why employees might prefer them versus why employers might have one preference over another.

Gratuity has one big advantage from an employee perspective: A 100% of the contri butions have to come from the company, with zero out-of-pocket cost for the employee. If that was the extent of it, it would make a lot of sense to pick gratuity. There is, however, one

very big downside: If the employer claims they fired an employee for a justifiable cause, they owe that employee nothing. Sure, the employee could sue them if they think the company does not have a defensible case, but how many people in Pakistan have the means to do so, both in terms of money and time?

From an employer’s perspective, the ability to not have to pay an employee anything in the case of a dismissal makes it enormously attractive, giving them leverage over their workforce. That leverage, however, is very cost ly. Not only does the company bear 100% of the cost of the benefit, but the benefit is designed to bias the company against their longest-ten ured employees. Think about it: The longer an employee stays, the more increments they get in their salary, and the bigger the multiplier against which that last salary will be multiplied in order to determine how much you owe your employee. For example, an employee who stays 10 years is owed 10 months salary, versus one who stayed only two years and is owed just two months’ salary.

Textile companies are discovering this problem firsthand, with their most experi enced floor managers suddenly becoming very expensive in terms of gratuity liabilities, forcing companies to think about their most productive employees in a negative light.

By contrast, in a Provident Fund, an employee has to make half the contributions, which reduces their monthly take-home salary, but here is the security. Once the money – both the employee contribution and the company’s contribution – hits the Provident Fund’s bank account, that money becomes the employee’s property and there is no circumstance under which the company can legally keep the money away from the employee, though they can – and often do – deduct any amounts the employee

may owe them.

From an employee’s perspective, the one advantage it has over gratuity is that, in general, the company will likely hand over the bulk of your Provident Fund, even after some deductions and delays.

From an employer’s perspective, the Provident Fund reduces the cost of employee retirement / end-of-service benefits by about half relative to gratuity. And the fact remains that, while it is technically a separate trust, a Provident Fund is fully controlled by a com pany’s management, which means that while the employee may have some legal rights, in practice, the company has a lot of control over the money. The most sophisticated employers realise that a Provident Fund is probably enough leverage and the cost savings relative to gratuity are worth it.

A further note on Provident Fund: The reduction of take-home pay is a crucial factor in both employer and employee preference; white collar workers are much more amenable to the idea, as for blue-collar employees earning the minimum wage, the difference is extremely material to their day-to-day finances. Indeed, the lack of required employee contributions for their blue-collar workforce is the more benevolent reason that some employers give for maintaining gratuity as their retirement benefit instead of a Provident Fund.

The retirement expenses bomb

Sohow did Corporate Pakistan collectively get itself into this mess? Well, the law makes the most expensive option for employers – and one that does not yield significant returns for employees – the default: Gratuity. It costs more on an annual

CORPORATE FINANCE

basis, and it has two separate factors driving its growth rate (salary increments and lengthening average tenure of the workforce), meaning gra tuity liability often starts to grow significantly faster than revenues.

Companies could cut back on this prob lem – halving the cost and capping its growth rate – by switching to a Provident Fund, but the problem with a Provident Fund is that it is really designed for large companies in mind and is very cumbersome to administer for a small or even mid-sized company. A company has to create a separate trust, with its own set of accounts and auditors, and compliance with a relatively complex set of regulatory require ments determined not just by the Securities and Exchange Commission of Pakistan (SECP) but also the Federal Board of Revenue (FBR), and the company’s relevant provincial labour laws.

Oh, and if any of these laws and regulations are violated, the board of directors of the company are personally liable in any potential litigation.

Pakistan’s largest companies – and some of the mid-sized ones – all have a Provident Fund, but many mid-to-small-sized companies are not able to offer such a benefit owing to its regulatory complexity and thus generally stuck with the more expensive option.

Even more confusingly, while smaller companies struggle to provide even one form of retirement benefit, many large companies offer both a Provident Fund and gratuity, even though the law in every province explicitly states that only one is required.

Why do companies offer both? Because they want to encourage their employees to stay longer, and do this by offering an optional version of gratuity. This is one where they can set a minimum number of years in service at a company before an employee becomes eligible to receive gratuity.

It is this optional form of gratuity that is becoming particularly expensive for companies that wanted to encourage low employee turnover, and perhaps wanted to provide financial security for their longest-serving employees in their retirement years.

Perhaps, most baffling of all is the fact that even a Provident Fund plus gratuity combination – with all the expenses it entails for a company – would generate less cash in retirement for employees than would a VPS.

One way to reduce that regulatory burden is to simply remove the need to manage the Provident Funds internally within the company’s management and pass the burden of managing the funds directly to employees: By letting them invest their Provident Funds into Voluntary Pension Schemes (VPS), a specially designated category of mutual funds designed for long-term savings, an arrangement allowed by all relevant regulations that govern Provident Funds. In such an arrangement, a company’s Provident Fund would then concern itself simply with collecting and disbursing company and employee contributions, making its regula tory burden considerably less complex.

Why employees might prefer a VPS-invested Provident Fund

Thatbrings us to the third option we mentioned earlier. Less than 1% of Pakistan’s corporate retirement assets are invested in VPS, a spe-

cially designated kind of mutual fund. But, in our admittedly biased view, they are the best form of retirement savings from an employee’s perspective.

The VPS basically gets rid of the biggest problem with the Provident Fund. Instead of an employee, maybe getting 100% of their Provident Fund amount, they will definitely get 100% of their Provident Fund amount invested in a VPS fund. Why? Because unlike the regular Provident Fund, where money is managed –and therefore controlled – by the company, in a VPS-invested Provident Fund, both the employer and employee contributions are de posited into a mutual fund account owned and controlled 100% by the employee.

Once that deposit is made, the employer has absolutely no say over it, just like they have no say over an employee’s post-tax salary after it has been deposited into their bank account.

But the real reason why employees should love the VPS is not even the fact that they would have 100% control over the money. It is the fact that they can get to invest their money the way they want to, and in accordance with their own risk tolerance and financial needs.

From an investment perspective, the sin gle biggest flaw with a Provident Fund is that it does not take into account any differences between the needs of individual employees, but rather is designed to offer the safest investments only. That sounds prudent until you realise that most Pakistani workers are very young and should be invested in high-return assets that also have higher risks.

The median age in Pakistan is 23 years, and the median age of the Pakistani labour force is 28 years, according to Elphinstone’s analysis of data from the 2021 Labour Force Survey, published by the Pakistan Bureau of Statistics (PBS). But the investment guide lines for the Provident Fund are designed for a 55-year-old, permitting very little investment in stocks and equity-based mutual funds.

Here is how much of a difference being able to invest in stocks could make for a young

TEXTILES16

person just entering the workforce. Imagine a 22-year-old who has just graduated from college. He starts making Rs50,000 a month as his starting salary. Let us assume that his employer provides him a choice. He can either keep his money invested in a Provident Fund, which is mostly invested in government bonds, or he can invest it in a VPS, where he can go up to 100% in a stock mutual fund.

Let us also assume that the employee would have a 6% matching contribution from their company if they were to put in 6% of their salary (a modest Rs 3,000 per month for this fresh graduate). What would the difference in performance be? If we were to take the histori cal average rates of return for the stock market and government bond markets since 1999, and then apply a long-term inflation adjustment, that Rs 3,000 per month starting investment by that employee could turn into Rs 1.4 crore – in today’s terms – in a Provident Fund, by the time they retire at age 65. If they invested that same money in a 100% stock market mutual fund, they could have Rs 14.5 crore – in today’s terms – by the time they retire. More than 10 times more money – adjusted for inflation!

Just by saving 6% of their salary each month, this employee would accumulate an amount of money that could yield them a signif icant amount of wealth and financial security.

Of course, these numbers are based on historical averages which do not guarantee future returns, and are only estimates. And employees in Pakistan tend to be risk-averse, meaning very few people will actually put 100% of their money in stocks, even though it might be an appropriate set of investments for them. Still, they highlight just how big a difference a re-allocation in savings can be, and how a person pursuing an asset allocation more appropriate for their needs can accumulate real wealth for themselves.

Even if one assumes that an employee does not want to take the risk of investing in

stocks, there is one more reason to prefer a VPS: in a regular Provident Fund, generally the employer decides whether the money is invested in a conventional fund or an Islamic fund, with very few companies offering employees a real choice. In the case of a VPS-invested fund, the employee is free to choose whichever option they prefer.

Why letting go of control may be cheaper – and better – for employers

Itis clear from the above analysis that an employee would be better off at a company that offered just a VPS-invested Provident Fund rather than a Provident Fund and gratuity combination that many large com panies offer. And such a combination would clearly be cheaper for the company to offer. So why do most companies not switch over? The current system is creating a massive liability while delivering an inferior set of benefits for their employees.

So why do companies not switch over?

Save themselves some money and make their employees more money. There are three reasons.

Firstly, there is the inertia. Traditional Provident Funds and gratuity are a familiar product. There is no need to explain anything to employees since most of them already understand it. Most Pakistani companies hesitate when trying new ideas, even if it is simply investing a Provident Fund in an individualised account.

Secondly, there is the small matter of the fact that most employees do not have the capability of determining what is the appropri ate set of funds they should be investing in, and most companies do not have capable in-house help. (Elphinstone was created in large part to help solve this exact problem.)

Thirdly, and perhaps most importantly, the direct control exercised by a company over traditional Provident Funds and gratuity is insurance against a bad employee, or a valuable employee leaving on bad terms. That insurance has some value to companies, though some companies appear to be paying hundreds of thousands of rupees per employee for an imperfect form of insurance that is surely too expensive at this point.

At some point, most companies in Pakistan will realise that the current system is not working and – unlike many other types of problems in Pakistan – this is one where current law allows for a solution that can be implemented relatively painlessly. When that happens, the first movers will be at an advantage; companies that switch earlier will have both higher profitability and the ability to attract talented employees by offering them more control and more resources over their corporate benefits.

When that happens, those who wait too long because they were too used to valuing their control over their employees will find themselves with lower profits and less talented employees, permanently rendered uncompeti tive against their more nimble rivals.n

CORPORATE FINANCE

Jo Dar gaya woh mar gaya

By Profit

Ishaq Dar hit the tarmac in an oversized sports coat fashioned over a checked shirt and the most high-waisted trousers in the entire Wild West. Af ter five years of self-exile, one would have expected a welcoming party. But as he walked across the Nur Khan Airbase in Chaklala, he was met only by the Rawalpindi press corps.

There were no garlands and no sloganeering. Dar walked confidently towards the reporters, thanked them for being there, expressed his gratitude for being back home, and stated he was there to fix the economy. And the first thing he brought up was how dollar prices had already gone down.

Why Dar’s actual return was so subdued is anyone’s guess. The league would like to claim it was because Dar was here to get down to business, not gloat and bask in the victory of his return. Others would say it was because the house of the Sharifs is divided over his return — since it took the strong-arming of Mian Nawaz to dismiss Miftah Ismail, who had formidably taken on the task of correcting the economic course when others would have baulked at having to. Political realities aside, Dar’s return marks a critical juncture in Pakistan’s current protracted economic ailment. He brings with him a very different style of fiscal management than the prudent if painful ways of Miftah Ismail and Abdul Hafeez Sheikh. The oh so famous ‘Dar-nomics’ are back, and that most likely means increased government spending, lower interest rates, and Dar stepping into the ring and wrestling the dollar himself if he needs to.

What will the coming days look like? What are Dar’s aims and what are the tools at his disposal to achieve them? To understand entirely, Profit presented this brief statement and two accompanying questions to a number of economists, academics, politicians, and analysts:

Ishaq Dar has said we need to revive the economy by reducing inflation. Profit wants to investigate what tools he has at his disposal to do this, and whether it will be a good idea. We would appreciate it if you could please answer these two questions:

1. Does Dar have the means to revive the economy?

2. Is this a good goal to pursue at this time?

These were their answers

Ammar H Khan

No. There is a global recession that is looming, and we do not have the tools, nor the financial capacity to move into a high-growth phase, when there is a recession globally. The answer to whether this is a good idea or not is the same.

If I were to propose one solution that would address a lot of underlying constraints to policy issues in Pakistan, it would be lack of expertise and skill required to solve problems i.e the dearth of human capital. Having capable experts drive key portfolios is key to solving the problems that actual retard export growth amongst other key policy issues. The identification of the right problem to solve is key to meaningful reforms. And there is a key contradiction at play here. Policy measures that will win back electoral prowess may not be the key policy issues that need attention. So the right goal to pursue is one that will actual start correcting for policy fundamentals unlike short term populist measures that will only hurt us in the long run.

What tools does Ishaq Dar have at his disposal, and is now the right time to use them?

Maha Rehman

18

Nadeem-ul-Haque

I say these each and every day and the answer is that at the core of it we do not want our economy to succeed. Ishaq Dar will come in with a few agenda items but there are no written, longterm, sustainable goals that anyone can find. You can tell the press all you want about your grand plans but until you write down your policies, forward them to the public for deliberation, what does it matter? The only written economic policy directives that come in are from the IMF and that is how I see things going as well. Dar Sb will do whatever the IMF tells him to do. The rest makes no difference. Remember, the economy is massive. That is why I personally do not listen to what politicians have to say anymore because they don’t mean any of it. Economies run and thrive on change and the rot sets in when there is stagnancy. We have been in a static situation for 70 years now where the loop keeps reviving itself instead of the economy. Like clockwork we keep going to the IMF and we will keep doing so. Of course there are things in the short run that need to be controlled. The budget deficit will be a key factor in the coming days but it is the bigger structural issues that really matter.

Sakib Sherani

The economy needs to be in stabilisation mode and any attempt to “revive” it will prove to be temporary and unsustainable. The “forced” appreciation of the Rupee is a political gimmick meant to generate a feel-good factor and earn bragging points ahead of the next election. It is not only unsustainable, it is irresponsible economic policy making, similar to what we have seen in Turkey or now in the UK.

Fawad Chaudhry

Khurram Hussain

The answer is no. Ishaq Dar does not have the means to revive the economy on his own and he will need external help to pull this off. There are, of course, a few ways he can try and go about trying to do this. One of the things we might expect in the days to come are lower interest rates, and it is no secret that he wants to lower the exchange rate as well, which has already seen a dip after his return. Normally these techniques are augmented with increased government spending. We have seen it before too when governments spend more to try and revive the economy.

The other question is whether this is a good idea or not, and the answer is no. The economy is still in the middle of a very hard fought stabilisation effort and trying to revive growth right now could aggravate its very real vulnerabilities.

Huzaima Bukhari

As the Finance Minister he definitely has the means. Monetary, trade and fiscal policies are all tools that can help revive an economy if used sensibly. As for the second question, reviving the economy is the most appropri ate goal at this stage.

Muhammad Sohail

Dar has limited tools to use considering global financial markets are bad and Pakistan is in an IMF program. However, some administra tive and other measures can help.

I have spoken to a number of economists and read many opinions on this, and from what I can gauge it looks like Ishaq Dar will have a problem balancing the local and international markets. For example, as soon as he said he would try to cater to the domestic markets by saying the government would manage both the currency and interest rates our bond market fell immediately. The problem is that this time around we do not have the same amount of money that we did last time he was finance minister when he spent $7 billion to keep the rupee at 100. To get this money, Dar will need international donors to manage the financial markets as well as the sentiments of local markets.

The gap is massive. Remittances have been falling steadily and that is because overseas Pakistanis do not trust this government. At the end of the day, the main reason behind this eco nomic instability is political instability, and that is about to increase by ten-times in the coming days. And when it does we will see the problems on the economic front increase manyfold.

The not-so-micro business of

By Ahtasam Ahmad

Mainstream

and social media has recently been awash with horror stories of the predatory practices of loan sharks

– many citing stories of high-interest rates and exploitation of poor borrowers.

On the face of it, it would seem that the criticism is correct. How can charging such exuberant rates from a person in need be anything but exploitation? So Profit went out

to understand the issue and the astronomical figures involved.

The sector says there is more to that figure than just plain profit and greed.

The microfinance sector, over the past decade, has emerged as a primary lender to the financially underserved segment of society. However, as the sector grew, it came into the public eye and has since been scrutinised for practices that raise questions over its ultimate goal.

A key player in the sector is microfinance banks (MFB) which are involved in approximately 75% of the country’s microfi

nance lending. Yet, some of these banks have a questionable approach when it comes to their operations, which are led by a fragile business model.

A constant criticism of these banks has been their relatively high-interest rates. They charge anywhere from 35%- 40% a year for lending out the money.

Kabeer Naqvi, President & CEO of U Microfinance Bank, says he understands why there is criticism, but that there is a need to understand the MFB model and the costs involved. There is the cost of borrower verification, setting up branches in remote areas

20

Microfinance U Microfinance Bank’s President & CEO explains the intricacies of operating at ground zero of financial inclusion

where microfinancing is needed more, among other costs. Then there is the cost of compliance with banking and finance laws.

“This adds to the cost especially when you take into account the small loan ticket size,” Naqvi tells Profit.

The reality of the matter is that the av erage loan size of these banks stood at around Rs60,000 as per a Pakistan Credit Rating Agency (PACRA) report published in 2021. Therefore, the advantages of economies of scale are missing in the sector.

As per, “The How & the Why of Microfinance Lending Rates”, a study conducted by Pakistan Microfinance Network in 2019, operational costs comprised around 22% of the average gross loan portfolio for the overall microfinance sector including Non-Banking Microfinance Companies. Additionally, the cost of funds for these institutions is also high as they have to offer premium rates in order to compete with conventional alternatives for attracting depositors.

“Yet, with a 35%-plus interest rate, we have a margin of only around 4-5% and that is not accounting for the adverse impact of ca lamities like locusts or the recent floods which significantly increase the default ratio in the sector,” Kabeer says.

Kabeer stated, “Recently, the sector has been subjected to a lot of criticism and cited as predatory lenders. The fact is that MFBs cater to a segment of society that, for the longest of time, was left at the mercy of local loan sharks who would charge exuberant interest rates of more than 100% and had tyrannical methods of recovery.”

“The need for a bank in the segment stems from the fact that the NGO model is not scalable. As long as you are not able to raise money from the affluent to lend to the excluded segment, there is no way that eight million people could have been served.”

Are MFBs sustainable?

Notlong ago, the sector was pleading for regulatory relaxation to the SBP after the pandemic shook its foundations - and there was more criticism for the sector. With so many appar ent issues involved, the question remains if the MFB model is sustainable or viable, and how can these issues be addressed.

“When Covid hit, the most vulnerable socio-economic sector was unfortunately our borrowers. The industry’s communication with SBP, which later came out in the media, was taken out of context. The figures we presented were representative of the worstcase scenario. It was an exercise to understand the magnitude of the challenge at hand. Yet, the SBP was very accommodating as it allowed

the industry to reschedule loans and other relaxations were also provided.”

As per sources, the microfinance depart ment of SBP has asked the banks to provide for earlier rescheduled loans, specifically that portfolio for which the interest has ballooned to levels of the principal amount.

“I cannot comment on other banks, but U Bank’s rescheduled portfolio is down from Rs12 billion in 2021 to Rs3 billion up till now. Further, we are the only bank in the country, scheduled or micro, that has implemented IFRS-9 and accelerated provisioning on loans. Therefore, the SBP was able to draw comfort from our portfolio quality,” Kabeer explained.

Despite the troubles, U Bank’s head honcho presents an optimistic outlook for the industry: “As far as the sustainability of the model is concerned, the sector has ventured into high ticket value financing like a Rs3 million housing loan or a tractor loan. When the disbursements of these products will pick pace, the interest yield will inevitably reduce. If the sector maintains the right balance between micro-consumer lending, MSME lending and high-ticket lending, you would witness a turn around in the next few years.”

The case of U Bank

UBank is operating like a commer cial bank. It has invested more in securities than it has lent and it has substantial borrowings, almost five to nine times the borrowing of other MFBs in the sector. Further, the effective tax rate for the bank was around 16%, the lowest in the past five years.

Kabeer told Profit, “The reason why U Bank’s balance sheet mix looks like an anomaly in the sector is purely a strategic one. Conventional microfinance lending is an extremely risky business, and coupled with our aggressive growth strategy of expanding branch operations, we needed to hedge the risk. That is primarily what drove our investing spree.”

“Further, our effective tax rate went down as the bank had carried tax losses that we decided to realise and the fact that taxation on treasury investment is only 15% half of the corporate tax rates also explains the effective tax rate.”

U Bank, through U Paisa, has a stake in the Mobile Financial Services segment like other telco-backed banks. However, when the pandemic started, the SBP issued a circular instructing banks to abolish Inter Bank Fund Transfer charges to promote digital payments. This was one of the main earning points for Mobile Financial Service Operators. Coupled with the market opening up to FinTechs and Commercial Banks venturing into the digital banking space, existing players are now challenged for the dominance of Pakistan’s mobile

banking market.

“U Bank’s strategy for growth is a bit different. To summarise what we are trying to achieve, we need to look at where the resourc es are being invested. The bank now has six verticals; Rural Retail, Urban Retail, Islamic Banking, Corporate Finance/Investments, Cor porate & MSME and Digital Banking,” Kabeer elaborated.

“On the digital front, we are aiming to leverage our existing customer base and shift it to digital accounts completely. Our AI-en abled application UBot and banking software Temenos Infinity will help us make that shift. So essentially, whosoever opens an account at the U Bank branch will be opening a digital Level 2 account.”

“This will serve as our pathway to venture into full-fledged digital banking space without entangling ourselves in the complexi ties of a digital bank license,” he added.

As per SBP’s Strategic Plan for Islamic Banking Industry 2021-25, “The plan identifies improving liquidity management by inspiring the industry to develop innovative products to cater to unserved/underserved sectors and regions. This will also enable the industry to achieve the target of 10% and 8% share of its private sector financing to SMEs and Agricul ture, respectively by 2025.”

“Islamic Banking has a huge potential in the country as the population resonates with the idea. U Bank has also ventured into this sphere and we are expanding. In the next few months, the bank will be inaugurating around 30 Islamic Banking branches which will focus on lending rather than parking money in Sukuks.”

However, the primary driver of growth in the country’s Islamic banking segment has been Meezan Bank which is likely to take any new entrant heads on.

While the MFBs have their share of liquidity issues, some commercial banks are not that well off either. The government, in the Memorandum of Economic and Financial Policies, earlier last month, stated, “We remain closely engaged with two undercapitalised private banks and are committed to ensuring compliance with the minimum capital require ments.”

“I am very clear that MFBs need to be operated like banks rather than just loan shops. The banks must invest, lend and raise funds, and work on product innovation. We recently converted U Bank’s Tier-2 capital into Tier-1 and also issued preference shares. All this was for growth financing that is necessary to compete as a challenger retail bank, especially when the total assets are fast approaching a figure of Rs150 billion which in no way is micro and is comparable in size to some small commercial banks,” Kabeer reaffirmed. n

NATIVE CONTENT

How digitalisation kept aid coming to flood-hit Pakistanis

A digital inclusion scheme that relies on basic tech has meant that financial aid has kept coming for millions of historically disenfranchised and underbanked people

By Zarrar Sehgal

Recent flooding in Pakistan has upturned the lives of close to 70 million people, affecting 16 million families. The Secretary-General of the United Nations, who has been moni toring the relief efforts, has termed the natural disaster ‘’unnatural’’ — citing climate change as an aggravating factor in the mass-scale suffering caused.

Already struggling with high inflation and still battling the COVID-19 pandemic, the flooding has only exacerbated the challenges facing Pakistan’s very poorest people.

The crisis has further highlighted the need to deliver humanitarian aid through an efficient and transparent process, where technology can be used as an enabler to ensure implementation, distribution and, more impor tantly, utilization.

Digitalization can be an effective tool for dealing with humanitarian crises such as the one unfolding in Pakistan. Today, we have the required resources, infrastructure and technology available and in place to activate initiatives like the World Bank’s innovative “financial inclusion” scheme and Pakistan’s “Asaan Mobile Account” (AMA) Scheme, which has set up millions of Pakistanis with bank accounts, allowing them to receive emergency fundings in the ongoing flooding crisis.

The common man’s independence starts with women’s financial inclusion

Launched in Pakistan under the slogan

Aam Aadmi Ki Azaadi — Urdu for “the common man’s independence” — the AMA scheme has already onboarded over 5.5 million accounts.

Notably, 44 percent of those who have signed up for the AMA scheme in Pakistan were women, despite them making up only 18 percent of overall bank account holders.

Pakistan ranked 145th worldwide — out of 146 countries analyzed — in economic participation and opportunity in the World

Economic Forum’s Gender Gap Report 2022. When it comes to the position of women in the economy, there is much work to do be done. While it is making progress, and Pakistan is “near equal rights” when it comes to access to financial services, there remains a significant economic inclusion gap between males and females in the countries.

The AMA scheme goes some way toward rectifying this and bringing the country’s 110 million women to economic and financial equality. Research suggests that encouraging financial inclusion is an essential tool for lifting people out of poverty — and so schemes like AMA, which enfranchise women into the system, can have far-reaching and long-lasting benefits to women and wider society.

In times of crisis, as Pakistan is experiencing now, this is critically important — everyone should have the means to access emergency government funds.

Many-to-many makes everyone more secure

Criticalto ensuring that the scheme has had maximum uptake and that This has been largely possible due to the interoperable infrastruc ture where the USSD (Unstructured Supple mentary Service Data) platform — similar to SMS texting — on which AMA is built does not require internet connection or a smart phone to access financial services.

The many-to-many USSD platform is also unique in that many financial institutions as well as telecom players operate as equal actors in its infrastructure. This robust foun dation ensures that in situations of emergency relief, the distribution and allocation of capital is based on transparency and that financial aid is not siphoned off to the wrong places — or the wrong hands.

In effect, the AMA scheme allows Pakistanis or their communities — many of them women — who are either cut off from the outside world by flooding or displaced by it to access emergency funding.

In flood-ravaged Pakistan, the respond ers supporting the relief efforts can simultaneously prepare lists of effected individuals,

gathering details such as identity numbers of the impacted families, and work in coordination with the authorities managing the national response to the disaster. This ensures that all those who need emergency funding can open accounts and access it quickly.

The government can instantly and credibly disburse funds in a transparent manner with real-time visibility and accountability.

Agent interoperability also assists with the flood response and force-multiplies the benefits to those affected by flooding, allowing them to readily access multiple agents of any of the participating banks and telecommunica tion providers.

The AMA scheme also provides the government with much-needed data on the disbursement of its relief funds — and this makes it a valuable replicable model for across the developing and developed world.

A replicable model for payments

Thetransparent collection of data and wider disbursement system is a “made to order” solution for any government seeking to transfer emergency cash directly to its citizens. Money can be sent directly to the victims of natural disasters, as Pakistan has done with its flooding victims, but there are many other potential use-cases.

Payments to refugees, for example, could benefit from this model. With very little in the way of expensive hardware required on either the government or recipient end, people fleeing war-torn areas like Ukraine would be able to receive money sent either from their home or host countries. In turn, those countries sending the money receive important data on numbers of refugees.

Schemes like Pakistan’s AMA initia tive allow anyone, even the very poorest, the financially excluded and minorities to open bank accounts and, if needed, access emergen cy funding.

As the world faces down natural disasters, conflicts and other instability, simple but effective ways like this that guarantee financial inclusion will allow some of the world’s most vulnerable to weather challenging times. n

Courtesy: World Economic Forum

23

OPINION

Khurram Husain

Will Dar recognise the limits of his power?

For the past 20 years every finance minister that Pakistan has had (with the exception of Hafeez Shaikh) has pushed the economy towards a catastrophe by pumping growth using artificial means such as depressed interest rates and fixed exchange rates. In every case they all re fused to acknowledge that the means they were using to pump growth were unsustainable, and steadfastly refused to correct course, leaving it to the next government to take the painful steps required to arrest the growth momentum, deflate the deficits (fiscal and external) that their policies had given rise to, and preside over a painful adjustment that involved sharp devaluations, interest rate hikes and spikes in the prices of fuel and power. In two instances, Shaikh was brought in to clean up the mess.

Now Ishaq Dar is back as finance minister and promising more of the same. He has laid out his priorities in brief remarks given to reporters as he entered his office in Q block after taking oath, saying the country needs to see lower interest rates and lower exchange rates in an effort to revive growth and combat inflation. But every body knows that the country does not have the resources to make this happen. A country cannot lower interest rates and the exchange rate simultaneously without giving rise to inflation and drawing down its foreign exchange reserves. If reserves are already low, and inflation is already high, the resources with which to “revive the economy” are simply not there.

he writer is former editor Profit

So what exactly does Dar expect to do with these con straints? One possibility could be that he is counting on the arrival of massive international support. But so far indications are that whatever support does come may be enough to keep things on an even keel, but grossly insufficient for purposes of “reviving the economy”. Another possibility is that he will extract more resources from the economy by taking a firm line against banks, exporters and money changers, by accusing them of “manipulating the exchange rate,” but even at its best, this course of action can shore up the rupee for a brief period only. At the end of the day, if the dollars are not there the rupee will have to slide.

Lowering interest rates can help release fiscal resources, but doing so carries its own costs. Hundreds of billions of rupees can be saved on debt service payments depending on how much interest rates are cut by, making it easier for the government to reduce re liance on taxes on fuel and power to raise resources to pay its bills. But lowering interest rates can also fuel inflation, and more importantly, run afoul of the commitments given to the IMF. Already the government is struggling to get banks to participate in treasury bills auction beyond limited three-month tenors. With rate cuts it will have to strongarm the banks into participating.

There is little doubt that Dar will mount an effort to do precisely this. He will try to shut down the dollar, weigh in on the State Bank, and strongarm vested interests in the economy to keep their ambitions in check. And it will work briefly. For a while the exchange rate will be reduced, and some fiscal space may well be opened up. Rates of the Petroleum Development Levy have already been cut in defiance of the commitments given to the IMF to raise these by Rs 5 per month for the next few months. The Consumer Price Index will register a few declines, even if marginal.

But it will be impossible to run the economy like this for any meaningful length of time without giving rise to destabilising deficits all over again, something the economy cannot afford at this point in time. Dar’s brief is to keep the IMF programme on the rails, prevent a default, bring down inflation to reduce the burden of adjustment on the citizenry, while doing whatever is possible to get the wheels of the economy to start moving again. These are contradictory objectives. They will pull him in opposing directions, and persisting down this road will destabilise the economy.

The question naturally arises: Will Dar have what it takes to realise the limits of his own power and correct course in time? A billion-dollar bond is maturing in December, for example. Will he honour that com mitment and make the repayment? Or might he turn to his creditors and tell them “I have the dollars, I would rather use them to help my people instead of handing them over to you. Can we please come to an agreement about repaying this money at a later date once things have settled down a bit at home?”

Consider his own track record to search for an answer, as well as the track record of every other finance minister from the past 20 years (with the exception of Shaikh). Shaukat Aziz ran the economy into the ground

24

by artificially pumping growth through a combination of low interest rates, fixed exchange rate and high fiscal spending. Even as the current account and fiscal deficits registered blowouts through the year 2007, he stead fastly refused to slow the economy or reduce the fuel subsidy bill (at that time there was a circular debt in the fuels segment in addition to power). His own advisor – Salman Shah –went public even with the catastrophic bill mounting on fuel subsidies, warning that the new government after the elections will face a massive bill (more than Rs 700 billion, which was an even more massive amount at that time compared to today). His efforts to try and persuade his bosses, Aziz initially, and then Musharraf during the months of the interim government, were in vain. There was no polit ical appetite to take a hit by hiking fuel prices massively at a time Musharraf was looking at going into elections.

Dar himself steadfastly refused to acknowledge reality in 2017 as the pressures on the current account deficit mounted to dangerous levels. Remember his angry tirade in July of that year when the State Bank unexpectedly delivered a devaluation of the rupee to ease the pressure on the reserves? He launched an

internal inquiry into that episode and brought in a pliant governor to ensure such a thing never happens again. All through that year as the pressures on the economy mounted he refused to acknowledge them, saying the trade deficit is temporary, that growth will sort out the deficits in due course, that it is alright to bridge these deficits with short term borrowing till the whole thing autocorrects once the CPEC related investments begin commercial operations.

Of course, things did not autocorrect, and ultimately the country had to undergo another round of a painful adjustment. But by then he was out of power and could stand on the sidelines and argue that had he been finance minister, he would not have allowed things to come to this. Incidentally, all finance ministers have said this once out of power.

Asad Umar had a brief stint as finance minister, but towards the end he too was refusing to acknowledge that the economy is veering into dangerous territory and with out an IMF programme it faced a potentially catastrophic meltdown. In his last days he had begun talking about a “homegrown programme” instead of going to the IMF, even arguing that the deficits had been sorted with Saudi and Chinese support that had come in

during those days. Of course, the deficits were not sorted, only bridged temporarily, and his own attempts to try and put together a “mini budget” in January 2019 to help meet the IMF partially were reversed before they were even announced, and instead of a set of new revenue measures, what he unveiled in that “mini bud get” was a set of tax cuts and further incentives for industry. He argued at the time that this was an “economic revival package” instead of a “mini budget”.

Our own history tells us that finance ministers, including Dar, have a hard time acknowledging the limits of their power. They power ahead with relief and incentive measures at a time when they cannot afford it, when doing so imperils the economy. This powering ahead is driven either by a refusal to acknowledge the dangers, or an inability to persuade their political bosses to take the hit that will have to be taken to stabilise things. Now that he is back in power, the economy is still teetering on the edge of danger, and he is once again talking about growth and relief. Will Dar have what it takes to acknowledge when he has done all that is possible and halt before things get out of hand? That is the big question hanging over the country now. n

COMMENT

Aga Khan University Hospital and Roche Diagnostics expand their partnership to extend access to innovative and quality testing across Pakistan!

it is infectious diseases or chronic health conditions, a large part of the value of diagnostics informa tion lies in prevention, early detection and management. In vitro diagnostic (IVD) testing provides critical information from prognosis and screening to disease progression and treatment pathways, enabling healthcare providers to make the best decisions on expected courses of action — with minimized uncertainty.

For example, early and accurate diagno sis can help identify changes in the body even before the disease occurs,buying clinicians time to make optimal treatment choices for patients. Ongoing patient monitoring helps physicians measure treatment effectiveness, potentially preventing or slowing disease progression.

As a developing country with 3% of its GDP allocated for total health expenditures, Pakistan faces many hurdles to maintain a proper healthcare system with effective and efficient testing and treatment capabilities. These challenges were exacerbated by the pandemic. The fact is, laboratory investigations are essential – not just for Covid-19 – but also for monitoring, ruling in/out other concomitant infections and diseases.

However, while diagnostics is critical to stemming the economic and societal costs of illnesses, access to quality testing remains a challenge. Although the government has invested to provide primary health centers within reasonable reach of most of the population, Pakistan still ranks 154 among 195 countries in terms of accessibility and quality of healthcare.

The need of the hour is to improve the effectiveness and efficiency of our healthcare

Whethersystem so that we can deal with a larger patient load, increase testing capabilities, and have the resources to treat patients accordingly. In this regard, the Aga Khan University Hospital has partnered with Roche Diagnostics and Sysmex to improve patient access to quality diagnostics and enhance testing capacity across Pakistan.

As part of this partnership, an agreement has been signed to install a new fully Automated Laboratory system in the Main Lab and 14 outreach centers of the Aga Khan University Hospital across Pakistan.

Connected with Roche’s cobas IT infin ity solutions, these latest, state-of-the art high throughput automated systems are designed to give laboratories full and transparent control over their operational processes, whether at single or multi-site operations.

Through this strategic collaboration between the Aga Khan University Hospital, Roche Diagnostics, and Sysmex, AKUH will be able to cater to the needs and enhance the capacity of its labs, not just in the main cities, but also in the remote areas of the country.

This agreement builds on Aga Khan University Hospital’s historic collaboration with Roche Diagnostics Pakistan. It also marks a significant milestone in evolving laboratory diagnostic workflows by increas ing automation and minimizing operation intervention in clinical laboratories to reduce errors, improve efficiency and enable faster test results to the patients.

Speaking at the ceremony, Dr. Sulaiman Shahabuddin, President AKU, congratulated and lauded the efforts of all the teams involved in achieving this milestone agreement. “All of us are playing an integral part in shaping the national health system,” said Dr. Shahabuddin, adding that cross-collaboration between different stakeholders is key in scaling up and reshaping lives through the provision of quality healthcare.

Welcoming this new partnership with Roche Diagnostics and Sysmex, Shagufta Has san, CFO and VP of Finance, AKU, expressed her gratitude and thanked all the stakeholders involved for all their hard work. Highlighting the high-quality standards of the Aga Khan University Hospital and its Outreach Health Network, she said, “AKU is Pakistan’s first aca demic medical centre to receive the prestigious Joint Commission International (JCI) and College of American Pathologists CAP accreditation. I am thankful to our teams working on the front lines, and providing access to quality healthcare to millions across Pakistan.”

Recognizing the immense contribution of AKUH towards setting high quality stan dards of healthcare excellence, Abdul Qayyum, Country Manager, Roche Diagnostics Pakistan said, “Expanding access to health services is an important step towards reducing health disparities. I must commend AKUH for their unwavering commitment to improve healthcare delivery where it truly matters most. I am proud of our long association with AKUH and look forward to jointly expanding testing capabilities beyond main cities to reach more patients across Pakistan. Together, we are truly embodying our shared vision of shaping healthcare and improving patient lives.”

“Healthcare excellence works with part ners to spread innovations and build capability so that everyone has safe and high-quality health care. Together we are spreading innovations that equitably deliver care where people live and when they need it.” shared Rizwan Feroz, Director S. Ejazuddin & Co., official distributors of Sysmex in Pakistan.

This momentous partnership will go a long way in strengthening diagnostic capacity, increasing patient access to high quality laboratory tests and supporting faster, more cost-effective treatment outcomes to improve patient care across Pakistan. n

Press Release

26 PAID CONTENT

OPINION

OPINION

Femme Finance

The economy of eating right

You don’t have to be wealthy to eat healthy… it’s all about getting the right information and advice

Islightly toasted my slice of sourdough and then spread the mashed avocado that I had scooped out of the skin. It was such a lush green. Next, I placed my fried egg on top and sprinkled the entire thing with pink salt and crushed red chilli flakes. It was so pretty: golden brown, bright green and orange speckled abundantly with dark red dots. When I bit into it, my heart skipped a beat. Soft, crunchy, juicy, tangy, it tasted like heaven; so cliché I know, but I have no other words to describe the experience. Not only was it a treat for the tastebuds, it was also healthy – a rare combination.

But this single experience cost me roughly Rs 600. Even if I eat like this five days a week, I will end up spending at least Rs 12,000 a month. On breakfast. For one person.

Eating healthy is an expensive business, particularly in a country where the food is ‘rich’ even though the people are poor . If you’re going to do it, you’re going to need to think seriously about your budget and your options.

When I first bemoaned how expensive it is to eat healthy, Arooj, my friend, who is a chef, rolled her eyes. “Who asked you to pay Rs 900 for an avocado,” she asked. And I promptly named

the celebrity nutritionist/trainer that I follow on Instagram. “Unfollow her right now,” she barked. “You live in Pakistan, not America.”

If you scroll through my Insta, you will find lots of videos showing recipes for quick, easy and clean eating. I don’t cook. I almost never have. It’s not that I don’t love anyone enough to cook for them but that I hate cooking more. So when I learn a new way of making something, I teach my cook how to make it for me. It’s always clean, sugar-free and, since the last one year, gluten-free too. And damn is it expensive.

For example, paying for quinoa – a healthy protein-heavy seed alternative to starchy grains – week after week. The damn thing finishes so fast, and I need heaps to fill my stomach.

Eating healthy costs money. Lots of it. This has been my single biggest complaint over the last few years. Ok, maybe not my single biggest one.

Even though I’ve now unfollowed so many celebrity chefs and trainers and nutritionists, and I try and eat as simply as I can, I feel like I still spend too much money on my food. And this is food that is made at home.

About four months ago, I went to Imtiaz store near Nuplex in Karachi for the first time. I saw local varieties of all kinds of oats, chia seeds, flax seed powder and even gluten free atta. Every thing was cheaper than most other stores. I can’t begin to explain my excitement. I picked up a box of everything along with all my other groceries. At the counter, I looked at the tiny screen with green numbers flashing on it. With great trepidation, I should add. The bill was tabled at Rs 17,453. Ok, at least it’s not the usual Rs 254,378,909. And most of the things like atta, oil, rice, cereals and so on will last me 10 to 12 days at the very least.

Working woman. Mother. Survivor. Teri maa, bhen.

The thing is, this isn’t enough if you’re genuinely trying to eat healthy. For people like me, who’ve struggled with various illnesses, eating right is a basic requirement. This diet includes a weight-appropriate amount of protein. And here’s the rub: Pro tein is expensive if you’re eating lean chicken or meat every day, even if it’s small quantities, because not everyone can have lots of chicken and meat in a day, or even eggs. For a family of five, it can still cost near Rs 50,000 a month just for protein. That’s a startling figure, I know; but, trust me, the inflation driven math supports it. This won’t break your bank, someone recently said to me. It won’t break mine but what about the average middle class woman who wants to eat healthy? She wouldn’t be able to afford it. Adding plant-based protein sometimes is great but what if your intake isn’t enough? Like in my case. I end up supplementing with protein shakes. My favourite is Optimum Nutrition whey protein and one large container costs almost Rs 18,000. It has 40 servings, and I restrict its use to five days a week. Now you do the math.

28

My childhood friend Nazish is an Ap plied Functional Medicine Coach, Hormone Health Expert and Health Food Enthusiast. I call upon her frequently for help with my diet for my gut issues and for advice on general wellness. Is eating healthy expensive, I ask her. “It’s a huge misconception,” she responds. “You don’t need to eat anything that isn’t indigenous. Palak bhindi or palak gosht (cooked right) make for a clean, healthy meal.”

You don’t need me or a nutritionist to tell you that palak and bhindi cost a lot less than quinoa and avocados.

What is ‘clean,’ I ask. “It is a term given to anything that isn’t junk. There are lots of ways of classifying it; anything that isn’t processed or coming out of a can is clean.”

So what about meat, I persist. “Even if you’re someone who can’t afford to eat beef, fish or mutton every single day you can still be healthy. It’s absolutely ridiculous to live in Pakistan and buy avocados.” I cringe, both physically and emotionally. But she continues: “It is the most ridiculous thing you can do to yourself and to your economy.”

What she explained next is going to fundamentally change the way I look at food. She explained that, as people whose families have lived in this region for centuries, our DNA is programmed to digest specific types of food. So, while quinoa and avocados may feel great and we may thrive on them, we will not derive as much benefit from them as we will from foods that our great, great, great grandparents have traditionally grown and eaten. “The body will always thrive on indig enous foods because it is coded in our DNA, the body absorbs nutrients from such foods really well.”

Why doesn’t anyone know this, I ask Arooj, indignantly. How can people not know and not talk about something so important.

“Eat seasonal and regional,” she snaps, “I’ve always been telling you that.”

“Be in sync with your environment,” my husband chimes in from the background. I ignore him.

“We aren’t built to eat blueberries out of season and what is not grown in our environment,” adds Arooj, also ignoring him.

Ok, so then what should I eat if I’m not having quinoa? Nazish says to have whole grains and seeds such as millet. Arooj says millet too, and adds barley, and chickpeas to the list. These are more widely available, locally grown and cheap.